UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22564

GMO Series Trust

(Exact name of the registrant as specified in charter)

| | |

| 40 Rowes Wharf, Boston, MA | | 02110 |

| (Address of principal executive offices) | | (Zip Code) |

J.B. Kittredge, Chief Executive Officer, 40 Rowes Wharf, Boston, MA 02110

(Name and address of agent for services)

Registrant’s telephone number, including area code: 617-346-7646

Date of fiscal year end: 04/30/13

Date of reporting period: 04/30/13

Item 1. Reports to Stockholders.

The annual reports for each series of the registrant for the periods ended April 30, 2013 are filed herewith.

GMO Series Trust

Annual Report

April 30, 2013

Benchmark-Free Allocation Series Fund

Global Asset Allocation Series Fund

Global Equity Allocation Series Fund

International Equity Allocation Series Fund

For a free copy of the Funds’ proxy voting guidelines, shareholders may call 1-617-346-7646 (collect) or visit the Securities and Exchange Commission’s website at www.sec.gov. Information regarding how the Funds voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 will be available on GMO’s website www.dc.gmo.com, or on the Securities and Exchange Commission’s website at www.sec.gov.

The Funds file their complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarter of each fiscal year on Form N-Q, which is available on the Commission’s website at www.sec.gov. The Funds’ Form N-Q may be reviewed and copied at the Commission’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

This report is prepared for the general information of shareholders. It is authorized for distribution to prospective investors only when preceded or accompanied by a prospectus for the GMO Series Trust, which contains a complete discussion of the risks associated with an investment in these Funds and other important information. The GMO Series Trust prospectus can be obtained at www.dc.gmo.com.

TABLE OF CONTENTS

i

Benchmark-Free Allocation Series Fund

(A Series of GMO Series Trust)

Management Discussion and Analysis of Fund Performance

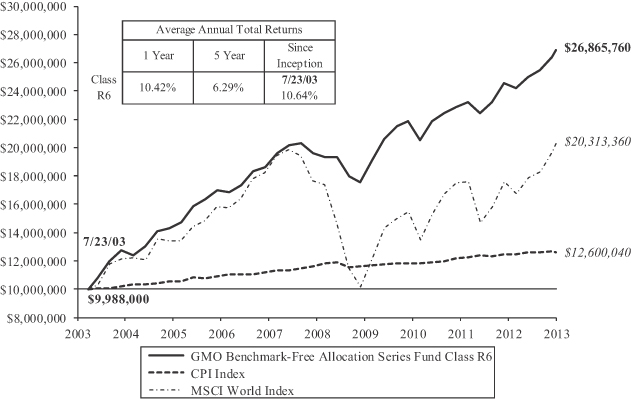

Although GMO Benchmark-Free Allocation Series Fund does not seek to control risk relative to any securities market index or benchmark, a discussion of the Fund’s performance relative to the CPI Index is included for comparative purposes.

Since inception on January 24, 2013, Class R6 shares of GMO Benchmark-Free Allocation Series Fund returned +3.5% for the fiscal year ended April 30, 2013, as compared with +0.1% for the CPI Index. The Fund’s exposures to global quality equities and Japanese equities drove most of that outperformance.

The views expressed herein are exclusively those of Grantham, Mayo, Van Otterloo & Co. LLC (“GMO”) as of the date of this report and are subject to change. GMO disclaims any responsibility to update such views. They are not meant as investment advice.

Comparison of Change in Value of a $10,000,000 Investment in

GMO Benchmark-Free Allocation Series Fund Class R6 Shares and the CPI Index

As of April 30, 2013

Performance data quoted represents past performance and is not indicative of future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance data may be lower or higher than the performance data provided herein. To obtain performance information up to the most recent month-end, visit www.gmo.com. Performance data shown above for GMO Benchmark-Free Allocation Series Fund (the “Fund”) reflect the performance data of GMO Benchmark-Free Allocation Fund (the “Institutional Fund”) through January 24, 2013 (the commencement date of the Fund), re-stated to reflect the additional fees and expenses of the Fund. Performance data shown above for the Fund is net of all fees after reimbursement from the Manager. The performance information shown above includes purchase premiums and/or redemption fees charged by the Institutional Fund in effect as of April 30, 2013. The figures assume a purchase at the beginning and redemption at the end of the stated period and reflect a transaction fee of .12% on the purchase and .12% on the redemption. Returns would have been lower had certain expenses not been reimbursed during the periods shown and do not include the effect of taxes on distributions and redemptions. All information is unaudited.

The Fund invests substantially all of its assets in shares of the Institutional Fund. Prior to January 1, 2012, the Institutional Fund served as a principal component of a broader GMO real return strategy. Beginning on January 1, 2012, the Institutional Fund has been managed as a stand alone investment vehicle.

MSCI data may not be reproduced or used for any other purpose. MSCI provides no warranties, has not prepared or approved this report, and has no liability hereunder.

1

Benchmark-Free Allocation Series Fund

(A Series of GMO Series Trust)

Investment Concentration Summary

April 30, 2013 (Unaudited)

| | | | |

| Asset Class Summary* | | % of Total Net Assets | |

Common Stocks | | | 60.2 | % |

Short-Term Investments | | | 26.6 | |

Futures Contracts | | | 12.9 | |

Debt Obligations | | | 9.5 | |

Preferred Stocks | | | 1.1 | |

Investment Funds | | | 0.4 | |

Loan Participations | | | 0.1 | |

Rights/Warrants | | | 0.0 | ^ |

Loan Assignments | | | 0.0 | ^ |

Options Purchased | | | 0.0 | ^ |

Swap Agreements | | | (0.0 | )^ |

Reverse Repurchase Agreements | | | (0.0 | )^ |

Written Options | | | (0.0 | )^ |

Forward Currency Contracts | | | (0.5 | ) |

Other | | | (10.3 | ) |

| | | | |

| | | 100.0 | % |

| | | | |

| | | | |

| Country/Region Summary** | | % of Investments | |

United States | | | 36.4 | % |

Emerging*** | | | 19.7 | |

United Kingdom | | | 12.9 | |

Japan | | | 8.2 | |

France | | | 4.8 | |

Germany | | | 3.4 | |

Spain | | | 2.4 | |

Italy | | | 2.4 | |

Australia | | | 2.0 | |

Switzerland | | | 2.0 | |

Hong Kong | | | 1.9 | |

Netherlands | | | 0.9 | |

Belgium | | | 0.5 | |

Singapore | | | 0.5 | |

Canada | | | 0.4 | |

Denmark | | | 0.2 | |

Austria | | | 0.2 | |

Ireland | | | 0.2 | |

Sweden | | | 0.2 | |

New Zealand | | | 0.2 | |

Finland | | | 0.2 | |

Greece | | | 0.1 | |

Norway | | | 0.1 | |

Portugal | | | 0.1 | |

Israel | | | 0.1 | |

| | | | |

| | | 100.0 | % |

| | | | |

| * | The table above incorporates aggregate indirect asset class exposure resulting from investments in shares of a series of GMO Trust (the “Institutional Fund”) and the series of GMO Trust in which the Institutional Fund invests (collectively referred to as the “Underlying Funds”) except for GMO Alpha Only Fund because of its short investment exposures. |

| ** | The table above incorporates aggregate indirect country exposure associated with investments in the Institutional Fund and Underlying Funds except for GMO Alpha Only Fund because of its short investment exposures. The table excludes short-term investments and includes exposure through the use of derivative financial instruments, if any. The table excludes exposure through forward currency contracts. |

| *** | The “Emerging” exposure is primarily comprised of: Argentina, Brazil, China, Colombia, Congo, Czech Republic, Dominican Republic, Egypt, Hungary, India, Indonesia, Iraq, Malaysia, Mexico, Panama, Peru, Philippines, Poland, Russia, South Africa, South Korea, Taiwan, Thailand, Turkey, Ukraine and Venezuela. |

2

Benchmark-Free Allocation Series Fund

(A Series of GMO Series Trust)

Schedule of Investments

(showing percentage of total net assets)

April 30, 2013

| | | | | | | | | | | | |

| | | Shares | | Description | | Value ($) |

| | | | | | | | | | | | |

| | | | | | | MUTUAL FUNDS — 98.9% | | | | | |

| | | |

| | | | | | | Affiliated Issuers — 98.9% | | | | | |

| | | | 5,977,807 | | | GMO Benchmark-Free Allocation Fund, Class III | | | | 158,352,116 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | TOTAL MUTUAL FUNDS (Cost $153,238,612) | | | | 158,352,116 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | TOTAL INVESTMENTS — 98.9%

(Cost $153,238,612) | | | | 158,352,116 | |

| | | | | | | Other Assets and Liabilities (net) — 1.1% | | | | 1,785,442 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | TOTAL NET ASSETS — 100.0% | | | | $160,137,558 | |

| | | | | | | | | | | | |

See accompanying notes to the financial statements.

3

Global Asset Allocation Series Fund

(A Series of GMO Series Trust)

Management Discussion and Analysis of Fund Performance

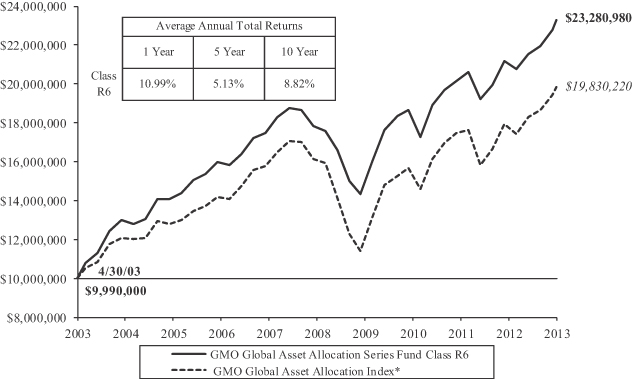

Since inception on July 31, 2012, Class R6 shares of GMO Global Asset Allocation Series Fund returned +11.4% for the fiscal year ended April 30, 2013, as compared with +12.4% for the Fund’s benchmark, the GMO Global Asset Allocation Index (65% MSCI ACWI [All Country World Index] and 35% Barclays U.S. Aggregate Index).

Underlying fund implementation detracted from relative performance, as six of the underlying equity funds underperformed their respective benchmarks.

Asset allocation added modestly to relative performance due to the Fund’s emphasis on quality stocks and an overweight to Japanese equities.

The views expressed herein are exclusively those of Grantham, Mayo, Van Otterloo & Co. LLC (“GMO”) as of the date of this report and are subject to change. GMO disclaims any responsibility to update such views. They are not meant as investment advice.

Comparison of Change in Value of a $10,000,000 Investment in

GMO Global Asset Allocation Series Fund Class R6 Shares and the

GMO Global Asset Allocation Index

As of April 30, 2013

Performance data quoted represents past performance and is not indicative of future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance data may be lower or higher than the performance data provided herein. To obtain performance information up to the most recent month-end, visit www.gmo.com. Performance data shown above for GMO Global Asset Allocation Series Fund (the “Fund”) reflect the performance data of GMO Global Asset Allocation Fund (the “Institutional Fund”) through July 31, 2012 (the commencement date of the Fund), re-stated to reflect the additional fees and expenses of the Fund. Performance data shown above for the Fund is net of all fees after reimbursement from the Manager. The performance information shown above includes purchase premiums and/or redemption fees charged by the Institutional Fund in effect as of April 30, 2013. The figures assume a purchase at the beginning and redemption at the end of the stated period and reflect a transaction fee of .10% on the purchase and .10% on the redemption. Returns would have been lower had certain expenses not been reimbursed during the periods shown and do not include the effect of taxes on distributions and redemptions. All information is unaudited.

The Fund invests substantially all of its assets in shares of the Institutional Fund.

| * | The GMO Global Asset Allocation Index is comprised of MSCI ACWI prior to June 30, 2002 and GMO Global Asset Allocation (Blend) Index** thereafter. |

| ** | The GMO Global Asset Allocation (Blend) Index is a composite benchmark computed by GMO and comprised of 48.75% S&P 500 Index, 16.25% MSCI ACWI ex-USA and 35% Barclays Capital U.S. Aggregate Index prior to March 30, 2007 and 65% MSCI ACWI and 35% Barclays Capital U.S. Aggregate Index thereafter. |

4

Global Asset Allocation Series Fund

(A Series of GMO Series Trust)

Investment Concentration Summary

April 30, 2013 (Unaudited)

| | | | |

| Asset Class Summary* | | % of Total Net Assets | |

Common Stocks | | | 66.8 | % |

Short-Term Investments | | | 17.6 | |

Debt Obligations | | | 11.9 | |

Futures Contracts | | | 6.3 | |

Preferred Stocks | | | 1.2 | |

Investment Funds | | | 0.1 | |

Loan Participations | | | 0.1 | |

Options Purchased | | | 0.0 | ^ |

Loan Assignments | | | 0.0 | ^ |

Rights/Warrants | | | 0.0 | ^ |

Written Options | | | (0.1 | ) |

Swap Agreements | | | (0.1 | ) |

Reverse Repurchase Agreements | | | (0.1 | ) |

Forward Currency Contracts | | | (0.2 | ) |

Other | | | (3.5 | ) |

| | | | |

| | | 100.0 | % |

| | | | |

| | | | |

| Country/Region Summary** | | % of Investments | |

United States | | | 40.6 | % |

Emerging*** | | | 16.5 | |

United Kingdom | | | 9.7 | |

Japan | | | 8.2 | |

France | | | 5.1 | |

Germany | | | 3.0 | |

Spain | | | 2.9 | |

Italy | | | 2.8 | |

Switzerland | | | 2.1 | |

Canada | | | 1.9 | |

Australia | | | 1.7 | |

Hong Kong | | | 1.1 | |

Sweden | | | 1.0 | |

New Zealand | | | 0.6 | |

Singapore | | | 0.6 | |

Netherlands | | | 0.5 | |

Belgium | | | 0.4 | |

Finland | | | 0.2 | |

Austria | | | 0.2 | |

Denmark | | | 0.2 | |

Ireland | | | 0.2 | |

Norway | | | 0.2 | |

Greece | | | 0.1 | |

Portugal | | | 0.1 | |

Israel | | | 0.1 | |

| | | | |

| | | 100.0 | % |

| | | | |

| * | The table above incorporates aggregate indirect asset class exposure resulting from investments in shares of a series of GMO Trust (the “Institutional Fund”) and the series of GMO Trust in which the Institutional Fund invests (collectively referred to as the “Underlying Funds”) except for GMO Alpha Only Fund because of its short investment exposures. |

| ** | The table above incorporates aggregate indirect country exposure associated with investments in the Institutional Fund and Underlying Funds except for GMO Alpha Only Fund because of its short investment exposures and GMO Special Situations Fund due to the short-term nature of its investments. The table excludes short-term investments and includes exposure through the use of derivative financial instruments, if any. The table excludes exposure through forward currency contracts. |

| *** | The “Emerging” exposure is primarily comprised of: Argentina, Brazil, China, Colombia, Congo, Czech Republic, Dominican Republic, Egypt, Hungary, India, Indonesia, Iraq, Malaysia, Mexico, Panama, Peru, Philippines, Poland, Russia, South Africa, South Korea, Taiwan, Thailand, Turkey, Ukraine and Venezuela. |

5

Global Asset Allocation Series Fund

(A Series of GMO Series Trust)

Schedule of Investments

(showing percentage of total net assets)

April 30, 2013

| | | | | | | | | |

| | | Shares | | Description | | Value ($) |

| | | | | | | | | |

| | | | MUTUAL FUNDS — 99.3% | | | | | |

| | | |

| | | | Affiliated Issuers — 99.3% | | | | | |

| | 52,124,613 | | GMO Global Asset Allocation Fund, Class III | | | | 588,486,882 | |

| | | | | | | | | |

| | | |

| | | | TOTAL MUTUAL FUNDS (Cost $556,974,873) | | | | 588,486,882 | |

| | | | | | | | | |

| | | |

| | | | TOTAL INVESTMENTS — 99.3%

(Cost $556,974,873) | | | | 588,486,882 | |

| | | | Other Assets and Liabilities (net) — 0.7% | | | | 3,928,503 | |

| | | | | | | | | |

| | | |

| | | | TOTAL NET ASSETS — 100.0% | | | | $592,415,385 | |

| | | | | | | | | |

See accompanying notes to the financial statements.

6

Global Equity Allocation Series Fund

(A Series of GMO Series Trust)

Management Discussion and Analysis of Fund Performance

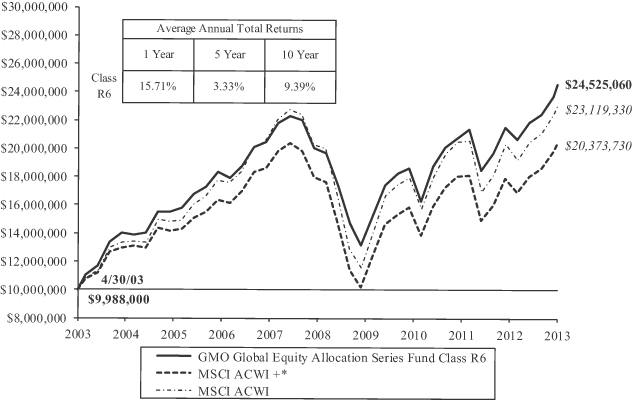

Since inception on September 4, 2012, Class R6 shares of GMO Global Equity Allocation Series Fund returned +15.3% for the fiscal year ended April 30, 2013, as compared with +16.6% for the Fund’s benchmark, the MSCI ACWI (All Country World Index).

Underlying fund implementation detracted from relative performance, as six of the eight underlying funds underperformed their respective benchmarks.

Asset allocation contributed positively to relative performance. The Fund’s overweight to Japanese equities in particular was a major contributor.

The views expressed herein are exclusively those of Grantham, Mayo, Van Otterloo & Co. LLC (“GMO”) as of the date of this report and are subject to change. GMO disclaims any responsibility to update such views. They are not meant as investment advice.

Comparison of Change in Value of a $10,000,000 Investment in

GMO Global Equity Allocation Series Fund Class R6 Shares and the MSCI ACWI +

As of April 30, 2013

Performance data quoted represents past performance and is not indicative of future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance data may be lower or higher than the performance data provided herein. To obtain performance information up to the most recent month-end, visit www.gmo.com. Performance data shown above for GMO Global Equity Allocation Series Fund (the “Fund”) reflect the performance data of GMO Global Equity Allocation Fund (the “Institutional Fund”) through September 4, 2012 (the commencement date of the Fund), re-stated to reflect the additional fees and expenses of the Fund. Performance data shown above for the Fund is net of all fees after reimbursement from the Manager. The performance information shown above includes purchase premiums and/or redemption fees charged by the Institutional Fund in effect as of April 30, 2013. The figures assume a purchase at the beginning and redemption at the end of the stated period and reflect a transaction fee of .12% on the purchase and .12% on the redemption. Returns would have been lower had certain expenses not been reimbursed during the periods shown and do not include the effect of taxes on distributions and redemptions. All information is unaudited.

The Fund invests substantially all of its assets in shares of the Institutional Fund.

| * | The MSCI ACWI + represents 75% S&P 500 Index and 25% MSCI ACWI ex-USA prior to May 30, 2008 and MSCI ACWI thereafter. |

MSCI data may not be reproduced or used for any other purpose. MSCI provides no warranties, has not prepared or approved this report, and has no liability hereunder.

7

Global Equity Allocation Series Fund

(A Series of GMO Series Trust)

Investment Concentration Summary

April 30, 2013 (Unaudited)

| | | | |

| Asset Class Summary* | | % of Total Net Assets | |

Common Stocks | | | 93.9 | % |

Short-Term Investments | | | 2.4 | |

Preferred Stocks | | | 1.5 | |

Futures Contracts | | | 0.1 | |

Investment Funds | | | 0.1 | |

Swap Agreements | | | 0.0 | ^ |

Rights/Warrants | | | 0.0 | ^ |

Private Equity Securities | | | 0.0 | ^ |

Forward Currency Contracts | | | (0.1 | ) |

Other | | | 2.1 | |

| | | | |

| | | 100.0 | % |

| | | | |

| | | | |

| Country/Region Summary** | | % of Investments | |

United States | | | 39.5 | % |

Emerging*** | | | 14.0 | |

Japan | | | 12.3 | |

United Kingdom | | | 10.4 | |

France | | | 5.7 | |

Germany | | | 3.4 | |

Spain | | | 3.3 | |

Italy | | | 3.1 | |

Australia | | | 2.1 | |

Switzerland | | | 1.8 | |

Singapore | | | 0.7 | |

Netherlands | | | 0.5 | |

Belgium | | | 0.5 | |

Hong Kong | | | 0.5 | |

Sweden | | | 0.3 | |

Denmark | | | 0.3 | |

Finland | | | 0.3 | |

Austria | | | 0.2 | |

Canada | | | 0.2 | |

Ireland | | | 0.2 | |

New Zealand | | | 0.2 | |

Norway | | | 0.2 | |

Portugal | | | 0.1 | |

Greece | | | 0.1 | |

Israel | | | 0.1 | |

| | | | |

| | | 100.0 | % |

| | | | |

| * | The table above incorporates aggregate indirect asset class exposure resulting from investments in shares of a series of GMO Trust (the “Institutional Fund”) and the series of GMO Trust in which the Institutional Fund invests (collectively referred to as the “Underlying Funds”). |

| ** | The table above incorporates aggregate indirect country exposure associated with investments in the Institutional Fund and Underlying Funds. The table excludes short-term investments and includes exposure through the use of derivative financial instruments, if any. The table excludes exposure through forward currency contracts. |

| *** | The “Emerging” exposure is primarily comprised of: Brazil, China, Czech Republic, Egypt, India, Indonesia, Malaysia, Mexico, Peru, Philippines, Poland, Russia, South Africa, South Korea, Taiwan, Thailand and Turkey. |

8

Global Equity Allocation Series Fund

(A Series of GMO Series Trust)

Schedule of Investments

(showing percentage of total net assets)

April 30, 2013

| | | | | | | | | | | | |

| | | Shares | | Description | | Value ($) |

| | | | | | | | | | | | |

| | | | | | | MUTUAL FUNDS — 98.2% | | | | | |

| | | |

| | | | | | | Affiliated Issuers — 98.2% | | | | | |

| | | | 158,168 | | | GMO Global Equity Allocation Fund, Class III | | | | 1,434,587 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | TOTAL MUTUAL FUNDS (Cost $1,366,088) | | | | 1,434,587 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | TOTAL INVESTMENTS — 98.2%

(Cost $1,366,088) | | | | 1,434,587 | |

| | | | | | | Other Assets and Liabilities (net) — 1.8% | | | | 26,851 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | TOTAL NET ASSETS — 100.0% | | | | $1,461,438 | |

| | | | | | | | | | | | |

See accompanying notes to the financial statements.

9

International Equity Allocation Series Fund

(A Series of GMO Series Trust)

Management Discussion and Analysis of Fund Performance

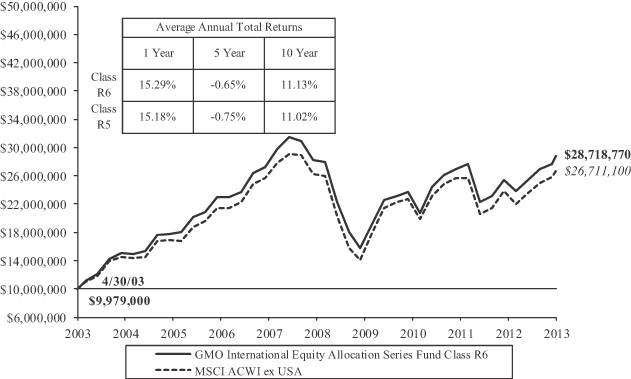

Class R6 shares of GMO International Equity Allocation Series Fund returned +15.8% for the fiscal year ended April 30, 2013, as compared with +14.1% for the MSCI ACWI (All Country World Index) ex-USA.

The impact from underlying fund implementation was negligible.

Asset allocation added to relative performance. The Fund’s exposure to international value stocks drove most of the outperformance.

The views expressed herein are exclusively those of Grantham, Mayo, Van Otterloo & Co. LLC (“GMO”) as of the date of this report and are subject to change. GMO disclaims any responsibility to update such views. They are not meant as investment advice.

Comparison of Change in Value of a $10,000,000 Investment in

GMO International Equity Allocation Series Fund Class R6 Shares and the

MSCI ACWI ex USA

As of April 30, 2013

Performance data quoted represents past performance and is not indicative of future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance data may be lower or higher than the performance data provided herein. To obtain performance information up to the most recent month-end, visit www.gmo.com. Performance data shown above for GMO International Equity Allocation Series Fund (the “Fund”) reflect the performance data of GMO International Equity Allocation Fund (the “Institutional Fund”) through March 30, 2012 for Class R6 and April 5, 2013 for Class R5 (the respective commencement dates of the Fund’s classes), re-stated to reflect the additional fees and expenses of the Fund. Performance data shown above for the Fund is net of all fees after reimbursement from the Manager. The performance information shown above includes purchase premiums and/or redemption fees charged by the Institutional Fund in effect as of April 30, 2013. The figures assume a purchase at the beginning and redemption at the end of the stated period and reflect a transaction fee of .21% on the purchase and .21% on the redemption. Returns would have been lower had certain expenses not been reimbursed during the periods shown and do not include the effect of taxes on distributions and redemptions. All information is unaudited.

The Fund invests substantially all of its assets in shares of the Institutional Fund.

MSCI data may not be reproduced or used for any other purpose. MSCI provides no warranties, has not prepared or approved this report, and has no liability hereunder.

10

International Equity Allocation Series Fund

(A Series of GMO Series Trust)

Investment Concentration Summary

April 30, 2013 (Unaudited)

| | | | |

| Asset Class Summary* | | % of Total Net Assets | |

Common Stocks | | | 93.3 | % |

Short-Term Investments | | | 2.8 | |

Preferred Stocks | | | 2.6 | |

Futures Contracts | | | 0.2 | |

Investment Funds | | | 0.2 | |

Swap Agreements | | | 0.0 | ^ |

Rights/Warrants | | | 0.0 | ^ |

Forward Currency Contracts | | | (0.1 | ) |

Other | | | 1.0 | |

| | | | |

| | | 100.0 | % |

| | | | |

| | | | |

| Country/Region Summary** | | % of Investments | |

Emerging*** | | | 24.4 | % |

Japan | | | 20.5 | |

United Kingdom | | | 16.8 | |

France | | | 8.2 | |

Germany | | | 6.1 | |

Spain | | | 4.7 | |

Italy | | | 4.7 | |

Switzerland | | | 3.1 | |

Australia | | | 2.9 | |

Singapore | | | 1.4 | |

Hong Kong | | | 1.2 | |

Netherlands | | | 1.0 | |

Sweden | | | 0.7 | |

Belgium | | | 0.7 | |

Denmark | | | 0.7 | |

Finland | | | 0.5 | |

Norway | | | 0.5 | |

Ireland | | | 0.4 | |

Canada | | | 0.3 | |

Austria | | | 0.3 | |

New Zealand | | | 0.2 | |

Greece | | | 0.2 | |

Portugal | | | 0.2 | |

Israel | | | 0.2 | |

United States | | | 0.1 | |

| | | | |

| | | 100.0 | % |

| | | | |

| * | The table above incorporates aggregate indirect asset class exposure resulting from investments in shares of a series of GMO Trust (the “Institutional Fund”) and the series of GMO Trust in which the Institutional Fund invests (collectively referred to as the “Underlying Funds”). |

| ** | The table above incorporates aggregate indirect country exposure associated with investments in the Institutional Fund and Underlying Funds. The table excludes short-term investments and includes exposure through the use of derivative financial instruments, if any. The table excludes exposure through forward currency contracts. |

| *** | The “Emerging” exposure is primarily comprised of: Brazil, China, Czech Republic, Egypt, India, Indonesia, Malaysia, Mexico, Peru, Philippines, Poland, Russia, South Africa, South Korea, Taiwan, Thailand and Turkey. |

11

International Equity Allocation Series Fund

(A Series of GMO Series Trust)

Schedule of Investments

(showing percentage of total net assets)

April 30, 2013

| | | | | | | | | | | | |

| Shares | | Description | | Value ($) |

| | | | | | | | | | | | |

| | | | | | | MUTUAL FUNDS — 99.4% | | | | | |

| | | |

| | | | | | | Affiliated Issuers — 99.4% | | | | | |

| | | | 27,589,336 | | | GMO International Equity Allocation Fund, Class III | | | | 302,379,125 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | TOTAL MUTUAL FUNDS (Cost $270,840,840) | | | | 302,379,125 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | TOTAL INVESTMENTS — 99.4%

(Cost $270,840,840) | | | | 302,379,125 | |

| | | | | | | Other Assets and Liabilities (net) — 0.6% | | | | 1,679,992 | |

| | | | | | | | | | | | |

| | | |

| | | | | | | TOTAL NET ASSETS — 100.0% | | | | $304,059,117 | |

| | | | | | | | | | | | |

See accompanying notes to the financial statements.

12

GMO Series Trust Funds

Statements of Assets and Liabilities — April 30, 2013

| | | | | | | | | | | | | | | | | | | | |

| | | Benchmark-

Free

Allocation

Series Fund | | Global Asset

Allocation

Series Fund | | Global Equity

Allocation

Series Fund | | International

Equity

Allocation

Series Fund |

Assets: | | | | | | | | | | | | | | | | | | | | |

Investments in affiliated issuers, at value (Notes 2 and 10)(a) | | | $ | 158,352,116 | | | | $ | 588,486,882 | | | | $ | 1,434,587 | | | | $ | 302,379,125 | |

Cash | | | | 1,896,079 | | | | | 4,034,379 | | | | | 19,955 | | | | | 1,723,690 | |

Receivable for Fund shares sold | | | | 20,460 | | | | | 199,731 | | | | | 7,919 | | | | | 23,511 | |

Receivable for reimbursement by Manager (Note 5) | | | | 250 | | | | | 329 | | | | | 534 | | | | | 247 | |

| | | | | | | | | | | | | | | | | | | | |

Total assets | | | | 160,268,905 | | | | | 592,721,321 | | | | | 1,462,995 | | | | | 304,126,573 | |

| | | | | | | | | | | | | | | | | | | | |

Liabilities: | | | | | | | | | | | | | | | | | | | | |

Payable for Fund shares repurchased | | | | 124,638 | | | | | 280,469 | | | | | — | | | | | 53,229 | |

Payable to affiliate for (Note 5): | | | | | | | | | | | | | | | | | | | | |

Administration fee | | | | 6,484 | | | | | 23,970 | | | | | 56 | | | | | 11,921 | |

Payable for 12b-1 fee – Class R5 | | | | — | | | | | — | | | | | — | | | | | 1,547 | |

Accrued expenses | | | | 225 | | | | | 1,497 | | | | | 1,501 | | | | | 759 | |

| | | | | | | | | | | | | | | | | | | | |

Total liabilities | | | | 131,347 | | | | | 305,936 | | | | | 1,557 | | | | | 67,456 | |

| | | | | | | | | | | | | | | | | | | | |

Net assets | | | $ | 160,137,558 | | | | $ | 592,415,385 | | | | $ | 1,461,438 | | | | $ | 304,059,117 | |

| | | | | | | | | | | | | | | | | | | | |

Net assets consist of: | |

Paid-in capital | | | $ | 155,024,054 | | | | $ | 560,226,415 | | | | $ | 1,366,265 | | | | $ | 272,245,155 | |

Distributions in excess of net investment income | | | | — | | | | | (93,768 | ) | | | | (208 | ) | | | | (47,031 | ) |

Accumulated net realized gain | | | | — | | | | | 770,729 | | | | | 26,882 | | | | | 322,708 | |

Net unrealized appreciation | | | | 5,113,504 | | | | | 31,512,009 | | | | | 68,499 | | | | | 31,538,285 | |

| | | | | | | | | | | | | | | | | | | | |

| | | $ | 160,137,558 | | | | $ | 592,415,385 | | | | $ | 1,461,438 | | | | $ | 304,059,117 | |

| | | | | | | | | | | | | | | | | | | | |

Net assets attributable to: | | | | | | | | | | | | | | | | | | | | |

Class R5 | | | $ | — | | | | $ | — | | | | $ | — | | | | $ | 23,189,830 | |

| | | | | | | | | | | | | | | | | | | | |

Class R6 | | | $ | 160,137,558 | | | | $ | 592,415,385 | | | | $ | 1,461,438 | | | | $ | 280,869,287 | |

| | | | | | | | | | | | | | | | | | | | |

Shares outstanding: | | | | | | | | | | | | | | | | | | | | |

Class R5 | | | | — | | | | | — | | | | | — | | | | | 2,114,021 | |

| | | | | | | | | | | | | | | | | | | | |

Class R6 | | | | 15,473,945 | | | | | 54,674,422 | | | | | 131,181 | | | | | 25,603,786 | |

| | | | | | | | | | | | | | | | | | | | |

Net asset value per share: | | | | | | | | | | | | | | | | | | | | |

Class R5 | | | $ | — | | | | $ | — | | | | $ | — | | | | $ | 10.97 | |

| | | | | | | | | | | | | | | | | | | | |

Class R6 | | | $ | 10.35 | | | | $ | 10.84 | | | | $ | 11.14 | | | | $ | 10.97 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | |

(a) Cost of investments – affiliated issuers: | | | $ | 153,238,612 | | | | $ | 556,974,873 | | | | $ | 1,366,088 | | | | $ | 270,840,840 | |

See accompanying notes to the financial statements.

13

GMO Series Trust Funds

Statements of Operations — Year Ended April 30, 2013

| | | | | | | | | | | | | | | | | | | | |

| | | Benchmark-

Free

Allocation

Series Fund* | | Global Asset

Allocation

Series Fund** | | Global Equity

Allocation

Series Fund*** | | International

Equity

Allocation

Series Fund |

Investment Income: | | | | | | | | | | | | | | | | | | | | |

Dividends from affiliated issuers (Note 10) | | | $ | — | | | | $ | 14,137,412 | | | | $ | 19,679 | | | | $ | 8,138,219 | |

| | | | | | | | | | | | | | | | | | | | |

Total investment income | | | | — | | | | | 14,137,412 | | | | | 19,679 | | | | | 8,138,219 | |

| | | | | | | | | | | | | | | | | | | | |

Expenses: | | | | | | | | | | | | | | | | | | | | |

Administration fee (Note 5) | | | | 18,918 | | | | | 171,460 | | | | | 258 | | | | | 123,746 | |

12b-1 fee – Class R5 (Note 5) | | | | — | | | | | — | | | | | — | | | | | 1,547 | **** |

Registration fees | | | | 2,705 | | | | | 2,998 | | | | | 3,000 | | | | | 3,000 | |

| | | | | | | | | | | | | | | | | | | | |

Total expenses | | | | 21,623 | | | | | 174,458 | | | | | 3,258 | | | | | 128,293 | |

| | | | | | | | | | | | | | | | | | | | |

Fees and expenses reimbursed by Manager (Note 5) | | | | (2,705 | ) | | | | (2,998 | ) | | | | (3,000 | ) | | | | (3,000 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net expenses | | | | 18,918 | | | | | 171,460 | | | | | 258 | | | | | 125,293 | |

| | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | | (18,918 | ) | | | | 13,965,952 | | | | | 19,421 | | | | | 8,012,926 | |

| | | | | | | | | | | | | | | | | | | | |

Realized and unrealized gain (loss): | | | | | | | | | | | | | | | | | | | | |

Net realized gain (loss) on: | | | | | | | | | | | | | | | | | | | | |

Investments in affiliated issuers | | | | — | | | | | 974,291 | | | | | 1,532 | | | | | 328,740 | |

Realized gains distributions from affiliated issuers (Note 10) | | | | — | | | | | — | | | | | 28,726 | | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

Net realized gain (loss) | | | | — | | | | | 974,291 | | | | | 30,258 | | | | | 328,740 | |

| | | | | | | | | | | | | | | | | | | | |

Change in net unrealized appreciation (depreciation) on: | | | | | | | | | | | | | | | | | | | | |

Investments in affiliated issuers | | | | 5,113,504 | | | | | 31,512,009 | | | | | 68,499 | | | | | 35,743,862 | |

| | | | | | | | | | | | | | | | | | | | |

Net realized and unrealized gain (loss) | | | | 5,113,504 | | | | | 32,486,300 | | | | | 98,757 | | | | | 36,072,602 | |

| | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in net assets resulting from operations | | | $ | 5,094,586 | | | | $ | 46,452,252 | | | | $ | 118,178 | | | | $ | 44,085,528 | |

| | | | | | | | | | | | | | | | | | | | |

| * | Period from January 24, 2013 (commencement of operations) through April 30, 2013. |

| ** | Period from July 31, 2012 (commencement of operations) through April 30, 2013. |

| *** | Period from September 4, 2012 (commencement of operations) through April 30, 2013. |

| **** | Period from April 5, 2013 (commencement of operations) through April 30, 2013. |

See accompanying notes to the financial statements.

14

GMO Series Trust Funds

Statements of Changes in Net Assets

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Benchmark-

Free Allocation

Series Fund | | Global Asset

Allocation

Series Fund | | Global Equity

Allocation

Series Fund | | International Equity Allocation

Series Fund |

| | | Period from

January 24, 2013

(commencement

of operations)

through

April 30, 2013 | | Period from

July 31, 2012

(commencement

of operations)

through

April 30, 2013 | | Period from

September 4, 2012

(commencement

of operations)

through

April 30, 2013 | | Year Ended

April 30, 2013 | | Period from

March 30, 2012

(commencement

of operations)

through

April 30, 2012 |

Increase (decrease) in net assets: | | | | | | | | | | | | | | | | | | | | | | | | | |

Operations: | | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | $ | (18,918 | ) | | | $ | 13,965,952 | | | | $ | 19,421 | | | | $ | 8,012,926 | | | | $ | (7,748 | ) |

Net realized gain (loss) | | | | — | | | | | 974,291 | | | | | 30,258 | | | | | 328,740 | | | | | — | |

Change in net unrealized appreciation (depreciation) | | | | 5,113,504 | | | | | 31,512,009 | | | | | 68,499 | | | | | 35,743,862 | | | | | (4,205,577 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in net assets from operations | | | | 5,094,586 | | | | | 46,452,252 | | | | | 118,178 | | | | | 44,085,528 | | | | | (4,213,325 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Distributions to shareholders from: | | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | | | | | | | | | | | | | | | | | | | | | | | |

Class R6 | | | | — | | | | | (14,067,683 | ) | | | | (23,005 | ) | | | | (8,065,989 | ) | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Net realized gains | | | | | | | | | | | | | | | | | | | | | | | | | |

Class R6 | | | | — | | | | | (195,599 | ) | | | | — | | | | | — | | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Net share transactions (Note 9): | | | | | | | | | | | | | | | | | | | | | | | | | |

Class R5 | | | | — | | | | | — | | | | | — | | | | | 21,976,142 | * | | | | — | |

Class R6 | | | | 155,042,972 | | | | | 560,226,415 | | | | | 1,366,265 | | | | | 62,733,574 | | | | | 187,543,187 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Increase (decrease) in net assets resulting from net share transactions | | | | 155,042,972 | | | | | 560,226,415 | | | | | 1,366,265 | | | | | 84,709,716 | | | | | 187,543,187 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Total increase (decrease) in net assets | | | | 160,137,558 | | | | | 592,415,385 | | | | | 1,461,438 | | | | | 120,729,255 | | | | | 183,329,862 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | |

| Net assets: | | | | | | | | | | | | | | | | | | | | | | | | | |

Beginning of period | | | | — | | | | | — | | | | | — | | | | | 183,329,862 | | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

End of period | | | $ | 160,137,558 | | | | $ | 592,415,385 | | | | $ | 1,461,438 | | | | $ | 304,059,117 | | | | $ | 183,329,862 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Distributions in excess of net investment income | | | $ | — | | | | $ | (93,768 | ) | | | $ | (208 | ) | | | $ | (47,031 | ) | | | $ | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| * | Period from April 5, 2013 (commencement of operations) through April 30, 2013. |

See accompanying notes to the financial statements.

15

GMO Series Trust Funds

Financial Highlights

(For a share outstanding throughout the period)

BENCHMARK-FREE ALLOCATION SERIES FUND

| | | | | |

| | | Class R6 Shares |

| | | Period from

January 24, 2013

(commencement

of operations)

through

April 30, 2013 |

Net asset value, beginning of period | | | $ | 10.00 | |

| | | | | |

Income (loss) from investment operations: | | | | | |

Net investment income (loss)† | | | | (0.00 | )(a) |

Net realized and unrealized gain (loss) | | | | 0.35 | |

| | | | | |

Total from investment operations | | | | 0.35 | |

| | | | | |

Net asset value, end of period | | | $ | 10.35 | |

| | | | | |

Total Return(b) | | | | 3.50 | %** |

Ratios/Supplemental Data: | | | | | |

Net assets, end of period (000’s) | | | $ | 160,138 | |

Net expenses to average daily net assets(c) | | | | 0.05 | %* |

Net investment income (loss) to average daily net assets | | | | (0.05 | )%* |

Portfolio turnover rate | | | | 0 | %** |

Fees and expenses reimbursed by the Manager to average daily net assets | | | | 0.01 | %* |

| (a) | Rounds to less than $0.01. |

| (b) | The total return would have been lower had certain expenses not been reimbursed during the period shown. |

| (c) | Net expenses exclude expenses incurred indirectly through investment in the Underlying Funds (Note 5). |

| † | Calculated using average shares outstanding throughout the period. |

See accompanying notes to the financial statements.

16

GMO Series Trust Funds

Financial Highlights

(For a share outstanding throughout the period)

GLOBAL ASSET ALLOCATION SERIES FUND

| | | | | |

| | | Class R6 Shares |

| | | Period from

July 31, 2012

(commencement

of operations)

through

April 30, 2013 |

Net asset value, beginning of period | | | $ | 10.00 | |

| | | | | |

Income (loss) from investment operations: | | | | | |

Net investment income (loss)(a)† | | | | 0.32 | |

Net realized and unrealized gain (loss) | | | | 0.79 | |

| | | | | |

Total from investment operations | | | | 1.11 | |

| | | | | |

Less distributions to shareholders: | | | | | |

From net investment income | | | | (0.27 | ) |

From net realized gains | | | | (0.00 | )(b) |

| | | | | |

Total distributions | | | | (0.27 | ) |

| | | | | |

Net asset value, end of period | | | $ | 10.84 | |

| | | | | |

Total Return(c) | | | | 11.36 | %** |

Ratios/Supplemental Data: | | | | | |

Net assets, end of period (000’s) | | | $ | 592,415 | |

Net expenses to average daily net assets(d) | | | | 0.05 | %* |

Net investment income (loss) to average daily net assets | | | | 4.07 | %* |

Portfolio turnover rate | | | | 6 | %** |

Fees and expenses reimbursed by the Manager to average daily net assets(e) | | | | 0.00 | %* |

| (a) | Net investment income is affected by the timing of the declaration of dividends by the underlying funds in which the fund invests. |

| (b) | Rounds to less than $0.01. |

| (c) | The total return would have been lower had certain expenses not been reimbursed during the period shown and assumes the effect of reinvested distributions. |

| (d) | Net expenses exclude expenses incurred indirectly through investment in the Underlying Funds (Note 5). |

| (e) | Fees and expenses reimbursed by the Manager to average daily net assets were less than 0.01%. |

| † | Calculated using average shares outstanding throughout the period. |

See accompanying notes to the financial statements.

17

GMO Series Trust Funds

Financial Highlights

(For a share outstanding throughout the period)

GLOBAL EQUITY ALLOCATION SERIES FUND

| | | | | |

| | | Class R6 Shares |

| | | Period from

September 4, 2012

(commencement

of operations)

through

April 30, 2013 |

Net asset value, beginning of period | | | $ | 10.00 | |

| | | | | |

Income (loss) from investment operations: | | | | | |

Net investment income (loss)† | | | | 0.26 | |

Net realized and unrealized gain (loss) | | | | 1.23 | |

| | | | | |

Total from investment operations | | | | 1.49 | |

| | | | | |

Less distributions to shareholders: | | | | | |

From net investment income | | | | (0.35 | ) |

| | | | | |

Total distributions | | | | (0.35 | ) |

| | | | | |

Net asset value, end of period | | | $ | 11.14 | |

| | | | | |

Total Return(a) | | | | 15.29 | %** |

Ratios/Supplemental Data: | | | | | |

Net assets, end of period (000’s) | | | $ | 1,461 | |

Net expenses to average daily net assets(b) | | | | 0.05 | %* |

Net investment income (loss) to average daily net assets | | | | 3.76 | %* |

Portfolio turnover rate | | | | 46 | %** |

Fees and expenses reimbursed by the Manager to average daily net assets | | | | 0.58 | %* |

| (a) | The total return would have been lower had certain expenses and purchase premiums and/or redemption fees not been reimbursed during the period shown and assumes the effect of reinvested distributions (Note 11). |

| (b) | Net expenses exclude expenses incurred indirectly through investment in the Underlying Funds (Note 5). |

| † | Calculated using average shares outstanding throughout the period. |

See accompanying notes to the financial statements.

18

GMO Series Trust Funds

Financial Highlights

(For a share outstanding throughout each period)

INTERNATIONAL EQUITY ALLOCATION SERIES FUND

| | | | | | | | | | | | | | | |

| | | Class R5 Shares | | Class R6 Shares |

| | | Period from

April 5, 2013

(commencement

of operations)

through

April 30, 2013 | | Year Ended

April 30, 2013 | | Period from

March 30, 2012

(commencement

of operations)

through

April 30, 2012 |

Net asset value, beginning of period | | | $ | 10.40 | | | | $ | 9.77 | | | | $ | 10.00 | |

| | | | | | | | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | |

Net investment income (loss)† | | | | (0.00 | )(a) | | | | 0.33 | | | | | (0.00 | )(a) |

Net realized and unrealized gain (loss) | | | | 0.57 | | | | | 1.18 | | | | | (0.23 | ) |

| | | | | | | | | | | | | | | |

Total from investment operations | | | | 0.57 | | | | | 1.51 | | | | | (0.23 | ) |

| | | | | | | | | | | | | | | |

Less distributions to shareholders: | | | | | | | | | | | | | | | |

From net investment income | | | | — | | | | | (0.31 | ) | | | | — | |

| | | | | | | | | | | | | | | |

Total distributions | | | | — | | | | | (0.31 | ) | | | | — | |

| | | | | | | | | | | | | | | |

Net asset value, end of period | | | $ | 10.97 | | | | $ | 10.97 | | | | $ | 9.77 | |

| | | | | | | | | | | | | | | |

Total Return | | | | 5.48 | %(b)** | | | | 15.77 | %(c) | | | | (2.30 | )%(b)** |

Ratios/Supplemental Data: | | | | | | | | | | | | | | | |

Net assets, end of period (000’s) | | | $ | 23,190 | | | | $ | 280,869 | | | | $ | 183,330 | |

Net expenses to average daily net assets(d) | | | | 0.15 | %* | | | | 0.05 | % | | | | 0.05 | * |

Net investment income (loss) to average daily net assets | | | | (0.15 | )%* | | | | 3.26 | % | | | | (0.05 | )* |

Portfolio turnover rate | | | | 3 | % | | | | 3 | % | | | | 0 | %** |

Fees and expenses reimbursed by the Manager to average daily net assets(e) | | | | 0.00 | %* | | | | 0.00 | % | | | | 0.00 | %* |

| (a) | Rounds to less than $0.01. |

| (b) | The total return would have been lower had certain expenses not been reimbursed during the periods shown. |

| (c) | The total return would have been lower had certain expenses not been reimbursed during the period shown and assumes the effect of reinvested distributions. |

| (d) | Net expenses exclude expenses incurred indirectly through investment in the Underlying Funds (Note 5). |

| (e) | Fees and expenses reimbursed by the Manager to average daily net assets were less than 0.01%. |

| † | Calculated using average shares outstanding throughout the period. |

See accompanying notes to the financial statements.

19

GMO Series Trust Funds

Notes to Financial Statements

April 30, 2013

Each of GMO Benchmark-Free Allocation Series Fund (commenced operations on January 24, 2013), Global Asset Allocation Series Fund (commenced operations on July 31, 2012), Global Equity Allocation Series Fund (commenced operations on September 4, 2012) and International Equity Allocation Series Fund (each a “Fund” and collectively the “Funds”) is a series of GMO Series Trust (the “Trust”). The Trust is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Trust was established as a Massachusetts business trust under the laws of The Commonwealth of Massachusetts on May 27, 2011. The Declaration of Trust permits the Trustees of the Trust (“Trustees”) to create an unlimited number of series of shares (“Funds”) and to subdivide Funds into classes. The Funds are diversified as that term is defined in the 1940 Act. The Funds are advised and managed by Grantham, Mayo, Van Otterloo & Co. LLC (the “Manager” or “GMO”).

Each Fund invests substantially all of its assets in shares of another fund that is a series of GMO Trust that is also managed by GMO (each an “Institutional Fund”). The performance and operations of each Fund are directly affected by the performance and operations of the relevant Institutional Fund. Each Institutional Fund is a fund of funds that invests primarily in shares of other GMO Funds (“Underlying Funds”). Information about the Institutional Funds for their fiscal years ended February 28, 2013 is contained in the Institutional Funds’ financial statements of the same date. Additional selected information about the Institutional Funds and Underlying Funds as of the date of this report can be found in Note 11, “Institutional Fund information”. The financial statements of the Institutional Funds and Underlying Funds are presented separately and can be obtained from the Securities and Exchange Commission’s (“SEC”) EDGAR database on its Internet site at www.sec.gov or by calling (617) 346-7646 (collect) or visiting www.gmo.com and should be read in conjunction with the Funds’ financial statements.

The following table provides information about each Fund’s benchmark (if any), investment objective and the portion of the corresponding Institutional Fund owned by the Fund:

| | | | | | | | |

| | | | |

| Fund Name | | Benchmark | | Investment Objective | | Percent of

Institutional Fund

Owned | |

| Benchmark-Free Allocation Series Fund | | Not Applicable | | Positive total return, not “relative” return | | | 2.7% | |

| Global Asset Allocation Series Fund | | GMO Global Asset Allocation Index (65% MSCI ACWI and 35% Barclays U.S. Aggregate Index) | | Total return greater than benchmark | | | 11.8% | |

| Global Equity Allocation Series Fund | | MSCI ACWI | | Total return greater than benchmark | | | 0.1% | |

International Equity Allocation Series Fund | | MSCI ACWI ex USA | | Total return greater than benchmark | | | 21.0% | |

| 2. | Significant accounting policies |

The following is a summary of significant accounting policies followed by each Fund in the preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”) and have been consistently followed by the Funds in preparing these financial statements. The preparation of financial statements in accordance with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates. The accounting records of the Funds are maintained in U.S. Dollars.

Portfolio valuation

Shares of the Institutional Funds are valued at their most recent net asset value. See Note 11 for details on Institutional Fund valuation policies.

20

GMO Series Trust Funds

Notes to Financial Statements — (Continued)

April 30, 2013

U.S. GAAP requires the Funds to disclose the fair value of their investments in a three-level hierarchy (Levels 1, 2 and 3). The valuation hierarchy is based upon the relative observability of inputs to the valuation of the Funds’ investments. The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers into or out of an investment’s assigned level within the fair value hierarchy. In addition, in periods of market dislocation, the observability of prices and inputs may be reduced for many instruments. This condition, as well as changes related to liquidity of investments, could cause a security to be reclassified between levels.

U.S. GAAP requires additional disclosures about fair value measurements for material Level 3 securities and derivatives, if any (determined by each category of asset or liability as compared to a Fund’s total net assets). At April 30, 2013, there were no Funds with classes of investments or derivatives with direct material Level 3 holdings.

The three levels are defined as follows:

Level 1 – Valuations based on quoted prices for identical securities in active markets.

Level 2 – Valuations determined using other significant direct or indirect observable inputs.

Level 3 – Valuations based primarily on inputs that are unobservable and significant.

Each Fund classified all of its investments, including investments in the Institutional Funds, as Level 1 as of April 30, 2013. For the summary of valuation inputs (including Level 3 inputs, if any) of the Institutional Funds and Underlying Funds, please refer to their most recent financial statements or for the net aggregate indirect exposure to these valuation methodologies as of the date of this report see Note 11 below.

The Funds had no transfers between levels of the fair value hierarchy during the year ended April 30, 2013.

Cash

Cash, if any, on the Statements of Assets and Liabilities consists of cash balances held with the custodian.

Taxes and distributions

Each Fund intends to qualify each tax year as a regulated investment company under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). Each Fund intends to distribute substantially all of its net investment income and substantially all of its net realized short-term and long-term capital gains, if any, after giving effect to any available capital loss carryforwards for U.S. federal income tax purposes. Therefore, each Fund makes no provision for U.S. federal income or excise taxes.

Each Fund’s policy is to declare and pay distributions of its net investment income, net realized short-term and long-term capital gains, if any, at least annually. Typically, distributions are reinvested in additional shares of each Fund, at net asset value, unless the shareholder elects to receive cash distributions. Distributions to shareholders are recorded by each Fund on the ex-dividend date.

Foreign taxes paid by the Institutional Funds may be treated, to the extent permissible under the Code and if each Fund so elects, as if paid by U.S. shareholders of each Fund.

Income and capital gain distributions for each Fund are determined in accordance with U.S. federal income tax regulations, which may differ from U.S. GAAP. Certain capital accounts in the financial statements are periodically adjusted for permanent differences in order to reflect their tax character. These adjustments have no impact on net assets or net asset value per share. Temporary differences that arise from recognizing certain items of income, expense, gain or loss in different periods for financial statement and tax purposes will likely reverse at some time in the future. Distributions in excess of net investment income or net realized gains are temporary over-distributions for financial statement purposes resulting from differences in the recognition or classification of income or distributions for financial statement and tax purposes.

21

GMO Series Trust Funds

Notes to Financial Statements — (Continued)

April 30, 2013

U.S. GAAP and tax accounting differences for each Fund primarily relate to reasons described in the following table:

| | | | | | | | | | | | | | | | |

| | | | | |

| Differences related to: | | Benchmark-Free

Allocation Series

Fund | | | Global Asset

Allocation Series

Fund | | | Global Equity

Allocation Series

Fund | | | International

Equity Allocation

Series Fund | |

Distribution character reclassification | | | | | | | | | | | X | | | | | |

| Losses on wash sale transactions | | | | | | | | | | | X | | | | | |

| Mutual fund distributions received | | | | | | | | | | | X | | | | | |

There are no significant differences | | | X | | | | X | | | | | | | | X | |

The tax character of distributions declared by each Fund to shareholders is as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Tax year ended April 30, 2013 | | | Tax year ended April 30, 2012 | |

| | | | | | | |

| Fund Name | | Ordinary

Income

(including

any net

short-term

capital gain)

($) | | | Net

Long-Term

Capital

Gain ($) | | | Total

Distributions

($) | | | Ordinary

Income

(including

any net

short-term

capital gain)

($) | | | Net

Long-Term

Capital

Gain ($) | | | Total

Distributions

($) | |

| Benchmark-Free Allocation Series Fund | | | — | | | | — | | | | — | | | | | | | | | | | | | |

| Global Asset Allocation Series Fund | | | 14,263,282 | | | | — | | | | 14,263,282 | | | | | | | | | | | | | |

| Global Equity Allocation Series Fund | | | 23,005 | | | | — | | | | 23,005 | | | | | | | | | | | | | |

| International Equity Allocation Series Fund | | | 8,065,989 | | | | — | | | | 8,065,989 | | | | — | | | | — | | | | — | |

Distributions in excess of tax basis earnings and profits, if significant, are reported in the Fund’s financial statements as a return of capital.

As of April 30, 2013, the components of distributable earnings on a tax basis and other tax attributes for each Fund consisted of the following:

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| Fund Name | | Undistributed

Ordinary Income

(including any

net short-term

capital gain) ($) | | | Undistributed

Net Long-Term

Capital Gain ($) | | | Late-Year

Ordinary Loss

Deferral ($) | | | Capital Loss

Carryforwards

($) | | | Post-October

Capital Losses

($) | |

| Benchmark-Free Allocation Series Fund | | | — | | | | — | | | | — | | | | — | | | | — | |

| Global Asset Allocation Series Fund | | | 770,729 | | | | — | | | | (93,768) | | | | — | | | | — | |

| Global Equity Allocation Series Fund | | | 2,441 | | | | 26,254 | | | | (208) | | | | — | | | | — | |

| International Equity Allocation Series Fund | | | 322,708 | | | | — | | | | (47,031) | | | | — | | | | — | |

22

GMO Series Trust Funds

Notes to Financial Statements — (Continued)

April 30, 2013

As of April 30, 2013, the Funds had no capital loss carryforwards available to offset future realized gains, if any, to the extent permitted by the Code. Utilization of late-year ordinary losses and losses realized subsequent to April 30, 2013, if any, could be subject to further limitations imposed by the Code related to share ownership activity.

As of April 30, 2013, the approximate cost for U.S. federal income tax purposes and gross and net unrealized appreciation (depreciation) in the value of investments were as follows:

| | | | | | | | | | | | | | | | |

| | | | | |

| Fund Name | | Aggregate

Cost ($) | | | Gross Unrealized

Appreciation ($) | | | Gross Unrealized

(Depreciation) ($) | | | Net Unrealized

Appreciation

(Depreciation) ($) | |

| Benchmark-Free Allocation Series Fund | | | 153,238,612 | | | | 5,113,504 | | | | — | | | | 5,113,504 | |

| Global Asset Allocation Series Fund | | | 556,974,873 | | | | 31,512,009 | | | | — | | | | 31,512,009 | |

| Global Equity Allocation Series Fund | | | 1,367,901 | | | | 66,686 | | | | — | | | | 66,686 | |

| International Equity Allocation Series Fund | | | 270,840,840 | | | | 31,538,285 | | | | — | | | | 31,538,285 | |

The Funds are subject to authoritative guidance related to the accounting and disclosure of uncertain tax positions under U.S. GAAP. This guidance sets forth a minimum threshold for the financial statement recognition of tax positions taken based on the technical merits of such positions. United States and non-U.S. tax rules (including the interpretation and application of tax laws) are subject to change. The Funds file tax returns and/or adopt certain tax positions in various jurisdictions. Non-U.S. taxes are provided for based on the Funds’ understanding of the prevailing tax rules of the non-U.S. markets in which they invest. Recently enacted tax rules, including the interpretation of tax laws (e.g., regulations pertaining to the U.S. Foreign Account Tax Compliance Act) and proposed legislation currently under consideration in various jurisdictions, including the U.S., might affect the way the Funds and their investors are taxed prospectively and/or retroactively. Prior to the expiration of the relevant statutes of limitations, if any, the Funds are subject to examination by U.S. federal, state, local and non-U.S. jurisdictions with respect to the tax returns they have filed and the tax positions they have adopted. The Funds’ U.S. federal income tax returns are generally subject to examination by the Internal Revenue Service for a period of three years after they are filed. State, local and/or non-U.S. tax returns and/or other filings may be subject to examination for different periods, depending upon the tax rules of each applicable jurisdiction.

Security transactions and related investment income

Security transactions are accounted for in the financial statements on trade date. For purposes of daily net asset value calculations, the Funds’ policy is that security transactions are generally accounted for on the following business day. The Manager may override that policy and a Fund may account for security transactions on trade date if it experiences significant purchases or redemptions or engages in significant portfolio transactions. Income dividends and capital gain distributions from the Institutional Funds are recorded on the ex-dividend date. Interest income is recorded on the accrual basis and is adjusted for the amortization of premiums and accretion of discounts. Non-cash dividends, if any, are recorded at the fair market value of the asset received. In determining the net gain or loss on securities sold, the Funds use the identified cost basis.

Expenses

Most of the expenses of the Trust are directly identifiable to an individual Fund. Fund investment income, common expenses and realized and unrealized gains and losses are allocated among the classes of shares of the Fund, if applicable, based on the relative net assets of each class. Each Fund incurs fees and expenses indirectly as a shareholder in the Institutional Funds and the Underlying Funds. Because the Underlying Funds owned by the Institutional Funds have different expense and fee levels and the Institutional Funds may own different proportions of the Underlying Funds at different times, the amount of fees and expenses indirectly incurred by a Fund may vary (See Note 5 and Note 11).

State Street Bank and Trust Company (“State Street”) serves as the Funds’ custodian, fund accounting agent and transfer agent. Prior to December 31, 2012, State Street’s fees may have been reduced by an earnings allowance calculated on the average daily cash balances each Fund maintains with State Street. During this same period, each Fund received the benefit of any earnings allowance; earnings allowances were reported as a reduction of expenses in the Statements of Operations. Effective January 1, 2013, any cash balances maintained at State Street are held in a Demand Deposit Account and interest income earned, if any, is shown as interest income in the Statement of Operations.

23

GMO Series Trust Funds

Notes to Financial Statements — (Continued)

April 30, 2013

Recent accounting guidance

In December 2011, the Financial Accounting Standards Board issued “Disclosures about Offsetting Assets and Liabilities”. In January 2013, an update was issued entitled “Clarifying the Scope of Disclosures about Offsetting Assets and Liabilities”. These pronouncements create new disclosure requirements requiring entities to disclose both gross and net information for derivatives, repurchase agreements, reverse repurchase agreements and securities borrowing and lending transactions that are either offset in the Statements of Assets and Liabilities or subject to enforceable master netting arrangements or similar agreements. The disclosure requirements are effective for annual reporting periods beginning on or after January 1, 2013 and interim periods within those annual periods. At April 30, 2013, the Funds held no investments or financial instruments directly that would be subject to offsetting or impacted by the new pronouncement.

| 3. | Investment and other risks |

The following chart identifies selected risks of investing in the Funds. Risks not marked for a particular Fund may, however, still apply to some extent to that Fund at various times.

| | | | | | | | | | | | | | | | |

| | | Benchmark-Free

Allocation Series

Fund | | | Global Asset

Allocation Series

Fund | | | Global Equity

Allocation Series

Fund | | | International

Equity Allocation

Series Fund | |

| Market Risk – Equity Securities Risk | | | — | | | | — | | | | — | | | | — | |

| Market Risk – Fixed Income Investments Risk | | | — | | | | — | | | | — | | | | — | |

| Market Risk – Asset-Backed Securities Risk | | | — | | | | — | | | | — | | | | — | |

| Credit Risk | | | — | | | | — | | | | — | | | | — | |

| Liquidity Risk | | | — | | | | — | | | | — | | | | — | |

| Smaller Company Risk | | | — | | | | — | | | | — | | | | — | |

| Derivatives Risk | | | — | | | | — | | | | — | | | | — | |

| Non-U.S. Investment Risk | | | — | | | | — | | | | — | | | | — | |

| Currency Risk | | | — | | | | — | | | | — | | | | — | |

| Focused Investment Risk | | | — | | | | — | | | | — | | | | — | |

| Options Risk | | | — | | | | — | | | | — | | | | — | |

| Real Estate Risk | | | — | | | | — | | | | — | | | | | |

| Leveraging Risk | | | — | | | | — | | | | — | | | | — | |

| Counterparty Risk | | | — | | | | — | | | | — | | | | — | |

| Short Sales Risk | | | — | | | | — | | | | — | | | | — | |

| Commodities Risk | | | — | | | | — | | | | — | | | | — | |

| Natural Resources Risk | | | — | | | | — | | | | — | | | | — | |

| Market Disruption and Geopolitical Risk | | | — | | | | — | | | | — | | | | — | |

| Large Shareholder Risk | | | — | | | | — | | | | — | | | | — | |

| Management and Operational Risk | | | — | | | | — | | | | — | | | | — | |

| Fund of Funds Risk | | | — | | | | — | | | | — | | | | — | |

| Non-Diversified Funds | | | — | | | | — | | | | — | | | | — | |

24

GMO Series Trust Funds

Notes to Financial Statements — (Continued)

April 30, 2013

Investing in mutual funds involves many risks. The risks of investing in a particular Fund depend on the types of investments in its portfolio and the investment strategies the Manager employs on its behalf. This section does not describe every potential risk of investing in the Funds. Funds could be subject to additional risks because of the types of investments they make and market conditions, which may change over time.

Because each Fund invests substantially all of its assets in an Institutional Fund, the most significant risks of investing in a Fund are the risks to which the Fund is exposed through its corresponding Institutional Fund (and, in turn, the Underlying Funds in which the Institutional Fund invests). Those risks include the risks summarized below. Some of the Underlying Funds are non-diversified companies under the 1940 Act and therefore a decline in the market value of a particular security held by those Underlying Funds may affect their performance more than if they were diversified. In addition to the risks to which each Fund is exposed through investment in its corresponding Institutional Fund, the Fund is subject to the risk that cash flows into or out of the Fund will cause its performance to be worse than the performance of its corresponding Institutional Fund.

References in this section to investments made by a Fund include those made by its corresponding Institutional Fund and Underlying Funds.

An investment in a Fund is not a bank deposit and, therefore, is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

• MARKET RISK. All of the Funds are subject to market risk, which is the risk that the market value of their holdings will decline. Market risks include:

Equities Risk — Funds that invest in equities run the risk that the market prices of those investments will decline. The market price of equities may decline for reasons that directly relate to the issuing company, such as poor management performance or reduced demand for its goods or services. They also may decline due to factors that affect a particular industry, such as a decline in demand, labor or raw material shortages, or increased production costs. In addition, market prices may decline as a result of general market conditions not specifically related to a company or industry, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates, or adverse investor sentiment generally. Equities generally have significant price volatility and the market price of equities can decline in a rapid or unpredictable manner.

Some of the Funds invest a substantial portion of their assets in equities and generally do not take temporary defensive positions. As a result, declines in stock market prices generally are likely to reduce the net asset values of those Funds’ shares.

If a Fund purchases equities at a discount from their value as determined by the Manager, the Fund runs the risk that the market prices of these investments will not appreciate to or will decline from that value for a variety of reasons, one of which may be the Manager’s overestimation of the value of those investments.

The market prices of equities trading at high multiples of current earnings often are more sensitive to changes in future earnings expectations than the market prices of equities trading at lower multiples.

Fixed Income Investments Risk — Funds that invest in fixed income securities (including bonds, notes, bills, synthetic debt instruments and asset-backed securities) are subject to various market risks. The market price of a fixed income investment can decline due to a number of market-related factors, including rising interest rates and widening credit spreads, or decreased liquidity stemming from the market’s uncertainty about the value of a fixed income investment (or class of fixed income investments). In addition, the market price of fixed income investments with complex structures, such as asset-backed securities and sovereign and quasi-sovereign debt instruments, can decline due to market uncertainty about their credit quality and the reliability of their payment streams. Some fixed income securities also are subject to unscheduled prepayment, and a Fund may be unable to invest prepayments at as high a yield as was provided by the fixed income security. When interest rates rise, these securities also may be repaid more slowly than anticipated, which could cause the market price of the Fund’s investment to decrease. During periods of economic uncertainty and change, the market price of a Fund’s investments in below investment grade securities (commonly referred to as “junk bonds”) may be particularly volatile. Often junk bonds are subject to greater sensitivity to interest rate and economic changes than higher rated bonds and can be more difficult to value, exposing a Fund to the risk that the price of which it sells them will be less than the value placed on them when they were held by the Fund. See “Credit Risk” and “Liquidity Risk” below for more information about these risks.

25

GMO Series Trust Funds

Notes to Financial Statements — (Continued)

April 30, 2013

A risk run by each Fund with a significant investment in fixed income securities is that an increase in prevailing interest rates will cause the market price of those securities to decline. The risk associated with increases in interest rates (also called “interest rate risk”) is generally greater for Funds investing in fixed income securities with longer durations and in some cases duration can increase.

The extent to which a fixed income security’s price changes with changes in interest rates is referred to as interest rate duration, which can be measured mathematically or empirically. A longer-maturity investment generally has longer interest rate duration because the investment’s fixed rate is locked in for a longer period of time. Floating-rate or adjustable-rate securities, however, generally have shorter interest rate durations because their interest rates are not fixed but rather float up and down as interest rates change. Conversely, inverse floating-rate securities have durations that move in the opposite direction from short-term interest rates and thus tend to underperform fixed rate securities when interest rates rise but outperform them when interest rates decline. Fixed income securities paying no interest, such as zero coupon and principal-only securities, create additional interest rate risk.

The market price of inflation indexed bonds (including Inflation-Protected Securities issued by the U.S. Treasury (“TIPS”)) normally changes when real interest rates change. Their value typically will decline during periods of rising real interest rates (i.e., nominal interest rate minus inflation) and increase during periods of declining real interest rates. Real interest rates may not fluctuate in the same manner as nominal interest rates. In some interest rate environments, such as when real interest rates are rising faster than nominal interest rates, the market price of inflation-indexed bonds may decline more than the price of non-inflation-indexed (or nominal) fixed income bonds with similar maturities. The market price of a Fund’s inflation-indexed bonds, however, will not necessarily change in the same proportion as changes in nominal interest rates, and short term increases in inflation may lead to a decline in their price. Moreover, if the index measuring inflation falls, the principal value of inflation-indexed bond investments will be adjusted downward, and, consequently, the interest they pay (calculated with respect to a smaller principal amount) will be reduced. In the case of TIPS, the U.S. government guarantees the repayment of the original bond principal upon maturity (as adjusted for inflation). Generally, when interest rates on short term U.S. Treasury obligations equal or approach zero, a Fund that invests a substantial portion of its assets in U.S. Treasury obligations will have a negative return unless the Manager waives or reduces its management fees.

Market risk for fixed income securities denominated in non-U.S. currencies is also affected by currency risk. See “Currency Risk” below.

Asset-Backed Securities Risk — Investments in asset-backed securities not only are subject to all of the market risks described above for fixed income securities but to other market risks as well.

Funds investing in asset-backed securities are exposed to the risk that these securities experience severe credit downgrades, illiquidity, defaults, and declines in market value. These risks are particularly acute during periods of adverse market conditions, such as those that occurred in 2008. Asset-backed securities may be backed by many types of assets, including pools of residential and commercial mortgages, automobile loans, educational loans, home equity loans, and credit-card receivables. They also may be backed by pools of corporate or sovereign bonds, bank loans made to corporations, or a combination of these bonds and loans (commonly referred to as “collateralized debt obligations” or “collateralized loan obligations”) and by the fees earned by service providers.