Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

1. Organization and Significant Accounting Policies

The Cavalier Funds (“Funds”) are series of the Starboard Investment Trust (“Trust”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. Each Fund is a separate, diversified series of the Trust.

The Cavalier Adaptive Income Fund seeks to achieve its investment objective by investing primarily in fixed income securities.

The Cavalier Fundamental Growth Fund seeks to achieve its investment objective by principally investing in stocks that the portfolio manager believes to have above-average growth potential relative to their peers.

The Cavalier Growth Opportunities Fund seeks to achieve its investment objective by investing in exchange-traded funds that are registered under the 1940 Act and not affiliated with the Fund that invest in equity securities of issuers from a number of countries throughout the world.

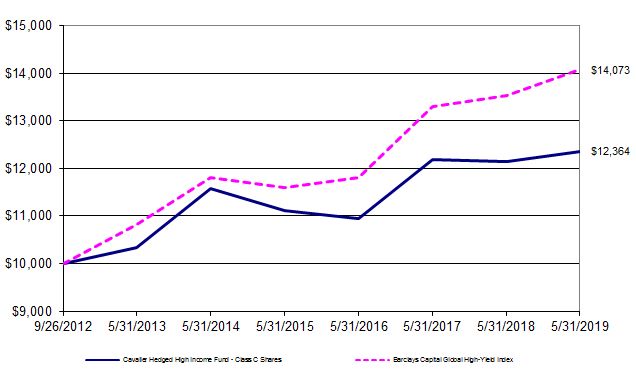

The Cavalier Hedged High Income Fund seeks to achieve its investment objective by investing other investment companies, including mutual and exchange-traded funds (“ETFs”) that are registered under the 1940 Act and not affiliated with the Fund or making direct investments in portfolio securities based upon institutional research.

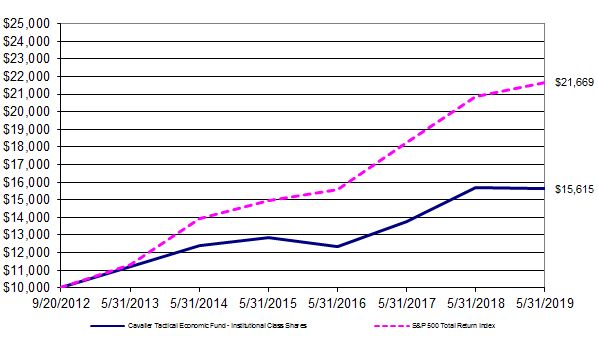

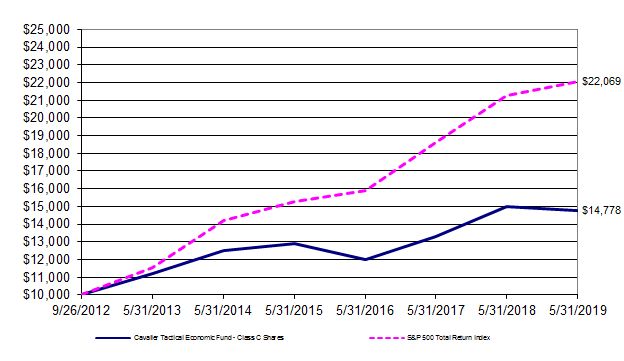

The Cavalier Tactical Economic Fund seeks to achieve its investment objective by investing in funds that are registered under the 1940 Act and not affiliated with the Fund, including ETFs.

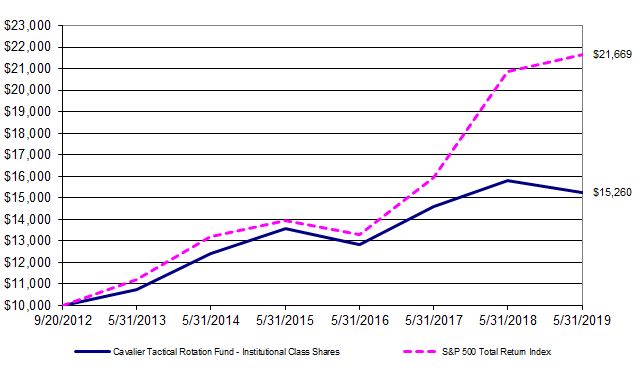

The Cavalier Tactical Rotation Fund seeks to achieve its investment objective by investing in ETFs that are registered under the 1940 Act and not affiliated with the Fund.

Each Fund currently has an unlimited number of authorized shares, which are divided into three classes – Institutional Class Shares, Class C Shares, and Class A Shares. Each class of shares has equal rights to assets of the Funds, and the classes are identical except for differences in ongoing distribution and service fees.

The Class C Shares and Class A Shares are subject to distribution plan fees as described in Note 4. Each Fund’s Class C Shares are sold without an initial sales charge; however, they are subject to a contingent deferred sales charge of 1.00% on shares redeemed within one year of the purchase date. This amount is paid to Capital Investment Group, Inc. (the “Distributor”). Income, expenses (other than distribution and service fees), and realized and unrealized gains or losses on investments are allocated to each class of shares based upon its relative net assets. All classes have equal voting privileges, except where otherwise required by law or when the Trustees determine that the matter to be voted on affects only the interests of the shareholders of a particular class. Class C Shares held longer than seven years will automatically convert into Institutional Class Shares. Class A Shares have an initial sales charge of 4.50%, but there is no automatic conversion of Class A Shares into any other Class of Shares.

As of May 31, 2019, the Cavalier Fundamental Growth Fund, the Cavalier Growth Opportunities Fund, the Cavalier Tactical Economic Fund, and the Cavalier Tactical Rotation Fund were the only Funds with active Class A Shares.

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

The Date of Initial Public Investment for each Fund and Class of Shares is as follows:

| Fund | Institutional Class Shares | Class C Shares | Class A Shares |

Cavalier Adaptive Income Fund | October 2, 2009 | February 25, 2011 | - |

| Cavalier Fundamental Growth Fund | October 17, 2013 | November 4, 2013 | March 13, 2018 |

| Cavalier Growth Opportunities Fund | September 20, 2012 | September 26, 2012 | April 16, 2018 |

| Cavalier Hedged High Income Fund | September 20, 2012 | September 26, 2012 | - |

| Cavalier Tactical Economic Fund | September 20, 2012 | September 26, 2012 | October 18, 2018 |

| (formerly known as “Cavalier Multi Strategy Fund”) | | | |

| Cavalier Tactical Rotation Fund | September 20, 2012 | September 26, 2012 | April 2, 2018 |

| | | | |

Fund Name Change

As of October 1, 2018, the Cavalier Tactical Economic Fund changed its name from the Cavalier Multi Strategy Fund per the annual Prospectus update filed on September 28, 2018.

The following is a summary of significant accounting policies consistently followed by the Funds. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The Funds follow the accounting and reporting guidance in the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification 946 “Financial Services – Investment Companies.”

Investment Valuation

Each Fund’s investments in securities are carried at fair value. Securities listed on an exchange or quoted on a national market system are valued at the last price as of 4:00 p.m. Eastern Time. Securities traded in the NASDAQ over-the-counter market are generally valued at the NASDAQ Official Closing Price. Other securities traded in the over-the-counter market and listed securities for which no sale was reported on that date are valued at the mean of the most recent bid and ask prices. Securities and assets for which representative market quotations are not readily available (e.g., if the exchange on which the portfolio security is principally traded closes early or if trading of the particular portfolio security is halted during the day and does not resume prior to each Fund’s net asset value calculation) or which cannot be accurately valued using each Fund’s normal pricing procedures are valued at fair value as determined in good faith under policies approved by the Board of Trustees (the “Trustees”). A portfolio security’s “fair value” price may differ from the price next available for that portfolio security using each Fund’s normal pricing procedures. Instruments with maturities of 60 days or less are valued at amortized cost, which approximates market value.

Underlying Funds

Open-End Funds - Open-end funds value securities in their portfolios for which market quotations are readily available at their market values (generally the last reported sale price) and all other securities and assets at their fair value to the methods established by the boards of directors of the open-end funds. Open-end funds are valued at their respective net asset values as reported by such investment companies.

Fair Value Measurement

Each Fund has adopted ASC Topic 820, Fair Value Measurements. ASC Topic 820 defines fair value, establishes a framework for measuring fair value and expands disclosure about fair value measurements.

Various inputs are used in determining the value of each Fund's investments. These inputs are summarized in the three broad levels listed below:

Level 1: Unadjusted quoted prices in active markets for identical securities

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

Level 2: Other significant observable inputs (including quoted prices for similar securities, interest rates, credit risk, etc.)

Level 3: Significant unobservable inputs (including each Fund’s own assumptions in determining fair value of investments)

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following tables summarize the inputs as of May 31, 2019 for each Fund’s investments measured at fair value:

Cavalier Adaptive Income Fund

| Assets | | Total | | Level 1 | | Level 2 | | Level 3 |

| Preferred Stock | $ | 500,000 | $ | - | $ | 500,000 | $ | - |

| Corporate Bond | | 227,243 | | - | | 227,243 | | - |

| Asset-Backed Securities | | 1,141,229 | | - | | 1,141,229 | | - |

| Collateralized Mortgage Obligations | | 16,026,736 | | - | | 16,026,736 | | - |

| Short-Term Investment | | 1,543,780 | | 1,543,780 | | - | | - |

| Total Assets | $ | 19,438,988 | $ | 1,543,780 | $ | 17,895,208 | $ | - |

Cavalier Fundamental Growth Fund

| Assets | | Total | | Level 1 | | Level 2 | | Level 3 |

| Common Stocks* | $ | 81,641,860 | $ | 81,641,860 | $ | - | $ | - |

| Short-Term Investment | | 1,409,027 | | 1,409,027 | | -

| | - |

| Total Assets | $ | 83,050,887 | $ | 83,050,887 | $ | - | $ | -

|

Cavalier Growth Opportunities Fund

| Assets | | Total | | Level 1 | | Level 2 | | Level 3 |

| Common Stocks* | $ | 4,411,301 | $ | 4,411,301 | $ | - | $ | - |

| Exchange-Traded Products* | | 43,477,284 | | 43,477,284 | | - | | - |

| Short-Term Investment | | 6,323,522 | | 6,323,522 | | -

| | -

|

| Total Assets | $ | 54,212,107 | $ | 54,212,107 | $ | - | $ | - |

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

Cavalier Hedged High Income Fund

| Assets | | Total | | Level 1 | | Level 2 | | Level 3 |

| Exchange-Traded Products* | $ | 10,259,337 | $ | 10,259,337 | $ | - | $ | - |

| Common Stocks* | | 1,630,293 | | 1,630,293 | | - | | - |

| Preferred Stocks* | | 3,000,000 | | - | | 3,000,000 | | - |

| Short-Term Investment | | 19,726,646 | | 19,726,646 | | - | | - |

| Total Assets | $ | 34,616,276 | $ | 31,616,276 | $ | 3,000,000 | $ | - |

Cavalier Tactical Economic Fund

| Assets | | Total | | Level 1 | | Level 2 | | Level 3 |

| Exchange-Traded Products* | $ | 15,313,959 | $ | 15,313,959 | $ | - | $ | - |

| Short-Term Investment | | 257,900 | | 257,900 | | - | | - |

| Total Assets | $ | 15,571,859 | $ | 15,571,859 | $ | - | $ | - |

Cavalier Tactical Rotation Fund

| Assets | | Total | | Level 1 | | Level 2 | | Level 3 |

| Exchange-Traded Products* | $ | 73,871,264 | $ | 73,871,264 | $ | - | $ | - |

| Short-Term Investment | | 26,826 | | 26,826 | | -

| | - |

| Total Assets | $ | 73,898,090 | $ | 73,898,090 | $ | - | $ | - |

*Refer to the Schedules of Investments for a breakdown by sector.

The Funds had no transfers into or out of Level 1, 2, or 3 during the year ended May 31, 2019. It is the Funds’ policy to recognize transfers at the end of the reporting period.

Investment Transactions and Investment Income

Investment transactions are accounted for as of the date purchased or sold (trade date). Dividend income is recorded on the ex-dividend date. Certain dividends from foreign securities will be recorded as soon as a Fund is informed of the dividend if such information is obtained subsequent to the ex-dividend date. Interest income is recorded on the accrual basis and includes accretion and amortization of discounts and premiums. Gains and losses are determined on the identified cost basis, which is the same basis used for federal income tax purposes.

Expenses

Each Fund bears expenses incurred specifically on its behalf as well as a portion of general expenses, which are allocated according to methods reviewed annually by the Trustees.

Distributions

Each Fund will distribute its income and realized gains to its shareholders every year. Income dividends paid by the Funds derived from net investment income, if any, will generally be paid monthly or quarterly, and capital gains distributions, if any, will be made at least annually. Dividends and distributions to shareholders are recorded on ex-date.

Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in the net assets from operations during the reporting period. Actual results could differ from those estimates.

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

Federal Income Taxes

No provision for income taxes is included in the accompanying financial statements, as each Fund intends to distribute to shareholders all taxable investment income and realized gains and otherwise continue to comply with Subchapter M of the Internal Revenue Code applicable to regulated investment companies.

2. Transactions with Related Parties and Service Providers

Advisor

Each Fund pays a monthly advisory fee to Cavalier Investments, LLC (the “Advisor”) based upon the average daily net assets and calculated at an annual rate.

See the table below for the advisory fee rates and amounts incurred by the Advisor for each Fund during fiscal year ended May 31, 2019:

| Fund | | Advisory Fee Rate June 1, 2018 - May 31, 2019 | Amount Incurred | Amount Waived by Advisor | Expenses Reimbursed by Advisor |

Cavalier Adaptive Income Fund | | 1.00% | $ 112,472 | $ 112,472 | $ 72,213 |

| Cavalier Fundamental Growth Fund | | 1.00% | 966,702 | 117,280 | - |

| Cavalier Growth Opportunities Fund | | 1.00% | 535,168 | 155,410 | - |

| Cavalier Hedged High Income Fund | | 1.00% | 314,448 | 124,783 | - |

| Cavalier Tactical Economic Fund | | 1.00% | 131,336 | 131,336 | 53,018 |

| Cavalier Tactical Rotation Fund | | 1.00% | 1,157,082 | 101,867 | - |

| | | | | | |

The Advisor has engaged sub-advisors to provide day to day portfolio management for some of the Funds. Each sub-advisor is paid directly by the Advisor based upon the average daily net assets and calculated at an annual rate. See the table below for the sub-advisory fee rates and amounts paid by the Advisor to the Sub-Advisor for each sub-advised Fund during the fiscal year ended May 31, 2019:

| Fund | Sub-Advisors |

| Sub-Advisory Fee Rate |

| Sub-Advisory Fee Received | |

Cavalier Adaptive Income Fund | | Buckhead Capital Management, LLC | 0.05% | | $ 5,659 | |

| Cavalier Fundamental Growth Fund | | Navellier & Associates, Inc. | 0.30% (on AUM over $20M) | | 229,828 | |

| Cavalier Growth Opportunities Fund | | Bluestone Capital Management, LLC | 0.30% | | 156,920 | |

| Cavalier Tactical Rotation Fund | | Julex Capital Management, LLC | 0.20% | | 230,883 | |

| | | | | | | |

All Due from Advisor amounts indicated in each Fund’s Statement of Assets and Liabilities were received on July 31, 2019.

Expense Limitation

The Advisor entered into a contractual agreement (the “Expense Limitation Agreement”) with the Trust, on behalf of the Funds, under which it has agreed to waive or reduce its fees and to assume other expenses of the Funds, if necessary, in amounts that limit the Funds’ total operating expenses (exclusive of (i) any front-end or contingent deferred loads; (ii) brokerage fees and commissions, (iii) acquired fund fees and expenses; (iv) fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including for example option and swap fees and expenses); (v) borrowing costs (such as interest and dividend expense on securities sold short); (vi) taxes; and (vii) extraordinary expenses, such as litigation expenses (which may include indemnification of Fund officers and Trustees and contractual indemnification of Fund service providers (other than the Advisor)) to not more than the following percentages of the average daily net assets of the Institutional Class Shares, Class C Shares, and Class A Shares of the Funds for the fiscal year from June 1, 2018 through May 31, 2019.

(Continued)

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

| Fund | | | Institutional Class Shares | Class C Shares | Class A Shares | |

Cavalier Adaptive Income Fund | | | 1.25% | 2.25% | 1.50% | |

| Cavalier Fundamental Growth Fund | | | 1.25% | 2.25% | 1.50% | |

| Cavalier Growth Opportunities Fund* | | | 1.25% | 2.25% | 1.50% | |

| Cavalier Hedged High Income Fund | | | 1.25% | 2.25% | 1.50% | |

| Cavalier Tactical Economic Fund | | | 1.25% | 2.25% | 1.50% | |

| Cavalier Tactical Rotation Fund | | | 1.25% | 2.25% | 1.50% | |

*For the period from June 1, 2018 through September 5, 2018, the Expense Limitation of the Cavalier Growth Opportunities Fund was 1.35% for the Institutional Class Shares, 2.35% for the Class C Shares, and 1.60% for the Class A Shares.

Administrator

Each Fund pays a monthly fee to The Nottingham Company (the “Administrator”) based upon the average daily net assets of each Fund and calculated at the annual rates as shown in the schedule below subject to a minimum of $2,000 per month. The Administrator also receives a fee as to procure and pay the Fund’s custodian, additional compensation for fund accounting and recordkeeping services, and additional compensation for certain costs involved with the daily valuation of securities and as reimbursement for out-of-pocket expenses. The Administrator also receives a miscellaneous compensation fee for peer group, comparative analysis, and compliance support totaling $150 per month.

A breakdown of these fees is provided in the following table:

| Administration Fees* | Custody Fees* | Fund Accounting Fees (base fee) (monthly fee) | Fund Accounting Fees (asset-based fee) | Blue Sky Administration Fees (annual) |

Average Net Assets | Annual

Rate | Average Net Assets | Annual Rate |

| First $250 million | 0.100% | First $200 million | 0.020% | $2,250 plus $500/additional share class | 0.01% | $150 per state |

| Next $250 million | 0.080% | Over $200 million | 0.009% | | | |

| Next $250 million | 0.060% | | | | | |

| Next $250 million | 0.050% | *Minimum monthly fees of $2,000 and $417 for Administration and Custody, respectively. |

| On the next $1 billion | 0.040% |

| On all assets over $2 billion | 0.035% | |

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

The Fund incurred the following amounts in Administration fees for the fiscal year ended May 31, 2019:

| Fund | | | | | |

Cavalier Adaptive Income Fund | | | | | $ 22,960 |

| Cavalier Fundamental Growth Fund | | | | | 96,021 |

| Cavalier Growth Opportunities Fund | | | | | 51,800 |

| Cavalier Hedged High Income Fund | | | | | 31,241 |

| Cavalier Tactical Economic Fund | | | | | 23,002 |

| Cavalier Tactical Rotation Fund | | | | | 114,123 |

The Funds incurred the following amounts in Fund Accounting fees for the fiscal year ended May 31, 2019:

| Fund | | | | | |

Cavalier Adaptive Income Fund | | | | | $ 34,120 |

| Cavalier Fundamental Growth Fund | | | | | 49,558 |

| Cavalier Growth Opportunities Fund | | | | | 43,966 |

| Cavalier Hedged High Income Fund | | | | | 36,146 |

| Cavalier Tactical Economic Fund | | | | | 38,039 |

| Cavalier Tactical Rotation Fund | | | | | 51,607 |

The Funds incurred the following amounts in Custody fees for the fiscal year ended May 31, 2019:

| Fund | | | | | |

Cavalier Adaptive Income Fund | | | | | $ 11,462 |

| Cavalier Fundamental Growth Fund | | | | | 32,080 |

| Cavalier Growth Opportunities Fund | | | | | 14,960 |

| Cavalier Hedged High Income Fund | | | | | 7,245 |

| Cavalier Tactical Economic Fund | | | | | 6,272 |

| Cavalier Tactical Rotation Fund | | | | | 35,104 |

Compliance Services

Cipperman Compliance Services, LLC provides services as the Trust’s Chief Compliance Officer. Cipperman Compliance Services, LLC is entitled to receive customary fees from the Funds for their services pursuant to the Compliance Services agreement with the Funds.

Transfer Agent

Nottingham Shareholder Services, LLC (“Transfer Agent”), an affiliate of the Administrator, serves as transfer, dividend paying, and shareholder servicing agent for the Funds. For its services, the Transfer Agent is entitled to receive compensation from the Funds pursuant to the Transfer Agent’s fee arrangements with the Funds.

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

The Funds incurred the following amounts in Transfer Agent fees for the fiscal year ended May 31, 2019:

| Fund | | | | | |

Cavalier Adaptive Income Fund | | | | | $ 27,000 |

| Cavalier Fundamental Growth Fund | | | | | 30,250 |

| Cavalier Growth Opportunities Fund | | | | | 33,000 |

| Cavalier Hedged High Income Fund | | | | | 27,000 |

| Cavalier Tactical Economic Fund | | | | | 30,726 |

| Cavalier Tactical Rotation Fund | | | | | 47,734 |

Distributor

Capital Investment Group, Inc. (the “Distributor”) serves as the Funds’ principal underwriter and distributor. For its services, the Distributor is entitled to receive compensation from the Funds pursuant to the Funds’ fee arrangements with the Distributor.

3. Trustees and Officers

The Board of Trustees is responsible for the management and supervision of the Funds. The Trustees approve all significant agreements between the Trust, on behalf of the Funds, and those companies that furnish services to the Funds; review performance of the Advisor and the Funds; and oversee activities of the Funds. Officers of the Trust and Trustees who are interested persons of the Trust or the Advisor will receive no salary or fees from the Trust. Trustees who are not “interested persons” of the Trust or the Advisor within the meaning of the Investment Company Act of 1940, as amended (the “Independent Trustees”) will receive $2,000 each year from each Fund. The Trust will reimburse each Trustee and officer of the Trust for his or her travel and other expenses related to attendance of Board meetings. Additional fees may also be incurred during the year as special meetings are necessary in addition to the regularly scheduled meetings of the Board of Trustees.

Certain officers of the Trust may also be officers of the Administrator.

4. Distribution and Service Fees

The Board of Trustees, including a majority of the Independent Trustees , adopted a distribution and service plan pursuant to Rule 12b-1 of the 1940 Act (the “Plan”) for the Class C Shares and Class A Shares. The 1940 Act regulates the manner in which a registered investment company may assume costs of distributing and promoting the sales of its shares and servicing of its shareholder accounts. The Plan provides that each Fund may incur certain costs, which may not exceed 1.00% per annum of the average daily net assets of the Class C Shares and 0.25% per annum of the average daily net assets of the Class A Shares for each year elapsed subsequent to adoption of the Plan, for payment to the Distributor and others for items such as advertising expenses, selling expenses, commissions, travel, or other expenses reasonably intended to result in sales of Class C Shares or Class A Shares or servicing of Class C or Class A shareholder accounts.

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

See the table below for the Distribution and Service Fees of the Class C Shares and Class A Shares for each Fund during the fiscal year ended May 31, 2019:

| Fund | | | | Amount Incurred |

| | | | | Class C Shares

| Class A Shares |

Cavalier Adaptive Income Fund | | | | $ 31,868

| $ - |

| Cavalier Fundamental Growth Fund | | | | 29,613

| 1,939 |

| Cavalier Growth Opportunities Fund | | | | 10,411

| 482 |

| Cavalier Hedged High Income Fund | | | | 9,345

| - |

| Cavalier Tactical Economic Fund | | | | 7,714

| 29 |

| Cavalier Tactical Rotation Fund | | | | 23,697

| 391 |

| | | | | | |

5. Purchases and Sales of Investment Securities

For the fiscal year ended May 31, 2019, the aggregate cost of purchases and proceeds from sales of investment securities (excluding short-term securities) were as follows:

| | | Purchases of Securities | Proceeds from Sales of Securities |

| Cavalier Adaptive Income Fund | | $ 13,820,141 | $ 2,964,268 |

| Cavalier Fundamental Growth Fund | | 115,274,374 | 114,651,801 |

| Cavalier Growth Opportunities Fund | | 142,550,312 | 128,957,782 |

| Cavalier Hedged High Income Fund | | 23,408,311 | 41,049,743 |

| Cavalier Tactical Economic Fund | | 25,507,908 | 19,891,550 |

| Cavalier Tactical Rotation Fund | | 423,065,275 | 467,732,238 |

| | | | |

There were no long-term purchases or sales of U.S. Government Obligations during the fiscal year ended May 31, 2019.

6. Federal Income Tax

Distributions are determined in accordance with Federal income tax regulations, which may differ from GAAP, and, therefore, may differ significantly in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences.

Management has reviewed all taxable years / periods that are open for examination (i.e., not barred by the applicable statute of limitations) by taxing authorities of all major jurisdictions, including the Internal Revenue Service. As of May 31,

2019, open taxable years consisted of the taxable years ended May 31, 2016 through May 31, 2019. No examination of tax returns is currently in progress for any of the Funds.

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

Reclassifications relate primarily to differing book/tax treatment of ordinary net investment losses, dividends paid/received, partnership adjustments, and PFIC mark-to-market adjustments and have no impact on the net assets of the Funds. For the year ended May 31, 2019, the following reclassifications were necessary:

| | Paid-In- Capital | |

| Distributable Earnings/Accumulated Loss |

| Cavalier Adaptive Income Fund | $ (15,812) | | | $ 15,812 |

| Cavalier Tactical Economic Fund | (1,250) | | | 1,250 |

| Cavalier Growth Opportunities Fund | (50,526) | | | 50,526 |

| Cavalier Fundamental Growth Fund | (698,067) | | | 698,067 |

| Cavalier Hedged High Income Fund | (112,923) | | | 112,923 |

Distributions during the fiscal years ended May 31, 2018 and May 31, 2019 were characterized for tax purposes as follows:

| | | Distributions from | |

| Fund | Fiscal year ended | Ordinary Income | Long-Term Capital Gains | Return of Capital |

| Cavalier Adaptive Income Fund | 05/31/2019 | $ 454,738 | $ - | $ - |

| | 05/31/2018 | 205,235 | - | 120,188 |

| Cavalier Fundamental Growth Fund | 05/31/2019 | 1,046,710 | 5,804,179 | - |

| | 05/31/2018 | 38,981 | 3,314,434 | - |

| Cavalier Growth Opportunities Fund | 05/31/2019 | 2,848,714 | 564,594 | - |

| | 05/31/2018 | 35,430 | - | - |

| Cavalier Hedged High Income Fund | 05/31/2019 | 1,434,166 | - | - |

| | 05/31/2018 | 421,036 | - | - |

| Cavalier Tactical Economic Fund | 05/31/2019 | 1,149,074 | 790,938 | - |

| | 05/31/2018 | 165,350 | - | - |

| Cavalier Tactical Rotation Fund | 05/31/2019 | 949,396 | 14,091,743 | - |

| | 05/31/2018 | 667,637 | - | - |

| | | | | - |

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

At May 31, 2019, the tax-basis cost of investments and components of distributable earnings were as follows:

| | | | Cavalier Adaptive Income Fund | Cavalier Fundamental Growth Fund | Cavalier Growth Opportunities Fund |

Cost of Investments | | | $19,219,491 | $76,959,375 | $54,896,461 |

| | | | | | |

| Gross Unrealized Appreciation | | | 345,267 | 10,567,761 | 1,146,184 |

| Gross Unrealized Depreciation | | | (125,765) | (4,476,249) | (1,830,538) |

| Net Unrealized Appreciation (Depreciation) | | | 219,497 | 6,091,512 | (684,354) |

| | | | | | |

Accumulated Ordinary Income (Loss) | | | - | - | - |

| Undistributed Long-Term Capital Gains | | | - | - | - |

| Accumulated Net Capital Losses | | | (168,790) | - | (1,347,866) |

| Deferred Post-October Losses | | | (2,306) | (7,816,468) | (313,381) |

| Late Year Losses | | | - | (39,124) | (126,550) |

| | | | | | |

Distributable Earnings (Accumulated Deficit) | | | $ 48,401 | $(1,764,080) | $ (2,472,151) |

| | | Cavalier Hedged High Income Fund | Cavalier Tactical Economic Fund | Cavalier Tactical Rotation Fund |

Cost of Investments | | $34,640,290 | $15,826,056 | $73,682,220 |

| | | | | |

| Gross Unrealized Appreciation | | 64,817 | 249,054 | 556,334 |

| Gross Unrealized Depreciation | | (88,831) | (503,251) | (338,464) |

| Net Unrealized Appreciation (Depreciation) | | (24,014) | (254,197) | 217,870 |

| | | | | |

| Accumulated Ordinary Income (Loss) | | - | - | 930,504 |

| Undistributed Long-Term Capital Gains | | - | - | - |

| Accumulated Net Capital Losses | | (1,910,290) | - | |

| Deferred Post-October Losses | | (875,319) | (38,987) | (7,576,381) |

| | | | | |

| Distributable Earnings (Accumulated Deficit) | | $(2,809,623) | $(293,184) | $(6,428,007) |

The difference between book-basis and tax-basis net unrealized appreciation (depreciation) is attributable to the deferral of losses from wash sales. Accumulated capital losses noted above represent net capital loss carryovers as of May 31, 2019 that are available to offset future realized capital gains, if any, and thereby reduce future taxable gain distributions. The Cavalier Adaptive Income Fund has a loss carryforward of $168,790, of which $52,870 is short term in nature and $115,920 is long term in nature. The Cavalier Growth Opportunities Fund has a loss carryforward of $1,347,866, all of which is short term in nature. The Cavalier Hedged High Income Fund has a loss carryforward of $1,910,290, of which $1,459,098 is short term in nature and $451,192 is long term in nature. The capital loss carryforwards have no expiration date.

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

In addition, realized losses reflected in the accompanying financial statements include net capital losses realized between November 1 and the Funds’ fiscal year-end that have not been recognized for tax purposes (Deferred Post-October Losses).

For tax purposes, the current late year losses of $39,124 in the Cavalier Fundamental Growth Fund were incurred during the period from January 1, 2019 through May 31, 2019. The current late year losses of $126,550 in the Cavalier Growth Opportunities Fund were incurred during the period from January 1, 2019 through May 31, 2019. The current late year losses of $2,306 in the Cavalier Adaptive Income Fund were incurred during the period from January 1, 2019 through May 31, 2019. The current late year losses of $875,319 in the Cavalier Hedged High Income Fund were incurred during the period from January 1, 2019 through May 31, 2019. The current late year losses of $38,987 in the Cavalier Tactical Economic Fund were incurred during the period from January 1, 2019 through May 31, 2019. The current late year losses of $7,576,381 in the Cavalier Tactical Rotation Fund were incurred during the period from January 1, 2019 through May 31, 2019. These losses will be recognized for tax purposes on the first business day of the Fund’s next fiscal year, June 1, 2019.

7. Concentration of Risk

The Cavalier Hedged High Income Fund currently invests a significant portion of its assets in the Goldman Sachs Access High Yield Corporate Bond ETF (“Goldman”). The Cavalier Hedged High Income Fund may redeem its investment from Goldman at any time if the Advisor determines that it is in the best interest of the Cavalier Hedged High Income Fund and its shareholders to do so. The performance of the Cavalier Hedged High Income Fund may be directly affected by the performance of Goldman. The financial statements of Goldman, including the portfolio of investments, can be found at Goldman’s website, www.gsam.com, or the Securities and Exchange Commission’s website, www.sec.gov, and should be read in conjunction with Goldman’s financial statements. As of May 31, 2019, the Cavalier Hedged Income Fund’s net assets invested in Goldman were 38.38%.

The Cavalier Tactical Economic Fund currently invests a significant portion of its assets in the iShares Core S&P 500 ETF (the “Core ETF”) The Cavalier Tactical Economic Fund may redeem its investment from the Core ETF at any time if the Advisor determines that it is in the best interest of the Cavalier Tactical Economic Fund and its shareholders to do so. The performance of the Cavalier Tactical Economic Fund may be directly affected by the performance of the Core ETF. The financial statements of the Core ETF, including the portfolio of investments, can be found at the Core ETF’s website, www.ishares.com, or the Securities and Exchange Commission’s website, www.sec.gov, and should be read in conjunction with the Core ETF’s financial statements. As of May 31, 2019, the Cavalier Tactical Economic Fund’s net assets invested in the Core ETF were 26.30%.

The Cavalier Tactical Economic Fund also currently invests a significant portion of its assets in the iShares Edge MSCI Min Vol USA ETF (the “MSCI ETF”) The Cavalier Tactical Economic Fund may redeem its investment from the MSCI ETF at any time if the Advisor determines that it is in the best interest of the Cavalier Tactical Economic Fund and its shareholders to do so. The performance of the Cavalier Tactical Economic Fund may be directly affected by the performance of the MSCI ETF. The financial statements of the MSCI ETF, including the portfolio of investments, can be found at the MSCI ETF’s website, www.ishares.com, or the Securities and Exchange Commission’s website, www.sec.gov, and should be read in conjunction with the MSCI ETF’s financial statements. As of May 31, 2019, the Cavalier Tactical Economic Fund’s net assets invested in the MSCI ETF were 28.34%.

8. Commitments and Contingencies

Under the Trust’s organizational documents, its officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Funds. In addition, in the normal course of business, the Trust entered into contracts with its service providers, on behalf of the Funds, and others that provide for general indemnifications. The Funds’ maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Funds. The Funds expect the risk of loss to be remote.

Cavalier Funds

Notes to Financial Statements

As of May 31, 2019

9. New Accounting Pronouncements

In August 2018, the Securities and Exchange Commission adopted amendments to certain disclosure requirements under Regulation S-X to conform to US GAAP, including: (i) an amendment to require presentation of the total, rather than the components, of distributable earnings on the Statement of Assets and Liabilities; and (ii) an amendment to require presentation of the total, rather than the components, of distributions to shareholders, except for tax return of capital distributions, if any, on the Statement of Changes in Net Assets. The amendments also removed the requirement for parenthetical disclosure of undistributed net investment income on the Statement of Changes in Net Assets. This amendment facilitates compliance of the disclosure of information without significantly altering the information provided to investors. These amendments have been adopted with these financial statements. The changes have been applied to the Fund’s financial statements as of the fiscal year ended May 31, 2019.

In August 2018, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2018-13, Fair Value Measurement (Topic 820) – Disclosure Framework–Changes to the Disclosure Requirements for Fair Value Measurement. The amendments eliminate certain disclosure requirements for fair value measurements for all entities, requires public entities to disclose certain new information, and modifies some disclosure requirements. The new guidance is effective for all entities for fiscal years beginning after December 15, 2019 and for interim periods within those fiscal years. An entity is permitted to early adopt either the entire standard or portions of the standard. The changes have been applied to the Fund’s financial statements as of the fiscal year ended May 31, 2019.

10. Subsequent Events

In accordance with GAAP, management has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date of issuance of the financial statements. This evaluation did not result in any subsequent events that necessitated disclosures and/or adjustments, other than the following items:

Distributions

Per share distributions during the subsequent period were as follows:

| | | | |

| Fund | Class | Record Date | Pay Date | Ordinary Income |

| Cavalier Adaptive Income Fund | Institutional | 6/26/2019 | 6/27/2019 | $ 0.03290 |

| Class C | 6/26/2019 | 6/27/2019 | 0.02477 |

| | | | | |

| | | | | |

| | Institutional | 6/26/2019 | 6/27/2019 | 0.01826 |

| Cavalier Hedged High Income Fund | Class C | 6/26/2019 | 6/27/2019 | 0.01029 |

| | | | | |

| | | | | |

Cavalier Funds

Additional Information

(Unaudited)

As of May 31, 2019

1. Proxy Voting Policies and Voting RecordA copy of the Advisor’s Disclosure Policy is included as Appendix B to the Fund’s Statement of Additional Information and is available, without charge, upon request, by calling 800-773-3863, and on the website of the Securities and Exchange Commission (“SEC”) at sec.gov. Information regarding how each Fund voted proxies relating to portfolio securities during the most recent twelve-month period ended June 30, is available (1) without charge, upon request, by calling the Funds at the number above and (2) on the SEC’s website at sec.gov.

2. Quarterly Portfolio Holdings

Each Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Each Fund’s Form N-Q is available on the SEC’s website at sec.gov. You may review and make copies at the SEC’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 800-SEC-0330. You may also obtain copies without charge, upon request, by calling the Fund at 800-773-3863.

3. Tax Information

We are required to advise you within 60 days of each Fund’s fiscal year-end regarding the federal tax status of certain distributions received by shareholders during each fiscal year.

Each of the funds listed below had the following distribution information for the fiscal year ended May 31, 2019.

| | Ordinary Income | Long-Term Capital Gains |

| Cavalier Adaptive Income Fund | $ 454,738 | $ - |

| Cavalier Fundamental Growth Fund | 1,046,713 | 5,804,176 |

| Cavalier Growth Opportunities Fund | 2,848,714 | 564,594 |

| Cavalier Hedged High Income Fund | 1,434,166 | - |

| Cavalier Tactical Economic Fund | 1,149,093 | 790,919 |

| Cavalier Tactical Rotation Fund | 1,204,238 | 13,836,901 |

Dividend and distributions received by retirement plans such as IRAs, Keogh-type plans, and 403(b) plans need not be reported as taxable income. However, many retirement plans may need this information for their annual information meeting.

4. Schedule of Shareholder Expenses

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including contingent deferred sales charges; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from December 1, 2018 through May 31, 2019.

Actual Expenses – The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (e.g., an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Cavalier Funds

Additional Information

(Unaudited)

As of May 31, 2019

Hypothetical Example for Comparison Purposes – The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Cavalier Adaptive Income Fund | Beginning Account Value December 1, 2018 | Ending Account Value May 31, 2019 | Expenses Paid During Period* | Annualized Expense Ratio* |

| Institutional Class Shares | | | | |

| Actual | $1,000.00 | $1,023.00 | $6.36 | 1.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,018.70 | $6.29 | 1.25% |

| Class C Shares | | | | |

| Actual | $1,000.00 | $1,017.60 | $11.42 | 2.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,013.71 | $11.30 | 2.25% |

| Cavalier Fundamental Growth Fund | Beginning Account Value December 1, 2018 | Ending Account Value May 31, 2019 | Expenses Paid During Period* | Annualized Expense Ratio* |

| Institutional Class Shares | | | | |

| Actual | $1,000.00 | $1,040.60 | $6.36 | 1.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,018.70 | $6.29 | 1.25% |

| Class C Shares | | | | |

| Actual | $1,000.00 | $1,036.42 | $11.42 | 2.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,013.71 | $11.30 | 2.25% |

| Class A Shares | | | | |

| Actual | $1,000.00 | $ 992.09 | $7.45 | 1.50% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,017.45 | $7.54 | 1.50% |

| Cavalier Growth Opportunities Fund | Beginning Account Value December 1, 2018 | Ending Account Value May 31, 2019 | Expenses Paid During Period* | Annualized Expense Ratio* |

| Institutional Class Shares | | | | |

| Actual | $1,000.00 | $ 992.70 | $6.21 | 1.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,018.70 | $6.29 | 1.25% |

| Class C Shares | | | | |

| Actual | $1,000.00 | $ 987.80 | $11.15 | 2.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,013.71 | $11.30 | 2.25% |

| Class A Shares | | | | |

| Actual | $1,000.00 | $ 961.64 | $7.34 | 1.50% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,017.45 | $7.54 | 1.50% |

Cavalier Funds

Additional Information

(Unaudited)

As of May 31, 2019

| Cavalier Hedged High Income Fund | Beginning Account Value December 1, 2018 | Ending Account Value May 31, 2019 | Expenses Paid During Period* | Annualized Expense Ratio* |

| Institutional Class Shares | | | | |

| Actual | $1,000.00 | $1,041.00 | $6.36 | 1.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,018.70 | $6.29 | 1.25% |

| Class C Shares | | | | |

| Actual | $1,000.00 | $1,042.30 | $11.46 | 2.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,013.71 | $11.30 | 2.25% |

| Cavalier Tactical Economic Fund | Beginning Account Value December 1, 2018 | Ending Account Value May 31, 2019 | Expenses Paid During Period* | Annualized Expense Ratio* |

| Institutional Class Shares | | | | |

| Actual | $1,000.00 | $1,002.50 | $6.24 | 1.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,018.70 | $6.29 | 1.25% |

| Class C Shares | | | | |

| Actual | $1,000.00 | $ 998.21 | $11.21 | 2.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,013.71 | $11.30 | 2.25% |

| Class A Shares | | | | |

| Actual | $1,000.00 | $1,001.20 | $7.48 | 1.50% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,017.45 | $7.54 | 1.50% |

| Cavalier Tactical Rotation Fund | Beginning Account Value December 1, 2018 | Ending Account Value May 31, 2019 | Expenses Paid During Period* | Annualized Expense Ratio* |

| Institutional Class Shares | | | | |

| Actual | $1,000.00 | $ 962.700 | $6.12 | 1.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,018.70 | $6.29 | 1.25% |

| Class C Shares | | | | |

| Actual | $1,000.00 | $ 958.00 | $10.98 | 2.25% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,013.71 | $11.30 | 2.25% |

| Class A Shares | | | | |

| Actual | $1,000.00 | $ 961.30 | $7.33 | 1.50% |

| Hypothetical (5% annual return before expenses) | $1,000.00 | $1,017.45 | $7.54 | 1.50% |

*Expenses are equal to the average account value over the period multiplied by each Fund’s annualized expense ratio, multiplied by the number of days in the most recent period divided by the number of days in the fiscal year (to reflect the six month period).

Cavalier Funds

Additional Information

(Unaudited)

As of May 31, 2019

5. Approval of Investment Advisory Agreement and Sub-Advisory Agreements

Investment Advisory Agreement with the Advisor

In connection with the quarterly Board meeting held on December 6, 2018, the Board, including a majority of the Independent Trustees, discussed the renewal of the management agreement pursuant to Rule 15a-4 of the Investment Company Act of 1940 between the Trust and the Advisor, with respect to each of the Funds (together, the "Investment Advisory Agreement").

The Trustees then reviewed the information prepared by Cavalier Investments (the “Advisor”) relating to the renewal of the Investment Advisory Agreement, including the Advisor’s Form ADV, experience, profitability with respect to the Funds, its financial strength and capability, and other pertinent information. The Trustees also reviewed, among other things, the Advisor’s income statement, fee and performance comparisons, and a copy of the current Investment Advisory Agreement.

The Trustees noted that the Cavalier Growth Opportunities Fund had become profitable, although it still reflects a loss for the Advisor for the one-year period. The Advisor discussed that the indirect expenses of the Advisor were allocated equally among the Funds because the amount of the Advisor’s time, effort, and resources devoted to each Fund was similar for each Fund. The Advisor also discussed the projected growth of the Funds with the Trustees.

In deciding on whether to approve the renewal of the Investment Advisory Agreement, the Trustees considered numerous factors, including:

(i) Nature, Extent, and Quality of Services. The Trustees considered the responsibilities of the Advisor under the Investment Advisory Agreement. The Trustees reviewed the services being provided by the Advisor to the Funds including, without limitation, the quality of its investment advisory services since the Advisor began managing Fund (including research and recommendations with respect to portfolio securities); its procedures for formulating investment recommendations and assuring compliance with the Funds’ investment objectives, policies and limitations; its coordination of services for the Funds among the Funds’ service providers; and its efforts to promote the Funds, grow the Funds’ assets, and assist in the distribution of Fund shares. The Trustees evaluated the Advisor’s staffing, personnel, and methods of operating; the education and experience of the Advisor’s personnel; the Advisor’s compliance program; and the financial condition of the Advisor.

After reviewing the foregoing information and further information in the memorandum from the Advisor (e.g., descriptions of the Advisor’s business, the Advisor’s compliance program, and the Advisor’s Form ADV), the Trustees concluded that the nature, extent, and quality of the services provided by the Advisor were satisfactory and adequate for the Funds.

(ii) Performance. The Trustees compared the performance of the Funds with the performance of its benchmark index, comparable funds with similar strategies managed by other investment advisers, and applicable peer group data (e.g., Morningstar/Lipper peer group average). The Trustees also considered the consistency of the Advisor’s management of the Funds with its investment objective, policies, and limitations. The Trustees made the following observations regarding the performance of each of the Funds.

Cavalier Adaptive Income Fund: The Trustees noted that the Fund had outperformed both its peer group and category for all periods shown.

Cavalier Fundamental Growth Fund: The Board noted that the Fund outperformed the peer group for all periods shown and outperformed the category since inception.

Cavalier Growth Opportunities Fund: The Trustees discussed that the Fund had outperformed its peer group but underperformed its category for all periods shown. They noted that the Fund is rated 5 Star by Morningstar for the 3 and 5 year periods and that the Fund is in the top 1% in the tactical category.

Cavalier Funds

Additional Information

(Unaudited)

As of May 31, 2019

Cavalier Hedged High Income Fund: The Trustees noted that the Fund had outperformed both its peer group and category for all periods shown.

Cavalier Tactical Economic Fund: The Trustees discussed that the Fund had outperformed its peer group for all periods shown but had underperformed the category average for all periods shown. They noted the Advisor’s explanation that the category was not well aligned with the Fund’s strategy.

Cavalier Tactical Rotation Fund: The Trustees noted that the Fund had outperformed the peer group for all periods shown and is rated 5 Star by Morningstar for the 3 and 5 year periods. They also discussed the Fund’s underperformance relative to its category and noted the Advisor’s explanation that the category was not well aligned with the Fund’s strategy.

After reviewing the investment performance of the Funds, the Advisor’s experience managing the Funds, the Advisor’s historical investment performance, and other factors, the Trustees concluded that the investment performance of the Funds and the Advisor was satisfactory.

(iii) Fees and Expenses. The Trustees noted the management fees for the Funds under the Investment Advisory Agreement. The Trustees noted that the management fee for each Fund was above average of the peer group and category. They further discussed that the Advisor believed this was due primarily to the small size of the Fund relative to those comparison groups. The Trustees considered the Advisor’s unique research and investment process in evaluating the reasonableness of its management fee.

Following this comparison, and upon further consideration and discussion of the foregoing, the Board concluded that the fees to be paid to the Advisor by the Funds were not unreasonable in relation to the nature and quality of the services provided by the Advisor and that they reflected charges that were within a range of what could have been negotiated at arm’s length.

(iv) Profitability. The Board reviewed the Advisor’s profitability analysis in connection with its management of the Funds over the past twelve months. The Board noted that the Advisor did not realize a profit for the prior twelve months of operations for any of the Funds except the Cavalier Fundamental Growth Fund and the Cavalier Tactical Rotation Fund. The Trustees discussed the profitability level of the Advisor, noting, among other factors and circumstances, that the level of profitability was a function of current and expected expenses, and it was important for the Advisor to make a profit in order to have adequate resources to operate the Funds. After discussion, the Trustees concluded that the Advisor’s level of profitability was not excessive.

(v) Economies of Scale. In this regard, the Trustees reviewed the Funds’ operational history and noted the Advisor’s advice that the size of the Funds had not provided an opportunity to realize economies of scale. The Trustees then reviewed the Funds’ fee arrangements for breakpoints or other provisions that would allow the Funds’ shareholders to benefit from economies of scale in the future as the Funds grow. The Trustees determined that the maximum management fee would stay the same regardless of the Funds’ asset levels but noted the Advisor’s willingness to consider breakpoints in the future as assets grow. The Trustees noted that the Funds were a relatively small size and economies of scale were unlikely to be achievable in the near future. It was pointed out that breakpoints in the advisory fee could be reconsidered in the future as the Funds grow.

Conclusion. Having reviewed and discussed in depth such information from the Advisor as the Trustees believed to be reasonably necessary to evaluate the terms of the Investment Advisory Agreement and as assisted by the advice of legal counsel, the Trustees concluded that approval of the Investment Advisory Agreement was in the best interest of the shareholders of the Fund.

Cavalier Funds

Additional Information

(Unaudited)

As of May 31, 2019

Sub-Advisory Agreement with Buckhead

In connection with the quarterly Board meeting held on September 5, 2018, the Board, including a majority of the Independent Trustees, discussed the renewal of the sub-advisory agreement, each between the Advisor and Buckhead Capital Management, LLC (“Buckhead”) (together, the "Sub-Advisory Agreement"), with respect the Cavalier Adaptive Income Fund (referred to in this section as the “Fund”).

The Trustees were assisted by legal counsel throughout the review process. The Trustees relied upon the advice of legal counsel and their own business judgment in determining the material factors to be considered in evaluating the Sub-Advisory Agreement and the weight to be given to each factor considered. The conclusions reached by the Trustees were based on a comprehensive evaluation of all of the information provided and were not the result of any one factor. Moreover, each Trustee may have afforded different weight to the various factors in reaching his conclusions with respect to the approval of the Sub-Advisory Agreement. In connection with their deliberations regarding approval of the Sub-Advisory Agreement, the Trustees reviewed materials prepared by Buckhead.

In deciding on whether to approve the Sub-Advisory Agreement, the Trustees considered numerous factors, including:

(i) Nature, Extent, and Quality of Services. The Trustees considered the responsibilities of Buckhead under the Investment Sub-Advisory Agreement. The Trustees reviewed the services being provided by Buckhead to the Cavalier Adaptive Income Fund including, without limitation, the quality of its investment advisory services (including research and recommendations with respect to portfolio securities); its procedures for formulating investment recommendations and assuring compliance with the Cavalier Adaptive Income Fund’s investment objectives, policies and limitations; its coordination of services for the Cavalier Adaptive Income Fund among the Cavalier Adaptive Income Fund’s service providers; and its efforts to promote the Cavalier Adaptive Income Fund, grow the Cavalier Adaptive Income Fund’s assets, and assist in the distribution of Cavalier Adaptive Income Fund shares. The Trustees evaluated Buckhead’s staffing, personnel, and methods of operating; the education and experience of Buckhead’s personnel; Buckhead’s compliance program; and the financial condition of Buckhead.

After reviewing the foregoing information and further information in the memorandum from Buckhead (e.g., descriptions of Buckhead’s business, Buckhead’s compliance program, and Buckhead’s Form ADV), the Trustees concluded that the nature, extent, and quality of the services provided by Buckhead were satisfactory and adequate for the Cavalier Adaptive Income Fund.

(ii) Performance. The Trustees compared the performance of the Cavalier Adaptive Income Fund with the performance of its benchmark index, comparable funds with similar strategies managed by other investment advisers, and applicable peer group data (e.g., Lipper peer group average). The Trustees noted that the Cavalier Adaptive Income Fund had outperformed the peer group average for one-year period although it underperformed for the 5 year and since inception periods. The Trustees noted that the performance attributable to Buckhead was only for the one-year period, as they only recently began managing the Cavalier Adaptive Income Fund. After reviewing the investment performance of the Cavalier Adaptive Income Fund, the Trustees concluded that the investment performance of the Cavalier Adaptive Income Fund and Buckhead was satisfactory.

(iii) Fees and Expenses. The Trustees first noted the management fee for the Cavalier Adaptive Income Fund under the Investment Sub-Advisory Agreement. The Trustees then compared the sub-advisory fee and expense ratio of the Cavalier Adaptive Income Fund to other comparable accounts managed by Buckhead. The Trustees noted that the management fee was lower than the other comparable accounts at lower asset levels.

Following this comparison, and upon further consideration and discussion of the foregoing, the Trustees concluded that the fees to be paid to Buckhead by the Cavalier Adaptive Income Fund were not unreasonable in relation to the nature and quality of the services provided by Buckhead and that they reflected charges that were within a range of what could have been negotiated at arm’s length.

Cavalier Funds

Additional Information

(Unaudited)

As of May 31, 2019

(iv) Profitability. The Board reviewed Buckhead’s profitability analysis in connection with its management of the Cavalier Adaptive Income Fund. The Trustees noted that Buckhead did not realize a profit as of June 30, 2018, the most recent quarter end.

(v) Economies of Scale. In this regard, the Trustees reviewed the Cavalier Adaptive Income Fund’s operational history and noted the Advisor’s advice that the size of the Cavalier Adaptive Income Fund had not provided an opportunity to realize economies of scale. The Trustees then reviewed the Cavalier Adaptive Income Fund’s fee arrangements for breakpoints or other provisions that would allow the Cavalier Adaptive Income Fund’s shareholders to benefit from economies of scale in the future as the Cavalier Adaptive Income Fund grows. The Trustees determined that the maximum management fee would stay the same regardless of the Cavalier Adaptive Income Fund’s asset levels. The Trustees noted that the Cavalier Adaptive Income Fund was a relatively small size and economies of scale were unlikely to be achievable in the near future. It was pointed out that breakpoints in the sub-advisory fee could be reconsidered in the future as the Cavalier Adaptive Income Fund grows.

Conclusion. Having reviewed and discussed in depth such information from Buckhead as the Trustees believed to be reasonably necessary to evaluate the terms of the Sub-Advisory Agreement and as assisted by the advice of legal counsel, the Trustees concluded that approval of the Sub-Advisory Agreement was in the best interest of the shareholders of the Fund.

Sub-Advisory Agreement with Julex

In connection with the special Board meeting held on September 5, 2018, the Board, including a majority of the Independent Trustees, discussed the renewal of the new sub-advisory agreement, each between the Advisor and Julex Capital Management, LLC. (“Julex”) (together, the "Sub-Advisory Agreement"), with respect the Cavalier Tactical Rotation Fund (referred to in this section as the “Fund”).

The Trustees were assisted by legal counsel throughout the review process. The Trustees relied upon the advice of legal counsel and their own business judgment in determining the material factors to be considered in evaluating the Sub-Advisory Agreement and the weight to be given to each factor considered. The conclusions reached by the Trustees were based on a comprehensive evaluation of all of the information provided and were not the result of any one factor. Moreover, each Trustee may have afforded different weight to the various factors in reaching his conclusions with respect to the approval of the Sub-Advisory Agreement. In connection with their deliberations regarding approval of the Sub-Advisory Agreement, the Trustees reviewed materials prepared by Julex.

In deciding on whether to approve the Sub-Advisory Agreement, the Trustees considered numerous factors, including:

(i) Nature, Extent, and Quality of Services. The Trustees considered the responsibilities of Julex under the proposed investment sub-advisory agreement. The Trustees reviewed the services to be provided by Julex to the Fund including without limitation: the quality of its investment advisory services (including research and recommendations with respect to portfolio securities); its procedures for formulating investment recommendations and assuring compliance with the Fund’s investment objectives and limitations; its coordination of services for the Fund among the Cavalier Tactical Rotation Fund’s service providers; and its efforts to promote the Fund, grow the Fund’s assets, and assist in the distribution of Fund shares. The Trustees evaluated Julex’s: staffing, personnel, and methods of operating; the education and experience of Julex’s personnel; Julex’s compliance program; and the financial condition of Julex.

After reviewing the foregoing information and further information in the memorandum from Julex (e.g., descriptions of Julex’s business, compliance program, and Form ADV), the Trustees concluded that the nature, extent, and quality of the services to be provided by Julex were satisfactory and adequate for the Fund.

(ii) Performance. The Trustees then discussed that Julex’s personnel had experience in advising mutual funds and pointed out the performance of Julex with certain other accounts using a similar strategy to that of the Cavalier Tactical Rotation Fund. They noted the sector composite used has a lot of overlap with the Fund’s strategy and outperformed its benchmark for the 1, 5, and since inception periods.

Cavalier Funds

Additional Information

(Unaudited)

The Trustees concluded that Julex was in a position to achieve satisfactory performance of the Fund.

(iii) Fees and Expenses. The Trustees noted the management fee rate for the Fund under the proposed investment sub-advisory agreement. The Trustees then compared the proposed sub-advisory fee rate and net expense ratio of the Fund to other comparable accounts managed by Julex. The Trustees noted that the maximum sub-advisory fee rate was lower than fee rates charged to other accounts using a comparable strategy managed by Julex as represented by Julex.

Following this comparison, and upon further consideration and discussion of the foregoing, the Trustees concluded that the fee rate to be paid to Julex was not unreasonable in relation to the nature and quality of the services to be provided by Julex and that they reflected charges that were within a range of what could have been negotiated at arm’s length.

(iv) Profitability. The Trustees reviewed Julex’s profitability analysis in connection with its proposed management of the Fund. The Trustees noted that Julex anticipated a very small profit during the first 12 months of managing the Fund and modest profit during the second 12 months of managing the Fund. The Trustees concluded that Julex’s expected level of profitability was not excessive.

(v) Economies of Scale. In this regard, the Trustees reviewed the Fund’s operational history and noted the Advisor’s advice that the Fund was not yet large enough to realize economies of scale. The Trustees then reviewed the Fund’s proposed fee arrangements for breakpoints or other provisions that would allow the Fund’s shareholders to benefit from economies of scale in the future as the Fund grows.

Conclusion. Having reviewed and discussed in depth such information from Julex as the Trustees believed to be reasonably necessary to evaluate the terms of the Sub-Advisory Agreement and as assisted by the advice of legal counsel, the Trustees concluded that approval of the Sub-Advisory Agreement was in the best interest of the shareholders of the Fund.

Sub-Advisory Agreement with Bluestone

In connection with the special Board meeting held on September 5, 2018, the Board, including a majority of the Independent Trustees, discussed the renewal of the sub-advisory agreement, each between the Advisor and Bluestone Capital Management, LLC (together, the "Sub-Advisory Agreement"), with respect the Cavalier Growth Opportunities Fund (referred to in this section as the “Fund”).

The Trustees were assisted by legal counsel throughout the review process. The Trustees relied upon the advice of legal counsel and their own business judgment in determining the material factors to be considered in evaluating the Sub-Advisory Agreement and the weight to be given to each factor considered. The conclusions reached by the Trustees were based on a comprehensive evaluation of all of the information provided and were not the result of any one factor. Moreover, each Trustee may have afforded different weight to the various factors in reaching his conclusions with respect to the approval of the Sub-Advisory Agreement. In connection with their deliberations regarding approval of the Sub-Advisory Agreement, the Trustees reviewed materials prepared by Beaumont.

In deciding on whether to approve the Sub-Advisory Agreement, the Trustees considered numerous factors, including:

(i) Nature, Extent, and Quality of Services. The Trustees considered the responsibilities of Bluestone under the proposed investment sub-advisory agreement. The Trustees reviewed the services to be provided by Bluestone to the Fund including without limitation: the quality of its investment advisory services (including research and recommendations with respect to portfolio securities); its procedures for formulating investment recommendations and assuring compliance with the Fund’s investment objectives and limitations; its coordination of services for the Fund among the Fund’s service providers; and its efforts to promote the Fund, grow the Fund’s assets, and assist in the distribution of Fund shares. The Trustees evaluated: Bluestone’s staffing, personnel, and methods of operating; the education and experience of Bluestone’s personnel; Bluestone’s compliance program; and the financial condition of Bluestone.

Cavalier Funds

Additional Information

(Unaudited)

As of May 31, 2019

The Trustees reviewed the financial statements for Bluestone and discussed the financial stability and profitability of the firm. The Trustees also considered potential benefits for Bluestone in managing the Fund, including promotion of Bluestone’s name, and the ability for Bluestone to place small accounts into the Fund.

After reviewing the foregoing information and further information in the memorandum from Bluestone (e.g., descriptions of Bluestone’s business, Bluestone’s compliance program, and Bluestone’s Form ADV), the Board concluded that the nature, extent, and quality of the services to be provided by Bluestone were satisfactory and adequate for the Fund.

(ii) Performance. The Trustees then discussed that Bluestone’s personnel had experience in advising mutual funds and highlighted the performance of Bluestone with certain other accounts using a similar strategy to that of the Fund. They noted that those accounts had outperformed the benchmark for the one-year, ten-year, and since-inception periods and performed in line with the benchmark for the five-year period. The Trustees concluded that Bluestone was positioned to achieve satisfactory performance of the Fund.

(iii) Fees and Expenses. The Trustees noted the management fee rate for the Fund under the proposed investment sub-advisory agreement. The Trustees then compared the proposed sub-advisory fee rate and net expense ratio of the Fund to other comparable accounts managed by Bluestone. The Trustees noted that the maximum sub-advisory fee rate was below fee rates charged to other accounts using a comparable strategy managed by Bluestone.

Following this comparison, and upon further consideration and discussion of the foregoing, the Trustees concluded that the fee rate to be paid to Bluestone was not unreasonable in relation to the nature and quality of the services to be provided by Bluestone and that they reflected charges that were within a range of what could have been negotiated at arm’s length.

(iv) Profitability. The Trustees reviewed Bluestone’s profitability analysis in connection with its proposed management of the Fund. The Trustees noted that Bluestone anticipated negative profitability during the first 12 months of managing the Fund and modest profit during the second 12 months of managing the Fund. The Trustees concluded that Bluestone’s expected level of profitability was not excessive.

(v) Economies of Scale. In this regard, the Trustees reviewed the Fund’s operational history and noted the Advisor’s advice that the Fund was not yet large enough to realize economies of scale. The Trustees then reviewed the Fund’s proposed fee arrangements for breakpoints or other provisions that would allow the Fund’s shareholders to benefit from economies of scale in the future as the Fund grows. The Trustees noted that the Fund was a relatively small size and economies of scale were unlikely to be achievable in the near future. It was also noted that no sub-advisory fee was payable until the Fund reached a certain asset level and that breakpoints in the advisory fee rate could be reconsidered in the future as the Fund grows.

Conclusion. Having reviewed and discussed in depth such information from Beaumont as the Trustees believed to be reasonably necessary to evaluate the terms of the Sub-Advisory Agreement and as assisted by the advice of legal counsel, the Trustees concluded that approval of the Sub-Advisory Agreement was in the best interest of the shareholders of the Funds.

Sub-Advisory Agreement with Navellier

In connection with the special Board meeting held on December 6, 2018, the Board, including a majority of the Independent Trustees, discussed the renewal of the sub-advisory agreement, each between the Advisor and Navellier & Associates, LLC (“Navellier”) (together, the "Sub-Advisory Agreement"), with respect the Cavalier Fundamental Growth Fund (referred to in this section as the “Fund”).

The Trustees were assisted by legal counsel throughout the review process. The Trustees relied upon the advice of legal counsel and their own business judgment in determining the material factors to be considered in evaluating the Sub-Advisory Agreement and the weight to be given to each factor considered. The conclusions reached by the Trustees were based on a comprehensive evaluation of all of the information provided and were not the result of any one factor. Moreover, each Trustee may have afforded different weight to the various factors in reaching his conclusions with respect to the approval of the Sub-Advisory Agreement. In connection with their deliberations regarding approval of the Sub-Advisory Agreement, the Trustees reviewed materials prepared by Navellier.

Cavalier Funds

Additional Information

(Unaudited)

As of May 31, 2019

In deciding on whether to approve the Sub-Advisory Agreement, the Trustees considered numerous factors, including:

(i) Nature, Extent, and Quality of Services. The Trustees considered the responsibilities of the Sub-Advisor under the Investment Advisory Agreement. The Trustees reviewed the services being provided by the Sub-Advisor to the Fund including, without limitation, the quality of its investment advisory services since the Sub-Advisor began managing Fund (including research and recommendations with respect to portfolio securities); and its procedures for formulating investment recommendations and assuring compliance with the Fund’s investment objectives, policies and limitations. The Trustees evaluated the Sub-Advisor’s staffing, personnel, and methods of operating; the education and experience of the Sub-Advisor’s personnel; the Sub-Advisor’s compliance program; and the financial condition of the Advisor.

After reviewing the foregoing information and further information in the memorandum from the Sub-Advisor (e.g., descriptions of the Sub-Advisor’s business, the Sub-Advisor’s compliance program, and the Sub-Advisor’s Form ADV), the Trustees concluded that the nature, extent, and quality of the services provided by the Sub-Advisor were satisfactory and adequate for the Fund.

(ii) Performance. The Trustees compared the performance of the Fund with the performance of its benchmark index, comparable funds with similar strategies managed by other investment advisers, and applicable peer group data (e.g., Morningstar/Lipper peer group average). The Trustees noted that the Fund outperformed its peer group for all periods shows and outperformed the category for all but the one-year period. The Trustees also considered the consistency of the Sub-Advisor’s management of the Fund with its investment objective, policies and limitations. After reviewing the investment performance of the Fund, the Sub-Advisor’s experience managing the Fund, the Sub-Advisor’s historical investment performance, and other factors, the Trustees concluded that the investment performance of the Fund and the Sub-Advisor was satisfactory.

(iii) Fees and Expenses. The Trustees noted the management fees for the Fund under the Investment Sub-Advisory Agreement. The Trustees discussed that the Sub-Advisory did not have any accounts using a comparable strategy to that of the Fund to which to compare the sub-advisory fee being charged by the Sub-Advisor, but that the overall management fee was not unreasonable in relation to the nature and quality of the services provided by the Sub-Advisor and Advisor. The Trustees considered the Sub-Advisor’s unique research and investment process in evaluating the reasonableness of its management fee.

Following this comparison, and upon further consideration and discussion of the foregoing, the Trustees concluded that the fees to be paid to the Sub-Advisor by the Fund were not unreasonable in relation to the nature and quality of the services provided by the Sub-Advisor and that they reflected charges that were within a range of what could have been negotiated at arm’s length.

(iv) Profitability. The Board reviewed the Sub-Advisor’s profitability analysis in connection with its management of the Fund over the past twelve months and noted that the Sub-Advisor had returned a profit. The Independent Trustees discussed the profitability level of the Sub-Advisor, noting, among other factors and circumstances, that the level of profitability was a function of current and expected expenses, and it was important for the Sub-Advisor to make a profit in order to have adequate resources to operate the Funds. After discussion, the Trustees concluded that the Sub-Advisor level of profitability was not excessive.

(v) Economies of Scale. In this regard, the Trustees reviewed the Fund’s operational history and noted the Advisor’s advice that the size of the Fund had not provided an opportunity to realize economies of scale. The Trustees then reviewed the Fund’s fee arrangements for breakpoints or other provisions that would allow the Fund’s shareholders to benefit from economies of scale in the future as the Fund grows. The Trustees determined that the maximum management fee would stay the same regardless of the Fund’s asset levels. The Trustees noted that the Fund was a relatively small size and economies of scale were unlikely to be achievable in the near future. It was pointed out that breakpoints in the advisory fee could be reconsidered in the future as the Fund grows.

Cavalier Funds

Additional Information

(Unaudited)

As of May 31, 2019