| OMB APPROVAL | |

OMB Number: 3235-0570 Expires: July 31, 2022 Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-22680 |

| Ultimus Managers Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

Khimmara Greer

| Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, Ohio 45246_ |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (513) 587-3400 |

| Date of fiscal year end: | May 31 | |

| Date of reporting period: | May 31, 2022 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

| (a) |

Institutional Class (ADLVX)

ANNUAL REPORT

May 31, 2022

Managed by

Adler Asset Management, LLC

For information or assistance in opening an account,

please call toll-free 1-800-408-4682.

| ADLER VALUE FUND | |

| LETTER TO SHAREHOLDERS (Unaudited) | June 13, 2022 |

Dear Shareholder,

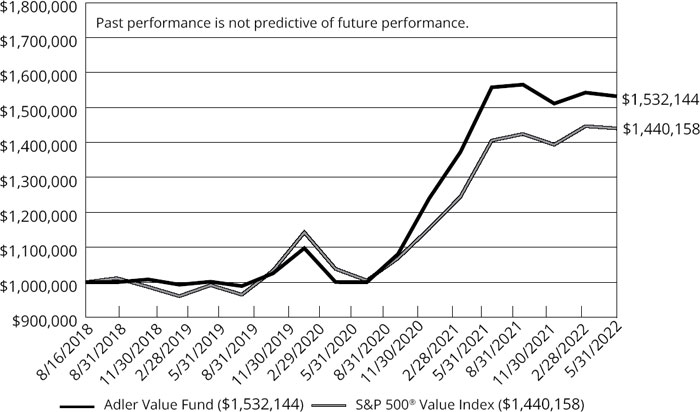

In mid-August 2018, the Adler Value Fund (the “Fund”) commenced operations. Adler Asset Management, LLC (the “Adviser”) is the Fund’s investment adviser. For the annual period ended May 31, 2022, the Fund’s total return was -1.64%. During the same period, the total return of the S&P 500 Value Index was 2.46%. During the annual period ended May 31, 2022, the Fund completed three years in operation. For the three years ended May 31, 2022, the Fund had an annualized total return of 15.71%. During the same period, the S&P 500 Value Index had an annualized total return of 14.30%

As the fiscal year progressed, equity, fixed-income, foreign exchange, and commodities markets increasingly reacted to economic data that either validated or refuted market expectations around three key themes:

| ● | Pace of Federal Reserve interest rate increases; |

| ● | Persistently high inflation; and |

| ● | Probability, timing, and severity of a potential recession. |

Investment Approach

In selecting investments for the Fund, the Adviser uses a focused-value strategy to invest in companies that, in its opinion, appear to be undervalued by the equity market but where catalysts exist, in the opinion of the Adviser, to close these valuation gaps. The Adviser seeks to exploit perceived market misjudgments in pricing by buying equity securities that appear to be undervalued because of a temporary aversion to these out-of-favor issuers.

The Adviser maintains a watch list of companies and reviews each company’s financial condition and prospects, including factors such as (but not limited to): expected future earnings, cash flow, the ability and willingness to return capital to shareholders, competitive position, quality of the business franchise, and the reputation, experience, and competence of a company’s management and board of directors. The Adviser considers these factors both while the company is on the watch list and also at the time of purchase. Not all companies, at the time of purchase, are on the Adviser’s watch list, and a company may be added to the Fund’s portfolio following a precipitating event.

When added to the Fund’s portfolio, a company will generally be trading at a significant discount to its 52-week or all-time high. The Adviser’s contrarian approach, buying what it believes are fundamentally sound companies that are out-of-favor with the market, is industry, sector and market capitalization agnostic, and typically will result in a portfolio containing the securities of fewer than thirty issuers.

1

Performance for the Annual Period

The Adviser attributes the Fund’s underperformance for the annual period to the impact of recession fears on some of the Fund’s holdings. Value stocks can and do operate in industries impacted by a potential economic slowdown with the equity market re-pricing certain stocks. The Adviser remains confident in the catalysts for the Fund’s holdings as we move through this period of economic uncertainty.

Portfolio Developments

Veoneer’s (VNE) $37.00 per share cash sale closed near the end of the annual period. VNE was the Fund’s largest holding reflecting the exercise of in-the-money call options and the purchase of additional shares to capitalize on an unusually large arbitrage spread prior to close.

Altice USA (ATUS) is one of the largest broadband communications and video services providers in the United States. ATUS has embarked on a multi-billion dollar build-out of its fiber network which is depressing free cash flow in the short-term. This impact on free cash flow has hurt the stock price which currently trades below the Fund’s cost. In addition, ATUS has a controlling shareholder. The Fund did well with another holding, Meredith Corporation, with a controlling shareholder. In this case, the Adviser has and continues to assess the degree of alignment of the controlling shareholder with minority shareholders of which the Fund is one.

In closing, I want to thank shareholders for their confidence in the Fund’s Adviser. The Adviser continues to assess companies that fit the Fund’s investment approach.

David Adler

Adler Asset Management, LLC

June 13, 2022

2

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month-end are available by calling 1-800-408-4682.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please visit the Fund’s website at www.adlervaluefund.com or call 1-800-408-4682 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time, and may no longer be held by the Fund. For a complete list of securities held by the Fund as of May 31, 2022, please see the Schedule of Investments section of the annual report. The opinions of the Fund’s adviser with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Fund and the market in general and statements of the Fund’s plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements, include, without limitation, general economic conditions, such as inflation, recession, and interest rates. Past performance is not a guarantee of future results.

3

| ADLER VALUE FUND |

| PERFORMANCE INFORMATION |

| May 31, 2022 (Unaudited) |

Comparison of the Change in Value of a $1,000,000 Investment in

Adler Value Fund - Institutional Class vs. the S&P 500® Value Index

| Average Annual Total Returns (for the periods ended May 31, 2022) | ||||||

| Since | ||||||

| 1 Year | 3 Year | Inception (b) | ||||

| Adler Value Fund - Institutional Class (a) | (1.64%) | 15.71% | 11.92% | |||

| S&P 500® Value Index (c) | 2.46% | 14.30% | 10.11% | |||

| (a) | The total returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. |

| (b) | The Fund commenced operations on August 16, 2018. |

| (c) | The S&P 500® Value Index measures value stocks drawn from the S&P 500® Index. Value is measured using three factors: the ratios of book value, earnings, and sales to price. |

4

| ADLER VALUE FUND |

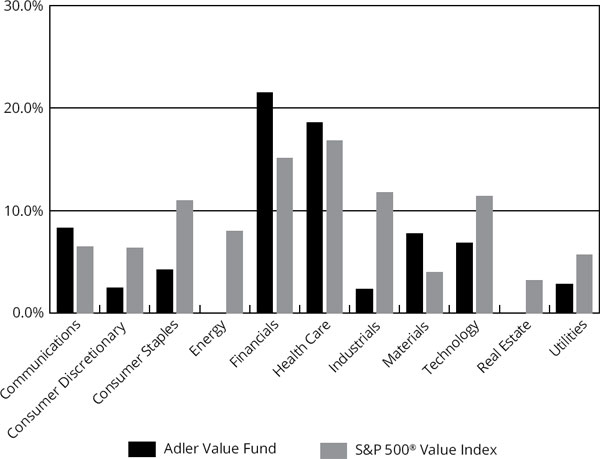

| PORTFOLIO INFORMATION |

| May 31, 2022 (Unaudited) |

Sector Diversification

(% of Net Assets)

| Top 10 Equity Holdings | ||

| % of Net | ||

| Security Description | Assets | |

| Pfizer, Inc | 5.6% | |

| Valvoline, Inc. | 4.6% | |

| Charles Schwab Corporation (The) | 4.2% | |

| Aflac, Inc. | 3.9% | |

| Cigna Corporation | 3.8% | |

| Bayer AG - ADR | 3.5% | |

| Jackson Financial, Inc. - Class A | 3.5% | |

| Equitable Holdings, Inc. | 3.4% | |

| MultiPlan Corporation | 3.3% | |

| O-I Glass, Inc. | 3.2% | |

5

| ADLER VALUE FUND |

| SCHEDULE OF INVESTMENTS |

| May 31, 2022 |

| COMMON STOCKS — 72.6% | Shares | Value | ||||||

| Communications — 8.3% | ||||||||

| Cable & Satellite — 1.5% | ||||||||

| Altice USA, Inc. - Class A (a) | 3,100 | $ | 35,278 | |||||

| Comcast Corporation - Class A | 600 | 26,568 | ||||||

| 61,846 | ||||||||

| Entertainment Content — 3.2% | ||||||||

| Paramount Global - Class B | 3,900 | 133,887 | ||||||

| Internet Media & Services — 0.9% | ||||||||

| Twitter, Inc. (a) | 1,000 | 39,600 | ||||||

| Publishing & Broadcasting — 2.7% | ||||||||

| iHeartMedia, Inc. - Class A (a) | 9,500 | 112,100 | ||||||

| Consumer Discretionary — 2.5% | ||||||||

| Automotive — 1.9% | ||||||||

| Tenneco, Inc. - Class A (a) | 4,700 | 81,357 | ||||||

| Leisure Facilities & Services — 0.6% | ||||||||

| Starbucks Corporation | 300 | 23,550 | ||||||

| Consumer Staples — 4.2% | ||||||||

| Beverages — 1.1% | ||||||||

| Diageo plc - ADR | 250 | 46,743 | ||||||

| Household Products — 3.1% | ||||||||

| Spectrum Brands Holdings, Inc. | 1,500 | 131,610 | ||||||

| Financials — 19.3% | ||||||||

| Banking — 2.5% | ||||||||

| Citigroup, Inc. | 2,000 | 106,820 | ||||||

| Broker-Dealers — 6.0% | ||||||||

| Charles Schwab Corporation (The) | 2,500 | 175,250 | ||||||

| XP, Inc. - Class A (a) | 3,395 | 76,761 | ||||||

| 252,011 | ||||||||

| Insurance — 10.8% | ||||||||

| Aflac, Inc. | 2,700 | 163,539 | ||||||

| Equitable Holdings, Inc. | 4,700 | 142,927 | ||||||

| Jackson Financial, Inc. - Class A | 4,000 | 145,640 | ||||||

| 452,106 | ||||||||

6

| ADLER VALUE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| COMMON STOCKS — 72.6% (Continued) | Shares | Value | ||||||

| Health Care — 18.6% | ||||||||

| Biotech & Pharma — 14.8% | ||||||||

| Bayer AG - ADR | 8,200 | $ | 146,124 | |||||

| Bristol-Myers Squibb Company | 1,500 | 113,175 | ||||||

| Pfizer, Inc. | 4,400 | 233,376 | ||||||

| Viatris, Inc. | 10,335 | 126,810 | ||||||

| 619,485 | ||||||||

| Health Care Facilities & Services — 3.8% | ||||||||

| Cigna Corporation | 600 | 160,974 | ||||||

| Industrials — 2.3% | ||||||||

| Industrial Support Services — 2.3% | ||||||||

| Grainger (W.W.), Inc. | 200 | 97,414 | ||||||

| Materials — 7.8% | ||||||||

| Chemicals — 4.6% | ||||||||

| Valvoline, Inc. | 5,800 | 194,068 | ||||||

| Containers & Packaging — 3.2% | ||||||||

| O-I Glass, Inc. (a) | 8,300 | 136,535 | ||||||

| Technology — 6.8% | ||||||||

| Technology & Electronics — 2.4% | ||||||||

| Corning, Inc. | 2,800 | 100,296 | ||||||

| Technology Hardware — 1.1% | ||||||||

| Diebold Nixdorf, Inc. (a) | 14,200 | 44,162 | ||||||

| Technology Services — 3.3% | ||||||||

| MultiPlan Corporation (a) | 28,000 | 140,000 | ||||||

| Utilities — 2.8% | ||||||||

| Electric Utilities — 2.8% | ||||||||

| PG&E Corporation (a) | 9,600 | 117,120 | ||||||

| Total Common Stocks (Cost $2,570,871) | $ | 3,051,684 | ||||||

7

| ADLER VALUE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| PREFERRED STOCKS — 2.2% | Shares | Value | ||||||

| Financials — 2.2% | ||||||||

| Banking — 2.2% | ||||||||

| Itau Unibanco Holding S.A. - ADR ($80,145) | 16,800 | $ | 92,064 | |||||

| PURCHASED OPTION | Notional | |||||||||||||||

| CONTRACTS — 5.1% | Strike Price | Contracts | Value | Value | ||||||||||||

| Call Option Contracts — 5.1% | ||||||||||||||||

| Altice USA, Inc. - Class A, 06/17/22 | $ | 18.00 | 20 | $ | 22,760 | $ | 50 | |||||||||

| Altice USA, Inc. - Class A, 06/17/22 | 25.00 | 10 | 11,380 | 25 | ||||||||||||

| Altice USA, Inc. - Class A, 01/20/23 | 10.00 | 30 | 34,140 | 9,300 | ||||||||||||

| Altice USA, Inc. - Class A, 01/20/23 | 11.00 | 10 | 11,380 | 2,500 | ||||||||||||

| Altice USA, Inc. - Class A, 01/20/23 | 12.00 | 20 | 22,760 | 4,000 | ||||||||||||

| Bristol-Myers Squibb Company, 06/17/22 | 57.50 | 20 | 150,900 | 36,750 | ||||||||||||

| Bristol-Myers Squibb Company, 06/17/22 | 65.00 | 4 | 30,180 | 4,400 | ||||||||||||

| Corning, Inc., 01/20/23 | 32.00 | 10 | 35,820 | 6,000 | ||||||||||||

| Corning, Inc., 01/20/23 | 35.00 | 10 | 35,820 | 4,000 | ||||||||||||

| Corning, Inc., 01/20/23 | 37.00 | 30 | 107,460 | 9,300 | ||||||||||||

| Diebold Nixdorf, Inc., 11/18/22 | 5.00 | 10 | 3,110 | 430 | ||||||||||||

| Diebold Nixdorf, Inc., 11/18/22 | 7.50 | 20 | 6,220 | 260 | ||||||||||||

| Equitable Holdings, Inc., 01/20/23 | 30.00 | 40 | 121,640 | 14,000 | ||||||||||||

| iHeartmedia, Inc. - Class A, 07/15/22 | 20.00 | 25 | 29,500 | 938 | ||||||||||||

| iHeartMedia, Inc. - Class A, 01/20/23 | 12.50 | 10 | 11,800 | 2,100 | ||||||||||||

| iHeartMedia, Inc. - Class A, 01/20/23 | 15.00 | 30 | 35,400 | 3,150 | ||||||||||||

| iHeartMedia, Inc. - Class A, 01/20/23 | 17.50 | 10 | 11,800 | 575 | ||||||||||||

| iHeartmedia, Inc. - Class A, 01/20/23 | 20.00 | 30 | 35,400 | 1,875 | ||||||||||||

| Itau Unibanco Holding S.A. - ADR, 01/20/23 | 4.50 | 10 | 5,480 | 1,768 | ||||||||||||

8

| ADLER VALUE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| PURCHASED OPTION | ||||||||||||||||

| CONTRACTS — 5.1% | Notional | |||||||||||||||

| (Continued) | Strike Price | Contracts | Value | Value | ||||||||||||

| Call Option Contracts — 5.1% | ||||||||||||||||

| (Continued) | ||||||||||||||||

| Itau Unibanco Holding S.A. - ADR, 01/20/23 | $ | 5.00 | 20 | $ | 10,960 | $ | 2,790 | |||||||||

| Jackson Financial, Inc. - Class A, 06/17/22 | 30.00 | 10 | 36,410 | 7,050 | ||||||||||||

| MultiPlan Corporation, 01/20/23 | 5.00 | 110 | 55,000 | 12,100 | ||||||||||||

| MultiPlan Corporation, 01/20/23 | 7.50 | 10 | 5,000 | 400 | ||||||||||||

| O-I Glass, Inc., 11/18/22 | 13.00 | 10 | 16,450 | 3,700 | ||||||||||||

| O-I Glass, Inc., 12/16/22 | 12.00 | 5 | 8,225 | 2,575 | ||||||||||||

| Paramount Global - Class B, 06/17/22 | 37.50 | 10 | 34,330 | 330 | ||||||||||||

| Paramount Global - Class B, 01/20/23 | 30.00 | 10 | 34,330 | 7,200 | ||||||||||||

| Pfizer, Inc., 01/20/23 | 47.00 | 20 | 106,080 | 16,450 | ||||||||||||

| Pfizer, Inc., 01/20/23 | 50.00 | 40 | 212,160 | 25,800 | ||||||||||||

| PG&E Corporation, 01/20/23 | 10.00 | 10 | 12,200 | 2,995 | ||||||||||||

| Valvoline, Inc., 12/16/22 | 30.00 | 20 | 66,920 | 11,400 | ||||||||||||

| Viatris, Inc., 01/20/23 | 10.00 | 10 | 12,270 | 2,750 | ||||||||||||

| Viatris, Inc., 01/20/23 | 12.50 | 50 | 61,350 | 7,000 | ||||||||||||

| Viatris, Inc., 01/20/23 | 15.00 | 160 | 196,320 | 9,600 | ||||||||||||

| Total Purchased Option Contracts (Cost $197,105) | $ | 1,590,955 | $ | 213,561 | ||||||||||||

| MONEY MARKET FUNDS — 19.9% | Shares | Value | ||||||

| Federated Hermes Treasury Obligations Fund – Service Shares, 0.41% (b) (Cost $836,318) | 836,318 | $ | 836,318 | |||||

| Investments at Value — 99.8% (Cost $3,684,439) | $ | 4,193,627 | ||||||

| Other Assets in Excess of Liabilities — 0.2% | 8,737 | |||||||

| Net Assets — 100.0% | $ | 4,202,364 | ||||||

| (a) | Non-income producing security. |

| (b) | The rate shown is the 7-day effective yield as of May 31, 2022. |

ADR - American Depository Receipt

AG - Aktiengesellschaft

plc - Public Limited Company

S.A. - Société anonyme

See accompanying notes to financial statements.

9

| ADLER VALUE FUND |

| STATEMENT OF ASSETS AND LIABILITIES |

| May 31, 2022 |

| ASSETS | ||||

| Investments in securities: | ||||

| At cost | $ | 3,684,439 | ||

| At value (Note 2) | $ | 4,193,627 | ||

| Receivable for capital shares sold | 750 | |||

| Receivable from Adviser (Note 4) | 8,778 | |||

| Dividends receivable | 8,200 | |||

| Tax reclaims receivable | 512 | |||

| Other assets | 3,665 | |||

| Total assets | 4,215,532 | |||

| LIABILITIES | ||||

| Payable to administrator (Note 4) | 7,030 | |||

| Other accrued expenses | 6,138 | |||

| Total liabilities | 13,168 | |||

| NET ASSETS | $ | 4,202,364 | ||

| NET ASSETS CONSIST OF: | ||||

| Paid-in capital | $ | 3,455,345 | ||

| Distributable earnings | 747,019 | |||

| NET ASSETS | $ | 4,202,364 | ||

| PRICING OF INSTITUTIONAL SHARES (Note 2) | ||||

| Net assets applicable to Institutional Shares | $ | 4,202,364 | ||

| Shares of Institutional Shares outstanding (no par value, unlimited number of shares authorized) | 151,729 | |||

| Net asset value, offering and redemption price per share (Note 2) | $ | 27.70 |

See accompanying notes to financial statements.

10

| ADLER VALUE FUND |

| STATEMENT OF OPERATIONS |

| For the Year Ended May 31, 2022 |

| INVESTMENT INCOME | ||||

| Dividends | $ | 185,134 | ||

| Foreign withholding tax on dividends | (1,598 | ) | ||

| Total investment income | 183,536 | |||

| EXPENSES | ||||

| Investment advisory fees (Note 4) | 40,980 | |||

| Fund accounting fees (Note 4) | 30,408 | |||

| Administration fees (Note 4) | 30,000 | |||

| Legal fees | 24,694 | |||

| Trustees��� fees and expenses (Note 4) | 17,817 | |||

| Audit and tax services fees | 16,995 | |||

| Registration and filing fees | 14,644 | |||

| Transfer agent fees (Note 4) | 12,000 | |||

| Compliance fees (Note 4) | 12,000 | |||

| Custodian and bank service fees | 8,976 | |||

| Printing of shareholder reports | 6,725 | |||

| Postage and supplies | 4,597 | |||

| Insurance expense | 3,344 | |||

| Other expenses | 8,298 | |||

| Total expenses | 231,478 | |||

| Less fee reductions and expense reimbursements by the Adviser (Note 4) | (180,253 | ) | ||

| Net expenses | 51,225 | |||

| NET INVESTMENT INCOME | 132,311 | |||

| REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS | ||||

| Net realized gains on investments transactions | 433,006 | |||

| Net change in unrealized appreciation (depreciation) on investments | (639,008 | ) | ||

| NET REALIZED AND UNREALIZED LOSSES ON INVESTMENTS | (206,002 | ) | ||

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (73,691 | ) |

See accompanying notes to financial statements.

11

| ADLER VALUE FUND |

| STATEMENTS OF CHANGES IN NET ASSETS |

| Year Ended | Year Ended | |||||||

| May 31, | May 31, | |||||||

| 2022 | 2021 | |||||||

| FROM OPERATIONS | ||||||||

| Net investment income | $ | 132,311 | $ | 6,671 | ||||

| Net realized gains (losses) from investment transactions | 433,006 | (3,828 | ) | |||||

| Net change in unrealized appreciation (depreciation) on investments | (639,008 | ) | 1,190,419 | |||||

| Net increase (decrease) in net assets resulting from operations | (73,691 | ) | 1,193,262 | |||||

| DISTRIBUTIONS TO SHAREHOLDERS (NOTE 2) | ||||||||

| Institutional Shares | (326,422 | ) | (33,750 | ) | ||||

| FROM CAPITAL SHARE TRANSACTIONS | ||||||||

| Institutional Shares | ||||||||

| Proceeds from shares sold | 556,469 | 1,143,090 | ||||||

| Net asset value of shares issued in reinvestment of distributions to shareholders | 326,422 | 33,750 | ||||||

| Payments for shares redeemed | (75,104 | ) | (30 | ) | ||||

| Net increase in Institutional Shares net assets from capital share transactions | 807,787 | 1,176,810 | ||||||

| TOTAL INCREASE IN NET ASSETS | 407,674 | 2,336,322 | ||||||

| NET ASSETS | ||||||||

| Beginning of year | 3,794,690 | 1,458,368 | ||||||

| End of year | $ | 4,202,364 | $ | 3,794,690 | ||||

| CAPITAL SHARES ACTIVITY | ||||||||

| Institutional Shares | ||||||||

| Shares sold | 18,654 | 49,491 | ||||||

| Shares reinvested | 11,295 | 1,359 | ||||||

| Shares redeemed | (2,634 | ) | (1 | ) | ||||

| Net increase in shares outstanding | 27,315 | 50,849 | ||||||

| Shares outstanding, beginning of year | 124,414 | 73,565 | ||||||

| Shares outstanding, end of year | 151,729 | 124,414 | ||||||

See accompanying notes to financial statements.

12

| ADLER VALUE FUND |

| INSTITUTIONAL SHARES |

| FINANCIAL HIGHLIGHTS |

Per Share Data for a Share Outstanding Throughout Each Period

| Year Ended | Year Ended | Period Ended | Period Ended | |||||||||||||

| May 31, | May 31, | May 31, | July 31, | |||||||||||||

| 2022 | 2021 | 2020(a) | 2019(b) | |||||||||||||

| Net asset value at beginning of period | $ | 30.50 | $ | 19.82 | $ | 20.41 | $ | 20.00 | ||||||||

| Income (loss) from investment operations: | ||||||||||||||||

| Net investment income | 0.95 | (c) | 0.07 | (c) | 0.49 | (d) | 0.15 | |||||||||

| Net realized and unrealized gains (losses) on investments | (1.35 | ) | 10.92 | (0.88 | ) | 0.26 | ||||||||||

| Total from investment operations | (0.40 | ) | 10.99 | (0.39 | ) | 0.41 | ||||||||||

| Less distributions from: | ||||||||||||||||

| Net investment income | (2.30 | ) | (0.31 | ) | (0.20 | ) | — | |||||||||

| Net realized gains | (0.10 | ) | — | — | — | |||||||||||

| Total distributions | (2.40 | ) | (0.31 | ) | (0.20 | ) | — | |||||||||

| Net asset value at end of period | $ | 27.70 | $ | 30.50 | $ | 19.82 | $ | 20.41 | ||||||||

| Total return (e) | (1.64 | %) | 55.78 | % | (2.01 | %) (f) | 2.05 | % (f) | ||||||||

| Net assets at end of period (000’s) | $ | 4,202 | $ | 3,795 | $ | 1,458 | $ | 1,447 | ||||||||

| Ratios/supplementary data: | ||||||||||||||||

| Ratio of total expenses to average net assets | 5.65 | % | 8.42 | % | 13.01 | % (g) | 11.82 | % (g) | ||||||||

| Ratio of net expenses to average net assets (h) | 1.25 | % | 1.25 | % | 1.25 | % (g) | 1.26 | % (g)(i) | ||||||||

| Ratio of net investment income to average net assets (h) | 3.23 | % (j) | 0.27 | % | 2.93 | % (d)(g) | 0.81 | % (g) | ||||||||

| Portfolio turnover rate | 45 | % | 0 | %(k) | 4 | % (f) | 0 | % | ||||||||

| (a) | Fund changed fiscal year to May 31. |

| (b) | Represents the period from the commencement of operations (August 16, 2018) through July 31, 2019. |

| (c) | Per share net investment income has been determined on the basis of average number of shares outstanding during the period. |

| (d) | During the period ended May 31, 2020, the Fund received a large special dividend distribution from NortonLifeLock, Inc. Had the Fund not received this special dividend distribution, the net investment income per share and ratio of net investment income to average net assets would have been $0.33 and 1.97%(g) lower, respectively. |

| (e) | Total return is a measure of the change in value of an investment in the Fund over the periods covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced fees and reimbursed expenses (Note 4). |

| (f) | Not annualized. |

| (g) | Annualized. |

| (h) | Ratio was determined after advisory fee reductions and expense reimbursements (Note 4). |

| (i) | Includes federal excise taxes of 0.01% of average net assets with respect to the period ended July 31, 2019. |

| (j) | During the year ended May 31, 2022, the Fund received a large special dividend distribution from Meredith Corporation. Had the Fund not received this special dividend distribution, the net investment income per share and ratio of net investment income to average net assets would have been $0.82 and 2.79% lower, respectively. |

| (k) | Percentage rounds to less than 1%. |

See accompanying notes to financial statements.

13

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS |

| May 31, 2022 |

1. Organization

Adler Value Fund (the “Fund”) is a non-diversified series of Ultimus Managers Trust (the “Trust”), an open-end investment company established as an Ohio business trust under a Declaration of Trust dated February 28, 2012. Other series of the Trust are not incorporated in this report.

The investment objective of the Fund is to seek to achieve long-term growth of capital.

The Fund currently offers one class of shares: Institutional Class shares (sold without any sales loads or distribution fees and subject to a $1,000,000 initial investment requirement).

2. Significant Accounting Policies

The Fund follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification Topic 946, “Financial Services – Investment Companies.” The following is a summary of the Fund’s significant accounting policies used in preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”).

New accounting pronouncements – In October 2020, the U.S. Securities and Exchange Commission (the “SEC”) adopted new regulations governing the use of derivatives by registered investment companies (“Rule 18f-4”). The Funds will be required to comply with the Rule 18f-4 by August 19, 2022. Once implemented, Rule 18f-4 will impose limits on the amount of derivatives a fund can enter into, eliminate the asset segregation framework currently used by funds to comply with Section 18 of the Investment Company Act of 1940, as amended, (the “1940 Act”), treat derivatives as senior securities and require funds whose use of derivatives is more than a limited specified exposure amount to establish and maintain a comprehensive derivatives risk management program and appoint a derivatives risk manager. The Fund is currently evaluating the impact, if any, of this provision.

Securities valuation – The Fund values its portfolio securities at market value as of the close of regular trading on the New York Stock Exchange (the “NYSE”) (normally 4:00 p.m. Eastern Time) on each day the NYSE is open for business. The Fund generally values its listed securities on the basis of the security’s last sale price on the security’s primary exchange, if available, otherwise at the exchange’s most recently quoted mean price. NASDAQ-listed securities are valued at the NASDAQ Official Closing Price. Option contracts are valued at the closing price on the exchanges on which they are primarily traded; if no closing price is available at the time of valuation, the option will be valued at the mean of the closing bid and ask prices for that day. Investments representing shares of money market funds and other open-end investment companies not traded on an exchange are valued at their net asset value (“NAV”) as reported by such companies. When using a quoted price and when the market is considered active, the security will be classified as Level 1 within the fair value hierarchy (see next page). In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund values its securities and other assets at fair value in accordance with

14

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

procedures established by and under the general supervision of the Board of Trustees of the Trust (the “Board”). Under these procedures, the securities will be classified as Level 2 or 3 within the fair value hierarchy, depending on the inputs used. Unavailable or unreliable market quotes may be due to the following factors: a substantial bid-ask spread; infrequent sales resulting in stale prices; insufficient trading volume; small trade sizes; a temporary lapse in any reliable pricing source; and actions of the securities or futures markets, such as the suspension or limitation of trading. As a result, the prices of securities used to calculate the Fund’s NAV may differ from quoted or published prices for the same securities.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

| ● | Level 1 – quoted prices in active markets for identical securities |

| ● | Level 2 – other significant observable inputs |

| ● | Level 3 – significant unobservable inputs |

The inputs or methods used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the Fund’s investments based on the inputs used to value the investments as of May 31, 2022:

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Common Stocks | $ | 3,051,684 | $ | — | $ | — | $ | 3,051,684 | ||||||||

| Preferred Stocks | 92,064 | — | — | 92,064 | ||||||||||||

| Purchased Option Contracts | 112,570 | 100,991 | — | 213,561 | ||||||||||||

| Money Market Funds | 836,318 | — | — | 836,318 | ||||||||||||

| Total | $ | 4,092,636 | $ | 100,991 | $ | — | $ | 4,193,627 | ||||||||

Refer to the Fund’s Schedule of Investments for a listing of the common and preferred stocks by sector and industry type. The Fund did not have any assets or liabilities that were measured at fair value on a recurring basis using significant unobservable inputs (Level 3) as of or during the year ended May 31, 2022.

Share valuation – The NAV per share of each class of the Fund is calculated daily by dividing the total value of the assets attributable to that class, less liabilities attributable to that class, by the number of shares outstanding of that class. The offering price and redemption price per share of each class of the Fund is equal to the NAV per share of such class.

15

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

Investment income – Dividend income is recorded on the ex-dividend date. Non-cash dividends included in dividend income, if any, are recorded at the fair value of the security received. Interest income is accrued as earned. Withholding taxes on foreign dividends, if any, have been recorded in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

Investment transactions – Investment transactions are accounted for on the trade date. Realized gains and losses on investments sold are determined on a specific identification basis.

Common expenses – Common expenses of the Trust are allocated among the Fund and the other series of the Trust based on the relative net assets of each series, the number of series in the Trust, or the nature of the services performed and the relative applicability to each series.

Distributions to shareholders – Distributions to shareholders arising from net investment income and realized capital gains, if any, are declared and paid annually to shareholders. The amount of distributions from net investment income and net realized capital gains are determined in accordance with federal income tax regulations, which may differ from GAAP. Dividends and distributions to shareholders are recorded on the ex-dividend date.

The tax character of distributions paid during the years ended May 31, 2022 and 2021 was as follows:

| Years | Ordinary | Long-Term | Total | |||||||||

| Ended | Income | Capital Gains | Distributions | |||||||||

| 5/31/2022 | $ | 313,110 | $ | 13,312 | $ | 326,422 | ||||||

| 5/31/2021 | 33,750 | — | 33,750 | |||||||||

Purchased option contracts – The Fund may use option contracts in any manner consistent with its investment objectives and as long as its use is consistent with relevant provisions of the 1940 Act. The Fund may use options for speculative purposes as well as for the purpose of seeking to reduce the overall investment risk that would otherwise be associated with the securities in which the Fund invests. When the Fund purchases a call or put option, an amount equal to the total premium (the premium plus the commission) paid by the Fund is recorded as an asset on the Fund’s Statement of Assets and Liabilities and is subsequently marked-to-market daily. Premiums paid in the purchase of options which expire are treated as realized losses. Premiums paid in the purchase of call options which are exercised increase the cost of the security purchased. Premiums paid in the purchase of put options which are exercised decrease the proceeds used to calculate the realized capital gain or loss on the sale of the security.

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of increase (decrease) in net assets from operations during the reporting period. Actual results could differ from those estimates.

16

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

Federal income tax – The Fund has qualified and intends to continue to qualify as a regulated investment company under the Internal Revenue Code of 1986, as amended (the “Code”). Qualification generally will relieve the Fund of liability for federal income taxes to the extent 100% of its net investment income and net realized capital gains are distributed in accordance with the Code.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also the Fund’s intention to declare as dividends in each calendar year amounts equal to at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the 12 months ended October 31) plus undistributed amounts from prior years.

The following information is computed on a tax basis for each item as of May 31, 2022:

| Tax cost of investments | $ | 3,684,442 | ||

| Gross unrealized appreciation | $ | 762,930 | ||

| Gross unrealized depreciation | (253,745 | ) | ||

| Net unrealized appreciation | 509,185 | |||

| Undistributed long-term gains | 257,372 | |||

| Accumulated capital and other losses | (19,538 | ) | ||

| Distributable earnings | $ | 747,019 |

Net qualified late year ordinary losses represent losses incurred after December 31, 2021. These losses are deemed to arise on the first day of the Fund’s next taxable year. For the year ended May 31, 2022, the Fund qualified late year ordinary losses of $19,538.

During the year ended May 31, 2022, the Fund utilized long-term capital loss carryforwards of $5,621 to offset current year capital gains.

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has reviewed the Fund’s tax positions for the current and all open tax periods (generally, three years) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements. The Fund identifies its major tax jurisdiction as U.S. federal.

3. Investment Transactions

During the year ended May 31, 2022, cost of purchases and proceeds from sales of investment securities, other than short-term investments, were $1,593,037 and $1,602,687, respectively.

4. Transactions with Related Parties

INVESTMENT ADVISORY AGREEMENT

The Fund’s investments are managed by Adler Asset Management, LLC (the “Adviser”) pursuant to the terms of an Investment Advisory Agreement. Under the Investment Advisory Agreement, the Fund pays the Adviser an investment advisory fee, computed and accrued daily and paid monthly, at the annual rate of 1.00% of its average daily net assets.

17

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

Pursuant to an Expense Limitation Agreement (“ELA”) between the Fund and the Adviser, the Adviser has agreed, until December 1, 2022, to reduce its investment advisory fees and reimburse other expenses to limit total annual operating expenses (exclusive of brokerage costs; taxes; interest; borrowing costs such as interest and dividends expenses on securities sold short; costs to organize the Fund; acquired fund fees and expenses; and extraordinary expenses such as litigation and merger or reorganization costs and other expenses not incurred in the ordinary course of the Fund’s business) to an amount not exceeding 1.25% of the Fund’s average daily net assets of the Institutional Class shares. Accordingly, during the year ended May 31, 2022, the Adviser did not collect any of its investment advisory fees and reimbursed other operating expenses totaling $139,273.

Under the terms of the ELA, investment advisory fee reductions and expense reimbursements by the Adviser are subject to repayment by the Fund for a period of three years after such fees and expenses were incurred, provided that the repayments do not cause the Fund’s total annual operating expenses to exceed the lesser of (i) the expense limitation then in effect, if any, and (ii) the expense limitation in effect at the time the expenses to be repaid were incurred. As of May 31, 2022, the Adviser may seek recoupment of investment advisory fee reductions and expense reimbursements no later than the dates as stated below:

| July 31, 2022 | $ | 27,579 | ||

| May 31, 2023 | 142,930 | |||

| May 31, 2024 | 179,743 | |||

| May 31, 2025 | 180,253 | |||

| Total | $ | 530,505 |

OTHER SERVICE PROVIDERS

Ultimus Fund Solutions, LLC (“Ultimus”) provides administration, fund accounting, compliance and transfer agency services to the Fund. The Fund pays Ultimus fees in accordance with the agreements for such services. In addition, the Fund pays out-of-pocket expenses including, but not limited to, postage, supplies, and certain costs related to the pricing of the Fund’s portfolio securities.

Under the terms of a Distribution Agreement with the Trust, Ultimus Fund Distributors, LLC (the “Distributor”) serves as principal underwriter to the Fund. The Distributor is a wholly-owned subsidiary of Ultimus. The Distributor is compensated by the Adviser (not the Fund) for acting as principal underwriter.

Certain officers and a Trustee of the Trust are also officers of Ultimus and are not paid by the Fund for serving in such capacities.

TRUSTEE COMPENSATION

Effective October 20, 2021, each member of the Board (a “Trustee”) who is not an “interested person” (as defined by the 1940 Act, as amended) of the Trust (“Independent Trustee”) receives a $1,300 annual retainer from the Fund, paid quarterly, except for the Board Chairperson

18

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

who receives a $1,700 annual retainer from the Fund, paid in quarterly installments. Each Independent Trustee also receives from the Fund a fee of $550 for each Board meeting attended plus reimbursement for travel and other meeting-related expenses. Prior to October 19, 2021, each Independent Trustee received a $1,300 annual retainer from the Fund, paid quarterly, except for the Board Chairperson who received a $1,500 annual retainer from the Fund, paid in quarterly installments. Each Independent Trustee also received from the Fund a fee of $500 for each Board meeting attended plus reimbursement for travel and other meeting-related expenses.

PRINCIPAL HOLDER OF FUND SHARES

As of May 31, 2022, the following shareholder owned of record 25% or more of the outstanding shares of the Fund:

| NAME OF RECORD OWNER | % Ownership |

| David R. Adler | 61% |

A beneficial owner of 25% or more of the Fund’s outstanding shares may be considered a controlling person. That shareholder’s vote could have a more significant effect on matters presented at a shareholders’ meeting.

5. Derivative Transactions

The location on the Statement of Assets and Liabilities of the derivative positions of the Fund are as follows:

| Average | ||||||||||||||||

| Fair Value | Monthly | |||||||||||||||

| Notional Value | ||||||||||||||||

| During the | ||||||||||||||||

| Type of | Asset | Liability | Year Ended | |||||||||||||

| Derivative | Risk | Location | Derivatives | Derivatives | May 31, 2022* | |||||||||||

| Equity call options purchased | Equity | Investments in securities at value | $ | 213,561 | $ | — | $ | 1,463,544 | ||||||||

| * | The average monthly notional value generally represents the Fund’s derivative activity throughout the year. |

19

| ADLER VALUE FUND |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

Realized and unrealized gains and losses associated with transactions in derivative instruments for the Fund during the year ended May 31, 2022 are recorded in the following locations on the Statement of Operations:

| Change in | ||||||||||||||

| Unrealized | ||||||||||||||

| Type of | Realized | Appreciation | ||||||||||||

| Derivative | Risk | Location | Losses | Location | (Depreciation) | |||||||||

| Equity call options purchased | Equity | Net realized gains on investment transactions | $ | (94,154 | ) | Net change in unrealized appreciation (depreciation) on investments | $ | 10,195 | ||||||

6. Contingencies and Commitments

The Fund indemnifies the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations, warranties, and general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

7. Subsequent Events

The Fund is required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statement of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events.

20

| ADLER VALUE FUND |

| REPORT OF INDEPENDENT REGISTERED |

| PUBLIC ACCOUNTING FIRM |

To the Board of Trustees of Ultimus Managers Trust

and the Shareholders of Adler Value Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Adler Value Fund, a series of shares of beneficial interest in Ultimus Managers Trust (the “Fund”), including the schedule of investments, as of May 31, 2022, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights as noted in the table below , and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of May 31, 2022, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and its financial highlights as presented in the table below, in conformity with accounting principles generally accepted in the United States of America.

| Fund | Financial Highlights Presented |

| Adler Value Fund | The financial highlights for each of the years in the two-year period May 31, 2022, the period from August 1, 2019 through May 31, 2020, and the period from August 16, 2018 (commencement of operations) to July 31, 2019 |

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities law and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risk of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the

21

| ADLER VALUE FUND |

| REPORT OF INDEPENDENT REGISTERED |

| PUBLIC ACCOUNTING FIRM (Continued) |

amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of May 31, 2022 by correspondence with the custodian and broker. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

BBD, LLP

We have served as the auditor of one or more of the Funds in the Ultimus Managers Trust since 2013.

Philadelphia, Pennsylvania

July 20, 2022

22

| ADLER VALUE FUND |

| ABOUT YOUR FUND’S EXPENSES (Unaudited) |

We believe it is important for you to understand the impact of costs on your investment. As a shareholder of the Fund, you incur ongoing costs, including management fees and other operating expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The expenses in the table below are based on an investment of $1,000 made at the beginning of the most recent period December 1, 2021) and held until the end of the period (May 31, 2022).

The table below illustrates the Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the fourth column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare the Fund’s ongoing costs with those of other mutual funds. It assumes that the Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Fund’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the SEC requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Fund does not charge sales loads.

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

23

| ADLER VALUE FUND |

| ABOUT YOUR FUND’S EXPENSES (Unaudited) (Continued) |

More information about the Fund’s expenses can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Fund’s prospectus.

| Beginning | Ending | |||

| Account Value | Account Value | Expenses | ||

| December 1, | May 31, | Net Expense | Paid During | |

| Institutional Class | 2021 | 2022 | Ratio(a) | Period(b) |

| Based on Actual Fund Return | $1,000.00 | $1,013.80 | 1.25% | $6.28 |

| Based on Hypothetical 5% Return (before expenses) | $1,000.00 | $1,018.70 | 1.25% | $6.29 |

| (a) | Annualized, based on the Fund’s most recent one-half year expenses. |

| (b) | Expenses are equal to the Fund’s annualized net expense ratio multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). |

24

| ADLER VALUE FUND |

| OTHER INFORMATION (Unaudited) |

A description of the policies and procedures that the Fund uses to vote proxies relating to portfolio securities is available without charge upon request by calling 1-800-408-4682, or on the SEC’s website at www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, 2022 is also available without charge upon request by calling 1-800-408-4682, or on the SEC’s website at www.sec.gov.

The Trust files a complete listing of portfolio holdings for the Fund with the SEC as of the end of the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. These filings are available upon request by calling 1-800-408-4682. Furthermore, you may obtain a copy of the filings on the SEC’s website at www.sec.gov and the Fund’s website at www.adlervaluefund.com.

25

| ADLER VALUE FUND |

| BOARD OF TRUSTEES AND EXECUTIVE OFFICERS |

| (Unaudited) |

The Board has overall responsibility for management of the Trust’s affairs. The Trustees serve during the lifetime of the Trust and until its termination, or until death, resignation, retirement, or removal. The Trustees, in turn, elect the officers of the Fund to actively supervise their day-to-day operations. The officers have been elected for an annual term. Each Trustee’s and officer’s address is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246. The following are the Trustees and executive officers of the Fund:

| Name and Year of Birth | Length of Time Served | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years | Number in Trust | Directorships of Public Companies Held by Trustee During Past 5 Years |

| Interested Trustees: | |||||

| David R. Carson* Year of Birth: 1958 | Trustee Since 2021

Officer Since 2013 | Trustee (2021 to present)

Vice President (2021 to present; and previously April 2013 to October 2013)

President and Principal Executive Officer of each of its series (2013 to 2021) | Vice President and Director of Client Strategies of Ultimus Fund Solutions, LLC (2013 to present); President of Unified Series Trust (2017 to present). | 26 | Interested Trustee of 21 series of the Unified Series Trust (a registered management company) (2020 to present). |

| Independent Trustees: | |||||

| Janine L. Cohen Year of Birth: 1952 | Since 2016 | Chairperson (2019 to present)

Trustee (2016 to present) | Retired since 2013; previously Chief Financial Officer from 2004 to 2013 and Chief Compliance Officer from 2008 to 2013 at AER Advisors, Inc. | 26 | none |

26

| ADLER VALUE FUND |

| BOARD OF TRUSTEES AND EXECUTIVE OFFICERS |

| (Unaudited) (Continued) |

| Name and Year of Birth | Length of Time Served | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years | Number of Funds in Trust Overseen by Trustee | Directorships of Public Companies Held by Trustee During Past 5 Years |

| Independent Trustees (Continued): | |||||

| David M. Deptula Year of Birth: 1958 | Since 2012 | Trustee | Vice President of Legal and Special Projects at Dayton Freight Lines, Inc. since February 2016 | 26 | none |

| Jacqueline A. Williams Year of Birth: 1954 | Since 2019 | Trustee | Managing Member of Custom Strategy Consulting, LLC (2017 to present); Managing Director of Global Investment Research (2005 to 2017), Cambridge Associates, LLC. | 26 | none |

| Clifford N. Schireson Year of Birth: 1953 | Since 2019 | Trustee | Retired; Founder of Schireson Consulting, LLC (2017 to present); Director of Institutional Services for Brandes Investment Partners, LP (2004-2017). | 26 | Trustee of the San Diego City Employees’ Retirement System (2019 to present). |

| Robert E. Morrison Year of Birth: 1957 | Since 2019 | Trustee | Managing Director, Midwest Trust and FCI Advisors (2022 to present); Senior Vice President and National Practice Lead for Investment, Huntington National Bank/ Huntington Private Bank (2014 to 2022); CEO, CIO, President of 5 Star Investment Management Company (2006 to 2014). | 26 | none |

| * | Mr. Carson is considered an “interested person” of the Trust within the meaning of Section 2(a)(19) of the 1940 Act because of his relationship with the Trust’s administrator, transfer agent, and distributor. Mr. Carson was President of the Trust from October 2013 to January 2021 and Vice President of the Trust from April 2013 to October 2013. |

27

| ADLER VALUE FUND |

| BOARD OF TRUSTEES AND EXECUTIVE OFFICERS |

| (Unaudited) (Continued) |

| Name and Year of Birth | Length of Time Served | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years |

| Executive Officers: | |||

| Todd E. Heim Year of Birth: 1967 | Since 2014 | President (2021 to present)

Vice President (2014 to 2021) | Vice President, Relationship Management (2018 to present) and Assistant Vice President, Client Implementation Manager of Ultimus Fund Solutions, LLC (2014 to 2018); Naval Flight Officer in United States Navy (1989 to 2017). |

| Jennifer L. Leamer Year of Birth: 1976 | Since 2014 | Treasurer (2014 to present)

Assistant Treasurer (April 2014 to October 2014) | Senior Vice President, Fund Accounting of Ultimus Fund Solutions, LLC (2014 to present). |

| Daniel D. Bauer Year of Birth: 1977 | Since 2016 | Assistant Treasurer (2016 to present) | Vice President, Fund Accounting (2022 to present) and Assistant Vice President, Fund Accounting of Ultimus Fund Solutions, LLC (2015 to 2022). |

| Angela A. Simmons Year of Birth: 1975 | Since 2022 | Assistant Treasurer (2022 to present) | Vice President, Financial Administration (2022 to present) and Assistant Vice President, Financial Administration (2015 to 2022) of Ultimus Fund Solutions, LLC. |

| Khimmara Greer Year of Birth: 1983 | Since 2021 | Secretary (2021 to present) | Vice President and Senior Legal Counsel of Ultimus Fund Solutions, LLC (2021 to present); Vice President, Asset Servicing – Regulatory Administration of The Bank of New York Mellon (2019 to 2021); Vice President and Counsel of State Street Bank and Trust Company (2015 to 2019). |

| David K. James Year of Birth: 1970 | Since 2021 | Assistant Secretary (2021 to present)

Secretary (2021 to 2021) | Executive Vice President and Chief Legal and Risk Officer of Ultimus Fund Solutions, LLC (2018 to present); Managing Director and Managing Counsel of State Street Bank and Trust Company (2009 to 2018). |

| Natalie S. Anderson Year of Birth: 1975 | Since 2016 | Assistant Secretary (2016 to present) | Legal Administration Manager (July 2016 to present) and Paralegal (January 2015 to June 2016) of Ultimus Fund Solutions, LLC. |

28

| ADLER VALUE FUND |

| BOARD OF TRUSTEES AND EXECUTIVE OFFICERS |

| (Unaudited) (Continued) |

| Name and Year of Birth | Length of Time | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years |

| Executive Officers (Continued): | |||

| Gweneth Gosselink Year of Birth: 1955 | Since 2020 | Chief Compliance Officer (2020 to present) | Assistant Vice President, Senior Compliance Officer of Ultimus Fund Solutions, LLC (December 2019 to present); CCO Consultant at GKG Consulting, LLC (December 2019 to present); Chief Operating Officer & CCO at Miles Capital, Inc. (June 2013 to December 2019). |

| Martin Dean Year of Birth: 1963 | Since 2019 | Assistant Chief Compliance Officer (2020 to present)

Interim Chief Compliance Officer (October 2019 to January 2020)

Assistant Chief Compliance Officer (2016 to 2017) | Senior Vice President, Head of Fund Compliance (February 2020 to present); Vice President & Director of Fund Compliance of Ultimus Fund Solutions, LLC (January 2016 to January 2020). |

Additional information about members of the Board and executive officers is available in the Fund’s Statement of Additional Information (“SAI”). To obtain a free copy of the SAI, please call toll free 1-800-408-4682.

29

| ADLER VALUE FUND |

| DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT |

| (Unaudited) |

The Board of Trustees (the “Board”), including the Independent Trustees voting separately, has reviewed and approved the continuance of the Fund’s Investment Advisory Agreement with Adler Asset Management, LLC (the “Adviser” or “Adler”) for an additional one-year term (the “Advisory Agreement”). The Board approved the continuance of the Advisory Agreement at a meeting held on January 18 and 19, 2022, at which all of the Trustees were present.

In deciding on whether to approve the continuation of the Advisory Agreement, the Board recalled its review of the materials related to the Fund and Adler at the meeting and throughout the preceding twelve months and its numerous discussions with Trust Management and Adler about the operations and performance of the Fund during that period. The Board further considered those materials and discussions and other numerous factors, including the following:

The nature, extent, and quality of the services provided by the Adviser. In this regard, the Board reviewed the services being provided by Adler to the Fund including, without limitation, its providing a continuous investment program for the Fund, adhering to the Fund’s investment restrictions, complying with the Trust’s policies and procedures and voting proxies on behalf of the Fund. The Board considered the qualifications and experience of Adler’s portfolio manager who is responsible for the day-to day management of the Fund’s portfolio. The Board concluded that the quality, extent, and nature of the services provided by Adler to the Fund were satisfactory.

The investment performance of the Fund. In this regard, the Board compared the performance of the Fund with the performance of its benchmark index, the custom peer group and Morningstar category. The Board concluded that the investment performance of the Fund has been satisfactory.

The costs of the services provided and profits realized by the Adviser and its affiliates from its relationship with the Fund. In this regard, the Board considered the Fund’s management fee proposed to be charged to the Fund and the Fund’s expense ratio, each as compared to the Fund’s peer group. The Board considered the revenue earned from the Fund and the current and anticipated profitability of the Fund to Adler, if any. The Board also considered Adler’s past fee reductions and expense reimbursements for the Fund and the indirect benefits that Adler received from its management of the Fund. The Board concluded that the advisory fee to be paid to Adler by the Fund is reasonable in light of the nature and quality of services provided by Adler.

The extent to which economies of scale would be realized as the Fund grows and whether advisory fee levels reflect these economies of scale for the benefit of the Fund’s investors. In this regard, the Board considered that the Fund’s fee arrangements with Adler involve both the advisory fee and an expense limitation agreement (the “ELA”). The Board determined that while the advisory fee rate remained the same as asset levels increased, the shareholders of the Fund

30

| ADLER VALUE FUND |

| DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT |

| (Unaudited) (Continued) |

have experienced benefits from the ELA and will continue to experience benefits from the ELA. The Board concluded that the advisory fee was reasonable in light of the information that was provided to the Trustees by Adler with respect to economies of scale.

After further discussion of the factors noted above and in reliance on the information provided by Adler and Trust Management, and taking into account the totality of all the factors discussed and information presented at the meeting and previous meetings, the Board indicated its agreement to approve the continuance of the Advisory Agreement. It was noted that in the Trustees’ deliberations regarding the approval of renewal the Advisory Agreement, the Trustees did not identify any particular information or factor that was all-important or controlling, and that each individual Trustee may have attributed different weights to the various factors listed above. After full consideration of the above factors as well as other factors, the Board unanimously concluded that approval of the continuance of the Advisory Agreement was in the best interests of the Fund and its shareholders.

31

This page intentionally left blank.

ADLER-AR-22

EVOLUTIONARY TREE INNOVATORS FUND

I Class Shares (INVNX)

A Class Shares (INVTX)

Annual Report

May 31, 2022

| EVOLUTIONARY TREE INNOVATORS FUND | |

| LETTER TO SHAREHOLDERS (Unaudited) | JUNE 17, 2022 |

Dear Fellow Shareholders,

We know it has been a volatile period in the markets during the first two quarters of 2022 and over the past year, particularly for growth and innovation-focused strategies. Given this environment, we felt it was important to provide our perspective on the drivers of this volatility and share why we have confidence in the portfolio and investing in quality innovative businesses.

For newer investors to the Evolutionary Tree Innovators Fund, we provide below a brief overview of our investment approach and why we focus on long-term drivers such as innovation versus trying to predict or side-step movements in the market or economy. For investors that are more familiar with our innovation-focused strategy, please jump to the sections on our perspective on the current environment and why we believe the underlying companies owned in the Fund are well positioned, as a group, to drive sustainable growth.

How Our Approach Enables Investors to Access Leading and Quality Innovative Businesses

The Evolutionary Tree Innovators Fund was launched to provide an attractive pathway for investing in important innovations and secular trends, or evolutionary shifts as we call them. The Fund and its adviser apply an innovation and evolution-focused framework to investing. We believe the development of innovation and its resultant pattern of evolutionary change is the primary engine of growth for companies, industries, and the economy—and, in turn, is the underlying driver of long-term wealth creation. While investors are currently focused on near-term macro drivers, such as the Fed, inflation, and the war in Ukraine, we believe innovation can still drive growth for leading innovators and remains critically important for long-term investors.

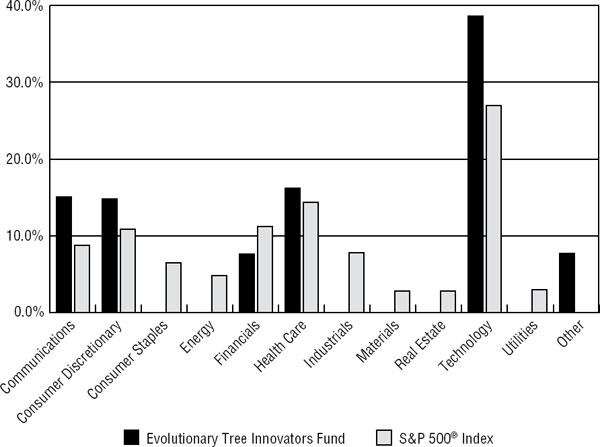

The Fund seeks to identify important innovations that are driving secular growth and evolutionary shifts for companies, industries, and the economy, and own the leading innovators at the forefront. The Fund defines an evolutionary shift as when an industry shifts from an old generation (of a product, service, or business model) over to a “next generation” or new offering that provides advantages versus the “old way” of doing things. The Fund invests in a focused portfolio of 25-35 quality innovative businesses.

Examples of innovations that we believe contribute to sustainable growth include technological innovation, product innovation, service or experience innovation, process or cost innovation, and/or business model innovation. In addition to contributing to sustaining growth for leading innovative businesses, new innovations may also enable innovators to take market share, create competitive advantage, and/or enhance profitability over time. Innovation is the root cause of value creation.

Perspective on Drivers of the Current Difficult Economic and Geopolitical Environment The current environment is highly unusual in that we have faced a succession of three different headwinds, which have created multiple storms affecting the markets and Fund performance. The first headwind was the Federal Reserve (“the Fed”) communicating a

1

tightening cycle of raising rates in November of 2021 in response to higher inflation. We certainly acknowledge the heightened inflation coming out of COVID as the economy has reopened and supply has not kept up with greater demand across sectors. However, a key driver of inflation is the labor shortage, and it is important to note that technology is a key solution to this issue, as it can raise worker productivity. Many of the companies in our portfolio, especially our enterprise software companies, are providing solutions to this issue and seeing strong demand as a result. A significant portion of the portfolio represents companies offering technology to improve labor productivity. We also believe that the Fed’s rate increases, which will slow the economy, coupled with supply chain improvement, will gradually ease inflation over time. Signs of that happening may stabilize the markets, though this may take some time.

The second headwind is that many digital companies that saw accelerated growth during COVID are now experiencing “tougher comparisons” with last year’s elevated results, leading to temporary deceleration in growth. We believe this is a short-term phenomenon and will ease as we move through the year, as comparisons get much easier in the second half of 2022.

Lastly, the third headwind was Putin’s War in Ukraine, which led to another leg down in the markets with substantial risk-off behavior by investors as they processed the risk of a possible wider war in Europe and even threats of nuclear war. These fears led to indiscriminate selling across the equity markets. We believe as the war likely stays limited to Ukraine, investors will lessen their focus on this headwind and re-focus on fundamentals. It is important to note that the portfolio’s exposure to Russia/Ukraine is quite low, with the typical company deriving 0-3% of revenues from these two countries. The bottom line is that this risk-off dynamic in the markets has driven valuations to attractive levels, in our opinion. Lastly, given our focus on companies with strong financial positions, their growth can typically be internally funded through their existing cash balance and free cash flow generation.

Despite these three headwinds, the underlying businesses are demonstrating solid business fundamentals, with 30-35% revenue growth and generally stable-to-improving operating margins, on a weighted-average basis over the past quarter and calendar year for the portfolio. With the pullback in prices relative to continued growth for portfolio companies, there is a growing disconnect between the underlying business results and the valuations of portfolio companies. While the timing is unknown, we believe strong business results will eventually be rewarded by the market.

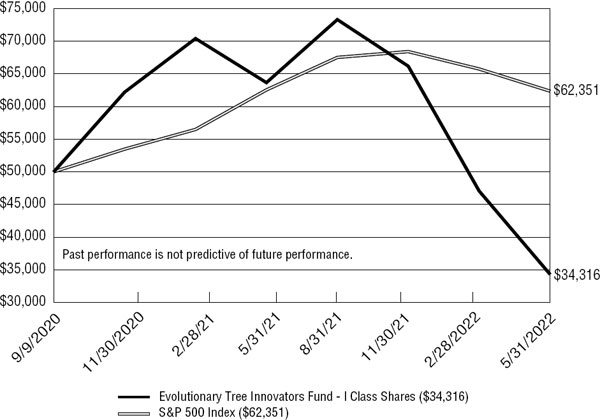

Perspective on the Bear Market and Fund Performance

We are witnessing growth, technology, and innovation stocks experiencing a deep bear market (with Class I experiencing a decline of 46.09% for the fiscal year ended 5/31/22 versus the broader S&P 500 Index return of -0.30%). While the broader indexes are now down around 15-25% year to date through the end of May, there is much greater and broader pain below the surface, revealing a severe bear market for the average growth stock. In fact, through May 31st about 50% of the Russell 1000 Growth constituents (of 498 stocks in the index) are down 30% or more from 52-week highs, 41% are down 35% or more, and 34% are down 40% or more. What is insulating the broader indexes is a

2

handful of megacap companies that now comprise 25-40% of the benchmarks, and these stocks have generally held up better than the average stock, though even these companies (so-called FAANG stocks) are now under pressure. We were not immune to this backdrop.

The Fund also generally owns faster-growing companies and has flexibility to own mid-caps and even small-caps, which positions it further down the industry S-curve, a goal of the Fund to access innovators earlier in their lifecycle. However, in the current market environment, where investors are shunning fast-growing companies and ones that are earlier in their profit cycle, the Fund has been negatively impacted performance-wise. We believe as investors eventually look beyond macro headwinds, particularly if inflation starts to ease (which we acknowledge may take some time), investors may re-embrace faster-growing innovative companies, which may lead to improved performance over time. We believe we own a collection of high-quality innovative companies, ones that meet our stringent criteria that includes companies with competitive advantages, strong management teams, and robust balance sheets. We actively avoid “hype” and “concept stocks” and believe that the current market has “thrown babies out with the bathwater”.

Quality Innovators: Resilient Fundamentals in the Face of Inflation

In our view, there are two important, but distinct, effects on the portfolio resulting from rising inflation and interest rates: 1) the impact to the fundamentals of the underlying businesses, and 2) the impact on the valuations investors are willing to pay for future cash flows. We will touch briefly on each.

As it relates to business fundamentals, we believe our portfolio companies are, on average, relatively more insulated from inflationary pressure given our focus on owning leading innovators in attractive industries with competitive advantages, which for many holdings provides them with pricing power.

Essential products and services, ones that are mission critical, are least likely to be cut if budgets get squeezed, while non-essential products and services are often the most impacted. Asset-light digital offerings, like many of our Internet and software businesses, are also less impacted by rising commodity prices and input costs, which is not the case for traditional product or durable goods companies. Additionally, highly innovative companies with unique and valuable products usually have pricing power and can pass some or all of the rising costs on to customers. For example, both HubSpot and ServiceNow, software-as-a-service leaders in marketing automation and service engagement platforms, respectively, are successfully moving their client base to higher priced tiers as they add more features to their platforms. Lastly, companies where there are few substitutes or alternatives, such as life-saving biotech treatments, are more protected than companies in competitive markets where customers may shift to lower-cost alternatives.

The second impact referenced above is the effect on stock valuations investors are willing to pay for future cash flows. As rates rise, so does the discount rate in financial models, which can reduce valuations. Since the Fed started signaling the need to increase interest rates in November 2021, the 10-Year Treasury rate has moved from 1.4% to 3.3%. In response, many innovative growth stocks are now down 30% to 70%+ from their highs. We think this suggests future interest rate hikes may have largely already been discounted by the market, if not overshooting on the downside relative to their fundamentals.

3

Historically, growth stocks tend to underperform once the Fed signals the need to increase rates. However, growth stocks can perform reasonably well during the period of rising rates. This is a classic example of the market discounting the news before the rate hikes take place. In the current environment, we believe it’s likely that most of the pullback from rising rates may already be priced in by the market.

Technology: A Solution to the Labor Shortage Issue By Improving Productivity For Businesses

The recent pullback in technology stocks has led some investors to surmise that growth at these companies has slowed dramatically or that many have experienced significant business issues. Worried about the impact of inflation on the economy and tech stock valuations, many investors have sold growth and tech stocks. Although we certainly acknowledge rising inflation, spurred on by a combination of reopening economies, labor shortages, and supply chain issues, we view technology as a solution in this challenging environment.

The investment ramifications for technology stocks during the current labor crisis are potentially profound. Specific technology companies, including those in enterprise software, are seeing sustained demand as companies of all sizes use technology platforms and solutions to make up for fewer workers by relying on improving productivity of existing workers. This is the role of technology, a role that is more (not less) relevant as today’s global economy experiences a shortage of workers. Furthermore, as companies feel pressure on their margins from rising input costs, they will search for ways to gain greater efficiencies. We believe that technology is the solution to driving both worker productivity and cost efficiencies.

The 2020s are Not 1999: The Cloud Era Is Different Than The Dotcom Era

In the current market environment, what has become a true bear market for growth and technology stocks, there seems to be an assumption that this era, what we call the Cloud Era, is similar to the Dotcom Era. We share the following viewpoints:

| 1. | The Cloud Era is built on more solid ground than investor perceptions versus past eras. |

| 2. | The quality of current software businesses is actually quite healthy and on a strong path of profitability, a point that seems to be overlooked by many investors that assume a similar outcome as the dotcom bust. |

| 3. | Software valuations have potentially corrected to attractive levels. |