UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-23015

SEI Catholic Values Trust

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, Pennsylvania 19456

(Address of principal executive offices) (Zip code)

c/o CT Corporation

155 Federal Street

Boston, MA 02110

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-342-5734

Date of fiscal year end: February 29, 2016

Date of reporting period: February 29, 2016

Item 1. Reports to Stockholders.

February 29, 2016

ANNUAL REPORT

SEI Catholic Values Trust

➤ Catholic Values Equity Fund

➤ Catholic Values Fixed Income Fund

| 1 | ||||

| 4 | ||||

| 8 | ||||

| 23 | ||||

| 24 | ||||

| 25 | ||||

| 26 | ||||

| 27 | ||||

| 37 | ||||

| 38 | ||||

| 41 | ||||

| 42 | ||||

| 43 | ||||

The Trust files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarter of each fiscal year on Form N-Q within sixty days after the end of the period. The Trust’s Forms N-Q are available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Trust uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how a Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-800-DIAL-SEI; and (ii) on the Commission’s website at http://www.sec.gov.

SEI CATHOLIC VALUES TRUST — FEBRUARY 29, 2016

To our Shareholders:

The Funds’ inaugural fiscal time period — from the start of the Funds commencement in April 2015 through the end of February 2016 — was notable for several key themes: energy-sector volatility spreading amid continued oil-price weakness, and central-bank policies diverging in the face of disinflationary pressures. The Federal Reserve (“Fed”) commenced rate increases, while the European Central Bank (“ECB”), Bank of Japan and People’s Bank of China deepened their commitments to accommodation — ultimately reinforcing the strong-U.S. dollar/weak-commodity-prices dynamic.

Geopolitical Events

Severe unrest continued in certain areas of the Middle East, driven by the opposing and overlapping interests of Islamic State, the Syrian regime, Syrian nationalists, Kurdish forces and the Iraqi military. Regional superpowers Iran, Saudi Arabia and Turkey also applied varying degrees of indirect influence. Broader involvement escalated, with Russia’s airpower commitment in early fall and a redoubled coalition of Western powers targeting Islamic State after a series of attacks by religious extremists across the globe. A U.S.-Russia-brokered ceasefire between the Syrian regime and nationalist rebels (excluding Islamic State and other terrorist groups) came into effect during the final days of the period. While the conflict that originated in Syria and Iraq appears to have influenced destabilizing events elsewhere in the Middle East and Northern Africa, and taken a terrible human toll, it has not had a significant impact on global markets or the economy. In fact, the price of oil continued to drop despite considerable regional instability.

Oil-price weakness remained primarily attributable to oversupply: the Organization of Petroleum Exporting Countries’ early December meeting yielded no production cuts; U.S. Congress approved the restoration of oil exports in mid-December; and Iran’s multi-lateral agreement on the scope of its nuclear program paved the way for its post-sanction return as a major low-cost oil supplier.

Economic Performance

In the U.S., economic growth during the second quarter of 2015 bordered on impressive, due in large part to strong consumer activity; both retail sales and consumer-spending measures registered significant spikes in May. The pace of growth essentially halved during the third quarter on modest inventory restocking amid slow sales and lackluster export activity. Fourth-quarter growth decelerated further, as industrial production and manufacturing came under pressure from the effects of U.S. dollar strength. The labor market consistently improved, with the unemployment rate declining to 4.9% in January; while the percentage of Americans participating in the labor force bottomed at a 38-year low in September, it rose slowly to finish the period above where it began. The Fed raised the federal funds rate in mid-December for the first time since 2006, leaving behind a near-zero interest rate that had been in place since late 2008.

Market Developments

Financial markets began the Funds’ recently completed fiscal period on generally positive footing, as U.S. dollar strength continued on the expectation of tighter Fed policy — which weighed on a long list of other currencies around the globe. Risk assets came under pressure in late spring, as China’s mainland stock exchanges gave back a significant portion of recent gains, with more-severe declines and a sharp volatility spike in late summer after China moderately devalued its currency. China’s decision to devalue the renminbi in late August was arguably the most significant market surprise of the period; choppy and opaque implementation, coupled with limited commitment to a market-determined exchange rate, has not engendered a great deal of confidence in China’s effectiveness in managing market pressures. As 2015 came to a close, the questionable health of U.S. energy companies, given a persistent multi-year oil-price decline, raised concerns among high-yield bond investors — resulting in a sharp selloff that likely discouraged equity investors and kept a lid on performance at year end. The year of 2016 began with a global flight to quality, benefitting safe-haven assets at the expense of risk assets. A trend reversal took place in mid-February, and

| SEI Catholic Values Trust / Annual Report / February 29, 2016 | 1 |

SEI CATHOLIC VALUES TRUST — FEBRUARY 29, 2016

Letter to Shareholders (Concluded)

risk assets rotated back into favor through the end of the period. Fourth-quarter 2015 earnings for domestically oriented companies outside of energy and commodities were strong, providing rationale for a cautiously optimistic outlook. The U.S. dollar ended the period 8.6% higher against a trade-weighted basket of currencies.

For the period ended February 29, 2016, the MSCI All-Country World Index, a proxy for global equities, fell 13.45% in U.S. dollar terms (though performance was generally better in local currencies), while the S&P 500 Index fell 5.59%, including dividends. Emerging-market equity returns were deeply negative in U.S. dollar terms, with the MSCI Emerging Markets Index falling 27.86%.

U.S. large caps (represented by the Russell 1000 Index) continued to outpace small caps, (represented by the Russell 2000 Index), delivering (6.7%) and (14.24%), respectively. Defensive and less-cyclically sensitive equity sectors (which typically exhibit lower volatility in challenging market environments compared to cyclically-sensitive sectors) fared relatively well. Consumer staples, utilities and telecommunications led (with positive returns in the U.S. and comparably small declines globally), while energy and materials lagged considerably.

Global fixed income, as measured by the Barclays Global Aggregate Bond Index, advanced 0.74% in U.S. dollar terms during the period. U.S. Treasurys delivered positive returns, despite headwinds from rising interest-rate expectations ahead of the Fed’s December move. Short-term Treasury rates increased over the full period, while intermediate-and long-term rates declined, resulting in a flatter yield curve.

U.S. investment-grade corporate debt produced negative returns for the period: the Barclays Investment Grade U.S. Corporate Index fell 1.11%. Meanwhile, the high-yield market swooned — particularly from November through January amid intensifying concerns about distressed energy debt — with the BofA Merrill Lynch U.S. High Yield Constrained Index plummeting 9.11% in the period.

Mortgage-backed securities (“MBS”) delivered positive returns: the Barclays U.S. Mortgage Backed Securities Index advanced 2.09%. MBS spreads were stable compared to the volatility of equity and fixed-income markets, thanks to a continued housing recovery.

Emerging-market debt delivered the most deeply negative performance among fixed-income market segments; but the decline was mostly limited to local-currency bonds, largely a casualty of U.S. dollar strength. The J.P. Morgan GBI Emerging Markets Global Diversified Index, which tracks local-currency-denominated emerging-market bonds, fell 12.37%; the J.P. Morgan EMBI Global Diversified Index, which tracks foreign-currency-denominated debt, declined 0.73%.

The persistent combination of subdued inflation and U.S. dollar strength continued to challenge inflation-sensitive assets such as Treasury inflation-protected securities and commodities. The latter were hit especially hard, with the price per barrel of West Texas Intermediate crude oil declining by more than 40% during the period.

Our View

We continue to expect equities to outperform fixed income over the coming months. Although opportunities appeared to be more promising in developed international equities outside the U.S. at the end of the period, recent market dynamics have brought U.S. equity valuations more closely in line with other developed markets; Japan, however, continues to sell at attractive valuations. While the eurozone economy should continue to be supported by ECB policy, new risks have materialized: an immigration crisis, the possibility that Britain may leave the European Union as well as concerns about the European banking system and the health of some peripheral eurozone countries.

We believe there is good reason to expect equities to show resilience once they adjust to the start of the Fed tightening cycle. Fed policy will likely remain benign relative to past tightening cycles, and the yield curve is far from inversion. The U.S. economy is certainly not at risk of overheating; there is no precedent for rate hikes to come in quick succession. As such, we continue to prefer a strategy of “buying on the dip” selectively.

| 2 | SEI Catholic Values Trust / Annual Report / February 29, 2016 |

Within fixed-income markets, commodity-related weakness and the likelihood of additional rate increases by the Fed have the potential to remain sources of both caution and opportunity. We expect these conditions to favor active management.

Sincerely,

William Lawrence, CFA

Managing Director, Portfolio Management Team

| SEI Catholic Values Trust / Annual Report / February 29, 2016 | 3 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI CATHOLIC VALUES TRUST — FEBRUARY 29, 2016 (Unaudited)

Catholic Values Equity Fund

I. Objective

The Catholic Values Equity Fund (the “Fund”) seeks long-term capital appreciation.

II. Investment Approach

The Fund uses a multi-manager approach, relying on a number of sub-advisers with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corporation (SIMC). The Fund utilized the following sub-advisers as of February 29, 2016: BlackRock Investment Management, LLC; Brandywine Global Investment Management, LLC; EAM Investors, LLC; EARNEST Partners LLC; Parametric Portfolio Associates LLC; Snow Capital Management, L.P.; and Waddell & Reed Investment Management Company There were no manager changes during the period.

III. Returns

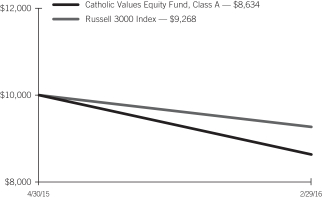

For the period from April 30, 2015 (the Fund’s inception date) through February 29, 2016, the Catholic Values Equity Fund, Class A returned -13.66%. The Fund’s primary benchmark — the Russell 3000 Index (USD) — returned -7.32%.

IV. Performance Discussion

Absolute performance faced significant challenges as equity markets slumped in summer 2015, and particularly in late August, as concerns about emerging markets and oil prices came to the forefront for investors. As noted in the enclosed shareholder letter, losses were more pronounced within energy and cyclical sectors, smaller-cap stocks and outside of the U.S. The Fund recovered most of its losses by early November, as data illustrated an improving domestic economy. This gave way to the Federal Open Market Committee’s modest rate hike in December, which, as the shareholder letter addressed, introduced a backdrop of monetary policy differences between the U.S. and other major developed nations that remained on an easing track. This dissonance led to strong U.S. dollar appreciation versus other currencies, which further exacerbated weakness among non-U.S. investments from a U.S. investor perspective. Concerns had resurfaced by the end of November, evidenced by the widening of spreads in high-yield energy-sector

names and emerging markets. The Fund slid along with equity markets through December and January as investors exercised the preference for safety assets. By early February, momentum shifted back in favor of a broad equity-market advance, which remained intact through the end of the period.

The Fund’s relative performance struggled during the period largely as a result of manager exposures to the trends listed above. Our non-U.S. manager, EARNEST Partners LLC, lagged due to its focus on China and emerging markets, which prompted the Fund’s underweight to the manager versus its strategic target for much of the period. Brandywine Global Investment Management and Snow Capital Management, L.P., domestic deep-value managers within large cap and small cap, respectively, were also challenged during the period. The Fund’s allocations to them led to losses resulting from the dislocation within energy and industrial names. Both managers added to distressed positions and upgraded their portfolio holdings — consistent with their expected management style during a challenging environment — and the Fund modestly added to its allocations late in the period to position for an expected rebound in valuations and on the belief that the market selloff was overdone.

Catholic Values Equity Fund:

AVERAGE ANNUAL TOTAL RETURN1

| Cumulative Inception to Date | ||||

| Class A | (13.66)% | |||

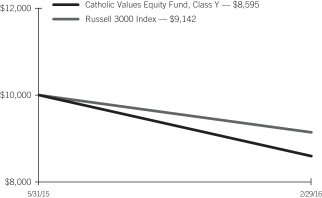

| Class Y | (14.05)% | |||

| Russell 3000 Index | (7.32)% | |||

| 4 | SEI Catholic Values Trust / Annual Report / February 29, 2016 |

Comparison of Change in the Value of a $10,000 Investment in the Catholic Values Equity Fund, Class A, versus the Russell 3000 Index

| 1 | For the period ended 2/29/2016. Past performance is no indication of future performance. Class A shares were offered beginning on 4/30/2015 and Class Y share were offered beginning 5/31/2015. The graph is based on only the Class A; performance for Class Y would be different due to differences in fee structures. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

Comparison of Change in the Value of a $10,000 Investment in the Catholic Values Equity Fund, Class Y, versus the Russell 3000 Index

| 1 | For the period ended 2/29/2016. Past performance is no indication of future performance. Class Y shares were offered beginning on 5/31/2015 and Class A share were offered beginning 4/30/2015. The graph is based on only the Class Y; performance for Class A would be different due to differences in fee structures. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| SEI Catholic Values Trust / Annual Report / February 29, 2016 | 5 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

SEI CATHOLIC VALUES TRUST — FEBRUARY 29, 2016

Catholic Values Fixed Income Fund

I. Objective

The Catholic Values Fixed Income Fund (the “Fund”) seeks a high level of current income with preservation of capital.

II. Investment Approach

The Fund uses a multi-manager approach, relying on a number of sub-advisers with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corporation (SIMC). The Fund utilized the following sub-advisers as of February 29, 2016: Income Research & Management; Western Asset Management Company; and Western Asset Management Company Limited. There were no manager changes during the period.

III. Returns

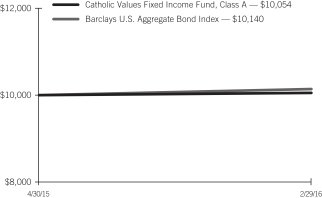

For the period from April 30, 2015 (the Fund’s inception date) through February 29, 2016, the Catholic Values Fixed Income Fund, Class A returned 0.54%. The Fund’s benchmark — the Barclays U.S. Aggregate Bond Index (USD) — returned 1.40%.

IV. Performance Discussion

Absolute performance over the period was driven by a number of sectors. U.S. Treasurys were one of the most significant contributors; as the enclosed shareholder letter notes, the yield curve flattened, with longer-maturity bonds outperforming shorter-maturity bonds. Credit spreads widened in the investment-grade sector, but the contribution to absolute return was positive outside of industrials, where energy and basics experienced negative returns. A meaningful exposure to mortgage-backed securities (MBS), specifically agency MBS, contributed significantly to performance. As addressed in the shareholder letter, the housing market continued to improve during the period.

The Fund’s underweight to U.S. Treasurys detracted from relative performance, as corporate credit underperformed Treasurys amid credit spread widening during the period. An underweight to MBS, coupled with issue selection within the sector, detracted from relative performance. Favorable active yield-curve and duration positioning contributed to relative performance. A yield-curve-flattening position benefitted as longer-dated bonds outperformed shorter-dated bonds.

For Western Asset Management, duration and yield-curve positioning were the most significant contributors to relative performance, while small positions in emerging-market debt and non-investment-grade corporate bonds detracted. For Income Research & Management, an overweight to corporate credit and an underweight to agency MBS detracted from relative performance.

The Fund used U.S. Treasury futures, Eurodollar Futures and to-be-announced (TBA) forward contracts to effectively manage duration, yield-curve and market exposures. (TBA contracts confer the obligation to buy or sell future debt obligations of the three U.S. government-sponsored agencies that issue or guarantee MBS — Fannie Mae, Freddie Mac and Ginnie Mae.) None of these had a meaningful impact on performance.

Catholic Values Fixed Income Fund:

AVERAGE ANNUAL TOTAL RETURN1

| Cumulative Inception to Date | ||||

| Class A | 0.54% | |||

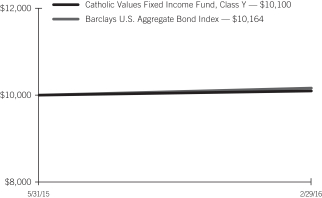

| Class Y | 1.00% | |||

| Barclays U.S. Aggregate Bond Index | 1.40% | |||

Comparison of Change in the Value of a $10,000 Investment in the Fixed Income Fund, Class A, versus the Barclays U.S. Aggregate Bond Index

| 1 | For the period ended 2/29/2016. Past performance is no indication of future performance. Class A shares were offered beginning on 4/30/2015 and Class Y share were offered beginning 5/31/2015. The graph is based on only the Class A; performance for Class Y would be different due to differences in fee structures. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| 6 | SEI Catholic Values Trust / Annual Report / February 29, 2016 |

Comparison of Change in the Value of a $10,000 Investment in the Fixed Income Fund, Class Y, versus the Barclays U.S. Aggregate Bond Index

| 1 | For the period ended 2/29/2016. Past performance is no indication of future performance. Class Y shares were offered beginning on 5/31/2015 and Class A share were offered beginning 4/30/2015. The graph is based on only the Class Y; performance for Class A would be different due to differences in fee structures. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. |

| SEI Catholic Values Trust / Annual Report / February 29, 2016 | 7 |

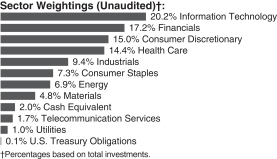

Catholic Values Equity Fund

February 29, 2016

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK — 74.2% |

| |||||||

Consumer Discretionary — 11.8% |

| |||||||

Abercrombie & Fitch, Cl A | 10,348 | $ | 301 | |||||

Amazon.com* | 3,200 | 1,768 | ||||||

Best Buy | 2,579 | 84 | ||||||

Big Lots | 4,527 | 183 | ||||||

Callaway Golf | 9,292 | 83 | ||||||

Carnival | 19,835 | 951 | ||||||

Chipotle Mexican Grill, Cl A* | 1,892 | 963 | ||||||

Comcast, Cl A | 16,026 | 925 | ||||||

Cracker Barrel Old Country Store | 315 | 47 | ||||||

Dave & Buster’s Entertainment* | 2,391 | 88 | ||||||

Dillard’s, Cl A | 2,455 | 205 | ||||||

Dollar General | 2,489 | 185 | ||||||

Domino’s Pizza | 2,418 | 322 | ||||||

Ford Motor | 24,722 | 309 | ||||||

Gap | 2,620 | 72 | ||||||

General Motors | 31,810 | 937 | ||||||

Genesco* | 2,431 | 160 | ||||||

Goodyear Tire & Rubber | 13,884 | 418 | ||||||

Hasbro | 2,175 | 165 | ||||||

Hilton Worldwide Holdings | 4,300 | 89 | ||||||

Home Depot | 12,243 | 1,520 | ||||||

John Wiley & Sons, Cl A | 1,814 | 79 | ||||||

Johnson Controls | 5,015 | 183 | ||||||

Kohl’s | 9,233 | 431 | ||||||

L Brands | 1,996 | 169 | ||||||

Liberty Global, Cl A* | 18,706 | 689 | ||||||

Lowe’s | 1,465 | 99 | ||||||

Macy’s | 12,827 | 554 | ||||||

Magna International | 20,727 | 805 | ||||||

McDonald’s | 1,030 | 121 | ||||||

Netflix* | 7,531 | 703 | ||||||

NIKE, Cl B | 20,308 | 1,251 | ||||||

Nordstrom | 1,997 | 103 | ||||||

Office Depot* | 13,586 | 69 | ||||||

PVH | 956 | 76 | ||||||

Ralph Lauren, Cl A | 1,477 | 134 | ||||||

Royal Caribbean Cruises | 1,916 | 143 | ||||||

Staples | 11,068 | 105 | ||||||

Starbucks | 9,814 | 571 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

Starwood Hotels & Resorts Worldwide | 914 | $ | 63 | |||||

Target | 2,839 | 223 | ||||||

Time Warner | 890 | 59 | ||||||

TJX | 1,445 | 107 | ||||||

TripAdvisor* | 3,562 | 223 | ||||||

Tupperware Brands | 3,740 | 187 | ||||||

VF | 3,024 | 197 | ||||||

Visteon | 1,449 | 101 | ||||||

VOXX International, Cl A* | 28,319 | 113 | ||||||

Walt Disney | 4,056 | 387 | ||||||

Wayfair, Cl A* | 2,227 | 87 | ||||||

Williams-Sonoma | 1,501 | 78 | ||||||

|

| |||||||

| 17,885 | ||||||||

|

| |||||||

Consumer Staples — 5.8% |

| |||||||

Altria Group | 1,949 | 120 | ||||||

Andersons | 8,408 | 226 | ||||||

Campbell Soup | 6,043 | 373 | ||||||

Clorox | 2,458 | 311 | ||||||

Coca-Cola | 8,967 | 387 | ||||||

Coca-Cola Enterprises | 3,388 | 164 | ||||||

Colgate-Palmolive | 1,477 | 97 | ||||||

Constellation Brands, Cl A | 4,666 | 660 | ||||||

Costco Wholesale | 6,339 | 951 | ||||||

CVS Health | 3,797 | 369 | ||||||

General Mills | 5,126 | 302 | ||||||

Hershey | 1,640 | 149 | ||||||

Kellogg | 3,207 | 237 | ||||||

Kimberly-Clark | 3,063 | 399 | ||||||

Kraft Heinz | 9,715 | 748 | ||||||

Kroger | 1,278 | 51 | ||||||

Molson Coors Brewing, Cl B | 4,960 | 423 | ||||||

Mondelez International, Cl A | 4,786 | 194 | ||||||

Omega Protein* | 8,571 | 204 | ||||||

PepsiCo | 6,149 | 601 | ||||||

Philip Morris International | 13,587 | 1,237 | ||||||

Procter & Gamble | 5,857 | 470 | ||||||

Sysco | 2,183 | 96 | ||||||

|

| |||||||

| 8,769 | ||||||||

|

| |||||||

Energy — 4.1% |

| |||||||

Apache | 10,394 | 398 | ||||||

Baker Hughes | 2,580 | 111 | ||||||

Cabot Oil & Gas | 17,962 | 361 | ||||||

California Resources | 1,054 | 1 | ||||||

CARBO Ceramics | 17,963 | 359 | ||||||

Chevron | 1,314 | 110 | ||||||

Cimarex Energy | 7,426 | 624 | ||||||

Concho Resources* | 1,485 | 134 | ||||||

ConocoPhillips | 4,113 | 139 | ||||||

Devon Energy | 24,776 | 488 | ||||||

EOG Resources | 7,081 | 458 | ||||||

Equities | 772 | 43 | ||||||

Exxon Mobil | 8,408 | 674 | ||||||

| 8 | SEI Catholic Values Trust / Annual Report / February 29, 2016 |

| Description | Shares | Market Value ($ Thousands) | ||||||

Halliburton | 9,022 | $ | 291 | |||||

Hess | 3,807 | 166 | ||||||

Newfield Exploration* | 3,310 | 90 | ||||||

Occidental Petroleum | 11,209 | 771 | ||||||

PBF Energy, Cl A | 12,780 | 386 | ||||||

Schlumberger | 2,097 | 150 | ||||||

Southwestern Energy* | 9,303 | 54 | ||||||

Spectra Energy | 6,476 | 189 | ||||||

Tidewater | 41,149 | 237 | ||||||

|

| |||||||

| 6,234 | ||||||||

|

| |||||||

Financials — 12.8% | ||||||||

Allied World Assurance Holdings | 1,601 | 52 | ||||||

Allstate | 5,134 | 326 | ||||||

American Equity Investment Life Holding | 8,447 | 115 | ||||||

American Express | 800 | 44 | ||||||

American Homes 4 Rent, Cl A‡ | 4,082 | 57 | ||||||

American International Group | 8,266 | 415 | ||||||

American Tower‡ | 9,838 | 907 | ||||||

Arthur J Gallagher | 2,146 | 85 | ||||||

Bancorp* | 38,209 | 182 | ||||||

Bank of America | 127,286 | 1,594 | ||||||

Bank of New York Mellon | 5,555 | 197 | ||||||

Berkshire Hathaway, Cl B* | 11,626 | 1,560 | ||||||

BlackRock, Cl A | 260 | 81 | ||||||

Blackstone Group LP (A) | 22,878 | 594 | ||||||

CBRE Group, Cl A* | 3,632 | 92 | ||||||

Chimera Investment‡ | 9,801 | 128 | ||||||

Chubb | 2,151 | 248 | ||||||

Citigroup | 52,602 | 2,044 | ||||||

Corporate Office Properties Trust‡ | 3,415 | 80 | ||||||

Crown Castle International‡ | 5,613 | 485 | ||||||

Everest Re Group | 3,089 | 575 | ||||||

FBR | 7,201 | 126 | ||||||

FCB Financial Holdings, Cl A* | 3,370 | 101 | ||||||

First Commonwealth Financial | 19,970 | 172 | ||||||

First Niagara Financial Group | 4,628 | 43 | ||||||

Goldman Sachs Group | 3,101 | 464 | ||||||

Green Dot, Cl A* | 32,877 | 679 | ||||||

Hartford Financial Services Group | 1,072 | 45 | ||||||

HCP‡ | 5,614 | 166 | ||||||

Highwoods Properties‡ | 2,412 | 105 | ||||||

HomeStreet* | 8,683 | 173 | ||||||

Jones Lang LaSalle | 1,215 | 124 | ||||||

JPMorgan Chase | 34,939 | 1,967 | ||||||

KKR LP (A) | 56,996 | 732 | ||||||

Legg Mason | 1,747 | 50 | ||||||

Manning & Napier, Cl A | 14,085 | 97 | ||||||

McGraw Hill Financial | 3,332 | 299 | ||||||

MetLife | 18,458 | 730 | ||||||

Morgan Stanley | 5,622 | 139 | ||||||

Morningstar | 1,265 | 100 | ||||||

Northern Trust | 9,913 | 589 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

ProAssurance | 3,709 | $ | 183 | |||||

Prologis‡ | 9,307 | 358 | ||||||

Santander Consumer USA Holdings* | 33,236 | 341 | ||||||

Spirit Realty Capital‡ | 3,947 | 42 | ||||||

State Street | 5,663 | 310 | ||||||

Synchrony Financial* | 4,252 | 115 | ||||||

T Rowe Price Group | 2,429 | 168 | ||||||

US Bancorp | 4,708 | 181 | ||||||

Wells Fargo | 13,758 | 645 | ||||||

Welltower‡ | 775 | 49 | ||||||

Weyerhaeuser‡ | 13,418 | 349 | ||||||

|

| |||||||

| 19,503 | ||||||||

|

| |||||||

Health Care — 10.2% | ||||||||

Abbott Laboratories | 4,644 | 180 | ||||||

ABIOMED* | 1,095 | 88 | ||||||

Akorn* | 6,740 | 179 | ||||||

Alexion Pharmaceuticals* | 2,899 | 408 | ||||||

Amgen | 2,040 | 290 | ||||||

Anacor Pharmaceuticals* | 853 | 54 | ||||||

Analogic | 5,743 | 431 | ||||||

Anthem | 2,173 | 284 | ||||||

Baxalta | 2,288 | 88 | ||||||

Biogen* | 2,683 | 696 | ||||||

BioMarin Pharmaceutical* | 713 | 58 | ||||||

BioSpecifics Technologies* | 1,868 | 66 | ||||||

Boston Scientific* | 5,660 | 96 | ||||||

Bruker | 8,311 | 216 | ||||||

Cambrex* | 7,064 | 272 | ||||||

Celgene* | 10,102 | 1,019 | ||||||

Charles River Laboratories International* | 3,356 | 246 | ||||||

Cigna | 1,258 | 176 | ||||||

Collegium Pharmaceutical* | 4,202 | 73 | ||||||

Cytokinetics* | 7,723 | 49 | ||||||

Dynavax Technologies* | 3,336 | 54 | ||||||

Express Scripts Holding* | 626 | 44 | ||||||

FibroGen* | 3,132 | 54 | ||||||

Gilead Sciences | 3,311 | 289 | ||||||

Horizon Pharma* | 19,452 | 334 | ||||||

Humana | 1,115 | 197 | ||||||

Integra LifeSciences Holdings* | 8,882 | 545 | ||||||

Intuitive Surgical* | 152 | 86 | ||||||

Kindred Healthcare | 19,833 | 208 | ||||||

Kite Pharma* | 1,227 | 55 | ||||||

Lannett* | 5,557 | 140 | ||||||

Lipocine* | 12,074 | 122 | ||||||

McKesson | 663 | 103 | ||||||

Medtronic | 17,704 | 1,370 | ||||||

Mettler-Toledo International* | 2,175 | 685 | ||||||

Molina Healthcare* | 1,432 | 89 | ||||||

NeoGenomics* | 25,277 | 161 | ||||||

Neurocrine Biosciences* | 2,220 | 82 | ||||||

Nevro* | 1,655 | 95 | ||||||

| SEI Catholic Values Trust / Annual Report / February 29, 2016 | 9 |

SCHEDULE OF INVESTMENTS

Catholic Values Equity Fund (Continued)

February 29, 2016

| Description | Shares | Market Value ($ Thousands) | ||||||

NxStage Medical* | 5,715 | $ | 85 | |||||

Ophthotech* | 1,685 | 76 | ||||||

OPKO Health* | 4,521 | 42 | ||||||

Otonomy* | 2,928 | 37 | ||||||

Pacira Pharmaceuticals* | 2,999 | 156 | ||||||

Portola Pharmaceuticals* | 2,681 | 75 | ||||||

Premier, Cl A* | 2,544 | 83 | ||||||

PTC Therapeutics* | 2,962 | 24 | ||||||

Quintiles Transnational Holdings* | 4,164 | 261 | ||||||

Regeneron Pharmaceuticals* | 327 | 126 | ||||||

ResMed | 1,742 | 99 | ||||||

Sirona Dental Systems* | 1,398 | 154 | ||||||

TESARO* | 1,602 | 65 | ||||||

TherapeuticsMD* | 22,954 | 140 | ||||||

United Therapeutics* | 3,544 | 432 | ||||||

UnitedHealth Group | 10,225 | 1,218 | ||||||

Varian Medical Systems* | 4,509 | 353 | ||||||

Vertex Pharmaceuticals* | 5,367 | 459 | ||||||

VWR* | 29,092 | 710 | ||||||

Waters* | 3,224 | 388 | ||||||

Zimmer Biomet Holdings | 929 | 90 | ||||||

Zoetis, Cl A | 18,515 | 760 | ||||||

|

| |||||||

| 15,515 | ||||||||

|

| |||||||

Industrials — 7.5% | ||||||||

3M | 4,377 | 687 | ||||||

Acacia Research | 67,646 | 214 | ||||||

ACCO Brands* | 50,936 | 372 | ||||||

Actuant, Cl A | 3,147 | 74 | ||||||

AGCO | 1,432 | 71 | ||||||

American Airlines Group | 18,274 | 749 | ||||||

Atlas Air Worldwide Holdings* | 8,409 | 304 | ||||||

Caterpillar | 7,837 | 531 | ||||||

Chicago Bridge & Iron | 5,939 | 199 | ||||||

Covanta Holding | 8,121 | 113 | ||||||

Crane | 2,776 | 136 | ||||||

CSX | 2,560 | 62 | ||||||

Cummins | 1,250 | 122 | ||||||

Deere | 2,505 | 201 | ||||||

Delta Air Lines | 26,179 | 1,263 | ||||||

Dover | 1,366 | 83 | ||||||

DXP Enterprises* | 2,768 | 38 | ||||||

Eaton | 8,416 | 477 | ||||||

Emerson Electric | 973 | 47 | ||||||

Illinois Tool Works | 1,299 | 122 | ||||||

Ingersoll-Rand | 4,588 | 255 | ||||||

Kansas City Southern | 3,370 | 275 | ||||||

LB Foster, Cl A | 18,738 | 257 | ||||||

ManpowerGroup | 3,623 | 281 | ||||||

Matson | 2,266 | 91 | ||||||

Nordson | 1,333 | 96 | ||||||

Owens Corning | 3,846 | 165 | ||||||

Parker-Hannifin | 926 | 94 | ||||||

Pitney Bowes | 2,185 | 40 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

Rockwell Automation | 1,196 | $ | 124 | |||||

Rockwell Collins | 8,450 | 740 | ||||||

Southwest Airlines | 2,354 | 99 | ||||||

Stanley Black & Decker | 2,756 | 259 | ||||||

Terex | 12,088 | 271 | ||||||

Titan Machinery* | 12,758 | 121 | ||||||

TransDigm Group* | 414 | 88 | ||||||

Triumph Group | 14,083 | 429 | ||||||

Union Pacific | 2,036 | 161 | ||||||

United Parcel Service, Cl B | 3,789 | 366 | ||||||

Waste Management | 1,918 | 107 | ||||||

Wesco Aircraft Holdings* | 41,595 | 532 | ||||||

WESCO International* | 1,213 | 53 | ||||||

WW Grainger | 1,538 | 334 | ||||||

Xylem | 7,036 | 263 | ||||||

|

| |||||||

| 11,366 | ||||||||

|

| |||||||

Information Technology — 16.4% |

| |||||||

Activision Blizzard | 5,389 | 171 | ||||||

Adobe Systems* | 13,208 | 1,125 | ||||||

Alliance Data Systems* | 1,019 | 214 | ||||||

Alphabet, Cl A* | 4,279 | 3,069 | ||||||

Alphabet, Cl C* | 851 | 594 | ||||||

Analog Devices | 1,606 | 85 | ||||||

Apple | 22,371 | 2,163 | ||||||

Applied Materials | 60,774 | 1,147 | ||||||

Applied Optoelectronics* | 5,229 | 94 | ||||||

Autobytel* | 5,003 | 96 | ||||||

Autodesk* | 1,781 | 92 | ||||||

Black Box | 16,909 | 224 | ||||||

Broadcom | 611 | 82 | ||||||

CA | 8,337 | 244 | ||||||

Cisco Systems | 46,043 | 1,205 | ||||||

Cognizant Technology Solutions, Cl A* | 8,683 | 495 | ||||||

eBay* | 10,272 | 244 | ||||||

Facebook, Cl A* | 20,827 | 2,227 | ||||||

GoDaddy, Cl A* | 1,847 | 58 | ||||||

HP | 8,538 | 91 | ||||||

Intel | 20,433 | 605 | ||||||

International Business Machines | 4,148 | 543 | ||||||

Juniper Networks | 4,590 | 113 | ||||||

Keysight Technologies* | 6,271 | 164 | ||||||

Lam Research | 3,278 | 240 | ||||||

Lexmark International, Cl A | 4,860 | 151 | ||||||

LogMeIn* | 1,471 | 75 | ||||||

MasterCard, Cl A | 9,053 | 787 | ||||||

Micron Technology* | 59,830 | 636 | ||||||

Microsoft | 50,591 | 2,574 | ||||||

National Instruments | 2,999 | 86 | ||||||

NetApp | 2,221 | 55 | ||||||

NVIDIA | 3,110 | 97 | ||||||

Open Text | 5,563 | 277 | ||||||

Oracle | 13,817 | 508 | ||||||

| 10 | SEI Catholic Values Trust / Annual Report / February 29, 2016 |

| Description | Shares | Market Value ($ Thousands) | ||||||

OSI Systems* | 8,049 | $ | 486 | |||||

QUALCOMM | 6,141 | 312 | ||||||

salesforce.com inc* | 8,447 | 572 | ||||||

SanDisk | 1,186 | 86 | ||||||

Silicon Graphics International* | 52,644 | 320 | ||||||

Solera Holdings | 1,471 | 82 | ||||||

Symantec | 14,140 | 273 | ||||||

Texas Instruments | 4,776 | 253 | ||||||

Visa, Cl A | 25,061 | 1,814 | ||||||

Xerox | 9,532 | 92 | ||||||

|

| |||||||

| 24,921 | ||||||||

|

| |||||||

Materials — 3.5% | ||||||||

Air Products & Chemicals | 5,522 | 731 | ||||||

Alcoa | 5,402 | 48 | ||||||

American Vanguard | 3,392 | 43 | ||||||

Ball | 5,110 | 338 | ||||||

Cabot | 1,966 | 88 | ||||||

Dow Chemical | 9,837 | 478 | ||||||

Eastman Chemical | 6,590 | 423 | ||||||

Ecolab | 2,953 | 303 | ||||||

FMC | 3,280 | 123 | ||||||

Louisiana-Pacific* | 16,388 | 260 | ||||||

LSB Industries* | 13,094 | 76 | ||||||

Mosaic | 2,170 | 58 | ||||||

PPG Industries | 1,218 | 118 | ||||||

Praxair | 6,686 | 681 | ||||||

Reliance Steel & Aluminum | 5,696 | 347 | ||||||

Sherwin-Williams | 3,191 | 863 | ||||||

Sonoco Products | 6,077 | 266 | ||||||

United States Steel | 10,810 | 99 | ||||||

|

| |||||||

| 5,343 | ||||||||

|

| |||||||

Telecommunication Services — 1.2% |

| |||||||

8x8* | 7,401 | 86 | ||||||

AT&T | 14,216 | 525 | ||||||

Level 3 Communications* | 8,004 | 389 | ||||||

Sprint* | 30,075 | 103 | ||||||

Verizon Communications | 13,416 | 681 | ||||||

|

| |||||||

| 1,784 | ||||||||

|

| |||||||

Utilities — 0.9% | ||||||||

AES | 8,725 | 86 | ||||||

American Water Works | 4,543 | 295 | ||||||

CMS Energy | 8,598 | 340 | ||||||

Eversource Energy | 1,974 | 107 | ||||||

Exelon | 5,725 | 180 | ||||||

PG&E | 1,952 | 111 | ||||||

Pinnacle West Capital | 678 | 47 | ||||||

Sempra Energy | 667 | 64 | ||||||

Xcel Energy | 5,348 | 211 | ||||||

|

| |||||||

| 1,441 | ||||||||

|

| |||||||

Total Common Stock | 112,761 | |||||||

|

| |||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

FOREIGN COMMON STOCK — 22.6% |

| |||||||

Australia — 0.3% | ||||||||

BHP Billiton ADR | 17,372 | $ | 393 | |||||

|

| |||||||

Austria — 1.0% | ||||||||

Conwert Immobilien Invest | 21,010 | 293 | ||||||

Erste Group Bank | 21,318 | 549 | ||||||

Schoeller-Bleckmann Oilfield Equipment | 4,428 | 251 | ||||||

voestalpine | 13,568 | 394 | ||||||

|

| |||||||

| 1,487 | ||||||||

|

| |||||||

Belgium — 0.8% | ||||||||

Anheuser-Busch InBev ADR | 11,072 | 1,234 | ||||||

|

| |||||||

Bermuda — 0.2% | ||||||||

Aspen Insurance Holdings | 2,284 | 102 | ||||||

Endurance Specialty Holdings | 1,490 | 93 | ||||||

Validus Holdings | 2,718 | 122 | ||||||

|

| |||||||

| 317 | ||||||||

|

| |||||||

Brazil — 0.4% | ||||||||

Banco Bradesco ADR | 42,658 | 226 | ||||||

Banco do Brasil | 29,100 | 100 | ||||||

Qualicorp | 84,007 | 270 | ||||||

|

| |||||||

| 596 | ||||||||

|

| |||||||

British Virgin Islands — 0.7% | ||||||||

Michael Kors Holdings* | 18,214 | 1,032 | ||||||

|

| |||||||

Canada — 1.7% | ||||||||

Canadian Natural Resources | 34,980 | 729 | ||||||

Canadian Pacific Railway | 3,720 | 451 | ||||||

Magna International | 11,610 | 450 | ||||||

Tencent Holdings ADR | 33,681 | 618 | ||||||

Thomson Reuters | 7,621 | 279 | ||||||

|

| |||||||

| 2,527 | ||||||||

|

| |||||||

China — 0.8% | ||||||||

Anhui Conch Cement, Cl H | 117,500 | 233 | ||||||

China Oilfield Services, Cl H | 360,000 | 265 | ||||||

Industrial & Commercial Bank of China, Cl H | 286,000 | 141 | ||||||

Mindray Medical International ADR | 15,068 | 419 | ||||||

Weichai Power, Cl H | 186,000 | 170 | ||||||

|

| |||||||

| 1,228 | ||||||||

|

| |||||||

Colombia — 0.1% | ||||||||

Bancolombia ADR | 6,273 | 189 | ||||||

|

| |||||||

Czech Republic — 0.0% | ||||||||

Komercni banka as | 384 | 72 | ||||||

|

| |||||||

| SEI Catholic Values Trust / Annual Report / February 29, 2016 | 11 |

SCHEDULE OF INVESTMENTS

Catholic Values Equity Fund (Concluded)

February 29, 2016

| Description | Shares | Market Value ($ Thousands) | ||||||

France — 0.7% | ||||||||

Societe Generale | 13,398 | $ | 472 | |||||

Sodexo | 6,175 | 628 | ||||||

|

| |||||||

| 1,100 | ||||||||

|

| |||||||

Germany — 0.3% | ||||||||

BASF | 4,063 | 266 | ||||||

Continental | 1,202 | 241 | ||||||

|

| |||||||

| 507 | ||||||||

|

| |||||||

Hong Kong — 0.8% | ||||||||

China Mobile ADR | 13,480 | 721 | ||||||

Orient Overseas International | 114,500 | 416 | ||||||

|

| |||||||

| 1,137 | ||||||||

|

| |||||||

India — 0.6% | ||||||||

HDFC Bank ADR | 10,729 | 567 | ||||||

ICICI Bank ADR | 59,095 | 335 | ||||||

|

| |||||||

| 902 | ||||||||

|

| |||||||

Indonesia — 0.1% | ||||||||

Indofood Sukses Makmur | 293,300 | 155 | ||||||

|

| |||||||

Ireland — 2.3% | ||||||||

Accenture, Cl A | 3,557 | 357 | ||||||

ICON* | 20,108 | 1,431 | ||||||

Jazz Pharmaceuticals* | 4,230 | 514 | ||||||

Mallinckrodt* | 5,918 | 385 | ||||||

Shire ADR | 5,499 | 858 | ||||||

|

| |||||||

| 3,545 | ||||||||

|

| |||||||

Israel — 0.5% | ||||||||

Orbotech* | 16,951 | 384 | ||||||

SodaStream International* | 25,808 | 385 | ||||||

|

| |||||||

| 769 | ||||||||

|

| |||||||

Japan — 2.2% | ||||||||

Denso | 17,700 | 657 | ||||||

Hitachi | 81,000 | 343 | ||||||

Nippon Steel & Sumitomo Metal | 12,900 | 223 | ||||||

Nomura Holdings ADR | 130,370 | 547 | ||||||

Secom | 7,700 | 548 | ||||||

Toyota Motor ADR | 9,490 | 988 | ||||||

|

| |||||||

| 3,306 | ||||||||

|

| |||||||

Netherlands — 1.9% | ||||||||

AerCap Holdings* | 18,370 | 656 | ||||||

Core Laboratories | 7,802 | 819 | ||||||

NXP Semiconductors* | 7,625 | 543 | ||||||

QIAGEN* | 24,556 | 519 | ||||||

Royal Dutch Shell, Cl A | 13,713 | 315 | ||||||

|

| |||||||

| 2,852 | ||||||||

|

| |||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

Norway — 1.0% | ||||||||

DNB | 66,835 | $ | 770 | |||||

Norsk Hydro | 112,860 | 449 | ||||||

Statoil ADR | 22,574 | 329 | ||||||

|

| |||||||

| 1,548 | ||||||||

|

| |||||||

Puerto Rico — 0.4% | ||||||||

OFG Bancorp | 94,860 | 552 | ||||||

Popular | 4,269 | 113 | ||||||

|

| |||||||

| 665 | ||||||||

|

| |||||||

South Korea — 0.5% | ||||||||

Hyundai Mobis | 2,326 | 468 | ||||||

Samsung Electronics | 369 | 352 | ||||||

|

| |||||||

| 820 | ||||||||

|

| |||||||

Spain — 0.6% | ||||||||

Amadeus IT Holding, Cl A | 21,065 | 851 | ||||||

|

| |||||||

Sweden — 0.4% | ||||||||

Getinge, Cl B | 30,689 | 681 | ||||||

|

| |||||||

Switzerland — 0.3% | ||||||||

Credit Suisse Group ADR | 33,036 | 440 | ||||||

|

| |||||||

Taiwan — 0.7% | ||||||||

Advanced Semiconductor Engineering | 416,000 | 475 | ||||||

Taiwan Semiconductor Manufacturing | 119,000 | 534 | ||||||

|

| |||||||

| 1,009 | ||||||||

|

| |||||||

Turkey — 0.4% | ||||||||

Akbank | 67,865 | 170 | ||||||

Turkiye Garanti Bankasi | 156,753 | 390 | ||||||

|

| |||||||

| 560 | ||||||||

|

| |||||||

United Kingdom — 2.9% | ||||||||

ARM Holdings ADR | 23,404 | 959 | ||||||

BP ADR | 37,346 | 1,087 | ||||||

Diageo | 28,498 | 738 | ||||||

HSBC Holdings | 11,770 | 75 | ||||||

ITV | 79,853 | 277 | ||||||

Rio Tinto ADR | 9,053 | 236 | ||||||

Shire | 20,948 | 1,106 | ||||||

|

| |||||||

| 4,478 | ||||||||

|

| |||||||

Total Foreign Common Stock | 34,400 | |||||||

|

| |||||||

| 12 | SEI Catholic Values Trust / Annual Report / February 29, 2016 |

| Description | Face Amount | Market Value ($ Thousands) | ||||||

U.S. TREASURY OBLIGATION — 0.1% |

| |||||||

United States Treasury Bill | ||||||||

0.437%, 08/18/2016 (B) | $ | 100 | $ | 100 | ||||

|

| |||||||

Total U.S. Treasury Obligation | 100 | |||||||

|

| |||||||

CASH EQUIVALENT — 2.0% |

| |||||||

SEI Daily Income Trust, Prime Obligation Fund, Cl A 0.300%**† | 3,009,631 | 3,010 | ||||||

|

| |||||||

Total Cash Equivalent | 3,010 | |||||||

|

| |||||||

Total Investments — 98.9% |

| $ | 150,271 | |||||

|

| |||||||

A list of the open futures contracts held by the Fund at February 29, 2016, is as follows:

| Type of Contract | Number of Contracts Long | Expiration Date | Unrealized Appreciation ($ Thousands) | |||||||||

Russell 2000 Index | 3 | Mar-2016 | $ | 5 | ||||||||

S&P 500 Index E-MINI | 13 | Mar-2016 | 33 | |||||||||

|

| |||||||||||

| $ | 38 | |||||||||||

|

| |||||||||||

For the period ended February 29, 2016, the total amount of all open futures contracts, as presented in the table above, are representative of the volume of activity for this derivative type during the period.

Percentages are based on a Net Assets of $151,872 ($ Thousands).

| * | Non-income producing security. |

| ** | Rate shown is the 7-day effective yield as of February 29, 2016. |

| † | Investment in Affiliated Security (see Note 2). |

| ‡ | Real Estate Investment Trust. |

| (A) | Security is a Master Limited Partnership. At February 29, 2016, such securities amounted to $1,326 ($ Thousands), or 0.87% of Net Assets (See Note 2). |

| (B) | Security, or portion thereof, has been pledged as collateral on open futures contracts. |

ADR — American Depositary Receipt

Cl — Class

LP — Limited Partnership

The following is a list of the level of inputs used as of February 29, 2016, in valuing the Fund’s investments and other financial instruments carried at value ($ Thousands):

| Investments in Securities | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Common Stock | $ | 112,761 | $ | — | $ | — | $ | 112,761 | ||||||||

Foreign Common Stock | 34,400 | — | — | 34,400 | ||||||||||||

U.S. Treasury Obligation | — | 100 | — | 100 | ||||||||||||

Cash Equivalent | 3,010 | — | — | 3,010 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total Investments in Securities | $ | 150,171 | $ | 100 | $ | — | $ | 150,271 | ||||||||

|

|

|

|

|

|

|

| |||||||||

| Other Financial Instruments | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Futures Contracts* | ||||||||||||||||

Unrealized Appreciation | $ | 38 | $ | — | $ | — | $ | 38 | ||||||||

|

|

|

|

|

|

|

| |||||||||

| * | Futures contracts are valued at the unrealized appreciation/ (depreciation) on the instrument. |

For the period ended February 29, 2016, there were no transfers between Level 1 and Level 2 assets and liabilities. For the period ended February 29, 2016, there were no transfers from Level 2 into Level 3 assets and liabilities.

For the period ended February 29, 2016, there were no Level 3 securities.

Amounts designated as “—” are $0.

The accompanying notes are an integral part of the financial statements.

| SEI Catholic Values Trust / Annual Report / February 29, 2016 | 13 |

SCHEDULE OF INVESTMENTS

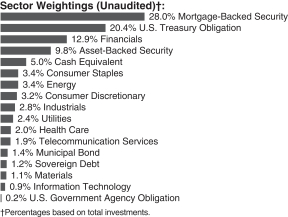

Catholic Values Fixed Income Fund

February 29, 2016

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

CORPORATE OBLIGATIONS — 35.3% |

| |||||||

Consumer Discretionary — 3.3% | ||||||||

1011778 BC ULC | ||||||||

6.000%, 04/01/2022 (A) | $ | 20 | $ | 21 | ||||

21st Century Fox America | ||||||||

6.150%, 02/15/2041 | 180 | 194 | ||||||

Amazon.com | ||||||||

4.950%, 12/05/2044 | 30 | 33 | ||||||

CCO Safari II | ||||||||

6.484%, 10/23/2045 (A) | 100 | 105 | ||||||

4.908%, 07/23/2025 (A) | 222 | 228 | ||||||

Comcast | ||||||||

6.400%, 05/15/2038 | 430 | 544 | ||||||

3.375%, 08/15/2025 | 150 | 157 | ||||||

Dollar Tree | ||||||||

5.750%, 03/01/2023 (A) | 180 | 192 | ||||||

Ford Motor | ||||||||

4.750%, 01/15/2043 | 170 | 156 | ||||||

General Motors | ||||||||

6.250%, 10/02/2043 | 40 | 39 | ||||||

4.200%, 03/01/2021 | 405 | 406 | ||||||

Historic TW | ||||||||

9.150%, 02/01/2023 | 100 | 129 | ||||||

L Brands | ||||||||

5.625%, 10/15/2023 | 10 | 11 | ||||||

McDonald’s MTN | ||||||||

3.700%, 01/30/2026 | 30 | 31 | ||||||

NCL | ||||||||

4.625%, 11/15/2020 (A) | 20 | 19 | ||||||

Netflix | ||||||||

5.500%, 02/15/2022 | 80 | 84 | ||||||

Time Warner | ||||||||

7.570%, 02/01/2024 | 101 | 123 | ||||||

4.750%, 03/29/2021 | 140 | 151 | ||||||

3.600%, 07/15/2025 | 135 | 132 | ||||||

Viacom | ||||||||

4.850%, 12/15/2034 | 220 | 174 | ||||||

|

| |||||||

| 2,929 | ||||||||

|

| |||||||

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

Consumer Staples — 3.5% | ||||||||

Altria Group | ||||||||

5.375%, 01/31/2044 | $ | 60 | $ | 68 | ||||

4.750%, 05/05/2021 | 50 | 55 | ||||||

2.850%, 08/09/2022 | 150 | 151 | ||||||

Anheuser-Busch InBev Finance | ||||||||

4.900%, 02/01/2046 | 386 | 414 | ||||||

3.650%, 02/01/2026 | 230 | 237 | ||||||

3.300%, 02/01/2023 | 50 | 51 | ||||||

2.650%, 02/01/2021 | 30 | 31 | ||||||

Anheuser-Busch InBev Worldwide | ||||||||

2.500%, 07/15/2022 | 150 | 148 | ||||||

Constellation Brands | ||||||||

4.750%, 11/15/2024 | 100 | 105 | ||||||

CVS Health | ||||||||

5.750%, 05/15/2041 | 70 | 82 | ||||||

5.125%, 07/20/2045 | 80 | 90 | ||||||

4.875%, 07/20/2035 | 20 | 22 | ||||||

3.875%, 07/20/2025 | 20 | 21 | ||||||

CVS Pass-Through Trust | ||||||||

7.507%, 01/10/2032 (A) | 428 | 508 | ||||||

Diageo Capital | ||||||||

4.828%, 07/15/2020 | 150 | 165 | ||||||

Kraft Foods Group | ||||||||

5.375%, 02/10/2020 | 30 | 33 | ||||||

3.500%, 06/06/2022 | 40 | 41 | ||||||

Kraft Heinz Foods | ||||||||

5.200%, 07/15/2045 (A) | 20 | 22 | ||||||

5.000%, 07/15/2035 (A) | 20 | 21 | ||||||

4.875%, 02/15/2025 (A) | 10 | 11 | ||||||

3.950%, 07/15/2025 (A) | 150 | 157 | ||||||

Mondelez International | ||||||||

4.000%, 02/01/2024 | 80 | 83 | ||||||

PepsiCo | ||||||||

4.600%, 07/17/2045 | 40 | 44 | ||||||

Pernod Ricard | ||||||||

4.450%, 01/15/2022 (A) | 200 | 212 | ||||||

Philip Morris International | ||||||||

4.500%, 03/20/2042 | 30 | 31 | ||||||

2.900%, 11/15/2021 | 50 | 52 | ||||||

2.500%, 08/22/2022 | 50 | 51 | ||||||

Reynolds American | ||||||||

5.850%, 08/15/2045 | 130 | 153 | ||||||

3.250%, 06/12/2020 | 11 | 11 | ||||||

Wm Wrigley Jr | ||||||||

3.375%, 10/21/2020 (A) | 30 | 31 | ||||||

|

| |||||||

| 3,101 | ||||||||

|

| |||||||

Energy — 3.5% | ||||||||

Anadarko Finance | ||||||||

7.500%, 05/01/2031 | 60 | 54 | ||||||

Anadarko Petroleum | ||||||||

6.200%, 03/15/2040 | 75 | 60 | ||||||

4.335%, 10/10/2036 | 1,000 | 352 | ||||||

| 14 | SEI Catholic Values Trust / Annual Report / February 29, 2016 |

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

Apache | ||||||||

4.250%, 01/15/2044 | $ | 50 | $ | 36 | ||||

BP Capital Markets | ||||||||

3.506%, 03/17/2025 | 90 | 87 | ||||||

Concho Resources | ||||||||

5.500%, 04/01/2023 | 40 | 37 | ||||||

ConocoPhillips | ||||||||

3.350%, 05/15/2025 | 200 | 177 | ||||||

Devon Energy | ||||||||

5.850%, 12/15/2025 | 30 | 26 | ||||||

5.000%, 06/15/2045 | 30 | 20 | ||||||

Devon Financing | ||||||||

7.875%, 09/30/2031 | 50 | 40 | ||||||

Ecopetrol | ||||||||

5.875%, 05/28/2045 | 100 | 70 | ||||||

Ensco | ||||||||

4.700%, 03/15/2021 | 20 | 11 | ||||||

Enterprise Products Operating | ||||||||

2.550%, 10/15/2019 | 130 | 126 | ||||||

Exxon Mobil | ||||||||

3.043%, 03/01/2026 | 40 | 40 | ||||||

Halliburton | ||||||||

3.800%, 11/15/2025 | 50 | 47 | ||||||

2.700%, 11/15/2020 | 10 | 10 | ||||||

Kinder Morgan | ||||||||

5.300%, 12/01/2034 | 20 | 16 | ||||||

Kinder Morgan Energy Partners | ||||||||

4.250%, 09/01/2024 | 40 | 35 | ||||||

4.150%, 02/01/2024 | 400 | 351 | ||||||

3.500%, 09/01/2023 | 30 | 25 | ||||||

MPLX | ||||||||

4.875%, 06/01/2025 (A) | 110 | 90 | ||||||

Noble Energy | ||||||||

5.250%, 11/15/2043 | 10 | 7 | ||||||

4.150%, 12/15/2021 | 50 | 44 | ||||||

Oasis Petroleum | ||||||||

7.250%, 02/01/2019 | 20 | 12 | ||||||

Occidental Petroleum | ||||||||

4.625%, 06/15/2045 | 20 | 19 | ||||||

3.125%, 02/15/2022 | 19 | 19 | ||||||

Petrobras Global Finance BV | ||||||||

6.850%, 06/05/2115 | 50 | 31 | ||||||

5.375%, 01/27/2021 | 250 | 187 | ||||||

Petroleos Mexicanos | ||||||||

6.875%, 08/04/2026 (A) | 20 | 21 | ||||||

6.625%, 06/15/2035 | 150 | 135 | ||||||

Pride International | ||||||||

6.875%, 08/15/2020 | 10 | 6 | ||||||

QEP Resources | ||||||||

5.250%, 05/01/2023 | 40 | 28 | ||||||

Range Resources | ||||||||

4.875%, 05/15/2025 (A) | 40 | 35 | ||||||

Schlumberger Holdings | ||||||||

4.000%, 12/21/2025 (A) | 30 | 30 | ||||||

3.000%, 12/21/2020 (A) | 283 | 278 | ||||||

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

Shell International Finance BV | ||||||||

4.375%, 05/11/2045 | $ | 50 | $ | 46 | ||||

Sinopec Group Overseas Development | ||||||||

4.375%, 04/10/2024 (A) | 200 | 212 | ||||||

SM Energy | ||||||||

6.125%, 11/15/2022 | 20 | 9 | ||||||

5.000%, 01/15/2024 | 30 | 12 | ||||||

Sunoco Logistics Partners Operations | ||||||||

3.450%, 01/15/2023 | 147 | 120 | ||||||

Valero Energy | ||||||||

6.125%, 02/01/2020 | 74 | 79 | ||||||

|

| |||||||

| 3,040 | ||||||||

|

| |||||||

Financials — 13.4% | ||||||||

ACE INA Holdings | ||||||||

4.350%, 11/03/2045 | 30 | 32 | ||||||

3.350%, 05/03/2026 | 10 | 10 | ||||||

2.300%, 11/03/2020 | 10 | 10 | ||||||

AgriBank FCB | ||||||||

9.125%, 07/15/2019 | 264 | 321 | ||||||

AIA Group MTN | ||||||||

3.200%, 03/11/2025 (A) | 200 | 198 | ||||||

Ally Financial | ||||||||

8.000%, 11/01/2031 | 50 | 55 | ||||||

American Express | ||||||||

2.650%, 12/02/2022 | 140 | 136 | ||||||

American International Group | ||||||||

4.800%, 07/10/2045 | 183 | 168 | ||||||

3.750%, 07/10/2025 | 80 | 79 | ||||||

Bank of America MTN | ||||||||

5.625%, 07/01/2020 | 150 | 166 | ||||||

5.000%, 01/21/2044 | 160 | 170 | ||||||

4.875%, 04/01/2044 | 150 | 156 | ||||||

4.000%, 01/22/2025 | 300 | 291 | ||||||

3.875%, 08/01/2025 | 40 | 41 | ||||||

2.600%, 01/15/2019 | 300 | 302 | ||||||

1.950%, 05/12/2018 | 229 | 228 | ||||||

Blackstone Holdings Finance | ||||||||

6.625%, 08/15/2019 (A) | 407 | 464 | ||||||

BNP Paribas MTN | ||||||||

4.375%, 09/28/2025 (A) | 200 | 194 | ||||||

Boston Properties | ||||||||

3.850%, 02/01/2023 | 200 | 206 | ||||||

Carlyle Holdings II Finance | ||||||||

5.625%, 03/30/2043 (A) | 235 | 247 | ||||||

CDP Financial | ||||||||

3.150%, 07/24/2024 (A) | 430 | 450 | ||||||

CIT Group | ||||||||

5.500%, 02/15/2019 (A) | 20 | 21 | ||||||

5.000%, 08/15/2022 | 20 | 20 | ||||||

| SEI Catholic Values Trust / Annual Report / February 29, 2016 | 15 |

SCHEDULE OF INVESTMENTS

Catholic Values Fixed Income Fund (Continued)

February 29, 2016

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

Citigroup | ||||||||

4.450%, 09/29/2027 | $ | 170 | $ | 167 | ||||

3.700%, 01/12/2026 | 170 | 174 | ||||||

2.150%, 07/30/2018 | 120 | 119 | ||||||

Cooperatieve Centrale Raiffeisen-Boerenleenbank | ||||||||

5.750%, 12/01/2043 | 250 | 276 | ||||||

Credit Agricole | ||||||||

8.125%, 12/31/2049 (A) (B) | 260 | 242 | ||||||

Credit Suisse Group Funding Guernsey | ||||||||

4.875%, 05/15/2045 | 250 | 228 | ||||||

Fifth Third Bancorp | ||||||||

2.875%, 07/27/2020 | 192 | 193 | ||||||

GLP Capital | ||||||||

4.875%, 11/01/2020 | 30 | 30 | ||||||

Goldman Sachs Group MTN | ||||||||

7.500%, 02/15/2019 | 185 | 211 | ||||||

6.750%, 10/01/2037 | 100 | 114 | ||||||

6.250%, 02/01/2041 | 50 | 60 | ||||||

5.375%, 03/15/2020 | 100 | 110 | ||||||

5.150%, 05/22/2045 | 30 | 29 | ||||||

4.750%, 10/21/2045 | 30 | 30 | ||||||

4.250%, 10/21/2025 | 30 | 30 | ||||||

3.850%, 07/08/2024 | 190 | 194 | ||||||

2.875%, 02/25/2021 | 131 | 131 | ||||||

HCP | ||||||||

4.250%, 11/15/2023 | 125 | 122 | ||||||

4.000%, 06/01/2025 | 150 | 142 | ||||||

Health Care | ||||||||

4.500%, 01/15/2024 | 200 | 204 | ||||||

HSBC Holdings | ||||||||

4.250%, 03/14/2024 | 200 | 197 | ||||||

Intercontinental Exchange | ||||||||

2.750%, 12/01/2020 | 165 | 168 | ||||||

Intesa Sanpaolo MTN | ||||||||

5.017%, 06/26/2024 (A) | 200 | 184 | ||||||

JPMorgan Chase | ||||||||

4.125%, 12/15/2026 | 150 | 152 | ||||||

3.125%, 01/23/2025 | 150 | 150 | ||||||

KKR Group Finance II | ||||||||

5.500%, 02/01/2043 (A) | 193 | 193 | ||||||

KKR Group Finance III | ||||||||

5.125%, 06/01/2044 (A) | 215 | 209 | ||||||

Liberty Mutual Group | ||||||||

4.250%, 06/15/2023 (A) | 200 | 205 | ||||||

MetLife | ||||||||

3.000%, 03/01/2025 | 175 | 167 | ||||||

Morgan Stanley MTN | ||||||||

6.625%, 04/01/2018 | 585 | 636 | ||||||

Navient MTN | ||||||||

8.000%, 03/25/2020 | 50 | 49 | ||||||

Prudential Financial MTN | ||||||||

7.375%, 06/15/2019 | 385 | 444 | ||||||

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

Quicken Loans | ||||||||

5.750%, 05/01/2025 (A) | $ | 30 | $ | 28 | ||||

Royal Bank of Scotland Group | ||||||||

5.125%, 05/28/2024 | 200 | 192 | ||||||

Teachers Insurance & Annuity Association of America | ||||||||

4.900%, 09/15/2044 (A) | 150 | 152 | ||||||

UBS Group Funding Jersey | ||||||||

4.125%, 09/24/2025 (A) | 200 | 199 | ||||||

Ventas Realty | ||||||||

4.125%, 01/15/2026 | 136 | 138 | ||||||

2.700%, 04/01/2020 | 215 | 213 | ||||||

WEA Finance | ||||||||

3.750%, 09/17/2024 (A) | 200 | 202 | ||||||

2.700%, 09/17/2019 (A) | 430 | 429 | ||||||

Wells Fargo | ||||||||

4.900%, 11/17/2045 | 50 | 51 | ||||||

4.650%, 11/04/2044 | 100 | 98 | ||||||

4.480%, 01/16/2024 | 200 | 212 | ||||||

4.300%, 07/22/2027 | 100 | 104 | ||||||

3.450%, 02/13/2023 | 160 | 162 | ||||||

|

| |||||||

| 11,705 | ||||||||

|

| |||||||

Health Care — 2.1% | ||||||||

Amgen | ||||||||

3.625%, 05/22/2024 | 60 | 62 | ||||||

Celgene | ||||||||

5.000%, 08/15/2045 | 60 | 62 | ||||||

3.875%, 08/15/2025 | 110 | 113 | ||||||

Cleveland Clinic Foundation | ||||||||

4.858%, 01/01/2114 | 236 | 250 | ||||||

DaVita HealthCare Partners | ||||||||

5.000%, 05/01/2025 | 50 | �� | 50 | |||||

Fresenius Medical Care US Finance II | ||||||||

4.750%, 10/15/2024 (A) | 50 | 51 | ||||||

Gilead Sciences | ||||||||

4.750%, 03/01/2046 | 50 | 53 | ||||||

3.650%, 03/01/2026 | 40 | 42 | ||||||

3.500%, 02/01/2025 | 50 | 52 | ||||||

Howard Hughes Medical Institute | ||||||||

3.500%, 09/01/2023 | 210 | 224 | ||||||

Kindred Healthcare | ||||||||

8.750%, 01/15/2023 | 30 | 27 | ||||||

Mallinckrodt International Finance | ||||||||

4.750%, 04/15/2023 | 30 | 26 | ||||||

Medtronic | ||||||||

3.500%, 03/15/2025 | 80 | 84 | ||||||

New York and Presbyterian Hospital | ||||||||

4.024%, 08/01/2045 | 465 | 461 | ||||||

Zimmer Biomet Holdings | ||||||||

4.450%, 08/15/2045 | 50 | 46 | ||||||

3.550%, 04/01/2025 | 230 | 227 | ||||||

|

| |||||||

| 1,830 | ||||||||

|

| |||||||

| 16 | SEI Catholic Values Trust / Annual Report / February 29, 2016 |

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

Industrials — 2.9% | ||||||||

Air Canada Pass Through Trust, | ||||||||

3.600%, 03/15/2027 (A) | $ | 215 | $ | 205 | ||||

American Airlines Pass-Through Trust, Ser 2013-1, Cl B | ||||||||

5.625%, 01/15/2021 (A) | 171 | 172 | ||||||

American Airlines Pass-Through Trust, Ser 2013-2, Cl A | ||||||||

4.950%, 01/15/2023 | 437 | 460 | ||||||

American Builders & Contractors Supply | ||||||||

5.750%, 12/15/2023 (A) | 30 | 31 | ||||||

Burlington Northern Santa Fe | ||||||||

3.000%, 04/01/2025 | 150 | 150 | ||||||

Canadian Pacific Railway | ||||||||

6.125%, 09/15/2115 | 127 | 133 | ||||||

Delta Air Lines Pass-Through Trust, | ||||||||

4.950%, 05/23/2019 | 349 | 367 | ||||||

Eaton | ||||||||

4.150%, 11/02/2042 | 70 | 67 | ||||||

Florida East Coast Holdings | ||||||||

6.750%, 05/01/2019 (A) | 30 | 30 | ||||||

International Lease Finance | ||||||||

5.875%, 08/15/2022 | 50 | 53 | ||||||

Siemens Financieringsmaatschappij | ||||||||

2.900%, 05/27/2022 (A) | 342 | 353 | ||||||

United Airlines Pass-Through Trust, Ser 2014-1, Cl A | ||||||||

4.000%, 04/11/2026 | 403 | 412 | ||||||

Waste Management | ||||||||

3.500%, 05/15/2024 | 70 | 72 | ||||||

West | ||||||||

5.375%, 07/15/2022 (A) | 30 | 27 | ||||||

|

| |||||||

| 2,532 | ||||||||

|

| |||||||

Information Technology — 1.0% | ||||||||

Apple | ||||||||

3.200%, 05/13/2025 | 80 | 83 | ||||||

Hewlett Packard Enterprise | ||||||||

4.400%, 10/15/2022 (A) | 160 | 156 | ||||||

Intel | ||||||||

3.700%, 07/29/2025 | 60 | 65 | ||||||

Juniper Networks | ||||||||

3.125%, 02/26/2019 | 128 | 128 | ||||||

Microsoft | ||||||||

4.450%, 11/03/2045 | 40 | 42 | ||||||

QUALCOMM | ||||||||

4.800%, 05/20/2045 | 50 | 46 | ||||||

Telefonaktiebolaget LM Ericsson | ||||||||

4.125%, 05/15/2022 | 190 | 196 | ||||||

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

Visa | ||||||||

4.300%, 12/14/2045 | $ | 50 | $ | 54 | ||||

3.150%, 12/14/2025 | 80 | 83 | ||||||

|

| |||||||

| 853 | ||||||||

|

| |||||||

Materials — 1.2% | ||||||||

Barrick | ||||||||

4.100%, 05/01/2023 | 181 | 169 | ||||||

BHP Billiton Finance USA | ||||||||

6.750%, 10/19/2075 (A) (B) | 200 | 193 | ||||||

5.000%, 09/30/2043 | 30 | 29 | ||||||

3.250%, 11/21/2021 | 100 | 100 | ||||||

Freeport-McMoRan | ||||||||

4.000%, 11/14/2021 | 60 | 41 | ||||||

3.550%, 03/01/2022 | 230 | 153 | ||||||

Glencore Funding | ||||||||

2.875%, 04/16/2020 (A) | 200 | 166 | ||||||

2.125%, 04/16/2018 (A) | 130 | 119 | ||||||

Rock-Tenn | ||||||||

4.000%, 03/01/2023 | 10 | 10 | ||||||

3.500%, 03/01/2020 | 20 | 21 | ||||||

Vale Overseas | ||||||||

4.375%, 01/11/2022 | 40 | 31 | ||||||

|

| |||||||

| 1,032 | ||||||||

|

| |||||||

Telecommunication Services — 1.9% |

| |||||||

AT&T | ||||||||

5.650%, 02/15/2047 | 170 | 176 | ||||||

3.400%, 05/15/2025 | 438 | 430 | ||||||

Rogers Communications | ||||||||

6.800%, 08/15/2018 | 185 | 206 | ||||||

Verizon Communications | ||||||||

6.550%, 09/15/2043 | 220 | 268 | ||||||

4.522%, 09/15/2048 | 465 | 424 | ||||||

3.500%, 11/01/2024 | 170 | 174 | ||||||

|

| |||||||

| 1,678 | ||||||||

|

| |||||||

Utilities — 2.5% | ||||||||

AES | ||||||||

5.500%, 03/15/2024 | 30 | 28 | ||||||

Berkshire Hathaway Energy | ||||||||

6.500%, 09/15/2037 | 97 | 121 | ||||||

3.500%, 02/01/2025 | 300 | 305 | ||||||

Duke Energy | ||||||||

3.750%, 04/15/2024 | 331 | 342 | ||||||

Electricite de France | ||||||||

3.625%, 10/13/2025 (A) | 137 | 139 | ||||||

Eversource Energy | ||||||||

3.150%, 01/15/2025 | 175 | 174 | ||||||

Exelon | ||||||||

5.625%, 06/15/2035 | 100 | 109 | ||||||

5.100%, 06/15/2045 (A) | 165 | 168 | ||||||

| SEI Catholic Values Trust / Annual Report / February 29, 2016 | 17 |

SCHEDULE OF INVESTMENTS

Catholic Values Fixed Income Fund (Continued)

February 29, 2016

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

FirstEnergy | ||||||||

7.375%, 11/15/2031 | $ | 220 | $ | 273 | ||||

Pacific Gas & Electric | ||||||||

6.050%, 03/01/2034 | 90 | 110 | ||||||

2.950%, 03/01/2026 | 285 | 287 | ||||||

Virginia Electric & Power | ||||||||

3.150%, 01/15/2026 | 124 | 127 | ||||||

|

| |||||||

| 2,183 | ||||||||

|

| |||||||

Total Corporate Obligations | 30,883 | |||||||

|

| |||||||

MORTGAGE-BACKED SECURITIES — 29.9% |

| |||||||

Agency Mortgage-Backed Obligations — 19.30% |

| |||||||

FHLMC | ||||||||

5.000%, 09/01/40 to 06/01/41 | 580 | 648 | ||||||

4.500%, 06/01/38 | 371 | 404 | ||||||

4.000%, 06/01/43 to 02/01/44 | 1,237 | 1,330 | ||||||

3.500%, 03/01/43 to 03/01/45 | 727 | 764 | ||||||

1.983%, 11/15/38 | 1,213 | 85 | ||||||

FHLMC ARM | ||||||||

2.392%, 03/01/37 (B) | 421 | 444 | ||||||

FHLMC CMO, Ser 2014-328, | ||||||||

1.989%, 02/15/38 (B) | 524 | 40 | ||||||

FHLMC CMO, Ser 2014-4415, | ||||||||

1.905%, 04/15/41 (B) | 803 | 58 | ||||||

FNMA | ||||||||

5.000%, 10/01/33 to 05/01/42 | 2,997 | 3,346 | ||||||

4.500%, 08/01/38 to 06/01/42 | 518 | 564 | ||||||

4.000%, 10/01/40 to 07/01/45 | 1,105 | 1,200 | ||||||

3.500%, 11/01/44 to 01/01/46 | 1,790 | 1,883 | ||||||

2.810%, 04/01/25 | 110 | 113 | ||||||

FNMA ARM | ||||||||

2.489%, 11/01/34 (B) | 193 | 202 | ||||||

2.303%, 05/01/38 (B) | 283 | 299 | ||||||

FNMA CMO, Ser 2013-52, Cl MD | ||||||||

1.250%, 06/25/43 | 271 | 266 | ||||||

FNMA CMO, Ser 2015-55, | ||||||||

1.712%, 08/25/55 (B) | 637 | 41 | ||||||

FNMA CMO, Ser 2015-56, | ||||||||

5.724%, 08/25/45 (B) | 384 | 99 | ||||||

FNMA TBA | ||||||||

5.000%, 03/01/37 | 400 | 443 | ||||||

4.500%, 02/18/19 | 800 | 869 | ||||||

3.500%, 04/01/41 | 400 | 422 | ||||||

3.000%, 03/25/26 | 1,200 | 1,251 | ||||||

2.500%, 03/01/26 | 200 | 205 | ||||||

GNMA | ||||||||

4.000%, 08/20/45 to 12/20/45 | 976 | 1,050 | ||||||

3.500%, 08/15/42 | 108 | 114 | ||||||

3.000%, 09/20/45 | 392 | 407 | ||||||

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

GNMA, Cl IO, IO | ||||||||

1.084%, 07/16/56 (B) | $ | 1,606 | $ | 120 | ||||

GNMA CMO, Ser 2012-34, | ||||||||

5.624%, 03/20/42 (B) | 258 | 56 | ||||||

GNMA CMO, Ser 2012-43, | ||||||||

6.175%, 04/16/42 (B) | 230 | 54 | ||||||

GNMA CMO, Ser 2014-118, | ||||||||

5.768%, 08/20/44 (B) | 445 | 107 | ||||||

|

| |||||||

| 16,884 | ||||||||

|

| |||||||

Non-Agency Mortgage-Backed Obligations — 10.6% |

| |||||||

BBCCRE Trust 2015-GTP, Ser GTP, Cl D | ||||||||

4.715%, 08/10/33 (A) (B) | 140 | 119 | ||||||

Bear Stearns Commercial Mortgage Securities Trust, | ||||||||

5.201%, 12/11/38 | 610 | 620 | ||||||

Bear Stearns Commercial Mortgage Securities Trust, | ||||||||

5.331%, 02/11/44 | 601 | 615 | ||||||

Chevy Chase Funding Mortgage-Backed Certificates, Ser 2004-2A, Cl B1 | ||||||||

0.704%, 05/25/35 (A) (B) | 426 | 334 | ||||||

Chevy Chase Funding Mortgage-Backed Certificates, Ser 2004-2A, Cl A1 | ||||||||

0.491%, 05/25/35 (A) (B) | 255 | 228 | ||||||

Commercial Mortgage Trust, Ser 2006-C7, Cl A4 | ||||||||

5.963%, 06/10/46 (B) | 168 | 168 | ||||||

Commercial Mortgage Trust, Ser 2014- CR18, Cl D | ||||||||

4.896%, 07/15/47 | 240 | 185 | ||||||

Credit Suisse Commercial Mortgage Trust, Ser 2006-C5, Cl A3 | ||||||||

5.311%, 12/15/39 | 565 | 569 | ||||||

CSAIL Commercial Mortgage Trust, Ser 2015-C2, Cl AS | ||||||||

3.849%, 06/15/57 | 210 | 213 | ||||||

First Horizon Mortgage Pass-Through Trust, Ser 2005-AR1, | ||||||||

2.608%, 04/25/35 (B) | 459 | 332 | ||||||

Freddie Mac Structured Agency Credit Risk Debt Notes, Ser 2015-HQ2, Cl M3 | ||||||||

3.433%, 05/25/25 (B) | 340 | 296 | ||||||

| 18 | SEI Catholic Values Trust / Annual Report / February 29, 2016 |

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

Greenwich Capital Commercial Mortgage Trust, | ||||||||

5.444%, 03/10/39 | $ | 366 | $ | 374 | ||||

GS Mortgage Securities Trust, Ser 2006-GG8, Cl A5 | ||||||||

5.622%, 11/10/39 | 220 | 205 | ||||||

GS Mortgage Securities Trust, Ser 2012-GC6, Cl AS | ||||||||

4.948%, 01/10/45 (A) | 200 | 224 | ||||||

GS Mortgage Securities Trust, Ser 2012-GCJ7, Cl A4 | ||||||||

3.377%, 05/10/45 | 247 | 259 | ||||||

Homestar Mortgage Acceptance, Ser 2004-5, Cl M2 | ||||||||

0.891%, 10/25/34 (B) | 367 | 340 | �� | |||||

IndyMac INDX Mortgage Loan Trust, Ser 2007-AR5, | ||||||||

2.782%, 05/25/37 (B) | 414 | 311 | ||||||

JP Morgan Chase Commercial Mortgage Securities Trust, Ser 2007-CB18, Cl A4 | ||||||||

5.440%, 06/12/47 | 586 | 598 | ||||||

JPMBB Commercial Mortgage Securities Trust, Ser 2015-C29, Cl C | ||||||||

4.202%, 05/15/48 (B) | 110 | 94 | ||||||

Morgan Stanley Bank of America Merrill Lynch Trust, Ser 2015-C23, Cl B | ||||||||

4.137%, 06/15/25 (B) | 100 | 98 | ||||||

Morgan Stanley Capital I Trust, Ser 2007-IQ16, Cl AJ | ||||||||

6.300%, 12/12/49 (B) | 260 | 237 | ||||||

Morgan Stanley Re-REMIC Trust, Ser 2009-GG10, Cl A4B | ||||||||

5.988%, 08/12/45 (A) (B) | 139 | 142 | ||||||

Morgan Stanley Re-REMIC Trust, Ser 2010-GG10, Cl A4B | ||||||||

5.988%, 08/15/45 (A) (B) | 182 | 189 | ||||||

Motel 6 Trust, | ||||||||

4.532%, 02/05/20 (A) | 230 | 219 | ||||||

MSCG Trust, | ||||||||

3.577%, 06/07/35 (A) (B) | 110 | 115 | ||||||

Reperforming Loan REMIC Trust, Ser 2005- R2, Cl 2A3 | ||||||||

8.000%, 06/25/35 (A) | 195 | 203 | ||||||

UBS-Citigroup Commercial Mortgage Trust, | ||||||||

2.804%, 01/10/45 | 645 | 648 | ||||||

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

Wachovia Bank Commercial Mortgage Trust, Ser 2006-C28, Cl A4 | ||||||||

5.572%, 10/15/48 | $ | 607 | $ | 613 | ||||

Wachovia Bank Commercial Mortgage Trust, Ser 2007-C31, Cl A5 | ||||||||

5.500%, 04/15/47 | 413 | 425 | ||||||

Wells Fargo Commercial Mortgage Trust, Ser 2015-C28, Cl AS | ||||||||

3.872%, 05/15/48 | 120 | 121 | ||||||

Wells Fargo Commercial Mortgage Trust, Ser 2015-C28, Cl A4 | ||||||||

3.540%, 05/15/48 | 180 | 186 | ||||||

|

| |||||||

| 9,280 | ||||||||

|

| |||||||

Total Mortgage-Backed Securities | 26,164 | |||||||

|

| |||||||

U.S. TREASURY OBLIGATIONS — 21.2% |

| |||||||

U.S. Treasury Bills (C) | ||||||||

2.400%, 03/24/16 | 486 | 486 | ||||||

U.S. Treasury Bonds | ||||||||

4.500%, 02/15/36 | 957 | 1,317 | ||||||

3.000%, 11/15/44 | 950 | 1,026 | ||||||

3.000%, 05/15/45 | 698 | 753 | ||||||

3.000%, 11/15/45 | 180 | 195 | ||||||

2.875%, 05/15/43 | 980 | 1,037 | ||||||

2.875%, 08/15/45 | 120 | 126 | ||||||

2.750%, 11/15/42 | 590 | 610 | ||||||

U.S. Treasury Inflation Indexed Bond | ||||||||

2.375%, 01/15/25 | 188 | 221 | ||||||

1.750%, 01/15/28 | 90 | 103 | ||||||

1.375%, 02/15/44 | 507 | 548 | ||||||

1.000%, 02/15/46 | 339 | 340 | ||||||

0.750%, 02/15/45 | 201 | 187 | ||||||

0.375%, 07/15/23 | 752 | 764 | ||||||

0.375%, 07/15/25 | 140 | 141 | ||||||

U.S. Treasury Notes | ||||||||

2.375%, 08/15/24 | 140 | 148 | ||||||

2.125%, 05/15/25 | 118 | 122 | ||||||

2.000%, 07/31/20 | 30 | 31 | ||||||

2.000%, 08/15/25 | 140 | 143 | ||||||

1.875%, 10/31/22 | 280 | 287 | ||||||

1.625%, 06/30/20 | 1,302 | 1,326 | ||||||

1.625%, 11/30/20 | 1,274 | 1,298 | ||||||

1.500%, 08/28/23 | 770 | 769 | ||||||

1.375%, 04/30/20 | 3,820 | 3,852 | ||||||

1.375%, 10/31/20 | 10 | 10 | ||||||

1.125%, 02/28/21 | 960 | 955 | ||||||

0.500%, 06/15/16 | 216 | 216 | ||||||

0.500%, 04/30/17 | 1,550 | 1,546 | ||||||

|

| |||||||

Total U.S. Treasury Obligations | 18,557 | |||||||

|

| |||||||

| SEI Catholic Values Trust / Annual Report / February 29, 2016 | 19 |

SCHEDULE OF INVESTMENTS

Catholic Values Fixed Income Fund (Continued)

February 29, 2016

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

ASSET-BACKED SECURITIES — 10.1% |

| |||||||

Mortgage Related Securities — 0.7% |

| |||||||

Bayview Financial Asset Trust, Ser 2007- SR1A, Cl M3 | ||||||||

1.371%, 03/25/37 (A) (B) | $ | 382 | $ | 306 | ||||

Master Asset-Backed Securities Trust, Ser 2006-FRE1, | ||||||||

0.717%, 12/25/35 (B) | 342 | 299 | ||||||

|

| |||||||

| 605 | ||||||||

|

| |||||||

Other Asset-Backed Securities — 9.4% |

| |||||||

Airspeed, Ser 2007-1A, Cl G1 | ||||||||

0.697%, 04/15/24 (A) (B) | 356 | 283 | ||||||

Citibank Credit Card Issuance Trust, Ser 2014-A6, Cl A6 | ||||||||

2.150%, 07/15/21 | 257 | 262 | ||||||

Colony American Homes, Ser 2014-1A, Cl A | ||||||||

1.576%, 05/17/31 (A) (B) | 496 | 484 | ||||||

Conseco Financial, Ser 1997-7, | ||||||||

7.030%, 07/15/28 | 242 | 231 | ||||||

DRB Prime Student Loan Trust, Ser 2015-B, Cl A1 | ||||||||

2.327%, 10/27/31 (A) (B) | 209 | 207 | ||||||

DRB Prime Student Loan Trust, Ser 2015-B, Cl A2 | ||||||||

3.170%, 07/25/31 (A) | 186 | 185 | ||||||

Ford Credit Floorplan Master Owner Trust A, Ser 2015-2, | ||||||||

1.980%, 01/15/22 | 825 | 829 | ||||||

GSAMP Trust, Ser 2004-SEA2, | ||||||||

1.677%, 03/25/34 (B) | 420 | 290 | ||||||

Invitation Homes Trust, Ser 2013-SFR1, Cl A | ||||||||

1.576%, 12/17/30 (A) (B) | 365 | 357 | ||||||

John Deere Owner Trust, | ||||||||

1.650%, 12/15/21 | 205 | 206 | ||||||

Nelnet Student Loan Trust, Ser 2008-3, Cl A4 | ||||||||

2.279%, 11/25/24 (B) | 120 | 120 | ||||||

NextGear Floorplan Master Owner Trust, Ser 2015-2A, Cl A | ||||||||

2.380%, 10/15/18 (A) | 293 | 293 | ||||||

RAMP Trust, Ser 2006-RZ3, | ||||||||

0.547%, 08/25/36 (B) | 470 | 338 | ||||||

SLM Student Loan Trust, Ser 2008-4, Cl A4 | ||||||||

2.269%, 07/25/22 (B) | 110 | 109 | ||||||

| Description | Face Amount ($ Thousands) | Market Value ($ Thousands) | ||||||

SLM Student Loan Trust, Ser 2008-5, Cl A4 | ||||||||

2.319%, 07/25/23 (B) | $ | 110 | $ | 110 | ||||

Small Business Administration, Ser 2010-20B, Cl 1 | ||||||||

4.140%, 02/01/30 | 187 | 205 | ||||||

Small Business Administration, Ser 2011-20H, Cl 1 | ||||||||

3.290%, 08/01/31 | 353 | 375 | ||||||

Small Business Administration, Ser 2013-20G, Cl 1 | ||||||||

3.150%, 07/01/33 | 930 | 974 | ||||||

Small Business Administration, Ser 2014-20C, Cl 1 | ||||||||

3.210%, 03/01/34 | 1,007 | 1,067 | ||||||

Small Business Administration, Ser 2015-20E, Cl 1 | ||||||||

2.770%, 05/01/35 | 1,050 | 1,069 | ||||||

Small Business Administration, Ser 2015-20F, Cl 1 | ||||||||

2.980%, 06/01/35 | 251 | 259 | ||||||

|

| |||||||

| 8,253 | ||||||||

|

| |||||||

Total Asset-Backed Securities | 8,858 | |||||||

|

| |||||||

MUNICIPAL BONDS — 1.4% | ||||||||

Florida — 0.2% | ||||||||

Florida State Board of Administration Finance, Ser A, RB | ||||||||

2.638%, 07/01/21 | 205 | 207 | ||||||

|

| |||||||

Indiana — 0.4% | ||||||||

Indianapolis Local Public Improvement Bond Bank, Build America Bonds, Ser B-2, RB | ||||||||

6.116%, 01/15/40 | 270 | 355 | ||||||

|

| |||||||

New Jersey — 0.4% | ||||||||

New Jersey Economic Development Authority, Ser YY, RB | ||||||||

4.197%, 06/15/19 | 350 | 356 | ||||||

|

| |||||||

Wisconsin — 0.4% | ||||||||

Wisconsin State, Ser A, RB, AGM | ||||||||

5.200%, 05/01/18 | 295 | 311 | ||||||