united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22208

Valued Advisers Trust

(Exact name of registrant as specified in charter)

Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, OH 45246

(Address of principal executive offices) (Zip code)

Ultimus Fund Solutions, LLC

Attn: Zachary Richmond

225 Pictoria Drive, Suite 450

Cincinnati, OH 45246

(Name and address of agent for service)

Registrant's telephone number, including area code: 513-587-3400

Date of fiscal year end: 10/31

Date of reporting period: 10/31/2023

Item 1. Reports to Stockholders.

(a)

DANA LARGE CAP EQUITY FUND

DANA EPIPHANY ESG SMALL CAP EQUITY FUND

DANA EPIPHANY ESG EQUITY FUND

Annual Report

October 31, 2023

Dana Investment Advisors, Inc.

20700 Swenson Drive, Suite 400

Waukesha, WI 53186

(855) 280-9648

www.danafunds.com

Management Discussion of Fund Performance (Unaudited)

Dear Fellow Shareholders,

At this time last year, we were eager to put the previous twelve months behind us. The Federal Reserve (“Fed”) had raised rates repeatedly in 2022 to fight inflation, and this pressured asset prices. While bear markets are never welcome, we wrote that they often create new opportunities for growth and value creation. The recovery in equities that started in October 2022 was fairly broad across market cap ranges through year end. However, this breadth gave way to a more narrow market focus in 2023. Large cap stocks, particularly mega-cap stocks, outperformed the smaller cap indexes in the New Year, a recurring theme that played out for much of 2023. After lagging the concentrated, strong performance of a handful of companies, many stocks now have better relative valuations across market cap ranges. We have confidence that Dana’s investment philosophy, which relies on fundamental analysis and valuation discipline, should serve us well. We remain thankful for your continued trust and support of the Dana Funds. We are happy to share this discussion and analysis of the prior twelve months in the financial markets and the Dana Funds performance.

Economic and Market Recap

The S&P 500® Index rose over 10% for the fiscal year ended October 31, 2023, but in March 2023, it touched a short-term low immediately following the collapse of Silicon Valley Bank. Investors were understandably concerned and moved out of riskier assets. However, the equity market quickly turned upward following Fed and U.S. Treasury actions. The S&P 500® Index finished the first quarter with a positive +7.50% return, pleasantly surprising investors. Market breadth was not as remarkable, and the S&P 500® Equal Weight Index gained only +2.93%, roughly in line with the Russell® 2000 Index return of +2.74%.

The Fed continued to dominate market psychology and persisted in raising rates through all three quarters of 2023, albeit at a much more modest pace compared to 2022. The economy remained resilient with GDP up 2.1% in Q2 and 4.9% in Q3, and equities rose during the second quarter. While mega-cap names continued to outperform, small cap stocks experienced a good rally as well. However, equities hit the pause button in Q3 and ultimately gave up ground due to increasing pressure on valuations caused by higher interest rates. By the end of the quarter, rates were at their highest level in over 15 years. Energy costs also rose in Q3 as oil moved from $70 to $90 a barrel. This added to concerns for all sectors with the exception of the Energy sector, the only sector to deliver a positive return in the S&P 500® Index during the third quarter.

Fed policy and interest rate expectations remain the dominant influence on the markets. The Fed seems to be on hold for now; indeed inflation as measured by CPI has fallen to much lower levels compared to 2022 and corporate earnings have been favorable. These factors have thus far overcome the geopolitical and economic concerns posed by the

1

Management Discussion of Fund Performance (Unaudited) (continued)

sudden war in Israel that began in early October. Many stocks have negative returns for the year and are increasingly attractive on a relative basis. We will continue to seek these opportunities as we remain vigilant on the impacts of a potentially escalating situation in the Middle East and the uncertainties in a U.S. presidential election next year.

Dana Large Cap Equity Fund (the “Large Cap Fund” or “Fund”) Discussion

Over the Fund’s fiscal year ended October 31, 2023, the S&P 500® Index returned +10.14% and the Dana Large Cap Equity Fund (DLCIX) gained +6.44%. The concentration of performance in mega-cap names drove returns in the cap-weighted S&P 500® Index. In fact, stocks deemed the “Magnificent 7” accounted for approximately 85% of the S&P 500® Index’s total return through the first three quarters of 2023, a staggering concentration. The Fund has held several of these stocks for a long period, including Apple, Inc. (AAPL), Microsoft Corp. (MSFT) and Alphabet, Inc. (GOOGL), and they have been very accretive over time. We added Meta Platforms, Inc. (META) back to the Fund and purchased AI champion NVIDIA Corp. (NVDA) partway through 2023.

Last year, we noted that there were some names in the portfolio that we felt had been unfairly punished; names where the fundamentals held up and valuation looked compelling, yet they underperformed. One such example was Adobe, Inc. (ADBE), the dominant provider of digital market software. Our patience paid off, and the stock rallied 67%, the second-best returning holding during the fiscal year. Broadcom, Inc. (AVGO) performed even better, and Dell Technologies, Inc. (DELL) rounded out the top three Fund performers, all of which are in the Technology sector. Despite these strong returns, the Fund’s holdings lagged this best performing benchmark sector due to the significant impact of not holding NVIDIA Corp. (NVDA) early in the year and, to a lesser extent, having a smaller weight in Microsoft Corp. (MSFT) versus the benchmark and holding security firm, Fortinet, Inc. (FTNT).

The Communications Sector’s performance is similar in that not holding Meta Platforms, Inc. (META) early on detracted from relative performance. Fund holding Alphabet, Inc. (GOOGL) was the strongest absolute and relative performer in this sector. Interpublic Group of Companies (IPG) weakened this year on lower revenue expectations largely driven by cutbacks in technology firms, and Verizon (VZ) had weak price action. We sold both stocks in October on their more uncertain outlooks.

The best relative performance sector for the Fund was Financials. The Fund’s Financial holdings delivered a positive return versus the benchmark’s sector holdings posting a negative return. Morgan Stanley (MS) and Visa, Inc. (V) were up double digits. The Fund’s Real Estate sector had the second-best relative return and again was positive versus a negative return for the benchmark’s sector holdings. Solid performance in stable cash flow

2

Management Discussion of Fund Performance (Unaudited) (continued)

generator Iron Mountain, Inc. (IRM) more than offset the weaker performing Gaming and Leisure Properties, Inc. (GLPI).

The persistence in the Fed and the economy proved to be a tug of war for investors. Valuations certainly fluctuated with the changes in expectations. We placed more trades than is typical for us to take advantage where we saw opportunities. With the concentrated performance in the largest cap names, many stocks in our universe experienced a negative return for the fiscal year and are flying “under the radar screen.” We believe it is likely this disparity will not persist for much longer and that we will see more relative valuation beyond those most heavily weighted benchmark stocks.

Dana Epiphany ESG Equity Fund (the “Epiphany ESG Fund” or “Fund”) Discussion

The Dana Epiphany ESG Equity Fund (ESGIX) posted a return of -0.71%, trailing the benchmark S&P 500® Index return of +10.14% during the fiscal year ended October 31, 2023. The Epiphany ESG Fund shares an investment philosophy that is common to all the Dana Funds, then adds a faith-based values component to security selection. This Fund has an all-cap universe, so it invests across stocks in the large, mid, and small market cap ranges. The frequent shifts in market dynamics, the persistence of the Fed, and extreme concentration of performance in a few mega-cap names impacted this Fund as well as the Dana Large Cap Equity Fund. While we are disappointed in the performance of this Fund over the past fiscal year, we know that value-oriented strategies have lagged in this more concentrated, growth-focused market. The Fund has strong valuation characteristics that we believe will be rewarded over time.

On a sector level, the Epiphany ESG Fund outperformed the benchmark S&P 500® Index in the Real Estate and Energy sectors. Iron Mountain, Inc. (IRM) had a double-digit return. In the Energy sector, we made some recent changes, one of which was adding Weatherford International plc (WFRD) to the Fund. This was the primary contributor to the Fund in this sector. Both the Real Estate and Energy sectors in the Fund delivered positive returns versus the negative returns of their corresponding benchmark sector holdings.

The two weakest sectors were Technology and Consumer Discretionary. Similar to the Large Cap Fund, there are names in the portfolio where the mega-cap, growth-oriented stocks accounted for a substantial share of the benchmark’s performance. NVIDIA Corp. (NVDA) was one such company that we did not own early on and detracted from performance. We have added NVDA and are excited about this semiconductor company that specializes in advanced chips suited for AI development, a field that is still at the early stages and growing rapidly. We also purchased CrowdStrike Holdings, Inc. (CRWD), a global leader in cybersecurity applications. The Consumer Discretionary sector was hurt by weakness in Crocs, Inc. (CROX). The company hit its July earning report, yet revenue projections were below expectations.

3

Management Discussion of Fund Performance (Unaudited) (continued)

The past year was challenging, especially for value-oriented active management, as market index performance was largely determined by a small group of mega-cap stocks with exceptionally strong returns. The vast majority of stocks posted returns well below the major broad market indexes (S&P 500, Russell 1000, Russell 3000), with value stocks and mid- and small-cap stocks, on average, lagging substantially behind the mega-cap-dominated indexes. We believe the market will become more balanced and recognize the steady and solid performance of businesses outside of the mega-cap darlings, and that the portfolio is well positioned with attractive stocks that will benefit from this change in dynamic going forward. We remain focused on our fundamental and value-oriented approach to stock selection and believe shareholders will be rewarded over time.

Dana Epiphany ESG Small Cap Equity Fund (the “Small Cap Fund” or “Fund”) Discussion

The Dana Epiphany ESG Small Cap Equity Fund (DSCIX) returned -0.81% compared +1.28% for the benchmark Morningstar US Small Core Index during the fiscal year ended October 31, 2023. This Fund also shares an investment philosophy that is common to all the Dana Funds, then adds a faith-based values component to security selection. The small cap portion of the market as measured by the Russell 2000® Index began to rally toward the end of 2022, yet consistently remained in the shadow of the larger cap indices for much of the fiscal year. This index pushed higher in the first half of 2023, but this quickly faded in the third quarter. Persistently higher interest rates and higher energy costs weighed heavily on smaller companies, and the collapse of Silicon Valley Bank early in the year put regional banks more at risk relative to larger banks. The range of sector returns was wide. Five of the eleven sectors in the Russell 2000® Index had double-digit declines, and the best performing sector, Energy, was only up a bit more than 6%. The Fund lagged the Morningingstar US Small Core Index benchmark, yet outperformed the Russell 2000® Index significantly.

Many Consumer Discretionary sector holdings performed quite well. These include Deckers Outdoor Corporation (DECK), Group 1 Automotive, Inc. (GPI), TopBuild Corp. (BLD), and Boot Barn Holdings, Inc. (BOOT). All delivered significant double-digit returns. Most of these companies raised revenue and earnings estimates. Fund holdings in the Industrial sector also delivered double-digit returns, including FTI Consulting, Inc. (FCN), EnerSys (ENS), and Clean Harbors, Inc. (CLH).

Communication Services sector holdings disappointed. Ooma, Inc. (OOMA) is a cloud phone system provider that offers low-cost subscription communication services for small businesses and residences. It has a strong balance sheet, yet missed consensus earnings estimates, and its price declined. TechTarget, Inc. (TTGT) was also weak. ADTRAN Holdings, Inc. (ADTN), a fiber networking company, and TransMedics Group, Inc.

4

Management Discussion of Fund Performance (Unaudited) (continued)

(TMDX), a unique health care company striving to improve transport for organ donations, were two of the largest detractors in the Fund. Also in Health Care, Lantheus Holdings, Inc. (LNTH), Travere Therapeutics, Inc. (TVTX), and Omnicell, Inc. (OMCL) declined, yet were more than offset by other Health Care holdings in the sector that soared. In particular, Horizon Therapeutics plc (HZNP) was taken over at a significant premium by Amgen, Inc. (AMGN). In Energy, Ovintiv, Inc. (OVV) and in Utilities, Clearway Energy, Inc. (CWEN) disappointed. Qvintiv, Inc. was replaced with Weatherford International PLC (WFRD) for its energy diversification and upside potential.

We see strong relative valuations in the small cap portion of the market in good quality stocks. Companies that manage their balance sheets and grow their EBITDA are companies that we want to know better because they can be great additions to our Strategy. Our relative value bias means we are exposed to dynamic market segments, while we continually watch valuation multiples. We are excited about the opportunities we see for the Dana Epiphany ESG Small Cap Equity Fund.

5

Investment Results (Unaudited)

Average Annual Total Returns(a) as of October 31, 2023

| One Year | Five Year | Ten Year | |

| Dana Large Cap Equity Fund | |||

| Institutional Class | 6.44% | 8.48% | 9.17% |

| Investor Class | 6.22% | 8.22% | 8.89% |

| S&P 500® Index(b) | 10.14% | 11.01% | 11.18% |

| Expense Ratios(c) | |||

| Institutional | Investor | ||

| Class | Class | ||

| Gross | 0.87% | 1.12% | |

| With Applicable Waivers | 0.73% | 0.98% | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Dana Large Cap Equity Fund (the “Large Cap Fund”) distributions or the redemption of Large Cap Fund shares. Current performance of the Large Cap Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-855-280-9648.

| (a) | Average annual total returns reflect any change in price per share and assume the reinvestment of all distributions. The Large Cap Fund’s returns reflect any fee reductions during the applicable period. If such reductions had not occurred, the quoted performance would have been lower. |

| (b) | The S&P 500® Index (“S&P Index”) is a widely recognized unmanaged index of equity securities and is representative of a broader domestic equity market and range of securities than is found in the Large Cap Fund’s portfolio. Individuals cannot invest directly in the S&P Index; however, an individual can invest in exchange-traded funds (“ETFs”) or other investment vehicles that attempt to track the performance of a benchmark index. |

| (c) | The expense ratios are from the Large Cap Fund’s prospectus dated February 28, 2023. Expense ratios with applicable waivers reflect that Dana Investment Advisors, Inc. (the “Adviser”) has contractually agreed to waive or limit its fees and to assume other expenses of the Large Cap Fund until February 29, 2024, so that total annual fund operating expenses do not exceed 0.73% of the Large Cap Fund’s average daily net assets. This operating expense limitation does not apply to brokerage fees and commissions, borrowing costs (such as interest and dividend expenses on securities sold short), taxes, extraordinary expenses, fees and expenses paid under a distribution plan adopted pursuant to Rule 12b-1, fees and expenses paid under a shareholder services plan, and indirect expenses (such as “Acquired Fund Fees and Expenses”). Each waiver or reimbursement of an expense by the Adviser is subject to repayment by the Large Cap Fund within three years following the date of such waiver or reimbursement, provided that the Large Cap Fund is able to make the repayment without exceeding the expense limitation in place at the time of the waiver or reimbursement and the expense limitation in place at the time of the repayment. This agreement may only be terminated by mutual consent of the Adviser and the Board of Trustees. Additional information pertaining to the Large Cap Fund’s expense ratios as of October 31, 2023 can be found in the financial highlights. |

6

Investment Results (Unaudited) (continued)

The Large Cap Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Large Cap Fund and may be obtained by calling the same number as above. Please read it carefully before investing.

The Large Cap Fund is distributed by Ultimus Fund Distributors, LLC, Member FINRA/SIPC.

7

Investment Results (Unaudited) (continued)

Average Annual Total Returns(a) as of October 31, 2023

| Since | |||

| Inception | |||

| One Year | Five Year | (11/3/15) | |

| Dana Epiphany ESG Small Cap Equity Fund | |||

| Institutional Class | (0.81)% | 4.31% | 4.05% |

| Morningstar US Small Core Index(b) | 1.28% | 5.64% | 6.58% |

| Expense Ratios(c) | |||

| Institutional | |||

| Class | |||

| Gross | 1.95% | ||

| With Applicable Waivers | 0.95% | ||

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Dana Epiphany ESG Small Cap Equity Fund (the “Small Cap Fund”) distributions or the redemption of Small Cap Fund shares. Current performance of the Small Cap Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-855-280-9648.

| (a) | Average annual total returns reflect any change in price per share and assume the reinvestment of all distributions. The Small Cap Fund’s returns reflect any fee reductions during the applicable period. If such reductions had not occurred, the quoted performance would have been lower. |

| (b) | The Morningstar US Small Core Index (“Morningstar Index”) provides a comprehensive depiction of the performance and fundamental characteristics of the Small Core segment of U.S. equity markets. The Morningstar Index does not incorporate Environmental, Social, or Governance (ESG) criteria. Individuals can not invest directly in the Morningstar Index; however, an individual can invest in ETFs or other investment vehicles that attempt to track the performance of a benchmark index. |

The Small Cap Fund is not sponsored, endorsed, sold or promoted by Morningstar, Inc. or any of its affiliates (all such entities, collectively, “Morningstar Entities”). The Morningstar Entities make no representation or warranty, express or implied, to individuals who invest in the Small Cap Fund or any member of the public regarding the advisability of investing in equity securities generally or in the Small Cap Fund in particular or the ability of the Small Cap Fund to track the Morningstar Indices or general equity market performance. THE MORNINGSTAR ENTITIES DO NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE MORNINGSTAR US SMALL CORE INDEX OR ANY DATA INCLUDED THEREIN AND MORNINGSTAR ENTITIES SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS, OR INTERRUPTIONS THEREIN.

| (c) | The expense ratios are from the Small Cap Fund’s prospectus dated February 28, 2023. Expense ratios with applicable waivers reflect that the Adviser has contractually agreed to waive or limit its fees and to assume other expenses of the Small Cap Fund until February 29, 2024, so that total annual fund operating expenses do not exceed 0.95% of the Small Cap Fund’s average daily net assets. This operating expense limitation does not apply to brokerage fees and commissions, borrowing costs (such as interest and dividend expenses on securities sold short), taxes, extraordinary expenses, |

8

Investment Results (Unaudited) (continued)

fees and expenses paid under a distribution plan adopted pursuant to Rule 12b-1, fees and expenses paid under a shareholder services plan, and indirect expenses (such as “Acquired Fund Fees and Expenses”). Each waiver or reimbursement of an expense by the Adviser is subject to repayment by the Small Cap Fund within three years following the date of such waiver or reimbursement, provided that the Small Cap Fund is able to make the repayment without exceeding the expense limitation in place at the time of the waiver or reimbursement and the expense limitation in place at the time of the repayment. This agreement may only be terminated by mutual consent of the Adviser and the Board of Trustees. Additional information pertaining to the Small Cap Fund’s expense ratios as of October 31, 2023 can be found in the financial highlights.

The Small Cap Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Small Cap Fund and may be obtained by calling the same number as above. Please read it carefully before investing.

The Small Cap Fund is distributed by Ultimus Fund Distributors, LLC, Member FINRA/SIPC.

9

Investment Results (Unaudited) (continued)

Average Annual Total Returns(a) as of October 31, 2023

| One Year | Five Year | Ten Year | |

| Dana Epiphany ESG Equity Fund | |||

| Institutional Class | (0.71)% | 6.50% | 6.92% |

| S&P 500® Index(b) | 10.14% | 11.01% | 11.18% |

| Expense Ratios(c) | |||

| Institutional | |||

| Class | |||

| Gross | 0.96% | ||

| With Applicable Waivers | 0.85% | ||

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Dana Epiphany ESG Equity Fund (the “Epiphany ESG Fund”) distributions or the redemption of Epiphany ESG Fund shares. Current performance of the Epiphany ESG Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-855-280-9648.

| (a) | Average annual total returns reflect any change in price per share and assume the reinvestment of all distributions. The Epiphany ESG Fund’s returns reflect any fee reductions during the applicable period. If such reductions had not occurred, the quoted performance would have been lower. |

| (b) | The S&P 500® Index (“S&P Index”) is a widely recognized unmanaged index of equity securities and is representative of a broader domestic equity market and range of securities than is found in the Epiphany ESG Fund’s portfolio. Individuals cannot invest directly in the S&P Index; however, an individual can invest in ETFs or other investment vehicles that attempt to track the performance of a benchmark index. |

| (c) | The expense ratios are from the Epiphany ESG Fund’s prospectus dated February 28, 2023. Expense ratios with applicable waivers reflect that the Adviser has contractually agreed to waive or limit its fees and to assume other expenses of the Epiphany ESG Fund until February 29, 2024, so that total annual fund operating expenses do not exceed 0.85% of the Epiphany ESG Fund’s average net assets. This operating expense limitation does not apply to brokerage fees and commissions, borrowing costs (such as interest and dividend expenses on securities sold short), taxes, extraordinary expenses, fees and expenses paid under a distribution plan adopted pursuant to Rule 12b-1, fees and expenses paid under a shareholder services plan, and indirect expenses (such as “Acquired Fund Fees and Expenses”). Each waiver or reimbursement of an expense by the Adviser is subject to repayment by the Epiphany ESG Fund within three years following the date of such waiver or reimbursement, provided that the Epiphany ESG Fund is able to make the repayment without exceeding the expense limitation in place at the time of the waiver or reimbursement and the expense limitation in place at the time of the repayment. This agreement may only be terminated by mutual consent of the Adviser and the Board of Trustees. Additional information pertaining to the Epiphany ESG Fund’s expense ratios as of October 31, 2023 can be found in the financial highlights. |

10

Investment Results (Unaudited) (continued)

The Epiphany ESG Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Epiphany ESG Fund and may be obtained by calling the same number as above. Please read it carefully before investing.

The Epiphany ESG Fund is distributed by Ultimus Fund Distributors, LLC, Member FINRA/SIPC.

11

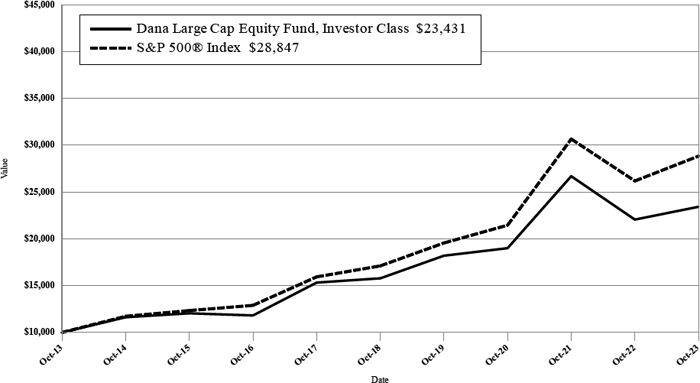

Investment Results (Unaudited) (continued)

Comparison of the Growth of a $10,000 Investment in the Dana Large Cap Equity Fund, Investor Class and the S&P 500® Index (Unaudited)

The chart above assumes an initial investment of $10,000 made on October 31, 2013 held through October 31, 2023. THE LARGE CAP FUND’S RETURN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on Large Cap Fund distributions or the redemption of Large Cap Fund shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Large Cap Fund, and to obtain performance data current to the most recent month end or to request a prospectus, please call (855) 280-9648. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Large Cap Fund before investing. The Large Cap Fund’s prospectus contains this and other information about the Large Cap Fund, and should be read carefully before investing.

The Large Cap Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

12

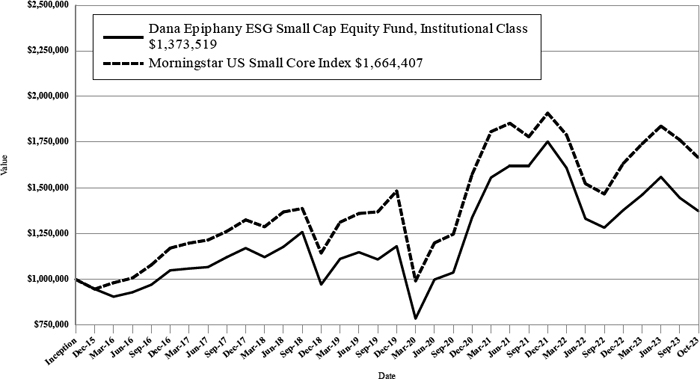

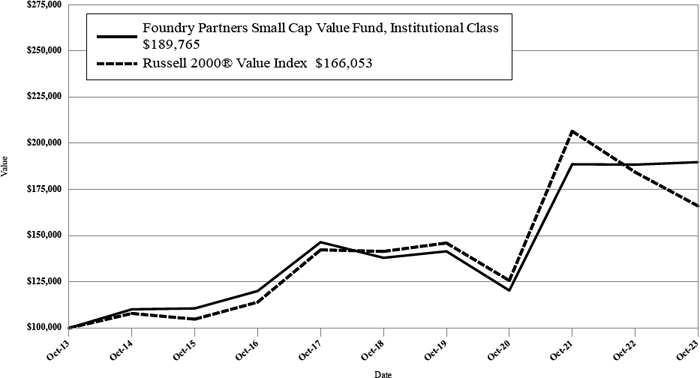

Investment Results (Unaudited) (continued)

Comparison of the Growth of a $1,000,000 Investment in the Dana Epiphany ESG Small Cap Equity Fund, Institutional Class and Morningstar US Small Core Index (Unaudited)

The chart above assumes an initial investment of $1,000,000 made on November 3, 2015 (commencement of Institutional Class operations) held through October 31, 2023. THE SMALL CAP FUND’S RETURN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on Small Cap Fund distributions or the redemption of Small Cap Fund shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Small Cap Fund, and to obtain performance data current to the most recent month end or to request a prospectus, please call (855) 280-9648. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Small Cap Fund before investing. The Small Cap Fund’s prospectus contains this and other information about the Small Cap Fund, and should be read carefully before investing.

The Small Cap Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

13

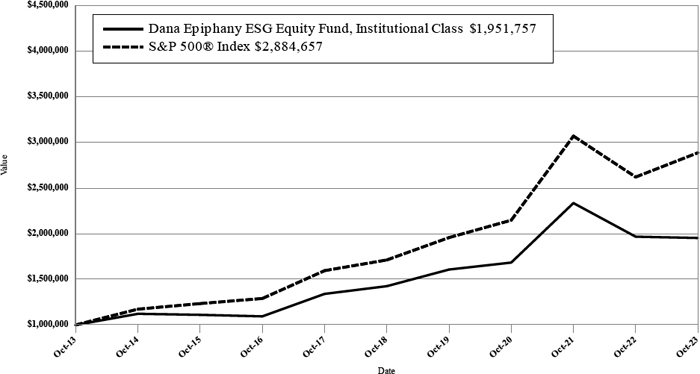

Investment Results (Unaudited) (continued)

Comparison of the Growth of a $1,000,000 Investment in the Dana Epiphany ESG Equity Fund, Institutional Class and the S&P 500® Index (Unaudited)

The chart above assumes an initial investment of $1,000,000 made on October 31, 2013 held through October 31, 2023. THE EPIPHANY ESG FUND’S RETURN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on Epiphany ESG Fund distributions or the redemption of Epiphany ESG Fund shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Epiphany ESG Fund, and to obtain performance data current to the most recent month end or to request a prospectus, please call (855) 280-9648. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Epiphany ESG Fund before investing. The Epiphany ESG Fund’s prospectus contains this and other information about the Epiphany ESG Fund, and should be read carefully before investing.

The Epiphany ESG Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

14

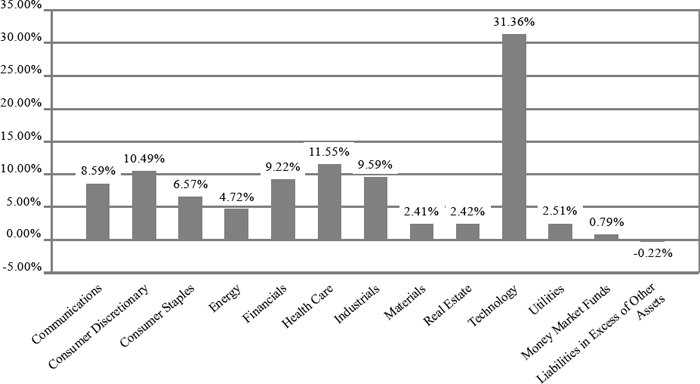

Fund Holdings (Unaudited)

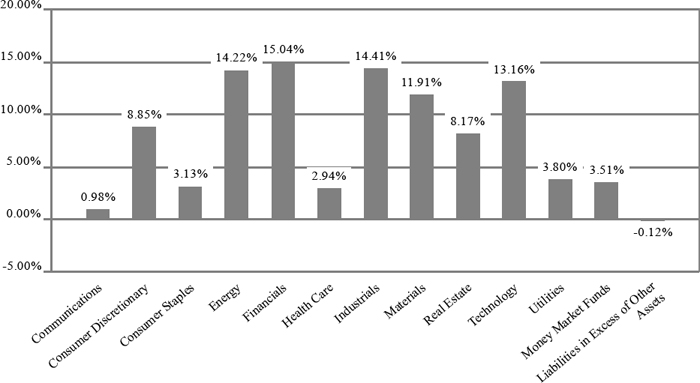

The following chart gives a visual breakdown of the Large Cap Fund by sector weighting as a percentage of net assets as of October 31, 2023.

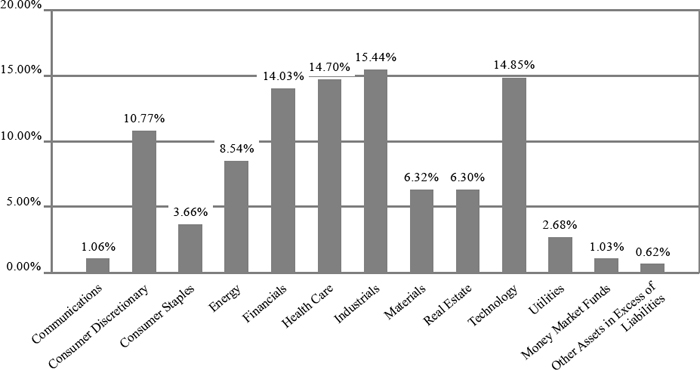

The following chart gives a visual breakdown of the Small Cap Fund by sector weighting as a percentage of net assets as of October 31, 2023.

15

Fund Holdings (Unaudited)

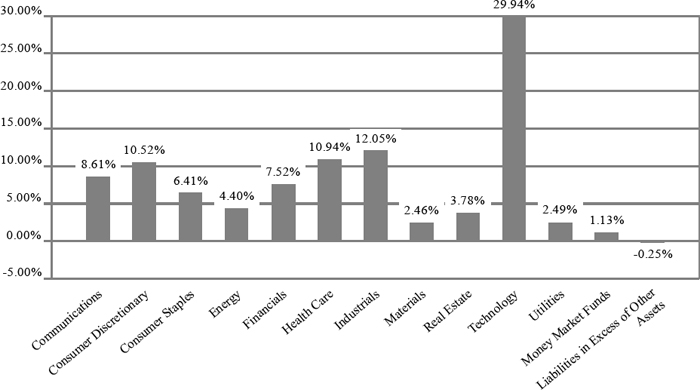

The following chart gives a visual breakdown of the Epiphany ESG Fund by sector weighting as a percentage of net assets as of October 31, 2023.

Availability of Portfolio Schedules (Unaudited)

The Large Cap Fund, the Small Cap Fund and the Epiphany ESG Fund (each a “Fund” and collectively the “Funds”) file their complete schedules of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Funds’ Form N-PORT reports are available on the SEC’s website at http://www.sec.gov and on the Funds’ website at http://www.danafunds.com.

16

| Dana Large Cap Equity Fund |

| Schedule of Investments |

| October 31, 2023 |

| COMMON STOCKS — 99.43% | Shares | Fair Value | ||||||

| Communications — 8.59% | ||||||||

| Alphabet, Inc., Class A(a) | 30,400 | $ | 3,772,032 | |||||

| Comcast Corp., Class A | 27,400 | 1,131,346 | ||||||

| Meta Platforms, Inc., Class A(a) | 3,400 | 1,024,318 | ||||||

| T-Mobile US, Inc.(a) | 7,200 | 1,035,792 | ||||||

| 6,963,488 | ||||||||

| Consumer Discretionary — 10.49% | ||||||||

| Amazon.com, Inc.(a) | 21,800 | 2,901,362 | ||||||

| Lululemon Athletica, Inc.(a) | 3,340 | 1,314,223 | ||||||

| Marriott International, Inc., Class A | 8,200 | 1,546,192 | ||||||

| PulteGroup, Inc. | 19,000 | 1,398,210 | ||||||

| Restaurant Brands International, Inc. | 20,000 | 1,344,000 | ||||||

| 8,503,987 | ||||||||

| Consumer Staples — 6.57% | ||||||||

| Kimberly-Clark Corp. | 11,000 | 1,316,040 | ||||||

| Kroger Co. (The) | 31,000 | 1,406,470 | ||||||

| Mondelez International, Inc., Class A | 17,800 | 1,178,538 | ||||||

| Sysco Corp. | 19,000 | 1,263,310 | ||||||

| Walmart, Inc. | 1,000 | 163,410 | ||||||

| 5,327,768 | ||||||||

| Energy — 4.72% | ||||||||

| Baker Hughes Co., Class A | 10,000 | 344,200 | ||||||

| Chevron Corp. | 500 | 72,865 | ||||||

| ConocoPhillips | 7,400 | 879,120 | ||||||

| Exxon Mobil Corp. | 1,000 | 105,850 | ||||||

| Marathon Petroleum Corp. | 7,800 | 1,179,750 | ||||||

| Pioneer Natural Resources Co. | 5,200 | 1,242,800 | ||||||

| 3,824,585 | ||||||||

| Financials — 9.22% | ||||||||

| American Express Co. | 8,600 | 1,255,858 | ||||||

| Bank of America Corp. | 5,000 | 131,700 | ||||||

| Bank of New York Mellon Corp. (The) | 37,000 | 1,572,500 | ||||||

| Interactive Brokers Group, Inc., Class A | 19,400 | 1,553,358 | ||||||

| JPMorgan Chase & Co. | 5,200 | 723,112 | ||||||

| Reinsurance Group of America, Inc. | 7,500 | 1,121,025 | ||||||

| Wells Fargo & Co. | 28,000 | 1,113,560 | ||||||

| 7,471,113 | ||||||||

| Health Care — 11.55% | ||||||||

| AbbVie, Inc. | 11,000 | 1,552,980 | ||||||

| Bristol-Myers Squibb Co. | 20,000 | 1,030,600 | ||||||

| Eli Lilly & Co. | 1,900 | 1,052,467 | ||||||

| IQVIA Holdings, Inc.(a) | 4,400 | 795,652 | ||||||

| McKesson Corp. | 3,800 | 1,730,368 | ||||||

| Merck & Co., Inc. | 15,000 | 1,540,500 | ||||||

| UnitedHealth Group, Inc. | 3,100 | 1,660,236 | ||||||

| 9,362,803 | ||||||||

See accompanying notes which are an integral part of these financial statements.

17

| Dana Large Cap Equity Fund |

| Schedule of Investments (continued) |

| October 31, 2023 |

| COMMON STOCKS — 99.43% - continued | Shares | Fair Value | ||||||

| Industrials — 9.59% | ||||||||

| Boston Scientific Corp.(a) | 24,000 | $ | 1,228,560 | |||||

| Caterpillar, Inc. | 5,700 | 1,288,485 | ||||||

| Huntington Ingalls Industries, Inc. | 5,000 | 1,099,100 | ||||||

| Lincoln Electric Holdings, Inc. | 8,600 | 1,503,280 | ||||||

| Norfolk Southern Corp. | 5,400 | 1,030,266 | ||||||

| Parker-Hannifin Corp. | 4,400 | 1,623,204 | ||||||

| 7,772,895 | ||||||||

| Materials — 2.41% | ||||||||

| Graphic Packaging Holding Co. | 43,000 | 924,930 | ||||||

| Linde PLC | 2,700 | 1,031,832 | ||||||

| 1,956,762 | ||||||||

| Real Estate — 2.42% | ||||||||

| Gaming and Leisure Properties, Inc. | 21,000 | 953,190 | ||||||

| Iron Mountain, Inc. | 17,000 | 1,004,190 | ||||||

| 1,957,380 | ||||||||

| Technology — 31.36% | ||||||||

| Accenture PLC, Class A | 3,200 | 950,688 | ||||||

| Adobe, Inc.(a) | 3,100 | 1,649,386 | ||||||

| Apple, Inc. | 27,000 | 4,610,790 | ||||||

| Broadcom, Inc. | 2,200 | 1,851,014 | ||||||

| CrowdStrike Holdings, Inc., Class A(a) | 4,700 | 830,819 | ||||||

| Dell Technologies, Inc., Class C | 25,000 | 1,672,750 | ||||||

| Fiserv, Inc.(a) | 9,600 | 1,092,000 | ||||||

| Microsoft Corp. | 12,600 | 4,260,187 | ||||||

| NVIDIA Corp. | 3,800 | 1,549,640 | ||||||

| Oracle Corp. | 9,400 | 971,960 | ||||||

| Palo Alto Networks, Inc.(a) | 4,200 | 1,020,684 | ||||||

| Salesforce, Inc.(a) | 5,400 | 1,084,482 | ||||||

| ServiceNow, Inc.(a) | 1,800 | 1,047,330 | ||||||

| Visa, Inc., Class A | 7,000 | 1,645,700 | ||||||

| Workday, Inc., Class A(a) | 5,600 | 1,185,576 | ||||||

| 25,423,006 | ||||||||

| Utilities — 2.51% | ||||||||

| CenterPoint Energy, Inc. | 37,000 | 994,560 | ||||||

| NextEra Energy, Inc. | 17,800 | 1,037,740 | ||||||

| 2,032,300 | ||||||||

| Total Common Stocks (Cost $65,990,383) | 80,596,087 | |||||||

See accompanying notes which are an integral part of these financial statements.

18

| Dana Large Cap Equity Fund |

| Schedule of Investments (continued) |

| October 31, 2023 |

| MONEY MARKET FUNDS - 0.79% | Shares | Fair Value | ||||||

| Fidelity Investments Money Market Government Portfolio, Institutional Class, 5.28%(b) | 643,800 | $ | 643,800 | |||||

| Total Money Market Funds (Cost $643,800) | 643,800 | |||||||

| Total Investments — 100.22% (Cost $66,634,183) | 81,239,887 | |||||||

| Liabilities in Excess of Other Assets — (0.22)% | (178,341 | ) | ||||||

| NET ASSETS — 100.00% | $ | 81,061,546 | ||||||

| (a) | Non-income producing security. |

| (b) | Rate disclosed is the seven day effective yield as of October 31, 2023. |

See accompanying notes which are an integral part of these financial statements.

19

| Dana Epiphany ESG Small Cap Equity Fund |

| Schedule of Investments |

| October 31, 2023 |

| COMMON STOCKS — 98.35% | Shares | Fair Value | ||||||

| Communications — 1.06% | ||||||||

| Ooma, Inc.(a) | 22,522 | $ | 245,715 | |||||

| Consumer Discretionary — 10.77% | ||||||||

| Bloomin’ Brands, Inc. | 17,389 | 405,859 | ||||||

| Boot Barn Holdings, Inc.(a) | 5,248 | 364,736 | ||||||

| Deckers Outdoor Corp.(a) | 829 | 494,963 | ||||||

| GMS, Inc.(a) | 7,493 | 438,190 | ||||||

| Group 1 Automotive, Inc. | 1,655 | 417,606 | ||||||

| Modine Manufacturing Co.(a) | 9,717 | 383,822 | ||||||

| 2,505,176 | ||||||||

| Consumer Staples — 3.66% | ||||||||

| e.l.f. Beauty, Inc.(a) | 4,142 | 383,673 | ||||||

| Simply Good Foods Co. (The)(a) | 12,519 | 466,834 | ||||||

| 850,507 | ||||||||

| Energy — 8.54% | ||||||||

| Chord Energy Corp. | 3,165 | 523,238 | ||||||

| EnerSys | 4,896 | 419,000 | ||||||

| Matador Resources Co. | 8,740 | 539,170 | ||||||

| Weatherford International PLC(a) | 5,434 | 505,851 | ||||||

| 1,987,259 | ||||||||

| Financials — 14.03% | ||||||||

| Atlantic Union Bancshares Corp. | 14,204 | 409,217 | ||||||

| AXIS Capital Holdings Ltd. | 7,161 | 408,893 | ||||||

| Evercore, Inc., Class A | 3,125 | 406,813 | ||||||

| Pinnacle Financial Partners, Inc. | 6,555 | 408,770 | ||||||

| Primerica, Inc. | 2,145 | 410,038 | ||||||

| SouthState Corp. | 6,153 | 406,713 | ||||||

| Stifel Financial Corp. | 7,137 | 406,809 | ||||||

| Wintrust Financial Corp. | 5,451 | 407,135 | ||||||

| 3,264,388 | ||||||||

| Health Care — 14.70% | ||||||||

| Alkermes PLC(a) | 6,709 | 162,291 | ||||||

| Axsome Therapeutics, Inc.(a) | 4,970 | 309,532 | ||||||

| Blueprint Medicines Corp.(a) | 5,945 | 349,923 | ||||||

| Cytokinetics, Inc.(a) | 6,287 | 219,165 | ||||||

| Deciphera Pharmaceuticals, Inc.(a) | 11,515 | 138,065 | ||||||

| Denali Therapeutics, Inc.(a) | 8,780 | 165,327 | ||||||

| DocGo, Inc.(a) | 73,299 | 435,396 | ||||||

| Ensign Group, Inc. (The) | 5,003 | 483,290 | ||||||

| Insmed, Inc.(a) | 5,656 | 141,739 | ||||||

| Lantheus Holdings, Inc.(a) | 7,623 | 492,446 | ||||||

| Madrigal Pharmaceuticals, Inc.(a) | 1,229 | 161,466 | ||||||

| TransMedics Group, Inc.(a) | 9,651 | 361,719 | ||||||

| 3,420,359 | ||||||||

| Industrials — 15.44% | ||||||||

| Applied Industrial Technologies, Inc. | 3,039 | 466,517 | ||||||

| Atkore, Inc.(a) | 3,266 | 405,898 | ||||||

See accompanying notes which are an integral part of these financial statements.

20

| Dana Epiphany ESG Small Cap Equity Fund |

| Schedule of Investments (continued) |

| October 31, 2023 |

| COMMON STOCKS — 98.35% - continued | Shares | Fair Value | ||||||

| Industrials — 15.44% - continued | ||||||||

| Cactus, Inc., Class A | 10,167 | $ | 477,239 | |||||

| Clean Harbors, Inc.(a) | 2,786 | 428,125 | ||||||

| FTI Consulting, Inc.(a) | 2,608 | 553,575 | ||||||

| Hub Group, Inc., Class A(a) | 5,832 | 400,950 | ||||||

| John Bean Technologies Corp. | 4,496 | 467,674 | ||||||

| TopBuild Corp.(a) | 1,707 | 390,493 | ||||||

| 3,590,471 | ||||||||

| Materials — 6.32% | ||||||||

| Advanced Drainage Systems, Inc. | 4,099 | 437,896 | ||||||

| Avient Corp. | 10,351 | 327,299 | ||||||

| Eagle Materials, Inc. | 2,304 | 354,609 | ||||||

| Element Solutions, Inc. | 19,272 | 351,328 | ||||||

| 1,471,132 | ||||||||

| Real Estate — 6.30% | ||||||||

| Agree Realty Corp. | 6,483 | 362,659 | ||||||

| Spirit Realty Capital, Inc. | 10,565 | 380,234 | ||||||

| STAG Industrial, Inc. | 10,552 | 350,537 | ||||||

| Tanger Factory Outlet Centers, Inc. | 16,460 | 371,173 | ||||||

| 1,464,603 | ||||||||

| Technology — 14.85% | ||||||||

| Axcelis Technologies, Inc.(a) | 2,849 | 363,248 | ||||||

| Box, Inc., Class A(a) | 18,619 | 462,869 | ||||||

| i3 Verticals, Inc., Class A(a) | 21,079 | 395,231 | ||||||

| Lattice Semiconductor Corp.(a) | 5,403 | 300,461 | ||||||

| Perficient, Inc. (a) | 7,536 | 438,520 | ||||||

| Perion Network Ltd.(a) | 9,765 | 248,031 | ||||||

| Tenable Holdings, Inc.(a) | 9,775 | 411,625 | ||||||

| Teradata Corp.(a) | 10,077 | 430,490 | ||||||

| Veeco Instruments, Inc.(a) | 16,890 | 404,346 | ||||||

| 3,454,821 | ||||||||

| Utilities — 2.68% | ||||||||

| Chesapeake Utilities Corp. | 3,323 | 294,451 | ||||||

| Clearway Energy, Inc., Class C | 15,133 | 328,537 | ||||||

| 622,988 | ||||||||

| Total Common Stocks (Cost $23,427,464) | 22,877,419 | |||||||

See accompanying notes which are an integral part of these financial statements.

21

| Dana Epiphany ESG Small Cap Equity Fund |

| Schedule of Investments (continued) |

| October 31, 2023 |

| MONEY MARKET FUNDS - 1.03% | Shares | Fair Value | ||||||

| Fidelity Investments Money Market Government Portfolio, Institutional Class, 5.28%(b) | 240,535 | $ | 240,535 | |||||

| Total Money Market Funds (Cost $240,535) | 240,535 | |||||||

| Total Investments — 99.38% (Cost $23,667,999) | 23,117,954 | |||||||

| Other Assets in Excess of Liabilities — 0.62% | 144,770 | |||||||

| NET ASSETS — 100.00% | $ | 23,262,724 | ||||||

| (a) | Non-income producing security. |

| (b) | Rate disclosed is the seven day effective yield as of October 31, 2023. |

See accompanying notes which are an integral part of these financial statements.

22

| Dana Epiphany ESG Equity Fund |

| Schedule of Investments |

| October 31, 2023 |

| COMMON STOCKS — 99.12% | Shares | Fair Value | ||||||

| Communications — 8.61% | ||||||||

| Alphabet, Inc., Class A(a) | 16,700 | $ | 2,072,136 | |||||

| Alphabet, Inc., Class C(a) | 4,600 | 576,380 | ||||||

| Comcast Corp., Class A | 31,000 | 1,279,990 | ||||||

| Interpublic Group of Cos., Inc. | 36,000 | 1,022,400 | ||||||

| Verizon Communications, Inc. | 5,000 | 175,650 | ||||||

| 5,126,556 | ||||||||

| Consumer Discretionary — 10.52% | ||||||||

| Amazon.com, Inc.(a) | 13,000 | 1,730,170 | ||||||

| BorgWarner, Inc. | 27,000 | 996,300 | ||||||

| Home Depot, Inc. (The) | 2,600 | 740,194 | ||||||

| Lululemon Athletica, Inc.(a) | 2,000 | 786,960 | ||||||

| PulteGroup, Inc. | 15,000 | 1,103,850 | ||||||

| Tapestry, Inc. | 33,000 | 909,480 | ||||||

| 6,266,954 | ||||||||

| Consumer Staples — 6.41% | ||||||||

| Darling Ingredients, Inc.(a) | 10,000 | 442,900 | ||||||

| General Mills, Inc. | 14,400 | 939,456 | ||||||

| Kimberly-Clark Corp. | 8,400 | 1,004,976 | ||||||

| Mondelez International, Inc., Class A | 9,000 | 595,890 | ||||||

| Sysco Corp. | 12,600 | 837,774 | ||||||

| 3,820,996 | ||||||||

| Energy — 4.40% | ||||||||

| ConocoPhillips | 3,000 | 356,400 | ||||||

| Ovintiv, Inc. | 7,000 | 336,000 | ||||||

| Pioneer Natural Resources Co. | 4,400 | 1,051,600 | ||||||

| Weatherford International PLC(a) | 9,400 | 875,046 | ||||||

| 2,619,046 | ||||||||

| Financials — 7.52% | ||||||||

| American Express Co. | 6,900 | 1,007,607 | ||||||

| Bank of New York Mellon Corp. (The) | 27,000 | 1,147,500 | ||||||

| Reinsurance Group of America, Inc. | 8,300 | 1,240,601 | ||||||

| Webster Financial Corp. | 28,600 | 1,085,942 | ||||||

| 4,481,650 | ||||||||

| Health Care — 10.94% | ||||||||

| Cigna Corp. | 4,500 | 1,391,400 | ||||||

| CVS Health Corp. | 16,400 | 1,131,764 | ||||||

| Elevance Health, Inc. | 2,500 | 1,125,225 | ||||||

| IQVIA Holdings, Inc.(a) | 5,700 | 1,030,731 | ||||||

| Waters Corp.(a) | 3,500 | 834,855 | ||||||

| Zoetis, Inc., Class A | 6,400 | 1,004,800 | ||||||

| 6,518,775 | ||||||||

| Industrials — 12.05% | ||||||||

| Boston Scientific Corp. (a) | 23,700 | 1,213,203 | ||||||

| CSX Corp. | 40,400 | 1,205,940 | ||||||

| Deere & Co. | 3,500 | 1,278,760 | ||||||

| Lincoln Electric Holdings, Inc. | 7,200 | 1,258,560 | ||||||

See accompanying notes which are an integral part of these financial statements.

23

| Dana Epiphany ESG Equity Fund |

| Schedule of Investments (continued) |

| October 31, 2023 |

| COMMON STOCKS — 99.12% - continued | Shares | Fair Value | ||||||

| Industrials — 12.05% - continued | ||||||||

| Regal-Beloit Corp. | 9,000 | $ | 1,065,690 | |||||

| TE Connectivity Ltd. | 9,800 | 1,154,930 | ||||||

| 7,177,083 | ||||||||

| Materials — 2.46% | ||||||||

| Graphic Packaging Holding Co. | 34,400 | 739,944 | ||||||

| Linde PLC | 1,900 | 726,104 | ||||||

| 1,466,048 | ||||||||

| Real Estate — 3.78% | ||||||||

| Hannon Armstrong Sustainable Infrastructure Capital, Inc. | 43,000 | 737,020 | ||||||

| Iron Mountain, Inc. | 13,800 | 815,166 | ||||||

| STAG Industrial, Inc. | 21,000 | 697,620 | ||||||

| 2,249,806 | ||||||||

| Technology — 29.94% | ||||||||

| Accenture PLC, Class A | 4,000 | 1,188,360 | ||||||

| Apple, Inc. | 15,000 | 2,561,550 | ||||||

| Cadence Design Systems, Inc.(a) | 5,600 | 1,343,160 | ||||||

| Cisco Systems, Inc. | 26,000 | 1,355,380 | ||||||

| CrowdStrike Holdings, Inc., Class A(a) | 5,200 | 919,204 | ||||||

| Fiserv, Inc.(a) | 8,800 | 1,001,000 | ||||||

| Microchip Technology, Inc. | 16,800 | 1,197,672 | ||||||

| Microsoft Corp. | 8,000 | 2,704,880 | ||||||

| NVIDIA Corp. | 2,700 | 1,101,060 | ||||||

| Salesforce, Inc.(a) | 5,600 | 1,124,648 | ||||||

| ServiceNow, Inc.(a) | 1,900 | 1,105,515 | ||||||

| Visa, Inc., Class A | 5,000 | 1,175,500 | ||||||

| Workday, Inc., Class A(a) | 5,000 | 1,058,550 | ||||||

| 17,836,479 | ||||||||

| Utilities — 2.49% | ||||||||

| NextEra Energy, Inc. | 13,400 | 781,220 | ||||||

| Portland General Electric Co. | 17,600 | 704,352 | ||||||

| 1,485,572 | ||||||||

| Total Common Stocks (Cost $59,970,647) | 59,048,965 | |||||||

| MONEY MARKET FUNDS - 1.13% | ||||||||

| Fidelity Investments Money Market Government Portfolio, Institutional Class, 5.28%(b) | 674,054 | 674,054 | ||||||

| Total Money Market Funds (Cost $674,054) | 674,054 | |||||||

| Total Investments — 100.25% (Cost $60,644,701) | 59,723,019 | |||||||

| Liabilities in Excess of Other Assets — (0.25)% | (147,290 | ) | ||||||

| NET ASSETS — 100.00% | $ | 59,575,729 | ||||||

| (a) | Non-income producing security. |

| (b) | Rate disclosed is the seven day effective yield as of October 31, 2023. |

See accompanying notes which are an integral part of these financial statements.

24

| Dana Funds |

| Statements of Assets and Liabilities |

| October 31, 2023 |

| Dana | ||||||||||||

| Epiphany | Dana | |||||||||||

| Dana Large | ESG Small | Epiphany | ||||||||||

| Cap Equity | Cap Equity | ESG Equity | ||||||||||

| Fund | Fund | Fund | ||||||||||

| Assets | ||||||||||||

| Investments in securities at fair value (cost $66,634,183, $23,667,999 and $60,644,701) (Note 3) | $ | 81,239,887 | $ | 23,117,954 | $ | 59,723,019 | ||||||

| Receivable for fund shares sold | 3,740 | 8,334 | 22,729 | |||||||||

| Receivable for investments sold | — | 597,140 | 2,264,708 | |||||||||

| Dividends receivable | 62,137 | 8,404 | 54,801 | |||||||||

| Receivable from Adviser (Note 4) | — | 566 | — | |||||||||

| Prepaid expenses | 24,941 | 19,103 | 12,923 | |||||||||

| Total Assets | 81,330,705 | 23,751,501 | 62,078,180 | |||||||||

| Liabilities | ||||||||||||

| Payable for fund shares redeemed | 197,976 | 12,428 | 31,878 | |||||||||

| Payable for investments purchased | — | 443,115 | 2,413,288 | |||||||||

| Payable to Adviser (Note 4) | 30,208 | — | 22,499 | |||||||||

| Accrued Distribution (12b-1) fees (Note 4) | 4,098 | — | — | |||||||||

| Payable to Administrator (Note 4) | 10,095 | 7,673 | 7,929 | |||||||||

| Payable to trustees (Note 4) | 2,000 | 2,000 | 2,000 | |||||||||

| Other accrued expenses | 24,782 | 23,561 | 24,857 | |||||||||

| Total Liabilities | 269,159 | 488,777 | 2,502,451 | |||||||||

| Net Assets | $ | 81,061,546 | $ | 23,262,724 | $ | 59,575,729 | ||||||

| Net Assets consist of: | ||||||||||||

| Paid-in capital | $ | 57,217,422 | $ | 23,897,060 | $ | 62,915,773 | ||||||

| Accumulated earnings (deficit) | 23,844,124 | (634,336 | ) | (3,340,044 | ) | |||||||

| Net Assets | $ | 81,061,546 | $ | 23,262,724 | $ | 59,575,729 | ||||||

| Institutional Class: | ||||||||||||

| Net Assets | $ | 62,264,736 | $ | 23,262,724 | $ | 59,575,729 | ||||||

| Shares outstanding (unlimited number of shares authorized, no par value) | 3,016,035 | 2,126,332 | 5,264,956 | |||||||||

| Net asset value, offering and redemption price per share (Note 2) | $ | 20.64 | $ | 10.94 | $ | 11.32 | ||||||

| Investor Class: | ||||||||||||

| Net Assets | $ | 18,796,810 | ||||||||||

| Shares outstanding (unlimited number of shares authorized, no par value) | 910,301 | |||||||||||

| Net asset value, offering and redemption price per share (Note 2) | $ | 20.65 | ||||||||||

See accompanying notes which are an integral part of these financial statements.

25

| Dana Funds |

| Statements of Operations |

| For the year ended October 31, 2023 |

| Dana Epiphany | Dana Epiphany | |||||||||||

| Dana Large Cap | ESG Small Cap | ESG Equity | ||||||||||

| Equity Fund | Equity Fund | Fund | ||||||||||

| Investment Income | ||||||||||||

| Dividend income | $ | 1,905,511 | $ | 322,522 | $ | 1,118,274 | ||||||

| Total investment income | 1,905,511 | 322,522 | 1,118,274 | |||||||||

| Expenses | ||||||||||||

| Investment Adviser fees (Note 4) | 637,750 | 188,796 | 415,988 | |||||||||

| Administration fees (Note 4) | 58,657 | 32,072 | 38,369 | |||||||||

| Distribution (12b-1) fees, Investor Class (Note 4) | 51,184 | — | — | |||||||||

| Fund accounting fees (Note 4) | 38,955 | 26,726 | 27,055 | |||||||||

| Registration expenses | 36,920 | 23,021 | 26,547 | |||||||||

| Transfer agent fees (Note 4) | 24,588 | 19,784 | 20,820 | |||||||||

| Legal fees | 19,849 | 19,837 | 19,849 | |||||||||

| Audit and tax preparation fees | 18,830 | 18,830 | 18,830 | |||||||||

| Custodian fees | 15,055 | 6,299 | 12,715 | |||||||||

| Printing and postage expenses | 10,270 | 7,209 | 9,541 | |||||||||

| Trustee fees (Note 4) | 7,753 | 7,753 | 7,753 | |||||||||

| Compliance service fees (Note 4) | 4,755 | 4,750 | 4,750 | |||||||||

| Insurance expenses | 4,590 | 3,467 | 4,243 | |||||||||

| Miscellaneous expenses | 23,760 | 23,681 | 23,308 | |||||||||

| Total expenses | 952,916 | 382,225 | 629,768 | |||||||||

| Fees contractually waived by Adviser (Note 4) | (185,548 | ) | (143,132 | ) | (85,812 | ) | ||||||

| Net operating expenses | 767,368 | 239,093 | 543,956 | |||||||||

| Net investment income | 1,138,143 | 83,429 | 574,318 | |||||||||

| Net Realized and Change in Unrealized Gain (Loss) on Investments | ||||||||||||

| Net realized gain (loss) on investment securities transactions | 9,293,059 | (72,141 | ) | (1,318,786 | ) | |||||||

| Net change in unrealized appreciation (depreciation) on investment securities | (3,532,624 | ) | (458,867 | ) | 619,220 | |||||||

| Net realized and change in unrealized gain (loss) on investments | 5,760,435 | (531,008 | ) | (699,566 | ) | |||||||

| Net increase (decrease) in net assets resulting from operations | $ | 6,898,578 | $ | (447,579 | ) | $ | (125,248 | ) | ||||

See accompanying notes which are an integral part of these financial statements

26

| Dana Funds |

| Statements of Changes in Net Assets |

| Dana Large Cap Equity Fund | ||||||||

| For the Year | For the Year | |||||||

| Ended October | Ended October | |||||||

| 31, 2023 | 31, 2022 | |||||||

| Increase (Decrease) in Net Assets due to: | ||||||||

| Operations | ||||||||

| Net investment income | $ | 1,138,143 | $ | 1,335,454 | ||||

| Net realized gain on investment securities transactions | 9,293,059 | 7,882,982 | ||||||

| Net change in unrealized depreciation of investment securities | (3,532,624 | ) | (32,144,030 | ) | ||||

| Net increase (decrease) in net assets resulting from operations | 6,898,578 | (22,925,594 | ) | |||||

| Distributions to Shareholders from Earnings (Note 2) | ||||||||

| Institutional Class | (7,243,857 | ) | (14,198,810 | ) | ||||

| Investor Class | (1,715,762 | ) | (3,218,987 | ) | ||||

| Total distributions | (8,959,619 | ) | (17,417,797 | ) | ||||

| Capital Transactions – Institutional Class | ||||||||

| Proceeds from shares sold | 4,190,683 | 14,475,937 | ||||||

| Reinvestment of distributions | 4,106,603 | 7,925,662 | ||||||

| Amount paid for shares redeemed | (26,796,119 | ) | (22,829,242 | ) | ||||

| Total – Institutional Class | (18,498,833 | ) | (427,643 | ) | ||||

| Capital Transactions – Investor Class | ||||||||

| Proceeds from shares sold | 191,295 | 368,279 | ||||||

| Reinvestment of distributions | 1,614,452 | 3,041,633 | ||||||

| Amount paid for shares redeemed | (2,489,366 | ) | (2,415,054 | ) | ||||

| Total – Investor Class | (683,619 | ) | 994,858 | |||||

| Net increase (decrease) in net assets resulting from capital transactions | (19,182,452 | ) | 567,215 | |||||

| Total Decrease in Net Assets | (21,243,493 | ) | (39,776,176 | ) | ||||

| Net Assets | ||||||||

| Beginning of year | 102,305,039 | 142,081,215 | ||||||

| End of year | $ | 81,061,546 | $ | 102,305,039 | ||||

| Share Transactions - Institutional Class | ||||||||

| Shares sold | 196,733 | 577,714 | ||||||

| Shares issued in reinvestment of distributions | 207,383 | 299,112 | ||||||

| Shares redeemed | (1,262,433 | ) | (959,176 | ) | ||||

| Total – Institutional Class | (858,317 | ) | (82,350 | ) | ||||

| Share Transactions - Investor Class | ||||||||

| Shares sold | 9,112 | 15,632 | ||||||

| Shares issued in reinvestment of distributions | 81,545 | 114,484 | ||||||

| Shares redeemed | (117,715 | ) | (101,487 | ) | ||||

| Total – Investor Class | (27,058 | ) | 28,629 | |||||

See accompanying notes which are an integral part of these financial statements.

27

| Dana Funds |

| Statements of Changes in Net Assets (continued) |

| Dana Epiphany ESG Small Cap | ||||||||

| Equity Fund | ||||||||

| For the Year | For the Year | |||||||

| Ended October | Ended October | |||||||

| 31, 2023 | 31, 2022 | |||||||

| Increase (Decrease) in Net Assets due to: | ||||||||

| Operations | ||||||||

| Net investment income | $ | 83,429 | $ | 9,163 | ||||

| Net realized gain (loss) on investment securities transactions | (72,141 | ) | 1,159,913 | |||||

| Net change in unrealized depreciation of investment securities | (458,867 | ) | (4,828,049 | ) | ||||

| Net decrease in net assets resulting from operations | (447,579 | ) | (3,658,973 | ) | ||||

| Distributions to Shareholders from Earnings (Note 2) | ||||||||

| Institutional Class | (1,212,675 | ) | (1,429,190 | ) | ||||

| Total distributions | (1,212,675 | ) | (1,429,190 | ) | ||||

| Capital Transactions – Institutional Class | ||||||||

| Proceeds from shares sold | 19,902,954 | 4,022,076 | ||||||

| Reinvestment of distributions | 1,202,030 | 1,400,259 | ||||||

| Amount paid for shares redeemed | (9,640,065 | ) | (4,314,843 | ) | ||||

| Total – Institutional Class | 11,464,919 | 1,107,492 | ||||||

| Net increase in net assets resulting from capital transactions | 11,464,919 | 1,107,492 | ||||||

| Total Increase (Decrease) in Net Assets | 9,804,665 | (3,980,671 | ) | |||||

| Net Assets | ||||||||

| Beginning of year | 13,458,059 | 17,438,730 | ||||||

| End of year | $ | 23,262,724 | $ | 13,458,059 | ||||

| Share Transactions - Institutional Class | ||||||||

| Shares sold | 1,680,428 | 291,572 | ||||||

| Shares issued in reinvestment of distributions | 110,815 | 95,256 | ||||||

| Shares redeemed | (823,320 | ) | (324,787 | ) | ||||

| Total – Institutional Class | 967,923 | 62,041 | ||||||

See accompanying notes which are an integral part of these financial statements

28

| Dana Funds |

| Statements of Changes in Net Assets (continued) |

| Dana Epiphany ESG Equity Fund | ||||||||

| For the Year | For the Year | |||||||

| Ended October | Ended October | |||||||

| 31, 2023 | 31, 2022 | |||||||

| Increase (Decrease) in Net Assets due to: | ||||||||

| Operations | ||||||||

| Net investment income | $ | 574,318 | $ | 678,437 | ||||

| Net realized loss on investment securities transactions | (1,318,786 | ) | (1,150,639 | ) | ||||

| Net change in unrealized appreciation (depreciation) of investment securities | 619,220 | (12,474,484 | ) | |||||

| Net decrease in net assets resulting from operations | (125,248 | ) | (12,946,686 | ) | ||||

| Distributions to Shareholders from Earnings (Note 2) | ||||||||

| Institutional Class | (576,674 | ) | (1,696,546 | ) | ||||

| Total distributions | (576,674 | ) | (1,696,546 | ) | ||||

| Capital Transactions – Institutional Class | ||||||||

| Proceeds from shares sold | 15,996,248 | 36,072,130 | ||||||

| Reinvestment of distributions | 571,181 | 1,650,842 | ||||||

| Amount paid for shares redeemed | (29,280,915 | ) | (17,645,598 | ) | ||||

| Total – Institutional Class | (12,713,486 | ) | 20,077,374 | |||||

| Net increase (decrease) in net assets resulting from capital transactions | (12,713,486 | ) | 20,077,374 | |||||

| Total Increase (Decrease) in Net Assets | (13,415,408 | ) | 5,434,142 | |||||

| Net Assets | ||||||||

| Beginning of year | 72,991,137 | 67,556,995 | ||||||

| End of year | $ | 59,575,729 | $ | 72,991,137 | ||||

| Share Transactions - Institutional Class | ||||||||

| Shares sold | 1,330,401 | 2,777,361 | ||||||

| Shares issued in reinvestment of distributions | 48,598 | 121,043 | ||||||

| Shares redeemed | (2,453,902 | ) | (1,394,549 | ) | ||||

| Total – Institutional Class | (1,074,903 | ) | 1,503,855 | |||||

See accompanying notes which are an integral part of these financial statements.

29

| Dana Large Cap Equity Fund – Institutional Class |

| Financial Highlights |

| (For a share oustanding during each year) |

| For the Years Ended October 31, | ||||||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Selected Per Share Data | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 21.26 | $ | 29.20 | $ | 21.25 | $ | 22.69 | $ | 22.35 | ||||||||||

| Investment operations: | ||||||||||||||||||||

| Net investment income | 0.27 | 0.28 | 0.17 | 0.23 | 0.38 | |||||||||||||||

| Net realized and unrealized gain (loss) on investments | 1.01 | (4.60 | ) | 8.39 | 0.86 | 2.46 | ||||||||||||||

| Total from investment operations | 1.28 | (4.32 | ) | 8.56 | 1.09 | 2.84 | ||||||||||||||

| Less distributions to shareholders from: | ||||||||||||||||||||

| Net investment income | (0.28 | ) | (0.25 | ) | (0.17 | ) | (0.23 | ) | (0.36 | ) | ||||||||||

| Net realized gains | (1.62 | ) | (3.37 | ) | (0.44 | ) | (2.30 | ) | (2.14 | ) | ||||||||||

| Total distributions | (1.90 | ) | (3.62 | ) | (0.61 | ) | (2.53 | ) | (2.50 | ) | ||||||||||

| Net asset value, end of year | $ | 20.64 | $ | 21.26 | $ | 29.20 | $ | 21.25 | $ | 22.69 | ||||||||||

| Total Return(a) | 6.44 | % | (17.16 | )% | 40.89 | % | 4.65 | % | 15.55 | % | ||||||||||

| Ratios and Supplemental Data: | ||||||||||||||||||||

| Net assets, end of year (000 omitted) | $ | 62,265 | $ | 82,373 | $ | 115,544 | $ | 91,379 | $ | 107,026 | ||||||||||

| Before waiver | ||||||||||||||||||||

| Ratio of expenses to average net assets | 0.91 | % | 0.87 | % | 0.86 | % | 0.91 | % | 0.85 | % | ||||||||||

| After waiver | ||||||||||||||||||||

| Ratio of expenses to average net assets | 0.73 | % | 0.73 | % | 0.73 | % | 0.73 | % | 0.73 | % | ||||||||||

| Ratio of net investment income to average net assets | 1.21 | % | 1.14 | % | 0.65 | % | 1.10 | % | 1.68 | % | ||||||||||

| Portfolio turnover rate(b) | 55 | % | 38 | % | 30 | % | 57 | % | 50 | % | ||||||||||

| (a) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

| (b) | Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing among the classes of shares. |

See accompanying notes which are an integral part of these financial statements.

30

| Dana Large Cap Equity Fund – Investor Class |

| Financial Highlights |

| (For a share oustanding during each year) |

| For the Years Ended October 31, | ||||||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Selected Per Share Data | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 21.26 | $ | 29.20 | $ | 21.26 | $ | 22.69 | $ | 22.35 | ||||||||||

| Investment operations: | ||||||||||||||||||||

| Net investment income | 0.20 | 0.22 | 0.10 | 0.18 | 0.30 | |||||||||||||||

| Net realized and unrealized gain (loss) on investments | 1.03 | (4.60 | ) | 8.39 | 0.87 | 2.50 | ||||||||||||||

| Total from investment operations | 1.23 | (4.38 | ) | 8.49 | 1.05 | 2.80 | ||||||||||||||

| Less distributions to shareholders from: | ||||||||||||||||||||

| Net investment income | (0.22 | ) | (0.19 | ) | (0.11 | ) | (0.18 | ) | (0.32 | ) | ||||||||||

| Net realized gains | (1.62 | ) | (3.37 | ) | (0.44 | ) | (2.30 | ) | (2.14 | ) | ||||||||||

| Total distributions | (1.84 | ) | (3.56 | ) | (0.55 | ) | (2.48 | ) | (2.46 | ) | ||||||||||

| Net asset value, end of year | $ | 20.65 | $ | 21.26 | $ | 29.20 | $ | 21.26 | $ | 22.69 | ||||||||||

| Total Return(a) | 6.22 | % | (17.38 | )% | 40.48 | % | 4.43 | % | 15.29 | % | ||||||||||

| Ratios and Supplemental Data: | ||||||||||||||||||||

| Net assets, end of year (000 omitted) | $ | 18,797 | $ | 19,932 | $ | 26,537 | $ | 24,615 | $ | 25,398 | ||||||||||

| Before waiver | ||||||||||||||||||||

| Ratio of expenses to average net assets | 1.16 | % | 1.12 | % | 1.11 | % | 1.16 | % | 1.10 | % | ||||||||||

| After waiver | ||||||||||||||||||||

| Ratio of expenses to average net assets | 0.98 | % | 0.98 | % | 0.98 | % | 0.98 | % | 0.98 | % | ||||||||||

| Ratio of net investment income to average net assets | 0.95 | % | 0.89 | % | 0.40 | % | 0.85 | % | 1.40 | % | ||||||||||

| Portfolio turnover rate(b) | 55 | % | 38 | % | 30 | % | 57 | % | 50 | % | ||||||||||

| (a) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

| (b) | Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing among the classes of shares. |

See accompanying notes which are an integral part of these financial statements.

31

| Dana Epiphany ESG Small Cap Equity Fund – Institutional Class |

| Financial Highlights |

| (For a share oustanding during each year) |

| For the Years Ended October 31, | ||||||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Selected Per Share Data | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 11.62 | $ | 15.91 | $ | 9.82 | $ | 10.24 | $ | 11.09 | ||||||||||

| Investment operations: | ||||||||||||||||||||

| Net investment income (loss) | 0.04 | 0.01 | (0.03 | ) | 0.01 | 0.01 | ||||||||||||||

| Net realized and unrealized gain (loss) on investments | (0.14 | ) | (3.02 | ) | 6.12 | (0.42 | ) | (0.05 | ) | |||||||||||

| Total from investment operations | (0.10 | ) | (3.01 | ) | 6.09 | (0.41 | ) | (0.04 | ) | |||||||||||

| Less distributions to shareholders from: | ||||||||||||||||||||

| Net investment income | (0.04 | ) | — | — | (0.01 | ) | — | |||||||||||||

| Net realized gains | (0.54 | ) | (1.28 | ) | — | — | (0.81 | ) | ||||||||||||

| Total distributions | (0.58 | ) | (1.28 | ) | — | (0.01 | ) | (0.81 | ) | |||||||||||

| Net asset value, end of year | $ | 10.94 | $ | 11.62 | $ | 15.91 | $ | 9.82 | $ | 10.24 | ||||||||||

| Total Return(a) | (0.81 | )% | (20.59 | )% | 62.02 | % | (4.04 | )% | 0.83 | % | ||||||||||

| Ratios and Supplemental Data: | ||||||||||||||||||||

| Net assets, end of year (000 omitted) | $ | 23,263 | $ | 13,458 | $ | 17,439 | $ | 9,861 | $ | 12,421 | ||||||||||

| Before waiver | ||||||||||||||||||||

| Ratio of expenses to average net assets | 1.52 | % | 1.95 | % | 2.05 | % | 2.58 | % | 1.88 | % | ||||||||||

| After waiver | ||||||||||||||||||||

| Ratio of expenses to average net assets | 0.95 | % | 0.95 | % | 0.95 | % | 0.95 | % | 0.95 | % | ||||||||||

| Ratio of net investment income (loss) to average net assets | 0.33 | % | 0.06 | % | (0.24 | )% | 0.02 | % | 0.11 | % | ||||||||||

| Portfolio turnover rate | 59 | % | 82 | % | 92 | % | 88 | % | 50 | % | ||||||||||

| (a) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

See accompanying notes which are an integral part of these financial statements.

32

| Dana Epiphany ESG Equity Fund – Institutional Class |

| Financial Highlights |

| (For a share outstanding during each year) |

| For the Years Ended October 31, | ||||||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Selected Per Share Data | ||||||||||||||||||||

| Net asset value, beginning of year | $ | 11.51 | $ | 13.97 | $ | 10.25 | $ | 11.58 | $ | 11.80 | ||||||||||

| Investment operations: | ||||||||||||||||||||

| Net investment income | 0.11 | 0.11 | 0.06 | 0.09 | 0.14 | |||||||||||||||

| Net realized and unrealized gain (loss) on investments | (0.19 | ) | (2.27 | ) | 3.87 | 0.47 | 1.15 | |||||||||||||

| Total from investment operations | (0.08 | ) | (2.16 | ) | 3.93 | 0.56 | 1.29 | |||||||||||||

| Less distributions to shareholders from: | ||||||||||||||||||||

| Net investment income | (0.11 | ) | (0.11 | ) | (0.06 | ) | (0.10 | ) | (0.12 | ) | ||||||||||

| Net realized gains | — | (0.19 | ) | (0.15 | ) | (1.79 | ) | (1.39 | ) | |||||||||||

| Total distributions | (0.11 | ) | (0.30 | ) | (0.21 | ) | (1.89 | ) | (1.51 | ) | ||||||||||

| Net asset value, end of year | $ | 11.32 | $ | 11.51 | $ | 13.97 | $ | 10.25 | $ | 11.58 | ||||||||||

| Total Return(a) | (0.71 | )% | (15.76 | )% | 38.70 | % | 4.76 | % | 12.76 | % | ||||||||||

| Ratios and Supplemental Data: | ||||||||||||||||||||

| Net assets, end of year (000 omitted) | $ | 59,576 | $ | 72,991 | $ | 67,557 | $ | 13,062 | $ | 5,079 | ||||||||||

| Before waiver | ||||||||||||||||||||

| Ratio of expenses to average net assets | 0.98 | % | 0.96 | % | 1.12 | % | 2.00 | % | 2.13 | % | ||||||||||

| After waiver | ||||||||||||||||||||

| Ratio of expenses to average net assets | 0.85 | % | 0.85 | % | 0.85 | % | 0.85 | % | 0.90 | % | ||||||||||

| Ratio of net investment income to average net assets | 0.90 | % | 0.91 | % | 0.57 | % | 0.89 | % | 1.19 | % | ||||||||||

| Portfolio turnover rate | 60 | % | 33 | % | 18 | % | 67 | % | 60 | % | ||||||||||

| (a) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

See accompanying notes which are an integral part of these financial statements.

33

| Dana Funds |

| Notes to the Financial Statements |

| October 31, 2023 |

NOTE 1. ORGANIZATION

The Dana Large Cap Equity Fund (the “Large Cap Fund”), the Dana Epiphany ESG Small Cap Equity Fund (the “Small Cap Fund”), and the Dana Epiphany ESG Equity Fund (the “Epiphany ESG Fund”) (each a “Fund” and collectively, the “Funds”) are each registered under the Investment Company Act of 1940, as amended (“1940 Act”), as an open-end diversified series of Valued Advisers Trust (the “Trust”). The Trust is a management investment company established under the laws of Delaware by an Agreement and Declaration of Trust dated June 13, 2008 (the “Trust Agreement”). The Trust Agreement permits the Board of Trustees (“Board”) to issue an unlimited number of shares of beneficial interest of separate series without par value. Each Fund is one of a series of funds currently authorized by the Board. The investment adviser to the Funds is Dana Investment Advisors, Inc. (the “Adviser”). Each Fund seeks long-term growth of capital.

The Large Cap Fund currently offers Investor Class shares and Institutional Class shares. The Small Cap Fund and Epiphany ESG Fund currently offer Institutional Class shares. Each share represents an equal proportionate interest in the assets and liabilities belonging to the Fund and is entitled to such dividends and distributions out of income belonging to the Fund as declared by the Board.

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES

The Funds are investment companies and follow accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”. The following is a summary of significant accounting policies followed by the Funds in the preparation of their financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”).

Regulatory update – Tailored Shareholder Reports for Mutual Funds and Exchange-Traded Funds (“ETFs”) – Effective January 24, 2023, the SEC adopted rule and form amendments to require mutual funds and ETFs to transmit concise and visually engaging streamlined annual and semiannual reports to shareholders that highlight key information. Other information, including financial statements, will no longer appear in a streamlined shareholder report but must be available online, delivered free of charge upon request, and filed on a semiannual basis on Form N-CSR. The rule and form amendments have a compliance date of July 24, 2024. At this time, management is evaluating the impact of these amendments on the shareholder reports for the Funds.

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of

34

| Dana Funds |

| Notes to the Financial Statements (continued) |

| October 31, 2023 |

assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Federal Income Taxes – The Funds make no provision for federal income or excise tax. Each Fund has qualified and intends to qualify each year as a regulated investment company (“RIC”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of its taxable income. Each Fund also intends to distribute sufficient net investment income and net capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Funds could incur a tax expense.

As of and during the fiscal year ended October 31, 2023, the Funds did not have any liabilities for any unrecognized tax benefits. The Funds recognize interest and penalties, if any, related to unrecognized tax benefits as income tax expense on the Statements of Operations when incurred. During the fiscal year ended October 31, 2023, the Funds did not incur any interest or penalties. Management of the Funds has reviewed tax positions taken in tax years that remain subject to examination by all major tax jurisdictions, including federal (i.e., the last three tax year ends and the interim tax period since then, as applicable). Management believes that there is no tax liability resulting from unrecognized tax benefits related to uncertain tax positions taken.

Expenses – Expenses incurred by the Trust that do not relate to a specific fund of the Trust are allocated to the individual funds based on each fund’s relative net assets or another appropriate basis (as determined by the Board). Expenses specifically attributable to any class are borne by that class. Income, realized gains and losses, unrealized appreciation and depreciation, and fund-wide expenses not allocated to a particular class shall be allocated to each class based on the net assets of that class in relation to the net assets of the entire fund.

Security Transactions and Related Income – The Funds follow industry practice and record security transactions on the trade date for financial reporting purposes. The specific identification method is used for determining gains or losses for financial statement and income tax purposes. Dividend income is recorded on the ex-dividend date and interest income is recorded on an accrual basis. Withholding taxes on foreign dividends, if any, have been provided for in accordance with the Funds’ understanding of the applicable country’s tax rules and rates.

The Funds may hold Real Estate Investment Trusts (“REITs”) which pay dividends to their shareholders based upon available funds from operations. It is possible for these dividends to exceed the REIT’s underlying taxable earnings and profits resulting in the

35

| Dana Funds |

| Notes to the Financial Statements (continued) |

| October 31, 2023 |

excess portion of such dividends being designated as a return of capital. Distributions received from REITs that represent a return of capital or capital gains are recorded as a reduction of the cost of the REITs or as a realized gain, respectively.

Dividends and Distributions – The Funds intend to distribute substantially all of their net investment income, if any, at least quarterly. The Funds intend to distribute their net realized long-term and short-term capital gains, if any, annually. Distributions to shareholders, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the year from net investment income or net realized capital gains may differ from their ultimate treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of the recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, they are reclassified in the components of the net assets based on their ultimate characterization for federal income tax purposes. Any such reclassifications will have no effect on net assets, results of operations or net asset value (“NAV”) per share of the Funds.

For the fiscal year end of October 31, 2023, the Funds made the following reclassifications to increase (decrease) the components of net assets:

| Accumulated | ||||||||

| Paid-In | Earnings | |||||||

| Capital | (Deficit) | |||||||

| Large Cap Fund | $ | — | $ | — | ||||

| Small Cap Fund | (4,035 | ) | 4,035 | |||||

| Epiphany ESG Fund | 24,564 | (24,564 | ) | |||||

Share Valuation – The NAV per share of each class of each Fund is calculated each day the New York Stock Exchange (“NYSE”) is open by dividing the total value of the assets attributable to that class, less liabilities attributable to that class, by the number of shares outstanding of that class.

NOTE 3. SECURITIES VALUATION AND FAIR VALUE MEASUREMENTS