Wells Fargo Commercial Mortgage Trust 2013-LC12

Filed: 9 Jul 13, 12:00am

| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-172366-08 | ||

|  |

| WELLS FARGO SECURITIES | RBS | |

Co-Lead Manager and Co-Bookrunner | Co-Lead Manager and Co-Bookrunner | |

Citigroup Co-Manager | ||

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Certificate Structure |

Expected Ratings (Fitch/KBRA/Moody’s)(1) | Approximate Initial Certificate Principal Balance or Notional Amount(2) | Approx. Initial Credit Support(3) | Pass- Through Rate Description | Weighted Average Life (Years)(4) | Expected Principal Window(4) | Certificate Principal to Value Ratio(5) | Certificate Principal U/W NOI Debt Yield(6) | |||||

| Offered Certificates | ||||||||||||

| A-1 | AAA(sf)/AAA(sf)/Aaa(sf) | $130,432,000 | 30.000% | (7) | 3.58 | 1 - 60 | 46.4% | 15.3% | ||||

| A-2 | AAA(sf)/AAA(sf)/Aaa(sf) | $80,000,000 | 30.000% | (7) | 7.79 | 94 - 94 | 46.4% | 15.3% | ||||

| A-3 | AAA(sf)/AAA(sf)/Aaa(sf) | $100,000,000 | 30.000% | (7) | 9.76 | 117 - 118 | 46.4% | 15.3% | ||||

| A-4 | AAA(sf)/AAA(sf)/Aaa(sf) | $326,055,000 | 30.000% | (7) | 9.81 | 118 - 119 | 46.4% | 15.3% | ||||

| A-5 | AAA(sf)/AAA(sf)/Aaa(sf) | $100,000,000 | 30.000% | (7) | 9.88 | 119 - 119 | 46.4% | 15.3% | ||||

| A-SB | AAA(sf)/AAA(sf)/Aaa(sf) | $149,929,000 | 30.000% | (7) | 7.80 | 60 - 117 | 46.4% | 15.3% | ||||

A-S(8) | AAA(sf)/AAA(sf)/Aaa(sf) | $116,257,000 | 21.750% | (7) | 9.89 | 119 - 120 | 51.9% | 13.7% | ||||

B(8) | AA-(sf)/AA-(sf)/Aa3(sf) | $88,072,000 | 15.500% | (7) | 9.96 | 120 - 120 | 56.0% | 12.7% | ||||

C(8) | A-(sf)/A-(sf)/A3(sf) | $56,367,000 | 11.500% | (7) | 9.96 | 120 - 120 | 58.7% | 12.1% | ||||

PEX(8) | A-(sf)/A-(sf)/A1(sf) | $260,696,000 | 11.500% | (7) | 9.93 | 119 - 120 | 58.7% | 12.1% | ||||

| X-A | AAA(sf)/AAA(sf)/Aaa(sf) | $1,102,673,000 | (9) | N/A | Variable(10) | N/A | N/A | N/A | N/A | |||

Non-Offered Certificates | ||||||||||||

| X-B | NR/NR/NR | $95,118,821 | (11) | N/A | Variable(12) | N/A | N/A | N/A | N/A | |||

A-3FL(13) | AAA(sf)/AAA(sf)/Aaa(sf) | $100,000,000 | (13) | 30.000% | LIBOR Plus(15) | 9.76 | 117 - 118 | 46.4% | 15.3% | |||

A-3FX(13) | AAA(sf)/AAA(sf)/Aaa(sf) | $0 | (13) | 30.000% | (7) | 9.76 | 117 - 118 | 46.4% | 15.3% | |||

| D | BBB-(sf)/BBB-(sf)/NR(sf) | $66,936,000 | 6.750% | (7) | 9.96 | 120 - 120 | 61.8% | 11.5% | ||||

| E | BB(sf)/BB(sf)/NR(sf) | $28,183,000 | 4.750% | (7) | 9.96 | 120 - 120 | 63.2% | 11.3% | ||||

| F | B(sf)/B(sf)/NR(sf) | $14,092,000 | 3.750% | (7) | 9.96 | 120 - 120 | 63.8% | 11.1% | ||||

| G | NR/NR/NR | $52,843,821 | 0.000% | (7) | 9.96 | 120 - 120 | 66.3% | 10.7% | ||||

Notes: | ||||||||||||||

| (1) | The expected ratings presented are those of Fitch Ratings, Inc. (“Fitch”), Kroll Bond Rating Agency, Inc. (“KBRA”) and Moody’s Investors Service, Inc. (“Moody’s”) which the depositor hired to rate the rated offered certificates. One or more other nationally recognized statistical rating organizations that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or otherwise, to rate or provide market reports and/or published commentary related to the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign or that its reports will not express differing, possibly negative, views of the mortgage loans and/or the offered certificates. See “Risk Factors—Risks Related to the Offered Certificates—Risks Related to the Offered Certificates—Ratings on the Certificates Have Substantial Limitations and Ratings” in the free writing prospectus, dated July 8, 2013 (the “Free Writing Prospectus”). | |||||||||||||

| (2) | The principal balances and notional amounts set forth in the table are approximate. The actual initial principal balances and notional amounts may be larger or smaller depending on the aggregate cut-off date principal balance of the mortgage loans definitively included in the pool of mortgage loans, which aggregate cut-off date principal balance may be as much as 5% larger or smaller than the amount presented in the Free Writing Prospectus. | |||||||||||||

| (3) | The approximate initial credit support with respect to the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4, A-5 and A-SB Certificates represents the approximate credit enhancement for the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4, A-5 and A-SB Certificates in the aggregate. No class of Certificates will provide any credit support to the Class A-3FL Certificates for any failure by the swap counterparty to make the payment under the related swap contract. The percentage indicated under the column “Approximate Initial Credit Support” with respect to the Class C Certificates and the Class PEX Certificates represents the approximate credit support for the Class C regular interest which will have an initial outstanding principal balance on the closing date of $56,367,000. | |||||||||||||

| (4) | Weighted Average Lives and Expected Principal Windows are calculated based on an assumed prepayment rate of 0% CPR and the “Structuring Assumptions” described on Annex B to the Free Writing Prospectus. | |||||||||||||

| (5) | The Certificate Principal to Value Ratio for each Class of Certificates (other than the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4, A-5 and A-SB Certificates and other than the Exchangeable Certificates) is calculated by dividing the aggregate principal balance of such class of certificates and all classes of certificates (other than the Exchangeable Certificates), if any, that are senior to such class, by the aggregate appraised value of approximately $2,124,575,075 (calculated as described in the Free Writing Prospectus) of the mortgaged properties securing the mortgage loans (excluding, with respect to each pari passu loan combination, a pro rata portion of the related appraised value allocated to the related companion loan based on its cut-off date principal balance). The Certificate Principal to Value Ratios for each of the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4, A-5 and A-SB Certificates are calculated by dividing the aggregate principal balance of the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4, A-5 and A-SB Certificates by such aggregate appraised value (excluding, with respect to each pari passu loan combination, a pro rata portion of the related appraised value allocated to the related companion loan based on its cut-off date principal balance). The Certificate Principal to Value Ratio for each of the Class A-S, Class B and Class C Certificates is calculated by dividing the aggregate principal balance of the Class A-S regular interest, the Class B regular interest or the Class C regular interest, as applicable, and all other classes of certificates (other than the Exchangeable Certificates) and the regular interests that are senior to such class, by such aggregate appraised value (excluding, with respect to each pari passu loan combination, a pro rata portion of the related appraised value allocated to the related companion loan based on its cut-off date principal balance). The Certificate Principal to Value Ratio of the Class PEX Certificates is equal to the Certificate Principal to Value Ratio of the Class C Certificates. In any event, however, excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan (unless such mortgage loans are cross-collateralized and the cross-collateralization remains in effect). | |||||||||||||

| (6) | The Certificate Principal U/W NOI Debt Yield for each Class of Certificates (other than the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4, A-5 and A-SB Certificates and other than the Exchangeable Certificates) is calculated by dividing the underwritten net operating income (which excludes, with respect to each pari passu loan combination, a pro rata portion of the related underwritten net operating income allocated to the related companion loan based on its cut-off date principal balance) for the mortgage pool of approximately $151,044,448 (calculated as described in the Free Writing Prospectus) by the aggregate certificate principal balance of such class of certificates and all classes of certificates (other than the Exchangeable Certificates), if any, that are senior to such class of certificates. The Underwritten NOI Debt Yield for each of the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4, A-5 and A-SB Certificates is calculated by dividing such mortgage pool underwritten net operating income (which excludes, with respect to each pari passu loan combination, a pro rata portion of the related underwritten net operating income allocated to the related companion loan based on its cut-off date principal balance) by the aggregate principal balance of the Class A-1, A-2, A-3, A-3FL, A-3FX, A-4, A-5 and A-SB Certificates. The Certificate Principal U/W NOI Debt Yield for each of the Class A-S, Class B and Class C Certificates is calculated by dividing the underwritten net operating income (which excludes, with respect to each pari passu loan combination, a pro rata portion of the related underwritten net operating income allocated to the related companion loan based on its cut-off date principal balance) for the mortgage pool of approximately $151,044,448 (calculated as described in the Free Writing Prospectus) by the aggregate principal balance of the Class A-S regular interest, the Class B regular interest or the Class C regular interest, as applicable, and all other classes of certificates (other than the | |||||||||||||

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Certificate Structure |

| Exchangeable Certificates) and the regular interests that are senior to such class. The Certificate Principal U/W NOI Debt Yield of the Class PEX Certificates is equal to the Certificate Principal U/W NOI Debt Yield for the Class C Certificates. In any event, however, cash flow from each mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan (unless such mortgage loans are cross-collateralized and the cross-collateralization remains in effect). | |||||||||||||||||||

| (7) | The pass-through rates for the Class A-1, A-2, A-3, A-3FX, A-4, A-5, A-SB, A-S, B, C, D, E, F and G Certificates and the Class A-3FX Regular Interest in each case will be one of the following: (i) a fixed rate per annum, (ii) the WAC Rate (as defined in the Free Writing Prospectus) for the related distribution date, (iii) a variable rate per annum equal to the lesser of (a) a fixed rate and (b) the WAC Rate for the related distribution date or (iv) a variable rate per annum equal to the WAC Rate for the related distribution date minus a specified percentage. The Class PEX Certificates will not have a pass-through rate, but will be entitled to receive the sum of the interest distributable on the Class PEX Components. The pass-through rate for the Class A-S Certificates, the Class A-S regular interest and the Class PEX Component A-S will, at all times, be the same. The pass-through rate for the Class B Certificates, the Class B regular interest and the Class PEX Component B will, at all times, be the same. The pass-through rate for the Class C Certificates, the Class C regular interest and the Class PEX Component C will, at all times, be the same. | ||||||||||||||||||

| (8) | The Class A-S, Class B, Class PEX and Class C Certificates are “Exchangeable Certificates”. On the closing date, the upper-tier REMIC of the issuing entity will issue the Class A-S, Class B and Class C regular interests (each a “regular interest”) which will have outstanding principal balances on the closing date of $116,257,000, $88,072,000 and $56,367,000, respectively. The regular interests will be held in a grantor trust for the benefit of the holders of the Class A-S, Class B, Class PEX and Class C Certificates. The Class A-S, Class B, Class PEX and Class C Certificates will, at all times, represent undivided beneficial ownership interests in a grantor trust that will hold those regular interests. Each class of the Class A-S, Class B and Class C Certificates will, at all times, represent an undivided beneficial ownership interest in a percentage of the outstanding certificate principal balance of the regular interest with the same alphabetical class designation. The Class PEX Certificates will, at all times, represent an undivided beneficial ownership interest in the remaining percentages of the outstanding certificate principal balances of the Class A-S, Class B and Class C regular interests and which portions of those regular interests are referred to in this Term Sheet as the Class PEX Component A-S, Class PEX Component B and Class PEX Component C (collectively, the “Class PEX Components”). Following any exchange of Class A-S, Class B and Class C Certificates for Class PEX Certificates or any exchange of Class PEX Certificates for Class A-S, Class B and Class C Certificates as described in the Free Writing Prospectus, the percentage interest of the outstanding certificate principal balances of the Class A-S, Class B and Class C regular interest that is represented by the Class A-S, Class B, Class PEX and Class C Certificates will be increased or decreased accordingly. The initial certificate principal balance of each of the Class A-S, Class B and Class C Certificates shown in the table represents the maximum certificate principal balance of such class without giving effect to any exchange. The initial certificate principal balance of the Class PEX Certificates is equal to the aggregate of the initial certificate principal balance of the Class A-S, Class B and Class C Certificates and represents the maximum certificate principal balance of the Class PEX Certificates that could be issued in an exchange. The certificate principal balances of the Class A-S, Class B and Class C Certificates to be issued on the closing date will be reduced, in required proportions, by an amount equal to the certificate principal balance of the Class PEX Certificates issued on the closing date. Distributions and allocations of payments and losses with respect to the Exchangeable Certificates are described in this Term Sheet under “Allocations and Distributions on the Class A-S, Class B, Class PEX and Class C Certificates” and under “Description of the Offered Certificates—Distributions” in the Free Writing Prospectus. The maximum certificate principal balance of the Class PEX Certificates is set forth in the table but is not included in the certificate principal balance of the certificates set forth on the cover page of this Term Sheet or on the top of the cover page of the Free Writing Prospectus. | ||||||||||||||||||

| (9) | The Class X-A Certificates are notional amount certificates. The Notional Amount of the Class X-A Certificates will be equal to the aggregate principal balance of the Class A-1, A-2, A-3, A-4, A-5, A-SB and A-S Certificates and the Class A-3FX Regular Interest outstanding from time to time (without regard to any exchange of Class A-S, Class B and Class C Certificates for Class PEX Certificates). The Class X-A Certificates will not be entitled to distributions of principal. | ||||||||||||||||||

| (10) | The pass-through rate for the Class X-A Certificates for any distribution date will be a per annum rate equal to the excess, if any, of (a) the WAC Rate for the related distribution date, over (b) the weighted average of the pass-through rates on the Class A-1, A-2, A-3, A-4, A-5, A-SB and A-S Certificates and the Class A-3FX Regular Interest for the related distribution date (without regard to any exchange of Class A-S, Class B and Class C Certificates for Class PEX Certificates), weighted on the basis of their respective aggregate principal balances outstanding immediately prior to that distribution date. | ||||||||||||||||||

| (11) | The Class X-B Certificates are notional amount certificates. The Notional Amount of the Class X-B Certificates will be equal to the aggregate principal balance of the Class E, F and G Certificates outstanding from time to time. The Class X-B Certificates will not be entitled to distributions of principal. | ||||||||||||||||||

| (12) | The pass-through rate for the Class X-B Certificates for any distribution date will be a per annum rate equal to the excess, if any, of (a) the WAC Rate for the related distribution date, over (b) the weighted average of the pass-through rates on the Class E, F and G Certificates for the related distribution date, weighted on the basis of their respective aggregate principal balances outstanding immediately prior to that distribution date. | ||||||||||||||||||

| (13) | The Class A-3FL Certificates will evidence a beneficial interest in a grantor trust that includes the Class A-3FX Regular Interest and an interest rate swap contract. Under certain circumstances, holders of the Class A-3FL Certificates may exchange all or a portion of their certificates for a like principal amount of Class A-3FX Certificates having the same pass-through rate as the Class A-3FX Regular Interest. The aggregate principal balance of the Class A-3FL Certificates may be adjusted from time to time as a result of such an exchange. The aggregate principal balance of the Class A-3FX Certificates and Class A-3FL Certificates will at all times equal the principal balance of the Class A-3FX Regular Interest. The principal balance of the Class A-3FX Certificates will initially be $0. | ||||||||||||||||||

| (14) | The ratings assigned to the Class A-3FL Certificates reflect only the receipt of up to the fixed rate of interest at a rate equal to the applicable pass-through rate for the Class A-3FX Regular Interest. The ratings of Fitch, KBRA and Moody’s do not address any shortfalls or delays in payments that investors in the Class A-3FL Certificates may experience as a result of the conversion of the pass-through Certificates from a floating interest rate to a fixed rate. | ||||||||||||||||||

| (15) | The pass-through rate on the Class A-3FL Certificates will be a per annum rate equal to LIBOR plus a specified percentage; provided, however, that under certain circumstances, the pass-through rate on the Class A-3FL Certificates may convert to the pass-through rate applicable to the Class A-3FX Regular Interest. The initial LIBOR rate will be determined two LIBOR Business Days prior to the Closing Date, and subsequent LIBOR rates for the Class A-3FL Certificates will be determined two LIBOR Business Days before the start of the related interest accrual period. | ||||||||||||||||||

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Issue Characteristics |

Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Cut-off Date Pool Balance | |||||

| Ladder Capital Finance LLC | 40 | 69 | $553,375,420 | 39.3% | |||||

| The Royal Bank of Scotland plc | 10 | 45 | 478,188,094 | 33.9 | |||||

Wells Fargo Bank, National Association | 33 | 36 | 377,603,308 | 26.8 | |||||

| Total | 83 | 150 | $1,409,166,822 | 100.0% | |||||

| Cut-off Date Balance: | $1,409,166,822 |

| Number of Mortgage Loans: | 83 |

| Average Cut-off Date Balance per Mortgage Loan: | $16,977,914 |

| Number of Mortgaged Properties: | 150 |

Average Cut-off Date Balance per Mortgaged Property(1): | $9,394,445 |

| Weighted Average Mortgage Interest Rate: | 4.334% |

| Ten Largest Mortgage Loans as % of Cut-off Date Pool Balance: | 56.2% |

| Weighted Average Original Term to Maturity or ARD (months): | 116 |

| Weighted Average Remaining Term to Maturity or ARD (months): | 115 |

Weighted Average Original Amortization Term (months)(2): | 343 |

Weighted Average Remaining Amortization Term (months)(2): | 342 |

| Weighted Average Seasoning (months): | 1 |

(1) Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. (2) Excludes any mortgage loan that does not amortize. | |

Weighted Average U/W Net Cash Flow DSCR(1): | 1.75x |

Weighted Average U/W Net Operating Income Debt Yield Ratio(1): | 10.7% |

Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 67.1% |

Weighted Average Balloon or ARD Loan-to-Value Ratio(1): | 57.2% |

| % of Mortgage Loans with Additional Subordinate Debt: | 10.0% |

% of Mortgage Loans with Single Tenants(2): | 3.2% |

(1) With respect to each pari passu loan combination, loan-to-value ratio, debt service coverage ratio, debt yield and cut-off date balance per square foot calculations include the related pari passu companion loan unless otherwise stated. (2) Excludes mortgage loans that are secured by multiple single tenant properties. | |

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Issue Characteristics |

| Real Estate Taxes: | 70.7% of the pool | |

| Insurance Premiums: | 61.6% of the pool | |

| Capital Replacements: | 61.3% of the pool | |

| TI/LC: | 47.1% of the pool(1) | |

(1) The percentage of Cut-off Date Balance for loans with TI/LC reserves is based on the aggregate principal balance allocable to office, retail, industrial, and mixed use properties. | ||

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Issue Characteristics |

| Securities Offered: | $1,147,112,000 approximate monthly pay, multi-class, commercial mortgage REMIC pass-through certificates consisting of eleven classes (Classes A-1, A-2, A-3, A-4, A-5, A-SB, A-S, B, C, PEX and X-A), which are offered pursuant to a registration statement filed with the SEC. | ||

| Mortgage Loan Sellers: | Ladder Capital Finance LLC (“LCF”); The Royal Bank of Scotland plc (“RBS”); Wells Fargo Bank, National Association (“WFB”). | ||

| Co-lead Bookrunning Managers: | Wells Fargo Securities, LLC and RBS Securities Inc. | ||

| Co-Manager: | Citigroup Global Markets Inc. | ||

| Rating Agencies: | Fitch Ratings, Inc., Kroll Bond Rating Agency, Inc. and Moody’s Investors Service, Inc. | ||

| Master Servicer: | Wells Fargo Bank, National Association | ||

| Special Servicer: | Rialto Capital Advisors, LLC | ||

| Certificate Administrator: | Wells Fargo Bank, National Association | ||

| Trustee: | U.S. Bank National Association | ||

| Trust Advisor: | Park Bridge Lender Services LLC | ||

| Cut-off Date: | The Cut-off Date with respect to each mortgage loan is the due date for the monthly debt service payment that is due in July 2013 (or, in the case of any mortgage loan that has its first due date in August 2013, the date that would have been its due date in July 2013 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month). | ||

| Expected Closing Date: | On or about July 30, 2013. | ||

| Determination Dates: | The 11th day of each month (or if that day is not a business day, the next succeeding business day), commencing in August 2013. | ||

| Distribution Dates: | The fourth business day following the Determination Date in each month, commencing in August 2013. | ||

| Rated Final Distribution Date: | The Distribution Date in July 2046. | ||

| Interest Accrual Period: | With respect to any Distribution Date, the calendar month preceding the month in which such Distribution Date occurs. | ||

| Day Count: | The Offered Certificates will accrue interest on a 30/360 basis. | ||

| Minimum Denominations: | $10,000 for each Class of Offered Certificates (other than the Class X-A Certificates) and $1,000,000 for the Class X-A Certificates. Investments may also be made in any whole dollar denomination in excess of the applicable minimum denomination. | ||

| Clean-up Call: | 1% | ||

| Delivery: | DTC, Euroclear and Clearstream Banking | ||

| ERISA/SMMEA Status: | Each Class of Offered Certificates is expected to be eligible for exemptive relief under ERISA. No Class of Offered Certificates will be SMMEA eligible. | ||

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. SEE THE “RISK FACTORS” SECTION OF THE FREE WRITING PROSPECTUS. | ||

| Bond Analytics Information: | The Certificate Administrator will be authorized to make distribution date settlements, CREFC® reports and certain supplemental reports (other than confidential information) available to certain financial modeling and data provision services, including Bloomberg Financial Markets L.P., Trepp LLC, Intex Solutions, Inc., Markit Group Limited, Interactive Data Corp. and BlackRock Financial Management, Inc. |

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Characteristics of the Mortgage Pool |

| A. Ten Largest Mortgage Loans |

| Mortgage Loan Seller | Mortgage Loan Name | City | State | Number of Mortgage Loans / Mortgaged Properties | Mortgage Loan Cut-off Date Balance ($) | % of Cut- off Date Pool Balance (%) | Property Type | Number of SF, Rooms, Pads or Beds | Cut-off Date Balance Per SF, Room, Pad or Bed ($) | Cut-off Date LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | ||||||||||||||

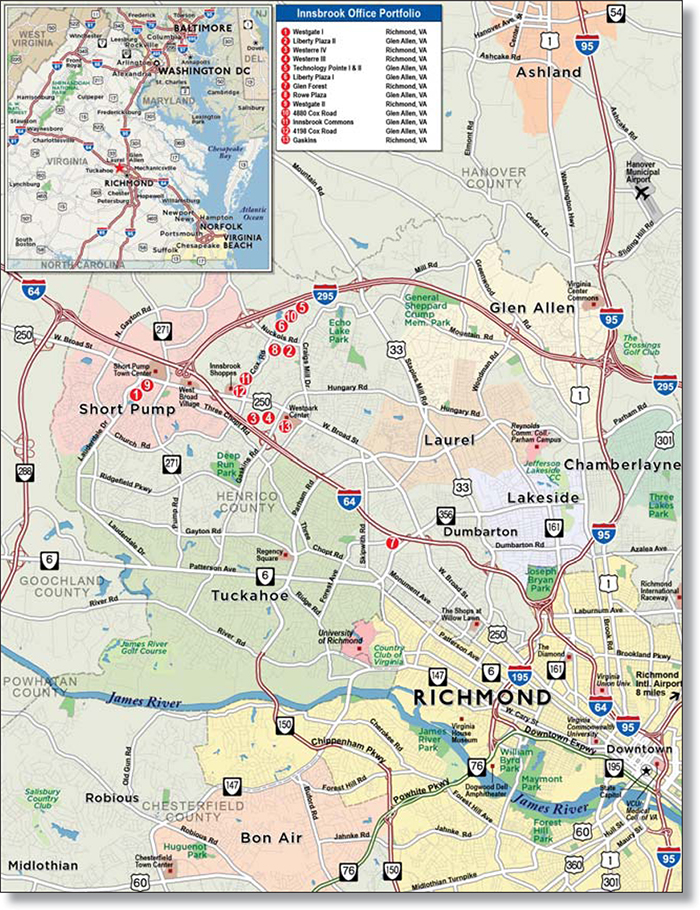

| LCF | Innsbrook Office Portfolio | Various | VA | 1 / 13 | $103,500,000 | 7.3% | Office | 994,040 | $104 | 74.8% | 63.8% | 1.59x | 10.8 | % | |||||||||||||

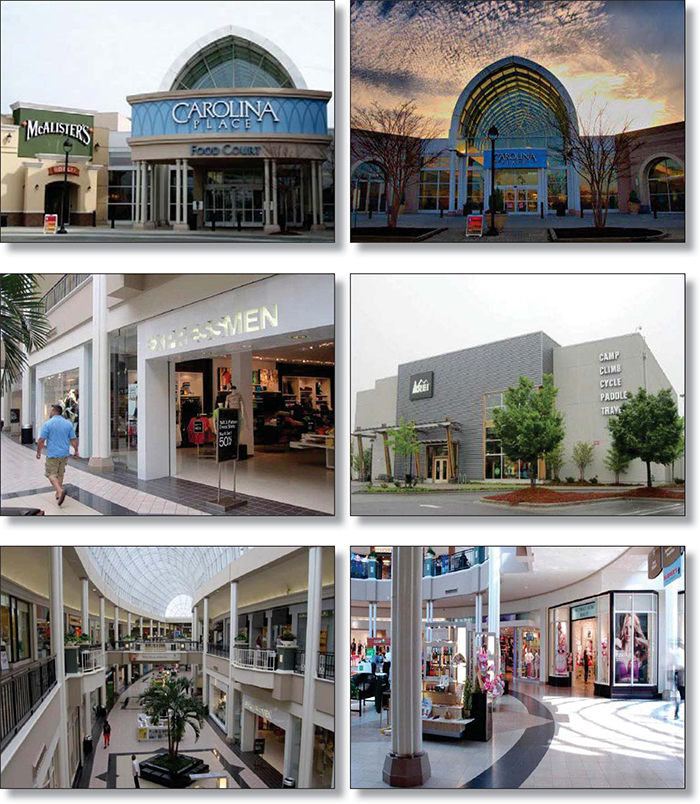

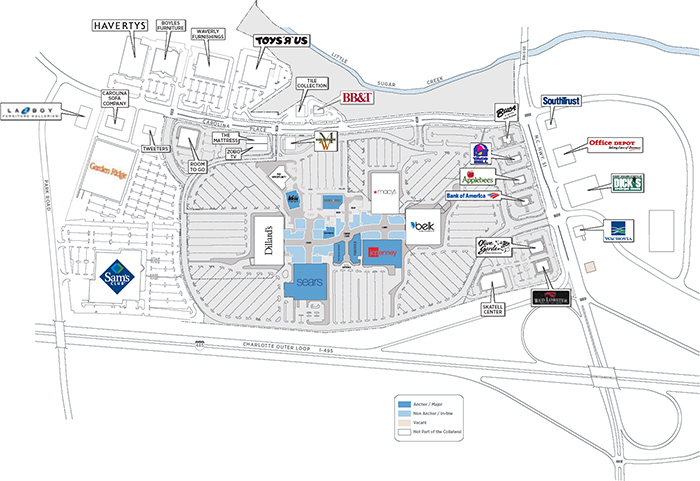

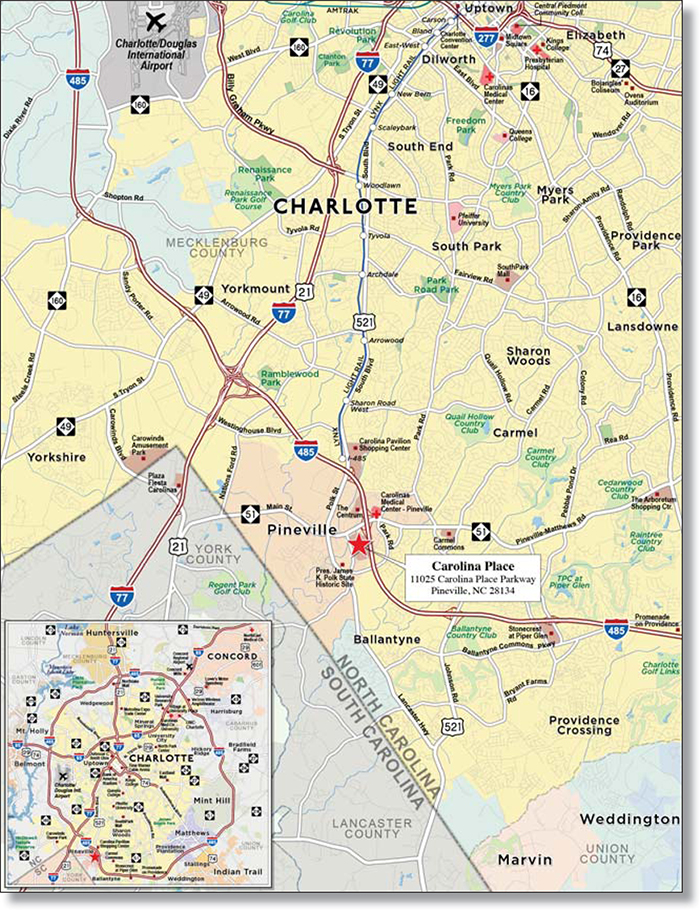

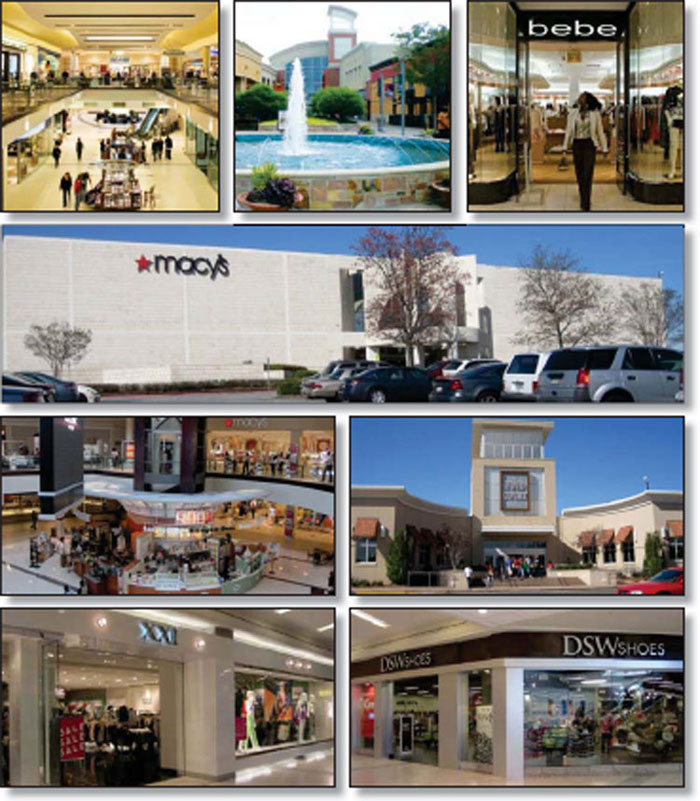

| RBS | Carolina Place | Pineville | NC | 1 / 1 | 90,000,000 | 6.4 | Retail | 647,511 | 270 | 66.5 | 57.3 | 1.71 | 10.1 | ||||||||||||||

| RBS | Cumberland Mall | Atlanta | GA | 1 / 1 | 90,000,000 | 6.4 | Retail | 541,527 | 295 | 63.0 | 63.0 | 2.49 | 9.7 | ||||||||||||||

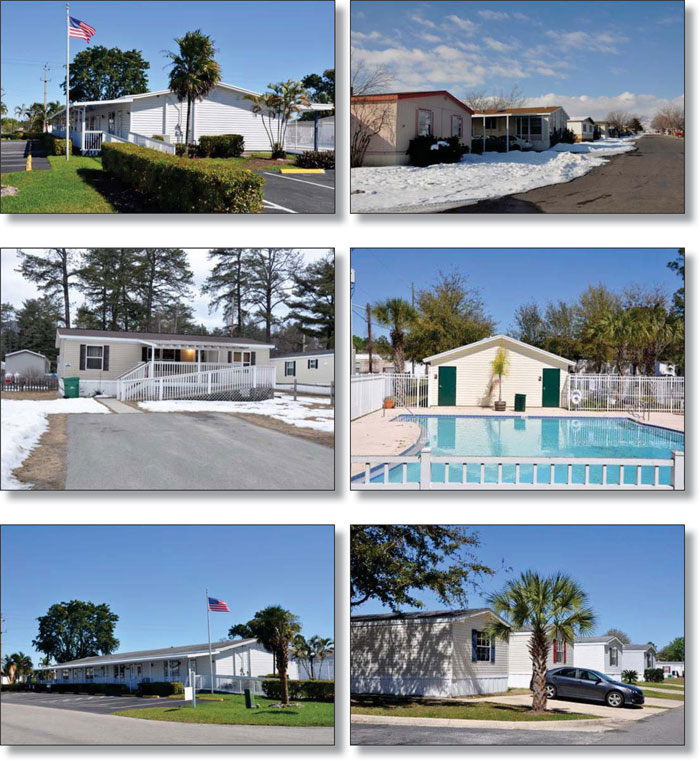

| RBS | RHP Portfolio V | Various | Various | 1 / 10 | 83,410,313 | 5.9 | Manufactured Housing Community | 2,416 | 34,524 | 73.7 | 63.5 | 1.43 | 8.4 | ||||||||||||||

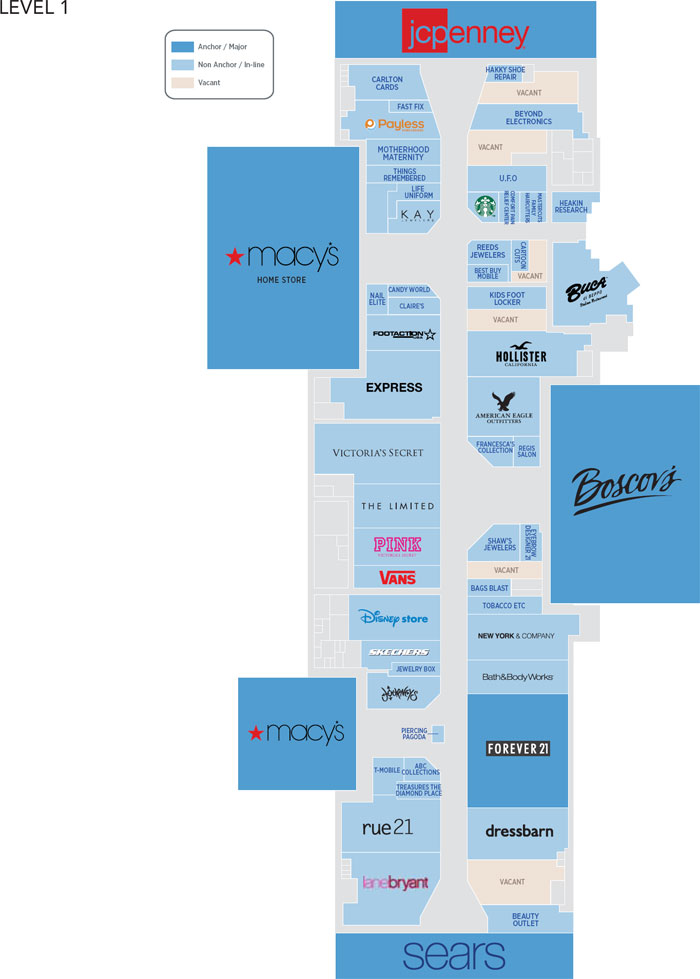

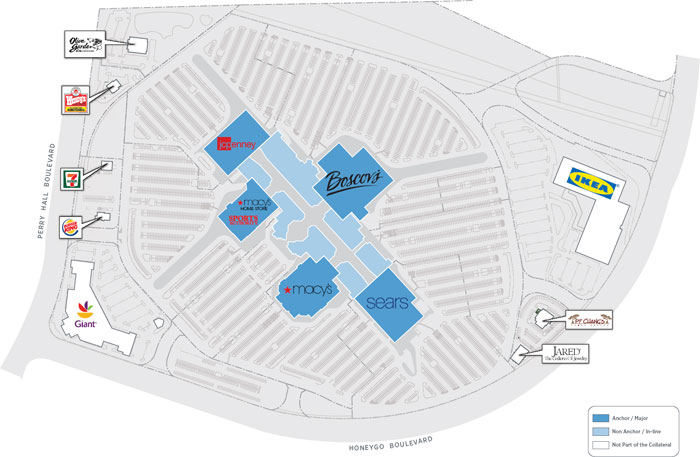

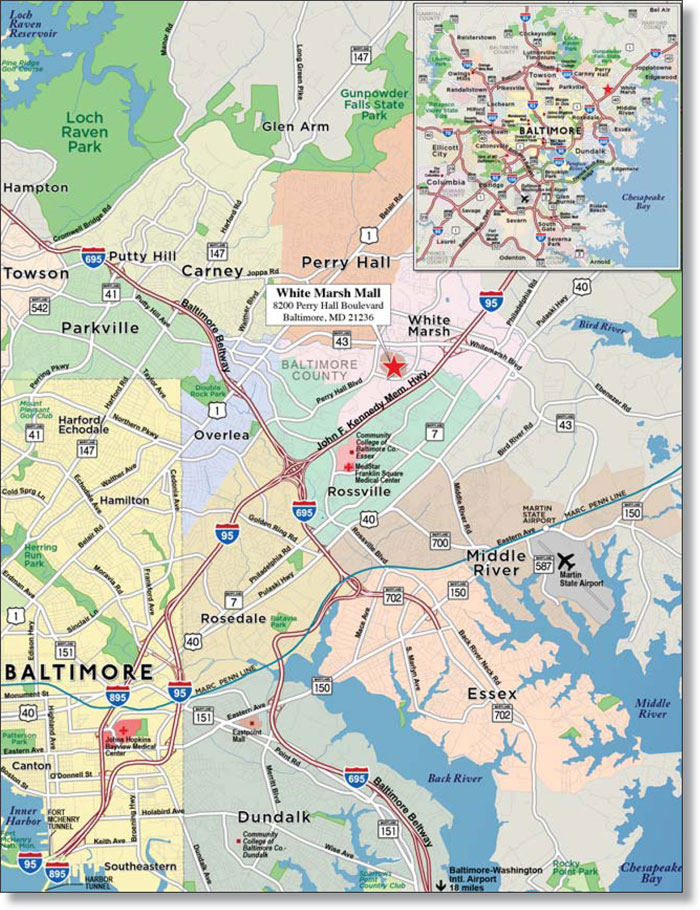

| WFB | White Marsh Mall | Baltimore | MD | 1 / 1 | 80,000,000 | 5.7 | Retail | 702,317 | 271 | 63.3 | 63.3 | 2.66 | 10.3 | ||||||||||||||

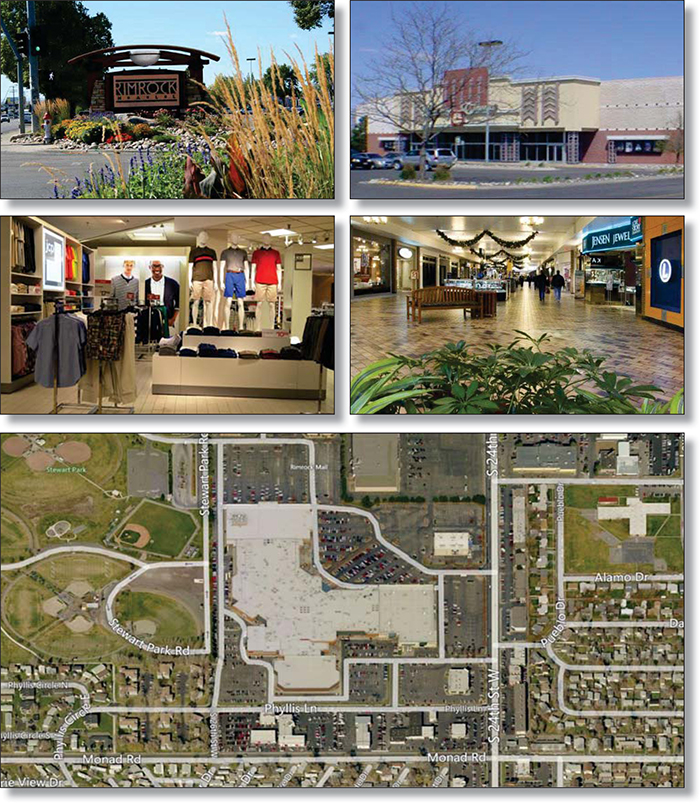

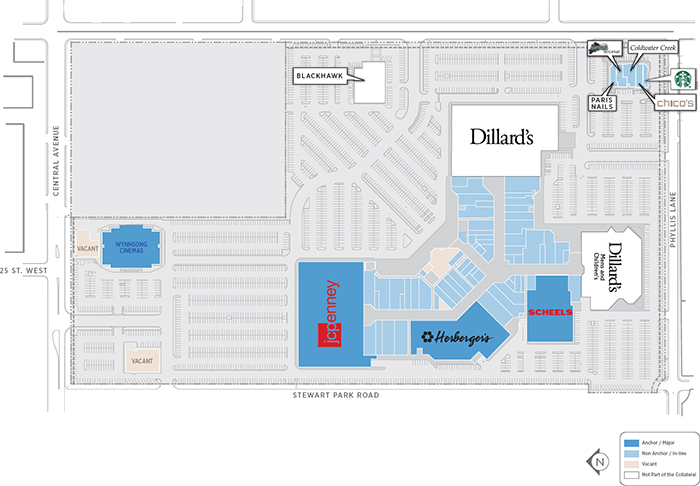

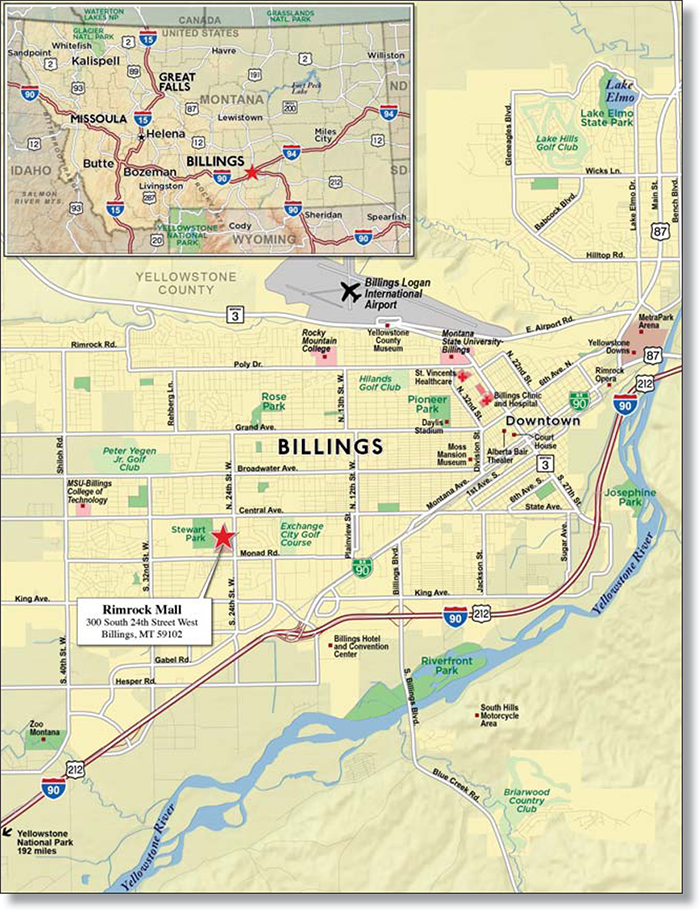

| RBS | Rimrock Mall | Billings | MT | 1 / 1 | 77,000,000 | 5.5 | Retail | 428,661 | 180 | 68.8 | 62.7 | 1.70 | 10.6 | ||||||||||||||

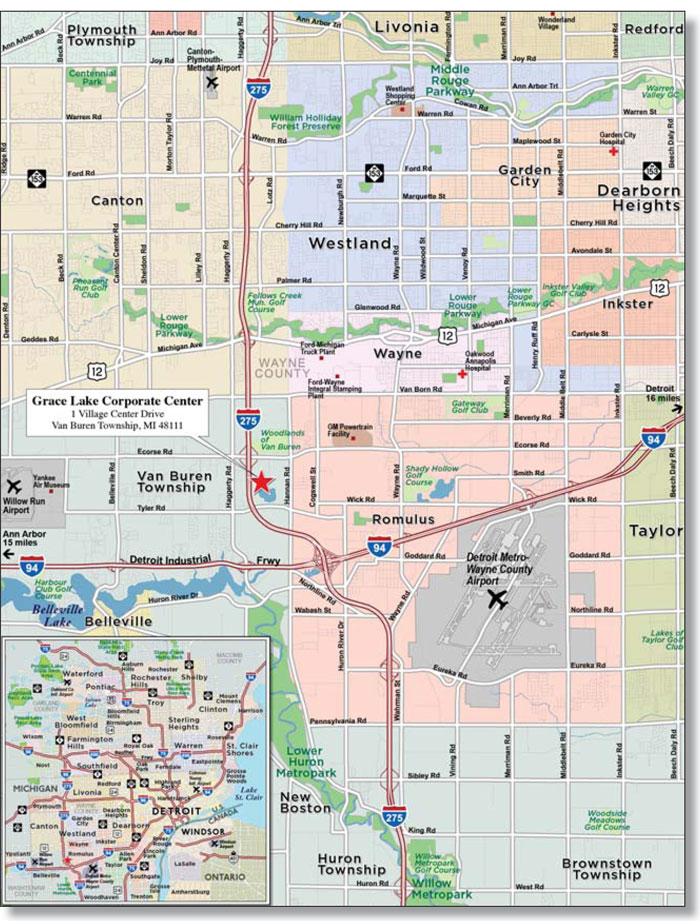

| LCF | Grace Lake Corporate Center | Van Buren | MI | 1 / 1 | 75,528,409 | 5.4 | Office | 882,949 | 86 | 61.5 | 42.6 | 1.60 | 12.1 | ||||||||||||||

| RBS | RHP Portfolio VI | Various | Various | 1 / 8 | 74,033,564 | 5.3 | Manufactured Housing Community | 1,769 | 41,851 | 73.7 | 63.5 | 1.45 | 8.4 | ||||||||||||||

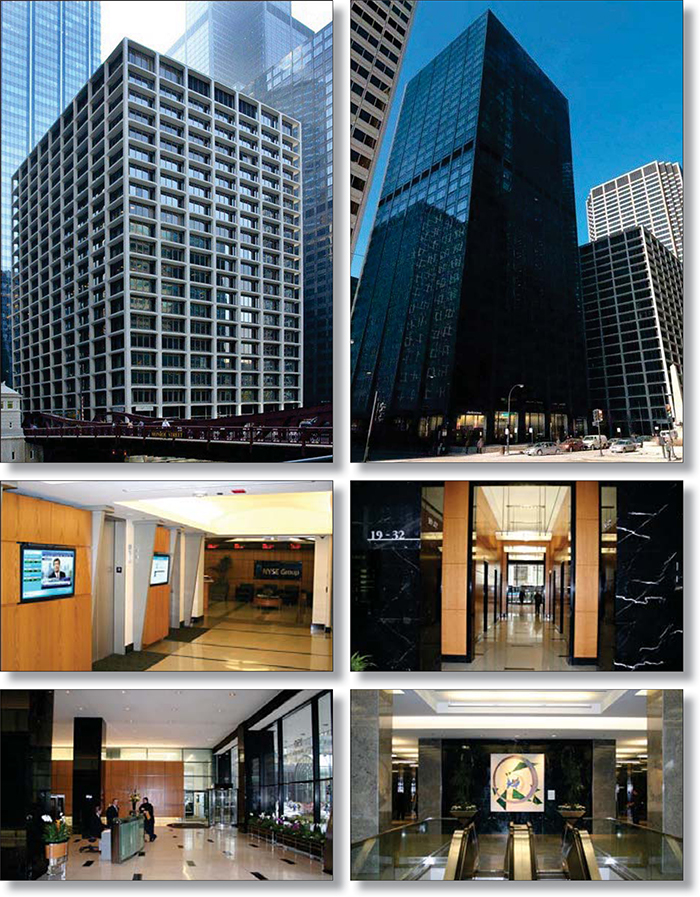

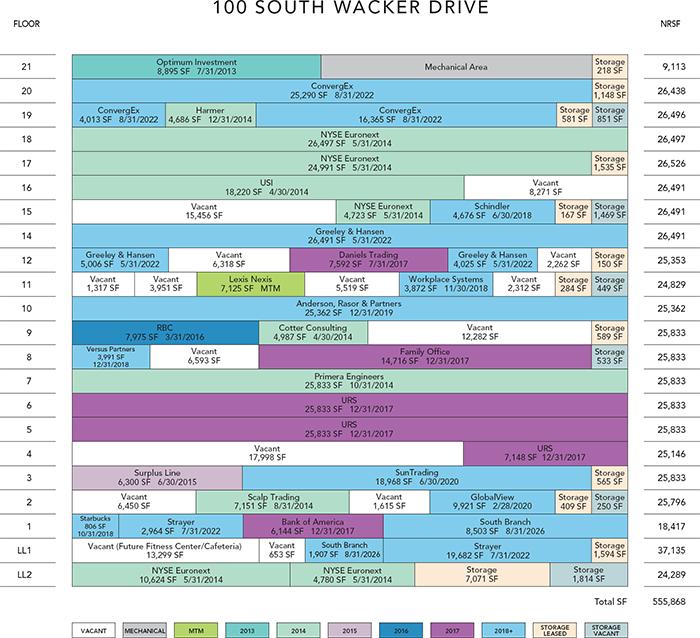

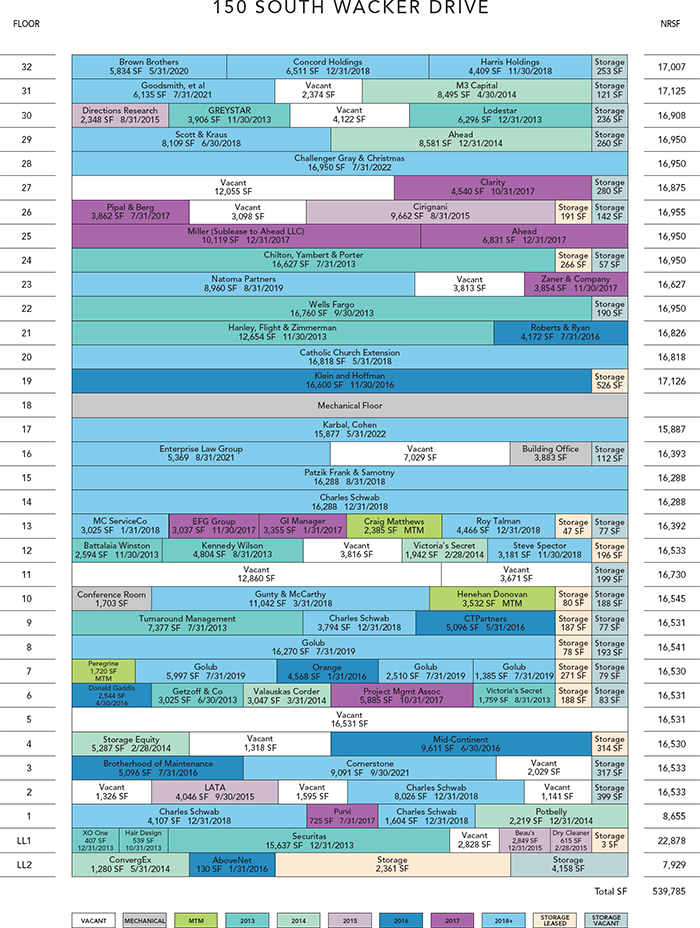

| WFB | 100 & 150 South Wacker Drive | Chicago | IL | 1 / 1 | 71,000,000 | 5.0 | Office | 1,095,653 | 128 | 66.4 | 60.2 | 1.56 | 10.7 | ||||||||||||||

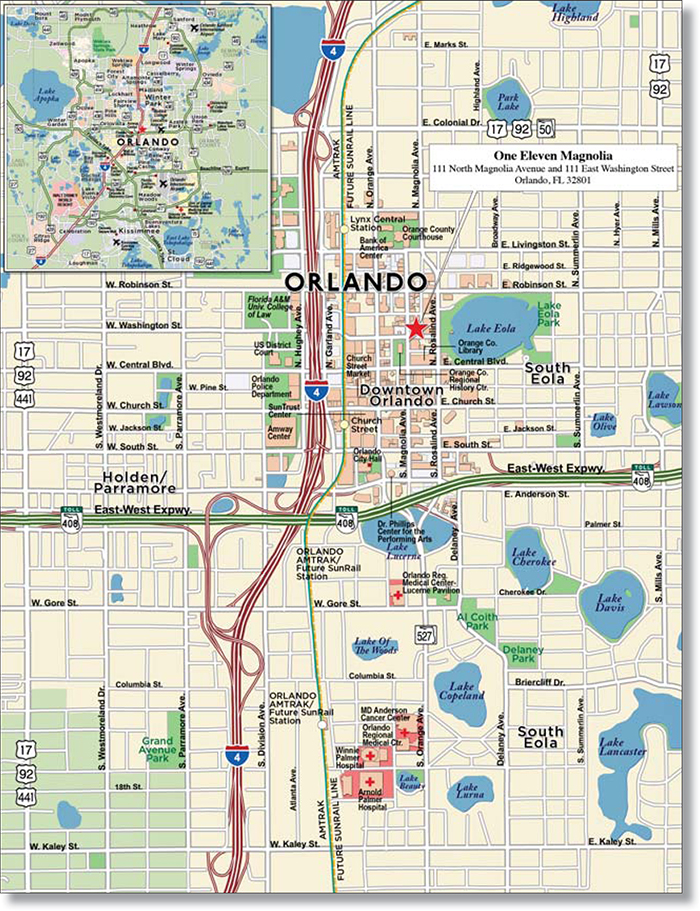

| LCF | One Eleven Magnolia | Orlando | FL | 1 / 1 | 46,900,000 | 3.3 | Mixed Use | 316,959 | 148 | 73.9 | 63.3 | 1.30 | 8.5 | ||||||||||||||

| Top Three Total/Weighted Average | 3 / 15 | $283,500,000 | 20.1% | 68.4% | 61.5% | 1.91x | 10.2 | % | |||||||||||||||||||

| Top Five Total/Weighted Average | 5 / 26 | $446,910,313 | 31.7% | 68.5% | 62.2% | 1.96x | 9.9 | % | |||||||||||||||||||

| Top Ten Total/Weighted Average | 10 / 38 | $791,372,286 | 56.2% | 68.5% | 60.4% | 1.78x | 10.0 | % | |||||||||||||||||||

| Non-Top Ten Total/Weighted Average | 73 / 112 | $617,794,536 | 43.8% | 65.3% | 53.1% | 1.71x | 11.6 | % | |||||||||||||||||||

| (1) | With respect to Carolina Place, Cumberland Mall, White Marsh Mall and 100 & 150 South Wacker Drive, each of which is part of a pari passu loan combination, Cut-off Date Balance per square foot, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan (unless otherwise stated) in total debt. With respect to each Mortgage Loan, debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. |

| Property Name | Mortgage Loan Seller | Related Notes in Loan Group (Original Balance) | Holder of Note | Whether Note is Lead Servicing for the Entire Loan Combination | Current Master Servicer Under Related Securitization PSA | Current Special Servicer Under Related Securitization PSA |

| Carolina Place | RBS | $90,000,000 | WFCM 2013-LC12 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| RBS | $85,000,000 | (1) | No | TBD | TBD | |

| Cumberland Mall | RBS | $90,000,000 | WFCM 2013-LC12 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| RBS | $70,000,000 | WFRBS 2013-C14 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | |

| White Marsh Mall | WFB | $80,000,000 | WFCM 2013-LC12 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| WFB | $110,000,000 | WFRBS 2013-C14 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | |

| 100 & 150 South Wacker Drive | WFB | $71,000,000 | WFCM 2013-LC12 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| WFB | $69,000,000 | WFRBS 2013-C14 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| (1) | The pari passu companion loan is currently held by the mortgage loan seller for the mortgage loan included in the WFCM 2013-LC12 trust. |

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Characteristics of the Mortgage Pool |

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | Mortgage Loan Cut-off Date Balance ($) | % of Cut- off Date Balance (%) | Mezzanine Debt Cut-off Date Balance ($) | Total Debt Interest Rate (%) | Mortgage Loan U/W NCF DSCR (x) | Total Debt U/W NCF DSCR (x) | Mortgage Loan Cut- off Date U/W NOI Debt Yield (%) | Total Debt Cut-off Date U/W NOI Debt Yield (%) | Mortgage Loan Cut-off Date LTV Ratio (%) | Total Debt Cut-off Date LTV Ratio (%) | ||||||||||

| 7 | LCF | Grace Lake Corporate Center | $75,528,409 | 5.4% | $2,994,780 | 4.749% | 1.60x | 1.51x | 12.1% | 11.6% | 61.5% | 64.0% | ||||||||||

| 12 | LCF | Durban Retail Portfolio | 29,741,369 | 2.1 | 2,599,256 | 5.868 | 1.45 | 1.25 | 10.2 | 9.4 | 74.9 | 81.5 | ||||||||||

| 19 | LCF | Oaks at Broad River | 15,765,000 | 1.1 | 1,885,000 | 5.820 | 1.25 | 1.02 | 8.5 | 7.6 | 70.5 | 79.0 | ||||||||||

| 43 | LCF | The Shops at Church Square | 7,184,826 | 0.5 | 999,973 | 6.570 | 1.72 | 1.29 | 13.0 | 11.4 | 64.2 | 73.1 | ||||||||||

| Total/Weighted Average | $128,219,604 | 9.1% | $8,479,009 | 5.260% | 1.53x | 1.37x | 11.3% | 10.5% | 65.9% | 70.6% | ||||||||||||

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Characteristics of the Mortgage Pool |

| Loan No. | Mortgage Loan Seller | Mortgage Loan or Mortgaged Property Name | City | State | Property Type | Mortgage Loan or Mortgaged Property Cut-off Date Balance ($) | % of Cut-off Date Pool Balance (%) | Previous Securitization | |

| 2 | RBS | Carolina Place | Pineville | NC | Retail | $90,000,000 | 6.4% | CGCMT 2005-C3 | |

| 4.01 | RBS | Country Club Mobile Estates | Holladay | UT | Manufactured Housing Community | 21,672,675 | 1.5 | CGCMT 2004-C1 | |

| 4.02 | RBS | Chalet North | Apopka | FL | Manufactured Housing Community | 17,028,530 | 1.2 | MLMT 2008-C1 | |

| 4.03 | RBS | Lakeview Estates | Layton | UT | Manufactured Housing Community | 11,919,971 | 0.8 | WBCMT 2004-C11 | |

| 11.01 | RBS | Brecksville | Brecksville | OH | Self Storage | 3,297,983 | 0.2 | LBUBS 2000-C5 | |

| 11.04 | RBS | Medina | Medina | OH | Self Storage | 2,735,827 | 0.2 | GSMS 2005-GG4 | |

| 11.12 | RBS | Peninsula | Peninsula (Boston Township) | OH | Self Storage | 1,311,698 | 0.1 | GSMS 2005-GG4 | |

| 11.13 | RBS | Sandusky | Sandusky | OH | Self Storage | 1,274,221 | 0.1 | GSMS 2005-GG4 | |

| 18 | WFB | Plaza De Oro Shopping Center | Murrieta | CA | Retail | 16,000,000 | 1.1 | JPMCC 2004-C1 | |

| 19 | LCF | Oaks at Broad River | Beaufort | SC | Multifamily | 15,765,000 | 1.1 | WBCMT 2007-C31 | |

| 21 | LCF | Shops at Bruckner | Bronx | NY | Retail | 14,421,486 | 1.0 | NASC 1998-D6 | |

| 25 | LCF | The Vineyards Apartments | St. Louis | MO | Multifamily | 11,718,430 | 0.8 | GECMC 2003-C1 | |

| 26 | WFB | Grand Forks Market Place | Grand Forks | ND | Retail | 11,500,000 | 0.8 | MLMT 2003-KEY1 | |

| 31 | WFB | Hampton Inn & Suites - Westgate | Spartanburg | SC | Hospitality | 10,180,896 | 0.7 | MSC 2006-HQ9 | |

| 32 | WFB | Carriage Way MHP | Chesterfield Township | MI | Manufactured Housing Community | 10,000,000 | 0.7 | BSCMS 2003-T12 | |

| 33 | WFB | 321 Santa Monica | Santa Monica | CA | Retail | 10,000,000 | 0.7 | JPMCC 2003-LN1 | |

| 45 | LCF | Greenville-Augusta Apartment Portfolio | Various | SC | Multifamily | 6,777,883 | 0.5 | JPMCC 2003-LN1, CSFB 2003-C3 | |

| 46 | LCF | North Reno Plaza | Reno | NV | Retail | 6,445,942 | 0.5 | JPMCC 2002-C2 | |

| 51 | WFB | Holiday Inn Express - Westgate | Spartanburg | SC | Hospitality | 6,038,668 | 0.4 | CSMC 2006-C2 | |

| 62 | WFB | Storage Depot - Mission, Sunshine & Alta Mesa | Various | TX | Self Storage | 4,891,913 | 0.3 | GECMC 2003-C2 | |

| 64 | WFB | Shoppes at North Augusta | North Augusta | SC | Retail | 4,188,683 | 0.3 | GCCFC 2004-GG1 | |

| 67 | WFB | Marlboro Industrial Park | Marlboro Township | NJ | Industrial | 3,994,519 | 0.3 | MSC 2004-HQ4 | |

| 74 | WFB | Walgreens - Taylorsville | Taylorsville | UT | Retail | 3,120,000 | 0.2 | WBCMT 2002-C2 | |

| 76 | WFB | Walgreens - Dickinson | Dickinson | TX | Retail | 2,950,000 | 0.2 | WBCMT 2003-C5 | |

| 77 | WFB | Berkshire Pointe | Reading | PA | Retail | 2,721,527 | 0.2 | CDCMT 2002-FX1 | |

| 80 | WFB | Cedar Lake MHC | Biloxi | MS | Manufactured Housing Community | 2,050,000 | 0.1 | JPMCC 2003-LN1 | |

| 81 | WFB | Spruce Grove | Lower Lake | CA | Self Storage | 1,544,967 | 0.1 | GECMC 2003-C2 | |

| Total | $293,550,817 | 20.8% | |||||||

| (1) | The table above represents the most recent securitization with respect to the mortgaged property securing the related mortgage loan, based on information provided by the related borrower or obtained through searches of a third-party database. While the above mortgage loans may have been securitized multiple times in prior transactions, mortgage loans are only listed in the above chart if the mortgage loan paid off a mortgage loan in another securitization. The information has not otherwise been confirmed by the mortgage loan sellers. |

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Characteristics of the Mortgage Pool |

Class A-1(1) | ||||||||||||||||

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut-off Date Pool Balance (%) | Mortgage Loan Balance at Maturity ($) | % of Class A-1 Certificate Principal Balance (%)(2) | SF/ Rooms/ Pads/ Units | Loan per SF/ Room/ Pad/ Unit ($) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | Cut-off Date LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) |

| 14 | WFB | Starwood Schulte Hotel Portfolio | Various | Hospitality | $19,700,000 | 1.4% | $18,317,685 | 14.0% | 260 | $75,769 | 2.07x | 13.8% | 58.1% | 54.0% | 12 | 60 |

| 17 | WFB | Doubletree Hotel – Los Angeles Norwalk | CA | Hospitality | 16,000,000 | 1.1 | 14,110,335 | 10.8 | 171 | 93,567 | 1.53 | 12.1 | 66.9 | 59.0 | 0 | 60 |

| 24 | LCF | Crowne Plaza Madison | WI | Hospitality | 12,097,763 | 0.9 | 10,960,444 | 8.4 | 226 | 53,530 | 1.60 | 14.0 | 61.7 | 55.9 | 0 | 50 |

| 43 | LCF | The Shops at Church Square | OH | Retail | 7,184,826 | 0.5 | 6,712,698 | 5.1 | 109,446 | 66 | 1.72 | 13.0 | 64.2 | 59.9 | 0 | 52 |

| Total/Weighted Average | $54,982,589 | 3.9% | $50,101,162 | 38.4% | 1.76x | 13.2% | 62.3% | 56.6% | 4 | 57 | ||||||

| (1) | The table above presents the mortgage loans whose balloon payments would be applied to pay down the principal balance of the Class A-1 Certificates, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Free Writing Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each class of Certificates, including the Class A-1 Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Free Writing Prospectus. |

| (2) | Reflects the percentage equal to the Mortgage Loan Balance at Maturity divided by the initial Class A-1 Certificate Principal Balance. |

Class A-2(1) | ||||||||||||||||

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut-off Date Pool Balance (%) | Mortgage Loan Balance at Maturity ($) | % of Class A-2 Certificate Principal Balance (%)(2) | SF/ Rooms/ Pads/ Units | Loan per SF / Room/ Pad/Unit ($) | U/W NCF DSCR (x)(3) | U/W NOI Debt Yield (%)(3) | Cut-off Date LTV Ratio (%)(3) | Balloon or ARD LTV Ratio (%)(3) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) |

| 5 | WFB | White Marsh Mall | MD | Retail | $80,000,000 | 5.7% | $80,000,000 | 100.0% | 702,317 | $271 | 2.66x | 10.3% | 63.3% | 63.3% | 94 | 94 |

| Total/Weighted Average | $80,000,000 | 5.7% | $80,000,000 | 100.0% | 2.66x | 10.3% | 63.3% | 63.3% | 94 | 94 | ||||||

| (1) | The table above presents the mortgage loan whose balloon payments would be applied to pay down the principal balance of the Class A-2 Certificates, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Free Writing Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each class of Certificates, including the Class A-2 Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Free Writing Prospectus. |

| (2) | Reflects the percentage equal to the Mortgage Loan Balance at Maturity divided by the initial Class A-2 Certificate Principal Balance. |

| (3) | With respect to each pari passu loan combination, loan-to-value ratio, debt service coverage ratio, debt yield and cut-off date balance per square foot calculations include the related pari passu companion loan unless otherwise stated. |

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Characteristics of the Mortgage Pool |

Class A-SB(1) | ||||||||||||||||

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut- off Date Pool Balance (%) | Mortgage Loan Balance at Maturity ($) | % of Class A-SB Certificate Principal Balance (%)(2) | SF/ Rooms/ Pads/ Units | Loan per SF/ Room/ Pad/ Unit ($) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) |

| 46 | LCF | North Reno Plaza | NV | Retail | $6,445,942 | 0.5% | $5,334,573 | 3.6% | 126,907 | 51 | 1.47x | 11.0% | 63.8% | 52.8% | 0 | 113 |

| 47 | LCF | Ravenswood Professional Office Building | IL | Office | 6,418,521 | 0.5 | 5,244,402 | 3.5 | 58,416 | 110 | 1.58 | 10.8 | 70.1 | 57.3 | 0 | 116 |

| 68 | LCF | Walgreens Aiken | SC | Retail | 3,885,000 | 0.3 | 3,885,000 | 2.6 | 14,550 | 267 | 2.15 | 9.3 | 63.2 | 63.2 | 114 | 114 |

| 70 | LCF | Walgreens Gray | TN | Retail | 3,453,000 | 0.2 | 3,453,000 | 2.3 | 14,550 | 237 | 2.15 | 9.3 | 64.2 | 64.2 | 114 | 114 |

| 71 | LCF | Walgreens Gallatin | TN | Retail | 3,322,000 | 0.2 | 3,322,000 | 2.2 | 14,820 | 224 | 2.15 | 9.3 | 63.9 | 63.9 | 114 | 114 |

| 72 | LCF | Walgreens Durant | OK | Retail | 3,250,000 | 0.2 | 3,250,000 | 2.2 | 14,550 | 223 | 2.14 | 9.4 | 65.0 | 65.0 | 115 | 115 |

| 75 | LCF | Walgreens Mount Airy | NC | Retail | 2,950,000 | 0.2 | 2,950,000 | 2.0 | 14,820 | 199 | 2.15 | 9.3 | 63.1 | 63.1 | 114 | 114 |

| 83 | LCF | Dollar General - Satsuma | FL | Retail | 721,500 | 0.1 | 721,500 | 0.5 | 9,026 | 80 | 1.97 | 11.4 | 65.0 | 65.0 | 106 | 106 |

| Total/Weighted Average | $30,445,963 | 2.2% | $28,160,475 | 18.8% | 1.88x | 10.0% | 65.2% | 60.2% | 66 | 114 | ||||||

| (1) | The table above presents the mortgage loans whose balloon payments would be applied to pay down the principal balance of the Class A-SB Certificates, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Free Writing Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each class of Certificates, including the Class A-SB Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-SB to the Free Writing Prospectus. |

| (2) | Reflects the percentage equal to the Mortgage Loan Balance at Maturity divided by the initial Class A-SB Certificate Principal Balance. |

| (3) | With respect to each pari passu loan combination, loan-to-value ratio, debt service coverage ratio, debt yield and cut-off date balance per square foot calculations include the related pari passu companion loan unless otherwise stated. |

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Characteristics of the Mortgage Pool |

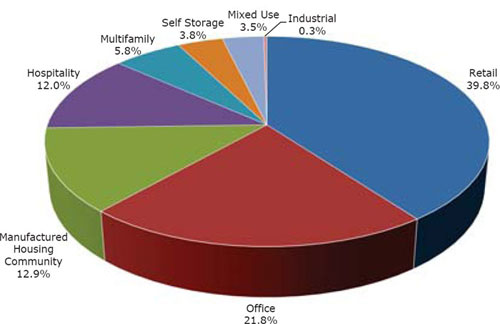

| Property Type | Number of Mortgaged Properties | Aggregate Cut- off Date Balance ($) | % of Cut- off Date Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon or ARD LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) | ||

| Retail | 49 | $561,243,521 | 39.8% | 65.1% | 58.0% | 1.93x | 10.4% | 9.9% | 4.184% | ||

| Regional Mall | 4 | 337,000,000 | 23.9 | 65.3 | 61.5 | 2.14 | 10.2 | 9.7 | 3.853 | ||

| Anchored | 16 | 136,431,356 | 9.7 | 65.2 | 53.3 | 1.57 | 11.0 | 10.2 | 4.827 | ||

| Single Tenant | 20 | 47,218,369 | 3.4 | 61.9 | 50.6 | 1.80 | 10.6 | 10.2 | 4.339 | ||

| Unanchored | 5 | 23,439,239 | 1.7 | 63.5 | 50.8 | 1.57 | 10.4 | 9.9 | 4.655 | ||

| Shadow Anchored | 4 | 17,154,558 | 1.2 | 70.3 | 56.3 | 1.64 | 10.6 | 10.1 | 4.502 | ||

| Office | 19 | 306,941,753 | 21.8 | 67.7 | 56.4 | 1.61 | 11.2 | 10.0 | 4.347 | ||

| Suburban | 14 | 188,478,409 | 13.4 | 69.4 | 55.2 | 1.58 | 11.3 | 10.2 | 4.496 | ||

| CBD | 3 | 103,194,823 | 7.3 | 64.0 | 57.8 | 1.67 | 11.1 | 9.6 | 4.046 | ||

| Flex | 1 | 8,850,000 | 0.6 | 74.8 | 63.8 | 1.59 | 10.8 | 9.6 | 4.444 | ||

| Medical Office | 1 | 6,418,521 | 0.5 | 70.1 | 57.3 | 1.58 | 10.8 | 9.9 | 4.665 | ||

| Manufactured Housing Community | 25 | 182,224,077 | 12.9 | 71.7 | 61.8 | 1.68 | 9.3 | 9.1 | 4.069 | ||

| Manufactured Housing Community | 25 | 182,224,077 | 12.9 | 71.7 | 61.8 | 1.68 | 9.3 | 9.1 | 4.069 | ||

| Hospitality | 19 | 169,405,258 | 12.0 | 65.6 | 52.0 | 1.75 | 13.4 | 11.8 | 4.746 | ||

| Limited Service | 11 | 79,671,026 | 5.7 | 66.9 | 49.3 | 1.81 | 13.8 | 12.4 | 4.651 | ||

| Full Service | 5 | 54,510,609 | 3.9 | 62.8 | 54.0 | 1.70 | 13.3 | 11.4 | 4.694 | ||

| Extended Stay | 3 | 35,223,622 | 2.5 | 67.1 | 55.2 | 1.67 | 12.7 | 11.1 | 5.041 | ||

| Multifamily | 13 | 82,163,307 | 5.8 | 67.0 | 53.6 | 1.42 | 10.0 | 9.3 | 4.805 | ||

| Garden | 9 | 56,996,223 | 4.0 | 67.4 | 53.6 | 1.47 | 10.8 | 9.9 | 4.920 | ||

| Student Housing | 4 | 25,167,084 | 1.8 | 65.9 | 53.5 | 1.30 | 8.3 | 8.0 | 4.545 | ||

| Self Storage | 22 | 53,894,387 | 3.8 | 67.4 | 54.3 | 1.69 | 10.6 | 10.2 | 4.437 | ||

| Self Storage | 22 | 53,894,387 | 3.8 | 67.4 | 54.3 | 1.69 | 10.6 | 10.2 | 4.437 | ||

| Mixed Use | 2 | 49,300,000 | 3.5 | 73.8 | 63.1 | 1.32 | 8.6 | 8.1 | 4.632 | ||

| Office/Retail/Multifamily | 1 | 46,900,000 | 3.3 | 73.9 | 63.3 | 1.30 | 8.5 | 8.0 | 4.622 | ||

| Office/Retail | 1 | 2,400,000 | 0.2 | 71.2 | 58.2 | 1.61 | 10.9 | 10.2 | 4.830 | ||

| Industrial | 1 | 3,994,519 | 0.3 | 67.8 | 54.5 | 1.67 | 11.1 | 9.9 | 4.280 | ||

| Flex | 1 | 3,994,519 | 0.3 | 67.8 | 54.5 | 1.67 | 11.1 | 9.9 | 4.280 | ||

| Total/Weighted Average | 150 | $1,409,166,822 | 100.0% | 67.1% | 57.2% | 1.75x | 10.7% | 10.0% | 4.334% | ||

| (1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated amounts (allocating the mortgage loan principal balance to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate). With respect to Carolina Place, Cumberland Mall, White Marsh Mall and 100 & 150 South Wacker Drive, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan (unless otherwise stated) in total debt. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property) that is allowed under the terms of any mortgage loan. See Annex A-1 to the Free Writing Prospectus. |

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Characteristics of the Mortgage Pool |

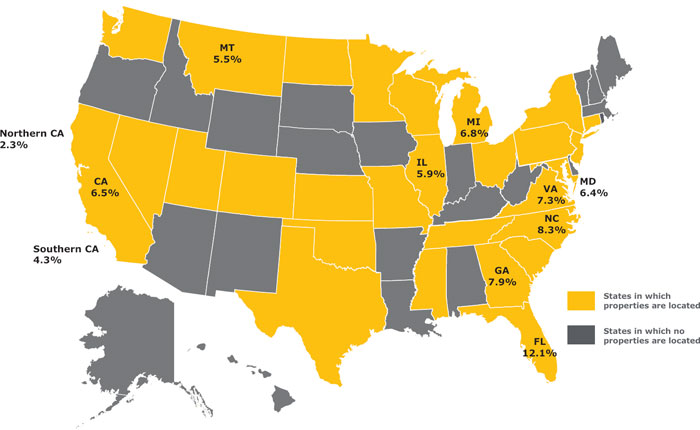

Location(2) | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($)(3) | % of Cut- off Date Balance | Weighted Average Cut- off Date LTV Ratio (%)(3) | Weighted Average Balloon or ARD LTV Ratio (%)(3) | Weighted Average U/W NCF DSCR (x) (3) | Weighted Average U/W NOI Debt Yield (%)(3) | Weighted Average U/W NCF Debt Yield (%)(3) | Weighted Average Mortgage Rate (%)(3) | |

| Florida | 16 | $170,757,385 | 12.1% | 72.3% | 61.6% | 1.40x | 9.1% | 8.6% | 4.633% | |

| North Carolina | 8 | 116,957,551 | 8.3 | 66.9 | 57.0 | 1.70 | 10.3 | 9.8 | 4.062 | |

| Georgia | 4 | 111,425,772 | 7.9 | 65.3 | 62.9 | 2.29 | 9.8 | 9.4 | 3.990 | |

| Virginia | 13 | 103,500,000 | 7.3 | 74.8 | 63.8 | 1.59 | 10.8 | 9.6 | 4.444 | |

| Michigan | 4 | 95,228,283 | 6.8 | 59.3 | 43.1 | 2.10 | 13.3 | 12.5 | 4.434 | |

| California | 10 | 92,178,590 | 6.5 | 62.4 | 50.6 | 1.56 | 10.4 | 9.7 | 4.393 | |

| Southern | 5 | 60,180,344 | 4.3 | 62.9 | 53.0 | 1.50 | 10.2 | 9.4 | 4.464 | |

| Northern | 5 | 31,998,247 | 2.3 | 61.4 | 46.2 | 1.66 | 10.9 | 10.4 | 4.261 | |

| Maryland | 2 | 90,485,059 | 6.4 | 63.5 | 61.9 | 2.55 | 10.3 | 9.9 | 3.706 | |

| Illinois | 3 | 83,290,779 | 5.9 | 66.9 | 59.7 | 1.56 | 10.6 | 9.0 | 4.055 | |

| Montana | 1 | 77,000,000 | 5.5 | 68.8 | 62.7 | 1.70 | 10.6 | 10.1 | 4.286 | |

Other(4) | 89 | 468,343,402 | 33.2 | 66.9 | 54.7 | 1.64 | 11.3 | 10.4 | 4.498 | |

| Total/Weighted Average | 150 | $1,409,166,822 | 100.0% | 67.1% | 57.2% | 1.75x | 10.7% | 10.0% | 4.334% |

| (1) | The Mortgaged Properties are located in 28 states. |

| (2) | For purposes of determining whether a mortgaged property is in Northern California or Southern California, Northern California includes areas with zip codes above 93600 and Southern California includes areas with zip codes of 93600 and below. |

| (3) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated amounts (allocating the mortgage loan principal balance to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate). With respect to Carolina Place, Cumberland Mall, White Marsh Mall and 100 & 150 South Wacker Drive, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan (unless otherwise stated) in total debt. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. See Annex A-1 to the Free Writing Prospectus. |

(4) | Includes 19 other states. |

Wells Fargo Commercial Mortgage Trust 2013-LC12 | Characteristics of the Mortgage Pool |

| CUT-OFF DATE BALANCE | LOAN PURPOSE | |||||||

| Number of | Number of | |||||||

| Range of Cut-off Date | Mortgage | Aggregate Cut- | % of Cut-off | Mortgage | Aggregate Cut- | % of Cut-off | ||

| Balances ($) | Loans | off Date Balance | Date Balance | Loan Purpose | Loans | off Date Balance | Date Balance | |

| 721,500 - 1,000,000 | 1 | $721,500 | 0.1% | Refinance | 59 | $923,389,690 | 65.5% | |

| 1,000,001 - 2,000,000 | 2 | 3,044,967 | 0.2 | Acquisition | 24 | 485,777,131 | 34.5 | |

| 2,000,001 - 3,000,000 | 6 | 15,171,527 | 1.1 | Total: | 83 | $1,409,166,822 | 100.0% | |

| 3,000,001 - 4,000,000 | 8 | 27,924,519 | 2.0 | |||||

| 4,000,001 - 5,000,000 | 7 | 31,433,999 | 2.2 | MORTGAGE RATE | ||||

| 5,000,001 - 6,000,000 | 8 | 45,932,246 | 3.3 | Number of | ||||

| 6,000,001 - 7,000,000 | 8 | 51,344,340 | 3.6 | Range of Mortgage Rates | Mortgage | Aggregate Cut- | % of Cut-off | |

| 7,000,001 - 8,000,000 | 4 | 30,919,581 | 2.2 | (%) | Loans | off Date Balance | Date Balance | |

| 8,000,001 - 9,000,000 | 3 | 25,537,315 | 1.8 | 3.658 - 3.750 | 3 | $180,000,000 | 12.8% | |

| 9,000,001 - 10,000,000 | 5 | 49,105,135 | 3.5 | 3.751 - 4.000 | 5 | 193,416,126 | 13.7 | |

| 10,000,001 - 15,000,000 | 12 | 143,707,186 | 10.2 | 4.001 - 4.250 | 14 | 270,604,442 | 19.2 | |

| 15,000,001 - 20,000,000 | 6 | 104,442,172 | 7.4 | 4.251 - 4.500 | 14 | 292,264,008 | 20.7 | |

| 20,000,001 - 30,000,000 | 2 | 57,741,369 | 4.1 | 4.501 - 4.750 | 18 | 240,557,600 | 17.1 | |

| 30,000,001 - 50,000,000 | 2 | 77,668,679 | 5.5 | 4.751 - 5.000 | 17 | 94,939,697 | 6.7 | |

| 50,000,001 - 80,000,000 | 5 | 377,561,973 | 26.8 | 5.001 - 5.250 | 5 | 49,867,533 | 3.5 | |

| 80,000,001 - 90,000,000 | 3 | 263,410,313 | 18.7 | 5.251 - 5.500 | 3 | 37,647,695 | 2.7 | |

| 90,000,001 - 103,500,000 | 1 | 103,500,000 | 7.3 | 5.501 - 5.980 | 4 | 49,869,721 | 3.5 | |

| Total: | 83 | $1,409,166,822 | 100.0% | Total: | 83 | $1,409,166,822 | 100.0% | |

| Average: | $16,977,914 | Weighted Average: | 4.334% | |||||

| UNDERWRITTEN NOI DEBT SERVICE COVERAGE RATIO | UNDERWRITTEN NOI DEBT YIELD | |||||||

| Number of | Number of | |||||||

| Range of U/W NOI | Mortgage | Aggregate Cut- | % of Cut-off | Range of U/W NOI | Mortgage | Aggregate Cut- | % of Cut-off | |

| DSCRs (x) | Loans | off Date Balance | Date Balance | Debt Yields (%) | Loans | off Date Balance | Date Balance | |

| 1.23 - 1.30 | 2 | $18,885,000 | 1.3% | 8.2 - 9.0 | 9 | $266,511,760 | 18.9% | |

| 1.31 - 1.40 | 5 | 96,594,256 | 6.9 | 9.1 - 10.0 | 15 | 208,615,821 | 14.8 | |

| 1.41 - 1.50 | 7 | 187,804,699 | 13.3 | 10.1 - 11.0 | 17 | 525,121,146 | 37.3 | |

| 1.51 - 1.60 | 8 | 94,593,146 | 6.7 | 11.1 - 12.0 | 14 | 81,419,773 | 5.8 | |

| 1.61 - 1.70 | 7 | 67,633,787 | 4.8 | 12.1 - 13.0 | 13 | 187,468,324 | 13.3 | |

| 1.71 - 1.80 | 14 | 409,599,633 | 29.1 | 13.1 - 14.0 | 8 | 89,265,383 | 6.3 | |

| 1.81 - 1.90 | 8 | 134,803,149 | 9.6 | 14.1 - 15.0 | 3 | 18,814,964 | 1.3 | |

| 1.91 - 2.00 | 8 | 64,962,496 | 4.6 | 15.1 - 22.3 | 4 | 31,949,649 | 2.3 | |

| 2.01 - 2.25 | 17 | 112,986,042 | 8.0 | Total: | 83 | $1,409,166,822 | 100.0% | |

| 2.26 - 2.50 | 4 | 41,304,613 | 2.9 | Weighted Average: | 10.7% | |||

| 2.51 - 2.75 | 1 | 90,000,000 | 6.4 | |||||

| 2.76 - 3.00 | 1 | 80,000,000 | 5.7 | UNDERWRITTEN NCF DEBT YIELD | ||||

| 3.01 - 5.97 | 1 | 10,000,000 | 0.7 | Number of | ||||

| Total: | 83 | $1,409,166,822 | 100.0% | Range of U/W NCF | Mortgage | Aggregate Cut- | % of Cut-off | |

| Weighted Average: | 1.88x | Debt Yields (%) | Loans | off Date Balance | Date Balance | |||

| 8.0 - 9.0 | 16 | $423,024,547 | 30.0% | |||||

| UNDERWRITTEN NCF DEBT SERVICE COVERAGE RATIO | 9.1 - 10.0 | 19 | 469,903,386 | 33.3 | ||||

| Number of | 10.1 - 11.0 | 18 | 197,664,583 | 14.0 | ||||

| Range of U/W NCF | Mortgage | Aggregate Cut- | % of Cut-off | 11.1 - 12.0 | 16 | 210,373,342 | 14.9 | |

| DSCRs (x) | Loans | off Date Balance | Date Balance | 12.1 - 13.0 | 7 | 57,436,350 | 4.1 | |

| 1.22 - 1.30 | 7 | $115,479,256 | 8.2% | 13.1 - 14.0 | 2 | 14,700,000 | 1.0 | |

| 1.31 - 1.40 | 4 | 28,260,822 | 2.0 | 14.1 - 15.0 | 4 | 26,064,613 | 1.8 | |

| 1.41 - 1.50 | 11 | 277,542,416 | 19.7 | 15.1 - 21.9 | 1 | 10,000,000 | 0.7 | |

| 1.51 - 1.60 | 13 | 333,693,862 | 23.7 | Total: | 83 | $1,409,166,822 | 100.0% | |

| 1.61 - 1.70 | 12 | 166,610,779 | 11.8 | Weighted Average: | 10.0% | |||

| 1.71 - 1.80 | 13 | 165,264,578 | 11.7 | |||||

| 1.81 - 1.90 | 3 | 19,810,220 | 1.4 | |||||

| 1.91 - 2.00 | 7 | 61,140,275 | 4.3 | |||||

| 2.01 - 2.50 | 11 | 151,364,613 | 10.7 | |||||

| 2.51 - 3.00 | 1 | 80,000,000 | 5.7 | |||||

| 3.01 - 5.86 | 1 | 10,000,000 | 0.7 | |||||

| Total: | 83 | $1,409,166,822 | 100.0% | |||||

| Weighted Average: | 1.75x | |||||||

| (1) | With respect to Carolina Place, Cumberland Mall, White Marsh Mall and 100 & 150 South Wacker Drive, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan (unless otherwise stated) in total debt. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. |

Wells Fargo Commercial Mortgage Trust 2013-LC12 | Characteristics of the Mortgage Pool |

| ORIGINAL TERM TO MATURITY OR ARD | CUT-OFF DATE LOAN-TO-VALUE RATIO | |||||||||||||

| Number of | Number of | |||||||||||||

| Range of Original Terms to | Mortgage | Aggregate Cut- | % of Cut-off | Range of Cut-off Date LTV | Mortgage | Aggregate Cut- | % of Cut-off | |||||||

| Maturity or ARD (months) | Loans | off Date Balance | Date Balance | Ratios (%) | Loans | off Date Balance | Date Balance | |||||||

| 60 | 4 | $54,982,589 | 3.9% | 38.5 - 45.0 | 2 | $24,421,486 | 1.7% | |||||||

| 85 - 120 | 77 | 1,327,538,134 | 94.2 | 45.1 - 50.0 | 1 | 3,200,000 | 0.2 | |||||||

| 121 - 126 | 2 | 26,646,099 | 1.9 | 50.1 - 55.0 | 3 | 18,734,964 | 1.3 | |||||||

| Total: | 83 | $1,409,166,822 | 100.0% | 55.1 - 60.0 | 10 | 98,763,143 | 7.0 | |||||||

| Weighted Average: | 116 months | 60.1 - 65.0 | 25 | 391,744,577 | 27.8 | |||||||||

| 65.1 - 70.0 | 18 | 368,893,439 | 26.2 | |||||||||||

| REMAINING TERM TO MATURITY OR ARD | 70.1 - 75.0 | 24 | 503,409,214 | 35.7 | ||||||||||

| Number of | Total: | 83 | $1,409,166,822 | 100.0% | ||||||||||

| Range of Remaining Terms | Mortgage | Aggregate Cut- | % of Cut-off | Weighted Average: | 67.1% | |||||||||

| to Maturity or ARD (months) | Loans | off Date Balance | Date Balance | |||||||||||

| 50 - 60 | 4 | $54,982,589 | 3.9% | BALLOON OR ARD LOAN-TO-VALUE RATIO | ||||||||||

| 85 - 120 | 79 | 1,354,184,233 | 96.1 | Number of | ||||||||||

| Total: | 83 | $1,409,166,822 | 100.0% | Range of Balloon or ARD | Mortgage | Aggregate Cut- | % of Cut-off | |||||||

| Weighted Average: | 115 months | LTV Ratios (%) | Loans | off Date Balance | Date Balance | |||||||||

| 21.5 - 35.0 | 2 | $17,541,486 | 1.2% | |||||||||||

ORIGINAL AMORTIZATION TERM(2) | 35.1 - 40.0 | 2 | 13,200,000 | 0.9 | ||||||||||

| Range of Original | Number of | 40.1 - 45.0 | 12 | 155,944,925 | 11.1 | |||||||||

| Amortization Terms | Mortgage | Aggregate Cut- | % of Cut-off | 45.1 - 50.0 | 10 | 71,537,942 | 5.1 | |||||||

| (months) | Loans | off Date Balance | Date Balance | 50.1 - 55.0 | 16 | 149,036,981 | 10.6 | |||||||

| Interest-Only | 9 | $197,581,500 | 14.0% | 55.1 - 60.0 | 20 | 245,324,863 | 17.4 | |||||||

| 180 | 1 | 3,120,000 | 0.2 | 60.1 - 65.0 | 21 | 756,580,625 | 53.7 | |||||||

| 181 - 240 | 3 | 25,631,486 | 1.8 | Total: | 83 | $1,409,166,822 | 100.0% | |||||||

| 241 - 300 | 23 | 249,536,642 | 17.7 | Weighted Average: | 57.2% | |||||||||

| 301 - 360 | 47 | 933,297,194 | 66.2 | |||||||||||

| Total: | 83 | $1,409,166,822 | 100.0% | AMORTIZATION TYPE | ||||||||||

Weighted Average(3): | 343 months | Number of | ||||||||||||

(2) The original amortization term shown for any mortgage loan that is interest-only for part of its term does not include the number of months in its interest-only period and reflects only the number of months as of the commencement of amortization remaining from the end of such interest-only period. | Mortgage | Aggregate Cut- | % of Cut-off | |||||||||||

| Type of Amortization | Loans | off Date Balance | Date Balance | |||||||||||

| Interest-only, Amortizing Balloon | 16 | $583,904,976 | 41.4% | |||||||||||

| (3) Excludes the non-amortizing loans. | Amortizing Balloon | 56 | 517,305,431 | 36.7 | ||||||||||

| Interest-only, Balloon | 3 | 180,000,000 | 12.8 | |||||||||||

REMAINING AMORTIZATION TERM(4) | Interest-only, Amortizing ARD | 1 | 103,500,000 | 7.3 | ||||||||||

| Range of Remaining | Number of | Interest-only, ARD | 6 | 17,581,500 | 1.2 | |||||||||

| Amortization Terms | Mortgage | Aggregate Cut- | % of Cut-off | Amortizing Balloon, ARD | 1 | 6,874,914 | 0.5 | |||||||

| (months) | Loans | off Date Balance | Date Balance | Total: | 83 | $1,409,166,822 | 100.0% | |||||||

| Interest-Only | 9 | $197,581,500 | 14.0% | |||||||||||

| 180 | 1 | 3,120,000 | 0.2 | ORIGINAL TERM OF INTEREST-ONLY PERIOD FOR PARTIAL IO LOANS | ||||||||||

| 181 - 240 | 3 | 25,631,486 | 1.8 | Number of | ||||||||||

| 241 - 300 | 23 | 249,536,642 | 17.7 | Mortgage | Aggregate Cut- | % of Cut-off | ||||||||

| 301 - 360 | 47 | 933,297,194 | 66.2 | IO Term (months) | Loans | off Date Balance | Date Balance | |||||||

| Total: | 83 | $1,409,166,822 | 100.0% | 1 - 6 | 2 | $26,646,099 | 1.9% | |||||||

Weighted Average(5): | 342 months | 7 - 12 | 3 | 31,000,000 | 2.2 | |||||||||

(4) The remaining amortization term shown for any mortgage loan that is interest-only for part of its term does not include the number of months in its interest-only period and reflects only the number of months as of the commencement of amortization remaining from the end of such interest-only period. | 13 - 18 | 1 | 15,765,000 | 1.1 | ||||||||||

| 19 - 24 | 5 | 190,550,000 | 13.5 | |||||||||||

| 25 - 36 | 3 | 247,443,877 | 17.6 | |||||||||||

| (5) Excludes the non-amortizing loans. | 37 - 60 | 3 | 176,000,000 | 12.5 | ||||||||||

| Total: | 17 | $687,404,976 | 48.8% | |||||||||||

| LOCKBOXES | Weighted Average: | 36 months | ||||||||||||

| Number of | % of Cut-off | |||||||||||||

| Mortgage | Aggregate Cut- | Date | SEASONING | |||||||||||

| Type of Lockbox | Loans | off Date Balance | Balance | Number of | ||||||||||

| Hard/Springing Cash Management | 20 | $473,556,789 | 33.6% | Mortgage | Aggregate Cut- | % of Cut-off | ||||||||

| Hard/Upfront Cash Management | 17 | 421,854,840 | 29.9 | Seasoning (months) | Loans | off Date Balance | Date Balance | |||||||

| Soft/Springing Cash Management | 12 | 291,832,518 | 20.7 | 0 | 26 | $428,678,879 | 30.4% | |||||||

| Springing (W/Out Estab. Account) | 20 | 133,605,789 | 9.5 | 1 - 3 | 45 | 904,113,292 | 64.2 | |||||||

| None | 9 | 40,898,983 | 2.9 | 4 - 6 | 7 | 41,955,693 | 3.0 | |||||||

| Soft/Upfront Cash Management | 2 | 27,483,430 | 2.0 | 7 - 9 | 3 | 21,599,695 | 1.5 | |||||||

| Springing (With Estab. Account) | 3 | 19,934,473 | 1.4 | 10 - 12 | 1 | 12,097,763 | 0.9 | |||||||

| Total: | 83 | $1,409,166,822 | 100.0% | 13 - 18 | 1 | 721,500 | 0.1 | |||||||

| Total: | 83 | $1,409,166,822 | 100.0% | |||||||||||

| PREPAYMENT PROVISION SUMMARY | Weighted Average: | 1 month | ||||||||||||

| Number of | % of Cut- | |||||||||||||

| Mortgage | Aggregate Cut- | off Date | ||||||||||||

| Prepayment Provision | Loans | off Date Balance | Balance | |||||||||||

| Lockout/Defeasance/Open | 66 | $984,980,081 | 69.9% | |||||||||||

| Lockout/YM%/Open | 7 | 191,983,755 | 13.6 | |||||||||||

| YM%/Defeasance or YM%/Open | 2 | 117,921,486 | 8.4 | |||||||||||

| Lockout/YM%/Defeasance or YM%/Open | 1 | 77,000,000 | 5.5 | |||||||||||

| Lockout/Defeasance or YM%/Open | 1 | 19,700,000 | 1.4 | |||||||||||

| YM/Defeasance or YM/Open | 6 | 17,581,500 | 1.2 | |||||||||||

| Total: | 83 | $1,409,166,822 | 100.0% | |||||||||||

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Certain Terms and Conditions |

| Interest Entitlements: | The interest entitlement of each Class of Offered Certificates on each Distribution Date generally will be the interest accrued during the related Interest Accrual Period on the related Certificate Principal Balance or Notional Amount at the related pass-through rate, net of any prepayment interest shortfalls allocated to that Class for such Distribution Date as described below. If prepayment interest shortfalls arise from voluntary prepayments (without special servicer consent) on particular non-specially serviced mortgage loans during any collection period, the Master Servicer is required to make a compensating interest payment to offset those shortfalls, generally up to an amount equal to the portion of its master servicing fees that accrue at one basis point per annum. The remaining amount of prepayment interest shortfalls will be allocated to reduce the interest entitlement on all Classes of Certificates (other than the Class X-A and Class X-B Certificates), pro rata, based on their respective amounts of accrued interest for the related Distribution Date (except with respect to the allocation among the Class A-S, Class B, Class PEX and Class C Certificates as described below under “Allocations and Distributions on the Class A-S, B, C and PEX Certificates”). If a Class receives less than the entirety of its interest entitlement on any Distribution Date, then the shortfall, excluding any shortfall due to prepayment interest shortfalls, will be added to its interest entitlement for the next succeeding Distribution Date. Interest entitlements on the Class D, C and B Certificates, in that order, may be reduced by certain Trust Advisor expenses (subject to the discussion below under “Allocations and Distributions on the Class A-S, B, C and PEX Certificates”). | |

| Principal Distribution Amount: | The Principal Distribution Amount for each Distribution Date generally will be the aggregate amount of principal received or advanced in respect of the mortgage loans, net of any non-recoverable advances and interest thereon that are reimbursed to the Master Servicer, the Special Servicer or the Trustee during the related collection period. Non-recoverable advances and interest thereon are reimbursable from principal collections and advances before reimbursement from other amounts. The Principal Distribution Amount may also be reduced, with a corresponding loss, to the Class D, C, B and A-S Certificates, then to the Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates and Class A-3FX Regular Interest (and therefore, to the Class A-3FX and A-3FL Certificates) (with any losses on the Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates and Class A-3FX Regular Interest (and therefore, on the Class A-3FX and A-3FL Certificates) allocated pro rata according to their respective Certificate Principal Balances immediately prior to that Distribution Date), in that order, in connection with certain Trust Advisor expenses to the extent that interest entitlements on the Class B, C and D Certificates are insufficient to absorb the effect of the expense on any particular Distribution Date, in each case except as discussed below under “Allocations and Distributions on the Class A-S, B, C and PEX Certificates”. | |

| Distributions: | On each Distribution Date, funds available for distribution from the mortgage loans, net of specified trust fees, expenses and reimbursements will generally be distributed in the following amounts and order of priority (in each case to the extent of remaining available funds): | |

1. Class A-1, A-2, A-3, A-4, A-5, A-SB, X-A and X-B Certificates and Class A-3FX Regular Interest: To interest on the Class A-1, A-2, A-3, A-4, A-5, A-SB, X-A and X-B Certificates and Class A-3FX Regular Interest, pro rata, according to their respective interest entitlements. | ||

2. Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates and Class A-3FX Regular Interest: To principal on the Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates (and the Class A-3FX Regular Interest) in the following amounts and order of priority: (i) first, to principal on the Class A-SB Certificates, in an amount up to the Principal Distribution Amount for such Distribution Date until their Certificate Principal Balance is reduced to the Class A-SB Planned Principal Balance; (ii) second, to principal on the Class A-1 Certificates until their Certificate Principal Balance is reduced to zero, up to the remainder of the Principal Distribution Amount for such Distribution Date; (iii) third, to principal on the Class A-2 Certificates until their Certificate Principal Balance is reduced to zero, up to the remainder of the Principal Distribution Amount for such Distribution Date; (iv) fourth, on a pro rata basis, to principal on the Class A-3 Certificates and the Class A-3FX Regular Interest (and therefore, to holders of the Class A-3FX and A-3FL Certificates) until their Certificate Principal Balance is reduced to zero, up to the remainder of the Principal Distribution Amount for such Distribution Date; (v) fifth, to principal on the Class A-4 Certificates until their Certificate Principal Balance is reduced to zero, up to the remainder of the Principal Distribution Amount for such Distribution Date; (vi) sixth, to principal on the Class A-5 Certificates until their Certificate Principal Balance is reduced to zero, up to the remainder of the Principal Distribution Amount for such Distribution Date; and (vii) seventh, to principal on the Class A-SB Certificates until their Certificate Principal Balance is reduced to zero, up to the remainder of the Principal Distribution Amount for such Distribution Date. However, if the Certificate Principal Balance of each and every Class of Principal |

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Certain Terms and Conditions |

| Balance Certificates, other than the Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates and Class A-3FX Regular Interest, has been reduced to zero as a result of the allocation of Mortgage Loan losses and expenses and any of the Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates and Class A-3FX Regular Interest remains outstanding, then the Principal Distribution Amount will be distributed on the Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates and Class A-3FX Regular Interest, pro rata, based on their respective outstanding Certificate Principal Balances, until their Certificate Principal Balances have been reduced to zero. |

3. Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates and Class A-3FX Regular Interest: To reimburse the holders of the Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates and the Class A-3FX Regular Interest (and, therefore, to reimburse the holders of the Class A-3FX and A-3FL Certificates), pro rata, for any previously unreimbursed losses (other than certain Trust Advisor expenses) on the mortgage loans that were previously allocated in reduction of the Certificate Principal Balances of such Classes. | ||

4. Class A-S regular interest: To make distributions on the Class A-S regular interest as follows: (a) first, to interest on Class A-S regular interest in the amount of the interest entitlement for that Class; (b) next, to the extent of the portion of the Principal Distribution Amount remaining after distributions in respect of principal to each Class with a higher distribution priority (in this case, the Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates and Class A-3FX Regular Interest), to principal on the Class A-S regular interest until its principal balance is reduced to zero; and (c) next, to reimburse the holders of the Class A-S regular interest for any previously unreimbursed losses (other than certain Trust Advisor expenses) on the mortgage loans that were previously allocated to that Class in reduction of its principal balance. 5. Class B regular interest: To make distributions on the Class B regular interest as follows: (a) first, to interest on Class B regular interest in the amount of the interest entitlement for that Class; (b) next, to the extent of the portion of the Principal Distribution Amount remaining after distributions in respect of principal to each Class with a higher distribution priority (in this case, the Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates, Class A-S regular interest and Class A-3FX Regular Interest), to principal on the Class B regular interest until its principal balance is reduced to zero; and (c) next, to reimburse the holders of the Class B regular interest for any previously unreimbursed losses (other than certain Trust Advisor expenses) on the mortgage loans that were previously allocated to that Class in reduction of its principal balance. 6. Class C regular interest: To make distributions on the Class C regular interest as follows: (a) first, to interest on Class C regular interest in the amount of the interest entitlement for that Class; (b) next, to the extent of the portion of the Principal Distribution Amount remaining after distributions in respect of principal to each Class with a higher distribution priority (in this case, the Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates, Class A-S and B regular interests and Class A-3FX Regular Interest), to principal on the Class C regular interest until its principal balance is reduced to zero; and (c) next, to reimburse the holders of the Class C regular interest for any previously unreimbursed losses (other than certain Trust Advisor expenses) on the mortgage loans that were previously allocated to that Class in reduction of its principal balance. | ||

7. After the Class A-1, A-2, A-3, A-4, A-5 and A-SB Certificates and Class A-S, B and C regular interests and Class A-3FX Regular Interest are paid all amounts to which they are entitled, the remaining funds available for distribution will be used to pay interest, principal and loss reimbursement amounts (other than certain Trust Advisor expenses) on the Class D, E, F and G Certificates sequentially in that order in a manner analogous to the Class C regular interest. Amounts distributed in respect of the Class A-3FX Regular Interest will generally be allocated between the Class A-3FX and A-3FL Certificates in accordance with their class percentage interests. | ||

| Allocations and Distributions on the Class A-S, B, C and PEX Certificates: | On the closing date, the upper-tier REMIC of the issuing entity will issue the Class A-S, Class B and Class C regular interests (each a “regular interest”) which will have outstanding principal balances on the closing date of $116,257,000, $88,072,000 and $56,367,000, respectively. The regular interests will be held in a grantor trust for the benefit of the holders of the Class A-S, B, C and PEX Certificates. The Class A-S, B, C and PEX Certificates will, at all times, represent undivided beneficial ownership interests in a grantor trust that will hold those regular interests. Each class of the Class A-S, B, C and PEX Certificates will, at all times, represent an undivided |

| Wells Fargo Commercial Mortgage Trust 2013-LC12 | Certain Terms and Conditions |

beneficial ownership interest in a percentage of the outstanding principal balance of the regular interest with the same alphabetical class designation. The Class PEX Certificates will, at all times, represent an undivided beneficial ownership interest in the remaining percentages of the outstanding principal balances of the Class A-S, B and C regular interests and which percentage interests are referred to in this Term Sheet as the “Class PEX Component A-S, Class PEX Component B and Class PEX Component C” (collectively, the “Class PEX Components”). Interest, principal, prepayment premiums, yield maintenance charges and voting rights that are allocated to the Class A-S, B or C regular interest will be distributed or allocated, as applicable, as between the Class A-S, B or C Certificates, as applicable, on the one hand, and Class PEX Component A-S, Class PEX Component B or Class PEX Component C, as applicable (and correspondingly, the Class PEX Certificates), on the other hand, pro rata, based on their respective percentage interests in the Class A-S, Class B or Class C regular interest, as applicable. In addition, any losses (including, without limitation, as a result of Trust Advisor expenses) that are allocated to the Class A-S, Class B or Class C regular interest will correspondingly be allocated as between the Class A-S, B or C Certificates, as applicable, on the one hand, and Class PEX Component A-S, Class PEX Component B or Class PEX Component C, as applicable (and correspondingly, the Class PEX Certificates), on the other hand, pro rata, based on their respective percentage interests in the Class A-S, Class B or Class C regular interest, as applicable. For a complete description of the allocations and distributions with respect to the Class A-S regular interest, the Class B regular interest and the Class C regular interest (and correspondingly the Class A-S, B, C and PEX Certificates and the Class PEX Component A-S, Class PEX Component B and Class PEX Component C), see “Description of the Offered Certificates” in the Free Writing Prospectus. See “Material Federal Income Tax Consequences” in the Free Writing Prospectus for a discussion of the tax treatment of the Exchangeable Certificates. | ||

Exchanging Certificates through Combination and Recombination: | If you own Class A-S, B and C Certificates, you will be able to exchange them for a proportionate interest in the Class PEX Certificates, and vice versa, as described in the Free Writing Prospectus. You can exchange your Exchangeable Certificates by notifying the Certificate Administrator. If Exchangeable Certificates are outstanding and held by certificateholders, those certificates will receive principal and interest that would otherwise have been payable on the same proportion of certificates exchanged therefor if those certificates were outstanding and held by certificateholders. Any such allocations of principal and interest between classes of Exchangeable Certificates will have no effect on the principal or interest entitlements of any other class of certificates. The Free Writing Prospectus describes the available combinations of Exchangeable Certificates eligible for exchange. | |