UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-22759

The Private Shares Fund

(Exact name of registrant as specified in charter)

88 Pine Street, 31st Floor, Suite 3101

New York, NY 10005

(Address of principal executive offices) (Zip code)

Cogency Global, Inc.

c/o The Private Shares Fund

850 New Burton Rd. Ste. 201

City of Dover, County of Kent, Delaware 19904

(Name and address of agent for service)

Copies to:

Dechert LLP

One Bush Street, Suite 1600

San Francisco, CA 94104-4446

Registrant's telephone number, including area code: (646) 839-5548

Date of fiscal year end: December 31

Date of reporting period: December 31, 2022

Item 1. Reports to Stockholders.

(a) The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended.

THE PRIVATE SHARES FUND

Table of Contents | |

Shareholder Letter | 2 |

Fund Performance | 7 |

Fund Performance & Portfolio Diversification | 10 |

Portfolio Composition | 11 |

Schedule of Investments | 13 |

Statement of Assets and Liabilities | 21 |

Statement of Operations | 22 |

Statements of Changes in Net Assets | 23 |

Statement of Cash Flows | 24 |

Financial Highlights | 25 |

Notes to the Financial Statements | 28 |

Report of Independent Registered Public Accounting Firm | 41 |

Trustees and Officers | 42 |

Additional Information | 43 |

1

THE PRIVATE SHARES FUND

Shareholder Letter

PORTFOLIO MANAGER 2022 COMMENTARY

The Private Shares Fund (the “Fund”) can report that through 2022, the Fund generated a one-year total return of 0.70% as measured by the Fund’s Institutional Class (PIIVX) and was able to achieve those returns with a significantly lower level of volatility than the broader market. While the returns are disappointing on an absolute basis, the Fund’s relative returns demonstrate resilience during a challenging year in the financial markets.

The National Venture Capital Association (NVCA) reported approximately 2,935 U.S. Venture Capital (VC)-backed deals closed in the fourth quarter of 2022, while total deal value fell to $36.2 billion, a twelve-quarter low. Despite the slowdown, full year 2022 VC deal activity has exceeded all prior years except for 2021 with an estimated $238 billion in total deal value across nearly 16,000 deals. Late-stage investment activity continued to moderate in the fourth quarter of 2022 with 936 deals closed representing $13.5 billion in total value, the lowest quarterly deal value for late-stage VC since the second quarter of 2018. However, full year 2022 late-stage investment activity far exceeded all prior 2021 levels with $93.7 billion in total deal value across 4,285 deals. While mega-deals (late-stage VC deals over $100 million) experienced a slowdown with 30 deals closed during the fourth quarter, this figure still far exceeds pre-2021 levels.

During the fourth quarter, the NVCA created a new category called venture-growth stage deals, which they define as any financing that is Series E or later, or any VC financing of a company that is at least seven years old and has raised at least six VC rounds. The purpose of this new category is to better distinguish the mitigated risk/reward profile of these more mature companies compared to other VC deals. For the full year 2022, venture-growth investment activity also slowed, but still far exceeded all prior 2021 levels with approximately $55 billion in total deal value across 845 deals.

Early-stage VC activity was mixed during the fourth quarter of 2022, with 1,330 deals closed representing $10.7 billion. Notably, aggregate investment of $68.4 billion through the fourth quarter of 2022 exceeded all pre-2021 full-year figures and total deal count of nearly 5,600 set a new record. This data continues to support a recent trend of larger investors entering companies at earlier stages in the traditional venture lifecycle, which has also resulted in larger median and average valuations. However, given that early-stage companies typically require less capital and have longer holding periods, current market conditions may be less problematic for this segment of the VC market.

2022 was the second most active year for all VC-related activity on record despite sustained macroeconomic and geopolitical headwinds, which may continue to have a meaningful impact over the coming quarters. Groups like nontraditional investors (e.g., crossover funds, sovereign wealth firms, family offices, etc.) that have been heavily involved in late-stage VC activity further reduced their participation in deals during Q4, a trend that may continue. That said, the significant levels of VC fundraising in recent years should serve as a backstop for the entire ecosystem. Along those lines, US VC fundraising set a new annual record in 2022 with $162.6 billion raised, taking the last 24-month total to roughly $316 billion.

VC exit activity for the fourth quarter of 2022 continued to moderate with respect to both count and value. NVCA estimates 281 exits occurred in Q4 2022 representing $5.2 billion in estimated exit value, notably lower than the $14.0 billion estimated for Q3. In aggregate, $71.4 billion in total exit value was generated in 2022, down roughly 90% compared to the $753.2 billion generated in 2021 and falling below $100 billion for the first time since 2016. Roughly half of the exits generated year-to-date involved acquisitions as the IPO market remains relatively frozen. Related, SPAC (special purpose acquisition company) activity is also at a near standstill, as many of the remaining SPACs have hit their two-year maturity and will likely lead to a large percentage deciding to shut down and return capital to investors. However, it is important to note that these exit trends are common during periods of increased market volatility and macroeconomic uncertainty.

While it is possible to see an increase in M&A activity as strategic and private equity buyers look to take advantage of dislocations without much competition from public offerings, increased regulatory scrutiny and rising rates may create more obstacles.

Overall, 2022 was a challenging year for the markets and economy. This was largely driven by a combination of rising inflation, aggressive Fed rate hikes and balance sheet tightening, ongoing labor market and supply chain challenges, increased geopolitical risks stemming from the Russia-Ukraine conflict, ongoing Covid-19 variants, and general concerns around a recession and the

2

THE PRIVATE SHARES FUND

Shareholder Letter (Continued)

impacts these measures may have on corporate growth rates and earnings. During the fourth quarter of 2022, the CBOE Volatility Index (VIX) increased in October but fell to more moderate levels in November and December. While it remains unclear whether there will be a soft or hard landing for the economy, we anticipate these challenges to persist into 2023, but with challenges comes opportunity.

As previously noted, while our portfolio of late-stage VC and growth companies is not immune to what may happen if these challenges persist over a longer time period, we have been pleased it’s overall performance and resiliency thus far and will continue to monitor developments. In our view, we believe the bigger implication will be that companies planning to raise capital may face greater pressure on valuation and terms, and it may take companies longer to exit. We prefer to see our companies remain disciplined, strengthen their balance sheets, right-size their cost structures and continue executing on their strategies in the private market rather than forcing exits and instead pursue liquidity options at a more optimal time.

As long-term investors in private market technology innovation and disruption, we believe the Fund could potentially continue to benefit from value creation across sectors including fintech, artificial intelligence, cyber-security, cloud, data storage and analytics, online education, supply chain optimization, e-commerce, digital health, and the space economy. It is important to acknowledge the record high levels of dry-powder available to support the VC ecosystem and increased maturity of market participants relative to prior cyclical rotations. Furthermore, we are encouraged to see companies reducing their headcount and burn levels and believe this will lead to better efficiency and profitability as they learn to do more with less. To that end, the Fund continued deploying capital during 2022 across existing holdings and new positions in a market environment where dislocations are creating more attractive entry points. We continue to focus on companies that have differentiated business models, are operated by seasoned management teams, backed by strong VCs, and have healthy balance sheets to help manage through market cycles.

Historically, the Fund’s Net Asset Value (NAV) has been relatively stable during periods of public market stress like those in 2016 and 2018, during which we were able to invest in some very strong names at attractive prices. Similarly, the Fund’s NAV has remained relatively stable over the last 12-18 months despite negative impacts by various macro developments, multiple contraction, etc., and we have continued investing throughout this cycle. It is the experience of the PMs that periods of increased volatility and uncertainty in the public equity markets and overall macro environment are often good catalysts for increasing the supply of opportunities in the private markets. In other words, these catalysts may improve supply and demand imbalances in favor of buyers and investors, as owners of illiquid assets tend to become more risk averse and prefer liquidity. These types of environments often result in more attractive risk-adjusted entry points. As a result, vintages involving periods of increased public market activity and macro uncertainty typically also generate outperformance. While this may appear a bit counter- intuitive, these environments could create buying and investing opportunities in the private markets while simultaneously maintaining discipline, relying upon our comprehensive diligence process and leveraging our relationships across the private market ecosystem.

NEW PORTFOLIO ADDITIONS

LOADSMART

With the goal of transforming the future of freight, Loadsmart leverages artificial intelligence, machine learning, and strategic partnerships to automate how freight is priced, booked, and shipped. Pairing advanced technologies with deep-seated industry experience, Loadsmart fuels growth, simplifies operational complexity, and bolsters efficiency for carriers and shippers alike.

COLOR HEALTH

Color is a provider in distributed healthcare and clinical testing. Color makes population-scale healthcare programs accessible, convenient, and cost-effective for everyone. Color works with health systems, employers, and national health initiatives around the world, including the million-person All of Us Research Program by the National Institutes of Health.

3

THE PRIVATE SHARES FUND

Shareholder Letter (Continued)

CONTRAST SECURITY

Contrast Security provides a modern and comprehensive Application Security Platform, removing security roadblock inefficiencies and empowering enterprises to write and release secure application code faster. Embedding code analysis and attack prevention directly into software with instrumentation, the Contrast platform automatically detects vulnerabilities while developers write code, eliminates false positives, and provides context-specific how-to-fix guidance for easy and fast vulnerability remediation. Doing so enables application and development teams to collaborate more effectively and to innovate faster while accelerating digital transformation initiatives. This is why a growing number of the world’s largest private and public sector organizations rely on Contrast to secure their applications in development and extend protection in production.

HYDROW

Hydrow is the Live Outdoor Reality (LOR)™ rower. With workouts led by world-class athletes, including some training for the U.S. National Rowing team, Hydrow delivers a live on-river rowing experience at-home that engages two times more of the body’s muscles than biking or running. Now more than ever, people’s over-scheduled, stressful lives leave little time for meaningful exercise and the soul-enriching opportunity to spend time outdoors. Hydrow’s innovative LOR technology brings balance and peace, while simultaneously delivering a challenging workout that burns up to 400 calories per 20-minute session.

DATABRICKS

Databricks is a data and AI company. More than 5,000 organizations worldwide — including Comcast, Condé Nast, H&M, and over 40% of the Fortune 500 — rely on the Databricks Lakehouse Platform to unify their data, analytics and AI. Databricks is headquartered in San Francisco, with offices around the globe. Founded by the original creators of Apache Spark™, Delta Lake and MLflow, Databricks is on a mission to help data teams solve the world’s toughest problems.

DEVOTED HEALTH

Devoted Health is on a mission to provide simple, seamless, and affordable healthcare. In other words, they want to offer the kind of plans and care they’d want for their own families. They support the health and wellness of their members with guides who help them navigate the healthcare system, by utilizing world-class technology that powers a simplified member experience, and partnerships with trusted providers.

CONSENSYS

ConsenSys is a leading Ethereum software company which enables developers, enterprises, and people worldwide to build next-generation applications, launch modern financial infrastructure, and access the decentralized web. Consensys’ suite of products serves millions of users, supports billions of blockchain-based queries for their clients, and has handled billions of dollars in digital assets. Ethereum is the largest programmable blockchain in the world, leading in business adoption, developer community, and DeFi activity.

XPLORE

Xplore is a provider of commercial space services intended to facilitate the flight of instruments out of earth’s orbit. The company’s services provide hosting of mission-critical payloads, communication relay services and delivery of datasets via its multi-mission spacecraft, serving national space agencies, national security agencies, sovereign space agencies and universities.

4

THE PRIVATE SHARES FUND

Shareholder Letter (Continued)

CEREBRAS SYSTEMS

Cerebras Systems is a team of pioneering computer architects, computer scientists, deep learning researchers, and subject matter experts of all types. They have come together to build a new class of computer system, designed for the singular purpose of accelerating AI and changing the future of AI work forever. The Cerebras CS-2 system, powered by the world’s largest processor – the WSE-2, enables customers to accelerate their deep learning by orders of magnitude over general purpose compute.

CLEARMOTION

ClearMotion builds products enabling a next-generation user experience in vehicles. The company’s proactive suspension and seating systems combine software and hardware to mitigate vehicle movement across uneven road surfaces. ClearMotion was founded out of MIT and has locations in the greater Boston area and Birmingham, UK.

ROOFSTOCK

Roofstock provides a digital real estate investing platform for single-family rental home sector. The company provides resources for investors to buy, manage, and sell investment homes online, including data analytics, property management oversight, and other tools. Roofstock’s marketplace empowers investors to own cash-flowing rental properties, diversify their investment portfolios, and build long-term wealth through real estate.

VOYAGER SPACE

Voyager Space operates a space-focused holding company intended to increase vertical integration and mission capability. Voyager’s long-term mission is to create a vertically integrated NewSpace company capable of delivering any space mission humans can conceive. The company centralizes core shared services and offers an alternative solution to traditional private capital models and replaces them with a longer-term approach as a provider of permanent capital, enabling commercial space companies to focus more on the development of innovative products and solutions.

UPGRADE

Upgrade, Inc. is a financial technology company offering credit, mobile banking and payment products to mainstream consumers. Upgrade has delivered over $12 billion in affordable credit to consumers through credit cards and loans since 2017. The company also offers reward checking accounts with debit cards to its customers.

FLEXPORT

Flexport is a modern freight forwarder. Flexport delivers a combination of advanced technology, physical logistics infrastructure and human expertise, providing fast and predictable transit times, visibility and control, and lower supply chain costs to logistics and supply chain professionals across the globe. First to market with a purpose-built cloud software and data analytics platform, Flexport today connects almost 10,000 clients and suppliers across more than 200 countries, including established global brands as well as emerging innovators. Flexport offers a full range of services, including ocean, air, truck and rail freight, drayage and cartage, warehousing, customs and trade advisory, financing, and insurance.

NANOTRONICS

Nanotronics is an advanced machines and intelligence company that helps customers across the public, private, and nonprofit sectors solve for the unique inspection and process control challenges of precision manufacturing. Deployed across fifteen countries and industry agnostic, Nanotronics works with leading-edge companies, from aerospace, to electronics, to healthcare, to drive up yield, reduce footprint and waste, lower costs, and speed up design iteration, while eliminating laborious manual inspections.

5

THE PRIVATE SHARES FUND

Shareholder Letter (Continued)

EPIC GAMES

Epic Games is a leading developer of gaming software and applications designed for gamers and game developers to publish and play immersive games. The company specializes in game engine developing technology and operates a game store that empowers others to make quality games and 3D content, providing game developers the ability to build high-fidelity, interactive experiences for PC, console, mobile, and virtual reality devices.

NORTHGATE GROWTH FUND III

Northgate Growth Fund III is a special-purpose vehicle that holds an underlying private fund investment.

6

THE PRIVATE SHARES FUND

Fund Performance

December 31, 2022 (Unaudited)

As of December 31, 2022, the Fund’s performance is as follows:

Total Return Information (Unaudited) |

The Private Shares Fund – Class A

(Inception Date: 03/25/2014) | Five

Years | Three

Years | One

Year | Annualized

Since Inception | Cumulative

Since Inception |

Returns based on Purchase Without Any Sales Charge (NAV) | 11.41% | 15.44% | 0.42% | 9.99% | 130.45% |

Returns based on Purchase With Maximum Sales Charge of 5.75% (POP) | 10.10% | 13.18% | -5.35% | 9.25% | 117.20% |

Fund Benchmark | | | | | |

Russell 2000® Index | 4.13% | 3.10% | -20.44% | 6.11% | 68.18% |

The Private Shares Fund – Class I

(Inception Date: 11/17/2017) | Five

Years | Three

Years | One

Year | Annualized

Since Inception | Cumulative

Since Inception |

Returns based on Purchase Without Any Sales Charge (NAV) | 11.69% | 15.72% | 0.70% | 11.80% | 77.00% |

Fund Benchmark | | | | | |

Russell 2000® Index | 4.13% | 3.10% | -20.44% | 4.64% | 26.17% |

The Private Shares Fund – Class L

(Inception Date: 05/11/2018) | Three

Years | One

Year | Annualized

Since Inception | Cumulative

Since Inception |

Returns based on Purchase Without Any Sales Charge (NAV) | 15.13% | 0.16% | 10.73% | 60.47% |

Returns based on Purchase With Maximum Sales Charge of 4.25% (POP) | 13.48% | -4.08% | 9.70% | 53.65% |

Fund Benchmark | | | | |

Russell 2000® Index | 3.10% | -20.44% | 3.35% | 16.52% |

Performance data quoted represents past performance and is no guarantee of future results. Public offering price (“POP”) performance assumes a maximum sales load of 5.75% (Class A) and 4.25% (Class L) on all sales. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than original cost. Current performance may be lower or higher than the performance data quoted. For performance as of the most recent month-end, please call 1-855-551-5510. Some of the Fund’s fees were waived or expenses reimbursed; otherwise, returns would have been lower. The Fund’s total annual expenses per the currently stated prospectus are 2.37% (Class A), 2.32% (Class I), and 2.60% (Class L). The Fund’s total net expenses are 2.53% (Class A), 2.28% (Class I), and 2.78% (Class L). Liberty Street Advisors, Inc. (the “Investment Adviser”) has contractually agreed to waive fees and/or reimburse (excluding taxes, interest, brokerage commissions, acquired fund fees and expenses, and extraordinary expenses) expenses such that the total expenses do not exceed 2.50% (Class A), 2.25% (Class I), and 2.75% (Class L) through May 2, 2023. Net expenses are applicable to investors.

7

THE PRIVATE SHARES FUND

Fund Performance (Continued)

December 31, 2022 (Unaudited)

DISCLOSURES

As of December 9, 2020, Liberty Street Advisors, Inc. became the adviser to the Fund. The Fund’s portfolio managers did not change. Effective April 30, 2021, the Fund changed its name from the “SharesPost 100 Fund” to “The Private Shares Fund.” Effective July 7, 2021, the Fund made changes to its investment strategy. In addition to directly investing in private companies, the Fund may also invest in private investments in public equity (“PIPEs”) where the issuer is a special purpose acquisition company (“SPAC”), and profit sharing agreements. The Fund’s investment thesis has not changed.

Investment in the Fund involves substantial risk. The Fund is not suitable for investors who cannot bear the risk of loss of all or part of their investment. The Fund is appropriate only for investors who can tolerate a high degree of risk and do not require a liquid investment. All investing involves risk including the possible loss of principal. Shares in the Fund are highly illiquid, and can be sold by shareholders only in the quarterly repurchase program of the Fund which allows for up to 5% of the Fund’s outstanding shares at NAV to be redeemed each quarter. Due to transfer restrictions and the illiquid nature of the Fund’s investments, you may not be able to sell your shares when, or in the amount that, you desire. The Fund intends to primarily invest in securities of private, late-stage, venture-backed growth companies. There are significant potential risks relating to investing in such securities. Because most of the securities in which the Fund invests are not publicly traded, the Fund’s investments will be valued by Liberty Street Advisors, Inc. (the “Investment Adviser”) as Valuation Designee pursuant to fair valuation procedures and methodologies approved by the Board of Trustees, as set forth in the prospectus. As a consequence, the value of the securities, and therefore the Fund’s Net Asset Value (NAV), may vary. There are significant potential risks associated with investing in venture capital and private equity-backed companies with complex capital structures. The Fund focuses its investments in a limited number of securities, which could subject it to greater risk than that of a larger, more varied portfolio. There is a greater focus in technology securities that could adversely affect the Fund’s performance. The Fund’s quarterly repurchase policy may require the Fund to liquidate portfolio holdings earlier than the Investment Adviser would otherwise do so and may also result in an increase in the Fund’s expense ratio. Portfolio holdings of private companies that become publicly traded likely will be subject to more volatile market fluctuations than when private, and the Fund may not be able to sell shares at favorable prices. Such companies frequently impose lock-ups that would prohibit the Fund from selling shares for a period of time after an initial public offering (IPO). Market prices of public securities held by the Fund may decline substantially before the Investment Adviser is able to sell the securities. The Fund may invest in private securities utilizing special purpose vehicles (“SPV”s), venture capital funds and other funds that invest in private companies and rely on exclusions from the 1940 Act under section 3(c)(1) or 3(c)(7) (“Private Funds”), private investments in public equity (“PIPE”) transactions where the issuer is a special purpose acquisition company (“SPAC”), and profit sharing agreements. The Fund will bear its pro rata portion of expenses on investments in SPVs and Private Funds and will have no direct claim against underlying portfolio companies. The Fund’s investments in Private Funds subject it to the risks associated with direct ownership of the securities in which the underlying funds invest, as well as additional risks specific to the Private Funds, including operational risk, legal and indemnification risks, and lock-ups and other restrictions on withdrawal. PIPE transactions involve price risk, market risk, expense risk, and the Fund may not be able to sell the securities due to lock-ups or restrictions. Profit sharing agreements may expose the Fund to certain risks, including that the agreements could reduce the gain the Fund otherwise would have achieved on its investment, may be difficult to value and may result in contractual disputes. Certain conflicts of interest involving the Fund and its affiliates could impact the Fund’s investment returns and limit the flexibility of its investment policies. This is not a complete enumeration of the Fund’s risks. Please read the Fund prospectus for other risk factors related to the Fund.

The Fund may not be suitable for all investors. We encourage you to consult with appropriate financial professionals before considering an investment in the Fund.

The Russell 2000 is an index measuring the performance of approximately 2,000 smallest-cap American companies in the Russell 3000 Index, which is made up of 3,000 of the largest U.S. stocks. It is a market-cap weighted index. CBOE Volatility Index measures the stock market’s expectation of volatility based on S&P 500 index options. One cannot invest in an index. A Special Purpose Acquisition Company (SPAC) is a company that has no commercial operations and is formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring or merging with an existing company.

8

THE PRIVATE SHARES FUND

Fund Performance (Continued)

December 31, 2022 (Unaudited)

The views expressed in this material reflect those of the Fund’s Investment Advisor as of the date this is written and may not reflect its views on the date this material is first published or anytime thereafter. These views are intended to assist in understanding the Fund’s investment methodology and do not constitute investment advice. This material may contain discussions about investments that may or may not be held by the Fund. All current and future holdings are subject to risk and to change.

The Fund is distributed by Foreside Fund Services, LLC

IMPORTANT DISCLOSURE

All investing involves risk including the possible loss of principal. Shares in the Fund are highly illiquid, and you may not be able to sell your shares when, or in the amount that, you desire. The Fund intends to primarily invest in securities of private, late-stage, venture-backed growth companies. There are significant potential risks relating to investing in such securities. Because most of the securities in which the Fund invests are not publicly traded, the Fund’s investments will be valued by the Investment Adviser, as Valuation Designee, pursuant to fair valuation procedures and methodologies approved by the Board of Trustees.

There are significant potential risks associated with investing in venture capital and private equity-backed companies with complex capital structures. The Fund focuses its investments on a limited number of securities, which could subject it to greater risk than that of a larger, more varied portfolio. There is a greater focus in technology securities which could adversely affect the Fund’s performance. The inclusion of various indices is for comparison purposes only. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

The Fund’s quarterly repurchase policy may require the Fund to liquidate portfolio holdings earlier than the Investment Adviser would otherwise do so, and may also result in an increase in the Fund’s expense ratio. This is not a complete enumeration of the Fund’s risks. Please read the Fund prospectus for other risk factors related to the Fund, its investment strategy and your investment in the Fund, and other additional details.

Holdings subject to change. Not a recommendation to buy, sell, or hold any specific security.

9

THE PRIVATE SHARES FUND

Fund Performance & Portfolio Diversification

December 31, 2022 (Unaudited)

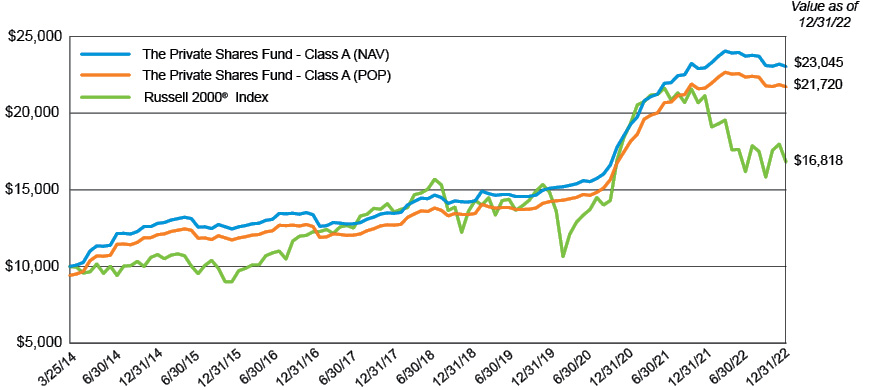

Growth of $10,000 Investment

This graph illustrates the hypothetical investment of $10,000 in the Class A from March 25, 2014 (Class inception) to December 31, 2022. The Total Return Information table and Growth of $10,000 Investment graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The Public Offering Price (“POP”) assumes an initial investment of $9,425 ($10,000 less the maximum sales load of 5.75%). The Net Asset Value (“NAV”) assumes no sales load.

Fund Sector Diversification

The following chart provides a visual breakdown of the Fund, by the industry sectors that the underlying securities represent, as a percentage of the total investments.

10

THE PRIVATE SHARES FUND

Portfolio Composition

December 31, 2022 (Unaudited)

Fund Holdings

11

THE PRIVATE SHARES FUND

Portfolio Composition (Continued)

December 31, 2022 (Unaudited)

Fund Holdings (Continued)

12

THE PRIVATE SHARES FUND

Schedule of Investments

December 31, 2022

| | Acquisition

Date | | Shares | | | Cost | | | Fair Value | |

COMMON STOCK IN PUBLIC COMPANIES(a) — 1.0% | | | | | | | | | | | | |

3D PRINTING — 0.1% | | | | | | | | | | | | | |

Fathom Digital Manufacturing, Corp. | Dec 2021 | | | 263,646 | | | $ | 2,636,460 | | | $ | 348,013 | |

| | | | | | | | | | | | | | |

CONSUMER WEB — 0.3% | | | | | | | | | | | | | |

Nextdoor Holding, Inc. | Nov 2018 | | | 925,479 | | | | 5,037,326 | | | | 1,906,487 | |

Wag Labs, Inc.(b) | Oct 2018 | | | 426,552 | | | | 2,314,001 | | | | 1,300,983 | |

| | | | | | | | 7,351,327 | | | | 3,207,470 | |

EDUCATION — 0.2% | | | | | | | | | | | | | |

Udemy, Inc. | Aug 2019 | | | 163,448 | | | | 1,648,103 | | | | 1,724,376 | |

| | | | | | | | | | | | | | |

FINANCE/PAYMENTS — 0.1% | | | | | | | | | | | | | |

Marqeta, Inc. | Jul 2018 | | | 194,514 | | | | 227,581 | | | | 1,188,481 | |

| | | | | | | | | | | | | | |

HARDWARE — 0.0% | | | | | | | | | | | | | |

Tempo Automation, Inc. | Aug 2019 | | | 93,787 | | | | 1,868,000 | | | | 72,216 | |

| | | | | | | | | | | | | | |

HEALTHCARE/BIOTECH — 0.2% | | | | | | | | | | | | | |

23andMe Holding Co. | Oct 2017 | | | 724,260 | | | | 4,436,112 | | | | 1,564,402 | |

| | | | | | | | | | | | | | |

SOFTWARE — 0.1% | | | | | | | | | | | | | |

SoundHound AI, Inc. | Sep 2016 | | | 736,112 | | | | 3,200,767 | | | | 1,302,918 | |

TOTAL COMMON STOCK IN PUBLIC COMPANIES | | | | | | | | 21,368,350 | | | | 9,407,876 | |

| | | | | | | | | | | | | |

COMMON STOCK IN PRIVATE COMPANIES(a),(b) — 39.3% | | | | | | | | | | | | |

3D PRINTING — 0.3% | | | | | | | | | | | | | |

Carbon, Inc. | Jun 2019 | | | 158,853 | | | | 2,125,214 | | | | 3,569,427 | |

| | | | | | | | | | | | | | |

ADVERTISING — 2.6% | | | | | | | | | | | | | |

GroundTruth, Inc. | Oct 2016 | | | 1,659,427 | | | | 446,424 | | | | 381,668 | |

NextRoll, Inc. | Mar 2017 | | | 2,367,054 | | | | 16,079,048 | | | | 22,131,955 | |

OpenX Software, Ltd. | Jun 2015 | | | 2,899,297 | | | | 2,615,386 | | | | 2,145,480 | |

WideOrbit, Inc. | Oct 2015 | | | 400,000 | | | | 1,100,000 | | | | 948,000 | |

| | | | | | | | 20,240,858 | | | | 25,607,103 | |

AEROSPACE — 5.3% | | | | | | | | | | | | | |

Axiom Space, Inc. | Mar 2021 | | | 29,543 | | | | 5,099,983 | | | | 4,990,699 | |

Relativity Space, Inc. | Oct 2021 | | | 437,922 | | | | 9,999,993 | | | | 9,835,728 | |

Space Exploration Technologies Corp. | May 2019 | | | 490,200 | | | | 10,049,100 | | | | 37,402,260 | |

| | | | | | | | 25,149,076 | | | | 52,228,687 | |

AGTECH — 0.5% | | | | | | | | | | | | | |

Farmer’s Business Network, Inc. | Sep 2021 | | | 87,500 | | | | 5,042,625 | | | | 5,337,500 | |

See accompanying Notes to the Financial Statements

13

THE PRIVATE SHARES FUND

Schedule of Investments (Continued)

December 31, 2022

| | | Acquisition

Date | | | Shares | | | Cost | | | Fair Value | |

COMMON STOCK IN PRIVATE COMPANIES(a),(b) — 39.3% (Continued) | | | | | | | | | | | | |

ANALYTICS/BIG DATA — 4.6% | | | | | | | | | | | | | | | | |

Baktus, Inc. | | | Apr 2015 | | | | 10,795 | | | $ | 1,500,951 | | | $ | 22,669 | |

Dataminr, Inc. | | | Sep 2015 | | | | 500,083 | | | | 5,671,336 | | | | 14,402,390 | |

Domino Data Lab, Inc. | | | Apr 2021 | | | | 330,000 | | | | 4,118,400 | | | | 5,134,800 | |

Dremio Corp.(c) | | | Dec 2021 | | | | 166,664 | | | | 1,018,383 | | | | 1,369,978 | |

INRIX, Inc. | | | May 2014 | | | | 133,238 | | | | 3,026,249 | | | | 6,200,630 | |

SingleStore, Inc. | | | May 2020 | | | | 2,148,366 | | | | 10,359,604 | | | | 13,792,510 | |

Tealium, Inc. | | | Sep 2020 | | | | 200,000 | | | | 1,300,000 | | | | 2,372,000 | |

ThoughtSpot, Inc. | | | Oct 2018 | | | | 162,087 | | | | 1,745,759 | | | | 1,998,533 | |

| | | | | | | | | | | 28,740,682 | | | | 45,293,510 | |

ARTIFICIAL INTELLIGENCE — 3.0% | | | | | | | | | | | | | | | | |

Brain Corp. | | | Dec 2020 | | | | 2,375,000 | | | | 9,540,000 | | | | 10,283,750 | |

Cerebras Systems, Inc. | | | Feb 2022 | | | | 309,813 | | | | 6,946,627 | | | | 6,648,587 | |

Nanotronics Imaging, Inc. | | | Aug 2022 | | | | 76,504 | | | | 7,803,408 | | | | 12,408,184 | |

| | | | | | | | | | | 24,290,035 | | | | 29,340,521 | |

CLEAN TECHNOLOGY — 0.0% | | | | | | | | | | | | | | | | |

WiTricity Holdings, Inc.(c) | | | Mar 2021 | | | | 166,667 | | | | 1,667 | | | | 500,001 | |

| | | | | | | | | | | | | | | | | |

E-COMMERCE — 0.6% | | | | | | | | | | | | | | | | |

1661, Inc. (d.b.a. GOAT)(c) | | | Sep 2021 | | | | 128,148 | | | | 760,724 | | | | 658,681 | |

CaaStle, Inc. | | | Mar 2022 | | | | 859,884 | | | | 2,742,746 | | | | 5,107,711 | |

| | | | | | | | | | | 3,503,470 | | | | 5,766,392 | |

EDUCATION — 1.7% | | | | | | | | | | | | | | | | |

Eruditus Learning Solutions Pte., Ltd.(c) | | | Aug 2021 | | | | 36,264 | | | | 5,092,426 | | | | 4,969,619 | |

Learneo, Inc. (f.k.a. Course Hero, Inc.) | | | Jun 2020 | | | | 270,000 | | | | 3,429,200 | | | | 9,379,800 | |

Udacity, Inc. | | | Nov 2018 | | | | 448,075 | | | | 2,884,586 | | | | 2,258,298 | |

| | | | | | | | | | | 11,406,212 | | | | 16,607,717 | |

ENTERPRISE SOFTWARE — 3.0% | | | | | | | | | | | | | | | | |

Algolia, Inc. | | | Jan 2020 | | | | 45,000 | | | | 420,000 | | | | 1,197,000 | |

Automation Anywhere, Inc. | | | Jul 2021 | | | | 189,449 | | | | 4,019,940 | | | | 2,286,649 | |

D2iQ, Inc. | | | Feb 2019 | | | | 165,000 | | | | 1,605,450 | | | | 270,600 | |

Docker, Inc. | | | May 2017 | | | | 2,500 | | | | 531,250 | | | | 74,150 | |

EquipmentShare.com, Inc. | | | Oct 2021 | | | | 694,800 | | | | 9,985,874 | | | | 10,755,504 | |

Motive Technologies, Inc. (f.k.a. Keep Truckin, Inc.) | | | May 2019 | | | | 788,562 | | | | 3,420,734 | | | | 6,253,297 | |

Tebra Technologies, Inc. (f.k.a. Kareo, Inc.) | | | Nov 2020 | | | | 190,007 | | | | 1,235,126 | | | | 1,540,805 | |

Trax, Ltd. | | | Mar 2020 | | | | 149,970 | | | | 5,100,000 | | | | 7,889,922 | |

| | | | | | | | | | | 26,318,374 | | | | 30,267,927 | |

See accompanying Notes to the Financial Statements

14

THE PRIVATE SHARES FUND

Schedule of Investments (Continued)

December 31, 2022

| | | Acquisition

Date | | | Shares | | | Cost | | | Fair Value | |

COMMON STOCK IN PRIVATE COMPANIES(a),(b) — 39.3% (Continued) | | | | | | | | | | | | |

FINANCE/PAYMENTS — 4.3% | | | | | | | | | | | | | | | | |

Betterment Holdings, Inc. | | | Mar 2021 | | | | 1,457,800 | | | $ | 14,999,995 | | | $ | 17,653,958 | |

Circle Internet Financial, Ltd. | | | Apr 2018 | | | | 290,200 | | | | 2,604,825 | | | | 14,155,956 | |

ConsenSys Software, Inc. | | | May 2022 | | | | 31,010 | | | | 3,703,824 | | | | 4,134,563 | |

Payward, Inc. (d.b.a. Kraken) | | | Jun 2021 | | | | 105,218 | | | | 5,079,228 | | | | 3,088,148 | |

Prosper Marketplace, Inc. | | | Jan 2016 | | | | 244,130 | | | | 1,307,998 | | | | 178,215 | |

Upgrade, Inc. | | | Apr 2022 | | | | 661,053 | | | | 2,900,002 | | | | 3,602,739 | |

| | | | | | | | | | | 30,595,872 | | | | 42,813,579 | |

FOODTECH — 0.6% | | | | | | | | | | | | | | | | |

Impossible Foods, Inc. | | | Oct 2022 | | | | 299,056 | | | | 3,050,371 | | | | 5,966,167 | |

| | | | | | | | | | | | | | | | | |

GAMES — 1.1% | | | | | | | | | | | | | | | | |

Epic Games | | | Nov 2022 | | | | 11,774 | | | | 7,650,039 | | | | 10,551,623 | |

| | | | | | | | | | | | | | | | | |

HEALTHCARE/BIOTECH — 2.8% | | | | | | | | | | | | | | | | |

Click Therapeutics, Inc. | | | Nov 2020 | | | | 1,000,000 | | | | 3,500,000 | | | | 3,250,000 | |

Color Health, Inc. | | | Feb 2022 | | | | 139,486 | | | | 10,039,927 | | | | 13,944,416 | |

Devoted Health, Inc. | | | Aug 2022 | | | | 177,776 | | | | 9,999,953 | | | | 9,999,900 | |

ZocDoc, Inc. | | | Feb 2015 | | | | 61,016 | | | | 1,321,708 | | | | 881,681 | |

| | | | | | | | | | | 24,861,588 | | | | 28,075,997 | |

HOSTING/STORAGE — 0.4% | | | | | | | | | | | | | | | | |

Rubrik, Inc. | | | Sep 2019 | | | | 126,281 | | | | 3,220,166 | | | | 3,718,975 | |

| | | | | | | | | | | | | | | | | |

SECURITY — 4.9% | | | | | | | | | | | | | | | | |

Arctic Wolf Networks, Inc. | | | Dec 2021 | | | | 1,747,151 | | | | 17,915,660 | | | | 16,265,976 | |

Code42 Software, Inc. | | | May 2016 | | | | 330,000 | | | | 754,500 | | | | 990,000 | |

Contrast Security, Inc. | | | Sep 2022 | | | | 31,250 | | | | 255,000 | | | | 430,625 | |

Exabeam, Inc. | | | Jul 2021 | | | | 54,500 | | | | 1,590,855 | | | | 1,367,405 | |

Lookout, Inc. | | | Jul 2022 | | | | 1,869,160 | | | | 10,000,006 | | | | 19,962,629 | |

Malwarebytes, Inc. | | | Dec 2019 | | | | 188,173 | | | | 1,129,038 | | | | 2,732,272 | |

Tanium, Inc. | | | Apr 2019 | | | | 640,000 | | | | 4,787,200 | | | | 6,508,800 | |

| | | | | | | | | | | 36,432,259 | | | | 48,257,707 | |

SOFTWARE — 2.8% | | | | | | | | | | | | | | | | |

Discord, Inc.(c) | | | Dec 2021 | | | | 45,694 | | | | 18,267,788 | | | | 21,680,432 | |

Mynd Management, Inc. | | | Dec 2021 | | | | 340,202 | | | | 6,130,637 | | | | 6,007,967 | |

| | | | | | | | | | | 24,398,425 | | | | 27,688,399 | |

TRANSPORTATION — 0.8% | | | | | | | | | | | | | | | | |

Flexport, Inc. | | | Jul 2022 | | | | 538,387 | | | | 7,260,075 | | | | 7,537,418 | |

TOTAL COMMON STOCK IN PRIVATE COMPANIES | | | | | | | | | | | 284,287,008 | | | | 389,128,650 | |

| | | | | | | | | | | | | | | | |

PREFERRED STOCK IN PRIVATE COMPANIES (a),(b) — 39.1% | | | | | | | | | | | | | | | | |

ADVERTISING — 0.0% | | | | | | | | | | | | | | | | |

GroundTruth, Inc., Preferred Series B-1 | | | Jan 2017 | | | | 600,000 | | | | 149,200 | | | | 138,000 | |

See accompanying Notes to the Financial Statements

15

THE PRIVATE SHARES FUND

Schedule of Investments (Continued)

December 31, 2022

| | | Acquisition

Date | | | Shares | | | Cost | | | Fair Value | |

PREFERRED STOCK IN PRIVATE COMPANIES(a),(b) — 39.1% (Continued) | | | | | | | | | | | | |

AEROSPACE — 3.5% | | | | | | | | | | | | | | | | |

Axiom Space, Inc., Preferred Series B | | | Dec 2020 | | | | 32,221 | | | $ | 2,019,958 | | | $ | 5,443,094 | |

Beta Technologies, Inc., Preferred Series A | | | Apr 2021 | | | | 40,944 | | | | 2,999,967 | | | | 4,215,185 | |

Beta Technologies, Inc., Preferred Series B | | | Apr 2022 | | | | 58,156 | | | | 5,999,954 | | | | 5,994,139 | |

Radian Aerospace, Inc., Preferred Series Seed 2 | | | Sep 2021 | | | | 607,336 | | | | 1,999,997 | | | | 1,998,135 | |

Relativity Space, Inc., Preferred Series E | | | Jul 2021 | | | | 437,922 | | | | 10,299,992 | | | | 9,923,312 | |

Voyager Space Holdings, Inc., Preferred Series B | | | Mar 2022 | | | | 192,061 | | | | 7,499,982 | | | | 7,499,982 | |

| | | | | | | | | | | 30,819,850 | | | | 35,073,847 | |

AGTECH — 1.8% | | | | | | | | | | | | | | | | |

CIBO Technologies, Inc., Preferred Series C(c) | | | Aug 2021 | | | | 600,000 | | | | 3,090,000 | | | | 2,928,000 | |

Farmer’s Business Network, Inc., Preferred Series G | | | Sep 2021 | | | | 160,880 | | | | 10,199,946 | | | | 9,910,208 | |

Invaio Sciences, Inc., Preferred Series C(c) | | | Mar 2021 | | | | 1,061,390 | | | | 5,150,000 | | | | 5,264,494 | |

| | | | | | | | | | | 18,439,946 | | | | 18,102,702 | |

ANALYTICS/BIG DATA — 3.0% | | | | | | | | | | | | | | | | |

Databricks, Inc., Preferred Series G(c) | | | Jul 2022 | | | | 182,664 | | | | 10,799,704 | | | | 11,608,297 | |

Dataminr, Inc., Preferred Series A | | | Apr 2019 | | | | 20,000 | | | | 198,000 | | | | 576,000 | |

Dataminr, Inc., Preferred Series B | | | Apr 2019 | | | | 87,496 | | | | 866,211 | | | | 2,519,885 | |

Dremio Corp., Preferred Series E(c) | | | Dec 2021 | | | | 469,594 | | | | 4,070,000 | | | | 3,930,502 | |

Heap, Inc., Preferred Series C | | | May 2019 | | | | 1,361,503 | | | | 4,999,997 | | | | 10,783,104 | |

Heap, Inc., Preferred Series D | | | Nov 2021 | | | | 84,047 | | | | 711,170 | | | | 689,185 | |

| | | | | | | | | | | 21,645,082 | | | | 30,106,973 | |

ARTIFICIAL INTELLIGENCE — 2.7% | | | | | | | | | | | | | | | | |

Nanotronics Imaging, Inc., Preferred Series F-2 | | | Apr 2022 | | | | 90,888 | | | | 15,300,066 | | | | 14,873,821 | |

VerbIT, Inc., Preferred Series A | | | Nov 2021 | | | | 47,640 | | | | 693,256 | | | | 663,953 | |

VerbIT, Inc., Preferred Series B | | | Nov 2021 | | | | 288,180 | | | | 4,194,173 | | | | 4,016,333 | |

VerbIT, Inc., Preferred Series E-1 | | | Nov 2021 | | | | 423,720 | | | | 6,166,668 | | | | 6,041,226 | |

VerbIT, Inc., Preferred Series Seed 2 | | | Nov 2021 | | | | 65,000 | | | | 945,904 | | | | 905,898 | |

| | | | | | | | | | | 27,300,067 | | | | 26,501,231 | |

CLEAN TECHNOLOGY — 0.4% | | | | | | | | | | | | | | | | |

WiTricity Holdings, Inc., Preferred Series A | | | Oct 2020 | | | | 1,000,000 | | | | 1,020,000 | | | | 3,000,000 | |

WiTricity Holdings, Inc., Preferred Series B | | | Jun 2022 | | | | 333,253 | | | | 999,999 | | | | 999,759 | |

| | | | | | | | | | | 2,019,999 | | | | 3,999,759 | |

CONSUMER WEB — 0.0% | | | | | | | | | | | | | | | | |

Trusper, Inc. (d.b.a. Musely), Preferred Series B | | | Oct 2014 | | | | 7,961 | | | | 100,012 | | | | 124,749 | |

See accompanying Notes to the Financial Statements

16

THE PRIVATE SHARES FUND

Schedule of Investments (Continued)

December 31, 2022

| | | Acquisition

Date | | | Shares | | | Cost | | | Fair Value | |

PREFERRED STOCK IN PRIVATE COMPANIES(a),(b) — 39.1% (Continued) | | | | | | | | | | | | |

E-COMMERCE — 5.8% | | | | | | | | | | | | | | | | |

1661, Inc. (d.b.a. GOAT), Preferred Series A-1(c) | | | Sep 2021 | | | | 112,563 | | | $ | 668,206 | | | $ | 578,574 | |

1661, Inc. (d.b.a. GOAT), Preferred Series A-5(c) | | | Sep 2021 | | | | 2,394 | | | | 14,211 | | | | 12,305 | |

1661, Inc. (d.b.a. GOAT), Preferred Series A-7(c) | | | Sep 2021 | | | | 146,495 | | | | 869,637 | | | | 752,984 | |

1661, Inc. (d.b.a. GOAT), Preferred Series B(c) | | | Sep 2021 | | | | 231,687 | | | | 1,375,362 | | | | 1,190,871 | |

1661, Inc. (d.b.a. GOAT), Preferred Series C(c) | | | Sep 2021 | | | | 237,913 | | | | 1,412,322 | | | | 1,222,873 | |

CaaStle, Inc., Preferred Series A-12 | | | Dec 2021 | | | | 1,740,786 | | | | 8,050,124 | | | | 10,583,979 | |

GrubMarket, Inc., Preferred Series D | | | Oct 2020 | | | | 440,742 | | | | 1,999,999 | | | | 6,318,653 | |

GrubMarket, Inc., Preferred Series E | | | Jun 2021 | | | | 1,520,838 | | | | 14,999,995 | | | | 21,803,342 | |

GrubMarket, Inc., Preferred Series F | | | Feb 2022 | | | | 697,526 | | | | 9,999,982 | | | | 10,000,012 | |

Lyst, Ltd., Preferred Series E | | | Jul 2021 | | | | 401,929 | | | | 5,172,500 | | | | 4,598,068 | |

| | | | | | | | | | | 44,562,338 | | | | 57,061,661 | |

EDUCATION — 0.6% | | | | | | | | | | | | | | | | |

Yanka Industries, Inc. (d.b.a. MasterClass), Preferred Series Seed 1 | | | Jul 2021 | | | | 193,100 | | | | 6,146,189 | | | | 5,590,245 | |

| | | | | | | | | | | | | | | | | |

ENTERPRISE SOFTWARE — 4.1% | | | | | | | | | | | | | | | | |

Checkr, Inc., Preferred Series A-1 | | | Mar 2020 | | | | 150,000 | | | | 1,405,000 | | | | 2,751,000 | |

Cohere Technologies, Inc., Preferred Series D-1 | | | Feb 2022 | | | | 279,571 | | | | 1,999,995 | | | | 1,909,470 | |

Cohere Technologies, Inc., Preferred Series D-2 | | | Dec 2020 | | | | 386,038 | | | | 2,071,233 | | | | 2,501,526 | |

EquipmentShare.com, Inc., Preferred Series E | | | May 2022 | | | | 323,064 | | | | 4,999,997 | | | | 5,001,031 | |

Motive Technologies, Inc. (f.k.a. Keep Truckin, Inc.), Preferred Series E | | | May 2021 | | | | 638,843 | | | | 4,599,996 | | | | 5,066,025 | |

Motive Technologies, Inc. (f.k.a. Keep Truckin, Inc.), Preferred Series F | | | Jun 2022 | | | | 1,923,076 | | | | 14,999,993 | | | | 15,249,993 | |

Ocrolus, Inc., Preferred Series C(c) | | | Aug 2021 | | | | 438,327 | | | | 3,062,500 | | | | 2,629,962 | |

Tebra Technologies, Inc. (f.k.a. Kareo, Inc.), Preferred Series Seed 2 | | | Nov 2020 | | | | 123,819 | | | | 804,870 | | | | 1,004,073 | |

Trax, Ltd., Pre IPO | | | Mar 2021 | | | | 76,722 | | | | 3,999,978 | | | | 4,036,344 | |

| | | | | | | | | | | 37,943,562 | | | | 40,149,424 | |

FINANCE/PAYMENTS — 5.3% | | | | | | | | | | | | | | | | |

Betterment Holdings, Inc., Preferred Series F | | | Sep 2021 | | | | 318,380 | | | | 3,999,999 | | | | 3,928,809 | |

ConsenSys Software, Inc., Preferred Series D(c) | | | Feb 2022 | | | | 35,699 | | | | 5,075,000 | | | | 4,886,122 | |

Fundbox, Ltd., Preferred Series C | | | Jun 2019 | | | | 439,552 | | | | 4,999,992 | | | | 6,197,683 | |

Fundbox, Ltd., Preferred Series D | | | Sep 2021 | | | | 531,914 | | | | 7,499,988 | | | | 7,499,988 | |

Payward, Inc. (d.b.a. Kraken), Preferred Series A | | | Nov 2021 | | | | 262,210 | | | | 13,768,164 | | | | 7,695,864 | |

Payward, Inc. (d.b.a. Kraken), Preferred Series Seed | | | Apr 2022 | | | | 67,000 | | | | 3,505,340 | | | | 1,966,450 | |

Prosper Marketplace, Inc., Preferred Series A | | | Jan 2016 | | | | 55,395 | | | | 305,781 | | | | 40,438 | |

Prosper Marketplace, Inc., Preferred Series A-1 | | | Jan 2016 | | | | 58,165 | | | | 116 | | | | 86,666 | |

Ripple Labs, Inc., Preferred Series A | | | Dec 2018 | | | | 42,000 | | | | 504,000 | | | | 2,367,540 | |

Upgrade, Inc., Preferred Series C-1 | | | Mar 2022 | | | | 3,290,000 | | | | 14,159,000 | | | | 17,930,500 | |

| | | | | | | | | | | 53,817,380 | | | | 52,600,060 | |

See accompanying Notes to the Financial Statements

17

THE PRIVATE SHARES FUND

Schedule of Investments (Continued)

December 31, 2022

| | | Acquisition

Date | | | Shares/

Principal | | | Cost | | | Fair Value | |

PREFERRED STOCK IN PRIVATE COMPANIES(a),(b) — 39.1% (Continued) | | | | | | | | | | | | |

FOODTECH — 1.3% | | | | | | | | | | | | | | | | |

Impossible Foods, Inc., Preferred Series E-1 | | | Nov 2022 | | | | 400,000 | | | $ | 4,080,000 | | | $ | 7,980,000 | |

Impossible Foods, Inc., Preferred Series H-1(c) | | | Nov 2021 | | | | 153,494 | | | | 3,746,778 | | | | 3,398,357 | |

Impossible Foods, Inc., Preferred Series H-2(c) | | | Nov 2021 | | | | 53,389 | | | | 1,303,222 | | | | 1,182,033 | |

| | | | | | | | | | | 9,130,000 | | | | 12,560,390 | |

HARDWARE — 0.3% | | | | | | | | | | | | | | | | |

Hydrow, Inc., Preferred Series D | | | Feb 2022 | | | | 435,304 | | | | 4,999,989 | | | | 2,612,520 | |

| | | | | | | | | | | | | | | | | |

HEALTHCARE/BIOTECH — 2.1% | | | | | | | | | | | | | | | | |

Click Therapeutics, Inc., Preferred Series A | | | Nov 2020 | | | | 60,087 | | | | 210,304 | | | | 195,283 | |

Collective Health, Inc., Preferred Series F | | | May 2021 | | | | 3,989,361 | | | | 3,120,000 | | | | 2,672,872 | |

Crossover Health Management Services, Inc., Preferred Series D | | | Mar 2021 | | | | 239,125 | | | | 8,503,127 | | | | 9,978,686 | |

Omada Health, Inc., Preferred Series E | | | Dec 2021 | | | | 1,334,400 | | | | 7,999,995 | | | | 7,752,864 | |

ZocDoc, Inc., Preferred Series A | | | Feb 2015 | | | | 35,000 | | | | 875,000 | | | | 505,750 | |

| | | | | | | | | | | 20,708,426 | | | | 21,105,455 | |

SECURITY — 3.9% | | | | | | | | | | | | | | | | |

Contrast Security, Inc., Preferred Series A | | | Jul 2022 | | | | 828,514 | | | | 10,300,003 | | | | 11,416,923 | |

Contrast Security, Inc., Preferred Series C | | | Nov 2022 | | | | 1,164,596 | | | | 7,649,998 | | | | 16,048,133 | |

Cybereason, Inc., Preferred Series F(c) | | | Jul 2021 | | | | 1,510,600 | | | | 7,631,457 | | | | 7,250,880 | |

Exabeam, Preferred Series A | | | Nov 2020 | | | | 80,000 | | | | 1,020,000 | | | | 2,007,200 | |

Lookout, Inc., Preferred Series A | | | Feb 2015 | | | | 204,000 | | | | 1,927,800 | | | | 2,178,720 | |

| | | | | | | | | | | 28,529,258 | | | | 38,901,856 | |

SOFTWARE — 1.0% | | | | | | | | | | | | | | | | |

Roofstock, Inc., Preferred Series E | | | Mar 2022 | | | | 339,154 | | | | 9,999,990 | | | | 9,482,746 | |

| | | | | | | | | | | | | | | | | |

TRANSPORTATION — 3.3% | | | | | | | | | | | | | | | | |

Clearmotion, Inc., Preferred Series A-4 | | | Mar 2022 | | | | 12,954,589 | | | | 908,932 | | | | 1,562,324 | |

Flexport, Inc., Preferred Series A | | | Jun 2022 | | | | 580,165 | | | | 8,489,030 | | | | 8,122,310 | |

Flexport, Inc., Preferred Series B-1 | | | Jul 2022 | | | | 69,790 | | | | 944,665 | | | | 977,060 | |

Flexport, Inc., Preferred Series D-3 | | | Jul 2022 | | | | 82,613 | | | | 1,117,776 | | | | 1,156,582 | |

Hyperloop Technologies, Inc., Preferred Series B-1 | | | Jun 2017 | | | | 1,381 | | | | 999,999 | | | | 4,920 | |

Hyperloop Technologies, Inc., Preferred Series C | | | May 2019 | | | | 4,330 | | | | 37,938 | | | | 15,426 | |

Loadsmart, Inc., Preferred Series D | | | Jan 2022 | | | | 500,000 | | | | 10,000,000 | | | | 9,915,000 | |

Neutron Holdings, Inc. (d.b.a. Lime), Preferred Series 1-D | | | Mar 2019 | | | | 20,618,556 | | | | 5,000,000 | | | | 1,649,485 | |

Turo, Inc., Preferred Series D-1 | | | Jun 2018 | | | | 628,035 | | | | 2,932,295 | | | | 9,445,646 | |

| | | | | | | | | | | 30,430,635 | | | | 32,848,753 | |

TOTAL PREFERRED STOCK IN PRIVATE COMPANIES | | | | | | | | 346,741,923 | | | | 386,960,371 | |

| | | | | | | | | | | | | | | | |

CONVERTIBLE NOTES OF PRIVATE COMPANIES(b) — 6.4% | | | | | | | | | | | | | |

AEROSPACE — 1.9% | | | | | | | | | | | | | | | | |

Axiom Space, Inc., 3.00% 8/11/2023 | | | Aug 2021 | | | $ | 15,000,000 | | | | 15,612,740 | | | | 18,367,928 | |

See accompanying Notes to the Financial Statements

18

THE PRIVATE SHARES FUND

Schedule of Investments (Continued)

December 31, 2022

| | | Acquisition

Date | | | Units/Principal/

Commitment | | | Cost | | | Fair Value | |

CONVERTIBLE NOTES OF PRIVATE COMPANIES(b) — 6.4% (Continued) | | | | | | | | | | | | |

HOSTING/STORAGE — 1.0% | | | | | | | | | | | | | | | | |

TMGcore, Inc., 4.00% 8/11/2026 | | | Dec 2021 | | | $ | 10,000,000 | | | $ | 10,000,000 | | | $ | 10,000,000 | |

| | | | | | | | | | | | | | | | | |

SOFTWARE — 2.0% | | | | | | | | | | | | | | | | |

Tradeshift Holdings, Inc., 6.00% 11/22/2023 (d) | | | Nov 2021 | | | $ | 5,000,000 | | | | 2,574,645 | | | | 5,000,000 | |

Tradeshift Holdings, Inc., 6.00% 6/15/2023 (d) | | | Jun 2021 | | | $ | 10,000,000 | | | | 5,451,896 | | | | 10,000,000 | |

Tradeshift Holdings, Inc., 7.00% 3/25/2024 | | | Mar 2022 | | | $ | 5,000,000 | | | | 2,461,948 | | | | 5,000,000 | |

| | | | | | | | | | | 10,488,489 | | | | 20,000,000 | |

TRANSPORTATION — 1.5% | | | | | | | | | | | | | | | | |

Neutron Holdings, Inc. (d.b.a. Lime), 4.00% 10/29/2025 | | | Oct 2021 | | | $ | 15,000,000 | | | | 15,000,000 | | | | 15,000,000 | |

Neutron Holdings, Inc. (d.b.a. Lime), 4.00% 6/1/2027 | | | Jun 2020 | | | $ | 253,169 | | | | 252,362 | | | | 253,169 | |

| | | | | | | | | | | 15,252,362 | | | | 15,253,169 | |

TOTAL CONVERTIBLE NOTES OF PRIVATE COMPANIES | | | | | | | | 51,353,591 | | | | 63,621,097 | |

| | | | | | | | | | | | | | | | |

WARRANTS OF PRIVATE COMPANIES — 1.1% | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

SOFTWARE — 1.1% | | | | | | | | | | | | | | | | |

Tradeshift Holdings, Inc., Exercise Price $0.001, Exercise Date 11/21/2031 | | | Nov 2021 | | | | 213,797 | | | | 2,425,355 | | | | 2,663,654 | |

Tradeshift Holdings, Inc., Exercise Price $0.001, Exercise Date 9/9/2031 | | | Dec 2021 | | | | 427,594 | | | | 4,570,844 | | | | 5,327,308 | |

Tradeshift Holdings, Inc., Exercise Price $0.001, Exercise Date 3/25/2032 | | | Mar 2022 | | | | 213,797 | | | | 2,538,052 | | | | 2,663,676 | |

| | | | | | | | | | | 9,534,251 | | | | 10,654,638 | |

TRANSPORTATION — 0.0% | | | | | | | | | | | | | | | | |

Clearmotion, Inc., Exercise Price $0.12, Exercise Date 3/9/2029 | | | Mar 2022 | | | | 5,181,836 | | | | 341,068 | | | | 447,711 | |

Neutron Holdings, Inc. (d.b.a. Lime), Exercise Price $0.01, Exercise Date 6/2/2027 | | | Jun 2020 | | | | 1,016,483 | | | | 807 | | | | 1,802 | |

| | | | | | | | | | | 341,875 | | | | 449,513 | |

TOTAL WARRANTS OF PRIVATE COMPANIES | | | | | | | | | | | 9,876,126 | | | | 11,104,151 | |

| | | | | | | | | | | | | | | | | |

SIMPLE AGREEMENT FOR FUTURE EQUITY OF PRIVATE COMPANIES(a),(b) — 0.1% | | | | | | | | |

AEROSPACE — 0.1% | | | | | | | | | | | | | | | | |

Xplore, Inc. | | | Feb 2022 | | | | 1,000,000 | | | | 1,000,000 | | | | 1,000,000 | |

TOTAL SIMPLE AGREEMENT FOR FUTURE EQUITY OF PRIVATE COMPANIES | | | 1,000,000 | | | | 1,000,000 | |

See accompanying Notes to the Financial Statements

19

THE PRIVATE SHARES FUND

Schedule of Investments (Continued)

December 31, 2022

| | | Acquisition

Date | | | Shares | | | Cost | | | Fair Value | |

SPECIAL PURPOSE VEHICLES/PRIVATE FUNDS(a),(b) — 0.1% | | | | | | | | | | | | | |

PRIVATE FUNDS — 0.1% | | | | | | | | | | | | | | | | |

Northgate Growth Fund III(f) | | | Dec 2022 | | | | 400,000 | | | $ | 400,000 | | | $ | 400,000 | |

TOTAL SPECIAL PURPOSE VEHICLES/PRIVATE FUNDS | | | | | | | | | 400,000 | | | | 400,000 | |

| | | | | | | | | | | | | | | | | |

SHORT-TERM INVESTMENTS — 12.6% | | | | | | | | | | | | | | | | |

DEMAND DEPOSIT — 12.6% | | | | | | | | | | | | | | | | |

Goldman Sachs Government Fund, 4.07%, (e) | | | | | | | | | | | 124,900,347 | | | | 124,900,347 | |

| | | | | | | | | | | | | | | | |

TOTAL SHORT-TERM INVESTMENTS | | | | | | | | | | | 124,900,347 | | | | 124,900,347 | |

| | | | | | | | | | | | | | | | |

TOTAL INVESTMENTS — 99.7% | | | | | | | | | | | 839,927,345 | | | | 986,522,492 | |

Other assets less liabilities — 0.3% | | | | | | | | | | | | | | | 2,764,791 | |

| | | | | | | | | | | | | | | | |

NET ASSETS — 100.0% | | | | | | | | | | | | | | $ | 989,287,283 | |

(a) | Equity positions are non-income producing and debt positions are income producing. |

(b) | Investments in private companies, and in some cases public companies, may be subject to restrictions on disposition imposed by the issuer. All positions held are non-controlled and non-affiliated investments, as defined by the Investment Company Act of 1940, as amended (“1940 Act”). As of December 31, 2022 restricted securities represented 86.28% of the net assets of the Fund. |

(c) | These securities have been purchased through Special Purpose Vehicles/Private Funds in which the Fund has a direct investment of ownership units of the Vehicles. The shares, cost basis and fair value stated are disclosed based on the underlying securities purchased by the Vehicle and the Fund’s ownership percentage. |

(d) | Denotes a variable rate security. The rate shown is the current interest rate as of December 31, 2022. |

(e) | Represents the 7-day effective yield as of December 31, 2022. |

(f) | These investments in Special Purpose Vehicles/Private Funds are expected to be invested into Portfolio Companies’ common and preferred shares. |

All issuers are based in the United States, except for Lyst, Ltd. and OpenX Software, Ltd., which are based in the UK, and Trax, Ltd., Eruditus Learning Solutions Pte., Ltd., and Fundbox, Ltd., which are based in the Cayman Islands, Singapore, and Israel, respectively.

See accompanying Notes to the Financial Statements

20

THE PRIVATE SHARES FUND

Statement of Assets and Liabilities

December 31, 2022

Assets: | | | | |

Investments, at fair value (cost $839,927,345) (Note 3) | | $ | 986,522,492 | |

Receivable for fund shares sold | | | 2,137,707 | |

Interest receivable | | | 2,848,602 | |

Prepaid expenses and other assets | | | 372,044 | |

Total assets | | | 991,880,845 | |

| | | | |

Liabilities: | | | | |

Advisory fees | | | 1,574,711 | |

Payable for shareholder servicing fees - Class L | | | 892 | |

Payable for shareholder servicing fees - Class A | | | 39,327 | |

Payable for investments purchased | | | 75,090 | |

Payable for audit and tax fees | | | 219,999 | |

Payable for transfer agent fees | | | 321,000 | |

Payable for 12b-1 fees - Class L | | | 892 | |

Other accrued liabilities | | | 361,651 | |

Total liabilities | | | 2,593,562 | |

Commitments and contingences (Note 9) | | | | |

Net assets | | $ | 989,287,283 | |

| | | | |

Net assets consist of: | | | | |

Capital stock (unlimited shares authorized, no par value) | | $ | 851,302,678 | |

Total distributable earnings | | | 137,984,605 | |

Net assets | | $ | 989,287,283 | |

| | | | |

Net assets: | | | | |

Class A | | $ | 178,576,857 | |

Class I | | | 807,234,330 | |

Class L | | | 3,476,096 | |

Total net assets | | $ | 989,287,283 | |

| | | | |

Shares outstanding: | | | | |

Class A | | | 4,316,217 | |

Class I | | | 19,245,141 | |

Class L | | | 85,149 | |

Total shares outstanding | | | 23,646,507 | |

| | | | | |

Net asset value, public offering price, and redemption proceeds per share: | | | | |

Class A - Net asset value and redemption proceeds per share | | $ | 41.37 | |

Class I - Net asset value and redemption proceeds per share | | $ | 41.94 | |

Class L - Net asset value and redemption proceeds per share | | $ | 40.82 | |

Class A - Public offering price per share(a) | | $ | 43.89 | |

Class L - Public offering price per share(b) | | $ | 42.63 | |

(a) | Computation of public offering price per share 100/94.25 of net asset value. (See Note 10). |

(b) | Computation of public offering price per share 100/95.75 of net asset value. (See Note 10). |

See accompanying Notes to the Financial Statements

21

THE PRIVATE SHARES FUND

Statement of Operations

For the year ended December 31, 2022

Investment Income: | | | | |

Dividends1 | | $ | 503,160 | |

Interest2 | | | 5,579,883 | |

Total investment income | | | 6,083,043 | |

| | | | | |

Expenses: | | | | |

Investment advisory fees (Note 5) | | | 18,224,852 | |

Transfer agent fees | | | 1,650,306 | |

Audit and tax fees | | | 517,100 | |

Legal fees3 | | | 515,982 | |

Fund accounting & administration fees | | | 368,575 | |

Printing & postage | | | 350,878 | |

Registration fees | | | 194,983 | |

Insurance fees | | | 186,697 | |

Trustee fees | | | 147,750 | |

Shareholder servicing fees - Class A | | | 121,262 | |

Miscellaneous expenses | | | 111,932 | |

Chief compliance officer fees | | | 90,000 | |

Custodian fees | | | 72,663 | |

SEC fees | | | 26,705 | |

Distribution fees - Class L | | | 11,122 | |

Shareholder servicing fees - Class L | | | 1,822 | |

Total expenses | | | 22,592,629 | |

Less: Net contractual waiver of fees and reimbursement of expenses (Note 4) | | | (441,827 | ) |

Net expenses | | | 22,150,802 | |

Net investment loss | | $ | (16,067,759 | ) |

| | | | |

Net realized loss on investments | | | (5,976,695 | ) |

Net change in unrealized gain on investments | | | 20,286,802 | |

Net realized & change in unrealized gain on investments | | | 14,310,107 | |

Net change in net assets from operations | | $ | (1,757,652 | ) |

1 | Includes paid-in-kind dividends of $503,160. |

2 | Includes paid-in-kind interest of $1,811,644. |

3 | Includes extraordinary expenses incurred during the fiscal year. Extraordinary expenses related to Legal expenses incurred in the amount of $92,234 were excluded from the contractual waiver of fees due to their nature. Please see Note 4 in the Notes to the Financial Statements for additional information. |

See accompanying Notes to the Financial Statements

22

THE PRIVATE SHARES FUND

Statements of Changes in Net Assets

| | | Year ended

December 31, 2022 | | | Year ended

December 31, 2021 | |

Operations: | | | | | | | | |

Net investment loss | | $ | (16,067,759 | ) | | $ | (11,695,427 | ) |

Net realized gain/loss on investments | | | (5,976,695 | ) | | | 65,538,431 | |

Net change in unrealized gain on investments | | | 20,286,802 | | | | 40,658,916 | |

Net change in net assets resulting from operations | | | (1,757,652 | ) | | | 94,501,920 | |

| | | | | | | | | |

Distributions to Shareholders: | | | | | | | | |

Distributions from long term capital gains | | | (14,486,991 | ) | | | (51,227,704 | ) |

Net change in net assets from distributions | | | (14,486,991 | ) | | | (51,227,704 | ) |

| | | | | | | | | |

Fund share transactions: | | | | | | | | |

Proceeds from shares issued - Class A | | | 64,299,732 | | | | 62,603,597 | |

Proceeds from shares issued - Class I | | | 439,954,802 | | | | 351,778,917 | |

Proceeds from shares issued - Class L | | | 1,615,901 | | | | 2,173,960 | |

Reinvested distributions - Class A | | | 951,826 | | | | 5,041,316 | |

Reinvested distributions - Class I | | | 5,539,070 | | | | 21,362,256 | |

Reinvested distributions - Class L | | | 50,276 | | | | 204,652 | |

Cost of shares repurchased - Class A | | | (42,652,800 | ) | | | (28,951,952 | ) |

Cost of shares repurchased - Class I | | | (190,815,002 | ) | | | (32,099,168 | ) |

Cost of shares repurchased - Class L | | | (1,896,389 | ) | | | (346,778 | ) |

Net change in net assets from fund share transactions | | | 277,047,416 | | | | 381,766,800 | |

Net change in net assets | | $ | 260,802,773 | | | $ | 425,041,016 | |

| | | | | | | | | |

Net assets: | | | | | | | | |

Beginning of year | | $ | 728,484,510 | | | $ | 303,443,494 | |

End of year | | $ | 989,287,283 | | | $ | 728,484,510 | |

| | | | | | | | |

Transactions in shares: | | | | | | | | |

Issuance of shares - Class A | | | 1,492,876 | | | | 1,500,815 | |

Issuance of shares - Class I | | | 10,118,688 | | | | 8,243,895 | |

Issuance of shares - Class L | | | 37,898 | | | | 52,196 | |

Reinvested distributions - Class A | | | 22,749 | | | | 120,808 | |

Reinvested distributions - Class I | | | 130,638 | | | | 506,455 | |

Reinvested distributions - Class L | | | 1,218 | | | | 4,955 | |

Repurchase of shares - Class A | | | (992,797 | ) | | | (690,399 | ) |

Repurchase of shares - Class I | | | (4,415,495 | ) | | | (745,246 | ) |

Repurchase of shares - Class L | | | (45,436 | ) | | | (8,342 | ) |

Net change in shares | | | 6,350,339 | | | | 8,985,137 | |

See accompanying Notes to the Financial Statements

23

THE PRIVATE SHARES FUND

Statement of Cash Flows

For the year ended December 31, 2022

Cash flows from operating activities: | | | | |

Net change in net assets from operations | | $ | (1,757,652 | ) |

Adjustments to reconcile net change in net assets from operations to net cash used in operating activities: | | | | |

Purchases of investments | | | (319,606,614 | ) |

Net sales of short-term investments | | | 51,017,789 | |

Proceeds from sales of investments | | | 24,350,527 | |

Net change in unrealized gain on investments | | | (20,286,802 | ) |

Net realized loss on investments | | | 5,976,695 | |

Change in operating assets and liabilities: | | | | |

Increase in interest receivable | | | (2,387,803 | ) |

Increase in prepaid expenses and other assets | | | (36,187 | ) |

Increase in net payable to adviser | | | 517,090 | |

Increase in other accrued liabilities | | | 223,943 | |

Net cash used in operating activities | | | (261,989,014 | ) |

| | | | | |

Cash flows from financing activities: | | | | |

Proceeds from shares issued, net of change in receivable for fund shares sold | | | 495,889,060 | |

Cost of shares redeemed | | | (225,954,227 | ) |

Cash distributions paid | | | (7,945,819 | ) |

Net cash provided by financing activities | | | 261,989,014 | |

| | | | | |

Net change in cash | | | — | |

| | | | |

Cash at beginning of year | | | — | |

Cash at end of year | | $ | — | |

| | | | | |

Supplemental disclosure of noncash financing activities | | | | |

Transfer in and out between share classes | | $ | 9,409,965 | |

Purchases of shares through reinvested distributions | | | 6,541,172 | |

See accompanying Notes to the Financial Statements

24

THE PRIVATE SHARES FUND

Financial Highlights – Class A

For a capital share outstanding throughout each period

| | | Year ended

December 31,

2022 | | Year ended

December 31,

2021 | | Year ended

December 31,

2020 | | Year ended

December 31,

2019 | | Year ended

December 31,

2018 |

Per share operating performance | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of year | | $ | 41.77 | | | $ | 36.33 | | | $ | 29.96 | | | $ | 28.44 | | | $ | 26.85 | |

| | | | | | | | | | | | | | | | | | | | |

Change in net assets from operations: | | | | | | | | | | | | | | | | | |

Net investment loss | | | (0.80 | ) | | | (0.88 | ) | | | (0.90 | ) | | | (0.88 | ) | | | (0.71 | ) |

Net realized and unrealized gain on investments | | | 0.98 | | | | 9.54 | | | | 7.98 | | | | 2.40 | | | | 2.30 | |

Total change in net assets from operations | | | 0.18 | | | | 8.66 | | | | 7.08 | | | | 1.52 | | | | 1.59 | |

| | | | | | | | | | | | | | | | | | | | |

Distributions: | | | | | | | | | | | | | | | | | | | | |

From net return of capital | | | — | | | | — | | | | (0.07 | ) | | | — | | | | — | |

From net realized gain on investments | | | (0.58 | ) | | | (3.22 | ) | | | (0.64 | ) | | | — | | | | — | |

Total distributions | | | (0.58 | ) | | | (3.22 | ) | | | (0.71 | ) | | | — | | | | — | |

Net increase (decrease) in net asset value | | | (0.40 | ) | | | 5.44 | | | | 6.37 | | | | 1.52 | | | | 1.59 | |

Net asset value, end of year | | $ | 41.37 | (f) | | $ | 41.77 | | | $ | 36.33 | | | $ | 29.96 | | | $ | 28.44 | |

| | | | | | | | | | | | | | | | | | | | |

Total return(a) | | | 0.42 | % | | | 23.85 | % | | | 23.69 | % | | | 5.34 | % | | | 5.92 | % |

| | | | | | | | | | | | | | | | | | | | |

Ratios and supplemental data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of year (in thousands) | | $ | 178,577 | | | $ | 158,433 | | | $ | 103,984 | | | $ | 108,068 | | | $ | 109,902 | |

Ratio of net expenses to average net assets | | | 2.51 | %(b)(c) | | | 2.51 | %(b)(d) | | | 2.50 | %(b) | | | 2.79 | %(b)(e) | | | 2.50 | %(b) |

Ratio of gross expenses before reimbursement to average net assets | | | 2.41 | % | | | 2.64 | % | | | 2.97 | % | | | 3.56 | % | | | 3.29 | % |

Ratio of net investment loss to average net assets | | | (1.89 | )% | | | (2.42 | )% | | | (2.48 | )% | | | (2.71 | )% | | | (2.44 | )% |

Portfolio turnover | | | 3.17 | % | | | 26.20 | % | | | 6.97 | % | | | 14.76 | % | | | 24.75 | % |

(a) | The Fund’s total investment returns do not include a sales load. |

(b) | The ratio of net expenses includes recoupment of previously waived and/or reimbursed fees of $184,461, or 0.10%, for the fiscal year ended December 31, 2022, and contractual waivers and expense reimbursements of $171,876, $492,357, $916,804, and $887,579, or 0.12%, 0.47%, 0.78%, and 0.79%, for the fiscal years ended December 31, 2021, 2020, 2019, and 2018, respectively. Please see Note 4 in the Notes to the Financial Statements for additional information. |

(c) | During the fiscal year ended December 31, 2022, there were legal expenses incurred by the Fund that were distinguishable in their characterization as being unusual in nature as well as not expected to be recurring in future periods. The exclusion of these extraordinary expenses from the Fund’s expense limitation agreement caused the expense ratio to exceed the contractual expense limit by $17,472 or 0.01%. |

(d) | During the fiscal year ended December 31, 2021, there were legal expenses incurred by the Fund that were distinguishable in their characterization as being unusual in nature as well as not expected to be recurring in future periods. The exclusion of these extraordinary expenses from the Fund’s expense limitation agreement caused the expense ratio to exceed the contractual expense limit by $17,584 or 0.01%. |

(e) | During the fiscal year ended December 31, 2019, there were certain expenses incurred by the Fund that were distinguishable in their characterization as being unusual in nature as well as not expected to be recurring in future periods. The exclusion of these extraordinary expenses from the Fund’s expense limitation agreement caused the expense ratio to exceed the contractual expense limit by $336,193 or 0.29%. |

(f) | The NAV per share has been adjusted from the published NAV of $41.75 for post-closing adjustments. |

See accompanying Notes to the Financial Statements

25

THE PRIVATE SHARES FUND

Financial Highlights – Class I

For a capital share outstanding throughout each period

| | | Year ended

December 31,

2022 | | Year ended

December 31,

2021 | | Year ended

December 31,

2020 | | Year ended

December 31,

2019 | | Year ended

December 31,

2018 |

Per share operating performance | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of year | | $ | 42.22 | | | $ | 36.61 | | | $ | 30.12 | | | $ | 28.51 | | | $ | 26.85 | |

| | | | | | | | | | | | | | | | | | | | |

Change in net assets from operations: | | | | | | | | | | | | | | | | | | | | |

Net investment loss | | | (0.65 | ) | | | (0.62 | ) | | | (0.47 | ) | | | (0.59 | ) | | | (0.20 | ) |

Net realized and unrealized gain on investments | | | 0.95 | | | | 9.45 | | | | 7.67 | | | | 2.20 | | | | 1.86 | |

Total change in net assets from operations | | | 0.30 | | | | 8.83 | | | | 7.20 | | | | 1.61 | | | | 1.66 | |

| | | | | | | | | | | | | | | | | | | | |

Distributions: | | | | | | | | | | | | | | | | | | | | |

From net return of capital | | | — | | | | — | | | | (0.07 | ) | | | — | | | | — | |

From net realized gain on investments | | | (0.58 | ) | | | (3.22 | ) | | | (0.64 | ) | | | — | | | | — | |

Total distributions | | | (0.58 | ) | | | (3.22 | ) | | | (0.71 | ) | | | — | | | | — | |

Net increase (decrease) in net asset value | | | (0.28 | ) | | | 5.61 | | | | 6.49 | | | | 1.61 | | | | 1.66 | |

Net asset value, end of year | | $ | 41.94 | (e) | | $ | 42.22 | | | $ | 36.61 | | | $ | 30.12 | | | $ | 28.51 | |

| | | | | | | | | | | | | | | | | | | | |

Total return | | | 0.70 | % | | | 24.13 | % | | | 23.97 | % | | | 5.65 | % | | | 6.18 | % |

| | | | | | | | | | | | | | | | | | | | |

Ratios and supplemental data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of year (in thousands) | | $ | 807,234 | | | $ | 566,272 | | | $ | 197,921 | | | $ | 82,992 | | | $ | 33,945 | |

Ratio of net expenses to average net assets | | | 2.26 | %(a)(b) | | | 2.26 | %(a)(c) | | | 2.25 | %(a) | | | 2.54 | %(a)(d) | | | 2.25 | %(a) |

Ratio of gross expenses before reimbursement to average net assets | | | 2.34 | % | | | 2.50 | % | | | 2.75 | % | | | 3.36 | % | | | 3.10 | % |

Ratio of net investment loss to average net assets | | | (1.62 | )% | | | (2.15 | )% | | | (2.24 | )% | | | (2.46 | )% | | | (2.17 | )% |

Portfolio turnover | | | 3.17 | % | | | 26.20 | % | | | 6.97 | % | | | 14.76 | % | | | 24.75 | % |

(a) | The ratio of net expenses includes contractual waivers and expense reimbursements of $631,951, $899,197, $567,388, $546,174, and $94,654, or 0.08%, 0.23%, 0.50%, 0.82%, and 0.85%, for the fiscal years ended December 31, 2022, 2021, 2020, 2019, and 2018, respectively. Please see Note 4 in the Notes to the Financial Statements for additional information. |

(b) | During the fiscal year ended December 31, 2022, there were legal expenses incurred by the Fund that were distinguishable in their characterization as being unusual in nature as well as not expected to be recurring in future periods. The exclusion of these extraordinary expenses from the Fund’s expense limitation agreement caused the expense ratio to exceed the contractual expense limit by $74,334 or 0.01%. |

(c) | During the fiscal year ended December 31, 2021, there were legal expenses incurred by the Fund that were distinguishable in their characterization as being unusual in nature as well as not expected to be recurring in future periods. The exclusion of these extraordinary expenses from the Fund’s expense limitation agreement caused the expense ratio to exceed the contractual expense limit by $48,772 or 0.01%. |

(d) | During the fiscal year ended December 31, 2019, there were certain expenses incurred by the Fund that were distinguishable in their characterization as being unusual in nature as well as not expected to be recurring in future periods. The exclusion of these extraordinary expenses from the Fund’s expense limitation agreement caused the expense ratio to exceed the contractual expense limit by $189,435 or 0.29%. |

(e) | The NAV per share has been adjusted from the published NAV of $42.32 for post-closing adjustments. |

See accompanying Notes to the Financial Statements

26

THE PRIVATE SHARES FUND

Financial Highlights – Class L

For a capital share outstanding throughout each period

| | | Year ended

December 31,

2022 | | Year ended

December 31,

2021 | | Year ended

December 31,

2020 | | Year ended

December 31,

2019 | | Period ended

December 31,

2018* |

Per share operating performance | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 41.33 | | | $ | 36.07 | | | $ | 29.83 | | | $ | 28.39 | | | $ | 28.37 | |

| | | | | | | | | | | | | | | | | | | | |

Change in net assets from operations: | | | | | | | | | | | | | | | | | | | | |

Net investment loss | | | (1.12 | ) | | | (0.82 | ) | | | (0.67 | ) | | | (0.58 | ) | | | (0.49 | ) |

Net realized and unrealized gain on investments | | | 1.19 | | | | 9.30 | | | | 7.62 | | | | 2.02 | | | | 0.51 | |

Total change in net assets from operations | | | 0.07 | | | | 8.48 | | | | 6.95 | | | | 1.44 | | | | 0.02 | |

| | | | | | | | | | | | | | | | | | | | |

Distributions: | | | | | | | | | | | | | | | | | | | | |

From net return of capital | | | — | | | | — | | | | (0.07 | ) | | | — | | | | — | |