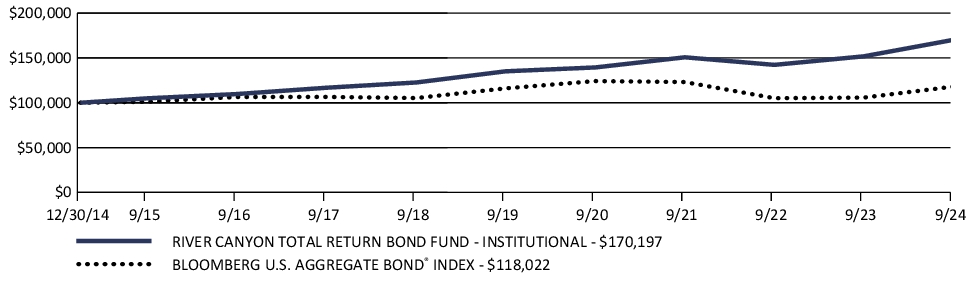

Advisers Investment Trust (the “Trust”) is a Delaware statutory trust operating under a Fifth Amended and Restated Agreement and Declaration of Trust (the “Trust Agreement”) dated March 9, 2023. The Trust was formerly an Ohio business trust, which commenced operations on December 20, 2011. On March 31, 2017, the Trust was converted to a Delaware statutory trust. As an open-end registered investment company, as defined in Financial Accounting Standards Board (“FASB”) Accounting Standards Update (“ASU”) 2013-08, the Trust follows accounting and reporting guidance under FASB Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”. The Trust Agreement permits the Board of Trustees (the “Trustees” or “Board”) to authorize and issue an unlimited number of shares of beneficial interest, at no par value, in separate series of the Trust. The River Canyon Total Return Bond Fund (the “Fund”) is a series of the Trust which is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and the Fund’s Institutional Shares class commenced operations on December 30, 2014. Prior to April 6, 2015 shares of the Fund were not registered under the Securities Act of 1933, as amended (the “1933 Act”). During that time, investments in the Fund were made only by individuals or entities that were “accredited investors” within the meaning of Regulation D under the 1933 Act, and shares were issued solely in private placement transactions that did not involve any “public offering” within the meaning of Section 4(a)(2) of the 1933 Act. Effective April 6, 2015, the Fund became publicly available for investment.

The investment objective of the Fund is to seek to maximize total return. The Fund has been managed as a diversified fund pursuant to Section 5(b) of the 1940 Act since July 2018. Effective April 26, 2021, the Fund determined to continue to be managed as a diversified fund.

Under the Trust's organizational documents, its officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust and Fund. In addition, in the normal course of business, the Trust enters into contracts with its vendors and others that provide for general indemnifications. The Fund's maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund.

A. Significant accounting policies are as follows:

Investments are recorded at fair value. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The valuation techniques employed by the Fund, as described below, maximize the use of observable inputs and minimize the use of unobservable inputs in determining fair value. These inputs are summarized in the following three broad levels:

• Level 1 —quoted prices in active markets for identical assets

• Level 2 —other significant observable inputs (including quoted prices of similar securities, interest rates, prepayment speeds, credit risk, etc.)

• Level 3 —significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. For example, certain short-term debt securities may be valued using amortized cost. Generally, amortized cost approximates the current value of a security, but since this valuation is not obtained from a quoted price in an active market, such securities would be reflected as Level 2 in the fair value hierarchy.

Security prices are generally provided by an approved independent third party pricing service as of the close of the New York Stock Exchange, normally at 4:00 p.m. Eastern Time, each business day on which the share price of the Fund is calculated.