As filed with the Securities and Exchange Commission on March 2, 2018

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22842

FORUM FUNDS II

Three Canal Plaza, Suite 600

Portland, Maine 04101

Jessica Chase, Principal Executive Officer

Three Canal Plaza, Suite 600

Portland, Maine 04101

207-347-2000

Date of fiscal year end: December 31

Date of reporting period: January 1, 2017 – December 31, 2017

| Phocas Real Estate Fund |

Annual Report

December 31, 2017

PHOCAS REAL ESTATE FUND A MESSAGE TO OUR SHAREHOLDERS (Unaudited) DECEMBER 31, 2017 |

Market Summary

The securitized commercial real estate market, as measured by the FTSE NAREIT All Equity REIT Index (the "Index" or the "Benchmark"), posted a positive total return in the fourth quarter of +2.5%. The positive performance in the quarter was driven by the growth in November and partially offset by the late decline in December. While the Index closed the year with a total return of +8.7%, the Phocas Real Estate Fund (the "Fund") underperformed the Benchmark with a return of 7.4%.

As REITs have largely been driven by the direction of the 10-year Treasury over the last several years, there is obvious concern that should rates move up, investors would prefer to be underweight REITs. That said, REIT valuations could be supported given a modest forecasted rise in interest rates on both short and long term. Looking ahead to 2018, the tax bill will likely have important impacts on the economy, financial markets and commercial real estate.

Performance Summary

With the exception of Retail and Health Care, most REIT portfolios are experiencing historically high levels of occupancy and solid fundamentals. Despite the recent indications of a healthy 2017 holiday shopping season, Retail REITs have suffered through store closure announcements, bankruptcies and general unfavorable investor sentiment. Healthcare has also been challenged by increased cost of capital and Skilled Nursing Facilities (SNF) tenant issues including concerns on reimbursement rates, unaffordable contracted rent bumps, and contracting margins.

Data Centers and Manufactured Homes continue to perform well for the Fund. We remain positive on the demand for outsourced data center providers, including IT outsourcing, IP traffic growth and expansion of cloud computing. Sun Communities (SUI) performed well as fundamentals remain very healthy and the company continues to source acquisitions opportunities.

The year's top performing real estate sectors were Infrastructure (+35.4%), Data Centers (+28.4%) Manufactured Homes (+24.9%), Timber (+21.9%) and Industrial (+20.6%). The outperformance from Infrastructure and Data Center REITs were driven by the growing demand for mobile and cloud data streaming. Industrial REIT demand is continuing to grow due to ecommerce expansion. Retail REITs, on the other hand, lagged the Index at -4.8%, as Shopping Centers ended 2017 with -11.4% returns overall and Regional malls were -2.7%. Other, more traditional REIT property sectors also underperformed during the year, Healthcare (+0.9%), Apartments (+3.7%) and Office (+5.2%).

Contributors

Despite the negative headlines and poor performance of the Retail sector, two of the top three performers in the fourth quarter were in fact Retail REITs. The share price of General Growth Properties (GGP, +14.9%) was driven higher due to the buyout proposal from Brookfield Asset Management (BAM) and then Unibal-Rodamco takeover of Westfield Corp. Regency Centers (REG, +12.4%) also outperformed in the fourth quarter as its reported third quarter earnings results beat consensus. REG continues to be a top quality company with high quality properties and strong demographic markets.

Detractors

The largest detractor in the quarter was SBRA Health Care (SBRA, -12.1%), which was driven by the headline risks of its tenant mix, SNF and Senior Housing (SH). Despite the industry risks, SBRA's fundamentals remain solid, and management showed confidence with its recent 5% increase to the annual dividend. Seritage Growth Properties (SRG, +11.6%) declined during the fourth quarter after being a top performer in the prior quarter. We expect SRG's share price to remain volatile given its connection to its largest tenant, Sears Holdings, and its widely known struggles. SRG is working to redevelop the department store space, and is viewed as a significant opportunity to improve the asset through retenanting and densification. Corporate Office Properties (OFC, -10.2%) also impaired the Fund's performance during the quarter. The dip in OFC's share price was directly linked to concern over a letter OFC received from the SEC regarding its 2016 10-K. The matter was addressed and viewed as a non-issue.

Fund Positioning

Against a backdrop of tax cuts for the rest of corporate America that should accelerate earnings either from faster economic growth or larger dividends and stock buybacks, we expect REITs to face skepticism given presumed better growth elsewhere. That said, we believe the more interesting part of investing will likely be later in the year, as the sugar high of the tax cuts wears off and investors measure the actual impact on the economy. With the view of a recession still years off, REITs could return to favor as the valuation gap widens and demand builds for companies to expand office space and hire more employees.

1 |

PHOCAS REAL ESTATE FUND A MESSAGE TO OUR SHAREHOLDERS (Unaudited) DECEMBER 31, 2017 |

From a portfolio positioning standpoint, we continue to favor a mix of growth oriented companies combined with selected REITs trading at deeper discounts to NAV and solid cash flow growth. While we don't expect any initial benefits, we believe that a few REIT sectors are well positioned to benefit from the changes in tax law, namely Office, Retail and Apartments.

Little has changed with the strategy of underweighting Healthcare, Freestanding, Suburban Office and Shopping Centers. In the current environment, Health Care REITs have several risks that make them less defensive today than in the past, particularly supply of Senior Housing and Skill Nursing reimbursement. The Fund remains overweight Office, preferring central business district holdings over suburban, as accelerating employment should drive strong same property NOI growth and lowered concessions.

Best Regards,

Phocas Financial Corporation

William Schaff, CFA James Murray, CFA

IMPORTANT RISKS AND DISCLOSURES

The views expressed in this report reflect those of the Fund's Portfolio Managers as of the date this report is first published and may not reflect their views anytime thereafter. These views are intended to assist shareholders in understanding the Fund's investment methodology and do not constitute investment advice. This report may contain discussions about investments that may or may not be held by the Fund as of the date this report is first published. All current and future holdings are subject to risk and to change. To the extent this report contains forward looking statements, unforeseen circumstances may cause actual results to differ materially from the views expressed as of the date this is written.

The Fund is exposed to the same risks that are associated with the direct ownership of real estate including, but not limited to, a general decline in the value of real estate, fluctuations in rental income, changes in interest rates, increases in property taxes, increasing operating costs, overbuilding, changes in zoning laws, and changes in consumer demand for real estate. The Fund may invest in foreign securities which involve political, economic and currency risks, greater volatility, and differences in accounting methods from investing solely in the U.S. These risks are magnified in emerging markets. The Fund is non-diversified, meaning it may invest its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund.

The FTSE NAREIT All Equity REITs Index is an unmanaged index of all tax qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property that also meet minimum size and liquidity criteria. One cannot invest directly in an index.

2 |

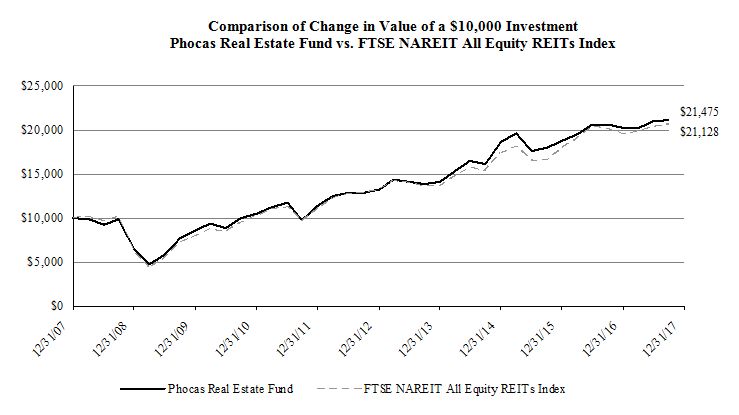

PHOCAS REAL ESTATE FUND PERFORMANCE CHART AND ANALYSIS (Unaudited) DECEMBER 31, 2017 |

The following chart reflects the change in the value of a hypothetical $10,000 investment, including reinvested dividends and distributions, in the Phocas Real Estate Fund (the "Fund") compared with the performance of the benchmark, the FTSE NAREIT All Equity REITs Index (the "NAREIT Equity Index"), over the past 10 fiscal years. The NAREIT Equity Index is an unmanaged index of all tax qualified REITs with more than 50% of total assets in qualifying real estate assets other than mortgages secured by real property that also meets minimum size and liquidity criteria. The total return of the NAREIT Equity Index includes the reinvestment of dividends and income. The total return of the Fund includes operating expenses that reduce returns, while the total return of the NAREIT Equity Index does not include expenses. The Fund is professionally managed, while the NAREIT Equity Index is unmanaged and is not available for investment.

| Average Annual Total Returns | |||||||||||

| Periods Ended December 31, 2017 | One Year | Five Years | Ten Years | ||||||||

| Phocas Real Estate Fund | 7.35 | % | 10.44 | % | 8.08 | % | |||||

| FTSE NAREIT All Equity REITs Index | 8.67 | % | 9.83 | % | 7.77 | % | |||||

Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than original cost. For the most recent month-end performance, please call (866) 746-2271. Shares redeemed within 90 days of purchase will be charged a 1.00% redemption fee. As stated in the Fund's current prospectus, the annual operating expense ratio (gross) is 2.17%. However, the Fund's Advisor has contractually agreed to waive its fee and/or reimburse expenses to limit total operating expenses (excluding all taxes, interest, portfolio transaction expenses, acquired fund fees and expenses, proxy expenses and extraordinary expenses) to 1.50%, through April 30, 2018 (the "Expense Cap"). The Advisor may be reimbursed by the Fund for fees waived and expenses reimbursed by the Advisor pursuant to the Expense Cap if such payment is made within three years of the fee waiver or expense reimbursement, is approved by the Board and does not cause the Net Annual Fund Operating Expenses of the Fund to exceed the lesser of (i) the current expense cap, or (ii) the Expense Cap in place at the time the fees were waived. During the period, certain fees were waived and/or expenses reimbursed; otherwise, returns would have been lower. The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns greater than one year are annualized.

The historical information shown above from December 31, 2007 through July 31, 2013, reflects the historical performance of the Phocas Real Estate Fund, a series of the Advisors Series Trust (the "Predecessor Fund"). Effective as of the close of business on July 31, 2013, the Predecessor Fund reorganized into the Fund. The Predecessor Fund had identical investment objectives and strategies to the fund and was managed by the same investment advisor.

3 |

PHOCAS REAL ESTATE FUND SCHEDULE OF INVESTMENTS DECEMBER 31, 2017 |

| Shares | Security Description | Value | |||

| Common Stock (REITs) - 96.6% | ||||||

| Apartments - 14.2% | ||||||

| 3,219 | AvalonBay Communities, Inc. | $ | 574,302 | |||

| 2,699 | Camden Property Trust | 248,470 | ||||

| 3,159 | Education Realty Trust, Inc. | 110,312 | ||||

| 1,975 | Essex Property Trust, Inc. | 476,706 | ||||

| 37,646 | Independence Realty Trust, Inc. | 379,848 | ||||

| 1,789,638 | ||||||

| Commercial Financing - 1.6% | ||||||

| 10,432 | Jernigan Capital, Inc. | 198,312 | ||||

| Data Centers - 8.3% | ||||||

| 5,701 | CoreSite Realty Corp. | 649,344 | ||||

| 7,172 | QTS Realty Trust, Inc., Class A | 388,436 | ||||

| 1,037,780 | ||||||

| Diversified - 3.6% | ||||||

| 12,758 | Colony NorthStar, Inc., Class A | 145,569 | ||||

| 4,002 | Vornado Realty Trust | 312,876 | ||||

| 458,445 | ||||||

| Diversified Financials - 1.4% | ||||||

| 4,592 | Iron Mountain, Inc. | 173,256 | ||||

| Freestanding - 2.4% | ||||||

| 7,473 | Seritage Growth Properties, Class A | 302,358 | ||||

| Health Care - 3.5% | ||||||

| 5,419 | Sabra Health Care, Inc. | 101,715 | ||||

| 5,320 | Welltower, Inc. | 339,256 | ||||

| 440,971 | ||||||

| Industrial - 9.5% | ||||||

| 10,021 | First Industrial Realty Trust, Inc. | 315,361 | ||||

| 19,505 | Rexford Industrial Realty, Inc. | 568,766 | ||||

| 11,313 | STAG Industrial, Inc. | 309,184 | ||||

| 1,193,311 | ||||||

| Infrastructure - 1.5% | ||||||

| 1,297 | American Tower Corp. | 185,043 | ||||

| Lodging/Resorts - 5.1% | ||||||

| 7,463 | Chatham Lodging Trust | 169,858 | ||||

| 12,729 | Pebblebrook Hotel Trust | 473,137 | ||||

| 642,995 | ||||||

| Manufactured Homes - 2.6% | ||||||

| 3,497 | Sun Communities, Inc. | 324,452 | ||||

| Office - 19.6% | ||||||

| 4,676 | Alexandria Real Estate Equities, Inc. | 610,639 | ||||

| 2,749 | Boston Properties, Inc. | 357,452 | ||||

| 7,084 | Corporate Office Properties Trust | 206,853 | ||||

| 11,639 | Hudson Pacific Properties, Inc. | 398,636 | ||||

| 4,243 | Kilroy Realty Corp. | 316,740 | ||||

| 9,740 | NorthStar Realty Europe Corp. | 130,808 | ||||

| 4,354 | SL Green Realty Corp. | 439,449 | ||||

| 2,460,577 | ||||||

| Shares | Security Description | Value | |||

| Regional Malls - 9.2% | ||||||

| 10,362 | GGP, Inc. | $ | 242,367 | |||

| 5,307 | Simon Property Group, Inc. | 911,424 | ||||

| 1,153,791 | ||||||

| Self Storage - 8.2% | ||||||

| 3,079 | Extra Space Storage, Inc. | 269,258 | ||||

| 27,957 | National Storage Affiliates Trust | 762,108 | ||||

| 1,031,366 | ||||||

| Shopping Centers - 4.9% | ||||||

| 13,217 | Acadia Realty Trust | 361,617 | ||||

| 3,653 | Regency Centers Corp. | 252,715 | ||||

| 614,332 | ||||||

| Single Family Homes - 1.0% | ||||||

| 5,630 | Invitation Homes, Inc. | 132,699 | ||||

Total Common Stock (REITs) (Cost $8,754,772) | 12,139,326 |

Investments, at value - 96.6% (Cost $8,754,772) | $ | 12,139,326 |

| Other Assets & Liabilities, Net – 3.4% | 428,356 | ||

| Net Assets – 100.0% | $ | 12,567,682 |

| REIT | Real Estate Investment Trust |

The following is a summary of the inputs used to value the Fund's investments as of December 31, 2017.

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used in the table below, please refer to the Security Valuation section in Note 2 of the accompanying Notes to Financial Statements.

| Valuation Inputs | Investments in Securities | |||

| Level 1 - Quoted Prices | $ | 12,139,326 | ||

| Level 2 - Other Significant Observable Inputs | - | |||

| Level 3 - Significant Unobservable Inputs | - | |||

| Total | $ | 12,139,326 | ||

The Level 1 value displayed in this table is Common Stock (REITs). Refer to this Schedule of Investments for a further breakout of each security by industry.

The Fund utilizes the end of period methodology when determining transfers. There were no transfers among Level 1, Level 2 and Level 3 for the year ended December 31, 2017.

See Notes to Financial Statements. | 4 |

PHOCAS REAL ESTATE FUND SCHEDULE OF INVESTMENTS DECEMBER 31, 2017 |

| PORTFOLIO HOLDINGS (Unaudited) | ||

| % of Total Investments | ||

| Apartments | 14.7 | % |

| Commercial Financing | 1.6 | % |

| Data Centers | 8.6 | % |

| Diversified | 3.8 | % |

| Diversified Financials | 1.4 | % |

| Freestanding | 2.5 | % |

| Health Care | 3.6 | % |

| Industrial | 9.8 | % |

| Infrastructure | 1.5 | % |

| Lodging/Resorts | 5.3 | % |

| Manufactured Homes | 2.7 | % |

| Office | 20.3 | % |

| Regional Malls | 9.5 | % |

| Self Storage | 8.5 | % |

| Shopping Centers | 5.1 | % |

| Single Family Homes | 1.1 | % |

| 100.0 | % |

See Notes to Financial Statements. | 5 |

PHOCAS REAL ESTATE FUND STATEMENT OF ASSETS AND LIABILITIES DECEMBER 31, 2017 |

| ASSETS | ||||||

| . | Investments, at value (Cost $8,754,772) | $ | 12,139,326 | |||

| Cash | 401,792 | |||||

| Receivables: | ||||||

| Fund shares sold | 3 | |||||

| Dividends and interest | 67,460 | |||||

| Prepaid expenses | 1,305 | |||||

| Total Assets | 12,609,886 | |||||

| LIABILITIES | ||||||

| Accrued Liabilities: | ||||||

| Investment advisor fees | 11,715 | |||||

| Trustees' fees and expenses | 20 | |||||

| Fund services fees | 6,533 | |||||

| Other expenses | 23,936 | |||||

| Total Liabilities | 42,204 | |||||

| NET ASSETS | $ | 12,567,682 | ||||

| COMPONENTS OF NET ASSETS | ||||||

| Paid-in capital | $ | 9,049,868 | ||||

| Undistributed net investment income | 23,894 | |||||

| Accumulated net realized gain | 109,366 | |||||

| Net unrealized appreciation | 3,384,554 | |||||

| NET ASSETS | $ | 12,567,682 | ||||

| SHARES OF BENEFICIAL INTEREST AT NO PAR VALUE (UNLIMITED SHARES AUTHORIZED) | 388,028 | |||||

NET ASSET VALUE, OFFERING AND REDEMPTION PRICE PER SHARE* | $ | 32.39 | ||||

| * | Shares redeemed or exchanged within 90 days of purchase are charged a 1.00% redemption fee. | |||||

See Notes to Financial Statements. | 6 |

PHOCAS REAL ESTATE FUND STATEMENT OF OPERATIONS YEAR ENDED DECEMBER 31, 2017 |

| INVESTMENT INCOME | |||||||

| Dividend income | . | $ | 450,291 | ||||

| Interest income | 1,596 | ||||||

| Total Investment Income | 451,887 | ||||||

| Advisor | |||||||

| EXPENSES | |||||||

| Investment advisor fees | 92,116 | ||||||

| Fund services fees | 94,400 | ||||||

| Custodian fees | 5,000 | ||||||

| Registration fees | 2,162 | ||||||

| Professional fees | 28,567 | ||||||

| Trustees' fees and expenses | 2,480 | ||||||

| Other expenses | 16,936 | ||||||

| Total Expenses | 241,661 | ||||||

| Fees waived and expenses reimbursed | (57,429 | ) | |||||

| Net Expenses | 184,232 | ||||||

| NET INVESTMENT INCOME | 267,655 | ||||||

| NET REALIZED AND UNREALIZED GAIN (LOSS) | |||||||

| Net realized gain on investments | 528,894 | ||||||

| Net change in unrealized appreciation (depreciation) on investments | 89,256 | ||||||

| NET REALIZED AND UNREALIZED GAIN | 618,150 | ||||||

| INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 885,805 | |||||

See Notes to Financial Statements. | 7 |

PHOCAS REAL ESTATE FUND STATEMENTS OF CHANGES IN NET ASSETS |

| # | 43100 | # | # | 42735 | |||||||

| For the Year Ended December 31, 2017 | For the Year Ended December 31, 2016 | ||||||||||

| OPERATIONS | |||||||||||

| Net investment income | $ | 267,655 | $ | 301,744 | |||||||

| Net realized gain | 528,894 | 25,119 | |||||||||

| Net change in unrealized appreciation (depreciation) | 89,256 | 527,384 | |||||||||

| Increase in Net Assets Resulting from Operations | 885,805 | 854,247 | |||||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM | |||||||||||

| Net investment income | (125,775 | ) | (133,353 | ) | |||||||

| Net realized gain | (598,603 | ) | (482,261 | ) | |||||||

| Total Distributions to Shareholders | (724,378 | ) | (615,614 | ) | |||||||

| CAPITAL SHARE TRANSACTIONS | |||||||||||

| Sale of shares | 599,046 | 1,686,936 | |||||||||

| Reinvestment of distributions | 724,378 | 615,614 | |||||||||

| Redemption of shares | (1,338,289 | ) | (1,171,733 | ) | |||||||

| Increase (Decrease) in Net Assets from Capital Share Transactions | (14,865 | ) | 1,130,817 | ||||||||

| Increase in Net Assets | 146,562 | 1,369,450 | |||||||||

| NET ASSETS | |||||||||||

| Beginning of Year | 12,421,120 | 11,051,670 | |||||||||

| End of Year (Including line (a)) | $ | 12,567,682 | $ | 12,421,120 | |||||||

| SHARE TRANSACTIONS | |||||||||||

| Sale of shares | 18,467 | 51,662 | |||||||||

| Reinvestment of distributions | 21,979 | 19,647 | |||||||||

| Redemption of shares | (41,176 | ) | (36,450 | ) | |||||||

| Increase (Decrease) in Shares | (730 | ) | 34,859 | ||||||||

| (a) | Undistributed net investment income | $ | 23,894 | $ | - | ||||||

See Notes to Financial Statements. | 8 |

PHOCAS REAL ESTATE FUND FINANCIAL HIGHLIGHTS |

| These financial highlights reflect selected data for a share outstanding throughout each year. | |||||||||||||||||||||

| For the Years Ended December 31, | |||||||||||||||||||||

| 2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||||

| NET ASSET VALUE, Beginning | |||||||||||||||||||||

| of Year | $ | 31.95 | $ | 31.23 | $ | 32.44 | $ | 24.66 | $ | 23.30 | |||||||||||

| INVESTMENT OPERATIONS | |||||||||||||||||||||

| Net investment income (a) | 0.72 | 0.83 | 0.57 | 0.45 | 0.46 | ||||||||||||||||

| Net realized and unrealized gain (loss) | 1.65 | 1.51 | (0.18 | ) | 7.35 | 1.09 | |||||||||||||||

| Total from Investment Operations | 2.37 | 2.34 | 0.39 | 7.80 | 1.55 | ||||||||||||||||

| DISTRIBUTIONS TO | |||||||||||||||||||||

| SHAREHOLDERS FROM | |||||||||||||||||||||

| Net investment income | (0.33 | ) | (0.35 | ) | (0.36 | ) | (0.02 | ) | (0.19 | ) | |||||||||||

| Net realized gain | (1.60 | ) | (1.27 | ) | (1.24 | ) | — | — | |||||||||||||

| Total Distributions to Shareholders | (1.93 | ) | (1.62 | ) | (1.60 | ) | (0.02 | ) | (0.19 | ) | |||||||||||

| NET ASSET VALUE, End of Year | $ | 32.39 | $ | 31.95 | $ | 31.23 | $ | 32.44 | $ | 24.66 | |||||||||||

| TOTAL RETURN | 7.35 | % | 7.64 | % | 1.28 | % | 31.65 | % | 6.64 | % | |||||||||||

| RATIOS/SUPPLEMENTARY DATA | |||||||||||||||||||||

| Net Assets at End of | |||||||||||||||||||||

| Year (000's omitted) | $12,568 | $12,421 | $11,052 | $10,782 | $7,492 | ||||||||||||||||

| Ratios to Average Net Assets: | |||||||||||||||||||||

| Net investment income | 2.18 | % | 2.57 | % | 1.75 | % | 1.59 | % | 1.83 | % | |||||||||||

| Net expenses | 1.50 | % | 1.50 | % | 1.50 | % | 1.50 | % | 1.50 | % | |||||||||||

| Gross expenses (b) | 1.97 | % | 2.17 | % | 2.30 | % | 2.93 | % | 3.85 | % | |||||||||||

| PORTFOLIO TURNOVER RATE | 25 | % | 26 | % | 30 | % | 18 | % | 29 | % | |||||||||||

| (a) | Calculated based on average shares outstanding during each year. | ||||||||||||||||||||

| (b) | Reflects the expense ratio excluding any waivers and/or reimbursements. | ||||||||||||||||||||

See Notes to Financial Statements. | 9 |

PHOCAS REAL ESTATE FUND NOTES TO FINANCIAL STATEMENTS DECEMBER 31, 2017 |

Note 1. Organization

The Phocas Real Estate Fund (the "Fund") is a a non-diversified portfolio of Forum Funds II (the "Trust"). The Trust is a Delaware statutory trust that is registered as an open-end, management investment company under the Investment Company Act of 1940, as amended (the "Act"). Under its Trust Instrument, the Trust is authorized to issue an unlimited number of the Fund's shares of beneficial interest without par value. The Fund commenced operations on September 29, 2006. The Fund seeks long-term total investment return through a combination of capital appreciation and current income.

On July 19, 2013, at a Special Meeting of Shareholders of the Phocas Real Estate Fund (the "Predecessor Fund"), a series of the Advisor Series Trust, the shareholders approved a proposal to reorganize the Predecessor Fund into the Fund, a newly created series of the Trust. The Fund is designed to be substantially similar from an investment perspective to the Predecessor Fund, and is managed by the same investment advisor. As a result of the reorganization, the Fund is now operating under the supervision of a different board of trustees. On August 1, 2013, the shares of the Predecessor Fund were, in effect, exchanged on a tax-free basis for shares of the Fund with the same aggregate value. No sales load, commission or other transactional fees were imposed on shareholders in connection with the tax-free exchange of their shares.

Note 2. Summary of Significant Accounting Policies

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board ("FASB") Accounting Standards Codification ("ASC") Topic 946, "Financial Services-Investment Companies". These financial statements are prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP"), which require management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent liabilities at the date of the financial statements, and the reported amounts of increases and decreases in net assets from operations during the fiscal year. Actual amounts could differ from those estimates. The following summarizes the significant accounting policies of the Fund:

Security Valuation – Securities are valued at market prices using the last quoted trade or official closing price from the principal exchange where the security is traded, as provided by independent pricing services on each Fund business day. In the absence of a last trade, securities are valued at the mean of the last bid and ask price provided by the pricing service. Shares of non-exchange traded open-end mutual funds are valued at net asset value ("NAV"). Short-term investments that mature in sixty days or less may be valued at amortized cost.

The Fund values its investments at fair value pursuant to procedures adopted by the Trust's Board of Trustees (the "Board") if (1) market quotations are not readily available or (2) the Advisor, as defined in Note 4, believes that the values available are unreliable. The Trust's Valuation Committee, as defined in the Fund's registration statement, performs certain functions as they relate to the administration and oversight of the Fund's valuation procedures. Under these procedures, the Valuation Committee convenes on a regular and ad hoc basis to review such investments and considers a number of factors, including valuation methodologies and significant unobservable inputs, when arriving at fair value.

The Valuation Committee may work with the Advisor to provide valuation inputs. In determining fair valuations, inputs may include market-based analytics that may consider related or comparable assets or liabilities, recent transactions, market multiples, book values and other relevant investment information. Advisor inputs may include an income-based approach in which the anticipated future cash flows of the investment are discounted in determining fair value. Discounts may also be applied based on the nature or duration of any restrictions on the disposition of the investments. The Valuation Committee performs regular reviews of valuation methodologies, key inputs and assumptions, disposition analysis and market activity.

Fair valuation is based on subjective factors and, as a result, the fair value price of an investment may differ from the security's market price and may not be the price at which the asset may be sold. Fair valuation could result in a different NAV than a NAV determined by using market quotes.

GAAP has a three-tier fair value hierarchy. The basis of the tiers is dependent upon the various "inputs" used to determine the value of the Fund's investments. These inputs are summarized in the three broad levels listed below:

Level 1 — Quoted prices in active markets for identical assets and liabilities

Level 2 – Prices determined using significant other observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). Short-term securities with maturities of sixty days or less are valued at amortized cost, which approximates market value, and are categorized as Level 2 in the hierarchy. Municipal securities, long-term U.S. government

10 |

PHOCAS REAL ESTATE FUND NOTES TO FINANCIAL STATEMENTS DECEMBER 31, 2017 |

obligations and corporate debt securities are valued in accordance with the evaluated price supplied by the pricing service and generally categorized as Level 2 in the hierarchy. Other securities that are categorized as Level 2 in the hierarchy include, but are not limited to, warrants that do not trade on an exchange, securities valued at the mean between the last reported bid and ask quotation and international equity securities valued by an independent third party with adjustments for changes in value between the time of the securities respective local market closes and the close of the U.S. market.

Level 3 — Significant unobservable inputs (including the Fund's own assumptions in determining the fair value of investments)

The aggregate value by input level, as of December 31, 2017, for the Fund's investments is included at the end of the Fund's Schedule of Investments.

Security Transactions, Investment Income and Realized Gain and Loss – Investment transactions are accounted for on the trade date. Dividend income is recorded on the ex-dividend date. Foreign dividend income is recorded on the ex-dividend date or as soon as possible after determining the existence of a dividend declaration after exercising reasonable due diligence. Income and capital gains on some foreign securities may be subject to foreign withholding taxes, which are accrued as applicable. Interest income is recorded on an accrual basis. Premium is amortized and discount is accreted using the effective interest method. Identified cost of investments sold is used to determine the gain and loss for both financial statement and federal income tax purposes.

Distributions to Shareholders – Distributions to shareholders of net investment income, if any, are declared and paid at least annually. Distributions to shareholders of net capital gains, if any, are declared and paid at least annually. Distributions to shareholders are recorded on the ex-dividend date. Distributions are based on amounts calculated in accordance with applicable federal income tax regulations, which may differ from GAAP. These differences are due primarily to differing treatments of income and gain on various investment securities held by the Fund, timing differences and differing characterizations of distributions made by the Fund.

Federal Taxes – The Fund intends to continue to qualify each year as a regulated investment company under Subchapter M of Chapter 1, Subtitle A, of the Internal Revenue Code of 1986, as amended ("Code"), and to distribute all of its taxable income to shareholders. In addition, by distributing in each calendar year substantially all of its net investment income and capital gains, if any, the Fund will not be subject to a federal excise tax. Therefore, no federal income or excise tax provision is required. The Fund files a U.S. federal income and excise tax return as required. The Fund's federal income tax returns are subject to examination by the Internal Revenue Service for a period of three fiscal years after they are filed. As of December 31, 2017, there are no uncertain tax positions that would require financial statement recognition, de-recognition or disclosure.

REITs – The Fund has made certain investments in real estate investment trusts ("REITs") which pay dividends to their shareholders based upon funds available from operations. It is quite common for these dividends to exceed the REIT's taxable earnings and profits resulting in the excess portion of such dividends being designated as a return of capital. The Fund may include the gross dividends from such REITs in income or may utilize estimates of any potential REIT dividend reclassifications in the Fund's annual distributions to shareholders and, accordingly, a portion of the Fund's distributions may be designated as a return of capital, require reclassification, or be under distributed on an excise basis and subject to excise tax.

Income and Expense Allocation – The Trust accounts separately for the assets, liabilities and operations of each of its investment portfolios. Expenses that are directly attributable to more than one investment portfolio are allocated among the respective investment portfolios in an equitable manner.

Redemption Fees – A shareholder who redeems or exchanges shares within 90 days of purchase will incur a redemption fee of 1.00% of the current NAV of shares redeemed or exchanged, subject to certain limitations. The fee is charged for the benefit of the remaining shareholders and will be paid to the Fund to help offset transaction costs. The fee is accounted for as an addition to paid-in capital. The Fund reserves the right to modify the terms of or terminate the fee at any time. There are limited exceptions to the imposition of the redemption fee. Redemption fees incurred for the Fund, if any, are reflected on the Statements of Changes in Net Assets.

Commitments and Contingencies – In the normal course of business, the Fund enters into contracts that provide general indemnifications by the Fund to the counterparty to the contract. The Fund's maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore, cannot be estimated; however, based on experience, the risk of loss from such claims is considered remote. The Fund has determined that none of these arrangements requires disclosure on the Fund's balance sheet.

11 |

PHOCAS REAL ESTATE FUND NOTES TO FINANCIAL STATEMENTS DECEMBER 31, 2017 |

Note 3. Cash – Concentration in Uninsured Account

For cash management purposes, the Fund may concentrate cash with the Fund's custodian. This typically results in cash balances exceeding the Federal Deposit Insurance Corporation ("FDIC") insurance limits. As of December 31, 2017, The Fund had $151,792 at MUFG Union Bank, N.A. that exceeded the FDIC insurance limit.

Note 4. Fees and Expenses

Investment Advisor – Phocas Financial Corporation (the "Advisor") is the investment advisor to the Fund. Pursuant to an investment advisory agreement, the Advisor receives an advisory fee, payable monthly, from the Fund at an annual rate of 0.75% of the Fund's average daily net assets.

Distribution – Foreside Fund Services, LLC serves as the Fund's distributor (the "Distributor"). The Fund has adopted a Distribution Plan (the "Plan") in accordance with Rule 12b-1 of the Act. Under the Plan, the Fund may pay the Distributor and/or any other entity as authorized by the Board a fee of up to 0.25% of the Fund's average daily net assets for providing distribution and/or shareholder services to the Fund. The Distributor is not affiliated with the Advisor or Atlantic Fund Administration, LLC (d/b/a Atlantic Fund Services) ("Atlantic") or their affiliates.

Other Service Providers – Atlantic provides fund accounting, fund administration, compliance and transfer agency services to the Fund. The fees related to these services are included in Fund services fees within the Statement of Operations. Atlantic also provides certain shareholder report production and EDGAR conversion and filing services. Pursuant to an Atlantic services agreement, the Fund pays Atlantic customary fees for its services. Atlantic provides a Principal Executive Officer, a Principal Financial Officer, a Chief Compliance Officer and an Anti-Money Laundering Officer to the Fund, as well as certain additional compliance support functions.

Trustees and Officers – The Trust pays each Independent Trustee an annual fee of $16,000 ($21,000 for the Chairman) for service to the Trust. The Independent Trustees and Chairman may receive additional fees for special Board meetings. The Independent Trustees are also reimbursed for all reasonable out-of-pocket expenses incurred in connection with their duties as Trustees, including travel and related expenses incurred in attending Board meetings. The amount of Independent Trustees' fees attributable to the Fund is disclosed in the Statement of Operations. Certain officers of the Trust are also officers or employees of the above named service providers, and during their terms of office received no compensation from the Fund.

Note 5. Expenses Reimbursed and Fees Waived

The Advisor has contractually agreed to waive its fee and/or reimburse certain expenses to limit total operating expenses (excluding all taxes, interest, portfolio transaction expenses, acquired fund fees and expenses, proxy expenses and extraordinary expenses) to 1.50% through April 30, 2018. Other fund service providers have voluntarily agreed to waive and reimburse a portion of their fees. These voluntary fee waivers and reimbursements may be reduced or eliminated at any time. For the year ended December 31, 2017, fees waived and expenses reimbursed were as follows:

| Investment Advisor Fees Waived | Other Waivers | Total Fees Waived | |||||

| $ | 41,429 | $ | 16,000 | $ | 57,429 | ||

The Fund may repay the Advisor for fees waived and expenses reimbursed pursuant to the expense cap if such payment is (1) made within three years of the fee waiver or expense reimbursement (2) is approved by the Board and (3) does not cause the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement of the Fund to exceed the lesser of (i) the then-current expense cap, or (ii) the expense cap in place at the time the fees/expenses were waived/reimbursed. As of December 31, 2017, $179,173 is subject to recapture by the Advisor.

Note 6. Security Transactions

The cost of purchases and proceeds from sales of investment securities (including maturities), other than short-term investments, during the year ended December 31, 2017 totaled $2,995,160 and $3,510,336, respectively.

12 |

PHOCAS REAL ESTATE FUND NOTES TO FINANCIAL STATEMENTS DECEMBER 31, 2017 |

Note 7. Federal Income Tax

Cost for federal income tax purposes is $8,751,111 and net unrealized appreciation consists of:

| Gross Unrealized Appreciation | $ | 3,657,638 | ||||

| Gross Unrealized Depreciation | (269,423 | ) | ||||

| Net Unrealized Appreciation | $ | 3,388,215 |

Distributions paid during the fiscal years ended as noted were characterized for tax purposes as follows:

| 2017 | 2016 | |||||

Ordinary Income | $ 149,516 | $ 78,381 | ||||

Long-Term Capital Gain | 574,862 | 537,233 | ||||

| $ 724,378 | $ 615,614 |

As of December 31, 2017, distributable earnings (accumulated loss) on a tax basis were as follows:

| Undistributed Ordinary Income | $ | 37,682 | ||||

| Undistributed Long-Term Gain | 91,917 | |||||

| Unrealized Appreciation | 3,388,215 | |||||

| Total | $ | 3,517,814 |

The difference between components of distributable earnings on a tax basis and the amounts reflected in the Statement of Assets and Liabilities are primarily due to wash sales and differences between book and tax treatment on distributions from REITs.

On the Statement of Assets and Liabilities, as a result of permanent book to tax differences, certain amounts have been reclassified for the year ended December 31, 2017. The following reclassification was the result of REIT distribution reallocation adjustments and has no impact on the net assets of the Fund.

| Undistributed Net Investment Income (Loss) | $ | (117,986 | ) | |||

| Accumulated Net Realized Gain (Loss) | 117,986 |

Note 8. Subsequent Events

Subsequent events occurring after the date of this report through the date these financial statements were issued have been evaluated for potential impact, and the Fund has had no such events.

13 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

To the Board of Trustees of Forum Funds II

and the Shareholders of Phocas Real Estate Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Phocas Real Estate Fund, a series of shares of beneficial interest in Forum Funds II (the "Fund"), including the schedule of investments, as of December 31, 2017, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, the financial highlights for each of the years in the five-year period then ended, and the related notes and schedules (collectively referred to as the "financial statements"). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of December 31, 2017, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and its financial highlights for each of the years in the five-year period then ended, in conformity with accounting principles generally accepted in the United States of America ("GAAP").

Basis for Opinion

These financial statements are the responsibility of the Fund's management. Our responsibility is to express an opinion on the Fund's financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) ("PCAOB") and are required to be independent with respect to the Fund in accordance with the U.S. federal securities law and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund's internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risk of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2017 by correspondence with the custodian. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

BBD, LLP

We have served as the auditor of one or more of the Funds in Forum Funds II since 2013.

Philadelphia, Pennsylvania

February 23, 2018

PHOCAS REAL ESTATE FUND

FOR MORE INFORMATION:

P.O. Box 588

Portland, ME 04112

(866) 746-2271 (toll free)

INVESTMENT ADVISOR

Phocas Financial Corporation

980 Atlantic Avenue, Suite 106

Alameda, CA 94501

TRANSFER AGENT

Atlantic Fund Services

P.O. Box 588

Portland, ME 04112

www.atlanticfundservices.com

DISTRIBUTOR

Foreside Fund Services, LLC

Three Canal Plaza, Suite 100

Portland, Maine 04101

www.foreside.com

This report is submitted for the general information of the shareholders of the Fund. It is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus, which includes information regarding the Fund's risks, objectives, fees and expenses, experience of its management, and other information.

215-ANR-1217

ITEM 2. CODE OF ETHICS.

| (a) | As of the end of the period covered by this report, Forum Funds II (the "Registrant") has adopted a code of ethics, which applies to its Principal Executive Officer and Principal Financial Officer (the "Code of Ethics"). |

| (c) | There have been no amendments to the Registrant's Code of Ethics during the period covered by this report. |

(d) There have been no waivers to the Registrant's Code of Ethics during the period covered by this report.

(e) Not applicable.

(f) (1) A copy of the Code of Ethics is being filed under Item 12(a) hereto.

ITEM 3. AUDIT COMMITTEE FINANCIAL EXPERT.

The Board of Trustees has determined that Mr. Mark Moyer is an "audit committee financial expert" as that term is defined under applicable regulatory guidelines. Mr. Moyer is a non- "interested" Trustee (as defined in Section 2(a)(19) under the Investment Company Act of 1940, as amended (the "Act")), and serves as Chairman of the Audit Committee.

ITEM 4. PRINCIPAL ACCOUNTANT FEES AND SERVICES.

(a) Audit Fees - The aggregate fees billed for each of the last two fiscal years (the "Reporting Periods") for professional services rendered by the Registrant's principal accountant for the audit of the Registrant's annual financial statements, or services that are normally provided by the principal accountant in connection with the statutory and regulatory filings or engagements for the Reporting Periods, were $13,400 in 2016 and $13,400 in 2017.

(b) Audit-Related Fees – The aggregate fees billed in the Reporting Periods for assurance and related services rendered by the principal accountant that were reasonably related to the performance of the audit of the Registrant's financial statements and are not reported under paragraph (a) of this Item 4 were $0 in 2016 and $0 in 2017.

(c) Tax Fees - The aggregate fees billed in the Reporting Periods for professional services rendered by the principal accountant to the Registrant for tax compliance, tax advice and tax planning were $3,000 in 2016 and $3,000 in 2017. These services consisted of review or preparation of U.S. federal, state, local and excise tax returns.

(d) All Other Fees - The aggregate fees billed in the Reporting Periods for products and services provided by the principal accountant to the Registrant, other than the services reported in paragraphs (a) through (c) of this Item, were $0 in 2016 and $0 in 2017.

(e) (1) The Audit Committee reviews and approves in advance all audit and "permissible non-audit services" (as that term is defined by the rules and regulations of the Securities and Exchange Commission) to be rendered to a series of the Registrant (each, a "Series"). In addition, the Audit Committee reviews and approves in advance all "permissible non-audit services" to be provided to an investment adviser (not including any sub-adviser) of a Series, or an affiliate of such investment adviser, that is controlling, controlled by or under common control with the investment adviser and provides on-going services to the Registrant ("Affiliate"), by the Series' principal accountant if the engagement relates directly to the operations and financial reporting of the Series. The Audit Committee considers whether fees paid by a Series' investment adviser or an Affiliate to the Series' principal accountant for audit and permissible non-audit services are consistent with the principal accountant's independence.

(e) (2) No services included in (b) - (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Not applicable

(g) The aggregate non-audit fees billed by the principal accountant for services rendered to the Registrant for the Reporting Periods were $0 in 2016 and $0 in 2017. There were no fees billed in either of the Reporting Periods for non-audit services rendered by the principal accountant to the Registrant's investment adviser or any Affiliate.

(h) During the Reporting Period, the Registrant's principal accountant provided no non-audit services to the investment advisers or any entity controlling, controlled by or under common control with the investment advisers to the series of the Registrant to which this report relates.

ITEM 5. AUDIT COMMITTEE OF LISTED REGISTRANTS.

Not applicable

ITEM 6. INVESTMENTS.

| (a) | Included as part of report to shareholders under Item 1. |

| (b) | Not applicable. |

ITEM 7. DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED-END

MANAGEMENT INVESTMENT COMPANIES.

Not applicable.

ITEM 8. PORTFOLIO MANAGERS OF CLOSED-END MANAGEMENT INVESTMENT COMPANIES.

Not applicable.

ITEM 9. PURCHASES OF EQUITY SECURITIES BY CLOSED-END MANAGEMENT INVESTMENT COMPANY AND AFFILIATED PURCHASERS.

Not applicable.

ITEM 10. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

The Registrant does not accept nominees to the board of trustees from shareholders.

ITEM 11. CONTROLS AND PROCEDURES

(a) The Registrant's Principal Executive Officer and Principal Financial Officer have concluded that the Registrant's disclosure controls and procedures (as defined in Rule 30a-3(c) under the Act are effective, based on their evaluation of the controls and procedures required by Rule 30a-3(b) under the Act and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934, as of a date within 90 days of the filing date of this report.

(b) There were no changes in the Registrant's internal control over financial reporting (as defined in

Rule 30a-3(d) under the Act) that occurred during the second fiscal quarter of the period covered by this report that have materially affected, or are reasonably likely to materially affect, the Registrant's internal control over financial reporting.

ITEM 12. EXHIBITS.

(a)(1) Code of Ethics (Exhibit filed herewith).

(a)(2) Certifications pursuant to Rule 30a-2(a) of the Act, and Section 302 of the Sarbanes-Oxley Act of 2002. (Exhibits filed herewith)

(a)(3) Not applicable.

(b) Certifications pursuant to Rule 30a-2(b) of the Act, and Section 906 of the Sarbanes-Oxley Act of 2002. (Exhibit filed herewith)

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Registrant Forum Funds II

| By | /s/ Jessica Chase | ||

| Jessica Chase, Principal Executive Officer | |||

| Date | February 26, 2018 |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the Registrant and in the capacities and on the dates indicated.

| By | /s/ Jessica Chase | ||

| Jessica Chase, Principal Executive Officer | |||

| Date | February 26, 2018 |

| By | /s/ Karen Shaw | ||

| Karen Shaw, Principal Financial Officer | |||

| Date | February 26, 2018 |