UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-22321

MAINSTAY FUNDS TRUST

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

30 Hudson Street

Jersey City, New Jersey 07302

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 576-7000

Date of fiscal year end: October 31

Date of reporting period: April 30, 2021

| Item 1. | Reports to Stockholders. |

MainStay Balanced Fund

Message from the President and Semiannual Report

Unaudited | April 30, 2021

Sign up for e-delivery of your shareholder reports. For full details on e-delivery, including who can participate and what you can receive via e-delivery,

please log in to newyorklifeinvestments.com/accounts.

| Not FDIC/NCUA Insured | Not a Deposit | May Lose Value | No Bank Guarantee | Not Insured by Any Government Agency |

This page intentionally left blank

Message from the President

With the approval of COVID-19 vaccines and the passage of relief packages by the U.S. Congress, economic prospects improved during the reporting period, and investor risk appetite increased, benefiting both equities and fixed-income markets. Despite some volatility stemming from a sell-off in longer-dated Treasury securities, the stock market and higher-risk segments of the fixed-income market posted gains for the six months ended April 30, 2021.

By the beginning of the reporting period, the economy had made tremendous progress from the second quarter of 2020, when economic activity plunged. But uncertainty about when vaccines would be available and how quickly they could be administered left investors unsure about the economic outlook.

With the approval of several vaccines in November, the outlook brightened and investors became less risk-averse. Anticipating the likely end of the pandemic and a continuation of the economic recovery, they began to see opportunities in investment-grade and high-yield bonds and more cyclical segments of the stock market. The $900 billion relief and stimulus package passed in December provided further assurance.

In January, the Federal Reserve opted to leave interest rates unchanged, pointing to some uncertainty about the pace of the global recovery. Officials also noted that inflation remained low, citing oil prices in particular.

In March, President Biden signed the $1.9 billion American Rescue Plan, which, among other provisions, called for payments of $1,400 for those earning less than $75,000 per year, plus $1,400 per dependent. This, combined with the Federal Reserve’s new tolerance for inflation and an anticipated $2 trillion infrastructure spending bill, added to growing concerns about higher prices. Supply shortages in some markets caused some prices to soar, heightening concerns further.

In fixed-income markets, an improving economic outlook and rising inflation expectations led to a sell-off in longer-term Treasuries, with the result that the yield on the 10-year note rose sharply, particularly in February and March. Investment grade corporate bonds were also affected. Early in the reporting period, they performed well as investors shifted out of Treasuries, but as the reporting period progressed, they faltered. Longer-dated securities issued in recent years at historically low interest rates became especially unattractive.

High-yield bonds remained steady, supported by more favorable yields and an improved economic outlook, which reduced their perceived risk. Municipal bonds produced modest gains, and

although the sell-off in Treasuries produced some volatility early in 2021, stronger-than-expected tax revenues, $350 billion in financial support from the federal government, and the possibility of an increase in federal income tax rates appeared to buoy the market late in the reporting period.

Inflation concerns and volatility in the Treasury market led to a shift in equities markets. Although the S&P 500® Index, a widely followed measure of U.S. equities, posted double-digit gains and hit a record high, the rise of Treasury yields disrupted valuations, especially those of growth stocks. Technology companies that saw their valuations soar amid the work-from-home trend in 2020 suffered large declines.

But the fiscal stimulus and continued accommodation from the Federal Reserve gave investors confidence the economic recovery would continue. Combined with the sky-high valuations in technology and growth stocks, this increased the appeal of more cyclical and value-oriented shares. As a result, value stocks outperformed growth stocks during the reporting period.

Reflecting the shift in investor sentiment, the performance of S&P 500® Index sectors varied widely. While the information technology sector kept up with the broader market, it lagged cyclical sectors such as energy and financials, which led the way. The shift was further reflected in the performance of small-cap stocks, which outperformed large caps. While developed markets kept pace with the U.S. market, lagging economic and pandemic recoveries appeared to weigh on emerging markets late in the reporting period.

With the lockdown restrictions lifting in the U.S. and the pandemic easing in many regions, we at New York Life Investments are looking forward to a return to a more normal economy. We anticipate that over the next several years, a variety of trends will likely offer long-term investors many attractive opportunities. With this in mind, we continue to develop products and services to help you to take advantage of these trends, manage your risks, and ultimately meet your investment goals.

Sincerely,

Kirk C. Lehneis

President

The opinions expressed are as of the date of this report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment. Past performance is no guarantee of future results.

Not part of the Semiannual Report

Investors should refer to the Fund’s Summary Prospectus and/or Prospectus and consider the Fund’s investment objectives, strategies, risks, charges and expenses carefully before investing. The Summary Prospectus and/or Prospectus contain this and other information about the Fund. You may obtain copies of the Fund’s Summary Prospectus, Prospectus and Statement of Additional Information free of charge, upon request, by calling toll-free 800-624-6782, by writing to NYLIFE Distributors LLC, Attn: MainStay Marketing Department, 30 Hudson Street, Jersey City, NJ 07302 or by sending an e-mail to MainStayShareholderServices@nylim.com. These documents are also available via the MainStay Funds’ website at newyorklifeinvestments.com. Please read the Fund’s Summary Prospectus and/or Prospectus carefully before investing.

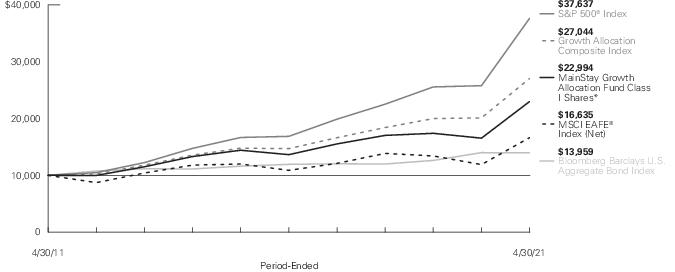

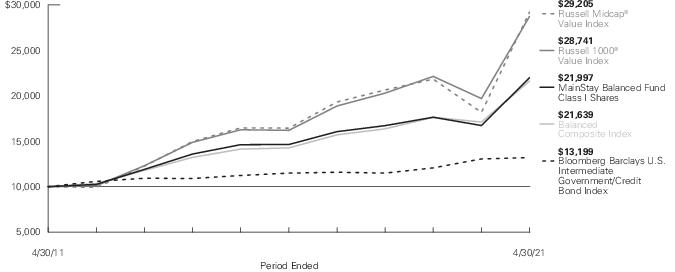

Investment and Performance Comparison (Unaudited)

Performance data quoted represents past performance. Past performance is no guarantee of future results. Because of market volatility and other factors, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate, and as a result, when shares are redeemed, they may be worth more or less than their original cost. The graph below depicts the historical performance of Class I shares of the Fund. Performance will vary from class to class based on differences in class-specific expenses and sales charges. For performance information current to the most recent month-end, please call 800-624-6782 or visit newyorklifeinvestments.com.

The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on distributions or Fund share redemptions. Total returns reflect maximum applicable sales charges as indicated in the table below, if any, changes in share price, and reinvestment of dividend and capital gain distributions. The graph assumes the initial investment amount shown below and reflects the deduction of all sales charges that would have applied for the period of investment. Performance figures may reflect certain fee waivers and/or expense limitations, without which total returns may have been lower. For more information on share classes and current fee waivers and/or expense limitations (if any), please refer to the Notes to Financial Statements.

| Average Annual Total Returns for the Period-Ended April 30, 20211 |

| Class | Sales Charge | | Inception

Date | Six

Months | One

Year | Five

Years | Ten

Years | Gross

Expense

Ratio2 |

| Class A Shares3 | Maximum 3% Initial Sales Charge | With sales charges | 1/2/2004 | 18.98% | 27.21% | 6.99% | 7.32% | 1.09% |

| | | Excluding sales charges | | 22.66 | 31.14 | 8.21 | 7.93 | 1.09 |

| Investor Class Shares3, 4 | Maximum 2.5% Initial Sales Charge | With sales charges | 2/28/2008 | 19.43 | 26.86 | 6.78 | 7.12 | 1.36 |

| | | Excluding sales charges | | 22.49 | 30.79 | 8.00 | 7.73 | 1.36 |

| Class B Shares5 | Maximum 5% CDSC | With sales charges | 1/2/2004 | 17.07 | 24.85 | 6.88 | 6.92 | 2.11 |

| | if Redeemed Within the First Six Years of Purchase | Excluding sales charges | | 22.07 | 29.85 | 7.19 | 6.92 | 2.11 |

| Class C Shares | Maximum 1% CDSC | With sales charges | 12/30/2002 | 21.05 | 28.82 | 7.19 | 6.92 | 2.11 |

| | if Redeemed Within One Year of Purchase | Excluding sales charges | | 22.05 | 29.82 | 7.19 | 6.92 | 2.11 |

| Class I Shares | No Sales Charge | | 5/1/1989 | 22.82 | 31.49 | 8.48 | 8.20 | 0.84 |

| Class R1 Shares | No Sales Charge | | 1/2/2004 | 22.73 | 31.30 | 8.38 | 8.09 | 0.94 |

| Class R2 Shares | No Sales Charge | | 1/2/2004 | 22.59 | 30.99 | 8.13 | 7.84 | 1.19 |

| Class R3 Shares | No Sales Charge | | 4/28/2006 | 22.44 | 30.69 | 7.83 | 7.55 | 1.44 |

| Class R6 Shares | No Sales Charge | | 12/15/2017 | 22.88 | 31.62 | 8.03 | N/A | 0.74 |

| 1. | Effective March 5, 2021, the Fund replaced the subadvisor to the equity portion of the Fund and modified its principal investment strategies. The past performance in the graph and table prior to that date reflects the Fund’s prior subadvisor and principal investment strategies for the equity portion of the Fund. |

| 2. | The gross expense ratios presented reflect the Fund’s “Total Annual Fund Operating Expenses” from the most recent Prospectus, as supplemented, and may differ from other expense ratios disclosed in this report. |

| 3. | Prior to November 4, 2019, the maximum initial sales charge was 5.5%, which is reflected in the average annual total return figures shown. |

| 4. | Prior to June 30, 2020, the maximum initial sales charge was 3.0%, which is reflected in the average annual total return figures shown. |

| 5. | Class B shares are closed to all new purchases as well as additional investments by existing Class B shareholders. |

The footnotes on the next page are an integral part of the table and graph and should be carefully read in conjunction with them.

| Benchmark Performance | Six

Months | One

Year | Five

Years | Ten

Years |

| Russell 1000® Value Index1 | 36.30% | 45.92% | 12.15% | 11.13% |

| Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index2 | -0.68 | 1.09 | 2.80 | 2.81 |

| Balanced Composite Index3 | 20.46 | 26.45 | 8.69 | 8.02 |

| Russell Midcap® Value Index4 | 41.41 | 60.70 | 12.18 | 11.31 |

| Morningstar Allocation - 50% to 70% Equity Category Average5 | 20.03 | 30.67 | 9.84 | 7.46 |

| 1. | The Fund has selected the Russell 1000® Value Index as its primary benchmark. The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000® Index companies with lower price-to-book ratios and lower expected growth values. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an index. |

| 2. | The Fund has selected the Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index as a secondary benchmark. The Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index measures the performance of U.S. dollar denominated U.S. treasuries, government related and investment grade U.S. corporate securities that have a remaining maturity of greater than one year and less than ten years. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an index. |

| 3. | The Fund has selected the Balanced Composite Index as an additional benchmark. The Balanced Composite Index consists of the Russell Midcap® Value Index and the Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index weighted 60% and 40%, respectively. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an index. |

| 4. | The Russell Midcap® Value Index, the Fund's prior primary benchmark, measures the performance of the mid-cap value segment of the U.S. equity universe. It includes those Russell Midcap® Index companies with lower price-to-book ratios and lower forecasted growth values. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an index. |

| 5. | The Morningstar Allocation – 50% to 70% Equity Category Average is representative of funds that seek to provide both income and capital appreciation by investing in multiple asset classes, including stocks, bonds, and cash. These portfolios are dominated by domestic holdings and have equity exposures between 50% and 70%. Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

The footnotes on the preceding page are an integral part of the table and graph and should be carefully read in conjunction with them.

Cost in Dollars of a $1,000 Investment in MainStay Balanced Fund (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the six-month period from November 1, 2020, to April 30, 2021, and the impact of those costs on your investment.

Example

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including exchange fees and sales charges (loads) on purchases (as applicable), and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from November 1, 2020, to April 30, 2021.

This example illustrates your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six months ended April 30, 2021. Simply divide your account value by $1,000 (for example, an

$8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in the Fund with the ongoing costs of investing in other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as exchange fees or sales charges (loads). Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Share Class | Beginning

Account

Value

11/1/20 | Ending Account

Value (Based

on Actual

Returns and

Expenses)

4/30/21 | Expenses

Paid

During

Period1 | Ending Account

Value (Based

on Hypothetical

5% Annualized

Return and

Actual Expenses)

4/30/21 | Expenses

Paid

During

Period1 | Net Expense

Ratio

During

Period2 |

| Class A Shares | $1,000.00 | $1,226.60 | $ 6.07 | $1,019.34 | $ 5.51 | 1.10% |

| Investor Class Shares | $1,000.00 | $1,224.90 | $ 7.56 | $1,018.00 | $ 6.85 | 1.37% |

| Class B Shares | $1,000.00 | $1,220.70 | $11.67 | $1,014.28 | $10.59 | 2.12% |

| Class C Shares | $1,000.00 | $1,220.50 | $11.67 | $1,014.28 | $10.59 | 2.12% |

| Class I Shares | $1,000.00 | $1,228.20 | $ 4.75 | $1,020.53 | $ 4.31 | 0.86% |

| Class R1 Shares | $1,000.00 | $1,227.30 | $ 5.25 | $1,020.08 | $ 4.76 | 0.95% |

| Class R2 Shares | $1,000.00 | $1,225.90 | $ 6.62 | $1,018.84 | $ 6.01 | 1.20% |

| Class R3 Shares | $1,000.00 | $1,224.40 | $ 8.05 | $1,017.56 | $ 7.30 | 1.46% |

| Class R6 Shares | $1,000.00 | $1,228.80 | $ 4.20 | $1,021.03 | $ 3.81 | 0.76% |

| 1. | Expenses are equal to the Fund’s annualized expense ratio of each class multiplied by the average account value over the period, divided by 365 and multiplied by 181 (to reflect the six-month period). The table above represents the actual expenses incurred during the six-month period. In addition to the fees and expenses which the Fund bears directly, it also indirectly bears a pro rata share of the fees and expenses of the underlying funds in which it invests. Such indirect expenses are not included in the above-reported expense figures. |

| 2. | Expenses are equal to the Fund's annualized expense ratio to reflect the six-month period. |

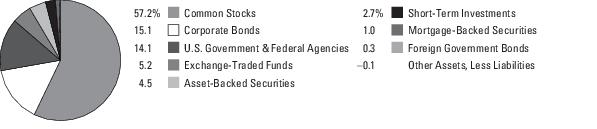

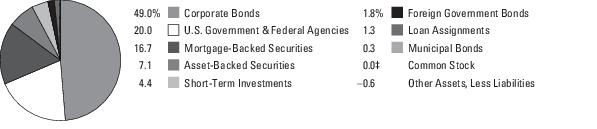

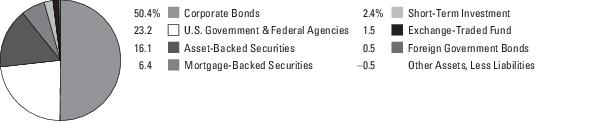

Portfolio Composition as of April 30, 2021 (Unaudited)

See Portfolio of Investments beginning on page 13 for specific holdings within these categories. The Fund's holdings are subject to change.

Top Ten Holdings or Issuers Held as of April 30, 2021 (excluding short-term investments) (Unaudited)

| 1. | U.S. Treasury Notes, 0.125%-1.25%, due 4/30/23–2/15/31 |

| 2. | iShares Russell 1000 Value ETF |

| 3. | iShares Intermediate Government/Credit Bond ETF |

| 4. | JPMorgan Chase & Co. |

| 5. | FFCB, 0.68%-2.09%, due 1/13/27–4/14/31 |

| 6. | Bank of America Corp. |

| 7. | Alphabet, Inc., Class C |

| 8. | Comcast Corp., Class A |

| 9. | Cisco Systems, Inc. |

| 10. | Pfizer, Inc. |

Portfolio Management Discussion and Analysis (Unaudited)

Questions answered by portfolio managers Jae S. Yoon, CFA, and Jonathan Swaney of New York Life Investment Management LLC, the Fund’s Manager; Kenneth Sommer and AJ Rzad, CFA, of NYL Investors LLC, the Fund’s fixed-income Subadvisor; Migene Kim, CFA, and Mona Patni of MacKay Shields LLC, (“MacKay Shields”), the Fund’s former equity Subadvisor; and portfolio manager Adam H. Illfelder of Wellington Management Company LLP (“Wellington”), the Fund’s current equity Subadvisor.

How did MainStay Balanced Fund perform relative to its benchmarks and peer group during the six months ended April 30, 2021?

For the six months ended April 30, 2021, Class I shares of MainStay Balanced Fund returned 22.82%, underperforming the 36.30% return of the Fund’s primary benchmark, the Russell 1000® Value Index. Over the same period, Class I shares outperformed the −0.68% return of the Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index, which is the Fund’s secondary benchmark, and the 20.46% return of the Balanced Composite Index, which is an additional benchmark of the Fund. During the reporting period, the Fund underperformed the 41.41% return of the Russell Midcap® Value Index, which was the Fund's former primary benchmark. For the six months ended April 30, 2021, Class I shares of the Fund outperformed the 20.03% return of the Morningstar Allocation –50% to 70% Equity Category Average.1

Were there any changes to the Fund during the reporting period?

At meetings held on January 21, January 25, and February 3, 2021, the Board of Trustees of MainStay Funds Trust considered and approved, among other related proposals: (i) appointing Wellington Management Company LLP as subadvisor to the equity portion of the Fund, and the related subadvisory agreement; (ii) modifying the Fund’s principal investment strategies, investment process and primary benchmark; and (iii) reducing the Fund’s contractual management fee. These changes, in addition to the Russell 1000® Value Index becoming the Fund’s primary benchmark, became effective on March 5, 2021. For more information on these and other changes, refer to the supplement dated February 5, 2021.

What factors affected relative performance in the equity portion of the Fund during the reporting period?

MacKay Shields

During the time MacKay Shields managed the equity portion of the Fund, benchmark-relative performance was undermined primarily by the equity portion of the Fund’s allocation to large-cap value stocks. The combination of signals used by our quantitative stock selection model supported the relative performance of the equity portion of the Fund’s mid-cap stock allocation, which benefited from the strong return of the market’s valuation premium.

Wellington

During the time Wellington managed the equity portion of the

Fund, performance relative to the Russell 1000® Value Index benefited primarily from security selection. Strong selection in the communication services and consumer discretionary sectors was partially offset by weaker selection in health care. Sector allocation, a result of our bottom-up stock selection process, also bolstered relative results due to underweight exposure to the energy and communication services sectors.

During the reporting period, which sectors were the strongest positive contributors to the relative performance of the equity portion of the Fund and which sectors were particularly weak?

MacKay Shields

During the time MacKay Shields managed the equity portion of the Fund, the strongest contributions to benchmark-relative performance came from positions in the utilities, financials and industrials sectors. (Contributions take weightings and total returns into account.) During the same period, the weakest contributors to benchmark-relative performance were the real estate, health care and communication services sectors.

Wellington

During the time Wellington managed the equity portion of the Fund, the communication services, energy and consumer discretionary sectors provided the strongest positive contributions to relative performance. Over the same period, the health care sector detracted most significantly from relative performance.

During the reporting period, which individual stocks made the strongest positive contributions to absolute performance in the equity portion of the Fund and which stocks detracted the most?

MacKay Shields

During the time MacKay Shields managed the equity portion of the Fund, the individual stocks that made the strongest positive contributions to the Fund’s absolute performance included regional banking firm Signature Bank, internet & direct marketing retailer Qurate Retail and copper miner Freeport-McMoRan. The stocks that detracted most significantly from absolute performance in the equity portion of the Fund included diversified utilities WEC Energy Group and Consolidated Edison, and gold miner Newmont.

Wellington

During the time Wellington managed the equity portion of the Fund, the top contributors to absolute performance included home improvement retailer The Home Depot and internet search provider Alphabet. Shares of The Home Depot rose over the

| 1. | See page 5 for other share class returns, which may be higher or lower than Class I share returns. See page 6 for more information on benchmark and peer group returns. |

reporting period on the tailwinds of strong fourth quarter 2020 earnings, reported in late February 2021. Positive U.S. housing trends supported builders and home improvement names. Shares of Alphabet rose to record highs after the company reported first-quarter 2021 results that widely exceeded most analysts’ revenue estimates. Top-line growth was driven by a surge in advertising sales related to travel and retail as businesses boosted digital advertising spending in the hopes of capitalizing on consumers eager to resume travel following the pandemic. Both positions were still held in the Fund as of the end of the reporting period.

During the same period, the most significant detractors from absolute performance were Eli Lilly, a U.S.-based pharmaceutical company, and Phillips 66, a diversified energy company. Shares of Eli Lilly came under pressure amid underwhelming Phase 2 data from an Alzheimer’s study that had produced positive headlines earlier in the year. The equity portion of the Fund maintained the position as of the end of the reporting period. Shares of Phillips 66 traded lower after the company released guidance for the first quarter of 2021 that was considerably worse than consensus due to winter storm impacts. The release pointed to the company’s midstream, chemicals and refining segments as seeing large disruptions from lower utilization and higher costs. The equity portion of the Fund reduced exposure to Phillips 66 during the reporting period.

What were some of the largest purchases and sales in the equity portion of the Fund during the reporting period?

MacKay Shields

During the time MacKay Shields managed the equity portion of the Fund, its largest initial purchase was in shares of real estate services and investment company CBRE Group, while the largest increased position size was in shares of automobile manufacturer Ford Motor Company. During the same period, the largest full sale by the equity portion of the Fund was its position in home improvement and building products company Masco, while the most significantly decreased position size was in semiconductor maker Skyworks Solutions.

Wellington

During the time Wellington managed the equity portion of the Fund, its largest initial purchase was in shares of Rio Tinto, a metals and mining corporation, while the largest increase in position size was in the cloud-based networking platform, F5 Networks. Rio Tinto is the second largest metals and mining company in the world and the largest producer of iron ore. In our view, the stock appeared undervalued with minimal balance sheet and execution risk, and significant exposure to a cyclical recovery. F5 has often been viewed by the investment community as “legacy tech” with a focus on hardware, but we believed its business model transition towards software and subscriptions was underappreciated and revenue had begun to reaccelerate.

During the same period, the largest full sale was its holding of Zimmer Biomet, a medical device company, and the largest decrease in position size was Lennar, the biggest homebuilder in the United States. Zimmer Biomet had outperformed, and we saw better risk-adjusted upside in the health care sector in large pharmaceutical names. Lennar was a beneficiary of the robust strength in the U.S. housing market during the pandemic, and the company’s valuation no longer appeared compelling in our process.

How did sector weightings change in the equity portion of the Fund during the reporting period?

MacKay Shields

The largest increases in benchmark-relative sector exposure during the time MacKay Shields managed the equity portion of the Fund occurred in industrials and utilities. Conversely, the most significant decreases in benchmark-relative sector exposure were in the materials and information technology sectors.

Wellington

During the time Wellington managed the equity portion of the Fund, the largest increases in active weight were in the materials, communication services and energy sectors, while the largest decreases were in the health care, consumer discretionary and information technology sectors.

How was the equity portion of the Fund positioned at the end of the reporting period?

MacKay Shields

At the end of the period when MacKay Shields managed the equity portion of the Fund, the most overweight positions in the equity portion of the Fund relative to the benchmark were in the health care and consumer staples sectors, while the most underweight benchmark-relative positions were in real estate and materials.

Wellington

As of April 30, 2021, the most overweight positions in the equity portion of the Fund relative to the Russell 1000® Value Index were in the health care, information technology and financials sectors. As of the same date, the equity portion of the Fund held its most significantly underweight positions in the consumer staples, communication services and energy sectors.

What factors affected the relative performance of the fixed-income portion of the Fund during the reporting period?

Relative to the Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index, the fixed-income portion of the Fund held overweight positions in U.S. government agencies, corporates, asset-backed securities and commercial mortgage-backed securities throughout the reporting period. To facilitate these overweight positions, the Fund maintained

underweight exposure to the Treasury sector. Option-adjusted spreads2 on the designated benchmark tightened 11 basis points during the reporting period. (A basis point is one one-hundredth of a percentage point.) The corporate sector was the best performing sector, led by the financials and industrials sectors. Overweight exposure to asset-backed securities was also accretive to performance, driven by both the floating-rate and fixed-rate subcomponents. Positioning in commercial mortgage-backed securities, particularly the non-agency subcomponent, also added to relative performance, as did overweight exposure to U.S. government agencies. Rates positioning in the intermediate part of the yield curve3 detracted from performance during the reporting period.

During the reporting period, how was the performance of the fixed-income portion of the Fund materially affected by investments in derivatives?

During the reporting period, the use of derivatives was limited to interest-rate derivatives designed to keep the duration4 of the fixed-income portion of the Fund in line with our target duration. Generally, interest-rate derivatives had a negative impact on performance.

What was the duration strategy of the fixed-income portion of the Fund during the reporting period?

During the reporting period, the fixed-income portion of the Fund generally maintained a duration close to that of the Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index. The fixed-income portion of the Fund adopted a significantly longer duration than the benchmark on one occasion in the beginning of the reporting period; this strategy positively impacted the Fund’s performance. Throughout the second half of the reporting period, the Fund was positioned with a shorter duration than the designated benchmark in the front end of the interest rate curve (0-1 year) and a longer duration than the designated benchmark in the intermediate part of the curve (2+ years). This curve positioning detracted from performance as interest rates moved higher and steeper during the reporting period. As of April 30, 2021, the effective duration of the fixed-income portion of the Fund was 4.12 years compared to a duration of 4.13 years for the benchmark.

During the reporting period, which sectors were the strongest positive contributors to the relative performance of the fixed-income portion of the Fund and which sectors were particularly weak?

During the reporting period, the fixed-income portion of the Fund maintained overweight exposure compared to the Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index in the industrials and financials sectors, both of which were accretive to the Fund’s relative performance. Among industrials, performance in the consumer cyclical and capital goods subsectors were particularly strong, with bonds issued by Ford Motor Credit, Nissan Motor, Boeing and Owens Corning among the fixed-income portion of the Fund’s strongest performers. Among financials, overweight exposure to the REIT (real estate investment trust) and finance company subsectors had the most positive impact on relative performance, particularly holdings in Vereit Operating Partnership, Highwoods Realty, and GE Capital Funding. Within securitized products, asset backed securities was the best performing sector, particularly AAA-rated5 collateralized loan obligations. In the CMBS (commercial mortgage-backed securities) sector, the fixed-income portion of the Fund’s overweight position relative to the benchmark in the non-agency subcomponent was also accretive to performance. Conversely, relatively underweight exposure to the sovereign, supranational and foreign agency subsectors detracted slightly from performance. The fixed-income portion of the Fund’s positioning in the energy, technology and transportation sectors also detracted from relative performance during the reporting period.

What were some of the largest purchases and sales in the fixed-income portion of the Fund during the reporting period?

The largest additions to the fixed-income portion of the Fund during the reporting period included bonds from Crown Castle International, Charles Schwab, Air Lease, Brighthouse Financial Global Funding and Truist Financial. These additions were based on attractive relative value opportunities, primarily on the new issue calendar. These additions increased the diversity of the fixed-income portion of the Fund while improving the yield profile.

The largest reductions during the reporting period included positions in Kinder Morgan, Becton Dickinson and Company, Cigna, Credit Suisse AG and Huntington Bancshares. These

| 2. | An option-adjusted spread is the measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to take into account an embedded option. |

| 3. | The yield curve is a line that plots the yields of various securities of similar quality—typically U.S. Treasury issues—across a range of maturities. The U.S. Treasury yield curve serves as a benchmark for other debt and is used in economic forecasting. |

| 4. | Duration is a measure of the price sensitivity of a fixed-income investment to changes in interest rates. Duration is expressed as a number of years and is considered a more accurate sensitivity gauge than average maturity. |

| 5. | An obligation rated ‘AAA’ has the highest rating assigned by Standard & Poor’s (“S&P”), and in the opinion of S&P, the obligor’s capacity to meet its financial commitment on the obligation is extremely strong. When applied to portfolio holdings, ratings are based solely on the creditworthiness of the bonds in the portfolio and are not meant to represent the security or safety of the portfolio. |

names were reduced due to lower yield profiles than opportunities in the new issue market.

How did the sector weightings of the fixed-income portion of the Fund change during the reporting period?

During the reporting period, the fixed-income portion of the Fund held overweight exposure to the industrials and financials sectors within the corporate sector. The corporate credit allocation increased during the first quarter of 2021 as the new issue calendar presented numerous opportunities to invest in intermediate corporate credit. The financials sector came under pressure as supply put upward pressure on credit spreads,6 resulting in modestly more attractive valuations.

Toward the end of the reporting period, we reduced the Fund’s weighting in the U.S. government callable agency sector. As the economy continued to heal from the pandemic and volatility fell sharply, option-adjusted spreads among U.S. government callable agencies tightened dramatically. The spread compression prompted us to reduce this sector’s weighting for the fixed-income portion of the Fund.

In the securitized products sector, the fixed-income portion of the Fund exited exposure to non-agency residential mortgage-backed securities entirely as we felt the sector had reached terminal value given the dollar prices and convexity7 associated with the securities.

How was the fixed-income portion of the Fund positioned at the end of the reporting period?

As of April 30, 2021, the fixed-income portion of the Fund held its most significantly overweight exposure relative to the Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index in asset-backed securities. In the corporate sector, the fixed-income portion of the Fund held overweight exposure to financials, industrials and utilities. The fixed-income portion of the Fund also held overweight positions in commercial mortgage-backed securities and U.S. government agencies. As of the same date, the fixed-income portion of the Fund held relatively underweight positions in the sovereign, supranational, foreign agency and foreign local government sectors, as well as in U.S. Treasury securities.

| 6. | The terms “spread” and “yield spread” may refer to the difference in yield between a security or type of security and comparable U.S. Treasury issues. The terms may also refer to the difference in yield between two specific securities or types of securities at a given time. |

| 7. | Convexity is a mathematical measure of the sensitivity of an interest-bearing bond to changes in interest rates. |

The opinions expressed are those of the portfolio managers as of the date of this report and are subject to change. There is no guarantee that any forecasts will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

Portfolio of Investments April 30, 2021† (Unaudited)

| | Principal

Amount | Value |

| Long-Term Bonds 35.0% |

| Asset-Backed Securities 4.5% |

| Automobile Asset-Backed Securities 0.3% |

| Ford Credit Floorplan Master Owner Trust | |

| Series 2018-4, Class A | | |

| 4.06%, due 11/15/30 | $ 1,000,000 | $ 1,136,746 |

| Toyota Auto Loan Extended Note Trust | |

| Series 2020-1A, Class A | | |

| 1.35%, due 5/25/33 (a) | 750,000 | 764,059 |

| | | 1,900,805 |

| Other Asset-Backed Securities 4.2% |

| 522 Funding CLO Ltd. | |

| Series 2021-7A, Class A | | |

| 1.27% (3 Month LIBOR + 1.07%), due 4/23/34 (a)(b) | 600,000 | 600,472 |

| Apidos CLO XXV | |

| Series 2016-25A, Class A1R | | |

| 1.358% (3 Month LIBOR + 1.17%), due 10/20/31 (a)(b) | 650,000 | 650,258 |

| Apidos CLO XXX | |

| Series XXXA, Class A2 | | |

| 1.79% (3 Month LIBOR + 1.60%), due 10/18/31 (a)(b) | 600,000 | 595,264 |

| Apidos CLO XXXII | |

| Series 2019-32A, Class A1 | | |

| 1.508% (3 Month LIBOR + 1.32%), due 1/20/33 (a)(b) | 600,000 | 600,701 |

| ARES XXXVIII CLO Ltd. | |

| Series 2015-38A, Class BR | | |

| 1.588% (3 Month LIBOR + 1.40%), due 4/20/30 (a)(b) | 600,000 | 593,117 |

| Benefit Street Partners CLO XVIII Ltd. | |

| Series 2019-18A, Class A | | |

| 1.524% (3 Month LIBOR + 1.34%), due 10/15/32 (a)(b) | 350,000 | 350,308 |

| Benefit Street Partners CLO XXIII Ltd. | |

| Series 2021-23A, Class A1 | | |

| 2.297% (3 Month LIBOR + 1.08%), due 4/25/34 (a)(b) | 1,000,000 | 1,000,396 |

| CAL Funding IV Ltd. | |

| Series 2020-1A, Class A | | |

| 2.22%, due 9/25/45 (a) | 1,188,021 | 1,195,393 |

| Cedar Funding IV CLO Ltd. | |

| Series 2014-4A, Class AR | | |

| 1.403% (3 Month LIBOR + 1.23%), due 7/23/30 (a)(b) | 1,500,000 | 1,501,255 |

| | Principal

Amount | Value |

| |

| Other Asset-Backed Securities (continued) |

| Cedar Funding XII CLO Ltd. | |

| Series 2020-12A, Class A | ��� | |

| 1.446% (3 Month LIBOR + 1.27%), due 10/25/32 (a)(b) | $ 800,000 | $ 800,432 |

| Dryden 76 CLO Ltd. | |

| Series 2019-76A, Class A1 | | |

| 1.518% (3 Month LIBOR + 1.33%), due 10/20/32 (a)(b) | 500,000 | 501,124 |

| HPS Loan Management Ltd. (a)(b) | |

| Series 11A-17, Class AR | | |

| 1.213% (3 Month LIBOR + 1.02%), due 5/6/30 | 1,050,000 | 1,046,913 |

| Series 10A-16, Class A1R | | |

| 1.328% (3 Month LIBOR + 1.14%), due 1/20/28 | 248,173 | 248,121 |

| Magnetite XVIII Ltd. | |

| Series 2016-18A, Class AR | | |

| 1.274% (3 Month LIBOR + 1.08%), due 11/15/28 (a)(b) | 600,000 | 599,999 |

| Magnetite XXIII Ltd. | |

| Series 2019-23A, Class A | | |

| 1.476% (3 Month LIBOR + 1.30%), due 10/25/32 (a)(b) | 350,000 | 350,758 |

| Magnetite XXVIII Ltd. | |

| Series 2020-28A, Class A | | |

| 1.446% (3 Month LIBOR + 1.27%), due 10/25/31 (a)(b) | 500,000 | 500,590 |

| Neuberger Berman Loan Advisers CLO 24 Ltd. | |

| Series 2017-24A, Class AR | | |

| 1.21% (3 Month LIBOR + 1.02%), due 4/19/30 (a)(b) | 350,000 | 349,464 |

| Neuberger Berman Loan Advisers CLO 35 Ltd. | |

| Series 2019-35A, Class A1 | | |

| 1.53% (3 Month LIBOR + 1.34%), due 1/19/33 (a)(b) | 900,000 | 901,774 |

| Oaktree CLO Ltd. | |

| Series 2020-1A, Class B | | |

| 2.774% (3 Month LIBOR + 2.59%), due 7/15/29 (a)(b) | 500,000 | 500,648 |

| Octagon Investment Partners 29 Ltd. | |

| Series 2016-1A, Class AR | | |

| 1.356% (3 Month LIBOR + 1.18%), due 1/24/33 (a)(b) | 500,000 | 499,015 |

| OHA Credit Funding 6 Ltd. | |

| Series 2020-6A, Class A1 | | |

| 1.838% (3 Month LIBOR + 1.65%), due 7/20/31 (a)(b) | 400,000 | 400,484 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

13

Portfolio of Investments April 30, 2021† (Unaudited) (continued)

| | Principal

Amount | Value |

| Asset-Backed Securities (continued) |

| Other Asset-Backed Securities (continued) |

| Palmer Square CLO Ltd. (a)(b) | |

| Series 2014-1A, Class A1R2 | | |

| 1.32% (3 Month LIBOR + 1.13%), due 1/17/31 | $ 250,000 | $ 250,050 |

| Series 2015-2A, Class A2R2 | | |

| 1.738% (3 Month LIBOR + 1.55%), due 7/20/30 | 250,000 | 250,039 |

| Progress Residential | |

| Series 2021-SFR3, Class A | | |

| 1.637%, due 5/17/26 (a) | 600,000 | 601,337 |

| Regatta XIV Funding Ltd. | |

| Series 2018-3A, Class A | | |

| 1.366% (3 Month LIBOR + 1.19%), due 10/25/31 (a)(b) | 400,000 | 400,048 |

| SMB Private Education Loan Trust (a) | |

| Series 2020-B, Class A1A | | |

| 1.29%, due 7/15/53 | 632,551 | 634,763 |

| Series 2020-PTB, Class A2A | | |

| 1.60%, due 9/15/54 | 800,000 | 809,976 |

| THL Credit Wind River CLO Ltd. | |

| Series 2017-4A, Class A | | |

| 1.332% (3 Month LIBOR + 1.15%), due 11/20/30 (a)(b) | 507,000 | 507,089 |

| Tiaa CLO III Ltd. | |

| Series 2017-2A, Class A | | |

| 1.334% (3 Month LIBOR + 1.15%), due 1/16/31 (a)(b) | 500,000 | 497,262 |

| TICP CLO X Ltd. | |

| Series 2018-10A, Class A | | |

| 1.188% (3 Month LIBOR + 1.00%), due 4/20/31 (a)(b) | 400,000 | 399,324 |

| TICP CLO XIII Ltd. | |

| Series 2019-13A, Class A | | |

| 1.484% (3 Month LIBOR + 1.30%), due 7/15/32 (a)(b) | 500,000 | 500,125 |

| TIF Funding II LLC | |

| Series 2021-1A, Class A | | |

| 1.65%, due 2/20/46 (a) | 882,563 | 865,739 |

| Triton Container Finance VIII LLC | |

| Series 2020-1A, Class A | | |

| 2.11%, due 9/20/45 (a) | 950,414 | 957,633 |

| Vantage Data Centers LLC | |

| Series 2020-1A, Class A2 | | |

| 1.645%, due 9/15/45 (a) | 1,400,000 | 1,394,697 |

| | Principal

Amount | Value |

| |

| Other Asset-Backed Securities (continued) |

| Voya CLO Ltd. | |

| Series 2019-1A, Class AR | | |

| 1.244% (3 Month LIBOR + 1.06%), due 4/15/31 (a)(b) | $ 400,000 | $ 400,218 |

| Westcott Park CLO Ltd. | |

| Series 2016-1A, Class AR | | |

| 1.398% (3 Month LIBOR + 1.21%), due 7/20/28 (a)(b) | 600,000 | 600,416 |

| | | 22,855,202 |

Total Asset-Backed Securities

(Cost $24,757,228) | | 24,756,007 |

| Corporate Bonds 15.1% |

| Aerospace & Defense 0.2% |

| Boeing Co. (The) | | |

| 3.10%, due 5/1/26 | 335,000 | 352,187 |

| 3.25%, due 2/1/28 | 450,000 | 470,376 |

| 3.625%, due 2/1/31 | 500,000 | 525,743 |

| | | 1,348,306 |

| Apparel 0.0% ‡ |

| Ralph Lauren Corp. | | |

| 1.70%, due 6/15/22 | 225,000 | 228,682 |

| Auto Manufacturers 1.3% |

| American Honda Finance Corp. | | |

| 0.55%, due 7/12/24 | 425,000 | 424,397 |

| Daimler Finance North America LLC (a) | | |

| 1.094% (3 Month LIBOR + 0.90%), due 2/15/22 (b) | 850,000 | 854,889 |

| 2.45%, due 3/2/31 | 350,000 | 350,518 |

| Ford Motor Credit Co. LLC | | |

| 3.087%, due 1/9/23 | 575,000 | 585,793 |

| 3.664%, due 9/8/24 | 1,275,000 | 1,327,466 |

| General Motors Financial Co., Inc. | | |

| 1.05%, due 3/8/24 | 275,000 | 275,580 |

| 1.25%, due 1/8/26 | 800,000 | 789,959 |

| 4.35%, due 4/9/25 | 980,000 | 1,086,192 |

| Hyundai Capital America (a) | | |

| 1.80%, due 1/10/28 | 275,000 | 266,881 |

| 2.375%, due 10/15/27 | 475,000 | 479,217 |

| Nissan Motor Co. Ltd. | | |

| 4.81%, due 9/17/30 (a) | 425,000 | 471,895 |

| Volkswagen Group of America Finance LLC | | |

| 1.25%, due 11/24/25 (a) | 450,000 | 448,875 |

| | | 7,361,662 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

| | Principal

Amount | Value |

| Corporate Bonds (continued) |

| Banks 3.2% |

| Banco Santander SA | | |

| 1.849%, due 3/25/26 | $ 1,200,000 | $ 1,210,064 |

| Bank of America Corp. | | |

| 1.734%, due 7/22/27 (c) | 3,345,000 | 3,376,060 |

| BNP Paribas SA | | |

| 2.588% (5 Year Treasury Constant Maturity Rate + 2.05%), due 8/12/35 (a)(b) | 675,000 | 646,037 |

| Citigroup, Inc. | | |

| 2.561%, due 5/1/32 (c) | 775,000 | 774,156 |

| 4.60%, due 3/9/26 | 1,250,000 | 1,428,678 |

| Goldman Sachs Group, Inc. (The) | | |

| 1.431%, due 3/9/27 (c) | 775,000 | 771,974 |

| JPMorgan Chase & Co. (c) | | |

| 1.578%, due 4/22/27 | 2,400,000 | 2,410,536 |

| 2.956%, due 5/13/31 | 750,000 | 770,447 |

| Lloyds Banking Group plc | | |

| 0.695% (1 Year Treasury Constant Maturity Rate + 0.55%), due 5/11/24 (b) | 650,000 | 650,797 |

| Mizuho Financial Group, Inc. | | |

| 0.817% (3 Month LIBOR + 0.63%), due 5/25/24 (b) | 1,150,000 | 1,155,005 |

| Morgan Stanley | | |

| 3.625%, due 1/20/27 | 220,000 | 243,944 |

| 4.35%, due 9/8/26 | 1,370,000 | 1,550,267 |

| Societe Generale SA | | |

| 1.488% (1 Year Treasury Constant Maturity Rate + 1.10%), due 12/14/26 (a)(b) | 975,000 | 964,591 |

| Standard Chartered plc | | |

| 0.991% (1 Year Treasury Constant Maturity Rate + 0.78%), due 1/12/25 (a)(b) | 300,000 | 298,792 |

| Truist Financial Corp. | | |

| 1.267%, due 3/2/27 (c) | 775,000 | 771,484 |

| UBS Group AG | | |

| 1.364% (1 Year Treasury Constant Maturity Rate + 1.08%), due 1/30/27 (a)(b) | 675,000 | 668,355 |

| | | 17,691,187 |

| Beverages 0.3% |

| Anheuser-Busch InBev Worldwide, Inc. | | |

| 4.75%, due 1/23/29 | 1,125,000 | 1,320,253 |

| | Principal

Amount | Value |

| |

| Beverages (continued) |

| Diageo Capital plc | | |

| 2.125%, due 4/29/32 | $ 475,000 | $ 463,616 |

| | | 1,783,869 |

| Building Materials 0.2% |

| Owens Corning | | |

| 3.95%, due 8/15/29 | 875,000 | 971,963 |

| Chemicals 0.5% |

| EI du Pont de Nemours and Co. | | |

| 1.70%, due 7/15/25 | 225,000 | 231,293 |

| LYB International Finance III LLC | | |

| 1.25%, due 10/1/25 | 225,000 | 224,874 |

| NewMarket Corp. | | |

| 4.10%, due 12/15/22 | 1,245,000 | 1,309,298 |

| Nutrien Ltd. | | |

| 3.625%, due 3/15/24 | 250,000 | 268,919 |

| Nutrition & Biosciences, Inc. | | |

| 1.832%, due 10/15/27 (a) | 475,000 | 469,269 |

| | | 2,503,653 |

| Diversified Financial Services 1.6% |

| Air Lease Corp. | | |

| 0.70%, due 2/15/24 | 1,650,000 | 1,637,060 |

| Aircastle Ltd. | | |

| 2.85%, due 1/26/28 (a) | 750,000 | 736,144 |

| Antares Holdings LP | | |

| 3.95%, due 7/15/26 (a) | 250,000 | 256,695 |

| Aviation Capital Group LLC | | |

| 1.95%, due 1/30/26 (a) | 650,000 | 637,210 |

| BOC Aviation USA Corp. | | |

| 1.625%, due 4/29/24 (a) | 225,000 | 225,917 |

| Charles Schwab Corp. (The) | | |

| 0.75%, due 3/18/24 | 2,150,000 | 2,164,107 |

| GE Capital Funding LLC | | |

| 4.05%, due 5/15/27 (a) | 1,850,000 | 2,069,607 |

| LSEGA Financing plc | | |

| 2.00%, due 4/6/28 (a) | 550,000 | 548,826 |

| Thirax 1 LLC | | |

| 0.968%, due 1/14/33 | 350,000 | 349,003 |

| | | 8,624,569 |

| Electric 1.3% |

| Berkshire Hathaway Energy Co. | | |

| 1.65%, due 5/15/31 | 675,000 | 637,237 |

| Commonwealth Edison Co | | |

| 3.10%, due 11/1/24 | 340,000 | 364,260 |

| DTE Electric Co. | | |

| 2.65%, due 6/15/22 | 625,000 | 637,128 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

15

Portfolio of Investments April 30, 2021† (Unaudited) (continued)

| | Principal

Amount | Value |

| Corporate Bonds (continued) |

| Electric (continued) |

| DTE Energy Co. | | |

| Series F | | |

| 1.05%, due 6/1/25 | $ 375,000 | $ 373,610 |

| Entergy Arkansas LLC | | |

| 3.70%, due 6/1/24 | 740,000 | 802,169 |

| Entergy Corp. | | |

| 4.00%, due 7/15/22 | 1,395,000 | 1,446,351 |

| FirstEnergy Transmission LLC | | |

| 4.35%, due 1/15/25 (a) | 1,410,000 | 1,537,682 |

| Pinnacle West Capital Corp. | | |

| 1.30%, due 6/15/25 | 775,000 | 778,882 |

| Southern California Edison Co. | | |

| Series 20C | | |

| 1.20%, due 2/1/26 | 550,000 | 545,442 |

| Tampa Electric Co. | | |

| 2.40%, due 3/15/31 | 275,000 | 276,512 |

| | | 7,399,273 |

| Electrical Components & Equipment 0.1% |

| Emerson Electric Co. | | |

| 1.80%, due 10/15/27 | 500,000 | 508,100 |

| Electronics 0.1% |

| Flex Ltd. | | |

| 3.75%, due 2/1/26 | 400,000 | 434,568 |

| Food 0.1% |

| Conagra Brands, Inc. | | |

| 4.85%, due 11/1/28 | 690,000 | 812,517 |

| Forest Products & Paper 0.1% |

| Georgia-Pacific LLC | | |

| 0.95%, due 5/15/26 (a) | 300,000 | 293,109 |

| Healthcare-Services 0.2% |

| Fresenius Medical Care U.S. Finance III, Inc. | | |

| 2.375%, due 2/16/31 (a) | 1,215,000 | 1,170,600 |

| Insurance 0.4% |

| Brighthouse Financial Global Funding | | |

| 1.00%, due 4/12/24 (a) | 1,475,000 | 1,477,390 |

| Guardian Life Global Funding | | |

| 1.25%, due 11/19/27 (a) | 775,000 | 754,177 |

| | | 2,231,567 |

| | Principal

Amount | Value |

| |

| Investment Companies 0.1% |

| Blackstone Secured Lending Fund | | |

| 2.75%, due 9/16/26 (a) | $ 375,000 | $ 377,442 |

| Iron & Steel 0.1% |

| Nucor Corp. | | |

| 2.00%, due 6/1/25 | 400,000 | 413,897 |

| Steel Dynamics, Inc. | | |

| 2.40%, due 6/15/25 | 275,000 | 287,696 |

| | | 701,593 |

| Machinery-Diversified 0.1% |

| Deere & Co. | | |

| 3.10%, due 4/15/30 | 625,000 | 676,274 |

| Media 0.1% |

| Discovery Communications LLC | | |

| 3.625%, due 5/15/30 | 200,000 | 214,034 |

| Thomson Reuters Corp. | | |

| 3.85%, due 9/29/24 | 450,000 | 489,004 |

| | | 703,038 |

| Mining 0.2% |

| Anglo American Capital plc (a) | | |

| 2.25%, due 3/17/28 | 700,000 | 696,073 |

| 5.625%, due 4/1/30 | 550,000 | 660,970 |

| | | 1,357,043 |

| Miscellaneous—Manufacturing 0.1% |

| Siemens Financieringsmaatschappij NV | | |

| 1.70%, due 3/11/28 (a) | 625,000 | 620,449 |

| Oil & Gas 0.2% |

| Valero Energy Corp. | | |

| 2.85%, due 4/15/25 | 925,000 | 976,355 |

| Oil & Gas Services 0.3% |

| Schlumberger Holdings Corp. | | |

| 3.75%, due 5/1/24 (a) | 1,395,000 | 1,503,584 |

| Packaging & Containers 0.3% |

| WRKCo, Inc. | | |

| 3.75%, due 3/15/25 | 1,295,000 | 1,417,233 |

| Pharmaceuticals 0.7% |

| AbbVie, Inc. | | |

| 2.95%, due 11/21/26 | 1,300,000 | 1,392,224 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

| | Principal

Amount | Value |

| Corporate Bonds (continued) |

| Pharmaceuticals (continued) |

| Bayer US Finance II LLC | | |

| 4.375%, due 12/15/28 (a) | $ 1,085,000 | $ 1,227,747 |

| Cigna Corp. | | |

| 2.375%, due 3/15/31 | 325,000 | 320,932 |

| CVS Health Corp. | | |

| 1.875%, due 2/28/31 | 705,000 | 666,927 |

| | | 3,607,830 |

| Pipelines 0.4% |

| Energy Transfer Partners LP | | |

| 5.875%, due 3/1/22 | 1,735,000 | 1,786,962 |

| Texas Eastern Transmission LP | | |

| 2.80%, due 10/15/22 (a) | 615,000 | 630,313 |

| | | 2,417,275 |

| Private Equity 0.1% |

| Apollo Management Holdings LP | | |

| 2.65%, due 6/5/30 (a) | 500,000 | 498,767 |

| Real Estate Investment Trusts 1.8% |

| American Campus Communities Operating Partnership LP | | |

| 3.30%, due 7/15/26 | 1,155,000 | 1,245,977 |

| Corporate Office Properties LP | | |

| 2.75%, due 4/15/31 | 370,000 | 365,193 |

| Crown Castle International Corp. | | |

| 1.05%, due 7/15/26 | 2,435,000 | 2,374,315 |

| Federal Realty Investment Trust | | |

| 1.25%, due 2/15/26 | 200,000 | 199,285 |

| Highwoods Realty LP | | |

| 3.875%, due 3/1/27 | 2,050,000 | 2,229,081 |

| Kimco Realty Corp. | | |

| 1.90%, due 3/1/28 | 290,000 | 286,437 |

| 2.80%, due 10/1/26 | 640,000 | 678,449 |

| Simon Property Group LP | | |

| 1.75%, due 2/1/28 | 475,000 | 466,463 |

| Spirit Realty LP | | |

| 2.70%, due 2/15/32 | 250,000 | 242,451 |

| 3.20%, due 2/15/31 | 225,000 | 230,805 |

| VEREIT Operating Partnership LP | | |

| 3.95%, due 8/15/27 | 1,195,000 | 1,331,217 |

| | | 9,649,673 |

| Retail 0.1% |

| Advance Auto Parts, Inc. | | |

| 1.75%, due 10/1/27 | 200,000 | 198,062 |

| | Principal

Amount | Value |

| |

| Retail (continued) |

| CK Hutchison International 21 Ltd. | | |

| 1.50%, due 4/15/26 (a) | $ 325,000 | $ 325,089 |

| | | 523,151 |

| Telecommunications 0.9% |

| AT&T, Inc. | | |

| 4.35%, due 3/1/29 | 1,080,000 | 1,225,843 |

| NTT Finance Corp. | | |

| 1.162%, due 4/3/26 (a) | 600,000 | 594,721 |

| T-Mobile US, Inc. | | |

| 2.55%, due 2/15/31 (a) | 1,100,000 | 1,082,103 |

| Verizon Communications, Inc. | | |

| 2.10%, due 3/22/28 | 450,000 | 454,085 |

| 3.376%, due 2/15/25 | 8,000 | 8,727 |

| 4.016%, due 12/3/29 | 1,156,000 | 1,307,274 |

| | | 4,672,753 |

Total Corporate Bonds

(Cost $80,910,717) | | 83,066,085 |

| Foreign Government Bonds 0.3% |

| Colombia 0.1% |

| Colombia Government Bond | | |

| 3.875%, due 4/25/27 | 350,000 | 373,814 |

| Mexico 0.1% |

| Mexico Government Bond | | |

| 3.75%, due 1/11/28 | 350,000 | 379,012 |

| Norway 0.0% ‡ |

| Equinor ASA | | |

| 1.75%, due 1/22/26 | 300,000 | 308,924 |

| Philippines 0.1% |

| Philippine Government Bond | | |

| 3.00%, due 2/1/28 | 325,000 | 347,645 |

| Poland 0.0% ‡ |

| Poland Government Bond | | |

| 5.00%, due 3/23/22 | 150,000 | 156,195 |

Total Foreign Government Bonds

(Cost $1,449,011) | | 1,565,590 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

17

Portfolio of Investments April 30, 2021† (Unaudited) (continued)

| | Principal

Amount | Value |

| Mortgage-Backed Securities 1.0% |

| Commercial Mortgage Loans (Collateralized Mortgage Obligations) 1.0% |

| Benchmark Mortgage Trust | |

| Series 2018-B1, Class A2 | | |

| 3.571%, due 1/15/51 | $ 300,000 | $ 310,851 |

| Series 2018-B2, Class A2 | | |

| 3.662%, due 2/15/51 | 250,000 | 259,683 |

| Citigroup Commercial Mortgage Trust | |

| Series 2020-GC46, Class A5 | | |

| 2.717%, due 2/15/53 | 1,000,000 | 1,043,124 |

| CLNY Trust | |

| Series 2019-IKPR, Class B | | |

| 1.593% (1 Month LIBOR + 1.478%), due 11/15/38 (a)(b) | 2,000,000 | 1,997,580 |

| CSMC WEST Trust | |

| Series 2020-WEST, Class A | | |

| 3.04%, due 2/15/35 (a) | 1,250,000 | 1,286,169 |

| UBS Commercial Mortgage Trust | |

| Series 2018-C8, Class A2 | | |

| 3.713%, due 2/15/51 | 800,000 | 833,056 |

Total Mortgage-Backed Securities

(Cost $5,656,129) | | 5,730,463 |

| U.S. Government & Federal Agencies 14.1% |

| Federal Home Loan Mortgage Corporation (Mortgage Pass-Through Securities) 4.8% |

| FFCB | | |

| 0.68%, due 1/13/27 | 950,000 | 931,089 |

| 0.90%, due 8/19/27 | 1,125,000 | 1,105,303 |

| 1.14%, due 8/20/29 | 1,300,000 | 1,255,586 |

| 1.23%, due 9/10/29 | 1,500,000 | 1,446,316 |

| 1.23%, due 7/29/30 | 1,125,000 | 1,081,503 |

| 1.25%, due 6/24/30 | 1,400,000 | 1,342,876 |

| 1.62%, due 4/6/28 | 600,000 | 597,059 |

| 1.67%, due 3/3/31 | 950,000 | 939,607 |

| 2.03%, due 1/21/28 | 1,200,000 | 1,265,732 |

| 2.04%, due 4/14/31 | 685,000 | 680,265 |

| 2.09%, due 4/1/31 | 875,000 | 868,884 |

| FHLB | | |

| 0.375%, due 9/4/25 | 1,060,000 | 1,045,085 |

| 0.90%, due 2/26/27 | 950,000 | 938,061 |

| 1.00%, due 7/28/28 | 950,000 | 923,463 |

| 2.50%, due 12/10/27 | 1,350,000 | 1,452,323 |

| 3.00%, due 3/10/28 | 500,000 | 553,802 |

| 3.125%, due 9/12/25 | 800,000 | 879,781 |

| 3.25%, due 6/9/28 | 1,200,000 | 1,355,167 |

| FHLMC | | |

| 0.375%, due 7/21/25 | 45,000 | 44,419 |

| | Principal

Amount | Value |

| |

| Federal Home Loan Mortgage Corporation (Mortgage Pass-Through Securities) (continued) |

| FHLMC (continued) | | |

| 0.375%, due 9/23/25 | $ 250,000 | $ 246,124 |

| 0.625%, due 12/17/25 | 1,125,000 | 1,120,365 |

| 0.85%, due 12/30/27 | 525,000 | 508,228 |

| 0.90%, due 11/23/27 | 900,000 | 877,428 |

| 1.42%, due 12/30/30 | 1,125,000 | 1,086,391 |

| FNMA | | |

| 0.50%, due 6/17/25 | 950,000 | 943,892 |

| 0.75%, due 10/8/27 | 1,000,000 | 968,386 |

| 0.875%, due 8/5/30 | 1,900,000 | 1,774,915 |

| | | 26,232,050 |

| United States Treasury Notes 9.3% |

| U.S. Treasury Notes | | |

| 0.125%, due 4/30/23 | 21,975,000 | 21,959,549 |

| 0.375%, due 4/15/24 | 20,090,000 | 20,115,113 |

| 0.75%, due 3/31/26 | 1,875,000 | 1,867,676 |

| 0.75%, due 4/30/26 | 2,890,000 | 2,876,453 |

| 1.125%, due 2/15/31 | 2,650,000 | 2,530,750 |

| 1.25%, due 4/30/28 | 1,530,000 | 1,524,023 |

| | | 50,873,564 |

Total U.S. Government & Federal Agencies

(Cost $77,150,902) | | 77,105,614 |

Total Long-Term Bonds

(Cost $189,923,987) | | 192,223,759 |

| |

| | Shares | |

| Common Stocks 57.2% |

| Aerospace & Defense 3.1% |

| General Dynamics Corp. | 21,069 | 4,007,956 |

| L3Harris Technologies, Inc. | 19,700 | 4,121,831 |

| Lockheed Martin Corp. | 9,581 | 3,646,145 |

| Raytheon Technologies Corp. | 61,213 | 5,095,370 |

| | | 16,871,302 |

| Auto Components 0.6% |

| Gentex Corp. | 101,699 | 3,577,771 |

| Banks 6.7% |

| Bank of America Corp. | 226,741 | 9,189,813 |

| JPMorgan Chase & Co. | 80,466 | 12,376,476 |

| M&T Bank Corp. | 26,723 | 4,213,950 |

| PNC Financial Services Group, Inc. (The) | 29,210 | 5,460,809 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

| | Shares | Value |

| Common Stocks (continued) |

| Banks (continued) |

| Truist Financial Corp. | 89,326 | $ 5,297,925 |

| | | 36,538,973 |

| Beverages 0.8% |

| Keurig Dr Pepper, Inc. | 127,702 | 4,578,117 |

| Biotechnology 0.3% |

| Biogen, Inc. (d) | 5,541 | 1,481,276 |

| Building Products 1.4% |

| Fortune Brands Home & Security, Inc. | 32,960 | 3,460,141 |

| Johnson Controls International plc | 65,969 | 4,112,507 |

| | | 7,572,648 |

| Capital Markets 2.6% |

| BlackRock, Inc. | 6,576 | 5,387,717 |

| Blackstone Group, Inc. (The) | 48,999 | 4,335,921 |

| LPL Financial Holdings, Inc. | 28,283 | 4,431,946 |

| | | 14,155,584 |

| Chemicals 1.5% |

| Celanese Corp. | 28,770 | 4,506,820 |

| FMC Corp. | 31,103 | 3,677,619 |

| | | 8,184,439 |

| Communications Equipment 2.2% |

| Cisco Systems, Inc. | 164,596 | 8,379,582 |

| F5 Networks, Inc. (d) | 19,337 | 3,611,378 |

| | | 11,990,960 |

| Containers & Packaging 0.8% |

| Sealed Air Corp. | 87,794 | 4,337,024 |

| Electric Utilities 1.4% |

| Entergy Corp. | 33,238 | 3,632,581 |

| Exelon Corp. | 94,218 | 4,234,157 |

| | | 7,866,738 |

| Electrical Equipment 0.8% |

| nVent Electric plc | 136,861 | 4,167,417 |

| Electronic Equipment, Instruments & Components 0.9% |

| Corning, Inc. | 114,350 | 5,055,413 |

| Equity Real Estate Investment Trusts 2.1% |

| Crown Castle International Corp. | 17,255 | 3,262,230 |

| | Shares | Value |

| |

| Equity Real Estate Investment Trusts (continued) |

| Gaming and Leisure Properties, Inc. | 104,176 | $ 4,843,141 |

| Host Hotels & Resorts, Inc. | 189,049 | 3,433,130 |

| | | 11,538,501 |

| Food Products 0.8% |

| Mondelez International, Inc., Class A | 73,212 | 4,452,022 |

| Health Care Equipment & Supplies 2.8% |

| Becton Dickinson and Co. | 18,737 | 4,661,953 |

| Boston Scientific Corp. (d) | 99,625 | 4,343,650 |

| Medtronic plc | 48,681 | 6,373,316 |

| | | 15,378,919 |

| Health Care Providers & Services 2.8% |

| Anthem, Inc. | 18,171 | 6,893,896 |

| Centene Corp. (d) | 53,141 | 3,280,925 |

| UnitedHealth Group, Inc. | 13,707 | 5,466,352 |

| | | 15,641,173 |

| Hotels, Restaurants & Leisure 0.6% |

| Booking Holdings, Inc. (d) | 1,283 | 3,163,981 |

| Household Durables 0.8% |

| Lennar Corp., Class A | 40,939 | 4,241,280 |

| Insurance 3.8% |

| Assurant, Inc. | 28,572 | 4,445,803 |

| Chubb Ltd. | 34,387 | 5,900,466 |

| MetLife, Inc. | 105,494 | 6,712,583 |

| Progressive Corp. (The) | 38,234 | 3,851,693 |

| | | 20,910,545 |

| Interactive Media & Services 1.6% |

| Alphabet, Inc., Class C (d) | 3,583 | 8,635,460 |

| IT Services 1.6% |

| Amdocs Ltd. | 56,742 | 4,354,381 |

| Global Payments, Inc. | 20,296 | 4,356,131 |

| | | 8,710,512 |

| Machinery 0.7% |

| Middleby Corp. (The) (d) | 21,872 | 3,965,831 |

| Media 1.5% |

| Comcast Corp., Class A | 150,943 | 8,475,449 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

19

Portfolio of Investments April 30, 2021† (Unaudited) (continued)

| | Shares | Value |

| Common Stocks (continued) |

| Metals & Mining 0.6% |

| Rio Tinto plc, Sponsored ADR (e) | 40,937 | $ 3,482,101 |

| Multi-Utilities 1.5% |

| Dominion Energy, Inc. | 56,800 | 4,538,320 |

| Sempra Energy | 28,668 | 3,943,857 |

| | | 8,482,177 |

| Oil, Gas & Consumable Fuels 1.5% |

| Phillips 66 | 48,661 | 3,937,161 |

| Pioneer Natural Resources Co. | 26,390 | 4,059,574 |

| | | 7,996,735 |

| Pharmaceuticals 4.2% |

| AstraZeneca plc, Sponsored (e) | 73,054 | 3,876,976 |

| Eli Lilly and Co. | 26,800 | 4,898,236 |

| Merck & Co., Inc. | 34,920 | 2,601,540 |

| Pfizer, Inc. | 211,080 | 8,158,242 |

| Roche Holding AG | 10,094 | 3,289,324 |

| | | 22,824,318 |

| Real Estate Management & Development 0.7% |

| CBRE Group, Inc., Class A (d) | 44,328 | 3,776,746 |

| Road & Rail 1.5% |

| Knight-Swift Transportation Holdings, Inc. | 89,710 | 4,227,135 |

| Union Pacific Corp. | 18,527 | 4,114,662 |

| | | 8,341,797 |

| Semiconductors & Semiconductor Equipment 2.6% |

| Analog Devices, Inc. | 22,805 | 3,492,814 |

| KLA Corp. | 9,193 | 2,899,013 |

| Micron Technology, Inc. (d) | 50,318 | 4,330,870 |

| Qorvo, Inc. (d) | 20,177 | 3,796,706 |

| | | 14,519,403 |

| Software 0.6% |

| VMware, Inc., Class A (d)(e) | 20,084 | 3,230,110 |

| Specialty Retail 1.8% |

| Home Depot, Inc. (The) | 18,031 | 5,836,094 |

| TJX Cos., Inc. (The) | 56,993 | 4,046,503 |

| | | 9,882,597 |

Total Common Stocks

(Cost $269,609,546) | | 314,027,319 |

| | Shares | | Value |

| Exchange-Traded Funds 5.2% |

| iShares iBoxx $ Investment Grade Corporate Bond ETF | 9,969 | | $ 1,307,434 |

| iShares Intermediate Government/Credit Bond ETF | 108,365 | | 12,506,524 |

| iShares Russell 1000 Value ETF | 92,220 | | 14,529,261 |

Total Exchange-Traded Funds

(Cost $26,801,324) | | | 28,343,219 |

| Short-Term Investments 2.7% |

| Affiliated Investment Company 0.8% |

| MainStay U.S. Government Liquidity Fund, 0.01% (f) | 4,391,582 | | 4,391,582 |

| Unaffiliated Investment Company 1.9% |

| BlackRock Liquidity FedFund, 0.05% (f)(g) | 10,458,688 | | 10,458,688 |

Total Short-Term Investments

(Cost $14,850,270) | | | 14,850,270 |

Total Investments

(Cost $501,185,127) | 100.1% | | 549,444,567 |

| Other Assets, Less Liabilities | (0.1) | | (690,888) |

| Net Assets | 100.0% | | $ 548,753,679 |

| † | Percentages indicated are based on Fund net assets. |

| ‡ | Less than one-tenth of a percent. |

| (a) | May be sold to institutional investors only under Rule 144A or securities offered pursuant to Section 4(a)(2) of the Securities Act of 1933, as amended. |

| (b) | Floating rate—Rate shown was the rate in effect as of April 30, 2021. |

| (c) | Fixed to floating rate—Rate shown was the rate in effect as of April 30, 2021. |

| (d) | Non-income producing security. |

| (e) | All or a portion of this security was held on loan. As of April 30, 2021, the aggregate market value of securities on loan was $10,589,187; the total market value of collateral held by the Fund was $10,830,457. The market value of the collateral held included non-cash collateral in the form of U.S. Treasury securities with a value of $371,769. The Fund received cash collateral with a value of $10,458,688. (See Note 2(I)) |

| (f) | Current yield as of April 30, 2021. |

| (g) | Represents a security purchased with cash collateral received for securities on loan. |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

Futures Contracts

As of April 30, 2021, the Fund held the following futures contracts1:

| Type | Number of

Contracts | Expiration

Date | Value at

Trade Date | Current

Notional

Amount | Unrealized

Appreciation

(Depreciation)2 |

| Long Contracts | | | | | |

| U.S. Treasury 2 Year Notes | 96 | June 2021 | $ 21,199,782 | $ 21,192,750 | $ (7,032) |

| U.S. Treasury 5 Year Notes | 13 | June 2021 | 1,622,132 | 1,611,188 | (10,944) |

| U.S. Treasury 10 Year Notes | 21 | June 2021 | 2,773,678 | 2,772,656 | (1,022) |

| Total Long Contracts | | | | | (18,998) |

| Short Contracts | | | | | |

| U.S. Treasury 10 Year Ultra Bonds | (28) | June 2021 | (4,142,327) | (4,075,313) | 67,014 |

| U.S. Treasury Long Bonds | (6) | June 2021 | (966,786) | (943,500) | 23,286 |

| Total Short Contracts | | | | | 90,300 |

| Net Unrealized Appreciation | | | | | $ 71,302 |

| 1. | As of April 30, 2021, cash in the amount of $65,810 was on deposit with a broker or futures commission merchant for futures transactions. |

| 2. | Represents the difference between the value of the contracts at the time they were opened and the value as of April 30, 2021. |

| Abbreviation(s): |

| ADR—American Depositary Receipt |

| CLO—Collateralized Loan Obligation |

| ETF—Exchange-Traded Fund |

| FFCB—Federal Farm Credit Bank |

| FHLB—Federal Home Loan Bank |

| FHLMC—Federal Home Loan Mortgage Corp. |

| FNMA—Federal National Mortgage Association |

| LIBOR—London Interbank Offered Rate |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

21

Portfolio of Investments April 30, 2021† (Unaudited) (continued)

The following is a summary of the fair valuations according to the inputs used as of April 30, 2021, for valuing the Fund’s assets and liabilities:

| Description | Quoted

Prices in

Active

Markets for

Identical

Assets

(Level 1) | | Significant

Other

Observable

Inputs

(Level 2) | | Significant

Unobservable

Inputs

(Level 3) | | Total |

| Asset Valuation Inputs | | | | | | | |

| Investments in Securities (a) | | | | | | | |

| Long-Term Bonds | | | | | | | |

| Asset-Backed Securities | $ — | | $ 24,756,007 | | $ — | | $ 24,756,007 |

| Corporate Bonds | — | | 83,066,085 | | — | | 83,066,085 |

| Foreign Government Bonds | — | | 1,565,590 | | — | | 1,565,590 |

| Mortgage-Backed Securities | — | | 5,730,463 | | — | | 5,730,463 |

| U.S. Government & Federal Agencies | — | | 77,105,614 | | — | | 77,105,614 |

| Total Long-Term Bonds | — | | 192,223,759 | | — | | 192,223,759 |

| Common Stocks | 314,027,319 | | — | | — | | 314,027,319 |

| Exchange-Traded Funds | 28,343,219 | | — | | — | | 28,343,219 |

| Short-Term Investments | | | | | | | |

| Affiliated Investment Company | 4,391,582 | | — | | — | | 4,391,582 |

| Unaffiliated Investment Company | 10,458,688 | | — | | — | | 10,458,688 |

| Total Short-Term Investments | 14,850,270 | | — | | — | | 14,850,270 |

| Total Investments in Securities | 357,220,808 | | 192,223,759 | | — | | 549,444,567 |

| Other Financial Instruments | | | | | | | |

| Futures Contracts (b) | 90,300 | | — | | — | | 90,300 |

| Total Investments in Securities and Other Financial Instruments | $ 357,311,108 | | $ 192,223,759 | | $ — | | $ 549,534,867 |

| Liability Valuation Inputs | | | | | | | |

| Other Financial Instruments | | | | | | | |

| Futures Contracts (b) | $ (18,998) | | $ — | | $ — | | $ (18,998) |

| (a) | For a complete listing of investments and their industries, see the Portfolio of Investments. |

| (b) | The value listed for these securities reflects unrealized appreciation (depreciation) as shown on the Portfolio of Investments. |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

Statement of Assets and Liabilities as of April 30, 2021 (Unaudited)

| Assets |

Investment in unaffiliated securities, at value

(identified cost $496,793,545) including securities on loan of $10,589,187 | $545,052,985 |

Investment in affiliated investment companies, at value

(identified cost $4,391,582) | 4,391,582 |

| Cash collateral on deposit at broker for futures contracts | 65,810 |

| Cash | 9,730,742 |

| Receivables: | |

| Investment securities sold | 3,033,240 |

| Dividends and interest | 810,356 |

| Fund shares sold | 306,757 |

| Variation margin on futures contracts | 6,058 |

| Securities lending | 2,754 |

| Other assets | 61,451 |

| Total assets | 563,461,735 |

| Liabilities |

| Cash collateral received for securities on loan | 10,458,688 |

| Payables: | |

| Investment securities purchased | 3,360,646 |

| Manager (See Note 3) | 289,438 |

| Fund shares redeemed | 255,341 |

| Transfer agent (See Note 3) | 152,865 |

| NYLIFE Distributors (See Note 3) | 108,630 |

| Shareholder communication | 44,944 |

| Custodian | 17,079 |

| Professional fees | 16,590 |

| Accrued expenses | 3,835 |

| Total liabilities | 14,708,056 |

| Net assets | $548,753,679 |

| Composition of Net Assets |

| Shares of beneficial interest outstanding (par value of $.001 per share) unlimited number of shares authorized | $ 15,271 |

| Additional paid-in-capital | 407,369,899 |

| | 407,385,170 |

| Total distributable earnings (loss) | 141,368,509 |

| Net assets | $548,753,679 |

| Class A | |

| Net assets applicable to outstanding shares | $315,841,789 |

| Shares of beneficial interest outstanding | 8,790,228 |

| Net asset value per share outstanding | $ 35.93 |

| Maximum sales charge (3.00% of offering price) | 1.11 |

| Maximum offering price per share outstanding | $ 37.04 |

| Investor Class | |

| Net assets applicable to outstanding shares | $ 49,266,142 |

| Shares of beneficial interest outstanding | 1,370,639 |

| Net asset value per share outstanding | $ 35.94 |

| Maximum sales charge (2.50% of offering price) | 0.92 |

| Maximum offering price per share outstanding | $ 36.86 |

| Class B | |

| Net assets applicable to outstanding shares | $ 10,914,781 |

| Shares of beneficial interest outstanding | 306,200 |

| Net asset value and offering price per share outstanding | $ 35.65 |

| Class C | |

| Net assets applicable to outstanding shares | $ 29,415,929 |

| Shares of beneficial interest outstanding | 825,497 |

| Net asset value and offering price per share outstanding | $ 35.63 |

| Class I | |

| Net assets applicable to outstanding shares | $138,834,110 |

| Shares of beneficial interest outstanding | 3,853,315 |

| Net asset value and offering price per share outstanding | $ 36.03 |

| Class R1 | |

| Net assets applicable to outstanding shares | $ 98,835 |

| Shares of beneficial interest outstanding | 2,747 |

| Net asset value and offering price per share outstanding | $ 35.98 |

| Class R2 | |

| Net assets applicable to outstanding shares | $ 1,981,559 |

| Shares of beneficial interest outstanding | 55,070 |

| Net asset value and offering price per share outstanding | $ 35.98 |

| Class R3 | |

| Net assets applicable to outstanding shares | $ 2,341,362 |

| Shares of beneficial interest outstanding | 65,266 |

| Net asset value and offering price per share outstanding | $ 35.87 |

| Class R6 | |

| Net assets applicable to outstanding shares | $ 59,172 |

| Shares of beneficial interest outstanding | 1,640 |

| Net asset value and offering price per share outstanding | $ 36.08 |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

23

Statement of Operations for the six months ended April 30, 2021 (Unaudited)

| Investment Income (Loss) |

| Income | |

| Dividends-unaffiliated (net of foreign tax withholding of $16,254) | $ 3,702,170 |

| Interest | 1,731,699 |

| Securities lending | 45,241 |

| Dividends-affiliated | 35 |

| Total income | 5,479,145 |

| Expenses | |

| Manager (See Note 3) | 1,831,815 |

| Distribution/Service—Class A (See Note 3) | 356,076 |

| Distribution/Service—Investor Class (See Note 3) | 61,616 |

| Distribution/Service—Class B (See Note 3) | 55,138 |

| Distribution/Service—Class C (See Note 3) | 157,878 |

| Distribution/Service—Class R2 (See Note 3) | 2,334 |

| Distribution/Service—Class R3 (See Note 3) | 5,515 |

| Transfer agent (See Note 3) | 398,337 |

| Registration | 58,515 |

| Professional fees | 45,295 |

| Shareholder communication | 35,635 |

| Custodian | 26,348 |

| Trustees | 5,611 |

| Insurance | 2,641 |

| Shareholder service (See Note 3) | 2,081 |

| Miscellaneous | 13,573 |

| Total expenses before waiver/reimbursement | 3,058,408 |

| Expense waiver/reimbursement from Manager (See Note 3) | (8,391) |

| Net expenses | 3,050,017 |

| Net investment income (loss) | 2,429,128 |