UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22652

First Trust Variable Insurance Trust

(Exact name of registrant as specified in charter)

120 East Liberty Drive, Suite 400

Wheaton, IL 60187

(Address of principal executive offices) (Zip code)

W. Scott Jardine, Esq.

First Trust Portfolios L.P.

120 East Liberty Drive, Suite 400

Wheaton, IL 60187

(Name and address of agent for service)

Registrant's telephone number, including area code: 630-765-8000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

(a) The Report to Shareholders is attached herewith.

(b)

First Trust Variable Insurance Trust

Annual Report

For the Year Ended

December 31, 2022

First Trust Variable Insurance Trust

Annual Report

December 31, 2022

Caution Regarding Forward-Looking Statements

This report contains certain forward-looking statements within the meaning of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended. Forward-looking statements include statements regarding the goals, beliefs, plans or current expectations of First Trust Advisors L.P. (“First Trust” or the “Advisor”), Energy Income Partners, LLC (“EIP” or the “Sub-Advisor”), and/or Stonebridge Advisors LLC (“Stonebridge” or the “Sub-Advisor”) and their respective representatives, taking into account the information currently available to them. Forward-looking statements include all statements that do not relate solely to current or historical fact. For example, forward-looking statements include the use of words such as “anticipate,” “estimate,” “intend,” “expect,” “believe,” “plan,” “may,” “should,” “would” or other words that convey uncertainty of future events or outcomes.

Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of any series of First Trust Variable Insurance Trust (the “Trust”) to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. When evaluating the information included in this report, you are cautioned not to place undue reliance on these forward-looking statements, which reflect the judgment of the Advisor and/or Sub-Advisor and their respective representatives only as of the date hereof. We undertake no obligation to publicly revise or update these forward-looking statements to reflect events and circumstances that arise after the date hereof.

Performance and Risk Disclosure

There is no assurance that any series (individually called a “Fund” and collectively the “Funds”) of the Trust will achieve its investment objectives. Each Fund is subject to market risk, which is the possibility that the market values of securities owned by the Fund will decline and that the value of the Fund’s shares may therefore be less than what you paid for them. Accordingly, you can lose money by investing in a Fund. See “Risk Considerations” in the Additional Information section of this report for a discussion of certain other risks of investing in the Funds.

Performance data quoted represents past performance, which is no guarantee of future results, and current performance may be lower or higher than the figures shown. For the most recent month-end performance figures, please visit www.ftportfolios.com or speak with your financial advisor. Investment returns and net asset value will fluctuate and Fund shares, when sold, may be worth more or less than their original cost.

The Advisor may also periodically provide additional information on Fund performance on each Fund’s web page at www.ftportfolios.com.

How to Read This Report

This report contains information that may help you evaluate your investment. It includes details about each Fund and presents data and analysis that provide insight into each Fund’s performance.

By reading the portfolio commentary by the portfolio management team of each Fund, you may obtain an understanding of how the market environment affected each Fund’s performance. The statistical information that follows may help you understand each Fund’s performance compared to that of relevant market benchmarks.

It is important to keep in mind that the opinions expressed by personnel of the Advisor and/or Sub-Advisors are just that: informed opinions. They should not be considered to be promises or advice. The opinions, like the statistics, cover the period through the date on the cover of this report. The material risks of investing in each Fund are spelled out in the prospectus, the statement of additional information, this report and other Fund regulatory filings.

First Trust Variable Insurance Trust

Annual Letter from the Chairman and CEO

December 31, 2022

Dear Shareholders,

First Trust is pleased to provide you with the annual report for the First Trust Variable Insurance Trust (the “Funds”), which contains detailed information about the Funds for the twelve months ended December 31, 2022.

The past year was filled with challenges, several of which surely tested the resolve of even the most seasoned investors. The year began with the same headwinds that existed at the end of 2021, namely: stubbornly high inflation and rising interest rates. When Russia invaded Ukraine in late February 2022, we added war, geopolitical tension, and potential food and energy shortages to the list. Considering the bleak backdrop at the start of the year, it probably does not surprise you to read that with a total return of -18.11%, 2022 was the worst year for the S&P 500® Index since 2008. Even the bond market struggled to provide a haven to weary investors. The Bloomberg U.S. Aggregate Bond Index posted a total return of -13.01% for the year; its worst total return in 45 years.

A common topic of discussion in 2022 was whether central banks around the world had tightened monetary policy enough to quell inflation without causing excess damage to their economies. In the U.S., the Federal Reserve (the “Fed”) described this as a “soft landing,” stating it was their intent to keep the labor market strong but to increase interest rates enough to bring inflation down to 2.0%. True to their word, over the course of seven interest rate hikes, the Fed increased the Federal Funds target rate (upper bound) from 0.25% (where it stood in March 2022) to 4.50% as of December 2022. This is the highest the Federal Funds rate has been since 2008.

The economic impact of the Fed’s tighter monetary policy quickly became evident. Excluding the economic contraction from COVID-19 in 2020, the U.S. experienced its first decline in the gross domestic product (“GDP”) growth rate since March 2014. Data from the U.S. Bureau of Economic Analysis indicates that annualized real GDP growth rates over the first three quarters of 2022 were -1.6%, -0.6%, and 3.2%, respectively. Thankfully, inflation, as measured by the trailing 12-month rate on the Consumer Price Index (“CPI”), appears to be responding to the Fed’s tightening. After peaking at 9.1% in June 2022, the CPI rate fell to 6.5% at the end of December 2022. For comparative purposes, the CPI rate has averaged 2.5% over the past 30 years. Job creation has provided a respite from dreary economic data in recent months, but that could quickly change. Nearly 125,000 employees have lost their jobs since June 2022 as more than 120 U.S. companies announced layoffs, according to Forbes. The jury is still out on whether the Fed will be able to pull off a soft landing, but the job market will tell the tale, in my opinion.

Since 1928, the S&P 500® Index has only fallen for two consecutive years on four occasions: The Great Depression, World War II, the oil crisis of the 1970s and the burst of the dot-com bubble in the early 2000s. As we enter 2023, the U.S. economy has significant obstacles to overcome to avoid a recession and another negative year. We will be watching and reporting on what transpires.

Thank you for giving First Trust the opportunity to play a role in your financial future. We value our relationship with you and will report on the Funds again in six months.

Sincerely,

James A. Bowen

Chairman of the Board of Trustees

Chief Executive Officer of First Trust Advisors L.P.

Portfolio Commentary and Performance Summary

First Trust/Dow Jones Dividend & Income Allocation Portfolio

Annual Report

December 31, 2022 (Unaudited)

Advisor

First Trust Advisors L.P. (“First Trust”) is a registered investment advisor based in Wheaton, IL and is the investment advisor to First Trust/Dow Jones Dividend & Income Allocation Portfolio (the “Fund”). In this capacity, First Trust is responsible for the selection and ongoing monitoring of the securities in the Fund’s portfolio and certain other services necessary for the management of the Fund.

Portfolio Management Team

Daniel J. Lindquist, Chairman of the Investment Committee and Managing Director, First Trust

David G. McGarel, Chief Investment Officer, Chief Operating Officer and Managing Director, First Trust

Jon C. Erickson, Senior Vice President, First Trust

Roger F. Testin, Senior Vice President, First Trust

Todd Larson, Senior Vice President, First Trust

Chris A. Peterson, Senior Vice President, First Trust

Eric Maisel, Senior Vice President, First Trust

Scott Skowronski, Senior Vice President, First Trust

First Trust/Dow Jones Dividend & Income Allocation Portfolio

For the year ended December 31, 2022, the Fund’s Class I Shares returned -12.20% versus -19.21% for the Russell 3000® Index, and -17.24% for the Blended Benchmark (50% Russell 3000® Index and 50% Bloomberg U.S. Corporate Investment-Grade Index), and -15.76% for the Bloomberg U.S. Corporate Investment-Grade Index. As of December 31, 2022, the total investments for the Fund were allocated as follows: Equities, 51.8% and Fixed Income, 48.2%.

Equities Commentary

For the twelve-month period ended December 31, 2022, U.S. equities had their worst yearly performance since 2008 as the Russell 3000® Index returned -19.21%, after gaining 99% over the previous three years (2019-2021.) Equities trended down most of the year with the Russell 3000® Index declining 24.63% through its closing low on October 14, 2022 though it rallied during the fourth quarter of 2022 posting the only positive quarter of the year. Throughout the year, equities confronted headwinds such as high inflation, rising interest rates, global coronavirus (“COVID-19”) policies, and war in Ukraine. The Federal Reserve’s (the “Fed”) Federal Open Market Committee raised its upper bound of the Federal Funds target rate seven times in 2022, taking it from 25 basis points (“bps”) at the start of the year to 4.5% by year-end, in its efforts to combat high inflation, with expectations to exceed 5.0% in the coming year. Weekly U.S. initial jobless claims averaged about 215 thousand throughout 2022 while unemployment fell from 3.9% to 3.5% over the course of the year. Consumer sentiment also declined throughout the year as the University of Michigan Consumer Sentiment Index hit an all-time low in June 2022, though trended up and recovered some of the decline in the second half of the year. The Technology industry (Russell 3000 Technology Index -34.66%) took the largest lumps as rising interest rates took their toll on growth companies, while the Consumer Discretionary industry (Russell 3000 Consumer Discretionary Index -34.56%) and Real Estate industry (Russell 3000 Real Estate Index -25.74%) followed close behind. The Energy industry (Russell 3000 Energy Index +59.75%) showed the strongest performance in 2022, with other value leaning industries, Consumer Staples (Russell 3000 Consumer Staples Index +2.89%) and Utilities (Russell 3000 Utilities Index -2.38%), posting the next best performances. Value stocks (Russell 3000 Value Index -7.98%) outperformed growth stocks (Russell 3000 Growth Index -28.97%) by more than 20%.

A portfolio factor attribution reveals that the largest factor exposures were small size, value, and dividend yield. Dividend yield and value were the best performing factors in 2022 and drove overall outperformance in the equity portion of the Fund versus the Russell 3000® Index. However, small size was the worst performing factor, mitigating some of that outperformance. We expect these three factors to remain the largest factor loadings heading into 2023.

The equity portion of the Fund has a quarterly rebalance in early January, April, July, and October. The selection process is focused on identifying stocks exhibiting dividend strength, capital strength and price stability. This process resulted in overweight positions in the Financials, Industrials, and Basic Materials industries, while the Technology, Health Care, and Energy industries were underweight.

The Technology, Industrials, Financials, Consumer Discretionary, and Basic Materials industries had a positive total attribution effect (allocation effect combined with selection effect), while the Energy, Utilities, Consumer Staples, and Health Care industries had a negative effect. The Technology, Financials, Industrials, Basic Materials, and Consumer Discretionary industries had a positive allocation effect while the Energy and Health Care industries had a negative effect. The Industrials, Consumer Discretionary, Financials, and Basic Materials industries had a positive selection effect. The equity portion of the Fund was boosted by both a positive allocation effect and positive selection effect.

Portfolio Commentary and Performance Summary (Continued)

First Trust/Dow Jones Dividend & Income Allocation Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

The Technology industry was the largest overall contributor to relative performance as the equity portion of the Fund was underweight the worst performing industry in the Blended Benchmark, which led to a large positive allocation effect. Further, the Fund had a positive selection effect within the Technology industry positions. Technology industry positions in the Fund included Amphenol Corp., Intel Corp., Microsoft Corp., Power Integrations, Inc., and Texas Instruments, Inc. The Industrials, Consumer Discretionary, Financials, and Basic Materials industries also contributed to positive relative performance. The Fund’s holdings in the Industrial industry included Deere & Co., Lockheed Martin Corp., and Northrop Grumman Corp., while Consumer Discretionary industry names included Dollar General Corp., Texas Roadhouse, Inc., and The TJX Cos., Inc. Financial industry names included Aflac, Inc., Raymond James Financial, Inc., and The Travelers Cos., Inc., while Basic Materials industry names included FMC Corp., Mueller Industries, Inc., and Reliance Steel & Aluminum Co., all of which posted positive returns while equities were broadly negative in 2022.

The Energy industry was the biggest detractor from relative performance as the equity portion of the Fund had no positions in the best performing industry in the Russell 3000® Index, which led to a negative allocation effect. The Energy industry made up less than 5% of the Russell 3000® Index. The Utilities, Consumer Staples, and Health Care industries also detracted from relative performance. The Fund had a negative allocation effect in all three industries due to being underweight the outperforming industries.

The Fund’s top five contributors to performance were Steel Dynamics Inc., Merck & Co., Inc., Northrop Grumman Corp, Lockheed Martin Corp., and Amgen, Inc. The top five detractors from performance were Intel Corp, T. Rowe Price Group, Inc., Zoetis, Inc., Ross Stores, Inc., and Cognizant Technology Solutions Corp.

Heading into 2023, equity returns are likely to remain choppy as elevated inflation has resulted in the Fed hiking interest rates to mitigate economic activity, which tends to be deflationary. If the Fed hikes too high and fast, economic recession risks grow. If they hike too low and slow, inflationary risks grow. Historically value and dividend yielding stocks tend to hold up well during a higher volatility equity market. The equity portion of the Fund currently has factor loading to both value and dividend yielding names which could offer both downside protection and upside participation.

Fixed Income Commentary

Coming into 2022, the U.S. economy benefited from low interest rates, a strong labor market, optimism around growth expectations, and hope that the reopening of global economies would alleviate supply chain disruptions, thereby easing inflation. At the time, markets expected two to three modest interest rate hikes by the end of 2022. However, as the Consumer Price Index (“CPI”) continued to rise, the Fed abandoned its view that inflation was “transitory” and began to aggressively tighten monetary policy.

Throughout the 12-month period ended December 31, 2022, inflation remained stubbornly elevated, with the June 2022 CPI (reported in July 2022) printing 9.1% on a year-over-year basis. While continuing to reiterate its commitment to a 2.0% inflation target, the Fed increased the Federal Funds target rate by 425 bps during the reporting period, moving the upper bound from 0.25% to 4.50% over the course of seven meetings. This interest rate hiking path included four meetings at which the Fed increased the Federal Funds target rate by a full 75 bps. The impact on the investment grade credit market was pronounced. For the 12-month period ended December 31, 2022, corporate bonds underperformed Treasuries by 125 bps. As measured by the Bloomberg U.S. Corporate Investment-Grade Index, spreads widened by 38 bps to 130 bps at year-end. Driven by the increase in U.S. Treasury rates, investment-grade corporate bonds also had a negative total return for the period, as the carry provided by corporate bonds failed to offset the year’s increase in interest rates and widening in credit spreads. The yield on the 10-Year U.S. Treasury, for example, increased from 1.51% to 3.88% over the course of the period, having reached a high of 4.23% in late October 2022.

The fixed-income portion of the Fund seeks to provide income along with preservation of capital. To accomplish this, the selection process is primarily value oriented, strongly emphasizes downside protection and focuses on free cash flow, leverage, interest coverage and revenue growth rates. This process resulted in overweight positions in Banking and Electric Utilities, U.S. Treasuries, and Communications bonds, while the Technology industry, Consumer Non-Cyclical, and Consumer Cyclical were the largest underweights.

For the reporting period, the total return for the bond portion of the Fund outperformed the Bloomberg U.S. Corporate Investment-Grade Index by 26 bps. The Fund maintained a duration underweight throughout the year, partially through hedging interest rate exposure with U.S. Treasury Futures, and this contributed beneficially to relative performance. Treasury yields increased during the year as inflation remained elevated and the Fed commenced an aggressive series of interest rate increases. Among credit quality and maturity cohorts, allocation to single-A credits, along with allocations in the 10- and 30-year maturity buckets, added the most to relative performance.

Portfolio Commentary and Performance Summary (Continued)

First Trust/Dow Jones Dividend & Income Allocation Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

Among the 18 fixed-income industry groups, allocations to Insurance, Real Estate Investment Trusts, and Capital Goods added the most to relative returns. Allocations to Banking, Consumer Cyclical, and Technology, by contrast, reduced relative returns. Overall, the allocation effect reduced relative performance. Within these industries, credit selection in Electric, Communications, and Insurance had the greatest positive impacts, while credit selection within Banking, Technology, and Energy reduced relative returns. Overall, credit selection within these industries added to relative performance. Issuer allocation reduced relative performance, with underweights to United Healthcare Group, Inc. and Oracle Corp., along with an overweight to FirstEnergy Transmission LLC having the greatest positive impact on relative returns. Security selection contributed to relative return, with selection among bonds of The Southern Co., NextEra Energy Capital Holdings, Inc., and Pacific Gas and Electric Co. contributing the most to relative returns.

As we begin 2023, our market framework centers on the Fed staying the course. Due to the persistence of the inflation data, and how far it is from the Fed’s target inflation rate, we do not believe the Fed can ease monetary policy through interest rate cuts until either (1) inflation has been tamed, or (2) a recession is near or already underway, absent any major financial market calamity. We therefore expect market volatility to continue as investors attempt to gauge the ultimate Federal Funds target rate as well as the likelihood, and timing of, a recession. Consequently, extending durations back to neutral is not yet warranted, in our view, although we do believe we are much closer to that point in the cycle where duration extension will be warranted. Additionally, we favor increasing credit quality while positioning in more defensive sectors with lower cyclicality. Accordingly, our focus for the fixed-income portion of the Fund will be on our process, and on issuers and sectors with credit profiles well suited to weather the upcoming challenges.

Portfolio Commentary and Performance Summary (Continued)

First Trust/Dow Jones Dividend & Income Allocation Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

| Return Comparison | | | | |

| | | Average Annual

Total Returns |

| | 1 Year

Ended

12/31/22 | 5 Years

Ended

12/31/22 | 10 Years

Ended

12/31/22 | Inception

(5/1/12)

to 12/31/22 |

| Fund Performance | | | | |

| First Trust/Dow Jones Dividend & Income Allocation Portfolio - Class I | -12.20% | 4.06% | 6.75% | 6.74% |

| Index Performance | | | | |

| Blended Benchmark(1) | -17.24% | 4.86% | 7.16% | 7.18% |

| Bloomberg U.S. Corporate Investment-Grade Index(2) | -15.76% | 0.45% | 1.96% | 2.42% |

| Russell 3000® Index(3) | -19.21% | 8.79% | 12.13% | 11.67% |

| Secondary Blended Benchmark(4) | -17.97% | 4.82% | 7.14% | 7.17% |

| Dow Jones Equal Weight U.S. Issued Corporate Bond IndexSM(5) | -16.85% | 0.49% | 1.99% | 2.49% |

| Dow Jones U.S. Total Stock Market IndexSM(6) | -19.53% | 8.65% | 12.03% | 11.57% |

| Return Comparison | | | |

| | | Average Annual

Total Returns |

| | 1 Year

Ended

12/31/22 | 5 Years

Ended

12/31/22 | Inception

(5/1/14)

to12/31/22 |

| Fund Performance | | | |

| First Trust/Dow Jones Dividend & Income Allocation Portfolio - Class II | -12.02% | 4.32% | 6.33% |

| Index Performance | | | |

| Blended Benchmark(1) | -17.24% | 4.86% | 6.18% |

| Bloomberg U.S. Corporate Investment-Grade Index(2) | -15.76% | 0.45% | 1.92% |

| Russell 3000® Index(3) | -19.21% | 8.79% | 10.10% |

| Secondary Blended Benchmark(4) | -17.97% | 4.82% | 6.17% |

| Dow Jones Equal Weight U.S. Issued Corporate Bond IndexSM(5) | -16.85% | 0.49% | 1.98% |

| Dow Jones U.S. Total Stock Market IndexSM(6) | -19.53% | 8.65% | 10.00% |

The returns for the Fund do not reflect the deduction of expenses associated with variable products, such as mortality and expense risk charges, separate account charges, and sales charges or the effect of taxes. These expenses would reduce the overall returns shown.

| (1) | The Blended Benchmark returns are a 50/50 split between the Russell 3000® Index and the Bloomberg U.S. Corporate Investment-Grade Index returns. The Blended Benchmark returns are calculated by using the monthly return of the two indices during each period shown above. At the beginning of each month the two indices are rebalanced to a 50-50 ratio to account for divergence from that ratio that occurred during the course of each month. The monthly returns are then compounded for each period shown above, giving the performance for the Blended Benchmark for each period shown above. |

| (2) | Bloomberg U.S. Corporate Investment-Grade Index measures the performance of investment grade U.S. corporate bonds. The index includes all publicly issued, dollar-denominated corporate bonds with a minimum of $250 million par outstanding that are investment grade-rated (Baa3/BBB- or higher). The index excludes bonds having less than one year to final maturity as well as floating rate bonds, non-registered private placements, structured notes, hybrids, and convertible securities. (Bloomberg). (The index reflects no deduction for fees, expenses or taxes). |

| (3) | The Russell 3000® Index is composed of 3,000 large U.S. companies, as determined by market capitalization. This index represents approximately 98% of the investable U.S. equity market. (Bloomberg). (The index reflects no deduction for fees, expenses or taxes). |

| (4) | The Secondary Blended Benchmark return is a 50/50 split between the Dow Jones U.S. Total Stock Market IndexSM and the Dow Jones Equal Weight U.S. Issued Corporate Bond IndexSM returns. The Secondary Blended Benchmark returns are calculated by using the monthly return of the two indices during each period shown above. At the beginning of each month the two indices are rebalanced to a 50-50 ratio to account for divergence from that ratio that occurred during the course of each month. The monthly returns are then compounded for each period shown above, giving the performance for the Secondary Blended Benchmark for each period shown above. |

| (5) | The Dow Jones Equal Weight U.S. Issued Corporate Bond IndexSM measures the return of readily tradable, high-grade U.S. corporate bonds. The index includes an equally weighted basket of 96 recently issued investment-grade corporate bonds with laddered maturities. (The index reflects no deduction for fees, expenses or taxes). |

| (6) | The Dow Jones U.S. Total Stock Market IndexSM measures all U.S. equity securities that have readily available prices. (The index reflects no deduction for fees, expenses or taxes). |

Portfolio Commentary and Performance Summary (Continued)

First Trust/Dow Jones Dividend & Income Allocation Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

Portfolio Commentary and Performance Summary (Continued)

First Trust/Dow Jones Dividend & Income Allocation Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

| Credit Quality(7) | % of Total

Fixed-Income

Investments |

| AAA | 7.4% |

| AA- | 11.4 |

| A+ | 10.6 |

| A | 15.0 |

| A- | 13.9 |

| BBB+ | 13.4 |

| BBB | 15.9 |

| BBB- | 11.5 |

| NR | 0.9 |

| Total | 100.0% |

| Top Equity Holdings | % of Total

Investments |

| Caterpillar, Inc. | 0.5% |

| Steel Dynamics, Inc. | 0.5 |

| Evercore, Inc., Class A | 0.4 |

| Air Products and Chemicals, Inc. | 0.4 |

| Toro (The) Co. | 0.4 |

| Columbia Sportswear Co. | 0.4 |

| Merck & Co., Inc. | 0.4 |

| BlackRock, Inc. | 0.4 |

| Deere & Co. | 0.4 |

| EMCOR Group, Inc. | 0.4 |

| Total | 4.2% |

| Top Fixed-Income Holdings by Issuer | % of Total

Investments |

| United States Treasury | 4.0% |

| Goldman Sachs Group (The), Inc. | 3.0 |

| JPMorgan Chase & Co. | 2.5 |

| Bank of America Corp. | 2.5 |

| Morgan Stanley | 2.0 |

| UnitedHealth Group, Inc. | 1.8 |

| Citigroup, Inc. | 1.6 |

| Duke Energy Corp. | 1.5 |

| T-Mobile USA, Inc. | 1.2 |

| Oracle Corp. | 1.2 |

| Total | 21.3% |

| Sector Allocation | % of Total

Investments |

| Common Stocks | |

| Financials | 16.1% |

| Industrials | 14.6 |

| Consumer Discretionary | 5.3 |

| Information Technology | 4.8 |

| Health Care | 4.4 |

| Materials | 4.0 |

| Consumer Staples | 2.2 |

| Total Common Stocks | 51.4% |

| Corporate Bonds and Notes | |

| Financials | 12.4 |

| Utilities | 9.5 |

| Health Care | 7.2 |

| Communication Services | 4.5 |

| Industrials | 3.2 |

| Information Technology | 2.6 |

| Energy | 2.4 |

| Consumer Staples | 0.5 |

| Materials | 0.3 |

| Real Estate | 0.1 |

| Total Corporate Bonds and Notes | 42.7% |

| U.S. Government Bonds and Notes | 4.0% |

| Foreign Corporate Bonds and Notes | |

| Financials | 0.5 |

| Industrials | 0.5 |

| Health Care | 0.3 |

| Energy | 0.2 |

| Total Foreign Corporate Bonds and Notes | 1.5% |

| Real Estate Investment Trusts | |

| Real Estate | 0.4 |

| Total Real Estate Investment Trusts | 0.4% |

| Total | 100.0% |

| Fund Allocation | % of Net Assets |

| Common Stocks | 50.8% |

| Corporate Bonds and Notes | 42.2 |

| U.S. Government Bonds and Notes | 4.0 |

| Foreign Corporate Bonds and Notes | 1.5 |

| Real Estate Investment Trusts | 0.3 |

| Net Other Assets and Liabilities(8) | 1.2 |

| Total | 100.0% |

| (7) | The credit quality and ratings information presented above reflect the ratings assigned by one or more nationally recognized statistical rating organizations (NRSROs), including S&P Global Ratings, Moody’s Investors Service, Inc., Fitch Ratings or a comparably rated NRSRO. For situations in which a security is rated by more than one NRSRO and the ratings are not equivalent, the highest rating is used. Sub-investment grade ratings are those rated BB+/Ba1 or lower. Investment grade ratings are those rated BBB-/Baa3 or higher. The credit ratings shown relate to the creditworthiness of the issuers of the underlying securities in the Fund, and not to the Fund or its shares. Credit ratings are subject to change. |

| (8) | Includes variation margin on futures contracts. |

Portfolio Commentary and Performance Summary (Continued)

First Trust Multi Income Allocation Portfolio

Annual Report

December 31, 2022 (Unaudited)

Advisor

First Trust is a registered investment advisor based in Wheaton, IL and is the investment advisor to the First Trust Multi Income Allocation Portfolio (the “Fund”). In this capacity, First Trust is responsible for the selection and ongoing monitoring of the securities in the Fund’s portfolio and certain other services necessary for the management of the Fund. First Trust manages the Fund’s fixed income investments, as well as a portion of the Fund’s equity investments.

Sub-Advisors

Stonebridge Advisors LLC (“Stonebridge” or the “Sub-Advisor”) is a sub-advisor to the Fund and is a registered investment advisor based in Wilton, CT. Stonebridge specializes in the management of preferred securities and North American equity income securities.

Energy Income Partners, LLC (“EIP” or the “Sub-Advisor”) is a sub-advisor to the Fund and is a registered investment advisor based in Westport, CT. EIP was founded in 2003 to provide professional asset management services in publicly traded, energy-related infrastructure companies with above average dividend payout ratios operating pipelines and related storage and handling facilities, electric power transmission and distribution as well as long contracted or regulated power generation from renewables and other sources. The corporate structure of the portfolio companies include C-corporations, partnerships and energy infrastructure and real estate investment trusts (“REITs”).

Portfolio Management Team

First Trust

Daniel J. Lindquist, Chairman of the Investment Committee and Managing Director, First Trust

David G. McGarel, Chief Investment Officer, Chief Operating Officer and Managing Director, First Trust

Jon C. Erickson, Senior Vice President, First Trust

Roger F. Testin, Senior Vice President, First Trust

William Housey, Senior Vice President, First Trust

Chris A. Peterson, Senior Vice President, First Trust

Todd Larson, Senior Vice President, First Trust

James Snyder, Senior Vice President, First Trust

Jeremiah Charles, Senior Vice President, First Trust

Stonebridge

Scott Fleming, Portfolio Manager, President and Chief Investment Officer of Stonebridge

Robert Wolf, Senior Portfolio Manager and Senior Vice President of Stonebridge

EIP

James J. Murchie, Co-Portfolio Manager, Co-Founder, Principal and CEO of EIP

Eva Pao, Co-Portfolio Manager, Co-Founder, Principal of EIP

John Tysseland, Co-Portfolio Manager, Principal of EIP

First Trust Multi Income Allocation Portfolio

For the year ended December 31, 2022, the Fund’s Class I Shares returned -7.52% versus -13.01% for the Bloomberg U.S. Aggregate Bond Index, -15.21% for the Broad Blended Benchmark (60% Bloomberg U.S. Aggregate Bond Index and 40% Russell 3000® Index) and -4.69% for the Asset Class Blended Benchmark (15% Dow Jones U.S. Select Dividend Index; 8% ICE BofA Fixed Rate Preferred Securities Index; 15% Alerian MLP Index; 15% S&P U.S. REIT Index; 8% ICE BofA U.S. High Yield Constrained Index; 15% Morningstar® LSTA® U.S. Leveraged Loan Index; 8% Bloomberg U.S. Corporate Investment-Grade Index; 8% ICE BofA U.S. MBS Index; and 8% ICE BofA U.S. Inflation-Linked Treasury Index).

The Fund invests in nine asset classes which are: dividend-paying stocks, preferred stocks, energy infrastructure companies and master limited partnerships (“MLPs”), real estate investment trusts (“REITs”), high yield or “junk” bonds, floating-rate loans, corporate bonds, mortgage-backed securities (“MBS”) and Treasury Inflation Protected Securities (“TIPS”). The weight assigned to each asset class is determined on a quarterly basis. As of December 31, 2022, the dividend-paying stocks were the highest-weighted asset class, while the TIPS asset class was the lowest-weighted asset class. As of December 31, 2022, the Fund held approximately 1.82% in cash. The MLP asset class had the most positive impact on the overall Fund performance for the year, while the REITs asset class had the largest negative impact on the overall Fund performance.

Portfolio Commentary and Performance Summary (Continued)

First Trust Multi Income Allocation Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

Dividend-paying stocks returned -6.18% (Gross of Fees) for the year ended December 31, 2022 and represented 17.3% of the portfolio as of December 31, 2022. US equities, as measured by the Russell 3000® Index, saw losses in 2022 amounting to -19.21% as the economy digested rising inflation and the Federal Reserve’s (the “Fed”) response to it. On a factor basis, value stocks dominated, with much of that relative performance versus the most expensive names by price to book coming from the second quarter of 2022. During the worst quarter of market performance overall, those expensive names suffered the most in the face of inflation and the related rising interest rates. Investors preferred quality names during the market downturn, with the Russell 3000® Index’s most extreme losses coming from the third of the market with the least quality. Size (small cap) as a factor was modestly positive for the year ended December 31, 2022, though the smallest names in the market took a beating in the first quarter of 2022 and never recovered parity with the rest of the market. Dividend payers in the Russell 3000® Index outperformed non-payers significantly over the year. On a sector basis, the dividend section of the portfolio carried throughout the year an overweight in the energy sector, which was far and away the year’s best performing sector. The Communication Services sector struggled during the year as struggling interactive media names like Meta Platforms Inc. dragged down the sector; the dividend section of the portfolio was beneficially underweight communication services.

The preferred securities returned -9.25% (Gross of Fees) for the year ended December 31, 2022 and represented 7.9% of the portfolio as of December 31, 2022. The preferred market was primarily affected by global central bank policies, interest rate volatility and geopolitical risks, with a secondary technical impact from exchange-traded funds and mutual fund outflows during the year. The Fund achieved negative performance given the general move higher in interest rates during the period, but this was mitigated by the Fund’s bias towards shorter duration, floating rate and variable rate securities, an overweight to the Energy sector and an underweight to both $25 par exchange-traded securities and non-U.S. bank contingent convertible capital securities.

The energy infrastructure companies and MLPs asset class returned 14.39% (Gross of Fees) for the year ended December 31, 2022 and represented 15.4% of the portfolio as of December 31, 2022. The performance of this asset class outperformed the overall performance of the Fund. Energy infrastructure companies and MLPs in the portfolio have generally had stable earnings historically, but negative sentiment around energy stocks in general weighed on valuations in the previous years. This negative sentiment faded with a sharp jump in the price of oil and natural gas in the first quarter of 2022. Continued earnings growth among the energy infrastructure companies and MLPs coupled with low valuations relative to the S&P 500® Index based on forward 12-month earnings expectations and improving sentiment all contributed to significant outperformance for the year.

REITs returned -24.70% (Gross of Fees) for the year ended December 31, 2022 and represented 12.8% of the portfolio as of December 31, 2022. Though REITs are typically viewed as a defensive asset, soaring inflation and the sharp rise in interest rates have been significant drags on their performance. The U.S. 10-year yield spiked from 1.51% to 3.88% in 2022, increasing financing costs for REITs across all sectors and driving down valuations. The portfolio benefitted from an underweight allocation in Industrial and Office REITs, as well as an overweight allocation in Specialized REITs. However, stock selection had a negative impact on total returns, particularly driven by Health Care REITs. Selections within Retail REITs had a significant impact on total returns. The top performing REITs in the portfolio by contribution to total return were Gaming and Leisure Properties, Inc., VICI Properties, Inc., and Kite Realty Group Trust. The worst performing REITs in the portfolio were Medical Properties Trust, Inc., Camden Property Trust, and Invitation Homes, Inc.

High-yield bonds returned -12.94% (Gross of Fees) for the year ended December 31, 2022 and represented 6.9% of the portfolio at year-end. High-yield bond spreads over U.S. Treasuries entered the year at T+311 basis points (“bps”), widened to T+589 bps in the second quarter of 2022, and subsequently tightened to T+483 bps at year-end. For historical context, year-end spreads were 68 bps below the long-term average of T+551 bps, dating back to December 1997. High-yield bond funds experienced record-setting outflows of approximately $47 billion in 2022; this compares to outflows of approximately $13 billion in 2021. A challenging macroenvironment, marked by the Fed’s rapid rate interest hikes, contributed to outflows and negatively impacted risk assets. Within the high-yield bond market, BB rated issues (-10.44%) outperformed both B rated issues (-10.56%) and CCC rated issues (-16.54%). The last twelve-month default rate of the JP Morgan High-Yield Bond universe increased from 0.27% to 0.84% throughout the course of the year. The current default rate remains well below the long-term average default rate of 3.05% (March 1999 - December 2022).

Senior loans returned -2.61% (Gross of Fees) for the year ended December 31, 2022 and represented 12.6% of the portfolio at year-end. Senior loan spreads over 3-month London Inter-Bank Offered Rate (“LIBOR”) entered the year at L+428, subsequently widened to L+665 in the third quarter, and finished the year at L+645, surpassing the historical average of L+516 bps (December 1997 - December 2022). The benchmark rate for senior loan coupons, 3-month LIBOR, entered the year at 0.21% before increasing to 4.77% at year-end. The move in 3-month LIBOR was largely driven by the Fed’s rapid interest rate hikes. Given market expectations for higher inflation and future interest rate hikes, the senior loan asset class experienced approximately $47 billion of inflows from retail investors in 2021. However, the senior loan asset class experienced outflows of approximately $11 billion in 2022 as inflation, as measured by the Consumer Price Index (“CPI”), cooled after peaking at 9.1% in the second quarter.

Portfolio Commentary and Performance Summary (Continued)

First Trust Multi Income Allocation Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

Corporate bonds returned -14.93% (Gross of Fees) for the year ended December 31, 2022 and represented 8.8% of the portfolio as of December 31, 2022. Throughout the full-year period, inflation remained stubbornly elevated with the CPI reaching a high of 9.1% on a year-over-year basis in June 2022. While continuing to reiterate its commitment to a 2.0% inflation target, the Fed increased the Federal Funds target rate by 425 bps and reached 4.50% at year-end 2022. This interest rate hiking path included four meetings at which the Fed increased the Federal Funds target rate by a full 75 bps. In response, Treasury yields increased dramatically. For example, the yield on the 10-Year U.S. Treasury increased from 1.51% to 3.88% over the course of the year and reached a high of 4.23% in late October 2022. The impact of higher yields on the investment grade credit market was pronounced as well. For the 12-month period ended December 31, 2022, the Bloomberg U.S. Corporate Investment-Grade Index returned -15.76%.

The MBS asset class returned -5.54% (Gross of Fees) for the year ended December 31, 2022 and represented 11.5% of the portfolio as of December 31, 2022. This dramatically outperformed its benchmark, the ICE BofA US Mortgage Backed Securities Index by over 630 bps, which returned -11.89% for the year. Over the course of the year, the sleeve maintained significantly less duration than its benchmark, which aided the performance of the asset class as interest rates across the curve rose over the year. Given our outlook on the broader bond markets, we plan to continue to actively manage the Fund versus the Index from duration and asset allocation standpoints.

TIPS returned -11.97% (Gross of Fees) for the year ended December 31, 2022 and represented 6.8% of the portfolio as of December 31, 2022. The environment of rising inflation was very supportive of U.S. TIPS during the early part of 2022 but that faded during the latter half as the rate of CPI inflation declined. The CPI reached a high of 9.1% in June 2022 before ending the year at 6.5%. The impact of rising yields, primarily in response to policy interest rate hikes by the Fed, had a negative impact on Treasury returns. For the 12-month period ended December 31, 2022, the ICE BofA U.S. Inflation-Linked Treasury Index returned -12.63%. This was slightly better than the return on nominal Treasury bonds. The ICE BofA U.S. Treasury Index returned -12.86% for the period. TIPS benefit from rising inflation, but it is a negative factor for nominal Treasury bonds.

Investment Climate

What a difference a year can make! While 2021 certainly had its share of headwinds, their impact on the U.S. financial markets was subdued. Much of that changed in 2022. Pressured by stubbornly high consumer prices, central banks around the world reacted by raising their target rates. This led to a selloff in global equity and fixed income markets amid growing concerns that the major economies could fall into recession. As this was unfolding Russia invaded Ukraine in late February 2022, resulting in disruptions to worldwide food and energy supplies and creating geopolitical strife across the globe. These factors, among others, continue to influence the investment climate that we find ourselves in today.

In response to stubbornly high inflation in the U.S., the Fed sprang into action in the first quarter of 2022. Over the course of seven rate hikes, the Fed increased the Federal Funds target rate (upper bound) from 0.25% (where it stood in March 2022), to 4.50% as of December 31, 2022. While it is our opinion that the full impact of these interest rate increases has yet to be realized, it appears that inflation is responding. One key measure of inflation is the CPI. The CPI stood at 6.5% on a trailing 12-month basis in December 2022, down 2.6 percentage points since peaking at 9.1% in June 2022. While this is a welcome improvement, the CPI rate still stands well above the Fed’s desired 2.0%, suggesting that further action by the Fed could be warranted, in our opinion.

The broader U.S. equity and fixed income markets struggled against the backdrop of tighter monetary policy in 2022. The S&P 500® Index posted a total return of -18.11% for the year, its lowest annual total return since 2008, according to data from Bloomberg. The increases in the Federal Funds target rate also impacted the fixed income markets. The yield on the benchmark 10-Year Treasury Note (“T-Note”) closed trading on December 31, 2022, at 3.88%, up 237 bps from its 1.51% close on December 31, 2021, according to Bloomberg. The yield stood 175 bps above its 2.13% average for the 10-year period ended December 31, 2022. Most bond investors likely know that as yields increase, prices fall. As indicated by the sizeable increase in the yield on the 10-Year T-Note, bond investors endured a challenging year of declines in 2022.

Portfolio Commentary and Performance Summary (Continued)

First Trust Multi Income Allocation Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

| Return Comparison | | | |

| | | Average Annual

Total Returns |

| | 1 Year

Ended

12/31/22 | 5 Years

Ended

12/31/22 | Inception

(5/1/14)

to 12/31/22 |

| Fund Performance | | | |

| First Trust Multi Income Allocation Portfolio - Class I | -7.52% | 3.50% | 3.90% |

| First Trust Multi Income Allocation Portfolio - Class II | -7.37% | 3.76% | 4.14% |

| Index Performance | | | |

| Broad Blended Benchmark(1) | -15.21% | 3.85% | 4.92% |

| Bloomberg U.S. Aggregate Bond Index(2) | -13.01% | 0.02% | 1.12% |

| Russell 3000® Index(3) | -19.21% | 8.79% | 10.11% |

| Asset Class Blended Benchmark(4) | -4.69% | 4.42% | 4.27% |

The returns for the Fund do not reflect the deduction of expenses associated with variable products, such as mortality and expense risk charges, separate account charges, and sales charges or the effect of taxes. These expenses would reduce the overall returns shown.

| (1) | The Broad Blended Benchmark returns are split between the Bloomberg U.S. Aggregate Bond Index (60%) and the Russell 3000® Index (40%). The Broad Blended Benchmark returns are calculated by using the monthly return of the two indices during each month shown above. At the beginning of each month the two indices are rebalanced to a 60% and 40% ratio, respectively, to account for divergence from that ratio that occurred during the course of each month. The monthly returns are then compounded for each period shown above, giving the performance for the Broad Blended Benchmark for each period shown above. |

| (2) | The Bloomberg U.S. Aggregate Bond Index represents the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Bonds included in the index are U.S. dollar denominated; have a fixed rate coupon; carry an investment-grade rating; have at least one year to final maturity; and meet certain criteria for minimum amount of outstanding par value. (The index reflects no deduction for fees, expenses or taxes). |

| (3) | The Russell 3000® Index is composed of 3,000 large U.S. companies, as determined by market capitalization. This index represents approximately 98% of the investable U.S. equity market. (Bloomberg). (The index reflects no deduction for fees, expenses or taxes). |

| (4) | The Asset Class Blended Benchmark is weighted to include nine indexes: Dow Jones U.S. Select Dividend TM Index (15%), ICE BofA Fixed Rate Preferred Securities Index (8%), Alerian MLP Index (15%), S&P U.S. REIT Index (15%), ICE BofA U.S. High Yield Constrained Index (8%), Morningstar® LSTA® U.S. Leveraged Loan Index (15%), Bloomberg U.S. Corporate Investment-Grade Index (8%), ICE BofA U.S. MBS Index (8%), and ICE BofA U.S. Inflation-Linked Treasury Index (8%).The Asset Class Benchmark returns are calculated by using the monthly return of the nine indices during each period shown above. At the beginning of each month the nine indices are rebalanced to a 15%, 8%, 15%, 15%, 8%, 15%, 8%, 8% and 8% ratio, respectively, to account for divergence from that ratio that occurred during the course of each month. The monthly returns are then compounded for each period shown above, giving the performance for the Asset Class Blended Benchmark for each period shown above. |

Portfolio Commentary and Performance Summary (Continued)

First Trust Multi Income Allocation Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

| Top Ten Holdings | % of Total

Investments |

| First Trust Senior Loan ETF | 12.7% |

| First Trust Tactical High Yield ETF | 6.9 |

| iShares iBoxx $ Investment Grade Corporate Bond ETF | 6.3 |

| First Trust Institutional Preferred Securities and Income ETF | 6.0 |

| iShares 7-10 Year Treasury Bond ETF | 4.2 |

| First Trust Low Duration Opportunities ETF | 3.2 |

| First Trust Limited Duration Investment Grade Corporate ETF | 2.7 |

| iShares MBS ETF | 2.7 |

| First Trust Preferred Securities and Income ETF | 1.9 |

| Magellan Midstream Partners, L.P. | 1.3 |

| Total | 47.9% |

| Sector Allocation | % of Total

Investments |

| Exchange-Traded Funds | 46.7% |

| Common Stocks | |

| Energy | 5.7 |

| Utilities | 5.0 |

| Health Care | 3.6 |

| Information Technology | 3.5 |

| Financials | 2.1 |

| Industrials | 2.0 |

| Consumer Discretionary | 1.6 |

| Consumer Staples | 1.2 |

| Materials | 0.5 |

| Communication Services | 0.3 |

| Total Common Stocks | 25.5% |

| Real Estate Investment Trusts | |

| Financials | 12.9 |

| Total Real Estate Investment Trusts | 12.9% |

| Master Limited Partnerships | |

| Energy | 6.2 |

| Utilities | 0.6 |

| Materials | 0.2 |

| Total Master Limited Partnerships | 7.0% |

| U.S. Government Bonds and Notes | 6.9% |

| U.S. Government Agency Mortgage-Backed Securities | 1.0% |

| Mortgage-Backed Securities | 0.0% * |

| Total | 100.0% |

| * | Amount is less than 0.1%. |

Portfolio Commentary and Performance Summary (Continued)

First Trust Dorsey Wright Tactical Core Portfolio

Annual Report

December 31, 2022 (Unaudited)

Advisor

First Trust is a registered investment advisor based in Wheaton, IL and is the investment advisor to First Trust Dorsey Wright Tactical Core Portfolio (the “Fund”). In this capacity, First Trust is responsible for the selection and ongoing monitoring of the securities in the Fund’s portfolio and certain other services necessary for the management of the Fund.

Portfolio Management Team

Daniel J. Lindquist, Chairman of the Investment Committee and Managing Director, First Trust

David G. McGarel, Chief Investment Officer, Chief Operating Officer and Managing Director, First Trust

Jon C. Erickson, Senior Vice President, First Trust

Roger F. Testin, Senior Vice President, First Trust

Todd Larson, Senior Vice President, First Trust

Chris A. Peterson, Senior Vice President, First Trust

Eric R. Maisel, Senior Vice President, First Trust

Scott Skowronski, Senior Vice President, First Trust

First Trust Dorsey Wright Tactical Core Portfolio

For the year ended December 31, 2022, the Fund’s Class I Shares returned -17.05% versus -18.11% for the S&P 500® Index, and -15.79% for the Broad Blended Benchmark: 60% S&P 500® Index and 40% Bloomberg U.S. Aggregate Bond Index.

The Fund seeks to provide total return. The Fund seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its net assets (including any investment borrowings) in exchange-traded funds (“ETFs”) and cash and cash equivalents that comprise the Dorsey Wright Tactical Tilt Moderate Core Index (the “Index”). It is expected that most of the ETFs in which the Fund invests will be advised by First Trust.

The Index is owned and was developed by Dorsey, Wright & Associates (the “Index Provider”). The Index is constructed pursuant to the Index Provider’s proprietary methodology, which considers the performance of four distinct asset classes relative to one another. The Index is designed to strategically allocate its investments among (i) domestic equity securities; (ii) international equity securities; (iii) fixed income securities; and (iv) cash and cash equivalents. The Index will gain exposure to the asset classes by investing in ETFs that invest in such assets. The Index Provider has retained Nasdaq, Inc. (“Nasdaq”) to calculate and maintain the Index.

The Index will utilize the Dynamic Asset Level Investing (“DALI”) asset allocation process developed by the Index Provider to allocate assets over the four asset classes. The asset class allocations are determined using a relative strength methodology that is based upon each asset class’s market performance and characteristics that offer the greatest potential to outperform the other asset classes at a given time. Relative strength is a momentum technique that relies on unbiased, unemotional, and objective data, rather than biased forecasting and subjective research. Relative strength is a way of recording historic performance patterns, and the Index Provider uses relative strength signals as a trend indicator for current momentum trends of each asset class against the others.

Performance Review

The Fund began 2022 with the following allocations to the four asset classes: domestic equity securities (73.0%), international equity securities (4.9%), fixed income securities (19.6%), and cash equivalents (2.5%). During 2022, the following allocation changes were made to the domestic equity securities: in July 2022 the allocation was decreased to 25%, in September 2022 the allocation was increased to 75%, in October 2022 the allocation decreased to 25% and in December 2022 the allocation was decreased to 20%. Most of the allocation changes to domestic equity securities involved an offsetting allocation change to cash equivalents. At the end of 2022, the Fund had the following allocations: domestic equity securities (20.1%), international equity securities (10.2%), fixed income securities (20.3%), and cash equivalents (49.4%). The selection impact from the Fund’s equity holdings was negative and the largest detracting holding was the First Trust Industrials/Producer Durables AlphaDEX® Fund. The Fund’s largest contributing holdings to performance in 2022 were the First Trust Nasdaq Oil & Gas ETF and the First Trust Enhanced Short Maturity ETF.

Portfolio Commentary and Performance Summary (Continued)

First Trust Dorsey Wright Tactical Core Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

| Return Comparison | | | |

| | | Average Annual

Total Returns |

| | 1 Year

Ended

12/31/22 | 5 Years

Ended

12/31/22 | Inception

(10/30/15)

to 12/31/22 |

| Fund Performance | | | |

| First Trust Dorsey Wright Tactical Core Portfolio - Class I | -17.05% | 3.13% | 4.55% |

| First Trust Dorsey Wright Tactical Core Portfolio - Class II | -16.81% | 3.28% | 4.71% |

| Index Performance | | | |

| Broad Blended Benchmark(1) | -15.79% | 5.96% | 7.10% |

| Bloomberg U.S. Aggregate Bond Index(2) | -13.01% | 0.02% | 0.79% |

| S&P 500® Index(3) | -18.11% | 9.42% | 10.99% |

The returns for the Fund do not reflect the deduction of expenses associated with variable products, such as mortality and expense risk charges, separate account charges, and sales charges or the effect of taxes. These expenses would reduce the overall returns shown.

| (1) | The Broad Blended Benchmark return is split between the Bloomberg U.S. Aggregate Bond Index (40%) and the S&P 500® Index (60%). The Broad Blended Benchmark returns are calculated by using the monthly return of the two indices during each period shown above. At the beginning of each month the two indices are rebalanced to a 40% and 60% ratio, respectively, to account for divergence from that ratio that occurred during the course of each month. The monthly returns are then compounded for each period shown above, giving the performance for the Broad Blended Benchmark for each period shown above. |

| (2) | The Bloomberg U.S. Aggregate Bond Index represents the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Bonds included in the index are U.S. dollar denominated; have a fixed rate coupon; carry an investment-grade rating; have at least one year to final maturity; and meet certain criteria for minimum amount of outstanding par value. (The index reflects no deduction for fees, expenses or taxes). |

| (3) | The S&P 500® Index is an unmanaged index of 500 stocks used to measure large-cap U.S. stock market performance. (The index reflects no deduction for fees, expenses or taxes). |

Portfolio Commentary and Performance Summary (Continued)

First Trust Dorsey Wright Tactical Core Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

| Top Ten Holdings | % of Total

Investments |

| First Trust Enhanced Short Maturity ETF | 49.0% |

| iShares Core U.S. Aggregate Bond ETF | 6.1 |

| SPDR Bloomberg Investment Grade Floating Rate ETF | 3.6 |

| SPDR Portfolio Short Term Corporate Bond ETF | 3.6 |

| SPDR Blackstone Senior Loan ETF | 3.6 |

| SPDR FTSE International Government Inflation-Protected Bond ETF | 3.5 |

| First Trust Mid Cap Value AlphaDEX® Fund | 2.7 |

| First Trust Mid Cap Core AlphaDEX® Fund | 2.7 |

| First Trust Small Cap Value AlphaDEX® Fund | 2.7 |

| First Trust Developed Markets ex-US AlphaDEX® Fund | 2.6 |

| Total | 80.1% |

Portfolio Commentary and Performance Summary (Continued)

First Trust Capital Strength Portfolio

Annual Report

December 31, 2022 (Unaudited)

Advisor

First Trust is a registered investment advisor based in Wheaton, IL and is the investment advisor to First Trust Capital Strength Portfolio (the “Fund”). In this capacity, First Trust is responsible for the selection and ongoing monitoring of the securities in the Fund’s portfolio and certain other services necessary for the management of the Fund.

Portfolio Management Team

Daniel J. Lindquist, Chairman of the Investment Committee and Managing Director, First Trust

David G. McGarel, Chief Investment Officer, Chief Operating Officer and Managing Director, First Trust

Jon C. Erickson, Senior Vice President, First Trust

Roger F. Testin, Senior Vice President, First Trust

Chris A. Peterson, Senior Vice President, First Trust

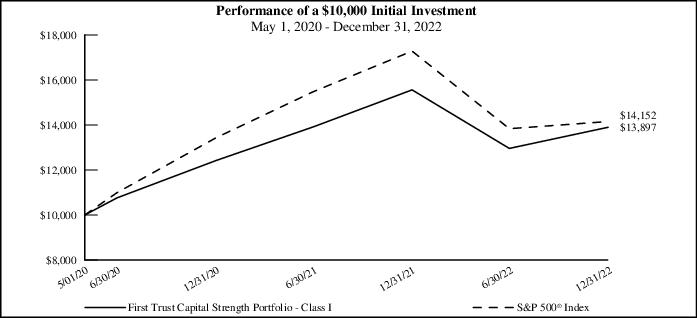

First Trust Capital Strength Portfolio

For the year ended December 31, 2022, the Fund’s Class I Shares returned -10.68% versus -18.11% for the S&P 500® Index (the “Benchmark”).

The Fund seeks to provide capital appreciation. The Fund seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its net assets (including investment borrowings) in the common stocks and real estate investment trusts that comprise The Capital Strength IndexSM (the “Index”). The Index seeks to provide exposure to well-capitalized companies with strong market positions that have the potential to provide their stockholders with a greater degree of stability and performance over time. The Index is rebalanced and reconstituted quarterly and the Fund will make corresponding changes to its portfolio shortly after the Index changes are made public.

For the year ended December 31, 2022, the Fund outperformed the Benchmark by nearly 7.5% as the quality and low volatility holdings selected by the methodology held up relatively well in a tough market environment. The Fund’s low volatility and quality tilts along with a tilt away from growth stocks drove much of the Fund’s outperformance along with strong sector allocation. The Fund held underweight positions in the Consumer Discretionary and Communications Services sectors which were heavily weighed down by their exposure to Alphabet, Inc., Amazon.com, Inc., and Tesla, Inc. while holding its largest weight in the Health Care sector which outperformed during the period. Stock selection was strong within the Information Technology sector and weak within the Consumer Staples sector and was negligible in aggregate.

| Return Comparison | | |

| | | Average Annual

Total Returns |

| | 1 Year Ended

12/31/22 | Inception (5/1/20)

to 12/31/22 |

| Fund Performance | | |

| First Trust Capital Strength Portfolio - Class I | -10.68% | 13.12% |

| First Trust Capital Strength Portfolio - Class II | -10.46% | 13.39% |

| Index Performance | | |

| S&P 500® Index(1) | -18.11% | 13.90% |

The returns for the Fund do not reflect the deduction of expenses associated with variable products, such as mortality and expense risk charges, separate account charges, and sales charges or the effect of taxes. These expenses would reduce the overall returns shown.

| (1) | The S&P 500® Index is an unmanaged index of 500 stocks used to measure large-cap U.S. stock market performance. (The index reflects no deduction for fees, expenses or taxes). |

Portfolio Commentary and Performance Summary (Continued)

First Trust Capital Strength Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

| Top Ten Holdings | % of Total

Investments |

| Air Products and Chemicals, Inc. | 2.4% |

| Hologic, Inc. | 2.2 |

| Procter & Gamble (The) Co. | 2.2 |

| Honeywell International, Inc. | 2.2 |

| Trane Technologies PLC | 2.2 |

| Merck & Co., Inc. | 2.2 |

| Monster Beverage Corp. | 2.2 |

| Emerson Electric Co. | 2.2 |

| Abbott Laboratories | 2.2 |

| Moody’s Corp. | 2.1 |

| Total | 22.1% |

| Sector Allocation | % of Total

Investments |

| Health Care | 32.0% |

| Industrials | 20.2 |

| Information Technology | 17.5 |

| Consumer Staples | 12.1 |

| Financials | 12.1 |

| Real Estate | 3.7 |

| Materials | 2.4 |

| Total | 100.0% |

Portfolio Commentary and Performance Summary (Continued)

First Trust International Developed Capital Strength Portfolio

Annual Report

December 31, 2022 (Unaudited)

Advisor

First Trust is a registered investment advisor based in Wheaton, IL and is the investment advisor to First Trust International Developed Capital Strength Portfolio (the “Fund”). In this capacity, First Trust is responsible for the selection and ongoing monitoring of the securities in the Fund’s portfolio and certain other services necessary for the management of the Fund.

Portfolio Management Team

Daniel J. Lindquist, Chairman of the Investment Committee and Managing Director, First Trust

David G. McGarel, Chief Investment Officer, Chief Operating Officer and Managing Director, First Trust

Jon C. Erickson, Senior Vice President, First Trust

Roger F. Testin, Senior Vice President, First Trust

Chris A. Peterson, Senior Vice President, First Trust

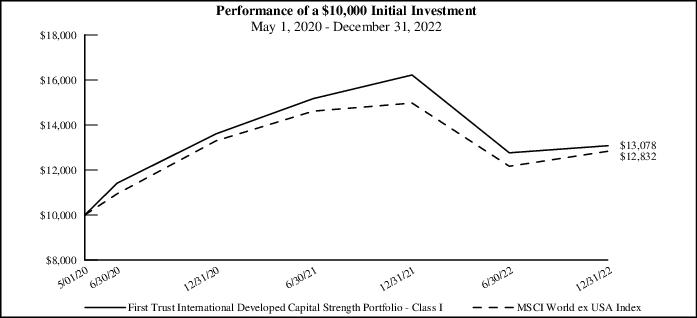

First Trust International Developed Capital Strength Portfolio

For the year ended December 31, 2022, the Fund’s Class I Shares returned -19.38% versus -14.29% for the MSCI World ex USA Index (the “Benchmark”).

The Fund seeks to provide capital appreciation. The Fund seeks to achieve its investment objective by investing, under normal market conditions, at least 80% of its net assets (including investment borrowings) in the common stocks that comprise The International Developed Capital Strength IndexSM (the “Index”). The Index seeks to provide exposure to well-capitalized non-U.S. companies in developed markets with strong market positions that have the potential to provide their stockholders with a greater degree of stability and performance over time. The Fund may invest in securities of any market capitalization. The Index is rebalanced and reconstituted semi-annually and the Fund will make corresponding changes to its portfolio shortly after the Index changes are made public.

For the year ended December 31, 2022, the Fund underperformed the Benchmark by over 5%. Fund performance tracked relatively closely to the Benchmark for much of the year before giving up sufficiently all of its relative performance in the last two months of the year. In the upward trending market, the low volatility and quality factors hampered Fund returns while risky stocks benefitted. On a country basis, poor relative performance in Australia and Japan would have been enough to explain nearly all of the Fund’s underperformance, all else equal. The Fund benefitted from an overweight allocation and strong stock selection in Canada during the period. On a sector basis, the Fund suffered from an underweight position in the Energy sector and poor selection within the Materials and Consumer Discretionary sectors. Strong stock selection within the Information Technology sector was the most prominent benefit to the Fund, particularly by owning Information Technology names that did not draw down as much as the broad sector in the Index.

| Return Comparison | | |

| | | Average Annual

Total Returns |

| | 1 Year Ended

12/31/22 | Inception (5/1/20)

to 12/31/22 |

| Fund Performance | | |

| First Trust International Developed Capital Strength Portfolio - Class I | -19.38% | 10.58% |

| First Trust International Developed Capital Strength Portfolio - Class II | -19.28% | 10.78% |

| Index Performance | | |

| MSCI World ex USA Index(1) | -14.29% | 9.80% |

The returns for the Fund do not reflect the deduction of expenses associated with variable products, such as mortality and expense risk charges, separate account charges, and sales charges or the effect of taxes. These expenses would reduce the overall returns shown.

| (1) | The MSCI World ex USA Index includes developed markets and is designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. |

Portfolio Commentary and Performance Summary (Continued)

First Trust International Developed Capital Strength Portfolio (Continued)

Annual Report

December 31, 2022 (Unaudited)

| Top Ten Holdings | % of Total

Investments |

| Hong Kong Exchanges & Clearing Ltd. | 2.4% |

| Merck KGaA | 2.3 |

| Shin-Etsu Chemical Co., Ltd. | 2.2 |

| Schindler Holding AG | 2.2 |

| Novartis AG | 2.2 |

| LVMH Moet Hennessy Louis Vuitton SE | 2.1 |

| L’Oreal S.A. | 2.1 |

| Zurich Insurance Group AG | 2.1 |

| Sampo Oyj, Class A | 2.1 |

| Carlsberg A.S., Class B | 2.1 |

| Total | 21.8% |

| Sector Allocation | % of Total

Investments |

| Industrials | 21.8% |

| Financials | 16.4 |

| Consumer Staples | 16.1 |

| Information Technology | 13.9 |

| Health Care | 12.1 |

| Consumer Discretionary | 11.6 |

| Materials | 4.2 |

| Real Estate | 2.0 |

| Communication Services | 1.9 |

| Total | 100.0% |

First Trust Variable Insurance Trust

Understanding Your Fund Expenses

December 31, 2022 (Unaudited)

As a shareholder of First Trust Dow/Jones Dividend & Income Allocation Portfolio, First Trust Multi Income Allocation Portfolio, First Trust Dorsey Wright Tactical Core Portfolio, First Trust Capital Strength Portfolio or First Trust International Developed Capital Strength Portfolio (each a “Fund” and collectively, the “Funds”), you incur two types of costs: (1) transaction costs; and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, if any, and other Fund expenses. This Example is intended to help you understand your ongoing costs of investing in the Funds and to compare these costs with the ongoing costs of investing in other funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held through the six-month period ended December 31, 2022.

Actual Expenses

The first three columns of the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the third column under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this six-month period.

Hypothetical Example for Comparison Purposes

The next three columns of the table below provide information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not each Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs such as sales charges (loads) or contingent deferred sales charges. Therefore, the hypothetical section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | Actual Expenses | | Hypothetical

(5% Return Before Expenses) | |

| | Beginning

Account

Value

7/1/2022 | Ending

Account

Value

12/31/2022 | Expenses Paid

During Period

7/1/2022 -

12/31/2022 (a) | | Beginning

Account

Value

7/1/2022 | Ending

Account

Value

12/31/2022 | Expenses Paid

During Period

7/1/2022 -

12/31/2022 (a) | Annualized

Expense

Ratios (b) |

First Trust/Dow Jones Dividend

& Income Allocation Portfolio |

Class I

| $ 1,000.00 | $ 1,031.90 | $ 6.15 | | $ 1,000.00 | $ 1,019.16 | $ 6.11 | 1.20% |

Class II

| $ 1,000.00 | $ 1,033.20 | $ 4.87 | | $ 1,000.00 | $ 1,020.42 | $ 4.84 | 0.95% |

First Trust Multi Income Allocation

Portfolio (c) |

Class I

| $ 1,000.00 | $ 1,023.30 | $ 4.23 | | $ 1,000.00 | $ 1,021.02 | $ 4.23 | 0.83% |

Class II

| $ 1,000.00 | $ 1,023.70 | $ 2.96 | | $ 1,000.00 | $ 1,022.28 | $ 2.96 | 0.58% |

First Trust Dorsey Wright Tactical

Core Portfolio (c) |

Class I

| $ 1,000.00 | $ 986.30 | $ 4.46 | | $ 1,000.00 | $ 1,020.72 | $ 4.53 | 0.89% |

Class II

| $ 1,000.00 | $ 988.40 | $ 3.21 | | $ 1,000.00 | $ 1,021.98 | $ 3.26 | 0.64% |

First Trust Variable Insurance Trust

Understanding Your Fund Expenses (Continued)

December 31, 2022 (Unaudited)

| | Actual Expenses | | Hypothetical

(5% Return Before Expenses) | |

| | Beginning

Account

Value

7/1/2022 | Ending

Account

Value

12/31/2022 | Expenses Paid

During Period

7/1/2022 -

12/31/2022 (a) | | Beginning

Account

Value

7/1/2022 | Ending

Account

Value

12/31/2022 | Expenses Paid

During Period

7/1/2022 -

12/31/2022 (a) | Annualized

Expense

Ratios (b) |

| First Trust Capital Strength Portfolio |

Class I

| $ 1,000.00 | $ 1,072.60 | $ 5.75 | | $ 1,000.00 | $ 1,019.66 | $ 5.60 | 1.10% |

Class II

| $ 1,000.00 | $ 1,073.10 | $ 4.44 | | $ 1,000.00 | $ 1,020.92 | $ 4.33 | 0.85% |

First Trust International Developed

Capital Strength Portfolio |

Class I

| $ 1,000.00 | $ 1,024.80 | $ 6.12 | | $ 1,000.00 | $ 1,019.16 | $ 6.11 | 1.20% |

Class II

| $ 1,000.00 | $ 1,024.80 | $ 4.85 | | $ 1,000.00 | $ 1,020.42 | $ 4.84 | 0.95% |

| (a) | Expenses are equal to the annualized expense ratios as indicated in the table multiplied by the average account value over the period (July 1, 2022 through December 31, 2022), multiplied by 184/365 (to reflect the six-month period). |

| (b) | These expense ratios reflect expense caps. First Trust Multi Income Allocation Portfolio expense ratios reflect an additional waiver. See Note 3 in the Notes to Financial Statements. |

| (c) | Annualized expense ratio and expenses paid during the six-month period do not include fees and expenses of the underlying funds in which the Fund invests. |

First Trust/Dow Jones Dividend & Income Allocation Portfolio

Portfolio of Investments

December 31, 2022

| Shares | | Description | | Value |

| COMMON STOCKS – 50.8% |

| | | Aerospace & Defense – 1.2% | | |

| 13,970 | | General Dynamics Corp.

| | $3,466,096 |

| 7,675 | | Lockheed Martin Corp.

| | 3,733,811 |

| 6,303 | | Northrop Grumman Corp.

| | 3,438,980 |

| | | | | 10,638,887 |

| | | Air Freight & Logistics – 1.1% | | |

| 33,568 | | Expeditors International of Washington, Inc.

| | 3,488,387 |

| 32,516 | | Forward Air Corp.

| | 3,410,603 |

| 18,350 | | United Parcel Service, Inc., Class B

| | 3,189,964 |

| | | | | 10,088,954 |

| | | Auto Components – 0.4% | | |

| 124,342 | | Gentex Corp.

| | 3,390,806 |

| | | Banks – 4.5% | | |

| 47,061 | | Commerce Bancshares, Inc.

| | 3,203,442 |

| 49,341 | | Community Bank System, Inc.

| | 3,106,016 |

| 117,073 | | CVB Financial Corp.

| | 3,014,630 |

| 50,635 | | Eagle Bancorp, Inc.

| | 2,231,485 |

| 216,688 | | First BanCorp

| | 2,756,271 |

| 69,848 | | First Commonwealth Financial Corp.

| | 975,777 |

| 70,864 | | First Financial Bankshares, Inc.

| | 2,437,722 |

| 187,614 | | Fulton Financial Corp.

| | 3,157,544 |

| 24,053 | | Lakeland Financial Corp.

| | 1,755,147 |

| 29,005 | | NBT Bancorp, Inc.

| | 1,259,397 |

| 89,384 | | Northwest Bancshares, Inc.

| | 1,249,588 |

| 34,614 | | OFG Bancorp

| | 953,962 |

| 41,138 | | Popular, Inc.

| | 2,728,272 |

| 44,455 | | Prosperity Bancshares, Inc.

| | 3,230,989 |

| 147,700 | | Regions Financial Corp.

| | 3,184,412 |

| 33,831 | | ServisFirst Bancshares, Inc.

| | 2,331,294 |

| 32,757 | | UMB Financial Corp.

| | 2,735,865 |

| 16,595 | | Westamerica BanCorp

| | 979,271 |

| | | | | 41,291,084 |

| | | Biotechnology – 0.4% | | |

| 13,152 | | Amgen, Inc.

| | 3,454,241 |

| | | Building Products – 1.1% | | |

| 61,020 | | A.O. Smith Corp.

| | 3,492,785 |

| 33,056 | | Allegion PLC

| | 3,479,475 |

| 41,078 | | UFP Industries, Inc.

| | 3,255,431 |

| | | | | 10,227,691 |

| | | Capital Markets – 4.4% | | |

| 11,765 | | Ameriprise Financial, Inc.

| | 3,663,268 |

| 5,387 | | BlackRock, Inc.

| | 3,817,390 |

| 16,735 | | CME Group, Inc.

| | 2,814,158 |

| 36,040 | | Evercore, Inc., Class A

| | 3,931,243 |

| 32,760 | | Hamilton Lane, Inc., Class A

| | 2,092,709 |

| 39,325 | | Houlihan Lokey, Inc.

| | 3,427,567 |

| 87,677 | | Moelis & Co., Class A

| | 3,364,166 |

| 11,934 | | Piper Sandler Cos.

| | 1,553,687 |

| 35,308 | | PJT Partners, Inc., Class A

| | 2,601,847 |

| 29,999 | | Raymond James Financial, Inc.

| | 3,205,393 |

| 60,434 | | SEI Investments Co.