Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22132

Aberdeen Funds

(Exact name of registrant as specified in charter)

1735 Market Street, 32nd Floor

Philadelphia, PA 19103

(Address of principal executive offices) (Zip code)

Ms. Andrea Melia

Aberdeen Asset Management Inc.

1735 Market Street, 32nd Floor

Philadelphia, PA 19103

(Name and address of agent for service)

Registrant’s telephone number, including area code: 866-667-9231

Date of fiscal year end: October 31

Date of reporting period: October 31, 2014

Table of Contents

Item 1. Reports to Shareholders.

Table of Contents

Aberdeen Funds

Equity Series

Annual Report

October 31, 2014

Aberdeen Asia-Pacific (ex-Japan) Equity Fund

Aberdeen Asia-Pacific Smaller Companies Fund

Aberdeen China Opportunities Fund

Aberdeen Emerging Markets Fund

Aberdeen Equity Long-Short Fund

Aberdeen Global Natural Resources Fund

Aberdeen Global Small Cap Fund

Aberdeen International Equity Fund

Aberdeen Latin American Equity Fund

Table of Contents

| Page 1 | ||||

| Page 2 | ||||

| Page 3 | ||||

| Page 9 | ||||

| Page 16 | ||||

| Page 21 | ||||

| Page 28 | ||||

| Page 36 | ||||

| Page 42 | ||||

| Page 48 | ||||

| Page 53 | ||||

| Page 59 | ||||

| Page 65 | ||||

| Page 70 | ||||

| Page 75 | ||||

| Page 80 | ||||

| Page 130 | ||||

| Page 150 | ||||

| Page 152 | ||||

| Page 153 | ||||

| Page 155 | ||||

| Page 159 | ||||

Investors should carefully consider a fund’s investment objectives, risks, fees, charges and expenses before investing any money. To obtain this and other fund information, please call 866-667-9231 to request a prospectus, or download a prospectus at www.aberdeen-asset.us. Please read it carefully before investing any money.

Investing in mutual funds involves risk, including possible loss of principal.

Aberdeen Funds is distributed by Aberdeen Fund Distributors LLC, Member FINRA, 1735 Market Street, 32nd Floor, Philadelphia, PA 19103.

Aberdeen Asset Management Inc. (AAMI) has been registered as an investment adviser under the Investment Advisers Act of 1940 since August 23, 1995.

Statement Regarding Availability of Quarterly Portfolio Schedule.

The complete schedule of portfolio holdings for each Fund of Aberdeen Funds is included in the Funds’ semi-annual and annual reports to shareholders. Aberdeen Funds also files complete schedules of portfolio holdings for each Fund with the Securities and Exchange Commission (the “Commission”) for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Form N-Q filings are available on the Commission’s website at http://www.sec.gov. The Funds’ Form N-Q filings may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330; and the Funds make the information on Form N-Q available to shareholders on www.aberdeen-asset.us or upon request without charge.

Statement Regarding Availability of Proxy Voting Record.

Information regarding the policies and procedures that the Funds use to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 1-866-667-9231. The information is also included in the Funds’ Statement of Additional Information, which is available on the Funds’ website at www.aberdeen-asset.us and on the Commission’s website at www.sec.gov.

Information relating to how each Fund voted proxies relating to portfolio securities held during the most recent twelve months ended June 30 is available by August 30 of the relevant year: (i) upon request and without charge by calling 1-866-667-9231; and (ii) on the Commission’s website at www.sec.gov.

Table of Contents

October 31, 2014

Dear Valued Shareholder,

Welcome to the Aberdeen Funds Annual Report covering the activities for the twelve-month period ended October 31, 2014.

Market overview

Global equity markets continued to be dominated by concerns over global economic growth levels during the reporting period, lagging their U.S. counterparts. Strong U.S. equity market performance buoyed global markets as deflationary pressures continued to cause headwinds in Europe. Meanwhile, emerging markets finished the period with weak returns as a strong sell-off in September overshadowed gains from earlier in the year. The fixed income universe was volatile over the period, as investment-grade core and total return bond markets delivered modest returns against the backdrop of struggling global equity markets and falling commodity prices. Meanwhile, the global high yield bond market came under significant pressure during the period after yields and spreads made new lows in late June.

Markets continue to brace for more headwinds as we enter 2015 given the environment of slow global growth, a potential U.S. interest rate hike on the horizon and falling oil prices. In the U.S., voters elected eight new Republican senators as the GOP will take control of both houses of Congress in January 2015. The implications of this shift remain unclear, but dramatic legislative moves are likely to be made regarding healthcare and government spending. In emerging markets, the election of pro-business candidate Narendra Modi as the new Prime Minister of India has buoyed the outlook for the world’s 10th largest economy. In Europe, tensions between Russia and the West continue to hinder Russian markets.

Anne Richards, Aberdeen Asset Management PLC’s (Aberdeen) Global Chief Investment Officer, provides you with a detailed insight on the investment marketplace in the Global Market Review and Outlook on the following page.

Aberdeen developments

As of April 1, 2014, Aberdeen Asset Management PLC completed the acquisition of Scottish Widows Investment Partnership (SWIP) from Lloyds Banking Group in the UK. During the period, the integration of SWIP into the wider Aberdeen group continued to progress. The acquisition combines Aberdeen and SWIP’s strengths across fixed income, real estate, active and quantitative equities, investment solutions and alternatives. The acquisition of SWIP will not have a direct impact on any funds in the Aberdeen Fund family but will significantly add to Aberdeen’s global investment capabilities.

During the period, Aberdeen reached an agreement with the European Tour and the Scottish Government to extend our sponsorship of the Aberdeen Asset Management Scottish Open through 2020.

Aberdeen received several industry awards during the period, including 12 Mutual Fund Education Association (MFEA) STAR Awards for financial communications in both digital and direct marketing categories.

Thank you for choosing Aberdeen Funds. We value your investment with us.

Kind Regards,

Yours sincerely,

/s/ Bev Hendry

Bev Hendry

President

Aberdeen Funds

2014 Annual Report

1

Table of Contents

In our opinion, the performances of the major global equity markets for the 12-month period ended October 31, 2014, might be best described as “all over the map” – literally. There was marked divergence in stock returns among geographical regions. On the surface, it appeared that global equities generally posted respectable gains, with the MSCI World Index, the developed-market benchmark, rising 9.3% (in U.S. dollars) over the period. However, the strength in the markets was concentrated on the western side of the Atlantic Ocean, with the U.S. broader-market S&P 500 Index climbing 17.3%. In contrast, the MSCI World ex US Index was up just 0.2% during the period, dragged down mainly by investors’ concerns about economic growth in Europe and the continued rise in the U.S. dollar against most major global currencies. Both the euro and the Japanese yen declined sharply against the U.S. dollar over the period, with the latter currency experiencing particular weakness. The upturn in the U.S. market was the primary contributor to the outperformance of developed markets versus their emerging counterparts, as measured by the MSCI Emerging Markets Index, which returned 1.0% for the reporting period. The sharp decline in oil prices over the annual period had a mixed effect on the global markets: Importing nations were notable beneficiaries, whereas exporters such as Russia came under pressure as lower oil prices may aggravate revenue shortfalls caused by a raft of Western sanctions.

Unlike many other regions, the U.S. equity market benefited from a generally improving economy over the reporting period. Healthy gross domestic product (GDP) growth in the fourth quarter of 2013 and the second and third quarters of 2014 offset a decline in the first quarter of the year, most likely attributable to bad weather-induced weakness in consumer spending. Additionally, the unemployment rate fell substantially during the period, although the labor participation rate declined to its lowest level in 36 years. Investors remained focused on U.S. monetary policy for much of the period. Former Federal Reserve (Fed) vice chair Janet Yellen succeeded Ben Bernanke as head of the Fed in February 2014. The Fed began to reduce its $85 billion-per-month asset purchase program in $10 billion increments in January 2014, and ended its tapering in late October.

United Kingdom (UK) stocks saw marginal gains while European equities ended the period modestly lower. Economic recovery in the Eurozone1 remains fragile and much slower-paced than in the U.S. and UK. The European labor market has continued to improve, albeit unevenly, as has household confidence; however, inflation expectations are dangerously low for the region. Late in the reporting period, the European Central Bank (ECB) announced that, if required, it would use “unconventional policy instruments” in support of the Eurozone economy. However, there are doubts over the scale and potential effectiveness of such measures. In Japan, the yen’s weakness lifted equity markets overall, but gains were pared because of doubts over the efficacy of Prime Minister Shinzo Abe’s “third arrow” stimulus measures, as well as the impact of the consumption tax hike that was implemented in April 2014.

Within the global emerging equity markets, strong performance in India and, to a lesser extent, China, was counterbalanced by notable weakness in Latin America and Russia. Indian stocks rallied after the business-friendly Bharatiya Janata Party (BJP), headed by Narendra Modi, swept into power as that country’s first single-party majority in 25 years. The Chinese market was bolstered by signs of an upturn in economic growth. Additionally, investors appeared to take a favorable view of a proposed pilot program for mutual market connectivity between Hong Kong and Shanghai, as it was seen as a significant step towards cross-border capital market integration. The program commenced operations shortly after the end of the reporting period in mid-November. In Latin America, Brazilian equities were hampered as investor sentiment soured in reaction to the nation’s bitterly-contested presidential election. Brazil’s incumbent president, Dilma Rousseff, whose policies generally are perceived as unfriendly to business, edged out her opponent, Aecio Neves, to secure a second term. Ongoing geopolitical tensions surrounding Russia’s expanded military presence in Ukraine had a negative impact on the Russian market for the period.

The global bond markets experienced periods of volatility over the reporting period, which increased more significantly in August and October. Concerns over faltering global economic growth, combined with heightened fears of potential deflation in Europe, drove much of the uncertainty. Nonetheless, the global fixed income markets collectively finished in positive territory for the period. Investment-grade bonds outperformed high yield securities, with the Bank of America Merrill Lynch Global Broad Market Corporate Index advancing 6.4% versus the 5.9% return of the Bank of America Merrill Lynch Global High Yield Constrained Index. Emerging markets debt, as measured by the J.P. Morgan EMBI Global Diversified Index, was the strongest-performing segment within the global fixed income universe, climbing 8.6% for the period, as investors focused on the yield differential between emerging and developed markets, rather than the geopolitical tensions between Russia and Ukraine.

Outlook

In our opinion, the global economic and monetary environment remains supportive of equities relative to fixed income and cash. We believe that the end to U.S. quantitative easing in late October, higher interest rates in 2015, and improvement in the U.S. economy could lead to continued strengthening of the U.S. dollar. Our overall view on interest rates is that they will remain low for an extended period. Confidence in the global recovery has improved somewhat, given the pick-up in U.S. economic activity. However, we feel that the picture is less rosy elsewhere in the developed world. The Eurozone continues to suffer from high debt and unemployment. We remain cautious about Japan, as the recovery in household consumption has been slower than expected. However, these conditions have led to unprecedented monetary stimulus in both regions, which we think may potentially create investment opportunities. We believe that prospects for emerging economies also remain mixed, with recent market developments highlighting sensitivities to U.S. monetary policy. At the corporate level, we observe efforts to boost margins through cost-cuts and reorganization, although this has yet to translate into a broader trend of improving profitability.

Anne Richards

Chief Investment Officer

Aberdeen Asset Management

| 1 | The Eurozone comprises 18 European Union member states that have adopted the euro as their common currency. |

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Annual Report 2014

2

Table of Contents

Aberdeen Asia-Pacific (ex-Japan) Equity Fund (Unaudited)

The Aberdeen Asia-Pacific (ex-Japan) Equity Fund (Class A shares at net asset value net of fees) returned 2.43% for the year ended October 31, 2014, versus the 4.24% return of its benchmark, the MSCI AC Asia Pacific ex-Japan Index, during the same period. For broader comparison, the average return of the Fund’s Lipper peer category of Pacific ex-Japan Funds (consisting of 50 funds) was 5.76% for the period.

Asian equities, ex-Japan, as measured by the MSCI AC Asia Pacific ex-Japan Index, posted gains over the reporting period. Political change in the Asia-Pacific region, global economic growth concerns and monetary policy from major global central banks continued to dictate market direction. The strongest performer in the region was the Indian market, which had fared poorly in 2013. The opposition Bharatiya Janata Party’s landslide election victory and hopes that the new government would accelerate reforms bolstered the local market to new highs. The Thai market extended gains as the military coup and the installation of coup leader general Prayuth Chan-ocha as prime minister brought some stability to a domestic situation that had previously been rocked by turmoil. China, as measured by the MSCI Zhong Hua Index, also outperformed the MSCI AC Asia Pacific ex-Japan Index despite investors’ persistent growth worries. Conversely, share prices in Australia fell on the back of weaker commodity prices, while market sentiment in Hong Kong was pressured by a disruptive pro-democracy movement and Singapore was dogged by worries over economic recovery. Indonesia also lagged, although voters elected market-friendly Joko Widodo as the country’s new president. Over the reporting period, equity markets priced in the gradual end to the U.S. Federal Reserve’s quantitative easing program, but the Bank of Japan’s surprise decision at the end of the period to expand its already massive stimulus plan provided a late jolt of confidence.

The Indian market performed well as election-related euphoria pushed the MSCI India Index1 to all-time highs. The Fund has a large exposure to the Indian market, which enhanced its performance over the reporting period relative to the Fund’s benchmark. Many of the Fund’s stocks also performed well. Top contributors to performance included holdings in Housing Development Finance Corp. (HDFC), UltraTech Cement and Hero MotoCorp. Mortgage lender HDFC was further lifted by hopes of better loan growth, while UltraTech gained on expectations of increased infrastructure spending. Meanwhile, motorcycle maker Hero MotoCorp enjoyed solid sales growth amid signs it was winning back market share from competitors. In contrast, the Korean market declined in the face of poor economic growth. Consequently, the Fund’s small position relative to the benchmark in this region bolstered performance for the period.

The biggest detractor from Fund performance among individual holdings was Standard Chartered. In October 2014, the lender issued its third profit warning in a year as it delivered its nine-month results, citing high impairment charges as some clients were hurt by weakening commodity markets. Investor sentiment was also dampened by speculation that U.S. regulators could reinvestigate alleged sanction violations against Standard Chartered. However, the company has peerless focus on emerging markets, replete with banking licenses and long-term customer relationships, in our opinion. Another detractor was Australia’s QBE Insurance. The company reported a net loss of US$254 million for the year ended December 2013 on the back of additional provisions, restructuring charges and a goodwill write-down in North America. Later, the company allocated additional reserves in Argentina. Nevertheless, we were encouraged that other parts of QBE continued to operate within expectations. The stock recouped some losses after management bolstered the company’s balance sheet with the placement of new shares and the chairman appointed new members to its board of directors.

Regarding significant changes to the Fund over the reporting period, we introduced three new holdings. In our view, Indian conglomerate ITC has a dominant position in the cigarettes sector and has been using robust cash flows from this business to invest in other growth opportunities such as fast-moving consumer goods. Yum! Brands is a leading multi-brand, quick-service restaurant operator, which generates more than half its revenues from Asia and, we believe, has good long-term potential in key markets such as China and India. In our view, the stock trades at a reasonable valuation relative to the sector, with a 2% yield. Another new holding was Australia-listed CSL, a leading player in the global plasma products market. We feel that the company has robust quality control and enjoys superior growth and returns because of its highly efficient collection and processing system, coupled with its commitment to research and development. The company is financially strong, in our opinion, and any excess free cash flows have been used for share buybacks. Elsewhere, we participated in the rights issues of both Bank of the Philippine Islands and Oversea-Chinese Banking Corp. Ltd. (OCBC), as we felt that they were attractively discounted. We believe that Bank of the Philippine Islands is poised to benefit from healthy loan demand, while Singapore’s OCBC is looking to bolster its balance sheet after acquiring Wing Hang Bank.

Conversely, we took profits from our positions in India following the local market’s solid performance. We sold GlaxoSmithKline Pharmaceuticals in India after the successful tender offer by its parent company, UK-based GlaxoSmithKline. We also exited Singapore Airlines. Although we think the company has a robust balance sheet and an enviable brand, we feel the challenging operating environment is not expected to improve soon. We believe there are better opportunities in a regional portfolio.

The divergence between major central banks’ monetary policies has become more pronounced, although how that translates into global capital flows is uncertain. In Asia, the slowdown in China remains a key concern and, in our opinion, should continue to sway market sentiment. In our opinion, weaker demand in mainland China has hurt major trading partners, and activity may potentially moderate further

| 1 | The MSCI India Index is designed to measure the performance of the large- and mid-cap segments of the Indian market. With 73 constituents, the index covers approximately 85% of the Indian equity universe. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index. |

2014 Annual Report

3

Table of Contents

Aberdeen Asia-Pacific (ex-Japan) Equity Fund (Unaudited) (concluded)

with the Chinese government trying to prevent runaway credit expansion. However, we believe that the government has the resources to employ selective stimulus to cushion the slowdown. Ultimately, in our view, selective stimulus may improve the quality of growth, even if it takes longer to achieve. Meanwhile, falling global oil prices have brought some reprieve to oil importing nations. In particular, India and Indonesia now have greater room to revise subsidies. We believe this may potentially help resolve fiscal imbalances that, until recently, have handcuffed government spending on crucial areas such as infrastructure. India did just that, hiking gas prices while eliminating diesel subsidies. Indonesia, under newly elected president Joko Widodo, has made tackling fuel subsidies a cornerstone of its economic rejuvenation plan. We think that Japan also may benefit as lower oil prices mitigate the impact of the weaker yen on energy imports.

Portfolio Management:

Aberdeen Asia-Pacific Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance data quoted represents past performance and current returns may be lower or higher. Class A Shares have up to a 5.75% front-end sales charge and a 0.25% 12b-1 fee. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, which may be higher or lower than the performance shown above, please call 866-667-9231 or go to www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal.

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Concentrating investments in the Asia-Pacific region subjects the Fund to more volatility and greater risk of loss than geographically diverse mutual funds.

Parts of the Asian-Pacific region may be subject to a greater degree of economic, political and social instability than is the case in the United States and Europe. Some Asian countries can be characterized as emerging markets or newly industrialized and may experience more volatile economic cycles than developed countries.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and political and economic risks. These risks are enhanced in emerging markets countries.

Equity stocks of small and mid-cap companies carry greater risk and more volatility than equity stocks of larger, more established companies.

Please read the prospectus for more detailed information regarding these and other risks.

Annual Report 2014

4

Table of Contents

Aberdeen Asia-Pacific (ex-Japan) Equity Fund (Unaudited)

Average Annual Total Return (For periods ended October 31, 2014) | 1 Yr. | Inception1 | ||||||||

Class A2 | w/o SC | 2.43% | 6.86% | |||||||

| w/SC3 | (3.44% | ) | 5.59% | |||||||

Class C2 | w/o SC | 1.67% | 6.44% | |||||||

| w/SC4 | 0.67% | 6.44% | ||||||||

Class R2,5 | w/o SC | 2.06% | 6.70% | |||||||

Institutional Service Class5 | w/o SC | 2.59% | 6.96% | |||||||

Institutional Class5 | w/o SC | 2.64% | 6.99% | |||||||

All figures showing the effect of a sales charge (SC) reflect the maximum charge possible because it has the most significant effect on performance data. The total returns shown above do not include the impact of financial statement rounding of the net asset value per share and/or financial statement adjustments.

| 1 | Fund commenced operations on November 16, 2009. |

| 2 | Returns before the first offering of Class A, Class C and Class R (February 28, 2012) are based on the previous performance of the Institutional Class. The performance of the Institutional Class is substantially similar to what Class A, Class C and Class R would have produced because all classes invest in the same portfolio of securities. Returns for Class A, Class C and Class R shares would only differ to the extent of the differences in expenses of the classes. |

| 3 | A 5.75% front-end sales charge was deducted. |

| 4 | A 1.00% contingent deferred sales charge (CDSC) was deducted from the one year return because it is charged when Class C shares are sold within the first year after purchase. |

| 5 | Not subject to any sales charges. |

2014 Annual Report

5

Table of Contents

Aberdeen Asia-Pacific (ex-Japan) Equity Fund (Unaudited)

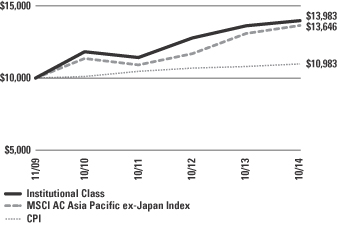

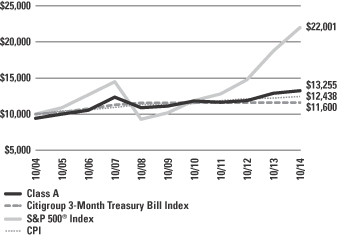

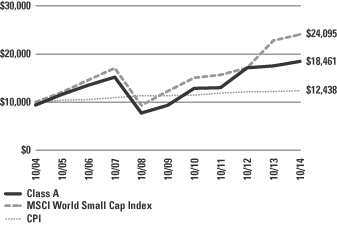

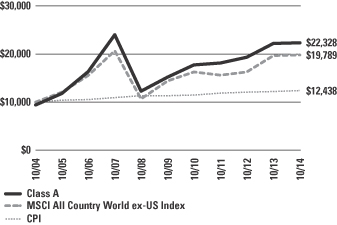

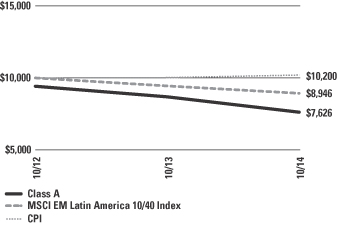

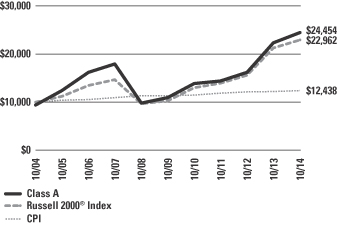

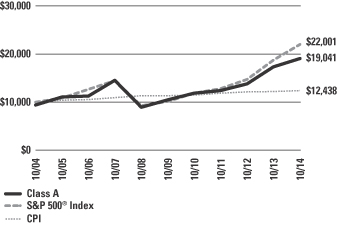

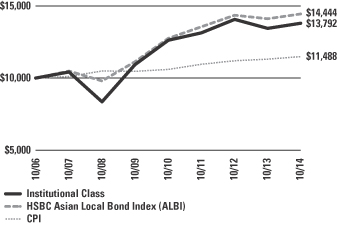

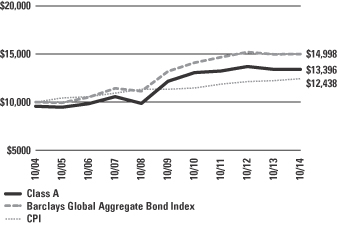

Performance of a $10,000 Investment (as of October 31, 2014)

Comparative performance of $10,000 invested in Institutional Class shares of the Aberdeen Asia-Pacific (ex-Japan) Equity Fund, the Morgan Stanley Capital International All Country (MSCI AC) Asia Pacific ex-Japan Index and the Consumer Price Index (CPI) since inception. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees, expenses, or sales charges. Investors cannot invest directly in market indexes.

The MSCI AC Asia Pacific ex-Japan Index is a free float-adjusted, market capitalization-weighted index that captures large and mid cap representation in the Asia Pacific region excluding Japan. The MSCI AC Asia Pacific ex-Japan Index consists of the following developed markets countries: Australia, Hong Kong, New Zealand and Singapore; and the following emerging markets countries: China, India, Indonesia, Korea, Malaysia, the Philippines, Taiwan and Thailand.

The CPI represents changes in prices of a basket of goods and services purchased for consumption by urban households.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and Performance graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Total returns reflect waivers and reimbursements in effect, without which returns would have been lower.

Portfolio Summary

October 31, 2014 (Unaudited)

| Asset Allocation | ||||

Common Stocks | 91.7% | |||

Preferred Stocks | 5.4% | |||

Repurchase Agreement | 3.2% | |||

Liabilities in excess of other assets | (0.3% | ) | ||

| 100.0% | ||||

The following chart summarizes the composition of the Fund’s portfolio, in industry classification standard sectors, expressed as a percentage of net assets. An industry classification standard sector can include more than one industry group. As of October 31, 2014, the Fund did not have more than 25% of its assets invested in any industry group. The sectors, as classified by S&P’s Global Industry Classification Standard Sectors, are comprised of several industry groups.

| Top Sectors | ||||

Financials | 39.3% | |||

Information Technology | 12.7% | |||

Materials | 11.9% | |||

Industrials | 9.9% | |||

Telecommunication Services | 7.4% | |||

Consumer Staples | 6.8% | |||

Consumer Discretionary | 4.5% | |||

Energy | 4.0% | |||

Health Care | 0.6% | |||

Other | 2.9% | |||

| 100.0% | ||||

| Top Holdings* | ||||

Samsung Electronics Co. Ltd., Preferred Shares | 5.4% | |||

Oversea-Chinese Banking Corp. Ltd. | 4.2% | |||

Jardine Strategic Holdings Ltd. | 3.8% | |||

Housing Development Finance Corp. Ltd. | 3.7% | |||

HSBC Holdings PLC | 3.6% | |||

BHP Billiton – London Listing | 3.6% | |||

Rio Tinto – London Listing | 3.5% | |||

Taiwan Semiconductor Manufacturing Co. Ltd. | 3.4% | |||

AIA Group Ltd. | 3.3% | |||

QBE Insurance Group Ltd. | 3.1% | |||

Other | 62.4% | |||

| 100.0% | ||||

| Top Countries | ||||

Hong Kong | 21.4% | |||

Singapore | 19.6% | |||

Australia | 12.8% | |||

India | 11.0% | |||

Republic of South Korea | 6.6% | |||

China | 6.1% | |||

Taiwan | 5.3% | |||

United States | 4.8% | |||

Thailand | 3.5% | |||

Philippines | 3.0% | |||

Other | 5.9% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, repurchase agreements are included as part of Other. |

Annual Report 2014

6

Table of Contents

Statement of Investments

October 31, 2014

Aberdeen Asia-Pacific (ex-Japan) Equity Fund

| Shares or Principal Amount | Value | |||||||

COMMON STOCKS (91.7%) | ||||||||

AUSTRALIA (12.8%) | ||||||||

Consumer Staples (2.0%) | ||||||||

Woolworths Ltd. (a) | 683,056 | $ | 21,677,162 | |||||

Financials (3.1%) | ||||||||

QBE Insurance Group Ltd. (a) | 3,282,150 | 33,339,761 | ||||||

Health Care (0.6%) | ||||||||

CSL Ltd. (a) | 95,000 | 6,707,274 | ||||||

Materials (7.1%) | ||||||||

BHP Billiton — London Listing (a) | 1,470,073 | 37,981,691 | ||||||

Rio Tinto — London Listing (a) | 791,740 | 37,672,135 | ||||||

| 75,653,826 | ||||||||

| 137,378,023 | ||||||||

CHINA (6.1%) | ||||||||

Energy (3.1%) | ||||||||

PetroChina Co. Ltd., H Shares (a) | 26,448,000 | 33,145,500 | ||||||

Telecommunication Services (3.0%) | ||||||||

China Mobile Ltd. (a) | 2,581,000 | 32,180,677 | ||||||

| 65,326,177 | ||||||||

HONG KONG (21.4%) | ||||||||

Consumer Discretionary (1.7%) | ||||||||

Global Brands Group Holding Ltd. (b) | 9,218,000 | 2,032,556 | ||||||

Li & Fung Ltd. (a) | 13,368,000 | 16,309,324 | ||||||

| 18,341,880 | ||||||||

Consumer Staples (1.5%) | ||||||||

Dairy Farm International Holdings Ltd. | 1,694,700 | 16,269,120 | ||||||

Financials (13.6%) | ||||||||

AIA Group Ltd. (a) | 6,365,800 | 35,523,868 | ||||||

Hang Lung Group Ltd. (a) | 2,827,000 | 14,222,817 | ||||||

Hang Lung Properties Ltd. (a) | 4,825,000 | 15,067,166 | ||||||

HSBC Holdings PLC (a) | 3,838,476 | 39,277,590 | ||||||

Swire Pacific Ltd., Class A (a) | 2,445,500 | 32,108,074 | ||||||

Swire Pacific Ltd., Class B (a) | 2,465,000 | 5,983,034 | ||||||

Swire Properties Ltd. (a) | 1,373,900 | 4,402,401 | ||||||

| 146,584,950 | ||||||||

Industrials (3.8%) | ||||||||

Jardine Strategic Holdings Ltd. (a) | 1,138,000 | 40,565,915 | ||||||

Information Technology (0.8%) | ||||||||

ASM Pacific Technology Ltd. (a) | 779,200 | 8,586,659 | ||||||

| 230,348,524 | ||||||||

INDIA (11.0%) | ||||||||

Consumer Discretionary (1.2%) | ||||||||

Hero MotoCorp Ltd. (a) | 257,000 | 12,829,140 | ||||||

Consumer Staples (0.5%) | ||||||||

ITC Ltd. (a) | 1,000,000 | 5,774,239 | ||||||

Financials (4.4%) | ||||||||

Housing Development Finance Corp. Ltd. (a) | 2,214,799 | 39,734,974 | ||||||

ICICI Bank Ltd. (a) | 246,200 | $ | 6,532,630 | |||||

ICICI Bank Ltd., ADR | 26,800 | 1,510,448 | ||||||

| 47,778,052 | ||||||||

Information Technology (2.7%) | ||||||||

Infosys Ltd. (a) | 432,250 | 28,673,558 | ||||||

Materials (2.2%) | ||||||||

Grasim Industries Ltd. (a) | 42,024 | 2,398,323 | ||||||

Grasim Industries Ltd., GDR (c) | 20,080 | 1,151,186 | ||||||

UltraTech Cement Ltd. (a) | 488,142 | 20,248,428 | ||||||

UltraTech Cement Ltd., GDR (c) | 330 | 13,705 | ||||||

| 23,811,642 | ||||||||

| 118,866,631 | ||||||||

INDONESIA (0.6%) | ||||||||

Consumer Staples (0.6%) | ||||||||

Unilever Indonesia Tbk PT (a) | 2,699,500 | 6,796,711 | ||||||

MALAYSIA (2.7%) | ||||||||

Consumer Staples (1.0%) | ||||||||

British American Tobacco Bhd (a) | 504,500 | 10,667,049 | ||||||

Financials (1.7%) | ||||||||

CIMB Group Holdings Bhd (a) | 6,020,999 | 11,889,312 | ||||||

Public Bank Bhd | 1,174,500 | 6,620,120 | ||||||

| 18,509,432 | ||||||||

| 29,176,481 | ||||||||

PHILIPPINES (3.0%) | ||||||||

Financials (3.0%) | ||||||||

Ayala Corp. (a) | 1,104,780 | 16,980,250 | ||||||

Ayala Land, Inc. (a) | 4,812,700 | 3,596,159 | ||||||

Bank of Philippine Islands (a) | 5,518,225 | 11,693,087 | ||||||

| 32,269,496 | ||||||||

REPUBLIC OF SOUTH KOREA (1.2%) | ||||||||

Consumer Staples (1.2%) | ||||||||

E-Mart Co. Ltd. (a) | 71,440 | 13,255,619 | ||||||

SINGAPORE (19.6%) | ||||||||

Financials (10.7%) | ||||||||

City Developments Ltd. (a) | 4,489,000 | 33,038,690 | ||||||

DBS Group Holdings Ltd. (a) | 1,102,075 | 15,853,806 | ||||||

Oversea-Chinese Banking Corp. Ltd. (a) | 5,836,829 | 44,961,716 | ||||||

United Overseas Bank Ltd. (a) | 1,173,235 | 21,019,291 | ||||||

| 114,873,503 | ||||||||

Industrials (6.0%) | ||||||||

Jardine Matheson Holdings Ltd. (a) | 155,200 | 9,300,812 | ||||||

Keppel Corp. Ltd. (a) | 3,894,000 | 28,555,529 | ||||||

Singapore Technologies Engineering Ltd. (a) | 9,323,000 | 27,218,937 | ||||||

| 65,075,278 | ||||||||

Information Technology (0.4%) | ||||||||

Venture Corp. Ltd. (a) | 738,000 | 4,445,270 | ||||||

See accompanying Notes to Financial Statements.

2014 Annual Report

7

Table of Contents

Statement of Investments (concluded)

October 31, 2014

Aberdeen Asia-Pacific (ex-Japan) Equity Fund

| Shares or Principal Amount | Value | |||||||

Telecommunication Services (2.5%) | ||||||||

Singapore Telecommunications Ltd. (a) | 9,073,000 | $ | 26,698,259 | |||||

| 211,092,310 | ||||||||

TAIWAN (5.3%) | ||||||||

Information Technology (3.4%) | ||||||||

Taiwan Semiconductor Manufacturing Co. Ltd. (a) | 8,488,000 | 36,794,381 | ||||||

Telecommunication Services (1.9%) | ||||||||

Taiwan Mobile Co. Ltd. | 6,234,100 | 20,229,338 | ||||||

| 57,023,719 | ||||||||

THAILAND (3.5%) | ||||||||

Energy (0.9%) | ||||||||

PTT Exploration & Production PCL, Foreign Shares (a) | 2,197,000 | 9,877,491 | ||||||

Materials (2.6%) | ||||||||

Siam Cement PCL, Foreign Shares (a) | 2,005,200 | 27,852,106 | ||||||

| 37,729,597 | ||||||||

UNITED KINGDOM (2.8%) | ||||||||

Financials (2.8%) | ||||||||

Standard Chartered PLC (a) | 1,969,676 | 29,648,855 | ||||||

UNITED STATES (1.6%) | ||||||||

Consumer Discretionary (1.6%) | ||||||||

Yum! Brands, Inc. | 240,000 | 17,239,200 | ||||||

Total Common Stocks | 986,151,343 | |||||||

PREFERRED STOCKS (5.4%) | ||||||||

REPUBLIC OF SOUTH KOREA (5.4%) | ||||||||

Information Technology (5.4%) | ||||||||

Samsung Electronics Co. Ltd., Preferred Shares (a) | 63,350 | 58,476,039 | ||||||

Total Preferred Stocks | 58,476,039 | |||||||

REPURCHASE AGREEMENT (3.2%) | ||||||||

UNITED STATES (3.2%) | ||||||||

Repurchase Agreement, Fixed Income Clearing Corp., 0.00%, dated 10/31/2014, due 11/03/2014, repurchase price $33,785,000 collateralized by U.S. Treasury Note, maturing 10/31/2021; total market value of $34,465,364 | $ | 33,785,000 | 33,785,000 | |||||

Total Repurchase Agreement | 33,785,000 | |||||||

Total Investments | 1,078,412,382 | |||||||

Liabilities in excess of other assets—(0.3)% | (2,999,997 | ) | ||||||

Net Assets—100.0% | $ | 1,075,412,385 | ||||||

| (a) | Fair Valued Security. Fair Values are determined pursuant to procedures approved by the Fund’s Board of Trustees. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (b) | Non-income producing security. |

| (c) | Denotes a security issued under Regulation S or Rule 144A. |

| (d) | See Notes to Financial Statements for tax unrealized appreciation/depreciation of securities. |

| ADR | American Depositary Receipt |

| GDR | Global Depositary Receipt |

See accompanying Notes to Financial Statements.

Annual Report 2014

8

Table of Contents

Aberdeen Asia-Pacific Smaller Companies Fund (Unaudited)

The Aberdeen Asia-Pacific Smaller Companies Fund (Class A shares at net asset value net of fees) returned 1.78% for the year ended October 31, 2014, versus the 2.68% return of its benchmark, the MSCI AC Asia Pacific ex-Japan Small Cap Index, during the same period. For broader comparison, the average return of the Fund’s Lipper peer category of Pacific Region Funds (consisting of 23 funds) was 2.96% for the period.

The MSCI AC Asia Pacific ex-Japan Small Cap Index rose during the reporting period. Political change in the Asia-Pacific region, global economic growth concerns and monetary policy from major global central banks continued to dictate market direction. The strongest performer in the region was the Indian market, which had fared poorly in 2013. The opposition Bharatiya Janata Party’s landslide election victory and hopes that the new government would accelerate reforms bolstered the local market to new highs. The Thai market extended gains as the military coup and the installation of coup leader general Prayuth Chan-ocha as prime minister brought some stability to a domestic situation that had previously been rocked by turmoil. China, as measured by the MSCI Zhong Hua Index, also outperformed the MSCI AC Asia Pacific ex-Japan Small Cap Index, despite investors’ persistent growth worries. Conversely, share prices in Australia fell on the back of weaker commodity prices, while market sentiment in Hong Kong was pressured by a disruptive pro-democracy movement and Singapore was dogged by worries over economic recovery. Indonesia also lagged, although voters elected market-friendly Joko Widodo as the country’s new president. Over the reporting period, equity markets priced in the gradual end to the U.S. Federal Reserve’s quantitative easing program, but the Bank of Japan’s surprise decision at the end of the period to expand its already massive stimulus plan provided a late jolt of confidence.

Fund performance for the reporting period benefited from its holdings in India and Thailand, which performed well. Holdings in Indian companies were among the biggest contributors to performance as election-related euphoria on the hopes of long overdue infrastructure reforms pushed local share prices to all-time highs, as evidenced by Fund holdings Container Corp. of India and Ramco Cements. Meanwhile, auto-related materials stocks Kansai Nerolac Paints and Castrol India were buoyant on investor expectations of a pick-up in consumer demand and industrial growth. Thai holdings, such as Hana Microelectronics and Bumrungrad Hospital, also enjoyed a good year despite the troubled domestic political situation.

Conversely, Giordano International was the biggest detractor from Fund performance. The apparel retailer’s share price fell amid weak retail conditions in China, one of its core markets. Nevertheless, we believe that its healthy balance sheet may provide a buffer against market downturn. Pacific Basin Shipping experienced subdued dry bulk rates amid sluggish demand, but the company has historically been disciplined in managing its assets within a highly cyclical industry and rates have started to improve.

Notable changes to the Fund during the period included the sale of industrial property company BWP Trust, Thai shopping mall owner Central Pattana, Singapore software solutions provider Silverlake Axis, and nickel producer Vale Indonesia. We felt that Australia exchange-listed BWP Trust’s growth prospects were diminishing, while the stock was trading above the company’s net asset value. Silverlake Axis and Central Pattana’s valuations were becoming less appealing, in our view. Regarding Vale Indonesia, in our view, the country’s regulatory regime had become increasingly uncertain.

Conversely, we initiated a position in Tesco Lotus Retail Growth Freehold & Leasehold Property, a fund that invests in Tesco Lotus shopping malls. We feel that it offers an attractive yield and stands to benefit from a recovery in Thai retail spending. Additionally, we supported the rights issues of Bank OCBC NISP and BS Financial. We felt that the rights issues would provide both banks with the capital flexibility to grow in the Indonesian and Korean markets, respectively, particularly for BS Financial after its acquisition of Kyongnam Bank.

The divergence between major central banks’ monetary policies has become more pronounced, although how that translates into global capital flows is uncertain. In Asia, the slowdown in China remains a key concern and, in our opinion, should continue to sway market sentiment. Weaker demand in mainland China has hurt major trading partners, and activity may potentially moderate further with the Chinese government trying to prevent runaway credit expansion. However, we believe that the government has the resources to employ selective stimulus to cushion the slowdown. Ultimately, in our view, the selective stimulus may improve the quality of growth, even if it takes longer to achieve. Meanwhile, falling global oil prices have brought some reprieve to oil importing nations. In particular, India and Indonesia now have greater room to revise subsidies. This may potentially help resolve fiscal imbalances that, until recently, have handcuffed government spending on crucial areas such as infrastructure. India did just that, hiking gas prices while eliminating diesel subsidies. Indonesia, under newly elected president Joko Widodo, has made tackling fuel subsidies a cornerstone of its economic rejuvenation plan. We think that Japan also may benefit as lower oil prices mitigate the impact of the weaker yen on energy imports.

Portfolio Management:

Aberdeen Asia-Pacific Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance data quoted represents past performance and current returns may be lower or higher. Class A Shares have up to a 5.75% front-end sales charge and a 0.25% 12b-1 fee. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, which may be higher or lower than the performance shown above, please call 866-667-9231 or go to www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal.

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

2014 Annual Report

9

Table of Contents

Aberdeen Asia-Pacific Smaller Companies Fund (Unaudited) (concluded)

Risk Considerations

Concentrating investments in the Asia-Pacific region subjects the Fund to more volatility and greater risk of loss than geographically diverse mutual funds.

Parts of the Asian-Pacific region may be subject to a greater degree of economic, political and social instability than is the case in the United States and Europe. Some Asian countries can be characterized as emerging markets or newly industrialized and may experience more volatile economic cycles than developed countries.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and political and economic risks. These risks are enhanced in emerging markets countries.

Equity stocks of small-cap companies carry greater risk, and more volatility than equity stocks of larger, more established companies.

Please read the prospectus for more detailed information regarding these and other risks.

Annual Report 2014

10

Table of Contents

Aberdeen Asia-Pacific Smaller Companies Fund (Unaudited)

Average Annual Total Return (For periods ended October 31, 2014) | 1 Yr. | Inception1 | ||||||||

Class A | w/o SC | 1.78% | 6.96% | |||||||

| w/SC2 | (4.04% | ) | 5.09% | |||||||

Class C | w/o SC | 1.16% | 6.19% | |||||||

| w/SC3 | 0.31% | 6.19% | ||||||||

Class R4 | w/o SC | 1.41% | 6.48% | |||||||

Institutional Service Class4 | w/o SC | 2.09% | 7.60% | |||||||

Institutional Class4 | w/o SC | 2.12% | 7.26% | |||||||

All figures showing the effect of a sales charge (SC) reflect the maximum charge possible because it has the most significant effect on performance data. The total returns shown above do not include the impact of financial statement rounding of the net asset value per share and/or financial statement adjustments.

| 1 | Fund commenced operations on June 28, 2011. |

| 2 | A 5.75% front-end sales charge was deducted. |

| 3 | A 1.00% contingent deferred sales charge (CDSC) was deducted from the one year return because it is charged when Class C shares are sold within the first year after purchase. |

| 4 | Not subject to any sales charges. |

2014 Annual Report

11

Table of Contents

Aberdeen Asia-Pacific Smaller Companies Fund (Unaudited)

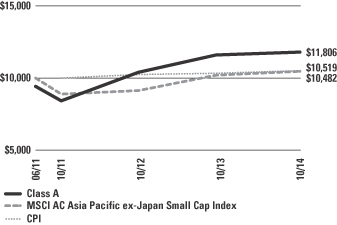

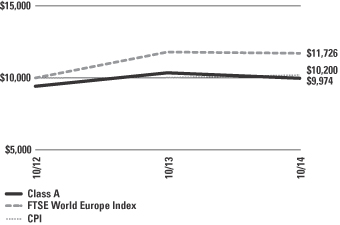

Performance of a $10,000 Investment (as of October 31, 2014)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Asia-Pacific Smaller Companies Fund, Morgan Stanley Capital International All Country (MSCI AC) Asia Pacific ex-Japan Small Cap Index and the Consumer Price Index (CPI) since inception. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees, expenses, or sales charges. Investors cannot invest directly in market indexes.

The MSCI AC Asia Pacific ex-Japan Small Cap Index is a free float-adjusted, small market capitalization-weighted index that captures small cap representation across the Asia Pacific region excluding Japan including the following developed markets countries: Australia, Hong Kong, New Zealand and Singapore; and the following emerging markets countries: China, India, Indonesia, Korea, Malaysia, the Philippines, Taiwan and Thailand.

The CPI represents changes in prices of a basket of goods and services purchased for consumption by urban households.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and Performance graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Total returns reflect waivers and reimbursements in effect, without which returns would have been lower.

Portfolio Summary (as a percentage of net assets)

October 31, 2014 (Unaudited)

| Asset Allocation | ||||

Common Stocks | 97.4% | |||

Repurchase Agreement | 2.7% | |||

Warrants | —% | |||

Liabilities in excess of other assets | (0.1% | ) | ||

| 100.0% | ||||

Amounts listed as “–” are 0% or round to 0%.

The following chart summarizes the composition of the Fund’s portfolio, in industry classification standard sectors, expressed as a percentage of net assets. An industry classification standard sector can include more than one industry group. As of October 31, 2014, the Fund did not have more than 25% of its assets invested in any industry group. The sectors, as classified by S&P’s Global Industry Classification Standard Sectors, are comprised of several industry groups.

| Top Sectors | ||||

Financials | 26.2% | |||

Consumer Discretionary | 21.6% | |||

Industrials | 14.6% | |||

Materials | 10.2% | |||

Consumer Staples | 9.9% | |||

Information Technology | 6.5% | |||

Health Care | 5.6% | |||

Utilities | 1.5% | |||

Telecommunication Services | 0.7% | |||

Energy | 0.6% | |||

Other | 2.6% | |||

| 100.0% | ||||

| Top Holdings* | ||||

Millennium & Copthorne Hotels PLC | 3.2% | |||

Aeon Co. (M) Bhd | 3.0% | |||

Dah Sing Financial Holdings Ltd. | 2.9% | |||

Venture Corp. Ltd. | 2.1% | |||

Oriental Holdings Bhd | 2.0% | |||

BS Financial Group, Inc. | 2.0% | |||

Shinsegae Co. Ltd. | 2.0% | |||

DGB Financial Group, Inc. | 1.9% | |||

Petra Foods Ltd. | 1.9% | |||

United Plantations Bhd | 1.9% | |||

Other | 77.1% | |||

| 100.0% | ||||

| Top Countries | ||||

Malaysia | 16.0% | |||

Singapore | 14.8% | |||

India | 12.3% | |||

Hong Kong | 11.7% | |||

Thailand | 10.8% | |||

Indonesia | 9.4% | |||

Republic of South Korea | 5.9% | |||

Australia | 3.9% | |||

United Kingdom | 3.2% | |||

China | 3.1% | |||

Other | 8.9% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, repurchase agreements are included as part of Other. |

Annual Report 2014

12

Table of Contents

Statement of Investments

October 31, 2014

Aberdeen Asia-Pacific Smaller Companies Fund

| Shares or Principal Amount | Value | |||||||

COMMON STOCKS (97.4%) | ||||||||

AUSTRALIA (3.9%) | ||||||||

Consumer Discretionary (1.1%) | ||||||||

ARB Corp. Ltd. (a) | 28,845 | $ | 334,604 | |||||

Financials (1.4%) | ||||||||

Shopping Centres Australasia Property Group, REIT (a) | 271,000 | 432,556 | ||||||

Industrials (1.4%) | ||||||||

Cabcharge Australia Ltd. (a) | 102,416 | 446,631 | ||||||

| 1,213,791 | ||||||||

CHINA (3.1%) | ||||||||

Energy (0.6%) | ||||||||

Green Dragon Gas Ltd. (b) | 22,576 | 180,574 | ||||||

Greka Engineering & Technology Ltd. (b) | 121,761 | 3,409 | ||||||

| 183,983 | ||||||||

Financials (1.3%) | ||||||||

Yanlord Land Group Ltd. (a) | 460,000 | 392,401 | ||||||

Materials (1.2%) | ||||||||

Yingde Gases Group Co. Ltd. (a) | 500,000 | 390,421 | ||||||

| 966,805 | ||||||||

HONG KONG (11.7%) | ||||||||

Consumer Discretionary (4.3%) | ||||||||

Cafe de Coral Holdings Ltd. (a) | 30,000 | 107,566 | ||||||

Giordano International Ltd. (a) | 800,000 | 407,552 | ||||||

Hongkong & Shanghai Hotels Ltd. (The) (a) | 355,520 | 562,990 | ||||||

Texwinca Holdings Ltd. (a) | 298,000 | 261,530 | ||||||

| 1,339,638 | ||||||||

Consumer Staples (1.0%) | ||||||||

Convenience Retail Asia Ltd. | 460,000 | 306,661 | ||||||

Financials (3.4%) | ||||||||

AEON Credit Service (Asia) Co. Ltd. (a) | 82,000 | 67,033 | ||||||

Dah Sing Financial Holdings Ltd. (a) | 141,738 | 882,563 | ||||||

Public Financial Holdings Ltd. (a) | 214,000 | 102,199 | ||||||

| 1,051,795 | ||||||||

Industrials (2.3%) | ||||||||

Hong Kong Aircraft Engineering Co. Ltd. (a) | 12,400 | 136,241 | ||||||

Pacific Basin Shipping Ltd. (a) | 1,218,000 | 582,994 | ||||||

| 719,235 | ||||||||

Telecommunication Services (0.7%) | ||||||||

Asia Satellite Telecommunications Holdings Ltd. (a) | 63,000 | 219,446 | ||||||

| 3,636,775 | ||||||||

INDIA (12.3%) | ||||||||

Consumer Staples (1.6%) | ||||||||

Godrej Consumer Products Ltd. | 31,887 | 499,598 | ||||||

Health Care (2.6%) | ||||||||

Piramal Enterprises Ltd. | 19,500 | 255,977 | ||||||

Sanofi India Ltd. | 9,993 | 539,549 | ||||||

| 795,526 | ||||||||

Industrials (1.6%) | ||||||||

Container Corp. of India (a) | 22,203 | 486,709 | ||||||

Information Technology (2.4%) | ||||||||

CMC Ltd. | 14,834 | 468,697 | ||||||

MphasiS Ltd. (a) | 45,196 | 294,475 | ||||||

| 763,172 | ||||||||

Materials (3.7%) | ||||||||

Castrol (India) Ltd. (a) | 57,485 | 386,152 | ||||||

Kansai Nerolac Paints Ltd. | 9,668 | 303,109 | ||||||

Ramco Cements Ltd. (The) | 82,732 | 465,806 | ||||||

| 1,155,067 | ||||||||

Utilities (0.4%) | ||||||||

Gujarat Gas Co. Ltd. | 14,500 | 114,205 | ||||||

| 3,814,277 | ||||||||

INDONESIA (9.4%) | ||||||||

Consumer Discretionary (1.1%) | ||||||||

Astra Otoparts Tbk PT (a) | 1,031,900 | 335,927 | ||||||

Consumer Staples (3.8%) | ||||||||

M.P. Evans Group PLC | 37,345 | 270,028 | ||||||

Multi Bintang Indonesia Tbk PT | 3,000 | 310,302 | ||||||

Petra Foods Ltd. | 197,000 | 584,238 | ||||||

| 1,164,568 | ||||||||

Financials (1.6%) | ||||||||

Bank OCBC NISP Tbk PT (b) | 1,496,895 | 160,713 | ||||||

Bank Permata Tbk PT | 2,613,561 | 320,072 | ||||||

| 480,785 | ||||||||

Industrials (1.4%) | ||||||||

AKR Corporindo Tbk PT (a) | 1,070,300 | 436,059 | ||||||

Materials (1.5%) | ||||||||

Holcim Indonesia Tbk PT (a) | 2,470,400 | 480,312 | ||||||

| 2,897,651 | ||||||||

MALAYSIA (16.0%) | ||||||||

Consumer Discretionary (6.4%) | ||||||||

Aeon Co. (M) Bhd | 815,200 | 929,391 | ||||||

Oriental Holdings Bhd | 283,900 | 630,937 | ||||||

Panasonic Manufacturing Malaysia Bhd | 23,600 | 136,323 | ||||||

Shangri-La Hotels Malaysia Bhd | 123,400 | 264,489 | ||||||

| 1,961,140 | ||||||||

Consumer Staples (3.5%) | ||||||||

Carlsberg Brewery Malaysia Bhd | 40,000 | 134,985 | ||||||

Guinness Anchor Bhd (a) | 34,300 | 134,961 | ||||||

United Malacca Bhd | 114,000 | 236,370 | ||||||

See accompanying Notes to Financial Statements.

2014 Annual Report

13

Table of Contents

Statement of Investments (continued)

October 31, 2014

Aberdeen Asia-Pacific Smaller Companies Fund

| Shares or Principal Amount | Value | |||||||

United Plantations Bhd (a) | 75,000 | $ | 583,846 | |||||

| 1,090,162 | ||||||||

Financials (3.4%) | ||||||||

Alliance Financial Group Bhd (a) | 321,600 | 468,723 | ||||||

Bursa Malaysia Bhd (a) | 59,600 | 146,677 | ||||||

SP Setia Bhd | 292,626 | 292,693 | ||||||

YNH Property Bhd | 234,993 | 147,886 | ||||||

| 1,055,979 | ||||||||

Industrials (1.1%) | ||||||||

Pos Malaysia Bhd (a) | 217,700 | 334,354 | ||||||

Materials (1.6%) | ||||||||

Batu Kawan Bhd (a) | 29,000 | 162,611 | ||||||

Tasek Corp. Bhd | 66,400 | 337,123 | ||||||

| 499,734 | ||||||||

| 4,941,369 | ||||||||

NETHERLANDS (0.6%) | ||||||||

Information Technology (0.6%) | ||||||||

ASM International NV (a) | 4,300 | 172,313 | ||||||

PHILIPPINES (2.8%) | ||||||||

Consumer Discretionary (0.8%) | ||||||||

Jollibee Foods Corp. (a) | 59,420 | 259,494 | ||||||

Financials (0.5%) | ||||||||

Cebu Holdings, Inc. | 1,329,500 | 152,726 | ||||||

Industrials (0.4%) | ||||||||

Asian Terminals, Inc. (a) | 444,200 | 123,644 | ||||||

Utilities (1.1%) | ||||||||

Manila Water Co., Inc. | 505,400 | 325,483 | ||||||

| 861,347 | ||||||||

REPUBLIC OF SOUTH KOREA (5.9%) | ||||||||

Consumer Discretionary (2.0%) | ||||||||

Shinsegae Co. Ltd. (a) | 3,240 | 601,042 | ||||||

Financials (3.9%) | ||||||||

BS Financial Group, Inc. (a) | 40,144 | 624,667 | ||||||

DGB Financial Group, Inc. (a) | 41,400 | 590,370 | ||||||

| 1,215,037 | ||||||||

| 1,816,079 | ||||||||

SINGAPORE (14.8%) | ||||||||

Financials (6.3%) | ||||||||

Ascendas Hospitality Trust, REIT | 405,000 | 222,250 | ||||||

Bukit Sembawang Estates Ltd. (a) | 110,000 | 454,745 | ||||||

CDL Hospitality Trusts, REIT (a) | 240,000 | 322,641 | ||||||

Far East Hospitality Trust, REIT | 650,000 | 419,942 | ||||||

Hong Leong Finance Ltd. (a) | 25,000 | 50,637 | ||||||

Wheelock Properties (Singapore) Ltd. (a) | 205,000 | 287,676 | ||||||

Yoma Strategic Holdings Ltd. (a)(b) | 346,000 | 180,422 | ||||||

| 1,938,313 | ||||||||

Health Care (1.9%) | ||||||||

Eu Yan Sang International Ltd. | 170,000 | 99,906 | ||||||

Raffles Medical Group Ltd. (a) | 165,315 | 489,421 | ||||||

| 589,327 | ||||||||

Industrials (3.9%) | ||||||||

ComfortDelGro Corp. Ltd. (a) | 230,000 | 472,881 | ||||||

SATS Ltd. (a) | 144,000 | 347,523 | ||||||

SBS Transit Ltd. | 9,500 | 12,275 | ||||||

Singapore Post Ltd. (a) | 241,000 | 369,904 | ||||||

| 1,202,583 | ||||||||

Information Technology (2.1%) | ||||||||

Venture Corp. Ltd. (a) | 110,000 | 662,574 | ||||||

Materials (0.6%) | ||||||||

Straits Trading Co. Ltd. (a) | 90,500 | 203,312 | ||||||

| 4,596,109 | ||||||||

SRI LANKA (2.9%) | ||||||||

Financials (0.4%) | ||||||||

Commercial Bank of Ceylon PLC (a) | 109,646 | 139,257 | ||||||

Industrials (2.5%) | ||||||||

Aitken Spence & Co. PLC | 234,381 | 188,186 | ||||||

John Keells Holdings PLC (a) | 292,192 | 575,720 | ||||||

| 763,906 | ||||||||

| 903,163 | ||||||||

THAILAND (10.8%) | ||||||||

Consumer Discretionary (2.7%) | ||||||||

BEC World PCL, Foreign Shares (a) | 318,200 | 471,522 | ||||||

Minor International PCL, Foreign Shares (a) | 330,000 | 352,043 | ||||||

| 823,565 | ||||||||

Financials (4.0%) | ||||||||

AEON Thana Sinsap Thailand PCL, NVDR | 119,000 | 396,423 | ||||||

Tesco Lotus Retail Growth Freehold & Leasehold Property Fund (c) | 390,000 | 153,270 | ||||||

Tisco Financial Group PCL, Foreign Shares (a) | 282,000 | 385,533 | ||||||

Tisco Financial Group PCL, NVDR (a) | 220,000 | 300,771 | ||||||

| 1,235,997 | ||||||||

Health Care (1.1%) | ||||||||

Bumrungrad Hospital PCL, Foreign Shares (a) | 85,700 | 350,002 | ||||||

Information Technology (1.4%) | ||||||||

Hana Microelectronics PCL, Foreign Shares (a) | 330,900 | 441,945 | ||||||

Materials (1.6%) | ||||||||

Siam City Cement PCL, Foreign Shares (a) | 39,000 | 502,932 | ||||||

| 3,354,441 | ||||||||

UNITED KINGDOM (3.2%) | ||||||||

Consumer Discretionary (3.2%) | ||||||||

Millennium & Copthorne Hotels PLC | 109,682 | 996,603 | ||||||

Total Common Stocks | 30,170,723 | |||||||

See accompanying Notes to Financial Statements.

Annual Report 2014

14

Table of Contents

Statement of Investments (concluded)

October 31, 2014

Aberdeen Asia-Pacific Smaller Companies Fund

| Shares or Principal Amount | Value | |||||||

WARRANTS (0.0%) | ||||||||

SRI LANKA (0.0%) | ||||||||

Industrials (0.0%) | ||||||||

John Keells Holdings PLC, expires 11/11/16 (b) | 7,564 | $ | 4,627 | |||||

John Keells Holdings PLC, expires 11/12/15 (b) | 7,564 | 4,338 | ||||||

| 8,965 | ||||||||

THAILAND (0.0%) | ||||||||

Consumer Discretionary (0.0%) | ||||||||

Minor International PLC, expires 11/03/17 (b) | 16,500 | 0 | ||||||

Total Warrants | 8,965 | |||||||

REPURCHASE AGREEMENT (2.7%) | ||||||||

UNITED STATES (2.7%) | ||||||||

Repurchase Agreement, Fixed Income Clearing Corp., 0.00%, dated 10/31/2014, due 11/03/2014, repurchase price $831,000, collateralized by U.S. Treasury Note, maturing 10/31/2021; total market value of $847,795 | $ | 831,000 | 831,000 | |||||

Total Repurchase Agreement | 831,000 | |||||||

Total Investments | 31,010,688 | |||||||

Liabilities in excess of other assets—(0.1)% | (37,368 | ) | ||||||

Net Assets—100.0% | $ | 30,973,320 | ||||||

| (a) | Fair Valued Security. Fair Values are determined pursuant to procedures approved by the Fund’s Board of Trustees. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (b) | Non-income producing security. |

| (c) | As of October 31, 2014, security is a closed-end fund incorporated in Thailand. |

| (d) | See Notes to Financial Statements for tax unrealized appreciation/depreciation of securities. |

| NVDR | Non-Voting Depositary Receipt |

| REIT | Real Estate Investment Trust |

See accompanying Notes to Financial Statements.

2014 Annual Report

15

Table of Contents

Aberdeen China Opportunities Fund (Unaudited)

The Aberdeen China Opportunities Fund (Class A shares at net asset value net of fees) returned -0.82% for the 12-month period ended October 31, 2014, versus the 7.87% return of its benchmark, the MSCI Zhong Hua Index, during the same period. For broader comparison, the average return of the Fund’s Lipper peer category of China Region Funds (consisting of 47 funds) was 6.19% for the period.

Equity markets in China and Hong Kong rallied during the reporting period. Stocks initially were boosted by optimism over details about the Chinese government’s Third Plenum1 reforms, which included liberalizing the financial sector. Towards the end of the first half of the period, however, the contraction in China’s manufacturing activity dragged equity markets lower. Liquidity was tight in the mainland, prompting the central bank to pump funds into the financial system. Concerns over shadow banking2 persisted, exacerbated by a landmark bond default. Further uncertainty was fuelled by the tumble of the yuan, the nation’s currency unit. But confidence recovered following the reform of state-owned enterprises. Investors were also excited over pilot schemes for the China (Shanghai) Pilot Free-Trade Zone as well as the Shanghai–Hong Kong Stock Connect program,3 as these were seen as significant steps towards cross-border capital market integration. On the economic front, China’s better-than-expected gross domestic product (GDP) growth data for the first half of 2014 also reassured markets, albeit this was driven by state-backed investment and lending. Gains were pared in anticipation of the end of quantitative easing in the U.S., which happened at the end of the reporting period, as well as political jitters over the ongoing pro-democracy protests in Hong Kong.

The lack of exposure to Tencent was the most notable detractor from Fund performance over the reporting period, relative to the Fund’s benchmark. The Chinese Internet company’s shares rallied as investors expected mobile gaming revenues to boost its growth prospects. Market sentiment towards the stock also strengthened after it bought a stake in a Chinese logistics operator in a bid to boost its e-commerce business, as well as in response to reports that it may invest in a restaurant and entertainment guide website. However, we feel that its valuation since has become more stretched and we remain cautious on the sector given our concerns regarding the variable interest entity4 structure.

Other detractors from Fund performance for the period included retailer Giordano, which was hurt by the challenging macroeconomic environment, as well as Standard Chartered. The lender’s stock price weakened after the third profit warning in a year as it delivered its results for the first nine months of its 2014 fiscal year. Management cited high impairment charges as some corporate and institutional clients were hurt by weakening commodity markets. Investor sentiment was also dampened by speculation that U.S. regulators could reinvestigate alleged sanction violations against Standard Chartered. Some of its problems are cyclical and, we believe, may be resolved in the medium term. In our opinion, more structural difficulties may require management to reprioritize investments, divest non-core businesses and streamline riskier portfolios.

The primary contributors to the Fund’s relative return for the review period included Green Dragon Gas (GDG) and Samsonite International. GDG’s shares climbed sharply after it agreed to a deal with China National Offshore Oil Corporation (CNOOC) regarding five of its production sharing contracts in China. The agreement will secure GDG’s interest and revenue share of approximately 1,600 wells drilled by CNOOC’s subsidiary, China United Coalbed Methane Corporation. Samsonite International saw healthy growth during the period across all businesses, particularly in Asia and the American Tourister brand.

The absence of a position in Industrial & Commercial Bank of China also had a positive impact on performance, relative to the Fund’s benchmark, as Chinese banks were dogged by worries over asset quality, particularly focused on the banks’ off-balance sheet items, which may potentially be de facto liabilities due to implicit guarantees. The lack of transparency on shadow banking assets also makes it difficult for investors to quantify potential losses, in our view.

During the reporting period, we initiated a position in global logistics company Kerry Logistics. We like the company for its integrated capabilities, which are hard to replicate, in our opinion. Additionally, the group continues to increase its substantial exposure to China, where it has the largest distribution network.

Against this, we exited the Fund’s position in Wing Hang Bank following its takeover by OCBC. We also exited the position in China Vanke’s H-shares,5 which rose substantially after being converted from the B-shares. We retain exposure to the company through its A-shares, which trade at a significant discount.

A fundamental restructuring of China’s economy lies ahead and this means a prolonged period of slower growth, in our opinion. Poor economic data arising from this may continue to sway market sentiment. Despite market movements, we feel that policymakers are unlikely to implement aggressive fiscal or credit policies. We think that monetary policy may continue to accommodate economic transition, while averting liquidity crises. Recently, the Chinese central bank raised the reference rate for the yuan, while the

| 1 | The Third Plenum of the 18th Chinese Communist Party Congress was held in November 2013. This plenum has historically been a platform for Chinese leaders to present their long-term vision for the economy. |

| 2 | Shadow banking refers to the financial intermediaries involved in facilitating the creation of credit across the global financial system, but whose members are not subject to regulatory oversight. The shadow banking system also refers to unregulated activities by regulated institutions. |

| 3 | Shanghai–Hong Kong Stock Connect is a pilot program that links the stock markets in Shanghai and Hong Kong. Under the program, investors in Hong Kong and Mainland China can trade and settle shares listed on the other market via the exchange and clearing house in their home market. |

| 4 | An entity in which equity investors do not have the characteristics of a controlling financial interest (i.e., they lack certain decision-making ability) or do not have sufficient equity at risk for the entity to finance its activities without additional subordinated financial support. |

| 5 | Shares of a company incorporated in the Chinese mainland that is listed on the Hong Kong Stock Exchange or other foreign exchange. |

Annual Report 2014

16

Table of Contents

Aberdeen China Opportunities Fund (Unaudited) (concluded)

Hong Kong Monetary Authority scrapped the yuan-conversion limit, both of which may potentially strengthen the currency and boost its global standing.

In our view, the developments that will be keenly monitored include the commencement of the Shanghai-Hong Kong Stock Connect program, which marks the first step towards the internationalization of the mainland’s capital markets. It expands investment choices for investors on both sides of the border and paves the way for the further opening up of the renminbi and China’s capital account.6 This may enhance Hong Kong’s position as the world’s primary offshore renminbi center and reinforces it as the gateway between China and international markets.

The ensuing euphoria resulting from the Shanghai-Hong Kong Stock Connect program will not change the way we identify investment opportunities. We have always followed a bottom-up, long-term investment strategy based on the thorough assessment of a company’s merits. However, we are carefully monitoring the impact of this new program on our holding in Hong Kong Exchanges and Clearing. If the new program is successful, there is scope for an expansion that includes the cross-border trading of even more asset classes.

Portfolio Management:

Aberdeen Asia-Pacific Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance data quoted represents past performance and current returns may be lower or higher. Class A Shares have up to a 5.75% front-end sales charge and a 0.25% 12b-1 fee. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, which may be higher or lower than the performance shown above, please call 866-667-9231 or go to www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal.

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Concentrating investments in China and Hong Kong subjects the Fund to more volatility and greater risk of loss than geographically diverse mutual funds.

Additional risks associated with investments in China and Hong Kong include exposure to currency fluctuations, less liquidity, expropriation, confiscatory taxation, nationalization, exchange control regulations (including currency blockage) and differing legal standards.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and political and economic risks. These risks are enhanced in emerging markets countries.

Equity stocks of small and mid-cap companies carry greater risk, and more volatility than equity stocks of larger, more established companies.

Please read the prospectus for more detailed information regarding these and other risks.

| 6 | Under China’s closed capital account, companies, banks and individuals cannot move money in or out of the country except in accordance with strict rules. The limit for individuals is currently $50,000 a year, while corporate investments need government approval. |

2014 Annual Report

17

Table of Contents

Aberdeen China Opportunities Fund (Unaudited)

Average Annual Total Return1 (For periods ended October 31, 2014) | 1 Yr. | 5 Yr. | 10 Yr. | |||||||||||

Class A | w/o SC | (0.82% | ) | 5.24% | 11.46% | |||||||||

| w/SC2 | (6.51% | ) | 4.00% | 10.80% | ||||||||||

Class C | w/o SC | (1.57% | ) | 4.49% | 10.64% | |||||||||

| w/SC3 | (2.55% | ) | 4.49% | 10.64% | ||||||||||

Class R4 | w/o SC | (1.25% | ) | 4.90% | 11.13% | |||||||||

Institutional Service Class4 | w/o SC | (0.56% | ) | 5.54% | 11.73% | |||||||||

Institutional Class4 | w/o SC | (0.65% | ) | 5.47% | 11.73% | |||||||||

All figures showing the effect of a sales charge (SC) reflect the maximum charge possible because it has the most significant effect on performance data. The total returns shown above do not include the impact of financial statement rounding of the net asset value per share and/or financial statement adjustments.

| 1 | Returns incorporate the performance of a predecessor fund (the “Predecessor Fund”) from inception to June 23, 2008. The Fund and the Predecessor Fund have substantially similar investment objectives and strategies. Please consult the Fund’s prospectus for more detail. |

| 2 | A 5.75% front-end sales charge was deducted. |

| 3 | A 1.00% contingent deferred sales charge (CDSC) was deducted from the one year return because it is charged when Class C shares are sold within the first year after purchase. |

| 4 | Not subject to any sales charges. |

Annual Report 2014

18

Table of Contents

Aberdeen China Opportunities Fund (Unaudited)

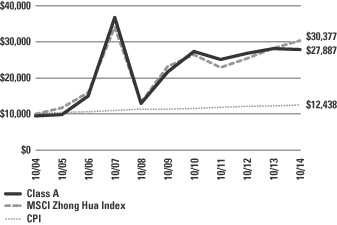

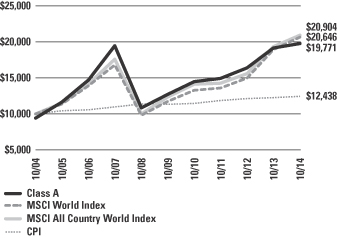

Performance of a $10,000 Investment (as of October 31, 2014)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen China Opportunities Fund, Morgan Stanley Capital International (MSCI) Zhong Hua Index and the Consumer Price Index (CPI) over a 10-year period ended October 31, 2014. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees, expenses, or sales charges. Investors cannot invest directly in market indexes.

The MSCI Zhong Hua Index is a free float-adjusted, market capitalization-weighted index that is an aggregate of the MSCI Hong Kong Index and the MSCI China Index. The MSCI Hong Kong Index is designed to measure the performance of the large and mid cap segments of the Hong Kong market. The MSCI China Index captures large and mid capitalization across China H shares, B shares, Red chips, and P chips.

The CPI represents changes in prices of a basket of goods and services purchased for consumption by urban households.

Investment returns and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and Performance graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Total returns reflect waivers and reimbursements in effect, without which returns would have been lower.

Portfolio Summary (as a percentage of net assets)

October 31, 2014 (Unaudited)

| Asset Allocation | ||||

Common Stocks | 99.0% | |||

Repurchase Agreement | 0.4% | |||

Other assets in excess of liabilities | 0.6% | |||

| 100.0% | ||||

The following chart summarizes the composition of the Fund’s portfolio, in industry classification standard sectors, expressed as a percentage of net assets. An industry classification standard sector can include more than one industry group. As of October 31, 2014, the Fund did not have more than 25% of its assets invested in any industry group. The sectors, as classified by S&P’s Global Industry Classification Standard Sectors, are comprised of several industry groups.

| Top Sectors | ||||

Financials | 36.9% | |||

Consumer Discretionary | 17.9% | |||

Industrials | 17.9% | |||

Energy | 8.7% | |||

Consumer Staples | 5.5% | |||

Telecommunication Services | 4.8% | |||

Materials | 3.2% | |||

Information Technology | 2.5% | |||

Utilities | 1.6% | |||

Other | 1.0% | |||

| 100.0% | ||||

| Top Holdings* | ||||

Jardine Strategic Holdings Ltd. | 8.3% | |||

Swire Pacific Ltd., Class B | 6.6% | |||

AIA Group Ltd. | 5.7% | |||

MTR Corp. Ltd. | 5.0% | |||

HSBC Holdings PLC | 4.8% | |||

Hang Lung Group Ltd. | 4.2% | |||

China Mobile Ltd. | 3.9% | |||

PetroChina Co. Ltd., H Shares | 3.7% | |||

CNOOC Ltd. | 3.4% | |||

Hongkong & Shanghai Hotels Ltd. (The) | 3.0% | |||

Other | 51.4% | |||

| 100.0% | ||||

| Top Countries | ||||

Hong Kong | 71.8% | |||

China | 24.4% | |||

United States | 3.2% | |||

Other | 0.6% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, repurchase agreements are included as part of Other. |

2014 Annual Report

19

Table of Contents

Statement of Investments

October 31, 2014

Aberdeen China Opportunities Fund

| Shares or Principal Amount | Value | |||||||

COMMON STOCKS (99.0%) | ||||||||

CHINA (24.4%) | ||||||||

Consumer Staples (2.8%) | ||||||||

China Resources Enterprise Ltd. (a) | 360,000 | $ | 856,257 | |||||

Energy (8.7%) | ||||||||

CNOOC Ltd. (a) | 651,000 | 1,017,720 | ||||||

Green Dragon Gas Ltd. (b) | 58,000 | 463,913 | ||||||

Greka Drilling Ltd. (a)(b) | 225,000 | 30,827 | ||||||

Greka Engineering & Technology Ltd. (b) | 174,000 | 4,871 | ||||||

PetroChina Co. Ltd., H Shares (a) | 894,000 | 1,120,390 | ||||||

| 2,637,721 | ||||||||

Financials (6.4%) | ||||||||

China Merchants Bank Co. Ltd., A Shares (a)(c) | 453,000 | 800,795 | ||||||

China Vanke Co. Ltd., A Shares (a)(c) | 438,000 | 673,003 | ||||||

Yanlord Land Group Ltd. (a) | 550,000 | 469,175 | ||||||

| 1,942,973 | ||||||||

Materials (2.6%) | ||||||||

Huaxin Cement Co. Ltd., B Shares | 298,240 | 321,503 | ||||||

Yingde Gases Group Co. Ltd. (a) | 597,000 | 466,162 | ||||||

| 787,665 | ||||||||

Telecommunication Services (3.9%) | ||||||||

China Mobile Ltd. (a) | 94,500 | 1,178,254 | ||||||

| 7,402,870 | ||||||||

HONG KONG (71.8%) | ||||||||