UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-22582

Western Asset Middle Market Income Fund Inc.

(Exact name of registrant as specified in charter)

620 Eighth Avenue, 49th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (888)777-0102

Date of fiscal year end: April 30

Date of reporting period: April 30, 2020

| ITEM 1. | REPORT TO STOCKHOLDERS. |

TheAnnual Report to Stockholders is filed herewith.

| | |

| Annual Report | | April 30, 2020 |

WESTERN ASSET

MIDDLE MARKET

INCOME FUND INC.

Beginning in April 2021, as permitted by regulations adopted by the Securities and Exchange Commission, the Fund intends to no longer mail paper copies of the Fund’s shareholder reports like this one, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary (such as a broker-dealer or bank). Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you invest through a financial intermediary and you already elected to receive shareholder reports electronically(“e-delivery”), you will not be affected by this change and you need not take any action. If you have not already electede-delivery, you may elect to receive shareholder reports and other communications from the Fund electronically by contacting your financial intermediary.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. That election will apply to all Legg Mason Funds held in your account at that financial intermediary. If you are a direct shareholder with the Fund, you can call the Fund at1-888-888-0151, or write to the Fund by regular mail at P.O. Box 505000, Louisville, KY 40233 or by overnight delivery to Computershare, 462 South 4th Street, Suite 1600, Louisville, KY 40202 to let the Fund know you wish to continue receiving paper copies of your shareholder reports. That election will apply to all Legg Mason Funds held in your account held directly with the fund complex.

|

| INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

Fund objectives

The Fund’s primary investment objective is to provide high income. As a secondary investment objective, the Fund seeks capital appreciation.

The Fund seeks to achieve its investment objectives by investing, under normal market conditions, at least 80% of its managed assets (the net assets of the Fund plus the principal amount of any borrowings and any preferred stock that may be outstanding) in securities, including loans, issued by middle market companies. For investment purposes, “middle market” refers to companies with annual revenues of between $100 million and $1 billion at the time of investment by the Fund. Securities of middle market issuers are typically considered below investment grade (also commonly referred to as “junk bonds”).

It is anticipated that the Fund will terminate on or before December 30, 2022.

| | |

| II | | Western Asset Middle Market Income Fund Inc. |

Letter from the chairman

.

Dear Shareholder,

We are pleased to provide the annual report of Western Asset Middle Market Income Fund Inc. for the twelve-month reporting period ended April 30, 2020. Please read on for Fund performance information and a detailed look at prevailing economic and market conditions during the Fund’s reporting period and to learn how those conditions have affected Fund performance.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our website, www.lmcef.com. Here you can gain immediate access to market and investment information, including:

| • | | Fund net asset values and performance, |

| • | | Market insights and commentaries from our portfolio managers, and |

| • | | A host of educational resources. |

We look forward to helping you meet your financial goals.

Sincerely,

Jane Trust, CFA

Chairman, President and Chief Executive Officer

May 29, 2020

| | |

| | |

| Western Asset Middle Market Income Fund Inc. | | III |

Fund overview

Q. What is the Fund’s investment strategy?

A.The Fund’s primary investment objective is to provide high income. As a secondary investment objective, the Fund seeks capital appreciation. The Fund seeks to achieve its investment objectives by investing, under normal market conditions, at least 80% of its managed assets (the net assets of the Fund plus the principal amount of any borrowings and any preferred stock that may be outstanding) in securities, including loans, issued by middle market companies. For investment purposes, “middle market” refers to companies with annual revenues of between $100 million and $1 billion at the time of investment by the Fund. Securities of middle market issuers are typically considered high yield. High yield securities are below investment grade quality (also commonly referred to as “junk bonds”).

The Fund may also invest up to 20% of its managed assets innon-middle market securities. Thenon-middle market securities the Fund expects to invest in include corporate debt securities rated investment grade or below investment grade of U.S. and foreign (including emerging markets) issuers and U.S. government debt securities.

No more than 10% of the Fund’s managed assets may be invested in any one issuer, except securities issued by the U.S. government and its agencies. The Fund may sell certain fixed income and equity securities short including, but not limited to, U.S. government debt securities, for hedging purposes. The Fund may invest all or a portion of its managed assets in illiquid securities.

The Fund is an actively managed portfolio consisting primarily of fixed income securities. The durationi of the Fund’s portfolio is anticipated to be between two and four years. However, the duration may change significantly at any time and is dependent on market conditions and investment opportunities available to the Fund. The Fund has a limited term. It is anticipated that the Fund will terminate on or before December 30, 2022. Although it has an anticipated term of eight years, the Fund’s term may be shorter or longer, depending on market conditions.

At Western Asset Management Company, LLC (“Western Asset”), the Fund’s subadviser, we utilize a fixed income team approach, with decisions derived from interaction among various investment management sector specialists. The sector teams are comprised of Western Asset’s senior portfolio management personnel, research analysts and anin-house economist. Under this team approach, management of client fixed income portfolios reflects a consensus of interdisciplinary views within the Western Asset organization. The individuals responsible for development of investment strategy,day-to-day portfolio management, oversight and coordination of the Fund are S. Kenneth Leech, Michael C. Buchanan, Christopher N. Jacobs and Christopher F. Kilpatrick.

Q. What were the overall market conditions during the Fund’s reporting period?

A.Fixed income markets, in general, posted mixed results over the twelve-months reporting period ended April 30, 2020. Most spread sectors(non-Treasuries) lagged equal duration Treasuries amid periods of heightened volatility. This was driven by a number of factors,

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 1 |

Fund overview (cont’d)

including extreme risk aversion as theCOVID-19 pandemic escalated, sharply falling global growth, aggressive monetary policy accommodation from the Federal Reserve Board (“Fed”),ii trade conflicts and a number of geopolitical issues.

Both short- and long-term U.S. Treasury yields moved sharply lower during the reporting period. The yield for thetwo-year Treasury note began the reporting period at 2.27% and ended the period at 0.20%, equaling the low for the period. The yield for thetwo-year Treasury note experienced a high for the period of 2.35% on May 2, 2019. The yield for theten-year Treasury began the reporting period at 2.51% and ended the period at 0.64%. The yield for theten-year Treasury peaked at 2.55% on May 2, 2019, and the low for the period of 0.58% occurred on April 21, 2020.

All told, the Bloomberg Barclays U.S. Aggregate Indexiii returned 10.84% for the twelve months ended April 30, 2020. Comparatively, riskier fixed-income securities, including high-yield bonds, produced weak results. Over the reporting period, the Bloomberg Barclays U.S. Corporate High Yield — 2% Issuer Cap Indexiv returned-4.08%. Elsewhere, the JPMorgan Emerging Markets Bond Index Globalv returned-3.31% for the twelve months ended April 30, 2020.

Q. How did we respond to these changing market conditions?

A.A number of adjustments were made to the Fund’s portfolio during the reporting period. We continued to favor higher rated loans and bonds by increasing the Fund’s allocations to senior secured bank loans and to securities rated B or higher.

During the reporting period, we utilized leverage in the Fund. We ended the period with liabilities as a percentage of gross assets of approximately 21%, versus 12% at the beginning of the period. While the Fund increased the amount of leverage deployed over the period, the use of leverage detracted from results in March and April 2020, given the negative performance of the Fund’s assets in the current market environment. The use of leverage is aligned with our view of the market opportunity available in below investment-grade debt given spread widening in recent months.

Performance review

For the twelve months ended April 30, 2020, Western Asset Middle Market Income Fund Inc. returned-22.94% based on its net asset value (“NAV”)vi. The Fund’s unmanaged benchmark, the Bloomberg Barclays U.S. Corporate High Yield – 2% Issuer Cap Caa Component Index, returned-20.05% for the same period. The Lipper High Yield (Leveraged)Closed-End Funds Category Averagevii returned –11.96% over the same time frame. Please note that Lipper performance returns are based on each fund’s NAV.

During the reporting period, the Fund made distributions to shareholders totaling $60.06 per share*. The performance table shows the Fund’s twelve-month total return based on its NAV as of April 30, 2020.Past performance is no guarantee of future results.

| * | For the tax character of distributions paid during the fiscal period ended April 30, 2020, please refer to page 39 of this report. |

| | |

| 2 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

| | | | |

| Performance Snapshotas of April 30, 2020 | |

| Price Per Share | | 12-Month Total Return** | |

| $527.84 (NAV) | | | -22.94 | %† |

All figures represent past performance and are not a guarantee of future results.

** Total return is based on changes in NAV. Return reflects the deduction of all Fund expenses, including management fees, operating expenses, and other Fund expenses. Return does not reflect the deduction of brokerage commissions or taxes that investors may pay on distributions or the disposition of shares.

† Total return assumes the reinvestment of all distributions at NAV.

Q. What were the leading contributors to performance?

A.The largest contributor to the Fund’s performance during the reporting period was security selection. In particular, the Fund’s positions in Option Care Health Inc., Air Medical Group Holdings, Inc., andFlexi-Van Leasing LLC contributed to performance. Option Care Health (formerly known as BioScrip) announced a merger and completed a refinancing of its debt in the third quarter of 2019. The company provides infusion and home health care management solutions, including products, services and condition-specific programs for many health conditions, such as chronic diseases, organ transplants, bleeding disorders, cancer and heart failure. Also, in the Health Care sector, Air Medical Group Holdings contributed to performance during the reporting period. The company provides emergency air, ground, managed medical transportation and community, industrial and fire medical services through its fleet of specially configured helicopters.Flexi-Van Leasing LLC provides truck chassis to shipping lines, trucking companies and other freight transportation firms. In January 2020 a private equity sponsor agreed to acquireFlexi-Van Leasing and called the existing 10.00% notes at a premium. Elsewhere, the Fund’s position in Bausch Health Companies, Inc. was additive for returns, as the company was viewed as a defensive selection by investors. Bausch Health Companies is a pharmaceutical firm with a significant contact lens business. We expect the company’s business performance to be less affected by the current economic slowdown than other issuers.

Q. What were the leading detractors from performance?

A.The largest detractor from performance during the reporting period was the Fund’s quality biases. Having an allocation to securities rated below B was a headwind for results as lower quality securities, represented by the benchmark, underperformed given the volatility in the reporting period, most notably in March and April 2020.

Investments in the Energy sector that negatively impacted performance included Oasis Petroleum, Inc. and Berry Corp. Oasis Petroleum is an oil and gas exploration and development company operating in diverse basins in the U.S. and owns midstream assets as well. Berry Corp. is also an oil and gas exploration and production company operating in California. Investments in both companies detracted from performance due to the combined forces of the change in the production outlook globally for oil and the reduction in demand

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 3 |

Fund overview (cont’d)

due to dramatically slower U.S. economic activity. Elsewhere, Techniplas, LLC was negative for results during the reporting period. The company is a global manufacturer of auto components offering fluid level indicators, vacuum boosters, brake fluid reservoirs, active grill shutters and air water separators among other parts. It performed poorly as a result of auto plant shutdowns and production stoppages. The company had been pursuing afollow-on strategic investment by a private equity sponsor, but after the plant closures in the industry the transaction was no longer viable.

The industry sectors detracting the most from the Fund’s returns during the reporting period were the Energy (both debt and equity positions) and Consumer Discretionary sectors, including the hotels, restaurants & leisure subsector. Historically described as a defensive consumer sector with stable cash flows, hard assets, and competition limited by state licensing, the property shutdowns and the uncertain outlook for when properties might reopen has changed the near-term outlook and securities prices for the hotel and gaming industries.

Looking for additional information?

The Fund’s daily NAV is availableon-line under the symbol “XWMFX” on most financial websites. In a continuing effort to provide information concerning the Fund, shareholders may call1-888-777-0102 (toll free), Monday through Friday from 8:00 a.m. to 5:30 p.m. Eastern Time, for the Fund’s current NAV and other information.

Thank you for your investment in Western Asset Middle Market Income Fund Inc. As always, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

Western Asset Management Company, LLC

May 29, 2020

RISKS: The Fund is anon-diversifiedclosed-end management investment company. An investment in the Fund involves a high degree of risk. The Fund should be considered an illiquid investment. This Fund is not publicly traded and is closed to new investors. The Fund does not intend to apply for an exchange listing, and it is highly unlikely that a secondary market will exist for the purchase and sale of the Fund’s shares. Investors could lose some or all of their investment. An investment in the Fund is not appropriate for all investors and is not intended to be a complete investment program. The Fund is designed as a long-term investment for investors who are prepared to hold the Fund’s Common Stock until the expiration of its term, and is not a trading vehicle. Because the Fund isnon-diversified, it may be more susceptible to economic, political or regulatory events than a diversified fund. Fixed income securities are subject to numerous risks, including but not limited to, credit, inflation, income, prepayment and interest rates risks. As interest rates rise, the value of fixed income securities falls. Middle market companies have additional risks due to their limited operating histories, limited financial resources, less predictable operating results, narrower product lines and other factors. Securities

| | |

| 4 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

of middle market issuers are typically considered high-yield. High-yield fixed income securities of below-investment-grade quality are regarded as having predominantly speculative characteristics with respect to the issuer’s capacity to pay interest and repay principal. High-yield bonds (“junk bonds”) are subject to higher credit risk and a greater risk of default. The Fund may invest all or a portion of its managed assets in illiquid securities. The Fund may make significant investments in securities for which there are no observable market prices. Investments in foreign securities involve risks, including the possibility of losses due to changes in currency exchange rates and negative developments in the political, economic or regulatory structure of specific countries or regions. These risks are greater in emerging markets. Emerging market countries tend to have economic, political and legal systems that are less developed and are less stable than those of more developed countries. Leverage may result in greater volatility of the net asset value of common shares and increases a shareholder’s risk of loss. Derivative instruments can be illiquid, may disproportionately increase losses and have a potentially large impact on Fund performance. Distributions are not guaranteed and are subject to change. The Fund may also invest in money market funds, including funds affiliated with the Fund’s manager and subadviser.

Portfolio holdings and breakdowns are as of April 30, 2020 and are subject to change and may not be representative of the portfolio managers’ current or future investments. Please refer to pages 8 through 16 for a list and percentage breakdown of the Fund’s holdings.

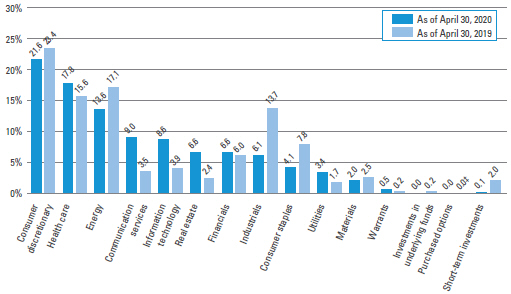

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. The Fund’s top five sector holdings (as a percentage of net assets) as of April 30, 2020 were: Consumer Discretionary (27.5%), Health Care (22.7%), Energy (17.4%), Communication Services (11.5%), and Information Technology (10.9%). The Fund’s portfolio composition is subject to change at any time.

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 5 |

Fund overview (cont’d)

| i | Duration is the measure of the price sensitivity of a fixed-income security to an interest rate change of 100 basis points. Calculation is based on the weighted average of the present values for all cash flows. |

| ii | The Federal Reserve Board (“Fed”) is responsible for the formulation of policies designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | The Bloomberg Barclays U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| iv | The Bloomberg Barclays U.S. Corporate High Yield — 2% Issuer Cap Index is an index of the 2% Issuer Cap component of the Bloomberg Barclays U.S. Corporate High Yield Index, which covers the U.S. dollar-denominated,non-investment grade, fixed-rate, taxable corporate bond market. |

| v | The JPMorgan Emerging Markets Bond Index Global (“EMBI Global”) tracks total returns for U.S.dollar-denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Eurobonds and local market instruments. |

| vi | Net asset value (“NAV”) is calculated by subtracting total liabilities, including liabilities associated with financial leverage (if any), from the closing value of all securities held by the Fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the market prices of securities in which the Fund has invested. However, the price at which an investor may buy or sell shares of the Fund is the Fund’s market price as determined by supply of and demand for the Fund’s shares. |

| vii | Lipper, Inc., a wholly-owned subsidiary of Reuters, provides independent insight on global collective investments. Returns are based on thetwo-month period ended April 30, 2020, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 38 funds in the Fund’s Lipper category. |

| | |

| 6 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

Fund at a glance†(unaudited)

Investment breakdown (%) as a percent of total investments

| † | The bar graph above represents the composition of the Fund’s investments as of April 30, 2020 and April 30, 2019 and does not include derivatives such as forward foreign currency contracts. The Fund is actively managed. As a result, the composition of the Fund’s investments is subject to change at any time. |

| ‡ | Represents less than 0.1%. |

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 7 |

Schedule of investments

April 30, 2020

Western Asset Middle Market Income Fund Inc.

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

| Corporate Bonds & Notes — 65.4% | | | | | | | | | | | | | | | | |

| Communication Services — 9.4% | | | | | | | | | | | | | | | | |

Diversified Telecommunication Services — 1.9% | | | | | | | | | | | | | |

Cogent Communications Group Inc., Senior Secured Notes | | | 5.375 | % | | | 3/1/22 | | | | 1,200,000 | | | $ | 1,224,540 | (a)(b) |

Windstream Services LLC/Windstream Finance Corp., Senior Secured Notes | | | 8.625 | % | | | 10/31/25 | | | | 1,350,000 | | | | 817,020 | *(a)(c) |

Total Diversified Telecommunication Services | | | | | | | | | | | | 2,041,560 | |

Entertainment — 1.0% | | | | | | | | | | | | | | | | |

Allen Media LLC/Allen MediaCo-Issuer Inc., Senior Notes | | | 10.500 | % | | | 2/15/28 | | | | 1,390,000 | | | | 1,038,608 | (a)(b) |

Wireless Telecommunication Services — 6.5% | | | | | | | | | | | | | | | | |

Block Communications Inc., Senior Notes | | | 4.875 | % | | | 3/1/28 | | | | 2,360,000 | | | | 2,359,292 | (a)(b) |

CSC Holdings LLC, Senior Notes | | | 10.875 | % | | | 10/15/25 | | | | 747,000 | | | | 810,981 | (a)(b) |

Sprint Communications Inc., Senior Notes | | | 11.500 | % | | | 11/15/21 | | | | 815,000 | | | | 912,433 | (b) |

Sprint Corp., Senior Notes | | | 7.875 | % | | | 9/15/23 | | | | 2,520,000 | | | | 2,845,206 | (b) |

Total Wireless Telecommunication Services | | | | | | | | | �� | | | 6,927,912 | |

Total Communication Services | | | | | | | | | | | | | | | 10,008,080 | |

| Consumer Discretionary — 17.2% | | | | | | | | | | | | | | | | |

Distributors — 0.7% | | | | | | | | | | | | | | | | |

American News Co. LLC, Secured Notes (8.500% Cash or 10.000% PIK) | | | 8.500 | % | | | 9/1/26 | | | | 750,000 | | | | 799,462 | (a)(d) |

Hotels, Restaurants & Leisure — 16.3% | | | | | | | | | | | | | | | | |

24 Hour Fitness Worldwide Inc., Senior Notes | | | 8.000 | % | | | 6/1/22 | | | | 2,500,000 | | | | 112,500 | (a)(b) |

Downstream Development Authority of the Quapaw Tribe of Oklahoma, Senior Secured Notes | | | 10.500 | % | | | 2/15/23 | | | | 3,510,000 | | | | 2,131,623 | (a)(b) |

Golden Entertainment Inc., Senior Notes | | | 7.625 | % | | | 4/15/26 | | | | 3,290,000 | | | | 2,503,526 | (a)(b) |

Golden Nugget Inc., Senior Notes | | | 8.750 | % | | | 10/1/25 | | | | 910,000 | | | | 524,388 | (a)(b) |

Jacobs Entertainment Inc., Secured Notes | | | 7.875 | % | | | 2/1/24 | | | | 3,818,000 | | | | 2,920,006 | (a)(b) |

Melco Resorts Finance Ltd., Senior Notes | | | 5.375 | % | | | 12/4/29 | | | | 1,550,000 | | | | 1,460,387 | (a)(b) |

Nathan’s Famous Inc., Senior Secured | | | | | | | | | | | | | | | | |

Notes | | | 6.625 | % | | | 11/1/25 | | | | 3,770,000 | | | | 3,656,900 | (a)(b) |

See Notes to Financial Statements.

| | |

| 8 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

Western Asset Middle Market Income Fund Inc.

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

Hotels, Restaurants & Leisure — continued | | | | | | | | | | | | | | | | |

Sugarhouse HSP Gaming Prop Mezz LP/ Sugarhouse HSP Gaming Finance Corp., Senior Secured Notes | | | 5.875 | % | | | 5/15/25 | | | | 3,000,000 | | | $ | 2,574,750 | (a)(b) |

Twin River Worldwide Holdings Inc., Senior Notes | | | 6.750 | % | | | 6/1/27 | | | | 1,900,000 | | | | 1,523,990 | (a)(b) |

Total Hotels, Restaurants & Leisure | | | | | | | | | | | | | | | 17,408,070 | |

Specialty Retail — 0.2% | | | | | | | | | | | | | | | | |

Michaels Stores Inc., Senior Notes | | | 8.000 | % | | | 7/15/27 | | | | 280,000 | | | | 194,502 | (a)(b) |

Total Consumer Discretionary | | | | | | | | | | | | | | | 18,402,034 | |

| Energy — 16.0% | | | | | | | | | | | | | | | | |

Energy Equipment & Services — 1.5% | | | | | | | | | | | | | | | | |

USA Compression Partners LP/USA Compression Finance Corp., Senior Notes | | | 6.875 | % | | | 4/1/26 | | | | 2,000,000 | | | | 1,619,400 | (b) |

Oil, Gas & Consumable Fuels — 14.5% | | | | | | | | | | | | | | | | |

Antero Midstream Partners LP/Antero Midstream Finance Corp., Senior Notes | | | 5.750 | % | | | 1/15/28 | | | | 1,990,000 | | | | 1,475,187 | (a)(b) |

Berry Petroleum Co. LLC, Senior Notes | | | 7.000 | % | | | 2/15/26 | | | | 3,650,000 | | | | 1,723,165 | (a)(b) |

Endeavor Energy Resources LP/EER Finance Inc., Senior Notes | | | 5.500 | % | | | 1/30/26 | | | | 1,200,000 | | | | 1,068,840 | (a)(b) |

Holly Energy Partners LP/Holly Energy Finance Corp., Senior Notes | | | 5.000 | % | | | 2/1/28 | | | | 2,050,000 | | | | 1,874,520 | (a)(b) |

Montage Resources Corp., Senior Notes | | | 8.875 | % | | | 7/15/23 | | | | 2,530,000 | | | | 2,078,521 | (b) |

Oasis Petroleum Inc., Senior Notes | | | 6.500 | % | | | 11/1/21 | | | | 4,088,000 | | | | 572,320 | (b) |

Oasis Petroleum Inc., Senior Notes | | | 6.875 | % | | | 3/15/22 | | | | 2,017,000 | | | | 310,114 | (b) |

Oasis Petroleum Inc., Senior Notes | | | 6.875 | % | | | 1/15/23 | | | | 800,000 | | | | 109,000 | (b) |

Shelf Drilling Holdings Ltd., Senior Notes | | | 8.250 | % | | | 2/15/25 | | | | 3,470,000 | | | | 1,093,050 | (a)(b) |

Teine Energy Ltd., Senior Notes | | | 6.875 | % | | | 9/30/22 | | | | 1,620,000 | | | | 1,566,621 | (a)(b) |

Transportadora de Gas del Sur SA, Senior Notes | | | 6.750 | % | | | 5/2/25 | | | | 3,000,000 | | | | 2,221,980 | (a)(b) |

Vesta Energy Corp., Senior Notes | | | 8.125 | % | | | 7/24/23 | | | | 3,800,000 | CAD | | | 1,351,342 | (a) |

Total Oil, Gas & Consumable Fuels | | | | | | | | | | | | | | | 15,444,660 | |

Total Energy | | | | | | | | | | | | | | | 17,064,060 | |

| Financials — 0.8% | | | | | | | | | | | | | | | | |

Diversified Financial Services — 0.8% | | | | | | | | | | | | | | | | |

Werner FinCo LP/Werner FinCo Inc., Senior Notes | | | 8.750 | % | | | 7/15/25 | | | | 1,000,000 | | | | 877,300 | (a)(b) |

See Notes to Financial Statements.

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 9 |

Schedule of investments (cont’d)

April 30, 2020

Western Asset Middle Market Income Fund Inc.

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

| Health Care — 8.8% | | | | | | | | | | | | | | | | |

Health Care Equipment & Supplies — 3.0% | | | | | | | | | | | | | | | | |

Immucor Inc., Senior Notes | | | 11.125 | % | | | 2/15/22 | | | | 3,554,000 | | | $ | 3,223,656 | (a)(b) |

Health Care Providers & Services — 4.4% | | | | | | | | | | | | | | | | |

Air Medical Group Holdings Inc., Senior Notes | | | 6.375 | % | | | 5/15/23 | | | | 1,050,000 | | | | 984,165 | (a)(b) |

LifePoint Health Inc., Senior Secured Notes | | | 4.375 | % | | | 2/15/27 | | | | 450,000 | | | | 425,812 | (a)(b) |

MPH Acquisition Holdings LLC, Senior Notes | | | 7.125 | % | | | 6/1/24 | | | | 2,000,000 | | | | 1,794,940 | (a)(b) |

US Renal Care Inc., Senior Notes | | | 10.625 | % | | | 7/15/27 | | | | 1,500,000 | | | | 1,495,650 | (a) |

Total Health Care Providers & Services | | | | | | | | | | | | | | | 4,700,567 | |

Pharmaceuticals — 1.4% | | | | | | | | | | | | | | | | |

Bausch Health Cos. Inc., Senior Notes | | | 5.875 | % | | | 5/15/23 | | | | 134,000 | | | | 133,203 | (a)(b) |

Bausch Health Cos. Inc., Senior Notes | | | 6.125 | % | | | 4/15/25 | | | | 280,000 | | | | 284,956 | (a)(b) |

Bausch Health Cos. Inc., Senior Notes | | | 9.000 | % | | | 12/15/25 | | | | 1,010,000 | | | | 1,106,455 | (a)(b) |

Total Pharmaceuticals | | | | | | | | | | | | | | | 1,524,614 | |

Total Health Care | | | | | | | | | | | | | | | 9,448,837 | |

| Industrials — 6.0% | | | | | | | | | | | | | | | | |

Commercial Services & Supplies — 3.0% | | | | | | | | | | | | | | | | |

GFL Environmental Inc., Senior Notes | | | 7.000 | % | | | 6/1/26 | | | | 342,000 | | | | 358,484 | (a)(b) |

GFL Environmental Inc., Senior Notes | | | 8.500 | % | | | 5/1/27 | | | | 414,000 | | | | 453,678 | (a)(b) |

GFL Environmental Inc., Senior Secured Notes | | | 5.125 | % | | | 12/15/26 | | | | 320,000 | | | | 334,800 | (a)(b) |

Waste Pro USA Inc., Senior Notes | | | 5.500 | % | | | 2/15/26 | | | | 2,090,000 | | | | 2,081,222 | (a)(b) |

Total Commercial Services & Supplies | | | | | | | | | | | | | | | 3,228,184 | |

Machinery — 0.2% | | | | | | | | | | | | | | | | |

Cleaver-Brooks Inc., Senior Secured Notes | | | 7.875 | % | | | 3/1/23 | | | | 180,000 | | | | 149,364 | (a)(b) |

Marine — 1.0% | | | | | | | | | | | | | | | | |

Navios Maritime Acquisition Corp./ Navios Acquisition Finance U.S. Inc., Senior Secured Notes | | | 8.125 | % | | | 11/15/21 | | | | 1,640,000 | | | | 1,075,266 | (a)(b) |

Trading Companies & Distributors — 1.8% | | | | | | | | | | | | | | | | |

Emeco Pty Ltd., Senior Secured Notes | | | 9.250 | % | | | 3/31/22 | | | | 1,978,824 | | | | 1,909,466 | (b) |

Total Industrials | | | | | | | | | | | | | | | 6,362,280 | |

| Information Technology — 0.0% | | | | | | | | | | | | | | | | |

Software — 0.0% | | | | | | | | | | | | | | | | |

Interface Special Holdings Inc., Senior Notes (19.000% PIK) | | | 19.000 | % | | | 11/1/23 | | | | 3,631,968 | | | | 54,480 | (a)(d)(e)(f) |

See Notes to Financial Statements.

| | |

| 10 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

Western Asset Middle Market Income Fund Inc.

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

| Materials — 2.6% | | | | | | | | | | | | | | | | |

Construction Materials — 1.8% | | | | | | | | | | | | | | | | |

U.S. Concrete Inc., Senior Notes | | | 6.375 | % | | | 6/1/24 | | | | 2,000,000 | | | $ | 1,898,900 | (b) |

Metals & Mining — 0.2% | | | | | | | | | | | | | | | | |

Northwest Acquisitions ULC/Dominion Finco Inc., Secured Notes | | | 7.125 | % | | | 11/1/22 | | | | 1,790,000 | | | | 185,712 | (a)(b) |

Paper & Forest Products — 0.6% | | | | | | | | | | | | | | | | |

Mercer International Inc., Senior Notes | | | 7.375 | % | | | 1/15/25 | | | | 720,000 | | | | 694,944 | (b) |

Total Materials | | | | | | | | | | | | | | | 2,779,556 | |

| Real Estate — 4.6% | | | | | | | | | | | | | | | | |

Real Estate Management & Development — 4.6% | | | | | | | | | | | | | |

Five Point Operating Co. LP/Five Point Capital Corp., Senior Notes | | | 7.875 | % | | | 11/15/25 | | | | 3,030,000 | | | | 2,946,675 | (a)(b) |

Kennedy-Wilson Inc., Senior Notes | | | 5.875 | % | | | 4/1/24 | | | | 2,000,000 | | | | 1,925,400 | (b) |

Total Real Estate | | | | | | | | | | | | | | | 4,872,075 | |

Total Corporate Bonds & Notes (Cost — $95,036,376) | | | | | | | | | | | | 69,868,702 | |

| Senior Loans — 56.8% | | | | | | | | | | | | | | | | |

| Communication Services — 2.1% | | | | | | | | | | | | | | | | |

Entertainment — 1.2% | | | | | | | | | | | | | | | | |

Allen Media LLC, Initial Term Loan (3 mo. USD LIBOR + 5.500%) | | | 7.231 | % | | | 2/10/27 | | | | 1,500,000 | | | | 1,327,500 | (f)(g)(h)(i) |

Media — 0.9% | | | | | | | | | | | | | | | | |

AppLovin Corp., Incremental Term Loan B | | | — | | | | 8/15/25 | | | | 1,000,000 | | | | 957,500 | (j) |

Total Communication Services | | | | | | | | | | | | | | | 2,285,000 | |

| Consumer Discretionary — 10.3% | | | | | | | | | | | | | | | | |

Commercial Services & Supplies — 1.7% | | | | | | | | | | | | | | | | |

KC Culinarte Intermediate LLC, First Lien Initial Term Loan (1 mo. USD LIBOR + 3.750%) | | | 4.750 | % | | | 8/25/25 | | | | 1,979,850 | | | | 1,795,477 | (f)(g)(h)(i) |

Hotels, Restaurants & Leisure — 5.3% | | | | | | | | | | | | | | | | |

Affinity Gaming LLC, Second Lien Initial Term Loan (3 mo. USD LIBOR + 8.250%) | | | 9.010 | % | | | 1/31/25 | | | | 3,990,000 | | | | 2,593,500 | (f)(g)(h)(i) |

CEC Entertainment Inc., Term Loan B (3 mo. USD LIBOR + 6.500%) | | | 7.572 | % | | | 8/17/26 | | | | 4,172,816 | | | | 2,197,684 | (g)(h)(i) |

Golden Entertainment Inc., First Lien Term Loan B (1 mo. USD LIBOR + 3.000%) | | | 3.750 | % | | | 10/21/24 | | | | 1,042,238 | | | | 859,846 | (f)(g)(h)(i) |

Total Hotels, Restaurants & Leisure | | | | | | | | | | | | | | | 5,651,030 | |

See Notes to Financial Statements.

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 11 |

Schedule of investments (cont’d)

April 30, 2020

Western Asset Middle Market Income Fund Inc.

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

Specialty Retail — 3.3% | | | | | | | | | | | | | | | | |

Isagenix International LLC, Term Loan (3 mo. USD LIBOR + 5.750%) | | | 7.017 | % | | | 6/16/25 | | | | 1,823,098 | | | $ | 680,243 | (g)(h)(i) |

Michaels Stores Inc., 2018 New Replacement Term Loan B (1 mo. USD LIBOR + 2.500%) | | | 3.500-3.568 | % | | | 1/30/23 | | | | 1,356,121 | | | | 1,118,800 | (g)(h)(i) |

Spencer Spirit IH LLC, Initial Term Loan | | | 6.570-13.000 | % | | | 6/19/26 | | | | 1,940,487 | | | | 1,765,844 | (g)(h)(i) |

Total Specialty Retail | | | | | | | | | | | | | | | 3,564,887 | |

Total Consumer Discretionary | | | | | | | | | | | | | | | 11,011,394 | |

| Consumer Staples — 5.2% | | | | | | | | | | | | | | | | |

Food Products — 5.2% | | | | | | | | | | | | | | | | |

8th Avenue Food & Provisions Inc., Second Lien Term Loan (1 mo. USD LIBOR + 7.750%) | | | 8.579 | % | | | 10/1/26 | | | | 2,720,000 | | | | 2,546,600 | (g)(h)(i) |

CSM Bakery Solutions LLC, Second Lien Term Loan (3 mo. USD LIBOR + 7.750%) | | | 9.100 | % | | | 7/5/21 | | | | 4,000,000 | | | | 3,066,668 | (g)(h)(i) |

Total Consumer Staples | | | | | | | | | | | | | | | 5,613,268 | |

| Energy — 0.5% | | | | | | | | | | | | | | | | |

Oil, Gas & Consumable Fuels — 0.5% | | | | | | | | | | | | | | | | |

Chesapeake Energy Corp., Term Loan A (2 mo. USD LIBOR + 8.000%) | | | 9.000 | % | | | 6/24/24 | | | | 1,500,000 | | | | 532,083 | (g)(h)(i) |

| Financials — 5.9% | | | | | | | | | | | | | | | | |

Diversified Financial Services — 1.5% | | | | | | | | | | | | | | | | |

GI Revelation Acquisition LLC, First Lien Term Loan (1 mo. USD LIBOR + 5.000%) | | | 5.404 | % | | | 4/16/25 | | | | 1,974,825 | | | | 1,611,127 | (g)(h)(i) |

Insurance — 4.4% | | | | | | | | | | | | | | | | |

AIS Holdco LLC, First Lien Term Loan (3 mo. USD LIBOR + 5.000%) | | | 5.760 | % | | | 8/15/25 | | | | 3,214,750 | | | | 2,788,796 | (f)(g)(h)(i) |

AmeriLife Group LLC, First Lien Delayed Draw Term Loan | | | — | | | | 3/18/27 | | | | 232,955 | | | | 213,153 | (j) |

AmeriLife Holdings LLC, First Lien Initial Term Loan (1 mo. USD LIBOR + 4.000%) | | | 4.985 | % | | | 3/18/27 | | | | 1,817,045 | | | | 1,662,597 | (g)(h)(i) |

Total Insurance | | | | | | | | | | | | | | | 4,664,546 | |

Total Financials | | | | | | | | | | | | | | | 6,275,673 | |

| Health Care — 13.7% | | | | | | | | | | | | | | | | |

Health Care Equipment & Supplies — 0.7% | | | | | | | | | | | | | |

Air Methods Corp., Initial Term Loan (3 mo. USD LIBOR + 3.500%) | | | 4.950 | % | | | 4/22/24 | | | | 988,876 | | | | 755,254 | (g)(h)(i) |

Health Care Providers & Services — 10.7% | | | | | | | | | | | | | |

Agiliti Health Inc., Term Loan (3 mo. USD LIBOR + 3.000%) | | | 4.438 | % | | | 1/4/26 | | | | 997,481 | | | | 947,607 | (f)(g)(h)(i) |

See Notes to Financial Statements.

| | |

| 12 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

Western Asset Middle Market Income Fund Inc.

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

Health Care Providers & Services — continued | | | | | | | | | | | | | | | | |

EyeCare Partners LLC, First Lien Initial Delayed Draw Term Loan | | | — | | | | 2/18/27 | | | | 359,459 | | | $ | 304,642 | (j) |

EyeCare Partners LLC, First Lien Initial Term Loan (3 mo. USD LIBOR + 3.750%) | | | 4.822 | % | | | 2/18/27 | | | | 1,540,541 | | | | 1,305,608 | (g)(h)(i) |

EyeCare Partners LLC, Second Lien Initial Term Loan (3 mo. USD LIBOR + 8.250%) | | | 9.139 | % | | | 2/4/28 | | | | 2,050,000 | | | | 1,737,375 | (g)(h)(i) |

Medical Solutions Holdings Inc., First Lien Closing Date Term Loan (1 mo. USD LIBOR + 4.500%) | | | 5.500 | % | | | 6/14/24 | | | | 2,019,850 | | | | 1,878,460 | (f)(g)(h)(i) |

MPH Acquisition Holdings LLC, Initial Term Loan (3 mo. USD LIBOR + 2.750%) | | | 4.200 | % | | | 6/7/23 | | | | 1,480,000 | | | | 1,366,885 | (g)(h)(i) |

Option Care Health Inc., First Lien Term Loan B (1 mo. USD LIBOR + 4.500%) | | | 4.904 | % | | | 8/6/26 | | | | 1,995,000 | | | | 1,890,263 | (g)(h)(i) |

Radnet Management Inc., First Lien Term Loan B1 (1 mo. USD LIBOR + 3.500%) | | | 4.500 | % | | | 6/30/23 | | | | 2,120,874 | | | | 1,981,692 | (g)(h)(i) |

Total Health Care Providers & Services | | | | | | | | | | | | | | | 11,412,532 | |

Pharmaceuticals — 2.3% | | | | | | | | | | | | | | | | |

Bausch Health Cos. Inc., Initial Term Loan (1 mo. USD LIBOR + 3.000%) | | | 3.718 | % | | | 6/2/25 | | | | 1,313,976 | | | | 1,273,462 | (g)(h)(i) |

Pearl Intermediate Parent LLC, Second Lien Initial Term Loan (1 mo. USD LIBOR + 6.250%) | | | 6.654 | % | | | 2/13/26 | | | | 1,350,000 | | | | 1,201,500 | (g)(h)(i) |

Total Pharmaceuticals | | | | | | | | | | | | | | | 2,474,962 | |

Total Health Care | | | | | | | | | | | | | | | 14,642,748 | |

| Industrials — 1.8% | | | | | | | | | | | | | | | | |

Building Products — 0.6% | | | | | | | | | | | | | | | | |

ACProducts Inc., First Lien Initial Term Loan (3 mo. USD LIBOR + 6.500%) | | | 8.192 | % | | | 8/18/25 | | | | 680,000 | | | | 612,000 | (g)(h)(i) |

Commercial Services & Supplies — 1.2% | | | | | | | | | | | | | | | | |

Garda World Security Corp., First Lien Term Loan B (3 mo. USD LIBOR + 4.750%) | | | 6.390 | % | | | 10/23/26 | | | | 1,374,131 | | | | 1,329,643 | (g)(h)(i) |

Total Industrials | | | | | | | | | | | | | | | 1,941,643 | |

| Information Technology — 10.9% | | | | | | | | | | | | | | | | |

Communications Equipment — 1.8% | | | | | | | | | | | | | | | | |

CommScope Inc., Initial Term Loan (1 mo. USD LIBOR + 3.250%) | | | 3.654 | % | | | 4/4/26 | | | | 2,044,862 | | | | 1,942,108 | (g)(h)(i) |

See Notes to Financial Statements.

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 13 |

Schedule of investments (cont’d)

April 30, 2020

Western Asset Middle Market Income Fund Inc.

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount† | | | Value | |

IT Services — 7.3% | | | | | | | | | | | | | | | | |

Access CIG LLC, Second Lien Initial Term Loan (1 mo. USD LIBOR + 7.750%) | | | 8.154 | % | | | 2/13/26 | | | | 3,470,984 | | | $ | 3,054,466 | (f)(g)(h)(i) |

Datto Inc., Term Loan (1 mo. USD LIBOR + 4.250%) | | | 4.654 | % | | | 4/2/26 | | | | 1,955,225 | | | | 1,842,799 | (g)(h)(i) |

Project Alpha Intermediate Holding Inc., 2019 Incremental Term Loan (3 mo. USD LIBOR + 4.250%) | | | 6.130 | % | | | 4/26/24 | | | | 2,950,213 | | | | 2,832,204 | (g)(h)(i) |

Total IT Services | | | | | | | | | | | | | | | 7,729,469 | |

Software — 1.8% | | | | | | | | | | | | | | | | |

DCert Buyer Inc., First Lien Initial Term Loan (1 mo. USD LIBOR + 4.000%) | | | 4.404 | % | | | 10/16/26 | | | | 2,030,000 | | | | 1,930,191 | (g)(h)(i) |

Total Information Technology | | | | | | | | | | | | | | | 11,601,768 | |

| Real Estate — 3.9% | | | | | | | | | | | | | | | | |

Equity Real Estate Investment Trusts (REITs) — 1.6% | | | | | | | | | | | | | |

Corecivic Inc., Term Loan (1 mo. USD LIBOR + 4.500%) | | | 5.500 | % | | | 12/12/24 | | | | 1,826,875 | | | | 1,708,129 | (g)(h)(i) |

Real Estate Management & Development — 2.3% | | | | | | | | | | | | | |

Coastal Construction Corp., Delayed Draw Term Loan | | | — | | | | 10/10/24 | | | | 670,000 | | | | 633,150 | (e)(f)(j) |

Coastal Construction Products LLC, Term Loan B (1 mo. USD LIBOR + 5.125%) | | | 6.125 | % | | | 9/4/24 | | | | 1,912,023 | | | | 1,806,861 | (e)(f)(g)(h)(i) |

Total Real Estate Management & Development | | | | | | | | | | | | 2,440,011 | |

Total Real Estate | | | | | | | | | | | | | | | 4,148,140 | |

| Utilities — 2.5% | | | | | | | | | | | | | | | | |

Electric Utilities — 2.5% | | | | | | | | | | | | | | | | |

Panda Temple Power LLC, Second Lien Term Loan (1 mo. USD LIBOR + 8.000% PIK) | | | 9.000 | % | | | 2/7/23 | | | | 2,775,142 | | | | 2,690,153 | (d)(f)(g)(h)(i) |

Total Senior Loans (Cost — $70,862,953) | | | | | | | | | | | | | | | 60,741,870 | |

| | | | |

| | | | | | | | | Shares | | | | |

| Common Stocks — 2.9% | | | | | | | | | | | | | | | | |

| Energy — 0.9% | | | | | | | | | | | | | | | | |

Oil, Gas & Consumable Fuels — 0.9% | | | | | | | | | | | | | | | | |

Berry Corp. | | | | | | | | | | | 98,271 | | | | 337,069 | |

Montage Resources Corp. | | | | | | | | | | | 92,531 | | | | 631,987 | * |

Total Energy | | | | | | | | | | | | | | | 969,056 | |

See Notes to Financial Statements.

| | |

| 14 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

Western Asset Middle Market Income Fund Inc.

| | | | | | | | | | | | | | | | |

| Security | | | | | | | | Shares | | | Value | |

| Health Care — 0.2% | | | | | | | | | | | | | | | | |

Health Care Providers & Services — 0.2% | | | | | | | | | | | | | | | | |

Option Care Health Inc. | | | | | | | | | | | 14,761 | | | $ | 211,086 | * |

| Utilities — 1.8% | | | | | | | | | | | | | | | | |

Electric Utilities — 1.8% | | | | | | | | | | | | | | | | |

Panda Temple Power LLC | | | | | | | | | | | 91,433 | | | | 1,965,810 | *(f) |

Total Common Stocks (Cost — $10,296,653) | | | | | | | | | | | | | | | 3,145,952 | |

| | | | |

| | | Rate | | | | | | | | | | |

| Preferred Stocks — 1.7% | | | | | | | | | | | | | | | | |

| Financials — 1.7% | | | | | | | | | | | | | | | | |

Capital Markets — 1.7% | | | | | | | | | | | | | | | | |

B Riley Financial Inc. (Cost — $1,997,500) | | | 6.875% | | | | | | | | 79,900 | | | | 1,835,303 | (b) |

| | | | |

| | | | | | Expiration

Date | | | Warrants | | | | |

| Warrants — 0.6% | | | | | | | | | | | | | | | | |

Option Care Health Inc. (Cost—$94,112) | | | | | | | 6/29/27 | | | | 65,920 | | | | 621,494 | *(e)(f) |

Total Investments before Short-Term Investments (Cost — $178,287,594) | | | | 136,213,321 | |

| | | | |

| | | Rate | | | | | | Shares | | | | |

| Short-Term Investments — 0.1% | | | | | | | | | | | | | | | | |

Dreyfus Government Cash Management, Institutional Shares

(Cost — $85,093) | | | 0.153% | | | | | | | | 85,093 | | | | 85,093 | |

Total Investments — 127.5% (Cost — $178,372,687) | | | | | | | | 136,298,414 | |

Liabilities in Excess of Other Assets — (27.5)% | | | | | | | | | | | | | | | (29,405,406 | ) |

Total Net Assets — 100.0% | | | | | | | | | | | | | | $ | 106,893,008 | |

See Notes to Financial Statements.

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 15 |

Schedule of investments (cont’d)

April 30, 2020

Western Asset Middle Market Income Fund Inc.

| † | Face amount denominated in U.S. dollars, unless otherwise noted. |

| * | Non-income producing security. |

| (a) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Directors. |

| (b) | All or a portion of this security is pledged as collateral pursuant to the loan agreement (Note 6). |

| (c) | The coupon payment on these securities is currently in default as of April 30, 2020. |

| (d) | Payment-in-kind security for which the issuer has the option at each interest payment date of making interest payments in cash or additional securities. |

| (e) | Security is valued in good faith in accordance with procedures approved by the Board of Directors (Note 1). |

| (f) | Security is valued using significant unobservable inputs (Note 1). |

| (g) | Interest rates disclosed represent the effective rates on senior loans. Ranges in interest rates are attributable to multiple contracts under the same loan. |

| (h) | Senior loans may be considered restricted in that the Fund ordinarily is contractually obligated to receive approval from the agent bank and/or borrower prior to the disposition of a senior loan. |

| (i) | Variable rate security. Interest rate disclosed is as of the most recent information available. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

| (j) | All or a portion of this loan is unfunded as of April 30, 2020. The interest rate for fully unfunded term loans is to be determined. |

| | |

Abbreviation(s) used in this schedule: |

| |

| CAD | | —Canadian Dollar |

| |

| LIBOR | | —London Interbank Offered Rate |

| |

| PIK | | —Payment-In-Kind |

| |

| USD | | —United States Dollar |

At April 30, 2020, the Fund had the following open forward foreign currency contracts:

| | | | | | | | | | | | | | |

Currency Purchased | | Currency Sold | | | Counterparty | | Settlement

Date | | | Unrealized

Depreciation | |

| CAD 308,750 | | USD | 222,916 | | | Citibank N.A. | | | 7/16/20 | | | $ | (1,064 | ) |

| USD 1,867,467 | | CAD | 2,600,000 | | | Citibank N.A. | | | 7/16/20 | | | | (761 | ) |

| Total | | | | | | | | | | | | $ | (1,825 | ) |

| | |

Abbreviation(s) used in this table: |

| |

| CAD | | — Canadian Dollar |

| |

| USD | | — United States Dollar |

See Notes to Financial Statements.

| | |

| 16 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

Statement of assets and liabilities

April 30, 2020

| | | | |

| |

| Assets: | | | | |

Investments, at value (Cost — $178,372,687) | | $ | 136,298,414 | |

Cash | | | 34,332 | |

Receivable for securities sold | | | 2,458,718 | |

Interest receivable | | | 2,370,587 | |

Prepaid expenses | | | 1,036 | |

Total Assets | | | 141,163,087 | |

| |

| Liabilities: | | | | |

Loan payable (Note 6) | | | 30,300,000 | |

Payable for securities purchased | | | 3,758,794 | |

Investment management fee payable | | | 127,134 | |

Interest payable | | | 11,046 | |

Directors’ fees payable | | | 2,001 | |

Unrealized depreciation on forward foreign currency contracts | | | 1,825 | |

Accrued expenses | | | 69,279 | |

Total Liabilities | | | 34,270,079 | |

| Total Net Assets | | $ | 106,893,008 | |

| |

| Net Assets: | | | | |

Par value ($0.001 par value; 202,512 shares issued and outstanding; 100,000,000 shares authorized) | | $ | 203 | |

Paid-in capital in excess of par value | | | 232,205,412 | |

Total distributable earnings (loss) | | | (125,312,607) | |

| Total Net Assets | | $ | 106,893,008 | |

| |

| Shares Outstanding | | | 202,512 | |

| |

| Net Asset Value | | | $527.84 | |

See Notes to Financial Statements.

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 17 |

Statement of operations

For the Year Ended April 30, 2020

| | | | |

| |

| Investment Income: | | | | |

Interest | | $ | 15,019,868 | |

Dividends | | | 329,306 | |

Income from paymentin-kind | | | 963,116 | |

Total Investment Income | | | 16,312,290 | |

| |

| Expenses: | | | | |

Investment management fee (Note 2) | | | 2,292,720 | |

Interest expense (Note 6) | | | 779,150 | |

Transfer agent fees | | | 112,219 | |

Audit and tax fees | | | 78,151 | |

Fund accounting fees | | | 75,091 | |

Legal fees | | | 55,745 | |

Shareholder reports | | | 47,239 | |

Directors’ fees | | | 36,010 | |

Custody fees | | | 5,939 | |

Insurance | | | 3,408 | |

Miscellaneous expenses | | | 13,553 | |

Total Expenses | | | 3,499,225 | |

Less: Fee waivers and/or expense reimbursements (Note 2) | | | (187,472) | |

Net Expenses | | | 3,311,753 | |

| Net Investment Income | | | 13,000,537 | |

| |

Realized and Unrealized Gain (Loss) on Investments, Forward Foreign Currency Contracts and Foreign Currency Transactions (Notes 1, 3 and 4): | | | | |

Net Realized Gain (Loss) From: | | | | |

Investment transactions | | | (11,753,578) | |

Forward foreign currency contracts | | | 153,974 | |

Foreign currency transactions | | | (10,426) | |

Net Realized Loss | | | (11,610,030) | |

Change in Net Unrealized Appreciation (Depreciation) From: | | | | |

Investments | | | (35,024,482) | |

Forward foreign currency contracts | | | (19,750) | |

Foreign currencies | | | (546) | |

Change in Net Unrealized Appreciation (Depreciation) | | | (35,044,778) | |

| Net Loss on Investments, Forward Foreign Currency Contracts and Foreign Currency Transactions | | | (46,654,808) | |

| Decrease in Net Assets From Operations | | $ | (33,654,271) | |

See Notes to Financial Statements.

| | |

| 18 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

Statements of changes in net assets

| | | | | | | | |

| For the Years Ended April 30, | | 2020 | | | 2019 | |

| | |

| Operations: | | | | | | | | |

Net investment income | | $ | 13,000,537 | | | $ | 17,096,536 | |

Net realized loss | | | (11,610,030) | | | | (4,222,411) | |

Change in net unrealized appreciation (depreciation) | | | (35,044,778) | | | | 1,953,843 | |

Increase (Decrease) in Net Assets From Operations | | | (33,654,271) | | | | 14,827,968 | |

| | |

| Distributions to Shareholders From (Note 1): | | | | | | | | |

Total distributable earnings | | | (13,130,243) | | | | (17,432,726) | |

Decrease in Net Assets From Distributions to Shareholders | | | (13,130,243) | | | | (17,432,726) | |

| | |

| Fund Share Transactions: | | | | | | | | |

Reinvestment of distributions (2,194 and 2,417 shares issued, respectively) | | | 1,444,128 | | | | 1,808,289 | |

Cost of shares repurchased through tender offer (30,808 and 32,435 shares repurchased, respectively) (Note 5) | | | (21,097,399) | | | | (24,195,474) | |

Decrease in Net Assets From Fund Share Transactions | | | (19,653,271) | | | | (22,387,185) | |

Decrease in Net Assets | | | (66,437,785) | | | | (24,991,943) | |

| | |

| Net Assets: | | | | | | | | |

Beginning of year | | | 173,330,793 | | | | 198,322,736 | |

End of year | | $ | 106,893,008 | | | $ | 173,330,793 | |

See Notes to Financial Statements.

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 19 |

Statement of cash flows

For the Year Ended April 30, 2020

| | | | |

| |

| Increase (Decrease) in Cash: | | | | |

| Cash Provided (Used) by Operating Activities: | |

Net decrease in net assets resulting from operations | | $ | (33,654,271) | |

Adjustments to reconcile net decrease in net assets resulting from operations to net cash provided (used) by operating activities: | | | | |

Purchases of portfolio securities | | | (101,052,764) | |

Sales of portfolio securities | | | 109,613,154 | |

Net purchases, sales and maturities of short-term investments | | | 4,084,049 | |

Payment-in-kind | | | (963,116) | |

Net amortization of premium (accretion of discount) | | | (1,470,502) | |

Decrease in receivable for securities sold | | | 474,160 | |

Decrease in interest receivable | | | 1,047,648 | |

Decrease in prepaid expenses | | | 262 | |

Increase in payable for securities purchased | | | 1,093,794 | |

Decrease in investment management fee payable | | | (58,929) | |

Decrease in Directors’ fees payable | | | (10,973) | |

Decrease in interest payable | | | (11,637) | |

Decrease in accrued expenses | | | (70,839) | |

Net realized loss on investments | | | 11,753,578 | |

Change in net unrealized appreciation (depreciation) of investments and forward foreign currency contracts | | | 35,044,232 | |

Net Cash Provided by Operating Activities* | | | 25,817,846 | |

| |

| Cash Flows From Financing Activities: | | | | |

Distributions paid on common stock | | | (11,686,115) | |

Proceeds from loan facility borrowings | | | 52,000,000 | |

Repayment of loan facility borrowings | | | (45,000,000) | |

Payment for shares repurchased through tender offer | | | (21,097,399) | |

Net Cash Used in Financing Activities | | | (25,783,514) | |

| Net Increase in Cash and Restricted Cash | | | 34,332 | |

| Cash and restricted cash at beginning of year | | | — | |

| Cash and restricted cash at end of year | | $ | 34,332 | |

| * | Included in operating expenses is cash of $790,787 paid for interest on borrowings. |

| | The following table provides a reconciliation of cash and restricted cash reported within the Statement of Assets and Liabilities that sums to the total of such amounts shown on the Statement of Cash Flows. |

| | | | |

| | | April 30, 2020 | |

Cash | | $ | 34,332 | |

Restricted cash | | | — | |

Total cash and restricted cash shown in the Statement of Cash Flows | | $ | 34,332 | |

| Non-Cash Financing Activities: | | | | |

Proceeds from reinvestment of distributions | | $ | 1,444,128 | |

See Notes to Financial Statements.

| | |

| 20 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

Financial highlights

| | | | | | | | | | | | | | | | | | | | |

| For a share of capital stock outstanding throughout each year ended April 30: | |

| | | 20201 | | | 20191 | | | 20181 | | | 20171 | | | 20161 | |

| | | | | |

| Net asset value, beginning of year | | | $749.94 | | | | $759.44 | | | | $799.71 | | | | $708.75 | | | | $915.01 | |

| | | | |

| Income (loss) from operations: | | | | | | | | | | | | | | | | | |

Net investment income | | | 60.08 | | | | 68.47 | | | | 76.58 | | | | 87.83 | | | | 86.64 | |

Net realized and unrealized gain (loss) | | | (222.12) | | | | (8.83) | | | | (38.51) | | | | 93.13 | | | | (202.90) | |

Total income (loss) from operations | | | (162.04) | | | | 59.64 | | | | 38.07 | | | | 180.96 | | | | (116.26) | |

| | | | | |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (60.06) | | | | (69.14) | | | | (78.34) | | | | (90.00) | | | | (90.00) | |

Total distributions | | | (60.06) | | | | (69.14) | | | | (78.34) | | | | (90.00) | | | | (90.00) | |

| | | | | |

| Net asset value, end of year | | | $527.84 | | | | $749.94 | | | | $759.44 | | | | $799.71 | | | | $708.75 | |

Total return, based on NAV2 | | | (22.94) | % | | | 8.20 | % | | | 5.04 | % | | | 26.72 | % | | | (12.74) | % |

| | | | | |

| Net assets, end of year (millions) | | | $107 | | | | $173 | | | | $198 | | | | $229 | | | | $222 | |

| | | | | |

| Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

Gross expenses | | | 2.31 | % | | | 2.29 | % | | | 2.36 | % | | | 2.45 | % | | | 1.83 | % |

Net expenses | | | 2.18 | 3 | | | 2.17 | 3 | | | 2.23 | 3 | | | 2.40 | 3 | | | 1.83 | |

Net investment income | | | 8.56 | | | | 8.98 | | | | 9.81 | | | | 11.37 | | | | 11.20 | |

| | | | | |

| Portfolio turnover rate | | | 56 | % | | | 28 | % | | | 32 | % | | | 51 | % | | | 39 | % |

| | | | |

| Supplemental data: | | | | | | | | | | | | | | | | | |

Loan Outstanding, End of Year (000s) | | | $30,300 | | | | $23,300 | | | | $47,400 | | | | $94,000 | | | | $53,000 | |

Asset Coverage Ratio for Loan Outstanding4 | | | 453 | % | | | 844 | % | | | 518 | % | | | 343 | % | | | 518 | % |

Asset Coverage, per $1,000 Principal Amount of Loan Outstanding4 | | | $4,528 | | | | $8,439 | | | | $5,184 | | | | $3,431 | | | | $5,181 | |

Weighted Average Loan (000s) | | | $31,672 | | | | $36,567 | | | | $58,175 | | | | $88,175 | | | | $53,000 | |

Weighted Average Interest Rate on Loan | | | 2.46 | % | | | 3.00 | % | | | 2.08 | % | | | 1.37 | % | | | 1.00 | % |

| 1 | Per share amounts have been calculated using the average shares method. |

| 2 | Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Reflects fee waivers and/or expense reimbursements. |

| 4 | Represents value of net assets plus the loan outstanding at the end of the period divided by the loan outstanding at the end of the period. |

See Notes to Financial Statements.

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 21 |

Notes to financial statements

1. Organization and significant accounting policies

Western Asset Middle Market Income Fund Inc. (the “Fund”) was incorporated in Maryland on June 29, 2011 and is registered as anon-diversified, limited-termclosed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund commenced operations on August 26, 2014. The Fund’s primary investment objective is to provide high income. As a secondary objective, the Fund seeks capital appreciation. The Fund seeks to achieve its investment objectives by investing, under normal market conditions, at least 80% of its managed assets (the net assets of the Fund plus the principal amount of any borrowings and any preferred stock that may be outstanding) in securities, including loans, issued by middle market companies. For investment purposes, “middle market” refers to companies with annual revenues of between $100 million and $1 billion at the time of investment by the Fund. Securities of middle market issuers are typically considered below investment grade (also commonly referred to as “junk bonds”). It is anticipated that the Fund will terminate on or before December 30, 2022. Upon its termination, it is anticipated that the Fund will have distributed substantially all of its net assets to stockholders, although securities for which no market exists or securities trading at depressed prices, if any, may be placed in a liquidating trust.

On October 31, 2019 and April 1, 2020, the Board of Directors of the Fund approved amendments to the Fund’s bylaws. The amended and restated bylaws were subsequently filed on Form8-K and are available on the Securities and Exchange Commission’s website at www.sec.gov.

The following are significant accounting policies consistently followed by the Fund and are in conformity with U.S. generally accepted accounting principles (“GAAP”). Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ. Subsequent events have been evaluated through the date the financial statements were issued.

(a) Investment valuation.The valuations for fixed income securities (which may include, but are not limited to, corporate, government, municipal, mortgage-backed, collateralized mortgage obligations and asset-backed securities) and certain derivative instruments are typically the prices supplied by independent third party pricing services, which may use market prices or broker/dealer quotations or a variety of valuation techniques and methodologies. The independent third party pricing services use inputs that are observable such as issuer details, interest rates, yield curves, prepayment speeds, credit risks/spreads, default rates and quoted prices for similar securities. Investments inopen-end funds are valued at the closing net asset value per share of each fund on the day of valuation. Equity securities for which market quotations are available are valued at the last reported sales price or official closing price on the primary market or exchange on which they trade. When

| | |

| 22 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

the Fund holds securities or other assets that are denominated in a foreign currency, the Fund will normally use the currency exchange rates as of 4:00 p.m. (Eastern Time). If independent third party pricing services are unable to supply prices for a portfolio investment, or if the prices supplied are deemed by the manager to be unreliable, the market price may be determined by the manager using quotations from one or more broker/ dealers or at the transaction price if the security has recently been purchased and no value has yet been obtained from a pricing service or pricing broker. When reliable prices are not readily available, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded, but before the Fund calculates its net asset value, the Fund values these securities as determined in accordance with procedures approved by the Fund’s Board of Directors.

The Board of Directors is responsible for the valuation process and has delegated the supervision of the daily valuation process to the Legg Mason North Atlantic Fund Valuation Committee (the “Valuation Committee”). The Valuation Committee, pursuant to the policies adopted by the Board of Directors, is responsible for making fair value determinations, evaluating the effectiveness of the Fund’s pricing policies, and reporting to the Board of Directors. When determining the reliability of third party pricing information for investments owned by the Fund, the Valuation Committee, among other things, conducts due diligence reviews of pricing vendors, monitors the daily change in prices and reviews transactions among market participants.

The Valuation Committee will consider pricing methodologies it deems relevant and appropriate when making fair value determinations. Examples of possible methodologies include, but are not limited to, multiple of earnings; discount from market of a similar freely traded security; discounted cash-flow analysis; book value or a multiple thereof; risk premium/yield analysis; yield to maturity; and/or fundamental investment analysis. The Valuation Committee will also consider factors it deems relevant and appropriate in light of the facts and circumstances. Examples of possible factors include, but are not limited to, the type of security; the issuer’s financial statements; the purchase price of the security; the discount from market value of unrestricted securities of the same class at the time of purchase; analysts’ research and observations from financial institutions; information regarding any transactions or offers with respect to the security; the existence of merger proposals or tender offers affecting the security; the price and extent of public trading in similar securities of the issuer or comparable companies; and the existence of a shelf registration for restricted securities.

For each portfolio security that has been fair valued pursuant to the policies adopted by the Board of Directors, the fair value price is compared against the last available and next available market quotations. The Valuation Committee reviews the results of such back testing monthly and fair valuation occurrences are reported to the Board of Directors quarterly.

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 23 |

Notes to financial statements (cont’d)

The Fund uses valuation techniques to measure fair value that are consistent with the market approach and/or income approach, depending on the type of security and the particular circumstance. The market approach uses prices and other relevant information generated by market transactions involving identical or comparable securities. The income approach uses valuation techniques to discount estimated future cash flows to present value.

GAAP establishes a disclosure hierarchy that categorizes the inputs to valuation techniques used to value assets and liabilities at measurement date. These inputs are summarized in the three broad levels listed below:

| • | | Level 1 — quoted prices in active markets for identical investments |

| • | | Level 2 — other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.) |

| • | | Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used in valuing the Fund’s assets and liabilities carried at fair value:

| | | | | | | | | | | | | | | | |

| ASSETS | |

| Description | | Quoted Prices

(Level 1) | | | Other Significant

Observable Inputs

(Level 2) | | | Significant

Unobservable

Inputs (Level 3) | | | Total | |

| Long-Term Investments†: | | | | | | | | | | | | | | | | |

Corporate Bonds & Notes: | | | | | | | | | | | | | | | | |

Information Technology | | | — | | | | — | | | $ | 54,480 | | | $ | 54,480 | |

Other Corporate Bonds & Notes | | | — | | | $ | 69,814,222 | | | | — | | | | 69,814,222 | |

Senior Loans: | | | | | | | | | | | | | | | | |

Communication Services | | | — | | | | 957,500 | | | | 1,327,500 | | | | 2,285,000 | |

Consumer Discretionary | | | — | | | | 5,762,571 | | | | 5,248,823 | | | | 11,011,394 | |

Financials | | | — | | | | 3,486,877 | | | | 2,788,796 | | | | 6,275,673 | |

Health Care | | | — | | | | 11,816,681 | | | | 2,826,067 | | | | 14,642,748 | |

Information Technology | | | — | | | | 8,547,302 | | | | 3,054,466 | | | | 11,601,768 | |

Real Estate | | | — | | | | 1,708,129 | | | | 2,440,011 | | | | 4,148,140 | |

Utilities | | | — | | | | — | | | | 2,690,153 | | | | 2,690,153 | |

Other Senior Loans | | | — | | | | 8,086,994 | | | | — | | | | 8,086,994 | |

Common Stocks: | | | | | | | | | | | | | | | | |

Utilities | | | — | | | | — | | | | 1,965,810 | | | | 1,965,810 | |

Other Common Stocks | | $ | 1,180,142 | | | | — | | | | — | | | | 1,180,142 | |

Preferred Stocks | | | 1,835,303 | | | | — | | | | — | | | | 1,835,303 | |

Warrants | | | — | | | | — | | | | 621,494 | | | | 621,494 | |

| Total Long-Term Investments | | | 3,015,445 | | | | 110,180,276 | | | | 23,017,600 | | | | 136,213,321 | |

| Short-Term Investments† | | | 85,093 | | | | — | | | | — | | | | 85,093 | |

| Total Investments | | $ | 3,100,538 | | | $ | 110,180,276 | | | $ | 23,017,600 | | | $ | 136,298,414 | |

| | |

| 24 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

| | | | | | | | | | | | | | | | |

|

LIABILITIES | |

| Description | | Quoted Prices

(Level 1) | | | Other Significant

Observable Inputs

(Level 2) | | | Significant

Unobservable

Inputs (Level 3) | | | Total | |

| Other Financial Instruments: | | | | | | | | | | | | | | | | |

Forward Foreign Currency Contracts | | | — | | | $ | 1,825 | | | | — | | | $ | 1,825 | |

| † | See Schedule of Investments for additional detailed categorizations. |

The following is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value:

| | | | | | | | | | | | | | | | | | | | |

| Investments in Securities | | Balance as of April 30,

2019 | | | Accrued

premiums/

discounts | | | Realized gain (loss)1 | | | Change in

unrealized

appreciation

(depreciation)2 | | | Purchases | |

| Corporate Bonds & Notes: | | | | | | | | | | | | | | | | | | | | |

Energy | | $ | 0 | * | | | — | | | $ | 0 | * | | | — | | | | — | |

Health Care | | | 4,246,529 | | | $ | 5,894 | | | | 650,219 | | | $ | (456,830) | | | $ | 183,577 | |

Information Technology | | | — | | | | — | | | | — | | | | — | | | | — | |

| Senior Loans: | | | | | | | | | | | | | | | | | | | | |

Communication Services | | | — | | | | 174 | | | | — | | | | (165,174) | | | | 1,492,500 | |

Consumer Discretionary | | | 1,902,735 | | | | 202,217 | | | | (2,026,840) | | | | 261,283 | | | | 948,438 | |

Consumer Staples | | | 4,342,650 | | | | 4,456 | | | | (1,154) | | | | 40,898 | | | | — | |

Financials | | | 5,211,484 | | | | 3,075 | | | | 443 | | | | (711,479) | | | | — | |

Health Care | | | — | | | | 2,751 | | | | 95 | | | | (94,011) | | | | 2,927,382 | |

Information Technology | | | — | | | | — | | | | — | | | | — | | | | — | |

Real Estate | | | 2,619,936 | | | | 4,423 | | | | 761 | | | | (91,270) | | | | — | |

Utilities | | | — | | | | — | | | | — | | | | — | | | | — | |

| Common Stocks: | | | | | | | | | | | | | | | | | | | | |

Utilities | | | 1,965,810 | | | | — | | | | — | | | | — | | | | — | |

| Warrants | | | 282,624 | | | | — | | | | (1) | | | | 370,242 | | | | 94,113 | |

| Total | | $ | 20,571,768 | | | $ | 222,990 | | | $ | (1,376,477) | | | $ | (846,341) | | | $ | 5,646,010 | |

| | |

| | |

| Western Asset Middle Market Income Fund Inc. 2020 Annual Report | | 25 |

Notes to financial statements (cont’d)

| | | | | | | | | | | | | | | | | | | | |

Investments in

Securities (cont’d) | | Sales | | | Transfers into Level 33 | | | Transfers out of Level 34 | | | Balance as of April 30,

2020 | | | Net change

in unrealized

appreciation

(depreciation)

for

investments

in securities

still held at

April 30, 20202 | |

| Corporate Bonds & Notes: | | | | | | | | | | | | | | | | | | | | |

Energy | | $ | (0) | * | | | — | | | | — | | | | — | | | | — | |

Health Care | | | (4,629,389) | | | | — | | | | — | | | | — | | | | — | |

Information Technology | | | — | | | $ | 54,480 | | | | — | | | $ | 54,480 | | | | — | |

| Senior Loans: | | | | | | | | | | | | | | | | | | | | |

Communication Services | | | — | | | | — | | | | — | | | | 1,327,500 | | | $ | (165,174) | |

Consumer Discretionary | | | (427,987) | | | | 4,388,977 | | | | — | | | | 5,248,823 | | | | (89,376) | |

Consumer Staples | | | (4,386,850) | | | | — | | | | — | | | | — | | | | — | |

Financials | | | (103,600) | | | | — | | | $ | (1,611,127) | | | | 2,788,796 | | | | (353,954) | |

Health Care | | | (10,150) | | | | — | | | | — | | | | 2,826,067 | | | | (94,011) | |

Information Technology | | | — | | | | 3,054,466 | | | | — | | | | 3,054,466 | | | | — | |

Real Estate | | | (93,839) | | | | — | | | | — | | | | 2,440,011 | | | | (91,270) | |

Utilities | | | — | | | | 2,690,153 | | | | — | | | | 2,690,153 | | | | — | |

| Common Stocks: | | | | | | | | | | | | | | | | | | | | |

Utilities | | | — | | | | — | | | | — | | | | 1,965,810 | | | | — | |

| Warrants | | | (125,484) | | | | — | | | | — | | | | 621,494 | | | | 527,381 | |

| Total | | $ | (9,777,299) | | | $ | 10,188,076 | | | $ | (1,611,127) | | | $ | 23,017,600 | | | $ | (266,404) | |

| * | Amount represents less than $1. |

| 1 | This amount is included in net realized gain (loss) from investment transactions in the accompanying Statement of Operations. |

| 2 | This amount is included in the change in net unrealized appreciation (depreciation) in the accompanying Statement of Operations. Change in unrealized appreciation (depreciation) includes net unrealized appreciation (depreciation) resulting from changes in investment values during the reporting period and the reversal of previously recorded unrealized appreciation (depreciation) when gains or losses are realized. |

| 3 | Transferred into Level 3 as a result of the unavailability of a quoted price in an active market for an identical investment or the unavailability of other significant observable inputs. |

| 4 | Transferred out of Level 3 as a result of the availability of a quoted price in an active market for an identical investment or the availability of other significant observable inputs. |

The following table summarizes the valuation techniques used and unobservable inputs approved by the Valuation Committee to determine the fair value of certain, material Level 3 investments. The table does not include Level 3 investments with values derived utilizing

| | |

| 26 | | Western Asset Middle Market Income Fund Inc. 2020 Annual Report |

prices from prior transactions or third party pricing information without adjustment (e.g., broker quotes, pricing services, net asset values).

| | | | | | | | | | | | | | | | |

| | | Fair Value at 4/30/20

(000’s) | | | Valuation Technique(s) | | | Unobservable Input(s) | | Range/Average | | Impact to Valuation

from an Increase in

Input* | |

| Senior Loans | | $ | 2,440 | | | | Market Approach | | | Yield to

Maturity | | 2.681% - 9.757%

range4.294% average | | | Decrease | |

| | | | | |