UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR/A

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number: | 811-02474 |

Midas Perpetual Portfolio, Inc.

(Exact name of registrant as specified in charter)

| 11 Hanover Square, New York, NY | 10005 |

| (Address of principal executive offices) | (Zipcode) |

John F. Ramírez, Esq.

11 Hanover Square

New York, NY 10005

(Name and address of agent for service)

Registrant's telephone number, including area code: 1-212-480-6432

Date of fiscal year end: 12/31

Date of reporting period: 1/1/10 - 12/31/10

The Commission may use the information provided on Form N-CSR/A in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR/A and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR/A unless the Form displays a current valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under clearance requirements of 44 U.S.C. sec. 3507.

Item 1. Report to Stockholders.

December 31

2010

ANNUAL REPORT

| |

| |

| | |

| Portfolio Commentary | |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| Financial Statements | |

| | |

| Schedule of Portfolio Investments | |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| 26 |

| | |

| Supplemental Information | |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| Opening Your Account | |

| | |

| |

| | |

| New Account Application | 37 |

| Midas Fund (Ticker: MIDSX) | | Midas Special Fund (Ticker: MISEX) | | Midas Perpetual Portfolio (Ticker: MPERX) |

| Seeks capital appreciation and protection against inflation and secondarily current income through investments primarily in precious metals and natural resource companies and bullion. | | Invests aggressively for capital appreciation in any security in any sector. | | Seeks to preserve and increase the purchasing power value of its shares over the long term by investing in gold, silver, Swiss franc assets, hard asset securities, large capitalization growth stocks, and dollar assets. |

| Got fiscal discipline? The Congressional Budget Office now estimates that the U.S. fiscal deficit for 2011 will reach $1.5 trillion. To deal with this problem, the U.S. government recently announced a plan for budget cuts of almost $500 billion. But, didn’t the same U.S. lawmakers also just approve a $858 billion tax cut? Does this mean the national debt of $14.1 trillion (about equal to our nation’s annual production of goods and services) is going $358 billion in the wrong direction? It shouldn’t. After World War II, Congress created debt ceiling legislation which currently limits our national debt to $14.3 trillion. Or does it? Consider that Congress also has raised the debt ceiling six times in the last three years. About three years ago, the debt limit was under $9 trillion. |  |

START REGULAR INVESTING NOW ... AND BUILD FOR YOUR FUTURE

Notwithstanding disarray in Washington, many Americans can and are doing something to provide for their long term financial goals. We were very pleased to read that, according to the U.S. Bureau of Economic Analysis, personal saving by Americans as a percentage of disposable personal income was 5.8% percent in 2010. From 1982 when it stood at about 11%, the U.S. savings rate had been in a fairly steady decline through 2005 when it hit bottom at 1.2%. Is this a positive trend in savings towards our longer term average of 7.1%?

In this connection, Midas offers an excellent free service to make regular investing fast and convenient. Sign up for the free Midas Bank Transfer Plan, and each month a fixed amount of money will be transferred from your bank account to the Midas fund you designate. You should then periodically review your overall portfolio. Known as “dollar cost averaging,” this steady plan can reduce the anxiety of investing in a rising or falling market or buying all your shares at market highs. This strategy cannot assure a profit or protect against loss in a declining market and you should consider your financial ability to continue your purchases through periods of low and volatile price levels. Volatility in markets highlights the importance of diversifying your portfolio across the Midas family of mutual funds to balance the returns offered by the different market sectors in which they invest.

DISCOVERING OPPORTUNITIES FOR LONG TERM PLANNING WITH MIDAS

Reasons for careful investment planning are compelling. Retirement is longer as life expectancies increase, and the promises of pensions, retirement plans, and even Social Security are becoming less reliable. During our working careers, we are being asked to pay a greater share of health insurance, more tuition costs, and sometimes for the care of elderly parents. Even with these challenges, we believe personal investment planning can be successful by following three simple steps. First, commit to a long term investing approach. Second, follow a regular investment plan as described above. Third, manage your investing risk by diversifying among the three Midas funds: Midas Special Fund for longer term, stock market oriented objectives, Midas Perpetual Portfolio, seeking to preserve and increase the purchasing power value of its shares over the long term, and Midas Fund for potential precious metals capital appreciation and a hedge against inflation.

It is with great sadness we announce the recent passing of Robert D. Anderson, Vice Chairman and a founder of the Midas funds family. His leadership, integrity, perseverance, and humor will be missed. He was a lifelong advocate of the Midas quality investing approach, careful personal financial planning, and the highest standards of shareholder service and communication.

As always, please call us at 1-800-400-MIDAS (6432) if you have any questions or would like further information, and we will be happy to speak with you with no obligation on your part. Thank you for investing with Midas.

Sincerely,

Thomas B. Winmill

President

We are very pleased to report that Midas Fund’s net asset value rose 47.91% in 2010, a gratifying result, especially on top of a total return of 83.88% in 2009. We credit these returns to our quality, “growth in gold and resources” investment approach, particularly given the relatively lackluster return for gold bullion in the same period of about 29% in 2010 and 25% in 2009. We are also delighted to welcome new shareholders attracted to Midas Fund by its track record of past performance, its policy of investing in securities of companies principally involved in mining, processing, distributing or otherwise dealing in gold, silver, platinum, or other natural resources, and its no charge shareholder services.

PRECIOUS METALS AND FINANCIAL MARKETS

In 2010, gold prices fluctuated between $1,058 and $1,421 per ounce, averaging about $1,225, and ending the period at $1,405 (all prices are based on the London p.m. fix). The strength of gold’s price in 2010 was remarkable given the U.S. Bureau of Labor Statistics reported only a 1.5% increase in the consumer price index (a measure of inflation). Recently, however, with increasing investor complacency over reports of continuing strength in the U.S. and other world economies, the gold price plunged over $86 per ounce to $1,319, until spreading political upheavals and violence in the Middle East appeared to propel the gold price back upwards.

We expect continuing volatility in the gold price in 2011, as offsetting and often contradictory economic information is received by investors. While unsettling geo-political events – what we call the “fear factor” – may drive future short term swings, we believe that the gold price has the potential to reach $1,600 by year end due to longer term factors: fundamental supply/demand and, more importantly, fiscal and monetary policies pursued by governments around the world. These government policies currently appear to have the potential to solidify gold’s role as an “alternative currency,” particularly to the currencies of nations with large debt and entitlement obligations. For example, official U.S. public debt is now about $14.1 trillion, or 96% of U.S. annual gross domestic product; including entitlement obligations, such as Medicare, the total debt probably exceeds $60 trillion. Furthermore, to battle deflation and unemployment, the Federal Reserve has kept interest rates low, which may exacerbate future inflation and currency debasement concerns.

INVESTMENT STRATEGIES AND OUTLOOK

With this economic and market backdrop in 2010, Midas Fund strategically re-balanced its portfolio towards higher quality senior and intermediate precious metals producers. As gold and silver prices increased, well managed producing mining companies showed dramatic earnings and cash flow growth, boosting their stock prices. Midas Fund particularly benefited from high acquisition bids for a number of portfolio holdings in the year. Disappointing mine production or reserve addition by a company in the Fund’s portfolio typically detracted from Fund performance. For the balance of 2011, Midas Fund expects to be invested in a global portfolio of primarily large and medium sized gold, silver, and platinum miners offering attractive valuations, and smaller companies with promising exploration potential, expanding production profiles, increasing cash flow, and/or other special growth features, although it may seek a more defensive position at times. Currently, the Fund is emphasizing global mining companies with production of gold, silver, and other metals, including copper, deemed to have both reasonable valuations and compelling quality and growth prospects.

TOP10 HOLDINGS AS OF DECEMBER 31, 2010

|

1 Northern Dynasty Minerals Ltd. 2 Barrick Gold Corp. 3 Avocet Mining PLC 4 Fresnillo plc 5 Freeport-McMoRan Copper & Gold, Inc. 6 Northgate Minerals Corp. 7 Newmont Mining Corp. 8 Kinross Gold Corp. 9 Eldorado Gold Corp. Ltd. 10 Impala Platinum Holdings Ltd.

Top Ten Holdings comprise approximately 39% of total assets. |

Portfolio Commentary

We are pleased to submit this 2010 Annual Report for Midas Special Fund and to welcome our new shareholders attracted to the Fund’s approach of seeking capital appreciation in quality companies. While the Fund’s investment policies permit it to invest in any security type and in any industry sector, in domestic or foreign companies, and in companies of any size to seek its investment objective, the Fund currently is focused on those companies with unique combinations of strength in operations, products, and finances that can potentially offer growth in addition to value. Interestingly, the Fund may invest defensively as well as employ speculative investment techniques such as borrowing money for investment purposes, a practice known as leveraging.

ECONOMIC AND FINANCIAL TRENDS

The Federal Reserve Open Market Committee (FOMC) recently noted that U.S. economic activity has been increasing at a moderate rate. Specifically, the pace of consumer spending picked up in the fourth quarter, exports rose, and the recovery in some business spending, particularly for computers and software, appeared to be continuing. In contrast, the FOMC sees residential and non-residential construction activity as still depressed. Encouragingly, manufacturing production appears to be showing gains and non-farm businesses adding workers, while inflation expectations and trends are viewed by the FOMC as relatively benign. Unemployment levels, however, remain high.

In other economies, the strength of recovery in 2010 was mixed. The world’s second largest economy, China, is estimated to have had GDP growth of around 10% and appears set to enjoy another year of strong growth in 2011. Yet, China currently also has problems with rising inflation and is suspected to be suffering from widespread non performing debt at local levels. Meanwhile, Japan, the world’s third largest economy, also showed healthy, if not as dramatic, recovery with 2010 GDP growth estimated at approximately 3%. Europe appears to be recovering slowly, although painfully. According to Eurostat, the European Union’s statistics agency, the 16 country euro area is estimated to have had relatively weak 1.7% GDP growth in 2010 and unemployment recently stood at 10.1%. Giving cause for some optimism, however, in November 2010 compared with October 2010, industrial new orders were up by 2.1% in the euro area.

INVESTMENT STRATEGY AND OUTLOOK

Given this comparatively benign economic environment, the Fund’s strategy in 2010 included maintaining its focus on larger, quality companies with attractive valuations, using fewer, but more concentrated, individual positions. At December 31, 2010, the Fund’s top ten holdings comprised approximately 87% of its total assets, with 28% of total assets in just one holding, Berkshire Hathaway, Inc. The Fund holds predominantly blue chip and other well known companies in its portfolio, including some of the strongest companies with global operations in insurance, technology, and banking. The Fund enjoyed a total return of 5.67% in 2010.

The current outlook, according to the International Monetary Fund (IMF), is for global output to expand by about 4.5% in 2011. Importantly, however, the IMF believes that the advanced economies’ growth will slow to 2.5% from 3.0% last year, while emerging markets may see 6.5% growth, down from 7.1% in 2010. As economic and financial news continue to suggest investment potential, the Fund may seek to employ its flexible investment strategy to enhance returns with leverage (borrowing at year end was slightly over 12% of net assets) and other speculative techniques, or may seek a defensive investment position.

TOP10 HOLDINGS AS OF DECEMBER 31, 2010 |

1 Berkshire Hathaway, Inc. Class B |

2 MasterCard, Inc. |

3 Google, Inc. |

4 Canadian Natural Resources Ltd |

5 JPMorgan Chase & Co. |

6 Apple Inc. |

7 Costco Wholesale Corp. |

8 Johnson & Johnson |

9 General Electric Company. |

10 The Goldman Sachs Group, Inc. |

| Top Ten Holdings comprise approximately 87% of total assets. |

We are delighted to submit this 2010 Annual Report for Midas Perpetual Portfolio and to welcome our new shareholders who have invested in the Fund directly or through one of the growing number of brokerage firms making the Fund available to their customers.

Investors who wish to invest all or a portion of their capital in a way that does not depend on any particular outcome for the economy should consider purchasing shares of the Fund. While the Fund’s objective is to preserve and increase the purchasing power value of its shares over the long term, the investment strategy of Midas Perpetual Portfolio acknowledges a broad range of economic possibilities and investing outlooks, and seeks to incorporate investments appropriate for each of them. Key to the pursuit of its investment objective, the Fund seeks to invest a fixed “Target Percentage” of its total assets of each of the following categories:

| Investment Category | Target Percentage |

| Gold | 20% |

| Silver | 5% |

| Swiss Franc Assets | 10% |

| Hard Asset Securities | 15% |

| Large Capitalization Growth Stocks | 15% |

| Dollar Assets | 35% |

| Total | 100% |

These investment categories, although subject to the risk of potential loss, have been chosen and weighted with the goal of providing downside protection to the overall portfolio in most foreseeable economic conditions. As a category outperforms the others and becomes overweighted, its weighting may be reduced back towards its target. This “re-balancing” activity normally may cause the Fund to reduce its exposure to sectors with potentially unsustainable investor enthusiasm, and increase its investment in sectors which might hold greater relative, although currently underappreciated, value for investors.

STRATEGIES AND OUTLOOK

Concerns over the weakness of the U.S. and global economic recoveries were accompanied by strength in silver and gold prices, and the Fund’s strategic allocations to those categories benefited significantly, while large capitalization growth stock prices stalled. The Fund’s holdings of Swiss franc assets and hard asset securities performed well as the U.S. dollar weakened. Defensively invested in money market funds, dollar asset holdings in the Fund avoided losses and potential depreciation from a scenario of rising interest rates. The outlook for potentially slowing growth in most of the world’s economies reinforces our view of the potential benefits, as well as challenges, of investing in a number of different investment categories.

CONTACT US FOR INFORMATION AND SERVICES

Since the Fund’s strategies reflect longer term wealth building goals, we believe that it can be especially appropriate for a program of steady monthly investing. To make regular investing in the Fund as easy, convenient, and affordable as possible, we offer the Midas Bank Transfer Plan. Midas Perpetual Portfolio’s long term investment objective also makes it attractive for investment through our Traditional or Roth IRAs, Health Savings Accounts, and also our Education Savings Accounts. For information, simply give us a call toll free at 1-800-400-MIDAS (6432) and we will be delighted to provide such information to you, a friend, or relative.

TOP 10 HOLDINGS AS OF DECEMBER 31, 2010 |

| 1 SSgA Money Market Fund |

| 2 SPDR Gold Trust |

| 3 Switzerland Government, 2.5% Notes, due 3/12/16 |

| 4 iShares Silver Trust |

| 5 Comcast Corp. |

| 6 Roche-Holding AG ADR |

| 7 Oracle Corp. |

| 8 E.I. du Pont de Nemours and Company |

| 9 Schlumberger Limited |

| 10 Rio Tinto Ltd. |

| Top Ten Holdings comprise approximately 61% of total assets. |

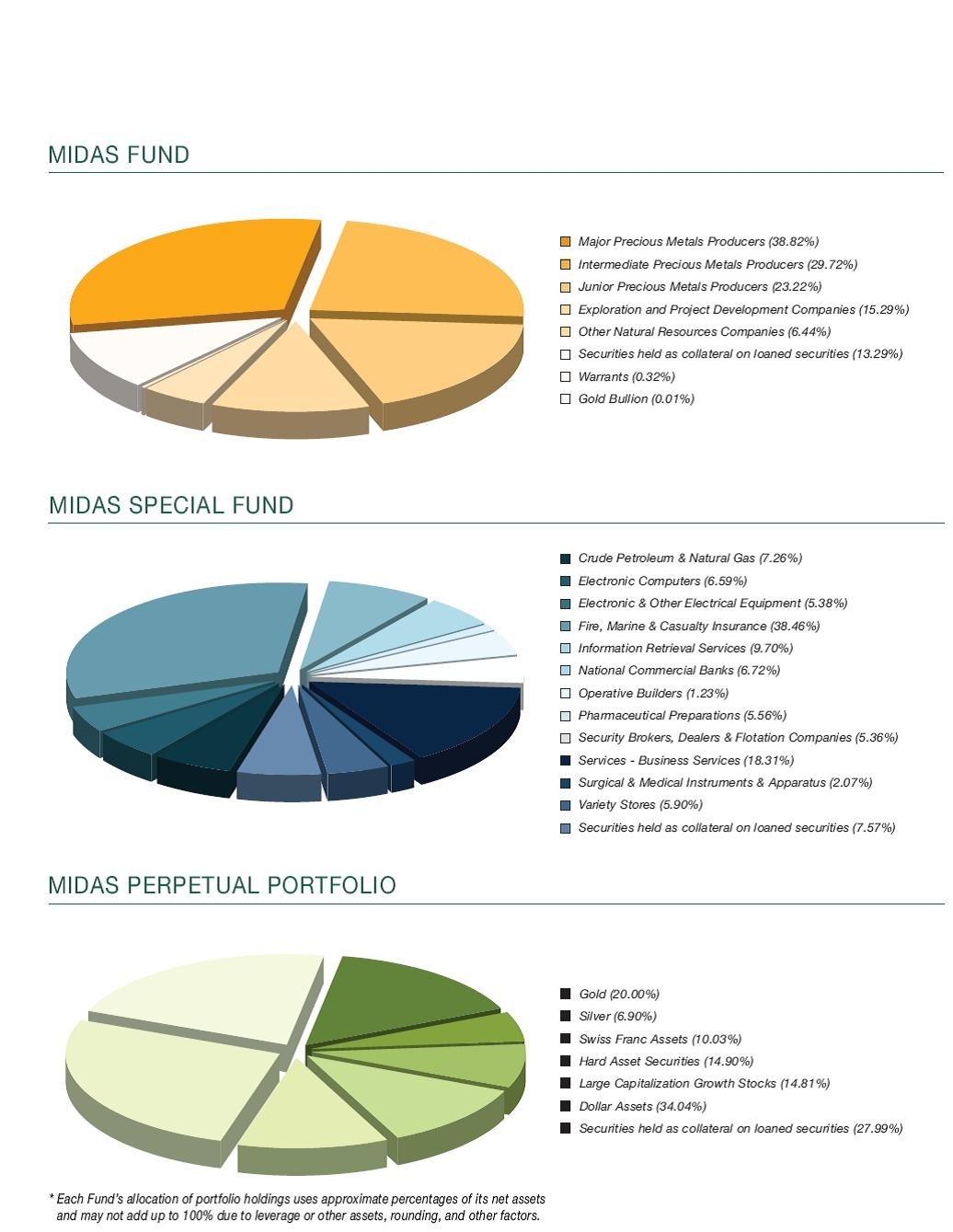

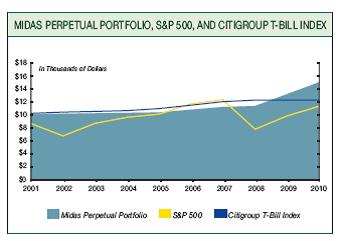

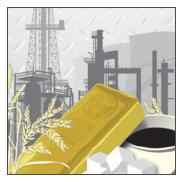

| Allocation of Portfolio Holdings* | December 31, 2010 (Unaudited) |

Table of Contents

| MIDAS Fund | Schedule of Portfolio Investments - December 31, 2010 |

| Common Stocks (113.49%) | | | | | | |

| Shares | | | | Cost | | | Value | |

| Major Precious Metals Producers (38.82%) | | | | | | |

| | 100,000 | | AngloGold Ashanti Ltd. ADR (a) | | $ | 4,479,423 | | | $ | 4,923,000 | |

| | 150,000 | | Barrick Gold Corp. (b) | | | 6,187,628 | | | | 7,977,000 | |

| | 60,000 | | Freeport-McMoRan Copper & Gold, Inc. (b) | | | 5,054,576 | | | | 7,205,400 | |

| | 291,453 | | Fresnillo plc (b) | | | 587,289 | | | | 7,611,335 | |

| | 90,000 | | Goldcorp Inc. | | | 3,796,193 | | | | 4,138,200 | |

| | 170,000 | | Impala Platinum Holdings Ltd. (b) | | | 5,222,171 | | | | 5,986,200 | |

| | 319,369 | | Kinross Gold Corp. (b) | | | 6,409,617 | | | | 6,055,236 | |

| | 100,755 | | Newcrest Mining Ltd. (a) | | | 2,220,469 | | | | 4,176,609 | |

| | 100,000 | | Newmont Mining Corp. | | | 5,940,870 | | | | 6,143,000 | |

| | | | | | | 39,898,236 | | | | 54,215,980 | |

| | | | | | | | | | | | |

| Intermediate Precious Metals Producers (29.72%) | | | | | | | | |

| | 350,000 | | African Barrick Gold plc | | | 3,061,809 | | | | 3,348,155 | |

| | 50,000 | | Agnico-Eagle Mines Ltd. | | | 3,557,835 | | | | 3,835,000 | |

| | 919,000 | | Aquarius Platinum Ltd. | | | 6,288,476 | | | | 5,064,709 | |

| | 275,400 | | Centerra Gold Inc. | | | 2,833,774 | | | | 5,498,854 | |

| | 325,000 | | Eldorado Gold Corp. Ltd. (b) | | | 5,655,700 | | | | 6,035,250 | |

| | 850,000 | | Golden Star Resources Ltd. (a) (c) | | | 3,999,471 | | | | 3,901,500 | |

| | 200,000 | | IAMGOLD Corp. (a) | | | 3,671,460 | | | | 3,560,000 | |

| | 575,000 | | Northam Platinum Ltd. | | | 1,552,969 | | | | 3,937,195 | |

| | 30,000 | | Randgold Resources Ltd. ADR (a) | | | 2,403,978 | | | | 2,469,900 | |

| | 300,000 | | Silvercorp Metals, Inc. (b) | | | 1,941,192 | | | | 3,849,000 | |

| | | | | | | 34,966,664 | | | | 41,499,563 | |

| | | | | | | | | | | | |

| Junior Precious Metals Producers (23.22%) | | | | | | | | |

| | 200,000 | | Alamos Gold Inc. (b) | | | 2,506,500 | | | | 3,808,182 | |

| | 135,000 | | Aurizon Mines Ltd. (c) | | | 797,838 | | | | 988,200 | |

| | 2,100,000 | | Avocet Mining PLC (c) | | | 3,548,756 | | | | 7,784,049 | |

| | 600,000 | | CGA Mining Ltd. (c) | | | 895,814 | | | | 1,871,886 | |

| | 500,000 | | Gold Wheaton Gold Corp. (c) | | | 1,723,593 | | | | 2,586,424 | |

| | 1,000,000 | | Great Basin Gold Ltd. (a) (c) | | | 2,816,753 | | | | 2,959,996 | |

| | 800,000 | | Jaguar Mining, Inc. (a) (c) | | | 3,972,073 | | | | 5,703,980 | |

| | 2,100,000 | | Northgate Minerals Corp. (a) (c) | | | 6,007,060 | | | | 6,720,000 | |

| | | | | | | 22,268,387 | | | | 32,422,717 | |

| | | | | | | | | | | | |

| Exploration and Project Development Companies (15.29%) | | | | | | | | |

| | 250,000 | | Corvus Gold Inc. (a) (c) | | | 290,236 | | | | 198,762 | |

| | 85,000 | | Detour Gold Corp. (b) (c) | | | 1,266,311 | | | | 2,497,006 | |

| | 500,000 | | Geomark Exploration Ltd. (c) | | | 174,406 | | | | 593,770 | |

| | 500,000 | | International Tower Hill Mines Ltd. (c) | | | 2,657,727 | | | | 5,035,000 | |

| | 37,699 | | Ivanhoe Nickel & Platinum Ltd. (c) (d) | | | 0 | | | | 0 | |

| | 600,000 | | Northern Dynasty Minerals Ltd. (a) (c) | | | 7,605,098 | | | | 8,574,000 | |

| | 1,500,000 | | Platinum Group Metals Ltd. (a) (c) | | | 3,159,430 | | | | 3,990,000 | |

| | 81,600 | | Sabina Gold & Silver Corp. (c) | | | 272,025 | | | | 460,701 | |

| | | | | | | 15,425,233 | | | | 21,349,239 | |

See notes to financial statements.

| MIDAS Fund | Schedule of Portfolio Investments continued |

| | Common Stocks - continued | | | | | | |

| | Shares | | | | Cost | | | Value | |

| | Other Natural Resources Companies (6.44%) | | | | | | |

| | | | | | | | | | | | | |

| | | 6,815,000 | | Farallon Mining Ltd. (c) | | $ | 4,812,369 | | | $ | 5,418,256 | |

| | | 445,000 | | Forsys Metals Corp. (c) | | | 2,112,343 | | | | 1,379,500 | |

| | | 550,000 | | Mercator Minerals Ltd. (a) (c) | | | 2,891,248 | | | | 2,197,454 | |

| | | | | | | | 9,815,960 | | | | 8,995,210 | |

| | Total common stocks | | | 122,374,480 | | | | 158,482,709 | |

| | | | | | | | | | |

| | Warrants (0.32%) (c) | | | | | | | | |

| | Units | | | | | | | | |

| | | 100,000 | | Kinross Gold Corp., expiring 9/07/11 | | | 105,450 | | | | - | |

| | | 142,900 | | Kinross Gold Corp., expiring 9/03/13 | | | 314,951 | | | | 577,052 | |

| | | 7,150 | | Kinross Gold Corp., expiring 9/17/14 (a) | | | 33,748 | | | | - | |

| | Total warrants | | | 577,052 | | | | 454,149 | |

| | | | | | | | | | |

| | Bullion Ounces (0.01%) (c) | | | | | | | | |

| | | 10 | | Gold | | | 14,189 | | | | 9,643 | |

| | Securities held as Collateral on Loaned Securities (13.29%) | | | | | | | | |

| | | 18,552,621 | | State Street Navigator Securities Lending Prime Portfolio | | | 18,552,621 | | | | 18,552,621 | |

| | | | | | | | | | | | | |

| | Total investments (127.11%) | | $ | 141,513,796 | | | | 177,503,668 | |

| | | | | | | | | | |

| | Liabilities in excess of other assets (-27.11%) | | | | | | | (37,859,985 | ) |

| | | | | | | | | | |

| | Net assets (100.00%) | | | | | | $ | 139,643,683 | |

| | | | | | | | | | |

| | (a) All or a portion of this security was on loan. | | | | | | | | |

| | (b) Fully or partially pledged as collateral on bank credit facility. | | | | | | | | |

| | (c) Non-income producing. | | | | | | | | |

| | (d) Illiquid and/or restricted security that has been fair valued. | | | | | | | | |

| | ADR means “American Depositary Receipt.” | | | | | | | | |

See notes to financial statements.

Table of Contents| Common Stocks (112.54%) | | | | |

| Shares | | Cost | | Value | |

| Crude Petroleum & Natural Gas (7.26%) | | | | |

| | | | | | | | | |

| | 20,000 | Canadian Natural Resources Ltd. | $ | 522,599 | | $ | 888,400 | |

| | | | | | | | | |

| Electronic Computers (6.59%) | | | | | | |

| | | | | | | | | |

| | 2,500 | Apple Inc. (a) (b) | | 477,375 | | | 806,400 | |

| | | | | | | | | |

| Electronic & Other Electrical Equipment (5.38%) | | | | | | |

| | | | | | | | | |

| | 36,000 | General Electric Company | | 435,510 | | | 658,440 | |

| | | | | | | | | |

| Fire, Marine & Casualty Insurance (38.46%) | | | | | | |

| | | | | | | | | |

| | 52,500 | Berkshire Hathaway, Inc. Class B (a) (b) | | 1,744,890 | | | 4,205,775 | |

| | 9,000 | The Travelers Companies, Inc. (c) | | 416,182 | | | 501,390 | |

| | | | | 2,161,072 | | | 4,707,165 | |

| | | | | | | | | |

| Information Retrieval Services (9.70%) | | | | | | |

| | | | | | | | | |

| | 2,000 | Google, Inc. - Class A (a) (b) | | 758,730 | | | 1,187,940 | |

| | | | | | | | | |

| National Commercial Banks (6.72%) | | | | | | |

| | | | | | | | | |

| | 19,400 | JPMorgan Chase & Co. (b) | | 691,858 | | | 822,948 | |

| | | | | | | | | |

| Operative Builders (1.23%) | | | | | | |

| | | | | | | | | |

| | 20,000 | PulteGroup, Inc. (a) (c) | | 444,535 | | | 150,400 | |

| | | | | | | | | |

| Pharmaceutical Preparations (5.56%) | | | | | | |

| | | | | | | | | |

| | 11,000 | Johnson & Johnson (b) | | 669,169 | | | 680,350 | |

| | | | | | | | | |

| Security Brokers, Dealers & Flotation Companies (5.36%) | | | | | | |

| | | | | | | | | |

| | 3,900 | The Goldman Sachs Group, Inc. (b) | | 865,343 | | | 655,824 | |

| | | | | | | | | |

| Services - Business Services (18.31%) | | | | | | |

| | | | | | | | | |

| | 10,000 | MasterCard, Inc. (b) | | 937,175 | | | 2,241,100 | |

| | | | | | | | | |

See notes to financial statements.

Table of Contents

| MIDAS Special Fund | Schedule of Portfolio Investments continued |

| Common Stocks - continued | | | | | | |

| Shares | | | | Cost | | | Value | |

| Surgical & Medical Instruments & Apparatus (2.07%) | | | | | | |

| | | | | | | | | | | | |

| | 3,000 | | Becton, Dickinson and Company (c) | | $ | 210,947 | | | $ | 253,560 | |

| | | | | | | | | | | | |

| Variety Stores (5.90%) | | | | | | | | |

| | | | | | | | | | | | |

| | 10,000 | | Costco Wholesale Corp. (b) | | | 692,696 | | | | 722,100 | |

| | | | | | | | | | | | |

| Total common stocks | | | 8,867,009 | | | | 13,774,627 | |

| | | | | | | | | |

| Securities held as Collateral on Loaned Securities (7.57%) | | | | | | | | |

| | | | | | | | | | | | |

| | 665,750 | | State Street Navigator Securities Lending Prime Portfolio | | | 665,750 | | | | 665,750 | |

| | 261,000 | | U.S. Government and U.S. Government Agency .44% - 4.00% | | | | | | | | |

| | | | due 4/30/11 - 12/28/12 | | | 260,545 | | | | 260,545 | |

| | | | | | | 926,295 | | | | 926,295 | |

| | | | | | | | | | | | |

| Total investments (120.11%) | | $ | 9,793,304 | | | | 14,700,922 | |

| | | | | | | | | | | | |

| Liabilities in excess of other assets (-20.11%) | | | | | | | (2,461,339 | ) |

| | | | | | | | | | | | |

| Net assets (100.00%) | | | | | | $ | 12,239,583 | |

(a) Non-income producing. (b) Fully or partially pledged as collateral on bank credit facility. (c) All or a portion of this security was on loan. | | | | | | | | |

See notes to financial statements.

| Shares | | | | Cost | | | Value | |

| Gold (20.00%) | | | | | | | | |

| | 15,310 | | SPDR Gold Trust (a) (b) | | $ | 1,326,145 | | | $ | 2,123,803 | |

| Silver (6.90%) | | | | | | | | | | |

| | 24,264 | | iShares Silver Trust (a) (b) | | | 272,282 | | | | 732,288 | |

| Swiss Franc Assets (10.03%) | | | | | | | | |

| | 932,000 | | Switzerland Government 2.50% Notes, due 3/12/16 (c) | | | 877,566 | | | | 1,065,510 | |

| Hard Asset Securities (14.90%) | | | | | | | | |

| Crude Petroleum & Natural Gas (2.59%) | | | | | | | | |

| | 1,219 | | Occidental Petroleum Corp. (b) | | | 73,137 | | | | 119,584 | |

| | 654 | | PetroChina Company Limited | | | 68,566 | | | | 85,994 | |

| | 1,838 | | Petroleo Brasileiro S.A. (b) | | | 67,908 | | | | 69,550 | |

| | | | | | | 209,611 | | | | 275,128 | |

| Gold Ores (2.06%) | | | | | | | | | | |

| | 2,051 | | Barrick Gold Corp. | | | 75,431 | | | | 109,072 | |

| | 2,385 | | Goldcorp Inc. | | | 75,217 | | | | 109,662 | |

| | | | | | | 150,648 | | | | 218,734 | |

| Industrial Gases (1.11%) | | | | | | | | |

| | 1,231 | | Praxair, Inc. (b) | | | 73,081 | | | | 117,524 | |

| Metal Mining (2.28%) | | | | | | | | |

| | 1,700 | | Rio Tinto Ltd. (b) | | | 120,006 | | | | 121,822 | |

| | 3,500 | | Vale S.A. ADR (b) | | | 121,959 | | | | 120,995 | |

| | | | | | | 241,965 | | | | 242,817 | |

| Petroleum Refining (1.53%) | | | | | | | | |

| | 1,408 | | ConocoPhillips | | | 72,945 | | | | 95,885 | |

| | 915 | | Exxon Mobil Corp. | | | 73,051 | | | | 66,905 | |

| | | | | | | 145,996 | | | | 162,790 | |

| Plastic Materials, Resins & Nonvulcanelastomers (1.37%) | | | | | | | | |

| | 2,907 | | E.I. du Pont de Nemours and Company (b) | | | 73,569 | | | | 145,001 | |

| Real Estate Investment Trusts (2.60%) | | | | | | | | |

| | 1,213 | | Federal Realty Investment Trust (b) | | | 75,091 | | | | 94,529 | |

| | 1,778 | | Health Care REIT, Inc. (b) | | | 74,180 | | | | 84,704 | |

| | 958 | | Public Storage (b) | | | 76,168 | | | | 97,160 | |

| | | | | | | 225,439 | | | | 276,393 | |

| Soybean Oil Mills (0.72%) | | | | | | | | |

| | 2,525 | | Archer-Daniels-Midland Company | | | 72,815 | | | | 75,952 | |

| Steel Works, Blast Furnaces & Rolling Mills (Coke Ovens) (0.64%) | | | | | | | | |

| | 1,558 | | Nucor Corp. (b) | | | 71,991 | | | | 68,272 | |

| Total hard asset securities | | | 1,265,115 | | | | 1,582,611 | |

See notes to financial statements.

Table of Contents

| MIDAS Perpetual Portfolio | Schedule of Portfolio Investments continued |

| Shares | | | | Cost | | | Value | |

| Large Capitalization Growth Stocks (14.81%) | | | | | | |

| Cable & Other Pay Television Services (1.57%) | | | | | | |

| | 8,000 | | Comcast Corp. (b) | | $ | 161,288 | | | $ | 166,480 | |

| Communications Equipment (1.06%) | | | | | | | | |

| | 5,559 | | Cisco Systems, Inc. (a) | | | 90,765 | | | | 112,459 | |

| Electronic Computers (0.79%) | | | | | | | | |

| | 2,000 | | Hewlett-Packard Company | | | 75,060 | | | | 84,200 | |

| Fire, Marine & Casualty Insurance (1.13%) | | | | | | | | |

| | 1,500 | | Berkshire Hathaway Inc. Class B (a) | | | 96,440 | | | | 120,165 | |

| Information Retrieval Services (1.03%) | | | | | | | | |

| | 184 | | Google, Inc. (a) | | | 75,235 | | | | 109,290 | |

| Life Insurance (0.76%) | | | | | | | | |

| | 1,316 | | China Life Insurance Company Ltd. ADR | | | 74,580 | | | | 80,500 | |

| Oil & Gas Field Services (1.20%) | | | | | | | | |

| | 1,533 | | Schlumberger Ltd. | | | 64,903 | | | | 128,005 | |

| Pharmaceutical Preparations (2.42%) | | | | | | | | |

| | 4,500 | | Roche-Holding AG ADR | | | 161,994 | | | | 164,925 | |

| | 2,851 | | Sanofi-Aventis ADR | | | 91,709 | | | | 91,888 | |

| | | | | | | 253,703 | | | | 256,813 | |

| Radio & TV Communications Equipment (0.77%) | | | | | | | | |

| | 1,667 | | QUALCOMM Inc. | | | 75,052 | | | | 82,500 | |

| Services-Prepackaged Software (2.36%) | | | | | | | | |

| | 3,261 | | Microsoft Corp. | | | 75,582 | | | | 91,047 | |

| | 5,096 | | Oracle Corp. | | | 90,696 | | | | 159,505 | |

| | | | | | | 166,278 | | | | 250,552 | |

| Telephone Communications (1.72%) | | | | | | | | |

| | 1,799 | | China Mobile Ltd. ADR (b) | | | 91,493 | | | | 89,266 | |

| | 1,359 | | Telefonica, S.A. ADR | | | 91,593 | | | | 92,983 | |

| | | | | | | 183,086 | | | | 182,249 | |

| Total large capitalization growth stocks | | | 1,316,390 | | | | 1,573,213 | |

| Dollar Assets (34.04%) | | | | | | | | |

| Money Market Fund | | | | | | | | |

| | 3,614,394 | | SSgA Money Market Fund, 0.01% (d) | | | 3,614,394 | | | | 3,614,394 | |

| SECURITIES HELD AS COLLATERAL ON LOANED SECURITIES (27.99%) | | | | | | | | |

| | 2,972,564 | | State Street Navigator Securities Lending Prime Portfolio | | | 2,972,564 | | | | 2,972,564 | |

| | | | | | | | | | | | |

| Total investments (128.67%) | | $ | 11,644,456 | | | | 13,664,383 | |

| | | | | | | | | | | | |

| Liabilities in excess of other assets (-28.67%) | | | | | | | (3,044,872 | ) |

| Net assets (100.00%) | | | | | | $ | 10,619,511 | |

| | | | | | | | | | | | |

(a) Non-income producing. | | | | | | | | |

| (b) All or a portion of this security was on loan. | | | | | | | | |

| (c) Principal amount denominated in Swiss Francs. | | | | | | | | |

| (d) Rate represents the 7 day annualized yield at December 31, 2010. | | | | | | | | |

| ADR means “American Depositary Receipt.” | | | | | | | |

See notes to financial statements.

Table of Contents

| December 31, 2010 | | Midas Fund | | | Midas Special Fund | | Midas Perpetual Portfolio | |

| Assets | | | | | | | | | |

| Investments at cost | | $ | 141,513,796 | | | $ | 9,793,304 | | | $ | 11,644,456 | |

| | | | |

| Investments at value | | $ | 177,503,668 | | | $ | 14,700,922 | | | $ | 13,664,383 | |

| Cash | | | - | | | | 5,835 | | | | - | |

| Receivables | | | | | | | | | | | | |

| Fund shares sold | | | 135,611 | | | | 38,987 | | | | 79,749 | |

| Dividends | | | 18,700 | | | | 6,315 | | | | 2,531 | |

| Income from securities loaned | | | 1,528 | | | | 223 | | | | 379 | |

| Interest | | | - | | | | - | | | | 13,883 | |

| Foreign withholding taxes reclaimed | | | - | | | | - | | | | 21,259 | |

| Other assets | | | 43,685 | | | | 8,605 | | | | 7,134 | |

| | | | |

| Total assets | | | 177,703,192 | | | | 14,760,887 | | | | 13,789,318 | |

| Liabilities | | | | | | | | | | | | |

| Bank line of credit | | | 18,993,272 | | | | 1,494,113 | | | | - | |

| Collateral on securities loaned, at value | | | 18,552,621 | | | | 926,295 | | | | 2,972,564 | |

| Payables | | | | | | | | | | | | |

| Accrued expenses | | | 233,112 | | | | 75,899 | | | | 56,419 | |

| Fund shares redeemed | | | 125,959 | | | | 2,298 | | | | 20,493 | |

| Investment management fees | | | 110,305 | | | | 10,055 | | | | - | |

| Distribution fees | | | 29,410 | | | | 10,285 | | | | 2,193 | |

| Administrative services | | | 14,830 | | | | 2,359 | | | | 1,037 | |

| Securities purchased | | | - | | | | - | | | | 117,101 | |

| | | | |

| Total liabilities | | | 38,059,509 | | | | 2,521,304 | | | | 3,169,807 | |

| | | | |

| Net assets | | $ | 139,643,683 | | | $ | 12,239,583 | | | $ | 10,619,511 | |

| | | | |

| Shares outstanding, $0.01 par value | | | 24,704,997 | | | | 830,662 | | | | 8,191,562 | |

| | | | | | | | | | | | | |

| Net asset value, offering, and redemption price per share | | $ | 5.65 | | | $ | 14.73 | | | $ | 1.30 | |

| | | | | | | | | | | | | |

| Net assets consist of | | | | | | | | | | | | |

| Paid in capital | | $ | 119,337,513 | | | $ | 11,721,716 | | | $ | 8,434,433 | |

| Accumulated undistributed net investment loss | | | (1,997,833 | ) | | | - | | | | - | |

| Accumulated net realized gain (loss) | | | (13,685,869 | ) | | | (4,389,751 | ) | | | 161,397 | |

| Net unrealized appreciation on investments | | | | | | | | | | | | |

| and foreign currencies | | | 35,989,872 | | | | 4,907,618 | | | | 2,023,681 | |

| | | | |

| | | $ | 139,643,683 | | | $ | 12,239,583 | | | $ | 10,619,511 | |

| | | | | | | | | | | | | |

See notes to financial statements.

Table of Contents

| | | Midas | | | Midas | | | Midas | |

| For the Year Ended December 31, 2010 | | Fund | | | Special Fund | | | Perpetual Portfolio | |

| Investment income | | | | | | | | | |

| Dividends | | $ | 815,192 | | | $ | 90,513 | | | $ | 64,667 | |

| Income from securities loaned | | | 58,821 | | | | 3,928 | | | | 3,201 | |

| Foreign tax withholding | | | (55,936 | ) | | | (1,374 | ) | | | (2,808 | ) |

| Interest | | | - | | | | - | | | | 14,398 | |

| | | | | | | | | | | | | |

| Total investment income | | | 818,077 | | | | 93,067 | | | | 79,458 | |

| | | | | | | | | | | | | |

| Expenses | | | | | | | | | | | | |

| Investment management | | | 1,145,898 | | | | 110,504 | | | | 44,078 | |

| Transfer agent | | | 431,700 | | | | 76,438 | | | | 40,603 | |

| Distribution | | | 286,474 | | | | 112,011 | | | | 22,039 | |

| Interest and fees on bank credit facility | | | 171,005 | | | | 42,643 | | | | 3,001 | |

| Administrative services | | | 129,915 | | | | 13,000 | | | | 8,599 | |

| Printing and postage | | | 82,759 | | | | 11,407 | | | | 11,224 | |

| Bookkeeping and pricing | | | 75,301 | | | | 24,069 | | | | 26,401 | |

| Legal | | | 70,029 | | | | 9,221 | | | | 4,910 | |

| Directors | | | 51,410 | | | | 12,236 | | | | 4,650 | |

| Interest and fees related to short sales | | | 47,834 | | | | - | | | | - | |

| Custodian | | | 39,281 | | | | 7,664 | | | | 1,930 | |

| Registration | | | 38,150 | | | | 29,890 | | | | 31,880 | |

| Insurance | | | 32,110 | | | | 3,182 | | | | 3,357 | |

| Auditing | | | 22,271 | | | | 19,387 | | | | 18,250 | |

| Other | | | 5,499 | | | | 1,371 | | | | 494 | |

| | | | | | | | | | | | | |

| Total expenses | | | 2,629,636 | | | | 473,023 | | | | 221,416 | |

| Less contractual fee waivers | | | | | | | | | | | | |

| Investment management | | | - | | | | - | | | | (44,078 | ) |

| Distribution | | | - | | | | - | | | | (6,883 | ) |

| | | | | | | | | | | | | |

| Net expenses | | | 2,629,636 | | | | 473,023 | | | | 170,455 | |

| | | | | | | | | | | | | |

| Net investment loss | | | (1,811,559 | ) | | | (379,956 | ) | | | (90,997 | ) |

| | | | | | | | | | | | | |

| Realized and Unrealized Gain (Loss) | | | | | | | | | | | | |

| Net realized gain (loss) on | | | | | | | | | | | | |

| Investments | | | 17,253,574 | | | | (664,083 | ) | | | 161,397 | |

| Foreign currencies | | | 106,232 | | | | - | | | | (341 | ) |

| Securities sold short | | | (86,423 | ) | | | - | | | | - | |

| Unrealized appreciation on | | | | | | | | | | | | |

| Investments | | | 28,951,224 | | | | 1,687,394 | | | | 913,265 | |

| Translation of assets and liabilities in foreign currencies | | | 1,779,227 | | | | - | | | | 98,792 | |

| Securities sold short | | | 275,514 | | | | - | | | | - | |

| | | | | | | | | | | | | |

| Net realized and unrealized gain | | | 48,279,348 | | | | 1,023,311 | | | | 1,173,113 | |

| | | | | | | | | | | | | |

| Net increase in net assets resulting from operations | | $ | 46,467,789 | | | $ | 643,355 | | | $ | 1,082,116 | |

| | | | | | | | | | | | | |

See notes to financial statements.

For The Years Ended December 31, 2010 and 2009 | | Midas Fund | | | Midas Special Fund | | | Midas Perpetual Portfolio | |

| | | 2010 | | | 2009 | | | 2010 | | | 2009 | | | 2010 | | | 2009 | |

| Operations | | | | | | | | | | | | | | | | | | |

| Net investment loss | | $ | (1,811,559 | ) | | $ | (1,563,178 | ) | | $ | (379,956 | ) | | $ | (313,847 | ) | | $ | (90,997 | ) | | $ | (92,745 | ) |

| Net realized gain (loss) | | | 17,273,383 | | | | 6,557,484 | | | | (664,083 | ) | | | (406,657 | ) | | | 161,056 | | | | 214,585 | |

| Unrealized appreciation | | | 31,005,965 | | | | 51,642,270 | | | | 1,687,394 | | | | 3,755,833 | | | | 1,012,057 | | | | 1,017,414 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net increase in net assets | | | | | | | | | | | | | | | | | | | | | | | | |

| resulting from operations | | | 46,467,789 | | | | 56,636,576 | | | | 643,355 | | | | 3,035,329 | | | | 1,082,116 | | | | 1,139,254 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Distributions to shareholders | | | | | | | | | | | | | | | | | | | | | | | | |

| Ordinary income | | | - | | | | (1,403,657 | ) | | | - | | | | - | | | | - | | | | - | |

| Net realized gains | | | - | | | | - | | | | - | | | | - | | | | - | | | | (135,764 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Total distributions | | | - | | | | (1,403,657 | ) | | | - | | | | - | | | | - | | | | (135,764 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Capital share transactions | | | | | | | | | | | | | | | | | | | | | | | | |

| Change in net assets resulting from | | | | | | | | | | | | | | | | | | | | | | | | |

capital share transactions (a) | | | (23,146,852 | ) | | | (16,447,053 | ) | | | 13,884 | | | | (365,286 | ) | | | 1,222,457 | | | | 113,439 | |

| Redemption fees | | | 11,801 | | | | 23,190 | | | | 626 | | | | 914 | | | | 4,281 | | | | 2,657 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Decrease in net assets resulting from | | | | | | | | | | | | | | | | | | | | | | | | |

| capital share transactions | | | (23,135,051 | ) | | | (16,423,863 | ) | | | 14,510 | | | | (364,372 | ) | | | 1,226,738 | | | | 116,096 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Total change in net assets | | | 23,332,738 | | | | 38,809,056 | | | | 657,865 | | | | 2,670,957 | | | | 2,308,854 | | | | 1,119,586 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets | | | | | | | | | | | | | | | | | | | | | | | | |

| Beginning of year | | | 116,310,945 | | | | 77,501,889 | | | | 11,581,718 | | | | 8,910,761 | | | | 8,310,657 | | | | 7,191,071 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

End of year (b) | | $ | 139,643,683 | | | $ | 116,310,945 | | | $ | 12,239,583 | | | $ | 11,581,718 | | | $ | 10,619,511 | | | $ | 8,310,657 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

(a) Capital share transactions were as follows: | | | | | | | | | | | | | | | | | | | | | | | | |

| Value | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares sold | | $ | 25,448,976 | | | $ | 22,434,540 | | | $ | 1,309,859 | | | $ | 542,044 | | | $ | 4,131,103 | | | $ | 2,087,424 | |

| Shares issued in reinvestment of distributions | | | - | | | | 1,302,755 | | | | - | | | | - | | | | - | | | | 133,543 | |

| Shares redeemed | | | (48,595,828 | ) | | | (40,184,348 | ) | | | (1,295,975 | ) | | | (907,330 | ) | | | (2,908,646 | ) | | | (2,107,528 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net increase (decrease) | | $ | (23,146,852 | ) | | $ | (16,447,053 | ) | | $ | 13,884 | | | $ | (365,286 | ) | | $ | 1,222,457 | | | $ | 113,439 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Number | | | | | | | | | | | | | | | | | | | | | | | | |

| Shares sold | | | 5,795,951 | | | | 7,680,094 | | | | 91,033 | | | | 49,797 | | | | 3,456,412 | | | | 1,864,840 | |

| Shares issued in reinvestment of distributions | | | - | | | | 489,199 | | | | - | | | | - | | | | - | | | | 119,860 | |

| Shares redeemed | | | (11,539,586 | ) | | | (14,517,372 | ) | | | (91,222 | ) | | | (79,232 | ) | | | (2,468,976 | ) | | | (1,969,285 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net increase (decrease) | | | (5,743,635 | ) | | | (6,348,079 | ) | | | (189 | ) | | | (29,435 | ) | | | 987,436 | | | | 15,415 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

(b) Undistributed net investment loss | | | | | | | | | | | | | | | | | | | | | | | | |

included in net assets | | $ | (1,997,833 | ) | | $ | (723,745 | ) | | $ | - | | | $ | - | | | $ | - | | | $ | - | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

See notes to financial statements.

Table of Contents

For The Year Ended December 31, 2010 | | Midas Fund | | | Midas Special Fund | | Midas Perpetual Portfolio | |

Cash flows from operating activities | | | | | | | | | |

Net increase in net assets resulting from operations | | $ | 46,467,789 | | | $ | 643,355 | | | $ | 1,082,116 | |

Adjustments to reconcile change in net assets | | | | | | | | | | | | |

resulting from operations to net cash provided | | | | | | | | | | | | |

by (used in) operating activities: | | | | | | | | | | | | |

Proceeds from sales of long term investments | | | 99,209,363 | | | | 913,518 | | | | 248,692 | |

Purchase of long term investments | | | (79,074,719 | ) | | | - | | | | (786,866 | ) |

Buy to cover investments held short | | | (11,425,957 | ) | | | - | | | | - | |

Proceeds from short sale of investments | | | 7,019,996 | | | | - | | | | - | |

Unrealized appreciation of investments and foreign currencies | | | (31,005,965 | ) | | | (1,687,394 | ) | | | (1,012,057 | ) |

Net realized (gain) loss on sales of investments, | | | | | | | | | | | | |

short sales, and foreign currencies | | | (17,273,383 | ) | | | 664,083 | | | | (161,056 | ) |

Net sales (purchases) of short term investments | | | 106,232 | | | | 5,199 | | | | (659,954 | ) |

Amortization of premium of investment securities | | | - | | | | - | | | | 5,996 | |

Increase in collateral for securities loaned | | | (1,585,762 | ) | | | (194,017 | ) | | | (2,972,564 | ) |

Decrease in receivable for investments sold | | | 1,330,847 | | | | - | | | | - | |

Decrease (increase) in dividends receivable | | | 40,732 | | | | (620 | ) | | | 3,835 | |

Decrease (increase) in securities lending income receivable | | | 8,519 | | | | 138 | | | | (379 | ) |

Increase in interest receivable | | | - | | | | - | | | | (283 | ) |

Increase in foreign withholding taxes reclaimed | | | - | | | | - | | | | (15,645 | ) |

| | | 3,487 | | | | 375 | | | | 1,070 | |

Increase in payable upon return of securities loaned | | | 1,585,762 | | | | 194,017 | | | | 2,972,564 | |

Increase in payable for investments purchased | | | - | | | | - | | | | 117,101 | |

(Decrease) increase in accrued expenses | | | (2,096 | ) | | | 3,487 | | | | 5,984 | |

Increase in investment management fees payable | | | 14,462 | | | | 526 | | | | - | |

Increase in distribution fees payable | | | 3,615 | | | | 608 | | | | 2,193 | |

Increase (decrease) in administrative services payable | | | 2,830 | | | | 394 | | | | (1,241 | ) |

| | | | |

Net cash provided by (used in) operating activities | | | 15,425,752 | | | | 543,669 | | | | (1,170,494 | ) |

| | | | |

Cash flows from financing activities | | | | | | | | | | | | |

Net shares (redeemed) sold | | | (23,152,543 | ) | | | (22,179 | ) | | | 1,169,532 | |

Borrowing on (repayment of) bank line of credit | | | 7,726,791 | | | | (515,655 | ) | | | - | |

| | | | |

Net cash (used in) provided by financing activities | | | (15,425,752 | ) | | | (537,834 | ) | | | 1,169,532 | |

| | | - | | | | 5,835 | | | | (962 | ) |

| | | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | - | | | | - | | | | 962 | |

| | | | |

| | $ | - | | | $ | 5,835 | | | $ | - | |

| | | | | | | | | | | | | |

Supplemental disclosure of cash flow information: | | | | | | | | | | | | |

Cash paid for interest and fees on bank line of credit | | | | | | | | | | | | |

| | $ | 218,506 | | | $ | 42,888 | | | $ | 447 | |

| | | | | | | | | | | | | |

See notes to financial statements.

| NOTES to Financial Statements | December 31, 2010 |

1 ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES The Midas Funds are Maryland corporations registered under the Investment Company Act of 1940, as amended (the “Act”), as open end management investment companies. The investment objectives of Midas Fund are primarily capital appreciation and protection against inflation and, secondarily, current income, and it invests primarily in precious metals and natural resource companies and bullion. Midas Special Fund’s investment objective is capital appreciation, which it seeks by investing aggressively in any security in any sector. The investment objective of Midas Perpetual Portfolio (formerly Midas Dollar Reserves) is to preserve and increase the purchasing power value of its shares over the long term with a policy of investing a fixed target percentage of its total assets in gold, silver, Swiss franc assets, hard asset securities, large capitalization growth stocks, and dollar assets. Prior to December 12, 2008, Midas Perpetual Portfolio operated as a money market fund. On December 29, 2008, the Fund changed its name to Midas Perpetual Portfolio, ceased operating as a money market fund, and began operating as a fluctuating net asset value fund pursuant to its current investment objective and policies. The Funds retain Midas Management Corporation as their Investment Manager.

Midas Fund and Midas Perpetual Portfolio each has authorized capital of one billion shares of common stock, par value $0.01 per share. Midas Special Fund has authorized capital of 500 million shares of common stock, par value $0.01. Each Fund offers only one class of shares. Each Fund’s shareholders are entitled to one vote for each whole share owned and a fractional vote for each fraction of a share owned. Voting rights are not cumulative. All shares of a Fund are fully paid and non-assessable and have no preemptive or conversion rights.

The Funds impose a short term trading redemption fee on any Fund shares that are redeemed or exchanged within 30 days following their purchase date. The redemption fee is 1% of the amount redeemed. Such fees are retained by the Funds for the benefit of the remaining shareholders and are accounted for as an addition to paid in capital.

The following is a summary of significant accounting policies consistently followed by each Fund in the preparation of its financial statements.

Valuation of Investments – Portfolio securities are valued by various methods depending on the primary market or exchange on which they trade. Most equity securities for which the primary market is the United States are valued at the official closing price, last sale price or, if no sale has occurred, at the closing bid price. Most equity securities for which the primary market is outside the United States are valued using the official closing price or the last sale price in the principal market in which they are traded. If the last sale price on the local exchange is unavailable, the last evaluated quote or closing bid price normally is used. Gold and silver bullion is valued at 4:00 p.m. ET, at the mean between the last bid and asked quotations of the Bloomberg Composite (NY) Spot Price for that metal. Debt obligations with remaining maturities of 60 days or less are valued at cost adjusted for amortization of premiums and accretion of discounts. Certain of the securities in which the Funds may invest are priced through pricing services that may utilize a matrix pricing system which takes into consideration factors such as yields, prices, maturities, call features, and ratings on comparable securities. Bonds may be valued according to prices quoted by a bond dealer that offers pricing services. Open end investment companies are valued at their net asset value. Foreign securities markets may be open on days when the U.S. markets are closed. For this reason, the value of any foreign securities owned by a Fund could change on a day when stockholders cannot buy or sell shares of the Fund. Securities for which market quotations are not readily available or reliable and other assets may be valued as determined in good faith by the Investment Manager under the direction of and pursuant to procedures established by a Fund’s Board of Directors. Due to the inherent uncertainty of valuation, these values may differ from the values that would have been used had a readily available market for the securities existed. These differences in valuation could be material. A security’s valuation may differ depending on the method used for determining value. The use of fair value pricing by a Fund may cause the net asset value of its shares to differ from the net asset value that would be calculated using market prices.

Foreign Currency Translation – Securities denominated in foreign currencies are translated into U.S. dollars at prevailing exchange rates. Realized gain or loss on sales of such investments in local currency terms is reported separately from gain or loss attributable to the change in foreign exchange rates for those investments.

Table of Contents

| NOTES to Financial Statements | continued |

Foreign Currency Contracts – Forward foreign currency contracts are marked to market and the change in market value is recorded by a Fund as an unrealized gain or loss. When a contract is closed, a Fund records a realized gain or loss equal to the difference between the value of the contract at the time it was opened and the value at the time it was closed. A Fund could be exposed to risk if the counterparties are unable to meet the terms of the contracts or if the value of the currency changes unfavorably.

Derivatives – Midas Fund and Midas Special Fund may use derivatives for a variety of reasons, such as to attempt to protect against possible changes in the value of their portfolio holdings or to generate potential gain. Derivatives are financial instruments that derive their values from other securities or commodities, or that are based on indices. Derivative instruments are marked to market with the change in value reflected in unrealized appreciation or depreciation. Upon disposition, a realized gain or loss is recognized accordingly, except when taking delivery of a security underlying a contract. In these instances, the recognition of gain or loss is postponed until the disposal of the security underlying the contract. Risk may arise as a result of the potential inability of the counterparties to meet the terms of their contracts. Derivative instruments include written options, purchased options, futures contracts, forward foreign currency exchange contracts, and swap agreements. For the year ended December 31, 2010, the Funds did not invest in any derivative instruments.

Short Sales – Midas Fund and Midas Special Fund may sell a security it does not own in anticipation of a decline in the market value of the security. When a Fund sells a security short, it must borrow the security sold short and deliver it to the broker/dealer through which it made the short sale. A Fund is liable for any dividends or interest paid on securities sold short. A gain, limited to the price at which a Fund sold the security short, or a loss, unlimited in size, will be recognized upon the termination of a short sale. Securities sold short result in off balance sheet risk as a Fund’s ultimate obligation to satisfy the terms of the sale of securities sold short may exceed the amount recognized in the Statement of Assets and Liabilities.

Investment Transactions – Investment transactions are accounted for on the trade date (the date the order to buy or sell is executed). Realized gains or losses are determined by specifically identifying the cost basis of the security sold.

Investment Income – Interest income is recorded on the accrual basis. Amortization of premium and accretion of discount on debt securities are included in interest income. Dividend income is recorded on the ex-dividend date or in the case of certain foreign securities, as soon as a Fund is notified. Taxes withheld on foreign dividends have been provided for in accordance with a Fund’s understanding of the applicable country’s tax rules and rates.

Expenses – Estimated expenses are accrued daily. Expenses directly attributable to a Fund are charged to that Fund. Expenses borne by the complex of related investment companies, which includes open end and closed end investment companies for which the Investment Manager and its affiliates serve as investment manager, that are not directly attributed to a Fund, are allocated among the Fund and the other investment companies in the complex on the basis of relative net assets, except where a more appropriate allocation of expenses can otherwise be made fairly.

Expense Reduction Arrangement – Through arrangements with the Funds’ custodian and cash management bank, credits realized as a result of uninvested cash balances are used to reduce custodian and transfer agent expenses. No credits were realized by the Funds during the period.

Distributions – Distributions to shareholders, are determined in accordance with income tax regulations, and recorded on the ex-dividend date.

Income Taxes – No provision has been made for U.S. income taxes because each Fund intends to qualify as a regulated investment company under the Internal Revenue Code and to distribute to shareholders substantially all taxable income and net realized gains. Foreign securities held by a Fund may be subject to foreign taxation. Foreign taxes, if any, are recorded based on the tax regulations and rates that exist in the foreign markets in which a Fund invests. The Funds recognize the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. The Funds have reviewed their tax positions and have concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax position taken on federal, state, and local income tax returns for all open tax years (2007 - 2009) or expected to be taken in the Funds’ 2010 tax returns.

Table of Contents

| NOTES to Financial Statements | continued |

Use of Estimates – In preparing financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”), management makes estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements, as well as the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Indemnifications – The Funds indemnify officers and directors for certain liabilities that might arise from their performance of their duties for the Funds. Additionally, in the normal course of business the Funds enter into contracts that contain a variety of representations and warranties and which may provide general indemnifications. The Funds’ maximum exposure under these arrangements is unknown, as it involves future claims that may be made against the Funds under circumstances that have not occurred.

Recently Issued Accounting Standards Updates – In January 2010, the Financial Accounting Standard Board released Accounting Standards Update (“ASU”) No. 2010-06, Improving Disclosures about Fair Value Measurements. Among the new disclosures and clarifications of existing disclosures the ASU requires the Funds to disclose separately the amounts of significant transfers in and out of Level 1 and Level 2 fair value measurements and to describe the reasons for the transfers. Significance shall be judged with respect to total earnings and total assets or total liabilities. The ASU requires the Level 3 roll forward reconciliation of beginning and ending balances to be prepared on a gross basis, in particular separately presenting information about purchases, sales, issuances, and settlements. The ASU also requires disclosure of the reasons for significant transfers in and out of Level 3. The Funds adopted the ASU on January 1, 2010, except for the Level 3 gross basis roll forward reconciliation which is effective for fiscal years beginning after December 15, 2010 and for interim periods within those fiscal years.

2 FEES AND TRANSACTIONS WITH RELATED PARTIES Under the investment management agreement of Midas Fund, the Investment Manager receives a management fee, payable monthly, based on the average daily net assets of the Fund at the annual rate of 1% on the first $200 million, .95% from $200 million to $400 million, .90% from $400 million to $600 million, .85% from $600 million to $800 million, .80% from $800 million to $1 billion, and .75% over $1 billion. Under the investment management agreement of Midas Special Fund, the Investment Manager receives a management fee, payable monthly, based on the average daily net assets of the Fund at the annual rate of 1% on the first $10 million, 7/8 of 1% from $10 million to $30 million, 3/4 of 1% from $30 million to $150 million, 5/8 of 1% from $150 million to $500 million, and 1/2 of 1% over $500 million. Under the investment management agreement of Midas Perpetual Portfolio, the Investment Manager receives a management fee, payable monthly, based on the average daily net assets of the Fund at the annual rate of .50% of the first $250 million, .45% from $250 million to $500 million, and .40% over $500 million.

The Investment Manager contractually agreed with Midas Perpetual Portfolio to waive its fee for the periods April 29, 2009 through April 29, 2010 and April 29, 2010 to December 31, 2010, and further contractually agreed to waive its fee for the year ending December 31, 2011.

Each Fund has adopted a plan of distribution pursuant to Rule 12b-1 under the Act. Under each plan, each Fund pays the Distributor, Midas Securities Group, Inc., an affiliate of the Investment Manager, a fee of .25% (Midas Fund and Midas Perpetual Portfolio) or 1.00% (Midas Special Fund) for distribution and shareholder services. A contractual fee waiver between the Distributor and Midas Perpetual Portfolio expired on April 29, 2010 and, subsequent to April 29, 2010, the Distributor began receiving the 0.25% fee from the Fund for distribution and shareholder services. The shareholder service fee is intended to cover personal services provided to the shareholders of the Funds and the maintenance of shareholder accounts. The distribution fee is to cover all other activities and expenses primarily intended to result in the sale of the Funds’ shares. In addition, Midas Fund, Midas Special Fund, and Midas Perpetual Portfolio each reimbursed the Distributor $140,193, $1,054, and $1,408, respectively, for payments made to certain brokers for record keeping services for the year ended December 31, 2010.

Certain officers and directors of the Funds are officers and directors of the Investment Manager and the Distributor.

| NOTES to Financial Statements | continued |

Pursuant to the investment management agreements, the Funds reimburse the Investment Manager for providing certain administrative services at cost comprised of compliance and accounting services. For the year ended December 31, 2010, the Funds incurred administrative services expenses as follows:

| | | Midas Fund | | Midas Special Fund | | Midas Perpetual Portfolio | |

| Compliance | | $ | 92,295 | | $ | 3,942 | | $ | 1,979 | |

| Accounting | | | 37,620 | | | 9,058 | | | 6,620 | |

| Total | | $ | 129,915 | | $ | 13,000 | | $ | 8,599 | |

3 DISTRIBUTIONS TO SHAREHOLDERS AND DISTRIBUTABLE EARNINGS The Funds paid no distributions for the year ended December 31, 2010. For the year ended December 31, 2009, Midas Fund paid a distribution of $1,403,657 comprised of ordinary income and Midas Perpetual Portfolio paid a distribution of $135,764 comprised of net realized gains. There was no distribution paid by Midas Special Fund for the year ended December 31, 2009.

At December 31, 2010, the components of distributable earnings on a tax basis were as follows:

| | | Midas Fund | | | Midas Special Fund | | | Midas Perpetual Portfolio | |

| Accumulated net investment income | | $ | 1,140,431 | | | $ | - | | | $ | - | |

| Accumulated net realized gain (loss) on investments | | | (13,685,848 | ) | | | (4,389,751 | ) | | | 161,397 | |

| Net unrealized appreciation | | | 32,851,587 | | | | 4,907,618 | | | | 2,023,681 | |

| Total | | $ | 20,306,170 | | | $ | 517,867 | | | $ | 2,185,078 | |

Federal income tax regulations permit post-October net capital losses, if any, to be deferred and recognized on the tax return of the next succeeding taxable year. The differences between book basis and tax basis unrealized appreciation is attributable primarily to the Passive Foreign Investment Company (“PFIC”) mark to market adjustments. GAAP requires certain components of net assets to be reclassified between financial and tax reporting. These reclassifications have no effect on net assets or net asset value per share. At December 31, 2010, permanent differences between book and tax accounting have been reclassified to paid in capital as follows:

| | | Midas Fund | | | Midas Special Fund | | | Midas Perpetual Portfolio | |

| Decrease in accumulated undistributed net investment loss | | $ | 537,471 | | | $ | 379,956 | | | $ | 90,997 | |

| (Increase) decrease in accumulated net realized gain (loss) on investments | | $ | (537,471 | ) | | $ | - | | | $ | 341 | |

| Decrease in paid in capital | | $ | - | | | $ | (379,956 | ) | | $ | (91,338 | ) |

Table of Contents

| NOTES to Financial Statements | continued |

At December 31, 2010, Midas Fund had net capital loss carryovers that may be used to offset future realized capital gains for federal income tax purposes of $13,685,848 expiring in 2017.

At December 31, 2010, Midas Special Fund had net capital loss carryovers that may be used to offset future realized gains for federal income tax purposes of $4,389,751, of which $1,823,745, $340,513, $1,154,753, $406,657, and $664,083 expire in 2011, 2014, 2016, 2017, and 2018, respectively.

4 FAIR VALUE MEASUREMENTS The Funds use a three level hierarchy for fair value measurements based on the transparency of inputs to the valuation of an asset or liability. Inputs may be observable or unobservable and refer broadly to the assumptions that market participants would use in pricing the asset or liability. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Funds. Unobservable inputs reflect a Fund’s own assumptions about the assumptions that market participants would use in pricing the asset or liability developed based on the best information available under the circumstances. A Fund’s investment in its entirety is assigned a level based upon the inputs which are significant to the overall valuation. The inputs or methodology used for valuing investments are not an indication of the risk associated with investing in those investments. The hierarchy of inputs is summarized below.

| • | Level 1 - unadjusted quoted prices in active markets for identical assets or liabilities including securities actively traded on a securities exchange. |

| • | Level 2 - observable inputs other than quoted prices included in level 1 that are observable for the asset or liability which may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates, and similar data. |

| • | Level 3 - unobservable inputs for the asset or liability including the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability. |

The following is a summary of the inputs used as of December 31, 2010 in valuing each Fund’s assets and liabilities carried at fair value. Refer to each Fund’s Schedule of Portfolio Investments for detailed information on specific investments.

| MIDAS FUND | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Assets | | | | | | | | | | | | |

| Common stocks | | $ | 158,482,709 | | | $ | - | | | $ | 0 | | | $ | 158,482,709 | |

| Warrants | | | 454,149 | | | | - | | | | - | | | | 454,149 | |

| Bullion | | | 14,189 | | | | - | | | | - | | | | 14,189 | |

| Securities held as collateral on loaned securities | | | 18,552,621 | | | | - | | | | - | | | | 18,552,621 | |

| Total investments | | $ | 177,503,668 | | | $ | - | | | $ | 0 | | | $ | 177,503,668 | |

| MIDAS SPECIAL FUND | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Assets | | | | | | | | | | | | |

| Common stocks | | $ | 13,774,627 | | | $ | - | | | $ | - | | | $ | 13,774,627 | |

| Securities held as collateral on loaned securities | | | 665,750 | | | | 260,545 | | | | - | | | | 926,295 | |

| Total investments | | $ | 14,440,317 | | | $ | 260,545 | | | $ | - | | | $ | 14,700,922 | |

| NOTES to Financial Statements | continued |

| MIDAS PERPETUAL PORTFOLIO | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Assets | | | | | | | | | | | | |

| Gold | | $ | 2,123,803 | | | $ | - | | | $ | - | | | $ | 2,123,803 | |

| Silver | | | 732,288 | | | | - | | | | - | | | | 732,288 | |

| Swiss Franc Assets | | | - | | | | 1,065,510 | | | | - | | | | 1,065,510 | |

| Hard Asset Securities | | | 1,582,611 | | | | - | | | | - | | | | 1,582,611 | |

| Large Capitalization Growth Stocks | | | 1,573,213 | | | | - | | | | - | | | | 1,573,213 | |

| Dollar Assets | | | 3,614,394 | | | | - | | | | - | | | | 3,614,394 | |

| Securities held as collateral on loaned securities | | | 2,972,564 | | | | - | | | | - | | | | 2,972,564 | |

| Total investments | | $ | 12,598,873 | | | $ | 1,065,510 | | | $ | - | | | $ | 13,664,383 | |

There were no transfers between Level 1 and Level 2 by the Funds during the year ended December 31, 2010.

There were no Level 3 investment purchases, sales, settlements, transfers in/out, or changes in unrealized appreciation/depreciation by the Funds for the year ended December 31, 2010. Midas Fund’s sole Level 3 investment consisted of Ivanhoe Nickel & Platinum Ltd. with a fair value of $0 as of December 31, 2010 and December 31, 2009, respectively.

5 INVESTMENT TRANSACTIONS At December 31, 2010, the aggregate gross unrealized appreciation and depreciation of investments, based on cost for federal income tax purposes, are summarized as follows:

| | | Federal Income | | | Gross Unrealized | | | Net Unrealized | |

| | | Tax Cost | | | Appreciation | | | Depreciation | | | Appreciation | |

| Midas Fund | | $ | 144,652,081 | | | $ | 36,419,399 | | | $ | (3,567,812 | ) | | $ | 32,851,587 | |

| Midas Special Fund | | $ | 9,793,304 | | | $ | 5,411,272 | | | $ | (503,654 | ) | | $ | 4,907,618 | |

| Midas Perpetual Portfolio | | $ | 11,644,456 | | | $ | 2,032,983 | | | $ | (13,056 | ) | | $ | 2,019,927 | |

Purchases and sales of securities, excluding short sale transactions and short term investments, for the year ended December 31, 2010 were as follows:

| | | Midas Fund | | | Midas Special Fund | | | Midas Perpetual Portfolio | |

| Purchases | | $ | 79,074,719 | | | $ | - | | | $ | 786,866 | |

| Proceeds | | $ | 99,209,363 | | | $ | 911,487 | | | $ | 248,692 | |

Table of Contents

| NOTES to Financial Statements | continued |

6 ILLIQUID AND RESTRICTED SECURITIES Midas Fund owns securities which have a limited trading market and/or certain restrictions on trading and, therefore, may be illiquid and/or restricted. Such securities have been valued at fair value in accordance with the procedures described in Note 1. Due to the inherent uncertainty of valuation, these values may differ from the values that would have been used had a readily available market for the securities existed. These differences in valuation could be material. Illiquid and/or restricted securities owned at December 31, 2010 were as follows:

| | Acquisition Date | | Cost | | | Value | |

| Ivanhoe Nickel & Platinum Ltd., common stock | 4/30/97 | | $ | 0 | | | $ | 0 | |

| Percent of net assets | | | | 0.0 | % | | | 0.0 | % |

7 BANK CREDIT FACILITIES The Funds (except Midas Perpetual Portfolio), Global Income Fund, Inc., and Foxby Corp. (the “Borrowers”) have entered into a committed secured line of credit facility, which is subject to annual renewal, with State Street Bank and Trust Company (“SSB”), the Funds’ custodian. Global Income Fund, Inc. and Foxby Corp. are closed end investment companies advised by an affiliate of the Investment Manager. The aggregate amount of the credit facility is $10,000,000. The borrowing of each Borrower is collateralized by the underlying investments of such Borrower. SSB will make revolving loans to a Borrower not to exceed in the aggregate outstanding at any time with respect to any one Borrower the least of $10,000,000, the maximum amount permitted pursuant to each Borrower’s investment policies, or as permitted under the Act. The commitment fee on this facility is 0.15% per annum on the unused portion of the commitment, based on a 360 day year. All loans under this facility will be available at the Borrower’s option of (i) overnight Federal funds or (ii) LIBOR (30, 60, 90 days), each as in effect from time to time, plus 1.50% per annum, calculated on the basis of actual days elapsed for a 360 day year.

The Funds have also entered into an uncommitted secured redemption facility, which is subject to annual renewal, with SSB with an aggregate amount available of $25,000,000. The borrowing of each Borrower is collateralized by the underlying investments of such Borrower. This facility carries no legal obligation on the part of SSB to lend any amount of money to the Funds at any time and the Borrower does not pay a commitment fee under this facility. SSB may make revolving loans to a Borrower not to exceed in the aggregate outstanding at any time with respect to any one Borrower the least of $25,000,000, the maximum amount permitted pursuant to the Borrower’s investment policies, or as permitted under the Act. All loans under this facility will be available at the overnight Federal Funds rate in effect from time to time plus 1.25%, calculated on the basis of actual days elapsed for a 360 day year.

The outstanding loan balance and the value of eligible collateral investments at December 31, 2010, and the weighted average interest rate and average daily amount outstanding under the committed and uncommitted facilities for the year ended December 31, 2010 were as follows:

| | | Midas Fund | | | Midas Special Fund | | | Midas Perpetual Portfolio | |

| Outstanding balance | | $ | 18,993,272 | | | $ | 1,494,113 | | | $ | 0 | |

| Value of eligible collateral | | $ | 48,703,336 | | | $ | 7,141,380 | | | $ | 0 | |

| Average daily amount outstanding | | $ | 8,485,613 | | | $ | 2,110,804 | | | $ | 0 | |

| Weighted average interest rate | | | 1.70 | % | | | 1.86 | % | | | 0.00 | % |

| NOTES to Financial Statements | continued |

8 SECURITIES LENDING The Funds may lend their securities to qualified financial institutions. The Funds receive compensation in the form of fees, or retain a portion of the returns on the investment of any cash received as collateral. The Funds receive as collateral cash deposits, U.S. Government securities, or bank letters of credit valued greater than the value of the securities on loan. Cash deposits are invested in a money market fund. The value of the loaned securities is determined based upon the most recent closing prices and any additional required collateral is delivered to the Funds on the next business day. Any increase or decrease in the value of the securities loaned that might occur and any interest earned or dividends declared on those securities during the term of the loan is retained by the Funds. The Funds have the right under the lending agreement to recover the securities from the borrower on demand. As with other extensions of credit, the Funds bear the risk of delay on recovery or loss of rights in the collateral should the borrower of the securities default.

The value of loaned securities and related collateral outstanding at December 31, 2010 were as follows:

| | | Midas Fund | | | Midas Special Fund | | | Midas Perpetual Portfolio | |

| Value of securities loaned | | $ | 17,987,269 | | | $ | 905,350 | | | $ | 2,934,549 | |

| Value of related collateral | | $ | 18,552,621 | | | $ | 926,295 | | | $ | 2,972,564 | |