UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-22321

MAINSTAY FUNDS TRUST

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

169 Lackawanna Avenue

Parsippany, New Jersey 07054

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 576-7000

Date of fiscal year end: June 30 (MainStay Cornerstone Growth Fund)

Date of reporting period: June 30, 2013

FORM N-CSR

The information presented in this Form N-CSR relates solely to the

MainStay Cornerstone Growth Fund, a series of the Registrant.

| Item 1. | Reports to Stockholders. |

MainStay Cornerstone Growth Fund

Message from the President and Annual Report

June 30, 2013

This page intentionally left blank

Message from the President

The stock market advanced during the 12 months ended June 30, 2013. But the climb was less than steady. In the United States, stocks progressed until shortly before the November election, then gave up much of their earlier gains. After that, domestic stocks rose relatively steadily, dipping occasionally for major events, including the fiscal cliff, the Boston marathon bombing, and suggestions that the Federal Reserve might taper its direct purchases of securities on the open market.

International stocks were also strong, but many emerging markets suffered from concerns about slower growth in China and falling prices for metals and other commodities.

The Federal Open Market Committee (“FOMC”) maintained the federal funds target rate in a near-zero target range, as it had done since December 2008. During the 12-month period, the FOMC reaffirmed that it would “continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month.” Nevertheless, the FOMC noted that it was “prepared to increase or reduce the pace of its purchases to maintain appropriate policy accommodation as the outlook for the labor market or inflation changes.”

During the reporting period, the FOMC also shifted from providing dates when it anticipated that the federal funds target might change to specifying the economic conditions under which an adjustment might be warranted.

Generally speaking, bonds did not fare as well as stocks during the reporting period. Interest rates rose when Federal Reserve Chairman Ben Bernanke outlined a plan for tapering the Federal Reserve’s quantitative easing and other accommodative strategies. The consequent drop in bond prices led U.S. government securities into negative territory. Many investors, however, lengthened maturities and lowered their risk threshold in hopes of earning extra yield. As a result, high-yield bonds, leveraged

loans, and convertible securities on the whole tended to provide positive single-digit returns.

With wide variations in the performance of various asset classes, some investors might be tempted to chase higher returns by shifting back and forth between stocks and bonds. Since no one can predict where the market will move next, however, we encourage investors to select an appropriate mix of investments for their risk tolerance and time horizon and to stick with that mix, making only minor adjustments over time.

At MainStay Funds, our portfolio managers use a similar approach. Careful security selection and thoughtful sell disciplines help them pursue the investment objectives of their respective Funds. Using the principal investment strategies outlined in the Prospectus, they focus primarily on providing long-term investment potential for our shareholders.

Has this approach proved successful? In its most recent rankings, Barron’s listed MainStay Funds as the #1 fund family over the past 10 years. We were also the only mutual fund family that has appeared in Barron’s top six for the past five consecutive years.

The pages that follow provide additional insight into the specific market events, investment decisions and securities that shaped MainStay Cornerstone Growth Fund during the 12 months ended June 30, 2013. We encourage you to read the accompanying annual report carefully and to evaluate your results with your long-term financial goals in mind.

Sincerely,

Stephen P. Fisher

President

The opinions expressed are as of the date of this report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

To qualify for the Lipper/Barron’s Fund Survey, a fund family must have at least three funds in Lipper’s general U.S.-stock category, one in world equity (which combines global and international funds), one mixed-equity fund (which holds stocks and bonds), two taxable-bond funds, and one tax-exempt fund. Fund loads and 12b-1 fees aren’t included in the calculation of returns because the aim is to measure the manager’s skill. Each fund’s return is measured against all funds in its Lipper category, resulting in a percentile ranking which is then weighted by asset size relative to the fund family’s other assets in its general classifications. Finally, the score is multiplied by the general classification weightings as determined by the entire Lipper universe of funds.

Source: Barron’s, 2/9/13. Overall, MainStay Funds ranked number 56 for the one-year period, 20 for the five-year period and one for the 10-year period ended December 31, 2012, out of 62, 53 and 46 fund families, respectively. MainStay ranked number three for the 10-year period in 2009, 2010 and 2011 from among 48, 46 and 45 fund families, respectively. MainStay ranked number six from among 48 fund families for the 10-year period in 2008.

According to Lipper Inc., the percentile ranks for MainStay Cornerstone Growth Fund Class A shares are 97, 32, 53 and 52 for the one-, three-, five-year and since-inception periods and are from among 724, 612, 552 and 486 large-cap growth funds, respectively. The Fund’s total-return percentile rank for the specified time period is relative to all funds that have the same Lipper category. The highest (or most favorable) percentile rank is 1 and the lowest (or least favorable) percentile rank is 100. The top-performing fund in a category will always receive a rank of 1. Percentile ranks within categories are most useful in those categories that have a large number of funds. Lipper Inc. is an independent monitor of fund performance. Past performance is no guarantee of future results, which will vary. For the most recent MainStay Funds performance, please visit our website at mainstayinvestments.com. All mutual funds are subject to market risk and will fluctuate in value.

Not part of the Annual Report

Investors should refer to the Fund’s Summary Prospectus and/or Prospectus and consider the Fund’s investment objectives, strategies, risks, charges and expenses carefully before investing. The Summary Prospectus and/or Prospectus contain this and other information about the Fund. You may obtain copies of the Fund’s Summary Prospectus, Prospectus and Statement of Additional Information free of charge, upon request, by calling toll-free 800-MAINSTAY (624-6782), by writing to NYLIFE Distributors LLC, Attn: MainStay Marketing Department, 169 Lackawanna Avenue, Parsippany, New Jersey 07054 or by sending an e-mail to MainStayShareholderServices@nylim.com. These documents are also available via the MainStay Funds’ website at mainstayinvestments.com/documents. Please read the Summary Prospectus and/or Prospectus carefully before investing.

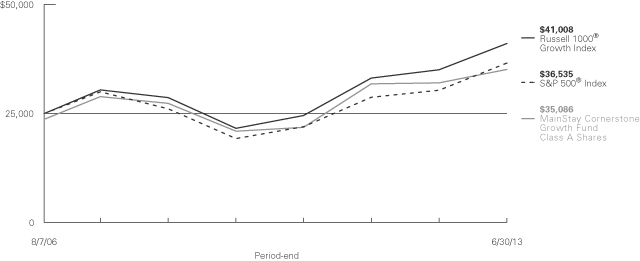

Investment and Performance Comparison1 (Unaudited)

Performance data quoted represents past performance. Past performance is no guarantee of future results. Because of market volatility, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate, and as a result, when shares are redeemed, they may be worth more or less than their original cost. The graph below depicts the historical performance of Class A shares of the Fund. Performance will vary from class to class based on differences in class-specific expenses and sales charges. For performance information current to the most recent month-end, please call 800-MAINSTAY (624-6782) or visit mainstayinvestments.com.

Average Annual Total Returns for the Period Ended June 30, 2013

| Class | Sales Charge | One Year | Five Year | Since Inception (8/7/06) | Gross Expense Ratio2 | |||||||||||||||

| Investor Class Shares3 | Maximum 5.5% Initial Sales Charge | With sales charges Excluding sales charges |

| 3.33 9.34 | %

|

| 3.88 5.06 | %

|

| 4.99 5.86 | %

|

| 1.58 1.58 | %

| ||||||

| Class A Shares4 | Maximum 5.5% Initial Sales Charge | With sales charges Excluding sales charges |

| 3.61 9.64 |

|

| 3.94 5.12 |

|

| 5.03 5.90 |

|

| 1.32 1.32 |

| ||||||

| Class B Shares3 | Maximum 5% CDSC if Redeemed Within First Six Years of Purchase | With sales charges Excluding sales charges |

| 3.51 8.51 |

|

| 3.93 4.28 |

|

| 5.06 5.06 |

|

| 2.33 2.33 |

| ||||||

| Class C Shares3 | Maximum 1% CDSC if Redeemed Within One Year of Purchase | With sales charges Excluding sales charges |

| 7.51 8.51 |

|

| 4.28 4.28 |

|

| 5.06 5.06 |

|

| 2.33 2.33 |

| ||||||

| Class | Sales Charge | One Year | Since Inception (11/2/09) | Gross Expense Ratio2 | ||||||||||||||||

| Class I Shares4 | No Sales Charge | 9.91 | % | 11.98 | % | 1.07 | % | |||||||||||||

| Class | Sales Charge | One Year | Five Year | Since Inception (8/7/06) | Gross Expense Ratio2 | |||||||||||||||

| Class R2 Shares3 | No Sales Charge | 9.50 | % | 5.01 | % | 5.79 | % | 1.42 | % | |||||||||||

| 1. | The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on distributions or Fund-share redemptions. Total returns reflect maximum applicable sales charges as indicated in the table above, changes in share price, and reinvestment of dividend and capital gain distributions. The graph assumes the initial investment amount being shown above and reflects the deduction of all sales charges that would have applied for the period of investment. Performance figures reflect certain fee waivers and/or expense limitations, without which total returns may have been lower. For more information on share classes and current fee waivers and/or expense limitations, please refer to the notes to the financial statements. |

| 2. | The gross expense ratios presented reflect the Fund’s “Total Annual Fund Operating Expenses” from the most recent Prospectus and may differ from other expense ratios disclosed in this report. |

| 3. | Performance figures for Investor Class shares, Class B shares, Class C shares and Class R2 shares, first offered as of the close of business on January 18, 2013 include the historical performance of Class A shares through January 18, 2013. Performance figures for Investor Class shares, Class B shares, Class C shares and Class R2 shares have been adjusted for differences in fees and expenses. Unadjusted, the performance for the newer classes would likely have been different. |

| 4. | Performance figures for Class A and Class I shares reflect the historical performance of Class A and Class I shares of the Keystone Large Cap Growth Fund (the predecessor to the Fund, which was subject to a different fee structure), for periods prior to January 11, 2013. Performance data for the classes varies based on differences in their fee and expense structures and the length of time these shares have been offered. Keystone Large Cap Growth Fund commenced operations, and Class A shares were first offered, on August 7, 2006. Class I shares were first offered on November 2, 2009. |

The footnotes on the next page are an integral part of the table and graph and should be carefully read in conjunction with them.

| mainstayinvestments.com | 5 |

| Benchmark Performance | One Year | Five Year | Since Inception | |||||||||

Russell 1000® Growth Index5 | 17.07 | % | 7.47 | % | 7.44 | % | ||||||

S&P 500® Index6 | 20.60 | 7.01 | 5.65 | |||||||||

Average Lipper Large-Cap Growth Fund7 | 15.85 | 5.29 | 5.95 | |||||||||

| 5. | The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000® Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 1000® Growth Index is the Fund’s broad-based securities market index for comparison purposes. Total returns assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an index. |

| 6. | The S&P 500® Index is a trademark of the McGraw-Hill Companies, Inc. The S&P 500® Index is widely regarded as the standard index for measuring large-cap U.S. stock market performance. The S&P 500® Index is the Fund’s secondary benchmark. Total returns assume reinvestment of all |

| dividends and capital gains. An investment cannot be made directly in an index. |

| 7. | The average Lipper large-cap growth fund is representative of funds that, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) above Lipper’s U.S. Diversified Equity large-cap floor. Large-cap growth funds typically have an above-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value, compared to the S&P 500® Index. This benchmark is a product of Lipper Inc. Lipper Inc. is an independent monitor of fund performance. Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

The footnotes on the preceding page are an integral part of the table and graph and should be carefully read in conjunction with them.

| 6 | MainStay Cornerstone Growth Fund |

Cost in Dollars of a $1,000 Investment in MainStay Cornerstone Growth Fund (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the period from January 1, 2013, to June 30, 2013, and the impact of those costs on your investment.

Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including exchange fees and sales charges (loads) on purchases (as applicable), and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other Funds. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from January 1, 2013, to June 30, 2013.

This example illustrates your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six months ended June 30, 2013. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then

multiply the result by the number under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in the Fund with the ongoing costs of investing in other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other Funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as exchange fees or sales charges (loads). Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Share Class | Beginning Account Value 1/1/131 | Ending Account Value (Based on Actual Returns and Expenses) 6/30/13 | Expenses During | Ending Account Value (Based on Hypothetical 5% Annualized Return and Actual Expenses) 6/30/13 | Expenses Paid During Period2 | |||||||||||||||

| Investor Class Shares3 | $ | 1,000.00 | $ | 1,015.10 | $ | 7.96 | $ | 1,014.40 | $ | 7.96 | ||||||||||

| Class A Shares | $ | 1,000.00 | $ | 1,051.30 | $ | 5.95 | $ | 1,019.00 | $ | 5.86 | ||||||||||

| Class B Shares3 | $ | 1,000.00 | $ | 1,011.60 | $ | 11.32 | $ | 1,011.10 | $ | 11.32 | ||||||||||

| Class C Shares3 | $ | 1,000.00 | $ | 1,011.60 | $ | 11.32 | $ | 1,011.10 | $ | 11.32 | ||||||||||

| Class I Shares | $ | 1,000.00 | $ | 1,052.60 | $ | 4.73 | $ | 1,020.20 | $ | 4.66 | ||||||||||

| Class R2 Shares3 | $ | 1,000.00 | $ | 1,017.10 | $ | 5.86 | $ | 1,016.50 | $ | 5.85 | ||||||||||

| 1. | Investor Class, Class B, Class C, and Class R2 shares were first offered as of the close of business on January 18, 2013. |

| 2. | Expenses are equal to the Fund’s annualized expense ratio of each class (1.77% for Investor Class, 1.17% for Class A, 2.52% for Class B, 2.52% for Class C, 0.93% for Class I and 1.30% for Class R2) multiplied by the average account value over the period, divided by 365 and multiplied by 181 for Class A and Class I and 163 days for Investor Class, Class B, Class C and Class R2 (to reflect the six-month period). The table above represents the actual expenses incurred during the six-month period. |

| 3. | Expenses paid during the period reflect ongoing costs for the period from inception through June 30, 2013. Had these shares been offered for the full six-month period ended June 30, 2013, and had the Fund provided a hypothetical 5% annualized return, expenses paid during the period would have been $8.85 for Investor Class, $12.57 for Class B and Class C, and $6.51 for Class R2 and the ending account value would have been $1,016.00 for Investor Class, $1,012.30 for Class B and Class C, and $1,018.30 for Class R2. |

| mainstayinvestments.com | 7 |

Industry Composition as of June 30, 2013 (Unaudited)

| Internet Software & Services | 11.0 | % | ||

| IT Services | 7.0 | |||

| Textiles, Apparel & Luxury Goods | 6.1 | |||

| Health Care Equipment & Supplies | 5.3 | |||

| Communications Equipment | 5.2 | |||

| Chemicals | 5.0 | |||

| Health Care Providers & Services | 4.7 | |||

| Software | 4.4 | |||

| Oil, Gas & Consumable Fuels | 3.8 | |||

| Beverages | 3.7 | |||

| Media | 3.7 | |||

| Computers & Peripherals | 3.6 | |||

| Specialty Retail | 3.3 | |||

| Biotechnology | 2.9 | |||

| Tobacco | 2.9 | |||

| Energy Equipment & Services | 2.7 | |||

| Construction & Engineering | 2.2 |

| Semiconductors & Semiconductor Equipment | 2.1 | % | ||

| Real Estate Investment Trusts | 2.0 | |||

| Trading Companies & Distributors | 2.0 | |||

| Internet & Catalog Retail | 1.9 | |||

| Metals & Mining | 1.9 | |||

| Auto Components | 1.7 | |||

| Machinery | 1.6 | |||

| Pharmaceuticals | 1.3 | |||

| Consumer Finance | 1.1 | |||

| Food Products | 1.1 | |||

| Diversified Financial Services | 1.0 | |||

| Aerospace & Defense | 0.9 | |||

| Capital Markets | 0.9 | |||

| Electrical Equipment | 0.9 | |||

| Multiline Retail | 0.8 | |||

| Short-Term Investment | 3.0 | |||

| Other Assets, Less Liabilities | –1.7 | |||

|

| |||

| 100.0 | % | |||

|

|

See Portfolio of Investments beginning on page 11 for specific holdings within these categories.

Top Ten Holdings as of June 30, 2013 (excluding short-term investment) (Unaudited)

| 1. | Google, Inc. Class A |

| 2. | QUALCOMM, Inc. |

| 3. | Western Union Co. (The) |

| 4. | Visa, Inc. Class A |

| 5. | Cobalt International Energy, Inc. |

| 6. | Sherwin-Williams Co. (The) |

| 7. | Diageo PLC, Sponsored ADR |

| 8. | Philip Morris International, Inc. |

| 9. | Hologic, Inc. |

| 10. | Walt Disney Co. (The) |

| 8 | MainStay Cornerstone Growth Fund |

Portfolio Management Discussion and Analysis (Unaudited)

Questions answered by portfolio manager Thomas G. Kamp, CFA, of Cornerstone Capital Management LLC, the Fund’s Subadvisor.

How did MainStay Cornerstone Growth Fund perform relative to its benchmark and peers during the 12 months ended June 30, 2013?

Excluding all sales charges, MainStay Cornerstone Growth Fund returned 9.34% for Investor Class shares, 9.64% for Class A shares and 8.51% for Class B and Class C shares for the 12 months ended June 30, 2013. Over the same period, Class I shares returned 9.91% and Class R2 shares returned 9.50%. During the 12 months ended June 30, 2013, all share classes underperformed the 17.07% return of the Russell 1000® Growth Index,1 which is the Fund’s broad-based securities-market index. Over the same period, all share classes underperformed the 15.85% return of the average Lipper2 large-cap growth fund. See page 5 for Fund returns with applicable sales charges.

What factors affected the Fund’s relative performance during the reporting period?

We entered the reporting period with caution. In our opinion, the U.S. government was following an unsustainable path that would likely lead to equity market volatility, especially in light of economic and political challenges elsewhere in the world. We have been and continue to be pessimistic about the prospects for meaningful spending cuts. As a result, we anticipated a series of cliffs, deadlines and Band-Aid solutions that would do little to solve our nation’s structural problems.

We underestimated the willingness of investors to ignore these structural problems by bidding valuations higher, in many cases on reduced earnings expectations. The lesson we must take away is “Don’t fight the Federal Reserve”—especially when central banks around the world seem to be aggressively monetizing their debt, injecting hundreds of billions of dollars of liquidity into the financial system.

Our cautionary stance resulted in the Fund’s underperformance of the Russell 1000® Growth Index in a robustly rising stock market. We sought safety in stocks we thought offered protection because of low valuations and high cash-flow generation. We sold or steered clear of many growth stocks because we viewed their valuations as high, but then saw their valuations rise.

During the reporting period, which sectors were the strongest positive contributors to the Fund’s relative performance and which sectors were particularly weak?

During the reporting period, information technology made the strongest positive sector contribution relative to the Russell 1000® Growth Index, primarily because of stock selection. (Contributions take weightings and total returns into account.) Financials also contributed modestly to relative returns, primarily as a result of stock selection.

The Fund’s weakest-contributing sector relative to the Russell 1000® Growth Index was consumer discretionary, primarily as a result of stock selection. In the health care sector, stock selection detracted from relative performance. The industrials sector was the third-weakest contributor, with stock selection and an underweight position hurting relative performance.

During the reporting period, which individual stocks made the strongest contributions to the Fund’s absolute performance and which stocks detracted the most?

Search engine company Google was the strongest positive contributor to the Fund’s absolute performance. The stock rallied on prospects for accelerated growth from mobile and new product opportunities.

Retail electronic payments company Visa was the next-strongest contributor to absolute performance. Visa continued to deliver high revenue growth with strong operating margin expansion and shareholder-friendly capital deployment. These fundamentals combined to generate high rates of earnings-per-share growth.

Global diversified technology and industrial company Johnson Controls was also a strong contributor to absolute performance during the reporting period. We trimmed the Fund’s position in the stock during the period as it approached what we viewed as its fair value. Nevertheless, we continue to see longer-term value in the stock, assuming execution in Europe and divestitures of underperforming segments.

Computers & peripherals company Apple was the weakest contributor to the Fund’s absolute performance, and the stock was no longer held in the Fund at the end of the reporting period. The weak contribution resulted from concerns about saturation of the high-end smart phone market, delays in striking a distribution deal with China Mobile, and iPhone inventory buildup in the distribution channel.

Online education company Apollo Group was the second-weakest contributor to the Fund’s absolute performance and was no longer held in the Fund at the end of the reporting period. We eliminated our position in Apollo Group because of a growing realization that the online education industry is facing increasing competition from traditional not-for-profit schools and because the company intends to invest in international operations.

Cardiovascular device company Edwards Lifesciences was another weak contributor during the reporting period. The company missed sales and earnings estimates and lowered 2013 guidance primarily because the outlook weakened for U.S. transcatheter heart valves, a key product and market. Nevertheless, we see potential in the company, and the Fund continued to hold the stock at the end of the reporting period.

| 1. | See footnote on page 6 for more information on the Russell 1000® Growth Index. |

| 2. | See footnote on page 6 for more information on Lipper Inc. |

| mainstayinvestments.com | 9 |

Did the Fund make any significant purchases or sales during the reporting period?

We eliminated our position in Apple because of concerns about saturation in the high-end smart phone market, delays in striking a distribution deal with China Mobile, and iPhone inventory buildup in the distribution channel.

We eliminated the Fund’s position in Chinese Internet search provider Baidu because of concerns that the incremental investments required to expand its mobile business and cloud services would lead to negative estimate revisions.

We also eliminated the Fund’s holdings in health benefit company WellPoint as the valuation recovered toward our price target. We anticipated that membership among small businesses would be volatile as the health care exchanges begin.

Finally, we eliminated our position in Apollo Group because of a growing realization that the online education industry is facing increasing competition from traditional not-for-profit schools and because the company intends to invest in international operations.

We added a position in Edwards Lifesciences during the reporting period. We anticipated accelerated procedure volume after a heavy period of training. Another new addition was biopharmaceutical company Gilead Sciences. We liked the promise of Sofusbuvir, a treatment for hepatitis C. We believed that the new drug might lead to high earnings growth and rising estimates for much of this decade. The Fund also added a position in industrial equipment company United Rentals. We were attracted to the stock because the company is focused on the United States market and has no exposure to China. The stock gave the Fund upside to nonresidential construction acceleration in addition to increases in industrial and energy capital expenditures. We also added professional social networking company LinkedIn. The company is a leading provider of human

resource recruiting services that is disintermediating traditional recruitment at a lower cost. The Internet company is leveraging its growing user base to drive advertising and revenue from subscriptions.

How did the Fund’s sector weightings change during the reporting period?

In the financials sector, the Fund moved from a significantly underweight position relative to the Russell 1000® Growth Index to a slightly overweight position during the reporting period. The Fund started the reporting period with a modestly underweight position in health care but moved to a meaningfully overweight position at the end of June. Another increase in sector weightings came in the materials sector, adding to an already meaningfully overweight position.

In the industrials sector, the Fund moved from an underweight position relative to the Russell 1000® Growth Index to a dramatically underweight position. The Fund cut its dramatically overweight position in the energy sector to a meaningfully overweight position. In the consumer discretionary sector, the Fund moved from a significantly overweight position to a modestly overweight position.

How was the Fund positioned at the end of June 2013?

As of June 30, 2013, the Fund held a significantly overweight position relative to the Russell 1000® Growth Index in information technology and significantly overweight positions in materials and energy. As of the same date, the Fund held significantly underweight positions in industrials and consumer staples and a significantly underweight position in telecommunication services. The telecommunication services underweight resulted from not owning any stocks in the sector because these stocks did not meet the Fund’s investment criteria.

The opinions expressed are those of the portfolio manager as of the date of this report and are subject to change. There is no guarantee that any forecasts made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

| 10 | MainStay Cornerstone Growth Fund |

Portfolio of Investments June 30, 2013

| Shares | Value | |||||||

| Common Stocks 98.7%† | ||||||||

Aerospace & Defense 0.9% | ||||||||

Textron, Inc. | 334,911 | $ | 8,724,432 | |||||

|

| |||||||

Auto Components 1.7% | ||||||||

Johnson Controls, Inc. | 496,463 | 17,768,411 | ||||||

|

| |||||||

Beverages 3.7% | ||||||||

Coca-Cola Co. (The) | 198,587 | 7,965,324 | ||||||

¨Diageo PLC, Sponsored ADR | 256,741 | 29,512,378 | ||||||

|

| |||||||

| 37,477,702 | ||||||||

|

| |||||||

Biotechnology 2.9% | ||||||||

Celgene Corp. (a) | 78,584 | 9,187,255 | ||||||

Gilead Sciences, Inc. (a) | 397,407 | 20,351,213 | ||||||

|

| |||||||

| 29,538,468 | ||||||||

|

| |||||||

Capital Markets 0.9% | ||||||||

Morgan Stanley | 368,533 | 9,003,261 | ||||||

|

| |||||||

Chemicals 5.0% | ||||||||

Mosaic Co. (The) | 378,582 | 20,371,497 | ||||||

¨Sherwin-Williams Co. (The) | 171,383 | 30,266,238 | ||||||

|

| |||||||

| 50,637,735 | ||||||||

|

| |||||||

Communications Equipment 5.2% | ||||||||

¨QUALCOMM, Inc. | 869,520 | 53,110,282 | ||||||

|

| |||||||

Computers & Peripherals 3.6% | ||||||||

NetApp, Inc. (a) | 627,680 | 23,713,751 | ||||||

Stratasys, Ltd. (a) | 153,622 | 12,864,306 | ||||||

|

| |||||||

| 36,578,057 | ||||||||

|

| |||||||

Construction & Engineering 2.2% | ||||||||

Fluor Corp. | 370,091 | 21,950,097 | ||||||

|

| |||||||

Consumer Finance 1.1% | ||||||||

Capital One Financial Corp. | 179,477 | 11,272,950 | ||||||

|

| |||||||

Diversified Financial Services 1.0% | ||||||||

CME Group, Inc. | 137,036 | 10,411,995 | ||||||

|

| |||||||

Electrical Equipment 0.9% | ||||||||

Rockwell Automation, Inc. | 112,890 | 9,385,675 | ||||||

|

| |||||||

Energy Equipment & Services 2.7% | ||||||||

Schlumberger, Ltd. | 382,322 | 27,397,194 | ||||||

|

| |||||||

Food Products 1.1% | ||||||||

Mondelez International, Inc. Class A | 392,535 | 11,199,024 | ||||||

|

| |||||||

| Shares | Value | |||||||

Health Care Equipment & Supplies 5.3% |

| |||||||

Edwards Lifesciences Corp. (a) | 392,173 | $ | 26,354,026 | |||||

¨Hologic, Inc. (a) | 1,440,941 | 27,810,161 | ||||||

|

| |||||||

| 54,164,187 | ||||||||

|

| |||||||

Health Care Providers & Services 4.7% | ||||||||

Catamaran Corp. (a) | 304,382 | 14,829,491 | ||||||

Express Scripts Holding Co. (a) | 366,223 | 22,592,297 | ||||||

WellPoint, Inc. | 123,089 | 10,073,604 | ||||||

|

| |||||||

| 47,495,392 | ||||||||

|

| |||||||

Internet & Catalog Retail 1.9% | ||||||||

Amazon.com, Inc. (a) | 50,578 | 14,045,005 | ||||||

Shutterfly, Inc. (a) | 99,923 | 5,574,704 | ||||||

|

| |||||||

| 19,619,709 | ||||||||

|

| |||||||

Internet Software & Services 11.0% | ||||||||

eBay, Inc. (a) | 309,917 | 16,028,907 | ||||||

¨Google, Inc. Class A (a) | 74,136 | 65,267,110 | ||||||

LinkedIn Corp. Class A (a) | 89,400 | 15,940,020 | ||||||

Zillow, Inc. Class A (a) | 253,185 | 14,254,316 | ||||||

|

| |||||||

| 111,490,353 | ||||||||

|

| |||||||

IT Services 7.0% | ||||||||

¨Visa, Inc. Class A | 177,485 | 32,435,384 | ||||||

¨ Western Union Co. (The) | 2,247,550 | 38,455,580 | ||||||

|

| |||||||

| 70,890,964 | ||||||||

|

| |||||||

Machinery 1.6% | ||||||||

Joy Global, Inc. | 344,378 | 16,712,664 | ||||||

|

| |||||||

Media 3.7% | ||||||||

Comcast Corp. Class A | 245,543 | 10,283,341 | ||||||

¨ Walt Disney Co. (The) | 434,982 | 27,469,113 | ||||||

|

| |||||||

| 37,752,454 | ||||||||

|

| |||||||

Metals & Mining 1.9% | ||||||||

Freeport-McMoRan Copper & Gold, Inc. | 691,041 | 19,079,642 | ||||||

|

| |||||||

Multiline Retail 0.8% | ||||||||

Dollar General Corp. (a) | 154,828 | 7,807,976 | ||||||

|

| |||||||

Oil, Gas & Consumable Fuels 3.8% | ||||||||

Anadarko Petroleum Corp. | 69,944 | 6,010,288 | ||||||

¨Cobalt International Energy, Inc. (a) | 1,210,712 | 32,168,618 | ||||||

|

| |||||||

| 38,178,906 | ||||||||

|

| |||||||

Pharmaceuticals 1.3% | ||||||||

Teva Pharmaceutical Industries, Ltd., Sponsored ADR | 335,740 | 13,161,008 | ||||||

|

| |||||||

Real Estate Investment Trusts 2.0% | ||||||||

Camden Property Trust | 289,880 | 20,042,303 | ||||||

|

| |||||||

| † | Percentages indicated are based on Fund net assets. |

| ¨ | Among the Portfolio’s 10 largest holdings, as of June 30, 2013, excluding short-term investment. May be subject to change daily. |

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | mainstayinvestments.com | 11 |

Portfolio of Investments June 30, 2013 (continued)

| Shares | Value | |||||||

| Common Stocks (continued) | ||||||||

Semiconductors & Semiconductor Equipment 2.1% |

| |||||||

Altera Corp. | 645,233 | $ | 21,286,237 | |||||

|

| |||||||

Software 4.4% | ||||||||

Citrix Systems, Inc. (a) | 363,792 | 21,947,571 | ||||||

Salesforce.com, Inc. (a) | 603,070 | 23,025,213 | ||||||

|

| |||||||

| 44,972,784 | ||||||||

|

| |||||||

Specialty Retail 3.3% | ||||||||

Dick’s Sporting Goods, Inc. | 405,456 | 20,297,127 | ||||||

TJX Cos., Inc. | 275,324 | 13,782,720 | ||||||

|

| |||||||

| 34,079,847 | ||||||||

|

| |||||||

Textiles, Apparel & Luxury Goods 6.1% |

| |||||||

Burberry Group PLC, Sponsored ADR | 313,860 | 12,931,032 | ||||||

Michael Kors Holdings, Ltd. (a) | 155,914 | 9,669,786 | ||||||

NIKE, Inc. Class B | 283,102 | 18,027,935 | ||||||

Ralph Lauren Corp. | 123,139 | 21,394,170 | ||||||

|

| |||||||

| 62,022,923 | ||||||||

|

| |||||||

Tobacco 2.9% | ||||||||

¨ Philip Morris International, Inc. | 337,582 | 29,241,353 | ||||||

|

| |||||||

Trading Companies & Distributors 2.0% |

| |||||||

United Rentals, Inc. (a) | 401,168 | 20,022,295 | ||||||

|

| |||||||

Total Common Stocks | 1,002,476,280 | |||||||

|

| |||||||

| Principal Amount | Value | |||||||

| Short-Term Investment 3.0% | ||||||||

Repurchase Agreement 3.0% | ||||||||

State Street Bank and Trust Co. | $ | 30,280,090 | $ | 30,280,090 | ||||

|

| |||||||

Total Short-Term Investment | 30,280,090 | |||||||

|

| |||||||

Total Investments | 101.7 | % | 1,032,756,370 | |||||

Other Assets, Less Liabilities | (1.7 | ) | (17,456,740 | ) | ||||

Net Assets | 100.0 | % | $ | 1,015,299,630 | ||||

| (a) | Non-income producing security. |

| (b) | As of June 30, 2013, cost is $983,602,514 for federal income tax purposes and net unrealized appreciation is as follows: |

Gross unrealized appreciation | $ | 82,462,870 | ||

Gross unrealized depreciation | (33,309,014 | ) | ||

|

| |||

Net unrealized appreciation | $ | 49,153,856 | ||

|

|

| The | following abbreviation is used in the above portfolio: |

| ADR | —American Depositary Receipt |

The following is a summary of the fair valuations according to the inputs used as of June 30, 2013, for valuing the Fund’s assets.

Asset Valuation Inputs

Description | Quoted Prices in Active Markets for Assets (Level 1) | Significant (Level 2) | Significant (Level 3) | Total | ||||||||||||

| Investments in Securities (a) | ||||||||||||||||

| Common Stocks | $ | 1,002,476,280 | $ | — | $ | — | $ | 1,002,476,280 | ||||||||

| Short-Term Investment | ||||||||||||||||

Repurchase Agreement | — | 30,280,090 | — | 30,280,090 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total Investments in Securities | $ | 1,002,476,280 | $ | 30,280,090 | $ | — | $ | 1,032,756,370 | ||||||||

|

|

|

|

|

|

|

| |||||||||

| (a) | For a complete listing of investments and their industries, see the Portfolio of Investments. |

The Fund recognizes transfers between levels as of the beginning of the period.

For the year ended June 30, 2013, the Fund did not have any transfers between Level 1 and Level 2 fair value measurements. (See Note 2)

As of June 30, 2013, the Fund did not hold any investments with significant unobservable inputs (Level 3). (See Note 2)

| 12 | MainStay Cornerstone Growth Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Statement of Assets and Liabilities as of June 30, 2013

| Assets | ||||

Investment in securities, at value | $ | 1,032,756,370 | ||

Receivables: | ||||

Investment securities sold | 1,898,682 | |||

Dividends and interest | 1,707,990 | |||

Fund shares sold | 1,328,995 | |||

Other assets | 174,050 | |||

|

| |||

Total assets | 1,037,866,087 | |||

|

| |||

| Liabilities | ||||

Payables: | ||||

Investment securities purchased | 19,230,141 | |||

Fund shares redeemed | 1,441,355 | |||

Transfer agent (See Note 3) | 1,113,337 | |||

Manager (See Note 3) | 514,258 | |||

NYLIFE Distributors (See Note 3) | 155,494 | |||

Professional fees | 65,789 | |||

Shareholder communication | 28,692 | |||

Custodian | 3,600 | |||

Trustees | 1,208 | |||

Accrued expenses | 12,583 | |||

|

| |||

Total liabilities | 22,566,457 | |||

|

| |||

Net assets | $ | 1,015,299,630 | ||

|

| |||

| Net Assets Consist of | ||||

Shares of beneficial interest outstanding (par value of $.001 per share) unlimited number of shares authorized | $ | 34,049 | ||

Additional paid-in capital | 921,706,488 | |||

|

| |||

| 921,740,537 | ||||

Undistributed net investment income | 806,187 | |||

Accumulated net realized gain (loss) on investments | 42,988,319 | |||

Net unrealized appreciation (depreciation) on investments | 49,764,587 | |||

|

| |||

Net assets | $ | 1,015,299,630 | ||

|

| |||

Investor Class | ||||

Net assets applicable to outstanding shares | $ | 233,119,650 | ||

|

| |||

Shares of beneficial interest outstanding | 7,864,455 | |||

|

| |||

Net asset value per share outstanding | $ | 29.64 | ||

Maximum sales charge (5.50% of offering price) | 1.73 | |||

|

| |||

Maximum offering price per share outstanding | $ | 31.37 | ||

|

| |||

Class A | ||||

Net assets applicable to outstanding shares | $ | 272,378,007 | ||

|

| |||

Shares of beneficial interest outstanding | 9,164,132 | |||

|

| |||

Net asset value per share outstanding | $ | 29.72 | ||

Maximum sales charge (5.50% of offering price) | 1.73 | |||

|

| |||

Maximum offering price per share outstanding | $ | 31.45 | ||

|

| |||

Class B | ||||

Net assets applicable to outstanding shares | $ | 55,523,655 | ||

|

| |||

Shares of beneficial interest outstanding | 1,879,517 | |||

|

| |||

Net asset value per share outstanding | $ | 29.54 | ||

|

| |||

Class C | ||||

Net assets applicable to outstanding shares | $ | 3,850,711 | ||

|

| |||

Shares of beneficial interest outstanding | 130,352 | |||

|

| |||

Net asset value and offering price per share outstanding | $ | 29.54 | ||

|

| |||

Class I | ||||

Net assets applicable to outstanding shares | $ | 450,402,173 | ||

|

| |||

Shares of beneficial interest outstanding | 15,010,053 | |||

|

| |||

Net asset value and offering price per share outstanding | $ | 30.01 | ||

|

| |||

Class R2 | ||||

Net assets applicable to outstanding shares | $ | 25,434 | ||

|

| |||

Shares of beneficial interest outstanding | 856 | |||

|

| |||

Net asset value and offering price per share outstanding (a) | $ | 29.70 | ||

|

|

| (a) | The difference in the NAV recalculation and NAV stated is caused by rounding differences. |

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | mainstayinvestments.com | 13 |

Statement of Operations for the year ended June 30, 2013

| Investment Income (Loss) | ||||

Income | ||||

Dividends (a) | $ | 9,561,599 | ||

Interest | 467 | |||

|

| |||

Total income | 9,562,066 | |||

|

| |||

Expenses | ||||

Manager (See Note 3) | 4,297,560 | |||

Transfer agent (See Note 3) | 1,875,244 | |||

Distribution/Service—Investor Class (See Note 3) | 265,096 | |||

Distribution/Service—Class A (See Note 3) | 341,615 | |||

Distribution and service—Class B (See Note 3) | 272,746 | |||

Distribution/Service—Class C (See Note 3) | 18,399 | |||

Distribution/Service—Class R2 (See Note 3) | 28 | |||

Administration and accounting (See Note 3) | 218,416 | |||

Shareholder communication | 133,460 | |||

Professional fees | 114,708 | |||

Registration | 85,284 | |||

Trustees | 58,411 | |||

Custodian | 31,775 | |||

Miscellaneous | 57,179 | |||

|

| |||

Total expenses before waiver/reimbursement | 7,769,921 | |||

Expense waiver/reimbursement from Manager (See Note 3) | (119,144 | ) | ||

|

| |||

Net expenses | 7,650,777 | |||

|

| |||

Net investment income (loss) | 1,911,289 | |||

|

| |||

| Realized and Unrealized Gain (Loss) on Investments | ||||

Net realized gain (loss) on investments | 58,502,775 | |||

Net change in unrealized appreciation (depreciation) on investments | (17,153,257 | ) | ||

|

| |||

Net realized and unrealized gain (loss) on investments | 41,349,518 | |||

|

| |||

Net increase (decrease) in net assets resulting from operations | $ | 43,260,807 | ||

|

| |||

| (a) | Dividends recorded net of foreign withholding taxes in the amount of $49,916. |

| 14 | MainStay Cornerstone Growth Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Statements of Changes in Net Assets

for the years ended June 30, 2013 and June 30, 2012

| 2013 | 2012* | |||||||

| Increase (Decrease) in Net Assets | ||||||||

Operations: | ||||||||

Net investment income (loss) | $ | 1,911,289 | $ | (225,794 | ) | |||

Net realized gain (loss) on investments | 58,502,775 | 21,596,363 | ||||||

Net change in unrealized appreciation (depreciation) on investments | (17,153,257 | ) | (19,331,846 | ) | ||||

|

| |||||||

Net increase (decrease) in net assets resulting from operations | 43,260,807 | 2,038,723 | ||||||

|

| |||||||

Dividends and distributions | ||||||||

From net investment income: | ||||||||

Class A | (72,827 | ) | — | |||||

Class I | (976,716 | ) | — | |||||

|

| |||||||

| (1,049,543 | ) | — | ||||||

|

| |||||||

From net realized gain on investments: | ||||||||

Class A | (2,913,456 | ) | (7,283,246 | ) | ||||

Class I | (23,470,802 | ) | (6,166,482 | ) | ||||

|

| |||||||

| (26,384,258 | ) | (13,449,728 | ) | |||||

|

| |||||||

Total dividends and distributions to shareholders | (27,433,801 | ) | (13,449,728 | ) | ||||

|

| |||||||

Capital share transactions: | ||||||||

Net proceeds from sale of shares | 224,733,585 | 236,561,174 | ||||||

Net asset value of shares issued in connection with the acquisition of MainStay Growth Equity Fund (See Note 9) | 539,595,303 | — | ||||||

Net asset value of shares issued to shareholders in reinvestment of dividends and distributions | 25,434,466 | 12,537,211 | ||||||

Cost of shares redeemed | (115,106,399 | ) | (211,414,962 | ) | ||||

|

| |||||||

Increase (decrease) in net assets derived from capital share transactions | 674,656,955 | 37,683,423 | ||||||

|

| |||||||

Net increase (decrease) in net assets | 690,483,961 | 26,272,418 | ||||||

| Net Assets | ||||||||

Beginning of year | 324,815,669 | 298,543,251 | ||||||

|

| |||||||

End of year | $ | 1,015,299,630 | $ | 324,815,669 | ||||

|

| |||||||

Undistributed net investment income at end of year | $ | 806,187 | $ | — | ||||

|

| |||||||

| * | This year was audited by a predecessor audit firm whose opinion was unqualified. |

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | mainstayinvestments.com | 15 |

Financial Highlights selected per share data and ratios

| Investor Class | ||||

| January 18, 2013** through June 30, | ||||

| 2013 | ||||

Net asset value at beginning of period | $ | 29.20 | † | |

|

| |||

Net investment income (loss) | (0.03 | )(a) | ||

Net realized and unrealized gain (loss) on investments | 0.47 | |||

|

| |||

Total from investment operations | 0.44 | |||

|

| |||

Net asset value at end of period | $ | 29.64 | ||

|

| |||

Total investment return | 1.51 | % (b)(c) | ||

Ratio of expenses to average net assets: | ||||

Before expense waivers and reimbursements | 1.77 | % †† | ||

After expense waivers and reimbursements | 1.77 | % †† | ||

Ratio of net investment income (loss) to average net assets: | ||||

Before expense waivers and reimbursements | (0.25 | %)†† | ||

After expense waivers and reimbursements | (0.25 | %)†† | ||

Portfolio turnover rate | 98 | % | ||

Net assets at end of period (in 000’s) | $ | 233,120 | ||

| ** | Inception date. |

| † | Based on the net asset value of Class A as of January 18, 2013. |

| †† | Annualized. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Total investment return is not annualized. |

| (c) | Total investment return may reflect adjustments to conform to generally accepted accounting principles. |

| Class A | ||||||||||||||||||||

Year ended June 30, | ||||||||||||||||||||

| 2013 | 2012*** | 2011*** | 2010*** | 2009*** | ||||||||||||||||

Net asset value at beginning of year | $ | 29.41 | $ | 30.71 | $ | 21.10 | $ | 20.24 | $ | 26.43 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net investment income (loss) (a) | 0.10 | (0.07 | ) | (0.18 | ) | (0.12 | ) | (0.06 | ) | |||||||||||

Net realized and unrealized gain (loss) on investments | 2.57 | 0.16 | 9.79 | 0.98 | (6.13 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations | 2.67 | 0.09 | 9.61 | 0.86 | (6.19 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Less dividends and distributions: | ||||||||||||||||||||

From net investment income | (0.06 | ) | — | — | — | — | ||||||||||||||

From net realized gain on investments | (2.30 | ) | (1.39 | ) | — | — | — | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total dividends and distributions | (2.36 | ) | (1.39 | ) | — | — | — | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value at end of year | $ | 29.72 | $ | 29.41 | $ | 30.71 | $ | 21.10 | $ | 20.24 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total investment return | 9.64 | % | 0.72 | % | 45.55 | % | 4.25 | % | (23.42 | %) | ||||||||||

Ratio of expenses to average net assets: | ||||||||||||||||||||

Before expense waivers and reimbursements | 1.21 | % | 1.34 | % | 1.33 | % | 1.39 | % | 1.54 | % | ||||||||||

After expense waivers and reimbursements | 1.19 | % | 1.34 | % | 1.40 | % | 1.48 | % | 1.50 | % | ||||||||||

Ratio of net investment income (loss) to average net assets: | ||||||||||||||||||||

Before expense waivers and reimbursements | 0.32 | % | (0.24 | %) | (0.58 | %) | (0.42 | %) | (0.37 | %) | ||||||||||

After expense waivers and reimbursements | 0.34 | % | (0.24 | %) | (0.65 | %) | (0.51 | %) | (0.33 | %) | ||||||||||

Portfolio turnover rate | 98 | % | 114 | % | 120 | % | 132 | % | 192 | % | ||||||||||

Net assets at end of year (in 000’s) | $ | 272,378 | $ | 35,680 | $ | 155,583 | $ | 171,330 | $ | 106,119 | ||||||||||

| *** | These years were audited by a predecessor audit firm whose opinion was unqualified. |

| (a) | Per share data based on average shares outstanding during the year. |

| 16 | MainStay Cornerstone Growth Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Financial Highlights selected per share data and ratios

| Class B | Class C | |||||||

| January 18, 2013** through June 30, | January 18, 2013** through June 30, | |||||||

2013 | 2013 | |||||||

Net asset value at beginning of period | $ | 29.20 | † | $ | 29.20 | † | ||

|

|

|

| |||||

Net investment income (loss) | (0.13 | )(a) | (0.13 | )(a) | ||||

Net realized and unrealized gain (loss) on investments | 0.47 | 0.47 | ||||||

|

|

|

| |||||

Total from investment operations | 0.34 | 0.34 | ||||||

|

|

|

| |||||

Net asset value at end of period | $ | 29.54 | $ | 29.54 | ||||

|

|

|

| |||||

Total investment return | 1.16 | % (b)(c) | 1.16 | % (b)(c) | ||||

Ratios of expenses to average net assets: | ||||||||

Before expense waivers and reimbursements | 2.52 | % †† | 2.52 | % †† | ||||

After expense waivers and reimbursements | 2.52 | % †† | 2.52 | % †† | ||||

Ratios of net investment income (loss) to average net assets: | ||||||||

Before expense waivers and reimbursements | (0.99 | %)†† | (1.00 | %)†† | ||||

After expense waivers and reimbursements | (0.99 | %)†† | (1.00 | %)†† | ||||

Portfolio turnover rate | 98 | % | 98 | % | ||||

Net assets at end of period (in 000’s) | $ | 55,524 | $ | 3,851 | ||||

| ** | Inception date. |

| † | Based on the net asset value of Class A as of January 18, 2013. |

| †† | Annualized. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Total investment return is not annualized. |

| (c) | Total investment return may reflect adjustments to conform to generally accepted accounting principles. |

| Class I | ||||||||||||||||

Year ended June 30, | November 2, 2009** through June 30, | |||||||||||||||

| 2013 | 2012*** | 2011*** | 2010*** | |||||||||||||

Net asset value at beginning of period | $ | 29.63 | $ | 30.84 | $ | 21.14 | $ | 22.64 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net investment income (loss) (a) | 0.17 | 0.00 | ‡ | (0.11 | ) | (0.04 | ) | |||||||||

Net realized and unrealized gain (loss) on investments | 2.61 | 0.18 | 9.81 | (1.46 | ) | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Total from investment operations | 2.78 | 0.18 | 9.70 | (1.50 | ) | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Less dividends and distributions: | ||||||||||||||||

From net investment income | (0.10 | ) | — | — | — | |||||||||||

From net realized gain on investments | (2.30 | ) | (1.39 | ) | — | — | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Total dividends and distributions | (2.40 | ) | (1.39 | ) | — | — | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Net asset value at end of period | $ | 30.01 | $ | 29.63 | $ | 30.84 | $ | 21.14 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total investment return | 9.91 | % | 1.02 | % | 45.88 | % | (6.63 | %)(b) | ||||||||

Ratio of expenses to average net assets: | ||||||||||||||||

Before expense waivers and reimbursements | 1.00 | % | 1.10 | % | 1.10 | % | 1.12 | % †† | ||||||||

After expense waivers and reimbursements | 0.97 | % | 1.10 | % | 1.14 | % | 1.20 | % †† | ||||||||

Ratio of net investment income (loss) to average net assets: | ||||||||||||||||

Before expense waivers and reimbursements | 0.55 | % | 0.01 | % | (0.34 | %) | (0.18 | %)†† | ||||||||

After expense waivers and reimbursements | 0.58 | % | 0.01 | % | (0.38 | %) | (0.26 | %)†† | ||||||||

Portfolio turnover rate | 98 | % | 114 | % | 120 | % | 132 | % | ||||||||

Net assets at end of period (in 000’s) | $ | 450,402 | $ | 289,136 | $ | 142,960 | $ | 7,518 | ||||||||

| ** | Inception date. |

| *** | These years were audited by a predecessor audit firm whose opinion was unqualified. |

| †† | Annualized. |

| ‡ | Less than one cent per share. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Total investment return is not annualized. |

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | mainstayinvestments.com | 17 |

Financial Highlights selected per share data and ratios

| Class R2 | ||||

| January 18, 2013** through June 30, | ||||

| 2013 | ||||

Net asset value at beginning of period | $ | 29.20 | † | |

|

| |||

Net investment income (loss) | 0.03 | (a) | ||

Net realized and unrealized gain (loss) on investments | 0.47 | |||

|

| |||

Total from investment operations | 0.50 | |||

|

| |||

Net asset value at end of period | $ | 29.70 | ||

|

| |||

Total investment return | 1.71 | %(b)(c) | ||

Ratio of expenses to average net assets: | ||||

Before expense waivers and reimbursements | 1.30 | %†† | ||

After expense waivers and reimbursements | 1.30 | %†† | ||

Ratio of net investment income (loss) to average net assets: | ||||

Before expense waivers and reimbursements | 0.23 | %†† | ||

After expense waivers and reimbursements | 0.23 | %†† | ||

Portfolio turnover rate | 98 | % | ||

Net assets at end of period (in 000’s) | $ | 25 | ||

| ** | Inception date. |

| † | Based on the net asset value of Class A as of January 18, 2013. |

| †† | Annualized. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Total investment return is not annualized. |

| (c) | Total investment return may reflect adjustments to conform to generally accepted accounting principles. |

| 18 | MainStay Cornerstone Growth Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Note 1–Organization and Business

MainStay Funds Trust (the “Trust”) was organized as a Delaware statutory trust on April 28, 2009, and is governed by a Declaration of Trust. The Trust is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company, and is comprised of thirty-four funds (collectively referred to as the “Funds”). These financial statements and notes relate only to the MainStay Cornerstone Growth Fund (the “Fund”), a diversified fund. The Fund is successor to Keystone Large Cap Growth Fund (the “Predecessor Fund”), which was a series of a different registered investment company for which Cornerstone Capital Management LLC, a Minnesota limited liability company and the predecessor entity to the Fund’s Subadvisor (as defined in Note 3(A)), served as investment adviser. The financial statements of the Fund reflect the historical results of corresponding shares of the Predecessor Fund prior to its reorganization on January 11, 2013. Upon the completion of the reorganization, the Class A and Class I shares of the Fund assumed the performance, financial and other information of the Predecessor Fund. All information and references to periods prior to January 11, 2013 refer to the Predecessor Fund.

The Fund currently offers six classes of shares. Investor Class, Class B, Class C and Class R2 were first offered as of the close of business on January 18, 2013. Class B shares were closed to new investors as of January 18, 2013, however, existing Class B shareholders continue to be able to add to their existing account. Class A shares commenced operations on August 7, 2006. Class I shares commenced operations on November 2, 2009. Investor Class and Class A shares are offered at net asset value (“NAV”) per share plus an initial sales charge. No sales charge applies to investments of $1 million or more (and certain other qualified purchases) in Investor Class and Class A shares, but a contingent deferred sales charge (“CDSC”) is imposed on certain redemptions made within one year of the date of purchase. Class B and Class C shares are offered at NAV without an initial sales charge, although a declining CDSC may be imposed on redemptions made within six years of the date of purchase of Class B shares and a 1.00% CDSC may be imposed on redemptions made within one year of the date of purchase of Class C shares. Class I and Class R2 shares are offered at NAV and are not subject to a sales charge. Depending upon eligibility, Class B shares convert to either Investor Class or Class A shares at the end of the calendar quarter eight years after the date they were purchased. Additionally, depending upon eligibility, Investor Class shares may convert to Class A shares and Class A shares may convert to Investor Class shares. The six classes of shares have the same voting (except for issues that relate solely to one class), dividend, liquidation and other rights, and the same terms and conditions, except that Class B and Class C shares are subject to higher distribution and/or service fee rates than Investor Class, Class A and Class R2 shares under a distribution plan pursuant to Rule 12b-1 under the 1940 Act. Class I shares are not subject to a distribution and/or service fee. Class R2 shares are subject to a shareholder service fee. This is in addition to any fees paid under a distribution plan, where applicable.

The Fund’s investment objective is to seek long-term growth of capital.

Note 2–Significant Accounting Policies

The Fund prepares its financial statements in accordance with generally accepted accounting principles (“GAAP”) in the United States of America and follows the significant accounting policies described below.

(A) Securities Valuation. Investments are valued as of the close of regular trading on the New York Stock Exchange (“Exchange”) (generally 4:00 p.m. Eastern time) on each day the Fund is open for business (“valuation date”).

The Board of Trustees (the “Board”) has adopted procedures for the valuation of the Fund’s securities and has delegated the responsibility for valuation determination under those procedures to the Valuation Committee of the Fund (the “Valuation Committee”). The Board has authorized the Valuation Committee to appoint a Valuation Sub-Committee (the “Sub-Committee”) to deal in the first instance with questions that arise or cannot be resolved under these procedures. The Sub-Committee meets (in person, via electronic mail or via teleconference) on an as-needed basis. The Valuation Committee meets at a later time, as necessary, to ensure that actions taken by the Sub-Committee were appropriate. The procedures recognize that, subject to the oversight of the Board and unless otherwise noted, the responsibility for day-to-day valuation of portfolio assets (including securities for which market prices are not readily available) rests with New York Life Investment Management LLC (“New York Life Investments” or the “Manager”), aided to whatever extent necessary by the Subadvisor (as defined in Note 3(A)) of the Fund.

To assess the appropriateness of security valuations, the Manager or the Fund’s third party service provider who is subject to oversight by the Manager regularly compares prior day prices, prices on comparable securities and the sale prices to the prior and current day prices and challenges prices exceeding certain tolerance levels with third party pricing services or broker sources. For those securities valued by recommendation, whether through a standardized fair valuation methodology or a fair valuation determination, the Valuation Committee reviews and affirms the reasonableness of the valuation based on such methodologies and determinations on a regular basis after considering all relevant information that is reasonably available.

“Fair value” is defined as the price that the Fund would receive upon selling an investment in an orderly transaction to an independent buyer in the principal or most advantageous market of the investment. Fair value measurements are determined within a framework that has established a three-tier hierarchy which maximizes the use of observable market data and minimizes the use of unobservable inputs to establish classification of fair value measurements for disclosure purposes. “Inputs” refers broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, such as the risk inherent in a particular valuation technique used to measure fair value using a pricing model and/or the risk inherent in the inputs for the valuation technique. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Fund. Unobservable inputs reflect the Fund’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the information available in the circumstances. The inputs or

| mainstayinvestments.com | 19 |

Notes to Financial Statements (continued)

methodology used for valuing securities may not be an indication of the risks associated with investing in those securities. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below.

| • | Level 1—quoted prices in active markets for identical investments |

| • | Level 2—other significant observable inputs (including quoted prices for similar investments in active markets, interest rates and yield curves, prepayment speeds, credit risks, etc.) |

| • | Level 3—significant unobservable inputs (including the Fund’s own assumptions about the assumptions that market participants would use in determining the fair value of investments) |

The aggregate value by input level, as of June 30, 2013, for the Fund’s investments is included at the end of the Fund’s Portfolio of Investments.

The valuation techniques used by the Fund to measure fair value maximize the use of observable inputs and minimize the use of unobservable inputs. The Fund may utilize third party vendor evaluations, whose prices may be derived from one or more of the following standard inputs:

• Broker Dealer Quotes | • Reported Trades | |

• Two-sided markets | • Issuer Spreads | |

• Bids/Offers | • Benchmark securities | |

• Industry and economic events | • Reference Data (corporate actions or material event notices) | |

• Equity and credit default swap curves | • Monthly payment information |

Securities for which market values cannot be determined using the methodologies described above are valued by methods deemed in good faith by the Fund’s Valuation Committee, following the procedures established by the Board, to represent fair value. Under these procedures, the Fund primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information. The Fund may also use an income-based valuation approach in which the anticipated future cash flows of the investment are discounted to calculate fair value. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. Due to the inherent uncertainty of valuations of such investments, the fair values may differ significantly from the values that would have been used had an active market existed. After the completion of the reorganization the Fund assumed the current fair value methodologies described in this note.

Equity and non-equity securities which may be valued in this manner include, but are not limited to: (i) a security for which the trading has been halted or suspended; (ii) a debt security that has recently gone into default and for which there is not a current market quotation; (iii) a security of an issuer that has entered into a restructuring; (iv) a security that has been de-listed from a national exchange; (v) a security for which the market price is not available from a third party pricing source or, if so provided, does not, in the opinion of the Fund’s Manager or Subadvisor reflect the security’s market value; and (vi) a security whose principal market has been temporarily closed at a time when, under normal conditions, it would be open. Securities for which market quotations or observable inputs are not readily available are generally categorized as Level 3 in the hierarchy. As of June 30, 2013, the Fund did not hold any securities that were fair valued in such a manner.

Certain events may occur between the time that foreign markets close, on which securities held by the Fund principally trade, and the time at which the Fund’s NAV is calculated. These events may include, but are not limited to, situations relating to a single issuer in a market sector, significant fluctuations in U.S. or foreign markets, natural disasters, armed conflicts, governmental actions or other developments not tied directly to the securities markets. Should the Manager or Subadvisor conclude that such events may have affected the accuracy of the last price of such securities reported on the local foreign market, the Manager or Subadvisor may, pursuant to procedures adopted by the Board, adjust the value of the local price to reflect the estimated impact on the price of such securities as a result of such events. In this instance, securities are generally categorized as Level 3 in the hierarchy. Additionally, foreign equity securities are also fair valued whenever the movement of a particular index exceeds certain thresholds. In such cases, the securities are fair valued by applying factors provided by a third party vendor in accordance with the Fund’s policies and procedures and are generally categorized as Level 2 in the hierarchy. As of June 30, 2013, the Fund did not hold any foreign equity securities.

Equity securities and Exchange Traded Funds are valued at the latest quoted sales prices as of the close of regular trading on the Exchange on each valuation date. Securities that are not traded on the valuation date are valued at the mean of the latest quoted bid and ask prices. Prices normally are taken from the principal market in which each security trades. Investments in other mutual funds are valued at their respective NAVs as of the close of the Exchange on the valuation date. These securities are generally categorized as Level 1 in the hierarchy.

Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments which mature in 60 days or less (“Short-Term Investments”) are valued at amortized cost. The amortized cost method involves valuing a security at its cost on the date of purchase and thereafter assuming a constant amortization to maturity of the difference between such cost and the value on maturity date. Amortized cost approximates the current fair value of a security. Securities valued at amortized cost are not valued using a quoted price in an active market. These securities are generally categorized as Level 2 in the hierarchy.

(B) Income Taxes. The Fund’s policy is to comply with the requirements of the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”), applicable to regulated investment companies and to distribute all of the taxable income to the shareholders of the Fund within the allowable time limits. Therefore, no federal, state and local income tax provision is required.

Management evaluates its tax positions to determine if the tax positions taken meet the minimum recognition threshold in connection with accounting for uncertainties in income tax positions taken or expected to be taken for the purposes of measuring and recognizing tax liabilities in the financial statements. Recognition of tax benefits of an uncertain tax position is required only when the position is “more likely than not” to be sustained assuming examination by taxing authorities. Management has analyzed the Fund’s tax positions taken on federal, state and local income tax returns for all open tax years (for up to three tax years), and has concluded that no provision for federal, state and local income tax is

| 20 | MainStay Cornerstone Growth Fund |

required in the Fund’s financial statements. The Fund’s federal, state and local income and federal excise tax returns for tax years for which the applicable statutes of limitations have not expired are subject to examination by the Internal Revenue Service and state and local departments of revenue.

(C) Dividends and Distributions to Shareholders. Dividends and distributions are recorded on the ex-dividend date. The Fund intends to declare and pay dividends of net investment income and distributions of net realized capital and currency gains, if any, annually. Unless the shareholder elects otherwise, all dividends and distributions are reinvested in the same class of shares of the Fund, at NAV. Dividends and distributions to shareholders are determined in accordance with federal income tax regulations and may differ from GAAP.

(D) Security Transactions and Investment Income. The Fund records security transactions on the trade date. Realized gains and losses on security transactions are determined using the identified cost method. Dividend income is recognized on the ex-dividend date and interest income is accrued as earned using the effective interest rate method. Discounts and premiums on Short-Term Investments are accreted and amortized, respectively, on the straight-line method.

Investment income and realized and unrealized gains and losses on investments of the Fund are allocated to separate classes of shares pro rata based upon their relative net assets on the date the income is earned or realized and unrealized gains and losses are incurred.

(E) Expenses. Expenses of the Trust are allocated to the individual Funds in proportion to the net assets of the respective Funds when the expenses are incurred, except where direct allocations of expenses can be made. Expenses (other than transfer agent expenses and fees incurred under the shareholder services plans and the distribution plans further discussed in Note 3(B)) are allocated to separate classes of shares pro rata based upon their relative net assets on the date the expenses are incurred. The expenses borne by the Fund, including those of related parties to the Fund, are shown in the Statement of Operations.

(F) Use of Estimates. In preparing financial statements in conformity with GAAP, management makes estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

(G) Repurchase Agreements. The Fund may enter into repurchase agreements to earn income. The Fund may enter into repurchase agreements only with financial institutions that are deemed by the Manager or Subadvisor to be creditworthy, pursuant to guidelines established by the Fund’s Board. During the term of any repurchase agreement, the Manager or Subadvisor will continue to monitor the creditworthiness of the seller. Under the 1940 Act, repurchase agreements are considered to be collateralized loans by a Fund to the seller secured by the securities transferred to the Fund.

When the Fund invests in repurchase agreements, the Fund’s custodian takes possession of the collateral pledged for investments in the repurchase agreement. The underlying collateral is valued daily on a mark-to-market basis to determine that the value, including accrued interest, exceeds the repurchase price. In the event of the seller’s default on the obligation to repurchase, the Fund has the right to liquidate the collateral and apply the proceeds in satisfaction of the obliga-

tion. Under certain circumstances, such as in the event of default or bankruptcy by the counterparty to the agreement, realization and/or retention of the collateral may be subject to legal proceedings and possible realized loss to the Fund.