The Funds are required by Subchapter M of the Internal Revenue Code of 1986, as amended, to advise their shareholders of the U.S. federal tax status of distributions received by the Funds’ shareholders in respect of such fiscal year. During the year ended April 30, 2023, the Polen Growth Fund, Polen Global Growth Fund, Polen International Growth Fund, Polen U.S. Small Company Growth Fund, Polen International Small Company Growth Fund , Polen Emerging Markets Growth Fund, Polen U.S. SMID Company Growth Fund, Polen Global SMID Company Growth Fund, Polen Emerging Markets ex China Growth Fund, Polen Bank Loan Fund and Polen Upper Tier High Yield Fund paid $0, $0, $414,209, $0, $0, $15,994, $0, $0, $0, $389,555 and $131,394 of ordinary income dividends and $646,213,431, $4,939,028, $0, $0, $0, $0, $0, $0, $0, $0 and $0 of long-term capital gains, respectively, to its shareholders.

The Polen Growth Fund, Polen Global Growth Fund, Polen International Growth Fund, Polen U.S. Small Company Growth Fund, Polen International Small Company Growth Fund, Polen Emerging Markets Growth Fund, Polen U.S. SMID Company Growth Fund, Polen Global SMID Company Growth Fund, Polen Emerging Markets ex China Growth Fund, Polen Bank Loan Fund and Polen Upper Tier High Yield Fund designated $646,213,431, $4,939,028, $0, $0, $0, $0, $0, $0, $0, $0 and $0, respectively, as long-term capital gains distributions during the year ended April 30, 2023. Distributable long-term gains are based on net realized long-term gains determined on a tax basis and may differ from such amounts for financial reporting purposes.

The Polen Growth Fund, Polen Global Growth Fund, Polen International Growth Fund, Polen U.S. Small Company Growth Fund, Polen International Small Company Growth Fund, Polen Emerging Markets Growth Fund, Polen U.S. SMID Company Growth Fund, Polen Global SMID Company Growth Fund, Polen Emerging Markets ex China Growth Fund, Polen Bank Loan Fund and Polen Upper Tier High Yield Fund designates 0.00%, 0.00%, 0.00%, 0.00%, 0.00%, 100.00%, 0.00%, 0.00%, 0.00%, 0.00% and 0.00%, respectively, of ordinary income distributions as qualified dividend income pursuant to the Jobs and Growth Tax Relief Reconciliation Act of 2003.

The percentage of ordinary income dividends qualifying for corporate dividends received deduction for the Polen Growth Fund, Polen Global Growth Fund, Polen International Growth Fund, Polen U.S. Small Company Growth Fund, Polen International Small Company Growth Fund, Polen Emerging Markets Growth Fund, Polen U.S. SMID Company Growth Fund, Polen Global SMID Company Growth Fund, Polen Emerging Markets ex China Growth Fund, Polen Bank Loan Fund and Polen Upper Tier High Yield Fund is 0.00%, 0.00%, 0.00%, 0.00%, 0.00%, 0.00%, 0.00%, 0.00%, 0.00%, 0.00% and 0.00%, respectively.

The Polen Growth Fund, Polen Global Growth Fund, Polen International Growth Fund, Polen U.S. Small Company Growth Fund, Polen International Small Company Growth Fund, Polen Emerging Markets Growth Fund, Polen U.S. SMID Company Growth Fund, Polen Global SMID Company Growth Fund, Polen Emerging Markets ex China Growth Fund, Polen Bank Loan Fund and Polen Upper Tier High Yield Fund designates 0.00%, 0.00%, 0.00%, 0.00%, 0.00%, 0.00%, 0.00%, 0.00%, 0.00%, 100.00% and 0.00%, respectively, of ordinary income distributions as qualified short-term gain pursuant to the American Jobs Creation Act of 2004.

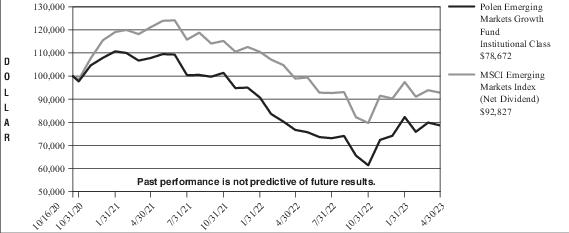

The Polen Emerging Markets Growth Fund paid foreign taxes of $79,864 and recognized foreign source income of $300,614.

All designations are based on financial information available as of the date of this annual report and, accordingly, are subject to change. For each item, it is the intention of the Funds to designate the maximum amount permitted under the Internal Revenue Code of 1986, as amended, and the regulations thereunder.

Because the Funds’ fiscal year is not the calendar year, another notification will be sent with respect to calendar year 2022. The second notification, which will reflect the amount, if any, to be used by calendar year taxpayers on their U.S. federal income tax returns, will be made in conjunction with Form 1099-DIV and will be mailed in January 2024.

Foreign shareholders will generally be subject to U.S. withholding tax on the amount of their ordinary income dividends. They will generally not be entitled to a foreign tax credit or deduction for the withholding taxes paid by the Funds, if any.

In general, dividends received by tax-exempt recipients (e.g., IRAs and Keoghs) need not be reported as taxable income for U.S. federal income tax purposes. However, some retirement trusts (e.g., corporate, Keogh and 403(b)(7) plans) may need this information for their annual information reporting.

Shareholders are advised to consult their own tax advisers with respect to the tax consequences of their investment in the Funds.