UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-22175 |

|

ALPS ETF TRUST |

(Exact name of registrant as specified in charter) |

|

1290 Broadway, Suite 1100, Denver, Colorado | | 80203 |

(Address of principal executive offices) | | (Zip code) |

|

Tané T. Tyler, Esq. ALPS ETF Trust 1290 Broadway, Suite 1100 Denver, Colorado 80203 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (303) 623-2577 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | January 1, 2009 – December 31, 2009 | |

| | | | | | | | | |

Item 1. Reports to Stockholders.

Table of Contents

ALPS Equal Sector Weight ETF

Table of CONTENTS

ALPS Equal Sector Weight ETF | www.alpsetfs.com

Table of Contents

| Shareholder Letter December 31, 2009 |

Dear Shareholders:

When ALPS launched its ETF Trust in 2008 our goal was to bring innovative solutions to the ETF industry that provide investors with access to a unique market segment or strategy. The ALPS Equal Sector Weight ETF, which was launched in July 2009, is the world’s first ETF to provide access to an Equal Sector Strategy.

Sectors are one of the most important drivers of risk and return in a portfolio. An equal sector strategy can minimize the negative impact of any one sector on the entire portfolio. At the same time by offering meaningful exposure to each sector of the market, it allows investors the ability to participate in market rallies regardless of where they occur. We believe the consistency of the historical returns delivered by an equal sector strategy combined with its transparency(1) and simplicity make it a viable alternative for US large-cap investing.

In the pages that follow our Fund managers have provided a performance overview. We thank you for your investment and for being a EQL shareholder.

| |

| |

Thomas A. Carter* | |

President, ALPS ETF Trust

* Registered representative of ALPS Distributors, Inc.

Ordinary brokerage commissions apply.

(1) ETFs are considered transparent because their portfolio holdings are disclosed daily.

Annual Report | December 31, 2009

2

Table of Contents

Performance Overview (Unaudited)

December 31, 2009

INVESTMENT OBJECTIVE

The Fund seeks investment results that replicate as closely as possible, before fees and expenses, the performance of the Banc of America Securities - Merrill Lynch Equal Sector Weight Index (the “Underlying Index”). The Fund’s investment objective is not fundamental and may be changed by the Board of Trustees without shareholder approval.

PRIMARY INVESTMENT STRATEGIES

The Adviser will seek to match the performance of the Underlying Index. The Underlying Index is an index of indexes comprised in equal proportions of the nine Select Sector SPDR Indexes (“The Underlying Sector Indexes”). In order to track the securities in the Underlying Index, the Fund will use a “fund of funds” approach, and seek to achieve its investment objective by investing at least 90% if its total assets in the shares of Select Sector SPDR exchange-traded funds (each, an “Underlying Sector ETF” and collectively, the “Underlying Sector ETFs”) that track the Underlying Sector Indexes of which the Underlying Index is comprised.

PERFORMANCE OVERVIEW

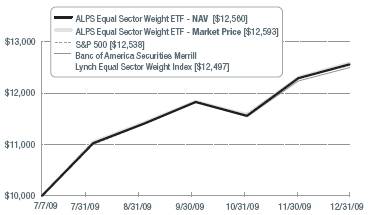

Since inception (7/7/09) the fund returned 25.60% while the Fund’s benchmark returned 24.97% and the S&P 500 returned 25.38% . While all sectors of the market showed positive performance in the period, the early cycle sectors performed the best. The primary drivers of performance in the Fund were the Consumer Discretionary, Materials and Technology sectors, which were up 34.1% and 33.5%, and 29.9% respectively. The worst performing sectors were the more defensive Healthcare, Consumer Staples and Utilities sectors, which were up 20.9%, 15.2% and 14.9% respectively.

Compared to the S&P 500 the fund benefited from its relative overweight in the Materials and Consumer Discretionary sectors and was negatively impacted by its underweight in the Technology sector and overweight in the Utilities sector. Overall, the Fund’s sector weights relative to the S&P 500 resulted in positive outperformance above the index in 5 of the 9 sectors.

3

Table of Contents

PERFORMANCE as of December 31, 2009

| | | | | | Since Inception | |

| | 1 Month | | 3 Month | | Cumulative* | |

ALPS Equal Sector Weight ETF | | | | | | | |

NAV | | 2.20 | % | 6.19 | % | 25.60 | % |

Market Price** | | 2.27 | % | 6.29 | % | 25.93 | % |

Banc of America Securities | | | | | | | |

Merrill Lynch Equal Sector | | | | | | | |

Weight Index | | 2.12 | % | 5.75 | % | 24.97 | % |

S&P 500 Total Return Index | | 1.93 | % | 6.04 | % | 25.38 | % |

Total Expense Ratio (per the current Prospectus) | | 0.55 | % | | | | |

Performance data quoted represents past performance. Past performance does not guarantee future results. Current performance may be higher or lower than actual data quoted. Call 1.866.675.2639 or visit www.alpsetfs.com for current month end performance. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

* The Fund commenced Investment Operations on July 6, 2009 with an Inception Date, the first day of trading on the Exchange, of July 7, 2009.

S&P 500 Index: the Standard & Poor’s composite index of 500 stocks, a widely recognized, unmanaged index of common stock prices.

** Market price returns are based on the midpoint of the bid/ask spread at 4 p.m. ET and do not represent the returns an investor would receive if shares were traded at other times.

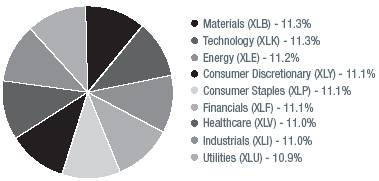

The following table shows the sector weights of both the Fund and the S&P 500 as of December 31, 2009:

SECTOR WEIGHTING COMPARISON as of December 31, 2009

| | EQL | | S&P 500 | |

Materials (XLB) | | 11.3 | % | 3.7 | % |

Technology (XLK) | | 11.3 | | 22.9 | |

Energy (XLE) | | 11.2 | | 11.7 | |

Consumer Discretionary (XLY) | | 11.1 | | 9.5 | |

Consumer Staples (XLP) | | 11.1 | | 11.2 | |

Financials (XLF) | | 11.1 | | 14.6 | |

Health Care (XLV) | | 11.0 | | 11.5 | |

Industrials (XLI) | | 11.0 | | 10.3 | |

Utilities (XLU) | | 10.9 | | 3.6 | |

Source: S&P 500.

4

Table of Contents

SECTOR ALLOCATION as of December 31, 2009

GROWTH OF $10,000 as of December 31, 2009

5

Table of Contents

| Disclosure of Fund Expenses For the Period Ended December 31, 2009 (Unaudited) |

Shareholder Expense Example: As a shareholder of the Fund, you incur two types of costs: (1) transaction costs which may include creation and redemption fees or brokerage charges and (2) ongoing costs, including management fees and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other funds. It is based on an investment of $1,000 invested at July 1, 2009 and held through the period ended December 31, 2009.

Actual Return: The first line of the table provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you incurred over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid during Period” to estimate the expenses attributable to your investment during this period.

Hypothetical 5% Return: The second line of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The expenses shown in the table are meant to highlight ongoing Fund costs only and do not reflect any transaction costs, such as creation and redemption fees, or brokerage charges. Therefore, the second table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these costs were included, your costs would have been higher.

| | | | | | | | Expenses | |

| | Beginning | | | | | | Paid During | |

| | Account | | Ending | | | | Period | |

| | Value | | Account Value | | Expense | | 07/01/09- | |

| | 07/01/09 | | 12/31/09 | | Ratio | | 12/31/09 | |

Actual(a) | | $ | 1,000.00 | | $ | 1,256.00 | | 0.34 | % | $ | 1.87 | |

Hypothetical(b) | | $ | 1,000.00 | | $ | 1,023.49 | | 0.34 | % | $ | 1.73 | |

(a) The “Actual” example in the table above is equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days the Fund was in existence in the most recent fiscal half year (178), then divided by 365.

(b) The “Hypothetical” example in the table above is equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), then divided by 365.

6

Table of Contents

Report of Independent Registered Public Accounting Firm

December 31, 2009

To the Board of Trustees and Shareholders of ALPS ETF Trust:

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of the ALPS Equal Sector Weight ETF (the “Fund”), which is part of the ALPS ETF Trust, as of December 31, 2009, and the related statement of operations, statement of changes in net assets, and the financial highlights for the period from July 7, 2009 (inception) to December 31, 2009. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2009, by correspondence with the custodian. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the ALPS Equal Sector Weight ETF as of December 31, 2009, the results of its operations, the changes in its net assets, and the financial highlights for the period from July 7, 2009 (inception) to December 31, 2009, in conformity with accounting principles generally accepted in the United States of America.

February 24, 2010

Denver, Colorado

7

Table of Contents

| Statement of Investments December 31, 2009 |

Security Description | | Shares | | Market Value | |

EXCHANGE TRADED FUNDS (99.94%) | | | | | |

Consumer Discretionary (11.07%) | | | | | |

Consumer Discretionary Select Sector SPDR Fund | | 52,071 | | $ | 1,550,154 | |

| | | | | |

Consumer Staples (11.10%) | | | | | |

Consumer Staples Select Sector SPDR Fund | | 58,768 | | 1,555,589 | |

| | | | | |

Energy (11.17%) | | | | | |

Energy Select Sector SPDR Fund | | 27,442 | | 1,564,468 | |

| | | | | |

Financials (11.13%) | | | | | |

Financial Select Sector SPDR Fund | | 108,356 | | 1,559,243 | |

| | | | | |

Healthcare (10.99%) | | | | | |

Health Care Select Sector SPDR Fund | | 49,541 | | 1,539,734 | |

| | | | | |

Industrials (10.98%) | | | | | |

Industrial Select Sector SPDR Fund | | 55,346 | | 1,538,065 | |

| | | | | |

Materials (11.34%) | | | | | |

Materials Select Sector SPDR Fund | | 48,132 | | 1,588,357 | |

| | | | | |

Technology (11.26%) | | | | | |

Technology Select Sector SPDR Fund | | 68,984 | | 1,577,664 | |

| | | | | |

Utilities (10.90%) | | | | | |

Utilities Select Sector SPDR Fund | | 49,240 | | 1,526,440 | |

| | | | | |

TOTAL EXCHANGE TRADED FUNDS

(Cost $12,528,125) | | | | 13,999,714 | |

| | | | | |

TOTAL INVESTMENTS (99.94%)

(Cost $12,528,125) | | | | 13,999,714 | |

| | | | | |

NET OTHER ASSETS AND LIABILITIES (0.06%) | | | | 8,513 | |

| | | | | |

NET ASSETS (100.00%) | | | | $ | 14,008,227 | |

See Notes to Financial Statements.

8

Table of Contents

Statement of Assets and Liabilities

December 31, 2009

ASSETS: | | | |

Investments, at value | | $ | 13,999,714 | |

Cash | | 12,538 | |

Total Assets | | 14,012,252 | |

| | | |

LIABILITIES: | | | |

Payable to advisor | | 4,025 | |

Total Liabilities | | 4,025 | |

NET ASSETS | | $ | 14,008,227 | |

| | | |

NET ASSETS CONSIST OF: | | | |

Paid-in capital | | $ | 12,530,970 | |

Undistributed net investment income | | 41 | |

Accumulated net realized gain on investments | | 5,627 | |

Net unrealized appreciation on investments | | 1,471,589 | |

NET ASSETS | | $ | 14,008,227 | |

| | | |

INVESTMENTS, AT COST | | $ | 12,528,125 | |

| | | |

PRICING OF SHARES | | | |

Net Assets | | $ | 14,008,227 | |

Shares of beneficial interest outstanding (Unlimited number of shares authorized, par value $0.01 per share) | | 450,000 | |

Net Asset Value, offering and redemption price per share | | $ | 31.13 | |

See Notes to Financial Statements.

9

Table of Contents

| Statement of Operations For the Period Ended July 7, 2009 (Inception) Through December 31, 2009 |

INVESTMENT INCOME: | | | |

Dividends | | $ | 140,472 | |

Total Investment Income | | 140,472 | |

| | | |

EXPENSES: | | | |

Investment advisory fee | | 17,698 | |

Total Expenses before Reimbursement | | 17,698 | |

Expenses Reimbursed by: | | | |

Investment advisor | | (1,435 | ) |

NET EXPENSES | | 16,263 | |

NET INVESTMENT INCOME | | 124,209 | |

| | | |

Net realized gain on investments | | 9,220 | |

Net change in unrealized appreciation on investments | | 1,471,589 | |

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS | | 1,480,809 | |

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 1,605,018 | |

See Notes to Financial Statements.

10

Table of Contents

Statement of Changes in Net Assets

| | For the Period Ended | |

| | July 7, 2009 (Inception) | |

| | through | |

| | December 31, 2009 | |

| | | |

OPERATIONS: | | | |

Net investment income | | $ | 124,209 | |

Net realized gain on investments | | 9,220 | |

Net change in unrealized appreciation on investments | | 1,471,589 | |

Net increase in net assets resulting from operations | | 1,605,018 | |

| | | |

DISTRIBUTIONS TO SHAREHOLDERS: | | | |

From net investment income | | (124,168 | ) |

From net realized gains on investments | | (3,593 | ) |

Total distributions | | (127,761 | ) |

| | | |

SHARE TRANSACTIONS: | | | |

Proceeds from sale of shares | | 12,530,970 | |

Net increase from share transactions | | 12,530,970 | |

Net increase in net assets | | 14,008,227 | |

| | | |

NET ASSETS: | | | |

Beginning of period | | — | |

End of period* | | $ | 14,008,227 | |

*Including undistributed net investment income of: | | $ | 41 | |

| | | |

OTHER INFORMATION: | | | |

SHARE TRANSACTIONS: | | | |

Beginning shares | | — | |

Sold | | 450,000 | |

Shares outstanding, end of period | | 450,000 | |

See Notes to Financial Statements.

11

Table of Contents

| Financial Highlights For a share outstanding throughout the period presented. |

| | For the Period Ended | |

| | July 7, 2009 (Inception) | |

| | through | |

| | December 31, 2009 | |

| | | |

NET ASSET VALUE, BEGINNING OF PERIOD | | $ | 25.04 | |

| | | |

INCOME FROM OPERATIONS: | | | |

Net investment income | | 0.31 | |

Net realized and unrealized gain on investments | | 6.10 | |

Total from Investment Operations | | 6.41 | |

| | | |

LESS DISTRIBUTIONS: | | | |

From net investment income | | (0.31 | ) |

From capital gains | | (0.01 | ) |

Total distributions | | (0.32 | ) |

NET INCREASE IN NET ASSET VALUE | | 6.09 | |

NET ASSET VALUE, END OF PERIOD | | $ | 31.13 | |

TOTAL RETURN(a) | | 25.60 | % |

| | | |

RATIOS/ SUPPLEMENTAL DATA: | | | |

Net assets, end of period (in 000s) | | $ | 14,008 | |

| | | |

RATIOS TO AVERAGE NET ASSETS: | | | |

Net investment income including reimbursement/waiver | | 2.60 | %(b) |

Net investment income excluding reimbursement/waiver | | 2.57 | %(b) |

Operating expenses including reimbursement/waiver | | 0.34 | %(b) |

Operating expenses excluding reimbursement/waiver | | 0.37 | %(b) |

PORTFOLIO TURNOVER RATE(c) | | 4 | % |

(a) Total return is calculated assuming an initial investment made at the net asset value at the beginning of the period and redemption at the net asset value on the last day of the period. The return presented does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption or sale of Fund shares. Total return calculated for a period of less than one year is not annualized.

(b) Annualized.

(c) Portfolio turnover is not annualized and does not include securities received or delivered from processing creations or redemptions.

See Notes to Financial Statements.

12

Table of Contents

Notes to Financial Statements

December 31, 2009

1. ORGANIZATION

The ALPS ETF Trust (the “Trust”) is an open-end management investment company organized as a Delaware statutory trust on September 13, 2007 and is registered with the Securities and Exchange Commission (“SEC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). As of the year end, the Trust consists of five separate portfolios. Each portfolio represents a separate series of the Trust. This report pertains solely to the ALPS Equal Sector Weight ETF (the “Fund”), which commenced Investment operations on July 6, 2009 and began trading on the exchange on July 7, 2009.

The Fund’s Shares are listed on the NYSE Arca. Unlike conventional mutual funds, the Fund issues and redeems Shares on a continuous basis, at NAV, only in large specified blocks of 50,000 Shares, each of which is called a “Creation Unit.” Creation Units are issued and redeemed principally in-kind for securities included in a specified index. Except when aggregated in Creation Units, Shares are not redeemable securities of the Fund. The investment objective of the Fund is to seek investment results that correspond generally to the price and yield (before the Fund’s fees and expenses) of the Banc of America Securities Merrill Lynch Equal Sector Weight Index.

2. SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of the financial statements. The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). The preparation of financial statements in conformity with U.S. GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the period. Actual results could differ from those estimates.

A. Portfolio Valuation

The Fund’s NAV is determined daily, as of the close of regular trading on the New York Stock Exchange (“NYSE”), normally 4:00 p.m. Eastern time, on each day the NYSE is open for trading. The NAV is computed by dividing the value of all assets of the Fund (including accrued interest and dividends), less all liabilities (including accrued expenses and dividends declared but unpaid), by the total number of shares outstanding.

The Fund’s investments are valued at market value or, in the absence of market value with respect to any portfolio securities, at fair value according to procedures

13

Table of Contents

| Notes to Financial Statements December 31, 2009 |

adopted by the Trust’s Board of Trustees. Portfolio securities listed on any exchange other than the NASDAQ Stock Market, Inc. (“NASDAQ”) are valued at the last sale price on the business day as of which such value is being determined. If there has been no sale on such day, the securities are valued at the mean of the most recent bid and asked prices on such day. Securities traded on the NASDAQ are valued at the NASDAQ Official Closing Price as determined by NASDAQ. Short-term investments that mature in less than 60 days are valued at amortized cost.

Certain securities may not be able to be priced by pre-established pricing methods. Such securities may be valued by the Board of Trustees or its delegate at fair value. These securities generally include, but are not limited to, restricted securities (securities which may not be publicly sold without registration under the Securities Act of 1933) for which a pricing service is unable to provide a market price; securities whose trading has been formally suspended; a security whose market price is not available from a pre-established pricing source; a security with respect to which an event has occurred that is most likely to materially affect the value of the security after the market has closed but before the calculation of the Fund’s NAV or make it difficult or impossible to obtain a reliable market quotation; and a security whose price, as provided by the pricing service, does not reflect the security’s “fair value.” As a general principle, the current “fair value” of a security would be the amount which the owner might reasonably expect to receive from the closing sale prices on the applicable exchange and fair value prices may not reflect the actual value of a security. A variety of factors may be considered in determining the fair value of such securities.

Valuing the Fund’s securities using fair value pricing will result in using prices for those securities that may differ from current market valuations. Use of fair value prices and certain market valuations could result in a difference between the prices used to calculate a Fund’s NAV and the prices used by the Index, which, in turn, could result in a difference between a Fund’s performance and the performance of the Index. No securities were valued using the Fund’s fair value procedures at December 31, 2009.

B. Securities Transactions and Investment Income

Securities transactions are recorded as of the trade date. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recorded on the ex-dividend date. Interest income, if any, is recorded on the accrual basis.

14

Table of Contents

Notes to Financial Statements

December 31, 2009

C. Federal Tax Information

The timing and character of income and capital gain distributions are determined in accordance with income tax regulations, which may differ from U.S. GAAP. Reclassifications are made to the Fund’s capital accounts for permanent tax differences to reflect income and gains available for distribution (or available capital loss carryforwards) under income tax regulations.

For the year ended December 31, 2009, there were no permanent book and tax differences.

D. Dividends and Distributions to Shareholders

Dividends from net investment income of the Fund, if any, are declared and paid quarterly or as the Board of Trustees may determine from time to time. Distributions of net realized capital gains earned by the Fund, if any, are distributed at least annually.

Distributions from income and capital gains are determined in accordance with income tax regulations, which may differ from U.S GAAP. These differences are primarily due to differing treatments of income and gains on various investment securities held by the Fund, timing differences and differing characterization of distributions made by the Fund.

The tax character of the distributions paid was as follows:

| | Period Ended

December 31, 2009 | |

Distributions paid from: | | | |

Ordinary Income | | $ | 127,761 | |

Total | | $ | 127,761 | |

As of December 31, 2009, the components of distributable earnings on a tax basis for the Fund were as follows:

Undistributed net investment income | | $ | 5,753 | |

Net unrealized appreciation on investments | | 1,471,504 | |

Total | | $ | 1,477,257 | |

The differences between book-basis and tax-basis are primarily due to the deferral of losses from wash sales.

15

Table of Contents

| Notes to Financial Statements December 31, 2009 |

E. Income Taxes

No provision for income taxes is included in the accompanying financial statements, as the Fund intends to distribute to shareholders all taxable investment income and realized gains and otherwise comply with Subchapter M of the Internal Revenue Code applicable to regulated investment companies.

The Fund evaluates tax positions taken (or expected to be taken) in the course of preparing the Fund’s tax returns to determine whether these positions meet a “more-likely-than-not” standard that, based on the technical merits, have a more than fifty percent likelihood of being sustained by a taxing authority upon examination. A tax position that meets the “more-likely-than-not” recognition threshold is measured to determine the amount of benefit to recognize in the financial statements.

Management of the Fund analyzes all open tax years, as defined by the Statute of Limitations, for all major jurisdictions, including federal tax authorities and certain state tax authorities. As of and during the fiscal year ended December 31, 2009, the Fund did not have a liability for any unrecognized tax benefits. The Fund will file income tax returns in the U.S. federal jurisdiction and Colorado. For the year ended December 31, 2009, the Fund’s returns will be open to examination by the appropriate taxing authority.

F. Fair Value Measurements

A three-tier hierarchy has been established to measure fair value based on the extent of use of “observable inputs” as compared to “unobservable inputs” for disclosure purposes and requires additional disclosures about these valuations measurements. Inputs refer broadly to the assumptions that market participants would use in pricing a security. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the security developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the security developed based on the best information available in the circumstances.

The three-tier hierarchy is summarized as follows:

Level 1 - quoted prices in active markets for identical securities

Level 2 - other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

Level 3 - significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

16

Table of Contents

Notes to Financial Statements

December 31, 2009

ALPS EQUAL SECTOR WEIGHT ETF

Assets:

Investments in

Securities at

Value | | Level 1 -

Quoted Prices | | Level 2 -

Other

Significant

Observable

Inputs | | Level 3 -

Significant

Unobservable

Inputs | | Total | |

Exchange Traded Funds | | $ | 13,999,714 | | $ | — | | $ | — | | $ | 13,999,714 | |

TOTAL | | $ | 13,999,714 | | $ | — | | $ | — | | $ | 13,999,714 | |

All securities of the Fund were valued using Level 1 inputs for the year ended December 31, 2009. Thus a reconciliation of assets in which significant unobservable inputs (Level 3) were used is not applicable for this Fund.

In April 2009, FASB issued “Determining Fair Value When the Volume and Level of Activity for the Asset or Liability Have Significantly Decreased and Identifying Transactions That Are Not Orderly,” which provides additional guidance for estimating fair value in accordance with Fair Value Measurements when the volume and level of activity for the asset or liability have significantly decreased as well as guidance on identifying circumstances that indicate a transaction is not orderly. Additionally, it amends the Fair Value Measurement Standard by expanding disclosure requirements for reporting entities surrounding the major categories of assets and liabilities carried at fair value. The required disclosures have been incorporated into the summary of inputs tables above. Applying this guidance did not have a material impact on the Fund’s financial statements.

3. INVESTMENT ADVISORY FEE AND OTHER AFFILIATED TRANSACTIONS

ALPS Advisors, Inc. (the “Investment Adviser”) acts as the Fund’s investment adviser pursuant to an Advisory Agreement with the Trust on behalf of the Fund (the “Advisory Agreement”). Pursuant to the Advisory Agreement, the Fund pays the Investment Adviser a unitary fee for the services and facilities it provides payable on a monthly basis at the annual rate of 0.37% of the Fund’s average daily net assets. ALPS Distributors Inc. (“ADI”) is both the distributor for the Fund as well as the Select Sector SPDR exchange traded funds (“Underlying Sector ETFs”) that the Fund invests in. As required by exemptive relief obtained by the Underlying Sector ETFs, the Investment Adviser will reimburse the Fund an amount equal to the distribution fee received by ADI from the Underlying Sector ETFs attributable to the Fund’s investment in the Underlying Sector ETFs, for so long as ADI acts as the distributor to the Fund and the Underlying Sector ETFs. From time to time, the Investment Adviser may waive all or a portion of its fee.

17

Table of Contents

| Notes to Financial Statements December 31, 2009 |

Out of the unitary management fee, the Investment Adviser pays substantially all expenses of the Fund, including the licensing fee of the Index provider, and the cost of transfer agency, custody, fund administration, legal, audit and other services, except for interest expenses, distribution fees or expenses, brokerage expenses, taxes and extraordinary expenses not incurred in the ordinary course of the Fund’s business. In addition, the Investment Adviser’s unitary management fee is designed to compensate the Investment Adviser for providing services for the Fund.

ALPS Fund Services, Inc. (“ALPS”), an affiliate of the Investment Adviser, is the administrator of the Fund.

The Bank of New York Mellon is the custodian, fund accounting agent and transfer agent for the Fund.

Each Trustee who is not an officer or employee of the Investment Adviser, or any of its affiliates (“Independent Trustees”) is paid a quarterly retainer of $3,500, $1,500 for each regularly scheduled Board meeting attended and $750 for each special meeting held outside of regularly scheduled meetings.

4. PURCHASES AND SALES OF SECURITIES

For the year ended December 31, 2009, the cost of purchases and proceeds from sales of investment securities, excluding in-kind transactions and short-term investments, were as follows:

| | Purchases | | Sales | |

ALPS Equal Sector Weight ETF | | $ | 453,255 | | $ | 467,144 | |

| | | | | | | |

For the year ended December 31, 2009, the cost of in-kind purchases and proceeds from in-kind sales were as follows:

| | Purchases | | Sales | |

ALPS Equal Sector Weight ETF | | $ | 12,532,794 | | $ | — | |

| | | | | | | |

Gains on in-kind transactions are generally not considered taxable gains for Federal income tax purposes.

18

Table of Contents

Notes to Financial Statements

December 31, 2009

As of December 31, 2009, the costs of investments for federal income tax purposes and accumulated net unrealized appreciation/(depreciation) on investments were as follows:

Gross Appreciation (excess of value over tax cost) | | $ | 1,471,504 | |

Net Unrealized Appreciation | | 1,471,504 | |

Cost of investments for income tax purposes | | 12,528,210 | |

5. CAPITAL SHARE TRANSACTIONS

Shares are created and redeemed by the Fund only in Creation Unit size aggregations of 50,000. Only Authorized Participants are permitted to purchase or redeem Creation Units from the Fund. Such transactions are generally permitted on an in-kind basis, with a balancing cash component to equate the transaction to the net asset value per unit of the Fund on the transaction date. Cash may be substituted equivalent to the value of certain securities generally when they are not available in sufficient quantity for delivery, not eligible for trading by the Authorized Participant or as a result of other market circumstances.

6. INDEMNIFICATIONS

Under the Trust’s organizational documents, its Officers and Trustees are in-demnified against certain liability arising out of the performance of their duties to the Trust. Additionally, in the normal course of business, the Trust enters into contracts with service providers that contain general indemnification clauses. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust that have not yet occurred.

7. SUBSEQUENT EVENTS

Management has evaluated whether any events or transactions occurred subsequent to December 31, 2009 through February 24, 2010, the date of issuance of the Fund’s financial statements, and determined that there were no material events or transactions that would require recognition or disclosure in the Funds’ financial statements.

19

Table of Contents

| Additional Information (Unaudited) December 31, 2009 |

PROXY VOTING POLICIES AND PROCEDURES

A description of the policies and procedures that the Fund uses to determine how to vote proxies and information on how the Fund voted proxies relating to portfolio securities during the period ending June 30, 2010 will be available (1) without charge, upon request, by calling (866) 513-5856; (2) on the Trust’s website located at http://www.alpsetfs.com; and (3) on the SEC’s website at http://www.sec.gov.

PORTFOLIO HOLDINGS

The Trust will file its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Trust’s Form N-Q will be available (1) by calling (866) 513-5856; (2) on the Trust’s website located at http://www.alpsetfs.com; (3) on the SEC’s website at http://www. sec.gov; and (4) for review and copying at the SEC’s Public Reference Room (“PRR”) in Washington D.C. Information regarding the operation of the PRR may be obtained by calling (800) SEC-0330.

TAX INFORMATION

Tax Designations

The Fund designates the following amounts for the fiscal year ended December 31, 2009:

Qualified Dividend Income | | 85.32 | % |

Corporate Dividends Received Deduction | | 83.89 | % |

20

Table of Contents

| Trustees & Officers (Unaudited) December 31, 2009 |

INDEPENDENT TRUSTEES

Name, Address

and Age of

Management

Trustee* | | Position(s)

Held

with Trust | | Term of Office

and Length of

Time Served** | | Principal Occupation(s)

During Past 5 Years | | Number of

Portfolios

in Fund

Complex

Overseen

by

Trustees*** | | Other

Directorships

Held by Trustees |

Mary K. Anstine,

age 69 | | Trustee | | Since March 2008 | | Ms. Anstine was President/ Chief Executive Officer of HealthONE Alliance, Denver, Colorado, and former Executive Vice President of First Interstate Bank of Denver. Ms. Anstine is also Trustee/Director of the following: AV Hunter Trust; Colorado Uplift Board. Ms. Anstine was formerly a Director of the Trust Bank of Colorado (later purchased and now known as Northern Trust Bank), HealthONE and Denver Area Council of the Boy Scouts of America and a member of the American Bankers Association Trust Executive Committee. | | 19 | | Ms. Anstine is a Trustee of ALPS Variable Insurance Trust (1 fund); Financial Investors Variable Insurance Trust (5 funds); Financial Investors Trust (7 funds); Reaves Utility Income Fund; and Westcore Trust (12 funds). |

| | | | | | | | | | |

Jeremy W. Deems,

age 33 | | Trustee | | Since March 2008 | | Mr. Deems is the Co-President and Chief Financial Officer of Green Alpha Advisors, LLC. Prior to joining Green Alpha Advisors, Mr. Deems was CFO and Treasurer of Forward Management, LLC, ReFlow Management Co., LLC, ReFlow Fund, LLC, a private investment fund, and Sutton Place Management, LLC, an administrative services company, from 2004 to June 2007. Prior to this, Mr. Deems served as Controller of Forward Management, LLC, ReFlow Management Co., LLC, ReFlow Fund, LLC and Sutton Place Management, LLC. | | 14 | | Mr. Deems is a Trustee of ALPS Variable Insurance Trust (1 fund); Financial Investors Trust (7 funds); and Reaves Utility Income Fund. |

22

Table of Contents

Name, Address

and Age of

Management

Trustee* | | Position(s)

Held

with Trust | | Term of Office

and Length of

Time Served** | | Principal Occupation(s)

During Past 5 Years | | Number of

Portfolios

in Fund

Complex

Overseen

by

Trustees*** | | Other

Directorships

Held by Trustees |

Rick A. Pederson,

age 57 | | Trustee | | Since March 2008 | | President, Foundation Properties, Inc. (a real estate investment management company), 1994 - present; Partner, Western Capital Partners (a prime lending company), 2000 - present; Partner, Bow River Capital Partners (investment manager), 2003 - present; Principal, The Pauls Corporation (real estate development), 2008 - present; Director, Guaranty Bank and Trust (a community bank), 1999 — 2007; Winter Park Recreational Association (an entity that operates, maintains and develops Winter Park Resort), 2002 — 2008; Neenan Co. (an integrated real estate development, architecture and construction company), 2002 — present; NexCore Properties LLC (a real estate investment company), 2004 — present; Urban Land Conservancy (a not-for-profit organization), 2004 — present. | | 9 | | Mr. Pederson is Trustee of Westcore Trust (12 funds) |

* The business address of the Trustee is c/o ALPS Advisors, Inc., 1290 Broadway, Suite 1100, Denver, Colorado 80203.

** This is the period for which the Trustee began serving the Trust. Each Trustee serves an indefinite term, until his successor is elected.

*** The Fund Complex includes all series of the Trust and any other investment companies for which ALPS Advisors, Inc. provides investment advisory services.

23

Table of Contents

INTERESTED TRUSTEE

Name, Address

and Age of

Management

Trustee* | | Position(s)

Held

with Trust | | Term of Office

and Length of

Time Served** | | Principal Occupation(s)

During Past 5 Years | | Number of

Portfolios

in Fund

Complex

Overseen

by

Trustees*** | | Other

Directorships

Held by Trustees |

Thomas A. Carter,

age 43 | | Trustee and President | | Since March 2008 | | Mr. Carter joined ALPS Fund Services, Inc. (“ALPS”) in 1994 and is currently President and Director of ALPS Advisors, Inc. (“AAI”), ALPS Distributors, Inc. (“ADI”) and FTAM Funds Distributor, Inc. (“FDI”) and Executive Vice President and Director of ALPS and ALPS Holdings, Inc. (“AHI”). Because of his position with AHI, ALPS, ADI, FDI and AAI, Mr. Carter is deemed an affiliate of the Fund as defined under the 1940 Act. Before joining ALPS, Mr. Carter was with Deloitte & Touche LLP, where he worked with a diverse group of clients, primarily within the financial services industry. Mr. Carter is a Certified Public Accountant and received his Bachelor of Science in Accounting from the University of Colorado at Boulder. | | 14 | | Mr. Carter is a Trustee of Financial Investors Variable Insurance Trust (5 funds) |

* The business address of the Trustee is c/o ALPS Advisors, Inc., 1290 Broadway, Suite 1100, Denver, Colorado 80203.

** This is the period for which the Trustee began serving the Trust. Each Trustee serves an indefinite term, until his successor is elected.

*** Mr. Carter is an interested person of the Trust because of his affiliation with ALPS.

24

Table of Contents

OFFICERS

Name, Address

and Age of

Executive Officer* | | Position(s)

Held

with Trust | | Length of

Time Served** | | Principal Occupation(s) During Past 5 Years |

Melanie Zimdars,

age 33 | | Chief Compliance Officer (“CCO”) | | Since December 2009 | | Ms. Zimdars currently serves as a Deputy Chief Compliance Officer with ALPS. Prior to joining ALPS in September 2009, Ms. Zimdars served as Principal Financial Officer, Treasurer and Secretary for the Wasatch Funds from February 2007 to December 2008. From November 2006 to February 2007, she served as Assistant Treasurer for the Wasatch Funds and served as a Senior Compliance Officer for Wasatch Advisors, Inc. since 2005. From 2001 until joining Wasatch in 2005, she was a Compliance Officer for U.S. Bancorp Fund Services, LLC. Because of her position with ALPS, Ms. Zimdars is deemed an affiliate of the Trust as defined under the 1940 Act. Ms. Zimdars is also the CCO of ALPS Variable Insurance Trust, Financial Investors Variable Insurance Trust, Liberty All-Star Growth Fund, Inc. and Liberty All-Star Equity Fund. |

| | | | | | |

Kimberly R. Storms,

age 37 | | Treasurer | | Since March 2008 | | Ms. Storms is Director of Fund Administration and Senior Vice President of ALPS. Ms. Storms joined ALPS in 1998 as Assistant Controller. Because of her position with ALPS, Ms. Storms is deemed an affiliate of the Trust as defined under the 1940 Act. Ms. Storms is also Treasurer of ALPS Variable Insurance Trust; Assistant Treasurer of the Liberty All-Star Equity Fund, Liberty All-Star Growth Fund and Financial Investors Trust; and Assistant Secretary of Ameristock Mutual Fund, Inc. |

| | | | | | |

William Parmentier,

age 57 | | Vice President | | Since March 2008 | | Mr. Parmentier is Chief Investment Officer, ALPS Advisors, Inc. (since 2006); President of the Liberty All-Star Funds (since April 1999); Senior Vice President (2005-2006), Banc of America Investment Advisors, Inc. |

| | | | | | |

Tané T. Tyler,

age 44 | | Secretary | | Since December 2008 | | Ms. Tyler is Senior Vice President, General Counsel and Secretary of ALPS. Ms. Tyler joined ALPS in 2004. She served as Secretary, Liberty All-Star Equity Fund and Liberty All-Star Growth Fund from December 2006-2008; Secretary, Reaves Utility Income Fund from December 2004—2007; Secretary, Westcore Funds from February 2005—2007; Secretary, First Funds from November 2004 to January 2007; Secretary, Financial Investors Variable Insurance Trust from December 2004—December 2006; Vice President and Associate Counsel, Oppenheimer Funds from January 2004 to August 2004; Vice President and Assistant General Counsel, INVESCO Funds from September 1991 to December 2003. |

25

Table of Contents

Name, Address

and Age of

Executive Officer* | | Position(s)

Held

with Trust | | Length of

Time Served** | | Principal Occupation(s) During Past 5 Years |

Monette R. Nickels,

age 38 | | Tax Officer | | Since December 2009 | | Ms. Nickels is Senior Vice President and Director of Tax Administration of ALPS. Ms. Nickels joined ALPS in 2004 as Director of Tax Administration. Because of her position with ALPS, Ms. Nickels is deemed an affiliate of the Trust as defined under the 1940 Act. Ms. Nickels is also Tax Officer of ALPS Variable Insurance Trust, Financial Investors Trust, Liberty All-Star Equity Fund, Liberty All-Star Growth Fund, Inc., and Financial Investors Variable Insurance Trust. |

* The business address of each Officer is c/o ALPS Advisors, Inc., 1290 Broadway, Suite 1100, Denver, Colorado 80203.

** This is the period for which the Officer began serving the Trust. Each Officer serves an indefinite term, until his successor is elected.

26

Table of Contents

Board Considerations Regarding Approval of

Investment Advisory Agreement

At an in-person meeting held on March 9, 2009, the Board of Trustees of the Trust (the “Board”), including the Trustees who are not “interested persons” of the Trust within the meaning of the 1940 Act, as amended (the “Independent Trustees”), evaluated a proposal to approve the Advisory Agreement between the Trust and the Investment Adviser with respect to the Funds. The Independent Trustees also met separately with their independent legal counsel to consider the Advisory Agreement.

In evaluating the Advisory Agreement, the Board considered various factors, including (i) the nature, extent and quality of the services expected to be provided by the Investment Adviser with respect to the Fund under the Advisory Agreement, (ii) costs to the Investment Adviser of its services; and (iii) the extent to which economies of scale would be realized if and as the Fund grows and whether the fee level in the Advisory Agreement reflects these economies of scale.

The Board of Trustees, including a majority of the independent trustees, determined that approval of the Advisory Agreement was in the best interests of the Fund. The Board of Trustees, including the independent trustees, did not identify any single factor or group of factors as all important or controlling and considered all factors together. In evaluating whether to approve the Advisory Agreement for the Fund, the Board considered numerous factors, as described below.

With respect to the nature, extent and quality of the services to be provided by the Adviser under the Advisory Agreement, the Board considered and reviewed information concerning the services proposed to be provided under the Advisory Agreement, the proposed investment parameters of the index for the Fund, financial information regarding the Adviser and its parent company, information describing the Adviser’s current organization and the background and experience of the persons who would be responsible for the day-to-day management of the Fund, the anticipated financial support of the Fund and the nature and quality of services provided to other exchange-traded (“ETFs”), open-end and closed-end funds by the Adviser. Based upon their review, the Board concluded that the Adviser was qualified to manage the Fund and oversee the services to be provided by other service providers and that the services to be provided by the Adviser to the Fund are expected to be satisfactory.

With respect to the costs of services to be provided and profits to be realized by the Adviser, the Board considered the resources involved in managing the Fund as well as the fact that the Adviser had agreed to pay all of the Fund’s expenses (except for interest expenses, distribution fees or expenses, brokerage expenses, taxes and extraordinary expenses such as litigation and other expenses not incurred in the ordinary course of the Fund’s business) out of the unitary advisory fee. The Board noted that because the Fund is newly organized, the Adviser

27

Table of Contents

represented that profitability information was not yet determinable. However, based upon the impact of the unitary advisory fee for the Fund, the Board concluded that profitability was not expected to be unreasonable.

The Board also reviewed information provided by the Adviser showing the proposed advisory fees for the Fund as compared to those of a peer group of ETFs compiled using Lipper comparative fee data. The Board noted the services to be provided by the Adviser for the annual advisory fee of 0.37% of the Fund’s average daily net assets. The Board also considered that the advisory fee was a unitary one and that, as set forth above, the Adviser had agreed to pay all of the Fund’s expenses (except for interest expenses, distribution fees or expenses, brokerage expenses, taxes and extraordinary expenses such as litigation and other expenses not incurred in the ordinary course of the Fund’s business) out of the unitary fee. The Board considered that, taking into account the impact of the Fund’s unitary advisory fee, the Fund’s expense ratios were expected to be within range of the expense ratios of the peer group of ETFs provided by the Adviser. The Board concluded that the Fund’s advisory fee was reasonable given the nature, extent and anticipated quality of the services to be provided under the Investment Adviser Agreement and the expense limitation by operation of the unitary advisory fee.

The Board considered the extent to which economies of scale would be realized as the Fund grows and whether fee levels reflect a reasonable sharing of such economies of scale for the benefit of Fund investors. Because the Fund is newly organized, the Board reviewed the Fund’s proposed unitary advisory fee and anticipated expenses, and determined to review economies of scale in the future when the Fund had attracted assets.

The Board considered benefits to be derived by the Adviser from its relationship with the Fund. The Board concluded that the advisory fees were reasonable, taking into account these benefits.

28

Table of Contents

| | SHAREHOLDER LETTER |

Dear Shareholders:

When ALPS launched its ETF Trust in 2008 our goal was to bring innovative solutions to the ETF industry that provide investors with access to a unique market segment or strategy. Our first portfolio — the Cohen & Steers Global Realty Majors ETF — is one of the first ETFs to provide investors with access to a diversified portfolio of global real estate securities. US real estate, while already a mainstream asset class, only covers 1/3 of the global real estate universe. Furthermore, the global market is growing at a rapid pace as foreign countries continue to securitize their private real estate holdings. As a result, a global real estate fund can provide investors with a wider range of opportunities than a purely domestic fund while preserving the diversification and income benefits of US REITs.

By partnering with Cohen & Steers, we have secured a best in breed real estate manager with a great track record and reputation. Furthermore, the transparency,(1) low cost and tax efficiency of the ETF structure provides access to global real estate in a very efficient manner. We believe access to global real estate, the benefits of the ETF structure, and the expertise of Cohen & Steers make for a powerful investment combination that will allow investors to build better portfolios.

In the pages that follow our Fund managers have provided a performance overview. We thank you for your investment and for being a GRI shareholder.

Thomas A. Carter*

President, ALPS ETF Trust

* Registered representative of ALPS Distributors, Inc.

Ordinary brokerage commissions apply.

(1) ETFs are considered transparent because their portfolio holdings are disclosed daily.

www.alpsetfs.com | 866.513.5856

2

Table of Contents

| PERFORMANCE OVERVIEW (Unaudited) |

FUND DESCRIPTION

The Cohen & Steers Global Realty Majors ETF (the “Fund”) seeks investment results that correspond generally to the performance (before the Fund’s fees and expenses) of an equity index called the Cohen & Steers Global Realty Majors Index (the “Index”). The Shares of the Fund are listed and trade on the NYSE Arca under the ticker symbol “GRI.” The Fund will normally invest substantially all of its assets in the 75 stocks that comprise the Cohen & Steers Global Realty Majors Index. The Fund began trading on May 9, 2008.

The Index is a free-float, market-cap-weighted total return index of selected real estate equity securities maintained by Cohen & Steers. It is quoted intraday on a real-time basis by the Chicago Mercantile Exchange under the symbol GRM. The Index’s free-float market capitalization approach and qualitative screening process emphasize companies that the Cohen & Steers Index Committee believes are leading the securitization of real estate globally.

PERFORMANCE OVERVIEW

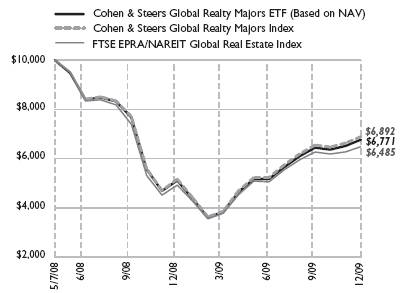

Global markets spent much of 2009 responding to the financial and credit market crises that began in 2008. After a challenging first two months, markets rallied, with momentum slowing in the 4th quarter. Much of the recovery that took place can be attributed to the ability of REITs to recapitalize and deleverage their balance sheets. These actions reassured investors that real estate stocks could not only meet debt maturities but could also take advantage of buying opportunities in the private market. Overall, real estate stocks posted very strong gains for the year with Asian Pacific securities leading the way up (+43.5%), followed by Europe (+40.4%) and North America (+28.0%) .

Hong Kong (+88.8%) and Singapore (+78.4%) were the strongest performers in Asia in 2009. Hong Kong benefited from flows from China, declining lending rates, and limited residential supply, along with an improving economic outlook. Singapore also saw an improving economic environment as well as a rebound in residential transaction volume aided by developers’ price cuts. Australia (+6.4%) and Japan (+4.1%) had much more modest returns and were slower to recover. After a very weak first half of the year, Japanese Real Estate Investment Trusts (“J-REITs”) had a sharp turn-around as bankruptcy fears started to subside. In Australia, the economic environment had changed so substantially by the end of the year that the country’s central bank reversed its monetary easing policy and raised short-term rates to 3.75% .

Europe real estate performance was lead by France which had the strongest gains of Europe’s major economies (+50.0%) . French real estate stocks were buoyed earlier in the year from the policy which ties rents to the cost of construction. The United Kingdom, whose real estate securities increased (+16.5%) in 2009, was primarily aided by capital raisings and improved balance sheets. The rally leveled off toward the

3

Table of Contents

middle of the year once most of the capital needs for the sector had been met and investors focused more on fundamentals, which remained weak. Property transactions for high quality real estate, however, were able to fetch attractive valuations signaling a decline in cap rates and improvement in fundamentals.

US real estate stocks had a total return of (+28.0%) in 2009, rebounding significantly from multi-year lows in March. Recapitalizations fueled the recovery as US public real estate companies raised $20 billion during the year. The hotel (+67.2%) and regional mall (+63.0%) sectors performed the best. Hotels were benefited from shorter leases which allowed them to respond more quickly to a changing economic environment. Stabilization in both consumer confidence and retail sales proved to be a boost to the mall sector. The more defensive health care (+24.6%), self-storage (+8.4%) and shopping center (-1.7%) sectors lagged their more economically sensitive counterparts during 2009’s early expansion rally.

For the twelve months ended December 31, 2009 the Fund’s market price increased 34.01% and the Fund’s net asset value (“NAV”) increased 32.51%. Over the same time period the Fund’s benchmark was up 31.75%.

| | Six | | One | | Since | |

Annualized | | Months | | Year | | Inception* | |

Fund Performance | | | | | | | |

NAV | | 30.89 | % | 32.51 | % | -21.02 | % |

Market Price | | 33.53 | % | 34.01 | % | -20.89 | % |

Index Performance | | | | | | | |

Cohen & Steers Global Realty Majors Index | | 32.63 | % | 33.36 | % | -20.20 | % |

FTSE EPRA/NAREIT Global Real Estate Index | | 28.22 | % | 31.75 | % | -23.09 | % |

* Fund Inception 5/7/08

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For most current month-end performance data please visit www.alpsetfs.com.

An investor cannot invest directly in an index.

NAV is an exchange-traded fund’s per-share value. The per-share dollar amount of the fund is derived by dividing the total value of all the securities in its portfolio, less any liabilities, by the number of fund shares outstanding.

Market Price is the price at which a share can currently be traded in the market.

Information detailing the number of days the Market Price of the Fund was greater than the Fund’s NAV and the number of days it was less than the Fund’s NAV can be obtained at www.alpsetfs.com.

FTSE EPRA/NAREIT Global Real Estate Index: An unmanaged market-weighted total return index that consists of many companies from developed markets whose floats are larger than $100 million and which derive more than half of their revenue from property-related activities.

4

Table of Contents

TOP 10 HOLDINGS as of December 31, 2009

Simon Property Group, Inc. | | 4.31 | % |

Mitsubishi Estate Co., Ltd. | | 4.11 | % |

Westfield Group | | 3.78 | % |

Sun Hung Kai Properties, Ltd. | | 3.76 | % |

Unibail-Rodamco | | 3.72 | % |

Mitsui Fudosan Co., Ltd. | | 3.54 | % |

Public Storage | | 2.80 | % |

Vornado Realty Trust | | 2.78 | % |

CapitaLand, Ltd. | | 2.41 | % |

Boston Properties, Inc. | | 2.36 | % |

Percent of Net Assets in Top Ten Holdings: | | 33.57 | % |

GEOGRAPHIC BREAKDOWN (% of Total Investments) as of December 31, 2009

United States | | 38.33 | % |

Hong Kong | | 14.90 | % |

Japan | | 12.85 | % |

Australia | | 9.36 | % |

United Kingdom | | 8.15 | % |

Singapore | | 6.06 | % |

France | | 5.87 | % |

Netherlands | | 2.23 | % |

Canada | | 0.81 | % |

Switzerland | | 0.51 | % |

Sweden | | 0.47 | % |

Belgium | | 0.46 | % |

GROWTH OF $10K as of December 31, 2009

Comparison of Change in Value of $10,000 Investment in Cohen & Steers Global Realty Majors ETF and Cohen & Steers Global Realty Majors Index.

5

Table of Contents

| Disclosure of Fund Expenses |

For the Period Ended December 31, 2009 (Unaudited) |

Shareholder Expense Example: As a shareholder of the Fund, you incur two types of costs: (1) transaction costs which may include creation and redemption fees or brokerage charges and (2) ongoing costs, including management fees and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other funds. It is based on an investment of $1,000 invested at July 1, 2009 and held through the period ended December 31, 2009.

Actual Return: The first line of the table provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you incurred over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid during Period” to estimate the expenses attributable to your investment during this period.

Hypothetical 5% Return: The second line of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The expenses shown in the table are meant to highlight ongoing Fund costs only and do not reflect any transaction costs, such as creation and redemption fees, or brokerage charges. Therefore, the second line is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these costs were included, your costs would have been higher.

| | Beginning | | Ending | | | | Expenses Paid | |

| | Account | | Account | | | | During | |

| | Value | | Value | | Expense | | Period(a) | |

| | 07/01/09 | | 12/31/09 | | Ratio | | 07/01/09-12/31/09 | |

Actual | | $ | 1,000.00 | | $ | 1,308.90 | | 0.55 | % | $ | 3.20 | |

Hypothetical | | $ | 1,000.00 | | $ | 1,022.43 | | 0.55 | % | $ | 2.80 | |

(a) Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), then divided by 365.

6

Table of Contents

| Report of Independent registered Public Accounting Firm |

To the Board of Trustees and Shareholders of ALPS ETF Trust:

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of the Cohen & Steers Global Realty Majors ETF (the “Fund”), which is part of the ALPS ETF Trust, as of December 31, 2009, the related statement of operations for the year then ended, and the statements of changes in net assets and the financial highlights for the year then ended and the period from May 7, 2008 (inception) to December 31, 2008. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2009, by correspondence with the custodian and brokers; where replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Cohen & Steers Global Realty Majors ETF as of December 31, 2009, the results of its operations for the year then ended, and the statements of changes in net assets and the financial highlights for the year then ended and the period from May 7, 2008 (inception) to December 31, 2008, in conformity with accounting principles generally accepted in the United States of America.

February 24, 2010

Denver, Colorado

7

Table of Contents

| SCHEDULE OF INVESTMENTS |

December 31, 2009 |

Security Description | | Shares | | Value | |

| | | | | |

COMMON STOCKS (101.25%) | | | | | |

Australia (9.48%) | | | | | |

CFS Retail Property Trust | | 68,986 | | $ | 117,881 | |

Commonwealth Property Office Fund | | 60,268 | | 52,576 | |

Dexus Property Group | | 162,309 | | 124,077 | |

Mirvac Group | | 94,988 | | 134,121 | |

Stockland Trust Group | | 79,773 | | 283,388 | |

Westfield Group | | 42,766 | | 482,308 | |

| | | | 1,194,351 | |

Belgium (0.47%) | | | | | |

Confinimmo | | 414 | | 58,573 | |

| | | | | |

Canada (0.82%) | | | | | |

Boardwalk Real Estate Investment Trust | | 837 | | 29,581 | |

RioCan Real Estate Investment Trust | | 3,913 | | 74,091 | |

| | | | 103,672 | |

France (5.93%) | | | | | |

Fonciere des Regions | | 885 | | 90,635 | |

ICADE | | 661 | | 63,304 | |

Klepierre | | 2,942 | | 119,835 | |

Unibail-Rodamco | | 2,150 | | 474,120 | |

| | | | 747,894 | |

Hong Kong (15.08%) | | | | | |

China Overseas Land & Investment, Ltd. | | 128,000 | | 270,723 | |

Hang Lung Properties, Ltd | | 65,000 | | 256,511 | |

Henderson Land Development Co., Ltd. | | 33,000 | | 248,541 | |

Hongkong Land Holdings, Ltd. | | 39,000 | | 193,050 | |

The Link Real Estate Investment Trust | | 73,000 | | 186,594 | |

Sun Hung Kai Properties, Ltd. | | 32,000 | | 479,956 | |

The Wharf Holdings, Ltd. | | 46,000 | | 265,474 | |

| | | | 1,900,849 | |

Japan (13.02%) | | | | | |

Aeon Mall Co., Ltd. | | 2,600 | | 50,104 | |

Japan Real Estate Investment Corp. | | 14 | | 102,863 | |

Japan Retail Fund Investment Corp. | | 12 | | 53,752 | |

Mitsubishi Estate Co., Ltd. | | 33,000 | | 523,915 | |

Mitsui Fudosan Co., Ltd. | | 27,000 | | 451,861 | |

Nippon Building Fund, Inc. | | 17 | | 128,922 | |

Nomura Real Estate Office Fund, Inc. | | 9 | | 48,724 | |

Sumitomo Realty & Development Co., Ltd. | | 15,000 | | 280,198 | |

| | | | 1,640,339 | |

| | | | | | |

8

Table of Contents

Security Description | | Shares | | Value | |

| | | | | |

Netherlands (2.26%) | | | | | |

Corio N.V. | | 2,478 | | $ | 169,553 | |

Eurocommercial Properties N.V. | | 1,127 | | 46,569 | |

Wereldhave N.V. | | 722 | | 69,094 | |

| | | | 285,216 | |

Singapore (6.14%) | | | | | |

Ascendas Real Estate Investment Trust | | 47,066 | | 74,423 | |

CapitaLand, Ltd. | | 103,000 | | 308,131 | |

CapitaMall Trust | | 85,347 | | 109,423 | |

City Developments, Ltd. | | 20,000 | | 164,678 | |

Kerry Properties, Ltd. | | 23,000 | | 117,165 | |

| | | | 773,820 | |

Sweden (0.47%) | | | | | |

Castellum AB | | 5,861 | | 59,512 | |

| | | | | |

Switzerland (0.52%) | | | | | |

PSP Swiss Property AG* | | 1,154 | | 65,305 | |

| | | | | |

United Kingdom (8.25%) | | | | | |

British Land Co., Plc | | 28,767 | | 222,981 | |

Derwent London Plc | | 3,028 | | 64,545 | |

Great Portland Estates Plc | | 11,206 | | 51,954 | |

Hammerson Plc | | 23,394 | | 160,178 | |

Land Securities Group Plc | | 25,310 | | 279,972 | |

Liberty International Plc | | 14,594 | | 121,371 | |

Segro Plc | | 25,035 | | 139,314 | |

| | | | 1,040,315 | |

United States (38.81%) | | | | | |

Alexandria Real Estate Equities, Inc. | | 1,420 | | 91,292 | |

AMB Property Corp. | | 4,739 | | 121,081 | |

Apartment Investment and Management Co. | | 3,792 | | 60,369 | |

AvalonBay Communities, Inc. | | 2,590 | | 212,665 | |

Boston Properties, Inc. | | 4,490 | | 301,144 | |

BRE Properties, Inc. | | 1,712 | | 56,633 | |

Brookfield Properties Corp. | | 8,153 | | 98,814 | |

Camden Property Trust | | 2,131 | | 90,290 | |

Digital Realty Trust, Inc. | | 2,467 | | 124,041 | |

Douglas Emmett, Inc. | | 4,144 | | 59,052 | |

Duke Realty Corp. | | 7,257 | | 88,318 | |

Equity Residential | | 8,877 | | 299,865 | |

Essex Property Trust, Inc. | | 914 | | 76,456 | |

Federal Realty Investment Trust | | 1,982 | | 134,221 | |

| | | | | | |

9

Table of Contents

Security Description | | Shares | | Value | |

| | | | | |

United States (continued) | | | | | |

HCP, Inc. | | 9,497 | | $ | 290,038 | |

Host Hotels & Resorts, Inc. | | 20,001 | | 233,412 | |

Kimco Realty Corp. | | 13,010 | | 176,025 | |

Liberty Property Trust | | 3,618 | | 115,812 | |

The Macerich Co. | | 3,164 | | 113,746 | |

Mack-Cali Realty Corp. | | 2,538 | | 87,739 | |

ProLogis | | 15,332 | | 209,895 | |

Public Storage | | 4,394 | | 357,891 | |

Regency Centers Corp. | | 2,602 | | 91,226 | |

Simon Property Group, Inc. | | 6,897 | | 550,380 | |

SL Green Realty Corp. | | 2,490 | | 125,098 | |

UDR, Inc. | | 4,878 | | 80,194 | |

Ventas, Inc. | | 5,072 | | 221,849 | |

Vornado Realty Trust | | 5,078 | | 355,155 | |

Weingarten Realty Investors | | 3,451 | | 68,295 | |

| | | | 4,890,996 | |

TOTAL COMMON STOCKS | | | | | |

(Cost $12,373,202) | | | | 12,760,842 | |

| | | | | |

WARRANTS (0.01%) | | | | | |

France (0.01%) | | | | | |

Fonciere des Regions, Warrants, strike price 65.00 EUR, Expires 12/31/10* | | 775 | | 655 | |

| | | | | |

TOTAL WARRANTS | | | | | |

(Cost $0) | | | | 655 | |

| | | | | |

TOTAL INVESTMENTS (101.26%) | | | | | |

(Cost $12,373,202) | | | | 12,761,497 | |

| | | | | |

NET LIABILITIES LESS OTHER ASSETS (-1.26%) | | | | (158,246 | ) |

| | | | | |

NET ASSETS (100.00%) | | | | $ | 12,603,251 | |

* Non-income producing security.

Common Abbreviations:

AB - | Aktiebolag is the Swedish equivalent of the term corporation. |

AG - | Aktiengesellschaft is a German term that refers to a corporation that is limited by shares, i.e., owned by sharholders. |

EUR - | Euro |

Ltd. - | Limited |

N.V. - | Naamloze Vennootschap is the Dutch term for a public limited liability corporation. |

Plc - | Public Limited Co. |

See Notes to Financial Statements.

10

Table of Contents

| | STATEMENT OF ASSETS & LIABILITIES |

| December 31, 2009 |

ASSETS: | | | |

Investments, at value | | $ | 12,761,497 | |

Cash | | 18,474 | |

Foreign currency, at value (Cost $22,658) | | 22,039 | |

Receivable for investments sold | | 156,128 | |

Receivable for shares sold | | 1,568,393 | |

Foreign tax reclaims | | 2,422 | |

Interest and dividends receivable | | 45,138 | |

Total Assets | | 14,574,091 | |

| | | |

LIABILITIES: | | | |

Distributions payable | | 364,000 | |

Payable for investments purchased | | 1,601,596 | |

Payable to advisor | | 5,244 | |

Total Liabilities | | 1,970,840 | |

NET ASSETS | | $ | 12,603,251 | |

| | | |

NET ASSETS CONSIST OF: | | | |

Paid-in capital | | $ | 13,920,377 | |

Overdistributed net investment income | | (294,951 | ) |

Accumulated net realized loss on investments and foreign currency transactions | | (1,410,212 | ) |

Net unrealized appreciation on investments and translation of assets and liabilities denominated in foreign currencies | | 388,037 | |

NET ASSETS | | $ | 12,603,251 | |

| | | |

INVESTMENTS, AT COST | | $ | 12,373,202 | |

| | | |

PRICING OF SHARES | | | |

Net Assets | | $ | 12,603,251 | |

Shares of beneficial interest outstanding (Unlimited number of shares authorized, par value $0.01 per share) | | 402,000 | |

Net Asset Value, offering and redemption price per share | | $ | 31.35 | |

See Notes to Financial Statements.

11

Table of Contents

| STATEMENT OF OPERATIONS |

For the Year Ended December 31, 2009 |

INVESTMENT INCOME: | | | |

Dividends(a) | | $ | 248,261 | |

Total Investment Income | | 248,261 | |

| | | |

EXPENSES: | | | |

Investment advisory fee | | 36,031 | |

Total Net Expenses | | 36,031 | |

NET INVESTMENT INCOME | | 212,230 | |

| | | |

Net realized loss on investments | | (1,180,517 | ) |

Net realized gain on foreign currency transactions | | 4,745 | |

Net change in unrealized appreciation on investments | | 2,833,445 | |

Net change in unrealized depreciation on translation of assets and liabilities in foreign currencies | | (1,351 | ) |

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS | | 1,656,322 | |

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 1,868,552 | |

(a) Net of foreign withholding tax of $15,715.

See Notes to Financial Statements.

12

Table of Contents

| STATEMENTS OF CHANGES IN NET ASSETS |

| | | | For the Period | |

| | For the | | May 7, 2008 | |

| | Year Ended | | (Inception) through | |

| | December 31, 2009 | | December 31, 2008 | |

OPERATIONS: | | | | | |

Net investment income | | $ | 212,230 | | $ | 93,943 | |

Net realized loss on investments and foreign currency transactions | | (1,175,772 | ) | (232,654 | ) |

Net change in unrealized appreciation/(depreciation) on investments and foreign currency | | 2,832,094 | | (2,444,057 | ) |

Net increase/(decrease) in net assets resulting from operations | | 1,868,552 | | (2,582,768 | ) |

| | | | | |

DISTRIBUTIONS TO SHAREHOLDERS: | | | | | |

From net investment income | | (504,174 | ) | (98,737 | ) |

Total distributions | | (504,174 | ) | (98,737 | ) |

| | | | | |

SHARE TRANSACTIONS: | | | | | |

Proceeds from sale of shares | | 6,176,164 | | 7,644,214 | |

Net increase from share transactions | | 6,176,164 | | 7,644,214 | |

Net increase in net assets | | 7,540,542 | | 4,962,709 | |

| | | | | |

NET ASSETS: | | | | | |

Beginning of period | | 5,062,709 | | 100,000 | |

End of period* | | $ | 12,603,251 | | $ | 5,062,709 | |

*Including overdistributed net investment income of: | | $ | (294,951 | ) | $ | (8,130 | ) |

| | | | | |

Other Information: | | | | | |

SHARE TRANSACTIONS: | | | | | |

Beginning shares | | 202,000 | | 2,000 | |

Sold | | 200,000 | | 200,000 | |

Shares outstanding, end of period | | 402,000 | | 202,000 | |

See Notes to Financial Statements.

13

Table of Contents

| FINANCIAL HIGHLIGHTS |

For the Shares Outstanding For the Period Presented |

| | | | For the Period | |

| | For the | | May 7, 2008 | |

| | Year Ended | | (Inception) through | |

| | December 31, 2009 | | December 31, 2008 | |

NET ASSET VALUE, BEGINNING OF PERIOD | | $ | 25.06 | | $ | 50.00 | |

| | | | | |

INCOME/(LOSS) FROM OPERATIONS: | | | | | |

Net investment income | | 0.98 | | 0.47 | |

Net realized and unrealized gain/(loss) on investments | | 7.00 | | (24.92 | ) |

Total from Investment Operations | | 7.98 | | (24.45 | ) |

| | | | | |

LESS DISTRIBUTIONS: | | | | | |

From net investment income | | (1.69 | ) | (0.49 | ) |

Total Distributions | | (1.69 | ) | (0.49 | ) |

NET INCREASE/(DECREASE) IN NET ASSET VALUE | | 6.29 | | (24.94 | ) |

NET ASSET VALUE, END OF PERIOD | | $ | 31.35 | | $ | 25.06 | |

TOTAL RETURN(a) | | 32.51 | % | (48.90 | )% |

| | | | | |

RATIOS/ SUPPLEMENTAL DATA: | | | | | |

Net assets, end of period (in 000s) | | $ | 12,603 | | $ | 5,063 | |

| | | | | |

RATIOS TO AVERAGE NET ASSETS: | | | | | |

Net investment income including reimbursement/waiver | | 3.24 | % | 3.49 | %(b) |

Operating expenses including reimbursement/waiver | | 0.55 | % | 0.55 | %(b) |

Operating expenses excluding reimbursement/waiver | | 0.55 | % | 0.55 | %(b) |

PORTFOLIO TURNOVER RATE(c) | | 18 | % | 18 | % |