UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22027

FundVantage Trust

(Exact name of registrant as specified in charter)

301 Bellevue Parkway

Wilmington, DE 19809

(Address of principal executive offices) (Zip code)

Joel L. Weiss

JW Fund Management LLC

100 Springdale Rd., Suite A3-416

Cherry Hill, NJ 08003

(Name and address of agent for service)

Registrant’s telephone number, including area code: 856-528-3500

Date of fiscal year end: April 30

Date of reporting period: April 30, 2020

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Reports to Shareholders are attached herewith.

DUPONT CAPITAL EMERGING MARKETS FUND

Annual Investment Adviser’s Report

April 30, 2020

(Unaudited)

Dear Fund Shareholder,

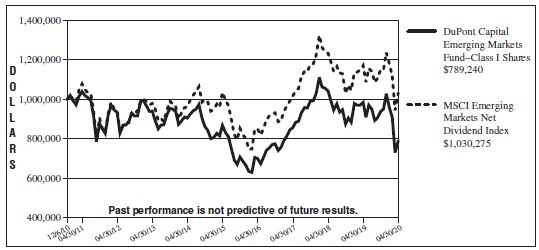

The DuPont Capital Emerging Markets Fund (the “Fund”) declined -19.80%, net of fees, for the twelve-month period ending April 30, 2020. The MSCI Emerging Markets Net Dividend Index “the Index”) fell -12.00% over the trailing twelve-months ending April 30, 2020.

After strong returns during calendar year 2019, the Fund sold off sharply due to the COVID-19 global health pandemic. The temporary closing of multiple economies across the globe caused economic activity to contract at the fastest pace on record. Federal governments and central banks reacted quickly with forceful fiscal and monetary policy. These policies were intended to supplement incomes and funnel liquidity into banks and financial markets to prevent a sharp credit contraction. So far, it would appear that these policies have been successful in thwarting a worst-case scenario from an economic perspective.

China, South Korea and Taiwan were among the better performing countries during this period. While each country was negatively impacted by the COVID-19 virus, they were reportedly able to quickly contain the outbreak and economic activity has been returning to pre-pandemic levels. Brazil, Mexico and South Africa have been among the hardest hit countries. Each of these countries was producing low levels of growth prior to the pandemic, which made the subsequent negative economic hit from the pandemic even more pernicious.

The health care and technology sectors performed the best, as their businesses have been less impacted or have benefited from the pandemic impacts. The technology sector has performed particularly well due to the widespread home-isolation measures. Energy, materials and financials were the worst performing economic sectors. Commodities fell into a tailspin due to collapsing demand and over-production, particularly in the oil industry. Financials were hurt by fears of large credit impairments stemming from the sharp decrease in employment and economic activity.

The Fund fell more than the benchmark due to its positioning in more economically sensitive companies and its value-oriented investment style, which has performed poorly due to investors current strong preference for companies with high growth rates.

From a country perspective the Fund has been negatively impacted by unfavorable stock selection in Russia, South Africa and South Korea. The underlying driver of negative relative performance within these countries were positions that have a higher degree of economic sensitivity. Russia was negatively impacted by a position in an energy company and a position in the country’s largest bank. Both companies are very profitable and extremely well capitalized, however their near-term earnings are expected to be negatively impacted by the current economic environment. Stock selection in South Korea was negatively impacted by a holding in an airline, which has since been sold, and positions in auto manufacturers. The Korean auto manufacturers held in the portfolio have experienced negative order levels, however their product portfolios are very strong and should perform well as the industry recovers. An energy producer and

1

DUPONT CAPITAL EMERGING MARKETS FUND

Annual Investment Adviser’s Report (Continued)

April 30, 2020

(Unaudited)

financial companies within South Africa detracted from relative performance due to weak energy prices and weakness in the South African economy. Partially offsetting these negative relative performance impacts were under allocations to India and Saudi Arabia. The Indian economy has struggled with problems within its financial sector and containment of COVID-19, while Saudi Arabia has been negatively impacted by falling oil prices.

The Fund’s investment strategy is to build a portfolio of companies that has better characteristics such as profitability, financial position and dividend potential than the benchmark, at a lower valuation. While characteristics such as lower debt levels aided relative performance, the Fund’s overallocation to economically sensitive areas of the market and under allocation to companies with the highest expected growth rates negatively impacted performance.

Investment Environment and Outlook

While the current outlook is uncertain due to the global health pandemic, there are signs of improvement and reasons for optimism regarding emerging market equities. Economic activity is returning to normal in countries such as China, South Korea and Taiwan that were the first to experience and exit the COVID-19 pandemic. These countries may provide helpful tools and templates for countries that are still in the midst of battling this health crisis. Many of the countries still battling the crisis are showing signs of stabilizing case loads and mortality rates. Additionally, the massive investment in health care across the globe should lead to better disease treatment and prevention not only for this pandemic but other current and future diseases.

We believe as economic activity progresses to normal levels emerging market equites and the Fund’s relative performance will improve. Valuation metrics within emerging market equites appear very attractive relative to long-term averages, which should provide a favorable starting point for returns going forward. The Fund’s valuation metrics are lower than the benchmark with better financial characteristics, and we believe this will lead to favorable performance as we exit this global health pandemic.

We appreciate your investment in the Fund and look forward to communicating with you in the future.

DuPont Capital Management Corporation

This letter is intended to assist shareholders in understanding how the Fund performed over the past twelve months from April 30, 2019 through April 30, 2020 and reflects the views of the investment adviser at the time of this writing. These views may change and do not guarantee future performance of the Fund or the markets.

2

DUPONT CAPITAL EMERGING MARKETS FUND

Annual Investment Adviser’s Report (Concluded)

April 30, 2020

(Unaudited)

Portfolio composition is subject to change. The current and future portfolio holdings of the Fund are subject to investment risks. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Mutual fund investing involves risks, including possible loss of principal. The Fund invests primarily in markets of emerging countries which are riskier than more developed markets and may be considered speculative. Emerging markets are riskier than more developed markets because they tend to develop unevenly or may never fully develop. Emerging markets are more likely to experience hyperinflation and currency valuations, which adversely affect returns to U.S. investors. In addition, many emerging markets have far lower trading volumes and less liquidity than developed markets.

Foreign securities are subject to political, social, and economic risks including instability in the country of the issuer of a security, variation in international trade patterns, the possibility of the imposition of exchange controls, expropriation, confiscatory taxation, limits on movement to currency or other assets and nationalization of assets.

3

DUPONT CAPITAL EMERGING MARKETS FUND

Annual Report

Performance Data

April 30, 2020

(Unaudited)

Comparison of Change in Value of $1,000,000 (investment minimum) Investment in the DuPont Capital Emerging

Markets Fund

Class I Shares vs MSCI Emerging Markets Net Dividend Index

| Average Annual Total Returns for the Periods Ended April 30, 2020 |

| |||||||||||||||||||

| 1 Year | 3 Year | 5 Year | Since Inception* | |||||||||||||||||

Class I Shares | -19.80 | % | -2.61 | % | -1.85 | % | -2.49 | % | ||||||||||||

MSCI Emerging Markets Net Dividend Index | -12.00 | % | 0.57 | % | -0.10 | % | 0.31 | %** | ||||||||||||

| * | The DuPont Capital Emerging Markets Fund (the “Fund”) commenced operations on December 6, 2010. |

| ** | Benchmark performance is from inception date of the Fund only and is not the inception date of the benchmark itself. |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained by calling (888) 447-0014.

As stated in the current prospectus dated September 1, 2019, the Fund’s “Total Annual Fund Operating Expenses” and “Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement” are 2.38% and 1.28%, respectively of the Fund’s average daily net assets, which may differ from the actual expenses incurred by the Fund for the period covered by this report. DuPont Capital Management Corporation (the “Adviser”) has contractually agreed to reduce its investment advisory fee and/or reimburse certain expenses of the Fund to the extent necessary

4

DUPONT CAPITAL EMERGING MARKETS FUND

Annual Report

Performance Data (Concluded)

April 30, 2020

(Unaudited)

to ensure that the Fund’s total operating expenses, excluding taxes, fees and expenses attributable to a distribution or service plan adopted by FundVantage Trust (the “Trust”), “Acquired Fund Fees and Expenses,” interest, extraordinary items, and brokerage commissions do not exceed 1.27% (on an annual basis) of the Fund’s average daily net assets (the “Expense Limitation”). The Expense Limitation will remain in place until August 31, 2020, unless the Board of Trustees (“Board of Trustees”) of the Trust approves its earlier termination. The Adviser is entitled to recover, subject to approval by the Board of Trustees, amounts reduced or reimbursed for a period of up to three (3) years from the date on which the Adviser reduced its compensation and/or assumed expenses for the Fund. The Adviser is permitted to seek reimbursement from the Fund, subject to certain limitations, for fees it waived and Fund expenses it paid to the extent the total annual fund operating expenses do not exceed the limits described above or any lesser limits in effect at the time of reimbursement. No recoupment will occur unless the Fund’s expenses are below the Expense Limitation amount. Total returns would be lower had such fees and expenses not been waived and/or reimbursed.

A 2.00% redemption fee applies to shares redeemed within 60 days of purchase. The redemption fee is not reflected in the returns shown above.

The Fund intends to evaluate performance as compared to that of the MSCI Emerging Markets Net Dividend Index. This index is a free float-adjusted market capitalization index and is designed to measure equity market performance of emerging markets. This index is net total return which reinvests dividends after the deduction of withholding taxes. The returns for this index do not include any transaction costs, management fees or other costs. It is impossible to invest directly in an index.

5

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Annual Investment Adviser’s Report

April 30, 2020

(Unaudited)

Dear Fund Shareholder,

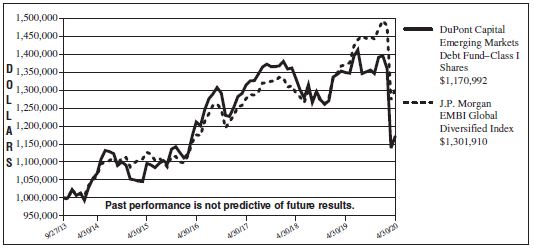

The DuPont Capital Emerging Markets Debt Fund (the “Fund”) returned -13.14%, net of fees, for the twelve-month period ending April 30, 2020. The J.P. Morgan Emerging Markets Bond Index Global Diversified Index (“the Index”) returned -4.97% over the trailing twelve-months ending April 30, 2020.

The U.S. economy was very healthy and grew moderately for the first ten months of the period until the global spread of COVID-19 decimated global economies in March and April. The rapidly spreading COVID-19 virus resulted in unprecedented lockdowns in most countries which essentially stopped many sectors of the global economy. Equity markets saw massive declines and gave up the strong gains of 2019. Yields on U.S. Treasuries moved to all-time lows and Central Banks across the globe moved quickly and aggressively to provide liquidity. The Federal Reserve cut rates by 150 bps points in less than two weeks to take the Funds Rate back to 0%. They also restarted Quantitative Easing by purchasing bonds, but this time also included investment grade corporate bonds. U.S. interest rates declined significantly over the twelve-month reporting period. The two-year Treasury declined by 207 basis points and closed at 0.20%, while the ten-year treasury fell 187 basis bps to 0.64%.

Emerging markets debt (“EMD”) performed very well in 2019 but experienced a sudden and massive decline in March due to the virus. The Fund’s index was down -13.85% just in March and returned -4.97% for the entire twelve-month period. EMD was supported by the monetary and fiscal stimulus but could not overcome the significant decline in global economic activity due to the virus. Oil prices were very volatile and collapsed in the 1st quarter of 2020. The decline was caused by a combination of much lower demand due to the weaker economy and a price war between Saudi Arabia and Russia. Over the last twelve months, the price per barrel fell from $63.9 to $18.8, a remarkable 70% decline. Overall commodity prices were much lower for the period. Local Currency EMD performed better than Hard Currency EMD, but both segments had negative returns.

Within U.S. Dollar EMD, investment grade sovereigns significantly outperformed lower quality sovereigns, partly due to the rise in Treasury prices. The best performing countries within US Dollar EMD included Russia, Qatar, Kuwait and Uruguay with returns above +10%. Lebanon, Ecuador, Argentina and Venezuela were the worst performing countries over the past twelve months which all experienced significant problems and will eventually restructure their debts. Europe was the strongest performing region. Spreads in EMD widened by 266 basis points during the last twelve months to 610 basis points over Treasuries, while the yield of the Index rose by 79 basis points and closed at 6.80%. The much wider spreads were partly offset by the much lower U.S. Treasury yields.

With regard to the performance of the Fund, the main negative drivers were overweights and positioning in Argentina, Venezuela and Lebanon. Our underweight to several higher quality countries also detracted from performance as these countries held much better when the market declined. In addition, our local

6

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Annual Investment Adviser’s Report (Continued)

April 30, 2020

(Unaudited)

currency position in Brazil hurt returns. An overweight and positioning in Brazil and Israel added to returns as did local currency positions in Poland and Russia.

Investment Environment and Outlook

EMD performed well in 2019, but suffered greatly in 2020, mostly due to COVID-19. Over the last twelve months, spreads have widened by 266 basis points while yields rose by 79 basis points to 6.80%. At current levels, we feel that valuations are very attractive, but the coronavirus creates significant uncertainty that can’t be measured. Economic growth has been decimated across the world and will remain weak for at least the next several months. Central Banks have responded in unprecedented ways with the Federal Reserve cutting rates back to 0% and also by providing a massive injection of liquidity. The U.S. government has also stepped in to provide the largest stimulus plan in history, estimated at over $2 trillion. We believe that EMD will recover and provide strong returns, but the timing is uncertain due to the impact of the virus, the volatility of oil prices and country specific events. We are gradually adding positions to the portfolio, mostly in US dollar sovereigns in higher quality countries in which we were underweight. Historically, our portfolios often lag the benchmark in the beginning stage of a recovery phase because higher quality credits (in which we are underweight) tend to rally first. As the rally has taken hold and has become more sustainable, the more attractive lower quality credits (that we are overweight) have risen strongly. This happened in the financial crisis of 2008/2009 and we are hopeful this situation will occur in 2020/2021.

Heading into May, the primary overweight exposures in the Fund include Brazil, Ukraine, Egypt, Argentina and Israel. In local currency bonds, the main positions are in Mexico, Poland and Brazil and the Fund’s total local currency exposure is close to 12%. The Fund is underweight several higher quality countries that the investment team believes are overvalued including Qatar, Panama, UAE, and the Philippines. The Fund has a large yield advantage when compared to the benchmark and a shorter duration.1

| 1 | Duration: Duration, expressed in years, is a measure of the average time-to-maturity of a bond. It is calculated as the weighted average of the time-to-maturity of its cashflows, weighted by the cashflows’ present value. Duration is also a useful measure of the sensitivity of a bond’s price to interest rate movements. As an example, if interest rates rise (fall) by 1%, a bond with a duration of 2 years will experience an approximate price decline (increase) of 2%, and a bond with a duration of 3 years will experience an approximate price decline (increase) of 3%. |

7

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Annual Investment Adviser’s Report (Concluded)

April 30, 2020

(Unaudited)

We appreciate your investment in the Fund and look forward to communicating with you in the future.

DuPont Capital Management Corporation

This letter is intended to assist shareholders in understanding how the Fund performed over the past twelve months from April 30, 2019 through April 30, 2020 and reflects the views of the investment adviser at the time of this writing. These views may change and do not guarantee future performance of the Fund or the markets.

Portfolio composition is subject to change. The current and future portfolio holdings of the Fund are subject to investment risks. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Mutual fund investing involves risks, including possible loss of principal. The Fund invests primarily in markets of emerging countries which are riskier than more developed markets and may be considered speculative. Emerging markets are riskier than more developed markets because they tend to develop unevenly or may never fully develop. Emerging markets are more likely to experience hyperinflation and currency valuations, which adversely affect returns to U.S. investors. In addition, many emerging markets have far lower trading volumes and less liquidity than developed markets. The Fund is non-diversified, which means that a large portion of the Fund’s assets may be invested in one or few companies or sectors. The Fund could fluctuate in value more than a diversified fund. Investing in foreign securities entails special risks, such as fluctuations in currency exchange rates and possible lax regulation of securities markets and accounting practices.

Foreign securities are subject to political, social, and economic risks including instability in the country of the issuer of a security, variation in international trade patterns, the possibility of the imposition of exchange controls, expropriation, confiscatory taxation, limits on movement to currency or other assets and nationalization of assets. The value of debt securities generally falls when interest rates rise. The Fund may invest without limit in below-investment grade debt securities commonly called “high yield” securities or “junk bonds.” Such securities may have greater default risk, less liquidity, and greater price volatility than investment-grade bonds.

8

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Annual Report

Performance Data

April 30, 2020

(Unaudited)

Comparison of Change in Value of $1,000,000 (investment minimum) Investment in the DuPont Capital Emerging

Markets Debt Fund

Class I Shares vs J.P. Morgan EMBI Global Diversified Index

| Average Annual Total Returns for the Periods Ended April 30, 2020 |

| |||||||||||||||||||

| 1 Year | 3 Year | 5 Year | Since Inception* | |||||||||||||||||

Class I Shares | -13.14 | % | -3.76 | % | 1.35 | % | 2.42 | % | ||||||||||||

J.P. Morgan EMBI Global Diversified Index | -4.97 | % | 0.67 | % | 2.94 | % | 4.10 | %** | ||||||||||||

| * | The DuPont Capital Emerging Markets Debt Fund (the “Fund”) commenced operations on September 27, 2013. |

| ** | Benchmark performance is from inception date of the Fund only and is not the inception date of the benchmark itself. |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained by calling (888) 447-0014.

As stated in the current prospectus dated September 1, 2019, the Fund’s “Total Annual Fund Operating Expenses” and “Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement” are 3.92% and 0.89%, respectively, of the Fund’s average daily net assets, which may differ from the actual expenses incurred by the Fund for the period covered by this report. DuPont Capital Management Corporation (the “Adviser”) has contractually agreed to reduce its investment advisory fee and/or reimburse certain expenses of the Fund to the extent necessary

9

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Annual Report

Performance Data (Concluded)

April 30, 2020

(Unaudited)

to ensure that the Fund’s total operating expenses, excluding taxes, fees and expenses attributable to a distribution or service plan adopted by FundVantage Trust (the “Trust”), “Acquired Fund Fees and Expenses,” interest, extraordinary items, and brokerage commissions do not exceed 0.89% (on an annual basis) of the Fund’s average daily net assets (the “Expense Limitation”). The Expense Limitation will remain in place until August 31, 2020, unless the Board of Trustees (“Board of Trustees”) of the Trust approves its earlier termination. The Adviser is entitled to recover, subject to approval by the Board of Trustees, amounts reduced or reimbursed for a period of up to three (3) years from the date on which the Adviser reduced its compensation and/or assumed expenses for the Fund. The Adviser is permitted to seek reimbursement from the Fund, subject to certain limitations, for fees it waived and Fund expenses it paid to the extent the total annual fund operating expenses do not exceed the limits described above or any lesser limits in effect at the time of reimbursement. No recoupment will occur unless the Fund’s expenses are below the Expense Limitation amount. Total returns would be lower had such fees and expenses not been waived and/or reimbursed.

A 2.00% redemption fee applies to shares redeemed within 60 days of purchase. The redemption fee is not reflected in the returns shown above.

The Fund intends to evaluate performance as compared to that of the J.P. Morgan Emerging Markets Bond Index Global Diversified (EMBI Global Diversified) Index. This index tracks the traded market for U.S.-dollar-denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities and includes Brady bonds, loans, Eurobonds and external debt instruments. It limits the weights of those Index countries with larger debt stock by only including specified portions of these countries eligible current face amounts of debt outstanding. The returns for the index do not include any transaction costs, management fees or other costs. It is impossible to invest directly in an index.

10

DUPONT CAPITAL FUNDS

Fund Expense Disclosure

April 30, 2020

(Unaudited)

As a shareholder of the Fund(s), you incur two types of costs: (1) transaction costs, including redemption fees; and (2) ongoing costs, including management fees and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

These examples are based on an investment of $1,000 invested at the beginning of the period from November 1, 2019 through April 30, 2020 and held for the entire period.

Actual Expenses

The first line for each Fund in the accompanying table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each Fund in the accompanying table provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not your Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the accompanying table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the second line of the accompanying table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

11

DUPONT CAPITAL FUNDS

Fund Expense Disclosure (Concluded)

April 30, 2020

(Unaudited)

| DuPont Capital Emerging Markets Fund | |||||||||||||||

| Beginning Account Value November 1, 2019 | Ending Account Value April 30, 2020 | Expenses Paid During Period* | |||||||||||||

Class I | |||||||||||||||

Actual | $ | 1,000.00 | $ | 840.90 | $ | 5.81 | |||||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.55 | 6.37 | ||||||||||||

| DuPont Capital Emerging Markets Debt Fund | |||||||||||||||

| Beginning Account Value November 1, 2019 | Ending Account Value April 30, 2020 | Expenses Paid During Period** | |||||||||||||

Class I | |||||||||||||||

Actual | $ | 1,000.00 | $ | 864.20 | $ | 4.13 | |||||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,020.44 | 4.47 | ||||||||||||

| * | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2020 of 1.27% for Class I Shares of the DuPont Capital Emerging Markets Fund, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (182), then divided by 366 to reflect the period. The DuPont Capital Emerging Markets Fund’s ending account value on the first line in the table is based on the actual total return for the six-month period ended April 30, 2020 for the Fund of (15.91)%. |

| ** | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2020 of 0.89% for Class I Shares of the DuPont Capital Emerging Markets Debt Fund, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (182), then divided by 366 to reflect the period. The DuPont Capital Emerging Markets Debt Fund’s ending account value on the first line in the table is based on the actual total return for the six-month period ended April 30, 2020 for the Fund of (13.58)%. |

12

DUPONT CAPITAL EMERGING MARKETS FUND

Portfolio Holdings Summary Table

April 30, 2020

(Unaudited)

The following table presents a summary by industry of the portfolio holdings of the Fund:

| % of Net Assets | Value | |||||||||

INDUSTRY CATEGORIES: | ||||||||||

Commercial Banks | 17.2 | % | $ | 3,724,282 | ||||||

Internet & Catalog Retail | 11.9 | 2,574,659 | ||||||||

Semiconductors & Semiconductor Equipment | 7.4 | 1,594,883 | ||||||||

Oil, Gas & Consumable Fuels | 6.6 | 1,415,724 | ||||||||

Technology Hardware, Storage & Peripherals | 6.2 | 1,335,005 | ||||||||

Interactive Media & Services | 6.0 | 1,298,010 | ||||||||

Insurance | 4.2 | 915,136 | ||||||||

Automobiles | 3.0 | 656,428 | ||||||||

Food Products | 2.5 | 546,530 | ||||||||

Construction & Engineering | 2.5 | 532,991 | ||||||||

Electronic Equipment, Instruments & Components | 2.4 | 519,555 | ||||||||

Machinery | 2.4 | 519,488 | ||||||||

Real Estate Management & Development | 2.3 | 502,377 | ||||||||

IT Services | 2.1 | 443,030 | ||||||||

Household Durables | 1.9 | 407,606 | ||||||||

Metals & Mining | 1.8 | 392,709 | ||||||||

Food & Staples Retailing | 1.8 | 391,304 | ||||||||

Building Products | 1.8 | 391,201 | ||||||||

Media | 1.7 | 363,477 | ||||||||

Specialty Retail | 1.6 | 336,934 | ||||||||

Auto Components | 1.4 | 299,161 | ||||||||

Pharmaceuticals | 1.2 | 254,332 | ||||||||

Wireless Telecommunication Services | 1.2 | 247,918 | ||||||||

Air Freight & Logistics | 0.9 | 204,974 | ||||||||

Industrial Conglomerates | 0.9 | 198,537 | ||||||||

Beverages | 0.7 | 151,073 | ||||||||

Entertainment | 0.5 | 110,025 | ||||||||

Consumer Finance | 0.5 | 96,810 | ||||||||

Chemicals | 0.3 | 72,029 | ||||||||

Personal Products | 0.3 | 70,212 | ||||||||

Diversified Consumer Services | 0.3 | 61,736 | ||||||||

Thrifts & Mortgage Finance | 0.2 | 32,828 | ||||||||

Hotels, Restaurants & Leisure | 0.1 | 18,579 | ||||||||

Exchange Traded Fund | 2.9 | 622,880 | ||||||||

Other Assets in Excess of Liabilities | 1.3 | 289,638 | ||||||||

|

|

|

| |||||||

NET ASSETS | 100.0 | % | $ | 21,592,061 | ||||||

|

|

|

| |||||||

Portfolio holdings are subject to change at any time.

The accompanying notes are an integral part of the financial statements.

13

DUPONT CAPITAL EMERGING MARKETS FUND

Portfolio of Investments

April 30, 2020

| Number of Shares | Value | |||||||

COMMON STOCKS — 93.3% |

| |||||||

Brazil — 2.2% | ||||||||

Banco do Brasil SA* | 53,900 | $ | 280,805 | |||||

Cia Brasileira de Distribuicao | 15,400 | 189,318 | ||||||

|

| |||||||

| 470,123 | ||||||||

|

| |||||||

China — 38.2% | ||||||||

Alibaba Group Holding, Ltd., SP ADR* | 8,426 | 1,707,697 | ||||||

China Communications Services Corp., Ltd., Class H | 590,000 | 420,560 | ||||||

China Construction Bank Corp., Class H | 836,000 | 671,027 | ||||||

China Lesso Group Holdings, Ltd. | 273,000 | 391,201 | ||||||

China Maple Leaf Educational Systems, Ltd. | 210,000 | 61,736 | ||||||

China Oriental Group Co., Ltd. | 638,000 | 192,814 | ||||||

China Overseas Land & Investment, Ltd. | 136,000 | 502,377 | ||||||

CNOOC, Ltd. | 314,000 | 347,165 | ||||||

Dali Foods Group Co., Ltd.(a) | 293,500 | 181,319 | ||||||

Dongfeng Motor Group Co., Ltd., Class H | 322,000 | 213,570 | ||||||

Haier Electronics Group Co., Ltd. | 148,000 | 407,606 | ||||||

Haitian International Holdings, Ltd. | 116,001 | 205,246 | ||||||

Industrial & Commercial Bank of China, Ltd., Class H | 236,000 | 158,240 | ||||||

JOYY, Inc., ADR* | 3,022 | 184,221 | ||||||

| Number of Shares | Value | |||||||

COMMON STOCKS — (Continued) |

| |||||||

China — (Continued) | ||||||||

LexinFintech Holdings, Ltd., ADR* | 11,484 | $ | 96,810 | |||||

Livzon Pharmaceutical Group, Inc., Class H | 57,070 | 254,332 | ||||||

Lonking Holdings, Ltd. | 515,000 | 174,491 | ||||||

PICC Property & Casualty Co., Ltd., Class H | 341,000 | 326,319 | ||||||

Ping An Insurance Group Co., of China Ltd., Class H | 46,000 | 468,108 | ||||||

Sinopec Engineering Group Co., Ltd., Class H | 234,500 | 112,431 | ||||||

Sinotrans, Ltd., Class H | 845,000 | 204,974 | ||||||

Tencent Holdings, Ltd. | 18,400 | 967,278 | ||||||

|

| |||||||

| 8,249,522 | ||||||||

|

| |||||||

Czech Republic — 0.8% | ||||||||

Komercni banka AS* | 7,937 | 168,064 | ||||||

|

| |||||||

Greece — 1.2% | ||||||||

JUMBO SA | 16,171 | 253,076 | ||||||

|

| |||||||

India — 5.4% | ||||||||

HCL Technologies, Ltd. | 61,773 | 443,030 | ||||||

ICICI Bank, Ltd., SP ADR | 15,798 | 154,188 | ||||||

Indiabulls Housing Finance, Ltd. | 18,852 | 32,828 | ||||||

Just Dial, Ltd.* | 27,308 | 146,511 | ||||||

Reliance Industries, Ltd., SP | 10,343 | 392,481 | ||||||

|

| |||||||

| 1,169,038 | ||||||||

|

| |||||||

Indonesia — 1.4% | ||||||||

Bank Rakyat Indonesia Persero Tbk PT | 634,484 | 115,405 | ||||||

The accompanying notes are an integral part of the financial statements.

14

DUPONT CAPITAL EMERGING MARKETS FUND

Portfolio of Investments (Continued)

April 30, 2020

| Number of Shares | Value | |||||||

COMMON STOCKS — (Continued) |

| |||||||

Indonesia — (Continued) | ||||||||

Media Nusantara Citra Tbk PT | 3,101,500 | $ | 189,143 | |||||

|

| |||||||

| 304,548 | ||||||||

|

| |||||||

Kazakhstan — 0.9% | ||||||||

Halyk Savings Bank of Kazakhstan JSC, GDR | 21,126 | 190,176 | ||||||

|

| |||||||

Malaysia — 0.9% | ||||||||

Bermaz Auto Bhd | 266,200 | 83,858 | ||||||

Malayan Banking Bhd | 58,860 | 103,303 | ||||||

|

| |||||||

| 187,161 | ||||||||

|

| |||||||

Mexico — 1.7% | ||||||||

Grupo Financiero Banorte SAB de CV, Class O | 59,100 | 161,795 | ||||||

Ternium SA, SP ADR | 14,709 | 199,895 | ||||||

|

| |||||||

| 361,690 | ||||||||

|

| |||||||

Russia — 3.9% | ||||||||

Ros Agro PLC, GDR | 16,726 | 141,095 | ||||||

Sberbank of Russia PJSC, SP ADR | 41,820 | 443,980 | ||||||

Tatneft PJSC, SP ADR | 5,952 | 265,153 | ||||||

|

| |||||||

| 850,228 | ||||||||

|

| |||||||

Saudi Arabia — 1.6% | ||||||||

Saudi British Bank (The) | 17,738 | 115,866 | ||||||

Saudia Dairy & Foodstuff Co. | 5,600 | 224,116 | ||||||

|

| |||||||

| 339,982 | ||||||||

|

| |||||||

South Africa — 7.7% | ||||||||

Absa Group, Ltd. | 25,401 | 125,358 | ||||||

Bid Corp., Ltd. | 15,499 | 201,986 | ||||||

MultiChoice Group, Ltd.* | 37,196 | 174,334 | ||||||

Naspers, Ltd., N Shares | 5,570 | 866,962 | ||||||

Nedbank Group, Ltd. | 14,162 | 82,330 | ||||||

| Number of Shares | Value | |||||||

COMMON STOCKS — (Continued) |

| |||||||

South Africa — (Continued) |

| |||||||

Old Mutual, Ltd. | 166,288 | $ | 120,709 | |||||

Sasol, Ltd.* | 15,177 | 72,029 | ||||||

Tsogo Sun Gaming, Ltd. | 131,399 | 18,579 | ||||||

|

| |||||||

| 1,662,287 | ||||||||

|

| |||||||

South Korea — 11.6% | ||||||||

Hyundai Mipo Dockyard Co., Ltd. | 5,524 | 139,751 | ||||||

Hyundai Mobis Co., Ltd. | 2,116 | 299,161 | ||||||

Hyundai Motor Co. | 3,200 | 247,336 | ||||||

Samsung Electronics Co., Ltd. | 32,468 | 1,335,005 | ||||||

Shinhan Financial Group Co., Ltd. | 13,696 | 347,229 | ||||||

SK Innovation Co., Ltd. | 1,858 | 149,884 | ||||||

|

| |||||||

| 2,518,366 | ||||||||

|

| |||||||

Taiwan — 11.9% | ||||||||

CTBC Financial Holding Co., Ltd. | 578,918 | 385,787 | ||||||

Hon Hai Precision Industry Co., Ltd. | 202,164 | 519,555 | ||||||

Novatek Microelectronics Corp. | 53,692 | 333,908 | ||||||

Taiwan Semiconductor Manufacturing Co., Ltd. | 125,000 | 1,260,975 | ||||||

TCI Co., Ltd. | 9,191 | 70,212 | ||||||

|

| |||||||

| 2,570,437 | ||||||||

|

| |||||||

Thailand — 0.9% | ||||||||

Kasikornbank PCL, NVDR | 34,071 | 89,324 | ||||||

Major Cineplex Group PCL | 245,900 | 110,025 | ||||||

|

| |||||||

| 199,349 | ||||||||

|

| |||||||

Turkey — 3.0% | ||||||||

KOC Holding AS | 90,481 | 198,537 | ||||||

The accompanying notes are an integral part of the financial statements.

15

DUPONT CAPITAL EMERGING MARKETS FUND

Portfolio of Investments (Concluded)

April 30, 2020

| Number of Shares | Value | |||||||

COMMON STOCKS — (Continued) |

| |||||||

Turkey — (Continued) | ||||||||

Tofas Turk Otomobil Fabrikasi AS | 61,190 | $ | 195,522 | |||||

Turkcell Iletisim Hizmetleri AS | 124,446 | 247,918 | ||||||

|

| |||||||

| 641,977 | ||||||||

|

| |||||||

TOTAL COMMON STOCKS (Cost $21,054,232) |

| 20,136,024 | ||||||

|

| |||||||

PREFERRED STOCKS — 2.5% |

| |||||||

Brazil — 1.8% | ||||||||

Itau Unibanco Holding SA | 31,163 | 131,405 | ||||||

Petroleo Brasileiro SA | 78,600 | 261,041 | ||||||

|

| |||||||

| 392,446 | ||||||||

|

| |||||||

Chile — 0.7% | ||||||||

Embotelladora Andina SA, Class B | 63,255 | 151,073 | ||||||

|

| |||||||

TOTAL PREFERRED STOCKS (Cost $651,604) |

| 543,519 | ||||||

|

| |||||||

EXCHANGE TRADED FUND — 2.9% |

| |||||||

iShares MSCI Emerging Market Index Fund | 17,000 | 622,880 | ||||||

|

| |||||||

TOTAL EXCHANGE TRADED FUND (Cost $620,939) |

| 622,880 | ||||||

|

| |||||||

| Value | ||||

TOTAL INVESTMENTS - 98.7% | $ | 21,302,423 | ||

OTHER ASSETS IN EXCESS OF | 289,638 | |||

|

| |||

NET ASSETS - 100.0% | $ | 21,592,061 | ||

|

| |||

| * | Non-income producing. |

| (a) | Securities exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities were purchased in accordance with the guidelines approved by the Fund’s Board of Trustees and may be resold, in transactions exempt from registration, to qualified institutional buyers. At April 30, 2020, these securities amounted to $573,800 or 2.66% of net assets. These securities have been determined by the Adviser to be liquid securities. |

ADR | American Depository Receipt | |

GDR | Global Depository Receipt | |

JSC | Joint Stock Company | |

NVDR | Non-voting Depository Receipt | |

PCL | Public Company Limited | |

PJSC | Public Joint Stock Company | |

PLC | Public Limited Company | |

SP ADR | Sponsored American Depository Receipt | |

SP GDR | Sponsored Global Depository Receipt |

The accompanying notes are an integral part of the financial statements.

16

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Portfolio Holdings Summary Table

April 30, 2020

(Unaudited)

The following table presents a summary by security type of the portfolio holdings of the Fund:

| % of Net Assets | Value | |||||||||

SECURITY TYPE: | ||||||||||

Foreign Government Bonds and Notes | 66.4 | % | $ | 4,173,286 | ||||||

Corporate Bonds and Notes | 17.9 | 1,124,305 | ||||||||

U.S. Treasury Obligations | 7.2 | 450,188 | ||||||||

Common Stocks | 0.0 | 88 | ||||||||

Other Assets in Excess of Liabilities | 8.5 | 531,856 | ||||||||

|

|

|

| |||||||

NET ASSETS | 100.0 | % | $ | 6,279,723 | ||||||

|

|

|

| |||||||

Portfolio holdings are subject to change at any time.

The accompanying notes are an integral part of the financial statements.

17

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Portfolio of Investments

April 30, 2020

Par* Value | Value | |||||||

CORPORATE BONDS AND NOTES — 17.9% |

| |||||||

Austria — 0.0% | ||||||||

OGX Austria GmbH | $ 200,000 | $ | 2 | |||||

|

| |||||||

China — 4.8% |

| |||||||

China Evergrande Group | 250,000 | 197,290 | ||||||

Sinochem Overseas Capital Co. Ltd. | 100,000 | 101,033 | ||||||

|

| |||||||

| 298,323 | ||||||||

|

| |||||||

Israel — 3.6% |

| |||||||

Israel Electric Corp., Ltd. | 200,000 | 224,024 | ||||||

|

| |||||||

Netherlands — 3.4% |

| |||||||

Petrobras Global Finance BV | 100,000 | 105,450 | ||||||

Petrobras Global Finance BV | 100,000 | 98,500 | ||||||

Petrobras Global Finance BV | 10,000 | 9,350 | ||||||

|

| |||||||

| 213,300 | ||||||||

|

| |||||||

Russia — 5.7% |

| |||||||

Gazprom PJSC Via Gaz Capital SA | 150,000 | 220,847 | ||||||

Russian Railways Via RZD Capital PLC | RUB | 10,000,000 | 139,684 | |||||

|

| |||||||

| 360,531 | ||||||||

|

| |||||||

Venezuela — 0.4% |

| |||||||

Petroleos de Venezuela SA | 300,000 | 11,250 | ||||||

Petroleos de Venezuela SA | 100,000 | 3,750 | ||||||

Par* Value | Value | |||||||

CORPORATE BONDS AND NOTES — (Continued) |

| |||||||

Venezuela — (Continued) |

| |||||||

Petroleos de Venezuela SA | $ 350,000 | $ | 13,125 | |||||

|

| |||||||

| 28,125 | ||||||||

|

| |||||||

TOTAL CORPORATE BONDS AND NOTES | 1,124,305 | |||||||

|

| |||||||

FOREIGN GOVERNMENT BONDS AND NOTES — 66.4% |

| |||||||

Argentina — 2.9% |

| |||||||

Argentine Republic Government International Bond 6.88%, 01/26/2027 | 460,000 | 115,005 | ||||||

Argentine Republic Government International Bond 5.88%, 01/11/2028 | 70,000 | 17,606 | ||||||

Argentine Republic Government International Bond 7.63%, 04/22/2046 | 190,000 | 46,552 | ||||||

|

| |||||||

| 179,163 | ||||||||

|

| |||||||

Brazil — 4.0% |

| |||||||

Brazil Notas Do Tesouro Nacional Serie F 10.00%, 01/01/2021 | BRL | 1,000,000 | 192,220 | |||||

Brazil Notas Do Tesouro Nacional Serie F 10.00%, 01/01/2027 | BRL | 290,000 | 60,960 | |||||

|

| |||||||

| 253,180 | ||||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

18

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Portfolio of Investments (Continued)

April 30, 2020

Par* Value | Value | |||||||

FOREIGN GOVERNMENT BONDS AND NOTES — (Continued) |

| |||||||

Costa Rica — 2.8% | ||||||||

Costa Rica Government International Bond 4.25%, 01/26/2023 | $ 200,000 | $ | 177,500 | |||||

|

| |||||||

Croatia — 3.5% | ||||||||

Croatia Government International Bond 6.00%, 01/26/2024 | 200,000 | 222,623 | ||||||

|

| |||||||

Dominican Republic — 2.9% |

| |||||||

Dominican Republic International Bond 7.45%, 04/30/2044 | 200,000 | 181,500 | ||||||

|

| |||||||

Ecuador — 0.9% |

| |||||||

Ecuador Government International Bond 7.88%, 01/23/2028 | 200,000 | 56,752 | ||||||

|

| |||||||

Egypt — 7.7% | ||||||||

Egypt Government International Bond 6.88%, 04/30/2040 | 100,000 | 82,752 | ||||||

Egypt Government International Bond 8.70%, 03/01/2049(c) | 250,000 | 224,048 | ||||||

Egypt Government International Bond 8.70%, 03/01/2049 | 200,000 | 179,239 | ||||||

|

| |||||||

| 486,039 | ||||||||

|

| |||||||

Hungary — 1.3% | ||||||||

Hungary Government International Bond 7.63%, 03/29/2041 | 50,000 | 80,000 | ||||||

|

| |||||||

Par* Value | Value | |||||||

FOREIGN GOVERNMENT BONDS AND NOTES — (Continued) |

| |||||||

Jordan — 3.0% |

| |||||||

Jordan Government International Bond 7.38%, 10/10/2047 | $ 200,000 | $ | 184,996 | |||||

|

| |||||||

Lebanon — 0.7% |

| |||||||

Lebanon Government International Bond 6.38%, 03/09/2020(b) | 50,000 | 7,875 | ||||||

Lebanon Government International Bond 6.00%, 01/27/2023(b) | 70,000 | 11,025 | ||||||

Lebanon Government International Bond 6.20%, 02/26/2025(b) | 175,000 | 27,562 | ||||||

|

| |||||||

| 46,462 | ||||||||

|

| |||||||

Malaysia — 0.6% |

| |||||||

Malaysia Government Bond 3.89%, 08/15/2029 | MYR | 150,000 | 37,735 | |||||

|

| |||||||

Mexico — 9.2% |

| |||||||

Mexican Bonos 10.00%, 12/05/2024 | MXN | 1,200,000 | 58,685 | |||||

Mexican Bonos 8.50%, 05/31/2029 | MXN | 500,000 | 23,420 | |||||

Mexican Bonos 10.00%, 11/20/2036 | MXN | 1,000,000 | 51,975 | |||||

Petroleos Mexicanos 6.50%, 06/02/2041 | 125,000 | 83,594 | ||||||

Petroleos Mexicanos 5.50%, 06/27/2044 | 200,000 | 128,500 | ||||||

Petroleos Mexicanos 5.63%, 01/23/2046 | 50,000 | 32,500 | ||||||

Petroleos Mexicanos 6.75%, 09/21/2047 | 25,000 | 17,187 | ||||||

The accompanying notes are an integral part of the financial statements.

19

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Portfolio of Investments (Continued)

April 30, 2020

Par* Value | Value | |||||||

FOREIGN GOVERNMENT BONDS AND NOTES — (Continued) |

| |||||||

Mexico — (Continued) |

| |||||||

Petroleos Mexicanos 7.69%, 01/23/2050 | $ | 250,000 | $ | 183,750 | ||||

|

| |||||||

| 579,611 | ||||||||

|

| |||||||

Morocco — 3.3% | ||||||||

Morocco Government International Bond 4.25%, 12/11/2022(c) | 200,000 | 207,899 | ||||||

|

| |||||||

Nigeria — 2.4% | ||||||||

Nigeria Government International Bond 6.50%, 11/28/2027(c) | 200,000 | 151,000 | ||||||

|

| |||||||

Oman — 2.4% | ||||||||

Oman Government International Bond 4.75%, 06/15/2026 | 200,000 | 152,170 | ||||||

|

| |||||||

Pakistan — 1.4% | ||||||||

Pakistan Government International Bond 7.88%, 03/31/2036 | 100,000 | 84,500 | ||||||

|

| |||||||

Romania — 0.9% | ||||||||

Romanian Government International Bond 6.13%, 01/22/2044 | 50,000 | 59,274 | ||||||

|

| |||||||

Saudi Arabia — 2.9% | ||||||||

Saudi Government International Bond 3.75%, 01/21/2055(c) | 200,000 | 183,484 | ||||||

|

| |||||||

South Africa — 2.4% | ||||||||

Eskom Holdings SOC Ltd. 6.75%, 08/06/2023 | 200,000 | 149,500 | ||||||

|

| |||||||

Par* Value | Value | |||||||

FOREIGN GOVERNMENT BONDS AND NOTES — (Continued) |

| |||||||

Turkey — 4.4% |

| |||||||

Turkey Government International Bond 7.38%, 02/05/2025 | $ | 100,000 | $ | 101,595 | ||||

Turkey Government International Bond 5.13%, 02/17/2028 | 200,000 | 173,460 | ||||||

|

| |||||||

| 275,055 | ||||||||

|

| |||||||

Ukraine — 6.7% | ||||||||

Privatbank CJSC Via UK SPV Credit Finance PLC 10.25%, 01/23/2018(b) | 160,000 | 43,440 | ||||||

Ukraine Government International Bond 0.00%, 05/31/2040(c)(d) | 50,000 | 36,902 | ||||||

Ukreximbank Via Biz Finance PLC, 6-M LIBOR + 7.00%, 8.75%, 02/09/2023(c)(d) | 105,000 | 98,721 | ||||||

Ukreximbank Via Biz Finance PLC 9.75%, 01/22/2025(c) | 250,000 | 241,780 | ||||||

|

| |||||||

| 420,843 | ||||||||

|

| |||||||

Venezuela — 0.1% | ||||||||

Venezuela Government International Bond 7.00%, 12/01/2018(a)(b) | 50,000 | 4,000 | ||||||

|

| |||||||

TOTAL FOREIGN GOVERNMENT BONDS AND NOTES | 4,173,286 | |||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

20

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Portfolio of Investments (Continued)

April 30, 2020

Par* Value | Value | |||||||

U.S. TREASURY OBLIGATIONS — 7.2% |

| |||||||

U.S. Treasury Notes — 7.2% | ||||||||

2.25%, 08/15/2027 | $ | 200,000 | $ | 224,766 | ||||

2.25%, 11/15/2027 | 200,000 | 225,422 | ||||||

TOTAL U.S. TREASURY OBLIGATIONS (Cost $396,359) | 450,188 | |||||||

|

| |||||||

| Number of Shares | ||||||||

COMMON STOCKS — 0.0% | ||||||||

Brazil — 0.0% | ||||||||

Dommo Energia SA, SP ADR(a) | 31 | 88 | ||||||

|

| |||||||

TOTAL COMMON STOCKS |

| 88 | ||||||

|

| |||||||

TOTAL INVESTMENTS - 91.5% |

| 5,747,867 | ||||||

OTHER ASSETS IN EXCESS OF LIABILITIES - 8.5% |

| 531,856 | ||||||

|

| |||||||

NET ASSETS - 100.0% | $ | 6,279,723 | ||||||

|

| |||||||

| * | Par amount denominated in USD unless otherwise noted. |

| (a) | Security is deemed illiquid at April 30, 2020 (Unaudited). |

| (b) | Securities are currently in default. Investments with a total aggregate value of $122,029 or 1.94% of net assets were in default as of April 30, 2020. |

| (c) | Securities exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities were purchased in accordance with the guidelines approved by the Fund’s Board of Trustees and may be resold, in transactions exempt from registration, to qualified institutional buyers. At April 30, 2020 these securities amounted to $1,379,108 or 21.96% of net assets. These securities have been determined by the Adviser to be liquid securities. |

| (d) | Variable rate investments. The rate shown is based on the latest available information as of April 30, 2020. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate or spread in their description. |

The accompanying notes are an integral part of the financial statements.

21

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Portfolio of Investments (Concluded)

April 30, 2020

Forward foreign currency contracts outstanding as of April 30, 2020 were as follows:

Currency Purchased | Currency Sold | Expiration | Counterparty | Unrealized | ||||||||

USD | 68,029 | EUR | 62,409 | 06/10/20 | CIBC | $(417) | ||||||

BRL | Brazilian Real | |

CIBC | Canadian Imperial Bank of Commerce | |

CJSC | Closed Joint Stock Company | |

EUR | Euro | |

LIBOR | London Interbank Offered Rate | |

MXN | Mexican Peso | |

MYR | Malaysian Ringgit | |

PJSC | Public Joint Stock Company | |

PLC | Public Limited Company | |

RUB | Russian Ruble | |

SP ADR | Sponsored American Depository Receipt | |

USD | United States Dollar | |

6-M | Six Months |

The accompanying notes are an integral part of the financial statements.

22

DUPONT CAPITAL FUNDS

Statements of Assets and Liabilities

April 30, 2020

| DuPont Capital Emerging Markets Fund | DuPont Capital Emerging Markets Debt Fund | |||||||||

Assets | ||||||||||

Investments, at value (Cost $22,326,775 and $7,848,317, respectively) | $ | 21,302,423 | $ | 5,747,867 | ||||||

Cash | — | 229,597 | ||||||||

Foreign currency (Cost $89,946 and $246,289, respectively) | 90,341 | 228,023 | ||||||||

Receivable for investments sold | 914,536 | — | ||||||||

Dividends and interest receivable | 41,034 | 114,355 | ||||||||

Receivable from Investment Adviser | 19,544 | 10,962 | ||||||||

Prepaid expenses and other assets | 23,076 | 9,145 | ||||||||

|

|

|

| |||||||

Total assets | 22,390,954 | 6,339,949 | ||||||||

|

|

|

| |||||||

Liabilities | ||||||||||

Due to Custodian | 718,173 | — | ||||||||

Payable for audit fees | 30,981 | 26,127 | ||||||||

Payable for custodian fees | 15,824 | 7,926 | ||||||||

Payable for administration and accounting fees | 13,499 | 12,726 | ||||||||

Payable for transfer agent fees | 10,356 | 9,410 | ||||||||

Payable for printing fees | 4,912 | 1,460 | ||||||||

Payable for legal fees | 3,470 | 1,175 | ||||||||

Payable for investments purchased | 1,472 | — | ||||||||

Unrealized depreciation on forward foreign currency contracts* | — | 417 | ||||||||

Accrued expenses | 206 | 985 | ||||||||

|

|

|

| |||||||

Total liabilities | 798,893 | 60,226 | ||||||||

|

|

|

| |||||||

Net Assets | $ | 21,592,061 | $ | 6,279,723 | ||||||

|

|

|

| |||||||

Net Assets consisted of: | ||||||||||

Capital stock, $0.01 par value | $ | 30,978 | $ | 8,682 | ||||||

Paid-in capital | 109,258,767 | 8,419,809 | ||||||||

Total distributable loss | (87,697,684 | ) | (2,148,768 | ) | ||||||

|

|

|

| |||||||

Net Assets | $ | 21,592,061 | $ | 6,279,723 | ||||||

|

|

|

| |||||||

Class I: | ||||||||||

Net asset value, offering and redemption price per share ($21,592,061 / 3,097,763 shares) and ($6,279,723 / 868,241 shares), respectively | $6.97 | $7.23 | ||||||||

| * | Primary risk exposure is foreign currency. |

The accompanying notes are an integral part of the financial statements.

23

DUPONT CAPITAL FUNDS

Statements of Operations

For the Year Ended April 30, 2020

| DuPont Capital Emerging Markets Fund | DuPont Capital Emerging Markets Debt Fund | |||||||||

Investment income | ||||||||||

Dividends | $ | 871,475 | $ | 1,516 | ||||||

Interest | — | 484,071 | ||||||||

Less: foreign taxes withheld | (98,344 | ) | — | |||||||

|

|

|

| |||||||

Total investment income | 773,131 | 485,587 | ||||||||

|

|

|

| |||||||

Expenses | ||||||||||

Advisory fees (Note 2) | 258,943 | 43,192 | ||||||||

Administration and accounting fees (Note 2) | 105,832 | 69,243 | ||||||||

Custodian fees (Note 2) | 42,673 | 22,847 | ||||||||

Legal fees | 40,801 | 12,187 | ||||||||

Trustees’ and officers’ fees | 38,590 | 18,352 | ||||||||

Audit fees | 36,048 | 26,898 | ||||||||

Transfer agent fees (Note 2) | 24,230 | 29,314 | ||||||||

Registration and filing fees | 16,820 | 22,171 | ||||||||

Printing and shareholder reporting fees | 1,213 | 8,130 | ||||||||

Other expenses | 18,056 | 11,588 | ||||||||

|

|

|

| |||||||

Total expenses before waivers and reimbursements | 583,206 | 263,922 | ||||||||

|

|

|

| |||||||

Less: waivers and reimbursements (Note 2) | (270,007 | ) | (199,854 | ) | ||||||

|

|

|

| |||||||

Net expenses after waivers and reimbursements | 313,199 | 64,068 | ||||||||

|

|

|

| |||||||

Net investment income | 459,932 | 421,519 | ||||||||

|

|

|

| |||||||

Net realized and unrealized gain/(loss) from investments | ||||||||||

Net realized gain/(loss) from investments(a) | (357,331 | ) | 1,219 | |||||||

Net realized gain/(loss) from foreign currency transactions | (17,368 | ) | 943 | |||||||

Net realized gain from forward foreign currency contracts* | — | 3,731 | ||||||||

Net change in unrealized appreciation/(depreciation) from investments(b) | (5,632,937 | ) | (1,352,148 | ) | ||||||

Net change in unrealized appreciation/(depreciation) from foreign currency translations | 983 | (19,705 | ) | |||||||

Net change in unrealized appreciation/(depreciation) from forward foreign currency contracts* | — | (1,324 | ) | |||||||

|

|

|

| |||||||

Net realized and unrealized loss from investments | (6,006,653 | ) | (1,367,284 | ) | ||||||

|

|

|

| |||||||

Net decrease in net assets resulting from operations | $ | (5,546,721 | ) | $ | (945,765 | ) | ||||

|

|

|

| |||||||

| * | Primary risk exposure is foreign currency. |

| (a) | Net realized gain (loss) on investments for the DuPont Capital Emerging Markets Fund was net of foreign capital gains tax withheld of $5,958. |

| (b) | Change in net unrealized appreciation/(depreciation) on investments for the DuPont Capital Emerging Markets Fund was net of a decrease in deferred foreign capital gains tax of $430. |

The accompanying notes are an integral part of the financial statements.

24

DUPONT CAPITAL EMERGING MARKETS FUND

Statements of Changes in Net Assets

| For the Year Ended April 30, 2020 | For the Year Ended April 30, 2019 | |||||||||

Increase/(decrease) in net assets from operations: | ||||||||||

Net investment income | $ | 459,932 | $ | 489,745 | ||||||

Net realized gain/(loss) from investments and foreign currency transactions | (374,699 | ) | 858,588 | |||||||

Net change in unrealized appreciation/(depreciation) from investments and foreign currency translations | (5,631,954 | ) | (2,863,680 | ) | ||||||

|

|

|

| |||||||

Net decrease in net assets resulting from operations | (5,546,721 | ) | (1,515,347 | ) | ||||||

|

|

|

| |||||||

Less dividends and distributions to shareholders from: | ||||||||||

Total distributable earnings | (485,243 | ) | (436,646 | ) | ||||||

|

|

|

| |||||||

Decrease in net assets from dividends and distributions to shareholders | (485,243 | ) | (436,646 | ) | ||||||

|

|

|

| |||||||

Increase/(decrease) in net assets derived from capital share transactions (Note 4) | 2,162,193 | (1,590,174 | ) | |||||||

|

|

|

| |||||||

Total decrease in net assets | (3,869,771 | ) | (3,542,167 | ) | ||||||

|

|

|

| |||||||

Net assets | ||||||||||

Beginning of year | 25,461,832 | 29,003,999 | ||||||||

|

|

|

| |||||||

End of year | $ | 21,592,061 | $ | 25,461,832 | ||||||

|

|

|

| |||||||

The accompanying notes are an integral part of the financial statements.

25

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Statements of Changes in Net Assets

| For the Year Ended April 30, 2020 | For the Year Ended April 30, 2019 | |||||||||

Increase/(decrease) in net assets from operations: | ||||||||||

Net investment income | $ | 421,519 | $ | 372,619 | ||||||

Net realized gain from investments, forward foreign currency contracts and foreign currency transactions | 5,893 | 18,638 | ||||||||

Net change in unrealized appreciation/(depreciation) from investments, forward foreign currency contracts and foreign currency translations | (1,373,177 | ) | (291,306 | ) | ||||||

|

|

|

| |||||||

Net increase/(decrease) in net assets resulting from operations | (945,765 | ) | 99,951 | |||||||

|

|

|

| |||||||

Less dividends and distributions to shareholders from: | ||||||||||

Total distributable earnings | (500,338 | ) | (388,320 | ) | ||||||

|

|

|

| |||||||

Decrease in net assets from dividends and distributions to shareholders | (500,338 | ) | (388,320 | ) | ||||||

|

|

|

| |||||||

Increase in net assets derived from capital share transactions (Note 4) | 466,072 | 976,392 | ||||||||

|

|

|

| |||||||

Total increase/(decrease) in net assets | (980,031 | ) | 688,023 | |||||||

|

|

|

| |||||||

Net Assets | ||||||||||

Beginning of year | 7,259,754 | 6,571,731 | ||||||||

|

|

|

| |||||||

End of year | $ | 6,279,723 | $ | 7,259,754 | ||||||

|

|

|

| |||||||

The accompanying notes are an integral part of the financial statements.

26

DUPONT CAPITAL EMERGING MARKETS FUND

Financial Highlights

Contained below is per share operating performance data for Class I shares outstanding, total investment return, ratios to average net assets and other supplemental data for the respective period. The total returns in the table represent the rate that an investor would have earned or lost on an investment in the Fund (assuming reinvestment of all dividends and distributions). This information has been derived from information provided in the financial statements and should be read in conjunction with the financial statements and the notes thereto.

| Class I | ||||||||||||||||||||

| For the Year Ended | ||||||||||||||||||||

| April 30, 2020 | April 30, 2019 | April 30, 2018 | April 30, 2017 | April 30, 2016 | ||||||||||||||||

Per Share Operating Performance | ||||||||||||||||||||

Net asset value, beginning of year | $ | 8.85 | $ | 9.55 | $ | 7.97 | $ | 6.64 | $ | 8.28 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net investment income(1) | 0.15 | 0.18 | 0.14 | 0.11 | 0.13 | |||||||||||||||

Net realized and unrealized gain/(loss) on investments | (1.88 | ) | (0.72 | ) | 1.59 | 1.32 | (1.73 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net increase/(decrease) in net assets resulting from operations | (1.73 | ) | (0.54 | ) | 1.73 | 1.43 | (1.60 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Dividends and distributions to shareholders from: | ||||||||||||||||||||

Net investment income | (0.15 | ) | (0.16 | ) | (0.15 | ) | (0.10 | ) | (0.04 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value, end of year | $ | 6.97 | $ | 8.85 | $ | 9.55 | $ | 7.97 | $ | 6.64 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total investment return(2) | (19.80 | )% | (5.46 | )% | 21.82 | % | 21.77 | % | (19.23 | )% | ||||||||||

Ratios/Supplemental Data | ||||||||||||||||||||

Net assets, end of year (in thousands) | $ | 21,592 | $ | 25,462 | $ | 29,004 | $ | 30,816 | $ | 54,137 | ||||||||||

Ratio of expenses to average net assets | 1.27 | % | 1.27 | % | 1.27 | % | 1.39 | % | 1.60 | % | ||||||||||

Ratio of expenses to average net assets without waivers and expense | 2.36 | % | 2.37 | % | 2.17 | % | 2.06 | % | 1.63 | % | ||||||||||

Ratio of net investment income to average net assets | 1.86 | % | 2.05 | % | 1.52 | % | 1.51 | % | 1.81 | % | ||||||||||

Portfolio turnover rate | 53 | % | 35 | % | 65 | % | 28 | % | 53 | % | ||||||||||

| (1) | The selected per share data was calculated using the average shares outstanding method for the year. |

| (2) | Total investment return is calculated assuming a purchase of shares on the first day and a sale of shares on the last day of each period reported and includes reinvestment of dividends and distributions, if any. |

| (3) | During the period, certain fees were waived and/or reimbursed. If such fee waivers and/or reimbursements had not occurred, the ratios would have been as indicated (See Note 2). |

The accompanying notes are an integral part of the financial statements.

27

DUPONT CAPITAL EMERGING MARKETS DEBT FUND

Financial Highlights

Contained below is per share operating performance data for Class I shares outstanding, total investment return, ratios to average net assets and other supplemental data for the respective period. The total returns in the table represent the rate that an investor would have earned or lost on an investment in the Fund (assuming reinvestment of all dividends and distributions). This information has been derived from information provided in the financial statements and should be read in conjunction with the financial statements and the notes thereto.

| Class I | |||||||||||||||||||||||||

| For the Year Ended | |||||||||||||||||||||||||

| April 30, 2020 | April 30, 2019 | April 30, 2018 | April 30, 2017 | April 30, 2016 | |||||||||||||||||||||

Per Share Operating Performance | |||||||||||||||||||||||||

Net asset value, beginning of year | $ | 8.91 | $ | 9.35 | $ | 9.79 | $ | 9.56 | $ | 9.77 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Net investment income(1) | 0.50 | 0.48 | 0.53 | 0.66 | 0.74 | ||||||||||||||||||||

Net realized and unrealized gain/(loss) on investments | (1.58 | ) | (0.40 | ) | (0.38 | ) | 0.11 | 0.21 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Net increase/(decrease) in net assets resulting from operations | (1.08 | ) | 0.08 | 0.15 | 0.77 | 0.95 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Dividends and distributions to shareholders from: | |||||||||||||||||||||||||

Net investment income | (0.60 | ) | (0.52 | ) | (0.59 | ) | (0.52 | ) | (0.98 | ) | |||||||||||||||

Net realized capital gains | (0.00 | )(2) | — | — | (0.02 | ) | (0.18 | ) | |||||||||||||||||

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Total dividends and distributions to shareholders | (0.60 | ) | (0.52 | ) | (0.59 | ) | (0.54 | ) | (1.16 | ) | |||||||||||||||

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Net asset value, end of year | $ | 7.23 | $ | 8.91 | $ | 9.35 | $ | 9.79 | $ | 9.56 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Total investment return(3) | (13.14 | )% | 1.16 | % | 1.46 | % | 8.45 | % | 10.82 | % | |||||||||||||||

Ratios/Supplemental Data | |||||||||||||||||||||||||

Net assets, end of year (in thousands) | $ | 6,280 | $ | 7,260 | $ | 6,572 | $ | 6,145 | $ | 5,810 | |||||||||||||||

Ratio of expenses to average net assets | 0.89 | % | 0.89 | % | 0.89 | % | 0.89 | % | 0.89 | % | |||||||||||||||

Ratio of expenses to average net assets without waivers and expense reimbursements(4) | 3.67 | % | 3.92 | % | 3.46 | % | 3.70 | % | 3.34 | % | |||||||||||||||

Ratio of net investment income to average net assets | 5.86 | % | 5.45 | % | 5.45 | % | 6.84 | % | 7.93 | % | |||||||||||||||

Portfolio turnover rate | 5 | % | 10 | % | 17 | % | 18 | % | 25 | % | |||||||||||||||

| (1) | The selected per share data was calculated using the average shares outstanding method for the year. |

| (2) | Amount is less than $0.005 per share. |

| (3) | Total investment return is calculated assuming a purchase of shares on the first day and a sale of shares on the last day of each period reported and includes reinvestment of dividends and distributions, if any. |

| (4) | During the period, certain fees were waived and/or reimbursed. If such fee waivers and/or reimbursements had not occurred, the ratios would have been as indicated (See Note 2). |

The accompanying notes are an integral part of the financial statements.

28

DUPONT CAPITAL FUNDS

Notes to Financial Statements

April 30, 2020

1. Organization and Significant Accounting Policies

The DuPont Capital Emerging Markets Fund is a diversified, open-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The DuPont Capital Emerging Markets Debt Fund is a non-diversified, open-end management investment company registered under the 1940 Act (the DuPont Capital Emerging Markets Fund and the DuPont Capital Emerging Markets Debt Fund are each a “Fund”, and together, the “Funds”). The DuPont Capital Emerging Markets Fund commenced operations on December 6, 2010 and the DuPont Capital Emerging Markets Debt Fund commenced operations on September 27, 2013. The Funds are each a separate series of FundVantage Trust (the “Trust”) which was organized as a Delaware statutory trust on August 28, 2006. The Trust is a “series trust” authorized to issue an unlimited number of separate series or classes of shares of beneficial interest. Each series is treated as a separate entity for certain matters under the 1940 Act, and for other purposes, and a shareholder of one series is not deemed to be a shareholder of any other series. The Funds are each authorized to issue and offer Class I Shares.

The Funds are investment companies and follow accounting and reporting guidance in the Financial Accounting Standards Board Accounting Standards Codification Topic 946.

Portfolio Valuation — Each Fund’s net asset value (“NAV”) is calculated once daily at the close of regular trading hours on the New York Stock Exchange (“NYSE”) (typically 4:00 p.m. Eastern time) on each day the NYSE is open. Securities held by each Fund are valued using the closing price or the last sale price on a national securities exchange or the National Association of Securities Dealers Automatic Quotation System (“NASDAQ”) market system where they are primarily traded. Equity securities listed on any national or foreign exchange market system will be valued at the last sale price. Equity securities traded in the over-the-counter market are valued at their closing price. If there were no transactions on that day, securities traded principally on an exchange will be valued at the mean of the last bid and ask prices prior to the market close. Prices for equity securities normally are supplied by an independent pricing service approved by the Trust’s Board of Trustees (“Board of Trustees”). Fixed income securities are valued based on market quotations, which are furnished by an independent pricing service approved by the FundVantage Board of Trustees. Fixed income securities having remaining maturities of 60 days or less are generally valued at amortized cost, provided such amounts approximates market value. Debt securities are valued on the basis of broker quotations or valuations provided by a pricing service, which utilizes information with respect to recent sales, market transactions in comparable securities, quotations from dealers, and various relationships between securities in determining value. Due to continued volatility in the current market, valuations developed through pricing techniques may materially vary from the actual amounts realized upon sale of the securities. Any assets held by the Funds that are denominated in foreign currencies are valued daily in U.S. dollars at the foreign currency exchange rates that are prevailing at the time that the Funds determine the daily NAV per share. Foreign securities may trade on weekends or other days when the Funds do not calculate NAV. As a result, the market value of these investments may change on days when you cannot buy or sell shares of the Funds. Foreign securities are valued

29

DUPONT CAPITAL FUNDS

Notes to Financial Statements (Continued)

April 30, 2020

based on prices from the primary market in which they are traded and are translated from the local currency into U.S. dollars using current exchange rates. Forward exchange contracts are valued at the forward rate. Investments in any mutual fund are valued at their respective NAVs as determined by those mutual funds each business day (which may use fair value pricing as disclosed in their prospectuses). If market quotations are unavailable or deemed unreliable, securities will be valued in accordance with procedures adopted by the Board of Trustees. Relying on prices supplied by pricing services or dealers or using fair valuation may result in values that are higher or lower than the values used by other investment companies and investors to price the same investments. In the event that market quotes are not readily available, and the security or asset cannot be valued pursuant to one of the valuation methods, the value of the security or asset will be determined in good faith by the Adviser. The Trust has established a Valuation Committee which performs certain functions including the oversight of the Adviser’s fair valuation determinations.

Fair Value Measurements — The inputs and valuation techniques used to measure fair value of each Fund’s investments are summarized into three levels as described in the hierarchy below:

● Level 1 | — | quoted prices in active markets for identical securities; | ||

● Level 2 | — | other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.); and | ||

● Level 3 | — | significant unobservable inputs (including each Fund’s own assumptions in determining the fair value of investments). | ||

The fair value of each Fund’s bonds is generally based on quotes received from brokers or independent pricing services. Bonds with quotes that are based on actual trades with a sufficient level of activity on or near the measurement date are classified as Level 2 assets.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. Transfers in and out are recognized at the value at the end of the period.

Significant events (such as movement in the U.S. securities market, or other regional and local developments) may occur between the time that foreign markets close (where the security is principally traded) and the time that each Fund calculates its NAV (generally, the close of the NYSE) that may impact the value of securities traded in these foreign markets. As a result, each Fund fair values foreign securities using an independent pricing service which considers the correlation of the trading patterns of the foreign security to the intraday trading in the U.S. markets for investments such as American Depositary Receipts, financial futures, exchange traded funds and certain indexes as well as prices for similar securities. Such fair valuations are categorized as Level 2 in the hierarchy.

30

DUPONT CAPITAL FUNDS

Notes to Financial Statements (Continued)

April 30, 2020

Securities listed on a non-U.S. exchange are generally fair valued daily by an independent fair value pricing service approved by the Board of Trustees and categorized as Level 2 investments within the hierarchy. The fair valuations for these securities may not be the same as quoted or published prices of the securities on their primary markets. Securities for which daily fair value prices from the independent fair value pricing service are not available are generally valued at the last quoted sale price at the close of an exchange on which the security is traded and categorized as Level 1 investments within the hierarchy. Values of foreign securities, currencies, and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars at the exchange rate of said currencies against the U.S. dollar, as of valuation time, as provided by an independent pricing service approved by the Board of Trustees.