| OMB APPROVAL | ||||||

| OMB Number: 3235-0570 Expires: January 31, 2017 Estimated average burden hours per response. . ...20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-22321

MAINSTAY FUNDS TRUST

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

169 Lackawanna Avenue

Parsippany, New Jersey 07054

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 576-7000

Date of fiscal year end: November 30

(MainStay Cushing MLP Premier Fund, MainStay Cushing Renaissance Advantage Fund and MainStay Cushing Royalty Energy Income Fund only)

Date of reporting period: November 30, 2015

FORM N-CSR

The information presented in this Form N-CSR relates solely to the

MainStay Cushing MLP Premier Fund, MainStay Cushing Renaissance Advantage Fund and MainStay

Cushing Royalty Energy Income Fund, each a series of the Registrant.

Item 1. Reports to Stockholders.

MainStay Cushing® Funds

Message from the President, Cushing® Asset Management, LP,

Annual Report Commentary and Annual Report

November 30, 2015

MainStay Cushing® MLP Premier Fund

MainStay Cushing® Renaissance Advantage Fund

MainStay Cushing® Royalty Energy Income Fund

This page intentionally left blank

Message from the President

The 12-month period ended November 30, 2015, was marked by increased market volatility, particularly after the People’s Bank of China devalued the Chinese yuan on August 11, 2015. Following the devaluation, many stock markets around the world dropped substantially.

Energy stocks were particularly affected during the reporting period. Crude oil prices continued an extended decline, reaching several successive low points during the reporting period.

The Cushing Asset Management, LP, Annual Report Commentary that follows provides an overview of some of Cushing’s views on upstream, midstream and downstream energy companies and partnerships. This commentary seeks to help investors better understand the dynamics of the energy markets during the reporting period.

The following annual report provides more information on the specific market forces, securities and investment decisions that most affected your MainStay Cushing Fund(s) during the 12 months ended November 30, 2015.

We encourage you to carefully review this report and use it as you consider ways to pursue your personal financial goals and objectives.

Sincerely,

Stephen P. Fisher

President

The opinions expressed are as of the date of this report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. Past performance is no guarantee of future results.

Not part of the Annual Report

Cushing Asset Management, LP, Annual Report Commentary

The one-year fiscal period ended November 30, 2015, proved to be challenging for energy-related equities. Weakness and volatility in crude oil prices appeared to be the main driver behind investor uncertainty during the year. Historically, global demand for crude oil has improved after previous downturns, and we believe that there were signs during the reporting period that the energy industry was taking steps to adapt during the corrective part of the cycle in anticipation of a future recovery. Crude oil prices appeared to be forming a bottom in early 2015, then rallied to over $60 per barrel in May and June, before finally declining to multi-year lows below $40 per barrel in the fourth quarter of 2015. We believe exploration and production (“E&P”) company management teams have reduced capital spending due to the precipitous drop in commodities much more quickly than in prior periods of falling prices. According to IHS Herold, E&P companies reduced their capital spending guidance for 2015 by 37% on average.1 The combination of spending cuts and steep production declines of shale reserves began impacting oil supplies towards the end of the period, as U.S. crude oil production declined month after month.2 In light of the 60% decline in the U.S. oil directed rig count since October 2014, the U.S. Energy Information Administration revised its most recent energy forecast and stated that it expects monthly U.S. production to generally decline through late 2016 before growth resumes.3

Midstream MLP Sector

For the period, the midstream energy space meaningfully underperformed the broader market and other energy-related indices. As measured by the Alerian MLP Index (AMZ), the performance of master limited partnerships (MLPs) declined 38.3%. To put that into greater perspective, prices of MLPs as of November 30, 2015 represented an astounding 44% decline since August of 2014, replicating the 44% peak-to-trough decline in 2008 from the global financial crisis.

We believe there were several negative catalysts currently working in unison. First, crude oil traded down to multi-year lows is an obvious headwind for the space (as of November 30, 2015, crude oil is priced at $42/bbl). Continued weakness in natural gas prices did not help matters either, as natural gas currently sits near $2/mmbtu. In addition to weak commodity prices, technical factors such as forced selling from closed-end funds due to leverage levels and even rumors of hedge funds targeting positions of leveraged closed-end funds (from the short side) exacerbated fundamental worries. Finally, credit and distribution reduction concerns all contributed to unprecedented weakness and volatility in the midstream MLP space.

Market weakness and price volatility impairs MLPs’ cost of capital, which in turn drives a negative feedback loop. Capital markets are of critical importance to MLPs, as they are typically

externally funded investment vehicles. In other words, the majority of cash flows earned from legacy assets are returned to unitholders in the form of distributions. Therefore, funding requirements for capital expenditures on growth projects are typically externally funded via the debt and equity capital markets. Even in a scenario where the underlying fundamentals of a business remain healthy, a “freezing” of the capital markets, or at least significantly higher debt and equity costs, can quickly lead to fundamental problems.

As of the end of the period, the midstream energy space as a whole was trading at deeply discounted valuations, regardless of the metric. Price to distributable cash flow (P/DCF) multiples, a common valuation tool for MLPs, and yield spreads were near levels experienced in late 2008, the darkest days of the great financial crisis. The vast majority of large cap MLPs were yielding 10-15%, levels we believe indicated the expectation for distribution cuts. The market appeared to be anticipating further distribution cuts, which is something we simply don’t see coming to fruition at this point. In fact, several management teams of MLPs reiterated the security of their current distribution rates, even in today’s market environment.

We believe the end of the 2015 calendar year will bring an end to several non-fundamental factors impacting the MLP market, such as tax harvesting and forced closed-end fund selling (i.e. year-end redemptions will likely be complete). Furthermore, January is historically an MLP distribution-paying month, and we believe short sellers in the space will be incrementally disposed to covering ahead of these expensive ex-dates (now significantly more expensive).

We believe a rally in prices for MLPs in 2016 and beyond will likely be largely dependent upon crude oil prices. While we believe crude oil prices will continue to face near-term headwinds (e.g. high inventory levels, relatively stable production volumes, etc.), we are incrementally more positive on prospects for a recovery in the second half of 2016. Crude oil production is a cyclical industry and we are monitoring for signs the balance between supply and demand is being restored. We are seeing encouraging signs on demand growth, and capital spending by E&P companies continues to be aggressively curtailed. Generally speaking, we believe sub-$40 per barrel oil prices are uneconomical across the globe. More importantly, we believe stabilization in crude oil prices will bring investor confidence back into the asset class. Referring back to the “negative feedback loop,” we mentioned above, many midstream MLPs continued to have little to no direct exposure to crude oil prices; however, negative energy sentiment damaged their ability to access reasonably priced capital, which is leading to the fundamental problems described above.

| 1. | “Outlook for Upstream Spending for U.S. E&Ps Continues to Drop.” IHS Herold. March 9, 2015. |

| 2. | “Natural Gas Gross Withdrawals and Production” Report. U.S. Energy Information Administration. October 30, 2015. |

| 3. | “Short-Term energy and Summer Fuels Outlook (STEO).” U.S. Energy Information Administration. October 2015. |

Not part of the Annual Report

In summary, we remain confident in our belief that the longer term outlook for the midstream MLP asset class is positive, but we acknowledge that volatility is likely to continue in the immediate near term. Almost all valuation metrics are significantly below long-term historical averages and sit at levels we find compelling.

Upstream Sector

Upstream MLPs and energy-related U.S. Royalty trusts, Canadian Royalty Trusts and Canadian E&P companies (collectively, “Energy Trusts”) as well as securities of other companies based in North America that are generally engaged in the same lines of business as those in which Energy Trusts and MLPs engage (“Other Energy Companies”) continued to suffer during the fiscal period due to the inherent sensitivity of these businesses to energy prices. Many were forced to reduce or suspend distributions in response to lower crude oil and natural gas liquids prices. As unit prices for Energy Trusts and Upstream MLPs fell, the total market capitalization of the subsector decreased significantly and business fundamentals for Energy Trusts and Upstream MLPs continued to deteriorate.

During the period, Energy Trusts and Upstream MLPs continued to underperform integrated energy companies and large capitalization E&P companies. The latter two sectors showed a high correlation to energy prices, and we believe companies in those sectors have relatively stronger fundamentals and growth prospects in this challenging energy price environment. These companies also generally have better leverage ratios as compared to Energy Trusts and Upstream MLPs in the current crude oil price environment and may offer better growth potential, as well as a potential price recovery in the event oil prices recover to higher levels if the global supply-demand balance improves in the coming quarters. Our deep “bottom-up” fundamental research seeks to assist us in identifying companies with strong fundamentals and attractive growth prospects in changing market conditions while seeking to manage portfolio risk.

It is difficult to predict where oil prices will be in the coming months. The swift and dramatic response by U.S. and Canadian energy producers to reduce capital expenditures by nearly 40% appeared to slow production growth in North America. Looking at the demand side of the issue, we have continued to see signs of demand growth globally as a result of lower overall energy prices. We believe both of these macro dynamics will continue to be supportive of higher crude oil prices in the long term.

In our view, management teams of Upstream MLPs and Energy Trusts and investors are beginning to appropriately recalibrate expectations related to lower commodity price assumptions. We also think energy investors will continue to remain cautious in this environment, as crude oil and energy equity prices remain volatile. We believe that the current environment continues to challenge the fundamentals of the Upstream MLP and Energy Trust business models, and we remain defensive on those sectors. By contrast, we see greater long-term opportunity in

integrated energy companies and large-capitalization E&P companies.

Although energy companies have been challenged by continued volatility within the energy sector and the fall in crude oil prices to say the least, we remain focused on the long-term fundamental attributes of the energy sector and the potential for attractive total returns based on current yield and growth potential. We remain confident that North American shale basins will be developed over time, albeit slower pace than previously projected.

We remain focused on the favorable long-term fundamental attributes of the broad upstream sector and the potential for attractive total returns based on current yield and expected distributions. We will continue to seek out stocks with attractive valuations and long-term growth opportunities, as well as those with near-term catalysts.

U.S. Energy Renaissance

During the reporting period, the U.S. Energy Renaissance continued to strengthen as the natural gas export theme and infrastructure build-out associated with the U.S. shale revolution moved forward. The beneficiaries of the Renaissance theme continued to be dynamic during the reporting period, shifting significantly with the dramatic decline in crude oil prices. Industries which may not have been as compelling in a high crude oil price environment became favorable at a West Texas Intermediate crude oil price of approximately $50-$60 per barrel.

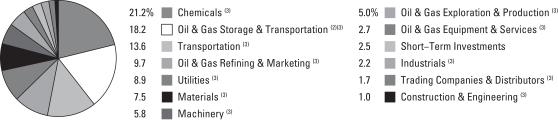

The MainStay Cushing Renaissance Advantage Fund focuses on companies that we believe have multi-year growth embedded in their business models with appropriate capital structures, good free cash flow growth and higher return on invested capital relative to their peers. Our theses on such names were not a function of their quarterly performance but a function of their underlying business fundamentals. We are believers in the multi-year growth in the transportation sector, industrial companies benefiting from energy and industrial developments and materials companies benefiting from lower feedstock prices.

On the macro economic front, there was no dearth of macro headwinds globally during the period. Clearly, China took center stage with the emerging market stock market collapse and the negative data points coming out of the second largest economy of the world. The market was led to think that a hard landing in China was around the corner. As a result, some of the Renaissance strategy’s core themes, such as LNG (“Liquefied Natural Gas”) demand, were questioned by the market, as Asia is projected to be a significant contributor to LNG demand growth in the next decade. Additionally, with the decline in crude oil prices, the sustainability of contracted LNG prices and volumes was also questioned, which was perceived as a negative read through for marine shipping companies that seek to be an integral part of the LNG value chain.

Not part of the Annual Report

We are aware of the negative macroeconomic concerns of certain investors, but we—as fundamental investors—would like to focus on positive fundamental developments. Firstly, we note that the economy has been in a declining crude oil price environment for four straight quarters and we have yet to see a single LNG contract that has been negotiated downwards, either in price or volume commitments. We realize some investors might focus on the increasing probability of this event happening in the near future. However, we note that most of these LNG contracts do not start for another couple of years and, most importantly, most of these contracts are long term in nature, with the contract duration ranging anywhere between 5-20 years. So, if we were to reverse engineer the bear thesis, one logical conclusion would be that the economic growth in emerging markets and, most importantly, the demand for LNG will be subdued for roughly the next decade. In our view, this would be a very draconian conclusion.

Fundamentals for crude oil prices continued to improve during the period, although at a slower pace than previously anticipated. Production in Non-US, Non-OPEC regions continued to decline and we finally started to see early signs of production decline in North America as well. Oil rig counts in North America continued to decline. Demand, on the other hand, surprised to the upside globally during the period. With oil prices at a nearly 60% discount to the five-year average, the beneficiaries within the scope of the U.S. Energy Renaissance shifted to those who benefitted from a lower price environment. The reduced price of crude oil resulted in significantly lower gasoline prices, which had a positive impact on operating expenses for companies with fuel expense as a high input cost in their operations, such as trucking companies, auto and auto part manufacturers, retail gas companies and airlines. Additionally, a low crude oil price environment has historically been a positive driver for domestic gross domestic product, which historically has driven additional growth opportunities for a majority of the industries within the scope of the Renaissance universe.

Due to the dynamic theme and broad scope of the U.S. Energy Renaissance, the industries and companies which see the greatest benefit can vary in different macroeconomic environments. As an example within the transportation sector, when crude oil prices were above $100 per barrel, the demand for crude oil trucking was very high due to a lack of pipeline infrastructure in developing shales. However, the decline in crude oil prices led to a decline in gasoline prices, as well as decreased demand for crude oil trucking. Trucking companies which focus on hauling consumer goods versus crude oil experienced increased margins relative to recent historical levels, without decreased volumes associated with crude oil.

Throughout the reporting period, the continued discount of U.S. natural gas prices to global natural gas prices helped several industries maintain a competitive advantage. The incentive to take advantage of the price arbitrage through exporting natural gas as LNG was the driving force behind multiple companies filing for permits to build LNG export facilities along the coasts (primarily the Gulf Coast). On the same note, U.S. industries that have a high energy input cost, such as the manufacturing, industrials and chemicals industries, continued to realize a significant competitive advantage through a reduction in operating expense as U.S. natural gas prices remained at a significant discount to natural gas prices around the world. This advantage not only drove higher margins for companies operating domestically, but also drove jobs back to the U.S. that had largely moved overseas for the past 20 years. The competitive price advantage incentivized domestic companies to increase their production capacity, which led to a significant expansion in manufacturing and chemical plants. This expansion created heightened demand for industrial companies involved with design, construction and supply.

To summarize, we believe that the fundamentals for the U.S. Energy Renaissance thesis have improved since the beginning of the reporting period. The benefit has shifted from only portions of the economy benefiting from low natural gas prices to an even larger portion of the economy benefitting from both low natural gas prices and low crude oil prices. As a result, our investment universe has broadened and we believe the markets are beginning to realize the potential benefits. We also believe both the demand fundamentals for LNG and the price for LNG have more upside potential than is being reflected by the current equity price in the entire LNG value chain. In addition to the LNG theme, other industries that are benefitting from the energy Renaissance continued their upward trajectory. U.S. petrochemical margins were steady, aided by low NGL prices across the board, despite the fall in crude oil prices. The LNG export facilities being built in North America continued to be on track. The U.S. refining industry continued to benefit both due to higher product demand and healthy margins due to lower crude oil prices. The industrial sector experienced a slowdown, particularly in industries that are levered to energy sector capex. While the market remained skeptical of energy fundamentals during the period, Energy Renaissance theme companies continued to secure contracts worth billions that show the long-term competitiveness of U.S. sourced energy and LNG. Through active management, we believe the portfolio holdings can be adapted to capitalize on the opportunities created by the U.S. Energy Renaissance as it plays out over the next several years.

The information provided herein represents the opinion of the portfolio manager and in not intended to be a forecast of future events, a guarantee of future results, nor investment advice. The opinions expressed are as of the date of this report and are subject to change.

Not part of the Annual Report

Investors should refer to each Fund’s Summary Prospectus and/or Prospectus and consider each Fund’s investment objectives, strategies, risks, charges and expenses carefully before investing. The Summary Prospectus and/or Prospectus contain this and other information about each Fund. You may obtain copies of each Fund’s Summary Prospectus, Prospectus and Statement of Additional Information free of charge, upon request, by calling toll-free 800-MAINSTAY (624-6782), by writing to NYLIFE Distributors LLC, Attn: MainStay Marketing Department, 169 Lackawanna Avenue, Parsippany, New Jersey 07054 or by sending an e-mail to MainStayShareholderServices@nylim.com. These documents are also available via the MainStay Funds’ website at mainstayinvestments.com/documents. Please read each Summary Prospectus and/or Prospectus carefully before investing.

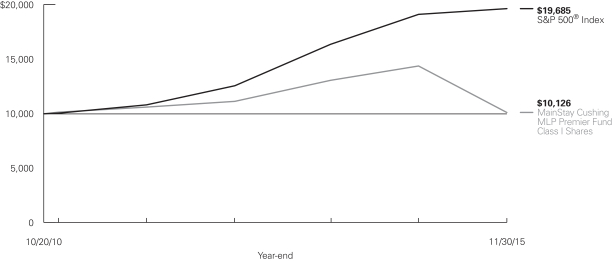

MainStay Cushing MLP Premier Fund

Investment and Performance Comparison1 (Unaudited)

Performance data quoted represents past performance. Past performance is no guarantee of future results. Because of market volatility, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate, and as a result, when shares are redeemed, they may be worth more or less than their original cost. The graph below depicts the historical performance of Class I shares of the Fund. Performance will vary from class to class based on differences in class-specific expenses and sales charges. For performance information current to the most recent month-end, please call 800-MAINSTAY (624-6782) or visit mainstayinvestments.com.

Average Annual Total Returns for the Year Ended November 30, 2015

| Class | Sales Charge | One Year | Since Inception (10/20/10) | Gross Expense Ratio2 | ||||||||||||

| Class A Shares3 | Maximum 5.5% Initial Sales Charge | With sales charge Excluding sales charge |

| –33.77 –29.92 | %

|

| –1.16 –0.01 | %

|

| 6.98 6.98 | %

| |||||

| Investor Class Shares4 | Maximum 5.5% Initial Sales Charge | With sales charge Excluding sales charge |

| –33.77 –29.91 |

| | –1.16 –0.01 | | | 6.97 6.97 | | |||||

| Class C Shares3 | Maximum 1% CDSC if Redeemed Within One Year of Purchase | With sales charge Excluding sales charge |

| –31.08 –30.43 |

| | –0.77 –0.77 | | | 7.72 7.72 | | |||||

| Class I Shares3 | No Sales Charge | –29.71 | 0.24 | 6.73 | ||||||||||||

| 1. | The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on distributions or Fund share redemptions. Total returns reflect maximum applicable sales charges as indicated in the table above, changes in share price, and reinvestment of dividend and capital gain distributions. The graph assumes the initial investment amount shown above and reflects the deduction of all sales charges that would have applied for the period of investment. Performance figures reflect certain fee waivers and/or expense limitations, without which total returns may have been lower. For more information on share classes and current fee waivers and/or expense limitations, please refer to the notes to the financial statements. |

| 2. | The gross expense ratios presented reflect the Fund’s “Total Annual Fund Operating Expenses” from the most recent Prospectus and may differ from other expense ratios disclosed in this report. |

| 3. | Performance figures for Class A shares, Class C shares and Class I shares reflect the historical performance of the then-existing Class A shares, Class C shares and Class I shares, respectively, of the Cushing® MLP Premier Fund (the predecessor to the Fund, which was subject to a different fee structure) for periods prior to July 11, 2014. The Cushing® MLP Premier Fund commenced operations on October 20, 2010. |

| 4. | Performance figures for Investor Class shares, first offered on July 11, 2014, include the historical performance of Class A shares through July 10, 2014, adjusted for differences in certain expenses and fees. Unadjusted, the performance shown for Investor Class shares would likely have been different. |

The footnotes on the next page are an integral part of the table and graph and should be carefully read in conjunction with them.

| 8 | MainStay Cushing MLP Premier Fund |

| Benchmark Performance | One Year | Since Inception | ||||||

S&P 500® Index5 | 2.75 | % | 14.16 | % | ||||

Average Lipper Energy MLP Fund6 | –32.52 | 2.31 | ||||||

| 5. | “S&P 500®” is a trademark of The McGraw-Hill Companies, Inc. The S&P 500® Index is widely regarded as the standard index for measuring large-cap U.S. stock market performance. The S&P 500® Index is the Fund’s primary benchmark. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an index. |

| 6. | The average Lipper Energy MLP Fund is representative of funds that invest primarily in Master Limited Partnerships (MLPs) engaged in the |

| transportation, storage and processing of minerals and natural resources. This benchmark is a product of Lipper Inc. Lipper Inc. is an independent monitor of fund performance. Results are based on average total returns of similar funds with all dividend and capital gain distributions reinvested. |

The footnotes on the preceding page are an integral part of the table and graph and should be carefully read in conjunction with them.

| 9 |

Cost in Dollars of a $1,000 Investment in MainStay Cushing MLP Premier Fund (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the six-month period from June 1, 2015, to November 30, 2015, and the impact of those costs on your investment.

Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including exchange fees and sales charges (loads) on purchases (as applicable), and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from June 1, 2015, to November 30, 2015.

This example illustrates your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six months ended November 30, 2015. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then

multiply the result by the number under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in the Fund with the ongoing costs of investing in other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other Funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as exchange fees or sales charges (loads). Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Share Class | Beginning Value | Ending Account Value (Based | Expenses During | Ending Account Value (Based on Hypothetical 5% Annualized Return and Actual Expenses) 11/30/15 | Expenses During | |||||||||||||||

| Class A Shares | $ | 1,000.00 | $ | 719.50 | $ | 6.42 | $ | 1,017.60 | $ | 7.54 | ||||||||||

| Investor Class Shares | $ | 1,000.00 | $ | 719.50 | $ | 6.47 | $ | 1,017.55 | $ | 7.59 | ||||||||||

| Class C Shares | $ | 1,000.00 | $ | 717.10 | $ | 9.64 | $ | 1,013.84 | $ | 11.31 | ||||||||||

| Class I Shares | $ | 1,000.00 | $ | 720.80 | $ | 5.35 | $ | 1,018.85 | $ | 6.28 | ||||||||||

| 1. | Expenses are equal to the Fund’s annualized expense ratio of each class (1.49% for Class A, 1.50% for Investor Class, 2.24% for Class C and 1.24% for Class I) multiplied by the average account value over the period, divided by 365 and multiplied by 183 for Class A, Investor Class, Class C, and Class I (to reflect the six-month period). Expenses for the six-month period ended excluded a net deferred tax benefit to the Fund that equaled 8.56% for Class A, 8.55% for Investor Class, 8.56% for Class C, and 8.56% for Class I. The table above represents the actual expenses incurred during the six-month period. |

| 10 | MainStay Cushing MLP Premier Fund |

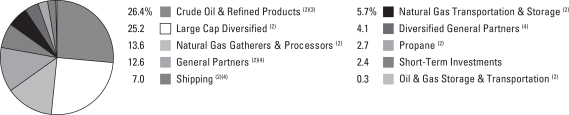

Portfolio Composition as of November 30, 2015(1) (Unaudited)

(Expressed as a Percentage of Total Investments)

See Portfolio of Investments beginning on page 14 for specific holdings within these categories.

Top Ten Holdings as of November 30, 2015 (excluding short-term investments)

| 1. | Enterprise Products Partners, L.P. |

| 2. | Tesoro Logistics, L.P. |

| 3. | Energy Transfer Partners, L.P. |

| 4. | EQT Midstream Partners, L.P. |

| 5. | Energy Transfer Equity, L.P. |

| 6. | Genesis Energy, L.P. |

| 7. | Sunoco Logistics Partners, L.P. |

| 8. | Williams Partners, L.P. |

| 9. | Shell Midstream Partners, L.P. |

| 10. | Kinder Morgan, Inc. |

| (1) | Fund holdings and sector allocations are subject to change, and there is no assurance that the Fund will continue to hold any particular security. |

| (2) | Master Limited Partnerships and Related Companies |

| (3) | Preferred Stock |

| (4) | Common Stock |

| 11 |

Portfolio Management Discussion and Analysis (Unaudited)

Questions answered by portfolio managers Jerry V. Swank and Kevin P. Gallagher, CFA, of Cushing Asset Management, LP, the Fund’s Subadvisor.

How did MainStay Cushing MLP Premier Fund perform relative to its primary benchmark and peers during the 12 months ended November 30, 2015?

Excluding all sales charges, MainStay Cushing MLP Premier Fund returned –29.92% for Class A shares, –29.91% for Investor Class shares and –30.43% for Class C shares for the 12 months ended November 30, 2015. Over the same period, Class I shares returned –29.71%. For the 12 months ended November 30, 2015, all share classes underperformed the 2.75% return of the S&P 500® Index,1 which is the Fund’s broad-based securities-market index. Over the same period, all share classes outperformed the –32.52% return of the Average Lipper2 Energy MLP Fund. See page 8 for Fund returns with applicable sales charges.

Were there any changes to the Fund?

Effective December 7, 2015, Daniel L. Spears no longer serves as a portfolio manager of the Fund. Jerry V. Swank and Kevin P. Gallagher will continue to manage the Fund.

What factors affected the Fund’s performance relative to the S&P 500® Index during the reporting period?

The most significant factors that affected the Fund’s performance relative to the S&P 500® Index during the reporting period were primarily related to significant declines in commodity prices (crude oil, natural gas and natural gas liquids). These declines were driven by supply/demand imbalances, which weakened the operational and financial outlook for—and investor sentiment toward—the energy industry overall, including energy infrastructure master limited partnerships (“MLPs”). The S&P 500® Index includes stocks across many sectors, while the Fund’s exposure is limited to the energy sector. In this weakened energy environment, which led to significant selling pressure on energy equities and Fund holdings, many MLPs experienced slower or reduced volumes, slower capital spending on organic growth projects, higher leverage, diminished access to—and higher costs for—debt and equity capital, and slowing distribution growth. Other technical factors that likely pressured MLP equities and Fund holdings during the latter part of the reporting period included year-end tax-loss selling (i.e. tax harvesting), slowing retail fund flows into MLP-related investment products compared to the prior year, and MLP position liquidations by public closed-end funds to meet leverage covenants. In addition, unlike the S&P 500® Index, the Fund is subject to fees and expenses and is taxed as a regular corporation for federal income tax purposes, which may have a negative effect on the Fund’s performance relative to the Index.

Which subsectors were the strongest contributors to the Fund’s absolute performance and which subsectors were particularly weak?

The top subsector contributors to the Fund’s absolute performance during the reporting period were MLPs in the natural gas transportation & storage subsector, upstream MLPs and shipping MLP general partners. (Contributions take weightings and total returns into account.) The performance of each of these subsectors was negative for the reporting period, but the impact was moderated by the Fund’s relatively modest average weightings, which were less than 5% for each subsector. The Fund sold its two holdings in upstream MLPs early in the reporting period, so the Fund’s average exposure to this subsector was just 0.1% for the 12 months ended November 30, 2015.

The subsectors that detracted the most from the Fund’s absolute performance were MLPs in the large-cap diversified, natural gas gatherers & processors, and MLP general partners subsectors. All of these subsectors had negative absolute returns for the reporting period. Of these subsectors, the most substantial weighting was in the large-cap diversified subsector, partly because we believe that many of these partnerships are in the best position to weather the industry downturn from an operations and financial perspective. The natural gas gatherers & processors subsector was hurt by slowing or reduced system throughput and lower commodity prices. The MLP general partners subsector suffered from investor concerns about slowing distribution growth at the underlying MLPs.

During the reporting period, which individual holdings made the strongest contributions to the Fund’s absolute performance and which holdings detracted the most?

The top contributor to the Fund’s absolute performance during the reporting period was Shell Midstream Partners, L.P., a “drop-down” MLP with expected multiyear double-digit distribution growth in the crude oil & refined products subsector. This was followed by Spectra Energy Partners L.P., a natural gas transportation & storage MLP with stable and growing cash flows driven by a large project backlog, and Crestwood Equity Partners, L.P., a holding that was sold from the Fund in December 2014 (at the time, it was classified in the MLP general partners subsector). The contribution from each of these positions was approximately zero. Throughout the reporting period, we used periods of MLP market weakness (including periods of investor concern about funding growth projects) to add to the Shell Midstream Partners position.

The position that detracted the most from the Fund’s absolute performance during the reporting period was Targa Resources Corp., an MLP general partner with interests in a commodity-

| 1. | See footnote on page 9 for more information on the S&P 500® Index. |

| 2. | See footnote on page 9 for more information on Lipper Inc. |

| 12 | MainStay Cushing MLP Premier Fund |

sensitive natural gas gatherers & processors MLP. This was followed by Plains All American Pipeline, L.P., a large-cap diversified MLP, and Kinder Morgan Inc., a large diversified midstream company. Each of these detractors had negative absolute performance driven by the deteriorating commodity price environment. The Fund reduced the size of its position in Targa Resources during the reporting period because of slowing distribution growth at the underlying MLP and the levered impact on general partner cash flows. Following the second quarter earnings call for Plains All American Pipeline, L.P., the Fund reduced its position. We believed that the MLP’s business was performing worse than expected (in part because of competition) and that the near-term outlook was unlikely to improve. The Fund reduced its position in Kinder Morgan through the reporting period because of slowing growth expectations and the company’s relatively high leverage. (The Fund completely exited the position after the end of the reporting period following a sizeable cut in Kinder Morgan’s dividend.)

Did the Fund make any significant purchases or sales during the reporting period?

During the reporting period, the Fund’s largest purchase was Enterprise Products Partners, L.P., a large-cap diversified MLP. We added to the Fund’s position in Enterprise Products Partners because we believed that this MLP had a strong ability to weather the volatile environment. Enterprise Products Partners, L.P. had a large and diverse footprint of integrated assets, a relatively low cost of capital, a good backlog of contracted fee-based projects, healthy cash flow coverage and a strong bal-

ance sheet. We also added to the Fund’s position in Tesoro Logistics, L.P., a crude oil & refined products MLP, throughout the reporting period because of its relatively high distribution yield and projected double-digit multiyear distribution growth driven by drop-down transactions from its supportive sponsor/parent as well as an inventory of organic projects.

During the reporting period, we sold shares of The Williams Companies Inc., an MLP general partner, after it announced a merger agreement with Energy Transfer Equity, L.P. We used the sale to reduce the Fund’s combined exposure to the pro forma merged entity. We also sold units of Regency Energy Partners, L.P., formerly a natural gas gatherers & processors MLP, because of its merger agreement with Energy Transfer Partners L.P.

How did the Fund’s subsector weightings change during the reporting period?

During the reporting period, we increased the Fund’s exposure to the crude oil & refined products and large-cap diversified MLP subsectors. We decreased the Fund’s exposure to the general partners and natural gas gatherers & processors subsectors.

How was the Fund positioned at the end of the reporting period?

As of November 30, 2015, the Fund’s largest MLP subsector positions were in large cap diversified and in crude oil & refined products. Together, these positions accounted for more than 50% of the Fund’s net assets.

The opinions expressed are those of the portfolio managers as of the date of this report and are subject to change. There is no guarantee that any forecasts will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

| 13 |

Portfolio of Investments November 30, 2015

| Shares | Value | |||||||

| Common Stocks 13.2%† | ||||||||

Diversified General Partners 4.1% |

| |||||||

United States 4.1% |

| |||||||

ONEOK, Inc. | 889,800 | $ | 26,231,304 | |||||

Williams Companies, Inc. | 759,700 | 27,774,632 | ||||||

|

| |||||||

| 54,005,936 | ||||||||

|

| |||||||

General Partners 5.8% |

| |||||||

United States 5.8% |

| |||||||

¨Kinder Morgan, Inc. | 2,088,432 | 49,224,342 | ||||||

Targa Resources Corporation | 708,100 | 27,828,330 | ||||||

|

| |||||||

| 77,052,672 | ||||||||

|

| |||||||

Shipping 3.3% | ||||||||

Bermuda 1.6% | ||||||||

Golar LNG Ltd. | 770,000 | 21,059,500 | ||||||

|

| |||||||

Republic of the Marshall Islands 1.7% |

| |||||||

Teekay Corporation | 830,000 | 23,107,200 | ||||||

|

| |||||||

| 44,166,700 | ||||||||

|

| |||||||

Total Common Stocks | 175,225,308 | |||||||

|

| |||||||

| MLPs and Related Companies 83.2% | ||||||||

Crude Oil & Refined Products 25.4% |

| |||||||

United States 25.4% |

| |||||||

Blueknight Energy Partners, L.P. (a) | 2,161,200 | 13,399,440 | ||||||

Enbridge Energy Partners, L.P. | 1,597,800 | 39,705,330 | ||||||

¨Genesis Energy, L.P. | 1,590,061 | 62,568,900 | ||||||

NuStar Energy, L.P. | 828,500 | 33,156,570 | ||||||

¨Shell Midstream Partners, L.P. | 1,497,987 | 52,234,807 | ||||||

¨Sunoco Logistics Partners, L.P. | 2,098,400 | 58,482,408 | ||||||

¨Tesoro Logistics, L.P. | 1,540,600 | 76,952,970 | ||||||

|

| |||||||

| 336,500,425 | ||||||||

|

| |||||||

General Partners 6.7% |

| |||||||

United States 6.7% |

| |||||||

¨Energy Transfer Equity, L.P. | 3,697,200 | 70,024,968 | ||||||

Plains GP Holdings, L.P. | 1,555,000 | 19,064,300 | ||||||

|

| |||||||

| 89,089,268 | ||||||||

|

| |||||||

Large Cap Diversified 25.2% |

| |||||||

United States 25.2% |

| |||||||

¨Energy Transfer Partners, L.P. | 2,005,312 | 76,622,972 | ||||||

¨Enterprise Products Partners, L.P. | 3,514,250 | 89,226,807 | ||||||

Magellan Midstream Partners, L.P. | 506,615 | 31,678,636 | ||||||

ONEOK Partners, L.P. | 1,121,600 | 33,905,968 | ||||||

Plains All American Pipeline, L.P. | 1,770,905 | 43,883,026 | ||||||

¨Williams Partners, L.P. | 2,111,603 | 57,900,154 | ||||||

|

| |||||||

| 333,217,563 | ||||||||

|

| |||||||

| Shares | Value | |||||||

Natural Gas Gatherers & Processors 13.5% |

| |||||||

United States 13.5% |

| |||||||

DCP Midstream Partners, L.P. | 541,000 | $ | 13,741,400 | |||||

Enable Midstream Partners, L.P. | 524,124 | 4,926,765 | ||||||

EnLink Midstream Partners, L.P. | 2,861,700 | 42,696,564 | ||||||

MarkWest Energy Partners, L.P. | 941,400 | 45,187,200 | ||||||

Targa Resources Partners, L.P. | 1,453,025 | 33,187,091 | ||||||

Western Gas Partners, L.P. | 828,600 | 39,789,372 | ||||||

|

| |||||||

| 179,528,392 | ||||||||

|

| |||||||

Natural Gas Transportation & Storage 5.7% |

| |||||||

United States 5.7% |

| |||||||

¨EQT Midstream Partners, L.P. | 1,110,000 | 75,091,500 | ||||||

|

| |||||||

Oil & Gas Storage & Transportation 0.3% |

| |||||||

United States 0.3% |

| |||||||

Spectra Energy Partners L.P. | 100,000 | 4,237,000 | ||||||

|

| |||||||

Propane 2.7% |

| |||||||

United States 2.7% |

| |||||||

NGL Energy Partners, L.P. | 2,018,652 | 35,427,343 | ||||||

|

| |||||||

Shipping 3.7% |

| |||||||

Republic of the Marshall Islands 3.7% |

| |||||||

Capital Product Partners, L.P. | 4,991,100 | 31,443,930 | ||||||

Golar LNG Partners, L.P. | 1,230,000 | 17,638,200 | ||||||

|

| |||||||

| 49,082,130 | ||||||||

|

| |||||||

Total MLPs and Related Companies | 1,102,173,621 | |||||||

|

| |||||||

| Preferred Stocks 1.0% | ||||||||

Crude Oil & Refined Products 1.0% |

| |||||||

United States 1.0% |

| |||||||

Blueknight Energy Partners, L.P. (a) | 1,902,541 | 13,013,381 | ||||||

|

| |||||||

Total Preferred Stocks | 13,013,381 | |||||||

|

| |||||||

| Short-Term Investments—Investment Companies 2.4% | ||||||||

United States 2.4% | ||||||||

Invesco Short-Term Treasury Portfolio Fund—Institutional Class, | 6,341,649 | 6,341,649 | ||||||

Fidelity Government Portfolio Fund—Institutional Class, | 6,341,648 | 6,341,648 | ||||||

Fidelity Money Market Portfolio— | 6,341,648 | 6,341,648 | ||||||

| † | Calculated as a percentage of net assets applicable to common shareholders. |

| ¨ | Among the Portfolio’s 10 largest holdings or issuers held, as of November 30, 2015, excluding short-term investments. May be subject to change daily. |

| 14 | MainStay Cushing MLP Premier Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

| Shares | Value | |||||||

| Short-Term Investments—Investment Companies (continued) | ||||||||

United States (continued) |

| |||||||

First American Prime Obligations Fund—Class Z, | 6,341,649 | $ | 6,341,649 | |||||

Invesco STIC Prime Portfolio, | 6,341,649 | 6,341,649 | ||||||

|

| |||||||

Total Short-Term Investments—Investment Companies | 31,708,243 | |||||||

|

| |||||||

Total Investments | 99.8 | % | 1,322,120,553 | |||||

Other Assets in Excess of Liabilities | 0.2 | 2,060,412 | ||||||

Net Assets | 100.0 | % | $ | 1,324,180,965 | ||||

| (a) | Illiquid security—As of November 30, 2015, the total market value of securities deemed illiquid under procedures approved by the Board of Trustees was $26,412,821, which represented 1.99% of the Fund’s net assets. |

| (b) | Rate reported is the current yield as of November 30, 2015. |

| (c) | As of November 30, 2015, cost was $1,436,380,112 for federal income tax purposes and net unrealized depreciation was as follows: |

Gross unrealized appreciation | $ | 492,113,759 | ||

Gross unrealized depreciation | (606,373,318 | ) | ||

|

| |||

Net unrealized depreciation | $ | (114,259,559 | ) | |

|

|

The following is a summary of the fair valuations according to the inputs used as of November 30, 2015, for valuing the Fund’s assets and liabilities.

Asset Valuation Inputs

Description | Quoted Prices in Active Markets for Assets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant (Level 3) | Total | ||||||||||||

| Investments in Securities (a) | ||||||||||||||||

Common Stocks | $ | 175,225,308 | $ | — | $ | — | $ | 175,225,308 | ||||||||

MLPs and Related Companies | 1,102,173,621 | — | — | 1,102,173,621 | ||||||||||||

Preferred Stock | 13,013,381 | — | — | 13,013,381 | ||||||||||||

Short-Term Investments | 31,708,243 | — | — | 31,708,243 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| Total Investments in Securities | $ | 1,322,120,553 | $ | — | $ | — | $ | 1,322,120,553 | ||||||||

|

|

|

|

|

|

|

| |||||||||

| (a) | For a complete listing of investments and their industries, see the Portfolio of Investments. |

The Fund recognizes transfers between the levels as of the beginning of the period.

For the year ended November 30, 2015, the Fund did not have any transfers between Level 1 and Level 2 fair value measurements (See Note 2).

As of November 30, 2015, the Fund did not hold any investments with significant unobservable inputs (Level 3) (See Note 2).

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 15 |

Statement of Assets and Liabilities as of November 30, 2015

| Assets | ||||

Investments, at value | $ | 1,322,120,553 | ||

Receivables: | ||||

Investments sold | 4,033,421 | |||

Fund shares sold | 11,824,984 | |||

Dividends and interest | 1,876 | |||

Prepaid expenses | 49,010 | |||

|

| |||

Total assets | 1,338,029,844 | |||

|

| |||

| Liabilities | ||||

Payables: | ||||

Fund shares redeemed | 7,031,768 | |||

Investments purchased | 4,255,465 | |||

Advisory fees (See Note 3) | 1,262,529 | |||

NYLIFE Distributors (See Note 3) | 553,988 | |||

Transfer agent (See Note 3) | 276,000 | |||

Shareholder communication | 70,438 | |||

Professional fees | 54,574 | |||

Custodian | 3,501 | |||

Trustees | 370 | |||

Accrued expenses | 81,365 | |||

Franchise taxes | 258,881 | |||

|

| |||

Total liabilities | 13,848,879 | |||

|

| |||

Net assets | $ | 1,324,180,965 | ||

|

| |||

| Composition of Net Assets | ||||

Shares of beneficial interest outstanding (par value of $.001 per share) unlimited number of shares authorized | $ | 92,889 | ||

Additional paid-in capital | 1,676,667,400 | |||

|

| |||

| 1,676,760,289 | ||||

Accumulated net investment loss, net of income taxes | (69,765,351 | ) | ||

Accumulated net realized gain (loss) on investments, net of income taxes | (56,218,817 | ) | ||

Net unrealized appreciation (depreciation) on investments, net of income taxes | (226,595,156 | ) | ||

|

| |||

Net assets | $ | 1,324,180,965 | ||

|

| |||

Class A | ||||

Net assets applicable to outstanding shares | $ | 317,903,246 | ||

|

| |||

Shares of beneficial interest outstanding | 21,967,819 | |||

|

| |||

Net asset value per share outstanding | $ | 14.47 | ||

Maximum sales charge (5.50% of offering price) | 0.80 | |||

|

| |||

Maximum offering price per share outstanding | $ | 15.27 | ||

|

| |||

Investor Class | ||||

Net assets applicable to outstanding shares | $ | 2,630,563 | ||

|

| |||

Shares of beneficial interest outstanding | 181,822 | |||

|

| |||

Net asset value per share outstanding | $ | 14.47 | ||

Maximum sales charge (5.50% of offering price) | 0.80 | |||

|

| |||

Maximum offering price per share outstanding | $ | 15.27 | ||

|

| |||

Class C | ||||

Net assets applicable to outstanding shares | $ | 553,891,725 | ||

|

| |||

Shares of beneficial interest outstanding | 40,115,163 | |||

|

| |||

Net asset value per share outstanding | $ | 13.81 | ||

|

| |||

Class I | ||||

Net assets applicable to outstanding shares | $ | 449,755,431 | ||

|

| |||

Shares of beneficial interest outstanding | 30,624,212 | |||

|

| |||

Net asset value per share outstanding | $ | 14.69 | ||

|

|

| 16 | MainStay Cushing MLP Premier Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Statement of Operations for the year ended November 30, 2015

| Investment Income (Loss) | ||||

Income | ||||

Dividends and distributions | $ | 22,236,475 | ||

Interest | 38,034 | |||

|

| |||

Total income | 22,274,509 | |||

|

| |||

Expenses | ||||

Manager (See Note 3) | 19,828,997 | |||

Distribution/Service—Class A (See Note 3) | 1,159,611 | |||

Distribution/Service—Investor Class (See Note 3) | 5,882 | |||

Distribution/Service—Class C (See Note 3) | 7,710,821 | |||

Transfer agent (See Note 3) | 1,505,243 | |||

Registration | 368,105 | |||

Professional fees | 245,165 | |||

Franchise tax | 517,762 | |||

Shareholder communication | 376,616 | |||

Trustees | 23,300 | |||

Custodian | 21,740 | |||

Miscellaneous | 35,476 | |||

|

| |||

Net expenses | 31,798,718 | |||

|

| |||

Net investment loss, before income taxes | (9,524,209 | ) | ||

Deferred tax benefit | 7,343,122 | |||

|

| |||

Net investment income (loss) | (2,181,087 | ) | ||

|

| |||

| Realized and Unrealized Gain (Loss) on Investments | ||||

Net realized gain (loss) on: | ||||

Investments, before income taxes | (127,225,171 | ) | ||

Deferred tax benefit | 46,981,594 | |||

|

| |||

Net realized gain (loss) on investments | (80,243,577 | ) | ||

|

| |||

Net change in unrealized appreciation (depreciation) on: | ||||

Investments, before income taxes | (606,373,036 | ) | ||

Deferred tax benefit, net of valuation allowance | 100,482,703 | |||

|

| |||

Net change in unrealized appreciation (depreciation) | (505,890,333 | ) | ||

|

| |||

Net realized and unrealized gain (loss) on investments | (586,133,910 | ) | ||

|

| |||

Net increase (decrease) in net assets resulting from operations | $ | (588,314,997 | ) | |

|

| |||

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 17 |

Statements of Changes in Net Assets

| Year ended November 30, 2015 | Year ended November 30, 2014 | |||||||

| Increase (Decrease) in Net Assets | ||||||||

Operations: | ||||||||

Net investment income (loss) | $ | (2,181,087 | ) | $ | (10,515,805 | ) | ||

Net realized gain (loss) on investments | (80,243,577 | ) | 35,136,178 | |||||

Net change in unrealized appreciation (depreciation) on investments | (505,890,333 | ) | 100,775,299 | |||||

|

| |||||||

Net increase (decrease) in net assets resulting from operations | (588,314,997 | ) | 125,395,672 | |||||

|

| |||||||

Dividends and distributions to shareholders: | ||||||||

From net investment income: | ||||||||

Class A | — | (14,189,873 | ) | |||||

Investor Class | — | (6,008 | ) | |||||

Class C | — | (20,166,403 | ) | |||||

Class I | — | (10,131,458 | ) | |||||

|

| |||||||

| — | (44,493,742 | ) | ||||||

|

| |||||||

From return of capital: | ||||||||

Class A | (31,601,906 | ) | (18,145,019 | ) | ||||

Investor Class | (172,126 | ) | (7,683 | ) | ||||

Class C | (55,256,642 | ) | (25,787,389 | ) | ||||

Class I | (38,732,047 | ) | (12,955,400 | ) | ||||

|

| |||||||

| (125,762,721 | ) | (56,895,491 | ) | |||||

|

| |||||||

Total dividends and distributions to shareholders | (125,762,721 | ) | (101,389,233 | ) | ||||

|

| |||||||

Capital share transactions: | ||||||||

Net proceeds from sale of shares | 753,559,128 | 1,058,742,376 | ||||||

Net asset value of shares issued to shareholders in reinvestment of dividends and distributions | 116,970,153 | 86,845,034 | ||||||

Cost of shares redeemed | (803,926,743 | ) | (475,289,126 | ) | ||||

|

| |||||||

Increase (decrease) in net assets derived from capital share transactions | 66,602,538 | 670,298,284 | ||||||

|

| |||||||

Net increase (decrease) in net assets | (647,475,180 | ) | 694,304,723 | |||||

| Net Assets | ||||||||

Beginning of year | 1,971,656,145 | 1,277,351,422 | ||||||

|

| |||||||

End of year | $ | 1,324,180,965 | $ | 1,971,656,145 | ||||

|

| |||||||

Accumulated net investment loss, net of income taxes | $ | (69,765,351 | ) | $ | (67,584,264 | ) | ||

|

| |||||||

| 18 | MainStay Cushing MLP Premier Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Financial Highlights selected per share data and ratios

| Year ended November 30, | ||||||||||||||||||||

| Class A | 2015 | 2014 | 2013*** | 2012*** | 2011*** | |||||||||||||||

Net asset value at beginning of year | $ | 22.15 | $ | 21.36 | $ | 19.48 | $ | 19.92 | $ | 20.28 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net investment income (loss) (a) | 0.03 | (0.09 | ) | (0.12 | ) | (0.13 | ) | (0.14 | ) | |||||||||||

Net realized and unrealized gain (loss) on investments | (6.37 | ) | 2.21 | 3.34 | 1.02 | 1.07 | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations | (6.34 | ) | 2.12 | 3.22 | 0.89 | 0.93 | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| Less dividends and distributions: | ||||||||||||||||||||

From net investment income | — | (0.59 | ) | — | — | — | ||||||||||||||

From return of capital | (1.34 | ) | (0.75 | ) | (1.34 | ) | (1.34 | ) | (1.30 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total dividends and distributions | (1.34 | ) | (1.34 | ) | (1.34 | ) | (1.34 | ) | (1.30 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Redemption fees retained (a)(b) | — | 0.01 | 0.00 | ‡ | 0.01 | 0.01 | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value at end of year | $ | 14.47 | $ | 22.15 | $ | 21.36 | $ | 19.48 | $ | 19.92 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total investment return (c) | (29.92 | %) | 10.00 | % | 16.91 | % | 4.56 | % | 4.55 | % | ||||||||||

| Ratios (to average net assets)/Supplemental Data: | ||||||||||||||||||||

Net investment income (loss) (including net deferred income tax benefit (expense)) (d) | 8.32 | % (e) | (6.46 | %) | (9.12 | %) | (2.95 | %) | (1.95 | %) | ||||||||||

Net investment income (loss) (excluding net deferred income tax benefit (expense)) (d) | (0.24 | %)(e) | (0.97 | %) | (1.18 | %) | (1.23 | %) | (1.29 | %) | ||||||||||

Net expenses (including net deferred income tax (benefit) expense) (d)(f) | (7.07 | %)(e) | 7.08 | % | 9.59 | % | 3.37 | % | 2.32 | % | ||||||||||

Expenses (before waiver/recoupment, including net deferred income tax (benefit) | (7.07 | %)(e) | 7.03 | % | 9.57 | % | 3.43 | % | 3.29 | % | ||||||||||

Portfolio turnover rate | 32.35 | % | 20.70 | % | 27.29 | % | 43.32 | % | 72.32 | % | ||||||||||

Net assets at end of year (in 000’s) | $ | 317,903 | $ | 531,607 | $ | 487,318 | $ | 306,054 | $ | 81,865 | ||||||||||

| *** | These years were audited by a predecessor audit firm whose opinion was unqualified. |

| ‡ | Less than one cent per share. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Redemption fees were only applicable prior to reorganization. (See Note 1) |

| (c) | Total investment return is calculated exclusive of sales charges and assumes the reinvestment of dividends and distributions. |

| (d) | For the year ended November 30, 2015, the Fund accrued $154,807,419 in net deferred income tax benefit, of which $39,834,200 is attributable to Class A. For the year ended November 30, 2014, the Fund accrued $70,224,241 in net deferred income tax expense, of which $30,305,000 is attributable to Class A. For the year ended November 30, 2013, the Fund accrued $77,002,011 in net deferred income tax expense, of which $31,765,943 is attributable to Class A. For the year ended November 30, 2012, the Fund accrued $7,120,938 in net deferred income tax expense, of which $3,616,649 is attributable to Class A. For the year ended November 30, 2011, the Fund accrued $452,365 in net deferred tax expense, of which $212,282 is attributable to Class A. |

| (e) | Ratios including/excluding net deferred income tax benefit (expense) includes applicable franchise tax expense for the period. For the year ended November 30, 2015, the Fund accrued $517,762 in franchise tax expense, of which $128,449 is attributable to Class A. |

| (f) | The ratio of expenses excluding net deferred income tax expense to average net assets before waiver and recoupment was 1.49%, 1.54%, 1.63%, 1.71% and 2.62% for the fiscal years ended November 30, 2015, 2014, 2013, 2012 and 2011, respectively. The ratio of expenses excluding net deferred income tax expense to average net assets after waiver and recoupment was 1.49%, 1.59%, 1.65%, 1.65%, and 1.65% for the fiscal years ended November 30, 2015, 2014, 2013, 2012 and 2011, respectively. |

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 19 |

Financial Highlights selected per share data and ratios

| Investor Class | Year ended November 30, 2015 | July 12, 2014** through November 30, 2014 | ||||||

Net asset value at beginning of period | $ | 22.15 | $ | 24.02 | ||||

|

|

|

| |||||

Net investment income (loss) (a) | (0.00 | )‡ | (0.03 | ) | ||||

Net realized and unrealized gain (loss) on investments | (6.34 | ) | (1.17 | ) | ||||

|

|

|

| |||||

Total from investment operations | (6.34 | ) | (1.20 | ) | ||||

|

|

|

| |||||

| Less dividends and distributions: | ||||||||

From net investment income | — | (0.29 | ) | |||||

From return of capital | (1.34 | ) | (0.38 | ) | ||||

|

|

|

| |||||

Total dividends and distributions | (1.34 | ) | (0.67 | ) | ||||

|

|

|

| |||||

Net asset value at end of period | $ | 14.47 | $ | 22.15 | ||||

|

|

|

| |||||

Total investment return (b) | (29.91 | %)(d) | (5.12 | %)(c)(d) | ||||

| Ratios (to average net assets)/Supplemental Data: | ||||||||

Net investment income (loss) (including net deferred income tax benefit (expense)) (e) | 8.17 | % (f) | 2.79 | % †† | ||||

Net investment income (loss) (excluding net deferred income tax benefit (expense)) (e) | (0.38 | %)(f) | (0.52 | %)†† | ||||

Net expenses (including net deferred income tax (benefit) expense) (e)(g) | (7.05 | %)(f) | (1.80 | %)†† | ||||

Expenses (before waiver/recoupment, including net deferred income tax (benefit) expense) (e)(g) | (7.05 | %)(f) | (1.80 | %)†† | ||||

Portfolio turnover rate | 32.35 | % | 20.70 | % | ||||

Net assets at end of period (in 000’s) | $ | 2,631 | $ | 1,310 | ||||

| ** | Inception date. |

| ‡ | Less than one cent per share. |

| †† | Annualized. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Total investment return is calculated exclusive of sales charges and assumes the reinvestment of dividends and distributions. |

| (c) | Total investment return is not annualized. |

| (d) | Total investment return may reflect adjustments to conform to generally accepted accounting principles. |

| (e) | For the year ended November 30, 2015, the Fund accrued $154,807,419 in net deferred income tax benefit, of which $202,049 is attributable to Investor Class. For the period from July 12, 2014 to November 30, 2014, the Fund accrued $70,224,241 in net deferred income tax expense, of which $17,830 of deferred income tax benefit is attributable to Investor Class. |

| (f) | Ratios including/excluding net deferred income tax benefit (expense) includes applicable franchise tax expense for the period. For the year ended November 30, 2015, the Fund accrued $517,762 in franchise tax expense, of which $830 is attributable to Investor Class. |

| (g) | The ratio of expenses excluding net deferred income tax expense to average net assets before waiver and recoupment was 1.50% and 1.51%, for the year ended November 30, 2015 and the period from July 12, 2014 to November 30, 2014. The ratio of expenses excluding net deferred income tax expense to average net assets after waiver and recoupment was 1.50% and 1.51% for the year ended November 30, 2015 and the period from July 12 to November 30, 2014, respectively. |

| 20 | MainStay Cushing MLP Premier Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

Financial Highlights selected per share data and ratios

| Year ended November 30, | ||||||||||||||||||||

| Class C | 2015 | 2014 | 2013*** | 2012*** | 2011*** | |||||||||||||||

Net asset value at beginning of year | $ | 21.36 | $ | 20.79 | $ | 19.14 | $ | 19.73 | $ | 20.26 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net investment income (loss) (a) | (0.12 | ) | (0.25 | ) | (0.27 | ) | (0.27 | ) | (0.29 | ) | ||||||||||

Net realized and unrealized gain (loss) on investments | (6.09 | ) | 2.16 | 3.26 | 1.02 | 1.06 | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations | (6.21 | ) | 1.91 | 2.99 | 0.75 | 0.77 | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| Less dividends and distributions: | ||||||||||||||||||||

From net investment income | — | (0.59 | ) | — | — | — | ||||||||||||||

From return of capital | (1.34 | ) | (0.75 | ) | (1.34 | ) | (1.34 | ) | (1.30 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total dividends and distributions | (1.34 | ) | (1.34 | ) | (1.34 | ) | (1.34 | ) | (1.30 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Redemption fees retained (a)(b) | — | 0.00 | ‡ | 0.00 | ‡ | 0.00 | ‡ | 0.00 | ‡ | |||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value at end of year | $ | 13.81 | $ | 21.36 | $ | 20.79 | $ | 19.14 | $ | 19.73 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total investment return (c) | (30.43 | %) | 9.19 | % | 16.05 | % | 3.82 | % | 3.69 | % | ||||||||||

| Ratios (to average net assets)/Supplemental Data: | ||||||||||||||||||||

Net investment income (loss) (including net deferred income tax benefit (expense)) (d) | 7.56 | % (e) | (5.80 | %) | (9.87 | %) | (3.70 | %) | (2.70 | %) | ||||||||||

Net investment income (loss) (excluding net deferred income tax benefit (expense)) (d) | (1.00 | %)(e) | (1.68 | %) | (1.93 | %) | (1.98 | %) | (2.04 | %) | ||||||||||

Net expenses (including net deferred income tax (benefit) expense) (d)(f) | (6.32 | %)(e) | 6.46 | % | 10.34 | % | 4.12 | % | 3.07 | % | ||||||||||

Expenses (before waiver/recoupment, including net deferred income tax (benefit) | (6.32 | %)(e) | 6.41 | % | 10.32 | % | 4.18 | % | 4.04 | % | ||||||||||

Portfolio turnover rate | 32.35 | % | 20.70 | % | 27.29 | % | 43.32 | % | 72.32 | % | ||||||||||

Net assets at end of year (in 000’s) | $ | 553,892 | $ | 859,193 | $ | 568,837 | $ | 252,473 | $ | 50,321 | ||||||||||

| ** | Inception date. |

| *** | These years were audited by a predecessor audit firm whose opinion was unqualified. |

| ‡ | Less than one cent per share. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Redemption fees were only applicable prior to reorganization. (See Note 1) |

| (c) | Total investment return is calculated exclusive of sales charges and assumes the reinvestment of dividends and distributions. |

| (d) | For the year ended November 30, 2015, the Fund accrued $154,807,419 in net deferred income tax benefit, of which $66,219,265 is attributable to Class C. For the year ended November 30, 2014, the Fund accrued $70,224,241 in net deferred income tax expense, of which $31,069,447 is attributable to Class C. For the year ended November 30, 2013, the Fund accrued $77,002,011 in net deferred income tax expense, of which $33,095,235 is attributable to Class C. For the year ended November 30, 2012, the Fund accrued $7,120,938 in net deferred income tax expense, of which $147,543 is attributable to Class C. For the year ended November 30, 2011, the Fund accrued $452,365 in net deferred income tax expense, of which $147,543 is attributable to Class C. |

| (e) | Ratios including/excluding net deferred income tax benefit (expense) includes applicable franchise tax expense for the period. For the year ended November 30, 2015, the Fund accrued $517,762 in franchise tax expense, of which $220,745 is attributable to Class C. |

| (f) | The ratio of expenses excluding net deferred income tax expense to average net assets before waiver and recoupment was 2.24% 2.29%, 2.38%, 2.46% and 3.37% for the fiscal years ended November 30, 2015, 2014, 2013, 2012 and 2011, respectively. The ratio of expenses excluding net deferred income tax expense to average net assets after waiver and recoupment was 2.24%, 2.34%, 2.40%, 2.40% and 2.40% for the fiscal years ended November 30, 2015, 2014, 2013, 2012 and 2011, respectively. |

| The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. | 21 |

Financial Highlights selected per share data and ratios

| Year ended November 30, | ||||||||||||||||||||

| Class I | 2015 | 2014 | 2013*** | 2012*** | 2011*** | |||||||||||||||

Net asset value at beginning of year | $ | 22.40 | $ | 21.54 | $ | 19.57 | $ | 19.96 | $ | 20.28 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net investment income (loss) (a) | 0.07 | (0.03 | ) | (0.07 | ) | (0.08 | ) | (0.09 | ) | |||||||||||

Net realized and unrealized gain (loss) on investments | (6.44 | ) | 2.22 | 3.36 | 1.02 | 1.07 | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations | (6.37 | ) | 2.19 | 3.29 | 0.94 | 0.98 | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| Less dividends and distributions: | ||||||||||||||||||||

From net investment income | — | (0.59 | ) | — | — | — | ||||||||||||||

From return of capital | (1.34 | ) | (0.75 | ) | (1.34 | ) | (1.34 | ) | (1.30 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total dividends and distributions | (1.34 | ) | (1.34 | ) | (1.34 | ) | (1.34 | ) | (1.30 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Redemption fees retained (a)(b) | — | 0.01 | 0.02 | 0.01 | 0.00 | ‡ | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value at end of year | $ | 14.69 | $ | 22.40 | $ | 21.54 | $ | 19.57 | $ | 19.96 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total investment return (c) | (29.71 | %) | 10.25 | % | 17.37 | % | 4.81 | % | 4.75 | % | ||||||||||

| Ratios (to average net assets)/Supplemental Data: | ||||||||||||||||||||

Net investment income (loss) (including net deferred income tax benefit (expense)) (d) | 8.53 | % (e) | (2.90 | %) | (8.87 | %) | (2.70 | %) | (1.70 | %) | ||||||||||

Net investment income (loss) (excluding net deferred income tax benefit (expense)) (d) | (0.02 | %)(e) | (0.62 | %) | (0.93 | %) | (0.98 | %) | (1.04 | %) | ||||||||||

Net expenses (including net deferred income tax (benefit) expense) (d)(f) | (7.31 | %)(e) | 3.61 | % | 9.34 | % | 3.12 | % | 2.07 | % | ||||||||||

Expenses (before waiver/recoupment, including net deferred income tax (benefit) | (7.31 | %)(e) | 3.57 | % | 9.32 | % | 3.18 | % | 3.04 | % | ||||||||||

Portfolio turnover rate | 32.35 | % | 20.70 | % | 27.29 | % | 43.32 | % | 72.32 | % | ||||||||||

Net assets at end of year (in 000’s) | $ | 449,755 | $ | 579,546 | $ | 221,196 | $ | 92,104 | $ | 27,847 | ||||||||||

| *** | These years were audited by a predecessor audit firm whose opinion was unqualified. |

| ‡ | Less than one cent per share. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Redemption fees were only applicable prior to reorganization. (See Note 1) |

| (c) | Total investment return is calculated exclusive of sales charges and assumes the reinvestment of dividends and distributions. Class I shares are not subject to sales charges. |

| (d) | For the year ended November 30, 2015, the Fund accrued $154,807,419 in net deferred income tax benefit, of which $48,551,905 is attributable to Class I. For the year ended November 30, 2014, the Fund accrued $70,224,241 in net deferred income tax expense, of which $8,867,624 is attributable to Class I. For the year ended November 30, 2013, the Fund accrued $77,002,011 in net deferred income tax expense, of which $12,140,833 is attributable to Class I. For the year ended November 30, 2012, the Fund accrued $7,120,938 in net deferred income tax expense, of which $1,072,968 is attributable to Class I. For the year ended November 30, 2011, the Fund accrued $452,365 in net deferred income tax expense, of which $92,540 is attributable to Class I. |

| (e) | Ratios including/excluding net deferred income tax benefit (expense) includes applicable franchise tax expense for the period. For the year ended November 30, 2015, the Fund accrued $517,762 in franchise tax expense, of which $167,738 is attributable to Class I. |

| (f) | The ratio of expenses excluding net deferred income tax expense to average net assets before waiver and recoupment was 1.24%, 1.29%, 1.38%, 1.46% and 2.37% for the fiscal years ended November 30, 2015, 2014, 2013, 2012 and 2011, respectively. The ratio of expenses excluding net deferred income tax expense to average net assets after waiver and recoupment was 1.24%, 1.33%, 1.40%, 1.40% and 1.40% for the fiscal years ended November 30, 2015, 2014, 2013, 2012 and 2011, respectively. |

| 22 | MainStay Cushing MLP Premier Fund | The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements. |

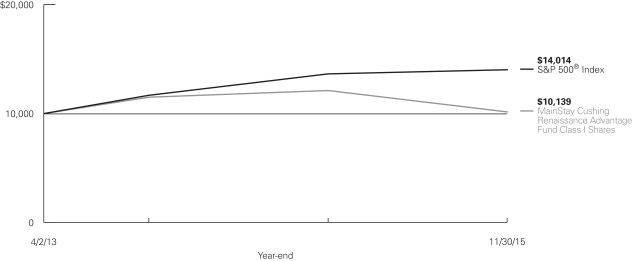

MainStay Cushing Renaissance Advantage Fund

Investment and Performance Comparison1 (Unaudited)

Performance data quoted represents past performance. Past performance is no guarantee of future results. Because of market volatility, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate, and as a result, when shares are redeemed, they may be worth more or less than their original cost. The graph below depicts the historical performance of Class I shares of the Fund. Performance will vary from class to class based on differences in class-specific expenses and sales charges. For performance information current to the most recent month-end, please call 800-MAINSTAY (624-6782) or visit mainstayinvestments.com.

Average Annual Total Returns for the Year Ended November 30, 2015

| Class | Sales Charge | One Year | Since | Gross | ||||||||||||

| Class A Shares3 | Maximum 5.5% Initial Sales Charge | With sales charge Excluding sales charge |

| –21.15 –16.57 | %

|

| –1.90 0.31 | %

|

| 1.76 1.76 | %

| |||||

| Investor Class Shares4 | Maximum 5.5% Initial Sales Charge | With sales charge Excluding sales charge | | –21.26 –16.68 | | | –1.92 0.29 | | | 1.88 1.88 | | |||||

| Class C Shares3 | Maximum 1% CDSC if Redeemed Within One Year of Purchase | With sales charge Excluding sales charge | | –18.09 –17.28 | | | –0.43 –0.43 | | | 2.63 2.63 | | |||||

| Class I Shares3 | No Sales Charge | –16.34 | 0.52 | 1.51 | ||||||||||||

| 1. | The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on distributions or Fund share redemptions. Total returns reflect maximum applicable sales charges as indicated in the table above, changes in share price, and reinvestment of dividend and capital gain distributions. The graph assumes the initial investment amount shown above and reflects the deduction of all sales charges that would have applied for the period of investment. Performance figures reflect certain fee waivers and/or expense limitations, without which total returns may have been lower. For more information on share classes and current fee waivers and/or expense limitations, please refer to the notes to the financial statements. |

| 2. | The gross expense ratios presented reflect the Fund’s “Total Annual Fund Operating Expenses” from the most recent Prospectus and may differ from other expense ratios disclosed in this report. |