UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-22175 |

|

ALPS ETF TRUST |

(Exact name of registrant as specified in charter) |

|

1290 Broadway, Suite 1100, Denver, Colorado | | 80203 |

(Address of principal executive offices) | | (Zip code) |

|

Craig Fidler

ALPS ETF Trust

1290 Broadway, Suite 1100

Denver, Colorado 80203 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (303) 623-2577 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | May 7, 2008 - June 30, 2008 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

ALPS ETF Trust | TABLE OF CONTENTS |

Shareholder Letter | 2 |

| |

Fund Description | 3 |

| |

Performance Overview | 3 |

| |

Disclosure of Fund Expenses | 6 |

| |

Financial Statements | |

| |

Schedule of Investments | 7 |

| |

Statement of Assets and Liabilities | 10 |

| |

Statement of Operations | 11 |

| |

Statement of Changes in Net Assets | 12 |

| |

Financial Highlights | 13 |

| |

Notes to Financial Statements | 14 |

| |

Additional Information | 20 |

Semi-Annual | June 30, 2008

1

ALPS ETF Trust | SHAREHOLDER LETTER |

June 30, 2008

Dear Shareholders,

ALPS Fund Services has established itself as a significant service provider to the exchange-traded fund (“ETF”) industry since ETFs were introduced on the American Stock Exchange in 1993. Given that history, it gave us great pleasure to launch the Cohen & Steers Global Realty Majors Exchange Traded Fund (AMEX: GRI) in May 2008.

Our new investment company, ALPS ETF Trust, had been searching for opportunities to partner with an asset manager or index provider to develop our first product. We found what we were looking for in Cohen & Steers, a best in class real estate investment trust manager whose experience in the real estate field made for a good complement to ALPS’ ETF knowledge.

ETFs provide investors with a transparent, low-cost and tax efficient way to obtain exposure to a variety of asset classes. Global real estate is an asset class that has been growing significantly in recent years, and one that we believe should have a place in every investor’s portfolio. Cohen & Steers has a long and distinguished reputation in managing real estate securities. The Fund also fits with the ALPS philosophy of moving beyond the traditional style boxes to obtain better diversification. We believe the advantages of ETFs, coupled with the attractiveness of global real estate and the expertise of Cohen & Steers will make GRI a suitable investment for a wide range of investors.

In the pages that follow, the fund managers provide a detailed analysis of this exciting new ETF. I encourage you to review their perspective and the rest of the information in the semi-annual report.

And of course, I thank you for being a GRI shareholder.

Tom Carter

President, ALPS ETF Trust

www.alpsetfs.com | 866.513.5856

2

ALPS ETF Trust | PERFORMANCE OVERVIEW |

FUND DESCRIPTION

The Cohen & Steers Global Realty Majors ETF (the “Fund”) seeks investment results that correspond generally to the performance (before the Fund’s fees and expenses) of an equity index called the Cohen & Steers Global Realty Majors Index (the “Index”). The Shares of the Fund are listed and trade on the American Stock Exchange under the ticker symbol “GRI.” The Fund will normally invest substantially all of its assets in the 75 stocks that comprise the Cohen & Steers Global Realty Majors Index. The Fund began trading on May 9, 2008.

The Index is a free-float, market-cap-weighted total return index of selected real estate equity securities maintained by Cohen & Steers. It is quoted intraday on a real-time basis by the Chicago Mercantile Exchange under the symbol GRM. The index’s free-float market capitalization approach and qualitative screening process emphasize companies that the Cohen & Steers Index Committee believes are leading the securitization of real estate globally.

PERFORMANCE OVERVIEW (as of June 30, 2008)

Real estate securities performed poorly in May and June as fears of increasing global inflation and slowing global economic growth persisted amongst investors. Initial hopes of interest rate cuts by the world’s central banks changed to concerns over the likelihood of rate hikes by year-end. Although global stock market declines were widespread, Europe suffered the most significant declines, followed by Asia Pacific and North America.

U.S. real estate securities stumbled in June although performance varied widely by property sector. The office REIT sector, which had been highly correlated with financial services stocks, started to rebound and was the best performer in the group. The hotel sector (15%) was the poorest performer, due in part to the rising cost and reduced availability of air travel.

Asian real estate securities outperformed their European peers in the 2nd quarter, but remained the poorest regional performer on a year-to-date basis. Japan was the standout, posting gains in excess of 5% for the quarter. Hong Kong and Singapore, down 10.8% and 10.9% respectively, were hampered by higher inflation and signs of softening in the economy. Despite solid property fundamentals in Australia, concern over higher future cap rates and lower occupancies moved the sector down 14.5% for the quarter.

3

European real estate securities were the worst performers in the second quarter, lead by Germany (24.5%) and the U.K. (22.6%). Despite better than expected economic growth in Germany, real estate stocks underperformed. Debt downgrades of homebuilders and the reluctance of banks to lend were major contributors to the continually worsening housing market in the U.K. While still negative in absolute terms, higher occupancies, rising rents and conservative financing all contributed to out-performance by both Dutch (11.5%) and French (10.9%) real estate securities for the quarter.

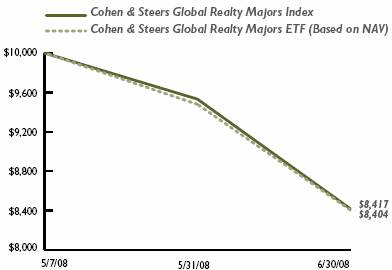

The Fund commenced operations in the middle of the second quarter on May 7, 2008. The Fund’s net asset value (“NAV”) declined 16.0% from inception through June 30, 2008, compared to declines of 15.8% for the Index and 14.9% for the Fund’s market price.

| | Cumulative Total Returns | |

| | Since Fund Inception | |

| | (May 7, 2008) | |

Fund Performance | | | |

NAV | | (15.96 | )% |

Market Price | | (14.90 | )% |

Index Performance | | | |

Cohen & Steers Global Realty Majors Index | | (15.83 | )% |

4

TOP 10 HOLDINGS as of June 30, 2008

Mitsubishi Estate Co., Ltd. | | 3.74 | % |

Simon Property Group, Inc. | | 3.69 | % |

Westfield Group | | 3.63 | % |

Unibail-Rodamco | | 3.55 | % |

Mitsui Fudosan Co., Ltd. | | 3.50 | % |

ProLogis | | 3.48 | % |

Sun Hung Kai Properties, Ltd. | | 2.85 | % |

Vornado Realty Trust | | 2.83 | % |

Land Securities Group Plc | | 2.73 | % |

Public Storage | | 2.57 | % |

Percent of Net Assets in Top Ten Holdings: | | 32.57 | % |

COUNTRY BREAKDOWN (% OF NET ASSETS) as of June 30, 2008

Australia | | 9.9 | % |

Belgium | | 0.3 | % |

Bermuda | | 2.0 | % |

Canada | | 1.0 | % |

France | | 5.3 | % |

Germany | | 0.9 | % |

Great Britain | | 8.6 | % |

Hong Kong | | 8.6 | % |

Japan | | 13.5 | % |

Netherlands | | 1.7 | % |

Singapore | | 3.3 | % |

Sweden | | 0.9 | % |

Switzerland | | 0.5 | % |

United States | | 41.1 | % |

GROWTH OF $10K as of June 30, 2008

Comparison of Change in Value of $10,000 Investment in Cohen & Steers Global Realty Majors ETF and Cohen & Steers Global Realty Majors Index.

5

ALPS ETF Trust | DISCLOSURE OF FUND EXPENSES |

| For the Period Ended June 30, 2008(a) (Unaudited) |

Shareholder Expense Example: As a shareholder of the Fund, you incur two types of costs: (1) transaction costs which may include creation and redemption fees or brokerage charges and (2) ongoing costs, including management fees and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other funds. It is based on an investment of $1,000 invested at May 9, 2008, the first day the Fund traded, and held through the period ended June 30, 2008.

Actual Return: The first line of the table provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you incurred over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first table under the heading entitled “Expenses Paid during Period” to estimate the expenses attributable to your investment during this period.

Hypothetical 5% Return: The second line of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The expenses shown in the table are meant to highlight ongoing Fund costs only and do not reflect any transaction costs, such as creation and redemption fees, or brokerage charges. Therefore, the second table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these costs were included, your costs would have been higher.

| | Beginning | | Ending | | | | Expenses Paid | |

| | Account | | Account | | | | During | |

| | Value | | Value | | Expense | | Period(b) | |

| | 5/7/08 | | 6/30/08 | | Ratio(a) | | 5/7/08-6/30/08 | |

Actual | | $ | 1,000.00 | | $ | 840.40 | | 0.55 | % | $ | 0.74 | |

Hypothetical | | $ | 1,000.00 | | $ | 1,006.44 | | 0.55 | % | $ | 0.80 | |

(a) | The Cohen & Steers Global Realty Majors ETF commenced operations on May 7, 2008. The Fund’s expenses have been annualized from the period May 9, 2008 through June 30, 2008. |

| |

(b) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (53), then divided by 366. |

6

ALPS ETF Trust | SCHEDULE OF INVESTMENTS |

| June 30, 2008 (Unaudited) |

Security Description | | Shares | | Value | |

| | | | | |

COMMON STOCKS (97.6%) | | | | | |

Australia (9.9%) | | | | | |

CFS Retail Property Trust* | | 17,348 | | $ | 30,799 | |

Dexus Property Group* | | 29,587 | | 39,183 | |

Goodman Group | | 16,298 | | 48,329 | |

GPT Group | | 20,229 | | 43,096 | |

Mirvac Group* | | 10,923 | | 31,027 | |

Stockland Trust Group | | 14,376 | | 74,360 | |

Westfield Group | | 9,946 | | 155,387 | |

| | | | 422,181 | |

Belgium (0.3%) | | | | | |

Confinimmo* | | 82 | | 14,922 | |

| | | | | |

Bermuda (2.0%) | | | | | |

Hongkong Land Holdings, Ltd. | | 13,000 | | 55,120 | |

Kerry Properties, Ltd. | | 6,000 | | 31,510 | |

| | | | 86,630 | |

Canada (1.0%) | | | | | |

RioCan REIT* | | 2,194 | | 42,948 | |

| | | | | |

France (5.3%) | | | | | |

Fonciere des Regions* | | 270 | | 33,096 | |

Klepierre* | | 810 | | 40,838 | |

Unibail-Rodamco | | 657 | | 152,082 | |

| | | | 226,016 | |

Germany (0.9%) | | | | | |

GAGFAH SA* | | 1,459 | | 20,735 | |

IVG Immobilien AG* | | 896 | | 17,674 | |

| | | | 38,409 | |

Great Britain (8.6%) | | | | | |

British Land Co., Plc | | 5,180 | | 73,039 | |

Brixton Plc* | | 2,386 | | 11,420 | |

Derwent London Plc* | | 776 | | 15,567 | |

Great Portland Estates Plc | | 2,229 | | 15,005 | |

Hammerson Plc | | 3,036 | | 53,926 | |

Land Securities Group Plc | | 4,780 | | 117,199 | |

Liberty International Plc* | | 2,818 | | 48,343 | |

Segro Plc | | 4,105 | | 32,147 | |

| | | | 366,646 | |

| | | | | | |

7

Security Description | | Shares | | Value | |

| | | | | |

Hong Kong (8.6%) | | | | | |

Hang Lung Properties, Ltd. | | 19,000 | | $ | 60,917 | |

Henderson Land Development Co., Ltd. | | 12,000 | | 74,794 | |

The Link REIT* | | 18,500 | | 42,137 | |

Sun Hung Kai Properties, Ltd. | | 9,000 | | 122,117 | |

The Wharf Holdings, Ltd. | | 16,000 | | 66,996 | |

| | | | 366,961 | |

Japan (13.5%) | | | | | |

Aeon Mall Co., Ltd. | | 1,100 | | 32,583 | |

Japan Real Estate Investment Corp.* | | 4 | | 42,262 | |

Japan Retail Fund Investment Corp. | | 3 | | 17,320 | |

Mitsubishi Estate Co., Ltd. | | 7,000 | | 160,464 | |

Mitsui Fudosan Co., Ltd. | | 7,000 | | 149,899 | |

Nippon Building Fund, Inc.* | | 4 | | 47,168 | |

Nomura Real Estate Office Fund, Inc.* | | 2 | | 15,075 | |

NTT Urban Development Corp.* | | 17 | | 22,291 | |

Sumitomo Realty & Development Co., Ltd. | | 4,000 | | 79,619 | |

Tokyo Tatemono Co., Ltd. | | 2,000 | | 12,962 | |

| | | | 579,643 | |

Netherlands (1.7%) | | | | | |

Corio N.V.* | | 526 | | 41,130 | |

Eurocommercial Properties N.V.* | | 272 | | 12,972 | |

Wereldhave N.V.* | | 178 | | 18,776 | |

| | | | 72,878 | |

Singapore (3.3%) | | | | | |

Ascendas Real Estate Investment Trust | | 6,000 | | 9,760 | |

CapitaLand, Ltd. | | 18,000 | | 75,516 | |

City Developments, Ltd. | | 7,000 | | 55,953 | |

| | | | 141,229 | |

Sweden (0.9%) | | | | | |

Castellum AB | | 1,500 | | 14,338 | |

Fabege AB* | | 1,400 | | 9,379 | |

Kungsleden AB | | 1,720 | | 12,753 | |

| | | | 36,470 | |

Switzerland (0.5%) | | | | | |

PSP Swiss Property AG* | | 394 | | 23,479 | |

| | | | | |

United States (41.1%) | | | | | |

Alexandria Real Estate Equities, Inc. | | 336 | | 32,706 | |

AMB Property Corp. | | 1,036 | | 52,194 | |

| | | | | | |

8

Security Description | | Shares | | Value | |

| | | | | |

United States (continued) | | | | | |

Apartment Investment and Management Co. | | 1,016 | | $ | 34,605 | |

AvalonBay Communities, Inc. | | 808 | | 72,041 | |

Boston Properties, Inc. | | 1,222 | | 110,249 | |

Brookfield Properties Corp. | | 2,181 | | 38,800 | |

Camden Property Trust | | 612 | | 27,087 | |

Developers Diversified Realty Corp. | | 1,292 | | 44,845 | |

Duke Realty Corp.* | | 1,540 | | 34,573 | |

Equity Residential | | 2,782 | | 106,467 | |

Essex Property Trust, Inc.* | | 276 | | 29,394 | |

Federal Realty Investment Trust | | 562 | | 38,778 | |

General Growth Properties, Inc. | | 2,796 | | 97,944 | |

HCP, Inc. | | 2,410 | | 76,662 | |

Host Hotels & Resorts, Inc. | | 5,448 | | 74,365 | |

Kimco Realty Corp. | | 2,594 | | 89,545 | |

Liberty Property Trust* | | 988 | | 32,752 | |

The Macerich Co. | | 760 | | 47,219 | |

ProLogis | | 2,744 | | 149,136 | |

Public Storage | | 1,366 | | 110,359 | |

Regency Centers Corp. | | 730 | | 43,158 | |

Simon Property Group, Inc. | | 1,758 | | 158,028 | |

SL Green Realty Corp. | | 572 | | 47,316 | |

UDR, Inc. | | 1,452 | | 32,496 | |

Ventas, Inc. | | 1,442 | | 61,386 | |

Vornado Realty Trust | | 1,378 | | 121,264 | |

| | | | 1,763,369 | |

| | | | | |

TOTAL COMMON STOCKS | | | | | |

(Cost $4,994,609) | | | | 4,181,781 | |

| | | | | |

TOTAL INVESTMENTS (97.6%) | | | | | |

(Cost $4,994,609) | | | | 4,181,781 | |

| | | | | |

NET OTHER ASSETS AND LIABILITIES (2.4%) | | | | 103,789 | |

| | | | | |

NET ASSETS (100.0%) | | | | $ | 4,285,570 | |

* Non-income producing security.

Common Abbreviations: |

AB – | Aktiebolag is the Swedish equivalent of the term corporation. |

AG – | Aktiengesellschaft is a German term that refers to a corporation that is limited by shares, i.e., owned by shareholders. |

Ltd. – | Limited |

N.V. – | Naamloze Vennootchap is the Dutch term for a public limited liability corporation. |

Plc – | Public Limited Co. |

REIT – | Real Estate Investment Trust |

| SA – Generally designates corporations in various countries, mostly those employing the civil law. This translates literally in all languages mentioned as anonymous company. |

See Notes to Financial Statements.

9

ALPS ETF Trust | STATEMENT OF ASSETS & LIABILITIES |

| June 30, 2008 (Unaudited) |

ASSETS: | | | |

Investments, at value | | $ | 4,181,781 | |

Cash | | 64,996 | |

Foreign currency, at value (Cost $60,912) | | 61,239 | |

Receivable for investments sold | | 71,991 | |

Foreign tax reclaims | | 88 | |

Interest and dividends receivable | | 19,654 | |

Total Assets | | 4,399,749 | |

| | | |

LIABIlITIES: | | | |

Payable for investments purchased | | 110,424 | |

Payable to advisor | | 3,755 | |

Total Liabilities | | 114,179 | |

NET ASSETS | | $ | 4,285,570 | |

| | | |

NET ASSETS CONSIST OF: | | | |

Paid-in capital | | $ | 5,099,704 | |

Undistributed net investment income | | 31,961 | |

Accumulated net realized loss on investments and foreign currency transactions | | (33,506 | ) |

Net unrealized depreciation on investments and translation of assets and liabilities denominated in foreign currencies | | (812,589 | ) |

NET ASSETS | | $ | 4,285,570 | |

| | | |

INVESTMENTS, AT COST | | $ | 4,994,609 | |

| | | |

PRICING OF SHARES | | | |

Net Asset Value, offering and redemption price per share | | $ | 42.02 | |

Net Assets | | $ | 4,285,570 | |

Shares of beneficial interest outstanding (Unlimited number of shares authorized, par value $0.01 per share) | | 102,000 | |

See Notes to Financial Statements.

10

ALPS ETF Trust | STATEMENT OF OPERATIONS |

| | For the Period | |

| | May 7, 2008(a) through | |

| | June 30, 2008 | |

| | (Unaudited) | |

INVESTMENT INCOME: | | | |

Dividends (b) | | $ | 35,718 | |

Total Investment Income | | 35,718 | |

| | | |

EXPENSES: | | | |

Investment advisory fee | | 3,757 | |

Total net expenses | | 3,757 | |

NET INVESTMENT INCOME: | | 31,961 | |

| | | |

Net realized loss on investments | | (31,480 | ) |

Net realized loss on foreign currency transactions | | (2,026 | ) |

Net change in unrealized depreciation on investments | | (812,828 | ) |

| | | |

Net change in unrealized appreciation on translation of assets and liabilities in foreign currencies | | 239 | |

NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | | (846,095 | ) |

NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | (814,134 | ) |

(a) | Inception date. |

(b) | Net of foreign withholding tax of $902. |

See Notes to Financial Statements.

11

ALPS ETF Trust | STATEMENT OF CHANGES IN NET ASSETS |

| | For the Period | |

| | May 7, 2008(a) through | |

| | June 30, 2008 | |

| | (Unaudited) | |

OPERATIONS: | | | |

Net investment income | | $ | 31,961 | |

Net realized loss on investments | | (31,480 | ) |

Net realized loss on foreign currency transactions | | (2,026 | ) |

Net change in unrealized depreciation on investments and foreign currency | | (812,589 | ) |

Net decrease in net assets resulting from operations | | (814,134 | ) |

| | | |

SHARE TRANSACTIONS: | | | |

Proceeds from sale of shares | | 4,999,704 | |

Net increase from share transactions | | 4,999,704 | |

Net increase in net assets | | 4,185,570 | |

| | | |

NET ASSETS: | | | |

Beginning of period | | 100,000 | |

End of period (including undistributed net investment income of $31,961) | | $ | 4,285,570 | |

| | | |

Other Information: | | | |

SHARE TRANSACTIONS: | | | |

Beginning Shares | | 2,000 | |

Sold | | 100,000 | |

Net increase in shares outstanding | | 102,000 | |

See Notes to Financial Statements.

12

ALPS ETF TRUST | | FINANCIAL HIGHLIGHTS |

For a Share Outstanding Throughout the Period Presented

| | For the Period | |

| | May 7, 2008(a) through | |

| | June 30, 2008 | |

| | (Unaudited) | |

NET ASSET VALUE, BEGINNING OF PERIOD | | $ | 50.00 | |

| | | |

INCOME/(LOSS) FROM OPERATIONS: | | | |

Net investment income | | 0.31 | |

Net realized and unrealized loss on investments | | (8.29 | ) |

Total from Investment Operations | | (7.98 | ) |

| | | |

NET DECREASE IN NET ASSET VALUE | | (7.98 | ) |

NET ASSET VALUE, END OF PERIOD | | $ | 42.02 | |

TOTAL RETURN | | (15.96 | )%(b) |

| | | |

RATIOS/ SUPPLEMENTAL DATA: | | | |

Net assets, end of period (in 000s) | | $ | 4,286 | |

| | | |

RATIOS TO AVERAGE NET ASSETS: | | | |

Net investment income including reimbursement/waiver | | 5.25 | %(c) |

Operating expenses including reimbursement/waiver | | 0.55 | %(c) |

Operating expenses excluding reimbursement/waiver | | 0.55 | %(c) |

PORTFOLIO TURNOVER RATE | | 16.55 | %(d) |

(a) | Inception date. |

(b) | Total return is calculated assuming an initial investment made at the net asset value at the beginning of the period and redemption at the net asset value on the last day of the period. The return presented does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption or sale of Fund shares. Total return calculated for a period of less than one year is not annualized. |

(c) | Annualized. |

(d) | Portfolio turnover is not annualized and does not include securities received or delivered from processing creations or redemptions. |

See Notes to Financial Statements.

13

ALPS ETF Trust | NOTES TO FINANCIAL STATEMENTS |

(Unaudited)

1. ORGANIZATION

The ALPS ETF Trust (the “Trust”) is an investment company organized as a Delaware statutory trust on September 13, 2007 and is registered with the Securities and Exchange Commission (“SEC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). The Trust consists of one separate ETF, the Fund, which commenced operations on May 7, 2008.

The Fund’s Shares are listed on the American Stock Exchange (“AMEX”). Unlike conventional mutual funds, the Fund issues and redeems Shares on a continuous basis, at NAV, only in large specified blocks of 50,000 Shares, each of which is called a “Creation Unit.” Creation Units are issued and redeemed principally in-kind for securities included in a specified index. Except when aggregated in Creation Units, Shares are not redeemable securities of the Fund. The investment objective of the Fund is to seek investment results that correspond generally to the price and yield (before the Fund’s fees and expenses) of the Cohen & Steers Global Realty Majors Index.

2. SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of the financial statements. The preparation of the financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

A. Portfolio Valuation

The Fund’s NAV is determined daily, as of the close of regular trading on the New York Stock Exchange (“NYSE”), normally 4:00 p.m. Eastern time, on each day the NYSE is open for trading. The NAV is computed by dividing the value of all assets of the Fund (including accrued interest and dividends), less all liabilities (including accrued expenses and dividends declared but unpaid), by the total number of shares outstanding.

The Fund’s investments are valued at market value or, in the absence of market value with respect to any portfolio securities, at fair value according to procedures adopted by the Trust’s Board of Trustees. Portfolio securities listed on any exchange other than the NASDAQ Stock Market, Inc. (“NASDAQ”) are valued at the last sale price on the business day as of which such value is being determined. If there has been no sale on such day, the securities are valued at the mean of the most recent bid and asked prices on such day. Securities traded on the NASDAQ are valued at the NASDAQ Official Closing Price as determined by NASDAQ. Portfolio securities traded on more than

14

ALPS ETF Trust | NOTES TO FINANCIAL STATEMENTS |

(Unaudited)

one securities exchange are valued at the last sale price on the business day as of which such value is being determined at the close of the exchange representing the principal market for such securities. Portfolio securities traded in the over-the-counter market, but excluding securities traded on the NASDAQ, are valued at the closing bid prices. Short-term investments that mature in less than 60 days are valued at amortized cost.

Certain securities may not be able to be priced by pre-established pricing methods. Such securities may be valued by the Board of Trustees or its delegate at fair value. These securities generally include, but are not limited to, restricted securities (securities which may not be publicly sold without registration under the Securities Act of 1933) for which a pricing service is unable to provide a market price; securities whose trading has been formally suspended; a security whose market price is not available from a pre-established pricing source; a security with respect to which an event has occurred that is most likely to materially affect the value of the security after the market has closed but before the calculation of the Fund’s NAV or make it difficult or impossible to obtain a reliable market quotation; and a security whose price, as provided by the pricing service, does not reflect the security’s “fair value.” As a general principle, the current “fair value” of a security would appear to be the amount which the owner might reasonably expect to receive from the closing sale prices on the applicable exchange and fair value prices may not reflect the actual value of a security. A variety of factors may be considered in determining the fair value of such securities.

Valuing the Fund’s securities using fair value pricing will result in using prices for those securities that may differ from current market valuations. Use of fair value prices and certain market valuations could result in a difference between the prices used to calculate a Fund’s NAV and the prices used by the Index, which, in turn, could result in a difference between a Fund’s performance and the performance of the Index.

B. Foreign Currency Translation and Foreign Investments

The accounting records of the Fund are maintained in U.S. dollars. Portfolio securities and other assets and liabilities denominated in a foreign currency are translated to U.S. dollars at the prevailing rates of exchange at period end. Amounts related to the purchases and sales of securities and investment income are translated into U.S. dollars at the prevailing exchange rate on the respective dates of transactions. The effects of changes in foreign currency exchange rates on portfolio investments are included in the net realized and unrealized gains and losses on investments. Net gains and losses on foreign currency transactions include disposition of foreign currencies, and currency gains and losses between the accrual and receipt dates of portfolio investment income and between the trade and settlement dates of portfolio investment transactions.

C. Securities Transactions and Investment Income

Securities transactions are recorded as of the trade date. Realized gains and

15

ALPS ETF Trust | NOTES TO FINANCIAL STATEMENTS |

(Unaudited)

losses from securities transactions are recorded on the identified cost basis. Dividend income is recorded on the ex-dividend date. Interest income, if any, is recorded on the accrual basis.

D. Dividends and Distributions to Shareholders

Dividends from net investment income of the Fund, if any, are declared and paid annually or as the Board of Trustees may determine from time to time. Distributions of net realized capital gains earned by the Fund, if any, are distributed at least annually.

Distributions from income and capital gains are determined in accordance with income tax regulations, which may differ from accounting principles generally accepted in the United States of America. These differences are primarily due to differing treatments of income and gains on various investment securities held by the Fund, timing differences and differing characterization of distributions made by the Fund.

There were no distributions paid during the period ended June 30, 2008.

As of June 30, 2008, the components of distributable earnings on a tax basis for the Fund were as follows:

Undistributed net investment income | | $ | 31,961 | |

Accumulated net realized loss on investments and foreign currencies | | (33,506 | ) |

Net unrealized depreciation on investments and translation of assets and liabilities denominated in foreign currencies | | (811,420 | ) |

Total | | $ | (812,965 | ) |

E. Income Taxes

The Fund intends to qualify as a regulated investment company by complying with the requirements under Subchapter M of the Internal Revenue Code of 1986, as amended, by distributing substantially all of its net investment income and net realized gains to shareholders. Accordingly, no provision has been made for federal and state income taxes.

In June 2006, Financial Accounting Standards Board Interpretation No. 48, “Accounting for Uncertainty in Income Taxes” – an interpretation of FASB 109 (“FIN 48”) was issued and is effective for fiscal years beginning after December 15, 2006. This interpretation prescribes a minimum threshold for financial statement recognition of the benefit of a tax position taken or expected to be taken in a tax return. As of June 30, 2008, management has evaluated the application of FIN 48 to the Fund, and has determined that there is no material impact resulting from the adoption of this interpretation on the Fund’s financial statements.

16

ALPS ETF Trust | NOTES TO FINANCIAL STATEMENTS |

(Unaudited)

F. New Accounting Pronouncements

In March, 2008, Statement of Financial Accounting Standards No. 161, “Disclosures about Derivative Instruments and Hedging Activities” (“SFAS 161”) was issued and is effective for fiscal years and interim periods beginning after November 15, 2008. SFAS 161 requires enhanced disclosures about Funds’ derivative and hedging activities. Management is currently evaluating the impact, if any, the adoption of SFAS 161 will have on the Fund’s financial statement disclosure.

G. Fair Value Measurements

The Fund has adopted Financial Accounting Standards Board Statement of Financial Accounting Standards No. 157, Fair Value Measurements (“FAS 157”). FAS 157 defines fair value, establishes a three-tier hierarchy to measure fair value based on the extent of use of “observable inputs” as compared to “unobservable inputs” for disclosure purposes and requires additional disclosures about these valuations measurements. Inputs refer broadly to the assumptions that market participants would use in pricing a security. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the security developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the security developed based on the best information available in the circumstances.

The three-tier hierarchy is summarized as follows:

1) Level 1 –quoted prices in active markets for identical securities

2) Level 2 – other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

3) Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The following is a summary of the inputs used as of June 30, 2008 in valuing the Fund’s assets:

| | | | Other Financial | |

| | | | Instruments* | |

| | | | - Unrealized | |

| | Investments in | | Appreciation | |

Valuation Inputs | | Securities at Value | | (Depreciation) | |

Level 1 - Quoted Prices | | $ | 4,181,781 | | $ | — | |

| | | | | |

Level 2 - Other Significant Observable Inputs | | $ | — | | $ | — | |

| | | | | |

Level 3 - Significant Unobservable Inputs | | $ | — | | $ | — | |

Total | | $ | 4,181,781 | | $ | — | |

* Other financial instruments include futures, forwards and swap contracts

17

ALPS ETF Trust | NOTES TO FINANCIAL STATEMENTS |

(Unaudited)

All securities of the Fund were valued using either Level 1 or Level 2 inputs during the period ended June 30, 2008. Thus a reconciliation of assets in which significant unobservable inputs (Level 3) were used is not applicable for the Fund.

3. INVESTMENT ADVISORY FEE AND OTHER AFFILIATED TRANSACTIONS

ALPS Advisers, Inc. (the “Investment Adviser”) acts as the Fund’s investment adviser pursuant to an advisory agreement with the Trust on behalf of the Fund (the “Advisory Agreement”). Pursuant to the Advisory Agreement, the Fund pays the Investment Adviser a unitary fee for the services and facilities it provides payable on a monthly basis at the annual rate of 0.55% of the Fund’s average daily net assets. From time to time, the Investment Adviser may waive all or a portion of its fee.

Out of the unitary management fee, the Investment Adviser pays substantially all expenses of the Fund, including the fees of the Sub-Adviser, the licensing fee of the Index provider, and the cost of transfer agency, custody, fund administration, legal, audit and other services, except for interest expenses, distribution fees or expenses, brokerage expenses, taxes and extraordinary expenses not incurred in the ordinary course of the Fund’s business.

The Investment Adviser’s unitary management fee is designed to pay substantially all of the Fund’s expenses and to compensate the Investment Adviser for providing services for the Fund.

Mellon Capital Management Corporation acts as the Fund’s sub-adviser (the “Sub-Adviser”) pursuant to a sub-advisory agreement with the Investment Adviser (the “Sub-Advisory Agreement”). According to this agreement, the Investment Adviser pays the Sub-Adviser on a monthly basis, an annual rate of 0.10% of the Fund’s average daily net assets. The Investment Adviser will pay the Sub-Adviser a minimum of $62,500 per year after the Fund’s first year of operations and a minimum of $125,000 per year after the Fund’s second year of operations.

ALPS Fund Services, Inc. (“ALPS”) is the administrator of the Fund.

The Bank of New York Mellon is the custodian, fund accounting agent and transfer agent for the Fund.

Each Trustee who is not an officer or employee of ALPS Advisers, Inc., any sub-adviser or any of their affiliates (“Independent Trustees”) is paid a quarterly retainer of $3,500 and $1,500 for each Board meeting attended.

18

ALPS ETF Trust | NOTES TO FINANCIAL STATEMENTS |

(Unaudited)

4. PURCHASES AND SALES OF SECURITIES

For the period ended June 30, 2008, the cost of purchases and proceeds from sales of investment securities, excluding short-term investments and in-kind transactions, were as follows:

| | Purchases | | Sales | |

Cohen & Steers Global Realty Majors ETF | | $ | 762,136 | | $ | 735,743 | |

| | | | | | | |

For the period ended June 30, 2008, the cost of in-kind purchases and proceeds from in-kind sales were as follows:

| | Purchases | | Sales | |

Cohen & Steers Global Realty Majors ETF | | $ | 4,999,697 | | $ | — | |

| | | | | | | |

Gains on in-kind transactions are not considered taxable for federal income tax purposes.

As of June 30, 2008, the costs of investments for federal income tax purposes and accumulated net unrealized appreciation/(depreciation) on investments were as follows:

Gross Appreciation (excess of value over tax cost) | | $ | 18,580 | |

Gross Depreciation (excess of tax cost over value) | | (830,000 | ) |

Net unrealized depreciation | | (811,420 | ) |

| | | |

Cost of investment for income tax purposes | | $ | 4,993,201 | |

5. CREATIONS, REDEMPTIONS AND TRANSACTION FEES

The Fund issues and redeems Shares at NAV only in large blocks of 50,000 Shares (each block of 50,000 Shares is called a “Creation Unit”) or multiples thereof. As a practical matter, only broker-dealers or large institutional investors with creation and redemption agreements called Authorized Participants (“APs”) can purchase or redeem these Creation Units. Purchasers of Creation Units at NAV must pay a standard Creation Transaction Fee of $1,500 per transaction. The value of a Creation unit as of first creation was approximately $2,500,000. An AP who holds Creation Units and wishes to redeem at NAV would also pay a standard Redemption Transaction Fee of $1,500 per transaction. If a Creation Unit is purchased or redeemed for cash, a variable fee of up to four times the standard Creation or Redemption Transaction Fee may be charged to the AP making the transaction.

The creation fee, redemption fee and variable fee are not expenses of the Fund and do not impact the Fund’s expense ratio.

19

ALPS ETF Trust | ADDITIONAL INFORMATION |

(Unaudited)

PROXY VOTING POLICIES AND PROCEDURES

A description of the policies and procedures that the Fund uses to determine how to vote proxies and information on how the Fund voted proxies relating to portfolio securities during the period ending June 30, 2008 is available (1) without charge, upon request, by calling (866) 513-5856; (2) on the Trust’s website located at http://www.alpsetfs.com; and (3) on the SEC’s website at http://www.sec.gov.

PORTFOLIO HOLDINGS

The Trust will file its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q beginning with the September 30, 2008 holdings. The Trust’s Form N-Q will be available (1) by calling (866) 513-5856; (2) on the Trust’s website located at http://www.alpsetfs.com; (3) on the SEC’s website at http://www.sec.gov; and (4) for review and copying at the SEC’s Public Reference Room (“PRR”) in Washington D.C. Information regarding the operation of the PRR may be obtained by calling (800) SEC-0330.

ADVISORY CONTRACT APPROVAL

At an in-person meeting held on March 26, 2008, The Board of Trustees of the Trust, including the Independent Trustees, evaluated proposals to approve the Advisory Agreement between the Trust and the Investment Adviser with respect to the Fund. The Trustees who are not “interested persons” of the Trust within the meaning of the 1940 Act, as amended (the “Independent Trustees”) also met separately with their independent legal counsel to consider the Agreement.

In evaluating the Advisory Agreement, the Board drew on materials provided to them by the Investment Adviser, The Bank of New York Mellon, the Trust’s Transfer Agent and Custodian, and ALPS Fund Services, Inc., the Trust’s Administrator. In deciding whether to approve the Advisory Agreement, the Board considered various factors, including (i) the nature, extent and quality of the services expected to be provided by the Investment Adviser with respect to the Fund under the Advisory Agreement, (ii) costs to the Investment Adviser of its services; and (iii) the extent to which economies of scale would be realized if and as the Fund grows and whether the fee level in the Advisory Agreement reflects these economies of scale.

The Board considered the nature, extent and quality of services to be provided by the Adviser. The Board reviewed the Advisory Agreement and the Investment Adviser’s anticipated responsibilities for managing investment operations of the Fund, in accordance with the Fund’s investment objective and policies, and applicable legal and regulatory requirements. The Board considered the background and experience of the Investment Adviser’s senior management, including those

20

individuals responsible for the portfolio management and compliance of the Fund. It also considered the efforts expended by ALPS in organizing the Trust and making arrangements for entities to provide services to the Fund. Since the Fund is newly organized, the Board did not consider investment performance of the Fund, but the Board did consider performance of the applicable index for the Fund. The Board concluded it was comfortable that the Investment Adviser had the capabilities and resources to oversee the operations of the Fund, including services to be provided by other service providers.

The Board considered whether the Investment Adviser benefited in other ways from its relationship with the Trust, noting that the Investment Adviser does not maintain soft-dollar arrangements in connection with the Trust’s brokerage transactions. The Board concluded that, to the extent that the Investment Adviser derives other benefits from its relationship with the Trust, those benefits are not so significant as to cause the Investment Adviser’s fees with respect to the Fund to be excessive.

The Board determined that the Investment Adviser is likely to realize economies of scale in managing the Fund as assets grow in size. However, the Board intends to continue to monitor fees as the Fund grows in size and assess whether fee breakpoints may be warranted.

The Board evaluated the Fund’s unitary fee through the review of comparative information with respect to fees paid by similar funds – i.e., ETFs tracking real estate equity indexes. The Board reviewed the universe of similar ETFs for the Fund based upon data from Lipper Analytical Services and related comparative information for similar ETFs. The Board considered limitations of the universe, notably the small number of ETFs in the universe and the fact that many were recently launched. The Board used a fund-by-fund analysis of the data and concluded, based on the information presented, that the Fund fees were fair and reasonable in light of those of its direct competitors.

The Board’s conclusions regarding the Advisory Agreement, including the independent Trustees voting separately, were as follows: (a) the nature and extent of the services expected to be provided by the Investment Adviser with respect to the Fund were appropriate; (b) the Investment Adviser’s fees for the Fund and the unitary fee, considered in relation to the services expected to be provided, were fair and reasonable; and (c) any additional benefits to the Investment Adviser were not of a magnitude to materially affect the Board’s conclusions.

At the same in person meeting, the Board also evaluated the proposal to approve the Sub-Advisory Agreement among the Investment Adviser, the Trust and

21

the Sub-Adviser with respect to the Fund. In deciding whether to approve the Sub-Advisory Agreement, the Board considered various factors, including (i) the nature, extent and quality of the services expected to be provided by the Sub-Adviser with respect to the Fund under the Sub-Advisory Agreement, (ii) the fees charged by the Sub-Adviser and any additional benefits received by the Sub-Adviser due to its relationship with the Investment Adviser and the Trust; and (iii) the extent to which economies of scale would be realized if and as the Fund grows and whether the fee levels in the Sub-Advisory Agreement reflect these economies of scale.

The Board considered, among other matters, the background and experience of the Sub-Adviser’s senior management and in particular the Sub-Adviser’s experience in investing in global real estate securities. The Board evaluated the Sub-Adviser’s proposed fee and determined that the Sub-Adviser is likely to realize economies of scale in managing the Fund as assets grow in size. The Board determined that such economies of scale are shared with the Fund by way of the relatively low advisory/sub-advisory fees and unitary fee structure of the Fund, although the Board intends to continue to monitor fees as the Fund grows in size and assess whether fee breakpoints may be warranted.

The Board’s conclusions in approving the Sub-Advisory Agreement, including the independent Trustees voting separately, were as follows: (a) the nature and extent of the services expected to be provided by the Sub-Adviser to the Fund were appropriate; (b) the Sub-Adviser’s fees for the Fund and the unitary fee, considered in relation to the services provided, were fair and reasonable; (c) any additional benefits to the Sub-Adviser were not of a magnitude to materially affect the Board’s conclusions; and (d) the fees expected to be paid to the Sub-Adviser adequately shared the economies of scale with the Fund.

22

RISK CONSIDERATIONS

You should consider the Fund’s investment objective, risks and charges carefully before investing. You can download the Fund’s prospectus at http://www.alpsetfs.com or contact ALPS Distributors, Inc. at 1-866-513-5856 to request a prospectus, which contains this and other information about the Fund. Read it carefully before you invest. ALPS Distributors, Inc. is the distributor of the Cohen & Steers Global Realty Majors ETF.

The Fund’s shares will change in value, and you could lose money by investing in the Fund. An investment in the Fund involves risks similar to those of investing in any fund of equity securities traded on an exchange. Investors buying or selling Fund shares on the secondary market may incur brokerage commissions. In addition, investors who sell Fund shares may receive less than the shares’ net asset value. Unlike shares of open-ended funds, investors are generally not able to purchase ETF shares directly from the Fund and individual ETF shares are not redeemable. However, specified large blocks of shares called creation units can be purchased from, or redeemed to, the Fund.

You should anticipate that the value of the Fund’s shares will decline, more or less, in correlation with any decline in the value of its corresponding Index.

The Fund’s return may not match the return of its corresponding Index for a number of reasons. For example, the Fund incurs operating expenses not applicable to its corresponding Index, and may incur costs in buying and selling securities, especially when rebalancing the Fund’s portfolio holdings to reflect changes in composition of its corresponding Index. In addition the Fund’s portfolio holdings may not exactly replicate the securities included in its corresponding Index or the ratios between the securities included in such Index.

The Fund is exposed to additional market risk due to its policy of investing principally in the securities included in its corresponding Index. As a result of this policy, securities held by the Fund will generally not be bought or sold in response to market fluctuations and the securities may be issued by companies concentrated in a particular industry. Therefore, the Fund will generally not sell a stock because the stock’s issuer is in financial trouble, unless that stock is removed or is anticipated to be removed from the Fund’s Index.

The Fund relies on a license and related sublicense that permits it to use its corresponding Index and associated trade names and trademarks in connection with the name and investment strategies of the Fund. Such license and related

23

sublicense may be terminated by the Index provider and, as a result, the Fund may lose its ability to use such intellectual property. In the event the license is terminated or the index provider does not have rights to license such intellectual property, it may have a significant effect on the operation of the Fund.

The value of an individual security or particular type of security can be more volatile than the market as a whole and can perform differently from the value of the market as a whole.

The Fund is not actively managed. The Fund may be affected by a general decline in certain market segments relating to its Index. The Fund invests in securities included in, or representative of, its index regardless of such investment’s merit. The Fund does not attempt to take defensive positions in declining markets.

The Fund invests in securities of foreign companies and, therefore, is subject to certain risks associated with possible adverse economic, political and social occurrences outside of the United States of America.

The Fund’s NAV is determined on the basis of the U.S. dollar. You may lose money if the local currency of a foreign market depreciates against the U.S. dollar, even if the local currency value of the Fund’s holdings goes up.

The Fund invests in securities of non-U.S. issuers. Investing in securities of non-U.S. issuers, which are generally denominated in non-U.S. currencies, may involve certain risks not typically associated with investing in securities of U.S. issuers such as there being less publicly available information about non-U.S. issuers or markets and non-U.S. markets being less smaller, less liquid and more volatile than the U.S. market. These risks may be more pronounced to the extent that the Fund invests a significant amount of its assets in companies located in one region.

The Fund invests in companies that are considered to be “passive foreign investment companies” and could be subject to U.S. federal income tax and additional interest charges on gains and certain distributions with respect to those equity interests.

The Fund invests in companies in the real estate industry, including real estate investment trusts and is subject to the risks associated with investing in real estate such as possible declines in the value of real estate, adverse general and local economic conditions and changes in interest rates and environmental problems.

24

Item 2. Code of Ethics.

Not Applicable to this Report.

Item 3. Audit Committee Financial Expert.

Not Applicable to this Report.

Item 4. Principal Accountant Fees and Services.

Not Applicable to this Report.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Schedule of Investments.

Schedule of Investments is included as part of the Report to Stockholders filed under Item 1 of this form.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

2

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to Vote of Security Holders.

No material changes to the procedures by which the shareholders may recommend nominees to the Registrant’s Board of Trustees have been implemented after the Registrant’s last provided disclosure in response to the requirements of Item 407(c)(2)(iv) of Regulation S-K (17 CFR 229.407) (as required by Item 22(b)(15) of Schedule 14A (17 CFR 240.14a-101)), or this Item.

Item 11. Controls and Procedures.

(a) The Registrant’s principal executive and principal financial officers, or persons performing similar functions, have concluded that the Registrant’s disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940, as amended (the “1940 Act”) (17 CFR 270.30a-3(c))) are effective, as of a date within 90 days of the filing date of the report that includes the disclosure required by this paragraph, based on their evaluation of these controls and procedures required by Rule 30a-3(b) under the 1940 Act (17 CFR 270.30a-3(b)) and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934, as amended (17 CFR 240.13a-15(b) or 240.15d-15(b)).

(b) No changes in the Registrant’s internal control over financial reporting (as defined in Rule 30a-3(d) under the 1940 Act (17 CFR 270.30a-3(d)) occurred during the Registrant’s second fiscal quarter of the period covered by this report that have materially affected, or are reasonably likely to materially affect, the Registrant’s internal control over financial reporting.

Item 12. Exhibits.

(a)(1) Not Applicable to this Report.

(a)(2) The certifications required by Rule 30a-2(a) of the Investment Company Act of 1940, as amended, and Section 302 of the Sarbanes-Oxley Act of 2002 are attached hereto as Ex99.Cert.

(a)(3) Not applicable.

(b) The certifications by the Registrant’s Principal Executive Officer and Principal Financial Officer, as required by Rule 30a-2(b) of the Investment Company Act of 1940, as amended, and Section 906 of the Sarbanes-Oxley Act of 2002 are attached hereto as Ex99.906Cert.

3

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

ALPS ETF TRUST |

|

By: | /s/ Thomas A. Carter | |

| Thomas A. Carter (Principal Executive Officer) |

| President |

| |

Date: | September 8, 2008 |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

By: | /s/ Thomas A. Carter | |

| Thomas A. Carter (Principal Executive Officer) |

| President |

| |

Date: | September 8, 2008 |

By: | /s/ Kimberly R. Storms | |

| Kimberly R. Storms (Principal Financial Officer) |

| Treasurer |

| |

Date: | September 8, 2008 |

4