UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-22920

The Advisors’ Inner Circle Fund III

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: (877) 446-3863

Date of fiscal year end: October 31, 2024

Date of reporting period: October 31, 2024

Item 1. Reports to Stockholders.

| (a) | A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR § 270.30e-1), is attached hereto. |

The Advisors' Inner Circle Fund III

FS Chiron Capital Allocation Fund

Annual Shareholder Report: October 31, 2024

This annual shareholder report contains important information about Class I Shares of the FS Chiron Capital Allocation Fund (the "Fund") for the period from November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://fsinvestments.com/investments/all-investments/ccapx/. You can also request this information by contacting us at 877-9-CHIRON(877-924-4766).

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| FS Chiron Capital Allocation Fund, Class I Shares | $127 | 1.16% |

How did the Fund perform in the last year?

For the fiscal year ended October 31, 2024, FS Chiron Capital Allocation Fund (the “Fund”) returned 19.45% (Class I shares), underperforming its benchmark return of 23.50% by 405bps. The Fund's blended benchmark is weighted 60% MSCI All Country World Index (MSCI ACWI Net) and 40% Bloomberg U.S. Aggregate Bond Index. While we measure the Fund against a blended benchmark, we do not manage to a static benchmark profile.

The Fund seeks to achieve its objective by allocating its assets among equity, debt, precious metals, and cash investments in markets around the globe. Subject to the allocation targets below, the combination of the Fund’s investments will vary from time to time both with respect to the types of securities and markets, in response to changing market and economic trends. In deciding between equity and debt investments, the Fund utilizes a “quantamental” approach, which combines quantitative and fundamental research.

Portfolio Positioning

To start the year, we saw improved market sentiment given a combination of positive seasonal impacts, investor sentiment that became less bearish, and falling interest rates. We were overweight large-cap stocks and underweight cyclical stocks. We reduced our fixed income on the back of lower rates. As we entered 2024, the Fund’s risk profile was roughly in line with the benchmark. Our largest sector overweights were to be defensives sectors– consumer staples, healthcare care and energy – and technology remained the top allocations on an absolute basis. In fixed income we were well below our 40% benchmark weight.

As we finished the first quarter of 2024 our model readings favored growth stocks, they also showed a preference for low-volatility and earnings quality, highlighting the Fund’s tilt toward GARP (growth at a reasonable price) names. The market was rewarding firms in any sector for strong free cash flow and growth metrics, a theme we were weaving throughout our portfolio. We maintained exposure to these companies while remaining balanced to cyclical and defensive companies with a preference for companies with attractive free cash flow margins and yields. During the second quarter we worked to minimize outsized risk in the portfolio while remaining invested. The equity portfolio was weighted towards large cap, low-beta, defensively oriented stocks. We reduced our emerging market holdings, with majority of the reduction coming in China. While sovereign bond exposure rose in June, we continued to prefer precious metals to bonds as a portfolio ballast, and we increased exposure to gold and silver, which we viewed as better diversifiers given market conditions.

To end the third quarter our models sat close to full Growth in developed markets, including the U.S. In most parts of the world cyclicals appeared to be fully priced in, advocating for a careful approach to risk-taking. The strongest signals in our models continued to be growth stocks over value stocks, and large caps over small caps. The Fund’s equity exposure remains at about 60%, in line with its benchmark.

To finish its fiscal year the top holdings in the portfolio continue to be comprised mostly of the largest, highest-quality technology firms, which we viewed as broadly resilient to both an economic growth scare and a rising-rate environment. Beyond this core, the book was largely balanced, with an underweight to cheap cyclicals and a slight overweight to defensives.

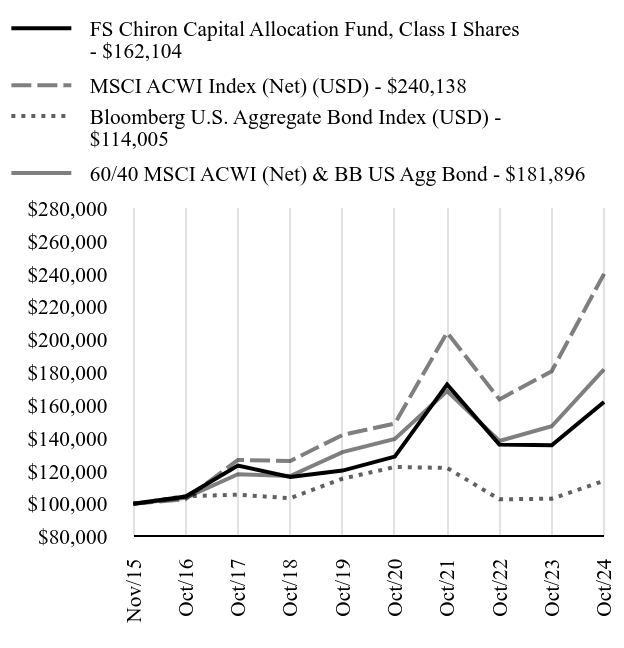

How did the Fund perform since inception?

Total Return Based on $100,000 Investment

| FS Chiron Capital Allocation Fund, Class I Shares - $162104 | MSCI ACWI Index (Net) (USD) - $240138 | Bloomberg U.S. Aggregate Bond Index (USD) - $114005 | 60/40 MSCI ACWI (Net) & BB US Agg Bond - $181896 |

|---|

| Nov/15 | $100000 | $100000 | $100000 | $100000 |

| Oct/16 | $104466 | $102898 | $104647 | $103746 |

| Oct/17 | $123280 | $126773 | $105591 | $118069 |

| Oct/18 | $116355 | $126117 | $103423 | $116912 |

| Oct/19 | $120266 | $141996 | $115326 | $131553 |

| Oct/20 | $128802 | $148937 | $122462 | $139485 |

| Oct/21 | $172774 | $204457 | $121876 | $168808 |

| Oct/22 | $136095 | $163653 | $102763 | $138350 |

| Oct/23 | $135707 | $180839 | $103129 | $147283 |

| Oct/24 | $162104 | $240138 | $114005 | $181896 |

Since its inception on November 30, 2015. The line graph represents historical performance of a hypothetical investment of $100,000 in the Fund since inception. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is not indicative of future performance.Call 877-9-CHIRON(877-924-4766) or visit https://fsinvestments.com/investments/all-investments/ccapx/ for current month-end performance.

Average Annual Total Returns as of October 31, 2024

| Fund/Index Name | 1 Year | 5 Years | Annualized Since Inception |

|---|

| FS Chiron Capital Allocation Fund, Class I Shares | 19.45% | 6.15% | 5.56% |

| MSCI ACWI Index (Net) (USD) | 32.79% | 11.08% | 10.31% |

| Bloomberg U.S. Aggregate Bond Index (USD) | 10.55% | -0.23% | 1.48% |

| 60/40 MSCI ACWI (Net) & BB US Agg Bond | 23.50% | 6.70% | 6.93% |

Key Fund Statistics as of October 31, 2024

| Total Net Assets (000's) | Number of Holdings | Total Advisory Fees Paid (000's) | Portfolio Turnover Rate |

|---|

| $408,954 | 87 | $4,613 | 171% |

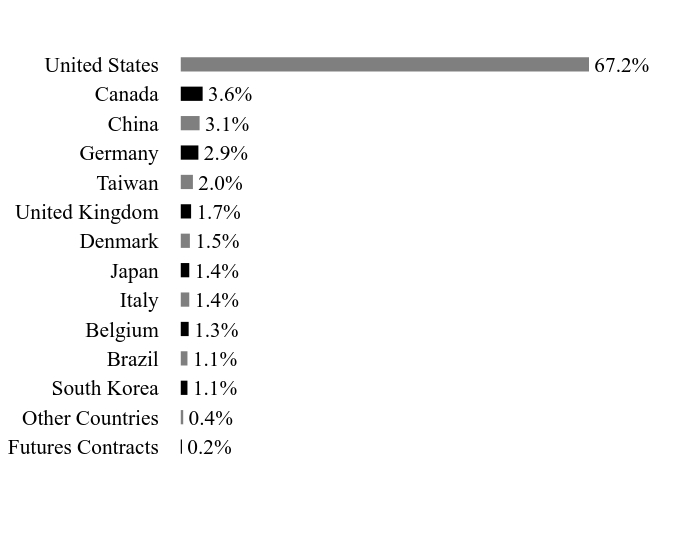

What did the Fund invest in?

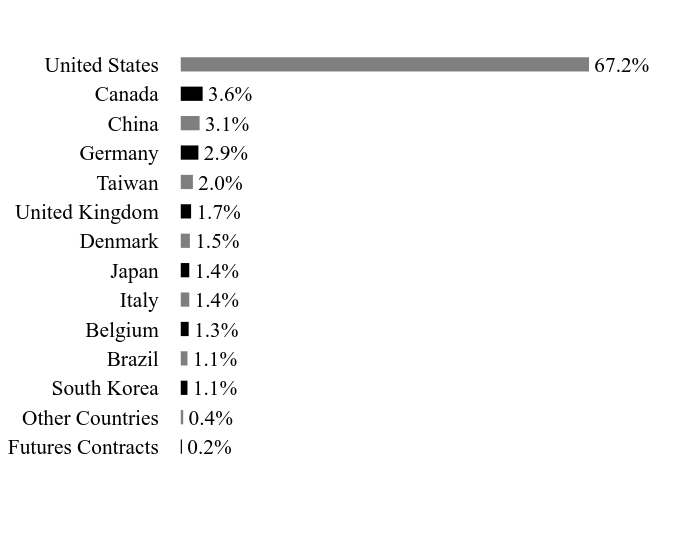

Country WeightingsFootnote Reference*

| Value | Value |

|---|

| Futures Contracts | 0.2% |

| Other Countries | 0.4% |

| South Korea | 1.1% |

| Brazil | 1.1% |

| Belgium | 1.3% |

| Italy | 1.4% |

| Japan | 1.4% |

| Denmark | 1.5% |

| United Kingdom | 1.7% |

| Taiwan | 2.0% |

| Germany | 2.9% |

| China | 3.1% |

| Canada | 3.6% |

| United States | 67.2% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | | | Percentage of Total Net Assets |

|---|

| U.S. Treasury Bill, 5.15%, 11/7/2024 | | | 10.1% |

| Jonah Energy, 7.20%, 12/10/2037, Cl A1 | | | 3.1% |

| NVIDIA | | | 2.6% |

| Apple | | | 2.5% |

| ServiceNow | | | 2.3% |

| Barrick Gold | | | 2.2% |

| Newmont | | | 2.1% |

| JPMorgan Chase | | | 2.0% |

| Taiwan Semiconductor Manufacturing ADR | | | 2.0% |

| Microsoft | | | 2.0% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy voting information, call or visit:

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds. Once implemented, if you would like to discontinue householding for your accounts, please call toll-free at 877-9-CHIRON(877-924-4766) to request individual copies of these documents. Once the Fund receives notice to stop householding, we will begin sending individual copies 30 days after receiving your request.

The Advisors' Inner Circle Fund III

FS Chiron Capital Allocation Fund / Class I Shares - CCAPX

Annual Shareholder Report: October 31, 2024

CHI-AR-TSR-2024-3

The Advisors' Inner Circle Fund III

FS Chiron Capital Allocation Fund

Annual Shareholder Report: October 31, 2024

This annual shareholder report contains important information about Class A Shares of the FS Chiron Capital Allocation Fund (the "Fund") for the period from November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://fsinvestments.com/investments/all-investments/ccpax/. You can also request this information by contacting us at 877-9-CHIRON(877-924-4766).

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| FS Chiron Capital Allocation Fund, Class A Shares | $154 | 1.41% |

How did the Fund perform in the last year?

For the fiscal year ended October 31, 2024, FS Chiron Capital Allocation Fund (the “Fund”) returned 19.14% (Class A shares), underperforming its benchmark return of 23.50% by 436bps. The Fund's blended benchmark is weighted 60% MSCI All Country World Index (MSCI ACWI Net) and 40% Bloomberg U.S. Aggregate Bond Index. While we measure the Fund against a blended benchmark, we do not manage to a static benchmark profile.

The Fund seeks to achieve its objective by allocating its assets among equity, debt, precious metals, and cash investments in markets around the globe. Subject to the allocation targets below, the combination of the Fund’s investments will vary from time to time both with respect to the types of securities and markets, in response to changing market and economic trends. In deciding between equity and debt investments, the Fund utilizes a “quantamental” approach, which combines quantitative and fundamental research.

Portfolio Positioning

To start the year, we saw improved market sentiment given a combination of positive seasonal impacts, investor sentiment that became less bearish, and falling interest rates. We were overweight large-cap stocks and underweight cyclical stocks. We reduced our fixed income on the back of lower rates. As we entered 2024, the Fund’s risk profile was roughly in line with the benchmark. Our largest sector overweights were to be defensives sectors– consumer staples, healthcare care and energy – and technology remained the top allocations on an absolute basis. In fixed income we were well below our 40% benchmark weight.

As we finished the first quarter of 2024 our model readings favored growth stocks, they also showed a preference for low-volatility and earnings quality, highlighting the Fund’s tilt toward GARP (growth at a reasonable price) names. The market was rewarding firms in any sector for strong free cash flow and growth metrics, a theme we were weaving throughout our portfolio. We maintained exposure to these companies while remaining balanced to cyclical and defensive companies with a preference for companies with attractive free cash flow margins and yields. During the second quarter we worked to minimize outsized risk in the portfolio while remaining invested. The equity portfolio was weighted towards large cap, low-beta, defensively oriented stocks. We reduced our emerging market holdings, with majority of the reduction coming in China. While sovereign bond exposure rose in June, we continued to prefer precious metals to bonds as a portfolio ballast, and we increased exposure to gold and silver, which we viewed as better diversifiers given market conditions.

To end the third quarter our models sat close to full Growth in developed markets, including the U.S. In most parts of the world cyclicals appeared to be fully priced in, advocating for a careful approach to risk-taking. The strongest signals in our models continued to be growth stocks over value stocks, and large caps over small caps. The Fund’s equity exposure remains at about 60%, in line with its benchmark.

To finish its fiscal year the top holdings in the portfolio continue to be comprised mostly of the largest, highest-quality technology firms, which we viewed as broadly resilient to both an economic growth scare and a rising-rate environment. Beyond this core, the book was largely balanced, with an underweight to cheap cyclicals and a slight overweight to defensives.

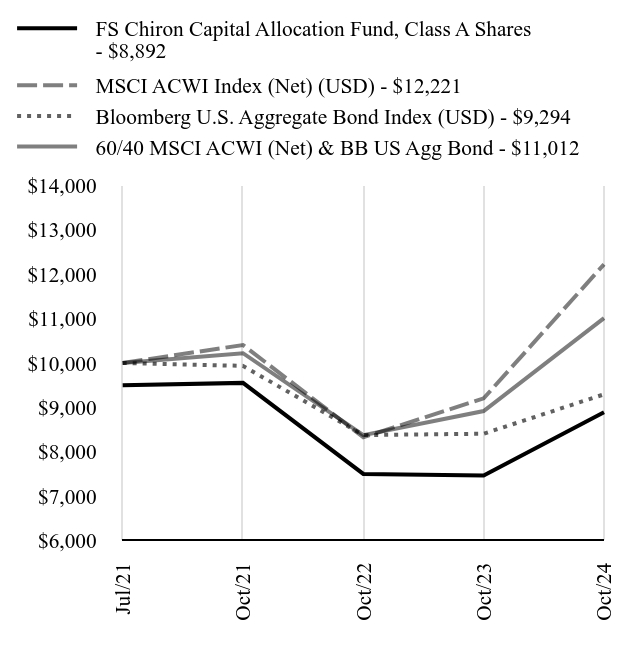

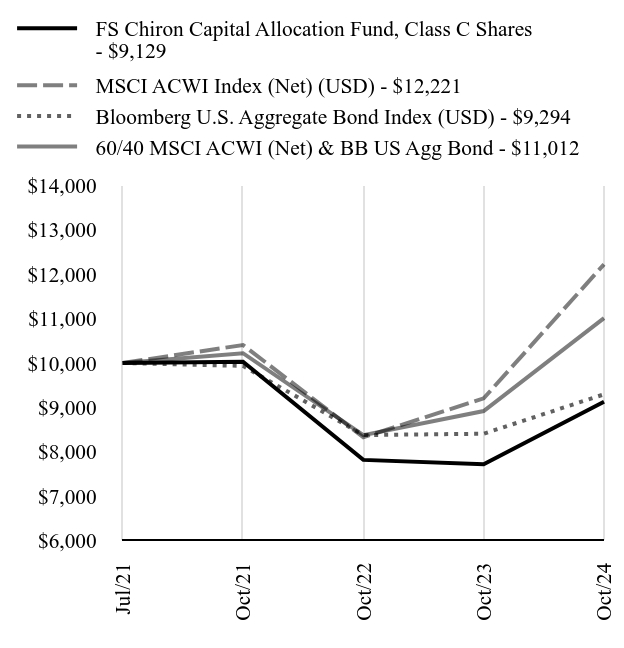

How did the Fund perform since inception?

Total Return Based on $10,000 Investment

| FS Chiron Capital Allocation Fund, Class A Shares - $8892 | MSCI ACWI Index (Net) (USD) - $12221 | Bloomberg U.S. Aggregate Bond Index (USD) - $9294 | 60/40 MSCI ACWI (Net) & BB US Agg Bond - $11012 |

|---|

| Jul/21 | $9500 | $10000 | $10000 | $10000 |

| Oct/21 | $9552 | $10405 | $9935 | $10220 |

| Oct/22 | $7502 | $8328 | $8377 | $8376 |

| Oct/23 | $7464 | $9203 | $8407 | $8917 |

| Oct/24 | $8892 | $12221 | $9294 | $11012 |

Since its inception on July 16, 2021. The line graph represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is not indicative of future performance.Call 877-9-CHIRON(877-924-4766) or visit https://fsinvestments.com/investments/all-investments/ccpax/ for current month-end performance.

Average Annual Total Returns as of October 31, 2024

| Fund/Index Name | 1 Year | Annualized Since Inception |

|---|

| FS Chiron Capital Allocation Fund | | |

| Class A Shares, With Load | 13.16% | -3.51% |

| Class A Shares, Without Load | 19.14% | -1.99% |

| MSCI ACWI Index (Net) (USD) | 32.79% | 6.27% |

| Bloomberg U.S. Aggregate Bond Index (USD) | 10.55% | -2.20% |

| 60/40 MSCI ACWI (Net) & BB US Agg Bond | 23.50% | 2.97% |

Key Fund Statistics as of October 31, 2024

| Total Net Assets (000's) | Number of Holdings | Total Advisory Fees Paid (000's) | Portfolio Turnover Rate |

|---|

| $408,954 | 87 | $4,613 | 171% |

What did the Fund invest in?

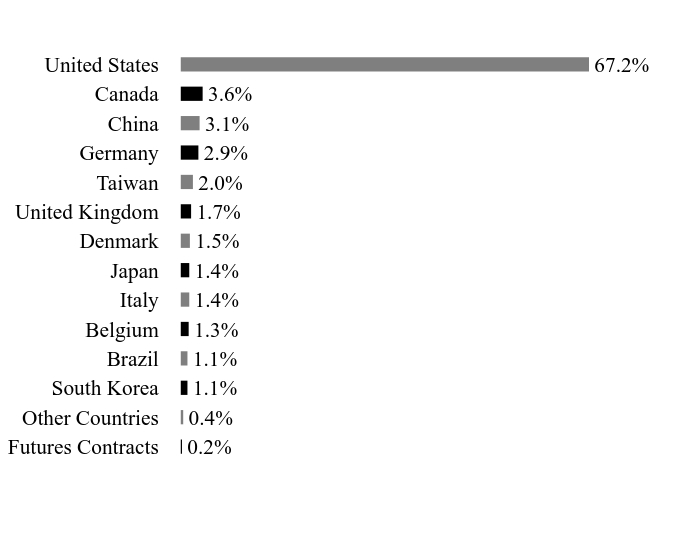

Country WeightingsFootnote Reference*

| Value | Value |

|---|

| Futures Contracts | 0.2% |

| Other Countries | 0.4% |

| South Korea | 1.1% |

| Brazil | 1.1% |

| Belgium | 1.3% |

| Italy | 1.4% |

| Japan | 1.4% |

| Denmark | 1.5% |

| United Kingdom | 1.7% |

| Taiwan | 2.0% |

| Germany | 2.9% |

| China | 3.1% |

| Canada | 3.6% |

| United States | 67.2% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | | | Percentage of Total Net Assets |

|---|

| U.S. Treasury Bill, 5.15%, 11/7/2024 | | | 10.1% |

| Jonah Energy, 7.20%, 12/10/2037, Cl A1 | | | 3.1% |

| NVIDIA | | | 2.6% |

| Apple | | | 2.5% |

| ServiceNow | | | 2.3% |

| Barrick Gold | | | 2.2% |

| Newmont | | | 2.1% |

| JPMorgan Chase | | | 2.0% |

| Taiwan Semiconductor Manufacturing ADR | | | 2.0% |

| Microsoft | | | 2.0% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy voting information, call or visit:

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds. Once implemented, if you would like to discontinue householding for your accounts, please call toll-free at 877-9-CHIRON(877-924-4766) to request individual copies of these documents. Once the Fund receives notice to stop householding, we will begin sending individual copies 30 days after receiving your request.

The Advisors' Inner Circle Fund III

FS Chiron Capital Allocation Fund / Class A Shares - CCPAX

Annual Shareholder Report: October 31, 2024

CHI-AR-TSR-2024-1

The Advisors' Inner Circle Fund III

FS Chiron Capital Allocation Fund

Annual Shareholder Report: October 31, 2024

This annual shareholder report contains important information about Class C Shares of the FS Chiron Capital Allocation Fund (the "Fund") for the period from November 1, 2023 to October 31, 2024. You can find additional information about the Fund at https://fsinvestments.com/investments/all-investments/ccpcx/. You can also request this information by contacting us at 877-9-CHIRON(877-924-4766).

What were the Fund costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| FS Chiron Capital Allocation Fund, Class C Shares | $236 | 2.16% |

How did the Fund perform in the last year?

For the fiscal year ended October 31, 2024, FS Chiron Capital Allocation Fund (the “Fund”) returned 18.24% (Class C shares), underperforming its benchmark return of 23.50% by 526bps. The Fund's blended benchmark is weighted 60% MSCI All Country World Index (MSCI ACWI Net) and 40% Bloomberg U.S. Aggregate Bond Index. While we measure the Fund against a blended benchmark, we do not manage to a static benchmark profile.

The Fund seeks to achieve its objective by allocating its assets among equity, debt, precious metals, and cash investments in markets around the globe. Subject to the allocation targets below, the combination of the Fund’s investments will vary from time to time both with respect to the types of securities and markets, in response to changing market and economic trends. In deciding between equity and debt investments, the Fund utilizes a “quantamental” approach, which combines quantitative and fundamental research.

Portfolio Positioning

To start the year, we saw improved market sentiment given a combination of positive seasonal impacts, investor sentiment that became less bearish, and falling interest rates. We were overweight large-cap stocks and underweight cyclical stocks. We reduced our fixed income on the back of lower rates. As we entered 2024, the Fund’s risk profile was roughly in line with the benchmark. Our largest sector overweights were to be defensives sectors– consumer staples, healthcare care and energy – and technology remained the top allocations on an absolute basis. In fixed income we were well below our 40% benchmark weight.

As we finished the first quarter of 2024 our model readings favored growth stocks, they also showed a preference for low-volatility and earnings quality, highlighting the Fund’s tilt toward GARP (growth at a reasonable price) names. The market was rewarding firms in any sector for strong free cash flow and growth metrics, a theme we were weaving throughout our portfolio. We maintained exposure to these companies while remaining balanced to cyclical and defensive companies with a preference for companies with attractive free cash flow margins and yields. During the second quarter we worked to minimize outsized risk in the portfolio while remaining invested. The equity portfolio was weighted towards large cap, low-beta, defensively oriented stocks. We reduced our emerging market holdings, with majority of the reduction coming in China. While sovereign bond exposure rose in June, we continued to prefer precious metals to bonds as a portfolio ballast, and we increased exposure to gold and silver, which we viewed as better diversifiers given market conditions.

To end the third quarter our models sat close to full Growth in developed markets, including the U.S. In most parts of the world cyclicals appeared to be fully priced in, advocating for a careful approach to risk-taking. The strongest signals in our models continued to be growth stocks over value stocks, and large caps over small caps. The Fund’s equity exposure remains at about 60%, in line with its benchmark.

To finish its fiscal year the top holdings in the portfolio continue to be comprised mostly of the largest, highest-quality technology firms, which we viewed as broadly resilient to both an economic growth scare and a rising-rate environment. Beyond this core, the book was largely balanced, with an underweight to cheap cyclicals and a slight overweight to defensives.

How did the Fund perform since inception?

Total Return Based on $10,000 Investment

| FS Chiron Capital Allocation Fund, Class C Shares - $9129 | MSCI ACWI Index (Net) (USD) - $12221 | Bloomberg U.S. Aggregate Bond Index (USD) - $9294 | 60/40 MSCI ACWI (Net) & BB US Agg Bond - $11012 |

|---|

| Jul/21 | $10000 | $10000 | $10000 | $10000 |

| Oct/21 | $10030 | $10405 | $9935 | $10220 |

| Oct/22 | $7818 | $8328 | $8377 | $8376 |

| Oct/23 | $7721 | $9203 | $8407 | $8917 |

| Oct/24 | $9129 | $12221 | $9294 | $11012 |

Since its inception on July 16, 2021. The line graph represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Returns shown are total returns, which assume the reinvestment of dividends and capital gains. The table and graph presented above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. Past performance is not indicative of future performance.Call 877-9-CHIRON(877-924-4766) or visit https://fsinvestments.com/investments/all-investments/ccpcx/ for current month-end performance.

Average Annual Total Returns as of October 31, 2024

| Fund/Index Name | 1 Year | Annualized Since Inception |

|---|

| FS Chiron Capital Allocation Fund, Class C Shares | 18.24% | -2.73% |

| MSCI ACWI Index (Net) (USD) | 32.79% | 6.27% |

| Bloomberg U.S. Aggregate Bond Index (USD) | 10.55% | -2.20% |

| 60/40 MSCI ACWI (Net) & BB US Agg Bond | 23.50% | 2.97% |

Key Fund Statistics as of October 31, 2024

| Total Net Assets (000's) | Number of Holdings | Total Advisory Fees Paid (000's) | Portfolio Turnover Rate |

|---|

| $408,954 | 87 | $4,613 | 171% |

What did the Fund invest in?

Country WeightingsFootnote Reference*

| Value | Value |

|---|

| Futures Contracts | 0.2% |

| Other Countries | 0.4% |

| South Korea | 1.1% |

| Brazil | 1.1% |

| Belgium | 1.3% |

| Italy | 1.4% |

| Japan | 1.4% |

| Denmark | 1.5% |

| United Kingdom | 1.7% |

| Taiwan | 2.0% |

| Germany | 2.9% |

| China | 3.1% |

| Canada | 3.6% |

| United States | 67.2% |

| Footnote | Description |

Footnote* | Percentages are calculated based on total net assets. |

| Holding Name | | | Percentage of Total Net Assets |

|---|

| U.S. Treasury Bill, 5.15%, 11/7/2024 | | | 10.1% |

| Jonah Energy, 7.20%, 12/10/2037, Cl A1 | | | 3.1% |

| NVIDIA | | | 2.6% |

| Apple | | | 2.5% |

| ServiceNow | | | 2.3% |

| Barrick Gold | | | 2.2% |

| Newmont | | | 2.1% |

| JPMorgan Chase | | | 2.0% |

| Taiwan Semiconductor Manufacturing ADR | | | 2.0% |

| Microsoft | | | 2.0% |

There were no material changes during the reporting period.

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the reporting period.

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy voting information, call or visit:

Rule 30e-1 of the Investment Company Act of 1940 permits funds to transmit only one copy of a proxy statement, annual report or semi-annual report to shareholders (who need not be related) with the same residential, commercial or electronic address, provided that the shareholders have consented in writing and the reports are addressed either to each shareholder individually or to the shareholders as a group. This process is known as “householding” and is designed to reduce the duplicate copies of materials that shareholders receive and to lower printing and mailing costs for funds. Once implemented, if you would like to discontinue householding for your accounts, please call toll-free at 877-9-CHIRON(877-924-4766) to request individual copies of these documents. Once the Fund receives notice to stop householding, we will begin sending individual copies 30 days after receiving your request.

The Advisors' Inner Circle Fund III

FS Chiron Capital Allocation Fund / Class C Shares - CCPCX

Annual Shareholder Report: October 31, 2024

CHI-AR-TSR-2024-2

Item 2. Code of Ethics.

The Registrant (also referred to as the “Trust”) has adopted a code of ethics that applies to the Registrant’s principal executive officer, principal financial officer, controller or principal accounting officer, and any person who performs a similar function. There have been no amendments to or waivers granted to this code of ethics during the period covered by this report.

Item 3. Audit Committee Financial Expert.

(a)(1) The Registrant’s board of trustees has determined that the Registrant has at least one audit committee financial expert serving on the audit committee.

(a)(2) The Registrant’s audit committee financial experts are Thomas P. Lemke and Jay Nadel, and each of Mr. Lemke and Mr. Nadel is “independent” as that term is defined in Form N-CSR Item 3 (a)(2).

Item 4. Principal Accountant Fees and Services.

Fees billed by PricewaterhouseCoopers LLP (“PwC”) related to the Trust.

PwC billed the Trust aggregate fees for services rendered to the Trust for the last two fiscal years as follows:

| | FYE October 31, 2024 | FYE October 31, 2023 |

| | | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval |

| (a) | Audit Fees(1) | $734,463 | None | None | $717,900 | None | None |

| (b) | Audit-Related Fees | None | None | None | None | None | None |

| (c) | Tax Fees | None | None | $559,700(2) | None | None | $807,756(2) |

| (d) | All Other Fees | None | None | $10,530(4) | None | None | $7,535(4) |

Fees billed by Ernst & Young LLP (“E&Y”) related to the Trust.

E&Y billed the Trust aggregate fees for services rendered to the Trust for the last two fiscal years as follows:

| | FYE October 31, 2024 | FYE October 31, 2023 |

| | | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval |

| (a) | Audit Fees(1) | $113,052 | None | None | $137,200 | None | None |

| (b) | Audit-Related Fees | None | None | None | None | None | None |

| (c) | Tax Fees | None | None | None | None | None | None |

| (d) | All Other Fees | None | None | None | None | None | None |

Fees billed by Deloitte & Touche LLP (“D&T”) related to the Trust.

D&T billed the Trust aggregate fees for services rendered to the Trust for the last two fiscal years as follows

| | FYE October 31, 2024 | FYE October 31, 2023 |

| | | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval |

| (a) | Audit Fees(1) | $30,000 | None | None | $30,624 | None | None |

| (b) | Audit-Related Fees | None | None | None | None | None | None |

| (c) | Tax Fees | None | None | None | None | None | None |

| (d) | All Other Fees | None | None | None | None | None | None |

Fees billed by KPMG (“KPMG”) related to the Trust.

KPMG billed the Trust aggregate fees for services rendered to the Trust for the last two fiscal years as follows

| | FYE October 31, 2024 | FYE October 31, 2023 |

| | | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Trust that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval |

| (a) | Audit Fees(1) | $45,000 | None | None | $363,625 | None | None |

| (b) | Audit-Related Fees | None | None | None | None | None | None |

| (c) | Tax Fees | None | None | None | None | None | None |

| (d) | All Other Fees | None | None | $154,000(3) | None | None | $282,908(3) |

Notes:

| (1) | Audit fees include amounts related to the audit of the Trust’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. |

| (2) | Tax return preparation fees for affiliates of the Funds. |

| (3) | Non-audit fees consist of SSAE No. 18 report over investment management activities and non-statutory audit reports of Legal & General Investment Management America, Inc. |

| (4) | Non-audit assurance engagements for service affiliates of the funds. |

(e)(1) The Trust’s Audit Committee has adopted and the Board of Trustees has ratified an Audit and Non-Audit Services Pre-Approval Policy (the “Policy”), which sets forth the procedures and the conditions pursuant to which services proposed to be performed by the independent auditor of the Funds may be pre-approved.

The Policy provides that all requests or applications for proposed services to be provided by the independent auditor must be submitted to the Registrant’s Chief Financial Officer (“CFO”) and must include a detailed description of the services proposed to be rendered. The CFO will determine whether such services:

| 1. | require specific pre-approval; |

| 2. | are included within the list of services that have received the general pre-approval of the Audit Committee pursuant to the Policy; or |

| 3. | have been previously pre-approved in connection with the independent auditor’s annual engagement letter for the applicable year or otherwise. In any instance where services require pre-approval, the Audit Committee will consider whether such services are consistent with SEC’s rules and whether the provision of such services would impair the auditor’s independence. |

Requests or applications to provide services that require specific pre-approval by the Audit Committee will be submitted to the Audit Committee by the CFO. The Audit Committee will be informed by the CFO on a quarterly basis of all services rendered by the independent auditor. The Audit Committee has delegated specific pre-approval authority to either the Audit Committee Chair or financial expert, provided that the estimated fee for any such proposed pre-approved service does not exceed $100,000 and any pre-approval decisions are reported to the Audit Committee at its next regularly-scheduled meeting.

Services that have received the general pre-approval of the Audit Committee are identified and described in the Policy. In addition, the Policy sets forth a maximum fee per engagement with respect to each identified service that has received general pre-approval.

All services to be provided by the independent auditor shall be provided pursuant to a signed written engagement letter with the Registrant, the investment adviser, or applicable control affiliate (except that matters as to which an engagement letter would be impractical because of timing issues or because the matter is small may not be the subject of an engagement letter) that sets forth both the services to be provided by the independent auditor and the total fees to be paid to the independent auditor for those services.

In addition, the Audit Committee has determined to take additional measures on an annual basis to meet the Audit Committee’s responsibility to oversee the work of the independent auditor and to assure the auditor's independence from the Registrant, such as (a) reviewing a formal written statement from the independent auditor delineating all relationships between the independent auditor and the Registrant, and (b) discussing with the independent auditor the independent auditor’s methods and procedures for ensuring independence.

(e)(2) Percentage of fees billed applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows (PwC):

| | FYE

October

31, 2024 | FYE

October

31, 2023 |

| Audit-Related Fees | None | None |

| Tax Fees | None | None |

| All Other Fees | None | None |

(e)(2) Percentage of fees billed applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows (E&Y):

| | FYE

October

31, 2024 | FYE

October

31, 2023 |

| Audit-Related Fees | None | None |

| Tax Fees | None | None |

| All Other Fees | None | None |

(e)(2) Percentage of fees billed applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows (D&T):

| | FYE

October

31, 2024 | FYE

October

31, 2023 |

| Audit-Related Fees | None | None |

| Tax Fees | None | None |

| All Other Fees | None | None |

(e)(2) Percentage of fees billed applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows (KPMG):

| | FYE

October

31, 2024 | FYE

October

31, 2023 |

| Audit-Related Fees | None | None |

| Tax Fees | None | None |

| All Other Fees | None | None |

(f) Not applicable.

(g) The aggregate non-audit fees and services billed by PwC for services rendered to the Registrant, and rendered to the Registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the Registrant for the last two fiscal-years-ended October 31st were $570,230 and $815,291 for 2024 and 2023, respectively.

(g) The aggregate non-audit fees and services billed by E&Y for services rendered to the Registrant, and rendered to the Registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the Registrant for the last two fiscal-years-ended October 31st were $0 and $0 for 2024 and 2023, respectively.

(g) The aggregate non-audit fees and services billed by D&T for services rendered to the Registrant, and rendered to the Registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the Registrant for the last two fiscal-years-ended October 31st were $0 and $0 for 2024 and 2023, respectively.

(g) The aggregate non-audit fees and services billed by KPMG for services rendered to the Registrant, and rendered to the Registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the Registrant for the last two fiscal-years-ended October 31st were $154,000 and $282,908 for 2024 and 2023, respectively.

(h) During the past fiscal year, all non-audit services provided by the Registrant’s principal accountant to either the Registrant’s investment adviser or to any entity controlling, controlled by, or under common control with the Registrant’s investment adviser that provides ongoing services to the Registrant were pre-approved by the Audit Committee of Registrant’s Board of Trustees. Included in the Audit Committee’s pre-approval of these non-audit service were the review and consideration as to whether the provision of these non-audit services is compatible with maintaining the principal accountant’s independence.

(i) Not applicable. The Registrant has not retained, for the preparation of the audit report on the financial statements included in the Form N-CSR, a registered public accounting firm that has a branch or office that is located in a foreign jurisdiction and that the Public Company Accounting Oversight Board (the “PCAOB”) has determined that the PCAOB is unable to inspect or investigate completely because of a position taken by an authority in the foreign jurisdiction.

(j) Not applicable. The Registrant is not a “foreign issuer,” as defined in 17 CFR § 240.3b-4.

Item 5. Audit Committee of Listed Registrants.

Not applicable to open-end management investment companies.

Item 6. Schedule of Investments.

(a) The Schedule of Investments is included as part of the Financial Statements and Other Information filed under Item 7 of this form.

(b) Not applicable.

Item 7. Financial Statements and Financial Highlights for Open-End Management Investment Companies.

Financial statements and financial highlights are filed herein.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON |

| | CAPITAL ALLOCATION FUND |

| | OCTOBER 31, 2024 |

TABLE OF CONTENTS

| Financial Statements (Form N-CSR Item 7) | |

| Consolidated Schedule of Investments | 1 |

| Consolidated Statement of Assets and Liabilities | 8 |

| Consolidated Statement of Operations | 10 |

| Consolidated Statements of Changes in Net Assets | 11 |

| Consolidated Financial Highlights | 13 |

| Notes to Consolidated Financial Statements | 16 |

| Report of Independent Registered Public Accounting Firm | 40 |

| Notice to Shareholders (Unaudited) | 42 |

| Approval of Investment Advisory Agreement (Form N-CSR Item 11)(Unaudited) | 43 |

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON |

| | CAPITAL ALLOCATION FUND |

| | OCTOBER 31, 2024 |

CONSOLIDATED SCHEDULE OF INVESTMENTS

(Percentages are based on Net Assets of $408,954 (000))

COMMON STOCK — 69.6%

| | | Shares | | | Fair Value (000) | |

| BELGIUM — 1.3% | | | | | | | | |

| Anheuser-Busch InBev | | | 92,055 | | | $ | 5,505 | |

| | | | | | | | | |

| BRAZIL — 1.1% | | | | | | | | |

| MercadoLibre* | | | 2,297 | | | | 4,679 | |

| | | | | | | | | |

| CANADA — 3.6% | | | | | | | | |

| Agnico Eagle Mines | | | 65,605 | | | | 5,661 | |

| Barrick Gold | | | 462,416 | | | | 8,934 | |

| | | | | | | | | |

| | | | | | | | 14,595 | |

| CHINA — 3.1% | | | | | | | | |

| Alibaba Group Holding ADR | | | 61,359 | | | | 6,012 | |

| Tencent Holdings | | | 128,900 | | | | 6,709 | |

| | | | | | | | | |

| | | | | | | | 12,721 | |

| DENMARK — 1.5% | | | | | | | | |

| Novo Nordisk, Cl B | | | 55,828 | | | | 6,212 | |

| | | | | | | | | |

| GERMANY — 2.9% | | | | | | | | |

| Deutsche Telekom | | | 147,489 | | | | 4,463 | |

| SAP | | | 31,486 | | | | 7,357 | |

| | | | | | | | | |

| | | | | | | | 11,820 | |

| ITALY — 1.4% | | | | | | | | |

| Ferrari | | | 11,609 | | | | 5,525 | |

| | | | | | | | | |

| JAPAN — 1.4% | | | | | | | | |

| Hitachi | | | 222,600 | | | | 5,749 | |

| | | | | | | | | |

| SOUTH KOREA — 1.1% | | | | | | | | |

| BNK Financial Group | | | 5,665 | | | | 39 | |

| DB Insurance | | | 1,245 | | | | 98 | |

| HD Hyundai | | | 1,368 | | | | 79 | |

| Hyundai Marine & Fire Insurance | | | 1,577 | | | | 35 | |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON |

| | CAPITAL ALLOCATION FUND |

| | OCTOBER 31, 2024 |

COMMON STOCK — continued

| | | Shares | | | Fair Value (000) | |

| SOUTH KOREA — (continued) | | | | | | | | |

| KEPCO Engineering & Construction | | | 657 | | | $ | 33 | |

| Korean Air Lines | | | 6,311 | | | | 109 | |

| KT | | | 4,291 | | | | 138 | |

| Samsung Biologics* | | | 1,259 | | | | 914 | |

| SK Hynix | | | 21,303 | | | | 2,876 | |

| | | | | | | | | |

| | | | | | | | 4,321 | |

| TAIWAN — 2.0% | | | | | | | | |

| Taiwan Semiconductor Manufacturing ADR | | | 43,099 | | | | 8,212 | |

| | | | | | | | | |

| UNITED KINGDOM — 1.7% | | | | | | | | |

| AstraZeneca | | | 21,507 | | | | 3,062 | |

| SSE | | | 171,936 | | | | 3,904 | |

| | | | | | | | | |

| | | | | | | | 6,966 | |

| | | | | | | | | |

| UNITED STATES — 48.5% | | | | | | | | |

| 3M | | | 16,824 | | | | 2,162 | |

| AbbVie | | | 10,752 | | | | 2,192 | |

| Alphabet, Cl C | | | 15,258 | | | | 2,635 | |

| Amazon.com* | | | 32,005 | | | | 5,966 | |

| American Tower | | | 33,570 | | | | 7,169 | |

| Apple | | | 45,939 | | | | 10,378 | |

| Arista Networks* | | | 9,914 | | | | 3,831 | |

| Berkshire Hathaway, Cl B* | | | 17,741 | | | | 8,000 | |

| Boston Scientific* | | | 12,149 | | | | 1,021 | |

| Caterpillar | | | 1,236 | | | | 465 | |

| Charles Schwab | | | 31,814 | | | | 2,253 | |

| Chipotle Mexican Grill, Cl A* | | | 135,416 | | | | 7,552 | |

| Colgate-Palmolive | | | 61,741 | | | | 5,786 | |

| Costco Wholesale | | | 4,872 | | | | 4,259 | |

| Cummins | | | 6,513 | | | | 2,142 | |

| Danaher | | | 3,916 | | | | 962 | |

| Duke Energy | | | 17,484 | | | | 2,016 | |

| Elevance Health | | | 3,014 | | | | 1,223 | |

| Energy Transfer | | | 343,777 | | | | 5,665 | |

| Exxon Mobil | | | 53,090 | | | | 6,200 | |

| Fiserv* | | | 11,247 | | | | 2,226 | |

| Freeport-McMoRan | | | 9,532 | | | | 429 | |

| General Electric | | | 28,701 | | | | 4,930 | |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON |

| | CAPITAL ALLOCATION FUND |

| | OCTOBER 31, 2024 |

COMMON STOCK — continued

| | | Shares | | | Fair Value (000) | |

| UNITED STATES — (continued) | | | | | | | | |

| HCA Healthcare | | | 12,727 | | | $ | 4,566 | |

| Home Depot | | | 5,937 | | | | 2,338 | |

| Interactive Brokers Group, Cl A | | | 8,391 | | | | 1,280 | |

| Intercontinental Exchange | | | 37,150 | | | | 5,790 | |

| International Business Machines | | | 9,850 | | | | 2,036 | |

| Intuitive Surgical* | | | 10,981 | | | | 5,532 | |

| JPMorgan Chase | | | 37,007 | | | | 8,213 | |

| Mastercard, Cl A | | | 3,037 | | | | 1,517 | |

| Meta Platforms, Cl A | | | 8,154 | | | | 4,628 | |

| Microsoft | | | 20,140 | | | | 8,184 | |

| Mondelez International, Cl A | | | 29,293 | | | | 2,006 | |

| Netflix* | | | 8,296 | | | | 6,272 | |

| Newmont | | | 188,988 | | | | 8,588 | |

| NVIDIA | | | 79,575 | | | | 10,565 | |

| PayPal Holdings* | | | 56,730 | | | | 4,499 | |

| Philip Morris International | | | 34,718 | | | | 4,607 | |

| Progressive | | | 20,194 | | | | 4,904 | |

| ServiceNow* | | | 10,241 | | | | 9,555 | |

| Simon Property Group | | | 2,528 | | | | 427 | |

| Uber Technologies* | | | 99,446 | | | | 7,165 | |

| Verizon Communications | | | 72,238 | | | | 3,043 | |

| Wynn Resorts | | | 34,683 | | | | 3,330 | |

| | | | | | | | | |

| | | | | | | | 198,507 | |

| TOTAL COMMON STOCK | | | | | | | | |

| (Cost $243,469) (000) | | | | | | | 284,812 | |

CORPORATE OBLIGATIONS — 5.9%

| | | Face Amount (000) | | | | | |

| MEXICO — 0.4% | | | | | | | | |

| Southern Copper | | | | | | | | |

| 3.875%, 04/23/25 | | $ | 1,600 | | | | 1,588 | |

| | | | | | | | | |

| UNITED STATES — 5.5% | | | | | | | | |

| American Tower | | | | | | | | |

| Callable 08/17/26 @ $100.000 | | | | | | | | |

| 1.450%, 09/15/26 | | | 2,600 | | | | 2,448 | |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON |

| | CAPITAL ALLOCATION FUND |

| | OCTOBER 31, 2024 |

CORPORATE OBLIGATIONS — continued

| | | Face Amount (000) | | | Fair Value (000) | |

| UNITED STATES — (continued) | | | | | | | | |

| Broadcom | | | | | | | | |

| Callable 07/15/26 @ $100.000 | | | | | | | | |

| 3.459%, 09/15/26 | | $ | 2,400 | | | $ | 2,351 | |

| Cheniere Energy | | | | | | | | |

| Callable 11/11/24 @ $101.156 | | | | | | | | |

| 4.625%, 10/15/28 | | | 2,500 | | | | 2,450 | |

| Flex | | | | | | | | |

| Callable 01/02/26 @ $100.000 | | | | | | | | |

| 3.750%, 02/01/26 | | | 1,700 | | | | 1,672 | |

| IQVIA | | | | | | | | |

| Callable 12/02/24 @ $100.000 | | | | | | | | |

| 5.000%, 10/15/26(A) | | | 3,100 | | | | 3,067 | |

| MPLX | | | | | | | | |

| Callable 11/15/24 @ $100.000 | | | | | | | | |

| 4.000%, 02/15/25 | | | 1,600 | | | | 1,594 | |

| PRA Health Sciences | | | | | | | | |

| Callable 07/15/25 @ $100.719 | | | | | | | | |

| 2.875%, 07/15/26(A) | | | 2,500 | | | | 2,413 | |

| Regal Rexnord | | | | | | | | |

| 6.050%, 02/15/26 | | | 1,600 | | | | 1,617 | |

| Scotts Miracle-Gro | | | | | | | | |

| Callable 08/03/26 @ $102.188 | | | | | | | | |

| 4.375%, 02/01/32 | | | 2,900 | | | | 2,624 | |

| Uber Technologies | | | | | | | | |

| Callable 12/02/24 @ $100.000 | | | | | | | | |

| 8.000%, 11/01/26(A) | | | 2,300 | | | | 2,300 | |

| | | | | | | | | |

| | | | | | | | 22,536 | |

| TOTAL CORPORATE OBLIGATIONS | | | | | | | | |

| (Cost $24,040) (000) | | | | | | | 24,124 | |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON |

| | CAPITAL ALLOCATION FUND |

| | OCTOBER 31, 2024 |

ASSET-BACKED SECURITY — 3.1%

| | | Face Amount (000) | | | Fair Value (000) | |

| UNITED STATES — 3.1% | | | | | | | | |

| Jonah Energy, Ser 2022-1, Cl A1 | | | | | | | | |

| Callable 11/10/26 @ $100.000 | | | | | | | | |

| 7.200%, 12/10/37(A) | | $ | 12,488 | | | $ | 12,533 | |

| | | | | | | | | |

| Total Asset-Backed Security | | | | | | | | |

| (Cost $12,330) (000) | | | | | | | 12,533 | |

| | | | | | | | | |

| U.S. TREASURY OBLIGATION — 10.1% | | | | | | | | |

| | | | | | | | | |

| U.S. Treasury Bill | | | | | | | | |

| 5.150%, 11/07/24(B) | | | 41,300 | | | | 41,268 | |

| | | | | | | | | |

| TOTAL U.S. TREASURY OBLIGATION | | | | | | | | |

| (Cost $41,265) (000) | | | | | | | 41,268 | |

| | | | | | | | | |

| TOTAL INVESTMENTS — 88.7% | | | | | | | | |

| (Cost $321,104) (000) | | | | | | $ | 362,737 | |

| * | Non-income producing security. |

| (A) | Securities sold within terms of a private placement memorandum, exempt from registration under Section 144A of the Securities Act of 1933, as amended, and may be sold only to dealers in that program or other "accredited investors." On October 31, 2024, the value of these securities amounted $20,313 (000) and represented 5.0% of net assets. |

| (B) | The rate reported on the Consolidated Schedule of Investments is the effective yield at the time of purchase. |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON |

| | CAPITAL ALLOCATION FUND |

| | OCTOBER 31, 2024 |

Open futures contracts held by the Fund at October 31, 2024 are as follows:

| Type of Contract | | Number of

Contracts | | | Expiration

Date | | | Notional Amount

(000) | | | Value (000) | | | Unrealized

Appreciation/

(Depreciation)

(000) | |

| Long Contracts | | | | | | | | | | | | | | | | | | |

| Euro-Bund 10-Year Bond | | 180 | | | Dec-2024 | | | $ | 26,732 | | | $ | 25,806 | | | $ | (377) | |

| Euro-Schatz | | 228 | | | Dec-2024 | | | | 27,071 | | | | 26,423 | | | | (186 | ) |

| Gold† | | 69 | | | Dec-2024 | | | | 16,996 | | | | 18,970 | | | | 1,974 | |

| Silver† | | 55 | | | Dec-2024 | | | | 8,960 | | | | 9,019 | | | | 59 | |

| U.S. 2-Year Treasury Note | | 103 | | | Dec-2024 | | | | 21,393 | | | | 21,212 | | | | (181) | |

| U.S. 5-Year Treasury Note | | 225 | | | Dec-2024 | | | | 24,705 | | | | 24,128 | | | | (577 | ) |

| | | | | | | | | $ | 125,857 | | | $ | 125,558 | | | $ | 712 | |

| † | Security, or a portion thereof, is held by the Chiron Capital Allocation Fund Ltd., as of October 31, 2024. |

ADR — American Depositary Receipt

Cl — Class

Ser — Series

The tables below set forth information about the Level within the fair value hierarchy at which the Fund’s investments and other financial instruments are measured at October 31, 2024:

| Investments in Securities | | Level 1 (000) | | | Level 2 (000) | | | Level 3 (000) | | | Total (000) | |

| Common Stock | | | | | | | | | | | | | | | | |

| Belgium | | $ | 5,505 | | | $ | — | | | $ | — | | | $ | 5,505 | |

| Brazil | | | 4,679 | | | | — | | | | — | | | | 4,679 | |

| Canada | | | 14,595 | | | | — | | | | — | | | | 14,595 | |

| China | | | 12,721 | | | | — | | | | — | | | | 12,721 | |

| Denmark | | | 6,212 | | | | — | | | | — | | | | 6,212 | |

| Germany | | | 11,820 | | | | — | | | | — | | | | 11,820 | |

| Italy | | | 5,525 | | | | — | | | | — | | | | 5,525 | |

| Japan | | | 5,749 | | | | — | | | | — | | | | 5,749 | |

| South Korea | | | 4,321 | | | | — | | | | — | | | | 4,321 | |

| Taiwan | | | 8,212 | | | | — | | | | — | | | | 8,212 | |

| United Kingdom | | | 6,966 | | | | — | | | | — | | | | 6,966 | |

| United States | | | 198,507 | | | | — | | | | — | | | | 198,507 | |

| Total Common Stock | | | 284,812 | | | | — | | | | — | | | | 284,812 | |

| Corporate Obligations | | | — | | | | 24,124 | | | | — | | | | 24,124 | |

| Asset-Backed Security | | | — | | | | 12,533 | | | | — | | | | 12,533 | |

| U.S. Treasury Obligation | | | — | | | | 41,268 | | | | — | | | | 41,268 | |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON |

| | CAPITAL ALLOCATION FUND |

| | OCTOBER 31, 2024 |

| Investments in Securities | | Level 1 (000) | | | Level 2 (000) | | | Level 3 (000) | | | Total (000) | |

| Total Investments in Securities | | $ | 284,812 | | | $ | 77,925 | | | $ | — | | | $ | 362,737 | |

| Other Financial Instruments | | Level 1 (000) | | | Level 2 (000) | | | Level 3 (000) | | | Total (000) | |

| Futures Contracts* | | | | | | | | | | | | | | | | |

| Unrealized Appreciation | | $ | 2,033 | | | $ | — | | | $ | — | | | $ | 2,033 | |

| Unrealized Depreciation | | | (1,321 | ) | | | — | | | | — | | | | (1,321 | ) |

| Total Other Financial Instruments | | $ | 712 | | | $ | — | | | $ | — | | | $ | 712 | |

| * | Futures contracts are valued at the unrealized appreciation (depreciation) on the instrument. |

Amounts designated as “—“ are either $0 or have been rounded to $0.

For more information on valuation inputs, see Note 2 – Significant Accounting Policies in the Notes to Financial Statements.

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON CAPITAL ALLOCATION FUND OCTOBER 31, 2024 |

| CONSOLIDATED STATEMENT OF ASSETS AND LIABILITIES ($ Thousands) | | | |

| Assets: | | | |

| Investments, at Fair Value (Cost $321,104) | | $ | 362,737 | |

| Foreign Currency, at Fair Value (Cost $1) | | | 1 | |

| Cash | | | 41,221 | |

| Cash Pledged as Collateral for Futures Contracts | | | 6,341 | |

| Receivable for Investments Sold | | | 3,424 | |

| Dividend and Interest Receivable | | | 1,289 | |

| Reclaim Receivable | | | 581 | |

| Receivable for Capital Shares Sold | | | 46 | |

| Prepaid Expenses | | | 29 | |

| Total Assets | | | 415,669 | |

| Liabilities: | | | | |

| Payable for Investment Securities Purchased | | $ | 5,069 | |

| Variation Margin Payable for Futures Contracts | | | 798 | |

| Payable Due to Adviser | | | 342 | |

| Payable for Capital Shares Redeemed | | | 319 | |

| Payable Due to Administrator | | | 26 | |

| Chief Compliance Officer Fees Payable | | | 3 | |

| Distribution Fees Payable (Class A) | | | 1 | |

| Other Accrued Expenses and Other Payables | | | 157 | |

| Total Liabilities | | | 6,715 | |

| Net Assets | | $ | 408,954 | |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON CAPITAL ALLOCATION FUND OCTOBER 31, 2024 |

| CONSOLIDATED STATEMENT OF ASSETS AND LIABILITIES ($ Thousands) (1) | | | |

| Net Assets Consist of: | | | |

| Paid-in Capital | | $ | 554,091 | |

| Total Accumulated Loss | | | (145,137 | ) |

| Net Assets | | $ | 408,954 | |

| Class I Shares: | | | | |

| Net Assets | | $ | 401,717 | |

| Outstanding Shares of Beneficial Interest (Unlimited Authorization - No Par Value) | | | 28,319 | |

| Net Asset Value, Offering and Redemption Price Per Share | | $ | 14.19 | |

| Class A Shares:(2) | | | | |

| Net Assets | | $ | 1,399 | |

| Outstanding Shares of Beneficial Interest (Unlimited Authorization - No Par Value) | | | 98 | |

| Net Asset Value, Offering and Redemption Price Per Share | | $ | 14.19 | ‡ |

Maximum Offering Price Per Share

($14.19/95.00%) | | | 14.94 | |

| Class C Shares:(3) | | | | |

| Net Assets | | $ | 5,838 | |

| Outstanding Shares of Beneficial Interest (Unlimited Authorization - No Par Value) | | | 413 | |

| Net Asset Value, Offering and Redemption Price Per Share | | $ | 14.14 | ‡ |

| (1) | Amounts shown In Thousands with the exception of Outstanding Shares of Beneficial Interest and Net Asset Value, Offering and Redemption Price Per Share. |

| (2) | Class A Shares purchases of $1,000 (000) or more may be subject to a 1.00% Contingent Deferred Sales Charge ("CDSC") if redeemed within 18 months of purchase. |

| (3) | Class C Shares may be subject to a 1.00% CDSC if redeemed within 12 months of purchase. |

| ‡ | Net Assets divided by Shares do not calculate to the stated NAV due to Net Assets and Shares being rounded. |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON CAPITAL ALLOCATION FUND FOR THE YEAR ENDED OCTOBER 31, 2024 |

| CONSOLIDATED STATEMENT OF OPERATIONS ($ Thousands) | | | |

| Investment Income: | | | |

| Dividends | | $ | 6,261 | |

| Interest | | | 8,917 | |

| Less: Foreign Taxes Withheld | | | (24 | ) |

| Total Investment Income | | | 15,154 | |

| Expenses: | | | | |

| Investment Advisory Fees | | | 4,613 | |

| Administration Fees | | | 345 | |

| Distribution Fees (Class A) | | | 4 | |

| Distribution Fees (Class C) | | | 58 | |

| Trustees' Fees | | | 19 | |

| Chief Compliance Officer Fees | | | 7 | |

| Transfer Agent Fees | | | 364 | |

| Professional Fees | | | 80 | |

| Registration and Filing Fees | | | 68 | |

| Printing Fees | | | 56 | |

| Custodian Fees | | | 12 | |

| Pricing Fees | | | 5 | |

| Other Expenses | | | 72 | |

| Total Expenses | | | 5,703 | |

| Net Investment Income | | | 9,451 | |

| Net Realized Gain (Loss) on: | | | | |

| Investments | | | 31,865 | |

| Futures Contracts | | | 6,004 | |

| Swap Contracts | | | (6,637 | ) |

| Foreign Currency Transactions | | | (298 | ) |

| Net Realized Gain | | | 30,934 | |

| Net Change in Unrealized Appreciation (Depreciation) on: | | | | |

| Investments | | | 50,157 | |

| Futures Contracts | | | 1,317 | |

| Swap Contracts | | | (397 | ) |

| Foreign Currency Translation | | | 26 | |

| Net Change in Unrealized Appreciation | | | 51,103 | |

| Net Realized and Unrealized Gain on Investments | | | 82,037 | |

| Net Increase in Net Assets Resulting from Operations | | $ | 91,488 | |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON CAPITAL ALLOCATION FUND |

CONSOLIDATED STATEMENTS OF CHANGES IN NET ASSETS

| | | Year Ended | | | Year Ended | |

| | | October 31, 2024 | | | October 31, 2023# | |

| Operations: | | | | | | |

| Net Investment Income | | $ | 9,451 | | | $ | 17,455 | |

| Net Realized Gain/(Loss) | | | 30,934 | | | | (2,035 | ) |

| Net Change in Unrealized Appreciation/(Depreciation) | | | 51,103 | | | | (9,623 | ) |

| Net Increase in Net Assets Resulting from Operations | | | 91,488 | | | | 5,797 | |

| Distributions: | | | | | | | | |

| Class I Shares | | | (8,713 | ) | | | (17,182 | ) |

| Class A Shares | | | (23 | ) | | | (90 | ) |

| Class C Shares | | | (48 | ) | | | (60 | ) |

| Return of Capital: | | | | | | | | |

| Class I Shares | | | – | | | | (575 | ) |

| Class A Shares | | | – | | | | (4 | ) |

| Class C Shares | | | – | | | | (5 | ) |

| Total Distributions | | | (8,784 | ) | | | (17,916 | ) |

| Capital Share Transactions: | | | | | | | | |

| Class I Shares | | | | | | | | |

| Issued | | | 50,671 | | | | 133,126 | |

| Reinvestment of Dividends | | | 7,143 | | | | 15,794 | |

| Redeemed | | | (314,111 | ) | | | (370,809 | ) |

| Net Decrease in Net Assets from Class I Share Transactions | | | (256,297 | ) | | | (221,889 | ) |

| Class A Shares | | | | | | | | |

| Issued | | | 274 | | | | 313 | |

| Reinvestment of Dividends | | | 17 | | | | 77 | |

| Redeemed | | | (2,883 | ) | | | (1,663 | ) |

| Net Decrease in Net Assets from Class A Share Transactions | | | (2,592 | ) | | | (1,273 | ) |

| Class C Shares | | | | | | | | |

| Issued | | | 750 | | | | 1,198 | |

| Reinvestment of Dividends | | | 47 | | | | 65 | |

| Redeemed | | | (1,572 | ) | | | (2,695 | ) |

| Net Decrease in Net Assets from Class C Share Transactions | | | (775 | ) | | | (1,432 | ) |

| Net Decrease in Net Assets from Capital Share Transactions | | | (259,664 | ) | | | (224,594 | ) |

| Total Decrease in Net Assets | | | (176,960 | ) | | | (236,713 | ) |

| Net Assets: | | | | | | | | |

| Beginning of Year | | | 585,914 | | | | 822,627 | |

| End of Year | | $ | 408,954 | | | $ | 585,914 | |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON CAPITAL ALLOCATION FUND |

CONSOLIDATED STATEMENTS OF CHANGES IN NET ASSETS

| | | Year Ended | | | Year Ended | |

| | | October 31, 2024 | | | October 31, 2023# | |

| Share Transactions: | | | | | | |

| Class I Shares | | | | | | |

| Issued | | | 3,757 | | | | 10,151 | |

| Reinvestment of Distributions | | | 534 | | | | 1,248 | |

| Redeemed | | | (23,603 | ) | | | (28,914 | ) |

| Net Decrease in Shares Outstanding from Share Transactions | | | (19,312 | ) | | | (17,515 | ) |

| Share Transactions: | | | | | | | | |

| Class A Shares | | | | | | | | |

| Issued | | | 20 | | | | 24 | |

| Reinvestment of Distributions | | | 1 | | | | 6 | |

| Redeemed | | | (227 | ) | | | (132 | ) |

| Net Decrease in Shares Outstanding from Share Transactions | | | (206 | ) | | | (102 | ) |

| Share Transactions: | | | | | | | | |

| Class C Shares | | | | | | | | |

| Issued | | | 55 | | | | 92 | |

| Reinvestment of Distributions | | | 3 | | | | 5 | |

| Redeemed | | | (118 | ) | | | (209 | ) |

| Net Decrease in Shares Outstanding from Share Transactions | | | (60 | ) | | | (112 | ) |

Amounts designated as "-" are $0 or have been rounded to $0.

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON CAPITAL ALLOCATION FUND |

CONSOLIDATED FINANCIAL HIGHLIGHTS

Selected Per Share Data & Ratios

For a Share Outstanding Throughout Each Year

Class I Shares

| | | Year Ended October 31, 2024 | | | Year Ended October 31, 2023# | | | Year Ended October 31, 2022# | | | Year Ended October 31, 2021# | | | Year Ended October 31, 2020# | |

| Net Asset Value, Beginning of Year | | $ | 12.10 | | | $ | 12.44 | | | $ | 16.56 | | | $ | 12.36 | | | $ | 11.63 | |

| Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

| Net Investment Income** | | | 0.26 | | | | 0.30 | | | | 0.25 | | | | (0.00)^^ | | | | 0.13 | |

| Net Realized and Unrealized Gain (Loss) | | | 2.08 | | | | (0.33 | ) | | | (3.62 | ) | | | 4.22 | | | | 0.68 | ‡‡ |

| Total from Investment Operations | | | 2.34 | | | | (0.03 | ) | | | (3.37 | ) | | | 4.22 | | | | 0.81 | |

| | | | | | | | | | | | | | | | | | | | | |

| Dividends and Distributions: | | | | | | | | | | | | | | | | | | | | |

| Net Investment Income | | | (0.25 | ) | | | (0.30 | ) | | | (0.20 | ) | | | (0.02 | ) | | | (0.08 | ) |

| Return of Capital | | | – | | | | (0.01 | ) | | | – | | | | – | | | | – | |

| Capital Gains | | | – | | | | – | | | | (0.55 | ) | | | – | | | | – | |

| | | | | | | | | | | | | | | | | | | | | |

| Total Dividends and Distributions | | | (0.25 | ) | | | (0.31 | ) | | | (0.75 | ) | | | (0.02 | ) | | | (0.08 | ) |

| Net Asset Value, End of Year | | $ | 14.19 | | | $ | 12.10 | | | $ | 12.44 | | | $ | 16.56 | | | $ | 12.36 | |

| Total Return‡ | | | 19.45 | % | | | (0.29 | )% | | | (21.23 | )% | | | 34.14 | % | | | 7.10 | % |

| | | | | | | | | | | | | | | | | | | | | |

| Ratios and Supplemental Data | | | | | | | | | | | | | | | | | | | | |

| Net Assets, End of Year (Thousands) | | $ | 401,717 | | | $ | 576,522 | | | $ | 810,364 | | | $ | 1,248,242 | | | $ | 539,694 | |

| Ratio of Expenses to Average Net Assets | | | 1.16 | % | | | 1.18 | % | | | 1.17 | % | | | 1.15 | % | | | 1.13 | % |

| Ratio of Expenses to Average Net Assets (Excluding Waivers) | | | 1.16 | % | | | 1.18 | % | | | 1.17 | % | | | 1.15 | % | | | 1.13 | % |

| Ratio of Net Investment Income (Loss) to Average Net Assets | | | 1.96 | % | | | 2.29 | % | | | 1.79 | % | | | (0.01 | )% | | | 1.18 | % |

| Portfolio Turnover Rate | | | 171 | % | | | 380 | % | | | 489 | % | | | 311 | % | | | 202 | % |

| ** | Per share data calculated using average shares method. |

| ^^ | Value is less than $(0.01) per share. |

| ‡ | Returns shown do not reflect the deductions of taxes that a shareholder would pay on Fund distributions or the redemption of Fund Shares, assumes reinvestments of dividends, and does not reflect the applicable sales charges, if applicable. |

| ‡‡ | The amount shown for the year ended October 31, 2020, for a share outstanding throughout the period does not accord with the aggregate net gains on investments for that period because of the sales and repurchase of Fund shares in relation to fluctuating market value of the investments of the Fund. |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON CAPITAL ALLOCATION FUND |

Selected Per Share Data & Ratios

For a Share Outstanding Throughout Each Year/Period

Class A Shares

| | | Year Ended October 31, 2024 | | | Year Ended October 31, 2023# | | | Year Ended October 31, 2022# | | | Period Ended October 31, 2021#* | |

| Net Asset Value, Beginning of Year/Period | | $ | 12.10 | | | $ | 12.42 | | | $ | 16.56 | | | $ | 16.47 | |

| Income from Investment Operations: | | | | | | | | | | | | | | | | |

| Net Investment Income (Loss)** | | | 0.22 | | | | 0.27 | | | | 0.18 | | | | (0.04 | ) |

| Net Realized and Unrealized Gain (Loss) | | | 2.08 | | | | (0.33 | ) | | | (3.59 | ) | | | 0.13 | |

| Total from Investment Operations | | | 2.30 | | | | (0.06 | ) | | | (3.41 | ) | | | 0.09 | |

| | | | | | | | | | | | | | | | | |

| Dividends and Distributions: | | | | | | | | | | | | | | | | |

| Net Investment Income | | | (0.21 | ) | | | (0.26 | ) | | | (0.18 | ) | | | – | |

| Return of Capital | | | – | | | | (0.00)^ | | | | – | | | | – | |

| Capital Gains | | | – | | | | – | | | | (0.55 | ) | | | – | |

| | | | | | | | | | | | | | | | | |

| Total Dividends and Distributions | | | (0.21 | ) | | | (0.26 | ) | | | (0.73 | ) | | | – | |

| Net Asset Value, End of Year/Period | | $ | 14.19 | | | $ | 12.10 | | | $ | 12.42 | | | $ | 16.56 | |

| Total Return‡ | | | 19.14 | % | | | (0.51 | )% | | | (21.46 | )% | | | 0.55 | %† |

| | | | | | | | | | | | | | | | | |

| Ratios and Supplemental Data | | | | | | | | | | | | | | | | |

| Net Assets, End of Year/Period (Thousands) | | $ | 1,399 | | | $ | 3,684 | | | $ | 5,039 | | | $ | 2,721 | |

| Ratio of Expenses to Average Net Assets | | | 1.41 | % | | | 1.43 | % | | | 1.43 | % | | | 1.55 | %†† |

| Ratio of Expenses to Average Net Assets (Excluding Waivers) | | | 1.41 | % | | | 1.43 | % | | | 1.43 | % | | | 1.55 | %†† |

| Ratio of Net Investment Income (Loss) to Average Net Assets | | | 1.61 | % | | | 2.05 | % | | | 1.26 | % | | | (0.83 | )%†† |

| Portfolio Turnover Rate | | | 171 | % | | | 380 | % | | | 489 | % | | | 311 | %† |

| * | Commenced operations on July 16, 2021. |

| ** | Per share data calculated using average shares method. |

| ^ | Value is less than $(0.01) per share. |

| ‡ | Returns shown do not reflect the deductions of taxes that a shareholder would pay on Fund distributions or the redemption of Fund Shares, assumes reinvestments of dividends, and does not reflect the applicable sales charges, if applicable. |

| † | Total Return and Portfolio Turnover Rate are for the period indicated and have not been annualized. |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON CAPITAL ALLOCATION FUND |

Selected Per Share Data & Ratios

For a Share Outstanding Throughout Each Year/Period

Class C Shares

| | | Year Ended October 31, 2024 | | | Year Ended October 31, 2023# | | | Year Ended October 31, 2022# | | | Period Ended October 31, 2021#* | |

| Net Asset Value, Beginning of Year/Period | | $ | 12.06 | | | $ | 12.34 | | | $ | 16.52 | | | $ | 16.47 | |

| Income from Investment Operations: | | | | | | | | | | | | | | | | |

| Net Investment Income (Loss)** | | | 0.12 | | | | 0.17 | | | | 0.05 | | | | (0.06 | ) |

| Net Realized and Unrealized Gain (Loss) | | | 2.07 | | | | (0.32 | ) | | | (3.56 | ) | | | 0.11 | |

| Total from Investment Operations | | | 2.19 | | | | (0.15 | ) | | | (3.51 | ) | | | 0.05 | |

| | | | | | | | | | | | | | | | | |

| Dividends and Distributions: | | | | | | | | | | | | | | | | |

| Net Investment Income | | | (0.11 | ) | | | (0.13 | ) | | | (0.12 | ) | | | – | |

| Return of Capital | | | – | | | | (0.00 | )^ | | | – | | | | – | |

| Capital Gains | | | – | | | | – | | | | (0.55 | ) | | | – | |

| | | | | | | | | | | | | | | | | |

| Total Dividends and Distributions | | | (0.11 | ) | | | (0.13 | ) | | | (0.67 | ) | | | – | |

| Net Asset Value, End of Year/Period | | $ | 14.14 | | | $ | 12.06 | | | $ | 12.34 | | | $ | 16.52 | |

| Total Return‡ | | | 18.24 | % | | | (1.24 | )% | | | (22.05 | )% | | | 0.30 | %† |

| | | | | | | | | | | | | | | | | |

| Ratios and Supplemental Data | | | | | | | | | | | | | | | | |

| Net Assets, End of Year/Period (Thousands) | | $ | 5,838 | | | $ | 5,708 | | | $ | 7,224 | | | $ | 3,340 | |

| Ratio of Expenses to Average Net Assets | | | 2.16 | % | | | 2.18 | % | | | 2.18 | % | | | 2.28 | %†† |

| Ratio of Expenses to Average Net Assets (Excluding Waivers) | | | 2.16 | % | | | 2.18 | % | | | 2.18 | % | | | 2.28 | %†† |

| Ratio of Net Investment Income (Loss) to Average Net Assets | | | 0.90 | % | | | 1.29 | % | | | 0.33 | % | | | (1.28 | )%†† |

| Portfolio Turnover Rate | | | 171 | % | | | 380 | % | | | 489 | % | | | 311 | %† |

| * | Commenced operations on July 16, 2021. |

| ** | Per share data calculated using average shares method. |

| ^ | Value is less than $(0.01) per share. |

| ‡ | Returns shown do not reflect the deductions of taxes that a shareholder would pay on Fund distributions or the redemption of Fund Shares, assumes reinvestments of dividends, and does not reflect the applicable sales charges, if applicable. |

| † | Total Return and Portfolio Turnover Rate are for the period indicated and have not been annualized. |

The accompanying notes are an integral part of the financial statements.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON CAPITAL ALLOCATION FUND OCTOBER 31, 2024 |

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Organization:

The Advisors’ Inner Circle Fund III (the “Trust”) is organized as a Delaware statutory trust under a Declaration of Trust dated December 4, 2013. The Trust is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company with 50 funds. The financial statements herein are those of the FS Chiron Capital Allocation Fund (the “Fund”). The investment objective of the FS Chiron Capital Allocation Fund is total return. Total return consists of capital growth and income. The Fund is classified as a diversified investment company. The financial statements of the remaining funds of the Trust are presented separately. The assets of each fund are segregated, and a shareholder’s interest is limited to the fund in which shares are held. The FS Chiron Capital Allocation Fund commenced operations on November 30, 2015.

As of October 31, 2024, the Fund had one wholly-owned subsidiary, Chiron Capital Allocation Fund Ltd. (hereinafter, the “Subsidiary”), which Subsidiary commenced operations on November 20, 2023, and through which Subsidiary the Fund may gain exposure to commodities. The consolidated financial statements include both the Fund’s accounts and the accounts of the Subsidiary. All intercompany balances have been eliminated in consolidation.

2. Significant Accounting Policies:

The accompanying financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”) and are presented in U.S. dollars which is the functional currency of the Fund. The Fund is an investment company and therefore applies the accounting and reporting guidance issued by the U.S. Financial Accounting Standards Board (“FASB”) in Accounting Standards Codification (“ASC”) Topic 946, Financial Services — Investment Companies. The following are significant accounting policies which are consistently followed in the preparation of the financial statements.

Use of Estimates —The preparation of financial statements requires management to make estimates and assumptions that affect the fair value of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates and such differences could be material.

Security Valuation — Securities listed on a securities exchange, market or automated quotation system for which quotations are readily available (except for securities traded on NASDAQ), including securities traded over the counter, are valued at the last quoted sale price on an exchange or market (foreign or domestic) on which they are traded on valuation date (or at approximately 4:00 pm Eastern Standard Time if a security’s primary exchange is normally open at that time), or, if there is no such reported sale on the valuation date, at the most independent, third- party pricing agents. Such values generally reflect the last reported sales price if the security is actively traded. The third-party pricing agents may also value debt securities at an evaluated bid price by employing methodologies that utilize actual market transactions, broker-supplied valuations, or other methodologies designed to identify the market value for such securities. Such methodologies generally consider such factors as security prices, yields, maturities, call features, ratings and developments relating to specific securities in arriving at valuations. On the first day a new debt security purchase is recorded, if a price is not available on the automated pricing feeds from our primary and secondary pricing vendors nor is it available from an independent broker, the security may be valued at its purchase price. Each day thereafter, the debt security will be valued according to the Trust’s Fair Value Procedures until an independent source can be secured. Debt obligations with remaining maturities of sixty days or less may be valued at their amortized cost, which approximates market value provided that it is determined the amortized cost continues to approximate fair value. Should existing credit, liquidity or interest rate conditions in the relevant markets and issuer specific circumstances suggest that amortized cost does not approximate fair value, then the amortized cost method may not be used. The prices for foreign securities are reported in local currency and converted to U.S. dollars using currency exchange rates.

| THE ADVISORS’ INNER CIRCLE FUND III | FS CHIRON CAPITAL ALLOCATION FUND OCTOBER 31, 2024 |

Securities for which market prices are not “readily available” are valued in accordance with fair value procedures (the "Fair Value Procedures") established by the Adviser and approved by the Trust's Board of Trustees (the “Board”). Pursuant to Rule 2a-5 under the 1940 Act, the Board has designated the Adviser as the "valuation designee" to determine the fair value of securities and other instruments for which no readily available market quotations are available. The Fair Value Procedures are implemented through a Fair Value Committee (the “Committee”) of the Adviser.

Swaps are marked-to-market daily based upon quotations from market makers and the resulting changes in market values, are recorded as an unrealized gain or loss in the Consolidated Statement of Operations.

Futures contracts that are traded on an exchange are valued at their last reported sales price as of the valuation date.