UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22649

iShares U.S. ETF Trust

(Exact name of registrant as specified in charter)

c/o: State Street Bank and Trust Company

100 Summer Street, 4th Floor, Boston, MA 02110

(Address of principal executive offices) (Zip code)

The Corporation Trust Company

1209 Orange Street, Wilmington, DE 19801

(Name and address of agent for service)

Registrant’s telephone number, including area code: (415) 670-2000

Date of fiscal year end: October 31, 2018

Date of reporting period: October 31, 2018

| Item 1. | Reports to Stockholders. |

Copies of the annual reports transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 are attached.

OCTOBER 31, 2018

| | | | |

2018 ANNUAL REPORT | | | |  |

iShares U.S. ETF Trust

iShares Short Maturity Bond ETF | NEAR | Cboe BZX

iShares Short Maturity Bond ETF | NEAR | Cboe BZX

iShares Short Maturity Municipal Bond ETF | MEAR | Cboe BZX

iShares Ultra Short-Term Bond ETF | ICSH | Cboe BZX

Table of Contents

Market Overview

iShares U.S. ETF Trust

U.S. Bond Market Overview

The U.S. bond market declined for the 12 months ended October 31, 2018 (“reporting period”). The Bloomberg Barclays U.S. Aggregate Bond Index, a broad measure of U.S. fixed-income performance, returned -2.05%. The negative return for U.S. bonds was primarily due to a stronger U.S. economy and higher interest rates. Driven in part by the stimulative effect of federal tax reform legislation, the U.S. economy grew by 3% for the 12 months ended September 2018, its highest year-over-year growth rate in more than three years. Key components of the strengthening economy included the job market, where the unemployment rate declined to its lowest level since December 1969; industrial production, which increased at its sharpest year-over-year pace in nearly eight years; and retail sales, which accelerated for much of the reporting period before slowing in the last two months.

Faster economic growth led to higher inflation, though it remained low by historical standards. As measured by the consumer price index, the year-over-year U.S. inflation rate rose to 2.9% in mid-2018 — its fastest rate in more than six years — before falling back to 2.3% by the end of the reporting period. By comparison, the long-term historical average inflation rate is 3.3%.

In this environment, the U.S. Federal Reserve Bank (“Fed”) continued its efforts to normalize monetary policy. The Fed increased short-term interest rates four times during the reporting period, increasing its short-term interest rate target to 2.25%, the highest level in more than a decade. In addition, the Fed reduced its holdings of U.S. Treasury and mortgage-backed securities by approximately 7% during the reporting period, after quadrupling its holdings in response to the 2008 financial crisis.

Interest rates increased broadly in response to the improving economy and higher inflation. Short-term interest rates increased the most, reflecting the Fed’s actions. For example, the yield of the two-year U.S. Treasury note increased from 1.60% to 2.87% during the reporting period. Longer-term interest rates rose to a lesser degree; the yield of the 30-year U.S. Treasury bond increased from 2.88% to 3.39%. These developments led to the narrowest yield difference, or spread, between short-term and longer-term U.S. Treasury securities in more than 11 years.

Higher interest rates had the most significant impact on U.S. Treasury securities, which typically have greater sensitivity to changes in interest rates compared with other higher-yielding sectors of the bond market. Consequently, the prices of U.S. Treasury bonds declined as interest rates increased during the reporting period. U.S. Treasury inflation-protected securities also declined but to a lesser degree as the inflation rate increased.

Corporate bonds posted mixed returns for the reporting period. Despite the positive economic environment, investment-grade corporate bonds declined the most among the major bond sectors. In addition to higher interest rates, investor concerns about high corporate debt levels, a decline in average credit quality, and relatively high valuations contributed to the weakness in investment-grade corporate bonds. In contrast, high-yield corporate bonds, which have lower credit ratings, performed relatively well, as their higher yields buffered price declines. Strong investor demand for yield, lower issuance levels, and limited interest rate sensitivity contributed to the positive performance of high-yield corporate bonds.

Among securitized bonds, asset-backed securities (bonds backed by credit card receivables, auto loans, and other debt) posted positive returns for the reporting period, benefiting from their higher yields and relatively short maturities. Mortgage-backed securities, both residential and commercial, declined but to a lesser degree than the broader bond market.

| | | | |

M A R K E T O V E R V I E W | | | 5 | |

| | |

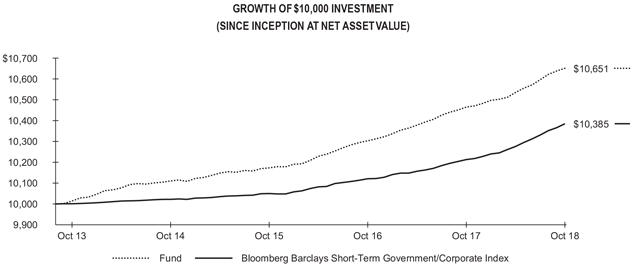

Fund Summary as of October 31, 2018 | | iShares® Short Maturity Bond ETF |

Investment Objective

The iShares Short Maturity Bond ETF (the “Fund”) seeks to maximize current income by investing, under normal circumstances, at least 80% of its net assets in a portfolio of U.S. dollar-denominated investment-grade fixed income securities and maintain a weighted average maturity that is less than three years. The Fund is an actively managed exchange-traded fund that does not seek to replicate the performance of a specified index.

Performance

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Average Annual Total Returns | | | | | | Cumulative Total Returns | |

| | | 1 Year | | | 5 Years | | | Since

Inception | | | | | | 1 Year | | | 5 Years | | | Since

Inception | |

Fund NAV | | | 1.78 | % | | | 1.24 | % | | | 1.24 | % | | | | | | | 1.78 | % | | | 6.36 | % | | | 6.51 | % |

Fund Market | | | 1.78 | | | | 1.24 | | | | 1.25 | | | | | | | | 1.78 | | | | 6.36 | | | | 6.53 | |

| Bloomberg Barclays Short-Term Government/Corporate Index | | | 1.68 | | | | 0.76 | | | | 0.74 | | | | | | | | 1.68 | | | | 3.84 | | | | 3.85 | |

The inception date of the Fund was 9/25/13. The first day of secondary market trading was 9/26/13.

The Bloomberg Barclays Short-Term Government/Corporate Index an unmanaged index that measures the performance of government and corporate securities with less than 1 year remaining to maturity.

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 12 for more information.

Expense Example

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Actual | | | Hypothetical 5% Return | | | | |

| Beginning

Account Value

(05/01/18) |

| |

| Ending

Account Value

(10/31/18) |

| |

| Expenses

Paid During

the Period |

(a) | |

| Beginning

Account Value

(05/01/18) |

| |

| Ending

Account Value

(10/31/18) |

| |

| Expenses

Paid During

the Period |

(a) | |

| Annualized

Expense

Ratio |

|

| | $ 1,000.00 | | | | $ 1,011.00 | | | | $ 1.27 | | | | $ 1,000.00 | | | | $ 1,023.90 | | | | $ 1.28 | | | | 0.25 | % |

| | (a) | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 12 for more information. | |

| | |

| 6 | | 2 0 1 8 I S H A R E S A N N U A L R E P O R T T O S H A R E H O L D E R S |

| | |

Fund Summary as of October 31, 2018 (continued) | | iShares® Short Maturity Bond ETF |

Portfolio Management Commentary

Short-term investment-grade bonds posted positive returns for the reporting period. While longer-term bond prices generally declined in the wake of four interest rate increases by the Fed, the shortest-term bonds are the least sensitive to interest rate changes.

The Fund performed well relative to the Bloomberg Barclays Short-Term Government/Corporate Index. The Fund’s performance relative to the broader short-term bond market benefited from overweight allocations to corporate credit and securitized products, including asset-backed securities (“ABSs”) and commercial mortgage-backed securities (“CMBSs”).

In the Fund’s corporate allocation, the largest contributors to the Fund’s performance were financial and industrial bonds. In general, corporate securities benefited from strong economic growth, tax reform, and healthy earnings. High demand from yield-seeking buyers also boosted corporate bonds.

Banks were the leading contributors to the Fund’s return. These issuers made up 23% of the Fund on average during the reporting period. Despite a flattening yield curve (the difference between short-term and long-term interest rates), banks generally benefited from increasing interest rates, as revenues from longer-term, higher-rate loans outpaced increases in deposit costs. In the industrial sector, overweight allocations to both the consumer non-cyclicals and consumer cyclicals industries were beneficial to the Fund’s performance, reflecting the strong economy, a decades-low unemployment rate, and healthy consumer spending.

Among securitized products, overweight positions in ABSs and CMBSs benefited the Fund, as investors seeking yield drove demand for these products. In addition, CMBSs benefited from falling delinquency rates for commercial loans. Rising property values and the easy availability of financing helped keep commercial mortgage defaults low.

For most of the reporting period, the Fund maintained a similar or shorter interest rate sensitivity (less price sensitivity to interest rate changes) relative to the Bloomberg Barclays Short-Term Government/Corporate Index. This position reflected expectations of interest rate increases by the Fed. By the end of the reporting period, the Fund moved to a slightly longer interest rate sensitivity relative to the broader market.

Portfolio Information

| | | | |

ALLOCATION BY INVESTMENT TYPE | |

| Investment Type | |

| Percent of

Total Investments |

(a) |

Corporate Bonds & Notes | | | 63.2 | % |

Asset-Backed Securities | | | 26.9 | |

Collaterized Mortgage Obligations | | | 4.8 | |

Commercial Paper | | | 2.1 | |

Certificates of Deposit | | | 1.9 | |

Repurchase Agreements | | | 0.7 | |

U. S. Government & Agency Obligations | | | 0.4 | |

| | | | |

ALLOCATION BY CREDIT QUALITY | |

| Moody’s Credit Rating* | |

| Percent of

Total Investments |

(a) |

Aaa | | | 20.1 | % |

Aa | | | 7.8 | |

A | | | 19.9 | |

Baa | | | 33.5 | |

Ba | | | 1.6 | |

P-1 | | | 3.1 | |

P-3 | | | 1.0 | |

Aaae | | | 0.5 | |

Not Rated | | | 12.5 | |

| | * | Credit quality ratings shown reflect the ratings assigned by Moody’s Investors Service (“Moody’s”), a widely used independent, nationally recognized statistical rating organization. Moody’s credit ratings are opinions of the credit quality of individual obligations or of an issuer’s general creditworthiness. Investment grade ratings are credit ratings of Baa or higher. Below investment grade ratings are credit ratings of Ba or lower. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | (a) | Excludes money market funds. |

| | |

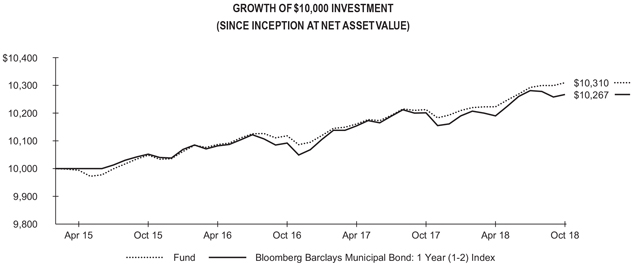

Fund Summary as of October 31, 2018 | | iShares® Short Maturity Municipal Bond ETF |

Investment Objective

The iShares Short Maturity Municipal Bond ETF (the “Fund”) seeks to maximize tax-free current income by investing, under normal circumstances, at least 80% of its net assets in municipal securities such that the interest on each bond is exempt from U.S. federal income taxes and the federal alternative minimum tax. Under normal circumstances, the effective duration of the Fund’s portfolio is expected to be 1.2 years or less, as calculated by the management team, and is not expected to exceed 1.5 years. The Fund is an actively managed exchange-traded fund that does not seek to replicate the performance of a specified index.

Performance

| | | | | | | | | | | | | | | | | | | | |

| | | Average Annual Total Returns | | | | | | Cumulative Total Returns | |

| | | 1 Year | | | Since

Inception | | | | | | 1 Year | | | Since

Inception | |

Fund NAV | | | 0.95 | % | | | 0.84 | % | | | | | | | 0.95 | % | | | 3.10 | % |

Fund Market | | | 1.01 | | | | 0.86 | | | | | | | | 1.01 | | | | 3.20 | |

| Bloomberg Barclays Municipal Bond: 1 Year (1-2) Index | | | 0.65 | | | | 0.72 | | | | | | | | 0.65 | | | | 2.67 | |

The inception date of the Fund was 3/3/15. The first day of secondary market trading was 3/5/15.

The Bloomberg Barclays Municipal Bond: 1 Year (1-2) Index is an unmanaged index comprised of national municipal bond issues having a maturity of at least one year and less than two years.

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 12 for more information.

Expense Example

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Actual | | | Hypothetical 5% Return | | | | |

| Beginning

Account Value

(05/01/18) |

| |

| Ending

Account Value

(10/31/18) |

| |

| Expenses

Paid During

the Period |

(a) | |

| Beginning

Account Value

(05/01/18) |

| |

| Ending

Account Value

(10/31/18) |

| |

| Expenses

Paid During

the Period |

(a) | |

| Annualized

Expense

Ratio |

|

| | $ 1,000.00 | | | | $ 1,008.50 | | | | $ 1.27 | | | | $ 1,000.00 | | | | $ 1,023.90 | | | | $ 1.28 | | | | 0.25% | |

| | (a) | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 12 for more information. | |

| | | | |

8 | | | 2 0 1 8 I S H A R E S A N N U A L R E P O R T T O S H A R E H O L D E R S | |

| | |

Fund Summary as of October 31, 2018 (continued) | | iShares® Short Maturity Municipal Bond ETF |

Portfolio Management Commentary

Short-term municipal bonds posted a positive return for the reporting period. While longer-term municipal bond prices generally declined in the wake of four interest rate increases by the Fed, short-term municipal bonds are the least sensitive to interest rate changes. The Fund further maintained a defensive strategy to minimize the effect of rising interest rates.

Supply and demand were mixed. Supply surged as tax reform led to a spike in refunding issuances in late 2017, but that spike was followed by lower-than-normal issuances in 2018. Tax reform also worked to boost demand for municipal bonds, particularly from investors in higher-income tax states such as New York and California. New limits to the deductibility of state income taxes made tax-exempt municipal bonds more attractive for investors from these areas. This helped to offset a decline in demand for municipal bonds from banks and other corporations, which have a smaller incentive to invest in tax-exempt securities following the reduction of the corporate tax rate.

The Fund performed well relative to the broader market, as represented by the Bloomberg Barclays Municipal Bond: 1 Year (1-2) Index. The Fund benefited from overweight positions in bonds rated in the A and BBB categories by Standard & Poor’s, as the higher yields for this class of credit offered attractive yields relative to higher-quality AAA-rated bonds. Strong demand from income investors and a wave of reinvested coupon and principal payments helped support the market for higher-yielding municipal bonds.

To mitigate the effect of rising interest rates, the Fund maintained an overweight allocation to variable-rate demand notes (“VRDNs”). Since interest rates on VRDN securities reset periodically, bondholders can benefit from these interest rate changes. Consequently, the overweight allocation to VRDNs contributed to the Fund’s relative return.

Overweight allocations to tax-backed state and local bonds and school district bonds also contributed to the Fund’s relative performance. On the downside, an underweight allocation to pre-refunded debt securities detracted from the Fund’s relative return.

Portfolio Information

| | | | |

ALLOCATION BY CREDIT QUALITY | |

| S&P Credit Rating* | |

| Percent of

Total Investments |

(a) |

AA | | | 20.9 | % |

AA- | | | 1.2 | |

A+ | | | 2.8 | |

A | | | 29.7 | |

A- | | | 1.8 | |

BBB+ | | | 14.2 | |

BBB | | | 0.3 | |

Not Rated | | | 29.1 | |

| | | | |

TEN LARGEST STATES | |

| State | |

| Percent of

Total Investments |

(a) |

New Jersey | | | 22.3 | % |

New York | | | 19.1 | |

Illinois | | | 8.7 | |

Wisconsin | | | 5.4 | |

Iowa | | | 5.2 | |

Texas | | | 4.8 | |

Washington | | | 4.4 | |

Virginia | | | 3.9 | |

Georgia | | | 3.8 | |

Connecticut | | | 3.2 | |

| | * | Credit quality ratings shown reflect the ratings assigned by Standard & Poor’s Ratings Service (“S&P”), a widely used independent, nationally recognized statistical rating organization. S&P credit ratings are opinions of the credit quality of individual obligations or of an issuer’s general creditworthiness. Investment grade ratings are credit ratings of BBB or higher. Below investment grade ratings are credit ratings of BB or lower. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | (a) | Excludes money market funds. |

| | |

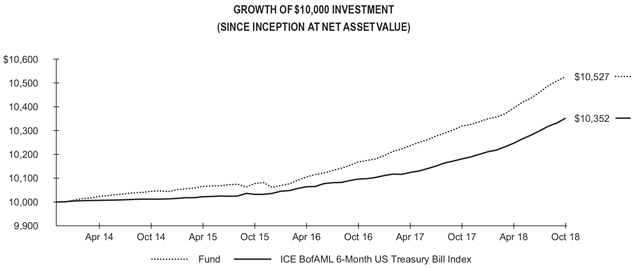

Fund Summary as of October 31, 2018 | | iShares® Ultra Short-Term Bond ETF |

Investment Objective

The iShares Ultra Short-Term Bond ETF (the “Fund”) seeks to provide current income consistent with preservation of capital by investing, under normal circumstances, at least 80% of its net assets in a portfolio of U.S. dollar-denominated investment-grade fixed- and floating-rate debt securities and maintain a dollar-weighted average maturity that is less than 180 days. The Fund is an actively managed exchange-traded fund that does not seek to replicate the performance of a specified index.

Performance

| | | | | | | | | | | | | | | | | | | | |

| | | Average Annual Total Returns | | | | | | Cumulative Total Returns | |

| | | 1 Year | | | Since

Inception | | | | | | 1 Year | | | Since

Inception | |

Fund NAV | | | 2.02 | % | | | 1.06 | % | | | | | | | 2.02 | % | | | 5.27 | % |

Fund Market | | | 2.08 | | | | 1.07 | | | | | | | | 2.08 | | | | 5.33 | |

| ICE BofAML 6-Month US Treasury Bill Index | | | 1.68 | | | | 0.71 | | | | | | | | 1.68 | | | | 3.52 | |

The inception date of the Fund was 12/11/13. The first day of secondary market trading was 12/13/13.

The ICE BofAML 6-Month US Treasury Bill Index is an unmanaged index that measures the performance of government securities with less than 6 months remaining to maturity.

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 12 for more information.

Expense Example

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Actual | | | Hypothetical 5% Return | | | | |

| Beginning

Account Value

(05/01/18) |

| |

| Ending

Account Value

(10/31/18) |

| |

| Expenses

Paid During

the Period |

(a) | |

| Beginning

Account Value

(05/01/18) |

| |

| Ending

Account Value

(10/31/18) |

| |

| Expenses

Paid During

the Period |

(a) | |

| Annualized

Expense

Ratio |

|

| | $ 1,000.00 | | | | $ 1,012.70 | | | | $ 0.41 | | | | $ 1,000.00 | | | | $ 1,024.80 | | | | $ 0.41 | | | | 0.08 | % |

| | (a) | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 12 for more information. | |

| | |

| 10 | | 2 0 1 8 I S H A R E S A N N U A L R E P O R T T O S H A R E H O L D E R S |

| | |

Fund Summary as of October 31, 2018 (continued) | | iShares® Ultra Short-Term Bond ETF |

Portfolio Management Commentary

Ultra-short-term bonds posted a positive return for the reporting period. While bond prices generally declined in the wake of four interest rate increases by the Fed, the shortest-term bonds are the least sensitive to interest rate changes. In addition, the Fund is designed to exhibit little share price volatility in most interest rate environments, as demonstrated during the reporting period.

The Fund performed well relative to the Bank of America Merrill Lynch 6-Month U.S. Treasury Bill Index. The largest contributor to the Fund’s return relative to the broader ultra-short-term bond market was an overweight allocation to corporate bonds. Corporate debt benefited from strong economic growth, tax reform, and healthy earnings. In addition, high demand from yield-seeking buyers boosted corporate bonds.

Within the corporate sector, banks were the largest contributors to the Fund’s return. These issuers made up 32% of the Fund on average during the reporting period. Despite a flattening yield curve (the difference between short-term and long-term interest rates), banks generally benefited from increasing interest rates, as revenues from longer-term, higher-rate loans outpaced increases in deposit costs. Bonds issued by industrial companies were also contributors to the Fund’s performance, as industrial production increased, driven by strong demand for consumer products and industrial goods.

Floating-rate notes (“floaters”), which offer some protection from rising interest rates, also contributed to the Fund’s return. Floaters periodically reset their interest rate paid to investors, therefore increasing their payments when interest rates are rising. Toward the end of the reporting period, the Fund reduced its allocation to fully valued floaters in the industrial sector in favor of more attractively valued fixed-rate securities. For example, yields on two-year Treasury notes reached their highest level since 2008 so the Fund added exposure to select maturities with attractive yields. The Fund also increased exposure to asset-backed securities, which offered an attractive risk-reward trade-off.

Portfolio Information

| | | | |

ALLOCATION BY INVESTMENT TYPE | |

| Investment Type | |

| Percent of

Total Investments |

(a) |

Corporate Bonds & Notes | | | 38.8 | % |

Commercial Paper | | | 35.6 | |

Certificates of Deposit | | | 18.8 | |

Repurchase Agreements | | | 4.6 | |

Asset-Backed Securities | | | 2.2 | |

| | | | |

ALLOCATION BY CREDIT QUALITY | |

| Moody’s Credit Rating* | |

| Percent of

Total Investments |

(a) |

Aaa | | | 1.7 | % |

Aa | | | 16.5 | |

A | | | 24.2 | |

Baa | | | 2.4 | |

P-1 | | | 30.9 | |

P-2 | | | 14.0 | |

Not Rated | | | 10.3 | |

| | * | Credit quality ratings shown reflect the ratings assigned by Moody’s Investors Service (“Moody’s”), a widely used independent, nationally recognized statistical rating organization. Moody’s credit ratings are opinions of the credit quality of individual obligations or of an issuer’s general creditworthiness. Investment grade ratings are credit ratings of Baa or higher. Below investment grade ratings are credit ratings of Ba or lower. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | (a) | Excludes money market funds. |

About Fund Performance

Past performance is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Performance data current to the most recent month-end is available at www.ishares.com. Performance results assume reinvestment of all dividends and capital gain distributions and do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. The investment return and principal value of shares will vary with changes in market conditions. Shares may be worth more or less than their original cost when they are redeemed or sold in the market. Performance for certain funds may reflect a waiver of a portion of investment advisory fees. Without such a waiver, performance would have been lower.

Net asset value or “NAV” is the value of one share of a fund as calculated in accordance with the standard formula for valuing mutual fund shares. The price used to calculate market return (“Market Price”) is determined by using the midpoint between the highest bid and the lowest ask on the primary stock exchange on which shares of a fund are listed for trading, as of the time that such fund’s NAV is calculated. Since shares of a fund may not trade in the secondary market until after the fund’s inception, for the period from inception to the first day of secondary market trading in shares of the fund, the NAV of the fund is used as a proxy for the Market Price to calculate market returns. Market and NAV returns assume that dividends and capital gain distributions have been reinvested at Market Price and NAV, respectively.

An index is a statistical composite that tracks a specified financial market or sector. Unlike a fund, an index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by a fund. These expenses negatively impact fund performance. Also, market returns do not include brokerage commissions that may be payable on secondary market transactions. If brokerage commissions were included, market returns would be lower.

Shareholder Expenses

As a shareholder of your Fund, you incur two types of costs: (1) transaction costs, including brokerage commissions on purchases and sales of fund shares and (2) ongoing costs, including management fees and other fund expenses. The expense example, which is based on an investment of $1,000 invested at the beginning of the period (or from the commencement of operations if less than 6 months) and held through the end of the period, is intended to help you understand your ongoing costs (in dollars and cents) of investing in your Fund and to compare these costs with the ongoing costs of investing in other funds.

Actual Expenses – The table provides information about actual account values and actual expenses. Annualized expense ratios reflect contractual and voluntary fee waivers, if any. To estimate the expenses that you paid on your account over the period, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period.”

Hypothetical Example for Comparison Purposes – The table also provides information about hypothetical account values and hypothetical expenses based on your Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as brokerage commissions paid on purchases and sales of fund shares. Therefore, the hypothetical examples are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | |

| 12 | | 2 0 1 8 I S H A R E S A N N U A L R E P O R T T O S H A R E H O L D E R S |

| | |

Schedule of Investments October 31, 2018 | | iShares® Short Maturity Bond ETF (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

|

Asset-Backed Securities | |

Adams Mill CLO Ltd., Series 2014-1A, Class A2, 3.54%, 07/15/26 (Call 01/15/19), (3 mo. LIBOR US + 1.100%)(a)(b) | | $ | 6,396 | | | $ | 6,396,913 | |

Ally Auto Receivables Trust, Class A2, 2.72%, 05/17/21 (Call 01/15/22) | | | 12,910 | | | | 12,891,868 | |

ALM VII Ltd., Series 2012-7A, Class A1R, 3.92%, 10/15/28 (Call 01/15/19), (3 mo. LIBOR US + 1.480%)(a)(b) | | | 9,000 | | | | 9,027,326 | |

ALM XII Ltd., Class A1R, 3.33%, 04/16/27 (Call 01/16/19), (3 mo. LIBOR US + 0.890%)(a)(b) | | | 3,735 | | | | 3,734,188 | |

ALM XVII Ltd., Class A1AR, 3.37%, 01/15/28 (Call 07/15/19), (3 mo. LIBOR US + 0.930%)(a)(b) | | | 22,500 | | | | 22,466,050 | |

American Express Credit Account Master Trust | | | | | | | | |

Series 2017-1, Class A, 1.93%, 09/15/22 | | | 10,500 | | | | 10,342,331 | |

Series 2017-4, Class A, 1.64%, 12/15/21 | | | 21,395 | | | | 21,266,835 | |

Americredit Automobile Receivables Trust, Class A2, 2.71%, 07/19/21 (Call 04/18/22) | | | 12,140 | | | | 12,120,745 | |

AmeriCredit Automobile Receivables Trust | | | | | | | | |

Series 2016-4, Class A3, 1.53%, 07/08/21

(Call 01/08/21) | | | 19,085 | | | | 18,976,760 | |

Series 2017-1, Class A3, 1.87%, 08/18/21

(Call 10/18/20) | | | 820 | | | | 815,097 | |

Series 2017-3, Class A3, 1.90%, 03/18/22

(Call 04/18/21) | | | 19,200 | | | | 18,965,182 | |

AMMC CLO 15 Ltd., Series 2014-15A, Class AXR, 3.58%, 12/09/26 (Call 12/09/18), (3 mo. LIBOR US + 1.250%)(a)(b) | | | 1,688 | | | | 1,688,847 | |

Arbor Realty Commercial Real Estate Notes Ltd., Series 2017-FL1, Class A, 3.58%, 04/15/27 (Call 11/15/19), (1 mo. LIBOR US + 1.300%)(a)(b) | | | 12,170 | | | | 12,198,800 | |

Ares XXIX CLO Ltd., Series 2014-1A, Class A1R, 3.64%, 04/17/26 (Call 01/17/19), (3 mo. LIBOR US + 1.190%)(a)(b) | | | 8,697 | | | | 8,700,083 | |

Atlas Senior Loan Fund III Ltd., Series 2013-1A, Class AR, 3.14%, 11/17/27 (Call 11/17/18), (3 mo. LIBOR US + 0.830%)(a)(b) | | | 4,350 | | | | 4,334,365 | |

Atlas Senior Loan Fund IV Ltd., Class A1RR, 2.99%, 02/17/26 (Call 11/15/18), (3 mo. LIBOR US + 0.680%)(a)(b) | | | 4,342 | | | | 4,341,330 | |

Avery Point IV CLO Ltd., 3.59%, 04/25/26 (Call 01/25/19), (3 mo. LIBOR US + 1.100%)(a)(b) | | | 5,494 | | | | 5,496,458 | |

BA Credit Card Trust, Class A1, 1.95%, 08/15/22 | | | 21,000 | | | | 20,688,072 | |

BlueMountain CLO Ltd., Series 2012-2A, Class AR, 3.74%, 11/20/28 (Call 11/20/18), (3 mo. LIBOR US + 1.420%)(a)(b) | | | 11,000 | | | | 11,006,065 | |

BMW Floorplan Master Owner Trust, Class A2, 2.60%, 05/15/23, (1 mo. LIBOR US + 0.320%)(a)(b) | | | 21,060 | | | | 21,092,807 | |

Cabela’s Credit Card Master Note Trust, Series 2014-2, Class A, 2.73%, 07/15/22, (1 mo. LIBOR US + 0.450%)(b) | | | 3,500 | | | | 3,506,718 | |

Capital One Multi-Asset Execution Trust, Series 2016-A1, Class A1, 2.73%, 02/15/22, (1 mo. LIBOR US + 0.450%)(b) | | | 38,000 | | | | 38,056,320 | |

Carlyle Global Market Strategies CLO Ltd. | | | | | | | | |

Series 2012-3A, Class A1R, 3.89%, 10/14/28 (Call 01/14/19),

(3 mo. LIBOR US +

1.450%)(a)(b) | | | 9,000 | | | | 9,002,208 | |

Series 2013-2A, Class AR, 3.33%, 01/18/29 (Call 01/18/19),

(3 mo. LIBOR US +

0.890%)(a)(b) | | | 6,210 | | | | 6,189,999 | |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | |

CarMax Auto Owner Trust | | | | | | | | |

Series 2015-1, Class A4, 1.83%, 07/15/20 (Call 04/15/19) | | $ | 20,647 | | | $ | 20,584,943 | |

Series 2018-2, Class A2, 2.73%, 08/16/21 (Call 12/15/21) | | | 11,660 | | | | 11,639,062 | |

Cedar Funding II CLO Ltd., Series 2013-1A, Class A1R, 3.56%, 06/09/30 (Call 06/09/19), (3 mo. LIBOR US + 1.230%)(a)(b) | | | 8,000 | | | | 8,010,822 | |

Cedar Funding VI CLO Ltd., Class AR, 3.56%, 10/20/28 (Call 10/20/19), (3 mo. LIBOR US + 1.090%)(a)(b) | | | 20,500 | | | | 20,499,287 | |

Chase Issuance Trust | | | | | | | | |

Series 2013-A9, Class A, 2.70%, 11/15/20, (1 mo. LIBOR US + 0.420%)(b) | | | 11,815 | | | | 11,817,214 | |

Series 2014-A5, Class A5, 2.65%, 04/15/21, (1 mo. LIBOR US + 0.370%)(b) | | | 7,000 | | | | 7,008,750 | |

Series 2016-A1, Class A, 2.69%, 05/15/21, (1 mo. LIBOR US + 0.410%)(b) | | | 36,750 | | | | 36,819,116 | |

Chesapeake Funding II LLC | | | | | | | | |

Series 2016-1A, Class A2, 3.43%, 03/15/28, (1 mo. LIBOR US + 1.150%)(a)(b) | | | 6,166 | | | | 6,182,494 | |

Series 2016-2A, Class A2, 3.28%, 06/15/28 (Call 08/15/19), (1 mo. LIBOR US + 1.000%)(a)(b) | | | 5,680 | | | | 5,695,801 | |

CIFC Funding Ltd. | | | | | | | | |

Class A, 3.71%, 04/20/30 (Call 04/20/19), (3 mo. LIBOR US + 1.240%)(a)(b) | | | 6,375 | | | | 6,383,178 | |

Class A1A, 3.59%, 10/17/30,

(3 mo. LIBOR US +

1.130%)(a)(b)(c) | | | 15,175 | | | | 15,175,000 | |

Series 2015-2A, Class AR, 3.22%, 04/15/27 (Call 01/15/19), (3 mo. LIBOR US + 0.780%)(a)(b) | | | 17,000 | | | | 16,923,019 | |

Citibank Credit Card Issuance Trust | | | | | | | | |

Series 2016-A1, Class A1, 1.75%, 11/19/21 | | | 14,385 | | | | 14,188,951 | |

Series 2017-A9, Class A9, 1.80%, 09/20/21 | | | 14,535 | | | | 14,387,788 | |

CNH Equipment Trust, Series 2017-B, Class A3, 1.86%, 09/15/22 (Call 08/15/21) | | | 19,320 | | | | 18,992,296 | |

Discover Card Execution Note Trust | | | | | | | | |

Series 2014-A1, Class A1, 2.71%, 07/15/21, (1 mo. LIBOR US + 0.430%)(b) | | | 6,760 | | | | 6,764,881 | |

Series 2016-A1, Class A1, 1.64%, 07/15/21 | | | 8,915 | | | | 8,898,081 | |

Drive Auto Receivables Trust | | | | | | | | |

Class A2, 2.64%, 09/15/20

(Call 02/15/22) | | | 8,803 | | | | 8,799,304 | |

Class A2, 2.75%, 10/15/20

(Call 05/15/22) | | | 12,000 | | | | 11,991,017 | |

Class A3, 3.01%, 11/15/21

(Call 05/15/22) | | | 35,660 | | | | 35,620,392 | |

Series 2017-2, Class B, 2.25%, 06/15/21 (Call 06/15/20) | | | 1,852 | | | | 1,850,045 | |

Dryden XXVI Senior Loan Fund, Series 2013-26A, Class AR, 3.34%, 04/15/29 (Call 10/15/19), (3 mo. LIBOR US + 0.900%)(a)(b) | | | 16,350 | | | | 16,283,261 | |

Enterprise Fleet Financing LLC

2.13%, 07/20/22(a) | | | 1,983 | | | | 1,971,595 | |

2.13%, 05/22/23(a) | | | 7,123 | | | | 7,054,346 | |

Series 2015-2, Class A3, 2.09%, 02/22/21(a) | | | 2,660 | | | | 2,651,608 | |

Series 2016-1, Class A2, 1.83%, 09/20/21(a) | | | 1,556 | | | | 1,555,387 | |

Series 2017-2, Class A2, 1.97%, 01/20/23(a) | | | 12,918 | | | | 12,819,745 | |

Ford Credit Floorplan Master Owner Trust | | | | | | | | |

Series 2014-2, Class A, 2.78%, 02/15/21, (1 mo. LIBOR US + 0.500%)(b) | | | 11,000 | | | | 11,018,987 | |

Series 2016-1, Class A2, 3.18%, 02/15/21, (1 mo. LIBOR US + 0.900%)(b) | | | 10,000 | | | | 10,027,891 | |

Series 2016-3, Class A2, 2.90%, 07/15/21, (1 mo. LIBOR US + 0.620%)(b) | | | 10,000 | | | | 10,033,200 | |

| | | | |

S C H E D U L E O F I N V E S T M E N T S | | | 13 | |

| | |

Schedule of Investments (continued) October 31, 2018 | | iShares® Short Maturity Bond ETF (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par

(000) | | | Value | |

| | | | | | | | |

Ford Credit Floorplan Master Owner Trust A, Series 2016-1, Class A1, 1.76%, 02/15/21 | | $ | 24,775 | | | $ | 24,702,003 | |

GM Financial Consumer Automobile Receivables Trust, Class A2, 2.93%, 11/16/21 (Call 09/16/22) | | | 23,250 | | | | 23,229,965 | |

GoldenTree Loan Opportunities IX Ltd., Class AR2, 3.62%, 10/29/29 (Call 10/29/20), (3 mo. LIBOR US +

1.110%)(a)(b)(c) | | | 16,680 | | | | 16,680,000 | |

Halcyon Loan Advisors Funding Ltd., Class AR, 3.57%, 07/25/27 (Call 07/25/19), (3 mo. LIBOR US + 1.080%)(a)(b)(c) | | | 16,185 | | | | 16,185,000 | |

Honda Auto Receivables Owner Trust | | | | | | | | |

Class A4, 3.16%, 08/19/24

(Call 07/18/21) | | | 5,705 | | | | 5,692,229 | |

Series 2015-3, Class A4, 1.56%, 10/18/21

(Call 12/18/18) | | | 6,596 | | | | 6,584,877 | |

Series 2015-4, Class A4, 1.44%, 01/21/22

(Call 02/21/19) | | | 6,025 | | | | 6,000,908 | |

Series 2016-2, Class A3, 1.39%, 04/15/20

(Call 08/15/19) | | | 3,991 | | | | 3,973,179 | |

Series 2016-2, Class A4, 1.62%, 08/15/22

(Call 08/15/19) | | | 18,000 | | | | 17,819,978 | |

John Deere Owner Trust, Series 2017-B, Class A3, 1.82%, 10/15/21 (Call 01/15/21) | | | 9,890 | | | | 9,750,321 | |

LCM XX LP, Class AR, 3.38%, 10/20/27, (3 mo. LIBOR US + 1.040%)(a)(b) | | | 13,750 | | | | 13,749,647 | |

LCM Xxiv Ltd., Series 24A, Class A, 3.78%, 03/20/30 (Call 04/20/19), (3 mo. LIBOR US + 1.310%)(a)(b) | | | 2,000 | | | | 2,008,520 | |

LoanCore Issuer Ltd., Class A, 3.41%, 05/15/28 (Call 05/15/20), (1 mo. LIBOR US + 1.130%)(a)(b) | | | 9,450 | | | | 9,467,590 | |

Madison Park Funding X Ltd., Series 2012-10A, Class AR, 3.92%, 01/20/29 (Call 01/20/19), (3 mo. LIBOR US + 1.450%)(a)(b) | | | 6,250 | | | | 6,259,436 | |

Madison Park Funding XIII Ltd., Class AR2, 3.40%, 04/19/30 (Call 01/19/19), (3 mo. LIBOR US + 0.950%)(a)(b) | | | 4,000 | | | | 3,992,073 | |

Marathon CRE Ltd., Class A, 3.43%, 06/15/28 (Call 07/15/20), (1 mo. LIBOR US + 1.150%)(a)(b) | | | 3,640 | | | | 3,642,941 | |

Mercedes-Benz Auto Receivables Trust, Series 2016-1, Class A3, 1.26%, 02/16/21 (Call 06/15/20) | | | 5,542 | | | | 5,496,079 | |

Mercedes-Benz Master Owner Trust | | | | | | | | |

Class A, 2.62%, 05/15/23,

(1 mo. LIBOR US +

0.340%)(a)(b) | | | 21,820 | | | | 21,859,101 | |

Series 2016-BA, Class A, 2.98%, 05/17/21, (1 mo. LIBOR US + 0.700%)(a)(b) | | | 11,375 | | | | 11,408,282 | |

Series 2017-BA, Class A, 2.70%, 05/16/22, (1 mo. LIBOR US + 0.420%)(a)(b) | | | 14,540 | | | | 14,581,398 | |

Navient Private Education Loan Trust | | | | | | | | |

Class A1, 2.63%, 12/15/59 (Call 12/15/27), (1 mo. LIBOR US + 0.350%)(a)(b) | | | 16,338 | | | | 16,345,501 | |

Series 2014-CT, Class A, 2.98%, 09/16/24 (Call 09/15/21), (1 mo. LIBOR US + 0.700%)(a)(b) | | | 955 | | | | 955,773 | |

Navient Private Education Refi Loan Trust | | | | | | | | |

Class A1, 2.58%, 12/15/59 (Call 07/15/28), (1 mo. LIBOR US + 0.300%)(a)(b) | | | 15,800 | | | | 15,800,000 | |

Class A1, 3.01%, 06/16/42 (Call 08/15/26)(a) | | | 24,306 | | | | 24,196,219 | |

Navient Student Loan Trust, Series 2015-2, Class A2, 2.70%, 08/27/29 (Call 02/25/27), (1 mo. LIBOR US + 0.420%)(b) | | | 2,028 | | | | 2,029,770 | |

Nissan Auto Receivables Owner Trust, Series 2016-B, Class A3, 1.32%, 01/15/21 (Call 09/15/20) | | | 15,105 | | | | 14,979,331 | |

| | | | | | | | |

| Security | | Par

(000) | | | Value | |

| | | | | | | | |

Nissan Master Owner Trust Receivables | | | | | | | | |

Class A, 2.60%, 10/17/22,

(1 mo. LIBOR US +

0.320%)(b) | | $ | 7,035 | | | $ | 7,044,136 | |

Series 2016-A, Class A1, 2.92%, 06/15/21, (1 mo. LIBOR US + 0.640%)(b) | | | 18,500 | | | | 18,556,258 | |

Series 2017-B, Class A, 2.71%, 04/18/22, (1 mo. LIBOR US + 0.430%)(b) | | | 22,513 | | | | 22,590,629 | |

OCP CLO Ltd., Class A1R, 3.56%, 10/18/28 (Call 10/15/19), (3 mo. LIBOR US + 1.120%)(a)(b) | | | 17,210 | | | | 17,209,392 | |

Octagon Investment Partners 24 Ltd., Series 2015-1A, Class A1R, 3.21%, 05/21/27 (Call 11/21/18), (3 mo. LIBOR US + 0.900%)(a)(b) | | | 18,600 | | | | 18,599,202 | |

OHA Credit Partners IX Ltd., Series 2013-9A, Class A1R, 3.48%, 10/20/25 (Call 01/20/19), (3 mo. LIBOR US + 1.010%)(a)(b) | | | 798 | | | | 798,199 | |

OZLM VIII Ltd., Series 2014-8A, Class A1AR, 3.58%, 10/17/26 (Call 01/17/19), (3 mo. LIBOR US + 1.130%)(a)(b) | | | 2,500 | | | | 2,500,564 | |

Palmer Square Loan Funding Ltd., Class A1, 3.15%, 11/15/26 (Call 11/15/19), (3 mo. LIBOR US + 0.900%)(a)(b) | | | 13,000 | | | | 12,998,700 | |

PFS Financing Corp., Series 2017-C, Class A, 2.75%, 10/15/21, (1 mo. LIBOR US + 0.470%)(a)(b) | | | 14,850 | | | | 14,858,206 | |

Prestige Auto Receivables Trust, Series 2016-2A, Class A2, 1.46%, 07/15/20 (Call 10/15/20)(a) | | | 31 | | | | 30,618 | |

Regatta VI Funding Ltd., 3.55%, 07/20/28 (Call 07/20/19), (3 mo. LIBOR US + 1.080%)(a)(b) | | | 15,130 | | | | 15,129,496 | |

Santander Drive Auto Receivables Trust | | | | | | | | |

Series 2017-2, Class A3, 1.87%, 12/15/20 (Call 04/15/20) | | | 2,015 | | | | 2,013,072 | |

Series 2017-3, Class A3, 1.87%, 06/15/21 (Call 10/15/20) | | | 11,130 | | | | 11,094,581 | |

SLM Private Credit Student Loan Trust, Series 2005-A, Class A3, 2.53%, 06/15/23 (Call 03/15/28), (3 mo. LIBOR US + 0.200%)(b) | | | 7,225 | | | | 7,215,204 | |

SLM Private Education Loan Trust | | | | | | | | |

Series 2011-C, Class A2A, 5.53%, 10/17/44 (Call 02/15/21), (1 mo. LIBOR US + 3.250%)(a)(b) | | | 635 | | | | 647,613 | |

Series 2012-E, Class A2B, 4.03%, 06/15/45 (Call 11/15/18), (1 mo. LIBOR US + 1.750%)(a)(b) | | | 863 | | | | 863,247 | |

Series 2013-A, Class A2B, 3.33%, 05/17/27 (Call 11/15/19), (1 mo. LIBOR US + 1.050%)(a)(b) | | | 58 | | | | 58,501 | |

Series 2013-C, Class A2B, 3.68%, 10/15/31 (Call 04/15/21),

(1 mo. LIBOR US +

1.400%)(a)(b) | | | 8,081 | | | | 8,123,680 | |

SLM Student Loan Trust,

Series 2011-2, Class A1, 2.88%, 11/25/27

(Call 09/25/31), (1 mo. LIBOR US +

0.600%)(b) | | | 437 | | | | 439,352 | |

SMB Private Education Loan Trust | | | | | | | | |

Class A1, 2.43%, 09/15/25,

(1 mo. LIBOR US + 0.300%)(a)(b) | | | 21,690 | | | | 21,683,447 | |

Class A1, 2.60%, 12/16/24,

(1 mo. LIBOR US + 0.320%)(a)(b) | | | 5,449 | | | | 5,450,698 | |

Class A1, 2.63%, 03/16/26,

(1 mo. LIBOR US + 0.350%)(a)(b) | | | 6,959 | | | | 6,959,702 | |

Series 2015-A, Class A2A, 2.49%, 06/15/27

(Call 03/15/27)(a) | | | 10,602 | | | | 10,449,755 | |

Series 2016-C, Class A1, 2.83%, 11/15/23, (1 mo. LIBOR US + 0.550%)(a)(b) | | | 376 | | | | 376,060 | |

| | |

| 14 | | 2 0 1 8 I S H A R E S A N N U A L R E P O R T T O S H A R E H O L D E R S |

| | |

Schedule of Investments (continued) October 31, 2018 | | iShares® Short Maturity Bond ETF (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par

(000) | | | Value | |

| | | | | | | | |

Series 2017-A, Class A2B, 3.18%, 09/15/34, (1 mo. LIBOR US + 0.900%)(a)(b) | | $ | 30,000 | | | $ | 30,218,535 | |

Series 2017-B, Class A1, 2.55%, 06/17/24, (1 mo. LIBOR US + 0.270%)(a)(b) | | | 2,646 | | | | 2,645,957 | |

SoFi Professional Loan Program LLC | | | | | | | | |

Series 16-C, Class A1, 3.38%, 10/27/36 (Call 10/25/24), (1 mo. LIBOR US + 1.100%)(a)(b) | | | 3,305 | | | | 3,354,753 | |

Series 16-C, Class A2A, 1.48%, 05/26/31 (Call 10/25/24)(a) | | | 359 | | | | 358,107 | |

Series 2014-A, Class A1, 3.88%, 06/25/25 (Call 10/25/19), (1 mo. LIBOR US + 1.600%)(a)(b) | | | 215 | | | | 216,169 | |

Series 2014-B, Class A1, 3.53%, 08/25/32

(Call 08/25/20), (1 mo. LIBOR US + 1.250%)(a)(b) | | | 187 | | | | 188,789 | |

Series 2014-B, Class A2, 2.55%, 08/27/29

(Call 08/25/20)(a) | | | 1,082 | | | | 1,070,529 | |

Series 2015-A, Class A1, 3.48%, 03/25/33 (Call 02/25/21), (1 mo. LIBOR US + 1.200%)(a)(b) | | | 536 | | | | 541,077 | |

Series 2015-B, Class A1, 3.33%, 04/25/35 (Call 07/25/22), (1 mo. LIBOR US + 1.050%)(a)(b) | | | 2,918 | | | | 2,956,501 | |

TCI-Flatiron CLO Ltd.,

Series 2016-1A, Class A, 4.00%, 07/17/28,

(3 mo. LIBOR US +

1.550%)(a)(b) | | | 6,850 | | | | 6,868,757 | |

TICP CLO I Ltd., Series 2015-1A, Class AR, 3.27%, 07/20/27 (Call 01/20/19), (3 mo. LIBOR US + 0.800%)(a)(b) | | | 4,015 | | | | 3,998,858 | |

Treman Park CLO Ltd., Class ARR, 1.00%, 10/20/28,

(3 mo. LIBOR US +

1.070%)(a)(b)(c) | | | 21,750 | | | | 21,750,000 | |

Wheels SPV 2 LLC | | | | | | | | |

Series 2015-1A, Class B, 1.88%, 04/20/26 (Call 01/20/21)(a) | | | 1,303 | | | | 1,291,984 | |

Series 2016-1A, Class A2, 1.59%, 05/20/25

(Call 10/20/19)(a) | | | 317 | | | | 316,139 | |

| | | | | | | | |

Total Asset-Backed Securities — 24.6%

(Cost: $1,225,902,493) | | | | 1,223,809,416 | |

| | | | | | | | |

Certificates of Deposit | | | | | | | | |

Barclays Bank PLC, 3.00%, 09/19/19 | | | 15,000 | | | | 15,000,366 | |

BNP Paribas SA/New York NY, 2.64%, 12/28/18, (3 mo. LIBOR US + 0.250%)(b) | | | 9,000 | | | | 9,004,223 | |

Commonwealth Bank of Australia/New York NY, 2.54%, 03/18/19, (3 mo. LIBOR US + 0.200%)(b) | | | 15,000 | | | | 15,014,175 | |

Credit SuisseAG/New York NY | | | | | | | | |

2.61%, 05/01/19, (3 mo. LIBOR US + 0.270%)(b) | | | 16,000 | | | | 16,011,136 | |

2.66%, 03/14/19, (3 mo. LIBOR US + 0.330%)(b) | | | 15,000 | | | | 15,008,505 | |

Royal Bank of Canada/New York NY, 2.50%, 02/07/19, (3 mo. LIBOR US + 0.160%)(b) | | | 15,000 | | | | 15,005,094 | |

| | | | | | | | |

| |

Total Certificates of Deposit — 1.7%

(Cost: $85,000,000) | | | | 85,043,499 | |

| | | | | | | | |

|

Collaterized Mortgage Obligations | |

|

Mortgage-Backed Securities — 4.4% | |

Americold LLC, Series 2010-ARTA, Class A1, 3.85%, 01/14/29(a) | | | 3,325 | | | | 3,339,564 | |

AOA Mortgage Trust, Class A, 2.96%, 12/13/29(a) | | | 6,920 | | | | 6,783,161 | |

Aventura Mall Trust, Series 2013-AVM, Class A, 3.74%, 12/05/32(a)(b) | | | 4,650 | | | | 4,702,113 | |

BAMLL Commercial Mortgage Securities Trust, Series 2014-FL1, Class A, 3.56%, 12/15/31, (1 mo. LIBOR US + 1.400%)(a)(b) | | | 1,406 | | | | 1,405,791 | |

| | | | | | | | |

| Security | | Par

(000) | | | Value | |

| | | | | | | | |

|

Mortgage-Backed Securities (continued) | |

Bancorp Commercial Mortgage Trust | | | | | | | | |

Class A, 3.18%, 09/15/35,

(1 mo. LIBOR US +

0.900%)(a)(b) | | $ | 6,753 | | | $ | 6,749,439 | |

Series 2016-CRE1, Class A, 3.59%, 11/15/33, (1 mo. LIBOR US + 1.430%)(a)(b) | | | 81 | | | | 81,026 | |

Bear Stearns Commercial Mortgage Securities Trust, Series 2005-PW10, Class AJ, 5.59%, 12/11/40(b) | | | 5,575 | | | | 5,871,743 | |

BSPRT Issuer Ltd., Series 2017-FL2, Class A, 3.10%, 10/15/34, (1 mo. LIBOR US + 0.820%)(a)(b)(c) | | | 1,443 | | | | 1,443,544 | |

BX Commercial MortgageTrust | | | | | | | | |

Class A, 2.95%, 03/15/37, (1 mo. LIBOR US + 0.671%)(a)(b) | | | 23,190 | | | | 23,117,188 | |

Class A, 3.03%, 11/15/35, (1 mo. LIBOR US + 0.750%)(a)(b) | | | 10,000 | | | | 9,994,900 | |

COMM MortgageTrust | | | | | | | | |

Series 2014-PAT, Class A, 3.08%, 08/13/27,

(1 mo. LIBOR US + 0.800%)(a)(b) | | | 13,570 | | | | 13,565,792 | |

Series 2014-TWC, Class A, 3.13%, 02/13/32,

(1 mo. LIBOR US + 0.850%)(a)(b) | | | 11,305 | | | | 11,301,441 | |

Commission Mortgage Trust, Series 2013-CR6, Class A3FL, 2.91%, 03/10/46, (1 mo. LIBOR US + 0.630%)(a)(b) | | | 9,874 | | | | 9,864,198 | |

Four Times Square Trust Commercial Mortgage Pass-Through Certificates, Series 2006-4TS, Class A, 5.40%, 12/13/28(a) | | | 11,117 | | | | 11,519,231 | |

Gosforth Funding PLC, Class A1, 2.71%, 08/25/60 (Call 08/25/23),

(3 mo. LIBOR US + 0.450%)(a)(b) | | | 11,200 | | | | 11,195,707 | |

GPMT Ltd., Series 2018-FL1, Class A, 3.18%, 11/21/35, (1 mo. LIBOR US + 0.900%)(a)(b) | | | 11,022 | | | | 11,001,678 | |

GS Mortgage Securities Corp. II, Series 2013-KING, Class A, 2.71%, 12/10/27(a) | | | 1,811 | | | | 1,799,988 | |

Hospitality Mortgage Trust, Series 2017-HIT, Class A, 3.13%, 05/08/30, (1 mo. LIBOR US + 0.850%)(a)(b) | | | 4,990 | | | | 4,990,033 | |

InTown Hotel Portfolio Trust, Series 2018-STAY, Class A, 2.98%, 01/15/33, (1 mo. LIBOR US + 0.700%)(a)(b) | | | 4,480 | | | | 4,477,262 | |

LMREC Inc., Series 2016-CRE2, Class A, 3.98%, 11/24/31, (1 mo. LIBOR US + 1.700%)(a)(b) | | | 3,410 | | | | 3,410,000 | |

Madison Avenue Trust, Series 2013-650M, Class A, 3.84%, 10/12/32(a) | | | 2,060 | | | | 2,069,040 | |

Morgan Stanley Capital I Trust | | | | | | | | |

Class A, 3.13%, 08/15/33, (1 mo. LIBOR US + 0.850%)(a)(b) | | | 6,860 | | | | 6,862,143 | |

Class A, 3.35%, 07/13/29(a) | | | 14,480 | | | | 14,454,531 | |

Series 2017-CLS, Class A, 2.98%, 11/15/34, (1 mo. LIBOR US + 0.700%)(a)(b) | | | 9,512 | | | | 9,506,084 | |

Natixis Commercial Mortgage Securities Trust, Series 2018-RIVA, Class A, 3.03%, 02/15/33, (1 mo. LIBOR US + 0.750%)(a)(b) | | | 7,500 | | | | 7,500,004 | |

Resource Capital Corp., Series 2017-CRE5, Class A, 3.09%, 07/15/34, (1 mo. LIBOR US + 0.800%)(a)(b) | | | 2,524 | | | | 2,524,490 | |

VNDO Mortgage Trust, Series 2013-PENN, Class A, 3.81%, 12/13/29(a) | | | 5,200 | | | | 5,233,400 | |

WFRBS Commercial Mortgage Trust, Series 2012-C8, Class AFL, 3.29%, 08/15/45, (1 mo. LIBOR US + 1.000%)(a)(b) | | | 23,192 | | | | 23,512,575 | |

| | | | | | | | |

| |

Total Collaterized Mortgage Obligations — 4.4%

(Cost: $219,517,310) | | | | 218,276,066 | |

| | | | | | | | |

| | | | |

S C H E D U L E O F I N V E S T M E N T S | | | 15 | |

| | |

Schedule of Investments (continued) October 31, 2018 | | iShares® Short Maturity Bond ETF (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par

(000) | | | Value | |

| | | | | | | | |

| | |

Commercial Paper | | | | | | | | |

| | |

Energy Transfer Partners LP, 3.01%, 11/13/18(d) | | $ | 25,000 | | | $ | 24,975,083 | |

Ford Motor Credit Co. LLC, 3.00%, 04/01/19(d) | | | 23,000 | | | | 22,695,168 | |

HSBC Bank PLC, 2.62%, 03/27/19,

(3 mo. LIBOR US + 0.240%)(a)(b) | | | 9,000 | | | | 9,005,698 | |

Kinder Morgan Inc./DE,

3.07%, 01/03/19(d) | | | 25,000 | | | | 24,866,563 | |

Toronto-Dominion Bank (The), 2.55%, 02/08/19, (1 mo. LIBOR US + 0.270%)(a)(b) | | | 15,000 | | | | 15,008,070 | |

| | | | | | | | |

| | |

Total Commercial Paper — 1.9%

(Cost: $96,556,969) | | | | | | | 96,550,582 | |

| | | | | | | | |

| | |

Corporate Bonds & Notes | | | | | | | | |

| | |

Advertising —0.3% | | | | | | | | |

Interpublic Group of Companies Inc. (The), 3.50%, 10/01/20 | | | 4,465 | | | | 4,460,063 | |

Omnicom Group Inc./Omnicom Capital Inc., 6.25%, 07/15/19 | | | 10,000 | | | | 10,219,160 | |

| | | | | | | | |

| | | | | | | 14,679,223 | |

Aerospace & Defense — 1.4% | | | | | | | | |

Lockheed Martin Corp., 4.25%, 11/15/19 | | | 16,004 | | | | 16,185,716 | |

Northrop Grumman Corp., 2.08%, 10/15/20 | | | 15,000 | | | | 14,642,923 | |

United Technologies Corp. 1.90%, 05/04/20 | | | 15,000 | | | | 14,682,846 | |

2.97%, 08/16/21 (Call 08/16/19), (3 mo. LIBOR US + 0.650%)(b) | | | 21,865 | | | | 21,888,709 | |

| | | | | | | | |

| | | | | | | 67,400,194 | |

Agriculture — 1.4% | | | | | | | | |

BAT Capital Corp.

2.30%, 08/14/20(a)(e) | | | 30,000 | | | | 29,358,134 | |

2.91%, 08/14/20, (3 mo. LIBOR US + 0.590%)(a)(b) | | | 24,000 | | | | 24,072,501 | |

Imperial Brands Finance PLC, 2.95%, 07/21/20(a)(e) | | | 15,000 | | | | 14,807,611 | |

| | | | | | | | |

| | | | | | | 68,238,246 | |

Auto Manufacturers — 4.9% | | | | | | | | |

American Honda Finance Corp., 2.59%, 06/16/20, (3 mo. LIBOR US + 0.260%)(b) | | | 10,000 | | | | 10,004,191 | |

BMW U.S. Capital LLC | | | | | | | | |

2.79%, 04/06/20, (3 mo. LIBOR US + 0.380%)(a)(b) | | | 4,415 | | | | 4,428,477 | |

3.25%, 08/14/20(a) | | | 13,665 | | | | 13,644,522 | |

Daimler Finance North America LLC

| | | | | | | | |

2.77%, 02/12/21, (3 mo. LIBOR US + 0.430%)(a)(b) | | | 5,000 | | | | 4,999,184 | |

2.87%, 05/05/20, (3 mo. LIBOR US + 0.530%)(a)(b)(e) | | | 15,500 | | | | 15,532,539 | |

3.15%, 07/05/19, (3 mo. LIBOR US + 0.740%)(a)(b) | | | 3,500 | | | | 3,510,187 | |

Ford Motor Credit Co. LLC

2.60%, 11/04/19(e) | | | 15,000 | | | | 14,819,828 | |

2.68%, 01/09/20(e) | | | 10,000 | | | | 9,853,470 | |

2.78%, 11/02/20, (3 mo. LIBOR US + 0.430%)(b) | | | 17,000 | | | | 16,780,360 | |

2.94%, 01/08/19(e) | | | 3,500 | | | | 3,499,152 | |

3.16%, 08/04/20(e) | | | 20,000 | | | | 19,651,819 | |

General Motors Financial Co. Inc.

3.20%, 07/13/20 (Call 06/13/20) | | | 50,000 | | | | 49,557,500 | |

3.26%, 04/09/21, (3 mo. LIBOR US + 0.850%)(b) | | | 10,000 | | | | 9,999,300 | |

3.50%, 07/10/19(e) | | | 15,000 | | | | 15,040,168 | |

Hyundai Capital America | | | | | | | | |

3.20%, 04/03/20, (3 mo. LIBOR US + 0.800%)(a)(b) | | | 6,890 | | | | 6,892,484 | |

3.34%, 09/18/20, (3 mo. LIBOR US + 1.000%)(a)(b)(e) | | | 3,000 | | | | 3,015,576 | |

Nissan Motor Acceptance Corp. | | | | | | | | |

3.02%, 01/13/20, (3 mo. LIBOR US + 0.580%)(a)(b) | | | 15,000 | | | | 15,047,340 | |

3.09%, 07/13/22, (3 mo. LIBOR US + 0.650%)(a)(b) | | | 12,500 | | | | 12,497,254 | |

| | | | | | | | |

| Security | | Par

(000) | | | Value | |

| | | | | | | | |

| |

Auto Manufacturers (continued) | | | | | |

Toyota Motor Credit Corp., 2.84%, 01/17/19,

(3 mo. LIBOR US + 0.390%)(b) | | $ | 3,840 | | | $ | 3,842,560 | |

Volkswagen Group of America Finance LLC,

2.13%, 05/23/19(a) | | | 12,500 | | | | 12,423,083 | |

| | | | | | | | |

| | | | | | | 245,038,994 | |

Banks — 22.8% | | | | | | | | |

ABN AMRO Bank NV, 3.08%, 01/18/19,

(3 mo. LIBOR US +

0.640%)(a)(b) | | | 4,700 | | | | 4,703,948 | |

Australia & New Zealand Banking Group Ltd., 2.82%, 08/19/20, (3 mo. LIBOR US +

0.500%)(a)(b) | | | 19,745 | | | | 19,828,462 | |

Australia & New Zealand Banking Group Ltd./New York NY, 2.70%, 11/16/20(e) | | | 15,000 | | | | 14,791,059 | |

Banco Santander SA, 3.55%, 04/12/23, (3 mo. LIBOR US + 1.120%)(b) | | | 10,000 | | | | 10,026,820 | |

Bank of America Corp. 3.05%, 10/01/21 (Call 10/01/20),

(3 mo. LIBOR US + 0.650%)(b) | | | 7,500 | | | | 7,526,194 | |

3.13%, 07/21/21 (Call 07/21/20),

(3 mo. LIBOR US + 0.660%)(b)(e) | | | 25,500 | | | | 25,610,470 | |

3.49%, 04/24/23 (Call 04/24/22),

(3 mo. LIBOR US + 1.000%)(b) | | | 7,500 | | | | 7,574,098 | |

3.63%, 01/20/23 (Call 01/20/22),

(3 mo. LIBOR US + 1.160%)(b) | | | 25,000 | | | | 25,390,894 | |

7.63%, 06/01/19 . | | | 10,000 | | | | 10,260,867 | |

Series L, 2.25%, 04/21/20(e) | | | 2,000 | | | | 1,971,034 | |

Bank of Montreal | | | | | | | | |

2.58%, 09/11/19, (3 mo. LIBOR US + 0.250%)(b) | | | 3,350 | | | | 3,354,553 | |

2.93%, 12/12/19, (3 mo. LIBOR US + 0.600%)(b) | | | 10,185 | | | | 10,240,695 | |

3.09%, 07/18/19, (3 mo. LIBOR US + 0.650%)(b) | | | 3,500 | | | | 3,513,929 | |

3.10%, 08/27/21, (3 mo. LIBOR US + 0.790%)(b) | | | 7,000 | | | | 7,088,165 | |

Bank of Nova Scotia (The), 2.96%, 09/19/22, (3 mo. LIBOR US + 0.620%)(b) | | | 10,000 | | | | 10,035,889 | |

Bank of Tokyo-Mitsubishi UFJ Ltd. (The), 2.83%, 09/09/19, (3 mo. LIBOR US + 0.450%)(b) | | | 6,000 | | | | 6,012,640 | |

Banque Federative du Credit Mutuel SA

2.20%, 07/20/20(a)(e) | | | 10,000 | | | | 9,789,764 | |

2.96%, 07/20/20, (3 mo. LIBOR US + 0.490%)(a)(b) | | | 3,215 | | | | 3,223,082 | |

Barclays PLC,

2.75%, 11/08/19(e) | | | 35,085 | | | | 34,840,177 | |

BB&T Corp., 2.90%, 06/15/20, (3 mo. LIBOR US + 0.570%)(b) | | | 9,403 | | | | 9,451,647 | |

BNP Paribas SA, 2.38%, 05/21/20(e) | | | 15,000 | | | | 14,798,705 | |

Capital One Financial Corp. | | | | | | | | |

2.97%, 10/30/20 (Call 09/30/20), (3 mo. LIBOR US + 0.450%)(b) | | | 5,000 | | | | 4,995,999 | |

3.10%, 05/12/20 (Call 04/12/20), (3 mo. LIBOR US + 0.760%)(b) | | | 15,505 | | | | 15,579,734 | |

Capital One N.A., 3.67%, 01/30/23 (Call 01/30/22), (3 mo. LIBOR US + 1.150%)(b) | | | 3,000 | | | | 3,019,376 | |

Citibank N.A., 2.83%, 06/12/20, (3 mo. LIBOR US + 0.500%)(b) | | | 7,060 | | | | 7,092,031 | |

Citigroup Inc.

2.05%, 06/07/19 | | | 10,000 | | | | 9,940,997 | |

2.45%, 01/10/20 (Call 12/10/19) | | | 10,000 | | | | 9,907,747 | |

2.50%, 07/29/19(e) | | | 10,000 | | | | 9,967,603 | |

2.65%, 10/26/20(e) | | | 25,000 | | | | 24,621,046 | |

3.20%, 01/10/20 (Call 12/10/19), (3 mo. LIBOR US + 0.790%)(b) | | | 8,286 | | | | 8,330,338 | |

3.20%, 10/27/22 (Call 09/27/22), (3 mo. LIBOR US + 0.690%)(b)(e) | | | 10,000 | | | | 9,995,836 | |

| | |

| 16 | | 2 0 1 8 I S H A R E S A N N U A L R E P O R T T O S H A R E H O L D E R S |

| | |

Schedule of Investments (continued) October 31, 2018 | | iShares® Short Maturity Bond ETF (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | | | | | | | |

Banks (continued) | | | | | | | | |

Citizens Bank N.A./Providence RI, 2.88%, 05/26/20, (3 mo. LIBOR US + 0.570%)(b) | | $ | 8,710 | | | $ | 8,734,089 | |

Commonwealth Bank of Australia/New York NY

2.30%, 03/12/20 | | | 15,000 | | | | 14,818,567 | |

2.40%, 11/02/20(e) | | | 20,000 | | | | 19,591,971 | |

Cooperatieve Rabobank UA, 3.23%, 09/26/23, (3 mo. LIBOR US + 0.860%)(a)(b)(e) | | | 10,000 | | | | 9,980,045 | |

Credit Suisse Group Funding Guernsey Ltd., 2.75%, 03/26/20(e) | | | 19,000 | | | | 18,801,226 | |

Danske Bank A/S

2.75%, 09/17/20(a)(e) | | | 20,000 | | | | 19,638,273 | |

2.83%, 03/02/20, (3 mo. LIBOR US + 0.510%)(a)(b) | | | 2,500 | | | | 2,497,014 | |

Deutsche Bank AG, 3.89%, 01/18/19, (3 mo. LIBOR US + 1.450%)(b) | | | 5,000 | | | | 5,003,135 | |

Deutsche Bank AG/London, 2.50%, 02/13/19(e) | | | 7,000 | | | | 6,983,561 | |

Deutsche Bank AG/New York NY | | | | | | | | |

3.28%, 01/22/21, (3 mo. LIBOR US + 0.815%)(b) | | | 5,000 | | | | 4,946,924 | |

4.25%, 02/04/21 | | | 9,905 | | | | 9,866,499 | |

Discover Bank

2.60%, 11/13/18(e) | | | 2,300 | | | | 2,299,591 | |

3.10%, 06/04/20 (Call 05/04/20) | | | 20,000 | | | | 19,842,856 | |

Fifth Third Bank/Cincinnati OH, 2.77%, 10/30/20 (Call 09/30/20),

(3 mo. LIBOR US + 0.250%)(b) | | | 10,000 | | | | 10,004,728 | |

Goldman Sachs Group Inc. (The) | | | | | | | | |

2.55%, 10/23/19 | | | 10,000 | | | | 9,934,468 | |

3.31%, 10/31/22 (Call 10/31/21),

(3 mo. LIBOR US + 0.780%)(b) | | | 4,000 | | | | 4,013,895 | |

3.37%, 06/05/23 (Call 06/05/22),

(3 mo. LIBOR US + 1.050%)(b) | | | 15,000 | | | | 15,099,750 | |

3.49%, 07/24/23 (Call 07/24/22),

(3 mo. LIBOR US + 1.000%)(b) | | | 5,000 | | | | 5,033,338 | |

3.53%, 09/15/20 (Call 08/15/20),

(3 mo. LIBOR US + 1.200%)(b) | | | 1,750 | | | | 1,774,341 | |

3.85%, 04/23/21 (Call 03/23/21),

(3 mo. LIBOR US + 1.360%)(b) | | | 7,000 | | | | 7,138,600 | |

4.08%, 02/25/21, (3 mo. LIBOR US + 1.770%)(b)(e) | | | 10,000 | | | | 10,274,803 | |

HSBC Bank PLC, 4.13%, 08/12/20(a)(e) | | | 10,000 | | | | 10,140,528 | |

HSBC Holdings PLC 2.92%, 05/18/21 (Call 05/18/20), (3 mo. LIBOR US + 0.600%)(b) | | | 24,695 | | | | 24,722,362 | |

3.97%, 05/25/21, (3 mo. LIBOR US + 1.660%)(b) | | | 10,000 | | | | 10,280,842 | |

4.57%, 03/08/21, (3 mo. LIBOR US + 2.240%)(b)(e) | | | 6,815 | | | | 7,078,713 | |

HSBC USA Inc., 2.35%, 03/05/20 | | | 15,000 | | | | 14,822,864 | |

Huntington National Bank (The)

2.20%, 11/06/18 (Call 10/06/18) | | | 5,000 | | | | 4,999,694 | |

2.20%, 04/01/19 (Call 03/01/19)(e) | | | 7,500 | | | | 7,481,473 | |

2.84%, 03/10/20, (3 mo. LIBOR US + 0.510%)(b) | | | 10,000 | | | | 10,029,157 | |

ING Bank NV, 2.92%, 08/15/19, (3 mo. LIBOR US + 0.610%)(a)(b) | | | 3,000 | | | | 3,007,879 | |

Intesa Sanpaolo SpA/New York NY, 3.08%, 07/17/19, (3 mo. LIBOR US + 0.630%)(b) | | | 6,990 | | | | 6,992,412 | |

JPMorgan Chase & Co. | | | | | | | | |

2.25%, 01/23/20 (Call 12/23/19)(e) | | | 4,000 | | | | 3,952,904 | |

2.88%, 03/09/21 (Call 03/09/20), (3 mo. LIBOR US + 0.550%)(b)(e) | | | 10,000 | | | | 10,012,850 | |

3.00%, 06/01/21 (Call 06/01/20), (3 mo. LIBOR US + 0.680%)(b) | | | 19,985 | | | | 20,014,977 | |

3.39%, 04/25/23 (Call 04/25/22), (3 mo. LIBOR US + 0.900%)(b) | | | 10,000 | | | | 10,055,000 | |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | | | | | | | |

Banks (continued) | | | | | | | | |

3.44%, 01/15/23 (Call 01/15/22), (3 mo. LIBOR US + 1.000%)(b) | | $ | 15,000 | | | $ | 15,143,113 | |

4.25%, 10/15/20(e) | | | 10,000 | | | | 10,155,384 | |

Lloyds Bank PLC

2.70%, 08/17/20 . | | | 20,000 | | | | 19,717,784 | |

3.47%, 01/22/19, (3 mo. LIBOR US + 1.000%)(b) | | | 1,020 | | | | 1,021,826 | |

Mitsubishi UFJ Financial Group Inc., 3.16%, 07/26/21, (3 mo. LIBOR US + 0.650%)(b) | | | 10,000 | | | | 10,039,598 | |

Mizuho Financial Group Inc. | | | | | | | | |

3.11%, 03/05/23, (3 mo. LIBOR US + 0.790%)(b) | | | 3,000 | | | | 3,000,523 | |

3.47%, 09/13/21, (3 mo. LIBOR US + 1.140%)(b)(e) | | | 20,000 | | | | 20,281,082 | |

Morgan Stanley

2.80%, 06/16/20(e) | | | 10,000 | | | | 9,910,831 | |

3.65%, 01/27/20, (3 mo. LIBOR US + 1.140%)(b) | | | 3,000 | | | | 3,028,852 | |

3.65%, 01/20/22 (Call 01/20/21), (3 mo. LIBOR US + 1.180%)(b) | | | 30,000 | | | | 30,337,712 | |

3.89%, 10/24/23 (Call 10/24/22), (3 mo. LIBOR US +

1.400%)(b)(e) | | | 5,000 | | | | 5,091,320 | |

7.30%, 05/13/19(e) | | | 10,000 | | | | 10,220,400 | |

Series 3NC2, 3.41%, 02/14/20 (Call 02/14/19), (3 mo. LIBOR US + 0.800%)(b) | | | 34,740 | | | | 34,781,271 | |

MUFG Bank Ltd.,

2.35%, 09/08/19(a)(e) | | | 10,000 | | | | 9,938,487 | |

National Australia Bank Ltd., 2.82%, 05/22/20, (3 mo. LIBOR US + 0.510%)(a)(b) | | | 10,000 | | | | 10,033,615 | |

Nordea Bank AB, 2.79%, 05/29/20, (3 mo. LIBOR US + 0.470%)(a)(b) | | | 15,000 | | | | 15,027,300 | |

Nordea Bank Abp, 3.25%, 08/30/23, (3 mo. LIBOR US + 0.940%)(a)(b) | | | 15,000 | | | | 14,986,530 | |

Royal Bank of Canada 2.70%, 03/02/20, (3 mo. LIBOR US + 0.380%)(b) | | | 5,000 | | | | 5,009,997 | |

3.03%, 12/10/18, (3 mo. LIBOR US + 0.700%)(b) | | | 2,300 | | | | 2,301,214 | |

Santander UK Group Holdings PLC, 2.88%, 10/16/20(e) | | | 10,000 | | | | 9,853,640 | |

Santander UK PLC, 2.35%, 09/10/19 | | | 10,000 | | | | 9,930,100 | |

Skandinaviska Enskilda Banken AB

| | | | | | | | |

2.63%, 11/17/20(a)(e) | | | 20,000 | | | | 19,626,600 | |

2.74%, 05/17/21, (3 mo. LIBOR US + 0.430%)(a)(b) | | | 10,000 | | | | 9,992,710 | |

Sumitomo Mitsui Banking Corp.

1.97%, 01/11/19 | | | 6,880 | | | | 6,868,458 | |

2.45%, 01/16/20 | | | 10,000 | | | | 9,900,872 | |

3.38%, 01/18/19, (3 mo. LIBOR US + 0.940%)(b) | | | 5,500 | | | | 5,507,257 | |

Sumitomo Mitsui Trust Bank Ltd., 3.35%, 10/18/19, (3 mo. LIBOR US + 0.910%)(a)(b) | | | 4,400 | | | | 4,427,869 | |

SunTrust Bank/Atlanta GA, 3.01%, 10/26/21 (Call 10/26/20), (3 mo. LIBOR US + 0.500%)(b) | | | 27,020 | | | | 27,023,459 | |

Svenska Handelsbanken AB

2.25%, 06/17/19 | | | 4,350 | | | | 4,328,321 | |

2.50%, 01/25/19 | | | 5,000 | | | | 4,997,100 | |

2.78%, 05/24/21, (3 mo. LIBOR US + 0.470%)(b)(e) | | | 12,500 | | | | 12,562,370 | |

UBS AG/London | | | | | | | | |

2.45%, 12/01/20

(Call 11/01/20)(a)(e) | | | 15,000 | | | | 14,673,390 | |

2.80%, 12/01/20 (Call 11/01/20),

(3 mo. LIBOR US +

0.480%)(a)(b) | | | 5,000 | | | | 5,004,180 | |

2.91%, 06/08/20 (Call 05/08/20),

(3 mo. LIBOR US +

0.580%)(a)(b) | | | 5,300 | | | | 5,318,232 | |

UBS AG/Stamford CT, 2.38%, 08/14/19 | | | 15,000 | | | | 14,916,988 | |

UBS Group Funding Switzerland AG, 3.53%, 05/23/23 (Call 05/23/22), (3 mo. LIBOR US + 1.220%)(a)(b)(e) | | | 20,000 | | | | 20,206,536 | |

| | | | |

S C H E D U L E O F I N V E S T M E N T S | | | 17 | |

| | |

Schedule of Investments (continued) October 31, 2018 | | iShares® Short Maturity Bond ETF (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | | | | | | | |

Banks (continued) | | | | | | | | |

Wells Fargo & Co. | | | | | | | | |

2.55%, 12/07/20 | | $ | 15,000 | | | $ | 14,702,340 | |

3.35%, 07/22/20, (3 mo. LIBOR US + 0.880%)(b) | | | 5,000 | | | | 5,042,151 | |

3.66%, 03/04/21, (3 mo. LIBOR US + 1.340%)(b) | | | 10,000 | | | | 10,203,079 | |

| | | | | | | | |

| | | | | | | 1,138,465,619 | |

Beverages — 0.2% | | | | | | | | |

Molson Coors Brewing Co., 1.90%, 03/15/19 | | | 9,425 | | | | 9,379,139 | |

| | | | | | | | |

Biotechnology — 0.5% | | | | | | | | |

Amgen Inc. | | | | | | | | |

2.20%, 05/22/19 (Call 04/22/19) | | | 3,000 | | | | 2,988,124 | |

2.79%, 05/11/20, (3 mo. LIBOR US + 0.450%)(b) | | | 8,100 | | | | 8,118,580 | |

5.70%, 02/01/19 | | | 4,000 | | | | 4,027,853 | |

Gilead Sciences Inc., 1.85%, 09/20/19 | | | 12,100 | | | | 11,976,527 | |

| | | | | | | | |

| | | | | | | 27,111,084 | |

Chemicals — 1.0% | | | | | | | | |

Dow Chemical Co. (The), 8.55%, 05/15/19(e) | | | 10,000 | | | | 10,285,128 | |

EI du Pont de Nemours & Co., 2.87%, 05/01/20, (3 mo. LIBOR US + 0.530%)(b) | | | 6,015 | | | | 6,042,420 | |

PPG Industries Inc., 2.30%, 11/15/19 (Call 10/15/19) | | | 10,868 | | | | 10,775,644 | |

Sherwin-Williams Co. (The), 2.25%, 05/15/20 | | | 25,000 | | | | 24,575,000 | |

| | | | | | | | |

| | | | | | | 51,678,192 | |

Computers — 0.6% | | | | | | | | |

Hewlett Packard Enterprise Co. | | | | | | | | |

3.06%, 10/05/21 (Call 09/20/19), (3 mo. LIBOR US + 0.720%)(b) | | | 20,000 | | | | 20,008,620 | |

3.60%, 10/15/20

(Call 09/15/20)(f) | | | 10,000 | | | | 10,020,757 | |

| | | | | | | | |

| | | | | | | 30,029,377 | |

Diversified Financial Services — 2.8% | |

AerCap Ireland Capital DAC/AerCap Global Aviation Trust

3.75%, 05/15/19 | | | 7,771 | | | | 7,786,194 | |

4.25%, 07/01/20(e) | | | 10,000 | | | | 10,062,209 | |

4.63%, 10/30/20 | | | 20,000 | | | | 20,304,958 | |

AIG Global Funding, 2.88%, 07/02/20, (3 mo. LIBOR US + 0.480%)(a)(b) | | | 3,695 | | | | 3,700,818 | |

American Express Co. | | | | | | | | |

2.85%, 10/30/20 (Call 09/29/20), (3 mo. LIBOR US + 0.330%)(b) | | | 7,750 | | | | 7,749,844 | |

2.96%, 02/27/23 (Call 01/27/23), (3 mo. LIBOR US + 0.650%)(b) | | | 4,000 | | | | 3,985,039 | |

American Express Credit Corp., 2.75%, 03/03/20 (Call 02/03/20), (3 mo. LIBOR US + 0.430%)(b) | | | 10,000 | | | | 10,029,448 | |

Federation des Caisses Desjardins du Quebec, 2.25%, 10/30/20(a) | | | 15,000 | | | | 14,665,140 | |

GE Capital International Funding Co. Unlimited Co., 2.34%, 11/15/20(e) | | | 25,000 | | | | 24,255,411 | |

Horsepower Finance Ltd., 2.15%, 12/02/19(g) | | | 10,000 | | | | 9,840,240 | |

International Lease Finance Corp.

5.88%, 04/01/19 | | | 3,225 | | | | 3,257,413 | |

6.25%, 05/15/19(e) | | | 23,238 | | | | 23,608,623 | |

| | | | | | | | |

| | | | | | | 139,245,337 | |

Electric — 1.1% | | | | | | | | |

Dominion Energy Inc.

1.88%, 12/15/18(a) | | | 10,000 | | | | 9,986,207 | |

Series A, 1.88%, 01/15/19 | | | 4,845 | | | | 4,838,022 | |

Duke Energy Florida LLC, 1.85%, 01/15/20 | | | 8,000 | | | | 7,881,075 | |

Duke Energy Progress LLC, 2.51%, 09/08/20, (3 mo. LIBOR US + 0.180%)(b) | | | 9,835 | | | | 9,848,923 | |

NextEra Energy Capital Holdings Inc., 2.30%, 04/01/19(e) | | | 5,000 | | | | 4,984,053 | |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | | | | | | | |

Electric (continued) | | | | | | | | |

Pacific Gas & Electric Co., 3.50%, 10/01/20 (Call 07/01/20)(e) | | $ | 10,000 | | | $ | 9,987,471 | |

Sempra Energy, 2.94%, 01/15/21 (Call 01/14/19), (3 mo. LIBOR US + 0.500%)(b) | | | 5,065 | | | | 5,065,215 | |

| | | | | | | | |

| | | | | | | 52,590,966 | |

Electronics — 0.1% | | | | | | | | |

Amphenol Corp., 2.55%, 01/30/19 (Call 12/30/18) | | | 4,500 | | | | 4,496,180 | |

| | | | | | | | |

| | |

Environmental Control — 0.2% | | | | | | | | |

Republic Services Inc., 5.50%, 09/15/19 | | | 7,964 | | | | 8,128,512 | |

| | | | | | | | |

| | |

Food — 2.1% | | | | | | | | |

Campbell Soup Co., 2.96%, 03/15/21, (3 mo. LIBOR US + 0.630%)(b) | | | 15,000 | | | | 14,943,535 | |

Conagra Brands Inc. | | | | | | | | |

2.91%, 10/09/20, (3 mo. LIBOR US + 0.500%)(b) | | | 7,000 | | | | 6,980,234 | |

3.22%, 10/22/20 (Call 10/22/19),

(3 mo. LIBOR US + 0.750%)(b) | | | 9,945 | | | | 9,950,559 | |

General Mills Inc., 2.98%, 04/16/21, (3 mo. LIBOR US + 0.540%)(b) | | | 21,636 | | | | 21,617,671 | |

Kraft Heinz Foods Co.

| | | | | | | | |

2.76%, 08/09/19, (3 mo. LIBOR US + 0.420%)(b) | | | 12,000 | | | | 12,010,038 | |

2.91%, 02/10/21, (3 mo. LIBOR US + 0.570%)(b)(e) | | | 4,010 | | | | 4,017,365 | |

Mondelez International Holdings Netherlands BV, 1.63%, 10/28/19 (Call 09/28/19)(a) | | | 7,500 | | | | 7,375,019 | |

Tyson Foods Inc.

| | | | | | | | |

2.65%, 08/15/19 (Call 07/15/19)(e) | | | 4,590 | | | | 4,577,091 | |

2.76%, 08/21/20, (3 mo. LIBOR US + 0.450%)(b) | | | 14,160 | | | | 14,185,369 | |

2.87%, 06/02/20, (3 mo. LIBOR US + 0.550%)(b) | | | 5,475 | | | | 5,486,148 | |

Wm Wrigley Jr Co., 2.90%, 10/21/19 (Call 09/21/19)(a) | | | 3,500 | | | | 3,491,460 | |

| | | | | | | | |

| | | | | | | 104,634,489 | |

Health Care - Products — 0.8% | | | | | | | | |

Becton Dickinson and Co.

2.68%, 12/15/19 . | | | 5,000 | | | | 4,965,396 | |

3.26%, 12/29/20 (Call 03/01/19),

(3 mo. LIBOR US + 0.875%)(b) | | | 28,505 | | | | 28,527,776 | |

Medtronic Inc., 3.13%, 03/15/20,

(3 mo. LIBOR US + 0.800%)(b) | | | 5,312 | | | | 5,355,858 | |

Stryker Corp., 2.00%, 03/08/19 | | | 1,115 | | | | 1,111,446 | |

| | | | | | | | |

| | | | | | | 39,960,476 | |

Health Care - Services — 0.8% | | | | | | | | |

Halfmoon Parent Inc., 3.20%, 09/17/20(a) | | | 30,000 | | | | 29,840,073 | |

UnitedHealth Group Inc., 2.70%, 07/15/20(e) | | | 10,000 | | | | 9,921,163 | |

| | | | | | | | |

| | | | | | | 39,761,236 | |

Housewares — 0.1% | | | | | | | | |

Newell Brands Inc., 2.60%, 03/29/19 | | | 7,000 | | | | 6,981,325 | |

| | | | | | | | |

| | |

Insurance — 0.9% | | | | | | | | |

Allstate Corp. (The), 2.82%, 03/29/21, (3 mo. LIBOR US + 0.430%)(b) | | | 5,710 | | | | 5,713,926 | |

American International Group Inc., 3.38%, 08/15/20 | | | 2,997 | | | | 2,991,586 | |

Metropolitan Life Global Funding I, 2.30%, 04/10/19(a) | | | 19,915 | | | | 19,864,490 | |

New York Life Global Funding, 1.55%, 11/02/18(a) | | | 4,750 | | | | 4,750,000 | |

Pricoa Global Funding I, 2.20%, 05/16/19(a) | | | 10,905 | | | | 10,864,817 | |

| | | | | | | | |

| | | | | | | 44,184,819 | |

Machinery — 0.4% | | | | | | | | |

Caterpillar Financial Services Corp., 2.82%, 05/15/23, (3 mo. LIBOR US + 0.510%)(b) | | | 10,000 | | | | 9,986,076 | |

| | |

| 18 | | 2 0 1 8 I S H A R E S A N N U A L R E P O R T T O S H A R E H O L D E R S |

| | |

Schedule of Investments (continued) October 31, 2018 | | iShares® Short Maturity Bond ETF (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | | | | | | | |

Machinery (continued) | | | | | | | | |

John Deere Capital Corp. 2.63%, 03/13/20, (3 mo. LIBOR US + 0.300%)(b) | | $ | 6,000 | | | $ | 6,009,699 | |

2.66%, 06/22/20, (3 mo. LIBOR US + 0.290%)(b) | | | 6,000 | | | | 6,012,600 | |

| | | | | | | | |

| | | | | | | 22,008,375 | |

Manufacturing — 0.2% | | | | | | | | |

Siemens Financieringsmaatschappij NV

2.15%, 05/27/20(a)(e) | | | 10,000 | | | | 9,838,991 | |

2.67%, 03/16/20, (3 mo. LIBOR US + 0.340%)(a)(b) | | | 2,000 | | | | 2,003,314 | |

| | | | | | | | |

| | | | | | | 11,842,305 | |

Media — 2.2% | | | | | | | | |

Charter Communications Operating LLC/Charter Communications Operating Capital, | | | | | | | | |

3.58%, 07/23/20 (Call 06/23/20) | | | 35,000 | | | | 34,942,375 | |

Comcast Corp., 2.85%, 10/01/21,

(3 mo. LIBOR US + 0.440%)(b) | | | 32,930 | | | | 32,942,085 | |

Discovery Communications LLC, 3.05%, 09/20/19, (3 mo. LIBOR US + 0.710%)(b)(e) | | | 30,000 | | | | 30,107,220 | |

Sky PLC, 2.63%, 09/16/19(a) | | | 1,425 | | | | 1,417,065 | |

Time Warner Cable LLC, 8.25%, 04/01/19 | | | 1,950 | | | | 1,989,557 | |

Warner Media LLC, 2.10%, 06/01/19 | | | 10,000 | | | | 9,946,915 | |

| | | | | | | | |

| | | | | | | 111,345,217 | |

Oil & Gas — 0.8% | | | | | | | | |

Chevron Corp., 2.53%, 03/03/20,

(3 mo. LIBOR US + 0.210%)(b) | | | 6,500 | | | | 6,511,902 | |

Ecopetrol SA, 7.63%, 07/23/19 | | | 16,000 | | | | 16,464,000 | |

Phillips 66, 3.19%, 04/15/20 (Call 12/10/18), (3 mo. LIBOR US + 0.750%)(a)(b) | | | 5,625 | | | | 5,625,993 | |

Sinopec Group Overseas Development 2014 Ltd., 2.75%, 04/10/19(g) | | | 12,000 | | | | 11,974,115 | |

| | | | | | | | |

| | | | | | | 40,576,010 | |

Pharmaceuticals — 4.9% | | | | | | | | |

AbbVie Inc., 2.50%, 05/14/20 (Call 04/14/20)(e) | | | 35,000 | | | | 34,542,892 | |

Allergan Funding SCS

2.45%, 06/15/19 | | | 18,783 | | | | 18,746,859 | |

3.00%, 03/12/20 (Call 02/12/20) | | | 43,000 | | | | 42,844,340 | |

3.59%, 03/12/20, (3 mo. LIBOR US + 1.255%)(b) | | | 20,505 | | | | 20,732,519 | |

AstraZeneca PLC, 1.95%, 09/18/19(e) | | | 6,500 | | | | 6,432,783 | |

Bayer U.S. Finance II LLC, 3.00%, 06/25/21 (Call 05/25/21),

(3 mo. LIBOR US + 0.630%)(a)(b) | | | 25,000 | | | | 25,009,388 | |

CVS Health Corp.

2.25%, 08/12/19 (Call 07/12/19) | | | 3,000 | | | | 2,981,646 | |

2.80%, 07/20/20 (Call 06/20/20) | | | 35,000 | | | | 34,644,947 | |

2.96%, 03/09/20, (3 mo. LIBOR US + 0.630%)(b)(e) | | | 5,318 | | | | 5,335,300 | |

3.05%, 03/09/21, (3 mo. LIBOR US + 0.720%)(b)(e) | | | 10,000 | | | | 10,053,227 | |

3.13%, 03/09/20 | | | 12,430 | | | | 12,401,499 | |

Shire Acquisitions Investments Ireland DAC, 1.90%, 09/23/19 | | | 30,000 | | | | 29,629,031 | |

| | | | | | | | |

| | | | | | | 243,354,431 | |

Pipelines — 1.9% | | | | | | | | |

Andeavor Logistics LP/Tesoro Logistics Finance Corp., 6.25%, 10/15/22 (Call 11/26/18) | | | 2,000 | | | | 2,062,500 | |

Enbridge Inc., 2.81%, 01/10/20, (3 mo. LIBOR US + 0.400%)(b) | | | 5,230 | | | | 5,221,774 | |

Energy Transfer Operating LP, 4.15%, 10/01/20 (Call 08/01/20) | | | 15,000 | | | | 15,127,807 | |

Kinder Morgan Inc./DE, 3.72%, 01/15/23, (3 mo. LIBOR US + 1.280%)(b) | | | 20,000 | | | | 20,338,525 | |

Spectra Energy Partners LP, 3.02%, 06/05/20, (3 mo. LIBOR US + 0.700%)(b) | | | 32,000 | | | | 32,086,123 | |

| | | | | | | | |

| Security | | Par (000) | | | Value | |

| | | | | | | | |

Pipelines (continued) | | | | | | | | |

TransCanada PipeLines Ltd., 2.13%, 11/15/19 | | $ | 2,540 | | | $ | 2,511,447 | |

Williams Companies Inc. (The), 5.25%, 03/15/20 | | | 15,000 | | | | 15,334,198 | |

| | | | | | | | |

| | | | | | | 92,682,374 | |

Real Estate Investment Trusts — 0.2% | |

American Tower Corp., 3.40%, 02/15/19 | | | 10,000 | | | | 10,011,282 | |

| | | | | | | | |

Retail — 0.2% | | | | | | | | |

Alimentation Couche-Tard Inc., 2.83%, 12/13/19 (Call 12/13/18),

(3 mo. LIBOR US + 0.500%)(a)(b)(e) | | | 8,600 | | | | 8,598,892 | |

Walgreens Boots Alliance Inc., 2.70%, 11/18/19 (Call 10/18/19) | | | 3,058 | | | | 3,042,435 | |

| | | | | | | | |

| | | | | | | 11,641,327 | |

Semiconductors — 1.0% | | | | | | | | |

Broadcom Corp./Broadcom Cayman Finance Ltd.

2.20%, 01/15/21(e) | | | 10,000 | | | | 9,664,305 | |

2.38%, 01/15/20 | | | 5,900 | | | | 5,831,184 | |

Intel Corp., 2.42%, 05/11/20, (3 mo. LIBOR US + 0.080%)(b) | | | 13,700 | | | | 13,695,623 | |

QUALCOMM Inc.

2.25%, 05/20/20 . | | | 10,000 | | | | 9,854,146 | |

3.25%, 01/30/23, (3 mo. LIBOR US + 0.730%)(b) | | | 10,000 | | | | 9,998,380 | |

| | | | | | | | |

| | | | | | | 49,043,638 | |

Software — 0.2% | | | | | | | | |