As filed with the Securities and Exchange Commission on August 8, 2012

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22492

MainGate Trust

(Exact name of registrant as specified in charter)

6075 Poplar Avenue, Suite 402, Memphis, TN 38119

(Address of principal executive offices) (Zip code)

Geoffrey P. Mavar

6075 Poplar Avenue, Suite 402, Memphis, TN 38119

(Name and address of agent for service)

(901) 537-1866

Registrant's telephone number, including area code

Date of fiscal year end: November 30

Date of reporting period: May 31, 2012

Item 1. Reports to Stockholders.

This Page Inentionally Blank

MainGate MLP Fund

Class A (AMLPX)

Class I (IMLPX)

6075 Poplar Avenue, Suite 402 | Memphis, TN 38119 | 855.MLP.FUND (855.657.3863) | www.maingatefunds.com

Semi-Annual Report

May 31, 2012

Table of Contents

| Letter to Shareholders | 5 |

| Hypothetical Growth of a $10,000 Investment | 9 |

| Average Annual Returns | 9 |

| Expense Example | 10 |

| Allocation of Portfolio Assets | 11 |

| Schedule of Investments | 11 |

| Statement of Assets and Liabilities | 12 |

| Statement of Operations | 12 |

| Statement of Changes in Net Assets | 13 |

| Financial Highlights: Class A Shares | 14 |

| Financial Highlights: Class I Shares | 15 |

| Notes to Financial Statements | 16 |

| Additional Information | 21 |

| Privacy Policy | 22 |

| Fund Service Providers | inside-back cover |

MainGate MLP Fund

The following discussion is based on our opinions and beliefs.

Dear Shareholders,

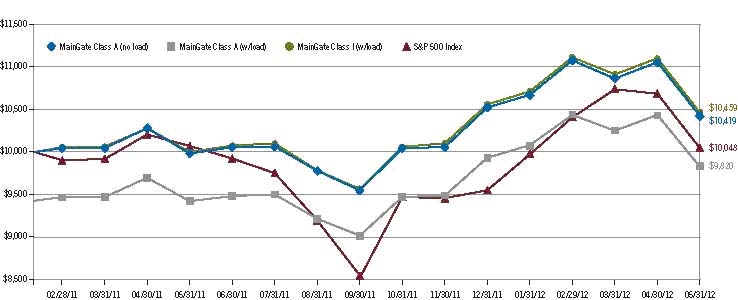

We thank you for your support and look forward to an exciting second half of the year. After the market experienced broad weakness during May, the first half of the year is off to a modest start for the MainGate MLP Fund. The Fund had the following performance through May 31, 2012.

| | CUMULATIVE RETURNS | AVG ANNUAL RETURNS |

| | 1 Month | 3 Months | 6 Months | 1 Year | Since Inception | Since Inception |

| MainGate MLP Fund – Class A without load | -5.77% | -5.96% | 3.36% | 4.29% | 4.19% | 3.25% |

| MainGate MLP Fund – Class A with 5.75% load | -11.16% | -11.33% | -2.62% | -1.71 | -1.80 | -1.41% |

| MainGate MLP Fund – Class I | -5.75% | -5.85% | 3.46% | 4.59% | 4.59% | 3.57% |

| S&P 500 Index | -6.01% | -3.53% | 6.23% | -0.41% | 0.48% | 0.37% |

Gross Expense Ratio = 19.34% | Net Expense Ratio = 10.03%: The Fund’s advisor contractually has agreed to waive a portion of Fund expenses through March 31, 2013. | Expense Cap = 1.50%: The Fund’s adviser contractually has agreed to cap the Fund’s total annual operating expenses (excluding fee and commissions; borrowing costs; current and deferred income tax expenses; acquired fund fees and expenses; 12-b fees; and extraordinary expenses) at 1.50% of the average daily net assets of each class through March 31, 2013.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will not fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 855-MLP-FUND (855-657-3863) or by visiting www.maingatefunds.com.

The MLP story remains bright over the long term. The MLP asset class offers investors the possibility of a solid total return from yield and growth. We expect that patient investors will have the opportunity to benefit from growth due to: (1) structural growth factors such as volume and rate increases, (2) accretive acquisitions, and (3) organic growth projects due to the renaissance of U.S. energy production from the shale basins.

All three factors should play a part in the growth story for MLPs in coming years. However, it is the potential for organic growth projects from the revolution in U.S. energy production that is the most exciting part of the MLP growth story. The shale revolution is firmly entrenched in the oil, natural gas, and natural gas liquids (NGL) markets. In the past few years, the development of U.S. shale resources has been the most important change in our quest for energy independence.

The shale revolution began with the development of the Barnett shale in Texas. Producers used a combination of horizontal drilling coupled with hydraulic fracturing (fracking) to allow oil and gas trapped in shale to be released and to flow freely to the wellhead. The development of other basins quickly followed with activity centered on the Fayetteville, Haynesville, Marcellus, and Eagle Ford shales. Shale basins may contain gas, NGLs, and/or oil. The Eagle Ford is loaded with all three. It has a dry gas window, a wet gas window, and an oil window. Producers have been developing all three areas of the Eagle Ford and MLPs have been there to provide the critical infrastructure and services that the producers need to bring those resources to market.

Exploration and Production (E&P) companies rely on the services that MLPs provide to develop new basins. When a basin is under development, MLPs team up with E&P companies to bring the production to market by gathering, processing, storing, and transporting the production from the wellhead to the end customers such as refineries, the petrochemical industry, or utilities. The MLP typically does not take possession of the commodity, but rather charges a toll or fee for the service. It is this fee-based, toll-taker business model that provides the potential for stable quarterly cash distributions to MLP unitholders like the Fund. When MLPs put in new infrastructure such as gathering lines, processing plants, storage facilities, and pipelines, those types of organic growth projects provide the opportunity for investors to enjoy higher future quarterly distributions from the cash flow generated once those projects go into service.

SEMI-ANNUAL REPORT 2012 • 5

The shale revolution is transforming many parts of the U.S. economy. For example, the electric utility industry has seen major changes in the past few years. The U.S. now generates as much electricity from natural gas as it does coal.

And the outlook for future natural gas demand looks bright with the issuance by the U.S. Environmental Protection Agency (EPA) in December 2011 of new mercury standards that will likely factor in to the potential conversion of up to 40% of the 1400 coal and oil fired power plants to natural gas generation in coming years1.

In addition to the changes taking place in the electric utility industry, the shale revolution is reshaping the petrochemical industry. The U.S. petrochemical industry is undergoing an industrial renaissance due to the cost advantage of shale based NGLs. Petrochemical companies have a choice of using either (1) naptha, which is a crude oil derivative, or (2) NGLs, such as ethane, as the feedstock for their petrochemical facilities. These plants convert the chosen feedstock into products which serve the plastics market. Because NGLs from the U.S. shale basins are viewed as a long-term cost advantaged feedstock, the petrochemical industry has committed to build five new, world class facilities. These plants are expected to have substantially higher profit margins when compared to European and Asian based naptha facilities.

Major New Ethane Cracker Constructions

| Company | Location | Estimated Startup | Ethylene tons/year (mm) | Ethylene lbs/year | Ethane Consumption (mbpd) |

| Exxon Mobil | Baytown, Texas | 2016 | 1.5 | 3,300 | 90.4 |

| Formosa Plastics | Point Comfort, Texas | 2016 | 0.8 | 1,760 | 48.2 |

| Dow Chemical | Freeport, Texas | 2016/2017 | 1.3 | 2,860 | 78.4 |

| ChevronPhillips | Cedar Bayou, Texas | 2017 | 1.5 | 3,300 | 90.4 |

| Royal Dutch Shell | Beaver County, PA | 2017* | 1.0* | 2,200* | 60.3* |

| Totals | | | 6.1 | 13,420 | 367.7 |

| Source: MLP Trader Weekly, Barclays Capital Inc., 06-11-1212 | *Not yet finalized. |

6 | MainGate MLP Fund EPA Issues New Regulation on Mercury, The Washington Post, 12-22-2011

MLPs are providing the midstream services and infrastructure that the petrochemical industry requires to ensure adequate NGL supply for these new facilities. The petrochemical industry has collectively committed to a multi-billion dollar set of long term investments, and MLPs will have to do their part in order for the petrochemical industry to enjoy the returns they expect from the construction of these new plants. For example, MLPs are building several new NGL pipelines to transport NGLs from production basins to market centers to meet this demand.

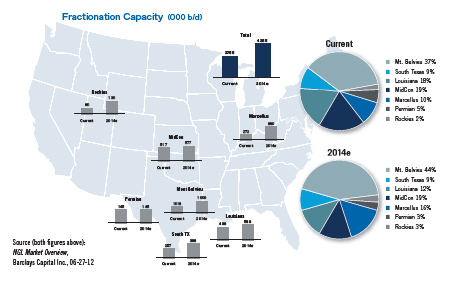

New Pipeline Corridors (2011–2014 Outlook)

In addition to the new NGL pipelines under construction by MLPs, there are numerous NGL fractionation facilities needed. A fractionator separates the various components of a mixed NGL stream into individual components such as ethane, propane, and butane. There are several fractionators under construction which should ensure that the petrochemical industry will have adequate NGL purity products, such as ethane, to meet the needs of these future petrochemical facilities.

SEMI-ANNUAL REPORT 2012 • 7

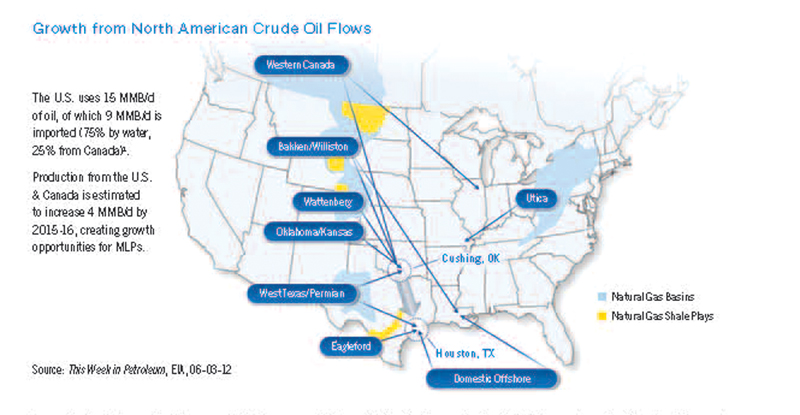

The crude oil market is also experiencing a revolution. The U.S. Energy Information Administration (EIA) estimates that North American crude oil production will grow by 4 million barrels per day (MMB/d) over the next five years2. With current U.S. waterborne crude imports of approximately 6.75 MMB/d, over 60% of those imports may be displaced based on the EIA estimates. This is a profound change with major implications. For example, U.S. demand for Middle Eastern crude, the U.S. balance of payments deficit, and U.S. foreign policy will all likely be impacted.

In order for this production growth to happen, MLPs will likely play a vital role. MLPs are involved in all of the major crude oil growth basins such as the Bakken, Eagle Ford, and Permian. There are numerous MLP organic growth projects that are ongoing that are designed to handle this changing flow of crude oil, with more expected in the future.

In summary, we see a bright future for MLPs as they play a critical role in the ongoing U.S. energy revolution.

The Fund’s portfolio is well positioned to benefit from potential future growth from new infrastructure that should serve as a critical link between the various shale basins and market centers for oil, NGLs, and natural gas.

Sincerely,

Geoffrey P. Mavar, Chairman Matthew G. Mead, CEO

Past performance is not a guarantee of future results.

Opinions expressed are those of MainGate and are subject to change, are not guaranteed, and should not be considered investment advice.

The information contained in this report is authorized for use when preceded or accompanied by a prospectus.

Mutual fund investing involves risk. Principal loss is possible. The Fund is nondiversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual security price volatility than a diversified fund. The Fund will invest in Master Limited Partnerships (MLPs) which concentrate investments in the natural resource sector and are subject to the risks of energy prices and demand and the volatility of commodity investments. Damage to facilities and infrastructure of MLPs may significantly affect the value of an investment and may incur environmental costs and liabilities due to the nature of their business. MLPs are subject to significant regulation and may be adversely affected by changes in the regulatory environment. Investments in smaller companies involve additional risks, such as limited liquidity and greater volatility. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. MLPs are subject to certain risks inherent in the structure of MLPs, including complex tax structure risks, limited ability for election or removal of management, limited voting rights, potential dependence on parent companies or sponsors for revenues to satisfy obligations, and potential conflicts of interest between partners, members and affiliates.

The Fund does not receive the same tax benefits of a direct investment in an MLP.

E&P refers to Exploration and Production energy MLPs which are engaged in the exploration and production of oil and gas properties.

The S&P 500 Index is a broad based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general. You cannot invest directly in an index.

Fund holdings and sector allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Please refer to the schedule of investments for a complete listing of fund holdings.

The MainGate MLP Fund is distributed by Quasar Distributors, LLC.

8

| MainGate MLP Fund 2 This Week in Petroleum, EIA, 06-03-12

Hypothetical Growth of a $10,000 Investment

unaudited

This chart illustrates the performance of a hypothetical $10,000 investment made in the Fund as of the Fund’s inception date on 2/17/11.

Assumes reinvestment of dividends and capital gains. This chart does not imply any future performance.

Average Annual Returns

May 31, 2012|unaudited

| | 1 Year | 5 Year | Since Inception | Inception Date |

| Class A (without sales load) | 4.29% | n/a | 3.25% | 2/17/11 |

| Class A (with sales load) | -1.71% | n/a | -1.41% | 2/17/11 |

| Class I | 4.59% | n/a | 3.57% | 2/17/11 |

| S&P 500 Index | -0.41% | n/a | 0.37% | 2/17/11 |

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 855.MLP.FUND (855.657.3863) or by visiting www.maingatefunds.com.

Class A and Class I shares were first available on February 17, 2011.

Class A performance has been restated to reflect the maximum sales charge of 5.75%. Class I is not subject to a sales charge.

The S&P 500 Index is a broad based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general. You cannot invest directly in an index.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of the Fund shares.

SEMI-ANNUAL REPORT 2012 • 9

Expense Example As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from December 1, 2011 to May 31, 2012. Actual Expenses For each class, the first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. | | Hypothetical Example for Comparison Purposes For each class, the second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect current and deferred income tax expense or any transactional costs, such as sales charges (loads) or exchange fees. Therefore, the second line of the table for each class is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these current and deferred income tax expense and transaction costs were included, your costs would have been higher. |

| | Beginning Account Value (12/01/2011) | Ending Account Value (05/31/2012) | Expenses Paid During Period(1) (12/01/2011 – 05/31/2012) | Net Annualized |

| Class A Actual | $1,000 | $1,033.60 | $8.90 | 1.75% |

| Class A Hypothetical (5% return before expenses) | $1,000 | $1,016.25 | $8.82 | 1.75% |

| Class I Actual | $1,000 | $1,034.60 | $7.63 | 1.50% |

| Class I Hypothetical (5% return before expenses) | $1,000 | $1,017.50 | $7.57 | 1.50% |

(1) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by 183 days (the number of days in the most recent period)/366 days (to reflect the period). |

(2) | Annualized expense ratio exlcudes current and deferred income tax expense. |

10 | MainGate MLP Fund

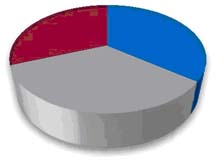

Allocation of Portfolio Assets

May 31, 2012|unaudited

(expressed as a percentage of total investments)

| Natural Gas Gathering/Processing* Crude/Refined Products Pipelines and Storage* Natural Gas/Natural Gas Liquid Pipelines and Storage* | 35.5% 33.9% 30.6% |  |

*Master Limited Partnerships and Related Companies

Schedule of Investments | May 31, 2012 | unaudited

Master Limited Partnerships and Related Companies, United States: 96.9%(1) | Shares | | Fair Value |

Crude/Refined Products Pipelines and Storage: 32.9%(1) | | | |

| Genesis Energy, L.P. | 160,000 | | $ | 4,603,200 |

Kinder Morgan Management, LLC(2) | 21,000 | | | 1,491,645 |

| Magellan Midstream Partners, L.P. | 53,000 | | | 3,646,930 |

| Oitanking Partners, L.P. | 124,500 | | | 3,871,950 |

| Plains All American Pipeline, L.P. | 80,000 | | | 6,282,400 |

| Sunoco Logistics Partners, L.P. | 43,000 | | | 1,448,240 |

| Tesoro Logistics, L.P | 112,000 | | | 3,531,360 |

| | | | | 24,875,725 |

Natural Gas/Natural Gas Liquid Pipelines and Storage: 29.6%(1) | | | |

| El Paso Pipeline Partners, L.P. | 93,500 | | | 3,067,735 |

| Energy Transfer Equity, L.P. | 97,000 | | | 3,524,010 |

| Enterprise Products Partners, L.P. | 124,000 | | | 6,046,240 |

| ONEOK Partners, L.P. | 30,000 | | | 1,638,000 |

| The Williams Companies, Inc.(3) | 119,000 | | | 3,633,070 |

| Western Gas Partners, L.P. | 52,000 | | | 2,292,680 |

| Williams Partners, L.P. | 42,000 | | | 2,221,800 |

| | | | | 22,423,535 |

Natural Gas Gathering/Processing: 34.4%(1) | | | | |

| Copano Energy, LLC | 232,100 | | | 6,220,280 |

Crosstex Energy, Inc.(3) | 350,000 | | | 4,728,500 |

| Crosstex Energy, L.P. | 48,000 | | | 748,320 |

| Eagle Rock Energy Partners, L.P. | 172,000 | | | 1,505,000 |

| MarkWest Energy Partners, L.P. | 70,000 | | | 3,355,800 |

| Regency Energy Partners, L.P. | 165,000 | | | 3,550,800 |

Targa Resources Corp.(3) | 84,000 | | | 3,724,560 |

| Targa Resources Partners, L.P. | 56,000 | | | 2,196,320 |

| | | | | 26,029,580 |

| | | | | |

| Total Master Limited Partnerships and Related Companies (Cost $72,910,098) | | | $ | 73,328,840 |

Total Investments: 96.9%(1) (Cost $72,910,098) | | | $ | 73,328,840 |

Other Assets in Excess of Liabilities: 3.1%(1) | | | | 2,362,681 |

Net Assets Applicable to Common Shareholders: 100.0%(1) | | | $ | 75,691,521 |

(1) Calculated as a percentage of net assets applicable to shareholders. (2) Security distributions are paid-in-kind. (3) MLP general partner interest.

See Accompanying Notes to the Financial Statements. SEMI-ANNUAL REPORT 2012 • 11

Statement of Assets and Liabilities

May 31, 2012 | unaudited

| Assets |

| Investments at fair value (cost $72,910,098) | $ | 73,328,840 | |

| Cash and cash equivalents | | 2,160,431 | |

| Receivable for Fund shares sold | | 338,343 | |

| Prepaid Expenses | | 50,113 | |

| Total assets | | 75,877,727 | |

| | | | |

| Liabilities | | | |

| Payable to Adviser | | 53,316 | |

| Deferred tax liability | | 41,498 | |

| Payable for Fund shares redeemed | | 4,510 | |

| Accrued expenses and other liabilities | | 86,882 | |

| Total liabilities | | 186,206 | |

| | | | |

| Net Assets aplicable to common shareholders | $ | 75,691,521 | |

| | | | |

| Net Assets Applicable to Common Stockholders Consist of | | | |

| Additional paid-in capital | $ | 75,623,813 | |

| Undistributed net investment loss, net of deferred taxes | | (163,857 | ) |

| Accumulated realized loss, net of deferred taxes | | (28,055 | ) |

| Net unrealized gain on investments, net of deferred taxes | | 259,620 | |

| Net assets applicable to common shareholders | $ | 75,691,521 | |

| Unlimited shares authorized | Class A | | | Class I | |

| Net assets | $ | 11,686,516 | | | $ | 64,005,005 | |

| Shares issued and outstanding | | 1,193,925 | | | | 6,514,079 | |

Net asset value, redemption price and minimum offering price per share | $ | 9.79 | | | $ | 9.83 | |

Maximum offering price per share ($9.79/0.9425) | $ | 10.39 | | | NA | |

Statement of Operations

December 1, 2011 – May 31, 2012 | unaudited

| Investment Income |

| Distributions received from master limited partnerships | $ | 1,786,914 | |

| Less: return of capital on distributions | | (1,726,719 | ) |

| Distribution income from master limited partnerships | | 60,195 | |

| Dividends from common stock | | 144,315 | |

| Total Investment Income | | 204,510 | |

Expenses | | | |

| Advisory fees | | 354,241 | |

| Professional fees | | 43,038 | |

| Reports to shareholders | | 40,152 | |

| Administrator fees | | 31,786 | |

| Transfer agent expense | | 28,505 | |

| Insurance expense | | 26,902 | |

| Registration fees | | 20,859 | |

| Trustees' fees | | 17,472 | |

| Compliance fees | | 17,160 | |

| Offering costs | | 12,092 | |

| Custodian fees and expenses | | 3,706 | |

| Fund accounting fees | | 549 | |

| 12b-1 shareholder servicing fee - Class A | | 11,362 | |

| Other expenses | | 5,643 | |

| Total Expenses | | 613,467 | |

| Less: expense reimbursement by Adviser | | (177,016 | ) |

| Net Expenses | | 436,451 | |

| Net Investment Loss, before Deferred Taxes | | (231,941 | ) |

| Deferred tax benefit | | 88,138 | |

| Net Investment Loss | | (143,803 | ) |

| | | | |

| Realized and Unrealized Loss on Investments | | | |

| Net realized loss on investments, before deferred taxes | | (23,414 | ) |

| Deferred tax benefit | | 8,897 | |

| Net realized loss on investments | | (14,517 | ) |

| Net change in unrealized depreciation of investments, before deferred taxes | | (610,064 | ) |

| Deferred tax benefit | | 231,824 | |

| Net change in unrealized depreciation of investments | | (378,240 | ) |

| Net Realized and Unrealized Loss on Investments | | (392,757 | ) |

| Decrease in Net Assets Applicable to Common Shareholders Resulting from Operations | $ | (536,560 | ) |

12 | MainGate MLP Fund See Accompanying Notes to the Financial Statements.

Statement of Changes in Net Assets

Operations | December 1, 2011 – May 31, 2012 unaudited | February 17, 2011(1) – November 30, 2011 |

| Net investment loss, net of deferred taxes | $(143,803) | $(20,054) |

| Net realized loss on investments, net deferred taxes | (14,517) | (13,538) |

| Net change in unrealized appreciation (depreciation) of investments, net of deferred taxes | (378,240) | 637,860 |

| Net increase (decrease) in net assets applicable to common shareholders resulting from operations | (536,560) | 604,268 |

Dividends and Distributions to Common Shareholders | | |

| Return of Capital | (1,744,681) | (233,071) |

| Total dividends and distribtuions to common shareholders | (1,744,681) | (233,071) |

Capital Share Transactions(Note 8) | | |

| Proceeds from shareholder subscriptions | 52,419,781 | 26,965,692 |

| Dividend reinvestments | 1,460,189 | 199,474 |

| Payments for redemptions | (1,802,671) | (1,640,900) |

| Net increase in net assets applicable to common shareholders from capital share transactions | 52,077,299 | 25,524,266 |

| Total increase in net assets applicable to common shareholders | 49,796,058 | 25,895,463 |

Net Assets | | |

| Beginning of period | 25,895,463 | $— |

| End of period | $75,691,521 | $25,895,463 |

| Undistributed net investment loss at the end of the period, net of income taxes | $(163,857) | $(20,054) |

(1) Commencement of operations.

See Accompanying Notes to the Financial Statements. SEMI-ANNUAL REPORT 2012 • 13

Financial Highlights: Class A Shares

| Per Common Share Data(2) | December 1, 2011 – May 31, 2012 unaudited | February 17, 2011(1) – November 30, 2011 |

| Net Asset Value, beginning of period | $9.76 | $— |

| Public offering price | | 10.00 |

| | | |

| Income from Investment Operations | | |

Net investment loss(3) | (0.04) | (0.05) |

Net realized and unrealized gain on investments(9) | 0.39 | 0.13 |

| Total increase from investment operations | 0.35 | 0.08 |

| Less Distributions to Common Shareholders | | |

| Return of Capital | (0.32) | (0.32) |

| Total distributions to common shareholders | (0.32) | (0.32) |

| Net Asset Value, end of period | $9.79 | $9.76 |

| Total Investment Return | 3.36%(4) | 0.80%(4) |

Supplemental Data and Ratios | | |

| Net assets applicable to common stockholders, end of period | $11,686,516 | $1,769,297 |

Ratio of expenses (including net deferred income tax (benefit) expense) to average net assets before waiver(5,6) | 1.21% | 19.59% |

Ratio of expenses (including net deferred income tax (benefit) expense) to average net assets after waiver(5,6) | 0.59% | 10.28% |

Ratio of expenses (excluding net deferred income tax (benefit) expense) to average net assets before waiver(5,6) | 2.37% | 11.06% |

Ratio of expenses (excluding net deferred income tax (benefit) expense) to average net assets after waiver(5,6) | 1.75% | 1.75% |

Ratio of net investment loss (including net deferred income tax benefit) to average net assets before waiver(5,7) | (1.34)% | (9.99)% |

Ratio of net investment loss (including net deferred income tax benefit) to average net assets after waiver(5,7) | (0.72)% | (0.68)% |

Ratio of net investment loss (excluding net deferred income tax benefit) to average net assets before waiver(5,7) | (1.65)% | |

Ratio of net investment loss (excluding net deferred income tax benefit) to average net assets after waiver(5,7) | (1.03)% | |

Portfolio turnover rate(8) | 71.46%(4) | 175.43%(4) |

| (1) | Commencement of operations. |

| (2) | Information presented relates to a share of common stock outstanding for the entire period. |

| (3) | Calculated using average shares outstanding method. |

| (5) | For periods less than one full year all income and expenses are annualized. |

| (6) | For the period from December 1, 2011 to May 31, 2012, the Fund accrued $328,859 in net deferred tax benefit, of which $52,741 is attributable to Class A. For the period from February 17, 2011 to November 30, 2011, the Fund accrued $370,357 in net deferred tax expense, of which $42,955 is attributable to Class A. |

| (7) | For the period from December 1, 2011 to May 31, 2012, the Fund accrued $88,138 in net deferred tax benefit, of which $14,135 is attributable to Class A. For the period from February 17, 2011 to November 30, 2011, the Fund accrued $12,291 in net deferred tax benefit, of which $1,426 is attributable to Class A. |

| (8) | Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing between the classes of shares issued. |

| (9) | Realized and unrealized gains and losses per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the period, and may not reconcile with the aggregate gains and losses in the Statement of Operations due to share transactions in the period. |

14 | MainGate MLP Fund See Accompanying Notes to the Financial Statements.

Financial Highlights: Class I Shares

| Per Common Share Data(2) | December 1, 2011 – May 31, 2012 unaudited | February 17, 2011(1) – November 30, 2011 |

| Net Asset Value, beginning of period | $9.79 | $— |

| Public offering price | | 10.00 |

| | | |

| Income from Investment Operations | | |

Net investment loss(3) | (0.02) | (0.03) |

Net realized and unrealized gain on investments(9) | 0.38 | 0.14 |

| Total increase from investment operations | 0.36 | 0.11 |

| Less Distributions to Common Shareholders | | |

| Return of Capital | (0.32) | (0.32) |

| Total distributions to common shareholders | (0.32) | (0.32) |

| Net Asset Value, end of period | $9.83 | $9.79 |

| Total Investment Return | 3.46%(4) | 1.10%(4) |

| | | |

| Supplemental Data and Ratios | | |

| Net assets applicable to common stockholders, end of period | $64,005,005 | $24,126,166 |

Ratio of expenses (including net deferred income tax (benefit) expense) to average net assets before waiver(5,6) | 0.96% | 19.34% |

Ratio of expenses (including net deferred income tax (benefit) expense) to average net assets after waiver(5,6) | 0.34% | 10.03% |

Ratio of expenses (excluding net deferred income tax (benefit) expense) to average net assets before waiver(5,6) | 2.12% | 10.81% |

Ratio of expenses (excluding net deferred income tax (benefit) expense) to average net assets after waiver(5,6) | 1.50% | 1.50% |

Ratio of net investment loss (including net deferred income tax benefit) to average net assets before waiver(5,7) | (1.09)% | (9.74)% |

Ratio of net investment loss (including net deferred income tax benefit) to average net assets after waiver(5,7) | (0.47)% | (0.43)% |

Ratio of net investment loss (excluding net deferred income tax benefit) to average net assets before waiver(5,7) | (1.40)% | (10.02)% |

Ratio of net investment loss (excluding net deferred income tax benefit) to average net assets after waiver(5,7) | (0.78)% | (0.72)% |

Portfolio turnover rate(8) | 71.46%(4) | 175.43%(4) |

| (1) | Commencement of operations. |

| (2) | Information presented relates to a share of common stock outstanding for the entire period. |

| (3) | Calculated using average shares outstanding method. |

| (4) | Not Annualized. |

| (5) | For periods less than one full year all income and expenses are annualized. |

| (6) | For the period from December 1, 2011 to May 31, 2012, the Fund accrued $328,859 in net deferred tax benefit, of which $276,118 is attributable to Class I. For the period from February 17, 2011 to November 30, 2011, the Fund accrued $370,357 in net deferred tax expense, of which $327,402 is attributable to Class I. |

| (7) | For the period from December 1, 2011 to May 31, 2012, the Fund accrued $88,138 in net deferred tax benefit, of which $74,003 is attributable to Class I. For the period from February 17, 2011 to November 30, 2011, the Fund accrued $12,291 in net deferred tax benefit, of which $10,865 is attributable to Class I. |

| (8) | Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing between the classes of shares issued. |

| (9) | Realized and unrealized gains and losses per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the period, and may not reconcile with the aggregate gains and losses in the Statement of Operations due to share transactions in the period. |

See Accompanying Notes to the Financial Statements. SEMI-ANNUAL REPORT 2012 • 15

Notes to Financial Statements

May 31, 2012|unaudited

1. Organization

MainGate MLP Fund (the “Fund”), a series of MainGate Trust (the “Trust”), is registered under the Investment Company Act of 1940 as an open-end, non-diversified investment company and was established under the laws of Delaware by an Agreement and Declaration of Trust dated November 3, 2010. The Fund’s investment objective is total return. The Fund commenced operations on February 17, 2011.

The Fund offers two classes of shares, Class A and Class I. Class A shares are subject to a 5.75% front-end sales charge. Class I shares have no sales charge.

2. Significant Accounting Policies

A. Use of Estimates.The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the recognition of distribution income and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

B. Investment Valuation.The Fund uses the following valuation methods to determine fair value as either current market value for investments for which market quotations are available, or if not available, a fair value, as determined in good faith pursuant to such policies and procedures as may be approved by the Trust’s Board of Trustees (“Board of Trustees”) from time to time. The valuation of the portfolio securities of the Fund currently includes the following processes:

| • | Equity Securities:Securities listed on a securities exchange or an automated quotation system for which quotations are readily available, including securities traded over the counter, will be valued at the last quoted sale price on the principal exchange on which they are traded on the valuation date (or at approximately 4:00 p.m. Eastern Time if a security’s principal exchange is normally open at that time), or, if there is no such reported sale on the valuation date, at the most recent quoted bid price. |

| • | Fixed Income Securities:Debt and fixed income securities will be priced by independent, third-party pricing agents approved by the Board of Trustees. These third-party pricing agents will employ methodologies that they believe are appropriate, including actual market transactions, broker-dealer supplied valuations, matrix pricing, or other electronic data processing techniques. These techniques generally consider such factors as security prices, yields, maturities, call features, ratings and developments relating to specific securities in arriving at valuations. Debt obligations with remaining maturities of sixty days or less will be valued at their amortized cost, which approximates fair market value. |

| • | Foreign Securities:Foreign securities are often principally traded on markets that close at different hours than U.S. markets. Such securities will be valued at their most recent closing prices on the relevant principal exchange even if the close of that exchange is earlier than the time of the Fund’s net asset value (“NAV”) calculation. However, securities traded in foreign markets which remain open as of the time of the NAV calculation will be valued at the most recent sales price as of the time of the NAV calculation. In addition, prices for certain foreign securities may be obtained from the Fund’s approved pricing sources. The Adviser must also monitor for the occurrence of significant events that may cast doubts on the reliability of previously obtained market prices for foreign securities held by the Fund. The prices for foreign securities will be reported in local currency and converted to U.S. dollars using currency exchange rates. Exchange rates will be provided daily by recognized independent pricing agents. The exchange rates used for the conversion will be captured as of the London close each day. |

C. Security Transactions, Investment Income and Expenses.Security transactions are accounted for on the date the securities are purchased or sold (trade date). Realized gains and losses are reported on a specific identified cost basis. Interest income is recognized on the accrual basis, including amortization of premiums and accretion of discounts. Distributions are recorded on the ex-dividend date. Distributions received from the Fund’s investments in master limited partnerships (“MLPs”) generally are comprised of ordinary income, capital gains and return of capital from the MLP. The Fund records investment income on the ex-date of the distributions. For financial statement purposes, the Fund uses return of capital and income estimates to allocate the dividend income received. Such estimates are based on historical information available from each MLP and other industry sources. These estimates may subsequently be revised based on information received from MLPs after their tax reporting periods are concluded, as the actual character of these distributions is not known until after the fiscal year end of the Fund.

The Fund estimates the allocation of investment income and return of capital for the distributions received from MLPs within the Statement of Operations. The Fund has estimated approximately 5% of the distributions to be from investment income with the remaining balance to be return of capital.

Expenses are recorded on the accrual basis. The Fund expensed organizational costs as incurred and amortizes offering costs over a one-year period from the commencement of operations. These costs consisted of legal fees pertaining to the Fund’s shares offered for sale, preparing the initial registration statement and printing the prospectus, and SEC and state registration fees. For the period February 17, 2011 (commencement of operations) through November 30, 2011, $43,784 of offering costs were amortized. For the period ended May 31, 2012, the remaining offering costs of $12,092 have been amortized and included in offering costs in the Statement of Operations.

D. Dividends and Distributions to Shareholders.Dividends and distributions to common shareholders will be recorded on the ex-dividend date. The character of dividends and distributions to common shareholders made during the period may differ from their ultimate characterization for federal income tax purposes. For the period ended May 31, 2012, the Fund’s dividends and distributions were expected to be comprised of 100% return of capital. The tax character of distributions paid for the period ended May 31, 2012 will be determined in early 2013.

E. Federal Income Taxation.The Fund, taxed as a corporation, is obligated to pay federal and state income tax on its taxable income. Currently, the maximum marginal regular federal income tax rate for a corporation is 35%. The Fund may be subject to a 20% federal alternative minimum tax on its federal alternative minimum taxable income to the extent that its alternative minimum tax exceeds its regular federal income tax.

The Fund invests its assets primarily in MLPs, which generally are treated as partnerships for federal income tax purposes. As a limited partner in the MLPs, the Fund reports its allocable share of the MLP’s taxable income in computing its own taxable income. The Fund’s tax expense or benefit is included in the Statement of Operations based on the component of income or gains (losses) to which such expense or benefit relates. Deferred income taxes reflect the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. A valuation allowance is recognized if, based on the weight of available evidence, it is more likely than not that some portion or all of the deferred income tax asset will not be realized.

The Fund’s policy is to classify interest and penalties associated with underpayment of federal and state income taxes as an income tax expense on the Statement of Operations. For the period ended May 31, 2012, the Fund did not have interest or penalties associated with underpayment of income taxes.

F. Cash and Cash Equivalents.The Fund considers all highly liquid investments purchased with initial maturity equal to or less than three months to be cash equivalents.

G. Cash Flow Information.The Fund intends to make quarterly distributions from investments, which include the amount received as cash distributions from MLPs and common stock dividends. These activities will be reported in the Statements of Changes in Net Assets.

H. Indemnifications.Under the Trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. In addition, in the normal course of business, the Trust may enter into contracts that provide general indemnification to other parties. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust that have not yet occurred, and may not occur. However, the Trust has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

I. Recent Accounting Pronouncement.In May 2011, the FASB issued ASU No. 2011-04 “Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements” in GAAP and the International Financial Reporting Standards (“IFRSs”). ASU No. 2011-04 amends FASB ASC Topic 820, Fair Value Measurements and Disclosures, to establish common requirements for measuring fair value and for disclosing information about fair value measurements in accordance with GAAP and IFRSs. ASU No. 2011-04 is effective for fiscal years beginning after December 15, 2011 and for interim periods within those fiscal years. Management is currently evaluating these amendments and does not believe they will have a material impact on the Fund’s financial statements.

3. Fair Value Measurements

Various inputs that are used in determining the fair value of the Fund’s investments are summarized in the three broad levels listed below:

| • | Level 1: | quoted prices in active markets for identical securities |

| • | Level 2: | other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| • | Level 3: | significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

SEMI-ANNUAL REPORT 2012 • 17

These inputs are summarized in the three broad levels that follow.

| | | Fair Value Measurements at Reporting Date Using: |

Description | Fair Value at May 31, 2012 | Quoted Prices in Active Markets for IdenticalAssets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) |

| Equity Securities | | | | |

Master Limited Partnerships and and Related Companies(1) | $73,328,840 | $73,328,840 | $ — | $ — |

| Total | | | $ — | $ — |

(1) All other industry classifications are identified in the Schedule of Investments.

The Fund did not hold Level 2 or Level 3 investments at any time during the period December 1, 2011 to May 31, 2012. There were no significant transfers into and out of Level 1 and Level 2 during the current period presented. It is the Fund’s policy to record transfers between Level 1 and Level 2 at the end of the reporting period.

4. Concentrations of Risk

The Fund’s investment objective is to seek to generate total return. The Fund seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its net assets, plus any borrowings for investment purposes, in MLP interests.

5. Agreements and Related Party Transactions

The Trust has entered into an Investment Advisory Agreement (the “Agreement”) with Chickasaw Capital Management, LLC (the “Adviser”). Under the terms of the Agreement, the Fund will pay the Adviser a fee, payable at the end of each calendar month, at an annual rate equal to 1.25% of the average daily net assets of the Fund.

The Adviser paid the initial organizational expenses of the Fund, which amounted to $51,184. The Adviser has agreed to waive its advisory fee and/or reimburse certain expenses of the Fund, until at least March 31, 2013, but only to the extent necessary so that the Fund’s total annual expenses, excluding brokerage fees and commissions; borrowing costs (such as (a) interest and (b) dividend expenses on securities sold short); taxes, including accrued deferred tax liability; any indirect expenses, such as acquired fund fees and expenses; 12b-1 fees, and extraordinary expenses, do not exceed 1.50% of the average daily net assets of each class of the Fund. Any payment by the Adviser of the Fund’s operating, organizational and offering expenses are subject to repayment by the Fund in the three fiscal years following the fiscal year in which the payment was made; provided that the Fund is able to make the repayment without exceeding the 1.50% expense limitation. For the period from February 17, 2011 (commencement of operations) to November 30, 2011, the Adviser waived and reimbursed expenses in the amount of $454,971, $403,787 after commencement and $51,184 related to organizational costs prior to commencement, which can be recouped on or before November 30 and February 3, 2014, respectively. For the period from December 1, 2011 to May 31, 2012, the Adviser waived expenses in the amount of $177,016, which can be recouped on or before November 30, 2015.

Certain Trustees and Officers of the Trust are also Officers of the Adviser.

The Fund has entered into a Rule 12b-1 distribution agreement with Quasar Distributors, LLC (“Quasar”). Class A shareholders pay Rule 12b-1 fees to Quasar at the annual rate of 0.25% of average daily net assets. For the period from December 1, 2011 through May 31, 2012, 12b-1 distribution expenses of $11,362 were accrued by Class A shares.

The Fund has engaged U.S. Bancorp Fund Services, LLC to serve as the Fund’s administrator. The Fund pays the administrator a monthly fee computed at an annual rate of 0.10% of the first $75,000,000 of the Fund’s average daily net assets, 0.08% on the next $250,000,000 of average daily net assets and 0.05% on the balance of the Fund’s average daily net assets, with a minimum annual fee of $64,000, imposed upon the Fund reaching certain asset levels.

U.S. Bancorp Fund Services, LLC serves as the Fund’s transfer agent, dividend paying agent, and agent for the automatic dividend reinvestment plan. The Fund pays the transfer agent a $30,000 flat fee, imposed upon the Fund reaching certain asset levels, plus transaction and other out-of-pocket charges.

U.S. Bank, N.A. serves as the Fund’s custodian. The Fund pays the custodian a monthly fee computed at an annual rate of 0.0075% of the first $250 million of market value and 0.0050% of the balance, with a minimum annual fee of $4,800, imposed upon Fund reaching certain asset levels.

6. Income Taxes

Deferred income taxes reflect the net tax effect of temporary differences between the carrying amount of assets and liabilities for financial reporting and tax purposes. A valuation allowance is recognized if, based on the weight of available evidence, it is more likely than not that some portion or all of a deferred income tax asset will not be realized. From time to time, as new information becomes available, the Fund will modify its estimate or assumption regarding the deferred tax liability or asset. Components of the Fund’s deferred tax assets and liabilities as of May 31, 2012, are as follows:

| Deferred tax assets: | |

| Net operating loss carryforward (tax basis) | $385,664 |

| Capital loss carryforward (tax basis) | 88,321 |

| Total deferred tax assets | 473,985 |

| Less: Deferred tax liabilities: | |

| Unrealized gain on investment securities (tax basis) | (515,483) |

| Net deferred tax asset (liability) | $(41,498) |

The net operating loss carryforward and capital loss carryforward are available to offset future taxable income. The Fund has the following net operating loss and capital loss amounts:

| Fiscal Year Ended Net Operating Loss | Amount | Expiration |

| November 30, 2011 | $55,821 | November 30, 2031 |

| November 30, 2012 | 959,083 | November 30, 2032 |

| Total Fiscal Year Ended Net Operating Loss | $1,014,904 | |

| | | |

| Fiscal Year Ended Capital Loss | | |

| November 30, 2011 | $143,751 | November 30, 2016 |

| November 30, 2012 | 88,673 | November 30, 2017 |

| Total Fiscal Year Ended Capital Loss | $232,424 | |

For corporations, capital losses can only be used to offset capital gains and cannot be used to offset ordinary income. The capital loss may be carried forward for 5 years and, accordingly, would begin to expire as of November 30, 2016. The net operating loss can be carried forward for 20 years and, accordingly, would begin to expire as of November 30, 2031.

Total income tax benefit (current and deferred) differs from the amount computed by applying the federal statutory income tax rate of 35% to net investment income and realized and unrealized gains (losses) on investments before taxes for the period ended May 31, 2012, as follows:

| Application of statutory income tax rate | $(302,897) |

| State income taxes (net of federal benefit) | (25,962) |

| Total tax expense | $(328,859) |

At May 31, 2012, the cost basis of investments was $71,972,306 and gross unrealized appreciation and depreciation of investments for federal income tax purposes were as follows:

| Gross unrealized appreciation | $1,994,870 |

| Gross unrealized depreciation | (638,336) |

| Net unrealized appreciation | $1,356,534 |

The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Fund’s tax positions, and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on U.S. tax returns and state tax returns filed since inception of the Fund. No income tax returns are currently under examination. The tax periods since inception remain subject to examination by the tax authorities in the United States. Due to the nature of the Fund’s investments, the Fund may be required to file income tax returns in several states. The Fund is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next 12 months.

7. Investment Transactions

For the period December 1, 2011 to May 31, 2012, the Fund purchased (at cost) and sold securities (proceeds) in the amount of $89,626,697 and $39,715,808 (excluding short-term securities), respectively.

SEMI-ANNUAL REPORT 2012 • 19

8. Common Stock

Transactions of shares of the Fund were as follows:

| | December 1, 2011 – May 31, 2012 unaudited | | February 17, 2011(1) – November 30, 2011 |

| | | | | | |

| Class A Shares | Amount | Shares | | Amount | Shares |

| Sold | $10,717,595 | 1,063,829 | | $3,253,057 | |

| Dividends Reinvested | 183,980 | 17,684 | | 19,579 | 2,080 |

| Redeemed | (712,645) | (68,808) | | (1,562,610) | |

| Net Increase | $10,188,930 | 1,012,705 | | $1,710,026 | 181,220 |

| | | | | | |

| Class I Shares | Amount | Shares | | Amount | Shares |

| Sold | $41,702,186 | 4,033,381 | | $23,712,635 | 2,449,150 |

| Dividends Reinvested | 1,276,209 | 122,559 | | 179,895 | 23,981 |

| Redeemed | (1,090,026) | (106,853) | | (78,290) | (8,139) |

| Net Increase | $41,888,369 | 4,049,087 | | $23,814,240 | 2,464,992 |

(1) Commencement of operations.

9. Subsequent Events

The Fund has adopted standards which establish general standards of accounting for disclosure of events that occur after the Statement of Assets & Liabilities date, but before the financial statements are issued. The Fund has performed an evaluation of subsequent events through the date the financial statements were issued.

The Fund declared a distribution of $0.1575 per share payable on July 25, 2012 to shareholders of record on July 23, 2012.

Additional Information

May 31, 2012|unaudited

Trustee and Officer Compensation

The Fund does not compensate any of its trustees who are interested persons nor any of its officers. For the period ended May 31, 2012, the aggregate compensation paid by the Fund to the independent trustees was $7,500. The Fund did not pay any special compensation to any of its trustees or officers. The Fund’s Statement of Additional Information includes additional information about the trustees and is available on the Fund’s Web site at www.maingatefunds.com or the SEC’s Web site at www.sec.gov.

Cautionary Note Regarding Forward-Looking Statements

This report contains “forward-looking statements” as defined under the U.S. federal securities laws. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will” and similar expressions identify forward-looking statements, which generally are not historical in nature. Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to materially differ from the Fund’s historical experience and its present expectations or projections indicated in any forward-looking statements. These risks include, but are not limited to, changes in economic and political conditions; regulatory and legal changes; MLP industry risk; concentration risk; energy sector risk; commodities risk; MLP and other tax risks, such as deferred tax assets and liabilities risk; and other risks discussed in the Fund’s filings with the SEC. You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. The Fund undertakes no obligation to update or revise any forward-looking statements made herein. There is no assurance that the Fund’s investment objectives will be attained.

Proxy Voting Policies

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities owned by the Fund and information regarding how the Fund voted proxies relating to the portfolio of securities during the period since inception through June 30, 2011 are available to shareholders without charge by visiting the SEC’s Web site at www.sec.gov.

Form N-Q

The Fund files its complete schedule of portfolio holdings for the first and third quarters of each fiscal year with the SEC on Form N-Q. The Fund’s Form N-Q and statement of additional information are available without charge by visiting the SEC’s Web site at www.sec.gov. In addition, you may review and copy the Fund’s Form N-Q at the SEC’s Public Reference Room in Washington D.C. You may obtain information on the operation of the Public Reference Room by calling (800) SEC-0330.

Householding

In an effort to decrease costs, the Fund intends to reduce the number of duplicate prospectuses, annual and semi-annual reports, proxy statements and other similar documents you receive by sending only one copy of each to those addresses shared by two or more accounts and to shareholders that the Transfer Agent reasonably believes are from the same family or household. Once implemented, if you would like to discontinue householding for your accounts, please call toll-free at 855.MLP.FUND (855.657.3863) to request individual copies of these documents. Once the Transfer Agent receives notice to stop householding, the Transfer Agent will begin sending individual copies thirty days after receiving your request. This policy does not apply to account statements.

SEMI-ANNUAL REPORT 2012 • 21

Privacy Policy

The following is a description of the Fund’s policies regarding disclosure of nonpublic personal information that you provide to the Fund or that the Fund collects from other sources. In the event that you hold shares of the Fund through a broker-dealer or other financial intermediary, the privacy policy of your financial intermediary would govern how your nonpublic personal information would be shared with nonaffiliated third parties.

Categories of Information the Fund Collects.The Fund collects the following nonpublic personal information about you:

• Information the Fund receives from you on applications or other forms, correspondence, or conversations (such as your name, address, phone number, social security number, and date of birth); and

• Information about your transactions with the Fund, its affiliates, or others (such as your account number and balance, payment history, cost basis information, and other financial information).

Categories of Information the Fund Discloses.The Fund does not disclose any nonpublic personal information about its current or former shareholders to unaffiliated third parties, except as required or permitted by law. The Fund is permitted by law to disclose all of the information it collects, as described above, to service providers (such as the Fund’s custodian, administrator, transfer agent, accountant and legal counsel) to process your transactions and otherwise provide services to you.

Confidentiality and Security.The Fund restricts access to your nonpublic personal information to those persons who require such information to provide products or services to you. The Fund maintains physical, electronic, and procedural safeguards that comply with federal standards to guard your nonpublic personal information.

Disposal of Information. The Fund, through its transfer agent, has taken steps to reasonably ensure that the privacy of your nonpublic personal information is maintained at all times, including in connection with the disposal of information that is no longer required to be maintained by the Fund. Such steps shall include, whenever possible, shredding paper documents and records prior to disposal, requiring off-site storage vendors to shred documents maintained in such locations prior to disposal, and erasing and/or obliterating any data contained on electronic media in such a manner that the information can no longer be read or reconstructed.

Fund Service Providers

May 31, 2012

Board of Trustees

Geoffrey P. Mavar*, Chairman of the Board

David C. Burns, Independent Trustee

Moss W. Davis, Independent Trustee

Marshall K. Gramm, Independent Trustee

Matthew G. Mead*, Interested Trustee

Robert A. Reed, Lead Independent Trustee

Barry A. Samuels, Independent Trustee

Darrison N. Wharton, Independent Trustee

Officers

Matthew G. Mead*, President and Chief Executive Officer

Geoffrey P. Mavar*, Treasurer and Chief Financial Officer

Salvatore Faia, Chief Compliance Officer

Debra McAdoo*, Secretary

Investment Advisor

Chickasaw Capital Management, LLC

6075 Poplar Avenue, Suite 402, Memphis, TN 38119

Distributor

Quasar Distributors, LLC

615 East Michigan Street, Milwaukee, WI 53202

Custodian

U.S. Bank, N.A.

1555 N. River Center Drive, Suite 302, Milwaukee, WI 53212

Transfer Agent

U.S. Bancorp Fund Services, LLC

615 East Michigan Street, 3rd Floor, Milwaukee, WI 53202

Administrator

U.S. Bancorp Fund Services, LLC

777 East Wisconsin Street, 5th Floor, Milwaukee, WI 53202

Legal Counsel

Thompson Couburn LLP

One U.S. Bank Plaza, St. Louis, MO 63101

Independent Registered Public Accounting Firm

Cohen Fund Audit Services, Ltd.

800 Westpoint Parkway, Suite 1100, Westlake, OH 44145

*Employed by Chickasaw Capital Management, LLC.

Item 2. Code of Ethics.

Not applicable for semi-annual reports.

Item 3. Audit Committee Financial Expert.

Not applicable for semi-annual reports.

Item 4. Principal Accountant Fees and Services.

Not applicable for semi-annual reports.

Item 5. Audit Committee of Listed Registrants.

Not applicable to registrants who are not listed issuers (as defined in Rule 10A-3 under the Securities Exchange Act of 1934).

Item 6. Investments.

| (a) | Schedule of Investments is included as part of the report to shareholders filed under Item 1 of this Form. |

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable to open-end investment companies.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable to open-end investment companies.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable to open-end investment companies.

Item 10. Submission of Matters to a Vote of Security Holders.

Not Applicable.

Item 11. Controls and Procedures.

| (a) | The Registrant’s President/Chief Executive Officer and Treasurer/Chief Financial Officer have reviewed the Registrant's disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940 (the “Act”)) as of a date within 90 days of the filing of this report, as required by Rule 30a-3(b) under the Act and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934. Based on their review, such officers have concluded that the disclosure controls and procedures are effective in ensuring that information required to be disclosed in this report is appropriately recorded, processed, summarized and reported and made known to them by others within the Registrant and by the Registrant’s service provider. |

| (b) | There were no changes in the Registrant's internal control over financial reporting (as defined in Rule 30a-3(d) under the Act) that occurred during the second fiscal quarter of the period covered by this report that has materially affected, or is reasonably likely to materially affect, the Registrant's internal control over financial reporting. |

Item 12. Exhibits.

| (a) | (1) Any code of ethics or amendment thereto, that is the subject of the disclosure required by Item 2, to the extent that the registrant intends to satisfy Item 2 requirements through filing an exhibit. Not Applicable. |

(2) A separate certification for each principal executive and principal financial officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. Filed herewith.

(3) Any written solicitation to purchase securities under Rule 23c-1 under the Act sent or given during the period covered by the report by or on behalf of the registrant to 10 or more persons. Not applicable to open-end investment companies.

| (b) | Certifications pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. Furnished herewith. |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

(Registrant) MainGate Trust

By (Signature and Title) /s/ Matthew G. Mead

Matthew G. Mead, President & Chief Executive Officer

Date 7/30/12

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

By (Signature and Title) /s/ Matthew G. Mead

Matthew G. Mead, President & Chief Executive Officer

Date 7/30/12

By (Signature and Title) /s/ Geoffrey P. Mavar

Geoffrey P. Mavar, Treasurer & Chief Financial Officer

Date 7/30/12