UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-22431

RiverPark Funds Trust

(Exact name of registrant as specified in charter)

156 West 56th Street, 17th Floor

New York, NY 10019

(Address of principal executive offices) (Zip code)

Morty Schaja

156 West 56th Street, 17th Floor

New York, NY 10019

(Name and address of agent for service)

With copies to:

Thomas R. Westle

Blank Rome LLP

405 Lexington Avenue

New York, NY 10174

Registrant’s telephone number, including area code: 212-484-2100

Date of fiscal year end: September 30, 2018

Date of reporting period: September 30, 2018

| Item 1. | Reports to Stockholders. |

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR § 270.30e-1), is attached hereto.

| |

Annual Report September 30, 2018

| |

RiverPark Large Growth Fund Retail Class and Institutional Class Shares

RiverPark/Wedgewood Fund Retail Class and Institutional Class Shares

RiverPark Short Term High Yield Fund Retail Class and Institutional Class Shares

RiverPark Long/Short Opportunity Fund Retail Class and Institutional Class Shares

RiverPark Strategic Income Fund Retail Class and Institutional Class Shares

| |

Investment Adviser:

|

|

|

Table of Contents

Management’s Discussion of Fund Performance and Analysis | |

RiverPark Large Growth Fund | 1 |

RiverPark/Wedgewood Fund | 3 |

RiverPark Short Term High Yield Fund | 5 |

RiverPark Long/Short Opportunity Fund | 8 |

RiverPark Strategic Income Fund | 12 |

Schedules of Investments | |

RiverPark Large Growth Fund | 15 |

RiverPark/Wedgewood Fund | 16 |

RiverPark Short Term High Yield Fund | 17 |

RiverPark Long/Short Opportunity Fund | 20 |

RiverPark Strategic Income Fund | 23 |

Statements of Assets and Liabilities | 28 |

Statements of Operations | 30 |

Statements of Changes in Net Assets | 32 |

Financial Highlights | 36 |

Notes to Financial Statements | 42 |

Report of Independent Registered Public Accounting Firm | 57 |

Trustees and Officers of the Trust | 58 |

Disclosure of Fund Expenses | 60 |

Approval of the Investment Advisory and Investment Sub-Advisory Agreements | 62 |

Notice to Shareholders | 66 |

The RiverPark Funds file their complete schedules of fund holdings with the Securities and Exchange Commission (the “Commission”) for the first and third quarters of each fiscal year on Form N-Q within sixty days after the end of the period. The Funds’ Forms N-Q are available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Funds use to determine how to vote proxies relating to fund securities, as well as information relating to how a Fund voted proxies relating to fund securities during the most recent period ended June 30 is available (i) without charge, upon request, by calling 888-564-4517; and (ii) on the Commission’s website at http://www.sec.gov.

|

|

Management’s Discussion of Fund Performance and Analysis

RiverPark Large Growth Fund (Unaudited)

For the fiscal year ended September 30, 2018, the RiverPark Large Growth Fund (the “Fund”) gained 22.68% and 22.34% on its Institutional Class Shares and Retail Class Shares, respectively, while the Russell 1000 Growth Index gained 26.30% and the S&P 500 Index gained 17.91%.

Investment results for the fiscal year were not uniform across quarters. The Institutional Class Shares gained 6.58% for the December quarter, 2.62% for the March quarter, 5.38% for the June quarter and 6.44% in the September quarter.

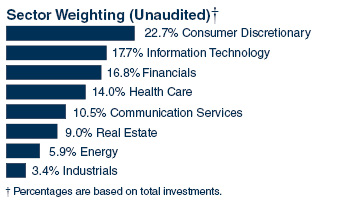

The Fund’s investment results were not uniform across sectors. During the period, the Fund’s best performing sectors were Information Technology, Health Care, Consumer Discretionary and Financials whereas the Fund’s worst performing sectors were Industrials, Energy, Real Estate and Communication Services. The Fund’s best performers during the period were Amazon, Adobe, MasterCard, Apple and Align Technologies whereas the Fund’s worst performers were Realogy, EBay, Dollarama, Cabot Oil & Gas and Schlumberger Ltd.

The RiverPark Large Growth Fund seeks to make investments in securities of large capitalization companies, which it defines as those in excess of $5 billion. The Fund invests in what it believes are exciting growth businesses with significant long-term growth potential, but patiently waits for opportunities to purchase these companies at attractive prices. RiverPark believes the style is best described as a “value orientation toward growth.” RiverPark believes that the current market environment provides it with an opportunity to own a diversified portfolio of growth stocks at attractive valuations. Management is cautiously optimistic that the Fund can achieve above average rates of return over the next few years.

This represents the manager’s assessment of the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

The Russell 1000 Growth Total Return Index measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

The S&P 500 Total Return Index is an unmanaged capitalization-weighted index generally representative of large companies in the U.S. stock market and based on price changes and reinvested dividends.

Morningstar Large Growth portfolios invest primarily in big U.S. companies that are projected to grow faster than other large-cap stocks.

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

1

|

|

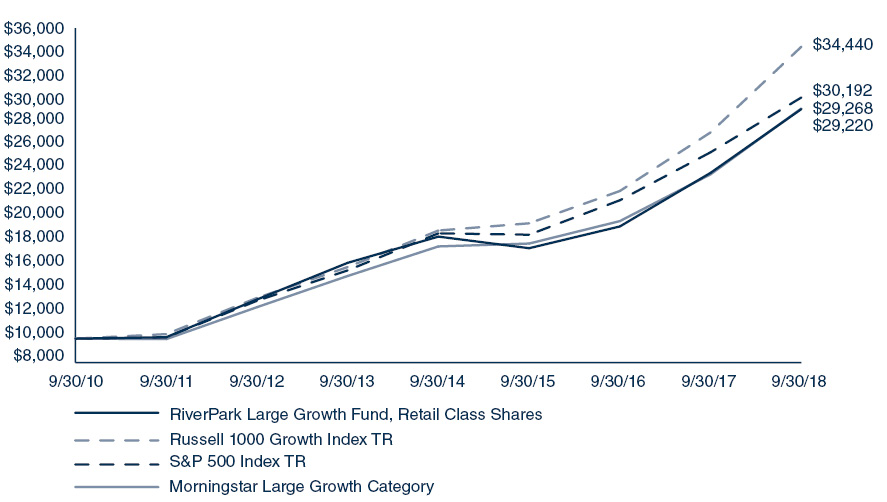

Comparison of Change in the Value of a $10,000 Investment in the RiverPark Large Growth Fund,

Retail Class Shares, versus the Russell 1000 Growth Index TR,

the S&P 500 Index TR and the Morningstar Large Growth Category

AVERAGE ANNUAL TOTAL RETURNS FOR THE | ||||

One Year Return | Annualized | Annualized | Annualized | |

Institutional Class Shares | 22.68% | 18.76% | 12.59% | 14.63% |

Retail Class Shares | 22.34% | 18.47% | 12.32% | 14.34% |

Russell 1000 Growth Index TR | 26.30% | 20.55% | 16.58% | 16.70% |

S&P 500 Index TR | 17.91% | 17.31% | 13.95% | 14.80% |

Morningstar Large Growth Category | 23.06% | 17.65% | 13.92% | 14.32% |

* | Fund commenced operations on September 30, 2010. |

Returns shown above are calculated assuming reinvestment of all dividends and distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on dividends or distributions or the redemption of shares from a fund. Returns reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. Effective July 31, 2016, the Fund fully recaptured previously waived investment advisory fees. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than a shareholder’s original cost. Performance of the Institutional Class Shares differs due to the differences in expenses. Current performance may be lower or higher than that shown here. Unlike the Fund’s comparative benchmarks, the Fund’s total returns are reduced by its annual operating expenses. Please note that one cannot invest directly in an unmanaged index.

2

|

|

Management’s Discussion of Fund Performance and Analysis

RiverPark/Wedgewood Fund (Unaudited)

For the fiscal year ended September 30, 2018, the RiverPark/Wedgewood Fund (the “Fund”) gained 22.69% and 22.37% on its Institutional Class Shares and Retail Class Shares, respectively, while the Russell 1000 Growth Index gained 26.30% and the S&P 500 Index gained 17.91%.

Investment results for the fiscal year were not uniform across quarters. The Institutional Class Shares gained 8.70% for the December quarter, lost 0.91% for the March quarter, gained 4.92% for the June quarter and gained 8.56% in the September quarter.

The Fund’s investment results were not uniform across sectors. During the period, the Fund’s best performing sectors were Information Technology, Consumer Discretionary, Industrials and Financials whereas the Fund’s worst performing sectors were Consumer Staples, Health Care, Energy and Communication Services. The Fund’s best performers during the period were Apple Inc., Edwards Lifesciences Corp, Qualcomm Inc., Visa Inc. and Ross Stores Inc. The Fund’s worst performers were Celgene Corp, Kraft Heinz Co, Schlumberger Ltd, Facebook Inc., and Ulta Beauty Inc.

The RiverPark/Wedgewood Fund seeks to make investments in about 19-21 companies, with market capitalizations in excess of $5 billion, which it believes have above-average growth prospects. The Fund invests in businesses that it believes are market leaders with a long-term sustainable competitive advantage. It patiently waits for opportunities to purchase what it believes are great businesses at attractive prices. While the Fund invests in growth, it believes that valuation is the key to generating attractive returns over the long-term. Unlike most growth investors, Wedgewood is not a momentum investor but rather a contrarian growth investor. Wedgewood is a firm that believes in investing as opposed to trading and generally experiences an annual portfolio turnover of less than 50%.Wedgewood believes that the current market environment provides it with an opportunity to own a portfolio of growth stocks at attractive valuations. Management is cautiously optimistic that the Fund can achieve above average rates of return over the next few years.

This represents the manager’s assessment of the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

The Russell 1000 Growth Total Return Index measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

The S&P 500 Total Return Index is an unmanaged capitalization-weighted index generally representative of large companies in the U.S. stock market and based on price changes and reinvested dividends.

Morningstar Large Growth portfolios invest primarily in big U.S. companies that are projected to grow faster than other large-cap stocks.

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

3

|

|

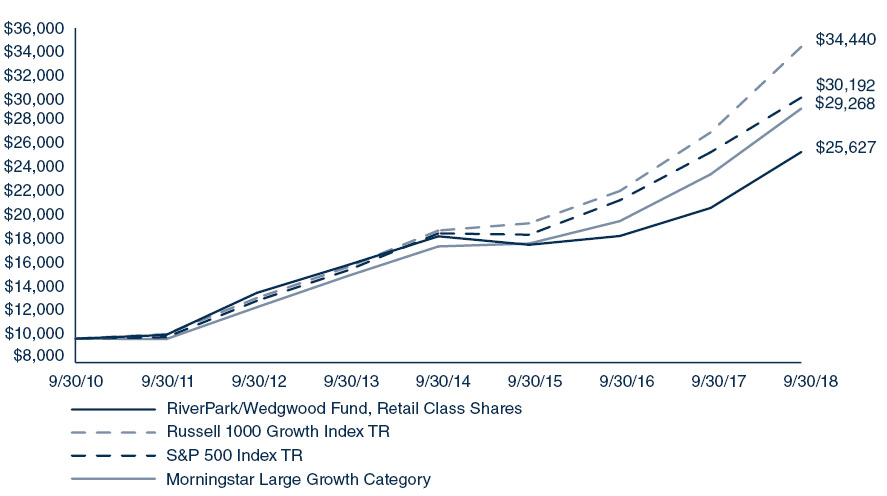

Comparison of Change in the Value of a $10,000 Investment in the RiverPark/Wedgewood Fund,

Retail Class Shares, versus the Russell 1000 Growth Index TR,

the S&P 500 Index TR and the Morningstar Large Growth Category

AVERAGE ANNUAL TOTAL RETURNS FOR THE | ||||

One Year Return | Annualized | Annualized | Annualized | |

Institutional Class Shares | 22.69% | 12.88% | 9.81% | 12.69% |

Retail Class Shares | 22.37% | 12.79% | 9.66% | 12.48% |

Russell 1000 Growth Index TR | 26.30% | 20.55% | 16.58% | 16.70% |

S&P 500 Index TR | 17.91% | 17.31% | 13.95% | 14.80% |

Morningstar Large Growth Category | 23.06% | 17.65% | 13.92% | 14.32% |

* | Fund commenced operations on September 30, 2010. |

Returns shown above are calculated assuming reinvestment of all dividends and distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on dividends or distributions or the redemption of shares from a fund. Returns reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. Effective June 30, 2013, the Fund fully recaptured previously waived investment advisory fees. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than a shareholder’s original cost. Performance of the Institutional Class Shares differs due to the differences in expenses. Current performance may be lower or higher than that shown here. Unlike the Fund’s comparative benchmarks, the Fund’s total returns are reduced by its annual operating expenses. Please note that one cannot invest directly in an unmanaged index.

4

|

|

Management’s Discussion of Fund Performance and Analysis

RiverPark Short Term High Yield Fund (Unaudited)

For the fiscal year ended September 30, 2018, the RiverPark Short Term High Yield Fund (the “Fund”) gained 2.79% and 2.53% on its Institutional Class Shares and Retail Class Shares, respectively, while the BofA Merrill Lynch 1-3 Year U.S. Corporate Bond Index gained 0.79%, the BofA Merrill Lynch 1-Year U.S. Treasury Index gained 1.08% and the BofA Merrill Lynch 0-3 Year U.S. High Yield Index Excluding Financials gained 4.90%.

Investment results for the Fiscal Year were largely consistent across quarters. The Institutional Class Shares gained 0.48% for the December quarter, 0.61% for the March quarter, 0.73% for the June quarter and 0.93% in the September quarter.

The Fund realized positive contributions from its investments in all five of its categories of investment. The Fund realized a contribution to its performance of 1.07% in the Short Term Maturities Category, 1.05% in Cushion Bonds, 0.73% in Redeemed Debt, 0.36% in Strategic Recap and 0.36% in Event Driven investments.

The Fund continues to strive for an attractive yield while maintaining a weighted average maturity of less than one year. As of September 30, 2018, 63% of the Fund’s invested portfolio is expected to mature or be repaid within 90 days, while 91% of the Fund’s invested portfolio is expected to mature or be repaid within 12 months. Over 28% of the invested portfolio is expected to be repaid as the result of a corporate event (redemption or early retirement due to an acquisition or recapitalization).

The RiverPark Short Term High Yield Fund focuses on short term high yield securities for which they believe credit ratings do not accurately reflect a company’s ability to meet their short term credit obligations. The RiverPark Short Term High Yield Fund seeks to make investments in fixed income securities of companies that have announced or, in Cohanzick’s opinion, will announce a funding event, reorganization or other corporate event that they believe will have a positive impact on a company’s ability to repay their debt. Additionally, the Fund will invest in securities in which it perceives there is limited near term risk of default. In Cohanzick’s view, the risks associated with investing in short term high yield debt are very different from investing in long-dated paper in which operating performance and business sustainability are of primary concern.

5

|

|

This represents the manager’s assessment of the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

The BofA Merrill Lynch 1-3 Year U.S. Corporate Bond Index is an unmanaged index comprised of U.S. dollar denominated investment grade corporate debt securities publicly issued in the U.S. domestic market with at least one year remaining term to final maturity.

The BofA Merrill Lynch 1-Year U.S. Treasury Index tracks the performance of U.S. dollar denominated sovereign debt publicly issued by the U.S. government in its domestic market with at least one year remaining term to final maturity.

The BofA Merrill Lynch 0-3 Year U.S. High Yield Index Excluding Financials considers all securities from the BofA Merrill Lynch U.S. High Yield Master II Index and the BofA Merrill Lynch U.S. High Yield, 0-1 Year Index, and then applies the following filters: securities greater than or equal to one month but less than 3 years to final maturity, and exclude all securities with Level 2 sector classification = Financial (FNCL).

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

6

|

|

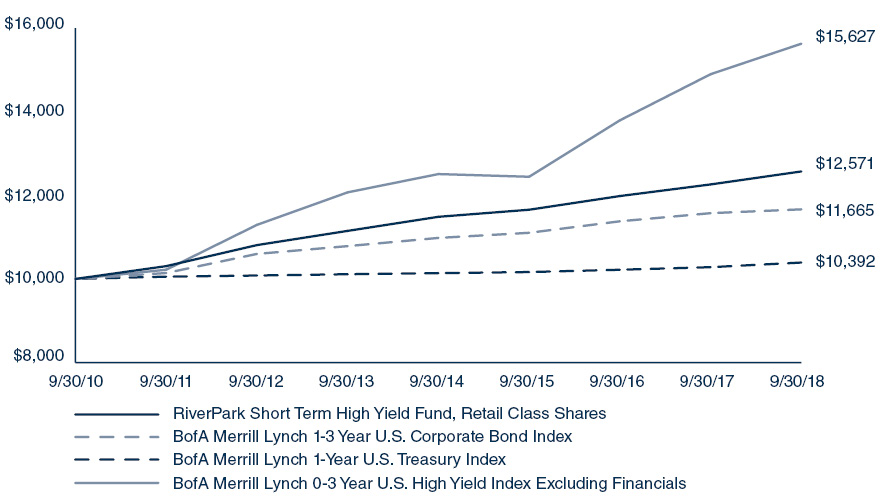

Comparison of Change in the Value of a $10,000 Investment in the RiverPark Short Term High Yield Fund,

Retail Class Shares, versus the BofA Merrill Lynch 1-3 Year U.S. Corporate Bond Index, the BofA Merrill Lynch

1-Year U.S. Treasury Index and the BofA Merrill Lynch 0-3 Year U.S. High Yield Index Excluding Financials

AVERAGE ANNUAL TOTAL RETURNS FOR THE | ||||

One Year Return | Annualized | Annualized | Annualized | |

Institutional Class Shares | 2.79% | 2.84% | 2.74% | 3.20% |

Retail Class Shares | 2.53% | 2.55% | 2.43% | 2.90% |

BofA Merrill Lynch 1-3 Year U.S. Corporate Bond Index | 0.79% | 1.66% | 1.58% | 1.94% |

BofA Merrill Lynch 1-Year U.S. Treasury Index | 1.08% | 0.74% | 0.55% | 0.48% |

BofA Merrill Lynch 0-3 Year U.S. High Yield Index Excluding Financials | 4.90% | 7.89% | 5.30% | 5.74% |

* | Fund commenced operations on September 30, 2010. |

Returns shown above are calculated assuming reinvestment of all dividends and distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on dividends or distributions or the redemption of shares from a fund. Returns reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. Effective September 30, 2013, the Fund fully recaptured previously waived investment advisory fees. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than a shareholder’s original cost. Performance of the Institutional Class Shares differs due to the differences in expenses. Current performance may be lower or higher than that shown here. Unlike the Fund’s comparative benchmarks, the Fund’s total returns are reduced by its annual operating expenses. Please note that one cannot invest directly in an unmanaged index.

7

|

|

Management’s Discussion of Fund Performance and Analysis

RiverPark Long/Short Opportunity Fund (Unaudited)

For the fiscal year ended September 30, 2018, the RiverPark Long/Short Opportunity Fund (the “Fund”) gained 14.19% and 14.06% on its Institutional Class Shares and Retail Class Shares respectively, while the S&P 500 Index gained 17.91% and the Morningstar Long/Short Equity Category gained 5.66%. The average gross and net month-end exposures of the Fund for the fiscal year were 163% and 59% (long 111%, short 52%), respectively.

The Fund’s long positions contributed approximately 23.9% for the fiscal year, as compared to the performance of the S&P 500 Index, which gained 17.91%. The Fund was negatively affected by its short positions, which detracted 7.6% for the fiscal year ended September 30, 2018. We still believe the Fund’s shorts are comprised of businesses facing major headwinds going forward and have flawed business models.

Investment results for the fiscal year were not uniform across quarters. The Institutional Class Shares gained 2.15% for the December quarter, 2.56% for the March quarter, 4.30% for the June quarter and 4.49% in the September quarter.

The Fund’s investment results were not uniform across sectors. During the period, the Fund’s best performing sectors were Information Technology, Health Care, Financials, Consumer Discretionary and Communication Services whereas the Fund’s worst performing sectors were Consumer Staples, Energy, Industrials, Real Estate and Materials. The Fund’s best performers during the period were Amazon Inc., Adobe Inc., MasterCard Inc., Illumina Inc. and Apple Inc. whereas the Fund’s worst performers were BJ’s Restaurants Inc., Southwestern Energy Co., CenturyLink Inc., Walmart Stores Inc. and Cimpress NV.

Derivatives as a category, which include total return swaps used to leverage the long positions and equity options, detracted approximately 0.25% from the Fund’s performance.

The RiverPark Long/Short Opportunity Fund seeks long-term capital appreciation while managing downside volatility by investing long in equity securities that the Fund’s investment adviser believes have above-average growth prospects and selling short equity securities the Adviser believes are competitively disadvantaged over the long-term. The Fund is an opportunistic long/short investment fund. The Fund’s investment goal is to achieve above average rates of return with less volatility and less downside risk as compared to U.S. equity markets. The Adviser believes the long book is currently comprised of businesses that are attractively priced as, on average, their businesses have experienced earnings growth in excess of their stock price gains. The Adviser believes the substantial appreciation of the short book, much of it due to valuation expansion along with or exceeding the market’s, has created an unusually attractive opportunity to short businesses that it believes are flawed at what it believes are full or excessive values.

8

|

|

This represents the manager’s assessment of the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

The S&P 500 Total Return Index is an unmanaged capitalization-weighted index generally representative of large companies in the U.S. stock market and based on price changes and reinvested dividends.

The Morningstar Long/Short Equity Category portfolios hold sizable stakes in both long and short positions in equities, exchange-traded funds and related derivatives. Some funds that fall into this category are market neutral - dividing their exposure equally between long and short positions in an attempt to earn a modest return that is not tied to the market’s fortunes. Other portfolios that are not market neutral will shift their exposure to long and short positions depending upon their macro outlook or the opportunities they uncover through bottom-up research.

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

9

|

|

Management’s Discussion of Fund Performance and Analysis

RiverPark Long/Short Opportunity Fund

Supplemental Disclosure (Unaudited):

The following represents a reconciliation of accounting principles generally accepted in the United States of America (“GAAP”) to non-GAAP exposure for underlying investments that are held by the Fund through investments in common stock and total return swap transactions as of September 30, 2018. The total non-GAAP exposure is calculated by using the common stock plus the notional swap and option values divided by the net asset value of the Fund as of September 30, 2018.

Common Stock and Total Return Swaps: | ||

GAAP | Non-GAAP | |

Alliance Data Systems | ||

Common Stock | 1.7% | 1.7% |

Equity Option | 0.1% | 1.3% |

1.8% | 3.0% | |

Amazon.com Inc | ||

Common Stock | 4.2% | 4.2% |

Total Return Swap | — | 0.1% |

4.2% | 4.3% | |

American Tower Corp | ||

Common Stock | 3.1% | 3.1% |

Total Return Swap | — | 0.2% |

3.1% | 3.3% | |

Apple Inc | ||

Common Stock | 2.7% | 2.7% |

Total Return Swap | — | 2.2% |

2.7% | 4.9% | |

Carmax Inc | ||

Common Stock | 2.4% | 2.4% |

Total Return Swap | — | 0.3% |

2.4% | 2.7% | |

CME Group Inc | ||

Common Stock | 2.9% | 2.9% |

Total Return Swap | — | 0.2% |

2.9% | 3.1% | |

Mastercard Inc | ||

Common Stock | 3.7% | 3.7% |

Total Return Swap | — | 0.1% |

3.7% | 3.8% | |

United Health Group Inc | ||

Common Stock | 2.1% | 2.1% |

Total Return Swap | — | 1.4% |

2.1% | 3.5% | |

Visa Inc | ||

Common Stock | 3.5% | 3.5% |

Total Return Swap | — | 0.1% |

3.5% | 3.6% | |

Remaining Underliers | ||

Common Stock | 70.7% | 70.7% |

Total Common Stock & | ||

Total Return Swaps | 97.1% | 102.9% |

Securities Sold Short, Not Yet Purchased: | ||

GAAP | Non-GAAP | |

Common Stock | (36.3%) | (36.3%) |

Total, Securities Sold Short, | ||

Not Yet Purchased | (36.3%) | (36.3%) |

10

|

|

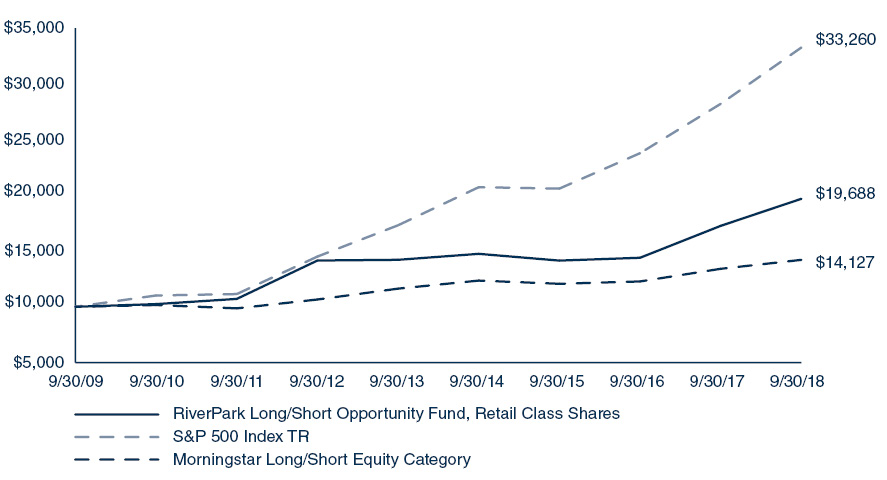

Comparison of Change in the Value of a $10,000 Investment in the RiverPark Long/Short Opportunity Fund,

Retail Class Shares, versus the S&P 500 Index and the Morningstar Long/Short Equity Category

AVERAGE ANNUAL TOTAL RETURNS FOR THE | ||||

One Year Return | Annualized | Annualized | Annualized | |

Institutional Class Shares | 14.19% | 11.87% | 6.94% | 7.96% |

Retail Class Shares | 14.06% | 11.65% | 6.73% | 7.82% |

S&P 500 Index TR | 17.91% | 17.31% | 13.95% | 14.28% |

Morningstar Long/Short Equity Category | 5.66% | 5.43% | 3.97% | 3.91% |

* | Fund commenced operations on March 30, 2012. The performance data quoted for periods prior to March 30, 2012 is that of the Predecessor Fund. The Predecessor Fund commenced operations on September 30, 2009. The Predecessor Fund was not a registered mutual fund and was not subject to the same investment and tax restrictions as the Fund. If it had been, the Predecessor Fund’s performance might have been lower. Performance shown for periods of one year and greater are annualized. |

For periods after March 30, 2012, the returns shown above are calculated assuming reinvestment of all dividends and distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on dividends or distributions or the redemption of shares from a fund. Returns reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than a shareholder’s original cost. Performance of the Institutional Class Shares differs due to the differences in expenses. Current performance may be lower or higher than that shown here. Unlike the Fund’s comparative benchmarks, the Fund’s total returns are reduced by its annual operating expenses. Please note that one cannot invest directly in an unmanaged index.

11

|

|

Management’s Discussion of Fund Performance and Analysis

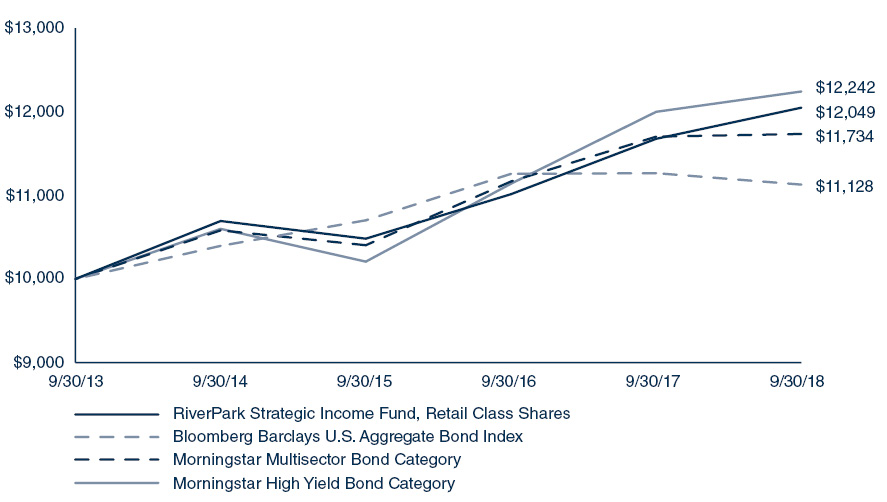

RiverPark Strategic Income Fund (Unaudited)

For the fiscal year ended September 30, 2018, the RiverPark Strategic Income Fund (the “Fund”) gained 3.46% and 3.19% on its Institutional Class Shares and Retail Class Shares, respectively, while the Bloomberg Barclays U.S. Aggregate Bond Index lost 1.22%, the Morningstar Multisector Bond Category gained 0.57%, and the Morningstar High Yield Bond Category gained 2.03%.

Investment results for the Fiscal Year were not uniform across quarters. The Institutional Class Shares gained 0.45% for the December quarter, 0.81% for the March quarter, 0.96% for the June quarter and 1.20% in the September quarter.

The Fund realized positive contributions from all seven of its categories of investment. The Fund realized a contribution to its performance of 1.00% in its Interest Rate Resets, 0.95% in RiverPark Short Term High Yield Bond Fund Overlap, 0.70% in Off the Beaten Path, 0.70% in Priority Based (Above the Fray), 0.61% in Buy & Hold “Money Good”, 0.16% in Other (ABS), and 0.06% in Hedges category of investments.

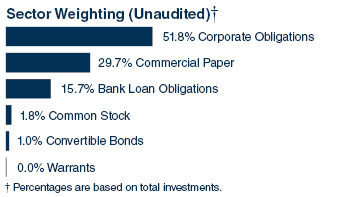

As of September 30, 2018, the Fund’s net assets were weighted by category as follows: 7.35% was held in RiverPark Short Term High Yield Bond Fund Overlap investments, 56.86% in the Buy & Hold “Money Good” category, 7.86% in Off The Beaten Path, 2.44% in Other (ABS), 2.64% in the Priority Based (Above the Fray), 22.32% in Interest Rate Resets (floaters, cushion bonds), -4.59% in Hedges, with the remaining 5.13% in cash and cash equivalents. Across all categories, 49.76% of the net assets was held in high yield securities and 43.29% was held in investment grade securities. The Fund held 112 positions as of this date, 5 of which were held in the RiverPark Short Term High Yield Bond Fund Overlap category and 107 of which were not.

RiverPark Strategic Income Fund seeks high current income and capital appreciation consistent with the preservation of capital by investing in investment grade and non-investment grade debt, preferred stock, convertible bonds, bank loans, high yield bonds and income producing equities that Cohanzick deems appropriate for the Fund’s investment objective. The Fund will primarily invest in both investment grade and non-investment grade “Money Good” securities, for which the enterprise value of the issuing company exceeds the value of the senior and equally ranked debt of the considered investment. Therefore, we believe the risk of loss of principal due to permanent impairment is minimal. The Fund expects to invest in securities that are not widely followed, which Cohanzick believes offer better returns with little or no additional credit risk.

Footnotes:

“Money Good” is a term used by the Adviser to describe debt it believes will be paid off in full under current market conditions and on a strict priority basis.

High yield and investment grade classification of securities was based on Bloomberg Composite Ratings comprised of Moody’s, Standard & Poors, Fitch & DBRS, Ltd.

12

|

|

This represents the manager’s assessment of the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

The Bloomberg Barclays U.S. Aggregate Bond Index is weighted according to market capitalization, which means the securities represented in the index are weighted according to the market size of the bond category.

The Morningstar Multisector Bond Category portfolios seek income by diversifying their assets among several fixed-income sectors, usually U.S. government obligations, U.S. corporate bonds, foreign bonds, and high-yield U.S. debt securities.

The Morningstar High Yield Bond Category primarily invest in U.S. high-income debt securities where at least 65% or more of bond assets are not rated or are rated by a major agency such as Standard & Poor’s or Moody’s at the level of BB and below.

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

13

|

|

Comparison of Change in the Value of a $10,000 Investment in the RiverPark Strategic Income Fund,

Retail Class Shares, versus the Bloomberg Barclays U.S. Aggregate Bond Index, the Morningstar Multisector

Bond Category and the Morningstar High Yield Bond Category

AVERAGE ANNUAL TOTAL RETURNS FOR THE | ||||

One Year Return | Annualized | Annualized | Annualized | |

Institutional Class Shares | 3.46% | 5.06% | 4.09% | 4.09% |

Retail Class Shares | 3.19% | 4.75% | 3.80% | 3.80% |

Bloomberg Barclays U.S. Aggregate Bond Index | -1.22% | 1.31% | 2.16% | 2.16% |

Morningstar Multisector Bond Category | 0.57% | 4.14% | 3.25% | 3.25% |

Morningstar High Yield Bond Category | 2.03% | 6.25% | 4.13% | 4.13% |

* | Fund commenced operations on September 30, 2013. |

Returns shown above are calculated assuming reinvestment of all dividends and distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on dividends or distributions or the redemption of shares from a fund. Returns reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. Effective March 31, 2014, the Fund fully recaptured previously waived investment advisory fees. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than a shareholder’s original cost. Performance of the Institutional Class Shares differs due to the differences in expenses. Current performance may be lower or higher than that shown here. Unlike the Fund’s comparative benchmarks, the Fund’s total returns are reduced by its annual operating expenses. Please note that one cannot invest directly in an unmanaged index.

14

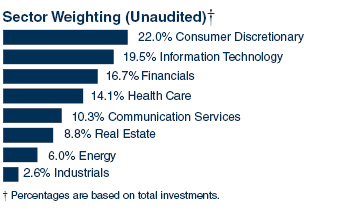

| RiverPark Large Growth Fund |

Description | Shares | Value (000) | ||||||

Schedule of Investments | ||||||||

Common Stock — 98.2%** | ||||||||

Communication Services – 10.1% | ||||||||

Alphabet, Cl A * | 1,157 | $ | 1,397 | |||||

Alphabet, Cl C * | 1,170 | 1,396 | ||||||

Facebook, Cl A * | 11,792 | 1,939 | ||||||

Walt Disney | 7,753 | 907 | ||||||

| 5,639 | ||||||||

Consumer Discretionary – 21.6% | ||||||||

adidas ADR | 11,446 | 1,398 | ||||||

Amazon.com * | 1,216 | 2,436 | ||||||

Booking Holdings * | 728 | 1,444 | ||||||

CarMax * | 20,067 | 1,498 | ||||||

Dollar Tree * | 12,215 | 996 | ||||||

Dollarama ^ | 27,978 | 881 | ||||||

eBay * | 24,856 | 821 | ||||||

NIKE, Cl B | 13,639 | 1,156 | ||||||

Ulta Beauty * | 4,867 | 1,373 | ||||||

| 12,003 | ||||||||

Energy – 5.8% | ||||||||

Cabot Oil & Gas, Cl A | 35,184 | 792 | ||||||

EOG Resources | 9,593 | 1,224 | ||||||

Schlumberger | 20,409 | 1,243 | ||||||

| 3,259 | ||||||||

Financials – 16.4% | ||||||||

BlackRock, Cl A | 2,951 | 1,391 | ||||||

Charles Schwab | 39,329 | 1,933 | ||||||

CME Group, Cl A | 9,965 | 1,696 | ||||||

TD Ameritrade Holding | 25,125 | 1,328 | ||||||

The Blackstone Group LP (a) | 73,010 | 2,780 | ||||||

| 9,128 | ||||||||

Health Care – 13.8% | ||||||||

Align Technology * | 1,979 | 774 | ||||||

Exact Sciences * | 19,771 | 1,560 | ||||||

Illumina * | 3,304 | 1,213 | ||||||

Intuitive Surgical * | 2,628 | 1,509 | ||||||

IQVIA Holdings * | 6,433 | 834 | ||||||

UnitedHealth Group | 6,802 | 1,810 | ||||||

| 7,700 | ||||||||

Industrials – 2.6% | ||||||||

Northrop Grumman | 4,538 | 1,440 | ||||||

Information Technology – 19.2% | ||||||||

Adobe Systems * | 5,276 | 1,424 | ||||||

Alliance Data Systems | 4,231 | 999 | ||||||

Apple | 10,803 | 2,439 | ||||||

Mastercard, Cl A | 9,651 | 2,148 | ||||||

salesforce.com * | 10,528 | 1,675 | ||||||

Visa, Cl A | 13,277 | 1,993 | ||||||

| 10,678 | ||||||||

Real Estate – 8.7% | ||||||||

American Tower REIT, Cl A | 11,403 | 1,657 | ||||||

CBRE Group, Cl A * | 26,512 | 1,169 | ||||||

Equinix REIT | 4,630 | 2,004 | ||||||

| 4,830 | ||||||||

Total Common Stock | ||||||||

(Cost $31,355) (000) | 54,677 | |||||||

Total Investments — 98.2% | ||||||||

(Cost $31,355) (000) | $ | 54,677 | ||||||

As of September 30, 2018, all of the Fund’s investments were considered Level 1 in accordance with the authoritative guidance on fair value measurements and disclosure under GAAP.

For the year ended September 30, 2018, there were no transfers between Level 1 and Level 2 assets and liabilities or between Level 2 and Level 3 assets and liabilities.

Percentages are based on Net Assets of $55,654 (000). |

* | Non-income producing security. |

** | More narrow industries are utilized for compliance purposes, whereas broad sectors are utilized for reporting purposes. |

^ | Traded in Canadian Dollar. |

(a) | Security considered Master Limited Partnership. At September 30, 2018, these securities amounted to $2,780 (000) or 5.0% of Net Assets. |

ADR — American Depositary Receipt

Cl — Class

LP — Limited Partnership

REIT — Real Estate Investment Trust

The accompanying notes are an integral part of the financial statements.

15

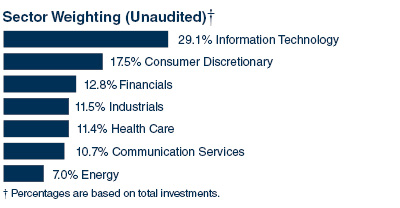

| RiverPark/Wedgewood Fund |

Description | Shares | Value (000) | ||||||

Schedule of Investments | ||||||||

Common Stock — 99.5%** | ||||||||

Communication Services – 10.7% | ||||||||

Alphabet, Cl A * | 10,325 | $ | 12,463 | |||||

Facebook, Cl A * | 94,095 | 15,475 | ||||||

| 27,938 | ||||||||

Consumer Discretionary – 17.4% | ||||||||

Booking Holdings * | 7,239 | 14,362 | ||||||

Ross Stores | 95,417 | 9,456 | ||||||

Tractor Supply | 167,565 | 15,228 | ||||||

Ulta Beauty * | 23,000 | 6,489 | ||||||

| 45,535 | ||||||||

Energy – 7.0% | ||||||||

Core Laboratories | 59,078 | 6,843 | ||||||

Schlumberger | 187,991 | 11,452 | ||||||

| 18,295 | ||||||||

Financials – 12.8% | ||||||||

Berkshire Hathaway, Cl B * | 106,692 | 22,844 | ||||||

Charles Schwab | 213,511 | 10,494 | ||||||

| 33,338 | ||||||||

Health Care – 11.3% | ||||||||

Celgene * | 122,913 | 10,999 | ||||||

Edwards Lifesciences * | 106,696 | 18,576 | ||||||

| 29,575 | ||||||||

Industrials – 11.4% | ||||||||

CH Robinson Worldwide | 95,599 | 9,361 | ||||||

Fastenal | 183,704 | 10,659 | ||||||

Old Dominion Freight Line | 60,600 | 9,772 | ||||||

| 29,792 | ||||||||

Information Technology – 28.9% | ||||||||

Apple | 112,080 | 25,301 | ||||||

Cognizant Technology Solutions, Cl A | 95,941 | 7,402 | ||||||

PayPal Holdings * | 123,321 | 10,833 | ||||||

QUALCOMM | 196,919 | 14,184 | ||||||

Visa, Cl A | 119,245 | 17,897 | ||||||

| 75,617 | ||||||||

Total Common Stock | ||||||||

(Cost $156,092) (000) | 260,090 | |||||||

Total Investments — 99.5% | ||||||||

(Cost $156,092) (000) | $ | 260,090 | ||||||

As of September 30, 2018, all of the Fund’s investments were considered Level 1 in accordance with the authoritative guidance on fair value measurements and disclosure under GAAP.

For the year ended September 30, 2018, there were no transfers between Level 1 and Level 2 assets and liabilities or between Level 2 and Level 3 assets and liabilities.

Percentages are based on Net Assets of $261,343 (000). |

* | Non-income producing security. |

** | More narrow industries are utilized for compliance purposes, whereas broad sectors are utilized for reporting purposes. |

Cl — Class

The accompanying notes are an integral part of the financial statements.

16

| RiverPark Short Term High Yield Fund |

Description | Face | Value (000) | ||||||

Schedule of Investments | ||||||||

Corporate Obligations — 70.9% | ||||||||

Communication Services – 8.4% | ||||||||

Level 3 Financing | ||||||||

6.125%, 01/15/21 | $ | 20,541 | $ | 20,721 | ||||

Qwest Capital Funding | ||||||||

6.500%, 11/15/18 | 20,569 | 20,673 | ||||||

Sprint Communications | ||||||||

9.000%, 11/15/18 (a) | 35,330 | 35,593 | ||||||

| 76,987 | ||||||||

Consumer Discretionary – 15.7% | ||||||||

CCO Holdings | ||||||||

5.250%, 03/15/21 | 12,600 | 12,687 | ||||||

GameStop | ||||||||

5.500%, 10/01/19 (a) | 17,228 | 17,250 | ||||||

International Game Technology | ||||||||

7.500%, 06/15/19 | 700 | 725 | ||||||

Lee Enterprises | ||||||||

9.500%, 03/15/22 (a) | 14,292 | 14,899 | ||||||

Lennar | ||||||||

4.125%, 12/01/18 | 16,523 | 16,502 | ||||||

Mediacom Broadband | ||||||||

5.500%, 04/15/21 | 21,734 | 22,006 | ||||||

MGM Resorts International | ||||||||

8.625%, 02/01/19 | 23,565 | 24,036 | ||||||

Michaels Stores | ||||||||

5.875%, 12/15/20 (a) | 18,531 | 18,642 | ||||||

Pinnacle Entertainment | ||||||||

5.625%, 05/01/24 | 5,126 | 5,440 | ||||||

TEGNA | ||||||||

5.125%, 10/15/19 | 5,123 | 5,132 | ||||||

William Carter | ||||||||

5.250%, 08/15/21 | 6,334 | 6,409 | ||||||

| 143,728 | ||||||||

Consumer Staples – 2.5% | ||||||||

Edgewell Personal Care | ||||||||

4.700%, 05/19/21 | 2,950 | 2,957 | ||||||

Spectrum Brands | ||||||||

6.625%, 11/15/22 | 4,392 | 4,513 | ||||||

Spectrum Brands Holdings | ||||||||

7.750%, 01/15/22 | 8,993 | 9,281 | ||||||

SUPERVALU | ||||||||

6.750%, 06/01/21 | 5,985 | 6,120 | ||||||

| 22,871 | ||||||||

Energy – 8.0% | ||||||||

NGL Energy Partners | ||||||||

6.875%, 10/15/21 | 57,312 | 58,387 | ||||||

NRG Energy | ||||||||

6.250%, 07/15/22 | 14,532 | 15,029 | ||||||

| 73,416 | ||||||||

Financials – 2.0% | ||||||||

Ally Financial | ||||||||

3.250%, 11/05/18 | 13,013 | 13,013 | ||||||

Intrepid Aviation Group Holdings | ||||||||

8.500%, 08/15/21 (a) | 4,866 | 4,903 | ||||||

| 17,916 | ||||||||

Health Care – 1.6% | ||||||||

Teva Pharmaceutical Finance Netherlands III BV | ||||||||

1.700%, 07/19/19 | 15,095 | 14,852 | ||||||

Industrials – 13.9% | ||||||||

Avis Budget Car Rental | ||||||||

5.125%, 06/01/22 (a) | 14,305 | 14,691 | ||||||

BlueLine Rental Finance | ||||||||

9.250%, 03/15/24 (a) | 13,466 | 14,190 | ||||||

Briggs & Stratton | ||||||||

6.875%, 12/15/20 | 8,667 | 9,208 | ||||||

Clean Harbors | ||||||||

5.125%, 06/01/21 | 15,807 | 15,886 | ||||||

FTI Consulting | ||||||||

6.000%, 11/15/22 | 3,044 | 3,122 | ||||||

HC2 Holdings | ||||||||

11.000%, 12/01/19 (a) | 16,253 | 16,416 | ||||||

Icahn Enterprises | ||||||||

6.000%, 08/01/20 | 22,028 | 22,456 | ||||||

Nielsen Finance | ||||||||

4.500%, 10/01/20 | 28,136 | 28,206 | ||||||

Xerium Technologies | ||||||||

9.500%, 08/15/21 | 2,954 | 3,110 | ||||||

| 127,285 | ||||||||

Information Technology – 8.0% | ||||||||

Anixter | ||||||||

5.625%, 05/01/19 | 15,756 | 15,992 | ||||||

BMC Software Finance | ||||||||

8.125%, 07/15/21 (a) | 29,829 | 30,493 | ||||||

Dell International | ||||||||

5.875%, 06/15/21 (a) | 3,475 | 3,588 | ||||||

The accompanying notes are an integral part of the financial statements.

17

| RiverPark Short Term High Yield Fund |

| Description | Face Amount (000) | Value (000) | ||||||

| Infor US | ||||||||

| 5.750%, 08/15/20 (a) | $ | 17,674 | $ | 17,939 | ||||

| NCR | ||||||||

| 4.625%, 02/15/21 | 4,681 | 4,646 | ||||||

| 72,658 | ||||||||

| Materials – 8.0% | ||||||||

| Cleveland-Cliffs | ||||||||

| 5.900%, 03/15/20 | 180 | 187 | ||||||

| Greif | ||||||||

| 7.750%, 08/01/19 | 20,219 | 20,987 | ||||||

| INVISTA Finance | ||||||||

| 4.250%, 10/15/19 (a) | 10,396 | 10,435 | ||||||

| Largo Resources | ||||||||

| 9.250%, 06/01/21 (a) | 5,546 | 5,823 | ||||||

| Lundin Mining | ||||||||

| 7.875%, 11/01/22 (a) | 21,454 | 22,428 | ||||||

| Reynolds Group Issuer | ||||||||

| 5.750%, 10/15/20 | 13,328 | 13,378 | ||||||

| 73,238 | ||||||||

| Real Estate – 2.8% | ||||||||

| Realogy Group | ||||||||

| 5.250%, 12/01/21 (a) | 14,130 | 14,218 | ||||||

| 4.500%, 04/15/19 (a) | 10,901 | 10,956 | ||||||

| 25,174 | ||||||||

| Total Corporate Obligations | ||||||||

| (Cost $648,670) (000) | 648,125 | |||||||

| Convertible Bonds — 13.4% | ||||||||

| B2Gold | ||||||||

| 3.250%, 10/01/18 | 6,575 | 6,605 | ||||||

| Clearway Energy | ||||||||

| 3.500%, 02/01/19 (a) | 16,383 | 16,424 | ||||||

| 3.250%, 06/01/20 (a) | 40,835 | 40,904 | ||||||

| Finisar | ||||||||

| 0.500%, 12/15/33 | 8,871 | 8,832 | ||||||

| Layne Christensen | ||||||||

| 4.250%, 11/15/18 | 10,794 | 10,869 | ||||||

| Macquarie Infrastructure | ||||||||

| 2.875%, 07/15/19 | 8,824 | 8,767 | ||||||

| Ship Finance International | ||||||||

| 5.750%, 10/15/21 | 7,850 | 7,819 | ||||||

| 0.250%, 09/15/19 | 6,570 | 6,378 | ||||||

| Yandex | ||||||||

| 1.125%, 12/15/18 | 15,809 | 15,718 | ||||||

| Total Convertible Bonds | ||||||||

| (Cost $122,045) (000) | 122,316 | |||||||

| Description | Face Amount (000)/ Shares | Value (000) | ||||||

| Commercial Paper (b) — 8.5% | ||||||||

| EI du Pont de Nemours | ||||||||

| 2.233%, 10/04/18 | $ | 20,000 | $ | 19,992 | ||||

| General Motors Financial | ||||||||

| 2.591%, 10/15/18 | 10,000 | 9,987 | ||||||

| 2.506%, 10/09/18 | 17,000 | 16,986 | ||||||

| Kraft Heinz Foods | ||||||||

| 2.471%, 10/23/18 | 17,638 | 17,608 | ||||||

| Walgreens Boots Alliance | ||||||||

| 2.410%, 10/22/18 | 13,215 | 13,194 | ||||||

| Total Commercial Paper | ||||||||

| (Cost $77,785) (000) | 77,767 | |||||||

| Preferred Stock — 0.5% | ||||||||

| Allstate | ||||||||

| 6.750% | 169,514 | 4,233 | ||||||

| Total Preferred Stock | ||||||||

| (Cost $4,292) (000) | 4,233 | |||||||

| Bank Loan Obligations — 3.9% | ||||||||

| Dell International | ||||||||

| 3.750%, VAR LIBOR USD 1 Month+1.500%, 12/31/18 | 9,874 | 9,877 | ||||||

| Eastman Kodak | ||||||||

| 8.592%, VAR LIBOR USD 1 Month+6.250%, 09/03/19 | 14,685 | 14,052 | ||||||

| Internap | ||||||||

| 7.900%, VAR LIBOR USD 1 Month+5.750%, 04/06/22 | 4,890 | 4,906 | ||||||

| Lee Enterprises | ||||||||

| 8.492%, VAR LIBOR USD 1 Month+6.250%, 03/31/19 | 482 | 481 | ||||||

| NCI Building Systems | ||||||||

| 4.076%, VAR LIBOR USD 1 Month+2.000%, 02/07/25 | 5,907 | 5,911 | ||||||

| Total Bank Loan Obligations | ||||||||

| (Cost $35,854) (000) | 35,227 | |||||||

| Total Investments — 97.2% | ||||||||

| (Cost $888,646) (000) | $ | 887,668 | ||||||

The accompanying notes are an integral part of the financial statements.

18

| RiverPark Short Term High Yield Fund |

The following is a list of the inputs used as of September 30, 2018 in valuing the Fund’s investments carried at value (000), in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP:

Investments in Securities | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Corporate Obligations | $ | — | $ | 648,125 | $ | — | $ | 648,125 | ||||||||

Convertible Bonds | — | 122,316 | — | 122,316 | ||||||||||||

Commercial Paper | — | 77,767 | — | 77,767 | ||||||||||||

Preferred Stock | 4,233 | — | — | 4,233 | ||||||||||||

Bank Loan Obligations | — | 35,227 | — | 35,227 | ||||||||||||

Total Investments in Securities | $ | 4,233 | $ | 883,435 | $ | — | $ | 887,668 | ||||||||

For the year ended September 30, 2018, there were no transfers between Level 1 and Level 2 assets and liabilities or between Level 2 and Level 3 assets and liabilities.

Percentages are based on Net Assets of $913,597 (000). |

(a) | Securities sold within terms of a private placement memorandum, exempt from registration under Section 144A of the Securities Act of 1933, as amended, and may be sold only to dealers in that program or other “accredited investors.” These securities have been determined to be liquid under guidelines established by the Board of Trustees. At September 30, 2018, these securities amounted to $309,792 (000) or 33.9% of Net Assets. |

(b) | Zero coupon security. The rate reported on the Schedule of Investments is the effective yield at time of purchase. |

LIBOR — London Interbank Offered Rate

USD — United States Dollar

VAR — Variable Rate

The accompanying notes are an integral part of the financial statements.

19

| RiverPark Long/Short Opportunity Fund |

Description | Shares | Value (000) | ||||||

Schedule of Investments | ||||||||

Common Stock — 97.0%** | ||||||||

Communication Services – 10.2% | ||||||||

Alphabet, Cl A * (a) | 2,250 | $ | 2,716 | |||||

Alphabet, Cl C * (a) | 2,284 | 2,726 | ||||||

Facebook, Cl A * | 22,738 | 3,740 | ||||||

Walt Disney | 14,471 | 1,692 | ||||||

| 10,874 | ||||||||

Consumer Discretionary – 22.0% | ||||||||

adidas ADR | 24,102 | 2,944 | ||||||

Amazon.com * (b) | 2,240 | 4,487 | ||||||

Booking Holdings * (a) | 1,439 | 2,855 | ||||||

CarMax * (a) (b) | 33,592 | 2,508 | ||||||

Dollar Tree * | 22,398 | 1,827 | ||||||

Dollarama ^ | 63,555 | 2,002 | ||||||

eBay * | 45,798 | 1,512 | ||||||

NIKE, Cl B | 31,220 | 2,645 | ||||||

Ulta Beauty * | 9,226 | 2,603 | ||||||

| 23,383 | ||||||||

Energy – 5.7% | ||||||||

Cabot Oil & Gas | 65,401 | 1,473 | ||||||

EOG Resources | 17,736 | 2,262 | ||||||

Schlumberger | 38,705 | 2,358 | ||||||

| 6,093 | ||||||||

Financials – 16.3% | ||||||||

BlackRock, Cl A | 5,597 | 2,638 | ||||||

Charles Schwab | 72,159 | 3,547 | ||||||

CME Group, Cl A (b) | 18,357 | 3,124 | ||||||

TD Ameritrade Holding | 47,923 | 2,532 | ||||||

The Blackstone Group LP (a) (c) | 144,645 | 5,508 | ||||||

| 17,349 | ||||||||

Health Care – 13.6% | ||||||||

Align Technology * | 3,648 | 1,427 | ||||||

Exact Sciences * | 36,427 | 2,875 | ||||||

Illumina * | 6,120 | 2,246 | ||||||

Intuitive Surgical * (a) | 5,199 | 2,984 | ||||||

IQVIA Holdings * | 11,489 | 1,491 | ||||||

Pacira Pharmaceuticals * | 25,118 | 1,235 | ||||||

UnitedHealth Group (b) | 8,312 | 2,211 | ||||||

| 14,469 | ||||||||

Industrials – 3.3% | ||||||||

Northrop Grumman | 10,934 | 3,470 | ||||||

Information Technology – 17.1% | ||||||||

Adobe Systems * | 9,745 | 2,631 | ||||||

Alliance Data Systems | 7,858 | 1,855 | ||||||

Apple (a) (b) | 12,638 | 2,853 | ||||||

Mastercard, Cl A (a) (b) | 17,739 | 3,949 | ||||||

salesforce.com * | 20,261 | 3,222 | ||||||

Visa, Cl A (b) | 24,738 | 3,713 | ||||||

| 18,223 | ||||||||

Real Estate – 8.8% | ||||||||

American Tower REIT, Cl A (a) (b) | 22,497 | 3,269 | ||||||

CBRE Group, Cl A * | 49,071 | 2,164 | ||||||

Equinix REIT (a) | 8,948 | 3,874 | ||||||

| 9,307 | ||||||||

Total Common Stock | ||||||||

(Cost $65,988) (000) | 103,168 | |||||||

Total Investments — 97.0% | ||||||||

(Cost $65,988) (000) | $ | 103,168 | ||||||

Schedule of Securities Sold Short, Not Yet Purchased | ||||||||

Common Stock — (36.3)% | ||||||||

Communication Services – (9.0)% | ||||||||

AT&T | (32,172 | ) | $ | (1,080 | ) | |||

CenturyLink | (55,271 | ) | (1,172 | ) | ||||

Cogent Communications Holdings | (19,145 | ) | (1,068 | ) | ||||

Discovery, Cl A* | (34,884 | ) | (1,116 | ) | ||||

Interpublic Group | (35,020 | ) | (801 | ) | ||||

Publicis Groupe | (17,512 | ) | (1,047 | ) | ||||

Verizon Communications | (23,760 | ) | (1,269 | ) | ||||

WPP | (69,376 | ) | (1,017 | ) | ||||

Zillow Group, Cl A* | (22,213 | ) | (982 | ) | ||||

| (9,552 | ) | |||||||

Consumer Discretionary – (4.6)% | ||||||||

Carnival | (12,743 | ) | (813 | ) | ||||

Gap | (16,774 | ) | (484 | ) | ||||

Garmin | (11,525 | ) | (807 | ) | ||||

Harley-Davidson | (18,007 | ) | (816 | ) | ||||

Michael Kors Holdings* | (7,170 | ) | (492 | ) | ||||

Ralph Lauren, Cl A | (5,019 | ) | (690 | ) | ||||

Tapestry | (16,157 | ) | (812 | ) | ||||

| (4,914 | ) | |||||||

Consumer Staples – (9.9)% | ||||||||

Church & Dwight | (13,361 | ) | (793 | ) | ||||

Clorox | (7,000 | ) | (1,053 | ) | ||||

Coca-Cola | (22,839 | ) | (1,055 | ) | ||||

Colgate-Palmolive | (11,734 | ) | (786 | ) | ||||

General Mills | (16,862 | ) | (724 | ) | ||||

The accompanying notes are an integral part of the financial statements.

20

| RiverPark Long/Short Opportunity Fund |

Description | Shares | Value (000) | ||||||

JM Smucker | (4,602 | ) | $ | (472 | ) | |||

Kellogg | (10,731 | ) | (751 | ) | ||||

Kimberly-Clark | (6,846 | ) | (778 | ) | ||||

Kroger | (16,763 | ) | (488 | ) | ||||

PepsiCo | (9,274 | ) | (1,037 | ) | ||||

Procter & Gamble | (16,020 | ) | (1,333 | ) | ||||

Spectrum Brands Holdings | (9,788 | ) | (732 | ) | ||||

Walmart | (5,527 | ) | (519 | ) | ||||

| (10,521 | ) | |||||||

Health Care – (1.0)% | ||||||||

Cerner* | (16,534 | ) | (1,065 | ) | ||||

Industrials – (1.9)% | ||||||||

Cimpress* | (5,762 | ) | (787 | ) | ||||

Stericycle* | (20,977 | ) | (1,231 | ) | ||||

| (2,018 | ) | |||||||

Information Technology – (4.4)% | ||||||||

CommScope Holding* | (34,070 | ) | (1,048 | ) | ||||

Flex* | (96,663 | ) | (1,268 | ) | ||||

International Business Machines | (7,098 | ) | (1,073 | ) | ||||

Western Union | (68,093 | ) | (1,298 | ) | ||||

| (4,687 | ) | |||||||

Real Estate – (5.5)% | ||||||||

Iron Mountain REIT | (36,843 | ) | (1,272 | ) | ||||

Kimco Realty | (61,223 | ) | (1,025 | ) | ||||

Regency Centers | (16,133 | ) | (1,043 | ) | ||||

Simon Property Group REIT | (7,129 | ) | (1,260 | ) | ||||

SL Green Realty REIT | (13,046 | ) | (1,272 | ) | ||||

| (5,872 | ) | |||||||

Total Common Stock | ||||||||

(Proceeds $37,884) (000) | (38,629 | ) | ||||||

Total Securities Sold Short, Not Yet Purchased | ||||||||

(Proceeds $37,884) (000) | $ | (38,629 | ) | |||||

Purchased Options (d) — 0.1% | ||||||||

Total Purchased Options | ||||||||

(Cost $202) (000) | $ | 118 | ||||||

The following is a list of the inputs used as of September 30, 2018 in valuing the Fund’s investments, securities sold short, not yet purchased and other financial instruments carried at value (000), in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP:

Investments in Securities | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Common Stock | $ | 103,168 | $ | — | $ | — | $ | 103,168 | ||||||||

Total Investments in Securities | $ | 103,168 | $ | — | $ | — | $ | 103,168 | ||||||||

Securities Sold Short, Not Yet Purchased | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Common Stock | $ | (38,629 | ) | $ | — | $ | — | $ | (38,629 | ) | ||||||

Total Securities Sold Short, Not Yet Purchased | $ | (38,629 | ) | $ | — | $ | — | $ | (38,629 | ) | ||||||

Other Financial Instruments | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Purchased Options | $ | 107 | $ | 11 | $ | — | $ | 118 | ||||||||

Total Return Swaps‡ | — | — | — | — | ||||||||||||

Total Other Financial Instruments | $ | 107 | $ | 11 | $ | — | $ | 118 | ||||||||

‡ | Total return swaps are valued at the unrealized appreciation (depreciation) on the instrument. The total return swaps reset monthly, as such there was $0 unrealized appreciation (depreciation) as of September 30, 2018. The swaps are considered Level 2. |

For the year ended September 30, 2018, there were no transfers between Level 1 and Level 2 assets and liabilities or between Level 2 and Level 3 assets and liabilities

The accompanying notes are an integral part of the financial statements.

21

| RiverPark Long/Short Opportunity Fund |

A list of open option contracts held by the Fund at September 30, 2018 was as follows:

Description | Number of | Notional | Exercise | Expiration | Value | ||||||||||||||

PURCHASED OPTIONS — 0.1% | |||||||||||||||||||

Call Options | |||||||||||||||||||

Alliance Data Systems* | 150 | $ | 3,542 | $ | 250.00 | 01/18/19 | $ | 107 | |||||||||||

Alliance Data Systems* | 150 | 3,542 | 300.00 | 01/18/19 | 11 | ||||||||||||||

Total Purchased Options | |||||||||||||||||||

(Cost $202) ($ Thousands) | $ | 7,084 | $ | 118 | |||||||||||||||

A list of open swap agreements held by the Fund at September 30, 2018 was as follows:

Total Return Swaps | |||||||||||||||||

Counterparty | Reference Entity/ | Fund Pays | Fund | Payment | Termination | Notional | Value | Net | |||||||||

Goldman Sachs | Amazon | USD-LIBOR-BBA 1 Month - 0.50% | Total Return | Monthly | 08/05/2019 | $ | 133 | $ | 132 | $ | — | ||||||

Goldman Sachs | American Tower | USD-LIBOR-BBA 1 Month - 0.50% | Total Return | Monthly | 08/05/2019 | 236 | 230 | — | |||||||||

Goldman Sachs | Apple | USD-LIBOR-BBA 1 Month - 0.50% | Total Return | Monthly | 08/05/2019 | 2,362 | 2,342 | — | |||||||||

Goldman Sachs | Carmax | USD-LIBOR-BBA 1 Month - 0.50% | Total Return | Monthly | 04/25/2019 | 298 | 286 | — | |||||||||

Goldman Sachs | Carmax | USD-LIBOR-BBA 1 Month - 0.50% | Total Return | Monthly | 04/25/2019 | 54 | 52 | — | |||||||||

Goldman Sachs | CME Group | USD-LIBOR-BBA 1 Month - 0.50% | Total Return | Monthly | 08/05/2019 | 215 | 209 | — | |||||||||

Goldman Sachs | Mastercard | USD-LIBOR-BBA 1 Month - 0.50% | Total Return | Monthly | 08/05/2019 | 153 | 158 | — | |||||||||

Goldman Sachs | UnitedHealth | USD-LIBOR-BBA 1 Month - 0.50% | Total Return | Monthly | 04/29/2019 | 1,009 | 1,000 | — | |||||||||

Goldman Sachs | UnitedHealth | USD-LIBOR-BBA 1 Month - 0.50% | Total Return | Monthly | 04/29/2019 | 499 | 494 | — | |||||||||

Goldman Sachs | Visa | USD-LIBOR-BBA 1 Month - 0.50% | Total Return | Monthly | 08/05/2019 | 75 | 77 | — | |||||||||

| $ | — | ||||||||||||||||

Percentages are based on Net Assets of $106,351 (000). |

* | Non-income producing security. |

** | More narrow industries are utilized for compliance purposes, whereas broad sectors are utilized for reporting purposes. |

^ | Traded in Canadian Dollar. |

(a) | All or a portion of this security has been committed as collateral for open short positions. The aggregate market value of the collateral at September 30, 2018 was $31,341 (000). |

(b) | Underlying security for a total return swap. |

(c) | Security considered Master Limited Partnership. At September 30, 2018, these securities amounted to $5,508 (000) or 5.2% of Net Assets. |

(d) | Refer to table below for details on Options Contracts. |

ADR — American Depositary Receipt

BBA — British Bankers Association

Cl — Class

LIBOR — London Interbank Offered Rate

LP — Limited Partnership

REIT — Real Estate Investment Trust

USD — United States Dollar

Amounts designated as “— “ are $0 or rounded to $0.

The accompanying notes are an integral part of the financial statements.

22

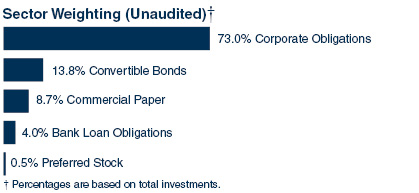

| RiverPark Strategic Income Fund |

Description | Face | Value (000) | ||||||

Schedule of Investments | ||||||||

Corporate Obligations — 51.1% | ||||||||

Communication Services – 2.0% | ||||||||

Inmarsat Finance | ||||||||

6.500%, 10/01/24 (a) | 1,876 | $ | 1,909 | |||||

Sprint | ||||||||

7.250%, 09/15/21 | 5,495 | 5,825 | ||||||

| 7,734 | ||||||||

Consumer Discretionary – 16.5% | ||||||||

American Axle & Manufacturing | ||||||||

6.500%, 04/01/27 | 786 | 781 | ||||||

Brunswick | ||||||||

4.625%, 05/15/21 | 5,951 | 5,910 | ||||||

Carrols Restaurant Group | ||||||||

8.000%, 05/01/22 | 7,408 | 7,734 | ||||||

Dollar Tree | ||||||||

3.036%, VAR ICE LIBOR USD 3 Month+0.700%, 04/17/20 | 5,848 | 5,857 | ||||||

Ford Motor Credit | ||||||||

3.124%, VAR ICE LIBOR USD 3 Month+0.790%, 06/12/20 | 4,828 | 4,828 | ||||||

Georg Jensen | ||||||||

6.000%, VAR EURIBOR EUR 3 Month+6.000%, 05/15/23 | EUR | 800 | 929 | |||||

Lee Enterprises | ||||||||

9.500%, 03/15/22 (a) | 8,721 | 9,091 | ||||||

Michaels Stores | ||||||||

5.875%, 12/15/20 (a) | 7,429 | 7,474 | ||||||

Netflix | ||||||||

4.875%, 04/15/28 (a) | 446 | 420 | ||||||

Nexteer Automotive Group | ||||||||

5.875%, 11/15/21 (a) | 2,405 | 2,461 | ||||||

Postmedia Network | ||||||||

8.250%, 07/15/21 (a) | CAD | 1,077 | 826 | |||||

Rivers Pittsburgh Borrower | ||||||||

6.125%, 08/15/21 (a) | 2,481 | 2,481 | ||||||

| Salem Media Group | ||||||||

| 6.750%, 06/01/24 (a) | 697 | 624 | ||||||

| SB Holdco | ||||||||

| 8.000%, VAR EURIBOR EUR 3 Month+8.000%, 07/13/22 | EUR | 1,700 | 1,984 | |||||

| Sirius XM Radio | ||||||||

| 5.000%, 08/01/27 (a) | 2,004 | 1,938 | ||||||

| SiTV | ||||||||

| 10.375%, 07/01/19 (a) | 1,575 | 925 | ||||||

| Tapestry | ||||||||

| 4.250%, 04/01/25 (f) | 4,731 | 4,695 | ||||||

| TEGNA | ||||||||

| 5.125%, 10/15/19 | 1,943 | 1,947 | ||||||

| Viacom | ||||||||

| 4.375%, 03/15/43 (f) | 3,393 | 2,972 | ||||||

| 63,877 | ||||||||

| Consumer Staples – 1.4% | ||||||||

| Cott Holdings | ||||||||

| 5.500%, 04/01/25 (a) | 4,125 | 4,037 | ||||||

| Fresh Market | ||||||||

| 9.750%, 05/01/23 (a) | 2,020 | 1,515 | ||||||

| 5,552 | ||||||||

| Energy – 1.3% | ||||||||

| Golar LNG Partners | ||||||||

| 6.710%, VAR ICE LIBOR USD 3 Month+4.400%, 05/22/20 | 3,400 | 3,357 | ||||||

| Jones Energy Holdings | ||||||||

| 9.250%, 03/15/23 | 1,185 | 723 | ||||||

| McDermott Technology Americas | ||||||||

| 10.625%, 05/01/24 (a) | 710 | 762 | ||||||

| Sanjel | ||||||||

| 7.500%, 06/19/19 (a) (b) (d) (g) | 2,700 | — | ||||||

| 4,842 | ||||||||

| Financials – 0.6% | ||||||||

| Bulk Industrier | ||||||||

| 7.590%, VAR NIBOR NOK 3 Month+6.500%, 05/26/21 | NOK | 12,000 | 1,479 | |||||

| Toll Road Investors Partnership | ||||||||

| 6.488%, 02/15/45 (a) (c) | 3,268 | 778 | ||||||

| Vostok New Ventures | ||||||||

| 6.150%, 06/14/22 | SEK | 1,000 | 114 | |||||

| 2,371 | ||||||||

| Health Care – 0.4% | ||||||||

| Bayer US Finance II | ||||||||

| 3.003%, VAR ICE LIBOR USD 3 Month+0.630%, 06/25/21 (a) | 255 | 256 | ||||||

The accompanying notes are an integral part of the financial statements.

23

| RiverPark Strategic Income Fund |

| Description | Face Amount (000) | Value (000) | ||||||

| Hadrian Merger Sub | ||||||||

| 8.500%, 05/01/26 (a) | $ | 1,452 | $ | 1,390 | ||||

| 1,646 | ||||||||

| Industrials – 18.1% | ||||||||

| America West Airlines Pass-Through Trust, Ser 2000-1 | ||||||||

| 8.057%, 07/02/20 | 222 | 237 | ||||||

| Borealis Finance | ||||||||

| 7.500%, 11/16/22 (a) | 5,046 | 5,008 | ||||||

| Chembulk Holding | ||||||||

| 8.000%, 02/02/23 (a) | 4,000 | 4,062 | ||||||

| Continental Airlines Pass-Through Trust, Ser 2000-2, Cl A1 | ||||||||

| 7.707%, 04/02/21 | 543 | 573 | ||||||

| Continental Airlines Pass-Through Trust, Ser 1999-2, Cl C2 | ||||||||

| 6.236%, 03/15/20 | 112 | 114 | ||||||

| Continental Airlines Pass-Through Trust, Ser 2007-1, Cl A | ||||||||

| 5.983%, 04/19/22 | 579 | 612 | ||||||

| Euronav Luxembourg | ||||||||

| 7.500%, 05/31/22 (a) | 1,600 | 1,580 | ||||||

| FXI Holdings | ||||||||

| 7.875%, 11/01/24 (a) | 3,627 | 3,468 | ||||||

| HC2 Holdings | ||||||||

| 11.000%, 12/01/19 (a) | 13,191 | 13,323 | ||||||

| Macquarie Infrastructure | ||||||||

| 2.000%, 10/01/23 | 3,050 | 2,749 | ||||||

| MAI Holdings | ||||||||

| 9.500%, 06/01/23 | 1,716 | 1,793 | ||||||

| MPC Container Ships Invest BV | ||||||||

| 7.116%, VAR ICE LIBOR USD 3 Month+4.750%, 09/22/22 | 4,000 | 4,098 | ||||||

| Mueller Industries | ||||||||

| 6.000%, 03/01/27 | 15,604 | 15,097 | ||||||

| Stolt-Nielsen | ||||||||

| 6.375%, 09/21/22 | 5,700 | 5,550 | ||||||

| Triumph Group | ||||||||

| 7.750%, 08/15/25 | 1,055 | 1,027 | ||||||

| Welbilt | ||||||||

| 9.500%, 02/15/24 | 5,203 | 5,710 | ||||||

| Xerium Technologies | ||||||||

| 9.500%, 08/15/21 | 4,949 | 5,210 | ||||||

| 70,211 | ||||||||

| Information Technology – 4.5% | ||||||||

| DXC Technology | ||||||||

| 3.271%, VAR ICE LIBOR USD 3 Month+0.950%, 03/01/21 | 3,504 | 3,504 | ||||||

| First Data | ||||||||

| 7.000%, 12/01/23 (a) | 5,909 | 6,168 | ||||||

| j2 Cloud Services | ||||||||

| 6.000%, 07/15/25 (a) | 542 | 559 | ||||||

| Trimble | ||||||||

| 4.750%, 12/01/24 | 4,099 | 4,156 | ||||||

| 4.150%, 06/15/23 | 3,070 | 3,075 | ||||||

| 17,462 | ||||||||

| Materials – 3.7% | ||||||||

| Ferroglobe | ||||||||

| 9.375%, 03/01/22 (a) | 3,679 | 3,895 | ||||||

| Hexion | ||||||||

| 10.375%, 02/01/22 (a) | 2,831 | 2,767 | ||||||

| 10.000%, 04/15/20 | 1,601 | 1,575 | ||||||

| INVISTA Finance | ||||||||

| 4.250%, 10/15/19 (a) | 4,499 | 4,516 | ||||||

| NOVA Chemicals | ||||||||

| 5.250%, 06/01/27 (a) | 1,804 | 1,685 | ||||||

| 14,438 | ||||||||

| Real Estate – 0.5% | ||||||||

| Avison Young Canada | ||||||||

| 9.500%, 12/15/21 (a) | 1,651 | 1,750 | ||||||

| Utilities – 2.1% | ||||||||

| Vistra Energy | ||||||||

| 7.375%, 11/01/22 | 7,694 | 8,002 | ||||||

| Total Corporate Obligations | ||||||||

| (Cost $202,705) (000) | 197,885 | |||||||

| Commercial Paper (c) — 29.2% | ||||||||

| AT&T | ||||||||

| 3.091%, 05/28/19 | 9,047 | 8,874 | ||||||

| Campbell Soup | ||||||||

| 2.526%, 10/18/18 | 8,100 | 8,089 | ||||||

| Comcast | ||||||||

| 2.426%, 10/30/18 | 9,984 | 9,962 | ||||||

| EI du Pont de Nemours | ||||||||

| 2.359%, 11/13/18 | 6,661 | 6,641 | ||||||

| General Motors Financial | ||||||||

| 2.605%, 10/24/18 | 7,488 | 7,473 | ||||||

| Keurig Dr Pepper | ||||||||

| 2.306%, 10/23/18 | 8,100 | 8,087 | ||||||

The accompanying notes are an integral part of the financial statements.

24

| RiverPark Strategic Income Fund |

| Description | Face Amount (000)/ Shares/ Number of Warrants | Value (000) | ||||||

| Kraft Heinz Foods | ||||||||

| 2.471%, 10/23/18 | $ | 7,588 | $ | 7,575 | ||||

| Mondelez International | ||||||||

| 2.378%, 11/05/18 | 10,247 | 10,221 | ||||||

| Nutrien | ||||||||

| 2.410%, 10/24/18 | 9,475 | 9,456 | ||||||

| Rockwell Collins | ||||||||

| 2.402%, 10/10/18 | 11,064 | 11,055 | ||||||

| Thomson Reuters | ||||||||

| 2.355%, 10/02/18 | 9,945 | 9,942 | ||||||

| Tyco International | ||||||||

| 2.404%, 10/25/18 | 10,326 | 10,307 | ||||||

| Walgreens Boots Alliance | ||||||||

| 2.410%, 10/22/18 | 5,685 | 5,676 | ||||||

| Total Commercial Paper | ||||||||

| (Cost $113,377) (000) | 113,358 | |||||||

| Common Stock — 1.7% | ||||||||

Appvion * (d)(g) | 116,300 | 2,266 | ||||||

Forum Merger II, Cl A * | 230,500 | 2,201 | ||||||

RA Parent * (d)(g) | 56 | 2,211 | ||||||

| Total Common Stock | ||||||||

| (Cost $7,607) (000) | 6,678 | |||||||

| Convertible Bonds — 1.0% | ||||||||

| Scorpio Tankers | ||||||||

| 2.375%, 07/01/19 (a) | 431 | 417 | ||||||

| Ship Finance International | ||||||||

| 5.750%, 10/15/21 | 3,397 | 3,383 | ||||||

| Total Convertible Bonds | ||||||||

| (Cost $3,793) (000) | 3,800 | |||||||

| Warrant — 0.0% | ||||||||

Forum Merger II* | 230,500 | 134 | ||||||

| Total Warrant | ||||||||

| (Cost $132) (000) | 134 | |||||||

| Bank Loan Obligations — 15.5% | ||||||||

| Appvion | ||||||||

| 8.070%, 06/12/26 (e) | 1,455 | 1,440 | ||||||

| BI-LO | ||||||||

| 10.338%, 05/15/24 | 1,525 | 1,525 | ||||||

| 10.335%, 05/15/24 | 1,587 | 1,587 | ||||||

| Description | Face Amount (000) | Value (000) | ||||||

| 10.310%, 05/15/24 | $ | 1,587 | $ | 1,587 | ||||

| 10.165%, 05/15/24 | 12 | 12 | ||||||

| Crestwood Holdings | ||||||||

| 9.765%, 02/28/23 (e) | 6,683 | 6,693 | ||||||

| Dell International | ||||||||

| 4.250%, VAR LIBOR USD 1 Month+2.000%, 09/07/23 | 5,148 | 5,158 | ||||||

| 4.000%, VAR LIBOR USD 1 Month+1.750%, 09/07/21 | 4,567 | 4,568 | ||||||

| Eastman Kodak | ||||||||

| 8.592%, VAR LIBOR USD 1 Month+6.250%, 09/03/19 | 5,198 | 4,974 | ||||||

| Envigo Holdings | ||||||||

| 10.840%, VAR LIBOR USD 1 Month+8.500%, 10/31/21 | 3,108 | 3,112 | ||||||

| Fram Group Holdings | ||||||||

| 8.826%, VAR LIBOR USD 1 Month+6.750%, 12/23/21 | 2,498 | 2,511 | ||||||

| Internap | ||||||||

| 7.900%, VAR LIBOR USD 1 Month+5.750%, 04/06/22 | 5,473 | 5,491 | ||||||

| Lee Enterprises | ||||||||

| 12.000%, 12/15/22 | 2,113 | 2,155 | ||||||

| 8.492%, VAR LIBOR USD 1 Month+6.250%, 03/31/19 | 66 | 66 | ||||||

| LSC Communications | ||||||||

| 7.576%, VAR LIBOR USD 1 Month+5.500%, 09/30/22 | 2,533 | 2,543 | ||||||

| McDermott International | ||||||||

| 7.242%, VAR LIBOR USD 1 Month+5.000%, 05/12/25 | 3,755 | 3,806 | ||||||

| Monitronics International | ||||||||

| 0.000%, 09/22/22 (h) | 1,434 | 1,395 | ||||||

| Prince Minerals | ||||||||

| 10.513%, 03/29/26 | 1,096 | 1,014 | ||||||

| Production Resource Group | ||||||||

| 9.320%, VAR LIBOR USD 1 Month+7.000%, 08/21/24 | 2,550 | 2,518 | ||||||

| Real Alloy Holding | ||||||||

| 12.386%, 12/31/49 (d) | 1,246 | 1,246 | ||||||

| 10.000%, 01/15/19 (b)(d) | 1,776 | — | ||||||

The accompanying notes are an integral part of the financial statements.

25

| RiverPark Strategic Income Fund |

| Description | Face Amount (000) | Value (000) | ||||||

| Tacala | ||||||||

| 5.549%, VAR LIBOR USD 1 Month+3.250%, 01/26/25 | $ | 734 | $ | 737 | ||||

| Young Innovations | ||||||||

| 6.386%, VAR LIBOR USD 1 Month+4.000%, 11/06/24 | 4,926 | 4,913 | ||||||

| Young Innovations | ||||||||

| 0.000%, 11/06/24 (h) | 886 | 883 | ||||||

| Total Bank Loan Obligations | ||||||||

| (Cost $59,494) (000) | 59,934 | |||||||

| Total Investments — 98.5% | ||||||||

| (Cost $387,108) (000) | $ | 381,789 | ||||||

| Schedule of Securities Sold Short, Not Yet Purchased | ||||||||

| Corporate Obligations — (3.7)% | ||||||||

| Communication Services – (0.5)% | ||||||||

| AT&T | ||||||||

| 4.250%, 03/01/27 | (2,000 | ) | $ | (1,978 | ) | |||

| Consumer Discretionary – (0.2)% | ||||||||

| Harley-Davidson | ||||||||

| 3.500%, 07/28/25 | (1,000 | ) | (959 | ) | ||||

| Consumer Staples – (1.3)% | ||||||||

| Conagra Brands | ||||||||

| 7.125%, 10/01/26 | (1,000 | ) | (1,151 | ) | ||||

| Kraft Heinz Foods | ||||||||

| 3.000%, 06/01/26 | (2,000 | ) | (1,829 | ) | ||||

| Molson Coors Brewing | ||||||||

| 5.000%, 05/01/42 | (1,000 | ) | (995 | ) | ||||

| Reckitt Benckiser Treasury Services | ||||||||

| 3.000%, 06/26/27 (a) | (1,000 | ) | (930 | ) | ||||

| (4,905 | ) | |||||||

| Industrials – (1.1)% | ||||||||

| General Electric | ||||||||

| 6.750%, 03/15/32 | (2,000 | ) | (2,422 | ) | ||||

| Trinity Industries | ||||||||

| 4.550%, 10/01/24 | (1,000 | ) | (971 | ) | ||||

| WW Grainger | ||||||||

| 4.600%, 06/15/45 | (1,000 | ) | (1,043 | ) | ||||

| (4,436 | ) | |||||||

| Information Technology – (0.3)% | ||||||||

| Lam Research | ||||||||

| 3.800%, 03/15/25 | (1,000 | ) | (994 | ) | ||||

| Description | Face Amount (000)/ Shares | Value (000) | ||||||

| Real Estate – (0.3)% | ||||||||

| DDR | ||||||||

| 4.700%, 06/01/27 ‡ | $ | (1,000 | ) | $ | (1,007 | ) | ||

| Total Corporate Obligations | ||||||||

| (Proceeds $14,699) (000) | (14,279 | ) | ||||||

| Exchange-Traded Fund — (1.1)% | ||||||||

| iShares iBoxx $High Yield Corporate Bond ETF | (50,000 | ) | (4,322 | ) | ||||

| Total Exchange-Traded Fund | ||||||||

| (Proceeds $4,373) (000) | (4,322 | ) | ||||||

| Total Securities Sold Short, Not Yet Purchased | ||||||||

| (Proceeds $19,072) (000) | $ | (18,601 | ) | |||||

A list of the open forward foreign currency contracts held by the Fund at September 30, 2018 is as follows (000):

Counterparty | Maturity | Currency | Currency to | Unrealized | |||||||

Brown Brothers Harriman | 10/05/18 | SEK | 1,030 | USD | 113 | $ | (3 | ) | |||

Brown Brothers Harriman | 10/05/18 | EUR | 2,532 | USD | 2,948 | 7 | |||||

Brown Brothers Harriman | 10/05/18 | NOK | 12,237 | USD | 1,455 | (48 | ) | ||||

Brown Brothers Harriman | 10/05/18 | CAD | 1,098 | USD | 831 | (19 | ) | ||||

| $ | (63 | ) | |||||||||

The following is a list of the inputs used as of September 30, 2018 in valuing the Fund’s investments, securities sold short, not yet purchased, and other financial instruments carried at value (000), in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP:

Investments in Securities | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Corporate Obligations | $ | — | $ | 197,885 | $ | — | $ | 197,885 | ||||||||

Commercial Paper | — | 113,358 | — | 113,358 | ||||||||||||

Common Stock | 2,201 | — | 4,477 | 6,678 | ||||||||||||

Convertible Bonds | — | 3,800 | — | 3,800 | ||||||||||||

Warrant | 134 | — | — | 134 | ||||||||||||

Bank Loan Obligations | — | 58,688 | 1,246 | 59,934 | ||||||||||||

Total Investments in Securities | $ | 2,335 | $ | 373,731 | $ | 5,723 | $ | 381,789 | ||||||||

The accompanying notes are an integral part of the financial statements.

26

| RiverPark Strategic Income Fund |

Securities Sold Short, Not Yet Purchased | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Corporate Obligations | $ | — | $ | (14,279 | ) | $ | — | $ | (14,279 | ) | ||||||

Exchange-Traded Fund | (4,322 | ) | — | — | (4,322 | ) | ||||||||||

Total Securities Sold Short, Not Yet Purchased | $ | (4,322 | ) | $ | (14,279 | ) | $ | — | $ | (18,601 | ) | |||||

Other Financial Instruments | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Forwards** | ||||||||||||||||

Unrealized Appreciation | $ | — | $ | 7 | $ | — | $ | 7 | ||||||||

Unrealized Depreciation | — | (70 | ) | — | (70 | ) | ||||||||||

Total Other Financial Instruments | $ | — | $ | (63 | ) | $ | — | $ | (63 | ) | ||||||

** | Forward contracts are valued at the unrealized appreciation (depreciation) on the instrument. See Note 2 in Notes to Financial Statements for additional information. |

The following is a reconciliation of the investments in which significant unobservable inputs (Level 3) were used in determining value (000):

| Corporate | Common | Bank Loan | Total | ||||||||||||

Beginning balance as of October 1, 2017 | $ | 14 | $ | — | $ | — | $ | 14 | ||||||||

Change in unrealized appreciation/ depreciation) | (14 | ) | (956 | ) | — | (970 | ) | |||||||||

Purchases | — | 6,407 | 1,478 | 7,885 | ||||||||||||

Sales | — | (974 | ) | (232 | ) | (1,206 | ) | |||||||||

Transfer into Level 3 | — | — | — | — | ||||||||||||

Transfer out of Level 3 | — | — | — | — | ||||||||||||

Ending balance as of September 30, 2018 | $ | — | $ | 4,477 | $ | 1,246 | $ | 5,723 | ||||||||

Change in unrealized gains/(losses) included in earnings related to securities still held at reporting date | $ | (14 | ) | $ | (956 | ) | $ | — | $ | (970 | ) | |||||

For the year ended September 30, 2018, there were no transfers between Level 1 and Level 2 assets and liabilities.

The following table summarizes the quantitative inputs and assumptions used for items categorized as material Level 3 investments as of September 30, 2018. The following disclosures also include qualitative information on the sensitivity of the fair value measurements to changes in the significant unobservable inputs.

Assets | Fair Value at | Valuation | Unobservable Inputs | Range | ||||||||||||

Common Stock | $ | 2,266 | Multiples and Comparables methods | 4.5x EBITDA; 30-50% haircut of EBITDA on comparables; recent emergence from bankruptcy | 4.5x - 9.0x multiple of EBITDA | |||||||||||

Common Stock | 2,211 | Multiples method | 5.4x of EBITDA; enterprise value | 5.4x - 8.8x multiple of EBITDA | ||||||||||||

Bank Loan Obligations | 1,246 | Multiples method | Low level of leverage and coupon of LIBOR+10% (totaling approximately 12.3% as of 9/30/18); purchaser willingness to backstop on emergence from bankruptcy | 2.15 - 2.22x net leverage | ||||||||||||

The unobservable inputs used to determine fair value of recurring Level 3 assets may have similar or diverging impacts on valuation. Significant increases and decreases in these inputs in isolation and interrelationships between those inputs could result in significantly higher or lower fair value measurement.

Percentages are based on Net Assets of $387,700 (000). |

* | Non-income producing security. |

† | In U.S. dollars unless otherwise indicated. |

‡ | Real Estate Investment Trust |

(a) | Securities sold within terms of a private placement memorandum, exempt from registration under Section 144A of the Securities Act of 1933, as amended, and may be sold only to dealers in that program or other “accredited investors.” These securities have been determined to be liquid under guidelines established by the Board of Trustees. At September 30, 2018, these securities amounted to $85,155 (000) or 22.0% of Net Assets. |

(b) | Security in default on interest payments. |

(c) | Zero coupon security. The rate reported on the Schedule of Investments is the effective yield at time of purchase. |