As filed with the Securities and Exchange Commission on 30 March 2018

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 20-F

(Mark One)

☐REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934

or

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended 31 December 2017

or

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

or

☐SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report

For the transition period from to

Commission file number: 001-35785

Sibanye Gold Limited

(Exact name of registrant as specified in its charter)

Republic of South Africa

(Jurisdiction of incorporation or organization)

Libanon Business Park

1 Hospital Street (off Cedar Avenue)

Libanon, Westonaria, 1780

South Africa.

011-27-11-278-9600

(Address of principal executive offices)

With copies to:

Charl Keyter

Chief Financial Officer

Sibanye Gold Limited

Tel: 011-27-11-278-9700

Fax: 011-27-11-278-9863

Libanon Business Park

1 Hospital Street (off Cedar Avenue)

Libanon, Westonaria, 1780

South Africa

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

and

Thomas B. Shropshire, Jr.

Linklaters LLP

Tel: 011-44-20-7456-3223

Fax: 011-44-20-7456-2222

One Silk Street

London EC2Y 8HQ

United Kingdom

Securities registered or to be registered pursuant to Section 12(b) of the Act

Title of Each Class

Ordinary shares of no par value each

American Depositary Shares, each representing four ordinary shares | Name of Each Exchange on Which Registered

New York Stock Exchange*

New York Stock Exchange |

*Not for trading, but only in connection with the registration of the American Depositary Shares pursuant to the requirements of the Securities and Exchange Commission. Securities registered or to be registered pursuant to Section 12(g) of the Act None (Title of Class) Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act None (Title of Class) Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock

as of the close of the period covered by the Annual Report 2,168,721,220 ordinary shares of no par value each |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act: Yes ☒ No ☐ If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒ Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections. Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐ Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files)*. Yes ☐ No ☐ Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one): Large accelerated filer ☒ Accelerated filer ☐ Non-accelerated filer ☐ Emerging growth company ☐ If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐ † The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing: |

U.S. GAAP ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow: Item 17 ☐ Item 18 ☐ If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒ (APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS) Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No ☐ |

* This requirement does not apply to the registrant

| | | | | | |

Item | | Form 20-F Caption | | Location in this document | | Page |

1 | | Identity of directors, senior management and advisers | | NA | | NA |

2 | | Offer statistics and expected timetable | | NA | | NA |

3 | | Key information | | | | |

| | (a) Selected financial data | | Annual Financial Report—Overview—Five-year financial performance | | 124-127 |

| | (b) Capitalisation and indebtedness | | NA | | NA |

| | (c) Reasons for the offer | | NA | | NA |

| | (d) Risk factors | | Further Information—Risk factors | | 220-237 |

4 | | Information on the Company | | | | |

| | (a) History and development of the Company | | Integrated Annual Report—Introduction—Corporate profile | | 12-14 |

| | | | Further Information—Additional information—Memorandum of incorporation | | 276 |

| | | | Annual Financial Report—Administrative details—Administrative and corporate information | | 219 |

| | | | Integrated Annual Report—View from the top—Perspective from the Chair | | 20-21 |

| | | | Integrated Annual Report—View from the top—Chief Executive’s review | | 22-25 |

| | | | Integrated Annual Report—View from the top—Chief Financial Officer’s report | | 26-27 |

| | | | Integrated Annual Report—Performance review—Delivering value from operations, projects and technology | | 35-46 |

| | | | Annual Financial Report—Overview—Five-year financial performance | | 124-127 |

| | | | Annual Financial Report—Overview—Management’s discussion and analysis of the financial statements—Recent platinum acquisitions | | 131-132 |

| | | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements—Note 13: Acquisitions | | 188-191 |

| | (b) Business overview | | Annual Financial Report—Overview—Management’s discussion and analysis of the financial statements—Introduction | | 128 |

| | | | Integrated Annual Report—Introduction—Corporate profile | | 12-14 |

| | | | Annual Financial Report—Overview—Management’s discussion and analysis of the financial statements—2017 financial performance compared with 2016 and 2015 | | 132-141 |

| | | | Annual Financial Report—Overview—Five-year financial performance | | 124-127 |

| | | | Annual Financial Report—Overview—Management’s discussion and analysis of the financial statements—Costs | | 130 |

| | | | Integrated Annual Report—View from the top—Perspective from the Chair | | 20-21 |

| | | | Further Information—Environmental and regulatory matters | | 268-272 |

| | (c) Organisational structure | | Integrated Annual Report—Introduction—Corporate profile | | 12-14 |

| | | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements—Note 1.3: Consolidation | | 165 |

| | (d) Property, plant and equipment | | Integrated Annual Report—Introduction—Corporate profile | | 12-14 |

| | | | Integrated Annual Report—Performance review—Delivering value from operations, projects and technology | | 35-46 |

| | | | Further Information—Additional information—Sibanye-Stillwater’s mining operations | | 238-254 |

| | | | Further Information—Reserves of Sibanye-Stillwater as of 31 December 2017 | | 255-263 |

| |

Sibanye-Stillwater | Form 20-F 2017 | 1 |

| | | | | | |

Item | | Form 20-F Caption | | Location in this document | | Page |

| | | | Further Information—Environmental and regulatory matters | | 268-272 |

| | | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements—Note 12: Property, plant and equipment | | 184-187 |

4A | | Unresolved staff comments | | NA | | NA |

5 | | Operating and financial review and prospects | | | | |

| | (a) Operating results | | Annual Financial Report—Overview—Management’s discussion and analysis of the financial statements | | 128-144 |

| | | | Annual Financial Report—Annual financial statements—Consolidated income statement | | 157 |

| | | | Annual Financial Report—Annual financial statements—Consolidated statement of financial position | | 158 |

| | | | Annual Financial Report—Annual financial statements—Consolidated statement of cash flows | | 160 |

| | | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements—Note 24: Borrowings and derivative financial instrument | | 199-205 |

| | | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements—Note 30: Fair value of financial assets and financial liabilities, and risk management | | 208-213 |

| | | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements—Note 31: Commitments | | 214 |

| | (b) Liquidity and capital resources | | Annual Financial Report—Overview—Management’s discussion and analysis of the financial statements—Liquidity and capital resources | | 141-142 |

| | (c) Research and development, patents and licences, etc. | | NA | | NA |

| | (d) Trend information | | Annual Financial Report—Overview—Management’s discussion and analysis of the financial statements | | 128-144 |

| | (e) Off-balance sheet arrangements | | Annual Financial Report—Overview—Management’s discussion and analysis of the financial statements—Off balance sheet arrangements and contractual commitments | | 143 |

| | (f) Tabular disclosure of contractual obligations | | Annual Financial Report—Overview—Management’s discussion and analysis of the financial statements—Off balance sheet arrangements and contractual commitments | | 143 |

| | (g) Safe harbour | | Forward-looking statements | | 8 |

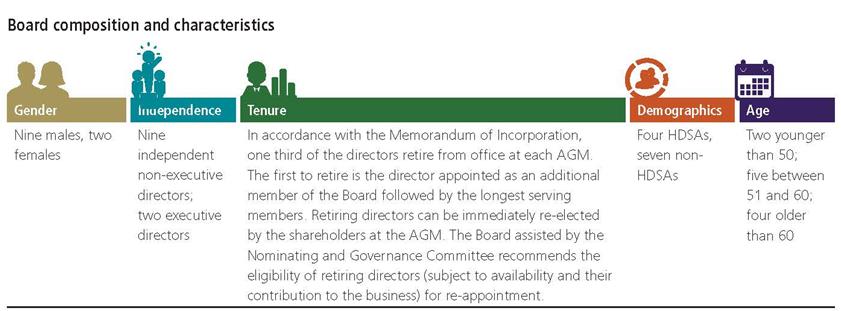

6 | | Directors, senior management and employees | | | | |

| | (a) Directors and senior management | | Integrated Annual Report—Leadership and governance—Board and Executive Committee | | 107-108 |

| | | | Further Information—Directors and Senior Management | | 264-267 |

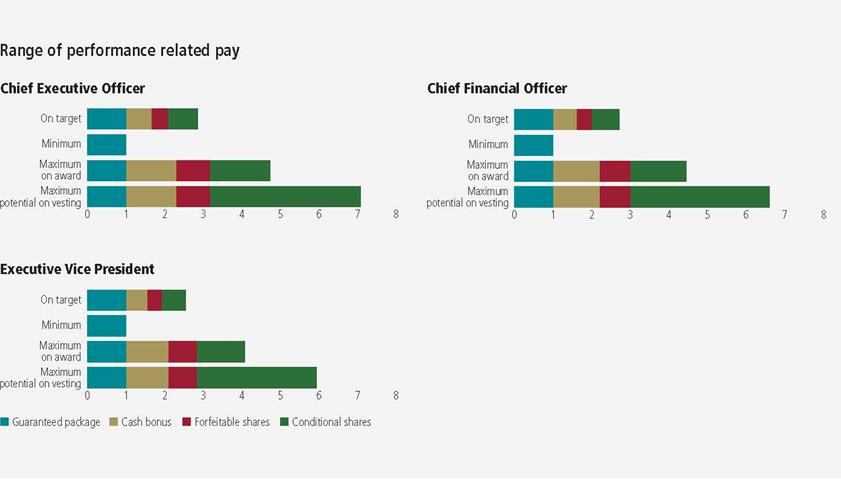

| | (b) Compensation | | Integrated Annual Report—Leadership and governance—Remuneration report | | 109-122 |

| | | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements—Note 33: Related-party transactions | | 214-216 |

| | (c) Board practices | | Integrated Annual Report—Accountability—Corporate governance report—Our Board, Governance Structures and Processes | | 95-103 |

| | | | Integrated Annual Report—Leadership and governance—Remuneration report—Executive directors’ contracts of employment | | 115 |

| | (d) Employees | | Integrated Annual Report—Performance overview—Superior value for the workforce | | 47-58 |

| |

Sibanye-Stillwater | Form 20-F 2017 | 2 |

| | | | | | |

Item | | Form 20-F Caption | | Location in this document | | Page |

| | (e) Share ownership | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements—Note 33: Related-party transactions | | 214-216 |

| | | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements—Note 6: Share-based payments | | 172-177 |

7 | | Major Shareholders and Related Party Transactions | | | | |

| | (a) Major shareholders | | Annual Financial Report—Administrative details—Shareholder information | | 217-218 |

| | | | Further Information—The listing | | 274-275 |

| | (b) Related party transactions | | Annual Financial Report—Accountability—Directors’ report—Directors’ and officers’ disclosure of interests in contracts | | 150-151 |

| | | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements—Note 33: Related-party transactions | | 214-216 |

| | (c) Interests of experts and counsel | | NA | | NA |

8 | | Financial information | | | | |

| | (a) Consolidated statements and other financial information | | Annual Financial Report—Overview—Management’s discussion and analysis of the financial statements | | 128-144 |

| | | | Annual Financial Report—Annual financial statements | | 157-216 |

| | | | Annual Financial Report—Director’s Report—Litigation | | 154-155 |

| | | | Annual Financial Report—Accountability—Directors’ report—Financial affairs—Dividend policy | | 151 |

| | | | Further Information—Additional information—Dividend policy and dividend distributions | | 273 |

| | (b) Significant changes | | NA | | NA |

9 | | The Offer and listing | | | | |

| | (a) Listing details | | Further Information—The listing | | 274-275 |

| | (b) Plan of distribution | | NA | | NA |

| | (c) Markets | | Further Information—The listing | | 274-275 |

| | (d) Selling shareholders | | NA | | NA |

| | (e) Dilution | | NA | | NA |

| | (f) Expenses of the issue | | NA | | NA |

10 | | Additional information | | | | |

| | (a) Share capital | | NA | | NA |

| | (b) Memorandum and articles of association | | Further Information—Additional information—Memorandum of Incorporation | | 276 |

| | (c) Material contracts | | Further Information—Additional information—Material contracts | | 276-277 |

| | (d) Exchange controls | | Further Information—Additional information—South African Exchange Control limitations affecting Security holders | | 282 |

| | | | Further Information—Environmental and regulatory matters—Exchange Controls | | 272 |

| | (e) Taxation | | Further Information—Additional information—Taxation | | 282-285 |

| | (f) Dividends and paying agents | | NA | | NA |

| | (g) Statement by experts | | NA | | NA |

| | (h) Documents on display | | Further Information—Additional information—Documents on display | | 285 |

| | (i) Subsidiary information | | NA | | NA |

11 | | Quantitative and qualitative disclosures about market risk | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements—Note 30.2: Risk management activities | | 209-213 |

12 | | Description of securities other than equity securities | | | | |

| |

Sibanye-Stillwater | Form 20-F 2017 | 3 |

| | | | | | |

Item | | Form 20-F Caption | | Location in this document | | Page |

| | (a) Debt securities | | NA | | NA |

| | (b) Warrants and rights | | NA | | NA |

| | (c) Other securities | | NA | | NA |

| | (d) American depositary shares | | Further Information—Additional information—American depositary shares | | 277-282 |

13 | | Defaults, dividend arrearages and delinquencies | | NA | | NA |

14 | | Material modifications to the rights of security holders and use of proceeds | | NA | | NA |

15 | | Controls and procedures | | Further Information—Controls and procedures | | 287 |

16A | | Audit Committee financial expert | | Annual Financial Report—Accountability—Corporate governance report—Board committees—Audit Committee | | 98 |

16B | | Code of ethics | | Annual Financial Report—Accountability—Corporate governance report—Code of ethics | | 92 |

| | | | Statement of responsibility by the Board of Directors | | 145 |

16C | | Principal accountant fees and services | | Annual Financial Report—Accountability—Report of the Audit Committee—Auditor independence and fees | | 148 |

16D | | Exemptions from the listing standards for audit committees | | NA | | NA |

16E | | Purchase of equity securities by the issuer and affiliated purchasers | | None | | |

16F | | Change in registrant’s certifying accountant | | NA | | NA |

16G | | Corporate governance | | Further Information—Additional information—JSE corporate governance practices compared with NYSE Listing Standards | | 286 |

16H | | Mine safety disclosure | | NA | | NA |

17 | | Financial statements | | NA | | NA |

18 | | Financial statements | | Financial Information—Report of independent registered public accounting firm | | 156 |

| | | | Annual Financial Report—Annual financial statements—Consolidated income statement | | 157 |

| | | | Annual Financial Report—Annual financial statements—Consolidated statement of other comprehensive income | | 157 |

| | | | Annual Financial Report—Annual financial statements—Consolidated statement of financial position | | 158 |

| | | | Annual Financial Report—Annual financial statements—Consolidated statement of changes in equity | | 159 |

| | | | Annual Financial Report—Annual financial statements—Consolidated statement of cash flows | | 160 |

| | | | Annual Financial Report—Annual financial statements—Notes to the consolidated financial statements | | 161-216 |

19 | | Exhibits | | Exhibits | | 288-289 |

| |

Sibanye-Stillwater | Form 20-F 2017 | 4 |

Historical Consolidated Financial Statements

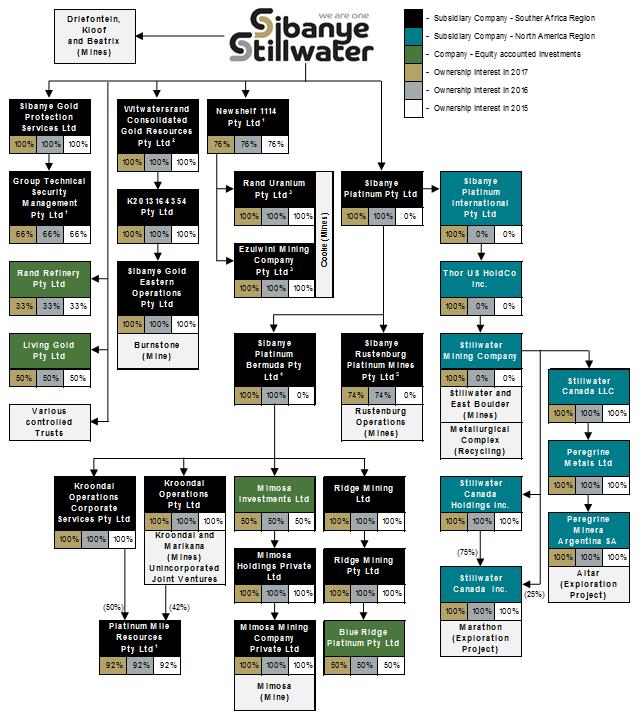

Sibanye Gold Limited (trading as Sibanye-Stillwater (Sibanye-Stillwater)), a South African domiciled global, precious metals mining company, which produces a mix of metals that includes gold and the platinum group metals (PGMs). Sibanye-Stillwater owns and operates a portfolio of high-quality operations and projects, which are grouped into two regions: the southern Africa region and the United States region. See Annual Financial Report—Overview—Management’s discussion and analysis of financial statements—Introduction.

Accordingly, the books of account of the Group (as defined below) are maintained in South African Rand and the Group’s annual financial statements are prepared in accordance with International Financial Reporting Standards (IFRS), as issued by the International Accounting Standards Board, as prescribed by law. These financial statements are distributed to shareholders and are submitted to the Johannesburg Stock Exchange (JSE) and the New York Stock Exchange (NYSE).

The consolidated financial statements of Sibanye-Stillwater as at and for the fiscal years ended 31 December 2017, 2016 and 2015 (the Consolidated Financial Statements) have been prepared using the historical results of operations, assets and liabilities attributable to Sibanye-Stillwater and all of its subsidiaries (the Sibanye-Stillwater Group, or the Group). The Consolidated Financial Statements have been prepared under the historical cost convention, except for financial assets and financial liabilities (including derivative financial instruments), which are measured at fair value through profit or loss or through the mark to market reserve in equity.

Non-IFRS Measures

The financial information in this annual report includes certain measures that are not defined by IFRS, including “adjusted earnings before interest, tax, depreciation and amortization” (adjusted EBITDA), “normalised earnings”, “operating cost”, “All-in sustaining cost”, “All-in sustaining cost margin”, “All-in cost”, “All-in cost margin”, “headline earnings per share”, “free cash flow” and “net debt” (each as defined below or in Annual Financial Report—Overview—Five-year financial performance. These measures are not measures of financial performance or cash flows under IFRS and may not be comparable to similarly titled measures of other companies. These measures have been included for the reasons described below or in Annual Financial Report—Overview—Five-year financial performance and should not be considered by investors as alternatives to costs of sales, net operating profit, profit before taxation, cash from operating activities or any other measure of financial performance presented in accordance with IFRS.

Operating costs is defined as the average cost of production and calculated by dividing the cost of sales, before amortisation and depreciation in a period by the tonnes milled/treated in the same period, and operating cost per kilogram (and ounce) is calculated by dividing the cost of sales, before amortisation and depreciation in a period by the gold produced in the same period. Free cash flow is defined as cash flows from operating activities before dividends paid, less additions to property, plant and equipment. Management considers free cash flow to be an indicator of cash available for repaying debt, funding exploration and paying dividends.

See Annual Financial Report—Overview—Five-year financial performance—Group operating statistics—Footnote 1, Annual Financial Report—Overview—Five-year financial performance—Group operating statistics—Footnote 2, Annual Financial Report—Overview—Five-year financial performance—Group operating statistics—Footnote 3, Annual Financial Report—Overview—Five-year financial performance—Group operating statistics—Footnote 4, Annual Financial Report—Overview—Five-year financial performance—Group financial statistics—Footnote 4 and Annual Financial Report—Overview—Five-year financial performance— Group financial statistics—Footnote 5 for more information.

Conversion Rates

Certain information in this annual report presented in Rand has been translated into US dollars. Unless otherwise stated, the conversion rate for these translations is R12.36/US$1.00 which was the closing rate on 31 December 2017. By including the US dollar equivalents, Sibanye-Stillwater is not representing that the Rand amounts actually represent the US dollar amounts shown or that these amounts could be converted into US dollars at the rates indicated.

The Acquisitions of STILLWATER, the Rustenburg Operations and Aquarius

On 9 December 2016, Sibanye-Stillwater announced it had reached a definitive agreement to acquire Stillwater Mining Company (Stillwater) for US$18 per share in cash, or US$2,200 million in aggregate (the Stillwater Transaction). On 25 April 2017, at the shareholders meeting of Sibanye-Stillwater, the Sibanye-Stillwater shareholders approved the proposed Stillwater Transaction by voting in favour of the various resolutions to give effect to the Stillwater Transaction and at the shareholders meeting of Stillwater, the requisite majority of Stillwater shareholders resolved to approve the Stillwater Transaction. Sibanye-Stillwater obtained control of Stillwater on this date. The effective date of the implementation of the Stillwater Transaction was 4 May 2017, when Sibanye-Stillwater took over legal ownership of Stillwater.

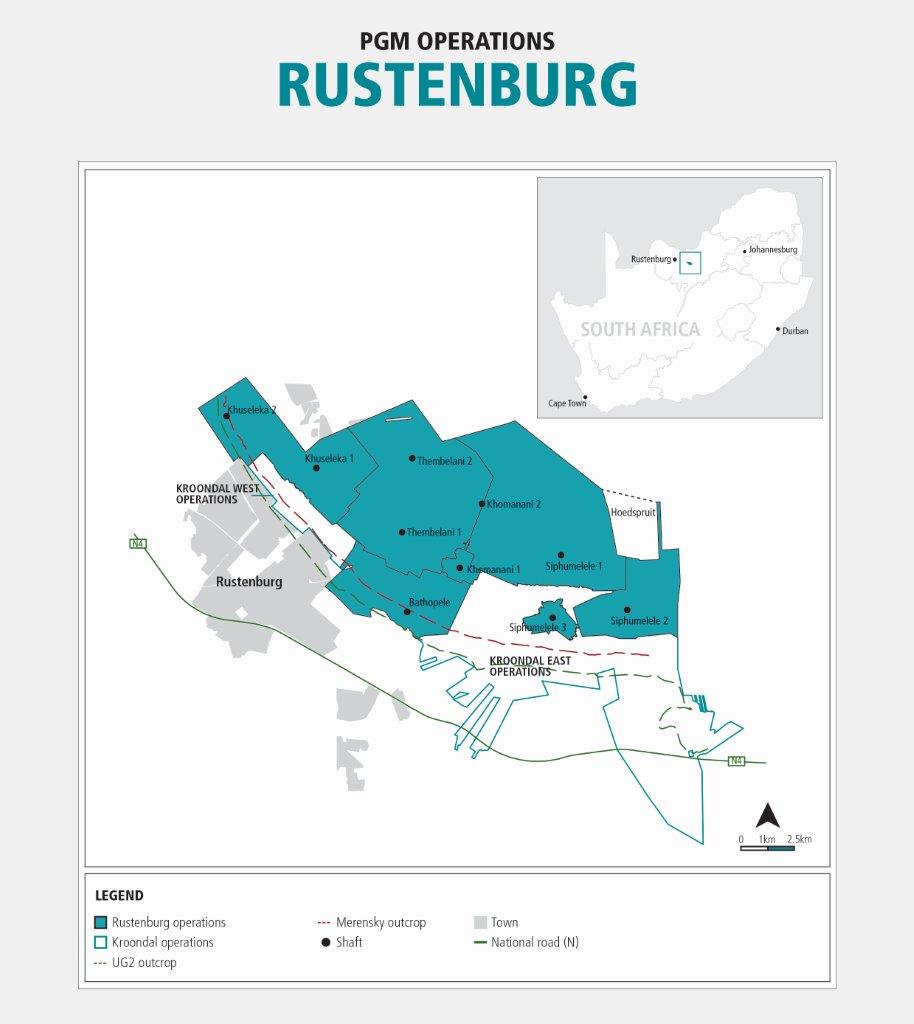

On 9 September 2015, Sibanye-Stillwater announced that it entered into an agreement with Rustenburg Platinum Mines Limited (RPM), a wholly owned subsidiary of Anglo American Platinum Limited (Anglo American Platinum) to acquire the Bathopele, Siphumelele (including Khomanani), and Thembelani (including Khuseleka) mining operations, two concentrating plants, an on-site chrome recovery plant, the Western Limb Tailings Retreatment Plant, associated surface infrastructure and related assets and liabilities on a going concern basis (the Rustenburg operations) (the Rustenburg operations Transaction). On 19 October 2016, Sibanye-Stillwater obtained consent in terms of section 11 of the Mineral and Petroleum Resources Development Act for the transfer of the mining right and prospecting right pursuant to the Rustenburg operations Transaction, and control of the Rustenburg operations on this date. The effective date of the implementation of the transaction was 1 November 2016, when Sibanye-Stillwater took over legal ownership and management of the Rustenburg operations.

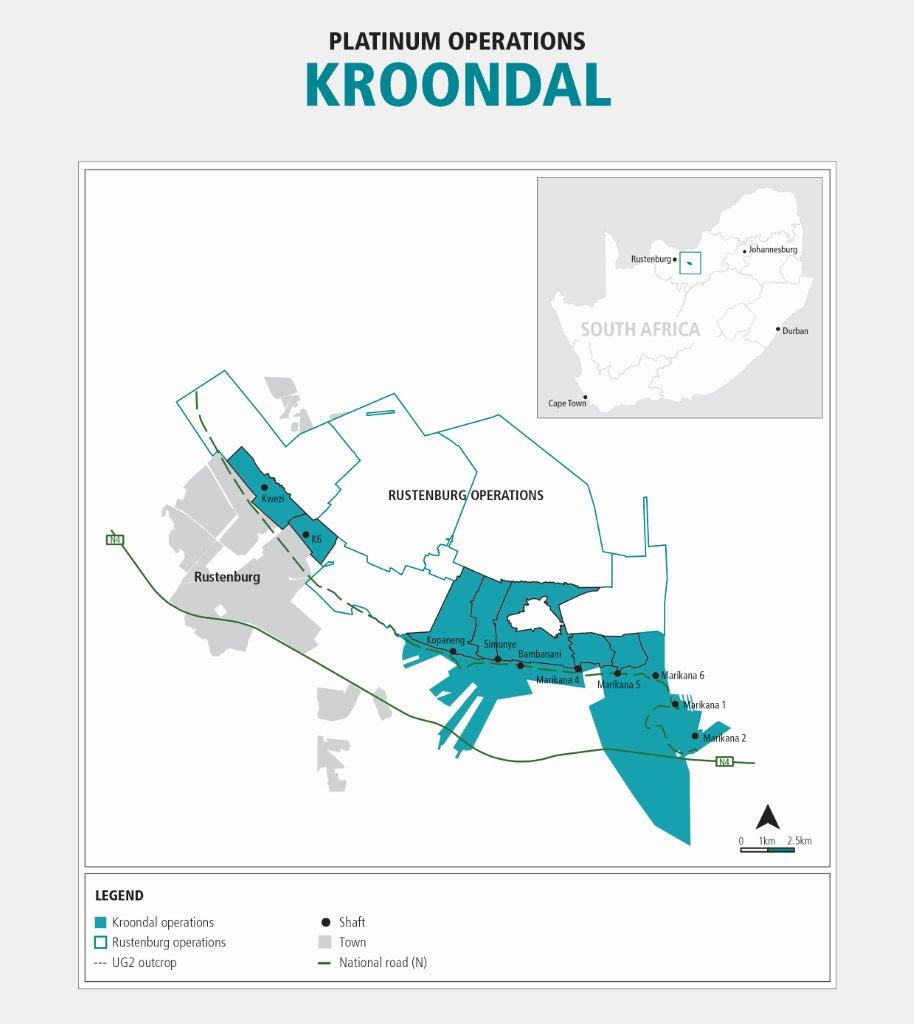

On 6 October 2015, Sibanye-Stillwater announced a cash offer of US$0.195 per share for the entire issued share capital of Aquarius Platinum Limited (Aquarius) (the Aquarius Transaction and, together with the Rustenburg operations Transaction and the Stillwater Transaction, the Acquisitions). Aquarius owns stakes in the Kroondal mine and Platinum Mile retreatment facilities near Rustenburg in South Africa and the Mimosa joint venture with Impala Platinum in Zimbabwe. The Aquarius Transaction was subject to the fulfilment of various conditions precedent which were completed on 12 April 2016, when Sibanye-Stillwater paid R4,301.5 million to the Aquarius shareholders and obtained control of Aquarius.

| |

Sibanye-Stillwater | Form 20-F 2017 | 5 |

market information

This annual report includes industry data about Sibanye-Stillwater’s markets obtained from industry surveys, industry publications, market research and other publicly available third-party information. Industry surveys and industry publications generally state that the information they contain has been obtained from sources believed to be reliable but that the accuracy and completeness of such information is not guaranteed. Sibanye-Stillwater and its advisers have not independently verified this data.

In addition, in many cases statements in this annual report regarding the gold and PGM mining industry, and Sibanye-Stillwater’s position in these industries have been made based on internal surveys, industry forecasts, market research, as well as Sibanye-Stillwater’s own experiences. While these statements are believed by Sibanye-Stillwater to be reliable, they have not been independently verified.

| |

Sibanye-Stillwater | Form 20-F 2017 | 6 |

In this annual report, all references to “we”, “us” and “our” refer to the Sibanye-Stillwater and the Sibanye-Stillwater Group, as applicable.

In this annual report, all references to “fiscal 2018” and “2018” are to the fiscal year ending 31 December 2018, all references to “fiscal 2017” and “2017” are to the audited fiscal year ended 31 December 2017, all references to “fiscal 2016” and “2016” are to the audited fiscal year ended 31 December 2016, and all references to “fiscal 2015” and “2015” are to the audited fiscal year ended 31 December 2015.

In this annual report, all references to “South Africa” are to the Republic of South Africa, all references to the “United States” and “US” are to the United States of America, its territories and possessions and any state of the United States and the District of Columbia, all references to the “United Kingdom” and “UK” are to the United Kingdom of Great Britain and Northern Ireland, all references to “Zimbabwe” are to the Republic of Zimbabwe, all references to “Canada” are to the Dominion of Canada and all references to “Argentina” are to the Republic of Argentina.

In this annual report, all references to the “DMR” are references to the South African Department of Mineral Resources, the government body responsible for regulating the mining industry in South Africa.

In this annual report, gold and PGM production figures are provided in kilograms, which are referred to as “kg”, or in troy ounces, which are referred as “ounces” or “oz”. Ore grades are provided in grams per metric ton, which are referred to as “grams per ton” or “g/t.” All references to “tons”, “tonnes” or “t” in this annual report are to metric tons.

In this annual report, “R”, “Rand” and “rand” refer to the South African Rand and “Rand cents” and “SA cents” refers to subunits of the South African Rand, “$”, “US$”, “US dollars” and “dollars” refer to United States dollars and “US cents” refers to subunits of the US dollar, “£”, “GBP” and “pounds sterling” refer to British pounds and “pence” refers to the subunits of the British pound.

This annual report contains references to the “total recordable injury frequency rate” (TRIFR). TRIFR includes the total number of fatalities, lost time injuries, medically treated injuries and restricted work injuries per million man hours.

| |

Sibanye-Stillwater | Form 20-F 2017 | 7 |

This annual report contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the US Securities Exchange Act of 1934, as amended (the Exchange Act) with respect to our financial condition, results of operations, business strategies, operating efficiencies, competitive position, growth opportunities for existing services, plans and objectives of management, markets for stock and other matters.

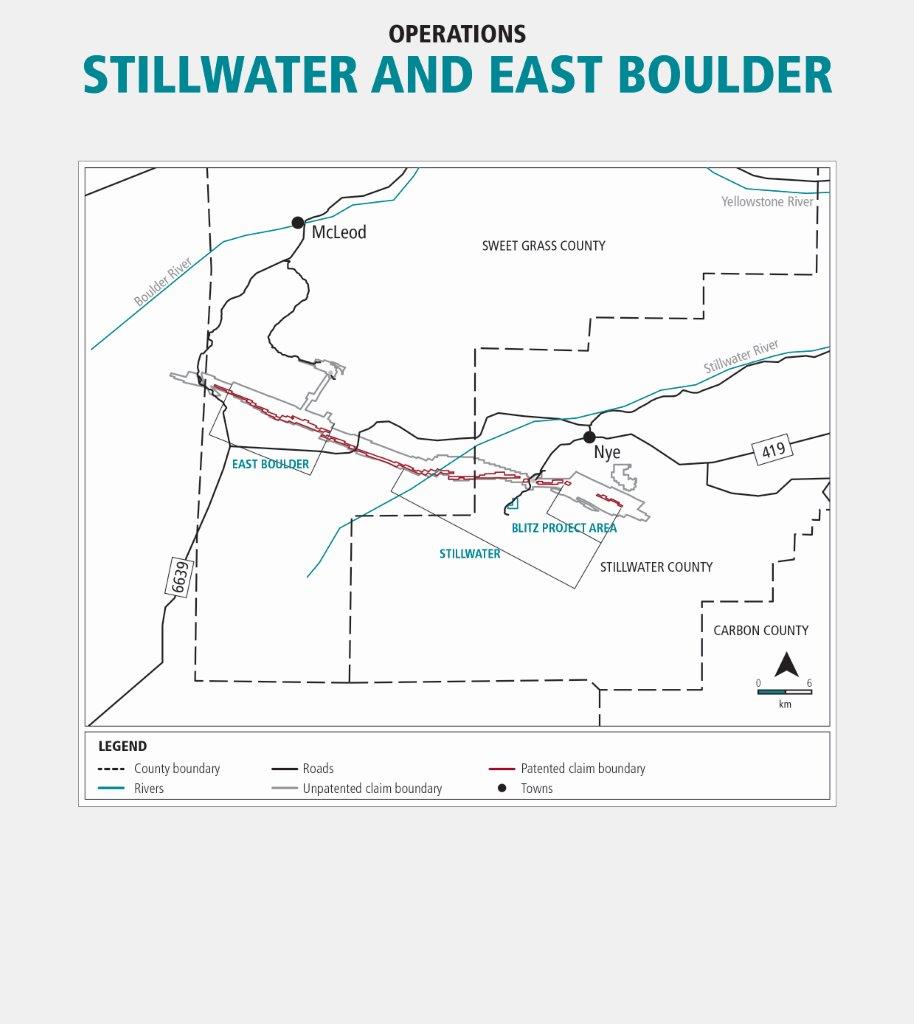

These forward-looking statements, including, among others, those relating to our future business prospects, revenues and income, the potential benefit of the Acquisitions (including statements regarding growth, cost savings, benefits from and access to international financing and financial re-ratings), PGM pricing expectations, levels of output, supply and demand, information relating to the Sibanye-Stillwater’s underground Blitz PGM project adjacent to the east of the existing Stillwater Mine designed to explore, define and extract the PGM resource along the far eastern extent of the J-M Reef (Blitz Project), and estimations or expectations of enterprise value, adjusted EBITDA and net asset values wherever they may occur in this annual report and the exhibits to this annual report, are necessarily estimates reflecting the best judgement of our senior management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. As a consequence, these forward-looking statements should be considered in light of various important factors, including those set forth in this annual report. Important factors that could cause actual results to differ materially from estimates or projections contained in the forward-looking statements include, without limitation:

| · | | changes in the market price of the minerals that it mines and sells; |

| · | | fluctuations in exchange rates, currency devaluations, inflation and other macro-economic monetary policies; |

| · | | the occurrence of labour disruptions and industrial actions; |

| · | | changes in relevant government regulations, particularly environmental, tax, health and safety regulations and new legislation affecting water, mining, mineral rights and business ownership, including any interpretation thereof which may be subject to dispute; |

| · | | power disruption, constraints and cost increases; |

| · | | the outcome and consequence of any potential or pending litigation or regulatory proceedings or environmental, health or safety issues; |

| · | | the occurrence of temporary stoppages of mines for safety incidents and unplanned maintenance; |

| · | | the occurrence of hazards associated with underground and surface mining; |

| · | | failure of Sibanye-Stillwater to comply with various lender covenants and restrictions and difficulties in obtaining additional financing or refinancing; |

| · | | the ability to achieve anticipated efficiencies and other cost savings in connection with, and the ability to successfully integrate, past and future acquisitions, as well as at existing operations; |

| · | | operating in new geographies and regulatory environments where Sibanye-Stillwater had no previous experience; |

| · | | Sibanye-Stillwater’s ability to implement its strategy and any changes thereto; |

| · | | Sibanye-Stillwater’s future financial position, plans, strategies, objectives, capital expenditures, projected costs and anticipated cost savings and financing plans; |

| · | | changes in assumptions underlying Sibanye-Stillwater’s estimation of its current mineral reserves; |

| · | | supply chain shortages and increases in the price of production inputs; |

| · | | economic, business, political and social conditions in South Africa, Zimbabwe, the United States and elsewhere; |

| · | | the ability of Sibanye-Stillwater to comply with requirements that it operates in a sustainable manner; |

| · | | failure of Sibanye-Stillwater’s information technology and communications systems; |

| · | | the success of Sibanye-Stillwater’s business strategy, exploration and development activities; |

| · | | the availability, terms and deployment of capital or credit; |

| · | | Sibanye-Stillwater’s ability to hire and retain senior management or sufficient technically skilled employees, as well as its ability to achieve sufficient representation of HDSAs in its management positions; |

| · | | the adequacy of Sibanye-Stillwater’s insurance coverage; |

| · | | uncertainty regarding the title to Sibanye-Stillwater’s properties; |

| · | | social unrest, sickness or natural or man-made disaster at informal settlements in the vicinity of Sibanye-Stillwater’s African operations; |

| · | | the impact of HIV, tuberculosis and other contagious diseases; and |

The foregoing factors and others described under “Risk Factors” should not be construed as exhaustive. There are other factors that may cause our actual results to differ materially from the forward-looking statements. Moreover, new risk factors emerge from time to time and it is not possible for us to predict all such risk factors. We cannot assess the impact of all risk factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Given these risks and uncertainties, you should not place undue reliance on forward-looking statements as a prediction of actual results.

We undertake no obligation to update publicly or release any revisions to these forward-looking statements to reflect events or circumstances after the date of this annual report or to reflect the occurrence of unanticipated events.

| |

Sibanye-Stillwater | Form 20-F 2017 | 8 |

| |

Sibanye-Stillwater | Form 20-F 2017 | 9 |

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 10 |

This integrated report covers the operational, financial and non-financial performance of the operations and activities of Sibanye Gold Limited, trading as Sibanye-Stillwater. It provides stakeholders with transparent insight into our strategy, our business and performance, and the progress made in delivering on our strategic objectives and our commitment to creating stakeholder value during the year to 31 December 2017. This report, which includes sustainable development- related information, is the primary report in our 2017 suite of reports and takes note of any material events since year-end and the date of approval by the Board.

SCOPE AND BOUNDARY

The scope and boundary of this report have been amended to take into account the regional organisational restructuring undertaken following the significant transformation the Group has undergone in the past two years (see Corporate profile) in order to ensure continued delivery on its strategic operating objectives.

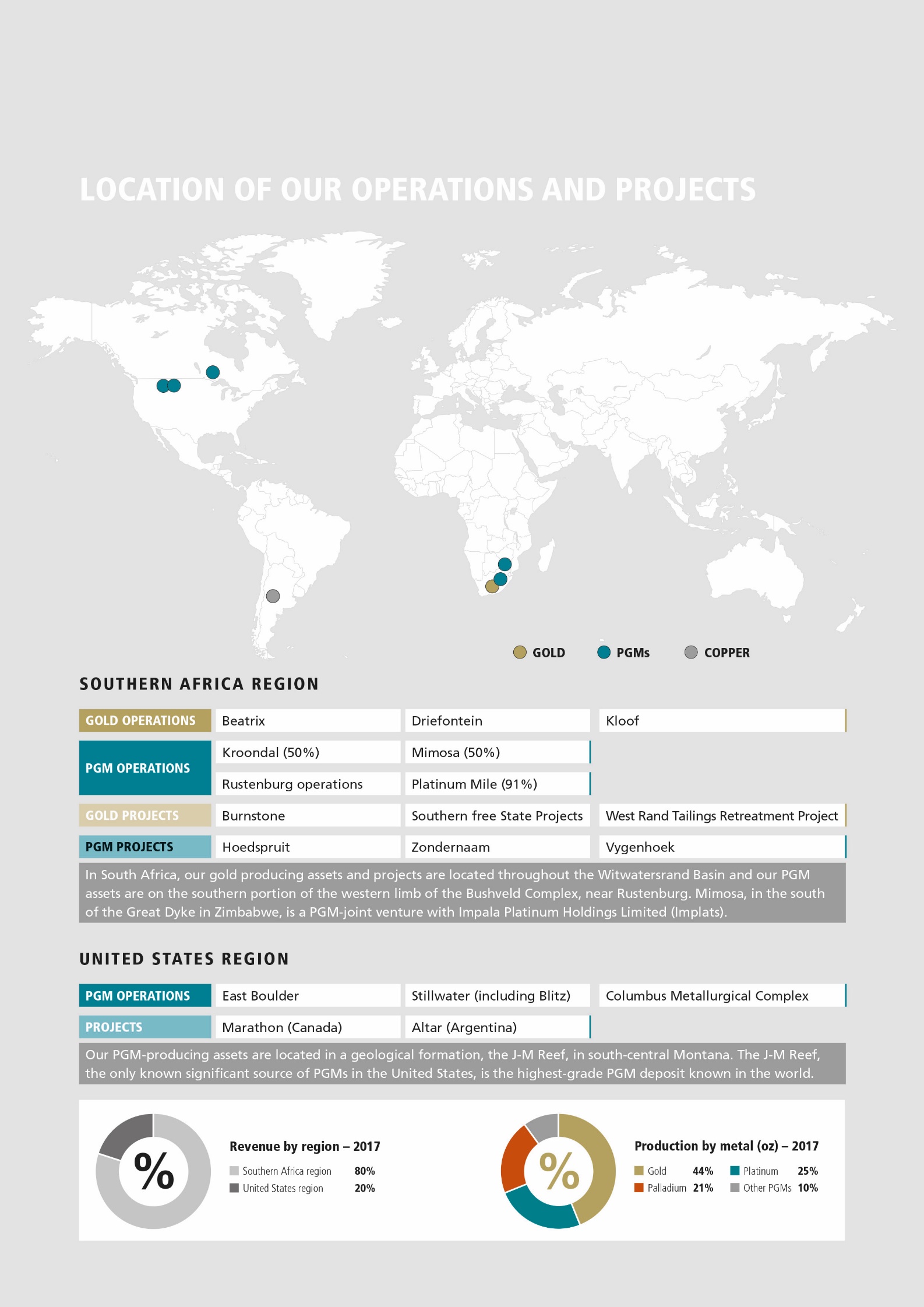

Sibanye-Stillwater’s operating assets are grouped regionally as follows:

Southern Africa (SA) region – gold and platinum group metal (PGM) mining operations and projects

United States (US) region – PGM mining operations and projects. Annual comparative data is provided where applicable. For the 2017 financial year, annual data is provided where possible by region, type of operation and at group level.

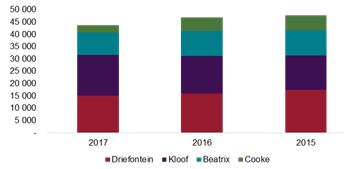

Note that the annual data provided at group-level for 2013 to 2015 is now comparable to that for the SA region’s gold operations for 2016 and 2017. Where data for previous years has been restated, this is indicated.

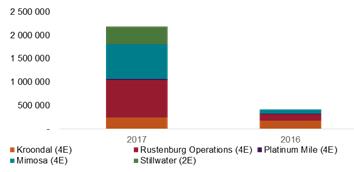

The 2016 data reported for the Platinum Division is now comparable to that reported for the SA region’s PGM operations, with Kroondal, Mimosa and Platinum Mile included for nine months of 2016 and the Rustenburg operation for two months. These operations were included for the full 12 months in 2017.

The US region’s PGM assets are those of the Stillwater Mining Company (Stillwater) which were acquired effective May 2017 and are included for eight months of the year (unless otherwise specified).

REPORTING PHILOSOPHY

In this integrated report, our primary report, the information provided is intended to inform stakeholders about Sibanye-Stillwater’s operating and financial performance and progress made in delivering on our strategy. While the principal audience for this report is investors and shareholders, we recognise that there are other stakeholders who have varied and specific information requirements, many of which we aim to fulfil, particularly as we do not produce a separate sustainable development report. Instead all non-financial reporting is either included in this integrated report or is available on the website, where referenced.

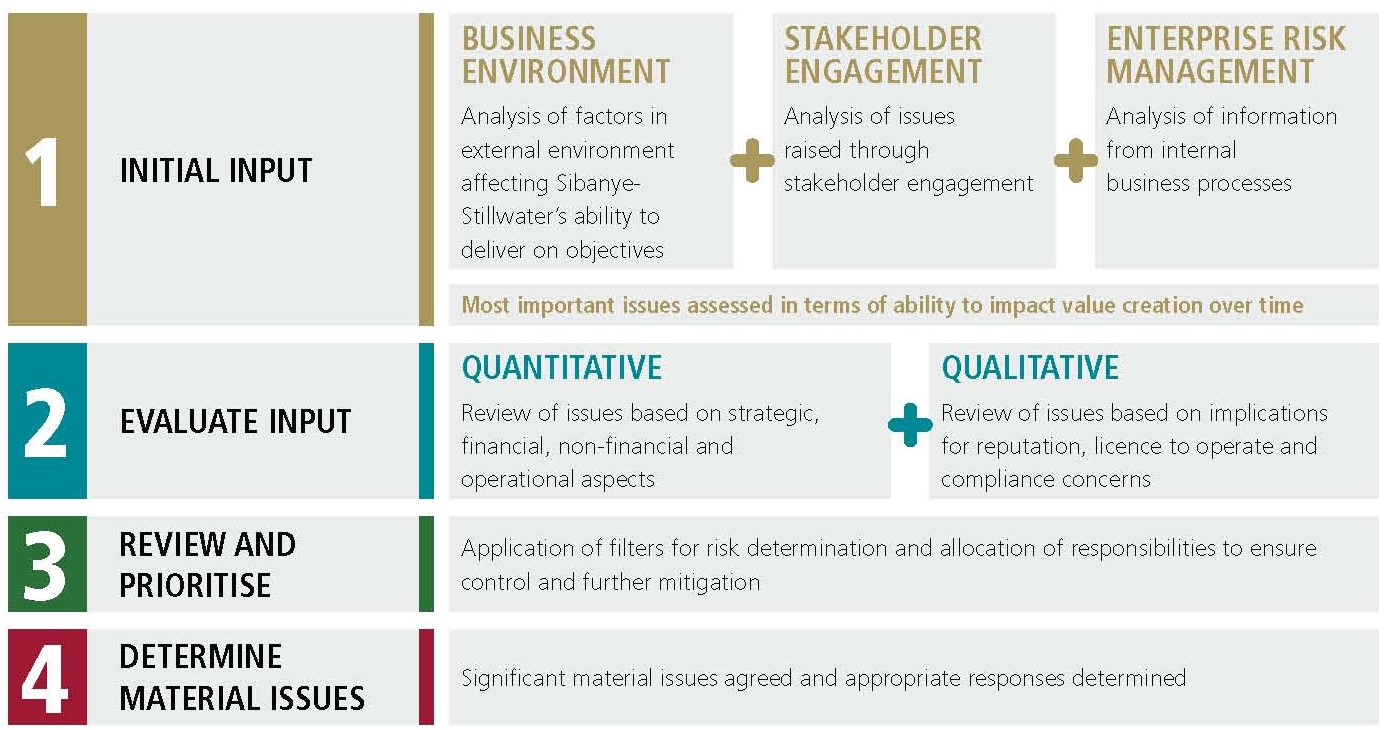

We have endeavoured to build on the information provided in the 2016 integrated report. This report describes what we accomplished in 2017 to create value, to improve lives and to achieve our strategic objectives. In so doing, we give an account of the impact of our activities and, more importantly, of those factors and risks, both in the external environment and internally, that have had an impact on our ability to achieve our strategic objectives and to create superior value in the past year. The process to determine the most material of these is described in –View from the top–Managing our material risks.

This report is intended to enable stakeholders to determine whether the material issues identified will affect the sustainability of Sibanye-Stillwater’s business and its ability to create and sustain value in the short, medium and long term.

APPROVAL AND ASSURANCE

Sibanye-Stillwater’s internal audit function provides an objective evaluation of the Group’s internal control processes and systems that have been devised to mitigate business risks and has ensured the accuracy of the information presented in these reports.

See Further Information—Controls and procedures for managements attestation on the effectiveness of Sibanye-Stillwater’s internal control over financial reporting as of 31 December 2017.

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 11 |

Sibanye-Stillwater, an independent, global, precious metals mining company, produces a unique mix of metals that includes gold and PGMs.

Globally, Sibanye-Stillwater, is the third largest producer of platinum and palladium, and features among the world’s top gold producing companies.

Domiciled in South Africa, Sibanye-Stillwater owns and operates a portfolio of high-quality operations and projects, which are located and managed in two regions: the Southern Africa (SA) region and the United States (US) region.

TRANSFORMING OUR COMPANY

Since its establishment in 2013, the company has transformed itself, geographically and by metal produced. From being a South African gold mining company, Sibanye-Stillwater is now an internationally competitive, diversified precious metals miner producing gold and PGMs. With the formal acquisition of Stillwater in May 2017, Sibanye Gold Limited was rebranded as Sibanye-Stillwater.

Our planned growth momentum continued in 2017 with the announcements towards year-end of the proposed acquisition of Lonmin plc (Lonmin), one of the largest PGM producers in South Africa, and the vending of certain of Sibanye-Stillwater’s surface gold tailings facilities and processing assets into DRDGOLD Limited (DRDGOLD), a world leader in the field, for a 38% shareholding.

OUR VALUE-CREATION JOURNEY

2013 | 2016 | 2017 | 2018 |

South African gold mining company with mature, short-life operations | Entry into the Southern African PGM sector | Becoming a global, precious metals miner | Our value-creation journey continues |

Implemented our operating model and reduced costs to: – improve flexibility and quality of mining – increase reserves – extend operating life – reduce debt/gearing – deliver consistent industry-leading returns | Value-accretive acquisitions at a low point in the PGM price cycle Innovative financing of strategic growth enhances value Implemented our operating model at the newly acquired PGM assets Consolidation synergies yielding superior value | Stillwater acquisition leads to creation of a globally competitive, South African- based mining company Successful refinancing of the bridge loan and US$1 billion rights offer, the US$1.05 billion bond issue and the US$450 million convertible bond | • Awaiting formal approval of: – Proposed acquisition of Lonmin – Planned partnership with DRDGOLD on retreatment of surface gold tailings |

ENTERPRISE VALUE1 R10 billion | ENTERPRISE VALUE1 R32 billion | ENTERPRISE VALUE1 R58 billion | |

1 Enterprise value, or EV, is a measure of a company’s total value, often used as a more comprehensive alternative to equity market capitalisation. Enterprise value is calculated as the market capitalisation plus debt and minority interests and preferred shares, minus total cash and cash equivalents. It is calculated as at 31 December of each year.

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 12 |

location of our operations and projects

LISTINGS

Sibanye-Stillwater has its primary listing on the JSE, South Africa, where it is included in the FTSE/JSE Responsible Investment Index. The company is also listed on the NYSE, with its shares quoted as American Depositary Receipts (ADRs). For further details, see Shareholder information as well as our corporate website, www.sibanyestillwater.com.

At 31 December 2017, Sibanye-Stillwater’s market capitalisation was R34.3 billion (US$2.7 billion) and 2016: R23.6 billion (US$1.7 billion).

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 13 |

OUR PRODUCTS

GOLD | PLATINUM GROUP METALS | BY-PRODUCTS |

In our SA region, Sibanye-Stillwater mines, extracts and processes gold-bearing ore to produce a beneficiated product, doré, which is then refined further at Rand Refinery Proprietary Limited (Rand Refinery) into gold bars with a purity of at least 99.5% in accordance with the London Bullion Market Association’s standards of Good Delivery. Sibanye-Stillwater holds a 33% interest in Rand Refinery, one of the largest global refiners of gold, and the largest in Africa, which then markets and sells the refined gold on international markets to customers around the world. The main sources of demand for gold are as a store of value (such as central bank holdings), as an investment (exchange traded funds, bars and coins), for jewellery and for various industrial purposes | At our PGM operations in South Africa and Zimbabwe, the primary PGMs produced are platinum, palladium and rhodium, which together with the gold occurring as a co- product, are referred to as 4E (3PGM+Au), by ratio approximately 58% platinum (Pt), 32% palladium (Pd), 8% rhodium (Rh) and 2% gold (Au). The PGM-bearing ore mined here is processed to produce PGMs-in- concentrate, which is currently processed further by third parties. The US operations primarily produce palladium and platinum (78% Pd and 22% Pt), which are referred to as 2E (or 2PGM). The PGM-bearing ore mined is processed, smelted and refined to produce a PGM-rich filter cake. A third party refines the filter cake further. The major sources of demand for PGMs are for autocatalytic convertors and jewellery. Together, these two areas account for around 72% of platinum demand while, for palladium, autocatalytic convertors account for 80% of demand for that metal.* | At our PGM operations, the minor PGMs – iridium and ruthenium – are produced as co-products. They, together with the three primary PGMs, are referred to as 6E (5PGM+Au). In addition, at the SA PGM operations, nickel, copper and chrome, among other minerals, are produced as by-products. |

| * Source: Johnson Matthey | |

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 14 |

OUR CORE PURPOSE

Sibanye-Stillwater’s mining improves lives

OUR VALUE PROPOSITION

| | |

Employees By providing employment, Sibanye-Stillwater enables those employed to earn an income, acquire skills and, with training and development, to advance in a work environment where their safety, health and wellbeing are priorities. | Shareholders Sibanye-Stillwater delivers value to shareholders by delivering superior returns through capital appreciation, spurred by operational efficiency, cost- efficient capital management and acquisitive growth. | In living our values, we show that we care about safe production, our stakeholders, our environment, our company and our future. Our approach is holistic. We are focused on delivery on all strategic imperatives critical to Sibanye-Stillwater’s long-term success |

Communities Sibanye-Stillwater contributes to communities, broader society (including suppliers), and the economy by investing in socio-economic development initiatives, employing those who reside in the vicinity of our operations and through preferential local procurement. | Government Sibanye-Stillwater contributes directly to the national fiscus by way of taxes and royalties paid, enabling government to provide social infrastructure and services. We also contribute indirectly through the payment by employees of personal income tax and of municipal rates and taxes. |

|

OUR VISION

Superior value creation for all our stakeholders through the responsible mining and beneficiation of our mineral resources.

OUR STRATEGY

In order to deliver on our vision to create superior value and improve lives, Sibanye-Stillwater aims to deliver sustained, positive cash flows to ensure robust profitability throughout the commodity cycle.

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 15 |

OUR THREE-YEAR STRATEGIC GOAL

OUR FOUR-STEP VALUE-ACCRETIVE PGM STRATEGY

APRIL 2016 | NOVEMBER 2016 | MAY 2017 | 2018 |

AQUARIUS | RUSTENBURG

OPERATIONS | STILLWATER | PROPOSED ACQUISITION OF LONMIN1 |

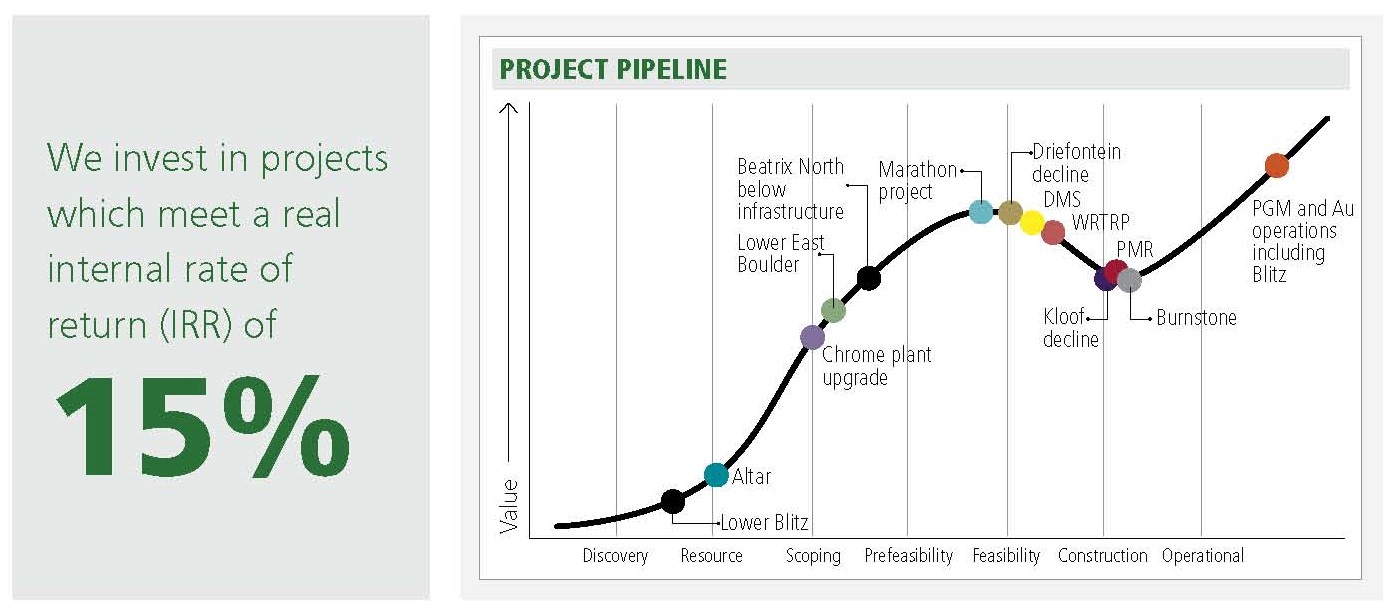

• Our first entry into the PGM sector was the acquisition of Aquarius Platinum Limited (Aquarius) and its Kroondal, Platinum Mile and Mimosa assets in Southern Africa • Aquarius managed efficient and productive assets • Since acquisition, these assets have increased their levels of operational performance | • Acquired the Rustenburg operation, located adjacent to Aquarius’ Kroondal mine, from Anglo American Platinum • A smart transaction structured to reduce risk and aligned with our outlook for the platinum price • Enabled realisation of significant synergies with Aquarius assets and Sibanye-Stillwater • Costs and operational synergies of more than R1 billion were achieved within 14 months, exceeding plan both in extent and time (R800m over three-four years) | • Acquired high-grade, low-cost assets and a world-class growth project • A palladium producer primarily, providing upside to a robust market • Facilitated geographic, commodity and currency diversification • Significant growth potential from the lower East Boulder and lower Blitz projects as well as from the 12.2km mineralised section between the Stillwater and East Boulder mines | • Proposed acquisition announced on 14 December 2017 • Located adjacent to our current PGM operations in South Africa • Potential to realise significant synergies • Given its smelting and refining facilities, this acquisition is aligned with our mine-to-market strategy for the SA region • Replacement value of smelting and refining facilities significantly exceeds acquisition cost • Sizeable resource provides long-term optionality from advanced brownfield and greenfield project pipeline • Subject to Competition Commission and shareholder approval |

At the end of 2016, Sibanye-Stillwater’s PGM (4E) Mineral Reserves totalled 23.2Moz | | At the end of 2017, PGM assets totalled: 2E: Mineral Reserves of 21.9Moz 4E: Mineral Reserves of 22.4Moz | Lonmin has a PGM Mineral Reserve of 31.8Moz (as at 30 September 2017) |

1 The full announcement is available at www.sibanyestillwater.com/investors/transactions/lonmin

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 16 |

Sibanye-Stillwater has a portfolio of gold and PGM assets that will enable it to sustainably conduct its business as a precious metals miner for many years. We conduct our business in a world in which various external factors have an impact, whether positive or negative, on the viability of our business.

Managing these factors and their related risks is vital to our business continuity. In addition, our mining activities have an impact on:

the environment, people, employees and local communities, and broader society. We build and maintain relationships with stakeholders to minimise and manage our risk. Our CARES values, governance framework and code of ethics, which speak to our role as a responsible corporate citizen, underpin all that we do.

| | |

OUR ASSETS | OUR PRIMARY BUSINESS ACTIVITIES | WE CREATE VALUE |

To ensure sustainable value creation, Sibanye-Stillwater has established a unique, global, diversified and long-life portfolio of precious metal assets. Sibanye-Stillwater is: • a top three global producer of platinum and palladium • the largest primary producer of palladium globally • a leading recycler of PGMs globally • the largest gold producer in South Africa | • Mining underground and surface resources • Processing and refining ore mined • PGM recycling • Sale of end products • Acquiring new, value-accretive assets • Supported by: – Community and social development initiatives – Environmental management and land rehabilitation | • Identifying value-accretive acquisition opportunities that are innovatively financed to optimise value for stakeholders • Focusing on safety, productivity, cost discipline and optimising operating capital so as to contribute to positive cash flows and, ultimately, to value creation • Investing in value-accretive organic growth projects to extend operating lives and optimise return on capital |

ATTRIBUTABLE OUTPUT 2017 VERSUS 2016 |

Gold (000oz) 2017: 1,403 2016: 1,512 | PGM (4E) (000oz) 2017: 1,194 2016: 412 | PGM (2E) (000oz) 2017: 376 |

OPERATING CONTEXT AND RISK | ENGAGING WITH STAKEHOLDERS | GOVERNANCE |

• Robust processes and systems are in place to identify and manage those factors likely to have a significant impact on our ability to create value • These systems and processes are supported by internal controls that ensure our response to mitigate any impact is effective and timely • Our top material risks have been identified, together with corresponding opportunities, see Material risks and opportunities | • Stakeholder engagement is critical both to the stability and sustainability of our business • Developing and maintaining constructive, positive relationships with stakeholders helps to ensure we maintain our social licence to operate | • Our strong, principled governance framework, underpinned by our values, is aimed at ensuring: • the long-term viability of our business to sustain value creation • that we conduct our business ethically for the benefit of all stakeholders (see Corporate governance) |

ATTRIBUTABLE OUTPUT 2017 VERSUS 2016 |

Platinum (000oz) 2017: 780 2016: 239 | Palladium (000oz) 2017: 663 2016: 136 | Chrome (000t) 2017: 736 2016: 274 |

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 17 |

CAPITAL RESOURCES USED, OUTCOMES AND IMPACTS – 2017

Various capital resources are used and affected during the conduct of our mining activities and in producing gold and PGMs. These capital resources, which are interdependent, are critical sustaining business and creating value

In 2017, Sibanye-Stillwater…

... used: | … did the following: | … achieved these milestones | … created value: |

HUMAN AND INTELLECTUAL CAPITAL |

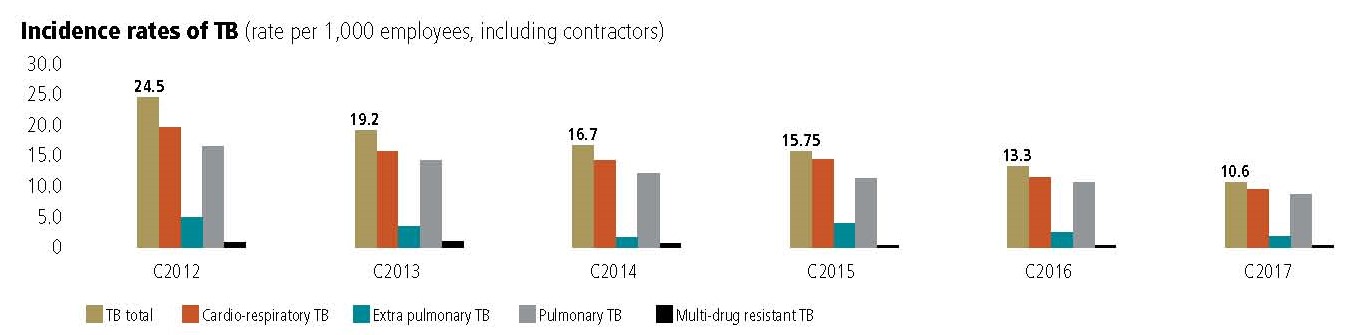

A skilled, motivated workforce, supported by training and development and relevant technologies, enhances our operational efficiency; we have a framework of policies, systems and processes in place to ensure employee safety, health and wellbeing | • Employed 66,472 (2016: 74,531) people (including contractors) – decline in total employee numbers from 2016 was due to cost optimisation undertaken that included retrenchment and downscaling of selected gold and PGM operations in the SA region • Prioritised employee engagement at newly-acquired assets • Initiated safety awareness campaigns and enhanced monitoring of safety compliance | • Improved safety performance: Fatalities: 11 (2016: 14) LTIFR: 5.78 per million hours worked (2016: 6.26) • 79.6 hours of training and skills development on average per employee in the SA region • Improved gender diversity: 13% of employees are female (2016: 12%) • Successfully implemented our organisational model and rolled out our values at newly acquired operations • Wage agreements finalised at Kroondal, Stillwater and East Boulder • Continued to progress the executive leadership development programme to ensure solid effective leadership | • Paid salaries and wages paid to employees totaling R18.5bn (2016: R9.3bn) equivalent to 42% of cost of sales before amortisation and depreciation • Spent R549m on training and development across the Group (2016: R403m), including R17.3m (US$1.3m) in the US region. The increase is mainly due to inclusion of SA PGM operations for 12 months in 2017 versus partial inclusion in 2016 • Began second phase of the Care for iMali indebtedness programme at the SA gold operations and by year-end, had reduced illegal garnishee deductions by R1.34m since 2015 • Improved health and wellbeing of employees – 12% decline in TB incidence (new and relapse) in the SA region |

FINANCIAL CAPITAL | | | |

Funds operating expenses, training and development, acquisition of natural resources and mining infrastructure, land rehabilitation, socio- economic initiatives and enhances the performance of manufactured capital. Availability of financial capital – is achieved through ensuring the right combination of equity, debt and operating cash flows –its efficient management is critical | • Had cash and cash equivalents of R968m at the beginning of the year • Acquired Stillwater for US$2.2bn (R29.3bn at R13.31/US$) • Raised US$2.65 billion bridge loan to conclude acquisition. • Net debt: adjusted EBITDA of 2.6 times following refinancing • Began the year with an enterprise value of R32bn | • Generated revenue of R46bn from sales of metals produced (2016: R31bn) • Incurred cost of sales of R36bn (2016: R25bn) • Capital expenditure of R6.1bn (2016: 4.1bn) for the Group • Bridge loan successfully refinance through a US$1 billion equity rights issue, US$1.05 billion corporate bonds and US$450 million convertible instruments, thereby ensuring a more appropriate capital structure • Debt of R26.0bn (2016: R6.3bn) | • Had cash and cash equivalents of R2,062m at year end • Acquisitions and capital restructuring has better positioned the company to unlock and create future value • Ended the year with an enterprise value of R58bn |

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 18 |

... used: | … did the following: | … achieved these milestones | … created value: |

NATURAL CAPITAL | | | |

Sustainable operations profitably accessing/ exploiting natural resources – economically viable ore-bodies – is fundamental to the sustainability of our business. In addition, natural resources – land, water, air – are impacted by our mining and processing activities | • Acquired PGM reserves (2E) of 21.903Moz with the Stillwater acquisition • Deposited 39.36Mt of waste (2016: 32.61Mt) • Replaced a substantial portion of depleted Mineral Reserves in the SA region, a result of mining and the removal of Cooke, under a tighter set of economic parameters, thus maintaining a sustainable production profile • Completed almost 20km of ore reserve development across the Group • Energy consumption was higher at 6.01TWh (2016: 4.72TWh), largely due to inclusion of SA PGM operations for full year, and acquisition of US PGM operations | • Mined/milled 36.08Mt of ore in total • Reported a 37% reduction in environmental incidents • Reduced energy intensity and GHG emissions by 43% and 41% respectively – the reduction was due to Cooke being placed on care and maintenance, the inclusion of SA PGM operations for a full year and acquisition of US PGM operations • Potable water consumption of 20,838Ml in the SA region (2016: 19,663Ml) | • With the acquisition of Stillwater have increased 2E PGM Mineral Reserves by 21.903Moz • DRDGOLD transaction establishes a commercial vehicle suited to securing long-term environmentally friendly tailings deposition on the West Rand |

SOCIAL AND RELATIONSHIP CAPITAL |

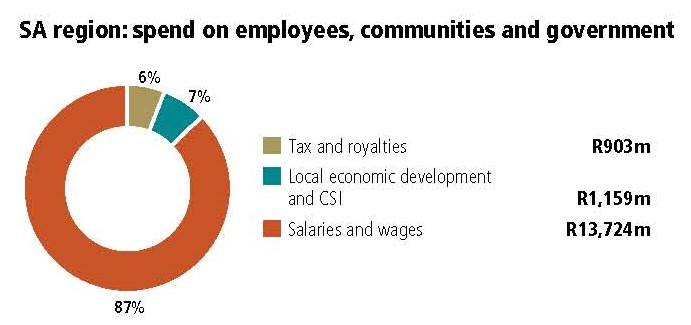

Given mining’s impact, stakeholder alignment is essential for operational sustainability and our ability to continue to deliver value to all our stakeholders. Honest, transparent stakeholder engagement ensures that we earn and maintain our social and legal licences to operate | • Engaged with key stakeholders on: – Mining Charter – Proposed acquisitions – Occupational lung disease – Community development – Safety • Continued with remaining SLP projects | • The Good Neighbour Agreement in force in the US region is a good example of how co-operation with stakeholders can be beneficial to maintaining a social licence to operate – aspects of which will be applied in the SA region • Enterprise development centres being established in the SA region | • Paid R903m to governments in taxes and royalties (2016: R1,733m) • Invested R1,161m in socio-economic development, of which R1,159m was in the SA region (2016: R656m) • Procurement spend of R24.7bn • BEE procurement spend in the SA region of R10.6bn or 79% of discretionary spend (2016: R7.6bn or 77% respectively) |

MANUFACTURED CAPITAL | | | |

Acquiring, maintaining and developing the infrastructure (plant, property and equipment) required by a mining company and optimised processes are essential to cost-efficient operations | • Spent R1.3bn at group level on sustaining capital, including maintenance, of which R1.1bn was in the SA region • Spent R593m on growth projects in the SA region • Acquisition of the Stillwater and East Boulder mines, the Blitz project and the Columbus Metallurgical Complex • Announced proposed acquisition of additional PGM assets (Lonmin) and of potential gold tailings retreatment partnership with DRDGOLD | • Blitz project commissioned three months ahead of schedule • Repositioned and diversified the Group geographically, operationally and with regard to product mix • Invested R13m in research and development • Invested R395m on further development of Burnstone | • Created a unique, leading, global precious metals producer • Became a top three global PGM producer • Plans in place to establish a full mine-to-market pipeline for PGM operations in the SA region |

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 19 |

It is a privilege to once again present this integrated report on behalf of the Sibanye-Stillwater Board to all of our stakeholders.

In recent years, the Company has undergone a significant strategic evolution from a single commodity, gold mining company with its asset base entirely located in South Africa, into a geographically diversified, uniquely positioned, international precious metals company.

Change of this magnitude is never easy and is often accompanied by periods of discomfort and uncertainty, and this has indeed been the case for Sibanye-Stillwater. The rapid execution of our strategy and growth to become a leading global PGM producer has resulted in the Group having to temporarily take on levels of debt that are well above those which have historically been maintained.

This rapid acquisition growth strategy and the resultant impact on the capital structure of the Group were carefully considered by management and the Board. While uncontrollable exogenous factors, such as the recent strength in the rand, present challenges, the Board is confident that, given the inherent flexibility of the broader Sibanye-Stillwater Group, there are no immediate material risks that cannot be dealt with. We are confident that management has sufficient operational and financial levers at its disposal to weather an extended period of rand strength, and that the Group is uniquely positioned to benefit substantially under more constructive market conditions and to deliver superior and sustainable value for shareholders and all other stakeholders.

One of the challenges identified by the Board during this period of rapid growth and change is maintaining the focus on safe delivering of operational targets and integration synergies. As a significant employer in South Africa, the safety of our employees is a priority and despite the improved safety performance across the Group in 2017, the recent spate of fatalities in 2018 is of concern. The Board has asked senior management to review the circumstances leading to these incidents and to take appropriate action. We are confident that there is proper focus on this aspect and plans are being made to mitigate future incidents.

In the CEO’s review, Neal Froneman provides significant detail on the transformative nature and benefits already accruing from recent acquisitions, as well as the strategic rationale of pending transactions, which were recently announced. The Group financial and operational performance for 2017 and outlook are also covered in detail elsewhere, so I will avoid repetition and provide a higher level overview on the company and the current operating environment.

It is not only Sibanye-Stillwater that has recently undergone significant change, but also the political and economic environment in which we operate.

South Africa has experienced a marked political shift, with the election in December 2017 of Cyril Ramaphosa as ANC president, in a tightly contested ANC elective and policy conference. It is still too early to ascertain what the effects will be of this change in leadership and possible political direction in the ANC on the fortunes of the country. Swift and decisive actions taken by the ANC in early 2018, most importantly resulting in the early resignation of the incumbent South African President Jacob Zuma, and apparent commitments to dealing with corruption and to stimulating investment and economic growth in South Africa, have been positively received by the market.

For the South African mining industry in particular, the appointment of Gwede Mantashe as Minister of Mineral Resources in February 2018 has been broadly welcomed. The mining industry’s relationship with the previous Minister was largely hostile and unproductive, and the appointment of a Minister with significant mining experience and a greater understanding of the dynamics of the industry is encouraging. The public recognition by Mr Ramaphosa of the critical importance of the mining industry to the success of the country also suggests a different approach to that which has stifled investment in the sector in recent years.

In February this year, the Chamber of Mines, on behalf of its members, agreed jointly with the Department of Mineral Resources (DMR) to postpone its court application, which was due to be heard by the High Court on 19 February 2018 in respect of the Reviewed Mining Charter that had been gazetted by the previous Minister of Mineral Resources, Mosebenzi Zwane, in June 2016. The postponement followed engagement with President Ramaphosa during which he indicated his commitment to resolving the impasse over the Mining Charter and to facilitating a process to develop a new Mining Charter that included all stakeholders and that was in the interests of the industry and the country as a whole.

Ideally, a new well-designed Mining Charter that is agreed on and supported by all parties in an inclusive process must be finalised as soon as possible. The mining industry believes that this inclusive process should involve meaningful engagement and negotiation with representation across a broad range of stakeholders, including government, business, labour and communities.

The South African mining industry, represented by the SA region: spend on employees, communities and government, Chamber of Mines, including our own Sibanye-Stillwater, remains ready and willing to play its part in building the South African mining industry and economy, while recommitting to further transformational progress and growth, to ensure the industry’s sustainability.

Despite publicly and in a forthright manner raising our concerns on the political and socio-economic outlook for South Africa under the previous regime, Sibanye-Stillwater has remained a proudly South African company and a mining champion, even as it has begun to reposition itself to be competitive in the global industry. In the five years since Gold Fields unbundled three mature, labour-intensive high-cost South African gold mines, which were perceived by the market as nearing the end of their operating lives, Sibanye-Stillwater has become the lowest cost producer of the major gold producers in South Africa, as well as a top three global PGM producer.

In this time, we have significantly extended the operating lives of our gold assets and newly-integrated PGM assets, thus maintaining sustainable, valuable employment. In addition we have invested over R15 billion (increasing potentially to R20 billion should the Lonmin transaction be approved) in growing our gold and PGM portfolio in the Southern Africa region and, in 2016, we committed in excess of about R3.5 billion towards capital to growth projects. This is in addition to the significant contribution of about R16 billion made in 2017 to the local economy in salaries and wages paid, local economic development expenditure, local procurement and the payment of state taxes and royalties. This is 37% more than we spent in 2016.

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 20 |

The Group currently employs more than 65,000 people in South Africa and should the Lonmin transaction be approved, will employ more than 85,000 people in South Africa. It would mark Sibanye-Stillwater as one of the largest employers in the country. As highlighted elsewhere in this report, given the multiplier effect that each job has in the economy, more than 1.4 million South Africans are beneficiaries (direct and indirect) of the jobs provided by Sibanye-Stillwater. Moreover, Sibanye-Stillwater is one of the state-owned utility Eskom’s largest consumers of electricity and therefore is critical to the ongoing viability of that financially troubled entity.

Sibanye-Stillwater’s fortunes are therefore inextricably linked to those of South Africa. Recent political events, which are generally perceived as positive for the South African mining industry, should have positive consequences for the Group. At this stage, these potential benefits are unquantifiable and have not yet been positively reflected in the relative ratings of South African mining companies. The positivity and euphoria following the recent political changes have, however, resulted in significant appreciation in the rand, which, assisted by US dollar weakness, appreciated by 10%, from an average of R13.3/US$ for 2017 to current levels of approximately R11.90/US$.

This recent relative strength in the currency is negatively impacting revenues and margins across the South African mining industry. While certain commodity prices have rebounded strongly in 2018, in some cases totally offsetting the stronger rand, precious metal prices in general have been less fortunate, with the dollar price of gold currently flat year-on-year. Despite the exceptional price gains for palladium and rhodium, the average South African basket price has only increased marginally owing to continued weakness in the platinum price.

The outlook for gold remains relatively muted, with expectations of the US Federal Reserve raising rates in the US, capping upside in 2018. Gold demand remains relatively firm, however, and the spectre of rising global inflation is likely to provide ongoing support below US$1,300/oz in our view. The outlook for PGMs is more positive. Supply deficits in palladium are expected to be sustained for some time while rhodium should benefit from higher loadings on catalysts, which will offset the negative impact that declining diesel vehicle sales are having. Platinum is expected to remain in surplus in 2018, albeit lower than in 2017, which should help to maintain current price levels in 2018. Thereafter, the platinum market is expected to return to deficit as supply from South Africa continues to decline with positive consequences for the price.

The recent rand strength, if sustained, and its impact on operating margins and cash flows in the SA region in 2018, will be offset partly by the already tangible diversification benefits being delivered by the US PGM operations. These are generating substantial operating cash flows, which will be further boosted by the Blitz project as this ramps up to full production in 2021.

As previously mentioned, management has at its disposal, and has already begun to apply, various operational and financial levers to weather and manage an extended period of rand strength. These include a full review of non-essential capital expenditure as well as of the operations, assessing innovative ways to significantly reduce debt and management’s forgoing salary increases in the short term. This review, once completed and acted on, will help to better position Sibanye-Stillwater to continue delivering value to all stakeholders. The Board is confident that the current environment, while challenging, does not pose a material risk to the sustainability of our business.

Sibanye-Stillwater has embraced the outcomes-based philosophy of King IV and begun the process of aligning our corporate governance structures and practices with the principles of King IV. While this process is still underway, we have nevertheless substantially adopted the disclosure requirements recommended by King IV to the extent possible in this integrated report. We are cognisant of our responsibilities, particularly given our Sibanye-Stillwater CARES values, to be ethical and to act responsibly in all that we do and in delivering on our strategy.

RECOGNITION

I would like to extend my thanks to those directors who resigned from the Board during the year – Messrs Christopher Chadwick, Robert Chan and Jiyu Yuan. Their support and contributions to Board deliberations were useful and insightful. I take this opportunity too, to welcome Mrs Savannah Danson, who joined our Board in May 2017.

Following what has been a highly successful 2017, we embark on 2018 full of confidence in the sustainability of our operations. I am personally grateful for the unstinting efforts of all our people to make ours the great company that it is. In particular, I extend my thanks to our CEO, Neal Froneman, and his team for leading the transformation of the company. Their strategic inputs have been invaluable in developing and transforming Sibanye-Stillwater to enable us to continue contributing to the welfare of all our stakeholders.

Sello Moloko

Chairman

29 March 2018

| |

Sibanye-Stillwater | Integrated Annual Report 2017 | 21 |

2017 will be recognised as a landmark year in the history of the company. Over the course of the past two years, primarily in 2017, the Group has fundamentally changed, from a gold mining company with its asset base located entirely in South Africa, into a geographically diversified, international precious metals company.

This transformation has been achieved in a relatively short, three-year period since we first expressed our interest in the PGM industry. In this time, we have established Sibanye-Stillwater as one of the top three global producers of platinum and palladium, while retaining our position as a leading global gold producer.

We have conclusively diversified our commodity mix as well as diversifying the geographical concentration of our operations. This has significantly reduced risk across the Group and is already delivering tangible benefits. To reflect the fundamental change in the Group, we have rebranded as Sibanye-Stillwater, which retains the value of both the Sibanye and Stillwater brands and better reflects our larger, internationally diversified profile.

What has remained constant through this period of change is our commitment to our core purpose, vision and CARES values. Our core purpose that “Our mining improves lives” captures the essence of how we operate, uplifting our employees’ and communities’ quality of life and contributing positively to broader society and the economy, not only through our operating activities, but also through the products we produce. PGMs, in particular, contribute through their superior catalytic properties to a cleaner and healthier environment. Our corporate vision of “creating superior value for all our stakeholders” and CARES values underpin our decisions and actions.

SAFETY

Safety is our principal value and we continue to focus significant effort and attention as well as resources on ensuring that our employees are able to work in a safe and conducive environment. Following a regression in our safety performance in the first half of 2016, we adopted a revised safety strategy in the SA region in the latter half of 2016 that was rolled out across all operations during 2017.

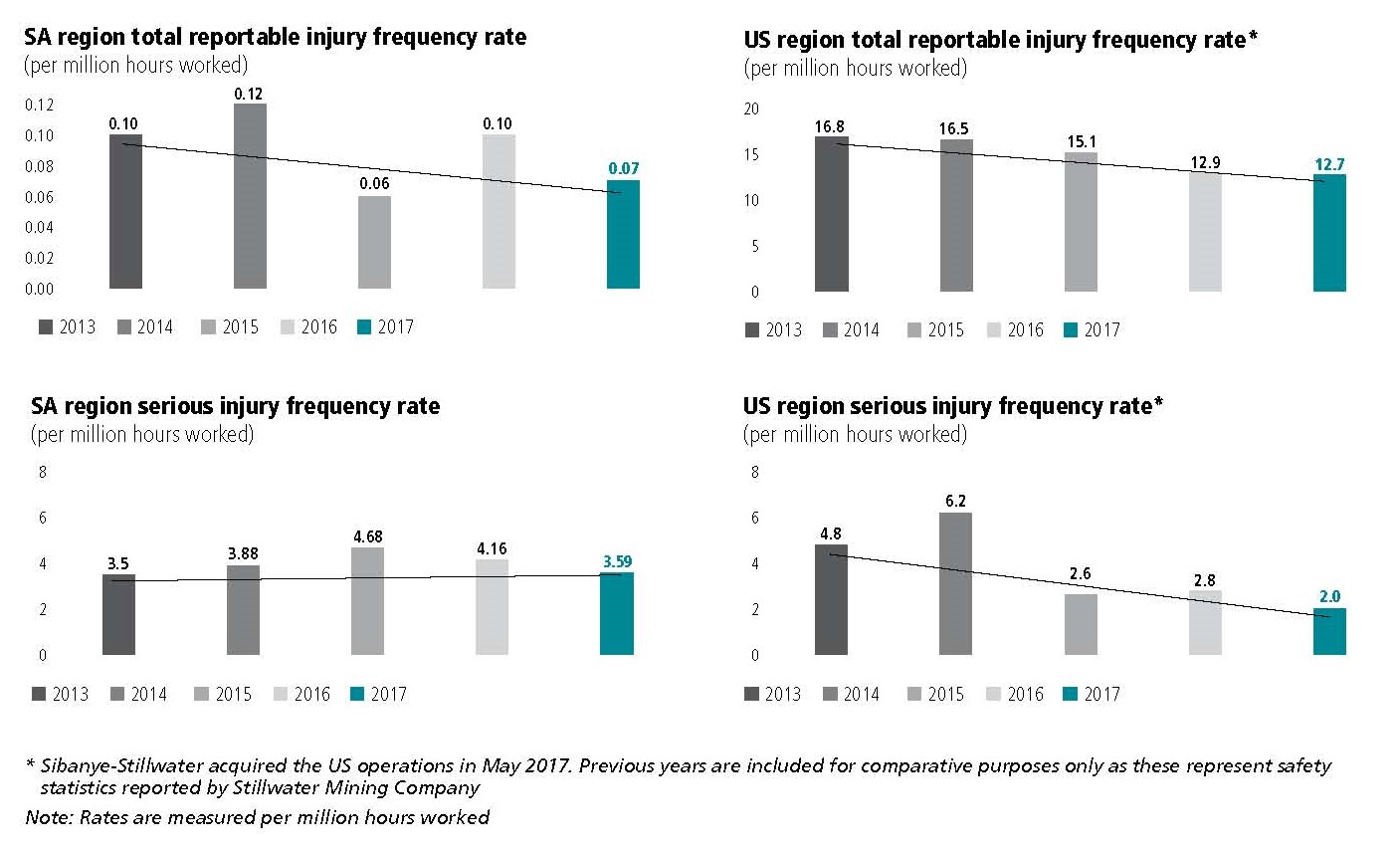

There was a significant improvement in all the main safety indicators across the region during 2017, with the SA region’s serious injury frequency rate (SIFR) improving by 14% to 3.59 per million hours worked, and the lost-time injury frequency rate (LTIFR) improving by 13% to 5.76 per million hours. Safety improvements continued through the year, with the SA gold operations, in the December 2017 quarter, recording their first fatality free quarter since March 2015.

We have now restored our leading position, among both gold and South African PGM peer companies, as the benchmark on most safety indices in the gold and PGM sectors.

Despite these improvements there were regrettably 11 fatalities in the SA region during 2017. These incidents have been thoroughly investigated and preventative action taken and rolled out where appropriate. On behalf of the Board and management, I extend my deepest condolences to the families, friends and colleagues of these employees: Sphampano Machenene, Mxolisi Cekiso, Mbuze Ncobela, Seabata Khetla, Andile Nkwenkwe, Nkosinathi Marumo, Thandisile Deku Rangwaga, Puseletso Molobogeng Mashego, Geraldo Sitoe, Sibongile Ganithuli and Moagisi Selaotswe. Consistent with our practice and policies, the families of the deceased have received, and will continue to receive, appropriate support from the company.

In the US region, the total recordable injury frequency rate (TRIFR) for 2017 was a record low of 12.7 per million hours worked, an improvement on the 12.9 reported for 2016 TRIFR. The East Boulder mine was free from lost day and serious injuries for the entire year and the US region reported no contractor injuries for the entire year.

ORGANISATIONAL RESTRUCTURING FOR EFFECTIVE DELIVERY

The significant increase in size and geographic spread of the company has required us to revise and restructure the organisation to ensure strategic alignment and delivery, role clarity and a continued focus on operational excellence.

During 2017, we transformed from a commodity-focused divisional structure, to a geographically regionalised structure, with separate regionally-focused executive teams in each region, namely, the SA region and the US region. These well-defined geographic regions are led by strong executive teams, which clearly understand the specific regional social and cultural issues, and are primarily responsible for continued delivery of operational and strategic goals. Strategy, finance, new business and other non-operational functions are the responsibility of the corporate office, which ensures that the regional leadership teams are able to focus on operational integration and delivery.

In the SA region, Robert van Niekerk was appointed Executive Vice President: SA region, where he is supported by a strong and experienced team. Robert has served as an executive of the Group since 2013, and has played a key role in improving organisational effectiveness, most recently driving the successful integration of the SA PGM operations. In the US region, Chris Bateman, previously CFO of Stillwater since 2014, was appointed as Executive Vice President: US region. He is also supported in this role by a regional executive team.

The effectiveness of this approach is evident in the successful integration of the SA PGM operations in 2017, which has exceeded expectations, and the efficient integration of the Stillwater operations, which have maintained operational consistency. Continued operational delivery and the successful integration of new acquisitions during periods of rapid growth and change, endorses the current organisational structure and operating model, which we are confident is appropriate for our current and future requirements.

2017 IN REVIEW – A YEAR OF OPPORTUNITY AND DELIVERY

Strategic review