UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22132

Exact name of registrant as specified in charter:

Aberdeen Funds

Address of principal executive offices:

1735 Market Street, 32nd Floor

Philadelphia, PA 19103

Name and address of agent for service:

Ms. Andrea Melia

Aberdeen Asset Management Inc.

1735 Market Street, 32nd Floor

Philadelphia, PA 19103

Registrant’s telephone number, including area code: 866-667-9231

Date of fiscal year end: October 31

Date of reporting period: October 31, 2017

Item 1. Reports to Shareholders.

Aberdeen Funds

Equity Series

Annual Report

October 31, 2017

Aberdeen Asia-Pacific (ex-Japan) Equity Fund

Aberdeen China Opportunities Fund

Aberdeen Emerging Markets Fund

Aberdeen Focused U.S. Equity Fund (formerly, Aberdeen Equity Long-Short Fund)

Aberdeen Global Equity Fund

Aberdeen International Equity Fund

Aberdeen International Small Cap Fund

Aberdeen Japanese Equities Fund

Aberdeen U.S. Mid Cap Equity Fund

Aberdeen U.S. Multi-Cap Equity Fund

Aberdeen U.S. Small Cap Equity Fund

| Page 2 | ||||

| Page 4 | ||||

| Page 10 | ||||

| Page 16 | ||||

| Page 24 | ||||

| Page 31 | ||||

| Page 37 | ||||

| Page 43 | ||||

| Page 49 | ||||

| Page 54 | ||||

| Page 60 | ||||

| Page 66 | ||||

| Page 72 | ||||

| Page 116 | ||||

| Page 134 | ||||

| Page 135 | ||||

| Page 137 | ||||

| Page 139 | ||||

| Page 142 | ||||

Investors should carefully consider a fund’s investment objectives, risks, fees, charges and expenses before investing any money. To obtain this and other fund information, please call 866-667-9231 to request a prospectus, or download a prospectus at www.aberdeen-asset.us. Please read it carefully before investing any money.

Investing in mutual funds involves risk, including possible loss of principal.

Aberdeen Funds is distributed by Aberdeen Fund Distributors LLC, Member FINRA, 1735 Market Street, 32nd Floor, Philadelphia, PA 19103.

Aberdeen Asset Management Inc. (“AAMI”) has been registered as an investment adviser under the Investment Advisers Act of 1940 since August 23, 1995.

Statement Regarding Availability of Quarterly Portfolio Schedule.

The complete schedule of portfolio holdings for each fund of Aberdeen Funds (each a “Fund” and collectively, the “Funds”) is included in the Funds’ semi-annual and annual reports to shareholders. Aberdeen Funds also files complete schedules of portfolio holdings for each Fund with the Securities and Exchange Commission (the “Commission”) for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Form N-Q filings are available on the Commission’s website at http://www.sec.gov. The Funds’ Form N-Q filings may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330; and the Funds make the information on Form N-Q available to shareholders on www.aberdeen-asset.us or upon request without charge.

Statement Regarding Availability of Proxy Voting Record.

Information regarding the policies and procedures that the Funds use to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 1-866-667-9231. The information is also included in the Funds’ Statement of Additional Information, which is available on the Funds’ website at www.aberdeen-asset.us and on the Commission’s website at www.sec.gov.

Information relating to how each Fund voted proxies relating to portfolio securities held during the most recent twelve months ended June 30 is available by August 30 of the relevant year: (i) upon request and without charge by calling 1-866-667-9231; and (ii) on the Commission’s website at www.sec.gov.

It appeared that the 12-month period ended October 31, 2017 saw the waning of the populist movement and a move towards the center in the global political arena. Early in the period in November 2016, Republican Donald Trump unexpectedly won the U.S. presidential election, defeating his Democratic party opponent, former U.S. Senator and Secretary of State Hillary Clinton. Trump’s victory seemed to be a continuation of the populist political movement that led to the UK’s vote to leave the European Union (known as Brexit) in June 2016. However, there appeared to be a change in voters’ sentiment in the spring of 2017, as candidates campaigning on a populist platform in the Netherlands and France lost national elections to more politically moderate opponents. Incumbent Prime Minister Mark Rutte’s People’s Party for Freedom and Democracy (VVD) won significantly more seats in the Dutch Parliament than Geert Wilders’ far-right Party for Freedom (PPV) in the Netherlands’ election in March 2017. Independent centrist candidate Emmanuel Macron subsequently claimed victory in the final round of the French presidential election in early May 2017, by a nearly two-to-one margin over far-right candidate Marine Le Pen. In the U.S., President Trump encountered numerous political challenges and obstacles to the fulfillment of his campaign promises – most notably the ongoing investigation of several members of his administration into possible collusion with the Russian government during the presidential election of 2016.

On the geopolitical front, in September 2017, North Korean leader Kim Jong Un claimed that the nation conducted a successful underground detonation of a hydrogen bomb, which reached a magnitude of 6.3 on the Richter scale, according to the U.S. Geological Survey. The following week, North Korea fired another intermediate-range ballistic missile which passed over the island of Hokkaido in Japan and subsequently landed in the Pacific Ocean. The launch from Pyongyang, North Korea’s capital, occurred after the United Nations Security Council unanimously adopted new sanctions against the nation.

The Morgan Stanley Capital International (MSCI) World Index,1 a global equity market benchmark, rose 23.4% for the 12-month period ended October 31, 2017. European large-cap stocks were the strongest performers among global developed markets, with the MSCI Europe Index up 27.0%. Shares of Asian and U.S. large-cap companies, as represented by the MSCI All Country (AC) Asia Pacific Index and the U.S. broader-market Standard & Poor’s (S&P) 500 Index, recorded corresponding gains of 23.7% and 23.6% over the period. Global emerging equity markets, as measured by the MSCI Emerging Markets Index, outperformed their developed-market counterparts, advancing 26.9% for the reporting period

Major U.S. equity indices moved sharply higher over the reporting period despite several periods of uncertainty surrounding the policies of the Trump administration. Most U.S. companies reported strong results and generally upbeat outlooks during the period. Corporate earnings generally were strong enough to support stocks across the market-capitalization ranges. U.S. small-cap stocks, as measured by the Russell 2000 Index, advanced 27.9% for the reporting period, outperforming the 23.6% and 21.1% returns of their large- and mid-cap counterparts, as measured by the S&P 500 Index and the Russell Midcap Index, respectively. Roughly 75% of S&P 500 Index companies posted better-than-expected earnings per share (EPS) for the third-quarter 2017 reporting season, while two-thirds exceeded consensus revenue estimates.2

Both European and UK stocks3 posted double-digit gains over the reporting period. In the Eurozone, the economic recovery, as well as investors’ positive views on the outcomes from elections in France and the Netherlands, strengthened the equity market. However, the rally was tempered by investors’ worries over rising secessionist fervor in the Catalonia region of Spain and its potential disruption to business operations. The UK market was hampered somewhat by Prime Minister Theresa May’s failed bid to secure a larger mandate from a snap election that resulted in a hung Parliament in June 2017.

The Asia-Pacific market also saw strong performance over the reporting period despite geopolitical tensions on the Korean peninsula and uncertainty regarding the prospect of major global central banks withdrawing monetary stimulus. China led the upturn in the region, buttressed by upbeat economic growth data, along with benchmark index provider MSCI’s decision to include A-shares4 in its influential indices and a sustained rise in Chinese internet stocks. Late in the reporting period, investors appeared to shrug off S&P’s downgrade of the country’s sovereign debt rating.5 Conversely, while Japanese equities rose sharply over the reporting period, they underperformed the overall Asia-Pacific region and their global developed-market counterparts due to investors’ concerns regarding external factors such as the volatile political environment in the U.S. and UK.

Emerging stock markets generally posted healthy gains for the reporting period. Within Latin America, Brazilian equities performed well despite a notable decline in May 2017, after President Michel Temer became implicated in a corruption scandal. Mexican stocks and the peso initially recovered from a post-U.S. election sell-off, but uncertainty over the fate of the North American Free Trade Agreement (NAFTA) and natural disasters capped gains towards the end of the reporting period. Economic growth in India slowed over the reporting period due to the lingering effects of the government’s demonetization,6 which it initiated in November 2016, while the Goods and Services Tax was implemented in July 2017.

Despite political risks in the U.S., Europe and the UK, global fixed-income markets garnered modestly positive returns over the reporting period amid an improving global economic backdrop. Investment-grade securities, as measured by the Bloomberg Barclays Global Aggregate Bond Index, returned 1.2% for the period. Global high-yield bonds outperformed their investment-grade counterparts by a wide margin, with the ICE Bank of America Merrill Lynch Global High Yield Constrained Index gaining 9.4% for the period. Global government bond yields moved higher after the U.S. presidential

| 2 | Annual Report 2017 |

Market Review (concluded)

election in November 2016, but slowly reversed direction throughout most of 2017; the 10-year U.S. Treasury yield rose 54 basis points to 2.38% over the reporting period. Donald Trump’s win in the November 2016 U.S. presidential election fueled expectations of increased fiscal spending and rising inflation, which halted the global bond market rally at that time. Towards the end of the reporting period, bond yields rose again as major global central banks edged closer towards ending the era of accommodative monetary policy. Both the U.S. Federal Reserve (Fed) and European Central Bank decided to start tapering their quantitative-easing programs. G107 currencies were mostly stronger against the U.S. dollar, while those in emerging markets ended with mixed performance.

Outlook

We believe that generally good economic conditions should support global equity prices. Business sentiment in the U.S. is likely to be buoyed by prospects of lower corporate taxes, in our view. Banks in the Eurozone anticipate healthier demand for loans from both businesses and households. Supporting this environment are still-low interest rates, increased capital expenditures, a favorable housing market, relatively low unemployment and rising consumer confidence. In Japan, investor sentiment improved following Prime Minister Shinzo Abe’s election victory in October 2017, which strengthened his mandate to implement reforms. However, we think that economic growth may moderate in China, as the Chinese Communist Party appears to be prioritizing stability over aggressive growth targets. For emerging markets, we think that future growth may be helped by structural reforms and a rebound in commodity prices. Crude oil prices are recovering, bolstered by growing demand, supply cuts, and stabilizing shale oil production. In addition to these developments, stock-market volatility, as measured by the CBOE Volatility Index,8 is at historical lows. In our view, equities now appear expensive in the U.S. While we do not think that valuations leave much room for upside, we also see little reason for a significant correction outside some external shock – which obviously is not out of the question given political instability both domestically and abroad. We believe that there is scope for improved earnings in Europe, while operational performance in Asia has been improving. We are cognizant that the move by major global central banks to exit quantitative easing, the unresolved Brexit issue in the UK, rising trade protectionism and geopolitical risks could dent corporate earnings growth. However, we believe that our bottom-up investment approach positions our equity portfolios well in the current global market environment. We will remain diligent in monitoring company valuations, financial performance and governance against their growth prospects in an effort to hold investments that we believe can withstand future challenges.

In early November 2017, the Bank of England raised its benchmark interest rate for the first time in a decade and indicated the beginning of a gradual increase in borrowing costs, as monetary policymakers seek to prevent a sustained rise in inflation without choking economic recovery. Meanwhile, the Fed grew more vocal about reducing its balance sheet. While we feel that global bond markets have taken this news in stride, we will not be surprised if the sell-off gathers pace. We do not think that such moves to drain liquidity from the global financial system will go unnoticed as risks to the nascent global economic recovery persist. In credit markets, valuations look expensive, so we will narrow our search to investment-grade companies that we believe have strong balance sheets, healthy cash flows and good management.

Aberdeen Standard Investments

| 1 | Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index. |

| 2 | Source: FactSet, “Earnings Insight,” November 2017. |

| 3 | The performance of UK stocks is measured by the MSCI United Kingdom Index. |

| 4 | A-shares are purchased and traded on the Shanghai and Shenzhen stock exchanges. |

| 5 | Standard & Poor’s credit ratings express the agency’s opinion about the ability and willingness of an issuer, such as a corporation or state or city government, to meet its financial obligations in full and on time. Typically, ratings are expressed as letter grades that range, for example, from “AAA” to “D” to communicate the agency’s opinion of relative level of credit risk. Ratings from “AA” to “CCC” may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. |

| 6 | Demonetization comprises the act of stripping specific denominations of a currency unit of their status as legal tender. The currency denominations are pulled from circulation and are replaced with new currency units. |

| 7 | The G10 nations, which consult and cooperate on economic, monetary and financial matters, include Belgium, Canada, France, Germany, Italy, Japan, the Netherlands, Sweden, Switzerland, the UK and the U.S. |

| 8 | The CBOE Volatility Index is a measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. |

| 2017 Annual Report | 3 |

Aberdeen Asia-Pacific (ex-Japan) Equity Fund (Unaudited)

The Aberdeen Asia-Pacific (ex-Japan) Equity Fund (Institutional Class shares net of fees) returned 28.21% for the 12-month period ended October 31, 2017, versus the 28.03% return of its benchmark, the Morgan Stanley Capital International (MSCI) All Country (AC) Asia Pacific ex Japan Index, during the same period. For broader comparison, the average return of the Fund’s category of Pacific ex-Japan Funds (comprising 40 funds), as measured by Lipper, Inc., was 26.51% for the period.

Asian equities posted solid gains over the 12-month reporting period, driven by improving corporate fundamentals across the region and a recovery in global trade. However, the upturn was capped by investors’ doubts over U.S. President Donald Trump’s ability to deliver on his economic agenda, geopolitical tensions on the Korean peninsula, and the prospect of major central banks withdrawing monetary stimulus.

China’s equity market outpaced the overall Asia-Pacific region. Upbeat economic growth data, along with benchmark index provider MSCI’s decision to include China A-shares1 in its influential indices and a sustained rise in Chinese internet stocks, drove the mainland market, despite Beijing’s increased regulatory scrutiny and efforts to tighten leverage. Meanwhile, a rally in the technology sector underpinned equity markets in Korea and Taiwan, with companies in the Apple supply chain among the beneficiaries. The Korean market also gained ground on investors’ hopes that tensions with China over the Terminal High Altitude Area Defense (THAAD) missile system would thaw after South Korean President Moon Jae-in took office in May 2017.

Conversely, the performance of equities in the Philippines, Malaysia and Indonesia trailed the overall Asia-Pacific region for the reporting period. Philippine stocks lagged after an extended run-up, hampered by President Rodrigo Duterte’s unpredictability and domestic political events. Both consumer spending and consumer confidence remained sluggish in Indonesia despite favorable economic conditions. The Malaysian economy continued to feel the impact of the Goods and Services tax enacted in April 2015, with inflation rising, while a weaker ringgit, the nation’s currency unit, increased the costs of imports.

The Fund’s modest outperformance versus its benchmark, the MSCI AC Asia Pacific ex Japan Index, over the reporting period was attributable mainly to positive stock selection in Australia, Singapore and India.

In Australia, shares of miners Rio Tinto and BHP Billiton rallied over the period as iron ore prices rebounded on the back of China’s improving macroeconomic outlook. The Fund’s other Australian holding, blood plasma manufacturer CSL, was also a strong contributor to the relative performance. We trimmed the Fund’s position in CSL after its stock price rose sharply in 2017, as the company reported strong earnings from its immunoglobulin and specialty products. We like CSL’s business, as we feel that the company has a decent growth pipeline and a wide moat2 in a sector that has consolidated.

The Fund’s holdings in Singapore-based banks Oversea-Chinese Banking Corp. (OCBC), DBS Group Holdings and United Overseas Bank (UOB) also performed well, as investors’ concerns regarding their asset quality eased and fee income improved. The companies’ third-quarter 2017 results demonstrated steady loan growth, backed by healthy levels of capital. The rally in the banks’ shares provided us with the opportunity to take some profits.

In India, shares of Grasim Industries outperformed after the conglomerate restructured its business and realized substantial hidden value in spinning off its financial holding company, Aditya Birla Capital. HDFC Bank benefited from the Indian government’s demonetization,3 posting solid income growth over the reporting period that was driven largely by an increase in net interest income.

In contrast, the Fund’s positioning in China weighed on the relative performance for the reporting period. The underweight exposure to the market relative to the benchmark MSCI AC Asia Pacific ex Japan Index detracted from performance as the MSCI China Index led the Asia-Pacific region’s gains. As we noted previously, China’s market rally was underpinned by the strong performance of internet stocks. Tencent Holdings and Alibaba stood out, buoyed by momentum trading4 and solid results. Therefore, the Fund’s underweight exposure to Tencent relative to the benchmark and the absence of a position in MSCI AC Asia Pacific ex Japan Index constituent Alibaba detracted from the Fund’s relative performance. We initiated a relatively small position in Tencent towards the end of the reporting period in September 2017. This reflects our growing conviction in, and comfort with, its business, corporate structure and governance. We think that the valuation reflects its high-quality growth potential. Tencent has succeeded in diversifying its presence in the Chinese internet space, creating a powerful ecosystem that leverages on the network effects of its various offerings, while at the same time navigating the migration of gaming from PC to mobile. We believe that this combination of an expanding ecosystem and a growing monetization5 of the user base will drive earnings growth. We are more circumspect regarding Alibaba. While the company has a strong competitive moat and impressive business model, we see potential downside risks from poor corporate governance.

The Fund’s holding in Indonesian conglomerate Astra International hampered the Fund’s relative performance for the reporting period. A more competitive environment had weighed on the company’s auto

| 4 | Annual Report 2017 |

| 1 | China A-shares are purchased and traded on the Shanghai and Shenzhen stock exchanges. |

| 2 | A business moat refers to the ability of a company to maintain competitive advantages over its competitors in an effort to protect its long-term profits and market share from competing firms. |

| 3 | Demonetization comprises the act of stripping specific denominations of a currency unit of their status as legal tender. The currency denominations are pulled from circulation and are replaced with new currency units. |

| 4 | Momentum trading seeks to capitalize on market volatility by focusing on stocks that are moving significantly in one direction on high volume. |

| 5 | Monetization comprises the conversion of an asset into money or legal tender. |

Aberdeen Asia-Pacific (ex-Japan) Equity Fund (Unaudited) (concluded)

business, although that proved to be temporary. Astra International reported improvement from all of its business segments in the third quarter of its 2017 fiscal year, led by earnings from heavy equipment distributor United Tractor. The conglomerate’s performance was also enhanced by its subsidiary, Permata Bank, which turned profitable in the third quarter due to lower credit costs.

Apart from the portfolio activity that we noted previously, we initiated a position in Yum China Holdings following the parent company’s (Yum! Brands) restructuring. We also established new positions in Hangzhou Hikvision Digital Technology Co., a large global video surveillance vendor; appliance manufacturer Midea Group Co., alcoholic beverage producer Kweichow Moutai Co.; Shanghai International Airport, a leading airport operator in China; consumer products maker Hindustan Unilever; and Indian private-sector lender Kotak Mahindra Bank. Conversely, we exited the Fund’s position in India-based ICICI Bank.

In the latter half of the reporting period, we initiated positions in China International Travel Services (CITS) and China Resources Land (CR Land). CITS is the mainland’s largest duty-free operator, which we believe is poised to benefit from rising consumer spending and growing demand for domestic travel. CR Land is a Hong Kong exchange-listed Chinese real estate developer that in our view has strong profitability, a substantial land bank, as well as a good business mix of property development and investment.

Elsewhere, we also introduced Bangkok Dusit Medical Services (BDMS), the largest private hospital group in Thailand with well-recognized brands and good management. It stands to benefit from the rising demand for healthcare domestically and medical tourism6 across the region, given its reputation in high-quality complex treatments.

In India, we exited the Fund’s position in software services company Infosys. While the dust appears to have settled somewhat, with one of its founders Nandan Nilekani returning as non-executive chairman following Vishal Sikka’s resignation as chief executive, we think that the company could continue to face uncertainty on strategy, board and management leadership. From a regional perspective, we feel that the company is now less attractive quality-wise when compared to other Asian holdings.

Asian markets continue to enjoy a “sweet spot” of improving economic growth prospects and favorable external conditions: corporate earnings have been improving amid growing evidence of a synchronized worldwide economic recovery. Global financial conditions remain relatively easy because of accommodative monetary policies, with the U.S. Federal Reserve raising rates gradually and continued quantitative easing in Japan. Consequently, global markets have recorded strong performance thus far in 2017. Many countries are expected to enjoy sustained economic growth into 2018, which we believe should benefit the Fund’s holdings.

Portfolio Management:

Aberdeen Asia-Pacific Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance data quoted represents past performance and current returns may be lower or higher. Class A Shares have up to a 5.75% front-end sales charge and a 0.25% 12b-1 fee. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, which may be higher or lower than the performance shown above, please call 866-667-9231 or go to www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal.

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Concentrating investments in the Asia-Pacific region subjects the Fund to more volatility and greater risk of loss than geographically diverse mutual funds.

Parts of the Asia-Pacific region may be subject to a greater degree of economic, political and social instability than is the case in the United States and Europe. Some Asian countries can be characterized as emerging markets or newly industrialized and may experience more volatile economic cycles than developed countries.

Foreign securities may be more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, currency exchange rates, political and economic risks. Fluctuation in currency exchange rates may impact the Fund’s returns more greatly to the extent the Fund does not hedge currency exposure or hedging techniques are unsuccessful. The foregoing risks are enhanced in emerging market countries.

Equity stocks of small- and mid-cap companies carry greater risk and more volatility than equity stocks of larger, more established companies.

Investing a significant portion of the Fund’s assets in securities of companies conducting business in a broadly related group of industries within an economic sector may make the Fund more vulnerable to unfavorable developments in that sector.

Please read the prospectus for more detailed information regarding these and other risks.

| 6 | Medical tourism is the process of traveling outside an individual’s country of residence for the purpose of receiving medical care. |

| 2017 Annual Report | 5 |

Aberdeen Asia-Pacific (ex-Japan) Equity Fund (Unaudited)

| Average Annual Total Return (For periods ended October 31, 2017) | 1 Yr. | 5 Yr. | Inception1 | |||||||||||

Class A2 | w/o SC | 27.84% | 5.27% | 5.55% | ||||||||||

| w/SC3 | 20.49% | 4.02% | 4.45% | |||||||||||

Class C2 | w/o SC | 27.07% | 4.55% | 4.81% | ||||||||||

| w/SC4 | 26.07% | 4.55% | 4.81% | |||||||||||

Class R2,5 | w/o SC | 27.56% | 5.02% | 5.28% | ||||||||||

Institutional Service Class5 | w/o SC | 28.02% | 5.49% | 6.66% | ||||||||||

Institutional Class5 | w/o SC | 28.21% | 5.53% | 6.69% | ||||||||||

All figures showing the effect of a sales charge (SC) reflect the maximum charge possible because it has the most significant effect on performance data. The total returns shown above do not include the impact of financial statement rounding of the net asset value (NAV) per share and/or financial statement adjustments.

| 1 | Fund commenced operations on November 16, 2009. |

| 2 | Returns before the first offering of Class A, Class C and Class R (February 28, 2012) are based on the previous performance of the Institutional Class. Returns of each class have not been adjusted to reflect the expenses applicable to the respective classes. Excluding the effect of any fee waivers or reimbursements, this performance is substantially similar to what Class A, Class C and Class R would have produced because all classes invest in the same portfolio of securities. Returns for Class A, Class C and Class R shares would only differ to the extent of the difference in expenses of the classes. |

| 3 | A 5.75% front-end sales charge was deducted. |

| 4 | A 1.00% contingent deferred sales charge (CDSC) was deducted from the one year return because it is charged when Class C shares are sold within the first year after purchase. |

| 5 | Not subject to any sales charges. |

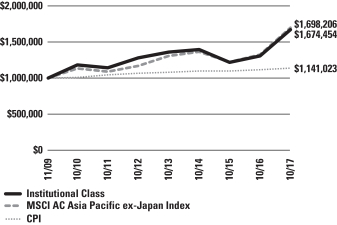

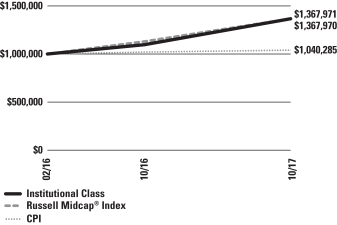

Performance of a $1,000,000 Investment* (as of October 31, 2017)

| * | Minimum Initial Investment |

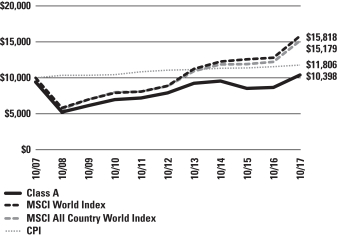

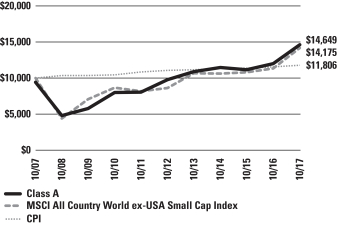

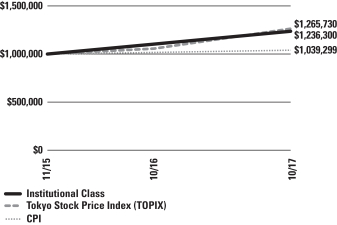

Comparative performance of $1,000,000 invested in Institutional Class shares of the Aberdeen Asia-Pacific (ex-Japan) Equity Fund, the Morgan Stanley Capital International All Country (MSCI AC) Asia Pacific ex-Japan Index and the Consumer Price Index (CPI) since inception. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees, expenses, or sales charges. Investors cannot invest directly in market indexes.

The MSCI AC Asia Pacific ex Japan Index captures large and mid cap representation across 4 of 5 Developed Markets countries (excluding Japan) and 9 Emerging Markets countries in the Asia Pacific region. With 710 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. Developed Markets countries in the index are: Australia, Hong Kong, New Zealand and Singapore. Emerging Markets countries in the Index are: China, India, Indonesia, Korea, Malaysia, Pakistan, the Philippines, Taiwan and Thailand.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and Performance graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Total returns reflect waivers and reimbursements in effect, without which returns would have been lower.

| 6 | Annual Report 2017 |

Aberdeen Asia-Pacific (ex-Japan) Equity Fund (Unaudited) (concluded)

Portfolio Summary (as a percentage of net assets)

October 31, 2017 (Unaudited)

| Asset Allocation | ||||

Common Stocks | 92.7% | |||

Preferred Stocks | 5.8% | |||

Short-Term Investment | 0.5% | |||

Other Assets in Excess of Liabilities | 1.0% | |||

| 100.0% | ||||

The following table summarizes the composition of the Fund’s portfolio, in Standard & Poor’s Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets. The GICS structure consists of 11 sectors, 24 industry groups, 68 industries and 157 sub-industries. As of October 31, 2017, the Fund did not have more than 25% of its assets invested in any industry group.

| Top Sectors | ||||

Financials | 29.2% | |||

Information Technology | 15.6% | |||

Materials | 10.3% | |||

Industrials | 9.0% | |||

Real Estate | 8.2% | |||

Consumer Discretionary | 8.1% | |||

Consumer Staples | 7.6% | |||

Telecommunication Services | 7.4% | |||

Health Care | 2.4% | |||

Energy | 0.7% | |||

Other | 1.5% | |||

| 100.0% | ||||

| Top Holdings* | ||||

Samsung Electronics Co. Ltd., Preferred Shares | 5.0% | |||

Taiwan Semiconductor Manufacturing Co. Ltd. | 4.0% | |||

Oversea-Chinese Banking Corp. Ltd. | 3.6% | |||

AIA Group Ltd. | 3.1% | |||

City Developments Ltd. | 3.1% | |||

Singapore Telecommunications Ltd. | 3.0% | |||

Jardine Strategic Holdings Ltd. | 3.0% | |||

Housing Development Finance Corp. Ltd. | 2.9% | |||

China Mobile Ltd. | 2.9% | |||

Ayala Corp. | 2.7% | |||

Other | 66.7% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, Short-Term Investments are included as part of Other. |

| Top Countries | ||||

Singapore | 16.5% | |||

China | 15.8% | |||

Hong Kong | 15.5% | |||

India | 12.7% | |||

Republic of South Korea | 9.4% | |||

United Kingdom | 6.3% | |||

Indonesia | 6.1% | |||

Taiwan | 5.5% | |||

Philippines | 4.1% | |||

Thailand | 2.8% | |||

Other | 5.3% | |||

| 100.0% | ||||

| 2017 Annual Report | 7 |

Statement of Investments

October 31, 2017

Aberdeen Asia-Pacific (ex-Japan) Equity Fund

| Shares or Principal Amount | Value | |||||||

COMMON STOCKS (92.7%) | ||||||||

AUSTRALIA (1.9%) | ||||||||

Health Care (1.9%) | ||||||||

CSL Ltd. (a) | 2,050 | $ | 218,245 | |||||

CHINA (15.8%) | ||||||||

Consumer Discretionary (4.3%) | ||||||||

China International Travel Service Corp. Ltd., A Shares (Stock Connect) (a)(b) | 25,399 | 158,697 | ||||||

Midea Group Co. Ltd., A Shares (Stock Connect) (a)(b) | 21,999 | 169,326 | ||||||

Yum China Holdings, Inc. (c) | 4,009 | 161,763 | ||||||

| 489,786 | ||||||||

Consumer Staples (1.8%) | ||||||||

Kweichow Moutai Co. Ltd., A Shares (Stock Connect) (a)(b) | 2,200 | 205,702 | ||||||

Energy (0.7%) | ||||||||

PetroChina Co. Ltd., H Shares (a) | 126,000 | 82,366 | ||||||

Industrials (1.2%) | ||||||||

Shanghai International Airport Co. Ltd., A Shares (Stock Connect) (a)(b) | 20,198 | 133,497 | ||||||

Information Technology (2.7%) | ||||||||

Hangzhou Hikvision Digital Technology Co. Ltd., A Shares (Stock Connect) (a)(b) | 31,900 | 189,214 | ||||||

Tencent Holdings Ltd. (a) | 2,500 | 112,363 | ||||||

| 301,577 | ||||||||

Materials (1.4%) | ||||||||

Anhui Conch Cement Co. Ltd., H Shares (a) | 36,500 | 156,355 | ||||||

Real Estate (0.8%) | ||||||||

China Resources Land Ltd. (a) | 32,000 | 95,503 | ||||||

Telecommunication Services (2.9%) | ||||||||

China Mobile Ltd. (a) | 32,000 | 321,868 | ||||||

| 1,786,654 | ||||||||

HONG KONG (15.5%) | ||||||||

Financials (7.2%) | ||||||||

AIA Group Ltd. (a) | 46,200 | 348,139 | ||||||

Hong Kong Exchanges & Clearing Ltd. (a) | 7,981 | 222,384 | ||||||

HSBC Holdings PLC (a) | 25,344 | 247,595 | ||||||

| 818,118 | ||||||||

Industrials (4.0%) | ||||||||

Jardine Strategic Holdings Ltd. (a) | 8,100 | 339,755 | ||||||

MTR Corp. Ltd. (a) | 18,459 | 107,016 | ||||||

| 446,771 | ||||||||

Real Estate (4.3%) | ||||||||

Hang Lung Group Ltd. (a) | 44,000 | 154,602 | ||||||

Swire Pacific Ltd., Class B (a) | 52,500 | 90,749 | ||||||

Swire Properties Ltd. (a) | 71,700 | 242,290 | ||||||

| 487,641 | ||||||||

| 1,752,530 | ||||||||

INDIA (12.7%) | ||||||||

Consumer Discretionary (1.2%) | ||||||||

Hero MotoCorp Ltd. (a) | 2,325 | 138,508 | ||||||

Consumer Staples (2.9%) | ||||||||

Hindustan Unilever Ltd. (a) | 3,000 | 57,405 | ||||||

ITC Ltd. (a) | 64,400 | 264,562 | ||||||

| 321,967 | ||||||||

Financials (4.9%) | ||||||||

Aditya Birla Capital Ltd. (c)(d) | 4,263 | 11,706 | ||||||

HDFC Bank Ltd. (a) | 3,830 | 107,106 | ||||||

Housing Development Finance Corp. Ltd. (a) | 12,508 | 328,625 | ||||||

Kotak Mahindra Bank Ltd. (a) | 6,900 | 109,436 | ||||||

| 556,873 | ||||||||

Information Technology (1.5%) | ||||||||

Tata Consultancy Services Ltd. (a) | 4,158 | 168,207 | ||||||

Materials (2.2%) | ||||||||

Grasim Industries Ltd. (a) | 12,870 | 244,522 | ||||||

| 1,430,077 | ||||||||

INDONESIA (6.1%) | ||||||||

Consumer Discretionary (2.6%) | ||||||||

Astra International Tbk PT (a) | 501,900 | 296,054 | ||||||

Consumer Staples (0.9%) | ||||||||

Unilever Indonesia Tbk PT | 28,600 | 104,594 | ||||||

Financials (2.6%) | ||||||||

Bank Central Asia Tbk PT (a) | 190,600 | 293,608 | ||||||

| 694,256 | ||||||||

MALAYSIA (1.9%) | ||||||||

Financials (1.9%) | ||||||||

CIMB Group Holdings Bhd (a) | 70,148 | 101,738 | ||||||

Public Bank Bhd (a) | 23,200 | 112,115 | ||||||

| 213,853 | ||||||||

PHILIPPINES (4.1%) | ||||||||

Financials (4.1%) | ||||||||

Ayala Corp. (a) | 15,360 | 306,511 | ||||||

Bank of the Philippine Islands | 80,515 | 152,842 | ||||||

| 459,353 | ||||||||

REPUBLIC OF SOUTH KOREA (3.6%) | ||||||||

Consumer Staples (1.2%) | ||||||||

Amorepacific Group (a) | 126 | 16,158 | ||||||

E-MART, Inc. (a) | 588 | 117,705 | ||||||

| 133,863 | ||||||||

Information Technology (2.4%) | ||||||||

NAVER Corp. (a) | 341 | 272,552 | ||||||

| 406,415 | ||||||||

See accompanying Notes to Financial Statements.

| 8 | Annual Report 2017 |

Statement of Investments (concluded)

October 31, 2017

Aberdeen Asia-Pacific (ex-Japan) Equity Fund

| Shares or Principal Amount | Value | |||||||

SINGAPORE (16.5%) | ||||||||

Financials (6.6%) | ||||||||

DBS Group Holdings Ltd. (a) | 13,715 | $ | 229,021 | |||||

Oversea-Chinese Banking Corp. Ltd. (a) | 46,693 | 407,799 | ||||||

United Overseas Bank Ltd. (a) | 6,174 | 111,537 | ||||||

| 748,357 | ||||||||

Industrials (3.8%) | ||||||||

Keppel Corp. Ltd. (a) | 48,100 | 264,756 | ||||||

Singapore Technologies Engineering Ltd. (a) | 63,800 | 162,879 | ||||||

| 427,635 | ||||||||

Real Estate (3.1%) | ||||||||

City Developments Ltd. (a) | 36,200 | 343,787 | ||||||

Telecommunication Services (3.0%) | ||||||||

Singapore Telecommunications Ltd. (a) | 124,900 | 343,720 | ||||||

| 1,863,499 | ||||||||

TAIWAN (5.5%) | ||||||||

Information Technology (4.0%) | ||||||||

Taiwan Semiconductor Manufacturing Co. Ltd. | 56,000 | 451,201 | ||||||

Telecommunication Services (1.5%) | ||||||||

Taiwan Mobile Co. Ltd. | 48,100 | 171,447 | ||||||

| 622,648 | ||||||||

THAILAND (2.8%) | ||||||||

Health Care (0.5%) | ||||||||

Bangkok Dusit Medical Services PCL, Foreign Shares (a) | 90,000 | 57,450 | ||||||

Materials (2.3%) | ||||||||

Siam Cement PCL (The), Foreign Shares (a) | 17,600 | 258,490 | ||||||

| 315,940 | ||||||||

UNITED KINGDOM (6.3%) | ||||||||

Financials (1.9%) | ||||||||

Standard Chartered PLC (a)(c) | 21,986 | 218,978 | ||||||

Materials (4.4%) | ||||||||

BHP Billiton PLC — London Listing (a) | 12,634 | 228,746 | ||||||

Rio Tinto PLC — London Listing (a) | 5,601 | 264,707 | ||||||

| 493,453 | ||||||||

| 712,431 | ||||||||

Total Common Stocks | 10,475,901 | |||||||

PREFERRED STOCKS (5.8%) | ||||||||

REPUBLIC OF SOUTH KOREA (5.8%) | ||||||||

Consumer Staples (0.8%) | ||||||||

Amorepacific Corp., Preferred Shares, 0.89% | 539 | 85,876 | ||||||

Information Technology (5.0%) | ||||||||

Samsung Electronics Co. Ltd., Preferred Shares, 1.20% (a) | 283 | 566,805 | ||||||

| 652,681 | ||||||||

Total Preferred Stocks | 652,681 | |||||||

SHORT-TERM INVESTMENT (0.5%) | ||||||||

UNITED STATES (0.5%) | ||||||||

State Street Institutional U.S. Government Money Market Fund, Institutional Class, 0.96% (e) | 57,879 | 57,879 | ||||||

Total Short-Term Investment | 57,879 | |||||||

Total Investments | 11,186,461 | |||||||

Other Assets in Excess of Liabilities—1.0% | 109,630 | |||||||

Net Assets—100.0% | $ | 11,296,091 | ||||||

| (a) | Fair Values are determined pursuant to procedures approved by the Fund’s Board of Trustees. Unless otherwise noted, securities are valued by applying valuation factors to the exchange traded price. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (b) | China A Shares. These shares are issued in local currency, traded in the local stock markets and are held through either a Qualified Foreign Institutional Investor (QFII) license or the Shanghai or Shenzhen Hong-Kong Stock Connect program. |

| (c) | Non-income producing security. |

| (d) | Shares received from spin off of Grasim Industries Ltd. and commenced trading on September 1, 2017. |

| (e) | Registered investment company advised by State Street Global Advisors. The rate shown is the current yield as of October 31, 2017. |

| (f) | See accompanying Notes to Financial Statements for tax unrealized appreciation/(depreciation) of securities. |

| PLC | Public Limited Company |

See accompanying Notes to Financial Statements.

| 2017 Annual Report | 9 |

Aberdeen China Opportunities Fund (Unaudited)

The Aberdeen China Opportunities Fund (Institutional Class shares net of fees) returned 23.62% for the 12-month period ended October 31, 2017, versus the 34.80% return of its benchmark, the Morgan Stanley Capital International (MSCI) Zhong Hua Index, during the same period. For broader comparison, the average return of the Fund’s peer category of China Region Funds (comprising 44 funds), as measured by Lipper, Inc., was 30.39% for the period.

The performance of equities in China and Hong Kong was buoyant over the reporting period. Despite early investor concerns over capital outflows, increased regulatory scrutiny and government curbs on leverage, Chinese equities recovered quickly amid upbeat corporate earnings and economic growth data, while worries over capital flight receded. Benchmark index provider MSCI’s decision to include China A-shares1 in its influential indices and a continued rise in Chinese internet stocks further propelled the mainland China market. In Hong Kong, sustained inflows from China and encouraging domestic economic data also bolstered investor sentiment.

The Fund recorded a positive return over the reporting period, but underperformed its benchmark, the MSCI Zhong Hua Index. Broadly, our buy-and-hold investment approach style was hampered by sector rotation and momentum trading,2 both of which were evident in the Chinese equity markets over the period.

The Fund’s positioning in the information technology (IT) sector was a key detractor from the relative performance for the reporting period. The IT sector rallied, driven by the sustained rise in domestic internet companies, notably Alibaba and Tencent Holdings, as momentum trading and solid corporate results boosted their share prices. Therefore, the Fund’s lack of exposure to Alibaba and the underweight allocation to Tencent relative to the benchmark weighed on performance. We initiated a relatively small position in Tencent Holdings in May 2017. This reflects our growing conviction in, and comfort with, its business, corporate structure and governance. We think that its valuation reflects its high-quality growth potential. Tencent has succeeded in diversifying its presence in the Chinese internet space, creating a powerful ecosystem that leverages on the network effects of its various offerings, while concurrently navigating the migration of gaming from PC to mobile. This combination of an expanding ecosystem and a growing monetization3 of the user base will drive earnings growth. We are more circumspect regarding Alibaba. While we think that the company has a strong competitive moat4 and impressive business model, we see potential downside risks from poor corporate governance.

However, within other technology subsectors, the Fund’s holdings in video-surveillance equipment manufacturer Hangzhou Hikvision Digital Technology Co. and semiconductor equipment supplier ASM Pacific Technology performed well over the reporting period. Shares of Hangzhou Hikvision rose on solid growth in both its domestic and overseas operations; the company is also branching out from its traditional video surveillance business. ASM Pacific Technology posted solid corporate results over the period that were driven by several factors, including increased output, ongoing cost reduction efforts, and a favorable product mix.

Shares of the Fund’s holdings in China Merchants Bank (CMB) and China Construction Bank (CCB) also rose on the back of positive results during the reporting period. The Chinese lenders generally saw declines in loan-loss provisions while asset quality and net interest margins stabilized. Global lender HSBC Holdings was another key contributor to Fund performance, aided by steady corporate results. Notably, the bank’s focus on Asia was successful, with the region generating over 70% of the company’s profits for the third quarter of its 2017 fiscal year.

Elsewhere, downbeat corporate results hurt the performance of the Fund’s holding in healthcare company Tong Ren Tang Technologies Co. (TRT) as a couple of its blockbuster products faced competition from cheaper alternatives. Nonetheless, TRT is a well-known traditional Chinese medicine maker in the mainland. We believe that its established brand is still able to differentiate it from other less trusted competitors in China.

Regarding portfolio activity over the reporting period, we initiated positions in Dah Sing Financial Holdings, as well as Chinese fast-food restaurant operator Yum China Holdings following the parent company’s (Yum! Brands) restructuring. We exited positions in Chinese industrial gas company Yingde Gases, Huaxin Cement Co. and Hung Hing Printing Group.

In addition to Tencent Holdings as previously noted, we established new positions in blood plasma products company China Biologic Products; China Construction Bank (CCB); automotive parts supplier Nexteer Automotive Group; and Chinese travel information provider Travelsky Technology. We think that China Biologic Products stands to benefit from structural growth in domestic demand for blood plasma products. We like the company’s direct sales model and initiated the holding at what we viewed as a reasonable valuation. We introduced CCB to the Fund after holding it in another Aberdeen China equity fund for some time, as we believe that it is one of the better managed state-owned lenders and is well positioned amid the government’s deleveraging campaign. Nexteer Automotive Group has benefited from the automotive industry’s move from hydraulic to electrical power steering, and has a growing business in Asia. Its financials are robust, while management is sensible and has a good track record, in our opinion. Travelsky Technology has a monopoly in China in airline-ticket distribution and is a proxy to the mainland’s growing tourism market fueled by rising affluence.

| 1 | China A-shares are purchased and traded on the Shanghai and Shenzhen stock exchanges. |

| 2 | Momentum trading seeks to capitalize on market volatility by focusing on stocks that are moving significantly in one direction on high volume. |

| 3 | Monetization comprises the conversion of an asset into money or legal tender. |

| 4 | A business moat refers to the ability of a company to maintain competitive advantages over its competitors in an effort to protect its long-term profits and market share from competing firms. |

| 10 | Annual Report 2017 |

Aberdeen China Opportunities Fund (Unaudited) (concluded)

Conversely, we exited the Fund’s relatively small positions in Hong Kong Aircraft Engineering Co., luxury hotel chain operator Hongkong & Shanghai Hotels, and knitted fabric and apparel maker Texwinca as we believe that the companies have deteriorating business prospects. Healthy global demand for its exports has led to generally better-than-expected economic growth in China. The slight moderation in growth in the third quarter of 2017 was attributable mainly to policy efforts to rein in leverage, reduce overcapacity5 and curb pollution. In a much-anticipated speech at the Communist Party’s 19th National Congress6 in October 2017, President Xi Jinping avoided specifying an economic growth target for 2020, instead espousing a near-term aim of a “moderately prosperous society,” while pushing for higher-quality growth. This was widely interpreted as a sign that the government will tolerate some deceleration in the economy in its pursuit of supply-side structural reforms, more equitable wealth distribution and financial stability.

At the corporate level, earnings growth for Chinese companies has recovered. Companies overall appear healthier, as do valuations, while the Chinese government continued to tweak supply-side policy. Many of the Fund’s holdings posted year-on-year earnings increases in the September quarter, which reflected fundamental growth rather than simply resulting from one-off gains or government subsidies. In our view, this suggested that the economy is bottoming out, with investors becoming optimistic and more willing to pay for future growth. Consequently, we have upgraded our forecasts across our Chinese holdings.7 Such supportive corporate fundamentals give us cause for optimism and confidence in our stock picks.

Portfolio Management:

Aberdeen Asia-Pacific Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance data quoted represents past performance and current returns may be lower or higher. Class A Shares have up to a 5.75% front-end sales charge and a 0.25% 12b-1 fee. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, which may be higher or lower than the performance shown above, please call 866-667-9231 or go to www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal.

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Concentrating investments in China and Hong Kong subjects the Fund to more volatility and greater risk of loss than geographically diverse mutual funds.

Additional risks associated with investments in China and Hong Kong include exposure to currency fluctuations, less liquidity, expropriation, confiscatory taxation, nationalization, exchange control regulations (including currency blockage) and differing legal standards.

Foreign securities may be more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, currency exchange rates, political and economic risks. Fluctuation in currency exchange rates may impact the Fund’s returns more greatly to the extent the Fund does not hedge currency exposure or hedging techniques are unsuccessful. The foregoing risks are enhanced in emerging market countries.

Equity stocks of small- and mid-cap companies carry greater risk, and more volatility than equity stocks of larger, more established companies.

Investing a significant portion of the Fund’s assets in securities of companies conducting business in a broadly related group of industries within an economic sector may make the Fund more vulnerable to unfavorable developments in that sector.

Please read the prospectus for more detailed information regarding these and other risks.

| 5 | Overcapacity occurs when the capacity to produce exceeds the demand. |

| 6 | The Chinese Communist Party sets its national policy goals and elects its leadership positions at the National Party Congress, which is held every five years. |

| 7 | Forecasts and estimates are offered as opinion and are not reflective of potential performance, are not guaranteed and actual events or results may differ materially. |

| 2017 Annual Report | 11 |

Aberdeen China Opportunities Fund (Unaudited)

| Average Annual Total Return1 (For periods ended October 31, 2017) | 1 Yr. | 5 Yr. | 10 Yr. | |||||||||||||

Class A | w/o SC | 23.15% | 3.61% | (1.39% | ) | |||||||||||

| w/SC2 | 16.04% | 2.39% | (1.97% | ) | ||||||||||||

Class C | w/o SC | 22.39% | 2.87% | (2.09% | ) | |||||||||||

| w/SC3 | 21.39% | 2.87% | (2.09% | ) | ||||||||||||

Class R4 | w/o SC | 22.77% | 3.24% | (1.69% | ) | |||||||||||

Institutional Service Class4 | w/o SC | 23.54% | 3.86% | (1.13% | ) | |||||||||||

Institutional Class4 | w/o SC | 23.62% | 3.89% | (1.14% | ) | |||||||||||

All figures showing the effect of a sales charge (SC) reflect the maximum charge possible because it has the most significant effect on performance data. The total returns shown above do not include the impact of financial statement rounding of the net asset value (NAV) per share and/or financial statement adjustments.

| 1 | Returns prior to June 23, 2008 reflect the performance of a predecessor fund (the “Predecessor Fund”). Returns of the Predecessor Fund have not been adjusted to reflect the expenses applicable to the respective classes. Aberdeen Asset Management Asia Limited began sub-advising the fund on January 1, 2009. Performance prior to this date reflects the performance of an unaffiliated sub-adviser. The Fund and the Predecessor Fund have substantially similar investment objectives and strategies. Please consult the Fund’s prospectus for more detail. |

| 2 | A 5.75% front-end sales charge was deducted. |

| 3 | A 1.00% contingent deferred sales charge (CDSC) was deducted from the one year return because it is charged when Class C shares are sold within the first year after purchase. |

| 4 | Not subject to any sales charges. |

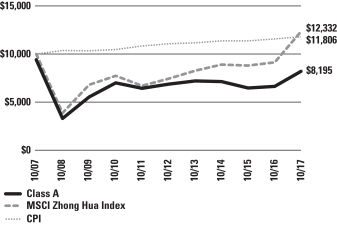

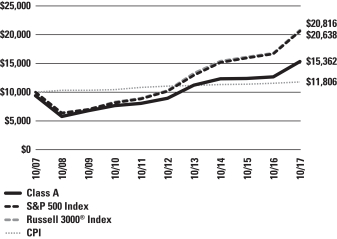

Performance of a $10,000 Investment (as of October 31, 2017)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen China Opportunities Fund, Morgan Stanley Capital International (MSCI) Zhong Hua Index and the Consumer Price Index (CPI) over a 10-year period ended October 31, 2017. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees, expenses, or sales charges. Investors cannot invest directly in market indexes.

The MSCI Zhong Hua Index is a composite index that comprises the MSCI China and MSCI Hong Kong Index. The index captures large and mid cap representation across all China securities (B shares, H shares, Red Chips, P Chips and foreign listed shares) as well as Hong Kong securities.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment returns and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and Performance graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Total returns reflect waivers and reimbursements in effect, without which returns would have been lower.

| 12 | Annual Report 2017 |

Aberdeen China Opportunities Fund (Unaudited) (concluded)

Portfolio Summary (as a percentage of net assets)

October 31, 2017 (Unaudited)

| Asset Allocation | ||||

Common Stocks | 98.7% | |||

Short-Term Investment | 0.2% | |||

Liabilities in Excess of Other Assets | 1.1% | |||

| 100.0% | ||||

The following table summarizes the composition of the Fund’s portfolio, in Standard & Poor’s Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets. The GICS structure consists of 11 sectors, 24 industry groups, 68 industries and 157 sub-industries. As of October 31, 2017, the Fund did not have more than 25% of its assets invested in any industry group.

| Top Sectors | ||||

Financials | 19.3% | |||

Industrials | 18.1% | |||

Consumer Discretionary | 16.6% | |||

Information Technology | 11.3% | |||

Real Estate | 10.9% | |||

Telecommunication Services | 6.3% | |||

Health Care | 5.6% | |||

Consumer Staples | 5.0% | |||

Energy | 3.6% | |||

Utilities | 2.0% | |||

Other | 1.3% | |||

| 100.0% | ||||

| Top Holdings* | ||||

AIA Group Ltd. | 5.3% | |||

MTR Corp. Ltd. | 4.5% | |||

Tencent Holdings Ltd. | 4.3% | |||

China Mobile Ltd. | 3.9% | |||

Hangzhou Hikvision Digital Technology Co. Ltd., A Shares | 3.9% | |||

Jardine Strategic Holdings Ltd. | 3.9% | |||

HSBC Holdings PLC | 3.6% | |||

China International Travel Service Corp. Ltd., A Shares | 3.5% | |||

Shanghai International Airport Co. Ltd., A Shares | 3.3% | |||

China Merchants Bank Co. Ltd., H Shares | 2.9% | |||

Other | 60.9% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, Short-Term Investments are included as part of Other. |

| Top Countries | ||||

Hong Kong | 48.7% | |||

China | 47.8% | |||

United States | 2.4% | |||

Other | 1.1% | |||

| 100.0% | ||||

| 2017 Annual Report | 13 |

Statement of Investments

October 31, 2017

Aberdeen China Opportunities Fund

| Shares or Principal Amount | Value | |||||||

COMMON STOCKS (98.7%) | ||||||||

CHINA (47.8%) | ||||||||

Consumer Discretionary (8.7%) | ||||||||

China International Travel Service Corp. Ltd., A Shares (a) | 74,000 | $ | 462,362 | |||||

China International Travel Service Corp. Ltd., A Shares (Stock Connect) (a)(b) | 200 | 1,250 | ||||||

Fuyao Glass Industry Group Co. Ltd., H Shares (a)(c) | 90,400 | 344,726 | ||||||

Nexteer Automotive Group Ltd. (a)(d) | 80,000 | 156,674 | ||||||

Yum China Holdings, Inc. (d) | 4,874 | 196,666 | ||||||

| 1,161,678 | ||||||||

Consumer Staples (3.0%) | ||||||||

Kweichow Moutai Co. Ltd., A Shares (a) | 2,400 | 93,501 | ||||||

Kweichow Moutai Co. Ltd., A Shares (Stock Connect) (a)(b) | 1,900 | 308,554 | ||||||

| 402,055 | ||||||||

Energy (3.6%) | ||||||||

CNOOC Ltd. (a) | 198,000 | 270,348 | ||||||

Green Dragon Gas Ltd. (d) | 53,000 | 42,587 | ||||||

PetroChina Co. Ltd., H Shares (a) | 254,000 | 166,039 | ||||||

| 478,974 | ||||||||

Financials (4.7%) | ||||||||

China Construction Bank Corp., Class H (a) | 260,000 | 232,366 | ||||||

China Merchants Bank Co. Ltd., H Shares (a) | 102,500 | 391,412 | ||||||

| 623,778 | ||||||||

Health Care (5.6%) | ||||||||

China Biologic Products Holdings, Inc. (d) | 600 | 46,626 | ||||||

CSPC Pharmaceutical Group Ltd. (a) | 196,000 | 340,988 | ||||||

Tong Ren Tang Technologies Co. Ltd., H Shares (a) | 251,000 | 352,768 | ||||||

| 740,382 | ||||||||

Industrials (5.5%) | ||||||||

China Conch Venture Holdings Ltd. (a) | 143,000 | 291,565 | ||||||

Shanghai International Airport Co. Ltd., A Shares (a)(b) | 66,500 | 439,526 | ||||||

| 731,091 | ||||||||

Information Technology (9.3%) | ||||||||

Hangzhou Hikvision Digital Technology Co. Ltd., A Shares (a)(b) | 87,375 | 518,234 | ||||||

Hangzhou Hikvision Digital Technology Co. Ltd., A Shares (Stock Connect) (a)(b) | 150 | 890 | ||||||

Tencent Holdings Ltd. (a) | 12,900 | 579,792 | ||||||

TravelSky Technology Ltd., H Shares (a) | 56,000 | 145,146 | ||||||

| 1,244,062 | ||||||||

Real Estate (3.5%) | ||||||||

China Resources Land Ltd. (a) | 90,000 | 268,604 | ||||||

Yanlord Land Group Ltd. (a)(e) | 149,600 | 196,582 | ||||||

| 465,186 | ||||||||

Telecommunication Services (3.9%) | ||||||||

China Mobile Ltd. (a) | 52,000 | 523,035 | ||||||

| 6,370,241 | ||||||||

HONG KONG (48.7%) | ||||||||

Consumer Discretionary (5.7%) | ||||||||

Aeon Stores (Hong Kong) Co. Ltd. (a) | 286,500 | 207,236 | ||||||

Giordano International Ltd. (a) | 224,000 | 126,642 | ||||||

Global Brands Group Holding Ltd. (a)(d) | 396,380 | 46,250 | ||||||

Shangri-La Asia Ltd. (a) | 188,000 | 374,317 | ||||||

| 754,445 | ||||||||

Consumer Staples (2.0%) | ||||||||

Convenience Retail Asia Ltd. (a) | 388,000 | 178,999 | ||||||

Dairy Farm International Holdings Ltd. (a) | 10,700 | 87,512 | ||||||

| 266,511 | ||||||||

Financials (14.6%) | ||||||||

AIA Group Ltd. (a) | 93,600 | 705,321 | ||||||

Dah Sing Banking Group Ltd. (a) | 59,840 | 132,432 | ||||||

Dah Sing Financial Holdings Ltd. (a) | 17,200 | 115,585 | ||||||

Hong Kong Exchanges & Clearing Ltd. (a) | 9,118 | 254,066 | ||||||

HSBC Holdings PLC (a) | 48,498 | 473,794 | ||||||

Standard Chartered PLC (HK Listing) (a)(d) | 27,348 | 271,471 | ||||||

| 1,952,669 | ||||||||

Industrials (12.6%) | ||||||||

Jardine Strategic Holdings Ltd. (a) | 12,300 | 515,925 | ||||||

Kerry Logistics Network Ltd. (a) | 225,000 | 310,229 | ||||||

MTR Corp. Ltd. (a) | 102,838 | 596,201 | ||||||

Pacific Basin Shipping Ltd. (a)(d) | 1,112,000 | 253,924 | ||||||

| 1,676,279 | ||||||||

Information Technology (2.0%) | ||||||||

ASM Pacific Technology Ltd. (a) | 17,900 | 261,169 | ||||||

Real Estate (7.4%) | ||||||||

Hang Lung Group Ltd. (a) | 70,000 | 245,957 | ||||||

Hang Lung Properties Ltd. (a) | 34,000 | 78,074 | ||||||

Swire Pacific Ltd., Class B (a) | 200,000 | 345,711 | ||||||

Swire Properties Ltd. (a) | 94,600 | 319,674 | ||||||

| 989,416 | ||||||||

Telecommunication Services (2.4%) | ||||||||

Asia Satellite Telecommunications Holdings Ltd. | 127,500 | 117,671 | ||||||

HKBN Ltd. (a) | 198,500 | 201,551 | ||||||

| 319,222 | ||||||||

Utilities (2.0%) | ||||||||

Hong Kong & China Gas Co. Ltd. (a) | 140,016 | 265,417 | ||||||

| 6,485,128 | ||||||||

UNITED STATES (2.2%) | ||||||||

Consumer Discretionary (2.2%) | ||||||||

Samsonite International SA (a) | 71,900 | 300,646 | ||||||

Total Common Stocks | 13,156,015 | |||||||

See accompanying Notes to Financial Statements.

| 14 | Annual Report 2017 |

Statement of Investments (concluded)

October 31, 2017

Aberdeen China Opportunities Fund

| Shares or Principal Amount | Value | |||||||

SHORT-TERM INVESTMENT (0.2%) | ||||||||

UNITED STATES (0.2%) | ||||||||

State Street Institutional U.S. Government Money Market Fund, Institutional Class, 0.96% (f) | 17,322 | $ | 17,322 | |||||

| 17,322 | ||||||||

Total Short-Term Investment | 17,322 | |||||||

Total Investments | 13,173,337 | |||||||

Liabilities in Excess of Other Assets—1.1% | 153,091 | |||||||

Net Assets—100.0% | $ | 13,326,428 | ||||||

| (a) | Fair Values are determined pursuant to procedures approved by the Fund’s Board of Trustees. Unless otherwise noted, securities are valued by applying valuation factors to the exchange traded price. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (b) | China A Shares. These shares are issued in local currency, traded in the local stock markets and are held through either a Qualified Foreign Institutional Investor (QFII) license or the Shanghai or Shenzhen Hong-Kong Stock Connect program. |

| (c) | Denotes a security issued under Regulation S or Rule 144A. |

| (d) | Non-income producing security. |

| (e) | All or a portion of the securities are on loan. The total value of all securities on loan is $187,328. The amount of securities on loan indicated may not correspond with the securities on loan identified because securities with pending sales are in the process of recall from the brokers. See Note 2(k) for additional information. |

| (f) | Registered investment company advised by State Street Global Advisors. The rate shown is the current yield as of October 31, 2017. |

| (g) | See accompanying Notes to Financial Statements for tax unrealized appreciation/(depreciation) of securities. |

| PLC | Public Limited Company |

See accompanying Notes to Financial Statements.

| 2017 Annual Report | 15 |

Aberdeen Emerging Markets Fund (Unaudited)

The Aberdeen Emerging Markets Fund (Institutional Class shares net of fees) returned 17.89% for the 12-month period ended October 31, 2017, versus the 26.91% return of its benchmark, the Morgan Stanley Capital International (MSCI) Emerging Markets Index, during the same period. For broader comparison, the average return of the Fund’s peer category of Emerging Markets Funds (comprising 355 funds), as measured by Lipper, Inc., was 22.71% for the period.

Emerging-market equities posted substantial gains over the reporting period. Stocks initially sold-off in a knee-jerk reaction to Donald Trump’s victory in the U.S. presidential election in November 2016. However, in the first 10 months of 2017, an improving global economy lifted corporate earnings, which resulted in continued inflows into the asset class. Upbeat investor sentiment helped emerging markets maintain their positive momentum despite three U.S. Federal Reserve rate hikes and rising geopolitical uncertainty in North Korea and the Middle East. Oil prices were volatile at the beginning of the reporting period, but firmed on higher demand and tighter inventories following an Organization of Petroleum Exporting Countries (OPEC)-led agreement to extend output cuts. Currencies broadly strengthened against the U.S. dollar over the period amid growing worries about the policies of the Trump administration, though gains were capped towards the end of the period on renewed hopes for U.S. tax reform.

Across geographic regions, China led the advance in the emerging Asian markets, attributable to better-than-expected economic growth and a sharp rise in shares of Chinese internet companies despite the government’s increased tightening of financial regulations. At the 19th Communist Party Congress1 in October 2017, President Xi Jinping consolidated his position, while also emphasizing more equitable economic growth outcomes. In India, economic growth slowed over the reporting period due to the lingering effects of the government’s demonetization2 in November 2016, while the Goods and Services Tax was implemented in July 2017. The Latin American equity market posted a healthy gain for the reporting period. Brazilian equities performed well despite a notable decline in May 2017, after President Michel Temer became implicated in a corruption scandal. Mexican stocks and the peso initially recovered from a post-U.S. election sell-off, but uncertainty over the fate of the North American Free Trade Agreement (NAFTA) and natural disasters capped gains towards the end of the reporting period. In the Europe, Middle East and Africa (EMEA) region, the Russian market’s performance was volatile, tracking oil prices, while South African stocks were hampered by domestic political turmoil.

The Fund’s underperformance relative to its benchmark, the MSCI Emerging Markets Index, was attributable largely to the underweight allocations to both China and the information technology sector. Notably, information technology is the benchmark’s largest-weighted sector, partly driven by benchmark provider MSCI’s inclusion of Chinese internet companies in the MSCI China Index in 2015. Major internet companies such as Tencent Holdings (which the Fund holds) and Alibaba (which the Fund does not own) have thrived in a closed market where U.S. companies such as Google, Facebook and Amazon have limited access. The share prices of both Tencent and Alibaba have increased significantly, driving the Chinese equity market higher. This factor weighed on the Fund’s relative performance over the reporting period despite the solid performance from other Fund holdings in mainland China, including alcoholic beverage producer Kweichow Moutai Co. and Hangzhou Hikvision Digital Technology Co., a large global video surveillance vendor, which were among the top individual stock contributors to Fund performance over the reporting period.

While we recognize the opportunities that Chinese internet businesses enjoy, we remain concerned over their corporate structures, known as variable interest entities (VIE),3 designed to circumvent domestic laws restricting direct foreign control. The Chinese government remains ambiguous about the structures’ legality, and investors appear to believe that, as an increasingly important part of stock markets and economic activity, the risk that the Chinese government may rule that VIE structures are illegal is becoming negligible. While we remain skeptical, we are more sympathetic to the notion that the risk today is lower than it was in the past.

Nonetheless, we are optimistic about the prospects for Tencent Holdings. Since the stock initially was listed on the Hong Kong Stock Exchange in 2004, we have conducted extensive due diligence regarding its corporate structure and founder, and have engaged management on these issues. We take greater comfort from its track record of treating minority shareholders fairly, and we like the company’s business moat4 and robust financials. Over time, we have come to appreciate Tencent’s disciplined capital allocation and ability to expand and monetize5 its social media-based ecosystem. Therefore, following further analysis and a meeting with senior management, we initiated a position in Tencent in September 2017. While we acknowledge that the stock is not cheap, we believe that its valuation reflects its high-quality growth potential.

Elsewhere in Asia, the Fund’s exposure to Hong Kong, which is not represented in the benchmark MSCI Emerging Markets Index, hampered the relative performance for the reporting period. The Fund’s holding in Hang Lung Group was among the key detractors from the relative performance due to investors’ concerns over the recovery of its property subsidiary. Shares of Indonesian conglomerate Astra International, a long-term Fund holding that has performed well, also fell as the company saw lower profit margins in the second quarter of its 2017 fiscal year, though we believe that the weakness should be temporary. Conversely, stock selection in India contributed to the Fund’s relative performance. Conglomerate Grasim Industries’ stock price rose on investors’ positive expectations about its restructuring into a broader conglomerate, while shares of consumer goods company Hindustan Unilever were buoyed by the market’s post-demonetization recovery.

| 1 | The Chinese Communist Party sets its national policy goals and elects its leadership positions at the National Party Congress, which is held every five years. |

| 2 | Demonetization comprises the act of stripping specific denominations of a currency of their status as legal tender. The currency denominations are pulled from circulation and are replaced with new currency units. |

| 3 | A variable interest entity is an entity in which an investor has a controlling interest that is not based on a majority of voting rights. |

| 4 | A business moat refers to the ability of a company to maintain competitive advantages over its competitors in an effort to protect its long-term profits and market share from competing firms. |

| 5 | Monetization comprises the conversion of an asset into money or legal tender. |

| 16 | Annual Report 2017 |

Aberdeen Emerging Markets Fund (Unaudited) (continued)

In Latin America, positive stock selection was outweighed by the negative impact of asset allocation. Mexican markets were roiled by Trump’s U.S. presidential election win, uncertainty over NAFTA negotiations and concerns over the impact of earthquakes on the economy. However, stock selection in Brazil bolstered Fund performance for the reporting period. The primary contributor was the absence of a position in state-owned oil company Petroleo Brasileiro (Petrobras), as its shares came under significant pressure during a sell-off in May 2017, when President Temer became implicated in a corruption scandal.

In the EMEA region, the Fund’s overweight to Turkey relative to the benchmark weighed on performance as the market underperformed its emerging-market peers in 2016, due to political uncertainty and a credit-rating6 downgrade. Stock selection in Russia also detracted from the Fund’s relative performance, with retailer Magnit a key laggard amid investors’ concerns over falling returns. Conversely, the underweight position in South Africa enhanced the Fund’s relative performance, given the ongoing political turmoil in the country and deteriorating domestic economy. The Fund’s lack of exposure to benchmark constituent Qatar also had a positive impact on performance due to heightened geopolitical tensions in the Middle East.

Regarding significant portfolio activity over the reporting period, apart from Tencent, as we previously noted, we also initiated holdings in five other mainland China-based companies: Yum China Holdings, a fast-food restaurant operator with a net cash balance sheet; Shanghai International Airport Co., a leading airport operator in China which we believe has attractive growth prospects; Hangzhou Hikvision Digital Technology Co.; which is expanding its global footprint amid increasing automation in surveillance; Midea Group Co., an appliance manufacturer, given our higher conviction about its quality; and China Resources Land, a property developer backed by a healthy balance sheet, in our view.

We also initiated positions in AMOREPACIFIC Corp., a fast-growing Korean cosmetics business with well-established brands and a growing presence overseas; Falabella, a Chile-based diversified retailer with a broad regional footprint in Latin America; and Kotak Mahindra Bank, which we believe is a well-managed Indian private-sector lender.

Conversely, we exited the Fund’s positions in Yum! Brands and reinvested the proceeds into its spun-off business, Yum China Holdings; Indian software company Infosys given our decreased confidence in the company’s prospects following the resignation of Vishal Sikka as chief executive officer (CEO) and our growing corporate governance concerns; and Argentinian steel-pipe maker Tenaris due to our lower conviction in the outlook for its business. We also sold the Fund’s holdings in mall operator Multiplan’s rights offering7 ahead of its upcoming capital-raising due to the stock’s relative price strength, as well as Malaysian financial services company CIMB, India’s ICICI Bank and Korean hypermarket operator E-Mart in view of what we believed were better opportunities elsewhere.

In our opinion, the synchronized global economic recovery should continue to underpin further gains in the global emerging markets, which outperformed their developed-market counterparts for the first 10 months of 2017. We think that Chinese economic growth may moderate, given the government’s focus on regulatory tightening and supply-side reform, but a sharp downturn seems unlikely as economic drivers appear resilient, and both fiscal and monetary policy remain accommodative. However, political risks remain, including Kurdish separatism exacerbating tensions in the Middle East, as well as unresolved domestic political crises in South Africa and Brazil. Elections in various developing countries over 2018 could add further uncertainty, in our view. Nevertheless, most emerging-market economies are benefiting from an improved global macroeconomic environment, with recovering growth supported by moderate inflation and healthy trade flows. While we feel that major global central banks’ monetary policy normalization and tighter liquidity could cause some concerns, their well-telegraphed changes should ensure stability. Emerging-market companies also have sustained earnings improvement attributable to stronger corporate fundamentals and consumers’ rising spending capacity. We think that the expansion of long-term trends such as the semiconductor super-cycle and rise of e-commerce provides an additional boost for several Fund holdings. We are cautiously optimistic and will remain disciplined in our investment approach and diligent in engaging the management teams of the Fund’s holdings in an effort to maintain the quality of the Fund’s portfolio.

Portfolio Management:

Aberdeen Global Emerging Markets Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance data quoted represents past performance and current returns may be lower or higher. Class A Shares have up to a 5.75% front-end sales charge and a 0.25% 12b-1 fee. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, which may be higher or lower than the performance shown above, please call 866-667-9231 or go to www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal.