As field with the U.S. Securities and Exchange Commission on January 9, 2020

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-22761

Stone Ridge Trust

(Exact name of registrant as specified in charter)

510 Madison Avenue, 21st Floor

New York, NY 10022

(Address of principal executive offices) (Zip code)

Stone Ridge Asset Management LLC

510 Madison Avenue, 21st Floor

New York, NY 10022

(Name and address of agent for service)

(855)609-3680

Registrant’s telephone number, including area code

Date of fiscal year end:October 31, 2019

Date of reporting period:October 31, 2019

Item 1. Reports to Stockholders.

Annual Report

October 31, 2019

Stone Ridge High Yield Reinsurance Risk Premium Fund

Stone Ridge U.S. Hedged Equity Fund

Beginning on January 1, 2021, as permitted by regulations adopted by the Commission, paper copies of the Funds’ shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from your financial intermediary or, if you invest directly through the Funds’ transfer agent, U.S. Bancorp Fund Services, LLC (the “Transfer Agent”), from the Transfer Agent. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications electronically by contacting your financial intermediary.

You may elect to receive all future reports in paper free of charge by contacting your financial intermediary or, if you invest directly through the Transfer Agent, by contacting the Transfer Agent at (855) 609-3680. Your election to receive reports in paper will apply to all funds held in your account if you invest through a financial intermediary or all funds within the fund complex if you invest directly through the Transfer Agent.

Shareholder Letter

“The advantages of nonaction. Few in the world attain these.”

- The Daodejing

“To see people who will notice a need in the world and do something about it. Those are my heroes.”

- Fred Rogers (aka Mr. Rogers)

“There is no cause to worry. The high tide of prosperity will continue.”

- Andrew Mellon, US Secretary of the Treasury, September 1929

“My centre is giving way, my right is in retreat; situation excellent. I am attacking.”

- Field Marshall Foch, Battle of the Marne, 1914

December 2019

Dear Fellow Shareholder,

The green light is a powerful symbol in our culture. Be aggressive. Charge. Do something. Go! But yellow and red lights are equally important. Slow down. Stop. Be still and think. Calm the mind. Wage peace with yourself.

In January, we instituted a “no device” policy for all meetings at Stone Ridge. It has coincided with the greatest burst of creativity we’ve experienced since the firm began. Email, text, Slack, and social media are each efficient dopamine delivery machines – which feels great in the moment – but the context switching inherent in the endless, tiny dopamine hits robs us of our ability to be creative at the level required to serve clients with breakthrough innovations. You can’t have a soaring career if you’re on drugs.

At Stone Ridge, to be engaged in the study of wonder, we must be engaged in the study of quiet. Have you ever taken a true detox from your electronics? Turned everything completely off, and out of reach, for a full day, weekend, or longer? Historically, I’ve done it1-2 times a year, but this year I decided to increase the dosage. The positive effect is so profound I now think of this strategy like a magic pill, up there in medicinal efficacy with good sleep and intense exercise. No downsides and the benefits compound.

Coined by computer scientist Cal Newport, Digital Minimalism is anot-so-secret weapon, available to all, followed by almost none. It creates the necessary, not sufficient, conditions for creativity to ignite. Working deeply, and free from dopamine addiction, true creatives free themselves from thinking merely outside the box. They understand the actual truth: there is no box.

One of my favorite parts of working at Stone Ridge is getting to glimpse occasional bursts of breathtaking creativity from brilliant colleagues emerging from deep work. When in flow, the firm runs on different fuel. It’s energizing and incredibly attractive to be around. There’s no insecurity, no lack. I think we create to experience moments when we feel like we are enough.

I gave up voicemail about 15 years ago and I’ve never had a social media account. I set an alarm to go off five minutes before meetings are scheduled to end, so in the interim I can lock in, and totally focus on the

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

2

Shareholder Letter

person I’m with. This year I stopped taking my phone to dinner. It would be impossible to overstate the benefit to my relationships, to my ability to connect, and to my enjoyment of meals.

A friend systematically takes at least three days to reply to most emails, and then does it as a batch. I wonder how many time-sensitive topics aren’t so time-sensitive after all? I wonder how extracting ourselves from the IV drip of continuous email-dopamine would impact our health? Would inserting a yellow light into our email practices shrink our lives? It would certainly shrink the noise. Would it amplify the signal?

The Triple Threat

At Stone Ridgeour singular purpose is financial security for all. Together, we innovate to prepare for an uncertain future. Our team finds virtue in our purpose. There is no finite end. There is no winning. There’s not even any competition. There is only progress, or not. There’s only helping people, or not.

Brimming with the most optimistic people I’ve ever been around, the team at Stone Ridge relentlessly seeks truth in data – not what we want to be true – and we see a monumental societal risk emerging. Increasingly long lifespans are colliding with low or negative interest rates, threatening our ability to generate enough retirement income to age with dignity, agency, and peace of mind. And while overall inflation may be subdued, unexpectedly high inflation always arrives unexpectedly. Even with only modest headline inflation today, prices for certain critical retiree purchases – including medical care, housing, and ongoing education – are rising rapidly.iWe call the combination of these risks – longevity risk, investment return risk, and inflation risk – the “Triple Threat”.

Low or negative rates are particularly insidious, because risk-free rates form the foundation of the total return to all asset classes: total return = risk-free rate + risk premium. In standard financial planning simulations, simply replacing the much higher historical risk-free rate with today’s much lower actual risk-free rate drives 75year-old male “failure rates” (atoo-anodyne academic term for running out of money before dying) from 3% to a sobering 47%.ii That’s arithmetic – not economic theory. Worse, that’s before considering any conservative adjustments to estimates of the future equity risk premium and/or inflation and/or the withdrawal %, just in case a retiree gets a bad draw (i.e., sequencing risk).

10,000 Baby Boomers turn 65 every day, underscoring the importance of tackling the Triple Threat with vigor, now. In 2035, retirees are forecast to outnumber minors for the first time in American history,iii weighing on economic growth (see, unfortunately, Japan). Achieving the peace of mind that comes from financial security can be boiled down to a singlenon-negotiable: high and reliable income, regardless of lifespan.

Retirement is all about income – assets are just an inefficient, and unreliable, means to an end. Spend too much and risk old age without dignity. Spend too little and risk youth without life. So traditional financial planning strategies can be useful, but never optimal, because we don’t know how long we’re going to live – i.e., we can never know how much is too much, how little is too little. Moving beyond a financial plan, the Triple Threat requires a longevity plan.

Live Long and Prosper: The Longevity Risk Premium

At Stone Ridge, our entire product development philosophy is six words: we build products we want ourselves. Our forthcoming longevity risk franchise – LIFEX for short – aims high, tackling our collective societal retirement challenge head on.

In building LIFEX, our first observation was as obvious as it was powerful:pooling longevity risk improves retirement outcomes.Pre-LIFEX, this pooling was primarily the domain of income annuities,

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

3

Shareholder Letter

which provide steady income for life and dramatically lower the risk of running out of money.iv However, despite their potentially life-changing financial and health benefits, income annuity usage has been limited in investor portfolios for a variety of reasons. Taking a very different approach – while still delivering the benefits of risk pooling – we’ve set out to change that.

Specifically, we believe that a product built specifically to address the Triple Threat, and the corresponding need for high and reliable retirement income – butdelivered in fund form, cheaply, easily, and with a click – will fundamentally transform retirement portfolios and create a higher level of financial security for all Americans. Our solution set – LIFEX – will be in ’40 Act fund form, offered on an annual rolling basis to50-85 year-olds, providing up to 25 years of steady income, uncorrelated to traditional portfolios.v To most broadly tackle the Triple Threat, LIFEX could have fixed payouts (i.e., constant) or, instead, inflation-linked payouts (i.e., adjusting annually based on CPI); it could take AAA risk or, instead, take higher-yieldingnon-AAA risk. Regardless of choice,LIFEX contains, and is built upon, the longevity risk premium.

The LIFEX investor experience will be straightforward. Investors purchase fund shares, just like any other ’40 Act fund. To make the payments actuarially fair, an investor’s purchase price is based on their age and gender. For every investor, one LIFEX share will distribute $1 of extremelytax-efficient income per year – paid monthly – for the life of the fund, so each investor can easily backsolve and purchase the right number of shares for their individual cash flow needs, supplemented as appropriate by Social Security. LIFEX distributions will be quite high relative to bond yields and will always subtotal to at least the amount invested, regardless of when an investor passes (akin to principal protection).vi Finally, as a “break glass” backup for an unexpected life emergency, or just a change of heart, LIFEX will offer quarterly liquidity (with a 2% repurchase fee to account for adverse selection).

Post-launch, some LIFEX investors pass away early, receiving fewer payments; others live longer and receive more payments. For the longer-lived investors, additional payments received in the later years translate into higher returns on their initial investment. That is,investors get paid more the longer they live. Such is the power of the longevity risk premium. To get a sense of the impact LIFEX can have on US retirement, for a 75year-old malepre-tax equivalent payout yields would be 9.4% with AAA assets, and 11.8% withnon-AAA assets, if LIFEX were to launch today.vii

The longevity risk premium is special for two reasons. First, it’s the only risk premium that’s truly reliable. Second, its magnitude is time-varying in the most valuable possible way: it increases with an investor’s lifespan.Pooling longevity risk among investors always increases payout yields for those alive, regardless of the underlying asset strategy.viii

Life Insurance is something we buy to protect our loved ones in case we die too soon. In the future, LIFEX will be something we buy to protect our loved ones in case we die too late. LIFEX is a breakthrough, and benefits from industry-leading actuarial services from New York Life and collaboration with the Director of the Stanford University Center on Longevity.

The Advantages of Nonaction

Our most important job is risk management – the safety of our clients’ wealth, and our own. We each work in risk management. Whether we choose it or not, it chooses us.

At Stone Ridge, our risk management philosophy can be expressed as an equation:

Risk Management = Diversification + Humility

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

4

Shareholder Letter

Notice the harmony between diversification and humility. The smaller the first, the smaller the second. The bigger the first, the bigger the second.

At Stone Ridge, the embodiment of our risk management philosophy is the 10/10 (“Ten Ten”) portfolio. In its purest unobtainable form, the 10/10 is 10 long-term allocations, each 10% weight, each with a persistent, pervasive, and intuitive risk premium, each uncorrelated with traditional markets, each uncorrelated with each other. Our 10/10 concept includes reinsurance, alternative lending, market insurance, drug royalty, SFR (single family rentals), private investments, and Bitcoin. That doesn’t (yet) add to 10. We remain on our journey.

The 10/10 honors our most important job. Its extraordinary diversification harmonizes with its quiet humility. Once set, tweaks or no tweaks have largely the same impact. Its stillness doesn’t mistake activity for achievement. This way, the 10/10 offers the advantages of nonaction, and seeks to deliver peace of mind.

Though the peace we seek isn’t really peaceof mind. It’s peacefrom mind. From the silent ruminations. “Do I have enough? Am I financially secure?” In the decades ahead, Stone Ridge will help as many people as possible answer those questions decisively and affirmatively.

We’re building the 10/10 so we don’t have to rely on stocks and bonds. We’re building LIFEX so we don’t have to rely on the 10/10. In financial planning language, the 10/10 is for wants and wishes. LIFEX is for needs. In longevity planning language, the 10/10 + LIFEX = offense against the Triple Threat.

“There is no cause to worry.”

On December 29, 1989 the Nikkei hit 38,957. Today, three decades later, it’s 23,783, and at one point it was down 82%.ix During this period, Japan has been in no wars. To inflate stock prices, the BOJ (Bank of Japan) has purchased 75% of all Japanese ETFs and is a top 10 holder in 90% of the Nikkei names.x Even net of dividends, 23,783 is clearly not the price they want, underscoring the impotence of any government in setting any long-term price for any good or service. So how is it possible that we are now entering the fourthdecade of a major global stock market index, in a free country, being cumulatively (very, very) down. How?

The sobering nature of risk is such that our feelings of safety reach their maximum when our actual risk is highest.Living under the influence of risk, what we want to be true doesn’t matter. In September 1929, the US Secretary of the Treasury said “There is no cause to worry. The high tide of prosperity will continue.” Similar sentiments were expressed in Tokyo trading rooms in December 1989. Similar sentiments are being expressed about US stocks today. They may be correct. We just don’t know.

Observation #1: the typical RIA portfolio holds about 50% equities, Japan is about an 8% weight in the global equity portfolio, so many investors have about a 4% allocation to Japan.xi

Over the last 25+ years, catastrophe reinsurance quota shares returned 11.5%/year with no correlation to anything.xii This period was far from a smooth ride, punctuated by Katrina/Rita/Wilma (2005), Tohoku/Christchurch (2011), Harvey/Irma/Maria (2017), Jebi/Cal Fire (2018), and Faxai/Hagibis (2019). Notably, the last 6 years – the period of our largest fund’s life (SRRIXxiii) – was a 17% percentile occurrence.xiv Far from great, far from unusual.

I wonder in what percentile of the true distribution the last30-years of the Nikkei performance lands? The reality is no one knows because the true distribution is unknowable. The more revealing and better

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

5

Shareholder Letter

question: what percentile would investors have estimated for such a future30-year performance on December 29, 1989? 0%-tile? This underscores the uncomfortable truth that, for investing in general – including assessing equity risk – we don’t know what we don’t know. If we did, markets wouldn’t crash. And they certainly wouldn’t have a positive risk premium.

Observation #2: the typical RIA portfolio that holds reinsurance, holds about a 3% position.xv

Observation #3: we’ve had significant repurchase requests in SRRIX. We’ve had zero investors ask us to take Japan out of the Elements Portfolios.

Japan returns are buried within an overall global equity allocation – out of sight, out of mind.30-years of cumulative red and counting? Not a topic. Are Japanese equities broken because of country demographics? We’ve never been asked that question.

SRRIX is its own line item – green its first three years, red its last three years. Positive 11.5% average quota share return the last 25 years?xii Drowned out by the availability bias of recent events. Reinsurance providing potentially life-changing diversificationxvi amidst a1930’s-style left tail in traditional markets? We can just hope that doesn’t happen (again).

“Situation Excellent. I am Attacking.”

At Stone Ridge, we believe in the reinsurance risk premium down to our toes and 2019 was marked by high levels of reinsurance-related productivity.

First, the “other” Stone Ridge reinsurance ’40 Act fund, SHRIXxvii, now has almost $1 billion AUM. Fully invested for more than 6 years, it’s outperformed every one of the 30+ funds in the Eurekahedge ILS Advisers Index and has been the only reinsurance fund in that group to “beat the market,” outperforming the Swiss Re Global Cat Bond Index.xviii Moreover, SHRIX has been profitable 24 out of 26 quarters, including 17 quarters in a row during one stretch,xix while delivering a risk premium comparable to the historical equity risk premium and multiples of the historical credit risk premium.xx

Notably, the same team manages SRRIX as SHRIX, with the same investment philosophy, market access, and execution discipline. SHRIX just takes (a lot) less risk so happened to do (a lot) better these last three years – both funds, each index-like, performed exactly as expected in light of industry events. In a textbook example of recency bias, SHRIX is growing while SRRIX – its own line item – is shrinking, for now.

Earning the reinsurance risk premium – or any risk premium – is impossible without the ability to resist recency bias. We share this foundational point in every introductory reinsurance meeting we have with potential investors, and I’ve written andre-written about this topic in past shareholder letters. If an investor can’t resist exiting after losses, it’s better to not invest in reinsurance at all – due to the left tail nature of the return distribution, market timing virtually guarantees a cumulative loss. The only way to earn the average is to stay in the trade.

The three-part fundamental thesis of reinsurance investing is clear. First, reinsurance has historically generated a significantly positive risk premium because it provides a valuable risk transfer service. Second, its returns have been uncorrelated to traditional financial assets. Third, its yields have been adaptive – that is, they have increased after losses. That’s it. We like simple at Stone Ridge.

Second, our 2020 executed quota shares experienced material elevation in rates, or improvements in terms & conditions, or both, versus those same trades in prior years. This is partly driven by the

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

6

Shareholder Letter

reinsurance market reacting to losses, and a lot driven by Stone Ridge-specific factors, as a function of our market leading size in quota shares. I credit our reinsurance team for world class execution.

Third, we’ve taken in significant capital for Stone Ridge quota shares from institutional investors, including one of the largest life insurance companies in the world, separate from SRRIX. 2020 executed Stone Ridge quota shares offer the most attractive rates and terms & conditions since the firm began, so it’s not surprising sophisticated institutional investors – exposed to the consequences of low or negative risk-free rates like all of us – like this entry point as part of a long-term reinsurance allocation.

Fourth, like catastrophe risk,non-catastrophe risk (e.g., D&O, E&O, General Liability) is experiencing material elevation in rates, or improvements in terms & conditions, or both. Working with a core set of our existing reinsurance partners, Stone Ridge also shares thisnon-catastrophe risk via quota shares, also separate from SRRIX. Underscoring the long-term power of reinsurance as a diversifier to traditional investments, new 2019non-SHRIX andnon-SRRIX Stone Ridge capital for catastrophe andnon-catastrophe risk, which we expect will grow substantially, will support about $1.5 billion of assets when fully deployed.

We now turn the reinsurance page on 2019 and move forward, never losing sight of the critical role reinsurance risk plays in financial security for all.

Notice a Need. Do Something.

Amidst a culture of creativity, our efforts at Stone Ridge are organized around a core set of beliefs we have about what willnot change. These are the things we believe are true today and we believe will be just as true decades from now. The irreplaceability of lifetime income. The critical role of financial advisors. The power of 10 uncorrelated risk premiums, eachanti-fad. The harmony of diversification and humility in risk management. Our “what will not change?” filter provides the necessary discipline for our creative process.

NobelPrize-winning physicist Arthur Compton said, “every useful discovery I ever made, I gambled that the truth was there, then acted on faith until I could prove its existence.” I like his attitude. Amidst uncertainty, but tethered by our discipline, we confidently invest in our shared future – ignoring press, eschewing focus groups – internally iterating ceaselessly. If one of our insights was hiding in plain sight after all, the result is valuable innovation for RIAs and their clients. Because nothing in business is easy or obvious, most of our ideas end up on the cutting room floor. A strength of the firm: we change our minds on a dime if an idea wasn’t good enough, or if we decide we got it wrong.

Compton-like, we got Flourish right.

Flourish believes people need people, not just technology. Flourish believes advisors have rightly earned the trust of their clients. Flourish believes clients want to feel authentic in their lives, connected to their loved ones and community, propelled by clear purpose.

Since launch in late 2018, the Flourish Cash numbers are astonishing, to me. 175 RIA firms have joined, we’ve experienced 55 consecutive weeks of record balances and counting, 53% of household invitations have been accepted and funded, the average balance is $152,190.xxi Flourish benefits clients with high cash rates, a beautiful front end, and simplicity – one RIA said, “Your website is one giant easy button.”xxii Flourish helps advisors help clients because the average client has 20% of their wealth in cashxxiii – likely far too high to reach their retirement goals. Flourish also has powerfulbuilt-in referral features with a growing list of amazing stories that helped new clients earn more and lifted advisor practices.

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

7

Shareholder Letter

Building on this momentum, here’s a sample of what’s coming next in Flourish:

First, Flourish Home.xxiv The target market here is narrow, but enormous: the growing segment of Americans who are risk-concentrated in their primary residence. A client’s home is often their largest individual asset, but it’s illiquid andindividual homes have volatility on par with equities.xxv Withpre-qualified andpre-populated applications, Home will provide a streamlined path for advisors to help suitable clients extract liquidity from their home without taking on debt or paying monthly interest. Clients essentially sell a portion of their home in atax-efficient manner – their choice of anywhere between5-20% – and do anything they want with the proceeds.

By purchasing LIFEX with the proceeds, for example, clients can transform an illiquid,non-cash-generating, “dead” asset – say 15% of their home – into one that immediately begins generating high monthly income (e.g., if LIFEX were to launch today, $200,000 unlocked from a partial home sale would generatepre-tax equivalent of $1,568/month (AAA assets) or $1,960/month(non-AAA assets) for a 75year-old male).xxvi Internally, we refer to this process as “cashlessly funding retirement income” and theHome-to-LIFEX workflow will be seamless within Flourish.

Second, Flourish Select. Three observations motivate this module. First, good companies are staying private longer. Select will help RIAs participate in thepre-IPO value creation process of “select” private companies. Second, some excellent, diversifying funds just don’t work in ’40 Act form. Select will help RIAs access “select” private funds that offer truly differentiated risks. Third, filling out complex paper subscription documents and getting physical signatures from clients is not operationally scalable for most RIAs, nor can all clients meet the large minimums required for many private investments. Select will provide a streamlined,all-electronic subscription process that feeds right into standard RIA reporting software – “streamlined” because we already have the relevant client information in Flourish Cash – and will create and manage feeder vehicles with low minimums.

Importantly, Select will not be a platform dispassionately connecting buyers and sellers. Instead, Stone Ridge will diligence and curate (that’s why we call it Select) – and invest in – all Flourish Select opportunities, soco-investors always know we have skin in the game. This doesn’t guarantee success – far from it – but it creates appropriate symmetry. If you give an opinion and someone follows it, the ethical path requires exposure to its consequences. And it has to be real exposure, not window dressing.

Stay tuned for Flourish Give, Flourish Advance, Flourish Invest, and…more.

In the years to come, we believe the leading RIAs will move beyond money management and beyond goal management. The client of the future will ask their advisor “help me discover a life I didn’t even know was possible.” Life management. Flourish can help.

OUR PARTNERSHIP

Stone Ridge is most proud of the 50/50 partnership we have with you. We are on the path together. You contribute the capital necessary to propel and sustain groundbreaking product development. We contribute our collective careers’ worth of experience in sourcing, structuring, execution, and risk management. Together, it works. In that spirit, I offer my deepest gratitude to you for sharing responsibility for your wealth with us this year. We look forward to serving you again in 2020.

Warmly,

Ross L. Stevens

Founder, CEO

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

8

Shareholder Letter

| i | The Unfinished Business of Health Reform by J. Bivens, Economic Policy Institute, October 2018 |

| ii | Assumes an investor holds a 60/40 portfolio, which means 60% equities (risk-free rate + equity risk premium) and 40% fixed income at risk-free rate. See table below for risk of failure at various withdrawal rates. Source: Historical risk-free rate from US Treasury10-year constant maturity rates, Morningstar, over past 65 years. Current risk-free rate is estimated based on current US and global risk-free rates. Equity risk premium based on lower end of range of Damodaran, Aswath, “Equity Risk Premiums (ERP): Determinants, Estimation and Implications”, April 2019. Future realized risk-free rate and equity risk premium may differ from historical and estimated values. Cash return is based on current national average savings account rate from FRED as of 7/21/2019. Average 20% allocation based on “UBS Investor Watch” 3Q 2017. Risk of failure is based on simulations assuming the stated returns and asset allocations (including cash), stated withdrawal as a percentage of initial assets and grown at 2% for inflation, and historical volatility. Risk of failure is % of simulations that resulted in negative portfolio value within 25 years. |

The New Arithmetic of Financial Planning

| | | | |

| | | Historical Risk-Free

Rate & Equity Risk

Premium | | Current Risk-Free Rate

& Historical Equity

Risk Premium |

Risk-Free Rate | | 5.9% | | 1.0% |

Equity Risk Premium | | 4.0% | | 4.0% |

Equity Return | | 9.9% | | 5.0% |

60/40 Return | | 8.3% | | 3.4% |

With 20% Cash @ 0.10% | | 6.6% | | 2.7% |

| | | Risk of Failure | | |

4% Withdrawals | | 3% | | 47% |

5% Withdrawals | | 16% | | 77% |

6% Withdrawals | | 40% | | 93% |

| iii | Source: U.S. Census Bureau, “Older people projected to outnumber children for first time in U.S. history,” September 6, 2018. Specifically, the Census Bureau projects that there will be 76.7 million people under the age of 18 and 78.0 million over the age of 65. |

| iv | Source:A Broader Framework for Determining an Efficient Frontier for Retirement Income by W. Pfau |

| v | LIFEX may end earlier than 25 years if the mortality experience is significantly lower than expected. |

| vi | Based on illustrative pricing discussed in endnote vii. Final terms will be determined prior to investment. |

| vii | Illustrative pricing. Final terms will be determined prior to investment. Payout yield is calculated as the annual sum of expected distributions divided by the investor’s expected price per share. |

| | Estimated using the Treasury yield curve as of 11/8/2019 and New York Life mortality expectations. AAA version uses estimated AAA CLO spreads as of 11/8/2019.Non-AAA version assumes risk premium strategies, combined, earn 4% excess returns net of fees with 5% volatility. Both versions may end earlier than 25 years if the mortality experience is significantly lower than expected. Because thenon-AAA version takes investment return risk, the probability that it terminates early may be higher than the AAA version.Pre-tax equivalent yields calculated assuming investor has $250,000 of taxable income: 25.1% federal tax rate, 4.7% state & local tax rate, and 18.8% long-term capital gains tax rate. |

| viii | Because longevity-pooled investments simply combine the underlying investment strategy with mortality pooling, they will always have a higher initial payout yield than is possible from the investment strategy alone. |

| ix | Source:https://tradingeconomics.com/japan/stock-market |

| x | Sources: FT, “BoJ’s dominance over ETFs raises concern on distorting influence”, and Barrons, “BoJ Now A Top 10 Shareholder In 90% of Nikkei 225.” |

| xi | Sources: Stone Ridge CIO Survey and MSCI. |

| xii | Stone Ridge analysis based on data from Bloomberg, Guy Carpenter, Aon and proprietary loss ratio data provided by global reinsurers. Analysis includes all reinsurers for which Stone Ridge has at least five consecutive years of loss ratio data (20 reinsurers as of 9/30/2019). These reinsurers include eight of the top ten global reinsurers as enumerated in AM Best’s 2019 “Top 50 World’s Largest Reinsurance Groups” (measured by net writtennon-life premium and excluding regional reinsurers and Berkshire Hathaway). Includes Stone Ridge estimates of 2019 performance through 12/25/19. |

| xiii | SRRIX is the ticker for the Stone Ridge Reinsurance Risk Premium Interval Fund. |

| xiv | Sources: AIR Worldwide, Bloomberg, Stone Ridge Analysis. Based on the rolling6-year average of remodeled historical natural disasters on current exposures provided by AIR Worldwide, trended for GDP and estimates for recent events. Perils included: US Tropical Cyclone; US Wildfire; Japan Typhoon; US, Canada, Japan, Europe, South America, India and Southeast Asia Earthquake; all events greater than $2.5B in 2018 US Dollars. |

| xv | Source: Stone Ridge CIO Survey. |

| xvi | Diversification does not assure a profit or protect against a loss in a declining market. |

| xvii | SHRIX is the ticker for the Stone Ridge High Yield Reinsurance Risk Premium Fund. |

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

9

Shareholder Letter

| xviii | The Eurekahedge ILS Advisers Index (the “Eurekahedge Index”) is ILS Advisers and Eurekahedge’s collaborative equally weighted index of 33 constituent hedge funds. The index is designed to provide a broad measure of the performance of underlying hedge fund managers that explicitly allocate to insurance linked investments and have at least 70% of their portfolio invested innon-life risk. One cannot invest directly in an index. The Swiss Re Global Cat Bond Index is Amarket-cap-weighted index that tracks the performance of all catastrophe bonds issued under Rule 144A. |

| xix | Source: Stone Ridge, as of 9/30/19. |

| xx | Investment grade credit risk premium estimated to be 0.50% for 1936-2014. Source:The Credit Risk Premium by A. Asvanunt and S. Richardson |

| xxi | Source: Stone Ridge, as of 12/25/19. Flourish Cash is a service offered by Stone Ridge Securities LLC, a registered broker-dealer and FINRA member. Stone Ridge Securities LLC is not a bank, but the cash balance in a Flourish Cash account is swept from the brokerage account to deposit account(s) at one or more third-party banks that have agreed to accept deposits from customers. Stone Ridge Asset Management LLC does not provide any services, including investment advisory services, in connection with Flourish Cash and does not provide any guarantees or financial support to Flourish Cash accounts. |

| xxii | This feedback may not be representative of other customers and is not a guarantee of future performance or success. |

| xxiii | Source: “UBS Investor Watch” 3Q 2017. |

| xxiv | Flourish is a platform for products and/or services offered through one or more affiliates of Stone Ridge Holdings Group LP (“Stone Ridge”). Flourish Select will be offered through Stone Ridge Securities LLC. Flourish Home and other Flourish modules will be offered through other Stone Ridge affiliates. |

| xxv | Source:2019 Volatility Index, Unison, July 2019 |

| xxvi | Based on illustrative pricing for a AAA version of LIFEX. Final terms will be determined prior to investment. Estimated using the Treasury yield curve and CLO spreads as of 11/8/2019 and New York Life mortality expectations. LIFEX may end earlier than 25 years if the mortality experience is significantly lower than expected. |

Risk Disclosures

The information herein regarding the Stone Ridge Longevity Risk Premium Fixed Income Fund 2019 (“LIFEX”) is not complete and may be changed. A registration statement relating to the securities of LIFEX has been filed with the Securities and Exchange Commission. The securities of LIFEX may not be sold until the registration statement becomes effective. This is not an offer to sell or the solicitation of an offer to buy securities and is not soliciting an offer to buy LIFEX’s securities in any state in which the offer, solicitation or sale would be unlawful.

The investment objective, risks, charges and expenses of LIFEX, a series of Stone Ridge Trust VII, must be considered carefully before investing. The prospectus, periodic reports and certain other regulatory filings contain this and other important information and may be obtained, when available, by visitingwww.sec.gov.

LIFEX’s prospectus, which includes a statement of additional information, can be obtained by visitingwww.sec.gov. The prospectus should be read carefully before investing.

The Stone Ridge Funds consist of the Stone Ridge High Yield Reinsurance Risk Premium Fund (the “High Yield Reinsurance Fund”), the Stone Ridge Reinsurance Risk Premium Interval Fund (“SRRIX” and, together with the High Yield Reinsurance Fund, the “Reinsurance Funds”), the Stone Ridge U.S. Hedged Equity Fund (the “Hedged Equity Fund”), the Stone Ridge All Asset Variance Risk Premium Fund (“AVRPX” and, together with the Hedged Equity Fund, the “VRP Funds”), the Stone Ridge Alternative Lending Risk Premium Fund (“LENDX”) and the Stone Ridge Residential Real Estate income Fund I, Inc. (“HOMEX and, together with the Reinsurance Funds, the VRP Funds and LENDX, the “Funds”).

The Elements Portfolios consist of the Elements U.S. Portfolio (“ELUSX”), Elements U.S. Small Cap Portfolio (“ELSMX”), Elements International Portfolio (“ELINX”), Elements International Small Cap Portfolio (“ELISX”), and Elements Emerging Markets Portfolio (“ELMMX”) (collectively, the “Portfolios,” and each a “Portfolio”).

The Funds and the Portfolios are generally sold to (i) institutional investors, including registered investment advisers (“RIAs”), that meet certain qualifications and have completed an educational program provided by Stone Ridge Asset Management LLC (the “Adviser”); (ii) clients of such institutional investors; and (iii) certain other eligible investors (as described in the relevant prospectus). Investors should carefully consider the Funds’ and the Portfolios’ risks and investment objectives, as an investment in the Funds and/or the Portfolios may not be appropriate for all investors and the Funds and the Portfolios are not designed to be a complete investment program. There can be no assurance that the Funds and/or the Portfolios will achieve their investment objectives. An investment in the Funds and/or the Portfolios involves a high degree of risk. It is possible that investing in a Fund and/or a Portfolio may result in a loss of some or all of the amount invested. Before making an investment/allocation decision, investors should (i) consider the suitability of this investment with respect to an investor’s or a client’s investment objectives and individual situation and (ii) consider factors such as an investor’s or a client’s net worth, income, age and risk tolerance. Investment should be avoided where an investor/client has a short-term investing horizon and/or cannot bear the loss of some or all of the investment. Before investing in a Fund and/or a Portfolio, an investor should read the discussion of the risks of investing in the Fund and/or a Portfolio in the relevant prospectus.

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

10

Shareholder Letter

Holdings and sector allocations are subject to change and are not a recommendation to buy or sell any security.

Investing in funds involves risks. Principal loss is possible.

The VRP Funds may invest in a variety of derivatives, including put and call options, futures contracts, options on futures contracts, swaps, swaptions, and other exchange-traded andover-the-counter derivatives contracts. The VRP Funds may invest in derivatives to generate income from premiums, for investment purposes, and for hedging and risk management purposes. A VRP Fund’s use of derivatives as part of its principal investment strategy to sell protection against the volatility of various underlying references involves the risk that, if the volatility of the underlying references is greater than expected, the VRP Fund will bear losses to the extent of its obligations under the relevant derivative contracts, which may not be outweighed by the amount of any premiums received for the sale of such derivative instruments. The use of derivatives involves risks that are in addition to, and potentially greater than, the risks of investing directly in securities and other more traditional assets. Derivatives also present other risks, including market risk, illiquidity risk, currency risk, and credit risk.

Economic, political, and issuer-specific events will cause the value of securities, and the Portfolio that owns them, to rise or fall. Because the value of your investment in a Portfolio will fluctuate, you may lose money, even over the long term. Securities of smaller companies are often less liquid than those of larger companies, and smaller companies are generally more vulnerable to adverse business or economic developments and may have more limited resources. Foreign securities prices may decline or fluctuate because of economic or political actions of foreign governments and/or less regulated or liquid securities markets and may give rise to foreign currency risk. Securities of companies that exhibit other factors such as value, momentum or quality may be riskier than securities of companies that do not exhibit those factors, and may perform differently from the market as a whole. If a Portfolio uses derivatives, such Portfolio will be directly exposed to the risks of that derivative, including the risk that the counterparty is unable or unwilling to perform its obligations. Derivatives are subject to a number of additional risks, including risks associated with liquidity, interest rates, market movements and valuation. Securities lending and similar transactions involve the risk that the counterparty may fail to return the securities in a timely manner or at all and that the value of collateral securing a securities loan or similar transaction falls.

The reinsurance industry relies on risk modeling to analyze potential risks in a single transaction and in a portfolio of transactions. The models are based on probabilistic simulations that generate thousands or millions of potential events based on historical data, scientific and meteorological principles and extensive data on current insured properties. Sponsors of reinsurance-related securities typically provide risk analytics and statistics at the time of issuance that typically include model results.

Event-linked bonds, catastrophe bonds and other reinsurance-related securities carry large uncertainties and major risk exposures to adverse conditions. If a trigger event, as defined within the terms of the bond, involves losses or other metrics exceeding a specific magnitude in the geographic region and time period specified therein, a Fund may lose a portion or all of its investment in such security. Such losses may be substantial. The reinsurance-related securities in which the Funds invest are considered “high yield” or “junk bonds.”

SHRIX and SRRIX may invest in reinsurance-related securities issued by foreign sovereigns and foreign entities that are corporations, partnerships, trusts or other types of business entities. Because the majority of reinsurance-related security issuers are domiciled outside the United States, each of SHRIX and SRRIX will normally invest significant amounts of its assets innon-U.S. entities. Accordingly, each of them may invest without limitation in securities issued bynon-U.S. entities, including those in emerging market countries. Foreign issuers could be affected by factors not present in the U.S., including expropriation, confiscatory taxation, lack of uniform accounting and auditing standards, less publicly available financial and other information, potential difficulties in enforcing contractual obligations, and increased costs to enforce applicable contractual obligations outside the U.S. These risks are greater in emerging markets.

The value of LENDX’s investments in whole loans and other alternative lending-related securities, such as shares, certificates, notes or other securities representing an interest in and the right to receive principal and interest payments due on whole loans or fractions of whole loans, is entirely dependent on the borrowers’ continued and timely payments. If a borrower is unable or fails to make payments on a loan for any reason, LENDX may be greatly limited in its ability to recover any outstanding principal or interest due, as (among other reasons) LENDX may not have direct recourse against the borrower or may otherwise be limited in its ability to directly enforce its rights under the loan, whether through the borrower or the platform through which such loan was originated, the loan may be unsecured or under-collateralized and/or it may be impracticable to commence a legal proceeding against the defaulting borrower. LENDX generally will need to rely on the efforts of the platforms, servicers or their designated collection agencies to collect on defaulted loans and there is no guarantee that such parties will be successful in their efforts to collect on loans. Even if a loan in which LENDX has investment exposure is secured, there can be no assurance that the collateral will, when recovered and liquidated, generate sufficient (or any) funds to offset any losses associated with the defaulting loan. Although LENDX conducts diligence on the platforms, LENDX generally does not have the ability to independently verify, and will not independently diligence or confirm the truthfulness of, the information provided by the platforms, other than payment information regarding loans and other alternative lending-related securities owned by LENDX, which LENDX will observe directly as payments are received. The default history for alternative lending borrowing arrangements is limited and future defaults may be higher than historical defaults.

In general, the value of a debt security is likely to fall as interest rates rise. LENDX may invest in below-investment grade securities, which are often referred to as “junk,” or in securities that are unrated but that have similar characteristics to junk bonds. Such

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

11

Shareholder Letter

instruments have predominantly speculative characteristics with respect to the issuer’s capacity to pay interest and repay principal. They may also be difficult to value and illiquid. LENDX’s investments in securitization vehicles or other special purpose entities that hold alternative lending-related securities (asset-backed securities) may involve risks that differ from or are greater than risks associated with other types of investments. The risks and returns for investors like LENDX in asset-backed securities depend on the tranche in which the investor holds an interest, and the value of an investment in LENDX may be more volatile and other risks tend to be compounded if and to the extent that LENDX is exposed to asset-backed securities directly or indirectly.

LENDX may invest directly or indirectly in the alternative lending-related securities of foreign issuers. Such investments may involve risks not ordinarily associated with exposure to alternative lending-related securities of U.S. issuers. The foreign alternative lending industry may be subject to less governmental supervision and regulation than exists in the U.S.; conversely, foreign regulatory regimes applicable to the alternative lending industry may be more complex and more restrictive than those in the U.S., resulting in higher costs associated with such investments, and such regulatory regimes may be subject to interpretation or change without prior notice to investors, such as LENDX. Foreign platforms may not be subject to accounting, auditing, and financial reporting standards and practices comparable to those in the U.S. Due to difference in legal systems, there may be difficulty in obtaining or enforcing a court judgment outside the U.S.

HOMEX is subject to risks typically associated with real estate, including: changes in global, national, regional or local economic, demographic or capital market conditions; future adverse national real estate trends, including increasing vacancy rates, declining rental rates and general deterioration of market conditions; changes in supply of or demand for similar properties in a given market or metropolitan area; reliance on tenants, managers and real estate operators that HOMEX works with in acquiring and managing assets to operate their businesses in an appropriate manner and in compliance with their contractual arrangements with HOMEX; changes in governmental rules, regulations and fiscal policies; bad acts of third parties; and unforeseeable events such as social unrest, civil disturbances, terrorism, earthquakes, hurricanes and other natural disasters. Many of these factors are beyond the control of HOMEX. Any negative changes in these factors could affect HOMEX’s performance and its ability to meet its obligations and make distributions to shareholders.

HOMEX’s portfolio will be concentrated at any time in the real estate industry, with a focus on single family rental investments, and may be heavily concentrated at any time in only a limited number of geographies or investments, and, as a consequence, the aggregate return of HOMEX may be substantially affected by the unfavorable performance of even a single investment. Concentration of investments in a particular type of asset or geography makes HOMEX more susceptible to fluctuations in value resulting from adverse economic or business conditions affecting that particular type of asset or geography.

HOMEX’s investment strategy involves sourcing assets through operators that purchase, renovate, maintain, and manage a large number of single family rental properties and leasing them to qualified residents through third-party property managers or leasing agents. When HOMEX purchases single family rental properties directly or indirectly through a real estate operator, the operator, or an affiliate of the operator, typically continues to act as the property manager of the properties. When HOMEX purchases debt instruments secured directly or indirectly by single family rental properties from an operator or bank originating such instruments, such entity typically continues to service the instruments. In the event that such operator is unable to act as the property manager or the servicer, as applicable, there is no assurance that a backup property manager or backup servicer will be able to assume responsibility in a timely or cost-effective manner; any resulting disruption or delay could jeopardize payments due to HOMEX in respect of its investments or increase the costs associated with HOMEX’s investments. A large proportion of HOMEX’s portfolio may consist of assets obtained from or through a small number of operators, potentially giving HOMEX high exposure to the risks associated with those operators.

HOMEX intends to continuously offer its shares during a subscription period of approximately two years after HOMEX commences investment operations (the “Subscription Period”). The Subscription Period is subject to extension, temporary suspension or early termination at the discretion of the Adviser. HOMEX expects to have a term of investment operations of approximately eight years, which may be extended by the Board without shareholder approval. At the end of such term, HOMEX expects the Adviser to recommend a plan of liquidation that, if approved by the Board, will be carried out without shareholder approval. The plan of liquidation may take up to twenty-four months to complete, and HOMEX may deviate from its investment strategies during this time. HOMEX may make investments that may not be realized prior to the date HOMEX is dissolved. HOMEX may attempt to sell, distribute, or otherwise dispose of investments at a time that may be disadvantageous, and as a result, the price obtained for such investments may be less than that which could have been obtained if the investments were held for a longer period of time. Moreover, HOMEX may be unsuccessful in realizing investments at the time of HOMEX’s dissolution. There can be no assurance that the winding up of HOMEX and the final distribution of its assets will be able to be executed expeditiously.

A Fund (or its subsidiaries) may obtain financing to make investments and may obtain leverage through derivative instruments that afford the Fund economic leverage. Therefore, the Funds are subject to leverage risk. Leverage magnifies a Fund’s exposure to declines in the value of one or more underlying reference instruments or creates investment risk with respect to a larger pool of assets than the Fund would otherwise have and may be considered a speculative technique. The value of an investment in a Fund will be more volatile and other risks tend to be compounded if and to the extent the Fund borrows or uses derivatives or other investments that have embedded leverage. This risk is enhanced for SHRIX and SRRIX because they invest substantially all their assets in reinsurance-related securities. Reinsurance-related securities can quickly lose all or much of their value if a triggering event occurs. Thus, to the extent assets subject to a triggering event are leveraged, the losses could substantially outweigh SHRIX’s or SRRIX’s investment and result in significant losses to the relevant Fund.

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

12

Shareholder Letter

Shareholders of LIFEX who die will have their fund shares redeemed for a redemption price that may be equal to $0, and will not be entitled to any further returns or distributions following such mandatory redemption. There can be no assurance that the applicable redemption price, plus the amount of any distributions received prior to death, will represent a positive return on investment for any shareholder who dies.

Unlike a traditional investment company with a perpetual existence, LIFEX is expected to be designed to have distributed most of its assets by the applicable fund liquidation date. Although the fund will seek to achieve a high level of distributions during the life of the fund, following the fund liquidation date there will be no further distributions made by the fund and shareholders may not be able to find a replacement investment that provides a similar level of distributions.

There can be no assurance that LIFEX will continue to make distributions until the planned fund liquidation date. Under certain circumstances, LIFEX may run out of assets to fund the planned distributions prior to the planned fund liquidation date. This risk is heightened by the novel nature of LIFEX. If the longevity of investors in LIFEX is materially better than assumed, the fund is likely to run out of assets prior to the fund liquidation date. In that case, the fund will liquidate early, and investors will not receive any returns or distributions following such early liquidation.

Shares of LIFEX will not be, and will not represent interests in, an insurance contract or an annuities contract. Investors in LIFEX will not benefit from the consumer protections provided by state insurance laws and regulations, including the protection afforded by state guaranty funds, and there is no insurance company or other third party that will be obligated to make distributions in the event the fund runs out of assets prior to the fund liquidation date.

The Funds may invest in illiquid or restricted securities, which may be difficult or impossible to sell at a time that a Fund would like without significantly changing the market value of the security.

Each Fund (other than HOMEX) intends to qualify for treatment as a regulated investment company (“RIC”) under the Internal Revenue Code. A Fund’s investment strategy will potentially be limited by its intention to qualify for treatment as a RIC. The tax treatment of certain of the Funds’ investments under one or more of the qualification or distribution tests applicable to RICs is not certain. An adverse determination or future guidance by the IRS might affect a Fund’s ability to qualify for such treatment.

If, in any year, a Fund (other than HOMEX) were to fail to qualify for treatment as a RIC under the Internal Revenue Code for any reason, and were unable to cure such failure, the Fund would be subject to tax on its taxable income at corporate rates, and all distributions from earnings and profits, including any distributions of nettax-exempt income and net long-term capital gains, would be taxable to shareholders as ordinary income.

HOMEX intends to elect to be taxed as and to qualify for treatment each year as a REIT under the Internal Revenue Code. HOMEX’s investment strategy will potentially be limited by its intention to qualify for treatment as a REIT. An adverse determination or future guidance by the IRS or a change in law might affect HOMEX’s ability to qualify for such treatment.

If, in any year, HOMEX were to fail to qualify for treatment as a REIT under the Internal Revenue Code for any reason, and were unable to cure such failure, HOMEX would be subject to tax on its taxable income at regular corporate rates, and all distributions to shareholders would be taxable as dividends to the extent of HOMEX’s current and accumulated earnings and profits, whether or not attributable to net capital gains.

For additional risks, please refer to the prospectus and statement of additional information.

SHRIX and HOMEX are classified asnon-diversified under the 1940 Act. Accordingly, each fund may invest a greater portion of its assets in the securities of a single issuer than if it were a diversified fund, which may subject it to a higher degree of risk associated with and developments affecting that issuer than a fund that invests more widely.

Each of AVRPX, SRRIX and LENDX has an interval fund structure pursuant to which each Fund, subject to applicable law, conducts quarterly repurchase offers of the Fund’s outstanding shares at net asset value (“NAV”), subject to approval of the Board of Trustees. In all cases, such repurchases will be for at least 5% and not more than 25% of the relevant Fund’s outstanding shares. Repurchase offers are currently expected to be 5% for SRRIX and LENDX and 25% for AVRPX.

HOMEX has an interval fund structure pursuant to which HOMEX conducts annual repurchase offers of the Fund’s outstanding shares at NAV, subject to approval of the Board of Directors. In all cases, such repurchases will be for at least 5% and not more than 25%, and are currently expected to be for 5%, of HOMEX’s outstanding shares.

In connection with any given repurchase offer, it is possible that a Fund may offer to repurchase only the minimum amount of 5% of its outstanding shares. It is possible that a repurchase offer may be oversubscribed, with the result that shareholders may only be able to have a portion of their shares repurchased. There is no assurance that you will be able to tender your Shares when or in the amount that you desire. The Funds’ shares are not listed, and the Funds do not currently intend to list their shares for trading on any national securities exchange; the shares are, therefore, not marketable, and you should consider the shares to be illiquid.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of a Fund or Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling855-609-3680.

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

13

Shareholder Letter

Standardized returns as of most recentquarter-end (09/30/2019): for VRLIX 1Yr= 1.26%, 5Yr= 5.10%, since inception(05/01/2013)= 6.41%; for SHRIX 1Yr= 2.97%, 5Yr= 3.55%, since inception(02/01/2013)= 4.71%; for SHRMX 1Yr= 2.77%, 5Yr= 3.40%, since inception(02/01/2013)= 4.55%; for SRRIX 1Yr=-6.80%, 5Yr= 0.03%, since inception(12/09/2013)= 1.35%; for AVRPX 1Yr=-6.12%, since inception(04/02/2015)= 2.13%; for LENDX 1Yr= 4.22%, since inception(06/01/2016)= 6.98%; for ELUSX 1Yr= 2.56%, since inception(03/31/2017)= 10.47%; for ELSMX 1Yr=-8.11%, since inception(03/31/2017)= 4.18%; for ELINX 1Yr=-5.19%, since inception(04/28/2017)= 2.23%; for ELISX 1Yr=-9.64%, since inception(04/28/2017)= 0.86%; for ELMMX 1Yr=-3.17%, since inception(05/31/2017)= 1.90%. As of 9/30/19,30-day SEC yield: SHRIX 4.68% (net), 4.71% (gross of subsidized expenses); SRRIX 0.00% (net), 0.00% (gross of subsidized expenses); LENDX 11.60% (net), 11.69% (gross of subsidized expenses). Results for the Funds and the Portfolios are annualized; all Fund and Portfolio returns reflect the reinvestment of dividends and other earnings and are net of fees and expenses. As a result of economic incentives received from platforms that may not be repeated, early LENDX performance was unusually strong and should not be extrapolated to future periods. Results for the Elements Portfolios reflect waivers of all of the Portfolios’ investment management fees and partial reimbursement of expenses by the Adviser. The Adviser has contractually agreed to waive its management fee entirely through September 30, 2022 and to pay or otherwise bear operating expenses as necessary to limit total annualized expenses, other than certain excluded expenses, of the Portfolios to 0.15% (for ELUSX and ELSMX) or 0.20% (for ELINX, ELISX and ELMMX) for the period from October 1, 2019 through September 30, 2020. Fee waiver and expense reimbursement may be discontinued in whole or in part after such dates. In the absence of fee waivers and reimbursements, returns for the Portfolios would have been lower.

Total Annual Fund Operating Expenses as disclosed in the most recent prospectus: for SRRIX, 2.45%; for ELUSX, 0.47%; for ELSMX, 0.73%; for ELINX, 0.70%; for ELISX, 0.99%; for ELMMX, 0.93%. Total Annual Fund Operating Expenses before fee waiver and/or expense reimbursement/(recoupment) as disclosed in the most recent prospectus: for SHRIX, 1.72%; for VRLIX, 1.28%; for AVRPX, 2.62%; for LENDX, 4.89%; for HOMEX, 2.79%. Total Annual Fund Operating Expenses after fee waiver and/or expense reimbursement/(recoupment) as disclosed in the most recent prospectus: for SHRIX, 1.67%; for VRLIX, 0.50%; for AVRPX, 2.62%; for LENDX, 4.97%; for HOMEX, 1.90%. Please see the financial highlights section of each Fund’s and each Portfolio’s shareholder report for more recent Fund Operating Expenses.

Information furnished by others, upon which all or portions of the information contained herein is based, is from sources believed to be reliable. Stone Ridge makes no representation as to the accuracy, adequacy or completeness of such information and it has accepted the information without further verification.

The information provided herein should not be construed in any way as tax, capital, accounting, legal or regulatory advice. Investors should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision. Opinions expressed are subject to change at any time and are not guaranteed and should not be considered investment advice.

The Funds’ and Portfolios’ investment objectives, risks, charges and expenses must be considered carefully before investing. The relevant prospectus contains this and other important information about the investment company. You can obtain an additional copy of the Funds’ and the Portfolios’ most recent periodic reports and certain other regulatory filings by calling855-609-3680 or visiting www.stoneridgefunds.com for the Funds and www.elementsfunds.com for the Portfolios. The Funds’ and the Portfolios’ prospectuses, which include a statement of additional information, can be found by visiting:

Stone Ridge High Yield Reinsurance Risk Premium Fund1:Prospectus andSAI

Stone Ridge Reinsurance Risk Premium Interval Fund2:Prospectus andSAI

Stone Ridge Post-Event Reinsurance Fund2:Prospectus andSAI

Stone Ridge U.S. Hedged Equity Fund1:Prospectus,SAI andSupplement

Stone Ridge All Asset Variance Risk Premium Fund2:Prospectus andSAI

Stone Ridge Alternative Lending Risk Premium Fund2:Prospectus andSAI

Elements Portfolios1:Prospectus andSAI

Stone Ridge Residential Real Estate Income Fund I, Inc.2:Prospectus andSAI

1Open-end fund,2Closed-end interval fund

The prospectuses should be read carefully before investing.

The Stone Ridge Funds (other than LIFEX) and the Elements Portfolios are distributed by ALPS Distributors, Inc. LIFEX is distributed by Stone Ridge Securities LLC. ALPS Distributors, Inc. is not affiliated with Stone Ridge Securities LLC or any other Stone Ridge entity.

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

14

| | | | |

| STONE RIDGE HIGH YIELD REINSURANCE RISK PREMIUM FUND | | | | |

|

|

| PERFORMANCE DATA (Unaudited) |

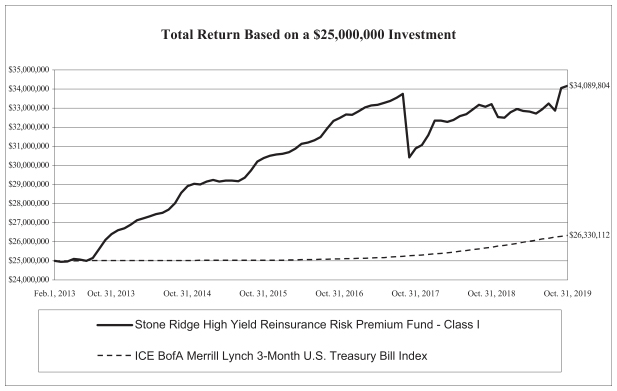

This chart assumes an initial gross investment of $25,000,000 made on February 1, 2013 (commencement of operations). Returns shown include the reinvestment of all dividends. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. In the absence of fee waivers and reimbursements, returns for the Fund would have been lower. Past performance is not predictive of future performance. Investment return and principal value will fluctuate, so that your shares, when redeemed, may be worth more or less than the original cost.

TheIntercontinental Exchange (ICE) Bank of America (BofA) Merrill Lynch3-Month U.S. Treasury Bill Index is an index of short-term U.S. Government securities with a remaining term to final maturity of less than three months. Index figures do not reflect any deduction of fees, taxes or expenses, and are not available for investment.

| | | | | | | | | | | | |

|

| AVERAGE ANNUAL TOTAL RETURNS (FOR PERIODS ENDED OCTOBER 31, 2019) | |

| | | 1-year

period

ended

10/31/2019 | | | 5-year

period

ended

10/31/2019 | | | Since

Inception

(02/01/13) | |

| | | |

Stone Ridge High Yield Reinsurance Risk Premium Fund — Class I | | | 2.87% | | | | 3.36% | | | | 4.70% | |

| | | |

Stone Ridge High Yield Reinsurance Risk Premium Fund — Class M | | | 2.78% | | | | 3.20% | | | | 4.54% | |

| | | |

ICE BofA Merrill Lynch3-Month U.S. Treasury Bill Index | | | 2.40% | | | | 1.02% | | | | 0.77% | |

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

15

| | | | |

| STONE RIDGE U.S. HEDGED EQUITY FUND | | | | |

|

|

| PERFORMANCE DATA (Unaudited) |

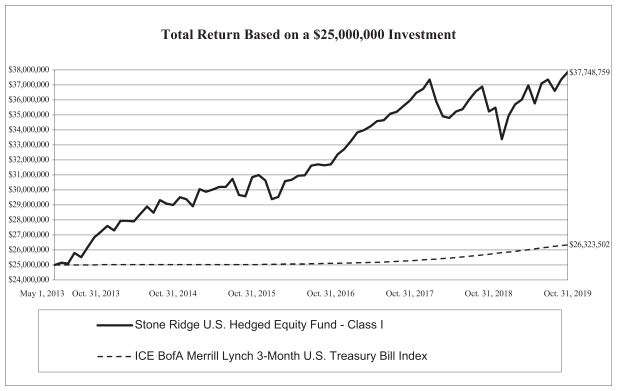

This chart assumes an initial gross investment of $25,000,000 made on May 1, 2013 (commencement of operations). Returns shown include the reinvestment of all dividends. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. In the absence of fee waivers and reimbursements, returns for the Fund would have been lower. Past performance is not predictive of future performance. Investment return and principal value will fluctuate, so that your shares, when redeemed, may be worth more or less than the original cost.

TheIntercontinental Exchange (ICE) Bank of America (BofA) Merrill Lynch3-Month U.S. Treasury Bill Index is an index of short-term U.S. Government securities with a remaining term to final maturity of less than three months. Index figures do not reflect any deduction of fees, taxes or expenses, and are not available for investment.

| | | | | | | | | | | | |

|

| AVERAGE ANNUAL TOTAL RETURNS (FOR PERIODS ENDED OCTOBER 31, 2019) | |

| | | 1-year

period

ended

10/31/2019 | | | 5-year

period

ended

10/31/2019 | | | Since

Inception

(05/01/13) | |

| | | |

Stone Ridge U.S. Hedged Equity Fund — Class I | | | 7.40% | | | | 5.43% | | | | 6.53% | |

| | | |

Stone Ridge U.S. Hedged Equity Fund — Class M | | | 7.24% | | | | 5.28% | | | | 6.37% | |

| | | |

ICE BofA Merrill Lynch3-Month U.S. Treasury Bill Index | | | 2.40% | | | | 1.02% | | | | 0.80% | |

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

16

| | |

| Management’s Discussion of Fund Performance | | |

Stone Ridge High Yield Reinsurance Risk Premium Fund is designed to capture the reinsurance risk premium by investing in a broad set of reinsurance-related securities, primarily focused on higher yielding catastrophe bonds. For the twelve months ended October 31, 2019, the Fund’s total return was 2.87% The Fund’s performance is largely based on the occurrence ornon-occurrence of natural ornon-natural catastrophe events or other loss events around the world, which impact the performance of reinsurance-related securities. The Fund’s exposures span many different regions and types of events covered. There were a number of natural andnon-natural catastrophes around the world (most significantly the Camp and Woolsey wildfires in California, Hurricane Dorian, and Typhoons Faxai and Hagibis in Japan) that negatively impacted many of the Fund’s risk exposures, and, therefore, negatively impacted Fund performance.

Stone Ridge U.S Hedged Equity Fund is designed to capture the returns of the variance risk premium in U.S. equity securities. For the 12 months ended October 31, 2019, the Fund’s total return was 7.40%. The Fund’s performance is almost entirely based on derivatives. Performance is materially affected by two primary factors: exposure to the equity securities underlying derivatives used by the Fund and exposure to the variance risk premium, which exists when the net premiums received by a seller of options and other derivatives, such as the Fund, exceed the net losses suffered on the resulting portfolio of derivative positions. The Fund’s performance is positively impacted by positive performance of the underlying equity securities or equity indices and by a positive variance risk premium. The variance risk premium is generally more likely to be positive during periods in which the “realized volatility” – the volatility actually experienced – of equity and equity index options is lower than the “implied volatility” – the expected level of volatility implied by an option’s price. Periods of positive performance for the Fund, such as the most recently completed fiscal year correspond to periods when the combination of underlying exposure and variance risk premium exposure is positive. This year, average realized volatility was lower than the implied volatility at which options were sold and equity indices exhibited positive performance.

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

17

| | | | |

| ALLOCATION OF PORTFOLIO HOLDINGS AT OCTOBER 31, 2019 (Unaudited) | | | | |

| | | | | | | | |

| STONE RIDGE HIGH YIELD REINSURANCE RISK PREMIUM FUND PORTFOLIO ALLOCATION BY YEAR OF SCHEDULED MATURITY | |

| | |

| 2019 | | | $103,281,933 | | | | 11.3% | |

| | |

| 2020 | | | 192,766,749 | | | | 21.0% | |

| | |

| 2021 | | | 186,605,871 | | | | 20.3% | |

| | |

| 2022 | | | 138,064,708 | | | | 15.0% | |

| | |

| 2023 | | | 138,196,005 | | | | 15.1% | |

| | |

| 2024 | | | 55,125,470 | | | | 6.0% | |

| | |

| 2025 | | | 6,063,401 | | | | 0.7% | |

| | |

| 2027 | | | 1,297,815 | | | | 0.1% | |

| | |

| 2034 | | | 3,340,239 | | | | 0.4% | |

| | |

| Not Applicable(1) | | | 82,807,594 | | | | 9.0% | |

| | |

| Other(2) | | | 9,883,864 | | | | 1.1% | |

| | | $917,433,649 | | | | | |

| | | | | | | | |

| STONE RIDGE U.S. HEDGED EQUITY FUND PORTFOLIO ALLOCATION BY ASSET TYPE | |

| | |

| Purchased Options | | | $1,375 | | | | 0.0% | |

| | |

| Short-Term Investments | | | 161,269,044 | | | | 100.5% | |

| | |

Liabilities in Excess of Other

Assets(3) | | | (808,255 | ) | | | (0.5% | ) |

| | | $160,462,164 | | | | | |

| | (1) | Preference shares do not have maturity dates. |

| | (2) | Cash, cash equivalents, short-term investments and liabilities in excess of other assets. |

| | (3) | Cash, cash equivalents and liabilities in excess of other assets. |

| | | | |

| | The accompanying Notes to the Financial Statements are an integral part of these Financial Statements. | | |

| | | | | | | | | | | | | | | | |

| | Stone Ridge Funds | | | | | | Annual Report | | | | | | October 31, 2019 | | |

| | | | |

18

| | |

| Schedule of Investments | | as of October 31, 2019 |

| | | | |

| STONE RIDGE HIGH YIELD REINSURANCE RISK PREMIUM FUND | | | | |

| | | | | | | | |

| | | PRINCIPAL

AMOUNT | | | VALUE | |

EVENT LINKED BONDS - 82.2% | |

Global - 22.9% | |

| Earthquake - 2.6% | |

Acorn Re2018-1 Class A

(3 Month Libor USD + 2.750%), 11/10/2021 (a)(b)(c)(d) (Cost: $5,587,000; Original Acquisition Date: 07/03/2018) | | $ | 5,587,000 | | | $ | 5,549,288 | |

IBRD CAR 116

(3 Month Libor USD + 2.500%), 02/15/2021 (a)(b)(c)(d) (Cost: $7,274,265; Original Acquisition Date: 10/30/2019) | | | 7,325,000 | | | | 7,279,585 | |

IBRD CAR 117

(3 Month Libor USD + 3.000%), 02/15/2021 (a)(b)(c)(d) (Cost: $2,339,518; Original Acquisition Date: 10/15/2019) | | | 4,634,000 | | | | 4,602,721 | |

IBRD CAR118-Class A

(3 Month Libor USD + 2.500%), 02/14/2020 (a)(b)(c)(d) (Cost: $2,356,547; Original Acquisition Date: 10/17/2019) | | | 3,387,000 | | | | 3,378,024 | |

IBRD CAR119-Class B

(3 Month Libor USD + 8.250%), 02/14/2020 (a)(b)(c)(d) (Cost: $1,500,000; Original Acquisition Date: 02/02/2018) | | | 1,500,000 | | | | 1,496,775 | |

IBRD CAR 120

(3 Month Libor USD + 6.000%), 02/15/2021 (a)(b)(c)(d) (Cost: $1,400,000; Original Acquisition Date: 02/02/2018) | | | 1,400,000 | | | | 1,384,810 | |

| | | | | | | | |

| | | | | | | 23,691,203 | |

| | | | | | | | |

| Mortality/Longevity/Disease - 2.5% | |

Benu Capital Class B

(3 Month Euribor + 3.350%), 01/08/2020 (a)(b)(c)(d)(e) (Cost: $12,884,938; Original Acquisition Date: 04/21/2015) | | EUR | 12,000,000 | | | | 13,407,687 | |

Chesterfield2014-1 4.500%,

12/15/2034 (c)(d)(f) (Cost: $3,343,750; Original Acquisition Date: 12/11/2014) | | $ | 3,343,750 | | | | 3,340,239 | |

IBRD CAR111-Class A

(6 Month Libor USD + 6.900%), 07/15/2020 (a)(b)(c)(d)(f) (Cost: $2,966,000; Original Acquisition Date: 06/28/2017) | | | 2,966,000 | | | | 2,968,966 | |

IBRD CAR112-Class B

(6 Month Libor USD + 11.500%), 07/15/2020 (a)(b)(c)(d)(f) (Cost: $871,000; Original Acquisition Date: 06/28/2017) | | | 871,000 | | | | 500,825 | |

| | | | | | | | |

| | | PRINCIPAL

AMOUNT | | | VALUE | |

| Mortality/Longevity/Disease - 2.5% (continued) | |

Vita Capital VI

(6 Month Libor USD + 2.900%), 01/08/2021 (a)(b)(c)(d)(e) (Cost: $3,000,000; Original Acquisition Date: 12/15/2015) | | $ | 3,000,000 | | | $ | 3,012,150 | |

| | | | | | | | |

| | | | | | | 23,229,867 | |

| | | | | | | | |

| Multiperil - 16.7% | |

Atlas Capital UK 2018 PLC

(3 Month Libor USD + 6.060%), 06/07/2022 (a)(b)(c)(d) (Cost: $8,750,000; Original Acquisition Date: 05/25/2018) | | | 8,750,000 | | | | 8,689,187 | |

Atlas Capital UK 2019 PLC2019-1

(3 Month Libor USD + 11.750%), 06/07/2023 (a)(b)(c)(d) (Cost: $4,436,000; Original Acquisition Date: 05/24/2019) | | | 4,436,000 | | | | 4,533,814 | |

Atlas IX2015-1

(3 Month Libor USD + 0.100%), 01/07/2021 (a)(b)(c)(d) (Cost: $1,528,465; Original Acquisition Date: 06/16/2017) | | | 1,528,197 | | | | 1,298,968 | |

Atlas IX2016-1

(3 Month Libor USD + 7.960%), 01/08/2020 (a)(b)(c)(d) (Cost: $25,951,075; Original Acquisition Date: 05/24/2017) | | | 25,948,000 | | | | 26,006,383 | |

Galilei Re2016-1 Class D1

(6 Month Libor USD + 5.600%), 01/08/2020 (a)(b)(c)(d) (Cost: $981,056; Original Acquisition Date: 05/21/2019) | | | 985,000 | | | | 987,906 | |

Galilei Re2016-1 Class E1

(6 Month Libor USD + 4.790%), 01/08/2020 (a)(b)(c)(d) (Cost: $1,471,752; Original Acquisition Date: 05/21/2019) | | | 1,477,000 | | | | 1,475,966 | |

Galileo Re2017-1 Class B

(3 Month Libor USD + 17.500%), 11/06/2020 (a)(b)(c)(d) (Cost: $2,074,000; Original Acquisition Date: 10/30/2017) | | | 2,074,000 | | | | 2,079,496 | |

Kendall Re2018-1 Class A

(3 Month Libor USD + 5.250%), 05/06/2021 (a)(b)(c)(d) (Cost: $10,014,744; Original Acquisition Date: 03/05/2019) | | | 10,029,000 | | | | 9,862,017 | |

Kilimanjaro Re2015-1 Class D

(T-Bill 3 Month + 9.250%),

12/06/2019 (a)(b)(c)(d)(e) (Cost: $10,000,000; Original Acquisition Date: 11/10/2015) | | | 10,000,000 | | | | 10,015,000 | |

Kilimanjaro Re2015-1 Class E

(T-Bill 3 Month + 6.750%),