UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22545

DREXEL HAMILTON MUTUAL FUNDS

(Exact name of registrant as specified in charter)

48 Wall Street, Suite 1100, New York, New York 10005

(Address of principal executive offices) (Zip code)

James A. Abate

48 Wall Street, Suite 1100

New York, New York 10005

(Name and address of agent for service)

Registrant’s telephone number, including area code: (855) 298-4236

Date of fiscal year end: September 30

Date of reporting period: October 1, 2012 – September 30, 2013

Item 1. Reports to Stockholders.

n Drexel Hamilton Centre American Equity Fund

(Ticker: DHAMX)

n Drexel Hamilton Centre Global Equity Fund

(Ticker: DHGLX)

n Drexel Hamilton Multi-Asset Real Return Fund

Investor Class (Ticker: DHMRX)

Institutional Class (Ticker: DHMUX)

Each a series of DREXEL HAMILTON MUTUAL FUNDS

| | |

| Drexel Hamilton Mutual Funds | | Shareholder Letter |

| | September 30, 2013 (Unaudited) |

November 2013

Dear Shareholder,

We present the annual report for the series of Drexel Hamilton Mutual Funds (the “Trust”) for the twelve-month period ending September 30, 2013.

The Net Asset Value (“NAV”) of the Drexel Hamilton Centre American Equity Fund (DHAMX) increased 12.30% for the twelve-month period ended September 30, 2013 and 32.40% since inception, and the NAV of the Drexel Hamilton Centre Global Equity Fund (DHGLX) increased 12.19% for the twelve-month period ended September 30, 2013 and 28.23% since inception. The Drexel Hamilton Multi-Asset Real Return Fund, Institutional Class, (DHMUX), launched on October 9, 2012, has returned 3.51% for the three-month period ended September 30, 2013 and 0.05% since inception. Additional performance and Fund information is available in the following Manager Commentary sections.

On September 13, 2013, the Board of Trustees approved and appointed Centre Asset Management, LLC (“Centre”) as the interim investment adviser to each series of the Trust (each, a “Fund” and together, the “Funds”). On September 14, 2013, the owners of Drexel Hamilton Investment Partners, LLC (“DHIP”), the Funds’ previous investment adviser, sold all of the membership units of DHIP to Centre. This transaction resulted in a change of control of DHIP, with Centre becoming sole owner of DHIP. The transaction also resulted in assignments of investment advisory agreement between DHIP and the Trust, on behalf of each Funds and the automatic termination of those agreements. In anticipation of the Centre acquisition, the Board of Trustees approved interim investment advisory agreements between Centre and the Trust on behalf of the Funds. Additionally, the Board of Trustees recommended shareholder approval of new investment advisory agreements. Centre has served as the investment sub-adviser to two of the Funds since their inception and James Abate and Jing Sun, two of Centre’s principals, have served as portfolio manager of the Drexel Hamilton Centre American Equity Fund and the Drexel Hamilton Centre Global Equity Fund, respectively, since their inception. The Board of Trustees believes that engaging Centre to serve as the investment adviser will maintain stability and continuity for the Funds. Each Fund’s investment advisory fee under that Fund’s interim advisory agreement and, if approved by Fund shareholders, the new investment advisory agreement will remain the same as the investment advisory fee under the Fund’s previous investment advisory agreement.

A Special Meeting of the Shareholders was held on October 31, 2013, at which shareholders of each Fund approved a new investment advisory agreement between the Trust, on behalf of the Fund, and Centre as the new investment adviser to the Fund.

The new investment advisory agreement does not result in changes to a Fund’s investment objectives or principal investment strategies, and does not cause any increase in the Fund’s investment advisory fee rates or total expenses. There will be continuity to management and service providers to the Trust and/or the Funds, including the administrator, transfer agent, custodian, independent registered public accounting firm and distributor of the Funds.

We have accomplished many significant milestones during this reporting period. By the time you receive this report, our newest fund, the Drexel Hamilton Multi-Asset Real Return Fund, launched on October 9, 2012, will have enjoyed its one year anniversary. The Drexel Hamilton Multi-Asset Real Return Fund seeks total return that exceeds U.S. inflation over a full inflation cycle by using a flexible allocation investment strategy that is diversified across various asset classes by dynamically shifting its allocation mix to maximize risk-adjusted returns and to preserve invested capital. The Drexel Hamilton Centre American Equity Fund and the Drexel Hamilton Centre Global Equity Fund are approaching their two year anniversaries in December 2013; each seeks capital growth through differentiated, fundamental investment processes.

Looking ahead to the upcoming months, the Trust intends to add a new actively managed U.S. Treasury fund to the stable of funds. We believe the addition of this new fixed income asset class product will add to our existing equity and multi-asset real return capabilities consistent with the Funds’ objective of offering fundamentally-driven, specialist active funds. Furthermore, the American and Global Equity Funds intend to offer two classes of shares so that all Funds offer Investor and Institutional Classes.

The Funds will continue to focus on high conviction, disciplined and research intensive processes in seeking long-term growth of capital or real return. We are committed to our shareholders for the long term by continuing to endeavor to provide consistent, risk-adjusted returns for our shareholders. We believe that the Funds are on the right track and look forward to striving to provide differentiation, value and performance.

Sincerely yours,

Andrew Bang

President

Past performance is no guarantee of future results and investment returns and principal value of each Fund will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

Andrew Bang is a registered representative of ALPS Distributors, Inc.

The statements and opinions expressed are those of the Adviser and are as of the date of this report.

| | |

| Annual Report | September 30, 2013 | | 1 |

| | |

| Drexel Hamilton Centre American Equity Fund | | Manager Commentary |

| | September 30, 2013 (Unaudited) |

Performance:

For the one year period ended September 30, 2013, the Drexel Hamilton Centre American Equity Fund delivered a positive absolute return but trailed its benchmark, the S&P 500® Index, on a relative basis mainly due to our mega-capitalization size bias and implementation of certain hedges and other investments that we deemed to be capital protective in nature. Despite being four plus years into economic expansion and exhaustion of further sustainable growth in revenue and earnings for most companies, early cycle sectors such as Consumer Discretionary and Financials, as well as mid-sized and smaller companies were the market leaders over the period. In fact, the equal-weighted1 S&P 500® Index delivered a total return nearly eight percentage points higher than the market capitalization weighted2 benchmark S&P 500® Index3 ; a situation normally associated with a robust economic backdrop.

Stocks that were strong performers within the Fund over this period included Delta Air Lines, Boston Scientific, LyondellBasell Industries, United Continental, Starbucks, Harley-Davidson, Citigroup, Visa, Honeywell, and Goldman Sachs. Stocks that were laggards included those mainly in the Materials and Technology sectors, such as Kinross Gold, Eldorado Gold, Goldcorp, Apple, and Broadcom, all of which remain in the Fund except for Broadcom.

Our principal overweight sectors were Technology and Health Care driven by bottom-up stock level opportunities and, from a performance impact perspective, the biased allocation attribution to Technology hurt while to Health Care helped the Fund. Our underweight posture in Financials hurt, but aside from very select opportunities, we maintain our general avoidance of most financial stocks as long-term investments, as regulatory scrutiny and increased capital requirements continue to depress returns on equity and intrinsic values.

As always, our process in managing the Fund is to focus bottom-up on each individual company’s growth outlook and capacity to create shareholder value. We analyze not only earnings, but we also strive to understand and link the capital allocation decisions being made today by each company and how they will lead to future earnings growth. In other words, we expect companies to invest in productive assets of the business, organically and through opportunistic purchases which, in turn, should provide the foundation for future revenue and profits growth that will create shareholder value. Alternatively, if companies cannot invest in productive assets due to a cyclical downturn or existing excess capacity, we expect these companies to “wisely contract” through the restructuring of their assets and other resources to regain their footing for future shareholder value creation. Our top-down views on interest rates and other fundamental economic indicators are important as many of those are inputs into our company models and, at the end of the day, reconciled with bottom-up information we gather and process from company performance. The end result is our attempt to find the best 45-70 stocks or so within the S&P 500® and weight those securities in a manner that delivers the Fund with competitive risk adjusted returns.

Economic and Market Review:

Despite the tepidness of US and global economic growth, we have not been surprised by the strength of the US stock market so far this year given that the Federal Reserve has continued to provide liquidity which, in turn, has translated into the overall price-earnings ratio4 (P/E) expanding against flat earnings. In simple terms, stocks have gone from being inexpensive to near fair value when compared to historical data, as the current P/E is around 17 times based on trailing earnings, up from around 14 times earnings one year ago.

The question to ask oneself now is whether the P/E can continue to expand on sheer monetary liquidity or will earnings growth revive heading into 2014 justifying the recent multiple expansion. In addressing the former, it has become a convention that the Federal Reserve’s distortive monetary policies are forcing investors into stocks as there is simply no other investment options to equities to achieve yield and capital growth relative to the liquid alternatives of cash, bonds, or commodities. Unlike the 1990’s, when a strong secular re-rating5 case could be made that transformational events, namely the fall of communism and opening up of vast international markets for growth and access to labor that would reduce costs, lower business cycle volatility due to automation and shift away from capital intensive industries, as well as the perception of better monetary and fiscal policies by the US government, this re-rating and crowding into equities seems more driven by stick rather than the carrot. Intertwined with this “there is no

| 1 | Equal Weighted – Index construction methodology, whereby all constituent stocks regardless of their size as measured by their market capitalization, are given equal weight inside the index. |

| 2 | Weighted Average Market Capitalization – Index construction methodology, whereby constituent stocks are given weights according to their weighted average market capitalization. Larger stocks therefore constitute a large portion of the index. The S&P 500 is an example of a well-known weighted average market capitalization index. |

| 3 | S&P 500 Index – The S&P 500 Index is a market capitalization weighted index consisting of 500 actively traded stocks in the U.S. equity markets. The index is designed to be the leading indicator of performance of the large capitalization U.S. equities universe. You cannot invest directly into an index. |

| 4 | Price to Earnings ratio – A valuation ratio of company’s current market share price compared to its earnings per share. |

| 5 | Re-rating – When the market changes its view of a company sufficiently to make calculation ratios or similar metrics higher or lower. |

| | |

| Drexel Hamilton Centre American Equity Fund | | Manager Commentary |

| | September 30, 2013 (Unaudited) |

alternative - TINA” environment has been the inconsistency that thus far this year, cyclicals have beaten more stable defensives as a style and smaller companies have outperformed larger companies; neither of which is consistent historically with a stock market rising due to a re-rating while earnings stagnate and inflation is low. The inference that we make from this observation is that investors are discounting a significant pickup in economic activity as well as a sharp re-acceleration of earnings. We find little evidence, top-down or bottom-up, of a consumer resurgence or corporate capital spending wave on the horizon to ignite higher revenue growth. Given this, we expect stock indexes to struggle to make further gains and the relative style and size performance winners of late to revert to losers, as profit margins and returns on equity seem to have peaked given a stagnant revenue backdrop and the hedges and other investments that we deemed to be capital protection in nature to be prudent.

Actions by the US Federal Reserve under its Chairman, Ben Bernanke, have been unprecedented in terms of using both the cost (interest rate) and quantity of money as stimulus tools. To fight the most recent recession, the Federal Reserve followed the standard prescription for a central bank and lowered its target short-term interest rate, attempting to ease financial conditions and support economic growth. In terms of existing non-traditional stimuli, the Federal Reserve has embarked on three distinct asset purchase programs, all in an effort to push down long-term interest rates as well as absorb lower quality assets from commercial banks. The latest version, QE3, has the Federal Reserve buying $85 billion worth of Treasury securities and other bonds from banks and primary dealers per month. In fact, the Federal Reserve alone has been the majority buyer of new treasury bonds issuance since the QE6 programs started. While QE has been effective in pushing long term interest rates down to record levels, it has not ignited commensurate loan growth nor inflation as the majority of the funds provided by the Federal Reserve have made their way right back to them as interest paying reserves; these deposits with Federal Reserve Banks now exceed $2.3 trillion dollars. In other words, QE stimulus has not made its way into the economy but has rather allowed the banks and primary dealers to capture the interest rate spread risk-free and boost financial assets in general. Unless the Federal Reserve discontinues paying interest on such deposits, it’s unlikely that banks will promote private sector lending in a meaningful way, particularly given new bank capital constraints such as Basel III7 and other anti-lending regulations, so this liquidity should continue to find its way into financial assets rather than being lent for productive assets. In fact, recent readings of commercial lending statistics by banks point to a contraction of new loans.

We are confident in our view that the Federal Reserve is unlikely to raise its target short-term interest rate and, although it may taper the level bond purchases or make them variable based on monthly conditions; it will maintain some type of QE program for the foreseeable future.

The natural question to ask oneself is then “What’s different this time?” The recoveries that followed the 2001 and 2008 recessions were uncharacteristically lackluster both in terms of economic growth and job creation. Indeed, the moniker given to these two recoveries has been “jobless.” Are there common threads between these recoveries? Moreover, has the U.S. economy fundamentally changed, resulting in a different pattern of growth during recoveries?

As students of demographics and natalism, we believe that, in a number of industrialized countries (including the US), assuming that fertility rates remain at or close to present levels, populations will start to decline and, in some cases, quite rapidly in the near future. The impact of this development on developed societies is that the aggregate demand for goods and services will decrease and increasing pension liabilities that can be crushing in terms of taxation on younger workers. Japan, the pathfinder of this phenomenon as it embraced Western family planning even before Europe and the US, shows the debilitative impact from an aging society and need to resort to new radical macroeconomic policies to combat its ill effects. With regard to near-term relevance to Federal Reserve policies, we see that the US Civilian Labor Force Participation Rate has dropped below a level that we last saw thirty years ago, as women began to join the workforce in earnest. A large part of the current fall in the unemployment rate from 10.0% to 7.3% has been due to this “dropping out” of the labor force, either due to discouragement, early retirement, or public assistance best evidenced by the fact that more persons have joined the rolls for social security disability payments than private sector payrolls since 2009. This collapse in the civilian workforce participation rate since the recovery began in June 2009 has never happened before during previous recoveries. Furthermore, productivity and the growth in average hourly wages have fallen significantly as inflation has slowed and competition for jobs domestically and from overseas limiting consumer consumption as evidenced by the latest drop in consumer spending being consistent only with past recessions.

Increasingly, we have more affinity to the “new normal” concept whereby economic growth in developed economies remain retarded by cyclical and secular influences and monetary policies remain hyper-active and non-traditional relative to anything seen by our generation of investors.

| 6 | QE – Quantitative Easing is a monetary policy by the government that is used to increase the money supply by buying government securities and other assets from the market. The goal is to decrease the interest rate and promote economic growth. |

| 7 | Basel III – A set of reforms and regulations designed to improve the supervision and risk management within the financial and banking sector. It is published by the Basel Committee on Banking Supervision. |

| | |

| Annual Report | September 30, 2013 | | 3 |

| | |

| Drexel Hamilton Centre American Equity Fund | | Manager Commentary |

| | September 30, 2013 (Unaudited) |

Outlook:

Given our outlook for earnings, valuation, and interest rates, we believe the best strategy to employ in the current environment where profitability will likely continue to come under pressure is a barbell one comprised mainly of leading mega-capitalization blue chips with the attributes that render them undervalued based upon their current multiples despite the recent re-rating. These companies, whose fundamentals we believe will stand out increasingly as the business cycle matures further, will distinguish themselves from the broad market through organic growth from innovation, pricing power and their global reach. US companies such as Exxon-Mobil, Johnson & Johnson, Proctor & Gamble, Nike, Starbucks, and Coca-Cola all exhibit these attributes. In addition, these US-listed global multi-national companies are an excellent way to capture the secular demand benefits from emerging economies. Combined with this portfolio component in a barbell approach, there remain selective companies in the US that continue to harvest growth in earnings and continue to enhance operations by streamlining labor forces and optimizing assets. US companies such as Lam Research, SanDisk, Avon Products, Urban Outfitters, Juniper Networks, Boston Scientific, NVidia, Sealed Air, Noble Corp., Express Scripts, Cardinal Health, Bemis, EOG Resources, HCA, Calpine, Cardinal Health, Bemis, IGT, Network Appliance, Schlumberger, and Devon Energy exhibit these attributes as do certain gold miners, which have curtailed capacity additions, namely Kinross and Goldcorp and we believe provide inverse positive optionality to potential stock market weakness in the event of a monetary or governmental policy mistake. Currently our mix between the former and latter groupings of companies is 70/30 versus 50/50 eighteen months ago.

Moving forward we are increasingly cautious about the overall market as the “stick rather than carrot driven TINA trade” into equities matures as well as our inference of the stock markets’ dependence upon a 2014 economic and profit recovery, which we do not see any evidence of. Furthermore, the ineffectiveness of traditional tools of macroeconomic policy, an oncoming demographic crisis, and other secular influences can lead to further non-traditional policies in developed economies, as most recently implemented in Japan that, in turn, could lead to mistakes and unintended consequences, especially if embraced collectively by the developed countries. Even if one were to ignore the top-down influences, our bottom-up selection highlights most favorably those leading mega-capitalization blue chips8 well exposed to global growth opportunities with defensive value attributes as well as those companies that continue to harvest growth in earnings and enhance operations by streamlining labor forces and optimizing assets in a company-specific manner.

| 8 | Blue Chips – A well-known, established and financially sound company. Blue chip companies are usually large capitalization companies with a track record of stable earnings and cash flow generation, as well as long term reliable growth prospects. |

| | |

| Drexel Hamilton Centre American Equity Fund | | Manager Commentary |

| | September 30, 2013 (Unaudited) |

SECTOR WEIGHTINGS

As a percentage of Net Assets

| | |

Information Technology | | 29.27% |

Health Care | | 17.05% |

Consumer Discretionary | | 13.30% |

Consumer Staples | | 10.03% |

Financials | | 8.64% |

Energy | | 7.46% |

Materials | | 6.39% |

Industrials | | 5.49% |

Telecommunication Services | | 1.06% |

Utilities | | 0.84% |

Calls | | 0.01% |

Cash and Cash Equivalents | | 0.46% |

Total | | 100.00% |

These allocations may not reflect the current or future positions of the portfolio.

GROWTH OF HYPOTHETICAL $10,000 INVESTMENT THROUGH

SEPTEMBER 30, 2013

This graph assumes an initial investment of $10,000 at December 21, 2011, the Fund’s inception date, and that any dividends ® and distributions are reinvested. This graph depicts the performance of the Fund versus the S&P 500 Index. Taxes on any Fund distributions or when shares are redeemed, if any, are not reflected. Unlike the Fund, an index is not available for investment, is unmanaged and does not have expenses that affect the results. The comparison is shown for illustrative purposes only.

TOTAL RETURNS – FOR THE PERIOD ENDED SEPTEMBER 30, 2013

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 1 Month | | 3 Month | | YTD | | 1 Year | | Since Inception* | | |

| Drexel Hamilton Centre American Equity Fund | | | | 2.67 | % | | | | 5.27 | % | | | | 15.21 | % | | | | 12.30 | % | | | | 17.10 | % | | |

S&P 500® Index | | | | 3.14 | % | | | | 5.25 | % | | | | 19.79 | % | | | | 19.34 | % | | | | 21.12 | % | | |

The performance information quoted above represents past performance, which is not a guarantee of future results, and does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total return includes reinvestment of dividends and capital gains, if any. Current performance may be lower or higher than the performance data quoted. For the most current month-end performance data please call 855-298-4236.

The total annual operating expense ratio (after expense reimbursements) as stated in the fee table of the most currently effective prospectus of the Fund, dated January 14, 2013, was 1.05%.

The Adviser has entered into a written expense limitation agreement under which it has agreed to limit for a period of two years from January 11, 2013 the total expenses of the existing class of shares of the Fund (including (but not limited to) investment advisory fees of the Adviser and distribution/service (Rule 12b-1) fees, but excluding interest, taxes, litigation, brokerage commissions, and extraordinary expenses not incurred in the ordinary course of the Fund’s business) to an annual rate of 1.05% of the average daily net assets of the Fund. This limitation may not be terminated and will remain in place through the end of the two-year period beginning after January 11, 2013. Without this waiver the total annual fund operating expenses of the Fund would have been 1.15%.

The S&P 500® Index is a commonly recognized, market-capitalization weighted index of 500 widely held securities, designed to measure broad U.S. equity performance. You cannot invest directly in an index.

* The Fund’s inception date was December 21, 2011.

| | |

| Annual Report | September 30, 2013 | | 5 |

| | |

| Drexel Hamilton Centre Global Equity Fund | | Manager Commentary |

| | September 30, 2013 (Unaudited) |

Performance:

For the one year period ended September 30, 2013, the Drexel Hamilton Centre Global Equity Fund delivered a positive absolute return but underperformed its benchmark, the MSCI All Country World (ACWI) Index1, on a relative basis. In general, the Fund’s underweighting of developed markets, particularly the US, and its bias towards higher growth, better valuation-supported emerging markets contributed to the relative underperformance. We maintain our bias and expect the future to reverse past fortunes.

Greece, Finland, Netherlands and Japan were some of the best performing markets globally during the 12-month period, while Indonesia, India, Brazil and South Africa were some of the worst performing markets. Regionally, Europe, followed by North America, outperformed the global market average as measured by the ACWI Index, while Asia Pacific ex-Japan underperformed the global market average. As noted, emerging markets as a group underperformed the global average but with mixed results: Indonesia, India, Brazil, Russia and South Africa were some of the worst performing markets while Greece and Argentina were some of the best performing markets globally.

During this period, our stock selection in Latin America contributed positively to the Fund’s relative performance. On the other hand, our stock selections in Asia, Europe, the U.S. and overweight posture in South America detracted from the Fund’s relative performance. Among the Fund’s stock holdings, Toyota Motor, Daiwa Securities and Fast Retailing of Japan; Daimler of Germany; Sands China and Tencent of China; and Compagnie Financiere Richemont of Switzerland all contributed positively to the Fund’s performance. On the negative side, America Movil of Mexico; Gazprom of Russia; SABESP, Vale and Petrobras of Brazil; China Shenhua Energy and China Life Insurance of China all detracted from Fund’s performance.

The Fund offers a unique investment vehicle for investors by focusing on large capitalization blue chips2 in the developed world and emerging blue chips in the developing countries. The Fund’s investment process combines bottom-up stock selection with structured portfolio construction and risk management that’s cognizant of secular growth forces. Our approach in managing the Fund is to focus bottom-up on each individual company’s growth outlook, not just on earnings, by understanding the capital allocation decisions being made today and how they will lead to future earnings growth. Our top-down views on macro outlooks of various markets, regions and global sectors etc. are important as many of those are inputs into our company models, and at the end of the day, are reconciled with the bottom-up information we gather and process from company performance and operating results.

Our disciplined economic-value-added3 based investment stock selection process and the unique dynamic GDP4-adjusted focused portfolio construction process ensure that the Fund is unencumbered by traditional market capitalization weighted benchmarks and goes where the bottom-up stock opportunities are globally. Consequently, the Fund is well positioned to extract value from the positive demographic trends and long-term economic growth in many developing economies as well as attractive investment opportunities in developed countries across the globe that we believe will lead to capital growth over a long-term investment horizon.

Economic and Market Review:

As we start the final quarter of 2013, global equity markets are on track to have another outstanding year. Although the bull market in global stocks that started in early 2009 is aging, it is still going strong. The 2008-2009 global financial crisis and the ensuing loose monetary policies and liquidity injections from the central banks of major economies all over the world have ushered in the age of the “new normal” with low interest rates, slow economic growth and anemic job creation. Nevertheless, there are signs of economic recovery in Europe and continued improvements in Japan, and even in some emerging markets, such as South Korea. In addition, China’s economy seems to have stabilized although the structural reforms needed for sustained long-term economic growth in China have not yet begun. With the determination of nearly all of the major central banks in the world to keep the interest rates super low for years to come, and valuations of fixed income assets looking unattractive, equities remain an attractive asset class for global investors in the foreseeable future. As the times are changing, investors must adapt with the changing times. It is no longer prudent to merely look at various regions and markets as monolithic groups. Rather it is more critical than ever before that

| 1 | MSCI All Country World Index (ACWI) – A market capitalization weighted index designed to track the performance of the broad global equity-market. The index is maintained by Morgan Stanley and the index constituents include both stocks from developing and emerging markets. |

| 2 | Blue Chips – A well-known, established and financially sound company. Blue chip companies are usually large capitalization companies with a track record of stable earnings and cash flow generation, as well as long term reliable growth prospects. |

| 3 | Economic Value Added (EVA) – An estimate of a firm’s economic profit – being the value created in excess of the required return of the company’s investors (being shareholders and debt holders). Quite simply, EVA is the profit earned by the firm less the cost of financing the firm’s capital. The idea is that value is created when the return on the firm’s economic capital employed is greater than the cost of that capital. |

| 4 | Gross Domestic Product (GDP) – The monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. |

| | |

| Drexel Hamilton Centre Global Equity Fund | | Manager Commentary |

| | September 30, 2013 (Unaudited) |

investors focus on individual companies and pick the right stocks. With changes come new risks, but also new opportunities. That is exactly how we approach investing globally. In line with our economic-value-added investment principle, we believe that a company’s ultimate worth is related to its propensity to create or destroy wealth in economic risk-adjusted terms rather than strictly nominal accounting terms. Furthermore, the company-specific cost of capital is a required component to the value today of that propensity for wealth creation or destruction. Based on our research within the economic-value-added investment principle framework, we identified many attractively valued, large capitalization blue chips in all corners of the world.

For instance, Companhia de Bebidas das Americas (AmBev) is one of our favorite stocks in Brazil. AmBev is the largest Latin American brewery and the sole distributor of Pepsi products in Brazil. We believe that Ambev’s leading market position, top-notch management, and strong cash flow generation will likely result in improved earnings growth despite the current tough operating environment. We think that AmBev will continue to focus on execution at the point of sales level and that sales volume will gradually improve from the very low base reported in the first quarter of 2013. Finally, we consider AmBev one of the major beneficiaries of the growing middle class and their increasing purchasing power, not only in Brazil but in many other developing markets as well.

In China, despite recent market declines, especially for stocks of large state-owned-enterprises (SOEs), we find a number of attractive investment opportunities in privately owned companies such as Hengan International Group. Hengan International Group is the largest producer of sanitary napkins and baby diapers in China. The company makes sanitary napkins, disposable baby diapers, adult diapers and other personal hygiene products and it is a private rather than state-owned company. We tend to stay away from SOEs since they are often very large, but persistent shareholder-value destroyers, caused by the state mandated over-investment. For Hengan International Group, safely outside the state control, we expect revenue growth to regain momentum this year and next and its profit margin should expand, especially in sanitary napkins product segment. Furthermore, we believe that Hengan International Group represents very attractive long-term risk-reward opportunity with excellent long-term growth potential, as the living standards of the Chinese population continue to improve.

In Japan, we believe that global leaders such as Toyota Motor, Murata Manufacturing Company and Fast Retailing, will continue to prosper whether the new economic policy platform being rolled out by the new Japanese Prime Minister, Shinzo Abe, dubbed “Abenomics”, will succeed or not. Murata Manufacturing is a global leader in electronic components-primarily in the manufacturing of ceramic passive electronic components, such as capacitors. The company has an overwhelming global market share in ceramic filters, high frequency parts and sensors. These electronic components are everywhere, in mobile phones, computers, cars, trucks, refrigerators, televisions, air conditioners, dishwashers, medical devices and the list goes on. Murata Manufacturing reported strong monthly orders for the first half of 2013, high utilization of its high end product lines and is likely to benefit from the future growth of the smart phone and tablet industry worldwide.

Outlook:

Currently, the Fund has overweight postures in Technology, Consumer Discretionary, and Consumer Staples; underweight postures in Industrials, Energy, Utilities, Healthcare and Materials; close to neutral postures in Financials and Telecommunication Services relative to the MSCI ACWI Index.

Recent purchases or additions in the Fund based on our fundamental research include Keyence, Hyundai Motor, Continental, and Schlumberger. Recent sells or reductions based on our disciplined investment process to take profit or remove stocks that no longer meet our fundamental investment and valuation criteria include Reliance Industries, China Life Insurance, China Shenhua Energy, and PetroChina.

Going forward, the Fund will continue to be anchored with and favor shareholder value creators, such as Google, Fast Retailing, MasterCard, Tencent and LVMH Moet Hennessy Louis Vuitton.

At the regional and country level, we think that the markets, especially those in selected emerging markets, Western Europe and Japan have already discounted many of the uncertainties and risks facing investors. Consequently, we see numerous investment opportunities for long-term global equity investors among the many attractively valued blue-chip large market capitalization multi-national companies all over the world. We believe that long-term global equity investors will be rewarded by focusing their investments, as we do in the Fund, in high quality blue chip stocks that have impressive track records of creating shareholder value, growing dividends in challenging operating environments, maintaining strong balance sheets, and are well positioned competitively in their respective industries.

In conclusion, the only constant in investing is that the market is ever changing, we believe investors should therefore concentrate on the fundamentals of the individual companies that are shareholder value creators, that make economic-value-added capital allocation decisions, that are market leaders in their respective industries, that are likely beneficiaries of secular changes and growth in different parts of the world, and that have exemplary management track records in delivering shareholder value and quality earnings growth even in challenging environments.

| | |

| Annual Report | September 30, 2013 | | 7 |

| | |

| Drexel Hamilton Centre Global Equity Fund | | Manager Commentary |

| | September 30, 2013 (Unaudited) |

SECTOR WEIGHTINGS

As a percentage of Net Assets

| | |

Financials | | 21.35% |

Information Technology | | 20.32% |

Consumer Discretionary | | 15.18% |

Consumer Staples | | 12.55% |

Health Care | | 8.94% |

Energy | | 6.17% |

Materials | | 5.38% |

Industrials | | 4.59% |

Telecommunication Services | | 3.61% |

Utilities | | 0.71% |

Cash and Cash Equivalents | | 1.20% |

Total | | 100.00% |

COUNTRY WEIGHTINGS

As a percentage of Net Assets

| | |

United States | | 27.30% |

Japan | | 10.82% |

Germany | | 10.35% |

France | | 7.58% |

Great Britain | | 6.89% |

Switzerland | | 5.77% |

China | | 4.24% |

Hong Kong | | 3.64% |

Brazil | | 3.19% |

Australia | | 2.72% |

Korea | | 2.64% |

Taiwan | | 2.52% |

Italy | | 2.33% |

Spain | | 1.84% |

Netherlands | | 1.36% |

Belgium | | 0.99% |

Denmark | | 0.90% |

Mexico | | 0.77% |

Greece | | 0.73% |

Russia | | 0.69% |

India | | 0.58% |

Singapore | | 0.53% |

Turkey | | 0.42% |

Cash and Cash Equivalents | | 1.20% |

Total | | 100.00% |

These sector and country allocations may not reflect the current or future positions of the portfolio.

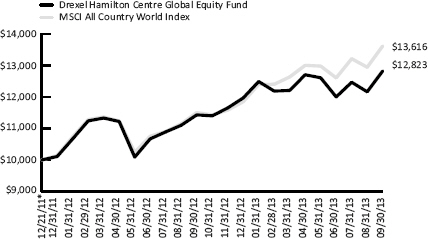

GROWTH OF HYPOTHETICAL $10,000 INVESTMENT THROUGH

SEPTEMBER 30, 2013

This graph assumes an initial investment of $10,000 at December 21, 2011, the Fund’s inception date, and that any dividends and distributions are reinvested. This graph depicts the performance of the Fund versus the MSCI All Country World Index. Taxes on any Fund distributions or when shares are redeemed, if any, are not reflected. Unlike the Fund, an index is not available for investment, is unmanaged and does not have expenses that affect the results. The comparison is shown for illustrative purposes only.

TOTAL RETURNS – FOR THE PERIOD ENDED SEPTEMBER 30, 2013

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 1 Month | | 3 Month | | YTD | | 1 Year | | Since Inception* | | |

| Drexel Hamilton Centre Global Equity Fund | | | | 5.43 | % | | | | 6.85 | % | | | | 7.14 | % | | | | 12.19 | % | | | | 15.01 | % | | |

| MSCI All Country World Index | | | | 5.20 | % | | | | 8.02 | % | | | | 14.92 | % | | | | 18.37 | % | | | | 18.96 | % | | |

The performance information quoted above represents past performance, which is not a guarantee of future results, and does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total return includes reinvestment of dividends and capital gains, if any. Current performance may be lower or higher than the performance data quoted. For the most current month-end performance data please call 855-298-4236.

The total annual operating expense ratio (after expense reimbursements) as stated in the fee table of the most currently effective prospectus of the Fund, dated January 14, 2013, was 1.25%.

The Adviser has entered into a written expense limitation agreement under which it has agreed to limit through January 31, 2014 the total operating expenses of the Fund, including investment advisory fees but excluding interest, taxes, litigation, brokerage commissions, other expenditures which are capitalized in accordance with generally accepted accounting principles and extraordinary expenses, to an annual rate of 1.25% of the average daily net assets of the Fund. Without this waiver the total annual fund operating expenses of the Fund would have been 3.04%.

Investing in the securities of foreign companies generally involves greater risk than investing in larger, more established domestic companies. Therefore, investments in the Fund may involve a greater degree of risk than investments in other mutual funds that invest in larger, more established domestic companies.

The MSCI (Morgan Stanley Capital International) All Country World Index is an unmanaged, free float-adjusted market capitalization weighted index composed of stocks of companies located in countries throughout the world. It is designed to measure equity market performance in global developed and emerging markets. You cannot invest directly in an index.

* The Fund’s inception date was December 21, 2011.

| | |

| Drexel Hamilton Multi-Asset Real Return Fund | | Manager Commentary |

| | September 30, 2013 (Unaudited) |

Performance:

For the period since October 9, 2012 (inception) through September 30, 2013, the Drexel Hamilton Multi-Asset Real Return Fund, Institutional Share Class, delivered an absolute return of 0.05%; the Investor Share Class, which launched on January 22, 2013, delivered a loss of 1.36%. Each result was slightly below the increase in the level of the CPI (Consumer Price Index)1. This was due mainly to the disappointing returns from the Fund’s allocation to Treasury Inflation Protected Securities (TIPS)2 and investments linked to commodities in general, as real interest rates rose during the period, dampening investor demand for such inflation protection securities.

Economic and Market Review:

The Drexel Hamilton Multi-Asset Real Return Fund strives to maintain purchasing power and deliver real returns, particularly in environments that exhibit inflationary conditions and potentially higher market volatility than in the recent past, using a fundamental process of asset allocation. In other words, the Fund is designed to maintain the purchasing power of today’s dollar plus deliver a real return on capital to investors through a tactical asset allocation strategy that employs multiple traditional asset classes with strong positive correlation with inflation. The allocation mix consists of Global Equities, Fixed Income (Treasuries and TIPS), commodity-linked instruments, and Cash and Cash Equivalents in an effort to maximize risk-adjusted returns.

The main fundamental input in the Fund’s asset allocation decision process is the level and the directional change in the equity risk premium (ERP)3 relative to other asset classes, simply defined as the excess return that the overall stock market is expected to provide over a risk-free rate indicating the relative valuation of risky assets versus the risk free alternative. Secondly, the overall trend in CPI and other proxies for inflation, namely currency and commodity prices, are used. Thirdly, historical and forecasted volatility for all asset classes are analyzed and modeled.

Currently, we see the implied risk premium for equities versus bonds as high given the distorted treasury yields due to the government’s quantitative easing (QE) programs which has resulted in asset price distortions and potentially a period of high volatility in the future. We note the following historical tendencies during high equity risk premium environments:

| | • | | Equities are undervalued |

| | • | | Earnings are overstated |

| | • | | Investors betting on rising instability |

| | • | | Higher inflationary expectations |

| | • | | Socio-economic instability |

The process remains flexible and allows the Fund to opportunistically shift to each of the various asset classes as conditions warrant based upon the ability of each asset class to perform best during particular market environments.

Global Equities, Treasury Bonds including Treasury Inflation-Protected Securities (TIPS), and commodity-linked instruments are part of the strategy to address inflation. Historically, the returns of these various asset classes move inversely or are less correlated to one another during different investment periods. This offers investors broader diversification and the ability to take advantage of the changes in asset class performance that may take place with changes in different inflationary environments. The Fund is designed to help mitigate the level of risk of delivering real returns that comes from concentrating in a single asset class. Additionally, we aim to overweight asset classes we believe are poised to perform based on our understanding of how different asset classes respond to inflation and changes in economic conditions. The result is a broadly diversified portfolio that can be used as a core holding or as a complementary allocation to existing equity or fixed income strategies.

| 1 | Consumer Price Index (CPI) – An economic measure that tracks the weighted average of prices of a basket of consumer goods and services. Changes in CPI are used to assess price changes associated with the cost of living. You cannot invest directly into an index. |

| 2 | Treasury Inflation Protected Securities (TIPS) – A fixed income treasury security that is indexed against inflation in order to protector investors’ real purchasing power. TIPS are considered low-risk investment backed by the guarantee of the U.S. Government and the par value moves in tandem with the inflation level, as measured by the Consumer Price Index. |

| 3 | Equity Risk Premium (ERP) – The excess return that that the overall stock market is expected to provide over the risk free rate. |

| | |

| Annual Report | September 30, 2013 | | 9 |

| | |

| Drexel Hamilton Multi-Asset Real Return Fund | | Manager Commentary |

| | September 30, 2013 (Unaudited) |

Outlook:

After years of stable inflation in the U.S., investors seem to be less concerned about the prospect of higher inflation in the future despite the U.S. Federal Reserve’s continuous massive QE4 programs. Actions by the U.S. Federal Reserve under its Chairman, Ben Bernanke, have been unprecedented and the Federal Reserve has embarked on three distinct asset purchase programs, all in an effort to push down long-term interest rates. The latest version, QE3, has the Federal Reserve buying $85 billion worth of Treasury securities and other bonds from banks and primary dealers per month. In fact, the Federal Reserve alone has been the majority buyer of new Treasury bonds issuance since the QE programs started. Despite recent talk by the Federal Reserve regarding the tapering of future asset purchases, the actual exit strategy remains undefined, with the potential for tremendous problems. Heightened global market volatility over the last decade and numerous economic recessions have added to investor concerns. The Fund is designed to address those concerns by diversifying risk, hedging against inflation and protecting against capital drawdowns. We believe that due to unprecedented monetary stimulus that’s been provided by the U.S. government and the Federal Reserve’s desire to prevent deflation at all costs, there are prospects of long-term risk of inflation increasing due to:

| | • | | increased debt loads burdening many developed markets |

| | • | | prolonged accommodative monetary policies |

| | • | | uncertain and poor fiscal conditions |

| | • | | increased stress on commodity supplies primarily from emerging markets |

We believe that the monetary stimuli will remain in force as central bankers embrace higher inflation targets with market expectations relatively benign regarding central bank “exit strategies” and discussion over tapering their asset purchases. We see a high potential for disruption and a future with higher inflationary expectations and we are thus positioned accordingly to weather the long-term risk of inflation and the loss of investors’ purchasing power.

All of these factors have created a myriad of outcomes over the next few years that are likely to cause a rise, perhaps a dramatic one, in inflation and the Drexel Hamilton Multi-Asset Real Return Fund will attempt to maintain investors’ purchasing power of today’s dollar in nominal terms plus deliver a positive real return on capital.

The statements and opinions expressed are those of Centre Asset Management, LLC and are as of the date of this report.

| 4 | QE – Quantitative Easing is a monetary policy by the government that is used to increase the money supply by buying government securities and other assets from the market. The goal is to decrease the interest rate and promote economic growth. |

| | |

| Drexel Hamilton Multi-Asset Real Return Fund | | Manager Commentary |

| | September 30, 2013 (Unaudited) |

ASSET TYPE WEIGHTINGS

As a percentage of Net Assets

| | |

Equity Holdings

(Open-End Funds) | | 52.30% |

U.S. Government Bonds | | 27.13% |

ETNs (Commodity Linked) | | 12.85% |

ETFs (Commodity Linked) | | 4.35% |

Cash and Cash Equivalents | | 3.37% |

Total | | 100.00% |

These allocations may not reflect the current or future positions of the portfolio.

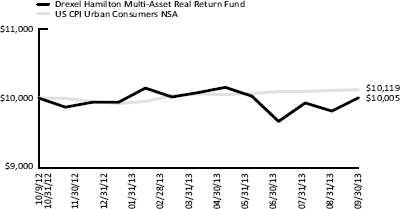

GROWTH OF HYPOTHETICAL $10,000 INVESTMENT THROUGH

SEPTEMBER 30, 2013

This graph assumes an initial investment of $10,000 at October 9, 2012, the Fund’s inception date, and that any dividends and distributions are reinvested. This graph depicts the performance of the Fund versus the US CPI Urban Consumers NSA Index. Unlike the Fund, an index is not available for investment and is unmanaged and does not have expenses that affect the results. The comparison is shown for illustrative purposes only.

CUMULATIVE TOTAL RETURNS – FOR THE PERIOD ENDED

SEPTEMBER 30, 2013

| | | | | | | | | | | | | | | | | | | | |

| | | 1 Month | | 3 Month | | YTD | | Since Inception* |

| Drexel Hamilton Multi-Asset Real Return Fund – Institutional Class | | | | 1.95 | % | | | | 3.51 | % | | | | 0.64 | % | | | | 0.05 | % |

| US CPI Urban Consumers NSA | | | | 0.12 | % | | | | 0.28 | % | | | | 1.98 | % | | | | 1.19 | % |

| Drexel Hamilton Multi-Asset Real Return Fund – Investor Class** | | | | 1.84 | % | | | | 3.52 | % | | | | – | | | | | -1.36 | % |

| US CPI Urban Consumers NSA | | | | 0.12 | % | | | | 0.28 | % | | | | – | | | | | 1.91 | % |

The performance information quoted above represents past performance, which is not a guarantee of future results, and does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total return includes reinvestment of dividends and capital gains, if any. Current performance may be lower or higher than the performance data quoted. For the most current month-end performance data please call 855-298-4236.

The total annual operating expense ratio (after expense reimbursements) as stated in the fee table of the most recent prospectus, dated January 14, 2013, was 1.81% for the Investor Class and 1.56% for the Institutional Class.

The Adviser has agreed, pursuant to a written expense limitation agreement, to reduce its advisory fees and/or reimburse other expenses of the Fund until January 31, 2014 to the extent necessary to limit the current operating expenses of each class of shares of the Fund (exclusive of any front-end or contingent deferred sales loads, taxes, leverage interest, brokerage commissions, expenses incurred in connection with any merger or reorganization, extraordinary expenses such as litigation and other expenses not incurred in the ordinary course of the Fund’s business, and acquired fund fees and expenses, except that, if an acquired fund is an underlying fund managed by the Adviser and such acquired fund is not subject to an effective expense limitation or fee waiver agreement at any time during the term of the expense limitation agreement relating to the Fund, then, for that time, the operating expenses of each class of shares of the Fund shall not exclude the amount of advisory fees included in such acquired fund’s fees and expenses to which the Fund would otherwise be subject), to 1.25% for Investor Class shares of the Fund and 1.00% for Institutional Class shares of the Fund. Without this waiver the total annual fund operating expenses of the Fund would be 2.37% for the Investor Class and 2.12% for the Institutional Class.

The US CPI Urban Consumers NSA Index is the annual percentage change in the Consumer Price Index (CPI). The CPI is an unmanaged index that represents the rate of inflation of U.S. consumer prices as determined by the U.S. Bureau of Labor Statistics.

* The Fund’s inception date was October 9, 2012.

** Investor’s class inception date was January 22, 2013.

| | |

| Annual Report | September 30, 2013 | | 11 |

| | |

| Drexel Hamilton Mutual Funds | | Disclosure of Fund Expenses |

| | September 30, 2013 (Unaudited) |

As a shareholder of a series of Drexel Hamilton Mutual Funds (each series, a “Fund” and together, the “Funds”), you will incur two types of costs: (1) transaction costs, including any applicable redemption fees; and (2) ongoing costs, including management fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on April 1, 2013 and held until September 30, 2013.

Actual Expenses. The first line of each table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line of the table below provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in a Fund to other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. The expenses shown in the table are meant to highlight ongoing Fund costs only and do not reflect transaction fees, such as redemption fees or exchange fees, if any. Therefore, the second line of each table below is useful in comparing ongoing costs only, and may not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | |

| | | BEGINNING ACCOUNT VALUE 04/01/13 | | ENDING ACCOUNT VALUE 09/30/13 | | EXPENSE RATIO(a) | | EXPENSES PAID DURING PERIOD 04/01/13-09/30/13 (b) |

Drexel Hamilton Centre American Equity Fund | | | | | | | | | | | | | | | | | | | | |

Actual | | | $ | 1,000.00 | | | | $ | 1,059.20 | | | | | 1.05% | | | | $ | 5.42 | |

Hypothetical (5% return before expenses) | | | $ | 1,000.00 | | | | $ | 1,019.80 | | | | | 1.05% | | | | $ | 5.32 | |

| | | | |

Drexel Hamilton Centre Global Equity Fund | | | | | | | | | | | | | | | | | | | | |

Actual | | | $ | 1,000.00 | | | | $ | 1,050.50 | | | | | 1.25% | | | | $ | 6.43 | |

Hypothetical (5% return before expenses) | | | $ | 1,000.00 | | | | $ | 1,018.80 | | | | | 1.25% | | | | $ | 6.33 | |

| | | | |

Drexel Hamilton Multi-Asset Real Return Fund | | | | | | | | | | | | | | | | | | | | |

| Institutional Class | | | | | | | | | | | | | | | | | | | | |

Actual | | | $ | 1,000.00 | | | | $ | 992.60 | | | | | 1.00% | | | | $ | 5.00 | |

Hypothetical (5% return before expenses) | | | $ | 1,000.00 | | | | $ | 1,020.05 | | | | | 1.00% | | | | $ | 5.06 | |

| | | | |

Investor Class | | | | | | | | | | | | | | | | | | | | |

Actual | | | $ | 1,000.00 | | | | $ | 990.50 | | | | | 1.25% | | | | $ | 6.24 | |

Hypothetical (5% return before expenses) | | | $ | 1,000.00 | | | | $ | 1,018.80 | | | | | 1.25% | | | | $ | 6.33 | |

| (a) | Annualized, based on the Fund’s most recent fiscal half year expenses. |

| (b) | Expenses are equal to the Portfolios’ annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (183), then divided by 365. |

| | |

| Drexel Hamilton Centre American Equity Fund | | Schedule of Investments |

| | September 30, 2013 |

| | | | | | | | |

| | | Shares | | | Value | |

| |

COMMON STOCKS (99.53%) | | | | | |

Consumer Discretionary (13.30%) | |

Automobiles (1.02%) | | | | | | | | |

Harley-Davidson, Inc. | | | 20,640 | | | $ | 1,325,913 | |

| | | | | | | | |

| |

Hotels Restaurants & Leisure (2.44%) | | | | | |

International Game Technology | | | 57,520 | | | | 1,088,854 | |

Starbucks Corp. | | | 26,960 | | | | 2,075,111 | |

| | | | | | | | |

| | | | | | | 3,163,965 | |

| | | | | | | | |

Internet & Catalog Retail (1.77%) | | | | | |

Amazon.com, Inc.(a) | | | 7,350 | | | | 2,297,904 | |

| | | | | | | | |

| | |

Media (4.29%) | | | | | | | | |

Comcast Corp., Class A | | | 52,670 | | | | 2,378,051 | |

Twenty-First Century Fox, Inc. | | | 44,170 | | | | 1,479,695 | |

Walt Disney Co. | | | 26,560 | | | | 1,712,854 | |

| | | | | | | | |

| | | | | | | 5,570,600 | |

| | | | | | | | |

Specialty Retail (2.53%) | | | | | | | | |

Home Depot, Inc. | | | 29,070 | | | | 2,204,959 | |

Urban Outfitters, Inc.(a) | | | 29,470 | | | | 1,083,612 | |

| | | | | | | | |

| | | | | | | 3,288,571 | |

| | | | | | | | |

Textiles, Apparel & Luxury

Goods (1.25%) | | | | | |

NIKE, Inc., Class B | | | 22,270 | | | | 1,617,693 | |

| | | | | | | | |

| | |

Total Consumer Discretionary | | | | | | | 17,264,646 | |

| | | | | | | | |

| | |

Consumer Staples (10.03%) | | | | | | | | |

Beverages (5.06%) | | | | | | | | |

Coca-Cola Co. | | | 90,200 | | | | 3,416,776 | |

PepsiCo, Inc. | | | 39,670 | | | | 3,153,765 | |

| | | | | | | | |

| | | | | | | 6,570,541 | |

| | | | | | | | |

Household Products (2.05%) | | | | | | | | |

Procter & Gamble Co. | | | 35,120 | | | | 2,654,721 | |

| | | | | | | | |

| | |

Personal Products (0.81%) | | | | | | | | |

Avon Products, Inc. | | | 51,040 | | | | 1,051,424 | |

| | | | | | | | |

| | |

Tobacco (2.11%) | | | | | | | | |

Philip Morris International, Inc. | | | 31,650 | | | | 2,740,573 | |

| | | | | | | | |

| | |

Total Consumer Staples | | | | | | | 13,017,259 | |

| | | | | | | | |

| | |

Energy (7.46%) | | | | | | | | |

Energy Equipment & Services (2.51%) | | | | | |

Noble Corp. | | | 25,200 | | | | 951,804 | |

Schlumberger, Ltd. | | | 26,000 | | | | 2,297,360 | |

| | | | | | | | |

| | | | | | | 3,249,164 | |

| | | | | | | | |

Oil, Gas & Consumable Fuels (4.95%) | | | | | |

EOG Resources, Inc. | | | 11,760 | | | | 1,990,733 | |

Exxon Mobil Corp. | | | 51,560 | | | | 4,436,222 | |

| | | | | | | | |

| | | | | | | 6,426,955 | |

| | | | | | | | |

Total Energy | | | | | | | 9,676,119 | |

| | | | | | | | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Financials (8.64%) | | | | | | | | |

Capital Markets (2.56%) | | | | | |

BlackRock, Inc. | | | 5,080 | | | $ | 1,374,750 | |

Goldman Sachs Group, Inc. | | | 6,310 | | | | 998,305 | |

State Street Corp. | | | 14,390 | | | | 946,142 | |

| | | | | | | | |

| | | | | | | 3,319,197 | |

| | | | | | | | |

Commercial Banks (1.14%) | | | | | |

US Bancorp | | | 40,330 | | | | 1,475,272 | |

| | | | | | | | |

| |

Consumer Finance (1.97%) | | | | | |

American Express Co. | | | 20,540 | | | | 1,551,181 | |

Capital One Financial Corp. | | | 14,700 | | | | 1,010,478 | |

| | | | | | | | |

| | | | | | | 2,561,659 | |

| | | | | | | | |

Diversified Financial

Services (2.97%) | | | | | |

Bank of America Corp. | | | 208,530 | | | | 2,877,714 | |

Citigroup, Inc. | | | 20,020 | | | | 971,170 | |

| | | | | | | | |

| | | | | | | 3,848,884 | |

| | | | | | | | |

Total Financials | | | | | | | 11,205,012 | |

| | | | | | | | |

| | |

Health Care (17.05%) | | | | | | | | |

Biotechnology (6.20%) | | | | | | | | |

Amgen, Inc. | | | 23,450 | | | | 2,624,993 | |

Biogen Idec, Inc.(a) | | | 8,310 | | | | 2,000,715 | |

Celgene Corp.(a) | | | 9,120 | | | | 1,403,842 | |

Gilead Sciences, Inc.(a) | | | 32,060 | | | | 2,014,650 | |

| | | | | | | | |

| | | | | | | 8,044,200 | |

| | | | | | | | |

Health Care Equipment &

Supplies (1.07%) | | | | | |

Boston Scientific Corp.(a) | | | 118,410 | | | | 1,390,133 | |

| | | | | | | | |

| |

Health Care Providers &

Services (2.75%) | | | | | |

Cardinal Health, Inc. | | | 20,610 | | | | 1,074,811 | |

Express Scripts Holding Co.(a) | | | 21,870 | | | | 1,351,129 | |

HCA Holdings, Inc. | | | 26,850 | | | | 1,147,838 | |

| | | | | | | | |

| | | | | | | 3,573,778 | |

| | | | | | | | |

Pharmaceuticals (7.03%) | | | | | |

AbbVie, Inc. | | | 34,570 | | | | 1,546,316 | |

Johnson & Johnson | | | 29,140 | | | | 2,526,147 | |

Merck & Co., Inc. | | | 58,500 | | | | 2,785,185 | |

Pfizer, Inc. | | | 78,820 | | | | 2,262,922 | |

| | | | | | | | |

| | | | | | | 9,120,570 | |

| | | | | | | | |

Total Health Care | | | | | | | 22,128,681 | |

| | | | | | | | |

| | |

Industrials (5.49%) | | | | | | | | |

Aerospace & Defense (2.51%) | | | | | |

Boeing Co. | | | 14,770 | | | | 1,735,475 | |

Honeywell International, Inc. | | | 18,280 | | | | 1,517,971 | |

| | | | | | | | |

| | | | | | | 3,253,446 | |

| | | | | | | | |

Airlines (0.93%) | | | | | | | | |

Delta Air Lines, Inc. | | | 51,210 | | | | 1,208,044 | |

| | | | | | | | |

| |

Construction & Engineering (0.85%) | | | | | |

Quanta Services, Inc.(a) | | | 40,200 | | | | 1,105,902 | |

| | | | | | | | |

| | |

| Annual Report | September 30, 2013 | | 13 |

| | |

| Drexel Hamilton Centre American Equity Fund | | Schedule of Investments |

| | September 30, 2013 |

| | | | | | | | |

| | | Shares | | | Value | |

Industrials (continued) | | | | | | | | |

Road & Rail (1.20%) | | | | | | | | |

Union Pacific Corp. | | | 10,010 | | | $ | 1,554,954 | |

| | | | | | | | |

| | |

Total Industrials | | | | | | | 7,122,346 | |

| | | | | | | | |

| | |

Information Technology (29.27%) | | | | | | | | |

Communication Equipment (4.72%) | | | | | | | | |

Cisco Systems, Inc. | | | 81,370 | | | | 1,905,686 | |

Juniper Networks, Inc.(a) | | | 50,320 | | | | 999,355 | |

QUALCOMM, Inc. | | | 47,790 | | | | 3,219,134 | |

| | | | | | | | |

| | | | | | | 6,124,175 | |

| | | | | | | | |

Computers & Peripherals (4.99%) | | | | | | | | |

Apple, Inc. | | | 9,010 | | | | 4,295,518 | |

NetApp, Inc. | | | 27,920 | | | | 1,189,950 | |

SanDisk Corp. | | | 16,550 | | | | 984,891 | |

| | | | | | | | |

| | | | | | | 6,470,359 | |

| | | | | | | | |

Internet Software & Services (4.96%) | | | | | | | | |

eBay, Inc.(a) | | | 37,670 | | | | 2,101,609 | |

Google, Inc., Class A(a) | | | 4,950 | | | | 4,335,755 | |

| | | | | | | | |

| | | | | | | 6,437,364 | |

| | | | | | | | |

IT Services (4.35%) | | | | | | | | |

International Business Machines Corp. | | | 10,970 | | | | 2,031,424 | |

Mastercard, Inc., Class A | | | 2,410 | | | | 1,621,400 | |

Visa, Inc., Class A | | | 10,420 | | | | 1,991,262 | |

| | | | | | | | |

| | | | | | | 5,644,086 | |

| | | | | | | | |

Semiconductor & Semiconductor Equipment (5.84%) | |

Intel Corp. | | | 103,440 | | | | 2,370,845 | |

Lam Research Corp.(a) | | | 22,540 | | | | 1,153,822 | |

Micron Technology, Inc.(a) | | | 83,130 | | | | 1,452,281 | |

NVIDIA Corp. | | | 69,510 | | | | 1,081,576 | |

Texas Instruments, Inc. | | | 37,930 | | | | 1,527,441 | |

| | | | | | | | |

| | | | | | | 7,585,965 | |

| | | | | | | | |

Software (4.41%) | | | | | | | | |

Microsoft Corp. | | | 98,910 | | | | 3,294,692 | |

Oracle Corp. | | | 73,170 | | | | 2,427,049 | |

| | | | | | | | |

| | | | | | | 5,721,741 | |

| | | | | | | | |

Total Information Technology | | | | | | | 37,983,690 | |

| | | | | | | | |

| | |

Materials (6.39%) | | | | | | | | |

Chemicals (0.81%) | | | | | | | | |

LyondellBasell Industries, Class A | | | 14,350 | | | | 1,050,851 | |

| | | | | | | | |

| | |

Containers & Packaging (1.51%) | | | | | | | | |

Bemis Co., Inc. | | | 24,650 | | | | 961,596 | |

Sealed Air Corp. | | | 36,640 | | | | 996,242 | |

| | | | | | | | |

| | | | | | | 1,957,838 | |

| | | | | | | | |

Metals & Mining (4.07%) | | | | | | | | |

Agnico Eagle Mines, Ltd. | | | 36,230 | | | | 959,008 | |

Eldorado Gold Corp. | | | 145,300 | | | | 974,963 | |

Goldcorp, Inc. | | | 40,960 | | | | 1,065,370 | |

IAMGOLD Corp. | | | 250,590 | | | | 1,190,302 | |

| | | | | | | | | | | | |

| | | | | | | Shares | | | Value | |

Materials (continued) | | | | | | | | |

Metals & Mining (continued) | | | | | | | | |

Kinross Gold Corp. | | | 215,640 | | | $ | 1,088,982 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 5,278,625 | |

| | | | | | | | | | | | |

Total Materials | | | | | | | 8,287,314 | |

| | | | | | | | | | | | |

| | |

Telecommunication Services (1.06%) | | | | | | | | |

Diversified Telecommunication (1.06%) | | | | | | | | |

Verizon Communications, Inc. | | | 29,360 | | | | 1,369,938 | |

| | | | | | | | | | | | |

| | |

Total Telecommunication Services | | | | | | | 1,369,938 | |

| | | | | | | | | | | | |

| | | | |

Utilities (0.84%) | | | | | | | | | | | | |

Independent Power Producers & Energy Traders (0.84%) | | | | | | | | |

Calpine Corp.(a) | | | 56,400 | | | | 1,095,852 | |

| | | | | | | | | | | | |

| | |

Total Utilities | | | | | | | 1,095,852 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | | |

TOTAL COMMON STOCKS (Cost $116,523,869) | | | | | | | 129,150,857 | |

| | | | | | | | | | | | | | | | |

| | | | |

| | | Expiration

Date | | | Exercise

Price | | | Contracts | | | Value | |

PURCHASED OPTIONS (0.01%) | | | | | | | | | | | | | |

Calls (0.01%) | | | | | | | | | | | | | | | | |

SPDR® Gold Shares: | | | | | | | | | | | | | | | | |

| | | 12/21/2013 | | | $ | 168.00 | | | | 480 | | | | 3,360 | |

| | | 1/18/2014 | | | | 168.00 | | | | 320 | | | | 4,480 | |

| | | | | | | | | | | | | | | | | |

TOTAL PURCHASED OPTIONS (Cost $666,122) | | | | | | | | 7,840 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | 7-Day Yield | | | Shares | | | Value | |

SHORT TERM INVESTMENTS (0.44%) | | | | | |

Money Market Fund (0.44%) | | | | | | | | | |

Dreyfus Treasury Prime Cash Management, Institutional Class | | | 0.00004 | % | | | 575,926 | | | | 575,926 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

TOTAL SHORT TERM INVESTMENTS (Cost $575,926) | | | | 575,926 | |

| | |

TOTAL INVESTMENTS (Cost $117,765,917) (99.98%) | | | | | | | $ | 129,734,623 | |

| | |

Other Assets In Excess Of Liabilities (0.02%) | | | | | | | | 30,098 | |

NET ASSETS (100.00%) | | | | | | | $ | 129,764,721 | |

| | | | | | | | | | | | | | | |

| (a) | Non-income producing security. |

| SPDR | - Standard & Poor’s Depositary Receipts. |

See Notes to Financial Statements.

| | |

| Drexel Hamilton Centre Global Equity Fund | | Schedule of Investments |

| | September 30, 2013 |

| | | | | | | | |

| | | Shares | | | Value | |

| |

COMMON STOCKS (96.08%) | | | | | | | | |

ASIA (27.69%) | | | | | | | | |

Australia (2.72%) | | | | | | | | |

Financials (0.75%) | | | | | | | | |

Australia & New Zealand Banking Group, Ltd. | | | 3,800 | | | $ | 109,115 | |

| | | | | | | | |

| | |

Materials (1.39%) | | | | | | | | |

BHP Billiton, Ltd. | | | 6,057 | | | | 201,951 | |

| | | | | | | | |

| |

Telecommunication Services (0.58%) | | | | | |

Telstra Corp., Ltd. | | | 18,000 | | | | 83,457 | |

| | | | | | | | |

| | |

Total Australia | | | | | | | 394,523 | |

| | | | | | | | |

| | |

China (4.24%) | | | | | | | | |

Consumer Staples (0.57%) | | | | | | | | |

Hengan International Group Co., Ltd. | | | 7,100 | | | | 83,030 | |

| | | | | | | | |

| | |

Energy (0.55%) | | | | | | | | |

CNOOC, Ltd. | | | 39,000 | | | | 79,348 | |

| | | | | | | | |

| | |

Financials (1.17%) | | | | | | | | |

Bank of China, Ltd., Class H | | | 173,700 | | | | 79,281 | |

China Overseas Land & Investment, Ltd. | | | 31,000 | | | | 91,331 | |

| | | | | | | | |

| | | | | | | 170,612 | |

| | | | | | | | |

Information Technology (1.04%) | | | | | |

Tencent Holdings, Ltd. | | | 2,880 | | | | 151,057 | |

| | | | | | | | |

| |

Telecommunication Services (0.91%) | | | | | |

China Mobile, Ltd. | | | 11,800 | | | | 131,831 | |

| | | | | | | | |

| | |

Total China | | | | | | | 615,878 | |

| | | | | | | | |

| | |

Hong Kong (3.64%) | | | | | | | | |

Consumer Discretionary (2.02%) | | | | | |

Li & Fung, Ltd. | | | 90,800 | | | | 132,058 | |

Sands China, Ltd. | | | 26,100 | | | | 161,360 | |

| | | | | | | | |

| | | | | | | 293,418 | |

| | | | | | | | |

Financials (1.62%) | | | | | | | | |

AIA Group, Ltd. | | | 28,300 | | | | 133,000 | |

Cheung Kong Holdings, Ltd. | | | 6,700 | | | | 102,022 | |

| | | | | | | | |

| | | | | | | 235,022 | |

| | | | | | | | |

Total Hong Kong | | | | | | | 528,440 | |

| | | | | | | | |

| | |

India (0.58%) | | | | | | | | |

Information Technology (0.58%) | | | | | |

Infosys, Ltd., Sponsored ADR | | | 1,750 | | | | 84,193 | |

| | | | | | | | |

| | |

Total India | | | | | | | 84,193 | |

| | | | | | | | |

| | |

Japan (10.82%) | | | | | | | | |

Consumer Discretionary (5.29%) | | | | | |

Denso Corp. | | | 2,180 | | | | 101,576 | |

Fast Retailing Co., Ltd. | | | 490 | | | | 183,697 | |

Honda Motor Co., Ltd. | | | 4,930 | | | | 187,329 | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Japan (continued) | | | | | | | | |

Consumer Discretionary (continued) | | | | | |

Toyota Motor Corp. | | | 4,650 | | | $ | 296,612 | |

| | | | | | | | |

| | | | | | | 769,214 | |

| | | | | | | | |

Financials (3.84%) | | | | | | | | |

Daiwa Securities Group, Inc. | | | 22,900 | | | | 205,016 | |

Mitsubishi UFJ Financial Group, Inc. | | | 26,300 | | | | 167,761 | |

Nomura Holdings, Inc. | | | 23,800 | | | | 185,228 | |

| | | | | | | | |

| | | | | | | 558,005 | |

| | | | | | | | |

Information Technology (1.69%) | | | | | |

Murata Manufacturing Co., Ltd. | | | 1,540 | | | | 117,347 | |

Yahoo Japan Corp. | | | 22,500 | | | | 127,499 | |

| | | | | | | | |

| | | | | | | 244,846 | |

| | | | | | | | |

Total Japan | | | | | | | 1,572,065 | |

| | | | | | | | |

| | |

Korea (2.64%) | | | | | | | | |

Consumer Discretionary (0.56%) | | | | | |

Hyundai Motor Co. | | | 350 | | | | 81,746 | |

| | | | | | | | |

| | |

Financials (0.50%) | | | | | | | | |

Shinhan Financial Group Co., Ltd. | | | 1,800 | | | | 73,110 | |

| | | | | | | | |

| |

Information Technology (1.58%) | | | | | |

Samsung Electronics Co., Ltd. | | | 180 | | | | 228,962 | |

| | | | | | | | |

| | |

Total Korea | | | | | | | 383,818 | |

| | | | | | | | |

| | |

Singapore (0.53%) | | | | | | | | |

Industrials (0.53%) | | | | | | | | |

Singapore Technologies Engineering, Ltd. | | | 23,300 | | | | 77,447 | |

| | | | | | | | |

| | |

Total Singapore | | | | | | | 77,447 | |

| | | | | | | | |

| | |

Taiwan (2.52%) | | | | | | | | |

Information Technology (2.52%) | | | | | |

Delta Electronics, Inc. | | | 16,800 | | | | 81,537 | |

MediaTek, Inc. | | | 9,800 | | | | 121,145 | |

Taiwan Semiconductor Manufacturing Co., Ltd. | | | 47,800 | | | | 162,475 | |

| | | | | | | | |

| | | | | | | 365,157 | |

| | | | | | | | |

Total Taiwan | | | | | | | 365,157 | |

| | | | | | | | |

| | |

TOTAL ASIA (Cost $3,418,705) | | | | | | | 4,021,521 | |

| |

| | |

EUROPE (38.98%) | | | | | | | | |

Belgium (0.99%) | | | | | | | | |

Consumer Staples (0.99%) | | | | | | | | |

Anheuser-Busch InBev NV | | | 1,448 | | | | 144,138 | |

| | | | | | | | |

| | |

Total Belgium | | | | | | | 144,138 | |

| | | | | | | | |

| | |

| Annual Report | September 30, 2013 | | 15 |

| | |

| Drexel Hamilton Centre Global Equity Fund | | Schedule of Investments |

| | September 30, 2013 |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Denmark (0.90%) | | | | | | | | |

Health Care (0.90%) | | | | | | | | |

Novo Nordisk A/S, Class B | | | 770 | | | $ | 130,729 | |

| | | | | | | | |

| | |

Total Denmark | | | | | | | 130,729 | |

| | | | | | | | |

| | |

France (7.58%) | | | | | | | | |

Consumer Discretionary (1.00%) | | | | | | | | |

LVMH Moet Hennessy Louis Vuitton SA | | | 740 | | | | 145,761 | |

| | | | | | | | |

| | |

Consumer Staples (2.24%) | | | | | | | | |

Danone SA | | | 1,210 | | | | 91,080 | |

L’Oreal SA | | | 1,360 | | | | 233,572 | |

| | | | | | | | |

| | | | | | | 324,652 | |

| | | | | | | | |

Financials (0.99%) | | | | | | | | |

BNP Paribas SA | | | 2,130 | | | | 144,079 | |

| | | | | | | | |

| | |

Health Care (2.46%) | | | | | | | | |

Essilor International SA | | | 1,700 | | | | 182,838 | |

Sanofi | | | 1,713 | | | | 173,738 | |

| | | | | | | | |

| | | | | | | 356,576 | |

| | | | | | | | |

Information Technology (0.89%) | | | | | | | | |

Dassault Systemes SA | | | 970 | | | | 129,494 | |

| | | | | | | | |

| | |

Total France | | | | | | | 1,100,562 | |

| | | | | | | | |

| | |

Germany (9.54%) | | | | | | | | |

Consumer Discretionary (3.17%) | | | | | | | | |

Adidas AG | | | 1,600 | | | | 173,555 | |

Daimler AG | | | 3,684 | | | | 287,172 | |

| | | | | | | | |

| | | | | | | 460,727 | |

| | | | | | | | |

Financials (1.19%) | | | | | | | | |

Muenchener Rueckversicherungs AG | | | 880 | | | | 171,969 | |

| | | | | | | | |

| | |

Health Care (1.27%) | | | | | | | | |

Bayer AG | | | 1,565 | | | | 184,536 | |

| | | | | | | | |

| | |

Industrials (1.73%) | | | | | | | | |

Siemens AG | | | 2,086 | | | | 251,331 | |

| | | | | | | | |

| | |

Information Technology (0.88%) | | | | | | | | |