UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-22321

MAINSTAY FUNDS TRUST

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

169 Lackawanna Avenue

Parsippany, New Jersey 07054

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212)576-7000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2013

FORM N-CSR

The information presented in this Form N-CSR relates solely to the

MainStay Marketfield Fund, a series of the Registrant.

| Item 1. | Reports to Stockholders. |

MainStay Marketfield Fund

Message from the President, Marketfield Asset Management LLC Year-End Commentary and Annual Report

December 31, 2013

This page intentionally left blank

Message from the President

We are pleased to present the annual report for MainStay Marketfield Fund and the Marketfield Asset Management LLC Year-End Commentary. The commentary was prepared by Michael Aronstein, President and Chief Investment Officer of Marketfield Asset Management LLC and the portfolio manager of MainStay Marketfield Fund.

Together, the commentary and the annual report contain specific information about the market events, macroeconomic trends and investment decisions that shaped MainStay Marketfield Fund during the reporting period.

We encourage you to read the following material carefully and to make thoughtful use of the information it contains.

We thank you for selecting MainStay Marketfield Fund, and we look forward to serving your investment needs for many years to come.

Sincerely,

Stephen P. Fisher

President

The opinions expressed are as of the date of this report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. Past performance is no guarantee of future results.

Not part of the Annual Report

Marketfield Asset Management LLC Year-End Commentary

During the last quarter, our monthly commentaries have begun to explore the question of inflation as a significant macroeconomic factor over the course of the next year. Our interest in this possibility is an outgrowth of a strong feeling that the Federal Reserve Board (FRB) is maintaining a radically expansive policy long past the point of propriety.

To the extent that we are correct in doubting the need for additional monetary stimulus, the consequences will be manifest in an environment that shows evidence of over-stimulation in the forms of excess activity and accelerating nominal prices.

On the other hand, if the popular view that rates deflation as the main macroeconomic risk is correct, then the FRB is entirely justified in its current policy path and we are wrong.

At the earliest stages of change in macroeconomic conditions, empirical evidence of the new, emergent regime is scant. The process of discernment is entirely theoretical. It is a function of human reason and the logical, scientific structures that derive from rational consideration.

Economic science and its related forecasting protocols, which we employ as a basis of our investment process, are logical, not empirical in form. Just as there is no need to measure thousands of triangles in order to prove the Pythagorean Theorem, we do not need studies to demonstrate that raising legal minimum wages above market rates reduces total employment or that subsidies provoke surpluses.

A reliance on theoretical processes to forecast economic change makes certain that we will spend a great deal of time defending views that most commentators find far-fetched or nonsensical.

From a practical, portfolio management standpoint, it is imperative that these theoretical musings about large-scale trend changes not be implemented before conditions are actually beginning to change. The risks of portfolio adjustments that are years too early outweigh any potential benefits of utilizing macroeconomic inputs in the asset allocation process. That said, it is important to act when markets are still incorporating the longer-term, macroeconomic factors that one believes to be on the way out. The difference in timing between insight and error comes out in the form of performance.

In the current cycle, plenty of intelligent commentators and managers made the point in 2009-2011 that the relentless monetary expansion undertaken by the FRB was bound to result in inflation. To the extent that they reacted by allocating funds to typical inflation sensitive assets e.g., mining stocks, precious metals, commodity indices, emerging market mineral exporters and inflation-indexed bonds, performance has been disastrous.

Now that these views have been fully discredited and customers have pulled a great deal of capital away from those who held and acted on them, conditions are ripe for change.

The early conflation of FRB policy and the consequent likelihood of inflation were not conceptually incorrect but incorrectly timed. We have said for decades that implementation of macroeconomic views that are several years in advance of market recognition is not a matter of too early but simply another way of being wrong.

Popular media presents an endless stream of heroic commentators who “called,” ex post, every great market dislocation since the 1929 crash. What is never mentioned is that these calls were generally three or four years before the actual event and thus useless in application. By the time such a long-touted event unfolds (if ever), the narrative behind the opinion has been so fully discredited by poor investment performance that clients have moved their assets elsewhere and the manager has become emotionally impaired.

The process of discrediting worries about inflation has been gathering momentum for the past three years. It appears to us to have reached full force with central bankers now uniformly anxious about their ability to create nominal price increases. This is somewhat the obverse of the sentiment that prevailed in 2008-2010, when we had countless discussions with advisors, analysts and business leaders who were concerned that the Fed could not muster enough firepower to prevent a tidal surge of default across fixed income markets and the entire banking system.

Now that nearly every measure of credit distress in the domestic financial system is at record lows, arguments for monetary impotence continue in different form. The fact that five years of balance sheet expansion by the Federal Reserve has not resulted in consumer price acceleration is taken as an indication that they are powerless to affect such an outcome. Prices of non-financial, “main street” goods and services did not respond quickly to the surge in dollar liquidity because the transmission mechanism within the economy was broken.

Households, governments and the banking systems that financed their credit adventures have been in the throes of secular balance sheet restructurings since the panic of 2008. Parallel restructurings and rationalizations in the elements of the real economy i.e., property markets and construction activity have likewise been in process.

The monetary pipeline was blocked by a full blown depression in U.S. home construction and the deflationary policies of the European Central Bank, which presided, ineptly, over the largest economic bloc in the world and did not change policy until the end of 2011. The Bank of Japan was similarly recalcitrant.

The combination of inappropriately tight monetary policy in two of the major developed world central banks, serious rationalization of government finances in the European periphery, U.S. states and municipalities and the draconian restructuring of the majority of the multinational banking system prevented the expansion of central bank liquidity from provoking more than spectacular asset inflation.

Not part of the Annual Report

The main defects in the transmission mechanism through the real economy are now largely healed. The question is how the inflationary process can migrate from assets’ prices to prices of consumers’ goods and services.

In order to address the question, one must begin with the morphology of asset inflations and central banks’ roles in provoking them.

We come at the issue from a perspective that considers inflationary processes to be monetary in origin. Our working definition of inflation is an inappropriately large (in relation to real economic activity) increase in money and credit.

Once such an increase has, as in the present case, come to pass, the discussion is entirely about consequences. The main focus of this letter is on the symptoms deriving from the inflation of money and credit that has already come to pass. We assume the impropriety of current FRB policy and will not further argue that point. Time and markets will tell if that basic assumption is correct.

Inflations are pernicious aspects of economies mainly because their effects are so uneven, or, in more popular parlance, unequal.

There would be little to object to in a circumstance where prices, wages and asset values were suddenly revised higher by 20%. Assuming this process was applied to bank balances and credit instruments, the resulting distortions would be manageable.

Unfortunately, the actual effects of monetary inflation are manifest throughout the global economy in highly uneven fashion. The process produces clear groups of winners and losers. The characteristics of the members in those categories vary from cycle to cycle. Beneficiaries range widely from owners of raw land (Japan 1980s, U.S. 2001-2007), to oil producers (1970s) and owners of residential property in financial centers (2010-present). Each of these episodes has countless subcategories comprising beneficiaries.

The main burdens in each case fall upon those who are not involved in the parts of the economy that are enjoying the boost from inflationary policy but are still in need of goods and services, the real cost of which continues to rise. There is a real transfer of wealth from the second group to the first. If it persists long enough, the disparity becomes extreme.

We can recall the height of the oil boom and the depth of the bond bear market in the early 1980s, when a two bedroom apartment in Manhattan cost less than a two bedroom starter home in Houston. Petroleum geologists, not fixed income managers, expected helicopter transport to work sites.

The effects of monetary inflations within the real economy arise in accordance with the different pathways of credit expansion at work in each cycle. At the outset of every inflationary cycle, there is always a collateral form that enjoys good fundamental

supply/demand characteristics available to transmit the monetary impulse. It is never the asset type that the central bank is attempting to repair.

Expansive monetary policy always follows periods of distress, when policymakers see something that needs to be rescued. The distressed assets are normally those that were the focus of enthusiasm in the prior cycle.

As monetary conditions are eased in response to the distress in a dying mania as took place in housing and housing finance in 2008-2009, that sector is never the beneficiary of the increased availability of credit. Bankers and investors will not willingly return to the collateral types that have just caused them the most extreme pain.

With the credit spigots open, there is always some unimpaired sector that can serve as collateral with no apparent risks. In the current cycle, emerging market economies gathered a disproportionate share of the global credit excess that began after the Panic of 2008. They were not involved in the U.S. and European property mania, had been growing steadily since 2002 and were, as a result, regarded as pristine borrowers.

The remarkable cycle of issuance in emerging market credit since 2009 strikes us as the primary locus of the inflation engendered by Federal Reserve policy.

It is difficult for observers to put the process in context because it is, like every important macroeconomic cycle, unique and without direct precedent. The inflationary mechanism utilized by the Fed in the present circumstance relies less upon the traditional avenue of expanding bank credit and more on the direct stimulation of fixed income markets.

By supporting bond prices at above market levels, the Fed is, in essence, maintaining a massive subsidy for issuers. There is little difference in form between QE 3 and the various agricultural price support programs undertaken by governments around the world. Their end result is always the same—a surplus of the item that is being held at above market prices.

All artificially elevated prices eventually provoke surplus production. The bond markets since the beginnings of QE have been no exception. Because the Fed has confined its purchases largely to high quality government and mortgage bonds, the field has been cleared for other issuers of lesser quality to jump into the void.

And jump they have.

We will not recapitulate the statistics regarding global fixed income issuance during the past three years. Suffice it to say that despite the Fed’s absorption of more than three trillion dollars of bonds from the open markets, the corpus of outstanding issues has still managed to grow.

In response to price declines in cotton and distress in the farm sector, the Chinese government introduced cotton price supports in 2011 and 2012. These were above world market levels.

Not part of the Annual Report

Today China is warehousing enough surplus cotton to supply more than half of the world’s annual needs. Unless wearing four pairs of underwear at once becomes the new fashion, the Chinese have a major problem.

The Federal Reserve has painted itself into a similar corner. Fixed income issuance since the onset of QE 2 has comprised a variety of overvalued and lesser quality instruments of little practical use. The old Wall Street admonition about learning the difference between eating sardines and trading sardines (which are never meant to be opened or consumed, merely passed back and forth among traders) is particularly apt as pertains to contemporary fixed income markets.

A ten-year bond with a 1.5% coupon is about as useful as teats on a bullfrog. It is a trading sardine with no practical, fundamental output value to the investor. It does not hold up next to cash as a safe haven. The only hope in owning it is to make a trading gain, which, on the heels of a 31-year bull market, is a dangerous business.

More egregious overvaluations were evident in the offerings from emerging market sovereign and corporate issuers. Their dollar bonds had the dual features of extraordinarily low rates and questionable credit fundamentals. Like Chinese cotton, Thai rice or U.S. sugar, price supports (by the FRB) have created a bond glut.

The inflationary aspect of the bond glut is the extraordinary flow of cash to issuers. For the past three years, it seemed as though anyone able to spell ‘bond’ was considered qualified to issue them.

The distortions in prices enabled by unprecedented and nearly unlimited access to credit markets have been profound. The most straightforward has been the corporate balance sheet arbitrage whereby companies have issued overpriced bonds and used the proceeds to buy back their own stock. This has been an obvious method of taking advantage of the implicit price supports offered by the Federal Reserve.

The capital structure arbitrage employed by developed market companies has been a meaningful factor in propelling equity prices and provoking resentment among those not enjoying the benefits.

The liquidity flood emanating from the fixed income markets has had the most striking effects within the developing world. The hyperinflationary spirals of property in Western financial centers, bad art and luxury goods are celebrated in ever-grander gatherings and heavier magazines.

The question at hand is whether this liquidity flood will now make its presence known in more prosaic aspects of the global economy.

An easy first look can be had directly within emerging market economies. Broad and accelerating inflation has become the norm. In China, Brazil, Russia, Indonesia and India, among

others, wages and prices are increasing at between 10 and 20% per annum. A portion of the increases in goods’ costs is attributable to the weakening currencies and the withdrawal of subsidies that have held prices of fuels, power and certain staples at artificially suppressed levels. The costs to central governments of maintaining payments to producers and importers to hold prices below market levels have exacerbated current account shortfalls and further weakened currencies and local bond markets. As these are withdrawn, costs of living increase rapidly for the lower and middle classes, and demands for legislated wage increases intensify. The process is self-reinforcing.

To the extent that these governments have sufficient reserves and are inclined to support their currencies in the face of current account shortfalls, that activity has the effect of tightening local capital markets’ liquidity (withdrawing local currency by purchasing it for dollars) and placing more stress on internal debtors.

The inflation, credit distress and capital outflows are consequences of the liquidity booms that proceeded in the aftermath of 2008. That process was and continues to be supported by the flood of dollar liquidity induced by the Federal Reserve.

The inflationary response to inflationary policy appears first in the developing world because they did not have the deflationary sinkholes opening in their economies between 2007 and 2010 that prevented anything other than asset inflation in the U.S. and Western Europe.

In order to consider the possible domestic influences of the inflation underway in emerging markets, we will go back four decades to look at a potential line of transmission.

During the explosive growth of the American consumer economy during the decades following the Second World War, a key input factor was an apparently limitless supply of cheap energy from domestic discoveries and from newly acquired allies in the Middle East.

In many regards, the repressed price of hydrocarbons was a crucial factor (along with our returning military personnel and the destruction of the rest of the world’s industrial capacity) in allowing the U.S. to vastly outperform every other economy on Earth. The development of a far-flung, suburban consumer infrastructure was enabled by the very low cost of automobile travel.

A generation after the end of World War II, the presence of inexpensive fuel was taken as a given throughout our economy.

The first oil shock in the early 1970s set the stage for a long, disruptive cycle of inflation and recession. It culminated with record high interest rates and a near collapse of the dollar. The oil supply shock, while real, was simply the proximate trigger for the generalized acceleration of inflation. The enabling fundamental was the Federal Reserve’s effort to head off a countervailing deflation in the non-energy related portions of the

Not part of the Annual Report

economy by inflating the money supply sufficiently to accommodate rising energy prices without that increase coming out of some other price.

Recall that in a stable monetary environment, a rise in the price of item A will be counterbalanced by falls in other prices. This is what the FRB of the early 1970s wished to prevent. In its stead, it provoked a much more serious and destabilizing trend, where rising prices and falling real incomes spread across all corners of the economy.

At present, there is a somewhat analogous system of external dependence and fears of deflationary chimera at work in the U.S. economy, although they do not involve OPEC and oil scarcity.

For more than two decades, we have come to rely on the extraordinarily inexpensive manufactured goods produced in the developing world. China is a particularly clear example of this. The trend of relocating global manufacturing capacity outside the developed world accelerated in the aftermath of the 1997-1998 Asian currency crisis. Their abrupt, involuntary devaluations further lowered costs and prices from the perspective of Western manufacturers and consumers.

The long migration of manufacturing capacity to Asia was abetted by the very loose monetary policy maintained by the Federal Reserve between 2001 and 2005. The process was then turbocharged by the radically accommodative policy measures arising in the aftermath of 2008 and continuing to this day.

The initial macroeconomic effects of the mass movement of capacity to low cost regions were deflationary for Western economies. These effects were particularly glaring in regions of the U.S. that had been devoted to traditional industrial processes. Wages, standards of living and overall measures of prosperity were relentlessly depressed.

The bankruptcies of two of the three remaining U.S. automobile manufacturers and the city in which they were headquartered probably marked the nadir. Readers should keep in mind that in 1926, some of the most expensive commercial property on the planet was on Dearborn Avenue in Detroit. Things change.

The processes by which labor unions and their legislative allies raised the costs of labor well beyond the growth of productivity created the basic incentive structure for companies (and consumers) to look overseas for greater value. The inevitable readjustment of wage levels from their artificially elevated heights two generations ago has been taken up by the mainstream economics community and much of the financial press as proof that there are fundamental flaws in labor markets that need administrative remedy.

The fact is that wage rates in the U.S. have finally adjusted back to levels at which they are well supported by productivity, and without political interference, should begin a cycle of real growth.

A similar cycle of wage deflation has been evident in parts of Europe since the onset of their crisis, and in much of the periphery, private labor costs are approaching levels where they are competitive on an international scale.

The extraordinary largess of the Federal Reserve has not, with some limited exceptions, raised U.S. wages, commodity prices or costs of retail goods, and in light of these facts the consensus view of the economy now holds deflation as a much more worrisome probability. Nearly every mainstream forecaster dismisses the possibility of a serious inflationary trend out of hand.

Price shocks that would undermine the accepted picture of economic risks in the U.S. and Europe have already progressed well beyond the embryonic stages in the parts of the emerging world that we have come to rely on for an endless supply of inexpensive manufactured goods.

Wage rates in China and most of developing Asia are continuing to grow at double-digit rates. Inadequate power and transportation infrastructure further undermines any cost advantages that have characterized the region since the mid 1990s.

Asia is the present day OPEC of manufactured products. We in the West have provided access to our robust consumer demand and manufacturing expertise in exchange for a generation of remarkably inexpensive consumer and intermediate goods. A sustained rise in prices from this corner will catch the investment community and central banks completely unprepared.

Most observers are discounting the risks inherent in inflationary processes now underway because their focus is on commodity prices and developed market wage rates. Both have been very subdued. In addition, anyone who has sounded the alarm regarding inflation since 2009 has been made to look quite foolish by markets and economic data flows. Most in that camp appear to have surrendered, a normal sign of trend change.

Commodity prices are still being depressed by the withdrawal of institutional investment capital that was sold the fiction of a “commodity super-cycle” right as it was ending some five years ago. The influx of passive capital to the strategy of owning large stocks of commodity inventory helped to create the final peak in prices. Large increases in productive capacity were the normal industry response to the price spikes. Both are being unwound and keeping most index contained commodities relatively docile.

Wages in the developed economies are in the midst of a long correction from unsustainably elevated levels. The process is complete in the vast majority of the private sector, particularly in manufacturing. The correction of unsustainably elevated public sector employment cost is underway, having progressed much farther in Greece and Detroit than in New York City. This is part of a long process of global cost rationalization that has made its way through the private sector and is just taking hold among governments.

Not part of the Annual Report

Price rises at the emerging economy end of the global supply chain would seem a natural prompt to capital and capacity migration back to the developed world. To some extent this is already underway. An important surprise will develop when it becomes clear that there is a great deal less spare capacity in developed economies than statistics would indicate.

Pressures on corporate managers to conserve equity capital (the apparent, real costs of which are high and difficult to determine) are substantial. There is a large cadre of analysts and “activists” leaning on managers to close, sell, reduce and rationalize capacity. Marginal facilities that are counted by statisticians as unused capacity may, in actuality, have no real productive value.

We suspect that the same is true in the labor force, where the skills mismatch between the unemployed and those needing workers capable of participating in modern manufacturing processes is insurmountable.

It is becoming quite clear that the popular imperative among central bankers in the developed world is to make monetary inflation manifest in prices and wages. The choruses of academia and politics are supporting them in this endeavor. A form of militant altruism has arisen as the new intellectual fashion among the very rich and powerful. Davos 2014 has become the Woodstock of guilt.

Present efforts to speed the migration of price increases from assets to goods and wages are not just superfluous but harmful. The tragic harm consists in the fact that the burdens of policy error will fall most heavily on those at the bottom of the economic ladder.

If there is just one thing about the relationship between economics and society that readers of this letter take away, it should be this; economic inefficiency kills prospects of the poor. Always and everywhere and in spite of good intentions (which are indeed pavement on the road to Hell).

In every cycle comprising unusual macroeconomic features, there are clear beneficiaries and victims. This one will be no different.

Companies with capacity that is difficult to replicate or substitute for will be at great advantage, assuming that they are able to compete for the labor required to satisfy additional demand.

Businesses that depend upon price advantages from emerging market inputs will begin to see cost pressures. Some will be able to pass these through, but few will have the ability to continue to take costs from their domestic labor force. Real wages at all points in the domestic economy look set to begin a long advance.

Commodities prices should be widely dispersed, with local supply/demand conditions playing a much larger role than institutional capital flows. Real costs of production in certain parts of the world will rise dramatically as the phenomenon of absurdly low wage rates in developing markets begins to abate.

In past cycles, equity valuations have not responded well to unanticipated increases in reported inflation. The negative response often takes time. At present, it is clear in the case of Emerging Market equities, where we have just entered year three of the bear market. Investors seem to be noticing, but there is still a stubborn adherence to the idea that the future of global economic progress will be led by the developing world. We continue to believe otherwise.

As 2013 drew to a close, our portfolio was continuing to move toward those companies that would fare better in a world where prices in the real economy started to catch up with prices of investment media. Our short portfolio remains concentrated in emerging market assets, where the benefits of the radical largess of Western central banks have been most profound and fundamentally unsupported.

As many of you are aware, the fund has experienced remarkable asset growth during the past year. We are acutely aware that this is not a good portent for ensuing performance. Our style and methods of execution remain deliberate and long-term, as they have been from day one. They are now matters of necessity as well as inclination, but the day-to-day processes within the firm have not changed. Results will continue to depend upon our ability to gain some differentiable insight into the complex macroeconomic processes that drive changes in capital assets’ pricing and output.

As always, we are extraordinarily grateful for your support and welcome your questions.

January 27, 2014

Michael C. Aronstein

President, CIO & Portfolio Manager

The information provided herein represents the opinion of the Portfolio Manager and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

Not part of the Annual Report

Investors should refer to the Fund’s Summary Prospectus and/or Prospectus and consider the Fund’s investment objectives, strategies, risks, charges and expenses carefully before investing. The Summary Prospectus and/or Prospectus contain this and other information about the Fund. You may obtain copies of the Fund’s Summary Prospectus, Prospectus and Statement of Additional Information free of charge, upon request, by calling toll-free 800-MAINSTAY (624-6782), by writing to NYLIFE Distributors LLC, Attn: MainStay Marketing Department, 169 Lackawanna Avenue, Parsippany, New Jersey 07054 or by sending an e-mail to MainStayShareholderServices@nylim.com. These documents are also available via the MainStay Funds’ website at mainstayinvestments.com/documents. Please read the Summary Prospectus and/or Prospectus carefully before investing.

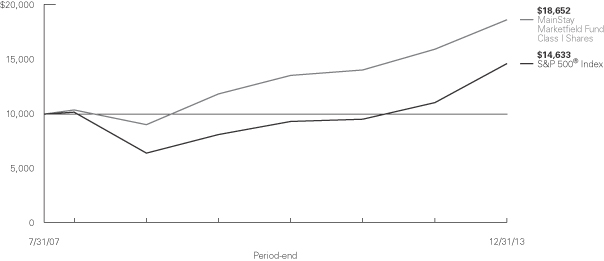

Investment and Performance Comparison1 (Unaudited)

Performance data quoted represents past performance. Past performance is no guarantee of future results. Because of market volatility, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate, and as a result, when shares are redeemed, they may be worth more or less than their original cost. The graph below depicts the historical performance of Class I shares of the Fund. Performance will vary from class to class based on differences in class-specific expenses and sales charges. For performance information current to the most recent month-end, please call 800-MAINSTAY (624-6782) or visit mainstayinvestments.com.

Average Annual Total Returns for the Period Ended December 31, 2013

| Class | Sales Charge | One Year | Five Years | Since Inception (7/31/07) | Gross Expense Ratio2 | |||||||||||||||

| Class A Shares3 | Maximum 5.5% Initial Sales Charge | With sales charges Excluding sales charges |

| 10.20 16.62 | %

|

| 14.00 15.30 | %

|

| 8.96 9.92 | %

|

| 4.15 4.15 | %

| ||||||

| Investor Class Shares3 | Maximum 5.5% Initial Sales Charge | With sales charges Excluding sales charges |

| 10.20 16.62 |

|

| 14.00 15.30 |

|

| 8.96 9.92 |

|

| 4.11 4.11 |

| ||||||

| Class C Shares3 | Maximum 1% CDSC if Redeemed Within One Year of Purchase | With sales charges Excluding sales charges | | 14.76 15.76 | | | 14.44 14.44 | | | 9.10 9.10 | |

| 4.90 4.90 |

| ||||||

| Class I Shares4 | No Sales Charge | 16.93 | 15.58 | 10.19 | 2.94 | |||||||||||||||

| Class R2 Shares3 | No Sales Charge | 16.58 | 15.18 | 9.80 | 3.91 | |||||||||||||||

| Class R6 Shares5 | No Sales Charge | 16.93 | 15.58 | 10.19 | 2.84 | |||||||||||||||

| Class P Shares6 | No Sales Charge | 16.87 | 15.57 | 10.18 | 2.94 | |||||||||||||||

| 1. | The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on distributions or Fund-share redemptions. Total returns reflect maximum applicable sales charges as indicated in the table above, changes in share price, and reinvestment of dividends and capital gain distributions. The graph assumes the initial investment amount shown above and reflects the deduction of all sales charges that would have applied for the period of investment. Performance figures reflect certain fee waivers and/or expense limitations, without which total returns may have been lower. For more information on share classes and current fee waivers and/or expense limitations, please refer to the notes to the financial statements. |

| 2. | The gross expense ratios presented reflect the Fund’s “Total Annual Fund Operating Expenses” from the most recent Prospectus and may differ from other expense ratios disclosed in this report. |

| 3. | Performance figures for Class A, Investor Class, Class C, and Class R2 shares, first offered on October 5, 2012 include the historical performance of Class I shares through October 4, 2012 and are adjusted to reflect |

| differences in fees and expenses. Performance data for the classes varies based on differences in their fee and expense structures. Marketfield Fund commenced operations on July 31, 2007. Unadjusted, the performance for the newer classes would likely have been different. |

| 4. | Performance figures for Class I shares reflect the historical performance of the then-existing shares of Marketfield Fund (the predecessor to the Fund, which was subject to a different fee structure, and for which a predecessor entity to Marketfield Asset Management LLC served as investment advisor) for periods prior to October 5, 2012. Marketfield Fund commenced operations on July 31, 2007. |

| 5. | Performance figures for Class R6 shares, first offered on June 17, 2013, include the historical performance of Class I shares through June 16, 2013. Performance for Class R6 would likely have been different because of differences in certain expenses attributable to each share class. |

| 6. | Performance figures for Class P shares, first offered on May 31, 2013, include the historical performance of Class I shares through May 30, 2013. |

The footnotes on the next page are an integral part of the table and graph and should be carefully read in conjunction with them.

| 10 | MainStay Marketfield Fund |

| Benchmark Performance | One Year | Five Years | Since Inception | |||||||||

S&P 500® Index7 | 32.39 | % | 17.94 | % | 6.11 | % | ||||||

Average Lipper Alternative Long/Short Equity Fund8 | 15.63 | 8.71 | 2.80 | |||||||||

| Performance for Class P shares would likely have been different because of differences in certain expenses attributable to each share class. |

| 7. | S&P 500® Index is a trademark of The McGraw-Hill Companies, Inc. The S&P 500® Index is widely regarded as the standard index for measuring large-cap U.S. stock market performance. The S&P 500® Index is the Fund’s broad-based securities market index for comparison purposes. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an Index. |

| 8. | The average Lipper alternative long/short equity fund is representative of funds that employ portfolio strategies combining long holdings of equities with short sales of equity, equity options, or equity index options. The funds may be either net long or net short, depending on the portfolio manager’s view of the market. This benchmark is a product of Lipper Inc. Lipper Inc. is an independent monitor of fund performance. Results are based on average total returns of similar funds with all dividend and capital gain distributions reinvested. |

The footnotes on the preceding page are an integral part of the table and graph and should be carefully read in conjunction with them.

| mainstayinvestments.com | 11 |

Cost in Dollars of a $1,000 Investment in MainStay Marketfield Fund (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the period from July 1, 2013, to December 31, 2013, and the impact of those costs on your investment.

Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including exchange fees and sales charges (loads) on purchases (as applicable), and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other Funds. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from July 1, 2013, to December 31, 2013. Shares are only sold in connection with variable life and annuity contracts and the example does not reflect any contract level or transactional fees or expenses. If these costs had been included, your costs would have been higher.

This example illustrates your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six months

ended December 31, 2013. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in the Fund with the ongoing costs of investing in other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other Funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as exchange fees or sales charges (loads). Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Share Class | Beginning Account Value 7/1/13 | Ending Account Value (Based on Actual Returns and Expenses) 12/31/13 | Expenses Paid During Period1 | Ending Account Value (Based on Hypothetical 5% Annualized Return and Actual Expenses) 12/31/13 | Expenses Paid During Period1 | |||||||||||||||

| Investor Class Shares | $ | 1,000.00 | $ | 1,085.30 | $ | 14.93 | $ | 1,010.90 | $ | 14.39 | ||||||||||

| Class A Shares | $ | 1,000.00 | $ | 1,086.00 | $ | 14.88 | $ | 1,010.90 | $ | 14.34 | ||||||||||

| Class C Shares | $ | 1,000.00 | $ | 1,081.70 | $ | 18.84 | $ | 1,007.10 | $ | 18.16 | ||||||||||

| Class I Shares | $ | 1,000.00 | $ | 1,087.60 | $ | 13.58 | $ | 1,012.20 | $ | 13.09 | ||||||||||

| Class R2 Shares | $ | 1,000.00 | $ | 1,085.50 | $ | 15.40 | $ | 1,010.40 | $ | 14.85 | ||||||||||

| Class R6 Shares | $ | 1,000.00 | $ | 1,087.60 | $ | 14.00 | $ | 1,011.80 | $ | 13.49 | ||||||||||

| Class P Shares | $ | 1,000.00 | $ | 1,087.00 | $ | 13.52 | $ | 1,012.20 | $ | 13.03 | ||||||||||

| 1. | Expenses are equal to the Fund’s annualized expense ratio of each class (2.84% for Investor Class, 2.83% for Class A, 3.59% for Class C, 2.58% for Class I, 2.93% for Class R2, 2.66% for Class R6 and 2.57% for Class P) multiplied by the average account value over the period, divided by 365 and multiplied by 184 (to reflect the six-month period). The table above represents the actual expenses incurred during the six-month period. |

| 12 | MainStay Marketfield Fund |

Country Composition as of December 31, 2013 (Unaudited)

| United States | 61.4 | % | ||

| Germany | 6.3 | |||

| Ireland | 4.9 | |||

| Japan | 4.6 | |||

| Italy | 4.1 | |||

| Spain | 3.1 | |||

| United Kingdom | 3.0 | |||

| Switzerland | 2.3 | |||

| Canada | 2.0 |

| Denmark | 1.0 | % | ||

| France | 1.0 | |||

| Mexico | 0.8 | |||

| Sweden | 0.2 | |||

| Other Assets, Less Liabilities | 34.7 | |||

| Investments Sold Short | –29.4 | |||

|

| |||

| 100.0 | % | |||

|

|

Industry Composition as of December 31, 2013 (Unaudited)

| Commercial Banks | 12.9 | % | ||

| Exchange-Traded Funds | 7.3 | |||

| Household Durables | 5.9 | |||

| Construction Materials | 5.1 | |||

| Metals & Mining | 4.8 | |||

| Chemicals | 4.3 | |||

| Machinery | 4.2 | |||

| Oil, Gas & Consumable Fuels | 3.4 | |||

| Automobiles | 2.8 | |||

| Electrical Equipment | 2.3 | |||

| Energy Equipment & Services | 2.2 | |||

| Industrial Conglomerates | 2.0 | |||

| Specialty Retail | 2.0 | |||

| Trading Companies & Distributors | 1.7 | |||

| Auto Components | 1.6 | |||

| Internet Software & Services | 1.4 | |||

| Food & Staples Retailing | 1.2 | |||

| Real Estate Management & Development | 1.2 | |||

| Aerospace & Defense | 1.0 | |||

| Building Products | 1.0 |

| Capital Markets | 1.0 | % | ||

| Consumer Finance | 1.0 | |||

| IT Services | 1.0 | |||

| Insurance | 1.0 | |||

| Road & Rail | 1.0 | |||

| Semiconductors & Semiconductor Equipment | 1.0 | |||

| Diversified Financial Services | 0.9 | |||

| Internet & Catalog Retail | 0.9 | |||

| Software | 0.9 | |||

| Transportation Infrastructure | 0.9 | |||

| Construction & Engineering | 0.8 | |||

| Purchased Options | 0.7 | |||

| Real Estate Investment Trusts | 0.6 | |||

| Commercial Services & Supplies | 0.5 | |||

| Investment in Money Market Fund | 14.2 | |||

| Other Assets, Less Liabilities | 34.7 | |||

| Investments Sold Short | –29.4 | |||

|

| |||

| 100.0 | % | |||

|

|

See Portfolio of Investments beginning on page 16 for specific holdings within these categories.

Top Ten Holdings or Issuers as of December 31, 2013 (excluding short-term investment) (Unaudited)

| 1. | Bank of Ireland |

| 2. | SPDR S&P Regional Banking |

| 3. | Sumitomo Mitsui Financial Group, Inc. |

| 4. | iShares MSCI Mexico Investable Market Index Fund |

| 5. | Facebook, Inc. Class A |

| 6. | ABB, Ltd. |

| 7. | Continental A.G. |

| 8. | Alcoa, Inc. |

| 9. | iShares Dow Jones US Home Construction Index Fund |

| 10. | BASF S.E. Corp. |

Top Five Short Positions as of December 31, 2013 (Unaudited)

| 1. | Vanguard FTSE Emerging Markets |

| 2. | Utilities Select Sector SPDR Fund |

| 3. | Allianz SE |

| 4. | iShares JP Morgan USD Emerging Markets Bond |

| 5. | JPMorgan Chase & Co. |

| mainstayinvestments.com | 13 |

Portfolio Management Discussion and Analysis (Unaudited)

Questions answered by portfolio manager Michael C. Aronstein of Marketfield Asset Management LLC, the Fund’s Subadvisor.

How did MainStay Marketfield Fund perform relative to its benchmark and peers during the 12 months ended December 31, 2013?

Excluding all sales charges, MainStay Marketfield Fund returned 16.62% for Class A and Investor Class shares and 15.76% for Class C shares for the 12 months ended December 31, 2013. Over the same period, Class I shares returned 16.93%, Class R2 shares returned 16.58%, Class R6 shares returned 16.93% and Class P shares returned 16.87%. During the 12 months ended December 31, 2013, all share classes underperformed the 32.39% return of the S&P 500® Index,1 which is the Fund’s broad-based securities-market index. Over the same period, all share classes outperformed the 15.63% return of the average Lipper2 alternative long/short equity fund. See page 10 for Fund returns with applicable sales charges.

What factors affected the Fund’s relative performance during the reporting period?

The Fund takes a top-down investment approach in which the portfolio manager identifies macroeconomic trends and themes, and then determines the most appropriate investment instruments or strategies to express those themes in the Fund.

Relative to the S&P 500® Index, the Fund’s net long position during the reporting period turned out to be not long enough. However, the Fund outperformed most of the relevant alternative indices. The Fund’s long Europe theme and its long Capital Spending Cycle theme were primary positive drivers of performance. The short Safe Haven Assets theme and the short Emerging Markets theme were the primary themes that pulled performance down.

During the reporting period, how was the Fund’s performance materially affected by investments in derivatives?

During the reporting period, we used short positions in various bond futures to express the Fund’s domestic and global interest-rate views. These positions had a negligible impact on performance. We also used puts in emerging-market securities as a way of creating short positions in these markets. We also used a number of long sovereign credit default swap3 positions in the Fund. These derivatives had an overall negative effect on the Fund’s performance.

During the reporting period, which investment themes were the strongest contributors to the Fund’s performance and which themes were particularly weak?

Several of our long themes provided positive contributions to the Fund’s performance. (Contributions take weightings and total returns into account.) Our Europe theme contributed 8.1% to performance. This theme suggests that Europe is broadening its economic recovery that was triggered by the European Central Bank’s 2011 monetary stimulus. Our Capital Spending theme contributed 7.5% to performance. This theme reflects our belief that the combination of the beginning of a broad capital spending cycle and the significant improvement in the global competiveness of U.S. manufacturing will benefit the U.S. industrial base. Our U.S. Housing Recovery theme added 4.8% to performance. This theme suggests that the U.S. housing market continues to recover supported by credit cycle strengthening and favorable inventory levels.

Other themes detracted from the Fund’s performance. Our short Safe Haven Assets theme detracted from performance by 3.4%. This theme’s rationale is that those assets that investors have considered to be “safe haven” assets are over-owned and overvalued, that interest rates have greater risk to the upside at current historic low yields, and that economic fears are subsiding. Our End of the PC Era theme detracted from performance by 1.7%. This theme reflects our view that the marketplace has become saturated with legacy computers and software and that the new technology era is likely to benefit consumer-driven web-based solutions and service providers. Our short Margin Pressures in Non-cyclical Businesses theme detracted from performance by 0.4%. This theme suggests that the Federal Reserve’s continued loose policy, combined with a recovery in the developed world economies, will give rise to pressures on wages and input costs.

During the reporting period, which individual stocks made the strongest contributions to the Fund’s absolute performance and which stocks detracted the most?

During 2013, the three strongest individual positive contributors to the Fund’s absolute performance were long holdings in commercial banking company Bank of Ireland, Internet software & services company Facebook, and Germany-based auto components company Continental AG.

Over the same period, the weakest contributions to the Fund’s absolute performance came from short holdings in China-based Internet software & services company Qihoo 360 Technology

| 1. | See footnote on page 11 for more information on the S&P 500® Index. |

| 2. | See footnote on page 11 for more information on Lipper Inc. |

| 3. | Credit default swaps are contracts where one party makes periodic payments to another party in exchange for the right to receive from that other party a payment equal to the par or other agreed-upon value of a particular debt obligation in the event of a default by the issuer of that debt obligation. |

| 14 | MainStay Marketfield Fund |

Co., Ltd., Germany-based insurance company Allianz SE, and U.K.-based financial services company Aberdeen Asset Management PLC.

Did the Fund make any significant purchases or sales during the reporting period?

During the reporting period, we initiated long exposure to Japan of 6%, which includes individual equities as well as Tokyo Price Index futures. We increased our long investment in the Bank of Ireland by purchasing Bank of Ireland Trust—Preferred Security 10.24%.

During the reporting period, we decreased our short emerging-market bond holding from 5% to 2%, and we covered our equity short holdings in India and Brazil.

How did the Fund’s sector weightings change during the reporting period?

Industrials ended 2012 at 32% of net assets compared to 15.2% at the end of 2013—a decrease of 16.8 percentage

points. Consumer discretionary ended 2012 at 16.5% of net assets compared to 10.7% at the end of 2013—a decrease of 5.8 percentage points. Materials ended 2012 at 7% of net assets compared to 14.2% at the end of 2013—an increase of 7.2 percentage points. Energy ended 2012 at 2% compared to 5.6% at the end of 2013—an increase of 3.6 percentage points. Financials ended 2012 at 2.6% compared to 9.8% at the end of 2013—an increase of 7.2 percentage points.

How was the Fund positioned at the end of the reporting period?

As of December 31, 2013, the equity portion of the Fund was 80% long and 30% short. The net equity exposure was long 50%.4 As of the same date, the futures portion of the Fund was 2% long and 14% short. The net futures exposure was short 12%.

| 4. | See Portfolio of Investments beginning on page 16 for information on specific holdings. |

The opinions expressed are those of the portfolio manager as of the date of this report and are subject to change. There is no guarantee that any forecasts made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

| mainstayinvestments.com | 15 |

Portfolio of Investments December 31, 2013

| Shares | Value | |||||||

| Common Stocks 70.9%† | ||||||||

Aerospace & Defense 1.0% |

| |||||||

Precision Castparts Corp. (a) | 702,059 | $ | 189,064,489 | |||||

|

| |||||||

Auto Components 1.6% | ||||||||

¨Continental A.G. | 1,134,505 | 248,781,608 | ||||||

ElringKlinger A.G. | 1,658,747 | 67,476,883 | ||||||

|

| |||||||

| 316,258,491 | ||||||||

|

| |||||||

Automobiles 2.8% |

| |||||||

Daimler A.G. | 2,329,310 | 201,558,666 | ||||||

Fiat Industrial S.p.A. (b) | 22,831,250 | 186,726,126 | ||||||

Ford Motor Co. | 9,974,810 | 153,911,318 | ||||||

|

| |||||||

| 542,196,110 | ||||||||

|

| |||||||

Building Products 1.0% |

| |||||||

Geberit A.G. | 614,769 | 186,418,939 | ||||||

|

| |||||||

Capital Markets 1.0% |

| |||||||

Daiwa Securities Group, Inc. | 19,027,959 | 189,719,466 | ||||||

|

| |||||||

Chemicals 3.9% |

| |||||||

Air Liquide S.A. | 1,318,450 | 186,457,698 | ||||||

¨BASF S.E. Corp. | 2,246,711 | 239,506,008 | ||||||

Potash Corporation of Saskatchewan, Inc. | 5,854,319 | 192,958,354 | ||||||

Sherwin-Williams Co. (The) (a) | 752,886 | 138,154,581 | ||||||

|

| |||||||

| 757,076,641 | ||||||||

|

| |||||||

Commercial Banks 11.7% |

| |||||||

Banco Bilbao Vizcaya Argentaria S.A. | 18,026,644 | 221,903,625 | ||||||

¨Bank of Ireland (b) | 1,024,050,774 | 355,014,073 | ||||||

¨Bank of Ireland, Sponsored ADR (b) | 3,389,402 | 48,841,283 | ||||||

Barclays PLC | 42,077,723 | 189,490,957 | ||||||

BB&T Corp. (a) | 5,103,628 | 190,467,397 | ||||||

CIT Group, Inc. (a) | 3,683,443 | 192,017,884 | ||||||

Fifth Third Bancorp (a) | 8,969,833 | 188,635,588 | ||||||

Grupo Financiero Banorte S.A.B. de C.V. Class O | 22,823,374 | 159,666,601 | ||||||

Lloyds Banking Group PLC (b) | 158,095,702 | 206,506,707 | ||||||

¨Sumitomo Mitsui Financial Group, Inc. | 5,571,889 | 286,768,952 | ||||||

UniCredit S.p.A. | 30,205,205 | 223,556,655 | ||||||

|

| |||||||

| 2,262,869,722 | ||||||||

|

| |||||||

Commercial Services & Supplies 0.5% |

| |||||||

Bilfinger S.E. | 893,532 | 100,219,237 | ||||||

|

| |||||||

Construction & Engineering 0.8% |

| |||||||

KBR, Inc. | 4,656,743 | 148,503,534 | ||||||

|

| |||||||

| Shares | Value | |||||||

Construction Materials 5.1% |

| |||||||

Buzzi Unicem S.p.A. | 10,458,073 | $ | 188,615,726 | |||||

CRH PLC | 7,840,070 | 197,727,484 | ||||||

Eagle Materials, Inc. (a) | 2,607,095 | 201,867,366 | ||||||

HeidelbergCement A.G. | 2,266,520 | 171,960,465 | ||||||

Taiheiyo Cement Corp. | 58,233,757 | 223,401,745 | ||||||

|

| |||||||

| 983,572,786 | ||||||||

|

| |||||||

Consumer Finance 1.0% |

| |||||||

Discover Financial Services | 3,485,591 | 195,018,816 | ||||||

|

| |||||||

Diversified Financial Services 0.9% |

| |||||||

CME Group, Inc. | 2,248,889 | 176,447,831 | ||||||

|

| |||||||

Electrical Equipment 2.3% |

| |||||||

¨ABB, Ltd. (b) | 9,618,365 | 253,168,780 | ||||||

Emerson Electric Co. | 2,709,197 | 190,131,445 | ||||||

|

| |||||||

| 443,300,225 | ||||||||

|

| |||||||

Energy Equipment & Services 2.2% |

| |||||||

Baker Hughes, Inc. | 3,459,321 | 191,162,078 | ||||||

Schlumberger, Ltd. (a) | 2,642,160 | 238,085,038 | ||||||

|

| |||||||

| 429,247,116 | ||||||||

|

| |||||||

Food & Staples Retailing 1.2% |

| |||||||

Costco Wholesale Corp. (a) | 1,893,207 | 225,310,565 | ||||||

|

| |||||||

Household Durables 5.9% |

| |||||||

D.R. Horton, Inc. (a) | 8,957,153 | 199,923,655 | ||||||

Mohawk Industries, Inc. (a)(b) | 1,317,929 | 196,239,628 | ||||||

PulteGroup, Inc. (a) | 9,994,004 | 203,577,862 | ||||||

Ryland Group, Inc. (The) (a) | 3,298,025 | 143,167,265 | ||||||

Sekisui House, Ltd. | 14,453,974 | 201,759,964 | ||||||

Toll Brothers, Inc. (a)(b) | 5,261,767 | 194,685,379 | ||||||

|

| |||||||

| 1,139,353,753 | ||||||||

|

| |||||||

Industrial Conglomerates 2.0% |

| |||||||

3M Co. (a) | 1,377,046 | 193,130,701 | ||||||

General Electric Co. (a) | 6,888,229 | 193,077,059 | ||||||

|

| |||||||

| 386,207,760 | ||||||||

|

| |||||||

Insurance 1.0% |

| |||||||

Assicurazioni Generali S.p.A. | 8,221,728 | 193,411,705 | ||||||

|

| |||||||

Internet & Catalog Retail 0.9% |

| |||||||

Amazon.com, Inc. (a)(b) | 462,682 | 184,512,955 | ||||||

|

| |||||||

Internet Software & Services 1.4% |

| |||||||

¨Facebook, Inc. Class A (a)(b) | 4,993,300 | 272,933,778 | ||||||

|

| |||||||

| † | Percentages indicated are based on Fund net assets. |

| ¨ | Among the Fund’s 10 largest holdings, as of December 31, 2013, excluding short-term investment. May be subject to change daily. |

| 16 | MainStay Marketfield Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

| Shares | Value | |||||||

| Common Stocks (continued) | ||||||||

IT Services 1.0% |

| |||||||

Amadeus IT Holding S.A. Class A | 4,572,000 | $ | 195,641,041 | |||||

|

| |||||||

Machinery 4.2% |

| |||||||

Cummins, Inc. (a) | 1,356,303 | 191,198,034 | ||||||

Deere & Co. (a) | 2,087,025 | 190,607,993 | ||||||

Ingersoll-Rand PLC (a) | 3,060,997 | 188,557,415 | ||||||

Joy Global, Inc. | 3,396,266 | 198,647,598 | ||||||

Scania AB Class B | 2,356,873 | 46,134,520 | ||||||

|

| |||||||

| 815,145,560 | ||||||||

|

| |||||||

Metals & Mining 4.8% |

| |||||||

¨Alcoa, Inc. (a) | 22,570,589 | 239,925,361 | ||||||

Freeport-McMoRan Copper & Gold, Inc. | 5,926,689 | 223,673,243 | ||||||

Steel Dynamics, Inc. (a) | 10,139,391 | 198,123,700 | ||||||

Teck Resources, Ltd. Class B (a) | 7,552,603 | 196,443,204 | ||||||

Walter Energy, Inc. | 4,932,820 | 82,032,797 | ||||||

|

| |||||||

| 940,198,305 | ||||||||

|

| |||||||

Oil, Gas & Consumable Fuels 3.4% |

| |||||||

Alpha Natural Resources, Inc. (a)(b) | 10,933,019 | 78,061,756 | ||||||

Apache Corp. (a) | 2,281,988 | 196,114,049 | ||||||

Chesapeake Energy Corp. (a) | 7,545,887 | 204,795,373 | ||||||

Devon Energy Corp. | 3,049,045 | 188,644,414 | ||||||

|

| |||||||

| 667,615,592 | ||||||||

|

| |||||||

Real Estate Investment Trusts 0.6% |

| |||||||

Green REIT PLC (b) | 28,477,636 | 56,492,752 | ||||||

Hibernia REIT PLC (b) | 34,883,746 | 56,147,771 | ||||||

|

| |||||||

| 112,640,523 | ||||||||

|

| |||||||

Real Estate Management & Development 1.2% |

| |||||||

Deutsche Wohnen A.G. | 5,741,449 | 110,855,557 | ||||||

St. Joe Co. (The) (b) | 6,130,622 | 117,646,636 | ||||||

|

| |||||||

| 228,502,193 | ||||||||

|

| |||||||

Road & Rail 1.0% |

| |||||||

DSV A/S | 5,695,640 | 186,747,461 | ||||||

|

| |||||||

Semiconductors & Semiconductor Equipment 1.0% |

| |||||||

Intel Corp. | 7,448,529 | 193,363,813 | ||||||

|

| |||||||

Software 0.9% |

| |||||||

Splunk, Inc. (b) | 2,667,543 | 183,180,178 | ||||||

|

| |||||||

Specialty Retail 2.0% |

| |||||||

Home Depot, Inc. (The) (a) | 2,341,800 | 192,823,812 | ||||||

Tractor Supply Co. | 2,476,634 | 192,137,266 | ||||||

|

| |||||||

| 384,961,078 | ||||||||

|

| |||||||

Trading Companies & Distributors 1.7% |

| |||||||

Beacon Roofing Supply, Inc. (a)(b) | 3,554,595 | 143,179,087 | ||||||

Wolseley PLC | 3,361,718 | 190,664,154 | ||||||

|

| |||||||

| 333,843,241 | ||||||||

|

| |||||||

| Shares | Value | |||||||

Transportation Infrastructure 0.9% |

| |||||||

Abertis Infraestructuras S.A. | 8,215,980 | $ | 182,538,904 | |||||

|

| |||||||

Total Common Stocks | 13,746,021,808 | |||||||

|

| |||||||

| Exchange-Traded Funds 7.3% (d) | ||||||||

¨iShares Dow Jones US Home Construction Index Fund (a) | 9,656,478 | 239,866,913 | ||||||

iShares MSCI Italy Index Fund | 13,068,013 | 203,730,323 | ||||||

iShares MSCI Japan Index Fund | 15,224,466 | 184,672,773 | ||||||

¨iShares MSCI Mexico Investable Market Index Fund (a) | 4,200,747 | 285,650,796 | ||||||

SPDR S&P Homebuilders (a) | 5,808,244 | 193,414,525 | ||||||

¨SPDR S&P Regional Banking (a) | 7,516,275 | 305,235,928 | ||||||

|

| |||||||

Total Exchange-Traded Funds | 1,412,571,258 | |||||||

|

| |||||||

| Preferred Stocks 1.6% | ||||||||

Chemicals 0.4% |

| |||||||

Fuchs Petrolub SE 1.81% | 840,221 | 82,114,532 | ||||||

|

| |||||||

Commercial Banks 1.2% | ||||||||

¨Bank of Ireland Trust—Preferred Security 10.24% (c) | 168,400,000 | 243,946,166 | ||||||

|

| |||||||

Total Preferred Stocks | 326,060,698 | |||||||

|

| |||||||

| Notional Amount | ||||||||

| Purchased Options 0.7% | ||||||||

Purchased Call Options 0.4% |

| |||||||

CNY/USD | ||||||||

Strike Price $6.321 | 1,401,000,000 | 888,234 | ||||||

Strike Price $6.722 | 1,401,000,000 | 1,340,757 | ||||||

| Number of Contracts | ||||||||

iShares Russell 2000 Index ETF | ||||||||

Strike Price $111.00 | 70,016 | 34,097,792 | ||||||

Strike Price $112.00 | 94,710 | 36,368,640 | ||||||

Vanguard FTSE Emerging Markets Strike Price $43.00 | 200,000 | 2,000,000 | ||||||

|

| |||||||

Total Purchased Call Options | 74,695,423 | |||||||

|

| |||||||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | mainstayinvestments.com | 17 |

Portfolio of Investments December 31, 2013 (continued)

| Notional Amount | Values | |||||||

| Purchased Options (continued) | ||||||||

Purchased Put Options 0.3% |

| |||||||

EUR/USD | 1,041,631,468 | $ | 19,780,742 | |||||

| Number of Contracts | ||||||||

30 Year United States Treasury Bond Futures | 28,918 | 40,665,938 | ||||||

iShares China Large Cap ETF | 94,470 | 2,078,340 | ||||||

iShares MSCI Emerging Markets | 236,441 | 8,511,876 | ||||||

|

| |||||||

Total Purchased Put Options | 71,036,896 | |||||||

|

| |||||||

Total Purchased Options (Cost $197,618,612) | 145,732,319 | |||||||

|

| |||||||

| Shares | ||||||||

| Short-Term Investment 14.2% | ||||||||

Money Market Fund 14.2% |

| |||||||

State Street Institutional Treasury Money Market Fund | 2,750,000,000 | 2,750,000,000 | ||||||

|

| |||||||

Total Short-Term Investment | 2,750,000,000 | |||||||

|

| |||||||

Total Investments, Before Investments Sold Short | 94.7 | % | 18,380,386,083 | |||||

|

| |||||||

| Common Stocks Sold Short (16.8%) | ||||||||

Beverages (1.2%) |

| |||||||

Coca-Cola Co. (The) | (5,602,494 | ) | (231,439,027 | ) | ||||

|

| |||||||

Capital Markets (3.3%) |

| |||||||

Aberdeen Asset Management PLC | (25,060,854 | ) | (207,497,595 | ) | ||||

Franklin Resources, Inc. | (3,122,898 | ) | (180,284,901 | ) | ||||

Invesco, Ltd. | (4,795,574 | ) | (174,558,894 | ) | ||||

Legg Mason, Inc. | (1,743,408 | ) | (75,803,380 | ) | ||||

|

| |||||||

| (638,144,770 | ) | |||||||

|

| |||||||

Diversified Financial Services (1.6%) |

| |||||||

JPMorgan Chase & Co. | (5,376,264 | ) | (314,403,919 | ) | ||||

|

| |||||||

| Shares | Values | |||||||

Food Products (3.3%) |

| |||||||

Danone | (3,222,286 | ) | $ | (231,929,162 | ) | |||

Kellogg Co. | (3,511,494 | ) | (214,446,938 | ) | ||||

Nestle S.A. | (2,613,789 | ) | (191,335,039 | ) | ||||

|

| |||||||

| (637,711,139 | ) | |||||||

|

| |||||||

Hotels, Restaurants & Leisure (1.2%) |

| |||||||

McDonald’s Corp. | (2,326,023 | ) | (225,694,012 | ) | ||||

|

| |||||||

Insurance (2.4%) |

| |||||||

Allianz SE | (2,623,510 | ) | (470,454,144 | ) | ||||

|

| |||||||

IT Services (1.0%) |

| |||||||

International Business Machines Corp. | (989,517 | ) | (185,603,703 | ) | ||||

|

| |||||||

Multiline Retail (1.0%) |

| |||||||

Target Corp. | (3,234,810 | ) | (204,666,429 | ) | ||||

|

| |||||||

Software (1.8%) |

| |||||||

Microsoft Corp. | (3,280,207 | ) | (122,778,148 | ) | ||||

Oracle Corp. | (2,250,814 | ) | (86,116,144 | ) | ||||

SAP A.G., Sponsored ADR | (1,699,966 | ) | (148,135,037 | ) | ||||

|

| |||||||

| (357,029,329 | ) | |||||||

|

| |||||||

Total Common Stocks Sold Short | (3,265,146,472 | ) | ||||||

|

| |||||||

| Exchange-Traded Funds Sold Short (12.6%) (d) | ||||||||

iShares iBoxx Investment Grade Corporate Bond | (754,366 | ) | (86,156,141 | ) | ||||

iShares JP Morgan USD Emerging Markets Bond | (3,872,623 | ) | (418,862,904 | ) | ||||

Market Vectors Emerging Markets Local Currency Bond | (759,501 | ) | (17,886,249 | ) | ||||

Utilities Select Sector SPDR Fund | (14,175,100 | ) | (538,228,547 | ) | ||||

Vanguard FTSE Emerging Markets | (33,602,717 | ) | (1,382,415,777 | ) | ||||

|

| |||||||

Total Exchange-Traded Funds Sold Short | (2,443,549,618 | ) | ||||||

|

| |||||||

Total Investments Sold Short | (29.4 | )% | (5,708,696,090 | ) | ||||

|

| |||||||

Total Investments, Net of Investments Sold Short | 65.3 | 12,671,689,993 | ||||||

Other Assets, Less Liabilities | 34.7 | 6,724,555,086 | ||||||

Net Assets | 100.0 | % | $ | 19,396,245,079 | ||||

| 18 | MainStay Marketfield Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

| Contracts Long | Unrealized Appreciation (Depreciation) (g) | |||||||

| Futures Contracts 0.1% | ||||||||

Futures Contracts Long | ||||||||

Topix Index March 2014 (f) | 2,933 | $ | 13,975,741 | |||||

|

| |||||||

Total Futures Contracts Long | 13,975,741 | |||||||

|

| |||||||

Futures Contracts Short | ||||||||

CAC 40 Index 10 Euro | (6,335 | ) | (16,555,091 | ) | ||||

Euro-Bund | (5,504 | ) | 16,278,946 | |||||

Euro-OAT | (5,864 | ) | 6,894,104 | |||||

United States Treasury Bond | (1,998 | ) | 5,502,432 | |||||

|

| |||||||

Total Futures Contracts Short | 12,120,391 | |||||||

|

| |||||||

Total Futures Contracts | $ | 26,096,132 | ||||||

| (a) | Security, or a portion thereof, is maintained in a segregated account at the Fund’s custodian as collateral for securities Sold Short (See Note 2(J)). |

| (b) | Non-income producing security. |

| (c) | May be sold to institutional investors only under Rule 144A or securities offered pursuant to Section 4(a)(2) of the Securities Act of 1933, as amended. |

| (d) | Exchange-Traded Fund—An investment vehicle that represents a basket of securities that is traded on an exchange. |

| (e) | As of December 31, 2013, cash in the amount of $6,284,632,232 is on deposit with broker for short sale transactions. |

| (f) | As of December 31, 2013, cash in the amount of $48,953,770 is on deposit with broker for futures transactions. |

| (g) | Represents the difference between the value of the contracts at the time they were opened and the value as of December 31, 2013. |

| (h) | As of December 31, 2013, cost is $15,842,520,296 for federal income tax purposes and net unrealized appreciation is as follows: |

Gross unrealized appreciation | $ | 2,670,043,946 | ||

Gross unrealized depreciation | (132,178,159 | ) | ||

|

| |||

Net unrealized appreciation | $ | 2,537,865,787 | ||

|

|

The following abbreviations are used in the above portfolio:

ADR—American Depositary Receipt

CNY—Chinese Yuan

EUR—Euro

ETF—Exchange-Traded Fund

SPDR—Standard & Poor’s Depositary Receipt

USD—United States Dollar

At December 31, 2013, the Fund held the following OTC credit default swap contracts:

Reference Entity | Counterparty | Termination Date | Buy/Sell Protection1 | Notional Amount (000)2 | (Pay)/ Receive Fixed Rate3 | Upfront Premiums Received/ (Paid) | Value | Unrealized Appreciation/ Depreciation4 | ||||||||||||||||||||||||

Federal Republic of Brazil | Citigroup | 3/20/2019 | Buy | $ | 945,424 | 1.00 | % | $ | (42,299,679 | ) | $ | 42,030,051 | $ | (269,628 | ) | |||||||||||||||||

Republic of South Africa | Citigroup | 3/20/2019 | Buy | $ | 236,356 | 1.00 | % | $ | (12,070,782 | ) | $ | 11,729,036 | $ | (341,746 | ) | |||||||||||||||||

| $ | 53,759,087 | $ | (611,374 | ) | ||||||||||||||||||||||||||||

| 1. | Buy—Fund pays premium and buys credit protection. If a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either (i) receive from the seller of protection an amount equal to the notional amount of the swap and deliver the referenced obligation or underlying securities comprising the referenced index or (ii) receive a net settlement amount in the form of cash or securities equal to the notional amount of the swap less the recovery value of the referenced obligation or underlying securities comprising the referenced index. |

| Sell—Fund receives premium and sells credit protection. If a credit event occurs, as defined under the terms of that particular swap agreement, the Fund will either (i) pay to the buyer of protection an amount equal to the notional amount of the swap and take delivery of the referenced obligation or underlying securities comprising the referenced index or (ii) pay a net settlement amount in the form of cash or securities equal to the notional amount of the swap less the recovery value of the referenced obligation or underlying securities comprising the referenced index. |

| 2. | The maximum potential amount the Fund could be required to pay as a seller of credit protection or receive as a buyer of credit protection if a credit event occurs as defined under the terms of that particular swap contract. |

| 3. | The annual fixed rate represents the interest received by the Fund (as a seller of protection) or paid by the Fund (as a buyer of protection) annually on the notional amount of the credit default swap contract. |

| 4. | Represents the difference between the value of the credit default swap contracts at the time they were opened and the value at December 31, 2013. |

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | mainstayinvestments.com | 19 |

Portfolio of Investments December 31, 2013 (continued)

The following is a summary of the fair valuations according to the inputs used as of December 31, 2013, for valuing the Fund’s assets and liabilities.

Asset Valuation Inputs

Description | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | ||||||||||||

| Investments in Securities (a) | ||||||||||||||||

| Common Stocks | $ | 13,746,021,808 | $ | — | $ | — | $ | 13,746,021,808 | ||||||||

| Exchange-Traded Funds | 1,412,571,258 | — | — | 1,412,571,258 | ||||||||||||

| Preferred Stocks | 82,114,532 | 243,946,166 | — | 326,060,698 | ||||||||||||

| Short-Term Investment | ||||||||||||||||

Money Market Fund | 2,750,000,000 | — | — | 2,750,000,000 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| Total Investments in Securities | 17,990,707,598 | 243,946,166 | — | 18,234,653,764 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| Other Financial Instruments | ||||||||||||||||

Futures Contracts Long (b) | 13,975,741 | — | — | 13,975,741 | ||||||||||||

Futures Contracts Short (b) | 28,675,482 | — | — | 28,675,482 | ||||||||||||

Purchased Call Options | 74,695,423 | — | — | 74,695,423 | ||||||||||||

Purchased Put Options | 71,036,896 | — | — | 71,036,896 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| Total Other Financial Instruments | 188,383,542 | — | — | 188,383,542 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| Total Investments in Securities and Other Financial Instruments | $ | 18,179,091,140 | $ | 243,946,166 | $ | — | $ | 18,423,037,306 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Liability Valuation Inputs

Description | Quoted Prices in Active Markets for Identical (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | ||||||||||||

| Investments in Securities Sold Short (a) | ||||||||||||||||

| Common Stocks Sold Short | $ | (3,265,146,472 | ) | $ | — | $ | — | $ | (3,265,146,472 | ) | ||||||

| Exchange-Traded Funds Sold Short | (2,443,549,618 | ) | — | — | (2,443,549,618 | ) | ||||||||||

|

|

|

|

|

|

|

| |||||||||

| Total Investments in Securities Sold Short | (5,708,696,090 | ) | — | — | (5,708,696,090 | ) | ||||||||||

|

|

|

|

|

|

|

| |||||||||

| Other Financial Instruments | ||||||||||||||||

Futures Contracts Short (b) | (16,555,091 | ) | — | — | (16,555,091 | ) | ||||||||||

Credit Default Swap Contracts (b) | — | (611,374 | ) | — | (611,374 | ) | ||||||||||

|

|

|

|

|

|

|

| |||||||||

| Total Other Financial Instruments | (16,555,091 | ) | (611,374 | ) | — | (17,166,465 | ) | |||||||||

|

|

|

|

|

|

|

| |||||||||

| Total Investments in Securities Sold Short and Other Financial Instruments | $ | (5,725,251,181 | ) | $ | (611,374 | ) | $ | — | $ | (5,725,862,555 | ) | |||||

|

|

|

|

|

|

|

| |||||||||

| (a) | For a complete listing of investments and their industries, see the Portfolio of Investments. |

| (b) | The value listed for these securities reflects unrealized appreciation (depreciation) as shown on the Portfolio of Investments. |

The Fund recognizes transfers between the levels as of the beginning of the period.

As of December 31, 2013, certain foreign securities with a market value of $909,364,735 were transferred from Level 2 to Level 1 as the prices of these securities were based on unadjusted quoted prices compared with the prior year prices which were adjusted for events after the market close. The December 31, 2012 prices were adjusted by applying factors provided by a third party vendor in accordance with the Fund’s policies and procedures. Fair values as of December 31,2013 for these securities were based on quoted prices in active markets for identical investments. (See Note 2)

As of December 31, 2013, the Portfolio did not hold any investments with significant unobservable inputs (Level 3). (See Note 2)

| 20 | MainStay Marketfield Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Statement of Assets and Liabilities as of December 31, 2013

| Assets | ||||

Investment in securities, at value | $ | 18,380,386,083 | ||

Cash collateral on deposit at broker | 6,333,586,002 | |||

Cash | 815,870,192 | |||

Cash denominated in foreign currencies | 60,424,498 | |||

Receivables: | ||||

Fund shares sold | 203,583,162 | |||

Investment securities sold | 59,671,408 | |||

Dividends and interest | 38,793,648 | |||

Premiums paid for swap contracts | 54,370,461 | |||

Other assets | 863,219 | |||

|

| |||

Total assets | 25,947,548,673 | |||

|

| |||

| Liabilities | ||||

Investments sold short (proceeds $5,427,910,964) | 5,708,696,090 | |||

Payables: | ||||

Investment securities purchased | 787,442,545 | |||

Manager (See Note 3) | 21,955,906 | |||

Fund shares redeemed | 18,272,168 | |||

Dividends on investments sold short | 7,925,792 | |||

Transfer agent (See Note 3) | 2,440,566 | |||

NYLIFE Distributors (See Note 3) | 1,628,391 | |||

Variation margin on futures contracts | 860,872 | |||

Shareholder communication | 196,824 | |||

Custodian | 118,632 | |||

Broker fees and charges on short sales | 103,558 | |||

Professional fees | 93,856 | |||

Trustees | 18,493 | |||

Unrealized depreciation on swap contracts | 611,374 | |||

Accrued expenses | 938,527 | |||

|

| |||

Total liabilities | 6,551,303,594 | |||

|

| |||

Net assets | $ | 19,396,245,079 | ||

|

| |||

| Composition of Net Assets | ||||

Shares of beneficial interest outstanding (par value of $.001 per share) unlimited number of shares authorized | $ | 1,048,858 | ||

Additional paid-in capital | 17,317,277,217 | |||

|

| |||

| 17,318,326,075 | ||||

Net investment loss | (22,363,209 | ) | ||

Accumulated net realized gain (loss) on investments, investments sold short, futures transactions, written options, swap transactions and foreign currency transactions | (219,184,224 | ) | ||

Net unrealized appreciation (depreciation) on investments, futures contracts, written options and swap contracts | 2,600,162,224 | |||