UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22969

PALMER SQUARE OPPORTUNISTIC INCOME FUND

(Exact name of registrant as specified in charter)

1900 Shawnee Mission Parkway Suite 315

Mission Woods, KS 66205

(Address of principal executive offices) (Zip code)

Scott Betz

Chief Compliance Officer

1900 Shawnee Mission Parkway Suite 315

Mission Woods, KS 66205

(Name and address of agent for service)

(816) 994-3200

Registrant's telephone number, including area code

Date of fiscal year end: July 31

Date of reporting period: July 31, 2021

Item 1. Report to Stockholders.

The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

Palmer Square Opportunistic Income Fund

(PSOIX)

ANNUAL REPORT

JULY 31, 2021

Palmer Square Opportunistic Income Fund

Table of Contents

| Letter to Shareholders | 1 |

| Fund Performance | 11 |

| Schedule of Investments | 12 |

| Statement of Assets and Liabilities | 33 |

| Statement of Operations | 34 |

| Statements of Changes of Net Assets | 35 |

| Financial Highlights | 36 |

| Notes to Financial Statements | 37 |

| Report of Independent Registered Public Accounting Firm | 53 |

| Supplemental Information | 54 |

| Expense Example | 56 |

This report and the financial statements contained herein are provided for the general information of the shareholders of the Palmer Square Opportunistic Income Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

www.palmersquarefunds.com

Palmer Square Opportunistic Income Fund (PSOIX)

July 2021

Fund Refresher

As a refresher, the Palmer Square Opportunistic Income Fund (“PSOIX” or the “Fund”) seeks to not only capture a high level of current income, but also long-term capital appreciation by investing with a flexible mandate to find the best relative value opportunities across corporate credit and structured credit.

Performance Summary

The Fund returned 17.96% (net of fees) for the fiscal year-ending 7/31/2021, driven by the strong rally in Collateralized Loan Obligation (“CLO”) debt as well as subordinated notes, bank loans and corporate bonds.

| Fund Performance Net of Fees as of 7/31/2021 (inception 8/29/2014*) |

| YTD 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014* | |

| PSOIX | 5.07% | 5.92% | 7.59% | -0.47% | 11.04% | 12.10% | -5.32% | -0.76% |

| Fund Performance Net of Fees as of 7/31/2021 (inception 8/29/2014) |

| 1 Year | 3 Years | 5 Years | Since Inception Annualized | |

| PSOIX | 17.96% | 5.28% | 7.28% | 4.92% |

Annual Expense Ratio: Gross 1.69% / Net 1.69%. The Fund’s advisor has contractually agreed to waive or reduce its management fees and/or reimburse expenses of the Fund to ensure that total annual Fund operating expenses (excluding taxes, leverage interest, brokerage commissions, dividend and interest expenses on short sales, acquired fund fees and expenses, expenses incurred in connection with any merger or reorganization, and extraordinary expenses such as litigation expenses) do not exceed 1.50% of the Fund’s average daily net assets. This agreement is in effect until December 1, 2021, and it may be terminated before that date only by the Fund’s Board of Trustees. The Fund’s advisor is permitted to seek reimbursement from the Fund, subject to certain limitations, of fees waived or payments made to the Fund for a period ending three full fiscal years after the date of the waiver or payment. The performance data quoted represents past performance and that past performance does not guarantee future results. Investment return and principal value will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information current to the most recent month-end please call 866-933-9033.

Portfolio Snapshot

Please refer to the table below for a portfolio snapshot by quarter.

| 6/30/2020 | 9/30/2020 | 12/31/2020 | 3/31/2021 | 7/31/2021 | |

| Interest Rate Duration* | 0.94 yrs | 0.70 yrs | 0.44 yrs | 0.52 yrs | 0.50 yrs |

| Spread Duration* | 3.95 yrs | 3.77 yrs | 3.31 yrs | 2.49 yrs | 2.33 yrs |

| Credit Spread | 751 | 748 | 647 | 565 | 599 |

| Weighted Average Price | $91.10 | $93.06 | $97.70 | $98.13 | $98.13 |

| Yield to Expected Call* | 7.88% | 7.85% | 6.82% | 6.08% | 6.40% |

| Yield to Maturity | 7.34% | 7.40% | 6.78% | 6.52% | 7.07% |

| Current Yield | 6.77% | 6.40% | 6.16% | 5.64% | 6.33% |

| 30-day SEC Yield* (net of fees) | 5.21% | 4.04% | 4.34% | 4.15% | 4.40% |

| 30-day SEC Yield* (gross of fees) | 5.26% | 4.09% | 4.42% | 4.24% | 4.40% |

| Beta vs. S&P 500 | 0.56 | 0.55 | 0.53 | 0.52 | 0.51 |

| Beta vs. Bloomberg Barclays U.S. Aggregate Bond Index | 0.40 | 0.34 | 0.38 | 0.33 | 0.33 |

Past performance does not guarantee future results. *Please see Notes and Disclosure for definitions.

Palmer Square Capital Management LLC 1900 Shawnee Mission Parkway, Suite 315, Mission Woods, KS 66205 www.palmersquarefunds.com

| 1 |

Allocation / Attribution Summary

6/30/2020 Allocation | 9/30/2020 Allocation | 12/31/2020 Allocation | 3/31/2021 Allocation | 7/31/2021 Allocation | 8/1/2020 to 7/31/2021 Gross Attribution | |

| CLO Debt | 68% | 72% | 72% | 72% | 71% | 12.39% |

| Bank Loans | 8% | 10% | 13% | 14% | 12% | 1.69% |

| High Yield Credit | 16% | 12% | 7% | 7% | 4% | 1.19% |

| Sub Notes | 3% | 4% | 3% | 1% | 6% | 3.16% |

| ABS/MBS* | 0% | 0% | 2% | 3% | 3% | 0.24% |

| IG Corp Debt* | 2% | 1% | 0% | 0% | 0% | 0.05% |

Please note the allocation above is on a gross exposure basis as a percent of NAV and does not include cash and/or hedges. Gross attribution does not include hedges, expenses and fees if applicable. Investment return and principal value will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. Attribution refers to the process of measuring returns generated by various sources. *Asset-Backed Securities (ABS), Mortgage-Backed Securities (MBS), Investment Grade Corporate Debt (IG Corp Debt).

Outlook - Potential Upside in CLO Debt

YTD Issuance Remains Elevated

| · | While demand has certainly increased significantly, supply has also been elevated. With the majority of the CLO market now out of its non-call period and AAAs near multi-year tights*, a large portion of the market was in the money for a refi or reset (tighter spreads means older deals can refinance their debt tranches (or modify the deal terms) at more attractive levels than they were originally priced). Coupled with a strong new issue market, CLO gross issuance is off to the busiest start of the year ever. YTD gross issuance is about $223bn ($83.6bn new issue, $72.4bn reset, $67.3bn refi). We expect this trend to continue in the near term as most deals issued in 2020 are exiting their 1 year non-calls in the next 3-6 months. The record setting supply led spreads to be mostly range bound, with AAAs 5-10bps (basis points*) wider* than their early February tights. Mezzanine is off the wides we saw in March/April on elevated supply, but still wider than the February tights. BBBs are currently in the 300-350bp range and BBs are 600- 650bps for higher quality deals. We view this as a significant buying opportunity and very attractive versus other areas of corporate and structured credit. |

Relative Value and Current Upside potential

| · | We see a lot of value in CLO debt at current levels, as spreads are wider from their YTD tights in early February and almost all other areas of corporate credit are at all time tights. If CLO debt levels return to their average post crisis spreads, total return potential is still very attractive. Please see the table below highlighting current price/spreads across the stack and potential upside from current levels. Yield to expected illustrates yields if spreads were to stay the same and the bonds pull to par with maturity. |

| CURRENT SPREAD AND YIELD LEVELS | |||

| Rating | Current Avg Price | Discount Margin | Yield to Expected |

| CLO AAA | $100.00 | 104 | 1.41% |

| CLO AA | $99.88 | 155 | 2.08% |

| CLO A | $99.73 | 201 | 2.67% |

| CLO BBB | $99.22 | 314 | 3.82% |

| CLO BB | $97.59 | 654 | 7.42% |

Source: Intex / Palmer Square as of 6/30/2021. Below investment grade ratings are subject to higher risks. Figures shown are not indicative of the performance of the Fund.

| * | Please see Notes and Disclosure for definitions. |

Palmer Square Capital Management LLC 1900 Shawnee Mission Parkway, Suite 315, Mission Woods, KS 66205 www.palmersquarefunds.com

| 2 |

| · | CLO BBs remain a significant allocation in the portfolio, and at current valuations appear to offer a lot of potential value on a standalone and relative basis. As compared to High Yield (HY) opportunities, CLO BBs on a historical basis still look very cheap. CLO BBs currently pick up 386bps of spread versus HY, which looking back to 2012 is a 95th percentile reading (meaning CLO BBs have been relatively cheaper only 5% of the time). |

CLO BB vs HY Spreads

Source: Bloomberg as of 6/30/2021. PCLOBBDM is the “Palmer Square CLO BB Discount Margin” index. LF98OAS is the “Barclays US Corp HY Average option adjusted spread” index. The chart is comparing spreads for CLO BBs and High Yield bonds. The CLO BB discount margin is the spread over 3mo LIBOR*. The spread for HY bonds is over equivalent “risk free”/ treasury securities.

Fundamentals Remain Positive

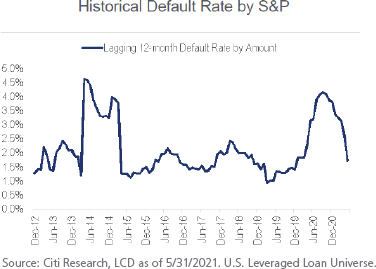

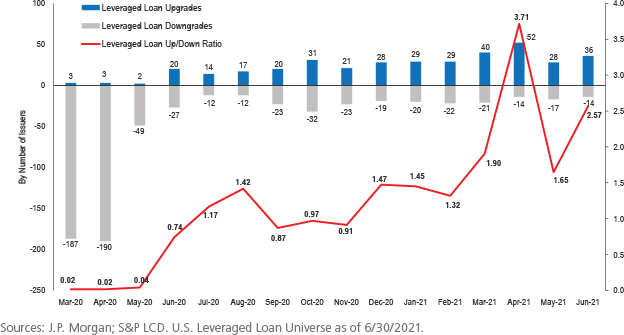

| · | As spreads have remained range bound on higher supply, underlying loan fundamentals have continued to be a tailwind and we expect that to continue. Defaults have continued to decline, with the LTM (last twelve months) U.S. leveraged loan default rate peaking at 4.26% in September 2020, it now sits at 1.70% and has continued to decline (Exhibit 1 below). We also continue to see loan upgrades as company earnings continue to surprise to the upside. The current rolling 3 month upgrade/downgrade ratio sits at 2.1x, which is the highest we have seen since 2011 (Exhibit 2 below). |

Exhibit 1 - Loan default rates continue to decline

| * | Please see Notes and Disclosure for definitions. |

Palmer Square Capital Management LLC 1900 Shawnee Mission Parkway, Suite 315, Mission Woods, KS 66205 www.palmersquarefunds.com

| 3 |

Exhibit 2 - Loan upgrade/downgrade ratio highest in 10 yrs

Summary

Given the portfolio positioning, we are confident in the outlook moving forward. We believe our portfolio is embedded with strong catalysts that can not only drive potential returns, but can also help mitigate a level volatility. More specifically, the portfolio has high current yield and the potential to generate price appreciation, and finally the portfolio has been providing low interest rate and relatively low spread duration*.

Please do not hesitate to contact us at investorrelations@palmersquarecap.com or 816-994-3200 should you desire more information. We would also be happy to set up a call and/or meeting at your convenience.

| * | Please see Notes and Disclosure for definitions. |

Palmer Square Capital Management LLC 1900 Shawnee Mission Parkway, Suite 315, Mission Woods, KS 66205 www.palmersquarefunds.com

| 4 |

APPENDIX: Summary Themes

| • | The Inflation Debate Remains Unsettled with Tapering on the Horizon; |

| • | The Great Reopening: Continued Tailwinds for Credit Fundamentals; |

| • | Current Positioning: Low Duration, High Income Potential. |

Theme I. The Inflation Debate Remains Unsettled with Tapering on the Horizon

| » | Inflation continued to be the dominant macro topic in the 2nd quarter, with divided opinions on whether it will be short lived or not. What is known is that the headline CPI (Consumer Price Index) has surged to 5.4% while the core measure, which excludes food and energy prices, is currently running at 4.5% y/y (as of 6/30/2021). This is the highest level of core inflation since the early 1990s. What remains unclear is how much of this run up in prices is transitory in nature and how much is structural and lasting. For sure, at least some appears to be transitory. U.S. lumber prices surged by 93% through early May, driven by a strong housing market and supply issues. But lumber prices are now 21% lower on the year. Similar price action can be seen in other basic materials such as copper and petrochemicals which have largely faded the Spring surge. But on the other hand, oil prices remain at the highs and U.S. house prices are at record high levels as well. We also know wages are increasing as companies struggle to hire and retain staff all the while dealing with, and passing through, other input cost inflation. Additionally, we view the transition of China’s economic model from export-led to domestic consumption-led as structurally inflationary for the world economy. The growing trends in ESG (environmental, social, and governance) and sustainability, while in almost all ways generally positive, also create inflationary pressures. So, at the margin, we still believe a non-trivial amount of this current surge in inflation is structural and could last longer than expected. The real question is if that is the case how will the bond market react. |

| » | The market reaction, at least in the 2nd quarter, appears to have a less hawkish view on inflation. Interest rates largely fell throughout the quarter with the 10Y treasury yield declining from 1.74% to 1.47%. What drove this move appears to be a host of factors, including a less hawkish view on Fed policy, technical factors related to the unwinding of hedges, a downshift in future growth assumptions, and foreign demand out of Europe and Asia. Also interesting is the curve flattened, both due to lower long bond yields but also due to higher front bond yields. In other words, the market is now pricing in a Fed hike sooner than previously expected, but also lowered expectations on long term growth and inflation. |

| » | Based on the last FOMC (Federal Open Market Committee) meeting the market now expects the Fed to outline plans for the tapering of purchases by the end of this year with a formal start in the 1st quarter of 2022. The market also expects the first rate hike to be towards the end of 2022. So the main question for fixed income investors is will above average inflation force the Fed to act earlier (or more forcefully). On that note we believe it will take a sustained period of 3%+ core inflation to force an earlier move by the Fed. If that is indeed the case, we think treasury yields will resume moving wider* throughout 2021. |

| * | Please see Notes and Disclosure for definitions. |

Palmer Square Capital Management LLC 1900 Shawnee Mission Parkway, Suite 315, Mission Woods, KS 66205 www.palmersquarefunds.com

| 5 |

Theme II. The Great Reopening: Continued Tailwinds for Credit Fundamentals

| » | We have highlighted in past investor letters how resilient corporate America was during the pandemic. Despite the initial fears of zero revenue, huge cash burns, liquidity shortfalls and resulting defaults/bankruptcies, U.S. companies (and all Western companies we follow for that matter) largely did a remarkable job of cutting costs, preserving cash, raising liquidity, and improvising their business models to weather the pandemic. While traditional measure of credit metrics such as leverage are admittedly close to record high levels, these are backward looking and, in most cases, fail to incorporate the likely substantial improvement in demand. And somewhat ironically, many businesses will exit the pandemic with leaner cost structures enabling margins to expand significantly in 2021. We think that many businesses will be more profitable compared to 2019 even with modestly lower revenue. |

| » | The credit tailwind is also showing up in credit ratings. The Agencies were very quick to downgrade companies at the onset of the pandemic. According to data from JPMorgan, almost half of all leveraged loan issuers were downgraded in 2020 with the bulk of those downgrades occurring in Mar/Apr. And in many cases the rating was not just downgraded, but the outlook was kept on Negative or even worse, Watch Negative which implies another downgrade is likely. However, as we have highlighted, companies performed much better than the agencies (and the market) expected. And this has led to net upgrades in the loan market for 10 of the last 12 months (see chart below). The HY and IG (investment grade) bond markets exhibited similar trends as well. And while credit ratings are a useful but not critical tool for fundamental credit investors such as ourselves, they do have fundamental impacts on CLO metrics, which in turn can and will affect the cash flows and trading prices of CLO debt and equity. As the global economy continues to recover from the pandemic, we see net upgrades continuing across all of corporate credit which is a positive technical tailwind for CLOs, bank loans and corporate bonds. |

| » | The resilient pandemic performance also showed itself in lower-than-expected defaults. The LTM (last twelve months) default rate peaked at 6.17% for HY in December and at 4.26% for loans in September, and both measures have been in decline since those peaks. This compares to peaks of 10.98% and 14.18% for HY and loans, respectively, in Nov 2009. On many levels, it could be argued the COVID-19 pandemic was a bigger macro shock than the GFC (global financial crisis) given broader impact in terms of geography and industry (the GFC was largely contained to the U.S. and European banking systems). The key difference, in our opinion, was the quicker response from central banks, governments and businesses that simultaneously kept the capital markets open and put a floor on aggregate demand. We see corporate defaults continuing their downward trend in 2021 which is yet another tailwind for corporate credit. |

| * | Please see Notes and Disclosure for definitions. |

Palmer Square Capital Management LLC 1900 Shawnee Mission Parkway, Suite 315, Mission Woods, KS 66205 www.palmersquarefunds.com

| 6 |

Theme III. Current Positioning: Low Duration, Relatively High Income

We believe our strategies are positioned to benefit our investors:

| · | Attractive yields; |

| · | Lower duration, higher quality bias; |

| · | Diversification potential; |

| · | Rotational ability to potentially take advantage of dislocations as they arise. |

| » | As we head into the 2nd half of 2021, the U.S. economy stands to benefit from the continued reopening of the country along with lingering fiscal stimulus and continued monetary support. While the pace of reopening could be uneven, there is clearly pent-up demand in various parts of the economy that should provide a steady source of organic growth. All this said, there are potential risks to highlight, and below we outline these themes and how the Fund aims to benefit. |

Palmer Square Capital Management LLC 1900 Shawnee Mission Parkway, Suite 315, Mission Woods, KS 66205 www.palmersquarefunds.com

| 7 |

Investment Considerations:

| » | First is the pace of reopening and economic recovery. The shape of the recovery was sharp initially with Q3 2020 GDP up 33.4% (effectively recovering 74% of the $2.2 trillion decline in 1H 2020) with Q4 2020 following at 4.3% and Q1 2021 accelerating back to 6.4%. And while the U.S. and European economies seems to be in decent shape (due to successes in vaccinations and inching closer to some form of herd immunity) emerging markets on the other hand continue to deal with surges in the Delta Variant that are causing health-related restrictions to be reintroduced which have both a direct economic cost as well as an indirect impact on the global supply chain. In summary, to the extent it takes longer than expected to reduce COVID-19 prevalence, the current jubilant market mood may quickly shift negatively leading to both technical and fundamental deterioration. In this event, the Fund has liquidity and trading flexibility enabling the team to maneuver through volatility and, just like in March and April of 2020, add risk at more attractive levels. |

| » | The second theme to focus on is interest rates. The debate on to what extent the current surge in inflation is transitory or structural remains inconclusive in our opinion. And while there are clearly some transitory factors at play, namely building materials, commodities and car prices, we also see a lot of structural inflationary forces at work. Companies are dealing with the current increases in labor and input costs by passing them along as much as possible to the end customer. These increases tend to be more sticky and less likely to be reversed. Furthermore, the evolution of China’s economic model from exporter to consumer along with the growing theme of ESG are also structurally inflationary. To what extent does elevated inflation alter the Fed’s reaction function is a whole other question. But the house view is still cautious on interest rates, especially after the retracement in the 2nd quarter. The Fund would be a net benefactor from rising rates, particularly if front end rates increase as that would increase the coupons on the floating rate component of the strategy. |

| » | The last theme to watch out for is asset bubbles. While somewhat isolated so far, there appears to be bubble-like behavior in certain “theme or meme” stocks like AMC, tech stocks in general, SPACs (special purpose acquisition company), “new economy” stocks in the online gambling and cannabis sectors, and crypto currencies just to name a few. A primary driver of these bubbles is the elevated level of U.S. savings, which in turn is due to direct-to-consumer stimulus measures. Eventually, the economy won’t need stimulus anymore and the pools of capital propping up these valuation levels will subside. The saying goes, nothing brings out sellers more than lower prices. As such, the risk is that some of these bubbles pop leading to declines in peripheral areas which in turn can lead to broad based risk reduction. But any such event would likely be a buying opportunity if it resulted in spread widening in the credit market. |

| * | Please see Notes and Disclosure for definitions. |

Palmer Square Capital Management LLC 1900 Shawnee Mission Parkway, Suite 315, Mission Woods, KS 66205 www.palmersquarefunds.com

| 8 |

Notes and Disclosure

This overview is for informational and comparative purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any interests in the Palmer Square Opportunistic Income Fund, the (“Fund”), and/or any other securities, or to provide any other advisory services. Any offer to invest in the funds will be made pursuant to the Fund’s prospectus, which will contain material information not contained herein and to which prospective investors are directed. Before investing, you should carefully read such materials in their entirety. This overview is not intended to replace such materials, and any information herein should not be relied upon for the purposes of investing in the Funds or for any other purpose. This overview is a summary and does not purport to be complete. The Palmer Square Opportunistic Income Fund is a closed-end fund.

Interest Rate Duration measures a portfolio’s sensitivity to changes in interest rates. Spread Duration measures the sensitivity of a bond price based on basis point changes of more than 100. Yield To Call is the yield of a bond or note if you were to buy and hold the security until the call date. Yield To Maturity is the rate of return anticipated on a bond if held until the end of its lifetime. Current Yield is annual income divided by price paid. Beta describes an investment’s volatility in relation to that of the stock or bond market as a whole. For example, the S&P 500 is typically considered to be “the equity market” and it has a beta of 1.0. Yield to Expected Call is a Yield to Call metric that assumes callable bonds are not called on their call date, but at some later date prior to maturity. Yield to Expected Call considers contractual terms in a bond’s indenture or other similar governing document. A bond may be called before or after this date, which has the potential to increase or decrease the Yield to Expected Call calculation. All else equal, when a bond’s price is below par, Yield to Expected Call is a more conservative yield metric than Yield to Call. If a bond is not callable, Yield to Expected Call calculates the bond’s Yield to Maturity. Basis points (BPS) refers to a common unit of measure for interest rates and other percentages in finance. The relationship between percentage changes and basis points can be summarized as follows: 1% change = 100 basis points and 0.01% = 1 basis point. The London Interbank Offered Rate (LIBOR) is a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans. Credit Spreads are the difference in yield between a U.S. Treasury bond and another debt security of the same maturity but different credit quality. Credit Spreads are often a good barometer of economic health - wide or widening (bearish sentiment) and narrowing/tight or tightening (bullish sentiment). The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index of publicly issued investment grade corporate, US Treasury and government agency securities with remaining maturities of one to three years. The S&P 500 Index is a market-value weighted index provided by Standard & Poor’s comprised of 500 stocks chosen for market size and industry group representation. JPMorgan Liquid Loan Index - is a market-weighted index that measures the performance of the most liquid issues in the investment grade, dollar-denominated corporate bond market. ICE BAML High Yield Index - tracks the performance of non-investment-grade corporate bonds. Unlike mutual funds, indices are not managed and do not incur fees or expenses. It is not possible to invest directly in an index.

The allocation and credit quality distribution figures shown are used for illustrative purposes only. Palmer Square does not guarantee to execute that allocation and credit quality distribution. Allocation and exposures information, as well as other referenced categorizations, reflect classifications determined by Palmer Square as well as certain Palmer Square assumptions based on estimated portfolio characteristic information. Allocation and credit quality distribution figures may not sum to 100%. Ratings listed herein are assigned by Standard & Poor’s (S&P) and Moody’s Investor Service (Moody’s). Credit quality ratings are measured on a scale with S&P’s credit quality ratings ranging from AAA (highest) to D (lowest) and Moody’s credit quality ratings ranging from Aaa (highest) to C (lowest). We use the higher of the two ratings. Credit ratings listed are subject to change. Please contact Palmer Square for more information.

Market opportunities and/or yields shown are for illustration purposes only and are subject to change without notice. Palmer Square does not represent that these or any other strategy/opportunity will prove to be profitable or that the Fund’s investment objective will be met. This material represents an assessment of the market environment at a specific point in time, is subject to change without notice, and should not be relied upon by the reader as research or investment advice. With regard to sources of information, certain of the economic and market information contained herein has been obtained from published sources and/or prepared by third parties. While such sources are believed to be reliable, Palmer Square or their employees or representatives do not assume any responsibility for the accuracy of such information. Palmer Square is under no obligation to verify its accuracy.

The performance presented here is past performance and not indicative of future returns. Different types of investments involve varying degrees of risk and there can be no assurance that any specific investment will be profitable. Please note that the performance of the funds may not be comparable to the performance of any index shown. Palmer Square has not verified, and is under no obligation to verify, the accuracy of these returns. Past performance does not guarantee future results.

Collateralized Loan Obligations Risk – The Fund may invest in CLOs. The Fund is subject to asset manager, legal and regulatory, limited recourse, liquidity, redemption, and reinvestment risks as a result of the structure of CLOs in which the Fund may invest. A CLO’s performance is linked to the expertise of the CLO manager and its ability to manage the CLO portfolio. Changes in the regulation of CLOs may adversely affect the value of the CLO investments held by the Fund and the ability of the Fund to execute its investment strategy. CLO debt is payable solely from the proceeds of the CLO’s underlying assets and, therefore, if the income from the underlying loans is insufficient to make payments on the CLO debt, no other assets will be available for payment. CLO debt securities may be subject to redemption and the timing of redemptions may adversely affect the returns on CLO debt. The CLO manager may not find suitable assets in which to invest and the CLO manager’s opportunities to invest may be limited.

Palmer Square Capital Management LLC 1900 Shawnee Mission Parkway, Suite 315, Mission Woods, KS 66205 www.palmersquarefunds.com

| 9 |

Notes and Disclosure cont’d

The risks of an investment in a collateralized debt obligation depend largely on the type of the collateral securities and the class of the debt obligation in which the Fund invests. Collateralized debt obligations are generally subject to credit, interest rate, valuation, prepayment and extension risks. These securities are also subject to risk of default on the underlying asset, particularly during periods of economic downturn. Defaults, downgrades, or perceived declines in creditworthiness of an issuer or guarantor of a debt security held by the Fund, or a counterparty to a financial contract with the Fund, can affect the value of the Fund’s portfolio. Credit loss can vary depending on subordinated securities and non-subordinated securities. If interest rates fall, an issuer may exercise its right to prepay their securities. If this happens, the Fund will not benefit from the rise in market price, and will reinvest prepayment proceeds at a later time. The Fund may lose any premium it paid on the security. If interest rates rise, repayments of fixed income securities may occur more slowly than anticipated by the market which may result in driving the prices of these securities down. The Fund is “non-diversified,” meaning the Fund may invest a larger percentage of its assets in the securities of a smaller number of issuers than a diversified fund. Investment in securities of a limited number of issuers exposes the Fund to greater market risk and potential losses than if its assets were diversified among the securities of a greater number of issuers. Foreign investments present additional risk due to currency fluctuations, economic and political factors, government regulations, differences in accounting standards and other factors. Investments in emerging markets involve even greater risks. High yield securities, commonly referred to as “junk bonds,” are rated below investment grade by at least one of Moody’s, S&P or Fitch (or if unrated, determined by the Fund’s advisor to be of comparable credit quality high yield securities). The Fund is new and has a limited history of operations.

The Palmer Square Opportunistic Income Fund is distributed by Foreside Fund Services LLC. Palmer Square Capital Management LLC (“Palmer Square”) is an SEC registered investment adviser with its principal place of business in the State of Kansas. Registration of an investment adviser does not imply a certain level of skill or training. Palmer Square and its representatives are in compliance with the current registration and notice filing requirements imposed upon registered investment advisers by those states in which Palmer Square maintains clients. Palmer Square may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements. Any subsequent, direct communication by Palmer Square with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about Palmer Square, including fees and services, send for our disclosure statement as set forth on Form ADV using the contact information herein or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you invest or send money.

This material must be preceded or accompanied by a prospectus. Please read the prospectus carefully before investing. For a prospectus, or summary prospectus, that contains this and other information about the Funds, call 866-933-9033 or visit our website at www. palmersquarefunds.com. Please read the prospectus, or summary prospectus carefully before investing.

Palmer Square Capital Management LLC 1900 Shawnee Mission Parkway, Suite 315, Mission Woods, KS 66205 www.palmersquarefunds.com

| 10 |

Palmer Square Opportunistic Income Fund

FUND PERFORMANCE at July 31, 2021 (Unaudited)

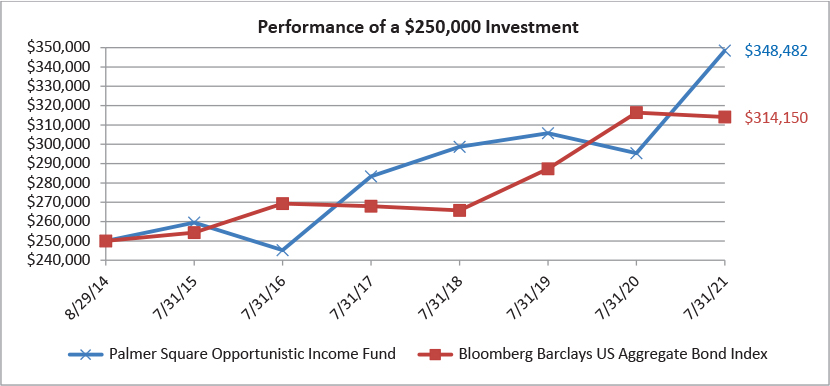

This graph compares a hypothetical $250,000 investment in the Fund’s shares, made at its inception, with a similar investment in the Bloomberg Barclays US Aggregate Bond Index. Results include the reinvestment of all dividends and capital gains.

The Bloomberg Barclays US Aggregate Bond Index is an unmanaged index of publicly issued investment grade corporate, US Treasury and government agency securities with remaining maturities of one to three years. The index does not reflect expenses, fees or sales charge, which would lower performance. The index is unmanaged and it is not possible to invest in an index.

| Average Annual Total Return as of July 31, 2021 | 1 Year | 5 Years | Since Inception | Inception Date |

| Palmer Square Opportunistic Income Fund | 17.96% | 7.28% | 4.92% | 8/29/14 |

| Bloomberg Barclays US Aggregate Bond Index | -0.70% | 3.13% | 3.36% | 8/29/14 |

The performance data quoted here represents past performance and past performance is not a guarantee of future results. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. The most recent month end performance may be obtained by calling (866) 933-9033.

Expense ratio for the Fund was 1.69%, which was the amount stated in the current prospectus dated December 1, 2020. For the Fund’s current one year expense ratios, please refer to the Financial Highlights Section of this report. The Advisor has contractually agreed to waive or reduce its fee and/or to absorb other operating expenses (excluding taxes, leverage interest, brokerage commissions, dividend and interest expenses on short sales, acquired fund fees and expenses, expenses incurred in connection with any merger or reorganization, and extraordinary expenses such as litigation expenses) do not exceed 1.50% of the Fund’s average daily net assets. In the absence of such waivers, the Fund’s returns would be lower. This agreement is in effect until December 1, 2021, and it may be terminated before that date only by the Fund’s Board of Trustees.

Returns reflect the reinvestment of distributions made by the Fund, if any. The graph and the performance table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| 11 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BANK LOANS — 11.1% | ||||||||

| 496,142 | Abe Investment Holdings, Inc. 4.625% (3-Month USD Libor+450 basis points), 2/19/20262,3,4 | $ | 496,142 | |||||

| 109,375 | Alphabet Holding Co., Inc. 7.842% (3-Month USD Libor+775 basis points), 8/15/20252,3,4 | 109,837 | ||||||

| 256,750 | Alterra Mountain Co. 5.500% (1-Month USD Libor+450 basis points), 8/1/20262,3,4 | 257,393 | ||||||

| 234,374 | American Consolidated Natural Resources, Inc. 17.000% (1-Month USD Libor+1,300 basis points), 9/16/20252,4 | 237,304 | ||||||

| 500,000 | American Rock Salt Co. LLC 4.750% (1-Month USD Libor+400 basis points), 6/11/20282,4 | 501,250 | ||||||

| 250,000 | 8.000% (1-Month USD Libor+725 basis points), 6/11/20292,4 | 250,000 | ||||||

| 496,165 | Amynta Agency Borrower, Inc. 4.604% (3-Month USD Libor+450 basis points), 2/28/20252,3,4 | 495,646 | ||||||

| 249,375 | Aruba Investments Holdings, LLC 4.750% (1-Month USD Libor+400 basis points), 11/24/20272,3,4 | 250,467 | ||||||

| 400,000 | 8.500% (1-Month USD Libor+775 basis points), 11/24/20282,3,4 | 404,000 | ||||||

| 500,000 | Avaya, Inc. 4.343% (1-Month USD Libor+425 basis points), 12/15/20272,3,4 | 501,563 | ||||||

| 298,502 | Canada Goose, Inc. 4.250% (1-Month USD Libor+350 basis points), 10/7/20272,3,4,5 | 299,682 | ||||||

| 299,250 | CCI Buyer, Inc. 4.750% (1-Month USD Libor+400 basis points), 12/17/20272,3,4 | 299,784 | ||||||

| 268,125 | CCS-CMGC Holdings, Inc. 5.592% (3-Month USD Libor+550 basis points), 10/1/20252,3,4 | 265,812 | ||||||

| 150,000 | 9.092% (3-Month USD Libor+900 basis points), 10/1/20262,3,4 | 146,687 | ||||||

| 493,750 | Delek U.S. Holdings, Inc. 6.500% (1-Month USD Libor+550 basis points), 3/30/20252,3,4 | 495,757 | ||||||

| 78,207 | Ditech Holding Corp. 8.499% (3-Month USD Libor+600 basis points), 6/30/2022*,2,4 | 15,756 | ||||||

| 746,250 | ECI Macola/Max Holding LLC 4.500% (1-Month USD Libor+375 basis points), 11/9/20272,3,4 | 747,742 | ||||||

| 350,000 | Flexential Intermediate Corp. 7.379% (3-Month USD Libor+725 basis points), 8/1/20252,3,4 | 318,938 | ||||||

| 502,279 | Forterra Finance LLC 4.000% (3-Month USD Libor+300 basis points), 10/25/20232,3,4 | 502,578 | ||||||

| 399,000 | Grab Holdings, Inc. 5.500% (1-Month USD Libor+450 basis points), 1/29/20262,3,4,5 | 402,491 | ||||||

| 597,000 | Great Outdoors Group LLC 5.000% (1-Month USD Libor+425 basis points), 3/5/20282,3,4 | 598,642 | ||||||

| 698,250 | Guidehouse LLP 4.646% (1-Month USD Libor+450 basis points), 5/1/20252,3,4 | 700,058 | ||||||

| 693,636 | Idera, Inc. 4.500% (1-Month USD Libor+375 basis points), 3/2/20282,3,4 | 692,769 | ||||||

| 12 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BANK LOANS (Continued) | ||||||||

| 682,234 | Inmar, Inc. 5.000% (3-Month USD Libor+400 basis points), 5/1/20242,3,4 | $ | 682,660 | |||||

| 247,442 | IRB Holding Corp. 2.953% (1-Month USD Libor+275 basis points), 2/5/20252,3,4 | 246,486 | ||||||

| 345,817 | Isagenix International LLC 6.750% (3-Month USD Libor+575 basis points), 6/14/20252,3,4 | 288,671 | ||||||

| 648,375 | Ivanti Software, Inc. 5.750% (1-Month USD Libor+475 basis points), 12/1/20272,3,4 | 648,826 | ||||||

| 268,766 | Kestrel Acquisition LLC 5.250% (3-Month USD Libor+425 basis points), 6/30/20252,3,4 | 230,578 | ||||||

| 199,591 | LBM Acquisition LLC 4.500% (1-Month USD Libor+375 basis points), 12/17/20272,3,4 | 198,032 | ||||||

| 497,500 | Life Time, Inc. 5.750% (1-Month USD Libor+475 basis points), 12/15/20242,3,4 | 497,813 | ||||||

| 473,305 | Lightstone Holdco LLC 4.750% (3-Month USD Libor+375 basis points), 1/30/20242,3,4 | 367,173 | ||||||

| 26,695 | 4.750% (3-Month USD Libor+375 basis points), 1/30/20242,3,4 | 20,709 | ||||||

| 597,000 | LogMeIn, Inc. 4.850% (1-Month USD Libor+475 basis points), 8/31/20272,3,4 | 595,367 | ||||||

| 500,000 | Magenta Buyer LLC 5.750% (1-Month USD Libor+500 basis points), 7/27/20282,3,4,6,7 | 498,283 | ||||||

| 248,062 | Mauser Packaging Solutions Holding Co. 3.381% (3-Month USD Libor+325 basis points), 4/3/20242,3,4 | 240,600 | ||||||

| 444,571 | McAfee LLC 3.840% (3-Month USD Libor+375 basis points), 9/29/20242,3,4 | 444,669 | ||||||

| 635,375 | Minotaur Acquisition, Inc. 4.854% (3-Month USD Libor+500 basis points), 3/29/20262,3,4 | 633,733 | ||||||

| 694,264 | National Mentor Holdings, Inc. 4.500% (1-Month USD Libor+375 basis points), 3/2/20282,3,4 | 693,976 | ||||||

| 32,230 | 4.500% (1-Month USD Libor+375 basis points), 3/2/20282,3,4,6,7 | 32,217 | ||||||

| 21,866 | 4.500% (1-Month USD Libor+375 basis points), 3/2/20282,3,4 | 21,857 | ||||||

| 398,344 | NeuStar, Inc. 9.000% (3-Month USD Libor+800 basis points), 8/8/20252,3,4 | 383,904 | ||||||

| 492,500 | Option Care Health, Inc. 3.842% (1-Month USD Libor+450 basis points), 8/6/20262,3,4 | 490,899 | ||||||

| 250,000 | Pluto Acquisition I, Inc. 4.135% (1-Month USD Libor+400 basis points), 6/20/20262,3,4 | 248,750 | ||||||

| 850,000 | PowerTeam Services LLC 8.250% (3-Month USD Libor+725 basis points), 3/6/20262,3,4 | 846,387 | ||||||

| 100,000 | Prairie ECI Acquiror LP 4.000% (3-Month USD Libor+475 basis points), 3/11/20262,3,4 | 97,202 | ||||||

| 325,000 | Quest Software U.S. Holdings, Inc. 8.379% (3-Month USD Libor+825 basis points), 5/18/20262,3,4 | 325,081 | ||||||

| 13 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BANK LOANS (Continued) | ||||||||

| 476,667 | Redstone Holdco 2 LP 8.500% (1-Month USD Libor+775 basis points), 4/27/20292,3,4 | $ | 470,511 | |||||

| 273,333 | 8.500% (1-Month USD Libor+775 basis points), 4/27/20292,3,4,6,7 | 269,803 | ||||||

| 400,000 | Renaissance Holdings Corp. 7.104% (3-Month USD Libor+700 basis points), 5/29/20262,3,4 | 401,392 | ||||||

| 396,970 | Rohm Holding GmbH 4.904% (1-Month USD Libor+500 basis points), 7/31/20262,3,4,5 | 396,473 | ||||||

| 576,016 | Sabert Corp. 5.500% (1-Month USD Libor+450 basis points), 12/10/20262,3,4 | 577,277 | ||||||

| 496,154 | Scientific Games International, Inc. 2.854% (1-Month USD Libor+275 basis points), 8/14/20242,3,4 | 489,505 | ||||||

| 343,698 | Serta Simmons Bedding LLC 3.500% (3-Month USD Libor+350 basis points), 11/8/20232,3,4 | 233,715 | ||||||

| 496,183 | Severin Acquisition LLC 3.339% (1-Month USD Libor+325 basis points), 8/1/20252,3,4 | 493,482 | ||||||

| 455,882 | SK Invictus Intermediate II Sarl 6.842% (3-Month USD Libor+675 basis points), 3/28/20262,3,4,5 | 455,955 | ||||||

| 248,121 | Surf Holdings LLC 3.628% (1-Month USD Libor+350 basis points), 3/5/20272,3,4 | 245,933 | ||||||

| 497,500 | U.S. Radiology Specialists, Inc. 6.250% (1-Month USD Libor+550 basis points), 12/15/20272,3,4 | 501,542 | ||||||

| 397,975 | U.S. Renal Care, Inc. 5.092% (3-Month USD Libor+500 basis points), 7/26/20262,3,4 | 398,934 | ||||||

| 389,492 | U.S. Silica Co. 5.000% (3-Month USD Libor+400 basis points), 5/1/20252,4 | 376,006 | ||||||

| 600,000 | Vision Solutions, Inc. 5.000% (1-Month USD Libor+425 basis points), 5/28/20282,3,4 | 598,548 | ||||||

| TOTAL BANK LOANS | ||||||||

| (Cost $23,352,787) | 23,633,247 | |||||||

| BONDS — 86.6% | ||||||||

| ASSET-BACKED SECURITIES — 75.4% | ||||||||

| 1,000,000 | AIMCO CLO Ltd. Series 2019-10A, Class E, 6.688% (3-Month USD Libor+655 basis points), 7/22/20323,4,8 | 1,000,547 | ||||||

| 1,000,000 | AIMCO CLO Series Series 2015-AA, Class DR, 2.576% (3-Month USD Libor+245 basis points), 1/15/20283,4,8 | 1,001,853 | ||||||

| 750,000 | Series 2015-AA, Class FR, 7.126% (3-Month USD Libor+700 basis points), 1/15/20283,4,8 | 747,492 | ||||||

| 1,050,000 | ALM Ltd. Series 2016-18A, Class DR, 5.626% (3-Month USD Libor+550 basis points), 1/15/20283,4,8 | 1,050,825 | ||||||

| 14 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| ASSET-BACKED SECURITIES (Continued) | ||||||||

| 1,000,000 | Anchorage Credit Funding Ltd. Series 2018-5A, Class DR, 5.500%, 4/25/20363,8 | $ | 1,006,656 | |||||

| 750,000 | Annisa CLO Series 2016-2A, Class DR, 3.134% (3-Month USD Libor+300 basis points), 7/20/20313,4,8 | 744,719 | ||||||

| 1,250,000 | Apidos CLO Series 2015-21A, Class DR, 5.334% (3-Month USD Libor+520 basis points), 7/18/20273,4,8 | 1,233,675 | ||||||

| 650,000 | Series 2016-24A, Class DR, 5.934% (3-Month USD Libor+580 basis points), 10/20/20303,4,8 | 614,250 | ||||||

| 750,000 | Series 2018-18A, Class E, 5.838% (3-Month USD Libor+570 basis points), 10/22/20303,4,8 | 714,532 | ||||||

| 925,000 | Series 2017-28A, Class D, 5.634% (3-Month USD Libor+550 basis points), 1/20/20313,4,8 | 888,000 | ||||||

| 1,500,000 | Series 2013-12A, Class DR, 2.726% (3-Month USD Libor+260 basis points), 4/15/20313,4,8 | 1,448,036 | ||||||

| 1,000,000 | Series XXXA, Class D, 5.734% (3-Month USD Libor+560 basis points), 10/18/20313,4,8 | 967,702 | ||||||

| 1,000,000 | Apidos CLO Series 2012-11A, Class DR3, 3.884% (3-Month USD Libor+375 basis points), 4/17/20343,4,8 | 1,004,580 | ||||||

| 1,000,000 | Ares CLO Ltd. Series 2020-58A, Class E, 7.156% (3-Month USD Libor+703 basis points), 1/15/20333,4,8 | 1,010,707 | ||||||

| 1,000,000 | ASSURANT CLO Ltd. Series 2019-5A, Class E, 7.466% (3-Month USD Libor+734 basis points), 1/15/20333,4,8 | 1,003,070 | ||||||

| 2,125,000 | Atrium Series 12A, Class DR, 2.938% (3-Month USD Libor+280 basis points), 4/22/20273,4,8 | 2,103,812 | ||||||

| 500,000 | Avery Point CLO Ltd. Series 2015-6A, Class E1, 5.676% (3-Month USD Libor+550 basis points), 8/5/20273,4,8 | 481,501 | ||||||

| 500,000 | Bain Capital Credit CLO Series 2018-1A, Class D, 2.838% (3-Month USD Libor+270 basis points), 4/23/20313,4,8 | 486,979 | ||||||

| 1,000,000 | Ballyrock CLO Ltd. Series 2019-1A, Class DR, 6.876% (3-Month USD Libor+675 basis points), 7/15/20323,4,8 | 999,997 | ||||||

| 750,000 | Bardot CLO Ltd. Series 2019-2A, Class D, 3.938% (3-Month USD Libor+380 basis points), 10/22/20323,4,8 | 751,552 | ||||||

| 15 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| ASSET-BACKED SECURITIES (Continued) | ||||||||

| 1,000,000 | Series 2019-2A, Class E, 7.088% (3-Month USD Libor+695 basis points), 10/22/20323,4,8 | $ | 1,007,236 | |||||

| 750,000 | Barings CLO Ltd. Series 2013-IA, Class FR, 6.884% (3-Month USD Libor+675 basis points), 1/20/20283,4,8 | 715,619 | ||||||

| 1,500,000 | Series 2017-1A, Class D, 3.734% (3-Month USD Libor+360 basis points), 7/18/20293,4,8 | 1,503,160 | ||||||

| 2,300,000 | Series 2017-1A, Class E, 6.134% (3-Month USD Libor+600 basis points), 7/18/20293,4,8 | 2,299,719 | ||||||

| 1,000,000 | Series 2017-1A, Class F, 7.584% (3-Month USD Libor+745 basis points), 7/18/20293,4,8 | 964,054 | ||||||

| 1,500,000 | Series 2019-1A, Class ER, 6.986% (3-Month USD Libor+686 basis points), 4/15/20363,4,8 | 1,502,324 | ||||||

| 750,000 | Barings Euro CLO Series 2020-1A, Class E, 6.900% (3-Month EUR Libor+690 basis points), 4/21/20333,4,8 | 893,855 | ||||||

| 1,000,000 | Series 2020-1X, Class F, 7.980% (3-Month EUR Libor+798 basis points), 4/21/20333,4 | 1,201,158 | ||||||

| 500,000 | Battalion CLO Ltd. Series 2016-10A, Class CR2, 3.575% (3-Month USD Libor+345 basis points), 1/25/20353,4,8 | 500,581 | ||||||

| 805,000 | Benefit Street Partners CLO Ltd. Series 2013-IIA, Class CR, 3.826% (3-Month USD Libor+370 basis points), 7/15/20293,4,8 | 807,369 | ||||||

| 750,000 | Series 2018-5BA, Class C, 3.064% (3-Month USD Libor+293 basis points), 4/20/20313,4,8 | 728,428 | ||||||

| 1,250,000 | Series 2018-14A, Class E, 5.484% (3-Month USD Libor+535 basis points), 4/20/20313,4,8 | 1,190,262 | ||||||

| 1,000,000 | Series 2020-21A, Class D, 4.476% (3-Month USD Libor+435 basis points), 7/15/20313,4,8 | 1,005,712 | ||||||

| 1,250,000 | Series 2019-17A, Class ER, 0.000% (3-Month USD Libor+635 basis points), 7/15/20323,4,8 | 1,250,000 | ||||||

| 1,250,000 | Series 2019-17A, Class E, 6.726% (3-Month USD Libor+660 basis points), 7/15/20323,4,8 | 1,251,754 | ||||||

| 500,000 | Canyon Capital CLO Ltd. Series 2014-1A, Class CR, 2.879% (3-Month USD Libor+275 basis points), 1/30/20313,4,8 | 480,769 | ||||||

| 500,000 | Carbone CLO Ltd. Series 2017-1A, Class D, 6.034% (3-Month USD Libor+590 basis points), 1/20/20313,4,8 | 488,683 | ||||||

| 1,303,000 | Carlyle U.S. CLO Ltd. Series 2019-3A, Class D, 7.164% (3-Month USD Libor+703 basis points), 10/20/20323,4,8 | 1,306,052 | ||||||

| 16 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| ASSET-BACKED SECURITIES (Continued) | ||||||||

| 2,000,000 | Catamaran CLO Ltd. Series 2013-1A, Class DR, 2.929% (3-Month USD Libor+280 basis points), 1/27/20283,4,8 | $ | 2,008,216 | |||||

| 1,000,000 | Cedar Funding CLO Ltd. Series 2019-10A, Class E, 7.134% (3-Month USD Libor+700 basis points), 10/20/20323,4,8 | 1,006,602 | ||||||

| 1,250,000 | Series 2020-12A, Class E, 6.125% (3-Month USD Libor+600 basis points), 10/25/20323,4,8 | 1,252,344 | ||||||

| 1,000,000 | CIFC European Funding CLO Series 3X, Class D, 3.600% (3-Month EUR Libor+360 basis points), 1/15/20343,4 | 1,199,560 | ||||||

| 750,000 | CIFC Funding Ltd. Series 2015-3A, Class DR, 2.634% (3-Month USD Libor+250 basis points), 4/19/20293,4,8 | 730,151 | ||||||

| 750,000 | Series 2018-1A, Class D, 2.784% (3-Month USD Libor+265 basis points), 4/18/20313,4,8 | 740,464 | ||||||

| 500,000 | Series 2018-3A, Class E, 5.634% (3-Month USD Libor+550 basis points), 7/18/20313,4,8 | 496,456 | ||||||

| 250,000 | Series 2018-5A, Class C, 3.126% (3-Month USD Libor+300 basis points), 1/15/20323,4,8 | 251,264 | ||||||

| 750,000 | Series 2019-5A, Class D, 6.966% (3-Month USD Libor+684 basis points), 10/15/20323,4,8 | 752,165 | ||||||

| 500,000 | Series 2019-6A, Class E, 7.526% (3-Month USD Libor+740 basis points), 1/16/20333,4,8 | 502,657 | ||||||

| 1,000,000 | Series 2019-2A, Class ER, 6.724% (3-Month USD Libor+659 basis points), 4/17/20343,4,8 | 1,018,778 | ||||||

| 500,000 | Crestline Denali CLO Ltd. Series 2016-1A, Class DR, 3.488% (3-Month USD Libor+335 basis points), 10/23/20313,4,8 | 484,350 | ||||||

| 1,000,000 | Cumberland Park CLO Ltd. Series 2015-2A, Class DR, 2.834% (3-Month USD Libor+270 basis points), 7/20/20283,4,8 | 1,004,794 | ||||||

| 2,500,000 | Series 2015-2A, Class ER, 5.784% (3-Month USD Libor+565 basis points), 7/20/20283,4,8 | 2,518,564 | ||||||

| 1,750,000 | Dartry Park CLO DAC Series 1X, Class CRR, 3.350% (3-Month EUR Libor+335 basis points), 1/28/20343,4 | 2,095,821 | ||||||

| 1,725,000 | Denali Capital CLO LLC Series 2013-1A, Class B1LR, 3.275% (3-Month USD Libor+315 basis points), 10/26/20273,4,8 | 1,724,495 | ||||||

| 17 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| ASSET-BACKED SECURITIES (Continued) | ||||||||

| 995,000 | Dryden CLO Ltd. Series 2018-57A, Class D, 2.706% (3-Month USD Libor+255 basis points), 5/15/20313,4,8 | $ | 976,185 | |||||

| 330,000 | Series 2018-57A, Class E, 5.356% (3-Month USD Libor+520 basis points), 5/15/20313,4,8 | 317,576 | ||||||

| 1,000,000 | Series 2018-70A, Class E, 6.176% (3-Month USD Libor+605 basis points), 1/16/20323,4,8 | 993,240 | ||||||

| 750,000 | Series 2020-85A, Class E, 7.876% (3-Month USD Libor+775 basis points), 10/15/20323,4,8 | 754,773 | ||||||

| 500,000 | Series 2020-78A, Class D, 3.134% (3-Month USD Libor+300 basis points), 4/17/20333,4,8 | 502,130 | ||||||

| 1,000,000 | Series 2020-77A, Class ER, 6.004% (3-Month USD Libor+587 basis points), 5/20/20343,4,8 | 993,168 | ||||||

| 1,000,000 | Series 2020-77A, Class FR, 7.724% (3-Month USD Libor+759 basis points), 5/20/20343,4,8 | 972,511 | ||||||

| 1,000,000 | Series 2020-86A, Class DR, 3.334% (3-Month USD Libor+320 basis points), 7/17/20343,4,8 | 1,000,014 | ||||||

| 1,500,000 | Dryden Senior Loan Fund Series 2012-25A, Class DRR, 3.126% (3-Month USD Libor+300 basis points), 10/15/20273,4,8 | 1,501,577 | ||||||

| 500,000 | Series 2016-45A, Class DR, 3.276% (3-Month USD Libor+315 basis points), 10/15/20303,4,8 | 500,922 | ||||||

| 1,500,000 | Series 2015-41A, Class ER, 5.426% (3-Month USD Libor+530 basis points), 4/15/20313,4,8 | 1,419,875 | ||||||

| 1,350,000 | Series 2015-40A, Class DR, 3.256% (3-Month USD Libor+310 basis points), 8/15/20313,4,8 | 1,357,250 | ||||||

| 1,075,000 | Eaton Vance CLO Ltd. Series 2015-1A, Class DR, 2.634% (3-Month USD Libor+250 basis points), 1/20/20303,4,8 | 1,051,794 | ||||||

| 850,000 | Series 2015-1A, Class ER, 5.734% (3-Month USD Libor+560 basis points), 1/20/20303,4,8 | 835,161 | ||||||

| 500,000 | Series 2014-1RA, Class E, 5.826% (3-Month USD Libor+570 basis points), 7/15/20303,4,8 | 479,814 | ||||||

| 750,000 | Series 2018-1A, Class D, 3.326% (3-Month USD Libor+320 basis points), 10/15/20303,4,8 | 752,925 | ||||||

| 1,250,000 | Series 2019-1A, Class ER, 6.626% (3-Month USD Libor+650 basis points), 4/15/20313,4,8 | 1,248,743 | ||||||

| 500,000 | Series 2020-2A, Class D, 4.226% (3-Month USD Libor+410 basis points), 10/15/20323,4,8 | 504,894 | ||||||

| 1,000,000 | Series 2020-2A, Class E, 7.446% (3-Month USD Libor+732 basis points), 10/15/20323,4,8 | 1,017,738 | ||||||

| 18 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| ASSET-BACKED SECURITIES (Continued) | ||||||||

| 1,500,000 | Series 2013-1A, Class D3R, 6.926% (3-Month USD Libor+680 basis points), 1/15/20343,4,8 | $ | 1,499,930 | |||||

| 5,425,000 | Flatiron CLO Ltd. Series 2017-1A, Class SUB, 0.000%, 5/15/20303,8,9 | 4,308,232 | ||||||

| 3,500,000 | Series 2018-1A, Class SUB, 0.000%, 4/17/20313,8,9 | 2,731,932 | ||||||

| 1,000,000 | Series 2020-1A, Class D, 3.945% (3-Month USD Libor+379 basis points), 11/20/20333,4,8 | 1,013,906 | ||||||

| 1,750,000 | Series 2020-1A, Class E, 8.005% (3-Month USD Libor+785 basis points), 11/20/20333,4,8 | 1,811,250 | ||||||

| 750,000 | Series 2021-1A, Class E, 6.151% (3-Month USD Libor+600 basis points), 7/19/20343,4,8 | 749,945 | ||||||

| 1,000,000 | Galaxy CLO Ltd. Series 2018-29A, Class E, 4.706% (3-Month USD Libor+455 basis points), 11/15/20263,4,8 | 1,000,001 | ||||||

| 500,000 | Series 2017-24A, Class E, 5.626% (3-Month USD Libor+550 basis points), 1/15/20313,4,8 | 491,096 | ||||||

| 500,000 | Goldentree Loan Management U.S. CLO Ltd. Series 2020-8A, Class F, 7.634% (3-Month USD Libor+750 basis points), 7/20/20313,4,8 | 499,972 | ||||||

| 1,500,000 | Goldentree Loan Opportunities Ltd. Series 2016-12A, Class ER, 5.534% (3-Month USD Libor+540 basis points), 7/21/20303,4,8 | 1,433,147 | ||||||

| 1,460,000 | GoldentTree Loan Management U.S. CLO Ltd. Series 2021-10A, Class E, 2.876% (3-Month USD Libor+620 basis points), 7/20/20343,4,8 | 1,460,000 | ||||||

| 750,000 | Series 2021-10A, Class F, 2.876% (3-Month USD Libor+779 basis points), 7/20/20343,4,8 | 727,500 | ||||||

| 1,000,000 | Griffith Park CLO DAC Series 1X, Class DR, 5.520% (3-Month EUR Libor+552 basis points), 11/21/20313,4 | 1,184,689 | ||||||

| 4,000,000 | Grippen Park CLO Ltd. Series 2017-1A, Class SUB, 0.000%, 1/20/20303,8,9 | 2,779,666 | ||||||

| 1,000,000 | Series 2017-1A, Class E, 5.834% (3-Month USD Libor+570 basis points), 1/20/20303,4,8 | 996,082 | ||||||

| 1,850,000 | Highbridge Loan Management Ltd. Series 7A-2015, Class DR, 2.556% (3-Month USD Libor+240 basis points), 3/15/20273,4,8 | 1,816,663 | ||||||

| 850,000 | Series 3A-2014, Class CR, 3.734% (3-Month USD Libor+360 basis points), 7/18/20293,4,8 | 848,681 | ||||||

| 875,000 | Series 5A-2015, Class DRR, 3.276% (3-Month USD Libor+315 basis points), 10/15/20303,4,8 | 839,747 | ||||||

| 19 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| ASSET-BACKED SECURITIES (Continued) | ||||||||

| 500,000 | HPS Loan Management Ltd. Series 8A-2016, Class ER, 5.634% (3-Month USD Libor+550 basis points), 7/20/20303,4,8 | $ | 478,455 | |||||

| 1,375,000 | Series 15A-19, Class E, 6.738% (3-Month USD Libor+660 basis points), 7/22/20323,4,8 | 1,378,694 | ||||||

| 1,000,000 | Invesco CLO Ltd. Series 2021-1A, Class E, 6.625% (3-Month USD Libor+646 basis points), 4/15/20343,4,8 | 995,133 | ||||||

| 500,000 | KKR CLO Ltd. Series 13, Class ER, 5.076% (3-Month USD Libor+495 basis points), 1/16/20283,4,8 | 498,800 | ||||||

| 1,000,000 | LCM LP Series 18A, Class DR, 2.934% (3-Month USD Libor+280 basis points), 4/20/20313,4,8 | 960,108 | ||||||

| 1,250,000 | Madison Park Funding Ltd. Series 2015-19A, Class CR, 2.288% (3-Month USD Libor+215 basis points), 1/22/20283,4,8 | 1,241,345 | ||||||

| 1,460,000 | Series 2015-19A, Class DR, 4.488% (3-Month USD Libor+435 basis points), 1/22/20283,4,8 | 1,402,993 | ||||||

| 500,000 | Magnetite Ltd. Series 2015-16A, Class ER, 5.134% (3-Month USD Libor+500 basis points), 1/18/20283,4,8 | 497,833 | ||||||

| 1,000,000 | Series 2019-22A, Class ER, 6.476% (3-Month USD Libor+635 basis points), 4/15/20313,4,8 | 1,001,935 | ||||||

| 1,050,000 | Series 2015-12A, Class FR, 8.076% (3-Month USD Libor+795 basis points), 10/15/20313,4,8 | 1,021,675 | ||||||

| 1,500,000 | Series 2015-14RA, Class F, 8.064% (3-Month USD Libor+793 basis points), 10/18/20313,4,8 | 1,447,109 | ||||||

| 750,000 | Series 2020-28A, Class E, 7.205% (3-Month USD Libor+708 basis points), 10/25/20313,4,8 | 753,186 | ||||||

| 1,075,000 | Series 2019-24A, Class E, 7.076% (3-Month USD Libor+695 basis points), 1/15/20333,4,8 | 1,080,850 | ||||||

| 800,000 | Milos CLO Ltd. Series 2017-1A, Class ER, 6.284% (3-Month USD Libor+615 basis points), 10/20/20303,4,8 | 790,453 | ||||||

| 1,000,000 | Mountain View CLO Ltd. Series 2015-10A, Class E, 4.979% (3-Month USD Libor+485 basis points), 10/13/20273,4,8 | 982,225 | ||||||

| 5,000,000 | Neuberger Berman CLO Ltd. Series 2015-20A, Class SUB, 0.000%, 1/15/20283,8,9 | 2,564,469 | ||||||

| 325,000 | Series 2016-22A, Class DR, 3.234% (3-Month USD Libor+310 basis points), 10/17/20303,4,8 | 325,437 | ||||||

| 20 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| ASSET-BACKED SECURITIES (Continued) | ||||||||

| 1,000,000 | Series 2016-22A, Class ER, 6.194% (3-Month USD Libor+606 basis points), 10/17/20303,4,8 | $ | 986,845 | |||||

| 1,000,000 | Neuberger Berman Loan Advisers CLO Ltd. Series 2017-26A, Class E, 6.034% (3-Month USD Libor+590 basis points), 10/18/20303,4,8 | 996,404 | ||||||

| 1,450,000 | Series 2019-32A, Class ER, 6.234% (3-Month USD Libor+610 basis points), 1/20/20323,4,8 | 1,448,599 | ||||||

| 500,000 | Series 2020-38A, Class D, 3.884% (3-Month USD Libor+375 basis points), 10/20/20323,4,8 | 500,995 | ||||||

| 1,550,000 | Series 2020-38A, Class E, 7.634% (3-Month USD Libor+750 basis points), 10/20/20323,4,8 | 1,561,827 | ||||||

| 528,045 | Series 2019-35A, Class D, 3.834% (3-Month USD Libor+370 basis points), 1/19/20333,4,8 | 531,430 | ||||||

| 1,000,000 | Neuberger Berman Loan Advisers Euro CLO Series 2021-1X, Class D, 3.000% (3-Month EUR Libor+300 basis points), 4/17/20343,4 | 1,183,925 | ||||||

| 1,000,000 | OCP CLO Ltd. Series 2020-18A, Class ER, 6.564% (3-Month USD Libor+643 basis points), 7/20/20323,4,8 | 1,000,098 | ||||||

| 1,000,000 | Series 2019-17A, Class ER, 6.634% (3-Month USD Libor+650 basis points), 7/20/20323,4,8 | 1,000,024 | ||||||

| 500,000 | Octagon Investment Partners Ltd. Series 2020-2A, Class D, 4.726% (3-Month USD Libor+460 basis points), 7/15/20333,4,8 | 500,613 | ||||||

| 500,000 | Series 2019-3A, Class ER, 6.876% (3-Month USD Libor+675 basis points), 7/15/20343,4,8 | 500,000 | ||||||

| 750,000 | Series 2020-1A, Class ER, 6.384% (3-Month USD Libor+625 basis points), 7/20/20343,4,8 | 749,543 | ||||||

| 1,750,000 | OHA Credit Funding Ltd. Series 2019-2A, Class DR, 3.434% (3-Month USD Libor+330 basis points), 4/21/20343,4,8 | 1,750,101 | ||||||

| 1,000,000 | Series 2019-2A, Class ER, 6.494% (3-Month USD Libor+636 basis points), 4/21/20343,4,8 | 998,969 | ||||||

| 750,000 | PPM CLO Ltd. Series 2019-3A, Class ER, 6.744% (3-Month USD Libor+661 basis points), 4/17/20343,4,8 | 750,000 | ||||||

| 1,000,000 | Recette CLO Ltd. Series 2015-1A, Class YRR, 0.100%, 4/20/20343,8 | 25,153 | ||||||

| 1,200,000 | Regatta Funding LP Series 2013-2A, Class CR2, 3.826% (3-Month USD Libor+370 basis points), 1/15/20293,4,8 | 1,205,014 | ||||||

| 21 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| ASSET-BACKED SECURITIES (Continued) | ||||||||

| 1,000,000 | Regatta Funding Ltd. Series 2018-4A, Class D, 6.625% (3-Month USD Libor+650 basis points), 10/25/20313,4,8 | $ | 997,384 | |||||

| 500,000 | Series 2019-1A, Class E, 6.976% (3-Month USD Libor+685 basis points), 10/15/20323,4,8 | 502,690 | ||||||

| 750,000 | Series 2019-2A, Class D, 4.026% (3-Month USD Libor+390 basis points), 1/15/20333,4,8 | 755,918 | ||||||

| 750,000 | Series 2016-1A, Class ER2, 6.535% (3-Month USD Libor+640 basis points), 6/20/20343,4,8 | 749,999 | ||||||

| 625,000 | Riserva CLO Ltd. Series 2016-3A, Class FRR, 8.644% (3-Month USD Libor+851 basis points), 1/18/20343,4,8 | 610,317 | ||||||

| 1,900,000 | Rockford Tower CLO Ltd. Series 2020-1A, Class E, 7.034% (3-Month USD Libor+690 basis points), 1/20/20323,4,8 | 1,910,311 | ||||||

| 1,000,000 | SOUND POINT CLO Ltd. Series 2019-1A, Class DR, 3.634% (3-Month USD Libor+350 basis points), 1/20/20323,4,8 | 1,000,000 | ||||||

| 1,250,000 | Symphony CLO Ltd. Series 2014-14A, Class E, 4.733% (3-Month USD Libor+460 basis points), 7/14/20263,4,8 | 1,245,518 | ||||||

| 875,000 | TCI-Flatiron CLO Ltd. Series 2017-1A, Class D, 2.906% (3-Month USD Libor+275 basis points), 11/18/20303,4,8 | 868,158 | ||||||

| 1,000,000 | Series 2016-1A, Class DR2, 3.734% (3-Month USD Libor+360 basis points), 1/17/20323,4,8 | 1,004,334 | ||||||

| 1,500,000 | Series 2016-1A, Class ER2, 7.134% (3-Month USD Libor+700 basis points), 1/17/20323,4,8 | 1,505,052 | ||||||

| 1,000,000 | TCI-Symphony CLO Ltd. Series 2016-1A, Class DR, 3.129% (3-Month USD Libor+300 basis points), 10/13/20293,4,8 | 1,004,508 | ||||||

| 1,000,000 | Thompson Park CLO Ltd. Series 2021-1A, Class E, 6.509% (3-Month USD Libor+631 basis points), 4/15/20343,4,8 | 993,546 | ||||||

| 750,000 | TICP CLO Ltd. Series 2017-8A, Class D, 6.684% (3-Month USD Libor+655 basis points), 10/20/20303,4,8 | 748,150 | ||||||

| 688,000 | Series 2016-5A, Class ER, 5.884% (3-Month USD Libor+575 basis points), 7/17/20313,4,8 | 669,914 | ||||||

| 560,000 | Series 2019-13A, Class ER, 6.326% (3-Month USD Libor+620 basis points), 4/15/20343,4,8 | 561,398 | ||||||

| 22 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| ASSET-BACKED SECURITIES (Continued) | ||||||||

| 500,000 | Treman Park CLO Ltd. Series 2015-1A, Class DRR, 2.784% (3-Month USD Libor+265 basis points), 10/20/20283,4,8 | $ | 502,659 | |||||

| 1,000,000 | Venture CLO Ltd. Series 2016-23A, Class ER, 6.084% (3-Month USD Libor+595 basis points), 7/19/20283,4,8 | 999,968 | ||||||

| 750,000 | Voya CLO Ltd. Series 2014-3A, Class CR, 2.775% (3-Month USD Libor+265 basis points), 7/25/20263,4,8 | 751,958 | ||||||

| 750,000 | Series 2015-1A, Class CR, 2.484% (3-Month USD Libor+235 basis points), 1/18/20293,4,8 | 727,553 | ||||||

| 500,000 | Series 2013-1A, Class CR, 3.076% (3-Month USD Libor+295 basis points), 10/15/20303,4,8 | 482,062 | ||||||

| 880,000 | Series 2016-1A, Class DR, 5.384% (3-Month USD Libor+525 basis points), 1/20/20313,4,8 | 817,187 | ||||||

| 1,000,000 | Series 2020-2A, Class E, 7.984% (3-Month USD Libor+785 basis points), 7/19/20313,4,8 | 1,005,233 | ||||||

| 1,500,000 | Series 2020-3A, Class E, 6.414% (3-Month USD Libor+628 basis points), 10/20/20313,4,8 | 1,507,545 | ||||||

| 500,000 | Series 2019-4A, Class E, 7.606% (3-Month USD Libor+748 basis points), 1/15/20333,4,8 | 503,826 | ||||||

| 750,000 | Wind River CLO Ltd. Series 2014-3A, Class DR2, 3.538% (3-Month USD Libor+340 basis points), 10/22/20313,4,8 | 735,540 | ||||||

| 1,000,000 | York CLO Ltd. Series 2016-1A, Class ER, 6.534% (3-Month USD Libor+640 basis points), 10/20/20293,4,8 | 1,003,886 | ||||||

| 750,000 | Series 2015-1A, Class DR, 2.738% (3-Month USD Libor+260 basis points), 1/22/20313,4,8 | 739,490 | ||||||

| 1,750,000 | Series 2018-1A, Class D, 3.488% (3-Month USD Libor+335 basis points), 10/22/20313,4,8 | 1,752,172 | ||||||

| 250,000 | Series 2019-1A, Class D, 4.138% (3-Month USD Libor+400 basis points), 7/22/20323,4,8 | 251,396 | ||||||

| 1,250,000 | Series 2019-2A, Class D, 3.938% (3-Month USD Libor+380 basis points), 1/22/20333,4,8 | 1,257,909 | ||||||

| TOTAL ASSET-BACKED SECURITIES | ||||||||

| (Cost $155,278,496) | 160,792,451 | |||||||

| COMMERCIAL MORTGAGE-BACKED SECURITIES — 5.0% | ||||||||

| 2,550,000 | AIMCO CLO Series Series 2015-AA, Class ER, 5.326% (3-Month USD Libor+520 basis points), 1/15/20283,4,8 | 2,542,499 | ||||||

| 23 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| COMMERCIAL MORTGAGE-BACKED SECURITIES (Continued) | ||||||||

| 1,875,000 | CSMC Series 2017-TIME, Class B, 3.653%, 11/13/20398,9 | $ | 1,711,472 | |||||

| 203,000 | DBUBS Mortgage Trust Series 2011-LC3A, Class PM2, 5.098%, 5/10/20443,8,9 | 202,596 | ||||||

| 955,000 | Elmwood CLO Ltd. Series 2020-2A, Class DR, 2.023% (3-Month USD Libor+310 basis points), 10/20/20343,4,8 | 955,056 | ||||||

| 650,000 | GS Mortgage Securities Corp. Series 2012-TMSQ, Class C, 3.458%, 12/10/20303,8,9 | 637,523 | ||||||

| 750,000 | Sixth Street CLO Ltd. Series 2021-17A, Class E, 6.369% (3-Month USD Libor+620 basis points), 1/20/20343,4,8 | 754,179 | ||||||

| 525,000 | U.S. USDC Series 2018-USDC, Class D, 4.493%, 5/13/20388,9 | 502,744 | ||||||

| 1,250,000 | Series 2018-USDC, Class E, 4.493%, 5/13/20388,9 | 1,102,634 | ||||||

| 1,210,793 | West Town Mall Trust Series 2017-KNOX, Class A, 3.823%, 7/5/20308 | 1,215,533 | ||||||

| 500,000 | WFLD Mortgage Trust Series 2014-MONT, Class D, 3.755%, 8/10/20313,8,9 | 397,833 | ||||||

| 750,000 | Worldwide Plaza Trust Series 2017-WWP, Class F, 3.596%, 11/10/20368,9 | 700,963 | ||||||

| TOTAL COMMERCIAL MORTGAGE-BACKED SECURITIES | ||||||||

| (Cost $10,319,104) | 10,723,032 | |||||||

| CORPORATE — 6.2% | ||||||||

| COMMUNICATIONS — 1.4% | ||||||||

| 500,000 | Endure Digital, Inc. 6.000%, 2/15/20293,8 | 486,277 | ||||||

| 255,000 | ION Trading Technologies Sarl 5.750%, 5/15/20283,5,8 | 264,466 | ||||||

| 1,000,000 | Scripps Escrow II, Inc. 5.375%, 1/15/20313,8 | 1,000,935 | ||||||

| 450,526 | Summer BC Holdco A Sarl 9.250%, 10/31/20273 | 580,853 | ||||||

| 750,000 | ViaSat, Inc. 5.625%, 9/15/20253,8 | 763,860 | ||||||

| 3,096,391 | ||||||||

| CONSUMER, CYCLICAL — 1.1% | ||||||||

| 500,000 | American Airlines Group, Inc. 3.750%, 3/1/20258 | 445,622 | ||||||

| 205,000 | Everi Holdings, Inc. 5.000%, 7/15/20293,8 | 209,869 | ||||||

| 24 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| CORPORATE (Continued) | ||||||||

| CONSUMER, CYCLICAL (Continued) | ||||||||

| 530,000 | GYP Holdings Corp. 4.625%, 5/1/20293,8 | $ | 537,046 | |||||

| 255,000 | International Game Technology PLC 5.250%, 1/15/20293,5,8 | 272,539 | ||||||

| 550,000 | Lions Gate Capital Holdings LLC 5.500%, 4/15/20293,8 | 563,769 | ||||||

| 395,000 | Shea Homes LP / Shea Homes Funding Corp. 4.750%, 4/1/20293,8 | 406,317 | ||||||

| 2,435,162 | ||||||||

| CONSUMER, NON-CYCLICAL — 1.3% | ||||||||

| 500,000 | CoreLogic, Inc. 4.500%, 5/1/20283,8 | 499,957 | ||||||

| 300,000 | Endo Dac / Endo Finance LLC / Endo Finco, Inc. 9.500%, 7/31/20273,5,8 | 301,335 | ||||||

| 169,000 | 6.000%, 6/30/20283,5,8 | 114,296 | ||||||

| 190,000 | Endo Luxembourg Finance Co. I Sarl / Endo US, Inc. 6.125%, 4/1/20293,5,8 | 189,097 | ||||||

| 70,000 | HCRX Investments Holdco LP 4.500%, 8/1/20293,8 | 71,488 | ||||||

| 500,000 | Modulaire Global Finance PLC 8.000%, 2/15/20233,5,8 | 515,375 | ||||||

| 500,000 | NESCO Holdings, Inc. 5.500%, 4/15/20293,8 | 516,887 | ||||||

| 500,000 | Team Health Holdings, Inc. 6.375%, 2/1/20253,8 | 464,382 | ||||||

| 2,672,817 | ||||||||

| ENERGY — 0.8% | ||||||||

| 500,000 | Crestwood Midstream Partners LP / Crestwood Midstream Finance Corp. 6.000%, 2/1/20293,8 | 520,687 | ||||||

| 350,000 | Genesis Energy LP / Genesis Energy Finance Corp. 7.750%, 2/1/20283 | 354,251 | ||||||

| 300,000 | Murray Energy Corp. 11.250%, 1/14/2022*,3,8,10 | 191 | ||||||

| 600,000 | Nabors Industries Ltd. 7.250%, 1/15/20263,5,8 | 561,975 | ||||||

| 450,000 | Peabody Energy Corp. 6.375%, 3/31/20253,8,11 | 355,756 | ||||||

| 1,792,860 | ||||||||

| 25 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Principal Amount1 | Value | |||||||

| BONDS (Continued) | ||||||||

| CORPORATE (Continued) | ||||||||

| FINANCIAL — 0.4% | ||||||||

| AmWINS Group, Inc. | ||||||||

| 550,000 | 4.875%, 6/30/20293,8 | $ | 561,687 | |||||

| Compass Group Diversified Holdings LLC | ||||||||

| 120,000 | 5.250%, 4/15/20293,8 | 124,650 | ||||||

| Iron Mountain, Inc. | ||||||||

| 165,000 | 5.000%, 7/15/20283,8 | 171,729 | ||||||

| 858,066 | ||||||||

| INDUSTRIAL — 0.9% | ||||||||

| FXI Holdings, Inc. | ||||||||

| 300,000 | 12.250%, 11/15/20263,8 | 341,672 | ||||||

| Plastipak Holdings, Inc. | ||||||||

| 350,000 | 6.250%, 10/15/20253,8 | 358,351 | ||||||

| PowerTeam Services LLC | ||||||||

| 550,000 | 9.033%, 12/4/20253,8 | 607,522 | ||||||

| Trident TPI Holdings, Inc. | ||||||||

| 512,000 | 6.625%, 11/1/20253,8 | 524,820 | ||||||

| 1,832,365 | ||||||||

| TECHNOLOGY — 0.3% | ||||||||

| Exela Intermediate LLC / Exela Finance, Inc. | ||||||||

| 230,000 | 10.000%, 7/15/20233,8 | 161,780 | ||||||

| Helios Software Holdings, Inc. | ||||||||

| 250,000 | 4.625%, 5/1/20283,8 | 246,875 | ||||||

| NCR Corp. | ||||||||

| 160,000 | 5.000%, 10/1/20283,8 | 164,984 | ||||||

| 573,639 | ||||||||

| TOTAL CORPORATE | ||||||||

| (Cost $13,407,375) | 13,261,300 | |||||||

| TOTAL BONDS | ||||||||

| (Cost $179,004,975) | 184,776,783 | |||||||

| Number of Shares | ||||||||

| COMMON STOCKS — 1.5% | ||||||||

| ENERGY — 0.8% | ||||||||

| 3,062 | Chevron Corp. | 311,742 | ||||||

| 4,045 | Diamondback Energy, Inc. | 311,991 | ||||||

| 5,479 | Exxon Mobil Corp. | 315,426 | ||||||

| 1,272 | Nabors Industries Ltd.*,5 | 111,313 | ||||||

| 12,590 | Occidental Petroleum Corp. | 328,599 | ||||||

| 26 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Number of Shares | Value | |||||||

| COMMON STOCKS (Continued) | ||||||||

| ENERGY (Continued) | ||||||||

| 3,913 | Phillips 66 | $ | 287,331 | |||||

| 1,666,402 | ||||||||

| FINANCIAL — 0.7% | ||||||||

| 7,083 | Equity Residential - REIT | 595,893 | ||||||

| 6,878 | SL Green Realty Corp. - REIT | 512,136 | ||||||

| 10,700 | Vornado Realty Trust - REIT | 465,450 | ||||||

| 1,573,479 | ||||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $3,273,623) | 3,239,881 | |||||||

Number of Contracts | ||||||||

| PURCHASED OPTION CONTRACTS — 0.1% | ||||||||

| PUT OPTIONS — 0.1% | ||||||||

| EQUITY — 0.1% | ||||||||

| 730 | iShares 20+ Year Treasury Bond ETF Exercise Price: $120.00, Notional Amount: $8,760,000, Expiration Date: August 20, 2021 | $ | 2,920 | |||||

| 730 | Exercise Price: $115.00, Notional Amount: $8,395,000, Expiration Date: October 15, 2021 | 14,965 | ||||||

| 146 | Exercise Price: $120.00, Notional Amount: $1,752,000, Expiration Date: October 15, 2021 | 2,409 | ||||||

| 1,361 | iShares iBoxx High Yield Corporate Bond ETF Exercise Price: $85.00, Notional Amount: $11,568,500, Expiration Date: August 20, 2021 | 16,332 | ||||||

| 851 | SPDR S&P 500 ETF Trust Exercise Price: $375.00, Notional Amount: $31,912,500, Expiration Date: September 17, 2021 | 112,757 | ||||||

| 340 | Exercise Price: $275.00, Notional Amount: $9,350,000, Expiration Date: January 21, 2022 | 56,270 | ||||||

| 991 | United Natural Foods, Inc. Exercise Price: $25.00, Notional Amount: $2,477,500, Expiration Date: August 20, 2021 | 12,388 | ||||||

| 218,041 | ||||||||

| TOTAL PUT OPTIONS | ||||||||

| (Cost $545,290) | 218,041 | |||||||

| TOTAL PURCHASED OPTION CONTRACTS | ||||||||

| (Cost $545,290) | 218,041 | |||||||

| 27 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Number of Shares | Value | |||||||

| WARRANTS — 0.0% | ||||||||

| ENERGY — 0.0% | ||||||||

| 508 | Nabors Industries Ltd., Expiration Date: June 11, 2026*,5 | $ | 3,302 | |||||

| TOTAL WARRANTS | ||||||||

| (Cost $—) | 3,302 | |||||||

| SHORT-TERM INVESTMENTS — 3.5% | ||||||||

| 1,596,057 | Fidelity Investments Money Market Funds - Treasury Portfolio - Class I, 0.01%11,12 | 1,596,057 | ||||||

| 5,734,917 | Federated Treasury Obligations Fund - Institutional Class, 0.01%12 | 5,734,917 | ||||||

| TOTAL SHORT-TERM INVESTMENTS | ||||||||

| (Cost $7,330,974) | 7,330,974 | |||||||

| TOTAL INVESTMENTS — 102.8% | ||||||||

| (Cost $213,507,649) | 219,202,228 | |||||||

| Liabilities in Excess of Other Assets — (2.8)% | (5,896,340 | ) | ||||||

| TOTAL NET ASSETS — 100.0% | $ | 213,305,888 | ||||||

Principal Amount | ||||||||

| SECURITIES SOLD SHORT — (1.0)% | ||||||||

| BONDS — (1.0)% | ||||||||

| CORPORATE — (1.0)% | ||||||||

| COMMUNICATIONS — (0.4)% | ||||||||

| $ | (700,000 | ) | Audacy Capital Corp. 6.500%, 5/1/20273,8 | (723,639 | ) | |||

| CONSUMER, CYCLICAL — (0.3)% | ||||||||

| (700,000 | ) | Staples, Inc. 10.750%, 4/15/20273,8 | (679,963 | ) | ||||

| CONSUMER, NON-CYCLICAL — (0.3)% | ||||||||

| (700,000 | ) | MPH Acquisition Holdings LLC 5.750%, 11/1/20283,8 | (680,645 | ) | ||||

| TOTAL CORPORATE | ||||||||

| (Proceeds $2,111,467) | (2,084,247 | ) | ||||||

| TOTAL BONDS | ||||||||

| (Proceeds $2,111,467) | (2,084,247 | ) | ||||||

| TOTAL SECURITIES SOLD SHORT | ||||||||

| (Proceeds $2,111,467) | $ | (2,084,247 | ) | |||||

| 28 |

Palmer Square Opportunistic Income Fund

SCHEDULE OF INVESTMENTS - Continued

As of July 31, 2021

Number of Contracts | Value | |||||||

| WRITTEN OPTION CONTRACTS — (0.0)% | ||||||||

| PUT OPTIONS — (0.0)% | ||||||||

| EQUITY — (0.0)% | ||||||||

| (851 | ) | SPDR S&P 500 ETF Trust Exercise Price: $300.00, Notional Amount: $(25,530,000), Expiration Date: September 17, 2021 | $ | (25,956 | ) | |||

| TOTAL PUT OPTIONS | ||||||||

| (Proceeds $45,073) | (25,956 | ) | ||||||

| TOTAL WRITTEN OPTION CONTRACTS | ||||||||

| (Proceeds $45,073) | (25,956 | ) | ||||||

REIT – Real Estate Investment Trusts

| * | Non-income producing security. |

| 1 | Local currency. |