Investor Presentation November 2011 Filed Pursuant to Rule 433 Registration Statement No. 333-173980 Dated November 23, 2011 |

Notices Please read the following notices before reviewing the information contained herein: The information in this document has been prepared solely for informational purposes and does not constitute an offer to sell or the solicitation of an offer to purchase any securities from any entities described herein. Any such offer will be made solely by means of the prospectus contained in the registration statement (collectively, the “Registration Statement”) filed by HomeStreet Inc. (the “Company”) with the Securities and Exchange Commission (the “SEC”). The information contained herein may not be used in connection with an offer or solicitation by anyone in any jurisdiction in which such offer or solicitation is not permitted by law or in which the person making the offer or solicitation is not qualified to do so or to any person to whom it is unlawful to make such offer or solicitation. All information herein is subject to revision. No representation or warranty can be given with respect to the accuracy or completeness of the information herein, or with respect to the terms of any future offer of securities conforming to the terms hereof. Any information herein shall be deemed superseded, amended, and supplemented in its entirety by the Registration Statement (and any free writing prospectus relating thereto) and any decision to invest in the securities offered thereby should be made solely in reliance upon the Registration Statement (and any free writing prospectus relating thereto). This document is confidential and is intended solely for the information of the person to whom it has been presented. It may not be retained, reproduced or distributed, in whole or in part, by any means (including electronically), without the prior written consent of the Company. Nothing contained herein should be construed as tax, accounting or legal advice. Neither the Company nor any of its affiliates or representatives accept any responsibility for the tax treatment of any investment in the securities of the Company. You (and each of your employees, representatives or other agents) may disclose to any and all persons, without limitation of any kind, this tax treatment and tax structure of the transactions contemplated by these materials and all materials of any kind (including opinions or other tax analyses) that are provided to you relating to such tax treatment and structure. For this purpose, the tax treatment of a transaction is the purported or claimed U.S. federal income tax treatment of the transaction and the tax structure of a transaction is any fact that may be relevant to understanding the purported or claimed U.S. federal income tax treatment of the transaction. INVESTING IS SPECULATIVE AND INVOLVES RISK OF LOSS. YOU SHOULD REVIEW CAREFULLY THE REGISTRATION STATEMENT, INCLUDING THE DESCRIPTION OF THE RISKS AND OTHER TERMS BEFORE MAKING A DECISION TO INVEST. The Company has filed a Registration Statement (including a prospectus) with the SEC for the offering to which this presentation relates. Before you invest, you should read the prospectus contained in the Registration Statement and other documents the Company has filed with the SEC for more complete information about the Company and the offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the Company, any underwriter or any dealer participating in the offering will arrange to send you the prospectus contained in the Registration Statement if you request it by calling FBR Capital Markets & Co. toll free at (800) 846 – 5050. The information contained herein contains forward-looking statements. These forward-looking statements are based on the Company’s current expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts, as well as a number of assumptions concerning future events. These statements are subject to risks, uncertainties, assumptions and other important factors set forth in the Registration Statement, many of which are outside the Company’s control, that could cause actual results to differ materially from the results discussed in the forward-looking statements. Actual results may vary materially from those expressed or implied, and there can be no assurance that estimated returns or projections will be realized or that actual returns will not be materially different than estimated herein. Accordingly, you are cautioned not to place undue reliance on such forward-looking statements. You should conduct your own analysis, using such assumptions as you deem appropriate, and should fully consider other available information, including the information described under “Forward-Looking Statements” and “Risk Factors” in the Registration Statement, in making a decision to invest. Past performance is not necessarily indicative of future results. All forward-looking statements are based on information available to the Company as of the date hereof and the Company assumes no obligation to, and expressly disclaims any obligation to, update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. To supplement the Company’s financial statements presented in accordance with generally accepted accounting principles (“GAAP”), the Company uses non-GAAP measures of certain components of financial performance. These non-GAAP measures are provided to enhance investors’ overall understanding of the Company’s current financial performance and its prospects for the future. Specifically, the Company believes the non-GAAP results provide useful information to both management and investors. These measures should be considered in addition to results prepared in accordance with GAAP, but should not be considered a substitute for, or superior to, GAAP results. |

Offering Summary (1) Assumes offering price of $23.00 per share (midpoint of proposed range of $22.00 and $24.00). Issuer HomeStreet Inc. Ticker NASDAQ: HMST Offering Type Initial public offering of common stock Offering Size $165,000,000 Overallotment Option 15% Shares Offered (1) 7,173,913 Pro Forma Shares (1) 8,524,787 Offering Range $22.00 – $24.00 Use of Proceeds Increase capital levels Fund growth in commercial banking activities General corporate purposes Underwriter FBR Capital Markets Anticipated Pricing Week of December 5, 2011 3 |

Investment Highlights Established and well-respected Pacific Northwest franchise Highly profitable conforming single family mortgage origination and servicing platform Significantly improved credit profile driven by aggressive problem asset resolution Management’s turnaround plan resulted in two consecutive quarters of profitability Commercial banking and diversified real estate lending provides loan and funding growth opportunities Offering designed to satisfy requirements of regulatory order Mid-teens normalized ROE driven by increased NIM and significant noninterest income 4 |

Established Pacific Northwest Franchise $2.3 billion institution with 20 deposit branches and nine lending centers – Average deposits per branch of $100 million (1) – No brokered deposits Largest community bank headquartered in Seattle Over 35,000 demand deposit accounts representing 60% of total accounts Improved competitive banking landscape in the PacNW HomeStreet Bank Branches (20) HomeStreet Loan Offices (9) Seattle Bellevue Tacoma Aberdeen Spokane Vancouver Portland Salem Honolulu Pearl City Maui W A S H I N G T O N O R E G O N # of Market State Branches Rank (2) Share (2) Washington 15 13 1.58% Oregon 2 27 0.47% Hawaii 3 7 1.32% 5 Source: HomeStreet Inc. and SNL Financial. (1) As of September 30, 2011. (2) As of June 30, 2011. |

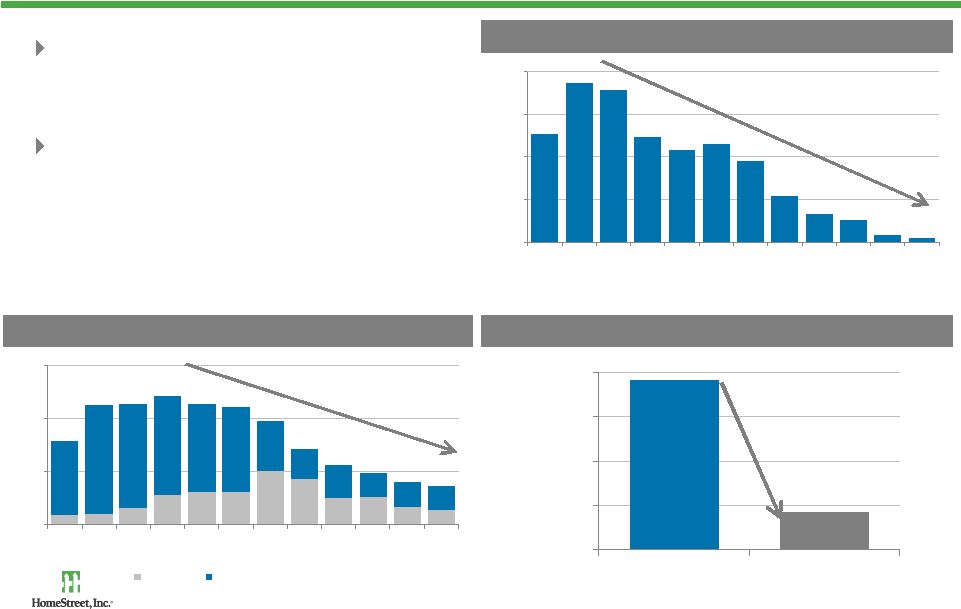

$177 $210 $336 $147 $99 $114 $142 $62 $276 $324 $478 $209 $0 $100 $200 $300 $400 $500 Q1 11 Q2 11 Q3 11 Oct 11 Highly Profitable Mortgage Origination Franchise 70% conventional / 30% government ; 70% purchase / 30% refinance 2009, 2010 and YTD 2011 (1) mortgage originations of $2.7, $2.1 and $1.3 billion 160 retail loan production officers (2) ; no brokered originations Joint venture with Windermere Real Estate Services, the largest real estate brokerage company in the Pacific Northwest Nominal repurchase claims and losses Net origination income of 110 bps in Q3; up to 182 bps in October Source: HomeStreet Inc. (1) As of October 31, 2011. (2) Includes Windermere Real Estate Services. (3) Represents single family held for sale production. 6 Single Family Closed Loan Production (3) ($ mm) HomeStreet Windermere |

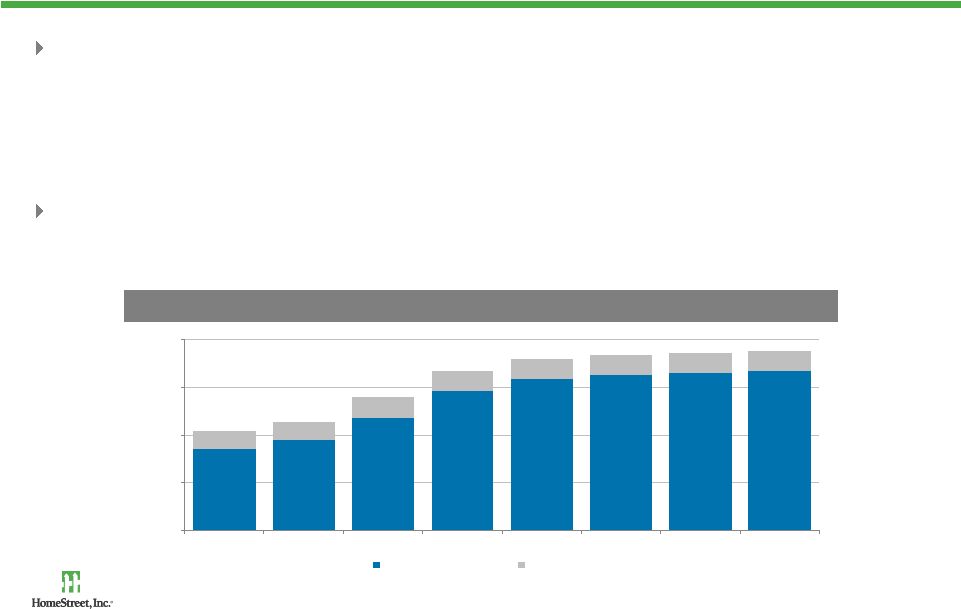

Growing & Profitable Servicing Platform Highly valuable SFR servicing portfolio relative to peers – Higher concentration of FHA/VA loans – – Low weighted average coupon (5.0%) resulting in lower prepayment speeds – Net servicing income of 26 bps year-to-date (2) Highly attractive multifamily servicing platform – Low prepayments and higher servicing fees – One of only 25 Fannie Mae DUS lenders nationwide Servicing Portfolio ($ mm) Source: S-1 filing and HomeStreet Inc. (1) Represents serious delinquency rate (loans over 90 days delinquent). (2) As of October 31, 2011. 7 $3,389 $3,775 $4,696 $5,821 $6,343 $6,521 $6,603 $6,705 $783 $793 $897 $881 $835 $843 $857 $829 $4,172 $4,569 $5,593 $6,702 $7,179 $7,364 $7,460 $7,534 $0 $2,000 $4,000 $6,000 $8,000 2006 2007 2008 2009 2010 Q1 2011 Q2 2011 Oct 2011 Single-family Multi-family / Other Delinquencies below 1%, less than 1/3 of Fannie Mae’s national average (1) |

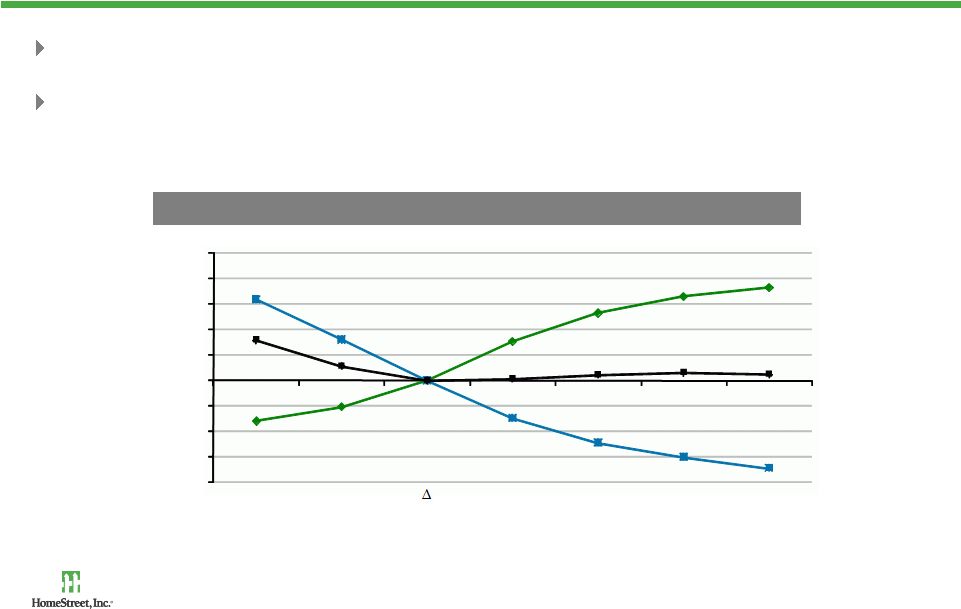

Highly Effective Hedging Strategy “Long position” in interest rates that offsets the “short position” of the MSRs Hedge strategy models maximum loss to $500,000 for a + / - 25 bps rate change, and $2 million for an extreme rate increase scenario MSR Interest Rate Shock Scenarios ($ mm) 8 MSR Asset Total Hedge Net Exposure -$80 -$60 -$40 -$20 $0 $20 $40 $60 $80 $100 -200 -100 0 +100 +200 +300 +400 in Interest Rates (bps) Source: HomeStreet Inc. As of October 31, 2011. Note: No hedging program can effectively hedge model risk (actual versus modeled prepayment rates) and basis risk (mortgage/swap rates spread). |

Source: S-1 filing. Seasoned Management Team Executive / Director Joined Company Years in Industry Relevant Experience Mark K. Mason Director, Vice Chairman, President and CEO Sept 2009 25 Seasoned banking executive with a proven track record of successfully implementing turnaround and growth strategies Former Chairman and CEO of Fidelity Federal Bank David E. Hooston EVP and CFO Aug 2009 30 Extensive turnaround, capital raising and M&A experience Previously was Managing Partner at Granite Bay Partners; Portfolio Manager at Belvedere Capital Partners and concurrently served as President, CFO and COO at Placer Sierra Bancshares and subsidiaries Jay C. Iseman EVP and Chief Credit Officer Aug 2009 20 Significant experience in troubled loan workouts, special assets and credit administration at major national banks Previously served as Senior Vice President and Senior Portfolio Manager of commercial special assets with Bank of America Godfrey B. Evans EVP, General Counsel and CAO Nov 2009 30 Significant experience in banking and corporate securities law, including recapitalization/ restructuring of financial institutions Previously served as General Counsel and CAO at Fidelity Federal Bank and corporate lawyer at Gibson, Dunn & Crutcher 9 |

Turnaround Progress Entered into C&D Developed plan to reduce classified assets, upgrade management, improve earnings and increase capital Restructured credit administration Accelerated problem asset resolution Instituted interest rate floors Expanded NIM – Improved asset yields – Reduced non-core funding – Restructured deposit products/pricing Filed $165 mm IPO Third party loan review confirms valuation / reserves Noncore funding (4) reduced by 88% (5) from 9/30/2009 Achieved two consecutive quarters of profitability Appointed new CEO, CFO, CAO Appointed new CCO 2009 2010 2011 Management Changes Management Actions Restructured Board (3) 10 Classified Assets $761 million (1) $482 million (1) 0.85% (2) $364 million $284 million 1.49% $213 million (5) $145 million (5) 2.51% (5) NPAs NIM Source: S-1 filing and HomeStreet Inc. (1) Represents peak levels in 2009. (2) Represents NIM for Q3 2009. (3) Contingent upon the successful closing of this offering and regulatory approval. (4) Noncore funding represents brokered deposits and FHLB borrowings.(5) As of or for the month ended October 31, 2011. |

Recent Developments Dramatic improvement in credit risk Q2 through October – NPAs down 25% – OREO down 50% – Classified assets decreased 23% Earned $15.3 million and $3.6 million in Q3 and October, respectively, driven by high mortgage banking revenue (1) – Pro forma adjusted ROE of ~21% on ~9.5% tangible equity (1) – NIM increased ~7% to 2.51% (2) – Operating efficiency ratio improved 22% to 57.2% (2)(3) Increased single family loan production by ~60% (4) – Continue to steal share from large mortgage originators Completed annual FDIC/DFI examination in September with no material findings Tangible book value increased 43% from $58.3 million to $83.2 million (5) 11 Source: S-1 filing and HomeStreet Inc. (1) October 2011 net income excludes provision expense, which will be determined at quarter end. Pro forma adjusted ROE for Q3 2011. Pro forma adjustments include: actual Q3 2011 net income of $15.3mm less hedge gains of $12.2mm plus REO expenses of $9.1mm = pro forma adjusted net income of $12.2mm. Annualized for ROE calculation. Denominator represents $232.7mm in pro forma tangible common equity. (2) From June 30, 2011 to October 31, 2011. (3) Noninterest expense adjusted for OREO expense. Noninterest income adjusted for hedge gains/losses and securities gains/losses. See Appendix for reconciliation of non-GAAP financial measures. (4) Represents growth from annualized three months ended Q2 2011 to annualized four months ended October 2011. (5) Represents tangible book value increase from June 30, 2011 to October 31, 2011. |

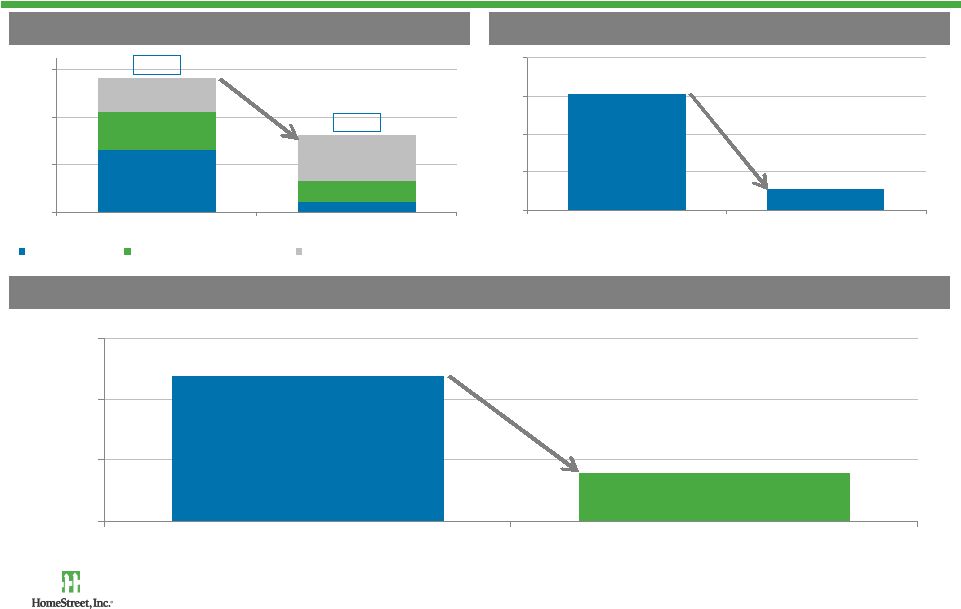

$581 $761 $738 $570 $526 $546 $484 $364 $299 $277 $225 $213 $200 $350 $500 $650 $800 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Oct 11 $37 $38 $63 $108 $123 $122 $202 $170 $99 $103 $64 $52 $278 $410 $389 $374 $327 $321 $189 $113 $124 $91 $95 $93 $314 $449 $452 $482 $450 $442 $391 $284 $223 $194 $159 $145 $0 $200 $400 $600 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Oct 11 OREO Nonperforming Loans $959 $211 $0 $250 $500 $750 $1,000 Q4 2008 Oct-11 (78%) Dramatic Credit Improvement NPAs down 70% and classified assets down 72% from 2009 peak levels (1) Driven by significantly reduced high risk construction loans Source: S-1 filing and HomeStreet Inc. (1) Represents change from peak levels. (70%) (72%) 12 Classified Assets ($ mm) Construction and Land Loans ($ mm) Nonperforming Assets ($ mm) |

Significant Credit Improvement Since Q2 Source: S-1 filing and HomeStreet Inc. (1) Assumes capital raise of $165 million, net of transaction expenses of $15 million. Assumes an additional $35.7 mm of trust preferred securities receive tier 1 capital treatment. Classified assets adjusted for $18.2 million of OREO contracted for sale and $38.6 million of current NPLs, paying as agreed. Represents holding company tier 1 capital. 13 $276.5 $213.4 $200 $225 $250 $275 $300 Q2 2011 Oct-11 (23%) $132.6 $88.2 $32.2 $18.2 $28.8 $38.6 $193.6 $145.0 $80 $120 $160 $200 Q2 2011 Oct-11 Adjusted NPAs OREO Contracted for Sale NPLs, Paying as Agreed (25%) 143% 47% 0.0% 60.0% 120.0% 180.0% Actual October 2011 Pro Forma Adjusted October 2011 (67%) Nonperforming Assets ($ mm) Classified Assets ($ mm) Classified Assets / (Tier 1 + ALLL) |

OREO declined 50% since Q2 driven by accelerated sales (1) – $24.8 million of OREO sold at an additional liquidation loss of $5.8 million Balances greater than 180 days decreased 55% (2) 38% or $19 million of existing OREO is already contracted for sale (3) $0 $30 $60 $90 $120 Q2 2011 Oct-11 Less than 90 Days 90 Days -180 Days Greater than 180 Days Aggressive OREO Sales 14 Source: S-1 filing and HomeStreet Inc. (1) As of October 31, 2011. (2) Decline from Q2 2011 through October 31, 2011 (3) As of November 18, 2011. Days in OREO ($ mm) $25.0 $6.3 $4.9 $12.8 $72.8 $32.7 $102.7 $51.8 (50%) |

Significant NPA Outflows Seven consecutive quarters of NPA outflows totaling ~$340 million (1) Only one commercial loan delinquency (2) NPA Migration 15 ($ in millions) Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Oct 11 Beginning Balance 482.0 $ 450.4 $ 442.2 $ 390.6 $ 283.7 $ 223.0 $ 193.6 $ 159.5 $ Additions to NPLs 20.7 83.5 37.8 22.3 28.9 14.2 20.9 2.3 Charge-Offs 11.7 20.6 36.2 14.6 2.1 4.7 7.7 1.1 OREO Sales 14.8 41.3 21.9 21.2 67.0 17.6 33.8 10.9 OREO Writedowns (1.2) 5.1 7.2 16.3 10.6 4.7 8.2 2.5 Principal Paydown, Payoff, Advances 10.2 17.6 19.0 10.9 5.6 6.0 2.4 1.8 Transferred Back to Accrual Status 16.6 7.1 5.1 66.2 4.3 10.6 2.9 0.4 Subtractions from NPAs 52.2 91.7 89.4 129.2 89.6 43.6 55.0 16.8 Net Inflows / (Outflows) (31.6) (8.2) (51.6) (106.9) (60.7) (29.4) (34.1) (14.4) Ending Balance 450.4 $ 442.2 $ 390.6 $ 283.7 $ 223.0 $ 193.6 $ 159.5 $ 145.0 $ Source: HomeStreet Inc. (1) Since Q4 2009. (2) As of November 18, 2011. |

Conservatively Marked Portfolio OREO has been sold to date at 64% (1) of unpaid principal balance NPAs currently carried at 55% (2) of UPB 16 Source: HomeStreet Inc. (1) Represents OREO sales since Q3 2009. (2) As of October 31, 2011. (3) Includes loan charge offs of $42.9 million and OREO writedowns of $25.7 million. (4) In addition to specific reserves of $23.0 million, the Company has remaining reserves of $29.1 million. ($ in millions) Category Unpaid Principal Balance LTD Charge Offs / Write Downs Carrying Value at 10/31/2011 Specific Reserves at 10/31/2011 CV - Specific Reserves CV - Specific Reserves % of Unpaid Principal Balance Remaining Reserves on all other Loans 1-4 Family 16.5 $ 1.6 $ 14.9 $ 0.6 $ 14.3 $ 86.7% Multifamily 5.2 0.0 5.2 0.0 5.2 100.0% CRE - Owner Occupied 7.9 0.5 7.4 0.2 7.2 90.8% CRE - Non Owner Occupied 3.4 0.4 3.0 0.0 3.0 86.9% C&I 2.1 0.2 2.0 0.4 1.6 73.4% Construction 63.1 5.3 57.8 21.7 36.1 57.2% Consumer 3.5 0.5 3.0 0.0 3.0 85.2% Nonperforming Loans 101.7 $ 8.5 $ 93.2 $ 23.0 $ 70.2 $ 69.1% 29.1 $ OREO 120.4 68.6 51.8 0.0 51.8 43.0% 0.0 Nonperforming Assets 222.1 $ 77.1 $ 145.0 $ 23.0 $ 122.1 $ 54.9% 29.1 $ (4) (3) Carrying Value of Nonperforming Assets |

Strong Reserves HomeStreet’s reserves / loans are 38% above peer averages (1)(2) Reserves ($ mm) Source: S-1 filing, HomeStreet Inc. and SNL Financial. (1) Company-identified peers include BANR, CACB, COBZ, COLB, CPF, CVBF, GBCI, PACW, PCBC, STSA, TCBK, UMPQ, WABC, WAL, WCBO and WFSL . Represents the median of peers’ reserves / loans ratio. Peers’ October data is unavailable. (2) As of September 30, 2011. 17 5.2% 5.0% 4.1% 4.0% 4.0% 4.1% 3.8% 3.7% 2.8% 2.9% 2.7% 2.8% 2.9% 2.8% 2.7% 2.0% 3.0% 4.0% 5.0% 6.0% Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Oct-11 Reserves / Loans Peer Reserves / Loans (1) |

$16.3 $13.3 $12 $13 $14 $15 $16 $17 Q2 2011 Oct 2011 Third Party Loan Review and Stress Tests Engaged Unicon Financial Services to review loan and OREO portfolios According to Unicon, reserves are adequate and carrying values are recoverable even in a high stress scenario Potential losses under HomeStreet’s stress scenario, which assumes further real estate market deterioration, declined 18% to $13.3 million since Q2 18 Source: Unicon Financial Services and HomeStreet Inc. (1) Unicon’s estimated losses are as of June 30, 2011. Unicon Stress Scenario (1) ($ mm) HomeStreet Stress Scenario ($ mm) (18%) $0.2 $1.5 $0.0 $0.5 $1.0 $1.5 $2.0 Low High |

Near Term Projected Credit Resolutions Approximately $45-$50 million of anticipated OREO sales in the next three quarters – ~40% is contracted for sale and scheduled to close by year end NPAs / Assets: 2.00% - 2.25% Total: $145 6.30% 19 Source: HomeStreet Inc. (1) Includes $22.4 million of chargeoffs of specific reserves existing as of October 31, 2011. Remaining chargeoffs primarily relate to anticipated migration of single family loans. (2) Net NPL outflows include NPL upgrades and anticipated additions to NPLs. Net NPLs $70.2 $45 - $50 OREO $51.8 General Reserves $3-$7 Additional: $3 - $5 $15 - $20 Specific Reserves $23.0 Specific Reserves $22.4 $0 $50 $100 $150 NPA Balance (10/31/2011) Utilization of Existing Reserves Anticipated OREO Sales Scheduled Principal Payoffs Net NPL Outflows Projected NPA Balance Mid 2012 Contracted as of 11/18/2011: $19 (1) (2) $25 - 30 |

Recapitalized HomeStreet Offering structured to meet regulatory order requirements Pro forma capital levels meet all Basel III requirements, if fully implemented Bank regulatory requirement of 10% and 12% Tier 1 Leverage and Total RBC, respectively 20 Well Pro Forma Capitalized 10/31/2011 Ratios (1) Tier 1 Leverage (2) 5.0% 4.2% 11.6% Tier 1 RBC (3) 6.0% 6.6% 19.0% Total RBC (3) 10.0% 10.2% 20.3% Note: The Company is not currently subject to holding company regulatory capital requirements. Holding company ratios are calculated for indicative purposes only, based on capital requirements for bank holding companies. Assumes an additional $35.7 mm of trust preferred securities receive tier 1 capital treatment. (1) Assumes capital raise of $165 million, net of transaction expenses of $15 million. (2) Pro forma tier 1 leverage calculation assumes the addition of 100% of net proceeds to average assets. (3) Pro forma tier 1 RBC and total RBC ratios assume 0% risk weighting assigned to net proceeds for risk weighted assets calculation. |

($5.1) ($9.4) ($5.4) ($14.4) ($7.4) $1.3 $15.3 $3.6 ($20) ($10) $0 $10 $20 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Oct 11 Return to Strong Profitability 21 Net Income ($ millions) $1.7 $6.4 $15.2 $12.7 $4.3 $9.2 $25.7 $6.0 $0 $10 $20 $30 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Oct 11 Earned $1.3 million and $15.3 million in Q2 and Q3 and $3.6 million in October (1) – Q3 and October ROAA of 2.67% and 1.85%, respectively Significant increase in noninterest income driven by higher originations and gain on sale margins (1) Pre-Tax Pre-Provision (2) ($ millions) Source: S-1 filing and HomeStreet Inc. (1) October 2011 net income excludes provision expense, which will be determined at quarter end. (2) Adjusted for OREO expense. See Appendix for reconciliation of non-GAAP financial measures. |

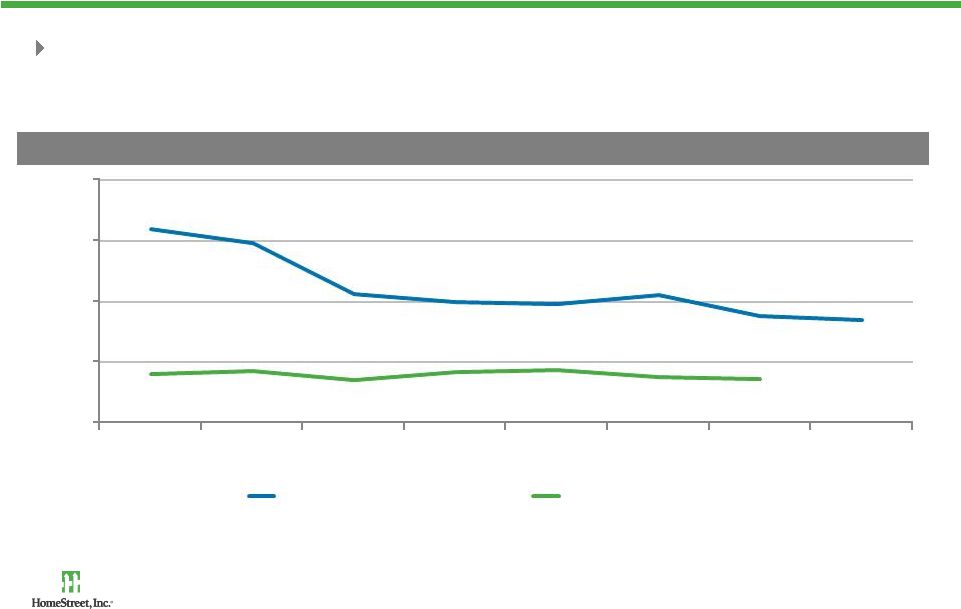

NIM increased 166 bps to 2.51% (1) from a low of 0.85% (2) Operating efficiency ratio improved to 57.2% from its peak of 154.6% (2) NIM Growth and Operating Efficiency 22 Net Interest Margin (%) Operating Efficiency Ratio (3) (%) 0.96% 1.16% 1.68% 2.34% 2.17% 2.35% 2.38% 2.51% 0.6% 1.1% 1.6% 2.1% 2.6% Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Oct 11 97.9% 102.4% 60.9% 72.3% 83.6% 73.2% 64.6% 57.2% 40% 60% 80% 100% 120% Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Oct 11 Source: S-1 filing and HomeStreet Inc. (1) As of October 31, 2011. (2) NIM low as of September 30, 2009. Operating efficiency peak as of September 30, 2009. (3) Noninterest expense adjusted for OREO expense. Noninterest income adjusted for hedge gains/losses and securities gains/losses. See Appendix for reconciliation of non-GAAP financial measures. |

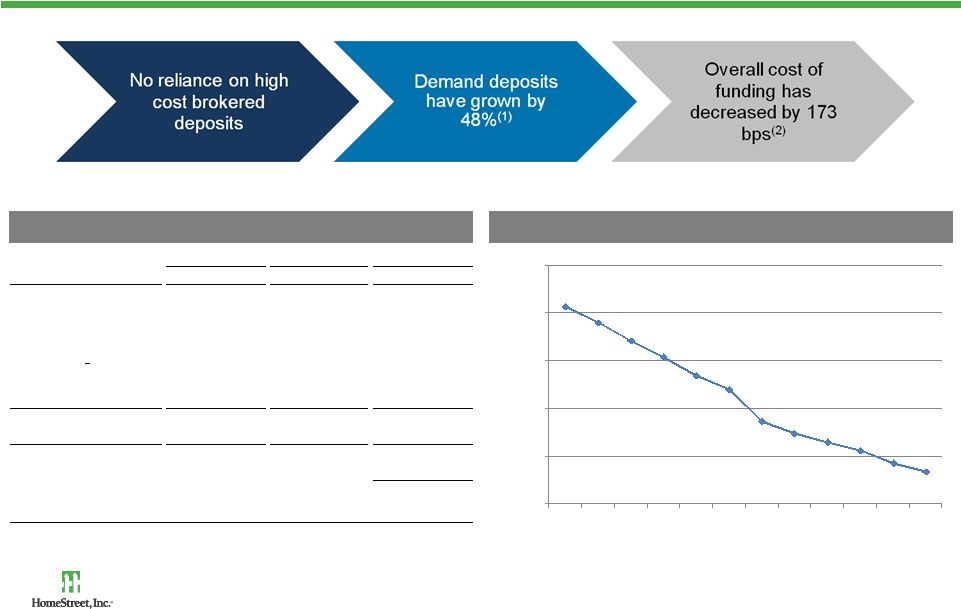

Efficient Retail Deposit Funding Base Source: S-1 filing and HomeStreet Inc. (1) Since Q4 2008 (2) Since Q1 2009. (3) Core deposits include transaction deposits, savings & MMDA deposits and time deposits less than $250,000. Bank Cost of Funding (%) Bank Funding Balances 23 3.07% 2.90% 2.71% 2.54% 2.35% 2.20% 1.87% 1.74% 1.65% 1.56% 1.43% 1.34% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Oct 11 ($ in millions) 9/30/2009 10/31/2011 Change Type of Deposits $ % $ % $ % Transaction 169.2 $ 5.6% 218.9 $ 10.4% 49.7 $ 29.4% Servicing Deposits 140.2 4.7% 221.3 10.5% 81.1 57.8% Savings & MMDA 439.5 14.6% 543.2 25.7% 103.7 23.6% Time Deposits $250k 1,166.6 38.9% 997.1 47.3% (169.5) (14.5)% Time Deposits > $250k 78.2 2.6% 71.4 3.4% (6.8) (8.7)% Brokered Deposits 326.9 10.9% 0.0 0.0% (326.9) (100.0)% Total Deposits 2,320.6 77.3% 2,051.9 97.3% (268.7) (11.6)% FHLB Advances 681.0 22.7% 57.9 2.7% (623.1) (91.5)% Total Funding 3,001.6 $ 100.0% 2,109.8 $ 100.0% (891.8) $ (29.7)% Change Cost of Total Deposits 2.4% 1.1% (1.3)% Core Deposits (3) 82.5% 96.5% 14.0% < |

Net Interest Margin Expansion Opportunities Source: HomeStreet Inc. (1) Margin expansion opportunities from 10/31/2011 net interest margin are based upon management’s assumptions of post recapitalization restructuring opportunities and will differ from future results. 24 (1) 2.51% 3.75% - 4.00% 0.20% - 0.30% 0.20% - 0.30% 0.80% - 0.90% 2% 3% 3% 4% 4% 10/31/2011 NIM Increased capital Increase in yields & reduction in NPLs Change in securities / loan / deposit mix Near Term Target NIM |

Earnings Potential Actual Normalizing Pro Forma ($ in millions) 9/30/2011 Adjustments (1) Normalized (1) Net Interest Income (2) 12.0 $ 10.2 $ 22.2 $ Provisions for Loan Losses (3) (1.0) (1.0) (2.0) Gain on Sale of Mortgage Loans (4) 16.1 (6.8) 9.3 Mortgage Servicing (4) 18.5 (12.2) 6.3 Other Noninterest Income (5) 2.7 (1.0) 1.6 Operating Revenue 48.2 (10.8) 37.5 OREO-Related Expense (6) 9.1 (9.0) 0.1 FDIC Assessment Fees (7) 1.3 (0.9) 0.3 Other Noninterest Expense (8) 22.2 (0.6) 21.7 Total Noninterest Expense 32.6 (10.5) 22.1 Pretax Income 15.6 (0.3) 15.4 Taxes (9) 0.4 5.3 5.7 Net Income 15.3 $ (5.6) $ 9.7 $ Net Interest Margin (2) 2.38% 3.89% Operating Efficiency Ratio (10) 64.6% 55.8% ROAA 2.7% 1.6% ROAE 83.0% 16.9% 25 Source: HomeStreet Inc. (1) These are not projections of future earnings, nor a complete listing of all potential impacts at the proposed recapitalization. Future results will differ from the opportunities outlined. (2) NIM reflects restructured balance sheet for securities, loans and deposits. (3) Provision for loan losses reflects providing for growth in loan portfolio to achieve target mix (i.e., 1/3 consumer, commercial real estate and C&I). (4) Single family gain on sale and servicing, as well as income from WMS adjustments reflect both reduction of volume to eliminate refinance activity and robust refinance "boom" margins which are consistent with Q2 2011 results. (5) Eliminated securities gains. (6) OREO expense adjusted to reflect reduction of OREO and substantial elimination of risk. (7) FDIC insurance fees reflect elimination of Regulatory Order at the Bank. (8) Adjusted salaries and benefits to reflect a decrease in commissions related to single family refinance boom, offset by increases in salaries and benefits to achieve loan and deposit mix changes. Aligned professional fees to reflect lower risk operating environment. Marketing expenses increased to achieve balance sheet restructuring of customers. (9) Assumes effective tax rate of 37%. (10) Noninterest expense adjusted for OREO expense. See Appendix for reconciliation of non-GAAP financial measures. |

Growth Strategies Organic growth opportunities driven by attractive market demographics – Job growth and housing recovery is expected to outpace the overall economy – Well educated workforce, high incomes and strong population trends Expand commercial and consumer banking activities – Commercial: lending, cash management, insurance – Consumer: mortgage loans, deposits, investments, insurance Expand single family mortgage banking activities – Increase retail, correspondent and internet production channels Expand multifamily mortgage banking through the Fannie Mae DUS program Restart traditional portfolio lending 26 |

HomeStreet Adjusted Book Value Per Share: $61.56 $23.00 $27.34 $(1.13) $1.77 $4.92 % of Stated Book: 37% P/ BV: 0.84x Price / Loss Adj. BV: 0.88x P/BV: 0.70x $32.90 Source: Derived from S-1 filings and HomeStreet Inc. (1) Net proceeds of $150.0 mm is calculated using gross capital raise of $165.0 mm less assumed capital raise expenses of $15.0 mm. Assumes offering price of $23.00 per share. (2) Based on estimated after-tax loan losses per management’s stress case scenario. Assumes effective tax rate of 37% on estimated losses of $15.3 million. (3) Actual realization of any DTA amount is not guaranteed, and actual results may differ (4) Based on historical 8 quarters of pre-provision earnings (10/1/2009 to 9/30/2011). Pre provision earnings calculated as pre tax income (loss) plus provision expense and REO related expense. Resulting earnings tax-effected at the rate of 37%. See Appendix for reconciliation of non-GAAP financial measures. P/ BV: 0.82x P/BV: 0.70x 27 (2 Years) 83.2 233.1 280.5 150.0 (9.6) 15.1 41.9 $0 $50 $100 $150 $200 $250 $300 $350 October 2011 Book Value New Capital Pro Forma Equity Estimated Stress Case Losses DTA Pre Provision Earnings Trailing Pro Forma Book Value (1) (2) (3) (4) |

Investment Highlights Established and well-respected Pacific Northwest franchise Highly profitable conforming single family mortgage origination and servicing platform Significantly improved credit profile driven by aggressive problem asset resolution Management’s turnaround plan resulted in two consecutive quarters of profitability Commercial banking and diversified real estate lending provides loan and funding growth opportunities Offering designed to satisfy requirements of regulatory order Mid-teens normalized ROE driven by increased NIM and significant noninterest income 28 |

Appendix |

Director Joined Relevant Experience David A. Ederer Chairman (since 2009) 2004 Currently serves as Chairman of Ederer Investment Company, a private investment company as well as Director in several other local foundations Mark K. Mason Vice Chairman 2009 Currently serves as President & CEO of HomeStreet Inc and HomeStreet Bank; former Chairman and CEO of Fidelity Federal Bank Scott Boggs (1)(2) 2006 Former Corporate Controller at Microsoft Corporation and adjunct accounting professor at Seattle University Albers School of Business Brian P. Dempsey (2) 1996 Previously served on the Board of Directors of Golden State Bancorp and Federal Home Loan Bank of Seattle and was President and Chairman of University Savings Bank Victor H. Indiek (1) 2011 Project Manager at Quantum Partners managing FDIC receiverships and previously President, CEO, CFO of Freddie Mac and CFO of American Savings Thomas E. King (1)(2) 2010 Consultant to banks; previously CEO or COO of San Diego Community Bank, Fullerton Community Bank, Bank of So. Cal, CapitolBank, credit & lending officer at Sec Pac George Kirk (1)(2) 2007 Former President and CEO of Port Blakely Communities and President of Skinner Development Company and Chair of Real Estate Dept at Davis Wright Tremaine LLP Michael J. Malone (1) 2011 CEO of Hunters Capital, member of the Board of Directors of Expeditors International; previously founder, Chairman and CEO of AEI/DMX Music Mary Oldshue (1)(2) 2007 Consultant in finance and business development, former Board Member of Metro One, former CFO of Pacific Development, a commercial real estate development company Doug Smith (1) 2011 President of Miller and Smith, a residential home building company Bruce W. Williams 1994 Previously served as President and CEO of Homestreet Inc and Homestreet Bank Pro Forma Board of Directors Source: S-1 filing (1) Appointment subject to regulatory approval. (2) Currently Director for HomeStreet Bank. Reflects date joined HomeStreet Bank’s Board. 30 |

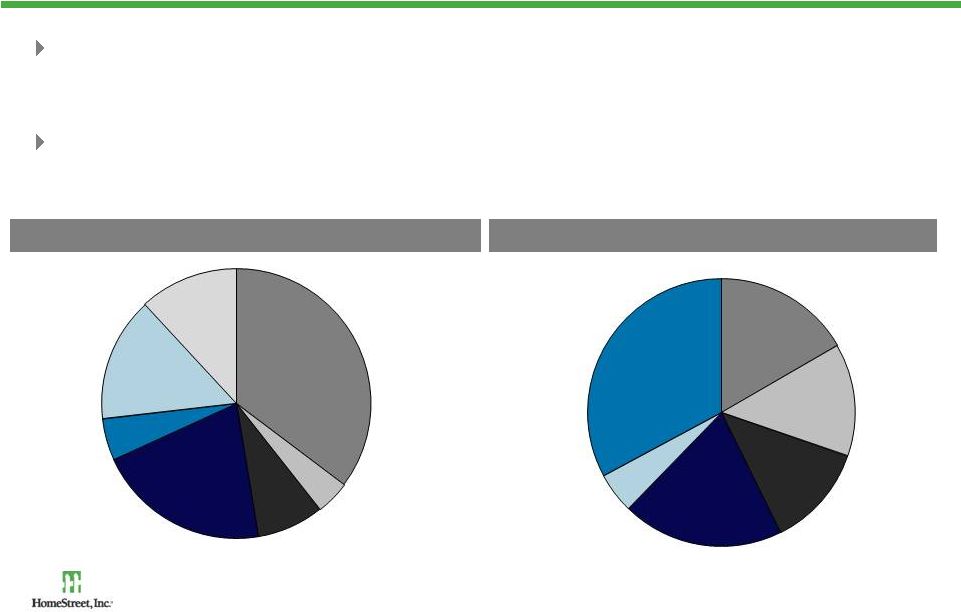

Loan Portfolio Characteristics New management team has focused on reducing exposure to real estate developers and higher risk property types Increased emphasis on business banking and multifamily mortgage lending October 2011 Loan Composition October 2011 CRE by Property Type 31 Source: HomeStreet Inc. Mixed Use $63 (14%) Office $91 (20%) Other $23 (5%) Retail $152 (33%) Industrial Warehouse $77 (16%) Multifamily $57 (12%) 1-4 Family $496 (35%) CRE - Non Owner Occupied $293 (21%) C&I $70 (5%) Consumer $166 (12%) Construction $211 (15%) Multifamily $57 (4%) CRE - Owner Occupied $112 (8%) |

Loan Portfolio Characteristics (cont.) Loan portfolio concentrated in the Puget Sound area, which has been less impacted by the economic downturn compared to eastern Washington Adjustable rate loans comprise approximately 67% of the loan portfolio October 2011 Loans by Geography October 2011 Loan Interest Rate Mix Source: HomeStreet Inc. 32 Fixed Rate 33% Adjustable Rate 67% Puget Sound Puget Sound 68% Idaho (Boise) 1% Oregon 17% Hawaii 3% Other 1% Washington Other 10% |

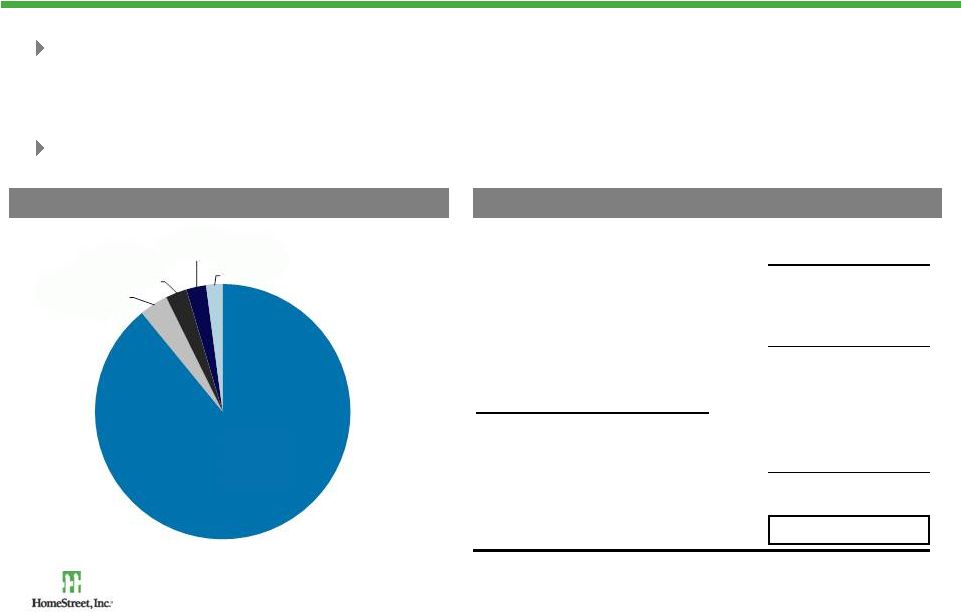

Strong Liquidity Position Proactively reduced brokered deposits and reliance on wholesale funding sources – Available capacity under FHLB and FRB of $248 million and $152 million, respectively Substantial excess liquidity with a primary liquidity ratio of 33% (1) Total Sources of Liquidity ($ mm) Funding Sources ($ mm) 33 Total Funding: $2,303 million Source: HomeStreet Inc. (1) Primary liquidity ratio is defined as net cash, short-term investments and other marketable assets as a percent of net deposits and short-term borrowings. Ratio as of October 31, 2011. (2) Represents market value of unpledged securities. October 31, 2011 Cash 306.3 $ Unpledged Securities 235.6 (2) Loans Held for Sale 132.0 Total On-Balance Sheet Liquidity 673.9 Additional Borrowing Capacity FHLB 248.3 FRB SF 151.9 Total Available Capacity 400.2 $ Total Direct Sources of Liquidity 1,074.1 $ Deposits $2,052 (89%) Capital $83 (4%) Borrowings $62 (3%) FHLB $58 (2%) Other $48 (2%) |

Mortgage Banking Platform 2009, 2010 and YTD 2011 (1) mortgage originations of $2.7, $2.1 and $1.3 billion Q3 2011 Mortgage Originations Source: S-1 filing and HomeStreet Inc. (1) As of October 31, 2011. (2) Excludes net MSR / hedge valuation gains/losses. (3) Basis points on closed loan production. 34 October 2011 Mortgage Originations Servicing Income (2) (bps) Year to Date 10/31/2011 Quarter Ended 9/30/2011 Month Ended 10/31/2011 Revenue 39 36 37 Cost of Servicing 13 9 15 Servicing Income 26 27 22 Quarter Ended 9/30/2011 ($ mm) HomeStreet Windermere Total Single Family Closed Loan Production 336 $ 142 $ 478 $ Rate Lock Commitments 462 169 631 Gain on Sale Income (bps) (3) Gross Revenue 403 185 338 Production Expense (222) (20) (228) Net Income 181 165 110 Month Ended 10/31/2011 ($ mm) HomeStreet Windermere Total Single Family Closed Loan Production 147 $ 62 $ 209 $ Rate Lock Commitments 144 52 196 Gain on Sale Income (bps) (3) Gross Revenue 380 275 349 Production Expense (162) (15) (167) Net Income 217 260 182 |

Balance Sheet 35 Source: S-1 filing and HomeStreet Inc. Month Ended Quarter Ended ($ in millions) 10/31/2011 9/30/2011 6/30/2011 3/31/2011 12/31/2010 Cash 306.3 $ 138.4 $ 108.2 $ 170.8 $ 72.6 $ Investments 282.7 339.5 315.7 304.4 313.5 Loans Held for Sale 132.0 226.6 121.2 82.8 212.6 Loans Held for Investment 1,401.1 1,413.4 1,451.9 1,562.7 1,602.7 Allowance for Loan Losses (52.0) (53.2) (59.7) (62.1) (64.2) Net Loans 1,349.1 1,360.2 1,392.2 1,500.6 1,538.5 Other Real Estate Owned 51.8 64.4 102.7 98.9 170.5 Mortgage Servicing Rights 80.7 74.1 94.3 96.0 87.2 Federal Home Loan Bank Stock 37.0 37.0 37.0 37.0 37.0 Other Assets 63.2 76.6 62.2 52.1 53.8 Total Assets 2,302.8 $ 2,316.8 $ 2,233.5 $ 2,342.6 $ 2,485.7 $ Deposits 2,051.9 $ 2,057.0 $ 1,993.7 $ 2,066.8 $ 2,129.7 $ Federal Home Loan Bank Borrowings 57.9 67.9 77.9 114.5 165.9 Other 109.8 111.6 103.6 110.1 131.3 Total Liabilities 2,219.6 2,236.5 2,175.2 2,291.4 2,426.9 Equity 83.2 80.3 58.3 51.2 58.8 Total Liabilities and Equity 2,302.8 $ 2,316.8 $ 2,233.5 $ 2,342.6 $ 2,485.7 $ |

Income Statement & Profitability Ratios 36 Month Ended Quarter Ended ($ in millions) 10/31/2011 9/30/2011 6/30/2011 3/31/2011 12/31/2010 Income Statement Net Interest Income 4.4 $ 12.0 $ 11.9 $ 11.6 $ 13.5 $ Provision for Loan Losses (1) 0.0 (1.0) (2.3) 0.0 (8.2) Total Noninterest Income (2) 9.7 37.3 18.9 14.5 28.1 Total Noninterest Expense (3) 10.5 32.6 27.3 33.5 46.5 Income / (Loss) Before Taxes 3.6 15.6 1.3 (7.4) (13.1) Provision / (Credit) for Taxes 0.0 0.4 (0.0) 0.0 1.3 Net Income (Loss) 3.6 $ 15.3 $ 1.3 $ (7.4) $ (14.4) $ Profitability Ratios Net Interest Margin 2.51% 2.38% 2.35% 2.17% 2.34% Operating Efficiency Ratio (4) 57.31% 47.74% 70.05% 83.31% 69.51% Return on Average Equity 52.23% 83.04% 8.97% (51.26)% (72.28)% Return on Average Assets 1.85% 2.67% 0.23% (1.25)% (2.23)% Average Loan Yield (5) 4.71% 4.85% 4.86% 4.82% 4.90% Average Cost of Deposits 1.24% 1.30% 1.44% 1.51% 1.58% Average Cost of Funds 1.40% 1.48% 1.61% 1.73% 1.78% Source: S-1 filing and HomeStreet Inc. (1) HomeStreet generally records provision expense at the end of each quarter. (2) Includes net MSR/hedge valuation (loss) gains of $(472,000), $12.2 million, $1.3 million, $91,000 and $1.6 million for October 2011, Q3 2011, Q2 2011, Q1 2011 and Q4 2010, respectively. (3) October OREO expenses were $2.4 million vs. $9.1 million in Q3 2011. (4) Noninterest expense adjusted for OREO expense. See Appendix for reconciliation of non-GAAP financial measures. (5) Before impact of nonaccrual loans. |

Asset Quality & Capital Adequacy 37 Source: S-1 filing and HomeStreet Inc. (1) Calculation based on Bank Tier 1 capital. Month Ended Quarter Ended ($ in millions) 10/31/2011 9/30/2011 6/30/2011 3/31/2011 12/31/2010 Asset Quality Net Charge Offs 1.1 $ 7.7 $ 4.7 $ 2.1 $ 14.6 $ Nonperforming Loans 93.2 95.1 90.9 124.1 113.2 Other Real Estate Owned 51.8 64.4 102.7 98.9 170.5 Nonperforming Assets 145.0 $ 159.5 $ 193.6 $ 223.0 $ 283.7 $ Classified Assets 213.4 $ 225.0 $ 276.5 $ 298.7 $ 363.9 $ NPLs / Total Loans 6.7% 6.7% 6.3% 7.9% 7.1% NPAs / Total Assets 6.3% 6.9% 8.7% 9.5% 11.4% Classified Assets / Total Assets 9.3% 9.7% 12.4% 12.8% 14.6% Total Delinquencies / Total Loans 11.1% 10.2% 9.1% 12.0% 11.1% Reserves / Loans 3.7% 3.8% 4.1% 4.0% 4.0% Reserves / NPLs 55.8% 55.9% 65.7% 50.1% 56.7% NPAs / Tier 1 + ALLL (1) 80.1% 89.0% 114.7% 131.3% 156.5% Classified Assets / Tier 1 + ALLL (1) 117.9% 125.6% 163.7% 175.9% 200.8% Bank Capital Adequacy Tier 1 Leverage Ratio 5.7% 5.6% 4.9% 4.5% 4.5% Risk Based Capital Ratio 10.5% 9.8% 8.7% 8.3% 8.2% |

15 Largest Nonperforming Loans 38 ID Loan Type Unpaid Principal Balance Partial Charge Offs Net Commitment Net Book Balance Specific Reserves Book Balance Net of Specific Reserves TDR Description 1 Construction/Land Development 21,809,726 $ - $ 21,875,566 $ 21,809,726 $ 11,442,592 $ 10,367,134 $ No • 340 acre Community in Thurston County, WA with 124 acres zoned for residential development and 215 acres zoned for Commercial. 2 Construction/Land Development 5,359,611 $ - $ 5,359,611 $ 5,359,611 $ 559,871 $ 4,799,741 $ No • 125 finished detached lots in Yakima (31), Clark (24) and Grant (70) Counties in WA. Construction/Land Development 2,950,403 $ - $ 2,950,403 $ 2,950,403 $ 358,252 $ 2,592,150 $ No • 557 residential detached lots with preliminary plat approval located in Yakima (58), Grant (475) and Clark (24) Counties in WA. Construction/Land Development 1,673,077 $ - $ 4,983,367 $ 1,673,077 $ 78,744 $ 1,594,333 $ No • 13 detached single family residences in Clark (9) and Grant (4) Counties in WA. TOTAL 9,983,091 $ - $ 13,293,381 $ 9,983,091 $ 996,867 $ 8,986,224 $ 3 Construction/Land Development 9,747,383 $ - $ 10,269,201 $ 9,747,383 $ 5,977,292 $ 3,770,091 $ Yes • 15 residential finished lots, 7.72 acres partially improved land, and 67.45 acres of raw land zoned for 300 residential lots in Lane County, OR. 4 Construction/ Land Development $ 4,399,850 - $ 4,399,850 $ 4,399,850 $ 2,047,601 $ 2,352,249 $ No • 63 Completed attached lots including four with foundations and three partially Completed townhomes (averaging 1,657sqft) located in Clark County, WA. Construction/Land Development $ 412,398 - $ 467,673 $ 412,398 $ - $ 412,398 $ No • Three substantially completed single family townhomes averaging 1,740sqft located in Clark County, WA. Home Equity $ 165,180 (50,680) $ 128,820 $ 114,500 $ 114,500 $ No • One single family residence in Clark County, WA. TOTAL 4,977,429 $ (50,680) $ 4,996,343 $ 4,926,748 $ 2,047,601 $ 2,879,147 $ 5 Construction/Land Development 6,537,385 $ (1,877,331) $ 4,737,943 $ 4,660,054 $ 428,418 $ 4,231,636 $ Yes • 17 single family residences in King County, WA. • One single family residences in Kitsap County, WA. 6 Construction/Land Development 1,403,929 $ - $ 1,403,929 $ 1,403,929 $ - $ 1,403,929 $ Yes • 6.88 acres of land in Multnomah County, OR for multi-family (rentals) development up to 147 units. Multifamily Residential 2,786,471 $ - $ 2,786,471 $ 2,786,471 $ - $ 2,786,471 $ Yes • 38 unit garden apartment in Multnomah County, OR. TOTAL 4,190,400 $ - $ 4,190,400 $ 4,190,400 $ - $ 4,190,400 $ |

15 Largest Nonperforming Loans (cont.) 39 ID Loan Type Unpaid Principal Balance Partial Charge Offs Net Commitment Net Book Balance Specific Reserves Book Balance Net of Specific Reserves TDR Description 7 Commercial Real Estate 3,797,619 $ - $ 3,797,619 $ 3,797,619 $ - $ 3,797,619 $ No • Five gas stations in King County, WA. 8 Construction/Land Development 2,817,054 $ - $ 2,817,054 $ 2,817,054 $ - $ 2,817,054 $ No • One 41,431sqft single-tenant retail building located in Pierce County, WA. 9 Construction/Land Development 347,471 $ (224,000) $ 123,471 $ 123,471 $ - $ 123,471 $ No • 51,299sqft of land with a farm house and several out buildings in Snohomish County, WA zoned for eight single family lots. Construction/Land Development 466,655 $ (272,637) $ 194,591 $ 194,018 $ 3,318 $ 190,700 $ No • 1.74 acres of land in Snohomish County, WA zoned for 20 townhomes. Multifamily Residential 2,404,240 $ - $ 2,470,524 $ 2,404,240 $ - $ 2,404,240 $ No • 13 unit apartment in Snohomish County, WA. TOTAL 3,218,366 $ (496,637) $ 2,788,586 $ 2,721,729 $ 3,318 $ 2,718,411 $ 10 Commercial Real Estate 2,262,430 $ - $ 2,262,430 $ 2,262,430 $ - $ 2,262,430 $ No • One gas station in Clackamas County, OR. 11 Commercial Real Estate 1,828,044 $ - $ 1,828,044 $ 1,828,044 $ - $ 1,828,044 $ No • Four industrial/warehouse buildings totaling 33,617sqft in King County, WA. 12 Construction/Land Development 1,500,000 $ (442,500) $ 1,057,500 $ 1,057,500 $ 422,925 $ 634,575 $ Yes • Subordinated deed of trust secured by Borrower's 5,600sqft single family personal residence and 36,202sqft office building, both located in King County, WA. 13 Commercial Business 119,158 $ - $ 119,158 $ 119,158 $ - $ 119,158 $ No • One furniture store in King County, WA. Commercial Real Estate 923,467 $ - $ 923,467 $ 923,467 $ - $ 923,467 $ No • One furniture store in King County, WA. TOTAL 1,042,625 $ - $ 1,042,625 $ 1,042,625 $ - $ 1,042,625 $ 14 Single Family 1,007,794 $ - $ 1,007,794 $ 1,007,794 $ 1,007,794 $ No • One Single family residence in San Juan County, WA. 15 Commercial Business 982,487 $ - $ 982,487 $ 982,487 $ - $ 982,487 $ No • Construction business in King County, WA. GRAND TOTAL 75,701,832 $ 76,946,972 $ 72,834,683 $ 21,319,013 $ 51,515,670 $ $ (2,867,148) |

10 Largest OREO Properties 40 Source: HomeStreet Inc. ID Description Location Property Type Sales Status Original Loan Balance LTD Charge- Offs Amount Transferred to OREO OREO Writedowns Carrying Value of OREO 1 40 acres of commercial land with zoning Thurston County, WA Construction/ Land Development Unsold $9,286,525 ($2,216,137) $7,070,388 $0 $7,070,388 2 101 finished condo lots and land for 90 future condo units Snohomish County, WA Construction/ Land Development Sold; set to close on or before 12/23/11 $13,008,596 ($5,968,427) $7,040,169 ($2,681,919) $4,358,250 3 Excess raw land planned for 344 residential lots, 298 multi-family units; and two finished commercial tracts totaling 13.72 acres (7.5 acres useable) Thurston County, WA Construction/ Land Development Unsold; Excess Land $9,447,348 $530,303 $9,977,651 ($6,032,865) $3,944,786 4 Raw land entitlements for 53 residential lots and 14 multi-family pads supporting 451 units Pierce County, WA Construction/ Land Development Sold; set to close on or before 11/30/11 $6,212,938 ($1,680,358) $4,532,580 ($993,555) $3,539,025 5 61 residential attached lots and 21 residential detached lots Pierce County, WA Construction/ Land Development Sold; set to close on or before 11/15/11 $6,516,372 ($4,583,431) $1,932,941 $0 $1,932,941 6 Two industrial buildings totaling 20,976 sqft Kitsap County, WA Commercial Real Estate Sold; set to close on or before 12/19/11 $2,193,458 ($41,775) $2,151,683 ($380,558) $1,771,125 7 71 residential detached lots and 29 residential attached lots Thurston County, WA Construction/ Land Development Unsold $4,000,000 $0 $4,000,000 ($2,387,448) $1,612,552 8 67 residential finished lots and land for 54 future lots Pierce County, WA Construction/ Land Development Sold; All lots and phases currently contracted and sold under separate PSA's. $16,187,150 ($13,992,725) $2,194,425 ($646,112) $1,548,313 9 68 residential finished lots Kitsap County, WA Construction/ Land Development Unsold $3,515,177 ($996,178) $2,518,999 ($1,186,397) $1,332,602 10 35 acres of raw land with partial entitlements for 333 future lots Kitsap County, WA Construction/ Land Development Unsold $4,461,390 ($997,822) $3,463,568 ($2,210,275) $1,253,293 $74,828,955 ($29,946,550) $44,882,405 ($16,519,129) $28,363,275 Sales Status Summary TOTAL Sold 46.4% 13,149,654 $ Unsold 53.6% 15,213,622 $ GRAND TOTAL |

Non-GAAP Reconciliation 41 Source: S-1 filing and HomeStreet Inc. (1) Assumes effective tax rate of 37%. Efficiency Ratio Month Ended Three Months Ended ($ in millions) 10/31/2011 9/30/2011 6/30/2011 3/31/2011 12/31/2010 9/30/2010 6/30/2010 3/31/2010 Noninterest expense $10.5 $32.6 $27.3 $33.5 $46.5 $32.0 $32.8 $20.9 Less: OREO expense $2.4 $9.1 $5.7 $11.8 $17.6 $9.2 $5.6 ($0.2) Adjusted noninterest expense $8.1 $23.5 $21.6 $21.7 $28.9 $22.8 $27.2 $21.1 Net interest income before provisions 4.4 12.0 11.9 11.6 13.5 10.3 8.1 7.1 Noninterest income 9.7 37.3 18.9 14.5 28.1 27.7 25.4 15.7 Less: Net hedge gain (loss) (0.5) 12.2 1.3 0.1 1.6 0.5 1.2 1.1 Less: Securities gain (loss) 0.4 0.6 0.0 0.0 0.0 0.1 5.8 0.2 Adjusted noninterest income 9.8 24.4 17.6 14.4 26.5 27.2 18.4 14.5 Adjusted operating revenue $14.2 $36.4 $29.5 $26.0 $40.0 $37.5 $26.5 $21.6 Operating efficiency ratio 57.2% 64.6% 73.2% 83.6% 72.3% 60.9% 102.4% 97.9% Efficiency ratio 74.7% 66.3% 88.4% 128.4% 111.8% 84.2% 97.8% 91.7% Pre-Tax, Pre-Provision Earnings Month 2 Year Total Ended Three Months Ended 12/31/2009 to ($ in millions) 10/31/2011 9/30/2011 6/30/2011 3/31/2011 12/31/2010 9/30/2010 6/30/2010 3/31/2010 12/31/2009 9/30/2011 Income / (loss) before income taxes $3.6 $15.6 $1.3 ($7.4) ($13.1) ($6.0) ($9.4) ($5.1) ($55.1) ($79.2) Add: Provision for loan losses 0.0 1.0 2.3 0.0 8.2 12.0 10.1 7.0 41.8 82.4 Add: OREO expenses 2.4 9.1 5.7 11.8 17.6 9.2 5.6 (0.2) 4.2 63.0 Pre-tax, pre-provision earnings 6.0 25.7 9.3 4.4 12.7 15.2 6.3 1.7 (9.1) 66.2 Less: Taxes (1) 2.2 9.5 3.4 1.6 4.7 5.6 2.3 0.6 (3.4) 24.3 Pre-provision earnings $3.8 $16.2 $5.9 $2.8 $8.0 $9.6 $4.0 $1.1 ($5.7) $41.9 |