UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934

Filed by the Registrant¨

Filed by a Party other than the Registrantx

Check the appropriate box:

| | | |

| ¨ | | Preliminary Proxy Statement |

| | |

| ¨ | | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| | |

| ¨ | | Definitive Proxy Statement |

| | |

| x | | Definitive Additional Materials |

| | |

| ¨ | | Soliciting Material Pursuant to §240.14a-12 |

Versum Materials, Inc.

(Name of the Registrant as Specified In Its Charter)

Merck KGaA

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| | | | | |

| x | | No fee required. |

| | |

| ¨ | | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| | | |

| | | (1) | | Title of each class of securities to which transaction applies: |

| | | (2) | | Aggregate number of securities to which transaction applies: |

| | | (3) | | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| | | (4) | | Proposed maximum aggregate value of transaction: |

| | | (5) | | Total fee paid: |

| | |

| ¨ | | Fee paid previously with preliminary materials. |

| | |

| ¨ | | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| | | |

| | | (1) | | Amount Previously Paid: |

| | | (2) | | Form, Schedule or Registration Statement No.: |

| | | (3) | | Filing Party: |

| | | (4) | | Date Filed: |

The following presentation was first used on April 2, 2019.

April 2, 2019 MERCK KGAA, DARMSTADT, GERMANY INVESTOR PRESENTATION

Disclaimer Publication of Merck KGaA, Darmstadt, Germany . In the United States and Canada the group of companies affiliated with Merck KGaA, Darmstadt, Germany, operates under individual business names (EMD Serono, Millipore Sigma, EMD Performance Materials) . To reflect such fact and to avoid any misconceptions of the reader of the publication certain logos, terms and business descriptions of the publication have been substituted or additional descriptions have been added . This version of the publication, therefore, slightly deviates from the otherwise identical version of the publication provided outside the United States and Canada . 2

3 Disclaimer Cautionary Statement Regarding Forward - Looking Statements This communication may contain forward - looking statements based on current assumptions and forecasts made by Merck KGaA, Darmstadt, Germany management . Various known and unknown risks, uncertainties and other factors could lead to material differences between the actual future results, financial situation, development or performance of the company and the estimates given here . These factors include Merck KGaA, Darmstadt, Germany’s ability to successfully complete the tender offer for all outstanding shares of common stock of Versum or realize the anticipated benefits of the transaction, delays in obtaining any approvals required for the transaction, or an inability to obtain them on the terms proposed or on the anticipated schedule, the failure of any of the conditions to the tender offer to be satisfied, and those discussed in Merck KGaA, Darmstadt, Germany’s public reports which are available on the Merck KGaA, Darmstadt, Germany website at www . emdgroup . com, and in the definitive proxy statement on Schedule 14 A filed by Merck KGaA, Darmstadt, Germany, with the Securities and Exchange Commission (the “SEC”) on March 22 , 2019 (the “Definitive Proxy Statement”) in opposition to the proposed business combination transaction between Versum Materials, Inc . (“Versum”) and Entegris, Inc . Merck KGaA, Darmstadt, Germany assumes no liability whatsoever to update these forward - looking statements or to conform them to future events or developments . Additional Important Information and Where to Find It This communication does not constitute an offer to buy or solicitation of an offer to sell any securities . Merck KGaA, Darmstadt, Germany and its wholly owned subsidiary EMD Performance Materials Holding, Inc . have commenced a tender offer for all outstanding shares of common stock of Versum and have filed with the SEC a tender offer statement on Schedule TO (including an Offer to Purchase, a Letter of Transmittal and related documents), which will be amended as necessary . These documents contain important information, including the terms and conditions of the tender offer . STOCKHOLDERS OF VERSUM ARE URGED TO READ THESE DOCUMENTS BEFORE MAKING ANY DECISION WITH RESPECT TO THE TENDER OFFER . Investors and security holders may also obtain free copies of these documents and other documents filed with respect to the tender offer through the website maintained by the SEC website at http : //www . sec . gov, or by contacting the proxy solicitor of Merck KGaA, Darmstadt, Germany, D . F . King & Co . , Inc . , at ( 212 ) 269 - 5550 for banks and brokers or at ( 800 ) 714 - 3312 for stockholders . Merck KGaA, Darmstadt, Germany also filed the Definitive Proxy Statement, the accompanying GREEN proxy card and other relevant documents with the SEC to be used to solicit proxies in opposition to the proposed business combination transaction between Versum and Entegris, Inc . Merck KGaA, Darmstadt, Germany and its directors and executive officers may be deemed to be participants in the solicitation of proxies from the holders of Versum common stock . Additional information regarding the participants in the proxy solicitation is contained in the Definitive Proxy Statement . STOCKHOLDERS OF VERSUM ARE URGED TO READ THE DEFINITIVE PROXY STATEMENT AND ALL RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING ALL PROXY MATERIALS, BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION . The Definitive Proxy Statement has been mailed to the stockholders of Versum . Investors and security holders may also obtain free copies of these documents and other documents filed with the SEC by Merck KGaA, Darmstadt, Germany through the website maintained by the SEC at http : //www . sec . gov, or by contacting the proxy solicitor of Merck KGaA, Darmstadt, Germany, D . F . King & Co . , Inc . , at ( 212 ) 269 - 5550 for banks and brokers or at ( 800 ) 714 - 3312 for stockholders .

Key topics to be addressed 4 Summary of Merck KGaA, Darmstadt, Germany’s superior proposal to acquire Versum Merck proposal provides superior value to Versum shareholders Market reaction supports our proposal Strong industrial logic in combination with Merck, KGaA, Darmstadt, Germany Flawed process run by Versum, with a one - track focus on Entegris Acquisition Versum’s poor governance around Entegris transaction Conclusion

SUMMARY OF MERCK KGAA, DARMSTADT, GERMANY’S SUPERIOR PROPOSAL TO ACQUIRE VERSUM

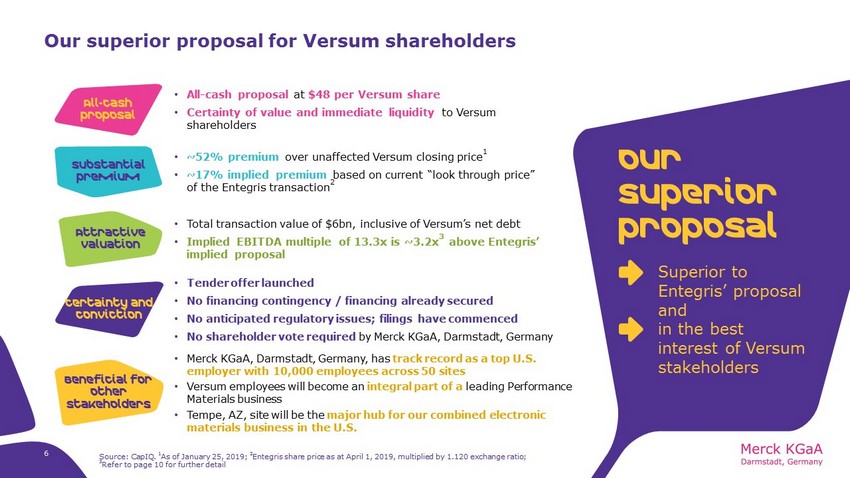

Our superior proposal for Versum shareholders 6 Our superior proposal • Superior to Entegris’ proposal and • in the best interest of Versum stakeholders All - cash proposal Substantial premium Attractive valuation Certainty and Conviction Beneficial for other stakeholders • ~52% premium over unaffected Versum closing price 1 • ~17% implied premium based on current “look through price” of the Entegris transaction 2 • Tender offer launched • No financing contingency / financing already secured • No anticipated regulatory issues; filings have commenced • No shareholder vote required by Merck KGaA, Darmstadt, Germany • All - cash proposal at $48 per Versum share • Certainty of value and immediate liquidity to Versum shareholders • Total transaction value of $ 6bn , inclusive of Versum’s net debt • Implied EBITDA multiple of 13.3x is ~3.2x 3 above Entegris’ implied proposal • Merck KGaA, Darmstadt, Germany, has track record as a top U.S. employer with 10,000 employees across 50 sites • Versum employees will become an integral part of a leading Performance Materials business • Tempe, AZ, site will be the major hub for our combined electronic materials business in the U.S. Source: CapIQ. 1 As of January 25, 2019; 2 Entegris share price as at April 1, 2019, multiplied by 1.120 exchange ratio; 3 Refer to page 10 for further detail

7 Significant discount to current trading Entegris’ deal is currently valued at a significant discount to Versum’s prevailing stock price and to our $48 bid Value proposition is inferior Analysis by Versum’s financial advisor, Lazard, clearly shows that our offer commands higher valuation than the Entegris merger consideration 1 , including assumed synergies Entegris acquisition was the result of a poorly run process Versum’s process was flawed, rushed and pre - conceived: Versum announced the transaction less than two months after its initial outreach and without meaningfully negotiating Entegris’ exchange ratio or contacting any other parties Newly found synergies are speculative and overly aggressive Versum’s newly claimed/discovered $50m of additional cost synergies and revenue synergies resulting in $50m additional EBITDA were unsubstantiated , speculative and illusory and market did not react materially to announcement 2 Versum stakeholders should be concerned Tactics employed by Versum and proposed Board composition are not in Versum stakeholders’ best interest Entegris acquisition is not in the best interest of Versum shareholders Source: CapIQ; 1 Based on DCF valuation of merger including synergies included in Lazard’s published financial analysis (released as part of E nte gris S - 4); 2 Versum share price closed up 0.5% on March 8, 2019 vs. prior close price

MERCK PROPOSAL PROVIDES SUPERIOR VALUE TO VERSUM SHAREHOLDERS

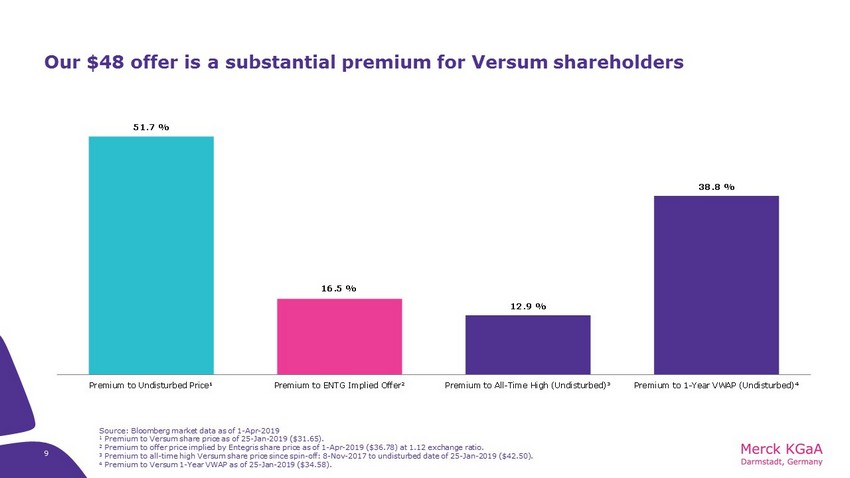

9 Our $48 offer is a substantial premium for Versum shareholders Source: Bloomberg market data as of 1 - Apr - 2019 1 Premium to Versum share price as of 25 - Jan - 2019 ($31.65). 2 Premium to offer price implied by Entegris share price as of 1 - Apr - 2019 ($36.78) at 1.12 exchange ratio. 3 Premium to all - time high Versum share price since spin - off: 8 - Nov - 2017 to undisturbed date of 25 - Jan - 2019 ($42.50). 4 Premium to Versum 1 - Year VWAP as of 25 - Jan - 2019 ($ 34.58). 51.7 % 16.5 % 12.9 % 38.8 % Premium to Undisturbed Price¹ Premium to ENTG Implied Offer² Premium to All-Time High (Undisturbed)³ Premium to 1 - Year VWAP (Undisturbed)⁴

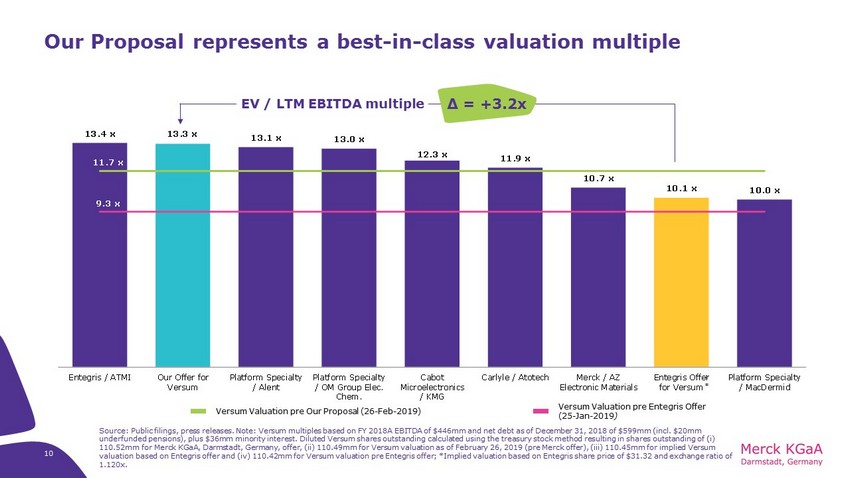

13.4 x 13.3 x 13.1 x 13.0 x 12.3 x 11.9 x 10.7 x 10.1 x 10.0 x Entegris / ATMI Our Offer for Versum Platform Specialty / Alent Platform Specialty / OM Group Elec. Chem. Cabot Microelectronics / KMG Carlyle / Atotech Merck / AZ Electronic Materials Entegris Offer for Versum Platform Specialty / MacDermid 11.7 x 9.3 x 10 Versum Valuation pre Our Proposal (26 - Feb - 2019) Versum Valuation pre Entegris Offer (25 - Jan - 2019 ) 1 Our Proposal represents a best - in - class valuation multiple EV / LTM EBITDA multiple Δ = +3.2 x * Source: Public filings, press releases. Note: Versum multiples based on FY 2018A EBITDA of $ 446mm and net debt as of December 31, 2018 of $ 599mm (incl. $ 20mm underfunded pensions), plus $ 36mm minority interest. Diluted Versum shares outstanding calculated using the treasury stock method resulting in shares outstandi ng of (i) 110.52mm for Merck KGaA, Darmstadt, Germany, offer, (ii) 110.49mm for Versum valuation as of February 26, 2019 (pre Merck offer), (iii) 110.45mm for implied Versum valuation based on Entegris offer and (iv) 110.42mm for Versum valuation pre Entegris offer; *Implied valuation based on Entegris share price of $31.32 and exchange ratio of 1.120x.

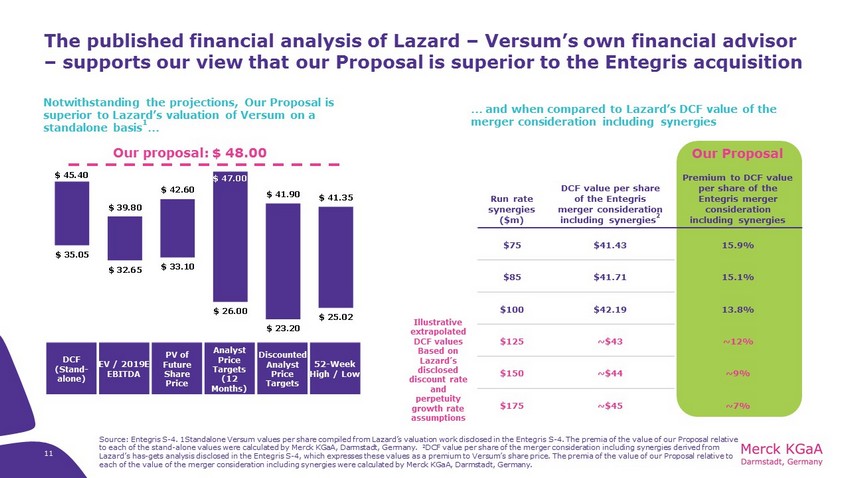

The published financial analysis of Lazard – Versum’s own financial advisor – supports our view that our Proposal is superior to the Entegris acquisition Notwithstanding the projections , Our Proposal is superior to Lazard’s valuation of Versum on a standalone basis 1 … 11 … and when compared to Lazard’s DCF value of the merger consideration including synergies DCF (Stand - alone) EV / 2019E EBITDA PV of Future Share Price Analyst Price Targets (12 Months) Discounted Analyst Price Targets 52 - Week High / Low Run rate synergies ($m) DCF value per share of the Entegris merger consideration including synergies 2 Our Proposal Premium to DCF value per share of the Entegris merger consideration including synergies $75 $41.43 15.9% $85 $41.71 15.1% $100 $42.19 13.8% $125 ~$43 ~12% $150 ~$44 ~9% $175 ~$45 ~7% $ 35.05 $ 32.65 $ 33.10 $ 26.00 $ 23.20 $ 25.02 $ 45.40 $ 39.80 $ 42.60 $ 47.00 $ 41.90 $ 41.35 Our Proposal: $48.00 Our proposal: $ 48.00 Source: Entegris S - 4. 1Standalone Versum values per share compiled from Lazard’s valuation work disclosed in the Entegris S - 4. T he premia of the value of our Proposal relative to each of the stand - alone values were calculated by Merck KGaA , Darmstadt, Germany. 2 DCF value per share of the merger consideration including synergies derived from Lazard’s has - gets analysis disclosed in the Entegris S - 4, which expresses these values as a premium to Versum’s share price. The premia of the value of our Proposal relative to each of the value of the merger consideration including synergies were calculated by Merck KGaA , Darmstadt, Germany. Illustrative extrapolated DCF values Based on Lazard’s disclosed discount rate and perpetuity growth rate assumptions

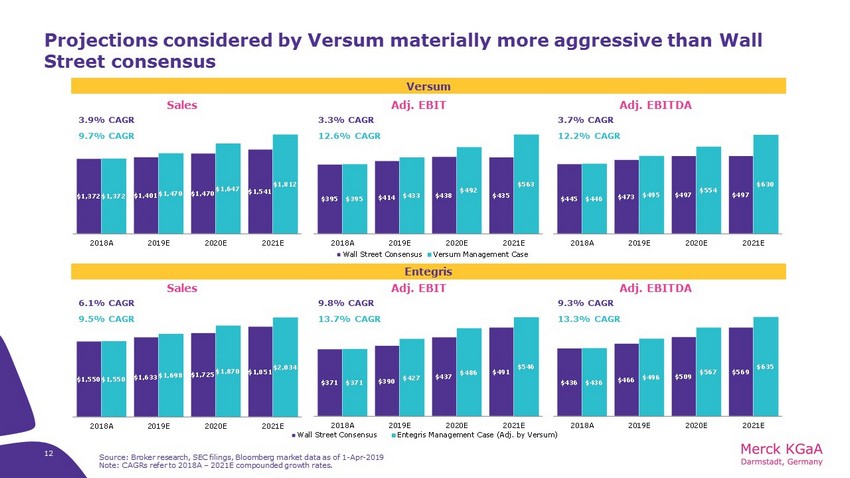

12 Projections considered by Versum materially more aggressive than Wall Street consensus Versum 12 Entegris Source: Broker research, SEC filings, Bloomberg market data as of 1 - Apr - 2019 Note: CAGRs refer to 2018A – 2021E compounded growth rates. Sales Adj. EBIT Adj. EBITDA 3.9 % CAGR 9.7% CAGR 3.3% CAGR 12.6% CAGR 3.7 % CAGR 12.2% CAGR Sales Adj. EBIT Adj. EBITDA 6.1 % CAGR 9.5% CAGR 9.8 % CAGR 13.7% CAGR 9.3 % CAGR 13.3% CAGR $371 $384 $423 $461 $371 $427 $486 $546 2018A 2019E 2020E 2021E Wall Street Consensus Entegris Management Case (Adj. by Versum) $436 $466 $509 $569 $436 $496 $567 $635 2018A 2019E 2020E 2021E $371 $390 $437 $491 $371 $427 $486 $546 2018A 2019E 2020E 2021E $1,550 $1,633 $1,725 $1,851 $1,550 $1,698 $1,870 $2,034 2018A 2019E 2020E 2021E $1,372 $1,401 $1,470 $1,541 $1,372 $1,470 $1,647 $1,812 2018A 2019E 2020E 2021E $395 $414 $438 $435 $395 $433 $492 $563 2018A 2019E 2020E 2021E Wall Street Consensus Versum Management Case $445 $473 $497 $497 $446 $495 $554 $630 2018A 2019E 2020E 2021E

13 Our Proposal provides certainty for Versum shareholders, and our unwavering commitment to the deal is exemplified by our actions We are committed to this deal Regulatory • No anticipated regulatory issues • Regulatory process is underway and we expect that regulatory clearances will be received in a timely manner Certainty • No shareholder vote required by our shareholders All - cash proposal • All - cash proposal at $48 per Versum share • Certainty of value and immediate liquidity to Versum shareholders Financing • Consummation of the Offer is not subject to any financing condition • We have entered into a Facilities Agreement with Bank of America Merrill Lynch, BNP Paribas Fortis and Deutsche Bank AG, providing fully committed financing to consummate the Tender Offer Proven Commitment Through Action • 27 - Feb : announced all - cash proposal • 5 - Mar : sent letter to Versum shareholders re - affirming proposal • March : met with Versum shareholders • 26 - Mar : Launched tender offer with committed financing Source: Public filings

MARKET REACTION SUPPORTS OUR PROPOSAL

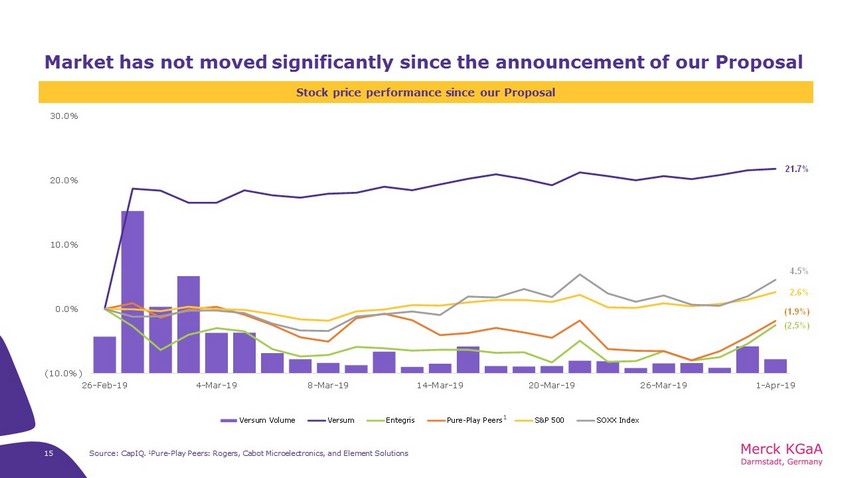

Source: CapIQ. 1 Pure - Play Peers: Rogers, Cabot Microelectronics, and Element Solutions 15 Market has not moved significantly since the announcement of our Proposal 1 Stock price performance since our Proposal 21.7% (2.5%) (1.9%) 2.6% 4.5% (10.0%) 0.0% 10.0% 20.0% 30.0% 26-Feb-19 4-Mar-19 8-Mar-19 14-Mar-19 20-Mar-19 26-Mar-19 1-Apr-19 Versum Volume Versum Entegris Pure-Play Peers S&P 500 SOXX Index

$50.40 $41.19 $48.00 0 2000 4000 6000 8000 10000 12000 14000 16000 18000 $20 $25 $30 $35 $40 $45 $50 $55 1-Jan-2019 11-Jan-2019 21-Jan-2019 31-Jan-2019 10-Feb-2019 20-Feb-2019 2-Mar-2019 12-Mar-2019 22-Mar-2019 1-Apr-2019 Volume Versum Stock Price Entegris Deal Value¹ Merck KGaA, Darmstadt, Germany Offer Market reaction supports view that our proposal is superior 25 - Jan - 19 Undisturbed d ate 28 - Jan - 19 Entegris acquisition announced 27 - Feb - 19 Our proposal announced 52% Premium to Undisturbed 16 % premium to Versum’s p re - our proposal High 8 - Mar - 19 Muted stock price reaction shows that market does not find “newly - found” synergies credible 16 Our offer price of $48 is at a 52% premium to Versum’s undisturbed price and a 16% premium to Versum’s 2019 - high price prior to our bid 51% of Versum shares have traded at or above $48 per share since announcement of our proposal Source: Capital IQ, market data as of 1 - Apr - 2019 ; 1 Entegris deal value is equal to the value of Entegris stock multiplied by the exchange ratio of 1.120x

$ 48.00 $ 50.40 $ 41.19 $ 37.14 $ 39.24 Our Offer for Versum Current Versum Price (1-Apr-2019) Current Implied Entegris Offer Implied Entegris Offer on Initial Combination Annoucement Implied Entegris Offer on Date "Newly Found" Synergies were Announced 17 Entegris acquisition could result in significant downside for Versum shareholders 1 2 3 (1 - Apr - 2019 ) (28 - Jan - 2019) (08 - Mar - 2019) Source: Bloomberg market data as of 1 - Apr - 2019 Note: All prices exclude the impact of synergies. 1 Offer price implied by Entegris share price as of 1 - Apr - 2019 ($36.78) at 1.12 exchange ratio. 2 Offer price implied by Entegris share price as of 28 - Jan - 2019 ($33.16 ) at 1.12 exchange ratio. 3 Offer price implied by Entegris share price as of 08 - Mar - 2019 ($35.05 ) at 1.12 exchange ratio.

$41.19 $50.40 $ 15 $ 20 $ 25 $ 30 $ 35 $ 40 $ 45 $ 50 $ 55 Sep-16 Nov-16 Jan-17 Apr-17 Jun-17 Aug-17 Oct-17 Dec-17 Mar-18 May-18 Jul-18 Sep-18 Nov-18 Jan-19 Apr-19 $ 48.00 $ 38.80 $ 49.93 $ 15 $ 20 $ 25 $ 30 $ 35 $ 40 $ 45 $ 50 $ 55 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Implied ENTG Offer Above VSM Price Implied Entegris Offer for Versum Versum Our Offer $ 48.00 18 Material downside risk to Versum shareholders in Entegris stock 1 $ 38.80 $ 49.93 $ 15 $ 20 $ 25 $ 30 $ 35 $ 40 $ 45 $ 50 $ 55 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Implied ENTG Offer Above VSM Price Implied Entegris Offer for Versum Versum Our Offer $ 48.00 Source: Bloomberg market data as of 1 - Apr - 2019 1 Entegris share price times 1.12 exchange ratio. The value to Versum shareholders implied by the 1.12 exchange ratio has never been above our $48 all - cash offer Since Versum’s spin off, the offer price from Entegris implied by the 1.12 exchange ratio has resulted in a higher per - share value on only 27% of trading days

STRONG INDUSTRIAL LOGIC IN COMBINATION WITH MERCK, KGAA, DARMSTADT, GERMANY

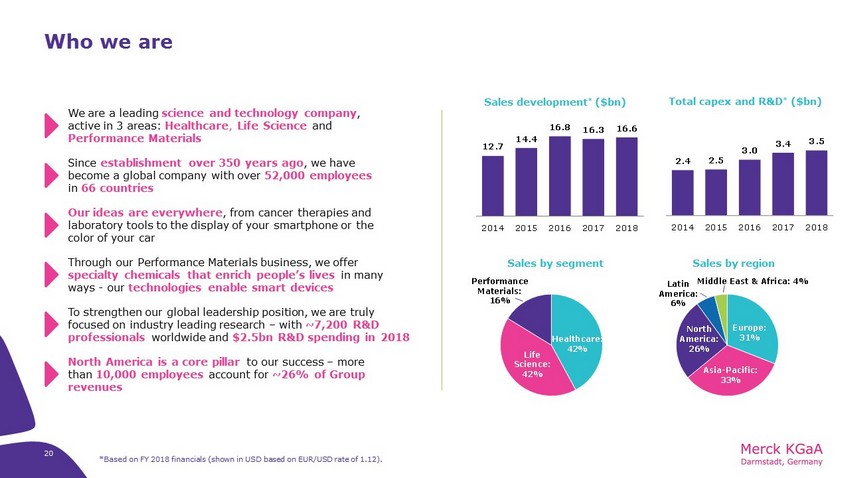

20 Sales by segment Sales by region Total capex and R&D * ($bn) Sales development * ($bn) Healthcare: 42% Life Science: 42% Performance Materials: 16% Europe: 31% Asia - Pacific: 33% Middle East & Africa: 4% Latin America: 6% North America: 26% We are a leading science and technology company , active in 3 areas: Healthcare , Life Science and Performance Materials Who we are Since establishment over 350 years ago , we have become a global company with over 52,000 employees in 66 countries Our ideas are everywhere , from cancer therapies and laboratory tools to the display of your smartphone or the color of your car Through our Performance Materials business, we offer specialty chemicals that enrich people’s lives in many ways - our technologies enable smart devices To strengthen our global leadership position, we are truly focused on industry leading research – with ~7,200 R&D professionals worldwide and $2.5bn R&D spending in 2018 North America is a core pillar to our success – more than 10,000 employees account for ~26% of Group revenues 12.7 14.4 16.8 16.3 16.6 2014 2015 2016 2017 2018 2.4 2.5 3.0 3.4 3.5 2014 2015 2016 2017 2018 *Based on FY 2018 financials (shown in USD based on EUR/USD rate of 1.12).

We have an outstanding track record of successful acquisitions and the financial flexibilities for further growth ▪ Strong track record of successful acquisitions, particularly in the U.S. ▪ Over the last 10 years, we have completed acquisitions in the U.S. with a total transaction value of ~$24bn 1 ▪ Successful acquisitions and integration of two large U.S. public companies ▪ We have significant experience in obtaining regulatory approvals both in the U.S. and globally Announced acquisition of for $2.5bn 2 Announced acquisition of for $17.0bn 2 Source: Market data as of April 1, 2019; 1 Values shown in USD based on EUR/USD rate of 1.12; 2 Values shown based on prevailing EUR/USD FX rates (February 28, 2010 = 1.37, December 5, 2013 = 1.37, September 22, 2014 = 1.28, April 19, 2018 = 1.24) Announced acquisition of for $7.2bn 2 3.5 x 2.6 x 2.3 x 1.8 x 2015 2016 2017 2018 Net Debt / EBITDA € 100.75 21 (~$ 49bn MCap) Announced divestment of Consumer Health for $4.2bn 2 M&A is part of our DNA and growth strategy … … leading to long - term value creation … … supported by our high cash generation € 20 € 30 € 40 € 50 € 60 € 70 € 80 € 90 € 100 € 110 € 120 2010 2011 2013 2015 2017 2019 Merck KGaA Share Price ( € )

22 Text slides and Textboxes Why Versum and Merck KGaA, Darmstadt, Germany, fit so well together – creating a leading electronic materials player 1 2 3 4 Create a leading player • Create one of the leading electronic materials players focused on the semiconductor and display industries with cutting - edge technology • Increase scale, product and services depth and truly global presence • Accelerate innovation with Versum R&D focused on the Advanced Materials segment (10 - 15% R&D rate) Capitalize on long - term growth trends • Electronics industry expected to benefit from data volume increase tailwinds , enabled through high purity semiconductor materials • Semiconductor Solutions business to comprise ~50% of pro - forma Performance Materials sales versus ~25% today Complementary offering • Complementary capabilities with very little product overlap • Manufacturing facilities in the U.S. strengthen our supply chain and supply reliability Value accretive to shareholders • ~$65 - 70m in annual cost synergies fully realized in 3rd year after closing (2022) • Expected to be EPS pre accretive in first year after closing, and to reported EPS in year 3 Note: Financials shown in USD based on EUR/USD FX rate of 1.12

FLAWED PROCESS RUN BY VERSUM, WITH A ONE - TRACK FOCUS ON ENTEGRIS ACQUISITION

Versum’s entire process to date has been rushed, flawed, and is not the result of a rigorous assessment Versum’s Flawed Process Rushed discussions between the parties Minimal due diligence and limited negotiation No other alternatives considered No apparent review of buyer landscape R ejection of our proposal even though exploring our proposal was a free option to maximize value 27 - Feb Our Proposal Our Proposal Rejected 01 - Mar 08 - Dec Versum & Entegris first discuss potential deal 1 8 - Dec Entegris board approves engagement with Versum 03 - Jan Parties enter into mutual non - disclosure & C.A. 28 - Jan Entegris Acquisition A nnounced 7 weeks from initial discussion to announcement Versum rejected our proposal 2 days after receipt , claiming they had undertaken “careful review and consideration” A typical review of our proposal could not have been conducted so swiftly, with a decision to reject as the outcome, without some form of underlying bias towards the existing deal 3 weeks of due diligence Newly - found synergies cast doubt on the credibility of financial projections and due diligence process 24 08 - Mar Newly - found synergies & new decision for presence in Tempe, AZ 17 - Jan Versum and Entegris agree 1.12x exchange ratio (following initial offer of 1.097x) The final exchange ratio represents only a 2% increase on the original offer Source: Versum DEFM14A, company filings

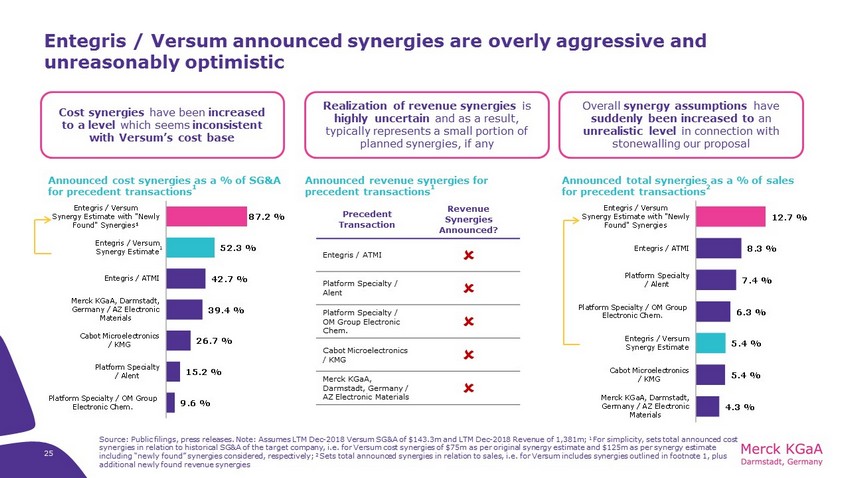

25 Cost synergies have been increased to a level which seems inconsistent with Versum’s cost base Entegris / Versum announced synergies are overly aggressive and unreasonably optimistic Announced cost synergies as a % of SG&A for precedent transactions 1 Announced total synergies as a % of sales for precedent transactions 2 Announced revenue synergies for precedent transactions 1 Realization of revenue synergies is highly uncertain and as a result, typically represents a small portion of planned synergies, if any Overall synergy assumptions have suddenly been increased to an unrealistic level in connection with stonewalling our proposal Precedent Transaction Revenue Synergies Announced? Entegris / ATMI Platform Specialty / Alent Platform Specialty / OM Group Electronic Chem. Cabot Microelectronics / KMG Merck KGaA, Darmstadt, Germany / AZ Electronic Materials 1 Source: Public filings, press releases. Note: Assumes LTM Dec - 2018 Versum SG&A of $143.3m and LTM Dec - 2018 Revenue of 1,381m; 1 For simplicity, sets total announced cost synergies in relation to historical SG&A of the target company, i.e. for Versum cost synergies of $75m as per original synerg y e stimate and $125m as per synergy estimate including “newly found” synergies considered, respectively; 2 Sets total announced synergies in relation to sales, i.e. for Versum includes synergies outlined in footnote 1, plus additional newly found revenue synergies 4.3 % 5.4 % 5.4 % 6.3 % 7.4 % 8.3 % 12.7 % Merck KGaA, Darmstadt, Germany / AZ Electronic Materials Cabot Microelectronics / KMG Entegris / Versum Synergy Estimate Platform Specialty / OM Group Electronic Chem. Platform Specialty / Alent Entegris / ATMI Entegris / Versum Synergy Estimate with "Newly Found" Synergies 9.6 % 15.2 % 26.7 % 39.4 % 42.7 % 52.3 % 87.2 % Platform Specialty / OM Group Electronic Chem. Platform Specialty / Alent Cabot Microelectronics / KMG Merck KGaA, Darmstadt, Germany / AZ Electronic Materials Entegris / ATMI Entegris / Versum Synergy Estimate Entegris / Versum Synergy Estimate with "Newly Found" Synergies¹

26 Versum’s new synergies are speculative and illusory Source: Public filings What this means Versum and Entegris are trying to salvage their deal by attempting to improve their value proposition – while ignoring associated execution risks and costs to achieve Further evidence of a poor process If the original process had been run properly, and not over such a hasty timeframe, a typical diligence exercise would have uncovered the purported synergies Synergies exceed Versum advisor’s own analysis Versum’s financial advisor, Lazard, included a synergy range of up to $100m in their independent analysis of the proposed transaction We would expect Lazard would have analyzed a range of potential synergies provided by the company New synergies miraculously uncovered On March 8, 2019, 8 days after filing their original proxy, the companies announced they had more than doubled the claimed synergies, while also strengthening a commitment to existing operational sites – this seems contradictory Further, the announcement provides little explanation as to the source of these synergies Timing appears opportunistic We believe that the timing of this announcement is opportunistic, and is an attempt to counter our superior proposal If management believed in these purported synergies, they should have included them in their original disclosure

$36.78 $ 25 $ 30 $ 35 $ 40 1-Jan 11-Jan 21-Jan 31-Jan 10-Feb 20-Feb 2-Mar 12-Mar 22-Mar 1-Apr Entegris Market seems skeptical of revised synergies 25 - Jan - 19 undisturbed date 27 At the announcement of the acquisition on 28 - Jan - 2019, Entegris / Versum predicted $75mm in synergies Initial Entegris / Versum announcement “Newly - found” synergies announced Source: Capital IQ, market data as of 1 - Apr - 2019 • ~5.5 weeks later, following Merck KGaA, Darmstadt, Germany’s offer, synergy estimates were more than doubled to $175mm • The market appears not to have given credit

“Following Versum’s spin - off from Air Products in 2016, the Versum board of directors, together with Versum’s senior management team, has from time to time considered... the possibility of a combination with Entegris... ... Versum’s senior management and the Versum board of directors were therefore generally familiar with Entegris , its business and its management team, and believed that a potential combination of the two companies on appropriate terms and at the right time could be an opportunity to enhance stockholder value... Entegris has considered ... prior to and following Versum’s spin off from Air Products in 2016, the possibility of a combination with Versum . As a result, the Entegris senior management and the Entegris board of directors were generally familiar with Versum, its management and its businesses” 28 Versum appears to have operated with a one - track process focused on the Entegris Acquisition Versum’s interest in an acquisition by Entegris has come at the expense of typical engagement with other bidders and the maximization of shareholder value The day after Merck presented its offer to Versum, Versum’s board implemented a poison pill – rejecting productive dialogue and putting up barriers to any deal apart from the one they were intent on Despite the superior terms of our all - cash proposal – that provides significant certainty for Versum shareholders – Versum has rejected our Proposal Versum and Entegris h ave contemplated a deal for y ears… ... a nd agreed to a deal only w eeks after beginning formal negotiations Source: Versum DEFM14A

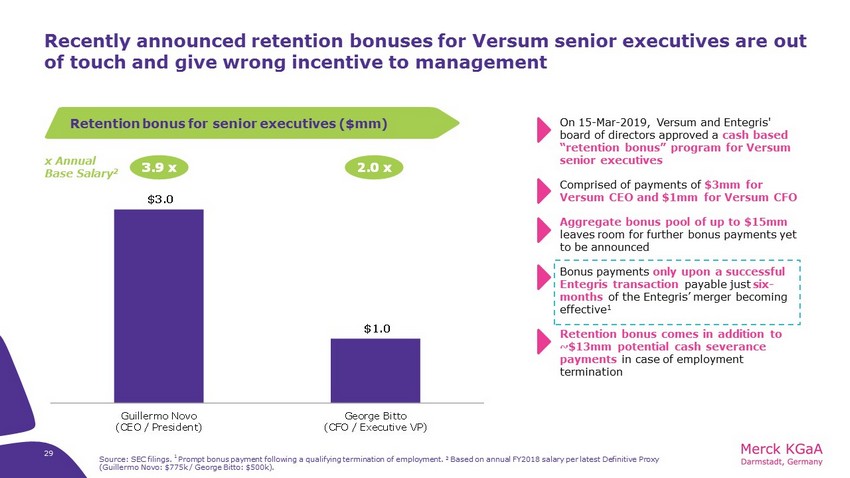

29 Recently announced retention bonuses for Versum senior executives are out of touch and give wrong incentive to management x Annual Base Salary 2 • On 15 - Mar - 2019, Versum and Entegris ' board of directors approved a cash based “retention bonus” program for Versum senior executives • Comprised of payments of $3mm for Versum CEO and $1mm for Versum CFO • Aggregate bonus pool of up to $15mm leaves room for further bonus payments yet to be announced • Bonus payments only upon a successful Entegris transaction payable just six - months of the Entegris’ merger becoming effective 1 • Retention bonus comes in addition to ~$13mm potential cash severance payments in case of employment termination Source: SEC filings. 1 Prompt bonus payment following a qualifying termination of employment. 2 Based on annual FY2018 salary per latest Definitive Proxy (Guillermo Novo: $775k / George Bitto : $500k). Retention bonus for senior executives ($mm) $3.0 $1.0 Guillermo Novo (CEO / President) George Bitto (CFO / Executive VP) 3.9 x 2.0 x

VERSUM’S POOR GOVERNANCE AROUND ENTEGRIS TRANSACTION

31 Pro Forma governance favors Entegris, and continues a number of structural characteristics of Entegris that are not best in class Versum 1 Versum 2 Versum 3 Versum 4 (Existing Chair) Entegris 1 Entegris 2 Entegris 3 Entegris 4 Entegris 5 (Existing CEO) 5 4 Proposed post - closing Board of Directors 1 Weighted Toward Entegris Entrenched Leadership Entegris Legacy • For three years following the close of the deal, to remove the chairman or CEO will require 75% of directors approval , resulting in leadership entrenchment • Entegris gains the CEO & CFO position and board control following the close of the transaction, weighting pro forma governance in Entegris’ favor • The company will retain both Entegris’ name as well as its current headquarters in Billerica, Massachusetts – indicating lack of commitment to the Tempe area Poor Corporate Governance • No independent lead director has been identified • Shareholders in the company will not be able to call special meetings or act by written consent • Supermajority standard to amend the bylaws of the combined company • Only three board committees ( no committee focused on environmental and sustainability initiatives ) Source: Versum DEFM14A 1 Per Versum DEFM14A, the combined board will be comprised of 4 Versum designees yet to be identified, 4 Entegris designees yet to be identified, and the Entegris CEO.

Aggressive adoption of poison pill is to the detriment of shareholder value Poison pill adoption as immediate reaction to our offer Poison pill out of step with governance best practices • Versum did not engage with us upon receipt of our proposal • Instead, Versum adopted a poison pill only one day after the receipt of our proposal • Poison pill amendment two weeks after its adoption to remove egregious provisions suggests hasty implementation of poison pill • Poison pill adopted to preclude shareholders from accepting our tender offer , not to allow Board to conduct a complete process 28 - Jan Entegris transaction announced 27 - Feb Our proposal made 01 - Mar Our proposal rejected 28 - Feb Poison pill adopted 14 - Mar Poison pill amended 2018 2004 ~53% ~1% % of S&P500 Companies with Shareholder Rights Plans 32 Source: SEC filings, Factset

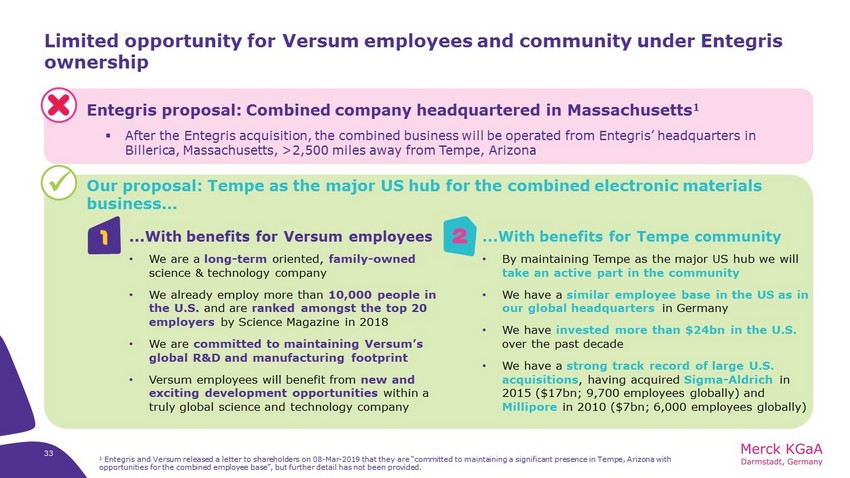

33 Limited opportunity for Versum employees and community under Entegris ownership ▪ After the Entegris acquisition, the combined business will be operated from Entegris’ headquarters in Billerica, Massachusetts, >2,500 miles away from Tempe, Arizona x Entegris proposal: Combined company headquartered in Massachusetts 1 Our proposal: Tempe as the major US hub for the combined electronic materials business... 1 2 ... With benefits for Versum employees • We are a long - term oriented, family - owned science & technology company • We already employ more than 10,000 people in the U.S. and are ranked amongst the top 20 employers by Science Magazine in 2018 • We are committed to maintaining Versum’s global R&D and manufacturing footprint • Versum employees will benefit from new and exciting development opportunities within a truly global science and technology company ...With benefits for Tempe community • By maintaining Tempe as the major US hub we will take an active part in the community • We have a similar employee base in the US as in our global headquarters in Germany • We have invested more than $ 24bn in the U.S. over the past decade • We have a strong track record of large U.S. acquisitions , having acquired Sigma - Aldrich in 2015 ($17bn; 9,700 employees globally) and Millipore in 2010 ($7bn; 6,000 employees globally) 1 Entegris and Versum released a letter to shareholders on 08 - Mar - 2019 that they are “committed to maintaining a significant presence in Tempe, Arizo na with opportunities for the combined employee base”, but further detail has not been provided.

CONCLUSION

35 Our proposal is superior We are the right owners of this asset The transaction process has been flawed We are committed to this deal Why Merck KGaA, Darmstadt, Germany, is the right owner of Versum • Leading science and technology company, active in 3 areas: Healthcare, Life Science and Performance Materials • Established over 350 years ago, and have become a global company with >52,000 employees in 66 countries • The current deal is not a result of a rigorous assessment, and the entire process to date has been rushed • Versum did not explore any other alternatives and rejected our proposal even though doing so was essentially a free option to maximize value • We have proven our unwavering commitment by taking all necessary actions to consummate the deal • Vote against the Entegris acquisition • All - cash proposal at $48 per Versum share • Significant premium over unaffected Versum closing price and “look through price” of Entegris transaction • No financing contingency and no anticipated regulatory issues

36 A compelling proposal for all stakeholders Providing leading - edge technology backed by the capabilities, scale and quality of Merck KGaA, Darmstadt, Germany Truly global footprint and close proximity to customers worldwide Combines innovation strength to better serve our customers in a rapidly evolving marketplace Combining the certainty of an all - cash transaction with an attractive premium A strategically and financially compelling transaction for our shareholders Delivers on strategy of building leading positions in attractive markets Meeting our disciplined financial M&A criteria Becoming an integral part of leading science and technology company Commitment to maintain Tempe, AZ presence as the major hub for the combined electronic materials business in the U.S. • ~ 52% premium to Versum’s unaffected closing price of $ 31.65 on January 25, 2019 • ~ 16% premium to Versum’s closing price of $ 41.40 on February 26, 2019 Merck KGaA, Darmstadt, Germany – the best strategic owner of Versum to the highest benefit of shareholders, employees and customers