united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22718

Two Roads Shared Trust

(Exact name of registrant as specified in charter)

225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246

(Address of principal executive offices) (Zip code)

The Corporation Trust Company

1209 Orange Street, Wilmington, DE 19801

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2619

Date of fiscal year end: 10/31

Date of reporting period: 10/31/22

ITEM 1. REPORTS TO SHAREHOLDERS.

EXPLANATORY NOTE

Amended to include Exhibit 13(a)(4) Change in Independent Registered Public Accounting Firm.

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Wealthfront Risk Parity Fund |

| Class W Shares (WFRPX) |

| |

| |

| |

| |

| |

| |

| |

| |

| Annual Report |

| October 31, 2022 |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| 1-877-910-4232 |

| www.wealthfront.com |

| |

| |

| |

| |

| |

| Distributed by Northern Lights Distributors, LLC |

| Member FINRA |

| |

| |

| |

| |

| |

| |

| |

| This report and the financial statements contained herein are submitted for the general information of shareholders and are not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus, which contains information about the Fund’s investment objective, risks, fees and expenses. Investors are reminded to read the prospectus carefully before investing in the Fund. |

Manager Discussion of Fund Performance

The past year has been an extremely challenging one for financial markets, with both equities and bonds declining significantly, breaking the long historical precedent of near-zero correlation between the two. Thus, it does not come as a surprise that the Wealthfront Risk Parity Fund (“the Fund”) performed poorly in the fiscal year of 2022 (November 1, 2021 to October 31, 2022*). Over this period, the Fund returned -24.99%, as every asset class the Fund held exposure to declined. The Fund’s benchmark** (a 60/40 blend of MSCI World Equity Index (Net) and the Bloomberg-Barclays Global Aggregate Bond Index) returned -19.20% over the same period. The disappointing relative performance was primarily driven by two factors: drawdowns in bond prices as interest rates increased, and the underperformance of foreign markets relative to the US.

The Fund follows a strategy which seeks to allocate risk equally to a broad range of asset classes, including: US, non-US Developed Markets, and Emerging Markets Equities; US and Emerging Markets Bonds; Treasury Inflation-Protected Securities (“TIPS”), and Real Estate. By utilizing this risk-balanced approach, the Adviser seeks to create a portfolio with a higher expected risk-adjusted return than any single asset class, and higher than that of a typical 60/40 equities/bonds portfolio. However, the allocation by risk, rather than by capital, tends to result in a portfolio with a significant allocation to lower risk (lower volatility) asset classes, such as high-quality bonds. The Fund employs leverage (taking positions in excess of net assets) to target an annualized volatility of 12%.

In the fiscal year of 2022, the Fund’s portfolio followed the pattern described above. On average over this period, 31.5% of the portfolio’s positions were in equities or real estate, with 69.5% allocated to fixed income. The Fund used an average of 1.48x leverage to achieve its target volatility. The Fund’s over exposure to bonds relative to its benchmark contributed to the Fund’s underperformance in the fiscal year 2022. Although equities experienced significant drawdowns, with the MSCI World Equity Index*** declining 18.48%, bonds fared even worse, with the Bloomberg Global Aggregate Bonds Index**** falling 20.79%. The relative underperformance of bonds was driven by a rapid increase in interest rates as economies across the globe sought to tame high inflation.

The Fund’s risk-balanced portfolio construction also tends to result in geographic allocations that are significantly different from the Fund’s benchmark. Within its equity allocation, the Fund’s weights on US, non-US developed, and emerging markets equities averaged approximately 29.3%, 32.7%, and 38.0%, respectively during fiscal year 2022. In contrast, the MSCI World Equity Index had approximately 70% of its weight in the US as of October 31, 2022, and no exposure to emerging markets. The same held true in the Fund’s fixed income exposures, which included approximately 28% exposure to emerging markets bonds, with the other 72% allocated to US fixed income.

In the fiscal year 2022, foreign developed and emerging markets underperformed the US in both the equity and fixed income portions of the Fund’s portfolio. The table below shows the ETFs

the fund uses to achieve exposure to each of the six underlying asset classes, and the total return of each of the ETFs in Fiscal 2022. The underperformance of foreign markets is clearly seen within the equity and fixed income categories.

| | Region | Instrument | Realized Return

(Nov 1, 2021 - Oct 31, 2022) |

| Equity | US

Foreign Developed

Emerging | SPDR S&P 500 ETF Trust

Vanguard FTSE Developed Markets ETF

Vanguard FTSE Emerging Markets ETF | -14.63%

-23.51%

-27.64% |

| Fixed Income | US

US TIPS

Emerging | iShares Core U.S. Aggregate Bond ETF

iShares TIPS Bond ETF

iShares J.P. Morgan USD Emerging Bonds ETF | -15.55%

-11.56%

-24.89% |

| Real Estate | US | Vanguard Real Estate ETF | -21.44% |

Source: CRSP

Aside from its exposure to these instruments, the Fund earns a positive return on treasury bills held as collateral, and pays fees to its swap counterparties to finance the exposures.

We believe that the behavior of markets in this period was atypical. Interest rates rose more rapidly than in any period over the last thirty years, causing severe losses in fixed income assets. The -15.55% return of the iShares Core US Aggregate ETF over this period was its single worst 12-month return since its inception in 2003. The outperformance of US equities relative to foreign equities, while a continuation of a pattern seen in 2021, was also atypical. For context, the performance difference between US stocks and Emerging Markets stocks in fiscal year 2022 was 16.42%, compared to an average performance of -2.04% over all twelve-month periods since the inception of the emerging markets index in 1999. Despite this year’s underperformance, we continue to believe in the fundamental premises of the strategy: that a risk-balanced approach implemented systematically at a low fee can yield higher performance in the long term.

9510-NLD 12/01/2022

DISCLOSURE

| * | The performance data quoted is historical. All year references are to the fiscal year of 2022 (November 1, 2021, through October 31, 2022) unless otherwise noted. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. The Fund’s estimated total annual fund operating expense ratio is 0.25% for Class W per the Fund’s Prospectus dated March 1, 2022. For performance information current to the most recent month-end, please call 1-877-910-4232. Performance numbers for periods longer than one year are annualized. |

| ** | The Blended Index is a customized blend of unmanaged indices, weighted as follows: 60% MSCI World Equity Index (Net) and 40% Bloomberg-Barclays Global Aggregate Bond Index, rebalanced monthly. Investors cannot invest directly in an index or benchmark. Index returns are gross of any fees, brokerage commissions or other expenses of investing. |

| *** | The MSCI World Equity Index (Net) is a broad global equity index that represents large and mid-cap equity performance across 23 developed markets countries. It covers approximately 85% of the free float-adjusted market capitalization in each country. Investors cannot invest directly in an index or benchmark. Index returns are gross of any fees, brokerage commissions or other expenses of investing. |

| **** | Bloomberg Barclays Global Aggregate Bond Index is a measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate, and securitized fixed-rate bonds from both developed and emerging markets issuers. Investors cannot invest directly into an index or benchmark. Index returns are gross of any fees, brokerage commissions or other expenses of investing. |

The views in this report are those of the Fund’s management. This report contains certain forward-looking statements about factors that may affect the performance of the Fund in the future. These statements are based on the Fund’s management’s predictions and expectations concerning certain future events such as the performance of the economy as a whole and of specific industry sectors. Management believes these forward- looking statements are reasonable, although they are inherently uncertain and difficult to predict.

| Wealthfront Risk Parity Fund |

| PORTFOLIO REVIEW (Unaudited) |

| October 31, 2022 |

| |

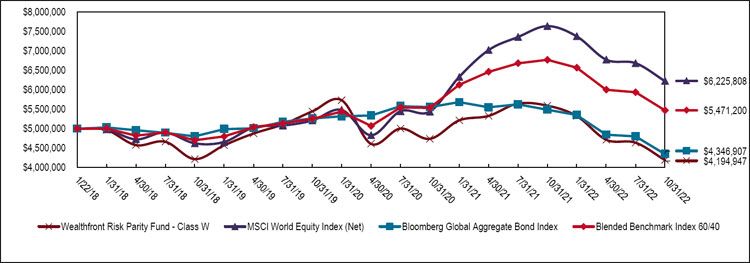

The Fund’s performance figures* for the periods ended October 31, 2022, compared to its benchmarks:

| | | Annualized |

| | One Year | Three Year | Since Inception (a) |

| Wealthfront Risk Parity Fund - Class W | (24.99)% | (8.31)% | (3.61)% |

| Bloomberg Global Aggregate Bond Index ** | (20.79)% | (6.16)% | (2.89)% |

| MSCI World Equity Index (Net) *** | (18.48)% | 6.11% | 4.70% |

| Blended Benchmark Index 60/40 **** | (19.20)% | 1.37% | 1.91% |

| | | | |

| (a) | Inception date is January 22, 2018. |

| * | The performance data quoted is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Total Returns for periods of less than one year are not annualized. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. The Fund’s estimated total annual fund operating expense ratio is 0.25% for Class W per the Fund’s Prospectus dated March 1, 2022. For performance information current to the most recent month-end, please call 1-877-910-4232. |

| ** | Bloomberg Global Aggregate Bond Index is a measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate, and securitized fixed-rate bonds from both developed and emerging markets issuers. Investors cannot invest directly into an index. Index returns are gross of any fees, brokerage commissions or other expenses of investing. |

| *** | MSCI World Equity Index (Net) is a broad global equity index that represents large and mid-cap equity performance across all 23 developed markets countries. It covers approximately 85% of the free float-adjusted market capitalization in each country. Investors cannot invest directly in an index or benchmark. Index returns are gross of any fees, brokerage commissions or other expenses of investing. |

| **** | The Blended Benchmark Index 60/40 represents a blend of 60% MSCI World Equity Index (Net) and 40% Bloomberg Global Aggregate Bond Index. |

Comparison of Change in Value of a $5,000,000 Investment

Since Inception January 22, 2018 through October 31, 2022

| Holdings by type of investment | | % of Net Assets | |

| Short Term Investments: | | | | |

| U.S. Treasury Securities | | | 109.4 | % |

| Money Market Fund | | | 2.6 | % |

| Other Assets Less Liabilities | | | (12.0 | )% |

| | | | 100.0 | % |

| | | | | |

Please refer to the Portfolio of Investments that follows in this annual report for a detail of the Fund’s holdings. Derivative exposure is included in “Other Assets and Liabilities.”

| Wealthfront Risk Parity Fund |

| PORTFOLIO OF INVESTMENTS |

| October 31, 2022 |

| Principal Amount | | | | | Yield Rate (%) | | Maturity | | Fair Value | |

| | | | | SHORT-TERM INVESTMENTS - 112.0% | | | | | | | | |

| | | | | U.S. TREASURY SECURITIES - 109.4% | | | | | | | | |

| $ | 174,000,000 | | | U.S. Treasury Bill | | 1.45 | | 11/3/2022 | | $ | 173,979,331 | |

| | 12,500,000 | | | U.S. Treasury Bill | | 2.34 | | 11/10/2022 | | | 12,491,984 | |

| | 67,000,000 | | | U.S. Treasury Bill | | 2.71 | | 11/17/2022 | | | 66,915,551 | |

| | 91,500,000 | | | U.S. Treasury Bill | | 3.20 | | 11/25/2022 | | | 91,300,141 | |

| | 135,000,000 | | | U.S. Treasury Bill | | 3.36 | | 12/1/2022 | | | 134,616,001 | |

| | 81,000,000 | | | U.S. Treasury Bill* | | 3.40 | | 12/8/2022 | | | 80,714,557 | |

| | 2,500,000 | | | U.S. Treasury Bill* | | 3.47 | | 12/15/2022 | | | 2,489,344 | |

| | 10,500,000 | | | U.S. Treasury Bill* | | 3.61 | | 12/22/2022 | | | 10,446,227 | |

| | 225,000,000 | | | U.S. Treasury Bill* | | 3.79 | | 1/5/2023 | | | 223,467,761 | |

| | 135,000,000 | | | U.S. Treasury Bill* | | 3.83 | | 12/29/2022 | | | 134,169,512 | |

| | 180,000,000 | | | U.S. Treasury Bill* | | 3.97 | | 1/12/2023 | | | 178,581,600 | |

| | 171,000,000 | | | U.S. Treasury Bill* | | 3.98 | | 1/19/2023 | | | 169,520,889 | |

| | 5,500,000 | | | U.S. Treasury Bill* | | 4.03 | | 1/26/2023 | | | 5,447,642 | |

| | | | | TOTAL U.S. TREASURY SECURITIES (Cost - $1,284,830,007) | | | 1,284,140,540 | |

| | | | | | | | | | | | | |

| Shares | | | | | | | | | | | |

| | | | | MONEY MARKET FUND - 2.6% | | | | | | | | |

| | 30,790,524 | | | First American Treasury Obligations Fund - Institutional Shares, 3.06% + (Cost - $30,790,524) | | | 30,790,524 | |

| | | | | | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 112.0% (Cost - $1,315,620,531) | | | $ | 1,314,931,064 | |

| | | | | LIABILITIES IN EXCESS OF OTHER ASSETS - NET - (12.0)% | | | (141,061,027 | ) |

| | | | | NET ASSETS - 100.0% | | | $ | 1,173,870,037 | |

| | | | | | | | | | | | | |

| + | Money market fund; interest rate reflects seven-day effective yield on October 31, 2022. |

| * | All or a portion of this security is segregated as collateral for swap contracts. |

| TOTAL RETURN SWAPS | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | Average | | | | | | Upfront | | | Unrealized | |

| Notional Amount | | | Number of | | | | | | Financing | | Termination | | | | payments/ | | | Appreciation/ | |

| at October 31, 2022 | | | Shares | | Description# | | Index | | Spread | | Date | | Counterparty | | receipts | | | (Depreciation)^ | |

| $ | 309,916,494 | | | 3,038,397 | | iShares Core U.S. Aggregate Bond ETF | | OBFR | | 23 bps | | 6/9/2023 | | JPM | | $ | — | | | $ | (21,775,798 | ) |

| | 21,683,125 | | | 223,158 | | iShares JPMorgan USD Emerging Markets Bond ETF | | OBFR | | 23 bps | | 5/8/2023 | | JPM | | | — | | | | (3,852,354 | ) |

| | 17,342,138 | | | 188,604 | | iShares JPMorgan USD Emerging Markets Bond ETF | | OBFR | | 23 bps | | 6/6/2023 | | JPM | | | — | | | | (2,310,175 | ) |

| | 67,245,780 | | | 742,473 | | iShares JPMorgan USD Emerging Markets Bond ETF | | OBFR | | 23 bps | | 6/9/2023 | | JPM | | | — | | | | (8,059,330 | ) |

| | 25,292,668 | | | 278,193 | | iShares JPMorgan USD Emerging Markets Bond ETF | | OBFR | | 23 bps | | 7/7/2023 | | JPM | | | — | | | | (3,186,875 | ) |

| | 71,410,680 | | | 583,494 | | iShares TIPS Bond ETF | | OBFR | | 10 bps | | 5/8/2023 | | JPM | | | — | | | | (6,842,259 | ) |

| | 76,110,316 | | | 628,216 | | iShares TIPS Bond ETF | | OBFR | | 10 bps | | 5/19/2023 | | JPM | | | — | | | | (6,573,247 | ) |

| | 22,028,038 | | | 182,292 | | iShares TIPS Bond ETF | | OBFR | | 10 bps | | 5/22/2023 | | JPM | | | — | | | | (1,848,973 | ) |

| | 64,818,372 | | | 549,978 | | iShares TIPS Bond ETF | | OBFR | | 10 bps | | 7/7/2023 | | JPM | | | — | | | | (5,131,457 | ) |

| | 83,061,176 | | | 713,952 | | iShares TIPS Bond ETF | | OBFR | | 10 bps | | 9/8/2023 | | JPM | | | — | | | | (6,568,796 | ) |

| | 4,017,890 | | | 8,935 | | SPDR S&P 500 ETF Trust | | OBFR | | 18 bps | | 4/24/2023 | | JPM | | | — | | | | (579,421 | ) |

| | 793,520 | | | 1,759 | | SPDR S&P 500 ETF Trust | | OBFR | | 18 bps | | 5/8/2023 | | JPM | | | — | | | | (116,469 | ) |

| | 14,143,534 | | | 32,964 | | SPDR S&P 500 ETF Trust | | OBFR | | 18 bps | | 6/6/2023 | | JPM | | | — | | | | (1,445,012 | ) |

| | 14,363,345 | | | 34,710 | | SPDR S&P 500 ETF Trust | | OBFR | | 18 bps | | 6/9/2023 | | JPM | | | — | | | | (988,604 | ) |

| | 47,815,781 | | | 114,559 | | SPDR S&P 500 ETF Trust | | OBFR | | 18 bps | | 7/6/2023 | | JPM | | | — | | | | (3,635,502 | ) |

| | 75,872 | | | 189 | | SPDR S&P 500 ETF Trust | | OBFR | | 18 bps | | 7/13/2023 | | JPM | | | — | | | | (2,951 | ) |

| | 2,544,341 | | | 6,142 | | SPDR S&P 500 ETF Trust | | OBFR | | 18 bps | | 9/8/2023 | | JPM | | | — | | | | (177,992 | ) |

| | 11,837,101 | | | 29,860 | | SPDR S&P 500 ETF Trust | | OBFR | | 18 bps | | 10/6/2023 | | JPM | | | — | | | | (305,284 | ) |

| | 10,493,624 | | | 28,919 | | SPDR S&P 500 ETF Trust | | OBFR | | 18 bps | | 11/3/2023 | | JPM | | | — | | | | 653,339 | |

| | 5,638,832 | | | 112,574 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 11/8/2022 | | JPM | | | — | | | | (1,204,574 | ) |

| | 1,786,459 | | | 36,964 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 3/1/2023 | | JPM | | | — | | | | (353,145 | ) |

| | 30,472,692 | | | 617,982 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 3/8/2023 | | JPM | | | — | | | | (6,385,510 | ) |

| | 5,923,995 | | | 126,446 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 4/3/2023 | | JPM | | | — | | | | (1,016,173 | ) |

| | 6,053,922 | | | 127,666 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 4/4/2023 | | JPM | | | — | | | | (1,099,506 | ) |

| | 5,214,346 | | | 111,728 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 4/10/2023 | | JPM | | | — | | | | (878,397 | ) |

| | 16,462,523 | | | 342,755 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 5/4/2023 | | JPM | | | — | | | | (3,187,319 | ) |

| | 7,893,038 | | | 162,911 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 5/5/2023 | | JPM | | | — | | | | (1,583,982 | ) |

| | | | | | | | | | | | | | | | | | | | | | | |

The accompanying notes are an integral part of these financial statements.

| Wealthfront Risk Parity Fund |

| PORTFOLIO OF INVESTMENTS (Continued) |

| October 31, 2022 |

| TOTAL RETURN SWAPS (Continued) | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | Average | | | | | | Upfront | | | Unrealized | |

| Notional Amount | | | Number of | | | | | | Financing | | Termination | | | | payments/ | | | Appreciation/ | |

| at October 31, 2022 | | | Shares | | Description# | | Index | | Spread | | Date | | Counterparty | | receipts | | | (Depreciation)^ | |

| $ | 26,807,140 | | | 557,094 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 5/8/2023 | | JPM | | $ | — | | | $ | (5,229,700 | ) |

| | 7,059,489 | | | 150,063 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 5/19/2023 | | JPM | | | — | | | | (1,246,269 | ) |

| | 3,053,035 | | | 66,733 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 6/6/2023 | | JPM | | | — | | | | (465,105 | ) |

| | 6,806,452 | | | 159,056 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 9/8/2023 | | JPM | | | — | | | | (695,442 | ) |

| | 2,113,859 | | | 57,839 | | Vanguard FTSE Developed Markets Index ETF | | OBFR | | 23 bps | | 11/3/2023 | | JPM | | | — | | | | 112,405 | |

| | 5,159,637 | | | 104,956 | | Vanguard FTSE Emerging Markets Stock Index ETF | | OBFR | | 23 bps | | 1/3/2023 | | JPM | | | — | | | | (1,348,272 | ) |

| | 32,868,913 | | | 660,658 | | Vanguard FTSE Emerging Markets Stock Index ETF | | OBFR | | 23 bps | | 1/6/2023 | | JPM | | | — | | | | (8,890,736 | ) |

| | 10,734,733 | | | 217,459 | | Vanguard FTSE Emerging Markets Stock Index ETF | | OBFR | | 23 bps | | 1/20/2023 | | JPM | | | — | | | | (2,835,572 | ) |

| | 11,672,812 | | | 256,657 | | Vanguard FTSE Emerging Markets Stock Index ETF | | OBFR | | 23 bps | | 5/19/2023 | | JPM | | | — | | | | (2,478,123 | ) |

| | 20,918,954 | | | 482,535 | | Vanguard FTSE Emerging Markets Stock Index ETF | | OBFR | | 23 bps | | 6/5/2023 | | JPM | | | — | | | | (3,608,754 | ) |

| | 43,494,564 | | | 1,050,119 | | Vanguard FTSE Emerging Markets Stock Index ETF | | OBFR | | 23 bps | | 9/8/2023 | | JPM | | | — | | | | (5,983,125 | ) |

| | 4,220,047 | | | 99,694 | | Vanguard FTSE Emerging Markets Stock Index ETF | | OBFR | | 23 bps | | 9/29/2023 | | JPM | | | — | | | | (653,197 | ) |

| | 15,191,248 | | | 419,416 | | Vanguard FTSE Emerging Markets Stock Index ETF | | OBFR | | 23 bps | | 11/24/2023 | | JPM | | | — | | | | (332,403 | ) |

| | 13,316,386 | | | 130,835 | | Vanguard Real Estate Index ETF | | OBFR | | 18 bps | | 11/4/2022 | | JPM | | | — | | | | (2,223,328 | ) |

| | 1,071,019 | | | 10,203 | | Vanguard Real Estate Index ETF | | OBFR | | 18 bps | | 3/1/2023 | | JPM | | | — | | | | (214,692 | ) |

| | 10,776,522 | | | 102,614 | | Vanguard Real Estate Index ETF | | OBFR | | 18 bps | | 3/8/2023 | | JPM | | | — | | | | (2,161,871 | ) |

| | 21,637,371 | | | 199,662 | | Vanguard Real Estate Index ETF | | OBFR | | 18 bps | | 5/4/2023 | | JPM | | | — | | | | (4,988,163 | ) |

| | 47,677,823 | | | 478,693 | | Vanguard Real Estate Index ETF | | OBFR | | 18 bps | | 7/6/2023 | | JPM | | | — | | | | (7,667,666 | ) |

| | 56,369 | | | 581 | | Vanguard Real Estate Index ETF | | OBFR | | 18 bps | | 7/10/2023 | | JPM | | | — | | | | (7,793 | ) |

| | 3,447,629 | | | 36,960 | | Vanguard Real Estate Index ETF | | OBFR | | 18 bps | | 8/22/2023 | | JPM | | | — | | | | (371,568 | ) |

| | 4,948,685 | | | 51,031 | | Vanguard Real Estate Index ETF | | OBFR | | 18 bps | | 9/8/2023 | | JPM | | | — | | | | (697,710 | ) |

| | | | | | | | | | | | | | | | | $ | — | | | $ | (140,442,850 | ) |

| | | | | | | | | | | | | | | | | | | | | | | |

| # | Each total return swap accesses a single exchange-traded fund as referenced below and settles to cash upon termination of the swap. |

| ^ | Includes accrued dividend and interest income, and swap fees. |

ETF - Exchange-Traded Fund

JPM - JP Morgan

OBFR - Overnight Bank Funding Rate

The accompanying notes are an integral part of these financial statements.

| Wealthfront Risk Parity Fund |

| STATEMENT OF ASSETS AND LIABILITIES |

| October 31, 2022 |

| ASSETS | | | | |

| Investment securities: | | | | |

| At cost | | $ | 1,315,620,531 | |

| At fair value | | $ | 1,314,931,064 | |

| Interest receivable | | | 368,900 | |

| Receivable for Fund shares sold | | | 395,429 | |

| Receivable for swap | | | 676 | |

| Prepaid expenses & other assets | | | 2,913 | |

| TOTAL ASSETS | | | 1,315,698,982 | |

| | | | | |

| LIABILITIES | | | | |

| Net unrealized depreciation on swap contracts | | | 140,442,850 | |

| Payable for Fund shares redeemed | | | 1,147,559 | |

| Advisory fees payable | | | 238,536 | |

| TOTAL LIABILITIES | | | 141,828,945 | |

| NET ASSETS | | $ | 1,173,870,037 | |

| | | | | |

| Net Assets Consist Of: | | | | |

| Paid in capital ($0 par value, unlimited shares authorized) | | $ | 1,475,582,183 | |

| Accumulated deficit | | | (301,712,146 | ) |

| NET ASSETS | | $ | 1,173,870,037 | |

| | | | | |

| Net Asset Value Per Share: | | | | |

| Class W Shares: | | | | |

| Net Assets | | $ | 1,173,870,037 | |

| Shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | | | 152,994,992 | |

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share | | $ | 7.67 | |

| | | | | |

The accompanying notes are an integral part of these financial statements.

| Wealthfront Risk Parity Fund |

| STATEMENT OF OPERATIONS |

| For the Year Ended October 31, 2022 |

| INVESTMENT INCOME | | | | |

| Interest | | $ | 11,590,213 | |

| | | | | |

| EXPENSES | | | | |

| Investment advisory fees | | | 3,339,559 | |

| Legal fees | | | 3,215 | |

| Trustees fees and expenses | | | 13,887 | |

| TOTAL EXPENSES | | | 3,356,661 | |

| | | | | |

| NET INVESTMENT INCOME | | | 8,233,552 | |

| | | | | |

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS AND SWAP CONTRACTS | | | | |

| Net realized loss on: | | | | |

| Investments | | | (1,014 | ) |

| Swap contracts | | | (162,101,876 | ) |

| | | | (162,102,890 | ) |

| | | | | |

| Net change in unrealized depreciation on: | | | | |

| Investments | | | (619,128 | ) |

| Swap contracts | | | (246,138,301 | ) |

| | | | (246,757,429 | ) |

| | | | | |

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS AND SWAP CONTRACTS | | | (408,860,319 | ) |

| | | | | |

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | (400,626,767 | ) |

| | | | | |

The accompanying notes are an integral part of these financial statements.

| Wealthfront Risk Parity Fund |

| STATEMENTS OF CHANGES IN NET ASSETS |

| | | Year Ended | | | Year Ended | |

| | | October 31, | | | October 31, | |

| | | 2022 | | | 2021 | |

| FROM OPERATIONS | | | | | | | | |

| Net investment income/(loss) | | $ | 8,233,552 | | | $ | (2,896,331 | ) |

| Net realized gain/(loss) from investments and swap contracts | | | (162,102,890 | ) | | | 109,029,994 | |

| Net change in unrealized appreciation/(depreciation) on investments and swap contracts | | | (246,757,429 | ) | | | 92,544,299 | |

| Net increase/(decrease) in net assets resulting from operations | | | (400,626,767 | ) | | | 198,677,962 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| Total distributions paid | | | (54,436,288 | ) | | | — | |

| | | | | | | | | |

| FROM SHARES OF BENEFICIAL INTEREST | | | | | | | | |

| Proceeds from shares sold: | | | 390,341,428 | | | | 738,795,595 | |

| Payments for shares redeemed: | | | (346,709,293 | ) | | | (327,172,768 | ) |

| Net increase in net assets from shares of beneficial interest | | | 43,632,135 | | | | 411,622,827 | |

| | | | | | | | | |

| TOTAL INCREASE/(DECREASE) IN NET ASSETS | | | (411,430,920 | ) | | | 610,300,789 | |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

| Beginning of year | | | 1,585,300,957 | | | | 975,000,168 | |

| End of year | | $ | 1,173,870,037 | | | $ | 1,585,300,957 | |

| | | | | | | | | |

| SHARE ACTIVITY | | | | | | | | |

| Shares sold | | | 42,028,562 | | | | 73,315,711 | |

| Shares redeemed | | | (38,668,333 | ) | | | (32,294,396 | ) |

| Net increase in shares of beneficial interest outstanding | | | 3,360,229 | | | | 41,021,315 | |

| | | | | | | | | |

The accompanying notes are an integral part of these financial statements.

| Wealthfront Risk Parity Fund |

| FINANCIAL HIGHLIGHTS |

| |

| Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Year/Period |

| | | Class W (1) | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Period Ended | |

| | | October 31, | | | October 31, | | | October 31, | | | October 31, | | | October 31, | |

| | | 2022 | | | 2021 | | | 2020 | | | 2019 | | | 2018 | |

| Net asset value, beginning of year/period | | $ | 10.59 | | | $ | 8.98 | | | $ | 10.59 | | | $ | 8.36 | | | $ | 10.00 | |

| Activity from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income/(loss) (2) | | | 0.05 | | | | (0.02 | ) | | | 0.05 | | | | 0.18 | | | | 0.11 | |

| Net realized and unrealized gain/(loss) on investments | | | (2.61 | ) | | | 1.63 | | | | (1.39 | ) | | | 2.23 | | | | (1.68 | ) (3) |

| Total from investment operations | | | (2.56 | ) | | | 1.61 | | | | (1.34 | ) | | | 2.41 | | | | (1.57 | ) |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | (0.04 | ) | | | — | | | | (0.05 | ) | | | (0.18 | ) | | | (0.07 | ) |

| Net realized gains | | | (0.32 | ) | | | — | | | | (0.22 | ) | | | — | | | | — | |

| Return of capital | | | — | | | | — | | | | (0.00 | ) (8) | | | — | | | | — | |

| Total distributions | | | (0.36 | ) | | | — | | | | (0.27 | ) | | | (0.18 | ) | | | (0.07 | ) |

| Net asset value, end of year/period | | $ | 7.67 | | | $ | 10.59 | | | $ | 8.98 | | | $ | 10.59 | | | $ | 8.36 | |

| Total return (4) | | | (24.92 | )% | | | 17.93 | % (9) | | | (12.94 | )% | | | 29.08 | % | | | (15.68 | )% |

| Net assets, end of year/period (000’s) | | $ | 1,173,870 | | | $ | 1,585,301 | | | $ | 975,000 | | | $ | 997,925 | | | $ | 758,869 | |

| Ratio of expenses to average net assets (5) | | | 0.24 | % | | | 0.24 | % | | | 0.24 | % | | | 0.24 | % | | | 0.27 | % (6) |

| Ratio of net investment income/(loss) to average net assets (5) | | | 0.59 | % | | | (0.21 | )% | | | 0.49 | % | | | 1.92 | % | | | 1.56 | % (6) |

| Portfolio Turnover Rate | | | 0 | % | | | 0 | % | | | 0 | % | | | 0 | % | | | 0 | % (7) |

| | | | | | | | | | | | | | | | | | | | | |

| (1) | The Wealthfront Risk Parity Fund commenced operations on January 22, 2018. |

| (2) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (3) | Net realized and unrealized gain/(loss) on investments per share are balancing amounts necessary to reconcile the change in net asset value per share for the period, and may not reconcile with aggregate gains/(losses) in the Statement of Operations due to the share transactions for the period. |

| (4) | Total returns are historical and assume changes in share price and reinvestment of dividends and distributions. Total returns for periods of less than one year are not annualized. |

| (5) | Does not include the expenses of other investment companies in which the Fund invests, if any. |

| (8) | Amount represents less than $0.005. |

| (9) | Includes adjustments in accordance with accounting principles generally accepted in the United States and, consequently the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

The accompanying notes are an integral part of these financial statements.

| Wealthfront Risk Parity Fund |

| NOTES TO FINANCIAL STATEMENTS |

| April 30, 2022 |

| |

Wealthfront Risk Parity Fund (the “Fund”) is a series of shares of beneficial interest of the Two Roads Shared Trust (the “Trust”), a statutory trust organized under the laws of the State of Delaware on June 8, 2012, and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a diversified, open-end management investment company. The Fund offers Class W shares. The Fund commenced investment operations for Class W shares on January 22, 2018. The Fund’s investment objective is to seek long-term total return, which consists of both capital appreciation and income.

On September 2, 2022, UBS Americas, Inc. (“UBS”) and Wealthfront Corporation, the Adviser’s parent company, mutually agreed to terminate their merger agreement, initially announced January 26, 2022, under which Wealthfront Corporation was to be acquired by UBS.

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies followed by the Fund in preparation of its financial statements. The policies are in conformity with U.S. generally accepted accounting principles in the United States of America (“U.S. GAAP”) . The preparation of the financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the period. Actual results could differ from those estimates. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies”.

Securities Valuation – Securities listed on an exchange are valued at the last reported sale price at the close of the regular trading session of the exchange on the business day the value is being determined, or in the case of securities listed on NASDAQ at the NASDAQ Official Closing Price. In the absence of a sale, such securities shall be valued at the mean between the current bid and ask prices on the primary exchange on the day of valuation. Debt securities, including U.S. government obligation (other than short-term obligations) are valued each day by an independent pricing service approved by the Trust’s Board of Trustees (the “Board”) based on methods which include consideration of: yields or prices of securities of comparable quality, coupon, maturity and type, indications as to values from dealers, and general market conditions or market quotations from a major market maker in the securities. Total return swaps on exchange-listed securities shall be valued at the last quoted sales price or, in the absence of a sale, at the mean between the current bid and ask prices on the day of valuation- on each underlying exchange-listed security. The independent- pricing service does not distinguish between smaller sized bond positions known as “odd lots” and larger institutional sized bond positions known as “round lots”. The Fund may fair value a particular bond if the adviser does not believe that the round lot value provided by the independent pricing service reflects fair value of the Fund’s holding. Short-term debt obligations having 60 days or less remaining until maturity, at the time of purchase, may be valued at amortized cost which approximates fair value.

Valuation of Underlying Funds – The Fund may invest in portfolios of open-end or closed-end investment companies (the “Underlying Funds”). The Underlying Funds value securities in their portfolios for which market quotations are readily available at their market values (generally the last reported sale price) and all other securities and assets at their fair value according to the methods established by the board of directors of the Underlying Funds.

Open-end investment companies are valued at their respective net asset values as reported by such investment companies. The shares of many closed -end investment companies, after their initial public offering, frequently trade at a price per share, which is different than the net asset value per share. The difference represents a market premium or market discount of such shares. There can be no assurances that the market discount or market premium on shares of any closed-end investment company purchased by the Fund will not change.

| Wealthfront Risk Parity Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| October 31, 2022 |

| |

The Fund may hold securities, such as private investments, interests in commodity pools, other non-traded securities or temporarily illiquid securities, for which market quotations are not readily available or are determined to be unreliable. These securities will be valued using the “fair value” procedures approved by the Board. The Board has designated the adviser as its valuation designee (the “Valuation Designee”) to execute these procedures. The Board may also enlist third party consultants such a valuation specialist at a public accounting firm, valuation consultant or financial officer of a security issuer on an as-needed basis to assist the Valuation Designee in determining a security-specific fair value. The Board is responsible for reviewing and approving fair value methodologies utilized by the Valuation Designee, approval of which shall be based upon whether the Valuation Designee followed the valuation procedures established by the Board.

Fair Valuation Process – The applicable investments are valued by the Valuation Designee pursuant to valuation procedures established by the Board. For example, fair value determinations are required for the following securities: (i) securities for which market quotations are insufficient or not readily available on a particular business day (including securities for which there is a short and temporary lapse in the provision of a price by the regular pricing source); (ii) securities for which, in the judgment of the Valuation Designee, the prices or values available do not represent the fair value of the instrument; factors which may cause the Valuation Designee to make such a judgment include, but are not limited to, the following: only a bid price or an asked price is available; the spread between bid and asked prices is substantial; the frequency of sales; the thinness of the market; the size of reported trades; and actions of the securities markets, such as the suspension or limitation of trading; (iii) securities determined to be illiquid; and (iv) securities with respect to which an event that affects the value thereof has occurred (a “significant event”) since the closing prices were established on the principal exchange on which they are traded, but prior to a Fund’s calculation of its net asset value. Specifically, interests in commodity pools or managed futures pools are valued on a daily basis by reference to the closing market prices of each futures contract or other asset held by a pool, as adjusted for pool expenses. Restricted or illiquid securities, such as private investments or non-traded securities are valued based upon the current bid for the security from two or more independent dealers or other parties reasonably familiar with the facts and circumstances of the security (who should take into consideration all relevant factors as may be appropriate under the circumstances). If a current bid from such independent dealers or other independent parties is unavailable, the Valuation Designee shall determine the fair value of such security using the following factors: (i) the type of security; (ii) the cost at date of purchase; (iii) the size and nature of the Fund’s holdings; (iv) the discount from market value of unrestricted securities of the same class at the time of purchase and subsequent thereto; (v) information as to any transactions or offers with respect to the security; (vi) the nature and duration of restrictions on disposition of the security and the existence of any registration rights; (vii) how the yield of the security compares to similar securities of companies of similar or equal creditworthiness; (viii) the level of recent trades of similar or comparable securities; (ix) the liquidity characteristics of the security; (x) current market conditions; and (xi) the market value of any securities into which the security is convertible or exchangeable.

The Fund utilizes various methods to measure the fair value of all of their investments on a recurring basis. U.S. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Fund has the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument in an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available; representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

| Wealthfront Risk Parity Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| October 31, 2022 |

| |

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following tables summarize the inputs used as of October 31, 2022 for the Fund’s assets and liabilities measured at fair value:

Wealthfront Risk Parity Fund

| Assets * | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| U.S. Treasury Securities | | $ | — | | | $ | 1,284,140,540 | | | $ | — | | | $ | 1,284,140,540 | |

| Money Market Fund | | | 30,790,524 | | | | — | | | | — | | | | 30,790,524 | |

| Total Assets | | $ | 30,790,524 | | | $ | 1,284,140,540 | | | $ | — | | | $ | 1,314,931,064 | |

| | | | | | | | | | | | | | | | | |

| Liabilities * | | | | | | | | | | | | | | | | |

| Swap Contracts | | $ | — | | | $ | 140,442,850 | | | $ | — | | | $ | 140,442,850 | |

| Total Liabilities | | $ | — | | | $ | 140,442,850 | | | $ | — | | | $ | 140,442,850 | |

| * | Refer to the Portfolio of Investments for classification. |

The Fund did not hold any Level 3 securities during the year ended October 31, 2022.

Security Transactions and Investment Income – Security transactions are accounted for on trade date basis. Interest income is recognized on an accrual basis. Discounts are accreted and premiums are amortized on securities purchased over the lives of the respective securities. Dividend income is recorded on the ex-dividend date. Realized gains or losses from sales of securities are determined by comparing the identified cost of the security lot sold with the net sales proceeds.

Dividends and Distributions to Shareholders – Dividends from net investment income are declared and distributed quarterly. Distributions from net realized capital gains are declared and distributed annually. Dividends from net investment income and distributions from net realized gains are recorded on ex- dividend date and determined in accordance with federal income tax regulations, which may differ from U.S. GAAP. These “book/tax” differences are considered either temporary (i.e., deferred losses, capital loss carry forwards) or permanent in nature. To the extent these differences are permanent in nature, such amounts are reclassified within the composition of net assets based on their federal tax-basis treatment. Temporary differences do not require reclassification.

Federal Income Taxes – It is the Fund’s policy to qualify as a regulated investment company by complying with the provisions of the Internal Revenue Code that are applicable to regulated investment companies and to distribute substantially all of their taxable income and net realized gains to shareholders. Therefore, no federal income tax provision has been recorded.

| Wealthfront Risk Parity Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| October 31, 2022 |

| |

The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Fund’s tax positions and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on returns filed for open tax years ended October 31, 2019-October 31, 2021, or is expected to be taken in the Fund’s October 31, 2022 year-end tax returns. The Fund identifies its major tax jurisdictions as U.S. Federal, Ohio, and foreign jurisdictions where the Fund makes significant investments. The Fund is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next twelve months.

Expenses – Expenses of the Trust that are directly identifiable to a specific fund are charged to that fund. Expenses, which are not readily identifiable to a specific fund, are allocated in such a manner as deemed equitable, taking into consideration the nature and type of expense and the relative sizes of the funds in the Trust.

Swap Agreements – The Fund may enter into various swap transactions for investment purposes or to manage interest rate, equity, or credit risk. These would be two-party contracts entered into primarily to exchange the returns (or differentials in rates of returns) earned or realized on particular pre-determined investments or instruments.

The gross returns to be exchanged or “swapped” between parties are calculated with respect to a notional amount, i.e., the return on or increase in value of a particular dollar amount invested at a particular interest rate, or in a “basket” of securities representing a particular index or market segment. Changes in the value of swap agreements are recognized as unrealized gains or losses in the Statement of Operations by “marking to market” on a daily basis to reflect the value of the swap agreement at the end of each day as reported by the swap counterparty. Net unrealized depreciation on swap contracts as shown on the statement of assets and liabilities as of October 31, 2022 includes changes in the fair value of the underlying, and receivables and payables for income and financing payments, respectively. Realized gains and losses from the decrease in notional value of the swap are recognized on trade date. A liquidation payment received or made at the termination of the swap agreement is recorded as a realized gain or loss on the Statement of Operations.

As of October 31, 2022, the unrealized depreciation on swap contracts subject to equity risk was $140,442,850. For the year ended October 31, 2022, the net change in unrealized depreciation on swap contracts subject to equity risk was $ 246,138,301. For the year ended October 31, 2022, the Fund had a realized loss of $162,101,876 on swap contracts subject to equity risk.

Offsetting of Financial Assets and Derivative Assets

The following table presents the Fund’s asset and liability derivatives available for offset under a master netting arrangement along with collateral pledged for these contracts as of October 31, 2022.

| | | | | | | | | | | | Gross Amounts Not Offset in the | | | | |

| | | | | | | | | | | | Statement of Assets & Liabilities | | | | |

| | | | | | Gross Amounts | | | Net Amount of | | | | | | | | | | |

| | | Gross Amounts | | | Offset in the | | | Assets/Liabilities | | | | | | | | | | |

| | | of Recognized | | | Statement of Assets | | | Present in the Statement | | | Financial | | | Cash Collateral | | | | |

| Description | | Assets/Liabilities | | | and Liabilities | | | of Assets and Liabilities | | | Instruments | | | Pledged | | | Total | |

| Assets | | | | | | | | | | | | | | | | | | | | | | | | |

| Swap Contracts | | $ | 765,744 | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

| Liabilities | | | | | | | | | | | | | | | | | | | | | | | | |

| Swap Contracts | | $ | 141,208,594 | | | $ | (765,744 | ) | | $ | 140,442,850 | (1) | | $ | 140,442,850 | (2) | | $ | — | | | $ | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | Net unrealized depreciation as presented in the Portfolio of Investments. |

| (2) | Total value of securities pledged as collateral to broker as of October 31, 2022 was $152,846,258. |

The notional value of the derivative instruments outstanding as of October 31, 2022 as disclosed in the Portfolio of Investments and the amounts of realized and changes in unrealized gains and losses on derivative instruments during the year ended October 31, 2022 as disclosed above and within the Statement of Operations serve as indicators of the volume of derivative activity for the Fund.

| Wealthfront Risk Parity Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| October 31, 2022 |

| |

Indemnification – The Trust indemnifies its officers and Trustees for certain liabilities that may arise from the performance of their duties to the Trust. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnities. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, the fund expects risk of loss due to these warranties and indemnities to be remote.

| 3. | INVESTMENT TRANSACTIONS AND ASSOCIATED RISKS |

For the year ended October 31, 2022, there were no aggregate purchases and sales of investments (excluding U.S. Government securities and short-term investments).

The Fund’s investments in securities, financial instruments and derivatives expose it to various risks, certain of which are discussed below. Please refer to the Fund’s prospectus and statement of additional information for further information regarding the risks associated with the Fund’s investments which include, but are not limited to commodities risk, correlation risk, counterparty credit risk, credit risk, cybersecurity risk, derivatives risk, emerging market risk, equity risk, fixed income securities risk (including call risk, credit risk, duration risk, interest rate risk, liquidity risk, and prepayment and extension risk), foreign (non U.S.) investment risk, forward and futures contract risk, gap risk, high portfolio turnover risk, interest rate risk, investment companies and exchange-traded funds risk (including other ETF risk and money market fund risk), leveraging risk, LIBOR risk, managed volatility strategy risk, management risk, market risk, market events risk, model and data risk, real estate investment trusts risk, regulatory risk, swap agreements risk, swap risk, tax risk, treasury inflation-protected securities (“TIPS”) risk, U.S. government securities risk and volatility risk.

Commodities Risk – Exposure to commodities markets may subject the Fund to greater volatility than investments in traditional securities. The value of commodity-linked derivative instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. The prices of energy, industrial metals, precious metals, agriculture, and livestock sector commodities may fluctuate widely due to factors such as changes in value, supply and demand and governmental regulatory policies. The commodity-linked securities in which the Fund invests may be issued by companies in the financial services sector, including the banking, brokerage and insurance sectors. As a result, events affecting issuers in the financial services sector may cause the Fund’s share value to fluctuate.

Correlation Risk – Because the Fund’s investment strategy seeks to balance risk across multiple asset classes, to the extent the asset classes become correlated in a way not anticipated by Wealthfront Strategies LLC (the “Adviser”), the Fund’s risk allocation process may result in magnified risks and loss instead of balancing (reducing) the risk of loss.

Counterparty Credit Risk – The Fund may enter into various types of derivative contracts. Many of these derivative contracts will be privately negotiated in the over- the-counter market. These contracts also involve exposure to credit risk, since contract performance depends in part on the financial condition of the counterparty. If a privately negotiated over-the-counter contract calls for payments by the Fund, the Fund must be prepared to make such payments when due. In addition, if a counterparty’s creditworthiness declines, or if a counterparty becomes the subject of insolvency proceedings, the Fund may not receive payments owed under the contract, or such payments may be delayed under such circumstances and the value of agreements with such counterparty can be expected to decline, potentially resulting in losses to the Fund. The Adviser considers factors such as counterparty credit ratings and financial statements among others when determining whether a counterparty is creditworthy. The Adviser regularly monitors the creditworthiness of each counterparty with which the Fund enters into a transaction. In addition, the Fund may enter into swap agreements with only a single counterparty or with a limited number of counterparties, which as a result increases the Fund’s exposure to counterparty risk. There is the risk that a counterparty refuses to continue to enter into swap agreements with the Fund in the future, or requires increased fees, which could impair the Fund’s ability to achieve its investment objective. A swap counterparty may also increase its collateral or margin requirements, due to regulatory requirements or otherwise, which may limit or restrict the Fund’s ability to use, or increase the cost to the Fund of, leverage and thereby reduce the Fund’s investment returns. If the Fund is not able to enter into a particular derivatives transaction, the Fund’s investment performance and risk profile could be adversely affected as a result. These risks are magnified by the Fund’s limited number of counterparties.

| Wealthfront Risk Parity Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| October 31, 2022 |

| |

Credit Risk – The risk that the Fund could lose money if the issuer or guarantor of a fixed income security, including as an asset of an ETF or as the issuer of the reference asset of a total return swap, is unwilling or unable to make timely payments to meet its contractual obligations on investments held by the Fund. In addition, the credit quality of securities held by the Fund may be lowered if an issuer’s financial condition changes, which may lower their value and may affect their liquidity.

Derivatives Risk – In general, a derivative instrument typically involves leverage, i.e., it provides exposure to potential gain or loss from a change in the level of the market price of the underlying security or commodity (or a basket or index) in a notional amount that exceeds the amount of cash or assets required to establish or maintain the derivative instrument. Adverse changes in the value or level of the underlying asset can result in a loss to the Fund substantially greater than the amount invested in the derivative itself. The use of derivative instruments also exposes the Fund to additional risks and transaction costs. A risk of the Fund’s use of derivatives is that the fluctuations in their values may not correlate perfectly with the overall securities markets. Derivative instruments may be more volatile than other instruments and may be subject to unanticipated market movements, which are potentially unlimited. Additionally, to the extent the Fund is required to segregate or “set aside” (often referred to as “asset segregation”) liquid assets or otherwise cover open positions with respect to certain derivative instruments, the Fund may be required to sell portfolio instruments to meet these asset segregation requirements. There is a possibility that segregation involving a large percentage of the Fund’s assets could impede portfolio management or the Fund’s ability to meet redemption requests or other current obligations. Certain derivatives require the Fund to make margin payments and the Fund may have to post additional margin if the value of the derivative position decreases in a manner adverse to the Fund.

Emerging Market Risk – Investing in emerging markets involves not only the risks described below with respect to investing in foreign securities, but also other risks, including exposure to economic structures that are generally less diverse and mature, and to political systems that can be expected to have less stability, than those of developed countries. The typically small size of the markets may also result in a lack of liquidity and in price volatility of these securities.

Emerging markets are riskier than more developed markets because they tend to develop unevenly and may never fully develop. Investments in emerging markets may be considered speculative and share the risks of foreign developed markets but to a greater extent. Emerging markets are more likely to experience hyperinflation and currency devaluations, which adversely affect returns to U.S. investors. In addition, many emerging financial markets have far lower trading volumes and less liquidity than developed markets, which may result in increased price volatility of emerging market investments.

Foreign (Non-U.S.) Investment Risk – Foreign (non-U.S.) securities present greater investment risks than investing in the securities of U.S. issuers and may experience more rapid and extreme changes in value than the securities of U.S. companies, due to less information about foreign (non-U.S.) companies in the form of reports and ratings than about U.S. issuers; different accounting, auditing and financial reporting requirements; smaller markets; nationalization; expropriation or confiscatory taxation; currency blockage; or political changes or diplomatic developments. Foreign (non-U.S.) securities may also be less liquid and more difficult to value than securities of U.S. issuers.

Interest Rate Risk – Generally, when interest rates rise, prices of fixed-income securities fall. However, market factors, such as the demand for particular fixed-income securities, may cause the price of certain fixed- income securities to fall while the prices of other securities rise or remain unchanged. Certain countries have experienced negative interest rates on certain fixed-income instruments. Very low or negative interest rates may magnify interest rate risk. Changing interest rates, including rates that fall below zero, may have unpredictable effects on markets, may result in heightened market volatility and may detract from Fund performance to the extent the Fund is exposed to such interest rates and/or volatility.

| Wealthfront Risk Parity Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| October 31, 2022 |

| |

Investment Companies and ETFs Risk – When the Fund invest in other investment companies, including ETFs, it will bear additional expenses based on its pro rata share of the other investment company’s or ETF’s operating expenses, including the potential duplication of management fees. The risk of owning an investment company or ETF generally reflects the risks of owning the underlying investments held by the investment company. The Fund will also bear brokerage costs when it purchases and sells ETFs. In addition to the risks associated with the underlying assets held by an ETF, investments in ETFs are subject to the following additional risks: (1) an ETF’s shares may trade above or below its net asset value; (2) an active trading market for the ETF’s shares may not develop or be maintained; (3) trading an ETF’s shares may be halted by the listing exchange; (4) a passively managed ETF may not track the performance of the reference asset; or underlying managed index and (5) a passively managed ETF may hold troubled securities. The Fund may invest in money market mutual funds. An investment in a money market mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Certain money market mutual funds are not required to preserve the value of the Fund’s investment at $1.00 per share.

LIBOR Risk – The Fund may invest in securities and other instruments whose interest payments are determined by references to the London Interbank Offered Rate (“LIBOR”).

The United Kingdom Financial Conduct Authority, which regulates LIBOR, announced its intention to cease its active encouragement of banks to provide the quotations needed to sustain LIBOR after 2021. ICE Benchmark Administration Limited, the administrator of LIBOR, ceased publication of certain LIBOR settings on a representative basis at the end of 2021 and is expected to cease publication of the remaining LIBOR settings on a representative basis after June 30, 2023. The U.S. Federal Reserve has begun publishing Secured Overnight Financing Rate (SOFR), a broad measure of secured overnight U.S. Treasury repo rates, that is intended to replace USD LIBOR. The unavailability of LIBOR presents risks to the Fund, including the risk that any pricing or adjustments to the Fund’s investments resulting from a substitute or alternate reference rate may adversely affect the Fund’s performance and/or NAV. It remains uncertain how such changes would be implemented and the effects such changes would have on the Fund, including any negative effects on the Fund’s liquidity and valuation of the Fund’s investments, issuers of instruments in which the Fund invests and financial markets generally.

Market Risk – Overall market risk may affect the value of individual instruments in which the Fund invests. The Fund is subject to the risk that the securities markets will move down, sometimes rapidly and unpredictably, based on overall economic conditions and other factors, which may negatively affect the Fund’s performance. Factors such as domestic and foreign (non-U.S.) economic growth and market conditions, real or perceived adverse economic or political conditions, inflation, changes in interest rate levels, lack of liquidity in the bond and other markets, volatility in the securities markets, adverse investor sentiment affect the securities markets and political events affect the securities markets. U.S. and foreign stock markets have experienced periods of substantial price volatility in the past and may do so again in the future. Securities markets also may experience long periods of decline in value. When the value of the Fund’s investments goes down, your investment in the Fund decreases in value and you could lose money.

Local, state, regional, national or global events such as war, acts of terrorism, the spread of infectious illness or other public health issues, recessions, or other events could have a significant impact on the Fund and its investments and could result in decreases to the Fund’s net asset value. Political, geopolitical, natural and other events, including war, terrorism, trade disputes, government shutdowns, market closures, natural and environmental disasters, epidemics, pandemics and other public health crises and related events and governments’ reactions to such events have led, and in the future may lead, to economic uncertainty, decreased economic activity, increased market volatility and other disruptive effects on U.S. and global economies and markets. Such events may have significant adverse direct or indirect effects on the Fund and its investments. For example, a widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, impact the ability to complete redemptions, and affect Fund performance. A health crisis may exacerbate other pre-existing political, social and economic risks. In addition, the increasing interconnectedness of markets around the world may result in many markets being affected by events or conditions in a single country or region or events affecting a single or small number of issuers.

| Wealthfront Risk Parity Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| October 31, 2022 |

| |

COVID-19 has resulted in travel restrictions, closed international borders, enhanced health screenings at ports of entry and elsewhere, disruption of and delays in healthcare service preparation and delivery, prolonged quarantines, cancellations, business and school closings, supply chain disruptions, and lower consumer demand, as well as general concern and uncertainty. The impact of COVID-19, and other infectious illness outbreaks that may arise in the future, could adversely affect the economies of many nations or the entire global economy, individual issuers and capital markets in ways that cannot necessarily be foreseen.

Model and Data Risk – Given the complexity of the investments and strategies of the Fund, the Adviser relies heavily on models, and information and data supplied by third parties (“Models and Data”). Models and Data are used to construct sets of transactions and investments and to provide risk management insights. The Fund may be exposed to additional risks when Models and Data prove to be incorrect or incomplete. Some of the models used by the Adviser for the Fund are predictive in nature. The use of predictive models has inherent risks. Because predictive models are usually constructed based on historical data supplied by third parties, the success of relying on such models may depend heavily on the accuracy and reliability of the supplied historical data. The Fund bears the risk that the models used by the Adviser will not be successful in determining the weighting of investment positions that will enable the Fund to achieve its investment objective.

Swap Risk – Swap agreements are subject to the risk that the counterparty to the swap will default on its obligation to pay the Fund and the risk that the Fund will not be able to meet its obligations to pay the counterparty to the swap. In addition, there is the risk that a swap may be terminated by the Fund or the counterparty in accordance with its terms. If a swap were to terminate, the Fund may be unable to implement its investment strategies and the Fund may not be able to seek to achieve its investment objective.

TIPS Risk – TIPS are debt instruments issued by the United States Department of the Treasury. The principal of TIPS increases with inflation and decreases with deflation, as measured by the Consumer Price Index. When TIPS mature, investors are paid the adjusted principal or original principal, whichever is greater. Interest payments on TIPS are unpredictable and will fluctuate as the principal and corresponding interest payments are adjusted for inflation. Inflation-indexed bonds generally pay a lower nominal interest rate than a comparable non-inflation-indexed bond. There can be no assurance that the CPI will accurately measure the real rate of inflation in the prices of goods and services. Any increases in the principal amount of TIPS will be considered taxable ordinary income, even though the Fund will not receive the principal until maturity. As a result, the Fund may make income distributions to shareholders that exceed the cash it receives. In addition, TIPS are subject to credit risk, interest rate risk, and duration risk.

U.S. Government Securities Risk – Treasury obligations may differ in their interest rates, maturities, times of issuance and other characteristics. Obligations of U.S. Government agencies and authorities are supported by varying degrees of credit but generally are not backed by the full faith and credit of the U.S. Government. No assurance can be given that the U.S. Government will provide financial support to its agencies and authorities if it is not obligated by law to do so. In addition, the value of U.S. Government securities may be affected by changes in the credit rating of the U.S. Government.

Volatility Risk – The Fund or an underlying fund may have investments that appreciate or decrease significantly in value over short periods of time. The value of an investment in the Fund’s or an underlying fund’s portfolio may fluctuate due to factors that affect markets generally or that affect a particular industry or sector. The value of an investment in the Fund’s portfolio may also be more volatile than the market as a whole. This volatility may affect the Fund’s net asset value per share, including by causing it to experience significant increases or declines in value over short periods of time. Events or financial circumstances affecting individual investments, industries or sectors may increase the volatility of the Fund. In addition, the Fund’s derivative investments can be highly volatile, and the Fund may experience large losses when buying, selling or holding such instruments. High volatility may have an adverse impact on the Fund.

| Wealthfront Risk Parity Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| October 31, 2022 |

| |

| 4. | INVESTMENT ADVISORY AGREEMENT AND TRANSACTION WITH RELATED PARTIES |

Wealthfront Strategies LLC serves as the Fund’s investment adviser. Pursuant to an advisory agreement with the Trust on behalf of the Fund, the Adviser, under the oversight of the Board, provides the investment management program for the Fund. Effective February 28, 2019, as compensation for its services and the related expenses borne by the Adviser, the Fund pays the Adviser a unitary fee computed and accrued daily, and paid monthly, based on the Fund’s average daily net assets at the annual rate of 0.24%. Pursuant to the advisory agreement, the Fund incurred $3,339,559 in advisory fees for the year ended October 31, 2022.

The Fund’s management fee is a “unitary” fee that includes all operating expenses payable by the Fund, except for the Fund’s pro rata portion of the fees and expenses associated with the Fund’s independent trustees (including independent trustees legal counsel fees), brokerage fees and commissions, taxes, borrowing costs (such as dividend expenses on securities sold short and interest), fees and expenses of other investment companies in which the Fund may invest, and such extraordinary or non-recurring expenses as may arise, including litigation expenses. The fee is computed daily and payable monthly.

The distributor of the Fund is Northern Lights Distributors, LLC (the “Distributor”), an affiliate of Ultimus Fund Solutions, LLC.

In addition, certain affiliates of the Distributor provide services to the Fund as follows:

Ultimus Fund Solutions, LLC (“UFS”)

UFS, an affiliate of the Distributor, provides administration, fund accounting, and transfer agent services to the Trust. Pursuant to separate servicing agreements with UFS, the Adviser, on behalf of the Fund, pays UFS customary fees for providing administration, fund accounting and transfer agency services to the Fund. Certain officers of the Trust are also officers of UFS, and are not paid any fees directly by the Fund for serving in such capacities.

Northern Lights Compliance Services, LLC (“NLCS”)

NLCS, an affiliate of UFS and the Distributor, provides a Chief Compliance Officer to the Trust, as well as related compliance services, pursuant to a consulting agreement between NLCS and the Trust. Under the terms of such agreement, NLCS receives customary fees from the Adviser on behalf of the Fund.

Blu Giant, LLC (“Blu Giant”), an affiliate of UFS and the Distributor, provides EDGAR conversion and filing services as well as print management services for the Fund on an ad-hoc basis. For the provision of these services, Blu Giant receives customary fees from the Adviser on behalf of the Fund.

| 5. | AGGREGATE UNREALIZED APPRECIATION AND DEPRECIATION – TAX BASIS |

The identified cost of investments in securities owned by the Fund for federal income tax purposes, and its respective gross unrealized depreciation at October 31, 2022, were as follows:

| Cost for Federal Tax purposes | | $ | 1,315,620,531 | |

| | | | | |

| Unrealized Appreciation | | $ | 1,097,031,776 | |

| Unrealized Depreciation | | | (1,238,164,093 | ) |

| Tax Net Unrealized Depreciation | | $ | (141,132,317 | ) |

| | | | | |

| Wealthfront Risk Parity Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| October 31, 2022 |

| |

| 6. | DISTRIBUTIONS TO SHAREHOLDERS AND TAX COMPONENTS OF CAPITAL |

The tax character of fund distributions paid for the year ended October 31, 2022 was as follows:

| | | Fiscal Year Ended | | | Fiscal Year Ended | |

| | | October 31, 2022 | | | October 31, 2021 | |

| Ordinary Income | | $ | 6,710,491 | | | $ | — | |

| Long-Term Capital Gain | | | 47,725,797 | | | | — | |

| | | $ | 54,436,288 | | | $ | — | |

| | | | | | | | | |

There were no Fund distributions for the year ended October 31, 2021.

As of October 31, 2022, the components of accumulated earnings/(deficit) on a tax basis were as follows:

| Undistributed | | | Undistributed | | | Post October Loss | | | Capital Loss | | | Other | | | Unrealized | | | Total | |

| Ordinary | | | Long-Term | | | and | | | Carry | | | Book/Tax | | | Appreciation/ | | | Distributable Earnings/ | |

| Income | | | Gains | | | Late Year Loss | | | Forwards | | | Differences | | | (Depreciation) | | | (Accumulated Deficit) | |

| $ | 1,523,061 | | | $ | — | | | $ | — | | | $ | (162,102,890 | ) | | $ | — | | | $ | (141,132,317 | ) | | $ | (301,712,146 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

At October 31, 2022, the Fund had capital loss carry forwards for federal income tax purposes available to offset future capital gains, as follows:

| Short-Term | | | Long-Term | | | Total | |

| $ | 114,174,026 | | | $ | 47,928,864 | | | $ | 162,102,890 | |

| | | | | | | | | | | |

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of the Fund creates presumption of control of the Fund, under Section 2(a) 9 of the 1940 Act. As of October 31, 2022, Wealthfront Brokerage Corporation, holding shares for the benefit of others in nominee name, held approximately 100% of the voting securities of the Fund.

Subsequent events after the date of the Statements of Assets and Liabilities have been evaluated through the date the financial statements were issued. Management has determined that no events or transactions occurred requiring adjustment or disclosure in the financial statements.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees of Two Roads Shared Trust and the Shareholders of Wealthfront Risk Parity Fund

Opinion on the Financial Statements and Financial Highlights

We have audited the accompanying statement of assets and liabilities of Wealthfront Risk Parity Fund (the “Fund”), one of the funds constituting the Two Roads Shared Trust (the “Trust”), including the portfolio of investments, as of October 31 2022, the related statements of operations, changes in net assets, and financial highlights for the year then ended, and the related notes. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Fund as of October 31, 2022, and the results of its operations, changes in its net assets, and the financial highlights for the year then ended in conformity with accounting principles generally accepted in the United States of America. The statement of changes in net assets for the year ended October 31, 2021 and the financial highlights for the each of the three years in the period ended October 31, 2021 and for the period from January 22, 2018 (commencement of operations) through October 31, 2018 were audited by other auditors whose report, dated December 28, 2021, expressed an unqualified opinion on those statements.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.