UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22582

Western Asset Middle Market Income Fund Inc.

(Exact name of registrant as specified in charter)

620 Eighth Avenue, 47th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

Gorge P. Hoyt.

Franklin Templeton

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (888) 777-0102

Date of fiscal year end: April 30

Date of reporting period: April 30, 2022

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Annual Report to Stockholders is filed herewith.

| | |

Annual Report | | April 30, 2022 |

WESTERN ASSET

MIDDLE MARKET

INCOME FUND INC.

|

| INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

Fund objectives

The Fund’s primary investment objective is to provide high income. As a secondary investment objective, the Fund seeks capital appreciation.

The Fund seeks to achieve its investment objectives by investing, under normal market conditions, at least 80% of its managed assets (the net assets of the Fund plus the principal amount of any borrowings and any preferred stock that may be outstanding) in securities, including loans, issued by middle market companies. For investment purposes, “middle market” refers to companies with annual revenues of between $100 million and $1 billion at the time of investment by the Fund. Securities of middle market issuers are typically considered below investment grade (also commonly referred to as “junk bonds”).

It is anticipated that the Fund will terminate on or before December 30, 2022.

| | |

II | | Western Asset Middle Market Income Fund Inc. |

Letter from the chairman

Dear Shareholder,

We are pleased to provide the annual report of Western Asset Middle Market Income Fund Inc. for the twelve-month reporting period ended April 30, 2022. Please read on for Fund performance information and a detailed look at prevailing economic and market conditions during the Fund’s reporting period and to learn how those conditions have affected Fund performance.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our website, www.franklintempleton.com. Here you can gain immediate access to market and investment information, including:

| • | | Fund prices and performance, |

| • | | Market insights and commentaries from our portfolio managers, and |

| • | | A host of educational resources. |

We look forward to helping you meet your financial goals.

Sincerely,

Jane Trust, CFA

Chairman, President and Chief Executive Officer

May 31, 2022

| | |

| Western Asset Middle Market Income Fund Inc. | | III |

Fund overview

Q. What is the Fund’s investment strategy?

A. The Fund’s primary investment objective is to provide high income. As a secondary investment objective, the Fund seeks capital appreciation. The Fund seeks to achieve its investment objectives by investing, under normal market conditions, at least 80% of its managed assets (the net assets of the Fund plus the principal amount of any borrowings and any preferred stock that may be outstanding) in securities, including loans, issued by middle market companies. For investment purposes, “middle market” refers to companies with annual revenues of between $100 million and $1 billion at the time of investment by the Fund. Securities of middle market issuers are typically considered high yield. High yield securities are below investment grade quality (also commonly referred to as “junk bonds”).

The Fund may also invest up to 20% of its managed assets in non-middle market securities. The non-middle market securities the Fund expects to invest in include corporate debt securities rated investment grade or below investment grade of U.S. and foreign (including emerging markets) issuers and U.S. government debt securities.

No more than 10% of the Fund’s managed assets may be invested in any one issuer, except securities issued by the U.S. government and its agencies. The Fund may sell certain fixed income and equity securities short including, but not limited to, U.S. government debt securities, for hedging purposes. The Fund may invest all or a portion of its managed assets in illiquid securities.

The Fund is an actively managed portfolio consisting primarily of fixed income securities. The duration of the Fund’s portfolio is anticipated to be between two and four years. However, the duration may change significantly at any time and is dependent on market conditions and investment opportunities available to the Fund. The Fund has a limited term. It is anticipated that the Fund will terminate on or before December 30, 2022. Although it has an anticipated term of eight years, the Fund’s term may be shorter or longer, depending on market conditions. Upon its termination, it is anticipated that the Fund will have distributed substantially all of its net assets to stockholders, although securities for which no market exists or securities trading at depressed prices, if any, may be placed in a liquidating trust. Securities placed in a liquidating trust may be held for an indefinite period of time until they can be sold or pay out all of their cash flows. The Fund cannot predict the amount of securities that will be required to be placed in a liquidating trust.

At Western Asset Management Company, LLC (“Western Asset”), the Fund’s subadviser, we utilize a fixed income team approach, with decisions derived from interaction among various investment management sector specialists. The sector teams are comprised of Western Asset’s senior portfolio management personnel, research analysts and an in-house economist. Under this team approach, management of client fixed income portfolios reflects a consensus of interdisciplinary views within the Western Asset organization. The individuals responsible for development of investment strategy, day-to-day portfolio management, oversight and coordination of the Fund are S. Kenneth Leech, Michael C. Buchanan, Christopher N. Jacobs and Christopher F. Kilpatrick.

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 1 |

Fund overview (cont’d)

Q. What were the overall market conditions during the Fund’s reporting period?

A. Fixed income markets experienced periods of volatility and, overall, declined over the twelve-month reporting period ended April 30, 2022. Volatility was driven by a number of factors, including the repercussions from the COVID-19 pandemic, the fluctuating global economy, sharply rising inflation and interest rates, central bank monetary policy tightening, and the war in Ukraine.

Short-term U.S. Treasury yields moved sharply higher, as the Federal Reserve Board (the “Fed”) began raising interest rates at its meeting in March 2022. The yield for the two-year Treasury note began the reporting period at 0.16% and ended the reporting period at 2.70%. The low of 0.13% occurred on June 2, 2021. The high of 2.72% took place on April 22, 2022. Long-term U.S. Treasury yields also moved higher, as rising inflation triggered expectations that the Fed would begin removing its monetary policy accommodation. The yield for the ten-year Treasury note began the reporting period at 1.65% and ended the reporting period at 2.89%. The low of 1.19% occurred on August 3 and August 4, 2021, and the high of 2.93% occurred on April 19, 2022.

All told, the Bloomberg U.S. Aggregate Indexi returned -8.51% for the twelve months ended April 30, 2022. Riskier fixed income securities, including high-yield bonds, also posted weak results. Over the reporting period, the Bloomberg U.S. Corporate High Yield — 2% Issuer Cap Indexii returned -5.22%. Elsewhere, the JPMorgan Emerging Markets Bond Index Global (“EMBI Global”)iii returned -12.98% for the twelve months ended April 30, 2022.

Q. How did we respond to these changing market conditions?

A. A number of adjustments were made to the Fund’s portfolio during the reporting period. From a sector perspective, we increased the Fund’s exposure to energy and increased its allocation to investment-grade corporate bonds, largely in the consumer non-cyclicals1 sector. Elsewhere, we reduced the Fund’s duration.

During the reporting period, we utilized leverage in the Fund. We ended the period with liabilities as a percentage of total assets of approximately 11%, versus 18% at the beginning of the period. The use of leverage modestly contributed to performance over the reporting period.

Performance review

For the twelve months ended April 30, 2022, Western Asset Middle Market Income Fund Inc. returned 0.73% based on its net asset value (“NAV”)iv. The Fund’s unmanaged benchmark, the Bloomberg U.S. High Yield — 2% Issuer Cap Caa Componentv, returned -4.15% for the same period. The Lipper High Yield (Leveraged) Closed-End Funds Category Averagevi returned -4.86% over the same time frame. Please note that Lipper performance returns are based on each fund’s NAV.

| 1 | Non-cyclicals consists of the following industries: consumer products, food/beverage, health care, pharmaceuticals, supermarkets and tobacco. |

| | |

2 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

During the twelve-month period, the Fund made distributions to shareholders totaling $34.33 per share.* The performance table shows the Fund’s twelve-month total return based on its NAV as of April 30, 2022. Past performance is no guarantee of future results.

| | | | |

| Performance Snapshot as of April 30, 2022 | |

| Price Per Share | | 12-Month

Total Return** | |

| $607.33 (NAV) | | | 0.73 | %† |

All figures represent past performance and are not a guarantee of future results.

| ** | Total return is based on changes in NAV. Return reflects the deduction of all Fund expenses, including management fees, operating expenses, and other Fund expenses. Return does not reflect the deduction of brokerage commissions or taxes that investors may pay on distributions or the disposition of shares. |

| † | Total returns assume the reinvestment of all distributions at NAV. |

Q. What were the leading contributors to performance?

A. The largest contributor to the Fund’s performance during the reporting period was its security selection. In particular, the Fund’s exposures to energy (Oasis Petroleum), consumer cyclicals2 (Jacobs Entertainment) and technology (Access CIG) added the most value.

Q. What were the leading detractors from performance?

A. Security selection in capital goods, including Waste Pro USA, and in consumer non-cyclicals, driven by Kraft Heinz, were the largest detractors from performance during the reporting period.

Looking for additional information?

The Fund’s daily NAV is available online under the symbol “XWMFX” on most financial websites. In a continuing effort to provide information concerning the Fund, shareholders may call 1-888-777-0102 (toll free), Monday through Friday from 8:00 a.m. to 5:30 p.m. Eastern Time, for the Fund’s current NAV and other information.

Thank you for your investment in Western Asset Middle Market Income Fund Inc. As always, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

Western Asset Management Company, LLC

May 12, 2022

| * | For the tax character of distributions paid during the fiscal period ended April 30, 2022, please refer to page 37 of this report. |

| 2 | Consumer cyclicals consists of the following industries: automotive, entertainment, gaming, home construction, lodging, retailers, restaurants, textiles, and other consumer services. |

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 3 |

Fund overview (cont’d)

RISKS: The Fund is a non-diversified closed-end management investment company. An investment in the Fund involves a high degree of risk. The Fund should be considered an illiquid investment. This Fund is not publicly traded and is closed to new investors. The Fund does not intend to apply for an exchange listing, and it is highly unlikely that a secondary market will exist for the purchase and sale of the Fund’s shares. Investors could lose some or all of their investment. An investment in the Fund is not appropriate for all investors and is not intended to be a complete investment program. The Fund is designed as a long-term investment for investors who are prepared to hold the Fund’s Common Stock until the expiration of its term and is not a trading vehicle. Because the Fund is non-diversified, it may be more susceptible to economic, political, or regulatory events than a diversified fund. Fixed income securities are subject to numerous risks, including but not limited to, credit, inflation, income, prepayment, and interest rates risks. As interest rates rise, the value of fixed income securities falls. Middle market companies have additional risks due to their limited operating histories, limited financial resources, less predictable operating results, narrower product lines and other factors. Securities of middle market issuers are typically considered high-yield. High-yield fixed income securities of below-investment-grade quality are regarded as having predominantly speculative characteristics with respect to the issuer’s capacity to pay interest and repay principal. High-yield bonds (“junk bonds”) are subject to higher credit risk and a greater risk of default. The Fund may invest all or a portion of its managed assets in illiquid securities. The Fund may make significant investments in securities for which there are no observable market prices. Investments in foreign securities involve risks, including the possibility of losses due to changes in currency exchange rates and negative developments in the political, economic or regulatory structure of specific countries or regions. These risks are greater in emerging markets. Emerging market countries tend to have economic, political, and legal systems that are less developed and are less stable than those of more developed countries. Leverage may result in greater volatility of the net asset value of common shares and increases a shareholder’s risk of loss. Derivative instruments can be illiquid, may disproportionately increase losses and have a potentially large impact on Fund performance. Distributions are not guaranteed and are subject to change. The Fund may also invest in money market funds, including funds affiliated with the Fund’s manager and subadvisers. For more information on Fund risks, see Summary of information regarding the Fund - Principal Risk Factors in this report.

Portfolio holdings and breakdowns are as of April 30, 2022 and are subject to change and may not be representative of the portfolio managers’ current or future investments. Please refer to pages 9 through 16 for a list and percentage breakdown of the Fund’s holdings.

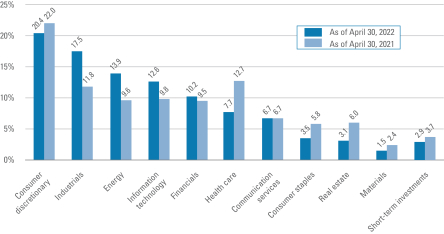

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. The Fund’s top five sector holdings (as a percentage of net assets) as of April 30, 2022 were: consumer discretionary (22.0%), industrials (19.0%), energy (15.0%), information technology (13.6%) and financials (11.1%). The Fund’s portfolio composition is subject to change at any time.

| | |

4 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

| i | The Bloomberg U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage-and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| ii | The Bloomberg U.S. Corporate High Yield — 2% Issuer Cap Index is an index of the 2% Issuer Cap component of the Bloomberg U.S. Corporate High Yield Index, which covers the U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market. |

| iii | The JPMorgan Emerging Markets Bond Index Global (“EMBI Global”) tracks total returns for U.S. dollar-denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Euro bonds and local market instruments. |

| iv | Net asset value (“NAV”) is calculated by subtracting total liabilities, including liabilities associated with financial leverage (if any), from the closing value of all securities held by the Fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the market prices of securities in which the Fund has invested. |

| v | The Bloomberg U.S. High Yield — 2% Issuer Cap Caa Component is an index of the 2% Issuer Cap Caa component of the Bloomberg U.S. High Yield Index, which covers the U.S. dollar denominated, noninvestment grade, fixed-rate, taxable corporate bond market. |

| vi | Lipper, Inc., a wholly-owned subsidiary of Refinitiv, provides independent insight on global collective investments. Returns are based on the twelve-month period ended April 30, 2022, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 38 funds in the Fund’s Lipper category. |

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 5 |

Fund at a glance† (unaudited)

Investment breakdown (%) as a percent of total investments

| † | The bar graph above represents the composition of the Fund’s investments as of April 30, 2022 and April 31, 2021. The Fund is actively managed. As a result, the composition of the Fund’s investments is subject to change at any time. |

| | |

6 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

Fund performance (unaudited)

| | | | |

| Net Asset Value | | | |

| Average annual total returns1 | | | |

| Twelve Months Ended 4/30/22 | | | 0.73 | % |

| Five Years Ended 4/30/22 | | | 2.58 | |

| Inception date of 8/26/14 through 4/30/22 | | | 2.45 | |

| |

| Cumulative total returns1 | | | |

| Inception date of 8/26/14 through 4/30/22 | | | 20.41 | % |

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower.

| 1 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. |

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 7 |

Fund performance (unaudited) (cont’d)

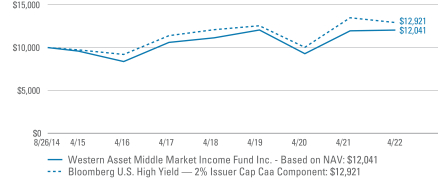

Historical performance

Value of $10,000 invested in

Western Asset Middle Market Income Fund Inc. vs. Bloomberg U.S. High Yield — 2% Issuer Cap Caa Component†— August 26, 2014 - April 30, 2022

All figures represent past performance and are not a guarantee of future results. Returns reflect the deduction of all Fund expenses, including management fees, operating expenses, and other Fund expenses. Returns do not reflect the deduction of brokerage commissions or taxes that investors may pay on distributions or the sale of shares.

| † | Hypothetical illustration of $10,000 invested in the Western Asset Middle Market Income Fund Inc. on August 26, 2014, assuming the reinvestment of all distributions, including returns of capital, if any, at net asset value and also assuming the reinvestment of all distributions, including returns of capital, if any, in additional shares in accordance with the Fund’s Dividend Reinvestment Plan through April 30, 2022. The hypothetical illustration also assumes a $10,000 investment in the Bloomberg U.S. High Yield — 2% Issuer Cap Caa Component. The Bloomberg U.S. High Yield — 2% Issuer Cap Caa Component (the “Index”) is an index of the 2% Issuer Cap Caa component of the Bloomberg U.S. High Yield Index, which covers the U.S. dollar denominated, non-investment grade, fixed-rate, taxable corporate bond market. The Index is unmanaged and is not subject to the same management and trading expenses as a mutual fund. Please note that an investor cannot invest directly in an index. |

| | |

8 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

Schedule of investments

April 30, 2022

Western Asset Middle Market Income Fund Inc.

(Percentages shown based on Fund net assets)

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount | | | Value | |

| Corporate Bonds & Notes — 61.9% | | | | | | | | | | | | | | | | |

| Communication Services — 5.6% | | | | | | | | | | | | | | | | |

Entertainment — 1.4% | | | | | | | | | | | | | | | | |

Allen Media LLC/Allen Media Co-Issuer Inc., Senior Notes | | | 10.500 | % | | | 2/15/28 | | | $ | 1,390,000 | | | $ | 1,256,379 | (a)(b) |

Media — 1.3% | | | | | | | | | | | | | | | | |

DISH DBS Corp., Senior Notes | | | 7.750 | % | | | 7/1/26 | | | | 1,000,000 | | | | 941,880 | |

Urban One Inc., Senior Secured Notes | | | 7.375 | % | | | 2/1/28 | | | | 220,000 | | | | 213,398 | (a) |

Total Media | | | | | | | | | | | | | | | 1,155,278 | |

Wireless Telecommunication Services — 2.9% | | | | | | | | | | | | | | | | |

Sprint Corp., Senior Notes | | | 7.875 | % | | | 9/15/23 | | | | 2,520,000 | | | | 2,649,264 | (b) |

Total Communication Services | | | | | | | | | | | | | | | 5,060,921 | |

| Consumer Discretionary — 15.4% | | | | | | | | | | | | | | | | |

Auto Components — 1.0% | | | | | | | | | | | | | | | | |

American Axle & Manufacturing Inc., Senior Notes | | | 6.500 | % | | | 4/1/27 | | | | 1,000,000 | | | | 933,075 | |

Distributors — 1.1% | | | | | | | | | | | | | | | | |

Accelerate360 Holdings LLC, Secured Notes | | | 8.000 | % | | | 3/1/28 | | | | 485,100 | | | | 508,239 | (a) |

American News Co. LLC, Secured Notes (8.500% Cash or 10.000% PIK) | | | 8.500 | % | | | 9/1/26 | | | | 470,628 | | |

| 528,271

| (a)(c)

|

Total Distributors | | | | | | | | | | | | | | | 1,036,510 | |

Diversified Consumer Services — 1.4% | | | | | | | | | | | | | | | | |

StoneMor Inc., Senior Secured Notes | | | 8.500 | % | | | 5/15/29 | | | | 1,270,000 | | | | 1,230,401 | (a)(b) |

Hotels, Restaurants & Leisure — 8.4% | | | | | | | | | | | | | | | | |

Carnival Corp., Senior Notes | | | 7.625 | % | | | 3/1/26 | | | | 150,000 | | | | 146,984 | (a) |

CCM Merger Inc., Senior Notes | | | 6.375 | % | | | 5/1/26 | | | | 2,000,000 | | | | 1,997,810 | (a)(b) |

Full House Resorts Inc., Senior Secured Notes | | | 8.250 | % | | | 2/15/28 | | | | 2,020,000 | | | | 2,002,810 | (a) |

Golden Entertainment Inc., Senior Notes | | | 7.625 | % | | | 4/15/26 | | | | 3,290,000 | | | | 3,368,680 | (a)(b) |

Total Hotels, Restaurants & Leisure | | | | | | | | | | | | | | | 7,516,284 | |

Household Durables — 1.3% | | | | | | | | | | | | | | | | |

CD&R Smokey Buyer Inc., Senior Secured Notes | | | 6.750 | % | | | 7/15/25 | | | | 350,000 | | | | 357,087 | (a) |

New Home Co. Inc., Senior Notes | | | 7.250 | % | | | 10/15/25 | | | | 820,000 | | | | 776,450 | (a) |

Total Household Durables | | | | | | | | | | | | | | | 1,133,537 | |

See Notes to Financial Statements.

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 9 |

Schedule of investments (cont’d)

April 30, 2022

Western Asset Middle Market Income Fund Inc.

(Percentages shown based on Fund net assets)

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount | | | Value | |

Specialty Retail — 2.2% | | | | | | | | | | | | | | | | |

Bath & Body Works Inc., Senior Notes | | | 6.625 | % | | | 10/1/30 | | | $ | 1,000,000 | | | $ | 996,500 | (a) |

Guitar Center Inc., Senior Secured Notes | | | 8.500 | % | | | 1/15/26 | | | | 1,000,000 | | | | 1,003,435 | (a) |

Total Specialty Retail | | | | | | | | | | | | | | | 1,999,935 | |

Total Consumer Discretionary | | | | | | | | | | | | | | | 13,849,742 | |

| Consumer Staples — 1.1% | | | | | | | | | | | | | | | | |

Food Products — 1.1% | | | | | | | | | | | | | | | | |

Kraft Heinz Foods Co., Senior Notes | | | 5.000 | % | | | 6/4/42 | | | | 1,000,000 | | | | 964,198 | |

| Energy — 13.7% | | | | | | | | | | | | | | | | |

Energy Equipment & Services — 1.3% | | | | | | | | | | | | | | | | |

Sunnova Energy Corp., Senior Notes | | | 5.875 | % | | | 9/1/26 | | | | 1,260,000 | | | | 1,154,594 | (a) |

Oil, Gas & Consumable Fuels — 12.4% | | | | | | | | | | | | | | | | |

Antero Midstream Partners LP/Antero Midstream Finance Corp., Senior Notes | | | 5.750 | % | | | 1/15/28 | | | | 1,990,000 | | | | 1,938,797 | (a)(b) |

Berry Petroleum Co. LLC, Senior Notes | | | 7.000 | % | | | 2/15/26 | | | | 4,450,000 | | | | 4,324,911 | (a)(b) |

Blue Racer Midstream LLC/Blue Racer Finance Corp., Senior Notes | | | 7.625 | % | | | 12/15/25 | | | | 490,000 | | | | 505,290 | (a) |

Chesapeake Energy Corp., Senior Notes | | | 5.500 | % | | | 2/1/26 | | | | 50,000 | | | | 49,635 | (a) |

CrownRock LP/CrownRock Finance Inc., Senior Notes | | | 5.000 | % | | | 5/1/29 | | | | 1,010,000 | | | | 989,770 | (a) |

EnLink Midstream LLC, Senior Notes | | | 5.625 | % | | | 1/15/28 | | | | 170,000 | | | | 168,645 | (a) |

Holly Energy Partners LP/Holly Energy Finance Corp., Senior Notes | | | 5.000 | % | | | 2/1/28 | | | | 2,050,000 | | | | 1,952,717 | (a)(b) |

MEG Energy Corp., Senior Notes | | | 7.125 | % | | | 2/1/27 | | | | 700,000 | | | | 712,142 | (a) |

Range Resources Corp., Senior Notes | | | 4.750 | % | | | 2/15/30 | | | | 350,000 | | | | 334,345 | (a) |

Summit Midstream Holdings LLC/ Summit Midstream Finance Corp., Secured Notes | | | 8.500 | % | | | 10/15/26 | | | | 200,000 | | | | 187,113 | (a) |

Total Oil, Gas & Consumable Fuels | | | | | | | | | | | | | | | 11,163,365 | |

Total Energy | | | | | | | | | | | | | | | 12,317,959 | |

| Financials — 3.9% | | | | | | | | | | | | | | | | |

Capital Markets — 1.1% | | | | | | | | | | | | | | | | |

TriplePoint Venture Growth BDC Corp. | | | 4.500 | % | | | 3/1/26 | | | | 1,000,000 | | | | 936,380 | (d)(e) |

Consumer Finance — 1.6% | | | | | | | | | | | | | | | | |

Midcap Financial Issuer Trust, Senior Notes | | | 6.500 | % | | | 5/1/28 | | | | 750,000 | | | | 648,038 | (a) |

Midcap Financial Issuer Trust, Senior Notes | | | 5.625 | % | | | 1/15/30 | | | | 1,000,000 | | | | 798,095 | (a) |

Total Consumer Finance | | | | | | | | | | | | | | | 1,446,133 | |

See Notes to Financial Statements.

| | |

10 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

Western Asset Middle Market Income Fund Inc.

(Percentages shown based on Fund net assets)

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount | | | Value | |

Thrifts & Mortgage Finance — 1.2% | | | | | | | | | | | | | | | | |

NMI Holdings Inc., Senior Secured Notes | | | 7.375 | % | | | 6/1/25 | | | $ | 1,060,000 | | | $ | 1,106,486 | (a) |

Total Financials | | | | | | | | | | | | | | | 3,488,999 | |

| Health Care — 3.3% | | | | | | | | | | | | | | | | |

Health Care Providers & Services — 3.3% | | | | | | | | | | | | | | | | |

Akumin Inc., Senior Secured Notes | | | 7.000 | % | | | 11/1/25 | | | | 1,090,000 | | | | 919,824 | (a) |

Cano Health LLC, Senior Notes | | | 6.250 | % | | | 10/1/28 | | | | 330,000 | | | | 304,879 | (a) |

Legacy LifePoint Health LLC, Senior Secured Notes | | | 4.375 | % | | | 2/15/27 | | | | 450,000 | | | | 416,810 | (a)(b) |

U.S. Renal Care Inc., Senior Notes | | | 10.625 | % | | | 7/15/27 | | | | 1,500,000 | | | | 1,297,155 | (a) |

Total Health Care | | | | | | | | | | | | | | | 2,938,668 | |

| Industrials — 13.1% | | | | | | | | | | | | | | | | |

Airlines — 1.1% | | | | | | | | | | | | | | | | |

Delta Air Lines Inc./SkyMiles IP Ltd., Senior Secured Notes | | | 4.750 | % | | | 10/20/28 | | | | 1,000,000 | | | | 989,758 | (a) |

Building Products — 0.5% | | | | | | | | | | | | | | | | |

CP Atlas Buyer Inc., Senior Notes | | | 7.000 | % | | | 12/1/28 | | | | 540,000 | | | | 451,759 | (a)(b) |

Commercial Services & Supplies — 2.1% | | | | | | | | | | | | | | | | |

Waste Pro USA Inc., Senior Notes | | | 5.500 | % | | | 2/15/26 | | | | 2,090,000 | | | | 1,861,950 | (a)(b) |

Construction & Engineering — 2.8% | | | | | | | | | | | | | | | | |

Brundage-Bone Concrete Pumping Holdings Inc., Secured Notes | | | 6.000 | % | | | 2/1/26 | | | | 620,000 | | | | 580,509 | (a) |

Empire Communities Corp., Senior Notes | | | 7.000 | % | | | 12/15/25 | | | | 1,120,000 | | |

| 1,062,611

| (a)

|

VM Consolidated Inc., Senior Notes | | | 5.500 | % | | | 4/15/29 | | | | 1,000,000 | | | | 896,220 | (a)(b) |

Total Construction & Engineering | | | | | | | | | | | | | | | 2,539,340 | |

Machinery — 2.0% | | | | | | | | | | | | | | | | |

ATS Automation Tooling Systems Inc., Senior Notes | | | 4.125 | % | | | 12/15/28 | | | | 280,000 | | | | 253,089 | (a) |

Titan International Inc., Senior Secured Notes | | | 7.000 | % | | | 4/30/28 | | | | 720,000 | | | | 706,493 | |

TriMas Corp., Senior Notes | | | 4.125 | % | | | 4/15/29 | | | | 1,000,000 | | | | 893,830 | (a) |

Total Machinery | | | | | | | | | | | | | | | 1,853,412 | |

Professional Services — 0.5% | | | | | | | | | | | | | | | | |

ZipRecruiter Inc., Senior Notes | | | 5.000 | % | | | 1/15/30 | | | | 460,000 | | | | 430,712 | (a) |

Trading Companies & Distributors — 3.1% | | | | | | | | | | | | | | | | |

Alta Equipment Group Inc., Secured Notes | | | 5.625 | % | | | 4/15/26 | | | | 1,890,000 | | | | 1,759,401 | (a) |

See Notes to Financial Statements.

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 11 |

Schedule of investments (cont’d)

April 30, 2022

Western Asset Middle Market Income Fund Inc.

(Percentages shown based on Fund net assets)

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount | | | Value | |

Trading Companies & Distributors — continued | | | | | | | | | | | | | | | | |

Foundation Building Materials Inc., Senior Notes | | | 6.000 | % | | | 3/1/29 | | | $ | 200,000 | | | $ | 162,978 | (a)(b) |

United Rentals North America Inc., Senior Notes | | | 3.875 | % | | | 2/15/31 | | | | 1,000,000 | | | | 883,400 | |

Total Trading Companies & Distributors | | | | | | | | | | | | | | | 2,805,779 | |

Transportation Infrastructure — 1.0% | | | | | | | | | | | | | | | | |

Carriage Purchaser Inc., Senior Notes | | | 7.875 | % | | | 10/15/29 | | | | 1,000,000 | | | | 878,800 | (a) |

Total Industrials | | | | | | | | | | | | | | | 11,811,510 | |

| Information Technology — 1.4% | | | | | | | | | | | | | | | | |

IT Services — 0.5% | | | | | | | | | | | | | | | | |

CPI CG Inc., Senior Secured Notes | | | 8.625 | % | | | 3/15/26 | | | | 468,000 | | | | 453,656 | (a)(b) |

Software — 0.9% | | | | | | | | | | | | | | | | |

Black Knight InfoServ LLC, Senior Notes | | | 3.625 | % | | | 9/1/28 | | | | 320,000 | | | | 297,192 | (a) |

Crowdstrike Holdings Inc., Senior Notes | | | 3.000 | % | | | 2/15/29 | | | | 530,000 | | | | 472,418 | |

Interface Special Holdings Inc., Senior Notes (19.000% PIK) | | | 19.000 | % | | | 11/1/23 | | | | 4,174,495 | | | | 0 | *(c)(d)(e)(f)(g) |

Total Software | | | | | | | | | | | | | | | 769,610 | |

Total Information Technology | | | | | | | | | | | | | | | 1,223,266 | |

| Materials — 1.1% | | | | | | | | | | | | | | | | |

Metals & Mining — 1.1% | | | | | | | | | | | | | | | | |

Mountain Province Diamonds Inc., Secured Notes | | | 8.000 | % | | | 12/15/22 | | | | 1,000,000 | | | | 985,200 | (a) |

| Real Estate — 3.3% | | | | | | | | | | | | | | | | |

Real Estate Management & Development — 3.3% | | | | | | | | | | | | | |

Five Point Operating Co. LP/Five Point Capital Corp., Senior Notes | | | 7.875 | % | | | 11/15/25 | | | | 3,030,000 | | | | 3,010,547 | (a)(b) |

Total Corporate Bonds & Notes (Cost — $62,625,848) | | | | | | | | | | | | 55,651,010 | |

| Senior Loans — 39.8% | | | | | | | | | | | | | | | | |

| Communication Services — 1.6% | | | | | | | | | | | | | | | | |

Entertainment — 1.6% | | | | | | | | | | | | | | | | |

Allen Media LLC, Term Loan B (3 mo. Term SOFR + 5.500%) | | | 6.151 | % | | | 2/10/27 | | | | 1,469,763 | | | | 1,459,475 | (h)(i)(j) |

| Consumer Discretionary — 6.6% | | | | | | | | | | | | | | | | |

Auto Components — 1.1% | | | | | | | | | | | | | | | | |

Autokiniton US Holdings Inc., Closing Date Term Loan B (the greater of 3 mo. USD LIBOR or 0.500% + 4.500%) | | | 5.000 | % | | | 4/6/28 | | | | 992,500 | | | | 979,101 | (h)(i)(j) |

See Notes to Financial Statements.

| | |

12 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

Western Asset Middle Market Income Fund Inc.

(Percentages shown based on Fund net assets)

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount | | | Value | |

Automobiles — 0.2% | | | | | | | | | | | | | | | | |

American Trailer World Corp., First Lien Initial Term Loan (the greater of 1 mo. USD LIBOR or 0.800% + 3.500%) | | | 4.300 | % | | | 3/3/28 | | | $ | 246,878 | | | $ | 230,963 | (h)(i)(j) |

Diversified Consumer Services — 1.1% | | | | | | | | | | | | | | | | |

Lakeshore Learning Materials, Initial Term Loan (the greater of 3 mo. USD LIBOR or 0.500% + 3.500%) | | | 4.000 | % | | | 9/29/28 | | | | 997,500 | | | | 987,730 | (h)(i)(j) |

Hotels, Restaurants & Leisure — 1.1% | | | | | | | | | | | | | | | | |

Pacific Bells LLC, Delayed Draw Term Loan (1 mo. Term SOFR + 4.614%) | | | 5.123 | % | | | 11/10/28 | | | | 10,309 | | | | 10,168 | (e)(h)(i)(j) |

Pacific Bells LLC, Initial Term Loan (the greater of 1 mo. USD LIBOR or 0.500% + 4.500%) | | | 5.000 | % | | | 11/10/28 | | | | 987,217 | | | | 973,642 | (e)(h)(i)(j) |

Total Hotels, Restaurants & Leisure | | | | | | | | | | | | | | | 983,810 | |

Specialty Retail — 3.1% | | | | | | | | | | | | | | | | |

ALCV Purchaser Inc., Initial Term Loan (the greater of 3 mo. USD LIBOR or 1.000% + 6.750%) | | | 7.750 | % | | | 4/15/26 | | | | 812,500 | | | | 811,484 | (e)(h)(i)(j) |

LS Group OpCo Acquisition LLC, Initial Term Loan (the greater of 3 mo. USD LIBOR or 0.750% + 3.250%) | | | 4.000 | % | | | 11/2/27 | | | | 987,500 | | | | 976,391 | (h)(i)(j) |

Rent-A-Center Inc., Term Loan B2 (1 mo. USD LIBOR + 3.250%) | | | 3.813 | % | | | 2/17/28 | | | | 997,481 | | | | 978,903 | (h)(i)(j) |

Total Specialty Retail | | | | | | | | | | | | | | | 2,766,778 | |

Total Consumer Discretionary | | | | | | | | 5,948,382 | |

| Consumer Staples — 2.7% | | | | | | | | | | | | | | | | |

Food Products — 2.7% | | | | | | | | | | | | | | | | |

8th Avenue Food & Provisions Inc., Second Lien Term Loan (1 mo. USD LIBOR + 7.750%) | | | 8.207 | % | | | 10/1/26 | | | | 2,720,000 | | | | 2,459,914 | (h)(i)(j) |

| Financials — 6.7% | | | | | | | | | | | | | | | | |

Capital Markets — 2.2% | | | | | | | | | | | | | | | | |

Cardinal Parent Inc., First Lien Initial Term Loan (the greater of 3 mo. USD LIBOR or 0.750% + 4.500%) | | | 5.250 | % | | | 11/12/27 | | | | 965,251 | | | | 960,039 | (h)(i)(j) |

Cowen Inc., Initial Term Loan (3 mo. USD LIBOR + 3.250%) | | | 4.635 | % | | | 3/24/28 | | | | 987,500 | | | | 964,052 | (h)(i)(j) |

Total Capital Markets | | | | | | | | | | | | | | | 1,924,091 | |

See Notes to Financial Statements.

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 13 |

Schedule of investments (cont’d)

April 30, 2022

Western Asset Middle Market Income Fund Inc.

(Percentages shown based on Fund net assets)

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount | | | Value | |

Insurance — 3.4% | | | | | | | | | | | | | | | | |

AmeriLife Holdings LLC, First Lien Term Loan (1 mo. USD LIBOR + 4.000%) | | | 4.457 | % | | | 3/18/27 | | | $ | 2,014,470 | | | $ | 1,997,679 | (h)(i)(j) |

Baldwin Risk Partners LLC, Term Loan B1 (the greater of 1 mo. USD LIBOR or 0.500% + 3.500%) | | | 4.000 | % | | | 10/14/27 | | | | 1,086,278 | | | | 1,079,038 | (h)(i)(j) |

Total Insurance | | | | | | | | | | | | | | | 3,076,717 | |

Mortgage Real Estate Investment Trusts (REITs) — 1.1% | | | | | | | | | | | | | |

Apollo Commercial Real Estate Finance Inc., Term Loan B1 (the greater of 1 mo. USD LIBOR or 0.500% + 3.500%) | | | 4.000 | % | | | 3/11/28 | | | | 990,000 | | | | 980,100 | (e)(h)(i)(j) |

Total Financials | | | | | | | | | | | | | | | 5,980,908 | |

| Health Care — 3.6% | | | | | | | | | | | | | | | | |

Health Care Providers & Services — 2.5% | | | | | | | | | | | | | | | | |

Agiliti Health Inc., Term Loan (the greater of 1 mo. USD LIBOR or 0.500% + 2.750%) | | | 3.250 | % | | | 1/4/26 | | | | 369,596 | | | | 366,824 | (e)(h)(i)(j) |

EyeCare Partners LLC, First Lien Initial Term Loan (3 mo. USD LIBOR + 3.750%) | | | 4.756 | % | | | 2/18/27 | | | | 1,864,841 | | | | 1,845,194 | (h)(i)(j) |

Total Health Care Providers & Services | | | | | | | | | | | | 2,212,018 | |

Health Care Technology — 1.1% | | | | | | | | | | | | | | | | |

Virgin Pulse Inc., First Lien Term Loan (the greater of 1 mo. USD LIBOR or 0.764% + 4.000%) | | | 4.764 | % | | | 4/6/28 | | | | 995,000 | | | | 973,548 | (h)(i)(j) |

Total Health Care | | | | | | | | | | | | | | | 3,185,566 | |

| Industrials — 5.8% | | | | | | | | | | | | | | | | |

Aerospace & Defense — 0.5% | | | | | | | | | | | | | | | | |

WP CPP Holdings LLC, First Lien Initial Term Loan (1 mo. USD LIBOR + 3.750%) | | | 4.750-4.990 | % | | | 4/30/25 | | | | 490,270 | | | | 464,531 | (h)(i)(j) |

Building Products — 2.1% | | | | | | | | | | | | | | | | |

CP Atlas Buyer Inc., Term Loan B (the greater of 1 mo. USD LIBOR or 0.764% + 3.750%) | | | 4.514 | % | | | 11/23/27 | | | | 990,131 | | | | 933,030 | (h)(i)(j) |

Potters Industries LLC, Initial Term Loan (3 mo. USD LIBOR + 4.000%) | | | 5.006 | % | | | 12/14/27 | | | | 990,000 | | | | 986,698 | (h)(i)(j) |

Total Building Products | | | | | | | | | | | | | | | 1,919,728 | |

Commercial Services & Supplies — 3.2% | | | | | | | | | | | | | | | | |

KC Culinarte Intermediate LLC, First Lien Initial Term Loan (the greater of 1 mo. USD LIBOR or 1.000% + 3.750%) | | | 4.750 | % | | | 8/25/25 | | | | 1,939,650 | | | | 1,854,189 | (h)(i)(j) |

See Notes to Financial Statements.

| | |

14 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

Western Asset Middle Market Income Fund Inc.

(Percentages shown based on Fund net assets)

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | Maturity

Date | | | Face

Amount | | | Value | |

Commercial Services & Supplies — continued | | | | | | | | | | | | | | | | |

LTR Intermediate Holdings Inc., Initial Term Loan (3 mo. USD LIBOR + 4.500%) | | | 5.506 | % | | | 5/5/28 | | | $ | 992,512 | | | $ | 983,411 | (h)(i)(j) |

Mister Car Wash Holdings Inc., First Lien Initial Term Loan (1 mo. USD LIBOR + 3.000%) | | | 3.764 | % | | | 5/14/26 | | | | 29,478 | | | | 29,283 | (h)(i)(j) |

Total Commercial Services & Supplies | | | | | | | | | | | | | | | 2,866,883 | |

Total Industrials | | | | | | | | 5,251,142 | |

| Information Technology — 12.2% | | | | | | | | | | | | | | | | |

IT Services — 8.1% | | | | | | | | | | | | | | | | |

Access CIG LLC, Second Lien Initial Term Loan (1 mo. USD LIBOR + 7.750%) | | | 8.207 | % | | | 2/27/26 | | | | 3,470,984 | | | | 3,450,748 | (h)(i)(j) |

Project Alpha Intermediate Holding Inc., 2021 Refinancing Term Loan (1 mo. USD LIBOR + 4.000%) | | | 4.770 | % | | | 4/26/24 | | | | 2,891,320 | | | | 2,888,790 | (h)(i)(j) |

Redstone Holdco 2 LP, First Lien Initial Term Loan (3 mo. USD LIBOR + 4.750%) | | | 5.934 | % | | | 4/27/28 | | | | 995,000 | | | | 959,862 | (h)(i)(j) |

Total IT Services | | | | | | | | | | | | | | | 7,299,400 | |

Software — 4.1% | | | | | | | | | | | | | | | | |

DCert Buyer Inc., First Lien Initial Term Loan (1 mo. USD LIBOR + 4.000%) | | | 4.764 | % | | | 10/16/26 | | | | 1,989,400 | | | | 1,983,561 | (h)(i)(j) |

Symplr Software Inc., First Lien Term Loan (3 mo. Term SOFR + 4.500%) | | | 5.251 | % | | | 12/22/27 | | | | 1,732,500 | | | | 1,722,105 | (h)(i)(j) |

Total Software | | | | | | | | | | | | | | | 3,705,666 | |

Total Information Technology | | | | | | | | 11,005,066 | |

| Materials — 0.6% | | | | | | | | | | | | | | | | |

Paper & Forest Products — 0.6% | | | | | | | | | | | | | | | | |

Schweitzer-Mauduit International Inc., Term Loan B (1 mo. USD LIBOR + 3.750%) | | | 4.563 | % | | | 4/20/28 | | | | 496,250 | | | | 491,699 | (h)(i)(j) |

Total Senior Loans (Cost — $36,307,896) | | | | | | | | 35,782,152 | |

| | | | |

| | | | | | | | | Shares | | | | |

| Common Stocks — 2.8% | | | | | | | | | | | | | | | | |

| Energy — 1.3% | | | | | | | | | | | | | | | | |

Oil, Gas & Consumable Fuels — 1.3% | | | | | | | | | | | | | | | | |

Oasis Petroleum Inc. | | | | | | | | | | | 8,804 | | | | 1,167,939 | (b) |

| Health Care — 1.5% | | | | | | | | | | | | | | | | |

Health Care Providers & Services — 1.5% | | | | | | | | | | | | | | | | |

Option Care Health Inc. | | | | | | | | | | | 44,396 | | | | 1,326,552 | * |

Total Common Stocks (Cost — $1,597,962) | | | | | | | | 2,494,491 | |

See Notes to Financial Statements.

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 15 |

Schedule of investments (cont’d)

April 30, 2022

Western Asset Middle Market Income Fund Inc.

(Percentages shown based on Fund net assets)

| | | | | | | | | | | | | | | | |

| Security | | Rate | | | | | | Shares | | | Value | |

| Preferred Stocks — 0.5% | | | | | | | | | | | | | | | | |

| Financials — 0.5% | | | | | | | | | | | | | | | | |

Capital Markets — 0.5% | | | | | | | | | | | | | | | | |

B Riley Financial Inc. (Cost — $500,000) | | | 6.000 | % | | | | | | | 20,000 | | | $ | 490,000 | (b) |

Total Investments before Short-Term Investments (Cost — $101,031,706) | | | | 94,417,653 | |

| Short-Term Investments — 3.1% | | | | | | | | | | | | | | | | |

Western Asset Premier Institutional Government Reserves, Premium Shares

(Cost — $2,820,845) | | | 0.198 | % | | | | | | | 2,820,845 | | | | 2,820,845 | (k) |

Total Investments — 108.1% (Cost — $103,852,551) | | | | 97,238,498 | |

Liabilities in Excess of Other Assets — (8.1)% | | | | | | | | | | | | | | | (7,305,559 | ) |

Total Net Assets — 100.0% | | | | $89,932,939 | |

| * | Non-income producing security. |

| (a) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Directors. |

| (b) | All or a portion of this security is pledged as collateral pursuant to the loan agreement (Note 6). |

| (c) | Payment-in-kind security for which the issuer has the option at each interest payment date of making interest payments in cash or additional securities. |

| (d) | Security is valued in good faith in accordance with procedures approved by the Board of Directors (Note 1). |

| (e) | Security is valued using significant unobservable inputs (Note 1). |

| (f) | The coupon payment on this security is currently in default as of April 30, 2022. |

| (g) | Value is less than $1. |

| (h) | Interest rates disclosed represent the effective rates on senior loans. Ranges in interest rates are attributable to multiple contracts under the same loan. |

| (i) | Senior loans may be considered restricted in that the Fund ordinarily is contractually obligated to receive approval from the agent bank and/or borrower prior to the disposition of a senior loan. |

| (j) | Variable rate security. Interest rate disclosed is as of the most recent information available. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

| (k) | In this instance, as defined in the Investment Company Act of 1940, an “Affiliated Company” represents Fund ownership of at least 5% of the outstanding voting securities of an issuer, or a company which is under common ownership or control with the Fund. At April 30, 2022, the total market value of investments in Affiliated Companies was $2,820,845 and the cost was $2,820,845 (Note 8). |

| | |

Abbreviation(s) used in this schedule: |

| |

| CPI | | — Consumer Price Index |

| |

| LIBOR | | — London Interbank Offered Rate |

| |

| PIK | | — Payment-In-Kind |

| |

| SOFR | | — Secured Overnight Financing Rate |

| |

| USD | | — United States Dollar |

See Notes to Financial Statements.

| | |

16 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

Statement of assets and liabilities

April 30, 2022

| | | | |

| |

| Assets: | | | | |

Investments in unaffiliated securities, at value (Cost — $101,031,706) | | $ | 94,417,653 | |

Investments in affiliated securities, at value (Cost — $2,820,845) | | | 2,820,845 | |

Receivable for securities sold | | | 2,820,305 | |

Interest and dividends receivable from unaffiliated investments | | | 1,127,461 | |

Dividends receivable from affiliated investments | | | 1,059 | |

Prepaid expenses | | | 16 | |

Total Assets | | | 101,187,339 | |

| |

| Liabilities: | | | | |

Loan payable (Note 6) | | | 11,000,000 | |

Investment management fee payable | | | 100,104 | |

Due to custodian | | | 47,430 | |

Interest expense payable | | | 13,861 | |

Directors’ fees payable | | | 2,031 | |

Accrued expenses | | | 90,974 | |

Total Liabilities | | | 11,254,400 | |

| Total Net Assets | | $ | 89,932,939 | |

| |

| Net Assets: | | | | |

Par value ($0.001 par value; 148,078 shares issued and outstanding; 100,000,000 shares authorized) | | | $148 | |

Paid-in capital in excess of par value | | | 198,442,096 | |

Total distributable earnings (loss) | | | (108,509,305) | |

| Total Net Assets | | | $89,932,939 | |

| |

| Shares Outstanding | | | 148,078 | |

| |

| Net Asset Value | | | $607.33 | |

See Notes to Financial Statements.

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 17 |

Statement of operations

For the Year Ended April 30, 2022

| | | | |

| |

| Investment Income: | | | | |

Interest | | $ | 7,608,225 | |

Dividends from unaffiliated investments | | | 158,037 | |

Dividends from affiliated investments | | | 1,898 | |

Total Investment Income | | | 7,768,160 | |

| |

| Expenses: | | | | |

Investment management fee (Note 2) | | | 1,596,233 | |

Interest expense (Note 6) | | | 205,236 | |

Transfer agent fees | | | 94,291 | |

Audit and tax fees | | | 74,981 | |

Fund accounting fees | | | 73,943 | |

Legal fees | | | 50,024 | |

Shareholder reports | | | 42,892 | |

Directors’ fees | | | 35,825 | |

Insurance | | | 1,649 | |

Custody fees | | | 582 | |

Miscellaneous expenses | | | 15,344 | |

Total Expenses | | | 2,191,000 | |

Less: Fee waivers and/or expense reimbursements (Note 2) | | | (128,933) | |

Net Expenses | | | 2,062,067 | |

| Net Investment Income | | | 5,706,093 | |

| |

| Realized and Unrealized Gain (Loss) on Investments and Foreign Currency Transactions (Notes 1 and 3): | | | | |

Net Realized Gain (Loss) From: | | | | |

Investment transactions in unaffiliated securities | | | (630,626) | |

Foreign currency transactions | | | 21,502 | |

Net Realized Loss | | | (609,124) | |

Change in Net Unrealized Appreciation (Depreciation) From: | | | | |

Investments in unaffiliated securities | | | (3,704,501) | |

Foreign currencies | | | (781) | |

Change in Net Unrealized Appreciation (Depreciation) | | | (3,705,282) | |

| Net Loss on Investments and Foreign Currency Transactions | | | (4,314,406) | |

| Increase in Net Assets From Operations | | $ | 1,391,687 | |

See Notes to Financial Statements.

| | |

18 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

Statements of changes in net assets

| | | | | | | | |

| For the Years Ended April 30, | | 2022 | | | 2021 | |

| | |

| Operations: | | | | | | | | |

Net investment income | | $ | 5,706,093 | | | $ | 7,201,376 | |

Net realized loss | | | (609,124) | | | | (17,652,442) | |

Change in net unrealized appreciation (depreciation) | | | (3,705,282) | | | | 39,168,262 | |

Increase in Net Assets From Operations | | | 1,391,687 | | | | 28,717,196 | |

| | |

| Distributions to Shareholders From (Note 1): | | | | | | | | |

Total distributable earnings | | | (5,702,945) | | | | (7,602,636) | |

Return of capital | | | — | | | | (22,218) | |

Decrease in Net Assets From Distributions to Shareholders | | | (5,702,945) | | | | (7,624,854) | |

| | |

| Fund Share Transactions: | | | | | | | | |

Reinvestment of distributions (945 and 1,452 shares issued, respectively) | | | 601,371 | | | | 855,300 | |

Cost of shares repurchased through tender offer (29,831 and 27,000 shares repurchased, respectively) | | | (18,969,476) | | | | (16,243,686) | |

Decrease in Net Assets From Fund Share Transactions | | | (18,368,105) | | | | (15,388,386) | |

| | |

| Capital Contributions: | | | | | | | | |

Capital contributions | | | — | | | | 15,338 | |

Increase (Decrease) in Net Assets | | | (22,679,363) | | | | 5,719,294 | |

| | |

| Net Assets: | | | | | | | | |

Beginning of year | | | 112,612,302 | | | | 106,893,008 | |

End of year | | $ | 89,932,939 | | | $ | 112,612,302 | |

See Notes to Financial Statements.

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 19 |

Statement of cash flows

For the Year Ended April 30, 2022

| | | | |

| |

| Increase (Decrease) in Cash: | | | | |

| Cash Flows from Operating Activities: | | | | |

Net increase in net assets resulting from operations | | $ | 1,391,687 | |

Adjustments to reconcile net increase in net assets resulting from operations to net cash provided (used) by operating activities: | | | | |

Purchases of portfolio securities | | | (16,314,860) | |

Sales of portfolio securities | | | 52,060,482 | |

Net purchases, sales and maturities of short-term investments | | | 2,488,154 | |

Payment-in-kind | | | (84,753) | |

Net amortization of premium (accretion of discount) | | | (103,938) | |

Increase in receivable for securities sold | | | (2,820,305) | |

Decrease in interest and dividends receivable | | | 290,177 | |

Decrease in prepaid expenses | | | 846 | |

Increase in dividends receivable from affiliated investments | | | (1,059) | |

Decrease in payable for securities purchased | | | (3,257,500) | |

Decrease in investment management fee payable | | | (26,238) | |

Decrease in Directors’ fees payable | | | (1,379) | |

Increase in interest expense payable | | | 7,988 | |

Increase in accrued expenses | | | 45,617 | |

Net realized loss on investments | | | 630,626 | |

Change in net unrealized appreciation (depreciation) of investments | | | 3,704,501 | |

Net Cash Provided in Operating Activities* | | | 38,010,046 | |

| |

| Cash Flows from Financing Activities: | | | | |

Distributions paid on common stock | | | (5,101,574) | |

Proceeds from loan facility borrowings | | | 3,000,000 | |

Repayment of loan facility borrowings | | | (17,000,000) | |

Increase in due to custodian | | | 47,430 | |

Payment for shares repurchased through tender offer | | | (18,969,476) | |

Net Cash Used by Financing Activities | | | (38,023,620) | |

| Net Decrease in Cash and Restricted Cash | | | (13,574) | |

| Cash and restricted cash at beginning of year | | | 13,574 | |

| Cash and restricted cash at end of year | | | — | |

| * | Included in operating expenses is cash of $197,248 paid for interest on borrowings. |

| | The following table provides a reconciliation of cash and restricted cash reported within the Statement of Assets and Liabilities that sums to the total of such amounts shown on the Statement of Cash Flows. |

| | | | |

| |

| | | | April 30, 2022 | |

| Cash | | | — | |

| Restricted cash | | | — | |

Total cash and restricted cash shown in the Statement of Cash Flows | | | — | |

| |

| Non-Cash Financing Activities: | | | | |

Proceeds from reinvestment of distributions | | $ | 601,371 | |

See Notes to Financial Statements.

| | |

20 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

Financial highlights

|

| For a share of capital stock outstanding throughout each year ended April 30: |

| | | | | | | | | | | | | | | | | | | | |

| | | 20221 | | | 20211 | | | 20201 | | | 20191 | | | 20181 | |

| | | | | |

| Net asset value, beginning of year | | $ | 636.36 | | | $ | 527.84 | | | $ | 749.94 | | | $ | 759.44 | | | $ | 799.71 | |

| | | | | |

| Income (loss) from operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 34.86 | | | | 37.49 | | | | 60.08 | | | | 68.47 | | | | 76.58 | |

Net realized and unrealized gain (loss) | | | (29.56) | | | | 110.00 | | | | (222.12) | | | | (8.83) | | | | (38.51) | |

Total income (loss) from operations | | | 5.30 | | | | 147.49 | | | | (162.04) | | | | 59.64 | | | | 38.07 | |

| | | | | |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (34.33) | | | | (38.93) | | | | (60.06) | | | | (69.14) | | | | (78.34) | |

Return of capital | | | — | | | | (0.12) | | | | — | | | | — | | | | — | |

Total distributions | | | (34.33) | | | | (39.05) | | | | (60.06) | | | | (69.14) | | | | (78.34) | |

| | | | | |

| Capital contributions | | | — | | | | 0.08 | 2 | | | — | | | | — | | | | — | |

| | | | | |

| Net asset value, end of year | | $ | 607.33 | | | $ | 636.36 | | | $ | 527.84 | | | $ | 749.94 | | | $ | 759.44 | |

Total return, based on NAV3 | | | 0.73 | % | | | 28.73 | %4 | | | (22.94) | % | | | 8.20 | % | | | 5.04 | % |

| | | | | |

| Net assets, end of year (000s) | | $ | 89,933 | | | $ | 112,612 | | | $ | 106,893 | | | $ | 173,331 | | | $ | 198,323 | |

| | | | | |

| Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

Gross expenses | | | 2.09 | % | | | 1.83 | % | | | 2.31 | % | | | 2.29 | % | | | 2.36 | % |

Net expenses5 | | | 1.97 | 6 | | | 1.72 | | | | 2.18 | | | | 2.17 | | | | 2.23 | |

Net investment income | | | 5.45 | | | | 6.29 | | | | 8.56 | | | | 8.98 | | | | 9.81 | |

| | | | | |

| Portfolio turnover rate | | | 14 | % | | | 62 | % | | | 56 | % | | | 28 | % | | | 32 | % |

| | | | | |

| Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Loan Outstanding, End of Year (000s) | | $ | 11,000 | | | $ | 25,000 | | | $ | 30,300 | | | $ | 23,300 | | | $ | 47,400 | |

Asset Coverage Ratio for Loan Outstanding7 | | | 918 | % | | | 550 | % | | | 453 | % | | | 844 | % | | | 518 | % |

Asset Coverage, per $1,000 Principal Amount of Loan Outstanding7 | | $ | 9,176 | | | $ | 5,504 | | | $ | 4,528 | | | $ | 8,439 | | | $ | 5,184 | |

Weighted Average Loan (000s) | | $ | 23,014 | | | $ | 16,859 | | | $ | 31,672 | | | $ | 36,567 | | | $ | 58,175 | |

Weighted Average Interest Rate on Loan | | | 0.88 | % | | | 0.87 | % | | | 2.46 | % | | | 3.00 | % | | | 2.08 | % |

| 1 | Per share amounts have been calculated using the average shares method. |

| 2 | Reimbursement from fund accounting agent for NAV error. |

| 3 | Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 4 | Includes the effect of a capital contribution. Absent the capital contribution, the total return would have been unchanged. |

| 5 | Reflects fee waivers and/or expense reimbursements. |

| 6 | The manager has agreed to waive the Fund’s management fee to an extent sufficient to offset the net management fee payable in connection with any investment in an affiliated money market fund. |

| 7 | Represents value of net assets plus the loan outstanding at the end of the period divided by the loan outstanding at the end of the period. |

See Notes to Financial Statements.

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 21 |

Notes to financial statements

1. Organization and significant accounting policies

Western Asset Middle Market Income Fund Inc. (the “Fund”) was incorporated in Maryland on June 29, 2011 and is registered as a non-diversified, limited-term closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund commenced operations on August 26, 2014. The Fund’s primary investment objective is to provide high income. As a secondary objective, the Fund seeks capital appreciation. The Fund seeks to achieve its investment objectives by investing, under normal market conditions, at least 80% of its managed assets (the net assets of the Fund plus the principal amount of any borrowings and any preferred stock that may be outstanding) in securities, including loans, issued by middle market companies. For investment purposes, “middle market” refers to companies with annual revenues of between $100 million and $1 billion at the time of investment by the Fund. Securities of middle market issuers are typically considered below investment grade (also commonly referred to as “junk bonds”). It is anticipated that the Fund will terminate on or before December 30, 2022. Upon its termination, it is anticipated that the Fund will have distributed substantially all of its net assets to stockholders, although securities for which no market exists or securities trading at depressed prices, if any, may be placed in a liquidating trust.

The following are significant accounting policies consistently followed by the Fund and are in conformity with U.S. generally accepted accounting principles (“GAAP”). Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ. Subsequent events have been evaluated through the date the financial statements were issued.

(a) Investment valuation. The valuations for fixed income securities (which may include, but are not limited to, corporate, government, municipal, mortgage-backed, collateralized mortgage obligations and asset-backed securities) and certain derivative instruments are typically the prices supplied by independent third party pricing services, which may use market prices or broker/dealer quotations or a variety of valuation techniques and methodologies. The independent third party pricing services typically use inputs that are observable such as issuer details, interest rates, yield curves, prepayment speeds, credit risks/spreads, default rates and quoted prices for similar securities. Investments in open-end funds are valued at the closing net asset value per share of each fund on the day of valuation. Equity securities for which market quotations are available are valued at the last reported sales price or official closing price on the primary market or exchange on which they trade. When the Fund holds securities or other assets that are denominated in a foreign currency, the Fund will normally use the currency exchange rates as of 4:00 p.m. (Eastern Time). If independent third party pricing services are unable to supply prices for a portfolio investment, or if the prices supplied are deemed by the manager to be unreliable, the market price may be determined by the manager using quotations from one or more

| | |

22 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

broker/dealers or at the transaction price if the security has recently been purchased and no value has yet been obtained from a pricing service or pricing broker. When reliable prices are not readily available, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded, but before the Fund calculates its net asset value, the Fund values these securities as determined in accordance with procedures approved by the Fund’s Board of Directors.

The Board of Directors is responsible for the valuation process and has delegated the supervision of the daily valuation process to the Global Fund Valuation Committee (the “Valuation Committee”). The Valuation Committee, pursuant to the policies adopted by the Board of Directors, is responsible for making fair value determinations, evaluating the effectiveness of the Fund’s pricing policies, and reporting to the Board of Directors. When determining the reliability of third party pricing information for investments owned by the Fund, the Valuation Committee, among other things, conducts due diligence reviews of pricing vendors, monitors the daily change in prices and reviews transactions among market participants.

The Valuation Committee will consider pricing methodologies it deems relevant and appropriate when making fair value determinations. Examples of possible methodologies include, but are not limited to, multiple of earnings; discount from market of a similar freely traded security; discounted cash-flow analysis; book value or a multiple thereof; risk premium/yield analysis; yield to maturity; and/or fundamental investment analysis. The Valuation Committee will also consider factors it deems relevant and appropriate in light of the facts and circumstances. Examples of possible factors include, but are not limited to, the type of security; the issuer’s financial statements; the purchase price of the security; the discount from market value of unrestricted securities of the same class at the time of purchase; analysts’ research and observations from financial institutions; information regarding any transactions or offers with respect to the security; the existence of merger proposals or tender offers affecting the security; the price and extent of public trading in similar securities of the issuer or comparable companies; and the existence of a shelf registration for restricted securities.

For each portfolio security that has been fair valued pursuant to the policies adopted by the Board of Directors, the fair value price is compared against the last available and next available market quotations. The Valuation Committee reviews the results of such back testing monthly and fair valuation occurrences are reported to the Board of Directors quarterly.

The Fund uses valuation techniques to measure fair value that are consistent with the market approach and/or income approach, depending on the type of security and the particular circumstance. The market approach uses prices and other relevant information

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 23 |

Notes to financial statements (cont’d)

generated by market transactions involving identical or comparable securities. The income approach uses valuation techniques to discount estimated future cash flows to present value.

GAAP establishes a disclosure hierarchy that categorizes the inputs to valuation techniques used to value assets and liabilities at measurement date. These inputs are summarized in the three broad levels listed below:

| • | | Level 1 — quoted prices in active markets for identical investments |

| • | | Level 2 — other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.) |

| • | | Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used in valuing the Fund’s assets carried at fair value:

| | | | | | | | | | | | | | | | |

| ASSETS | |

| Description | | Quoted Prices

(Level 1) | | | Other Significant

Observable Inputs

(Level 2) | | | Significant

Unobservable

Inputs (Level 3) | | | Total | |

| Long-Term Investments†: | | | | | | | | | | | | | | | | |

Corporate Bonds & Notes: | | | | | | | | | | | | | | | | |

Financials | | | — | | | $ | 2,552,619 | | | $ | 936,380 | | | $ | 3,488,999 | |

Information Technology | | | — | | | | 1,223,266 | | | | 0 | * | | | 1,223,266 | |

Other Corporate Bonds & Notes | | | — | | | | 50,938,745 | | | | — | | | | 50,938,745 | |

Senior Loans: | | | | | | | | | | | | | | | | |

Consumer Discretionary | | | — | | | | 4,153,088 | | | | 1,795,294 | | | | 5,948,382 | |

Financials | | | — | | | | 5,000,808 | | | | 980,100 | | | | 5,980,908 | |

Health Care | | | — | | | | 2,818,742 | | | | 366,824 | | | | 3,185,566 | |

Other Senior Loans | | | — | | | | 20,667,296 | | | | — | | | | 20,667,296 | |

Common Stocks | | $ | 2,494,491 | | | | — | | | | — | | | | 2,494,491 | |

Preferred Stocks | | | 490,000 | | | | — | | | | — | | | | 490,000 | |

| Total Long-Term Investments | | | 2,984,491 | | | | 87,354,564 | | | | 4,078,598 | | | | 94,417,653 | |

| Short-Term Investments† | | | 2,820,845 | | | | — | | | | — | | | | 2,820,845 | |

| Total Investments | | $ | 5,805,336 | | | $ | 87,354,564 | | | $ | 4,078,598 | | | $ | 97,238,498 | |

| † | See Schedule of Investments for additional detailed categorizations. |

| * | Amount represents less than $1. |

| | |

24 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

The following is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value:

| | | | | | | | | | | | | | | | | | | | |

Investments in Securities | | Balance as of April 30, 2021 | | | Accrued

premiums/

discounts | | | Realized

gain (loss)1 | | | Change in

unrealized

appreciation

(depreciation)2 | | | Purchases | |

| Corporate Bonds & Notes: | | | | | | | | | | | | | | | | | | | | |

Financials | | $ | 976,900 | | | | — | | | | — | | | $ | (40,520) | | | | — | |

Information Technology | | | 0 | * | | | — | | | | — | | | | — | | | | — | |

Materials | | | 0 | * | | | — | | | $ | (1,151,780) | | | | 1,151,780 | | | | — | |

| Senior Loans: | | | | | | | | | | | | | | | | | | | | |

Communication Services | | | 295,236 | | | $ | 93 | | | | 903 | | | | (2,100) | | | | — | |

Consumer Discretionary | | | 995,000 | | | | 2,953 | | | | 2,500 | | | | (5,185) | | | $ | 1,030,825 | |

Financials | | | 8,170,905 | | | | 4,800 | | | | (52,002) | | | | 10,780 | | | | — | |

Health Care | | | 2,613,256 | | | | 6,584 | | | | 26,743 | | | | (24,705) | | | | — | |

Industrials | | | 1,998,750 | | | | 2,364 | | | | 158 | | | | (13,675) | | | | — | |

Information Technology | | | 4,066,067 | | | | (1,232) | | | | (18,873) | | | | (29,815) | | | | — | |

Materials | | | 1,498,450 | | | | 640 | | | | 34 | | | | (3,675) | | | | — | |

| Total | | $ | 20,614,564 | | | $ | 16,202 | | | $ | (1,192,317) | | | $ | 1,042,885 | | | $ | 1,030,825 | |

| | | | | | | | | | | | | | | | | | | | |

Investments in Securities (cont’d) | | Sales | | | Transfers

into

Level 3 | | | Transfers

out of

Level 33 | | | Balance as of

April 30, 2022 | | | Net change in

unrealized

appreciation

(depreciation)

for investments

in securities

still held at

April 30, 20222 | |

Corporate Bonds & Notes: | | | | | | | | | | | | | | | | | | | | |

Financials | | | — | | | | — | | | | — | | | $ | 936,380 | | | $ | (40,520) | |

Information Technology | | | — | | | | — | | | | — | | | | 0 | * | | | — | |

Materials | | $ | (0) | * | | | — | | | | — | | | | — | | | | — | |

| Senior Loans: | | | | | | | | | | | | | | | | | | | | |

Communication Services | | | (294,132) | | | | — | | | | — | | | | — | | | | — | |

Consumer Discretionary | | | (230,799) | | | | — | | | | — | | | | 1,795,294 | | | | (5,185) | |

Financials | | | (4,192,652) | | | | — | | | $ | (2,961,731) | | | | 980,100 | | | | (7,469) | |

Health Care | | | (2,255,054) | | | | — | | | | — | | | | 366,824 | | | | (6,497) | |

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 25 |

Notes to financial statements (cont’d)

| | | | | | | | | | | | | | | | | | | | |

Investments in Securities (cont’d) | | Sales | | | Transfers into Level 3 | | | Transfers out of Level 33 | | | Balance as of April 30, 2022 | | | Net change in unrealized appreciation (depreciation) for investments in securities still held at April 30, 20222 | |

| Industrials | | $ (17,488) | | | — | | | $(1,970,109) | | | — | | | — | |

Information Technology | | | (565,399) | | | | — | | | | (3,450,748) | | | | — | | | | — | |

| Materials | | | (1,003,750) | | | | — | | | | (491,699) | | | | — | | | | — | |

| Total | | $ | (8,559,274) | | | | — | | | $ | (8,874,287) | | | $ | 4,078,598 | | | $ | (59,671) | |

| * | Amount represents less than $1. |

| 1 | This amount is included in net realized gain (loss) from investment transactions in the accompanying Statement of Operations. |

| 2 | This amount is included in the change in net unrealized appreciation (depreciation) in the accompanying Statement of Operations. Change in unrealized appreciation (depreciation) includes net unrealized appreciation (depreciation) resulting from changes in investment values during the reporting period and the reversal of previously recorded unrealized appreciation (depreciation) when gains or losses are realized. |

| 3 | Transferred out of Level 3 as a result of the availability of a quoted price in an active market for an identical investment or the availability of other significant observable inputs. |

(b) Loan participations. The Fund may invest in loans arranged through private negotiation between one or more financial institutions. The Fund’s investment in any such loan may be in the form of a participation in or an assignment of the loan. In connection with purchasing participations, the Fund generally will have no right to enforce compliance by the borrower with the terms of the loan agreement related to the loan, or any rights of off-set against the borrower and the Fund may not benefit directly from any collateral supporting the loan in which it has purchased the participation.

The Fund assumes the credit risk of the borrower, the lender that is selling the participation and any other persons interpositioned between the Fund and the borrower. In the event of the insolvency of the lender selling the participation, the Fund may be treated as a general creditor of the lender and may not benefit from any off-set between the lender and the borrower.

(c) Cash flow information. The Fund invests in securities and distributes dividends from net investment income and net realized gains, which are paid in cash and may be reinvested at the discretion of shareholders. These activities are reported in the Statements of Changes in Net Assets and additional information on cash receipts and cash payments is presented in the Statement of Cash Flows.

(d) Foreign currency translation. Investment securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollar amounts based upon prevailing exchange rates on the date of valuation. Purchases and sales of investment

| | |

26 | | Western Asset Middle Market Income Fund Inc. 2022 Annual Report |

securities and income and expense items denominated in foreign currencies are translated into U.S. dollar amounts based upon prevailing exchange rates on the respective dates of such transactions.

The Fund does not isolate that portion of the results of operations resulting from fluctuations in foreign exchange rates on investments from the fluctuations arising from changes in market prices of securities held. Such fluctuations are included with the net realized and unrealized gain or loss on investments.

Net realized foreign exchange gains or losses arise from sales of foreign currencies, including gains and losses on forward foreign currency contracts, currency gains or losses realized between the trade and settlement dates on securities transactions, and the difference between the amounts of dividends, interest, and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in the values of assets and liabilities, other than investments in securities, on the date of valuation, resulting from changes in exchange rates.

Foreign security and currency transactions may involve certain considerations and risks not typically associated with those of U.S. dollar denominated transactions as a result of, among other factors, the possibility of lower levels of governmental supervision and regulation of foreign securities markets and the possibility of political or economic instability.

(e) Credit and market risk. The Fund invests in high-yield and emerging market instruments that are subject to certain credit and market risks. The yields of high-yield and emerging market debt obligations reflect, among other things, perceived credit and market risks. The Fund’s investments in securities rated below investment grade typically involve risks not associated with higher rated securities including, among others, greater risk related to timely and ultimate payment of interest and principal, greater market price volatility and less liquid secondary market trading. The consequences of political, social, economic or diplomatic changes may have disruptive effects on the market prices of investments held by the Fund. The Fund’s investments in non-U.S. dollar denominated securities may also result in foreign currency losses caused by devaluations and exchange rate fluctuations.

(f) Foreign investment risks. The Fund’s investments in foreign securities may involve risks not present in domestic investments. Since securities may be denominated in foreign currencies, may require settlement in foreign currencies or may pay interest or dividends in foreign currencies, changes in the relationship of these foreign currencies to the U.S. dollar can significantly affect the value of the investments and earnings of the Fund. Foreign investments may also subject the Fund to foreign government exchange restrictions, expropriation, taxation or other political, social or economic developments, all of which affect the market and/or credit risk of the investments.

| | |

| Western Asset Middle Market Income Fund Inc. 2022 Annual Report | | 27 |