Exhibit (c)(6)

Preliminary Draft –Subject to Change The Conflicts Committee of the Board of Directors of Tallgrass Energy GP, LLC Discussion Materials December 16, 2019

Preliminary Draft –Subject to Change Table of Contents Section Executive Summary I TGE Situation Analysis II Overview of TGE III Valuation of TGE Shares IV A. Historical Growth Capital Expenditure Case B. TGE Financial Projections Appendix A. Weighted Average Cost of Capital B. TGE Shareholder Tax Impact C. Overview of TGE by Business Segment

Preliminary Draft –Subject to Change These materials have been prepared by Evercore Group L.L.C. (“Evercore”) for the Conflicts Committee of the Board of Directors (the “Conflicts Committee”) of Tallgrass Energy GP, LLC, the general partner of Tallgrass Energy, LP (“TGE” or the “Partnership”), to whom such materials are directly addressed and delivered and may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with Evercore. These materials are based on information provided by or on behalf of the Partnership and/or other potential transaction participants, from public sources or otherwise reviewed by Evercore. Evercore assumes no responsibility for independent investigation or verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance prepared by or reviewed with the management of the Partnership and/or other potential transaction participants or obtained from public sources, Evercore has assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such management (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). No representation or warranty, express or implied, is made as to the accuracy or completeness of such information and nothing contained herein is, or shall be relied upon as, a representation, whether as to the past, the present or the future. These materials were designed for use by specific persons familiar with the business and affairs of the Partnership . These materials are not intended to provide the sole basis for evaluating, and should not be considered a recommendation with respect to, any transaction or other matter. These materials have been developed by and are proprietary to Evercore and were prepared exclusively for the benefit and internal use of the Conflicts Committee of the Partnership. These materials were compiled on a confidential basis for use by the Conflicts Committee of the Partnership in evaluating the potential transaction described herein and not with a view to public disclosure or filing thereof under state or federal securities laws, and may not be reproduced, disseminated, quoted or referred to, in whole or in part, without the prior written consent of Evercore. These materials do not constitute an offer or solicitation to sell or purchase any securities and are not a commitment by Evercore (or any affiliate) to provide or arrange any financing for any transaction or to purchase any security in connection therewith. Evercore assumes no obligation to update or otherwise revise these materials. These materials may not reflect information known to other professionals in other business areas of Evercore and its affiliates. Evercore and its affiliates do not provide legal, accounting or tax advice. Accordingly, any statements contained herein as to tax matters were neither written nor intended by Evercore or its affiliates to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer. Each person should seek legal, accounting and tax advice based on his, her or its particular circumstances from independent advisors regarding the impact of the transactions or matters described herein.

Preliminary Draft –Subject to Change I. Executive Summary

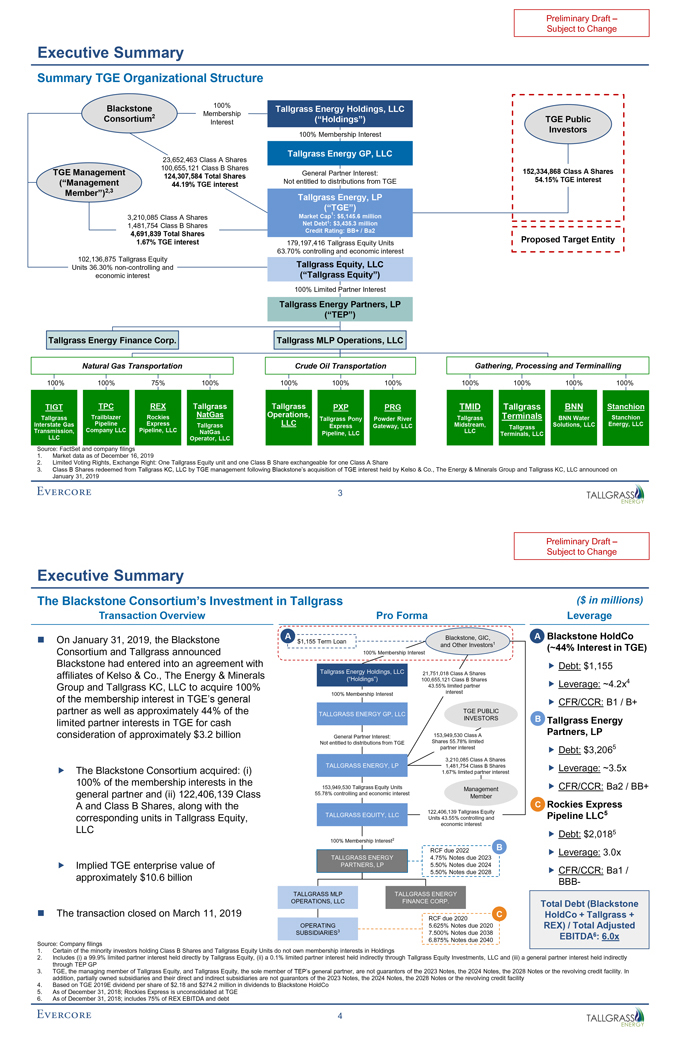

Preliminary Draft –Subject to Change Executive Summary Overview of the Materials ï® Evercore Group L.L.C. (“Evercore”) is pleased to provide the materials herein to the Conflicts Committee of the Board of Directors (the “Conflicts Committee”) of Tallgrass Energy GP, LLC (“TGE GP” or the “General Partner”), the general partner of Tallgrass Energy, LP (“Tallgrass”, “TGE” or the “Partnership”), regarding the proposed acquisition by Blackstone Infrastructure Partners (“Blackstone” or “BIP”), its partners and respective affiliates (collectively, the “Blackstone Consortium”) of all Class A shares representing limited partner interests in the Partnership (each, a “Class A Share”) from the current holders of such shares other than Class A Shares held by the Blackstone Consortium, the General Partner or their respective affiliates (the “Proposed Transaction”), in exchange for $22.45 in cash per Class A Share (the “Proposed Consideration”) ï,„ The Proposed Consideration represents a 56.4% premium to the closing price of $14.35 per Class A Share on August 27, 2019, the day of the Blackstone Consortium’s original offer of $19.50 per Class A Share (the “Initial Offer”), a 22.7% premium to TGE’s30-day volume-weighted average price (“VWAP”), a 13.4% premium to TGE’s60-day VWAP and an 8.2% premium to TGE’s90-day VWAP as of August 27, 2019 • The Proposed Consideration represents a 15.1% increase from the Initial Offer ï® The materials herein review the Proposed Transaction, including the following: ï,„ An executive summary, including an overview of the Proposed Transaction detailing summary proposed terms, an overview of the Partnership’s current summary organizational structure and ownership and certain agreements with TGE management, an analysis of financial metrics implied by the Proposed Transaction, changes since the December 8, 2019 materials presented to the Conflicts Committee and a review of Evercore’s evaluation process ï,„ An overview of TGE’s current market situation ï,„ An overview of TGE including: (i) a review of the financial projections for TGE as provided by TGE management (the “TGE Financial Projections”) and (ii) a review of financial projections for TGE based on the TGE Financial Projections assuming $350.0 million of annual growth capital expenditures (the “Historical Growth Capital Expenditure Case”) ï,„ A valuation of the TGE shares ï,„ In the Appendix, a review of TGE’s weighted average cost of capital, the potential tax impact of the Proposed Transaction to TGE shareholders and a review of TGE’s assets by segment 1

Preliminary Draft –Subject to Change Executive Summary Overview of Proposed Transaction Evercore has been asked by the Conflicts Committee, whether, in Evercore’s opinion, as of the date of the Opinion opinion, the Proposed Consideration is fair, from a financial point of view, to the unaffiliated holders of Requested: Class A Shares ï® Tallgrass Energy, LP Counterparties ï® Blackstone Infrastructure Partners, its partners and respective affiliates ï® The Blackstone Consortium proposes to acquire all publicly owned Class A Shares from the holders of Proposed such shares other than the Blackstone Consortium, the General Partner or their respective affiliates Transaction ï® TGE will cease to be publicly traded Summary be suspended and will not ï® The dividend with respect to the quarter ending December 31, 2019 will be paid if the Proposed Transaction closes ï® Holders of Class A Shares other than the Blackstone Consortium, the General Partner and their Consideration respective affiliates (the “Unaffiliated Class A Shareholders”) will receive $22.45 in cash for each Class A Share held ï® Requires approval of the Conflicts Committee ï® Requires approval from over 50.0% of TGE shareholders, including both Class A Shares and the Class B shares, which hold 100% of the voting power of Tallgrass Energy Holdings, LLC and are exchangeable, together with an equivalent number of Tallgrass Equity, LLC (“Tallgrass Equity”) units, Timing and Approvals for Class A Shares (the “Class B Shares”), owned by the Blackstone Consortium, TGE management and their respective affiliatesï® The Blackstone Consortium owns 100% of the membership interest in Tallgrass Energy Holdings, LLC ï® Requires a minimum of 7.6% of the Unaffiliated Class A Shareholders to approve Otherï® The Proposed Transaction is structured to be taxable to the Unaffiliated Class A Shareholders Source: TGE management and company filings 2

Preliminary Draft –Subject to Change Executive Summary Summary TGE Organizational Structure Blackstone 100% Tallgrass Energy Holdings, LLC 2 Membership Consortium Interest (“Holdings”) TGE Public Investors 100% Membership Interest Tallgrass Energy GP, LLC 23,652,463 Class A Shares 100,655,121 Class B Shares TGE Management General Partner Interest: 152,334,868 Class A Shares 124,307,584 Total Shares (“Management Not entitled to distributions from TGE 54.15% TGE interest 44.19% TGE interest Member”)2,3 Tallgrass Energy, LP (“TGE”) Market Cap1: $5,145.6 million 3,210,085 Class A Shares 1 1,481,754 Class B Shares Net Debt : $3,435.3 million Credit Rating: BB+ / Ba2 4,691,839 Total Shares 1.67% TGE interest 179,197,416 Tallgrass Equity Units Proposed Target Entity 63.70% controlling and economic interest 102,136,875 Tallgrass Equity Units 36.30%non-controlling and Tallgrass Equity, LLC economic interest (“Tallgrass Equity”) 100% Limited Partner Interest Tallgrass Energy Partners, LP (“TEP”) Tallgrass Energy Finance Corp. Tallgrass MLP Operations, LLC Natural Gas Transportation Crude Oil Transportation Gathering, Processing and Terminalling 100% 100% 75% 100% 100% 100% 100% 100% 100% 100% 100% TIGT TPC REX Tallgrass Tallgrass PXP PRG TMID Tallgrass BNN Stanchion Trailblazer Rockies NatGas Operations, Terminals Stanchion Tallgrass Tallgrass Pony Powder River Tallgrass BNN Water Interstate Gas Pipeline Express Tallgrass LLC Express Gateway, LLC Midstream, Solutions, LLC Energy, LLC Tallgrass Transmission, Company LLC Pipeline, LLC NatGas LLC Pipeline, LLC Terminals, LLC LLC Operator, LLC Source: FactSet and company filings 1. Market data as of December 16, 2019 2. Limited Voting Rights, Exchange Right: One Tallgrass Equity unit and one Class B Share exchangeable for one Class A Share 3. Class B Shares redeemed from Tallgrass KC, LLC by TGE management following Blackstone’s acquisition of TGE interest held by Kelso & Co., The Energy & Minerals Group and Tallgrass KC, LLC announced on January 31, 2019 3

Preliminary Draft –Subject to Change Executive Summary The Blackstone Consortium’s Investment in Tallgrass ($ in millions) Transaction Overview Pro Forma Leverage ï® On January 31, 2019, the Blackstone A Blackstone, GIC, Aï® Blackstone HoldCo $1,155 Term Loan 1 and Other Investors (~44% Interest in TGE) Consortium and Tallgrass announced 100% Membership Interest Blackstone had entered into an agreement with ï,„ Debt: $1,155 affiliates of Kelso & Co., The Energy & Minerals Tallgrass Energy Holdings, LLC 21,751,018 Class A Shares (“Holdings”) 100,655,121 Class B Shares 4 Group and Tallgrass KC, LLC to acquire 100% 43.55% limited partner ï,„ Leverage: ~4.2x of the membership interest in TGE’s general 100% Membership Interest interest ï,„ CFR/CCR: B1 / B+ partner as well as approximately 44% of the TGE PUBLIC TALLGRASS ENERGY GP, LLC limited partner interests in TGE for cash INVESTORS Bï® Tallgrass Energy consideration of approximately $3.2 billion 153,949,530 Class A Partners, LP General Partner Interest: Shares 55.78% limited Not entitled to distributions from TGE partner interestï,„ Debt: $3,2065 3,210,085 Class A Shares ï,„ The Blackstone Consortium acquired: (i) TALLGRASS ENERGY, LP 1,481,754 Class B Sharesï,„ Leverage: ~3.5x 1.67% limited partner interest 100% of the membership interests in the 153,949,530 Tallgrass Equity Units Managementï,„ CFR/CCR: Ba2 / BB+ general partner and (ii) 122,406,139 Class 55.78% controlling and economic interest Member A and Class B Shares, along with the Cï® Rockies Express 122,406,139 Tallgrass Equity 5 TALLGRASS EQUITY, LLC Pipeline LLC corresponding units in Tallgrass Equity, Units 43.55% controlling and economic interest LLC 5 2ï,„ Debt: $2,018 100% Membership Interest B RCF due 2022ï,„ Leverage: 3.0x TALLGRASS ENERGY 4.75% Notes due 2023ï,„ Implied TGE enterprise value of PARTNERS, LP 5.50% Notes due 2024 5.50% Notes due 2028ï,„ CFR/CCR: Ba1 / approximately $10.6 billionBBB- TALLGRASS MLP TALLGRASS ENERGY OPERATIONS, LLC FINANCE CORP. Total Debt (Blackstone ï® The transaction closed on March 11, 2019 C HoldCo + Tallgrass + RCF due 2020 OPERATING 5.625% Notes due 2020 REX) / Total Adjusted SUBSIDIARIES3 7.500% Notes due 2038 6.875% Notes due 2040 EBITDA6: 6.0x Source: Company filings 1. Certain of the minority investors holding Class B Shares and Tallgrass Equity Units do not own membership interests in Holdings 2. Includes (i) a 99.9% limited partner interest held directly by Tallgrass Equity, (ii) a 0.1% limited partner interest held indirectly through Tallgrass Equity Investments, LLC and (iii) a general partner interest held indirectly through TEP GP 3. TGE, the managing member of Tallgrass Equity, and Tallgrass Equity, the sole member of TEP’s general partner, are not guarantors of the 2023 Notes, the 2024 Notes, the 2028 Notes or the revolving credit facility. In addition, partially owned subsidiaries and their direct and indirect subsidiaries are not guarantors of the 2023 Notes, the 2024 Notes, the 2028 Notes or the revolving credit facility 4. Based on TGE 2019E dividend per share of $2.18 and $274.2 million in dividends to Blackstone HoldCo 5. As of December 31, 2018; Rockies Express is unconsolidated at TGE 6. As of December 31, 2018; includes 75% of REX EBITDA and debt 4

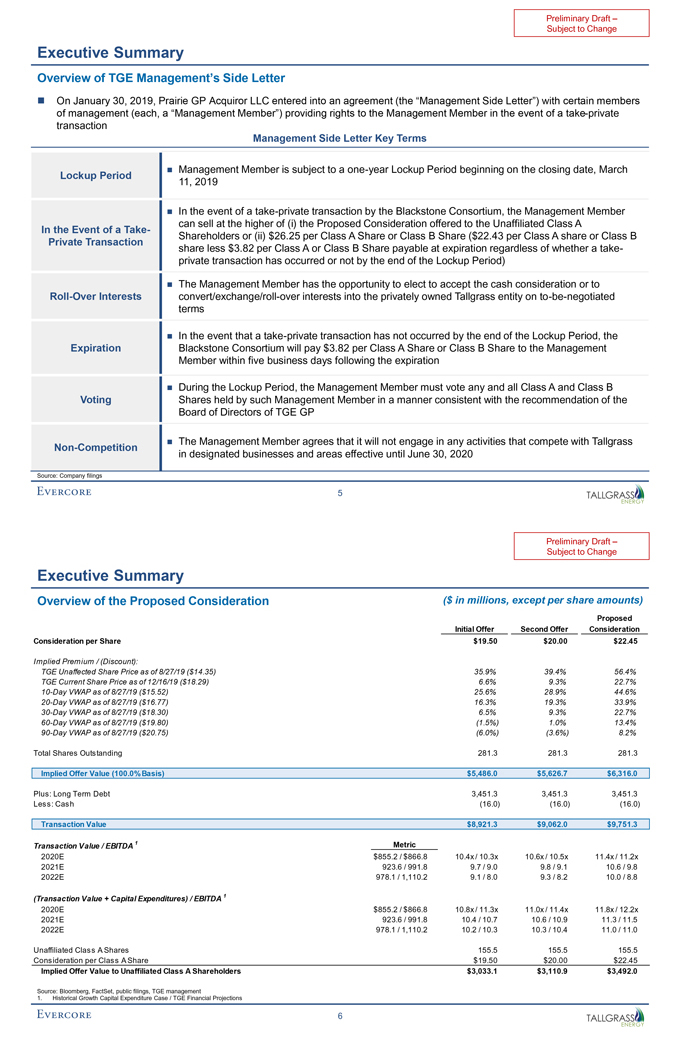

Preliminary Draft –Subject to Change Executive Summary Overview of TGE Management’s Side Letter ï® On January 30, 2019, Prairie GP Acquiror LLC entered into an agreement (the “Management Side Letter”) with certain members of management (each, a “Management Member”) providing rights to the Management Member in the event of a take-private transaction Management Side Letter Key Terms ï® Management Member is subject to aone-year Lockup Period beginning on the closing date, March Lockup Period 11, 2019 ï® In the event of a take-private transaction by the Blackstone Consortium, the Management Member can sell at the higher of (i) the Proposed Consideration offered to the Unaffiliated Class A In the Event of a Take- Shareholders or (ii) $26.25 per Class A Share or Class B Share ($22.43 per Class A share or Class B Private Transaction share less $3.82 per Class A or Class B Share payable at expiration regardless of whether a take-private transaction has occurred or not by the end of the Lockup Period) ï® The Management Member has the opportunity to elect to accept the cash consideration or to Roll-Over Interests convert/exchange/roll-over interests into the privately owned Tallgrass entity onto-be-negotiated terms ï® In the event that a take-private transaction has not occurred by the end of the Lockup Period, the Expiration Blackstone Consortium will pay $3.82 per Class A Share or Class B Share to the Management Member within five business days following the expiration ï® During the Lockup Period, the Management Member must vote any and all Class A and Class B Voting Shares held by such Management Member in a manner consistent with the recommendation of the Board of Directors of TGE GP ï® The Management Member agrees that it will not engage in any activities that compete with TallgrassNon-Competition in designated businesses and areas effective until June 30, 2020 Source: Company filings 5

Preliminary Draft –Subject to Change Executive Summary Overview of the Proposed Consideration ($ in millions, except per share amounts) Proposed Initial Offer Second Offer Consideration Consideration per Share $19.50 $20.00 $22.45 Implied Premium / (Discount): TGE Unaffected Share Price as of 8/27/19 ($14.35) 35.9% 39.4% 56.4% TGE Current Share Price as of 12/16/19 ($18.29) 6.6% 9.3% 22.7%10-Day VWAP as of 8/27/19 ($15.52) 25.6% 28.9% 44.6%20-Day VWAP as of 8/27/19 ($16.77) 16.3% 19.3% 33.9%30-Day VWAP as of 8/27/19 ($18.30) 6.5% 9.3% 22.7%60-Day VWAP as of 8/27/19 ($19.80) (1.5%) 1.0% 13.4%90-Day VWAP as of 8/27/19 ($20.75) (6.0%) (3.6%) 8.2% Total Shares Outstanding 281.3 281.3 281.3 Implied Offer Value (100.0% Basis) $5,486.0 $5,626.7 $6,316.0 Plus: Long Term Debt 3,451.3 3,451.3 3,451.3 Less: Cash (16.0) (16.0) (16.0) Transaction Value $8,921.3 $9,062.0 $9,751.3 Transaction Value / EBITDA 1 Metric 2020E $855.2 / $866.8 10.4x / 10.3x 10.6x / 10.5x 11.4x / 11.2x 2021E 923.6 / 991.8 9.7 / 9.0 9.8 / 9.1 10.6 / 9.8 2022E 978.1 / 1,110.2 9.1 / 8.0 9.3 / 8.2 10.0 / 8.8 (Transaction Value + Capital Expenditures) / EBITDA 1 2020E $855.2 / $866.8 10.8x / 11.3x 11.0x / 11.4x 11.8x / 12.2x 2021E 923.6 / 991.8 10.4 / 10.7 10.6 / 10.9 11.3 / 11.5 2022E 978.1 / 1,110.2 10.2 / 10.3 10.3 / 10.4 11.0 / 11.0 Unaffiliated Class A Shares 155.5 155.5 155.5 Consideration per Class A Share $19.50 $20.00 $22.45 Implied Offer Value to Unaffiliated Class A Shareholders $3,033.1 $3,110.9 $3,492.0 Source: Bloomberg, FactSet, public filings, TGE management 1. Historical Growth Capital Expenditure Case / TGE Financial Projections 6

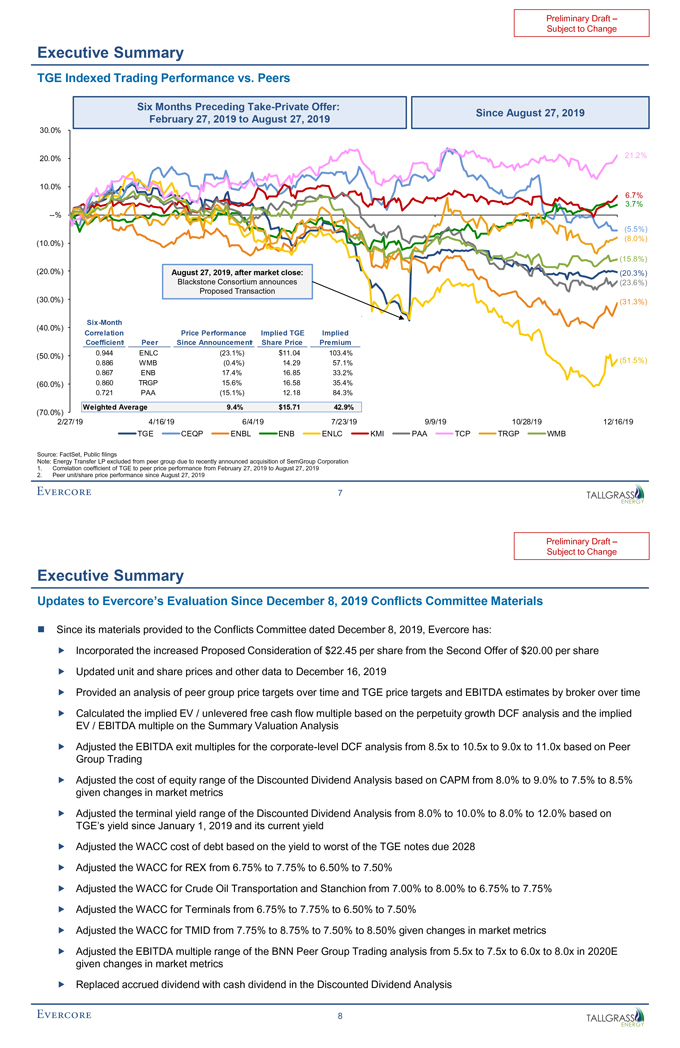

Preliminary Draft –Subject to Change Executive Summary TGE Indexed Trading Performance vs. Peers Six Months Preceding Take-Private Offer: Since August 27, 2019 February 27, 2019 to August 27, 2019 30.0% 20.0% 21.2% 10.0% 6.7% 3.7% —% (5.5%) (8.0%) (10.0%) (15.8%) (20.0%) August 27, 2019, after market close: (20.3%) Blackstone Consortium announces (23.6%) Proposed Transaction (30.0%) (31.3%)Six-Month (40.0%) Correlation Price Performance Implied TGE Implied Coefficient1 Peer Since Announcement2 Share Price Premium (50.0%) 0.944 ENLC (23.1%) $11.04 103.4% 0.886 WMB (0.4%) 14.29 57.1% (51.5%) 0.867 ENB 17.4% 16.85 33.2% (60.0%) 0.860 TRGP 15.6% 16.58 35.4% 0.721 PAA (15.1%) 12.18 84.3% Weighted Average 9.4% $15.71 42.9% (70.0%) 2/27/19 4/16/19 6/4/19 7/23/19 9/9/19 10/28/19 12/16/19 TGE CEQP ENBL ENB ENLC KMI PAA TCP TRGP WMB Source: FactSet, Public filings Note: Energy Transfer LP excluded from peer group due to recently announced acquisition of SemGroup Corporation 1. Correlation coefficient of TGE to peer price performance from February 27, 2019 to August 27, 2019 2. Peer unit/share price performance since August 27, 2019 7

Preliminary Draft –Subject to Change Executive Summary Updates to Evercore’s Evaluation Since December 8, 2019 Conflicts Committee Materials ï® Since its materials provided to the Conflicts Committee dated December 8, 2019, Evercore has: ï,„ Incorporated the increased Proposed Consideration of $22.45 per share from the Second Offer of $20.00 per shareï,„ Updated unit and share prices and other data to December 16, 2019 ï,„ Provided an analysis of peer group price targets over time and TGE price targets and EBITDA estimates by broker over timeï,„ Calculated the implied EV / unlevered free cash flow multiple based on the perpetuity growth DCF analysis and the implied EV / EBITDA multiple on the Summary Valuation Analysis ï,„ Adjusted the EBITDA exit multiples for the corporate-level DCF analysis from 8.5x to 10.5x to 9.0x to 11.0x based on Peer Group Trading ï,„ Adjusted the cost of equity range of the Discounted Dividend Analysis based on CAPM from 8.0% to 9.0% to 7.5% to 8.5% given changes in market metrics ï,„ Adjusted the terminal yield range of the Discounted Dividend Analysis from 8.0% to 10.0% to 8.0% to 12.0% based on TGE’s yield since January 1, 2019 and its current yield ï,„ Adjusted the WACC cost of debt based on the yield to worst of the TGE notes due 2028ï,„ Adjusted the WACC for REX from 6.75% to 7.75% to 6.50% to 7.50% ï,„ Adjusted the WACC for Crude Oil Transportation and Stanchion from 7.00% to 8.00% to 6.75% to 7.75%ï,„ Adjusted the WACC for Terminals from 6.75% to 7.75% to 6.50% to 7.50%ï,„ Adjusted the WACC for TMID from 7.75% to 8.75% to 7.50% to 8.50% given changes in market metrics ï,„ Adjusted the EBITDA multiple range of the BNN Peer Group Trading analysis from 5.5x to 7.5x to 6.0x to 8.0x in 2020E given changes in market metrics ï,„ Replaced accrued dividend with cash dividend in the Discounted Dividend Analysis 8

Preliminary Draft –Subject to Change Executive Summary Evercore Evaluation Process ï® In connection with its review of the Proposed Transaction, Evercore has, among other things: ï,„ Reviewed certain publicly available historical business and financial information relating to the Partnership that we deemed relevant, including as set forth in the Annual Report on Form10-K for the year ended December 31, 2018, the Quarterly Reports on Form10-Q for the quarters ended March 31, 2019, June 30, 2019 and September 30, 2019, and certain Current Reports on Form8-K, in each case as filed with or furnished to the U.S. Securities and Exchange Commission by the Partnership since December 31, 2018; ï,„ Reviewed certain internal projected financial and operating data and assumptions relating to the Partnership that were prepared and furnished to us by management of the Partnership the (the “TGE Financial Projections”);ï,„ Reviewed a financial scenario, at the request of the Conflicts Committee, based on the Tallgrass Financial Projections and total annual growth capital expenditures of $350.0 million (the “Historical Growth Capital Expenditure Case”), which senior management of the Partnership confirmed represented a more reasonable current assumption with respect to annual growth capital expenditures than is included in the TGE Financial Projections; ï,„ Discussed with management of the Partnership their assessment of the past and current operations of the Partnership, the current financial condition of the Partnership, the prospects of the Partnership and the historical and projected financial and operating data and assumptions relating to the Partnership (including management’s views of the risks and uncertainties of achieving such projections); ï,„ Reviewed the reported prices and the historical trading activity of the Class A Shares; ï,„ Performed a discounted cash flow analysis for the Partnership based on forecasts and other data provided by management of the Partnership; ï,„ Performed a discounted dividends analysis on the Partnership based on forecasts and other data prepared and furnished to us by management of the Partnership; ï,„ Performed asum-of-the-parts analysis on the Partnership based on the sum of the valuation of each of TGE’s business segments; ï,„ Compared the financial performance of the Partnership and its stock market trading multiples with those of certain other publicly traded partnerships and companies that we deemed relevant; ï,„ Reviewed a draft of the Merger Agreement, dated December 16, 2019; and ï,„ Performed such other analyses and examinations, held such other discussions, reviewed such other information and considered such other factors that we deemed appropriate. 9

Preliminary Draft –Subject to Change II. TGE Situation Analysis

Preliminary Draft –Subject to Change TGE Situation Analysis Summary Market Data ($ in millions, except per share amounts) Market Capitalization Balance Sheet and Credit Data As of December 16, 2019 As of September 30, 2019 Total Shares Outstanding1 281.3 Cash and Marketable Securities $16.0 Share Price $18.29 Short-Term Debt —Total Equity Value $5,145.6 Long-Term Debt 3,451.3 Plus: Net Debt 3,435.3 Total Debt $3,451.3 Enterprise Value $8,580.9 Net Debt $3,435.3 Historical Growth Capital Plus: Shareholders’ Equity 1,848.9 Expenditure Case / Net Book Capitalization $5,284.2 TGE Financial Projections Consensus Data Revolver Availability / Total Revolver Capacity $782.9 / $2,250.0 Metric Yield/Multiple Metric Yield/Multiple Net Debt / Net Book Cap 65.0% Dividend Yield 2 3 Net Debt / 2020E EBITDA 4.0x2 / 4.0x3 Current $2.20 / $2.20 12.0% / 12.0% $2.20 12.0% Net Debt / 2021E EBITDA 3.7x / 3.5x 2020E 2.25 / 2.25 12.3% / 12.3% 2.20 12.0% 2021E 2.25 / 2.25 12.3% / 12.3% 2.20 12.0% Current Ratings (Senior Unsecured): 2022E 2.25 / 2.26 12.3% / 12.3% NM Moody’s Ba2 (Stable) EV/EBITDA S&P BB+ (Positive) 2020E $855.2 / $866.8 10.0x / 9.9x $867.2 9.9x FitchBBB- (Stable) 2021E 923.6 / 991.8 9.3 / 8.7 892.7 9.6 2022E 978.1 / 1,110.2 8.8 / 7.7 947.5 9.1 Share Price and Dividend Information $30.00 $2.50 Di $25.00 $2.25 vi ic e r $20.00 $2.00 dend P e har $15.00 $1.75per S S $10.00 $1.50 e har $5.00 $1.25 $— $1.00 6/30/18 9/27/18 12/25/18 3/24/19 6/21/19 9/18/19 12/16/19 Source: FactSet and Partnership filings Dividend per Share Share Price 1. Includes 179.2 million Class A Shares and 102.1 million Class B Shares 2. Based on Historical Growth Capital Expenditure Case 3. Based on TGE Financial Projections 10

Preliminary Draft –Subject to Change TGE Situation Analysis TGE Trading Performance Since the MLPBuy-In 6/30/18: 8/1/18: 11/13/18: 11/26/18: 6/28/19: 8/27/19: TEGPstock-for-unit Announces plans to develop Announces expansion of Announces commercial TGE and Kinder Morgan, Inc. TGE announces merger with TEP closes, Seahorse Pipeline and PXP’s mainline capacity and agreement with (“KMI”) announce joint tariff receipt of take-private forming TGE Plaquemines Liquids associated binding open unaffiliated third-party open season to increase crude proposal from the Terminal season shipper for Seahorse oil capacity out of the Bakken Blackstone Pipeline Formation Consortium for 7/10/18: 8/15/18: 10/15/18: $19.50 per share Announces Announces binding TGE and Silver Creek 1/31/19: 3/11/19: 6/20/19: binding open open season for Midstream, LLC agree BIP enters into a BIP closes Energy Transfer 11/25/2019: season for the Seahorse Pipeline to expand the Powder definitive agreement to purchase of announces the DAPL CEO David Dehaemers Iron Horse River Gateway JV acquire a controlling controlling expansion Jr. retires and steps Pipeline interest in TGE from interest in down as CEO 9/11/18: Kelso & Co., the Energy TGE for 6/10/19: Announces Investment Grade & Minerals Group and approximately Phillips 66 and Bridger credit ratings upgrade from Fitch Tallgrass KC, LLC $3.2 billion announce Liberty Pipeline for TGE and REX $30.00 5/1/19: 25,000 Announces open season for further $27.50 22,500 PXP expansion $25.00 20,000 $22.50 17,500 V l o e $20.00 15,000 umes Shar i( n t Per $17.50 12,500 ous h rice P $15.00 10,000 and ) s $12.50 7,500 $10.00 5,000 $7.50 2,500 $5.00--6/30/2018 10/14/2018 1/29/2019 5/16/2019 8/31/2019 12/16/2019 TGE Volume TGE Price Source: FactSet, TGE public filings 11

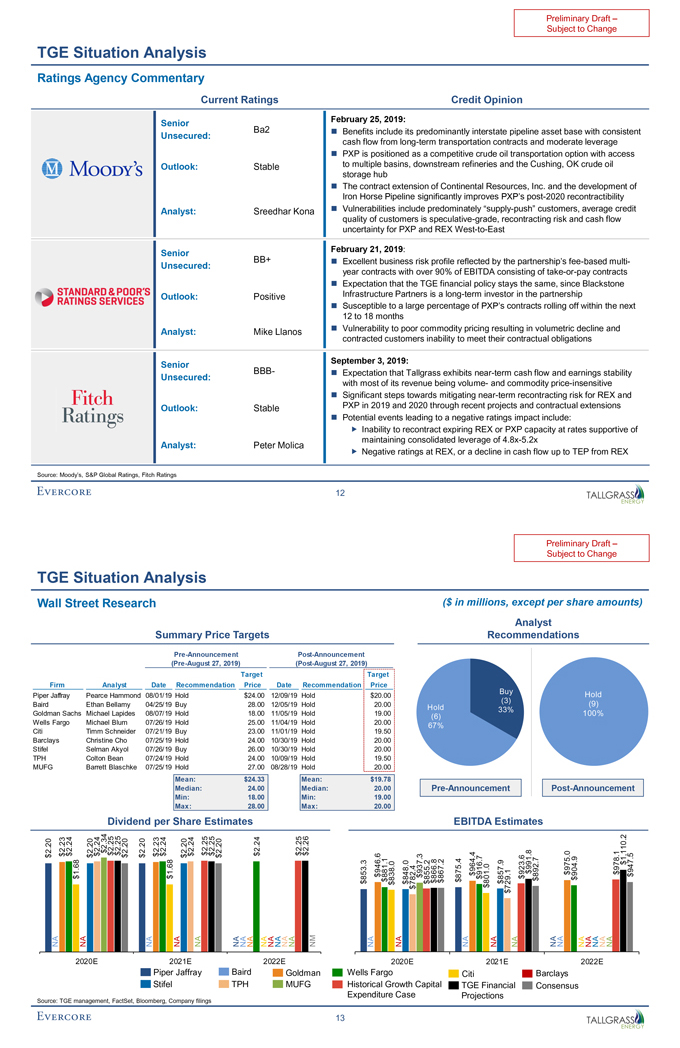

Preliminary Draft –Subject to Change TGE Situation Analysis Ratings Agency Commentary Current Ratings Credit Opinion February 25, 2019: Senior Ba2ï® Benefits include its predominantly interstate pipeline asset base with consistent Unsecured: cash flow from long-term transportation contracts and moderate leverageï® PXP is positioned as a competitive crude oil transportation option with access Outlook: Stable to multiple basins, downstream refineries and the Cushing, OK crude oil storage hubï® The contract extension of Continental Resources, Inc. and the development of Iron Horse Pipeline significantly improves PXP’s post-2020 recontractibility Analyst: Sreedhar Konaï® Vulnerabilities include predominately “supply-push” customers, average credit quality of customers is speculative-grade, recontracting risk and cash flow uncertainty for PXP and REXWest-to-East February 21, 2019: Senior BB+ï® Excellent business risk profile reflected by the partnership’sfee-based multi- Unsecured: year contracts with over 90% of EBITDA consisting oftake-or-pay contractsï® Expectation that the TGE financial policy stays the same, since Blackstone Outlook: Positive Infrastructure Partners is a long-term investor in the partnership ï® Susceptible to a large percentage of PXP’s contracts rolling off within the next 12 to 18 months Analyst: Mike Llanosï® Vulnerability to poor commodity pricing resulting in volumetric decline and contracted customers inability to meet their contractual obligations September 3, 2019: Senior BBB-ï® Expectation that Tallgrass exhibits near-term cash flow and earnings stability Unsecured: with most of its revenue being volume- and commodity price-insensitiveï® Significant steps towards mitigating near-term recontracting risk for REX and Outlook: Stable PXP in 2019 and 2020 through recent projects and contractual extensionsï® Potential events leading to a negative ratings impact include:ï,„ Inability to recontract expiring REX or PXP capacity at rates supportive of maintaining consolidated leverage of4.8x-5.2x Analyst: Peter Molica ï,„ Negative ratings at REX, or a decline in cash flow up to TEP from REX Source: Moody’s, S&P Global Ratings, Fitch Ratings 12

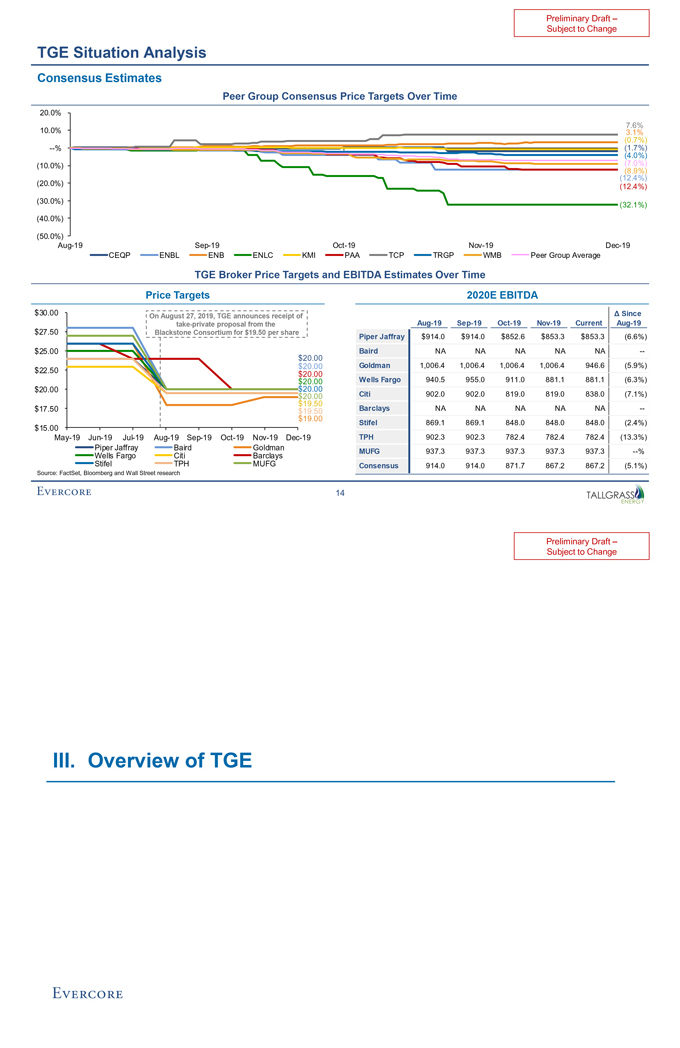

Preliminary Draft –Subject to Change TGE Situation Analysis Wall Street Research ($ in millions, except per share amounts) Analyst Summary Price Targets RecommendationsPre-Announcement Post-Announcement(Pre-August 27, 2019) (Post-August 27, 2019) Target Target Firm Analyst Date Recommendation Price Date Recommendation Price Buy Piper Jaffray Pearce Hammond 08/01/19 Hold $24.00 12/09/19 Hold $20.00 Hold (3) (9) Baird Ethan Bellamy 04/25/19 Buy 28.00 12/05/19 Hold 20.00 Hold 33% Goldman Sachs Michael Lapides 08/07/19 Hold 18.00 11/05/19 Hold 19.00 (6) 100% Wells Fargo Michael Blum 07/26/19 Hold 25.00 11/04/19 Hold 20.00 67% Citi Timm Schneider 07/21/19 Buy 23.00 11/01/19 Hold 19.50 Barclays Christine Cho 07/25/19 Hold 24.00 10/30/19 Hold 20.00 Stifel Selman Akyol 07/26/19 Buy 26.00 10/30/19 Hold 20.00 TPH Colton Bean 07/24/19 Hold 24.00 10/09/19 Hold 19.50 MUFG Barrett Blaschke 07/25/19 Hold 27.00 08/28/19 Hold 20.00 Mean: $24.33 Mean: $19.78 Median: 24.00 Median: 20.00Pre-Announcement Post-Announcement Min: 18.00 Min: 19.00 Max: 28.00 Max: 20.00 Dividend per Share Estimates EBITDA Estimates 2.34 2.232.24 2.24$2.252.25 2.232.24 2.24 2.252.25 2.24 2.252.26 2.20 2.20 2.20 2.20 2.20 2.20 $$ $ $$ $$ $ $$ $ $$ $ $ $ $ $ $ 1,110.2 $ 946.6 937.3 964.4 991.8 975.0 978.1 947.5 1.68 1.68 $916.7 923.6$892.7 $904.9 $ $ $ $881.1 $ 866.8867.2 875.4 857.9 $ $ 853.3 838.0 848.0 855.2 $ $ $ $ $ $$$ $ 801.0 $ $ $782.4 $ $ 729.1 $ NA NA NA NA N A NANANA NANANANANA NM NA NA NA NA NA NANA NANANANANA 2020E 2021E 2022E 2020E 2021E 2022E Piper Jaffray Baird Goldman Wells Fargo Citi Barclays Stifel TPH MUFG Historical Growth Capital TGE Financial Consensus Source: TGE management, FactSet, Bloomberg, Company filings Expenditure Case Projections 13

Preliminary Draft –Subject to Change TGE Situation Analysis Consensus Estimates Peer Group Consensus Price Targets Over Time 20.0% 7.6% 10.0% 3.1% (0.7%) —% (1.7%) (4.0%) (10.0%) (7.0%) (8.9%) (12.4%) (20.0%) (12.4%) (30.0%) (32.1%) (40.0%) (50.0%)Aug-19Sep-19Oct-19Nov-19Dec-19 CEQP ENBL ENB ENLC KMI PAA TCP TRGP WMB Peer Group Average TGE Broker Price Targets and EBITDA Estimates Over Time Price Targets 2020E EBITDA $30.00 On August 27, 2019, TGE announces receipt of Ä Since take-private proposal from theAug-19Sep-19Oct-19Nov-19 CurrentAug-19 $27.50 Blackstone Consortium for $19.50 per share Piper Jaffray $914.0 $914.0 $852.6 $853.3 $853.3 (6.6%) $25.00 $20.00 Baird NA NA NA NA NA —$20.00 Goldman 1,006.4 1,006.4 1,006.4 1,006.4 946.6 (5.9%) $22.50 $20.00 $20.00 Wells Fargo 940.5 955.0 911.0 881.1 881.1 (6.3%) $20.00 $20.00 $20.00 Citi 902.0 902.0 819.0 819.0 838.0 (7.1%) $19.50 $17.50 $19.50 Barclays NA NA NA NA NA —$19.00 Stifel 869.1 869.1 848.0 848.0 848.0 (2.4%) $15.00May-19Jun-19Jul-19Aug-19Sep-19Oct-19Nov-19Dec-19 TPH 902.3 902.3 782.4 782.4 782.4 (13.3%) Piper Jaffray Baird Goldman MUFG 937.3 937.3 937.3 937.3 937.3 —% Wells Fargo Citi Barclays Stifel TPH MUFG Consensus 914.0 914.0 871.7 867.2 867.2 (5.1%) Source: FactSet, Bloomberg and Wall Street research 14

Preliminary Draft –Subject to Change III. Overview of TGE

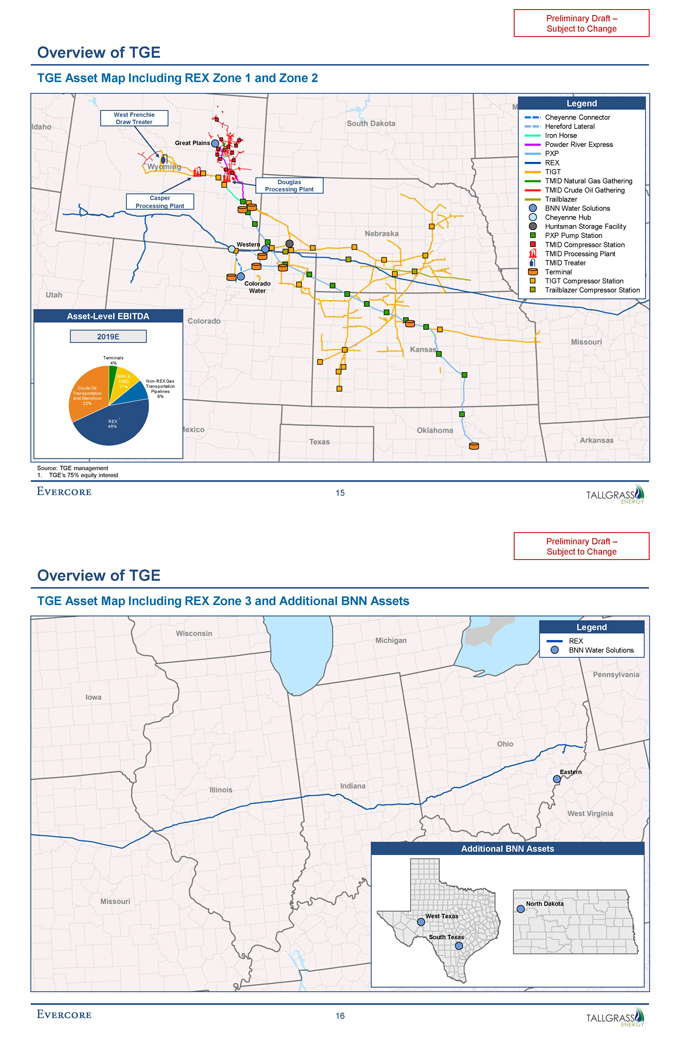

Preliminary Draft –Subject to Change Overview of TGE TGE Asset Map Including REX Zone 1 and Zone 2 Legend West Frenchie Cheyenne Connector Draw Treater Hereford Lateral Iron Horse Great Plains Powder River Express PXP REX TIGT Douglas TMID Natural Gas Gathering Processing Plant TMID Crude Oil Gathering Casper Trailblazer Processing Plant BNN Water Solutions Cheyenne Hub Huntsman Storage Facility PXP Pump Station Western TMID Compressor Station TMID Processing Plant TMID Treater Terminal Colorado TIGT Compressor Station Water Trailblazer Compressor Station Asset-Level EBITDA 2019E Terminals 4% BNN & TMIDNon-REX Gas Crude Oil 11% Transportation Transportation Pipelines and Stanchion 8% 32% 1 1 REX 46% Source: TGE management 1. TGE’s 75% equity interest 15

Overview of TGE TGE Asset Map Including REX Zone 3 and Additional BNN Assets Legend REX BNN Water Solutions Eastern Additional BNN Assets North Dakota West Texas South Texas 16

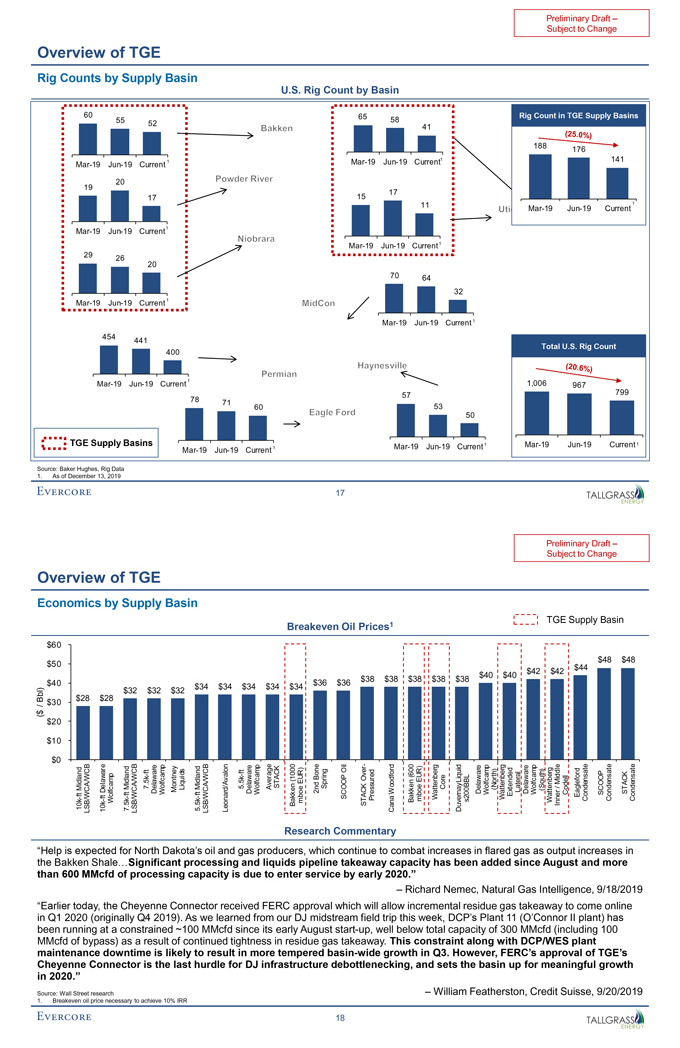

Preliminary Draft –Subject to Change Overview of TGE Rig Counts by Supply Basin U.S. Rig Count by Basin 60 65 Rig Count in TGE Supply Basins 55 58 52 41 188 176Mar-19Jun-19 Current 1Mar-19Jun-19 Current1 141 20 19 17 17 15 11Mar-19Jun-19 Current 1Mar-19Jun-19 Current1Mar-19Jun-19 Current1 29 26 20 70 64 32Mar-19Jun-19 Current 1Mar-19Jun-19 Current 1 454 441 Total U.S. Rig Count 400Mar-19Jun-19 Current 1 1,006 967 57 799 78 71 53 60 50 TGE Supply Basins 1Mar-19Jun-19 Current 1Mar-19Jun-19 Current 1Mar-19Jun-19 Current Source: Baker Hughes, Rig Data 1. As of December 13, 2019 17

Preliminary Draft –Subject to Change Overview of TGE Economics by Supply Basin TGE Supply Basin Breakeven Oil Prices1 $60 $48 $48 $50 $42 $42 $44 $40 $40 $38 $38 $38 $38 $38 $40 $36 $36 $34 $34 $34 $34 $34 l) b $32 $32 $32 B $28 $28 / $30 $ ( $20 $10 $0 e r—e r ne Oil e r mp are ft ft p and — o ng (600 iquid al WCB w l WCB k 1000 ( UR) B P Ov ded / m / EUR) L er E Middle 7.5k elawa 5.5 STACK Spri K tenberg Core tenberg ten elawa/ Midland Mid Liquids Midland Average t (North) t (South) Montney Lat Dela lfca D Wolfcamp Delaware Wolfcamp oe 2nd COO Woodford Delaware Wolfcamp D Wolfca Codell SCOOP STACK ft o—ft ft—Ex attenberg Eagleford — ft S Pressured mboe Wa Wa Condensate Condensate Condensate W k mb Bakken s200BBL W 10k LSB/WCA k 10 7.5 LSB/WCA 5.5k LSB/WCA/WCB Leonard/Avalon Bakken STAC Cana Duvernay Inner Research Commentary “Help is expected for North Dakota’s oil and gas producers, which continue to combat increases in flared gas as output increases in the Bakken Shale…Significant processing and liquids pipeline takeaway capacity has been added since August and more than 600 MMcfd of processing capacity is due to enter service by early 2020.” – Richard Nemec, Natural Gas Intelligence, 9/18/2019 “Earlier today, the Cheyenne Connector received FERC approval which will allow incremental residue gas takeaway to come online in Q1 2020 (originally Q4 2019). As we learned from our DJ midstream field trip this week, DCP’s Plant 11 (O’Connor II plant) has been running at a constrained ~100 MMcfd since its early Auguststart-up, well below total capacity of 300 MMcfd (including 100 MMcfd of bypass) as a result of continued tightness in residue gas takeaway. This constraint along with DCP/WES plant maintenance downtime is likely to result in more tempered basin-wide growth in Q3. However, FERC’s approval of TGE’s Cheyenne Connector is the last hurdle for DJ infrastructure debottlenecking, and sets the basin up for meaningful growth in 2020.” Source: Wall Street research – William Featherston, Credit Suisse, 9/20/2019 1. Breakeven oil price necessary to achieve 10% IRR 18

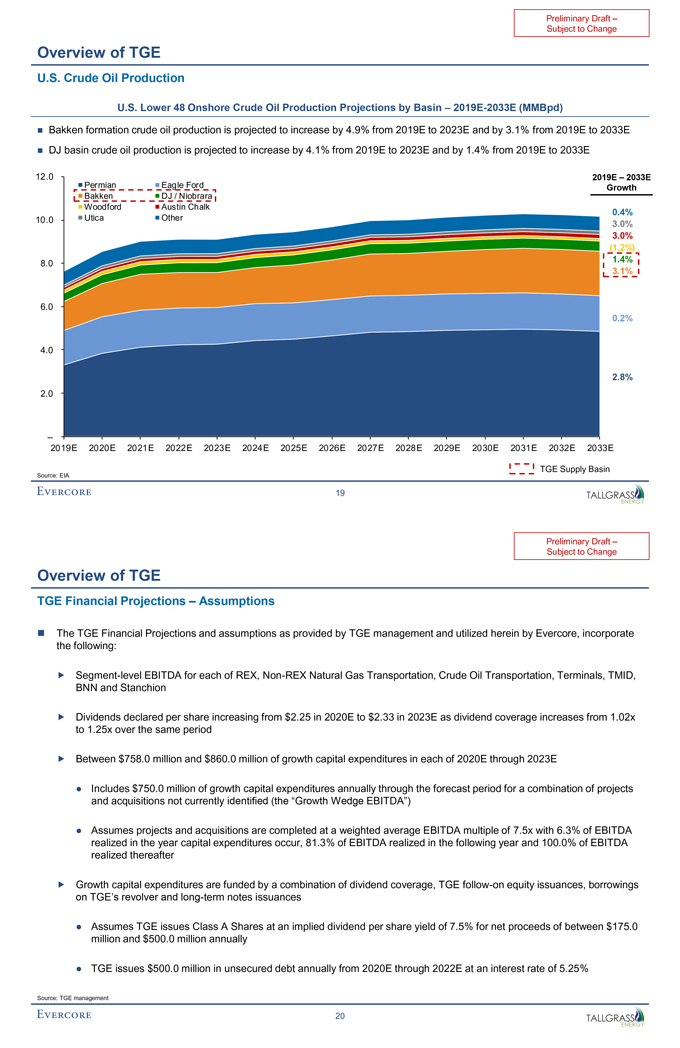

Preliminary Draft –Subject to Change Overview of TGE U.S. Crude Oil Production U.S. Lower 48 Onshore Crude Oil Production Projections by Basin – 2019E-2033E (MMBpd) ï® Bakken formation crude oil production is projected to increase by 4.9% from 2019E to 2023E and by 3.1% from 2019E to 2033Eï® DJ basin crude oil production is projected to increase by 4.1% from 2019E to 2023E and by 1.4% from 2019E to 2033E 12.0 2019E – 2033E Permian Eagle Ford Growth Bakken DJ / Niobrara Woodford Austin Chalk 0.4% 10.0 Utica Other 3.0% 3.0% (1.2%) 1.4% 8.0 3.1% 6.0 0.2% 4.0 2.8% 2.0 — 2019E 2020E 2021E 2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E 2031E 2032E 2033E Source: EIA TGE Supply Basin 19

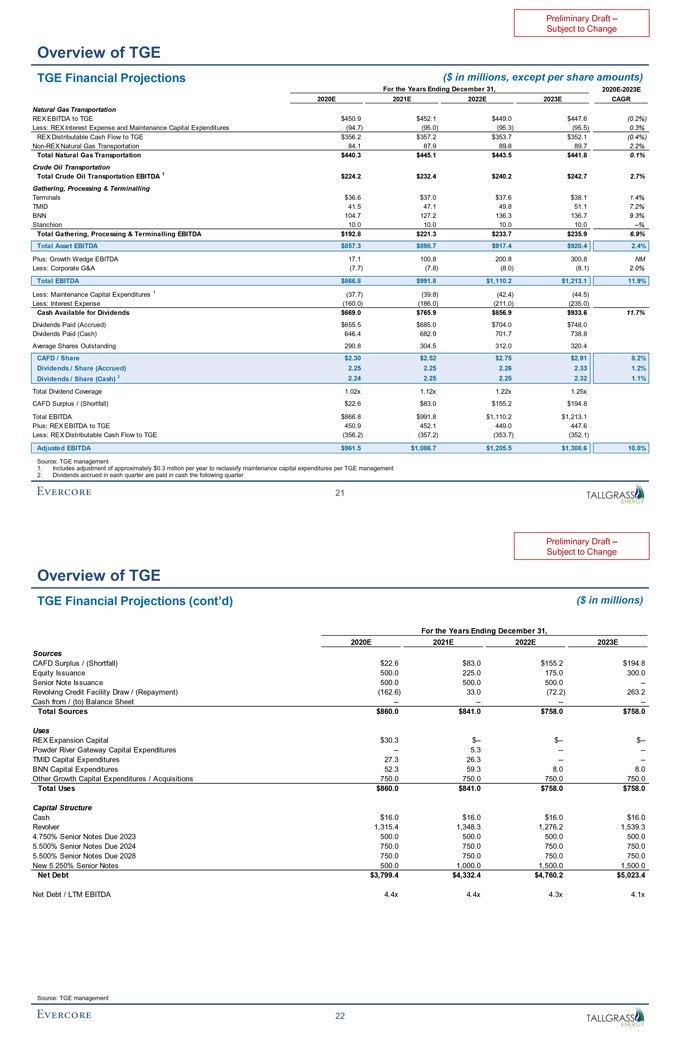

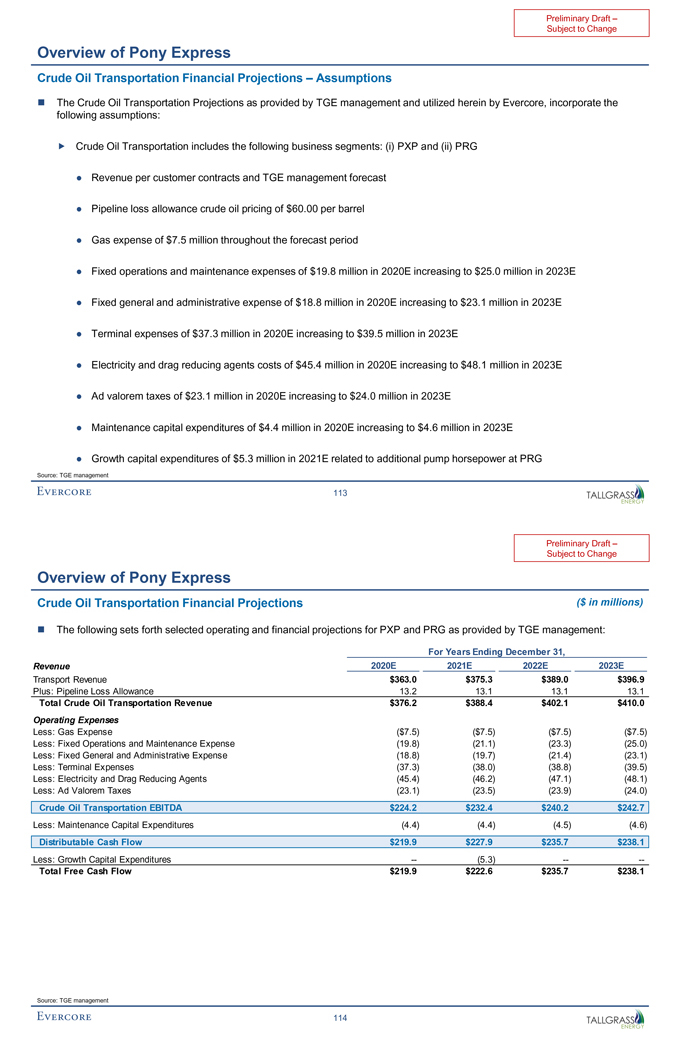

Subject to Change Overview of TGE TGE Financial Projections – Assumptions ï® The TGE Financial Projections and assumptions as provided by TGE management and utilized herein by Evercore, incorporate the following: ï,„ Segment-level EBITDA for each of REX,Non-REX Natural Gas Transportation, Crude Oil Transportation, Terminals, TMID, BNN and Stanchion ï,„ Dividends declared per share increasing from $2.25 in 2020E to $2.33 in 2023E as dividend coverage increases from 1.02x to 1.25x over the same period ï,„ Between $758.0 million and $860.0 million of growth capital expenditures in each of 2020E through 2023E • Includes $750.0 million of growth capital expenditures annually through the forecast period for a combination of projects and acquisitions not currently identified (the “Growth Wedge EBITDA”) • Assumes projects and acquisitions are completed at a weighted average EBITDA multiple of 7.5x with 6.3% of EBITDA realized in the year capital expenditures occur, 81.3% of EBITDA realized in the following year and 100.0% of EBITDA realized thereafter ï,„ Growth capital expenditures are funded by a combination of dividend coverage, TGEfollow-on equity issuances, borrowings on TGE’s revolver and long-term notes issuances • Assumes TGE issues Class A Shares at an implied dividend per share yield of 7.5% for net proceeds of between $175.0 million and $500.0 million annually • TGE issues $500.0 million in unsecured debt annually from 2020E through 2022E at an interest rate of 5.25% Source: TGE management 20

Preliminary Draft –Subject to Change Overview of TGE TGE Financial Projections ($ in millions, except per share amounts) For the Years Ending December 31, 2020E-2023E 2020E 2021E 2022E 2023E CAGR Natural Gas Transportation REX EBITDA to TGE $450.9 $452.1 $449.0 $447.6 (0.2%) Less: REX Interest Expense and Maintenance Capital Expenditures (94.7) (95.0) (95.3) (95.5) 0.3% REX Distributable Cash Flow to TGE $356.2 $357.2 $353.7 $352.1 (0.4%)Non-REX Natural Gas Transportation 84.1 87.9 89.8 89.7 2.2% Total Natural Gas Transportation $440.3 $445.1 $443.5 $441.8 0.1% Crude Oil Transportation Total Crude Oil Transportation EBITDA 1 $224.2 $232.4 $240.2 $242.7 2.7% Gathering, Processing & Terminalling Terminals $36.6 $37.0 $37.6 $38.1 1.4% TMID 41.5 47.1 49.8 51.1 7.2% BNN 104.7 127.2 136.3 136.7 9.3% Stanchion 10.0 10.0 10.0 10.0 —% Total Gathering, Processing & Terminalling EBITDA $192.8 $221.3 $233.7 $235.9 6.9% Total Asset EBITDA $857.3 $898.7 $917.4 $920.4 2.4% Plus: Growth Wedge EBITDA 17.1 100.8 200.8 300.8 NM Less: Corporate G&A (7.7) (7.8) (8.0) (8.1) 2.0% Total EBITDA $866.8 $991.8 $1,110.2 $1,213.1 11.9% Less: Maintenance Capital Expenditures 1 (37.7) (39.8) (42.4) (44.5) Less: Interest Expense (160.0) (186.0) (211.0) (235.0) Cash Available for Dividends $669.0 $765.9 $856.9 $933.6 11.7% Dividends Paid (Accrued) $655.5 $685.0 $704.0 $748.0 Dividends Paid (Cash) 646.4 682.9 701.7 738.8 Average Shares Outstanding 290.8 304.5 312.0 320.4 CAFD / Share $2.30 $2.52 $2.75 $2.91 8.2% Dividends / Share (Accrued) 2.25 2.25 2.26 2.33 1.2% Dividends / Share (Cash) 2 2.24 2.25 2.25 2.32 1.1% Total Dividend Coverage 1.02x 1.12x 1.22x 1.25x CAFD Surplus / (Shortfall) $22.6 $83.0 $155.2 $194.8 Total EBITDA $866.8 $991.8 $1,110.2 $1,213.1 Plus: REX EBITDA to TGE 450.9 452.1 449.0 447.6 Less: REX Distributable Cash Flow to TGE (356.2) (357.2) (353.7) (352.1) Adjusted EBITDA $961.5 $1,086.7 $1,205.5 $1,308.6 10.8% Source: TGE management 1. Includes adjustment of approximately $0.3 million per year to reclassify maintenance capital expenditures per TGE management 2. Dividends accrued in each quarter are paid in cash the following quarter 21

Preliminary Draft –Subject to Change Overview of TGE TGE Financial Projections (cont’d) ($ in millions) For the Years Ending December 31, 2020E 2021E 2022E 2023E Sources CAFD Surplus / (Shortfall) $22.6 $83.0 $155.2 $194.8 Equity Issuance 500.0 225.0 175.0 300.0 Senior Note Issuance 500.0 500.0 500.0 —Revolving Credit Facility Draw / (Repayment) (162.6) 33.0 (72.2) 263.2 Cash from / (to) Balance Sheet -———- Total Sources $860.0 $841.0 $758.0 $758.0 Uses REX Expansion Capital $30.3 $— $— $—Powder River Gateway Capital Expenditures — 5.3 -—-TMID Capital Expenditures 27.3 26.3-—-BNN Capital Expenditures 52.3 59.3 8.0 8.0 Other Growth Capital Expenditures / Acquisitions 750.0 750.0 750.0 750.0 Total Uses $860.0 $841.0 $758.0 $758.0 Capital Structure Cash $16.0 $16.0 $16.0 $16.0 Revolver 1,315.4 1,348.3 1,276.2 1,539.3 4.750% Senior Notes Due 2023 500.0 500.0 500.0 500.0 5.500% Senior Notes Due 2024 750.0 750.0 750.0 750.0 5.500% Senior Notes Due 2028 750.0 750.0 750.0 750.0 New 5.250% Senior Notes 500.0 1,000.0 1,500.0 1,500.0 Net Debt $3,799.4 $4,332.4 $4,760.2 $5,023.4 Net Debt / LTM EBITDA 4.4x 4.4x 4.3x 4.1x Source: TGE management 22

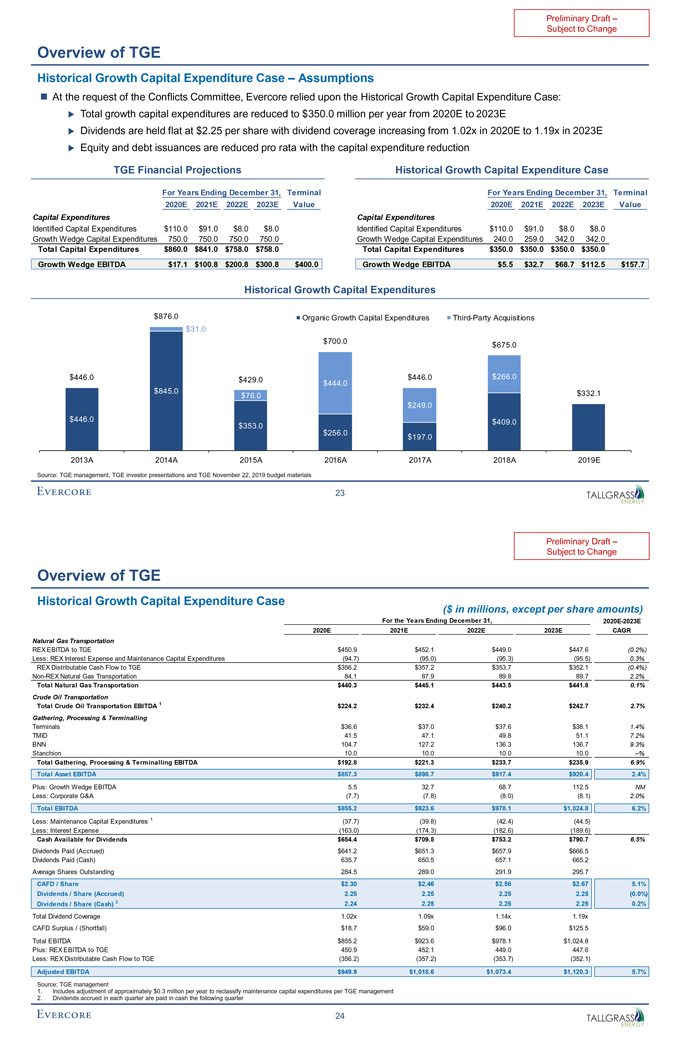

Preliminary Draft –Subject to Change Overview of TGE Historical Growth Capital Expenditure Case – Assumptions ï® At the request of the Conflicts Committee, Evercore relied upon the Historical Growth Capital Expenditure Case:ïµ Total growth capital expenditures are reduced to $350.0 million per year from 2020E to 2023E ïµ Dividends are held flat at $2.25 per share with dividend coverage increasing from 1.02x in 2020E to 1.19x in 2023Eïµ Equity and debt issuances are reduced pro rata with the capital expenditure reduction TGE Financial Projections Historical Growth Capital Expenditure Case For Years Ending December 31, Terminal For Years Ending December 31, Terminal 2020E 2021E 2022E 2023E Value 2020E 2021E 2022E 2023E Value Capital Expenditures Capital Expenditures Identified Capital Expenditures $110.0 $91.0 $8.0 $8.0 Identified Capital Expenditures $110.0 $91.0 $8.0 $8.0 Growth Wedge Capital Expenditures 750.0 750.0 750.0 750.0 Growth Wedge Capital Expenditures 240.0 259.0 342.0 342.0 Total Capital Expenditures $860.0 $841.0 $758.0 $758.0 Total Capital Expenditures $350.0 $350.0 $350.0 $350.0 Growth Wedge EBITDA $17.1 $100.8 $200.8 $300.8 $400.0 Growth Wedge EBITDA $5.5 $32.7 $68.7 $112.5 $157.7 Historical Growth Capital Expenditures $876.0 Organic Growth Capital Expenditures Third-Party Acquisitions $31.0 $700.0 $675.0 $446.0 $429.0 $444.0 $446.0 $266.0 $845.0 $332.1 $76.0 $249.0 $446.0 $353.0 $409.0 $256.0 $197.0 2013A 2014A 2015A 2016A 2017A 2018A 2019E Source: TGE management, TGE investor presentations and TGE November 22, 2019 budget materials 23

Preliminary Draft –Subject to Change Overview of TGE Historical Growth Capital Expenditure Case ($ in millions, except per share amounts) For the Years Ending December 31, 2020E-2023E 2020E 2021E 2022E 2023E CAGR Natural Gas Transportation REX EBITDA to TGE $450.9 $452.1 $449.0 $447.6 (0.2%) Less: REX Interest Expense and Maintenance Capital Expenditures (94.7) (95.0) (95.3) (95.5) 0.3% REX Distributable Cash Flow to TGE $356.2 $357.2 $353.7 $352.1 (0.4%)Non-REX Natural Gas Transportation 84.1 87.9 89.8 89.7 2.2% Total Natural Gas Transportation $440.3 $445.1 $443.5 $441.8 0.1% Crude Oil Transportation Total Crude Oil Transportation EBITDA 1 $224.2 $232.4 $240.2 $242.7 2.7% Gathering, Processing & Terminalling Terminals $36.6 $37.0 $37.6 $38.1 1.4% TMID 41.5 47.1 49.8 51.1 7.2% BNN 104.7 127.2 136.3 136.7 9.3% Stanchion 10.0 10.0 10.0 10.0 —% Total Gathering, Processing & Terminalling EBITDA $192.8 $221.3 $233.7 $235.9 6.9% Total Asset EBITDA $857.3 $898.7 $917.4 $920.4 2.4% Plus: Growth Wedge EBITDA 5.5 32.7 68.7 112.5 NM Less: Corporate G&A (7.7) (7.8) (8.0) (8.1) 2.0% Total EBITDA $855.2 $923.6 $978.1 $1,024.8 6.2% Less: Maintenance Capital Expenditures 1 (37.7) (39.8) (42.4) (44.5) Less: Interest Expense (163.0) (174.3) (182.6) (189.6) Cash Available for Dividends $654.4 $709.5 $753.2 $790.7 6.5% Dividends Paid (Accrued) $641.2 $651.3 $657.9 $666.5 Dividends Paid (Cash) 635.7 650.5 657.1 665.2 Average Shares Outstanding 284.5 289.0 291.9 295.7 CAFD / Share $2.30 $2.46 $2.58 $2.67 5.1% Dividends / Share (Accrued) 2.25 2.25 2.25 2.25 (0.0%) Dividends / Share (Cash) 2 2.24 2.25 2.25 2.25 0.2% Total Dividend Coverage 1.02x 1.09x 1.14x 1.19x CAFD Surplus / (Shortfall) $18.7 $59.0 $96.0 $125.5 Total EBITDA $855.2 $923.6 $978.1 $1,024.8 Plus: REX EBITDA to TGE 450.9 452.1 449.0 447.6 Less: REX Distributable Cash Flow to TGE (356.2) (357.2) (353.7) (352.1) Adjusted EBITDA $949.9 $1,018.6 $1,073.4 $1,120.3 5.7% Source: TGE management 1. Includes adjustment of approximately $0.3 million per year to reclassify maintenance capital expenditures per TGE management 2. Dividends accrued in each quarter are paid in cash the following quarter 24

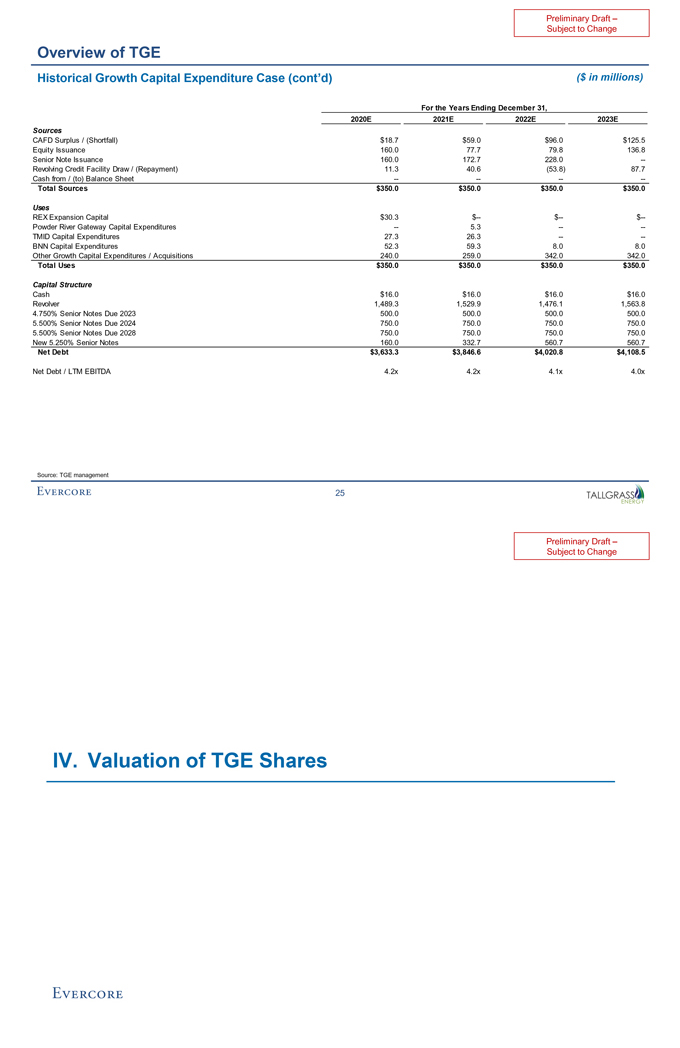

Preliminary Draft –Subject to Change Overview of TGE Historical Growth Capital Expenditure Case (cont’d) ($ in millions) For the Years Ending December 31, 2020E 2021E 2022E 2023E Sources CAFD Surplus / (Shortfall) $18.7 $59.0 $96.0 $125.5 Equity Issuance 160.0 77.7 79.8 136.8 Senior Note Issuance 160.0 172.7 228.0 —Revolving Credit Facility Draw / (Repayment) 11.3 40.6 (53.8) 87.7 Cash from / (to) Balance Sheet -———- Total Sources $350.0 $350.0 $350.0 $350.0 Uses REX Expansion Capital $30.3 $— $— $—Powder River Gateway Capital Expenditures — 5.3 -—-TMID Capital Expenditures 27.3 26.3-—-BNN Capital Expenditures 52.3 59.3 8.0 8.0 Other Growth Capital Expenditures / Acquisitions 240.0 259.0 342.0 342.0 Total Uses $350.0 $350.0 $350.0 $350.0 Capital Structure Cash $16.0 $16.0 $16.0 $16.0 Revolver 1,489.3 1,529.9 1,476.1 1,563.8 4.750% Senior Notes Due 2023 500.0 500.0 500.0 500.0 5.500% Senior Notes Due 2024 750.0 750.0 750.0 750.0 5.500% Senior Notes Due 2028 750.0 750.0 750.0 750.0 New 5.250% Senior Notes 160.0 332.7 560.7 560.7 Net Debt $3,633.3 $3,846.6 $4,020.8 $4,108.5 Net Debt / LTM EBITDA 4.2x 4.2x 4.1x 4.0x Source: TGE management 25

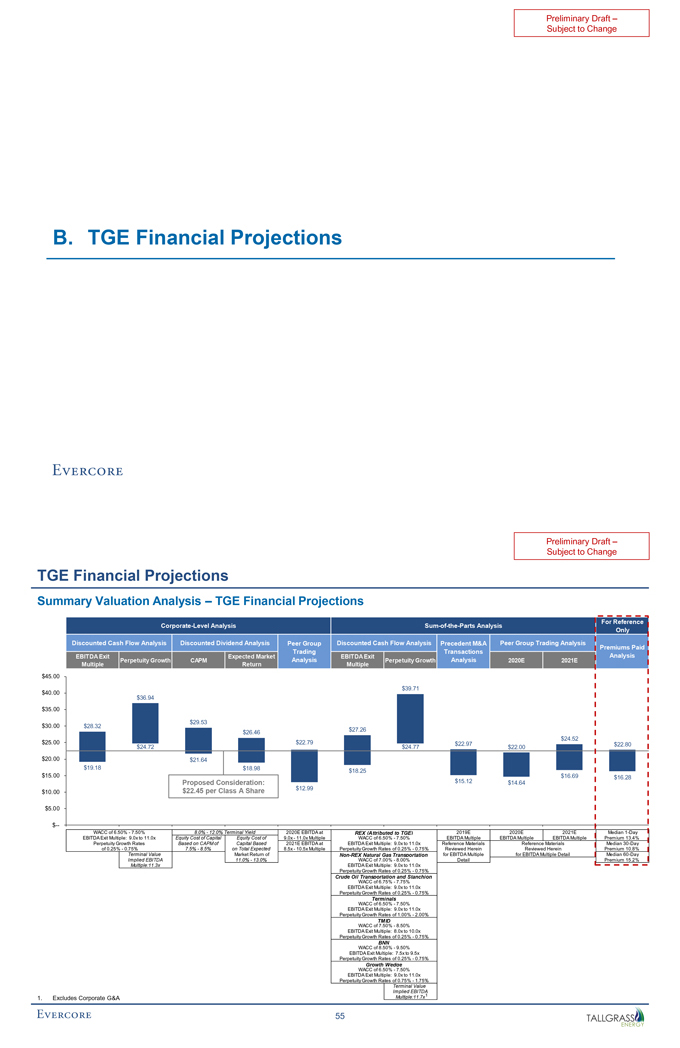

Preliminary Draft –Subject to Change IV. Valuation of TGE Shares

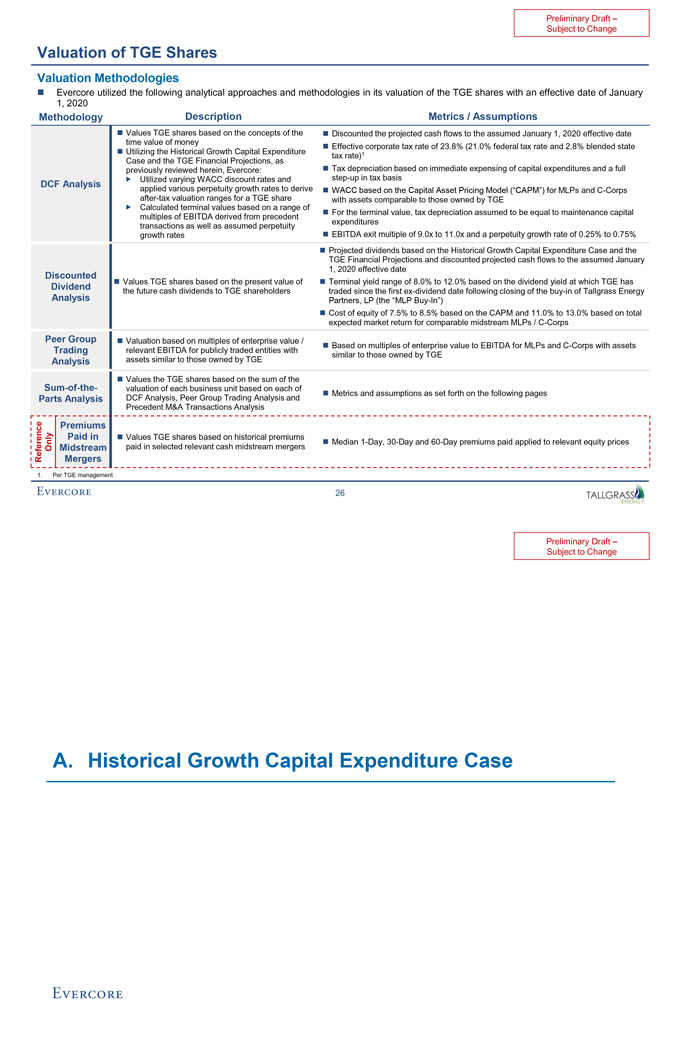

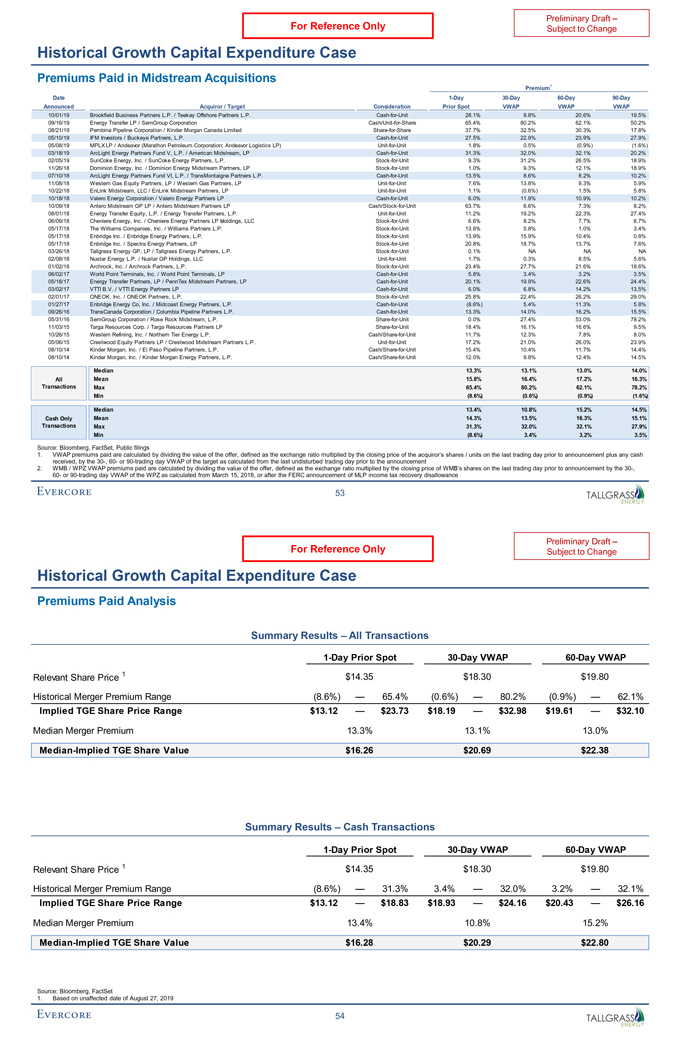

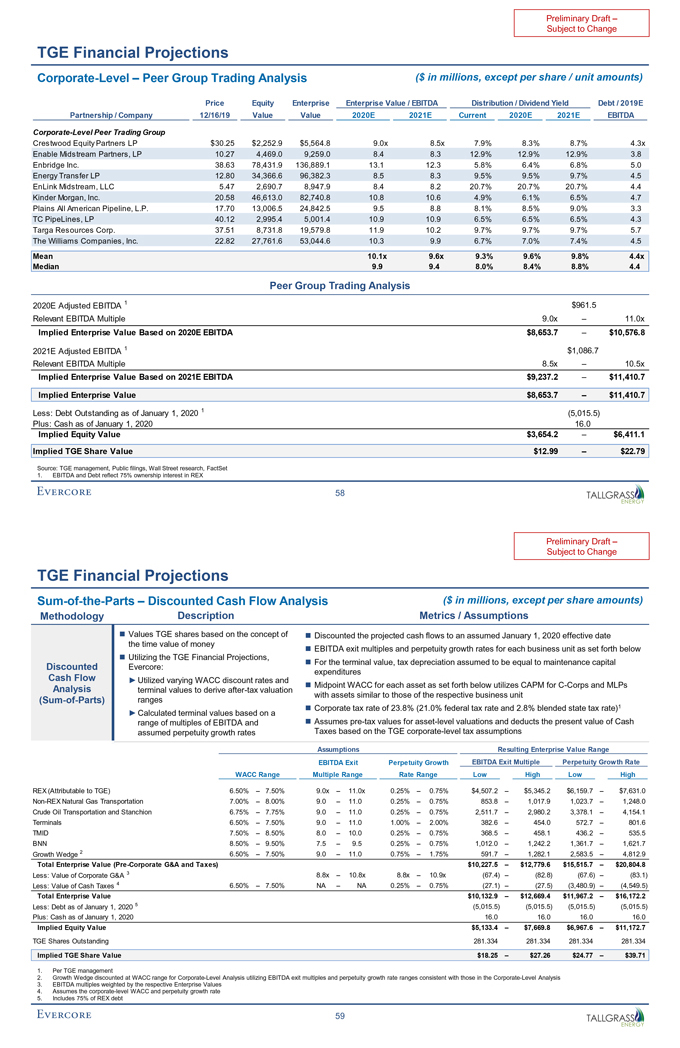

Preliminary Draft –Subject to Change Valuation of TGE Shares Valuation Methodologies ï® Evercore utilized the following analytical approaches and methodologies in its valuation of the TGE shares with an effective date of January 1, 2020 Methodology Description Metrics / Assumptions ï® Values TGE shares based on the concepts of theï® Discounted the projected cash flows to the assumed January 1, 2020 effective date time value of moneyï® Effective corporate tax rate of 23.8% (21.0% federal tax rate and 2.8% blended state ï® Utilizing the Historical Growth Capital Expenditure 1 tax rate) Case and the TGE Financial Projections, as previously reviewed herein, Evercore:ï® Tax depreciation based on immediate expensing of capital expenditures and a full ï,„ Utilized varying WACC discount rates andstep-up in tax basis DCF Analysis applied various perpetuity growth rates to derive ï® WACC based on the Capital Asset Pricing Model (“CAPM”) for MLPs andC-Corpsafter-tax valuation ranges for a TGE share with assets comparable to those owned by TGE ï,„ Calculated terminal values based on a range of ï® For the terminal value, tax depreciation assumed to be equal to maintenance capital multiples of EBITDA derived from precedent expenditures transactions as well as assumed perpetuity growth ratesï® EBITDA exit multiple of 9.0x to 11.0x and a perpetuity growth rate of 0.25% to 0.75%ï® Projected dividends based on the Historical Growth Capital Expenditure Case and the TGE Financial Projections and discounted projected cash flows to the assumed January 1, 2020 effective date Discounted ï® Values TGE shares based on the present value of ï® Terminal yield range of 8.0% to 12.0% based on the dividend yield at which TGE has Dividend the future cash dividends to TGE shareholders traded since the firstex-dividend date following closing of thebuy-in of Tallgrass Energy Analysis Partners, LP (the “MLPBuy-In”) ï® Cost of equity of 7.5% to 8.5% based on the CAPM and 11.0% to 13.0% based on total expected market return for comparable midstream MLPs /C-Corps Peer Group ï® Valuation based on multiples of enterprise value / ï® Based on multiples of enterprise value to EBITDA for MLPs andC-Corps with assets Trading relevant EBITDA for publicly traded entities with similar to those owned by TGE Analysis assets similar to those owned by TGE ï® Values the TGE shares based on the sum of theSum-of-the- valuation of each business unit based on each of ï® Metrics and assumptions as set forth on the following pages Parts Analysis DCF Analysis, Peer Group Trading Analysis and Precedent M&A Transactions Analysis Premiums Paid in ï® Values TGE shares based on historical premiums ï® Median1-Day,30-Day and60-Day premiums paid applied to relevant equity prices Only Midstream paid in selected relevant cash midstream mergers Reference Mergers 1. Per TGE management 26

Preliminary Draft –Subject to Change A. Historical Growth Capital Expenditure Case

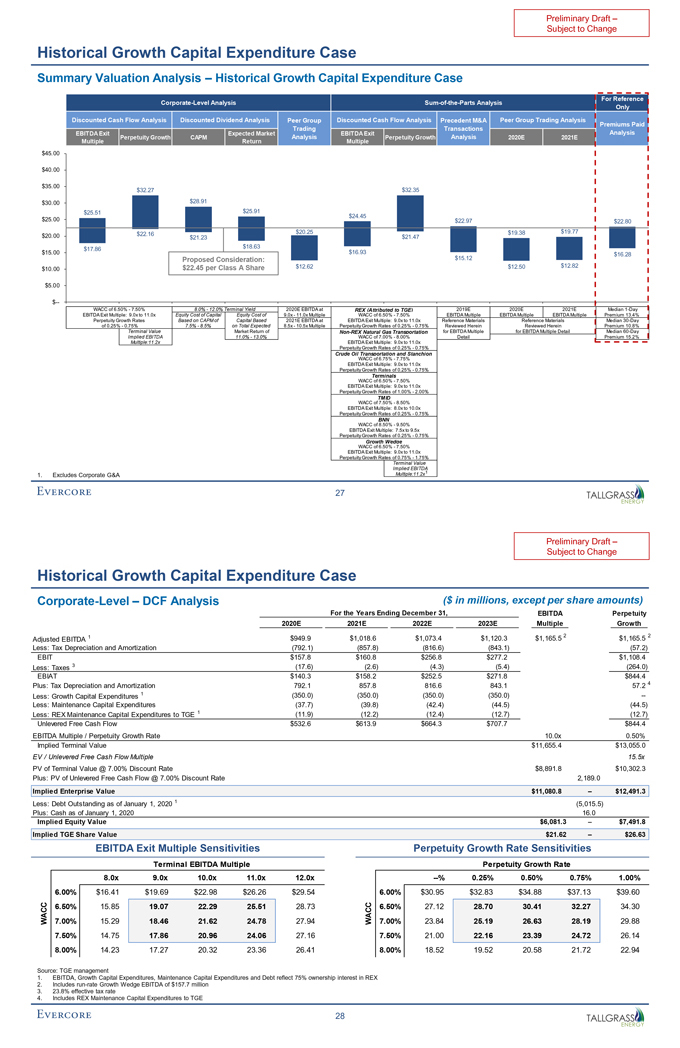

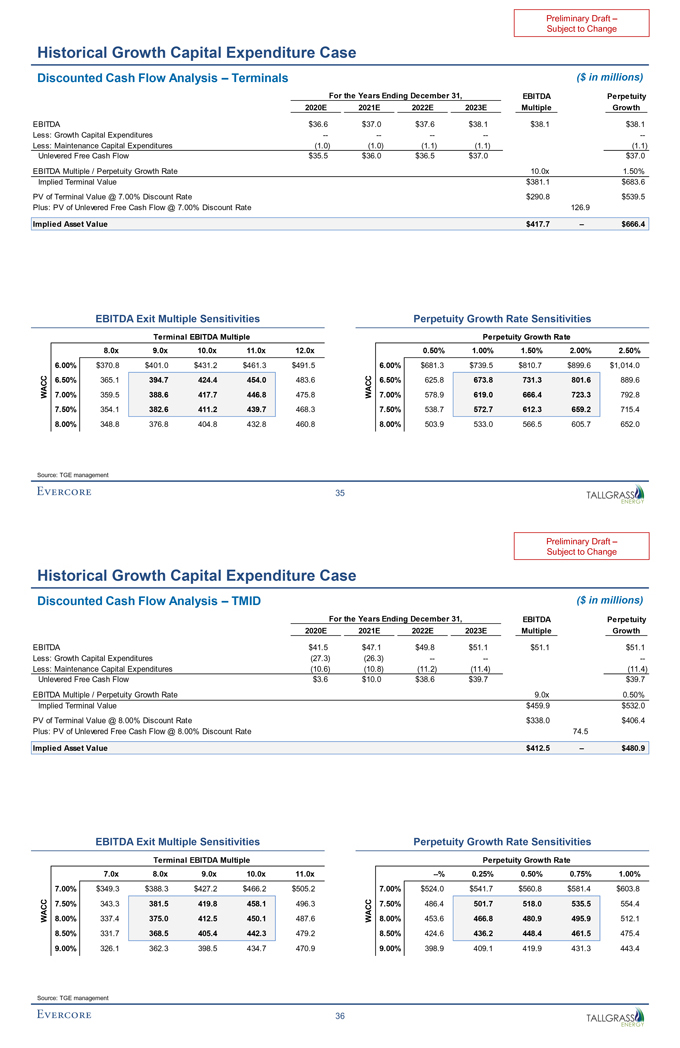

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure Case Summary Valuation Analysis – Historical Growth Capital Expenditure Case For Reference Corporate-Level AnalysisSum-of-the-Parts Analysis Only Discounted Cash Flow Analysis Discounted Dividend Analysis Peer Group Discounted Cash Flow Analysis Precedent M&A Peer Group Trading Analysis Premiums Paid Trading Transactions EBITDA Exit Expected Market EBITDA Exit Analysis Perpetuity Growth CAPM Analysis Perpetuity Growth Analysis 2020E 2021E Multiple Return Multiple $45.00 $40.00 $35.00 $32.27 $32.35 $30.00 $28.91 $25.51 $25.91 $24.45 $25.00 $22.97 $22.80 $22.16 $20.25 $19.38 $19.77 $20.00 $21.23 $21.47 $18.63 $17.86 $15.00 $16.93 $16.28 Proposed Consideration: $15.12 $22.45 per Class A Share $12.62 $12.50 $12.82 $10.00 $5.00 $— WACC of 6.50%—7.50% 8.0%—12.0% Terminal Yield 2020E EBITDA at REX (Attributed to TGE) 2019E 2020E 2021E Median1-Day EBITDA Exit Multiple: 9.0x to 11.0x Equity Cost of Capital Equity Cost of 9.0x—11.0x Multiple WACC of 6.50%—7.50% EBITDA Multiple EBITDA Multiple EBITDA Multiple Premium 13.4% Perpetuity Growth Rates Based on CAPM of Capital Based 2021E EBITDA at EBITDA Exit Multiple: 9.0x to 11.0x Reference Materials Reference Materials Median30-Day of 0.25%—0.75% 7.5%—8.5% on Total Expected 8.5x—10.5x Multiple Perpetuity Growth Rates of 0.25%—0.75% Reviewed Herein Reviewed Herein Premium 10.8% Terminal Value Market Return ofNon-REX Natural Gas Transportation for EBITDA Multiple for EBITDA Multiple Detail Median60-Day Implied EBITDA 11.0%—13.0% WACC of 7.00%—8.00% Detail Premium 15.2% Multiple:11.2x EBITDA Exit Multiple: 9.0x to 11.0x Perpetuity Growth Rates of 0.25%—0.75% Crude Oil Transportation and Stanchion WACC of 6.75%—7.75% EBITDA Exit Multiple: 9.0x to 11.0x Perpetuity Growth Rates of 0.25%—0.75% Terminals WACC of 6.50%—7.50% EBITDA Exit Multiple: 9.0x to 11.0x Perpetuity Growth Rates of 1.00%—2.00% TMID WACC of 7.50%—8.50% EBITDA Exit Multiple: 8.0x to 10.0x Perpetuity Growth Rates of 0.25%—0.75% BNN WACC of 8.50%—9.50% EBITDA Exit Multiple: 7.5x to 9.5x Perpetuity Growth Rates of 0.25%—0.75% Growth Wedge WACC of 6.50%—7.50% EBITDA Exit Multiple: 9.0x to 11.0x Perpetuity Growth Rates of 0.75%—1.75% Terminal Value Implied EBITDA 1 1. Excludes Corporate G&A Multiple:11.2x 27

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure Case Corporate-Level – DCF Analysis ($ in millions, except per share amounts) For the Years Ending December 31, EBITDA Perpetuity 2020E 2021E 2022E 2023E Multiple Growth 1 $949.9 $1,018.6 $1,073.4 $1,120.3 $1,165.5 2 $1,165.5 2 Adjusted EBITDA Less: Tax Depreciation and Amortization (792.1) (857.8) (816.6) (843.1) (57.2) EBIT $157.8 $160.8 $256.8 $277.2 $1,108.4 Less: Taxes 3 (17.6) (2.6) (4.3) (5.4) (264.0) EBIAT $140.3 $158.2 $252.5 $271.8 $844.4 Plus: Tax Depreciation and Amortization 792.1 857.8 816.6 843.1 57.2 4 Less: Growth Capital Expenditures 1 (350.0) (350.0) (350.0) (350.0) —Less: Maintenance Capital Expenditures (37.7) (39.8) (42.4) (44.5) (44.5) Less: REX Maintenance Capital Expenditures to TGE 1 (11.9) (12.2) (12.4) (12.7) (12.7) Unlevered Free Cash Flow $532.6 $613.9 $664.3 $707.7 $844.4 EBITDA Multiple / Perpetuity Growth Rate 10.0x 0.50% Implied Terminal Value $11,655.4 $13,055.0 EV / Unlevered Free Cash Flow Multiple 15.5x PV of Terminal Value @ 7.00% Discount Rate $8,891.8 $10,302.3 Plus: PV of Unlevered Free Cash Flow @ 7.00% Discount Rate 2,189.0 Implied Enterprise Value $11,080.8 – $12,491.3 Less: Debt Outstanding as of January 1, 2020 1 (5,015.5) Plus: Cash as of January 1, 2020 16.0 Implied Equity Value $6,081.3 – $7,491.8 Implied TGE Share Value $21.62 – $26.63 EBITDA Exit Multiple Sensitivities Perpetuity Growth Rate Sensitivities Terminal EBITDA Multiple Perpetuity Growth Rate 8.0x 9.0x 10.0x 11.0x 12.0x —% 0.25% 0.50% 0.75% 1.00% 6.00% $16.41 $19.69 $22.98 $26.26 $29.54 6.00% $30.95 $32.83 $34.88 $37.13 $39.60 ACC 6.50% 15.85 19.07 22.29 25.51 28.73 ACC 6.50% 27.12 28.70 30.41 32.27 34.30 W 7.00% 15.29 18.46 21.62 24.78 27.94 W 7.00% 23.84 25.19 26.63 28.19 29.88 7.50% 14.75 17.86 20.96 24.06 27.16 7.50% 21.00 22.16 23.39 24.72 26.14 8.00% 14.23 17.27 20.32 23.36 26.41 8.00% 18.52 19.52 20.58 21.72 22.94 Source: TGE management 1. EBITDA, Growth Capital Expenditures, Maintenance Capital Expenditures and Debt reflect 75% ownership interest in REX 2. Includesrun-rate Growth Wedge EBITDA of $157.7 million 3. 23.8% effective tax rate 4. Includes REX Maintenance Capital Expenditures to TGE 28

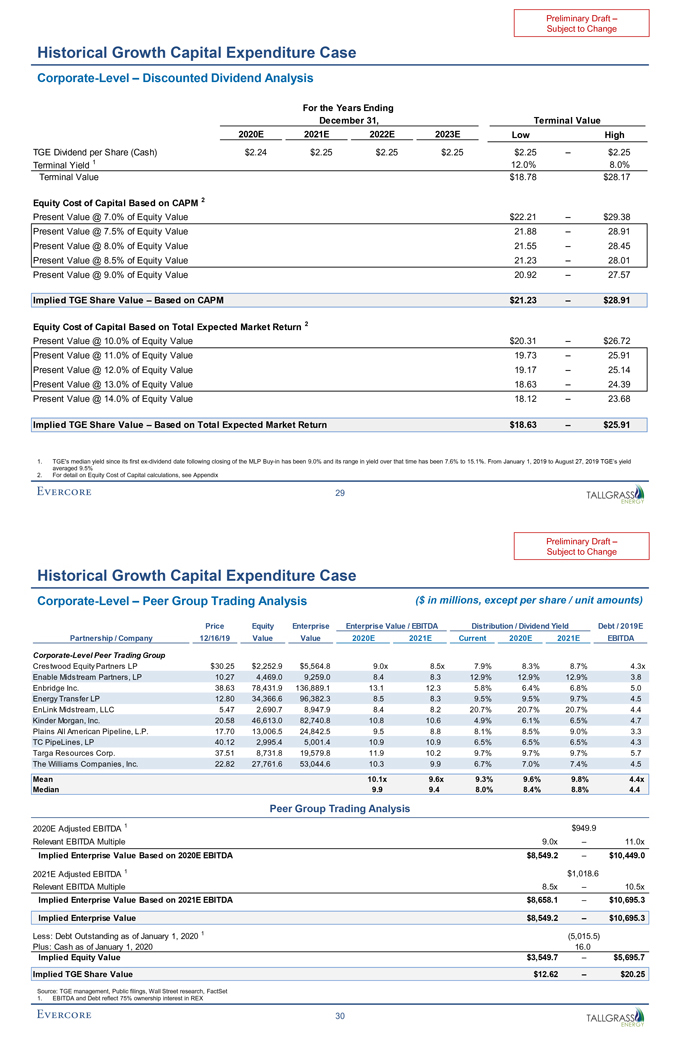

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure Case Corporate-Level – Discounted Dividend Analysis For the Years Ending December 31, Terminal Value 2020E 2021E 2022E 2023E Low High TGE Dividend per Share (Cash) $2.24 $2.25 $2.25 $2.25 $2.25 – $2.25 Terminal Yield 1 12.0% 8.0% Terminal Value $18.78 $28.17 Equity Cost of Capital Based on CAPM 2 Present Value @ 7.0% of Equity Value $22.21 – $29.38 Present Value @ 7.5% of Equity Value 21.88 – 28.91 Present Value @ 8.0% of Equity Value 21.55 – 28.45 Present Value @ 8.5% of Equity Value 21.23 – 28.01 Present Value @ 9.0% of Equity Value 20.92 – 27.57 Implied TGE Share Value – Based on CAPM $21.23 – $28.91 Equity Cost of Capital Based on Total Expected Market Return 2 Present Value @ 10.0% of Equity Value $20.31 – $26.72 Present Value @ 11.0% of Equity Value 19.73 – 25.91 Present Value @ 12.0% of Equity Value 19.17 – 25.14 Present Value @ 13.0% of Equity Value 18.63 – 24.39 Present Value @ 14.0% of Equity Value 18.12 – 23.68 Implied TGE Share Value – Based on Total Expected Market Return $18.63 – $25.91 1. TGE’s median yield since its firstex-dividend date following closing of the MLPBuy-in has been 9.0% and its range in yield over that time has been 7.6% to 15.1%. From January 1, 2019 to August 27, 2019 TGE’s yield averaged 9.5% 2. For detail on Equity Cost of Capital calculations, see Appendix 29

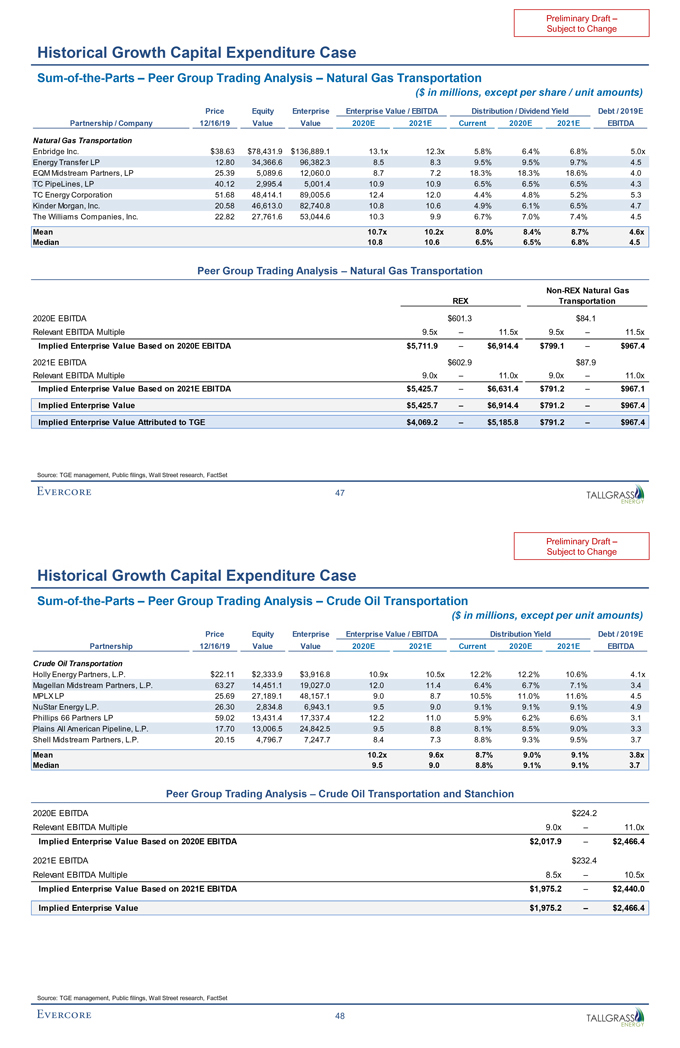

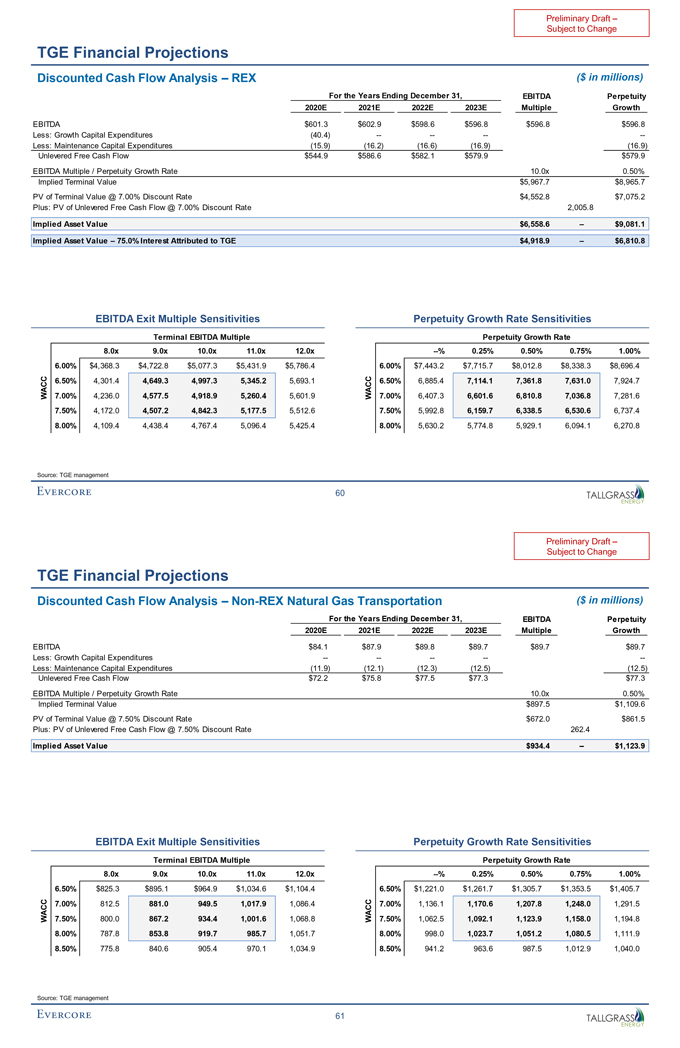

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure Case Corporate-Level – Peer Group Trading Analysis ($ in millions, except per share / unit amounts) Price Equity Enterprise Enterprise Value / EBITDA Distribution / Dividend Yield Debt / 2019E Partnership / Company 12/16/19 Value Value 2020E 2021E Current 2020E 2021E EBITDA Corporate-Level Peer Trading Group Crestwood Equity Partners LP $30.25 $2,252.9 $5,564.8 9.0x 8.5x 7.9% 8.3% 8.7% 4.3x Enable Midstream Partners, LP 10.27 4,469.0 9,259.0 8.4 8.3 12.9% 12.9% 12.9% 3.8 Enbridge Inc. 38.63 78,431.9 136,889.1 13.1 12.3 5.8% 6.4% 6.8% 5.0 Energy Transfer LP 12.80 34,366.6 96,382.3 8.5 8.3 9.5% 9.5% 9.7% 4.5 EnLink Midstream, LLC 5.47 2,690.7 8,947.9 8.4 8.2 20.7% 20.7% 20.7% 4.4 Kinder Morgan, Inc. 20.58 46,613.0 82,740.8 10.8 10.6 4.9% 6.1% 6.5% 4.7 Plains All American Pipeline, L.P. 17.70 13,006.5 24,842.5 9.5 8.8 8.1% 8.5% 9.0% 3.3 TC PipeLines, LP 40.12 2,995.4 5,001.4 10.9 10.9 6.5% 6.5% 6.5% 4.3 Targa Resources Corp. 37.51 8,731.8 19,579.8 11.9 10.2 9.7% 9.7% 9.7% 5.7 The Williams Companies, Inc. 22.82 27,761.6 53,044.6 10.3 9.9 6.7% 7.0% 7.4% 4.5 Mean 10.1x 9.6x 9.3% 9.6% 9.8% 4.4x Median 9.9 9.4 8.0% 8.4% 8.8% 4.4 Peer Group Trading Analysis 2020E Adjusted EBITDA 1 $949.9 Relevant EBITDA Multiple 9.0x – 11.0x Implied Enterprise Value Based on 2020E EBITDA $8,549.2 – $10,449.0 2021E Adjusted EBITDA 1 $1,018.6 Relevant EBITDA Multiple 8.5x – 10.5x Implied Enterprise Value Based on 2021E EBITDA $8,658.1 – $10,695.3 Implied Enterprise Value $8,549.2 – $10,695.3 Less: Debt Outstanding as of January 1, 2020 1 (5,015.5) Plus: Cash as of January 1, 2020 16.0 Implied Equity Value $3,549.7 – $5,695.7 Implied TGE Share Value $12.62 – $20.25 Source: TGE management, Public filings, Wall Street research, FactSet 1. EBITDA and Debt reflect 75% ownership interest in REX 30

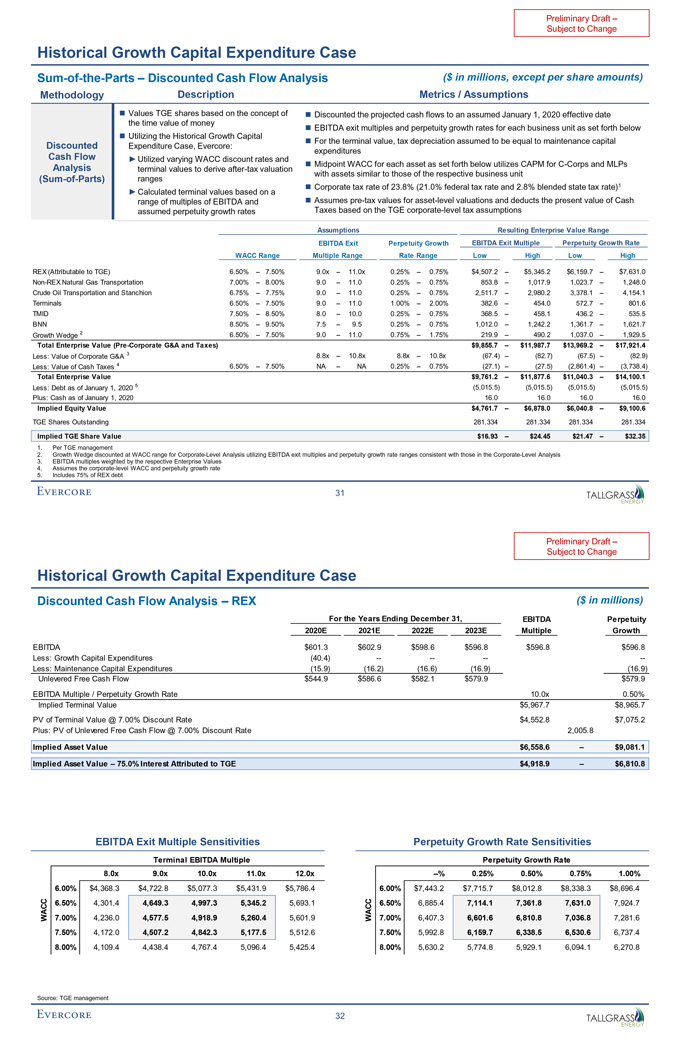

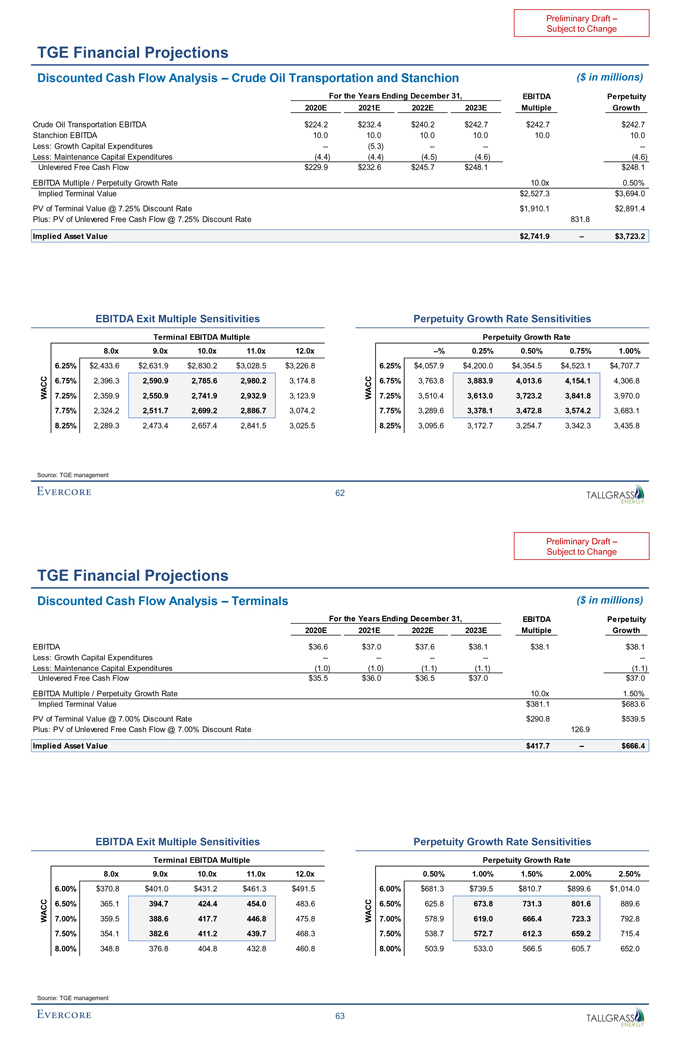

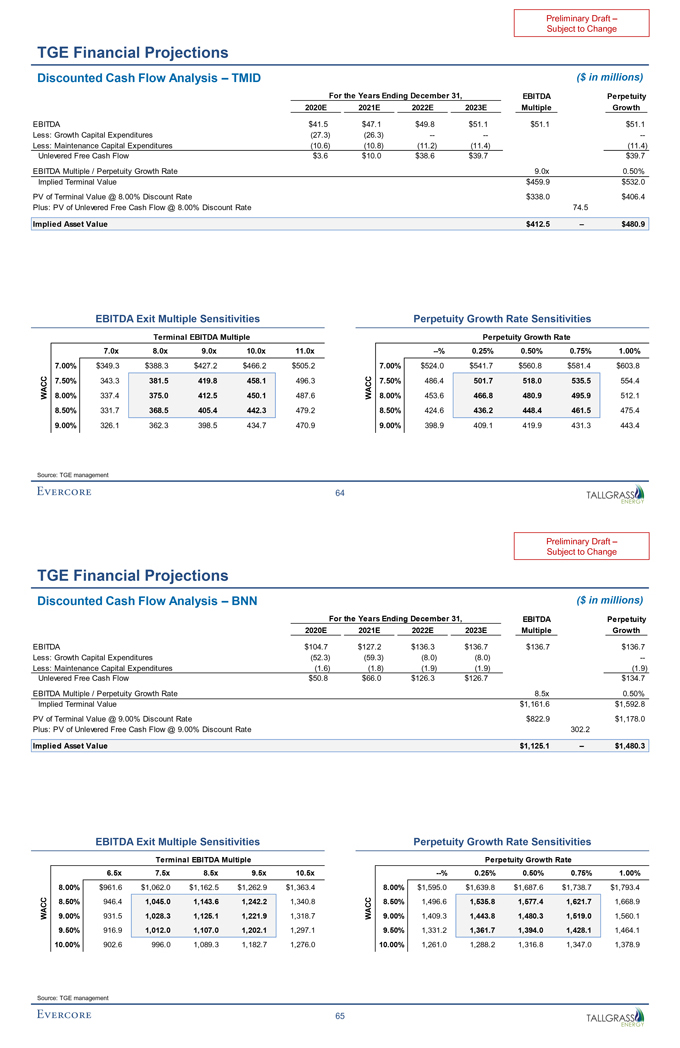

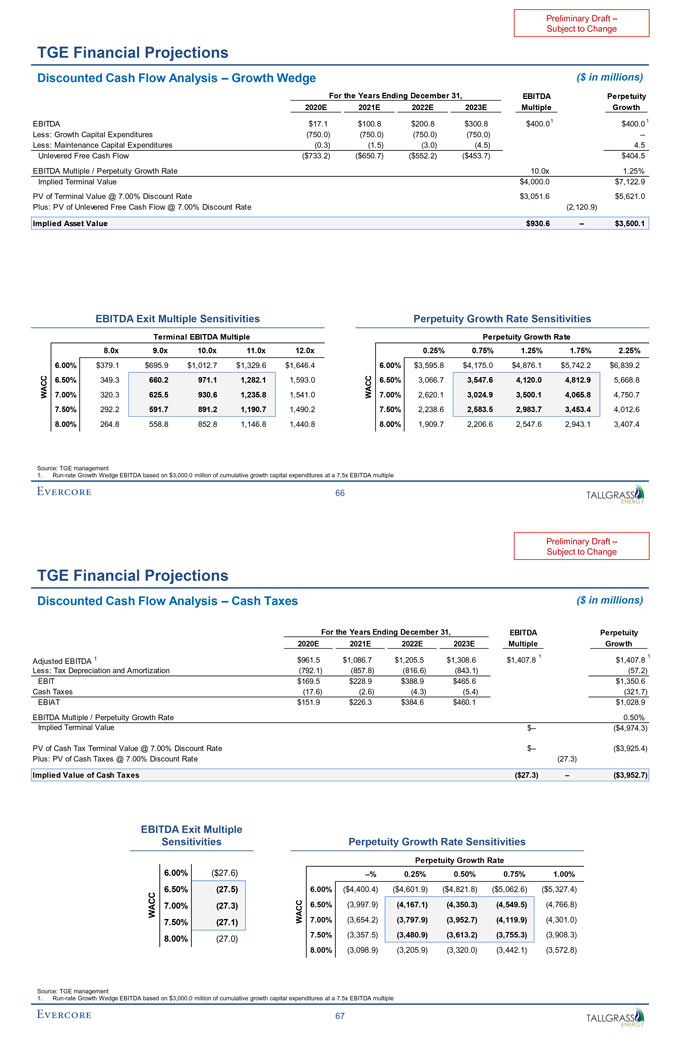

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure CaseSum-of-the-Parts – Discounted Cash Flow Analysis ($ in millions, except per share amounts) Methodology Description Metrics / Assumptions ï® Values TGE shares based on the concept of ï® Discounted the projected cash flows to an assumed January 1, 2020 effective date the time value of money ï® EBITDA exit multiples and perpetuity growth rates for each business unit as set forth belowï® Utilizing the Historical Growth Capital ï® For the terminal value, tax depreciation assumed to be equal to maintenance capital Discounted Expenditure Case, Evercore: expenditures Cash Flow â–º Utilized varying WACC discount rates and below utilizes CAPM forC-Corps and MLPs Analysisï® Midpoint WACC for each asset as set forth terminal values to deriveafter-tax valuation with assets similar to those of the respective business unit(Sum-of-Parts) ranges â–º Calculated terminal values based on a ï® Corporate tax rate of 23.8% (21.0% federal tax rate and 2.8% blended state tax rate)1 range of multiples of EBITDA andï® Assumespre-tax values for asset-level valuations and deducts the present value of Cash assumed perpetuity growth rates Taxes based on the TGE corporate-level tax assumptions Assumptions Resulting Enterprise Value Range EBITDA Exit Perpetuity Growth EBITDA Exit Multiple Perpetuity Growth Rate WACC Range Multiple Range Rate Range Low High Low High REX (Attributable to TGE) 6.50% – 7.50% 9.0x – 11.0x 0.25% – 0.75% $4,507.2 – $5,345.2 $6,159.7 – $7,631.0Non-REX Natural Gas Transportation 7.00% – 8.00% 9.0 – 11.0 0.25% – 0.75% 853.8 – 1,017.9 1,023.7 – 1,248.0 Crude Oil Transportation and Stanchion 6.75% – 7.75% 9.0 – 11.0 0.25% – 0.75% 2,511.7 – 2,980.2 3,378.1 – 4,154.1 Terminals 6.50% – 7.50% 9.0 – 11.0 1.00% – 2.00% 382.6 – 454.0 572.7 – 801.6 TMID 7.50% – 8.50% 8.0 – 10.0 0.25% – 0.75% 368.5 – 458.1 436.2 – 535.5 BNN 8.50% – 9.50% 7.5 – 9.5 0.25% – 0.75% 1,012.0 – 1,242.2 1,361.7 – 1,621.7 Growth Wedge 2 6.50% – 7.50% 9.0 – 11.0 0.75% – 1.75% 219.9 – 490.2 1,037.0 – 1,929.5 Total Enterprise Value(Pre-Corporate G&A and Taxes) $9,855.7 – $11,987.7 $13,969.2 – $17,921.4 Less: Value of Corporate G&A 3 8.8x – 10.8x 8.8x – 10.8x (67.4) – (82.7) (67.5) – (82.9) Less: Value of Cash Taxes 4 6.50% – 7.50% NA – NA 0.25% – 0.75% (27.1) – (27.5) (2,861.4) – (3,738.4) Total Enterprise Value $9,761.2 – $11,877.6 $11,040.3 – $14,100.1 Less: Debt as of January 1, 2020 5 (5,015.5) (5,015.5) (5,015.5) (5,015.5) Plus: Cash as of January 1, 2020 16.0 16.0 16.0 16.0 Implied Equity Value $4,761.7 – $6,878.0 $6,040.8 – $9,100.6 TGE Shares Outstanding 281.334 281.334 281.334 281.334 Implied TGE Share Value $16.93 – $24.45 $21.47 – $32.35 1. Per TGE management 2. Growth Wedge discounted at WACC range for Corporate-Level Analysis utilizing EBITDA exit multiples and perpetuity growth rate ranges consistent with those in the Corporate-Level Analysis 3. EBITDA multiples weighted by the respective Enterprise Values 4. Assumes the corporate-level WACC and perpetuity growth rate 5. Includes 75% of REX debt 31

Subject to Change Historical Growth Capital Expenditure Case Discounted Cash Flow Analysis – REX ($ in millions) For the Years Ending December 31, EBITDA Perpetuity 2020E 2021E 2022E 2023E Multiple Growth EBITDA $601.3 $602.9 $598.6 $596.8 $596.8 $596.8 Less: Growth Capital Expenditures (40.4) -———-Less: Maintenance Capital Expenditures (15.9) (16.2) (16.6) (16.9) (16.9) Unlevered Free Cash Flow $544.9 $586.6 $582.1 $579.9 $579.9 EBITDA Multiple / Perpetuity Growth Rate 10.0x 0.50% Implied Terminal Value $5,967.7 $8,965.7 PV of Terminal Value @ 7.00% Discount Rate $4,552.8 $7,075.2 Plus: PV of Unlevered Free Cash Flow @ 7.00% Discount Rate 2,005.8 Implied Asset Value $6,558.6 – $9,081.1 Implied Asset Value – 75.0% Interest Attributed to TGE $4,918.9 – $6,810.8 EBITDA Exit Multiple Sensitivities Perpetuity Growth Rate Sensitivities Terminal EBITDA Multiple Perpetuity Growth Rate 8.0x 9.0x 10.0x 11.0x 12.0x —% 0.25% 0.50% 0.75% 1.00% 6.00% $4,368.3 $4,722.8 $5,077.3 $5,431.9 $5,786.4 6.00% $7,443.2 $7,715.7 $8,012.8 $8,338.3 $8,696.4 6.50% 4,301.4 4,649.3 4,997.3 5,345.2 5,693.1 6.50% 6,885.4 7,114.1 7,361.8 7,631.0 7,924.7 WACC 7.00% 4,236.0 4,577.5 4,918.9 5,260.4 5,601.9 WACC 7.00% 6,407.3 6,601.6 6,810.8 7,036.8 7,281.6 7.50% 4,172.0 4,507.2 4,842.3 5,177.5 5,512.6 7.50% 5,992.8 6,159.7 6,338.5 6,530.6 6,737.4 8.00% 4,109.4 4,438.4 4,767.4 5,096.4 5,425.4 8.00% 5,630.2 5,774.8 5,929.1 6,094.1 6,270.8 Source: TGE management 32

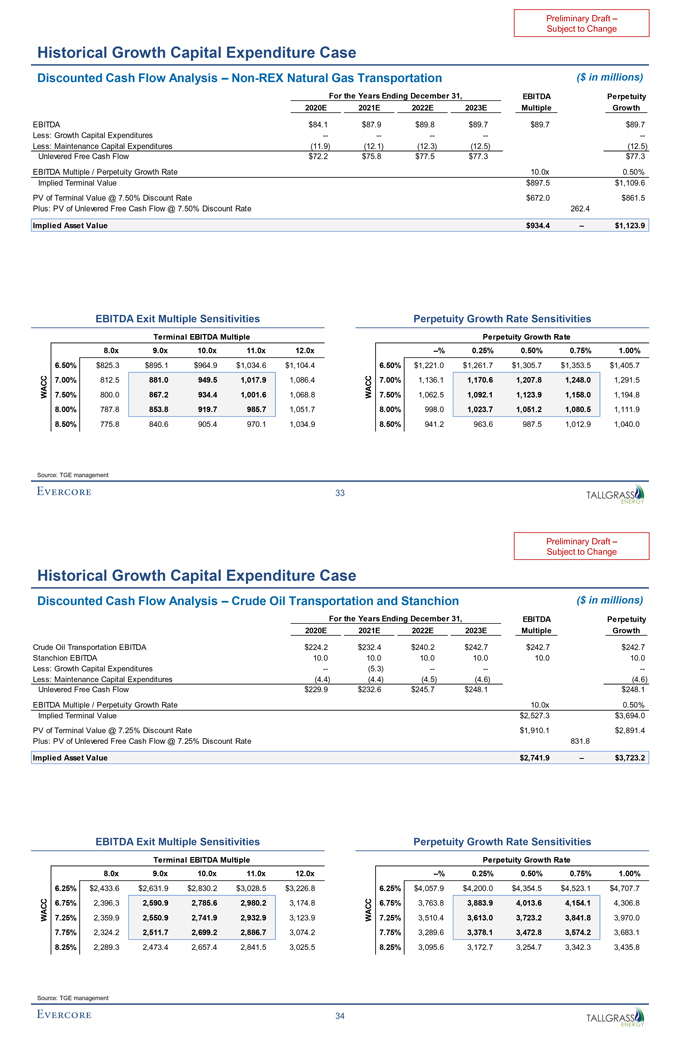

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure Case Discounted Cash Flow Analysis –Non-REX Natural Gas Transportation ($ in millions) For the Years Ending December 31, EBITDA Perpetuity 2020E 2021E 2022E 2023E Multiple Growth EBITDA $84.1 $87.9 $89.8 $89.7 $89.7 $89.7 Less: Growth Capital Expenditures -————-Less: Maintenance Capital Expenditures (11.9) (12.1) (12.3) (12.5) (12.5) Unlevered Free Cash Flow $72.2 $75.8 $77.5 $77.3 $77.3 EBITDA Multiple / Perpetuity Growth Rate 10.0x 0.50% Implied Terminal Value $897.5 $1,109.6 PV of Terminal Value @ 7.50% Discount Rate $672.0 $861.5 Plus: PV of Unlevered Free Cash Flow @ 7.50% Discount Rate 262.4 Implied Asset Value $934.4 – $1,123.9 EBITDA Exit Multiple Sensitivities Perpetuity Growth Rate Sensitivities Terminal EBITDA Multiple Perpetuity Growth Rate 8.0x 9.0x 10.0x 11.0x 12.0x —% 0.25% 0.50% 0.75% 1.00% 6.50% $825.3 $895.1 $964.9 $1,034.6 $1,104.4 6.50% $1,221.0 $1,261.7 $1,305.7 $1,353.5 $1,405.7 7.00% 812.5 881.0 949.5 1,017.9 1,086.4 7.00% 1,136.1 1,170.6 1,207.8 1,248.0 1,291.5 WACC 7.50% 800.0 867.2 934.4 1,001.6 1,068.8 WACC 7.50% 1,062.5 1,092.1 1,123.9 1,158.0 1,194.8 8.00% 787.8 853.8 919.7 985.7 1,051.7 8.00% 998.0 1,023.7 1,051.2 1,080.5 1,111.9 8.50% 775.8 840.6 905.4 970.1 1,034.9 8.50% 941.2 963.6 987.5 1,012.9 1,040.0 Source: TGE management 33

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure Case Discounted Cash Flow Analysis – Crude Oil Transportation and Stanchion ($ in millions) For the Years Ending December 31, EBITDA Perpetuity 2020E 2021E 2022E 2023E Multiple Growth Crude Oil Transportation EBITDA $224.2 $232.4 $240.2 $242.7 $242.7 $242.7 Stanchion EBITDA 10.0 10.0 10.0 10.0 10.0 10.0 Less: Growth Capital Expenditures — (5.3) -——-Less: Maintenance Capital Expenditures (4.4) (4.4) (4.5) (4.6) (4.6) Unlevered Free Cash Flow $229.9 $232.6 $245.7 $248.1 $248.1 EBITDA Multiple / Perpetuity Growth Rate 10.0x 0.50% Implied Terminal Value $2,527.3 $3,694.0 PV of Terminal Value @ 7.25% Discount Rate $1,910.1 $2,891.4 Plus: PV of Unlevered Free Cash Flow @ 7.25% Discount Rate 831.8 Implied Asset Value $2,741.9 – $3,723.2 EBITDA Exit Multiple Sensitivities Perpetuity Growth Rate Sensitivities Terminal EBITDA Multiple Perpetuity Growth Rate 8.0x 9.0x 10.0x 11.0x 12.0x —% 0.25% 0.50% 0.75% 1.00% 6.25% $2,433.6 $2,631.9 $2,830.2 $3,028.5 $3,226.8 6.25% $4,057.9 $4,200.0 $4,354.5 $4,523.1 $4,707.7 6.75% 2,396.3 2,590.9 2,785.6 2,980.2 3,174.8 6.75% 3,763.8 3,883.9 4,013.6 4,154.1 4,306.8 WACC 7.25% 2,359.9 2,550.9 2,741.9 2,932.9 3,123.9 WACC 7.25% 3,510.4 3,613.0 3,723.2 3,841.8 3,970.0 7.75% 2,324.2 2,511.7 2,699.2 2,886.7 3,074.2 7.75% 3,289.6 3,378.1 3,472.8 3,574.2 3,683.1 8.25% 2,289.3 2,473.4 2,657.4 2,841.5 3,025.5 8.25% 3,095.6 3,172.7 3,254.7 3,342.3 3,435.8 Source: TGE management 34

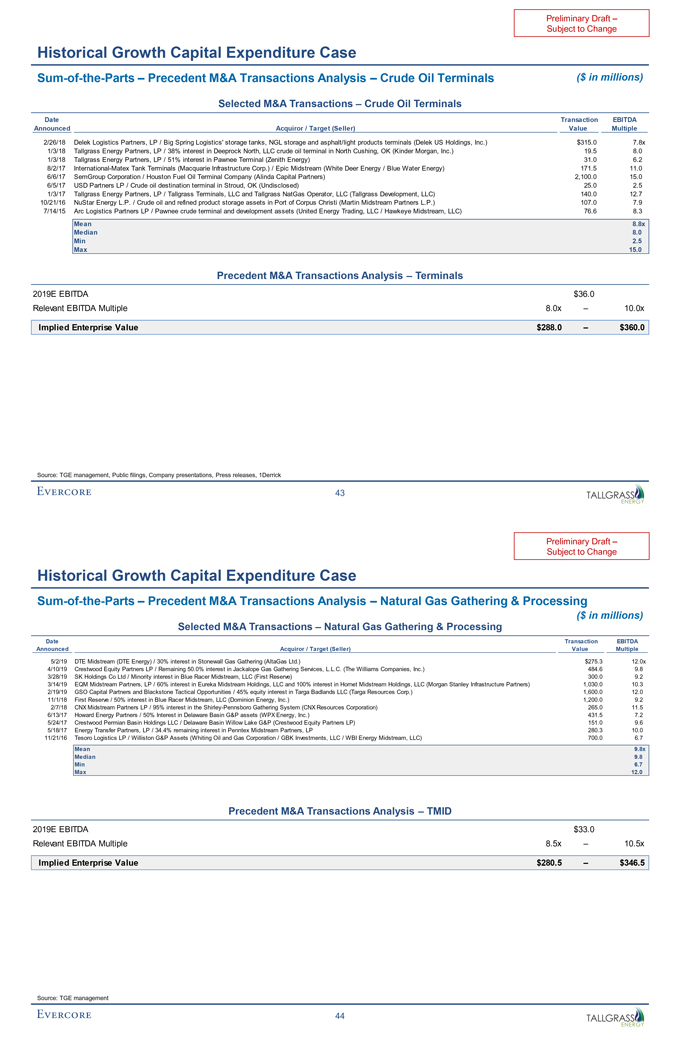

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure Case Discounted Cash Flow Analysis – Terminals ($ in millions) For the Years Ending December 31, EBITDA Perpetuity 2020E 2021E 2022E 2023E Multiple Growth EBITDA $36.6 $37.0 $37.6 $38.1 $38.1 $38.1 Less: Growth Capital Expenditures -————-Less: Maintenance Capital Expenditures (1.0) (1.0) (1.1) (1.1) (1.1) Unlevered Free Cash Flow $35.5 $36.0 $36.5 $37.0 $37.0 EBITDA Multiple / Perpetuity Growth Rate 10.0x 1.50% Implied Terminal Value $381.1 $683.6 PV of Terminal Value @ 7.00% Discount Rate $290.8 $539.5 Plus: PV of Unlevered Free Cash Flow @ 7.00% Discount Rate 126.9 Implied Asset Value $417.7 – $666.4 EBITDA Exit Multiple Sensitivities Perpetuity Growth Rate Sensitivities Terminal EBITDA Multiple Perpetuity Growth Rate 8.0x 9.0x 10.0x 11.0x 12.0x 0.50% 1.00% 1.50% 2.00% 2.50% 6.00% $370.8 $401.0 $431.2 $461.3 $491.5 6.00% $681.3 $739.5 $810.7 $899.6 $1,014.0 6.50% 365.1 394.7 424.4 454.0 483.6 6.50% 625.8 673.8 731.3 801.6 889.6 WACC 7.00% 359.5 388.6 417.7 446.8 475.8 WACC 7.00% 578.9 619.0 666.4 723.3 792.8 7.50% 354.1 382.6 411.2 439.7 468.3 7.50% 538.7 572.7 612.3 659.2 715.4 8.00% 348.8 376.8 404.8 432.8 460.8 8.00% 503.9 533.0 566.5 605.7 652.0 Source: TGE management 35

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure Case Discounted Cash Flow Analysis – TMID ($ in millions) For the Years Ending December 31, EBITDA Perpetuity 2020E 2021E 2022E 2023E Multiple Growth EBITDA $41.5 $47.1 $49.8 $51.1 $51.1 $51.1 Less: Growth Capital Expenditures (27.3) (26.3) -——-Less: Maintenance Capital Expenditures (10.6) (10.8) (11.2) (11.4) (11.4) Unlevered Free Cash Flow $3.6 $10.0 $38.6 $39.7 $39.7 EBITDA Multiple / Perpetuity Growth Rate 9.0x 0.50% Implied Terminal Value $459.9 $532.0 PV of Terminal Value @ 8.00% Discount Rate $338.0 $406.4 Plus: PV of Unlevered Free Cash Flow @ 8.00% Discount Rate 74.5 Implied Asset Value $412.5 – $480.9 EBITDA Exit Multiple Sensitivities Perpetuity Growth Rate Sensitivities Terminal EBITDA Multiple Perpetuity Growth Rate 7.0x 8.0x 9.0x 10.0x 11.0x —% 0.25% 0.50% 0.75% 1.00% 7.00% $349.3 $388.3 $427.2 $466.2 $505.2 7.00% $524.0 $541.7 $560.8 $581.4 $603.8 C AC 7.50% 343.3 381.5 419.8 458.1 496.3 C AC 7.50% 486.4 501.7 518.0 535.5 554.4 W 8.00% 337.4 375.0 412.5 450.1 487.6 W 8.00% 453.6 466.8 480.9 495.9 512.1 8.50% 331.7 368.5 405.4 442.3 479.2 8.50% 424.6 436.2 448.4 461.5 475.4 9.00% 326.1 362.3 398.5 434.7 470.9 9.00% 398.9 409.1 419.9 431.3 443.4 Source: TGE management 36

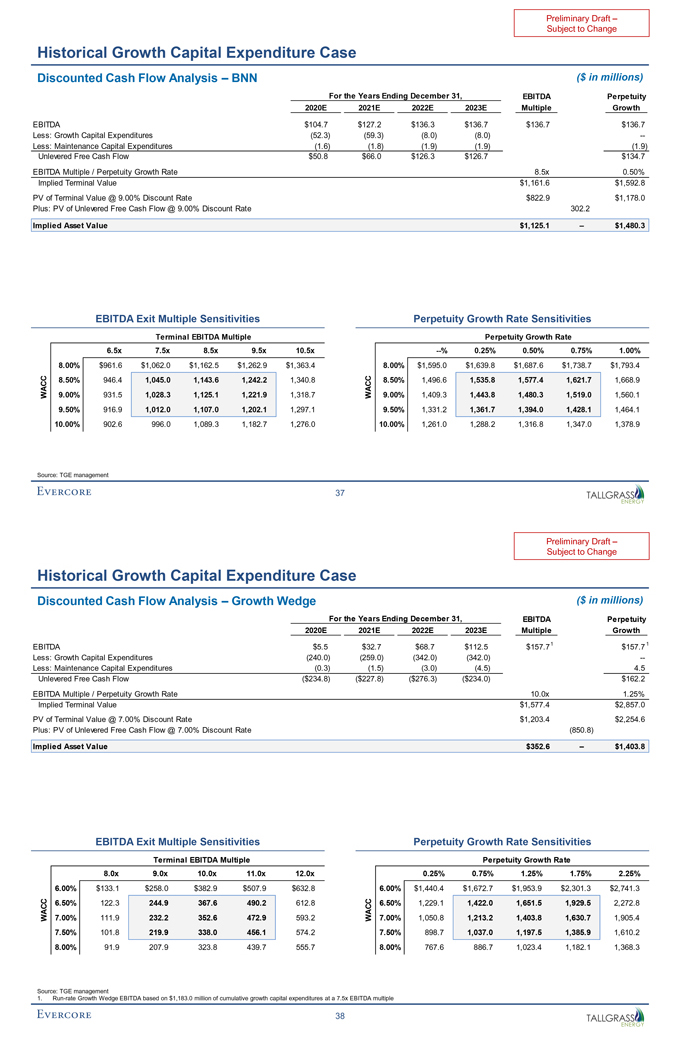

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure Case Discounted Cash Flow Analysis – BNN ($ in millions) For the Years Ending December 31, EBITDA Perpetuity 2020E 2021E 2022E 2023E Multiple Growth EBITDA $104.7 $127.2 $136.3 $136.7 $136.7 $136.7 Less: Growth Capital Expenditures (52.3) (59.3) (8.0) (8.0) —Less: Maintenance Capital Expenditures (1.6) (1.8) (1.9) (1.9) (1.9) Unlevered Free Cash Flow $50.8 $66.0 $126.3 $126.7 $134.7 EBITDA Multiple / Perpetuity Growth Rate 8.5x 0.50% Implied Terminal Value $1,161.6 $1,592.8 PV of Terminal Value @ 9.00% Discount Rate $822.9 $1,178.0 Plus: PV of Unlevered Free Cash Flow @ 9.00% Discount Rate 302.2 Implied Asset Value $1,125.1 – $1,480.3 EBITDA Exit Multiple Sensitivities Perpetuity Growth Rate Sensitivities Terminal EBITDA Multiple Perpetuity Growth Rate 6.5x 7.5x 8.5x 9.5x 10.5x —% 0.25% 0.50% 0.75% 1.00% 8.00% $961.6 $1,062.0 $1,162.5 $1,262.9 $1,363.4 8.00% $1,595.0 $1,639.8 $1,687.6 $1,738.7 $1,793.4 C 8.50% 946.4 1,045.0 1,143.6 1,242.2 1,340.8 C 8.50% 1,496.6 1,535.8 1,577.4 1,621.7 1,668.9 WAC 9.00% 931.5 1,028.3 1,125.1 1,221.9 1,318.7 WAC 9.00% 1,409.3 1,443.8 1,480.3 1,519.0 1,560.1 9.50% 916.9 1,012.0 1,107.0 1,202.1 1,297.1 9.50% 1,331.2 1,361.7 1,394.0 1,428.1 1,464.1 10.00% 902.6 996.0 1,089.3 1,182.7 1,276.0 10.00% 1,261.0 1,288.2 1,316.8 1,347.0 1,378.9 Source: TGE management 37

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure Case Discounted Cash Flow Analysis – Growth Wedge ($ in millions) For the Years Ending December 31, EBITDA Perpetuity 2020E 2021E 2022E 2023E Multiple Growth EBITDA $5.5 $32.7 $68.7 $112.5 $157.71 $157.7 1 Less: Growth Capital Expenditures (240.0) (259.0) (342.0) (342.0) —Less: Maintenance Capital Expenditures (0.3) (1.5) (3.0) (4.5) 4.5 Unlevered Free Cash Flow ($234.8) ($227.8) ($276.3) ($234.0) $162.2 EBITDA Multiple / Perpetuity Growth Rate 10.0x 1.25% Implied Terminal Value $1,577.4 $2,857.0 PV of Terminal Value @ 7.00% Discount Rate $1,203.4 $2,254.6 Plus: PV of Unlevered Free Cash Flow @ 7.00% Discount Rate (850.8) Implied Asset Value $352.6 – $1,403.8 EBITDA Exit Multiple Sensitivities Perpetuity Growth Rate Sensitivities Terminal EBITDA Multiple Perpetuity Growth Rate 8.0x 9.0x 10.0x 11.0x 12.0x 0.25% 0.75% 1.25% 1.75% 2.25% 6.00% $133.1 $258.0 $382.9 $507.9 $632.8 6.00% $1,440.4 $1,672.7 $1,953.9 $2,301.3 $2,741.3 6.50% 122.3 244.9 367.6 490.2 612.8 6.50% 1,229.1 1,422.0 1,651.5 1,929.5 2,272.8 WACC 7.00% 111.9 232.2 352.6 472.9 593.2 WACC 7.00% 1,050.8 1,213.2 1,403.8 1,630.7 1,905.4 7.50% 101.8 219.9 338.0 456.1 574.2 7.50% 898.7 1,037.0 1,197.5 1,385.9 1,610.2 8.00% 91.9 207.9 323.8 439.7 555.7 8.00% 767.6 886.7 1,023.4 1,182.1 1,368.3 Source: TGE management 1.Run-rate Growth Wedge EBITDA based on $1,183.0 million of cumulative growth capital expenditures at a 7.5x EBITDA multiple 38

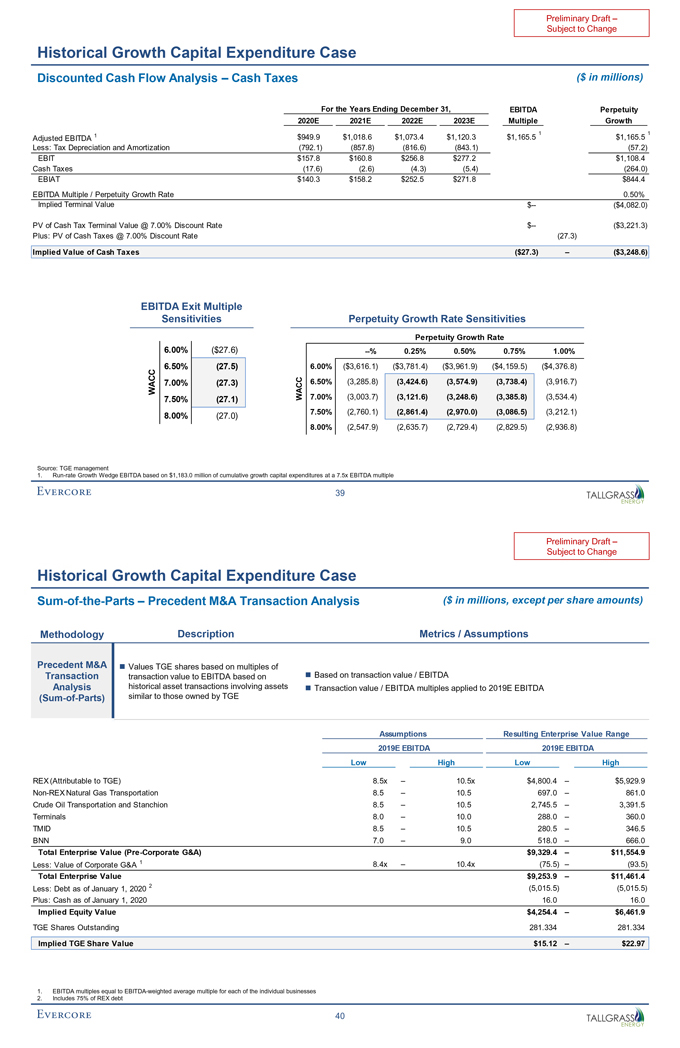

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure Case Discounted Cash Flow Analysis – Cash Taxes ($ in millions) For the Years Ending December 31, EBITDA Perpetuity 2020E 2021E 2022E 2023E Multiple Growth 1 1 Adjusted EBITDA 1 $949.9 $1,018.6 $1,073.4 $1,120.3 $1,165.5 $1,165.5 Less: Tax Depreciation and Amortization (792.1) (857.8) (816.6) (843.1) (57.2) EBIT $157.8 $160.8 $256.8 $277.2 $1,108.4 Cash Taxes (17.6) (2.6) (4.3) (5.4) (264.0) EBIAT $140.3 $158.2 $252.5 $271.8 $844.4 EBITDA Multiple / Perpetuity Growth Rate 0.50% Implied Terminal Value $— ($4,082.0) PV of Cash Tax Terminal Value @ 7.00% Discount Rate $— ($3,221.3) Plus: PV of Cash Taxes @ 7.00% Discount Rate (27.3) Implied Value of Cash Taxes ($27.3) – ($3,248.6) EBITDA Exit Multiple Sensitivities Perpetuity Growth Rate Sensitivities Perpetuity Growth Rate 6.00% ($27.6) —% 0.25% 0.50% 0.75% 1.00% C 6.50% (27.5) 6.00% ($3,616.1) ($3,781.4) ($3,961.9) ($4,159.5) ($4,376.8) C 6.50% (3,285.8) (3,424.6) (3,574.9) (3,738.4) (3,916.7) WA 7.00% (27.3) 7.50% (27.1) WACC 7.00% (3,003.7) (3,121.6) (3,248.6) (3,385.8) (3,534.4) 7.50% (2,760.1) (2,861.4) (2,970.0) (3,086.5) (3,212.1) 8.00% (27.0) 8.00% (2,547.9) (2,635.7) (2,729.4) (2,829.5) (2,936.8) Source: TGE management 1.Run-rate Growth Wedge EBITDA based on $1,183.0 million of cumulative growth capital expenditures at a 7.5x EBITDA multiple 39

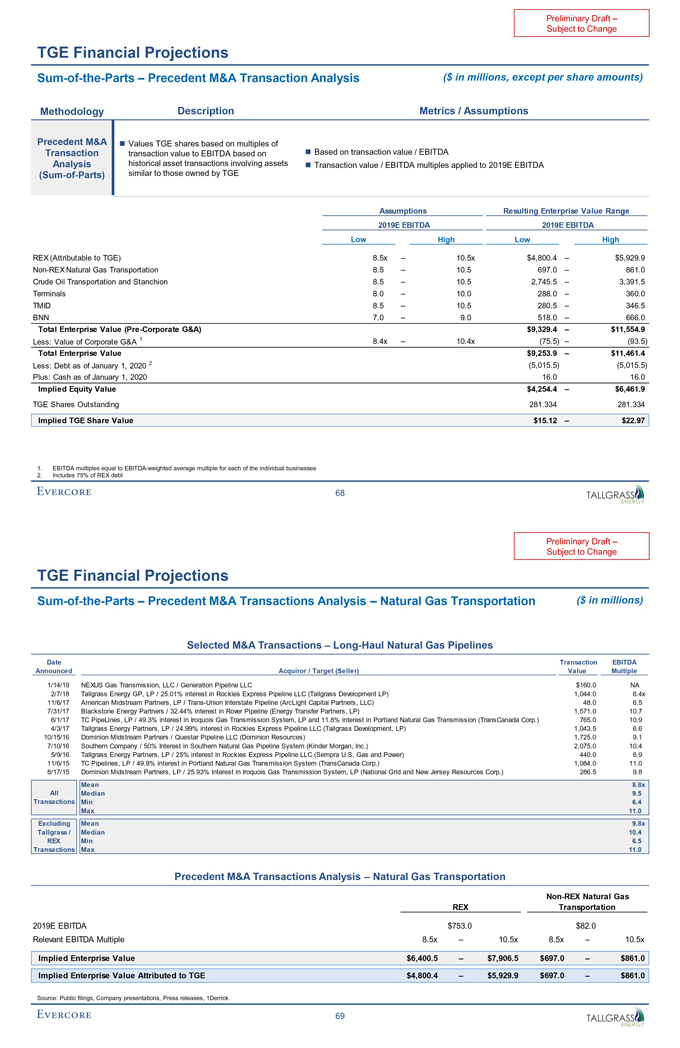

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure CaseSum-of-the-Parts – Precedent M&A Transaction Analysis ($ in millions, except per share amounts) Methodology Description Metrics / Assumptions Precedent M&A ï® Values TGE shares based on multiples of Transaction transaction value to EBITDA based on ï® Based on transaction value / EBITDA Analysis historical asset transactions involving assetsï® Transaction value / EBITDA multiples applied to 2019E EBITDA(Sum-of-Parts) similar to those owned by TGE Assumptions Resulting Enterprise Value Range 2019E EBITDA 2019E EBITDA Low High Low High REX (Attributable to TGE) 8.5x – 10.5x $4,800.4 – $5,929.9Non-REX Natural Gas Transportation 8.5 – 10.5 697.0 – 861.0 Crude Oil Transportation and Stanchion 8.5 – 10.5 2,745.5 – 3,391.5 Terminals 8.0 – 10.0 288.0 – 360.0 TMID 8.5 – 10.5 280.5 – 346.5 BNN 7.0 – 9.0 518.0 – 666.0 Total Enterprise Value(Pre-Corporate G&A) $9,329.4 – $11,554.9 Less: Value of Corporate G&A 1 8.4x – 10.4x (75.5) – (93.5) Total Enterprise Value $9,253.9 – $11,461.4 Less: Debt as of January 1, 2020 2 (5,015.5) (5,015.5) Plus: Cash as of January 1, 2020 16.0 16.0 Implied Equity Value $4,254.4 – $6,461.9 TGE Shares Outstanding 281.334 281.334 Implied TGE Share Value $15.12 – $22.97 1. EBITDA multiples equal to EBITDA-weighted average multiple for each of the individual businesses 2. Includes 75% of REX debt 40

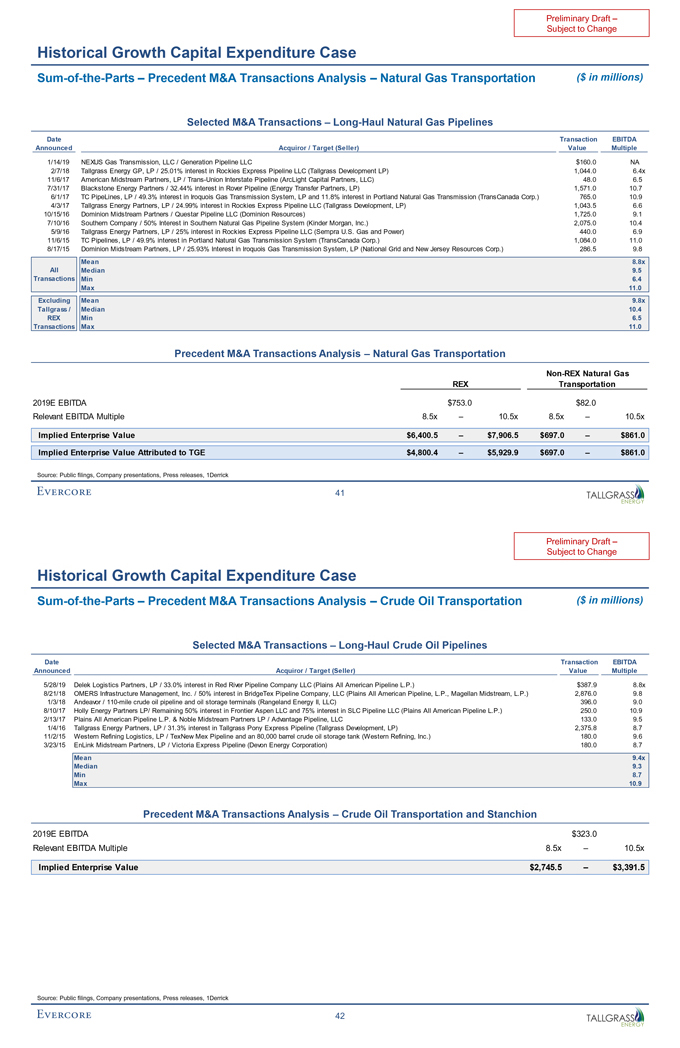

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure CaseSum-of-the-Parts – Precedent M&A Transactions Analysis – Natural Gas Transportation ($ in millions) Selected M&A Transactions – Long-Haul Natural Gas Pipelines Date Transaction EBITDA Announced Acquiror / Target (Seller) Value Multiple 1/14/19 NEXUS Gas Transmission, LLC / Generation Pipeline LLC $160.0 NA 2/7/18 Tallgrass Energy GP, LP / 25.01% interest in Rockies Express Pipeline LLC (Tallgrass Development LP) 1,044.0 6.4x 11/6/17 American Midstream Partners, LP / Trans-Union Interstate Pipeline (ArcLight Capital Partners, LLC) 48.0 6.5 7/31/17 Blackstone Energy Partners / 32.44% interest in Rover Pipeline (Energy Transfer Partners, LP) 1,571.0 10.7 6/1/17 TC PipeLines, LP / 49.3% interest in Iroquois Gas Transmission System, LP and 11.8% interest in Portland Natural Gas Transmission (TransCanada Corp.) 765.0 10.9 4/3/17 Tallgrass Energy Partners, LP / 24.99% interest in Rockies Express Pipeline LLC (Tallgrass Development, LP) 1,043.5 6.6 10/15/16 Dominion Midstream Partners / Questar Pipeline LLC (Dominion Resources) 1,725.0 9.1 7/10/16 Southern Company / 50% Interest in Southern Natural Gas Pipeline System (Kinder Morgan, Inc.) 2,075.0 10.4 5/9/16 Tallgrass Energy Partners, LP / 25% interest in Rockies Express Pipeline LLC (Sempra U.S. Gas and Power) 440.0 6.9 11/6/15 TC Pipelines, LP / 49.9% interest in Portland Natural Gas Transmission System (TransCanada Corp.) 1,084.0 11.0 8/17/15 Dominion Midstream Partners, LP / 25.93% Interest in Iroquois Gas Transmission System, LP (National Grid and New Jersey Resources Corp.) 286.5 9.8 Mean 8.8x All Median 9.5 Transactions Min 6.4 Max 11.0 Excluding Mean 9.8x Tallgrass / Median 10.4 REX Min 6.5 Transactions Max 11.0 Precedent M&A Transactions Analysis – Natural Gas TransportationNon-REX Natural Gas REX Transportation 2019E EBITDA $753.0 $82.0 Relevant EBITDA Multiple 8.5x – 10.5x 8.5x – 10.5x Implied Enterprise Value $6,400.5 – $7,906.5 $697.0 – $861.0 Implied Enterprise Value Attributed to TGE $4,800.4 – $5,929.9 $697.0 – $861.0 Source: Public filings, Company presentations, Press releases, 1Derrick 41

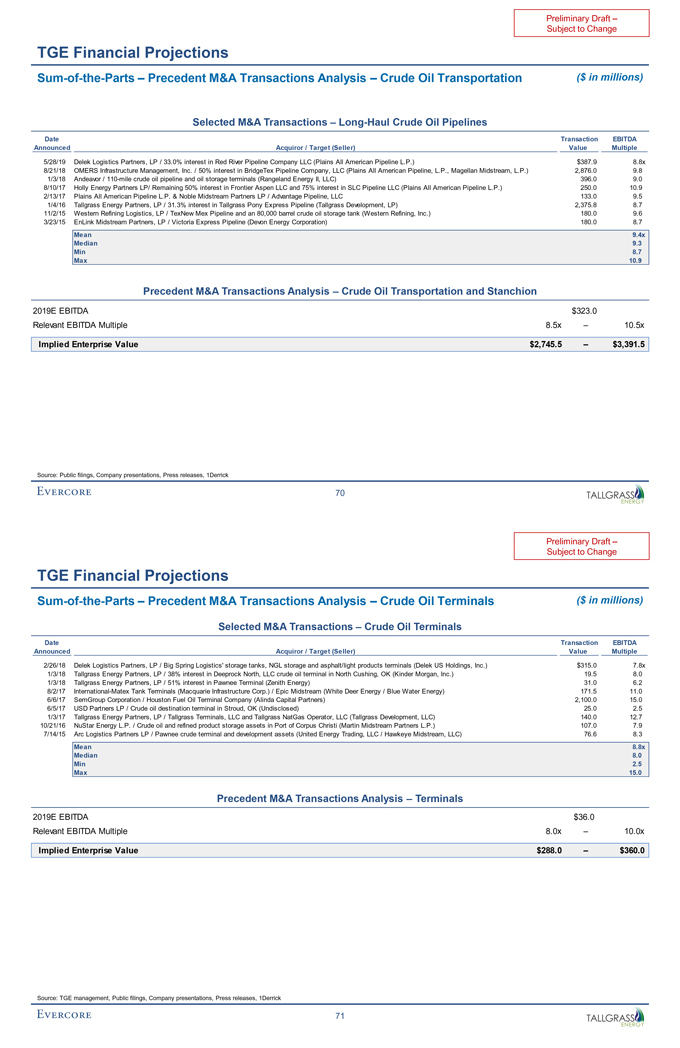

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure CaseSum-of-the-Parts – Precedent M&A Transactions Analysis – Crude Oil Transportation ($ in millions) Selected M&A Transactions – Long-Haul Crude Oil Pipelines Date Transaction EBITDA Announced Acquiror / Target (Seller) Value Multiple 5/28/19 Delek Logistics Partners, LP / 33.0% interest in Red River Pipeline Company LLC (Plains All American Pipeline L.P.) $387.9 8.8x 8/21/18 OMERS Infrastructure Management, Inc. / 50% interest in BridgeTex Pipeline Company, LLC (Plains All American Pipeline, L.P., Magellan Midstream, L.P.) 2,876.0 9.8 1/3/18 Andeavor /110-mile crude oil pipeline and oil storage terminals (Rangeland Energy II, LLC) 396.0 9.0 8/10/17 Holly Energy Partners LP/ Remaining 50% interest in Frontier Aspen LLC and 75% interest in SLC Pipeline LLC (Plains All American Pipeline L.P.) 250.0 10.9 2/13/17 Plains All American Pipeline L.P. & Noble Midstream Partners LP / Advantage Pipeline, LLC 133.0 9.5 1/4/16 Tallgrass Energy Partners, LP / 31.3% interest in Tallgrass Pony Express Pipeline (Tallgrass Development, LP) 2,375.8 8.7 11/2/15 Western Refining Logistics, LP / TexNew Mex Pipeline and an 80,000 barrel crude oil storage tank (Western Refining, Inc.) 180.0 9.6 3/23/15 EnLink Midstream Partners, LP / Victoria Express Pipeline (Devon Energy Corporation) 180.0 8.7 Mean 9.4x Median 9.3 Min 8.7 Max 10.9 Precedent M&A Transactions Analysis – Crude Oil Transportation and Stanchion 2019E EBITDA $323.0 Relevant EBITDA Multiple 8.5x – 10.5x Implied Enterprise Value $2,745.5 – $3,391.5 Source: Public filings, Company presentations, Press releases, 1Derrick 42

Preliminary Draft –Subject to Change Historical Growth Capital Expenditure CaseSum-of-the-Parts – Precedent M&A Transactions Analysis – Crude Oil Terminals ($ in millions) Selected M&A Transactions – Crude Oil Terminals Date Transaction EBITDA Announced Acquiror / Target (Seller) Value Multiple 2/26/18 Delek Logistics Partners, LP / Big Spring Logistics’ storage tanks, NGL storage and asphalt/light products terminals (Delek US Holdings, Inc.) $315.0 7.8x 1/3/18 Tallgrass Energy Partners, LP / 38% interest in Deeprock North, LLC crude oil terminal in North Cushing, OK (Kinder Morgan, Inc.) 19.5 8.0 1/3/18 Tallgrass Energy Partners, LP / 51% interest in Pawnee Terminal (Zenith Energy) 31.0 6.2 8/2/17 International-Matex Tank Terminals (Macquarie Infrastructure Corp.) / Epic Midstream (White Deer Energy / Blue Water Energy) 171.5 11.0 6/6/17 SemGroup Corporation / Houston Fuel Oil Terminal Company (Alinda Capital Partners) 2,100.0 15.0 6/5/17 USD Partners LP / Crude oil destination terminal in Stroud, OK (Undisclosed) 25.0 2.5 1/3/17 Tallgrass Energy Partners, LP / Tallgrass Terminals, LLC and Tallgrass NatGas Operator, LLC (Tallgrass Development, LLC) 140.0 12.7 10/21/16 NuStar Energy L.P. / Crude oil and refined product storage assets in Port of Corpus Christi (Martin Midstream Partners L.P.) 107.0 7.9 7/14/15 Arc Logistics Partners LP / Pawnee crude terminal and development assets (United Energy Trading, LLC / Hawkeye Midstream, LLC) 76.6 8.3 Mean 8.8x Median 8.0 Min 2.5 Max 15.0 Precedent M&A Transactions Analysis – Terminals 2019E EBITDA $36.0 Relevant EBITDA Multiple 8.0x – 10.0x Implied Enterprise Value $288.0 – $360.0 Source: TGE management, Public filings, Company presentations, Press releases, 1Derrick 43