UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number: 811-22375

PIMCO Equity Series

(Exact name of registrant as specified in charter)

650 Newport Center Drive, Newport Beach, CA 92660

(Address of principal executive office)

Trent W. Walker

Treasurer (Principal Financial & Accounting Officer)

PIMCO Equity Series

650 Newport Center Drive, Newport Beach, CA 92660

(Name and address of agent for service)

Copies to:

Brendan C. Fox

Dechert LLP

1900 K Street, N.W.

Washington, D.C. 20006

Registrant’s telephone number, including area code: (888) 877-4626

Date of fiscal year end: June 30

Date of reporting period: December 31, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507

| Item 1. | Reports to Shareholders. |

The following are copies of the reports transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR 270.30e-1).

| | • | | PIMCO Equity Series Funds |

| | • | | PIMCO Equity Series RAE Fundamental Funds | |

| | • | | PIMCO Equity Series RealPath® Blend Funds |

| | • | | PIMCO RAFI Dynamic Multi-Factor U.S. Equity ETF |

| | • | | PIMCO RAFI Dynamic Multi-Factor Emerging Markets Equity ETF |

| | • | | PIMCO RAFI Dynamic Multi-Factor International Equity ETF |

PIMCO Equity Series®

Semiannual

Report

December 31, 2017

PIMCO Dividend and Income Fund

PIMCO EqS® Long/Short Fund

Table of Contents

This material is authorized for use only when preceded or accompanied by the current PIMCO Equity Series prospectus. The Shareholder Reports for the other series of the PIMCO Equity Series are printed separately.

Chairman’s Letter

Dear Shareholder,

Please find enclosed the Semiannual Report for the PIMCO Equity Series covering the six-month reporting period ended December 31, 2017. The following pages contain specific details about the investment performance of each fund and a discussion of the factors that most affected performance during the reporting period.

Highlights of the financial markets during the six-month reporting period include:

| | ∎ | | During the reporting period, geopolitical concerns remained an investor focus but the global economy provided a solid fundamental backdrop with robust consumer confidence in both the eurozone and the U.S. This environment gave room for developed market central banks to adopt a more “dovish taper”. The European Central Bank (“ECB”), for example, announced a tapering in its monthly asset purchases, but President Mario Draghi emphasized the ECB’s overall accommodative stance. In September, the Federal Reserve (“Fed”) provided details on its plan to unwind its balance sheet and kept rates on hold through its November meeting, but raised the Federal Funds Rate in December by 0.25% to a range of 1.25% to 1.50% (marking the third rate increase during 2017, following rate increases in March and in June). The Bank of England (“BOE”) raised its policy rate and suggested reduced stimulus on the horizon and the Bank of Canada (“BOC”) raised interest rates twice after a seven-year gap. Furthermore, President Xi Jinping was extended a second five-year term following the 19th National Party Congress in China, while Japan’s Prime Minister Shinzo Abe won a decisive victory in snap elections. |

| | ∎ | | As a result, many developed market yield curves flattened over the reporting period as front-end rates moved higher alongside less accommodative monetary policy. In the U.S., solid growth momentum and the Fed’s three rate hikes throughout the year pushed the two-year yield to its highest level in nearly a decade. In turn, this drove the spread between two-year and 10-year rates to its narrowest level since November 2007. Front-end yields also moved higher in the U.K. and Canada as the BOE and BOC both raised policy rates for the first time in years. |

| | ∎ | | Global stock markets reached new highs as increasingly solid economic data, rising corporate earnings, and non-restrictive central bank policy underpinned robust risk sentiment. U.S. equities, as represented by the S&P 500 Index, returned 11.42% over the reporting period. Developed market equities outside the U.S. and Canada, as represented by the MSCI EAFE Net Dividend Index (USD Hedged) and the MSCI EAFE Net Dividend Index (USD Unhedged), returned 7.92% and 9.86%, respectively, over the reporting period. Japanese equities, as represented by the Nikkei 225 Index (in JPY), returned 14.63% over the reporting period and European equities, as represented by the MSCI Europe Index (in EUR), returned 3.34% over the reporting period. |

| | ∎ | | EM equities, as represented by the MSCI Emerging Markets Index (Net Dividends in USD), returned 15.92% over the reporting period as fundamentals remained healthy in select economies. Emerging markets benefited from broad-based and synchronized global growth, robust liquidity conditions, rising commodity prices, and a weak U.S. dollar. |

| | ∎ | | U.S. Treasuries, as represented by the Bloomberg Barclays U.S. Treasury Index, returned 0.43% for the reporting period. Yields rose across the majority of the yield curve through 10-year maturities, but declined across 20- and 30-year maturities. The benchmark 10-year U.S. Treasury note yielded 2.40% at the end of the reporting period, up from 2.31% on June 30, 2017. The Bloomberg Barclays U.S. Aggregate Index, a widely used index of U.S. investment-grade bonds, returned 1.24% for the reporting period. |

If you have any questions regarding the funds, please contact your account manager or financial adviser, or call one of our shareholder associates at 888.87.PIMCO. We also invite you to visit our website at www.pimco.com to learn more about our views and global thought leadership.

Thank you for the assets you have placed with us. We deeply value your trust, and we work diligently to meet your broad investment needs.

| | |

| | Sincerely,

Brent R. Harris Chairman of the Board,

PIMCO Equity Series February 21, 2018 |

Past performance is no guarantee of future results. Unless otherwise noted, index returns reflect the reinvestment of income distributions and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. It is not possible to invest directly in an unmanaged index.

| | | | | | |

| | SEMIANNUAL REPORT | | DECEMBER 31, 2017 | | 3 |

Important Information About the Funds

PIMCO Equity Series (the “Trust”) is an open-end management investment company that includes PIMCO Dividend and Income Fund and PIMCO EqS® Long/Short Fund (each, a “Fund” and collectively, the “Funds”).

We believe that equity funds have an important role to play in a well-diversified investment portfolio. It is important to note, however, that equity funds are subject to notable risks. Among other things, equity and equity-related securities may decline in value due to both real and perceived general market, economic, and industry conditions.

The values of equity securities, such as common stocks and preferred securities, have historically risen and fallen in periodic cycles and may decline due to general market conditions, which are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment generally. Equity securities may also decline due to factors that affect a particular industry or industries, such as labor shortages, increased production costs and competitive conditions within an industry. In addition, the value of an equity security may decline for a number of reasons that directly relate to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s goods or services, as well as the historical and prospective earnings of the issuer and the value of its assets. Different types of equity securities may react differently to these developments and a change in the financial condition of a single issuer may affect securities markets as a whole.

During a general downturn in the securities markets, multiple asset classes, including equity securities, may decline in value simultaneously. The market price of equity securities owned by a Fund may go up or down, sometimes rapidly or unpredictably. Equity securities generally have greater price volatility than fixed income securities and common stocks generally have the greatest appreciation and depreciation potential of all equity securities.

The Funds may be subject to various risks as described in each Fund’s prospectus and in the Principal Risks in the Notes to Financial Statements.

The geographical classification of foreign (non-U.S.) securities in this report are classified by the country of incorporation of a holding. In certain instances, a security’s country of incorporation may be different from its country of economic exposure.

On each individual Fund Summary page in this Shareholder Report, the Average Annual Total Return table and Cumulative Returns chart measure performance assuming that any dividend and capital gain distributions were reinvested. Returns do not reflect the deduction of taxes that a shareholder would pay on (i) Fund distributions or (ii) the redemption of Fund shares. The Cumulative Returns chart and Average Annual Total Return table reflect any sales load that would have applied at the time of purchase or any Contingent Deferred Sales Charge (“CDSC”) that would have applied if a full redemption occurred on the last business day of the period shown in the Cumulative Returns chart. Class A shares are subject to an initial sales charge. A CDSC may be imposed in certain circumstances on Class A shares that are purchased without an initial sales charge and then redeemed during the first 12 months after purchase. Class C shares are subject to a 1% CDSC, which may apply in the first year. The Cumulative Returns chart reflects only Institutional Class performance. Performance may vary by share class based on each class’s expense ratios. Performance shown is net of fees and expenses. The minimum initial investment amount for Institutional Class and Class P shares is $1,000,000. The minimum initial investment amount for Class A, Class C and Class D shares is $1,000. Each Fund measures its performance against at least one broad-based securities market index (“benchmark index”). The benchmark index does not take into account fees, expenses, or taxes. A Fund’s past performance, before and after taxes, is not necessarily an indication of how the Fund will perform in the future. There is no assurance that any Fund, including any Fund that has experienced high or unusual performance for one or more periods, will experience similar levels of performance in the future. High performance is defined as a significant increase in either 1) a Fund’s total return in excess of that of the Fund’s benchmark between reporting periods or 2) a Fund’s total return in excess of the Fund’s historical returns between reporting periods. Unusual performance is defined as a significant change in a Fund’s performance as compared to one or more previous reporting periods.

The following table discloses the inception dates of each Fund and its respective share classes along with each Fund’s diversification status as of period end:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Fund Name | | | | | Fund

Inception | | | Institutional

Class | | | Class P | | | Class D | | | Class A | | | Class C | | | Diversification

Status |

PIMCO Dividend and Income Fund | | | | | | | 12/14/11 | | | | 12/14/11 | | | | 12/14/11 | | | | 12/14/11 | | | | 12/14/11 | | | | 12/14/11 | | | Diversified |

PIMCO EqS® Long/Short Fund | | | | | | | 04/20/12 | | | | 04/20/12 | | | | 04/30/12 | | | | 04/30/12 | | | | 04/30/12 | | | | 04/30/12 | | | Non-diversified |

An investment in a Fund is not a bank deposit and is not guaranteed or insured by the Federal Deposit Insurance Corporation (“FDIC”) or any other government agency. It is possible to lose money on investments in a Fund.

The Trustees are responsible generally for overseeing the management of the Trust. The Trustees authorize the Trust to enter into service agreements with the Adviser, the Distributor, the Administrator and other service providers in order to provide, and in some cases authorize service providers to procure through other parties, necessary or desirable services on behalf of the Trust and the Funds. Shareholders are not parties to or third-party beneficiaries of such service agreements. Neither a Fund’s prospectus nor a Fund’s summary prospectus, the Trust’s Statement of Additional Information (“SAI”), any contracts filed as exhibits to the Trust’s registration statement, nor any other communications, disclosure documents or regulatory filings (including this report) from or on behalf of the Trust or a Fund creates a contract between or among any shareholder of a Fund, on the one hand, and the Trust, a Fund, a service provider to the Trust or a Fund, and/or the Trustees or officers of the Trust, on the other hand. The Trustees (or the Trust and its officers, service providers or other delegates acting under authority of the Trustees) may amend the most recent prospectus or use a new prospectus, summary prospectus or SAI with respect to a Fund or the Trust, and/or amend, file and/or issue any other communications, disclosure documents or regulatory filings, and may amend or enter into any contracts to which the Trust or a Fund is a party, and interpret the investment objective(s), policies, restrictions and contractual provisions applicable to any Fund, without shareholder

input or approval, except in circumstances in which shareholder approval is specifically required by law (such as changes to fundamental investment policies) or where a shareholder approval requirement is specifically disclosed in the Trust’s then-current prospectus or SAI.

PIMCO has adopted written proxy voting policies and procedures (“Proxy Policy”) as required by Rule 206(4)-6 under the Investment Advisers Act of 1940, as amended. The Proxy Policy has been adopted by the Trust as the policies and procedures that PIMCO will use when voting proxies on behalf of a Fund. A description of the policies and procedures that PIMCO uses to vote proxies relating to portfolio securities of a Fund, and information about how the Fund voted proxies relating to portfolio securities held during the most recent twelve-month period ended June 30th, are available without charge, upon request, by calling the Trust at (888) 87-PIMCO, on the Fund’s website at www.pimco.com, and on the Securities and Exchange Commission’s (“SEC”) website at www.sec.gov.

The Trust files a complete schedule of each Fund’s holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. A copy of a Fund’s Form N-Q is available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. A Fund’s Form N-Q is also available without charge, upon request, by calling the Trust at (888) 87-PIMCO and on the Fund’s website at www.pimco.com. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

| | | | | | |

| | SEMIANNUAL REPORT | | DECEMBER 31, 2017 | | 5 |

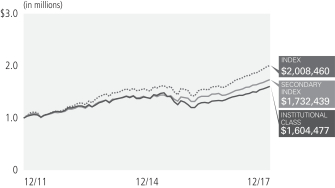

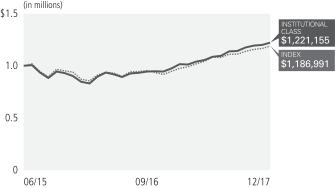

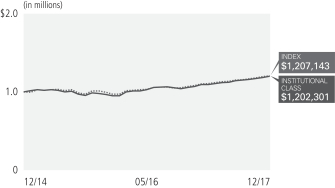

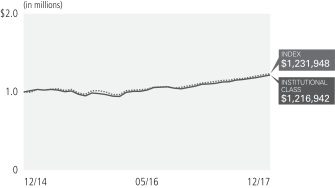

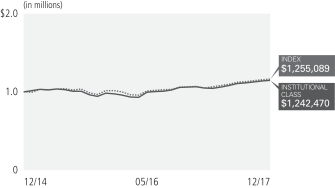

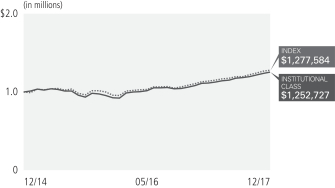

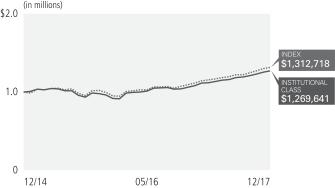

PIMCO Dividend and Income Fund

Cumulative Returns Through December 31, 2017

$1,000,000 invested at the end of the month when the Fund’s Institutional Class commenced operations.

Investment Objective and Strategy Overview

PIMCO Dividend and Income Fund seeks to provide current income that exceeds the average yield on global stocks, and as a secondary objective, seeks to provide long-term capital appreciation, by investing under normal circumstances at least 80% of its assets in a diversified portfolio of income-producing investments, and will typically invest between 60-80% of its assets in equity and equity-related securities (such portion of the Fund’s portfolio, the “Equity Sleeve”) providing exposure to a portfolio of stocks (the “RAE Income Global Portfolio”) through investment in the securities that comprise the RAE Income Global Portfolio. The stocks for the Equity Sleeve are selected by the Fund’s sub-adviser, Research Affiliates, LLC, from a broad universe of global equities. Fund strategies may change from time to time. Please refer to the Fund’s current prospectus for more information regarding the Fund’s strategy.

| | | | | | | | | | | | | | | | | | |

| Average Annual Total Return for the period ended December 31, 2017 | |

| | | | | 6 Months* | | | 1 Year | | | 5 Year | | | Fund Inception

(12/14/11) | |

| | PIMCO Dividend and Income Fund Institutional Class | | | 9.28% | | | | 16.20% | | | | 7.01% | | | | 8.50% | |

| | PIMCO Dividend and Income Fund Class P | | | 9.22% | | | | 16.08% | | | | 6.93% | | | | 8.43% | |

| | PIMCO Dividend and Income Fund Class D | | | 9.10% | | | | 15.81% | | | | 6.65% | | | | 8.14% | |

| | PIMCO Dividend and Income Fund Class A | | | 9.11% | | | | 15.73% | | | | 6.64% | | | | 8.13% | |

| | PIMCO Dividend and Income Fund Class A (adjusted) | | | 3.15% | | | | 9.39% | | | | 5.45% | | | | 7.12% | |

| | PIMCO Dividend and Income Fund Class C | | | 8.65% | | | | 14.84% | | | | 5.83% | | | | 7.31% | |

| | PIMCO Dividend and Income Fund Class C (adjusted) | | | 7.65% | | | | 13.84% | | | | 5.83% | | | | 7.31% | |

| | MSCI World Index± | | | 10.61% | | | | 22.40% | | | | 11.64% | | | | 12.92% | |

| | 75% MSCI World Index/25% Bloomberg Barclays Global Aggregate USD Unhedged±± | | | 8.64% | | | | 18.49% | | | | 8.93% | | | | 10.07% | |

All Fund returns are net of fees and expenses.

* Cumulative return.

± The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of 23 developed market country indices.

±± The benchmark is a blend of 75% MSCI World Index/25% Bloomberg Barclays Global Aggregate USD Unhedged. The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of 23 developed market country indices. Bloomberg Barclays Global Aggregate (USD Unhedged) Index provides a broad-based measure of the global investment-grade fixed income markets. The three major components of this index are the U.S. Aggregate, the Pan-European Aggregate, and the Asian-Pacific Aggregate Indices. The index also includes Eurodollar and Euro-Yen corporate bonds, Canadian Government securities, and USD investment grade 144A securities.

It is not possible to invest directly in an unmanaged index.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Differences in the Fund’s performance versus the index and related attribution information with respect to particular categories of securities or individual positions may be attributable, in part, to differences in the pricing methodologies used by the Fund and the index. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1.00% CDSC on Class C shares. For performance data current to the most recent month-end, visit www.pimco.com or via (888) 87-PIMCO.

The Fund’s total annual operating expense ratio in effect as of period end, were 0.81% for the Institutional Class shares, 0.91% for the Class P shares, 1.16% for the Class D shares, 1.16% for the Class A shares, and 1.91% for the Class C shares. Details regarding any changes to the Fund’s operating expenses, subsequent to period end, can be found in the Fund’s current prospectus, as supplemented.

| | | | | | | | |

| Institutional Class - PQIIX | | Class P - PQIPX | | Class D - PQIDX | | Class A - PQIZX | | Class C - PQICX |

Geographic Breakdown as of 12/31/20171§

| | | | | | | | |

United States | | | | | | | 50.5% | |

Japan | | | | | | | 10.1% | |

United Kingdom | | | | | | | 8.4% | |

France | | | | | | | 5.6% | |

Germany | | | | | | | 4.6% | |

Australia | | | | | | | 3.3% | |

Spain | | | | | | | 2.3% | |

Netherlands | | | | | | | 1.9% | |

Switzerland | | | | | | | 1.8% | |

Canada | | | | | | | 1.5% | |

Cayman Islands | | | | | | | 1.2% | |

Italy | | | | | | | 1.2% | |

Other | | | | | | | 5.5% | |

Sector Breakdown as of 12/31/20171§

| | | | | | | | |

Financials | | | | | | | 24.4% | |

Industrials | | | | | | | 8.5% | |

Energy | | | | | | | 6.9% | |

U.S. Treasury Obligations | | | | | | | 6.7% | |

Consumer Discretionary | | | | | | | 6.5% | |

Health Care | | | | | | | 6.2% | |

Asset-Backed Securities | | | | | | | 5.7% | |

Utilities | | | | | | | 5.5% | |

Information Technology | | | | | | | 5.1% | |

Consumer Staples | | | | | | | 4.5% | |

U.S. Government Agencies | | | | | | | 3.9% | |

Materials | | | | | | | 3.9% | |

Telecommunication Services | | | | | | | 3.8% | |

Non-Agency Mortgage-Backed Securities | | | | | | | 3.2% | |

Loan Participations and Assignments | | | | | | | 1.1% | |

Other | | | | | | | 2.0% | |

1 % of Investments, at value.

§ Geographic and Sector Breakdown and % of Investments exclude securities sold short, financial derivative instruments and short-term instruments, if any.

Fund Insights

The following affected performance during the reporting period:

| » | | Security selection in the industrial sector contributed to relative returns, as the Fund’s holdings outperformed the benchmark index. |

| » | | Overweight exposure to, and security selection in, the energy sector contributed to relative returns, as the sector and the Fund’s holdings outperformed the benchmark index. |

| » | | Overweight exposure to, and security selection in, the materials sector contributed to relative returns, as the sector and the Fund’s holdings outperformed the benchmark index. |

| » | | Holdings of non-agency mortgage-backed securities contributed to absolute returns, as these securities generated positive total returns. |

| » | | Underweight exposure to, and security selection in, the information technology sector detracted from relative returns, as the sector and the Fund’s holdings underperformed the benchmark index. |

| » | | Security selection in the financial sector detracted from relative returns, as the Fund’s holdings underperformed the benchmark index. |

| » | | Exposure to U.S. duration detracted from absolute returns, as yields generally rose. |

| | | | | | |

| | SEMIANNUAL REPORT | | DECEMBER 31, 2017 | | 7 |

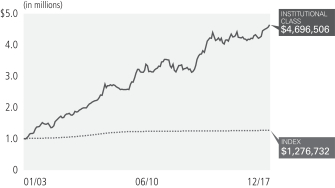

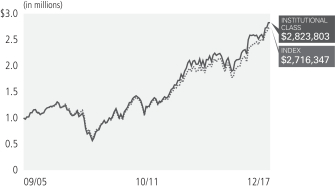

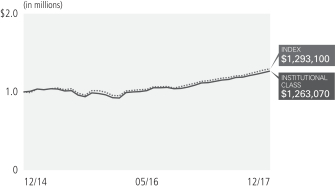

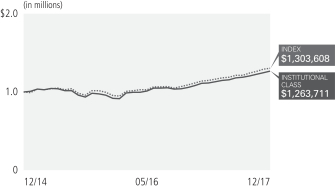

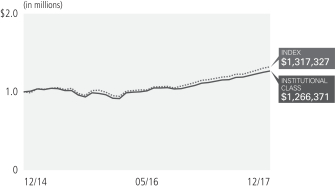

PIMCO EqS® Long/Short Fund

Cumulative Returns Through December 31, 2017

$1,000,000 invested at the end of the month when the Fund’s Institutional Class commenced operations.

Investment Objective and Strategy Overview

PIMCO EqS® Long/Short Fund seeks long-term capital appreciation by investing under normal circumstances in long and short positions of equity and equity-related securities, including common and preferred securities (and securities convertible into, or that PIMCO expects to be exchanged for, common or preferred securities), utilizing a fundamental investing style that integrates bottom-up and top-down research. The Fund will normally invest a substantial portion of its assets in equity and equity-related securities. The Fund may also invest in fixed income securities of varying maturities, cash and cash equivalents. Fund strategies may change from time to time. Please refer to the Fund’s current prospectus for more information regarding the Fund’s strategy.

| | | | | | | | | | | | | | | | | | | | | | |

| Average Annual Total Return for the period ended December 31, 2017* | |

| | | | | 6 Months** | | | 1 Year | | | 5 Year | | | 10 Year | | | Fund Inception

(01/01/03) | |

| | PIMCO EqS® Long/Short Fund Institutional Class | | | 1.34% | | | | 9.95% | | | | 8.41% | | | | 5.72% | | | | 10.96% | |

| | PIMCO EqS® Long/Short Fund Class P | | | 1.27% | | | | 9.83% | | | | 8.31% | | | | 5.67% | | | | 10.92% | |

| | PIMCO EqS® Long/Short Fund Class D | | | 1.20% | | | | 9.55% | | | | 8.02% | | | | 5.50% | | | | 10.80% | |

| | PIMCO EqS® Long/Short Fund Class A | | | 1.20% | | | | 9.66% | | | | 8.04% | | | | 5.51% | | | | 10.81% | |

| | PIMCO EqS® Long/Short Fund Class A (adjusted) | | | (4.36)% | | | | 3.61% | | | | 6.83% | | | | 4.91% | | | | 10.39% | |

| | PIMCO EqS® Long/Short Fund Class C | | | 0.81% | | | | 8.74% | | | | 7.23% | | | | 5.05% | | | | 10.49% | |

| | PIMCO EqS® Long/Short Fund Class C (adjusted) | | | (0.15)% | | | | 7.74% | | | | 7.23% | | | | 5.05% | | | | 10.49% | |

| | 3 Month USD LIBOR Index± | | | 0.66% | | | | 1.20% | | | | 0.54% | | | | 0.82% | | | | 1.65% | |

All Fund returns are net of fees and expenses.

** Cumulative return.

± The 3 Month USD LIBOR (London Interbank Offered Rate) Index is an average interest rate, determined by the ICE Benchmark Administration, that banks charge one another for the use of short-term money (3 months) in England’s Eurodollar market.

It is not possible to invest directly in an unmanaged index.

* For periods prior to April 20, 2012, the Fund’s performance reflects the performance when the Fund was a partnership, net of actual fees and expenses charged to individual partnership accounts in the aggregate. If the performance had been restated to reflect the applicable fees and expenses of each share class, the performance may have been higher or lower. The Fund began operations as a partnership on January 1, 2003 and, on April 20, 2012, was reorganized into a newly-formed fund that was registered as an investment company under the Investment Company Act of 1940. Prior to the reorganization, the Fund had an investment objective, investment strategies, investment guidelines, and restrictions that were substantially similar to those currently applicable to the Fund; however, the Fund was not registered as an investment company under the Investment Company Act of 1940 and was not subject to its requirements or requirements imposed by the Internal Revenue Code of 1986 which, if applicable, may have adversely affected its performance. The performance of Class P, D, A and C shares for the period from April 20, 2012 to April 30, 2012 is based on the performance of the Institutional Class shares of the Fund. The performance of each class of shares will differ as a result of the different levels of fees and expenses applicable to each class of shares.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Differences in the Fund’s performance versus the index and related attribution information with respect to particular categories of securities or individual positions may be attributable, in part, to differences in the pricing methodologies used by the Fund and the index. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1.00% CDSC on Class C shares. For performance data current to the most recent month-end, visit www.pimco.com or via (888) 87-PIMCO.

The Fund’s total annual operating expense ratio in effect as of period end, were 1.87% for the Institutional Class shares, 1.97% for the Class P shares, 2.22% for the Class D shares, 2.22% for the Class A shares, and 2.97% for the Class C shares. Details regarding any changes to the Fund’s operating expenses, subsequent to period end, can be found in the Fund’s current prospectus, as supplemented.

| | | | | | | | |

| Institutional Class - PMHIX | | Class P - PMHBX | | Class D - PMHDX | | Class A - PMHAX | | Class C - PMHCX |

Top 10 Holdings as of 12/31/20171§

| | | | | | | | |

Alphabet, Inc. ‘C’ | | | | | | | 4.9% | |

American Express Co. | | | | | | | 4.4% | |

Berkshire Hathaway, Inc. ‘B’ | | | | | | | 4.3% | |

Johnson & Johnson | | | | | | | 4.1% | |

SPDR S&P Oil & Gas Exploration & Production ETF | | | | | | | 3.5% | |

Union Pacific Corp. | | | | | | | 3.1% | |

Norfolk Southern Corp. | | | | | | | 3.1% | |

SPDR S&P Regional Banking ETF | | | | | | | 3.0% | |

Facebook, Inc. ‘A’ | | | | | | | 2.9% | |

Discover Financial Services | | | | | | | 2.9% | |

Sector Breakdown as of 12/31/20172§

| | | | | | | | |

Financials | | | | | | | 16.1% | |

Health Care | | | | | | | 13.4% | |

Energy | | | | | | | 11.6% | |

Industrials | | | | | | | 10.1% | |

Information Technology | | | | | | | 9.3% | |

Consumer Discretionary | | | | | | | 7.5% | |

Materials | | | | | | | 2.7% | |

Other | | | | | | | (1.5% | ) |

1 % of Investments, at value.

2 % of net exposure (Investments, at value less Securities Sold Short). Financial derivative instruments and short-term instruments are not taken into consideration.

§ Top 10 Holdings and Sector Breakdown and % of Investments exclude securities sold short, financial derivative instruments and short-term instruments, if any.

Fund Insights

The following affected performance during the reporting period:

| » | | The Fund’s long position in Berkshire Hathaway Inc. contributed to absolute returns, as the price of that security rose. |

| » | | The Fund’s long position in Union Pacific Corporation contributed to absolute returns, as the price of that security rose. |

| » | | The Fund’s long position in Alphabet Inc. contributed to absolute returns, as the price of that security rose. |

| » | | The Fund’s short equity positions detracted from absolute returns, as the prices of these securities generally rose. |

| » | | The Fund’s long position in Newell Brands Inc. detracted from absolute returns, as the price of that security fell. |

| » | | The Fund’s long position in Signature Bank detracted from absolute returns, as the price of that security fell. |

| | | | | | |

| | SEMIANNUAL REPORT | | DECEMBER 31, 2017 | | 9 |

Expense Examples

Example

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and exchange fees and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses. The Example is intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period indicated, which for all Funds and share classes is from July 1, 2017 to December 31, 2017 unless noted otherwise in the table and footnotes below.

Actual Expenses

The information in the table under the heading “Actual” provides information about actual account values and actual expenses. You may use this information, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60), then multiply the result by the number in the appropriate row for your share class, in the column entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information in the table under the heading “Hypothetical (5% return before expenses)” provides information about hypothetical account values and hypothetical expenses based on a Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in a Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) on purchase payments and exchange fees. Therefore, the information under the heading “Hypothetical (5% return before expenses)” is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Expense ratios may vary from period to period because of various factors such as an increase in expenses that are not covered by the management fees, such as fees and expenses of the independent trustees and their counsel, extraordinary expenses and interest expense.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | Actual | | | | | | Hypothetical

(5% return before expenses) | | | | | | | |

| | | | | | Beginning

Account Value

(07/01/17) | | | Ending

Account Value

(12/31/17) | | | Expenses Paid

During Period* | | | | | | Beginning

Account Value

(07/01/17) | | | Ending

Account Value

(12/31/17) | | | Expenses Paid

During Period* | | | | | | Net Annualized

Expense Ratio** | |

PIMCO Dividend and Income Fund | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Institutional Class | | | | | | $ | 1,000.00 | | | $ | 1,092.80 | | | $ | 4.41 | | | | | | | $ | 1,000.00 | | | $ | 1,020.86 | | | $ | 4.26 | | | | | | | | 0.84 | % |

| Class P | | | | | | | 1,000.00 | | | | 1,092.20 | | | | 4.93 | | | | | | | | 1,000.00 | | | | 1,020.36 | | | | 4.76 | | | | | | | | 0.94 | |

| Class D | | | | | | | 1,000.00 | | | | 1,091.00 | | | | 6.24 | | | | | | | | 1,000.00 | | | | 1,019.10 | | | | 6.02 | | | | | | | | 1.19 | |

| Class A | | | | | | | 1,000.00 | | | | 1,091.10 | | | | 6.24 | | | | | | | | 1,000.00 | | | | 1,019.10 | | | | 6.02 | | | | | | | | 1.19 | |

| Class C | | | | | | | 1,000.00 | | | | 1,086.50 | | | | 10.15 | | | | | | | | 1,000.00 | | | | 1,015.34 | | | | 9.80 | | | | | | | | 1.94 | |

PIMCO EqS® Long/Short Fund | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Institutional Class | | | | | | $ | 1,000.00 | | | $ | 1,013.40 | | | $ | 9.69 | | | | | | | $ | 1,000.00 | | | $ | 1,015.44 | | | $ | 9.70 | | | | | | | | 1.92 | % |

| Class P | | | | | | | 1,000.00 | | | | 1,012.70 | | | | 10.19 | | | | | | | | 1,000.00 | | | | 1,014.94 | | | | 10.20 | | | | | | | | 2.02 | |

| Class D | | | | | | | 1,000.00 | | | | 1,012.00 | | | | 11.45 | | | | | | | | 1,000.00 | | | | 1,013.69 | | | | 11.46 | | | | | | | | 2.27 | |

| Class A | | | | | | | 1,000.00 | | | | 1,012.00 | | | | 11.45 | | | | | | | | 1,000.00 | | | | 1,013.69 | | | | 11.46 | | | | | | | | 2.27 | |

| Class C | | | | | | | 1,000.00 | | | | 1,008.10 | | | | 15.20 | | | | | | | | 1,000.00 | | | | 1,009.93 | | | | 15.22 | | | | | | | | 3.02 | |

* Expenses Paid During Period are equal to the net annualized expense ratio for the class, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period).

** Net Annualized Expense Ratio is reflective of any applicable contractual fee waivers and/or expense reimbursements or voluntary fee waivers. Details regarding fee waivers, if any, can be found in Note 9, Fees and Expenses, in the Notes to Financial Statements.

(THIS PAGE INTENTIONALLY LEFT BLANK)

| | | | | | |

| | SEMIANNUAL REPORT | | DECEMBER 31, 2017 | | 11 |

Financial Highlights

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | Investment Operations | | | | | | Less Distributions(b) | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Selected Per Share Data for the Year or

Period Ended^: | |

Net Asset Value

Beginning of

Year or

Period | | | Net Investment

Income (Loss)(a) | | | Net Realized/

Unrealized

Gain (Loss) | | | Total | | | | | | From Net

Investment

Income | | | From Net

Realized

Capital Gains | | | Tax Basis

Return of

Capital | | | Total | |

| | | | | | | | | |

PIMCO Dividend and Income Fund | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Institutional Class | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

07/01/2017 - 12/31/2017+ | | $ | 11.09 | | | $ | 0.15 | | | $ | 0.88 | | | $ | 1.03 | | | | | | | $ | (0.24 | ) | | $ | 0.00 | | | $ | 0.00 | | | $ | (0.24 | ) |

06/30/2017 | | | 9.94 | | | | 0.30 | | | | 1.08 | | | | 1.38 | | | | | | | | (0.23 | ) | | | 0.00 | | | | 0.00 | | | | (0.23 | ) |

06/30/2016 | | | 12.29 | | | | 0.43 | | | | (1.58 | ) | | | (1.15 | ) | | | | | | | (0.44 | ) | | | (0.76 | ) | | | 0.00 | | | | (1.20 | ) |

06/30/2015 | | | 13.12 | | | | 0.47 | | | | (0.50 | ) | | | (0.03 | ) | | | | | | | (0.46 | ) | | | (0.34 | ) | | | 0.00 | | | | (0.80 | ) |

06/30/2014 | | | 11.60 | | | | 0.44 | | | | 1.54 | | | | 1.98 | | | | | | | | (0.46 | ) | | | 0.00 | | | | 0.00 | | | | (0.46 | ) |

06/30/2013 | | | 10.47 | | | | 0.54 | | | | 1.03 | | | | 1.57 | | | | | | | | (0.42 | ) | | | (0.02 | ) | | | 0.00 | | | | (0.44 | ) |

| Class P | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

07/01/2017 - 12/31/2017+ | | | 11.11 | | | | 0.15 | | | | 0.87 | | | | 1.02 | | | | | | | | (0.23 | ) | | | 0.00 | | | | 0.00 | | | | (0.23 | ) |

06/30/2017 | | | 9.96 | | | | 0.30 | | | | 1.07 | | | | 1.37 | | | | | | | | (0.22 | ) | | | 0.00 | | | | 0.00 | | | | (0.22 | ) |

06/30/2016 | | | 12.30 | | | | 0.39 | | | | (1.54 | ) | | | (1.15 | ) | | | | | | | (0.43 | ) | | | (0.76 | ) | | | 0.00 | | | | (1.19 | ) |

06/30/2015 | | | 13.13 | | | | 0.46 | | | | (0.50 | ) | | | (0.04 | ) | | | | | | | (0.45 | ) | | | (0.34 | ) | | | 0.00 | | | | (0.79 | ) |

06/30/2014 | | | 11.62 | | | | 0.44 | | | | 1.52 | | | | 1.96 | | | | | | | | (0.45 | ) | | | 0.00 | | | | 0.00 | | | | (0.45 | ) |

06/30/2013 | | | 10.48 | | | | 0.54 | | | | 1.03 | | | | 1.57 | | | | | | | | (0.41 | ) | | | (0.02 | ) | | | 0.00 | | | | (0.43 | ) |

| Class D | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

07/01/2017 - 12/31/2017+ | | | 11.09 | | | | 0.13 | | | | 0.88 | | | | 1.01 | | | | | | | | (0.22 | ) | | | 0.00 | | | | 0.00 | | | | (0.22 | ) |

06/30/2017 | | | 9.94 | | | | 0.27 | | | | 1.07 | | | | 1.34 | | | | | | | | (0.19 | ) | | | 0.00 | | | | 0.00 | | | | (0.19 | ) |

06/30/2016 | | | 12.29 | | | | 0.36 | | | | (1.54 | ) | | | (1.18 | ) | | | | | | | (0.41 | ) | | | (0.76 | ) | | | 0.00 | | | | (1.17 | ) |

06/30/2015 | | | 13.12 | | | | 0.46 | | | | (0.53 | ) | | | (0.07 | ) | | | | | | | (0.42 | ) | | | (0.34 | ) | | | 0.00 | | | | (0.76 | ) |

06/30/2014 | | | 11.61 | | | | 0.40 | | | | 1.53 | | | | 1.93 | | | | | | | | (0.42 | ) | | | 0.00 | | | | 0.00 | | | | (0.42 | ) |

06/30/2013 | | | 10.47 | | | | 0.46 | | | | 1.09 | | | | 1.55 | | | | | | | | (0.39 | ) | | | (0.02 | ) | | | 0.00 | | | | (0.41 | ) |

| Class A | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

07/01/2017 - 12/31/2017+ | | | 11.08 | | | | 0.13 | | | | 0.88 | | | | 1.01 | | | | | | | | (0.22 | ) | | | 0.00 | | | | 0.00 | | | | (0.22 | ) |

06/30/2017 | | | 9.94 | | | | 0.27 | | | | 1.07 | | | | 1.34 | | | | | | | | (0.20 | ) | | | 0.00 | | | | 0.00 | | | | (0.20 | ) |

06/30/2016 | | | 12.29 | | | | 0.39 | | | | (1.57 | ) | | | (1.18 | ) | | | | | | | (0.41 | ) | | | (0.76 | ) | | | 0.00 | | | | (1.17 | ) |

06/30/2015 | | | 13.12 | | | | 0.43 | | | | (0.50 | ) | | | (0.07 | ) | | | | | | | (0.42 | ) | | | (0.34 | ) | | | 0.00 | | | | (0.76 | ) |

06/30/2014 | | | 11.61 | | | | 0.42 | | | | 1.51 | | | | 1.93 | | | | | | | | (0.42 | ) | | | 0.00 | | | | 0.00 | | | | (0.42 | ) |

06/30/2013 | | | 10.47 | | | | 0.48 | | | | 1.07 | | | | 1.55 | | | | | | | | (0.39 | ) | | | (0.02 | ) | | | 0.00 | | | | (0.41 | ) |

| Class C | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

07/01/2017 - 12/31/2017+ | | | 11.06 | | | | 0.09 | | | | 0.86 | | | | 0.95 | | | | | | | | (0.17 | ) | | | 0.00 | | | | 0.00 | | | | (0.17 | ) |

06/30/2017 | | | 9.92 | | | | 0.18 | | | | 1.07 | | | | 1.25 | | | | | | | | (0.11 | ) | | | 0.00 | | | | 0.00 | | | | (0.11 | ) |

06/30/2016 | | | 12.27 | | | | 0.31 | | | | (1.57 | ) | | | (1.26 | ) | | | | | | | (0.33 | ) | | | (0.76 | ) | | | 0.00 | | | | (1.09 | ) |

06/30/2015 | | | 13.10 | | | | 0.34 | | | | (0.51 | ) | | | (0.17 | ) | | | | | | | (0.32 | ) | | | (0.34 | ) | | | 0.00 | | | | (0.66 | ) |

06/30/2014 | | | 11.59 | | | | 0.33 | | | | 1.51 | | | | 1.84 | | | | | | | | (0.33 | ) | | | 0.00 | | | | 0.00 | | | | (0.33 | ) |

06/30/2013 | | | 10.46 | | | | 0.40 | | | | 1.06 | | | | 1.46 | | | | | | | | (0.31 | ) | | | (0.02 | ) | | | 0.00 | | | | (0.33 | ) |

| | | | | | | | | |

PIMCO EqS® Long/Short Fund | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Institutional Class | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

07/01/2017 - 12/31/2017+ | | $ | 12.26 | | | $ | (0.02 | ) | | $ | 0.18 | | | $ | 0.16 | | | | | | | $ | 0.00 | | | $ | (0.64 | ) | | $ | 0.00 | | | $ | (0.64 | ) |

06/30/2017 | | | 11.69 | | | | (0.04 | ) | | | 1.20 | | | | 1.16 | | | | | | | | (0.36 | ) | | | (0.23 | ) | | | 0.00 | | | | (0.59 | ) |

06/30/2016 | | | 12.07 | | | | (0.17 | ) | | | (0.07 | ) | | | (0.24 | ) | | | | | | | 0.00 | | | | (0.14 | ) | | | 0.00 | | | | (0.14 | ) |

06/30/2015 | | | 11.92 | | | | 0.02 | | | | 0.18 | | | | 0.20 | | | | | | | | 0.00 | | | | (0.05 | ) | | | 0.00 | | | | (0.05 | ) |

06/30/2014 | | | 11.09 | | | | (0.10 | ) | | | 1.60 | | | | 1.50 | | | | | | | | (0.06 | ) | | | (0.61 | ) | | | 0.00 | | | | (0.67 | ) |

06/30/2013 | | | 9.71 | | | | 0.15 | | | | 1.27 | | | | 1.42 | | | | | | | | (0.04 | ) | | | 0.00 | | | | 0.00 | | | | (0.04 | ) |

| Class P | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

07/01/2017 - 12/31/2017+ | | | 12.19 | | | | (0.03 | ) | | | 0.18 | | | | 0.15 | | | | | | | | 0.00 | | | | (0.64 | ) | | | 0.00 | | | | (0.64 | ) |

06/30/2017 | | | 11.63 | | | | (0.05 | ) | | | 1.19 | | | | 1.14 | | | | | | | | (0.35 | ) | | | (0.23 | ) | | | 0.00 | | | | (0.58 | ) |

06/30/2016 | | | 12.02 | | | | (0.18 | ) | | | (0.07 | ) | | | (0.25 | ) | | | | | | | 0.00 | | | | (0.14 | ) | | | 0.00 | | | | (0.14 | ) |

06/30/2015 | | | 11.88 | | | | 0.02 | | | | 0.17 | | | | 0.19 | | | | | | | | 0.00 | | | | (0.05 | ) | | | 0.00 | | | | (0.05 | ) |

06/30/2014 | | | 11.08 | | | | (0.08 | ) | | | 1.56 | | | | 1.48 | | | | | | | | (0.07 | ) | | | (0.61 | ) | | | 0.00 | | | | (0.68 | ) |

06/30/2013 | | | 9.70 | | | | (0.05 | ) | | | 1.47 | | | | 1.42 | | | | | | | | (0.04 | ) | | | 0.00 | | | | 0.00 | | | | (0.04 | ) |

| Class D | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

07/01/2017 - 12/31/2017+ | | | 12.07 | | | | (0.04 | ) | | | 0.18 | | | | 0.14 | | | | | | | | 0.00 | | | | (0.64 | ) | | | 0.00 | | | | (0.64 | ) |

06/30/2017 | | | 11.53 | | | | (0.08 | ) | | | 1.18 | | | | 1.10 | | | | | | | | (0.33 | ) | | | (0.23 | ) | | | 0.00 | | | | (0.56 | ) |

06/30/2016 | | | 11.95 | | | | (0.20 | ) | | | (0.08 | ) | | | (0.28 | ) | | | | | | | 0.00 | | | | (0.14 | ) | | | 0.00 | | | | (0.14 | ) |

06/30/2015 | | | 11.84 | | | | (0.02 | ) | | | 0.18 | | | | 0.16 | | | | | | | | 0.00 | | | | (0.05 | ) | | | 0.00 | | | | (0.05 | ) |

06/30/2014 | | | 11.06 | | | | (0.12 | ) | | | 1.57 | | | | 1.45 | | | | | | | | (0.06 | ) | | | (0.61 | ) | | | 0.00 | | | | (0.67 | ) |

06/30/2013 | | | 9.70 | | | | (0.10 | ) | | | 1.48 | | | | 1.38 | | | | | | | | (0.02 | ) | | | 0.00 | | | | 0.00 | | | | (0.02 | ) |

| | | | | | | | |

| 12 | | PIMCO EQUITY SERIES | | | | | See Accompanying Notes | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | Ratios/Supplemental Data | |

| | | | | | | | | | Ratios to Average Net Assets | | | | |

Net Asset

Value End of

Year or

Period | | | Total Return | | | Net Assets

End of Year or

Period (000s) | | | Expenses | | | Expenses

Excluding

Waivers | | | Expenses

Excluding

Interest

Expense | | | Expenses

Excluding

Interest

Expense and

Waivers | | | Net

Investment

Income (Loss) | | | Portfolio

Turnover

Rate | |

| | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| $ | 11.88 | | | | 9.28 | % | | $ | 25,279 | | | | 0.84 | %* | | | 0.85 | %* | | | 0.80 | %* | | | 0.81 | %* | | | 2.66 | %* | | | 40 | % |

| | 11.09 | | | | 14.01 | | | | 23,087 | | | | 0.80 | | | | 0.81 | | | | 0.79 | | | | 0.80 | | | | 2.88 | | | | 93 | |

| | 9.94 | | | | (9.06 | ) | | | 31,840 | | | | 0.83 | (c) | | | 1.00 | (c) | | | 0.83 | (c) | | | 1.00 | (c) | | | 4.03 | | | | 114 | |

| | 12.29 | | | | (0.12 | ) | | | 68,607 | | | | 0.83 | | | | 1.00 | | | | 0.83 | | | | 1.00 | | | | 3.70 | | | | 98 | |

| | 13.12 | | | | 17.23 | | | | 90,408 | | | | 0.84 | | | | 1.00 | | | | 0.84 | | | | 1.00 | | | | 3.56 | | | | 79 | |

| | 11.60 | | | | 15.17 | | | | 69,203 | | | | 0.83 | | | | 1.00 | | | | 0.83 | | | | 1.00 | | | | 4.66 | | | | 75 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 11.90 | | | | 9.22 | | | | 28,342 | | | | 0.94 | * | | | 0.95 | * | | | 0.90 | * | | | 0.91 | * | | | 2.56 | * | | | 40 | |

| | 11.11 | | | | 13.86 | | | | 24,731 | | | | 0.90 | | | | 0.91 | | | | 0.89 | | | | 0.90 | | | | 2.79 | | | | 93 | |

| | 9.96 | | | | (9.05 | ) | | | 34,120 | | | | 0.93 | (c) | | | 1.10 | (c) | | | 0.93 | (c) | | | 1.10 | (c) | | | 3.53 | | | | 114 | |

| | 12.30 | | | | (0.22 | ) | | | 169,790 | | | | 0.93 | | | | 1.10 | | | | 0.93 | | | | 1.10 | | | | 3.64 | | | | 98 | |

| | 13.13 | | | | 17.05 | | | | 158,122 | | | | 0.94 | | | | 1.10 | | | | 0.94 | | | | 1.10 | | | | 3.53 | | | | 79 | |

| | 11.62 | | | | 15.15 | | | | 85,724 | | | | 0.93 | | | | 1.10 | | | | 0.93 | | | | 1.10 | | | | 4.62 | | | | 75 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 11.88 | | | | 9.10 | | | | 8,132 | | | | 1.19 | * | | | 1.20 | * | | | 1.15 | * | | | 1.16 | * | | | 2.33 | * | | | 40 | |

| | 11.09 | | | | 13.59 | | | | 8,117 | | | | 1.15 | | | | 1.16 | | | | 1.14 | | | | 1.15 | | | | 2.51 | | | | 93 | |

| | 9.94 | | | | (9.38 | ) | | | 10,623 | | | | 1.18 | (c) | | | 1.35 | (c) | | | 1.18 | (c) | | | 1.35 | (c) | | | 3.37 | | | | 114 | |

| | 12.29 | | | | (0.47 | ) | | | 41,094 | | | | 1.18 | | | | 1.35 | | | | 1.18 | | | | 1.35 | | | | 3.59 | | | | 98 | |

| | 13.12 | | | | 16.78 | | | | 32,523 | | | | 1.19 | | | | 1.35 | | | | 1.19 | | | | 1.35 | | | | 3.19 | | | | 79 | |

| | 11.61 | | | | 14.91 | | | | 23,204 | | | | 1.18 | | | | 1.35 | | | | 1.18 | | | | 1.35 | | | | 4.00 | | | | 75 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 11.87 | | | | 9.11 | | | | 143,218 | | | | 1.19 | * | | | 1.20 | * | | | 1.15 | * | | | 1.16 | * | | | 2.32 | * | | | 40 | |

| | 11.08 | | | | 13.54 | | | | 144,912 | | | | 1.15 | | | | 1.16 | | | | 1.14 | | | | 1.15 | | | | 2.53 | | | | 93 | |

| | 9.94 | | | | (9.38 | ) | | | 167,857 | | | | 1.18 | (c) | | | 1.35 | (c) | | | 1.18 | (c) | | | 1.35 | (c) | | | 3.67 | | | | 114 | |

| | 12.29 | | | | (0.49 | ) | | | 296,317 | | | | 1.18 | | | | 1.35 | | | | 1.18 | | | | 1.35 | | | | 3.39 | | | | 98 | |

| | 13.12 | | | | 16.78 | | | | 320,719 | | | | 1.19 | | | | 1.35 | | | | 1.19 | | | | 1.35 | | | | 3.34 | | | | 79 | |

| | 11.61 | | | | 14.91 | | | | 117,579 | | | | 1.18 | | | | 1.35 | | | | 1.18 | | | | 1.35 | | | | 4.18 | | | | 75 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 11.84 | | | | 8.65 | | | | 133,967 | | | | 1.94 | * | | | 1.95 | * | | | 1.90 | * | | | 1.91 | * | | | 1.58 | * | | | 40 | |

| | 11.06 | | | | 12.70 | | | | 140,710 | | | | 1.90 | | | | 1.91 | | | | 1.89 | | | | 1.90 | | | | 1.75 | | | | 93 | |

| | 9.92 | | | | (10.07 | ) | | | 195,393 | | | | 1.93 | (c) | | | 2.10 | (c) | | | 1.93 | (c) | | | 2.10 | (c) | | | 2.91 | | | | 114 | |

| | 12.27 | | | | (1.23 | ) | | | 358,171 | | | | 1.93 | | | | 2.10 | | | | 1.93 | | | | 2.10 | | | | 2.67 | | | | 98 | |

| | 13.10 | | | | 15.97 | | | | 353,287 | | | | 1.94 | | | | 2.10 | | | | 1.94 | | | | 2.10 | | | | 2.67 | | | | 79 | |

| | 11.59 | | | | 14.08 | | | | 86,879 | | | | 1.93 | | | | 2.10 | | | | 1.93 | | | | 2.10 | | | | 3.42 | | | | 75 | |

| | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| $ | 11.78 | | | | 1.34 | % | | $ | 197,381 | | | | 1.92 | %* | | | 1.93 | %* | | | 1.50 | %* | | | 1.51 | %* | | | (0.32 | )%* | | | 132 | % |

| | 12.26 | | | | 10.38 | | | | 188,022 | | | | 1.86 | | | | 1.87 | | | | 1.49 | | | | 1.50 | | | | (0.32 | ) | | | 251 | |

| | 11.69 | | | | (2.02 | ) | | | 243,341 | | | | 2.44 | | | | 2.45 | | | | 1.50 | | | | 1.51 | | | | (1.46 | ) | | | 672 | |

| | 12.07 | | | | 1.74 | | | | 299,808 | | | | 1.91 | | | | 1.92 | | | | 1.49 | | | | 1.50 | | | | 0.20 | | | | 450 | (d) |

| | 11.92 | | | | 13.59 | | | | 545,346 | | | | 2.02 | | | | 2.04 | | | | 1.48 | | | | 1.50 | | | | (0.82 | ) | | | 522 | |

| | 11.09 | | | | 14.66 | | | | 329,610 | | | | 2.65 | | | | 2.75 | | | | 1.40 | | | | 1.50 | | | | 1.45 | | | | 528 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 11.70 | | | | 1.27 | | | | 118,022 | | | | 2.02 | * | | | 2.03 | * | | | 1.60 | * | | | 1.61 | * | | | (0.42 | )* | | | 132 | |

| | 12.19 | | | | 10.28 | | | | 138,946 | | | | 1.96 | | | | 1.97 | | | | 1.59 | | | | 1.60 | | | | (0.44 | ) | | | 251 | |

| | 11.63 | | | | (2.11 | ) | | | 249,973 | | | | 2.54 | | | | 2.55 | | | | 1.60 | | | | 1.61 | | | | (1.51 | ) | | | 672 | |

| | 12.02 | | | | 1.66 | | | | 207,511 | | | | 2.01 | | | | 2.02 | | | | 1.59 | | | | 1.60 | | | | 0.16 | | | | 450 | (d) |

| | 11.88 | | | | 13.40 | | | | 277,661 | | | | 2.00 | | | | 2.02 | | | | 1.58 | | | | 1.60 | | | | (0.71 | ) | | | 522 | |

| | 11.08 | | | | 14.77 | | | | 15,664 | | | | 3.94 | | | | 4.04 | | | | 1.50 | | | | 1.60 | | | | (0.48 | ) | | | 528 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 11.57 | | | | 1.20 | | | | 49,915 | | | | 2.27 | * | | | 2.28 | * | | | 1.85 | * | | | 1.86 | * | | | (0.66 | )* | | | 132 | |

| | 12.07 | | | | 9.93 | | | | 46,418 | | | | 2.21 | | | | 2.22 | | | | 1.84 | | | | 1.85 | | | | (0.70 | ) | | | 251 | |

| | 11.53 | | | | (2.37 | ) | | | 62,130 | | | | 2.79 | | | | 2.80 | | | | 1.85 | | | | 1.86 | | | | (1.74 | ) | | | 672 | |

| | 11.95 | | | | 1.41 | | | | 44,227 | | | | 2.26 | | | | 2.27 | | | | 1.84 | | | | 1.85 | | | | (0.19 | ) | | | 450 | (d) |

| | 11.84 | | | | 13.13 | | | | 77,934 | | | | 2.31 | | | | 2.33 | | | | 1.83 | | | | 1.85 | | | | (1.01 | ) | | | 522 | |

| | 11.06 | | | | 14.31 | | | | 12,421 | | | | 3.95 | | | | 4.05 | | | | 1.75 | | | | 1.85 | | | | (0.97 | ) | | | 528 | |

| | | | | | |

| | SEMIANNUAL REPORT | | DECEMBER 31, 2017 | | 13 |

Financial Highlights (Cont.)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | Investment Operations | | | | | | Less Distributions(b) | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Selected Per Share Data for the Year or

Period Ended^: | |

Net Asset Value

Beginning of

Year or

Period | | | Net Investment

Income (Loss)(a) | | | Net Realized/

Unrealized

Gain (Loss) | | | Total | | | | | | From Net

Investment

Income | | | From Net

Realized

Capital Gains | | | Tax Basis

Return of

Capital | | | Total | |

| | | | | | | | | |

PIMCO EqS® Long/Short Fund (Cont.) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Class A | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

07/01/2017 - 12/31/2017+ | | $ | 12.05 | | | $ | (0.04 | ) | | $ | 0.18 | | | $ | 0.14 | | | | | | | $ | 0.00 | | | $ | (0.64 | ) | | $ | 0.00 | | | $ | (0.64 | ) |

06/30/2017 | | | 11.52 | | | | (0.08 | ) | | | 1.18 | | | | 1.10 | | | | | | | | (0.34 | ) | | | (0.23 | ) | | | 0.00 | | | | (0.57 | ) |

06/30/2016 | | | 11.94 | | | | (0.21 | ) | | | (0.07 | ) | | | (0.28 | ) | | | | | | | 0.00 | | | | (0.14 | ) | | | 0.00 | | | | (0.14 | ) |

06/30/2015 | | | 11.83 | | | | (0.02 | ) | | | 0.18 | | | | 0.16 | | | | | | | | 0.00 | | | | (0.05 | ) | | | 0.00 | | | | (0.05 | ) |

06/30/2014 | | | 11.05 | | | | (0.12 | ) | | | 1.57 | | | | 1.45 | | | | | | | | (0.06 | ) | | | (0.61 | ) | | | 0.00 | | | | (0.67 | ) |

06/30/2013 | | | 9.70 | | | | (0.00 | ) | | | 1.38 | | | | 1.38 | | | | | | | | (0.03 | ) | | | 0.00 | | | | 0.00 | | | | (0.03 | ) |

| Class C | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

07/01/2017 - 12/31/2017+ | | | 11.65 | | | | (0.08 | ) | | | 0.17 | | | | 0.09 | | | | | | | | 0.00 | | | | (0.64 | ) | | | 0.00 | | | | (0.64 | ) |

06/30/2017 | | | 11.20 | | | | (0.16 | ) | | | 1.13 | | | | 0.97 | | | | | | | | (0.29 | ) | | | (0.23 | ) | | | 0.00 | | | | (0.52 | ) |

06/30/2016 | | | 11.69 | | | | (0.29 | ) | | | (0.06 | ) | | | (0.35 | ) | | | | | | | 0.00 | | | | (0.14 | ) | | | 0.00 | | | | (0.14 | ) |

06/30/2015 | | | 11.67 | | | | (0.11 | ) | | | 0.18 | | | | 0.07 | | | | | | | | 0.00 | | | | (0.05 | ) | | | 0.00 | | | | (0.05 | ) |

06/30/2014 | | | 10.98 | | | | (0.20 | ) | | | 1.55 | | | | 1.35 | | | | | | | | (0.05 | ) | | | (0.61 | ) | | | 0.00 | | | | (0.66 | ) |

06/30/2013 | | | 9.69 | | | | 0.01 | | | | 1.29 | | | | 1.30 | | | | | | | | (0.01 | ) | | | 0.00 | | | | 0.00 | | | | (0.01 | ) |

| ^ | A zero balance may reflect actual amounts rounding to less than $0.01 or 0.01%. |

| (a) | Per share amounts based on average number of shares outstanding during the year or period. |

| (b) | The tax characterization of distributions is determined in accordance with Federal income tax regulations. The actual tax characterization of distributions paid is determined at the end of the fiscal year. See Note 2, Distributions to Shareholders, in the Notes to Financial Statements for more information. |

| (c) | Effective June 16, 2016, the Fund’s Investment advisory fee was decreased by 0.20% to an annual rate of 0.49%. |

| (d) | The amount previously reported as 763% in the Fund’s annual report has been restated, as above. |

| | | | | | | | |

| 14 | | PIMCO EQUITY SERIES | | | | | See Accompanying Notes | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | Ratios/Supplemental Data | |

| | | | | | | | | | Ratios to Average Net Assets | | | | |

Net Asset

Value End of

Year or

Period | | | Total Return | | | Net Assets

End of Year or

Period (000s) | | | Expenses | | | Expenses

Excluding

Waivers | | | Expenses

Excluding

Interest

Expense | | | Expenses

Excluding

Interest

Expense and

Waivers | | | Net

Investment

Income (Loss) | | | Portfolio

Turnover

Rate | |

| | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| $ | 11.55 | | | | 1.20 | % | | $ | 83,496 | | | | 2.27 | %* | | | 2.28 | %* | | | 1.85 | %* | | | 1.86 | %* | | | (0.67 | )%* | | | 132 | % |

| | 12.05 | | | | 9.97 | | | | 88,636 | | | | 2.21 | | | | 2.22 | | | | 1.84 | | | | 1.85 | | | | (0.67 | ) | | | 251 | |

| | 11.52 | | | | (2.38 | ) | | | 147,582 | | | | 2.79 | | | | 2.80 | | | | 1.85 | | | | 1.86 | | | | (1.79 | ) | | | 672 | |

| | 11.94 | | | | 1.41 | | | | 172,843 | | | | 2.26 | | | | 2.27 | | | | 1.84 | | | | 1.85 | | | | (0.18 | ) | | | 450 | (d) |

| | 11.83 | | | | 13.17 | | | | 382,160 | | | | 2.27 | | | | 2.29 | | | | 1.83 | | | | 1.85 | | | | (0.98 | ) | | | 522 | |

| | 11.05 | | | | 14.27 | | | | 24,759 | | | | 3.62 | | | | 3.72 | | | | 1.75 | | | | 1.85 | | | | (0.03 | ) | | | 528 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 11.10 | | | | 0.81 | | | | 80,290 | | | | 3.02 | * | | | 3.03 | * | | | 2.60 | * | | | 2.61 | * | | | (1.42 | )* | | | 132 | |

| | 11.65 | | | | 9.07 | | | | 91,557 | | | | 2.96 | | | | 2.97 | | | | 2.59 | | | | 2.60 | | | | (1.41 | ) | | | 251 | |

| | 11.20 | | | | (3.03 | ) | | | 145,358 | | | | 3.54 | | | | 3.55 | | | | 2.60 | | | | 2.61 | | | | (2.52 | ) | | | 672 | |

| | 11.69 | | | | 0.66 | | | | 140,719 | | | | 3.01 | | | | 3.02 | | | | 2.59 | | | | 2.60 | | | | (0.95 | ) | | | 450 | (d) |

| | 11.67 | | | | 12.26 | | | | 214,485 | | | | 3.00 | | | | 3.02 | | | | 2.58 | | | | 2.60 | | | | (1.71 | ) | | | 522 | |

| | 10.98 | | | | 13.41 | | | | 9,530 | | | | 4.04 | | | | 4.14 | | | | 2.50 | | | | 2.60 | | | | 0.13 | | | | 528 | |

| | | | | | |

| | SEMIANNUAL REPORT | | DECEMBER 31, 2017 | | 15 |

Statements of Assets and Liabilities

| | | | | | | | |

| (Amounts in thousands†, except per share amounts) | | PIMCO

Dividend and

Income

Fund | | | PIMCO

EqS®

Long/Short

Fund | |

| | |

Assets: | | | | | | | | |

Investments, at value | | | | | | | | |

Investments in securities* | | $ | 356,613 | | | $ | 446,850 | |

Investments in Affiliates | | | 5,299 | | | | 85,566 | |

Financial Derivative Instruments | | | | | | | | |

Exchange-traded or centrally cleared | | | 70 | | | | 94 | |

Over the counter | | | 209 | | | | 269 | |

Cash | | | 1,048 | | | | 1 | |

Deposits with counterparty | | | 1,068 | | | | 109,453 | |

Foreign currency, at value | | | 501 | | | | 716 | |

Receivable for investments sold | | | 58,485 | | | | 23,600 | |

Receivable for Fund shares sold | | | 992 | | | | 663 | |

Interest and/or dividends receivable | | | 1,569 | | | | 426 | |

Dividends receivable from Affiliates | | | 4 | | | | 145 | |

Reimbursement receivable from PIMCO | | | 4 | | | | 6 | |

Other assets | | | 1 | | | | 1 | |

Total Assets | | | 425,863 | | | | 667,790 | |

| | |

Liabilities: | | | | | | | | |

Borrowings & Other Financing Transactions | | | | | | | | |

Payable for reverse repurchase agreements | | $ | 9,126 | | | $ | 0 | |

Payable for sale-buyback transactions | | | 5,380 | | | | 0 | |

Payable for short sales | | | 3,001 | | | | 106,320 | |

Financial Derivative Instruments | | | | | | | | |

Exchange-traded or centrally cleared | | | 32 | | | | 175 | |

Over the counter | | | 343 | | | | 256 | |

Payable for investments purchased | | | 68,022 | | | | 30,168 | |

Payable for investments in Affiliates purchased | | | 4 | | | | 145 | |

Deposits from counterparty | | | 40 | | | | 260 | |

Payable for Fund shares redeemed | | | 561 | | | | 533 | |

Accrued investment advisory fees | | | 145 | | | | 482 | |

Accrued supervisory and administrative fees | | | 116 | | | | 238 | |

Accrued distribution fees | | | 89 | | | | 65 | |

Accrued servicing fees | | | 61 | | | | 36 | |

Other liabilities | | | 5 | | | | 8 | |

Total Liabilities | | | 86,925 | | | | 138,686 | |

| | |

Net Assets | | $ | 338,938 | | | $ | 529,104 | |

| | |

Net Assets Consist of: | | | | | | | | |

Paid in capital | | $ | 411,624 | | | $ | 499,574 | |

Undistributed (overdistributed) net investment income | | | (563 | ) | | | (482 | ) |

Accumulated undistributed net realized gain (loss) | | | (110,405 | ) | | | 2,532 | |

Net unrealized appreciation (depreciation) | | | 38,282 | | | | 27,480 | |

| | |

Net Assets | | $ | 338,938 | | | $ | 529,104 | |

| | |

Cost of investments in securities | | $ | 318,071 | | | $ | 414,789 | |

Cost of investments in Affiliates | | $ | 5,297 | | | $ | 85,557 | |

Cost of foreign currency held | | $ | 502 | | | $ | 712 | |

Proceeds received on short sales | | $ | 2,989 | | | $ | 102,332 | |

Cost or premiums of financial derivative instruments, net | | $ | (200 | ) | | $ | (3,368 | ) |

| | |

* Includes repurchase agreements of: | | $ | 186 | | | $ | 524 | |

| † | A zero balance may reflect actual amounts rounding to less than one thousand. |

| | | | | | | | |

| 16 | | PIMCO EQUITY SERIES | | | | | See Accompanying Notes | |

December 31, 2017 (Unaudited)

| | | | | | | | |

| | | PIMCO

Dividend and

Income Fund | | | PIMCO

EqS®

Long/Short

Fund | |

| | |

Net Assets: | | | | | | | | |

Institutional Class | | $ | 25,279 | | | $ | 197,381 | |

Class P | | | 28,342 | | | | 118,022 | |

Class D | | | 8,132 | | | | 49,915 | |

Class A | | | 143,218 | | | | 83,496 | |

Class C | | | 133,967 | | | | 80,290 | |

| | |

Shares Issued and Outstanding: | | | | | | | | |

Institutional Class | | | 2,128 | | | | 16,759 | |

Class P | | | 2,381 | | | | 10,087 | |

Class D | | | 685 | | | | 4,315 | |

Class A | | | 12,065 | | | | 7,233 | |

Class C | | | 11,311 | | | | 7,234 | |

| | |

Net Asset Value Per Share Outstanding: | | | | | | | | |

Institutional Class | | $ | 11.88 | | | $ | 11.78 | |

Class P | | | 11.90 | | | | 11.70 | |

Class D | | | 11.88 | | | | 11.57 | |

Class A | | | 11.87 | | | | 11.55 | |

Class C | | | 11.84 | | | | 11.10 | |

| | | | | | |

| | SEMIANNUAL REPORT | | DECEMBER 31, 2017 | | 17 |

Statements of Operations

(Unaudited)

| | | | | | | | |

| Six Months Ended December 31, 2017 | | | | | | |

| (Amounts in thousands†) | | PIMCO

Dividend and

Income

Fund | | | PIMCO

EqS®

Long/Short

Fund | |

| | |

Investment Income: | | | | | | | | |

Interest | | $ | 2,040 | | | $ | 593 | |

Dividends, net of foreign taxes* | | | 3,921 | | | | 2,709 | |

Dividends from Investments in Affiliates | | | 8 | | | | 1,027 | |

Total Income | | | 5,969 | | | | 4,329 | |

| | |

Expenses: | | | | | | | | |

Investment advisory fees | | | 833 | | | | 2,821 | |

Supervisory and administrative fees | | | 669 | | | | 1,396 | |

Distribution and/or servicing fees - Class D | | | 10 | | | | 61 | |

Distribution fees - Class C | | | 513 | | | | 323 | |

Servicing fees - Class A | | | 181 | | | | 107 | |

Servicing fees - Class C | | | 171 | | | | 108 | |

Dividends on short sales | | | 0 | | | | 1,049 | |

Trustee fees | | | 10 | | | | 16 | |

Interest expense | | | 64 | | | | 93 | |

Miscellaneous expense | | | 13 | | | | 20 | |

Total Expenses | | | 2,464 | | | | 5,994 | |

Waiver and/or Reimbursement by PIMCO | | | (10 | ) | | | (16 | ) |

Net Expenses | | | 2,454 | | | | 5,978 | |

| | |

Net Investment Income (Loss) | | | 3,515 | | | | (1,649 | ) |

| | |

Net Realized Gain (Loss): | | | | | | | | |

Investments in securities | | | 10,097 | | | | 15,183 | |

Investments in Affiliates | | | 0 | | | | (34 | ) |

Exchange-traded or centrally cleared financial derivative instruments | | | 85 | | | | (3,351 | ) |

Over the counter financial derivative instruments | | | (248 | ) | | | (1,525 | ) |

Short sales | | | (1 | ) | | | (5,336 | ) |

Foreign currency | | | 9 | | | | 79 | |

| | |

Net Realized Gain (Loss) | | | 9,942 | | | | 5,016 | |

| | |

Net Change in Unrealized Appreciation (Depreciation): | | | | | | | | |

Investments in securities | | | 15,800 | | | | 5,639 | |

Investments in Affiliates | | | 2 | | | | 5 | |

Exchange-traded or centrally cleared financial derivative instruments | | | (184 | ) | | | (282 | ) |

Over the counter financial derivative instruments | | | 0 | | | | 1,126 | |

Short sales | | | (12 | ) | | | (3,320 | ) |

Foreign currency assets and liabilities | | | 0 | | | | (133 | ) |

| | |

Net Change in Unrealized Appreciation (Depreciation) | | | 15,606 | | | | 3,035 | |

| | |

Net Increase (Decrease) in Net Assets Resulting from Operations | | $ | 29,063 | | | $ | 6,402 | |

| | |

* Foreign tax withholdings - Dividends | | $ | 145 | | | $ | 12 | |

| † | A zero balance may reflect actual amounts rounding to less than one thousand. |

| | | | | | | | |

| 18 | | PIMCO EQUITY SERIES | | | | | See Accompanying Notes | |

Statements of Changes in Net Assets

| | | | | | | | | | | | | | | | |

| | | PIMCO

Dividend and Income Fund | | | PIMCO

EqS® Long/Short Fund | |

| | | | |

| (Amounts in thousands†) | | Six Months Ended

December 31, 2017

(Unaudited) | | | Year Ended

June 30, 2017 | | | Six Months Ended

December 31, 2017

(Unaudited) | | | Year Ended

June 30, 2017 | |

| | | | |

Increase (Decrease) in Net Assets from: | | | | | | | | | | | | | | | | |

| | | | |

Operations: | | | | | | | | | | | | | | | | |

Net investment income (loss) | | $ | 3,515 | | | $ | 8,411 | | | $ | (1,649 | ) | | $ | (4,055 | ) |

Net realized gain (loss) | | | 9,942 | | | | 10,969 | | | | 5,016 | | | | 77,048 | |

Net change in unrealized appreciation (depreciation) | | | 15,606 | | | | 27,793 | | | | 3,035 | | | | (15,261 | ) |

| | | | |

Net Increase (Decrease) in Net Assets Resulting from Operations | | | 29,063 | | | | 47,173 | | | | 6,402 | | | | 57,732 | |

| | | | |

Distributions to Shareholders: | | | | | | | | | | | | | | | | |

From net investment income | | | | | | | | | | | | | | | | |

Institutional Class | | | (486 | ) | | | (525 | ) | | | 0 | | | | (5,009 | ) |

Class P | | | (542 | ) | | | (468 | ) | | | 0 | | | | (4,762 | ) |

Class D | | | (148 | ) | | | (156 | ) | | | 0 | | | | (1,056 | ) |

Class A | | | (2,629 | ) | | | (2,620 | ) | | | 0 | | | | (3,239 | ) |

Class C | | | (1,996 | ) | | | (1,732 | ) | | | 0 | | | | (2,934 | ) |

From net realized capital gains | | | | | | | | | | | | | | | | |

Institutional Class | | | 0 | | | | 0 | | | | (9,995 | ) | | | (3,352 | ) |

Class P | | | 0 | | | | 0 | | | | (6,284 | ) | | | (3,145 | ) |

Class D | | | 0 | | | | 0 | | | | (2,640 | ) | | | (852 | ) |

Class A | | | 0 | | | | 0 | | | | (4,412 | ) | | | (2,245 | ) |

Class C | | | 0 | | | | 0 | | | | (4,484 | ) | | | (2,370 | ) |

| | | | |

Total Distributions(a) | | | (5,801 | ) | | | (5,501 | ) | | | (27,815 | ) | | | (28,964 | ) |

| | | | |

Portfolio Share Transactions: | | | | | | | | | | | | | | | | |

Net increase (decrease) resulting from Portfolio share transactions** | | | (25,881 | ) | | | (139,948 | ) | | | (3,062 | ) | | | (323,573 | ) |

| | | | |

Total Increase (Decrease) in Net Assets | | | (2,619 | ) | | | (98,276 | ) | | | (24,475 | ) | | | (294,805 | ) |

| | | | |

Net Assets: | | | | | | | | | | | | | | | | |

Beginning of period | | | 341,557 | | | | 439,833 | | | | 553,579 | | | | 848,384 | |

End of period* | | $ | 338,938 | | | $ | 341,557 | | | $ | 529,104 | | | $ | 553,579 | |

| | | | |

* Including undistributed (overdistributed) net investment income of: | | $ | (563 | ) | | $ | 1,723 | | | $ | (482 | ) | | $ | 1,167 | |

| † | A zero balance may reflect actual amounts rounding to less than one thousand. |

| ** | See Note 13, Shares of Beneficial Interest, in the Notes to Financial Statements. |

| (a) | The tax characterization of distributions is determined in accordance with Federal income tax regulations. The actual tax characterization of distributions paid is determined at the end of the fiscal year. See Note 2, Distributions to Shareholders, in the Notes to Financial Statements for more information. |

| | | | | | |

| | SEMIANNUAL REPORT | | DECEMBER 31, 2017 | | 19 |

Statement of Cash Flows

| | | | |

| Six Months Ended December 31, 2017 (Unaudited) | | | |

| (Amounts in thousands) | | PIMCO

EqS® Long/Short

Fund | |

| |

Cash Flows Provided by (Used for) Operating Activities: | | | | |

| |

Net increase (decrease) in net assets resulting from operations | | $ | 6,402 | |

| |

Adjustments to Reconcile Net Increase (Decrease) in Net Assets from Operations to Net Cash Provided by (Used for) Operating Activities: | | | | |

Purchases of long-term securities | | | (494,225 | ) |

Proceeds from sales of long-term securities | | | 470,657 | |

(Purchases) Proceeds from sales of short-term portfolio investments, net | | | 62,359 | |

(Increase) decrease in deposits with counterparty | | | (9,667 | ) |

(Increase) decrease in receivable for investments sold | | | (7,301 | ) |

(Increase) decrease in interest and/or dividends receivable | | | 324 | |

(Increase) decrease in dividends receivable from Affiliates | | | 47 | |

Proceeds from (Payments on) exchange-traded or centrally cleared financial derivative instruments | | | (3,621 | ) |

Proceeds from (Payments on) over the counter financial derivative instruments | | | (1,525 | ) |

Increase (Decrease) in reimbursement receivable from PIMCO | | | (3 | ) |

Increase (decrease) in payable for investments purchased | | | 17,035 | |

Increase (decrease) in deposits from counterparty | | | 260 | |

Increase (decrease) in accrued investment advisory fees | | | (22 | ) |

Increase (decrease) in accrued supervisory and administrative fees | | | (11 | ) |

Increase (decrease) in accrued distribution fees | | | (5 | ) |

Increase (decrease) in accrued servicing fees | | | (3 | ) |

Proceeds from (Payments on) short sales transactions, net | | | (94 | ) |

Proceeds from (Payments on) foreign currency transactions | | | (54 | ) |

Increase (decrease) in other liabilities | | | (44 | ) |

Net Realized (Gain) Loss | | | | |

Investments in securities | | | (15,183 | ) |

Investments in Affiliates | | | 34 | |

Exchange-traded or centrally cleared financial derivative instruments | | | 3,351 | |

Over the counter financial derivative instruments | | | 1,525 | |

Short sales | | | 5,336 | |

Foreign currency | | | (79 | ) |

Net Change in Unrealized (Appreciation) Depreciation | | | | |

Investments in securities | | | (5,639 | ) |

Investments in Affiliates | | | (5 | ) |

Exchange-traded or centrally cleared financial derivative instruments | | | 282 | |

Over the counter financial derivative instruments | | | (1,126 | ) |

Short sales | | | 3,320 | |

Foreign currency assets and liabilities | | | 133 | |

Net amortization (accretion) on investments | | | (237 | ) |

| |

Net Cash Provided by (Used for) Operating Activities | | | 32,221 | |

| |

Cash Flows Received from (Used for) Financing Activities: | | | | |

Proceeds from shares sold | | | 81,055 | |

Payments on shares redeemed | | | (112,748 | ) |

Cash distributions paid* | | | (47 | ) |

| |

Net Cash Received from (Used for) Financing Activities | | | (31,740 | ) |

| |

Net Increase (Decrease) in Cash and Foreign Currency | | | 481 | |

| |

Cash and Foreign Currency: | | | | |

Beginning of period | | | 236 | |

End of period | | $ | 717 | |

| |

* Reinvestment of distributions | | $ | 27,768 | |

| |

Supplemental Disclosure of Cash Flow Information: | | | | |

Interest expense paid during the period | | $ | 159 | |

A Statement of Cash Flows is presented when the Fund has a significant amount of borrowing during the period, based on the average total borrowing outstanding in relation to total assets or when substantially all of the Fund’s investments are not classified as Level 1 or 2 in the fair value hierarchy.

| | | | | | | | |

| 20 | | PIMCO EQUITY SERIES | | | | | See Accompanying Notes | |

Schedule of Investments PIMCO Dividend and Income Fund

December 31, 2017 (Unaudited)

| | | | | | | | | | | | |

| | | | | PRINCIPAL

AMOUNT

(000S) | | | | | MARKET

VALUE

(000S) | |

| INVESTMENTS IN SECURITIES 105.2% | |

| |

| ASSET-BACKED SECURITIES 6.1% | |

| |

| CAYMAN ISLANDS 1.3% | |

NewMark Capital Funding CLO Ltd. | |

2.607% (US0003M + 1.120%) due 06/02/2025 ~ | | $ | | | 836 | | | $ | | | 838 | |

OZLM Ltd. | |

2.653% (US0003M + 1.300%) due 04/17/2026 ~ | | | | | 1,000 | | | | | | 1,006 | |

Palmer Square CLO Ltd. | |

2.573% (US0003M + 1.220%) due 10/17/2027 ~ | | | | | 700 | | | | | | 703 | |

TICP CLO Ltd. | |

2.551% (US0003M + 1.180%) due 04/26/2026 ~ | | | | | 1,100 | | | | | | 1,102 | |

TruPS Financials Note Securitization Ltd. | |

2.861% (US0003M + 1.570%) due 09/20/2039 ~ | | | | | 600 | | | | | | 591 | |

| | | | | | | | | | | | |

Total Cayman Islands | | | 4,240 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| NETHERLANDS 0.2% | |

Pallas CDO BV | |

0.000% due 07/16/2082 • | | EUR | | | 594 | | | | | | 709 | |

| | | | | | | | | | | | |

Total Netherlands | | | 709 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| UNITED STATES 4.6% | |

Conseco Finance Corp. | |

6.280% due 09/01/2030 | | $ | | | 483 | | | | | | 508 | |

Credit Suisse First Boston Mortgage Securities Corp. | |

2.172% (US0001M + 0.620%) due 01/25/2032 ~ | | | | | 1,453 | | | | | | 1,392 | |

EMC Mortgage Loan Trust | |

2.852% (LIBOR01M + 1.300%) due 02/25/2041 ~ | | | | | 39 | | | | | | 38 | |

HSI Asset Securitization Corp. Trust | |

1.722% (US0001M + 0.170%) due 12/25/2036 ~ | | | | | 5,120 | | | | | | 2,319 | |

Morgan Stanley Home Equity Loan Trust | |

1.652% (US0001M + 0.100%) due 12/25/2036 ~ | | | | | 1,955 | | | | | | 1,205 | |

1.972% (US0001M + 0.420%) due 12/25/2035 ~ | | | | | 3,600 | | | | | | 3,569 | |

Navient Student Loan Trust | |

2.602% (US0001M + 1.050%) due 12/27/2066 ~ | | | | | 732 | | | | | | 741 | |

Progress Residential Trust | |

2.960% (LIBOR01M + 1.500%) due 09/17/2033 ~ | | | | | 991 | | | | | | 1,003 | |

Residential Asset Securities Corp. Trust | |

2.437% (US0001M + 0.885%) due 01/25/2034 ~ | | | | | 1,743 | | | | | | 1,740 | |

Structured Asset Investment Loan Trust | |

1.702% (US0001M + 0.150%) due 09/25/2036 ~ | | | | | 3,326 | | | | | | 3,183 | |

| | | | | | | | | | | | |

| Total United States | | | 15,698 | |

| | | | | | | | | | | | |

| Total Asset-Backed Securities (Cost $19,223) | | | 20,647 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| LOAN PARTICIPATIONS AND ASSIGNMENTS 1.1% | |

| |

| CANADA 0.0% | |

B.C. Unlimited Liability Co. | |

3.819% (LIBOR03M + 2.250%) due 02/16/2024 ~ | | | | | 10 | | | | | | 10 | |

| | | | | | | | | | | | |

Total Canada | | | 10 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| IRELAND 0.0% | |

Avolon Holdings Ltd. | |