UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________

FORM N-CSR

________

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-22431

RiverPark Funds Trust

(Exact name of registrant as specified in charter)

________

156 West 56th Street, 17th Floor

New York, NY 10019

(Address of principal executive offices) (Zip code)

Morty Schaja

156 West 56th Street, 17th Floor

New York, NY 10019

(Name and address of agent for service)

With copies to:

Thomas R. Westle

Blank Rome LLP

405 Lexington Avenue

New York, NY 10174

Registrant’s telephone number, including area code: 212-484-2100

Date of fiscal year end: September 30, 2020

Date of reporting period: September 30, 2020

Item 1. Reports to Stockholders.

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR § 270.30e-1), is attached hereto.

| |

Annual Report September 30, 2020 | |

Investment Adviser: | RiverPark Large Growth Fund Retail Class Shares and Institutional Class Shares Wedgewood Fund (Formerly, RiverPark/Wedgewood Fund) Retail Class Shares and Institutional Class Shares RiverPark Short Term High Yield Fund Retail Class Shares and Institutional Class Shares RiverPark Long/Short Opportunity Fund Retail Class Shares and Institutional Class Shares RiverPark Strategic Income Fund Retail Class Shares and Institutional Class Shares RiverPark Floating Rate CMBS Fund Retail Class Shares and Institutional Class Shares

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports no longer will be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically by contacting your financial intermediary, or, if you are a direct investor, by calling 888-564-4517.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can follow the instructions included with this disclosure, if applicable, or you can contact your financial intermediary to inform it that you wish to continue receiving paper copies of your shareholder reports. If you invest directly with the Funds, you can inform the Funds that you wish to continue receiving paper copies of your shareholder reports by calling 888-564-4517.Your election to receive reports in paper will apply to all funds held with your financial intermediary if you invest through a financial intermediary or all RiverPark Funds if you invest directly with the Funds. |

|

|

Table of Contents

Management’s Discussion of Fund Performance and Analysis | |

RiverPark Large Growth Fund | 1 |

Wedgewood Fund | 3 |

RiverPark Short Term High Yield Fund | 5 |

RiverPark Long/Short Opportunity Fund | 8 |

RiverPark Strategic Income Fund | 13 |

RiverPark Floating Rate CMBS Fund | 16 |

Schedules of Investments | |

RiverPark Large Growth Fund | 19 |

Wedgewood Fund | 20 |

RiverPark Short Term High Yield Fund | 21 |

RiverPark Long/Short Opportunity Fund | 24 |

RiverPark Strategic Income Fund | 27 |

RiverPark Floating Rate CMBS Fund | 35 |

Statements of Assets and Liabilities | 38 |

Statements of Operations | 40 |

Statements of Changes in Net Assets | 42 |

Financial Highlights | 46 |

Notes to Financial Statements | 52 |

Report of Independent Registered Public Accounting Firm | 69 |

Trustees and Officers of the Trust | 70 |

Disclosure of Fund Expenses | 72 |

Approval of the Investment Advisory and Investment Sub-Advisory Agreements | 74 |

Review of Liquidity Risk Management Program | 78 |

Notice to Shareholders | 79 |

The RiverPark Funds file their complete schedules of fund holdings with the Securities and Exchange Commission (the “Commission”) for the first and third quarters of each fiscal year on Form N-Q or as an exhibit to its reports on Form N-PORT within sixty days after the end of the period. The Funds’ Forms N-Q and Form N-PORT reports are available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Funds use to determine how to vote proxies relating to fund securities, as well as information relating to how a Fund voted proxies relating to fund securities during the most recent period ended June 30 is available (i) without charge, upon request, by calling 888-564-4517; and (ii) on the Commission’s website at http://www.sec.gov.

|

|

Management’s Discussion of Fund Performance and Analysis

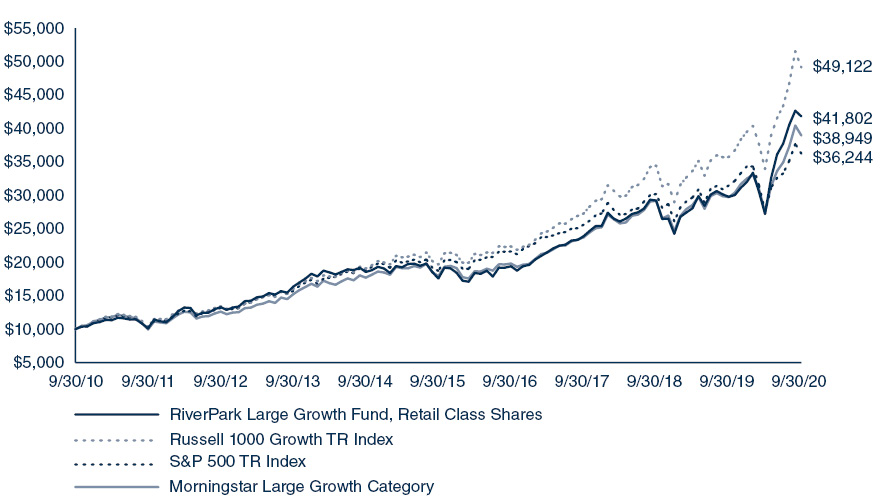

RiverPark Large Growth Fund (Unaudited)

For the fiscal year ended September 30, 2020, the RiverPark Large Growth Fund (the “Fund”) gained 40.78% and 40.38% on its Institutional Class Shares and Retail Class Shares, respectively, while the Russell 1000 Growth Total Return (TR) Index gained 37.53% and the S&P 500 Total Return (TR) Index gained 15.15%.

Investment results for the fiscal year were not uniform across quarters. The Institutional Class Shares gained 7.55% for the December quarter, lost 14.87% for the March quarter, gained 38.72% for the June quarter, and gained 10.84% in the September quarter.

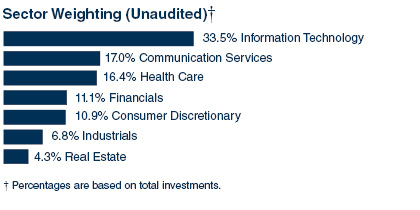

The Fund’s investment results were not uniform across sectors. The Fund’s best performing sectors during the period were Information Technology, Communication Services, Health Care and Consumer Discretionary. The Fund’s worst performing sectors were Energy, Consumer Staples, Industrials and Real Estate. The Fund’s best performers were Amazon, Apple, Shopify, Pinterest and Snap Inc. The Fund’s worst performers were Palo Alto Networks, Smile Direct Club, Five Below, Ulta Beauty and Teradata Corp.

The RiverPark Large Growth Fund seeks to make investments in securities of large capitalization companies, which it defines as those in excess of $5 billion. The Fund invests in what it believes are exciting growth businesses with significant long-term growth potential, but patiently waits for opportunities to purchase these companies at attractive prices. RiverPark believes the style is best described as a “value orientation toward growth.” RiverPark believes that the current market environment provides it with an opportunity to own a diversified portfolio of growth stocks at attractive valuations. We are cautiously optimistic that we can achieve our long-term objective of realizing above average rates of return over the next few years.

This represents the manager’s assessment of the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

The Russell 1000 Growth Total Return (TR) Index measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

The S&P 500 Total Return (TR) Index is an unmanaged capitalization-weighted index generally representative of large companies in the U.S. stock market and based on price changes and reinvested dividends.

Morningstar Large Growth portfolios invest primarily in big U.S. companies that are projected to grow faster than other large-cap stocks.

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

1

|

|

Comparison of Change in the Value of a $10,000 Investment in the RiverPark Large Growth Fund,

Retail Class Shares, versus the Russell 1000 Growth TR Index, the S&P 500 TR Index

and the Morningstar Large Growth Category

AVERAGE ANNUAL TOTAL RETURNS FOR THE | |||||

One Year Return | Annualized | Annualized | Annualized | Annualized | |

Institutional Class Shares | 40.78% | 20.85% | 19.23% | 15.67% | 15.67% |

Retail Class Shares | 40.38% | 20.51% | 18.92% | 15.38% | 15.38% |

Russell 1000 Growth TR Index | 37.53% | 21.67% | 20.10% | 17.25% | 17.25% |

S&P 500 TR Index | 15.15% | 12.28% | 14.15% | 13.74% | 13.74% |

Morningstar Large Growth Category | 31.02% | 17.99% | 16.80% | 14.56% | 14.56% |

* | Fund commenced operations on September 30, 2010. |

Returns shown above are calculated assuming reinvestment of all dividends and distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on dividends or distributions or the redemption of shares from a fund. Returns reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. Effective July 31, 2016, the Fund fully recaptured previously waived investment advisory fees. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than a shareholder’s original cost. Performance of the Institutional Class Shares differs due to the differences in expenses. Current performance may be lower or higher than that shown here. Unlike the Fund’s comparative benchmarks, the Fund’s total returns are reduced by its annual operating expenses. Please note that one cannot invest directly in an unmanaged index.

2

|

|

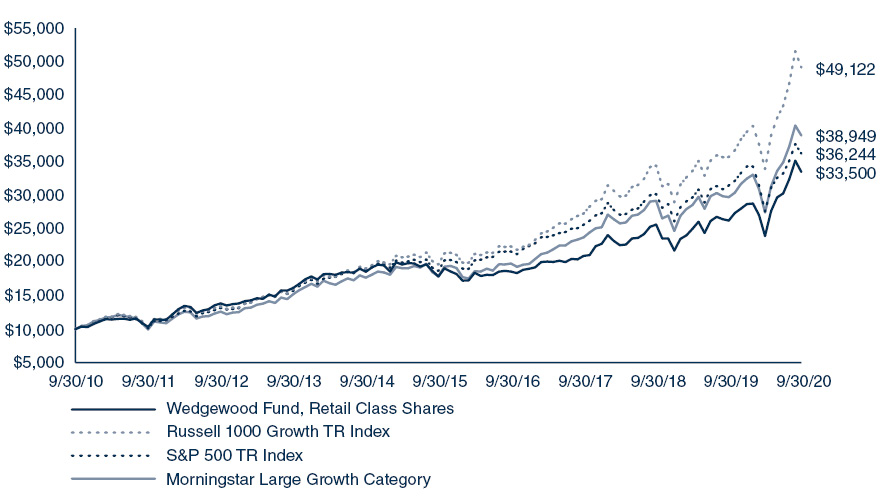

Management’s Discussion of Fund Performance and Analysis

Wedgewood Fund (formerly, RiverPark/Wedgewood Fund) (Unaudited)

For the fiscal year ended September 30, 2020, the Wedgewood Fund (the “Fund”) gained 28.14% and 27.74% on its Institutional Class Shares and Retail Class Shares, respectively, while the Russell 1000 Growth Total Return (TR) Index gained 37.53% and the S&P 500 Total Return (TR) Index gained 15.15%.

Investment results for the fiscal year were not uniform across quarters. The Institutional Class Shares gained 9.37% for the December quarter, lost 16.46% for the March quarter, gained 26.60% for the June quarter, and gained 10.77% in the September quarter.

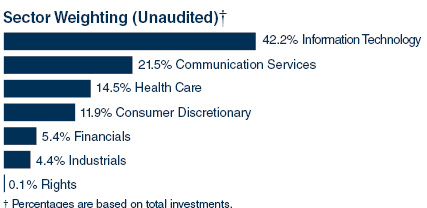

The Fund’s investment results were not uniform across sectors. The Fund’s best performing sectors during the period were Information Technology, Communication Services, Financials and Consumer Discretionary. The Fund’s worst performing sectors were Health Care and Industrials. The Fund’s best performers were Apple, Facebook, Nvidia, PayPal and Tractor Supply. The Fund’s worst performers were Celgene, Booking Holdings, C.H. Robinson Worldwide, Fleetcor Technologies and Starbucks.

The Wedgewood Fund seeks to make investments in about 19-21 companies, with market capitalizations in excess of $5 billion, which it believes have above-average growth prospects. The Fund invests in businesses that it believes are market leaders with a long-term sustainable competitive advantage. It patiently waits for opportunities to purchase what it believes are great businesses at attractive prices. While the Fund invests in growth it believes that valuation is the key to generating attractive returns over the long-term. Unlike most growth investors, Wedgewood is not a momentum investor but rather a contrarian growth investor. Wedgewood is a firm that believes in investing as opposed to trading and generally experiences an annual portfolio turnover of less than 50%.Wedgewood believes that the current market environment provides it with an opportunity to own a portfolio of growth stocks at attractive valuations. We are cautiously optimistic that we can achieve our long-term objective of realizing above average rates of return over the next few years.

This represents the manager’s assessment of the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

The Russell 1000 Growth Total Return (TR) Index measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

The S&P 500 Total Return (TR) Index is an unmanaged capitalization-weighted index generally representative of large companies in the U.S. stock market and based on price changes and reinvested dividends.

Morningstar Large Growth portfolios invest primarily in big U.S. companies that are projected to grow faster than other large-cap stocks.

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

3

|

|

Comparison of Change in the Value of a $10,000 Investment in the Wedgewood Fund,

Retail Class Shares, versus the Russell 1000 Growth TR Index,

the S&P 500 TR Index and the Morningstar Large Growth Category

AVERAGE ANNUAL TOTAL RETURNS FOR THE | |||||

One Year Return | Annualized | Annualized | Annualized | Annualized | |

Institutional Class Shares | 28.14% | 17.29% | 13.59% | 13.08% | 13.08% |

Retail Class Shares | 27.74% | 16.95% | 13.41% | 12.85% | 12.85% |

Russell 1000 Growth TR Index | 37.53% | 21.67% | 20.10% | 17.25% | 17.25% |

S&P 500 TR Index | 15.15% | 12.28% | 14.15% | 13.74% | 13.74% |

Morningstar Large Growth Category | 31.02% | 17.99% | 16.80% | 14.56% | 14.56% |

* | Fund commenced operations on September 30, 2010. |

Returns shown above are calculated assuming reinvestment of all dividends and distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on dividends or distributions or the redemption of shares from a fund. Returns reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. Effective June 30, 2013, the Fund fully recaptured previously waived investment advisory fees. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than a shareholder’s original cost. Performance of the Institutional Class Shares differs due to the differences in expenses. Current performance may be lower or higher than that shown here. Unlike the Fund’s comparative benchmarks, the Fund’s total returns are reduced by its annual operating expenses. Please note that one cannot invest directly in an unmanaged index.

4

|

|

Management’s Discussion of Fund Performance and Analysis

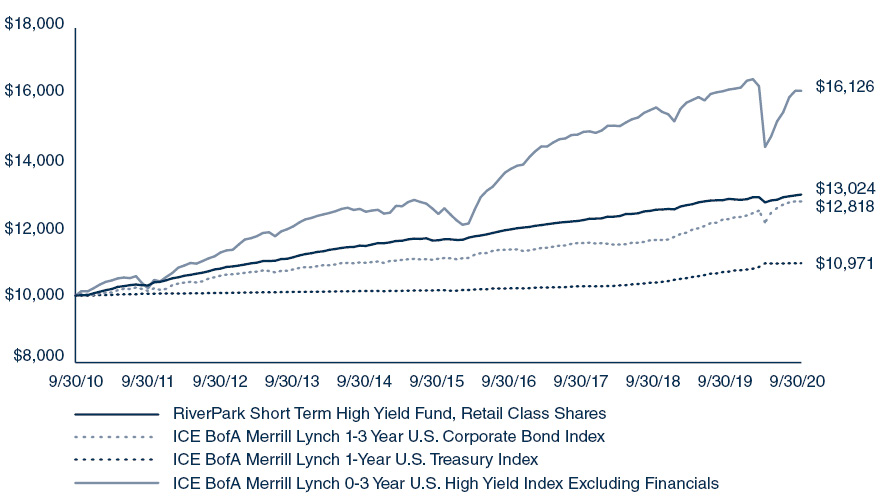

RiverPark Short Term High Yield Fund (Unaudited)

For the fiscal year ended September 30, 2020, the RiverPark Short Term High Yield Fund (the “Fund”) gained 1.26% and 1.01% on its Institutional Class Shares and Retail Class Shares, respectively, while the ICE BofA Merrill Lynch 1-3 Year U.S. Corporate Bond Index gained 4.31%, the ICE BofA Merrill Lynch 1-Year U.S. Treasury Index gained 2.37% and the ICE BofA Merrill Lynch 0-3 Year U.S. High Yield Index Excluding Financials lost 0.23%.

Investment results for the fiscal year were not uniform across quarters. The Institutional Class Shares gained 0.09% for the December quarter, lost 0.67% for the March quarter, gained 1.17% for the June quarter and gained 0.68% in the September quarter.

The Fund realized positive contributions from its investments in all five of its categories of investment. The Fund realized a contribution to its performance of 0.92% in the Redeemed Debt Category, 0.55% in Cushion Bonds, 0.39% in Short Term Maturities, 0.16% in Strategic Recap and 0.07% in Event-Driven investments.

The Fund continues to strive for an attractive yield while maintaining a weighted average maturity of less than one year. As of September 30, 2020, 71% of the Fund’s invested portfolio is expected to mature or be repaid within 90 days, while 87% of the Fund’s invested portfolio is expected to mature or be repaid within 12 months. As of the same date, over 63% of the invested portfolio is expected to be repaid as the result of a corporate event (redemption or early retirement due to an acquisition or recapitalization).

The RiverPark Short Term High Yield Fund focuses on short term high yield securities for which they believe credit ratings do not accurately reflect a company’s ability to meet their short term credit obligations. The RiverPark Short Term High Yield Fund seeks to make investments in fixed income securities of companies that have announced or, in Cohanzick’s opinion, will announce a funding event, reorganization or other corporate event that they believe will have a positive impact on a company’s ability to repay their debt. Additionally, the Fund will invest in securities in which it perceives there is limited near term risk of default. In Cohanzick’s view, the risks associated with investing in short term high yield debt are very different from investing in long-dated paper in which operating performance and business sustainability are of primary concern.

5

|

|

This represents the manager’s assessment of the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

The ICE BofA Merrill Lynch 1-3 Year U.S. Corporate Index is a subset of the ICE BofA Merrill Lynch U.S. Corporate Master Index tracking the performance of U.S. dollar denominated investment grade rated corporate debt publicly issued in the U.S. domestic market. This subset includes all securities with a remaining term to maturity of less than 3 years.

The ICE BofA Merrill Lynch 1-Year U.S. Treasuries Index is an unmanaged index that tracks the performance of the direct sovereign debt of the U.S. Government having a maturity of at least one year and less than three years.

The ICE BofA Merrill Lynch 0-3 Year U.S. High Yield Index Excluding Financials considers all securities from the ICE BofA Merrill Lynch US High Yield Master II Index and the ICE BofA Merrill Lynch U.S. High Yield 0-1 Year Index, and then applies the following filters: securities greater than or equal to one month but less than 3 years to final maturity, and exclude all securities with Level 2 sector classification = Financial (FNCL).

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

6

|

|

Comparison of Change in the Value of a $10,000 Investment in the RiverPark Short Term High Yield Fund,

Retail Class Shares, versus the ICE BofA Merrill Lynch 1-3 Year U.S. Corporate Bond Index, the ICE BofA Merrill Lynch

1-Year U.S. Treasury Index and the ICE BofA Merrill Lynch 0-3 Year U.S. High Yield Index Excluding Financials

AVERAGE ANNUAL TOTAL RETURNS FOR THE | |||||

One Year Return | Annualized | Annualized | Annualized | Annualized | |

Institutional Class Shares | 1.26% | 2.29% | 2.52% | 2.96% | 2.96% |

Retail Class Shares | 1.01% | 2.03% | 2.25% | 2.68% | 2.68% |

ICE BofA Merrill Lynch 1-3 Year U.S. Corporate Bond Index | 4.31% | 3.46% | 2.91% | 2.51% | 2.51% |

ICE BofA Merrill Lynch 1-Year U.S. Treasury Index | 2.37% | 2.19% | 1.54% | 0.93% | 0.93% |

ICE BofA Merrill Lynch 0-3 Year U.S. High Yield Index Excluding Financials | -0.23% | 2.67% | 5.32% | 4.89% | 4.89% |

* | Fund commenced operations on September 30, 2010. |

Returns shown above are calculated assuming reinvestment of all dividends and distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on dividends or distributions or the redemption of shares from a fund. Returns reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. Effective September 30, 2013, the Fund fully recaptured previously waived investment advisory fees. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than a shareholder’s original cost. Performance of the Institutional Class Shares differs due to the differences in expenses. Current performance may be lower or higher than that shown here. Unlike the Fund’s comparative benchmarks, the Fund’s total returns are reduced by its annual operating expenses. Please note that one cannot invest directly in an unmanaged index.

7

|

|

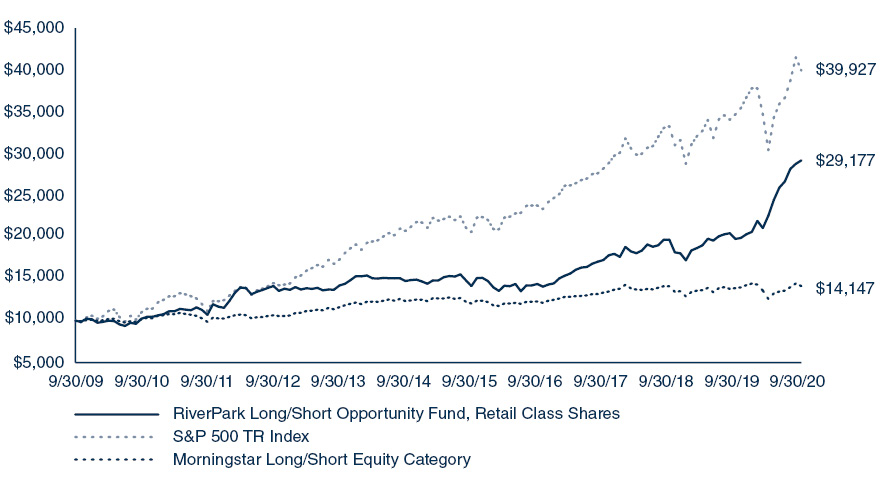

Management’s Discussion of Fund Performance and Analysis

RiverPark Long/Short Opportunity Fund (Unaudited)

For the fiscal year ended September 30, 2020, the RiverPark Long/Short Opportunity Fund (the “Fund”) gained 47.71% and 47.47% on its Institutional Class Shares and Retail Class Shares respectively, while the S&P 500 Total Return (TR) Index gained 15.15% and the Morningstar Long/Short Equity Category gained 1.78%. The average gross and net month-end exposures of the Fund for the fiscal year were 146% and 58% (long 102%, short 44%), respectively.

The Fund’s long positions contributed approximately 51.6% for the fiscal year, as compared to the performance of the broad stock market as measured by the S&P 500 Total Return (TR) Index which gained 15.15%.The Fund’s short positions detracted approximately 1.0% for the fiscal year ended September 30, 2020.

Investment results for the fiscal year were fairly uniform posting gains across all four quarters. The Institutional Class Shares gained 4.26% for the December quarter, 9.48% for the March quarter, 18.17% for the June quarter, and 9.50% in the September quarter.

The Fund’s investment results were not uniform across sectors. The Fund’s best performing sectors during the period were Information Technology, Communication Services, Health Care, Energy and Consumer Discretionary. The Fund’s worst performing sectors were Consumer Staples, Industrials, Real Estate and Materials. The Fund’s best performers were Pinterest, Apple, Amazon, Snap Inc. and Bill.com Holdings. The Fund’s worst performers were The Gap Inc, Palo Alto Networks, Sysco Corp, Deere & Co and Aramark.

Derivatives, which were used for the Fund’s short positions and to leverage the long positions contributed approximately 5.93% to the Fund’s performance.

The RiverPark Long/Short Opportunity Fund seeks long-term capital appreciation while managing downside volatility by investing long in equity securities that the Fund’s investment adviser believes have above-average growth prospects and selling short equity securities the Adviser believes are competitively disadvantaged over the long-term. The Fund is an opportunistic long/short investment fund. The Fund’s investment goal is to achieve above average rates of return with less volatility and less downside risk as compared to U.S. equity markets. We believe the long book is currently comprised of businesses that are attractively priced as, on average, their businesses have experienced earnings growth in excess of their stock price gains. We believe the substantial appreciation of the short book, much of it due to valuation expansion along with or exceeding the market’s, has created an unusually attractive opportunity to short businesses that we believe are flawed at what we believe are full or excessive values.

8

|

|

This represents the manager’s assessment of the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

The S&P 500 Total Return (TR) Index is an unmanaged capitalization-weighted index generally representative of large companies in the U.S. stock market and based on price changes and reinvested dividends.

The Morningstar Long/Short Equity Category portfolios hold sizable stakes in both long and short positions. Some funds that fall into this category are market neutral - dividing their exposure equally between long and short positions in an attempt to earn a modest return that is not tied to the market’s fortunes. Other portfolios that are not market neutral will shift their exposure to long and short positions depending upon their macro outlook or the opportunities they uncover through bottom-up research.

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

9

|

|

Management’s Discussion of Fund Performance and Analysis

RiverPark Long/Short Opportunity Fund

Supplemental Disclosure (Unaudited):

The following represents a reconciliation of accounting principles generally accepted in the United States of America (“GAAP”) to non-GAAP exposure for underlying investments that are held by the Fund through investments in common stock and total return swap transactions as of September 30, 2020. The total non-GAAP exposure is calculated by using the common stock plus the notional swap values divided by the net asset value of the Fund as of September 30, 2020.

Reconciliation of GAAP to Non-GAAP Long/Short Exposure by Underlier

as of September 30, 2020

Common Stock and Total Return Swaps: | ||

GAAP | Non-GAAP | |

Alphabet, Cl A | ||

Common Stock | 1.7% | 1.7% |

Total Return Swap | — | 0.1% |

1.7% | 1.8% | |

Alphabet, Cl C | ||

Common Stock | 1.7% | 1.7% |

Total Return Swap | — | 0.1% |

1.7% | 1.8% | |

Autodesk Inc | ||

Common Stock | 1.2% | 1.2% |

Total Return Swap | — | 1.2% |

1.2% | 2.4% | |

DexCom | ||

Common Stock | 2.3% | 2.3% |

Total Return Swap | — | 0.1% |

2.3% | 2.4% | |

Exact Sciences | ||

Common Stock | 3.5% | 3.5% |

Total Return Swap | — | 0.7% |

3.5% | 4.2% | |

Illumina | ||

Common Stock | 1.5% | 1.5% |

Total Return Swap | — | 0.9% |

1.5% | 2.4% | |

Intuitive Surgical | ||

Common Stock | 1.9% | 1.9% |

Total Return Swap | — | 1.0% |

1.9% | 2.9% | |

Lockheed Martin | ||

Common Stock | 0.8% | 0.8% |

Total Return Swap | — | 1.2% |

0.8% | 2.0% | |

GAAP | Non-GAAP | |

Mastercard, Cl A | ||

Common Stock | 1.9% | 1.9% |

Total Return Swap | — | 0.6% |

1.9% | 2.5% | |

NIKE, Cl B | ||

Common Stock | 2.2% | 2.2% |

Total Return Swap | — | 0.6% |

2.2% | 2.8% | |

PayPal Holdings | ||

Common Stock | 2.9% | 2.9% |

Total Return Swap | — | 0.1% |

2.9% | 3.0% | |

Pinterest, Cl A | ||

Common Stock | 3.2% | 3.2% |

Total Return Swap | — | 0.1% |

3.2% | 3.3% | |

ServiceNow | ||

Common Stock | 2.3% | 2.3% |

Total Return Swap | — | 0.1% |

2.3% | 2.4% | |

Shopify, Cl A | ||

Common Stock | 1.7% | 1.7% |

Total Return Swap | — | 1.2% |

1.7% | 2.9% | |

Snap, Cl A | ||

Common Stock | 3.4% | 3.4% |

Total Return Swap | — | 0.1% |

3.4% | 3.5% | |

Twilio, Cl A | ||

Common Stock | 2.0% | 2.0% |

Total Return Swap | — | 0.2% |

2.0% | 2.2% | |

10

|

|

Common Stock and Total Return Swaps (continued): | ||

GAAP | Non-GAAP | |

Uber Technologies | ||

Common Stock | 2.1% | 2.1% |

Total Return Swap | — | 0.3% |

2.1% | 2.4% | |

Visa, Cl A | ||

Common Stock | 1.4% | 1.4% |

Total Return Swap | — | 1.1% |

1.4% | 2.5% | |

GAAP | Non-GAAP | |

Walt Disney | ||

Common Stock | 1.6% | 1.6% |

Total Return Swap | — | 0.3% |

1.6% | 1.9% | |

Remaining Underliers Common Stock | 52.3% | 52.3% |

Total Common Stock & Total Return Swaps | 91.6% | 101.6% |

Securities Sold Short, Not Yet Purchased and Total Return Swaps: | ||

Common Stock | 0.0% | -31.5% |

Total Securities Sold Short, Not Yet Purchased | 0.0% | -31.5% |

* | See pages 24-26 of the Schedule of Investments, which presents a complete listing of the securities held by the Fund as of September 30, 2020. |

11

|

|

Comparison of Change in the Value of a $10,000 Investment in the RiverPark Long/Short Opportunity Fund,

Retail Class Shares, versus the S&P 500 TR Index and the Morningstar Long/Short Equity Category

AVERAGE ANNUAL TOTAL RETURNS FOR THE | |||||

One Year Return | Annualized | Annualized | Annualized | Annualized | |

Institutional Class Shares | 47.71% | 19.33% | 15.81% | 11.21% | 10.38% |

Retail Class Shares | 47.47% | 19.12% | 15.58% | 11.04% | 10.22% |

S&P 500 TR Index | 15.15% | 12.28% | 14.15% | 13.74% | 13.40% |

Morningstar Long/Short Equity Category | 1.78% | 1.90% | 3.25% | 3.37% | 3.20% |

* | Fund commenced operations on March 30, 2012. The performance data quoted for periods prior to March 30, 2012 is that of the Predecessor Fund. The Predecessor Fund commenced operations on September 30, 2009. The Predecessor Fund was not a registered mutual fund and was not subject to the same investment and tax restrictions as the Fund. If it had been, the Predecessor Fund’s performance might have been lower. Performance shown for periods of one year and greater are annualized. |

For periods after March 30, 2012, the returns shown above are calculated assuming reinvestment of all dividends and distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on dividends or distributions or the redemption of shares from a fund. Returns reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than a shareholder’s original cost. Performance of the Institutional Class Shares differs due to the differences in expenses. Current performance may be lower or higher than that shown here. Unlike the Fund’s comparative benchmarks, the Fund’s total returns are reduced by its annual operating expenses. Please note that one cannot invest directly in an unmanaged index.

12

|

|

Management’s Discussion of Fund Performance and Analysis

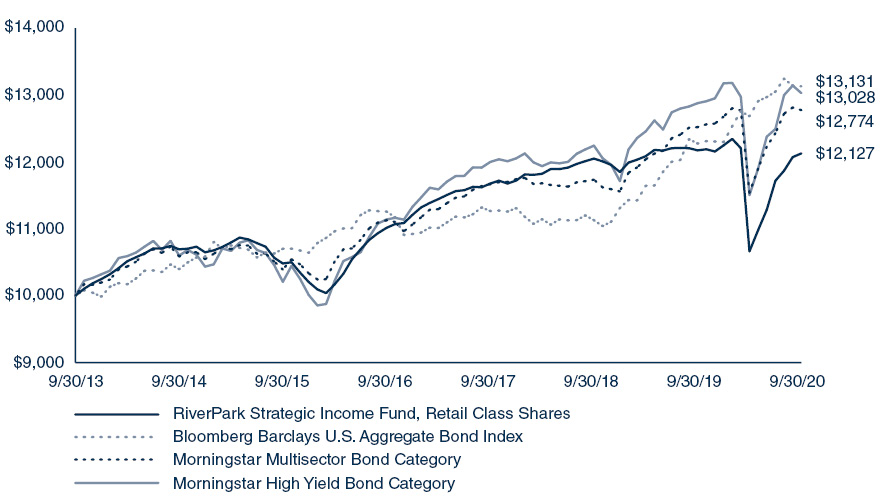

RiverPark Strategic Income Fund (Unaudited)

For the fiscal year ended September 30, 2020, the RiverPark Strategic Income Fund (the “Fund”) lost 0.10% and 0.36% on its Institutional Class Shares and Retail Class Shares, respectively, while the Bloomberg Barclays U.S. Aggregate Bond Index gained 6.98%, the Morningstar Multisector Bond Category gained 2.03%, and the Morningstar High Yield Bond Category gained 1.17%.

Investment results for the Fiscal Year were not uniform across quarters. The Institutional Class Shares gained 0.68% for the December quarter, lost 12.86% for the March quarter, gained 9.83% for the June quarter, and gained 3.68% in the September quarter.

The Fund realized positive contributions from four of its eight categories of investment. The Fund realized a contribution to its performance of 2.64% in Other (ABS) category, 0.89% in Buy & Hold “Money Good”, 0.52% in RiverPark Short Term High Yield Bond Fund Overlap, and 0.26% in Short Term Securities. Whereas the Fund lost 0.01% in Off the Beaten Path, 0.05% in Interest Rate Resets, 0.16% in Hedges, and 3.23% in the Priority Based (Above the Fray) category of investments.

As of September 30, 2020, the Fund’s net assets were weighted by category as follows: 35.89% in the Buy & Hold “Money Good” category, 19.37% in Off The Beaten Path, 17.33% in Other (ABS), 2.34% in the Priority Based (Above the Fray), 12.57% in Interest Rate Resets (floaters, cushion bonds), 5.25% in Short Term Securities, -3.10% in Hedges, with the remaining 10.35% in cash and cash equivalents. Across all categories, 87% of the net assets were held in high yield securities and 3% was held in investment grade securities. The Fund held 119 positions as of this date, none of which were held in the RiverPark Short Term High Yield Bond Fund Overlap category.

RiverPark Strategic Income Fund seeks high current income and capital appreciation consistent with the preservation of capital by investing in investment grade and non-investment grade debt, preferred stock, convertible bonds, bank loans, high yield bonds and income producing equities that Cohanzick deems appropriate for the Fund’s investment objective. The Fund will primarily invest in both investment grade and non-investment grade “Money Good” securities, for which the enterprise value of the issuing company exceeds the value of the senior and equally ranked debt of the considered investment. Therefore, we believe the risk of loss of principal due to permanent impairment is minimal. The Fund expects to invest in securities that are not widely followed, which Cohanzick believes offer better returns with little or no additional credit risk.

Footnotes:

“Money Good” is a term used by the Adviser to describe debt it believes will be paid off in full under current market conditions and on a strict priority basis.

High yield and investment grade classification of securities was based on Bloomberg Composite Ratings

13

|

|

This represents the manager’s assessment of the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based unmanaged index of investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, Mortgage-Backed Securities (agency fixed-rate and hybrid adjustable-rate mortgages pass-throughs), asset backed securities, and commercial backed securities.

The Morningstar Multisector Bond Category portfolios seek income by diversifying their assets among several fixed-income sectors, usually U.S. government obligations, U.S. corporate bonds, foreign bonds, and high-yield U.S. debt securities.

The Morningstar High Yield Bond Category portfolios seek income by diversifying their assets among several fixed-income sectors, usually U.S. government obligations, U.S. corporate bonds, foreign bonds, and high-yield U.S. debt securities.

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

14

|

|

Comparison of Change in the Value of a $10,000 Investment in the RiverPark Strategic Income Fund,

Retail Class Shares, versus the Bloomberg Barclays U.S. Aggregate Bond Index, the Morningstar Multisector

Bond Category and the Morningstar High Yield Bond Category

AVERAGE ANNUAL TOTAL RETURNS FOR THE | ||||

One Year Return | Annualized | Annualized | Annualized | |

Institutional Class Shares | -0.10% | 1.50% | 3.22% | 3.06% |

Retail Class Shares | -0.36% | 1.27% | 2.96% | 2.79% |

Bloomberg Barclays U.S. Aggregate Bond Index | 6.98% | 5.24% | 4.18% | 3.97% |

Morningstar Multisector Bond Category | 2.03% | 3.07% | 4.22% | 3.56% |

Morningstar High Yield Bond Category | 1.17% | 2.78% | 5.00% | 3.85% |

* | Fund commenced operations on September 30, 2013. |

Returns shown above are calculated assuming reinvestment of all dividends and distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on dividends or distributions or the redemption of shares from a fund. Returns reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. Effective March 31, 2014, the Fund fully recaptured previously waived investment advisory fees. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than a shareholder’s original cost. Performance of the Institutional Class Shares differs due to the differences in expenses. Current performance may be lower or higher than that shown here. Unlike the Fund’s comparative benchmarks, the Fund’s total returns are reduced by its annual operating expenses. Please note that one cannot invest directly in an unmanaged index.

15

|

|

Management’s Discussion of Fund Performance and Analysis

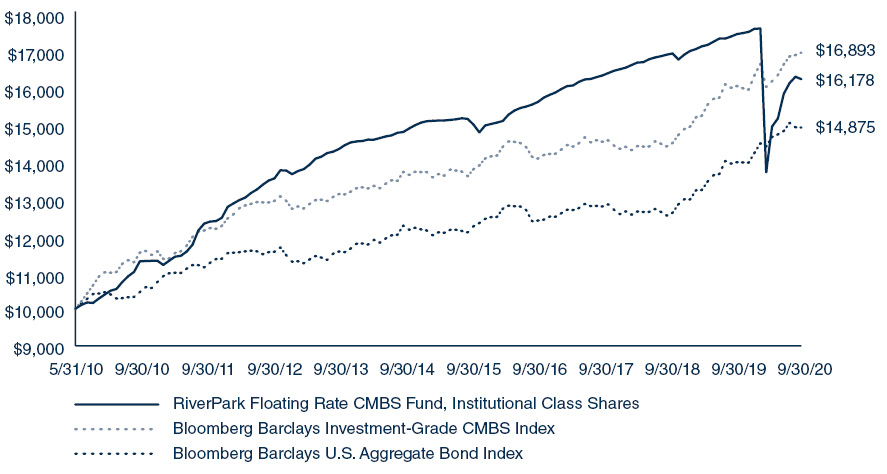

RiverPark Floating Rate CMBS Fund (Unaudited)

For the fiscal year ended September 30, 2020, the RiverPark Floating Rate CMBS Fund (the “Fund”) lost 6.63% and 6.96% on its Institutional Class Shares and Retail Class Shares respectively, while the Bloomberg Barclays U.S. Investment-Grade CMBS Index gained 5.95% and the Bloomberg Barclays U.S. Aggregate Bond Index gained 6.98%.

The Fund strives for an attractive yield while maintaining a portfolio that is substantially comprised of floating rate CMBS investments with a weighted average maturity of less than five years. As of September 30, 2020, the weighted average coupon for the Fund was 2.61%, 93% of the Fund’s invested portfolio was in floating rate securities with the remaining 7% in fixed rate, and the weighted average maturity of the portfolio was just over of 2.5 years.

Investment results for the Fiscal Year were not uniform across quarters. The Institutional Class Shares gained 0.72% for the December quarter, lost 21.63% for the March quarter, gained 15.42% for the June quarter, and gained 2.49% in the September quarter.

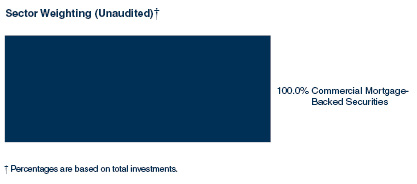

The RiverPark Floating Rate CMBS Fund emphasizes floating rate Single Asset / Single Borrower (SASB) loans that are structured as Commercial Mortgage Backed Securities (CMBS). The RiverPark Floating Rate CMBS Fund seeks to make investments in larger ($500+ million) securitizations of income producing commercial real estate loans secured by institutional quality assets with well regarded sponsors. The Fund emphasizes investments that have conservative credit metrics. As of September 30, 2020, all of the Fund’s investments were paying monthly coupons.

The RiverPark Floating Rate CMBS Fund emphasizes floating rate Single Asset / Single Borrower (SASB) loans that are structured as Commercial Mortgage Backed Securities (CMBS). The RiverPark Floating Rate CMBS Fund seeks to make investments in larger ($500+ million) securitizations of income producing commercial real estate loans secured by institutional quality assets with well-regarded sponsors. The Fund emphasizes investments that have conservative credit metrics including a weighted average loan-to-value ratio (LTV) of below 50% and a weighted average Debt Coverage Ratio of 4x. As of September 30, 2017, all of the Fund’s investments were performing.

This represents the manager’s assessment of the market environment at a specific point in time and should not be relied upon by the reader as research or investment advice.

The Bloomberg Barclays U.S. Investment-Grade CMBS Index measures the market of US Agency and US Non-Agency conduit and fusion CMBS deals with a minimum current deal size of $300mn.

16

|

|

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, mortgage-backed securities (agency fixed-rate and hybrid ARM pass-throughs), asset-backed securities and commercial back securities (agency and nonagency).

Loan-to-Value Ratio (or LTV): In order to calculate the Loan-to-Value Ratio at the Fund’s level in the capital structure (also referred to as “attachment point”), the Total Loan is divided by the underlying value of the commercial real estate securing the Fund’s investment. The Loan-to-Value Ratio is important to understanding the amount of credit support that protects the Fund’s investment. For example, if the Total Loan is $200 million and the property is appraised at $400 million, then the Loan-to-Value ratio would be 50%. A lower Loan-to-Value Ratio indicates that our investment has more credit support than a loan with a higher LTV.

Weighted Average Coupon is used to determine the gross interest rates of multiple mortgages that underline the CMBS. The Weighted Average Coupon represents the average interest rate of different pools of mortgages with varying interest rates.

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs, or expenses. Indexes are unmanaged and one cannot invest directly in an index.

17

|

|

Comparison of Change in the Value of a $10,000 Investment in the RiverPark Floating Rate CMBS Fund,

Institutional Class Shares, versus the Bloomberg Barclays U.S. Investment-Grade CMBS Index and Bloomberg Barclays U.S. Aggregate Bond Index

AVERAGE ANNUAL TOTAL RETURNS FOR THE | |||||

One Year Return | Annualized | Annualized | Annualized | Annualized | |

Institutional Class Shares | -6.63% | -0.01% | 1.41% | 4.64% | 4.76% |

Retail Class Shares | -6.96% | -0.29% | 1.20% | 4.52% | 4.65% |

Bloomberg Barclays U.S. Investment-Grade CMBS Index | 5.95% | 5.28% | 4.21% | 4.51% | 5.21% |

Bloomberg Barclays U.S. Aggregate Bond Index | 6.98% | 5.24% | 4.18% | 3.64% | 3.92% |

* | Fund commenced operations on September 30, 2016. The performance data quoted for period prior to September 30, 2016 is that of the Predecessor Fund. The Predecessor Fund commenced operations on May 31, 2010. The Predecessor Fund was not a registered mutual fund and was not subject to the same investment and tax restrictions as the Fund. If it had been, the Predecessor Fund’s performance might have been lower. Performance shown for periods of one year and greater are annualized. |

Furthermore, on November 12, 2018 the Interval Fund reorganized as an open-end mutual fund with daily liquidity. The performance data for the Retail Class Shares for periods prior to November 12, 2018, but after September 30, 2016 is that of the Institutional Class Shares adjusted to reflect the higher expense ratio applicable to the Retail Class Shares.

For periods after September 30, 2016, the returns shown above are calculated assuming reinvestments of all dividends and distributions. Returns do not reflect the deduction of taxes that a shareholder would pay on dividends or distributions or the redemption of shares from a fund. Returns reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than a shareholder’s original cost. Performance of the Institutional Class Shares differs due to the differences in expenses. Current performance may be lower or higher than that shown here. Unlike the Fund’s comparative benchmarks, the Fund’s total returns are reduced by its annual operating expenses. Please note that one cannot invest directly in an unmanaged index.

18

| RiverPark Large Growth Fund September 30, 2020 |

Description | Shares | Value (000) | ||||||

Schedule of Investments | ||||||||

Common Stock — 99.2%** | ||||||||

Communication Services – 16.8% | ||||||||

Alphabet, Cl A * | 783 | $ | 1,148 | |||||

Alphabet, Cl C * | 783 | 1,151 | ||||||

Facebook, Cl A * | 6,304 | 1,651 | ||||||

Pinterest, Cl A * | 52,860 | 2,194 | ||||||

Snap, Cl A * | 85,094 | 2,222 | ||||||

Twitter * | 24,987 | 1,112 | ||||||

Walt Disney | 10,505 | 1,303 | ||||||

| 10,781 | ||||||||

Consumer Discretionary – 10.8% | ||||||||

Amazon.com * | 1,064 | 3,350 | ||||||

NIKE, Cl B | 14,159 | 1,777 | ||||||

Vail Resorts | 8,425 | 1,803 | ||||||

| 6,930 | ||||||||

Financials – 11.0% | ||||||||

Apollo Global Management, Cl A | 34,104 | 1,526 | ||||||

Blackstone Group, Cl A (a) | 56,283 | 2,938 | ||||||

CME Group, Cl A | 5,461 | 914 | ||||||

KKR | 49,008 | 1,683 | ||||||

| 7,061 | ||||||||

Health Care – 16.3% | ||||||||

DexCom * | 3,551 | 1,464 | ||||||

Exact Sciences * | 25,560 | 2,606 | ||||||

Illumina * | 4,895 | 1,513 | ||||||

Intuitive Surgical * | 2,715 | 1,926 | ||||||

IQVIA Holdings * | 8,899 | 1,403 | ||||||

Zoetis, Cl A | 9,098 | 1,504 | ||||||

| 10,416 | ||||||||

Industrials – 6.8% | ||||||||

Lockheed Martin | 3,293 | 1,262 | ||||||

Northrop Grumman | 4,049 | 1,278 | ||||||

Uber Technologies * | 49,544 | 1,807 | ||||||

| 4,347 | ||||||||

Information Technology – 33.2% | ||||||||

Adobe * | 3,232 | 1,585 | ||||||

Apple | 22,020 | 2,550 | ||||||

Autodesk * | 6,917 | 1,598 | ||||||

Bill.Com Holdings * | 12,863 | 1,290 | ||||||

Mastercard, Cl A | 4,959 | 1,677 | ||||||

Microsoft | 14,792 | 3,111 | ||||||

PayPal Holdings * | 9,510 | 1,874 | ||||||

RingCentral, Cl A * | 4,519 | 1,241 | ||||||

ServiceNow * | 3,444 | 1,670 | ||||||

Shopify, Cl A * | 1,638 | 1,676 | ||||||

Twilio, Cl A * | 5,883 | 1,454 | ||||||

Visa, Cl A | 7,781 | 1,556 | ||||||

| 21,282 | ||||||||

Real Estate – 4.3% | ||||||||

American Tower REIT, Cl A | 5,351 | 1,294 | ||||||

Equinix REIT | 1,904 | 1,447 | ||||||

| 2,741 | ||||||||

Total Common Stock | ||||||||

(Cost $34,207) (000) | 63,558 | |||||||

Total Investments — 99.2% | ||||||||

(Cost $34,207) (000) | $ | 63,558 | ||||||

As of September 30, 2020, all of the Fund’s investments were considered Level 1 in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP.

For the year ended September 30, 2020, there were no transfers in or out of Level 3.

Percentages are based on Net Assets of $64,094 (000). |

* | Non-income producing security. |

** | More narrow industries are utilized for compliance purposes, whereas broad sectors are utilized for reporting purposes. |

(a) | Security considered Master Limited Partnership. At September 30, 2020, these securities amounted to $2,938 (000) or 4.6% of Net Assets. |

Cl — Class

REIT — Real Estate Investment Trust

The accompanying notes are an integral part of the financial statements.

19

| Wedgewood Fund September 30, 2020 |

Description | Shares | Value (000) | ||||||

Schedule of Investments | ||||||||

Common Stock — 98.9%** | ||||||||

Communication Services – 21.3% | ||||||||

Alphabet, Cl A * | 2,280 | $ | 3,342 | |||||

Electronic Arts * | 16,520 | 2,154 | ||||||

Facebook, Cl A * | 13,892 | 3,638 | ||||||

| 9,134 | ||||||||

Consumer Discretionary – 11.8% | ||||||||

Starbucks | 21,234 | 1,824 | ||||||

Tractor Supply | 22,656 | 3,248 | ||||||

| 5,072 | ||||||||

Financials – 5.4% | ||||||||

First Republic Bank | 10,388 | 1,133 | ||||||

S&P Global | 3,230 | 1,165 | ||||||

| 2,298 | ||||||||

Health Care – 14.4% | ||||||||

Alcon* | 18,756 | 1,068 | ||||||

Bristol-Myers Squibb | 30,566 | 1,843 | ||||||

Edwards Lifesciences * | 41,135 | 3,283 | ||||||

| 6,194 | ||||||||

Industrials – 4.3% | ||||||||

Copart * | 17,533 | 1,844 | ||||||

Information Technology – 41.7% | ||||||||

Apple | 27,836 | 3,224 | ||||||

CDW | 17,450 | 2,086 | ||||||

Keysight Technologies * | 18,033 | 1,781 | ||||||

Microsoft | 11,493 | 2,417 | ||||||

Motorola Solutions | 17,254 | 2,706 | ||||||

PayPal Holdings * | 15,365 | 3,027 | ||||||

Visa, Cl A | 13,415 | 2,683 | ||||||

| 17,924 | ||||||||

Total Common Stock | ||||||||

(Cost $32,871) (000) | 42,466 | |||||||

Rights — 0.1% | ||||||||

Health Care – 0.1% | ||||||||

Bristol Myers Squid CVR *(a) | 9,400 | 21 | ||||||

Total Rights | ||||||||

(Cost $20) (000) | 21 | |||||||

Total Investments — 99.0% | ||||||||

(Cost $32,891) (000) | $ | 42,487 | ||||||

As of September 30, 2020, all of the Fund’s investments were considered Level 1 in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP.

For the year ended September 30, 2020, there were no transfers in or out of Level 3.

Percentages are based on Net Assets of $42,930 (000). |

* | Non-income producing security. |

** | More narrow industries are utilized for compliance purposes, whereas broad sectors are utilized for reporting purposes. |

(a) | No rate available. |

Cl — Class

CVR — Contingent Value Right

The accompanying notes are an integral part of the financial statements.

20

| RiverPark Short Term High Yield Fund September 30, 2020 |

Description | Face | Value (000) | ||||||

Schedule of Investments | ||||||||

Corporate Obligations — 84.7% | ||||||||

Communication Services – 15.2% | ||||||||

CenturyLink | ||||||||

6.450%, 06/15/21 | 10,781 | $ | 11,075 | |||||

Cogent Communications Group | ||||||||

5.375%, 03/01/22 (a) | 1,087 | 1,113 | ||||||

Consolidated Communications | ||||||||

6.500%, 10/01/22 | 28,656 | 28,694 | ||||||

DISH DBS | ||||||||

6.750%, 06/01/21 | 9,663 | 9,914 | ||||||

Linkem | ||||||||

7.000%, VAR Euribor 3 Month+7.000%, 08/09/22 | EUR | 21,306 | 24,763 | |||||

Netflix | ||||||||

5.375%, 02/01/21 | 3,206 | 3,246 | ||||||

Sirius XM Radio | ||||||||

3.875%, 08/01/22 (a) | 6,947 | 7,029 | ||||||

TEGNA | ||||||||

4.875%, 09/15/21 (a) | 23,168 | 23,202 | ||||||

| 109,036 | ||||||||

Consumer Discretionary – 9.6% | ||||||||

APX Group | ||||||||

7.875%, 12/01/22 | 13,289 | 13,314 | ||||||

Carvana | ||||||||

8.875%, 10/01/23 (a) | 825 | 862 | ||||||

Emeco Pty | ||||||||

9.250%, 03/31/22 | 6,000 | 6,281 | ||||||

KFC Holding | ||||||||

5.000%, 06/01/24 (a) | 10,818 | 11,112 | ||||||

KGA Escrow | ||||||||

7.500%, 08/15/23 (a) | 18,026 | 18,684 | ||||||

L Brands | ||||||||

6.625%, 04/01/21 | 15,317 | 15,786 | ||||||

Penske Automotive Group | ||||||||

5.750%, 10/01/22 | 3,070 | 3,070 | ||||||

| 69,109 | ||||||||

Consumer Staples – 7.0% | ||||||||

Energizer Holdings | ||||||||

6.375%, 07/15/26 (a) | 22,391 | 24,089 | ||||||

Ingles Markets | ||||||||

5.750%, 06/15/23 | 4,693 | 4,774 | ||||||

JBS USA LUX | ||||||||

5.875%, 07/15/24 (a) | 21,255 | 21,695 | ||||||

| 50,558 | ||||||||

Energy – 7.1% | ||||||||

CITGO Petroleum | ||||||||

6.250%, 08/15/22 (a) | 14,326 | 14,252 | ||||||

CNX Resources | ||||||||

5.875%, 04/15/22 | 33,165 | 33,248 | ||||||

NuStar Logistics | ||||||||

6.750%, 02/01/21 | 3,673 | 3,718 | ||||||

| 51,218 | ||||||||

Financials – 5.7% | ||||||||

Quicken Loans | ||||||||

5.750%, 05/01/25 (a) | 39,508 | 40,693 | ||||||

Health Care – 3.0% | ||||||||

Hologic | ||||||||

4.375%, 10/15/25 (a) | 2,256 | 2,308 | ||||||

Tenet Healthcare | ||||||||

8.125%, 04/01/22 | 17,456 | 19,418 | ||||||

| 21,726 | ||||||||

Industrials – 9.6% | ||||||||

Altera Shuttle Tankers | ||||||||

7.125%, 08/15/22 | 2,800 | 2,857 | ||||||

BMC East | ||||||||

5.500%, 10/01/24 (a) | 7,111 | 7,320 | ||||||

Briggs & Stratton | ||||||||

6.875%, 12/15/20 (b) | 388 | 20 | ||||||

Great Lakes Dredge & Dock | ||||||||

8.000%, 05/15/22 | 6,433 | 6,620 | ||||||

Hawaiian Airlines 2013-1 Class B Pass-Through Certificates | ||||||||

4.950%, 01/15/22 | 6,731 | 6,078 | ||||||

HC2 Holdings | ||||||||

11.500%, 12/01/21 (a) | 9,133 | 8,722 | ||||||

Icahn Enterprises | ||||||||

6.250%, 02/01/22 | 6,362 | 6,443 | ||||||

Nielsen Luxembourg SARL | ||||||||

5.500%, 10/01/21 (a) | 5,109 | 5,123 | ||||||

Uber Technologies | ||||||||

7.500%, 11/01/23 (a) | 15,418 | 16,080 | ||||||

XPO Logistics | ||||||||

6.500%, 06/15/22 (a) | 9,849 | 9,896 | ||||||

| 69,159 | ||||||||

The accompanying notes are an integral part of the financial statements.

21

| RiverPark Short Term High Yield Fund |

Description | Face | Value (000) | ||||||

Information Technology – 11.7% | ||||||||

Dell International | ||||||||

5.875%, 06/15/21 (a) | 24,514 | $ | 24,575 | |||||

MagnaChip Semiconductor | ||||||||

6.625%, 07/15/21 | 23,756 | 23,756 | ||||||

Qorvo | ||||||||

5.500%, 07/15/26 | 15,387 | 16,345 | ||||||

VeriSign | ||||||||

4.625%, 05/01/23 | 3,630 | 3,656 | ||||||

Xerox | ||||||||

4.500%, 05/15/21 | 15,944 | 16,179 | ||||||

| 84,511 | ||||||||

Materials – 14.7% | ||||||||

BHP Billiton Finance USA | ||||||||

6.250%, VAR USD Swap Semi 30/360 5 Yr Curr+4.971%, 10/19/75 | 7,000 | 7,002 | ||||||

First Quantum Minerals | ||||||||

7.250%, 05/15/22 (a) | 18,991 | 19,018 | ||||||

Hudbay Minerals | ||||||||

7.250%, 01/15/23 (a) | 35,820 | 36,511 | ||||||

IAMGOLD | ||||||||

7.000%, 04/15/25 (a) | 33,883 | 35,703 | ||||||

Louisiana-Pacific | ||||||||

4.875%, 09/15/24 | 5,786 | 5,957 | ||||||

Reynolds Group Issuer | ||||||||

7.000%, 07/15/24 (a) | 1,827 | 1,860 | ||||||

| 106,051 | ||||||||

Real Estate – 1.1% | ||||||||

SBA Communications | ||||||||

4.000%, 10/01/22 | 8,041 | 8,116 | ||||||

Total Corporate Obligations | ||||||||

(Cost $609,996) (000) | 610,177 | |||||||

Convertible Bonds — 1.8% | ||||||||

Energy – 0.9% | ||||||||

Ship Finance International | ||||||||

5.750%, 10/15/21 | 6,340 | 6,262 | ||||||

Industrials – 0.3% | ||||||||

Dycom Industries | ||||||||

0.750%, 09/15/21 | 2,089 | 2,045 | ||||||

| Description | Shares/ Face Amount (000)‡ | Value (000) | ||||||

| Real Estate – 0.6% | ||||||||

| VEREIT | ||||||||

| 3.750%, 12/15/20 | 4,578 | $ | 4,586 | |||||

| Total Convertible Bonds | ||||||||

| (Cost $12,978) (000) | 12,893 | |||||||

| Common Stock — 1.0% | ||||||||

| Financials – 1.0% | ||||||||

| Subversive Capital Acquisition, Cl A * | 732,170 | 7,227 | ||||||

| Information Technology – 0.0% | ||||||||

| Internap Holding LLC * (c) (d) | 529,593 | 5 | ||||||

| Total Common Stock | ||||||||

| (Cost $9,648) (000) | 7,232 | |||||||

| Municipal Bond — 0.8% | ||||||||

| New York – 0.8% | ||||||||

| Metropolitan Transportation Authority, RB | ||||||||

| 5.000%, 11/15/20 | 5,812 | 5,826 | ||||||

| Total Municipal Bond | ||||||||

| (Cost $5,834) (000) | 5,826 | |||||||

| Bank Loan Obligations — 9.4% | ||||||||

| Communication Services – 2.6% | ||||||||

| Cincinnati Bell Inc., Tranche B Term Loan, 1st Lien | ||||||||

| 4.250%, 10/2/2024 (e) | 15,832 | 15,822 | ||||||

| Intelsat Jackson, Term Loan, 1st Lien DIP | ||||||||

| 6.500%, 07/13/22 (e) | 3,010 | 3,058 | ||||||

| 18,880 | ||||||||

| Consumer Discretionary – 2.5% | ||||||||

| First Brands Group, LLC, Tranche B-3 Term Loan, 1st Lien | ||||||||

| 8.500%, VAR LIBOR+7.500%, 02/02/24 | 5,085 | 5,003 | ||||||

| Golden Nugget Online Gaming, Inc., 2020 Buyback Term Loan | ||||||||

| 13.000%, VAR LIBOR+12.000%, 10/04/23 | 11,189 | 12,867 | ||||||

| 17,870 | ||||||||

The accompanying notes are an integral part of the financial statements.

22

| RiverPark Short Term High Yield Fund |

| Description | Face Amount (000)‡ | Value (000) | ||||||

| Environmental Services – 0.8% | ||||||||

| Advanced Disposal Services, Inc. (fka ADS Waste Holdings, Inc.), Additional Term Loan, 1st Lien | ||||||||

| 3.000%, 11/10/23 (e) | 5,844 | $ | 5,829 | |||||

| Industrials – 1.5% | ||||||||

| WCA Waste Corporation, 1st Lien | ||||||||

| 4.750%, 08/11/23 (e) | 10,530 | 10,508 | ||||||

| Information Technology – 2.0% | ||||||||

| CPA Global, 1st Lien | ||||||||

| 3.261%, 11/1/2024 (e) | 13,268 | 13,247 | ||||||

| Internap Holding LLC, Second Out Term Loan, 1st Lien | ||||||||

| 8.250%, VAR LIBOR+6.500%, 05/08/25 | 2,405 | 1,202 | ||||||

| 14,449 | ||||||||

| Total Bank Loan Obligations | ||||||||

| (Cost $68,375) (000) | 67,536 | |||||||

| Total Investments — 97.7% | ||||||||

| (Cost $706,831) (000) | $ | 703,664 | ||||||

A list of the open forward foreign currency contracts held by the Fund at September 30, 2020, is as follows (000):

| Counterparty | Maturity Date | Currency to Deliver | Currency to Receive | Unrealized Appreciation | ||||||||||||||

| Brown Brothers Harriman | 10/06/20 | EUR | 21,398 | USD | 25,244 | $ | 154 | |||||||||||

| $ | 154 | |||||||||||||||||

The following is a list of the inputs used as of September 30, 2020 in valuing the Fund’s investments and other financial instruments carried at value (000), in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP:

Investments in | Level 1 | Level 2 | Level 3(1) | Total | ||||||||||||

Corporate Obligations | $ | — | $ | 610,177 | $ | — | $ | 610,177 | ||||||||

Convertible Bonds | — | 12,893 | — | 12,893 | ||||||||||||

Common Stock | 7,227 | — | 5 | 7,232 | ||||||||||||

Municipal Bond | — | 5,826 | — | 5,826 | ||||||||||||

Bank Loan Obligations | — | 67,536 | — | 67,536 | ||||||||||||

Total Investments in Securities | $ | 7,227 | $ | 696,432 | $ | 5 | $ | 703,664 | ||||||||

| Other Financial Instruments | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Forwards Contracts* | ||||||||||||||||

| Unrealized Appreciation | $ | — | $ | 154 | $ | — | $ | 154 | ||||||||

| Total Other Financial Instruments | $ | — | $ | 154 | $ | — | $ | 154 | ||||||||

* | Forward contracts are valued at the unrealized appreciation on the instrument. See Note 2 in Notes to Financial Statements for additional information. |

For the year ended September 30, 2020, there were no transfers in or out of Level 3.

(1) | A reconciliation of Level 3 investments is presented when the Fund has a significant amount of Level 3 investments at the beginning and/or end of the period in relation to the net assets. Management has concluded that Level 3 investments are not material in relation to net assets. |

‡ | In U.S. Dollar unless otherwise indicated. |

Percentages are based on Net Assets of $719,881 (000). |

* | Non-income producing security. |

(a) | Securities sold within terms of a private placement memorandum, exempt from registration under Section 144A of the Securities Act of 1933, as amended, and may be sold only to dealers in that program or other “accredited investors.” These securities have been determined to be liquid under guidelines established by the Board of Trustees. At September 30, 2020, these securities amounted to $361,612 (000) or 50.2% of Net Assets. |

(b) | Security in default on interest payments. |

(c) | Level 3 security in accordance with fair value hierarchy. |

(d) | Securities considered illiquid. The total value of such securities as of September 30, 2020 was $5 (000) and represented 0.0% of Net Assets. |

(e) | Variable or floating rate security, the interest rate of which adjusts periodically based on changes in current interest rates and prepayments on the underlying pool of assets. |

Cl — Class

DIP — Debtor in Possession

EUR — Euro

EURIBOR— Euro London Interbank Offered Rate

LIBOR— London Interbank Offered Rate

LLC — Limited Liability Company

RB — Revenue Bond

USD — U.S. Dollar

VAR— Variable Rate

The accompanying notes are an integral part of the financial statements.

23

| RiverPark Long/Short Opportunity Fund September 30, 2020 |

Description | Shares | Value (000) | ||||||

Schedule of Investments | ||||||||

Common Stock — 91.6%** | ||||||||

Communication Services – 17.0% | ||||||||

Alphabet, Cl A *(a) | 4,217 | $ | 6,180 | |||||

Alphabet, Cl C *(a) | 4,212 | 6,190 | ||||||

Facebook, Cl A * | 50,233 | 13,156 | ||||||

Pinterest, Cl A *(a) | 285,926 | 11,869 | ||||||

Snap, Cl A *(a) | 482,755 | 12,605 | ||||||

Twitter * | 154,755 | 6,887 | ||||||

Walt Disney (a) | 48,158 | 5,975 | ||||||

| 62,862 | ||||||||

Consumer Discretionary – 9.6% | ||||||||

Amazon.com * | 5,777 | 18,190 | ||||||

NIKE, Cl B (a) | 65,554 | 8,230 | ||||||

Vail Resorts | 42,692 | 9,135 | ||||||

| 35,555 | ||||||||

Financials – 11.4% | ||||||||

Apollo Global Management, Cl A | 233,649 | 10,456 | ||||||

Blackstone Group, Cl A (b) (c) | 312,649 | 16,320 | ||||||

CME Group, Cl A | 33,709 | 5,640 | ||||||

KKR | 281,698 | 9,673 | ||||||

| 42,089 | ||||||||

Health Care – 16.4% | ||||||||

DexCom *(a) | 20,486 | 8,445 | ||||||

Exact Sciences *(a) | 127,931 | 13,042 | ||||||

Illumina *(a) | 17,785 | 5,497 | ||||||

Intuitive Surgical *(a) | 9,927 | 7,044 | ||||||

IQVIA Holdings * | 50,650 | 7,984 | ||||||

SmileDirectClub, Cl A * | 820,959 | 9,589 | ||||||

Zoetis, Cl A | 54,861 | 9,072 | ||||||

| 60,673 | ||||||||

Industrials – 4.9% | ||||||||

Lockheed Martin (a) | 7,490 | 2,871 | ||||||

Northrop Grumman | 23,440 | 7,395 | ||||||

Uber Technologies *(a) | 209,433 | 7,640 | ||||||

| 17,906 | ||||||||

Information Technology – 28.5% | ||||||||

Adobe * | 17,526 | 8,595 | ||||||

Apple | 129,724 | 15,024 | ||||||

Autodesk *(a) | 18,731 | 4,327 | ||||||

Bill.Com Holdings * | 71,680 | 7,190 | ||||||

Mastercard, Cl A (a) | 20,679 | 6,993 | ||||||

Microsoft | 82,261 | 17,302 | ||||||

PayPal Holdings *(a) | 54,764 | 10,790 | ||||||

RingCentral, Cl A * | 28,563 | 7,844 | ||||||

ServiceNow *(a) | 17,332 | 8,406 | ||||||

Shopify, Cl A *(a) | 6,206 | 6,349 | ||||||

Twilio, Cl A *(a) | 29,230 | 7,222 | ||||||

Visa, Cl A (a) | 25,568 | 5,113 | ||||||

| 105,155 | ||||||||

Real Estate – 3.8% | ||||||||

American Tower REIT, Cl A | 27,525 | 6,654 | ||||||

Equinix REIT | 9,809 | 7,456 | ||||||

| 14,110 | ||||||||

Total Common Stock | ||||||||

(Cost $252,143) (000) | 338,350 | |||||||

Total Investments — 91.6% | ||||||||

(Cost $252,143) (000) | $ | 338,350 | ||||||

The accompanying notes are an integral part of the financial statements.

24

| RiverPark Long/Short Opportunity Fund |

A list of open swap agreements held by the Fund at September 30, 2020 was as follows:

Equity Swap Agreements | ||||||||||||||||||||||

Company Reference | Counterparty | Receive (Pay) | Payment | Termination | Notional | Value | Net Unrealized | |||||||||||||||

Alphabet Inc-Cl A | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 10/13/21 | $ | 251 | $ | 241 | $ | (10 | ) | |||||||||||

Alphabet Inc-Cl C | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 10/13/21 | 247 | 237 | (10 | ) | ||||||||||||||

Ametek Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 04/13/21 | (2,213 | ) | (2,543 | ) | (330 | ) | ||||||||||||

Aramark | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (2,143 | ) | (2,281 | ) | (138 | ) | ||||||||||||

ATT Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 03/03/21 | (3,508 | ) | (3,314 | ) | 194 | |||||||||||||

Autodesk Inc | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 10/28/20 | 2,760 | 4,209 | 1,449 | |||||||||||||||

Baker Hughes Co | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (2,235 | ) | (1,897 | ) | 338 | |||||||||||||

Boston Properties Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 05/19/21 | (2,726 | ) | (2,379 | ) | 347 | |||||||||||||

Caterpillar Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (1,819 | ) | (2,211 | ) | (392 | ) | ||||||||||||

Centurylink Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 08/26/21 | (2,366 | ) | (2,352 | ) | 14 | |||||||||||||

Cerner Corp | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 06/03/21 | (1,607 | ) | (1,705 | ) | (98 | ) | ||||||||||||

Church Dwight Co Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/08/21 | (1,927 | ) | (2,399 | ) | (472 | ) | ||||||||||||

Core Laboratories N.V. | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (2,208 | ) | (1,459 | ) | 749 | |||||||||||||

Dexcom Inc | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 04/27/21 | 204 | 389 | 185 | |||||||||||||||

Discovery Inc - A | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 05/17/21 | (2,076 | ) | (2,108 | ) | (32 | ) | ||||||||||||

Dish Network Corp-A | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/01/21 | (1,497 | ) | (1,344 | ) | 153 | |||||||||||||

Edgewell Personal Care Co | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 06/03/21 | (3,180 | ) | (3,101 | ) | 79 | |||||||||||||

Exact Sciences Corp | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 04/07/21 | 1,675 | 2,476 | 801 | |||||||||||||||

Federal Realty Invs Trust | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 05/17/21 | (2,548 | ) | (2,323 | ) | 225 | |||||||||||||

Gap Inc/The | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (2,324 | ) | (3,271 | ) | (947 | ) | ||||||||||||

Gartner Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 05/12/21 | (2,576 | ) | (2,742 | ) | (166 | ) | ||||||||||||

Halliburton Co | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (1,923 | ) | (1,752 | ) | 171 | |||||||||||||

Harley-Davidson Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 05/17/21 | (2,800 | ) | (2,944 | ) | (144 | ) | ||||||||||||

Hp Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 05/19/21 | (2,426 | ) | (2,960 | ) | (534 | ) | ||||||||||||

Idex Corp | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 05/05/21 | (2,172 | ) | (2,587 | ) | (415 | ) | ||||||||||||

Illumina Inc | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 01/13/21 | 3,017 | 3,151 | 134 | |||||||||||||||

Intel Corp | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 05/19/21 | (1,693 | ) | (1,457 | ) | 236 | |||||||||||||

Interpublic Group Of Cos Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 04/14/21 | (1,940 | ) | (1,978 | ) | (38 | ) | ||||||||||||

Intuitive Surgical Inc | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 03/09/21 | 3,397 | 3,844 | 447 | |||||||||||||||

Iron Mountain Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 06/03/21 | (3,668 | ) | (3,890 | ) | (222 | ) | ||||||||||||

Kimberly-Clark Corp | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/08/21 | (2,106 | ) | (2,244 | ) | (138 | ) | ||||||||||||

Klepierre | Goldman Sachs International | Fed Funds - (1.00)% | Maturity | 08/11/21 | (2,061 | ) | (1,591 | ) | 470 | |||||||||||||

Kohls Corp | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (2,040 | ) | (1,733 | ) | 307 | |||||||||||||

Kraft Heinz Co/The | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/01/21 | (2,389 | ) | (2,300 | ) | 89 | |||||||||||||

Kroger Co | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/01/21 | (2,093 | ) | (2,198 | ) | (105 | ) | ||||||||||||

Lockheed Martin Corp | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 04/21/21 | 3,972 | 4,403 | 431 | |||||||||||||||

Masimo Corp | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 09/01/21 | (2,820 | ) | (3,124 | ) | (304 | ) | ||||||||||||

Mastercard Inc - A | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 04/07/21 | 2,184 | 2,304 | 120 | |||||||||||||||

Medical Properties Trust Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 06/03/21 | (2,162 | ) | (2,114 | ) | 48 | |||||||||||||

National Oilwell Varco Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (3,066 | ) | (2,261 | ) | 805 | |||||||||||||

Nielsen Holdings Plc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/01/21 | (2,150 | ) | (2,135 | ) | 15 | |||||||||||||

Nike Inc -Cl B | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 08/25/21 | 1,690 | 2,176 | 486 | |||||||||||||||

Omnicom Group | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 04/14/21 | (2,126 | ) | (2,031 | ) | 95 | |||||||||||||

Paypal Holdings Inc | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 04/15/21 | 286 | 544 | 258 | |||||||||||||||

Pinterest Inc- Class A | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 04/07/21 | 79 | 281 | 202 | |||||||||||||||

Publicis Groupe | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 03/26/21 | (1,862 | ) | (1,858 | ) | 4 | |||||||||||||

Regency Centers Corp | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 06/03/21 | (2,230 | ) | (1,942 | ) | 288 | |||||||||||||

Schlumberger Ltd | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (2,167 | ) | (1,774 | ) | 393 | |||||||||||||

Servicenow Inc | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 04/15/21 | 218 | 385 | 167 | |||||||||||||||

Shopify Inc - Class A | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 04/21/21 | 1,567 | 4,579 | 3,012 | |||||||||||||||

Simon Property Group Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (3,000 | ) | (2,777 | ) | 223 | |||||||||||||

Sl Green Realty Corp | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (2,968 | ) | (2,907 | ) | 61 | |||||||||||||

Snap Inc - A | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 04/08/21 | 91 | 265 | 174 | |||||||||||||||

Snap-On Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 06/03/21 | (1,710 | ) | (1,877 | ) | (167 | ) | ||||||||||||

The accompanying notes are an integral part of the financial statements.

25

| RiverPark Long/Short Opportunity Fund |

Equity Swap Agreements | ||||||||||||||||||||||

Company Reference | Counterparty | Receive (Pay) | Payment | Termination | Notional | Value | Net Unrealized | |||||||||||||||

Sysco Corp | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | $ | (2,031 | ) | $ | (2,316 | ) | $ | (285 | ) | |||||||||

Tapestry Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (1,990 | ) | (2,196 | ) | (206 | ) | ||||||||||||

Trimble Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 06/03/21 | (2,408 | ) | (2,762 | ) | (354 | ) | ||||||||||||

Twilio Inc - A | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 01/13/21 | 290 | 797 | 507 | |||||||||||||||

Uber Technologies Inc | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 04/07/21 | 843 | 1,149 | 306 | |||||||||||||||

Ventas Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 06/03/21 | (1,916 | ) | (2,219 | ) | (303 | ) | ||||||||||||

Verizon Communications Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 04/22/21 | (2,671 | ) | (2,857 | ) | (186 | ) | ||||||||||||

Visa Inc-Class A Shares | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 08/25/21 | 4,069 | 4,082 | 14 | |||||||||||||||

Vornado Realty Trust | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (2,674 | ) | (2,399 | ) | 275 | |||||||||||||

Walmart Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 07/14/21 | (2,517 | ) | (2,803 | ) | (286 | ) | ||||||||||||

Walt Disney Co/The | Goldman Sachs International | Fed Funds - 0.50% | Maturity | 04/07/21 | 828 | 973 | 145 | |||||||||||||||

Welltower Inc | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 06/03/21 | (2,028 | ) | (2,170 | ) | (142 | ) | ||||||||||||

Western Union Co | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 05/12/21 | (3,035 | ) | (3,182 | ) | (147 | ) | ||||||||||||

WPP PLC | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 03/26/21 | (2,419 | ) | (2,194 | ) | 225 | |||||||||||||

Zebra Technologies Corp-Cl A | Goldman Sachs International | Fed Funds - (0.50%) | Maturity | 03/03/21 | (2,344 | ) | (2,388 | ) | (44 | ) | ||||||||||||

| $ | 8,027 | |||||||||||||||||||||

The following is a list of the inputs used as of September 30, 2020 in valuing the Fund’s investments and other financial instruments carried at value (000), in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP:

Investments in | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Common Stock | $ | 338,350 | $ | — | $ | — | $ | 338,350 | ||||||||

Total Investments in Securities | $ | 338,350 | $ | — | $ | — | $ | 338,350 | ||||||||

Other Financial | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Equity Swaps‡ | ||||||||||||||||

Unrealized Appreciation | $ | — | $ | 14,642 | $ | — | $ | 14,642 | ||||||||

Unrealized Depreciation | — | (6,615 | ) | — | (6,615 | ) | ||||||||||

Total Other Financial Instruments | $ | — | $ | 8,027 | $ | — | $ | 8,027 | ||||||||

‡ | Equity Swaps are valued at the unrealized appreciation (depreciation) on the instrument. |

For the year ended September 30, 2020, there were no transfers in or out of Level 3.

Percentages are based on Net Assets of $369,183 (000). |

* | Non-income producing security. |

** | More narrow industries are utilized for compliance purposes, whereas broad sectors are utilized for reporting purposes. |

† | Inclusive of accrued dividends and interest related to Total Return Swaps. |

(a) | Underlying security for a Total Return Swap. |

(b) | Security considered Master Limited Partnership. At September 30, 2020, these securities amounted to $16,320 (000) or 4.4% of Net Assets. |

(c) | This security or a partial position of this security has been committed as collateral for Total Return Swaps. The aggregate market value of the collateral as of September 30, 2020 was $10,048 (000). |

Cl — Class

REIT — Real Estate Investment Trust

Amounts designated as “— “ are $0 or rounded to $0.

The accompanying notes are an integral part of the financial statements.

26

| RiverPark Strategic Income Fund September 30, 2020 |

| Description | Face Amount (000)‡ | Value (000) | ||||||

| Schedule of Investments | ||||||||

| Corporate Obligations — 58.2% | ||||||||

| Communication Services – 11.8% | ||||||||

| Connect Finco SARL | ||||||||

| 6.750%, 10/01/26 (a) | 5,517 | $ | 5,544 | |||||

| DISH DBS | ||||||||

| 6.750%, 06/01/21 | 2,939 | 3,016 | ||||||

| Linkem | ||||||||

| 7.000%, VAR Euribor 3 Month+7.000%, 08/09/22 (a) | EUR | 8,896 | 10,339 | |||||

| ORBCOMM | ||||||||

| 8.000%, 04/01/24 (a) | 1,011 | 985 | ||||||

| T-Mobile USA | ||||||||

| 6.000%, 03/01/23 | 2,442 | 2,451 | ||||||

| 22,335 | ||||||||

| Consumer Discretionary – 14.1% | ||||||||

| Anagram International | ||||||||

| 15.000%, 08/15/25 (a) | 1,528 | 1,604 | ||||||

| APX Group | ||||||||

| 7.875%, 12/01/22 | 5,433 | 5,443 | ||||||

| At Home Holding III | ||||||||

| 8.750%, 09/01/25 (a) | 3,303 | 3,458 | ||||||

| Diamond Sports Group | ||||||||

| 12.750%, 12/01/26 (a) | 1,084 | 873 | ||||||

| Ferrellgas | ||||||||

| 10.000%, 04/15/25 (a) | 1,567 | 1,700 | ||||||

| FXI Holdings | ||||||||

| 12.250%, 11/15/26 (a) | 2,965 | 3,170 | ||||||

| Georg Jensen | ||||||||

| 6.000%, VAR Euribor 3 Month+6.000%, 05/15/23 | EUR | 300 | 299 | |||||

| Hercules Achievement | ||||||||

| 9.000%, VAR ICE LIBOR USD 3 Month+8.000%, 12/22/24 (a) | 3,185 | 3,030 | ||||||

| Jacktel | ||||||||

| 10.000%, 12/04/23 (a) | 1,700 | 391 | ||||||

| Lifefit Group Midco GmbH | ||||||||

| 7.500%, VAR Euribor 3 Month+7.500%, 07/26/23 | EUR | 1,160 | 1,374 | |||||

| SB Holdco | ||||||||

| 8.000%, VAR Euribor 3 Month+8.000%, 07/13/22 | EUR | 1,300 | 1,535 | |||||

| Tapestry | ||||||||

| 4.250%, 04/01/25 (e) | 3,491 | 3,648 | ||||||

| 26,525 | ||||||||

| Energy – 8.7% | ||||||||

| CITGO Petroleum | ||||||||

| 6.250%, 08/15/22 (a) | 4,730 | 4,705 | ||||||

| Golar LNG Partners | ||||||||

| 6.506%, VAR ICE LIBOR USD 3 Month+6.250%, 11/22/21 | 969 | 819 | ||||||

| Martin Midstream Partners | ||||||||

| 11.500%, 02/28/25 (a) | 1,845 | 1,679 | ||||||

| 10.000%, 02/29/24 (a) | 1,920 | 1,997 | ||||||

| Oasis Petroleum | ||||||||

| 6.875%, 01/15/23 (b) | 1,112 | 261 | ||||||

| 6.250%, 05/01/26 (a) (b) | 2,065 | 494 | ||||||