UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22264

The Motley Fool Funds Trust

(Exact name of registrant as specified in charter)

Motley Fool Asset Management, LLC

2000 Duke Street, Suite 175

Alexandria, VA 22314

(Address of principal executive offices) (Zip code)

Peter E. Jacobstein

Motley Fool Asset Management, LLC

2000 Duke Street, Suite 175

Alexandria, VA 22314

(Name and address of agent for service)

Registrant’s telephone number, including area code: (703) 302-1100

Date of fiscal year end: October 31

Date of reporting period: October 31, 2011

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

A N N U A L R E P O R T

| | |

A series of The Motley Fool Funds Trust | | October 31, 2011 |

| | |

| | | |

Motley Fool Independence Fund & Motley Fool Great America Fund present:

Top 10 Reasons to

Read This Report

| | 10. | A free Motley Fool Funds ball cap and the chance to win lunch with Portfolio Manager Bill Mann. Really! |

| | 9. | A list of the Motley Fool Funds Guiding Principles. Now in an exciting new font! (Kidding – it’s the same font.) |

| | 8. | Unusual use of the word “autodidact.” |

| | 7. | A list of every single holding of both funds as of October 31, 2011, from the $7.38 million in Yum! Brands in the Independence Fund to the $117,440 in Varian Medical Systems in the Great America Fund. |

| | 6. | OK, don’t read it. It’s just that we worked really hard on it. And it’s just about your money. Which is pretty important. |

| | 5. | A whole lot of stimulating boilerplate! |

| | 4. | A section about expenses, which has been carefully and humorlessly reviewed by our auditors.* |

| | 3. | The fascinating story of Frank H. Brown’s monumental influence on your life. |

| | 2. | Interesting graphs of the relative performance of our funds vs. their benchmarks, as required by mutual fund law.** |

| | 1. | A not completely gratuitous reference to J. Martin Troost’s The Sex Lives of Cannibals. |

* Our auditors may have great senses of humor. We don’t really know.

| ** Full | disclosure: We don’t actually find these graphs interesting. |

Hello, and welcome to the annual report. Throughout, the Funds have included comments to help you understand the annual report, teach you some things to look for in a fund, and to make you chuckle a little. Our investment adviser is an affiliate of The Motley Fool, LLC (“The Motley Fool”), a publisher of investment information and analysis. Like The Motley Fool, our goal is to educate, amuse, and enrich you. Don’t forget to visit www.FoolFunds.com and sign up for our e-newsletter Declarations, featuring Bill Mann’s monthly Letter to Shareholders.

Hello, and welcome to the annual report. Throughout, the Funds have included comments to help you understand the annual report, teach you some things to look for in a fund, and to make you chuckle a little. Our investment adviser is an affiliate of The Motley Fool, LLC (“The Motley Fool”), a publisher of investment information and analysis. Like The Motley Fool, our goal is to educate, amuse, and enrich you. Don’t forget to visit www.FoolFunds.com and sign up for our e-newsletter Declarations, featuring Bill Mann’s monthly Letter to Shareholders.

Motley Fool Independence Fund

During the year ended October 31, 2011, the Motley Fool Independence Fund returned 1.9% versus its benchmark index, which returned 2.3%.

During the year ended October 31, 2011, the Motley Fool Independence Fund returned 1.9% versus its benchmark index, which returned 2.3%.

We set up best and worst case scenarios for all companies we analyze. Way to nail the worst case, Hellenic Exchanges!

We continued to find little value in European banks. That’s why we didn’t own any.

Motley Fool Great America Fund

During the year ended October 31, 2011, the Motley Fool Great America Fund returned 10.5% and outperformed its benchmark index by 2.6%.

Remember what we said about European banks for Indy? Yeah, we didn’t hold any American ones in Great America either.

Buying Schweitzer-Mauduit: helpful. Buying Joe’s Jeans: not helpful.

This report has been prepared for shareholders of Motley Fool Independence Fund and Motley Fool Great America Fund. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current prospectus, which contains more complete information about the Funds. Investors are reminded to read the prospectus carefully before investing. Past performance is no guarantee of future results. Share prices will fluctuate and there may be a gain or loss when shares are redeemed. Fund shares are distributed by BNY Mellon Distributors Inc., 760 Moore Rd., King of Prussia, PA 19406.

| | | | |

| 2 | | | | The Motley Fool Funds Trust |

TABLE OF CONTENTS

Letter from the President

| | |

President Peter Jacobstein | | Dear Fellow Shareholder: |

| | What happens when a long-time critic of the mutual fund industry creates a mutual fund? |

| | You get Motley Fool Funds. |

| | For 15 years, The Motley Fool was a harsh detractor of mutual fund industry practices that we believed were harmful to individual shareholders. Yet our criticism of mutual funds only seemed to make more people ask us: “can’t YOU manage my money for me?” |

| | So after years of study and soul-searching, we concluded that the best way we could help these investors was to create a mutual fund ourselves — but one that was true to our principles. |

This isn’t just a marketing slogan for us. We built Motley Fool Funds from the

| | | | |

| The Motley Fool Funds Trust | | | | 3 |

ground up to be a different kind of mutual fund company. Simply put: We want to be the most shareholder-friendly fund company in the business.

To make sure we’re serving you as well as possible, we focus on three critical areas:

1. The way we manage your money: We invest according to Foolish investment principles.

| | • | | We do extensive bottoms-up research on every company we hold. |

| | • | | We strive to buy stocks we can hold for the long-term — to hold down our trading costs and your tax bill. |

| | • | | We invest alongside you: Our Portfolio Managers invest their own money in our funds, and The Motley Fool has put $1 million of the company’s money into each fund as well. |

2. The fees we charge shareholders: We charge simple, fair fees that ensure our interests are always aligned with yours.

| | • | | We don’t charge loads or 12b-1 fees, ever. |

| | • | | We keep our fees for each fund below their category average. |

| | • | | Our management fees are performance-based. That means if our funds perform better, we earn more; if our funds perform worse, we earn less. |

3. The way we communicate with shareholders: We want you to know how we’re investing your money. And we want to make all our shareholders better investors.

| | • | | Our portfolio team writes a monthly email, Declarations, for all shareholders (sign up for free at FoolFunds.com), so you always know what we’re thinking and how we’re managing your money. |

| | • | | We give you multiple ways to interact with the portfolio team, including: |

n “Question Authority” online Q&A with the team

n Semi-annual conference calls

n Annual in-person shareholder meeting

| | • | | We write in plain English, not Wall Street jargon. |

At Motley Fool Funds, we want to change money management for the better. My

| | | | |

| 4 | | | | The Motley Fool Funds Trust |

team and I work hard every day to live our values.

Thank you for your investment in Motley Fool Funds, and for your continued confidence in us.

|

| Sincerely, |

|

|

Peter Jacobstein

President, Motley Fool Asset Management

PS: If you’re not already receiving our monthly newsletter, Declarations, I urge you to sign up today at FoolFunds.com. Full of investing insights, observations on the economy, travel tips, and witty asides, it’s always entertaining, and you’re guaranteed to learn something new every month.

| | | | |

| The Motley Fool Funds Trust | | | | 5 |

Letter to Shareholders

| | |

Portfolio Manager Bill Mann | | Dear Fellow Motley Fool Funds Shareholder: |

| | For the year ended October 31, 2011, the Motley Fool Independence Fund generated a return of 1.9% versus a return of 2.3% for the MSCI World, its benchmark. The Motley Fool Great America Fund had a return of 10.5% versus a return of 7.9% for the Russell Midcap Index. |

Had you simply tuned out over the past year, you might be excused for thinking that those returns suggest fairly benign market conditions. In actuality, they’ve been anything but. As global economic conditions have grown scarier, markets worldwide have displayed remarkable levels of volatility, with daily national index moves of 3, 4, even 5% becoming commonplace, particularly starting in June. The American stock market suffered a stomach-churning decline of more than 20%, only to rally rapidly through October. Stock movements in the U.S. were nothing compared to those in a multitude of international markets, with countries as diverse as Austria, Argentina, Greece, and Egypt suffering declines approaching 40%.

The Independence Fund ended the fiscal year trailing its benchmark by a fraction of a percent. We closed out our first year in the Great America Fund with a rather strong showing.

In 2010, the Independence Fund bested its benchmark, and I made the same claim then as I do now: We make no effort whatsoever to mimic the weightings of companies, industries, or geographies of our indexes, and as such we view our one-year relative performance to be an exercise in randomness as much as anything else. Whether the story is good or bad, our message is the same: If you find us worrying too much about our benchmarks, you should find someone else to manage your money because that would be a sign that we have lost our focus.

All in all, my own assessment is that we had a good year. There are some decisions that I’d like to have back — for example, selling Chipotle and buying Joe’s Jeans — but my regrets are due more to bad decisions than bad outcomes. If you make good decisions, on the balance the outcomes tend to take care of themselves. Good decisions are the result of having a good process in place. This is not to say that even good processes are lapse-free. Regarding Joe’s Jeans, for example, I undervalued the dynamic that had its chief designer being paid a percentage of gross (instead of net) profits, which put his interests ahead of — and at odds with — those of minority shareholders. This wasn’t just a bad outcome. It was a mistake.

| | | | |

| 6 | | | | The Motley Fool Funds Trust |

By the same measure, I’m proud of our process in investing in WeMade Entertainment, a Korean purveyor of online games, most notably the wildly profitable Legends of Mir II. Korean companies tend to offer analytical challenges, in no small part because they tend to only report results in Korean. Anthony Arsta’s primary research on this company was nothing short of spectacular, and the results for shareholders have been more than satisfactory.

We have made hundreds of investing decisions over the last year, none of which were conducted in consideration of the composition of our benchmarks. Despite this, our end-of-year scorecard shows that our funds tracked their benchmarks quite closely. One thing that volatility tends to cause among asset classes is increased correlation — even for ones that should move in the opposite direction. Through September and October, for example, the Treasury, equity, and precious metal markets all moved in lockstep with one another. In times when investing is generally rational, this should not happen. I feel very safe in declaring the market environment in which we currently operate as being highly irrational.

Two things I want you to do

I hope to convince you to do two things today. The first is fairly simple. We constantly look for ways to make the Fool Funds family extremely shareholder-friendly, and one way we do that is to communicate obsessively with our members and other folks who are interested in what we have to say. We do this through our monthly email, Declarations, which includes our shareholder letters (wholly written by our portfolio team), Question Authority (where we answer questions from our shareholders), dispatches from our travels, and our quarterly conference calls and annual live meeting. If you aren’t getting Declarations, please email contest@FoolFunds.com to sign up, even if you’re not a current shareholder (OK, especially if you’re not a current shareholder). To show our thanks, we’ll send a Motley Fool Funds ball cap to everyone who emails us (make sure you provide your postal address) and you’ll be entered in our contest. Grand prize: Lunch with me and another member of our portfolio team at a restaurant in your town. Sweet, right? (For complete contest rules, visit FoolFunds.com/help/contest.aspx.)

The reason we’re going to such lengths to encourage you to sign up is simple: We believe that mutual funds work best when the largest number of shareholders possible is aligned in philosophy and temperament with those who are managing their money. Even the best performing mutual funds deliver poor results for shareholders who buy and sell at the wrong time. It is important — very important — that you know what we are thinking and why.

That’s the first thing I want you to do today. I’ll tell you about the second in a moment.

The dismal lives of economic prognosticators

I’d like to invite you to a basketball game. It’s just your standard game: two teams,

| | | | |

| The Motley Fool Funds Trust | | | | 7 |

basket at each end, tall people, cheerleaders, all the trappings. Except in this game, the scoring system is quite different.

Rather than counting baskets made, a team of basketball experts determines the score based upon a large set of statistical measures: baskets attempted, turnovers, times shoelaces tied (TST), injuries, scoring balance, fan happiness, concession stand sales, fatigue measurements, etc. At the end of the game, the experts tell you which team won.

There are two other factors you should know about how scoring is measured. First, the measurements are all backward-looking. The experts who score the game have access to almost none of the information in real time, so they can only guess at the score at any point during the game. Second, the statistics they use are all prone to substantial revision. A team that thought it had won might be informed days or weeks later that the result had been reversed due to a revision to the sports drink-to-pretzel ratio.

Is this something that you’d like to watch? Frankly, it sounds like a pretty miserable experience, fraught with error and uncertainty. And yet, the process I describe is similar to that of economic analysis. In 1992, lousy economic data essentially scuppered George H. W. Bush’s re-election efforts. Cold comfort when much of those indicators were later revised higher. Given these two factors (the dependency on statistics that are rear-view and prone to substantial revision), is there any wonder that consensus among economists is so rare, even on events that happened years prior?

All hail Alaska

If economists cannot agree on events that took place years ago, and can’t access important data to determine what is happening right this second, what hope do we have that their forecasts are accurate? Past experience should suggest “very little,” but that doesn’t stop people from either making bold forecasts, or consuming them (I’m sure the former is a condition of the latter). Economic forecasts are little more than guesses made on bad data and historical inferences.

Which, of course, is why the story of Frank H. Brown is so important.

Who is Frank H. Brown, you ask? It’s a name that is associated with an event that has made the lives of millions of people around the world both better and different. Thanks to Frank H. Brown, many items in your daily life cost a fraction of what they would otherwise, if they were available at all.

Frank H. Brown was the world’s first container ship. It plied the Inside Passage route from Seattle and the Pacific Northwest up to Juneau and Skagway, Alaska. For centuries, shipping had been done essentially the same way: each parcel carried individually. This not only wasn’t very efficient, but it also left the packages exposed to the elements, so spoilage was quite common.

| | | | |

| 8 | | | | The Motley Fool Funds Trust |

In the 1950s, employees of the shipping company looked at all of these odd-shaped packages going to various places in Alaska and thought it might be wise to combine them into metal containers that could be offloaded in each port. They immediately noticed two benefits: the cargo hold was substantially more efficient to load and unload, and far fewer items were arriving at their destination damaged. This insight led to one of the most underrated developments of the last century: the standard-sized shipping container.

The advent of the shipping container spawned a massive industry (several of them, actually), and has transformed the very concept of product availability. (Don’t believe this is a big deal? Pick up a copy of Sex Lives of Cannibals by J. Martin Troost to read a modern account of living in Kiribati, a small South Pacific country that is too economically small to warrant regular shipments of products generally available all over the world. And no, that wasn’t a ploy to write the word “sex” into an annual letter.)

Containerized shipping makes goods all over the world cheaper to deliver and has unleashed massive amounts of economic activity, creating millions of jobs and shrinking the distance between producer and consumer. Fresh mangoes in Toledo? Frank H. Brown. Korean televisions in Estonia? Frank H. Brown. Enfamil in Zimbabwe? Frank H. Brown.

You might wonder why I’m bringing this up. Think back again to our miserable basketball game and the even more miserable practice of economic forecasting. Could experts have predicted the origin of something as transformative as the shipping container? Not a chance. Economists can only see what they know to look for, and then guess what this means about the future. Along comes something amazing, like the shipping container or the vacuum cleaner or the heart stent, created by someone for whom “this is how things are done” is merely a challenge, and whole new avenues of economic activity result.

Home of the autodidacts

And where, in all likelihood is the person who is creating the next amazing something? That’s a bit of a trick question, because there are probably thousands of amazing somethings rather than one big one. Nonetheless, a ridiculously large number — way too high to be coincidence — of these creative minds are residents of the United States.

This is the reason, despite an economy so miserable that thousands of Americans chose this fall to engage in long-term occupation protests in cities throughout the country, that great investors like Warren Buffett have invested billions of dollars into American companies over the last year. Buffett has often said that few fortunes will be made betting against the future of America, and I completely agree. The conditions that made the invention of the container ship or the stent or the UPC code have not been revoked.

| | | | |

| The Motley Fool Funds Trust | | | | 9 |

“But wait,” you must certainly be saying, “I constantly hear how the American education system is failing.” There is some truth to this, but unlike the educational systems in many countries, the American system doesn’t favor learning by rote. Education in many other countries is focused on preparing students for the standardized tests that play far larger roles in their college placements than the equivalent SAT or ACT do in the U.S.

Even more important, the center of the bell curve is far less relevant to the potential for future economic growth than the right tail, the high achievers. This is where you find those who go on to create the heart stents, the Netflixes, the Facebooks, and hundreds of other innovations that generate trillions of dollars in economic value.

The great news here is that America’s ability to turn out creative entrepreneurs hasn’t been revoked, sad headlines harkening the end of days be damned. The even better news is that while the United States is statistically very good at producing entrepreneurs, we by no means have a monopoly. I have full confidence in predicting that many of the elements that will help the global economy emerge from its malaise are, at this moment, not being tracked by economists.

The best time to invest

This is where I attempt to convince you to do one more thing. Warren Buffett has famously noted that the best time to buy is when there is “blood in the streets.” Sir John Templeton said to “buy on the cannons, sell on the trumpets.” I, like you, look at the three large pillars of the global economy — the U.S., China, and Europe — with the alarming realization that each one is shakier than the next. Pundits seem to have come to the same gloomy consensus: There’s no way out of this massive balance sheet mess. Certainly there are going to be plenty of reckonings to be had for a generation’s worth of miserable fiscal management.

But history will show that many of the biggest bargains in the stock market come during times of despair. It’s a pretty simple concept: where there are few shoppers, there are likely to be price inefficiencies. This dynamic shows up in the returns of shareholders in mutual funds versus the funds themselves. According to a Wall Street Journal article from December 2009, the CGM Focus Fund rose more than 18% per year through the decade, yet its typical shareholder lost 11% annually over the same period, a result that is entirely a function of shareholders buying when things were great, and selling when they weren’t.

What I want you to do is this: Get out there and invest.

In order to profit from market freak-outs, you need to invest into them. I am not asking you to invest in our funds specifically — I’m simply asking you to invest in something. Do it because few other people are, because everything looks like it will come apart at the seams. Sure, it’s possible that things will remain bad for a while. I wouldn’t argue otherwise, because I can’t. There is both literal and figurate

| | | | |

| 10 | | | | The Motley Fool Funds Trust |

blood running in the streets these days. As citizens we can and should be highly concerned and outraged. But by the same measure, many of the great investors have gifted us with clear instructions on what we should do during times of economic and political duress: Get out there and look for opportunities to buy. There is an inherent logic to making investments in the world’s great companies when the market has cast them aside.

Which is what your investment team here at Fool Funds is doing.

As always, the entire team here at Motley Fool Asset Management joins me in thanking you for entrusting us with your money. We are humbled by your trust.

Foolishly,

William H. Mann, III

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by the Annual Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time and may no longer be held by the Fund. The opinions of the Adviser with respect to those securities may change at any time.

| | | | |

| The Motley Fool Funds Trust | | | | 11 |

Motley Fool Independence Fund Portfolio Characteristics (Unaudited)

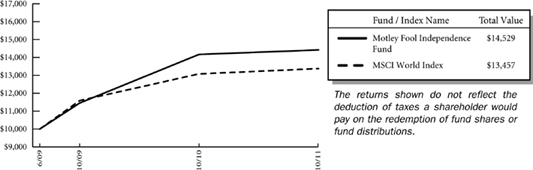

At October 31, 2011, the Motley Fool Independence Fund (the “Fund”) had an audited net asset value of $14.15 per share attributed to 14,010,532 shares outstanding. This compares with an unaudited net asset value as of June 16, 2009 of $10.00 per share attributed to 100,000 shares outstanding. From the Fund’s launch on June 16, 2009 to October 31, 2011 the Fund had a total return of 17.03% versus a return of 13.32% over the same period for its benchmark, MSCI World Index. The graph below shows the performance of $10,000 invested in the Fund at inception. The results shown below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Average Annual Total Returns as of 10/31/2011

| | | | |

| | | Fund* | | Benchmark** |

| | | |

One Year | | 1.91% | | 2.30% |

| | |

Since Inception | | 17.03% | | 13.32% |

| | |

Inception Date | | 06/16/2009 | | |

| | |

Total Annual Fund Operating Expenses Before Expense Limitation (February 28, 2011 Prospectus) | | 2.20% | | |

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained at www.FoolFunds.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. *These returns reflect expense waivers by the Fund’s investment adviser. Without these waivers, returns would have been lower.

**The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of the following 24 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States. The MSCI World Index is not available for direct investment. The Fund may invest in countries that are not included within the MSCI World Index (such as emerging market countries) and its investment portfolio is not weighted in terms of countries or issuers the same as the MSCI World Index. For this reason, the Fund’s investment performance should not be expected to track, and may exceed or trail, the MSCI World Index. Since Inception returns for the Benchmark reflect the performance based on the Inception Date of the Fund.

| | | | |

| 12 | | | | Motley Fool Independence Fund |

The investment objective of the Independence Fund is to achieve long-term capital appreciation. The Fund pursues this objective by investing primarily in common stocks of companies located anywhere in the world. The Fund invests in areas of the market that, in the view of Motley Fool Asset Management, LLC (the “Adviser”), offer the greatest potential for long-term capital appreciation. The Fund may invest in other types of securities and in other asset classes when, in the judgment of the Adviser, such investments offer attractive potential returns. As such, the Fund’s performance will deviate significantly from its benchmark from time to time. It is the view of the Adviser that this deviation is less meaningful over shorter time frames and is more relevant over multi-year periods.

Because the Independence Fund is free to invest in companies of any size around the world, at times, the Fund may be heavily invested in small-cap stocks and foreign securities, each of which presents extra risk. Small-cap stocks tend to be more volatile and less liquid than their large-cap counterparts. Fluctuations in currency exchange rates can cause losses when investing in foreign securities, with emerging markets presenting additional risks of illiquidity, political instability, and lax regulation. You are strongly encouraged to read more about the Fund’s strategies and risks in the prospectus.

The Independence Fund invests in securities of companies the Adviser believes are undervalued. Unlike mutual funds that are constrained by a style-box, the Fund may invest in any company, country, market, industry or sector where the Adviser’s analysis suggests that there is opportunity for gains that outweigh risks. In identifying investments for the Fund, the Adviser looks for companies it believes the market has irrationally undervalued and looks for companies that have high-quality businesses with strong market positions, manageable leverage, and robust streams of free cash flow. The following tables show the top 11 holdings and top 10 sectors and countries in which the Fund was invested at fiscal year-end. Portfolio holdings are subject to change without notice.

Certain mutual fund ratings and review services have created style boxes, which look more or less like a tic-tac-toe board; arranging funds by the size of the companies they typically invest in (large-, mid-, and small-cap) along one axis, and along a “value” to “growth” basis on the other axis. This may be a helpful way – at times – to think about certain investment opportunities, but we don’t believe we’ll improve your returns by limiting ourselves to any one portion of that style box.

| | | | |

Top Eleven Holdings* | | % of Net

Assets | |

| |

Telefonica SA | | | 3.72 | % |

Yum! Brands, Inc. | | | 3.49 | |

WellPoint, Inc. | | | 3.26 | |

Denbury Resources, Inc. | | | 2.87 | |

POSCO | | | 2.71 | |

Loews Corp. | | | 2.64 | |

HCC Insurance Holdings, Inc. | | | 2.42 | |

Lukoil OAO | | | 2.31 | |

Brookfield Asset Management, Inc. | �� | | 2.29 | |

Google, Inc. | | | 2.24 | |

Markel Corp. | | | 2.18 | |

| | | | |

| | | 30.13 | % |

| | | | |

| * | As of the date of the report the fund had a holding of 0.68% in the BNY Mellon Cash Reserve. |

| | | | |

| Motley Fool Independence Fund | | | | 13 |

The Motley Fool Independence Fund uses the Global Industry Classification StandardSM (“GICSSM”) as the basis for the classification of securities on the Schedule of Investments (“SOI”).We believe that this makes the SOI classifications more standard with the rest of the industry.

| | | | |

| Top Ten Sectors | | % of Net Assets | |

| | | | | |

| |

Financials | | | 22.19 | % |

Consumer Staples | | | 14.54 | |

Health Care | | | 13.03 | |

Information Technology | | | 10.20 | |

Consumer Discretionary | | | 9.01 | |

Industrials | | | 7.96 | |

Energy | | | 6.98 | |

Materials | | | 5.34 | |

Telecommunications | | | 5.19 | |

Utilities | | | 2.81 | |

| | | | |

| | | 97.25 | % |

| | | | |

| | | | |

| Top Eleven Countries | | % of Net Assets | |

| | | | | |

United States* | | | 50.35 | % |

Japan | | | 5.83 | |

South Korea | | | 4.06 | |

Spain | | | 3.72 | |

Brazil | | | 3.43 | |

Bermuda | | | 3.11 | |

Canada | | | 2.91 | |

Hong Kong | | | 2.71 | |

Russia | | | 2.31 | |

United Kingdom | | | 2.28 | |

Singapore | | | 1.78 | |

| | | | |

| | | 82.49 | % |

| | | | |

| * | As of the date of the report the fund had a holding of 0.68% in the BNY Mellon Cash Reserve. |

| | | | |

| 14 | | | | Motley Fool Independence Fund |

About Your Expenses

As a shareholder of the Independence Fund, you incur ongoing costs, including advisory fees and other Fund expenses. This example is intended to help you to understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. It is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from May 1, 2011 to October 31, 2011.

Actual Expenses

The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you incurred over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses attributable to your investment during this period.

Hypothetical Example for Comparison Purposes

The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the Independence Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. Thus, you should not use the hypothetical account values and expenses to estimate the actual ending account balance or your expenses for the period. Rather, these figures are provided to enable you to compare the ongoing costs of investing in the Fund as compared to the costs of investing in other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only. Therefore, the second section of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds.

Do you know how many times a fund, or the market, has returned a smooth 5% over a long period of time? Never. But we have to pick some example. In reality the market’s returns are always far bumpier, with the market returning 20% one year, followed by a loss of 10% the next year, followed by a 3% gain, etc. These variations affect actual expenses as well. Happily, over almost all time periods of 20 years or longer, according to the research of University of Pennsylvania’s Jeremy Siegel and others, the domestic market’s returns have been at least 5% per year on average.

| | | | | | | | | | | | | | | | |

| | | Beginning

Account Value

05/01/11 | | | Ending

Account Value

10/31/11 | | | Annualized

Expense Ratio(1) | | | Expenses Paid

During Period(2) | |

| | |

Actual | | $ | 1,000 | | | $ | 905.88 | | | | 1.43 | % | | $ | 6.87 | |

Hypothetical | | $ | 1,000 | | | $ | 1,018.00 | | | | 1.43 | % | | $ | 7.27 | |

| (1) | These ratios reflect expenses waived by the Fund’s investment Adviser. Without these Waivers, the Fund’s expenses would have been higher and the ending account values would have been lower. |

| (2) | Expenses are equal to the Fund’s annualized expense ratio for the period May 1, 2011 to October 31, 2011, multiplied by the average account value over the period, multiplied by the number of days (184) in the most recent fiscal half-year, then divided by 365. |

| | | | |

| Motley Fool Independence Fund (Unaudited) | | 15 |

The Motley Fool Funds Trust

Motley Fool Independence Fund

Schedule of Investments

at October 31, 2011

| | | | | | | | |

| Issues | | Shares | | | Value (Note 2) | |

| | |

| | |

Equity Securities — 95.51% | | | | | | | | |

Beverages — 0.75% | | | | | | | | |

Coca-Cola Icecek AS (Turkey) | | | 110,000 | | | $ | 1,483,505 | |

| | | | | | | | |

| | |

Capital Markets — 0.75% | | | | | | | | |

INTL FCStone, Inc. (United States)* | | | 61,513 | | | | 1,491,075 | |

| | | | | | | | |

| | |

Chemicals — 1.80% | | | | | | | | |

Innophos Holdings, Inc. (United States) | | | 81,164 | | | | 3,570,404 | |

| | | | | | | | |

| | |

Commercial Banks — 2.44% | | | | | | | | |

Banco Latinoamericano de Comercio Exterior SA (Panama) | | | 98,265 | | | | 1,596,806 | |

Qatar Islamic Bank (Qatar) | | | 146,650 | | | | 3,249,739 | |

| | | | | | | | |

| | |

| | | | | | | 4,846,545 | |

| | | | | | | | |

| | |

Commercial Services & Supplies — 3.05% | | | | | | | | |

De La Rue PLC (United Kingdom) | | | 190,900 | | | | 2,586,118 | |

Multiplus SA (Brazil) | | | 204,600 | | | | 3,455,981 | |

| | | | | | | | |

| | |

| | | | | | | 6,042,099 | |

| | | | | | | | |

| | |

Communications Equipment — 2.70% | | | | | | | | |

Cisco Systems, Inc. (United States) | | | 68,000 | | | | 1,260,040 | |

Infinera Corp. (United States)* | | | 561,100 | | | | 4,101,641 | |

| | | | | | | | |

| | |

| | | | | | | 5,361,681 | |

| | | | | | | | |

| | |

Construction & Engineering — 0.35% | | | | | | | | |

KHD Humboldt Wedag International AG (Germany)* | | | 109,586 | | | | 686,118 | |

| | | | | | | | |

| | |

Containers & Packaging — 0.68% | | | | | | | | |

Crown Holdings, Inc. (United States)* | | | 40,000 | | | | 1,351,600 | |

| | | | | | | | |

| | |

Diversified Consumer Services — 0.04% | | | | | | | | |

MegaStudy Co., Ltd (South Korea) | | | 800 | | | | 88,480 | |

| | | | | | | | |

| | |

Diversified Financial Services — 0.65% | | | | | | | | |

Hellenic Exchanges SA (Greece) | | | 264,077 | | | | 1,289,924 | |

| | | | | | | | |

| | |

Diversified Telecommunication Services — 3.72% | | | | | | | | |

Telefonica SA (Spain)(a) | | | 345,359 | | | | 7,380,322 | |

| | | | | | | | |

| | |

Electric Utilities — 2.81% | | | | | | | | |

Brookfield Infrastructure Partners LP (Bermuda) | | | 163,127 | | | | 4,092,857 | |

See Notes to Financial Statements.

| | | | |

| 16 | | | | Motley Fool Independence Fund |

| | | | | | | | |

| Issues | | Shares | | | Value (Note 2) | |

| | |

| | |

Equity Securities (continued) | | | | | | | | |

Electric Utilities (continued) | | | | | | | | |

Otter Tail Corp. (United States) | | | 75,725 | | | $ | 1,469,822 | |

| | | | | | | | |

| | |

| | | | | | | 5,562,679 | |

| | | | | | | | |

| | |

Electrical Equipment — 0.48% | | | | | | | | |

Legrand SA (France) | | | 27,209 | | | | 961,795 | |

| | | | | | | | |

| | |

Food & Staples Retailing — 4.02% | | | | | | | | |

Costco Wholesale Corp. (United States) | | | 29,558 | | | | 2,460,703 | |

Olam International Ltd. (Singapore) | | | 1,765,139 | | | | 3,535,746 | |

Wal-Mart de Mexico SAB de CV, Series V (Mexico) | | | 768,098 | | | | 1,982,635 | |

| | | | | | | | |

| | |

| | | | | | | 7,979,084 | |

| | | | | | | | |

| | |

Food Products — 5.13% | | | | | | | | |

BRF - Brasil Foods SA (Brazil)(a) | | | 158,704 | | | | 3,340,719 | |

Cresud SACIF y A (Argentina)(a) | | | 238,196 | | | | 2,765,456 | |

Nestle SA (Switzerland) | | | 38,694 | | | | 2,237,972 | |

PT Nippon Indosari Corpindo Tbk (Indonesia) | | | 4,795,000 | | | | 1,834,658 | |

| | | | | | | | |

| | |

| | | | | | | 10,178,805 | |

| | | | | | | | |

| | |

Health Care Equipment & Supplies — 6.25% | | | | | | | | |

Becton, Dickinson and Co. (United States) | | | 50,200 | | | | 3,927,146 | |

Covidien PLC (Ireland) | | | 41,000 | | | | 1,928,640 | |

Natus Medical, Inc. (United States)* | | | 243,900 | | | | 2,097,540 | |

Nihon Kohden Corp. (Japan) | | | 133,481 | | | | 3,116,252 | |

Zimmer Holdings, Inc. (United States)* | | | 25,000 | | | | 1,315,750 | |

| | | | | | | | |

| | |

| | | | | | | 12,385,328 | |

| | | | | | | | |

| | |

Health Care Providers & Services — 3.26% | | | | | | | | |

WellPoint, Inc. (United States) | | | 93,697 | | | | 6,455,723 | |

| | | | | | | | |

| | |

Hotels, Restaurants & Leisure — 5.43% | | | | | | | | |

Arcos Dorados Holdings, Inc. (Argentina) | | | 8,000 | | | | 187,200 | |

McDonald’s Corp. (United States) | | | 19,177 | | | | 1,780,585 | |

Penn National Gaming, Inc. (United States)* | | | 52,083 | | | | 1,874,988 | |

Yum! Brands, Inc. (United States) | | | 129,132 | | | | 6,917,601 | |

| | | | | | | | |

| | |

| | | | | | | 10,760,374 | |

| | | | | | | | |

| | |

Household Products — 1.83% | | | | | | | | |

Unicharm Corp. (Japan) | | | 80,800 | | | | 3,618,540 | |

| | | | | | | | |

| | |

Insurance — 10.41% | | | | | | | | |

Berkshire Hathaway, Inc. (United States)* | | | 33 | | | | 3,859,350 | |

See Notes to Financial Statements.

| | | | |

| Motley Fool Independence Fund | | | | 17 |

| | | | | | | | |

| Issues | | Shares | | | Value (Note 2) | |

| | |

| | |

Equity Securities (continued) | | | | | | | | |

Insurance (continued) | | | | | | | | |

Berkshire Hathaway, Inc., Class B (United States)* | | | 4,600 | | | $ | 358,156 | |

Enstar Group Ltd. (Bermuda)* | | | 22,510 | | | | 2,070,245 | |

HCC Insurance Holdings, Inc. (United States) | | | 180,200 | | | | 4,795,122 | |

Loews Corp. (United States) | | | 131,690 | | | | 5,228,093 | |

Markel Corp. (United States)* | | | 11,200 | | | | 4,328,800 | |

| | | | | | | | |

| | |

| | | | | | | 20,639,766 | |

| | | | | | | | |

| | |

Internet Software & Services — 2.24% | | | | | | | | |

Google, Inc. (United States)* | | | 7,500 | | | | 4,444,800 | |

| | | | | | | | |

| | |

IT Services — 1.55% | | | | | | | | |

Paychex, Inc. (United States) | | | 105,702 | | | | 3,080,156 | |

| | | | | | | | |

| | |

Leisure Equipment & Products — 1.55% | | | | | | | | |

Shimano, Inc. (Japan) | | | 62,000 | | | | 3,064,674 | |

| | | | | | | | |

| | |

Machinery — 1.30% | | | | | | | | |

Flowserve Corp. (United States) | | | 27,700 | | | | 2,567,513 | |

| | | | | | | | |

| | |

Metals & Mining — 2.71% | | | | | | | | |

POSCO (South Korea)(a) | | | 62,491 | | | | 5,369,227 | |

| | | | | | | | |

| | |

Oil, Gas & Consumable Fuels — 6.98% | | | | | | | | |

Denbury Resources, Inc. (United States)* | | | 362,200 | | | | 5,686,540 | |

Lukoil OAO (Russia)(a) | | | 79,350 | | | | 4,578,495 | |

Occidental Petroleum Corp. (United States) | | | 22,645 | | | | 2,104,626 | |

Total Gabon (Gabon) | | | 3,470 | | | | 1,460,398 | |

| | | | | | | | |

| | |

| | | | | | | 13,830,059 | |

| | | | | | | | |

| | |

Pharmaceuticals — 3.53% | | | | | | | | |

Astellas Pharma, Inc. (Japan) | | | 17,000 | | | | 621,748 | |

Astrazeneca PLC (United Kingdom)(a) | | | 40,100 | | | | 1,921,191 | |

Chugai Pharmaceutical Co., Ltd. (Japan) | | | 36,000 | | | | 563,893 | |

Dr. Reddy’s Laboratories Ltd. (India)(a) | | | 100,177 | | | | 3,320,868 | |

Santen Pharmaceutical Co., Ltd. (Japan) | | | 15,250 | | | | 569,032 | |

| | | | | | | | |

| | |

| | | | | | | 6,996,732 | |

| | | | | | | | |

| | |

Professional Services — 2.17% | | | | | | | | |

Bureau Veritas SA (France) | | | 800 | | | | 62,074 | |

Huron Consulting Group, Inc. (United States)* | | | 117,518 | | | | 4,231,823 | |

| | | | | | | | |

| | |

| | | | | | | 4,293,897 | |

| | | | | | | | |

See Notes to Financial Statements.

| | | | |

| 18 | | | | Motley Fool Independence Fund |

| | | | | | | | |

| Issues | | Shares | | | Value (Note 2) | |

| | |

| | |

Equity Securities (continued) | | | | | | | | |

Real Estate Investment Trusts — 2.93% | | | | | | | | |

Annaly Capital Management, Inc. (United States) | | | 219,989 | | | $ | 3,706,815 | |

DuPont Fabros Technology, Inc. (United States) | | | 101,000 | | | | 2,099,790 | |

| | | | | | | | |

| | |

| | | | | | | 5,806,605 | |

| | | | | | | | |

| | |

Real Estate Management & Development — 5.00% | | | | | | | | |

Brookfield Asset Management, Inc. (Canada) | | | 156,374 | | | | 4,534,846 | |

Cheung Kong Holdings Ltd. (Hong Kong) | | | 170,337 | | | | 2,111,486 | |

Henderson Land Development Co., Ltd. (Hong Kong) | | | 596,764 | | | | 3,261,929 | |

| | | | | | | | |

| | |

| | | | | | | 9,908,261 | |

| | | | | | | | |

| | |

Semiconductors & Semiconductor Equipment — 1.32% | | | | | | | | |

Formfactor, Inc. (United States)* | | | 233,100 | | | | 1,393,938 | |

NVIDIA Corp. (United States)* | | | 82,000 | | | | 1,213,600 | |

| | | | | | | | |

| | |

| | | | | | | 2,607,538 | |

| | | | | | | | |

| | |

Software — 2.39% | | | | | | | | |

DuzonBizon Co., Ltd. (South Korea)* | | | 184,180 | | | | 1,164,544 | |

Fundtech Ltd. (Israel) | | | 93,102 | | | | 2,142,277 | |

Wemade Entertainment Co., Ltd. (South Korea) | | | 29,507 | | | | 1,430,569 | |

| | | | | | | | |

| | |

| | | | | | | 4,737,390 | |

| | | | | | | | |

| | |

Specialty Retail — 0.09% | | | | | | | | |

Best Buy Co., Inc. (United States) | | | 7,000 | | | | 183,610 | |

| | | | | | | | |

| | |

Textiles, Apparel & Luxury Goods — 1.90% | | | | | | | | |

Under Armour, Inc. (United States)* | | | 44,705 | | | | 3,773,549 | |

| | | | | | | | |

| | |

Tobacco — 1.06% | | | | | | | | |

Philip Morris International, Inc. (United States) | | | 30,072 | | | | 2,101,131 | |

| | | | | | | | |

| | |

Trading Companies & Distributors — 0.62% | | | | | | | | |

MFC Industrial Ltd. (Canada) | | | 174,514 | | | | 1,226,833 | |

| | | | | | | | |

| | |

Wireless Telecommunication Services — 1.62% | | | | | | | | |

American Tower Corp. (United States)* | | | 16,686 | | | | 919,398 | |

SBA Communications Corp. (United States)* | | | 60,000 | | | | 2,285,400 | |

| | | | | | | | |

| | | | | | | 3,204,798 | |

| | | | | | | | |

| | |

Total Equity Securities (Cost $ 175,674,755) | | | | | | | 189,330,620 | |

| | | | | | | | |

See Notes to Financial Statements.

| | | | |

| Motley Fool Independence Fund | | | | 19 |

| | | | | | | | |

| Issues | | Shares | | | Value (Note 2) | |

| | |

| | |

Exchange Traded Note — 0.70% | | | | | | | | |

American International Group, Inc. (United States) | | | 56,950 | | | $ | 1,379,329 | |

| | | | | | | | |

Total Exchange Traded Note (Cost $ 1,253,490) | | | | | | | 1,379,329 | |

| | | | | | | | |

| | |

Participatory Note — 1.74% | | | | | | | | |

Food Products — 1.74% | | | | | | | | |

Almarai Co. (Saudi Arabia) 144A | | | 145,000 | | | | 3,460,344 | |

| | | | | | | | |

Total Participatory Note (Cost $ 3,576,755) | | | | | | | 3,460,344 | |

| | | | | | | | |

| | |

Other Investments — 0.68% | | | | | | | | |

Temporary Cash Investment — 0.68% | | | | | | | | |

BNY Mellon Cash Reserve | | | 1,347,465 | | | | 1,347,465 | |

| | | | | | | | |

| | |

Total Other Investments (Cost $ 1,347,465) | | | | | | | 1,347,465 | |

| | | | | | | | |

| | |

Total Investment Portfolio (Cost 181,852,465) — 98.63% | | | | | | | 195,517,758 | |

Other Assets in Excess of Liabilities — 1.37% | | | | | | | 2,714,588 | |

| | | | | | | | |

| | |

NET ASSETS — 100.00% | | | | | | | | |

(Applicable to 14,010,532 shares outstanding) | | | | | | $ | 198,232,346 | |

| | | | | | | | |

| * | Non-income producing security. |

| (a) | ADR — American Depositary Receipts |

| 144A | Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. Total market value of Rule 144A securities is $3,460,344 and represents 1.74% of net assets as of October 31, 2011. |

LP — Limited Partnership

| PLC | — Public Limited Company |

See Notes to Financial Statements.

| | | | |

| 20 | | | | Motley Fool Independence Fund |

Statement of Assets and Liabilities

| | | | | | |

| | | As of October 31, 2011 | | | |

| |

| | |

Assets: | | | | | | |

Investments in securities of unaffiliated issuers,

at value (at cost, $181,852,465) | | $ | 195,517,758 | | | |

Foreign currency, at value

(at cost, $1,803,162) | | | 1,806,929 | | | |

Receivables: | | | | | | |

Dividends and Tax Reclaims | | | 227,461 | | | |

Interest | | | 38 | | | |

Investment securities sold | | | 1,682,397 | | | |

Shares of beneficial interest sold | | | 185,082 | | | |

Prepaid expenses and other assets | | | 23,988 | | | |

| | | | | | |

Total Assets | | | 199,443,653 | | | |

| | | | | | |

| | |

Liabilities | | | | | | |

Payables: | | | | | | |

Cash overdraft | | | 3 | | | |

Investment securities purchased | | | 604,260 | | | |

Shares of beneficial interest redeemed | | | 290,323 | | | |

Accrued expenses: | | | | | | |

Audit fees | | | 16,965 | | | |

Accounting and administration fees | | | 56,429 | | | |

Advisory fees | | | 134,134 | | | |

Custodian fees | | | 12,158 | | | |

Legal fees | | | 18,065 | | | |

Transfer agent fees | | | 28,949 | | | |

Trustee fees | | | 2,787 | | | |

Other expenses | | | 47,234 | | | |

| | | | | | |

Total Liabilities | | | 1,211,307 | | | |

| | | | | | |

Net Assets | | $ | 198,232,346 | | | |

| | | | | | |

The accompanying notes are an integral part of these financial statements.

| | | | |

| Motley Fool Independence Fund | | | | 21 |

Statement of Assets and Liabilities

| | | | | | |

| | | As of October 31, 2011 | | | |

| |

| | |

Net Assets Consist of: | | | | | | |

Paid-in-Capital | | $ | 183,969,169 | | | |

Undistributed Net Investment Income | | | 599,663 | | | |

Accumulated Net Realized Gain (Loss) | | | (4,519 | ) | | |

Net Unrealized Appreciation (Depreciation) on

Investments, Foreign Currencies, and Assets and

Liabilities denominated in Foreign Currencies | | | 13,668,033 | | | |

| | | | | | |

Net Assets | | $ | 198,232,346 | | | |

| | | | | | |

| | |

Net Asset Value: | | | | | | |

$0.001 par value, unlimited shares authorized | | | | | | |

Net assets applicable to capital shares outstanding | | $ | 198,232,346 | | | |

Shares outstanding | | | 14,010,532 | | | |

| | | | | | |

Net asset value, offering and redemption price per

share | | $ | 14.15 | | | |

| | | | | | |

The accompanying notes are an integral part of these financial statements.

| | | | |

| 22 | | | | Motley Fool Independence Fund |

Statement of Operations

| | | | | | |

| | | Year Ended

October 31, 2011 | | | |

| |

| | |

Investment Income | | | | | | |

Dividends | | $ | 4,178,278 | | | |

Interest | | | 29,137 | | | |

Less foreign taxes withheld | | | (263,644 | ) | | |

| | | | | | |

Total Investment Income | | | 3,943,771 | | | |

| | | | | | |

| | |

Expenses | | | | | | |

Accounting and administration fees | | | 189,491 | | | |

Blue sky fees | | | 28,370 | | | |

Shareholder account-related services | | | 126,946 | | | |

Chief Compliance Officer fees | | | 23,532 | | | |

Custodian fees | | | 72,905 | | | |

Investment advisory fees | | | 1,849,271 | | | |

Professional fees | | | 77,057 | | | |

Shareholder reporting fees | | | 21,133 | | | |

Transfer agent fees | | | 372,540 | | | |

Trustee fees | | | 47,236 | | | |

Other expenses | | | 31,593 | | | |

| | | | | | |

Total expenses | | | 2,840,074 | | | |

| | | | | | |

Expenses waived/reimbursed net of amount

recaptured | | | (271,178 | ) | | |

| | | | | | |

Net expenses | | | 2,568,896 | | | |

| | | | | | |

Net Investment Income | | | 1,374,875 | | | |

| | | | | | |

| | |

Realized and Unrealized Gain (Loss) | | | | | | |

| | |

Net realized gain (loss) from: | | | | | | |

Investment securities | | | 137,987 | | | |

Foreign currency transactions | | | (147,572 | ) | | |

| | | | | | |

Net realized loss on investments and foreign

currency transactions | | | (9,585 | ) | | |

| | | | | | |

Change in net unrealized appreciation

(depreciation) on: | | | | | | |

Investment securities | | | (3,041,600 | ) | | |

Foreign currency translations | | | 3,634 | | | |

| | | | | | |

Change in net unrealized appreciation

(depreciation) on investments, foreign

currencies, and assets and liabilities

denominated in foreign currencies | | | (3,037,966 | ) | | |

| | | | | | |

Net realized and unrealized loss | | | (3,047,551 | ) | | |

| | | | | | |

| | |

Net Decrease in Net Assets Resulting from

Operations | | $ | (1,672,676 | ) | | |

| | | | | | |

The accompanying notes are an integral part of these financial statements.

| | | | |

| Motley Fool Independence Fund | | | | 23 |

Statements of Changes in Net Assets

| | | | | | | | | | |

| | | Year Ended October 31, 2011 | | | Year Ended October 31, 2010 | | | |

| |

| | | |

Operations: | | | | | | | | | | |

Net Investment Income | | $ | 1,374,875 | | | $ | 1,069,735 | | | |

Net Realized Gain/(Loss) on Investments and

Foreign Currency Transactions | | | (9,585 | ) | | | 805,287 | | | |

Change in Net Unrealized Appreciation/

(Depreciation) on Investments and Foreign

Currency Translation | | | (3,037,966 | ) | | | 15,586,918 | | | |

| | | | | | | | | | |

Net increase/(decrease) in net assets resulting from

operations | | | (1,672,676 | ) | | | 17,461,940 | | | |

| | | | | | | | | | |

| | | |

Dividends and Distributions to Shareholders: | | | | | | | | | | |

Dividends from net investment income | | | (1,465,155 | ) | | | (95,696 | ) | | |

Distributions from net realized capital gains | | | (1,105,695 | ) | | | (295,167 | ) | | |

| | | | | | | | | | |

Total dividends and distributions | | | (2,570,850 | ) | | | (390,863 | ) | | |

| | | | | | | | | | |

| | | |

Capital Share Transactions: | | | | | | | | | | |

Proceeds from shares sold (7,313,429 and 7,468,879

shares, respectively) | | | 108,513,048 | | | | 93,888,742 | | | |

Reinvestment of dividends and distributions

(175,447 and 31,228 shares, respectively) | | | 2,522,930 | | | | 384,097 | | | |

Value of shares redeemed (2,559,545 and 1,069,514

shares, respectively) | | | (37,047,015 | ) | | | (13,409,649 | ) | | |

| | | | | | | | | | |

Redemption and small-balance account fees | | | 80,714 | | | | 45,165 | | | |

| | | | | | | | | | |

Net increase from capital share transactions | | | 74,069,677 | | | | 80,908,355 | | | |

| | | | | | | | | | |

Total increase in net assets | | | 69,826,151 | | | | 97,979,432 | | | |

| | | | | | | | | | |

| | | |

Net Assets: | | | | | | | | | | |

Beginning of Period | | | 128,406,195 | | | | 30,426,763 | | | |

| | | | | | | | | | |

End of Period* | | $ | 198,232,346 | | | $ | 128,406,195 | | | |

| | | | | | | | | | |

*Including undistributed net investment income | | $ | 599,663 | | | $ | 867,782 | | | |

| | | | | | | | | | |

The accompanying notes are an integral part of these financial statements.

| | | | |

| 24 | | | | Motley Fool Independence Fund |

Financial Highlights

| | | | | | | | | | | | |

| | | Years ended October 31, | |

| | | 2011 | | | 2010(1) | | | 2009(2)(3) | |

Net Asset Value, Beginning of Period | | $ | 14.14 | | | $ | 11.48 | | | $ | 10.00 | |

| | | | | | | | | | | | |

| | | |

Income From Investment Operations (4) | | | | | | | | | | | | |

Net Investment Income | | | 0.11 | | | | 0.16 | | | | 0.02 | |

Net Gains on Securities (Realized and Unrealized) | | | 0.15 | | | | 2.59 | | | | 1.46 | |

| | | | | | | | | | | | |

Total From Investment Operations | | | 0.26 | | | | 2.75 | | | | 1.48 | |

| | | | | | | | | | | | |

| | | |

Less Distributions | | | | | | | | | | | | |

Net Investment Income | | | (0.15 | ) | | | (0.02 | ) | | | — | |

Net Realized Capital Gains | | | (0.11 | ) | | | (0.08 | ) | | | — | |

| | | | | | | | | | | | |

Total Distributions | | | (0.26 | ) | | | (0.10 | ) | | | — | |

| | | | | | | | | | | | |

| | | |

Redemption Fees | | | 0.01 | | | | 0.01 | | | | — | * |

| | | | | | | | | | | | |

| | | |

Net Asset Value, End of Period | | $ | 14.15 | | | $ | 14.14 | | | $ | 11.48 | |

| | | | | | | | | | | | |

Total Return(5)(6) | | | 1.91 | % | | | 24.18 | % | | | 14.80 | % |

Net Assets, End of Period (thousands) | | $ | 198,232 | | | $ | 128,406 | | | $ | 30,427 | |

| | | |

Ratios/Supplemental Data | | | | | | | | | | | | |

| | | |

Ratio of Expenses to Average Net Assets | | | 1.43 | % | | | 1.38 | % | | | 1.35 | % |

Ratio of Expenses to Average Net Assets (Before Waivers and Reimbursement of Expenses and/or Recapture of Previously Waived Fees) | | | 1.58 | % | | | 2.20 | % | | | 7.01 | % |

Ratio of Net Investment Income to Average Net Assets | | | 0.76 | % | | | 1.29 | % | | | 0.41 | % |

Ratio of Income to Average Net Assets (Before Waivers and Reimbursement of Expenses and/or Recapture of Previously Waived Fees) | | | 0.61 | % | | | 0.47 | % | | | (5.25 | )% |

Portfolio Turnover | | | 37 | % | | | 37 | % | | | 50 | % |

| * | Amount represents less than $0.005 per share. |

| (1) | Due to a clerical error, Net Gains on Securities (Realized and Unrealized) and Total From Investment Operations for the year ended October 31, 2010 were reported in the 2010 Annual Report as $2.39 and $2.55, respectively. Such amounts have been revised as shown above. |

| (2) | Because of commencement of operations and related preliminary transaction costs, these ratios are not necessarily indicative of future ratios. |

| (3) | Commenced operations on June 16, 2009. All ratios for the period have been annualized. Total return and portfolio turnover for the period have not been annualized. |

| (4) | Per share data calculated using average shares outstanding method. |

| (5) | During the years ended October 31, 2011 and October 31, 2010, 0.07% and 0.08%, respectively, of the Fund’s total return was attributable to redemption and small-balance account fees received as referenced in Note 4. Excluding this item, the total return would have been 1.84% and 24.10%, respectively. For the period ended October 31, 2009, redemption and small-balance account fees received had no effect on the Fund’s total return. |

| (6) | Total return reflects the rate an investor would have earned on an investment in the Fund during each period, assuming reinvestment of all distributions. |

The accompanying notes are an integral part of these financial statements.

| | | | |

| Motley Fool Independence Fund | | | | 25 |

Motley Fool Great America Fund Portfolio Characteristics (Unaudited)

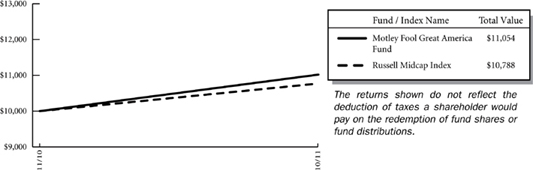

At October 31, 2011, the Motley Fool Great America Fund (the “Fund”) had an audited net asset value of $11.04 per share attributed to 5,043,986 shares outstanding. This compares with an unaudited net asset value as of November 1, 2010 of $10.00 per share attributed to 102,000 shares outstanding. From the Fund’s launch on November 1, 2010 to October 31, 2011 the Fund had a total return of 10.54% versus a return of 7.88% over the same period for its benchmark, Russell Midcap Index. The graph below shows the performance of $10,000 invested in the Fund at inception. The results shown below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Let’s be serious though. A graph of the performance of any investment over one year tells you virtually nothing. In about five years, they’ll actually tell you quite a bit about how well we’re managing your money.

Average Annual Total Returns as of 10/31/2011

| | | | | | |

| | | Fund* | | Benchmark** | |

| | |

Since Inception | | 10.54% | | | 7.88 | % |

Inception Date | | 11/01/2010 | | | | |

Total Annual Fund Operating Expenses Before Expense Limitation (February 28, 2011 Prospectus) | | 2.30% | | | | |

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained at www.FoolFunds.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

*These returns reflect expense waivers by the Fund’s investment adviser. Without these waivers, returns would have been lower.

** The Russell Midcap Index is an unmanaged, free float-adjusted, market capitalization weighted index that is designed to measure the performance of the mid-cap segment of the U.S. equity universe. The Russell Midcap Index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Russell Midcap Index represents approximately 27% of the total market capitalization of the Russell 1000 companies. The Fund may invest in companies that are not included within the Russell Midcap Index and its investment portfolio is not weighted in terms of issuers the same as the Russell Midcap Index. For this reason, the Fund’s investment performance should not be expected to track, and may exceed or trail, the Russell Midcap Index. Since Inception returns for the Benchmark reflect the performance based on the Inception Date of the Fund.

| | | | |

| 26 | | | | Motley Fool Great America Fund |

The investment objective of the Great America Fund is to achieve long-term capital appreciation. The Fund pursues this objective by investing primarily in common stocks of companies organized in the United States. The Fund employs a value-based Investment strategy and seeks long-term growth of capital by acquiring securities of companies at prices the investment adviser, Motley Fool Asset Management, LLC (the “Adviser”), believes to be significantly below their intrinsic value. The Fund may invest in other types of securities and in other asset classes when, in the judgment of the Adviser, such investments offer attractive potential returns. As such, the Fund’s performance will deviate significantly from its benchmark from time to time. It is the view of the Adviser that this deviation is less meaningful over shorter time frames and is more relevant over multi-year periods.

Although the Great America Fund may invest in companies with any market capitalization, the Adviser expects that investments in the securities of companies having smaller- and mid-market capitalizations will be important components of the Fund’s investment program. Investments in securities of these companies may involve greater risk than do investments in larger, more established companies. Small-and mid-cap stocks tend to be more volatile and less liquid than their large-cap counterparts. You are strongly encouraged to read more about the Fund’s strategies and risks in the prospectus.

The Great America Fund invests in securities of companies the Adviser believes are undervalued. Unlike mutual funds that hew to their benchmark, the Fund may invest in any company, industry or sector where the Adviser’s analysis suggests that there is opportunity for gains that outweigh risks. In identifying investments for the Fund, the Adviser looks for companies it believes the market has irrationally undervalued and looks for companies that have high-quality businesses with strong market positions, manageable leverage, and robust streams of free cash flow. The following tables show the top 11 holdings and top 10 sectors in which the Fund was invested at fiscal year-end. Portfolio holdings are subject to change without notice.

Certain mutual fund ratings and review services have created style boxes, which look more or less like a tic-tac-toe board; arranging funds by the size of the companies they typically invest in (large-, mid-, and small-cap) along one axis, and along a “value” to “growth” basis on the other axis. This may be a helpful way - at times - to think about certain investment opportunities, but we don’t believe we’ll improve your returns by limiting ourselves to any one portion of that style box.

| | | | |

| Top Eleven Holdings* | | % of Net

Assets | |

| | |

| |

Big Lots, Inc. | | | 4.60 | % |

HCC Insurance Holdings, Inc. | | | 4.16 | |

Berkshire Hathaway, Inc. | | | 3.57 | |

Schweitzer-Mauduit International, Inc. | | | 3.54 | |

Horsehead Holding Corp. | | | 3.35 | |

Thor Industries, Inc. | | | 3.32 | |

WellPoint, Inc. | | | 3.24 | |

Markel Corp. | | | 3.12 | |

Trimas Corp. | | | 3.04 | |

Under Armour, Inc. | | | 3.03 | |

Denbury Resources, Inc. | | | 2.99 | |

| | | | |

| | | 37.96 | % |

| | | | |

| * | As of the date of the report the fund had a holding of 0.87% in the BNY Mellon Cash Reserve. |

| | | | |

| Motley Fool Great America Fund | | | | 27 |

| | | | |

| Top Ten Sectors | | % of Net

Assets | |

| | |

| |

Financials | | | 22.73 | % |

Consumer Discretionary | | | 21.52 | |

Materials | | | 11.88 | |

Information Technology | | | 10.77 | |

Health Care | | | 9.91 | |

Industrials | | | 9.91 | |

Telecommunication Services | | | 4.85 | |

Energy | | | 4.14 | |

Consumer Staples | | | 2.91 | |

| | | | |

| | | 98.62 | % |

| | | | |

| | | | |

| 28 | | | | Motley Fool Great America Fund |

About Your Expenses

As a shareholder of the Great America Fund, you incur ongoing costs, including advisory fees and other Fund expenses. This example is intended to help you to understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. It is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from May 1, 2011 to October 31, 2011.

Actual Expenses

The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you incurred over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses attributable to your investment during this period.

Hypothetical Example for Comparison Purposes

The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. Thus, you should not use the hypothetical account values and expenses to estimate the actual ending account balance or your expenses for the period. Rather, these figures are provided to enable you to compare the ongoing costs of investing in the Fund as compared to the costs of investing in other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only. Therefore, the second section of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds.

Do you know how many times a fund, or the market, has returned a smooth 5% over a long period of time? Never. But we have to pick some example. In reality, the market’s returns are always far bumpier, with the market returning 20% one year, followed by a loss of 10% the next year, followed by a 3% gain, etc. These variations affect actual expenses as well. Happily, over almost all time periods of 20 years or longer, according to the research of University of Pennsylvania’s Jeremy Siegel and others, the domestic market’s returns have been at least 5% per year on average.

| | | | | | | | | | | | | | | | |

| | | Beginning Account Value 05/01/2011 | | | Ending

Account Value

10/31/11 | | | Annualized

Expense Ratio(1) | | | Expenses Paid

During Period(2) | |

| | |

| | | | |

Actual | | $ | 1,000 | | | $ | 920.77 | | | | 1.35 | % | | $ | 6.54 | |

Hypothetical | | $ | 1,000 | | | $ | 1,018.40 | | | | 1.35 | % | | $ | 6.87 | |

| (1) | These ratios reflect expenses waived by the Fund’s investment Adviser. Without these Waivers, the Fund’s expenses would have been higher and the ending account values would have been lower. |

| (2) | Expenses are equal to the Fund’s annualized expense ratio for the period May 1, 2011 to October 31, 2011, multiplied by the average account value over the period, multiplied by the number of days (184) in the most recent fiscal half-year, then divided by 365. |

| | | | |

| Motley Fool Great America Fund (Unaudited) | | 29 |

The Motley Fool Funds Trust

Motley Fool Great America Fund

Schedule of Investments

at October 31, 2011

| | | | | | | | |

| Issues | | Shares | | | Value

(Note 2) | |

| | |

Equity Securities — 98.62% | | | | | | | | |

Auto Components — 1.33% | | | | | | | | |

Drew Industries, Inc. (United States) | | | 30,811 | | | $ | 740,388 | |

| | | | | | | | |

Automobiles — 3.32% | | | | | | | | |

Thor Industries, Inc. (United States) | | | 69,988 | | | | 1,850,483 | |

| | | | | | | | |

Beverages — 1.85% | | | | | | | | |

Heckmann Corp. (United States)* | | | 172,000 | | | | 1,030,280 | |

| | | | | | | | |

Capital Markets — 3.49% | | | | | | | | |

Diamond Hill Investment Group, Inc. (United States) | | | 15,453 | | | | 1,163,302 | |

INTL FCStone, Inc. (United States)* | | | 32,300 | | | | 782,952 | |

| | | | | | | | |

| | | | | | | 1,946,254 | |

| | | | | | | | |

Chemicals — 1.07% | | | | | | | | |

Innophos Holdings, Inc. (United States) | | | 13,500 | | | | 593,865 | |

| | | | | | | | |

Communications Equipment — 5.64% | | | | | | | | |

Cisco Systems, Inc. (United States) | | | 87,000 | | | | 1,612,110 | |

Infinera Corp. (United States)* | | | 209,490 | | | | 1,531,372 | |

| | | | | | | | |

| | | | | | | 3,143,482 | |

| | | | | | | | |

Containers & Packaging — 2.72% | | | | | | | | |

Crown Holdings, Inc. (United States)* | | | 44,800 | | | | 1,513,792 | |

| | | | | | | | |

Diversified Telecommunication Services — 2.65% | | | | | | | | |

Level 3 Communications, Inc. (United States)* | | | 55,250 | | | | 1,474,622 | |

| | | | | | | | |

Energy Equipment & Services — 1.14% | | | | | | | | |

Dresser-Rand Group, Inc. (United States)* | | | 13,180 | | | | 637,912 | |

| | | | | | | | |

Health Care Equipment & Supplies — 2.92% | | | | | | | | |

Natus Medical, Inc. (United States)* | | | 175,700 | | | | 1,511,020 | |

Varian Medical Systems, Inc. (United States)* | | | 2,000 | | | | 117,440 | |

| | | | | | | | |

| | | | | | | 1,628,460 | |

| | | | | | | | |

Health Care Providers & Services — 6.99% | | | | | | | | |

Laboratory Corp. of America Holdings (United States)* | | | 8,920 | | | | 747,942 | |

Quest Diagnostics, Inc. (United States) | | | 24,000 | | | | 1,339,200 | |

WellPoint, Inc. (United States) | | | 26,200 | | | | 1,805,180 | |

| | | | | | | | |

| | | | | | | 3,892,322 | |

| | | | | | | | |

Hotels, Restaurants & Leisure — 5.02% | | | | | | | | |

International Speedway Corp. (United States) | | | 23,760 | | | | 566,914 | |

See Notes to Financial Statements.

| | | | |

| 30 | | | | Motley Fool Great America Fund |

| | | | | | | | |

| Issues | | Shares | | | Value

(Note 2) | |

| | |

Equity Securities (continued) | | | | | | | | |

Hotels, Restaurants & Leisure (continued) | | | | | | | | |

Penn National Gaming, Inc. (United States)* | | | 30,617 | | | $ | 1,102,212 | |

Red Robin Gourmet Burgers, Inc. (United States)* | | | 45,000 | | | | 1,128,150 | |

| | | | | | | | |

| | | | | | | 2,797,276 | |

| | | | | | | | |

Insurance — 13.05% | | | | | | | | |

Berkshire Hathaway, Inc. (United States)* | | | 17 | | | | 1,988,150 | |

Berkshire Hathaway, Inc., Class B (United States)* | | | 3,000 | | | | 233,580 | |

HCC Insurance Holdings, Inc. (United States) | | | 87,000 | | | | 2,315,070 | |

Loews Corp. (United States) | | | 25,000 | | | | 992,500 | |

Markel Corp. (United States)* | | | 4,500 | | | | 1,739,250 | |

| | | | | | | | |

| | | | | | | 7,268,550 | |

| | | | | | | | |

Internet & Catalog Retail — 0.65% | | | | | | | | |

Liberty Interactive Corp. (United States)* | | | 22,000 | | | | 361,460 | |

| | | | | | | | |

Internet Software & Services — 1.86% | | | | | | | | |

Google, Inc. (United States)* | | | 1,750 | | | | 1,037,120 | |

| | | | | | | | |

IT Services — 2.41% | | | | | | | | |

Paychex, Inc. (United States) | | | 46,000 | | | | 1,340,440 | |

| | | | | | | | |

Machinery — 6.30% | | | | | | | | |

Flow International Corp. (United States)* | | | 523,400 | | | | 1,355,606 | |

Flowserve Corp. (United States) | | | 4,950 | | | | 458,816 | |

Trimas Corp. (United States)* | | | 86,800 | | | | 1,691,732 | |

| | | | | | | | |

| | | | | | | 3,506,154 | |

| | | | | | | | |

Metals & Mining — 3.35% | | | | | | | | |

Horsehead Holding Corp. (United States)* | | | 214,700 | | | | 1,863,596 | |

| | | | | | | | |

Multiline Retail — 4.60% | | | | | | | | |

Big Lots, Inc. (United States)* | | | 68,000 | | | | 2,562,920 | |

| | | | | | | | |

Oil, Gas & Consumable Fuels — 2.99% | | | | | | | | |

Denbury Resources, Inc. (United States)* | | | 106,100 | | | | 1,665,770 | |

| | | | | | | | |

Paper & Forest Products — 4.75% | | | | | | | | |

KapStone Paper and Packaging Corp. (United States)* | | | 41,200 | | | | 675,680 | |

Schweitzer-Mauduit International, Inc. (United States) | | | 28,000 | | | | 1,968,960 | |

| | | | | | | | |

| | | | | | | 2,644,640 | |

| | | | | | | | |

Personal Products — 1.06% | | | | | | | | |

Female Health Co. (United States) | | | 129,500 | | | | 589,225 | |

| | | | | | | | |

Professional Services — 3.36% | | | | | | | | |

Barrett Business Services, Inc. (United States) | | | 46,200 | | | | 733,194 | |

See Notes to Financial Statements.

| | | | |

| Motley Fool Great America Fund | | | | 31 |

| | | | | | | | |

| Issues | | Shares | | | Value (Note 2) | |

| | |

| | |

Equity Securities (continued) | | | | | | | | |

Professional Services (continued) | | | | | | | | |

Huron Consulting Group, Inc. (United States)* | | | 31,550 | | | $ | 1,136,116 | |

| | | | | | | | |

| | | | | | | 1,869,310 | |

| | | | | | | | |

| | |

Real Estate Investment Trusts — 6.18% | | | | | | | | |

Annaly Capital Management, Inc. (United States) | | | 39,000 | | | | 657,150 | |

DuPont Fabros Technology, Inc. (United States) | | | 57,550 | | | | 1,196,464 | |

Retail Opportunity Investments Corp. (United States) | | | 139,560 | | | | 1,590,984 | |

| | | | | | | | |

| | | | | | | 3,444,598 | |

| | | | | | | | |

| | |

Road & Rail — 0.26% | | | | | | | | |

Zipcar, Inc. (United States)* | | | 7,000 | | | | 143,150 | |

| | | | | | | | |

| | |

Semiconductors & Semiconductor Equipment — 0.86% | | | | | | | | |

Formfactor, Inc. (United States)* | | | 80,000 | | | | 478,400 | |

| | | | | | | | |

| | |