united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22718

Two Roads Shared Trust

(Exact name of registrant as specified in charter)

17605 Wright Street, Suite 102, Omaha, NE 68137

(Address of principal executive offices) (Zip code)

Richard Malinowski, Gemini Fund Services, LLC.

80 Arkay Drive Suite 110, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2600

Date of fiscal year end: 10/31

Date of reporting period: 10/31/18

ITEM 1. REPORTS TO SHAREHOLDERS.

|

| Anfield Universal Fixed Income Fund |

| Class A Shares (AFLEX) |

| Class C Shares (AFLKX) |

| Class I Shares (AFLIX) |

| October 31, 2018 |

| Annual Report |

| Advised by: |

| Anfield Capital Management |

| 4041 MacArthur Blvd. |

| Suite 155 |

| Newport Beach, CA 92660 |

| www.AnfieldFunds.com |

| Distributed by Northern Lights Distributors, LLC |

| Member FINRA |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Fund’s website www.AnfieldCapital.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by following the instructions included with paper Fund documents that have been mailed to you.

December 2018

Letter to Shareholders of the Anfield Universal Fixed Income Fund (AFLIX)

The Universal Fixed Income Fund completed its fifth fiscal year on October 31, 2018, and we are pleased to report that the Fund has achieved favorable performance in pursuing its investment objectives. We are proud to report that the Fund’s assets grew nicely - to approximately $232 million - at fiscal year-end, delivering competitive returns of 3.25%, 2.59% and 3.61% from A, C and I shares respectively, net of all fees and expenses, for the year ended October 31, 2018.

Fund performance was driven largely by mortgage-backed and asset-backed positions, as well as its investment grade and high yield corporate positions. These selections not only performed well, but also limited the Fund’s volatility to a low 1.33% for the year ended October 31, 2018.

The year was not without its challenges; the confluence of tighter credit at home and uncertain rate cycles abroad limited options for exposure to sovereign fixed income, including U.S. Treasuries. However, we converted uncertainty into opportunity by targeting duration between 1 to 3 years - a lucrative tactic, it turned out, given the sequential interest rate hike that will no doubt make 2018 memorable. Overall, we believe the Fund remains well positioned for the economic and market environment we see going forward, with a blend of conservative, defensive positions and carefully selected exposures designed to capitalize on a range of yield and price enhancement.

Finally - and in the spirit of teamwork that defines our work here at Anfield Capital Management - I would like to thank the entire dedicated staff without whom the head line portfolio management team of Cyrille Conseil, CFA; Peter Van de Zilver, CFA; and David Young, CFA, could not succeed with such consistency.

Economic and Financial Market Commentary

| ● | Stocks took a beating in October as the Dow Jones, S&P, and Nasdaq indices shed 6%, 7% and 9% for the month, respectively. Of the 500 stocks in the S&P 500, nearly 400 saw declines. |

| ● | US Treasury yields tumbled in late October due to a decline in inflation expectations—despite a 25% surge in oil prices—and a quest for safe havens amid plunging stock prices. |

| ● | FactSet Research reported that, with 48% of the companies in the S&P 500 reporting results for the third quarter (as of the end of October 2018), 77% of companies have reported a positive EPS surprise. The blended earnings growth rate for the S&P 500 was on track for 22.5% average growth for the quarter, which would mark the third highest earnings growth since Q3 2010. |

| ● | The burden of servicing the US budget nearly doubled in October, to $779 Billion, an all-time high. The increase, attributed largely to tax cuts and defense outlays, was on track to reach $895 billion in November—$222 billion or 39% more than the previous year. Meanwhile, the US federal debt increased by $1.80 trillion in fiscal year 2018, according to data released by the Treasury Department. |

| ● | Despite growing fears about the debt problem, the US economy expanded at a 3.5% pace in the third quarter thanks to consumer spending, restocking of businesses inventories and governments expenditures, marking the strongest back-to-back quarters of growth since 2014, according to the Commerce Department. |

| ● | The IMF issued its report on global growth downgrades led by China, which is expected to slow by 20bps to 6.2%. Emerging market and developing economies’ growth was downgraded 20bps and 40bps in 2018 and 2019, respectively, as the report warned that growth in major economies has peaked. |

| ● | Growth in the Eurozone, meanwhile, fell to its slowest pace in more than four years, according to Bloomberg. Following a rally sparked after Moody’s cut Italian debt ratings less than the markets feared (one notch above junk—Baa3), the euro weakened on the news that German business activity slowed to its lowest rate in nearly four years as France’s manufacturing PMI index hit a 25-month low. |

| ● | The Bank of Japan held interest rates at -0.1% while trimming its inflation forecasts. It also vowed to purchase 10-year Japanese government bonds to maintain the yield at “around zero percent.” In doing so, Tokyo will drift further behind the rest of the developed world in policy normalizing in its battle to stoke inflation in line with its 2% target. |

1

Current Fixed Income Investment Strategy

| ● | Maintain a defensive position relative to interest rates, as we expect rates to continue to normalize from their low levels. |

| ● | Emphasize high quality yield enhancing corporate credit / MBS / ABS fixed income allocations |

| ● | Remain vigilant as asset markets reach new highs. Explore deeper in the credit stack on a selective basis targeting single ‘B’ names, BB rated CLO tranches, and non-agency MBS |

| ● | Our investment strategy is summarized below: |

| Directional (top-down macro) | Defensive, positioned for higher rates; target duration between 1 to 3 years |

| Yield Curve | 1 – 5 years (short-intermediate) mainly driven by directional, duration, sector, and yield views |

| Sector | Emphasize all grade yield enhancing corporate credits with strong cash positions and improving fundamentals & MBS and ABS allocations |

| Security Selection | Active and selective |

| Liquidity | Continue to focus on strong liquidity—which tends to be undervalued in uncertain markets |

| Volatility | Target between 1% and 2% annualized standard deviation (risk) |

On behalf of the entire staff at Anfield Capital Management, we thank you for your continued support, trust and confidence.

David Young, CFA

CEO & Founder

The views in this report are those of the Fund’s management. This report contains certain forward-looking statements about factors that may affect the performance of the Fund in the future. These statements are based on the Fund’s management’s predictions and expectations concerning certain future events such as the performance of the economy as a whole and of specific industry sectors. Management believes these forward-looking statements are reasonable, although they are inherently uncertain and difficult to predict.

8603-NLD-12/27/2018

2

| Anfield Universal Fixed Income Fund |

| PORTFOLIO REVIEW (Unaudited) |

| October 31, 2018 |

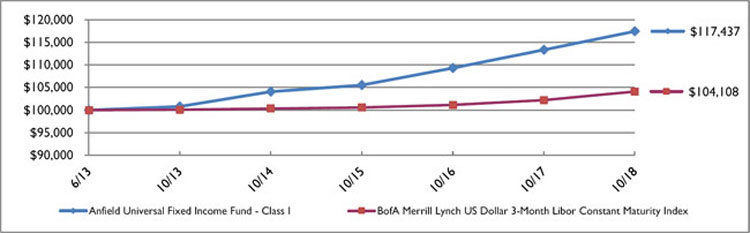

The Fund’s performance figures* for the periods ended October 31, 2018, compared to its benchmark:

| Since | |||

| 1 Year | 5 Year | Inception(a) | |

| Class A | 3.25% | 2.84% | 2.81% |

| Class A with 5.75% load | (2.66)% | 1.64% | 1.67% |

| Class C | 2.59% | 2.00% | 2.03% |

| Class I | 3.61% | 3.10% | 3.05% |

| BofA Merrill Lynch US Dollar 3-Month Libor Constant Maturity Index(b) | 1.85% | 0.79% | 0.76% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. The Advisor has contractually agreed to waive fees and/or reimburse expenses to the Fund until at least March 1, 2019 but only to the extent necessary to maintain the Fund’s total annual operating expenses (excluding any front-end or contingent deferred loads; brokerage fees and commissions, acquired fund fees and expenses; borrowing costs (such as interest and dividend expense on securities sold short); taxes; and extraordinary expenses, such as litigation expenses) at 1.50%, 2.25%, and 1.25% for Class A, Class C, and Class I shares, respectively, per the most recent prospectus dated February 28, 2018. Without waiver or reimbursement the gross expenses and fees are 1.54%, 2.29% and 1.29% for Class A, Class C, and Class I shares, respectively, per the most recent prospectus dated February 28, 2018. These fee waivers and expense reimbursements by the Advisor are subject to possible recoupment from the Fund in future years on a rolling three year basis (within the three years after the fees have been waived or expenses reimbursed) if such recoupment can be achieved within the foregoing expense limits. The expense limits in effect prior to their expiration on March 1, 2018 were 1.20%, 1.95% and 0.95% for Class A, Class C and Class I shares. Please review the Fund’s most recent prospectus dated February 28, 2018 for more detail on the expense waiver. For performance information current to the most recent month-end, please call toll-free 1-866-866-4848. |

| (a) | Anfield Universal Fixed Income Fund commenced investment operations on June 28, 2013. |

| (b) | The BofA Merrill Lynch US Dollar 3-Month LIBOR Constant Maturity Index is designed to track the performance of a synthetic asset paying LIBOR to a stated maturity. The index is based on the assumed purchase at par of a synthetic instrument having exactly its stated maturity and with a coupon equal to that day’s fixing rate. That issue is assumed to be sold the following business day (priced at a yield equal to the current day fixing rate) and rolled into a new instrument. |

Comparison of the Change in Value of a $100,000 Investment *

| * | Performance shown is for class I shares. The performance of the Fund’s other classes may be greater or less than the line shown due to differences in loads and fees paid by shareholders in different share classes. |

| Top Allocations | % of Net Assets | |||

| Bonds & Notes | 94.0 | % | ||

| Mutual Funds | 3.3 | % | ||

| Preferred Stocks | 0.6 | % | ||

| Exchange Traded Fund | 0.2 | % | ||

| Closed End Fund | 0.1 | % | ||

| Other Assets Less Liabilities * | 1.8 | % | ||

| 100.0 | % | |||

| * Derivatives are included in other assets less liabilities. | ||||

Please refer to the Schedule of Investments in this annual report for a detailed analysis of the Fund’s holdings.

3

| Anfield Universal Fixed Income Fund |

| SCHEDULE OF INVESTMENTS |

| October 31, 2018 |

| Shares | Fair Value | |||||||||||||||

| CLOSED END FUND - 0.1% | ||||||||||||||||

| DEBT FUND - 0.1% | ||||||||||||||||

| 13,898 | BlackRock Floating Rate Income Strategies Fund, Inc. | $ | 180,257 | |||||||||||||

| TOTAL CLOSED END FUND (Cost $202,950) | 180,257 | |||||||||||||||

| EXCHANGE TRADED FUND - 0.2% | ||||||||||||||||

| DEBT FUND - 0.2% | ||||||||||||||||

| 16,900 | Invesco Senior Loan ETF | 388,869 | ||||||||||||||

| TOTAL EXCHANGE TRADED FUND (Cost $419,079) | 388,869 | |||||||||||||||

| MUTUAL FUNDS - 3.3% | ||||||||||||||||

| DEBT FUNDS - 3.3% | ||||||||||||||||

| 203,556 | Fidelity Floating Rate High Income Fund - Institutional Class | 1,954,133 | ||||||||||||||

| 549,222 | Vanguard Short-Term Investment Grade Fund - Institutional Class | 5,717,403 | ||||||||||||||

| TOTAL MUTUAL FUNDS (Cost $7,819,386) | 7,671,536 | |||||||||||||||

| Par Value | Coupon Rate (%) | Maturity | Spread | Rate | ||||||||||||

| BONDS & NOTES - 94.0% | ||||||||||||||||

| AGENCY COLLATERAL CMO - 14.8% | ||||||||||||||||

| $ | 1,755,402 | Fannie Mae Interest Strip * | 2.5000 | 2/25/2028 | 125,299 | |||||||||||

| 825,476 | Fannie Mae Interest Strip * | 3.5000 | 11/25/2041 | 163,666 | ||||||||||||

| 552,348 | Fannie Mae Interest Strip *# | 4.0000 | 11/25/2041 | 114,285 | ||||||||||||

| 1,109,789 | Fannie Mae Interest Strip *# | 4.5000 | 11/25/2040 | 281,147 | ||||||||||||

| 922,947 | Fannie Mae Interest Strip *# | 4.5000 | 7/25/2042 | 275,328 | ||||||||||||

| 529,624 | Fannie Mae Interest Strip *# | 4.5000 | 7/25/2042 | 134,954 | ||||||||||||

| 1,085,374 | Fannie Mae Interest Strip * | 5.5000 | 5/25/2033 | 210,189 | ||||||||||||

| 719,432 | Fannie Mae Interest Strip * | 5.5000 | 8/25/2035 | 151,092 | ||||||||||||

| 442,824 | Fannie Mae Interest Strip * | 5.5000 | 4/25/2036 | 84,721 | ||||||||||||

| 672,195 | Fannie Mae Interest Strip * | 5.5000 | 6/25/2037 | 137,087 | ||||||||||||

| 1,008,994 | Fannie Mae Interest Strip * | 5.5000 | 1/25/2038 | 273,661 | ||||||||||||

| 548,115 | Fannie Mae Interest Strip * | 7.0000 | 2/25/2037 | 136,191 | ||||||||||||

| 428,710 | Fannie Mae Interest Strip *# | 7.0000 | 8/25/2038 | 105,071 | ||||||||||||

| 23,911,462 | Fannie Mae REMICS *~ | 0.0300 | 6/25/2045 | Monthly US LIBOR | +6.20% | 44,172 | ||||||||||

| 435,353 | Fannie Mae REMICS * | 3.0000 | 8/25/2030 | 31,796 | ||||||||||||

| 3,795,867 | Fannie Mae REMICS * | 3.5000 | 5/25/2044 | 549,831 | ||||||||||||

| 6,037,234 | Fannie Mae REMICS * | 3.5000 | 12/25/2044 | 1,001,719 | ||||||||||||

| 7,354,259 | Fannie Mae REMICS * | 3.5000 | 11/25/2045 | 1,328,650 | ||||||||||||

| 4,062,835 | Fannie Mae REMICS * | 3.5000 | 2/25/2046 | 743,126 | ||||||||||||

| 935,338 | Fannie Mae REMICS * | 3.5000 | 10/25/2047 | 190,047 | ||||||||||||

| 3,805,441 | Fannie Mae REMICS * | 3.5000 | 12/25/2047 | 759,713 | ||||||||||||

| 1,733,943 | Fannie Mae REMICS * | 3.5000 | 12/25/2047 | 326,960 | ||||||||||||

| 3,487,176 | Fannie Mae REMICS * | 3.5000 | 1/25/2048 | 645,894 | ||||||||||||

| 473,894 | Fannie Mae REMICS *~ | 3.8686 | 4/25/2045 | Monthly US LIBOR | +6.15% | 76,518 | ||||||||||

| 5,555,430 | Fannie Mae REMICS *~ | 4.0000 | 4/25/2041 | 740,312 | ||||||||||||

| 2,332,934 | Fannie Mae REMICS * | 4.0000 | 10/25/2041 | 313,952 | ||||||||||||

| 4,127,097 | Fannie Mae REMICS * | 4.0000 | 5/25/2044 | 618,282 | ||||||||||||

| 4,966,776 | Fannie Mae REMICS * | 4.0000 | 5/25/2047 | 874,796 | ||||||||||||

| 3,324,390 | Fannie Mae REMICS * | 4.0000 | 10/25/2047 | 642,506 | ||||||||||||

| 6,540,131 | Fannie Mae REMICS * | 4.0000 | 3/25/2048 | 1,639,364 | ||||||||||||

| 2,449,113 | Fannie Mae REMICS * | 4.0000 | 5/25/2048 | 518,114 | ||||||||||||

| 2,454,940 | Fannie Mae REMICS * | 4.0000 | 5/25/2048 | 531,385 | ||||||||||||

| 454,430 | Fannie Mae REMICS *~ | 4.1686 | 12/25/2037 | Monthly US LIBOR | +6.45% | 53,520 | ||||||||||

| 1,911,806 | Fannie Mae REMICS *~ | 4.2386 | 9/25/2037 | Monthly US LIBOR | +6.52% | 257,757 | ||||||||||

See accompanying notes to financial statements.

4

| Anfield Universal Fixed Income Fund |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2018 |

| Par Value | Coupon Rate (%) | Maturity | Spread | Rate | Fair Value | |||||||||||

| BONDS & NOTES - 94.0% (Continued) | ||||||||||||||||

| AGENCY COLLATERAL CMO - 14.8% (Continued) | ||||||||||||||||

| $ | 2,048,751 | Fannie Mae REMICS *~ | 4.2686 | 6/25/2038 | Monthly US LIBOR | +6.55% | $ | 110,641 | ||||||||

| 1,345,392 | Fannie Mae REMICS *~ | 4.3486 | 11/25/2036 | Monthly US LIBOR | +6.63% | 193,390 | ||||||||||

| 771,363 | Fannie Mae REMICS *~ | 4.3686 | 3/25/2036 | Monthly US LIBOR | +6.65% | 80,183 | ||||||||||

| 707,734 | Fannie Mae REMICS *~ | 4.3686 | 12/25/2036 | Monthly US LIBOR | +6.65% | 101,349 | ||||||||||

| 242,783 | Fannie Mae REMICS *~ | 4.4286 | 7/25/2035 | Monthly US LIBOR | +6.71% | 28,636 | ||||||||||

| 750,121 | Fannie Mae REMICS *~ | 4.4786 | 5/25/2037 | Monthly US LIBOR | +6.76% | 102,929 | ||||||||||

| 1,664,653 | Fannie Mae REMICS *~ | 4.4786 | 6/25/2037 | Monthly US LIBOR | +6.76% | 196,638 | ||||||||||

| 1,897,805 | Fannie Mae REMICS * | 4.5000 | 2/25/2043 | 375,349 | ||||||||||||

| 1,271,608 | Fannie Mae REMICS * | 4.5000 | 9/25/2043 | 219,950 | ||||||||||||

| 1,711,656 | Fannie Mae REMICS * | 4.5000 | 12/25/2047 | 406,052 | ||||||||||||

| 3,954,496 | Fannie Mae REMICS * | 4.5000 | 10/25/2048 | 868,516 | ||||||||||||

| 838,163 | Fannie Mae REMICS * | 6.0000 | 12/25/2039 | 170,808 | ||||||||||||

| 375,682 | Fannie Mae REMICS * | 6.0000 | 3/25/2040 | 84,613 | ||||||||||||

| 231,787 | Fannie Mae REMICS *~ | 7.5000 | 10/25/2023 | Monthly US LIBOR | +16.00% | 28,099 | ||||||||||

| 34,215,032 | Freddie Mac REMICS * | 0.2088 | 8/15/2044 | 364,180 | ||||||||||||

| 1,871,427 | Freddie Mac REMICS *~ | 1.1000 | 3/15/2034 | Monthly US LIBOR | +7.10% | 72,987 | ||||||||||

| 1,709,191 | Freddie Mac REMICS * | 3.0000 | 6/15/2041 | 225,096 | ||||||||||||

| 557,480 | Freddie Mac REMICS * | 3.5000 | 4/15/2033 | 60,532 | ||||||||||||

| 2,352,080 | Freddie Mac REMICS * | 3.5000 | 4/15/2038 | 220,270 | ||||||||||||

| 1,516,958 | Freddie Mac REMICS * | 3.5000 | 3/15/2043 | 201,179 | ||||||||||||

| 1,466,417 | Freddie Mac REMICS * | 3.5000 | 3/15/2043 | 224,972 | ||||||||||||

| 1,106,961 | Freddie Mac REMICS * | 3.5000 | 3/15/2043 | 166,593 | ||||||||||||

| 1,083,925 | Freddie Mac REMICS * | 3.5000 | 6/15/2043 | 146,140 | ||||||||||||

| 1,624,544 | Freddie Mac REMICS * | 3.5000 | 7/15/2043 | 239,247 | ||||||||||||

| 879,411 | Freddie Mac REMICS * | 3.5000 | 2/15/2044 | 147,752 | ||||||||||||

| 3,061,878 | Freddie Mac REMICS * | 3.5000 | 4/15/2044 | 486,940 | ||||||||||||

| 910,893 | Freddie Mac REMICS * | 3.5000 | 4/15/2046 | 156,740 | ||||||||||||

| 1,107,020 | Freddie Mac REMICS *~ | 3.8205 | 12/15/2044 | Monthly US LIBOR | +6.10% | 160,239 | ||||||||||

| 899,744 | Freddie Mac REMICS * | 4.0000 | 12/15/2041 | 128,648 | ||||||||||||

| 2,054,652 | Freddie Mac REMICS * | 4.0000 | 4/15/2043 | 446,257 | ||||||||||||

| 6,174,821 | Freddie Mac REMICS * | 4.0000 | 8/15/2043 | 904,869 | ||||||||||||

| 1,699,458 | Freddie Mac REMICS * | 4.0000 | 1/15/2044 | 255,952 | ||||||||||||

| 1,337,966 | Freddie Mac REMICS * | 4.0000 | 9/15/2044 | 163,706 | ||||||||||||

| 1,146,606 | Freddie Mac REMICS * | 4.0000 | 3/15/2045 | 249,893 | ||||||||||||

| 1,820,222 | Freddie Mac REMICS * | 4.0000 | 12/15/2046 | 337,026 | ||||||||||||

| 4,256,349 | Freddie Mac REMICS *~ | 4.2205 | 10/15/2041 | Monthly US LIBOR | +6.50% | 671,705 | ||||||||||

| 848,808 | Freddie Mac REMICS *~ | 4.4705 | 5/15/2029 | Monthly US LIBOR | +6.75% | 84,547 | ||||||||||

| 5,861,248 | Freddie Mac REMICS * | 4.5000 | 12/15/2044 | 989,045 | ||||||||||||

| 1,055,817 | Freddie Mac REMICS *~ | 4.7205 | 1/15/2032 | Monthly US LIBOR | +7.00% | 142,735 | ||||||||||

| 235,121 | Freddie Mac REMICS *~ | 4.9705 | 3/15/2032 | Monthly US LIBOR | +7.25% | 29,390 | ||||||||||

| 1,028,184 | Freddie Mac REMICS *~ | 5.4205 | 7/15/2034 | Monthly US LIBOR | +7.70% | 135,920 | ||||||||||

| 85,290 | Freddie Mac REMICS * | 5.5000 | 7/15/2040 | 70 | ||||||||||||

| 287,532 | Freddie Mac REMICS *~ | 5.6005 | 6/15/2031 | Monthly US LIBOR | +7.88% | 46,207 | ||||||||||

| 171,586 | Freddie Mac REMICS *~ | 6.5000 | 3/15/2032 | Monthly US LIBOR | 34,628 | |||||||||||

| 3,406 | Freddie Mac REMICS ~ | 9.4410 | 2/15/2019 | Monthly US LIBOR | +14.00% | 3,420 | ||||||||||

| 59,475 | Freddie Mac REMICS ~ | 15.0033 | 2/15/2032 | Monthly US LIBOR | +20.93% | 75,877 | ||||||||||

| 1,056,065 | Freddie Mac Strips *# | 4.3680 | 1/15/2043 | 262,480 | ||||||||||||

| 702,134 | Freddie Mac Strips *# | 4.4000 | 12/15/2039 | 153,245 | ||||||||||||

| 636,426 | Freddie Mac Strips *# | 4.5170 | 12/15/2040 | 150,355 | ||||||||||||

| 1,187,299 | Freddie Mac Strips * | 5.0000 | 6/15/2038 | 248,992 | ||||||||||||

| 300,905 | Freddie Mac Strips *~ | 5.4205 | 8/15/2036 | Monthly US LIBOR | +7.70% | 47,641 | ||||||||||

See accompanying notes to financial statements.

5

| Anfield Universal Fixed Income Fund |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2018 |

| Par Value | Coupon Rate (%) | Maturity | Spread | Rate | Fair Value | |||||||||||

| BONDS & NOTES - 94.0% (Continued) | ||||||||||||||||

| AGENCY COLLATERAL CMO - 14.8% (Continued) | ||||||||||||||||

| $ | 21,167,572 | Government National Mortgage Association *~ | 0.1500 | 9/16/2034 | Monthly US LIBOR | +6.70% | $ | 115,178 | ||||||||

| 3,200,195 | Government National Mortgage Association * | 3.0000 | 6/20/2041 | 401,407 | ||||||||||||

| 277,823 | Government National Mortgage Association * | 3.0000 | 7/20/2041 | 36,081 | ||||||||||||

| 5,142,307 | Government National Mortgage Association * | 3.0000 | 8/20/2041 | 535,548 | ||||||||||||

| 955,869 | Government National Mortgage Association * | 3.0000 | 7/20/2043 | 150,869 | ||||||||||||

| 1,516,500 | Government National Mortgage Association * | 3.5000 | 10/20/2039 | 214,338 | ||||||||||||

| 3,359,861 | Government National Mortgage Association * | 3.5000 | 8/20/2040 | 251,703 | ||||||||||||

| 1,540,830 | Government National Mortgage Association * | 3.5000 | 3/20/2044 | 236,140 | ||||||||||||

| 666,196 | Government National Mortgage Association * | 3.5000 | 4/20/2044 | 126,069 | ||||||||||||

| 2,253,363 | Government National Mortgage Association * | 3.5000 | 8/20/2044 | 286,267 | ||||||||||||

| 2,257,037 | Government National Mortgage Association * | 3.5000 | 12/20/2045 | 407,222 | ||||||||||||

| 3,214,285 | Government National Mortgage Association * | 3.5000 | 9/20/2046 | 723,861 | ||||||||||||

| 2,866,075 | Government National Mortgage Association * | 3.5000 | 3/20/2047 | 449,596 | ||||||||||||

| 4,783,334 | Government National Mortgage Association * | 3.5000 | 1/20/2048 | 951,421 | ||||||||||||

| 539,831 | Government National Mortgage Association *~ | 3.8204 | 1/20/2046 | Monthly US LIBOR | +6.10% | 72,919 | ||||||||||

| 491,788 | Government National Mortgage Association *~ | 3.9204 | 12/20/2042 | Monthly US LIBOR | +6.20% | 54,870 | ||||||||||

| 241,906 | Government National Mortgage Association * | 4.0000 | 12/16/2026 | 23,427 | ||||||||||||

| 877,634 | Government National Mortgage Association * | 4.0000 | 12/20/2040 | 112,400 | ||||||||||||

| 3,885,849 | Government National Mortgage Association * | 4.0000 | 11/20/2044 | 553,071 | ||||||||||||

| 1,294,119 | Government National Mortgage Association * | 4.0000 | 7/20/2045 | 194,862 | ||||||||||||

| 6,658,887 | Government National Mortgage Association * | 4.0000 | 11/20/2047 | 1,037,650 | ||||||||||||

| 891,959 | Government National Mortgage Association *~ | 4.0203 | 8/16/2038 | Monthly US LIBOR | +6.30% | 64,943 | ||||||||||

| 393,661 | Government National Mortgage Association *~ | 4.4203 | 6/16/2042 | Monthly US LIBOR | +6.70% | 56,376 | ||||||||||

| 882,069 | Government National Mortgage Association * | 4.5000 | 3/20/2044 | 187,858 | ||||||||||||

| 3,083,117 | Government National Mortgage Association * | 4.5000 | 8/20/2045 | Monthly US LIBOR | +6.70% | 613,144 | ||||||||||

| 514,017 | Government National Mortgage Association * | 4.5000 | 4/20/2046 | 103,102 | ||||||||||||

| 1,785,073 | Government National Mortgage Association * | 5.0000 | 2/16/2040 | 397,885 | ||||||||||||

| 503,473 | Government National Mortgage Association * | 5.0000 | 12/20/2047 | 118,833 | ||||||||||||

| 797,629 | Government National Mortgage Association * | 5.5000 | 7/20/2047 | 197,525 | ||||||||||||

| 1,138,564 | Government National Mortgage Association *# | 6.0000 | 1/20/2040 | 257,976 | ||||||||||||

| 34,416,274 | ||||||||||||||||

| AGRICULTURE - 0.2% | ||||||||||||||||

| 285,000 | Reynolds American, Inc. ^ | 6.8750 | 5/1/2020 | 299,134 | ||||||||||||

| 225,000 | Reynolds American, Inc. ^ | 8.1250 | 6/23/2019 | 231,990 | ||||||||||||

| 531,124 | ||||||||||||||||

| AIRLINES - 2.8% | ||||||||||||||||

| 992,517 | America West Airlines 2001-1 Pass Through Trust | 7.1000 | 4/2/2021 | 1,050,083 | ||||||||||||

| 383,662 | American Airlines 2011-1 Class A Pass Through Trust | 5.2500 | 1/31/2021 | 393,503 | ||||||||||||

| 353,670 | American Airlines 2013-2 Class B Pass Through Trust ^ | 5.6000 | 7/15/2020 | 359,417 | ||||||||||||

| 2,050,000 | American Airlines Group, Inc. ^ | 4.6250 | 3/1/2020 | 2,057,688 | ||||||||||||

| 291,242 | Continental Airlines 2000-1 Class A-1 Pass Through Trust | 8.0480 | 11/1/2020 | 301,260 | ||||||||||||

| 467,928 | Continental Airlines 2004-ERJ1 Pass Through Trust | 9.5580 | 9/1/2019 | 478,456 | ||||||||||||

| 1,203,614 | Continental Airlines 2007-1 Class A Pass Through Trust | 5.9830 | 4/19/2022 | 1,260,064 | ||||||||||||

| 436,778 | Continental Airlines 2010-1 Class A Pass Through Trust | 4.7500 | 7/12/2022 | 445,044 | ||||||||||||

| 31,339 | Delta Air Lines 2010-2 Class A Pass Through Trust | 4.9500 | 5/23/2019 | �� | 31,503 | |||||||||||

| 169,912 | United Airlines 2014-1 Class B Pass Through Trust | 4.7500 | 4/11/2022 | 171,186 | ||||||||||||

| 46,165 | Virgin Australia 2013-1B Pass Through Trust ^ | 6.0000 | 10/23/2020 | 46,742 | ||||||||||||

| 6,594,946 | ||||||||||||||||

See accompanying notes to financial statements.

6

| Anfield Universal Fixed Income Fund |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2018 |

| Par Value | Coupon Rate (%) | Maturity | Spread | Rate | Fair Value | |||||||||||

| BONDS & NOTES - 94.0% (Continued) | ||||||||||||||||

| AUTO MANUFACTURERS - 2.9% | ||||||||||||||||

| $ | 750,000 | Daimler Finance North America LLC ^ | 1.7500 | 10/30/2019 | $ | 739,633 | ||||||||||

| 4,350,000 | Fiat Chrysler Automobiles NV | 4.5000 | 4/15/2020 | 4,377,188 | ||||||||||||

| 1,145,000 | Ford Motor Credit Co. LLC | 2.5970 | 11/4/2019 | 1,131,524 | ||||||||||||

| 500,000 | General Motors Financial Co., Inc. | 4.3750 | 9/25/2021 | 504,782 | ||||||||||||

| 6,753,127 | ||||||||||||||||

| AUTO PARTS & EQUIPMENT - 0.2% | ||||||||||||||||

| 500,000 | Aptiv PLC | 3.1500 | 11/19/2020 | 494,697 | ||||||||||||

| BANKS - 8.1% | ||||||||||||||||

| 268,000 | Bank of America Corp. # | 4.0423 | 11/18/2020 | Quarterly US LIBOR | +1.72% | 270,967 | ||||||||||

| 500,000 | Bank of America Corp. # | 4.1461 | 9/28/2020 | Quarterly US LIBOR | +1.76% | 507,035 | ||||||||||

| 500,000 | Barclays Bank PLC # | 3.5596 | 2/22/2021 | Quarterly US LIBOR | +1.25% | 492,421 | ||||||||||

| 1,125,000 | BPCE SA | 2.5000 | 7/15/2019 | 1,120,881 | ||||||||||||

| 1,414,000 | Capital One NA | 2.4000 | 9/5/2019 | 1,404,401 | ||||||||||||

| 250,000 | Citigroup, Inc. ~ | 3.5841 | 12/15/2020 | Quarterly US LIBOR | +1.25% | 253,137 | ||||||||||

| 450,000 | Citigroup, Inc. # | 3.7880 | 8/11/2020 | Quarterly US LIBOR | +1.45% | 454,010 | ||||||||||

| 1,900,000 | Citigroup, Inc. # | 5.8750 | 3/27/2020 | Quarterly US LIBOR | +4.06% | 1,928,500 | ||||||||||

| 6,500,000 | Credit Agricole SA ^# | 8.3750 | 10/13/2019 | Quarterly US LIBOR | +6.98% | 6,760,000 | ||||||||||

| 787,000 | Discover Bank | 8.7000 | 11/18/2019 | 826,487 | ||||||||||||

| 250,000 | Goldman Sachs Group, Inc. # | 3.7114 | 8/26/2020 | Quarterly US LIBOR | +1.40% | 251,595 | ||||||||||

| 344,000 | Goldman Sachs Group, Inc. ~ | 3.7863 | 7/15/2020 | Quarterly US LIBOR | +1.35% | 346,351 | ||||||||||

| 252,000 | HSBC Bank USA NA | 4.8750 | 8/24/2020 | 257,982 | ||||||||||||

| 2,093,545 | Jacobs Douwe Egberts | 4.5625 | 11/1/2025 | 2,101,395 | ||||||||||||

| 263,000 | JPMorgan Chase & Co. ~ | 3.0093 | 10/29/2020 | Quarterly US LIBOR | +0.50% | 258,398 | ||||||||||

| 400,000 | Manufacturers & Traders Trust Co. # | 2.9613 | 12/1/2021 | Quarterly US LIBOR | +0.64% | 398,227 | ||||||||||

| 500,000 | National Westminster Bank PLC ~ | 2.6250 | 2/28/2019 | Quarterly US LIBOR | +0.25% | 410,090 | ||||||||||

| 700,000 | Wells Fargo & Co. # | 6.1041 | 3/15/2019 | Quarterly US LIBOR | +3.77% | 706,125 | ||||||||||

| 18,748,002 | ||||||||||||||||

| BEVERAGES - 2.1% | ||||||||||||||||

| 400,000 | Coca-Cola European Partners PLC | 3.2500 | 8/19/2021 | 394,637 | ||||||||||||

| 350,000 | Coca-Cola Femsa SAB de CV | 2.3750 | 11/26/2018 | 349,588 | ||||||||||||

| 1,263,000 | Constellation Brands, Inc. | 2.0000 | 11/7/2019 | 1,249,375 | ||||||||||||

| 1,344,000 | Constellation Brands, Inc. | 3.8750 | 11/15/2019 | 1,352,752 | ||||||||||||

| 1,560,000 | Molson Coors Brewing Co. | 2.2500 | 3/15/2020 | 1,536,538 | ||||||||||||

| 4,882,890 | ||||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS - 0.8% | ||||||||||||||||

| 258,354 | Alternative Loan Trust 2004-35T2 * | 6.0000 | 2/25/2035 | 56,904 | ||||||||||||

| 15,117 | Banc of America Funding 2004-D Trust # | 3.8804 | 6/25/2034 | 14,995 | ||||||||||||

| 13,656 | Banc of America Mortgage 2004-A Trust # | 3.8578 | 2/25/2034 | 13,740 | ||||||||||||

| 36,047 | Banc of America Mortgage 2004-C Trust # | 4.1458 | 4/25/2034 | 36,516 | ||||||||||||

| 11,034,106 | BCAP LLC Trust 2007-AA2 *# | 0.4467 | 4/25/2037 | 168,282 | ||||||||||||

| 28,949 | Bear Stearns ARM Trust 2003-4 # | 4.4006 | 7/25/2033 | 29,331 | ||||||||||||

| 25,148 | Bear Stearns Asset Backed Securities Trust 2003-AC5 | 5.5000 | 10/25/2033 | 25,768 | ||||||||||||

| 17,810 | Chase Mortgage Finance Trust Series 2007-A1 # | 4.2574 | 2/25/2037 | 17,949 | ||||||||||||

| 77,988 | CHL Mortgage Pass-Through Trust 2004-7 # | 4.0241 | 5/25/2034 | 78,442 | ||||||||||||

| 24,711 | Citigroup Global Markets Mortgage Securities VII, Inc. ^ | 6.0000 | 9/25/2033 | 24,758 | ||||||||||||

| 65,873 | Citigroup Mortgage Loan Trust 2006-4 | 0.0000 | 12/25/2035 | 66,205 | ||||||||||||

| 37,779 | Deutsche Mortgage Securities, Inc. Mortgage Loan Trust 2004-4 ~ | 2.7314 | 6/25/2034 | Monthly US LIBOR | +0.45% | 35,515 | ||||||||||

| 7,445 | First Horizon Alternative Mortgage Securities Trust 2006-FA1 ~ | 3.0314 | 4/25/2036 | Monthly US LIBOR | +0.75% | 7,464 | ||||||||||

| 67,418 | GSR Mortgage Loan Trust 2004-14 # | 4.5479 | 12/25/2034 | 69,090 | ||||||||||||

See accompanying notes to financial statements.

7

| Anfield Universal Fixed Income Fund |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2018 |

| Par Value | Coupon Rate (%) | Maturity | Spread | Rate | Fair Value | |||||||||||

| BONDS & NOTES - 94.0% (Continued) | ||||||||||||||||

| COLLATERALIZED MORTGAGE OBLIGATIONS - 0.8% (Continued) | ||||||||||||||||

| $ | 424,062 | GSR Mortgage Loan Trust 2004-2F *~ | 5.3686 | 1/25/2034 | Monthly US LIBOR | +7.65% | $ | 46,041 | ||||||||

| 31,079 | GSR Mortgage Loan Trust 2004-6F | 5.5000 | 5/25/2034 | 31,436 | ||||||||||||

| 132,034 | Impac CMB Trust Series 2004-4 ~ | 3.1814 | 9/25/2034 | Monthly US LIBOR | +0.90% | 126,584 | ||||||||||

| 18,185 | Impac CMB Trust Series 2004-5 ~ | 3.2014 | 10/25/2034 | Monthly US LIBOR | +0.92% | 18,363 | ||||||||||

| 103,746 | Impac CMB Trust Series 2004-6 ~ | 3.1064 | 10/25/2034 | Monthly US LIBOR | +0.83% | 98,256 | ||||||||||

| 108,754 | JP Morgan Mortgage Trust 2005-A1 # | 4.2724 | 2/25/2035 | 108,743 | ||||||||||||

| 14,646 | Lehman XS Trust Series 2005-1 ~ | 3.7560 | 7/25/2035 | Monthly US LIBOR | +1.50% | 14,624 | ||||||||||

| 19,196 | MASTR Alternative Loan Trust 2003-7 | 6.5000 | 12/25/2033 | 20,166 | ||||||||||||

| 935,897 | MASTR Alternative Loan Trust 2007-HF1 * | 7.0000 | 10/25/2047 | 245,283 | ||||||||||||

| 34,000 | MASTR Asset Securitization Trust 2005-2 | 5.3500 | 11/25/2035 | 35,666 | ||||||||||||

| 52,925 | Morgan Stanley Mortgage Loan Trust 2004-10AR # | 4.4059 | 11/25/2034 | 52,378 | ||||||||||||

| 17,815 | Morgan Stanley Mortgage Loan Trust 2004-7AR # | 4.3460 | 9/25/2034 | 18,357 | ||||||||||||

| 92,650 | RAMP Series 2004-SL3 Trust | 7.5000 | 12/25/2031 | 94,118 | ||||||||||||

| 37,750 | Structured Asset Securities Corp. # | 4.4578 | 9/25/2026 | 38,032 | ||||||||||||

| 36,066 | Structured Asset Securities Corp. Mo Pa Th Ce Se 1998-3 Tr ~ | 3.2814 | 3/25/2028 | Monthly US LIBOR | +1.00% | 36,114 | ||||||||||

| 44,558 | Wells Fargo Mortgage Backed Securities 2005-12 Trust | 5.5000 | 11/25/2035 | 11,954 | ||||||||||||

| 110,074 | Wilshire Funding Corp. # | 7.2500 | 8/25/2027 | 107,960 | ||||||||||||

| 1,749,034 | ||||||||||||||||

| COMMERCIAL SERVICES - 1.2% | ||||||||||||||||

| 2,735,000 | Nielsen Finance LLC | 4.5000 | 10/1/2020 | 2,735,000 | ||||||||||||

| COMPUTERS - 3.7% | ||||||||||||||||

| 2,888,000 | Dell, Inc. | 5.8750 | 6/15/2019 | 2,927,710 | ||||||||||||

| 4,070,000 | EMC Corp. | 2.6500 | 6/1/2020 | 3,961,155 | ||||||||||||

| 1,629,000 | Leidos Holdings, Inc. | 4.4500 | 12/1/2020 | 1,625,742 | ||||||||||||

| 8,514,607 | ||||||||||||||||

| DIVERSIFIED FINANCIAL SERVICES - 5.6% | ||||||||||||||||

| 1,130,000 | AerCap Ireland Capital DAC | 4.5000 | 5/15/2021 | 1,142,877 | ||||||||||||

| 375,000 | Ally Financial, Inc. | 3.3500 | 5/15/2019 | 373,858 | ||||||||||||

| 1,816,000 | Ally Financial, Inc. | 3.5000 | 1/27/2019 | 1,816,000 | ||||||||||||

| 2,881,000 | Ally Financial, Inc. | 3.7500 | 11/18/2019 | 2,888,491 | ||||||||||||

| 200,000 | GTP Acquisition Partners I LLC ^ | 2.3500 | 6/15/2020 | 195,618 | ||||||||||||

| 500,000 | ILFC E-Capital Trust I ^# | 4.7800 | 12/21/2065 | Monthly US LIBOR | +1.55% | 443,750 | ||||||||||

| 1,602,000 | International Lease Finance Corp. | 5.8750 | 4/1/2019 | 1,618,267 | ||||||||||||

| 1,926,000 | Navient Corp. | 5.5000 | 1/15/2019 | 1,935,630 | ||||||||||||

| 2,571,000 | Synchrony Financial | 3.0000 | 8/15/2019 | 2,560,985 | ||||||||||||

| 12,975,476 | ||||||||||||||||

| ELECTRIC - 1.1% | ||||||||||||||||

| 420,000 | EDP Finance BV ^ | 5.2500 | 1/14/2021 | 431,092 | ||||||||||||

| 1,642,000 | Electricite de France SA ^ | 4.6000 | 1/27/2020 | 1,670,264 | ||||||||||||

| 450,000 | Entergy Corp. | 5.1250 | 9/15/2020 | 459,795 | ||||||||||||

| 100,000 | PPL Capital Funding, Inc. # | 5.0511 | 3/30/2067 | Quarterly US LIBOR | +2.67% | 97,500 | ||||||||||

| 2,658,651 | ||||||||||||||||

| ENVIRONMENTAL CONTROL - 0.4% | ||||||||||||||||

| 1,000,000 | Waste Management, Inc. | 4.7500 | 6/30/2020 | 1,024,094 | ||||||||||||

| FOOD - 0.4% | ||||||||||||||||

| 902,000 | Wm Wrigley Jr. Co. ^ | 2.9000 | 10/21/2019 | 899,927 | ||||||||||||

| FOREST PRODUCTS & PAPER - 0.3% | ||||||||||||||||

| 775,000 | Carter Holt Harvey Ltd. + | 9.5000 | 12/1/2024 | 748,991 | ||||||||||||

See accompanying notes to financial statements.

8

| Anfield Universal Fixed Income Fund |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2018 |

| Par Value | Coupon Rate (%) | Maturity | Spread | Rate | Fair Value | |||||||||||

| BONDS & NOTES - 94.0% (Continued) | ||||||||||||||||

| HEALTHCARE-PRODUCTS - 0.9% | ||||||||||||||||

| $ | 1,700,000 | Zimmer Biomet Holdings, Inc. | 2.7000 | 4/1/2020 | $ | 1,682,298 | ||||||||||

| 322,000 | Zimmer Biomet Holdings, Inc. | 4.6250 | 11/30/2019 | 325,967 | ||||||||||||

| 2,008,265 | ||||||||||||||||

| HEALTHCARE-SERVICES - 0.2% | ||||||||||||||||

| 500,000 | Quest Diagnostics, Inc. | 4.7500 | 1/30/2020 | 508,994 | ||||||||||||

| HOME EQUITY ASSET BACKED SECURITIES - 1.8% | ||||||||||||||||

| 84,956 | Aames Mortgage Trust 2001 1 Mortgage Pass Thr Certs Se 01 1 < | 8.0880 | 6/25/2031 | 90,253 | ||||||||||||

| 81,787 | ABFC 2002-OPT1 Trust ~ | 3.6764 | 4/25/2032 | Monthly US LIBOR | +1.40% | 82,208 | ||||||||||

| 117,071 | ACE Securities Corp Home Equity Loan Trust Series 2003-OP1 ~ | 4.7564 | 12/25/2033 | Monthly US LIBOR | +2.48% | 112,631 | ||||||||||

| 54,472 | AFC Trust Series 2000-1 ~ | 3.0114 | 3/25/2030 | Monthly US LIBOR | +0.73% | 52,239 | ||||||||||

| 36,851 | Ameriquest Mort Sec Inc Asst Back Pas Thr Certs Ser 2003-9 ~ | 4.9912 | 9/25/2033 | Monthly US LIBOR | +3.00% | 36,931 | ||||||||||

| 27,896 | Ameriquest Mortgage Securities Asset-Backed Pass-Thr Ctfs Ser 2003 12 | 3.4064 | 1/25/2034 | Monthly US LIBOR | +1.13% | 27,929 | ||||||||||

| 14,567 | Ameriquest Mortgage Securities Asset-Backed Pass-Thr Ctfs Ser 2003 12 | 4.8314 | 1/25/2034 | Monthly US LIBOR | +2.55% | 14,786 | ||||||||||

| 7,745 | Ameriquest Mortgage Securities, Inc. Asst-Back Pass-Thr Ctfs Ser 2003- | 5.0554 | 12/25/2033 | 8,013 | ||||||||||||

| 54,862 | Amresco Residential Securities Corp Mortgage Loan Trust 1998-1 # | 7.0000 | 1/25/2028 | 55,244 | ||||||||||||

| 191,395 | Asset Backed Securities Corp Home Equity Loan Trust Series 2003-HE6 | 4.7564 | 11/25/2033 | Monthly US LIBOR | +2.48% | 192,817 | ||||||||||

| 135,000 | Bear Stearns Asset Backed Securities I Trust 2004-BO1 ~ | 6.2814 | 10/25/2034 | Monthly US LIBOR | +4.00% | 129,923 | ||||||||||

| 442,059 | Bear Stearns Asset Backed Securities I Trust 2004-FR3 ~ | 4.3814 | 9/25/2034 | Monthly US LIBOR | +2.10% | 433,927 | ||||||||||

| 244,442 | Bear Stearns Asset Backed Securities I Trust 2004-HE7 ~ | 4.9814 | 8/25/2034 | Monthly US LIBOR | +2.70% | 238,931 | ||||||||||

| 24,497 | Bear Stearns Asset Backed Securities Trust 2003-ABF1 ~ | 3.0214 | 1/25/2034 | Monthly US LIBOR | +0.74% | 24,019 | ||||||||||

| 155,469 | CDC Mortgage Capital Trust 2004-HE1 ~ | 4.0814 | 6/25/2034 | Monthly US LIBOR | +1.80% | 142,279 | ||||||||||

| 178,754 | CDC Mortgage Capital Trust 2004-HE3 ~ | 4.0814 | 11/25/2034 | Monthly US LIBOR | +1.80% | 158,478 | ||||||||||

| 90,360 | Citigroup Global Markets Mortgage Securities VII, Inc. ~ | 2.8414 | 9/25/2028 | Monthly US LIBOR | +0.56% | 90,022 | ||||||||||

| 24,658 | Conseco Finance Corp. # | 7.2200 | 3/15/2028 | 25,245 | ||||||||||||

| 61,035 | Credit Suisse First Boston Mortgage Securities Corp. < | 6.9900 | 2/25/2031 | 62,456 | ||||||||||||

| 40,000 | GSAA Trust < | 5.2950 | 11/25/2034 | 40,321 | ||||||||||||

| 64,512 | Home Equity Asset Trust ~ | 4.4314 | 3/25/2034 | Monthly US LIBOR | +2.15% | 63,628 | ||||||||||

| 195,285 | Home Equity Asset Trust 2004-4 ~ | 4.2314 | 10/25/2034 | Monthly US LIBOR | +1.95% | 189,988 | ||||||||||

| 42,603 | Meritage Mortgage Loan Trust 2003-1 ~ | 4.6064 | 11/25/2033 | Monthly US LIBOR | +2.33% | 42,584 | ||||||||||

| 36,156 | Meritage Mortgage Loan Trust 2003-1 ~ | 4.9814 | 11/25/2033 | Monthly US LIBOR | +2.70% | 34,442 | ||||||||||

| 64,104 | Merrill Lynch Mortgage Investors Trust Series 2003-OPT1 ~ | 4.4564 | 7/25/2034 | Monthly US LIBOR | +2.18% | 60,179 | ||||||||||

| 21,821 | Morgan Stanley ABS Capital I, Inc. Trust 2003-HE1 ~ | 5.6564 | 5/25/2033 | Monthly US LIBOR | +3.38% | 21,662 | ||||||||||

| 484,745 | Morgan Stanley ABS Capital I, Inc. Trust 2004-OP1 ~ | 4.1564 | 11/25/2034 | Monthly US LIBOR | +1.88% | 460,865 | ||||||||||

| 69,909 | New Century Home Equity Loan Trust ^~ | 3.4064 | 10/25/2033 | Monthly US LIBOR | +1.13% | 69,616 | ||||||||||

| 191,413 | New Century Home Equity Loan Trust Series 2003-B ~ | 4.7564 | 11/25/2033 | Monthly US LIBOR | +2.48% | 192,683 | ||||||||||

| 102,375 | NovaStar Mortgage Funding Trust Series 2003-4 ~ | 3.3464 | 2/25/2034 | Monthly US LIBOR | +1.07% | 101,998 | ||||||||||

| 1,843 | NovaStar Mortgage Funding Trust Series 2004-1 ~ | 3.8564 | 6/25/2034 | Monthly US LIBOR | +1.58% | 1,812 | ||||||||||

| 114,740 | NovaStar Mortgage Funding Trust Series 2004-2 ~ | 4.5314 | 9/25/2034 | Monthly US LIBOR | +2.25% | 106,497 | ||||||||||

| 19,753 | Option One Mortgage Accept Corp. Asset Back Certs Ser 2003 5 ~ | 2.9214 | 8/25/2033 | Monthly US LIBOR | +0.64% | 19,438 | ||||||||||

| 69,939 | Saxon Asset Securities Trust 2002-1 ~ | 4.0814 | 11/25/2031 | Monthly US LIBOR | +1.80% | 62,315 | ||||||||||

| 50,181 | Saxon Asset Securities Trust 2003-3 ~ | 4.3911 | 12/25/2033 | Monthly US LIBOR | +2.40% | 46,689 | ||||||||||

| 108,051 | Securitized Asset Backed Receivables LLC Trust 2004-OP1 ~ | 3.9314 | 2/25/2034 | Monthly US LIBOR | +1.65% | 106,882 | ||||||||||

| 260,479 | Securitized Asset Backed Receivables LLC Trust 2004-OP1 ~ | 4.3064 | 2/25/2034 | Monthly US LIBOR | +2.03% | 257,289 | ||||||||||

| 152,589 | Security National Mortgage Loan Trust 2007-1 ^~ | 2.6365 | 4/25/2037 | Monthly US LIBOR | +0.35% | 150,529 | ||||||||||

| 46,538 | Terwin Mortgage Trust 2004-16SL ^~ | 6.5564 | 10/25/2034 | Monthly US LIBOR | +4.28% | 46,460 | ||||||||||

| 114,760 | Terwin Mortgage Trust Series TMTS 2003-2HE ~ | 4.4314 | 7/25/2034 | Monthly US LIBOR | +2.15% | 117,974 | ||||||||||

| 4,172,182 | ||||||||||||||||

| INSURANCE - 0.1% | ||||||||||||||||

| 300,000 | Aspen Insurance Holdings Ltd. | 4.6500 | 11/15/2023 | 302,572 | ||||||||||||

See accompanying notes to financial statements.

9

| Anfield Universal Fixed Income Fund |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2018 |

| Par Value | Coupon Rate (%) | Maturity | Spread | Rate | Fair Value | |||||||||||

| BONDS & NOTES - 94.0% (Continued) | ||||||||||||||||

| INVESTMENT COMPANIES - 0.3% | ||||||||||||||||

| $ | 776,000 | Ares Capital Corp. | 4.8750 | 11/30/2018 | $ | 777,110 | ||||||||||

| LODGING - 2.1% | ||||||||||||||||

| 3,494,000 | MGM Resorts International | 5.2500 | 3/31/2020 | 3,546,410 | ||||||||||||

| 1,232,000 | MGM Resorts International | 8.6250 | 2/1/2019 | 1,247,400 | ||||||||||||

| 4,793,810 | ||||||||||||||||

| MEDIA - 3.0% | ||||||||||||||||

| 700,000 | Cablevision Systems Corp. | 8.0000 | 4/15/2020 | 734,125 | ||||||||||||

| 739,000 | Charter Communications Operating LLC | 4.4640 | 7/23/2022 | 748,271 | ||||||||||||

| 500,000 | CSC Holdings LLC | 8.6250 | 2/15/2019 | 506,250 | ||||||||||||

| 750,000 | DIRECTV Holdings LLC | 5.0000 | 3/1/2021 | 772,541 | ||||||||||||

| 1,015,000 | Discovery Communications LLC ^ | 2.7500 | 11/15/2019 | 1,008,065 | ||||||||||||

| 500,000 | NBCUniversal Enterprise, Inc. ^ | 1.9740 | 4/15/2019 | 497,996 | ||||||||||||

| 1,245,000 | Time Warner Cable LLC | 5.0000 | 2/1/2020 | 1,265,299 | ||||||||||||

| 1,335,000 | Time Warner Cable LLC | 8.2500 | 4/1/2019 | 1,362,221 | ||||||||||||

| 6,894,768 | ||||||||||||||||

| MINING - 0.1% | ||||||||||||||||

| 262,000 | Newmont Mining Corp. | 5.1250 | 10/1/2019 | 266,295 | ||||||||||||

| MISCELLANEOUS - 0.8% | ||||||||||||||||

| 2,000,000 | General Electric, Co. # | 5.0000 | 1/21/2021 | Quarterly US LIBOR | +3.33% | 1,855,000 | ||||||||||

| OIL & GAS - 2.5% | ||||||||||||||||

| 630,000 | BG Energy Capital PLC ^ | 4.0000 | 12/9/2020 | 637,160 | ||||||||||||

| 1,000,000 | Gazprom OAO Via Gaz Capital SA | 9.2500 | 4/23/2019 | 1,024,170 | ||||||||||||

| 666,000 | Petrobras Global Finance BV ~ | 4.5763 | 1/15/2019 | Quarterly US LIBOR | +2.14% | 667,006 | ||||||||||

| 417,000 | Petrobras Global Finance BV ~ | 5.2141 | 3/17/2020 | Quarterly US LIBOR | +2.88% | 426,904 | ||||||||||

| 3,000,000 | Unit Corp. | 6.6250 | 5/15/2021 | 2,992,500 | ||||||||||||

| 5,747,740 | ||||||||||||||||

| OTHER ASSET BACKED SECURITIES - 20.1% | ||||||||||||||||

| 850,000 | ACIS CLO 2017-7 Ltd. ^~ | 4.2910 | 5/1/2027 | Quarterly US LIBOR | +1.75% | 851,597 | ||||||||||

| 2,000,000 | AMMC CLO 16 Ltd. ^~ | 8.4963 | 4/14/2029 | Quarterly US LIBOR | +6.06% | 2,004,824 | ||||||||||

| 145,531 | Amortizing Residential Collateral Trust 2002-BC6 ~ | 4.0814 | 8/25/2032 | Monthly US LIBOR | +1.80% | 133,888 | ||||||||||

| 2,000,000 | Arch Street CLO Ltd. ^~ | 8.7690 | 10/20/2028 | Quarterly US LIBOR | +6.30% | 1,992,500 | ||||||||||

| 1,000,000 | Bain Capital Credit CLO 2017-2 ^~ | 4.3363 | 1/15/2029 | Quarterly US LIBOR | +1.90% | 1,002,012 | ||||||||||

| 172,776 | Bear Stearns Asset Backed Securities Trust 2003-SD3 ~ | 5.1314 | 10/25/2033 | Monthly US LIBOR | +2.85% | 170,596 | ||||||||||

| 7,130 | Bear Stearns Asset Backed Securities Trust 2006-SD2 ~ | 2.6614 | 6/25/2036 | Monthly US LIBOR | +0.38% | 7,145 | ||||||||||

| 21,133 | Bravo Mortgage Asset Trust ^~ | 2.5214 | 7/25/2036 | Monthly US LIBOR | +0.24% | 21,121 | ||||||||||

| 1,600,000 | Brigade Debt Funding I Ltd. ^ | 6.3000 | 4/25/2036 | 1,568,474 | ||||||||||||

| 191,211 | Carrington Mortgage Loan Trust Series 2004-NC2 ~ | 4.0814 | 8/25/2034 | Monthly US LIBOR | +1.80% | 188,856 | ||||||||||

| 2,000,000 | Catamaran CLO 2013-1 Ltd. ^~ | 9.6593 | 1/27/2028 | Quarterly US LIBOR | +7.15% | 1,906,592 | ||||||||||

| 6,660 | Chase Funding Trust Series 2002-2 | 5.5990 | 9/25/2031 | 6,784 | ||||||||||||

| 1,597,500 | CIFC Funding 2015-III Ltd. ^~ | 4.9496 | 4/19/2029 | Quarterly US LIBOR | +2.50% | 1,551,738 | ||||||||||

| 230,773 | Countrywide Asset-Backed Certificates ~ | 2.7814 | 8/25/2034 | Monthly US LIBOR | +0.50% | 229,432 | ||||||||||

| 77,728 | Countrywide Asset-Backed Certificates ^~ | 5.6564 | 3/25/2032 | Monthly US LIBOR | +3.38% | 77,035 | ||||||||||

| 22,904 | Countrywide Home Equity Loan Trust ~ | 2.4995 | 4/15/2030 | Monthly US LIBOR | +0.22% | 22,846 | ||||||||||

| 202,549 | Credit-Based Asset Servicing & Securitization LLC ~ | 3.8917 | 3/25/2034 | Monthly US LIBOR | +2.78% | 203,747 | ||||||||||

| 233,733 | Credit-Based Asset Servicing & Securitization LLC ~ | 4.0064 | 7/25/2035 | Monthly US LIBOR | +1.73% | 233,786 | ||||||||||

| 70,895 | CWABS Inc Asset-Backed Certificates Trust 2004-6 ~ | 3.1814 | 11/25/2034 | Monthly US LIBOR | +0.90% | 71,688 | ||||||||||

| 49,111 | CWABS Inc Asset-Backed Certificates Trust 2004-6 ~ | 3.4814 | 11/25/2034 | Monthly US LIBOR | +1.20% | 50,420 | ||||||||||

| 1,000,000 | Denali Capital CLO XI Ltd. ^ | 8.0790 | 10/20/2028 | Quarterly US LIBOR | +5.61% | 1,000,000 | ||||||||||

See accompanying notes to financial statements.

10

| Anfield Universal Fixed Income Fund |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2018 |

| Par Value | Coupon Rate (%) | Maturity | Spread | Rate | Fair Value | |||||||||||

| BONDS & NOTES - 94.0% (Continued) | ||||||||||||||||

| OTHER ASSET BACKED SECURITIES - 20.1% (Continued) | ||||||||||||||||

| $ | 2,400,000 | ECP CLO 2015-7 Ltd. ^~ | 4.4390 | 4/22/2030 | Quarterly US LIBOR | +1.97% | $ | 2,350,037 | ||||||||

| 1,000,000 | Elevation CLO 2017-7 Ltd. ^~ | 4.3363 | 7/15/2030 | Quarterly US LIBOR | +1.90% | 979,764 | ||||||||||

| 17,897 | Equity One Mortgage Pass-Through Trust 2002-5 < | 5.8030 | 11/25/2032 | 18,763 | ||||||||||||

| 232,969 | Finance America Mortgage Loan Trust 2004-2 ~ | 3.2564 | 8/25/2034 | Monthly US LIBOR | +0.98% | 233,986 | ||||||||||

| 89,165 | Finance America Mortgage Loan Trust 2004-2 ~ | 4.3814 | 8/25/2034 | Monthly US LIBOR | +2.10% | 87,357 | ||||||||||

| 43,273 | First Franklin Mortgage Loan Trust 2002-FF1 ~ | 3.3810 | 4/25/2032 | Monthly US LIBOR | +1.13% | 43,000 | ||||||||||

| 2,000,000 | Fortress Credit BSL VI Ltd. ^~ | 4.2973 | 7/23/2031 | Quarterly US LIBOR | +1.77% | 1,983,398 | ||||||||||

| 1,000,000 | Fortress Credit Opportunities VII CLO Ltd. ^~ | 7.9641 | 12/15/2028 | Quarterly US LIBOR | +5.63% | 1,016,708 | ||||||||||

| 2,000,000 | Greywolf CLO II Ltd. ^~ | 4.5863 | 10/15/2029 | Quarterly US LIBOR | +2.15% | 1,998,633 | ||||||||||

| 1,500,000 | Halcyon Loan Advisors Funding 2015-2 Ltd. ^~ | 8.1899 | 7/25/2027 | Quarterly US LIBOR | +5.70% | 1,494,114 | ||||||||||

| 2,000,000 | Halcyon Loan Advisors Funding 2015-3 Ltd. ^~ | 8.3946 | 10/18/2027 | Quarterly US LIBOR | +5.95% | 1,959,361 | ||||||||||

| 1,000,000 | KVK CLO 2013-1 Ltd. ^~ | 5.3863 | 1/15/2028 | Quarterly US LIBOR | +2.95% | 997,729 | ||||||||||

| 1,000,000 | KVK CLO 2016-1 Ltd. ^~ | 4.6863 | 1/15/2029 | Quarterly US LIBOR | +2.25% | 1,011,838 | ||||||||||

| 500,000 | KVK CLO 2018-1 Ltd. ^~ | 3.9813 | 5/20/2029 | Quarterly US LIBOR | +1.65% | 499,389 | ||||||||||

| 66,916 | Long Beach Mortgage Loan Trust 2003-2 ~ | 5.1314 | 6/25/2033 | Monthly US LIBOR | +2.85% | 66,991 | ||||||||||

| 18,785 | Long Beach Mortgage Loan Trust 2004-1 ~ | 3.1064 | 2/25/2034 | Monthly US LIBOR | +0.83% | 18,850 | ||||||||||

| 2,000,000 | Marathon CLO V Ltd. ^~ | 8.0619 | 11/21/2027 | Quarterly US LIBOR | +5.75% | 1,964,571 | ||||||||||

| 140,029 | Merrill Lynch Mortgage Investors Trust Series 2004-WMC5 ~ | 4.2314 | 7/25/2035 | Monthly US LIBOR | +1.95% | 140,592 | ||||||||||

| 132,522 | Morgan Stanley ABS Capital I, Inc. Trust 2004-NC7 ~ | 4.0064 | 7/25/2034 | Monthly US LIBOR | +17.25% | 129,131 | ||||||||||

| 2,450,000 | Oaktree CLO 2014-1 ^~ | 8.6380 | 5/13/2029 | Quarterly US LIBOR | +6.30% | 2,456,756 | ||||||||||

| 1,500,000 | Octagon Investment Partners XX Ltd. ^~ | 7.5880 | 8/12/2026 | Quarterly US LIBOR | +5.25% | 1,482,474 | ||||||||||

| 223,805 | RAMP Series 2002-RS3 Trust ~ | 3.2564 | 6/25/2032 | Monthly US LIBOR | +0.98% | 207,904 | ||||||||||

| 1,000,000 | Sound Point CLO IX Ltd. ^~ | 8.9690 | 7/20/2027 | Quarterly US LIBOR | +6.50% | 982,221 | ||||||||||

| 190,556 | Specialty Underwriting & Residential Finance Trust Series 2004-BC4 ~ | 3.4814 | 10/25/2035 | Monthly US LIBOR | +1.20% | 177,877 | ||||||||||

| 289,597 | Structured Asset Investment Loan Trust 2004-7 ~ | 3.4064 | 8/25/2034 | Monthly US LIBOR | +1.13% | 282,618 | ||||||||||

| 109,279 | Structured Asset Securities Corp 2005-WF1 ~ | 4.1864 | 2/25/2035 | Monthly US LIBOR | +1.91% | 107,109 | ||||||||||

| 89,566 | Structured Asset Securities Corp 2005-WF1 ~ | 4.3364 | 2/25/2035 | Monthly US LIBOR | +2.10% | 75,894 | ||||||||||

| 405,482 | Symphony CLO II Ltd. ^~ | 3.8114 | 10/25/2020 | Quarterly US LIBOR | +1.50% | 405,904 | ||||||||||

| 1,000,000 | Symphony CLO XIV Ltd. ^~ | 4.2863 | 7/14/2026 | Quarterly US LIBOR | +1.85% | 1,004,145 | ||||||||||

| 2,000,000 | Tralee CLO V Ltd. ^~ | 4.9588 | 10/20/2028 | Quarterly US LIBOR | +2.20% | 2,006,600 | ||||||||||

| 1,000,000 | Trinitas CLO I Ltd. ^~ | 7.1863 | 4/15/2026 | Quarterly US LIBOR | +4.75% | 985,325 | ||||||||||

| 2,000,000 | Tryon Park CLO Ltd. ^~ | 5.1363 | 4/15/2029 | Quarterly US LIBOR | +2.70% | 1,981,030 | ||||||||||

| 1,000,000 | Venture XVI CLO Ltd. ^~ | 4.9463 | 1/15/2028 | Quarterly US LIBOR | +2.51% | 989,439 | ||||||||||

| 2,000,000 | Venture XVI CLO Ltd. ^~ | 7.4663 | 1/15/2028 | Quarterly US LIBOR | +5.03% | 1,930,000 | ||||||||||

| 1,380,000 | Zais CLO 5 Ltd. ^~ | 4.8363 | 10/15/2028 | Quarterly US LIBOR | +2.40% | 1,384,807 | ||||||||||

| 46,749,396 | ||||||||||||||||

| PHARMACEUTICALS - 0.6% | ||||||||||||||||

| 1,000,000 | Allergan Funding SCS | 3.0000 | 3/12/2020 | 996,710 | ||||||||||||

| 500,000 | Zoetis, Inc. | 3.4500 | 11/13/2020 | 500,845 | ||||||||||||

| 1,497,555 | ||||||||||||||||

| PIPELINES - 4.7% | ||||||||||||||||

| 1,313,000 | DCP Midstream Operating LP | 2.7000 | 4/1/2019 | 1,306,435 | ||||||||||||

| 300,000 | DCP Midstream Operating LP ^# | 5.8500 | 5/21/2043 | Quarterly US LIBOR | +3.85% | 270,000 | ||||||||||

| 822,000 | Energy Transfer Operating LP | 4.1500 | 10/1/2020 | 829,351 | ||||||||||||

| 3,615,000 | IFM US Colonial Pipeline 2 LLC ^ | 6.4500 | 5/1/2021 | 3,795,897 | ||||||||||||

| 3,065,000 | Midcontinent Express Pipeline LLC ^ | 6.7000 | 9/15/2019 | 3,140,783 | ||||||||||||

| 395,000 | Plains All American Pipeline LP | 2.6000 | 12/15/2019 | 391,541 | ||||||||||||

| 535,000 | Plains All American Pipeline LP | 5.0000 | 2/1/2021 | 546,259 | ||||||||||||

| 731,000 | Plains All American Pipeline LP | 5.7500 | 1/15/2020 | 749,010 | ||||||||||||

| 11,029,276 | ||||||||||||||||

See accompanying notes to financial statements.

11

| Anfield Universal Fixed Income Fund |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2018 |

| Par Value | Coupon Rate (%) | Maturity | Spread | Rate | Fair Value | |||||||||||

| BONDS & NOTES - 94.0% (Continued) | ||||||||||||||||

| REITs (REAL ESTATE INVESTMENT TRUSTS) - 4.4% | ||||||||||||||||

| $ | 150,000 | American Tower Trust I ^ | 3.0700 | 3/15/2023 | $ | 145,489 | ||||||||||

| 500,000 | Crown Castle International Corp. | 2.2500 | 9/1/2021 | 479,853 | ||||||||||||

| 764,000 | Crown Castle International Corp. | 3.4000 | 2/15/2021 | 759,568 | ||||||||||||

| 2,942,000 | GLP Capital LP / GLP Financing II, Inc. | 4.8750 | 11/1/2020 | 2,982,452 | ||||||||||||

| 1,277,000 | Government Properties Income Trust | 3.7500 | 8/15/2019 | 1,281,256 | ||||||||||||

| 1,304,000 | iStar, Inc. | 5.0000 | 7/1/2019 | 1,305,630 | ||||||||||||

| 1,489,000 | PotlatchDeltic Corp. | 7.5000 | 11/1/2019 | 1,542,915 | ||||||||||||

| 1,422,000 | SBA Tower Trust ^ | 2.8980 | 10/15/2019 | 1,418,518 | ||||||||||||

| 400,000 | SBA Tower Trust ^ | 3.1560 | 10/8/2020 | 396,625 | ||||||||||||

| 10,312,306 | ||||||||||||||||

| RETAIL - 0.1% | ||||||||||||||||

| 250,000 | Advance Auto Parts, Inc. | 5.7500 | 5/1/2020 | 257,466 | ||||||||||||

| SAVINGS & LOANS - 0.2% | ||||||||||||||||

| 500,000 | First Niagara Financial Group, Inc. | 7.2500 | 12/15/2021 | 545,325 | ||||||||||||

| SEMICONDUCTORS - 0.2% | ||||||||||||||||

| 500,000 | NXP BV / NXP Funding LLC ^ | 4.1250 | 6/15/2020 | 499,400 | ||||||||||||

| SOFTWARE - 0.4% | ||||||||||||||||

| 800,000 | Dun & Bradstreet Corp. | 4.2500 | 6/15/2020 | 807,644 | ||||||||||||

| TELECOMMUNICATIONS - 6.9% | ||||||||||||||||

| 400,000 | CenturyLink, Inc. | 6.1500 | 9/15/2019 | 406,000 | ||||||||||||

| 1,121,000 | Frontier Communications Corp. | 7.1250 | 3/15/2019 | 1,129,407 | ||||||||||||

| 1,557,000 | Nokia OYJ | 5.3750 | 5/15/2019 | 1,572,414 | ||||||||||||

| 3,738,000 | Sprint Capital Corp. | 6.9000 | 5/1/2019 | 3,796,275 | ||||||||||||

| 1,420,000 | Sprint Communications, Inc. | 7.0000 | 8/15/2020 | 1,473,250 | ||||||||||||

| 487,000 | Sprint Communications, Inc. ^ | 9.0000 | 11/15/2018 | 488,583 | ||||||||||||

| 2,469,000 | Sprint Spectrum Co. LLC ^ | 3.3600 | 9/20/2021 | 2,450,482 | ||||||||||||

| 4,701,000 | Telecom Italia Capital SA | 7.1750 | 6/18/2019 | 4,789,144 | ||||||||||||

| 16,105,555 | ||||||||||||||||

| TOTAL BONDS & NOTES (Cost $216,025,163) | 218,857,499 | |||||||||||||||

| MUNICIPAL BOND - 0.0% | ||||||||||||||||

| WASHINGTON - 0.0% | ||||||||||||||||

| 95,000 | Grant County Public Utility District No. 2 | 5.2900 | 1/1/2020 | 96,283 | ||||||||||||

| TOTAL MUNICIPAL BOND (Cost $97,319) | 96,283 | |||||||||||||||

See accompanying notes to financial statements.

12

| Anfield Universal Fixed Income Fund |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2018 |

| Shares | Coupon Rate (%) | Spread | Rate | Fair Value | ||||||||||

| PREFERRED STOCKS - 0.6% | ||||||||||||||

| BANKS - 0.6% | ||||||||||||||

| 7,400 | Citigroup, Inc. # | 6.8750 | Quarterly US LIBOR | +4.13% | $ | 202,242 | ||||||||

| 40,000 | Citigroup, Inc. # | 7.1250 | Quarterly US LIBOR | +4.04% | 1,090,400 | |||||||||

| 5,000 | Northern Trust Corp. | 5.8500 | 127,200 | |||||||||||

| TOTAL PREFERRED STOCKS (Cost $1,467,670) | 1,419,842 | |||||||||||||

| TOTAL INVESTMENTS - 98.2% (Cost $226,031,567) | $ | 228,614,286 | ||||||||||||

| OTHER ASSETS LESS LIABILITIES - 1.8% | 4,307,614 | |||||||||||||

| TOTAL NET ASSETS - 100.0% | $ | 232,921,900 | ||||||||||||

CLO - Collateralized Loan Obligation

CMO - Collateralized Mortgage Obligation

LP - Limited Partnership

PLC - Public Limited Company

REMIC - Real Estate Mortgage Investment Conduits

| * | Interest Only Securities |

| # | Variable Rate Securities |

| ~ | Floating Rate Securities |

| ^ | 144A Security - Security exempt from registration under Rule 144A of the Securities Act of 1933. The 144A securities represent 31.35% of total net assets. The securities may be resold in transactions exempt from registration typically only to qualified institutional buyers. Unless otherwise indicated, these securities are not considered to be illiquid. |

| + | As of October 31, 2018 fair valued securities by the Valuation Committee had a market value of $748,991 and represented 0.32% of total net assets. |

| < | STEP Securities |

FUTURES CONTRACTS

| Long | Unrealized | |||||||||||||

| Contracts | Description | Maturity | Counterparty | Notional Value ** | Loss | |||||||||

| 106 | 10-Year US Treasury Note Future | December 2018 | Interactive Brokers | $ | 12,554,375 | $ | (161,438 | ) | ||||||

| Short | Unrealized | |||||||||||||

| Contracts | Description | Maturity | Counterparty | Notional Value ** | Gain | |||||||||

| 106 | US Treasury Long Bond Future | December 2018 | Interactive Brokers | $ | 14,641,250 | $ | 727,695 | |||||||

| Net Unrealized Gain from Futures Contracts | $ | 566,257 | ||||||||||||

| ** | The amounts shown are the underlying reference notional amounts to stock exchange indices and equities upon which the fair value of the futures contracts held by Anfield Universal Fixed Income Fund are based. Notional values do not represent the current fair value of, and are not necessarily indicative of the future cash flows of Anfield Universal Fixed Income Fund’s futures contracts. Further, the underlying price changes in relation to the variables specified by the notional values affects the fair value of these derivative financial instruments. The notional values as set forth within this schedule do not purport to represent economic value at risk to Anfield Universal Fixed Income Fund. |

See accompanying notes to financial statements.

13

Anfield Universal Fixed Income Fund

STATEMENT OF ASSETS AND LIABILITIES

October 31, 2018

| ASSETS | ||||

| Investment securities: | ||||

| At cost | $ | 226,031,567 | ||

| At fair value | $ | 228,614,286 | ||

| Receivable for securities sold | 1,240,337 | |||

| Dividends and interest receivable | 2,620,173 | |||

| Deposits for futures contracts | 296,369 | |||

| Net unrealized appreciation on futures contracts | 566,257 | |||

| Receivable for Fund shares sold | 258,165 | |||

| Prepaid expenses and other assets | 64,822 | |||

| TOTAL ASSETS | 233,660,409 | |||

| LIABILITIES | ||||

| Due to custodian | 373,697 | |||

| Investment advisory fees payable | 150,126 | |||

| Payable to related parties | 24,600 | |||

| Payable for Fund shares repurchased | 150,890 | |||

| Distribution (12b-1) fees payable | 5,686 | |||

| Accrued expenses and other liabilities | 33,510 | |||

| TOTAL LIABILITIES | 738,509 | |||

| NET ASSETS | $ | 232,921,900 | ||

| Composition of Net Assets: | ||||

| Paid in capital | $ | 229,036,053 | ||

| Accumulated earnings | 3,885,847 | |||

| NET ASSETS | $ | 232,921,900 |

See accompanying notes to financial statements.

14

Anfield Universal Fixed Income Fund

STATEMENT OF ASSETS AND LIABILITIES (Continued)

October 31, 2018

| Net Asset Value Per Share: | ||||

| Class A Shares: | ||||

| Net Assets | $ | 23,942,398 | ||

| Shares of beneficial interest outstanding (a) | 2,326,044 | |||

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share | $ | 10.29 | ||

| Maximum offering price per share | ||||

| (net asset value plus maximum sales charge of 5.75%) | $ | 10.92 | ||

| Class C Shares: | ||||

| Net Assets | $ | 799,026 | ||

| Shares of beneficial interest outstanding (a) | 77,595 | |||

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share | $ | 10.30 | ||

| Class I Shares: | ||||

| Net Assets | $ | 208,180,476 | ||

| Shares of beneficial interest outstanding (a) | 20,207,140 | |||

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share | $ | 10.30 |

| (a) | Unlimited number of shares of beneficial interest authorized, no par value. |

See accompanying notes to financial statements.

15

Anfield Universal Fixed Income Fund

STATEMENT OF OPERATIONS

For the Year Ended October 31, 2018

| INVESTMENT INCOME | ||||

| Dividends | $ | 314,989 | ||

| Interest | 6,328,427 | |||

| TOTAL INVESTMENT INCOME | 6,643,416 | |||

| EXPENSES | ||||

| Investment advisory fees | 1,439,620 | |||

| Distribution (12b-1) fees: | ||||

| Class A | 71,159 | |||

| Class C | 2,656 | |||

| Administration fees | 242,194 | |||

| Transfer agent fees | 107,026 | |||

| Shareholder service fees | 104,789 | |||

| Registration fees | 56,175 | |||

| Accounting services fees | 47,466 | |||

| Legal fees | 43,646 | |||

| Printing and postage expenses | 32,613 | |||

| Compliance officer fees | 26,915 | |||

| Custodian fees | 23,119 | |||

| Audit fees | 20,000 | |||

| Trustees fees and expenses | 12,098 | |||

| Insurance expense | 12,022 | |||

| Other expenses | 8,575 | |||

| TOTAL EXPENSES | 2,250,073 | |||

| Less: Fees waived by the Advisor | (128,740 | ) | ||

| NET EXPENSES | 2,121,333 | |||

| NET INVESTMENT INCOME | 4,522,083 | |||

| NET REALIZED AND UNREALIZED GAIN (LOSS) FROM INVESTMENTS | ||||

| Net realized gain from investments | 1,506,216 | |||

| Net realized loss from futures contracts | (203,675 | ) | ||

| Net change in unrealized appreciation on investments | 151,381 | |||

| Net change in unrealized appreciation on futures contracts | 566,257 | |||

| NET REALIZED AND UNREALIZED GAIN FROM INVESTMENTS | 2,020,179 | |||

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 6,542,262 |

See accompanying notes to financial statements.

16

Anfield Universal Fixed Income Fund

STATEMENTS OF CHANGES IN NET ASSETS

| For the | For the | |||||||

| Year Ended | Year Ended | |||||||

| October 31, 2018 | October 31, 2017 | |||||||

| FROM OPERATIONS | ||||||||

| Net investment income | $ | 4,522,083 | $ | 2,122,781 | ||||

| Net realized gain from investments | 1,506,216 | 339,441 | ||||||

| Net realized loss from futures contracts | (203,675 | ) | — | |||||

| Net change in unrealized appreciation on investments | 151,381 | 1,689,600 | ||||||

| Net change in unrealized appreciation on futures contracts | 566,257 | — | ||||||

| Net increase in net assets resulting from operations | 6,542,262 | 4,151,822 | ||||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

| From net investment income: | ||||||||

| Class A | — | (216,876 | ) | |||||

| Class C | — | (895 | ) | |||||

| Class I | — | (1,892,307 | ) | |||||

| Total Distributions Paid* | ||||||||

| Class A | (689,290 | ) | — | |||||

| Class C | (4,615 | ) | — | |||||

| Class I | (3,988,007 | ) | — | |||||

| Total distributions to shareholders | (4,681,912 | ) | (2,110,078 | ) | ||||

| FROM SHARES OF BENEFICIAL INTEREST | ||||||||

| Proceeds from shares sold: | ||||||||

| Class A | 22,447,380 | 26,499,998 | ||||||

| Class C | 722,975 | 25,200 | ||||||

| Class I | 131,333,426 | 55,426,342 | ||||||

| Net asset value of shares issued in reinvestment of distributions: | ||||||||

| Class A | 390,830 | 164,864 | ||||||

| Class C | 4,556 | 865 | ||||||

| Class I | 2,809,120 | 1,572,707 | ||||||

| Payments for shares redeemed: | ||||||||

| Class A | (30,553,245 | ) | (6,520,077 | ) | ||||

| Class C | (9,955 | ) | (55,433 | ) | ||||

| Class I | (37,836,098 | ) | (26,417,843 | ) | ||||

| Net increase in net assets from shares of beneficial interest | 89,308,989 | 50,696,623 | ||||||

| TOTAL INCREASE IN NET ASSETS | 91,169,339 | 52,738,367 | ||||||

| NET ASSETS | ||||||||

| Beginning of the year | 141,752,561 | 89,014,194 | ||||||

| End of the year ** | $ | 232,921,900 | $ | 141,752,561 | ||||

| * | Distributions from net investment income and net realized capital gains are combined for the year ended October 31, 2018. See “New Accounting Pronouncements” in the Notes to Financial Statements for more information. The dividends and distributions to shareholders for the year ended October 31, 2017 have not been reclassified to conform to the current year presentation. |

| ** | Net Assets- End of Year includes distributions in excess of net investment income of $458,325 as of October 31, 2017. |

See accompanying notes to financial statements.

17

Anfield Universal Fixed Income Fund

STATEMENTS OF CHANGES IN NET ASSETS (Continued)

| For the | For the | |||||||

| Year Ended | Year Ended | |||||||

| October 31, 2018 | October 31, 2017 | |||||||

| SHARE ACTIVITY | ||||||||

| Class A: | ||||||||

| Shares Sold | 2,196,343 | 2,613,285 | ||||||

| Shares Reinvested | 38,295 | 16,355 | ||||||

| Shares Redeemed | (2,986,396 | ) | (647,052 | ) | ||||

| Net increase (decrease) in shares of beneficial interest outstanding | (751,758 | ) | 1,982,588 | |||||

| Class C: | ||||||||

| Shares Sold | 70,551 | 2,490 | ||||||

| Shares Reinvested | 445 | 86 | ||||||

| Shares Redeemed | (973 | ) | (5,493 | ) | ||||

| Net increase (decrease) in shares of beneficial interest outstanding | 70,023 | (2,917 | ) | |||||

| Class I: | ||||||||

| Shares Sold | 12,834,050 | 5,488,999 | ||||||

| Shares Reinvested | 275,121 | 155,989 | ||||||

| Shares Redeemed | (3,696,821 | ) | (2,613,054 | ) | ||||

| Net increase in shares of beneficial interest outstanding | 9,412,350 | 3,031,934 | ||||||

See accompanying notes to financial statements.

18

Anfield Universal Fixed Income Fund

FINANCIAL HIGHLIGHTS

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout each Year

| Class A | ||||||||||||||||||||

| Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | ||||||||||||||||

| October 31, | October 31, | October 31, | October 31, | October 31, | ||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| Net asset value, beginning of year | $ | 10.21 | $ | 10.03 | $ | 10.00 | $ | 10.18 | $ | 10.08 | ||||||||||

| Activity from investment operations: | ||||||||||||||||||||

| Net investment income (1) | 0.23 | 0.16 | 0.30 | 0.29 | 0.23 | |||||||||||||||

| Net realized and unrealized gain (loss) on investments (2) | 0.10 | 0.19 | 0.03 | (0.17 | ) | 0.06 | ||||||||||||||

| Total from investment operations | 0.33 | 0.35 | 0.33 | 0.12 | 0.29 | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income | (0.25 | ) | (0.17 | ) | (0.30 | ) | (0.30 | ) | (0.19 | ) | ||||||||||

| Net asset value, end of year | $ | 10.29 | $ | 10.21 | $ | 10.03 | $ | 10.00 | $ | 10.18 | ||||||||||

| Total return (3) | 3.25 | % | 3.56 | % | 3.32 | % | 1.16 | % | 2.91 | % | ||||||||||

| Net assets, at end of year (000)s | $ | 23,942 | $ | 31,421 | $ | 10,988 | $ | 5,430 | $ | 3,749 | ||||||||||

| Ratio of gross expenses to average net assets (4)(5)(6) | 1.46 | % | 1.52 | % | 1.59 | % | 1.76 | % | 2.01 | % | ||||||||||

| Ratio of net expenses to average net assets (5)(6) | 1.38 | % | 1.20 | % | 1.20 | % | 1.20 | % | 1.37 | % | ||||||||||

| Ratio of net investment income to average net assets (5)(6) | 2.25 | % | 1.55 | % | 2.99 | % | 2.84 | % | 2.26 | % | ||||||||||

| Portfolio Turnover Rate | 50 | % | 43 | % | 45 | % | 26 | % | 22 | % | ||||||||||

| (1) | Per share amounts calculated using the average shares method, which more appropriately represents the per share data for the period. |

| (2) | Net realized and unrealized gain (loss) on investments per share are balancing amounts necessary to reconcile the change in net asset value per share for the period, and may not reconcile with aggregate gains (losses) in the statement of operations due to the share transactions for the period. |

| (3) | Total return shown excludes the effect of applicable sales charges. Total returns are historical in nature and assume changes in sale price, reinvestment of dividends and capital gain distributions. Had the Advisor not waived a portion of the Fund’s expenses, total returns would have been lower. |

| (4) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the Advisor. |

| (5) | The ratios of expenses to average net assets and net investment income (loss) to average net assets do not reflect the expenses of the underlying investment companies in which the Fund invests. |

| (6) | Ratio calculated for each share class as a whole, therefore an individual investor’s ratio may vary. |

See accompanying notes to financial statements.

19

Anfield Universal Fixed Income Fund

FINANCIAL HIGHLIGHTS

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout each Year

| Class C | ||||||||||||||||||||

| Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | ||||||||||||||||

| October 31, | October 31, | October 31, | October 31, | October 31, | ||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| Net asset value, beginning of year | $ | 10.22 | $ | 10.04 | $ | 10.01 | $ | 10.19 | $ | 10.08 | ||||||||||

| Activity from investment operations: | ||||||||||||||||||||

| Net investment income (1) | 0.18 | 0.10 | 0.24 | 0.22 | 0.16 | |||||||||||||||

| Net realized and unrealized gain (loss) on investments (2) | 0.08 | 0.18 | 0.01 | (0.18 | ) | 0.01 | ||||||||||||||

| Total from investment operations | 0.26 | 0.28 | 0.25 | 0.04 | 0.17 | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income | (0.18 | ) | (0.10 | ) | (0.22 | ) | (0.22 | ) | (0.06 | ) | ||||||||||

| Total distributions | (0.18 | ) | (0.10 | ) | (0.22 | ) | (0.22 | ) | (0.06 | ) | ||||||||||

| Net asset value, end of year | $ | 10.30 | $ | 10.22 | $ | 10.04 | $ | 10.01 | $ | 10.19 | ||||||||||

| Total return (3) | 2.59 | % | 2.80 | % | 2.52 | % | 0.45 | % | 1.68 | % | ||||||||||

| Net assets, at end of year (000)s | $ | 799 | $ | 77 | $ | 105 | $ | 165 | $ | 100 | ||||||||||

| Ratio of gross expenses to average net assets (4)(5)(6) | 2.21 | % | 2.27 | % | 2.34 | % | 2.51 | % | 2.76 | % | ||||||||||

| Ratio of net expenses to average net assets (5)(6) | 2.13 | % | 1.95 | % | 1.95 | % | 1.95 | % | 2.12 | % | ||||||||||

| Ratio of net investment income to average net assets (5)(6) | 1.72 | % | 0.98 | % | 2.45 | % | 2.16 | % | 1.53 | % | ||||||||||

| Portfolio Turnover Rate | 50 | % | 43 | % | 45 | % | 26 | % | 22 | % | ||||||||||

| (1) | Per share amounts calculated using the average shares method, which more appropriately represents the per share data for the period. |

| (2) | Net realized and unrealized gain (loss) on investments per share are balancing amounts necessary to reconcile the change in net asset value per share for the period, and may not reconcile with aggregate gains (losses) in the statement of operations due to the share transactions for the period. |

| (3) | Total returns are historical in nature and assume changes in sale price, reinvestment of dividends and capital gain distributions. Had the Advisor not waived a portion of the Fund’s expenses, total returns would have been lower. |

| (4) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the Advisor. |

| (5) | The ratios of expenses to average net assets and net investment income (loss) to average net assets do not reflect the expenses of the underlying investment companies in which the Fund invests. |

| (6) | Ratio calculated for each share class as a whole, therefore an individual investor’s ratio may vary. |

See accompanying notes to financial statements.

20

Anfield Universal Fixed Income Fund

FINANCIAL HIGHLIGHTS

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout each Year

| Class I | ||||||||||||||||||||

| Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | ||||||||||||||||

| October 31, | October 31, | October 31, | October 31, | October 31, | ||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||

| Net asset value, beginning of year | $ | 10.21 | $ | 10.04 | $ | 10.01 | $ | 10.19 | $ | 10.08 | ||||||||||

| Activity from investment operations: | ||||||||||||||||||||

| Net investment income (1) | 0.26 | 0.19 | 0.32 | 0.31 | 0.24 | |||||||||||||||

| Net realized and unrealized gain (loss) on investments (2) | 0.10 | 0.18 | 0.03 | (0.17 | ) | 0.09 | ||||||||||||||

| Total from investment operations | 0.36 | 0.37 | 0.35 | 0.14 | 0.33 | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income | (0.27 | ) | (0.20 | ) | (0.32 | ) | (0.32 | ) | (0.22 | ) | ||||||||||

| Net realized gains | — | — | — | — | (0.00 | ) (7) | ||||||||||||||

| Total distributions | (0.27 | ) | (0.20 | ) | (0.32 | ) | (0.32 | ) | (0.22 | ) | ||||||||||

| Net asset value, end of year | $ | 10.30 | $ | 10.21 | $ | 10.04 | $ | 10.01 | $ | 10.19 | ||||||||||

| Total return (3) | 3.61 | % | 3.70 | % | 3.56 | % | 1.42 | % | 3.25 | % | ||||||||||

| Net assets, at end of year (000)s | $ | 208,180 | $ | 110,254 | $ | 77,921 | $ | 50,777 | $ | 38,133 | ||||||||||

| Ratio of gross expenses to average net assets (4)(5)(6) | 1.21 | % | 1.27 | % | 1.34 | % | 1.51 | % | 1.76 | % | ||||||||||

| Ratio of net expenses to average net assets (5)(6) | 1.13 | % | 0.95 | % | 0.95 | % | 0.95 | % | 1.12 | % | ||||||||||

| Ratio of net investment income to average net assets (5)(6) | 2.54 | % | 1.93 | % | 3.19 | % | 3.11 | % | 2.38 | % | ||||||||||

| Portfolio Turnover Rate | 50 | % | 43 | % | 45 | % | 26 | % | 22 | % | ||||||||||

| (1) | Per share amounts calculated using the average shares method, which more appropriately represents the per share data for the period. |

| (2) | Net realized and unrealized gain (loss) on investments per share are balancing amounts necessary to reconcile the change in net asset value per share for the period, and may not reconcile with aggregate gains (losses) in the statement of operations due to the share transactions for the period. |

| (3) | Total returns are historical in nature and assume changes in sale price, reinvestment of dividends and capital gain distributions. Had the Advisor not waived a portion of the Fund’s expenses, total returns would have been lower. |

| (4) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the Advisor. |

| (5) | The ratios of expenses to average net assets and net investment income (loss) to average net assets do not reflect the expenses of the underlying investment companies in which the Fund invests. |

| (6) | Ratio calculated for each share class as a whole, therefore an individual investor’s ratio may vary. |

| (7) | Amount represents less than $0.005. |

See accompanying notes to financial statements.

21

Anfield Universal Fixed Income Fund

NOTES TO FINANCIAL STATEMENTS

October 31, 2018

| 1. | ORGANIZATION |

The Anfield Universal Fixed Income Fund (the “Fund”), is a series of shares of beneficial interest of the Two Roads Shared Trust (the “Trust”), a statutory trust organized under the laws of the State of Delaware on June 8, 2012, and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a diversified, open-end management investment company. The Fund commenced operations on June 28, 2013. The investment objective is to seek current income.