united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22447

Equinox Funds Trust

(Exact name of registrant as specified in charter)

17605 Wright Street Omaha, Nebraska 68130

(Address of principal executive offices) (Zip code)

James Ash, Gemini Fund Services, LLC.

80 Arkay Drive, Suite 110, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2619

Date of fiscal year end: 9/30

Date of reporting period: 9/30/17

Item 1. Reports to Stockholders.

| EQUINOX CAMPBELL STRATEGY FUND |

| |

| |

| |

| |

| CLASS A SHARES: EBSAX |

| |

| CLASS C SHARES: EBSCX |

| |

| CLASS I SHARES: EBSIX |

| |

| CLASS P SHARES: EBSPX |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| ANNUAL REPORT |

| |

| SEPTEMBER 30, 2017 |

| |

| |

| |

| |

| |

| |

| |

| |

| 1-888-643-3431 |

| WWW.EQUINOXFUNDS.COM |

| |

| |

| |

This report and the financial statements contained herein are submitted for the general information of shareholders and are not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus. Nothing herein contained is to be considered an offer to buy shares of the Equinox Campbell Strategy Fund. Such offering is made only by prospectus, which includes details as to offering price and other material information.

Distributed by Northern Lights Distributors, LLC

Member FINRA

| EQUINOX CAMPBELL STRATEGY FUND |

| Annual Letter to Shareholders for the year ended September 30, 2017 |

| |

The Equinox Campbell Strategy Fund (the “Fund”) was launched on the Equinox Alternative Strategy Platform (“EASP”) on March 8, 2013 (except for Class C Shares, as shown in the table below).

The Fund’s investment objective is to seek long-term capital appreciation, which is pursued by investing (a) directly or (b) indirectly through its wholly-owned subsidiary, in a combination of

| (i) | derivative instruments such as swap agreements1 that provide exposure to the managed futures program of Campbell & Company, Inc. (the “Campbell Program”)2; and |

| (ii) | a fixed-income portfolio. |

PERFORMANCE OF THE FUND (as of 9/30/2017)

| NAME | TICKER | 12 MO RETURN

(10/1/16-9/30/17) |

CUMULATIVE

RETURN SINCE

INCEPTION | INCEPTION

DATE |

| Equinox Campbell Strategy Fund - A | EBSAX | -7.60% | 1.03% | 3/8/2013 |

Equinox Campbell Strategy Fund – A

(with 5.75% maximum sales charge) | EBSAX | -12.93% | -4.78% | 3/8/2013 |

| Equinox Campbell Strategy Fund - C | EBSCX | -8.32% | 2.49% | 2/11/2014 |

| Equinox Campbell Strategy Fund - I | EBSIX | -7.45% | 2.23% | 3/8/2013 |

| Equinox Campbell Strategy Fund - P | EBSPX | -7.36% | 2.23% | 3/8/2013 |

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

Investments in Managed Futures are speculative, involve substantial risk, and are not suitable for all investors.

Returns of the Fund’s shares for the fiscal year are shown in the table above. The Fund’s primary investment allocation is to the Campbell Program, which is a diversified intermediate

| 1 | A swap is a derivative contract through which two parties exchange financial instruments. Most swaps involve cash flows based on a notional principal amount that both parties agree to. Usually, the principal does not change hands. Each cash flow comprises one leg of the swap. One cash flow is generally fixed, while the other is variable – that is, based on a benchmark interest rate, floating currency exchange rate or index price. The most common kind of swap is an interest rate swap. Swaps do not trade on exchanges, and retail investors do not generally engage in swaps. Rather, swaps are over-the-counter contracts between businesses or financial institutions. |

| 2 | A “Managed Futures Program” generally is a trading program that a CTA uses to guide its investments in futures, forwards, options or spot contracts. Please see the Fund’s Prospectus for a detailed description of the Fund’s investment strategy. |

| 47 Hulfish Street, Suite 510, Princeton, NJ 08542 • T 609.430.0404 • F 609.454.5010 • www.equinoxfunds.com |

to long-term multi-strategy (but predominantly trend-following) program. The Fund had negative performance for the fiscal year, but is still in positive territory since inception. As shown on page 2, the Campbell Program’s (and consequently the Fund’s) market exposure continues to be diversified across six sectors. As of the fiscal year-end, Currencies, Equity Indices, and Interest Rates, in that order, represent the largest gross exposures, and total almost 83% (vs. 70% last year), while the physical commodity sectors, Metals, Agricultural Commodities, and Energy (in that order) total the remaining 17%.

It is worth noting that the Campbell Program has long-term target risk exposures to various sectors. The actual sector risk exposures at any time are a function of the signals generated by the trading models: when there are more trends in markets, whether up or down, actual sector risk exposures will tend to be higher. It is also worth distinguishing between “gross” and “net” risk exposures: for example, a sector that has long positions whose risk exposure is 10% and short positions whose risk exposure is –15% will be shown as having a gross risk exposure of 25%, even though its “net” exposure would be only –5% (short).

SECTOR ALLOCATION (as of 9/30/2017)

| CURRENCIES | EQUITY

INDICES | INTEREST

RATES | AGRICULTURAL

COMMODITIES | ENERGY | METALS | TOTAL |

| 38.7% | 28.9% | 15.0% | 4.1% | 3.8% | 9.5% | 100.0% |

In terms of sector attribution, Equity Indices were the only positive contributor to performance. Agricultural Commodities, Energy, Interest Rates, Metals, and Currencies, in that order, all detracted from performance. Clearly, it was not a favorable market environment for most Commodity Trading Advisor (CTA) strategies, including trend-following.

SECTOR ATTRIBUTION (10/1/2016 TO 9/30/2017)

| CURRENCIES | EQUITY

INDICES | INTEREST

RATES | AGRICULTURAL

COMMODITIES | ENERGY | METALS | TOTAL |

| -0.23% | 13.14% | -4.70% | -8.02% | -6.13% | -1.68% | -7.60% |

FUND PERFORMANCE HIGHLIGHTS

The fund’s performance for the year was driven mainly by four months.

October 2016

The Fund returned [–3.06%] in October, a difficult month for trend-following strategies.

Trend-following strategies were responsible for most of the losses. Rising yields in the US and Europe led to losses for long positions held by longer-term (greater than 3-month average

| 47 Hulfish Street, Suite 510, Princeton, NJ 08542 • T 609.430.0404 • F 609.454.5010 • www.equinoxfunds.com |

holding period) strategies. Time-horizon diversification was helpful, however, as both short- term and medium-term trend strategies outperformed in all four sectors. Non-trend following strategies contributed positively during the month. Cross sector strategies, which use information from one asset class to trade markets in another asset class, posted significant gains in foreign exchange, with further gains in equities and fixed-income. Short-term mean- reversion and carry strategies posted small negative returns.

Sector performance diverged dramatically. Performance in equity indices, which represented the largest risk exposure for the program during October, was approximately flat. Net long positioning benefited from the risk-on sentiment early in the month, yielding early gains. As the month progressed, however, sector gains were erased as uncertainty surrounding the impending US election drove investors out of risky assets. Global equities sold off for five consecutive days to end the month, while equity implied volatility (VIX) rose by more than 30% during the same period. Concurrent with the month-end sell-off in equities, global bonds also moved lower. For the fourth consecutive month, global stocks and bonds (as proxied by the MSCI World Index and JPM Global Aggregate Bond Index, respectively) moved in the same direction.

Though equity indices and fixed income both retreated in October, the sell-off was much more significant for bonds. The 2.6% monthly decline for the JPM Bond Index was the largest in several years. While fixed income was a negative contributor to performance, short and medium-term trend strategies limited losses in the sector. These more reactive strategies helped drive net sector exposure short by month-end, marking the first time the portfolio had been net short fixed income in recent history.

The currency and commodity sectors were, respectively, the largest positive and negative contributors to profit and loss (P&L) in October. Net long dollar positions profited as the US Dollar strengthened against other traded currencies. The US Dollar Index (DXY) rose more than 3%, and the British Pound (–5.3%) and Swedish Krona (–5.0%) were the biggest losses vs the USD.

Difficulties in the commodity sector continued to plague performance. Year-to-date, performance has been dominated by losses in the energy complex, with trend-based strategies getting chopped up amidst the frequent reversals in the space. In October, short positions in corn and natural gas contributed significantly to P&L.

January 2017

Broad reversals in the last few trading days of the month led to negative performance (–2.89%). Short-term mean reversion strategies provided some profits, but it was a rough month for trend models, particularly those with 1-3month lookbacks, which incurred appreciable losses from reversals in currency and commodity markets.

| 47 Hulfish Street, Suite 510, Princeton, NJ 08542 • T 609.430.0404 • F 609.454.5010 • www.equinoxfunds.com |

Returns in the equity sector were positive albeit volatile. A sizable net long position led to gains in the early part of the month and again in the days following the presidential inauguration, as markets ramped higher. However, a month-end sell-off erased some of those profits. Overall positioning in the equity sector remained long, with net exposure moving higher by month-end.

Fixed-income sector performance was slightly negative, with losses in long-term rates more than offsetting small gains in short-term rates. Markets seemed mostly to react to country- specific events; most contracts traded lower, but Australian futures were higher while US futures were little changed. A net long position in European contracts led to some small losses, and net short exposure in Asia and North America also had some impact.

Performance in the commodity sector was negative. There was significant dispersion in returns across the complex, with large gains in base metals and losses in energy and grains. One of the most difficult markets was Reformulated Gasoline Blendstock for Oxygen Blending (RBOB) Gasoline, where a large long position suffered losses as prices declined rapidly throughout the month. The portfolio was well-positioned in industrial metals, with long positions in Copper, Aluminum and Nickel all profiting as those markets moved higher on bullish fundamentals.

Finally, the currency sector was a significant detractor from performance. Coming off a very strong fourth quarter, which included 3 consecutive monthly gains and a cumulative increase of more than 7%, the USD Index reversed course and finished the month of January about 2.6% lower. With the exception of Turkish Lira, our entire universe of currencies strengthened versus the greenback as investors pared back their bullish dollar bets amid worries that Trump was focusing more on protectionism than pro-growth economic policies. Some of the largest long USD/short Forex (FX) positions that suffered losses were the Japanese Yen, Swedish Krona and Canadian Dollar. By the end of the month, shorter-term models significantly reduced USD exposure, and even established long positions in certain currencies, such as the New Zealand and Australian Dollars.

February 2017

Trend-based strategies were the primary drivers of strong gains (+4.15%) during February, driven largely by the continued positive momentum in global equities. Long equity index positions in both medium-term and long-term trend-following models profited as global markets moved higher, although net exposure was reduced somewhat as the month progressed. While trend strategies represented the majority of the gains, net profits from macro strategies, including both multi-asset carry and cross sector investments, also boosted performance.

The rise in global equities was the dominant theme in February, as better-than-expected economic data and a potentially favorable political environment in the US promoted “risk-on”

| 47 Hulfish Street, Suite 510, Princeton, NJ 08542 • T 609.430.0404 • F 609.454.5010 • www.equinoxfunds.com |

sentiment. In tandem with the rally, volatility continued to decline to historically low levels – the MSCI World Index daily volatility (annualized) was just 4% during February, compared to an average of 11% over the prior 5 years. Notably, equity volatility was lower than both fixed- income and currency volatility during January and February. This had not occurred since at least January 2000.

A notable development during February was the divergence in net positioning between trend and macro strategies, which were both profitable despite their differing views. This was largely driven by changing signals within the trend portfolio, which flipped signs (of net exposure) in several sectors during the month. In the currency sector, trend strategies responded to the recent USD weakness and established a small net short position in early February, while macro strategies maintained a net long USD position. Trend strategies also repositioned somewhat in the fixed-income sector, reducing net short exposure throughout the month to finish nearly (net) flat. Macro strategies, however, maintained a long position in fixed-income. In the equity sector, macro strategies remained relatively uncommitted, with a small net short position serving to moderate long positions from trend-following.

June 2017

Sharp trend reversals at month-end led to a dramatic shift in performance for the managed futures asset class in general and for the Fund, which was down –3.82%. The sell-off in global fixed-income, which began on June 27 on the heels of comments from the European Central Bank’s (ECB) Mario Draghi at the Forum on Central Banking, was the main driver of the disappointing results for the month.

Trend-following strategies, which at this point held net long positions in the fixed-income sector, incurred broad losses, most notably in Europe. Unfortunately, macro and other non- trend models, which are normally less correlated to trend, also became broadly aligned with trend-following and lost money during the late-month reversal. Losses were only marginally mitigated by short-term strategies, which were quickest to react to the shift and ended up moderately profitable.

Three broad themes contributed to the month’s (and hence the quarter’s) poor results.

| 1. | Trend Reversals: While fixed-income markets reversed in the wake of Draghi’s comments, the reversals extended to other sectors as well, notably commodities (energies and grains) and currencies. As an example, Sugar fell 26% in Q2 through June 26th, before rallying nearly 8% in the last four trading days. |

| 2. | Volatility Expansion: Market volatility had been extremely compressed in 2017 until the last days of June. As of June 26th, realized volatility (63-day trailing) for more than 30 traded markets was in the bottom decile of its historical distribution, and below the average for many others. CTAs typically use realized volatility as an input to forecast market volatility. In June, this resulted in volatility forecasts that were severely |

| 47 Hulfish Street, Suite 510, Princeton, NJ 08542 • T 609.430.0404 • F 609.454.5010 • www.equinoxfunds.com |

understated. Forward-looking implied volatility measures also did not anticipate the spike in volatility. As one example of several: historical volatility estimates indicate that the 4-day sell-off in Bunds was a 4-sigma event (one that should occur roughly once in about 100,000 observations).

| 3. | Correlation breakdown: There was a marked shift in the correlation structure between equities and fixed-income, particularly in Europe. For example, the daily correlation (63- day rolling) between the DAX Index and the Bund had been negative and declining for the entire second quarter, before reversing and rising sharply at the end of June. Thus, anticipated risk mitigation from long positions in both markets/sectors did not materialize, as both sold off concurrently. Global stocks and bonds experienced similar, albeit less extreme, shifts in correlation. |

MARKET COMMENTARY AND OUTLOOK

The major drivers of the Fund’s negative performance have already been discussed. After three good years, bonds have started showing signs of stress, as the Fed starts to downsize its balance sheet, and rate hikes loom on the horizon. Global equity markets, however, continue their upward march, and we are now in the ninth year of the bull run, with most global indices at or near all-time highs. Energy prices have been volatile, and may continue to do so, especially given the specter of Trump’s reneging on the Iran deal.

The VIX® Index, known to investors as the “fear index,” has remained in an extremely narrow range since January 2017. After recording only 9 readings below 10% in the 27 years since its inception (in 1990), the Index proceeded to record 24 readings below 10% during the first nine months of 2017. Noted academic and industry pundits began to question the value of the VIX® as a predictor of market uncertainty; one academic called the low levels of the VIX® “the biggest financial mystery of our time.” Many people are now deriding the VIX® as “a fake fear index,” and contending that it is time to switch to other more useful indicators.

The rationale for these types of statements is that there is still rampant uncertainty in the markets. In the US, it centers mainly on Trump’s healthcare, fiscal, and tax policies, and the escalating Russia scandal and its potential outcome(s). In addition, US-North Korea tensions have added a new dimension to previously existing geopolitical stresses. Surprisingly, equity markets have continued to rally but not without an occasional case of the jitters. The Fed itself has remarked that equity prices are “quite high relative to standard valuation measures.” The widely followed Cyclically Adjusted Price-to-earnings (CAPE) Ratio stands at a historical high of almost 31.0, according to creator Nobel laureate Robert Shiller, who has commented that the U.S. stock market “hasn’t been this overvalued except a couple of times around 1929 (the Great Depression) and around 2000.” We are well above the 2007 valuations right before the global financial crisis; still, to be fair, Shiller has also expressed his belief the market could still have room to run. Meanwhile, other market professionals have expressed concerns about increases in the level and volatility of interest rates.

| 47 Hulfish Street, Suite 510, Princeton, NJ 08542 • T 609.430.0404 • F 609.454.5010 • www.equinoxfunds.com |

We are a little leery of beginning to sound like a “broken record” in repeating that we believe there is still a lot of latent uncertainty in the markets. In the US, concerns about the Trump administration and the potential outcome of multiple investigations into Russia-related financial and electoral scandals continue, as do the geopolitical stresses in Europe and the Middle East. Climate change continues to rear its ugly head, this year in the form of an unprecedented hurricane season. Surprisingly, equity markets continue to scale new heights while raising the question: how much longer? Opinions about the Fed’s policy on interest rates and its impact still seem likely to evolve over time, depending on the strength of the economy and evidence of inflation.

Investors should bear in mind that Commodity Trading Advisor (CTA) programs have historically offered useful diversification benefits, with the potential for attractive risk-adjusted returns over the long run. In fact, managed futures have historically tended to perform well in a wide variety of market conditions, perhaps particularly so during periods of equity market turbulence and volatility expansion. We continue to believe that a significant and strategic allocation to the asset class, while not a “hedge” for equities, nonetheless has the potential to serve investors well in the long run.

Although the Fund has been in operation for a short period of time, the Campbell Program itself has a track record dating back to 1998. It has historically offered useful diversification benefits, along with what we view as attractive risk-adjusted long-term returns over multiple market cycles. In our opinion, the Fund and the managed futures asset class should continue to offer these potential benefits in a market environment that is still challenging and a geopolitical outlook that remains fraught with uncertainty. In fact, managed futures, although not a hedge for equities in the true sense of the word, have historically displayed the ability to earn what has been termed as “crisis alpha:” positive returns during periods when equity markets have collapsed and volatility has increased.

Difficult market conditions, the prevailing climate of economic and geopolitical uncertainty, and the unpredictable nature of financial markets all pose challenges for investors. The Campbell program is, we believe, positioned to potentially perform well under these conditions. As always, we encourage investors to focus on holding a portfolio that blends traditional assets with a strategic and meaningful allocation to alternative assets, appropriate for their long-term goals. A well-balanced portfolio may display lower volatility, while also affording opportunities for potential long-term growth. We believe that the managed futures asset class should play an important role in such a portfolio.

Thank you for investing in the Equinox Campbell Strategy Fund.

| 47 Hulfish Street, Suite 510, Princeton, NJ 08542 • T 609.430.0404 • F 609.454.5010 • www.equinoxfunds.com |

DEFINITIONS OF TERMS AND INDICES

Alpha is a measure of performance on a risk-adjusted basis. Alpha takes the volatility (price risk) of a fund and compares its risk-adjusted performance to a benchmark index. The excess return of the fund relative to the return of the benchmark index is a fund’s alpha.

A Bund is a debt security issued by Germany’s federal government, and it is the German equivalent of a U.S. Treasury Bond.

Carry Trade is a strategy in which traders borrow a currency that has a low interest rate and use the funds to buy a different currency that is paying a higher interest rate.

A Commodity Trading Advisor (“CTA”) is a trader who may invest in more than 150 global futures markets. They seek to generate profit in both bull or bear markets, due to their ability to go long (buy) futures positions, in anticipation of rising markets, or go short (sell) futures positions, in anticipation of falling markets.

Crisis Alpha refers to the fact that some strategies earn superior risk-adjusted returns during crises.

The Cyclically Adjusted Price-to-Earnings Ratio is a valuation measure usually applied to the US S&P 500 equity market. It is defined as price divided by the average of ten years of earnings, adjusted for inflation.

DAX Index is a stock index that represents 30 of the largest and most liquid German companies that trade on the Frankfurt Exchange.

Forex (FX) is the market in which currencies are traded. The Forex market is the largest, most liquid market in the world.

Gilts are bonds that are issued by the British government, and they are generally considered low-risk investments.

J.P. Morgan (JPM) Global Aggregate Bond Index is a comprehensive global investment grade benchmark.

J.P.M. Bond Index covers a variety of asset classes ranging from flagship coverage of emerging.

Long Position refers to the buying of a security such as a stock, commodity or currency, with the expectation that the asset will rise in value.

Mean-Reversion is the theory suggesting that prices and returns eventually move back toward the mean or average.

MSCI World Index is the MSCI World is a market cap weighted stock market index of 1,652 ‘world’ stocks

Reformulated Gasoline Blendstock for Oxygen Blending (RBOB) is the term given to unleaded gas futures.

S&P 500® Index is an American stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ

Short Position is a position whereby an investor sells borrowed securities in anticipation of a price decline and is required to return an equal number of shares at some point in the future.

Trend-Following is an investment strategy based on the technical analysis of market prices, rather than on the fundamental strengths of the companies.

US Dollar Index is a measure of the value of the US dollar relative to the value of a basket of currencies

| 47 Hulfish Street, Suite 510, Princeton, NJ 08542 • T 609.430.0404 • F 609.454.5010 • www.equinoxfunds.com |

of the majority of the US’s most significant trading partners.

The VIX® Index (VIX) is a forward-looking measure of equity market volatility. Since its introduction, the VIX is considered by many to be the world’s premier barometer of investor sentiment and market volatility.

Investors cannot directly invest in an index and unmanaged index returns do not reflect any fees, expenses or sales charges.

5846-NLD-11/07/2017

| 47 Hulfish Street, Suite 510, Princeton, NJ 08542 • T 609.430.0404 • F 609.454.5010 • www.equinoxfunds.com |

| Equinox Campbell Strategy Fund |

| PORTFOLIO REVIEW (Unaudited) |

| September 30, 2017 |

| |

The Fund’s performance figures* for the periods ended September 30, 2017, as compared to its benchmarks:

| | | | | Annualized |

| | | | | | | Since Inception | | Since Inception |

| | | One Year | | Three Year | | (03/08/2013)** | | (02/11/2014)+ |

| Equinox Campbell Strategy Fund | | | | | | | | |

| Class A with Load | | (12.93)% | | (4.72)% | | (1.07)% | | N/A |

| Class A | | (7.60)% | | (2.83)% | | 0.22% | | N/A |

| Class C | | (8.32)% | | (3.50)% | | N/A | | 0.68% |

| Class I | | (7.45)% | | (2.56)% | | 0.48% | | N/A |

| Class P | | (7.36)% | | (2.56)% | | 0.48% | | N/A |

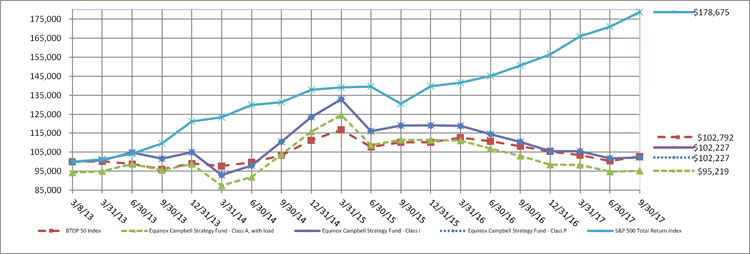

| S&P 500 Total Return Index ^ | | 18.61% | | 10.81% | | 13.56% | | 11.69% |

| BTOP 50 Index *** | | (4.95)% | | (0.18)% | | 0.61% | | 1.30% |

| | | | | | | | | |

| * | The performance data quoted is historical. The performance comparison includes reinvestment of all dividends and capital gains and has been adjusted for Class A maximum applicable sales charge of 5.75%. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on portfolio distributions or on the redemptions of portfolio shares. Performance figures for periods greater than one year are annualized. The returns would have been lower had the Advisor not waived its fees or reimbursed a portion of the Fund’s expenses. Per the fee table in the Fund’s prospectus dated February 1, 2017, the Fund’s “Total Annual Fund Operating Expenses” are 1.25%, 2.00%, 1.00% and 1.00% and the Fund’s “Total Annual Fund Operating Expenses (after Fee Waiver and/or Expense Reimbursement)” are 1.17%, 1.92%, 0.92% and 0.92% for Class A, Class C, Class I, and Class P shares, respectively, of the Fund’s average daily net assets. These expenses may differ from the actual expenses incurred by the Fund for the period covered by this report. Additional information regarding the Fund’s expense ratios is available in the Financial Highlights. For performance information current to the most recent month-end please call 1-888-643-3431. |

| ** | Commencement of operations was March 4, 2013. Start of performance is March 8, 2013. |

| + | Commencement of operations was February 11, 2014. |

| ^ | The S&P 500 Total Return Index is a widely accepted, unmanaged index of U.S. stock market performance which does not take into account charges, fees and other expenses. Investors cannot invest directly in an index. |

| *** | The Barclay BTOP50 Index (“BTOP50 Index”) seeks to replicate the overall composition of the managed futures industry with regard to trading style and overall market exposure. The BTOP50 Index employs a top-down approach in selecting its constituents. The largest investable trading advisor programs, as measured by assets under management, are selected for inclusion in the BTOP50 Index. In each calendar year the selected trading advisors represent, in aggregate, no less than 50% of the investable assets of the Barclay CTA Universe. For 2017, there are 20 funds in the BTOP50 Index. Investors cannot invest directly in an index. |

Comparison of the Change in Value of a $100,000 Investment

| Holdings by Asset Class | | % of Net Assets | |

| U.S. Treasury Notes | | | 64.8 | % |

| Short-Term Investments | | | 35.3 | % |

| Other Assets Less Liabilities | | | (0.1 | )% |

| | | | 100.0 | % |

| | | | | |

Please refer to the Consolidated Portfolio of Investments in this annual report for a detail of the Fund’s holdings. The value of the Fund’s derivative positions that provide exposure to a managed futures program is included in “other assets less liabilities;” however, the portfolio composition detailed above does not include derivatives exposure. See the accompanying notes for more information on the impact of the Fund’s derivative positions on the consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED PORTFOLIO OF INVESTMENTS |

| September 30, 2017 |

| Principal Amount | | | | | Coupon Rate % | | Maturity Date | | Fair Value | |

| | | | | U.S. TREASURY NOTES - 64.8% | | | | | | | | |

| $ | 100,000,000 | | | United States Treasury Note | | 0.7500 | | 10/31/2017 | | $ | 99,977,500 | |

| | 40,000,000 | | | United States Treasury Note | | 0.8750 | | 1/15/2018 | | | 39,968,471 | |

| | 100,000,000 | | | United States Treasury Note | | 1.0000 | | 3/15/2018 | | | 99,910,529 | |

| | | | | TOTAL U.S. TREASURY NOTES (Cost $239,970,085) | | | 239,856,500 | |

| | | | | | | | | |

| Shares | | | | | | | | | | | |

| | | | | SHORT-TERM INVESTMENTS - 35.3% | | | | |

| | | | | MONEY MARKET FUNDS - 35.3% | | | | |

| | 63,232,060 | | | Goldman Sachs Funds PLC - US$ Liquid Reserves Fund - Administration Share Class, 0.94%* + | | | 63,232,060 | |

| | 67,225,533 | | | JPMorgan Liquidity Funds - US Dollar Liquidity Fund - Premier Share Class, 1.20%* + | | | 67,225,533 | |

| | | | | TOTAL SHORT-TERM INVESTMENTS (Cost - $130,457,593) | | | 130,457,593 | |

| | | | | | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 100.1% (Cost $370,427,678) | | $ | 370,314,093 | |

| | | | | OTHER ASSETS LESS LIABILITIES - NET - (0.1)% | | | (450,748 | ) |

| | | | | TOTAL NET ASSETS - 100.0% | | $ | 369,863,345 | |

| | | | | | | | | | | | | |

| * | Pledged as collateral for swap contract. |

| + | All or a portion of this investment is a holding of Equinox Campbell Strategy Fund Limited. |

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED PORTFOLIO OF INVESTMENTS (Continued) |

| September 30, 2017 |

| Notional Value at | | | | | | | | | Variable Rate | | | | | Unrealized |

| September 30, 2017 | | | Description | | Counterparty | | Fixed Rate Paid | | Received | | Maturity Date | | | Depreciation |

| $ | 440,781,000 | | | | | Campbell Systematic

Trading Program | | Deutsche Bank | | 0.35% of the

notional value | | Total returns of

the Campbell

Systematic Trading

Program | | | 3/7/2018 | | | $(86,280,900) |

| Total Return Swap Top 50 Holdings ^ |

| |

| FUTURES CONTRACTS |

| Short Contracts | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | Unrealized | |

| | | | | | | | | Notional Value at | | | Appreciation/ | |

| Number of Contracts | | Description | | Counterparty | | Expiration Date | | | September 30, 2017 | | | | (Depreciation) | |

| 196 | | 2 Year Euro-Schatz Future | | Deutsche Bank | | Dec-17 | | $ | 25,960,654 | | | $ | 4,141 | |

| 467 | | 2 Year U.S. Treasury Notes Future | | Deutsche Bank | | Dec-17 | | | 100,721,423 | | | | 29,328 | |

| 1,153 | | 3 Month Sterling | | Deutsche Bank | | Dec-18 | | | 191,579,609 | | | | 105,242 | |

| 1,706 | | 3 Year Australian Treasury Bond Future | | Deutsche Bank | | Dec-17 | | | 402,627,641 | | | | 325,868 | |

| 640 | | 5 Year U.S. Treasury Notes Future | | Deutsche Bank | | Dec-17 | | | 75,205,191 | | | | 121,269 | |

| 29 | | 10 Year Australian Treasury Bond Future | | Deutsche Bank | | Dec-17 | | | 22,042,024 | | | | (1,599 | ) |

| 424 | | 10 Year Canadian Govt Bond Future | | Deutsche Bank | | Dec-17 | | | 46,036,120 | | | | 441,101 | |

| 828 | | 10 Year U.S. Treasury Notes Future | | Deutsche Bank | | Dec-17 | | | 103,796,098 | | | | 642,739 | |

| 527 | | 90 Day Bank Accepted Bill Future | | Deutsche Bank | | Mar-18 | | | 99,062,220 | | | | (29,122 | ) |

| 146 | | Copper Grade A Future | | Deutsche Bank | | Dec-17 | | | 23,833,697 | | | | 109,271 | |

| 1,834 | | Eurodollar | | Deutsche Bank | | Dec-18 | | | 449,830,491 | | | | 231,672 | |

| 592 | | Henry Hub Natural Gas Future | | Deutsche Bank | | Oct-17 | | | 17,864,814 | | | | 72,969 | |

| 171 | | Long Gilt Future | | Deutsche Bank | | Dec-17 | | | 28,408,921 | | | | 1,836 | |

| 433 | | Primary High Grade Aluminium Future | | Deutsche Bank | | Dec-17 | | | 23,037,651 | | | | (82,161 | ) |

| 502 | | Three Month Canadian Bankers Acceptance Future | | Deutsche Bank | | Dec-17 | | | 98,777,814 | | | | (132,578 | ) |

| | | | | | | | | | | | | | | |

| Long Contracts |

| 334 | | 10 Year Australian Treasury Bond Future | | Deutsche Bank | | Dec-17 | | | 253,863,314 | | | | (433,744 | ) |

| 108 | | 10 Year Japanese Goverment Bond Future | | Deutsche Bank | | Dec-17 | | | 144,128,252 | | | | (908,968 | ) |

| 735 | | 3 Month Euro (EURIBOR) | | Deutsche Bank | | Dec-18 | | | 217,486,747 | | | | (11,089 | ) |

| 214 | | AEX Index Future | | Deutsche Bank | | Oct-17 | | | 27,102,356 | | | | 473,889 | |

| 342 | | CAC 40 | | Deutsche Bank | | Oct-17 | | | 21,449,514 | | | | 431,312 | |

| 301 | | CME E-Mini Russell 2000 Index | | Deutsche Bank | | Dec-17 | | | 22,466,742 | | | | 1,164,737 | |

| 254 | | Copper Grade A Future | | Deutsche Bank | | Dec-17 | | | 41,464,103 | | | | (1,514,554 | ) |

| 48 | | DAX Index Future | | Deutsche Bank | | Dec-17 | | | 18,118,314 | | | | 354,564 | |

| 510 | | E-Mini Dow | | Deutsche Bank | | Dec-17 | | | 56,898,463 | | | | 1,149,338 | |

| 302 | | E-Mini S&P 500 | | Deutsche Bank | | Dec-17 | | | 37,917,438 | | | | 516,319 | |

| 139 | | E-Mini S&P MidCap 400 | | Deutsche Bank | | Dec-17 | | | 24,991,177 | | | | 850,586 | |

| 584 | | EURO STOXX 50 Index Future | | Deutsche Bank | | Dec-17 | | | 24,655,007 | | | | 476,807 | |

| 930 | | Euro-BOBL Future | | Deutsche Bank | | Dec-17 | | | 144,108,070 | | | | (308,486 | ) |

| 758 | | Euro-BUND Future | | Deutsche Bank | | Dec-17 | | | 144,182,890 | | | | (899,229 | ) |

| 313 | | Euro-OAT Futures | | Deutsche Bank | | Dec-17 | | | 57,366,960 | | | | (268,582 | ) |

| 776 | | MSCI Taiwan Index Future | | Deutsche Bank | | Oct-17 | | | 29,914,681 | | | | 47,040 | |

| 221 | | Nikkei 225 Future | | Deutsche Bank | | Dec-17 | | | 39,921,560 | | | | 1,084,205 | |

| 588 | | Primary High Grade Aluminium Future | | Deutsche Bank | | Dec-17 | | | 31,284,385 | | | | 470,532 | |

| 146 | | S&P Canada 60 Index Future | | Deutsche Bank | | Dec-17 | | | 21,508,337 | | | | 335,595 | |

| 1,033 | | S&P CNX Nifty Index Future | | Deutsche Bank | | Oct-17 | | | 20,328,218 | | | | (104,452 | ) |

| 234 | | TOPIX Future | | Deutsche Bank | | Dec-17 | | | 34,812,939 | | | | 1,007,694 | |

| | | | | | | | | | | | | | | |

| + | This investment is a holding of Equinox Campbell Strategy Fund Limited. |

| ^ | This investment is a not a direct holding of Equinox Campbell Strategy Fund Limited. The top 50 holdings were determined based on the absolute notional values of the positions within the underlying swap basket. |

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED PORTFOLIO OF INVESTMENTS (Continued) |

| September 30, 2017 |

| Total Return Swap Top 50 Holdings ^ | |

| | |

| FORWARD FOREIGN CURRENCY CONTRACTS |

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | Unrealized | |

| | | | | | Currency to | | | | | | Foreign Currency | | | | | Appreciation/ | |

| Settlement Date | | | Counterparty | | Deliver/Receive | | Value | | In Exchange For | | Value | | U.S. Dollar Value | | | (Depreciation) | |

| | 12/20/2017 | | | Deutsche Bank | | CAD | | 81,328,578 | | USD | | 65,580,284 | | | 65,123,686 | | | $ | (456,598 | ) |

| | 12/20/2017 | | | Deutsche Bank | | CNH | | 154,659,263 | | USD | | 23,538,761 | | | 23,155,072 | | | | (383,689 | ) |

| | 12/20/2017 | | | Deutsche Bank | | HUF | | 7,282,081,919 | | USD | | 28,492,748 | | | 27,793,259 | | | | (699,489 | ) |

| | 12/20/2017 | | | Deutsche Bank | | ILS | | 93,200,451 | | USD | | 26,275,480 | | | 26,464,388 | | | | 188,907 | |

| | 12/20/2017 | | | Deutsche Bank | | INO | | 1,228,676,370 | | USD | | 18,963,954 | | | 18,645,704 | | | | (318,250 | ) |

| | 12/20/2017 | | | Deutsche Bank | | MXN | | 480,173,524 | | USD | | 26,437,276 | | | 26,085,654 | | | | (351,622 | ) |

| | 12/20/2017 | | | Deutsche Bank | | NOK | | 496,069,337 | | USD | | 63,886,192 | | | 62,388,981 | | | | (1,497,211 | ) |

| | 12/20/2017 | | | Deutsche Bank | | PLN | | 74,530,369 | | USD | | 20,942,828 | | | 20,452,250 | | | | (490,578 | ) |

| | 12/20/2017 | | | Deutsche Bank | | SEK | | 340,560,297 | | USD | | 42,998,468 | | | 41,948,086 | | | | (1,050,382 | ) |

| | 12/20/2017 | | | Deutsche Bank | | TRY | | 90,651,123 | | USD | | 25,583,423 | | | 24,894,656 | | | | (688,767 | ) |

| | 12/20/2017 | | | Deutsche Bank | | USD | | 64,863,575 | | AUD | | 81,578,512 | | | 82,524,824 | | | | (946,311 | ) |

| | 12/20/2017 | | | Deutsche Bank | | USD | | 81,341,568 | | EUR | | 67,882,120 | | | 68,670,983 | | | | (788,863 | ) |

| | 12/20/2017 | | | Deutsche Bank | | USD | | 26,714,191 | | NZD | | 37,140,217 | | | 37,076,270 | | | | 63,947 | |

| | 12/20/2017 | | | Deutsche Bank | | USD | | 43,343,092 | | GBP | | 33,141,271 | | | 31,920,971 | | | | 1,220,300 | |

| | | | | | | | | | | | | | | | | | | | | |

| ^ | This investment is a not a direct holding of Equinox Campbell Strategy Fund Limited. The top 50 holdings were determined based on the absolute notional values of the positions within the underlying swap basket. |

AUD - Austrailian Dollar

BRO - Brazilian Real

CAD - Canadian Dollar

EUR - Euro

GBP - Pound Sterling

INO - Indian Rupee

JPY - Japanese Yen

MXN - Mexican Peso

SGO - Singapore Dollar

USD - U.S. Dollar

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED STATEMENT OF ASSETS AND LIABILITIES |

| September 30, 2017 |

| ASSETS | | | | |

| Investment securities: | | | | |

| At cost | | $ | 370,427,678 | |

| At fair value | | $ | 370,314,093 | |

| Cash | | | 56,796,348 | |

| Receivable for swap | | | 29,283,802 | |

| Interest receivable | | | 432,242 | |

| Receivable for fund shares sold | | | 53,182 | |

| Prepaid expenses & other assets | | | 35,129 | |

| TOTAL ASSETS | | | 456,914,796 | |

| | | | | |

| LIABILITIES | | | | |

| Unrealized depreciation on swap contract | | | 86,280,900 | |

| Payable for fund shares redeemed | | | 229,442 | |

| Advisory fee payable | | | 355,959 | |

| Distribution (12b-1) fees payable | | | 24,881 | |

| Payable to related parties | | | 23,210 | |

| Accrued expenses and other liabilities | | | 137,059 | |

| TOTAL LIABILITIES | | | 87,051,451 | |

| NET ASSETS | | $ | 369,863,345 | |

| | | | | |

| Net Assets Consist Of: | | | | |

| Paid in capital | | $ | 514,030,971 | |

| Accumulated net investment loss | | | (86,824,188 | ) |

| Accumulated net realized gain from investments and swap contract | | | 29,051,047 | |

| Net unrealized depreciation on investments and swap contract | | | (86,394,485 | ) |

| NET ASSETS | | $ | 369,863,345 | |

| | | | | |

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED STATEMENT OF ASSETS AND LIABILITIES (Continued) |

| September 30, 2017 |

| Net Asset Value Per Share: | | | | |

| Class A Shares: | | | | |

| Net Assets | | $ | 24,091,896 | |

| Shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | | | 2,573,758 | |

| Net asset value (Net Assets ÷ Shares Outstanding) and redemption price per share | | $ | 9.36 | |

| Maximum offering price per share (maximum sales charges of 5.75%) (a) | | $ | 9.93 | |

| | | | | |

| Class C Shares: | | | | |

| Net Assets | | $ | 22,792,443 | |

| Shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | | | 2,491,922 | |

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share (a) | | $ | 9.15 | |

| | | | | |

| Class I Shares: | | | | |

| Net Assets | | $ | 279,211,985 | |

| Shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | | | 29,575,048 | |

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share | | $ | 9.44 | |

| | | | | |

| Class P Shares: | | | | |

| Net Assets | | $ | 43,767,021 | |

| Shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | | | 4,636,046 | |

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share | | $ | 9.44 | |

| | | | | |

| (a) | A contingent deferred sales charge (“CDSC”) of 1.00% is assessed on certain redemptions of Class A shares made within 12 months after a purchase of Class A shares where no initial sales charge was paid at the time of purchase as part of an investment of $1,000,000 or more. A CDSC of 1.00% is assessed on redemptions of Class C shares made within one year after a purchase of such shares. |

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED STATEMENT OF OPERATIONS |

| For the Year Ended September 30, 2017 |

| INVESTMENT INCOME | | | | |

| Interest | | $ | 3,947,505 | |

| | | | | |

| EXPENSES | | | | |

| Investment advisory fees | | | 4,221,400 | |

| Distribution (12b-1) fees | | | | |

| Class A | | | 96,562 | |

| Class C | | | 336,594 | |

| Transfer agent fees | | | 500,200 | |

| Non 12b-1 sharesholder services fees | | | 117,098 | |

| Insurance expense | | | 233,198 | |

| Printing and postage expenses | | | 114,809 | |

| Administrative services fees | | | 206,427 | |

| Registration fees | | | 97,198 | |

| Legal fees | | | 249,592 | |

| Custodian fees | | | 49,701 | |

| Accounting services fees | | | 66,268 | |

| Audit and tax fees | | | 65,306 | |

| Compliance officer fees | | | 19,703 | |

| Trustees fees and expenses | | | 56,543 | |

| Other expenses | | | 379 | |

| TOTAL EXPENSES | | | 6,430,978 | |

| | | | | |

| Less: Fees waived by the Advisor | | | (947,515 | ) |

| | | | | |

| NET EXPENSES | | | 5,483,463 | |

| NET INVESTMENT LOSS | | | (1,535,958 | ) |

| | | | | |

| REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS | | | | |

| Net realized gain/(loss) on: | | | | |

| Investments | | | (194,068 | ) |

| Swap contract | | | 6,917,662 | |

| | | | 6,723,594 | |

| Net change in unrealized depreciation on: | | | | |

| Investments | | | (258,665 | ) |

| Swap contract | | | (62,323,546 | ) |

| | | | (62,582,211 | ) |

| | | | | |

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | | | (55,858,617 | ) |

| | | | | |

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | (57,394,575 | ) |

| | | | | |

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED STATEMENT OF CHANGES IN NET ASSETS |

| | | For the Year Ended | | | For the Year Ended | |

| | | September 30, | | | September 30, | |

| | | 2017 | | | 2016 | |

| FROM OPERATIONS | | | | | | | | |

| Net investment loss | | $ | (1,535,958 | ) | | $ | (7,676,325 | ) |

| Net realized gain on investments and swap contract | | | 6,723,594 | | | | 19,376,731 | |

| Net change in unrealized depreciation on investments and swap contract | | | (62,582,211 | ) | | | (98,396,934 | ) |

| Net decrease in net assets resulting from operations | | | (57,394,575 | ) | | | (86,696,528 | ) |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| From net investment income: | | | | | | | | |

| Class A | | | — | | | | (1,476,041 | ) |

| Class C | | | — | | | | (904,271 | ) |

| Class I | | | — | | | | (20,401,555 | ) |

| Class P | | | — | | | | (2,308,829 | ) |

| From distributions to shareholders | | | — | | | | (25,090,696 | ) |

| FROM SHARES OF BENEFICIAL INTEREST | | | | | | | | |

| Proceeds from shares sold: | | | | | | | | |

| Class A | | | 5,704,431 | | | | 27,276,547 | |

| Class C | | | 2,345,438 | | | | 19,152,099 | |

| Class I | | | 79,514,822 | | | | 306,992,752 | |

| Class P | | | 15,856,183 | | | | 38,923,617 | |

| Net asset value of shares issued in reinvestment of distributions: | | | | | | | | |

| Class A | | | — | | | | 1,386,845 | |

| Class C | | | — | | | | 880,201 | |

| Class I | | | — | | | | 2,890,148 | |

| Class P | | | — | | | | 2,230,239 | |

| Redemption fee proceeds: | | | | | | | | |

| Class A | | | — | | | | 4 | |

| Class C | | | — | | | | 3 | |

| Class I | | | — | | | | 50 | |

| Class P | | | — | | | | 6 | |

| Payments for shares redeemed: | | | | | | | | |

| Class A | | | (42,329,431 | ) | | | (39,682,974 | ) |

| Class C | | | (24,955,847 | ) | | | (18,518,884 | ) |

| Class I | | | (510,361,202 | ) | | | (452,313,473 | ) |

| Class P | | | (65,539,014 | ) | | | (38,210,616 | ) |

| Net decrease in net assets from shares of beneficial interest | | | (539,764,620 | ) | | | (148,993,436 | ) |

| | | | | | | | | |

| TOTAL DECREASE IN NET ASSETS | | | (597,159,195 | ) | | | (260,780,660 | ) |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

| Beginning of Period | | | 967,022,540 | | | | 1,227,803,200 | |

| End of Period* | | $ | 369,863,345 | | | $ | 967,022,540 | |

| * Includes accumulated net investment loss of: | | $ | (86,824,188 | ) | | $ | (92,142,708 | ) |

| | | | | | | | | |

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED STATEMENTS OF CHANGES IN NET ASSETS (Continued) |

| | | For the Year Ended | | | For the Year Ended | |

| | | September 30, | | | September 30, | |

| | | 2017 | | | 2016 | |

| | | | | | | |

| SHARE ACTIVITY | | | | | | | | |

| Class A: | | | | | | | | |

| Shares Sold | | | 590,750 | | | | 2,487,331 | |

| Shares Reinvested | | | — | | | | 125,734 | |

| Shares Redeemed | | | (4,384,329 | ) | | | (3,686,250 | ) |

| Net decrease in shares of beneficial interest outstanding | | | (3,793,579 | ) | | | (1,073,185 | ) |

| | | | | | | | | |

| Class C: | | | | | | | | |

| Shares Sold | | | 247,544 | | | | 1,768,365 | |

| Shares Reinvested | | | — | | | | 80,605 | |

| Shares Redeemed | | | (2,638,728 | ) | | | (1,769,690 | ) |

| Net increase/(decrease) in shares of beneficial interest outstanding | | | (2,391,184 | ) | | | 79,280 | |

| | | | | | | | | |

| Class I: | | | | | | | | |

| Shares Sold | | | 8,173,840 | | | | 28,062,871 | |

| Shares Reinvested | | | — | | | | 260,843 | |

| Shares Redeemed | | | (52,569,300 | ) | | | (42,045,767 | ) |

| Net decrease in shares of beneficial interest outstanding | | | (44,395,460 | ) | | | (13,722,053 | ) |

| | | | | | | | | |

| Class P: | | | | | | | | |

| Shares Sold | | | 1,631,107 | | | | 3,559,088 | |

| Shares Reinvested | | | — | | | | 201,467 | |

| Shares Redeemed | | | (6,767,806 | ) | | | (3,577,599 | ) |

| Net increase/(decrease) in shares of beneficial interest outstanding | | | (5,136,699 | ) | | | 182,956 | |

| | | | | | | | | |

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED FINANCIAL HIGHLIGHTS |

| |

| Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Period |

| | | Class A | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Period Ended | |

| | | September 30, | | | September 30, | | | September 30, | | | September 30, | | | September 30, | |

| | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 (1) | |

| Net asset value, beginning of period | | $ | 10.13 | | | $ | 11.17 | | | $ | 11.01 | | | $ | 10.14 | | | $ | 10.00 | |

| Activity from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss (2) | | | (0.04 | ) | | | (0.09 | ) | | | (0.13 | ) | | | (0.11 | ) | | | (0.07 | ) |

| Net realized and unrealized gain/(loss) on investments and swap contract | | | (0.73 | ) | | | (0.74 | ) | | | 0.97 | | | | 0.98 | (3) | | | 0.21 | (3) |

| Total from investment operations | | | (0.77 | ) | | | (0.83 | ) | | | 0.84 | | | | 0.87 | | | | 0.14 | |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | — | | | | (0.21 | ) | | | (0.68 | ) | | | — | | | | — | |

| Net asset value, end of period | | $ | 9.36 | | | $ | 10.13 | | | $ | 11.17 | | | $ | 11.01 | | | $ | 10.14 | |

| Total return (4) | | | (7.60 | )% | | | (7.60 | )% | | | 7.48 | % | | | 8.58 | % | | | 1.40 | % |

| Net assets, at end of period (000’s) | | $ | 24,092 | | | $ | 64,528 | | | $ | 83,077 | | | $ | 34,976 | | | $ | 14,427 | |

| Ratio of net expenses to average net assets including interest expense (6)(10)(11) | | | 1.15 | % | | | 1.17 | % | | | 1.15 | % | | | 1.15 | % (8) | | | 1.18 | % (7)(8) |

| Ratio of net investment loss to average net assets | | | (0.45 | )% | | | (0.83 | )% | | | (1.08 | )% | | | (1.10 | )% | | | (1.13 | )% (7)(9) |

| Portfolio Turnover Rate | | | 0 | % | | | 0 | % | | | 0 | % | | | 0 | % | | | 871 | % (5) |

| | | | | | | | | | | | | | | | | | | | | |

| (1) | | The Equinox Campbell Strategy Fund Class A commenced operations on March 4, 2013. Start of Performance was March 8, 2013. |

| | | |

| (2) | | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| | | |

| (3) | | Realized and unrealized gains per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the period, and may not reconcile with the aggregate gains and losses in the statement of operations due to the timing of share transactions for the period. |

| | | |

| (4) | | Total returns are historical and assume changes in share price and reinvestment of dividends and distributions. Total returns for periods of less than one year are not annualized. Total returns shown exclude the effect of the maximum applicable sales charges of 5.75% and, if applicable, wire redemption fees. Had the Advisor not waived its fees or reimbursed a portion of the Fund’s expenses, the returns would have been lower. |

| | | |

| (5) | | Not annualized. |

| (6) | | Represents the ratio of expenses to average net assets net of fee waivers and/or expense reimbursements by the Advisor. Had these waivers not been in place, the expense ratio would have been: | | | 1.33 | % | | | 1.25 | % | | | 1.24 | % | | | 1.30 | % (8) | | | 2.07 | % (7)(8) |

| | | | | | | | | | | | | | | | | | | | | | | |

| (7) | | Annualized. | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| (8) | | Does not include the expenses of other investment companies in which the Fund invests, if any. | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| (9) | | Recognition of net investment income by the Fund is affected by the timing of the declaration of dividends by the underlying exchange traded funds in which the Fund invests. | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| (10) | | Ratio of gross expenses to average net assets excluding interest expense (6). | | | 1.33 | % | | | 1.23 | % | | | 1.24 | % | | | 1.30 | % (8) | | | 2.07 | % (7)(8) |

| | | | | | | | | | | | | | | | | | | | | | | |

| (11) | | Ratio of net expenses to average net assets excluding interest expense. | | | 1.15 | % | | | 1.15 | % | | | 1.15 | % | | | 1.15 | % (8) | | | 1.18 | % (7)(8) |

| | | | | | | | | | | | | | | | | | | | | | | |

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED FINANCIAL HIGHLIGHTS |

| |

| Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Period |

| | | Class C | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Period Ended | |

| | | September 30, | | | September 30, | | | September 30, | | | September 30, | |

| | | 2017 | | | 2016 | | | 2015 | | | 2014 (1) | |

| Net asset value, beginning of period | | $ | 9.98 | | | $ | 11.03 | | | $ | 10.96 | | | $ | 9.61 | |

| Activity from investment operations: | | | | | | | | | | | | | | | | |

| Net investment loss (2) | | | (0.11 | ) | | | (0.17 | ) | | | (0.21 | ) | | | (0.12 | ) |

| Net realized and unrealized gain/(loss) on investments and swap contract | | | (0.72 | ) | | | (0.72 | ) | | | 0.97 | | | | 1.47 | |

| Total from investment operations | | | (0.83 | ) | | | (0.89 | ) | | | 0.76 | | | | 1.35 | |

| Less distributions from: | | | | | | | | | | | | | | | | |

| Net investment income | | | — | | | | (0.16 | ) | | | (0.69 | ) | | | — | |

| Net asset value, end of period | | $ | 9.15 | | | $ | 9.98 | | | $ | 11.03 | | | $ | 10.96 | |

| Total return (3) | | | (8.32 | )% | | | (8.16 | )% | | | 6.72 | % | | | 14.05 | % |

| Net assets, at end of period (000’s) | | $ | 22,792 | | | $ | 48,712 | | | $ | 52,977 | | | $ | 11,829 | |

| Ratio of net expenses to average net assets including interest expense (5)(8)(9) | | | 1.90 | % | | | 1.92 | % | | | 1.90 | % | | | 1.90 | % (6)(7) |

| Ratio of net investment loss to average net assets | | | (1.19 | )% | | | (1.58 | )% | | | (1.82 | )% | | | (1.84 | )% (6)(7) |

| Portfolio Turnover Rate | | | 0 | % | | | 0 | % | | | 0 | % | | | 0 | % (4) |

| | | | | | | | | | | | | | | | | |

| (1) | | The Equinox Campbell Strategy Fund Class C commenced operations on February 11, 2014. |

| | | |

| (2) | | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| | | |

| (3) | | Total returns are historical and assume changes in share price and reinvestment of dividends and distributions. Total returns for periods of less than one year are not annualized. Total returns shown exclude the effect of the maximum applicable sales charge and, if applicable, wire redemption fees. Had the Advisor not waived its fees or reimbursed a portion of the Fund’s expenses, the returns would have been |

| | | |

| (4) | | Not annualized. |

| (5) | | Represents the ratio of expenses to average net assets net of fee waivers and/or expense reimbursements by the Advisor. Had these waivers not been in place, the expense ratio would have been: | | | 2.08 | % | | | 2.00 | % | | | 1.99 | % | | | 2.17 | % (6)(7) |

| | | | | | | | | | | | | | | | | | | |

| (6) | | Annualized. | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| (7) | | Does not include the expenses of other investment companies in which the Fund invests, if any. | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| (8) | | Ratio of gross expenses to average net assets excluding interest expense (5). | | | 2.08 | % | | | 1.98 | % | | | 1.99 | % | | | 2.17 | % (6)(7) |

| | | | | | | | | | | | | | | | | | | |

| (9) | | Ratio of net expenses to average net assets excluding interest expense. | | | 1.90 | % | | | 1.90 | % | | | 1.90 | % | | | 1.90 | % (6)(7) |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED FINANCIAL HIGHLIGHTS |

| |

| Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Period |

| | | Class I | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Period Ended | |

| | | September 30, | | | September 30, | | | September 30, | | | September 30, | | | September 30, | |

| | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 (1) | |

| Net asset value, beginning of period | | $ | 10.20 | | | $ | 11.22 | | | $ | 11.05 | | | $ | 10.16 | | | $ | 10.00 | |

| Activity from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss (2) | | | (0.02 | ) | | | (0.06 | ) | | | (0.09 | ) | | | (0.08 | ) | | | (0.05 | ) |

| Net realized and unrealized gain/(loss) on investments and swap contract | | | (0.74 | ) | | | (0.73 | ) | | | 0.96 | | | | 0.97 | | | | 0.21 | (3) |

| Total from investment operations | | | (0.76 | ) | | | (0.79 | ) | | | 0.87 | | | | 0.89 | | | | 0.16 | |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | — | | | | (0.23 | ) | | | (0.70 | ) | | | — | | | | — | |

| Net asset value, end of period | | $ | 9.44 | | | $ | 10.20 | | | $ | 11.22 | | | $ | 11.05 | | | $ | 10.16 | |

| Total return (4) | | | (7.45 | )% | | | (7.20 | )% | | | 7.72 | % | | | 8.76 | % | | | 1.60 | % |

| Net assets, at end of period (000’s) | | $ | 279,212 | | | $ | 754,171 | | | $ | 984,152 | | | $ | 612,173 | | | $ | 295,031 | |

| Ratio of net expenses to average net assets including interest expense (6)(10)(11) | | | 0.90 | % | | | 0.92 | % | | | 0.90 | % | | | 0.90 | % (8) | | | 0.91 | % (7)(8) |

| Ratio of net investment loss to average net assets | | | (0.20 | )% | | | (0.58 | )% | | | (0.81 | )% | | | (0.85 | )% | | | (0.87 | )% (7)(9) |

| Portfolio Turnover Rate | | | 0 | % | | | 0 | % | | | 0 | % | | | 0 | % | | | 871 | % (5) |

| | | | | | | | | | | | | | | | | | | | | |

| (1) | | The Equinox Campbell Strategy Fund Class I commenced operations on March 4, 2013. Start of Performance was March 8, 2013. |

| | | |

| (2) | | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| | | |

| (3) | | Realized and unrealized gains per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the period, and may not reconcile with the aggregate gains and losses in the statement of operations due to the timing of share transactions for the period. |

| | | |

| (4) | | Total returns are historical and assume changes in share price and reinvestment of dividends and distributions. Total returns for periods of less than one year are not annualized. Total returns would be lower absent fee waivers. |

| | | |

| (5) | | Not annualized. |

| (6) | | Represents the ratio of expenses to average net assets net of fee waivers and/or expense reimbursements by the Advisor. Had these waivers not been in place, the expense ratio would have been: | | | 1.07 | % | | | 1.00 | % | | | 0.99 | % | | | 1.05 | % (8) | | | 1.58 | % (7)(8) |

| | | | | | | | | | | | | | | | | | | | | | | |

| (7) | | Annualized. | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| (8) | | Does not include the expenses of other investment companies in which the Fund invests, if any. | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| (9) | | Recognition of net investment income by the Fund is affected by the timing of the declaration of dividends by the underlying exchange traded funds in which the Fund invests. | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| (10) | | Ratio of gross expenses to average net assets excluding interest expense (6). | | | 1.07 | % | | | 0.98 | % | | | 0.99 | % | | | 1.05 | % (8) | | | 1.58 | % (7)(8) |

| | | | | | | | | | | | | | | | | | | | | | | |

| (11) | | Ratio of net expenses to average net assets excluding interest expense. | | | 0.90 | % | | | 0.90 | % | | | 0.90 | % | | | 0.90 | % (8) | | | 0.91 | % (7)(8) |

| | | | | | | | | | | | | | | | | | | | | | | |

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| CONSOLIDATED FINANCIAL HIGHLIGHTS |

| |

| Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Period |

| | | Class P | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Period Ended | |

| | | September 30, | | | September 30, | | | September 30, | | | September 30, | | | September 30, | |

| | | 2017 | | | 2016 | | | 2015 | | | 2014 | | | 2013 (1) | |

| Net asset value, beginning of period | | $ | 10.19 | | | $ | 11.22 | | | $ | 11.05 | | | $ | 10.16 | | | $ | 10.00 | |

| Activity from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss (2) | | | (0.02 | ) | | | (0.06 | ) | | | (0.13 | ) | | | (0.08 | ) | | | (0.05 | ) |

| Net realized and unrealized gain/(loss) on investments and swap contract | | | (0.73 | ) | | | (0.74 | ) | | | 1.00 | | | | 0.97 | | | | 0.21 | (3) |

| Total from investment operations | | | (0.75 | ) | | | (0.80 | ) | | | 0.87 | | | | 0.89 | | | | 0.16 | |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | — | | | | (0.23 | ) | | | (0.70 | ) | | | — | | | | — | |

| Net asset value, end of period | | $ | 9.44 | | | $ | 10.19 | | | $ | 11.22 | | | $ | 11.05 | | | $ | 10.16 | |

| Total return (4) | | | (7.36 | )% | | | (7.29 | )% | | | 7.72 | % | | | 8.76 | % | | | 1.60 | % |

| Net assets, at end of period (000’s) | | $ | 43,767 | | | $ | 99,612 | | | $ | 107,596 | | | $ | 37,153 | | | $ | 8,340 | |

| Ratio of net expenses to average net assets including interest expense (6)(10)(11) | | | 0.90 | % | | | 0.92 | % | | | 0.90 | % | | | 0.90 | % (9) | | | 0.92 | % (7)(8) |

| Ratio of net investment loss to average net assets | | | (0.19 | )% | | | (0.58 | )% | | | (1.09 | )% | | | (0.85 | )% | | | (0.87 | )% (7)(9) |

| Portfolio Turnover Rate | | | 0 | % | | | 0 | % | | | 0 | % | | | 0 | % | | | 871 | % (5) |

| | | | | | | | | | | | | | | | | | | | | |

| (1) | | The Equinox Campbell Strategy Fund Class P commenced operations on March 4, 2013. Start of Performance was March 8, 2013. |

| | | |

| (2) | | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| | | |

| (3) | | Realized and unrealized gains per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the period, and may not reconcile with the aggregate gains and losses in the statement of operations due to the timing of share transactions for the period. |

| | | |

| (4) | | Total returns are historical and assume changes in share price and reinvestment of dividends and distributions. Total returns for periods of less than one year are not annualized. Total returns would be lower absent fee waivers. |

| | | |

| (5) | | Not annualized. |

| (6) | | Represents the ratio of expenses to average net assets net of fee waivers and/or expense reimbursements by the Advisor. Had these waivers not bee in place, the expense ratio would have been: | | | 1.07 | % | | | 1.00 | % | | | 1.00 | % | | | 1.06 | % (8) | | | 1.97 | % (7)(8) |

| | | | | | | | | | | | | | | | | | | | | | | |

| (7) | | Annualized. | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| (8) | | Does not include the expenses of other investment companies in which the Fund invests, if any | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| (9) | | Recognition of net investment income by the Fund is affected by the timing of the declaration of dividends by the underlying exchange traded funds in which the Fund invests | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| (10) | | Ratio of gross expenses to average net assets excluding interest expense (6) | | | 1.07 | % | | | 0.98 | % | | | 1.00 | % | | | 1.06 | % (8) | | | 1.97 | % (7)(8) |

| | | | | | | | | | | | | | | | | | | | | | | |

| (11) | | Ratio of net expenses to average net assets excluding interest expense | | | 0.90 | % | | | 0.90 | % | | | 0.90 | % | | | 0.90 | % (8) | | | 0.92 | % (7)(8) |

| | | | | | | | | | | | | | | | | | | | | | | |

See accompanying notes to consolidated financial statements.

| Equinox Campbell Strategy Fund |

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| September 30, 2017 |

The Equinox Campbell Strategy Fund (the “Fund”) is a non-diversified series of shares of beneficial interest of Equinox Funds Trust (the “Trust”), a statutory trust organized under the laws of the State of Delaware on June 2 2010, and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Fund began operations on March 4, 2013. The Fund currently offers Class A, Class C, Class I, and Class P shares. Class A, Class I, and Class P shares commenced operations on March 4, 2013. Class C commenced operations on February 11, 2014. The investment objective of the Fund is to achieve long term capital appreciation.

Class C, Class I, and Class P shares are offered at net asset value. Class A shares are offered at net asset value plus a maximum sales charge of 5.75%. A contingent deferred sales charge (“CDSC”) of 1.00% is assessed on certain redemptions of Class A shares made within 12 months after a purchase of Class A shares where no initial sales charge was paid at the time of purchase as part of an investment of $1,000,000 or more. A CDSC of 1.00% is assessed on redemptions of Class C shares made within one year after a purchase of such shares. Each class represents an interest in the same assets of the Fund and classes are identical except for differences in their sales charge structures and ongoing service and distribution charges. All classes of shares have equal voting privileges except that each class has exclusive voting rights with respect to its service and/or distribution plans. The Fund’s income, expenses (other than class specific distribution fees) and realized and unrealized gains and losses are allocated proportionately each day based upon the relative net assets of each class.

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies followed by the Fund in preparation of its consolidated financial statements. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of the consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of income and expenses for the period. Actual results could differ from those estimates. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies” including FASB Accounting Standard Update ASU 2013-08.

Security Valuation – Securities, including exchange traded funds, listed on an exchange are valued at the last reported sale price at the close of the regular trading session of the exchange on the business day the value is being determined, or in the case of securities listed on NASDAQ at the NASDAQ Official Closing Price (“NOCP”). In the absence of a sale such securities shall be valued at the mean between the current bid and ask prices on the primary exchange on the day of valuation. Debt securities (other than short-term obligations) are valued each day by an independent pricing service approved by the Board of Trustees (the “Board”) using methods which include current market quotations from a major market maker in the securities and based on methods which include the consideration of yields or prices of securities of comparable quality, coupon, maturity and type. Short-

| Equinox Campbell Strategy Fund |

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued) |

| September 30, 2017 |

term debt obligations having 60 days or less remaining until maturity, at time of purchase, may be valued at amortized cost. Investments in open-end investment companies are valued at net asset value. Investments in swap contracts are reported at fair value based on daily price reporting from the swap counterparty.

The Fund may hold securities, such as private investments, interests in commodity pools, other non-traded securities or temporarily illiquid securities, for which market quotations are not readily available or are determined to be unreliable. These securities will be valued using the “fair value” procedures approved by the Board. The Board has delegated execution of these procedures to a fair value team composed of one or more representatives from each of the (i) Trust, (ii) administrator, and (iii) Advisor. The team may also enlist third party consultants such as a valuation specialist at a public accounting firm, valuation consultant or financial officer of a security issuer on an as-needed basis to assist in determining a security-specific fair value. The Board reviews and ratifies the execution of this process and the resultant fair value prices at least quarterly to assure the process produces reliable results.

Fair Valuation Process – As noted above, the fair value team is composed of one or more representatives from each of the (i) Trust, (ii) administrator, and (iii) Advisor. The applicable investments are valued collectively via inputs from each of these groups. For example, fair value determinations are required for the following securities: (i) securities for which market quotations are insufficient or not readily available on a particular business day (including securities for which there is a short and temporary lapse in the provision of a price by the regular pricing source), (ii) securities for which, in the judgment of the advisor, the prices or values available do not represent the fair value of the instrument. Factors which may cause the Advisor to make such a judgment include, but are not limited to, the following: only a bid price or an ask price is available; the spread between bid and ask prices is substantial; the frequency of sales; the thinness of the market; the size of reported trades; and actions of the securities markets, such as the suspension or limitation of trading; (iii) securities determined to be illiquid; (iv) securities with respect to which an event that will affect the value thereof has occurred (a “significant event”) since the closing prices were established on the principal exchange on which they are traded, but prior to a Fund’s calculation of its net asset value. Specifically, interests in commodity pools or managed futures pools are valued on a daily basis by reference to the closing market prices of each futures contract or other asset held by a pool, as adjusted for pool expenses. Restricted or illiquid securities, such as private investments or non-traded securities are valued via inputs from the Advisor based upon the current bid for the security from two or more independent dealers or other parties reasonably familiar with the facts and circumstances of the security (who should take into consideration all relevant factors as may be appropriate under the circumstances). If the Advisor is unable to obtain a current bid from such independent dealers or other independent parties, the fair value team shall determine the fair value of such security using the following factors: (i) the type of security; (ii) the cost at date of purchase; (iii) the size and nature of the Fund’s holdings; (iv) the discount from market value of unrestricted securities of the same class at the time of purchase and subsequent thereto; (v) information as to any transactions or offers with respect to the security; (vi) the nature and duration of restrictions on disposition of the security and the existence of any registration rights; (vii) how the yield of the security compares to similar securities of companies of similar or equal creditworthiness; (viii) the level of recent trades of similar or comparable securities;

| Equinox Campbell Strategy Fund |

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued) |

| September 30, 2017 |

(ix) the liquidity characteristics of the security; (x) current market conditions; and (xi) the market value of any securities into which the security is convertible or exchangeable.

The Fund utilizes various methods to measure the fair value of all of their investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Fund has the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument in an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

| Equinox Campbell Strategy Fund |

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued) |

| September 30, 2017 |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following tables summarize the inputs used as of September 30, 2017 for the Fund’s assets and liabilities measured at fair value:

| Assets | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |