Paracorp Inc.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Matisse Discounted Closed-End Fund Strategy (the “Fund”). The Fund’s shares are not deposits or obligations of, or guaranteed by, any depository institution. The Fund’s shares are not insured by the FDIC, Federal Reserve Board or any other agency, and are subject to investment risks, including possible loss of principal amount invested. Neither the Fund nor the Fund’s distributor is a bank.

The Matisse Discounted Closed-End Fund Strategy is distributed by Capital Investment Group, Inc., Member FINRA/SIPC, 100 E. Six Forks Road, Suite 200, Raleigh, NC, 27609. There is no affiliation between the Matisse Discounted Closed-End Fund Strategy, including its principals, and Capital Investment Group, Inc.

Beginning on January 1, 2021, paper copies of the Fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Fund’s website at https://www.nottinghamco.com/fundpages/Matisse, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

As of January 1, 2019, you may, notwithstanding the availability of shareholder reports online, elect to receive all future shareholder reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Fund, you can call 800-773-3863 to let the Fund know you wish to continue receiving paper copies of your shareholder reports.

(Unaudited)

Dear Fellow Shareholders of the Matisse Discounted Closed-End Fund Strategy:

Please find enclosed for your review the Annual Report for the Matisse Discounted Closed-End Fund Strategy (the “Fund”) for the year ending March 31, 2019. The Fund formally launched on October 31, 2012.

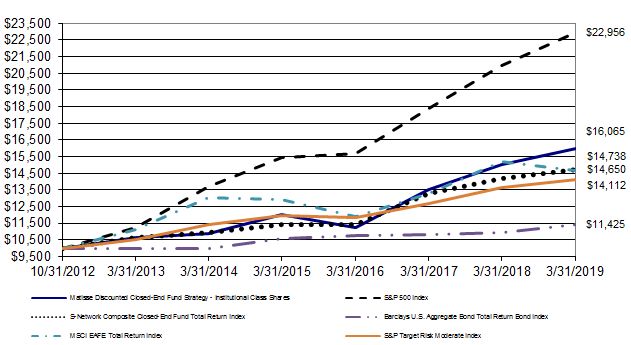

As you can see from the table below, Fund performance for the most recent twelve-month period was positive, ahead of most benchmarks, and behind the S&P 500.

Three major factors contributed during the twelve-month period to the Fund’s performance relative to these indexes:

| · | First, on the positive side, during the 12-month period, discounts on closed-end funds narrowed (for most types of funds), as the US universe moved from an average discount of 6.44% to 5.85% per Bloomberg, giving the Fund approximately a 0.6% tailwind during the 12-month period. As usual, the Fund was able to supplement this tailwind through our ongoing trading, replacing Closed-End Funds (“CEFs”) whose discounts had narrowed with more attractively discounted CEFs. Discount movement, including this “capture” activity, contributed approximately 4.3% to the Fund’s return during the period, with the entirety of this occurring in the first quarter. |

| · | Second, on a negative note, during the 12-month period, the US dollar was strong vs. most foreign currencies, rising 8% vs. a trade-weighted developed market currency basket, for example, and 12% vs. an emerging market currency basket. The Fund’s non-USD exposure averaged more than 30% during the period (due to the most attractively discounted Equity CEFs being in that space), which is higher than most peers and benchmarks. This factor therefore detracted about 2 percentage points from returns. |

| · | Third, on a related negative note, the Fund was hurt by our higher-than-peer exposure to Emerging Market stocks, as the MSCI Emerging Market Index fell 7% during the period, a stark contrast to the S&P 500’s 9% gain. |

| · | Offsetting these negative factors, we had several individual success stories, as two of our holdings, under pressure from us, liquidated at NAV, and therefore moved from mid-teens discounts to NAV during the period. |

Even after our 16% gain in the first quarter, we believe our current portfolio is still very well-positioned for the future. As of quarter-end, our CEF portfolio traded at a weighted average discount of 15.7%, and, here in early May, that discount is greater than 17%. We continue to own several “special situations” in our portfolio: CEFs whose wide discounts may narrow (although of course there is no guarantee) due to activism, tender offers, or liquidation. The broad CEF universe, too, is currently about a percentage point more discounted than its long-run average. So “coiled springs” abound. See “Portfolio positioning” below.

The Fund’s longer-term performance has been excellent. Per Morningstar, in our Tactical Allocation category, as of March 31, 2019, our 3-year return ranks in the top 2% (out of 256 funds), and our 5-year return also ranks in the top 2% (out of 208 funds). (Our 1-year performance is in the top 3% out of 272 funds.)

Average Annual Total Returns

Period ended March 31, 2019 | One year | Five year annualized | Annualized since inception1 | Net Expense Ratio2, 3 | Gross Expense Ratio3 |

Matisse Discounted Closed-End Fund Strategy – Institutional Class Shares

| +6.53% | +7.63% | +7.58% | 2.65% | 2.69% |

S&P 500 Index4

| +9.50% | +10.91% | +13.84% | N/A | N/A |

S-Network Composite Closed-End Fund Total Return Index4

| +4.11% | +6.13% | +6.23% | N/A | N/A |

S&P Target Risk Moderate Index4

| +3.53% | +4.37% | +5.52% | N/A | N/A |

MSCI EAFE Total Return Index4

| -3.55% | +2.33% | +6.14% | N/A | N/A |

Barclays US Aggregate Bond Total Return Index4 | +4.48% | +2.74% | +2.10% | N/A | N/A |

The performance information quoted above represents past performance and past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling the Fund at 800-773-3863. Fee waivers and expense reimbursements have positively impacted Fund performance.

1The Inception date of the Institutional Class Shares is October 31, 2012.

2 The Fund’s Advisor has entered into an Expense Limitation Agreement with the Fund under which it has agreed to waive or reduce its fees in an amount that limits the Fund's annual operating expenses (exclusive of acquired fund fees and expenses, interest, taxes, brokerage fees and commissions, and extraordinary expenses) to not more than 1.25% of the average daily net assets of the Fund through July 31, 2019. The Expense Limitation Agreement may be terminated by the Board at any time. The Advisor cannot recoup from the Fund any amounts paid by the Advisor under the Expense Limitation Agreement. Further, net annual operating expenses for the Fund may exceed those contemplated by the waiver due to acquired fund fees and other expenses that are not waived under the Expense Limitation Agreement. Performance would have been lower without this expense limitation.

3 Net and gross expense ratios are from the Fund’s prospectus dated August 1, 2018.

4You cannot invest directly in this index. This index does not have an investment advisor and does not pay any commissions, expenses, or taxes. If this index did pay commissions, expenses, or taxes, its returns would be lower. Performance returns for the indexes shown in this table are since the Inception date of October 31, 2012.

Portfolio positioning

As usual, the Fund owns highly discounted CEFs in many different asset classes and sectors. On a lookthrough basis, our portfolio of CEFs was about 80% allocated to stocks as of quarter-end, of which about half were US stocks. This represents an increase in the overall equity exposure of our portfolio from recent periods (as we are finding more opportunities at the margin in equity CEFs). As usual, the Fund’s portfolio is tilted towards large-cap stocks. These exposures are in-line with our Strategy’s long-term ranges.

One of our more interesting positions is Pershing Square Holdings, a 7.7% position for the Fund at quarter-end. This closed-end fund’s shares trade overseas (London and Amsterdam), but it is managed by US hedge fund manager Bill Ackman and contains mostly US stocks. Despite excellent underlying performance (a 37% at-NAV return in the first quarter), fund and manager share purchases, and the implementation of a regular quarterly dividend, the fund still traded at a shocking 27% discount to NAV at quarter-end. We expect this discount will not persist for long.

Another holding, Eagle Growth & Income, a 6% position for us at quarter-end, closed the quarter at a 15.5% discount to NAV, even though it is scheduled to terminate (at NAV) in 2027. While we wait (and attempt to rally other owners of the fund to move up its termination date), the fund pays a regular monthly cash distribution that works out to about 6% a year.

There are similar deals across our portfolio. As of quarter-end, we owned 4 large positions that traded for less than $.80 on the dollar. We will continue to pressure the boards of these funds---and of other funds---to do the right thing for shareholders by taking positive steps aimed at moving share prices much closer to NAVs.

Our outlook

We will continue to focus primarily on diligently capturing inefficiencies created by other participants in the niche, retail-dominated closed-end fund space. However, we are also watching several interesting developments as “clues” to guide us in how to “lean” our lookthrough portfolio allocation. (As always, we’ll make our primary decision based on the attractiveness of the discounts we see.)

| · | Following last year’s tax cut, the US economy is performing well, and unemployment, at 3.6%, is at its lowest level since 1969! Inflation, by most measures, is right around 2%, and the Fed has paused its rate hiking campaign with the Fed Funds target at 2.25-2.5%. This Fed pause brought the 10-year Treasury yield back to around 2.4% at quarter-end, making the yield curve flat as a pancake. |

| · | Despite the rates pause, attractive CEF discounts seem to imply that the retail investor herd still fears higher rates. The herd doesn’t seem to notice that the US economic expansion is now the longest on record, that US government deficits have spiked, that nearly all other types of debt are also at record levels (consumer, corporate, mortgage), that demographics favor lower rates, and that interest rates in most foreign countries (with lower credit quality than the US) are materially lower than those in the US. Rates could be “lower for longer”. (Japan, anyone?) If that environment continues, discounted Closed-End Funds, with their regular cash distributions, and (in some cases) embedded low-cost leverage, should perform well in a low-return world. |

| · | Valuations on US stocks still concern us. The S&P 500 traded at a trailing price per earnings ratio (“PE”) of 19 at quarter-end, and the tech love affair continues, with the Nasdaq 100 at a 23 PE at quarter-end rising to a 25 PE at the date of this letter (early May). Foreign stocks, however---especially stocks in many emerging markets---are substantially cheaper, and foreign currencies appear to be undervalued by many metrics (for example, purchasing power parity) vs. the US dollar, supporting our overweight to Emerging Market and Foreign Developed stocks. |

We appreciate your interest in, and investment in, the Fund. We’ll continue to keep you updated on the important developments we see in the misunderstood, retail-dominated world of closed-end funds. Check our Strategy website, www.matissecap.com/closed-end-funds , for updates, and feel free to contact us at 503-210-3005 to discuss the Matisse Discounted Closed-End Fund Strategy and our investment approach.

Sincerely,

Eric Boughton, CFA Portfolio ManagerMatisse Funds

| Bryn Torkelson Founder & CIO Matisse Funds |

| |

(RCMAT0519001)

Matisse Discounted Closed-End Fund Strategy

Notes to Financial Statements

As of March 31, 2019

1. Organization and Significant Accounting Policies

The Matisse Discounted Closed-End Fund Strategy (“Fund”) is a series of the Starboard Investment Trust (“Trust”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Fund is a separate diversified series of the Trust.

The Fund’s investment advisor, Deschutes Portfolio Strategies, LLC, dba Matisse Capital, (the “Advisor”), seeks to achieve the Fund’s investment objective of long-term capital appreciation and income by investing in unaffiliated closed-end funds that pay regular periodic cash distributions, the interests of which typically trade at substantial discounts relative to their underlying net asset values.

The following is a summary of significant accounting policies consistently followed by the Fund. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The Fund follows the accounting and reporting guidance in the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification 946 “Financial Services – Investment Companies,” and Financial Accounting Standards Update (“ASU”) 2013-08.

Investment Valuation

The Fund’s investments in securities are carried at fair value. Securities listed on an exchange or quoted on a national market system are valued at the last sales price as of 4:00 p.m. Eastern Time. Securities traded in the NASDAQ over-the-counter market are generally valued at the NASDAQ Official Closing Price. Other securities traded in the over-the-counter market and listed securities for which no sale was reported on that date are valued at the mean of the most recent bid and ask prices. Instruments with maturities of 60 days or less are valued at amortized cost, which approximates market value. Investments in open-end investment companies are valued at their respective net asset values as reported by such investment companies. Securities and assets for which representative market quotations are not readily available (e.g., if the exchange on which the security is principally traded closes early or if trading of the particular security is halted during the day and does not resume prior to the Fund’s net asset value calculation) or which cannot be accurately valued using the Fund’s normal pricing procedures are valued at fair value as determined in good faith under policies approved by the Trustees. A security’s “fair value” price may differ from the price next available for that security using the Fund’s normal pricing procedures.

Fair Value Measurement

Various inputs are used in determining the value of the Fund's investments. These inputs are summarized in the three broad levels listed below:

Level 1: Unadjusted quoted prices in active markets for identical securities

Level 2: Other significant observable inputs (including quoted prices for similar securities, interest rates, credit risk, etc.)

Level 3: Significant unobservable inputs (including the Fund’s own assumptions in determining fair value of investments)

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

(Continued)

Matisse Discounted Closed-End Fund Strategy

Notes to Financial Statements

As of March 31, 2019

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following table summarizes the inputs as of March 31, 2019 for the Fund’s investments measured at fair value:

| | | |

| Investments in Securities (a) | | Total | | Level 1 | | Level 2 | | Level 3 |

| Closed-End Funds | $ | 49,246,224 | $ | 49,214,221 | $ | - | $ | 32,003 |

| Short-Term Investment | | 366,702 | | 366,702 | | - | | - |

| Total Assets | $ | 49,612,926 | $ | 49,580,923 | $ | - | $ | 32,003 |

| | | | | | | | | |

| (a) | The Fund had one transfer into Level 3 and out of Level 1 during the fiscal year ended March 31, 2019. The aggregate value of such securities is 0.07% of net assets, and they have been fair valued under procedures approved by the Fund’s Board of Trustees. The Level 3 security is fair valued at $1 per share, which is the estimated amount of cash to be distributed to holders with the final liquidation. The weighted average for each unobservable input is 100%. |

The table below presents a reconciliation of all Level 3 fair value measurements existing at March 31, 2019:

| | | | | | |

| Opening Balance at 3/31/18 | | | $ | 1,168,462 | |

| Purchases | | | | 118,750 | |

| Principal payments/sales | | | | (1,362,106) | |

| Accrued discounts (premiums) | | | | - | |

| Realized gains | | | | 370,873 | |

| Net change in appreciation | | | | (263,976) | |

| Ending Balance at 3/31/19 | | | $

| 32,003 | |

| | | | | | |

Investment Transactions and Investment Income

Investment transactions are accounted for as of the date purchased or sold (trade date). Dividend income is recorded on the ex-dividend date. Certain dividends from foreign securities will be recorded as soon as the Fund is informed of the dividend if such information is obtained subsequent to the ex-dividend date. Gains and losses are determined on the identified cost basis, which is the same basis used for federal income tax purposes.

Distributions

The Fund may declare and distribute dividends from net investment income, if any, monthly or quarterly. Distributions from capital gains, if any, are generally declared and distributed annually. Dividends and distributions to shareholders are recorded on ex-date.

Expenses

The Fund bears expenses incurred specifically on its behalf as well as a portion of general expenses, which are allocated according to methods reviewed annually by the Trustees.

Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in the net assets from operations during the reporting period. Actual results could differ from those estimates.

Federal Income Taxes

No provision for income taxes is included in the accompanying financial statements, as the Fund intends to distribute to shareholders all taxable investment income and realized gains and otherwise comply with Subchapter M of the Internal Revenue Code applicable to regulated investment companies.

Matisse Discounted Closed-End Fund Strategy

Notes to Financial Statements

As of March 31, 2019

2. Transactions with Related Parties and Service Providers

Advisor

The Fund pays a monthly fee to the Advisor calculated at the annual rate of 0.99% of the Fund’s average daily net assets. For the fiscal year ended March 31, 2019, $664,994 in advisory fees were incurred, of which $104,446 in advisory fees were waived by the Advisor.

The Advisor has entered into a contractual agreement (the “Expense Limitation Agreement”) with the Trust, on behalf of the Fund, under which it has agreed to waive or reduce its fees and to assume other expenses of the Fund, if necessary, in amounts that limit the Fund’s total operating expenses (exclusive of acquired fund fees and expenses, interest, taxes, brokerage fees and commissions, and extraordinary expenses) to not more than 1.25% of the average daily net assets of the Fund. The current term of the Expense Limitation Agreement remains in effect until July 31, 2019. While there can be no assurance that the Expense Limitation Agreement will continue after that date, it is expected to continue from year-to-year thereafter. The Advisor cannot recoup from the Fund any expenses paid by the Advisor under the Expense Limitation Agreement.

Administrator

The Fund pays a monthly fee to the Fund’s administrator, The Nottingham Company (“the Administrator”), based upon the average daily net assets of the Fund and calculated at the annual rates as shown in the schedule below which is subject to a minimum of $2,000 per month. The Administrator also receives a fee to procure and pay the Fund’s custodian, additional compensation for fund accounting and recordkeeping services, and additional compensation for certain costs involved with the daily valuation of securities and as reimbursement for out-of-pocket expenses. The Administrator also receives a miscellaneous compensation fee for peer group, comparative analysis, and compliance support totaling $350 per month. As of March 31, 2019, the Administrator received $4,200 in miscellaneous expenses.

A breakdown of these fees is provided in the following table:

| Administration Fees* | Custody Fees* | | Fund Accounting Fees (asset-based fee)

| Blue Sky Administration Fees (annual) |

Average Net Assets | Annual Rate | Average Net Assets | Annual Rate | (Average

monthly) | Net Assets

| Annual Rate | Per state |

| First $100 million | 0.100% | First $200 million | 0.020% | $2,250 $500/ additional class | First $50 million | 0.02% | $150 |

| Next $100 million | 0.090% | Over $200 million | 0.009% | Next $50 million | 0.015% | |

| Next $100 million | 0.080% | | | | Over $100 million | 0.01% | |

| Next $100 million | 0.070% | | *Minimum monthly fees of $2,000 and $417 for Administration and Custody, respectively. |

| Next $100 million | 0.060% | |

| Over $500 million | 0.050% | |

| Over $750 million | 0.040% | | |

| Over $1 billion | 0.030% | | |

(Continued)

Matisse Discounted Closed-End Fund Strategy

Notes to Financial Statements

As of March 31, 2019

The Fund incurred $67,279 in administration fees, $19,136 in custody fees, and $31,888 in fund accounting fees for the fiscal year ended March 31, 2019.

Compliance Services

Cipperman Compliance Services, LLC provides services as the Trust’s Chief Compliance Officer. Cipperman Compliance Services, LLC is entitled to receive customary fees from the Fund for their services pursuant to the Compliance Services agreement with the Fund.

Transfer Agent

Nottingham Shareholder Services, LLC (“Transfer Agent”) serves as transfer, dividend paying, and shareholder servicing agent for the Fund. For its services, the Transfer Agent is entitled to receive compensation from the Fund pursuant to the Transfer Agent’s fee arrangements with the Fund.

Distributor

Capital Investment Group, Inc. (the “Distributor”) serves as the Fund’s principal underwriter and distributor. For its services, the Distributor is entitled to receive compensation from the Fund pursuant to the Distributor’s fee arrangements with the Fund.

Because the underlying funds have varied expense and fee levels and the Fund may own different proportions of underlying funds at different times, the amount of fees and expense incurred indirectly by the Fund will vary.

3. Trustees and Officers

The Board of Trustees is responsible for the management and supervision of the Fund. The Trustees approve all significant agreements between the Trust, on behalf of the Fund, and those companies that furnish services to the Fund; review performance of the Advisor and the Fund; and oversee activities of the Fund. Officers of the Trust and Trustees who are interested persons of the Trust or the Advisor will receive no salary or fees from the Trust. Trustees who are not “interested persons” of the Trust or the Advisor within the meaning of the 1940 Act (the “Independent Trustees”) receive $2,000 each year from each Fund. The Trust will reimburse each Trustee and officer of the Trust for his or her travel and other expenses relating to attendance of Board meetings. Additional fees may also be incurred during the year as special meetings are necessary in addition to the regularly scheduled meetings of the Board of Trustees.

Certain officers of the Trust may also be officers of the Administrator.

4. Purchases and Sales of Investment Securities

For the fiscal year ended March 31, 2019, the aggregate cost of purchases and proceeds from sales of investment securities (excluding short-term securities) were as follows:

| Purchases of Securities | Proceeds from Sales of Securities |

| $37,853,082 | $78,224,369 |

5. Federal Income Tax

Distributions are determined in accordance with Federal income tax regulations, which may differ from GAAP, and, therefore, may differ significantly in amount or character from net investment income and realized gains for financial reporting purposes. The general ledger is adjusted for permanent book/tax differences to reflect tax character but is not adjusted for temporary differences.

Management has reviewed the Fund’s tax positions to be taken on the federal income tax returns during the open years ended March 31, 2016 through March 31, 2018, and the yet to be filed March 31, 2019 return, and determined that the Fund does not have a liability for uncertain tax positions. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the fiscal year, the Fund did not incur any interest or penalties.

Matisse Discounted Closed-End Fund Strategy

Notes to Financial Statements

As of March 31, 2019

Distributions during the year ended were characterized for tax purposes as follows:

| | March 31, 2019 | March 31, 2018 |

Ordinary Income

| $ 1,528,869 | $ 1,669,951 |

Tax-Exempt Income

| 426,221

| 428,335 |

Long-Term Capital Gain

| 5,641,151

| 1,676,646 |

As of the fiscal year ended March 31, 2019, the following reclassifications were made:

| Accumulated distributable earnings | $(1,724,745) |

| Paid-in capital | 1,724,745 |

At March 31, 2019, the tax-basis cost of investments and components of distributable earnings were as follows:

| Cost of Investments | $ | 49,403,533 |

| | | |

| Unrealized Appreciation | $ | 1,550,233 |

| Unrealized Depreciation | | (1,340,840) |

| Net Unrealized Appreciation | $ | 209,393 |

| | | |

| Undistributed Long-Term Gains | | 4,555,003 |

| | | |

| Distributable Earnings | $ | 4,764,396 |

The difference between components of distributable earnings on a tax basis and the amounts reflected in the Statement of Assets and Liabilities are primarily due to wash sale losses. The Fund also had an adjustment relating to mark-to-market appreciation on PFIC lots totaling $688,594 as of the fiscal year ended March 31, 2019.

6. Beneficial Ownership

The beneficial ownership, either directly or indirectly, of 25% or more of the voting securities of a fund creates a presumption of control of a fund, under Section 2(a)(9) of the Investment Company Act of 1940. As of March 31, 2019, Charles Schwab & Co., Inc. held 75.23% of the Fund. The Fund has no knowledge as to whether all or any portion of the shares owned of record by Charles Schwab & Co., Inc. are also owned beneficially.

7. Commitments and Contingencies

Under the Trust’s organizational documents, its officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of business, the Trust entered into contracts with its service providers, on behalf of the Fund, and others that provide for general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund. The Fund expects risk of loss to be remote.

8. New Accounting Pronouncements

In August 2018, the Securities and Exchange Commission adopted amendments to certain disclosure requirements under Regulation S-X to conform to US GAAP, including: (i) an amendment to require presentation of the total, rather than the components, of distributable earnings on the Statement of Assets and Liabilities; and (ii) an amendment to require presentation of the total, rather than the components, of distributions to shareholders, except for tax return of capital distributions, if any, on the Statement of Changes in Net Assets. The amendments also removed the requirement for parenthetical disclosure of undistributed net investment income on the Statement of Changes in Net Assets. This amendment facilitates compliance of the disclosure of information without significantly altering the information provided to investors. These amendments have been adapted with these financial statements. The changes have been applied to the Fund’s financial statements as of the fiscal year ended March 31, 2019.

Matisse Discounted Closed-End Fund Strategy

Notes to Financial Statements

As of March 31, 2019

In August 2018, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2018-13, Fair Value Measurement (Topic 820) – Disclosure Framework–Changes to the Disclosure Requirements for Fair Value Measurement. The amendments eliminate certain disclosure requirements for fair value measurements for all entities, requires public entities to disclose certain new information, and modifies some disclosure requirements. The new guidance is effective for all entities for fiscal years beginning after December 15, 2019 and for interim periods within those fiscal years. An entity is permitted to early adopt either the entire standard or portions of the standard. The changes have been applied to the Fund’s financial statements as of the fiscal year ended March 31, 2019.

9. Borrowings

The Fund established a borrowing agreement with Goldman Sachs for investment purposes subject to the limitations of the 1940 Act for borrowings by registered investment companies.

Interest is based on the Federal Funds rate plus 1.00%. The average borrowing during the fiscal year was $3,611,362, and the average interest rate during the year was 3.25%.

Interest expense is charged directly to the Fund based upon actual amounts borrowed by the Fund. The Fund had no borrowings as of the fiscal year ended March 31, 2019. Total interest expense for the year was $95,431 as reflected in the Statement of Operations.

10. Subsequent Events

In accordance with GAAP, management has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date of issuance of the financial statements. This evaluation did not result in any subsequent events that necessitated disclosures and/or adjustments.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees of Starboard Investment Trust

and the Shareholders of Matisse Discounted Closed‐End Fund Strategy

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Matisse Discounted Closed- End Fund Strategy, a series of shares of beneficial interest in Starboard Investment Trust (the “Fund”), including the schedule of investments, as of March 31, 2019, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the five-year period then ended, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of March 31, 2019, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and its financial highlights for each of the years in the five-year period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund's management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities law and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risk of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of March 31, 2019 by correspondence with the custodian and brokers. Our audits also included evaluating the principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

BBD, LLP

We have served as the auditor of one or more of the Funds in the Starboard Investment Trust since 2012.

Philadelphia, Pennsylvania

May 30, 2019

Matisse Discounted Closed-End Fund Strategy

Additional Information

(Unaudited)

As of March 31, 2019

1. Proxy Voting Policies and Voting Record

A copy of the Advisor’s Disclosure Policy is included as Appendix B to the Fund’s Statement of Additional Information and is available, without charge, upon request, by calling 800-773-3863, and on the website of the Securities and Exchange Commission (“SEC”) at sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available (1) without charge, upon request, by calling the Fund at the number above and (2) on the SEC’s website at sec.gov.

2. Quarterly Portfolio Holdings

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the SEC’s website at sec.gov. You may review and make copies at the SEC’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 800-SEC-0330. You may also obtain copies without charge, upon request, by calling the Fund at 800-773-3863.

3. Tax Information

We are required to advise you within 60 days of the Fund’s fiscal year-end regarding federal tax status of certain distributions received by shareholders during each fiscal year. The following information is provided for the Fund’s fiscal year ended March 31, 2019.

During the fiscal year, the Fund paid $1,528,869 in income distributions and $5,641,151 in long-term capital gain distributions. The Fund also paid $426,221 in tax-exempt distributions during the fiscal year ended March 31, 2019.

Dividend and distributions received by retirement plans such as IRAs, Keogh-type plans, and 403(b) plans need not be reported as taxable income. However, many retirement plans may need this information for their annual information meeting.

4. Schedule of Shareholder Expenses

As a shareholder of the Fund, you incur ongoing costs, including management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from October 1, 2018 through March 31, 2019.

Actual Expenses – The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (e.g., an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes – The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Matisse Discounted Closed-End Fund Strategy

Additional Information

(Unaudited)

As of March 31, 2019

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Institutional Class Shares | Beginning Account Value October 1, 2018 | Ending Account Value March 31, 2019 | Expenses Paid During Period* |

Actual Hypothetical (5% annual return before expenses) | | | |

| $1,000.00 | $1,077.30 | $6.47 |

| $1,000.00 | $1,018.70 | $6.29 |

*Expenses are equal to the average account value over the period multiplied by the Fund’s annualized net expense ratio of 1.25%, multiplied by the number of days in the most recent period divided by the number of days in the fiscal year (to reflect the six month period).

5. Approval of Advisory Agreement

In connection with the regular Board meeting held on March 14, 2019, the Board, including a majority of the Independent Trustees, discussed the approval of a management agreement between the Trust and the Advisor, with respect to the Fund (the "Investment Advisory Agreement").

The Trustees were assisted by legal counsel throughout the review process. The Trustees relied upon the advice of legal counsel and their own business judgment in determining the material factors to be considered in evaluating the Investment Advisory Agreement and the weight to be given to each factor considered. The conclusions reached by the Trustees were based on a comprehensive evaluation of all of the information provided and were not the result of any one factor. Moreover, each Trustee may have afforded different weight to the various factors in reaching his conclusions with respect to the approval of the Investment Advisory Agreement. In connection with their deliberations regarding approval of the Investment Advisory Agreement, the Trustees reviewed materials prepared by the Advisor.

In deciding on whether to approve the Investment Advisory Agreement, the Trustees considered numerous factors, including:

| (i) | Nature, Extent, and Quality of Services. The Trustees considered the responsibilities of the Advisor under the Investment Advisory Agreement. The Trustees reviewed the services being provided to Fund including, without limitation, the quality of its investment advisory services since the Fund’s inception (including research and recommendations with respect to portfolio securities); its procedures for formulating investment recommendations and assuring compliance with the Fund’s investment objectives, policies and limitations; its coordination of services for the Fund among the service providers; and its efforts to promote the Fund, grow the assets, and assist in the distribution of shares. The Trustees evaluated the Advisor’s staffing, personnel, and methods of operating; the education and experience of the Advisor’s personnel; the Advisor’s compliance program; and the financial condition of the Advisor. |

The Trustees noted that the Advisor did not anticipate any changes in personnel or strategy during the renewal term.

After reviewing the foregoing information and further information in the memorandum from the Advisor (e.g., descriptions of the Advisor’s business, the compliance program, and Form ADV), the Board concluded that the nature, extent, and quality of the services provided by the Advisor were satisfactory and adequate.

| (ii) | Performance. The Trustees compared the performance of the Fund with the performance of its benchmark index, comparable funds with similar strategies managed by other investment advisers, applicable peer group data (e.g., Morningstar category average), and separately managed accounts of the Advisor using the same strategy as the Fund. The Board noted the strength of the Fund’s and the strategy’s performance for most periods since inception despite some period of underperformance. After reviewing the investment performance of the Fund, the Advisor’s experience managing the Fund, the Advisor’s historical investment performance, and other factors, the Board concluded that the investment performance of the Fund and the Advisor was satisfactory. |

Matisse Discounted Closed-End Fund Strategy

Additional Information

(Unaudited)

As of March 31, 2019

| (iii) | Fees and Expenses. The Trustees noted the management fee for the Fund under the Investment Advisory Agreement. The Trustees then compared the advisory fee and expense ratio of the Fund to other comparable funds and other similar accounts managed by the Advisor. Trust Counsel noted that the management fee was higher than the peer group and category averages but was within the range of fees charged to the separate accounts managed by the Advisor using the same strategy. The expense ratio was higher than the peer group average but lower than the category average. The Board noted that the Fund was much smaller than its peers, so it had not yet realized economies of scale. |

Following this comparison, and upon further consideration and discussion of the foregoing, the Board concluded that the fees to be paid to the Advisor by the Fund were not unreasonable in relation to the nature and quality of the services provided by the Advisor and that they reflected charges that were within a range of what could have been negotiated at arm’s length.

| (iv) | Profitability. The Board reviewed the Advisor’s profitability analysis in connection with its management of the Fund. The Board noted that the Advisor did realize a profit from the Fund for the twelve months ended December 31, 2018. The Board considered the quality of the Advisor’s service to the Fund, and after further discussion, concluded that the Advisor’s level of profitability was not excessive. |

| (v) | Economies of Scale. In this regard, the Trustees reviewed the Fund’s operational history and noted that the size of the Fund had not provided an opportunity to realize economies of scale. The Trustees then reviewed the Fund’s fee arrangements for breakpoints or other provisions that would allow shareholders to benefit from economies of scale in the future as the Fund grows. The Trustees determined that the management fee would stay the same regardless of the Fund’s asset levels and therefore, did not reflect economies of scale. The Trustees noted that the Fund was a relatively small size and economies of scale were unlikely to be achievable in the near future. It was pointed out that breakpoints in the advisory fee could be reconsidered in the future as the Fund grows. |

Conclusion. Having reviewed and discussed in depth such information from the Advisor as the Trustees believed to be reasonably necessary to evaluate the terms of the Investment Advisory Agreement and as assisted by the advice of legal counsel, the Trustees concluded that renewal of the Investment Advisory Agreement was in the best interest of the shareholders of the Fund.

6. Information about Trustees and Officers

The business and affairs of the Fund and the Trust are managed under the direction of the Board of Trustees of the Trust. Information concerning the Trustees and officers of the Trust and Fund is set forth below. Generally, each Trustee and officer serves an indefinite term or until certain circumstances such as their resignation, death, or otherwise as specified in the Trust’s organizational documents. Any Trustee may be removed at a meeting of shareholders by a vote meeting the requirements of the Trust’s organizational documents. The Statement of Additional Information of the Fund includes additional information about the Trustees and officers and is available, without charge, upon request by calling the Fund toll-free at 800-773-3863. The address of each Trustee and officer,

Matisse Discounted Closed-End Fund Strategy

Additional Information

(Unaudited)

As of March 31, 2019

Name, Age

and Address | Position

held with

Fund or Trust | Length of Time Served | Principal Occupation

During Past 5 Years | Number of Portfolios in Fund Complex Overseen by Trustee | Other Directorships

Held by Trustee

During Past 5 Years |

| Independent Trustees |

James H. Speed, Jr.

Date of Birth: 06/1953 | Independent Trustee, Chairman | Trustee since 7/09, Chair since 5/12 | Previously President and CEO of NC Mutual Insurance Company (insurance company) from 2003 to 2015. | 15 | Independent Trustee of the Brown Capital Management Mutual Funds for all its series, Hillman Capital Management Investment Trust for all its series, Centaur Mutual Funds Trust for all its series, Chesapeake Investment Trust for all its series, Leeward Investment Trust for all its series, and WST Investment Trust for all its series (all registered investment companies). Member of Board of Directors of M&F Bancorp. Member of Board of Directors of Investors Title Company. Previously, Board of Directors of NC Mutual Life Insurance Company. |

Theo H. Pitt, Jr.

Date of Birth: 04/1936 | Independent Trustee | Since 9/10 | Senior Partner, Community Financial Institutions Consulting (financial consulting) since 1999; Partner, Pikar Properties (real estate) since 2001. | 15 | Independent Trustee of World Funds Trust for all its series, Chesapeake Investment Trust for all its series, DGHM Investment Trust for all its series, Leeward Investment Trust for all its series and Hillman Capital Management Investment Trust for all its series (all registered investment companies). |

Michael G. Mosley

Date of Birth: 01/1953 | Independent Trustee | Since 7/10 | Owner of Commercial Realty Services (real estate) since 2004. | 15 | None. |

J. Buckley Strandberg

Date of Birth: 03/1960 | Independent Trustee | Since 7/09 | President of Standard Insurance and Realty since 1982. | 15 | None. |

| Other Officers |

Katherine M. Honey

Date of Birth: 09/1973 | President and Principal Executive Officer | Since 05/15 | EVP of The Nottingham Company since 2008. | n/a | n/a |

Ashley E. Harris Date of Birth: 03/1984 | Treasurer, Assistant Secretary and Principal Financial Officer | Since 05/15 | Fund Accounting Manager and Financial Reporting, The Nottingham Company since 2008. | n/a | n/a |

Matisse Discounted Closed-End Fund Strategy

Additional Information

(Unaudited)

As of March 31, 2019

Name, Age

and Address | Position

held with

Fund or Trust | Length of Time Served | Principal Occupation

During Past 5 Years | Number of Portfolios in Fund Complex Overseen by Trustee | Other Directorships

Held by Trustee

During Past 5 Years |

Robert G. Schaaf

Date of Birth: 09/1988 | Secretary | Since 09/18 | General Counsel of The Nottingham Company since 2018; Daughtry, Woodard, Lawrence & Starling (08/2015 – 01/2018); JD/MBA Candidate, Wake Forest University (07/2011 – 05/2015). | n/a | n/a |

Stacey Gillespie

Date of Birth: 05/1974 | Chief Compliance Officer | Since 03/16 | Compliance Director, Cipperman Compliance Services, LLC (09/15-present). Formerly, Chief Compliance Officer of Boenning & Scattergood, Inc. (2013-2015) and Director of Investment Compliance at Boenning & Scattergood, Inc. (2007-2013). | n/a | n/a |

Matisse Discounted Closed-End Fund Strategy

is a series of

The Starboard Investment Trust

| For Shareholder Service Inquiries: | For Investment Advisor Inquiries: |

| |

| Nottingham Shareholder Services | Deschutes Portfolio Strategies |

| 116 South Franklin Street | 4949 Meadows Road |

| Post Office Box 69 | Suite 200 |

| Rocky Mount, North Carolina 27802-0069 | Lake Oswego, Oregon 97035 |

| |

| Telephone: | Telephone: |

| |

| 800-773-3863 | 800-773-3863 |

| | |

| World Wide Web @: | World Wide Web @: |

| | |

| ncfunds.com | matissefunds.com |

| | |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.