UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22468

Ashmore Funds

(Exact name of registrant as specified in charter)

c/o Ashmore Investment Advisors Limited

61 Aldwych

London WC2B 4AE

England

(Address of principal executive offices) (Zip code)

Corporation Service Company

84 State Street

Boston, MA 20109

(Name and address of agent for service)

Registrant’s telephone number, including area code: 011-44-20-3077-6000

Date of fiscal year end: October 31

Date of reporting period: October 31, 2014

Item 1. Reports to Stockholders.

2

ASHMORE FUNDS

ANNUAL FINANCIAL STATEMENTS

October 31, 2014

ASHMORE FUNDS

TABLE OF CONTENTS

ASHMORE FUNDS

TABLE OF CONTENTS

This material is authorized for use only when preceded or accompanied by the current Ashmore Funds prospectuses. Investors should consider the investment objectives, principal risks, charges and expenses of these Funds carefully before investing. This and other information is contained in the Funds’ prospectus. Please read the prospectus carefully before you invest or send money.

A Fund’s past performance is not necessarily an indication of how the Fund will perform in the future.

An investment in a Fund is not a deposit of a bank and is not guaranteed or insured by the Federal Deposit Insurance Corporation or any other government agency. It is possible to lose money on investments in the Funds.

ASHMORE FUNDS

INVESTMENT MANAGER’S REPORT

For the period November 1, 2013 to October 31, 2014

Overview

The year to October 31, 2014 saw significant volatility across the different investment themes, but for many Emerging Market (“EM”) economies, it also saw improvements to fundamental positions which were already attractive relative to developed markets (strong economic growth, significant external foreign exchange balances and low levels of corporate debt).

In the final months of 2013, EM US dollar fixed income markets outperformed local currency markets, as currency depreciation in countries with larger current account deficits imposed pressure. Local currencies underperformed with significant dispersion between countries.

In the first quarter of 2014, the situation in Crimea brought volatility to Russia, Ukraine and other countries in the region; while fractious politics in Turkey and Thailand contaminated the overall mood in EM during the first weeks of January. Despite the increased geopolitical and political risk, EM assets performed well as the central banks of Turkey, Brazil, India and South Africa raised interest rates in order to control local inflation in the wake of strong foreign currency exchange (“FX”) depreciation experienced in recent years. This change in monetary policy was decisive in reducing FX volatility, which in combination with compelling levels of real interest rates, pushed investors to cover their short EM FX positions leading to a rebound in local currencies and local currency bonds.

The second quarter of 2014 yielded strong performance across nearly all EM asset classes with both equities and fixed income outperforming their developed world peers. Solid equity performance is frequently associated with a sell-off of fixed income assets; however, the effects of a weaker than expected economic recovery in most of the world and accommodative policy makers meant that fixed income assets also performed well. Within EM fixed income markets, high yield bonds outperformed investment grade issues across all asset classes. Over the quarter, the MSCI EM index rose 5.6% with the MSCI Frontier Markets index up 10.5%.

EM performance was supported by ample global liquidity and the stabilisation of political risks: In India the Bharatiya Janata Party (“BJP”) led by Narendra Modi won parliamentary elections by a landslide, delivering a strong mandate for Modi to enact his mantra of “less government, more governance”. In Ukraine, Petro Poroshenko won the May 25 presidential election with a clear majority in the first round. In China, targeted easing measures aided exports and supported a recovery in the wider Chinese economy. Furthermore, the World Bank International Comparison Project (“ICP”) revealed that the Chinese economy would surpass the United States in 2014 on a Purchasing Power Parity (“PPP”) basis.

The final quarter of the fiscal year saw growing divergence in economic conditions between the United States and the rest of the world, particularly the Eurozone. On the one hand, investors braced themselves for a scenario whereby the Federal Open Market Committee (“FOMC”) would start to hike interest rates in Q2/Q3 2015, causing volatility across all asset classes and particularly currencies. In contrast, declining inflation expectations in the Eurozone, the slowdown in economic activity in the core economies, and lower confidence due to concerns over the contagion from a weaker Russian economy in Europe, led the European Central Bank (“ECB”) to ease more than expected at its August meeting, where it cut rates by 10 basis points (“bps”), bringing the refinancing and deposit rates down to 0.05% and -0.20% respectively.

In EM fixed income, local currencies suffered from a strong US dollar and weak commodity prices. The difference in performance over the quarter between the JP Morgan GBI-EM Global Diversified index (which declined 5.7%) and the US dollar hedged version of the index (which only declined by 0.7%) serve to illustrate the extent to which underperformance was driven by FX. In fact, EM local interest rates only rose by a modest 20 bps. Within the US dollar space, corporate debt outperformed both EM sovereign debt and its developed market peers, with the JP Morgan CEMBI Broad Diversified index down 0.1% and the JP Morgan EMBI Global Diversified index down 0.6%. In October, EM fixed income performed well despite general market volatility. Investment Grade (“IG”) outperformed High Yield (“HY”) once more, largely driven by US Treasury yields. The strong decline of the Ruble (“RUB”) dragged the JP Morgan ELMI+ index down 0.5% during the final month of the period.

3

ASHMORE FUNDS

INVESTMENT MANAGER’S REPORT (CONTINUED)

Portfolio Overviews

Ashmore Emerging Markets Corporate Debt Fund

The Ashmore Emerging Markets Corporate Debt Fund (“the Fund”) seeks to achieve its objective by investing principally in the debt instruments of EM corporate issuers, which may be denominated in any currency, including the local currency of the issuer. EM corporates operate in an environment that typically consists of higher growth and maturing capital markets. In many cases, EM corporates are characterised by new and growing businesses in industries such as mobile communications, technology and food production. We expect these industries to benefit from the developing economies in which they operate. Increased “south/south” trade (i.e., trade between EM countries as opposed to trade with developed markets) has resulted in a material structural change for EM corporates and has helped them to broaden their customer bases. We continue to focus efforts on companies that are less followed by the market, which potentially allows us to add maximum value based on our views, research and global EM network capabilities.

Over the period, the Fund’s Institutional Class underperformed its benchmark. Despite the Fund’s recent underperformance, EM corporate credit remains in positive territory with the JP Morgan CEMBI BD index showing positive returns of 6.92% for the year and IG outperforming HY. The recent outperformance of IG credits is strongly linked to a marked flattening of the US Treasury yield curve, which has supported long dated IG bonds. In October, the 2 year Treasury yields tightened 8 bps while the 5 year and 10 year yields both tightened 15 bps. A number of idiosyncratic credit developments, mostly in the HY space, also contributed to the underperformance of EM HY credits. The Fund’s top contributors for the period were positions in India, Jamaica and China. Positions in Ukraine, Russia and South Africa were the largest detractors from performance.

At October 31, 2014, total EM corporate debt issuance year to date stood at just shy of US $300bn, putting 2014 on track for another record year. October itself saw new issuance continue to grow with over US $31bn printed during the month. Whilst positive, to put this in perspective it represents a 23% decrease compared to October 2013, mainly due to Europe which has lagged historical highs due to the political situation in Ukraine. Issuance in October came predominantly from Asia (64%) and Latin America (27%), with 62% of the US $31.7bn of new issuance coming from IG credits and 38% from HY.

A key trend during the period was the underperformance of EM corporates vs. US corporates. In 2014, EM outperformed the US in the IG space, but underperformed the US in the HY space. At the fiscal year end, EM HY corporates were trading at 240 bps above US HY credit, a widening of 42 bps compared to September, while EM IG corporates were trading at 90 bps above US IG, a tightening of 2 bps compared to September. There continues to be impressive spread pick-up (of 90%) in EM and we believe the yield differential remains attractive from a historical perspective. We believe that spread pick-up and attractive credit fundamentals in EM will be an important driver of EM credit inflows for the remainder of 2014.

Ashmore Emerging Markets Local Currency Bond Fund

The Ashmore Emerging Markets Local Currency Bond Fund (“the Fund”) seeks to achieve its objective by investing principally in the debt instruments of sovereign and quasi-sovereign EM issuers, denominated in the local currency of the issuer. The Fund’s returns have historically been driven by EM currency appreciation, interest rate positioning and credit worthiness. We believe EM currencies are currently supported by stronger growth, more robust fundamentals and higher interest rates than developed markets, and we expect many developed markets to use a gradual depreciation of their currencies as part of a strategy to de-leverage and reduce their enormous debt burdens. In terms of bonds, we continue to find attractive opportunities across EM countries: EM monetary policymakers are acting in an idiosyncratic fashion to meet their particular domestic needs and local expertise is increasingly necessary to help understand the dynamics that drive local decision-making.

Over the period, the Fund’s Institutional Class underperformed its benchmark. The Fund’s top contributors for the period were gains from positions in Turkey, Malaysia and Poland. Positions in Russia, Uruguay and Czech Republic were the largest detractors from performance.

Recent performance was driven by a decline in commodity prices with the CRB index down 2.4% in October, albeit with large deviations across sectors: energy declined sharply with Brent and WTI oil prices down 9% and 10.8% at US $84.8 and US $80.5, respectively, after Saudi Arabia conceded discounts to Chinese clients in order to preserve market share.

4

ASHMORE FUNDS

INVESTMENT MANAGER’S REPORT (CONTINUED)

Turkey is perhaps the country which benefitted the most from the decline in oil prices, as nearly all of its 6.6% current account deficit (down from 9.7% in 2011) is due to energy imports, which tend to be inelastic to price adjustments. The Central Bank kept interest rates unchanged at 8.25%, avoiding a cut in rates while inflation remained above the base rate. Turkey’s Consumer Price Index surprised on the downside in October, declining from 9.54% to 8.86% (core CPI from 9.68% to 9.25%) and the unemployment rate moved up from 9.1% to 9.8%.

In Russia, the currency declined in line with the collapse of oil prices. FX reserves declined to US $439bn, which represents a decline of US $78bn from the same period last year, raising concerns that a more interventionist Central Bank could lead to a faster erosion of FX reserves. Despite this, the Central Bank maintained its orthodox inflation-targeting approach, allowing the RUB to float in order to compensate for deteriorating terms of trade. The monetary authority hiked rates by 150 bps to 9.5% on the last day of October in order to rein in inflation which had climbed from 7.6% to 8.0% due to the pass-through from a weaker RUB. The current account balance reached a better than expected US $11.4bn surplus during Q3 2014.

Ashmore Emerging Markets Currency Fund

The Ashmore Emerging Markets Currency Fund (“the Fund”) seeks to achieve its objective by investing principally in derivatives and other instruments that provide investment exposure to the local currencies of EM countries. The Fund also has the flexibility to invest in debt securities issued by Sovereigns and Quasi-Sovereigns and denominated in the local currency of the issuer.

The current environment continues to reflect what we believe is a better fiscal and growth picture in EM compared to the developed markets. Putting aside periods of market dislocation when positioning tends to be based to a greater extent on technical and emotional factors rather than fundamentals, in our view the real drivers of long-term currency performance, including relative interest rates and growth, clearly favour EM. We believe that the deleveraging process across the developed world is perhaps half complete. At a sovereign level, the heavy debt burdens of developed market countries are clear – no more so than in the US, which continually bumps up against its multi-trillion dollar debt ceiling. In our view, a basket of EM currencies not only provides superior diversification, but also allows us to invest in currencies that we consider to be best positioned to benefit from positive domestic and regional trends.

Over the period, the Fund’s Institutional Class outperformed its benchmark. The best performing EM currencies were the Chinese renminbi, Czech koruna and Hong Kong dollar. The Brazilian real, Mexican nuevo peso and Indian rupee were the largest detractors from performance.

Eastern European currencies underperformed towards the end of the period, principally the RUB which was affected by lower oil prices. The same factor led Latin America and Middle East/Africa to outperform as lower energy prices are positive for a number of countries in those regions including Turkey and South Africa.

Brazil’s Consumer Price Index rose to 6.75% in September, overshooting the high end of the generous 2.5% - 6.5% inflation band. The government posted a shocking primary budget deficit of BRL 25.5bn, driving the nominal deficit close to 4% of GDP and increasing the pressure on the government to change its economic policies. In October, the Brazilian Central Bank surprised the market by hiking rates by 25 bps to 11.25% mentioning concerns over inflation due to the weaker BRL. Meanwhile the Chinese renminbi continued its gradual appreciation against the US dollar.

Ashmore Emerging Markets Debt Fund

The Ashmore Emerging Markets Debt Fund (“the Fund”) seeks to achieve its objective by investing principally in debt instruments of, and derivative instruments related to, sovereign, quasi-sovereign and corporate EM issuers, which may be denominated in any currency, including the local currency of the issuer. The Fund typically invests at least 50% of its net assets in debt instruments of sovereign or quasi-sovereign issuers denominated in hard currencies (i.e. the US dollar or any currency of a nation in the G-7).

Over the period, the Fund’s Institutional Class underperformed its benchmark. Positions in Ukraine, Ivory Coast and Indonesia were amongst the Fund’s best performing positions, whereas positions in Venezuela, Argentina and Jamaica detracted.

5

ASHMORE FUNDS

INVESTMENT MANAGER’S REPORT (CONTINUED)

The main index (the JPMorgan EMBI Global Diversified Index) recovered from weakness in 2013 to post a healthy rise of 8.55% during the reporting period. Falling US Treasury yields provided a strong boost to performance and general demand for higher yielding assets supported the gains. Both the IG and HY areas advanced. The sovereign external debt market continued this strong performance in October, led by declining US Treasury yields, with the JP Morgan EMBI GD index rising 1.70% month on month. The IG index was up 2.0% and the HY index was up 1.2%. Credit spreads tightened by 3 bps, with IG 11 bps tighter and HY 2 bps tighter.

Ukraine’s performance was volatile during the period, tracking the separatist conflict in the East of the country. The end of the reporting period saw some progress with attempts to stabilise the conflict: In the second weekend of October, Russian President Vladimir Putin ordered troops to pull back from Ukraine’s border, and Ukrainian President Petro Poroshenko stated his belief that a full ceasefire could soon be achieved. Furthermore, the gas price for the payment of Ukrainian arrears to Gazprom and a new price for supply during the winter were agreed, establishing the free flow of gas to Europe. Finally, parliamentary elections were held, with pro-European parties securing 311 seats in the Rada and the pro-Russian opposition winning 112 seats. 27 seats remained vacant for the representatives of cities in the Donetsk region. However, progress lapsed towards the end of the month when Russian leaders stated that they would “respect” results from elections organised by rebel leaders in the separatist-controlled areas of Ukraine, in defiance of the Ukrainian government.

Venezuela’s underperformance during the period continued through October on the back of declining oil prices with Venezuelan 2026 bonds declining as much as US $10 during the month. Valuations recovered from the middle of October as oil prices stabilised and expectations over further macro adjustments increased. Vice President for the Economy Rodolfo Marco Torres reaffirmed that authorities would draft proposals for adjusting the fiscal accounts via FX devaluation and potentially also through fuel price increases. The prompt repayment of the October 2016 Venezuelan state oil company (PDVSA) bonds, with a total outstanding value of US $1.6bn, improved the technical position and added to confidence concerning the ability and willingness of the country to serve its obligations.

Ashmore Emerging Markets Total Return Fund

The Ashmore Emerging Markets Total Return Fund (“the Fund”) seeks to achieve its objective by investing principally in the debt instruments of sovereign, quasi-sovereign, and corporate issuers, which may be denominated in any currency, including the local currency of the issuer. The Fund tactically allocates assets between external debt, corporate debt and local currency.

Over the period, the Fund’s Institutional Class underperformed its benchmark. Local currency was the main contributor to relative performance with corporate debt and external debt as the main detractors. Geographically, the Fund’s best performing positions were exposures to China, Singapore and Poland whereas exposures to Russia, Ukraine and Argentina were the main detractors.

Chinese trade balances, which recovered swiftly following a deficit in February 2014, deteriorated to US $31bn in September on the back of a rebound in imports. However, this concealed a double digit increase in export volumes. At the end of the reporting period, other activity numbers were mixed with a decline in retail sales but improved industrial production numbers. Q3 2014 GDP declined from 7.5% to 7.3%, better than expected by the market, while China’s Consumer Price Index declined to 1.6%. The FX reserves held by the People’s Bank of China (“PBOC”) declined by US $100bn in September to $3.89 trillion, largely due to the diversification of the portfolio, which holds meaningful exposures to currencies other than the US dollar.

Towards the end of the reporting year, Russian bond spreads reversed the 140 bps of tightening observed in May-June and finished September at 320 bps. The RUB was negatively impacted as economic sanctions and counter-sanctions took their toll on the economy, pushing investors to reduce their exposure and also pushing locals to withdraw money (albeit at a reduced rate after Russian banks repatriated assets for fears of an asset freeze). Economic performance was mixed with industrial production performing surprisingly well (up 2.8% year on year) but consumption and investment showed signs of weakness (fixed asset investment was down approximately 3% year on year). Meanwhile inflation continued to rise, owing in part to import bans on specific goods and food products imposed by the government.

EM corporate debt underperformed sovereign debt for the reporting period, restricted by lower interest rates and a flatter yield curve in the US. Nevertheless, EM corporates could ultimately outperform sovereign debt for the calendar year if US interest rates move higher later in 2014. The spreads on corporate credit proved resilient in

6

ASHMORE FUNDS

INVESTMENT MANAGER’S REPORT (CONTINUED)

the face of US Treasury yield volatility in 2013 and we believe that they are likely to continue to do so for some time, supported by stronger growth this year in both EM and developed markets.

Ashmore Emerging Markets Equity Fund

The Ashmore Emerging Markets Equity Fund (“the Fund”) seeks to achieve its objective by investing principally in equity securities and equity-related investments of EM issuers, which may be denominated in any currency, including the local currency of the issuer.

Global and local macro events dominated sentiment in EM for the reporting year: the spectre of rising US interest rates; a slower global recovery; elections in countries including India, Brazil and Indonesia; and the Russia/Ukraine conflict, amongst others. The MSCI EM index (Net) returned 0.6% in US dollar terms for the year ended October 31, 2014. On a regional basis, EM Eastern Europe was by far the weakest, led primarily by declines in Russia and Hungary. EM Asia, especially India and Taiwan, was the bright spot.

Geographically, the Fund’s overweights in China and India added value, as did exposures to Saudi Arabia and the United Arab Emirates (“UAE”) (which entered the MSCI EM index effective May 2014), and the Fund also benefitted from an underweight exposure to Chile. On a stock selection basis, holdings in India and China outperformed, with auto-maker Maruti Suzuki and internet services company Baidu Inc. contributing the most to their respective country portfolios.

Holdings in South Korea and Brazil detracted the most from performance. Sluggish demand and weakened consumer spending after the May ferry disaster weighed on export-driven and local South Korean stock, although we believe that domestic policies and a US recovery will help drive earnings higher. Stock specific events also weighed on certain holdings: Hyundai Motors fell sharply, detracting from portfolio performance, after announcing plans to pay heavily for new corporate headquarters in Seoul’s swanky Gangnam district. The seller of the property and beneficiary of this overpayment was Korea Electric Power Corp., a stock which is also held by the Fund. In Brazil, stocks were buffeted by significant volatility especially in the lead up to the elections, which concluded in October 2014. During this period, we held stocks where in our view a strong fundamental story was selling at a discount to intrinsic value.

We expect improving global growth and a strengthening of trade ties to benefit Mexico and certain EM countries in East Asia. Lower energy and commodity prices should help companies in the transport and manufacturing industries, but may also hurt prospects in Europe, the Middle East and Africa (“EMEA”), South Africa and Brazil. While monitoring the macro environment, the ultimate focus of our investment process is to seek companies trading at a discount to their long-term fundamental value with a focus on quality and growth consistent with our objective of seeking long-term capital appreciation.

Ashmore Emerging Markets Small-Cap Equity Fund

The Ashmore Emerging Markets Small-Cap Equity Fund (“the Fund”) seeks to achieve its objective by investing principally in equity securities and equity-related investments of small-capitalization EM issuers, which may be denominated in any currency, including the local currency of the issuer.

The MSCI EM Small Cap index (Net) returned 3.2% in US dollar terms for the year to 31 October 2014, outperforming the large cap index (MSCI EM index). Small caps in India, and in the new index entrants UAE and Qatar led returns during the period, while those in Eastern Europe and Latin America generally lagged.

The Fund’s exposures to Saudi Arabia and Turkey, together with a lack of exposure to a sharply lower Greek market added the most value during the reporting period. Allocations in Mexico and the UAE also contributed positively to performance. The Fund’s overall underperformance was driven by stock specific factors, largely attributable to certain holdings in China, Brazil and South Korea. In China, performance was impacted by the replacement of the company chairman at Hydoo, a logistics centre operator (and joint venture with Amazon); and by unfounded accusations in a purported research report by a short seller of 21Vianet (a provider of cloud infrastructure services). Regarding the latter, we re-visited our original investment thesis and conducted extensive additional independent reviews with company management, the founders and other industry sources. Our conclusion is that the report was unfounded. We subsequently added to the stock following its sharp decline. A longer than anticipated turnaround at Iochpe-Maxion in Brazil due to a slowdown in domestic auto sales also contributed to the underperformance.

7

ASHMORE FUNDS

INVESTMENT MANAGER’S REPORT (CONTINUED)

We retained our largest overweight in China, with a focus on the secular growth in mobile usage and what we believe are well positioned, well capitalized and well managed property stocks selling marginally above 3x earnings. We also favour component manufacturers in Taiwan (which are benefitting from mobile phone and PC sales), Indonesian property stocks, and mortgage providers (which have fallen sharply since the presidential election), together with a host of other interesting companies that tap into the EM growth stories. Our search for value in the context of growth and quality drives our conviction in our current holdings. Our prudent approach to long term investing focuses on seeking mispriced opportunities in the marketplace today.

Ashmore Emerging Markets Frontier Equity Fund

The Ashmore Emerging Markets Frontier Equity Fund (“the Fund”), which launched on November 5, 2013, seeks to achieve its objective by investing principally in equity securities and equity-related investments in frontier market issuers, which may be denominated in any currency, including the local currency of the issuer.

The MSCI Frontier Markets Index (Net) returned 21.2% in US dollar terms over the period from the inception of the Fund through October 2014, significantly outperforming EM small caps as well as the broader EM universe. Entrants that were removed from the index during the period, Qatar and the UAE, led returns together with Bangladesh and Argentina, while Estonia, Bahrain and Nigeria lagged.

The Fund’s underweights relative to the index in Nigeria and Kuwait, together with exposure in Saudi Arabia, added the most overall value during the reporting period. Despite this, the Fund’s performance lagged that of the index, driven by exposure in Ghana, which experienced significant currency volatility, as well as stock selection in Qatar and the UAE. We believe that market moves in Qatar and the UAE were primarily technical, positioned to benefit from the upgrade of those markets to EM status. Stocks that were tipped for inclusion in the EM index, some of which we did not own for valuation reasons, saw significant moves ahead of and following the index announcement. By the end of the period, on top of weak oil prices, the Gulf Cooperation Council (“GCC”) markets had to absorb significant new issuance, all of which required pre-funding, which drew liquidity away from other stocks.

While we reduced our overall exposure to the Middle East during the reporting period, we continue to maintain an allocation to selected stocks as a result of what we believe are attractive valuations in the context of growth and quality. We have increased the Fund’s allocation to Argentina where we believe the equity market may offer attractive risk-adjusted opportunities. The country continues to show signs of normalisation after consecutive managed currency devaluations, the gradual elimination of domestic fuel and other utility subsidies, along with marginally constructive negotiations with sovereign creditors.

Global headlines were decidedly negative for a good part of the reporting period and it is times like these when we are the most excited about the potential for significant mispricing opportunities. Our process, which is centred on fundamental research, allows us to dial-in to the key drivers of earnings in our businesses. Our outlook for the frontier markets universe remains positive, as markets continue to open up and bring new opportunities.

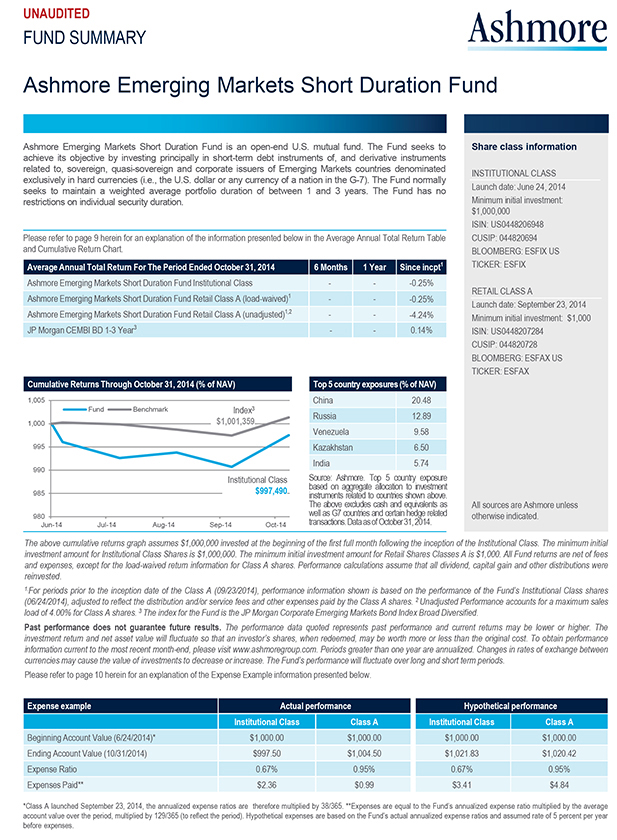

Ashmore Emerging Markets Short Duration Fund

The Ashmore Emerging Markets Short Duration Fund (“the Fund”), which launched on June 24, 2014, seeks to achieve its objective by investing principally in short-term debt instruments of, and derivative instruments related to, sovereign, quasi-sovereign and corporate EM issuers, denominated exclusively in hard currencies (i.e. the US dollar or any currency of a nation in the G-7). The Fund seeks to maintain a weighted average portfolio duration of between 1 and 3 years but has no restrictions on individual security duration.

Since the launch of the Fund in June 2014, its Institutional Class has underperformed its benchmark. The Fund’s top contributors for the period were gains from positions in South Africa, Venezuela and China. Positions in Russia, Mongolia and the UAE were the main detractors from performance.

The reporting period saw high volatility and weak market sentiment. An up-turn in US Treasury volatility as well as a number of other EM related worries (the Brazilian elections, the China slow down, the ongoing Russia/Ukraine conflict situation) all contributed to a widening in EM spreads. IG and HY credits reacted similarly, with both sectors widening. HY credits underperformed in this move, widening 19 bps during October compared to IG credits which finished the month only 4 bps wider.

8

IMPORTANT INFORMATION ABOUT THE FUNDS

Ashmore Investment Advisors Limited

This commentary may include statements that constitute “forward-looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the Funds and market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are those of Ashmore Investment Advisors Limited as of the date indicated and are subject to change at any time based upon economic, market, or other conditions and Ashmore Investment Advisors Limited undertakes no obligation to update the views expressed herein. Any discussions of specific securities or markets should not be considered a recommendation to buy or sell or invest in those securities or markets. The views expressed above may not be relied upon as investment advice or as an indication of the Funds’ trading intent. Information about the Funds’ holdings, asset allocation or country diversification is historical and is not an indication of future portfolio composition, which may vary. Direct investment in any index is not possible. The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses applicable to mutual fund investments. In addition, the returns do not reflect certain charges that an investor in the Funds may pay. If these additional fees were reflected, the performance shown would have been lower.

The following disclosure provides important information regarding each Fund’s Average Annual Total Return table and Cumulative Returns chart, which appear on each Fund’s individual page in this report (the “Shareholder Report” or “Report”). Please refer to this information when reviewing the table and chart for a Fund.

On each individual Fund Summary page in this Report, the Average Annual Total Return table and Cumulative Returns chart measure performance assuming that all dividend and capital gain distributions were reinvested. Returns do not reflect the deduction of taxes that a shareholder would pay on (i) Fund distributions or (ii) the redemption of Fund shares. The Cumulative Returns Chart reflects only Institutional Class performance. Performance for Class A and Class C shares is typically lower than Institutional Class performance due to the lower expenses paid by Institutional Class shares. Except for the load-waived performance for the Class A and C shares of each Fund (as applicable), performance shown is net of fees and expenses. The load-waived performance for Class A and Class C shares does not reflect the sales charges shareholders of those classes may pay in connection with a purchase or redemption of Class A and Class C shares. The load-waived performance of those share classes is relevant only to shareholders who purchased Class A or Class C shares on a load-waived basis. The figures in the line graph are calculated at net asset value and assume the investment of $1,000,000 at the beginning of the first full month following the inception of the Institutional Class. Each Fund measures its performance against a broad-based securities market index (“benchmark index”). Each benchmark index does not take into account fees, expenses or taxes.

For periods prior to the inception date of the Class A and Class C shares (if applicable), performance information shown is based on the performance of the Fund’s Institutional Class shares, adjusted to reflect the distribution and/or service fees and other expenses paid by the Class A and Class C shares, respectively.

A Fund’s past performance, before and after taxes, is not necessarily an indication of how the Fund will perform in the future.

An investment in a Fund is not a deposit of a bank and is not guaranteed or insured by the Federal Deposit Insurance Corporation or any other government agency. It is possible to lose money on investments in the Funds.

9

IMPORTANT INFORMATION ABOUT THE FUNDS (CONTINUED)

The following disclosure provides important information regarding each Fund’s Expense Example, which appears on each Fund’s individual page in this Shareholder Report. Please refer to this information when reviewing the Expense Example for a Fund.

EXPENSE EXAMPLE

Fund Expenses

As a shareholder of the Funds, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period, from May 1, 2014 or the inception date (if later), through October 31, 2014.

Actual Expenses

The information in the table under the heading “Actual Performance” provides information based on actual performance and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = $8.60), then multiply the result by the number in the appropriate column for your share class, in the row titled “Expenses Paid” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information in the table under the heading “Hypothetical Performance” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the information under the heading “Hypothetical Performance” is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

10

11

12

13

14

15

16

17

18

19

ASHMORE FUNDS

STATEMENTS OF ASSETS AND LIABILITIES

As of October 31, 2014

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Ashmore

Emerging Markets

Corporate Debt

Fund | | | | Ashmore

Emerging Markets

Local Currency

Bond Fund | | | | Ashmore

Emerging Markets

Currency Fund |

ASSETS: | | | | | | | | | | | | | | | | | | | |

Investments in securities, at value | | | $ | 344,963,211 | | | | | | $ | 65,653,571 | | | | | | $ | 2,148,452 | |

Investments in fully funded total return swaps, at value | | | | — | | | | | | | 3,983,456 | | | | | | | — | |

Deposit held at broker | | | | — | | | | | | | 69,385 | | | | | | | — | |

Cash | | | | 13,537,167 | | | | | | | 30,144,302 | | | | | | | 7,316,152 | |

Cash held at broker for collateral | | | | — | | | | | | | 1,368,835 | | | | | | | 217,218 | |

Foreign currency, at value | | | | 209,763 | | | | | | | — | | | | | | | 9,508 | |

Unrealized appreciation on forward foreign currency exchange contracts | | | | 221,188 | | | | | | | 1,187,592 | | | | | | | 376,377 | |

Unrealized appreciation on interest rate swap contracts | | | | — | | | | | | | 287,968 | | | | | | | — | |

Receivable for securities and currencies sold | | | | 6,070,222 | | | | | | | 91,523 | | | | | | | — | |

Receivable for fund shares sold | | | | 190,716 | | | | | | | 129,620 | | | | | | | — | |

Receivable from Investment Manager | | | | 36,448 | | | | | | | 37,829 | | | | | | | — | |

Interest and dividends receivable | | | | 6,676,794 | | | | | | | 1,171,708 | | | | | | | 35,643 | |

Other assets | | | | 13,719 | | | | | | | 3,902 | | | | | | | 5,075 | |

Total Assets | | | | 371,919,228 | | | | | | | 104,129,691 | | | | | | | 10,108,425 | |

LIABILITIES: | | | | | | | | | | | | | | | | | | | |

Reverse repurchase agreements at cost | | | | — | | | | | | | — | | | | | | | — | |

Unrealized depreciation on forward foreign currency exchange contracts | | | | 67,735 | | | | | | | 1,083,542 | | | | | | | 413,068 | |

Variable margin payables on centrally cleared swap contracts | | | | — | | | | | | | 4,647 | | | | | | | — | |

Unrealized depreciation on interest rate swap contracts | | | | — | | | | | | | 94,713 | | | | | | | — | |

Payable for securities and currencies purchased | | | | 2,573,482 | | | | | | | 300,903 | | | | | | | — | |

Payable for when-issued securities | | | | — | | | | | | | — | | | | | | | — | |

Payable for fund units redeemed | | | | 1,624,496 | | | | | | | — | | | | | | | — | |

Distributions payable | | | | 278,571 | | | | | | | 42,047 | | | | | | | 801 | |

Investment Manager fee payable | | | | 347,136 | | | | | | | 82,037 | | | | | | | 8,392 | |

Trustees’ fees payable | | | | — | | | | | | | 5,051 | | | | | | | 4,508 | |

Other liabilities | | | | 128,270 | | | | | | | 109,904 | | | | | | | 63,084 | |

Total Liabilities | | | | 5,019,690 | | | | | | | 1,722,844 | | | | | | | 489,853 | |

Net Assets | | | $ | 366,899,538 | | | | | | $ | 102,406,847 | | | | | | $ | 9,618,572 | |

NET ASSETS: | | | | | | | | | | | | | | | | | | | |

Paid in capital | | | $ | 380,723,967 | | | | | | $ | 110,327,416 | | | | | | $ | 9,951,503 | |

Undistributed (distributions in excess of) net investment income (loss) | | | | 1,054,040 | | | | | | | (238,153 | ) | | | | | | 52,033 | |

Accumulated net realized gain (loss) | | | | 1,663,670 | | | | | | | (2,113,945 | ) | | | | | | (232,804 | ) |

Net unrealized appreciation (depreciation) | | | | (16,542,139 | ) | | | | | | (5,568,471 | ) | | | | | | (152,160 | ) |

Net Assets | | | $ | 366,899,538 | | | | | | $ | 102,406,847 | | | | | | $ | 9,618,572 | |

| | | | | |

Net Assets: | | | | | | | | | | | | | | | | | | | |

Class A | | | $ | 1,703,562 | | | | | | $ | 897,340 | | | | | | $ | 911 | |

Class C | | | | 421,271 | | | | | | | 146,829 | | | | | | | 887 | |

Institutional Class | | | | 364,774,705 | | | | | | | 101,362,678 | | | | | | | 9,616,774 | |

| | | | | |

Shares Issued and Outstanding (no par value, unlimited shares authorized): | | | | | | | | | | | | | | | | | | | |

Class A | | | | 190,457 | | | | | | | 106,374 | | | | | | | 111 | |

Class C | | | | 47,076 | | | | | | | 17,430 | | | | | | | 111 | |

Institutional Class | | | | 39,238,824 | | | | | | | 11,609,245 | | | | | | | 1,170,877 | |

| | | | | |

Net Asset Value and Redemption Price Per Share (Net Asset Per Share Outstanding): | | | | | | | | | | | | | | | | | | | |

Class A | | | $ | 8.94 | | | | | | $ | 8.44 | | | | | | $ | 8.21 | |

Class C | | | | 8.95 | | | | | | | 8.42 | | | | | | | 8.00 | |

Institutional Class | | | | 9.30 | | | | | | | 8.73 | | | | | | | 8.21 | |

| | | | | |

Cost of Investments in securities | | | $ | 361,627,227 | | | | | | $ | 71,278,593 | | | | | | $ | 2,262,521 | |

Cost of Investments in fully funded total return swaps | | | $ | — | | | | | | $ | 4,196,591 | | | | | | $ | — | |

Cost of foreign currency held | | | $ | 213,911 | | | | | | $ | — | | | | | | $ | 9,459 | |

See accompanying notes to the financial statements.

20

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | |

| | | Ashmore

Emerging Markets

Debt Fund | | | | | Ashmore

Emerging Markets

Total Return Fund | | | | | Ashmore

Emerging Markets

Equity Fund | | | | | Ashmore

Emerging Markets

Small-Cap Equity Fund | | | | | Ashmore

Emerging Markets

Frontier Equity Fund | | | | | Ashmore

Emerging Markets

Short Duration Fund | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | $6,026,650 | | | | | | $ 883,981,947 | | | | | | $10,041,774 | | | | | | $49,140,253 | | | | | | $6,701,859 | | | | | | $19,841,075 | |

| | | — | | | | | | 20,526,445 | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | — | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | 157,960 | | | | | | 79,578,735 | | | | | | 93,692 | | | | | | 208,843 | | | | | | 423,869 | | | | | | 1,502,840 | |

| | | — | | | | | | 2,871,922 | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | 3,805 | | | | | | 843,868 | | | | | | 8,085 | | | | | | 271,668 | | | | | | 116,419 | | | | | | — | |

| | | 9,630 | | | | | | 6,269,887 | | | | | | — | | | | | | — | | | | | | — | | | | | | 7,490 | |

| | | — | | | | | | 167,816 | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | — | | | | | | 4,158,945 | | | | | | 304,236 | | | | | | 154,200 | | | | | | 47,023 | | | | | | — | |

| | | — | | | | | | 46,554 | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | 2,722 | | | | | | 276,577 | | | | | | 36,389 | | | | | | 144,654 | | | | | | 52,679 | | | | | | 36,080 | |

| | | 100,371 | | | | | | 15,350,727 | | | | | | 11,489 | | | | | | 4,213 | | | | | | 1,194 | | | | | | 334,644 | |

| | | | 5,201 | | | | | | 1,410 | | | | | | 6,427 | | | | | | 8,776 | | | | | | 6,164 | | | | | | 55,266 | |

| | | | 6,306,339 | | | | | | 1,014,074,833 | | | | | | 10,502,092 | | | | | | 49,932,607 | | | | | | 7,349,207 | | | | | | 21,777,395 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 617,403 | | | | | | 2,280,668 | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | 5,767 | | | | | | 7,403,695 | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | — | | | | | | — | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | — | �� | | | | | 87,113 | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | 5,908 | | | | | | 3,981,506 | | | | | | 83,996 | | | | | | 420,284 | | | | | | 565 | | | | | | 220,430 | |

| | | — | | | | | | 9,061,168 | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | — | | | | | | 201,449 | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | 3,050 | | | | | | 447,989 | | | | | | — | | | | | | — | | | | | | — | | | | | | 12,247 | |

| | | 4,228 | | | | | | 834,704 | | | | | | 9,816 | | | | | | 61,790 | | | | | | 9,204 | | | | | | 11,753 | |

| | | 4,028 | | | | | | 24,209 | | | | | | 482 | | | | | | 1,118 | | | | | | 80 | | | | | | 10,035 | |

| | | | 53,616 | | | | | | 424,856 | | | | | | 72,669 | | | | | | 131,562 | | | | | | 48,907 | | | | | | 47,524 | |

| | | | 694,000 | | | | | | 24,747,357 | | | | | | 166,963 | | | | | | 614,754 | | | | | | 58,756 | | | | | | 301,989 | |

| | | | $5,612,339 | | | | | | $ 989,327,476 | | | | | | $10,335,129 | | | | | | $49,317,853 | | | | | | $7,290,451 | | | | | | $21,475,406 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | $6,503,267 | | | | | | $1,050,468,933 | | | | | | $11,483,225 | | | | | | $48,533,881 | | | | | | $6,425,278 | | | | | | $21,836,822 | |

| | | (15,453 | ) | | | | | 232,021 | | | | | | 22,784 | | | | | | 45,071 | | | | | | (38,601 | ) | | | | | 18,576 | |

| | | (856,050 | ) | | | | | (16,876,349 | ) | | | | | (1,147,676 | ) | | | | | 1,619,597 | | | | | | 791,752 | | | | | | (36,187 | ) |

| | | | (19,425 | ) | | | | | (44,497,129 | ) | | | | | (23,204 | ) | | | | | (880,696 | ) | | | | | 112,022 | | | | | | (343,805 | ) |

| | | | $5,612,339 | | | | | | $ 989,327,476 | | | | | | $10,335,129 | | | | | | $49,317,853 | | | | | | $7,290,451 | | | | | | $21,475,406 | |

| | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | $ 37,816 | | | | | | $ 8,351,323 | | | | | | $ 29,711 | | | | | | $ 332,084 | �� | | | | | $ 9,218 | | | | | | $ 200,717 | |

| | | 1,191 | | | | | | 1,027,567 | | | | | | 1,063 | | | | | | 76,967 | | | | | | 1,020 | | | | | | — | |

| | | 5,573,332 | | | | | | 979,948,586 | | | | | | 10,304,355 | | | | | | 48,908,802 | | | | | | 7,280,213 | | | | | | 21,274,689 | |

| | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 4,328 | | | | | | 954,853 | | | | | | 3,214 | | | | | | 35,523 | | | | | | 905 | | | | | | 20,100 | |

| | | 137 | | | | | | 117,587 | | | | | | 102 | | | | | | 7,726 | | | | | | 101 | | | | | | — | |

| | | 642,470 | | | | | | 110,404,262 | | | | | | 1,159,828 | | | | | | 4,203,795 | | | | | | 641,537 | | | | | | 2,167,923 | |

| | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | $ 8.74 | | | | | | $ 8.75 | | | | | | $ 9.24 | | | | | | $ 9.35 | | | | | | $ 10.19 | | | | | | $ 9.99 | |

| | | 8.70 | | | | | | 8.74 | | | | | | 10.46 | | | | | | 9.96 | | | | | | 10.15 | | | | | | — | |

| | | | 8.68 | | | | | | 8.88 | | | | | | 8.88 | | | | | | 11.63 | | | | | | 11.35 | | | | | | 9.81 | |

| | | | | | | | | | | |

| | | $6,049,041 | | | | | | $ 924,397,719 | | | | | | $10,064,998 | | | | | | $50,018,574 | | | | | | $6,589,660 | | | | | | $20,191,374 | |

| | | $ — | | | | | | $ 23,318,414 | | | | | | $ — | | | | | | $ — | | | | | | $ — | | | | | | $ — | |

| | | | $ 3,830 | | | | | | $ 839,059 | | | | | | $ 8,096 | | | | | | $ 271,867 | | | | | | $ 116,007 | | | | | | $ — | |

See accompanying notes to the financial statements.

21

ASHMORE FUNDS

STATEMENTS OF OPERATIONS

For the Year Ended October 31, 2014

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Ashmore

Emerging Markets

Corporate Debt

Fund | | | | Ashmore

Emerging Markets

Local Currency

Bond Fund | | | | Ashmore

Emerging Markets

Currency Fund |

| | | | | |

INVESTMENT INCOME: | | | | | | | | | | | | | | | | | | | |

Interest, net of foreign tax withholdings* | | | $ | 20,060,884 | | | | | | $ | 4,583,483 | | | | | | $ | 200,996 | |

Dividends, net of foreign tax withholdings* | | | | — | | | | | | | — | | | | | | | — | |

Total Income | | | | 20,060,884 | | | | | | | 4,583,483 | | | | | | | 200,996 | |

| | | | | |

EXPENSES: | | | | | | | | | | | | | | | | | | | |

Investment Manager fees | | | | 3,104,502 | | | | | | | 777,840 | | | | | | | 103,251 | |

Administration fees | | | | 63,678 | | | | | | | 19,721 | | | | | | | 3,216 | |

Custody fees | | | | 50,707 | | | | | | | 91,379 | | | | | | | 27,194 | |

Professional fees | | | | 102,344 | | | | | | | 76,447 | | | | | | | 75,322 | |

Trustees’ fees | | | | 33,759 | | | | | | | 13,292 | | | | | | | 4,960 | |

Offering expenses and registration fees | | | | 52,200 | | | | | | | 47,584 | | | | | | | 43,646 | |

Insurance fees | | | | 6,422 | | | | | | | 7,523 | | | | | | | 3,697 | |

Printing fees | | | | 20,184 | | | | | | | 20,184 | | | | | | | 21,162 | |

Distribution fees - Class A | | | | 13,754 | | | | | | | 3,365 | | | | | | | 2 | |

Distribution fees - Class C | | | | 2,378 | | | | | | | 1,519 | | | | | | | 9 | |

Other | | | | 27,316 | | | | | | | 23,446 | | | | | | | 18,072 | |

Total Expenses | | | | 3,477,244 | | | | | | | 1,082,300 | | | | | | | 300,531 | |

Less expenses reimbursed by the Investment Manager | | | | (296,575 | ) | | | | | | (282,751 | ) | | | | | | (194,785 | ) |

Net Expenses | | | | 3,180,669 | | | | | | | 799,549 | | | | | | | 105,746 | |

Net Investment Income | | | | 16,880,215 | | | | | | | 3,783,934 | | | | | | | 95,250 | |

NET REALIZED AND UNREALIZED GAINS (LOSSES): | | | | | | | | | | | | | | | | | | | |

NET REALIZED GAIN (LOSS) ON: | | | | | | | | | | | | | | | | | | | |

Investments in securities | | | | 2,091,383 | | | | | | | (5,208,900 | ) | | | | | | (436,792 | ) |

Forward foreign currency exchange contracts | | | | 1,013,345 | | | | | | | (627,142 | ) | | | | | | (22,614 | ) |

Interest rate swap contracts | | | | — | | | | | | | (46,948 | ) | | | | | | (131 | ) |

Purchased options | | | | — | | | | | | | (60,630 | ) | | | | | | (36,378 | ) |

Foreign exchange transactions | | | | (391,965 | ) | | | | | | (156,270 | ) | | | | | | (638,371 | ) |

Net Realized Gain (Loss) | | | | 2,712,763 | | | | | | | (6,099,890 | ) | | | | | | (1,134,286 | ) |

NET CHANGE IN UNREALIZED APPRECIATION

(DEPRECIATION) ON: | | | | | | | | | | | | | | | | | | | |

Investments in securities | | | | (13,998,633 | ) | | | | | | (2,727,312 | ) | | | | | | 19,674 | |

Forward foreign currency exchange contracts | | | | 179,220 | | | | | | | 67,657 | | | | | | | 153,910 | |

Investments in fully funded total return swaps | | | | — | | | | | | | 592,075 | | | | | | | — | |

Interest rate swap contracts | | | | — | | | | | | | 331,266 | | | | | | | — | |

Purchased option contracts | | | | — | | | | | | | 60,589 | | | | | | | 36,353 | |

Foreign exchange translations | | | | (25,279 | ) | | | | | | (49,759 | ) | | | | | | (20 | ) |

Change in Net Unrealized Appreciation (Depreciation) | | | | (13,844,692 | ) | | | | | | (1,725,484 | ) | | | | | | 209,917 | |

Net Realized and Unrealized Gains (Losses) | | | | (11,131,929 | ) | | | | | | (7,825,374 | ) | | | | | | (924,369 | ) |

Net Increase (Decrease) in Net Assets Resulting from Operations | | | $ | 5,748,286 | | | | | | $ | (4,041,440 | ) | | | | | $ | (829,119 | ) |

* Foreign Tax Withholdings | | | $ | 34,442 | | | | | | $ | 78,955 | | | | | | $ | — | |

| 1 | The Fund commenced investment operations on November 5, 2013. |

| 2 | The Fund commenced investment operations on June 24, 2014. |

See accompanying notes to the financial statements.

22

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | |

| | | Ashmore

Emerging Markets

Debt Fund | | | | | Ashmore

Emerging Markets

Total Return Fund | | | | | Ashmore

Emerging Markets

Equity Fund | | | | | Ashmore

Emerging Markets

Small-Cap Equity Fund | | | | | Ashmore

Emerging Markets

Frontier Equity

Fund1 | | | | | Ashmore

Emerging Markets

Short Duration

Fund2 | |

| | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | $ 437,515 | | | | | | $ 48,107,357 | | | | | | $ — | | | | | | $ — | | | | | | $ — | | | | | | $ 377,525 | |

| | | | — | | | | | | — | | | | | | 206,912 | | | | | | 637,954 | | | | | | 158,755 | | | | | | — | |

| | | | 437,515 | | | | | | 48,107,357 | | | | | | 206,912 | | | | | | 637,954 | | | | | | 158,755 | | | | | | 377,525 | |

| | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 59,411 | | | | | | 7,799,080 | | | | | | 113,826 | | | | | | 565,125 | | | | | | 97,792 | | | | | | 44,420 | |

| | | 1,732 | | | | | | 183,728 | | | | | | 2,411 | | | | �� | | 8,773 | | | | | | 1,199 | | | | | | 1,367 | |

| | | 5,296 | | | | | | 329,017 | | | | | | 72,232 | | | | | | 147,407 | | | | | | 29,702 | | | | | | 1,407 | |

| | | 70,197 | | | | | | 185,570 | | | | | | 65,196 | | | | | | 69,322 | | | | | | 73,000 | | | | | | 48,000 | |

| | | 3,995 | | | | | | 113,057 | | | | | | 1,602 | | | | | | 5,080 | | | | | | 855 | | | | | | 10,603 | |

| | | 46,126 | | | | | | 89,985 | | | | | | 41,719 | | | | | | 63,517 | | | | | | 139,873 | | | | | | 73,028 | |

| | | 3,499 | | | | | | 36,794 | | | | | | 1,658 | | | | | | 3,250 | | | | | | 1,475 | | | | | | 2,099 | |

| | | 21,162 | | | | | | 20,184 | | | | | | 20,184 | | | | | | 20,184 | | | | | | 42,819 | | | | | | 15,000 | |

| | | 22 | | | | | | 20,062 | | | | | | 77 | | | | | | 920 | | | | | | 11 | | | | | | 52 | |

| | | 11 | | | | | | 9,074 | | | | | | 11 | | | | | | 360 | | | | | | 78 | | | | | | — | |

| | | | 15,205 | | | | | | 76,300 | | | | | | 14,440 | | | | | | 19,046 | | | | | | 10,458 | | | | | | 5,000 | |

| | | | 226,656 | | | | | | 8,862,851 | | | | | | 333,356 | | | | | | 902,984 | | | | | | 397,262 | | | | | | 200,976 | |

| | | | (165,889 | ) | | | | | (875,987 | ) | | | | | (217,452 | ) | | | | | (328,428 | ) | | | | | (298,073 | ) | | | | | (155,228 | ) |

| | | | 60,767 | | | | | | 7,986,864 | | | | | | 115,904 | | | | | | 574,556 | | | | | | 99,189 | | | | | | 45,748 | |

| | | | 376,748 | | | | | | 40,120,493 | | | | | | 91,008 | | | | | | 63,398 | | | | | | 59,566 | | | | | | 331,777 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | (816,133 | ) | | | | | (23,002,494 | ) | | | | | (93,120 | ) | | | | | 1,800,961 | | | | | | 791,752 | | | | | | (36,187 | ) |

| | | 12,134 | | | | | | (1,448,263 | ) | | | | | (1,467 | ) | | | | | 1,379 | | | | | | (5,548 | ) | | | | | 18,337 | |

| | | — | | | | | | (91,420 | ) | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | — | | | | | | (189,973 | ) | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | | (1,975 | ) | | | | | (2,204,583 | ) | | | | | (6,302 | ) | | | | | (40,313 | ) | | | | | (23,166 | ) | | | | | 1,115 | |

| | | | (805,974 | ) | | | | | (26,936,733 | ) | | | | | (100,889 | ) | | | | | 1,762,027 | | | | | | 763,038 | | | | | | (16,735 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 467,778 | | | | | | (14,579,031 | ) | | | | | (370,307 | ) | | | | | (3,544,559 | ) | | | | | 112,199 | | | | | | (350,299 | ) |

| | | 3,863 | | | | | | (831,849 | ) | | | | | — | | | | | | — | | | | | | — | | | | | | 7,490 | |

| | | — | | | | | | (493,123 | ) | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | — | | | | | | 122,961 | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | — | | | | | | 189,845 | | | | | | — | | | | | | — | | | | | | — | | | | | | — | |

| | | | (900 | ) | | | | | (248,861 | ) | | | | | 26 | | | | | | (3,610 | ) | | | | | (177 | ) | | | | | (996 | ) |

| | | | 470,741 | | | | | | (15,840,058 | ) | | | | | (370,281 | ) | | | | | (3,548,169 | ) | | | | | 112,022 | | | | | | (343,805 | ) |

| | | | (335,233 | ) | | | | | (42,776,791 | ) | | | | | (471,170 | ) | | | | | (1,786,142 | ) | | | | | 875,060 | | | | | | (360,540 | ) |

| | | | $ 41,515 | | | | | | $ (2,656,298 | ) | | | | | $(380,162 | ) | | | | | $(1,722,744 | ) | | | | | $ 934,626 | | | | | | $ (28,763 | ) |

| | | | $ — | | | | | | $ 302,841 | | | | | | $ 27,122 | | | | | | $ 64,237 | | | | | | $ 8,737 | | | | | | $ 1,586 | |

See accompanying notes to the financial statements.

23

ASHMORE FUNDS

STATEMENTS OF CHANGES IN NET ASSETS

For the Year Ended October 31, 2014

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Ashmore Emerging Markets Corporate Debt Fund | | | Ashmore Emerging Markets Local Currency Bond Fund | | | Ashmore Emerging Markets Currency Fund | |

| | | 2014 | | | 2013 | | | 2014 | | | 2013 | | | 2014 | | | 2013 | |

OPERATIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | $ | 16,880,215 | | | $ | 4,429,761 | | | $ | 3,783,934 | | | $ | 4,179,567 | | | $ | 95,250 | | | $ | 83,284 | |

Net realized gain (loss) | | | 2,712,763 | | | | (278,667 | ) | | | (6,099,890 | ) | | | (2,260,660 | ) | | | (1,134,286 | ) | | | 657,976 | |

Net change in unrealized appreciation (depreciation) | | | (13,844,692 | ) | | | (2,789,397 | ) | | | (1,725,484 | ) | | | (5,774,539 | ) | | | 209,917 | | | | (756,475 | ) |

Net Increase (Decrease) in Net Assets Resulting from Operations | | | 5,748,286 | | | | 1,361,697 | | | | (4,041,440 | ) | | | (3,855,632 | ) | | | (829,119 | ) | | | (15,215 | ) |

| | | | | | |

DISTRIBUTIONS TO CLASS A SHAREHOLDERS: | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (321,596 | ) | | | (129,218 | ) | | | — | | | | (34,973 | ) | | | — | | | | — | |

From net realized gain | | | — | | | | (8,260 | ) | | | — | | | | — | | | | (59 | ) | | | (30 | ) |

Tax return of capital | | | — | | | | (926 | ) | | | (62,760 | ) | | | (27,984 | ) | | | (5 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total Distributions to Class A Shareholders | | | (321,596 | ) | | | (138,404 | ) | | | (62,760 | ) | | | (62,957 | ) | | | (64 | ) | | | (30 | ) |

| | | | | | |

DISTRIBUTIONS TO CLASS C SHAREHOLDERS: | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (12,291 | ) | | | (3,894 | ) | | | — | | | | (1,828 | ) | | | — | | | | — | |

From net realized gain | | | — | | | | (203 | ) | | | — | | | | — | | | | (60 | ) | | | (30 | ) |

Tax return of capital | | | — | | | | (48 | ) | | | (5,740 | ) | | | (1,463 | ) | | | (2 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total Distributions to Class C Shareholders | | | (12,291 | ) | | | (4,145 | ) | | | (5,740 | ) | | | (3,291 | ) | | | (62 | ) | | | (30 | ) |

| | | | | | |

DISTRIBUTIONS TO INSTITUTIONAL CLASS SHAREHOLDERS: | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (16,331,560 | ) | | | (4,260,824 | ) | | | — | | | | (2,046,475 | ) | | | — | | | | (118,078 | ) |

From net realized gain | | | — | | | | (216,214 | ) | | | — | | | | — | | | | (621,904 | ) | | | (1,809,756 | ) |

Tax return of capital | | | — | | | | (59,552 | ) | | | (3,812,854 | ) | | | (1,618,141 | ) | | | (97,215 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total Distributions to Institutional Class Shareholders | | | (16,331,560 | ) | | | (4,536,590 | ) | | | (3,812,854 | ) | | | (3,664,616 | ) | | | (719,119 | ) | | | (1,927,834 | ) |

FUND SHARE TRANSACTIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in net assets resulting from Class A share transactions | | | (1,191,492 | ) | | | 2,556,553 | | | | (1,082,599 | ) | | | 1,842,673 | | | | 63 | | | | 32 | |

Net increase (decrease) in net assets resulting from Class C share transactions | | | 280,805 | | | | 128,015 | | | | 33,307 | | | | 116,253 | | | | 58 | | | | 30 | |

Net increase (decrease) in net assets resulting from Institutional Class share transactions | | | 192,159,009 | | | | 169,037,926 | | | | 26,615,002 | | | | 17,286,849 | | | | (24,481,009 | ) | | | (30,769,274 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Net Increase (Decrease) in Net Assets Resulting from Fund Share Transactions | | | 191,248,322 | | | | 171,722,494 | | | | 25,565,710 | | | | 19,245,775 | | | | (24,480,888 | ) | | | (30,769,212 | ) |

Total Increase (Decrease) in Net Assets | | | 180,331,161 | | | | 168,405,052 | | | | 17,642,916 | | | | 11,659,279 | | | | (26,029,252 | ) | | | (32,712,321 | ) |

NET ASSETS: | | | | | | | | | | | | | | | | | | | | | | | | |

Net Assets at the Beginning of the Year | | | 186,568,377 | | | | 18,163,325 | | | | 84,763,931 | | | | 73,104,652 | | | | 35,647,824 | | | | 68,360,145 | |

Net Assets at the End of the Year | | $ | 366,899,538 | | | $ | 186,568,377 | | | $ | 102,406,847 | | | $ | 84,763,931 | | | $ | 9,618,572 | | | $ | 35,647,824 | |

Undistributed (Distributions in Excess of) Net Investment Income (Loss) | | $ | 1,054,040 | | | $ | (191,916 | ) | | $ | (238,153 | ) | | $ | (29,724 | ) | | $ | 52,033 | | | $ | 454,881 | |

| 1 | Formerly the Ashmore Emerging Markets Sovereign Debt Fund. |

| 2 | The Fund commenced investment operations on November 5, 2013. |

| 3 | The Fund commenced investment operations on June 24, 2014. |

See accompanying notes to the financial statements.

24

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Ashmore Emerging Markets Debt Fund1 | | | Ashmore Emerging Markets Total Return Fund | | | Ashmore Emerging Markets Equity Fund | | | Ashmore Emerging Markets Small-Cap Equity Fund | | | Ashmore Emerging Markets Frontier Equity Fund2 | | | Ashmore Emerging Markets Short Duration Fund3 | |

2014 | | | 2013 | | | 2014 | | | 2013 | | | 2014 | | | 2013 | | | 2014 | | | 2013 | | | 2014 | | | 2014 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | $ 376,748 | | | | $ 1,607,319 | | | | $ 40,120,493 | | | | $ 28,102,512 | | | | $ 91,008 | | | | $ 73,841 | | | | $ 63,398 | | | | $ 49,879 | | | | $ 59,566 | | | | $ 331,777 | |

| | (805,974 | ) | | | 779,457 | | | | (26,936,733 | ) | | | 8,318,150 | | | | (100,889 | ) | | | 373,010 | | | | 1,762,027 | | | | 1,929,398 | | | | 763,038 | | | | (16,735 | ) |

| | 470,741 | | | | (3,717,674 | ) | | | (15,840,058 | ) | | | (43,239,875 | ) | | | (370,281 | ) | | | 308,603 | | | | (3,548,169 | ) | | | 1,914,326 | | | | 112,022 | | | | (343,805 | ) |

|

41,515 |

| | | (1,330,898 | ) | | | (2,656,298 | ) | | | (6,819,213 | ) | | | (380,162 | ) | | | 755,454 | | | | (1,722,744 | ) | | | 3,893,603 | | | | 934,626 | | | | (28,763 | ) |

| | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (509 | ) | | | (413 | ) | | | (288,037 | ) | | | (377,693 | ) | | | (255 | ) | | | (100 | ) | | | (353 | ) | | | (844 | ) | | | (46 | ) | | | (1,102 | ) |

| | (244 | ) | | | (43 | ) | | | (108,474 | ) | | | (64,653 | ) | | | — | | | | — | | | | (21,546 | ) | | | (13,704 | ) | | | — | | | | — | |

| | (5 | ) | | | — | | | | (106,644 | ) | | | — | | | | — | | | | (20 | ) | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (758 | ) | | | (456 | ) | | | (503,155 | ) | | | (442,346 | ) | | | (255 | ) | | | (120 | ) | | | (21,899 | ) | | | (14,548 | ) | | | (46 | ) | | | (1,102 | ) |

| | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (57 | ) | | | (40 | ) | | | (27,681 | ) | | | (32,382 | ) | | | (8 | ) | | | (6 | ) | | | (59 | ) | | | (40 | ) | | | (5 | ) | | | — | |

| | (175 | ) | | | (3 | ) | | | (12,431 | ) | | | (9,191 | ) | | | — | | | | — | | | | (873 | ) | | | (52 | ) | | | — | | | | — | |

| | (1 | ) | | | — | | | | (10,249 | ) | | | — | | | | — | | | | (1 | ) | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (233 | ) | | | (43 | ) | | | (50,361 | ) | | | (41,573 | ) | | | (8 | ) | | | (7 | ) | | | (932 | ) | | | (92 | ) | | | (5 | ) | | | — | |

| | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (375,103 | ) | | | (1,614,231 | ) | | | (29,319,267 | ) | | | (26,448,591 | ) | | | (85,433 | ) | | | (67,762 | ) | | | (40,881 | ) | | | (72,503 | ) | | | (69,402 | ) | | | (331,551 | ) |

| | (821,133 | ) | | | (126,668 | ) | | | (8,728,838 | ) | | | (8,496,687 | ) | | | — | | | | — | | | | (1,986,719 | ) | | | (1,116,480 | ) | | | — | | | | — | |

| | (3,339 | ) | | | — | | | | (10,855,322 | ) | | | — | | | | — | | | | (6,759 | ) | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (1,199,575 | ) | | | (1,740,899 | ) | | | (48,903,427 | ) | | | (34,945,278 | ) | | | (85,433 | ) | | | (74,521 | ) | | | (2,027,600 | ) | | | (1,188,983 | ) | | | (69,402 | ) | | | (331,551 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | |

| | 37,063 | | | | (11,850 | ) | | | (1,485,743 | ) | | | 7,948,290 | | | | 2,329 | | | | 25,333 | | | | 81,303 | | | | (106,768 | ) | | | 9,051 | | | | 200,994 | |

| | | | | | | | | | |

| | 232 | | | | 44 | | | | 115,811 | | | | 510,771 | | | | 8 | | | | 8 | | | | 68,695 | | | | 10,478 | | | | 4,549 | | | | — | |

| | | | | | | | | | |

| | (22,272,165 | ) | | | (2,949,787 | ) | | | 369,085,194 | | | | 189,754,435 | | | | 943,935 | | | | 404,751 | | | | 22,294,208 | | | | 14,455,333 | | | | 6,411,678 | | | | 21,635,828 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | |

|

(22,234,870 |

) | | | (2,961,593 | ) | | | 367,715,262 | | | | 198,213,496 | | | | 946,272 | | | | 430,092 | | | | 22,444,206 | | | | 14,359,043 | | | | 6,425,278 | | | | 21,836,822 | |

| | (23,393,921 | ) | | | (6,033,889 | ) | | | 315,602,021 | | | | 155,965,086 | | | | 480,414 | | | | 1,110,898 | | | | 18,671,031 | | | | 17,049,023 | | | | 7,290,451 | | | | 21,475,406 | |

| | | | | | | | | | |

| | 29,006,260 | | | | 35,040,149 | | | | 673,725,455 | | | | 517,760,369 | | | | 9,854,715 | | | | 8,743,817 | | | | 30,646,822 | | | | 13,597,799 | | | | — | | | | — | |

| | $ 5,612,339 | | | | $29,006,260 | | | | $989,327,476 | | | | $673,725,455 | | | | $10,335,129 | | | | $9,854,715 | | | | $49,317,853 | | | | $30,646,822 | | | | $7,290,451 | | | | $21,475,406 | |

| | | | | | | | | | |

| | $ (15,453 | ) | | | $ (22,533 | ) | | | $ 232,021 | | | | $ 2,693,049 | | | | $ 22,784 | | | | $ (507 | ) | | | $ 45,071 | | | | $ (2,074 | ) | | | $ (38,601 | ) | | | $ 18,576 | |

See accompanying notes to the financial statements.

25

ASHMORE FUNDS

FINANCIAL HIGHLIGHTS

Ashmore Emerging Markets Corporate Debt Fund

| | | | | | | | | | | | | | | | |

| | | Class A | |

| | | | |

| | | Year Ended October 31,

2014 | | | Year Ended October 31,

2013 | | | Year Ended October 31,

2012 | | | Period Ended October 31,

20111 | |

| | | | |

Net asset value at beginning of period | | | $9.25 | | | | $9.69 | | | | $9.09 | | | | $10.00 | |

| | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | |

Net investment income (loss)2 | | | 0.55 | | | | 0.51 | | | | 0.67 | | | | 0.32 | |

Net realized and unrealized gain (loss) | | | (0.31) | | | | (0.35) | | | | 0.67 | | | | (0.86) | |

| | | | | | | | | | | | | | | | |

Total from investment operations | | | 0.24 | | | | 0.16 | | | | 1.34 | | | | (0.54) | |

| | | | |

Less distributions: | | | | | | | | | | | | | | | | |

| | | | |

From net investment income | | | (0.55) | | | | (0.52) | | | | (0.69) | | | | (0.37) | |

From net realized gain | | | — | | | | (0.07) | | | | (0.05) | | | | — | |

Tax return of capital | | | — | | | | (0.01) | | | | — | | | | — | |

| | | | | | | | | | | | | | | | |

| | | | |

Total distributions | | | (0.55) | | | | (0.60) | | | | (0.74) | | | | (0.37) | |

| | | | | | | | | | | | | | | | |

Net asset value at end of period | | | $8.94 | | | | $9.25 | | | | $9.69 | | | | $9.09 | |

| | | | | | | | | | | | | | | | |

| | | | |

Total return3 | | | 2.53% | | | | 1.63% | | | | 15.54% | | | | (5.44%) | |

| | | | |

Portfolio turnover rate4 | | | 82% | | | | 49% | | | | 50% | | | | 22% | |

| | | | |

Net assets, end of period (in thousands) | | | $1,704 | | | | $2,852 | | | | $485 | | | | $1 | |

| | | | |

Ratios to average net assets:5 | | | | | | | | | | | | | | | | |

Total expenses to average net assets: | | | | | | | | | | | | | | | | |

Total expenses before reimbursements | | | 1.53% | | | | 1.71% | | | | 2.89% | | | | 4.36% | |

Total expenses after reimbursements | | | 1.45% | | | | 1.45% | | | | 1.45% | | | | 1.45% | |

| | | | |

Net investment income to average net assets: | | | | | | | | | | | | | | | | |

Net investment income before reimbursements | | | 5.79% | | | | 5.15% | | | | 5.19% | | | | 4.35% | |

Net investment income after reimbursements | | | 5.87% | | | | 5.41% | | | | 6.63% | | | | 7.26% | |

See accompanying notes to the financial statements.

26

ASHMORE FUNDS

FINANCIAL HIGHLIGHTS

Ashmore Emerging Markets Corporate Debt Fund

| | | | | | | | | | | | | | | | |

| | | Class C | |

| | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Period Ended | |

| | | October 31, | | | October 31, | | | October 31, | | | October 31, | |

| | | 2014 | | | 2013 | | | 2012 | | | 20111 | |

| | | | |

Net asset value at beginning of period | | | $ 9.25 | | | | $ 9.70 | | | | $ 9.09 | | | | $ 10.00 | |

| | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | |

Net investment income (loss)2 | | | 0.48 | | | | 0.44 | | | | 0.60 | | | | 0.28 | |

Net realized and unrealized gain (loss) | | | (0.30) | | | | (0.36) | | | | 0.68 | | | | (0.86) | |

| | | | | | | | | | | | | | | | |

Total from investment operations | | | 0.18 | | | | 0.08 | | | | 1.28 | | | | (0.58) | |

| | | | |

Less distributions: | | | | | | | | | | | | | | | | |

| | | | |

From net investment income | | | (0.48) | | | | (0.45) | | | | (0.62) | | | | (0.33) | |

From net realized gain | | | — | | | | (0.07) | | | | (0.05) | | | | — | |

Tax return of capital | | | — | | | | (0.01) | | | | — | | | | — | |

| | | | | | | | | | | | | | | | |

| | | | |

Total distributions | | | (0.48) | | | | (0.53) | | | | (0.67) | | | | (0.33) | |

| | | | | | | | | | | | | | | | |

Net asset value at end of period | | | $ 8.95 | | | | $ 9.25 | | | | $ 9.70 | | | | $ 9.09 | |

| | | | | | | | | | | | | | | | |

| | | | |

Total return3 | | | 1.87% | | | | 0.80% | | | | 14.78% | | | | (5.78%) | |

| | | | |

Portfolio turnover rate4 | | | 82% | | | | 49% | | | | 50% | | | | 22% | |

| | | | |

Net assets, end of period (in thousands) | | | $421 | | | | $150 | | | | $27 | | | | $1 | |

| | | | |

Ratios to average net assets:5 | | | | | | | | | | | | | | | | |

Total expenses to average net assets: | | | | | | | | | | | | | | | | |

Total expenses before reimbursements | | | 2.28% | | | | 2.46% | | | | 3.60% | | | | 5.12% | |

Total expenses after reimbursements | | | 2.20% | | | | 2.20% | | | | 2.20% | | | | 2.20% | |

| | | | |

Net investment income to average net assets: | | | | | | | | | | | | | | | | |

Net investment income before reimbursements | | | 5.15% | | | | 4.42% | | | | 4.73% | | | | 3.59% | |

Net investment income after reimbursements | | | 5.23% | | | | 4.68% | | | | 6.13% | | | | 6.51% | |

See accompanying notes to the financial statements.

27

ASHMORE FUNDS

FINANCIAL HIGHLIGHTS

Ashmore Emerging Markets Corporate Debt Fund

| | | | | | | | | | | | | | | | |

| | | Institutional Class | |

| | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Period Ended | |

| | | October 31, | | | October 31, | | | October 31, | | | October 31, | |

| | | 2014 | | | 2013 | | | 2012 | | | 20116 | |

| | | | |

Net asset value at beginning of period | | | $ 9.61 | | | | $ 10.07 | | | | $ 9.43 | | | | $ 10.00 | |

| | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | |

Net investment income (loss)2 | | | 0.59 | | | | 0.55 | | | | 0.73 | | | | 0.63 | |

Net realized and unrealized gain (loss) | | | (0.31) | | | | (0.36) | | | | 0.70 | | | | (0.60) | |

| | | | | | | | | | | | | | | | |

Total from investment operations | | | 0.28 | | | | 0.19 | | | | 1.43 | | | | 0.03 | |

| | | | |

Less distributions: | | | | | | | | | | | | | | | | |

| | | | |

From net investment income | | | (0.59) | | | | (0.57) | | | | (0.74) | | | | (0.60) | |

From net realized gain | | | — | | | | (0.07) | | | | (0.05) | | | | — | |

Tax return of capital | | | — | | | | (0.01) | | | | — | | | | — | |

| | | | | | | | | | | | | | | | |

| | | | |

Total distributions | | | (0.59) | | | | (0.65) | | | | (0.79) | | | | (0.60) | |

| | | | | | | | | | | | | | | | |

Net asset value at end of period | | | $ 9.30 | | | | $ 9.61 | | | | $ 10.07 | | | | $ 9.43 | |

| | | | | | | | | | | | | | | | |

| | | | |

Total return3 | | | 2.91% | | | | 1.91% | | | | 15.97% | | | | 0.27% | |

| | | | |

Portfolio turnover rate4 | | | 82% | | | | 49% | | | | 50% | | | | 22% | |

| | | | |

Net assets, end of period (in thousands) | | | $364,775 | | | | $183,567 | | | | $17,651 | | | | $11,824 | |

| | | | |

Ratios to average net assets:5 | | | | | | | | | | | | | | | | |

Total expenses to average net assets: | | | | | | | | | | | | | | | | |

Total expenses before reimbursements | | | 1.28% | | | | 1.46% | | | | 2.66% | | | | 3.78% | |

Total expenses after reimbursements | | | 1.17% | | | | 1.17% | | | | 1.17% | | | | 1.17% | |

| | | | |

Net investment income to average net assets: | | | | | | | | | | | | | | | | |

Net investment income before reimbursements | | | 6.14% | | | | 5.37% | | | | 6.16% | | | | 4.60% | |

Net investment income after reimbursements | | | 6.25% | | | | 5.66% | | | | 7.65% | | | | 7.21% | |

| 1 | Class A and Class C commenced investment operations on May 12, 2011. |

| 2 | Per share amounts are based on average number of shares outstanding during the period. |

| 3 | Assumes investment at net asset value at the beginning of the period, reinvestment of all distributions at net asset value on distribution date, and a complete redemption of the investment at net asset value at the end of the period excluding the impact of sales charges. Total return is not annualized for periods less than one year. |

| 4 | The portfolio turnover rate is calculated by dividing the lesser of cost of purchases or proceeds from sales of long term portfolio securities by the monthly average of the value of the long term portfolio securities. Portfolio turnover is not annualized for periods less than one year. |

| 5 | Annualized for periods less than one year. |

| 6 | The Institutional Class commenced investment operations on December 8, 2010. |

See accompanying notes to the financial statements.

28

ASHMORE FUNDS

FINANCIAL HIGHLIGHTS

Ashmore Emerging Markets Local Currency Bond Fund

| | | | | | | | | | | | | | | | |

| | | Class A | |

| | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Period Ended | |