UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22023

Nuveen Managed Accounts Portfolios Trust

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: July 31

Date of reporting period: July 31, 2009

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Mutual Funds

Nuveen Managed Accounts Portfolios Trust

Dependable, tax-free income because it’s not what you earn, it’s what you keep.®

Annual Report

July 31, 2009

|

Municipal Total

Return Managed

Accounts Portfolio |

LIFE IS COMPLEX.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Investments Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund dividends and statements from your financial advisor or brokerage account.

OR

www.nuveen.com/accountaccess

If you receive your Nuveen Fund dividends and statements directly from Nuveen.

| | | | | | |

| Must be preceded by or accompanied by a prospectus. | | NOT FDIC INSURED | | MAY LOSE VALUE | | NO BANK GUARANTEE |

Chairman’s

Letter to Shareholders

Dear Shareholder,

The financial markets in which your Fund operates continue to reflect the larger economic crosscurrents. The illiquidity that infected global credit markets over the last year appears to be slowly but steadily receding. The major institutions that are the linchpin of the international financial system are strengthening their capital structures, but many still struggle with losses in their various portfolios. There are encouraging signs of recovery in European and Asian economies, while the U.S. economy continues to feel the impact of job losses and an over-borrowed consumer. Global trends include modestly increasing trade and increased concern about the ability of the U.S. government to address its substantial budgetary deficits. Identifying those developments that will define the future is never easy, but rarely is it more difficult than at present.

After considerable volatility in the first few months of 2009, both the fixed-income and equity markets have seen a partial recovery. A fundamental component of a successful long-term investment program is a commitment to remain invested during market downturns in order to share in the rewards of the inevitable recovery. Another component is to re-evaluate investment disciplines and tactics and to confirm their validity following periods of extreme volatility and market dislocation, such as we have recently experienced. Your Board carried out an intensive review of investment performance with these objectives in mind during April and May of this year as part of the annual management contract renewal process. I encourage you to read the description of this process in the Annual Investment Management Agreement Approval Process section of this report.

Remaining invested through market downturns and reconfirming the appropriateness of a long term investment strategy is as important for our shareholders as it is for professional investment managers. For that reason, I again encourage you to remain in communication with your financial consultant on these subjects. For recent developments on all your Nuveen Funds, please visit the Nuveen web site: www.nuveen.com.

On behalf of the other members of your Fund’s Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Robert P. Bremner

Chairman of the Nuveen Fund Board

September 21, 2009

Portfolio Manager’s Comments

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not Intended as recommendations of individual investments. The forward looking statements and other views expressed herein are those of the portfolio manager as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Fund disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

The Nuveen Municipal Total Return Managed Account Portfolio is managed by Nuveen Asset Management, an affiliate of Nuveen Investments, Inc. The Portfolio is overseen by Marty Doyle, who has 20 years of investment experience and has managed the Portfolio since its inception in 2007. Here Marty discusses the general market environment, his investment strategy and the performance of the Portfolio for the twelve-month period ended July 31, 2009.

What were the general market conditions during the reporting period?

During this reporting period, downward pressure on the economy continued. In an effort to improve overall economic conditions, the Federal Reserve (Fed) continued to cut interest rates, lowering the fed funds rate from 2.00% on August 1, 2008, to a target range of zero to 0.25% in December 2008, its lowest level on record. In March 2009, the Fed announced that, in addition to maintaining the current target rate, it would buy $300 billion in long-term Treasury securities in an effort to support private credit markets and up to an additional $750 billion (for a total of $1.25 trillion) in agency mortgage-backed securities to bolster the housing market. (At its August 2009 meeting, following the end of this reporting period, the Fed continued to keep the fed funds rate unchanged.)

Additionally, the federal government passed a $700 billion financial industry rescue package in October 2008, which was followed by a $787 billion stimulus package in February 2009. The Fed’s efforts and the stimulus package were in part a response to the decline in U.S. economic growth, as measured by the U.S. gross domestic product (GDP). Over the four quarters ended June 30, 2009, the GDP experienced its longest decline since quarterly records began in 1947 and the worst recession in 50 years. While housing prices provided something of a bright spot in May and June 2009 by posting their first positive monthly returns after three years of decline, the depth of the housing slump continued to be a source of concern. In the labor markets, July 2009 marked the 19th consecutive month of job losses, with a total of 6.7 million jobs lost since the recession began in December 2007. The national unemployment rate for July 2009 was 9.4%, up from 5.8% in July 2008. At the same time, inflation remained subdued, as the Consumer Price Index (CPI), reflecting a 28% drop in energy prices, fell 2.1% year-over-year as of July 2009, the largest twelve-month decline since 1950. The core CPI (which excludes food and energy) rose 1.5% over this same period, within the Fed’s unofficial objective of 2.0% or lower for this measure.

During this period, the nation’s financial institutions and markets experienced significant turmoil and reductions in demand for many types of securities, which decreased valuations. In the municipal market, this negative impact was felt across all credit ratings, reducing the net asset values of municipal bond funds. In addition, some of the dealer

firms that make markets in bonds were unwilling to commit capital to purchase bonds or continue serving as dealers. The reduction in dealer involvement was accompanied by significant selling pressure by investors, especially institutional investors, predominantly related to lower-rated securities.

Municipal bond prices were further negatively impacted by concerns that a supply overhang (such as a large backlog of new issues that had been postponed) would cause selling pressure to persist. Additionally, greater price volatility, including wider credit spreads (i.e., lower quality bonds fell in price more than higher quality bonds); greatly reduced liquidity (i.e., the ability to sell bonds at prices close to their carrying values), particularly for lower quality bonds; and a lack of price transparency (i.e., the ability to accurately determine the price at which a bond would likely trade) weighed down the market for much of the period.

Market conditions began to show general signs of improvement in mid-December 2008, and municipal bonds were on an improving trend during the first seven months of 2009. Another positive impact was the reduced supply of tax-exempt municipal debt available in the marketplace, part because of the introduction of “Build America” bonds in April 2009. This new class of taxable municipal debt – created as part of the February 2009 economic stimulus package – provides municipal issuers with a federal subsidy equal to 35% of the security’s interest payments. For many borrowers, these bonds offered an attractive alternative to issuing traditional tax-exempt debt. The Build America bond program got off to a quick start, effectively diverting high-grade tax-exempt new-issue supply into the taxable market. Therefore, a combination of lower issuance along with higher demand provided additional support for municipal bond prices.

Over the twelve months ended July 31, 2009, municipal bond issuance nationwide totaled $389.2 billion, a drop of approximately 16% compared with the twelve-month period ended July 31, 2008. While market conditions during this period impacted the demand for municipal bonds, investors, especially from the retail sector, continued to be attracted by the high tax-equivalent yields of the municipal bond market relative to taxable bonds.

How did the Portfolio perform during the twelve-month period ended July 31, 2009? What strategies were used to manage the Portfolio during the reporting period? How did these strategies influence performance?

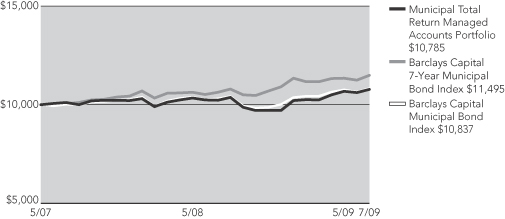

The Municipal Total Return Managed Accounts Portfolio underperformed the Barclays Capital 7-Year Municipal Bond Index and slightly outperformed the Barclays Capital Municipal Bond Index during the twelve-month reporting period. The table on page four provides performance information for the one-year and since inception periods ended July 31, 2009.

| 1 | The Barclays Capital 7-Year Municipal Bond Index is an unmanaged index composed of a broad range of investment-grade municipal bonds with maturity dates of approximately seven years and does not reflect any initial or ongoing expenses. This index more closely compares to the duration of the bonds in the Fund’s portfolio. You cannot invest directly in an index. |

| 2 | The Barclays Capital Municipal Bond Index is an unmanaged index composed of a broad range of investment-grade municipal bonds. The index does not reflect any initial or ongoing expenses. You cannot invest directly in an index. |

The Portfolio uses a value-oriented strategy and looks for higher-yielding and undervalued municipal bonds that offer the potential for above-average total return. The Portfolio invests in various types of municipal securities, including investment grade (rated BBB/Baa or better), below investment grade (rated BB/Ba or lower), high yield, and unrated municipal securities. The Portfolio focuses on securities with intermediate to longer-term maturities. This investment strategy did not change during the reporting period.

One factor that contributed to the Portfolio’s relative underperformance was its comparatively lower average credit quality. In a generally unfavorable market environment, lower rated securities generally underperformed their higher rated counterparts. The Portfolio continued to add mid-grade and high yield holdings during the period. Additionally, the Portfolio also had a comparatively lower weighting in shorter maturities (6 years or less), which tended to outperform longer maturities over the full period. We found the most value in the A and BBB rated tax-backed and essential service revenue bonds.

We continued to focus on diversification, and looked to add exposure across the entire yield curve, credit ranges and industry sectors. We also looked for opportunities to purchase undervalued credits in sectors and maturities that experienced elevated volatility during the period.

We remained relatively conservative with our long-term targets with respect to higher yield and longer duration weightings. We gradually increased exposure to longer maturities and slightly lower grade holdings (some to replace prior holdings that became pre-refunded) to increase the portfolio’s income component and long-term return prospects.

Class A Shares – Average Annual Total Returns

As of 7/31/09

| | | | |

| | | 1-Year | | Since

Inception (5/31/07) |

Municipal Total Return Managed Accounts Portfolio | | 5.35% | | 3.50% |

Barclays Capital 7-Year Municipal Bond Index1 | | 8.01% | | 6.64% |

Barclays Capital Municipal Bond Index2 | | 5.11% | | 3.77% |

Returns quoted represent past performance which is no guarantee of future results. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Current performance may be higher or lower than the performance shown. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Capital gains, if any, are subject to tax. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Please see the Fund’s Spotlight Page later in this report for more complete performance data and expense ratios.

Municipal Total Return Managed Accounts Portfolio

Growth of an Assumed $10,000 Investment

The graph does not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of shares.

The index comparisons show the change in value of a $10,000 investment in the Municipal Total Return Managed Accounts Portfolio compared with the corresponding index. The Barclays Capital 7-Year Municipal Bond Index is an unmanaged index comprised of a broad range of investment-grade municipal bonds with maturity dates of approximately seven years. The Barclays Capital Municipal Bond Index is an unmanaged index comprised of a broad range of investment-grade municipal bonds. The index returns assume reinvestment of dividends and do not reflect any initial or ongoing expenses. You cannot invest directly in an index. The Municipal Total Return Managed Accounts Portfolio’s returns include reinvestment of all dividends and distributions. The performance data quoted represents past performance, which is not indicative of future results. Current performance may be lower or higher than the performance shown.

Fund Spotlight as of 7/31/09 Municipal Total Return Managed Accounts Portfolio

| | | | | | | | |

| Quick Facts | | | | | | | | |

| | | | | | | | | |

NAV | | | | | | | | $9.80 |

Latest Monthly Dividend1 | | | | | | | | $.0389 |

Inception Date | | | | | | | | 5/31/07 |

Returns quoted represent past performance which is no guarantee of future results. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Current performance may be higher or lower than the performance shown. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Fund returns assume reinvestment of dividends and capital gains. Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

| | |

| Average Annual Total Returns as of 7/31/09 |

| |

| | | NAV |

1-Year | | 5.35% |

Since Inception | | 3.50% |

|

| Average Annual Total Returns as of 6/30/09 |

| |

| | | NAV |

1-Year | | 3.65% |

Since Inception | | 2.90% |

| |

| Tax-Free Yields | | |

| |

| | | NAV |

Dividend Yield2 | | 4.76% |

SEC 30-Day Yield2 | | 4.91% |

Taxable-Equivalent Yield3 | | 6.82% |

| | | | | | |

| Expense Ratios | | | | | | |

| | | Gross

Expense

Ratio | | Net

Expense

Ratio | | As of

Date |

| | | 0.44% | | 0.00% | | 7/31/08 |

The expense ratios shown factor in Total Annual Fund Operating Expenses. The Adviser has agreed irrevocably during the existence of the Fund to waive all fees and pay or reimburse all expenses of the Fund, except for interest expense, taxes, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses.

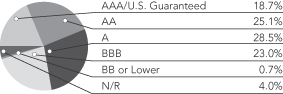

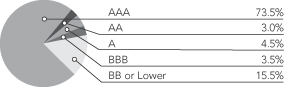

Bond Credit Quality4

| | |

| Portfolio Statistics |

| Net Assets ($000) | | $92,354 |

| Average Effective Maturity on Securities (Years) | | 13.54 |

| Average Duration | | 5.95 |

| 1 | Paid August 3, 2009. This is the latest monthly tax-exempt dividend declared during the period ended July 31, 2009. |

| 2 | Dividend Yield is the most recent dividend per share (annualized) divided by the appropriate price per share. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. The Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium. |

| 3 | The Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis at a specified tax rate. With respect to investments that generate qualified dividend income that is taxable at a maximum rate of 15%, the Taxable-Equivalent Yield is lower. The Taxable-Equivalent Yield is based on the Fund’s SEC 30-Day Yield on the indicated date and a federal income tax rate of 28%. |

| 4 | As a percentage of total long-term investments as of July 31, 2009. Holdings are subject to change. |

Fund Spotlight as of 7/31/09 Municipal Total Return Managed Accounts Portfolio

| | |

| Industries1 | | |

Tax Obligation/General | | 16.9% |

Tax Obligation/Limited | | 16.4% |

Education and Civic Organizations | | 14.6% |

Health Care | | 14.2% |

Transportation | | 10.1% |

Utilities | | 7.3% |

Water and Sewer | | 7.0% |

Other | | 13.5% |

| | |

| States1 | | |

California | | 11.8% |

Illinois | | 10.7% |

Pennsylvania | | 6.5% |

Indiana | | 5.4% |

New York | | 4.7% |

Texas | | 4.7% |

Michigan | | 4.2% |

Florida | | 3.9% |

North Carolina | | 3.8% |

Georgia | | 3.8% |

Wisconsin | | 3.6% |

Missouri | | 3.6% |

New Jersey | | 3.4% |

Massachusetts | | 3.1% |

Alabama | | 2.8% |

Puerto Rico | | 2.1% |

South Carolina | | 2.1% |

Virgin Islands | | 2.0% |

Nevada | | 1.8% |

Idaho | | 1.6% |

Other | | 14.4% |

| 1 | As a percentage of total long-term investments as of July 31, 2009. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | Hypothetical Performance |

| | | Actual Performance | | (5% annualized return before expenses) |

| Beginning Account Value (2/01/09) | | | | $ | 1,000.00 | | | | | | | | $ | 1,000.00 | | | | |

| Ending Account Value (7/31/09) | | | | $ | 1,054.90 | | | | | | | | $ | 1,024.79 | | | | |

| Expenses Incurred During Period | | | | $ | — | | | | | | | | $ | — | | | | |

Expenses are equal to the Fund’s annualized net expense ratio of 0.00% multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Report of

Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of

Nuveen Managed Accounts Portfolios Trust

In our opinion, the accompanying statement of assets and liabilities, including the portfolio of investments, and the related statements of operations, of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Municipal Total Return Managed Accounts Portfolio (a series of the Nuveen Managed Accounts Portfolios Trust, hereafter referred to as the “Fund”) at July 31, 2009, the results of its operations for the year then ended, the changes in its net assets for each of the two years then ended and the financial highlights for the periods indicated in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audit, which included confirmation of securities at July 31, 2009 by correspondence with the custodian and brokers, provides a reasonable basis for our opinion.

PRICEWATERHOUSECOOPERS LLP

Chicago, IL

September 25, 2009

Portfolio of Investments

Municipal Total Return Managed Accounts Portfolio

July 31, 2009

| | | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | | | Optional Call Provisions (2) | | Ratings (3) | | | Value |

| | | | | | | | | | | | | |

| | | Alabama – 2.8% | | | | | | | | | | |

| | | | | |

| $ | 1,020 | | Alabama 21st Century Authority, Tobacco Settlement Revenue Bonds, Series 2001, 5.500%, 12/01/10 | | | | No Opt. Call | | A– | | | $ | 1,031,618 |

| | | | | |

| | 850 | | Alabama State Board of Education, Revenue Bonds, Faulkner State Community College, Series 2009, 6.125%, 10/01/28 | | | | 10/18 at 100.00 | | A2 | | | | 912,127 |

| | | | | |

| | 100 | | City of Birmingham, Alabama, Water and Sewer Revenue Warrants, Series 1998-A, 4.750%, 1/01/29 – MBIA Insured | | | | 1/10 at 100.00 | | A | | | | 95,005 |

| | | | | |

| | 445 | | The Special Care Facilities Financing Authority of the City of Birmingham, Alabama, Medical Center East Health Care Facility Revenue Bonds, Series 1986 Refunding, 7.250%, 7/01/15 – MBIA Insured (ETM) | | | | 1/10 at 100.00 | | A | (4) | | | 523,120 |

| | 2,415 | | Total Alabama | | | | | | | | | | 2,561,870 |

| | | Alaska – 0.7% | | | | | | | | | | |

| | | | | |

| | 145 | | Alaska Municipal Bond Bank Authority, General Obligation Bonds, Series 2006-2, 5.500%, 12/01/21 – MBIA Insured (Alternative Minimum Tax) | | | | 12/16 at 100.00 | | A+ | | | | 145,178 |

| | | | | |

| | 500 | | Alaska Student Loan Corporation, Senior Lien Student Loan Revenue Bonds, Series 2006A-2, 5.000%, 6/01/14 (Alternative Minimum Tax) | | | | No Opt. Call | | AAA | | | | 514,000 |

| | 645 | | Total Alaska | | | | | | | | | | 659,178 |

| | | Arizona – 0.1% | | | | | | | | | | |

| | | | | |

| | 100 | | Yuma County Industrial Development Authority, Arizona, Exempt Revenue Bonds, Far West Water & Sewer Inc. Refunding, Series 2007A, 6.500%, 12/01/17 (Alternative Minimum Tax) | | | | No Opt. Call | | N/R | | | | 89,449 |

| | | Arkansas – 1.1% | | | | | | | | | | |

| | | | | |

| | 950 | | Arkansas Development Finance Authority, Single Family Mortgage Revenue Bonds, GNMA/FNMA Mortgage-Backed Securities Program, Series 2000F, 6.250%, 7/01/31 (Alternative Minimum Tax) | | | | 7/10 at 100.00 | | AAA | | | | 969,865 |

| | | California – 11.6% | | | | | | | | | | |

| | | | | |

| | 850 | | Bay Area Toll Authority, California, Revenue Bonds, San Francisco Bay Area Toll Bridge, Series 2008-F1, 5.500%, 4/01/43 | | | | 4/18 at 100.00 | | AA | | | | 865,640 |

| | | | | |

| | 385 | | California County Tobacco Securitization Agency, Tobacco Settlement Asset-Backed Bonds, Golden Gate Tobacco Funding Corporation, Turbo, Series 2002A, 5.750%, 6/01/30 (Pre-refunded 6/01/12) | | | | 6/12 at 100.00 | | BBB | (4) | | | 420,320 |

| | | | | |

| | 250 | | California Health Facilities Financing Authority, Revenue Bonds, Cedars-Sinai Medical Center, Series 2005, 5.000%, 11/15/10 | | | | No Opt. Call | | A2 | | | | 257,615 |

| | | | | |

| | 100 | | California Health Facilities Financing Authority, Revenue Bonds, Kaiser Permanente System, Series 1993A, 5.400%, 5/01/28 (ETM) | | | | 5/10 at 100.00 | | AAA | | | | 100,819 |

| | | | | |

| | 250 | | California Municipal Finance Authority, Revenue Refunding Bonds, Biola University, Series 2008A, 5.000%, 10/01/18 | | | | No Opt. Call | | Baa1 | | | | 239,860 |

| | | | | |

| | 720 | | California, Various Purpose General Obligation Bonds, Series 1997, 5.625%, 10/01/21 – BHAC Insured | | | | 10/09 at 100.00 | | AAA | | | | 724,183 |

| | | | | |

| | 225 | | Daly City Housing Development Finance Agency, California, Mobile Home Park Revenue Bonds, Franciscan Mobile Home Park Refunding, Series 2007A, 5.250%, 12/15/23 | | | | 12/17 at 100.00 | | A– | | | | 200,144 |

| | | | | |

| | 1,000 | | Gilroy Unified School District, Santa Clara County, California, General Obligation Bonds, Series 2009A, 6.000%, 8/01/25 – AGC Insured | | | | No Opt. Call | | AAA | | | | 1,125,728 |

| | | | | |

| | | Golden State Tobacco Securitization Corporation, California, Tobacco Settlement Asset-Backed Revenue Bonds, Series 2005A: | | | | | | | | | | |

| | 325 | | 4.000%, 6/01/12 – AMBAC Insured | | | | No Opt. Call | | A– | | | | 326,898 |

| | 500 | | 5.000%, 6/01/17 | | | | 6/17 at 100.00 | | A– | | | | 477,790 |

| | | | | |

| | 1,000 | | Peralta Community College District, Alameda County, California, General Obligation Bonds, Series 2004C, 5.500%, 8/01/24 – MBIA Insured | | | | 8/12 at 102.00 | | AA– | | | | 1,067,408 |

| | | | | |

| | 850 | | Public Utilities Commission of the City and County of San Francisco, California, Water Revenue Bonds, Series 2006A, 5.000%, 11/01/25 – FSA Insured | | | | 5/16 at 100.00 | | AAA | | | | 871,463 |

Portfolio of Investments

Municipal Total Return Managed Accounts Portfolio (continued)

July 31, 2009

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | | | Optional Call Provisions (2) | | Ratings (3) | | Value |

| | | | | | | | | | | | |

| | | California (continued) | | | | | | | | | |

| | | | | |

| $ | 600 | | San Francisco Airports Commission, California, Revenue Bonds, San Francisco International Airport, Second Series 2000, Issue 26A, 5.000%, 5/01/15 – FGIC Insured | | | | 5/10 at 101.00 | | A1 | | $ | 603,534 |

| | | | | |

| | 750 | | San Francisco Unified School District, California, General Obligation Bonds, Series 2007A, 3.000%, 6/15/26 – FSA Insured | | | | 6/17 at 100.00 | | AAA | | | 571,620 |

| | | | | |

| | 1,000 | | San Gorgonio Memorial Healthcare District, Riverside County, California, General Obligation Bonds, Series 2009C, 7.000%, 8/01/27 (WI/DD, Settling 8/11/09) | | | | 8/17 at 100.00 | | Baa1 | | | 1,028,300 |

| | | | | |

| | 1,000 | | State of California $4,000,000,000 Various Purpose General Obligation Bonds, 6.500%, 4/01/33 – MBIA Insured | | | | 4/19 at 100.00 | | A | | | 1,084,258 |

| | | | | |

| | 750 | | Western Municipal Water District Facilities Authority, California, Water Revenue Bonds, Series 2009B, 5.000%, 10/01/34 | | | | 10/19 at 100.00 | | AA+ | | | 728,003 |

| | 10,555 | | Total California | | | | | | | | | 10,693,583 |

| | | Colorado – 1.2% | | | | | | | | | |

| | | | | |

| | 500 | | Colorado Health Facilities Authority, Colorado, Revenue Bonds, Valley View Hospital Association, Series 2008, 5.750%, 5/15/36 | | | | 5/18 at 100.00 | | BBB | | | 436,715 |

| | | | | |

| | 75 | | Colorado Health Facilities Authority, Colorado, Revenue Bonds, Yampa Valley Medical Center, Series 2007, 5.000%, 9/15/15 | | | | No Opt. Call | | BBB | | | 73,354 |

| | | | | |

| | 200 | | Colorado Health Facilities Authority, Revenue Bonds, Evangelical Lutheran Good Samaritan Society, Series 2006, 5.250%, 6/01/17 | | | | 6/16 at 100.00 | | A– | | | 205,412 |

| | | | | |

| | 150 | | Denver City and County, Colorado, Airport System Revenue Refunding Bonds, Series 2001A, 5.500%, 11/15/14 – FGIC Insured | | | | 11/11 at 100.00 | | A+ | | | 155,912 |

| | | | | |

| | 300 | | E-470 Public Highway Authority, Colorado, Senior Revenue Bonds, Series 2007B-1, 5.500%, 9/01/24 – MBIA Insured | | | | 9/15 at 100.00 | | A | | | 276,558 |

| | 1,225 | | Total Colorado | | | | | | | | | 1,147,951 |

| | | District of Columbia – 0.3% | | | | | | | | | |

| | | | | |

| | 300 | | District of Columbia Tobacco Settlement Corporation, Tobacco Settlement Asset-Backed Bonds, Series 2001, 6.750%, 5/15/40 | | | | 5/11 at 101.00 | | BBB | | | 252,414 |

| | | Florida – 3.8% | | | | | | | | | |

| | | | | |

| | 25 | | Beacon Lakes Community Development District, Florida, Special Assessment Bonds, Series 2007A, 6.000%, 5/01/38 | | | | 5/17 at 100.00 | | N/R | | | 15,880 |

| | | | | |

| | 25 | | Boynton Village Community Development District, Florida, Special Assessment Bonds, Series 2007-A1, 5.750%, 5/01/37 | | | | 5/17 at 100.00 | | N/R | | | 15,862 |

| | | | | |

| | 360 | | Brevard County, Florida, General Obligation Bonds, South Brevard Recreation, Series 2007, 5.000%, 7/01/22 – AMBAC Insured | | | | No Opt. Call | | N/R | | | 348,016 |

| | | | | |

| | 750 | | Florida Board of Education, Lottery Revenue Bonds, Series 2006A, 5.000%, 7/01/21 – AMBAC Insured | | | | 7/15 at 101.00 | | AAA | | | 774,075 |

| | | | | |

| | 490 | | Florida Housing Finance Corporation, Homeowner Mortgage Revenue Bonds, Series 2008-1, 6.450%, 1/01/39 (Alternative Minimum Tax) | | | | 7/17 at 100.00 | | AA+ | | | 512,109 |

| | | | | |

| | 280 | | Highlands County Health Facilities Authority, Florida, Hospital Revenue Bonds, Adventist Health System, Series 2005D, 5.000%, 11/15/35 | | | | No Opt. Call | | A+ | | | 248,570 |

| | | | | |

| | 750 | | Jacksonville, Florida, Excise Taxes Revenue Refunding Bonds, Series 2003C, 5.250%, 10/01/19 – MBIA Insured (Alternative Minimum Tax) | | | | 10/13 at 100.00 | | Aa3 | | | 739,785 |

| | | | | |

| | 680 | | Miami-Dade County, Florida, Aviation Revenue Bonds, Miami International Airport, Refunding Series 2003E, 5.250%, 10/01/13 – MBIA Insured (Alternative Minimum Tax) | | | | No Opt. Call | | AA | | | 705,282 |

| | | | | |

| | 75 | | Seminole Tribe of Florida, Special Obligation Bonds, Series 2007A, 5.750%, 10/01/22 | | | | 10/17 at 100.00 | | BBB | | | 70,489 |

| | | | | |

| | 75 | | Tolomato Community Development District, Florida, Special Assessment Bonds, Series 2007, 6.375%, 5/01/17 | | | | No Opt. Call | | N/R | | | 62,278 |

| | 3,510 | | Total Florida | | | | | | | | | 3,492,346 |

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | | | Optional Call Provisions (2) | | Ratings (3) | | Value |

| | | | | | | | | | | | |

| | | Georgia – 3.7% | | | | | | | | | |

| | | | | |

| $ | 650 | | Atlanta Development Authority, Georgia, Educational Facilities Revenue Bonds, Science Park LLC Project, Series 2007, 5.250%, 7/01/27 | | | | 7/17 at 100.00 | | A1 | | $ | 667,973 |

| | | | | |

| | 500 | | Atlanta, Georgia, Water and Wastewater Revenue Bonds, Series 2009A, 6.000%, 11/01/22 | | | | 11/19 at 100.00 | | A | | | 508,675 |

| | | | | |

| | 500 | | Gwinnett County Development Authority, Georgia, Certificates of Participation, County Public Schools Project, Series 2006, 5.250%, 1/01/19 – MBIA Insured | | | | No Opt. Call | | AA+ | | | 555,255 |

| | | | | |

| | 60 | | Houston County Hospital Authority, Georgia, Revenue Bonds, Houston Healthcare Project, Series 2007, 5.250%, 10/01/18 | | | | 10/17 at 100.00 | | A2 | | | 60,911 |

| | | | | |

| | 500 | | La Grange-Troup County Hospital Authority, Georgia, Revenue Anticipation Certificates, Series 2008A, 5.500%, 7/01/38 | | | | 7/18 at 100.00 | | A+ | | | 495,685 |

| | | | | |

| | 350 | | Municipal Electric Authority of Georgia, Project One Subordinate Lien Revenue Bonds, Series 2008A, 5.250%, 1/01/21 | | | | No Opt. Call | | A | | | 379,736 |

| | | | | |

| | 750 | | Private Colleges and Universities Authority, Georgia, Revenue Bonds, Emory University, Series 2008C, 5.000%, 9/01/38 | | | | 9/18 at 100.00 | | AA | | | 757,605 |

| | 3,310 | | Total Georgia | | | | | | | | | 3,425,840 |

| | | Guam – 0.5% | | | | | | | | | |

| | | | | |

| | 500 | | Guam Government, General Obligation Bonds, 2009 Series A, 5.750%, 11/15/14 | | | | No Opt. Call | | B+ | | | 498,175 |

| | | Idaho – 1.6% | | | | | | | | | |

| | | | | |

| | 750 | | Boise-Kuna Irrigation District, Ada and Canyon Counties, Idaho Arrowrock Hydroelectric Project Revenue Bonds, Series 2008, 7.375%, 6/01/34 | | | | 6/18 at 100.00 | | A3 | | | 820,365 |

| | | | | |

| | | Idaho Housing and Finance Association, Single Family Mortgage Revenue Bonds, Series 2008A-1: | | | | | | | | | |

| | 130 | | 5.625%, 7/01/28 (Alternative Minimum Tax) | | | | 1/17 at 100.00 | | Aaa | | | 134,246 |

| | 500 | | 6.250%, 7/01/38 (Alternative Minimum Tax) | | | | 1/17 at 100.00 | | Aaa | | | 517,270 |

| | 1,380 | | Total Idaho | | | | | | | | | 1,471,881 |

| | | Illinois – 10.4% | | | | | | | | | |

| | | | | |

| | 685 | | Chicago, Illinois, General Obligation Refunding Bonds, Series 1992, 6.250%, 1/01/11 – AMBAC Insured | | | | No Opt. Call | | AA– | | | 711,736 |

| | | | | |

| | 500 | | Chicago, Illinois, Second Lien General Airport Revenue Refunding Bonds, O’Hare International Airport, Series 1999, 5.500%, 1/01/16 – AMBAC Insured (Alternative Minimum Tax) | | | | 1/10 at 101.00 | | AA– | | | 505,715 |

| | | | | |

| | 255 | | Green Oaks Village, Illinois, General Obligation Bonds, Series 2009, 5.500%, 12/01/28 | | | | No Opt. Call | | AAA | | | 274,574 |

| | | | | |

| | 200 | | Illinois Development Finance Authority, Revenue Bonds, Adventist Health System – Sunbelt Obligated Group, Series 1997A, 5.500%, 11/15/14 – MBIA Insured | | | | No Opt. Call | | AA | | | 210,410 |

| | | | | |

| | 750 | | Illinois Finance Authority, Revenue Bonds, Children’s Memorial Hospital, Series 2008B, 5.500%, 8/15/21 | | | | 8/18 at 100.00 | | A– | | | 768,765 |

| | | | | |

| | 650 | | Illinois Finance Authority, Revenue Bonds, Elmhurst Memorial Healthcare, Series 2008A, 5.625%, 1/01/37 | | | | 1/18 at 100.00 | | Baa1 | | | 531,525 |

| | | | | |

| | 750 | | Illinois Finance Authority, Revenue Bonds, Illinois Institute of Technology, Refunding Series 2006A, 5.000%, 4/01/17 | | | | 4/16 at 100.00 | | Baa2 | | | 711,008 |

| | | | | |

| | 1,000 | | Illinois Finance Authority, Revenue Bonds, Illinois Institute of Technology, Series 2009, 6.250%, 2/01/19 | | | | No Opt. Call | | N/R | | | 1,011,410 |

| | | | | |

| | 150 | | Illinois Finance Authority, Revenue Bonds, Roosevelt University, Series 2007, 5.400%, 4/01/27 | | | | 4/17 at 100.00 | | Baa1 | | | 141,825 |

| | | | | |

| | 100 | | Illinois Finance Authority, Revenue Bonds, Sherman Health Systems, Series 2007A, 5.500%, 8/01/37 | | | | 8/17 at 100.00 | | Baa1 | | | 75,837 |

| | | | | |

| | 700 | | Illinois Finance Authority, Revenue Refunding Bonds, Silver Cross Hospital and Medical Centers, Series 2008A, 6.000%, 8/15/23 | | | | 8/18 at 100.00 | | BBB | | | 668,682 |

Portfolio of Investments

Municipal Total Return Managed Accounts Portfolio (continued)

July 31, 2009

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | | | Optional Call Provisions (2) | | Ratings (3) | | Value |

| | | | | | | | | | | | |

| | | Illinois (continued) | | | | | | | | | |

| | | | | |

| $ | 75 | | Illinois Finance Authority, Student Housing Revenue Bonds, Educational Advancement Fund Inc., University Center Project, Series 2006B, 5.000%, 5/01/13 | | | | No Opt. Call | | Baa3 | | $ | 73,454 |

| | | | | |

| | | Illinois Health Facilities Authority, Revenue Refunding Bonds, Elmhurst Memorial Healthcare, Series 2002: | | | | | | | | | |

| | 665 | | 6.250%, 1/01/17 | | | | 1/13 at 100.00 | | Baa1 | | | 676,790 |

| | 60 | | 5.500%, 1/01/22 | | | | 1/13 at 100.00 | | Baa1 | | | 56,248 |

| | | | | |

| | 205 | | Kane County, Illinois, Community Unit School District 304 Geneva, General Obligation Bonds, Series 2008, 5.250%, 1/01/23 - FSA Insured | | | | 1/18 at 100.00 | | AAA | | | 219,221 |

| | | | | |

| | 250 | | Lombard Public Facilities Corporation, Illinois, Second Tier Conference Center and Hotel Revenue Bonds, Series 2005B, 5.250%, 1/01/30 | | | | 1/16 at 100.00 | | AA | | | 251,070 |

| | | | | |

| | | Markham, Illinois, General Obligation Bonds, Series 2008A: | | | | | | | | | |

| | 225 | | 4.750%, 2/01/17 | | | | No Opt. Call | | BBB | | | 217,019 |

| | 500 | | 4.750%, 2/01/18 | | | | No Opt. Call | | BBB | | | 476,440 |

| | | | | |

| | 500 | | Metropolitan Pier and Exposition Authority, Illinois, Revenue Bonds, McCormick Place Hospitality Facility, Series 1996A, 7.000%, 7/01/26 (ETM) | | | | No Opt. Call | | AAA | | | 652,735 |

| | | | | |

| | 250 | | Regional Transportation Authority, Cook, DuPage, Kane, Lake, McHenry and Will Counties, Illinois, General Obligation Bonds, Series 1991, 6.700%, 11/01/21 – FGIC Insured | | | | No Opt. Call | | AA+ | | | 306,573 |

| | | | | |

| | 250 | | Saint Clair County High School District 203, O’Fallon, Illinois, General Obligation Bonds, Series 2007, 5.750%, 12/01/26 – AMBAC Insured | | | | 12/17 at 100.00 | | A+ | | | 268,623 |

| | | | | |

| | 750 | | Southwestern Illinois Development Authority, Local Government Program Bonds, St. Clair County Community Unit School District 19 Mascoutah, Series 2009, 5.750%, 2/01/29 – AGC Insured | | | | No Opt. Call | | AAA | | | 818,190 |

| | 9,470 | | Total Illinois | | | | | | | | | 9,627,850 |

| | | Indiana – 5.3% | | | | | | | | | |

| | | | | |

| | 250 | | Central Nine Career Charter School Building Corporation, Indiana, General Obligation Bonds, Series 2007, 5.500%, 1/15/17 | | | | No Opt. Call | | A | | | 273,795 |

| | | | | |

| | 670 | | East Chicago Multi-School Building Corporation, Lake County, Indiana, First Mortgage Bonds, Series 2008, 6.000%, 7/15/16 | | | | No Opt. Call | | AA+ | | | 786,419 |

| | | | | |

| | 750 | | Franklin Community Multi-School Building Corporation, Marion County, Indiana, First Mortgage Revenue Bonds, Series 2007A, 5.000%, 7/15/20 – FGIC Insured | | | | No Opt. Call | | A | | | 803,400 |

| | | | | |

| | 350 | | Indiana Bond Bank, Special Program Gas Revenue Bonds, JP Morgan Ventures Energy Corporation Guaranteed, Series 2007A, 5.000%, 10/15/17 | | | | No Opt. Call | | Aa3 | | | 342,923 |

| | | | | |

| | | Indiana Finance Authority, Revenue Bonds, Children’s Museum Project, Series 2008: | | | | | | | | | |

| | 500 | | 5.000%, 10/01/26 | | | | 7/18 at 100.00 | | Aa3 | | | 501,050 |

| | 280 | | 5.000%, 10/01/28 | | | | 7/18 at 100.00 | | Aa3 | | | 272,244 |

| | | | | |

| | 500 | | Jasper County, Indiana, Pollution Control Revenue Refunding Bonds, Northern Indiana Public Service Company Project, Series 1994A Remarketed, 4.150%, 8/01/10 – MBIA Insured | | | | No Opt. Call | | AA | | | 502,825 |

| | | | | |

| | 250 | | Merrillville Multi-School Building Corporation, Lake County, Indiana, First Mortgage Revenue Bonds, Series 2008, 5.250%, 7/15/22 | | | | 1/18 at 100.00 | | A | | | 260,970 |

| | | | | |

| | 300 | | Portage Redevelopment District, Indiana, Tax Increment Revenue Bonds, Series 2008, 5.250%, 1/15/19 – CIFG Insured | | | | 1/18 at 100.00 | | BBB+ | | | 306,066 |

| | | | | |

| | 75 | | Portage, Indiana, Revenue Bonds, Series 2006, 5.000%, 7/15/23 | | | | 7/16 at 100.00 | | BBB+ | | | 68,174 |

| | | | | |

| | 650 | | Tri-Creek Middle School Building Corporation, Indiana, First Mortgage Bonds, Series 2008, 6.000%, 1/15/16 – FSA Insured | | | | No Opt. Call | | AAA | | | 768,469 |

| | 4,575 | | Total Indiana | | | | | | | | | 4,886,335 |

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | | | Optional Call Provisions (2) | | Ratings (3) | | Value |

| | | | | | | | | | | | |

| | | Kansas – 0.9% | | | | | | | | | |

| | | | | |

| $ | 835 | | Wyandotte County-Kansas City Unified Government, Kansas, Sales Tax Special Obligation Bonds, Redevelopment Project Area B, Series 2005, 4.750%, 12/01/16 | | | | 12/15 at 100.00 | | N/R | | $ | 818,250 |

| | | Kentucky – 0.8% | | | | | | | | | |

| | | | | |

| | 500 | | Kentucky Economic Development Finance Authority, Louisville Arena Project Revenue Bonds, Louisville Arena Authority, Inc., Series 2008A-1, 5.750%, 12/01/28 – AGC Insured | | | | 6/18 at 100.00 | | AAA | | | 521,760 |

| | | | | |

| | 250 | | Louisville and Jefferson County Metropolitan Government, Kentucky, General Revenue Bonds, Bellarmine University, Series 2008A, 6.000%, 5/01/28 | | | | 5/18 at 100.00 | | Baa2 | | | 253,195 |

| | 750 | | Total Kentucky | | | | | | | | | 774,955 |

| | | Maine – 0.4% | | | | | | | | | |

| | | | | |

| | 410 | | South Berwick, Maine, Education Revenue Bonds, Berwick Academy Issue, Series 1998, 5.250%, 8/01/13 | | | | 8/10 at 100.00 | | BBB | | | 410,357 |

| | | Massachusetts – 3.1% | | | | | | | | | |

| | | | | |

| | 750 | | Massachusetts Bay Transportation Authority, Senior Lien Sales Tax Revenue Bonds, Series 2004B, 5.250%, 7/01/18 | | | | No Opt. Call | | AAA | | | 881,145 |

| | | | | |

| | 250 | | Massachusetts Development Finance Agency, Revenue Bonds, Boston Architectural College, Series 2006, 5.000%, 1/01/37 – ACA Insured | | | | 1/17 at 100.00 | | N/R | | | 156,908 |

| | | | | |

| | 750 | | Massachusetts Development Finance Agency, Revenue Bonds, The Sabis International Charter School Issue, Series 2009, 8.000%, 4/15/31 | | | | 10/19 at 100.00 | | BBB | | | 796,620 |

| | | | | |

| | 750 | | Massachusetts Educational Financing Authority, Education Loan Revenue Bonds, Series 2008H, 6.125%, 1/01/22 – AGC Insured (Alternative Minimum Tax) | | | | 1/18 at 100.00 | | AAA | | | 769,470 |

| | | | | |

| | 300 | | Massachusetts Health and Educational Facilities Authority Revenue Bonds, Quincy Medical Center Issue, Series A (2008), 6.250%, 1/15/28 | | | | 1/18 at 100.00 | | N/R | | | 221,760 |

| | 2,800 | | Total Massachusetts | | | | | | | | | 2,825,903 |

| | | Michigan – 4.1% | | | | | | | | | |

| | | | | |

| | 250 | | Garden City Hospital Finance Authority, Michigan, Revenue Bonds, Garden City Hospital Obligated Group, Series 2007A, 4.875%, 8/15/27 | | | | 8/17 at 100.00 | | N/R | | | 139,098 |

| | | | | |

| | 500 | | Kent Hospital Finance Authority, Michigan, Revenue Bonds, Spectrum Health System, Series 2008A, 5.500%, 1/15/47 (Mandatory put 1/15/15) | | | | 1/15 at 100.00 | | AA | | | 517,580 |

| | | | | |

| | 750 | | Michigan Higher Education Facilities Authority, Limited Obligation Revenue Bonds, Alma College Project, Series 2008, 5.500%, 6/01/28 | | | | 6/18 at 100.00 | | A3 | | | 749,940 |

| | | | | |

| | 150 | | Michigan Higher Education Facilities Authority, Revenue Bonds, Kalamazoo College Project, Series 2007, 5.000%, 12/01/33 | | | | 12/17 at 100.00 | | A1 | | | 142,110 |

| | | | | |

| | 200 | | Michigan Higher Education Student Loan Authority, Revenue Bonds, Series 2003, XVII-I, 4.750%, 3/01/18 – AMBAC Insured (Alternative Minimum Tax) | | | | 3/14 at 100.00 | | AA | | | 185,692 |

| | | | | |

| | 80 | | Michigan State Building Authority, Revenue Bonds, Facilities Program, Series 2001I, 4.750%, 10/15/25 | | | | 10/09 at 100.00 | | A+ | | | 78,839 |

| | | | | |

| | 30 | | Michigan State Hospital Finance Authority, Hospital Revenue Bonds, Detroit Medical Center Obligated Group, Series 1998A, 5.250%, 8/15/23 | | | | 8/09 at 100.00 | | Ba3 | | | 20,437 |

| | | | | |

| | 130 | | Michigan State Hospital Finance Authority, Hospital Revenue Refunding Bonds, Detroit Medical Center Obligated Group, Series 1997A, 5.250%, 8/15/27 – AMBAC Insured | | | | 8/09 at 100.00 | | BB– | | | 83,587 |

| | | | | |

| | 875 | | Michigan State Hospital Finance Authority, Hospital Revenue Refunding Bonds, Trinity Health Credit Group, Series 2000A, 6.000%, 12/01/27 – AMBAC Insured | | | | 12/10 at 101.00 | | AA | | | 893,786 |

| | | | | |

| | 15 | | Michigan State Hospital Finance Authority, Revenue Refunding Bonds, Detroit Medical Center Obligated Group, Series 1993A, 6.250%, 8/15/13 | | | | 8/09 at 100.00 | | BB– | | | 14,767 |

| | | | | |

| | 300 | | Michigan Tobacco Settlement Finance Authority, Tobacco Settlement Asset-Backed Revenue Bonds, Series 2008A, 6.875%, 6/01/42 | | | | 6/18 at 100.00 | | Baa3 | | | 225,438 |

Portfolio of Investments

Municipal Total Return Managed Accounts Portfolio (continued)

July 31, 2009

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | | | Optional Call Provisions (2) | | Ratings (3) | | Value |

| | | | | | | | | | | | |

| | | Michigan (continued) | | | | | | | | | |

| | | | | |

| $ | 700 | | Royal Oak Hospital Finance Authority, Michigan, Hospital Revenue Bonds, William Beaumont Hospital, Refunding Series 2009V, 6.250%, 9/01/14 | | | | No Opt. Call | | A1 | | $ | 760,802 |

| | 3,980 | | Total Michigan | | | | | | | | | 3,812,076 |

| | | Missouri – 3.5% | | | | | | | | | |

| | | | | |

| | 1,000 | | Carroll County Public Water Supply District 1, Missouri, Water System Revenue Bonds, Refunding Series 2009, 5.625%, 3/01/34 | | | | 3/18 at 100.00 | | A | | | 1,009,020 |

| | | | | |

| | 1,000 | | Missouri Development Finance Board, Independence, Infrastructure Facilities Revenue Bonds, Water System Improvement Projects, Series 2009C, 5.750%, 11/01/29 | | | | No Opt. Call | | A+ | | | 1,011,620 |

| | | | | |

| | 600 | | Missouri Development Finance Board, Infrastructure Facilities Leasehold Revenue Bonds, Independence Electric System Projects, Series 2009D, 5.750%, 6/01/34 | | | | No Opt. Call | | A+ | | | 606,744 |

| | | | | |

| | 287 | | Saint Louis, Missouri, Tax Increment Financing Revenue Notes, Marquette Building Redevelopment Project, Series 2008-A, 6.500%, 1/23/28 | | | | No Opt. Call | | N/R | | | 183,496 |

| | | | | |

| | 360 | | Sikeston, Missouri, Electric System Revenue Bonds, Series 1992, 6.200%, 6/01/10 – MBIA Insured | | | | No Opt. Call | | A | | | 365,753 |

| | | | | |

| | 75 | | St. Louis County Industrial Development Authority, Missouri, Revenue Bonds, Friendship Village of West County, Series 2007A, 5.250%, 9/01/15 | | | | No Opt. Call | | N/R | | | 73,180 |

| | 3,322 | | Total Missouri | | | | | | | | | 3,249,813 |

| | | Nebraska – 0.6% | | | | | | | | | |

| | | | | |

| | 500 | | Douglas County Hospital Authority 2, Nebraska, Health Facilities Revenue Refunding Bonds, Children’s Hospital Obligated Group, Series 2008, 6.125%, 8/15/31 | | | | 8/17 at 100.00 | | A2 | | | 512,890 |

| | | Nevada – 1.8% | | | | | | | | | |

| | | | | |

| | 800 | | Clark County, Nevada, Passenger Facility Charge Revenue Bonds, Las Vegas-McCarran International Airport, Series 2007A-2, 5.000%, 7/01/26 – AMBAC Insured | | | | 7/17 at 100.00 | | Aa3 | | | 781,224 |

| | | | | |

| | 815 | | Clark County, Nevada, Subordinate Lien Airport Revenue Bonds, Series 2007A1, 5.000%, 7/01/19 – AMBAC Insured (Alternative Minimum Tax) | | | | 7/17 at 100.00 | | Aa3 | | | 785,937 |

| | | | | |

| | 100 | | Sparks Local Improvement District 3, Legends at Sparks Marina, Nevada, Limited Obligation Improvement Bonds, Series 2008, 6.750%, 9/01/27 | | | | 9/18 at 100.00 | | N/R | | | 78,194 |

| | 1,715 | | Total Nevada | | | | | | | | | 1,645,355 |

| | | New Jersey – 3.3% | | | | | | | | | |

| | | | | |

| | 600 | | New Jersey Economic Development Authority, Cigarette Tax Revenue Bonds, Series 2004, 5.625%, 6/15/19 | | | | 6/10 at 100.00 | | BBB | | | 558,822 |

| | | | | |

| | 500 | | New Jersey Economic Development Authority, School Facilities Construction Bonds, Series 2007-T3, 5.000%, 9/01/20 (Mandatory put 9/01/14) – FSA Insured | | | | 9/14 at 100.00 | | AAA | | | 543,615 |

| | | | | |

| | 350 | | New Jersey Health Care Facilities Finance Authority, Revenue Bonds, AHS Hospital Corporation, Series 2008A, 5.125%, 7/01/22 | | | | 7/18 at 100.00 | | A1 | | | 351,600 |

| | | | | |

| | | New Jersey Housing and Mortgage Finance Agency, Single Family Housing Revenue Bonds, Series 2008X: | | | | | | | | | |

| | 735 | | 4.850%, 4/01/16 (Alternative Minimum Tax) | | | | No Opt. Call | | AA | | | 758,130 |

| | 805 | | 5.000%, 4/01/17 (Alternative Minimum Tax) | | | | No Opt. Call | | AA | | | 824,932 |

| | 2,990 | | Total New Jersey | | | | | | | | | 3,037,099 |

| | | New Mexico – 0.8% | | | | | | | | | |

| | | | | |

| | 500 | | Albuquerque, New Mexico, Airport Revenue Bonds, Subordinate Lien Refunding Series 2008E, 5.500%, 7/01/13 | | | | No Opt. Call | | A1 | | | 544,405 |

| | | | | |

| | 250 | | Farmington, New Mexico, Pollution Control Revenue Bonds, Public Service Company of New Mexico San Juan Project, Series 2007A, 5.150%, 6/01/37 – FGIC Insured (Alternative Minimum Tax) | | | | 6/12 at 100.00 | | Baa3 | | | 176,813 |

| | 750 | | Total New Mexico | | | | | | | | | 721,218 |

| | | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | | | Optional Call Provisions (2) | | Ratings (3) | | | Value |

| | | | | | | | | | | | | |

| | | New York – 4.6% | | | | | | | | | | |

| | | | | |

| $ | 620 | | Dormitory Authority of the State of New York, Consolidated Revenue Bonds, City University System, Series 1993B, 6.000%, 7/01/14 | | | | No Opt. Call | | AA– | | | $ | 675,316 |

| | | | | |

| | 750 | | Dormitory Authority of the State of New York, Revenue Bond, Court Facilities Lease, New York City Issue, Series 2005A, 5.500%, 5/15/25 – AMBAC Insured | | | | No Opt. Call | | AA– | | | | 805,868 |

| | | | | |

| | 100 | | New York City Industrial Development Agency, New York, Civic Facility Revenue Bonds, Special Needs Facilities Pooled Program, Series 2008A-1, 5.700%, 7/01/13 | | | | No Opt. Call | | N/R | | | | 91,975 |

| | | | | |

| | 500 | | New York State Environmental Facilities Corporation, State Clean Water and Drinking Water Revolving Funds Revenue Bonds, Pooled Loan Issue, Series 2005B, 5.500%, 10/15/27 | | | | No Opt. Call | | AAA | | | | 595,575 |

| | | | | |

| | 435 | | New York State Mortgage Agency, Homeowner Mortgage Revenue Refunding Bonds, Series 87, 5.150%, 4/01/17 | | | | 9/09 at 100.00 | | Aa1 | | | | 440,685 |

| | | | | |

| | 500 | | New York State Tobacco Settlement Financing Corporation, Tobacco Settlement Asset-Backed and State Contingency Contract-Backed Bonds, Series 2003A-1, 5.250%, 6/01/20 – AMBAC Insured | | | | 6/13 at 100.00 | | AA– | | | | 517,610 |

| | | | | |

| | 450 | | Saratoga County Water and Sewer Authority, New York, Revenue Bonds, Series 2008, 5.000%, 9/01/38 | | | | 9/18 at 100.00 | | AA | | | | 449,982 |

| | | | | |

| | 640 | | Triborough Bridge and Tunnel Authority, New York, General Purpose Revenue Bonds, Series 2008C, 5.000%, 11/15/27 | | | | 11/18 at 100.00 | | Aa2 | | | | 667,987 |

| | 3,995 | | Total New York | | | | | | | | | | 4,244,998 |

| | | North Carolina – 3.7% | | | | | | | | | | |

| | | | | |

| | 100 | | Albemarle Hospital Authority, North Carolina, Health Care Facilities Revenue Bonds, Series 2007, 5.250%, 10/01/21 | | | | 10/17 at 100.00 | | N/R | | | | 91,359 |

| | | | | |

| | 1,000 | | Charlotte, North Carolina, Airport Revenue Bonds, Series 1999B, 6.000%, 7/01/16 – MBIA Insured (Alternative Minimum Tax) | | | | 7/11 at 100.00 | | A+ | | | | 1,011,250 |

| | | | | |

| | 250 | | Metropolitan Sewerage District of Buncombe County, North Carolina, Sewerage System Revenue Refunding Bonds, Series 1993A, 5.375%, 7/01/13 – FGIC Insured (ETM) | | | | 10/09 at 100.00 | | Aa3 | (4) | | | 273,990 |

| | | | | |

| | 350 | | North Carolina Eastern Municipal Power Agency, Power System Revenue Refunding Bonds, Series 1993B, 6.000%, 1/01/22 – FGIC Insured | | | | No Opt. Call | | Baa1 | | | | 386,166 |

| | | | | |

| | 500 | | North Carolina Eastern Municipal Power Agency, Power System Revenue Refunding Bonds, Series 2008A, 5.250%, 1/01/20 | | | | 1/18 at 100.00 | | BBB+ | | | | 513,665 |

| | | | | |

| | 740 | | North Carolina Medical Care Commission, Revenue Bonds, Maria Parham Medical Center, Series 2003, 5.500%, 10/01/17 – RAAI Insured | | | | No Opt. Call | | BBB– | | | | 660,095 |

| | | | | |

| | 500 | | North Carolina Municipal Power Agency 1, Catawba Electric Revenue Bonds, Series 2008C, 5.250%, 1/01/19 | | | | 1/18 at 100.00 | | A2 | | | | 534,685 |

| | 3,440 | | Total North Carolina | | | | | | | | | | 3,471,210 |

| | | Ohio – 1.4% | | | | | | | | | | |

| | | | | |

| | 95 | | Buckeye Tobacco Settlement Financing Authority, Ohio, Tobacco Settlement Asset-Backed Revenue Bonds, Senior Lien, Series 2007A-2, 5.125%, 6/01/24 | | | | 6/17 at 100.00 | | BBB | | | | 78,256 |

| | | | | |

| | 240 | | Cuyahoga County, Ohio, Revenue Refunding Bonds, Cleveland Clinic Health System, Series 2003A, 6.000%, 1/01/32 | | | | 7/13 at 100.00 | | Aa2 | | | | 249,900 |

| | | | | |

| | 200 | | Huron County, Ohio, Hospital Facilities Revenue Bonds, Fisher-Titus Medical Center, Series 2007, 5.250%, 12/01/17 | | | | 6/17 at 100.00 | | A | | | | 206,464 |

| | | | | |

| | 750 | | Lorain, Ohio, General Obligation Bonds, Pellet Terminal Improvement Series 2008, 6.750%, 12/01/23 | | | | 12/18 at 100.00 | | Baa2 | | | | 762,458 |

| | 1,285 | | Total Ohio | | | | | | | | | | 1,297,078 |

| | | Oregon – 0.1% | | | | | | | | | | |

| | | | | |

| | 150 | | Oregon Facilities Authority, Revenue Bonds, University of Portland Projects, Series 2007A, 5.500%, 4/01/27 | | | | 4/18 at 100.00 | | BBB+ | | | | 142,401 |

Portfolio of Investments

Municipal Total Return Managed Accounts Portfolio (continued)

July 31, 2009

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | | | Optional Call Provisions (2) | | Ratings (3) | | Value |

| | | | | | | | | | | | |

| | | Pennsylvania – 6.4% | | | | | | | | | |

| | | | | |

| $ | 430 | | City of Erie Higher Education Building Authority (Commonwealth of Pennsylvania) College Revenue Bonds, Series 2008 (Mercyhurst College Project), 5.350%, 3/15/28 | | | | 9/18 at 100.00 | | BBB | | $ | 387,292 |

| | | | | |

| | 250 | | Delaware County Authority, Pennsylvania, Revenue Bonds, Neumann College, Series 2008, 6.000%, 10/01/25 | | | | 10/18 at 100.00 | | BBB | | | 254,025 |

| | | | | |

| | 1,250 | | Lackawanna County, Pennsylvania, General Obligation Notes, Series 2009B, 6.000%, 9/15/32 – AGC Insured | | | | 9/19 at 100.00 | | AAA | | | 1,252,711 |

| | | | | |

| | 100 | | Lancaster County Hospital Authority, Pennsylvania, Revenue Bonds, Brethren Village Project, Series 2008A, 5.200%, 7/01/12 | | | | 7/10 at 101.00 | | N/R | | | 97,092 |

| | | | | |

| | 755 | | Lehigh County General Purpose Authority, Pennsylvania, Hospital Revenue Bonds, St. Luke’s Hospital of Bethlehem, Series 1992, 6.125%, 7/01/12 – AMBAC Insured | | | | 10/09 at 100.00 | | Baa1 | | | 756,072 |

| | | | | |

| | 500 | | Pennsylvania Economic Development Financing Authority, Exempt Facilities Revenue Refunding Bonds, Exelon Generation Company, LLC Project, Series 2009A, 5.000%, 12/01/42 (Mandatory put 6/01/12) | | | | 6/12 at 100.00 | | A3 | | | 504,695 |

| | | | | |

| | 375 | | Pennsylvania State University, General Revenue Bonds, Series 2005, 5.000%, 9/01/35 | | | | 9/15 at 100.00 | | AA | | | 379,294 |

| | | | | |

| | 870 | | Philadelphia Municipal Authority, Philadelphia, Pennsylvania, Lease Revenue Bonds, Series 2009, 6.000%, 4/01/23 | | | | No Opt. Call | | Baa1 | | | 887,165 |

| | | | | |

| | 850 | | Pittsburgh, Pennsylvania, General Obligation Bonds, Refunding Series 2008A, 5.000%, 9/01/13 | | | | No Opt. Call | | Baa1 | | | 874,922 |

| | | | | |

| | 500 | | Warwick School District, Bucks County, Pennsylvania, General Obligation Bonds, Series 2009, 4.375%, 2/01/25 – AGC Insured | | | | 2/18 at 100.00 | | AAA | | | 503,070 |

| | 5,880 | | Total Pennsylvania | | | | | | | | | 5,896,338 |

| | | Puerto Rico – 2.1% | | | | | | | | | |

| | | | | |

| | 275 | | Puerto Rico Highway and Transportation Authority, Highway Revenue Bonds, Series 2003G, 5.250%, 7/01/18 – FGIC Insured | | | | 7/13 at 100.00 | | BBB | | | 266,615 |

| | | | | |

| | 135 | | Puerto Rico Highway and Transportation Authority, Highway Revenue Bonds, Series 2007N, 5.500%, 7/01/21 | | | | No Opt. Call | | BBB | | | 129,415 |

| | | | | |

| | 1,000 | | Puerto Rico, General Obligation Refunding Bonds, Series 2002, 5.500%, 7/01/14 – FGIC Insured | | | | No Opt. Call | | BBB– | | | 1,029,190 |

| | | | | |

| | 500 | | Puerto Rico, The Children’s Trust Fund, Tobacco Settlement Asset-Backed Refunding Bonds, Series 2002, 5.000%, 5/15/11 – BHAC Insured | | | | No Opt. Call | | BBB | | | 499,060 |

| | 1,910 | | Total Puerto Rico | | | | | | | | | 1,924,280 |

| | | Rhode Island – 1.2% | | | | | | | | | |

| | | | | |

| | 200 | | Rhode Island Housing & Mortgage Finance Corporation, Homeownership Opportunity Bond Program, 2007 Series 57-B, 5.150%, 4/01/22 (Alternative Minimum Tax) | | | | 4/17 at 100.00 | | AA+ | | | 202,512 |

| | | | | |

| | 250 | | Rhode Island Student Loan Authority, Student Loan Program Revenue Bonds, Series 2008A, 6.750%, 12/01/28 (Alternative Minimum Tax) | | | | 12/17 at 100.00 | | A | | | 251,153 |

| | | | | |

| | 670 | | Rhode Island Tobacco Settlement Financing Corporation, Tobacco Settlement Asset-Backed Bonds, Series 2002A, 6.000%, 6/01/23 | | | | 6/12 at 100.00 | | BBB | | | 624,628 |

| | 1,120 | | Total Rhode Island | | | | | | | | | 1,078,293 |

| | | South Carolina – 2.0% | | | | | | | | | |

| | | | | |

| | 500 | | Berkeley County School District, South Carolina, Installment Purchase Revenue Bonds, Series 2006, 5.125%, 12/01/30 | | | | 12/16 at 100.00 | | A– | | | 500,115 |

| | | | | |

| | 400 | | Piedmont Municipal Power Agency, South Carolina, Electric Revenue Bonds, Series 2008A-3, 5.250%, 1/01/19 | | | | 1/18 at 100.00 | | A– | | | 413,164 |

| | | | | |

| | 740 | | South Carolina JOBS Economic Development Authority, Hospital Refunding and Improvement Revenue Bonds, Palmetto Health Alliance, Series 2003C, 6.000%, 8/01/13 | | | | No Opt. Call | | BBB+ | | | 769,052 |

| | | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | | | Optional Call Provisions (2) | | Ratings (3) | | | Value |

| | | | | | | | | | | | | |

| | | South Carolina (continued) | | | | | | | | | | |

| | | | | |

| | | Tobacco Settlement Revenue Management Authority, South Carolina, Tobacco Settlement Asset-Backed Bonds, Series 2001B: | | | | | | | | | | |

| $ | 195 | | 6.000%, 5/15/22 (Pre-refunded 5/15/12) | | | | 5/12 at 100.00 | | BBB | (4) | | $ | 205,175 |

| | 10 | | 6.375%, 5/15/28 (Pre-refunded 5/15/16) | | | | 5/16 at 100.00 | | BBB | (4) | | | 11,032 |

| | 1,845 | | Total South Carolina | | | | | | | | | | 1,898,538 |

| | | Tennessee – 0.9% | | | | | | | | | | |

| | | | | |

| | 145 | | Shelby County Health, Educational and Housing Facilities Board, Tennessee, Hospital Revenue Refunding Bonds, Methodist Healthcare, Series 1995, 5.250%, 8/01/15 – MBIA Insured | | | | No Opt. Call | | A | (4) | | | 161,882 |

| | | | | |

| | 1,000 | | Sullivan County Health Educational and Housing Facilities Board, Tennessee, Revenue Bonds, Wellmont Health System, Series 2006C, 5.250%, 9/01/36 | | | | 9/16 at 100.00 | | BBB+ | | | | 686,200 |

| | 1,145 | | Total Tennessee | | | | | | | | | | 848,082 |

| | | Texas – 4.5% | | | | | | | | | | |

| | | | | |

| | 500 | | City of Dallas, Texas, Counties of Dallas, Denton, Collin, and Rockwall, Waterworks and Sewer System Revenue Bonds, Series 1998 Refunding, 5.000%, 10/01/29 – FSA Insured | | | | 10/09 at 100.00 | | Aa2 | | | | 500,460 |

| | | | | |

| | 500 | | Dallas-Fort Worth International Airport, Texas, Auction Rate Revenue Bonds, Series 2004-A1, 5.750%, 11/01/18 – MBIA Insured (Alternative Minimum Tax) | | | | 11/09 at 100.00 | | A+ | | | | 501,015 |

| | | | | |

| | 350 | | Forney Independent School District, Kaufman County, Texas, General Obligation Bonds, Series 2008, 0.000%, 8/15/25 | | | | 8/17 at 65.60 | | AAA | | | | 154,609 |

| | | | | |

| | 500 | | Grapevine-Colleyville Independent School District, Tarrant and Dallas Counties, Texas, General Obligation Bonds, Series 2005A, 5.250%, 8/15/22 – FGIC Insured | | | | 8/15 at 100.00 | | AA | | | | 536,080 |

| | | | | |

| | 650 | | Houston, Texas, Subordinate Lien Airport System Revenue Refunding Bonds, Series 1998A, 6.000%, 7/01/13 – FGIC Insured (Alternative Minimum Tax) | | | | 7/10 at 100.00 | | A | | | | 654,355 |

| | | | | |

| | 380 | | North Texas Municipal Water District, Water System Revenue Bonds, Series 2006, 5.000%, 9/01/20 – FGIC Insured | | | | 9/16 at 100.00 | | AAA | | | | 413,163 |

| | | | | |

| | | North Texas Thruway Authority, First Tier System Revenue Refunding Bonds, Series 2008A: | | | | | | | | | | |

| | 200 | | 6.000%, 1/01/19 | | | | 1/18 at 100.00 | | A2 | | | | 218,184 |

| | 325 | | 6.000%, 1/01/23 – MBIA Insured | | | | 1/18 at 100.00 | | A | | | | 350,561 |

| | | | | |

| | 375 | | North Texas Thruway Authority, Second Tier System Revenue Refunding Bonds, Series 2008, 5.750%, 1/01/38 | | | | 1/18 at 100.00 | | A3 | | | | 359,310 |

| | | | | |

| | 540 | | Port of Port Arthur Navigation District, Texas, General Obligation Bonds, Port Improvement Series 2008B, 4.375%, 3/01/15 (Alternative Minimum Tax) | | | | No Opt. Call | | A | | | | 530,593 |

| | 4,320 | | Total Texas | | | | | | | | | | 4,218,330 |

| | | Utah – 1.1% | | | | | | | | | | |

| | | | | |

| | 750 | | Intermountain Power Agency, Utah, Power Supply Revenue Refunding Bonds, Series 2008A, 5.250%, 7/01/20 | | | | 7/13 at 100.00 | | A+ | | | | 775,403 |

| | | | | |

| | 100 | | Utah State Charter School Finance Authority, Revenue Bonds, Channing Hall Project, Series 2007A, 5.750%, 7/15/22 | | | | 7/15 at 102.00 | | N/R | | | | 81,736 |

| | | | | |

| | 140 | | Utah State Charter School Finance Authority, Revenue Bonds, Summit Academy Project, Series 2007A, 5.125%, 6/15/17 | | | | No Opt. Call | | BBB– | | | | 125,481 |

| | 990 | | Total Utah | | | | | | | | | | 982,620 |

| | | Virgin Islands – 2.0% | | | | | | | | | | |

| | | | | |

| | 300 | | Virgin Islands Public Finance Authority, Gross Receipts Taxes Loan Note, Series 2006, 5.000%, 10/01/16 – FGIC Insured | | | | No Opt. Call | | A | | | | 294,180 |

| | | | | |

| | 1,000 | | Virgin Islands Public Finance Authority, Matching Fund Revenue Loan

Note – Diageo Project, Series 2009A, 6.750%, 10/01/19 | | | | No Opt. Call | | Baa3 | | | | 1,046,360 |

| | | | | |

| | 500 | | Virgin Islands Public Finance Authority, Senior Lien Revenue Refunding Bonds, Matching Fund Loan Note, Series 1998A, 5.500%, 10/01/22 | | | | 10/09 at 100.50 | | BBB | | | | 472,980 |

| | 1,800 | | Total Virgin Islands | | | | | | | | | | 1,813,520 |

Portfolio of Investments

Municipal Total Return Managed Accounts Portfolio (continued)

July 31, 2009

| | | | | | | | | | | | | | |

Principal

Amount (000) | | | | Description (1) | | | | Optional Call Provisions (2) | | Ratings (3) | | Value |

| | | | | | | | | | | | | | |

| | | | | Virginia – 1.3% | | | | | | | | | |

| | | | | | |

| $ | 140 | | | | Fairfax County Water Authority, Virginia, Water Revenue Refunding Bonds, Series 1977, 5.800%, 1/01/16 (ETM) | | | | No Opt. Call | | AAA | | $ | 154,707 |

| | | | | | |

| | 100 | | | | Metropolitan Washington D.C. Airports Authority, Airport System Revenue Bonds, Series 2002A, 5.250%, 10/01/32 – FGIC Insured (Alternative Minimum Tax) | | | | 10/12 at 100.00 | | AA– | | | 94,244 |

| | | | | | |

| | 815 | | | | Virginia College Building Authority, Educational Facilities Revenue Bonds, Washington and Lee University, Series 2001, 5.750%, 1/01/34 | | | | No Opt. Call | | AA | | | 934,585 |

| | 1,055 | | | | Total Virginia | | | | | | | | | 1,183,536 |

| | | | | Washington – 0.2% | | | | | | | | | |

| | | | | | |

| | 100 | | | | Kalispel Indian Tribe, Washington, Priority Distribution Bonds, Series 2008, 6.625%, 1/01/28 | | | | No Opt. Call | | N/R | | | 75,357 |

| | | | | | |

| | 75 | | | | Skagit County Public Hospital District 1 , Washington, Skagit Valley Hospital, Series 2007, 5.750%, 12/01/28 | | | | 12/17 at 100.00 | | Baa2 | | | 65,069 |

| | 175 | | | | Total Washington | | | | | | | | | 140,426 |

| | | | | Wisconsin – 3.5% | | | | | | | | | |

| | | | | | |

| | | | | Badger Tobacco Asset Securitization Corporation, Wisconsin, Tobacco Settlement Asset-Backed Bonds, Series 2002: | | | | | | | | | |

| | 70 | | | | 6.125%, 6/01/27 (Pre-refunded 6/01/12) | | | | 6/12 at 100.00 | | AAA | | | 76,138 |

| | 320 | | | | 6.375%, 6/01/32 (Pre-refunded 6/01/12) | | | | 6/12 at 100.00 | | AAA | | | 361,440 |

| | | | | | |

| | 860 | | | | Wisconsin Health and Educational Facilities Authority, Revenue Bonds, Sisters of the Sorrowful Mother - Ministry Corporation, Series 1993D, 5.500%, 8/15/19 – MBIA Insured | | | | 8/09 at 100.00 | | A+ | | | 860,129 |

| | | | | | |

| | 860 | | | | Wisconsin Health and Educational Facilities Authority, Revenue Bonds, Wheaton Franciscan Services Inc., Series 2006B, 5.000%, 8/15/12 | | | | No Opt. Call | | BBB+ | | | 850,695 |

| | | | | | |

| | 1,000 | | | | Wisconsin State, General Fund Annual Appropriation Revenue Bonds, Series 2009A, 6.000%, 5/01/27 | | | | 5/19 at 100.00 | | AA– | | | 1,114,748 |

| | 3,110 | | | | Total Wisconsin | | | | | | | | | 3,263,150 |

| | | | | Wyoming – 0.3% | | | | | | | | | |

| | | | | | |

| | 250 | | | | Wyoming Municipal Power Agency Power Supply System Revenue Bonds, 2008 Series A, 5.500%, 1/01/28 | | | | 1/18 at 100.00 | | A2 | | | 258,318 |

| $ | 89,457 | | | | Total Long-Term Investments (cost $89,067,695) – 97.7% | | | | | | | | | 90,245,771 |

| | | | | | | | | | | | | | |

| | | | | Short-Term Investments – 2.5% | | | | | | | | | |

| | | | | | |

| $ | 2,267 | | | | State Street Global Advisors Money Market Fund, Tax Free Obligation | | | | N/A | | N/A | | | 2,267,059 |

| | | | | Total Short-Term Investments (cost $2,267,059) | | | | | | | | | 2,267,059 |

| | | | | Total Investments (cost $91,334,754) – 100.2% | | | | | | | | | 92,512,830 |

| | | | | Other Assets Less Liabilities – (0.2)% | | | | | | | | | (159,274) |

| | | | | Net Assets – 100% | | | | | | | | $ | 92,353,556 |

| | (1) | | All percentages shown in the Portfolio of Investments are based on net assets. |

| | (2) | | Optional Call Provisions (not covered by the report of independent registered public accounting firm): Dates (month and year) and prices of the earliest optional call or redemption. There may be other call provisions at varying prices at later dates. Certain mortgage-backed securities may be subject to periodic principal paydowns. |

| | (3) | | Ratings (not covered by the report of independent registered public accounting firm): Using the higher of Standard & Poor’s Group (“Standard & Poor’s”) or Moody’s Investor Service, Inc. (“Moody’s”) rating. Ratings below BBB by Standard & Poor’s or Baa by Moody’s are considered to be below investment grade. |

| | (4) | | Backed by an escrow or trust containing sufficient U.S. Government or U.S. Government agency securities which ensure the timely payment of principal and interest. Such investments are normally considered to be equivalent to AAA rated securities. |

| | WI/DD | | Purchased on a when-issued or delayed delivery basis. |

| | (ETM) | | Escrowed to maturity. |

See accompanying notes to financial statements.

Statement of Assets and Liabilities

July 31, 2009

| | | | |

Assets | | | | |

Investments, at value (cost $91,334,754) | | $ | 92,512,830 | |

Cash | | | 1,169 | |

Receivables: | | | | |

From Adviser | | | 82,632 | |

Interest | | | 1,076,788 | |

Investments sold | | | 90,000 | |

Shares sold | | | 34,056 | |

Other assets | | | 14 | |

Total assets | | | 93,797,489 | |

Liabilities | | | | |

Payables: | | | | |

Dividends | | | 304,432 | |

Investments purchased | | | 1,020,400 | |

Shares redeemed | | | 59,886 | |

Accrued other expenses | | | 59,215 | |

Total liabilities | | | 1,443,933 | |

Net assets | | $ | 92,353,556 | |

Shares outstanding | | | 9,419,505 | |

Net asset value per share | | $ | 9.80 | |

Net Assets Consist of: | | | | |

Capital paid-in | | $ | 92,113,199 | |

Undistributed (Over-distribution of) net investment income | | | 3,860 | |

Accumulated net realized gain (loss) from investments | | | (941,579 | ) |

Net unrealized appreciation (depreciation) of investments | | | 1,178,076 | |

Net assets | | $ | 92,353,556 | |

See accompanying notes to financial statements.

Statement of Operations

Year Ended July 31, 2009

| | | | |

Investment Income | | $ | 3,650,578 | |

Expenses | | | | |

Shareholders’ servicing agent fees and expenses | | | 4,948 | |

Custodian’s fees and expenses | | | 27,529 | |

Trustees’ fees and expenses | | | 2,277 | |

Professional fees | | | 59,677 | |

Shareholders’ reports – printing and mailing expenses | | | 42,318 | |

Federal and state registration fees | | | 39,720 | |

Other expenses | | | 2,109 | |

Total expenses before expense reimbursement | | | 178,578 | |

Expense reimbursement | | | (178,578 | ) |

Net expenses | | | — | |

Net investment income | | | 3,650,578 | |

Realized and Unrealized Gain (Loss) | | | | |

Net realized gain (loss) from investments | | | (856,243 | ) |

Change in net unrealized appreciation (depreciation) of investments | | | 1,870,917 | |

Net realized and unrealized gain (loss) | | | 1,014,674 | |

Net increase (decrease) in net assets from operations | | $ | 4,665,252 | |

See accompanying notes to financial statements.

Statement of Changes in Net Assets

| | | | | | | | |

| | | Year Ended

7/31/09 | | | Year Ended

7/31/08 | |

Operations | | | | | | | | |

Net investment income | | $ | 3,650,578 | | | $ | 809,706 | |

Net realized gain (loss) from investments | | | (856,243 | ) | | | (83,223 | ) |

Change in net unrealized appreciation (depreciation) of investments | | | 1,870,917 | | | | (727,908 | ) |

Net increase (decrease) in net assets from operations | | | 4,665,252 | | | | (1,425 | ) |

Distributions to Shareholders | | | | | | | | |

From net investment income | | | (3,639,392 | ) | | | (852,133 | ) |

Decrease in net assets from distributions to shareholders | | | (3,639,392 | ) | | | (852,133 | ) |

Fund Share Transactions | | | | | | | | |

Proceeds from sale of shares | | | 68,531,320 | | | | 47,631,290 | |

Proceeds from shares issued to shareholders due to reinvestment of

distributions | | | 238,828 | | | | — | |

| | | | 68,770,148 | | | | 47,631,290 | |

Cost of shares redeemed | | | (26,471,891 | ) | | | (3,326,839 | ) |

Net increase (decrease) in net assets from Fund share transactions | | | 42,298,257 | | | | 44,304,451 | |

Capital contribution from Adviser | | | 5,184 | | | | 4,480 | |

Net increase (decrease) in net assets | | | 43,329,301 | | | | 43,455,373 | |

Net assets at the beginning of year | | | 49,024,255 | | | | 5,568,882 | |

Net assets at the end of year | | | 92,353,556 | | | | 49,024,255 | |

Undistributed (Over-distribution of) net investment income at the

end of year | | $ | 3,860 | | | $ | (6,272 | ) |

See accompanying notes to financial statements.

Notes to Financial Statements

1. General Information and Significant Accounting Policies

The Nuveen Managed Accounts Portfolios Trust (the “Trust”) is an open-end management investment company registered under the Investment Company Act of 1940, as amended. The Trust is comprised of the Municipal Total Return Managed Accounts Portfolio (the “Fund”), among others. The Trust was organized as a Massachusetts business trust on November 14, 2006.