UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number | | 811-23075 |

Nuveen High Income November 2021 Target Term Fund

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Gifford R. Zimmerman

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: December 31

Date of reporting period: June 30, 2018

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Closed-End Funds

30 June 2018

Nuveen Closed-End Funds

| | |

| JHY | | Nuveen High Income 2020 Target Term Fund |

| JHD | | Nuveen High Income December 2019 Target Term Fund |

| JHA | | Nuveen High Income December 2018 Target Term Fund |

| JHB | | Nuveen High Income November 2021 Target Term Fund |

Semiannual Report

Life is Complex

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready—no more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your email!

www.investordelivery.com

If you receive your Nuveen Fund dividends and statements from your financial advisor or brokerage account.

or

www.nuveen.com/client-access

If you receive your Nuveen Fund dividends and statements directly from Nuveen.

Table of Contents

3

Chairman’s Letter to Shareholders

Dear Shareholders,

I am honored to serve as the new independent chairman of the Nuveen Fund Board, effective July 1, 2018. I’d like to gratefully acknowledge the stewardship of my predecessor William J. Schneider and, on behalf of my fellow Board members, reinforce our commitment to the legacy of strong, independent oversight of your Funds.

The increase in market volatility this year reflects greater uncertainty among investors. The global economic outlook is less clear cut than it was in 2017. U.S. growth is again decoupling from that of the rest of the world, and the U.S. dollar and interest rates have risen in response. Trade concern rhetoric and the imposition of tariffs between the U.S. and its major trading partners has recently dampened business sentiment and could pose a risk to growth expectations going forward. A host of other geopolitical concerns, including the ongoing Brexit and North American Free Trade Agreement negotiations, North Korea relations and rising populism around the world, remain on the horizon.

Despite these risks, global growth remains intact, albeit at a slower pace, providing support to corporate earnings. Fiscal stimulus, an easing regulatory environment and robust consumer spending recently helped boost the U.S. economy’s momentum. Subdued inflation pressures have kept central bank policy accommodative, even as Europe moves closer to winding down its monetary stimulus and the Federal Reserve remains on a moderate tightening course.

Headlines and political noise will continue to obscure underlying fundamentals at times and cause temporary bouts of volatility. We encourage you to work with your financial advisor to evaluate your goals, timeline and risk tolerance if short-term market fluctuations are a concern. On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Terence J. Toth

Chairman of the Board

August 24, 2018

4

Portfolio Managers’ Comments

Nuveen High Income 2020 Target Term Fund (JHY)

Nuveen High Income December 2019 Target Term Fund (JHD)

Nuveen High Income December 2018 Target Term Fund (JHA)

Nuveen High Income November 2021 Target Term Fund (JHB)

Nuveen High Income 2020 Target Term Fund (JHY), Nuveen High Income December 2019 Target Term Fund (JHD), Nuveen High Income December 2018 Target Term Fund (JHA), and Nuveen High Income November 2021 Target Term Fund (JHB) are closed-end funds that are advised by Nuveen Fund Advisors, LLC (NFAL) and feature portfolio management by Nuveen Asset Management, LLC (NAM). The Funds’ portfolio managers are John T. Fruit, CFA, and Jeffrey T. Schmitz, CFA.

On January 16, 2018, the Nuveen High Income December 2018 Target Term Fund (JHA) entered the wind-up period in anticipation of its termination date. The Fund is a “target term” Fund that will cease its investment operations and liquidate its portfolio on December 1, 2018 and distribute the net proceeds to shareholders, unless the term is extended for a period of up to six months by a vote of the Fund’s Board of Trustees.

During the wind-up period, the Fund may deviate from its investment objectives and policies, and may invest up to 100% of its managed assets in high quality, short-term securities. High quality, short-term securities for this Fund include securities rated investment grade (BBB-/Baa3 or higher or unrated but judged by the Fund’s subadviser to be of comparable quality) with a final or remaining maturity of 397 days or less. Consequently, for the remainder of its term, the Fund will invest at least 80% of its managed assets in below investment grade securities; and short-term investment grade securities that have a final or remaining maturity of 397 days or less, as long as the maturity does not occur later than June 1, 2019. These expanded investment parameters will provide the Fund with additional flexibility to reinvest the proceeds of matured or called portfolio securities in higher quality, short-term securities. As the Fund gets closer to its termination date, we will begin to transition its remaining below investment grade portfolio holdings to high quality, short-term securities to enhance its ability to efficiently liquidate its portfolio at termination.

Here the Funds’ portfolio management team discusses key investment strategies and the Fund’s performance for the six-month reporting period ended June 30, 2018.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

5

Portfolio Managers’ Comments (continued)

Nuveen High Income 2020 Target Term Fund (JHY)

What key strategies were used to manage the Fund during this six-month reporting period ended June 30, 2018?

The Fund has an objective to provide a high level of current income and to return the original $9.85 net asset value (NAV) per common share on or about November 1, 2020. The Fund will seek to achieve its investment objectives by investing primarily in shorter maturity, high yield (below investment grade) corporate debt securities. High yield bonds typically offer higher yields than investment grade bonds, in exchange for greater credit risk. Bonds with shorter maturities have lower duration (or interest rate sensitivity) than longer maturity bonds, which may help mitigate price declines if rates rise.

The Fund may invest in other types of securities including senior loans, convertible securities and other types of debt instruments and derivatives that provide comparable economic exposure to the corporate debt market. At least 80% of its managed assets will be in corporate debt securities and separately, at least 80% in securities that, at the time of investment, are rated below investment grade or are unrated but judged by the portfolio managers to be of comparable quality. No more than 15% will be in securities rated CCC+/Caa1 or lower at the time of investment. Up to 30% may be in securities of non-U.S. issuers, including up to 20% in emerging market issuers and up to 10% may be in non-U.S. dollar denominated securities.

The Fund seeks to identify securities across diverse sectors and industries that the managers believe are undervalued or mispriced. In seeking to return the original NAV on or about November 1, 2020, the Fund intends to utilize various portfolio and cash flow management techniques, including setting aside a portion of its net investment income, possibly retaining gains and limiting the longest maturity of any holding to no later than May 1, 2021. The Fund also uses leverage.

How did the Fund perform during this six-month reporting period ended June 30, 2018?

The table in the Performance Overview and Holding Summaries section of this report provides total return performance for the Fund for the six-month, one-year and since inception periods ended June 30, 2018. For the six-month reporting period ended June 30, 2018, the Fund underperformed the Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index based on the Fund’s total return at NAV.

High yield bonds traded in a fairly tight range during the first half of the reporting period, despite the mostly rate induced sell-off at the end of the first quarter. The yield for the benchmark index (as measured by yield-to-worst) bounced between 6.35% and 6.75% on the back of modest interest rate volatility and a generally supportive technical backdrop. After surging to more than 2.90% in mid-May, the 5-year Treasury yield rallied back to around 2.70% toward the end of the reporting period after the sell-off in emerging markets and slowing growth concerns in Europe and China created a bid for dollar assets. Strong U.S. economic and employment data was also supportive of U.S. corporate debt, easing spread pressure on high yield bonds.

Spreads for lower quality issues (CCCs) tightened modestly since the beginning of the reporting period due to improving fundamentals and less sensitivity to rates, while spreads for single-B and BB rated securities were marginally wider. This led to much better performance out of the CCC rated segment during the reporting period. However, the size of the CCC index has been shrinking since the bottom of the last credit cycle and represents just 14% of the high yield index, thereby making it hard for the segment to drive returns in the overall market.

Overall, thin supply, stabilizing fund flows and a small rally in rates helped high yield hold its ground in the face of escalating trade friction and deterioration of the global growth story. Demand for short-duration high yield also remained strong in the context of the Federal Reserve raising its expectations for the federal funds rate. Despite the shift in central bank policy that represents a reversal of the friendly monetary backdrop, the global yield environment has remained

6

under pressure from demand for yield outstripping supply. This backdrop has contributed to a period of heavy refinancing activity, due to the high level of portfolio securities being called or tendered as companies looked to take advantage of the strong credit environment and nominally low all-in yields to extend maturities.

The Fund seeks to protect against credit losses to help ensure the goal of returning its original NAV. While the Fund is designed to own more or less a static portfolio of high yield bonds, at times we have to add new securities to replace ones that have been called away or tendered. As we replace these bonds, we seek to maximize the Fund’s yield within the maturity, diversification and credit quality constraints described at the outset of the strategy. We may also look to maximize the Fund’s yield through opportunistic sales of securities that we believe have reached their upside potential, investing the proceeds in other securities that have a more attractive yield or credit profile. Our goal is to monetize some holdings at a gain, which should help to offset any realized or mark-to-market losses that may occur elsewhere in the portfolio. We believe the Fund’s focus on shorter-dated maturities, coupled with limitations to CCC rated securities, should result in lower volatility and help buffer its NAV performance during periods of weakness for the high yield market.

The Fund underperformed the benchmark during the reporting period, largely as a result of having a higher average quality rating and shorter duration than the index. More importantly, credit performance within the Fund continued to be strong and suffered little in the way of credit deterioration. The Fund’s NAV declined marginally during the reporting period as an increase in interest rates caused some minor mark-to-market declines in Fund holdings. Given the strong credit environment, however, we saw little in the way of credit deterioration among portfolio credits and the Fund had no defaults across the entire portfolio.

While we continue to attempt to maximize portfolio yield where achievable, we do so within the context of protecting the Fund’s credit quality and positioning the portfolio to alleviate the effects of early calls or redemptions. We have seen and expect to see additional call activity given the most recent downward trend in rates and the propensity for issuers to refinance their short-term debt and replace it with longer maturities. However, as a result of tightening credit spreads in the high yield market, the Fund’s NAV has stayed stable and remains near the original NAV at inception. As of the end of the reporting period, the Fund was on track to return its original NAV as described in its prospectus.

Nuveen High Income December 2019 Target Term Fund (JHD)

What key strategies were used to manage the Fund during this six-month reporting period ended June 30, 2018?

The Fund has an objective to provide a high level of current income and to return the original $9.86 net asset value (NAV) per common share on or about December 1, 2019. The Fund will seek to achieve its investment objectives by investing primarily in shorter maturity, high yield (below investment grade) corporate debt securities. High yield bonds typically offer higher yields than investment grade bonds, in exchange for greater credit risk. Bonds with shorter maturities have lower duration (or interest rate sensitivity) than longer maturity bonds, which may help mitigate price declines if rates rise.

The Fund may invest in other types of securities including senior loans, convertible securities and other types of debt instruments and derivatives that provide comparable economic exposure to the corporate debt market. At least 80% of its managed assets will be in corporate debt securities and separately, at least 80% in securities that, at the time of investment, are rated below investment grade or are unrated but judged by the portfolio managers to be of comparable quality. No more than 15% will be in securities rated CCC+/Caa1 or lower at the time of investment. Up to 30% may be in securities of non-U.S. issuers, including up to 20% in emerging market issuers and up to 10% may be in non-U.S. dollar denominated securities.

7

Portfolio Managers’ Comments (continued)

The Fund seeks to identify securities across diverse sectors and industries that the managers believe are undervalued or mispriced. In seeking to return the original NAV on or about December 1, 2019, the Fund intends to utilize various portfolio and cash flow management techniques, including setting aside a portion of its net investment income, possibly retaining gains and limiting the longest maturity of any holding to no later than June 1, 2020. The Fund also uses leverage.

How did the Fund perform during this six-month reporting period ended June 30, 2018?

The table in the Performance Overview and Holding Summaries section of this report provides total return performance for the Fund for the six-month, one-year and since inception periods ended June 30, 2018. For the six-month reporting period ended June 30, 2018, the Fund underperformed the Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index based on the Fund’s total return at NAV.

High yield bonds traded in a fairly tight range during the first half of the reporting period, despite the mostly rate induced sell-off at the end of the first quarter. The yield for the benchmark index (as measured by yield-to-worst) bounced between 6.35% and 6.75% on the back of modest interest rate volatility and a generally supportive technical backdrop. After surging to more than 2.90% in mid-May, the 5-year Treasury yield rallied back to around 2.70% toward the end of the reporting period after the sell-off in emerging markets and slowing growth concerns in Europe and China created a bid for dollar assets. Strong U.S. economic and employment data was also supportive of U.S. corporate debt, easing spread pressure on high yield bonds.

Spreads for lower quality issues (CCCs) tightened modestly since the beginning of the reporting period due to improving fundamentals and less sensitivity to rates, while spreads for single-B and BB rated securities were marginally wider. This led to much better performance out of the CCC rated segment during reporting period. However, the size of the CCC index has been shrinking since the bottom of the last credit cycle and represents just 14% of the high yield index, thereby making it hard for the segment to drive returns in the overall market.

Overall, thin supply, stabilizing fund flows and a small rally in rates helped high yield hold its ground in the face of escalating trade friction and deterioration of the global growth story. Demand for short-duration high yield also remained strong in the context of the Federal Reserve raising its expectations for the federal funds rate. Despite the shift in central bank policy that represents a reversal of the friendly monetary backdrop, the global yield environment has remained under pressure from demand for yield outstripping supply. This backdrop has contributed to a period of heavy refinancing activity, which surely had knock-on effects for our Fund due to the high level of portfolio securities being called or tendered as companies looked to take advantage of the strong credit environment and nominally low all-in yields to extend maturities. But it has also resulted in strong credit conditions, and by extension a continued period of low realized and projected default rates, which are estimated to remain around 2.5% for the foreseeable future.

The Fund seeks to protect against credit losses to help ensure the goal of returning its original NAV. While the Fund is designed to own more or less a static portfolio of high yield bonds, at times we have to add new securities to replace ones that have been called away or tendered. As we replace these bonds, we seek to maximize the Fund’s yield within the maturity, diversification and credit quality constraints described at the outset of the strategy. We may also look to maximize the Fund’s yield through opportunistic sales of securities that we believe have reached their upside potential, investing the proceeds in other securities that have a more attractive yield or credit profile. Our goal is to monetize some holdings at a gain, which should help to offset any realized or mark-to-market losses that may occur elsewhere in the portfolio. We believe the Fund’s focus on shorter-dated maturities, coupled with limitations to CCC rated securities, should result in lower volatility and help buffer its NAV performance during periods of weakness for the high yield market.

The Fund underperformed the benchmark during the reporting period, largely as a result of having a higher average quality rating and shorter duration than the index. More importantly, credit performance within the Fund continued to

8

be strong and suffered little in the way of credit deterioration. We began the Fund’s deleveraging process in April 2018 as current yields available on suitable new investments in most cases were not attractive enough to deploy the use of leverage. The elimination of leverage is also consistent with the wind-up period and the systematic liquidation of assets in anticipation of the Fund’s termination in December 2019.

We continue to hold a modest percentage of portfolio assets that mature within the three-month window after the Fund’s stated maturity, in accordance with prospectus guidelines, that we plan to liquidate shortly before the Fund’s maturity date. We may continue to reinvest the proceeds of called and matured securities into higher quality and short-dated instruments as we get closer to the stated maturity date. Reinvesting in shorter-duration and higher quality securities also resulted in a lower portfolio yield and concurrently a reduction in the dividend being paid by the Fund, which will continue as we approach the termination date. All of these outcomes are consistent with our expectations and with the guidelines we set forth in the prospectus at the Fund’s inception.

While we continue to attempt to maximize portfolio yield where achievable, we do so within the context of protecting the Fund’s credit quality and positioning the portfolio to alleviate the effects of early calls or redemptions. We have seen and expect to see additional call activity given the most recent downward trend in rates and the propensity for issuers to refinance their short-term debt and replace it with longer maturities. However, as a result of tightening credit spreads in the high yield market, the Fund’s NAV has remained stable and remains above the original NAV at inception. As of the end of the reporting period, the Fund was on track to return its original NAV as described in its prospectus.

Nuveen High Income December 2018 Target Term Fund (JHA)

What key strategies were used to manage the Fund during this six-month reporting period ended June 30, 2018?

The Fund has an objective to provide a high level of current income and to return the original $9.86 net asset value (NAV) per common share on or about December 1, 2018. The Fund will seek to achieve its investment objectives by investing primarily in shorter maturity, high yield (below investment grade) corporate debt securities. High yield bonds typically offer higher yields than investment grade bonds, in exchange for greater credit risk. Bonds with shorter maturities have lower duration (or interest rate sensitivity) than longer maturity bonds, which may help mitigate price declines if rates rise.

The Fund may invest in other types of securities including senior loans, convertible securities and other types of debt instruments and derivatives that provide comparable economic exposure to the corporate debt market. At least 80% of its managed assets will be in corporate debt securities and separately, at least 80% in securities that, at the time of investment, are rated below investment grade or are unrated but judged by the portfolio managers to be of comparable quality. No more than 15% will be in securities rated CCC+/Caa1 or lower at the time of investment. Up to 30% may be in securities of non-U.S. issuers, including up to 20% in emerging market issuers and up to 10% may be in non-U.S. dollar denominated securities.

The Fund seeks to identify securities across diverse sectors and industries that the managers believe are undervalued or mispriced. In seeking to return the original NAV on or about December 1, 2018, the Fund intends to utilize various portfolio and cash flow management techniques, including setting aside a portion of its net investment income, possibly retaining gains and limiting the longest maturity of any holding to no later than June 1, 2019.

How did the Fund perform during this six-month reporting period ended June 30, 2018?

The table in the Performance Overview and Holding Summaries section of this report provides total return performance for the Fund for the six-month, one-year and since inception periods ended June 30, 2018. For the six-month reporting period ended June 30, 2018, the Fund underperformed the Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index based on the Fund’s total return at NAV.

9

Portfolio Managers’ Comments (continued)

High yield bonds traded in a fairly tight range during the first half of the reporting period, despite the mostly rate induced sell-off at the end of the first quarter. The yield for the benchmark index (as measured by yield-to-worst) bounced between 6.35% and 6.75% on the back of modest interest rate volatility and a generally supportive technical backdrop. After surging to more than 2.90% in mid-May, the 5-year Treasury yield rallied back to around 2.70% toward the end of the reporting period after the sell-off in emerging markets and slowing growth concerns in Europe and China created a bid for dollar assets. Strong U.S. economic and employment data was also supportive of U.S. corporate debt, easing spread pressure on high yield bonds.

Spreads for lower quality issues (CCCs) tightened modestly since the beginning of the reporting period due to improving fundamentals and less sensitivity to rates, while spreads for single-B and BB rated securities were marginally wider. This led to much better performance out of the CCC rated segment during the reporting period. However, the size of the CCC index has been shrinking since the bottom of the last credit cycle and represents just 14% of the high yield index, thereby making it hard for the segment to drive returns in the overall market.

Overall, thin supply, stabilizing fund flows and a small rally in rates helped high yield hold its ground in the face of escalating trade friction and deterioration of the global growth story. Demand for short-duration high yield also remained strong in the context of the Federal Reserve raising its expectations for the federal funds rate. Despite the shift in central bank policy that represents a reversal of the friendly monetary backdrop, the global yield environment has remained under pressure from demand for yield outstripping supply. This backdrop has contributed to a period of heavy refinancing activity, which surely had knock-on effects for our Fund due to the high level of portfolio securities being called or tendered as companies looked to take advantage of the strong credit environment and nominally low all-in yields to extend maturities. But it has also resulted in strong credit conditions, and by extension a continued period of low realized and projected default rates, which are estimated to remain around 2.5% for the foreseeable future.

The Fund seeks to protect against credit losses to help ensure the goal of returning its original NAV. While the Fund is designed to own more or less a static portfolio of high yield bonds, at times we have to add new securities to replace ones that have been called away or tendered. As we replace these bonds, we seek to maximize the Fund’s yield within the maturity, diversification and credit quality constraints described at the outset of the strategy. We may also look to maximize the Fund’s yield through opportunistic sales of securities that we believe have reached their upside potential, investing the proceeds in other securities that have a more attractive yield or credit profile. Our goal is to monetize some holdings at a gain, which should help to offset any realized or mark-to-market losses that may occur elsewhere in the portfolio. We believe the Fund’s focus on shorter-dated maturities, coupled with limitations to CCC rated securities, should result in lower volatility and help buffer its NAV performance during periods of weakness for the high yield market.

The Fund underperformed the benchmark during the reporting period, largely as a result of the wind-up process we began early in the reporting period, which has resulted in a much higher average quality and shorter duration than the index. More importantly, credit performance within the Fund continued to be strong and suffered little in the way of credit deterioration. We have completed the Fund’s deleveraging process with an eye toward better protecting the Fund’s NAV in light of the approaching December 2018 maturity date. This has largely entailed moving into securities that are higher quality in nature and with maturities that largely coincide with the Fund’s stated maturity date. We continue to hold a modest percentage of portfolio assets that mature within a three-month window after the stated maturity, in accordance with prospectus guidelines, which we plan to liquidate shortly before the Fund’s maturity date. As of June 30, 2018, more than 65% of the portfolio’s assets were invested in investment grade securities, and we anticipate that figure will increase as we get closer to the stated maturity date and as other securities mature, get called or are sold.

10

As a result of stable credit spreads in the high yield market, the Fund’s NAV has stayed stable and remains near the original NAV at inception. As of the end of the reporting period, the Fund was on track to return its original NAV as described in its prospectus.

Nuveen High Income November 2021 Target Term Fund (JHB)

What key strategies were used to manage the Fund during this six-month reporting period ended June 30, 2018?

The Fund has an objective to provide a high level of current income and to return the original $9.85 net asset value (NAV) per common share on or about November 1, 2021. The Fund will seek to achieve its investment objectives by investing primarily in shorter maturity, high yield (below investment grade) corporate debt securities. High yield bonds typically offer higher yields than investment grade bonds, in exchange for greater credit risk. Bonds with shorter maturities have lower duration (or interest rate sensitivity) than longer maturity bonds, which may help mitigate price declines if rates rise.

The Fund may invest in other types of securities including senior loans, convertible securities and other types of debt instruments and derivatives that provide comparable economic exposure to the corporate debt market. At least 80% of its managed assets will be in corporate debt securities and separately, at least 80% in securities that, at the time of investment, are rated below investment grade or are unrated but judged by the portfolio managers to be of comparable quality. No more than 15% will be in securities rated CCC+/Caa1 or lower at the time of investment. Up to 30% may be in securities of non-U.S. issuers, including up to 20% in emerging market issuers, and up to 10% may be in non-U.S. dollar denominated securities.

The Fund seeks to identify securities across diverse sectors and industries that the managers believe are undervalued or mispriced. In seeking to return the original NAV on or about November 1, 2021, the Fund intends to utilize various portfolio and cash flow management techniques, including setting aside a portion of its net investment income, possibly retaining gains and limiting the longest maturity of any holding to no later than May 1, 2022. The Fund also uses leverage.

How did the Fund perform during this six-month reporting period ended June 30, 2018?

The table in the Performance Overview and Holding Summaries section of this report provides total return performance for the Fund for the six-month, one-year and since inception periods ended June 30, 2018. For the six-month reporting period ended June 30, 2018, the Fund underperformed the Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index based on the Fund’s total return at NAV.

High yield bonds traded in a fairly tight range during the first half of the reporting period, despite the mostly rate induced sell-off at the end of the first quarter. The yield for the benchmark index (as measured by yield-to-worst) bounced between 6.35% and 6.75% on the back of modest interest rate volatility and a generally supportive technical backdrop. After surging to more than 2.90% in mid-May, the 5-year Treasury yield rallied back to around 2.70% toward the end of the reporting period after the sell-off in emerging markets and slowing growth concerns in Europe and China created a bid for dollar assets. Strong U.S. economic and employment data was also supportive of U.S. corporate debt, easing spread pressure on high yield bonds.

Spreads for lower quality issues (CCCs) tightened modestly since the beginning of the reporting period due to improving fundamentals and less sensitivity to rates, while spreads for single-B and BB rated securities were marginally wider. This led to much better performance out of the CCC rated segment during the reporting period. However, the size of the CCC index has been shrinking since the bottom of the last credit cycle and represents just 14% of the high yield index, thereby making it hard for the segment to drive returns in the overall market.

11

Portfolio Managers’ Comments (continued)

Overall, thin supply, stabilizing fund flows and a small rally in rates helped high yield hold its ground in the face of escalating trade friction and deterioration of the global growth story. Demand for short-duration high yield also remained strong in the context of the Federal Reserve raising its expectations for the federal funds rate. Despite the shift in central bank policy that represents a reversal of the friendly monetary backdrop, the global yield environment has remained under pressure from demand for yield outstripping supply. This backdrop has contributed to a period of heavy refinancing activity, which surely had knock-on effects for our Fund due to the high level of portfolio securities being called or tendered as companies looked to take advantage of the strong credit environment and nominally low all-in yields to extend maturities. But it has also resulted in strong credit conditions, and by extension a continued period of low realized and projected default rates, which are estimated to remain around 2.5% for the foreseeable future.

The Fund seeks to protect against credit losses to help ensure the goal of returning its original NAV. While the Fund is designed to own more or less a static portfolio of high yield bonds, at times we have to add new securities to replace ones that have been called away or tendered. As we replace these bonds, we seek to maximize the Fund’s yield within the maturity, diversification and credit quality constraints described at the outset of the strategy. We may also look to maximize the Fund’s yield through opportunistic sales of securities that we believe have reached their upside potential, investing the proceeds in other securities that have a more attractive yield or credit profile. Our goal is to monetize some holdings at a gain, which should help to offset any realized or mark-to-market losses that may occur elsewhere in the portfolio. We believe the Fund’s focus on shorter-dated maturities, coupled with limitations to CCC rated securities, should result in lower volatility and help buffer its NAV performance during periods of weakness for the high yield market.

The Fund underperformed the benchmark during the reporting period, largely due to a higher average quality and shorter duration than the index. More importantly, credit performance within the Fund continued to be strong and suffered little in the way of credit deterioration. The Fund’s NAV declined marginally during the reporting period as an increase in interest rates caused some minor mark-to-market declines in Fund holdings.

While we continue to attempt to maximize portfolio yield where achievable, we do so within the context of protecting the Fund’s credit quality and positioning the portfolio to alleviate the effects of early calls or redemptions. We have seen and expect to see additional call activity given the most recent downward trend in rates and the propensity for issuers to refinance their short-term debt and replace it with longer maturities. However, as a result of tightening credit spreads in the high yield market, the Fund’s NAV has stayed stable and remains near the original NAV at inception. As of the end of the reporting period, the Fund was on track to return its original NAV as described in its prospectus.

12

Fund Leverage

IMPACT OF THE FUNDS’ LEVERAGE STRATEGIES ON PERFORMANCE

One important factor impacting the returns of JHY’s, JHD’s and JHB’s common shares relative to their comparative benchmarks was the Funds’ use of leverage through bank borrowings. JHA no longer use leverage. The Funds use leverage because our research has shown that, over time, leveraging provides opportunities for additional income and total return, particularly in the recent market environment where short-term market rates are at or near historical lows, meaning that the short-term rates the Fund has been paying on its leveraging instruments in recent years have been much lower than the interest the Fund has been earning on its portfolio securities that it has bought with the proceeds of that leverage.

However, use of leverage can expose Fund common shares to additional price volatility. When a Fund uses leverage, the Fund common shares will experience a greater increase in their net asset value if the securities acquired through the use of leverage increase in value, but will also experience a correspondingly larger decline in their net asset value if the securities acquired through leverage decline in value, which will make the shares’ net asset value more volatile, and total return performance more variable, over time.

In addition, common share income in levered funds will typically decrease in comparison to unlevered funds when short-term interest rates increase and increase when short-term interest rates decrease. Over the last few quarters, short-term interest rates have indeed increased from their extended lows after the 2007-09 financial crisis. This increase has reduced common share net income, and also reduced potential for long-term total returns. Nevertheless, the ability to effectively borrow at current short-term rates is still resulting in enhanced common share income, and management believes that the advantages of continuation of leverage outweigh the associated increase in risk and volatility described above.

The Funds’ use of leverage had a positive impact on performance during this reporting period.

As of June 30, 2018, the Funds’ percentages of leverage are shown in the accompanying table.

| | | | | | | | | | | | | | | | |

| | | JHY | | | JHD | | | JHA | | | JHB | |

Effective Leverage* | | | 28.72 | % | | | 6.71 | % | | | — | | | | 25.52 | % |

Regulatory Leverage* | | | 28.72 | % | | | 6.71 | % | | | — | | | | 25.52 | % |

| * | Effective Leverage is a Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of certain derivative and other investments in a Fund’s portfolio that increase the Fund’s investment exposure. Regulatory leverage consists of preferred shares issued or borrowings of a Fund. Both of these are part of a Fund’s capital structure. A Fund, however, may from time to time borrow on a typically transient basis in connection with its day-to-day operations, primarily in connection with the need to settle portfolio trades. Such incidental borrowings are excluded from the calculation of a Fund’s effective leverage ratio. Regulatory leverage is subject to asset coverage limits set forth in the Investment Company Act of 1940. |

THE FUNDS’ REGULATORY LEVERAGE

Bank Borrowings

As noted above, the following Funds employ leverage through the use of bank borrowings. The Funds’ bank borrowing activities are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Current Reporting Period | | | | | | Subsequent to the Close of

the Reporting Period | |

| Fund | | January 1, 2018 | | | Draws | | | Paydowns | | | June 30, 2018 | | | Average Balance

Outstanding | | | | | | Draws | | | Paydowns | | | August 27,

2018 | |

JHY | | $ | 44,000,000 | | | $ | 17,500,000 | | | $ | — | | | $ | 61,500,000 | | | $ | 52,301,105 | | | | | | | $ | — | | | $ | — | | | $ | 61,500,000 | |

JHD | | $ | 63,500,000 | | | $ | — | | | $ | (44,000,000 | ) | | $ | 19,500,000 | | | $ | 44,969,613 | | | | | | | $ | — | | | $ | (7,300,000 | ) | | $ | 12,200,000 | |

JHB | | $ | 190,000,000 | | | $ | — | | | $ | — | | | $ | 190,000,000 | | | $ | 190,000,000 | | | | | | | $ | — | | | $ | — | | | $ | 190,000,000 | |

Refer to Notes to Financial Statements, Note 8 – Borrowing Arrangements for further details.

13

Share Information

DISTRIBUTION INFORMATION

The following information regarding the Funds’ distributions is current as of June 30, 2018. Each Fund’s distribution levels may vary over time based on each Fund’s investment activity and portfolio investment value changes.

During the current reporting period, the Funds’ distributions to shareholders were as shown in the accompanying table.

| | | | | | | | | | | | | | | | |

| | | Per Share Amounts | |

| Monthly Distributions (Ex-Dividend Date) | | JHY | | | JHD | | | JHA | | | JHB | |

January 2018 | | $ | 0.0470 | | | $ | 0.0415 | | | $ | 0.0325 | | | $ | 0.0500 | |

February | | | 0.0470 | | | | 0.0415 | | | | 0.0325 | | | | 0.0500 | |

March | | | 0.0440 | | | | 0.0375 | | | | 0.0300 | | | | 0.0465 | |

April | | | 0.0440 | | | | 0.0375 | | | | 0.0300 | | | | 0.0465 | |

May | | | 0.0440 | | | | 0.0375 | | | | 0.0300 | | | | 0.0465 | |

June 2018 | | | 0.0420 | | | | 0.0350 | | | | 0.0270 | | | | 0.0465 | |

Total Distributions from Net Investment Income | | $ | 0.2680 | | | $ | 0.2305 | | | $ | 0.1820 | | | $ | 0.2860 | |

| | | | |

Current Distribution Rate* | | | 5.03 | % | | | 4.27 | % | | | 3.28 | % | | | 5.84 | % |

| * | Current distribution rate is based on the Fund’s current annualized monthly distribution divided by the Fund’s current market price. The Fund’s monthly distributions to its shareholders may be comprised of ordinary income, net realized capital gains and, if at the end of the fiscal year the Fund’s cumulative net ordinary income and net realized gains are less than the Fund’s distributions, a return of capital for tax purposes. |

Each Fund in this report seeks to pay regular monthly dividends out of its net investment income at a rate that reflects its past and projected net income performance. To permit each Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net income actually earned by the Fund during the period. If a Fund has cumulatively earned more than it has paid in dividends, it will hold the excess in reserve as undistributed net investment income (UNII) as part of the Fund’s net asset value. Conversely, if a Fund has cumulatively paid in dividends more than it has earned, the excess will constitute a negative UNII that will likewise be reflected in the Fund’s net asset value. Each Fund will, over time, pay all its net investment income as dividends to shareholders.

As of June 30, 2018, the Funds had positive UNII balances, based upon our best estimate, for tax purposes and positive UNII balances for financial reporting purposes.

All monthly dividends paid by each Fund during the current reporting period were paid from net investment income. If a portion of the Fund’s monthly distributions was sourced from or comprised of elements other than net investment income, including capital gains and/or a return of capital, shareholders would have received a notice to that effect. For financial reporting purposes the composition and per share amounts of each Fund’s dividends for the reporting period are presented in this report’s Statement of Changes in Net Assets and Financial Highlights, respectively. For income tax purposes, distribution information for each Fund as of its most recent tax year end is presented in Note 6 – Income Tax Information within the Notes to Financial Statements of this report.

14

EQUITY SHELF PROGRAM

During the current reporting period, JHY was authorized by the Securities and Exchange Commission to issue additional shares through an equity shelf program (“Shelf Offering”). Under this program JHY, subject to market conditions, may raise additional capital from time to time in varying amounts and offering methods at a net price at or above the Fund’s NAV per share. Under the Shelf Offering, the Fund was authorized to issue additional shares as shown in the accompanying table.

| | | | |

| | | JHY | |

Additional authorized shares | | | 3,400,000 | |

During the current reporting period, JHY sold shares through its Shelf Offering at a weighted average premium to its NAV per share as shown in the accompanying table.

| | | | |

| | | JHY | |

Shares sold through Shelf Offering | | | 15,181 | |

Weighted average premium to NAV per share sold | | | 1.20 | % |

Refer to the Notes to Financial Statements, Note 4 – Fund Shares, Equity Shelf Programs and Offering Costs for further details of Shelf Offerings and the Fund’s transactions.

SHARE REPURCHASES

During August 2018 (subsequent to the close of the reporting period), the Funds’ Board of Trustees reauthorized an open-market share repurchase program, allowing each Fund to repurchase an aggregate of up to approximately 10% of its outstanding shares.

As of June 30, 2018, and since the inception of the Funds’ repurchase programs, the Funds have cumulatively repurchased and retired their outstanding shares as shown in the accompanying table.

| | | | | | | | | | | | | | | | |

| | | JHY | | | JHD | | | JHA | | | JHB | |

Shares cumulatively repurchased and retired | | | — | | | | — | | | | — | | | | — | |

Shares authorized for repurchase | | | 1,495,000 | | | | 2,705,000 | | | | 2,930,000 | | | | 5,585,000 | |

OTHER SHARE INFORMATION

As of June 30, 2018, and during the current reporting period, the Funds’ share prices were trading at premium/(discount) to their NAVs as shown in the accompanying table.

| | | | | | | | | | | | | | | | |

| | | JHY | | | JHD | | | JHA | | | JHB | |

NAV | | $ | 9.75 | | | $ | 10.02 | | | $ | 9.96 | | | $ | 9.92 | |

Share price | | $ | 10.01 | | | $ | 9.83 | | | $ | 9.88 | | | $ | 9.56 | |

Premium/(Discount) to NAV | | | 2.67 | % | | | (1.90 | )% | | | (0.80 | )% | | | (3.63 | )% |

6-month average premium/(discount) to NAV | | | 0.22 | % | | | (2.30 | )% | | | (1.48 | )% | | | (3.80 | )% |

JHY, JHD, JHA and JHB each have an investment objective to return $9.85, $9.86, $9.86 and $9.85, respectively (the original net asset value following each Fund’s initial public offering (the “Original NAV”)) to shareholders on or about the end of the Fund’s term. There can be no assurance that the Funds will be able to return the Original NAV to shareholders, and such return is not backed or otherwise guaranteed by the Funds’ investment adviser, Nuveen Fund Advisors, LLC (the “Adviser”), or any other entity.

Each Fund’s ability to return Original NAV to common shareholders on or about the termination date will depend on market conditions and the success of various portfolio and cash flow management techniques. Each Fund currently

15

Share Information (continued)

intends to set aside and retain in its net assets a portion of its net investment income and possibly all or a portion of its gains. This will reduce the amounts otherwise available for distribution prior to the liquidation of each Fund, and the Fund may incur taxes on such retained amount, which will reduce the overall amounts that the Fund would have otherwise been able to distribute. Such retained income or gains, net of any taxes, would constitute a portion of the liquidating distribution returned to investors at the end of each Fund’s term. In addition, each Fund’s investment in shorter term and lower yielding securities, especially as the Fund nears the end of its term, may reduce investment income and, therefore, the monthly dividends during the period prior to termination. Investors that purchase shares in the secondary market (particularly if their purchase price differs meaningfully from the Original NAV) may receive more or less than their original investment.

16

Risk Considerations

Fund shares are not guaranteed or endorsed by any bank or other insured depository institution, and are not federally insured by the Federal Deposit Insurance Corporation.

Nuveen High Income 2020 Target Term Fund (JHY)

Investing in closed-end funds involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. Closed-end fund shares may frequently trade at a discount or premium to their net asset value. Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, derivatives risk, liquidity risk, and income risk. As interest rates rise, bond prices fall. Lower credit debt securities may be more likely to fail to make timely interest or principal payments and may be subject to higher liquidity risk. Leverage increases return volatility and magnifies the Fund’s potential return and its risks; there is no guarantee a fund’s leverage strategy will be successful. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. The risks of foreign investments are magnified in emerging markets. These and other risk considerations including the Fund’s limited term and call risk are described in more detail on the Fund’s web page at www.nuveen.com/JHY.

Nuveen High Income December 2019 Target Term Fund (JHD)

Investing in closed-end funds involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. Closed-end fund shares may frequently trade at a discount or premium to their net asset value. Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, derivatives risk, liquidity risk, and income risk. As interest rates rise, bond prices fall. Lower credit debt securities may be more likely to fail to make timely interest or principal payments and may be subject to higher liquidity risk. Leverage increases return volatility and magnifies the Fund’s potential return and its risks; there is no guarantee a fund’s leverage strategy will be successful. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. The risks of foreign investments are magnified in emerging markets. These and other risk considerations including the Fund’s limited term and call risk are described in more detail on the Fund’s web page at www.nuveen.com/JHD.

Nuveen High Income December 2018 Target Term Fund (JHA)

Investing in closed-end funds involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. Closed-end fund shares may frequently trade at a discount or premium to their net asset value. Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, derivatives risk, liquidity risk, and income risk. As interest rates rise, bond prices fall. Lower credit debt securities may be more likely to fail to make timely interest or principal payments and may be subject to higher liquidity risk. Leverage increases return volatility and magnifies the Fund’s potential return and its risks; there is no guarantee a fund’s leverage strategy will be successful. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. The risks of foreign investments are magnified in emerging markets. These and other risk considerations including the Fund’s limited term and call risk are described in more detail on the Fund’s web page at nuveen.com/JHA.

Nuveen High Income November 2021 Target Term Fund (JHB)

Investing in closed-end funds involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. Closed-end fund shares may frequently trade at a discount or premium to their net asset value. Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, derivatives risk, liquidity risk, and income risk. As interest rates rise, bond prices fall. Lower credit debt

17

Risk Considerations (continued)

securities may be more likely to fail to make timely interest or principal payments and may be subject to higher liquidity risk. Leverage increases return volatility and magnifies the Fund’s potential return and its risks; there is no guarantee a fund’s leverage strategy will be successful. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. The risks of foreign investments are magnified in emerging markets. These and other risk considerations including the Fund’s limited term and call risk are described in more detail on the Fund’s web page at www.nuveen.com/JHB.

18

THIS PAGE INTENTIONALLY LEFT BLANK

19

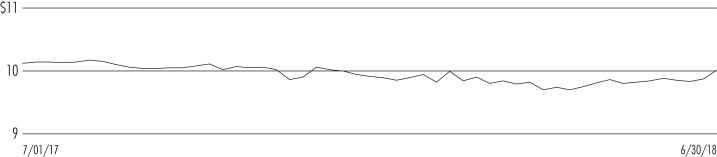

| | |

| JHY | | Nuveen High Income 2020 Target Term Fund Performance Overview and Holding Summaries as of June 30, 2018 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of June 30, 2018

| | | | | | | | | | | | |

| | | Cumulative | | | Average Annual | |

| | | 6-Month | | | 1-Year | | | Since

Inception | |

| JHY at NAV | | | 1.31% | | | | 3.90% | | | | 6.46% | |

| JHY at Share Price | | | 3.79% | | | | 4.97% | | | | 6.66% | |

| Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index | | | 1.93% | | | | 4.00% | | | | 6.04% | |

Since inception returns are from 7/28/15. Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Share Price Performance — Weekly Closing Price

20

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Corporate Bonds | | | 130.5% | |

| Convertible Bonds | | | 3.6% | |

| Sovereign Debt | | | 3.0% | |

| Repurchase Agreements | | | 0.6% | |

| Other Assets Less Liabilities | | | 2.6% | |

Net Assets Plus Borrowings | | | 140.3% | |

| Borrowings | | | (40.3)% | |

Net Assets | | | 100% | |

Country Allocation

(% of total investments)1

| | | | |

| United States | | | 76.9% | |

| Canada | | | 4.3% | |

| Japan | | | 1.9% | |

| Bermuda | | | 1.9% | |

| Netherlands | | | 1.5% | |

| Brazil | | | 1.5% | |

| Hong Kong | | | 1.4% | |

| Luxembourg | | | 1.4% | |

| Argentina | | | 1.2% | |

| Zambia | | | 1.2% | |

| Other | | | 6.8% | |

Total | | | 100% | |

Portfolio Composition

(% of total investments)

| | | | |

| Oil, Gas & Consumable Fuels | | | 7.1% | |

| Metals & Mining | | | 6.3% | |

| Specialty Retail | | | 5.1% | |

| Airlines | | | 5.0% | |

| Diversified Financial Services | | | 4.9% | |

| Media | | | 4.5% | |

| Household Durables | | | 4.3% | |

| Independent Power & Renewable Electricity Producers | | | 4.0% | |

| Hotels, Restaurants & Leisure | | | 3.8% | |

| Diversified Telecommunication Services | | | 3.7% | |

| Health Care Providers & Services | | | 3.6% | |

| Consumer Finance | | | 3.5% | |

| Equity Real Estate Investment Trusts | | | 3.4% | |

| Commercial Services & Supplies | | | 3.1% | |

| Aerospace & Defense | | | 2.9% | |

| Technology Hardware, Storage & Peripherals | | | 2.8% | |

| Building Products | | | 2.3% | |

| Banks | | | 2.1% | |

| Wireless Telecommunication Services | | | 2.1% | |

| Road & Rail | | | 1.8% | |

| Internet & Direct Marketing Retail | | | 1.6% | |

| Other | | | 19.5% | |

| Sovereign Debt | | | 2.2% | |

| Repurchase Agreements | | | 0.4% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term investments)

| | | | |

| A | | | 0.1% | |

| BBB | | | 9.3% | |

| BB or Lower | | | 88.3% | |

| N/R (not rated) | | | 2.3% | |

Total | | | 100% | |

Top Five Issuers

(% of total investments)

| | | | |

| CenturyLink Inc. | | | 2.4% | |

| L Brands Inc. | | | 1.9% | |

| Hertz Global Holdings Inc. | | | 1.8% | |

| NuStar Logistics LP | | | 1.8% | |

| HCA Healthcare Inc. | | | 1.7% | |

| 1 | Includes 10.2% (as a percentage of total investments) in emerging markets countries. |

21

| | |

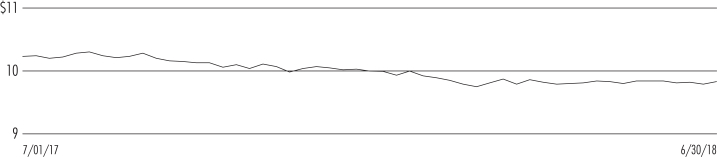

| JHD | | Nuveen High Income December 2019 Target Term Fund Performance Overview and Holding Summaries as of June 30, 2018 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of June 30, 2018

| | | | | | | | | | | | |

| | | Cumulative | | | Average Annual | |

| | | 6-Month | | | 1-Year | | | Since

Inception | |

| JHD at NAV | | | 0.70% | | | | 2.55% | | | | 6.17% | |

| JHD at Share Price | | | 0.42% | | | | 1.48% | | | | 4.58% | |

| Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index | | | 1.93% | | | | 4.00% | | | | 8.66% | |

Since inception returns are from 5/10/16. Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Share Price Performance — Weekly Closing Price

22

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Corporate Bonds | | | 96.5% | |

| Convertible Bonds | | | 3.9% | |

| Sovereign Debt | | | 2.9% | |

| Repurchase Agreements | | | 0.2% | |

| Other Assets Less Liabilities | | | 3.7% | |

Net Assets Plus Borrowings | | | 107.2% | |

| Borrowings | | | (7.2)% | |

Net Assets | | | 100% | |

Country Allocation

(% of total investments)1

| | | | |

| United States | | | 69.6% | |

| Canada | | | 4.7% | |

| Japan | | | 3.5% | |

| United Kingdom | | | 3.2% | |

| Luxembourg | | | 2.5% | |

| Italy | | | 2.2% | |

| Israel | | | 2.2% | |

| Spain | | | 2.0% | |

| Hong Kong | | | 1.8% | |

| Australia | | | 1.5% | |

| Other | | | 6.8% | |

Total | | | 100% | |

Portfolio Composition

(% of total investments)

| | | | |

| Oil, Gas & Consumable Fuels | | | 11.4% | |

| Independent Power & Renewable Electricity Producers | | | 5.7% | |

| Household Durables | | | 5.5% | |

| Technology Hardware, Storage & Peripherals | | | 5.2% | |

| Hotels, Restaurants & Leisure | | | 5.0% | |

| Equity Real Estate Investment Trusts | | | 4.9% | |

| Media | | | 4.8% | |

| Airlines | | | 4.8% | |

| Health Care Providers & Services | | | 4.3% | |

| Metals & Mining | | | 3.5% | |

| Banks | | | 3.4% | |

| Consumer Finance | | | 3.1% | |

| Automobiles | | | 3.0% | |

| Diversified Financial Services | | | 2.9% | |

| Diversified Telecommunication Services | | | 2.8% | |

| Pharmaceuticals | | | 2.8% | |

| Chemicals | | | 2.7% | |

| Specialty Retail | | | 2.4% | |

| Other | | | 18.8% | |

| Sovereign Debt | | | 2.9% | |

| Repurchase Agreements | | | 0.1% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term investments)

| | | | |

| A | | | 0.2% | |

| BBB | | | 20.2% | |

| BB or Lower | | | 77.5% | |

| N/R (not rated) | | | 2.1% | |

Total | | | 100% | |

Top Five Issuers

(% of total investments)

| | | | |

| EMC Corporation | | | 2.8% | |

| Tenet Healthcare Corporation | | | 2.3% | |

| CenturyLink Inc. | | | 2.2% | |

| Sprint Corporation | | | 2.1% | |

| HCA Healthcare Inc. | | | 2.0% | |

| 1 | Includes 8.4% (as a percentage of total investments) in emerging markets countries. |

23

| | |

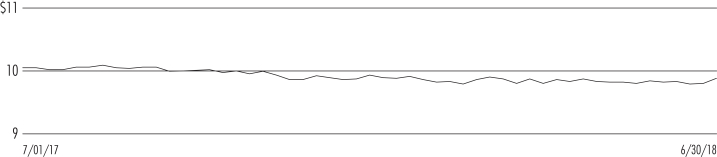

| JHA | | Nuveen High Income December 2018 Target Term Fund Performance Overview and Holding Summaries as of June 30, 2018 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of June 30, 2018

| | | | | | | | | | | | |

| | | Cumulative | | | Average Annual | |

| | | 6-Month | | | 1-Year | | | Since

Inception | |

| JHA at NAV | | | 0.92% | | | | 2.45% | | | | 5.41% | |

| JHA at Share Price | | | 1.55% | | | | 2.38% | | | | 4.55% | |

| Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index | | | 1.93% | | | | 4.00% | | | | 7.62% | |

Since inception returns are from 11/12/15. Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Share Price Performance — Weekly Closing Price

24

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Corporate Bonds | | | 87.7% | |

| Convertible Bonds | | | 6.5% | |

| Sovereign Debt | | | 2.4% | |

| Repurchase Agreements | | | 0.5% | |

| Other Assets Less Liabilities | | | 2.9% | |

Net Assets | | | 100% | |

Country Allocation

(% of total investments)1

| | | | |

| United States | | | 73.5% | |

| Japan | | | 4.9% | |

| Germany | | | 3.0% | |

| United Kingdom | | | 2.8% | |

| Ireland | | | 2.6% | |

| India | | | 2.4% | |

| Luxembourg | | | 1.9% | |

| Switzerland | | | 1.5% | |

| Mexico | | | 1.1% | |

| South Africa | | | 1.1% | |

| Other | | | 5.2% | |

Total | | | 100% | |

Portfolio Composition

(% of total investments)

| | | | |

| Oil, Gas & Consumable Fuels | | | 7.6% | |

| Automobiles | | | 6.9% | |

| Diversified Telecommunication Services | | | 5.8% | |

| Banks | | | 5.3% | |

| Consumer Finance | | | 4.8% | |

| Electronic Equipment, Instruments & Components | | | 4.8% | |

| Equity Real Estate Investment Trusts | | | 4.8% | |

| Health Care Providers & Services | | | 3.9% | |

| Media | | | 3.9% | |

| Household Durables | | | 3.7% | |

| Machinery | | | 3.7% | |

| Capital Markets | | | 3.6% | |

| Electric Utilities | | | 3.2% | |

| Technology Hardware, Storage & Peripherals | | | 2.9% | |

| Hotels, Restaurants & Leisure | | | 2.6% | |

| Commercial Services & Supplies | | | 2.6% | |

| Wireless Telecommunication Services | | | 2.5% | |

| Diversified Financial Services | | | 2.5% | |

| Trading Companies & Distributors | | | 2.1% | |

| Other | | | 19.7% | |

| Sovereign Debt | | | 2.5% | |

| Repurchase Agreements | | | 0.6% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term investments)

| | | | |

| AA | | | 4.9% | |

| A | | | 15.1% | |

| BBB | | | 45.1% | |

| BB or Lower | | | 31.4% | |

| N/R (not rated) | | | 3.5% | |

Total | | | 100% | |

Top Five Issuers

(% of total investments)

| | | | |

| HCA Healthcare Inc. | | | 2.7% | |

| Sprint Corporation | | | 2.5% | |

| AerCap Holdings NV | | | 2.5% | |

| Jaguar Land Rover Automotive PLC | | | 2.4% | |

| Qwest Communications International Inc. | | | 2.3% | |

| 1 | Includes 10.0% (as a percentage of total investments) in emerging markets countries. |

25

| | |

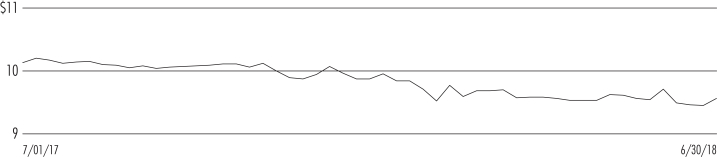

| JHB | | Nuveen High Income November 2021 Target Term Fund Performance Overview and Holding Summaries as of June 30, 2018 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of June 30, 2018

| | | | | | | | | | | | |

| | | Cumulative | | | Average Annual | |

| | | 6-Month | | | 1-Year | | | Since

Inception | |

| JHB at NAV | | | 0.86% | | | | 3.47% | | | | 6.11% | |

| JHB at Share Price | | | (1.13)% | | | | 0.34% | | | | 3.25% | |

| Bloomberg Barclays U.S. High Yield 1-5 Year Cash Pay 2% Issuer Capped Index | | | 1.93% | | | | 4.00% | | | | 6.46% | |

Since inception returns are from 8/23/16. Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Share Price Performance — Weekly Closing Price

26

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Corporate Bonds | | | 129.6% | |

| Sovereign Debt | | | 1.6% | |

| Convertible Bonds | | | 0.7% | |

| Other Assets Less Liabilities | | | 2.4% | |

Net Assets Plus Borrowings | | | 134.3% | |

| Borrowings | | | (34.3)% | |

Net Assets | | | 100% | |

Country Allocation

(% of total investments)1

| | | | |

| United States | | | 73.8% | |

| Canada | | | 4.4% | |

| Luxembourg | | | 2.9% | |

| United Kingdom | | | 2.7% | |

| Japan | | | 2.1% | |

| China | | | 1.5% | |

| Brazil | | | 1.4% | |

| Italy | | | 1.3% | |

| Israel | | | 0.9% | |

| Bermuda | | | 0.9% | |

| Other | | | 8.1% | |

Total | | | 100% | |

Portfolio Composition

(% of total investments)

| | | | |

| Oil, Gas & Consumable Fuels | | | 11.9% | |

| Media | | | 7.8% | |

| Metals & Mining | | | 6.1% | |

| Diversified Financial Services | | | 5.5% | |

| Health Care Providers & Services | | | 5.2% | |

| Household Durables | | | 4.8% | |

| Equity Real Estate Investment Trusts | | | 3.9% | |

| Hotels, Restaurants & Leisure | | | 3.6% | |

| Specialty Retail | | | 3.4% | |

| Consumer Finance | | | 3.3% | |

| Independent Power & Renewable Electricity Producers | | | 3.2% | |

| Commercial Services & Supplies | | | 3.1% | |

| Aerospace & Defense | | | 2.9% | |

| Wireless Telecommunication Services | | | 2.6% | |

| Technology Hardware, Storage & Peripherals | | | 2.4% | |

| Chemicals | | | 2.3% | |

| Airlines | | | 2.2% | |

| Pharmaceuticals | | | 2.0% | |

| Diversified Telecommunication Services | | | 2.0% | |

| Banks | | | 1.5% | |

| Other | | | 19.1% | |

| Sovereign Debt | | | 1.2% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term investments)

| | | | |

| BBB | | | 7.0% | |

| BB or Lower | | | 90.7% | |

| N/R (not rated) | | | 2.3% | |

Total | | | 100% | |

Top Five Issuers

(% of total investments)

| | | | |

| CenturyLink Inc. | | | 1.6% | |

| Bombardier Inc. | | | 1.2% | |

| Icahn Enterprises LP | | | 1.2% | |

| iStar Inc. | | | 1.2% | |

| Cequel Communications Holdings I LLC | | | 1.2% | |

| 1 | Includes 10.1% (as a percentage of total investments) in emerging markets countries. |

27

Shareholder Meeting Report

The annual meeting of shareholders was held in the offices of Nuveen on April 11, 2018 for JHY, JHD, JHA and JHB; at this meeting the shareholders were asked to elect Board Members.

| | | | | | | | | | | | | | | | |

| | | JHY | | | JHD | | | JHA | | | JHB | |

| | | Common

Shares | | | Common

Shares | | | Common

Shares | | | Common

Shares | |

Approval of the Board Members was reached as follows: | | | | | | | | | | | | | | | | |

Margo L. Cook | | | | | | | | | | | | | | | | |

For | | | 13,817,130 | | | | 23,455,104 | | | | 24,496,648 | | | | 48,981,010 | |

Withhold | | | 134,545 | | | | 652,872 | | | | 1,463,578 | | | | 723,361 | |

Total | | | 13,951,675 | | | | 24,107,976 | | | | 25,960,226 | | | | 49,704,371 | |

Jack B. Evans | | | | | | | | | | | | | | | | |

For | | | 13,831,408 | | | | 23,471,008 | | | | 24,516,862 | | | | 48,966,316 | |

Withhold | | | 120,267 | | | | 636,968 | | | | 1,443,364 | | | | 738,055 | |

Total | | | 13,951,675 | | | | 24,107,976 | | | | 25,960,226 | | | | 49,704,371 | |

Albin F. Moschner | | | | | | | | | | | | | | | | |

For | | | 13,830,929 | | | | 23,484,288 | | | | 24,534,562 | | | | 48,972,573 | |

Withhold | | | 120,746 | | | | 623,688 | | | | 1,425,664 | | | | 731,798 | |

Total | | | 13,951,675 | | | | 24,107,976 | | | | 25,960,226 | | | | 49,704,371 | |

William J. Schneider | | | | | | | | | | | | | | | | |

For | | | 13,831,408 | | | | 23,463,806 | | | | 24,524,721 | | | | 48,957,796 | |

Withhold | | | 120,267 | | | | 644,170 | | | | 1,435,505 | | | | 746,575 | |

Total | | | 13,951,675 | | | | 24,107,976 | | | | 25,960,226 | | | | 49,704,371 | |

28

| | |

| JHY | | Nuveen High Income 2020 Target Term

Fund Portfolio of Investments June 30, 2018 |

| | | (Unaudited) |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| |

| | | | LONG-TERM INVESTMENTS – 137.1% (99.6% of Total Investments) | |

| |

| | | | CORPORATE BONDS – 130.5% (94.8% of Total Investments) | |

| |

| | | | Aerospace & Defense – 4.1% | |

| | | | | |

| $ | 200 | | | Alcoa Inc. | | | 6.150% | | | | 8/15/20 | | | | BBB– | | | $ | 208,100 | |

| | 550 | | | Alcoa Inc. | | | 5.400% | | | | 4/15/21 | | | | BBB– | | | | 565,125 | |

| | 1,250 | | | Bombardier Inc., 144A | | | 7.750% | | | | 3/15/20 | | | | B | | | | 1,318,750 | |

| | 1,500 | | | TransDigm Inc. | | | 5.500% | | | | 10/15/20 | | | | B– | | | | 1,500,000 | |

| | 2,700 | | | Triumph Group Inc. | | | 4.875% | | | | 4/01/21 | | | | B– | | | | 2,598,750 | |

| | 6,200 | | | Total Aerospace & Defense | | | | | | | | | | | | | | | 6,190,725 | |

| |

| | | | Airlines – 6.9% | |

| | | | | |

| | 250 | | | Air Canada 2015-1C Pass-Through Trust, 144A | | | 5.000% | | | | 3/15/20 | | | | BB+ | | | | 251,700 | |

| | 2,344 | | | Air Canada, 144A | | | 7.750% | | | | 4/15/21 | | | | BB | | | | 2,502,220 | |

| | 2,325 | | | American Airlines Group Inc., 144A | | | 4.625% | | | | 3/01/20 | | | | BB– | | | | 2,313,375 | |

| | 128 | | | Continental Airlines 1999-1 Class A Pass-Through Trust | | | 6.545% | | | | 2/02/19 | | | | A+ | | | | 128,895 | |

| | 3,000 | | | Delta Air Lines Inc. | | | 3.400% | | | | 4/19/21 | | | | Baa3 | | | | 2,986,272 | |

| | 2,372 | | | Virgin Australia Holdings Limited, 144A | | | 8.500% | | | | 11/15/19 | | | | B– | | | | 2,395,720 | |

| | 10,419 | | | Total Airlines | | | | | | | | | | | | | | | 10,578,182 | |

| |

| | | | Banks – 2.8% | |

| | | | | |

| | 2,315 | | | CIT Group Inc. | | | 4.125% | | | | 3/09/21 | | | | BB+ | | | | 2,300,531 | |