UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 20-F

(Mark One)

[ ] | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

[X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009.

OR

[ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

[ ] | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number: 001-33840

WSP HOLDINGS LIMITED

(Exact Name of Registrant as Specified in Its Charter)

N/A

(Translation of Registrant’s Name Into English)

Cayman Islands

(Jurisdiction of Incorporation or Organization)

No. 38 Zhujiang Road

Xinqu, Wuxi

Jiangsu Province

People’s Republic of China

(Address of Principal Executive Offices)

Yip Kok Thi

WSP Holdings Limited

No. 38 Zhujiang Road

Xinqu, Wuxi

Jiangsu Province

People’s Republic of China

Phone: +86-510-8536-0401

Email: info@wsphl.com

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class | Name of exchange on which each class is to be registered |

American Depositary Shares, each representing two ordinary shares, par value $0.0001 per share | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the Issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

205,789,800 ordinary shares, par value $0.0001 per share, as of December 31, 2009.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes[ ] No [X]

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes [ ] No [X]

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or such shorter period that the registrant was required to submit and post such files).

Yes [ ] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer [ ] Accelerated filer [X] Non-accelerated filer [ ]

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

US GAAP[X]

International Financial Reporting Standards as issued by the

Other [ ]

International Accounting Standards Board [ ]

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 [ ] Item 18 [ ]

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes [ ] No [ ]

TABLE OF CONTENTS

Page

INTRODUCTION

1

PART I

2

Item 1.

Identity of Directors, Senior Management and Advisers

2

Item 2.

Offer Statistics and Expected Timetable

2

Item 3.

Key Information

2

Item 4.

Information on the Company

21

Item 4A.

Unresolved Staff Comments

41

Item 5.

Operating and Financial Review and Prospects

41

Item 6.

Directors, Senior Management and Employees

62

Item 7.

Major Shareholders and Related Party Transactions

73

Item 8.

Financial Information

74

Item 9.

The Offer and Listing

76

Item 10.

Additional Information

77

Item 11.

Quantitative and Qualitative Disclosures About Market Risk

88

Item 12.

Description of Securities Other than Equity Securities

89

PART II

91

Item 13.

Defaults, Dividend Arrearages and Delinquencies

91

Item 14.

Material Modifications to the Rights of Security Holders and Use of Proceeds

91

Item 15.

Controls and Procedures

91

Item 16A.

Audit Committee Financial Expert

92

Item 16B.

Code of Ethics

92

Item 16C.

Principal Accountant Fees and Services

92

Item 16D.

Exemptions from the Listing Standards for Audit Committees

93

Item 16E.

Purchases of Equity Securities by the Issuer and Affiliated Purchasers

93

Item 16F.

Change in Registrant’s Certifying Accountant

93

Item 16G.

Corporate Governance

93

PART III

93

Item 17.

Financial Statements

93

Item 18.

Financial Statements

93

Item 19.

Exhibits

94

i

INTRODUCTION

Unless the context otherwise requires, in this annual report on Form 20-F,

·

“we,” “us,” “our company,” “our” or “WSP Holdings” refers to WSP Holdings Limited, which, unless otherwise required under the context, includes its predecessor entities and its consolidated subsidiaries;

·

“ADSs” refers to our American depositary shares, each of which represents two ordinary shares;

·

“China” or “PRC” refers to the People’s Republic of China, excluding, for the purpose of this annual report on Form 20-F only, Taiwan, Hong Kong and Macau;

·

“Oil Country Tubular Goods,” or “OCTG,” refers to pipes and other tubular products used in the exploration, drilling and extraction of oil, gas and other hydrocarbon products. OCTG mainly consist of casing, tubing and drill pipes. Unless otherwise indicated, discussions relating to OCTG in this annual report on Form 20-F are limited to these three types of OCTG;

·

“Production capacity” refers to the maximum production capacity that can be achieved at the optimal level of operations of a production line, calculated using an estimated product mix for such production line, which may differ from its actual product mix;

·

“RMB” or “Renminbi” refers to the legal currency of China, “HK$” refers to the legal currency of Hong Kong, and “$,” “US$” or “U.S. dollars” refers to the legal currency of the United States; and

·

“shares” or “ordinary shares” refers to our ordinary shares, par value $0.0001 per share.

Names of certain companies provided in this annual report are translated or transliterated from their original Chinese legal names.

Discrepancies in any table between the amounts identified as total amounts and the sum of the amounts listed therein are due to rounding.

This annual report on Form 20-F includes our audited consolidated financial statements for the years ended December 31, 2007, 2008 and 2009.

We use U.S. dollars as the reporting currency in our financial statements and in this annual report. When reporting our operating results and financial position, we use the monthly average exchange rate for the year and the exchange rate at the balance sheet date, respectively, as published by the People’s Bank of China. With respect to amounts not recorded in our consolidated financial statements included elsewhere in this annual report, all translations from Renminbi amounts into U.S. dollars were made at the noon buying rate in New York, New York for cable transfers in Renminbi per U.S. dollar as certified for customs purposes by the Federal Reserve Bank of New York, or the noon buying rate, on December 31, 2009, which wasRMB6.8259 to $1.00. We make no representation that the Renminbi amounts in this annual report could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China— Fluctuations in exchange rates could adversely affect our business as well as result in foreign currency exchange losses.” On July 9, 2010, the noon buying rate was RMB6.7720 to $1.00.

1

PART I

Item 1.

IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

Item 2.

OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

Item 3.

KEY INFORMATION

A.

Selected Financial Data

The following selected consolidated financial data should be read in conjunction with our consolidated financial statements and notes to those consolidated financial statements included elsewhere in this annual report and “Item 5. Operating and Financial Review and Prospects.” The selected consolidated statement of operations data for the years ended December 31, 2007, 2008 and 2009 and the selected consolidated balance sheet data as of December 31, 2008 and 2009 are derived from our audited consolidated financial statements, which are included elsewhere in this annual report. The selected consolidated statement of operations data for the years ended December 31, 2005 and December 31, 2006 and the selected consolidated balance sheet data as of December 31, 2005, 2006 and 2007 are derived from our audited consolidated financial statements, which are not included in this annual report. Our consolidated financial statements are prepared and presented in accordance with United States generally accepted accounting principles, or U.S. GAAP. Our historical results do not necessarily indicate our results expected for any future periods.

| For the year ended December 31, | ||||||||

(in thousands, except for share and per share data) | 2005 | 2006 | 2007 | 2008 | 2009 | ||||

Selected Consolidated Income Statement Data: |

|

|

|

|

| ||||

Net revenues | $241,012 | $366,501 | $483,783 | $912,090 | $577,029 | ||||

Cost of revenues | (198,550) | (281,106) | (357,997) | (703,531) | (496,656) | ||||

Gross profit | 42,462 | 85,395 | 125,786 | 208,559 | 80,373 | ||||

Selling and marketing expenses | (2,056) | (4,102) | (8,578) | (22,770) | (18,244) | ||||

General and administrative expenses | (6,356) | (9,799) | (13,591) | (41,740) | (44,798) | ||||

Other operating (expenses) income, net | (499) | (549) | (32) | 2,589 | 2,559 | ||||

Income from operations | 33,551 | 70,945 | 103,585 | 146,638 | 19,890 | ||||

Interest income (expense), net | (1,901) | (1,735) | (10,541) | (15,319) | (17,026) | ||||

Other income (expense) | (86) | 4 | 212 | 767 | 767 | ||||

Exchange differences | 741 | 357 | (1,898) | (6,984) | 218 | ||||

Income from continuing operations before provision for income taxes | 32,305 | 69,571 | 91,358 | 125,102 | 3,849 | ||||

Provision for income taxes | (4,198) | (10,582) | (15,188) | (24,405) | (2,137) | ||||

2

| For the year ended December 31, | ||||||||

(in thousands, except for share and per share data) | 2005 | 2006 | 2007 | 2008 | 2009 | ||||

Net income from continuing operations before earnings in equity investments | 28,107 | 58,989 | 76,170 | 100,697 | 1,712 | ||||

Earnings (loss) in equity investments | 266 | 67 | — | 1 | (105) | ||||

Net income from continuing operations

| 28,373 | 59,056 | 76,170 | 100,698 | 1,607 | ||||

Net income (expense) from discontinued operations | (4,104) | 233 | — | — | — | ||||

Net income | 24,269 | 59,289 | 76,170 | 100,698 | 1,607 | ||||

Less: Net income (loss) attributable to the non-controlling interests(1) | (47) | 371 | (1,609) | (1,349) | 2,568 | ||||

Net income attributable to WSP Holdings Limited | $24,316 | $58,918 | $74,561 | $99,349 | $4,175 | ||||

Net income per share—basic |

|

|

|

|

| ||||

Income from continuing operations | $0.31 | $0.40 | $0.49 | $0.48 | $0.02 | ||||

Loss on discontinued operations | (0.04) | — | — | — | — | ||||

Net income per share | $0.27 | $0.40 | $0.49 | $0.48 | $0.02 | ||||

Net income per share—diluted |

|

|

|

|

| ||||

Income from continuing operations | $0.31 | $0.40 | $0.48 | $0.48 | $0.02 | ||||

Loss on discontinued operations | (0.04) | — | — | — | — | ||||

Net income per share | $0.27 | $0.40 | $0.48 | $0.48 | $0.02 | ||||

Weighted average ordinary shares used in computation of earnings per share: |

|

|

|

|

| ||||

Basic | 91,315,420 | 145,954,406 | 153,561,644 | 205,663,247 | 205,789,800 | ||||

Diluted | 91,315,420 | 145,954,406 | 153,738,133 | 205,663,247 | 205,789,800 | ||||

____________________

(1)

We adopted Financial Accounting Standards Board, or FASB, Accounting Standards Codification, or ASC, Topic 810-10-65, Transition Related to FASB Statement No. 160, Non-controlling Interests in Consolidated Financial Statements — an amendment of ARB No. 51, or ASC 810-10-65, on January 1, 2009 retrospectively. Non-controlling interest, formerly referred to as minority interest, has been reclassified in accordance with ASC 810-10-65.

3

The following table presents a summary of our consolidated balance sheet data as of December 31, 2005, 2006, 2007, 2008 and 2009:

____________________

(1)

We adopted ASC 810-10-65 (formerly FASB Statement No. 160, Non-controlling Interests) on January 1, 2009, retrospectively. Non-controlling interest, formerly referred to as minority interest, has been reclassified in accordance with ASC 810-10-65.

B.

Capitalization and Indebtedness

Not Applicable.

C.

Reasons for the Offer and Use of Proceeds

Not Applicable.

D.

Risk Factors

Declines in domestic and international oil and natural gas prices, or domestic and international exploration, drilling and production activities, would adversely affect our profitability.

Demand for our OCTG products depends significantly on the number of domestic and worldwide oil and gas wells drilled, completed and reworked, as well as the depth and drilling conditions of these wells. The level of such drilling activities in turn depends on the level of capital spending by major oil and gas companies. A decline in domestic and worldwide oil and gas exploration, drilling and production activities would adversely affect our results of operations. Capital spending on OCTG used for oil and natural gas exploration, drilling and production activities is driven in part by the prevailing prices for oil and natural gas and the perceived stability and sustainability of those prices. The current global credit and economic crisis has reduced worldwide demand for energy and resulted in significantly lower crude oil and natural gas prices. A substantial or extended decline in oil and natural gas prices can reduce our customers’ activities and their spending on our products. If the current global economic conditions and the availability of credit worsen or continue for an extended period, this could reduce our customers’ levels of expenditures and have a significant adverse effect on our revenue and operating results.

4

The reduction in cash flows being experienced by our customers resulting from declines in commodity prices, together with reduced availability of credit and increased costs of borrowing due to tightening of the credit markets, could have significant adverse effects on the financial conditions of some of our customers. This could result in project modifications, delays or cancellations, general business disruptions, and delays in, or nonpayment of, amounts that are owed to us, which could have a significant adverse effect on our results of operations and cash flows.

In addition, oil and natural gas prices are subject to significant volatility due to numerous factors beyond our control, including, but not limited to, changes in the supply and demand for oil and natural gas, market uncertainty, world events, regulatory control (including by the PRC government), political developments in petroleum producing regions and the price and availability of alternative energy sources. We cannot assure you that oil and natural gas prices will not decline further or that such prices will remain at sufficiently high levels to support levels of investment in exploration, drilling and production activities that will sustain demand for our products. Any further decline in the price of oil and natural gas, even for a short period of time, may reduce or curtail expenditures by oil and gas companies in connection with exploration, drilling and production activities, which may result in lower sales volumes and prices for our products in the PRC and overseas and materially and adversely affect our results of operations and financial condition.

Our results of operations may be adversely affected by increases in steel prices.

Steel is the principal raw material for our products. Cost for raw materials accounted for 80.9%, 77.9% and 74.4% of our cost of revenues in 2007, 2008 and 2009, respectively. Any increase in the price of steel could reduce our profit margin if we are unable to pass such increased costs on to our customers. From the end of 2003 to mid-2008, the price of steel increased substantially due in part to increasing demand, which significantly affected our gross margin. However, the price of steel declined towards the end of the third quarter of 2008 and the decline continued in the fourth quarter of 2008. The price of steel was volatile in the first quarter of 2009 and has been basically on an upwards trend since the second quarter of 2009. We expect the price of steel to experience continued volatility in 2010. The price of steel has had, and will continue to have, a significant impact on our cost of revenues. If we are unable to manage our purchases of steel at prices acceptable to us or if the price of steel increase significantly and we are not able to pass on all or part of any such price increases to our customers, our profit margins may decrease and our results of operations would be materially and adversely affected.

Measures such as initiation of anti-dumping and anti-subsidy proceedings and imposition of anti-dumping and/or countervailing duties by governments in our overseas markets could materially and adversely affect our export sales.

Anti-dumping and anti-subsidy proceedings have been initiated by some countries in relation to steel products, resulting in anti-dumping and/or countervailing duties being imposed by those countries on steel products. Those and other similar measures could trigger trade disputes in the international steel product markets that could adversely affect our exports.

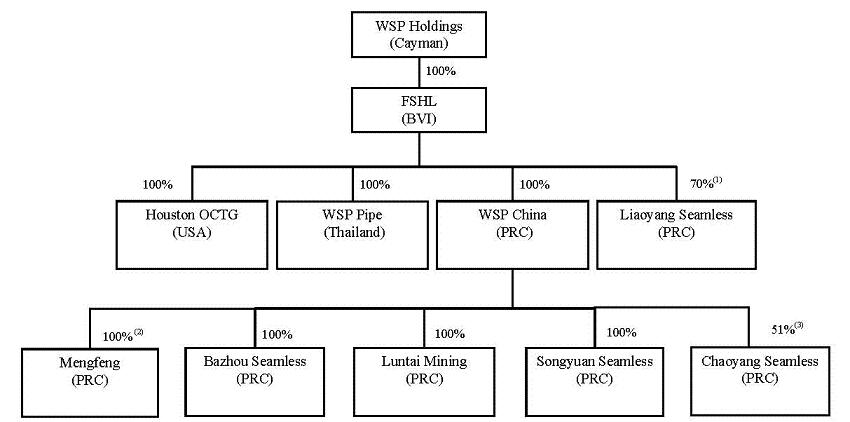

In April 2009, seven U.S. companies and the United Steelworkers Union filed a petition with the U.S. International Trade Commission, or the ITC, and the U.S. Department of Commerce, or the DOC, alleging that China-based OCTG manufacturers unfairly dumped OCTG products in the U.S. market and that Chinese producers were benefitting from massive government subsidies. Wuxi Seamless Oil Pipes Company Limited, or WSP China, was named as one of the major exporters of OCTG products from China. In June 2009, we were included as one of the mandatory respondent companies to the United States government’s countervailing duty investigation. On September 8, 2009, a preliminary determination was issued with a countervailing duty rate of 24.92% assigned to WSP China. On December 7, 2009, the DOC published its final determination in the countervailing duties investigation with a rate of 14.61% assigned to WSP China. The rate was subsequently changed to 14.95% in January 2010 due to certain ministerial errors made by the DOC. We were not selected as a mandatory respondent to the anti-dumping investigation and participated in this case as a separate rate respondent. In November 2009, we received a preliminary dumping rate of 36.53%, which was based on the average dumping rates of other OCTG producers that were selected as mandatory respondents. In December 2009, this rate was amended to 96.51% due to certain ministerial errors made by the DOC. On April 9, 2010, the DOC announced its final determination in the anti-dumping investigation with a rate of 29.94% assigned to WSP China. In May 2009, this rate was amended to 32.07%, after correcting certain ministerial errors. The anti-dumping and countervailing duties are applied to all Chinese exports of OCTG products to the United States starting from the date of the DOC’s preliminary determinations. WSP China did not export OCTG products to the United States after the date of the DOC’s preliminary determinations. The anti-dumping and countervailing duties will apply to us if WSP China exports OCTG products to the United States in the future and we are not subject to any other penalties or fines. In 2007 and 2008, products exported to the United States accounted for22.7% and 34.3%of our net revenues, respectively.In 2009, products exported to the United States

5

accounted for 9.0% of our net revenues. The decrease in export revenue of products exported to the United States as a percentage of our net revenues mainly was attributable to the effect of anti-dumping and countervailing duties on the subject goods. As a result of the proceedings, our sales in the U.S. suffered and our results of operations have been materially and adversely affected.

We cannot assure you that there will not be similar actions taken in the future in other countries against Chinese-made seamless OCTG products. If there were any action filed against us regarding the products we sell, even without merit, it would divert significant company resources and management attention and could have an adverse impact on the prices and sales of our products in the relevant countries. It could also adversely affect our business prospects and results of operations. If any decision is entered against us in such an action, we may be subject to additional tariff liabilities and our overseas sales would be materially and adversely affected.

Restrictive covenants under our facility agreements and any future indebtedness may limit the manner in which we operate and an event of default under any of our facility agreements and any future indebtedness may adversely affect our operations; and our financial leverage may hinder our ability to expand and materially affect our results of operations .

Our facility agreements with certain commercial banks, contain, and any future indebtedness we incur may contain, various covenants and conditions that limit our ability to, among other things:

| • | incur or guarantee additional debts; |

| • | secure loans, make capital expenditures or engage in investments and acquisitions; |

| • | enter into transactions with affiliates; |

| • | create liens; |

| • | merge or consolidate with other companies; and |

| • | transfer or sell all or substantially all of the assets. |

As a result of these covenants, we are limited in the manner in which we conduct our business and may be unable to engage in certain business activities. Some of the facility agreements also include certain financial covenants that, among other things, require us to maintain debt to assets ratio. A failure to maintain the financial covenants, or a breach of any of the other restrictive covenants, would result in a default under the relevant facility agreements. Upon the occurrence of any default under any of the facility agreements, the lender could elect to declare all borrowings outstanding, together with accrued and unpaid interests and fees, to be due and payable, or could require us to apply all of our available cash to repay these borrowings. If the lender accelerates the repayment of borrowings, we may not have sufficient cash or assets to repay the loans under the facility agreements. Even if we are able to obtain new financing, we may not be on commercially reasonable terms, or terms that are acceptable to us. Similarly, one credit line agreement entered into between WSP China and Bank of China requires WSP China to maintain minimum monthly sales amount and annual sales amount, respectively, and a failure to maintain the financial results would result in a reduction of the total amount of bank credit under such credit line agreement. In 2009 WSP China failed to maintain the minimum annual sales amount required under this agreement, as a result of which Bank of China reduced the total amount of bank credit available to us under such agreement in 2010.

In addition, our failure to comply with the financial or other covenants under the facility agreements could lead us to seek a waiver of the covenants contained in the facility agreements. Based on the financial position and results of Bazhou Seamless, as of and for the year ended December 31, 2009, Bazhou Seamless failed to meet the financial covenant as to the maximum debt to assets ratio under the facility agreement with Bank of China and China Construction Bank, respectively. We agreed to implement measures to address such breaches and obtained a waiver of such breaches from each of the lenders. However, we cannot assure you that we will be able to comply with the covenants contained in the facility agreements in the future, and if we breach the covenants, we cannot assure you that we would be able to obtain waiver of the breaches of covenants contained in the facility agreements or obtain alternative financing at commercially reasonable terms. Furthermore, we cannot assure you that any default under the existing facility agreements will not result in a cross-default in our other loans with banks in the PRC. Such event of default may result in a substantially amount of our debt becoming immediately due, which would have a material adverse effect on our financial condition and results of operations.

We rely largely on operating cash flow and short-term borrowings for the working capital needs of our operations. As of December 31, 2009, our total bank and other borrowings amounted to $695.5 million, of which $432.5 million were short-term bank borrowings. Our substantial indebtedness could have important consequences to you. For example, it could:

| • | limit our ability to satisfy our obligations under our debt; |

| • | increase our vulnerability to adverse general economic and industry conditions; |

| • | require us to dedicate a substantial portion of our cash flow from operations to servicing and repaying our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures and other general corporate purposes; |

| • | limit our flexibility in planning for or reacting to changes in our businesses and the industry in which we operate; |

| • | place us at a competitive disadvantage compared to our competitors that have less debt; |

| • | impair our ability to develop business opportunities or make strategic acquisitions; and |

| • | increase the cost of additional financing. |

Our ability to make scheduled payments under our financing agreements and any future financing transactions and our ability to refinance our debts, if necessary, will depend, among other things, on our future operating performance. See below for a discussion on the risks regarding our ability to service our debts.

Our financial statements indicate that there is a going concern uncertainty, which could adversely affect our ability to meet our ongoing financing needs as well as to obtain third party financing.

We experienced a significant decline in sales in the United States due to the anti-dumping and countervailing duty on seamless pipes made in China and are required to repay a significant amount of short-term borrowings. The existence of these conditions raise the issue about our ability to continue as a going concern. We cannot assure you that our business will generate sufficient cash flow from operations in the future to service our debts and make necessary capital expenditures, in which case we may (i) seek additional financing, (ii) seek to refinance some or all of our debts or (iii) dispose of certain assets. The existence of a going concern uncertainty could affect our ability to obtain financing from third parties or could result in increased costs of such financing. See Note 2 to our financial statements for more details. We cannot assure you that financing will be available in the amounts we need or on terms acceptable to us, if at all. The incurrence of debt would divert cash for working capital and capital expenditures to service debt obligations and could result in operating and financial covenants that restrict our operations and our ability to pay dividends to our shareholders. In the event that we are unable to meet our liabilities when they become due or if our creditors take legal actions against us for payment, we may have to liquidate long-term assets to repay our creditors. We may have difficulty converting our long-term assets into current assets in such a situation and may suffer material losses upon the sale of our long-term assets.

We depend on a limited number of customers, and any loss of these customers could materially and adversely affect our revenue and profitability.

Our customers include oil and gas companies in the PRC and abroad. Aggregate sales attributable to our five largest customers represented approximately 55.8%, 46.5% and 61.7% of our net revenues for the years ended December 31, 2007, 2008 and 2009, respectively. We cannot assure you that we will be able to maintain or improve our relationships with these customers, or that we will be able to continue to supply products to these customers at current levels or at all. In addition, our business is affected by competition in the oil and gas industry, and any decline in our major customers’ businesses in these markets could lead to a decline in purchase orders from these customers. If any of our key customers were to substantially reduce the size or amount of the orders they place with us or were to terminate their business relationship with us entirely, we cannot assure you that we would be able to obtain orders from other customers to replace any such lost sales on comparable terms or at all. If any of these relationships were to be so altered and we were unable to obtain replacement orders, our business, results of operations and financial condition would be materially and adversely affected.

Our sales contracts typically have a term of less than six months and, as a result, customers may reduce their orders or terminate their relationships with us almost immediately.

Sales of our products are typically conducted through sales contracts with a term of less than six months. As a result, our customers may choose to terminate their relationship with us after completion of the shipment or expiration of the contract, as the case may be. Our customers are also not obligated to continue placing orders with us at historical levels or at all. If any of our customers, particularly our key customers, were to materially reduce their orders with us or were to terminate entirely their business relationship with us with short notice, we might not have sufficient time to locate alternative customers and our business and results of operations could be materially and adversely affected.

We cannot assure you that our products will pass periodic inspection by the American Petroleum Institute, or API, or the qualification processes of potential customers, and any failure by us to pass such inspection or qualifications would adversely affect our business prospects and results of operations.

We have obtained certificates from API to use the official API monogram on our products to demonstrate that our products meet API standards. These certificates are subject to periodic inspections by API. Furthermore, our growth strategies include increasing our sales in the PRC domestic market, as well as expanding into international markets such as North America, the Middle East, Asia, Africa and Russia. It is standard industry practice that an OCTG manufacturer must first pass a qualification process to become an approved supplier of an oil and gas company before providing OCTG products to that company. We cannot assure you that we will be able to obtain the necessary certifications from API or approvals for new products from our existing customers or approvals from any new customers. Even if we can ultimately secure such approvals or certifications, we cannot assure you that such certifications and approvals can be obtained in a timely manner or can be maintained. If we fail to become an approved supplier of our potential customers, or if we are unable to obtain or maintain such approval in a timely manner, we may not be able to execute our expansion plans and our business prospects and results of operations may be materially and adversely affected.

If we are unable to compete effectively in the OCTG industry, our revenue and profits may decrease.

We face intense competition in the domestic and international markets in which we operate.

6

Domestically, we face competition from a number of manufacturers that produce OCTG that are similar to ours. Our major domestic competitors include Tianjin Pipe (Group) Corporation, Shanghai Baosteel Group Corporation and Pangang Group Chengdu Iron & Steel Co., Ltd., which are mostly state-owned enterprises. We also face competition from international manufacturers, such as Tenaris in Argentina, Vallourec & Mannesmann Tubes in France, TMK in Russia, Sumitomo and JFE in Japan and U.S. Steel in the United States. Our major competitors may have longer operating history, larger customer base, stronger customer relationships, greater brand or name recognition and greater financial, technical, marketing and public relations resources than we do. Some of our competitors may also be better positioned to develop superior product features and technological innovations and be able to better adapt to market trends than we are.

Our ability to compete depends on, among other things, high product quality, short lead-time, timely delivery, competitive pricing, wide range of product offerings and superior customer service and support. Increased competition may require us to reduce our prices or increase our costs and may have a material adverse effect on our financial condition and results of operations. Any decrease in the quality of our products or the level of our service to our customers or any occurrence of a price war among our competitors and us may adversely affect our business and results of operations. If we are unable to remain competitive, we may not be able to increase or even maintain our current share of the OCTG market in China or overseas or continue to achieve our current level of profitability.

We cannot assure you that we will be successful in implementing our future expansion plans, in particular our plans for international expansion and overseas sales, or in managing our growth.

A principal component of our future strategy is to continue to grow by expanding our production

7

capacity and further developing our overseas sales. For example, as a part of our international expansion strategy, in April 2008, we established our wholly-owned subsidiary, Houston OCTG Group, Inc., in Houston, Texas. In April 2009, WSP China established Chaoyang Seamless Oil Steel Casting Pipes Co., Ltd., or Chaoyang Seamless, in Chaoyang, Liaoning Province, China. In February 2010, we acquired WSP Pipe Company Limited, or WSP Pipe, a company in the Thai-Chinese Rayong Industrial Zone, Thailand from Mr. Piao Longhua, our chairman and chief executive officer. Our future growth will depend on a number of factors, including but not limited to, our ability to manage expansion and overseas operations, obtain any required financing, achieve operational efficiency, and secure sufficient access to raw materials. Some of these factors are beyond our control. As a result, we may not be able to successfully manage our growth or expand our operations, which could have a material adverse effect on our business, financial condition and results of operations.

In addition, we may need to increase the number of our employees and enhance our operational and financial systems to handle the increased complexity and the expanded geographical coverage of our operations associated with our growth. We cannot assure you that we will be able to attract and retain qualified management staff and employees or that our current operational and financial systems and controls will be adequate to accommodate future growth. This could have a material adverse effect on our business, financial condition and results of operations.

We face risks associated with the marketing, distribution and sale of our products internationally, and if we are unable to manage these risks effectively, they could impair our ability to expand our business overseas.

Our international expansion focuses are mature markets in terms of OCTG production. In order to succeed, we need to take market share away from the existing suppliers of seamless OCTG in these markets. We cannot assure you that we will be able to do so in these competitive markets.

Moreover, our plans for international expansion may be hindered by the following:

·

cultural differences and other difficulties in staffing and managing overseas operations;

·

inherent difficulties and delays in contract enforcement and collection of receivables through the use of foreign legal systems;

·

volatility in currency exchange rates;

·

the risk that foreign countries may impose withholding taxes (or otherwise tax our foreign income or place restrictions on repatriation of profit);

·

the risk of barriers, such as anti-dumping and other tariffs or other restrictions being imposed on foreign trade;

·

changes in the political, regulatory, or economic conditions in a foreign country or region; and

·

the burden of complying with foreign laws and regulations.

If we are unable to manage these risks effectively, our ability to conduct or expand our business overseas would be impaired, which may in turn materially and adversely affect our business, financial condition, results of operations and prospects.

Our business depends on our ability to attract and retain members of our senior management team and other key personnel.

Our future success is dependent on the efforts, performance and abilities of key members of our management team, particularly Mr. Piao Longhua, our chairman and chief executive officer. Mr. Piao founded our company and has extensive industry experience. We do not maintain key person insurance on any of our management personnel. As the OCTG industry in the PRC becomes more competitive, we expect the competition for management and other skilled personnel to intensify. Failure to attract and retain qualified employees or the loss of any member of our senior management may result in a loss of organizational focus, poor operating execution or an inability to identify and execute potential strategic initiatives such as overseas

8

expansion and new product offerings. This could, in turn, materially and adversely affect our business, financial condition and results of operations.

Our business relies on our ability to retain and attract experienced sales staff and our ability to maintain and expand our existing sales networks both domestically and overseas.

Our experienced sales staff constitutes an essential part of our business. In the domestic PRC market, our sales staff possesses strong technical backgrounds in the OCTG industry, which enable them to provide and deliver on-site technical support to our customers. We rely on our four sales offices located in the Daqing, Changqing, Xinjiang and Sichuan oilfields to directly sell our products to the major oilfields in the PRC. In addition to providing on-site services to our customers throughout the sales process and after-sales support, our sales staff also helps us maintain good relationships with our customers. Internationally, we sell our products through our distributors and sales agents. The loss of services of any of our experienced sales staff without timely replacement, the inability to attract and retain sales personnel, or the loss of any of our major distributors or sales agents may have an adverse effect on our business. If we are unable to maintain our existing sales network, our operations may be materially and adversely affected.

We depend on a limited number of suppliers for a majority of our raw material requirements, and interruption of raw material delivery could prevent us from delivering our products in a timely manner to our customers in the required quantities, and in turn result in order cancellations, decreased revenue and loss of market share.

Our operations depend on our ability to obtain adequate and quality supplies of our primary raw materials, namely, round steel billets and green pipes, in a timely manner. If our suppliers fail to meet our quality standards or our quantity demands, our production and sales volume and our results of operation may be adversely affected. Through our upstream acquisition of Tuoketuo County Mengfeng Special Steel Co., Ltd., or Mengfeng, from Hebei Bishi Industry Group Co., Ltd., or Hebei Bishi, in July 2008, establishment of Chaoyang Seamless in April 2009, and acquisition of certain tangible and intangible assets from a sponge iron and steel billet company in Liaoning province through Chaoyang Seamless, we expect to stabilize the supply, quality and cost of our raw materials. However, before our own steel manufacturing facilities are substantially utilized, we will continue to rely on major suppliers to supply round billets to us. See “Item 4. Information on the Company—B. Business Overview—Manufacturing—Suppliers of raw materials.” We cannot guarantee that our long-term arrangements with these suppliers will provide us with a reliable supply of raw materials. If there is any supply shortage, we may be unable to deliver our products in a timely manner to our customers in the required quantities, which in turn could result in order cancellations, decreased revenue and loss of market share.

Significant product liability claims made against us, regardless of their success, could harm our business reputation, results of operations and financial condition.

Our OCTG products are sold primarily for use in oil and gas exploration, drilling and extraction activities. These activities are subject to inherent risks, including well failures, line pipe leaks and fires that could result in death, personal injury, property damage, pollution or loss of production, all of which could result in liability claims being made against us. We typically offer warranties on our products for a period of up to one year. During the warranty period, faulty products will be repaired or replaced by us, or returned to us. Actual defects or allegations of defects in our products may give rise to claims against us for losses and expose us to claims for damages. For instance, we are subject to multiple lawsuits alleging defective casing pipes used in an oil and gas well operations the United States. See “—We are subject to litigation proceedings brought by third-parties. If any of the proceedings against us is successful, it may have an adverse effect on our financial condition and operating results.” and “Item 8. Financial Information—A. Consolidated Statements and Other Financial Information—Legal proceedings” for further information about the lawsuits. Any such claim, regardless of merit, could cause us to incur significant costs, divert our management’s attention, harm our business reputation or cause significant disruption to our operations. Furthermore, we can provide no assurance that we will be able to successfully defend against such claims, and we do not have any product liability insurance covering our products, except insurance covering those products sold in North America. If any such claims were successful, we could be subject to substantial liabilities, which could materially and adversely affect our results of operations and our financial condition.

We may be unable to prevent possible resales or transfers of our products to countries, governments, entities, or persons targeted by United States economic sanctions, especially when we sell our products to distributors over which we have limited control.

9

The U.S. Department of the Treasury’s Office of Foreign Assets Control, or OFAC, administers certain laws and regulations, or U.S. Economic Sanctions Laws, that impose restrictions upon U.S. persons and, in some instances, foreign entities owned or controlled by U.S. persons, with respect to activities or transactions with certain countries, governments, entities and individuals that are the subject of U.S. Economic Sanctions Laws, or Sanctions Targets. U.S. persons are also generally prohibited from facilitating such activities or transactions. We believe that U.S. Economic Sanctions Laws under their current terms are not applicable to our activities, however, we have nonetheless decided to adopt commercially reasonable measures to prevent any sales of our products to Sanctions Targets. If we become subject to U.S. Economic Sanctions Laws, a violation of these laws and regulations could subject us to fines, penalties and other sanctions. In the three years ended December 31, 2009, we did not have any direct sales to Sanctions Targets. However, we sell our products in international markets primarily through independent non-U.S. distributors who are responsible for interacting with the end customers of our products. We have limited control over these independent non-U.S. distributors, and these distributors may breach their covenant to us not to resell our products to Sanctions Targets. In addition, we do not always know the end customers to whom our distributors resell our products. See “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Internal control over distribution of our products.” Although we have adopted a written policy to prevent future direct or indirect sales to Sanctions Targets and have begun to implement internal control mechanisms to enforce such policy when possible, we cannot assure you that our measures will be able to prevent future sales or resales of our products, directly or indirectly, to Sanctions Targets.

If our products are sold or re-sold, directly or indirectly, to Sanctions Targets, we may fail to comply with U.S. Economic Sanctions Laws and we may be subject to civil or criminal penalties and other remedial measures, which could have an adverse impact on our business, results of operations, financial conditions and liquidity. In addition, our reputation could be adversely affected. Some of our U.S. investors may be required to sell their interests in our company under the laws of certain U.S. states or under internal investment policies or may decide for reputational reasons to sell such interests, and some U.S. institutional investors may forego the purchase of our ADSs, all of which could materially and adversely affect the value of our ADSs and your investment in us.

If we are unable to continue developing our production technology or adopt new production technology, our business and prospects may be harmed.

The OCTG industry is competitive and the production technology underlying the industry is evolving. As customers’ needs, related technologies and market trends are subject to change, we cannot assure you that we will be able to correctly predict the trends in a timely manner, develop or adopt competitive technology on a timely basis, or respond effectively to competitive industry conditions and changing customer demands.

Responding and adapting to technological developments and changes in the OCTG industry and the integration of new technologies or industry standards may require substantial investment of resources, time and capital. Even if we implement such measures, there can be no assurance that we will succeed in adequately responding and adapting to such technological and industry changes. In the event that we are unable to respond successfully to technological and industry changes, our business, results of operations and competitiveness may be materially and adversely affected.

Failure to protect our intellectual property rights may materially and adversely affect our competitive position and operations, and we may be exposed to infringement or misappropriation claims by third parties.

Our success is in part attributable to the technologies, know-how and other intellectual properties that we have developed or acquired. See “Item 4. Information on the Company—B. Business Overview—Intellectual property rights” for information relating to our patents and trademarks. Although we rely upon a combination of trade secrets, confidentiality policies, non-disclosure and other contractual arrangements, and patent and trademark laws to protect our intellectual property rights, there can be no assurance that the steps we have taken to protect our intellectual property rights are adequate to prevent or deter infringement or other misappropriation of our intellectual property. We may not be able to detect unauthorized uses or take appropriate and timely steps to enforce our intellectual property rights. Any significant infringement of our proprietary technologies and processes or our intellectual property rights could weaken our competitive position and have an adverse effect on our operations. To protect our intellectual property rights, we may have to commence legal proceedings against any misappropriation or infringement. However, there can be no assurance that we will prevail in such proceedings. Furthermore, as we only hold PRC patents, if third parties manufacture and sell products using our technology outside of the PRC in competition against us, we would not have a legal cause of action against them.

10

Furthermore, we may be subject to litigation involving claims of patent infringement or the violation of other intellectual property rights of third parties. The defense of intellectual property suits, patent opposition proceedings and related legal and administrative proceedings can be both costly and time-consuming and may significantly divert the efforts and resources of our technical and management personnel. An adverse determination in any such litigation or proceedings to which we may become a party could subject us to significant liability to third parties, require us to seek licenses from third parties, to pay ongoing royalties, or to redesign our products or subject us to injunctions prohibiting the manufacture and sale of our products or the use of our technologies, which could materially and adversely affect our business, financial condition or results of operations. Protracted litigation could also result in our customers or potential customers deferring or limiting their purchase or use of our products until resolution of such litigation, which could adversely affect our business.

Failure to maintain an effective quality control system at our manufacturing facilities could have a material adverse effect on our business and operations.

The performance, quality and safety of our products are critical to the success of our business. These factors depend significantly on the effectiveness of our quality control systems, which in turn depend on a number of factors, including the design of our quality control systems, our quality-training program, and our ability to ensure that our employees adhere to the quality control policies and guidelines. Any significant failure or deterioration of our quality control systems could have a material adverse effect on our business reputation, results of operations and financial condition.

If disruptions in our transportation network occur or our shipping costs substantially increase, we may be unable to deliver our products in a timely manner and our cost of revenues could increase.

We are highly dependent upon transportation systems, including train, truck and ocean shipping, to deliver our products. The transportation network is potentially exposed to disruption from a variety of causes, including labor disputes or port strikes, acts of war or terrorism and natural disasters. If our delivery times or our shipping costs increase unexpectedly for any reasons, our revenues and results of operation could be materially and adversely affected.

Our growth strategies require significant capital investments and may require us to seek external financing, which may not be available on terms favorable to us.

Our business operations and growth strategies require substantial capital investments, the availability of which depends on our ability to generate cash flow from operations, borrow funds on satisfactory terms and raise funds in the capital markets. Our ability to arrange for financing to support our capital expenditures and the cost of such financing are dependent on numerous factors, including general economic and capital markets conditions, interest rates and credit availability from banks or other lenders, many of which are beyond our control. In addition, increases in interest rates or failure to obtain external financing on terms favorable to us will affect our financing costs and our results of operations. We may not be able to obtain financing in amounts or on terms acceptable to us, if at all, especially in the current global credit and economic crisis, which may have an adverse effect on our operating results and financial condition.

We may not be successful in our future acquisitions and investments.

If we are presented with appropriate opportunities, we may acquire additional businesses or assets as part of our growth strategy. Future acquisitions, investments and joint ventures may expose us to potential risks, and the success of our acquisitions, investments and joint ventures depend on a number of factors, including:

·

our ability to identify suitable opportunities for acquisitions, investments or joint ventures;

·

whether we are able to reach an acquisition, investment or joint venture agreement on terms that are satisfactory to us;

·

the extent to which we are able to exercise control over the acquired company or business;

11

·

the economic, business or other strategic objectives and goals of the acquired company or business compared to those of our company;

·

the diversion of management attention and resources from our existing business;

·

our ability to finance the acquisition, investment or joint venture; and

·

our ability to integrate successfully the acquired company or business.

If we fail to make acquisitions or investments or form joint ventures that are strategically important to us, our growth and business prospects may be limited. If we encounter difficulties in integrating the business we acquired, our financial condition and results of operations may be materially and adversely affected.

If we fail to establish or maintain an effective system of internal controls, we may be unable to accurately report our financial results or prevent fraud, and investor confidence and the market price of our ADSs may be adversely impacted.

We are subject to reporting obligations under the U.S. securities law. The Securities and Exchange Commission, or the SEC, as required by Section 404 of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, has adopted rules requiring every public company to include a management report on such company’s internal control over financial reporting in its annual report, which must also contain management’s assessment of the effectiveness of the company’s internal control over financial reporting. In addition, an independent registered public accounting firm must attest to the effectiveness of the company’s internal control over financial reporting.

In connection with the preparation of this annual report on Form 20-F, we carried out an evaluation of the effectiveness of our internal control over financial reporting. Based on this evaluation, our chief executive officer and chief financial officer concluded that our internal control over financial reporting was not effective due to a material weakness, as defined by Auditing Standard 5, “An Audit of Internal Control Over Financial Reporting That Is Integrated with An Audit of Financial Statements.” See “Item 15. Control and Procedures.” The material weakness identified was that the control procedures to ensure that a new type of sales transaction involving trading in iron ore and certain bill financing transactions were appropriately communicated internally and in a timely manner to those charged with maintaining the Group's books and records and approved by senior management did not operate effectively.

We have implemented measures to address this material weakness. We cannot assure you that any significant deficiency or material weakness in our internal control over financial reporting will not be identified in the future. If we fail to maintain effective internal control over financial reporting in the future, we and our independent registered public accounting firm may not be able to conclude that we have effective internal control over financial reporting at a reasonable assurance level. This could in turn result in the loss of investor confidence in the reliability of our financial statements and negatively impact the trading price of our ADSs. Furthermore, we have incurred and anticipate that we will continue to incur considerable costs and use significant management time and other resources in an effort to comply with Section 404 and other requirements of the Sarbanes-Oxley Act.

We entered into certain bill financing arrangements which were not in compliance with relevant PRC laws and regulations, and we cannot assure you that there will not be any legal or regulatory action taken against us which would result in material adverse effect on our business conditions and cash flows.

In the past, we obtained funding for our business operations through issuing bank and commercial acceptance notes in amounts that were greater than the actual amounts of our total purchases from the relevant suppliers to take advantage of the lower discounted interest rates of bank and commercial acceptance notes. We ceased to conduct this kind of bill financing since the second quarter of 2010 and settled almost all of the bank and commercial acceptance notes involved in the overstated bill financing, with the remaining amount to be settled at the repayment dates. We have strengthened our internal controls system and implemented various rectifying measures to ensure that such bill financing activities will not occur in the future. See “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Bill financing.”

Based on advice from our PRC counsel, we believe that there is no legal basis for any PRC regulatory

12

authority to impose administrative or criminal liability on us or our senior management or directors in relation to this bill financing. Notwithstanding the opinion we received, we cannot assure you that relevant governmental agencies will not decide to take actions or impose penalties on us contrary to the legal advice we have obtained. Any actions by regulators could cause a disruption to our business operations and impact future financing by us with any of the commercial banks, which may have an adverse effect on our business conditions and cash flows. We have also obtained the written confirmations from all endorsing banks that they will not take any legal action against us. However, we cannot assure you that the endorsing banks will not take any legal action despite the confirmations we received due to unforeseen reasons, which would cause a disruption to our business and impact our long-term relationships with the banks and impact our future financing plans.

We may have excess inventory or otherwise sustain loss as a result of our entering into a five-year supply agreement with an iron ore pellets supplier, which could materially and adversely affect our financial condition and results of operations.

In November 2009, we entered into a five-year supply agreement with an iron ore pellets supplier to purchase iron ore pellets. Under this agreement, we have committed to purchase a minimum amount of 300,000 tons of iron ore pellets on a yearly basis from 2010 through 2014. Chinese steel companies heavily rely on imported iron ore for their raw material needs. In recent years, the prices for iron ore pellets under multi-year supply agreements are generally lower than the prices on the spot market. Given the strong demand for iron ore pellets in the Chinese market in the past few years, we expect to resell some of the iron ore pellets purchased under our five-year supply agreements on the spot market for profit. If we are not able to resell the purchased iron ore pellets within a short-period of time or do not generate sufficient profit from the resale of the iron ore pellets, we may overstock our inventory of raw materials or be unable to recover the costs for purchasing the iron ore pellets. If the price of such raw materials rapidly decline and we are forced to make an impairment on our inventory of iron ore pellets, or if we are forced to sell our stock at a reduced price to improve the aging of our inventory, our results of operations would be materially and adversely affect.

Our ability to distribute future dividends will be subject to various factors, some of which are beyond our control, and we may not be able to fulfill our dividend policy in the future.

In March 2009, we declared a cash dividend in the amount of $0.15 per ordinary share, or $0.30 per ADS, and a one-time special cash dividend in the amount of $0.225 per ordinary share, or $0.45 per ADS, out of our annual profits for the years ended December 31, 2007 and 2008.Our ability to distribute future dividends will be subject to various factors including, but not limited to, available cash and distributable reserves, investment requirements, and cash flow and working capital requirements, as well as the withholding tax obligations for dividend distribution under the PRC tax taw. These factors depend on other factors that are beyond our control, including a possible economic downturn and delays in the payments made by customers. If we encounter any of these problems or others, we may not be able to declare and pay dividends in the future as currently planned.

We are not required to pay dividends. Our shareholders or ADS holders also do not have contractual or other rights to require us to pay dividends. Our board may decide at any time, in its discretion, to decrease the amount of dividends under the dividend policy, change or revoke our dividend policy, or discontinue any payment of dividends.

Our ability to make distributions or other payments to our shareholders depends primarily on payments from WSP China, whose ability to make such payments is subject to PRC regulations. Under PRC laws and accounting rules, dividends may be paid only out of distributable profits. Distributable profits with respect to WSP China refers to its after-tax profits as determined under PRC accounting standards, less any recovery of accumulated losses and allocations to statutory funds that it is required to make. For example, it is required to allocate 10% of its after-tax profit to statutory reserves until such reserves reach 50% of WSP China’s registered capital. Allocations to these statutory reserves and funds can only be used for specific purposes and are not transferable to us in the form of loans, advances or cash dividends. The calculation of distributable profits of WSP China under PRC accounting standards differs in many respects from the equivalent calculation under U.S. GAAP. As a result, WSP China may not be able to pay dividends to us in any given year if it does not have distributable profits as determined under PRC accounting standards, even if we have profits for the relevant year as determined under U.S. GAAP. Accordingly, if we do not receive dividend distributions from WSP China, our liquidity, financial condition and ability to make dividend distributions will be materially and adversely affected.

Further, our dividend policy, to the extent implemented, will significantly restrict our cash reserves and may adversely affect our ability to fund unexpected capital expenditures. We may be required to borrow money or raise capital by issuing equity securities, which we may not be able to do so on attractive terms or at all. If we are unable to fulfill our dividend policy, or pay dividends at levels anticipated by investors, the market price of our ADSs may be negatively affected and the value of your investment may be reduced.

Our business is substantially dependent on the continuing devotion of our chairman and chief executive officer, and our business may be materially and adversely affected if we lose his service.

Mr. Piao Longhua, our chairman and chief executive officer, is a director and controlling shareholder of several private companies, including Eastar Industries, Inc., Expert Master Holdings Limited, or EMH, Lianyungang Eastar Photonics Technologies Co., Ltd., Regalia Investments Holdings Ltd., WSP Pipe LLC, Wuxi Huayi Investment Company Limited, Wuxi Longhua Steel Pipes Company Limited, or Wuxi Longhua and Cambodian WS Mining Industry Holding Ltd. The changing business environment may demand more of Mr. Piao’s time outside of our company. We cannot assure you that Mr. Piao will be able to devote substantially all of his time to our business given his duties to other companies. In addition, although none of these companies currently engages in the production and sale of OCTG products, we cannot assure you that they will not enter

13

into such business in the future. See “Item 6. Directors, Senior Management and Employees—C. Board Practices—Code of business conduct and ethics” for more details on our code of business conduct and ethics with respect to conflict of interests. If Mr. Piao is not able to devote a substantial amount of his time to our business, or if any dispute arises between Mr. Piao and us, we cannot assure you that we will be able to find a suitable replacement in a timely manner or at all, and our business may be adversely and materially affected.

Control or significant influence by our existing shareholders may limit your ability to affect the outcome of decisions requiring the approval of shareholders.

EMH owns approximately 50.9% of our issued share capital as of the date of this annual report. Mr. Piao, our chairman and chief executive officer, is the sole shareholder of EMH, and has control over our business, including matters relating to our management and policies and certain matters requiring the approval of our shareholders, such as election of directors, approval of significant corporate transactions and the timing and distribution of dividends. Furthermore, our articles of association contain a quorum requirement of at least a majority of our total outstanding shares present in person or by proxy. EMH, with an aggregate shareholding sufficient to constitute a quorum, could approve by itself actions that require a majority vote at shareholder meetings, which may not be in the best interest of our other shareholders. Furthermore, UMW China Ventures (L) Ltd., or UMW Ventures, which beneficially owns approximately 22.5% of our issued share capital as of the date of this annual report will have significant influence over our business. UMW Ventures is a wholly-owned subsidiary of UMW Holdings Berhad, or UMW. Our vice chairman, Abdul Halim bin Harun, was nominated by UMW. To the extent the interests of EMH or UMW conflict with the interests of other shareholders, the interests of other shareholders may be disadvantaged and harmed. Moreover, we have in the past entered into related party transactions with affiliates of EMH and UMW, and we expect to continue to enter into related party transactions, subject to our audit committee’s review and approval, if applicable.

We have limited insurance coverage in China.

The insurance industry in China is still at an early stage of development. Insurance companies in China offer limited commercial insurance products. We have determined that balancing the risks of disruption or liability from our business, or the loss or damage to our property, including our facilities, equipment and office furniture, the cost of insuring for these risks on the one hand, and the difficulties associated with acquiring such insurance on commercially reasonable terms on the other hand, makes it impractical for us to have such insurance. As a result, we only maintain property insurance with respect to our operations that covers general property, plant and equipment, and shipping and transportation. We do not have any product liability insurance covering our products, except for property liability insurance covering our products sold in North America. We do not maintain business interruption or key-man insurance in China. Consequently, any uninsured occurrence of loss or damage to property, litigation or business disruption may result in our incurring substantial costs and the diversion of resources, which could have an adverse effect on our operating results. The occurrence of certain incidents including fire, severe weather, earthquake, war, flooding, power outages and the consequences resulting from them may not be covered adequately, or may not be covered at all, by our insurance policies. If we were to incur substantial liabilities that were not covered by our insurance, or if our business operations were interrupted for more than a short period of time, we could incur costs and losses that could materially and adversely affect our results of operations.

We may not be able to obtain the necessary PRC government authorization, the land use rights certificate or the building ownership certificate for some of our properties and plants.

Pursuant to an agreement entered into in July 2008 with Hebei Bishi, WSP China acquired Mengfeng, a company located in Inner Mongolia, China. However, we have not obtained the necessary PRC government authorization for Mengfeng’s blast furnace project, the land use rights certificate for a piece of property of approximately 344,631 square meters and any of the ownership certificates for Mengfeng’s buildings. In addition, we do not have the land use rights certificate or the building ownership certificate for plants or facilities owned by five of our other subsidiaries with a gross floor area of approximately 567,146 square meters. We are in the process of obtaining PRC government authorization, the land use rights certificate or the building ownership certificate for these properties. However, there is no assurance that we will be able to obtain them. If we fail to obtain such authorization or certificates in a timely manner, or at all, we may be subject to severe penalties and fines, which could materially and adversely affect our financial condition and results of operations.

14

Economic and political conditions and instability in Thailand may adversely affect our operations.

WSP Pipe’s operations is subject to the changing economic and political conditions in Thailand. Our results of operations may be influenced in part by the political situation in Thailand, which is unstable. The political upheavals may have a severe adverse effect on Thailand’s economic and democratic development. Current and future political instability in Thailand could have a material adverse effect on our businesses and operations. In addition, we can not assure you that the Thai government would not amend foreign ownership rules or impose additional restrictions on foreign ownership that would have an adverse effect on our business.

We are subject to litigation proceedings brought by third-parties. If any of the proceedings against us is successful, it may have an adverse effect on our financial condition and operating results.

We are subject to litigation proceedings brought by third-parties. For instance, in December 2008, SB International, Inc., a Texas corporation, brought a case in a district court in Dallas County, Texas, against us, Mr. Longhua Piao and certain others, alleging that, among other things, the defendants interfered with the plaintiff’s contracts and business relations with its customers. There is no specific amount of damages claimed in the petition. Separately, there is another lawsuit brought against us in a district court in Lavaca County, Texas, alleging that we supplied defective products for a failed operation in an oil and gas well. Moreover, in August 2009, Western Oil & Gas Development Corp. brought a lawsuit against us in a district court in Canadian County, Oklahoma, alleged that a casing pipe provided by us caused damages to its well. In April 2010, Penn Virginia Oil & Gas L.P., filed a lawsuit against us in a district court in Panola County, Texas, alleging that a casing pipe provided by us caused a failed operation in an oil and gas well. In May 2010, WSP China was subject to a lawsuit in the district court in Desoto Parish, Louisiana, as the manufacturer of a casing pipe used in an alleged oil and gas well operation failure. See “Item 8. Financial Information—A. Consolidated Statements and Other Financial Information—Legal proceedings” for further information about the lawsuits. We are also subject to some other litigation proceedings brought by third-parties, which we believe are not material. We believe that the allegations in these cases are without merit and we intend to vigorously defend ourselves against the claims. The outcome of the these cases, like other litigation proceedings, is uncertain. We cannot assure you that in the future we will not be subject to litigation proceedings brought by third-parties arising from our operations or products. Regardless of their merit, litigation and other preparations undertaken to defend such cases can be costly, and we may incur substantial costs and expenses in doing so. They may also divert the attention of our management from our business and operations. If any of the cases against us is successful, it may result in substantial monetary liabilities, which may have a material adverse effect on our financial condition and operating results.

Risks related to doing business in China

The PRC’s economic, political and social conditions, as well as governmental policies, could affect the financial markets in China, our liquidity and access to capital and our ability to operate our business.

Substantially all of our business operations are conducted in China. Accordingly, our results of operations, financial condition and prospects are subject to a significant degree to economic, political and legal developments in China. China’s economy differs from the economies of developed countries in many respects, including with respect to the amount of government involvement, level of development, growth rate, control of foreign exchange and allocation of resources. While the PRC economy has experienced significant growth in the past 30 years, growth has been uneven across different regions and among various economic sectors of China. The PRC government has implemented various measures to encourage economic development and guide the allocation of resources. Some of these measures benefit the overall PRC economy, but may have a negative effect on us. For example, our financial condition and results of operations may be adversely affected by government control over capital investments or changes in tax regulations that are applicable to us. More generally, if the business environment in China deteriorates from the perspective of domestic or international investors, our business in China may also be adversely affected.

Uncertainties with respect to the PRC legal system could materially and adversely affect us.

We conduct our business primarily through our subsidiaries in China. PRC laws and regulations govern our operations in China. Our subsidiaries are generally subject to laws and regulations applicable to foreign investments in China and, in particular, laws applicable to wholly foreign-owned enterprises. The PRC legal system is based on written statutes. Prior court decisions may be cited for reference but have limited precedential value.

15