| OMB APPROVAL |

OMB Number: 3235-0570

Expires: July 31, 2022

Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-22680 |

| Ultimus Managers Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

Khimmara Greer

| Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, Ohio 45246_ |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (513) 587-3400 |

| Date of fiscal year end: | February 28 | |

| Date of reporting period: | February 28, 2022 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

| (a) |

BLUEPRINT ADAPTIVE GROWTH

ALLOCATION FUND

Investor Class (BLUPX)

Institutional Class (BLUIX)

Annual Report

February 28, 2022

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND | |

| LETTER TO SHAREHOLDERS | March 15, 2022 |

Dear Shareholders,

Our previous letter in the third quarter of 2021 occurred amid ten consecutive positive return months. Low volatility uptrends in growth-oriented U.S. equities were the primary catalyst in driving both U.S. stocks and the Fund higher. While these trends generally continued right up until the turning of the calendar, conditions have certainly shifted as we have entered and progressed into 2022.

Multi-decade highs in inflation have necessitated stark changes in monetary policy. This pivot from dovish to hawkish policy has accelerated already entrenched downtrends among fixed income instruments while also dampening equity demand for forward-looking markets. Add into the mix significant uncertainty from the Russian invasion of Ukraine and one has a recipe for an equity market correction.

For the end of the fiscal year ended on February 28, the Institutional Class finished up 6.3% versus the Morningstar Global Allocation Total Return Index (the Fund’s benchmark) return of 2.6%. The Fund’s outperformance was driven by overweight allocations to real estate, growth, and technology-oriented U.S. equities. In addition, the Fund’s focus on price trends allowed it to sidestep declines in international equities and higher duration fixed income assets. Positions that underperformed were held to a minimum but included alternatives and volatility hedges. That said, these are precisely the allocations performing best so far in 2022.

Looking ahead, equity markets will likely struggle to gain positive footing until the uncertainty around the timing and severity of interest rate hikes is better understood. Similarly, the most significant conflict on European soil in many decades has the potential to keep investors on edge for the foreseeable future. Either of these scenarios alone pose a serious threat to the global economic picture but together they could have significantly negative consequences. On the other hand, a measure of certainty or even perceived certainty is all that is needed to support buying that would be the basis for future gains.

The Blueprint Adaptive Growth Allocation Fund benefits from its ability to quickly adjust to these changing conditions. It is not always positioned perfectly for the circumstances at hand but is very rarely out of step. This seemingly small edge in our favor is aimed to provide advisors, their clients, and other investors the foundation to achieve their financial goals.

Thank you for your continued confidence and support of the Blueprint Adaptive Growth Allocation Fund.

Best,

|  |

| Jon Robinson | Brandon Langley |

Blueprint Fund Management, LLC

www.blueprintmutualfunds.com

1

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month-end are available by calling 1-866-983-4525.

An investor should consider the investment objectives, risks, charges, and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please visit the Fund’s website at www.blueprintmutualfunds.com or call 1-866-983-4525 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time, and may no longer be held by the Fund. For a complete list of securities held by the Fund as of February 28th, 2022, please see the Schedule of Investments section of the annual report. The opinions of the Fund’s adviser with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Fund and the market in general and statements of the Fund’s plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward- looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements include, without limitation, general economic conditions, such as inflation, recession, and interest rates.

2

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| PORTFOLIO INFORMATION |

| February 28, 2022 (Unaudited) |

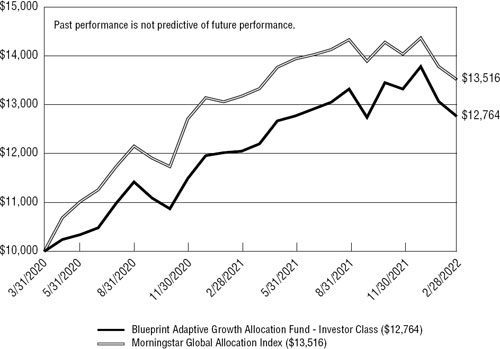

Comparison of the Change in Value of a $10,000 Investment in

Blueprint Adaptive Growth Allocation Fund - Investor Class (a) (since inception on

3/31/2020) versus the Morningstar Global Allocation Index

| Average Annual Total Returns (b) | ||||

| (for the periods ended February 28, 2022) | ||||

| Since | ||||

| Inception | ||||

| 1 Year | (3/31/2020) | |||

| Blueprint Adaptive Growth Allocation Fund - Investor Class | 5.95% | 13.59% | ||

| Blueprint Adaptive Growth Allocation Fund - Institutional Class | 6.29% | 13.94% | ||

| Morningstar Global Allocation Index (c) | 2.60% | 17.04% | ||

| (a) | The line graph above represents performance of the Investor Class only, which will vary from the performance of the Institutional Class based on the difference in fees paid by shareholders in the different classes. |

| (b) | The Fund’s total returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (c) | The Morningstar Global Allocation Index measures the performance of a multi-asset class portfolio of global equities, global bonds and cash. This portfolio is held in a static allocation that is appropriate for investors who seek average exposure to global equity market risk and returns. |

3

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| PORTFOLIO INFORMATION |

| February 28, 2022 (Unaudited) |

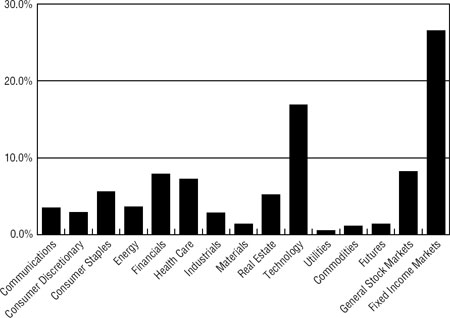

Sector Diversification (% of Net Assets)

| Top 10 Equity Holdings | |

| % of | |

| Net Assets | |

| Apple, Inc. | 8.0% |

| iShares Core S&P Total U.S. Stock Market ETF | 5.2% |

| iShares Floating Rate Bond ETF | 5.0% |

| ClearShares Ultra-Short Maturity ETF | 5.0% |

| SPDR Bloomberg 1-3 Month T-Bill ETF | 4.9% |

| iShares Short Treasury Bond ETF | 4.9% |

| PIMCO Enhanced Short Maturity Active Exchange-Traded Fund | 4.0% |

| Microsoft Corporation | 3.6% |

| JPMorgan Ultra-Short Income ETF | 2.9% |

| iShares Core MSCI Emerging Markets ETF | 2.8% |

4

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| SCHEDULE OF INVESTMENTS |

| February 28, 2022 |

| COMMON STOCKS — 56.4% | Shares | Value | ||||||

| Communications — 3.5% | ||||||||

| Internet Media & Services — 2.9% | ||||||||

| Alphabet, Inc. - Class A (a) | 379 | $ | 1,023,732 | |||||

| Alphabet, Inc. - Class C (a) | 363 | 979,309 | ||||||

| Booking Holdings, Inc. (a) | 138 | 299,770 | ||||||

| 2,302,811 | ||||||||

| Telecommunications — 0.6% | ||||||||

| T-Mobile US, Inc. (a) | 912 | 112,368 | ||||||

| Verizon Communications, Inc. | 7,342 | 394,045 | ||||||

| 506,413 | ||||||||

| Consumer Discretionary — 2.9% | ||||||||

| Apparel & Textile Products — 0.2% | ||||||||

| LVMH Moet Hennessy Louis Vuitton S.A. - ADR | 1,040 | 151,580 | ||||||

| Automotive — 1.4% | ||||||||

| Ford Motor Company | 4,576 | 80,355 | ||||||

| Tesla, Inc. (a) | 1,032 | 898,284 | ||||||

| Toyota Motor Corporation - ADR | 833 | 152,397 | ||||||

| 1,131,036 | ||||||||

| Leisure Facilities & Services — 0.3% | ||||||||

| McDonald’s Corporation | 1,118 | 273,653 | ||||||

| Retail - Discretionary — 1.0% | ||||||||

| Home Depot, Inc. (The) | 1,722 | 543,859 | ||||||

| Lowe’s Companies, Inc. | 1,072 | 236,976 | ||||||

| 780,835 | ||||||||

| Consumer Staples — 5.6% | ||||||||

| Beverages — 2.0% | ||||||||

| Anheuser-Busch InBev S.A./N.V. - ADR | 2,448 | 151,360 | ||||||

| Coca-Cola Company (The) | 11,060 | 688,375 | ||||||

| Diageo plc - ADR | 764 | 152,563 | ||||||

| PepsiCo, Inc. | 3,922 | 642,188 | ||||||

| 1,634,486 | ||||||||

| Food — 0.5% | ||||||||

| Mondelez International, Inc. - Class A | 4,139 | 271,022 | ||||||

| Nestlé S.A. - ADR | 1,173 | 152,525 | ||||||

| 423,547 | ||||||||

5

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| COMMON STOCKS — 56.4% (Continued) | Shares | Value | ||||||

| Consumer Staples — 5.6% (Continued) | ||||||||

| Household Products — 1.5% | ||||||||

| Colgate-Palmolive Company | 1,467 | $ | 112,886 | |||||

| Procter & Gamble Company (The) | 7,081 | 1,103,857 | ||||||

| 1,216,743 | ||||||||

| Retail - Consumer Staples — 0.6% | ||||||||

| Costco Wholesale Corporation | 1,001 | 519,769 | ||||||

| Tobacco & Cannabis — 1.0% | ||||||||

| Altria Group, Inc. | 6,555 | 336,206 | ||||||

| Philip Morris International, Inc. | 4,505 | 455,320 | ||||||

| 791,526 | ||||||||

| Energy — 3.6% | ||||||||

| Oil & Gas Producers — 3.6% | ||||||||

| BP plc - ADR | 10,561 | 308,487 | ||||||

| Chevron Corporation | 5,200 | 748,800 | ||||||

| ConocoPhillips | 2,885 | 273,671 | ||||||

| Enbridge, Inc. | 7,147 | 308,608 | ||||||

| Exxon Mobil Corporation | 11,051 | 866,619 | ||||||

| Shell plc - ADR | 2,352 | 123,221 | ||||||

| TotalEnergies SE - ADR | 5,968 | 301,563 | ||||||

| 2,930,969 | ||||||||

| Financials — 7.9% | ||||||||

| Asset Management — 0.2% | ||||||||

| Brookfield Asset Management, Inc. - Class A | 2,821 | 154,140 | ||||||

| Banking — 4.1% | ||||||||

| Bank of America Corporation | 21,729 | 960,422 | ||||||

| Bank of Nova Scotia (The) | 4,248 | 307,300 | ||||||

| BNP Paribas S.A. - ADR | 5,176 | 150,104 | ||||||

| HSBC Holdings plc - ADR | 8,899 | 307,372 | ||||||

| Mitsubishi UFJ Financial Group, Inc. - ADR | 49,466 | 304,711 | ||||||

| Royal Bank of Canada | 2,770 | 305,863 | ||||||

| Toronto-Dominion Bank (The) | 3,778 | 304,847 | ||||||

| U.S. Bancorp | 2,287 | 129,307 | ||||||

| Wells Fargo & Company | 10,139 | 541,118 | ||||||

| 3,311,044 | ||||||||

6

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| COMMON STOCKS — 56.4% (Continued) | Shares | Value | ||||||

| Financials — 7.9% (Continued) | ||||||||

| Institutional Financial Services — 0.3% | ||||||||

| Bank of New York Mellon Corporation (The) | 1,207 | $ | 64,152 | |||||

| Morgan Stanley | 2,099 | 190,463 | ||||||

| 254,615 | ||||||||

| Insurance — 2.6% | ||||||||

| Allianz SE - ADR | 6,716 | 151,849 | ||||||

| American International Group, Inc. | 2,362 | 144,649 | ||||||

| Berkshire Hathaway, Inc. - Class B (a) | 5,159 | 1,658,360 | ||||||

| MetLife, Inc. | 2,263 | 152,866 | ||||||

| 2,107,724 | ||||||||

| Specialty Finance — 0.7% | ||||||||

| American Express Company | 1,688 | 328,383 | ||||||

| Capital One Financial Corporation | 1,276 | 195,573 | ||||||

| 523,956 | ||||||||

| Health Care — 7.2% | ||||||||

| Biotech & Pharma — 4.5% | ||||||||

| AbbVie, Inc. | 4,513 | 666,886 | ||||||

| Amgen, Inc. | 1,099 | 248,902 | ||||||

| AstraZeneca plc - ADR | 5,064 | 308,296 | ||||||

| Bristol-Myers Squibb Company | 6,959 | 477,875 | ||||||

| Eli Lilly & Company | 1,022 | 255,449 | ||||||

| Johnson & Johnson | 4,364 | 718,183 | ||||||

| Novo Nordisk A/S - ADR | 1,483 | 152,675 | ||||||

| Pfizer, Inc. | 7,262 | 340,878 | ||||||

| Roche Holding AG - ADR | 3,206 | 151,419 | ||||||

| Sanofi - ADR | 5,850 | 306,833 | ||||||

| 3,627,396 | ||||||||

| Health Care Facilities & Services — 1.9% | ||||||||

| CVS Health Corporation | 3,202 | 331,887 | ||||||

| UnitedHealth Group, Inc. | 2,508 | 1,193,482 | ||||||

| 1,525,369 | ||||||||

| Medical Equipment & Devices — 0.8% | ||||||||

| Abbott Laboratories | 2,965 | 357,638 | ||||||

| Thermo Fisher Scientific, Inc. | 556 | 302,464 | ||||||

| 660,102 | ||||||||

7

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| COMMON STOCKS — 56.4% (Continued) | Shares | Value | ||||||

| Industrials — 2.8% | ||||||||

| Aerospace & Defense — 1.2% | ||||||||

| Airbus SE - ADR (a) | 4,789 | $ | 151,764 | |||||

| General Dynamics Corporation | 640 | 150,048 | ||||||

| Lockheed Martin Corporation | 678 | 294,116 | ||||||

| Raytheon Technologies Corporation | 3,896 | 400,119 | ||||||

| 996,047 | ||||||||

| Diversified Industrials — 0.1% | ||||||||

| Emerson Electric Company | 958 | 89,017 | ||||||

| Electrical Equipment — 0.2% | ||||||||

| ABB Ltd. - ADR | 4,523 | 152,335 | ||||||

| Transportation & Logistics — 1.3% | ||||||||

| Canadian National Railway Company | 1,230 | 152,508 | ||||||

| Union Pacific Corporation | 2,037 | 501,000 | ||||||

| United Parcel Service, Inc. - Class B | 1,900 | 399,798 | ||||||

| 1,053,306 | ||||||||

| Materials — 1.4% | ||||||||

| Chemicals — 0.7% | ||||||||

| Dow, Inc. | 2,600 | 153,296 | ||||||

| DuPont de Nemours, Inc. | 1,937 | 149,866 | ||||||

| Linde plc | 844 | 247,494 | ||||||

| 550,656 | ||||||||

| Metals & Mining — 0.7% | ||||||||

| BHP Group Ltd. - ADR | 4,509 | 305,665 | ||||||

| Rio Tinto plc - ADR | 3,891 | 305,755 | ||||||

| 611,420 | ||||||||

| Real Estate — 4.1% | ||||||||

| REITs — 4.1% | ||||||||

| American Campus Communities, Inc. | 612 | 32,932 | ||||||

| AvalonBay Communities, Inc. | 669 | 159,617 | ||||||

| Boston Properties, Inc. | 1,380 | 168,788 | ||||||

| Cousins Properties, Inc. | 622 | 24,028 | ||||||

| Duke Realty Corporation | 1,978 | 104,834 | ||||||

| Equity Residential | 1,592 | 135,798 | ||||||

| Essex Property Trust, Inc. | 311 | 98,640 | ||||||

| Extra Space Storage, Inc. | 642 | 120,792 | ||||||

| Federal Realty Investment Trust | 341 | 40,095 | ||||||

| Host Hotels & Resorts, Inc. (a) | 7,590 | 138,669 | ||||||

| Invitation Homes, Inc. | 2,744 | 103,723 | ||||||

8

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| COMMON STOCKS — 56.4% (Continued) | Shares | Value | ||||||

| Real Estate — 4.1% (Continued) | ||||||||

| REITs — 4.1% (Continued) | ||||||||

| Kilroy Realty Corporation | 1,008 | $ | 72,193 | |||||

| Mid-America Apartment Communities, Inc. | 386 | 78,979 | ||||||

| Prologis, Inc. | 5,185 | 756,232 | ||||||

| Public Storage | 1,373 | 487,442 | ||||||

| Realty Income Corporation | 2,679 | 177,055 | ||||||

| Regency Centers Corporation | 847 | 55,809 | ||||||

| Simon Property Group, Inc. | 1,798 | 247,333 | ||||||

| Sun Communities, Inc. | 506 | 91,586 | ||||||

| UDR, Inc. | 1,310 | 71,880 | ||||||

| Welltower, Inc. | 2,022 | 168,412 | ||||||

| 3,334,837 | ||||||||

| Technology — 16.9% | ||||||||

| Semiconductors — 2.2% | ||||||||

| Broadcom, Inc. | 1,105 | 649,121 | ||||||

| NVIDIA Corporation | 2,390 | 582,802 | ||||||

| QUALCOMM, Inc. | 3,099 | 532,997 | ||||||

| 1,764,920 | ||||||||

| Software — 3.6% | ||||||||

| Microsoft Corporation | 9,886 | 2,953,838 | ||||||

| Technology Hardware — 8.7% | ||||||||

| Apple, Inc. | 39,248 | 6,480,629 | ||||||

| Cisco Systems, Inc. | 6,648 | 370,759 | ||||||

| Nintendo Company Ltd. - ADR | 2,421 | 153,903 | ||||||

| 7,005,291 | ||||||||

| Technology Services — 2.4% | ||||||||

| Accenture plc - Class A | 904 | 285,682 | ||||||

| Mastercard, Inc. - Class A | 2,905 | 1,048,182 | ||||||

| Visa, Inc. - Class A | 2,763 | 597,140 | ||||||

| 1,931,004 | ||||||||

| Utilities — 0.5% | ||||||||

| Electric Utilities — 0.5% | ||||||||

| Constellation Energy Corporation | 778 | 35,773 | ||||||

| Duke Energy Corporation | 1,209 | 121,396 | ||||||

| Exelon Corporation | 3,306 | 140,703 | ||||||

| Southern Company (The) | 1,616 | 104,668 | ||||||

| 402,540 | ||||||||

| Total Common Stocks (Cost $39,707,559) | $ | 45,672,925 | ||||||

9

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| EXCHANGE-TRADED FUNDS — 38.3% | Shares | Value | ||||||

| ClearShares Ultra-Short Maturity ETF | 40,136 | $ | 4,015,410 | |||||

| iShares Core MSCI Emerging Markets ETF | 39,548 | 2,263,332 | ||||||

| iShares Core S&P Total U.S. Stock Market ETF | 43,064 | 4,223,717 | ||||||

| iShares Core U.S. REIT ETF | 14,001 | 853,501 | ||||||

| iShares Floating Rate Bond ETF | 79,330 | 4,019,651 | ||||||

| iShares Gold Trust (a) | 23,975 | 870,532 | ||||||

| iShares MSCI Mexico ETF | 659 | 33,174 | ||||||

| iShares MSCI Saudi Arabia ETF | 700 | 32,613 | ||||||

| iShares MSCI South Africa ETF | 624 | 32,860 | ||||||

| iShares MSCI Taiwan ETF | 507 | 32,408 | ||||||

| iShares MSCI Thailand ETF | 404 | 32,300 | ||||||

| iShares Short Treasury Bond ETF (a) | 35,761 | 3,944,081 | ||||||

| JPMorgan Ultra-Short Income ETF | 46,258 | 2,329,784 | ||||||

| PIMCO Enhanced Short Maturity Active Exchange-Traded Fund | 31,820 | 3,215,093 | ||||||

| ProShares Ultra VIX Short-Term Futures ETF (a) | 65,000 | 1,140,100 | ||||||

| SPDR Bloomberg 1-3 Month T-Bill ETF (a) | 43,162 | 3,945,438 | ||||||

| Total Exchange-Traded Funds (Cost $28,753,592) | $ | 30,983,994 | ||||||

| MONEY MARKET FUNDS — 4.3% | Shares | Value | ||||||

| First American Government Obligations Fund - Class X, 0.03% (b) (Cost $3,459,898) | $ | 3,459,898 | $ | 3,459,898 | ||||

| Investments at Value — 99.0% (Cost $71,921,049) | $ | 80,116,817 | ||||||

| Other Assets in Excess of Liabilities — 1.0% | 773,952 | |||||||

| Net Assets — 100.0% | $ | 80,890,769 | ||||||

| (a) | Non-income producing security. |

| (b) | The rate shown is the 7-day effective yield as of February 28, 2022. |

A/S - Aktieselskab

ADR - American Depositary Receipt

AG - Aktiengesellschaft

N.V. - Naamloze Vennootschap

plc - Public Limited Company

S.A. - Societe Anonyme

SE - Societe Europaea

See accompanying notes to financial statements.

10

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| STATEMENT OF ASSETS AND LIABILITIES |

| February 28, 2022 |

| ASSETS | ||||

| Investments: | ||||

| At cost | $ | 71,921,049 | ||

| At value (Note 2) | $ | 80,116,817 | ||

| Receivable for capital shares sold | 1,477,762 | |||

| Receivable for investment securities sold | 11,953,695 | |||

| Dividends and interest receivable | 83,644 | |||

| Tax reclaims receivable | 181 | |||

| Other assets | 15,695 | |||

| Total assets | 93,647,794 | |||

| LIABILITIES | ||||

| Payable for capital shares redeemed | 985,735 | |||

| Payable for investment securities purchased | 11,701,046 | |||

| Payable to the Adviser (Note 4) | 43,802 | |||

| Payable to administrator (Note 4) | 13,057 | |||

| Accrued distribution fees (Note 4) | 411 | |||

| Other accrued expenses and liabilities | 12,974 | |||

| Total liabilities | 12,757,025 | |||

| NET ASSETS | $ | 80,890,769 | ||

| NET ASSETS CONSIST OF: | ||||

| Paid-in capital | $ | 75,020,352 | ||

| Distributable earnings | 5,870,417 | |||

| NET ASSETS | $ | 80,890,769 | ||

| NET ASSET VALUE PER SHARE: | ||||

| INVESTOR CLASS | ||||

| Net assets applicable to Investor Class | $ | 858,330 | ||

| Investor Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 67,640 | |||

| Net asset value, offering price and redemption price per share (Note 2) | $ | 12.69 | ||

| INSTITUTIONAL CLASS | ||||

| Net assets applicable to Institutional Class | $ | 80,032,439 | ||

| Institutional Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 6,283,097 | |||

| Net asset value, offering price and redemption price per share (Note 2) | $ | 12.74 |

See accompanying notes to financial statements.

11

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| STATEMENT OF OPERATIONS |

| For the Year Ended February 28, 2022 |

| INVESTMENT INCOME | ||||

| Dividend income (net of foreign withholding taxes of $7,033) | $ | 1,226,664 | ||

| Interest | 97 | |||

| Total Investment Income | $ | 1,226,761 | ||

| EXPENSES | ||||

| Investment advisory fees (Note 4) | 647,283 | |||

| Administration fees (Note 4) | 68,209 | |||

| Registration and filing fees | 46,149 | |||

| Fund accounting fees (Note 4) | 39,320 | |||

| Legal fees | 32,709 | |||

| Transfer agent fees - Institutional Class (Note 4) | 18,000 | |||

| Transfer agent fees - Investor Class (Note 4) | 12,000 | |||

| Audit and tax services fees | 17,460 | |||

| Trustees’ fees and expenses (Note 4) | 17,403 | |||

| Compliance service fees (Note 4) | 12,000 | |||

| Custodian and bank service fees | 11,717 | |||

| Offering costs (Note 2) | 9,900 | |||

| Postage and supplies | 8,678 | |||

| Printing of shareholder reports | 8,387 | |||

| Insurance expense | 3,651 | |||

| Distribution fees - Investor Class (Note 4) | 1,092 | |||

| Other expenses | 22,318 | |||

| Total Expenses | 976,276 | |||

| Fee reductions by the Adviser (Note 4) | (113,574 | ) | ||

| Net Expenses | 862,702 | |||

| NET INVESTMENT INCOME | 364,059 | |||

| REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS AND FOREIGN CURRENCIES | ||||

| Net realized losses from: | ||||

| Investments | (1,889,349 | ) | ||

| Foreign currency transactions | (351 | ) | ||

| Net change in unrealized appreciation (depreciation) on investments: | 4,250,753 | |||

| NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS AND FOREIGN CURRENCIES | 2,361,053 | |||

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 2,725,112 |

See accompanying notes to financial statements.

12

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| STATEMENTS OF CHANGES IN NET ASSETS |

| Year Ended | Period Ended | |||||||

| February 28, | February 28, | |||||||

| 2022 | 2021 (a) | |||||||

| FROM OPERATIONS | ||||||||

| Net investment income | $ | 364,059 | $ | 41,476 | ||||

| Net realized losses from: | ||||||||

| Investments | (1,889,349 | ) | (408,741 | ) | ||||

| Foreign currency transactions | (351 | ) | — | |||||

| Net change in unrealized appreciation (depreciation) on investments and foreign currencies | 4,250,753 | 3,945,015 | ||||||

| Net increase in net assets resulting from operations | 2,725,112 | 3,577,750 | ||||||

| FROM DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | ||||||||

| Investor Class | (2,772 | ) | (63 | ) | ||||

| Institutional Class | (365,245 | ) | (111,204 | ) | ||||

| Decrease in net assets from distributions to shareholders | (368,017 | ) | (111,267 | ) | ||||

| CAPITAL SHARE TRANSACTIONS | ||||||||

| Investor Class | ||||||||

| Proceeds from shares sold | 892,113 | 70,056 | ||||||

| Net asset value of shares issued in reinvestment of distributions to shareholders | 2,772 | 63 | ||||||

| Payments for shares redeemed | (89,685 | ) | (64 | ) | ||||

| Net increase in Investor Class net assets from capital share transactions | 805,200 | 70,055 | ||||||

| Institutional Class | ||||||||

| Proceeds from shares sold | 39,522,452 | 54,668,532 | ||||||

| Net asset value of shares issued in reinvestment of distributions to shareholders | 365,216 | 110,988 | ||||||

| Payments for shares redeemed | (15,504,692 | ) | (4,970,560 | ) | ||||

| Net increase in Institutional Class net assets from capital share transactions | 24,382,976 | 49,808,960 | ||||||

| TOTAL INCREASE IN NET ASSETS | 27,545,271 | 53,345,498 | ||||||

| NET ASSETS | ||||||||

| Beginning of period | 53,345,498 | — | ||||||

| End of period | $ | 80,890,769 | $ | 53,345,498 | ||||

| (a) | Represents the period from the commencement of operations (March 31, 2020) through February 28, 2021. |

See accompanying notes to financial statements.

13

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| STATEMENTS OF CHANGES IN NET ASSETS (Continued) |

| Year Ended | Period Ended | |||||||

| February 28, | February 28, | |||||||

| 2022 | 2021 (a) | |||||||

| CAPITAL SHARES ACTIVITY | ||||||||

| Investor Class | ||||||||

| Shares sold | 68,431 | 6,015 | ||||||

| Shares issued in reinvestment of distributions to shareholders | 202 | 5 | ||||||

| Shares redeemed | (7,007 | ) | (6 | ) | ||||

| Net increase in shares outstanding | 61,626 | 6,014 | ||||||

| Shares outstanding at beginning of period | 6,014 | — | ||||||

| Shares outstanding at end of period | 67,640 | 6,014 | ||||||

| Institutional Class | ||||||||

| Shares sold | 3,030,556 | 4,833,392 | ||||||

| Shares issued in reinvestment of distributions to shareholders | 26,503 | 9,319 | ||||||

| Shares redeemed | (1,196,884 | ) | (419,789 | ) | ||||

| Net increase in shares outstanding | 1,860,175 | 4,422,922 | ||||||

| Shares outstanding at beginning of period | 4,422,922 | — | ||||||

| Shares outstanding at end of period | 6,283,097 | 4,422,922 | ||||||

| (a) | Represents the period from the commencement of operations (March 31, 2020) through February 28, 2021. |

See accompanying notes to financial statements.

14

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| INVESTOR CLASS |

| FINANCIAL HIGHLIGHTS |

Per Share Data for a Share Outstanding Throughout Each Period

| Year Ended | Period Ended | |||||||

| February 28, | February 28, | |||||||

| 2022 | 2021(a) | |||||||

| Net asset value at beginning of period | $ | 12.02 | $ | 10.00 | ||||

| Income (loss) from investment operations: | ||||||||

| Net investment income (loss) (b)(c) | 0.04 | (0.02 | ) | |||||

| Net realized and unrealized gains on investments and foreign currencies | 0.68 | 2.07 | ||||||

| Total from investment operations | 0.72 | 2.05 | ||||||

| Less distributions from: | ||||||||

| Net investment income | (0.05 | ) | (0.03 | ) | ||||

| Net asset value at end of period | $ | 12.69 | $ | 12.02 | ||||

| Total return (d) | 5.95 | % | 20.48 | % (e) | ||||

| Net assets at end of period | $ | 858,330 | $ | 72,305 | ||||

| Ratios/supplementary data: | ||||||||

| Ratio of total expenses to average net assets (f) | 6.96 | % | 104.34 | % (g) | ||||

| Ratio of net expenses to average net assets (f)(h) | 1.50 | % (i) | 1.60 | % (g)(i) | ||||

| Ratio of net investment income (loss) to average net assets (c)(f)(h) | 0.30 | % | (0.16 | %) (g) | ||||

| Portfolio turnover rate | 130 | % | 95 | % (e) | ||||

| (a) | Represents the period from the commencement of operations (March 31, 2020) through February 28, 2021. |

| (b) | Per share net investment income (loss) has been determined on the basis of average number of shares outstanding during the period. |

| (c) | Recognition of net investment income (loss) by the Fund is affected by the timing of the declaration of the dividends by the underlying companies in which the Fund invests. |

| (d) | Total return is a measure of the change in value of an investment in the Fund over the periods covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would have been lower had the Adviser not reduced advisory fees and reimbursed expenses (Note 4). |

| (e) | Not annualized. |

| (f) | Ratio does not include expenses of the investment companies in which the Fund invests. |

| (g) | Annualized. |

| (h) | Ratio was determined after advisory fees reductions and expense reimbursements (Note 4). |

| (i) | Includes costs to organize the Fund of less than 0.005% and 0.10% for the year ended February 28, 2022 and period ended February 28, 2021, respectively, which are excluded from the Expense Limitation Agreement (Note 4). |

See accompanying notes to financial statements.

15

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| INSTITUTIONAL CLASS |

| FINANCIAL HIGHLIGHTS |

Per Share Data for a Share Outstanding Throughout Each Period

| Year Ended | Period Ended | |||||||

| February 28, | February 28, | |||||||

| 2022 | 2021 (a) | |||||||

| Net asset value at beginning of period | $ | 12.04 | $ | 10.00 | ||||

| Income from investment operations: | ||||||||

| Net investment income (b)(c) | 0.07 | 0.02 | ||||||

| Net realized and unrealized gains on investments | 0.69 | 2.06 | ||||||

| Total from investment operations | 0.76 | 2.08 | ||||||

| Less distributions from: | ||||||||

| Net investment income | (0.06 | ) | (0.04 | ) | ||||

| Net asset value at end of period | $ | 12.74 | $ | 12.04 | ||||

| Total return (d) | 6.29 | % | 20.80 | % (e) | ||||

| Net assets at end of period (000’s) | $ | 80,032 | $ | 53,273 | ||||

| Ratios/supplementary data: | ||||||||

| Ratio of total expenses to average net assets (f) | 1.40 | % | 1.93 | % (g) | ||||

| Ratio of net expenses to average net assets (f)(h) | 1.26 | % (i) | 1.35 | % (g)(i) | ||||

| Ratio of net investment income to average net assets (c)(f)(h) | 0.54 | % | 0.20 | % (g) | ||||

| Portfolio turnover rate | 130 | % | 95 | % (e) | ||||

| (a) | Represents the period from the commencement of operations (March 31, 2020) through February 28, 2021. |

| (b) | Per share net investment income has been determined on the basis of average number of shares outstanding during the period. |

| (c) | Recognition of net investment income by the Fund is affected by the timing of the declaration of the dividends by the underlying companies in which the Fund invests. |

| (d) | Total return is a measure of the change in value of an investment in the Fund over the period covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would have been lower had the Adviser not reduced advisory fees and reimbursed expenses (Note 4). |

| (e) | Not annualized. |

| (f) | Ratio does not include expenses of the investment companies in which the Fund invests. |

| (g) | Annualized. |

| (h) | Ratio was determined after advisory fees reductions and expense reimbursements (Note 4). |

| (i) | Includes costs to organize the Fund of 0.01% and 0.10% for the year ended February 28, 2022 and period ended February 28, 2021, respectively, which are excluded from the Expense Limitation Agreement (Note 4). |

See accompanying notes to financial statements.

16

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| NOTES TO FINANCIAL STATEMENTS |

| February 28, 2022 |

1. Organization

Blueprint Adaptive Growth Allocation Fund (formerly Blueprint Growth Fund) (the “Fund”) is a diversified series of Ultimus Managers Trust (the “Trust”). The Trust is an open-end management investment company established as an Ohio business trust under a Declaration of Trust dated February 28, 2012. Other series of the Trust are not incorporated in this report. The Fund commenced operations on March 31, 2020.

The investment objective of the Fund is to seek capital appreciation while managing risk.

The Fund currently offers two classes of shares: Investor Class shares (sold without any sales loads, but subject to a distribution and/or shareholder servicing fee of up to 0.25% of the average daily net assets attributable to Investor Class shares and requiring a $5,000 initial investment) and Institutional Class shares (sold without any sales loads and distribution and/or shareholder servicing fees and requiring a $15,000 initial investment). Each share class represents an ownership interest in the same investment portfolio.

2. Significant Accounting Policies

The following is a summary of the Fund’s significant accounting policies used in the preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The Fund follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification Topic 946, “Financial Services – Investment Companies.”

Securities valuation – The Fund values its portfolio securities at fair value as of the close of regular trading on the New York Stock Exchange (the “NYSE”) (normally 4:00 p.m. Eastern time) on each business day the NYSE is open for business. The Fund values its listed securities, including common stocks and exchange-traded funds (“ETFs”), on the basis of the security’s last sale price on the security’s primary exchange, if available, otherwise at the exchange’s most recently quoted mean price. NASDAQ-listed securities are valued at the NASDAQ Official Closing Price. When using a quoted price and when the market for the security is considered active, the security will be classified as Level 1 within the fair value hierarchy (see below). In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund values its securities and other assets at fair value in accordance with procedures established by and under the general supervision of the Board of Trustees of the Trust (the “Board”). Under these procedures, the securities will be classified as Level 2 or 3 within the fair value hierarchy, depending on the inputs used. Unavailable or unreliable market quotes may be due to the following factors: a substantial bid-ask spread; infrequent sales resulting in stale prices; insufficient trading volume; small trade sizes; a temporary lapse in any reliable pricing source; and actions of the securities or futures markets, such as the

17

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

suspension or limitation of trading. As a result, the prices of securities used to calculate the Fund’s net asset value (“NAV”) may differ from quoted or published prices for the same securities.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

| ● | Level 1 – quoted prices in active markets for identical securities |

| ● | Level 2 – other significant observable inputs |

| ● | Level 3 – significant unobservable inputs |

The inputs or methods used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the Fund’s investments and the inputs used to value the investments as of February 28, 2022:

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Common Stocks | $ | 45,672,925 | $ | — | $ | — | $ | 45,672,925 | ||||||||

| Exchange-Traded Funds | 30,983,994 | — | — | 30,983,994 | ||||||||||||

| Money Market Funds | 3,459,898 | — | — | 3,459,898 | ||||||||||||

| Total | $ | 80,116,817 | $ | — | $ | — | $ | 80,116,817 | ||||||||

Refer to the Fund’s Schedule of Investments for a listing of the common stocks by sector and industry type. The Fund did not hold any derivative instruments or any assets or liabilities that were measured at fair value on a recurring basis using significant unobservable inputs (Level 3) as of or during the year ended February 28, 2022.

Cash – The Fund’s cash, if any, is held in a bank account with balances which, at times, may exceed United States federally insured limits set by the Federal Deposit Insurance Corporation. The Fund maintains these balances with a high quality financial institution and may incur charges on cash overdrafts.

Share valuation – The NAV per share of each class of the Fund is calculated daily by dividing the total value of the assets attributable to that class, less liabilities attributable to that class, by the number of shares outstanding of that class. The offering price and redemption price per share of each class of the Fund is equal to the NAV per share of such class.

18

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

Investment income – Dividend income is recorded on the ex-dividend date. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the security received. Interest income is accrued as earned. Withholding taxes on foreign dividends, if any, have been recorded in accordance with the Fund’s understanding of the applicable country’s rules and tax rates.

Investment transactions – Investment transactions are accounted for on the trade date. Realized gains and losses on investments sold are determined on a specific identification basis.

Offering costs – The Adviser advanced some of the Fund’s initial offering costs and was subsequently reimbursed by the Fund. Costs of $29,700 incurred in connection with the offering and initial registration had been deferred and were subsequently amortized on a straight-line basis over the first twelve months after commencement of operations. As of February 28, 2022, there were no unamortized offering costs remaining in the Fund.

Common expenses – Common expenses of the Trust are allocated among the Fund and the other series of the Trust based on the relative net assets of each series, the number of series in the Trust, or the nature of the services performed and the relative applicability to each series.

Allocation between Classes – Investment income earned, realized capital gains and losses, and unrealized appreciation and depreciation are allocated daily to each Class of the Fund based upon its proportionate share of total net assets of the Fund. Class-specific expenses are charged directly to the Class incurring the expense. Common expenses which are not attributable to a specific Class are allocated daily to the Class of shares of the Fund based upon its proportionate share of total net assets of the Fund.

Distributions to shareholders – The Fund distributes to shareholders any net investment income dividends and net realized capital gains on an annual basis. The amount of such dividends and distributions are determined in accordance with federal income tax regulations, which may differ from GAAP. Dividends and distributions to shareholders are recorded on the ex-dividend date. The tax character of distributions paid to shareholders by the Fund during the year ended February 28, 2022 and period ended February 28, 2021, was ordinary income.

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of increase (decrease) in net assets from operations during the reporting period. Actual results could differ from those estimates.

19

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

Federal tax – The Fund has qualified and intends to continue to qualify as a regulated investment company under the Internal Revenue Code of 1986, as amended (the “Code”). Qualification generally will relieve the Fund of liability for federal income taxes to the extent 100% of its net investment income and net realized capital gains are distributed in accordance with the Code.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also the Fund’s intention to declare as dividends in each calendar year equal to at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the twelve months ended October 31) plus undistributed amounts from prior years.

The following information is computed on a tax basis for each item as of February 28, 2022:

| Cost of portfolio investments | $ | 72,274,804 | ||

| Gross unrealized appreciation | $ | 8,286,680 | ||

| Gross unrealized depreciation | (444,667 | ) | ||

| Net unrealized appreciation | 7,842,013 | |||

| Accumulated capital and other losses | (1,971,596 | ) | ||

| Distributable earnings | $ | 5,870,417 | ||

The difference between the federal income tax cost of portfolio investments and the financial statement cost of portfolio investments is due to certain timing differences in the recognition of capital gains or losses under income tax regulations and GAAP. These “book/tax” differences are temporary in nature and are primarily due to the tax deferral of losses on wash sales and adjustments to basis for grantor trusts.

Net qualified late year losses, incurred after December 31, 2021 and within the taxable year, are deemed to arise on the first day of the Fund’s next taxable year. For the year ended February 28, 2022, the Fund deferred $41,466 of late year ordinary losses to March 1, 2022 for federal tax purposes.

As of February 28, 2022, the Fund had short-term capital loss carryforwards of $1,930,130 for federal income tax purposes. These capital loss carryforwards, which do not expire, may be utilized in future years to offset net realized capital gains, if any.

For the year ended February 28, 2022, the Fund reclassified $26,701 of distributable earnings against paid-in capital on the Statement of Assets and Liabilities. Such reclassification, the result of permanent differences between the financial statement and income tax reporting requirements, had no effect on the Fund’s net assets or NAV per share.

20

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” of being sustained assuming examination by tax authorities. Management has reviewed the Fund’s tax positions for all open tax years and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements. The Fund identifies its major tax jurisdiction as U.S. Federal. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax on the Statement of Operations. During the year ended February 28, 2022, the Fund did not incur any interest of penalties.

3. Investment Transactions

During the year ended February 28, 2022, cost of purchases and proceeds from sales of investment securities, other than short-term investments, amounted to $108,189,229 and $86,544,626, respectively.

4. Transactions with Related Parties

ADVISORY AND SUB-ADVISORY AGREEMENTS

Pursuant to the terms of the Advisory Agreement, Blueprint Fund Management, LLC (the “Adviser”) serves as the investment adviser to the Fund. The Adviser provides the Fund with the selection of a sub-investment advisor and the compliance and managerial oversight of that sub-adviser and its services to the Fund. The Fund pays the Adviser an investment advisory fee, computed and accrued daily and paid monthly, at the annual rate of 0.95% of average daily net assets.

Blueprint Investment Partners, LLC (the “Sub-Adviser”) serves as the Funds sub-adviser. Pursuant to the Sub-Advisory Agreement, the Sub-Adviser provides the Fund with a continuous program of investing the Fund’s assets and determining the composition of the Fund’s portfolio. For its services, the Adviser pays the Sub-Adviser an investment sub-advisory fee computed at the annual rate of 0.20% of the Fund’s average daily net assets. The Fund does not directly pay the sub-advisory fee.

Pursuant to an Expense Limitation Agreement (“ELA”) between the Fund and the Adviser, the Adviser has agreed contractually, until June 30, 2023, to reduce its advisory fees and reimburse other expenses to the extent necessary to limit total annual fund operating expenses (excluding brokerage costs, taxes, interest, borrowing costs such as interest and dividend expenses on securities sold short, acquired fund fees and expenses, costs to organize the Fund, extraordinary expenses such as litigation and merger or reorganization costs and other expenses not incurred in the ordinary course of the Fund’s business) to 1.50% and 1.25% of average daily net assets for Investor Class and Institutional Class shares, respectively. Accordingly, during the year ended February 28, 2022, the Adviser reduced its investment advisory fees in the amount of $46,870, and, in addition, reimbursed other operating expenses of $66,704.

21

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

Advisory fee reductions and expense reimbursements by the Adviser are subject to repayment by the Fund for a period of three years after such fees and expenses were incurred, provided that the repayments do not cause total annual fund operating expenses (exclusive of such reductions and reimbursements) to exceed (i) the expense limitation then in effect, if any, and (ii) the expense limitation in effect at the time the expenses to be repaid were incurred. Prior to June 30, 2023, the agreement may not be modified or terminated without the approval of the Board. After June 30, 2023, the ELA may continue from year-to-year provided such continuance is approved by the Board. The ELA may be terminated by the Adviser, or the Board, without approval by the other party, at the end of the then current term upon not less than 90 days’ notice to the other parties as set forth in the ELA. As of February 28, 2022, the Adviser may seek repayment of expense reimbursements no later than the dates below:

| February 29, 2024 | $ | 141,841 | ||

| February 28, 2025 | 113,574 | |||

| Total | $ | 255,415 | ||

OTHER SERVICE PROVIDERS

Ultimus Fund Solutions, LLC (“Ultimus”) provides administration, fund accounting, compliance and transfer agency services to the Fund. The Fund pays Ultimus fees in accordance with the agreements for such services. In addition, the Fund pays out-of-pocket expenses including, but not limited to, postage, supplies and certain costs related to the pricing of the Fund’s portfolio securities.

Under the terms of a Distribution Agreement with the Trust, Ultimus Fund Distributors, LLC (the “Distributor”) serves as principal underwriter to the Fund. The Distributor is a wholly-owned subsidiary of Ultimus. The Distributor is compensated partially by the Adviser and partially by the Investor Class shares of the Fund for acting as principal underwriter.

A Trustee and certain officers of the Trust are also officers of Ultimus.

DISTRIBUTION PLAN

The Fund has adopted a plan of distribution (the “Plan”), pursuant to Rule 12b-1 under the Investment Company Act of 1940, as amended (the “1940 Act”) which permits Investor Class shares of the Fund to make payments to securities dealers and other financial organizations (including payments directly to the Adviser and the Distributor) for expenses related to the distribution and servicing of the Fund’s Investor Class shares. The annual limitation for payment of expenses pursuant to the Plan is 0.25% of the Fund’s average daily net assets allocable to Investor Class shares. The Fund has not adopted a plan of distribution with respect to Institutional Class shares. During the year ended February 28, 2022, Investor Class shares of the Fund incurred $1,092 of distribution fees under the Plan.

22

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

TRUSTEE COMPENSATION

Effective October 20, 2021, each member of the Board (a “Trustee”) who is not an “interested person” (as defined by the 1940 Act, as amended) of the Trust (“Independent Trustee”) receives a $1,300 annual retainer from the Fund, paid quarterly, except for the Board Chairperson who receives a $1,700 annual retainer from the Fund, paid in quarterly installments. Each Independent Trustee also receives from the Fund a fee of $550 for each Board meeting attended plus reimbursement for travel and other meeting-related expenses. Prior to October 20, 2021, each Independent Trustee received a $1,300 annual retainer from the Fund, paid quarterly, except for the Board Chairperson who received a $1,500 annual retainer from the Fund, paid in quarterly installments. Each Independent Trustee also received from the Fund a fee of $500 for each Board meeting attended plus reimbursement for travel and other meeting-related expenses.

PRINCIPAL HOLDERS OF FUND SHARES

As of February 28, 2022, the following shareholders owned of record 25% or more of the outstanding shares of the Fund:

| NAME OF RECORD OWNER | % OWNERSHIP |

| National Financial Services, LLC (for the benefit of its customers) | 48% |

| TD Ameritrade, Inc. (for the benefit of its customers) | 31% |

A beneficial owner of 25% or more of the Fund’s outstanding shares may be considered a controlling person. That shareholder’s vote could have a more significant effect on matters presented at a shareholders’ meeting.

5. Contingencies and Commitments

The Fund indemnifies the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

6. Investment in Other Investment Companies

The Fund may invest a significant portion of its assets in shares of one or more investment companies, including ETFs, open-end mutual funds and money market mutual funds. The Fund will incur additional indirect expenses (acquired fund fees and expenses) to the extent it invests in shares of other investment companies. As of February 28, 2022, the Fund had 38.3% of the value of its net assets invested in ETFs.

23

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

7. Subsequent Events

The Fund is required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statement of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events.

24

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

To the Shareholders of Blueprint Adaptive Growth Allocation Fund and

Board of Trustees of Ultimus Managers Trust

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Blueprint Adaptive Growth Allocation Fund (formerly Blueprint Growth Fund) (the “Fund”), a series of Ultimus Managers Trust, as of February 28, 2022, the related statement of operations for the year then ended, the statements of changes in net assets, the related notes, and the financial highlights for each of the two periods in the period then ended (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of February 28, 2022, the results of its operations for the year then ended, and the changes in net assets and the financial highlights for each of the two periods in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of February 28, 2022, by correspondence with the custodian and broker; when replies were not received from the broker, we performed other auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the Fund’s auditor since 2020.

COHEN & COMPANY, LTD.

Cleveland, Ohio

April 27, 2022

25

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| ABOUT YOUR FUND’S EXPENSES (Unaudited) |

We believe it is important for you to understand the impact of costs on your investment. As a shareholder of the Fund, you incur ongoing costs, including management fees, class-specific expenses (such as distribution fees) and other operating expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The expenses in the table below are based on an investment of $1,000 made at the beginning of the most recent period (September 1, 2021) and held until the end of the period (February 28, 2022).

The table below illustrates the Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the fourth column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare the Fund’s ongoing costs with those of other mutual funds. It assumes that the Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Fund’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the U.S. Securities and Exchange Commission (the “SEC”) requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Fund does not charge transaction fees, such as purchase or redemption fees, nor does it carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

26

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| ABOUT YOUR FUND’S EXPENSES (Unaudited) (Continued) |

More information about the Fund’s expenses can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Fund’s prospectus.

| Beginning | Ending | |||

| Account Value | Account Value | Expenses | ||

| September 1, | February 28, | Net Expense | Paid During | |

| 2021 | 2022 | Ratio(a) | Period(b) | |

| Investor Class | ||||

| Based on Actual Fund Return | $1,000.00 | $ 958.20 | 1.50% | $7.28 |

| Based on Hypothetical 5% Return (before expenses) | $1,000.00 | $ 1,017.36 | 1.50% | $7.50 |

| Institutional Class | ||||

| Based on Actual Fund Return | $1,000.00 | $ 960.00 | 1.25% | $6.07 |

| Based on Hypothetical 5% Return (before expenses) | $1,000.00 | $ 1,018.60 | 1.25% | $6.26 |

| (a) | Annualized, based on the Fund’s most recent one-half year expenses. |

| (b) | Expenses are equal to the Fund’s annualized net expense ratio multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). |

27

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| OTHER INFORMATION (Unaudited) |

A description of the policies and procedures that the Fund uses to vote proxies relating to portfolio securities is available without charge upon request by calling toll-free 1-866-983-4525, or on the SEC’s website at www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available without charge upon request by calling toll-free 1-866-983-4525, or on the SEC’s website at www.sec.gov.

The Trust files a complete listing of portfolio holdings for the Fund with the SEC as of the end of the first and third quarters of each fiscal year as an exhibit to Form N-PORT. These filings are available upon request by calling 1-866-983-4525. Furthermore, you may obtain a copy of the filings on the SEC’s website at www.sec.gov and on the Fund’s website www.blueprintmutualfunds.com.

| FEDERAL TAX INFORMATION (Unaudited) |

Dividends Received Deduction

For corporate shareholders, 100% of ordinary income dividends paid during the period ended February 28, 2022 qualify for the corporate dividends received deduction.

Qualified Dividend Income

The Fund has designated the maximum amount allowable of their net taxable income as qualified dividend income as provided in the Jobs and Growth Tax Relief Reconciliation Act of 2003. This amount was reflected on Form 1099-DIV for the calendar year 2021.

28

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| BOARD OF TRUSTEES AND EXECUTIVE OFFICERS (Unaudited) |

The Board has overall responsibility for management of the Trust’s affairs. The Trustees serve during the lifetime of the Trust and until its termination, or until death, resignation, retirement, or removal. The Trustees, in turn, elect the officers of the Fund to actively supervise their day-to-day operations. The officers have been elected for an annual term. Each Trustee’s and officer’s address is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246. The following are the Trustees and executive officers of the Fund:

| Name and Year of Birth | Length of Time Served | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years | Number of Funds in Trust Overseen by Trustee | Directorships of Public Companies Held by Trustee During Past 5 Years |

| Interested Trustees: | |||||

| David R. Carson* Year of Birth: 1958 | Trustee Since 2021 Officer Since February 2012 | Trustee (January 2021 to present) Vice President (January 2021 to present; and previously April 2013 to October 2013) President and Principal Executive Officer of each of its series (October 2013 to January 2021) | Vice President and Director of Client Strategies of Ultimus Fund Solutions, LLC (2013 to present); President of Unified Series Trust (January 2017 to present). | 26 | Interested Trustee of 21 series of the Unified Series Trust (a registered management company) (January 2017 to present). |

| Independent Trustees: | |||||

| Janine L. Cohen Year of Birth: 1952 | Since January 2016 | Chairperson (October 2019 to present) Trustee (January 2016 to present) | Retired since 2013; previously Chief Financial Officer from 2004 to 2013 and Chief Compliance Officer from 2008 to 2013 at AER Advisors, Inc. | 26 | n/a |

29

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| BOARD OF TRUSTEES AND EXECUTIVE OFFICERS (Unaudited) (Continued) |

| Name and Year of Birth | Length of Time Served | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years | Number of Funds in Trust Overseen by Trustee | Directorships of Public Companies Held by Trustee During Past 5 Years |

| Independent Trustees (Continued): | |||||

| David M. Deptula Year of Birth: 1958 | Since June 2012 | Trustee | Vice President of Legal and Special Projects at Dayton Freight Lines, Inc. since February 2016; Vice President of Tax Treasury at The Standard Register, Inc. from November 2011 to 2016. | 26 | n/a |

| Jacqueline A. Williams Year of Birth: 1954 | Since June 2019 | Trustee | Managing Member of Custom Strategy Consulting, LLC (2017 to present); Managing Director of Global Investment Research (2005 to 2017), Cambridge Associates, LLC. | 26 | n/a |

| Clifford N. Schireson Year of Birth: 1953 | Since June 2019 | Trustee | Retired; Founder of Schireson Consulting, LLC (2017 to 2021); Director of Institutional Services for Brandes Investment Partners, LP (2004-2017). | 26 | Trustee of the San Diego City Employees’ Retirement System (August 2019 to present). |

| Robert E. Morrison Year of Birth: 1957 | Since June 2019 | Trustee | Managing Director, Midwest Trust and FCI Advisors (2022 to present); Senior Vice President and National Practice Lead for Investment, Huntington National Bank/ Huntington Private Bank (2014 to 2022); CEO, CIO, President of 5 Star Investment Management Company (2006 to 2014). | 26 | Independent Trustee and Chairman of the Ultimus Managers Trust (2012 to 2014). |

| * | Mr. Carson is considered an “interested person” of the Trust within the meaning of Section 2(a)(19) of the 1940 Act because of his relationship with the Trust’s administrator, transfer agent, and distributor. Mr. Carson was President of the Trust from October 2013 to January 2021 and Vice President of the Trust from April 2013 to October 2013. |

30

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| BOARD OF TRUSTEES AND EXECUTIVE OFFICERS (Unaudited) (Continued) |

| Name and Year of Birth | Length of Time Served | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years |

| Executive Officers: | |||

| Todd E. Heim Year of Birth: 1967 | Since 2014 | President (January 2021 to present) Vice President (2014 to January 2021) | Relationship Management Director and Vice President of Ultimus Fund Solutions, LLC (2018 to present); Client Implementation Manager and Assistant Vice President of Ultimus Fund Solutions, LLC (2014 to 2018); Naval Flight Officer of United States Navy (May 1989 to June 2017). |

| Jennifer L. Leamer Year of Birth: 1976 | Since 2014 | Treasurer (2014 to present) Assistant Treasurer (April 2014 to October 2014) | Senior Vice President, Fund Accounting of Ultimus Fund Solutions, LLC (2014 to present). |

| Daniel D. Bauer Year of Birth: 1977 | Since 2016 | Assistant Treasurer (April 2016 to present) | Assistant Vice President, Fund Accounting (September 2015 to present); Fund Accounting Manager (March 2012 to August 2015) of Ultimus Fund Solutions, LLC. |

| Angela A. Simmons Year of Birth: 1975 | Since 2022 | Assistant Treasurer (January 2022 to present) | Vice President, Financial Administration (2022 to present) and Assistant Vice President, Financial Administration (2015 to 2022) of Ultimus Fund Solutions, LLC. |

| Khimmara Greer Year of Birth: 1983 | Since 2021 | Secretary (October 2021 to present) | Vice President and Senior Legal Counsel of Ultimus Fund Solutions, LLC (2021 to present); Vice President, Asset Servicing – Regulatory Administration of The Bank of New York Mellon (2019 to 2021); Vice President and Counsel of State Street Bank and Trust Company (2015 to 2019); and Regulatory Advisor – Fund Regulatory Services of JPMorgan Chase Bank (2014 to 2015). |

| David K. James Year of Birth: 1970 | Since 2021 | Assistant Secretary (October 2021 to present) Secretary (July 2021 to October 2021) | Executive Vice President and Chief Legal and Risk Officer of Ultimus Fund Solutions, LLC (2018 to present); Managing Director and Managing Counsel of State Street Bank and Trust Company (2009 to 2018). |

| Natalie S. Anderson Year of Birth: 1975 | Since 2016 | Assistant Secretary (April 2016 to present) | Legal Administration Manager (July 2016 to present) and Paralegal (January 2015 to June 2016) of Ultimus Fund Solutions, LLC. |

31

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| BOARD OF TRUSTEES AND EXECUTIVE OFFICERS (Unaudited) (Continued) |

| Name and Year of Birth | Length of Time Served | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years |

| Executive Officers (Continued): | |||

| Gweneth Gosselink Year of Birth: 1955 | Since 2020 | Chief Compliance Officer (January 2020 to present) | Assistant Vice President, Compliance Officer of Ultimus Fund Solutions, LLC (December 2019 to present); CCO Consultant at GKG Consulting, LLC (December 2019 to present); Chief Operating Officer & CCO at Miles Capital, Inc. (June 2013 to December 2019). |

| Martin Dean Year of Birth: 1963 | Since 2019 | Assistant Chief Compliance Officer (January 2020 to present) Interim Chief Compliance Officer (October 2019 to January 2020) Assistant Chief Compliance Officer (January 2016 to 2017) | Senior Vice President, Head of Fund Compliance of Ultimus Fund Solutions, LLC (January 2016 to present). |

Additional information about members of the Board and executive officers is available in the Fund’s Statement of Additional Information (“SAI”). To obtain a free copy of the SAI, please call toll free 1-866-561-3087.

32

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT AND SUB-ADVISORY AGREEMENT (Unaudited) |

The Board of Trustees (the “Board”), including the Independent Trustees voting separately, has reviewed and approved the Fund’s Investment Advisory Agreement with Blueprint Fund Management, LLC (the “Adviser” or “Blueprint Management”) for an additional one-year term (the “Advisory Agreement”) and the Sub-Advisory Agreement between Blueprint Management and Blueprint Partners, LLC (the “Sub-Adviser” or “Blueprint Partners”), on behalf of the Fund, for an additional one-year term (the “Sub-Advisory Agreement” and together with the Advisory Agreement, the “Blueprint Advisor Agreements”)). The Board approved the Agreement at a meeting held on January 18-19, 2022, at which all of the Trustees were present.

In deciding on whether to approve the continuation of the Advisory Agreement, the Board recalled its review of the materials related to the Fund and Blueprint Management at the meeting and throughout the life of the Fund and its numerous discussions with Trust management and Blueprint Management about the operations and performance of the Fund during that period. The Board further considered those materials and discussions and other numerous factors, including the following:

The nature, extent, and quality of the services provided by the Adviser. In this regard, the Board reviewed the services being provided by Blueprint Management to the Fund including, without limitation, its providing a continuous investment program for the Fund, adhering to the Fund’s investment restrictions, complying with the Trust’s policies and procedures and voting proxies on behalf of the Fund. The Board considered the qualifications and experience of Blueprint Management’s portfolio managers who are responsible for the day-to day management of the Fund’s portfolio, as well as the qualifications of other individuals at Blueprint Management who provide services to the Fund. The Board concluded that the quality, extent, and nature of the services provided by Blueprint Management to the Fund were satisfactory.

The investment performance of the Fund. In this regard, the Board compared the performance of the Fund with the performance of its benchmark index, custom peer group, and Morningstar category. The Board concluded that the investment performance of the Fund has been satisfactory

The costs of the services provided and profits realized by the Adviser and its affiliates from their relationship with the Fund. In this regard, the Board considered the Fund’s management fee proposed to be charged to the Fund and the Fund’s expense ratio, each as compared to the Fund’s peer group. The Board considered the revenue earned from the Fund and the current and anticipated profitability of the Fund to Blueprint Management, if any. The Board also considered Blueprint Management’s past fee reductions and expense reimbursements for the Fund and the indirect benefits that Blueprint Management received from its management of the Fund. The Board concluded that the advisory fee to be paid to Blueprint Management by the Fund is reasonable in light of the nature and quality of services provided by Blueprint Management.

33

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT AND SUB-ADVISORY AGREEMENT (Unaudited) (Continued) |

The extent to which economics of scale would be realized as the Fund grows and whether advisory fee levels reflect these economies of scale for the benefit of the Fund’s investors. In this regard, the Board considered that the Fund’s fee arrangements with Blueprint Management involve both the advisory fee and the expense limitation agreement (the “ELA”). The Board determined that while the advisory fee rate remained the same as asset levels increased, the shareholders of the Fund have experienced benefits from the ELA and will continue to experience benefits from the ELA. The Board concluded that the advisory fee was reasonable in light of the information that was provided to the Trustees by Blueprint Management with respect to economies of scale.

In deciding on whether to approve the continuation of the Sub-Advisory Agreement, the Board recalled its review of the materials related to the Fund and Blueprint Partners at the meeting and throughout the life of the Fund and its numerous discussions with Trust management and Blueprint Partners about the operations and performance of the Fund during that period. The Board further considered those materials and discussions and numerous other factors, including:

The nature, extent, and quality of the services provided by the Sub-Adviser. In this regard, the Board reviewed the services being provided by Blueprint Partners under the Sub-Advisory Agreement to the Fund including, without limitation, its providing a continuous investment program for the Fund, adhering to the Fund’s investment restrictions, complying with the Trust’s policies and procedures and voting proxies on behalf of the Fund. The Board considered the qualifications and experience of Blueprint Partners’ portfolio managers who are responsible for the day-to day management of the Fund’s portfolio, as well as the qualifications of other individuals at Blueprint Partners who provide services to the Fund. The Board concluded that the quality, extent, and nature of the services provided by Blueprint Partner to the Fund were satisfactory.

The investment performance of the Fund. In this regard, the Board compared the performance of the Fund with the performance of its benchmark index, custom peer group, and Morningstar category. The Board concluded that the investment performance of the Fund has been satisfactory

The costs of the services provided and profits realized by the Sub-Adviser and its affiliates from its relationship with the Fund. In this regard, the Board considered that Blueprint Partners’ compensation for sub-advising the Fund is solely the responsibility of Blueprint Management, and that the Fund is not responsible for paying Blueprint Partners. The Board considered the revenue earned by Blueprint Partners under the Sub-Advisory Agreement and the common ownership and relationship with Blueprint Management. The Board concluded that the sub-advisory fee to be paid to Blueprint Partners would not increase fees paid by the Fund and is reasonable in light of the nature and quality of services provided by Blueprint Partners.

34

| BLUEPRINT ADAPTIVE GROWTH ALLOCATION FUND |

| DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT AND SUB-ADVISORY AGREEMENT (Unaudited) (Continued) |