In November 2010, the Company issued 20,000,000 shares of common stock for $60,000 to investors ($0.003 per share – 33 investors).

The methodologies, approaches and assumptions that the Company used are consistent with the American Institute of Certified Public Accountants, “Practice Guide on Valuation of Privately-Held Company Equity Securities Issued as Compensation”, considering numerous objective and subjective factors to determine common stock fair market value at each issuance date, including but not limited to the following factors: (a) arm’s length private transactions; (b) shares issued for cash as a basis to determine the value for shares issued for services to non-related third parties; and (c) fair value of service provided to non-related third parties as a basis to determine value per share. With respect to the sale of the securities identified above, the Company has relied on the exemption provisions of Section 4(2), Regulation S or Section 3(a) 10 of the Securities Act of 1933, as amended. The sale was made to a sophisticated or accredited investor, as defined in Rule 502, or were issued pursuant to a specific exemption.

In connection with the asset purchase, the Company also issued 40,000 shares of common stock to a former supplier of the vendor for mining related information of the assets purchased valued at $20,000 along with cash consideration of CDN$20,000.

On March 17, 2014, the Company increased the authorized amount of common stock from 150,000,000 common shares to 500,000,000 common shares. There were no changes to the authorized amount of preferred stock.

As of March 31, 2014, the Company has 94,626,000 shares of common stock issued and outstanding.

On August 12, 2013, the Company approved and enacted the 2013 Stock Incentive Plan (the “Plan”). Under the 2013 Stock Incentive Plan, the Company may grant options or share awards to its full-time employees, executive officers, directors and consultants up to a maximum of 8,000,000 common shares. Under the Plan, the exercise price of each option has been established at $0.25. Stock options vest as stipulated in the stock option agreement and their maximum term is 8 years.

The following table summarizes information about the Company’s stock options as of March 31, 2014 and December 31, 2013:

The following table summarizes the ranges of exercise prices of outstanding and exercisable options held by officers and directors as of March 31, 2014:

There were no stock options granted during the three months ended March 31, 2014. The fair value of the stock options granted during the year ended December 31, 2013 amounted to $239,930 and was determined using the Black-Scholes option–pricing model using the following weighted-average assumptions:

Stock options-based compensation expense included in the condensed consolidated statements of operations and comprehensive loss for the three months ended March 31, 2014 and 2013 was $29,991 and $0, respectively.

The following table summarizes the ranges of exercise prices of outstanding warrants as of March 31, 2014:

Fixed assets consist of the following as of March 31, 2014 and December 31, 2013:

As of March 31, 2014 and 2013, only the computers, office equipment and vehicle have been placed into service. Depreciation for the three months ended March 31, 2014 and 2013 was $3,656 and $1,392, respectively.

Deferred finance fees result from the issuance of share warrants as finders’ fees in connection with flow-through financing completed on December 23, 2013 and described in Note 4. The fair value of the warrants amounted to $25,431 and was determined using the Black-Scholes option–pricing model. The deferred financing fees are being amortized over the life of the warrants which is 2 years. Amortization of deferred financing fees for the three months ended March 31, 2014 and 2013 was $3,179 and $0, respectively.

As of March 31, 2014, there is no provision for income taxes, current or deferred.

At December 31, 2013, the Company had a net operating loss carry forward in the approximate amount of $4,200,000 available to offset future taxable income through 2034. The Company has established a valuation allowance equal to the full amount of the deferred tax assets due to the uncertainty of the utilization of the operating losses in future periods.

The Company entered into a promissory note with an investor on May 13, 2011 in the amount of CDN$500,000 that matures on May 31, 2014. The note had a default interest rate of 5% per annum should repayment not occur by the maturity date and the Company be in default of the promissory note agreement. In connection with the promissory note, the Company issued 1,000,000 shares of stock valued at CDN$3,000 in June 2011 for prepaid interest.

On March 4, 2013, 754 2542 Canada Inc. executed an agreement with the Company whereby 754 2542 Canada Inc. agreed to accept 2,500,000 shares of common stock in satisfaction of all amounts due and owing 754 2542 Canada Inc. pursuant to the promissory note executed between the parties on May 13, 2011. As a result, the promissory note has been converted, and the Company recorded a loss on conversion of this note of $125,000 in the consolidated statement of operations in 2013.

The Company had the following financial commitments, represented by rental lease agreements, as of March 31, 2014:

Rent expense under the lease agreements for the three months ended March 31, 2014 and 2013 were $9,329 and $5,151, respectively.

The Company adopted certain provisions of ASC Topic 820. ASC 820 defines fair value, provides a consistent framework for measuring fair value under generally accepted accounting principles and expands fair value financial statement disclosure requirements. ASC 820’s valuation techniques are based on observable and unobservable inputs. Observable inputs reflect readily obtainable data from independent sources, while unobservable inputs reflect our market assumptions. ASC 820 classifies these inputs into the following hierarchy:

Level 1 inputs: Quoted prices for identical instruments in active markets.

Level 2 inputs: Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations whose inputs are observable or whose significant value drivers are observable.

Level 3 inputs: Instruments with primarily unobservable value drivers.

The following table represents the fair value hierarchy for those financial assets and liabilities measured at fair value on a recurring basis as of March 31, 2014:

On October 30, 2013 and November 27, 2013, the Company entered into binding agreements for the asset acquisitions of an undivided one hundred percent (100%) interest in certain mineral claims and mining assets located in the Province of Quebec’s Montauban and Chavigny townships near Grondines West, in the county of Portneuf, specifically Mining Lease BM 748 and Mining Concession Miniere CM 410. The purchase price was CDN$75,000 together with the issuance of 1,050,000 common shares of the Company. The common shares for the acquisition were valued at their fair market value on the day they were issued which totaled $496,860. In connection with the asset purchase, the Company also issued 40,000 shares of common stock to a former supplier of the vendor for mining related information of the assets purchased valued at $20,000 along with cash consideration of CDN$20,000. The Company had been awaiting confirmation of the contemplated transaction from a bankruptcy court in Montreal, Quebec overviewing the financial restructuring of the vendor. The bankruptcy court approved the transaction on April 17, 2014 and have been included in Mining rights on the consolidated balance sheet as at March 31, 2014.

On April 14, 2014, the Company entered into an asset purchase agreement for an undivided one hundred percent (100%) interest in fifty seven (57) mining claims located in the Province of Quebec’s Montauban and Chavigny townships near Grondines West, in the county of Portneuf. The purchase price was CDN$50,000. The transfer of the mining claims is currently being completed by the Province of Quebec.

ITEM 2 -MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

DNA Precious Metals, Inc., a Nevada corporation (the “Company”), is an exploratory stage mining company. The Company may also be referred to as “we”, “our” or “us”, unless the context provides for otherwise.

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations discusses significant factors that have affected our financial position and operations during the three month period ended March 31, 2014 and 2013. This discussion also includes events that occurred after the end of the last fiscal quarter end and contains both historical and forward-looking statements.

When used in this discussion, the words “expect(s)”, “feel(s)”,”believe(s)”, “will”, “may”, “anticipate(s)” “intend(s)” and similar expressions are intended to identify forward-looking statements. Such statements are subject to certain risks and uncertainties, which could cause actual results to differ materially from those projected.

Background

We are a Nevada corporation organized on June 2, 2006. We were originally incorporated under the name, Celtic Capital, Inc. On October 20, 2008, we changed our name to Entertainment Education Arts, Inc. On May 12, 2010, we changed our name to DNA Precious Metals, Inc. to accurately reflect our new business plan.

Our Business

We are an exploration stage mining company initially involved in the business of processing tailings from previously extracted ore. Our Montauban Mining Project is located in the Montauban and Chavigny townships near Grondines-West in Portneauf County, Quebec, Canada (the “Property”). Our business objective is to identify proven reserves of gold, silver and other base metals, construct a mill, build out the Property’s infrastructure and place the mine into production. The Property does not contain any known ore reserves according to the definition of ore reserves under Industry Guide 7 promulgated by the Securities and Exchange Commission (“SEC”) as well as various SEC mining related leases. Further work is required on the Property before a final determination may be made regarding the economic and legal feasibility of a mining venture relative to the Property. There is no assurance that a commercially viable deposit will be proven through our exploration efforts. The funds we spend on our properties may be unsuccessful in measuring ore reserves that meet SEC guidelines.

PROPERTY DESCRIPTION AND LOCATION

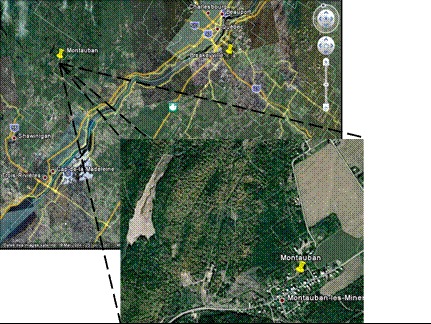

The Montauban Mine Property is composed of 15 mining claims totaling 340.36 hectares located in the Montauban-les-Mines sector of the Notre-Dame-de-Montauban municipality, in the Montauban Township, Portneuf County, Province of Quebec. The Property is located 120 km east of Quebec City and 80 km north of Trois-Rivières. The Montauban Tailings are located one kilometer west of Montauban-les-Mines with multiple land accesses. Manpower, water and electric power are easily available within the very same distance.

Figure I: Montauban Mine Property Location Map

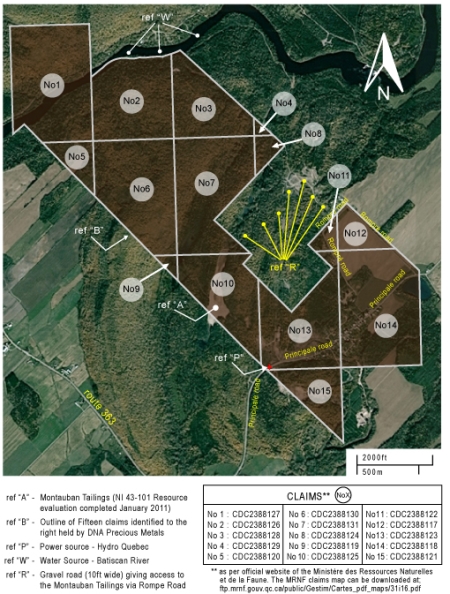

Pertinent data concerning the claims are presented in table I, these coming from the Quebec Government Ministry of Natural Resources GESTIM website.

Table I: List of Claims

| | Claim Number | Area in Hectares |

| | | |

| 1) | CDC 2388117 | 9.35 ha | |

| 2) | CDC 2388118 | 16.78 ha | |

| 3) | CDC 2388119 | 2.07 ha | |

| 4) | CDC 2388120 | 8.97 ha | |

| 5) | CDC 2388121 | 0.57 ha | |

| 6) | CDC 2388122 | 4.15 ha | |

| 7) | CDC 2388123 | 17.81 ha | |

| 8) | CDC 2388124 | 4.27 ha | |

| 9) | CDC 2388125 | 33.28 ha | |

| 10) | CDC 2388126 | 43.34 ha | |

| 11) | CDC 2388127 | 56.93 ha | |

| 12) | CDC 2388128 | 28.45 ha | |

| 13) | CDC 2388129 | 1.02 ha | |

| 14) | CDC 2388130 | 48.23 ha | |

| 15) | CDC 2388131 | 48.01 ha | |

Figure II: Claim Reference Map

The mining residues on the Montauban Mine Property are considered by the Quebec Government Authorities as toxic wastes. There are no environmental liabilities as such to our Company. However, the Company will have to obtain the necessary permits from the Quebec Government Authorities to realize any further fieldwork having an impact on the environment, especially if re-mobilization of mining residues is contemplated.

On September 14, 2012, the Company received a Certificate of Authorization, from the Quebec Provincial Government, with respect to operating a gravity-metric circuit to process the mining residues, or tailings, located on the Montauban Mine Property. On March 13, 2014, the Company received another Certificate of Authorization, also from the Quebec Provincial Government, with respect to operating a cyanization circuit to process the mining residues located on the Montauban Mine Property. Previously, on February 28, 2014, the Company received approval, from the Quebec Provincial Government, for the Restoration Plan on the Montauban Mine Property which will be implemented subsequent to the Company’s processing of the mining residues (tailings) on the site (see Note 11 to the consolidated financial statements, Subsequent Events). The two (2) Certificates of Authorization issued to the Company will allow for the construction and installation of equipment facilities to recuperate mica and precious metals (gold and silver) from the mining residues (tailings) located on the Montauban Mine Property.

MEASUREMENTS AND GLOSSARY

Conversion Table

For ease of reference in reviewing our business, we are providing you with conversion information and abbreviations:

| 1 acre | | = 0.4047 hectare | | 1 mile | | = 1.6093 kilometers |

| 1 foot | | = 0.3048 meter | | 1 troy ounce | | = 31.1035 grams |

| 1 gram per metric ton | | = 0.0292 troy ounce/ short ton | | 1 square mile | | = 2.59 square kilometers |

| 1 short ton (2000 pounds) | | = 0.9072 ton | | 1 square kilometer | | = 100 hectares |

| 1 ton | | = 1,000 kg or 2,204.6 lbs | | 1 kilogram | | = 2.204 pounds or 32.151 troy oz |

| 1 hectare | | = 10,000 square meters | | 1 hectare | | = 2.471 acres |

The following abbreviations may be used herein:

| Au | | = gold | | m2 | | = square meter |

| G | | = gram | | m3 | | = cubic meter |

| g/t | | = grams per ton | | Mg | | = milligram |

| Ha | | = hectare | | mg/m3 | | = milligrams per cubic meter |

| Km | | = kilometer | | T or t | | = ton |

| Km2 | | = square kilometers | | Oz | | = troy ounce |

| Kg | | = kilogram | | Ppb | | = parts per billion |

| M | | = meter | | Ma | | = million years |

Mining Terms

The following mining terms are used throughout this filing:

| | a) | SEC Industry Guide 7 Definitions |

| exploration stage | An “exploration stage” prospect, which is not in either the development or production stage. |

| development stage | A “development stage” project is one which there is ongoing preparation of an established commercially mineable deposit for its extraction but which is not yet in production. This stage occurs after completion of a feasibility study. |

| | |

mineralized material | The term “mineralized material” refers to material that is not included in the reserve as it does not meet all of the criteria for adequate demonstration for economic or legal extraction. |

| | |

| probable reserve | The term “probable reserve” refers to reserves for which quantity and grade and/or quality are computed from information similar to that used for proven (measured) reserves, but the sites for inspection, sampling, and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation. |

| production stage | A “production stage” project is actively engaged in the process of extraction and beneficiation of mineral reserves to produce a marketable metal or mineral product. | |

| | |

| proven reserve | The term “proven reserve” refers to reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well-established. |

| | |

| Reserve | The term “reserve” refers to that part of a mineral deposit, which could be economically and legally extracted or produced at the time of the reserve determination. Reserves must be supported by a feasibility study done to bankable standards that demonstrates the economic extraction (“bankable standards” implies that the confidence attached to the costs and achievements developed in the study is sufficient for the project to be eligible for external debt financing). A reserve includes adjustments to the in-situ tons and grade to include diluting materials and allowances for losses that might occur when the material is mined. |

| alteration | Any change in the mineral composition of a rock brought about by physical or chemical means. |

| | |

| assay | A measure of the valuable mineral content. |

| | |

| dip | The angle that a structural surface, a bedding or fault plane, makes with the horizontal, measured perpendicular to the strike of the structure. |

| | |

| disseminated | Where minerals occur as scattered particles in the rock. |

| | |

| fault | A surface or zone of rock fracture along which there has been displacement. |

| | |

feasibility study | A comprehensive study of a mineral deposit in which all geological, engineering, legal, operating, economic, social, environmental and other relevant factors are considered in sufficient detail that it could reasonably serve as the basis for a final decision by a financial institution to finance the development of the deposit for mineral production. |

| | |

| formation | A distinct layer of sedimentary rock of similar composition. |

| geochemistry | The study of the distribution and amounts of the chemical elements in minerals, ores, rocks, solids, water and the atmosphere. |

| | |

| geophysics | The study of the mechanical, electrical and magnetic properties of the earth’s crust. |

| | |

geophysical surveys | A survey method used primarily in the mining industry as an exploration tool, applying the methods of physics and engineering to the earth’s surface. |

| geotechnical | The study of ground stability. |

| | |

| grade | Quantity of metal per unit weight of host rock. |

| heap leach | A mineral processing method involving the crushing and stacking of an ore on an impermeable liner upon which solutions are sprayed to dissolve metals i.e. gold, copper, etc.; the solutions containing the metals are then collected and treated to recover the metals. |

| host rock | The rock in which a mineral or an ore body may be contained. |

| | |

| in-situ | In its natural position. |

| | |

| lithology | The character of the rock described in terms of its structure, color, mineral composition, grain size and arrangement of tits component parts, all those visible features that in the aggregate impart individuality to the rock. |

| | |

mapped or geological mapping | The recording of geologic information including rock units and the occurrence of structural features and mineral deposits on maps. |

| | |

| mineral | A naturally occurring inorganic crystalline material having a definite chemical composition. |

| | |

| mineralization | A natural accumulation or concentration in rocks or soil of one or more potentially economic minerals, also the process by which minerals are introduced or concentrated in a rock. |

| | |

| outcrop | That part of a geologic formation or structure that appears at the surface of the earth. |

| | |

open pit or open cut | Surface mining in which the ore is extracted from a pit or quarry, the geometry of the pit may vary with the characteristics of the ore body. |

| | |

| ore | Mineral bearing rock that can be mined and treated profitably under current or immediately foreseeable economic conditions. |

| | |

| ore body | A mostly solid and fairly continuous mass of mineralization estimated to be economically mineable. |

| | |

| ore grade | The average weight of the valuable metal or mineral contained in a specific weight of ore i.e. grams per ton of ore. |

| | |

| oxide | Gold bearing ore, which results from the oxidation of near surface sulfide ore. |

| | |

preliminary assessment | A study that includes an economic analysis of the potential viability of Mineral Resources taken at an early stage of the project prior to the completion of a preliminary feasibility study. |

| QA/QC | Quality Assurance/Quality Control is the process of controlling and assuring data quality for assays and other exploration and mining data. |

| | |

| quartz | A mineral composed of silicon dioxide, SiO2 (silica). |

| rock | Indurated naturally occurring mineral matter of various compositions. |

| | |

sampling analytical variance/ precision | An estimate of the total error induced by sampling, sample preparation and analysis. |

| | |

| sediment | Particles transported by water, wind or ice. |

| | |

sedimentary rock | Rock formed at the earth’s surface from solid particles, whether mineral or organic, which have been moved from their position of origin and re-deposited. |

| strike | The direction or trend that a structural surface, e.g. a bedding or fault plane, takes as it intersects the horizontal. |

| | |

| strip | To remove overburden in order to expose ore. |

| | |

| tailings | The residue from an ore crushing plant. |

| | |

| orphan site | Tailings residues from former mining operations that the Quebec government has taken responsibility for remediation / restoration. |

DRILLING SUMMARY

A systematical sampling program was developed to provide an accurate and homogeneous grid of data to estimate the Montauban Tailings potential. A 24-hole percussion drilling campaign was performed totaling 143.1 meters. This percussion drilling campaign was considered part of completing a previous 25-hole drilling campaign performed earlier. A total of 49 holes totaling 302.3 meters of drilling were completed. No proven or indicated reserves were identified.

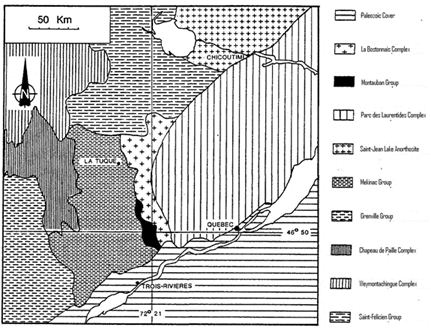

GEOLOGY

Regional geology consists of three main rock groups: the basement crust, the supracrustal rocks and the intrusive rocks which were respectively identified as the Mekinac Group, the Montauban Group and the La Bostonnais Complex

The Montauban Group is composed of Helikian supracrustal rocks. Those are various gneiss, quartzites, amphibolites, metabasalts and calcosilicated rocks reaching less than 2 kilometers in thickness. The Montauban deposit is located in the upper part of this unit.

The Montauban Group is bordered to the East by the La Bostonnais Complex, an intrusive rocks complex formed of basic, tonalitic and felsic igneous rocks. To the West, the Montauban Group is in contact with the Mekinac Group mostly composed of charnockitic migmatites.

The Montauban Deposit is a three-kilometer long mineralized formation with a geology that is fairly complex being located within an extensively folded sequence of amphibolite facies rocks that are sandwiched between intrusions of granodioritic to gabbroic composition. In the mine area, these metamorphic rocks strike roughly North-South and dip ±60° to the East and consist of migmatitic biotite gneiss, amphibolite, quartzofeldspathic biotite gneiss and quartzite.

Locally, the Montauban mineralization is contained within a thin complex package of biotite gneiss, nodular sillimanite gneiss, cordierite-antophyllite gneiss, calc-silicate rocks and rocks as meta-exhalites (tourmalinite and, along strike iron formation and carbonate rocks).

The Montauban deposit is distributed within numerous different zones along the strike length of the mineralization, from South to North we have the zones: South, Tétreault, A, C, North and Montauban. All zones are zinc bearing with the exception of the South and North zones, which are gold bearing.

MINERALIZATION

The base metal mineralization found in Montauban is massive to semi-massive sulphides, coarsely grained and mostly composed of sphalerite, galena, pyrrhotite, pyrite and chalcopyrite with minor quantities of cubanite, tetrahedrite and molybdenite.

The gold bearing mineralization is marginal and consists of disseminated pyrrhotite, galena, sphalerite and chalcopyrite with a large range of minor sulphides, sulphosalts and native minerals.

MONTAUBAN TAILINGS

The Montauban Mine Property covers a total area of 53,093 m² and amounts to a total volume of 250,750 m³. Since this volume is composed of tailings and that the water table is located within most of the blocks derived from each hole, the specific gravity of the material had to be evaluated to estimate the tonnage that is present on site. The estimation of the specific gravity was performed on the last drilling campaign 24 holes since no recovery evaluation is available from the first drilling campaign. Recovery of tailings in the sampling process averaged about 76% from the last percussion drilling campaign. Recoveries were ranging from 40 to 100 %, the lowest values being associated to the high water content of the deepest samples, the water table being at a depth of about 4,6 m (15 ft.) within the pile of tailings. The averaged recovery was in the order of 81 % (68 samples) for the upper portion of the tailings and it dropped to below 64 % (27 samples) for the deeper portion (below the water table). The specific gravity is then estimated to be 1, 71 g/cm³.

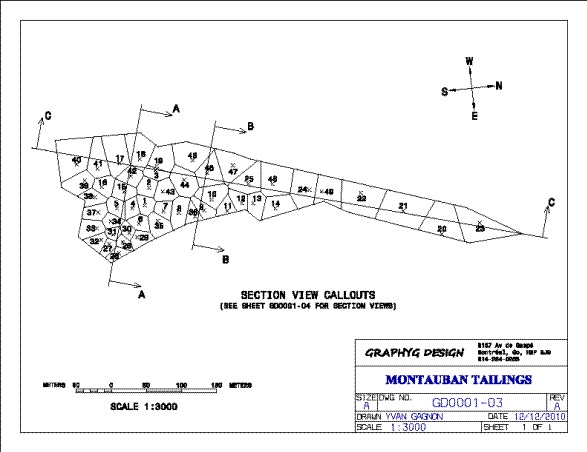

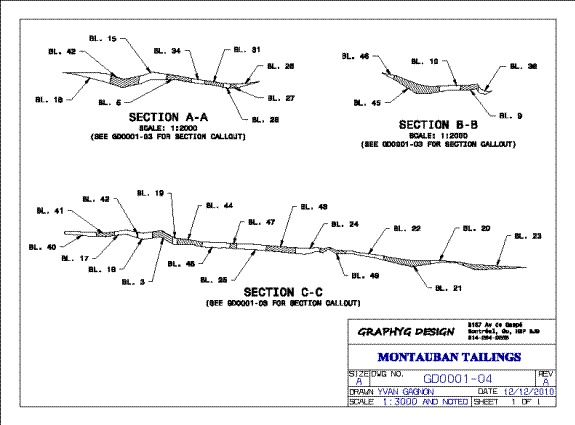

Montauban Mine Property Hole Location Plan

The above graph shows the typical sections of the Montauban Mine Property where it is clear that the drainage is towards the North (to the right on section C-C). It is also clear that the thickness is variable but not so thick compared to the value that should be reached if the whole production was to be still onsite. About 1.2 million tons were produced in the past; such a tonnage should be averaging over 13 meters in the Tailings pile. It is clear on site that an important fraction of the tailings was washed away through drainage.

Montauban Mine Property Typical Sections

Figure X: Montauban Mine Property View Looking South

A total of 49 blocks were defined from the two previous percussion-drilling campaigns. The drilling pattern is essentially regular with a hole each and every 30-meter on average. The block volumes were calculated with the help of the computer-modeling program that defined one polygon for each and every hole drilled. The perimeter of the tailings was mapped with the help of a GPS device, this perimeter is the limit where the surface meshing of the holes’ collars meets the meshing of the bottom of the holes. The block size is fairly regular averaging 8,740 tons, the smallest block being # 26 at 1 342 tons and the biggest one being # 21 at 24 334 tons.

To these metals one should add the mica content of the Montauban Mine Property, with the mica being mostly composed of the phlogopite type with some muscovite and minor amounts of biotite. The mica content is estimated to be at least 10 % of the total volume. The mica is an industrial mineral that is valued according to the market conditions.

DRILLING RESULTS

The distribution of metals within the tailings is not homogeneous. It was demonstrated with the 49 holes drilled on the Montauban Mine Property that recoveries dropped from 81 to less than 64 % below the 4,6 m (15 ft.) horizon, which is more or less the location of the water table within the Tailings. The impact is seen on metal content when gold is 67 % richer over this horizon, silver is up 73 %, Copper also up 63 %, and the winner being lead with a jump of 149 %. The only one being evenly distributed is zinc.

Example of Block 15 Showing Richer Upper Portion of Montauban Mine Property

MILL CONSTRUCTION

We are constructing a mill to process mining residues. Our focus will be to produce gold and silver concentrate in addition to the mica product. By extracting mica and producing the gold and silver concentrate, we will reduce the sulphide content of the tailings and thus lowering the environmental impact and cost for the project closure at the end of the operation.

Presently, there are no similar mills in the area surrounding our mining claims. The on-site mill production equipment to be constructed and installed will incorporate a closed cyanization circuit and separation equipment consisting of spiral classifiers and Nelson concentrators in addition to other equipment. Test work to date has indicated that this configuration will effectively segregate the mica and produce a gold/silver concentrate. There is a risk however that the plant will not effectively separate the components as planned. There is also a risk that the process being used is not ideal or optimal and that a different process may enhance or increase recovery of values. We intend to continue testing to improve the recuperation and extraction process. We have incorporated flexibility into our mill building design to allow for alternative/additional precious metal extraction processes to be installed. Initial testing results indicate that recovery of mica, gold and silver is possible but economic feasibility has not been proven and there is the associated risk that the operation as planned will not be profitable either with respect to our own mining operations or refining tailings or other mining concentrates from other mining companies in close proximity to our operations.

We anticipate that the mill will be able to process 1,000 tonnes per day. By constructing our own mill we will be able to reduce transportation costs.

PROPERTY DEVELOPMENT

The Company has completed construction of all access roads to and from the new milling facility. The hydropower source to the milling facility totaling 1.3 kilometers has been completed. The main power line consists of 2,500 amperes total output power and has been brought inside the newly erected 16,000 sq./ft. steel structure building.

We have also secured the necessary mining permits. On September 14, 2012, the Company received a Certificate of Authorization, from the Quebec Provincial Government, with respect to operating a gravity-metric circuit to process the mining residues, or tailings, located on the Montauban Mine Property. On March 13, 2014, the Company received another Certificate of Authorization, also from the Quebec Provincial Government, with respect to operating a cyanization circuit to process the mining residues located on the Montauban Mine Property. Previously, on February 28, 2014, the Company received approval, from the Quebec Provincial Government, for the Restoration Plan on the Montauban Mine Property which will be implemented subsequent to the Company’s processing of the mining residues (tailings) on the site. The two (2) Certificates of Authorization issued to the Company will allow for the construction and installation of equipment facilities to recuperate mica and precious metals (gold and silver) from the mining residues (tailings) located on the Montauban Mine Property.

Following an economic analysis of the project, our management made an assessment of the feasibility of the Anacon project and made a decision to commercially extract the gold, silver and other base metals located on the Property.

We have prepared a proposal to the Ministry of Natural Resources and Wildlife in Quebec to correct the environmental problems caused by the presence of tailings from previous operations on additional nearby tailings sites, Montauban United and Tetrault 1&2. These additional resource residues sites will increase the project life if we go into production.

SUBSEQUENT EVENTS

On October 30, 2013 and November 27, 2013, the Company entered into binding agreements for the asset acquisitions of an undivided one hundred percent (100%) interest in certain mineral claims and mining assets located in the Province of Quebec’s Montauban and Chavigny townships near Grondines West, in the county of Portneuf, specifically Mining Lease BM 748 and Mining Concession Miniere CM 410. The purchase price was CDN$75,000 together with the issuance of 1,050,000 common shares of the Company. The common shares for the acquisition were valued at their fair market value on the day they were issued which totaled $496,860. In connection with the asset purchase, the Company also issued 40,000 shares of common stock to a former supplier of the vendor for mining related information of the assets purchased valued at $20,000 along with cash consideration of CDN$20,000. The Company had been awaiting confirmation of the contemplated transaction from a bankruptcy court in Montreal, Quebec overviewing the financial restructuring of the vendor. The bankruptcy court approved the transaction on April 17, 2014 and have been included in Mining rights on the consolidated balance sheet as at March 31, 2014.

On April 14, 2014, the Company entered into an asset purchase agreement for an undivided one hundred percent (100%) interest in fifty seven (57) mining claims located in the Province of Quebec’s Montauban and Chavigny townships near Grondines West, in the county of Portneuf. The purchase price was CDN$50,000. The transfer of the mining claims is currently being completed by the Province of Quebec.

On April 28, 2014, the Company entered into a Securities Purchase Agreement (“SPA”), with a U.S.-based private equity fund, under which the Company issued a Secured Convertible Promissory Note (the “Promissory Note”) in the amount of $552,500. The Promissory Note includes an original issue discount of $50,000 (“OID”), calculated at 10% of the principal amount ($500,000), plus an additional $2,500 (“Transaction Expense Amount”) to cover the investor’s due diligence and legal fees in connection therewith. The principal amount will be paid to the investor in six (6) tranches of an initial amount under the Promissory Note of $250,000 and five (5) additional amounts of $50,000, with each of the additional amounts represented by Investor Notes (collectively, the Promissory Note and Investor Notes, the “Notes”). The initial $250,000 in cash was paid to the Company on April 29, 2014. Payment of the Notes will be made on a monthly basis, beginning six months after the issue date when the Company received the initial $250,000, in the amount of $34,531 per month plus all accrued but unpaid interest and other costs, fees or charges payable, for sixteen (16) months until the balance is paid in full. The Notes are convertible into common stock, at the option of the investor, at a price of $0.40 per share subject to adjustment in the case of a default, reorganization or recapitalization. In the event the Company elects to prepay all or any portion of the Notes, the Company is required to pay to the investor an amount in cash equal to 125% of the outstanding balance of the Notes, plus accrued interest and any other amounts owing. Interest accrues at the rate of 10% per annum. If the Company fails to repay the Notes when due, or if other events of default thereunder apply, a default interest rate of 22% per annum will apply. In addition, if the Company fails to issue stock to the investor within three trading days of receipt of a notice of conversion, the Company must pay a penalty equal to the greater of greater of $500 per day and 2% of the applicable conversion amount or installment amount, as applicable (but, in any event, the cumulative amount of such late fees shall not exceed the applicable conversion amount or installment amount). The Notes are secured by an interest in all right, title, interest, claims and demands of the Company in and to the property described in the Security Agreement, and all replacements, proceeds, products, and accessions thereof. The Notes are convertible into shares of our common stock in six tranches, consisting of (i) an initial tranche in an amount equal to $277,500 and any interest, costs, fees or charges accrued thereon or added thereto under the terms of this Note and the other Transaction Documents (as defined in the Securities Purchase Agreement), and (ii) five (5) additional tranches, each in the amount of $55,000, plus any interest, costs, fees or charges accrued thereon or added thereto under the terms of this Note and the other Transaction Documents. Except in the case of a Company default, the Notes are convertible by the investor at a price of $.40 per share. Concurrently with the Securities Purchase Agreement, the Company also issued to the investor a warrant (the "Warrant") to purchase 693,750 shares of the Company’s common stock at an exercise price of $.75 per share subject to adjustment as more fully set forth in the warrant agreement. The warrant also contains a cashless exercise provision. The warrant is for a term of two (2) years.

OUR PLAN OF OPERATIONS GOING FORWARD

We will need additional production financing, including working capital requirements, of $6 million to commence production. We have no commitments for additional financing.

We will also further define further the local potential of other resources such as additional tailings and/or underground resources underneath the Property or close-by in the Montauban area.

COMPARISON OF OPERATING RESULTS FOR THE THREE MONTHS ENDED MARCH 31, 2014 AND 2013 AND FROM JUNE 2, 2006 (INCEPTION) TO MARCH 31, 2014

Three Months Ended March 31, 2014 and 2013:

We have not generated revenues from operations and do not anticipate generating any revenues from operations until we have obtained additional debt or equity financing to complete the infrastructure of the mill site and acquire milling equipment essential to the processing of gold, silver and other base metals located on the Montauban Property. There are no assurances that we will obtain the needed financing or in the amount we need to conduct our processing activities.

The condensed consolidated financial statements for the three-month period ended March 31, 2014, included in this report, reflect total operations and other expenses of $596,096, representing a decrease of $288,745 compared to the three-month period ended March 31, 2013 when total operations and other expenses were $884,841. The decrease is mainly attributable to lower amount charged for the cost of common shares and stock options granted to our management as these expenses were mostly absorbed in the prior year, to lower wages and related expenses of $22,915, to lower professional fees of $35,747, to higher exploration costs of $85,099 and to higher general and administrative expenses of $81,800. We also recognized a loss on conversion of the promissory note of $125,000 during the three month period ended March 31, 2013.

We had engineering costs of $112,682 for the three month period ended March 31, 2014, representing an increase of $85,099 compared to the three month period ended March 31, 2013 when engineering costs were $27,583. The primary reason for the increase in engineering costs for the three months ended March 31, 2014 compared to the three months ended March 31, 2013 is attributable to the additional mining studies and drilling costs incurred in the current quarter. As mentioned above, the Company has now received all of its operating permits from the Ministry of Durable Development of the Environmental Parks (“MDDEP”) of the Quebec Provincial government. With the issuance of all necessary mining permits and approval of the restoration plan and upon obtaining additional financing, we will proceed with the installation of a custom designed milling circuit for the treatment of the mining residues on the Anacon Property.

From June 2, 2006 (Inception) Through March 31, 2014:

Since our inception on June 2, 2006, our expenses totaled $5,306,618 consisting primarily of $985,296 in exploration costs, $1,181,434 in wages and related expenses, $1,399,933 in shares and options issued as compensation expense and $772,864 in professional fees.

SOURCE OF FUNDS

We will require additional debt or equity funding to complete the mill and the infrastructure to otherwise conduct operations. In 2012, we filed a registration statement with the Securities and Exchange Commission offering 12 million shares of our common stock at $.25 per share. As of September 30, 2013, we sold a total of 9,428,000 shares of our common stock from the registration statement and secured $2,357,000 in financing. In the third quarter of 2013, we raised $110,000 from equity securities private placements and an additional $442,000 in the fourth quarter of 2013 from equity securities private placements. Prior to the effective date of the Registration Statement, we secured funding through the sales of both debt and equity securities in the form of private placements.

On April 28, 2014, the Company entered into a Securities Purchase Agreement (“SPA”), with a U.S.-based private equity fund, under which the Company issued a Secured Convertible Promissory Note (the “Promissory Note”) in the amount of $552,500. The Promissory Note includes an original issue discount of $50,000 (“OID”), calculated at 10% of the principal amount ($500,000), plus an additional $2,500 (“Transaction Expense Amount”) to cover the investor’s due diligence and legal fees in connection therewith. The principal amount will be paid to the investor in six (6) tranches of an initial amount under the Promissory Note of $250,000 and five (5) additional amounts of $50,000, with each of the additional amounts represented by Investor Notes (collectively, the Promissory Note and Investor Notes, the “Notes”). The initial $250,000 in cash was paid to the Company on April 29, 2014. We will require additional funding to complete construction of the mill and complete the build- out of the infrastructure. On a going forward basis, there can be no assurance that we will be able to secure additional capital. Until such time as we can fully implement our business plan, it is unlikely that we will be able to reverse our continuing losses in which case you may lose your entire investment.

LIQUIDITY AND CAPITAL RESOURCES

Assets and Liabilities

As of March 31, 2014, total assets were $2,605,426. We had current assets represented by cash totaling $57,801, prepaid expenses totaling $159,725 and sales tax receivable totaling $58,023. Current assets as of December 31, 2013 totaled $1,374,306. We also had net fixed assets as of March 31, 2014 totaling $1,276,704, mining claims totaling $1,031,271 and net deferred financing fees of $21,902. Total assets as of December 31, 2013 were $2,690,691 when we had cash totaling $535,934, prepaid deposit totaling $612,431, prepaid expenses totaling $190,514, sales tax receivable totaling $35,427, net fixed assets totaling $1,276,304, mining claims totaling $15,000 and net deferred financing fees totaling $25,081. There was not a significant change in total assets between December 31, 2013 and March 31, 2014. Total assets as of March 31, 2013 were $2,293,204. The primary reason for the significant increase of $321,477 in our total assets between March 31, 2013 and March 31, 2014 is attributable to purchases of mining rights resulting in an increase of $1,016,271 and offset by a decrease in cash of $572,162.

Current liabilities, represented by accounts payable and accrued expenses, totaled $143,518 as of March 31, 2014. There were no long-term liabilities. Current liabilities at December 31, 2013 totaled $186,729. Current liabilities at March 31, 2013 totaled $302,958. Accounts payable and accrued liabilities decreased by $43,211 from December 31, 2013 to March 31, 2014 and by $159,440 from March 31, 2013 to March 31, 2014, and is mainly attributable to reductions in amounts owed to suppliers and contractors.

We have a working capital surplus of $132,031 as of March 31, 2014 as compared to a working capital surplus of $1,187,577 as of December 31, 2013, representing a decrease of $1,055,546. This decrease is mainly attributable to a decrease in prepaid deposit, represented by mining rights that have been re-classified as such on the consolidated balance sheet as at March 31, 2014, of $612,431 and by a decrease in cash of $478,133 as of March 31, 2014. We have invested most of our funds to complete the infrastructure, purchase equipment and commence construction on the mill.

As of March 31, 2014, the cost of fixed assets totaled $1,289,822 and consisted of the mill building at a cost value of $1,089,415, land at a cost value of $111,587, mill equipment at a cost value of $43,115, computer equipment at a cost of $5,857, office equipment at a cost value of $14,711 and a vehicle at a cost value of $25,127. As of March 31, 2014, net fixed assets totaled $1,276,704. As of December 31, 2013, the cost of fixed assets totaled $1,285,766 and consisted of the mill building at a cost value of $1,089,415, land at a cost value of $108,974, mill equipment at a cost value of $43,115, computer equipment at a cost value of $4,424, office equipment at a cost value of $14,711 and a vehicle at a cost value $25,127. As of December 31, 2013, net fixed assets totaled $1,276,304.

As of March 31, 2014, we had an accumulated deficit totaling $5,306,618 as compared to $4,710,522 as of December 31, 2013. The $596,096 increase in the accumulated deficit is attributable to the loss recorded for the three months ended March 31, 2014.

The success of our mining operations business and the ability to continue as a going concern will be dependent upon our ability to obtain additional and adequate financing to commence profitable commercial activities in the extraction of gold, silver and other base metals and meet anticipated performance specifications on a continuous and long term commercial basis.

Going Concern

Our consolidated financial statements have been prepared on a going concern basis. The going concern basis of presentation assumes that we will continue in operation for the foreseeable future and be able to realize assets and discharge its liabilities and commitments in the normal course of business. We have not generated revenues since our inception and we have generated losses totaling $2,937,475 and $797,126 for the years ended December 31, 2013 and 2012, respectively, losses totaling $596,096 and $884,841 for the three months ended March 31, 2014 and 2013, respectively, and losses of $5,306,618 since our inception on June 2, 2006. We have had very little operating history to date.

Our continuation as a going concern is dependent upon, amongst other things, continued financial support from our shareholders, attaining a satisfactory revenue level, attainment of profitable operations and the generation of cash from operations and the ability to secure new financing arrangements and new capital to carry out our business plan. These matters are dependent on a number of items outside of our control and there exists material uncertainties that may cast significant doubt about our ability to continue as a going concern. There are no assurances that we will achieve profitability or be capable of sustaining profitable operations. Our consolidated financial statements do not include any adjustments relating to the recoverability and classification of the carrying amounts of assets or the amount and classification of liabilities that might result if we are unable to continue as a going concern. These factors raise substantial doubt regarding our ability to continue as a going concern.

Off-Balance Sheet Arrangements

We are not currently a party to, or otherwise involved with, any off-balance sheet arrangements that have or are reasonably likely to have a current or future material effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources.

ITEM 3 – QUANTITATIVE AND QUALITATIVE DISCLOSURE ABOUT MARKET RISK

Foreign Currency Exchange Rate Risk

We hold cash balances in both U.S. and Canadian dollars. We transact most of our financing in U.S. dollars and operational business in Canadian dollars. Some of our operational expenses denominated in Canadian dollars include building costs, labor costs and materials and supplies. As a result, currency exchange fluctuations may impact our operating costs. We do not manage our foreign currency exchange rate risk through the use of financial or derivative instruments, forward contracts or hedging activities.

In general, we do not believe that any weakening or strengthening of the U.S. dollar as compared to the Canadian dollar will have a positive or adverse material effect on our results of operations.

Interest Rate Risk

Our investment policy for our cash and cash equivalents is focused on the preservation of capital and supporting our liquidity requirements. We do not use interest rate derivative instruments to manage exposure to interest rate changes. We do not believe that interest rate fluctuations will have any effect on our results of operations.

Cyber-security Risk

We do not believe that we are subject to any undue cyber-security risk that may have an adverse material effect on our results of operations.

ITEM 4 – CONTROLS AND PROCEDURES

| (a) | Evaluation of Disclosure Controls and Procedures |

Our management, with the participation of our President & Chief Executive Officer and our Chief Financial Officer, evaluated the effectiveness of the design and operation of our disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Exchange Act) and determined that our disclosure controls and procedures were effective as of the end of the period covered by this Quarterly Report on Form 10-Q. The evaluation considered the procedures designed to ensure that the information required to be disclosed by us in reports filed or submitted under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms and communicated to our management as appropriate to allow timely decisions regarding required disclosure.

| (b) | Changes in Internal Control over Financial Reporting |

During the period covered by this Quarterly Report on Form 10-Q, there was no change in our internal control over financial reporting (as such term is defined in Rules 13a-15(d) and 13d-15(d) under the Exchange Act) that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

| (c) | Inherent Limitations of Disclosure Controls and Internal Controls over Financial Reporting |

Because of its inherent limitations, internal controls over financial reporting may not prevent or detect misstatements. Projections of any evaluation or effectiveness to future periods are subject to risks that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

PART III - OTHER INFORMATION

ITEM 1 – LEGAL PROCEEDINGS

None.

As a Smaller Reporting Company, we are not required to include risk factors in our Forms 10-Q. Nonetheless, the reader may review the risk factors included in our most recent Form 10-K for the fiscal year ended December 31, 2013 that was filed with the SEC on March 26, 2014.

ITEM 1B – UNRESOLVED STAFF COMMENTS

None.

ITEM 2 – UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS

We have issued shares of our common stock for services rendered, capital formation and corporate acquisitions. We relied on the exemption provisions of Section 4(2) of the Securities Act. We have also offered shares pursuant to the exemption provisions of Regulation S.

In May 2010, we issued to 28 purchasers residing in Canada an aggregate of 18,000,000 shares of our common stock at a purchase price of $.003 per share for a total of $54,000. Those shares were issued in transactions which qualify for that exemption from the registration and prospectus delivery requirements of the Securities Act of 1933, as amended (“Securities Act”), as specified by the provisions of Regulation S. Accordingly, none of those purchasers are U.S. persons as that term is defined in Regulation S. No underwriters were used, thus no commissions or other remuneration was paid. The securities were sold in an offshore transaction relying on Rule 903 of Regulation S of the Securities Act. We, any distributor, any of their respective affiliates or any person acting on behalf of any of the foregoing made no directed selling efforts in the United States. We are subject to Category 3 of Rule 903 of Regulation S and accordingly we implemented the offering restrictions required by Category 3 of Rule 903 of Regulations S by including a legend on all offering materials and documents which stated that the shares have not been registered under the Securities Act and may not be offered or sold in the United States or to US persons unless the shares are registered under the Securities Act, or an exemption from the registration requirements of the Securities Act is available.

In June 2010, we offered and sold to 5 United States purchasers 2,000,000 shares of our common stock at a purchase price of $.003 per share for a total of $6,000. The transactions did not involve a public offering of our securities and, therefore, were exempt from the registration and prospectus delivery requirements of the Securities Act pursuant to the provisions of Section 4(2) of the Securities Act. In connection with the offer and sale of those 2,000,000 shares, no general solicitation or advertising was used. The purchasers had pre-existing relationships with us on the dates we sold the 2,000,000 shares to them. No commission was paid in connection with the offer and sale of these 2,000,000 shares.

In 2011, we: (a) issued 5,000,000 common stock shares to acquire mining rights at a value of $15,000; (b) issued 5,000,000 shares of common stock to board members for services at a value of $15,000; (c) issued 1,000,000 shares of common stock for payment of interest on the promissory note of $3,000; (d) sold 3,350,000 common stock shares in a private placement of our securities totaling $670,000; (e) issued 1,500,000 common stock shares as consideration in employment agreements valued at $1,500,000; and (f) issued 250,000 common stock shares valued at $50,000 for engineering services. We relied on the exemption provisions of Securities Act Section 4(2) in issuing these securities.

There were no sales of unregistered securities in 2012. During the fiscal year ended December 31, 2012, we sold a total of 7,852,000 shares of our registered common stock for $1,963,000 with 6,924,000 of these shares being issued during the year ended December 31, 2012 and the remaining 928,000 shares were issued in during the three month period ended March 31, 2013. Also during the three month period ended March 31, 2013, we sold an additional 1,576,000 shares of our registered common stock for $394,000 and issued the shares during the three month period ended March 31, 2013. We used the proceeds from the sale of the 9,428,000 shares in 2012 and 2013 for working capital purposes including but not limited to the mill site building, infrastructure build-out, purchase of machines and equipment, wages and professional fees.

During the three months ended September 30, 2013, we sold 440,000 shares of our unregistered stock for $110,000. 400,000 of the shares were issued during the three months ended September 30, 2013 and the remaining 40,000 shares were issued in October 2013. During the three months ended December 31, 2013, we sold and issued 1,768,000 shares of our unregistered stock for $442,000.

With respect to the sale of the securities identified above, we relied on the exemption provisions of Section 4(2), Regulation S or Section 3(a) 10 of the Securities Act, as amended.

At all relevant times, the securities were offered subject to the following terms and conditions:

| | · | The sale was made to a sophisticated or accredited investor, as defined in Rule 502 or were issued pursuant to a specific exemption; |

| | · | We gave the purchaser the opportunity to ask questions and receive answers concerning the terms and conditions of the offering and to obtain any additional information which we possessed or could acquire without unreasonable effort or expense that is necessary to verify the accuracy of information furnished; |

| | · | At a reasonable time prior to the sale of securities, we advised the purchaser of the limitations on resale in the manner contained in Rule 502(d)2; and |

| | · | Neither we nor any person acting on our behalf sold the securities by any form of general solicitation or general advertising. |

ITEM 3 – DEFAULTS UPON SENIOR SECURITIES

None.

ITEM 4 – MINE SAFETY DISCLOSURE

Not applicable. We have no operational mines, in production or otherwise. We are subject to certain mining rules and regulations as promulgated by the Quebec Provincial government and other local municipalities and we have never been cited for any mining violations.

ITEM 5 – OTHER INFORMATION

Exhibit No. | | Description |

| | | |

| 31.1 | | Rule 13a-14(a)/15d14(a) Certifications of Mark Holbrook Chief Executive Officer and Director (attached hereto) |

| | | |

| 31.2 | | Rule 13a-14(a)/15d14(a) Certifications of Cora J. Holbrook, the CFO (attached hereto) |

| | | |

| 32.1 | | Section 1350 Certifications of Mark Holbrook, the President, Chief Executive Officer and Director (attached hereto) |

| | | |

| 32.2 | | Section 1350 Certifications Cora Holbrook (attached hereto) |

| | | |

| 101.INS** | | XBRL INSTANCE DOCUMENT |

| | | |

| 101.SCH** | | XBRL TAXONOMY EXTENSION SCHEMA |

| | | |

| 101.CAL** | | XBRL TAXONOMY EXTENSION CALCULATION LINKBASE |

| | | |

| 101.DEF** | | XBRL TAXONOMY EXTENSION DEFINITION LINKBASE |

| | | |

| 101.LAB** | | XBRL TAXONOMY EXTENSION LABEL LINKBASE |

| 101.PRE** | | XBRL TAXONOMY EXTENSION PRESENTATION LINKBASE |

_____________

** XBRL (Extensible Business Reporting Language) information is furnished and not filed or a part of a registration statement or prospectus for purposes of Sections 11 or 12 of the Securities Act of 1933, as amended, is deemed not filed for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, and otherwise is not subject to liability under these sections.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has caused this report to be been signed on its behalf by the undersigned thereunto duly authorized.

| | DNA Precious Metals, Inc. | |

| | | | |

| | | | |

| Date: May13, 2014 | By: | /s/ James Chandik | |

| | | James Chandik, President & Chief Executive Officer | |

| | | | |

| | | | |

| Date: May13, 2014 | By: | /s/ Tony J. Giuliano | |

| | | Tony J. Giuliano, Chief Financial Officer | |

| | | | |