Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-Q

QUARTERLY SCHEDULE OF PORTFOLIO HOLDINGS

OF REGISTERED MANAGEMENT INVESTMENT COMPANY

Investment Company Act file number: 811-22167

Allianz Funds Multi-Strategy Trust

(Exact name of registrant as specified in charter)

1633 Broadway,

New York, NY 10019

(Address of principal executive offices) (Zip code)

Lawrence G. Altadonna

1633 Broadway,

New York, NY 10019

(Name and address of agent for service)

Registrant’s telephone number, including area code: 212-739-3371

Date of fiscal year end: November 30, 2013

Date of reporting period: May 31, 2013

Table of Contents

Item 1. Report to Shareholders

Allianz Multi-Strategy Funds

SHARE CLASSES A, B, C, D, R, P, INSTITUTIONAL, R6, ADMINISTRATIVE

Semiannual Report

May 31, 2013

AllianzGI Retirement 2015 Fund

AllianzGI Retirement 2020 Fund

AllianzGI Retirement 2025 Fund

AllianzGI Retirement 2030 Fund

AllianzGI Retirement 2035 Fund

AllianzGI Retirement 2040 Fund

AllianzGI Retirement 2045 Fund

AllianzGI Retirement 2050 Fund

AllianzGI Retirement 2055 Fund

AllianzGI Retirement Income Fund

AllianzGI Global Allocation Fund

AllianzGI Global Growth Allocation Fund

AllianzGI Behavioral Advantage Large Cap Fund

AllianzGI China Equity Fund

AllianzGI Convertible Fund

AllianzGI Disciplined Equity Fund

AllianzGI Dynamic Emerging Multi-Asset Fund

AllianzGI Global Managed Volatility Fund

AllianzGI Global Water Fund

AllianzGI High Yield Bond Fund

AllianzGI International Small-Cap Fund

AllianzGI Micro Cap Fund

AllianzGI Multi-Asset Real Return Fund

AllianzGI NFJ Emerging Markets Value Fund

AllianzGI NFJ Global Dividend Value Fund

AllianzGI NFJ International Small-Cap Value Fund

AllianzGI NFJ International Value II Fund

AllianzGI Redwood Fund

AllianzGI Short Duration High Income Fund

AllianzGI Structured Alpha Fund

AllianzGI Ultra Micro Cap Fund

AllianzGI U.S. Emerging Growth Fund

AllianzGI U.S. Equity Hedged Fund

This material is authorized for use only when preceded or accompanied by the current Allianz Multi-Strategy Funds prospectus. Investors should consider the investment objectives, risks, charges and expenses of each Fund carefully before investing. This and other information is contained in the Funds’ prospectuses. Please read the prospectus carefully before you invest or send money.

Table of Contents

A Word About Risk: A fund may be subject to various risks as described in its prospectus. Some of those risks may include, but are not limited to, the following: derivatives risk, small company risk, foreign investment risk and specific sector investment risks. Use of derivative instruments may involve certain costs and risks such as liquidity risk, interest rate risk, market risk, credit risk, management risk and the risk that a fund is unable to close out a position when it is most advantageous to do so. Portfolios investing in derivatives could lose more than the principal amount invested in those instruments. Investing in foreign securities may entail risk due to foreign economic and political developments; this risk may be enhanced when investing in emerging markets. Smaller companies may be more volatile than larger companies and may entail more risk. Concentrating investments in individual sectors may add additional risk and additional volatility compared to a diversified equity portfolio. AllianzGI target-date funds seek to manage risk and return by blending two separately-managed portfolios: a return-generating portfolio for growth potential, and a defensive portfolio for principal protection. The balance grows increasingly defensive over time until the target date is reached, after which the Fund’s assets roll into a retirement income strategy. The principal value of the Funds is not guaranteed at any time, including the target date. Please refer to the Fund’s applicable current prospectus for complete details.

Table of Contents

Brian S. Shlissel

President

Dear Shareholder,

The US economy continued to expand throughout the six-month fiscal reporting period ended May 31, 2013. In contrast, growth in many other developed countries moderated and in certain situations, fell into recession. Demand for equities and lower rated, higher yielding fixed income securities was generally solid as investors looked to generate incremental returns in the low interest rate environment.

Six Months in Review

For the six-month fiscal reporting period ended May 31, 2013, US stocks, as measured by the Standard & Poor’s 500 Index, rose 16.43%. Two measures of stock performance in developed international and global markets, the MSCI EAFE (Europe, Australasia and Far East) Index and the MSCI World Index, advanced 11.39% and 13.26% respectively, in dollar-denominated terms. The MSCI Emerging Markets Index rose 1.30%, in dollar-denominated terms.

With respect to bonds, the Barclays US Credit Index declined 0.86%, the Barclays US High Yield Index rose 5.79%, the Barclays US Government Bond Index decreased 1.35%, and the broader US bond market, as measured by the Barclays US Aggregate Index, fell 1.05%.

The US economy continued to grow during the six-month fiscal reporting period, however the pace of expansion was far from robust. Gross domestic product (“GDP”), the value of goods and services produced in the country, the broadest measure of economic activity and the principal indicator of economic performance, grew at an annual pace of 3.1% during the third quarter of 2012 before declining to an annual rate of 0.4% during the fourth quarter of 2012. GDP growth, however rebounded to a 1.8% annual rate during the first quarter of 2013.

While US economic data was mixed at times, there were continued signs of recovery in the housing market. In addition, while unemployment remains elevated, the unemployment rate dropped from 7.8% in November 2012 to 7.6% in May 2013. Elsewhere, despite concerns related to higher tax rates, the “fiscal cliff” and sequestration, consumer spending held up relatively well during the six-month reporting period.

The Federal Reserve (the “Fed”) initiated a number of actions to support the economy and reduce unemployment. In September 2012, prior to the beginning of the fiscal reporting period, the Fed introduced a third round of “quantitative easing” which entailed the purchase of $40 billion of mortgage securities each month. Toward the end of 2012, the Fed revealed that it

| 2 | May 31, 2013 | | Semiannual Report |

Table of Contents

would continue the purchase of $40 billion of mortgage securities each month, in addition to purchasing $45 billion per month of longer-term Treasuries on an open-ended basis. At its meeting in December 2012, the Fed indicated that it expected to keep the Fed Funds rate in the 0.0% to 0.25% range, “…as long as the unemployment rate remains above 6.5%,” provided that inflation remains well contained. The Fed maintained this stance at its meetings in January, March and May 2013.

Outlook

From a global economic perspective, key US economic indicators are continuing their slow but steady improvement. Japan’s economic growth also appears to be accelerating, perhaps from witnessing the initial impact of the new economic policies under Prime Minister Abe. However, growth in Asia (ex-Japan) and Latin America appears to be stagnating and euro-zone economies are experiencing a double-dip

recession, with the current retrenchment lasting longer than the sharp downturn at the onset of the financial crisis.

While US unemployment remains well above the Fed’s 6.5% target, recently there has been an increase in market volatility and rising Treasury yields. This was partially triggered by expectations that the Fed may begin tapering the amount of quantitative easing. We expect that the Fed will want more evidence that the economy is on solid footing prior to adjusting monetary policy and that tapering could be more of an issue in 2014. That being said,

there may continue to be periods of heightened volatility given incoming economic data and the market’s attempts to anticipate future Fed actions.

On behalf of Allianz Global Investors Fund Management and our Sub-Advisers, thank you for investing with us. We encourage you to consult with your financial advisor and to visit our website, us.allianzgi.com, for additional information. We remain dedicated to serving your investment needs.

Sincerely,

Brian S. Shlissel

President

Past performance is no guarantee of future results. Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. It is not possible to invest directly in an index.

Receive this report electronically and eliminate paper mailings.

To enroll, go to us.allianzgi.com/edelivery.

| Semiannual Report | | May 31, 2013 | 3 |

Table of Contents

Unaudited

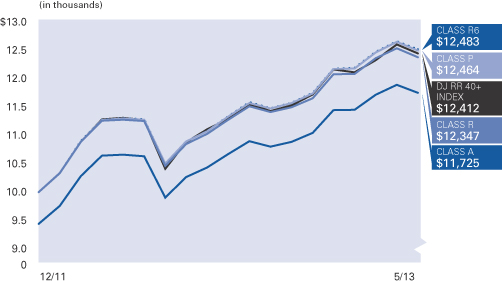

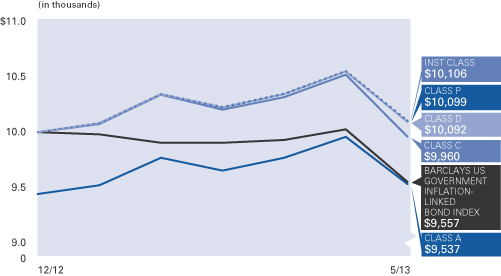

AllianzGI Retirement 2015 Fund (formerly Allianz Global Investors Solutions 2015 Fund)

For the period of December 1, 2012 through May 31, 2013, as provided by the Allianz Global Investors US Multi Asset Group.

Portfolio Insights

For the reporting period ended May 31, 2013, Class A shares at Net Asset Value (“NAV”) of the AllianzGI Retirement 2015 Fund (the “Fund”) returned 1.78% outperforming the Dow Jones Real Return 2015 Index (the “benchmark index”) which returned -0.27%.

What Happened

For the six months ended May 31, 2013, the dominant theme for global market returns has been central bank policy. Quantitative Easing (QE) has gone global and is the single most dominant force in global markets. Turning from QE to the fundamentals of economic growth and earnings, in the US, the economy continued to grow, albeit at a slower pace than initially expected, with first quarter GDP expanding at 2.4%. In Europe, the struggle for growth remains a persistent theme, which has forced the European Central Bank (ECB) to take more unconventional policy actions including, in early May, raising the prospect of introducing negative interest rates on deposits at the ECB. Further evidence of a slowdown in emerging markets, mainly the BRICs, continued to trickle in during the period.

During the past six months, there have been three major market-moving events. First, the most radical quantitative easing experiment to date was announced and then implemented in Japan following the election of Shinzo Abe to Prime Minister in December. A second new theme is the uncertainty surrounding the timing and size of the Federal Reserve’s (the “Fed’s”) beginning of the end of QE, the so-called “taper,” when the Fed reduces its monthly bond purchases from its current rate of $85 billion. Third, on the fiscal front in the US, the threat of a sequester and fear of a government shutdown ended with the sequester slowing government spending while tax revenues are up in a growing (even if slowly) economy, producing a rapidly improving fiscal position. The US federal deficit is now on track to decline from more than 10% of GDP to around 4% of GDP by the end of the fiscal year (based on Congressional Budget Office projections).

Quantitative easing around the world drove risk asset returns in the developed world. For the period, equities returned 47.7% in Japan, 16.5% in the US and 13.3% in Europe (all equity returns based on MSCI indexes, local currency). The link

between central bank asset purchases and equity performance has strengthened significantly since quantitative easing was first initiated: in the US, since November 2008, the correlation between the Fed’s balance sheet and the S&P 500 Index is over .90 (whereas in the five years leading up to the financial crisis, the correlation is less than 0.2).1

The questions surrounding the taper—both when and how quickly the Fed will put the brakes on asset purchases—also resulted in higher volatility across asset markets for the period, while core fixed income generally sold off toward the end of the period and equities rallied. Within fixed income, high yield and convertibles stand out as exceptions returning 5.50% and 14.57% for the period, respectively. US Treasuries suffered as the 10-year yield increased from a low of 1.59% on December 6, 2012 to an intraday high of 2.23% on May 29, 2013—a pronounced move given that that the yield had remained well below 2 percent since April 2012.

When interpreting economic evidence through the prism of the taper, not only is good economic data good for equity returns but bad economic data has also been good news for developed market equities—when it signifies that the Fed will continue to provide liquidity to markets for longer. For most of the rest of the world in equity and commodity markets returns were flat to down. Emerging market equities returned 1.5%. The broad commodity futures were down 8.5% in the period with precious metals suffering the biggest decline, down 22.8% and gold futures down 18.9% (returns based on DJ UBS Commodity Index, Sub Precious Metals Index and Gold Index).

Portfolio Review

During the six month period, the Fund held overweight positions in US small-cap equities, US

and non-US fixed-income assets and short-term Treasury inflation protected securities (TIPS). The Fund held underweights in US large- cap and non-US equities, including emerging markets and in real return assets, including real estate and commodities as well as in intermediate-term TIPS.

In the return generating part of portfolio, the equity holdings underperformed their benchmark. This was mostly due to underperformance in large cap equities as a result of both allocation and fund selection effects. The Fund was underweight US large cap equities in a period in which the Russell 1000 Index returned 16.68%. Selection effects in US small cap also detracted. Positive fund selection in international equities and emerging markets contributed to performance, helping to offset the negative effect from being underweight those sectors. Exposure to underlying funds implementing managed volatility strategies was a contributor to performance during the period as well.

In the defensive part of the portfolio, the Fund’s aggregate nominal bond positions outperformed the fixed income benchmark mainly due to fund selection and an overweight in agency and non-agency mortgage backed securities. The PIMCO Income Fund was up 6.58% in the period, with an excess return of 7.63% percentage points versus the Barclays US Aggregate Bond Index. A large allocation to the PIMCO Income Fund as well as the PIMCO Mortgage Opportunities Fund enabled the portfolios to gain exposure to the recovery in the housing market in the US and was part of the rationale for the underweight in equities.

The TIPS portion of the fixed income portfolio also contributed to performance due to asset allocation—a large underweight to intermediate term TIPS—and fund selection. Within the Fixed Income universe, TIPS overall underperformed Treasuries as the Barclays US Treasury US TIPS TR Index returned -4.57% versus the Barclays Aggregate Bond Treasury TR Index which was down 1.05%.

The Fund outperformed in commodities, due to a combination of being underweight the commodity benchmark, which was down 8.49% (based on the DJ UBS Commodity Total Return Index) for the period and positive fund selection.

1. Correlation is a measure of how two or more items move together. Perfect positive and negative correlation are 1 and -1, respectively. Zero indicates no correlation.

| 4 | May 31, 2013 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Retirement 2015 Fund (formerly Allianz Global Investors Solutions 2015 Fund) (cont’d)

In real estate, the Fund underperformed its benchmark. Fund selection and a tilt toward global REITs detracted from performance in this sector. For the quarter, the S&P United States Property Index outperformed the S&P Europe Property Index by more than 4%.

Outlook

Economic theory tells us that 10-year treasury yields will, in time, match long-term nominal GDP, at around 4% given the Fed’s 2% target inflation. However, the paths to get there and the timing remain uncertain. One virtuous path entails global growth accelerating and economic data steadily improving. The other path is dominated by eroding pricing power and a lack of improvement in the labor market. Both paths will lead to higher interest rates. But the first would be associated with good returns in

equities while the second would be associated with equity losses.

More broadly, we are either experiencing the great rotation into equity market outperformance and global growth or the early stages of another global slowdown. An expansion in global growth would be led by the US and emerging markets and would be associated with a recovery in Europe and an escape from deflation in Japan. In such a scenario, we would expect earnings to grow and valuations to continue to improve.

Chairman Bernanke, in particular, has stated that the risks to taking stimulus out of the economy too soon outweigh the risks of keeping quantitative easing in place too long. Thus, should the global economy slow, the Fed, along

with other developed country central banks will likely err on the side of maintaining low to negative real rates.

If evidence mounts that suggests that the world is healing and growth is accelerating, we are prepared to systematically add to risk assets, targeting those with the most attractive valuations. We are positioned to be liquidity suppliers. The portfolios are overweight high-quality dividend-paying stocks, overweight US stocks and remain underweight euro-zone stocks. The portfolios are modestly underweight commodities and real estate, as well as underweight nominal duration. All of the portfolios are within their benchmark-determined risk budgets.

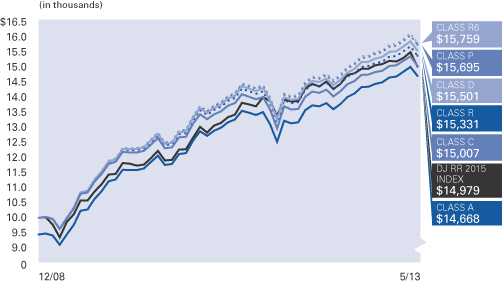

Average Annual Total Return for the period ended May 31, 2013

| 6 Month* | 1 Year | Since Inception† | ||||||||||||

| AllianzGI Retirement 2015 Fund Class A | 1.78% | 8.03% | 10.46% | |||||||||||

| AllianzGI Retirement 2015 Fund Class A (adjusted) | –3.82% | 2.09% | 9.05% | ||||||||||

| AllianzGI Retirement 2015 Fund Class C | 1.38% | 7.20% | 9.62% | |||||||||||

| AllianzGI Retirement 2015 Fund Class C (adjusted) | 0.39% | 6.20% | 9.62% | ||||||||||

| AllianzGI Retirement 2015 Fund Class D | 1.69% | 7.88% | 10.42% | ||||||||||

| AllianzGI Retirement 2015 Fund Class R | 1.60% | 7.67% | 10.15% | ||||||||||

| AllianzGI Retirement 2015 Fund Class P | 1.92% | 8.37% | 10.74% | ||||||||||

| AllianzGI Retirement 2015 Fund Class R6 | 2.00% | 8.46% | 10.84% | ||||||||||

| AllianzGI Retirement 2015 Fund Administrative Class | 1.77% | 8.05% | 10.51% | |||||||||||

| Dow Jones Real Return 2015 Index | –0.27% | 5.23% | 9.57% | ||||||||||

| Lipper Mixed-Asset Target 2015 Funds Average | 5.14% | 12.61% | 11.33% | |||||||||||

† The Fund began operations on 12/29/08. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on 12/31/08.

* Cumulative return.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares and the contingent deferred sales charge (CDSC) of 1% on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 94 and 95 for more information. The Fund’s gross expense ratios are 1.16% for Class A shares, 1.91% for Class C shares, 1.16% for Class D shares, 1.41% for Class R shares, 0.76% for Class P shares, 0.66% for Class R6 shares and 1.01% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least 3/31/14. The Fund’s expense ratios net of this reduction are 0.97% for Class A shares, 1.72% for Class C shares, 1.07% for Class D shares, 1.32% for Class R shares, 0.67% for Class P shares, 0.57% for Class R6 shares and 0.92% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated April 1, 2013, as supplemented to date.

| Semiannual Report | | May 31, 2013 | 5 |

Table of Contents

Unaudited

AllianzGI Retirement 2015 Fund (formerly Allianz Global Investors Solutions 2015 Fund) (cont’d)

Cumulative Returns Through May 31, 2013

Fund Allocation (as of May 31, 2013)

| PIMCO Real Return | 30.1% | |||

| PIMCO Income | 9.1% | |||

| PIMCO Foreign Bond (U.S. Dollar-Hedged) | 6.9% | |||

| PIMCO Mortgage Opportunities | 6.0% | |||

| PIMCO Short-Term | 6.0% | |||

| PIMCO Floating Income | 4.0% | |||

| AllianzGI Income & Growth | 4.0% | |||

| Wells Fargo Advantage Short-Term High Yield Bond | 3.6% | |||

| Other | 29.7% | |||

| Cash & Equivalents — Net | 0.6% |

| Shareholder Expense Example | Actual Performance | |||||||||||||

| Class A | Class C | Class D | Class R | Class P | Class R6 | Administrative Class | ||||||||

| Beginning Account Value (12/1/12) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

| Ending Account Value (5/31/13) | $1,017.80 | $1,013.80 | $1,016.90 | $1,016.00 | $1,019.20 | $1,020.00 | $1,017.70 | |||||||

| Expenses Paid During Period | $2.06 | $5.82 | $2.56 | $3.82 | $0.55 | $0.05 | $1.81 | |||||||

| Hypothetical Performance | ||||||||||||||

| (5% return before expenses) | ||||||||||||||

| Class A | Class C | Class D | Class R | Class P | Class R6 | Administrative Class | ||||||||

| Beginning Account Value (12/1/12) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

| Ending Account Value (5/31/13) | $1,022.89 | $1,019.15 | $1,022.39 | $1,021.14 | $1,024.38 | $1,024.88 | $1,023.14 | |||||||

| Expenses Paid During Period | $2.07 | $5.84 | $2.57 | $3.83 | $0.56 | $0.05 | $1.82 | |||||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.41% for Class A, 1.16% for Class C, 0.51% for Class D, 0.76% for Class R, 0.11% for Class P, 0.01% for Class R6 and 0.36% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. The expense ratio excludes the expenses of the Underlying Funds, which based upon the allocation of the Fund’s assets among the Underlying Funds are indirectly borne by the shareholders of the Fund.

| 6 | May 31, 2013 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | May 31, 2013 | 7 |

Table of Contents

Unaudited

AllianzGI Retirement 2020 Fund (formerly Allianz Global Investors Solutions 2020 Fund)

For the period of December 1, 2012 through May 31, 2013, as provided by the Allianz Global Investors US Multi Asset Group.

Portfolio Insights

For the reporting period ended May 31, 2013, Class A shares at NAV of the AllianzGI Retirement 2020 Fund (the “Fund”) returned 2.18% outperforming the Dow Jones Real Return 2020 Index (the “benchmark index”) which returned 0.38%.

For the six months ended May 31, 2013, the dominant theme for global market returns has been central bank policy. Quantitative Easing (QE) has gone global and is the single most dominant force in global markets. Turning from QE to the fundamentals of economic growth and earnings, in the US, the economy continued to grow, albeit at a slower pace than initially expected, with first quarter GDP expanding at 2.4%. In Europe, the struggle for growth remains a persistent theme, which has forced the European Central Bank (ECB) to take more unconventional policy actions including, in early May, raising the prospect of introducing negative interest rates on deposits at the ECB. Further evidence of a slowdown in emerging markets, mainly the BRICs, continued to trickle in during the period.

During the past six months, there have been three major market-moving events. First, the most radical quantitative easing experiment to date was announced and then implemented in Japan following the election of Shinzo Abe to Prime Minister in December. A second new theme is the uncertainty surrounding the timing and size of the Federal Reserve’s (the “Fed’s”) beginning of the end of QE, the so-called “taper,” when the Fed reduces its monthly bond purchases from its current rate of $85 billion. Third, on the fiscal front in the US, the threat of a sequester and fear of a government shutdown ended with the sequester slowing government spending while tax revenues are up in a growing (even if slowly) economy, producing a rapidly improving fiscal position. The US federal deficit is now on track to decline from more than 10% of GDP to around 4% of GDP by the end of the fiscal year (based on Congressional Budget Office projections).

Quantitative easing around the world drove risk asset returns in the developed world. For the period, equities returned 47.7% in Japan, 16.5% in the US and 13.3% in Europe (all equity returns based on MSCI indexes, local currency). The link between central bank asset purchases and equity

performance has strengthened significantly since quantitative easing was first initiated: in the US, since November 2008, the correlation

between the Fed’s balance sheet and the S&P 500 Index is over .90 (whereas in the five years leading up to the financial crisis, the correlation is less than 0.2).

The questions surrounding the taper—both when and how quickly the Fed will put the brakes on asset purchases—also resulted in higher volatility across asset markets for the period, while core fixed income generally sold off toward the end of the period and equities rallied. Within fixed income, high yield and convertibles stand out as exceptions returning 5.50% and 14.57% for the period, respectively. US Treasuries suffered as the 10-year yield increased from a low of 1.59% on December 6, 2012 to an intraday high of 2.23% on May 29, 2013—a pronounced move given that that the yield had remained well below 2 percent since April 2012.

When interpreting economic evidence through the prism of the taper, not only is good economic data good for equity returns but bad economic data has also been good news for developed market equities—when it signifies that the Fed will continue to provide liquidity to markets for longer. For most of the rest of the world in equity and commodity markets returns were flat to down. Emerging market equities returned 1.5%. The broad commodity futures were down 8.5% in the period with precious metals suffering the biggest decline, down 22.8% and gold futures down 18.9% (returns based on DJ UBS Commodity Index, Sub Precious Metals Index and Gold Index).

Portfolio Review

During the six month period and relative to its benchmark index, the Fund held overweight positions in US small-cap equities, US and non-US fixed-income assets and short-term Treasury inflation protected securities (TIPS). The Fund held underweights in US large- cap and non-US equities, including emerging markets and in real return assets, including real estate and commodities as well as in intermediate-term TIPS.

In the return generating part of portfolio, the equity holdings underperformed their benchmark. This was mostly due to underperformance in large cap equities as a result of both allocation and fund selection effects. The Fund was underweight US large cap in a period in which the Russell 1000 Index returned 16.68%. Selection effects in US small cap also detracted. Positive fund selection in international equities and emerging markets contributed to performance, helping to offset the negative effect from being underweight those sectors. Exposure to underlying funds implementing managed volatility strategies was a contributor to performance during the period as well.

In the defensive part of the portfolio, the Fund’s aggregate nominal bond positions outperformed the fixed income benchmark mainly due to fund selection and an overweight in agency and non-agency mortgage backed securities. The PIMCO Income Fund was up 6.58% in the period, with an excess return of 7.63% percentage points versus the Barclays US Aggregate Bond Index. A large allocation to the PIMCO Income Fund as well as the PIMCO Mortgage Opportunities Fund enabled the portfolios to gain exposure to the recovery in the housing market in the US and was part of the rationale for the underweight in equities.

The TIPS portion of the fixed income portfolio also contributed to performance due to asset allocation—a large underweight to intermediate term TIPS—and fund selection. Within the Fixed Income universe, TIPS overall underperformed Treasuries as the Barclays US Treasury US TIPS TR Index returned -4.57% versus the Barclays Aggregate Bond Treasury TR Index which was down 1.05%.

The Fund outperformed in commodities, due to a combination of being underweight the commodity benchmark, which was down 8.49% (based on the DJ UBS Commodity Total Return Index) for the period and positive fund selection.

In real estate, the Fund underperformed its benchmark. Fund selection and a tilt toward global REITs detracted from performance in this sector. For the quarter, the S&P United States Property Index outperformed the S&P Europe Property Index by more than 4%.

| 8 | May 31, 2013 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Retirement 2020 Fund (formerly Allianz Global Investors Solutions 2020 Fund) (cont’d)

Outlook

Economic theory tells us that 10-year treasury yields will, in time, match long-term nominal GDP, at around 4% given the Fed’s 2% target inflation. However, the paths to get there and the timing remain uncertain. One virtuous path entails global growth accelerating and economic data steadily improving. The other path is dominated by eroding pricing power and a lack of improvement in the labor market. Both paths will lead to higher interest rates. But the first would be associated with good returns in equities while the second would be associated with equity losses.

More broadly, we are either experiencing the great rotation into equity market

outperformance and global growth or the early stages of another global slowdown. An expansion in global growth would be led by the US and emerging markets and would be associated with a recovery in Europe and an escape from deflation in Japan. In such a scenario, we would expect earnings to grow and valuations to continue to improve.

Chairman Bernanke, in particular, has stated that the risks to taking stimulus out of the economy too soon outweigh the risks of keeping quantitative easing in place too long. Thus, should the global economy slow, the Fed, along with other developed country central banks will likely err on the side of maintaining low to negative real rates.

If evidence mounts that suggests that the world is healing and growth is accelerating, we are prepared to systematically add to risk assets, targeting those with the most attractive valuations. We are positioned to be liquidity suppliers. The portfolios are overweight high-quality dividend-paying stocks, overweight US stocks and remain underweight euro-zone stocks. The portfolios are modestly underweight commodities and real estate, as well as underweight nominal duration. All of the portfolios are within their benchmark-determined risk budgets.

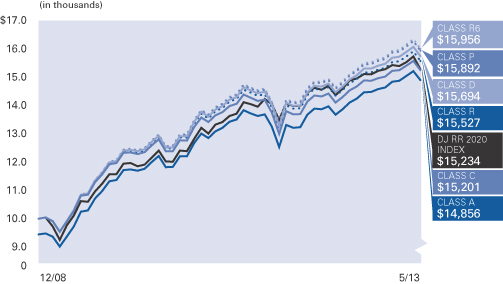

Average Annual Total Return for the period ended May 31, 2013

| 6 Month* | 1 Year | Since Inception† | ||||||||||||

| AllianzGI Retirement 2020 Fund Class A | 2.18% | 8.89% | 10.78% | |||||||||||

| AllianzGI Retirement 2020 Fund Class A (adjusted) | –3.44% | 2.90% | 9.37% | ||||||||||

| AllianzGI Retirement 2020 Fund Class C | 1.82% | 8.04% | 9.93% | |||||||||||

| AllianzGI Retirement 2020 Fund Class C (adjusted) | 0.82% | 7.04% | 9.93% | ||||||||||

| AllianzGI Retirement 2020 Fund Class D | 2.16% | 8.80% | 10.73% | ||||||||||

| AllianzGI Retirement 2020 Fund Class R | 1.99% | 8.51% | 10.47% | ||||||||||

| AllianzGI Retirement 2020 Fund Class P | 2.34% | 9.25% | 11.06% | ||||||||||

| AllianzGI Retirement 2020 Fund Class R6 | 2.36% | 9.32% | 11.15% | ||||||||||

| AllianzGI Retirement 2020 Fund Administrative Class | 2.23% | 8.91% | 10.83% | |||||||||||

| Dow Jones Real Return 2020 Index | 0.38% | 6.30% | 10.00% | ||||||||||

| Lipper Mixed-Asset Target 2020 Funds Average | 6.04% | 13.89% | 11.99% | |||||||||||

† The Fund began operations on 12/29/08. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on 12/31/08.

* Cumulative return.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares and the contingent deferred sales charge (CDSC) of 1% on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 94 and 95 for more information. The Fund’s gross expense ratios are 1.20% for Class A shares, 1.95% for Class C shares, 1.20% for Class D shares, 1.45% for Class R shares, 0.80% for Class P shares, 0.70% for Class R6 shares and 1.05% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least 3/31/14. The Fund’s expense ratios net of this reduction are 0.99% for Class A shares, 1.74% for Class C shares, 1.09% for Class D shares, 1.34% for Class R shares, 0.69% for Class P shares, 0.59% for Class R6 shares and 0.94% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated April 1, 2013, as supplemented to date.

| Semiannual Report | | May 31, 2013 | 9 |

Table of Contents

Unaudited

AllianzGI Retirement 2020 Fund (formerly Allianz Global Investors Solutions 2020 Fund) (cont’d)

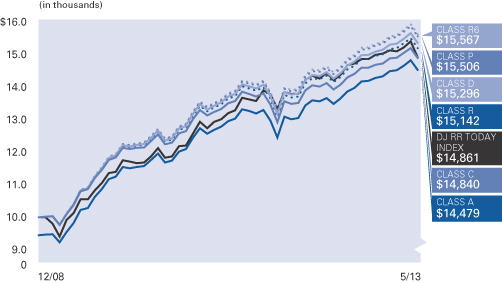

Cumulative Returns Through May 31, 2013

Fund Allocation (as of May 31, 2013)

PIMCO Real Return | 30.1% | |||

PIMCO Income | 9.0% | |||

PIMCO Mortgage Opportunities | 6.0% | |||

PIMCO Foreign Bond (U.S. Dollar-Hedged) | 5.5% | |||

PIMCO Floating Income | 4.5% | |||

AllianzGI Income & Growth | 4.0% | |||

AllianzGI NFJ Dividend Value | 3.7% | |||

AllianzGI NFJ Global Dividend Value | 3.6% | |||

Other | 32.8% | |||

Cash & Equivalents — Net | 0.8% |

| Shareholder Expense Example | Actual Performance | |||||||||||||

| Class A | Class C | Class D | Class R | Class P | Class R6 | Administrative Class | ||||||||

Beginning Account Value (12/1/12) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

Ending Account Value (5/31/13) | $1,021.80 | $1,018.20 | $1,021.60 | $1,019.90 | $1,023.40 | $1,023.60 | $1,022.30 | |||||||

Expenses Paid During Period | $2.17 | $5.94 | $2.67 | $3.93 | $0.66 | $0.15 | $1.92 | |||||||

Hypothetical Performance | ||||||||||||||

(5% return before expenses) | ||||||||||||||

Class A | Class C | Class D | Class R | Class P | Class R6 | Administrative | ||||||||

Beginning Account Value (12/1/12) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

Ending Account Value (5/31/13) | $1,022.79 | $1,019.05 | $1,022.29 | $1,021.04 | $1,024.28 | $1,024.78 | $1,023.04 | |||||||

Expenses Paid During Period | $2.17 | $5.94 | $2.67 | $3.93 | $0.66 | $0.15 | $1.92 | |||||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.43% for Class A, 1.18% for Class C, 0.53% for Class D, 0.78% for Class R, 0.13% for Class P, 0.03% for Class R6 and 0.38% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. The expense ratio excludes the expenses of the Underlying Funds, which based upon the allocation of the Fund’s assets among the Underlying Funds are indirectly borne by the shareholders of the Fund.

| 10 | May 31, 2013 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | May 31, 2013 | 11 |

Table of Contents

Unaudited

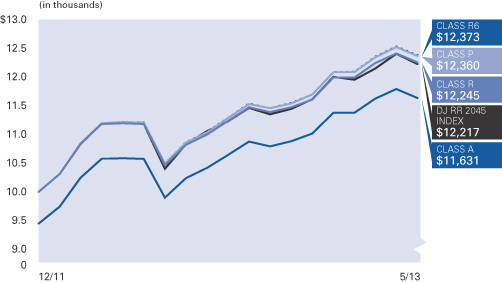

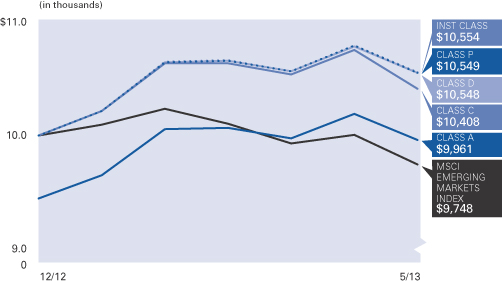

AllianzGI Retirement 2025 Fund (formerly Allianz Global Investors Solutions 2025 Fund)

For the period of December 1, 2012 through May 31, 2013, as provided by the Allianz Global Investors US Multi Asset Group.

Portfolio Insights

For the reporting period ended May 31, 2013, Class A shares at NAV of the AllianzGI Retirement 2025 Fund (the “Fund”) returned 2.43% outperforming the Dow Jones Real Return 2025 Index (the “benchmark index”) which returned 1.36%.

What Happened

For the six months ending May 31, 2013 the dominant theme for global market returns has been central bank policy. Quantitative Easing (QE) has gone global and is the single most dominant force in global markets. Turning from QE to the fundamentals of economic growth and earnings, in the US, the economy continued to grow, albeit at a slower pace than initially expected, with first quarter GDP expanding at 2.4%. In Europe, the struggle for growth remains a persistent theme, which has forced the European Central Bank (ECB) to take more unconventional policy actions including, in early May, raising the prospect of introducing negative interest rates on deposits at the ECB. Further evidence of a slowdown in emerging markets, mainly the BRICs, continued to trickle in during the period.

During the past six months, there have been three major market-moving events. First, the most radical quantitative easing experiment to date was announced and then implemented in Japan following the election of Shinzo Abe to Prime Minister in December. A second new theme is the uncertainty surrounding the timing and size of the Federal Reserve’s (the “Fed’s”) beginning of the end of QE, the so-called “taper,” when the Fed reduces its monthly bond purchases from its current rate of $85 billion. Third, on the fiscal front in the US, the threat of a sequester and fear of a government shutdown ended with the sequester slowing government spending while tax revenues are up in a growing (even if slowly) economy, producing a rapidly improving fiscal position. The US federal deficit is now on track to decline from more than 10% of GDP to around 4% of GDP by the end of the fiscal year (based on Congressional Budget Office projections).

Quantitative easing around the world drove risk asset returns in the developed world. For the period, equities returned 47.7% in Japan, 16.5% in the US and 13.3% in Europe (all equity returns based on MSCI indexes, local currency). The link between central bank asset purchases and equity performance has strengthened significantly

since quantitative easing was first initiated: in the US, since November 2008, the correlation between the Fed’s balance sheet and the S&P 500 Index is over .90 (whereas in the five years leading up to the financial crisis, the correlation is less than 0.2).

The questions surrounding the taper—both when and how quickly the Fed will put the brakes on asset purchases—also resulted in higher volatility across asset markets for the period, while core fixed income generally sold off toward the end of the period and equities rallied. Within fixed income, high yield and convertibles stand out as exceptions returning 5.50% and 14.57% for the period, respectively. US Treasuries suffered as the 10-year yield increased from a low of 1.59% on December 6, 2012 to an intraday high of 2.23% on May 29, 2013—a pronounced move given that that the yield had remained well below 2 percent since April 2012.

When interpreting economic evidence through the prism of the taper, not only is good economic data good for equity returns but bad economic data has also been good news for developed market equities—when it signifies that the Fed will continue to provide liquidity to markets for longer. For most of the rest of the world in equity and commodity markets returns were flat to down. Emerging market equities returned 1.5%. The broad commodity futures were down 8.5% in the period with precious metals suffering the biggest decline, down 22.8% and gold futures down 18.9% (returns based on DJ UBS Commodity Index, Sub Precious Metals Index and Gold Index).

Portfolio Review

During the six month period, and relative to its benchmark index, the Fund held overweight positions in US small-cap equities, US and non-US fixed-income assets and short-term Treasury inflation protected securities (TIPS). The Fund held underweights in US large- cap and non-US

equities, including emerging markets and in real return assets, including real estate and commodities as well as in intermediate-term TIPS.

In the return generating part of portfolio, the equity holdings underperformed their benchmark. This was mostly due to underperformance in large cap equities as a result of both allocation and fund selection effects. The Fund was underweight US large cap in a period in which the Russell 1000 Index returned 16.68%. Selection effects in US small cap also detracted. Positive fund selection in international equities and emerging markets contributed to performance, helping to offset the negative effect from being underweight those sectors. Exposure to underlying funds implementing managed volatility strategies was a contributor to performance during the period as well.

In the defensive part of the portfolio, the Fund’s aggregate nominal bond positions outperformed the fixed income benchmark mainly due to fund selection and an overweight in agency and non-agency mortgage backed securities. The PIMCO Income Fund was up 6.58% in the period, with an excess return of 7.63% percentage points versus the Barclays US Aggregate Bond Index. A large allocation to the PIMCO Income Fund as well as the PIMCO Mortgage Opportunities Fund enabled the portfolios to gain exposure to the recovery in the housing market in the US and was part of the rationale for the underweight in equities.

The TIPS portion of the fixed income portfolio also contributed to performance due to asset allocation—a large underweight to intermediate term TIPS—and fund selection. Within the Fixed Income universe, TIPS overall underperformed Treasuries as the Barclays US Treasury US TIPS TR Index returned -4.57% versus the Barclays Aggregate Bond Treasury TR Index which was down 1.05%.

The Fund outperformed in commodities, due to a combination of being underweight the commodity benchmark, which was down 8.49% (based on the DJ UBS Commodity Total Return Index USD) for the period and positive fund selection.

In real estate, the Fund underperformed its benchmark. Fund selection and a tilt toward global REITs detracted from performance in this

| 12 | May 31, 2013 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Retirement 2025 Fund (formerly Allianz Global Investors Solutions 2025 Fund) (cont’d)

sector. For the quarter, the S&P United States Property Index outperformed the S&P Europe Property Index by more than 4%.

Outlook

Economic theory tells us that 10-year treasury yields will, in time, match long-term nominal GDP, at around 4% given the Fed’s 2% target inflation. However, the paths to get there and the timing remain uncertain. One virtuous path entails global growth accelerating and economic data steadily improving. The other path is dominated by eroding pricing power and a lack of improvement in the labor market. Both paths will lead to higher interest rates. But the first would be associated with good returns in equities while the second would be associated with equity losses.

More broadly, we are either experiencing the great rotation into equity market outperformance and global growth or the early stages of another global slowdown. An expansion in global growth would be led by the US and emerging markets and would be associated with a recovery in Europe and an escape from deflation in Japan. In such a scenario, we would expect earnings to grow and valuations to continue to improve.

Chairman Bernanke, in particular, has stated that the risks to taking stimulus out of the economy too soon outweigh the risks of keeping quantitative easing in place too long. Thus, should the global economy slow, the Fed, along with other developed country central banks will

likely err on the side of maintaining low to negative real rates.

If evidence mounts that suggests that the world is healing and growth is accelerating, we are prepared to systematically add to risk assets, targeting those with the most attractive valuations. We are positioned to be liquidity suppliers. The portfolios are overweight high-quality dividend-paying stocks, overweight US stocks and remain underweight euro-zone stocks. The portfolios are modestly underweight commodities and real estate, as well as underweight nominal duration. All of the portfolios are within their benchmark-determined risk budgets.

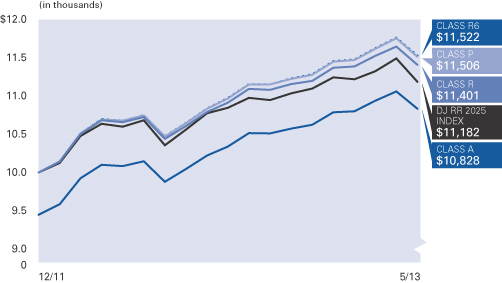

Average Annual Total Return for the period ended May 31, 2013

| 6 Month* | 1 Year | Since Inception† | ||||||||||||

| AllianzGI Retirement 2025 Fund Class A | 2.43% | 9.63% | 9.85% | |||||||||||

| AllianzGI Retirement 2025 Fund Class A (adjusted) | –3.20% | 3.60% | 5.64% | ||||||||||

| AllianzGI Retirement 2025 Fund Class R | 2.23% | 9.22% | 9.46% | ||||||||||

| AllianzGI Retirement 2025 Fund Class P | 2.55% | 9.94% | 10.17% | ||||||||||

| AllianzGI Retirement 2025 Fund Class R6 | 2.64% | 10.03% | 10.28% | ||||||||||

| AllianzGI Retirement 2025 Fund Administrative Class | 2.50% | 9.62% | 9.90% | |||||||||||

| Dow Jones Real Return 2025 Index | 1.36% | 7.98% | 8.02% | ||||||||||

| Lipper Mixed-Asset Target 2025 Funds Average | 8.05% | 17.17% | 14.05% | |||||||||||

† The Fund began operations on 12/19/11. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on 12/31/11.

* Cumulative return.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 94 and 95 for more information. The Fund’s gross expense ratios are 1.22% for Class A shares, 1.47% for Class R shares, 0.82% for Class P shares, 0.72% for Class R6 shares and 1.07% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least 3/31/14. The Fund’s expense ratios net of this reduction are 1.01% for Class A shares, 1.36% for Class R shares, 0.71% for Class P shares, 0.61% for Class R6 shares and 0.96% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated April 1, 2013, as supplemented to date.

| Semiannual Report | | May 31, 2013 | 13 |

Table of Contents

Unaudited

AllianzGI Retirement 2025 Fund (formerly Allianz Global Investors Solutions 2025 Fund) (cont’d)

Cumulative Returns Through May 31, 2013

Fund Allocation (as of May 31, 2013)

| PIMCO Real Return | 26.7% | |||

| PIMCO Income | 7.6% | |||

| PIMCO Mortgage Opportunities | 6.1% | |||

| PIMCO Foreign Bond (U.S. Dollar-Hedged) | 5.1% | |||

| PIMCO Floating Income | 4.5% | |||

| AllianzGI NFJ Global Dividend Value | 4.2% | |||

| AllianzGI Income & Growth | 4.0% | |||

| AllianzGI NFJ Dividend Value | 3.8% | |||

| Other | 37.3% | |||

| Cash & Equivalents — Net | 0.7% |

| Shareholder Expense Example | Actual Performance | |||||||||

| Class A | Class R | Class P | Class R6 | Administrative Class | ||||||

| Beginning Account Value (12/1/12) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (5/31/13) | $1,024.30 | $1,022.30 | $1,025.50 | $1,026.40 | $1,025.00 | |||||

| Expenses Paid During Period | $2.17 | $3.93 | $0.66 | $0.15 | $1.92 | |||||

| Hypothetical Performance | ||||||||||

| (5% return before expenses) | ||||||||||

| Class A | Class R | Class P | Class R6 | Administrative Class | ||||||

| Beginning Account Value (12/1/12) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (5/31/13) | $1,022.79 | $1,021.04 | $1,024.28 | $1,024.78 | $1,023.04 | |||||

| Expenses Paid During Period | $2.17 | $3.93 | $0.66 | $0.15 | $1.92 | |||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.43% for Class A, 0.78% for Class R, 0.13% for Class P, 0.03% for Class R6 and 0.38% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. The expense ratio excludes the expenses of the Underlying Funds, which based upon the allocation of the Fund’s assets among the Underlying Funds are indirectly borne by the shareholders of the Fund.

| 14 | May 31, 2013 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | May 31, 2013 | 15 |

Table of Contents

Unaudited

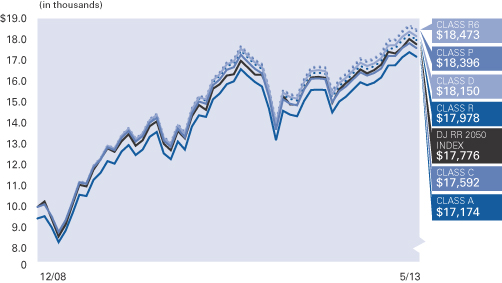

AllianzGI Retirement 2030 Fund (formerly Allianz Global Investors Solutions 2030 Fund)

For the period of December 1, 2012 through May 31, 2013, as provided by the Allianz Global Investors US Multi Asset Group.

Portfolio Insights

For the reporting period ended May 31, 2013, Class A shares at NAV of the AllianzGI Retirement 2030 Fund (the “Fund”) returned 3.94% outperforming the Dow Jones Real Return 2030 Index (the “benchmark index”) which returned 2.70%.

What Happened

For the six months ending May 31, 2013 the dominant theme for global market returns has been central bank policy. Quantitative Easing (QE) has gone global and is the single most dominant force in global markets. Turning from QE to the fundamentals of economic growth and earnings, in the US, the economy continued to grow, albeit at a slower pace than initially expected, with first quarter GDP expanding at 2.4%. In Europe, the struggle for growth remains a persistent theme, which has forced the European Central Bank (ECB) to take more unconventional policy actions including, in early May, raising the prospect of introducing negative interest rates on deposits at the ECB. Further evidence of a slowdown in emerging markets, mainly the BRICs, continued to trickle in during the period.

During the past six months, there have been three major market-moving events. First, the most radical quantitative easing experiment to date was announced and then implemented in Japan following the election of Shinzo Abe to Prime Minister in December. A second new theme is the uncertainty surrounding the timing and size of the Federal Reserve’s (the “Fed’s”) beginning of the end of QE, the so-called “taper,” when the Fed reduces its monthly bond purchases from its current rate of $85 billion. Third, on the fiscal front in the US, the threat of a sequester and fear of a government shutdown ended with the sequester slowing government spending while tax revenues are up in a growing (even if slowly) economy, producing a rapidly improving fiscal position. The US federal deficit is now on track to decline from more than 10% of GDP to around 4% of GDP by the end of the fiscal year (based on Congressional Budget Office projections).

Quantitative easing around the world drove risk asset returns in the developed world. For the period, equities returned 47.7% in Japan, 16.5% in the US and 13.3% in Europe (all equity returns based on MSCI indexes, local currency). The link between central bank asset purchases and equity performance has strengthened significantly

since quantitative easing was first initiated: in the US, since November 2008, the correlation between the Fed’s balance sheet and the S&P 500 Index is over .90 (whereas in the five years leading up to the financial crisis, the correlation is less than 0.2).

The questions surrounding the taper—both when and how quickly the Fed will put the brakes on asset purchases—also resulted in higher volatility across asset markets for the period, while core fixed income generally sold off toward the end of the period and equities rallied. Within fixed income, high yield and convertibles stand out as exceptions returning 5.50% and 14.57% for the period, respectively. US Treasuries suffered as the 10-year yield increased from a low of 1.59% on December 6, 2012 to an intraday high of 2.23% on May 29, 2013—a pronounced move given that that the yield had remained well below 2 percent since April 2012.

When interpreting economic evidence through the prism of the taper, not only is good economic data good for equity returns but bad economic data has also been good news for developed market equities—when it signifies that the Fed will continue to provide liquidity to markets for longer. For most of the rest of the world in equity and commodity markets returns were flat to down. Emerging market equities returned 1.5%. The broad commodity futures were down 8.5% in the period with precious metals suffering the biggest decline, down 22.8% and gold futures down 18.9% (returns based on DJ UBS Commodity Index, Sub Precious Metals Index and Gold Index).

Portfolio Review

During the six month period, and relative to its benchmark index, the Fund held overweight positions in US small-cap equities and US and non-US fixed-income assets. The Fund held underweights in US large- cap and non-US equities, including emerging markets and in real

return assets, including real estate and commodities as well as in intermediate-term Treasury inflation protected securities (TIPS).

In the return generating part of portfolio, the equity holdings underperformed their benchmark. This was mostly due to underperformance in large cap equities as a result of both allocation and fund selection effects. The Fund was underweight US large cap in a period in which the Russell 1000 Index returned 16.68%. Selection effects in US small cap also detracted. Positive fund selection in international equities and emerging markets contributed to performance, helping to offset the negative effect from being underweight those sectors. Exposure to underlying funds implementing managed volatility strategies was a contributor to performance during the period as well.

In the defensive part of the portfolio, the Fund’s aggregate nominal bond positions outperformed the fixed income benchmark mainly due to fund selection and an overweight in agency and non-agency mortgage backed securities. The PIMCO Income Fund was up 6.58% in the period, with an excess return of 7.63% percentage points versus the Barclays US Aggregate Bond Index. A large allocation to the PIMCO Income Fund as well as the PIMCO Mortgage Opportunities Fund enabled the portfolios to gain exposure to the recovery in the housing market in the US and was part of the rationale for the underweight in equities.

The TIPS portion of the fixed income portfolio also contributed to performance due to asset allocation—a large underweight to intermediate term TIPS—and fund selection. Within the Fixed Income universe, TIPS overall underperformed Treasuries as the Barclays US Treasury US TIPS TR Index returned -4.57% versus the Barclays Aggregate Bond Treasury TR Index which was down 1.05%.

The Fund outperformed in commodities, due to a combination of being underweight the commodity benchmark, which was down 8.49% (based on the DJ UBS Commodity Total Return Index) for the period and positive fund selection. In real estate, the Fund underperformed its benchmark. Fund selection and a tilt toward global REITs detracted from performance in this sector. For the quarter, the S&P United States

| 16 | May 31, 2013 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Retirement 2030 Fund (formerly Allianz Global Investors Solutions 2030 Fund) (cont’d)

Property Index outperformed the S&P Europe Property Index by more than 4%.

Outlook

Economic theory tells us that 10-year treasury yields will, in time, match long-term nominal GDP, at around 4% given the Fed’s 2% target inflation. However, the paths to get there and the timing remain uncertain. One virtuous path entails global growth accelerating and economic data steadily improving. The other path is dominated by eroding pricing power and a lack of improvement in the labor market. Both paths will lead to higher interest rates. But the first would be associated with good returns in equities while the second would be associated with equity losses.

More broadly, we are either experiencing the great rotation into equity market outperformance and global growth or the early stages of another global slowdown. An expansion in global growth would be led by the US and emerging markets and would be associated with a recovery in Europe and an escape from deflation in Japan. In such a scenario, we would expect earnings to grow and valuations to continue to improve.

Chairman Bernanke, in particular, has stated that the risks to taking stimulus out of the economy too soon outweigh the risks of keeping quantitative easing in place too long. Thus, should the global economy slow, the Fed, along with other developed country central banks will

likely err on the side of maintaining low to negative real rates.

If evidence mounts that suggests that the world is healing and growth is accelerating, we are prepared to systematically add to risk assets, targeting those with the most attractive valuations. We are positioned to be liquidity suppliers. The portfolios are overweight high-quality dividend-paying stocks, overweight US stocks and remain underweight euro-zone stocks. The portfolios are modestly underweight commodities and real estate, as well as underweight nominal duration. All of the portfolios are within their benchmark-determined risk budgets.

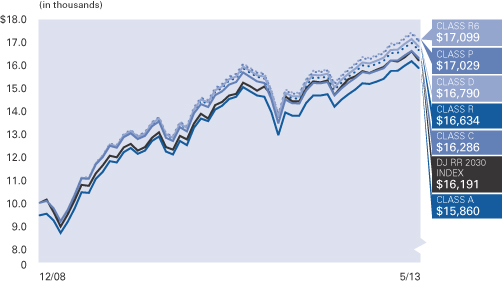

Average Annual Total Return for the period ended May 31, 2013

| 6 Month* | 1 Year | Since Inception† | ||||||||||||

| AllianzGI Retirement 2030 Fund Class A | 3.94% | 11.97% | 12.43% | |||||||||||

| AllianzGI Retirement 2030 Fund Class A (adjusted) | –1.78% | 5.81% | 11.00% | ||||||||||

| AllianzGI Retirement 2030 Fund Class C | 3.55% | 11.11% | 11.68% | |||||||||||

| AllianzGI Retirement 2030 Fund Class C (adjusted) | 2.55% | 10.11% | 11.68% | ||||||||||

| AllianzGI Retirement 2030 Fund Class D | 3.87% | 11.87% | 12.44% | ||||||||||

| AllianzGI Retirement 2030 Fund Class R | 3.82% | 11.63% | 12.21% | ||||||||||

| AllianzGI Retirement 2030 Fund Class P | 4.11% | 12.36% | 12.80% | ||||||||||

| AllianzGI Retirement 2030 Fund Class R6 | 4.16% | 12.46% | 12.90% | ||||||||||

| AllianzGI Retirement 2030 Fund Administrative Class | 4.03% | 12.06% | 12.58% | |||||||||||

| Dow Jones Real Return 2030 Index | 2.70% | 10.32% | 11.52% | ||||||||||

| Lipper Mixed-Asset Target 2030 Funds Average | 8.83% | 18.43% | 13.55% | |||||||||||

† The Fund began operations on 12/29/08. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on 12/31/08.

* Cumulative return.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares and the contingent deferred sales charge (CDSC) of 1% on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 94 and 95 for more information. The Fund’s gross expense ratios are 1.32% for Class A shares, 2.07% for Class C shares, 1.32% for Class D shares, 1.57% for Class R shares, 0.92% for Class P shares, 0.82% for Class R6 shares and 1.17% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least 3/31/14. The Fund’s expense ratios net of this reduction are 1.03% for Class A shares, 1.78% for Class C shares, 1.13% for Class D shares, 1.38% for Class R shares, 0.73% for Class P shares, 0.63% for Class R6 shares and 0.98% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated April 1, 2013, as supplemented to date.

| Semiannual Report | | May 31, 2013 | 17 |

Table of Contents

Unaudited

AllianzGI Retirement 2030 Fund (formerly Allianz Global Investors Solutions 2030 Fund) (cont’d)

Cumulative Returns Through May 31, 2013

Fund Allocation (as of May 31, 2013)

PIMCO Real Return | 16.4% | |||

PIMCO Income | 7.1% | |||

PIMCO Mortgage Opportunities | 6.1% | |||

AllianzGI NFJ Global Dividend Value | 5.0% | |||

AllianzGI NFJ International Value | 5.0% | |||

PIMCO Foreign Bond (U.S. Dollar-Hedged | 4.5% | |||

PIMCO Floating Income | 4.5% | |||

AllianzGI Income & Growth | 4.5% | |||

Other | 46.1% | |||

Cash & Equivalents — Net | 0.8% |

| Shareholder Expense Example | Actual Performance | |||||||||||||

| Class A | Class C | Class D | Class R | Class P | Class R6 | Administrative Class | ||||||||

Beginning Account Value (12/1/12) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

Ending Account Value (5/31/13) | $1,039.40 | $1,035.50 | $1,038.70 | $1,038.20 | $1,041.10 | $1,041.60 | $1,040.30 | |||||||

Expenses Paid During Period | $1.73 | $5.53 | $2.24 | $3.51 | $0.20 | $— | $1.48 | |||||||

Hypothetical Performance | ||||||||||||||

(5% return before expenses) | ||||||||||||||

Class A | Class C | Class D | Class R | Class P | Class R6 | Administrative | ||||||||

Beginning Account Value (12/1/12) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

Ending Account Value (5/31/13) | $1,023.24 | $1,019.50 | $1,022.74 | $1,021.49 | $1,024.73 | $1,024.93 | $1,023.49 | |||||||

Expenses Paid During Period | $1.72 | $5.49 | $2.22 | $3.48 | $0.20 | $— | $1.46 | |||||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.34% for Class A, 1.09% for Class C, 0.44% for Class D, 0.69% for Class R, 0.04% for Class P, 0.00% for Class R6 and 0.29% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. The expense ratio excludes the expenses of the Underlying Funds, which based upon the allocation of the Fund’s assets among the Underlying Funds are indirectly borne by the shareholders of the Fund.

| 18 | May 31, 2013 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | May 31, 2013 | 19 |

Table of Contents

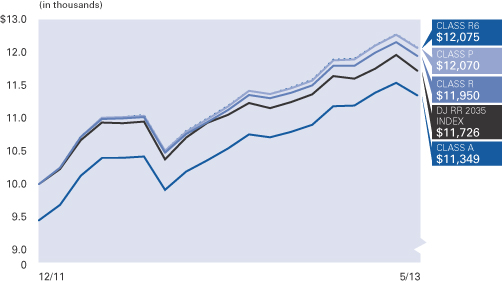

Unaudited

AllianzGI Retirement 2035 Fund (formerly Allianz Global Investors Solutions 2035 Fund)

For the period of December 1, 2012 through May 31, 2013, as provided by the Allianz Global Investors US Multi Asset Group.

Portfolio Insights

For the reporting period ended May 31, 2013, Class A shares at NAV of the AllianzGI Retirement 2035 Fund (the “Fund”) returned 5.14% outperforming the Dow Jones Real Return 2035 Index (the “benchmark index”) which returned 4.25%.

What Happened

For the six months ended May 31, 2013, the dominant theme for global market returns has been central bank policy. Quantitative Easing (QE) has gone global and is the single most dominant force in global markets. Turning from QE to the fundamentals of economic growth and earnings, in the US, the economy continued to grow, albeit at a slower pace than initially expected, with first quarter GDP expanding at 2.4%. In Europe, the struggle for growth remains a persistent theme, which has forced the European Central Bank (ECB) to take more unconventional policy actions including, in early May, raising the prospect of introducing negative interest rates on deposits at the ECB. Further evidence of a slowdown in emerging markets, mainly the BRICs, continued to trickle in during the period.

During the past six months, there have been three major market-moving events. First, the most radical quantitative easing experiment to date was announced and then implemented in Japan following the election of Shinzo Abe to Prime Minister in December. A second new theme is the uncertainty surrounding the timing and size of the Federal Reserve’s (the “Fed’s”) beginning of the end of QE, the so-called “taper,” when the Fed reduces its monthly bond purchases from its current rate of $85 billion. Third, on the fiscal front in the US, the threat of a sequester and fear of a government shutdown ended with the sequester slowing government spending while tax revenues are up in a growing (even if slowly) economy, producing a rapidly improving fiscal position. The US federal deficit is now on track to decline from more than 10% of GDP to around 4% of GDP by the end of the fiscal year (based on Congressional Budget Office projections).

Quantitative easing around the world drove risk asset returns in the developed world. For the period, equities returned 47.7% in Japan, 16.5% in the US and 13.3% in Europe (all equity returns based on MSCI indexes, local currency). The link between central bank asset purchases and equity performance has strengthened significantly

since quantitative easing was first initiated: in the US, since November 2008, the correlation between the Fed’s balance sheet and the S&P 500 Index is over .90 (whereas in the five years leading up to the financial crisis, the correlation is less than 0.2).

The questions surrounding the taper—both when and how quickly the Fed will put the brakes on asset purchases—also resulted in higher volatility across asset markets for the period, while core fixed income generally sold off toward the end of the period and equities rallied. Within fixed income, high yield and convertibles stand out as exceptions returning 5.50% and 14.57% for the period, respectively. US Treasuries suffered as the 10-year yield increased from a low of 1.59% on December 6, 2012 to an intraday high of 2.23% on May 29, 2013—a pronounced move given that that the yield had remained well below 2 percent since April 2012.

When interpreting economic evidence through the prism of the taper, not only is good economic data good for equity returns but bad economic data has also been good news for developed market equities—when it signifies that the Fed will continue to provide liquidity to markets for longer. For most of the rest of the world in equity and commodity markets returns were flat to down. Emerging market equities returned 1.5%. The broad commodity futures were down 8.5% in the period with precious metals suffering the biggest decline, down 22.8% and gold futures down 18.9% (returns based on DJ UBS Commodity Index, Sub Precious Metals Index and Gold Index).

Portfolio Review

During the six month period, and relative to its benchmark index, the Fund held overweight positions in US and non-US small-cap equities and US and non-US fixed-income assets. The Fund held underweights in US and non-US large-cap, emerging markets equities and in real

return assets, including real estate and commodities as well as in intermediate-term Treasury inflation protected securities (TIPS).

In the return generating part of portfolio, the equity holdings underperformed their benchmark. This was mostly due to underperformance in large cap equities as a result of both allocation and fund selection effects. The Fund was underweight US large cap in a period in which the Russell 1000 Index returned 16.68%. Selection effects in US small cap also detracted. Positive fund selection in international equities and emerging markets contributed to performance, helping to offset the negative effect from being underweight those sectors. Exposure to underlying funds implementing managed volatility strategies was a contributor to performance during the period as well.

In the defensive part of the portfolio, the Fund’s aggregate nominal bond positions outperformed the fixed income benchmark mainly due to fund selection and an overweight in agency and non-agency mortgage backed securities. The PIMCO Income Fund was up 6.58% in the period, with an excess return of 7.63% percentage points versus the Barclays US Aggregate Bond Index. A large allocation to the PIMCO Income Fund as well as the PIMCO Mortgage Opportunities Fund enabled the portfolios to gain exposure to the recovery in the housing market in the US and was part of the rationale for the underweight in equities.

The TIPS portion of the fixed income portfolio also contributed to performance due to asset allocation—a large underweight to intermediate term TIPS—and fund selection. Within the Fixed Income universe, TIPS overall underperformed Treasuries as the Barclays US Treasury US TIPS TR Index returned -4.57% versus the Barclays Aggregate Bond Treasury TR Index which was down 1.05%.

The Fund outperformed in commodities, due to a combination of being underweight the commodity benchmark, which was down 8.49% (based on the DJ UBS Commodity Total Return Index) for the period and positive fund selection.

In real estate, the Fund underperformed its benchmark. Fund selection and a tilt toward

| 20 | May 31, 2013 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Retirement 2035 Fund (formerly Allianz Global Investors Solutions 2035 Fund) (cont’d)

global REITs detracted from performance in this sector. For the quarter, the S&P United States Property Index outperformed the S&P Europe Property Index by more than 4%.

Outlook

Economic theory tells us that 10-year treasury yields will, in time, match long-term nominal GDP, at around 4% given the Fed’s 2% target inflation. However, the paths to get there and the timing remain uncertain. One virtuous path entails global growth accelerating and economic data steadily improving. The other path is dominated by eroding pricing power and a lack of improvement in the labor market. Both paths will lead to higher interest rates. But the first would be associated with good returns in equities while the second would be associated with equity losses.

More broadly, we are either experiencing the great rotation into equity market outperformance and global growth or the early stages of another global slowdown. An expansion in global growth would be led by the US and emerging markets and would be associated with a recovery in Europe and an escape from deflation in Japan. In such a scenario, we would expect earnings to grow and valuations to continue to improve.

Chairman Bernanke, in particular, has stated that the risks to taking stimulus out of the economy too soon outweigh the risks of keeping quantitative easing in place too long. Thus, should the global economy slow, the Fed, along with other developed country central banks will likely err on the side of maintaining low to negative real rates.

If evidence mounts that suggests that the world is healing and growth is accelerating, we are prepared to systematically add to risk assets, targeting those with the most attractive valuations. We are positioned to be liquidity suppliers. The portfolios are overweight high-quality dividend-paying stocks, overweight US stocks and remain underweight euro-zone stocks. The portfolios are modestly underweight commodities and real estate, as well as underweight nominal duration. All of the portfolios are within their benchmark-determined risk budgets.

Average Annual Total Return for the period ended May 31, 2013

| 6 Month* | 1 Year | Since Inception† | ||||||||||||

| AllianzGI Retirement 2035 Fund Class A | 5.14% | 14.47% | 13.48% | |||||||||||

| AllianzGI Retirement 2035 Fund Class A (adjusted) | –0.64% | 8.17% | 9.13% | ||||||||||

| AllianzGI Retirement 2035 Fund Class R | 4.95% | 14.07% | 13.09% | ||||||||||

| AllianzGI Retirement 2035 Fund Class P | 5.33% | 14.86% | 13.85% | ||||||||||

| AllianzGI Retirement 2035 Fund Class R6 | 5.33% | 14.93% | 13.90% | ||||||||||

| AllianzGI Retirement 2035 Fund Administrative Class | 5.21% | 14.54% | 13.52% | |||||||||||

| Dow Jones Real Return 2035 Index | 4.25% | 13.04% | 11.62% | ||||||||||

| Lipper Mixed-Asset Target 2035 Funds Average | 10.48% | 20.97% | 16.62% | |||||||||||

† The Fund began operations on 12/19/11. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on 12/31/11.

* Cumulative return.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 94 and 95 for more information. The Fund’s gross expense ratios are 1.34% for Class A shares, 1.59% for Class R shares, 0.94% for Class P shares, 0.84% for Class R6 shares and 1.19% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least 3/31/14. The Fund’s expense ratios net of this reduction are 1.06% for Class A shares, 1.41% for Class R shares, 0.76% for Class P shares, 0.66% for Class R6 shares and 1.01% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated April 1, 2013, as supplemented to date.

| Semiannual Report | | May 31, 2013 | 21 |

Table of Contents

Unaudited

AllianzGI Retirement 2035 Fund (formerly Allianz Global Investors Solutions 2035 Fund) (cont’d)

Cumulative Returns Through May 31, 2013

Fund Allocation (as of

May 31, 2013)

| PIMCO Real Return | 9.1% | |||

| PIMCO Income | 6.6% | |||

| AllianzGI NFJ International Value | 5.9% | |||

| AllianzGI NFJ Global Dividend Value | 5.4% | |||

| PIMCO Mortgage Opportunities | 5.0% | |||

| AllianzGI NFJ Dividend Value | 5.0% | |||

| AllianzGI Income & Growth | 4.7% | |||

| AllianzGI NFJ Mid-Cap Value | 4.6% | |||

| Other | 53.0% | |||

| Cash & Equivalents — Net | 0.7% |

| Shareholder Expense Example | Actual Performance | |||||||||

Class A | Class R | Class P | Class R6 | Administrative | ||||||

Beginning Account Value (12/1/12) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

Ending Account Value (5/31/13) | $1,051.40 | $1,049.50 | $1,053.30 | $1,053.30 | $1,052.10 | |||||

Expenses Paid During Period | $1.84 | $3.63 | $0.31 | $— | $1.59 | |||||

| Hypothetical Performance | ||||||||||

| (5% return before expenses) | ||||||||||

Class A | Class R | Class P | Class R6 | Administrative | ||||||

Beginning Account Value (12/1/12) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

Ending Account Value (5/31/13) | $1,023.14 | $1,021.39 | $1,024.63 | $1,024.93 | $1,023.39 | |||||

Expenses Paid During Period | $1.82 | $3.58 | $0.30 | $— | $1.56 | |||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.36% for Class A, 0.71% for Class R, 0.06% for Class P, 0.00% for Class R6 and 0.31% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. The expense ratio excludes the expenses of the Underlying Funds, which based upon the allocation of the Fund’s assets among the Underlying Funds are indirectly borne by the shareholders of the Fund.

| 22 | May 31, 2013 | | Semiannual Report |

Table of Contents

(THIS PAGE INTENTIONALLY LEFT BLANK)

| Semiannual Report | | May 31, 2013 | 23 |

Table of Contents

Unaudited

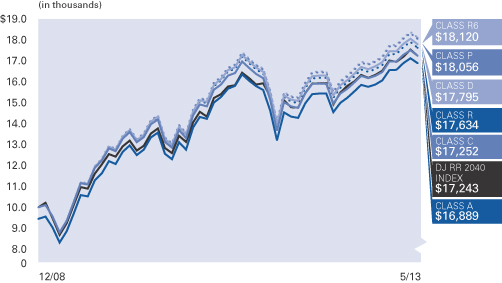

AllianzGI Retirement 2040 Fund (formerly Allianz Global Investors Solutions 2040 Fund)

For the period of December 1, 2012 through May 31, 2013, as provided by the Allianz Global Investors US Multi Asset Group.

Portfolio Insights

For the reporting period ended May 31, 2013, Class A shares at NAV of the AllianzGI Retirement 2040 Fund (the “Fund”) returned 6.41% outperforming the Dow Jones Real Return 2040 Index (the “benchmark index”) which returned 5.66%.

What Happened