record levels, the MSCI World index up 4% and the MSCI Europe and Asia indices up 6% and 5%, respectively. Emerging market equities continued to outperform developed markets, supported by a healthy rebound in global trade and a weaker U.S. dollar, with the MSCI Emerging Markets Index up 7% for the quarter. Stock market volatility remains subdued, with the CBOE Volatility Index continuing to trade at its lowest level in over 20 years, ending the third quarter down another 15%.

Though equities outperformed most asset classes, fixed income posted modest gains driven by strong investor demand and low volatility, with the Bloomberg Barclays U.S. Aggregate index up 0.8%, U.S. investment grade corporates up 1.3% and high yield corporates up 2% for the third quarter of 2017. The U.S. Federal Reserve held rates steady in September, keeping the targeted range for its benchmark interest rate at1.0-1.25%, and also announced the beginning of a plan to shrink the central bank’s $4.5 trillion balance sheet, leading to rising treasury yields across the curve. High yield spreads tightened 26 basis points and while issuance volume declined 2% from the second quarter, year to date issuance volume was still up 13% year over year. Global equity capital markets activity for both initial public offerings andfollow-on offerings hit a two year high, with year to date activity up 20% year over year, driven by continued strong market conditions and investor optimism.

Energy markets also rebounded significantly during the third quarter, with West Texas Intermediate Crude up 12% to $52 per barrel, driven by unexpectedly strong demand and signs of slowing U.S. production. The S&P 500 Energy Index was up 6% for the quarter while other commodities saw more subdued performance, with the Bloomberg Commodity Index up 2% and the Henry Hub Natural Gas spot price ended the third quarter of 2017 slightly down by 1%. Despite overall positive momentum in the third quarter of 2017, however, oil and gas prices remain at relatively low levels.

While the overall economic backdrop is positive, the U.S. dollar continued to weaken, with the U.S. dollar index down 3% during the quarter. The euro was up 4% versus the U.S. dollar, while the pound rose 3% and the Japanese yen was flat.

Political uncertainty, notably in the U.S. and Europe, also weighed on worldwide merger and acquisition (“M&A”) activity, particularly for larger transactions, with announced volume declining 5% year over year to the lowest third-quarter level since 2013. However, global private equity-backed M&A volume increased 25% year over year, reaching $212 billion, the highest level since 2007.

Although geopolitical risks continue to influence outlook, the general view for continued global economic expansion is positive, bolstered by historically low volatility and inflation and strong corporate earnings. Near-term risk of a recession is generally viewed as low, although less accommodative monetary policy may constrain growth potential. Although there continues to be uncertainty regarding regulatory and tax policy reform in the U.S., such reform could be a potential driver of growth in the medium-term.

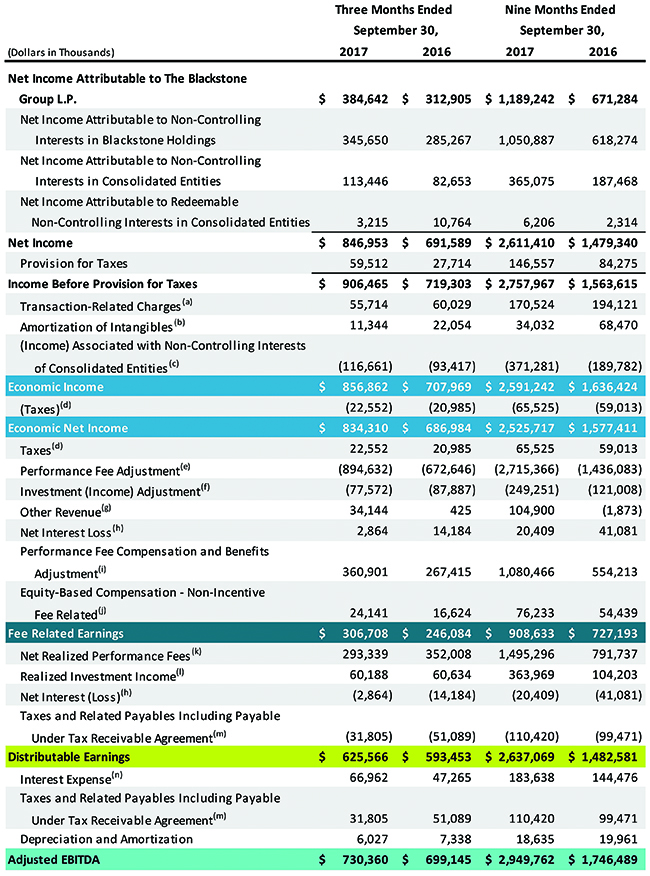

Significant Transactions

On September 25, 2017, Blackstone commenced a cash tender offer for any and all of its 6.625% senior notes maturing on August 15, 2019 (the “2019 Notes”). On September 29, 2017, the cash tender offer expired and $259.7 million aggregate principal amount of the 2019 Notes were validly tendered. Payment for the tendered notes was made on October 4, 2017. On November 1, 2017, in accordance with the make-whole provision under the indenture governing the 2019 Notes, Blackstone redeemed the remainder of the 2019 Notes that were not tendered.

On October 2, 2017, Blackstone issued $300 million in aggregate principal amount of 3.150% senior notes maturing on October 2, 2027 and $300 million in aggregate principal amount of 4.000% senior notes maturing on October 2, 2047. Blackstone intends to use the proceeds from these notes, together with cash on hand or available liquidity, to repurchase all of its 2019 Notes.

On October 16, 2017, Blackstone closed on its previously announced acquisition of Harvest Fund Advisors LLC (“Harvest”). Harvest primarily invests capital raised from institutional investors in separately managed accounts and pooled vehicles, investing in public master limited partnerships holding U.S. midstream energy assets.

64