Note 1. Organization

Baywood ValuePlus Fund and Baywood SociallyResponsible Fund (individually, a "Fund" and collectively, the "Funds") are diversified portfolios of Forum Funds II (the "Trust"). The Trust is a Delaware statutory trust that is registered as an open-end, management investment company under the Investment Company Act of 1940, as amended (the "Act"). Under its Trust Instrument, the Trust is authorized to issue an unlimited number of each Fund's shares of beneficial interest without par value. The Baywood ValuePlus Fund commenced operations on December 2, 2013, through a reorganization of a collective investment trust into the Baywood ValuePlus Fund. The collective investment trust was previously managed by the Baywood ValuePlus Fund's Advisor and portfolio management team. This collective investment trust was organized and commenced operations on June 27, 2008. The Baywood ValuePlus Fund currently offers two classes of shares: Investor Shares and Institutional Shares. The Baywood ValuePlus Fund seeks to achieve long-term capital appreciation by investing in undervalued equity securities.

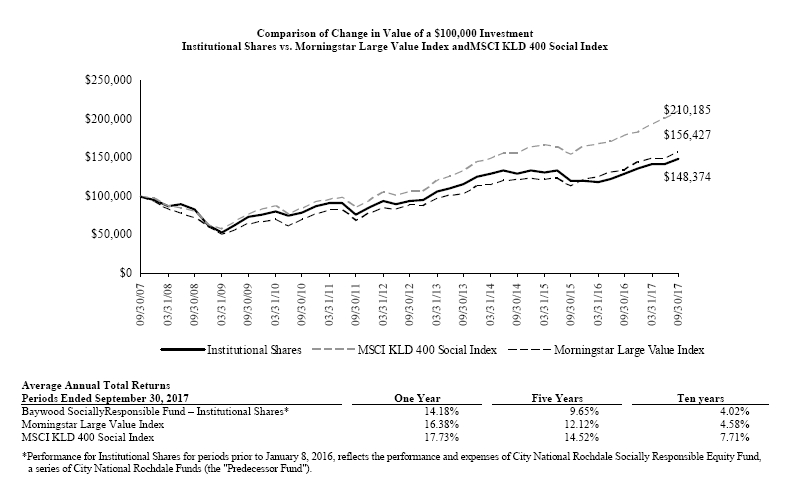

The Baywood SociallyResponsible Fund commenced operations on January 3, 2005. The Baywood SociallyResponsible Fund currently offers two classes of shares: Investor Shares and Institutional Shares. The Baywood SociallyResponsible Fund seeks to provide long-term capital growth.

On December 7, 2015, at a special meeting of shareholders of Baywood SociallyResponsible Fund, formerly City National Rochdale Socially Responsible Equity Fund, a series of City National Rochdale Funds (the "Predecessor Fund"), the shareholders approved a proposal to reorganize the Predecessor Fund into the Baywood SociallyResponsible Fund, a newly created series of the Forum Funds II. The Predecessor Fund was sub-advised by the Fund's Advisor, SKBA Capital Management, LLC, with the same portfolio managers as Baywood SociallyResponsible Fund. The Baywood SociallyResponsible Fund is managed in a manner that is in all material respects equivalent to the management of the Predecessor Fund, including the investment objective, strategies, guidelines and restrictions. The primary purpose of the reorganization was to move the Predecessor Fund to a newly created series of Forum Funds II. As a result of the reorganization, the Baywood SociallyResponsible Fund is now operating under the supervision of a different board of trustees. On January 8, 2016, the Baywood SociallyResponsible Fund acquired all of the assets, subject to liabilities, of the Predecessor Fund. The shares of the Predecessor Fund were, in effect, exchanged on a tax-free basis for Shares of the Baywood SociallyResponsible Fund with the same aggregate value. No commission or other transactional fees were imposed on shareholders in connection with the tax-free exchange of their shares.

Note 2. Summary of Significant Accounting Policies

The Funds are investment companies and follow accounting and reporting guidance under Financial Accounting Standards Board ("FASB") Accounting Standards Codification ("ASC") Topic 946, "Financial Services-Investment Companies". These financial statements are prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP"), which require management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent liabilities at the date of the financial statements, and the reported amounts of increases and decreases in net assets from operations during the fiscal year. Actual amounts could differ from those estimates. The following summarizes the significant accounting policies of each Fund:

Security Valuation – Securities are valued at market prices using the last quoted trade or official closing price from the principal exchange where the security is traded, as provided by independent pricing services on each Fund business day. In the absence of a last trade, securities are valued at the mean of the last bid and ask price provided by the pricing service. Shares of non-exchange-traded open-end mutual funds are valued at net asset value ("NAV"). Short-term investments that mature in 60 days or less may be valued at amortized cost.

Each Fund values its investments at fair value pursuant to procedures adopted by the Trust's Board of Trustees (the "Board") if (1) market quotations are not readily available or (2) the Advisor, as defined in Note 3, believes that the values available are unreliable. The Trust's Valuation Committee, as defined in each Fund's registration statement, performs certain functions as they relate to the administration and oversight of each Fund's valuation procedures. Under these procedures, the Valuation Committee convenes on a regular and ad hoc basis to review such investments and considers a number of factors, including valuation methodologies and significant unobservable inputs, when arriving at fair value.

The Valuation Committee may work with the Advisor to provide valuation inputs. In determining fair valuations, inputs may include market-based analytics that may consider related or comparable assets or liabilities, recent transactions, market multiples, book values and other relevant investment information. Advisor inputs may include an income-based approach in which the anticipated future cash flows of the investment are discounted in determining fair value. Discounts may also be applied based on the nature or duration of any restrictions on the disposition of the investments. The Valuation Committee performs regular reviews

of valuation methodologies, key inputs and assumptions, disposition analysis and market activity.

Fair valuation is based on subjective factors and, as a result, the fair value price of an investment may differ from the security's market price and may not be the price at which the asset may be sold. Fair valuation could result in a different NAV than a NAV determined by using market quotes.

GAAP has a three-tier fair value hierarchy. The basis of the tiers is dependent upon the various "inputs" used to determine the value of each Fund's investments. These inputs are summarized in the three broad levels listed below:

Level 1 — Quoted prices in active markets for identical assets and liabilities

Level 2 – Prices determined using significant other observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). Short-term securities with maturities of sixty days or less are valued at amortized cost, which approximates market value, and are categorized as Level 2 in the hierarchy. Municipal securities, long-term U.S. government obligations and corporate debt securities are valued in accordance with the evaluated price supplied by the pricing service and generally categorized as Level 2 in the hierarchy. Other securities that are categorized as Level 2 in the hierarchy include, but are not limited to, warrants that do not trade on an exchange, securities valued at the mean between the last reported bid and ask quotation and international equity securities valued by an independent third party with adjustments for changes in value between the time of the securities respective local market closes and the close of the U.S. market.

Level 3 — Significant unobservable inputs (including each Fund's own assumptions in determining the fair value of investments)

The aggregate value by input level, as of September 30, 2017, for each Fund's investments is included at the end of each Fund's Schedule of Investments.

Security Transactions, Investment Income and Realized Gain and Loss – Investment transactions are accounted for on the trade date. Dividend income is recorded on the ex-dividend date. Foreign dividend income is recorded on the ex-dividend date or as soon as possible after determining the existence of a dividend declaration after exercising reasonable due diligence. Income and capital gains on some foreign securities may be subject to foreign withholding taxes, which are accrued as applicable. Interest income is recorded on an accrual basis. Premium is amortized and discount is accreted using the effective interest method. Identified cost of investments sold is used to determine the gain and loss for both financial statement and federal income tax purposes.

Distributions to Shareholders – Distributions to shareholders of net investment income, if any, are declared and paid at least annually. Distributions to shareholders of net capital gains, if any, are declared and paid at least annually. Distributions to shareholders are recorded on the ex-dividend date. Distributions are based on amounts calculated in accordance with applicable federal income tax regulations, which may differ from GAAP. These differences are due primarily to differing treatments of income and gain on various investment securities held by each Fund, timing differences and differing characterizations of distributions made by each Fund.

Federal Taxes – Each Fund intends to continue to qualify each year as a regulated investment company under Subchapter M of Chapter 1, Subtitle A, of the Internal Revenue Code of 1986, as amended ("Code"), and to distribute all of its taxable income to shareholders. In addition, by distributing in each calendar year substantially all of its net investment income and capital gains, if any, the Fund will not be subject to a federal excise tax. Therefore, no federal income or excise tax provision is required. Each Fund files a U.S. federal income and excise tax return as required. Each Fund's federal income tax returns are subject to examination by the Internal Revenue Service for a period of three fiscal years after they are filed. As of September 30, 2017, there are no uncertain tax positions that would require financial statement recognition, de-recognition or disclosure.

Income and Expense Allocation – The Trust accounts separately for the assets, liabilities and operations of each of its investment portfolios. Expenses that are directly attributable to more than one investment portfolio are allocated among the respective investment portfolios in an equitable manner.

The Fund's class-specific expenses are charged to the operations of that class of shares. Income and expenses (other than expenses attributable to a specific class) and realized and unrealized gains or losses on investments are allocated to each class of shares based on the class' respective net assets to the total net assets of each Fund.

Commitments and Contingencies – In the normal course of business, each Fund enters into contracts that provide general indemnifications by each Fund to the counterparty to the contract. Each Fund's maximum exposure under these arrangements is dependent on future claims that may be made against each Fund and, therefore, cannot be estimated; however, based on experience,

the risk of loss from such claims is considered remote.

Note 3. Fees and Expenses

Investment Advisor – SKBA Capital Management, LLC (the "Advisor") is the investment advisor to the Funds. Pursuant to an Investment Advisory Agreement, the Advisor receives an advisory fee at an annual rate of 0.50% and 0.70% of the average daily net assets of Baywood ValuePlus Fund and Baywood SociallyResponsible Fund, respectively.

Distribution – Foreside Fund Services, LLC serves as each Fund's distributor (the "Distributor"). The Funds have adopted a Distribution Plan (the "Plan") in accordance with Rule 12b-1 of the Act. Under the Plan, each Fund may pay the Distributor and/or any other entity as authorized by the Board a fee of up to 0.25% of each Fund's average daily net assets of Investor Shares for providing distribution and/or shareholder services to the Funds.

The Distributor is not affiliated with the Advisor or Atlantic Fund Administration, LLC (d/b/a Atlantic Fund Services) ("Atlantic") or their affiliates.

Other Service Providers – Atlantic provides fund accounting, fund administration, compliance and transfer agency services to each Fund. The fees related to these services are included in Fund services fees within the Statement of Operations. Atlantic also provides certain shareholder report production and EDGAR conversion and filing services. Pursuant to an Atlantic services agreement, each Fund pays Atlantic customary fees for its services. Atlantic provides a Principal Executive Officer, a Principal Financial Officer, a Chief Compliance Officer and an Anti-Money Laundering Officer to each Fund, as well as certain additional compliance support functions.

Trustees and Officers – The Trust pays each Independent Trustee an annual fee of $16,000 ($21,000 for the Chairman) for service to the Trust. The Independent Trustees and Chairman may receive additional fees for special Board meetings. The Independent Trustees are also reimbursed for all reasonable out-of-pocket expenses incurred in connection with their duties as Trustees, including travel and related expenses incurred in attending Board meetings. The amount of Independent Trustees' fees attributable to each Fund is disclosed in the Statements of Operations. Certain officers of the Trust are also officers or employees of the above named service providers, and during their terms of office received no compensation from each Fund.

Note 4. Expenses Reimbursed and Fees Waived

The Advisor has contractually agreed to waive its fee and/or reimburse certain expenses to limit total operating expenses (excluding all taxes, interest, portfolio transaction expenses, acquired fund fees and expenses, proxy expenses and extraordinary expenses) for Investor Shares to 0.95% and Institutional Shares to 0.70% through January 31, 2018, for Baywood ValuePlus Fund. The Advisor also has contractually agreed to waive its fees and/or reimburse certain expenses to limit total operating expenses (excluding all taxes, interest, portfolio transaction expenses, acquired fund fees and expenses, proxy expenses and extraordinary expenses) for Investor Shares to 1.14% and Institutional Shares to 0.89% through January 31, 2018, for Baywood SociallyResponsible Fund. Other Fund service providers have voluntarily agreed to waive and reimburse a portion of their fees. These voluntary fee waivers and reimbursements may be reduced or eliminated at any time. For the year ended September 30, 2017, fees waived and expenses reimbursed were as follows:

| | Investment Advisor Fees Waived | | Investment Advisor Expenses Reimbursed | | Other Waivers | | Total Fees Waived and Expenses Reimbursed |

Baywood ValuePlus Fund | $ | 11,515 | | $ | 121,849 | | $ | 45,000 | | $ | 178,364 |

Baywood SociallyResponsible Fund | | 79,891 | | | 59,988 | | | 45,000 | | | 184,879 |

The Advisor may be reimbursed by the Funds for fees waived and expenses reimbursed by the Advisor pursuant to the expense cap if such payment is approved by the Board, and does not cause the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement to exceed the lesser of (i) the then-current expense cap, or (ii) the expense cap in place at the time the fees/expenses were waived or reimbursed. As of September 30, 2017, $415,124 and $230,924 in the Baywood ValuePlus Fund and Baywood SociallyResponsible Fund, respectively, is subject to recapture by the Advisor. Other Waivers are not eligible for recoupment.

Note 5. Security Transactions

The cost of purchases and proceeds from sales of investment securities (including maturities), other than short-term investments

during the year ended September 30, 2017, were as follows:

| | | Purchases | | Sales |

Baywood ValuePlus Fund | | $ | 1,055,730 | | $ | 1,234,811 |

Baywood SociallyResponsible Fund | | | 4,490,867 | | | 12,542,736 |

Note 6. Federal Income Tax

As of September 30, 2017, the cost of investments and the components of net unrealized appreciation were as follows:

| | | | Tax Cost of Investment | | | | Gross Unrealized Appreciation | | | | Gross Unrealized Depreciation | | | | Net Unrealized Appreciation | |

Baywood ValuePlus Fund | | $ | 2,063,377 | | | $ | 380,171 | | | $ | (19,536 | ) | | $ | 360,635 | |

Baywood SociallyResponsible Fund | | | 7,483,194 | | | | 947,527 | | | | (154,748 | ) | | | 792,779 | |

Distributions paid during the fiscal years ended as noted were characterized for tax purposes as follows:

| | | Ordinary Income | | Long-Term Capital Gain | | Total |

Baywood ValuePlus Fund |

| 2017 | | $ | 46,824 | | | $ | 38,818 | | | $ | 85,642 | |

| 2016 | | | 222,678 | | | | 61,442 | | | | 284,120 | |

| 2015 | | | 229,854 | | | | 2,129,193 | | | | 2,359,047 | |

Baywood SociallyResponsible Fund |

| 2017 | | | 130,282 | | | | 71,027 | | | | 201,309 | |

| 2016 | | | 752,147 | | | | 1,906,441 | | | | 2,658,588 | |

Equalization debits included in the distributions were as follows:

| | | Ordinary Income | | Long-Term Capital Gain | | Total | |

Baywood SociallyResponsible Fund | |

| 2017 | | $ | - | | | $ | 71,027 | | | $ | 71,027 | |

As of September 30, 2017, distributable earnings (accumulated loss) on a tax basis were as follows:

| | | Undistributed Ordinary Income | | Undistributed Long-Term Gain | | | Unrealized Appreciation | | Total |

Baywood ValuePlus Fund | | $ | 40 | | | $ | 73,877 | | | | $ | 360,635 | | | $ | 434,552 | |

Baywood SociallyResponsible Fund | | | 1,691 | | | | 112,413 | | | | | 792,779 | | | | 906,883 | |

The difference between components of distributable earnings on a tax basis and the amounts reflected in the Statements of Assets and Liabilities are primarily due to wash sales and equity return of capital.

On the Statements of Assets and Liabilities, as a result of permanent book to tax differences, certain amounts have been reclassified for the year ended September 30, 2017. The following reclassifications were the result of partnerships, equalization, equity return of capital, prior year adjustments for real estate investment trusts, distribution reclassifications, and reclassification of income from a taxable corporate action and have no impact on the net assets of each Fund.

| | Undistributed Net Investment Income (Loss) | | Accumulated Net Realized Gain (Loss) | | Paid-in-Capital |

Baywood ValuePlus Fund | | $ | (3,645 | ) | | $ | 3,645 | | | $ | - | |

Baywood SociallyResponsible Fund | | | 46,715 | | | | (25,176 | ) | | | (21,539 | ) |

Note 7. Subsequent Events

Subsequent events occurring after the date of this report through the date these financial statements were issued have been evaluated for potential impact, and each Fund has had no such events.

Investment Advisory Agreement Approval

At the September 14, 2017 Board meeting, the Board, including the Independent Trustees, considered the approval of the continuance of the investment advisory agreement between the Advisor and the Trust pertaining to the Funds (the "Advisory Agreement"). In preparation for the September meeting, the Board was presented with a range of information to assist in its deliberations. The Board requested and reviewed written responses from the Advisor to a letter circulated on the Board's behalf concerning the Advisor's personnel, operations, financial condition, performance, and services provided to the Funds by the Advisor. During its deliberations, the Board received an oral presentation from the Advisor and discussed the materials with the Advisor, independent legal counsel to the Independent Trustees ("Independent Legal Counsel"), and, as necessary, with the Trust's administrator, Atlantic Fund Services. The Independent Trustees also met in executive session with Independent Legal Counsel while deliberating.

At the September meeting, the Board reviewed, among other matters, the topics discussed below:

Nature, Extent and Quality of Services

Based on written materials received, a presentation from senior representatives of the Advisor and a discussion with the Advisor about the Advisor's personnel, operations and financial condition, the Board considered the quality of services provided by the Advisor under the Advisory Agreement. In this regard, the Board considered information regarding the experience, qualifications and professional background of the portfolio manager and other personnel at the Advisor with principal responsibility for the Funds, as well as the investment philosophy and decision-making process of those professionals and the capability and integrity of the Advisor's senior management and staff.

The Board considered also the adequacy of the Advisor's resources. The Board noted the Advisor's representation that the firm is financially stable and has the operational capability and necessary staffing and experience to continue providing quality investment advisory services to the Funds. Based on the presentation and the materials provided by the Advisor in connection with the Board's consideration of the renewal of the Advisory Agreement, the Board concluded that, overall, it was satisfied with the nature, extent and quality of services to be provided to the Fund under the Advisory Agreement.

Performance

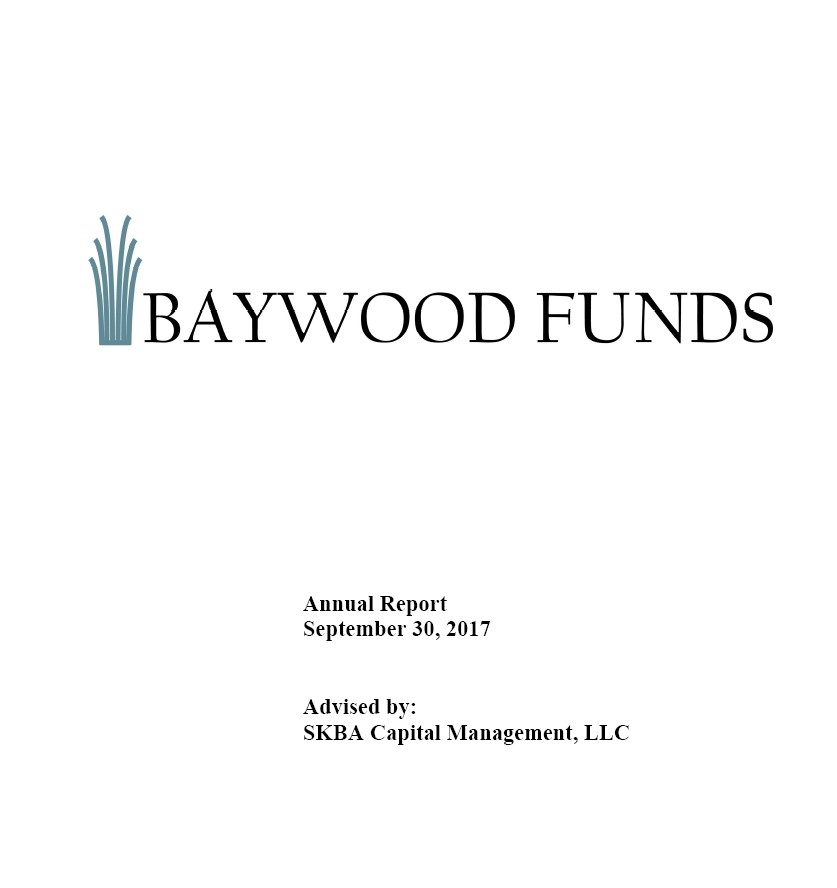

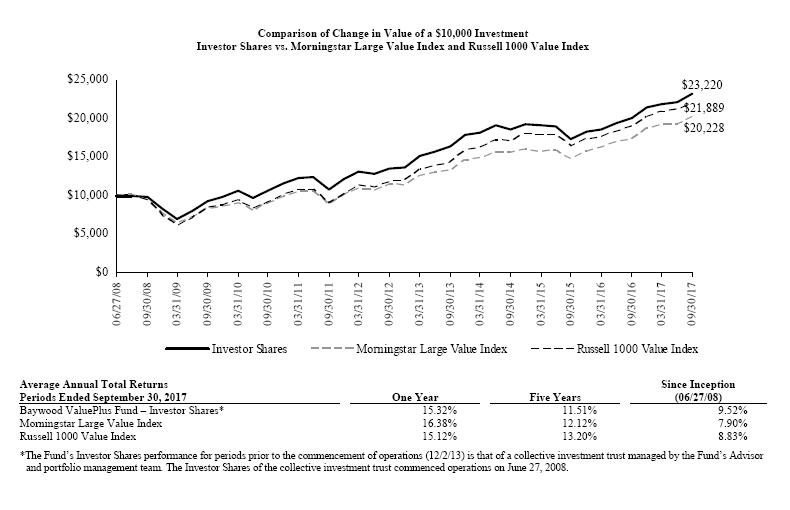

In connection with a presentation by the Advisor regarding its approach to managing the Funds, the Board reviewed the performance of the Funds compared to their respective benchmarks. The Board observed that the ValuePlus Fund underperformed the Russell 1000 Value Index, the primary benchmark index for the ValuePlus Fund, for the one-, three- and five-year periods ended June 30, 2017. The Board also considered the ValuePlus Fund's performance relative to an independent peer group of funds identified by Broadridge Financial Solutions, Inc. ("Broadridge") believed to have characteristics similar to those of the Funds. Based on the information provided by Broadridge, the Board observed that the ValuePlus Fund underperformed the median of the Broadridge peers for the one-year period ended June 30, 2017, and outperformed the median of the Broadridge peers for three-year period ended June 30, 2017. The Board noted the Advisor's representation that the ValuePlus Fund's underperformance relative to its primary benchmark index and peers over the one-year period could be attributed, in part, to the ValuePlus Fund's overweight exposure in the energy sector during a period in which energy stocks underperformed the overall market . The Board noted the Advisor's representation that the ValuePlus Fund underperformed the benchmark over the three- and five-year periods as a result of such periods having been marked by high absolute returns, an environment in which the ValuePlus Fund's strategy tended to underperform.

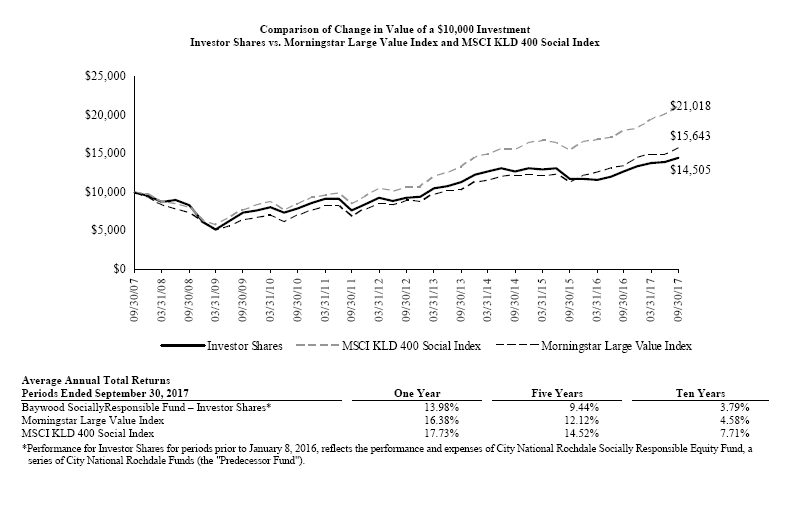

The Board observed that the SociallyResponsible Fund had underperformed the MSCI KLD 400 Social Index, the primary benchmark index, for the one-, three-, five- and 10-year periods ended June 30, 2017. The Board noted the Advisor's representation that the primary benchmark index was not an ideal comparison because it is comprised of companies with growth oriented strategies, which outperformed value investing in general over the last five years. The Board observed that the SociallyResponsible Fund underperformed the median of its Broadridge peers for the one-, three-, and five-year periods ended June 30, 2017. The Board noted the Advisor's representation that the SociallyResponsible Fund's underperformance relative to the Broadridge peers could be attributed, in part, to the SociallyResponsible Fund having a different set of characteristics than the Broadridge peers due to the "socially responsible" criteria, which will cause the SociallyResponsible Fund to perform differently than peers that do not have such "socially responsible" constraints and conditions. The Board noted also the Advisor's representation that the Advisor had recently implemented a change in the investment strategy for the SociallyResponsible Fund, which provided additional flexibility in the management of the portfolio.

Based on the foregoing and other relevant factors, the Board concluded that the Advisor's management of each Fund could benefit each Fund and their respective shareholders.

Compensation

The Board evaluated the Advisor's compensation for providing advisory services to the Funds and analyzed comparative information on actual advisory fee rates and actual total expenses of the Funds' respective Broadridge peer groups. The Board noted that the Advisor's actual advisory fee rate and actual total expense ratio for each of the Funds was less than the median of their respective Broadridge peers. Based on the foregoing, the Board concluded that the Advisor's advisory fee rate charged to the Fund was reasonable.

Cost of Services and Profitability

The Board considered information provided by the Advisor regarding the costs of services and its profitability with respect to the Fund. In this regard, the Board considered the Advisor's resources devoted to the Fund, as well as the Advisor's discussion of costs and profitability. The Board noted the Advisor's representation that, as a result of the contractual expense limitation arrangement in place for the Funds, the Advisor was not earning any profit from its mutual fund operations but that the Advisor was willing to continue subsidizing the Funds in an effort to support growth initiatives. The Board noted that based on other applicable considerations, the Board concluded that the Advisor's costs of services and profits attributable to management of the Fund were reasonable in the context of all factors considered.

Economies of Scale

The Board evaluated whether the Funds would benefit from any economies of scale. In this respect, the Board noted the Advisor's representation that economies of scale could be experienced by shareholders of the Funds upon reaching significantly higher asset levels but that, in light of the Funds' current asset levels, breakpoints in the advisory fee were not believed by the Advisor to be appropriate at this time. Based on the foregoing information, the Board concluded that economies of scale were not a material factor in approving the Advisory Agreement.

Other Benefits

The Board noted the Advisor's representation that, aside from its contractual advisory fees, it does not benefit in a material way from its relationship with the Funds. Based on the foregoing representation, the Board concluded that other benefits received by the Advisor from its relationship with the Funds were not a material factor to consider in approving the continuation of the Advisory Agreement.

Conclusion

The Board did not identify any single factor as being of paramount importance, and different Trustees may have given different weight to different factors. The Board reviewed a memorandum from Fund counsel discussing the legal standards applicable to its consideration of the Advisory Agreement. Based on its review, including consideration of each of the factors referenced above, the Board determined, in the exercise of its reasonable business judgment, that the advisory arrangement, as outlined in the Advisory Agreement, was fair and reasonable in light of the services performed or to be performed, expenses incurred or to be incurred and such other matters as the Board considered relevant.

Proxy Voting Information

A description of the policies and procedures that each Fund uses to determine how to vote proxies relating to securities held in each Fund's portfolio is available, without charge and upon request, by calling (855) 409-2297 and on the U.S. Securities and Exchange Commission's (the "SEC") website at www.sec.gov. Each Fund's proxy voting record for the most recent twelve-month period ended June 30 is available, without charge and upon request, by calling (855) 409-2297 and on the SEC's website at www.sec.gov.

Availability of Quarterly Portfolio Schedules

Each Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. These filings are available, without charge and upon request on the SEC's website at www.sec.gov or may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330.

Shareholder Expense Example

As a shareholder of the Fund, you incur ongoing costs, including management fees, distribution (12b-1) fees (for Investor Shares only) and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2017 through September 30, 2017.

Actual Expenses – The first line under each share class of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes – The second line under each share class of the table below provides information about hypothetical account values and hypothetical expenses based on each Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not each Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds.

| | Beginning | | Ending | | Expenses | | Annualized |

| | Account Value | | Account Value | | Paid During | | Expense |

| | April 1, 2017 | | September 30, 2017 | | Period* | | Ratio* |

Baywood ValuePlus Fund | | | | | | | | | | | |

| Investor Shares | | | | | | | | | | | |

| Actual | $ | 1,000.00 | | $ | 1,060.27 | | $ | 4.91 | | 0.95 | % |

| Hypothetical (5% return before expenses) | $ | 1,000.00 | | $ | 1,020.31 | | $ | 4.81 | | 0.95 | % |

| Institutional Shares | | | | | | | | | | | |

| Actual | $ | 1,000.00 | | $ | 1,061.93 | | $ | 3.62 | | 0.70 | % |

| Hypothetical (5% return before expenses) | $ | 1,000.00 | | $ | 1,021.56 | | $ | 3.55 | | 0.70 | % |

Baywood SociallyResponsible Fund | | | | | | | | | | | |

| Investor Shares | | | | | | | | | | | |

| Actual | $ | 1,000.00 | | $ | 1,049.01 | | $ | 5.86 | | 1.14 | % |

| Hypothetical (5% return before expenses) | $ | 1,000.00 | | $ | 1,019.35 | | $ | 5.77 | | 1.14 | % |

| Institutional Shares | | | | | | | | | | | |

| Actual | $ | 1,000.00 | | $ | 1,049.15 | | $ | 4.57 | | 0.89 | % |

| Hypothetical (5% return before expenses) | $ | 1,000.00 | | $ | 1,020.61 | | $ | 4.51 | | 0.89 | % |

| | | | | | | | | | | | |

| * | Expenses are equal to each Fund's annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (183) divided by 365 to reflect the half-year period. |

Federal Tax Status of Dividends Declared during the Fiscal Year

For federal income tax purposes, dividends from short-term capital gains are classified as ordinary income. The Baywood ValuePlus Fund designates 100.00% of its income dividend distributed as qualifying for the corporate dividends-received deduction (DRD) and 100.00% for the qualified dividend rate (QDI) as defined in Section 1(h)(11) of the Internal Revenue Code. The Baywood SociallyResponsible Fund designates 100.00% of its income dividend distributed as DRD and 100.00% for QDI.

Trustees and Officers of the Trust

The Board is responsible for oversight of the management of the Trust's business affairs and of the exercise of all the Trust's powers except those reserved for the shareholders. The following table provides information about each Trustee and certain officers of the Trust. Each Trustee and officer holds office until the person resigns, is removed, or is replaced. Unless otherwise noted, the persons have held their principal occupations for more than five years. The address for all Trustees and officers is Three Canal Plaza, Suite 600, Portland, Maine 04101. Mr. Keffer and Mr. Hong are considered Interested Trustees due to their affiliation with Atlantic. Each Fund's Statement of Additional Information includes additional information about the Trustees and is available, without charge and upon request, by calling (855) 409-2297.

| Name and Year of Birth | Position(s) with the Trust | Length of Time Served | Principal Occupation(s) During Past Five Years | Number of Series of Fund Complex¹ Overseen by Trustee | Other Directorships Held by Trustee |

| Independent Trustees | | | | | |

David Tucker Born: 1958 | Chairman of the Board; Trustee; Chairman, Nominating Committee and Qualified Legal Compliance Committee | Since 2013 | Director, Blue Sky Experience (a charitable endeavor) since 2008; Senior Vice President & General Counsel, American Century Companies (an investment management firm) 1998-2008. | 45 | Trustee, Forum Funds, Forum ETF Trust and U.S. Global Investors Funds |

Mark D. Moyer Born: 1959 | Trustee; Chairman, Audit Committee | Since 2013 | Chief Financial Officer, Freedom House (a NGO advocating political freedom and democracy), since 2017; Independent Consultant providing interim CFO services, principally to non-profit organizations, 2011-2017; Chief Financial Officer, Institute of International Education (a NGO administering international educational exchange programs), 2008- 2011; Chief Financial Officer and Chief Restructuring Officer, Ziff Davis Media Inc. (an integrated media company) 2005- 2008; Adjunct Professor of Accounting, Fairfield University 2009-2012. | 24 | Trustee, Forum ETF Trust and U.S. Global Investors Funds |

Jennifer Brown-Strabley Born: 1964 | Trustee | Since 2013 | Principal, Portland Global Advisors 1996-2010. | 24 | Trustee, Forum ETF Trust and U.S. Global Investors Funds |

| Interested Trustees | | | | | |

Stacey E. Hong Born: 1966 | Trustee | Since 2013 | President, Atlantic since 2008. | 24 | Trustee, U.S. Global Investors Funds |

John Y. Keffer2 Born: 1942 | Trustee | Since 2013 | Chairman, Atlantic since 2008; President, Forum Investment Advisors, LLC since 2011; President, Forum Foundation (a charitable organization) since 2005; President, Forum Trust, LLC (a non-depository trust company chartered in the State of Maine) since 1997. | 45 | Trustee, Forum Funds, Forum ETF Trust and U.S. Global Investors Funds; Director, Wintergreen Fund, Inc. |

| Officers | | | | | |

Jessica Chase Born: 1970 | President; Principal Executive Officer | Since 2015 | Senior Vice President, Atlantic since 2008. | N/A | N/A |

Karen Shaw Born: 1972 | Treasurer; Principal Financial Officer | Since 2013 | Senior Vice President, Atlantic since 2008. | N/A | N/A |

Zachary Tackett Born: 1988 | Vice President; Secretary; Anti-Money Laundering Compliance Officer | Since 2014 | Counsel, Atlantic since 2014; Intern Associate, Coakley & Hyde, PLLC, 2010-2013. | N/A | N/A |

Michael J. McKeen Born: 1971 | Vice President | Since 2013 | Senior Vice President, Atlantic since 2008. | N/A | N/A |

Timothy Bowden Born: 1969 | Vice President | Since 2013 | Manager, Atlantic since 2008. | N/A | N/A |

Geoffrey Ney Born: 1975 | Vice President | Since 2013 | Manager, Atlantic since 2013; Senior Fund Accountant, Atlantic, 2008-2013. | N/A | N/A |

Todd Proulx Born: 1978 | Vice President | Since 2013 | Manager, Atlantic since 2013; Senior Fund Accountant, Atlantic, 2008-2013. | N/A | N/A |

Carlyn Edgar Born: 1963 | Chief Compliance Officer | Since 2013 | Senior Vice President, Atlantic since 2008. | N/A | N/A |

1The Fund Complex includes the Trust, Forum Funds, Forum ETF Trust and U.S. Global Investors Funds and is overseen by different Boards of Trustees. 2Atlantic is a subsidiary of Forum Holdings Corp. I, a Delaware corporation that is wholly owned by Mr. Keffer. |